Being Virtuous and Prosperous: SRI’s Conflicting Goals : Dialectics of Investor Protection Rules...

23

Page1 Being Virtuous and Prosperous: SRI’s Conflicting Goals 1 : Dialectics of Investor Protection Rules (investor-state dispute settlement– ISDS) in Canada-European Union: Comprehensive Economic and Trade Agreement (CE-CETA) - Trends, Tensions and Contradictions [This paper was submitted as an LL.M paper for “t he Financial Srvice Industry & the Public Interest course] -RAJIV RANJAN 2 Abstract: 1 The title “Being Virtuous and Prosperous: SRI’s Conflicting Goals” is an adaption from an article by Benjamin J. Richardson and Wess Craig- at http:/ /papers .ssrn.com/sol3/papers.cfm?abstract_id=1463936 (also course reading), and used here to describe a paradigm to discuss CE-CETA 2 Is pursuing his second LL.M in Banking Law and Financial Regulation from Osgoode Hall Law School, York University, Toronto, after his first masters in International Business Law and is a member of Federal Revenue Service of India since 1991.

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Being Virtuous and Prosperous: SRI’s Conflicting Goals : Dialectics of Investor Protection Rules...

Page1

Being Virtuous and Prosperous: SRI’s Conflicting Goals1: Dialectics of Investor ProtectionRules (investor-state dispute settlement– ISDS) in Canada-European Union: ComprehensiveEconomic and Trade Agreement (CE-CETA) - Trends, Tensions and Contradictions

[This paper was submitted as an LL.M paper for “the Financial Srvice Industry & the Public Interest course]

-RAJIV RANJAN2

Abstract:

1 The title “Being Virtuous and Prosperous: SRI’s Conflicting Goals” is an adaption from an article by Benjamin J. Richardson and Wess Craig- at http://papers .ssrn.com/sol3/papers.cfm?abstract_id=1463936 (also course reading), and used here to describe a paradigm to discuss CE-CETA2 Is pursuing his second LL.M in Banking Law and Financial Regulation from Osgoode Hall Law School, York University, Toronto, after his first mastersin International Business Law and is a member of Federal Revenue Service of India since 1991.

Page2

“Transnational corporations [Countries] can support this effort [potential of international investment

with other financial resources for sustainable development] by creating decent jobs, generating

exports, promoting rights, respecting the environment, encouraging local content, paying fair taxes

and transferring capital, technology and business contacts to spur development”.3

-Ban Ki-moon

Introduction:

The universe of 3,268 (till 2014) International Investment Agreements

(IIA)4 shapes and pushes the two engines of globalization, commodity trade and capital

flows. With global FDI flows soaring to $1.6 trillion5 (2014), of which the triad combine

of 28 Member-European Union, America and Canada sharing more than 55%, the

international community necessity concurrent to define a set of Sustainable Development

Goals (SDG) ,inter alia, co-opting a bunch of SRI principles6 of the financial community,

to address7 common global economic, social and environmental challenges. It is crucial to

develop a general-equilibrium framework integrating the prosperity, rated in GDP scores

with sustainable development growth.

This paper situates this paradigm in this universe of 3,268 IIAs with Canada-

specific assessment of Canada-European Union: Comprehensive Economic and Trade

Agreement (CETA), with a dispute resolution mechanism called inter-state dispute

resolution (ISDS)8. ISDS engages cutting edge provisions9 of IIAs to settle transnational

trade and investment disputes over health, environment, financial and other domestic

safeguards to alleviate political and non-commercial risks. “IIAs are about governance for

3 Preface to World Investment Report 2014: Investing in the SDGs: An Action Plan- at http://unctad.org/en/PublicationsLibrary/wir2014_en.pdfaccessed on March 28, 2015-4 Recent Trends in IIAs and ISDS- IIA Issue Note No.1, February, 2015 at http://unctad.org/en/PublicationsLibrary/webdiaepcb2015d1_en.pdf accessedon April 5, 20155 Supra, note1- “After the 2012 slump, global FDI returned to growth, with inflows rising 9 per cent in 2013, to $1.45 trillion. UNCTAD projects that FDIflows could rise to $1.6 trillion in 2014, $1.7 trillion in 2015 and $1.8 trillion in 2016, with relatively larger increases in developed countries. Fragility insome emerging markets and risks related to policy uncertainty and regional instability may negatively affect the expected upturn in FDI .Developingeconomies maintain their lead in 2013. FDI flows to developed countries increased by 9 per cent to $566 billion, leaving them at 39 per cent of globalflows, while those to developing economies reached a new high of $778 billion, or 54 per cent of the total”6 London Principles of Sustainable Finance (2002)- a seven-principles integrated approach to economic prosperity, social wellbeing, and the environmentat http://www.cityoflondon.gov.uk/services/environment-and-planning/sustainability/Documents/pdfs/SUS_lonprinciples.pdf (accessed on April 12,2015); United Nations Principles for Responsible Investment(UNPRI-2006)- a six- principles(ESG-Environment, Social and Government) “developed byan international group of institutional investors reflecting the increasing relevance of environmental, social and corporate governance issues to investmentpractices” at http://www.unpri.org/about-pri/the-six-principles/ accessed on April 12, 2015; Equator Principles( 2003)- “The Equator Principles is a riskmanagement framework, adopted by financial institutions, for determining, assessing and managing environmental and social risk in projects and isprimarily intended to provide a minimum standard for due diligence to support responsible risk decision-making in the area of international project financedebt” at http://www.equator-principles.com/ accessed on April 12, 2015.7 Supra Note 2, Fig. iv.12 at pg. 1748 Preface to World Investment Report- United Nations Conference on Trade and Development Investing in the SDGs: An Action Plan athttp://unctad.org/en/pages/ diae/world% 20investment% 20report/wir-series.aspx, accessed on March 28, 20159 Expropriations- The process of expropriation "occurs when a public agency (for example, the provincial government and its agencies, regional districts,municipalities, school boards and utilities) takes private property for a purpose deemed to be in the public interest"- athttp://en.wikipedia.org/wiki/Expropriation; Fair and Equitable Treatment (FET) –“Broadly to include a variety of specific requirements including aState’s obligation to act consistently, transparently, reasonably, without ambiguity, arbitrariness or discrimination, in an even-handed manner, to ensuredue process in decision-making and respect investors’ legitimate expectation” FAIR AND EQUITABLE TREATMENT -UNCTAD Series on Issues inInternational Investment Agreements II at http://unctad.org/en/Docs/unctaddiaeia2011d5_en.pdf, accessed on April 15, 2015; National Treatment-“National treatment can be defined as a principle whereby a host country extends to foreign investors treatment that is at least as favourable as thetreatment that it accords to national investors in like circumstances. In this way the national treatment standard seeks to ensure a degree of competitiveequality between national and foreign investors”-National Treatment- UNCTAD Series on Issues in International Investment Agreements athttp://unctad.org/en/pages/PublicationArchive.aspx?publicationid=340 II , accessed on April 12, 2015

