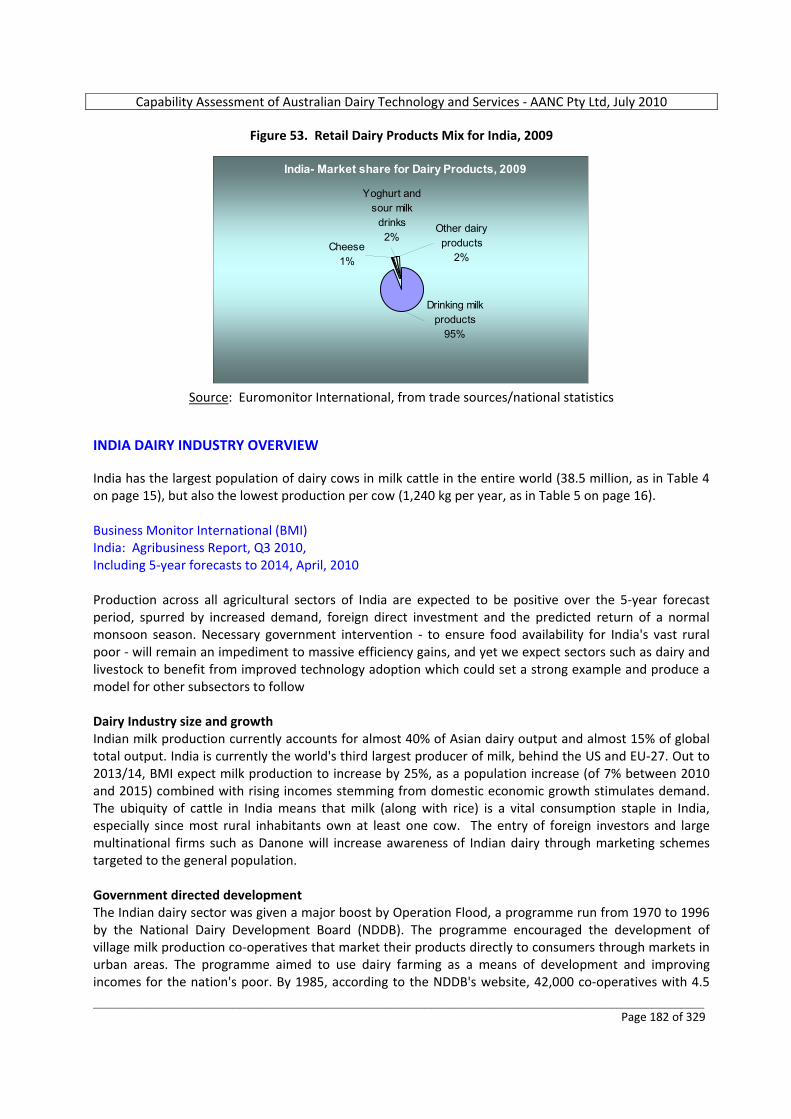

Capability Assessment of Australian Dairy Technology and ...

329

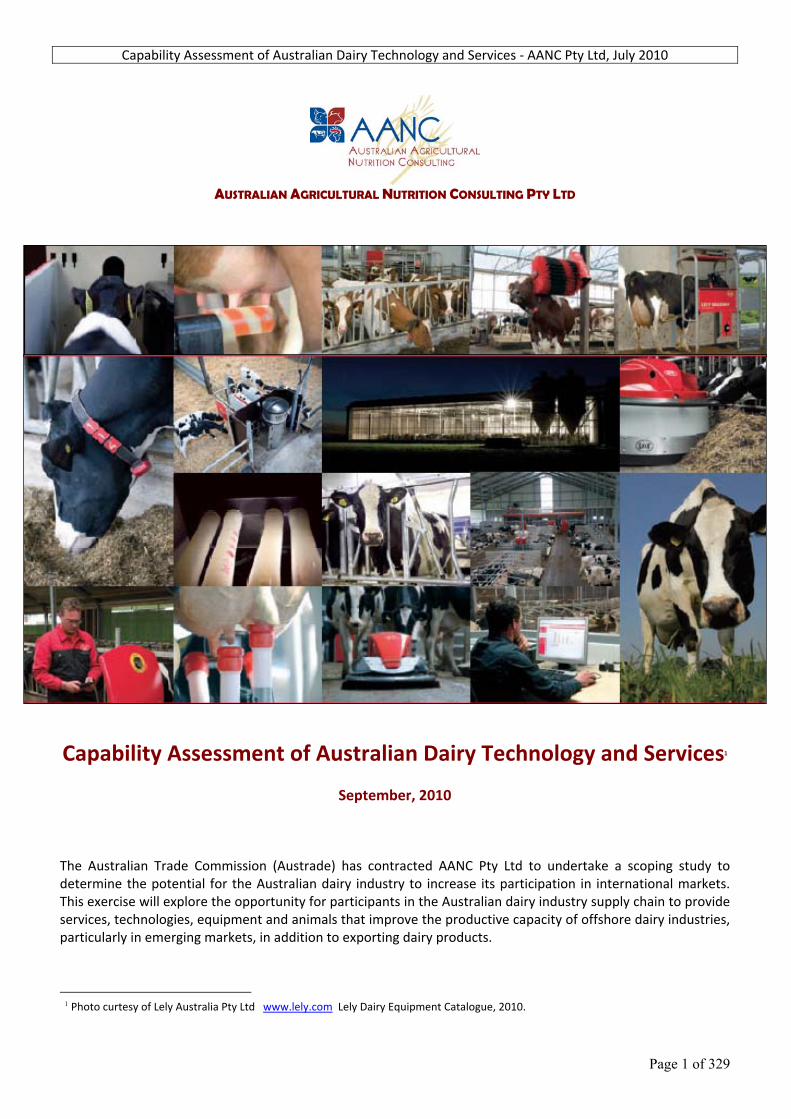

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010 Page 1 of 329 AUSTRALIAN AGRICULTURAL NUTRITION CONSULTING PTY LTD Capability Assessment of Australian Dairy Technology and Services 1 September, 2010 The Australian Trade Commission (Austrade) has contracted AANC Pty Ltd to undertake a scoping study to determine the potential for the Australian dairy industry to increase its participation in international markets. This exercise will explore the opportunity for participants in the Australian dairy industry supply chain to provide services, technologies, equipment and animals that improve the productive capacity of offshore dairy industries, particularly in emerging markets, in addition to exporting dairy products. 1 Photo curtesy of Lely Australia Pty Ltd www.lely.com Lely Dairy Equipment Catalogue, 2010.

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Capability Assessment of Australian Dairy Technology and ...

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 1 of 329

AUSTRALIAN AGRICULTURAL NUTRITION CONSULTING PTY LTD

Capability Assessment of Australian Dairy Technology and Services1

September, 2010

The Australian Trade Commission (Austrade) has contracted AANC Pty Ltd to undertake a scoping study to determine the potential for the Australian dairy industry to increase its participation in international markets. This exercise will explore the opportunity for participants in the Australian dairy industry supply chain to provide services, technologies, equipment and animals that improve the productive capacity of offshore dairy industries, particularly in emerging markets, in addition to exporting dairy products.

1 Photo curtesy of Lely Australia Pty Ltd www.lely.com Lely Dairy Equipment Catalogue, 2010.

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 2 of 329

Table of Contents

LIST OF ACRONYMS............................................................................................................................................................. 4

EXECUTIVE SUMMARY....................................................................................................................................................... 5

1. OVERVIEW OF THE AUSTRALIAN DAIRY INDUSTRY ........................................................................................... 9

1.1 Australia’s position as supplier to the global market – where we fit in production and supply................................. 14

Australia’s position in International Dairy Food product markets .................................................................................... 16

Australia’s Live Export Markets for Dairy Cattle ............................................................................................................... 22

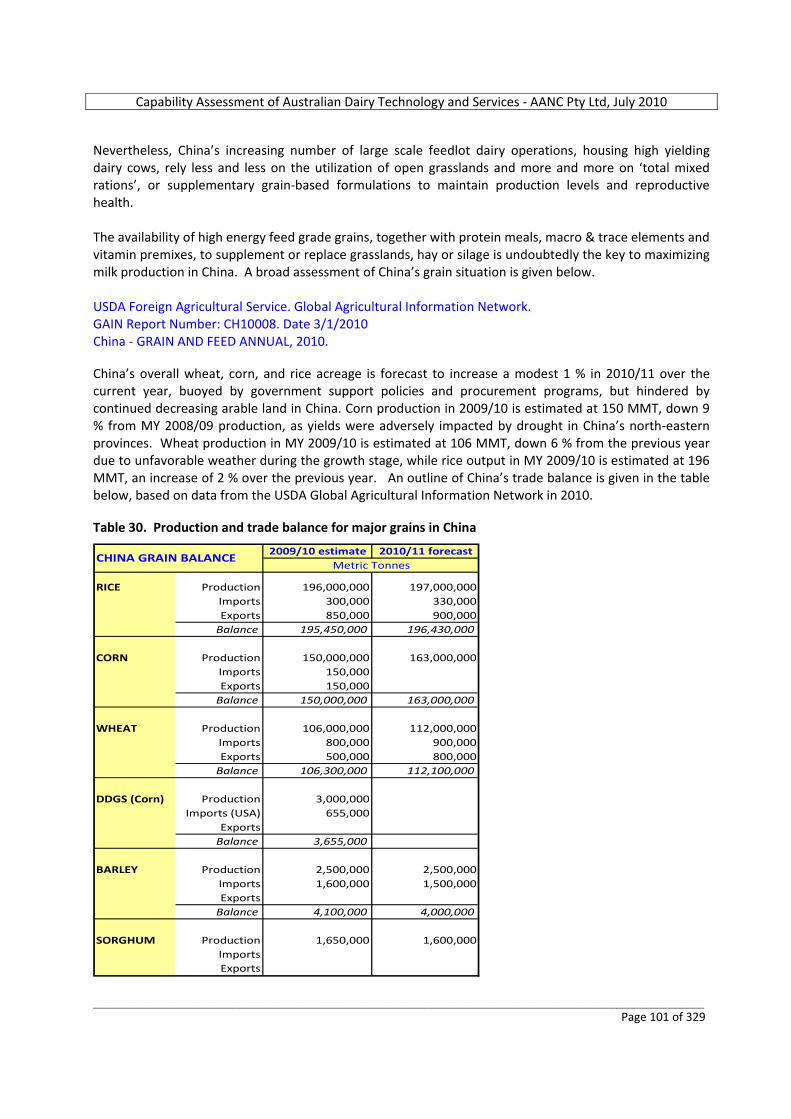

Australia’s position in Exported Dairy Technology & Equipment Markets ..................................................................... 32

1.2 Global Recognition – What AUSTRALIAN DAIRY PROFESSIONALS are considered best at ............................. 37

2. MAPPING THE SUPPLY CHAIN.................................................................................................................................... 46

3. CLUSTER APPROACHES................................................................................................................................................ 48

Examples of cluster approaches by services/equipment/technology suppliers................................................................... 48

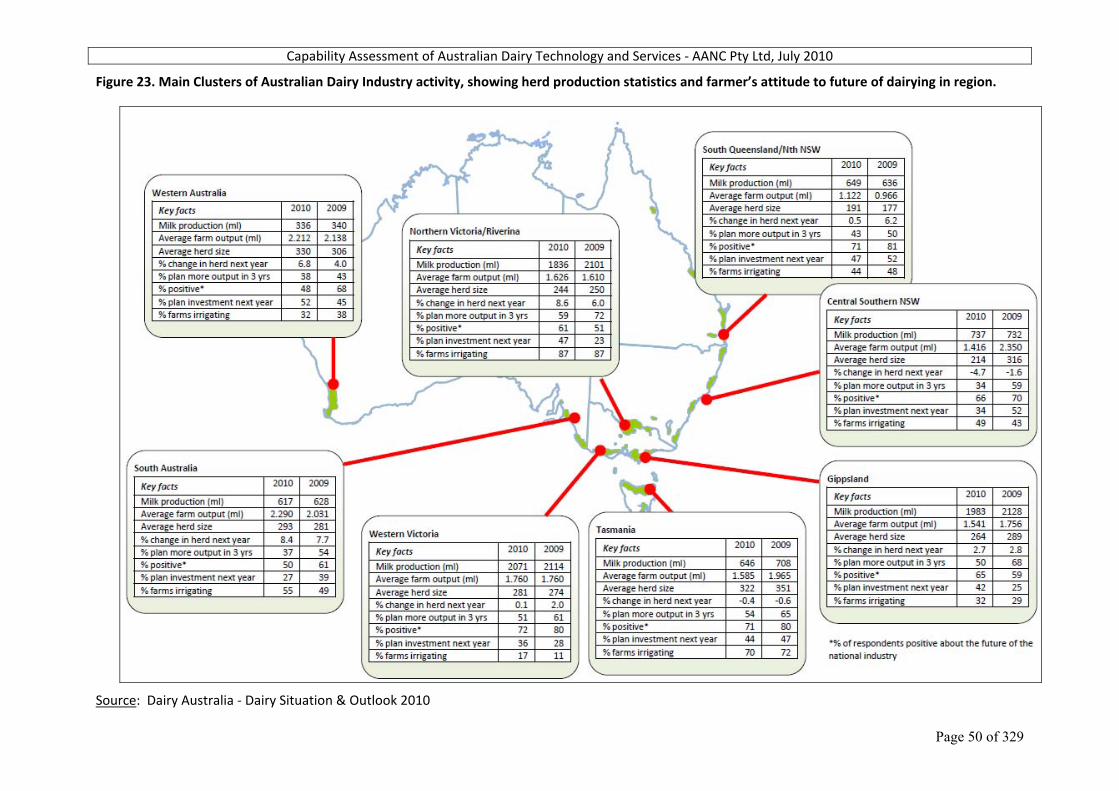

Potential for further cluster approaches ............................................................................................................................... 49

4. POTENTIAL FOR OUTWARD INVESTMENT BY AUSTRALIAN DAIRY PRODUCT EXPORTERS............... 51

Case studies of Outward Investment by Australian dairy product exporters ................................................................... 52

Potential for further Outward Investment (by market, by supply chain capabilities), including barriers ..................... 53

5. POTENTIAL FOR OUTWARD INVESTMENT BY THE AUSTRALIAN AGRIBUSINESS INVESTOR COMMUNITY (EXCLUDING DAIRY PRODUCT EXPORTERS)................................................................................. 61

Case studies of Outward Investment ..................................................................................................................................... 61

Potential for further Outward Investment (by market, by supply chain capabilities), including barriers. .................... 62

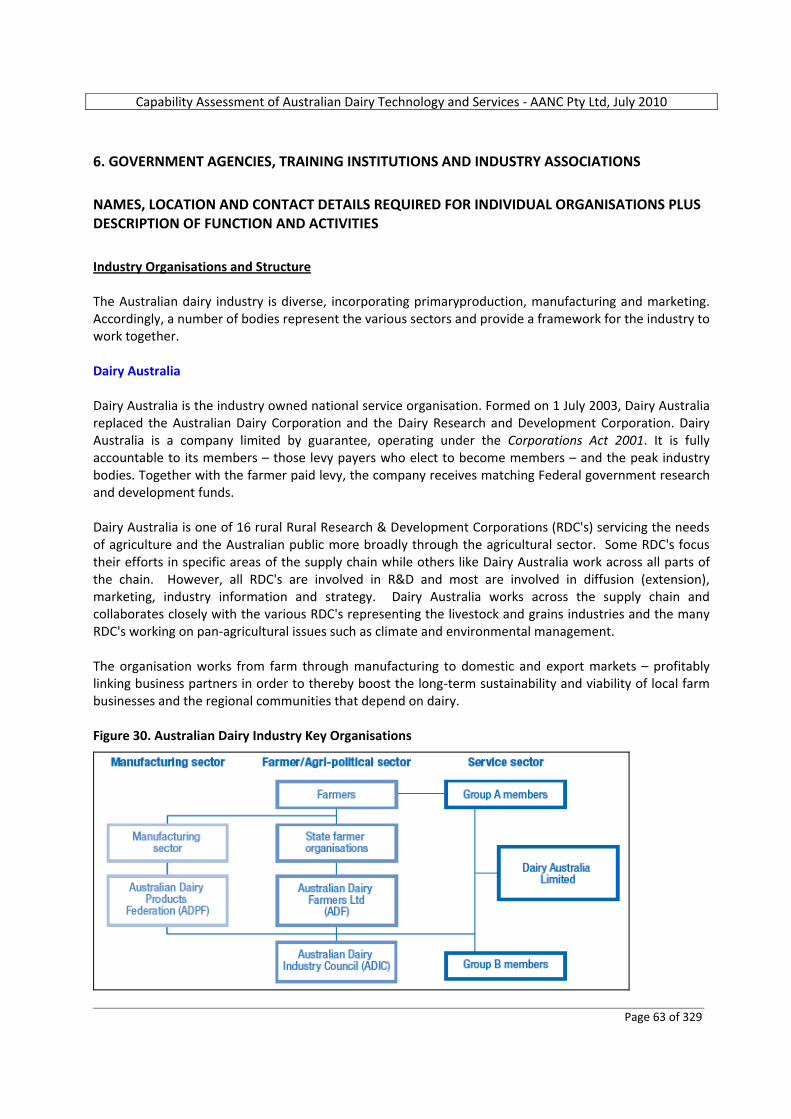

6. GOVERNMENT AGENCIES, TRAINING INSTITUTIONS AND INDUSTRY ASSOCIATIONS ......................... 63

Names, location and contact details required for individual organisations plus description of function and activities. 63

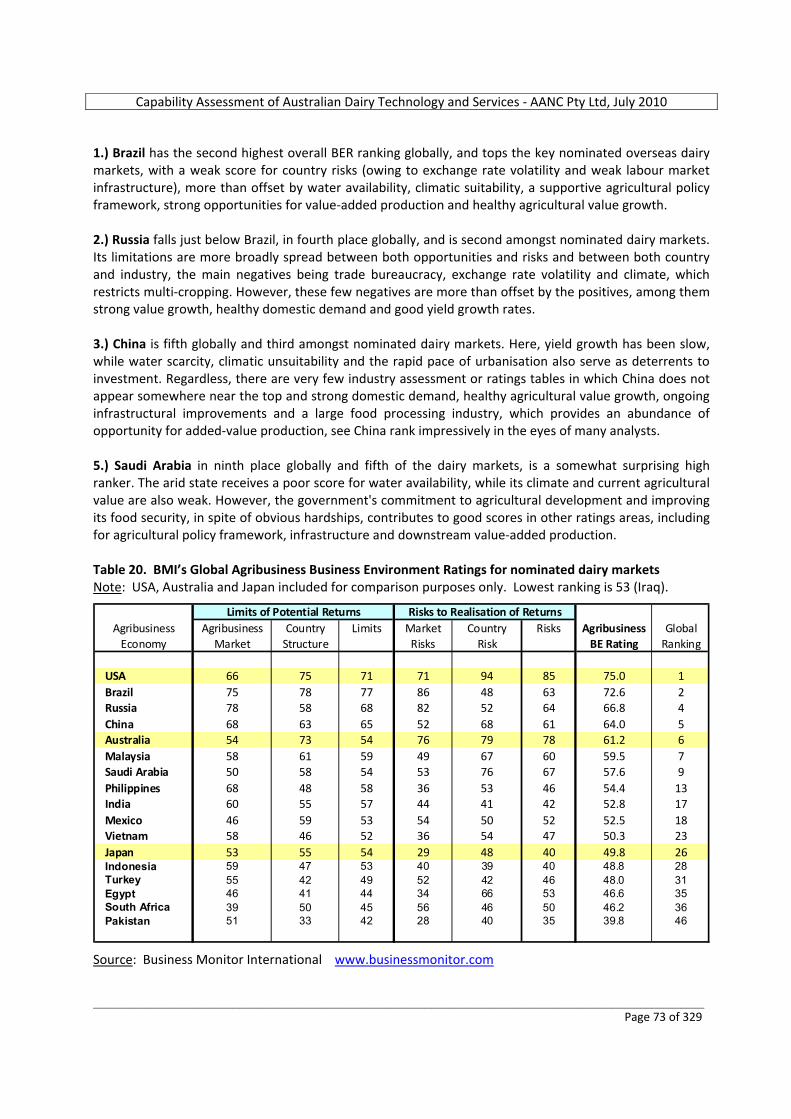

7. POTENTIAL IN NOMINATED OVERSEAS MARKETS ............................................................................................ 70

