GABA B receptor deficiency causes failure of neuronal homeostasis in hippocampal networks

Upload

independentCategory

view

8download

0

CHAPTER ONE

1.0 INTRODUCTION

1.1 Background of the Study

Education is a means through which young and

old members the society are taught about the

expected behaviour of the society and the rules

of polity, the values, skills attitudes and

knowledge that equip the individual to achieve

personal and society development and progress.

Ozigi (1998)

According to Danladi (2006), education is a

process of teaching and learning in which

students acquire practical knowledge, value and

skills for effective participation in the

society. He further said asserted that , the

process of acquiring the relevant knowledge,

1

attitude, values and skills must be made as

concrete as possible for easy learning.

History of Financial Accounting

There is no accurate record as to when

accounts started, but available information

suggests that record keeping is as old as man.

The starting point can be linked to the merchants

in the Babylonian and Assyrian civilizations,

about 4000 years B C. The strategy for keeping

records then was to make marks on the wall,

stone, papyrus or wax tablets, it was highly

primitive.

The history of accounting is not complete

without mentioning the name of an Italian monk

and Mathematician LUCCA PACIOLO. In 1494, the

crucial event in accounting was the introduction

of double entry book system in Italy described as

“Italian Method”. In his famous treatise Summa

2

De. Arithmetical Geometrical Proportion et

proportionalita in 1994 in Venice. Reverend

father Lucca Paciolo by giving insight into the

reasoning behind accounting records. He

postulated that all entries must have a double-

entry one a debtor, and one a creditor. Even

though during this period the records were

prepared to show statement for the business

rather than the owner, but the yearly preparation

was still lacking.

After paciolo, a Dutchman advocated the

profit and loss account at yearly interval. The

level of civilization and technological

advancement helped in the development of modern

method of accounting.

During the industrial revolution there was

need to sophisticated accounting methods.

Different professional bodies were formed e.g.

3

ICA Scotland in 1854. ICA England and Wales in

1880, etc. With the development of new methods

ownership was separated from management. Since

the discovery of the double entry principle,

there has been tremendous development in

accounting theories and methods. The introduction

of micro and mini computers have brought enhanced

performance but the fundamental principles remain

unchanged.

In Nigeria, record keeping has antecedents in

the ancient kingdoms and Empire and prominent

then was the periodic contributions which were

recorded on the wall. But the granting of royal

character to Royal Niger Company was the turning

point period in record keeping. The governing

accounting principles in Nigeria as almost the

same as the one’s in Britain.

4

In 1965, the institute of chartered

Accountants of Nigeria was established and

affiliated with the professional institutes in

Britain and USA. Many Nigerians came back as

professional accountants and became members. The

institute was charged with the responsibilities

of regulating accounting procedures and practice

in Nigeria.

In 1982, Nigeria Accounting standard Board was

established to set standards to guide accounting

operations. Members include Accounting Teachers

Association, Chamber of Commerce, Central Bank of

Nigeria, Finance Ministry of Nigeria, etc. Now in

Nigeria/ there are two recognized bodies namely

institute of Chartered Accountants of Nigeria

(ICAN), Association of National Accountants of

Nigeria (ANA)

1.2 Statement of the Problem

5

The primary objective of financial accounting

in the secondary school curriculum is to prepare

the students for Senior Secondary School

Certificate Examination (SSCE) which will enable

the holders pursue further education or to go

into lower clerical work in the office. It is as

a result that the government, teachers and

parents have been given support to ensure that

student’s performance in both internal and

external examination has improved.

However, the researcher through discussion

with some of the financial accounting teachers in

secondary schools and through interaction with

some of the students offering financial

accounting at secondary school level realized

that financial accounting has not recorded a

remarkable success. Many of the students that

offered the subject in SSCE have failed woefully.

6

Some of them that secured clerical job have not

been able to adjust to the practical working of

financial accounting and finally some of those

that gained admission for further studies have

not been able to cope up due to their poor

foundation in financial accounting.

For example WAEC (2010) analysis of

percentage performance of candidate in ten

popular subjects in WAEC for 2008, 2009 and 2010

revealed 52.48%,58.21% and 51.85% respectively,

failed financial accounting. However, of recent

the reverse is the case since there is low

enrolment of students for accounting in Senior

Secondary and low number of accounting teachers

in Senior Secondary. It is as a result of this

problem that the researcher intends to

investigate on the Cause of student failure in

financial accounting.

7

1.3 Purpose of the Study

The aim and objective of the study is to find

out the causes of student’s failure in financial

accounting at SSCE level in Government Secondary

Schools in Okigwe Local Government Area of Imo

State, Nigeria.

Therefore, the study intends to:

i. Assess the effectiveness of teacher’s

attitude on students academic performance in

financial accounting.

ii. Assess the method used by financial

accounting teachers as it affects the

learning of financial accounting in secondary

schools.

iii.Determine peer groups and parental influences

and their effects on the learning of

financial accounting in secondary schools.

8

iv. Evaluate the impact of available

infrastructural facilities as they affect the

learning of financial accounting in the

secondary schools

1.4 Research Questions

Based on the specific objectives, the researcher

deducted the following research questions:

1. To what extent does the teacher’s attitude

affect student’s performance in financial

accounting?

2. To what extent does the method used in

teaching financial accounting affect the

learning of financial accounting in secondary

schools?

3. To what extent does peer groups and parental

influence affect the learning of financial

accounting in secondary schools?

9

4. To what extent do available infrastructural

facilities affect the learning of financial

accounting in secondary schools?

1.5 Basic Assumptions

The following assumptions were made for the

study:

i. That all teachers teaching financial

accounting are professionals

ii. That the secondary school syllabus in

financial accounting is adequate for purpose

of achieving its objective

iii.That the students entry behaviour in

accounting is adequate to enable them cope

with instruction in financial accounting.

iv. That the West African Examination Council

(WAEC) and the National Examination Council

(NECO) syllabus in financial accounting cover

10

adequately the area required to benefit

students

1.6 Scope of the Study

This study is meant to analyze the causes of

student’s failure in financial accounting at SSCE

level in Okigwe Local Government. This study is

limited to Government owned Secondary Schools in

Okigwe Local Government Area of Imo State

1.7 Significance of the Study

Since the research contributes to development

of knowledge, as such, interested students or

researchers who may want to carry out similar

study will find this work very worthwhile.

Similarly, this study will also be helpful to

policy makers in formulation of educational

policy in near future. In the same vein Federal

11

and State Ministry of Education and other

institutions within the study location will

benefit from this study by identifying the Causes

of student failure in financial accounting at the

SSCE level in Okigwe local Government Area of Imo

state.

Thus using such information to current

imbalances by proper funding of educational

sector. It is hoped that the study will serve as

an open door policy to government for finding

solution to the failure of financial accounting.

Conclusively, this study wishes to create

awareness among parents, state and federal

government in the need to sensitize, providing

conducive atmosphere for proper learning and

fabulous performance where necessary.

12

1.8 Operational Definition of Terms

Financial Accounting: is the field of accountancy

concerned with the preparation of financial

statements for decision makers, such as

stakeholders, suppliers, banks, employees,

government agencies, owners, and other

stakeholders. It is also reporting of the

financial position and performance of a firm

through financial statements issued to external

users on a periodic basis.

Industrial Revolution: is the totality of the changes

in economic and social organization that began

about 1760 in England and later in other

countries, characterized chiefly by the

replacement of hand tools with power-driven

machines, as the power loom and steam engine, and

by the concentration of industry in large

establishment.

13

Bookkeeping: is the recording of financial

transactions. Transactions include sales,

purchases, income, and payments by individual or

organization. Bookkeeping is usually performed by

a bookkeeper. Bookkeeping should not be confused

with accounting. The accounting process is

usually performed by an accountant.

