Business Accounting - Dr. Nishikant Jha

1108

Business Accounting v. 2.0

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Business Accounting - Dr. Nishikant Jha

Business Accounting

v. 2.0

www.princexml.com

Prince - Non-commercial License

This document was created with Prince, a great way of getting web content onto paper.

This is the book Business Accounting (v. 2.0).

This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/3.0/) license. See the license for more details, but that basically means you can share this book as long as youcredit the author (but see below), don't make money from it, and do make it available to everyone else under thesame terms.

This book was accessible as of December 29, 2012, and it was downloaded then by Andy Schmitz(http://lardbucket.org) in an effort to preserve the availability of this book.

Normally, the author and publisher would be credited here. However, the publisher has asked for the customaryCreative Commons attribution to the original publisher, authors, title, and book URI to be removed. Additionally,per the publisher's request, their name has been removed in some passages. More information is available on thisproject's attribution page (http://2012books.lardbucket.org/attribution.html?utm_source=header).

For more information on the source of this book, or why it is available for free, please see the project's home page(http://2012books.lardbucket.org/). You can browse or download additional books there.

ii

Table of Contents

About the Authors................................................................................................................. 1

Acknowledgments ................................................................................................................. 4

Preface..................................................................................................................................... 6

Chapter 1: What Is Financial Accounting, and Why Is It Important? ...................... 10Making Good Financial Decisions about an Organization ....................................................................... 11

Incorporation and the Trading of Capital Shares..................................................................................... 21

Using Financial Accounting for Wise Decision Making ........................................................................... 31

End-of-Chapter Exercises ............................................................................................................................ 40

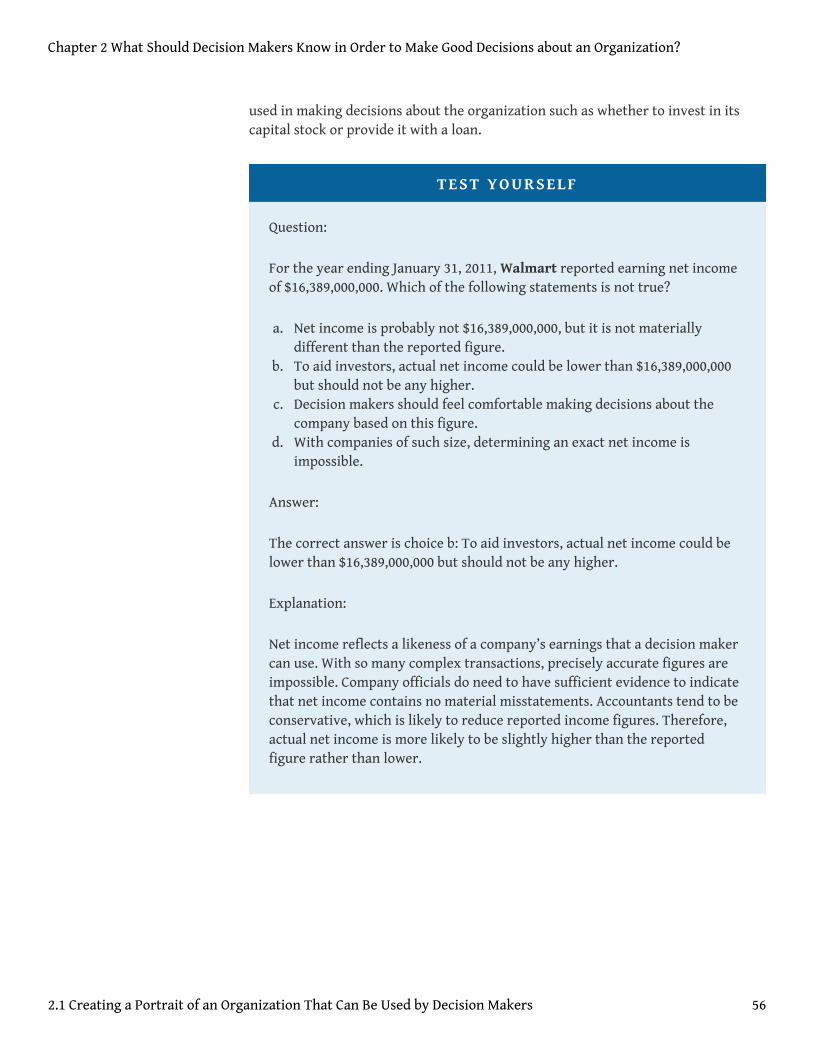

Chapter 2: What Should Decision Makers Know in Order to Make Good Decisions

about an Organization? ..................................................................................................... 50Creating a Portrait of an Organization That Can Be Used by Decision Makers.....................................51

Dealing with Uncertainty............................................................................................................................ 58

The Need for Accounting Standards .......................................................................................................... 62

Four Essential Terms Encountered in Financial Accounting .................................................................. 72

End-of-Chapter Exercises ............................................................................................................................ 86

Chapter 3: How Is Financial Information Delivered to Decision Makers Such as

Investors and Creditors? ................................................................................................... 96Construction of Financial Statements Beginning with the Income Statement .....................................97

Reported Profitability and the Impact of Conservatism........................................................................ 107

Increasing the Net Assets of a Company.................................................................................................. 117

Reporting a Balance Sheet and a Statement of Cash Flows ................................................................... 126

End-of-Chapter Exercises .......................................................................................................................... 136

Chapter 4: How Does an Organization Accumulate and Organize the Information

Necessary to Create Financial Statements?................................................................. 155The Essential Role of Transaction Analysis ............................................................................................. 156

Understanding the Effects Caused by Common Transactions .............................................................. 164

Double-Entry Bookkeeping ....................................................................................................................... 174

Recording Transactions Using Journal Entries ....................................................................................... 181

Connecting the Journal to the Ledger...................................................................................................... 191

End-of-Chapter Exercises .......................................................................................................................... 206

iii

Chapter 5: Why Is Financial Information Adjusted Prior to the Production of

Financial Statements? ...................................................................................................... 220The Need for Adjusting Entries ................................................................................................................ 221

Preparing Various Adjusting Entries ....................................................................................................... 229

Preparation of Financial Statements ....................................................................................................... 240

End-of-Chapter Exercises .......................................................................................................................... 248

Chapter 6: Why Should Decision Makers Trust Financial Statements? ................ 269The Need for the Securities and Exchange Commission........................................................................ 270

The Role of the Independent Auditor in Financial Reporting............................................................... 277

Performing an Audit .................................................................................................................................. 284

The Need for Internal Control .................................................................................................................. 291

The Purpose and Content of an Independent Auditor’s Report............................................................ 296

End-of-Chapter Exercises .......................................................................................................................... 302

Chapter 7: In Financial Reporting, What Information Is Conveyed about

Receivables? ....................................................................................................................... 312Accounts Receivable and Net Realizable Value ...................................................................................... 313

Accounting for Uncollectible Accounts ................................................................................................... 320

The Problem with Estimations ................................................................................................................. 327

The Actual Estimation of Uncollectible Accounts .................................................................................. 335

Reporting Foreign Currency Balances ..................................................................................................... 345

A Company’s Vital Signs—Accounts Receivable ..................................................................................... 352

End-of-Chapter Exercises .......................................................................................................................... 360

Chapter 8: How Does a Company Gather Information about Its Inventory? ........ 382Determining and Reporting the Cost of Inventory ................................................................................ 383

Perpetual and Periodic Inventory Systems ............................................................................................. 391

The Calculation of Cost of Goods Sold...................................................................................................... 400

Reporting Inventory at Lower of Cost or Market ................................................................................... 409

Determining Inventory on Hand .............................................................................................................. 416