Page3

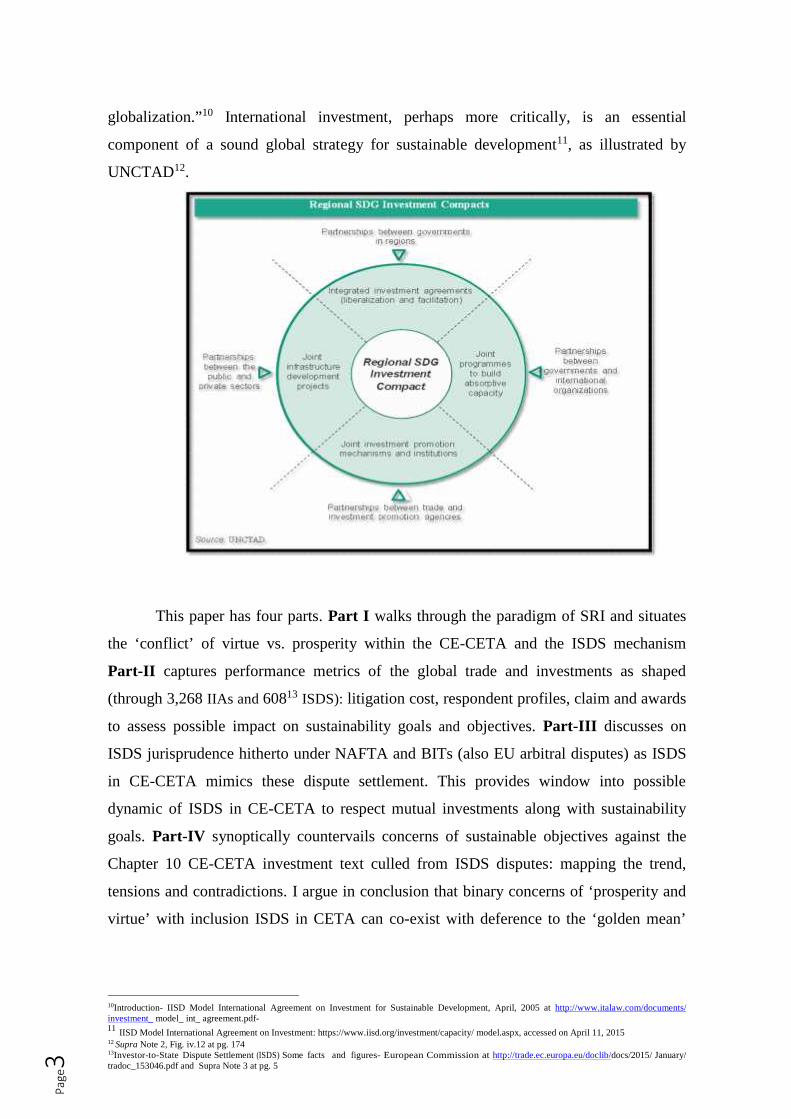

globalization.”10 International investment, perhaps more critically, is an essential

component of a sound global strategy for sustainable development11, as illustrated by

UNCTAD12.