Parental Influence: is the effect of parents have on

their children. The parent-child relationship is

the most important relationship the child has.

Different parental styles lead to various ways

the interact with their children and is an

important component that shapes the child’s views

about themselves and their world. Parents must be

aware of the way they influence their children

every day.

SSCE: Senior school certificate examination

14

ICAN: Institute of chartered accountant of

Nigeria

ANAN: Association of national accountant of

Nigeria

CHAPTER TWO

2.0 REVIEW OF RELATED LITERATURE

2.1 Introduction

15

A lot have been written on student’s

performance in the senior secondary certificate

examination (SSCE). The reason for this chapter

is to view related literature on the causes of

students’ failure in financial accounting at SSCE

level. The review is organized into the following

sub-headings:

Historical background of accounting, concepts

of financial accounting, types of accounting,

objectives of financial accounting, qualities of

a good financial accounting teacher, methods of

teaching financial accounting, the roles of

instructional materials in teaching financial

accounting, teachers attitude as its effects on

students performance, students learning attitude

and its effect on their performances, problems

affecting accounting education, empirical

studies, summary of literature review.

16

2.2 Historical Background of Accounting

The development of accounting dates back to

the earliest days of human agriculture and

civilization (the Sumerians in Mesopotamia, and

Egyptian old Kingdom). An ancient economic

thought of the near east facilitated the creation

of accurate records of the quantities and

relative values of agricultural products, methods

that were formalized in the trading and monetary

system by 2000 BC. Simply accounting is motivated

in the Christian Bible (Matthew 25:19). In the

parable of the talents. The Islamic Quran also

mentions simple accounting for trade and credit

arrangements (Quran 2:282).

In the twelfth-century A.D, the Arab writer,

Ibn Taymiyyah mentioned in his book Hisba

(literally, ‘’Verification’’ or ‘’Calculation’’)17

detailed accounting systems used by Muslims as

early in themed Seventy century A.D. these

accounting practices were influenced by the Roman

and the Persian civilization that Muslims

interacted with. The most detailed example Ibn

Taymiyyah provides of a complex governmental

accounting system is the ‘’Divan of Umar’’ has

been described in detail by various Islamic

historians and was used by Muslim rulers in the

middle East with modification and enhancement

until the fall of the Othman Empire.

Luca Pacioli (1445-1517), also known as Friar

Luca dal Borgo, is regarded as the “Father of

accounting’’. His summa de arithmetica,

geometrica, proportioni et proportionlita (summa

on arithmetic, geometry, proportions and

proportionality, venice 1494), was a textbook for

use in the Abbaco schools of Northern Italy where

18

the sons of Merchants and craftsmen were

educated. It was compendium of the mathematical

knowledge of his time, and includes the first

printed description of the method of keeping

accounts that Venetian merchants used at that

time, known as the double entry bookkeeping

system.

Pacioli codified rather than invented the

double entry system of keeping records. He

described the use of journals and ledgers and

warned: “A person should not go to sleep at night

until the debits equalled the credits”. He

demonstrated year-end closing entries and

proposed that a trail balance be used to prove a

balanced ledger

2.3 Concept of Financial Accounting

19

The term accounting has been defined by

prominent business educators and scholars among

which:

Asaolu (1998) defined accounting as “the art

of accurate bookkeeping, or records of

transactions from such records, certain

accounting data are prepared with the view to

controlling such business through prompt

detection of any impending financial hazards”.

The committee of American Accounting

Association (1996) in Richard (2000) defined

financial accounting as “the process of

identifying, measuring and communicating economic

information to permit informed judgments and

decision by users of information”.

Akintelure (2003) defined accounting as “the

recording classifying, and summarizing of

financial transactions or events in terms of20

money and reporting the result to management and

other users of accounting information”.

Udoh (2004) defined financial accounting as

“a discipline concerned with recording, analyzing

and forecasting of incomes and wealth of business

and other entities”.

Igben (2007) defined financial accounting as

“the process of collecting, recording, presenting

and analyzing/ interpreting financial information

for the users of financial statements”.

In the same vein, Aliyu (2010) classified

accounting into three segments such as accounting

measures, accounting analysis and accounting

system. In his definition, accounting measures is

the financial progress and proportion of the

organizational units of the business and the

business as a whole, by breaking the complex

business activities into identifiable measurable21

financial transaction. He defined accounting

analysis as “recording, summarizing and reporting

a multitude transaction in such a manner that

those who are concerned with the affairs of

entity.

Finally, accounting system is simply the art

of collecting financial transactions to be

reported to users, groups, which can also provide

safeguard in the administration of business

assets”. From the definitions above, we can infer

that accounting is the language implored in the

business transaction since data recorded,

classified and summarized must be communicated to

form the basis of decision making through the

aspects of management accounting.

2.4 Types of Accounting

2.4.1 Financial accounting: it is a major branch of

accounting involving the collection, recording22

and extraction of financial information, and the

summary of it in the form of a periodic profit or

loss account, a balance sheet and a cash flow

statement in accordance with legal, professional,

and capital market requirement.

2.4.2 Management Accounting: is another branch of

accounting performed within an organization to

provide information only accessible to its

decision maker.

2.4.3 Open Book Accounting: is an accounting

principle that aim to improve accounting

transparency of organizations.

2.4.4 Tax Accounting: is the accounting needed to

comply with jurisdictional tax regulations.

2.4.5 Accounting Scholarship: is the academic

discipline which studies the theory of

accountancy.

23

2.5 Objectives of Financial Accounting

The fundamental of accounting objectives

could be based on the basic concepts under

limping the measurement and disclosure of

business transaction and events. Stating the

objectives of accounting would be easier when

considering the general purpose of financial

statements where all users (external) had same

needs and interest.

The reasons for offering accounting in the

senior secondary school level are in four fold

according to Nolan (2007).

i. To enable students obtain a background in

bookkeeping and accounting.

ii. To enable the students to obtain a marketable

skills by which he/she can earn his/her

24

living in an appropriate business or

governments job.

iii.To enable students to understand that

systematic and accurately kept records are

the basis for financial decision that has to

be made by businessmen, government officials

and others.

iv. To enable students manage wisely his/her own

Personal business affairs with particular

emphasis on the wise planning of his/her

income and expenditure.

Similarly, Daniel (2002) observed that, the

focus of accounting education is the social and

economic welfare of the individual student and

the society at large. He further added that

accounting education furnishes the students with

the ability to develop their own business and

become self reliant.25

Aliyu (2006) stated that objectives of financial

accounting in general includes among others to:-

i. Aid in the development of desirable character

traits

ii. Develop the ability to correlate arithmetic,

spelling, business law, penmanship, economic

and commercial correspondence with each other

and with their practical usage in everybody

business

iii.Develop an appreciation of the needs for

giving careful attention to details in

transaction business and in recording the

necessary data.

iv. Develop the ability to understand, prepare

and control personal budget.

v. Develop an understanding of the need for

record keeping in modern business. These

26

objectives are to serve as a guide to the

teacher to enable him accommodates students

with varying interest and background.

2.6 Qualities of A Good Financial Accounting

Teacher

A good financial accounting teacher must

possess the qualities of a good teacher as

stated in Aliyu (2006).

He must be Qualified

The teacher must have the requirement in

terms of academic qualifications as laid down by

the governing council or authority of the

educational institutions.

He must Know His Subject

27

The teacher must possess an in-depth mastery

of the subject matter. However, it is important

for the teacher to note that; through preparation

of every lesson is essential. Each step has to be

planned, new work grafted into the old and

suitable examples provided.

He must be Discipline

True discipline is a state of mind. It is a

form of order maintained by individual as a

result of individual-self respect and self-

restraint. Discipline must be firm from the first

day of the lesson in all the classes.

He must have Suitable Instructional Manner.

The teacher must possess good voice

production and eye contact.