End-of-Chapter Exercises .......................................................................................................................... 424

iv

Chapter 9: Why Does a Company Need a Cost Flow Assumption in Reporting

Inventory? .......................................................................................................................... 445The Necessity of Adopting a Cost Flow Assumption .............................................................................. 446

The Selection of a Cost Flow Assumption for Reporting Purposes ....................................................... 457

Problems with Applying LIFO ................................................................................................................... 464

Merging Periodic and Perpetual Inventory Systems with a Cost Flow Assumption...........................472

Applying LIFO and Averaging to Determine Reported Inventory Balances ........................................ 479

Analyzing Reported Inventory Figures.................................................................................................... 490

End-of-Chapter Exercises .......................................................................................................................... 500

Chapter 10: In a Set of Financial Statements, What Information Is Conveyed

about Property and Equipment?.................................................................................... 526The Reporting of Property and Equipment............................................................................................. 527

Determining Historical Cost and Depreciation Expense........................................................................ 534

Recording Depreciation Expense for a Partial Year ............................................................................... 542

Alternative Depreciation Patterns and the Recording of a Wasting Asset .......................................... 549

Recording Asset Exchanges and Expenditures That Affect Older Assets ............................................. 561

Reporting Land Improvements and Impairments in the Value of Property and Equipment ............571

End-of-Chapter Exercises .......................................................................................................................... 581

Chapter 11: In a Set of Financial Statements, What Information Is Conveyed

about Intangible Assets?.................................................................................................. 605Identifying and Accounting for Intangible Assets.................................................................................. 606

Balance Sheet Reporting of Intangible Assets ........................................................................................ 614

Recognizing Intangible Assets Owned by a Subsidiary .......................................................................... 622

Accounting for Research and Development............................................................................................ 631

Acquiring an Asset with Future Cash Payments ..................................................................................... 638

End-of-Chapter Exercises .......................................................................................................................... 653

Chapter 12: In a Set of Financial Statements, What Information Is Conveyed

about Equity Investments?.............................................................................................. 677Accounting for Investments in Trading Securities ................................................................................ 678

Accounting for Investments in Securities That Are Classified as Available-for-Sale .........................688

Accounting for Investments by Means of the Equity Method............................................................... 697

Reporting Consolidated Financial Statements........................................................................................ 709

End-of-Chapter Exercises .......................................................................................................................... 720

v

Chapter 13: In a Set of Financial Statements, What Information Is Conveyed

about Current and Contingent Liabilities? .................................................................. 745The Basic Reporting of Liabilities............................................................................................................. 746

Reporting Current Liabilities Such as Gift Cards .................................................................................... 753

Accounting for Contingencies .................................................................................................................. 760

Accounting for Product Warranties......................................................................................................... 771

End-of-Chapter Exercises .......................................................................................................................... 782

Chapter 14: In a Set of Financial Statements, What Information Is Conveyed

about Noncurrent Liabilities Such as Bonds? ............................................................. 804Debt Financing ........................................................................................................................................... 805

Issuance of Notes and Bonds..................................................................................................................... 810

Accounting for Zero-Coupon Bonds......................................................................................................... 820

Pricing and Reporting Term Bonds.......................................................................................................... 832

Issuing and Accounting for Serial Bonds................................................................................................. 841

Bonds with Other Than Annual Interest Payments................................................................................ 852

End-of-Chapter Exercises .......................................................................................................................... 859

Chapter 15: In a Set of Financial Statements, What Information Is Conveyed

about Other Noncurrent Liabilities?............................................................................. 879Accounting for Leases................................................................................................................................ 880

Operating Leases versus Capital Leases ................................................................................................... 890

Recognition of Deferred Income Taxes.................................................................................................... 899

Reporting Postretirement Benefits .......................................................................................................... 907

End-of-Chapter Exercises .......................................................................................................................... 918

Chapter 16: In a Set of Financial Statements, What Information Is Conveyed

about Shareholders’ Equity? .......................................................................................... 941Selecting a Legal Form for a Business ...................................................................................................... 942

The Issuance of Common Stock ................................................................................................................ 948

Issuing and Accounting for Preferred Stock and Treasury Stock......................................................... 957

The Issuance of Cash and Stock Dividends.............................................................................................. 967

The Computation of Earnings per Share ................................................................................................. 978

End-of-Chapter Exercises .......................................................................................................................... 986

vi

Chapter 17: In a Set of Financial Statements, What Information Is Conveyed by

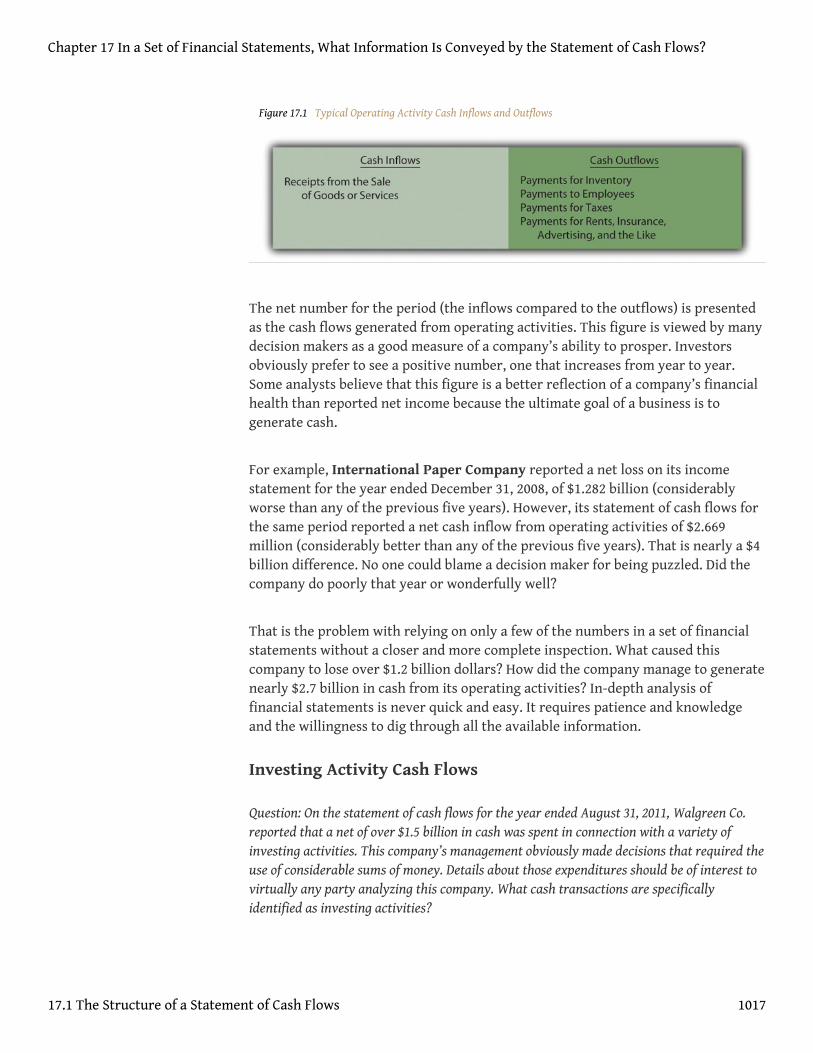

the Statement of Cash Flows?....................................................................................... 1012The Structure of a Statement of Cash Flows ......................................................................................... 1013

Cash Flows from Operating Activities: The Direct Method ................................................................. 1024

Cash Flows from Operating Activities: The Indirect Method .............................................................. 1036

Cash Flows from Investing and Financing Activities ........................................................................... 1046

Appendix: Comprehensive Illustration—Statement of Cash Flows .................................................... 1063

End-of-Chapter Exercises ........................................................................................................................ 1074

Appendix: Present Value Tables .................................................................................. 1099

vii

About the Authors

Joe Ben Hoyle, University of Richmond

Joe Hoyle is an associate professor of accounting at theRobins School of Business at the University ofRichmond. In 2006, he was named by BusinessWeek asone of twenty-six favorite undergraduate businessprofessors in the United States. In 2007, he was selectedas the Virginia Professor of the Year by the CarnegieFoundation for the Advancement of Teaching and theCouncil for the Advancement and Support of Education.In 2009, he was judged to be one of the one hundredmost influential members of the accounting professionby Accounting Today.