This paper has four parts. Part I walks through the paradigm of SRI and situates

the ‘conflict’ of virtue vs. prosperity within the CE-CETA and the ISDS mechanism

Part-II captures performance metrics of the global trade and investments as shaped

(through 3,268 IIAs and 60813 ISDS): litigation cost, respondent profiles, claim and awards

to assess possible impact on sustainability goals and objectives. Part-III discusses on

ISDS jurisprudence hitherto under NAFTA and BITs (also EU arbitral disputes) as ISDS

in CE-CETA mimics these dispute settlement. This provides window into possible

dynamic of ISDS in CE-CETA to respect mutual investments along with sustainability

goals. Part-IV synoptically countervails concerns of sustainable objectives against the

Chapter 10 CE-CETA investment text culled from ISDS disputes: mapping the trend,

tensions and contradictions. I argue in conclusion that binary concerns of ‘prosperity and

virtue’ with inclusion ISDS in CETA can co-exist with deference to the ‘golden mean’

10Introduction- IISD Model International Agreement on Investment for Sustainable Development, April, 2005 at http://www.italaw.com/documents/investment_ model_ int_ agreement.pdf-11 IISD Model International Agreement on Investment: https://www.iisd.org/investment/capacity/ model.aspx, accessed on April 11, 201512 Supra Note 2, Fig. iv.12 at pg. 17413Investor-to-State Dispute Settlement (ISDS) Some facts and figures- European Commission at http://trade.ec.europa.eu/doclib/docs/2015/ January/tradoc_153046.pdf and Supra Note 3 at pg. 5

Page4

doctrine between investor protection and sustainable goals, canvassed also through multi-

lateral initiatives like those of UNCTAD14.

Part-I: SRI Paradigm and Chapter 10 (Investment) of CE-CETA including ISDS-

Though having a catholic pedigree until 1990s, SRI eventually turned into “a

legitimate investment strategy”15. Be it the profit-current (business case SRI) or ethics-

triggered socially responsible investment, both call for re-engineering of norms and

governance standards. A stand-alone application of either strategy is problematic due to

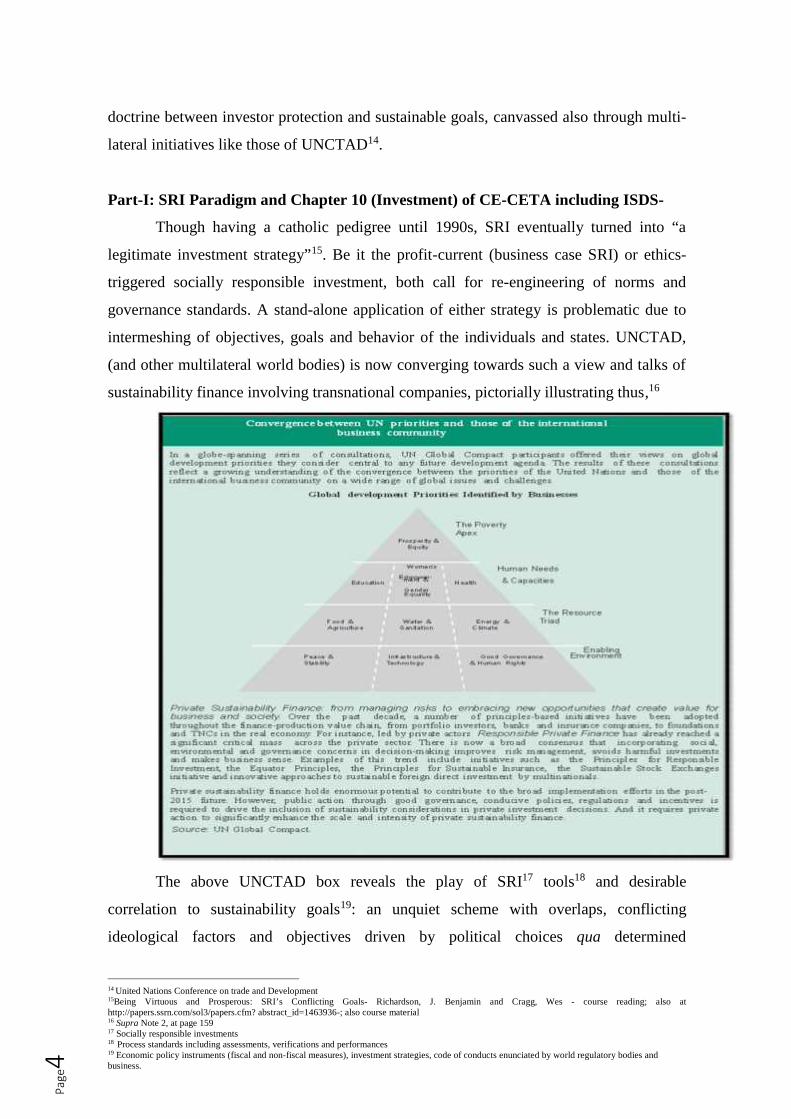

intermeshing of objectives, goals and behavior of the individuals and states. UNCTAD,

(and other multilateral world bodies) is now converging towards such a view and talks of

sustainability finance involving transnational companies, pictorially illustrating thus,16

The above UNCTAD box reveals the play of SRI17 tools18 and desirable

correlation to sustainability goals19: an unquiet scheme with overlaps, conflicting

ideological factors and objectives driven by political choices qua determined

14 United Nations Conference on trade and Development15Being Virtuous and Prosperous: SRI’s Conflicting Goals- Richardson, J. Benjamin and Cragg, Wes - course reading; also athttp://papers.ssrn.com/sol3/papers.cfm? abstract_id=1463936-; also course material16 Supra Note 2, at page 15917 Socially responsible investments18 Process standards including assessments, verifications and performances19 Economic policy instruments (fiscal and non-fiscal measures), investment strategies, code of conducts enunciated by world regulatory bodies andbusiness.

Page5

technological or economic outcomes.20 ISDS under CE-CETA has to meet this challenge.