Byron (2006) outlines four (4) major qualities of

a good financial accounting teacher such as;

28

knowledgeable, interest, communication skills and

respect for students.

2.7 Methods of Teaching Financial Accounting

There are many teaching methods which the

teacher can implore to deliver his teaching.

These includes; lecture methods, class teaching

method, project methods, questioning methods,

individual group and pupils activities,

assignment method, demonstration method, etc.

Bawa and Guwa (2006) are of the viewed that

all the below listed teaching methods are

generally accepted in teaching all subjects.

Project method

Class teaching method

Questioning and problem method

Assignment method

Individual, Group and pupil Activities

29

Lecture method

Project Method

It is common to hear people saying that they

have this project to execute at a particular

period of time. At times we hear of abandon

project or that students are writing projects.

The question one may want to ask is what does the

term project means.

It simply means planned activities or idea to be

carried out by an individual or a group of

persons. It is a special assignment set out plan

of activities to be carried out, having in mind

particular goal to be achieved.

Class Teaching Method

Very similar to the lecture method except for

the number of students involve is smaller. It is

30

commonly practice in secondary schools. It’s

advantage include saving time by teaching the

whole class at the same time. The pupil

interaction fosters spirit of cooperation and

healthy competition.

Questioning and Problem Method

Generally, questions help to reveal the minds

of both the teachers and students on particular

issues. When students ask questions, he exposes

his ignorance or level of understanding and

teacher is then able to assist him or her. When a

teacher asks question he seeks t ample the

knowledge of students and then assess whether or

not the set out objectives of the lesson are been

31

achieved. The question can either be from the

students to the teacher or vise versa.

Assignment Method

Individual, Group and Pupil Activities

The teaching and learning process generally

involves two groups of people that is, the

teacher on one hand the learner on the other

hand. For the success of the process, both the

teachers and students have roles to perform. The

teachers activities are to ensure that the desire

knowledge, skills, attitudes are transferred to

the learner. The student’s activities are those

that can be carried out by some individuals in

groups or by the entire class

Lecture Method

This involves a teacher and a larger group of

students at the same time. The teacher comes to

32

the class with his facts and dishes them out. The

students are largely passive listeners. This

method is also referred to as teacher-centred-

method. Its common in the higher institutions of

learning such as colleges of education,

polytechnics and universities.

Brown (1982) said lecture method does not

provide students with enough opportunity to

practice their skills. Therefore financial

accounting teachers should not adopt this method

in secondary schools since financial accounting

involves critical thinking and skills.

2.8 The Roles of Instructional Materials in Teaching

Financial Accounting.

According to martin (2004), instructional

technology is a systematic way of designing and

evaluating the total process of teaching-learning

in terms of specific objectives based upon reach33

in human, communication learning and combine both

human and non human resources to bring about

effective instruction. Therefore, it is expected

to use accurate instructional materials in

disseminating knowledge to improve student

performance in financial accounting. A textbook

on financial accounting present information rules

and principles, methodology that are used as the

basis for the subjects being taught and acts as a

guideline for effective teaching.

Awojobi (2001) says that, although, well

organized curriculum and good teaching methods

are important, effective teaching in financial

accounting depends on accurate supply and use of

instructional materials. Instructional materials

are very good assets in the teaching learning

situation.

34

In the same vein, Aliyu (2001) observed that

most setbacks for our financial accounting in

Nigeria are being caused by poor prescription or

selection of appropriate textbook and teaching

materials.

Therefore, the use of instructional materials

will assist in teaching and arouse the interest

of the learners. This also agrees with Peter

(2009) and Martin (2010) that a well designed

instructional material and available teaching

aids may be necessary in improving the quality of

teaching because lack of relevant modern textbook

written by well read educational personnel on

financial accounting subject has a barrier to

effective teaching of the subject.

2.9 Teachers Attitude on Student’s Performance in

Financial Accounting

35

The teacher is described as a director of

learning and provides opportunities for the

students to absorb facts, skills and knowledge.

The teacher’s attitude towards the teaching

of financial accounting will go a long way to

determine whether the students will be interested

in the subject or not (Aliyu 2001). Even their

performance in the subject during examination

depends so much on the teacher’s attitude.

The demonstration of mastery of financial

accounting by the teachers should arouse the

interest of the students, for subject teacher’s

attitude towards the teaching of financial

accounting in the classroom, should be that of a

continuously motivating students to arouse their

interest in learning which also will enhance

performance. Anderson (1974) opined that teacher

is a director of learning he has the

36

responsibility of motivating his students to work

towards the accomplishment of the desired

objectives. When students are motivated, they

tend to put in their best hence motivation has

been described as a force or device behind a

person’s action which causes a person to begin

his activity and fellow it through.

Amune (1998) further stated that motivation

is an incentive to work towards a goal.

2.10Student Learning Attitude and its Effects on

their Performance

No students can succeed in academics or

perform well without willingness to learn and

that is more reason why poor performance these

days could be attributed to lack of willingness.

Block et al (1975) assert that “attitude

affects teaching and learning in the classroom

37

and the kind of attitude a child possess can

affect his school works and learning”. Students

should cultivate a good and progressive attitude

which will enhance their learning capability.

2.11 Problems Affecting Accounting Education in

Nigeria

2.11.1 Insufficient Manpower

Nolan et al (1975) studied the staffing

situation of business schools in America. They

found out that accounting teachers were

insufficient because there were equally

attractive opportunities for them in the world of

business. This is also applicable to the

situation in our colleges, since the attainment

of educational objectives is the teachers.

Therefore, insufficient accounting teacher is a

38

major setback affecting accounting education both

in Nigerian and beyond.

2.11.2 Remuneration

Adeyanju (2005) and Daniel (2006)

stated that improved conditions of services will

help teachers in their profession in addition to

their salaries”. He added, poor condition to

service and lack of incentives would in no doubt

have a direct or an indirect influence on the

performance of the students. It is a well known

fact, that teachers in Nigeria have not given due

recognition at all levels despite their

contribution to move the teachers remained

stagnant with the non-implementation of the

teachers’ salaries scale (TSS).

2.11.3 Teachers were not Equally Motivated.

39

According to victel (1953) in (Daniel 2000),

believes that works is a stimulus variable. He

said that stimulus variable is those incentive

inherent in any given career. Among such

incentives included the various job related

factors which have the possibility of affecting

his productivity positively or negatively.

According to Tonne (1989), “standard of

achievement in principles of accounting depends

on accuracy, competency and honesty in business

teachers”. He further indicated that the

accounting teachers must always be sufficiently

aware of variation in current business practice

so that memorization of details from textbooks

does not over shadow the rest of the course. But

most of the accounting teachers have hardly

attended course, workshop and seminars which

affect their level of effectiveness.

40

2.11.4 Inadequate Instructional Materials:

Saleh (2003), assert that “Equipment and teaching

materials like teaching aids, accounting laboratory

equipment, and textbooks has become an impediment

for accounting in secondary schools”. Teaching

materials are hardly provided in this noble

profession.

Awojobi (2001) pointed out that “instructional

materials are very good assets in teaching/learning

situation, therefore should be carefully evaluated

to ensure that their effectiveness and reliability

meet the anticipated instructional objectives”.

Ellis (2001) classified the variety of

instructional materials in business education which

are lacking as Equipment/facilities, Audio/visual,

Reading resources/materials and Community

resources.

41

2.12Empirical Studies

In this section, two (2) related literature

is reviewed for the purpose of this study. The

works include:

Onyeka (2008) carried a research on the topic

“factors affecting effective teaching of

financial accounting in senior secondary schools

in Kaduna State”. The purpose of the research was

to determine how adequate facilities provided

affect teaching and learning of financial

accounting. Survey method was adopted for the

study and his sample population was 130 students

and 4 teachers out of 200 students and 4 teachers

maintain the same number in his findings, he

realized that students’ poor performance was as a

result of some certain constraint.