Joe has two market-leading textbooks published with McGraw-Hill—AdvancedAccounting (11th edition, 2012) and Essentials of Advanced Accounting (5th edition,2012), both coauthored with Tom Schaefer of the University of Notre Dame and TimDoupnik of the University of South Carolina.

At the Robins School of Business, Joe teaches Fundamentals of Financial Accounting,Intermediate Financial Accounting I, Intermediate Financial Accounting II, andAdvanced Financial Accounting. He earned his BA degree in accounting from DukeUniversity and his MA degree in business and economics, with a minor in education,from Appalachian State University. He has written numerous articles and continuesto make many presentations around the country on teaching excellence. Hemaintains a blog on teaching at http://www.joehoyle-teaching.blogspot.com/.

Joe also has three decades of experience operating his own CPA (Certified PublicAccountant) Exam review programs. In 2008, he created CPA Review for Free(http://www.CPAreviewforFREE.com), which provides thousands of free questionsto help accountants around the world prepare for the CPA Exam.

Joe and his wife, Sarah, have four children and four grandchildren.

1

C. J. Skender, University of North Carolina at ChapelHill

C. J. Skender has received two dozen teaching awards atthe University of North Carolina’s Kenan-FlaglerBusiness School (fourteen awards), at Duke University’sFuqua School of Business (five awards), and at NorthCarolina State University (five awards). He has beenincluded among the outstanding Fuqua faculty in foureditions of the Businessweek Guide to the Best BusinessSchools. His classes were highlighted in Businessweek(http://www.businessweek.com) and Sports Illustrated(http://sportsillustrated.cnn.com) in 2006. C. J. wasfeatured in “The Last Word” in the April 2008 Journal ofAccountancy. He was voted best professor in The Daily TarHeel: Carolina’s Finest annual awards issue in 2011.

C. J. has served as a training consultant on three continents for organizations, suchas GlaxoSmithKline, IBM, Siemens, Starwood, and Wells Fargo. He was inductedinto the Wells Fargo Hall of Fame in 2003 for lifetime achievement. C. J. hasdeveloped and delivered various executive education seminars as well as CPA, CMA(Certified Management Accountant), and CIA (Certified Internal Auditor) reviewcourses. For six years, he lectured simultaneously in the state, Carolina, and DukeCPA preparatory classes. For seven years, C. J. taught financial accounting andmanagerial accounting on cable television in the Research Triangle area. Hisscholarly work has been published in TAXES and the Journal of Accounting Education.

C. J. Skender was born in Harrisburg, Pennsylvania, in 1954. He captained threesports at Susquehanna Township High School. C. J. holds academic degrees fromLehigh University and Duke University. He attended Lehigh on a basketballscholarship and graduated magna cum laude. C. J. worked as an auditor for DeloitteHaskins & Sells in Philadelphia. He has attained eleven professional designations inaccounting, financial planning, insurance, and management. C. J. has taught morethan five hundred sections of college courses and more than twenty-five thousandstudents in his academic career. He was tapped into the Golden Chain Honor Societyat North Carolina State University in 1985 and was named Alumni DistinguishedProfessor there in 1992. C. J. was presented the Outstanding Educator Award by theNorth Carolina Association of Certified Public Accountants in 1995. At theUniversity of North Carolina, he has received three Weatherspoons (2000, 2004, and2007) as well as the James M. Johnston Teaching Excellence Award in 2005.

About the Authors

2

C. J. and his wife, Mary Anne, are the parents of two sons and one daughter: Charles(1979), Timothy (1983), and Corey (1987). They have one granddaughter: Riley(2010). C. J. and his wife reside in Raleigh, North Carolina.

About the Authors

3

Acknowledgments

A textbook of this size owes a genuine debt of gratitude to a long list of wonderfulpeople. We want to acknowledge the time, energy, ideas, and patience invested byeach of the following individuals.

Second Edition Book Development and Support

A warm thank you to Jeff Shelstad, Michael Boezi, Pam Hersperger, Becky Knauer,Chrissy Chimi, Ellen Bohnstengel, and Jason Kypros.

Textbook Reviewers

• James John Aitken, Central Michigan University• Pervaiz Alam, Kent State University• Somer Anderson, Fontbonne University• Jane Austin, Oklahoma City University• Richard Baldwin, Johnson & Wales University, Friedman Center,

Graduate School• Sheila Bedford, American University• Bruce Branson, North Carolina State University• Rada Brooks, University of California, Berkeley, Haas School of

Business• Helen Brubeck, San Jose State University• Charles Bunn, Wake Technical Community College• Stan Clark, University of Southern Mississippi• Sue Cunningham, Rowan Cabarrus Community College• Betty David, Francis Marion University• Carolyn Dreher, Southern Methodist University, Cox School of Business• Wilbert Harri, Pima Community College• Lori Holder-Webb, Simmons College School of Management• Ethan Kinory, Baruch College, City University of New York• Pamela Legner, College of DuPage• Randall Lewis, Spring Arbor University• Chao-Shin Liu, University of Notre Dame• Jane Mooney, Simmons College• Jason Nielsen, Harrisburg Area Community College• Larry Sayler, Greenville College• Rachel Siegel, Lyndon State College• David Sulzen, Ferrum College

4

• Diane Tanner, University of North Florida• Steven Thoede, Texas State University• Robin Thomas, North Carolina State University• Joyce van der Laan Smith, Richmond University• Wendy Wilson, Southern Methodist University• Gregory Yost, University of West Florida

The authors also appreciate the efforts of Claude Laflamme and Mike Donohue fromLyryx Learning. Their team helped develop the FLYX product that accompanies thistextbook.

Acknowledgments

5

Preface

How to Use This Book: From the Authors to the Students

If we have done our job properly during the creation of this textbook, it will be likeno other educational material that you have ever experienced. We literally set outto rethink the nature, structure, and purpose of college textbooks. Every featurethat you find here was designed to enhance student learning. We want this materialto be presented in a manner that is both innovative and effective.

The two of us have taught in college for over sixty years. Year in and year out,financial accounting has always seemed to us to be both interesting and relevant toeveryday life. We believe it is knowledge well worth acquiring. From the day westarted this project, we hoped to share our enthusiasm with you, to develop a bookthat you will find to be both readable and worth reading.

Historically, textbooks have been presented as dry monologues, a one-wayconversation that often seems to talk to the teacher more than to the student.“Boring” and “confusing” should never be synonymous with any aspect ofeducation. Instead, we seek to promote an active dialogue. Authors, teachers, andstudents should work together to create an environment where educationflourishes. We want you, the student, to understand the nature of our endeavor.After all, the only reason that this book exists is to aid you in learning financialaccounting. If you do not read the chapters because you find them boring or if youdo not understand the material that is included, no one benefits. We will havewasted our time.

We view this textbook as a guide. In constructing these seventeen chapters, we haveworked to lead you on a voyage through the world of business and financialreporting. We want to help you attain a usable knowledge of the principles offinancial accounting as well as an appreciation for its importance and logic. Bylearning its theory, presentation, and procedures, individuals become capable ofusing financial accounting to make prudent business decisions. That is an importantgoal regardless of the direction of your career. We have relied on our experience asteachers to highlight the aspects of this material that make it interesting, logical,and relevant.