FINAL RANKING OF NOMINATED COUNTRIES AS POTENTIAL NEW MARKETS FOR AUSTRALIAN DAIRY TECHNOLOGY AND SERVICES ......................................................................................................................... 71

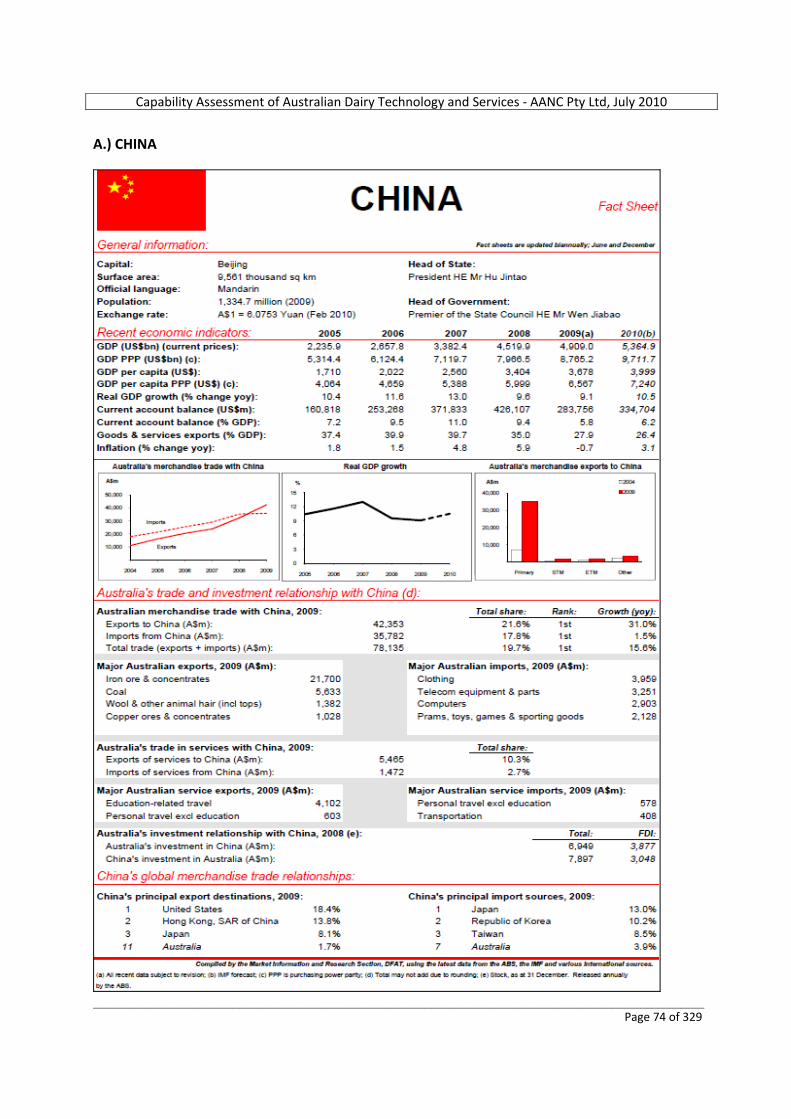

A.) CHINA ............................................................................................................................................................................... 74

B.) RUSSIAN FEDERATION.............................................................................................................................................. 109

C.) THE PHILIPPINES........................................................................................................................................................ 136

D.) BRAZIL ........................................................................................................................................................................... 160

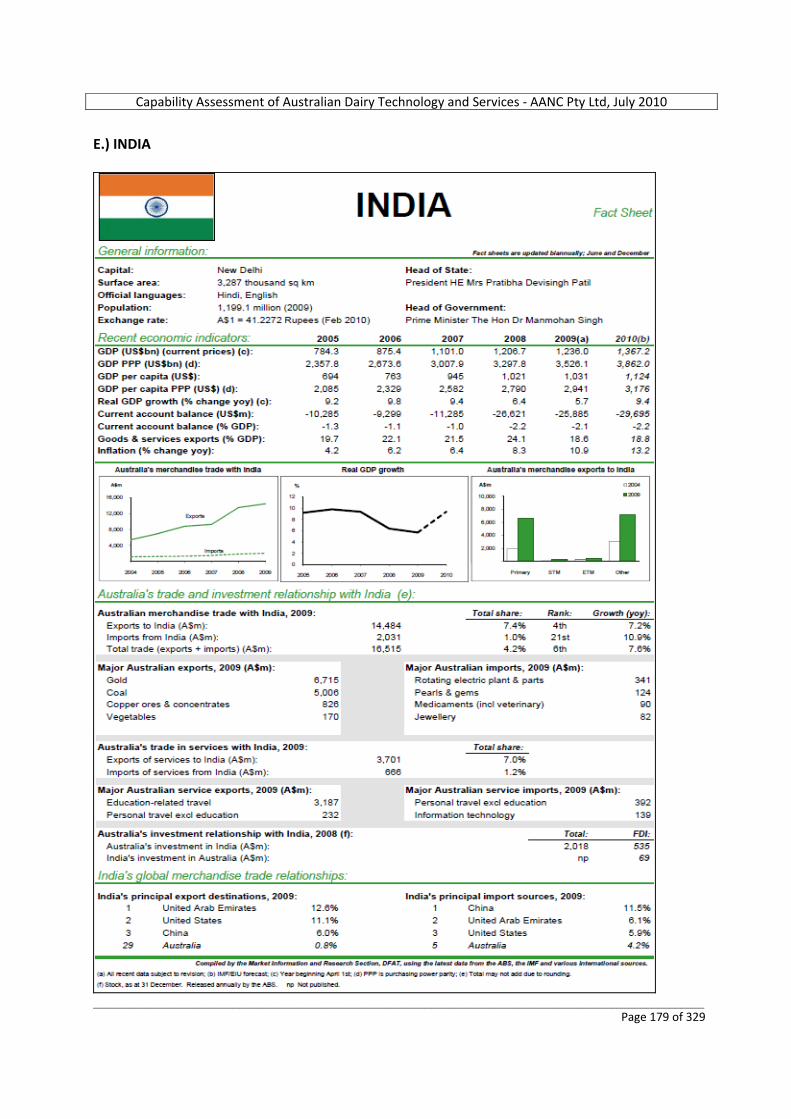

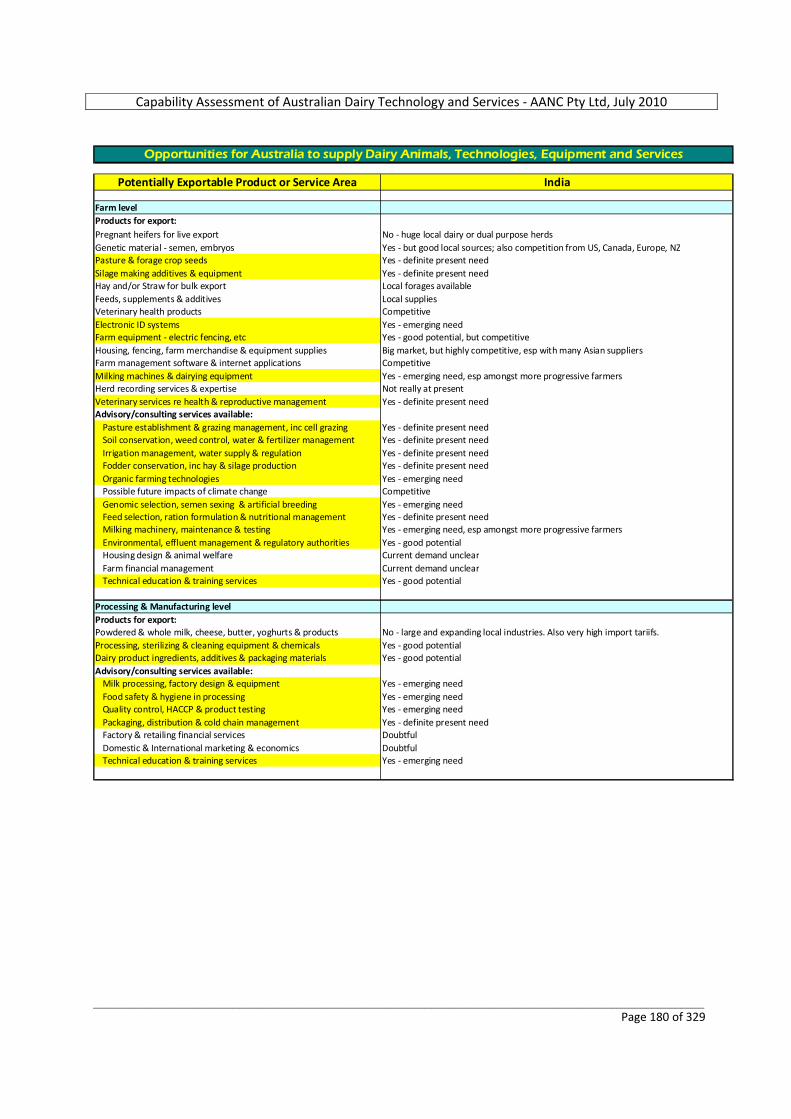

E.) INDIA............................................................................................................................................................................... 179

F.) INDONESIA .................................................................................................................................................................... 200

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 3 of 329

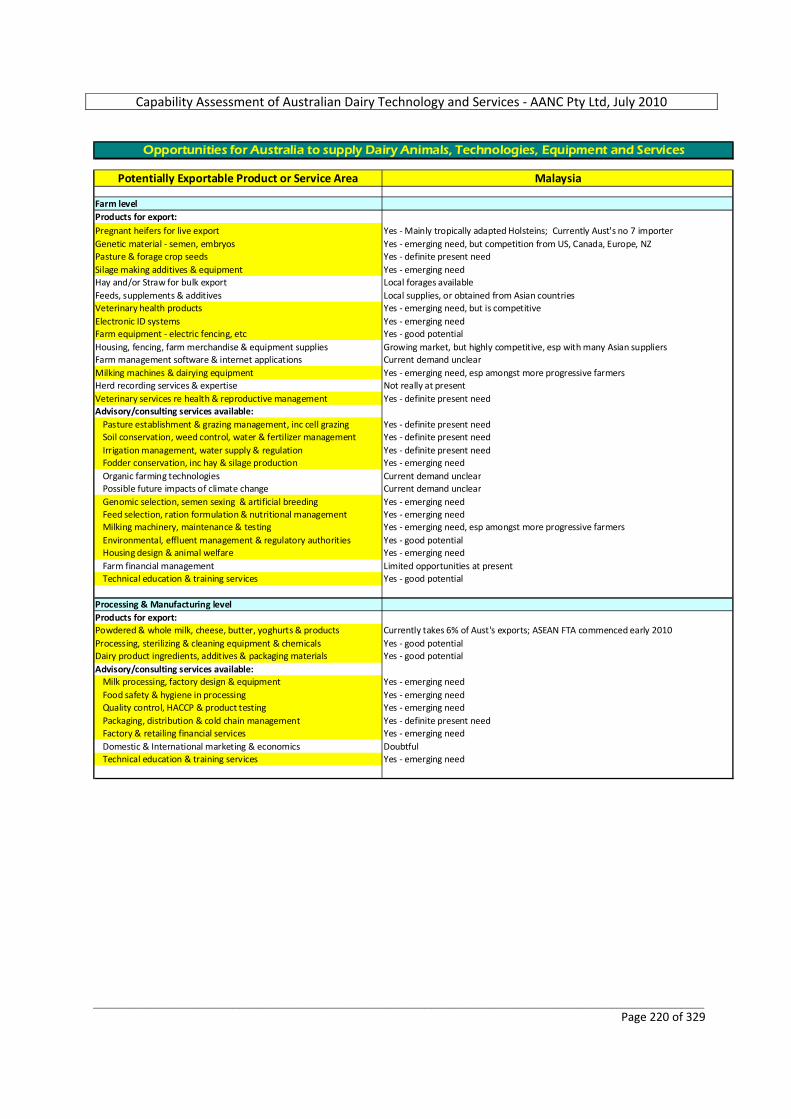

G.) MALAYSIA..................................................................................................................................................................... 219

H.) VIETNAM ....................................................................................................................................................................... 231

I.) PAKISTAN ....................................................................................................................................................................... 249

J.) MEXICO........................................................................................................................................................................... 264

K.) SAUDI ARABIA ............................................................................................................................................................. 279

L.) EGYPT............................................................................................................................................................................. 292

M.) SOUTH AFRICA ........................................................................................................................................................... 307

N.) TURKEY.......................................................................................................................................................................... 322

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 4 of 329

LIST OF ACRONYMS ABS Australian Bureau of Statistics ABARE Australian Bureau of Agriculture & Resource Economics ACIAR Australian Centre for International Agricultural Research ADIC Australian Dairy Industry Council ADF Australian Dairy Farmers Ltd ADG Average daily gain AFIA Australian Fodder Industry Association AFTA ASEAN Free Trade Area AMF Anhydrous milk fat ASEAN Association of South East Asian Nations BMI Business Monitor International BMP Butter milk powder CAGR Compound annual growth rate COGS Cost of goods sold CAP European Union’s Common Agricultural Policy CSIRO Commonwealth Scientific and Industrial Research Organisation DA Dairy Australia DAFF Department of Agriculture, Fisheries & Forestry DDGS Dried distillers grains plus solubles DIAA Dairy Industry Association of Australia EU European Union EU‐27 European Union 27 member states (additional 12 accession countries since May 2004) FAO Food and Agriculture Organisation of the United Nations FCR Food conversion ratio FDI Foreign direct investment FOB Free on board FTA Free Trade Agreement GDP Gross domestic product HACCP Hazard analysis critical control point IFC International Finance Corporation IMF International Monetary Fund LW Live weight MFN Most favoured nation MLA Meat & Livestock Australia MT Metric tonnes MMT Million metric tonnes NDM Nonfat dry milk OECD Organisation for Economic Cooperation and Development SMP Skim milk powder SNF Solids non fat SWOT Strengths, weaknesses, opportunities, threats WB World Bank WMP Whole milk powder WTO World Trade Organisation UNDP United Nations Development Project UHT Ultra high temperature USDA United States Department of Agriculture VAT Value added tax

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 5 of 329

EXECUTIVE SUMMARY Mapping of the Supply Chain for Australia’s Dairy Technology and Services This capability assessment of Australian dairy technology and services, as commissioned by Austrade, began with an overview of the Australian Dairy Industry and a detailed mapping of key participants in the supply chain, as it currently exists within this country. Industry associations, research bodies, Government agencies, academic and technical training institutions were included in this listing, which extended from the dairy farm‐gate level up to manufacturing and retail. This work was presented as spreadsheets in an Excel file, which forms an addendum to this report. Current Status of the Australian Dairy Industry The dairy industry is Australia's third largest rural industry, and is therefore a major economic contributor to many regional communities throughout the country. The industry is also Australia’s largest processed food exporter, and has achieved a ten‐fold growth in exports since the 1980’s. The Australian dairy industry is now one of the world’s most efficient producers of high quality dairy products. According to the industry’s peak body, Dairy Australia, the dairy industry in 2008/09 consisted of approximately 8,000 dairy farms, 1.6 million cows in milk averaging 5,750 litres per cow per year, and a direct employment of more than 60,000 people on farms and in local manufacturing and distribution. Many more downstream jobs and productive investments are created by the economic activity of the industry, with ABARE estimating a regional economic multiplier of 2.5. The industry has a farm‐gate value of $4 billion, and a wholesale value‐added worth of $12 billion. Over two‐thirds of the 9.4 billion litres of milk produced in 2008/09 was produced in Victoria, 10 % in New South Wales and 7 % in Tasmania. Just over half the milk produced in Australia during 2008/09 was consumed by the domestic market, the remainder being exported as either drinking milk or manufactured products. Australia’s key export markets for dairy products in 2008/09 were Japan, Singapore, China and the Philippines. A reduction in dairy farm numbers since deregulation of the industry in the 1990’s has been more than offset by an increase in average herd size and productivity, the effect being that the volume of milk produced by the 8,000 farms in 2009 is over 70 % above the volume produced by the 22,000 farms in 1980. Australia’s global position regarding Milk Production, Live Exports, and Dairy Food Exports In terms of numbers of cows in milk, Australia with 1.6 million falls well short of India (38.5 million) and Brazil (17.6 million), while New Zealand has 4.5 million. Regarding total milk production, Australia’s 9.5 billion litres falls well below the USA’s world leading 85 billion litres, followed by India with 48 billion, while New Zealand produces 17 billion litres per year. However, yields per cow per year in Australia at 5,750 litres compare favourably with many countries including New Zealand (3,800 litres) and Russia (3,470 litres), although they fall well short of the USA on 9,500 and Canada on 8,400 litres. Australia has long held an enviable global position as the world’s largest live exporter of beef and dairy cattle and sheep. Not only can we supply the numbers, but we can also supply the healthiest animals in the world, with an extremely valuable ‘disease free’ status with regards the most serious exotic diseases of livestock, including the greatly feared FMD, BSE and TB. During 2009, Australia live exported nearly 33,000 dairy cattle (mainly pregnant heifers) to China, and over 16,000 head to Indonesia, these numbers far exceeding our main competitor, New Zealand, or any other live exporting country.

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 6 of 329

With regards to dairy food product exports, approximately 45% of total Australian production was exported in 2008/09, with our key markets being SE Asia (worth $890 million), other parts of Asia ($618 million), and Japan ($554 million). On a global basis, Australia’s exports comprise 9% of total world trade in dairy products, with the front runners here being the European Union on 31%, New Zealand 28% and the USA with 10%. Exports of Hay and Dairy Machinery Australia is one of the world’s largest exporters of hay and straw, having peaked in 2005/06 with the shipping of almost 700,000 tonnes of mainly cereal hay (92%) and straw (8%) to mostly Asian countries, with Japan in fact completely dominating the market by taking 85%. South Korea and Taiwan took most of the remainder. Japan uses large volumes of imported hay for its 840,000 dairy cows, which happen to be the world’s second highest producers at 9,350 litres per cow per year, just under the USA. Australia does have a growing export market for ‘Milking Machines and Dairy Machinery’, although with severe competition from traditional manufacturers in Europe, the USA, Canada and Scandinavian countries, our share of world trade was only 0.9% in 2008. China was our main customer for these items. Key areas of Australia’s Dairy Industry Expertise Throughout this study, 14 key areas of Australian dairy industry expertise were identified which would appear to be highly competitive at a global level in terms of the supply of live animals, technologies, equipment, dairy products and/or advisory or consulting services. These areas are summarized below. 1.) Reputation as a premium supplier of whole milk, milk powder, butter, cheese, UHT lines and other dairy

products. 2.) World leaders in the sourcing and live export by ship and air of ‘disease free’ pregnant dairy heifers, with

lesser numbers of mature cows and bulls. 3.) Expertise in soil conservation, efficiency of water useage and proficiency in irrigation management. 4.) Proficiency in pasture & grazing management, weed control, fodder conservation and ruminant nutrition. 5.) Expertise in hay making. 6.) Expertise in livestock genetic research, breed development and reproductive physiology, with particular

specialist experience in tropical environments. 7.) Expertise in electronic animal identification, as well as live animal and food product traceability systems. 8.) Expertise in modern dairy farming techniques, such as semi‐automated dairy cow management systems,

high tech milking machinery and equipment (such as robotic milking machines and transponder‐based feeding systems), modern approaches to internal climate control and effluent management, solar water pumping, GPS laser leveling, electric fencing, web cam and remote scanning telemetry, water bore management, weed control, and natural resource management.