He concluded that teachers teaching

accounting are not qualified and professional to42

handle the subject perfectly. He recommended that

accounting teachers should adopt relevant and

better methods of teaching.

From the work of Onyeka (2008) reviewed, it

is very important in this study, because it help

the researcher in selecting the research design,

however, he would have used the whole population

as the number of students used so as to give the

researcher a reliable result.

Abdul (2005) carried out research on “an

evaluation of the problem of the problem

associated with teaching and learning of

financial accounting in senior secondary

schools”. The purpose of the study was to

determine the adequacy of accounting teachers as

it affects the learning of financial accounting.

The researcher used analytical research as the

design, and a sample population of 90 students

43

and 10 teachers out of 461 students and 24

teachers. Some of the findings includes: Methods

of teaching have a long way to determine the

performance of students in financial accounting

and also infrastructures available are

dilapidated.

From the work of Abdul (2005) reviewed above,

the works was found important to the research

study, as it drew the researchers attention to

the method of teaching financial accounting as it

affects the learning of financial accounting

which from the major area of this research work.

2.13 Summary of Literature Review

It was highlighted that the need for

accounting arises as the business owners,

managers, suppliers wanted to know more about the

existing business, the need to provide qualified

teachers to handle the subject, use of adequate44

instructional materials/textbooks, and adequate

remuneration for teachers is important in order

to boost their morale.

Different method of teaching are explained

which are generally accepted for teaching of all

courses including financial accounting. The

teachers and students positive attitude towards

accounting also contribute greatly to students

performance.

Therefore, in connection with this facts made

the researchers go into the causes of students’

failure in financial accounting at the SSCE

examinations. A case study of some selected

government owned secondary schools in Okigwe

Local Government of Imo State.

45

CHAPTER THREE

3.0 RESEARCH DESIGN AND METHODS

3.1 Introduction

In this chapter, research design, area of study,

population,

Sample / sampling procedures, instrumentation and

method of data collection are discussed,

3.2 Research Design

The research design is a survey; questionnaire

will be used as research instrument to collect data

from the respondents.

3.3 Population of Study

46

The research population is made up of all Senior

Secondary Schools in Okigwe Local Government of Imo

State.

3.4 Sample and Sampling Techniques

Five schools out of the Senior Secondary Schools

offering financial accounting in okigwe Local

Government Area were randomly selected. This include:

1.Ezinachi Community Secondary School

2 Federal Government College, Okigwe

3. Ihube Boys High School

4. Ugkwaku Community Secondary School

5. Okigwe National Grammer School,Umuoka

From each schools, 20 financial accounting students

were selected randomly to fill the questionnaires.

All the financial accounting teachers in the five

schools were purposely selected (to answer

questionnaires) as samples, because there were few

financial accounting teachers in the schools.

47

3.5 Instrumentation

Questionnaire was used as instrument for

collecting data. The questions are expected to be

given a “yes or no” answer. The questions therein

required respondent to indicate their degree of

agreement or disagreement in them. Part A (question

for student) were made up of 11 items while that of

teachers were made up of 10 items.

3.6 Validity and Reliability of the Instrument

Questionnaires was validated by the supervisor.

The reliability of the questionnaires was attested to

the fact that the respondent were not asked to give

their names, this added to the chance of getting

sincere responses.

3.7 Procedure for Data Collection

The method of data collection for the research

was through distribution of questionnaires. The

48

researcher distributed the questionnaire by himself

to ensure 100 percent return of the questionnaires.

3.8 Method of Data Analysis

The statistical method used to analyse the

data collected was simple percentage and the table

will serve as frame work on which interpretation and

conclusion were based.

Formula; _Mean = X = fx∑ X 100

f∑ 1

Where ;

fx∑ = Total Number of Responses

f∑ = Total Number of Frequency

100 = Percentage of Responses

The statistical analysis “SA” and “A” was grouped as

agreed and all the “SD” and “D” was grouped as

49

disagreed. Scores from 2.50 above was accepted, while

scores from 2.49 below was rejected.

CHAPTER FOUR

4.0 DATA PRESENTATION, ANALYSIS AND DISCUSSION OF

RESULTS

4.1 Introduction

This chapter presents the analysis of data,

interpretation and results of the study. The

analysis was based on the information collected

using a structured questionnaire. The

presentation of responses from the respondents

were given in tables and also interpreted.

50

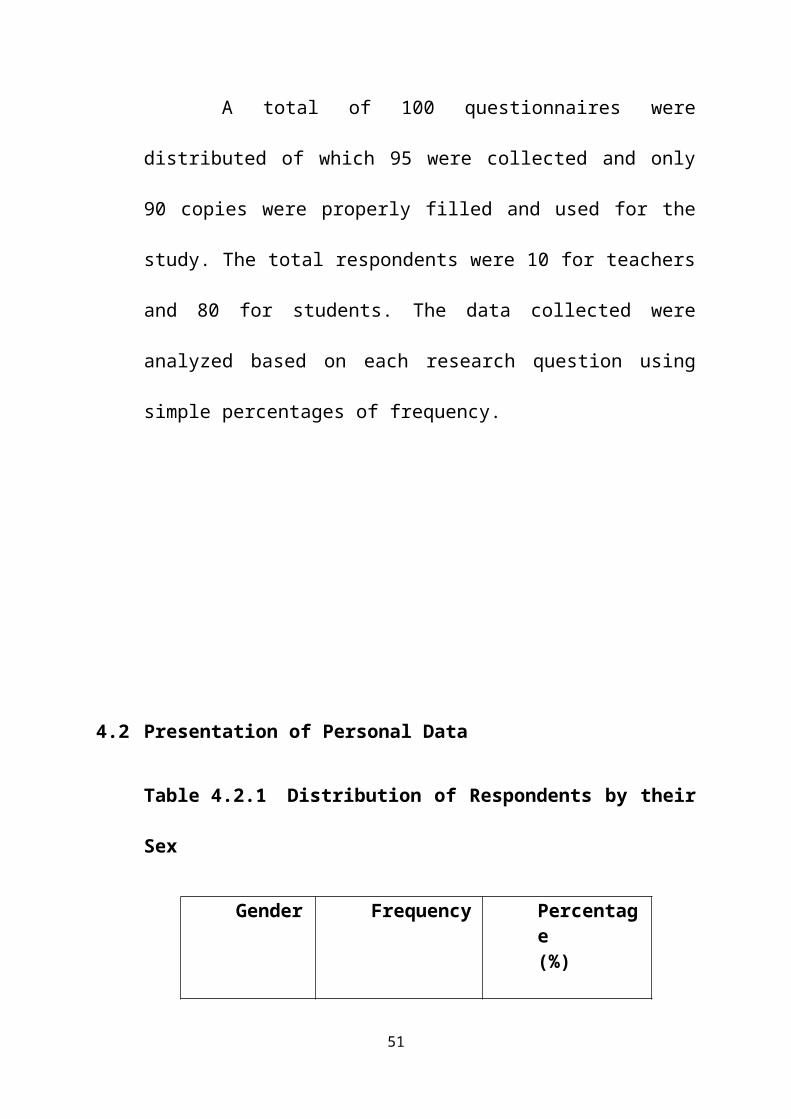

A total of 100 questionnaires were

distributed of which 95 were collected and only

90 copies were properly filled and used for the

study. The total respondents were 10 for teachers

and 80 for students. The data collected were

analyzed based on each research question using

simple percentages of frequency.