6

Talk, though, is cheap. Saying that this book is different and interesting does notmake it so. Be a wise consumer. When someone tries to sell you something, forcethem to back up their claims.

So How Does This Book Work? What Makes It Special?

1. Every chapter is introduced with a short video in which one of theauthors provides an overview of the material and a discussion of itsimportance. Thus, students are never forced to begin reading blindly,struggling to put new subjects into an understandable context. Evenbefore the first written word, each chapter is explained through theopening video. Simply put, this introduction makes the subject mattermore understandable and your reading more interesting and efficient.We attempt to remove the mystery from every aspect of financialaccounting because we want you to be an effective learner.

2. This textbook is written entirely in a question-and-answer format. TheSocratic method has been used successfully for thousands of years tohelp students develop critical thinking skills. We do that here on everypage of every chapter. A question is posed and the answer is explained.Then, the next logical question is put forth to lead you through thematerial in a carefully constructed sequential pattern. Topics arepresented and analyzed as through a conversation. This format breakseach chapter down into easy-to-understand components. A chapter isnot thirty pages of seemingly unending material. Instead, it is twentyto forty questions and answers that put the information intomanageable segments with each new question logically following theprevious one.

3. All college textbooks present challenging material. However, that is noexcuse for allowing readers to become lost. Educational materialsshould be designed to enhance learning and not befuddle students. Atkey points throughout each chapter, we have placed multiple-choice(“Test Yourself”) questions along with our own carefully constructedanswers. These questions allow you to pause at regular intervals toverify that you understand the material that has been covered.Immediate feedback is always a key ingredient in successful learning.These questions and answers are strategically placed throughout everychapter to permit ongoing review and reinforcement of knowledge.

4. For a course such as financial accounting, each subject should relate insome manner to the real world of business. Therefore, every chapterincludes a discussion with a successful investment analyst about thematerial that has been presented. This expert provides an honest andopen assessment of financial accounting straight from the daily worldof high finance and serious business decisions. Every question, every

Preface

7

answer, and every topic need to connect directly to the world we allface. Students should always be curious about the relevance of everyaspect of a textbook’s coverage. We believe that it is helpful to considerthis material from the perspective of a person already working in thebusiness environment of the twenty-first century.

5. In many chapters, we talk about the current evolution occurring infinancial accounting as the United States considers the possibility ofmoving from following U.S. rules (U.S. GAAP) to internationalstandards (IFRS). The world is getting smaller as companies and theiroperations become more global. At the same time, technology makesthe amount of available information from around the world almostbeyond comprehension. Accountants work to help make this mass ofinformation easier to understand and manage. Consequently,throughout this textbook, we interview one of the partners of a largeinternational accounting firm about the impact of possibly changingfinancial accounting in this country so that all reporting abides byinternational accounting rules rather than solely U.S. standards.

6. Each chapter ends with a final video. However, instead of merelyrehashing the material one last time in a repetitive fashion, wechallenge you to select the five most important elements of eachchapter. Some coverage is simply more important than others. That isa reasonable expectation. Part of a successful education is gaining theinsight to make such evaluations. Then, we provide you with our owntop five. The lists do not need to match; in fact, it is unlikely that theywill be the same. That is not the purpose. This exercise shouldencourage you to weigh the significance of the material. What reallymakes a difference based on your understanding of financialaccounting? In what areas should you focus your attention?

Is This Book Unique?

We truly believe so. We believe that it has an educationally creative structure thatwill promote your learning and make the educational process more effective andmore interesting:

• Opening videos for the chapters• Socratic method used consistently throughout the book• Embedded multiple-choice questions• Discussions with both an investment analyst and an international

accounting expert• Closing videos establishing top-five lists for each chapter

Preface

8

• Two end-of-chapter “video problems” in each chapter where questionsare posed and a video is available so students can watch one of theauthors explain his version of the answer

• A “research assignment” at the end of each chapter designed to helpstudents uncover and analyze the wealth of information available onthe Internet

In addition, all the end-of-chapter material in the second edition (questions, true orfalse, multiple-choice, and problems) has been rewritten and expanded. The sheernumber of available end-of-chapter material has been doubled and, in somechapters, tripled.

Every page of this book, every word in fact, has been created to encourage andenhance your understanding. We want you to benefit from our coverage, but just asimportantly, we want you to enjoy the process. When presented correctly, learningcan be fun and, we believe, should be fun.

Please feel free to contact us if you have any suggestions for improvement. Wewould love to hear from you.

Finally, this book is dedicated to our wives and our families. It is also dedicated tothe thousands of wonderful teachers across the world who walk into countlesscollege classrooms each day and make learning happen for their students. Youmake the world a better place to be.

Joe Hoyle, University of Richmond ([email protected])

C. J. Skender, University of North Carolina at Chapel Hill

Preface

9

Chapter 1

What Is Financial Accounting, and Why Is It Important?

Video Clip

(click to see video)

In this video, Professor Joe Hoyle introduces the essential points covered in Chapter 1 "What Is FinancialAccounting, and Why Is It Important?".

10

1.1 Making Good Financial Decisions about an Organization

LEARNING OBJECTIVES

At the end of this section, students should be able to meet the followingobjectives:

1. Define “financial accounting.”2. Understand the connection between financial accounting and the

communication of information about an organization.3. Explain the importance of gaining an understanding of financial

accounting.4. List decisions that an individual might make about an organization.5. Differentiate between financial accounting and managerial accounting.6. Provide reasons for individuals to study the financial accounting

information supplied by their employers.

Financial Accounting and Information

Question: In the June 30, 2011, edition of The Wall Street Journal, numerous headlinesdescribed the recent activities of various business organizations. Here are just a few:

“TMX and LSE Give Up on Planned Merger”

“Ally Financial Faces Charge for Mortgage Losses”

“HomeAway Jumps 49% in Debut”

“Ad-Seller Acquiring Myspace for a Song”

Millions of individuals around the world read such stories each day with rapt interest. Fromteen-agers to elderly billionaires, this type of information is analyzed obsessively. How arethese people able to understand all the data and details being provided? For most, the secretis straightforward: a strong knowledge of financial accounting.

This textbook provides an introduction to financial accounting. A logical place to begin suchan exploration is to ask the obvious question: What is financial accounting?

Chapter 1 What Is Financial Accounting, and Why Is It Important?

11

Answer: In simplest terms, financial accounting1 is the communication ofinformation about a business or other type of organization (such as a charity orgovernment) so that individuals can assess its financial health and future prospects.No single word is more relevant to financial accounting than “information.”Whether it is gathering monetary information about a specific organization, puttingthat information into a format designed to enhance communication, or analyzingthe information that is conveyed, financial accounting is intertwined withinformation.

In today’s world, information is king. Financial accounting provides the rules andstructure for the conveyance of financial information about businesses (and otherorganizations) to maximize clarity and understanding. Although a wide array oforganizations present financial information to interested parties, this bookprimarily focuses on the reporting of businesses because that is where the widestuse of financial accounting occurs.

organization → reports information based on the principles of financial accounting→ interested individuals assess financial health and future prospects

At any point in time, some businesses are poised to prosper while others teeter onthe verge of failure. Many people want to be able to evaluate the degree of successachieved to date by a particular organization as well as its prospects for the future.They seek information and the knowledge that comes from understanding thatinformation. How well did The Coca Cola Company do last year, and how wellshould this business do in the coming year? Those are simple questions to ask, butthe answers can make the difference between earning millions and losing millions.

Financial accounting provides data that these individuals need and want.