9.) Efficiency of labour usage in dairy farming. 10.) Good knowledge of environmental regulation, including effluent & compost management. 11.) Good knowledge of organic and biodynamic farming systems. 12.) Good knowledge of food safety & hygiene standards, milk processing, UHT methodolgy and shelf‐life

preservation techniques. 13.) High level skills in software development, for farming applications, dairy herd improvement schemes, milk

factory and sales management, inventory control, environmental management, etc. 14.) Highly regarded standards of teaching and higher education.

Composition of future Austrade Trade Missions to Developing Dairy Markets The supply chain mapping exercise performed as a key component of this industry capability assessment can be used as a guide to the composition of future Austrade Trade Missions to foreign developing countries which

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 7 of 329

have expressed an interest in establishing ‘greenfields’ integrated dairy operations. Members of such a trade mission could be individuals drawn from the following specialist categories.

Farm level • Consultants ‐ Dairy Farm design & layout • Consultants ‐ Pastures, Crops & Farm Management • Fencing requirements • Pasture & forage crop seeds • Pasture & forage crop protection • Silage making additives & equipment • Farm sheds, silos, steel yards, etc • Farm merchandise & equipment • Milking machinery, maintenance & testing • Irrigation management, water supply & regulation • Environmental, effluent mgt & regulatory authorities • Live Export Agents • Australian Livestock Export Corporation • Artificial Breeding ‐ AI, embryos, genomic selection • Dairy Breed Societies ‐ Holstein Australia; Jersey Australia • Consultants ‐ Health, Nutrition & Herd Management • (ASSUME ALL FEEDS SOURCED LOCALLY, with micro‐additives imported as required) • Veterinary health products • Veterinary services re health & reproductive management • Herd Management Software

Processing & Manufacturing level • Dairy product manufacturing consultants/trainers • Equipment suppliers • Packaging suppliers • Engineering consultants • Refrigeration/cold chain specialists • Dairy foods sales & marketing consultants

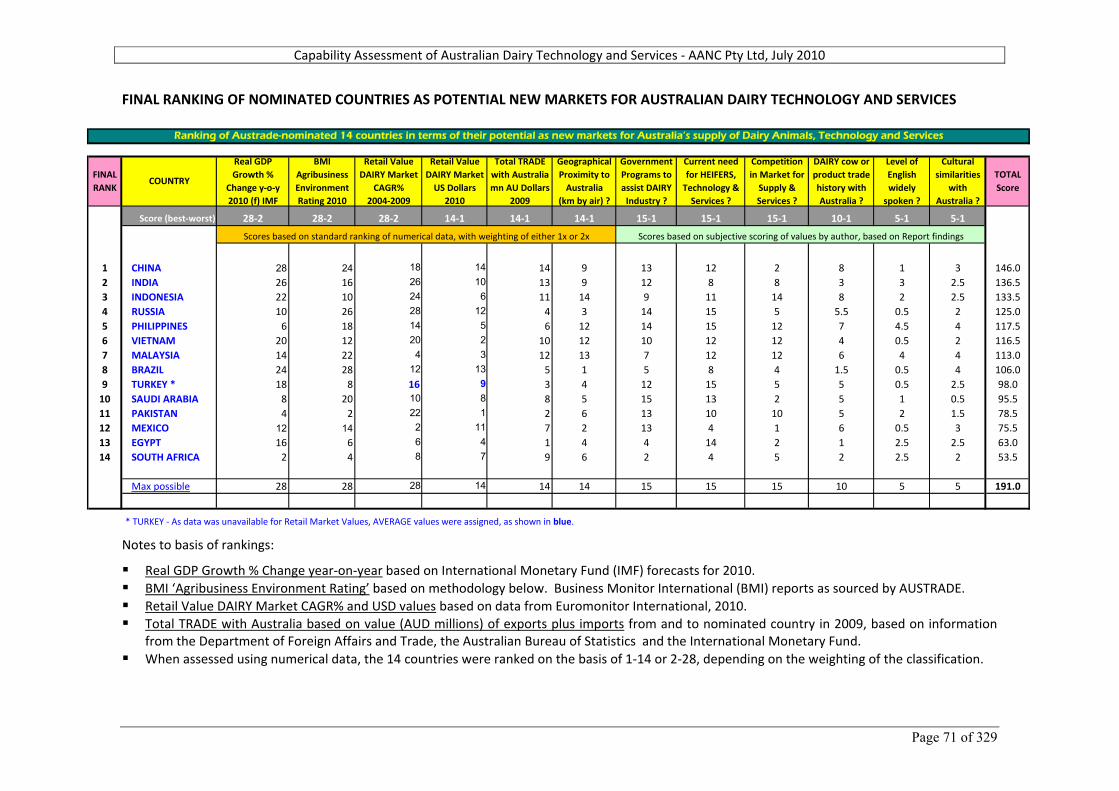

Potential for outward investment by Australian agribusiness and dairy product exporters Key factors for consideration when examining the potential for outward investment into overseas markets by Australian dairy product exporters and other agribusiness investors were discussed as a secondary component of this report. Potential held by 14 nominated Overseas Markets for Australian Dairy Live Animals, Technology and Services Finally, a large desktop study was undertaken into the potential held by 13 overseas markets nominated by Austrade as showing good potential for the Australian dairy industry. Turkey was later added to this list. It was not possible in the time allocated to fully assess all aspects of each of these countries, but worthwhile indicative data was obtained and presented, with the assistance of Austrade Australian and offshore office personnel. Based on various country specific agricultural sector and dairy industry factors, as well as broader country specific economic, business, political, trade history, geographic and cultural factors, a comprehensive matrix was constructed by which all 14 countries were assigned scores for 12 different categories, most of which were based on solid economic data, others on educated subjective estimates by the author following the desktop study. Business Monitor International’s ‘Global Agribusiness Environment Ratings’ formed one of the 12 categories that were ultimately used to produce a final total score for each country. These scores were then ranked to form an ordered listing of countries showing the most potential for Australian exporters of dairy live animals, technology and services. This list is shown below.

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 8 of 329

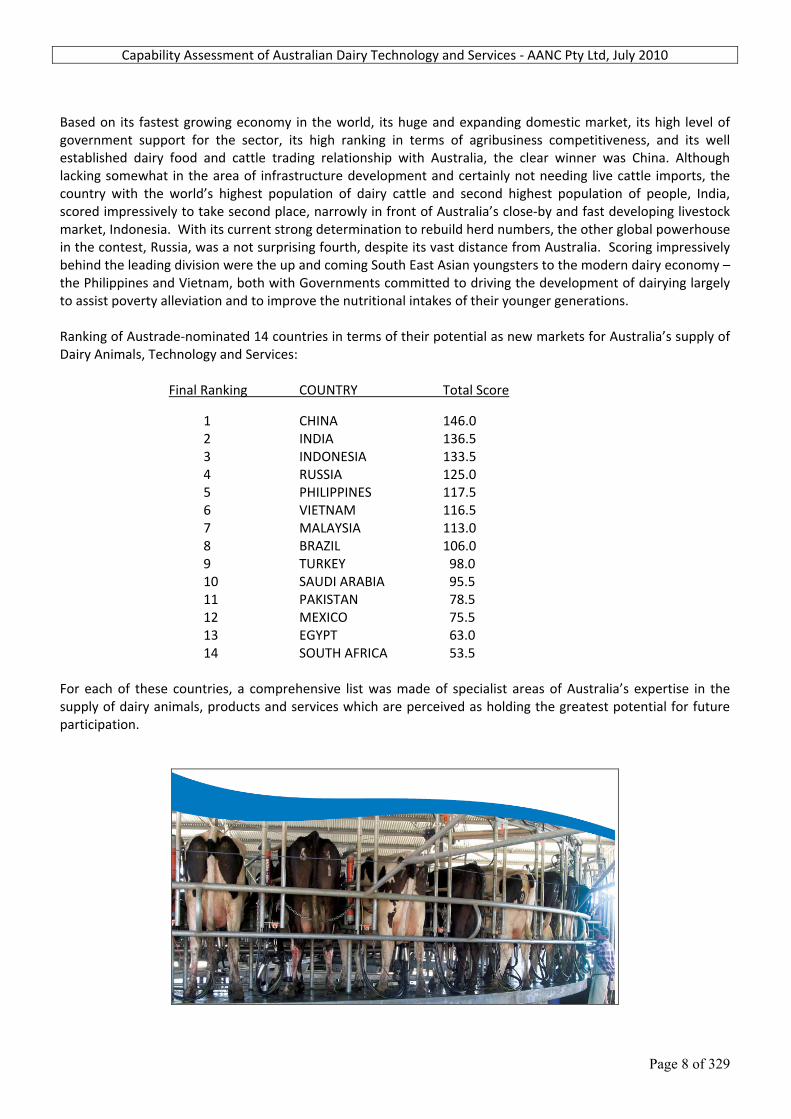

Based on its fastest growing economy in the world, its huge and expanding domestic market, its high level of government support for the sector, its high ranking in terms of agribusiness competitiveness, and its well established dairy food and cattle trading relationship with Australia, the clear winner was China. Although lacking somewhat in the area of infrastructure development and certainly not needing live cattle imports, the country with the world’s highest population of dairy cattle and second highest population of people, India, scored impressively to take second place, narrowly in front of Australia’s close‐by and fast developing livestock market, Indonesia. With its current strong determination to rebuild herd numbers, the other global powerhouse in the contest, Russia, was a not surprising fourth, despite its vast distance from Australia. Scoring impressively behind the leading division were the up and coming South East Asian youngsters to the modern dairy economy – the Philippines and Vietnam, both with Governments committed to driving the development of dairying largely to assist poverty alleviation and to improve the nutritional intakes of their younger generations. Ranking of Austrade‐nominated 14 countries in terms of their potential as new markets for Australia’s supply of Dairy Animals, Technology and Services:

Final Ranking COUNTRY Total Score

1 CHINA 146.0 2 INDIA 136.5 3 INDONESIA 133.5 4 RUSSIA 125.0 5 PHILIPPINES 117.5

6 VIETNAM 116.5 7 MALAYSIA 113.0 8 BRAZIL 106.0 9 TURKEY 98.0 10 SAUDI ARABIA 95.5 11 PAKISTAN 78.5 12 MEXICO 75.5 13 EGYPT 63.0 14 SOUTH AFRICA 53.5

For each of these countries, a comprehensive list was made of specialist areas of Australia’s expertise in the supply of dairy animals, products and services which are perceived as holding the greatest potential for future participation.

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 9 of 329

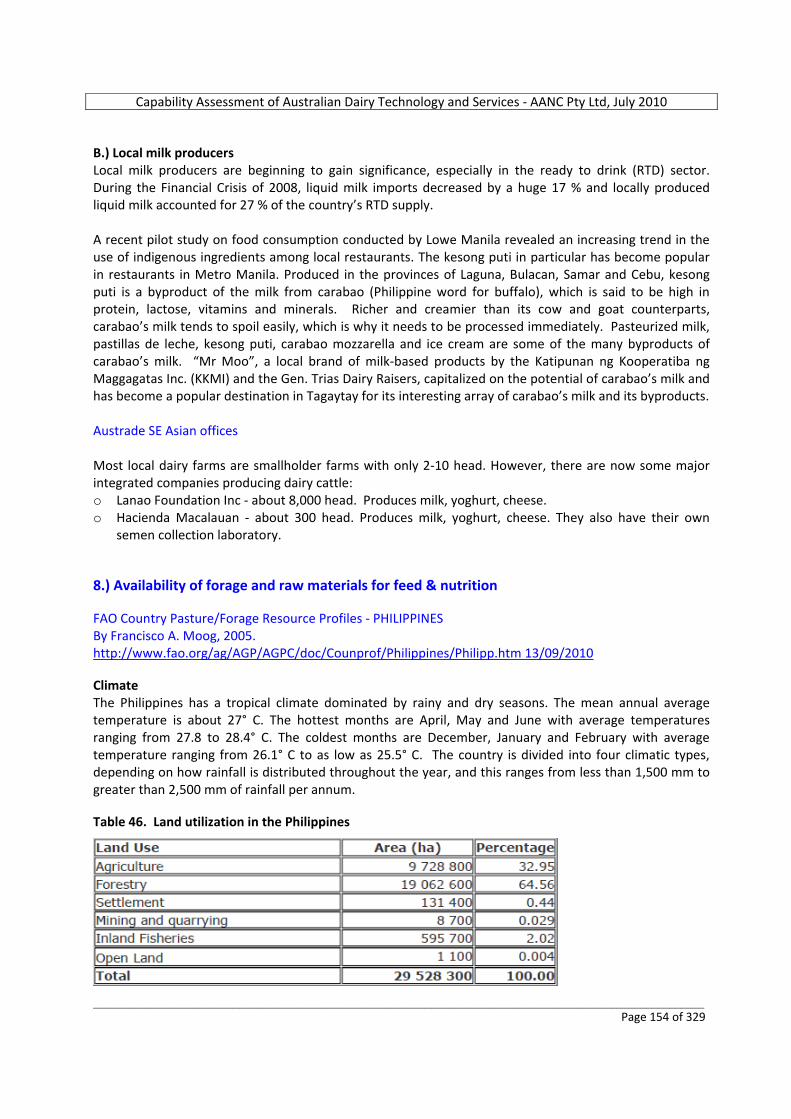

1. OVERVIEW OF THE AUSTRALIAN DAIRY INDUSTRY o The dairy industry is Australia's third largest rural industry, and is therefore a major economic contributor to

many regional communities throughout the country. o The dairy industry is Australia’s largest processed food exporter. o The dairy industry in Australia is one of the world’s most efficient producers of high quality dairy products. o The dairy industry has achieved a ten‐fold growth in exports since the 1980’s.

The Australian dairy industry consists of about 8,000 dairy farms and directly employs more than 60,000 people, on farms and in local manufacturing and distribution. Many more downstream jobs and productive investments are created by the economic activity of the industry, with ABARE estimating a regional economic multiplier of 2.5. The industry has a farm‐gate value of $4 billion. A reduction in dairy farm numbers since deregulation of the industry has been more than offset by an increase in average herd size and productivity, the effect being that the volume of milk produced by the 8,000 farms in 2009 is over 70 per cent above the volume produced by the 22,000 farms in 1980. Over two‐thirds of the 9.4 billion litres of milk produced in 2008‐09 was produced in Victoria, 10 per cent in New South Wales and 7 per cent in Tasmania. Just over half the milk produced in Australia during 2008‐09 was consumed by the domestic market; the remainder being exported as either drinking milk or manufactured products. Table 1. Snapshot of Australia’s Domestic Dairy Industry (2008/09)

National Dairy Herd • 1.6 million cows (in milk) Average Herd Size • 200 cows

Number of Dairy Farms • 8,000 farms Milk Production • 9,388 million litres

Average Annual Milk Production Per Cow • 5,750 litres Dairy ‐ Australia's 3rd Largest Rural Industry • $4.0 billion value at farm‐gate

Dairy ‐ Major Value‐Added Food Industry • $12.0 billion value at wholesale

Milk Utilisation

• Cheese 33 per cent Drinking milk 24 per cent SMP/butter 25 per cent WMP 12 per cent Casein/butter 4 per cent Other 2 per cent

Production Of Main Commodities (Tonnes) • Milk Powders 359,600

Cheese 342,000 Butter (CBE) 148,500

Dairy ‐ Major Export Industry • $2.9 billion

9 per cent of world dairy trade Percentage Of Australian Milk Production Exported • 45 per cent

Major Markets For Australian Dairy Products (Tonnes)

• Australia 2,604,000 (including 2,178,600 of drinking milk) Japan 106,000 Singapore 80,000 China 61,269 Philippines 50,000

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 10 of 329

National Dairy Herd • 1.6 million cows (in milk)

Per Capita Consumption • Drinking milk 104 Ltr

Cheese 12 kgs

Dairy Industry Workforce • Direct employment of approximately 40,000

people ABARE estimates a regional economic multiplier of 2.5 from the

dairy industry

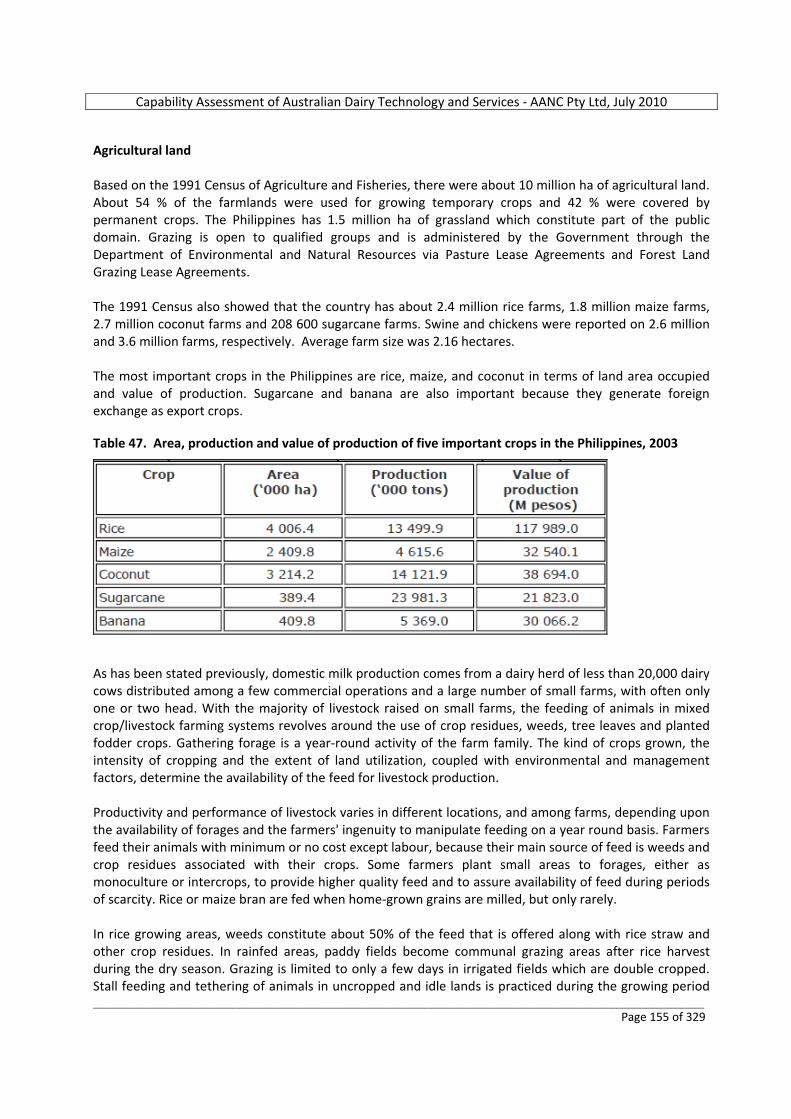

Source: Dairy Australia: Australian Dairy Industry in Focus 2009 Australia’s climate and natural resources are generally favourable to dairying and allow the industry to be predominantly pasture‐based, with approximately 75% of cattle feed requirements coming from grazing years with ‘traditional’ seasonal conditions. This results in efficient, low cost, high‐quality milk production. Most dairy production regions are located in coastal areas, where pasture growth generally depends on natural rainfall. Nevertheless, the inland irrigation schemes in northern Victoria and southern NSW are significant, accounting for around a quarter of national milk production. Feedlot‐based dairying remains the exception in Australia, although the use of supplementary feed – grains, hay and silage – is widespread and has increased significantly in recent seasons as farmers have had to adapt to drier conditions in many dairying regions. According to Dairy Australia’s 2009 National Dairy Farmer Survey, some 93% of dairy farms fed an average of 1.5 tonnes of grain, grain mixes or feed concentrates per cow during the 2008/09 season. Owner‐operated farms dominate the Australian dairy industry. Corporate farms make up just 2% of the total, with share farmers involved in 18% of local farms in 2007/08. The number of dairy farms has halved over the past two decades – to 7,920 in 2009. Falling farm numbers reflect a long‐term trend observed in agriculture around the world, as reduced price support and changing business practices have encouraged a shift to larger, more efficient operating systems. The average herd size has increased from 85 cows in 1980 to over 200 in 2008/09. The dominant dairy breed in Australia is the Holstein Friesian, accounting for approximately 67% of all dairy cattle, followed by the Jersey at more than 10% and then the Holstein/Jersey cross. More than 85% of dairy farmers use artificial insemination and access some of the best genetic material in the world. Improvements in herd genetics, pasture management practices and supplementary feeding regimes have seen the average yield per cow increase from 2,850 litres a year to around 5,750 litres over the past three decades. Table 2 below details the increase in productivity per cow on a state by state basis since 1980. However, in trying to ascertain the most productive dairying regions, figures such as those below are confusing in that the level of grain, concentrate, hay or silage supplementation of cows is not indicated, nor the quality of pasture on offer each year – as determined largely by seasonal rainfall. In general, productivity has increased similarly across all six states. Figure 1 below illustrates quite dramatically how the large bulk of milk produced in Australia is now produced in Victoria, with that state currently producing over 60 % of the nation’s total. The reason for this is largely due to the more favourable climatic and pastoral conditions for Holstein Friesian dominated dairy herds in the cooler, temperate pasture regions of the lower south eastern corner of the country. Victoria also has extensive grain and hay producing areas, plus advanced cold chain milk collection and processing infrastructure, together with a vast array of dairy support industries and services.