This right to regulate is quite often spoken in terms of “regulatory chill”21, and earns

infamy for ISDS as the constrain factor. Sovereigns’ right to regulate expresses through

through three explicit factors (1) definitions of specific protections; (2) general

exceptions; and (3) preambular language.22

The transnational universe of IIAs and ISDS is compounded further by perpetual

hegemonic “zero-sum” game of the States.23 But, development barren of suitable SRI

content is pouring wine down a bottomless casket: a “sure recipe for economic and

political disaster”24- a skewed economy which “dynamics…pushes alternatively towards

convergence and divergence”25. This is not Goldman Sachs’ “God’s work”26. UNCTAD27

(box below) provides clue to adopt balanced political choices to arrive at the “golden

mean”.

20 Reading “Capital”: Introduction; course material The Economist, Feb.27, 2014-21 “A State actor will fail to enact or enforce bona fide regulatory measures because of a perceived or actual threat of investment arbitration”- Para 68 TheImpact of Investor-State-Dispute Settlement (ISDS) in the Transatlantic Trade and Investment Partnership, Study prepared for the Minister for ForeignTrade and Development Cooperation, Ministry of Foreign Affairs, The Netherlands, 24/06/2014 (see P127, para 283)http://www.rijksoverheid.nl/documenten-en-publicaties/rapporten/2014/06/24/the-impact-of-investor-state-dispute-settlement-isds-in-the-ttip.htmlaccessed on April 8, 201522 Ibid, at para 90: CE-CETA in its preamble states….. “Reaffirming their commitment to promote sustainable development and the development ofinternational trade in such a way as to contribute to sustainable development in its economic, social and environmental dimensions; Determined toimplement this Agreement in a manner consistent with the enhancement of the levels of labour and environmental protection and the enforcement of theirlabour and environmental laws and policies, building on their international commitments on labour and environment matters; Encourage enterprisesoperating within their territory or subject to their jurisdiction to respect internationally recognized standards and principles of corporate socialresponsibility, notably the OECD Guidelines for multinational enterprises and to pursue best practices of responsible business conduct;23 It backfires though- Rubin Richard- “U.S. Companies Are Stashing $2.1 Trillion Overseas to Avoid Taxes”- USA reports $2.1 trillion of profitsstockpiled abroad with domestic availability of only $1.9 trillion, and despite all-Obama noise to mop “$268 billion over six years, to use forinfrastructure” through non-fiscal taxation is a far cry at http://www.bloomberg.com/news/articles/2015-03-04/ accessed on March 8,015, also on myFacebook post24 Soto de Hernando- The Mystery of Capital- Why capitalism triumphs in the West and fails everywhere else- Black Swan book- ed. 200125 Supra, Note 19.26 Arlidge, John- I'm doing 'God's work'. Meet Mr. Goldman Sachs- the Sunday Times published: 8 November 2009 – at http://www.thesundaytimes.co.uk/ sto/news/world_news/article189615.ece; and also course material27 Supra , note 2, Table IIIA, at pg. 131

Page6

Part-II: Performance metrics: FDI flows IIAs and ISDS and sustainability goals-

contextualizing CE-CETA

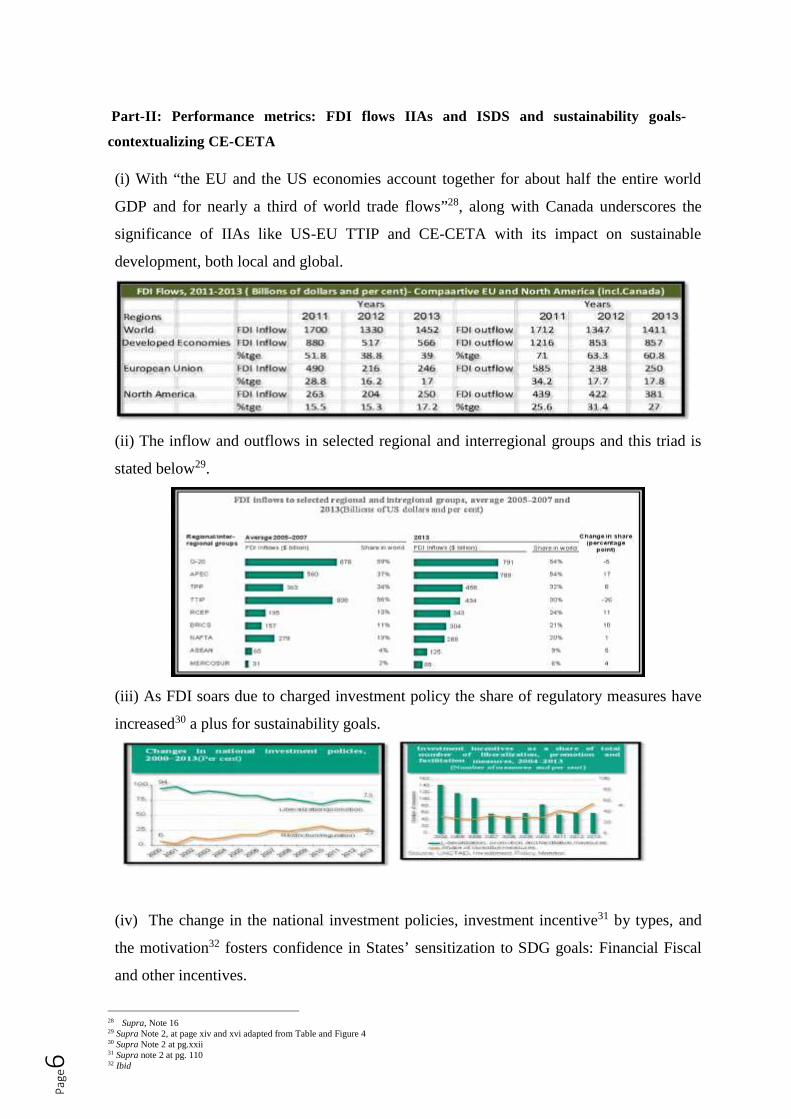

(i) With “the EU and the US economies account together for about half the entire world

GDP and for nearly a third of world trade flows”28, along with Canada underscores the

significance of IIAs like US-EU TTIP and CE-CETA with its impact on sustainable

development, both local and global.