Financial Accounting and Wise Decision Making

Question: Every semester, most college students are enrolled in several courses as well asparticipate in numerous outside activities. All of these compete for the hours that make upeach person’s day. Why should a student invest valuable time to learn the principles offinancial accounting? Why should anyone be concerned with the information communicatedabout an organization? What makes financial accounting important?

1. The communication offinancial information about abusiness or other type oforganization to externalaudiences to help them assessits financial health and futureprospects.

Chapter 1 What Is Financial Accounting, and Why Is It Important?

1.1 Making Good Financial Decisions about an Organization 12

Answer: Many possible benefits can be gained from acquiring a strong knowledge offinancial accounting because it provides the accepted methods for communicatingrelevant information about an organization. In this book, justification for theserious study that is required to master this subject matter is simple andstraightforward. Obtaining a working knowledge of financial accounting and itsunderlying principles enables a person to understand the information conveyedabout an organization so that better decisions can be made.

Around the world each day, millions of individuals make critical judgments aboutthe businesses and other organizations they encounter. Developing the ability toanalyze financial information and then making use of that knowledge to arrive atsound decisions can be critically important. Whether an organization is as giganticas Walmart or as tiny as a local convenience store, individuals have many, variedreasons for studying the information that is available.

As just a single example, a recent college graduate looking at full-time employmentopportunities might want to determine the probability that Company A will have abrighter economic future than Company B. Although such decisions can never becorrect 100 percent of the time, knowledge of financial accounting and theinformation being communicated greatly increases the likelihood of success. As KofiAnnan, former secretary-general of the United Nations, has said, “Knowledge ispower. Information is liberating.”See http://www.deepsky.com/~madmagic/kofi.html.

Thus, the ultimate purpose of this book is to provide students with a richunderstanding of the rules and nuances of financial accounting so they can evaluateavailable information about organizations and then make good decisions. In theworld of business, most successful individuals have developed this ability and areable to use it to achieve their investing and career objectives.

Common Decisions about Organizations

Question: Knowledge of financial accounting assists individuals in making informeddecisions about businesses and other organizations. What kinds of evaluations are typicallymade? For example, assume that a former student—one who recently graduated fromcollege—has been assigned the task of analyzing financial data provided by the AcmeCompany. What real-life decisions could a person be facing where an understanding offinancial accounting would be beneficial?

Chapter 1 What Is Financial Accounting, and Why Is It Important?

1.1 Making Good Financial Decisions about an Organization 13

Answer: The number of possible judgments that an individual might need to makeabout a business or other organization is close to unlimited. However, many ofthese decisions deal with the current financial health and prospects for futuresuccess. In order to analyze available data to make such assessments, a workingknowledge of financial accounting is invaluable. The more in-depth theunderstanding is of those principles, the more likely the person will be able to usethe information to arrive at the best possible choices. Common examples includethe following:

• Should a bank loan money to the Acme Company? The college graduatemight be employed by a bank to work in its corporate lendingdepartment. Assume, for example, that the Acme Company is a localbusiness that has applied to the bank for a large loan so that it canexpand. The graduate has been instructed by bank management toprepare an assessment of Acme to determine if it is likely to befinancially healthy in the future so that it will be able to repay theborrowed money when due. A correct decision to provide the loaneventually earns a profit for the bank because Acme will be required topay an extra amount (known as interest2) on the money borrowed.Conversely, an incorrect analysis of the information could lead to asubstantial loss if the loan is granted and Acme is unable to fulfill itsobligation. Bank officials must weigh the potential for profit againstthe risk of loss. That is a daily challenge in virtually all businesses. Theformer student’s career with the bank might depend on the ability toanalyze financial accounting data and then make appropriate choicesabout the actions to be taken. Should a loan be made to this company?

• Should another business make sales on credit to the Acme Company?The college graduate might hold a job as a credit analyst for amanufacturing company that sells its products to retail stores. Assumethat Acme is a relatively new retailer that wants to buy goods(inventory) on credit from this manufacturer to sell in its stores. Theformer student must judge whether to permit Acme to buymerchandise now but wait until later to remit the money. If paymentsare received on a timely basis, the manufacturer will have found a newoutlet for its merchandise. Profits will likely increase. Unfortunately,Acme could also make expensive purchases but then be unable to makepayment, creating significant losses for the manufacturer. Again, thepossibility of profit must be measured against the chance for loss.

• Should an individual invest money to become one of the owners of theAcme Company? The college graduate might be employed by a firmthat provides financial advice to its clients. Assume that the firm ispresently considering whether to recommend acquisition of ownershipshares of Acme as a good investment strategy. The former student hasbeen assigned to gather and evaluate relevant financial information as

2. The charge for using moneyover time, often associatedwith long-term loans; even ifnot specifically mentioned inthe debt agreement, financialaccounting rules require it tobe computed and reportedbased on a reasonable rate.

Chapter 1 What Is Financial Accounting, and Why Is It Important?

1.1 Making Good Financial Decisions about an Organization 14

a basis for this decision. If Acme is poised to become larger and moreprofitable, its ownership shares will likely rise in value over time,earning money for the firm’s clients. Conversely, if the prospects forAcme appear to be dim, the value of these shares might start to drop(possibly precipitously) so that the investment firm should avoidsuggesting the purchase of an ownership interest in this business.

Success in life—especially in business—frequently results from being able to makeappropriate decisions. Many economic choices, such as those described earlier,depend on a person’s ability to understand and make use of financial informationabout organizations. That financial information is produced and presented inaccordance with the rules and principles underlying financial accounting.

Chapter 1 What Is Financial Accounting, and Why Is It Important?

1.1 Making Good Financial Decisions about an Organization 15

TEST YOURSELF

Question:

James Esposito is a college student who has just completed a class infinancial accounting. He earned a good grade and wants to make use of hisknowledge. He wants to invest $10,000 that he recently inherited from adistant uncle. In which of the following decisions is Esposito most likely tohave used his understanding of financial accounting?

a. He decides to deposit the money in a bank to earn interest.b. He decides to buy ownership shares in Microsoft Corporation in hopes

that they will appreciate in value.c. He decides to trade in his old car and buy a new one that uses less

gasoline.d. He decides to buy a new computer so that he can make money by typing

papers for his classmates.

Answer:

The correct answer is choice b: He decides to buy ownership shares inMicrosoft Corporation in hopes that they will appreciate in value.

Explanation:

All of these are potentially good economic decisions. However, financialaccounting focuses on conveying data to help reflect the financial healthand prospects of organizations. His decision to buy ownership shares ofMicrosoft rather than any other company indicates that he believes thatMicrosoft is poised to grow and prosper. This decision is exactly the typethat investors around the world make each day with the use of theirknowledge of financial accounting.

Financial Accounting versus Managerial Accounting

Question: A great number of possible decisions could be addressed in connection with anybusiness. Is an understanding of financial accounting relevant to all decisions made about anorganization? What about the following?

• Should a business buy a building to serve as its new headquarters or rent afacility instead?

Chapter 1 What Is Financial Accounting, and Why Is It Important?

1.1 Making Good Financial Decisions about an Organization 16

• What price should a data processing company charge customers for itsservices?

• Should advertisements to alert the public about a new product be carried onthe Internet or on television?

Answer: Decisions such as these three are extremely important for the success ofany organization. However, these examples are not made about the reportingorganization. Rather, they are made within the organization in connection withsome element of its operations.