4.2 Presentation of Personal Data

Table 4.2.1 Distribution of Respondents by their

Sex

Gender Frequency Percentage(%)

51

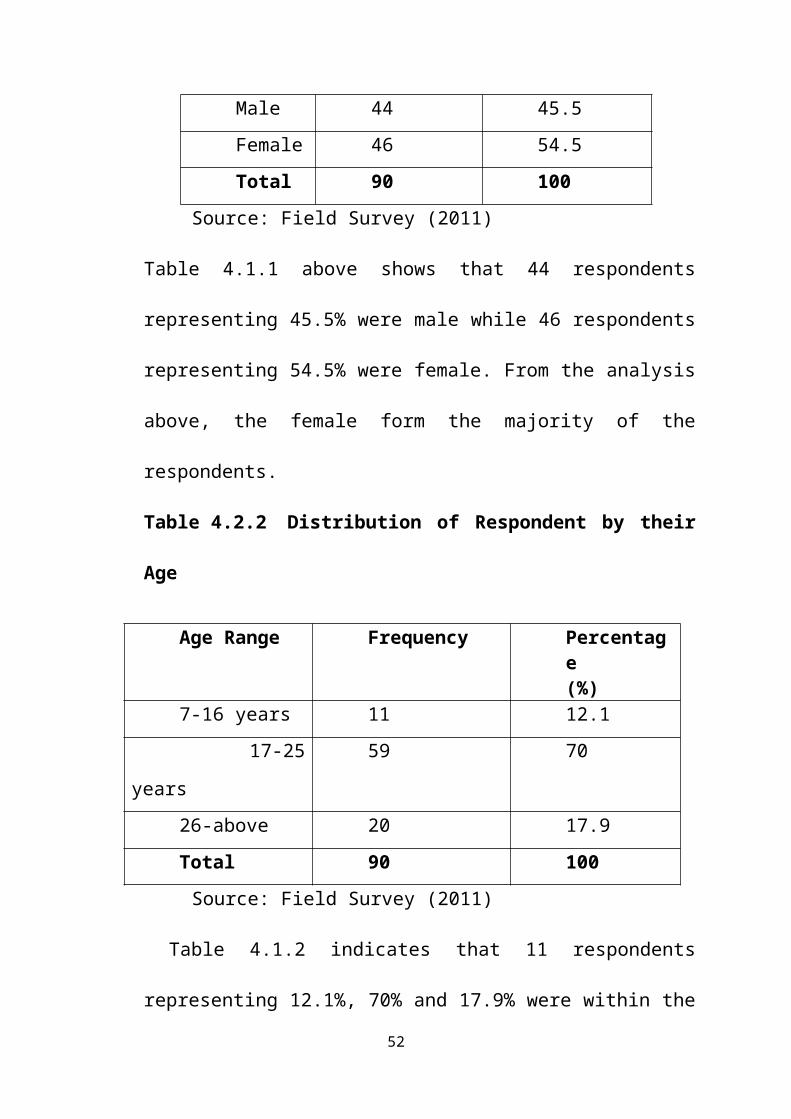

Male 44 45.5Female 46 54.5Total 90 100

Source: Field Survey (2011)

Table 4.1.1 above shows that 44 respondents

representing 45.5% were male while 46 respondents

representing 54.5% were female. From the analysis

above, the female form the majority of the

respondents.

Table 4.2.2 Distribution of Respondent by their

Age

Age Range Frequency Percentage(%)

7-16 years 11 12.1 17-25

years

59 70

26-above 20 17.9Total 90 100Source: Field Survey (2011)

Table 4.1.2 indicates that 11 respondents

representing 12.1%, 70% and 17.9% were within the

52

age range of 7-16, 17-25 and 26-above years

respectively.

Table 4.2.3 Distribution of Respondents by

their Marital Status

Status Frequency Percentage(%)

Married 4 4.0Single 86 96Total 90 100

Source: Field Survey (2011).

Table 4.1.3 indicates that 4 respondents

representing 4.0% were married, while 90

respondents representing 96% were single.

53

4.3 Answers to Research Questions

4.3.1 Research Question 1: To what extent does

teacher’s attitude affect students’ performance

in financial accounting?

Table 4.3.1: Extent of the effect of teachers

attitude as it affect students’

performance

(N=90)

S/N Questionnaire Items SA

4

A

3

D

2

SD

1

Mean _(X)

Decision

1 Students’ performancein financial accountingis not encouraging

38 28 18 6 3.08 Accepted

54

2 Financial accountingteachers are friendly

34 23 15 18 2.81 Accepted

3 Students find it easyto ask question formore explanation infinancial accountingclasses.

16 17 31 26 2.26 Rejected

4 Teachers do not oftengive students exerciseto solve

35 21 13 21 2.78 Accepted

5 Teachers are regularduring financialaccounting lesson

30 37 17 6 3.01 Accepted

Sectional mean 3.49 Accepted

Source: Field survey (2011)

Table 4.3.1 above shows the sectional mean score to

be 3.49. This reveals that teachers attitude affect

students’ performance in financial accounting. Item 1

(Students’ performance in financial accounting is not

encouraging) with a mean score of 3.08, shows that

students’ performance in financial accounting is not

encouraging.

Item 2 (Financial accounting teachers are friendly)

with a mean score of 2.81, shows that teachers are

55

not friendly to their students. Item 3 (Students find

it easy to ask question for more explanation in

financial accounting classes) with a mean score of

2.26, shows that the assertion is not true. Item 4

(Teachers do not often give students exercise to

solve) with a mean score of 2.78, shows that teacher

do not often give their students exercise during

lesson. Item 5 (Teachers are regular during financial

accounting lesson) with a mean score of 3.01, shows

that teachers are not regular during financial

accounting lessons.

4.3.2 Research Question 2: To what extent does the

method used in teaching financial accounting affect

the learning of the subject in secondary school?

Table 4.3.2: Extent of teaching Method as it affects

the learning of the subject56

(N=90)S/N Questionnaire Item SA

4

A

3

SD

2

D

1

Mean _(x)

Decision

6 Teachers do notapply differentmethod in teachingin the class

8 15 29 38 1.92 Rejected

7 Financialaccounting teachersdo encouragestudents to studyaccounting at home

18 41 23 8 2.77 Accepted

8 Teachers spendreasonable time toprepare theirlesson

22 27 28 13 2.64 Accepted

9 Accounting teachershas made thesubject difficultfor students tounderstand

14 21 33 22 2.30 Rejected

10 Teachers adoptstudents-centredmethods in theirteaching offinancialaccounting

36

20 18 16 2.84 Accepted

Sectional Mean 2.49 Rejected

Table 4.3.2 above shows the sectional mean score

to be 2.49. This reveals that the method used in

57

teaching financial accounting does not affect the

learning of the subject in secondary school.

Item 6 (Teachers do not apply different method in

teaching in the class) with a mean score of 1.92,

shows that the assertion is not true. Item 7

(Financial accounting teachers do encourage students

to study accounting at home) with a mean score of

2.77, shows that financial accounting teachers do

encourage their students to study accounting at home.

Item 8 (Teachers spend reasonable time to prepare

their lesson) with a mean score of 2.64, shows that

teachers spend reasonable time to prepare their

lesson. Item 9 (Accounting teachers has made the

subject difficult for students to understand) with a

mean score of 2.30, shows that the assertion is not

true. Item 10 (Teachers adopt students-centred

methods in their teaching of financial accounting)

with a mean score of 2.84, shows that teachers

58

adopt student-centred methods in their teaching of

financial accounting.

Research Question Three: To what extent does peer

group and parental influences affect the learning of

financial accounting in secondary schools?

Table 4.3.3: Extent of peer group and parental

influence as it affects the learning of

the subject.

(N=90)S/N Questionnaire Items SA

4A3

SD2

D1

Mean _(x)

Decision

11 Parents do not alwaysencourage theirchildren to read athome

13 25 44 21 1.95 Rejected

12 Students don’t ask fromtheir friends what isthought in theirabsence

29 37 19 5 3.00 Accepted

13 Parents don’t payschool and registrationfees on time therefore,children were sent home

26 33 13 18 2.80 Accepted

59

during lessons14 Students are usually

involved in a lot ofdomestic activitiesafter school, likegoing to the farm,market and hawking.