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 11 of 329

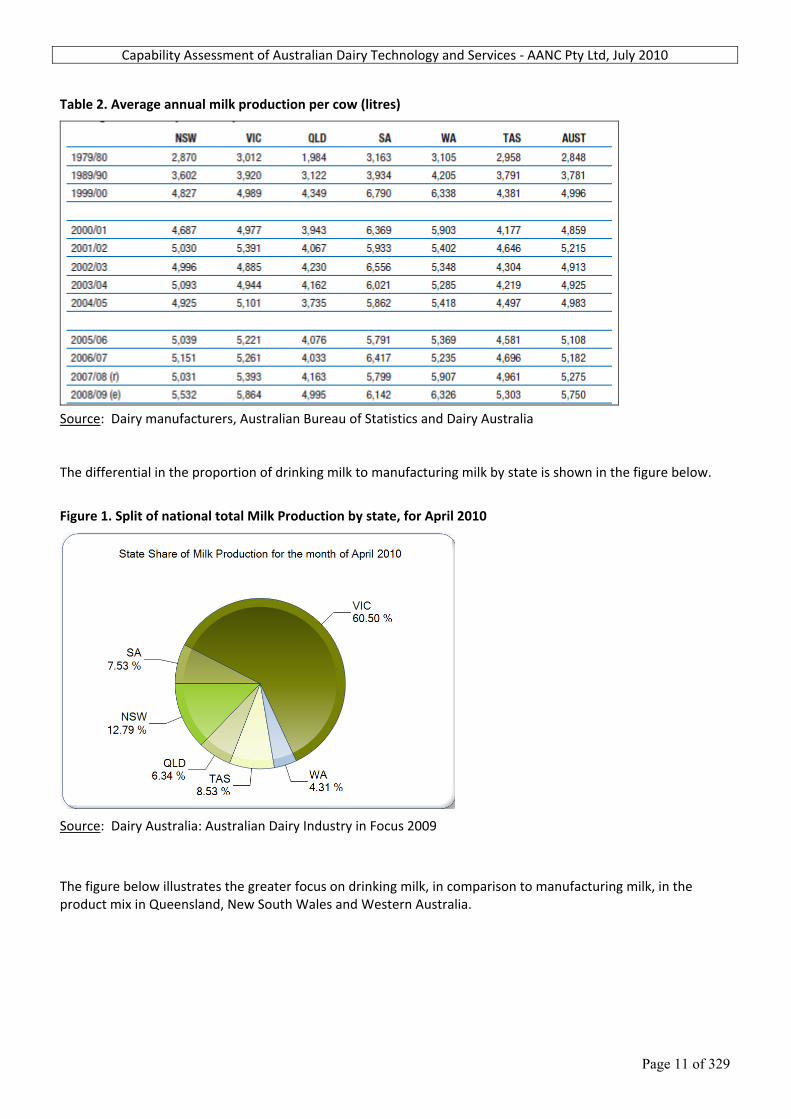

Table 2. Average annual milk production per cow (litres)

Source: Dairy manufacturers, Australian Bureau of Statistics and Dairy Australia The differential in the proportion of drinking milk to manufacturing milk by state is shown in the figure below.

Figure 1. Split of national total Milk Production by state, for April 2010

Source: Dairy Australia: Australian Dairy Industry in Focus 2009

The figure below illustrates the greater focus on drinking milk, in comparison to manufacturing milk, in the product mix in Queensland, New South Wales and Western Australia.

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 12 of 329

Figure 2. Drinking Milk vs Manufacturing Milk split by state, 2008/09

Source: Dairy Australia: Australian Dairy Industry in Focus 2009 The Australian dairy manufacturing sector is quite diverse and includes farmer‐owned co‐operatives, public, private and multi‐national companies. Co‐operatives no longer dominate the industry and now account for approximately 40% of Australia’s milk production. The largest is Murray Goulburn, accounting for some 37% of national milk output. Major multi‐national dairy companies have operated in the Australian dairy industry for many years and currently include Fonterra, National Foods and Parmalat. The former Bonlac cooperative is now owned by Fonterra, and the Dairy Farmers Group has been acquired by National Foods. Fonterra (20 %),together with Murray Goulburn (the largest remaining farmer owned cooperative, supplying 37 % of Australia's milk) are the prominent market players in the manufacturing milk market, as shown in Figure 3. Figure 3. Market share of total Milk volume by Australian manufacturers, 2008/09

Manufacturer's Share of Total Milk Volume, May 2010

United DP, 2%

Parmalat, 6%

Tatura, 3%

Warrnambool, 8%

National Foods, 15%

Fonterra, 20%

Murray Goulburn, 37%

Others, 8%

Source: Information derived from Dairy Australia The remaining milk produced in Australia is sold into the domestic drinking milk market which, like the manufacturing milk market, is dominated by two players – National Foods and Parmalat, as shown in Figure 4.

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 13 of 329

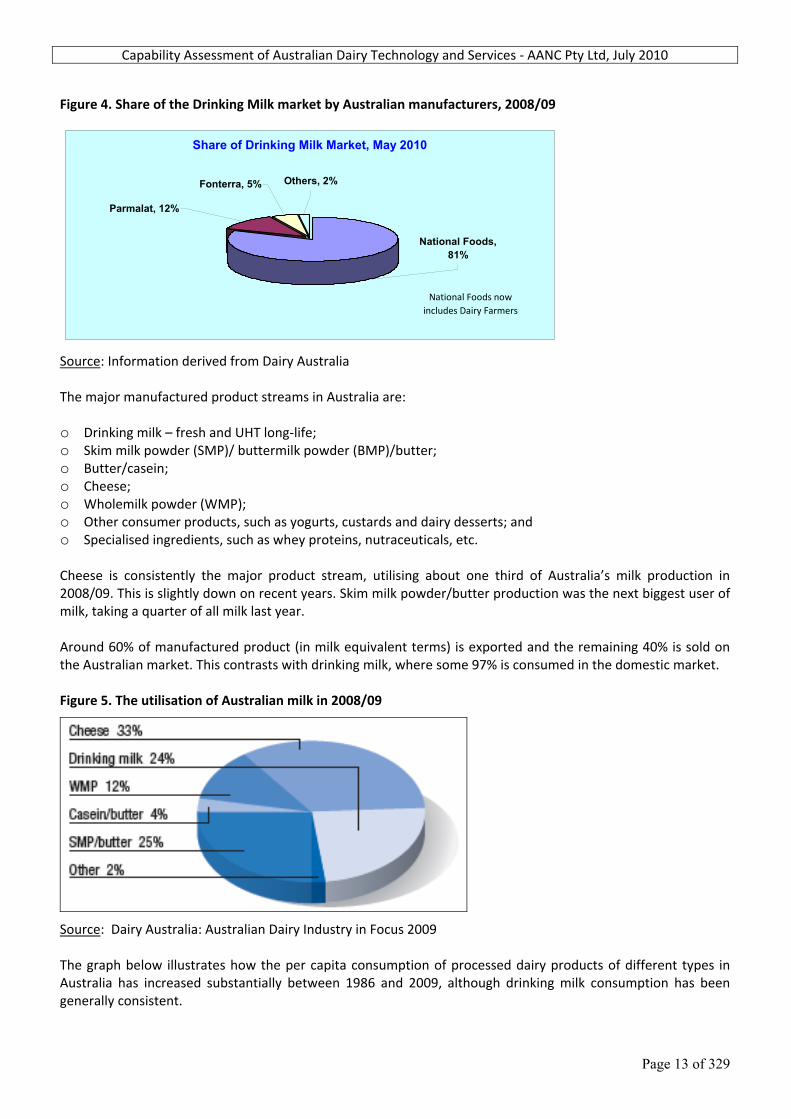

Figure 4. Share of the Drinking Milk market by Australian manufacturers, 2008/09

Share of Drinking Milk Market, May 2010

Parmalat, 12%

Fonterra, 5% Others, 2%

National Foods, 81%

National Foods now includes Dairy Farmers

Source: Information derived from Dairy Australia The major manufactured product streams in Australia are: o Drinking milk – fresh and UHT long‐life; o Skim milk powder (SMP)/ buttermilk powder (BMP)/butter; o Butter/casein; o Cheese; o Wholemilk powder (WMP); o Other consumer products, such as yogurts, custards and dairy desserts; and o Specialised ingredients, such as whey proteins, nutraceuticals, etc. Cheese is consistently the major product stream, utilising about one third of Australia’s milk production in 2008/09. This is slightly down on recent years. Skim milk powder/butter production was the next biggest user of milk, taking a quarter of all milk last year. Around 60% of manufactured product (in milk equivalent terms) is exported and the remaining 40% is sold on the Australian market. This contrasts with drinking milk, where some 97% is consumed in the domestic market. Figure 5. The utilisation of Australian milk in 2008/09

Source: Dairy Australia: Australian Dairy Industry in Focus 2009 The graph below illustrates how the per capita consumption of processed dairy products of different types in Australia has increased substantially between 1986 and 2009, although drinking milk consumption has been generally consistent.

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 14 of 329

Figure 6. Per capita consumption of dairy products in Australia (litres or kg per head per year)

Source: Dairy Australia: Australian Dairy Industry in Focus 2009

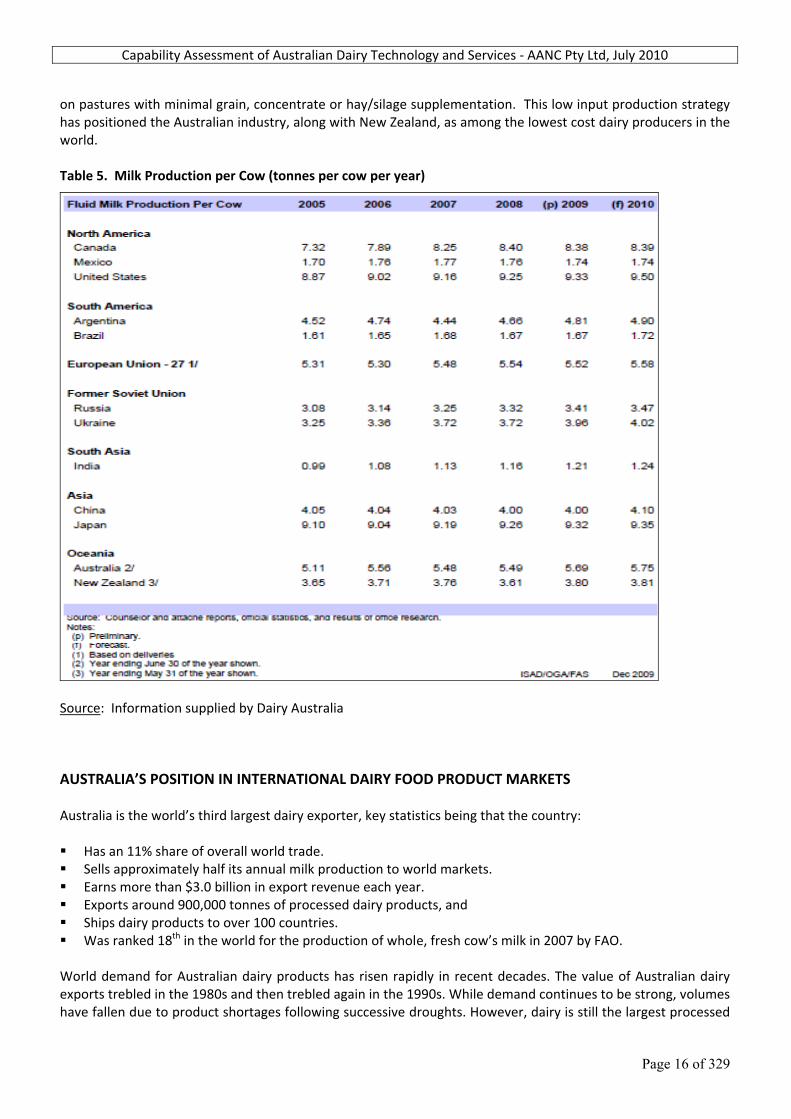

1.1 AUSTRALIA’S POSITION AS SUPPLIER TO THE GLOBAL MARKET – WHERE WE FIT IN PRODUCTION AND SUPPLY Portrayals of Australia’s position as a world competitor in terms of total milk production, herd numbers, and milk yield per cow, are given in the tables below. (Information supplied by Dairy Australia.) Table 3. Cow’s Milk Production for Selected Countries (‘000 tonnes)

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 15 of 329

From the above, it is apparent that according to 2010 forecasts, the world’s leading milk producers are currently: 1.) The expanded EU, 2.) The USA, 3.) India, 4.) Russia, 5.) China, 6.) Brazil. It is worth noting that New Zealand is forecast to produce almost twice the milk volume of Australia in 2010. The table below highlights that New Zealand has roughly three times the number of dairy cows as has Australia. It also shows the huge numbers of cows in India and Brazil, relative to their total production levels, which is explained by their generally low outputs per cow, commonly due to poor nutrition levels and the fact that calves are often reared on these cows whilst being milked. Table 4. Cow Numbers (cows in milk) for Selected Countries (‘000 head)

Source: Information supplied by Dairy Australia Milk production per cow is shown in Table 5 below, but from this data, the Australian dairy herd appears to have a lower level of production than the US herd ‐ typically 5,000 to 6,000 litres per 300 day lactation compared to a US level of 8,000 to 10,000 litres. However, this is because most cows in Australia, unlike in the US, are grazed

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 16 of 329

on pastures with minimal grain, concentrate or hay/silage supplementation. This low input production strategy has positioned the Australian industry, along with New Zealand, as among the lowest cost dairy producers in the world. Table 5. Milk Production per Cow (tonnes per cow per year)

Source: Information supplied by Dairy Australia

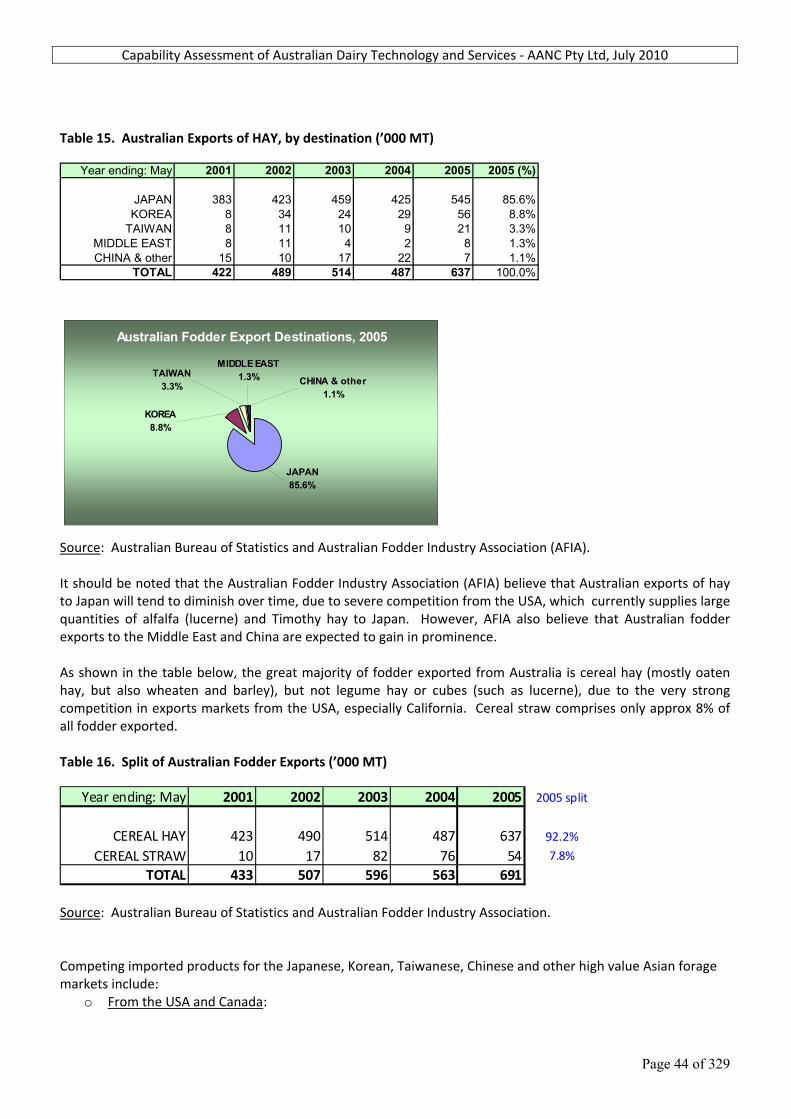

AUSTRALIA’S POSITION IN INTERNATIONAL DAIRY FOOD PRODUCT MARKETS Australia is the world’s third largest dairy exporter, key statistics being that the country: Has an 11% share of overall world trade. Sells approximately half its annual milk production to world markets. Earns more than $3.0 billion in export revenue each year. Exports around 900,000 tonnes of processed dairy products, and Ships dairy products to over 100 countries. Was ranked 18th in the world for the production of whole, fresh cow’s milk in 2007 by FAO.

World demand for Australian dairy products has risen rapidly in recent decades. The value of Australian dairy exports trebled in the 1980s and then trebled again in the 1990s. While demand continues to be strong, volumes have fallen due to product shortages following successive droughts. However, dairy is still the largest processed

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 17 of 329

food exporter in Australia, and there is significant potential for further expansion with a return to normal seasons, with Australian dairy producers being amongst the most efficient in the world.