The general term “accounting” refers to the communication of financialinformation for decision-making purposes. Accounting is then further subdividedinto (a) financial accounting and (b) managerial accounting3.Tax accounting isanother distinct branch of accounting. It is less focused on decision making andmore on providing information needed by a business to comply with allgovernment rules and regulations. Even in tax accounting, though, decision makingis important as businesses seek to take all possible legal actions to minimize taxpayments. Financial accounting is the subject explored in this textbook. It focuseson conveying relevant data (primarily to external parties) about an organization(such as Motorola Mobility or Starbucks) as a whole so that wise decisions can bemade. Thus, questions such as the following all fall within the discussion offinancial accounting:

• Do we loan money to the Acme Company?• Do we sell on credit to the Acme Company?• Do we recommend that our clients buy the ownership shares of the

Acme Company?

These decisions pertain to an overall evaluation of the financial health and futureprospects of the Acme Company.

Managerial accounting is the subject of other books and other courses. This secondbranch of accounting refers to the communication of information within anorganization so that internal decisions (such as whether to buy or rent a building)can be made in an appropriate manner. Individuals studying an organization as awhole have different goals than do internal parties making operational decisions.Thus, many unique characteristics have developed in connection with each of thesetwo branches of accounting. Financial accounting and managerial accounting haveevolved independently over the decades to address the specific needs of the users

3. The communication offinancial information within anorganization so internaldecisions can be made in anappropriate manner.

Chapter 1 What Is Financial Accounting, and Why Is It Important?

1.1 Making Good Financial Decisions about an Organization 17

being served and the decisions being made. This textbook is designed to explainthose attributes that are fundamental to attaining a useable understanding offinancial accounting.

It is not that one of these areas of accounting is more useful or more important thanthe other. Financial accounting and managerial accounting have simply beencreated to achieve different objectives. They both do their jobs well, but they do nothave the same jobs.

TEST YOURSELF

Question:

Janet Wineston is vice president of the State Bank of Main Street. Here arefour decisions that she made at her job today. Which of these decisions waslikely to have required her to make use of her knowledge of financialaccounting?

a. She gave one of the tellers who works at the bank a pay raise.b. She hired an advertising consultant to produce a television commercial

for the bank.c. She granted a $300,000 loan to one company but not another.d. She decided on the rate of interest that would be paid to customers on a

new type of savings account.

Answer:

The correct answer is choice c: She granted a $300,000 loan to one companybut not another.

Explanation:

Financial accounting focuses on decisions about organizations. When moneywas loaned to one company but not the other, Wineston was makingdecisions about both. She must have viewed one as more financially healthythan the other. Her other three decisions all relate to internal operations.Accounting information can certainly help in arriving at proper choices forthese three, but it is managerial accounting that is designed to produce theneeded data for such decisions.

Chapter 1 What Is Financial Accounting, and Why Is It Important?

1.1 Making Good Financial Decisions about an Organization 18

Financial Accounting Information and Company Employees

Question: Financial accounting refers to the conveyance of information about anorganization as a whole and is most frequently distributed to assist outside decision makers.Does a person who is employed by an organization care about the financial accounting datathat is reported? Why should an employee in the marketing or personnel department of theAcme Company be interested in the financial information that this business generates anddistributes?

Answer: Financial accounting is designed to portray the overall financial conditionand prospects of an organization. Virtually every employee should be interested instudying that information to judge future employment prospects. A business that isdoing well will possibly award larger pay raises or perhaps significant end-of-yearcash bonuses. A financially healthy organization can afford to hire new employees,buy additional equipment, or pursue major new initiatives. Conversely, when abusiness is struggling and prospects are dim, employees might anticipate layoffs,pay cuts, or reductions in resources.

Thus, although financial accounting information is directed to outside decisionmakers, employees should be keenly interested in the financial health of their ownorganization. No one wants to be clueless as to whether their employer is headedfor prosperity or bankruptcy. In reality, employees are often the most avid readersof the financial accounting information distributed by employers because theresults can have such an immediate and direct impact on their jobs and, hence,their lives.

Chapter 1 What Is Financial Accounting, and Why Is It Important?

1.1 Making Good Financial Decisions about an Organization 19

KEY TAKEAWAY

Financial accounting encompasses the rules and procedures covering theconveyance of monetary information to describe a business or otherorganization. Individuals who attain a sufficient level of knowledge offinancial accounting can then utilize this information to make decisionsbased on the organization’s perceived financial health and future prospects.Such decisions might include assessing employment potential, lendingmoney, granting credit, and buying or selling ownership shares. However,financial accounting does not address issues that are purely of an internalnature, such as whether an organization should buy or lease equipment orthe level of pay raises. Information to guide such internal decisions isgenerated according to managerial accounting rules and procedures that areintroduced in other books and courses. Although financial accounting is notdirected toward the inner workings of an organization, most employees areinterested in the resulting information because it helps them assess thefuture of their employer.

Chapter 1 What Is Financial Accounting, and Why Is It Important?

1.1 Making Good Financial Decisions about an Organization 20

1.2 Incorporation and the Trading of Capital Shares

LEARNING OBJECTIVES

At the end of this section, students should be able to meet the followingobjectives:

1. Define incorporation.2. Explain the popularity of investing in the capital stock of a corporation.3. Discuss the necessity and purpose of a board of directors.4. List the potential benefits gained from acquiring capital stock.

The Ownership Shares of an Incorporated Business

Question: In discussing possible decisions that could be made about a business organization,ownership shares were mentioned. Virtually every day, on television, in newspapers, or onthe Internet, mention is made that the shares of one company or another have gone up ordown in price because of trading on one of the stock markets. Why does a person acquireownership shares of a business such as Capital One or Intel?

Answer: In the United States, as well as in many other countries, owners of abusiness can apply to the state government to become identified as an entity legallyset apart from its owners. This process is referred to as incorporation4. Therefore,a corporation5 is an organization that has been formally recognized by the stategovernment as a separate legal entity that can act independently of its owners. Abusiness that has not been incorporated is either a sole proprietorship6 (oneowner) or a partnership7 (more than one owner). These businesses are not separatefrom their ownership.

As will be discussed in detail in a later chapter, several advantages are gained fromincorporation. One is especially important in connection with the study of financialaccounting. A corporation has the ability to obtain monetary resources by selling(also known as issuing) capital shares that allow investors to become owners. Theyare then known as stockholders8 or shareholders9.

4. Legal process by which ownersof an organization apply to astate government to have itidentified as an entity legallyseparate from its owners (acorporation); corporations arethe legal form of mostbusinesses of any size in theUnited States.

5. An organization that has beenformally recognized by thestate government as a separatelegal entity so that it can sellownership shares to raisemoney for capital expendituresand operations.

6. An unincorporated businesscreated, owned, and operatedby a single individual; thebusiness is not legally separatefrom its owner.

7. An unincorporated businesscreated, owned, and operatedby more than one individual;the business is not legallyseparate from its owners.

8. Individuals or organizationsthat hold the ownership sharesof capital stock of acorporation; same asshareholders.

9. Individuals or organizationsthat hold the ownership sharesof capital stock of acorporation; same asstockholders.

Chapter 1 What Is Financial Accounting, and Why Is It Important?

21

Millions of corporations operate in the United States. The Walt Disney Companyand General Electric are just two well-known examples of corporations. They existas legal entities completely distinct from the multitude of individuals andorganizations that possess their ownership shares (also known as equity or capitalstock10).

Any investor who acquires one or more shares of the capital stock of a corporationbecomes an owner and has all of the rights that are specified by the stategovernment or on the stock certificate. The number of shares and owners can bestaggering. At the end of 2010, stockholders held over 2.3 billion shares of TheCoca-Cola Company. Thus, possession of one share of the capital stock of TheCoca-Cola Company provided a person with approximately a 1/2,300,000,000thpart of the ownership.