32 22 17 19 2.74 Accepted

15 Parents decide thechoice of financialaccounting for theirchildren

25 34 23 8 2.84 Accepted

Sectional mean 2.67Accepted

Table 4.3.3 shows the sectional mean score to be

2.67. This reveals that peer group and parental

influences affect the learning of financial

accounting in secondary schools. Item 11 (Parents do

not always encourage their children to read at home)

with a mean score of 1.95, shows that the assertion

is not true. Item 12 (Students don’t ask from their

friends what is thought in their absence) with a mean

score of 3.00, shows that students do not ask their

friend from what is thought in their absence. Item 13

60

(Parents don’t pay school and registration fees on

time therefore, children were sent home during

lessons) with a mean score of 2.80, shows that

parents do not pay school and registration fees on

time therefore, children were sent home during

lesson. Item 14 (Students are usually involved in a

lot of domestic activities after school, like going

to the farm, market and hawking) with a mean score of

2.74, shows that students are usually involved in a

lot of domestic activities after school, like going

to the farm, market and hawking. Item 15 (Parents

decide the choice of financial accounting for their

children) with a mean score of 2.84, shows that

parents decide the choice of financial accounting for

their children.

Research Question Four: To what extent does

availability of infrastructural facilities affect the

61

learning of financial accounting in secondary

schools?

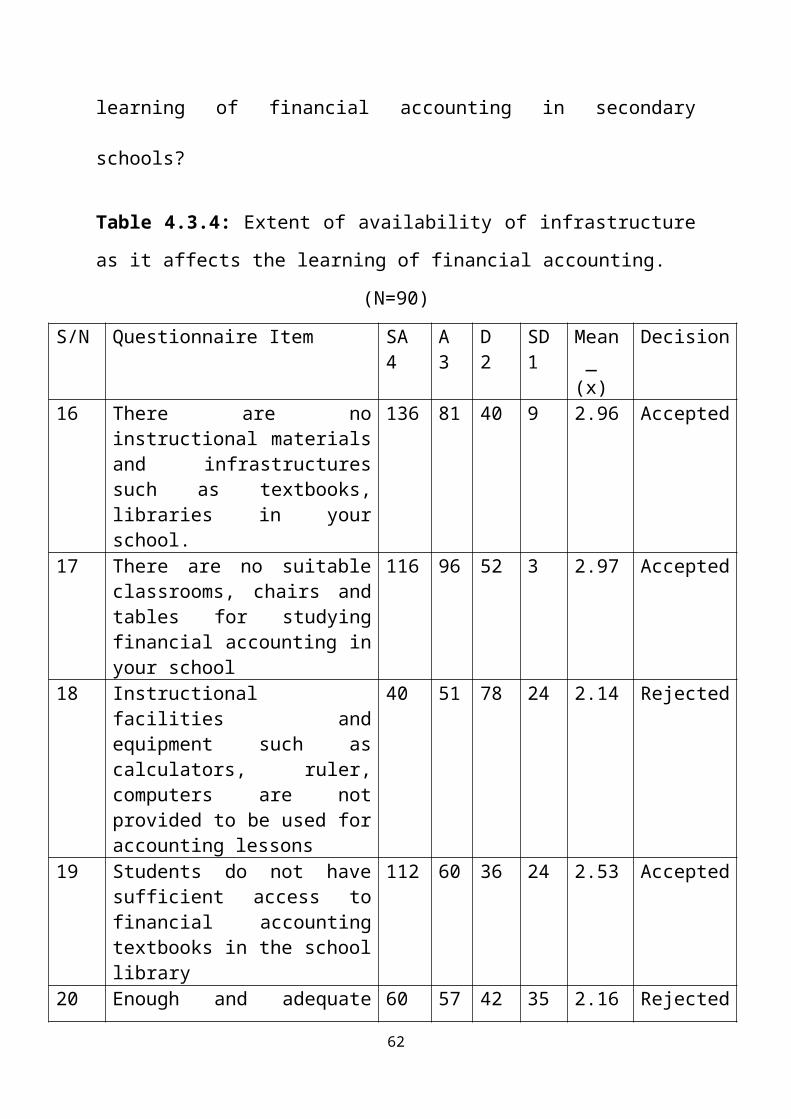

Table 4.3.4: Extent of availability of infrastructure

as it affects the learning of financial accounting.

(N=90)

S/N Questionnaire Item SA4

A3

D2

SD1

Mean _(x)

Decision

16 There are noinstructional materialsand infrastructuressuch as textbooks,libraries in yourschool.

136 81 40 9 2.96 Accepted

17 There are no suitableclassrooms, chairs andtables for studyingfinancial accounting inyour school

116 96 52 3 2.97 Accepted

18 Instructionalfacilities andequipment such ascalculators, ruler,computers are notprovided to be used foraccounting lessons

40 51 78 24 2.14 Rejected

19 Students do not havesufficient access tofinancial accountingtextbooks in the schoollibrary

112 60 36 24 2.53 Accepted

20 Enough and adequate 60 57 42 35 2.16 Rejected

62

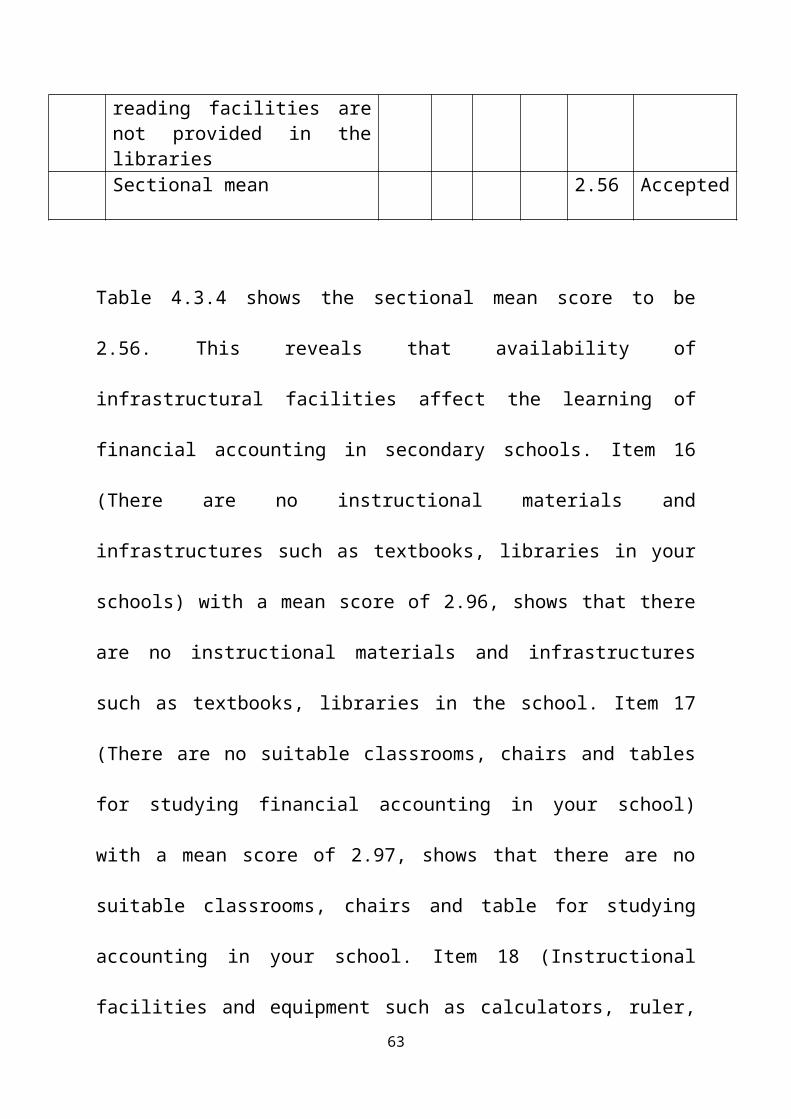

reading facilities arenot provided in thelibrariesSectional mean 2.56 Accepted

Table 4.3.4 shows the sectional mean score to be

2.56. This reveals that availability of

infrastructural facilities affect the learning of

financial accounting in secondary schools. Item 16

(There are no instructional materials and

infrastructures such as textbooks, libraries in your

schools) with a mean score of 2.96, shows that there

are no instructional materials and infrastructures

such as textbooks, libraries in the school. Item 17

(There are no suitable classrooms, chairs and tables

for studying financial accounting in your school)