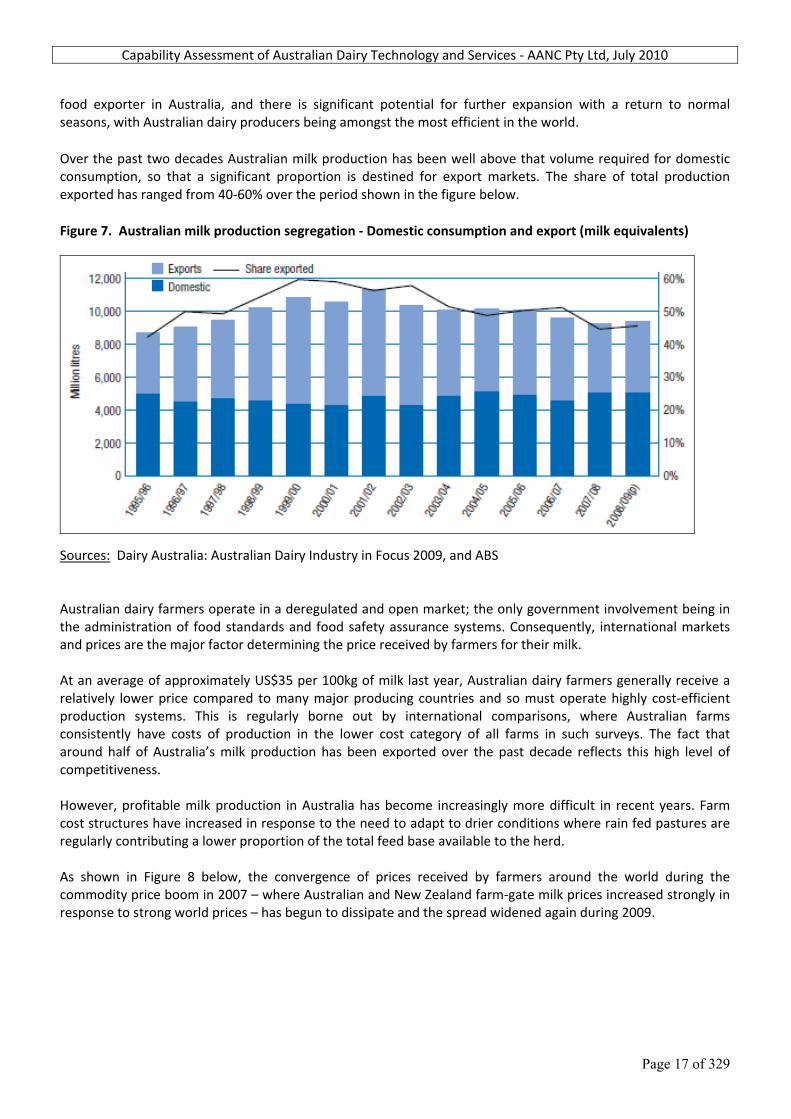

Over the past two decades Australian milk production has been well above that volume required for domestic consumption, so that a significant proportion is destined for export markets. The share of total production exported has ranged from 40‐60% over the period shown in the figure below.

Figure 7. Australian milk production segregation ‐ Domestic consumption and export (milk equivalents)

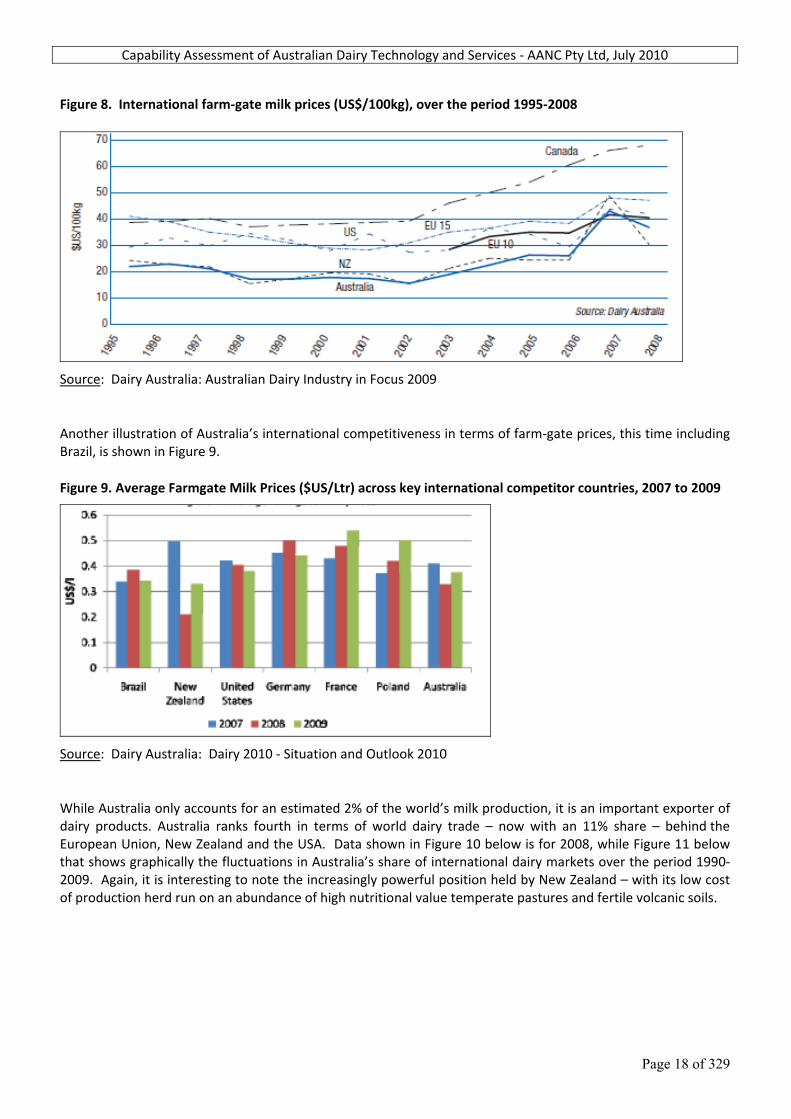

Sources: Dairy Australia: Australian Dairy Industry in Focus 2009, and ABS Australian dairy farmers operate in a deregulated and open market; the only government involvement being in the administration of food standards and food safety assurance systems. Consequently, international markets and prices are the major factor determining the price received by farmers for their milk. At an average of approximately US$35 per 100kg of milk last year, Australian dairy farmers generally receive a relatively lower price compared to many major producing countries and so must operate highly cost‐efficient production systems. This is regularly borne out by international comparisons, where Australian farms consistently have costs of production in the lower cost category of all farms in such surveys. The fact that around half of Australia’s milk production has been exported over the past decade reflects this high level of competitiveness. However, profitable milk production in Australia has become increasingly more difficult in recent years. Farm cost structures have increased in response to the need to adapt to drier conditions where rain fed pastures are regularly contributing a lower proportion of the total feed base available to the herd. As shown in Figure 8 below, the convergence of prices received by farmers around the world during the commodity price boom in 2007 – where Australian and New Zealand farm‐gate milk prices increased strongly in response to strong world prices – has begun to dissipate and the spread widened again during 2009.

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 18 of 329

Figure 8. International farm‐gate milk prices (US$/100kg), over the period 1995‐2008

Source: Dairy Australia: Australian Dairy Industry in Focus 2009

Another illustration of Australia’s international competitiveness in terms of farm‐gate prices, this time including Brazil, is shown in Figure 9.

Figure 9. Average Farmgate Milk Prices ($US/Ltr) across key international competitor countries, 2007 to 2009

Source: Dairy Australia: Dairy 2010 ‐ Situation and Outlook 2010

While Australia only accounts for an estimated 2% of the world’s milk production, it is an important exporter of dairy products. Australia ranks fourth in terms of world dairy trade – now with an 11% share – behind the European Union, New Zealand and the USA. Data shown in Figure 10 below is for 2008, while Figure 11 below that shows graphically the fluctuations in Australia’s share of international dairy markets over the period 1990‐2009. Again, it is interesting to note the increasingly powerful position held by New Zealand – with its low cost of production herd run on an abundance of high nutritional value temperate pastures and fertile volcanic soils.

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 19 of 329

Figure 10. Exporters’ share of world trade in 2008 in Dairy Products (milk equivalents)

Sources: Dairy Australia: Australian Dairy Industry in Focus 2009, and ABS Figure 11. Exporters’ share of international trade in Dairy Products (milk equivalents), from 1990‐2009

Exporter's Share of the International Market

0

10

20

30

40

50

60

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

% li

tres

milk

equ

ival

ents

Australia EU NZ USA Other

Source: Dairy Australia, personal communication, 2010

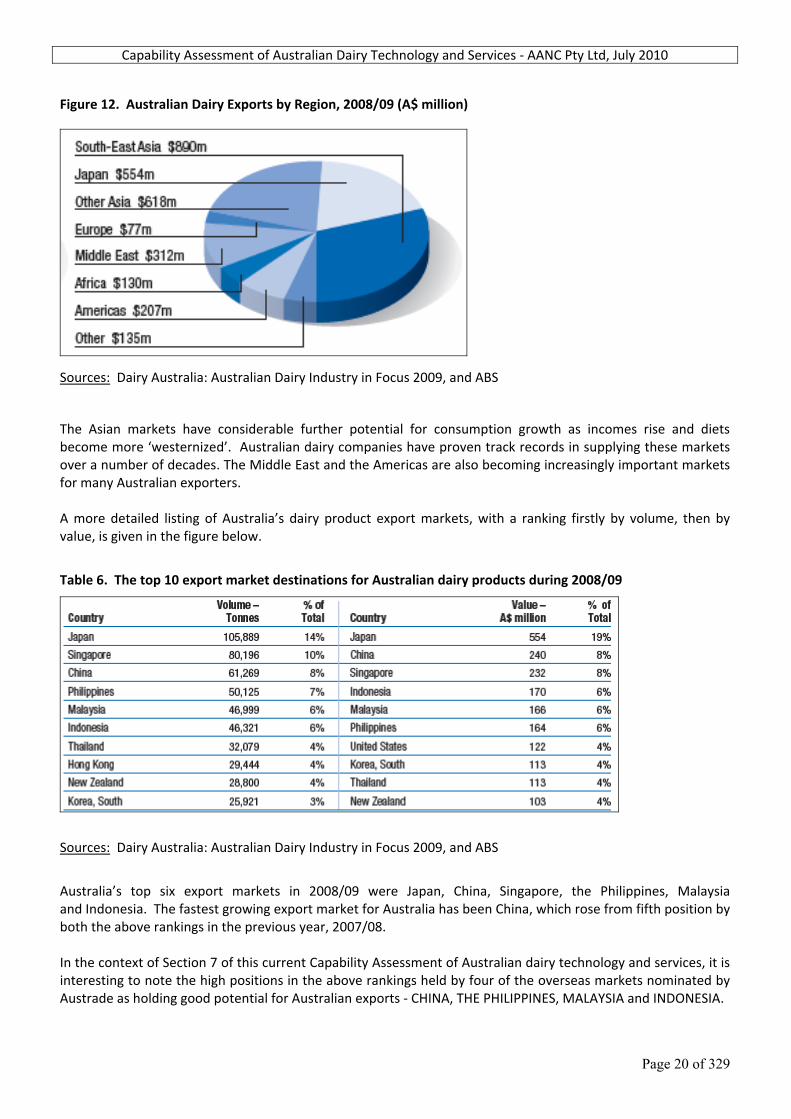

Australian exports are currently concentrated in Asia, which represented 71% of the total dairy exports value of A$2.9 billion in 2008/09. Japan is the single most important export market for Australia, accounting for 19% of exports by value. This concentration of exports in South East Asia or other parts of Asia reflects both Australia’s geographic proximity to these markets and the extent to which Australia is excluded from other major markets by direct restrictions (as in the case of the European Union) or the impact of the export subsidy programs of major competitor countries.

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 20 of 329

Figure 12. Australian Dairy Exports by Region, 2008/09 (A$ million)

Sources: Dairy Australia: Australian Dairy Industry in Focus 2009, and ABS

The Asian markets have considerable further potential for consumption growth as incomes rise and diets become more ‘westernized’. Australian dairy companies have proven track records in supplying these markets over a number of decades. The Middle East and the Americas are also becoming increasingly important markets for many Australian exporters. A more detailed listing of Australia’s dairy product export markets, with a ranking firstly by volume, then by value, is given in the figure below.

Table 6. The top 10 export market destinations for Australian dairy products during 2008/09

Sources: Dairy Australia: Australian Dairy Industry in Focus 2009, and ABS

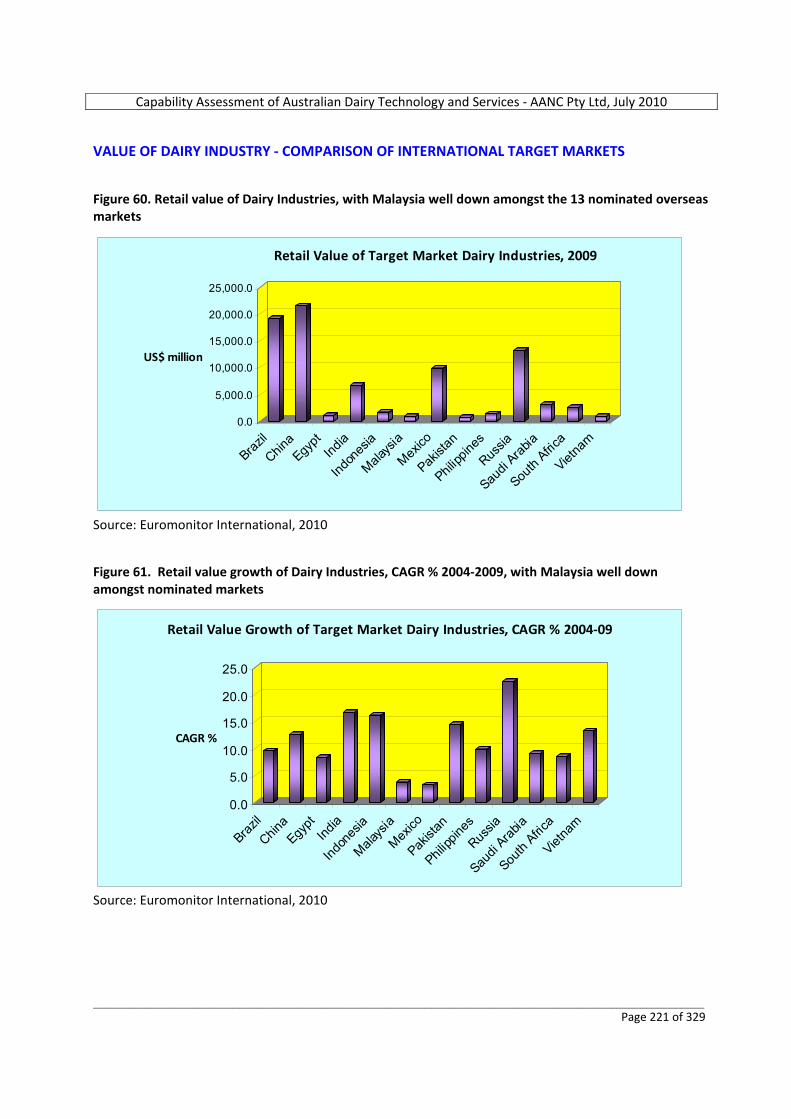

Australia’s top six export markets in 2008/09 were Japan, China, Singapore, the Philippines, Malaysia and Indonesia. The fastest growing export market for Australia has been China, which rose from fifth position by both the above rankings in the previous year, 2007/08. In the context of Section 7 of this current Capability Assessment of Australian dairy technology and services, it is interesting to note the high positions in the above rankings held by four of the overseas markets nominated by Austrade as holding good potential for Australian exports ‐ CHINA, THE PHILIPPINES, MALAYSIA and INDONESIA.

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 21 of 329

The table below shows the relative importance, by value, of various dairy product types in different export regions. A comparison with product values in the Australian domestic market is also shown.

Table 7. Value of Australian Dairy Exports by region, by product, 2008/09 (A$ million)

Sources: Dairy Australia: Australian Dairy Industry in Focus 2009, and ABS

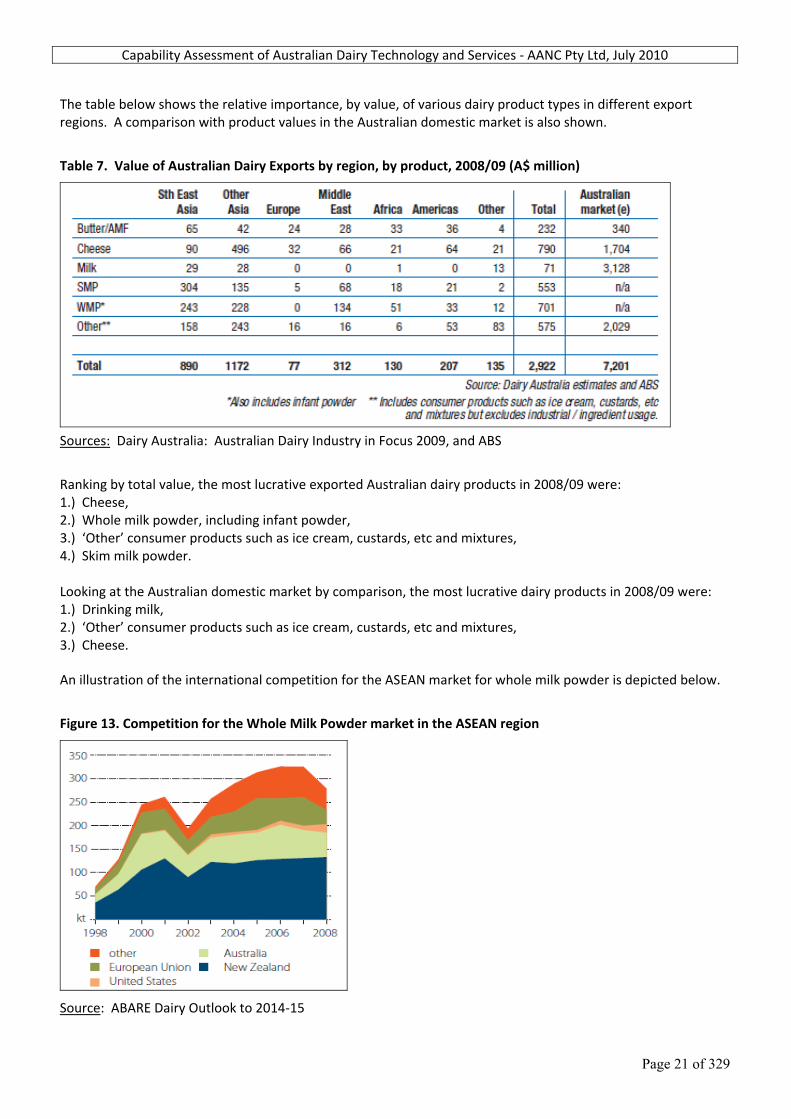

Ranking by total value, the most lucrative exported Australian dairy products in 2008/09 were: 1.) Cheese, 2.) Whole milk powder, including infant powder, 3.) ‘Other’ consumer products such as ice cream, custards, etc and mixtures, 4.) Skim milk powder. Looking at the Australian domestic market by comparison, the most lucrative dairy products in 2008/09 were: 1.) Drinking milk, 2.) ‘Other’ consumer products such as ice cream, custards, etc and mixtures, 3.) Cheese. An illustration of the international competition for the ASEAN market for whole milk powder is depicted below.

Figure 13. Competition for the Whole Milk Powder market in the ASEAN region

Source: ABARE Dairy Outlook to 2014‐15

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 22 of 329

AUSTRALIA’S LIVE EXPORT MARKETS FOR DAIRY CATTLE

An important additional dimension to Australia’s position as a supplier to the global market is the number of dairy cattle (principally pregnant heifers) exported live to various nations of the world.

“The Australian dairy industry is internationally recognised as one of the world’s most competitive and integral parts of the global food market. The nation’s enviable disease free status has seen it dominate the supply of dairy cattle to China, South East Asia, Middle East and Mexico for the past 10 years.” ‐ Landmark Global Exports, quote from website: www.landmarkglobalexports.com.au

Australia’s World Leadership in Live Exporting Australia is a world leader in the export of commercial livestock, exporting on average over 500,000 cattle (approx 60,000 of these being dairy heifers), 4 million sheep and 50,000 goats each year by sea and by air (LiveCorp statistics, www.livecorp.com.au). The country’s leadership in this market is attributed to a number of factors: 1.) The Australian livestock industry is underpinned by a solid commitment to food safety, product quality,

animal health and welfare. Our industry is one of the most stringently controlled in the world, with independently audited food safety systems in place across the whole supply chain.

2.) According to MLA‐Livecorp, Australia has the world’s highest livestock export standards, ensuring animals

arrive at overseas destinations in premium condition. 3.) Australia’s diverse climatic conditions ensure that livestock can be bred and reared to be well suited to

either tropical or temperate climates. 4.) Australia has an animal health status superior to almost all other nations of the world, with the country

being officially recognized by the international animal health authority, the OIE, as being “free” from all major exotic diseases of farm animals. Australian Live Export Protocols, involving pre‐loading inspection of all animals and the issuing of Health Certificates by AQIS accredited veterinarians, the cleaning of ships, and accreditation of all exporters, helps guarantee the critically important “disease free” status of all beef and dairy cattle, sheep and goats exported from Australia to many countries of the world.