One of the great advantages of incorporation is the ease by which most capital stockcan be exchanged. For most companies, investors are able to buy or sell ownershipshares on stock exchanges in a matter of moments. In contrast, sole proprietorshipsand partnerships rarely sell capital shares. Without the separation provided byincorporation, a clear distinction between owner and business does not exist. Forexample, debts incurred by a business that is a sole proprietorship or partnershipmay ultimately have to be satisfied by the owner personally. Thus, individuals tendto avoid making investments in unincorporated businesses unless they can beinvolved directly in the management. However, partnerships and soleproprietorships still remain popular because they are easy to create and offerpossible income tax benefits as will be described in a later chapter.

If traded on a stock exchange, shares of the capital stock of a corporationcontinually go up and down in value based on myriad factors, including theperceived financial health and future prospects of the organization. As an example,during trading on July 1, 2011, the price of an ownership share of Intel rose by $0.37to $22.53, while a share of Capital One went up by $0.98 to $52.65.

For countless individuals and groups around the world, the most popular method ofinvestment is through the purchase and sell of these capital shares of corporateownership. Although many other types of investment opportunities are available(such as the acquisition of gold or land), few come close to evoking the level ofinterest of capital stock.The most prevalent form of capital stock is common stockso that these two terms have come to be used somewhat interchangeably. As will bediscussed in a later chapter, the capital stock of some corporations is made up ofboth common stock and preferred stock. On the New York Stock Exchange11 alone,billions of shares are bought and sold every business day at a wide range of prices.

10. Ownership (equity) shares ofstock in a corporation that areissued to raise monetaryfinancing for capitalexpenditures and operations.

11. Organized stock market thatefficiently matches buyers andsellers of capital stock at amutually agreed-upon priceallowing ownership incompanies to change handseasily. The New York StockExchange is the largest stockexchange in the world followedby NASDAQ, the London StockExchange, the Tokyo StockExchange, and the ShanghaiStock Exchange.

Chapter 1 What Is Financial Accounting, and Why Is It Important?

1.2 Incorporation and the Trading of Capital Shares 22

As of June 30, 2011, an ownership share of Sprint Nextel was trading for $5.39,while a single share of Berkshire Hathaway sold for $116,105.00.

TEST YOURSELF

Question:

Ray Nesbitt owns a store in his hometown of Charlotte, North Carolina, thatsells food and a variety of other goods. He has always operated this store as asole proprietorship because he was the only owner. Recently, he went to hislawyer and began the legal process of turning his business into acorporation. Which of the following is the most likely reason for this action?

a. He can sell a wider variety of goods as a corporation.b. He has plans to build a second, and maybe a third, store in the area.c. The store has reached a size where incorporation has become

mandatory.d. He hopes his son will one day decide to become a member of the

management.

Answer:

The correct answer is choice b: He has plans to build a second, and maybe athird, store in the area.

Explanation:

One of the most important reasons to incorporate a business is thatadditional sources of capital can be tapped by issuing stock. Nesbitt may beplanning to get the money needed to build the new stores by encouragingothers to acquire stock and become owners. There is no size limit forincorporation, and the decision has little or nothing to do with operations.Neither the selection of goods nor the members of the management team isaffected by the legal form of the business.

The Operational Structure of a Corporation

Question: The owners of most small corporations can operate their businesses effectively asboth stockholders and managers. For example, two friends might each own half of the capitalstock of a bakery or a retail clothing store. Those individuals probably work together tomanage this business on a day-to-day basis.

Chapter 1 What Is Financial Accounting, and Why Is It Important?

1.2 Incorporation and the Trading of Capital Shares 23

Because of the number of people who can be involved, large corporations offer a significantlydifferent challenge. How do millions of investors possessing billions of capital shares of acorporation ever serve in any reasonable capacity as the owners and managers of thatbusiness?

Answer: Obviously, a great many corporations like The Coca-Cola Company havean enormous quantity of capital shares held by tens of thousands of investors.Virtually none of these owners can expect to have any impact on the dailyoperations of the business. A different operational structure is needed. In a vastnumber of such organizations, stockholders vote to elect a representative group tooversee operations. This body—called the board of directors12A story produced byNational Public Radio on the roles played by a board of directors can be found athttp://www.npr.org/templates/story/story.php?storyId=105576374.—is made up ofapproximately ten to twenty-five knowledgeable individuals.

As shown in Figure 1.1 "Company Operational Structure", the board of directorshires the members of management who run the business on a daily basis. The boardthen meets periodically (often quarterly) to review operating, investing, andfinancing results as well as to approve strategic policy initiatives.

Figure 1.1 Company Operational Structure

Occasionally, the original founders of a business (or their descendants) continue tohold enough shares to influence or actually control operating and other significantdecisions of a business. Or wealthy outside investors might acquire enough sharesto gain this same level of power. Such owners have genuine authority within thecorporation. Even that degree of control, though, is normally carried out through

12. A group that oversees themanagement of a corporation;the members are voted to thisposition by stockholders; ithires the management to runthe company on a daily basisand then meets periodically toreview operating, investing,and financing results and alsoto approve policy and strategy.

Chapter 1 What Is Financial Accounting, and Why Is It Important?

1.2 Incorporation and the Trading of Capital Shares 24

membership on the board of directors. For example, at the end of 2010, the FordMotor Company had fifteen members on its board of directors, three of whomwere named Ford. Except in rare circumstances, the hierarchy of owners, board ofdirectors, management, and employees remains intact. Thus, most stockholders arenot involved with the operating decisions of any large corporation.

Predicting the Appreciation of Capital Stock Values

Question: The acquisition of capital shares of a corporation is an extremely popularinvestment strategy for a wide range of the population. A buyer becomes one of the owners ofthe business. Why spend money in this way especially since very few stockholders can everhope to hold enough shares to participate in managing or influencing operations? Ownershipshares sometimes cost small amounts but can also require hundreds if not thousands ofdollars. What is the potential benefit of buying capital stock issued by a businessorganization such as PepsiCo or Chevron?

Answer: Capital shares of thousands of corporations trade each day on marketsaround the world such as the New York Stock Exchange or NASDAQ (NationalAssociation of Securities Dealers Automated Quotations)13. One party is lookingto sell shares whereas another is seeking shares to buy. Stock markets match upthese buyers and sellers so that a mutually agreed-upon price can be negotiated.This bargaining process allows the ownership interests of these companies tochange hands with relative ease.

When investors believe a business is financially healthy and its future is bright, theyexpect prosperity and growth to continue. If that happens, the negotiated price forthe capital shares of the corporation should rise over time. Investors around theworld attempt to anticipate such movements in order to buy the stock at a low priceand sell later at a higher one. Conversely, if predictions are not optimistic, then abusiness’s share price is likely to drop so that owners will experience losses in thevalue of their investments.

Financial accounting information plays an invaluable role in this market process asmillions of investors attempt to assess the financial condition and prospects ofvarious business organizations on an ongoing basis. Being able to understand andmake use of reported financial data helps improve the investor’s knowledge of acorporation and, thus, the chance of making wise decisions about the buying andselling of capital shares. Ignorance often leads to poor decisions and much lesslucrative outcomes.

13. An electronic market thatallows for the trading of capitalshares in approximately threethousand companies, providinginstantaneous price quotationsto efficiently match buyers andsellers allowing ownership incompanies to change hands.

Chapter 1 What Is Financial Accounting, and Why Is It Important?

1.2 Incorporation and the Trading of Capital Shares 25

In the United States, such investment gains—if successfully generated—areespecially appealing to individuals when ownership shares are held for over twelvemonths before being sold. For income tax purposes, the difference between the buyand sale prices for such investments is referred to as a long-term capital gain orloss. Under certain circumstances, significant tax reductions are attributed to long-term capital gains.This same tax benefit is not available to corporate taxpayers,only individuals. The U.S. Congress created this tax incentive to encourageadditional investment so that businesses could more easily obtain money forgrowth purposes. When businesses prosper and expand, the entire economy tendsto do better.