(ii) The inflow and outflows in selected regional and interregional groups and this triad is

stated below29.

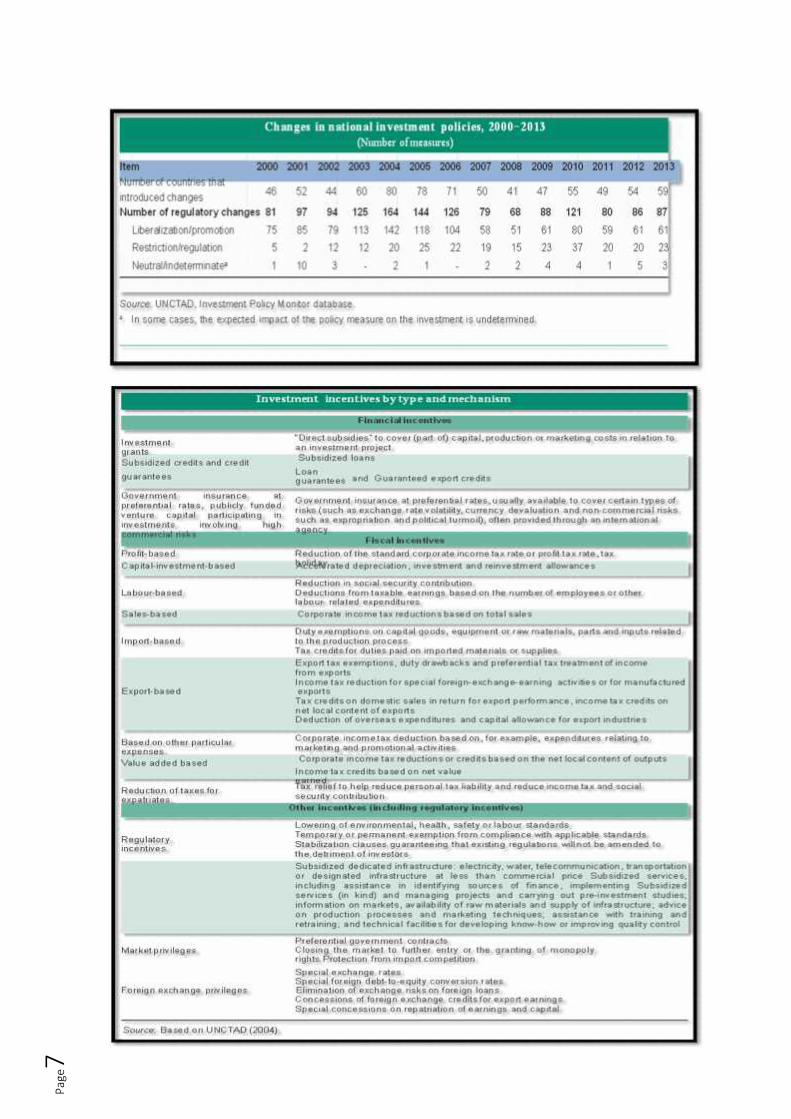

(iii) As FDI soars due to charged investment policy the share of regulatory measures have

increased30 a plus for sustainability goals.

(iv) The change in the national investment policies, investment incentive31 by types, and

the motivation32 fosters confidence in States’ sensitization to SDG goals: Financial Fiscal

and other incentives.

28 Supra, Note 1629 Supra Note 2, at page xiv and xvi adapted from Table and Figure 430 Supra Note 2 at pg.xxii31 Supra note 2 at pg. 11032 Ibid

Page7

Page8

(v) The spurt in IIAs and ISDS: bodes well for ISDS in CE-CETA.

(vi) Claiming/Litigating Investor profile33: constitutes a motley of companies,

associations and individuals34.

(vii) Case profile35: disputes relate to administrative acts36 - 260+37 ISDS cases (90%38)

relate to administrative measures with legislative acts (10%)39 in exceptional cases

subjected to ISDS.

(viii) USE OF ISDS: 356 concluded ISDS cases out of 608 known numbers indicate-

(a) that over 50% cases (327) were brought by EU investors from all EU MemberStates40.

33 Gaukrodger, D. and K. Gordon (2012), "Investor-State Dispute Settlement: A Scoping Paper for the Investment Policy Community", OECDWorking Papers on International Investment, 2012/03, OECD Publishing (see P17- 19) http://www.oecd-ilibrary.org/docserver/download/5k46b1r85j6f.pdf?expire accessed on April 8, 2015- “Investor claimants range from individuals with quite limited international experience (e.g. anassociation of retirees) to major multinational enterprises with tens of thousands of employees and global operations”.34 OECD Research for 100 decided cases between 2006-2011-(a) Medium and large enterprises [48% having employees-size in the range of 100-10,000]; (b)large Multinationals [8%- top 100 TNCs UNCTAD List]; (c) Individuals and very small corporations [22%- 1-2 foreign projects]; and (d)30% [ insufficient information]35 Supra Note 4 at pg.7- 'the two types of State conduct most frequently challenged by investors in 2014 were: (i) cancellations oralleged violations of contracts or concessions (at least nine cases); and (ii) revocations or denials of licenses or permits (at least sixcase)”36 Cancellation of licenses or permits, land zoning37 Supra Note 23-a June 2014 study commissioned by the Dutch Government38 Supra Note 2939 Ibid40 Except Estonia, Slovakia, Romania, Bulgaria, Malta and Ireland.