5.) The Australian Federal Government tightly controls the livestock export industry through legislation and

regulation. All livestock exporters must have an operations and governance manual as a requirement of their Australian livestock export licence. This manual acts as a quality assurance manual, covering all aspects of the Australian Standards for the Export of Livestock. Exporters are audited by the Federal Government twice a year.

6.) The Australian livestock industry, through Meat and Livestock Australia (MLA) and LiveCorp, provide after

sales technical support for buyers of the country’s livestock.

Location of dairy animals for export

It is important to note that dairy animal selection is generally restricted to Victoria, southern New South Wales and South Australia because these regions are free of the Bluetongue virus, which is transmitted to sheep, goats, deer and cattle by insects. In fact dairy cattle for export must be sourced outside the “Bluetongue Zone”. The position of this zone actually changes every year, according to seasonal conditions and prevailing entomological factors. BTV free regions happen to span the area of Australia with the highest number of dairy cows.

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 23 of 329

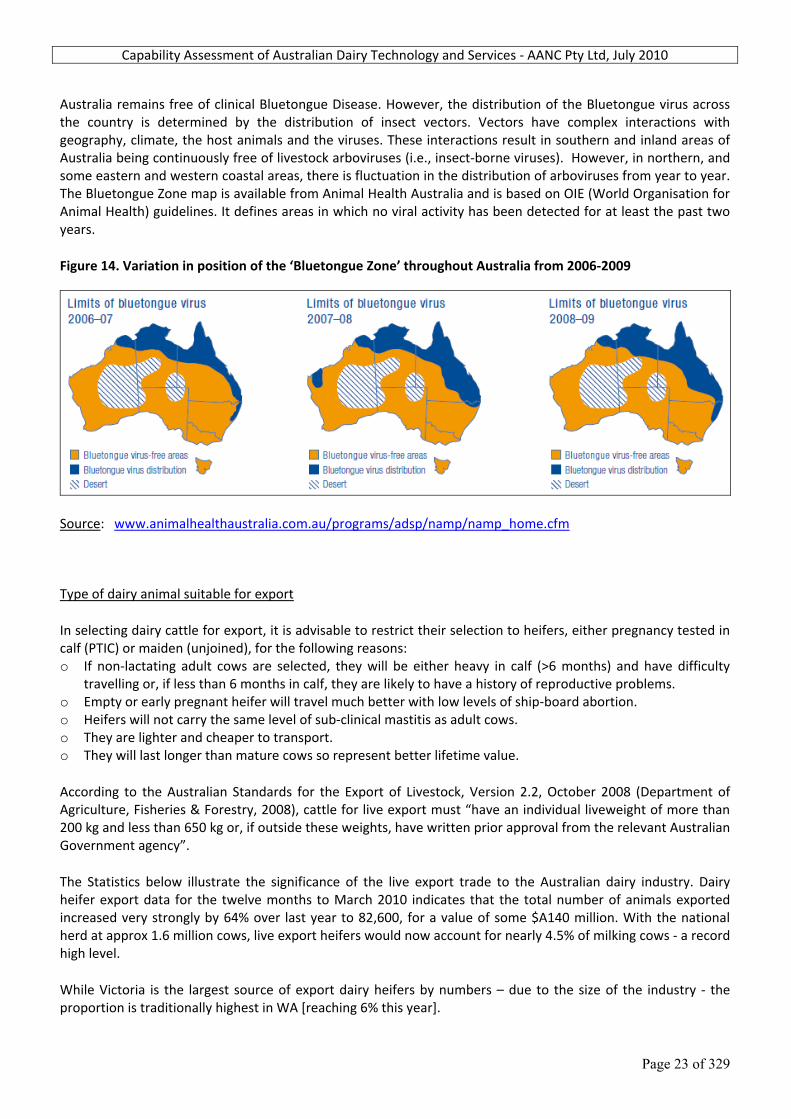

Australia remains free of clinical Bluetongue Disease. However, the distribution of the Bluetongue virus across the country is determined by the distribution of insect vectors. Vectors have complex interactions with geography, climate, the host animals and the viruses. These interactions result in southern and inland areas of Australia being continuously free of livestock arboviruses (i.e., insect‐borne viruses). However, in northern, and some eastern and western coastal areas, there is fluctuation in the distribution of arboviruses from year to year. The Bluetongue Zone map is available from Animal Health Australia and is based on OIE (World Organisation for Animal Health) guidelines. It defines areas in which no viral activity has been detected for at least the past two years.

Figure 14. Variation in position of the ‘Bluetongue Zone’ throughout Australia from 2006‐2009

Source: www.animalhealthaustralia.com.au/programs/adsp/namp/namp_home.cfm

Type of dairy animal suitable for export

In selecting dairy cattle for export, it is advisable to restrict their selection to heifers, either pregnancy tested in calf (PTIC) or maiden (unjoined), for the following reasons: o If non‐lactating adult cows are selected, they will be either heavy in calf (>6 months) and have difficulty

travelling or, if less than 6 months in calf, they are likely to have a history of reproductive problems. o Empty or early pregnant heifer will travel much better with low levels of ship‐board abortion. o Heifers will not carry the same level of sub‐clinical mastitis as adult cows. o They are lighter and cheaper to transport. o They will last longer than mature cows so represent better lifetime value.

According to the Australian Standards for the Export of Livestock, Version 2.2, October 2008 (Department of Agriculture, Fisheries & Forestry, 2008), cattle for live export must “have an individual liveweight of more than 200 kg and less than 650 kg or, if outside these weights, have written prior approval from the relevant Australian Government agency”.

The Statistics below illustrate the significance of the live export trade to the Australian dairy industry. Dairy heifer export data for the twelve months to March 2010 indicates that the total number of animals exported increased very strongly by 64% over last year to 82,600, for a value of some $A140 million. With the national herd at approx 1.6 million cows, live export heifers would now account for nearly 4.5% of milking cows ‐ a record high level.

While Victoria is the largest source of export dairy heifers by numbers – due to the size of the industry ‐ the proportion is traditionally highest in WA [reaching 6% this year].

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 24 of 329

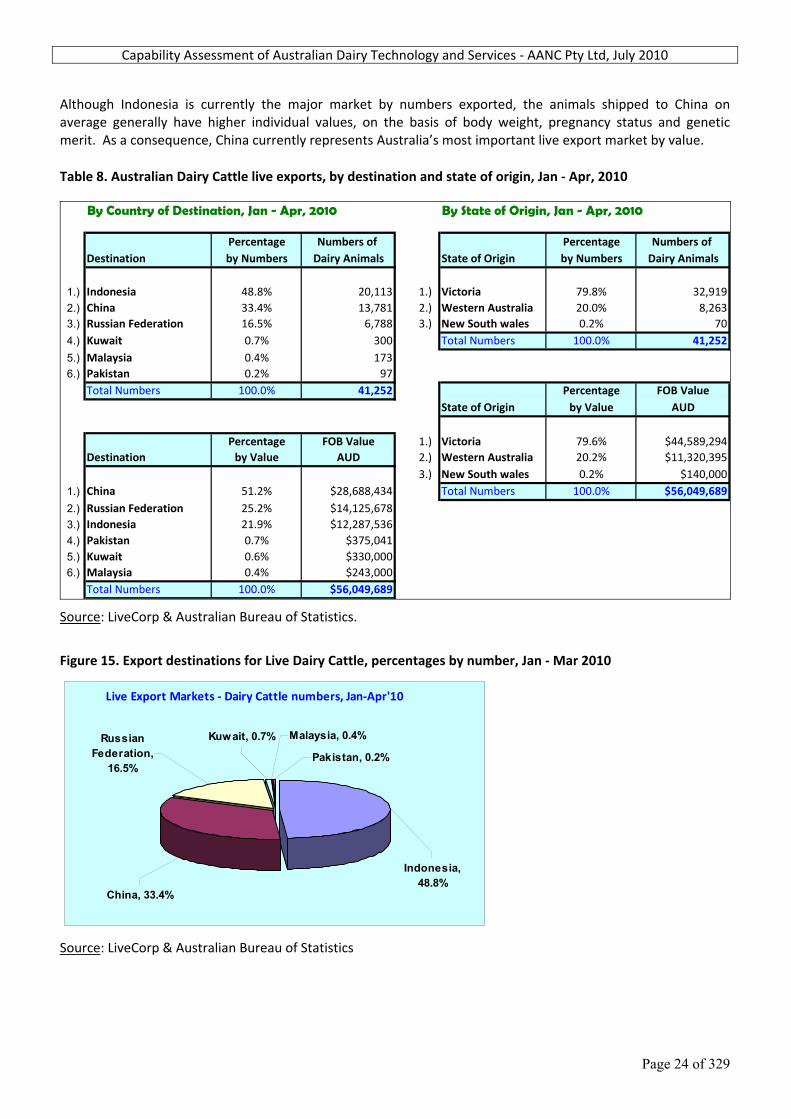

Although Indonesia is currently the major market by numbers exported, the animals shipped to China on average generally have higher individual values, on the basis of body weight, pregnancy status and genetic merit. As a consequence, China currently represents Australia’s most important live export market by value.

Table 8. Australian Dairy Cattle live exports, by destination and state of origin, Jan ‐ Apr, 2010

By Country of Destination, Jan - Apr, 2010 By State of Origin, Jan - Apr, 2010

Percentage Numbers of Percentage Numbers of Destination by Numbers Dairy Animals State of Origin by Numbers Dairy Animals

1.) Indonesia 48.8% 20,113 1.) Victoria 79.8% 32,9192.) China 33.4% 13,781 2.) Western Australia 20.0% 8,2633.) Russian Federation 16.5% 6,788 3.) New South wales 0.2% 704.) Kuwait 0.7% 300 Total Numbers 100.0% 41,2525.) Malaysia 0.4% 1736.) Pakistan 0.2% 97

Total Numbers 100.0% 41,252 Percentage FOB ValueState of Origin by Value AUD

Percentage FOB Value 1.) Victoria 79.6% $44,589,294Destination by Value AUD 2.) Western Australia 20.2% $11,320,395

3.) New South wales 0.2% $140,0001.) China 51.2% $28,688,434 Total Numbers 100.0% $56,049,6892.) Russian Federation 25.2% $14,125,6783.) Indonesia 21.9% $12,287,5364.) Pakistan 0.7% $375,0415.) Kuwait 0.6% $330,0006.) Malaysia 0.4% $243,000

Total Numbers 100.0% $56,049,689

Source: LiveCorp & Australian Bureau of Statistics.

Figure 15. Export destinations for Live Dairy Cattle, percentages by number, Jan ‐ Mar 2010

Live Export Markets ‐ Dairy Cattle numbers, Jan‐Apr'10

Pakistan, 0.2%

Malaysia, 0.4%Kuwait, 0.7%

Indonesia, 48.8%

Russian Federation,

16.5%

China, 33.4%

Source: LiveCorp & Australian Bureau of Statistics

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 25 of 329

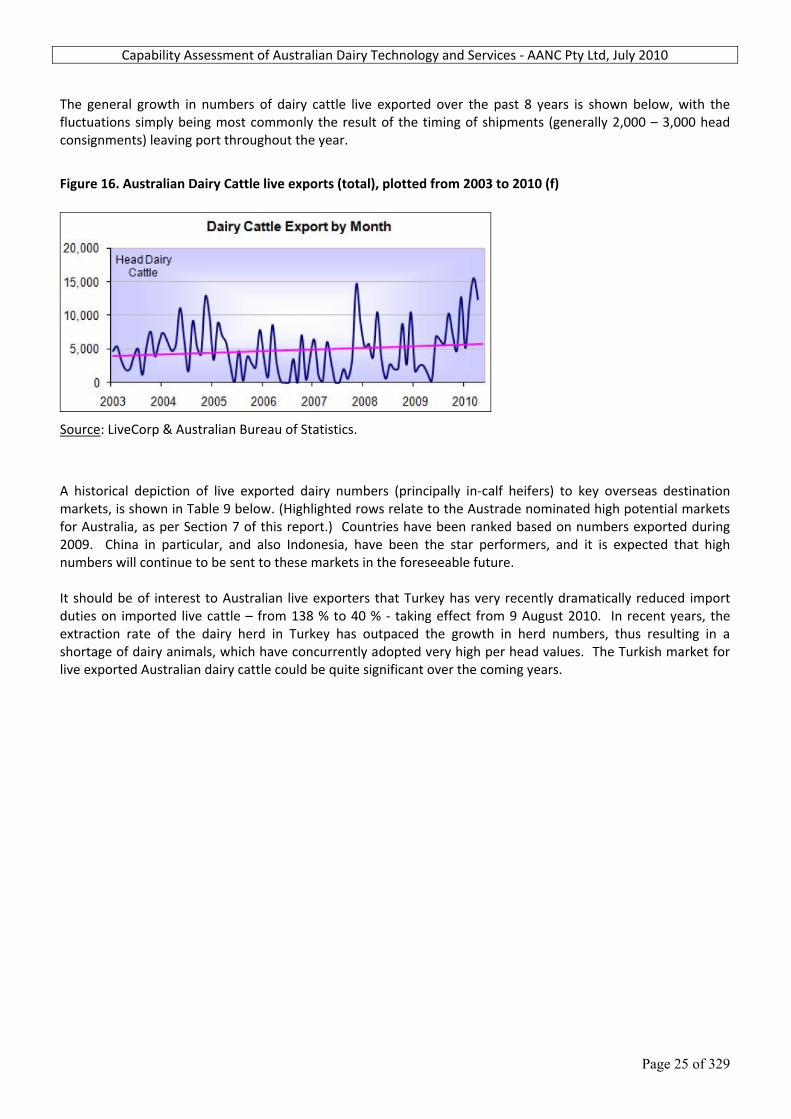

The general growth in numbers of dairy cattle live exported over the past 8 years is shown below, with the fluctuations simply being most commonly the result of the timing of shipments (generally 2,000 – 3,000 head consignments) leaving port throughout the year.

Figure 16. Australian Dairy Cattle live exports (total), plotted from 2003 to 2010 (f)

Source: LiveCorp & Australian Bureau of Statistics.