with a mean score of 2.97, shows that there are no

suitable classrooms, chairs and table for studying

accounting in your school. Item 18 (Instructional

facilities and equipment such as calculators, ruler,63

computers are not provided to be used for accounting

lessons) with a mean score of 2.14, shows that the

assertion is not true. Item 19 (Students do not have

sufficient access to financial accounting textbooks

in the school library) with a mean score of 2.53,

show that students do not have sufficient access to

financial accounting textbooks in the school. Item 20

(Enough and adequate reading facilities are not

provided in the libraries) with a mean score of 2.16,

shows that the assertion is not true.

4.4 Discussion of Findings

This study is on the causes of students’

failure in financial accounting at the SSCE level

in Okigwe local government of Imo State, four

research questions were stated, data was

64

collected and analysed from the questionnaire

used out to respondents. The findings in research

question one in table 4.3.1 shows that more of

the proposed factors enumerated relating to

teachers attitude is accepted. The learning of

financial accounting depends on the way it is

presented to the students, the way the students

actively interacts with the learning experiences

presented to them and the environment within

which the learning takes place. Teachers attitude

towards the teaching of financial accounting

plays a significant role in shaping the attitude

of students towards the learning of the subject.

Students’ positive attitude towards the learning

of the subject. Students’ positive attitude

towards financial accounting could be enhanced by

teachers’ enthusiasms, resourcefulness and

helpful behaviour, teachers’ thorough knowledge

65

of the subject matter and their making it quite

interesting. It is on the premise that the

attitude of the teacher, his/her disposition to

the subject, students, and classroom environment

could make or unmake the attitude of the students

to want to learn or not. Hence the financial

accounting teacher should be psychological

prepared to teach the subject given that every

other requirement is met.

From research question two in table 4.3.2, it

was discovered that the methods used in teaching

financial accounting is not the right method to

be used. This is because of the fact that

financial accounting like any other calculating

subjects requires constant practice and learning

by observation. It will be preferable to learn if

the teachers in question take their time to give

their students assignment at the end of every

66

lesson, ensure that those assignment are

collected, marked and make corrections were

necessary and also, it will be of great benefit

to the student if field trips like excursion are

organised by the teachers so that they will be

able to see in a practical form what has been

learnt in the classroom.

The third research question in table 4.3.3

was to find out how peer group and parental

influence affect the students’ performance. It

was revealed from the table that almost if not

all the factors enumerated relating to it was

affected. This is to show that peer groups and

parental influence play a vital role in a child

academic performance. Also, from the data

analysis table results obtained, we can as well

say that domestic work at home, late payment of

school fees, and parents deciding for their

67

children the choice of study for their children,

among others could determine the performance of

the students.

From table 4.3.4, it can be conclusively said

that lack of infrastructural facilities

contributed to the development of students

negative attitude towards financial accounting

which has led to a high level of failure recorded

in the senior school certificate examination.

There are few current text books of financial

accounting and other learning materials such as

computers, calculators, rule sheet and other

related materials in the schools.

68

CHAPTER FIVE

5.0 SUMMARY, CONCLUSION AND RECOMMENDATIONS

5.1 Introduction

This chapter presents the summary, conclusion

and recommendations.

5.2 Summary

The research work was on the causes of

students’ failure in financial accounting at SSCE

level in Government Secondary Schools in Okigwe

local Government of Imo State. Survey research

design was used. The population of the study was

ninety (90) comprising of ten (10) teachers and

eighty (80) students drawn from five selected

secondary schools in Okigwe local Government of

Imo state.

This entire research work is distributed over

five chapters each chapter bearing its own

significance in solving the research problem. The

breakdown of the chapters and their content are

this;

69

In the first chapter of this research work,

the researcher introduces the research topic; the

causes of students’ failure in financial

accounting at SSCE level in Government Secondary

Schools in Okigwe local Government of Imo State.

This chapter listed the question which the

researcher hopes to find solutions to.

The second chapter reviewed the related

literature on the topic and examined the concept

of financial accounting, the objectives of

financial accounting, qualities of a good

financial accounting teacher and methods of

teaching financial accounting.

The third chapter deals with the research

procedure and methodology adopted in finding

answers to the research questions in chapter one.

It laid emphasis on the method of data

collection, presentation and analysis. It also

70

bore a sample of the questionnaire used in

collection the data used in this study.

The interpretation of the data collected and

its analysis is done in the fourth chapter of

this study. The data collected through the

questionnaire were tabulated for easy computation

and analysis. Decisions were drawn from the

results obtained after the analysis. The findings

adequately answer the research question in

chapter one of the study. The summary, conclusion

and recommendations is found in this last chapter

which is chapter five of this study.

5.3 Conclusion

Based on the analysis of the responses to

this finding. It could be concluded thus,

teachers negative attitude during financial

accounting lessons will make the students develop

71

hatred for the subject which will latter affect

their performance and the number of the students

wishing to study accounting at the higher level.

Teachers methodology used in the teaching

financial accounting could affect the learning of

the subject. The employment of necessary teaching

aids and stimulating learning atmosphere that

could arouse interest and understanding ion the

learners can be of great help.

Further more, peer group and parental

influence affects students performance in

financial accounting. Therefore, negative

parental and peer group perception can lead to

poor performance of students in financial

accounting.

The researcher concludes that lack of

infrastructural facilities contribute to the

development of students negative attitude towards

financial accounting. This might lead to their

inability to learn some of the basic principles.

Similarly, the lack of adequate exposure to

learning materials could make the products or

graduate of the program me to be job seekers

instead of job creators.

72

5.4 Recommendations

1. To improve on teacher’s attitude, the

following recommendations were given:

i. Teachers should be more friendly with

the students. This will make them feel free

and will in turn, encourage them to approach

the teachers to help them in problem.

ii. Negative and discouraging statement to

students should be avoided in accounting

classes.

iii. Teachers should be very patient with the

students and provide more explanation to

their questions during accounting lectures.

iv. Teachers of financial accounting should

attend all their lessons bearing in mind that

it is a task for them to perform their duties

therefore they should dedicate themselves to

such functions.

2 To provide teaching learning and create

interest of the learner. The following

recommendations were given:73

i. Teachers should involve students in the

course of teaching financial accounting.

Their participation will make them feel

free with the teachers and will in turn

encourage them to approach the teacher

to help them to approach the teacher to

help them In solving difficult exercises

outside the normal financial accounting

lessons.

ii. Teachers should give students assignment

at the end of every lesson. This will

make them create time for the study of

financial accounting thereby getting

them use to the terms.

iii.Teachers should make sure that

assignment given are collected marked,

scored, recorded and corrections be made

in the class. This will make the

74

students to be properly groomed and

dedicated to work extra mile when at

home.

iv. Teachers should organize students to on

for excursion (field trip). This will

enable them see the importance of the

subject as the trip will aid them clear

their conscience and exposed the

students to real life situation of the

subject.