Page9

(b) Investors - the Netherlands, the UK, Germany, France, Spain and Italy havelaunched 236 cases (72% of EU based cases and 39% at global level).

(c) Challenges to EU Member States have been rare from non-EU investors withtotal of 29 cases with investors from Russia, Norway, Switzerland, India,Israel, Turkey, Lebanon, US and Canada.

(d) Challenge to EU Member States have been most frequently by EU basedinvestors (99 cases, mainly against Czech Republic, Slovakia, Hungary, Poland,Estonia, Hungary, Romania, Spain).

(e) Most-challenged countries under ISDS - 10 nos. from both developing anddeveloped countries41:

(ix) Success rate of ISDS42:

In favour of States , 132,38%

In favour of Investors,101, 29%

Settled, 87, 25%

Discontinued, 29, 8%

Results of 356 concluded ISDS cases

(x) Claim grants: Investors are on average granted only a small part of their original

claim: against an average amount claim of $343 million (approx.), the average awarded

damages was US$ lO.4 million.43

41 Argentina (56 cases), Venezuela (36), the Czech Republic (29), Egypt (24), Canada (23), Mexico and Ecuador (21), India and Ukraine (16), Poland andthe United States (15).42 Supra note 4 at pg. 843 Towards an EU-US trade deal: European Commission at http://trade.ec.europa. eu/doclib/ docs/2015/January/tradoc_ 153046. pdfaccessed on April 9, 2015 at pg.9

Page10

(xi) Arbitration cost44 : the average legal and arbitration costs for a claimant are around

$8 million: 82% (for legal counsel), 16% (arbitrator fee) and 2% (institutional cost).

Thus, ISDS cannot be wished away in CE-CETA, EU being the main user, as well as its

wide platform accessibility

Part-III- ISDS jurisprudence- NAFTA and EU-BIT arbitration: Global trends

NAFTA ISDS lags behind global ISDS trends: the per annum ISDS case since inception

of NAFTA is just 4 (total 73) covering 3 countries (US, Canada and Mexico), global ISDS

averages at 15 (total 276) covering over 150 countries of which more than 50% involves

EU. Obviously, global ISDS experiences would be more revealing for adoption rather

than NAFTA ISDS. But “ISDS faces a crisis of legitimacy”45, with regulatory chills46 as it

“prevents governments from exercising their sovereignty by restraining policy space

associated with the environment, health, natural resources, and human rights, among other

policy areas”47. The following tables cull information from resources, demonstrating

environmental (sustainability) goals as supportive48 of economic interests. It is not a threat

to policy space notwithstanding instances of “countries withdrawing or threatened to

withdraw from the ICSID Convention because of perceived biases in ISDS”49. The ISDS