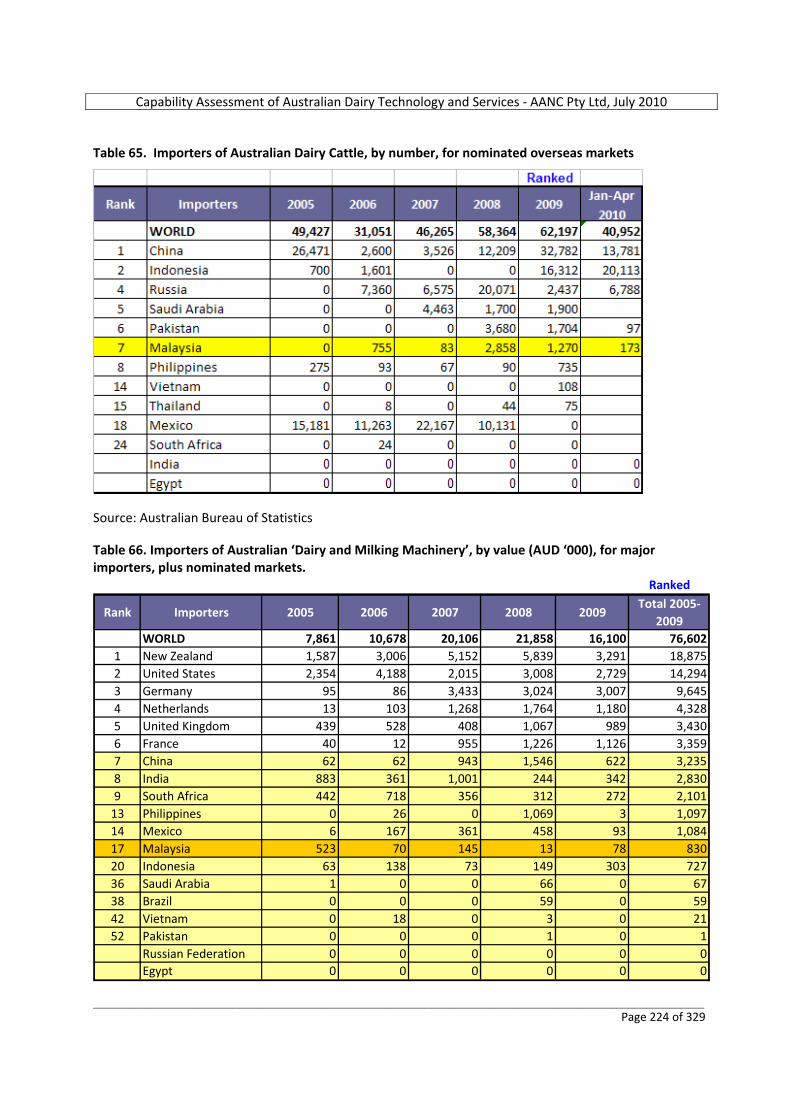

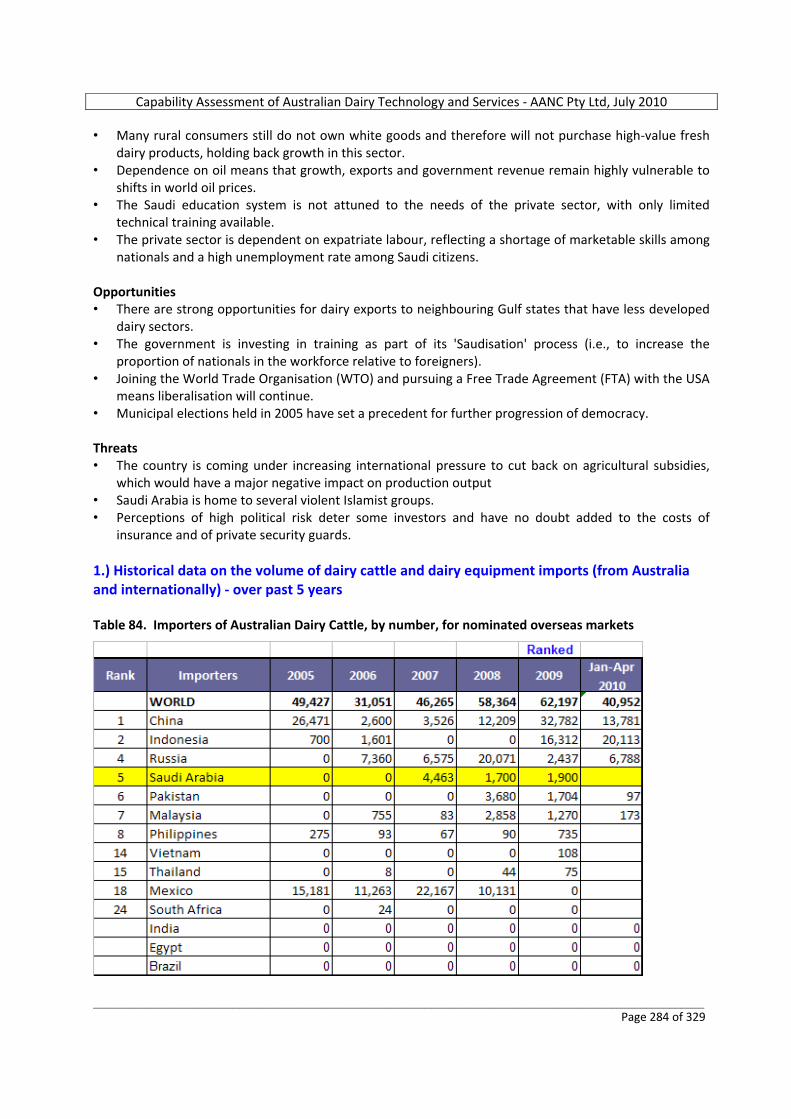

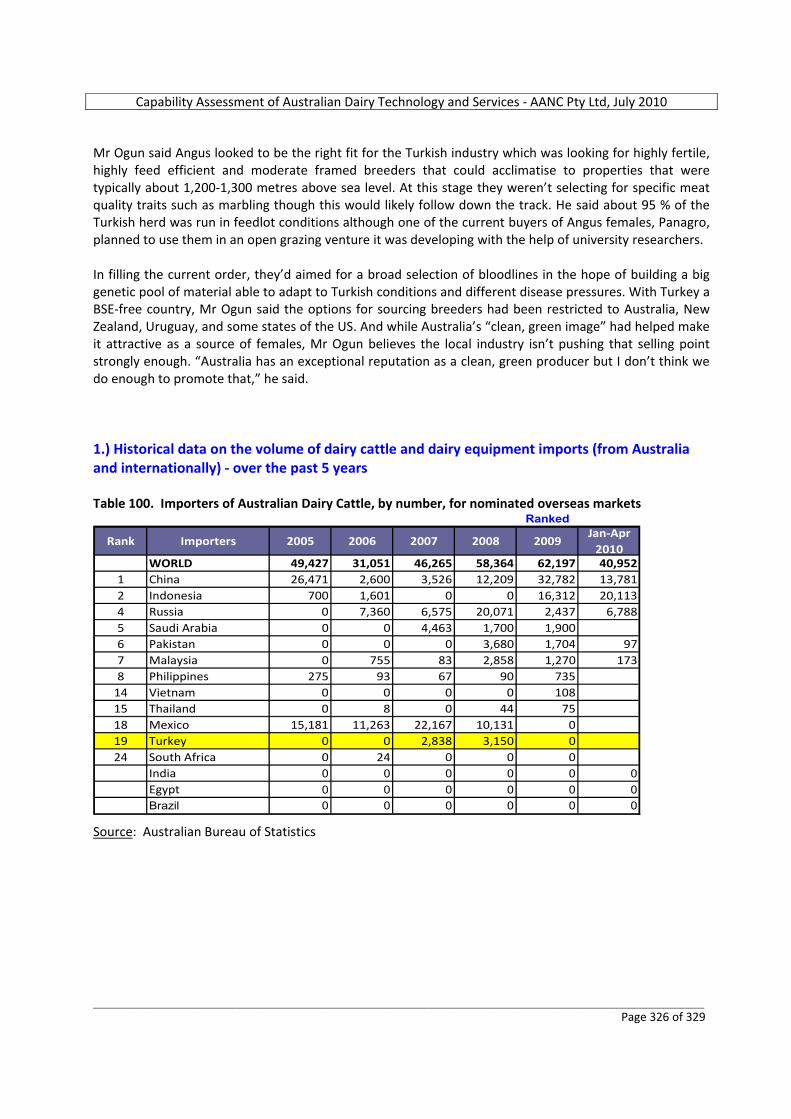

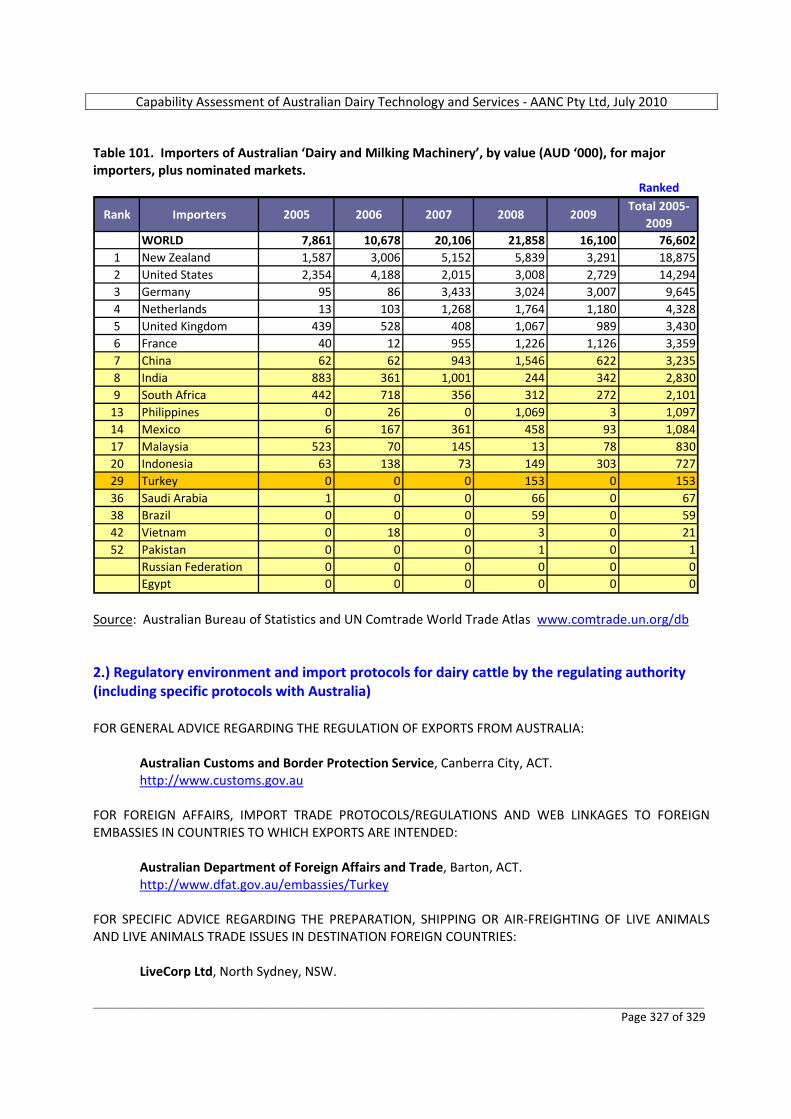

A historical depiction of live exported dairy numbers (principally in‐calf heifers) to key overseas destination markets, is shown in Table 9 below. (Highlighted rows relate to the Austrade nominated high potential markets for Australia, as per Section 7 of this report.) Countries have been ranked based on numbers exported during 2009. China in particular, and also Indonesia, have been the star performers, and it is expected that high numbers will continue to be sent to these markets in the foreseeable future. It should be of interest to Australian live exporters that Turkey has very recently dramatically reduced import duties on imported live cattle – from 138 % to 40 % ‐ taking effect from 9 August 2010. In recent years, the extraction rate of the dairy herd in Turkey has outpaced the growth in herd numbers, thus resulting in a shortage of dairy animals, which have concurrently adopted very high per head values. The Turkish market for live exported Australian dairy cattle could be quite significant over the coming years.

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 26 of 329

Table 9. Australian Dairy Cattle live export numbers by destination, Jan 2005 to Apr, 2010 (Highlighted are the nominated high potential markets for Australia, as per Section 7 of this report.)

Ranked

Rank Importers 2005 2006 2007 2008 2009Jan‐Apr

2010WORLD 49,427 31,051 46,265 58,364 62,197 41,252

1 China 26,471 2,600 3,526 12,209 32,782 13,7812 Indonesia 700 1,601 0 0 16,312 20,1133 Kuwait 3,039 3,331 4,479 3,936 3,434 3004 Russia 0 7,360 6,575 20,071 2,437 6,7885 Saudi Arabia 0 0 4,463 1,700 1,9006 Pakistan 0 0 0 3,680 1,704 977 Malaysia 0 755 83 2,858 1,270 1738 Philippines 275 93 67 90 7359 Oman 250 350 0 0 374

10 Japan 662 978 0 0 34011 Qatar 31 0 0 223 30012 United Arab Emirates 2,818 1,825 328 272 26813 Singapore 0 0 0 0 14914 Vietnam 0 0 0 0 10815 Thailand 0 8 0 44 7516 New Zealand 0 0 0 0 517 New Caledonia 0 0 0 0 418 Mexico 15,181 11,263 22,167 10,131 019 Turkey 0 0 2,838 3,150 020 Jordan 0 0 1,200 0 021 Brunei Darussalam 0 740 0 0 022 Taiwan 0 70 539 0 023 Iraq 0 30 0 0 024 South Africa 0 24 0 0 025 Bangladesh 0 13 0 0 026 Chile 0 10 0 0 0

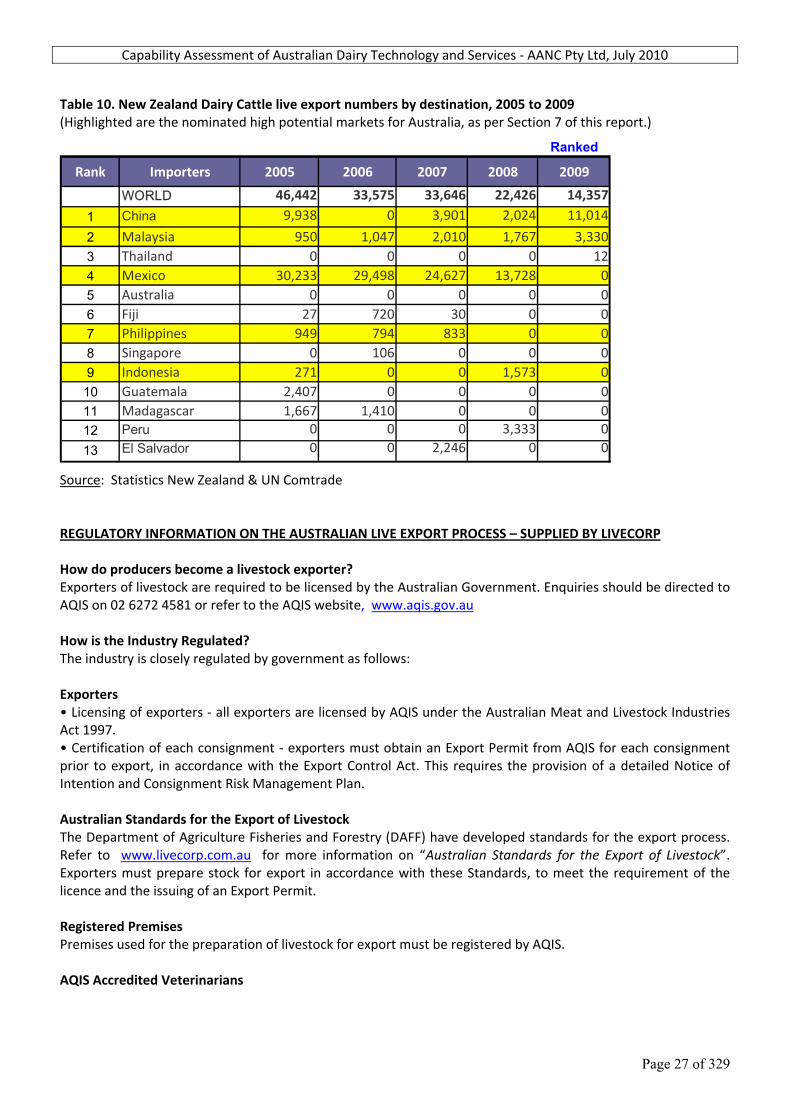

Source: Australian Bureau of Statistics. By way of comparison, Table 10 below details live exports of dairy cattle from New Zealand. It should be appreciated that, as shown previously, New Zealand has approximately three times the number of cows as has Australia, and that it currently exports large numbers to China ‐ Australia’s number one live export destination. Until 2009, New Zealand was also highly competitive in supplying heifers to Mexico. The country is very actively involved in promoting its dairy cattle, dairy products and advisory services in China and several parts of SE Asia and other countries. New Zealand can also boast equally as well or better than Australia, its clean, green, disease free image to foreign countries. Although exported numbers are currently well below Australia, New Zealand should be regarded a substantial on‐going competitor to Australia in our pursuit of offshore markets.

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 27 of 329

Table 10. New Zealand Dairy Cattle live export numbers by destination, 2005 to 2009 (Highlighted are the nominated high potential markets for Australia, as per Section 7 of this report.)

Ranked

Rank Importers 2005 2006 2007 2008 2009

WORLD 46,442 33,575 33,646 22,426 14,357

1 China 9,938 0 3,901 2,024 11,014

2 Malaysia 950 1,047 2,010 1,767 3,3303 Thailand 0 0 0 0 124 Mexico 30,233 29,498 24,627 13,728 05 Australia 0 0 0 0 06 Fiji 27 720 30 0 07 Philippines 949 794 833 0 08 Singapore 0 106 0 0 09 Indonesia 271 0 0 1,573 010 Guatemala 2,407 0 0 0 011 Madagascar 1,667 1,410 0 0 012 Peru 0 0 0 3,333 0

13 El Salvador 0 0 2,246 0 0

Source: Statistics New Zealand & UN Comtrade REGULATORY INFORMATION ON THE AUSTRALIAN LIVE EXPORT PROCESS – SUPPLIED BY LIVECORP How do producers become a livestock exporter? Exporters of livestock are required to be licensed by the Australian Government. Enquiries should be directed to AQIS on 02 6272 4581 or refer to the AQIS website, www.aqis.gov.au How is the Industry Regulated? The industry is closely regulated by government as follows: Exporters • Licensing of exporters ‐ all exporters are licensed by AQIS under the Australian Meat and Livestock Industries Act 1997. • Certification of each consignment ‐ exporters must obtain an Export Permit from AQIS for each consignment prior to export, in accordance with the Export Control Act. This requires the provision of a detailed Notice of Intention and Consignment Risk Management Plan. Australian Standards for the Export of Livestock The Department of Agriculture Fisheries and Forestry (DAFF) have developed standards for the export process. Refer to www.livecorp.com.au for more information on “Australian Standards for the Export of Livestock”. Exporters must prepare stock for export in accordance with these Standards, to meet the requirement of the licence and the issuing of an Export Permit. Registered Premises Premises used for the preparation of livestock for export must be registered by AQIS. AQIS Accredited Veterinarians

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 28 of 329

Only AQIS accredited veterinarians may undertake veterinary functions in an approved export program. Refer to AQIS website www.aqis.gov.au/live export/accredited veterinarians for more information. Ships Livestock ships must be approved by the Australian Maritime Safety Authority as meeting the requirements of Marine Order 45. Prevention of Cruelty Legislation State legislation on the prevention of cruelty to animals applies to the handling, management and transport of animals. Airfreight Airfreight requirements are in accordance with the Australian Standards for the Export of Livestock and IATA (International Air Transport Association) Live Animal Regulations. Licensing (responsibility of AQIS) An exporter must have a licence. Without a license an exporter cannot export. Each consignment needs an Export Permit to obtain a customs release from Australia. Without an Export Permit the ship or aircraft cannot leave Australia. Failure to observe government orders under the AMLI Act can result in the loss of licence. State Prevention of Cruelty to Animals Acts are to be observed at all times and failure in basic animal welfare can see a consignment stopped by AQIS. Customer Country Protocols (responsibility of AQIS) Some customer countries have protocols requiring an Import Permit, which in turn requires a Health Certificate from AQIS. This Health Certificate guarantees that all health protocol conditions have been met. Without this, entry into the country concerned may be prevented and as a result the consignment would be prevented from leaving Australia. Where protocols do not apply, AQIS/Customs can, should problems arise, withhold the issuance of an Export Permit, preventing the consignment from leaving Australia. Shipboard (responsibility of AMSA) Each livestock vessel is licensed by the Australian Maritime Safety Authority (AMSA). If a vessel fails to comply with the provisions of Marine Order 43 of the Navigation Act, the vessel may be barred from loading future consignments and penalties will apply to the shipping company. False declarations supplied to any Government department are covered under the various “Oath Acts” and penalties apply. Sanctions include loss of a ship’s licence to carry livestock. In addition, the ship is subject to additional engineering inspection and scrutiny by AMSA on arrival back in Australia. EXAMPLE OF THE DAIRY LIVE EXPORT PROCESS Document prepared by Austock Exports and Precision Beef : “Exporting Dairy Cows to China - A description of the process and the role of the exporter.” Two Australian companies, Austock Exports and Precision Beef, have joined forces to provide a more comprehensive service to their overseas clients. This document is intended to provide prospective clients in China with an overview of the steps associated with selecting and transporting dairy cattle to that country. 1. Cattle selection A number of issues associated with identifying and selecting the appropriate cattle are discussed below. 1.1. Customer’s requirements

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 29 of 329

Understanding the customer’s objectives and desired outcomes is fundamental to establishing a successful business relationship. In this case, Austock and Precision Beef will ascertain how the end user intends to manage the cattle, looking at issues such as: o whether they are to be housed or grazed, o the numbers are to be run under each management unit, o the level of nutrition the cows will have access to, o the level of expertise within the management and operations team, o the end market for the milk and the requirements of the milk processor. We will also seek to fully understand any other non-production related specification such as colour, markings, etc. This knowledge will then enable us to identify probable sources of cattle for the client to inspect with the highest likelihood of efficient, trouble-free selection. 1.2. Quality characteristics The Australian dairy herd has a lower level of production than the US herd - typically 5,000 to 6,000 litres per 300 day lactation compared to the US level of 8,000 to 10,000 litres. This is because most cows in Australia are grazed on pasture with minimal grain supplementation. This low input/medium output strategy has positioned the Australian industry, along with New Zealand’s, as the lowest cost producers in the world. However, most heifers presented for selection will be derived from North American genetics. This means that, if placed on total mixed rations similar to those fed in the US, one can expect similar levels of production to those achieved there, ie, 6,000 to 8,000 litres for heifers and 8,000 to 10,000 litres for mature cows. Other criteria upon which to base selection include: - Temperament, - Udder and teat conformation and placement, - Feet and leg conformation, - Body length and depth. 1.3. Contract to supply cattle Austock and Precision Beef require a supply contract describing the number and class of stock to be supplier, price and payment terms to be in place before selection commences. 1.4. Selection process Selecting sufficient cattle to fill a boat (1,500 to 2,300 head) is a significant undertaking. Typically, we would inspect between 20 and 50 heifers per farm and would be hopeful of selecting between 60% and 80% of presented animals. Bearing in mind that we need to select 10% to 20% more than we anticipate shipping to provide a contingency against those animals that fail the quarantine protocols, we will need to visit 50 to 100 farms to get a full consignment. This means the client may need to stay in Australia for between two and four weeks. 2. Veterinary testing and quarantine 2.1. On-farm testing The Chinese authorities require the following tests to be carried out on the farm of origin before the animals are transported to the quarantine depot: Disease Number of tests Bluetongue 2 Tuberculosis (TB) 1 Johnes - ELISA 1 - Intra-dermal 1 Akabane 1 Infectious Bovine Rhinotracheitis (IBR) 1 Bovine viral diarrhea (BVD) 1 Leukosis (EBL) 1 Leptospira 1 These tests take 4 days to complete but, given the number of farm visits that must be undertaken, it would be prudent to budget three weeks for this phase.