Chapter 1 What Is Financial Accounting, and Why Is It Important?

1.2 Incorporation and the Trading of Capital Shares 26

TEST YOURSELF

Question:

Mr. and Mrs. Randolph Ostar buy one thousand shares of a well-knowncompany at $25 per share on July 1, Year One. They hold no otherinvestments. The stock is traded on the New York Stock Exchange, and theprice goes up over time to $36 per share. On June 27, Year Two, the couple isconsidering the sale of these shares so that they can buy a new car. At thelast moment, they postpone these transactions for one week. What is themost likely reason for this delay?

a. Automobile prices tend to go down after July 1 each year.b. It normally takes several weeks to sell the shares of a large corporation.c. Laws delay the immediate use of money from the sale of investments for

several weeks.d. They are hoping to reduce the amount of income taxes to be paid.

Answer:

The correct answer is choice d: They are hoping to reduce the amount ofincome taxes to be paid.

Explanation:

For individuals who own stock, gains on the sale of capital assets (such asthese shares) are taxed at low rates, but only if long-term (held for over oneyear). The Ostars anticipate making an $11,000 profit ($36 − $25 × 1,000shares). Currently, the shares have been held for slightly less than one year.If sold in June, the gain is short-term and taxed at a higher rate. By holdingthem for just one more week, the gain becomes long-term, and a significantamount of tax money is saved.

The Receipt of Dividends

Question: Investors acquire ownership shares of selected corporations hoping that the stockprice will rise over time. This investment strategy is especially tempting because long-termcapital gains are often taxed at a relatively low rate. Is the possibility for appreciation invalue the only reason that investors choose to acquire capital shares?

Chapter 1 What Is Financial Accounting, and Why Is It Important?

1.2 Incorporation and the Trading of Capital Shares 27

Answer: Many corporations—although certainly not all—pay cash dividends14 totheir stockholders periodically. A dividend is a reward for being an owner of abusiness that is prospering. It is not a required payment; it is a sharing of profitswith the stockholders. As an example, for 2010, Duke Energy reported earningprofits (net income) of $1.32 billion. During that same period, the corporationdistributed total cash dividends of approximately $1.28 billion to the owners of itscapital stock.The receipt of cash dividends is additionally appealing to stockholdersbecause, in most cases, they are taxed at the same reduced rates as are applied tonet long-term capital gains.

The board of directors determines whether to pay dividends. Some boards prefer toleave money within the business to stimulate future growth and additional profits.For example, Google Inc. reported profits (net income) for 2010 of $8.51 billion butdistributed no dividends to its owners. Newer companies often choose to pay lessdividends than older companies as they try to grow quickly to a desired size.

Not surprisingly, a variety of investing strategies abound. Many investors acquireownership shares almost exclusively in hopes of benefiting from an anticipatedappreciation of stock prices. Another large segment of the investing public is morelikely to be drawn to the possibility of dividend payments. Unless an owner has thechance to influence or control the operations of a business, only these two potentialbenefits can accrue from the ownership of capital shares: appreciation in the valueof the stock price and cash dividends.

Annual Rate of Return on an Investment in Capital Stock

Question: An investor can put money into a savings account at a bank and earn a small butrelatively risk-free profit. For example, $100 could be invested on January 1 and then beworth $102 at the end of the year because interest is added to the balance. The extra $2means that the investor earned an annual return of 2 percent ($2 increase/$100 investment).This computation helps in comparing one possible investment opportunity against another.How is the annual rate of return computed when the capital stock of a corporation isacquired as an investment and then held for a period of time?

Answer: Capital stock investments are certainly not risk free. Profits can be high,but losses always loom as a possibility. The annual rate of return measures thoseprofits and losses in the past and is often anticipated for the future as a way ofmaking investment decisions.

14. Distributions made by acorporation to its shareholdersas a reward when income hasbeen earned; decision to pay ismade by the board of directors;shareholders often receivefavorable tax treatment whencash dividends are collected.

Chapter 1 What Is Financial Accounting, and Why Is It Important?

1.2 Incorporation and the Trading of Capital Shares 28

To illustrate, assume that on January 1, Year One, an investor spends $100 for oneownership share of the Ace Company and another $100 for a share of the BaseCompany. During the year, Ace distributes a dividend of $1.00 per share to each ofits owners while Base pays a dividend of $5.00 per share. On December 31, thecapital stock of the Ace Company is selling on a stock market for $108 per sharewhereas the stock of the Base Company has a price of only $91 per share.

This investor now holds a total value of $109 as a result of the purchase of the shareof the Ace Company: the cash dividend of $1 and a share of capital stock worth $108.In one year, the total value has risen by $9 ($109 less $100) so that the annual ratereturn was 9 percent ($9 increase/$100 investment).

The shares of the Base Company did not perform as well. At the end of the year, thetotal value of this investment is only $96: the cash dividend of $5 plus one share ofstock worth $91. That is a drop of $4 during the year ($96 less $100). The annual rateof return on this investment is a negative 4 percent ($4 decrease/$100 investment).

As a result of this first year, buying a share of Ace obviously proved to be a betterinvestment than buying a share of Base because of the higher annual rate of return.However, a careful analysis of the financial accounting data available at the start ofthe year might have helped this investor realize in advance that the rate of returnon the investment in Ace would be higher. An assessment of the financial healthand future prospects of both businesses could have shown that a higher return wasexpected in connection with the investment in Ace.

Therefore, estimating the annual rate of return is important for investors because ithelps them select from among multiple investment opportunities. This computationprovides a method for quantifying the financial benefit earned in the past andexpected in the future. Logically, investors should simply choose the investmentthat provides the highest anticipated rate of return. However, as with allpredictions, the risk that actual actions will not follow the expected course must betaken into consideration. Investing often breaks down to anticipating profits whilemeasuring the likelihood and amount of potential losses.

Chapter 1 What Is Financial Accounting, and Why Is It Important?

1.2 Incorporation and the Trading of Capital Shares 29

KEY TAKEAWAY

Incorporation allows an organization to be viewed legally as a separateentity apart from its ownership. In most large corporations, few owners areable to be involved in the operational decision making. Instead, stockholderselect a board of directors to oversee the business and direct the work ofmanagement. Corporations can issue shares of capital stock that give theholder an ownership right and enables the business to raise monetary funds.If the organization is financially healthy and prospering, these shares canincrease in value over time—possibly by a significant amount. In addition, aprofitable organization may well share its good fortune with its ownershipthrough the distribution of cash dividends. Investors often attempt toestimate the annual rate of return that can be expected from an investmentas a way of comparing it to other investment alternatives. This computationtakes the profit for the year (stock appreciation and dividends) and dividesit by the amount of the investment at the start of the period.

Chapter 1 What Is Financial Accounting, and Why Is It Important?

1.2 Incorporation and the Trading of Capital Shares 30

1.3 Using Financial Accounting for Wise Decision Making

LEARNING OBJECTIVES

At the end of this section, students should be able to meet the followingobjectives:

1. List the predictions that investors and potential investors want to makeabout a business organization.

2. List the predictions that creditors and potential creditors want to makeabout a business organization.

3. Explain the reporting of monetary amounts as a central focus offinancial accounting.

4. Explain how financial accounting information is enhanced and clarifiedby verbal explanations.

5. Understand the function played by the annual report published by manybusinesses and other organizations.

Financial Accounting Information and Investments in CapitalStock

Question: Investors are interested (sometimes almost obsessively interested) in the financialinformation that is produced by a business organization according to the rules andprinciples of financial accounting. They want to use this information to make wise investingdecisions. What do investors actually hope to learn about a business by analyzing publishedfinancial information?