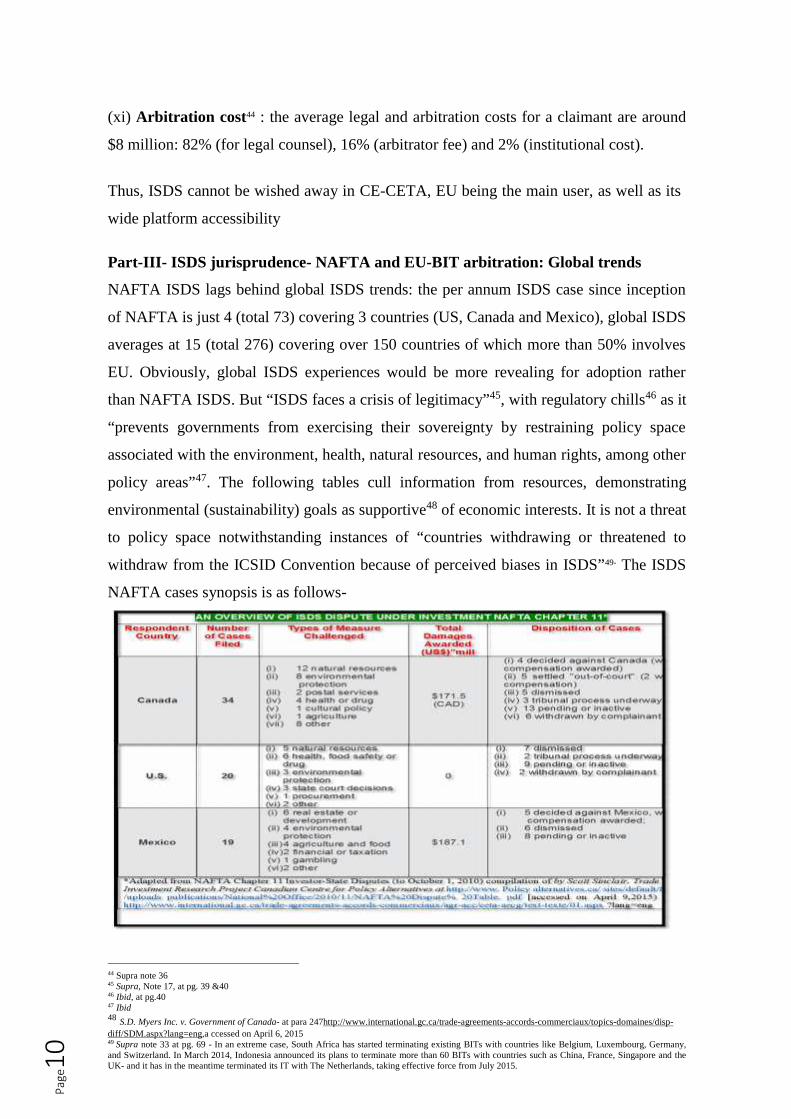

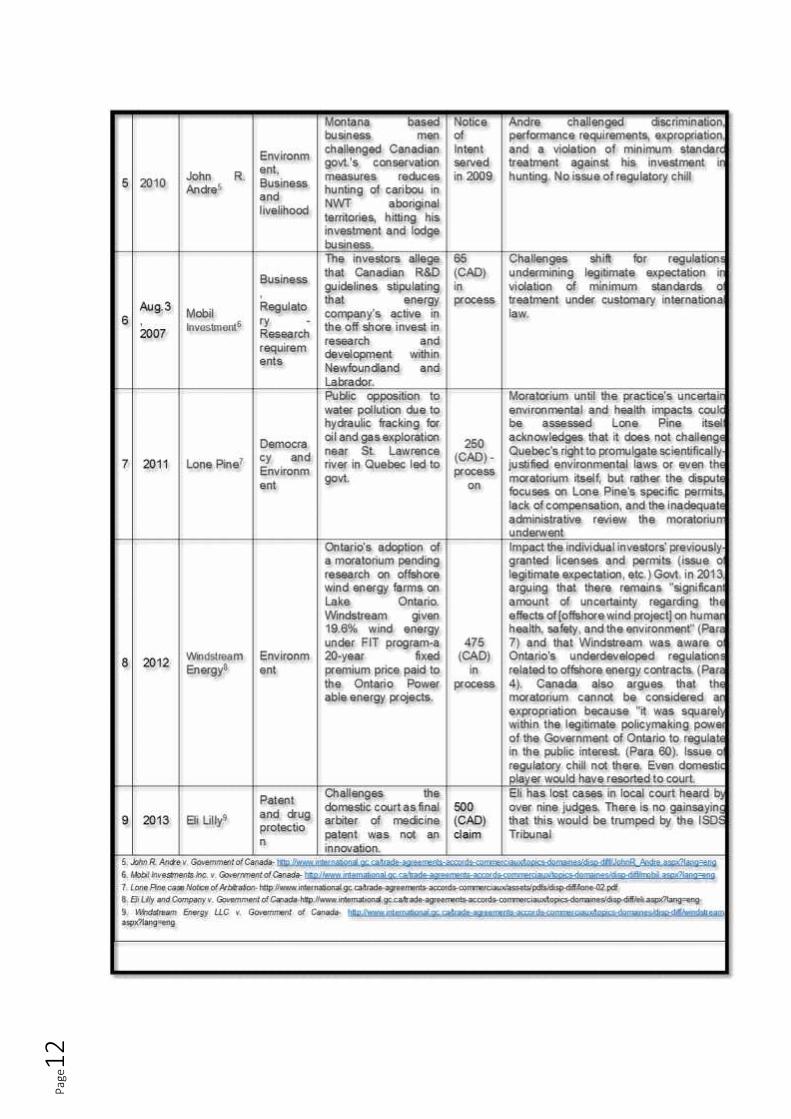

NAFTA cases synopsis is as follows-

44 Supra note 3645 Supra, Note 17, at pg. 39 &4046 Ibid, at pg.4047 Ibid48 S.D. Myers Inc. v. Government of Canada- at para 247http://www.international.gc.ca/trade-agreements-accords-commerciaux/topics-domaines/disp-diff/SDM.aspx?lang=eng,a ccessed on April 6, 201549 Supra note 33 at pg. 69 - In an extreme case, South Africa has started terminating existing BITs with countries like Belgium, Luxembourg, Germany,and Switzerland. In March 2014, Indonesia announced its plans to terminate more than 60 BITs with countries such as China, France, Singapore and theUK- and it has in the meantime terminated its IT with The Netherlands, taking effective force from July 2015.