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 30 of 329

2.2. Quarantine depot Once the on-farm testing is complete, animals which pass the tests must be transported to a central quarantine depot and stay there for at least 30 days as mandated by the Chinese authorities. A further battery of tests and treatments must be conducted during this period. Disease Number of tests Bluetongue 1 Akabane 1 Infectious Bovine Rhinotracheitis (IBR) 1 Internal parasites 1 External parasites 2 Leptospira 1 Nutritional management at this stage is critical to ensure that the pregnant animal receives the nutrients she needs for foetus development while at the same time controlling weight gain so that freight costs are minimized. 2.3. Chinese veterinarian The Chinese government requires that a Chinese veterinarian supervises the testing process. This involves inspecting the laboratory that will conduct the tests and approving their methods, overseeing a number of the blood sampling and other veterinary procedures, inspecting and approving the quarantine depot, liaising with the Australian quarantine authorities (AQIS) and supervising the dispatch. The quarantine phase cannot commence until he arrives. It is the responsibility of the Chinese client to arrange for the Chinese veterinarian to come to Australia and to cover his costs while here. 3. Transport and delivery 3.1. Freight Two options exist for transporting live cattle to China, air freight or sea freight. Air freight has the advantage of speed with less than 24 hour elapsing between dispatch from the depot until the cattle are unloaded in China. It also enables to importer to bring in smaller numbers. Typically, an aircraft will carry approximately 200 pregnant heifers. The major drawback to air freight is cost, which generally is in excess of USD1,200 per head. Sea freight is much cheaper; around USD250 to USD300 per head. However, it needs large numbers of cattle (1,500 to 2,500 head per shipment) to be effective and obviously takes longer to get there - between 15 and 20 days, depending on the vessel. 3.2. Import permit It is the client’s responsibility to secure the necessary permits from the Chinese government. The Australian authorities are unlikely to allow the quarantine testing to commence without those permits in place. 3.3. Customs and quarantine in China On arrival in China, the cattle must under go a further quarantine period and veterinary tests. It is the responsibility of the importer to fund this. It is also the client’s responsibility to ensure that all customs and quarantine measures are in place for the consignments arrival in China, including the provision of quarantine facilities. 4. Austock’s role 4.1. Selection Precision Beef’s principal, Dr Shane Blakeley, is a veterinarian with experience in managing large dairy operations and is familiar with the criteria by which superior dairy cattle are selected. He will work in close association with a subsidiary company of the Victorian Dairyfarmers Organisation that has been specially established to identify stock suitable for export to China. It is also wise to have provisional approval for the Chinese veterinarian’s visit. 4.2. Testing and quarantine Dr Blakeley will supervise and coordinate the on-farm and depot quarantine process. He will also oversee the management, nutrition and animal health of the cattle while they are in the depot. 4.3. Transport Austock is fully familiar with the shipping function and will organize the transport of the stock to the wharf or airport, chartering the ship or aircraft, generation of customs, quarantine and shipping documentation, provision of ship-board fodder and bedding, on-board supervision of the cattle during transit.

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 31 of 329

4.4. Documentation The export of livestock from Australia generates a considerable amount of documentation. Austock staff coordinate this on a daily basis and can confidently fulfill this task for Chinese clients. 5. Payment terms Austock is prepared to supply cattle on a CIF, C&F or FOB basis against a letter of credit acceptable to the ANZ Banking Corporation. However, whichever scenario is employed, the letter of credit must be configured in a way which enables Austock to draw down funds against that LC over the quarantine and depot period. This is needed to pay the farmers for the cattle once they are delivered to the depot and to pay for the veterinary tests, depot charges, freight to ship or aircraft and, if the contract is C&F or CIF, to pay the deposit on the ship or plane. All draw-downs would be against documentation agreed to by both parties. The balance would then be payable on presentation of loading documents and health certificates. 6. After-sales service Austock and Precision Beef are well positioned to offer a range of after-sales services. 6.1. Operations review Austock and Precision Beef personnel would accompany the cattle to China and, while in the country, we would be happy to provide an overview of the clients existing operations, free of charge, along with a series of recommendations for management’s consideration. 6.2. Fee based consultancy Dr Blakeley’s veterinary and dairy management experience provides him with the skills to offer consultancy advice on areas associated with nutrition, genetics and animal health. More importantly, he has specialized in developing management systems to ensure the efficient, profitable operation of beef and dairy businesses. These systems cover business strategy and planning, operating procedures, human resource management, marketing and customer relations and financial management. He is also expert in designing and supervising the construction of dairy feedlots. These services would be charged at a rate agreed to by both parties. 6.3. Contract management Austock and Precision Beef jointly manage two beef cattle feedlots in the Philippines and is negotiating with another concern on a similar project in Indonesia. We would be interested in discussing a similar arrangement with Chinese dairy and beef enterprises. 6.4. Supply of equipment and genetic material We are also able to source dairy equipment and superior dairy genetic material in the form of semen and embryos for our Chinese clients.

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 32 of 329

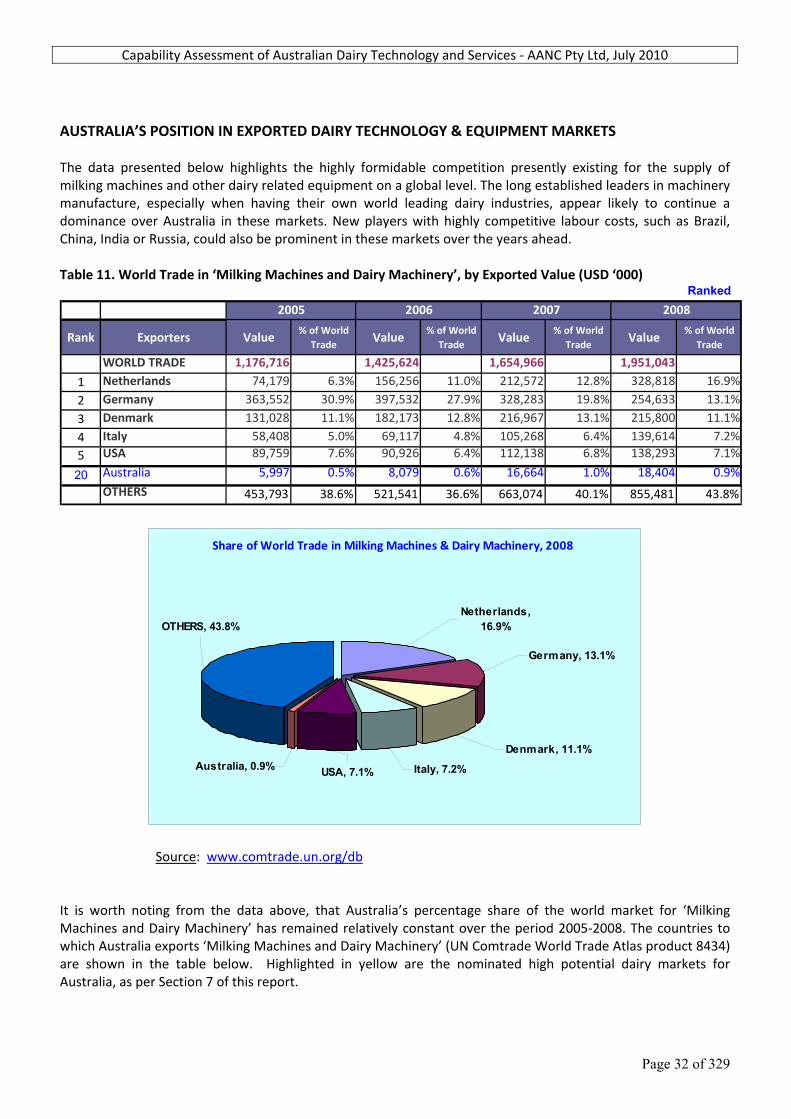

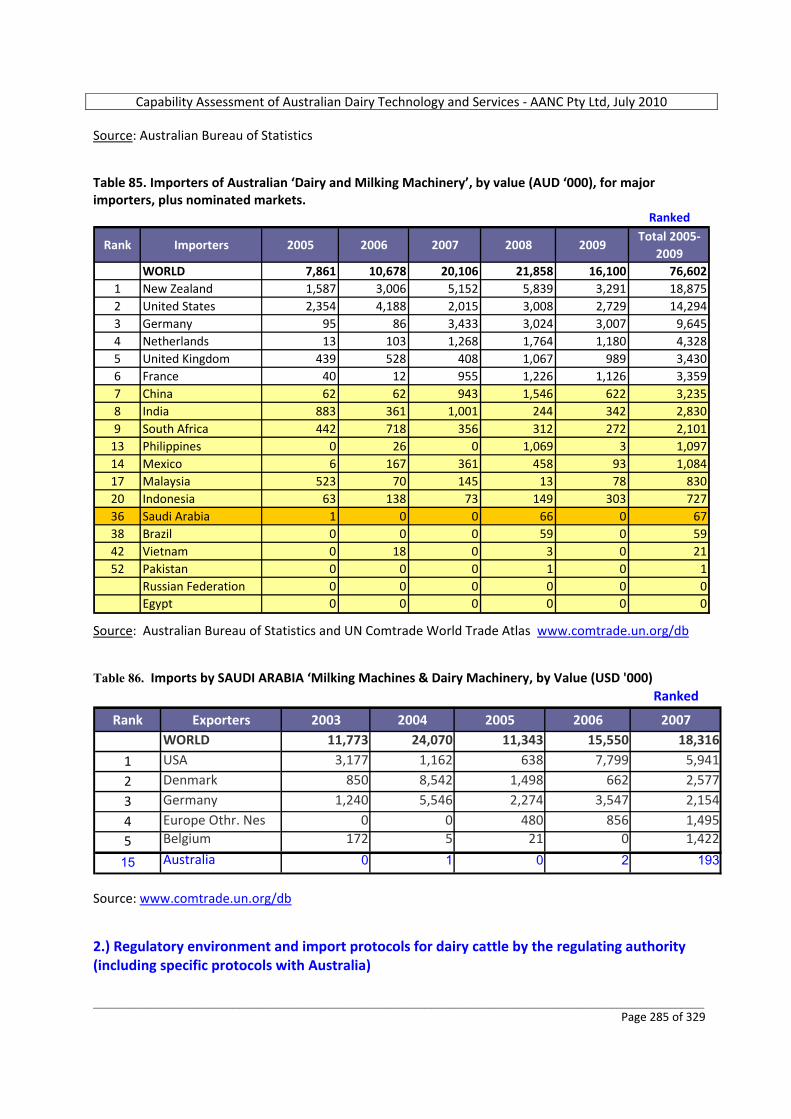

AUSTRALIA’S POSITION IN EXPORTED DAIRY TECHNOLOGY & EQUIPMENT MARKETS The data presented below highlights the highly formidable competition presently existing for the supply of milking machines and other dairy related equipment on a global level. The long established leaders in machinery manufacture, especially when having their own world leading dairy industries, appear likely to continue a dominance over Australia in these markets. New players with highly competitive labour costs, such as Brazil, China, India or Russia, could also be prominent in these markets over the years ahead. Table 11. World Trade in ‘Milking Machines and Dairy Machinery’, by Exported Value (USD ‘000)

Ranked

Rank Exporters Value% of World

TradeValue

% of World Trade

Value% of World

TradeValue

% of World Trade

WORLD TRADE 1,176,716 1,425,624 1,654,966 1,951,043

1 Netherlands 74,179 6.3% 156,256 11.0% 212,572 12.8% 328,818 16.9%

2 Germany 363,552 30.9% 397,532 27.9% 328,283 19.8% 254,633 13.1%

3 Denmark 131,028 11.1% 182,173 12.8% 216,967 13.1% 215,800 11.1%

4 Italy 58,408 5.0% 69,117 4.8% 105,268 6.4% 139,614 7.2%

5 USA 89,759 7.6% 90,926 6.4% 112,138 6.8% 138,293 7.1%

20 Australia 5,997 0.5% 8,079 0.6% 16,664 1.0% 18,404 0.9%

OTHERS 453,793 38.6% 521,541 36.6% 663,074 40.1% 855,481 43.8%

2005 2006 2007 2008

Share of World Trade in Milking Machines & Dairy Machinery, 2008

OTHERS, 43.8%Netherlands,

16.9%

Germany, 13.1%

Denmark, 11.1%

Italy, 7.2%USA, 7.1%Australia, 0.9%

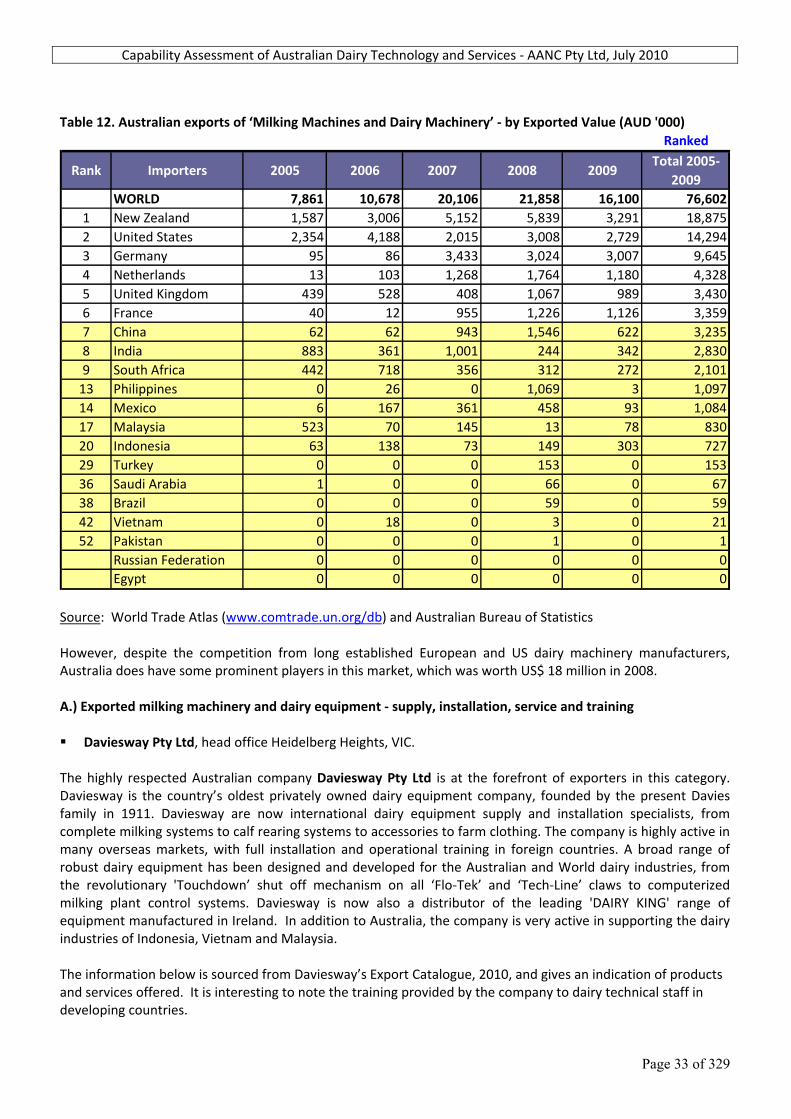

Source: www.comtrade.un.org/db It is worth noting from the data above, that Australia’s percentage share of the world market for ‘Milking Machines and Dairy Machinery’ has remained relatively constant over the period 2005‐2008. The countries to which Australia exports ‘Milking Machines and Dairy Machinery’ (UN Comtrade World Trade Atlas product 8434) are shown in the table below. Highlighted in yellow are the nominated high potential dairy markets for Australia, as per Section 7 of this report.

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 33 of 329

Table 12. Australian exports of ‘Milking Machines and Dairy Machinery’ ‐ by Exported Value (AUD '000)

Ranked

Rank Importers 2005 2006 2007 2008 2009Total 2005‐

2009WORLD 7,861 10,678 20,106 21,858 16,100 76,602

1 New Zealand 1,587 3,006 5,152 5,839 3,291 18,8752 United States 2,354 4,188 2,015 3,008 2,729 14,2943 Germany 95 86 3,433 3,024 3,007 9,6454 Netherlands 13 103 1,268 1,764 1,180 4,3285 United Kingdom 439 528 408 1,067 989 3,4306 France 40 12 955 1,226 1,126 3,3597 China 62 62 943 1,546 622 3,2358 India 883 361 1,001 244 342 2,8309 South Africa 442 718 356 312 272 2,101

13 Philippines 0 26 0 1,069 3 1,09714 Mexico 6 167 361 458 93 1,08417 Malaysia 523 70 145 13 78 83020 Indonesia 63 138 73 149 303 72729 Turkey 0 0 0 153 0 15336 Saudi Arabia 1 0 0 66 0 6738 Brazil 0 0 0 59 0 5942 Vietnam 0 18 0 3 0 2152 Pakistan 0 0 0 1 0 1

Russian Federation 0 0 0 0 0 0Egypt 0 0 0 0 0 0

Source: World Trade Atlas (www.comtrade.un.org/db) and Australian Bureau of Statistics However, despite the competition from long established European and US dairy machinery manufacturers, Australia does have some prominent players in this market, which was worth US$ 18 million in 2008. A.) Exported milking machinery and dairy equipment ‐ supply, installation, service and training Daviesway Pty Ltd, head office Heidelberg Heights, VIC.

The highly respected Australian company Daviesway Pty Ltd is at the forefront of exporters in this category. Daviesway is the country’s oldest privately owned dairy equipment company, founded by the present Davies family in 1911. Daviesway are now international dairy equipment supply and installation specialists, from complete milking systems to calf rearing systems to accessories to farm clothing. The company is highly active in many overseas markets, with full installation and operational training in foreign countries. A broad range of robust dairy equipment has been designed and developed for the Australian and World dairy industries, from the revolutionary 'Touchdown’ shut off mechanism on all ‘Flo‐Tek’ and ‘Tech‐Line’ claws to computerized milking plant control systems. Daviesway is now also a distributor of the leading 'DAIRY KING' range of equipment manufactured in Ireland. In addition to Australia, the company is very active in supporting the dairy industries of Indonesia, Vietnam and Malaysia. The information below is sourced from Daviesway’s Export Catalogue, 2010, and gives an indication of products and services offered. It is interesting to note the training provided by the company to dairy technical staff in developing countries.

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 34 of 329

EXPORT CATALOGUE

Indonesia Indonesia Romania

MOBILE MILKING MACHINE LINE BUCKET MILKER LINE MILKER EZI MILKER DOUBLE UP MILKER ROTARY MILKER CLAWS – CLAW BOWLS UNIONS, CONNECTORS & PVC TUBING LINERS & SHELLS PULSATORS CALF REARING PRODUCTS PUMPS IPC WASH JETTERS FILTERS PLATE HEAT EXCHANGES (MILK COOLERS) TEAT SPRAYERS – MASTITIS DETECTOR STRIP & DIP CUPS DETERGENTS & TEAT DIPS STAINLESS STEEL MANUFACTURING & FABRICATION BUCKETS – DAIRY WEAR

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 35 of 329

It is presently not clear which Australian other companies are participating in export markets for “milking machinery and dairy equipment”, although Lely Australia Pty Ltd is the Australian agent for the powerful European and US based dairy company ‘The Lely Group’, manufacturer and supplier of high tech and innovative products for the dairy sector. The Lely ‘Astronaut A3’ robotic milking system is at the cutting edge of industry technology. Other innovative products and systems offered to world markets by The Lely Group are illustrated below. Figure 17. Computer automated robotic sweepers for feed lanes and slatted walking areas

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 36 of 329

Figure 18. State of the art dairy cow living environment featuring free stalls and slatted walking areas

Figure 19. Transponder operated calf milk replacer feeding system and robotic lane sweeper

Capability Assessment of Australian Dairy Technology and Services ‐ AANC Pty Ltd, July 2010

Page 37 of 329

B.) Exported dairy product manufacturing equipment ‐ supply, installation, service and training Australia’s exports of ‘Milking Machines and Dairy Machinery’ would include machinery and equipment for dairy product manufacturing industries in offshore markets. Within the scope of the current assessment, it has not been possible to ascertain through the Bureau of Statistics or other agencies exactly which Australian companies are currently participating in these markets, but the following are a sample of prominent dairy manufacturers or associates which would appear to have the potential to export products or services under this category.

o Aggreko Australia Pacific Braeside, VIC www.aggreko.com.au o Sepak Industries Australia Ingleburn, NSW www.sepak.com.au o APV Australia Clayton South, VIC www.apv.com o Crown Stainless Dandenong South, VIC www.crownsheetmetal.co.nz o Diverse Welding Services Malaga, WA www.diversewelding.com o Flex Pack Service & Supplies Oakleigh, VIC www.flexpackservice.com.au o JL Lennard Silverwater, NSW www.jllennard.com.au o Teralba Industries Campbelltown, NSW www.teralba.com o WR and D Wells South Melbourne, VIC www.wrdwells.com o Spray Nozzle Engineering Mentone, VIC www.spraynozzle.com.au o Tasweld Engineering Warrnambool, VIC www.tasweldengineering.com.au

For further detail on each of these companies the reader is referred to EXCEL SUPPORT FILE: “Australian Dairy Industry Supply Chain Ver 4.xls”