3. With regard to the findings of research

question three, the researcher recommended

that:

i. Parents should always encourage their

children by way of checking their work

at home, not giving them too much of

domestic assignments to allow them

study even at home and more so, by

75

paying their school fees and

registration regularly and early. This

will help them not to be driven away

during lessons.

ii. Students should always inquire from

their colleagues what they were taught

while away and also form study groups so

that they can put each other properly in

difficult areas.

iii.Parents and teachers should adopt

control measures to prevent influence of

peer groups.

iv. Students should try as much as possible

to avoid keeping bad company to be able

to face their academics properly.

v. parents should assist the school

authority in creating an awareness and

76

development of accounting knowledge to

the students and also help in the

administration of discipline on the

students.

4. To solve the problem of infrastructural

facilities, the researcher recommended that:

i. instructional materials such as

chalkboard, rulers, accounting ledger

book, and calculator should be provided.

Equipment like adding machines and

computers should also be made available.

These items are necessarily needed in

order to facilitate the teaching

learning process in financial

accounting.

ii. the use of archaic i.e outdated

financial accounting textbooks should be

77

discouraged and replaced with current

ones that have simple illustration for

both teachers and students uses

iii.libraries should be sited in a conducive

environment. The library is very

important in any academic environment,

due to the role it plays in the

provision of information, therefore, it

should be provided with adequate

facilities such as current textbooks,

journals, periodicals relevant to the

study of financial accounting.

5.5 Suggestions for further research

This research work was carried out on “the

causes of students’ failure in financial

78

accounting in the SSCE. A case study of some

selected public senior secondary schools in

okigwe local government of Imo state”. Knowing

the limitations of the study:

The researcher wishes to suggest that further

study be conducted on the influence of Teachers

Methodology as it affect the teaching/Learning of

Financial Accounting in secondary schools in

Nigeria.

REFERENCES

Adewumi, P. (2000). “Factors Affecting Teaching and

Learning of Financial accounting in secondary Schools”. A

79

Case study of Ofa Local Government Area of

Kwara State. Unpublished undergraduate

project, A.B.U, Zaria.

Aliyu, M.M. (2006). “Subject Method for Business

Teachers”. Vendaico Int’l Ltd. Business centre

28, Sulu Gambari Rd, Illorin.

Igben, R.O. (2009). “Financial Accounting Made Simple”.

Roi Publishers Isolo, Lagos.

Asaolu,E.A. (1998). “Students Attitude Towards Education”.

Institute of Education O.A.U. Ife.

Awojobi, A.O (2001). “Evaluation of Instructional Materials

in Business Education”. National Association of

Business Education Book of Reading Vol. No3.

Bawa, M.R. And Guga, A. (2006). “A Curriculum and

Instruction”. A.B.U Printing Press, Zaria.

80

Block, J.H. and Anderson L.W. (1975). “Mastering

Hearing in Classroom Instructions”. Macmillan

Publishers Coy. Newyork.

Brain, A.N. (2006). “Emphasis on Teaching”.

Spectrum Books Ltd, North London.

Daniel, Z. (2002). “Factors Affecting Students

Performance In Financial Accounting at Senior Secondary

Schools Certificate Examination”. Kaduna State

Unpublished Undergraduate Project Work.

Eliss, A.E. (2001). “Evaluation of Instructional System”.

Gordonard Breach Science publication,

Newyork.

Martin, A. (2004). “Problems and Prospects of Financial

Accounting in Secondary Schools”. University of

Ibadan publisher, Nigeria.

81

Richard, L. and David Pen, (2000). “Advanced

Financial Accounting”. By T.J International ltd,

Southampton, England.

Saleh, V. (2003). “Education in Nigeria Development”.

Vanguard LTD, Lagos, Nigeria.

Udoh, A.A. (2004.) “Fundamental of Financial Accounting”.

Ishola and Sons, Sabon Gari, Zaria.

Colin Drury. (2004). “Management and cost accounting”. (6)

Thomson Learning, London.

The Holy Bible (New Testament).

The Holy Quran (2:282).

WEB:

http://en.wikipedia.org/wiki/history of financial accounting

http://dictionary.reference.com/browse/accountancy

http://news.bbc.co.uk/i/hi/business/1688550.stm.

http:// studyandexam.com/causes-of-student-failure-in-exam.html

82

APPENDIX

QUESTIONNAIRE

Faculty of Education

Department of Educational Management Studies Accounting Education) University of Abuja.Dear respondent,

QUESTIONNAIRE ON THE CAUSES OF STUDENT’S FAILURE INFINANCIAL ACCOUNTING AT THE SSCE LEVEL IN GOVERNMENTSECONDARY SCHOOLS IN OKIGWE LOCAL GOVERNMENT AREA OFIMO STATE.

83

The researcher is a final year student of the

above named institution and department conducting a

research on the causes of student’s failure in

financial accounting at the SSCE level in Okigwe

local government of Imo state.

The researcher would appreciate your kind

cooperation in responding to these questions.

Respondents are to note that the information

given will be used purely for academic purposes and

these responses will be treated strictly as

confidential.

Thanks for your cooperation.

Yours faithfully

Nwosu Campbell Sunday.

QUESTIONNAIRE FOR DATA COLLECTION ON THE CAUSES OF

STUDENTS’ FAILURE IN FINANCIAL ACCOUNTING AT THE SSCE

LEVEL.

SECTION A (TEACHERS).

84

Respondent are expected to answer from the following

options (strongly agree, agree, disagree and strongly

disagree).

1. Teachers are over utilized because they are in

short supply.

( )

2. Teachers have low motivation because they are

poorly remunerated by the government. (

)

3. The presence of teacher-centred activities is the

reason for the boredom in the financial

accounting class.( )

4. Monitoring students progress in the financial

accounting class is difficult, due to the

overcrowded nature of the class.(

)

85

5. Students do not involve in activities that could

improve their English language competence because

they are lazy.

( )

6. Teachers are not very qualified. (

)

7. Teachers do not spend reasonable time to prepare

their lesson. ( )

8. The time to cover the syllabus is not enough. (

)

86

QUESTIONNAIRE FOR DATA COLLECTION ON THE CAUSES OF

STUDENTS’ FAILURE IN FINANCIAL ACCOUNTING AT THE SSCE

LEVEL.

SECTION B (STUDENTS)

Respondent are expected to answer from the following

options (strongly agree, agree, disagree and strongly

disagree).

1. Student’s performance in financial accounting is

not encouraging. ( )

87

2. Financial accounting teachers are friendly. (

)

3. Students find it easy to ask question for more

explanation in financial accounting classes. (

)

4. Teachers do not often give students exercise to

solves.

( )

5. Teachers are regular during financial accounting

lesson.

( )

6. Teachers do not apply different methods of

teaching in the class. ( )

7. Financial accounting teachers do encourage

students to study accounting at home. (

)

88

8. Teachers spend reasonable time to prepare their

lesson.

( )

9. Accounting teacher’s has made the subject

difficult for students to understand. (

)

10. Teachers adopted student-centred methods in their

teaching of financial accounting. (

)

11. Parents don not always encourage their children

to read at home. ( )

12. Students do not ask from their friend from what

is thought in their absence. ( )

13. Parents do not pay school and registration fees

on time therefore, children were sent home during

lesson.

89

( )

14. Students are usually involved in a lot of

domestic activities after school, like going to

the farm, market and hawking.

( )

15. Parents decide the choice of financial accounting

for their children.( )

16. There are no instructional materials and

infrastructures such as textbooks, libraries in

your school. ( )

17. There are no suitable classrooms, chairs and

table for studying accounting in your school. (

)

18. Instructional facilities and equipment such as

calculators, rule sheets and computers are not

provided to be used for accounting lesson. (

)

90

19. Students do not have sufficient access to

financial accounting textbooks in your school. (

)

20. Enough and adequate reading facilities are not

provided in your libraries. ( )

91

Copyright © 2022 FDOKUMEN