Page11

Page12

Page13

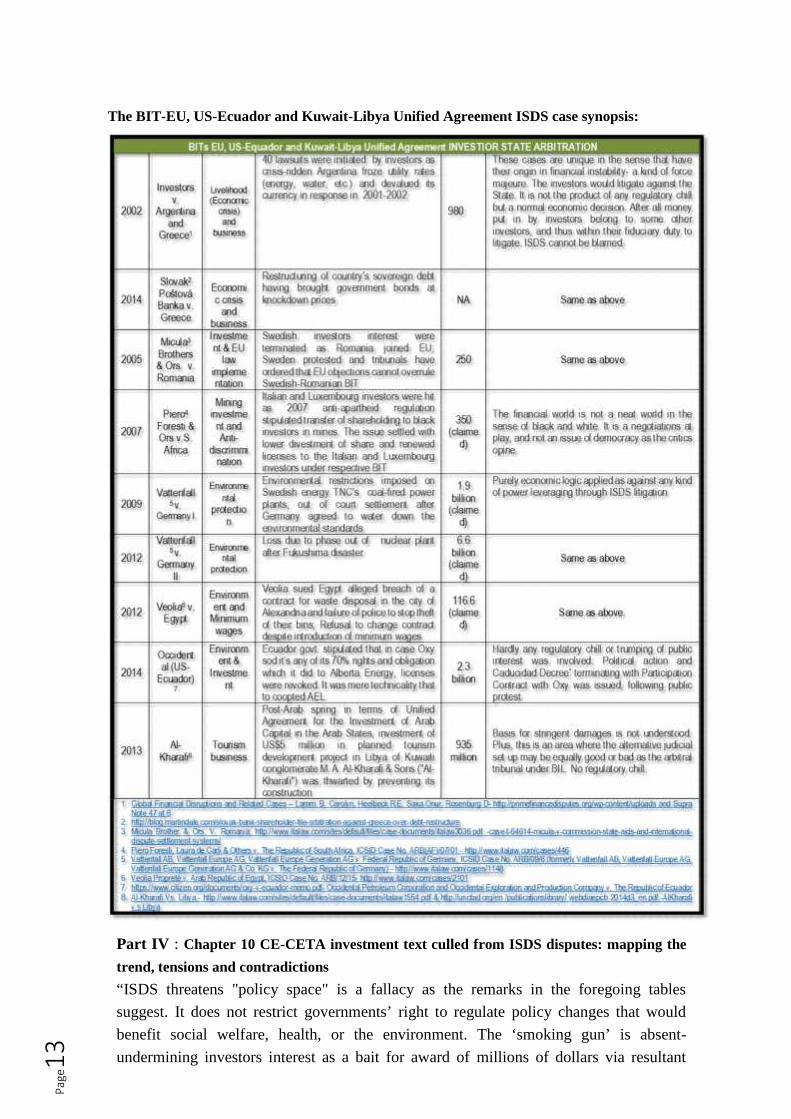

The BIT-EU, US-Ecuador and Kuwait-Libya Unified Agreement ISDS case synopsis:

Part IV : Chapter 10 CE-CETA investment text culled from ISDS disputes: mapping the

trend, tensions and contradictions

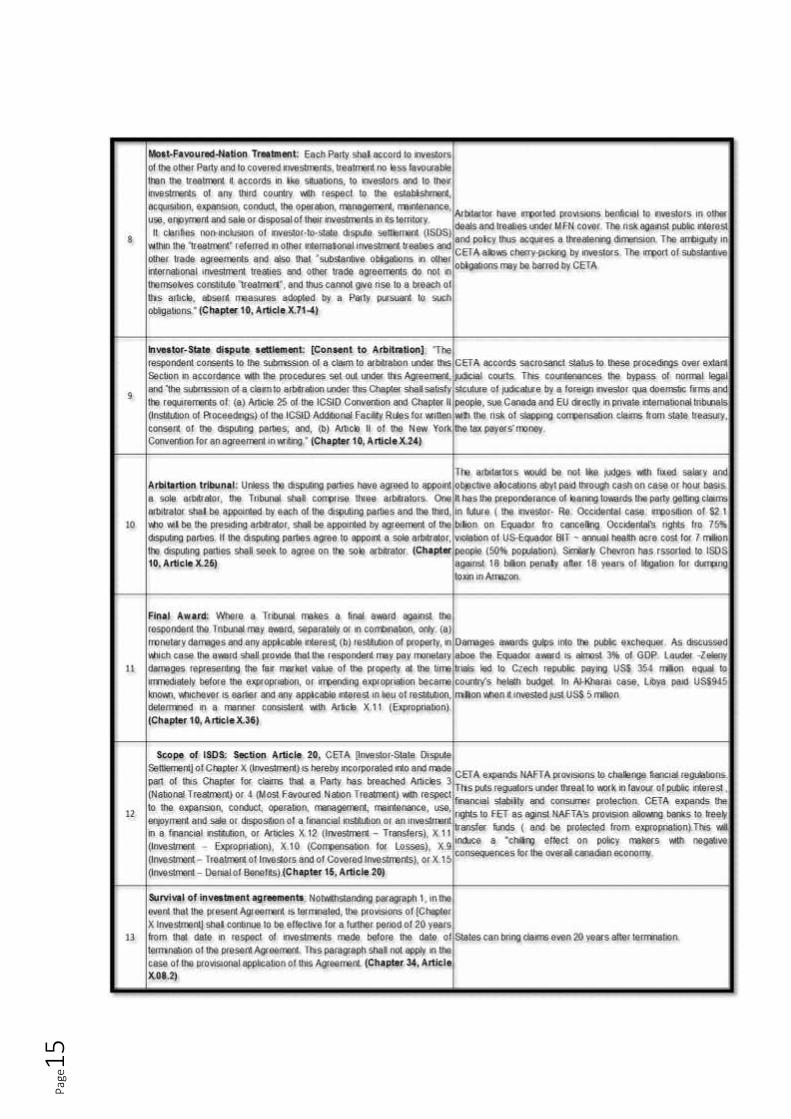

“ISDS threatens "policy space" is a fallacy as the remarks in the foregoing tables

suggest. It does not restrict governments’ right to regulate policy changes that would

benefit social welfare, health, or the environment. The ‘smoking gun’ is absent-undermining investors interest as a bait for award of millions of dollars via resultant

Page14

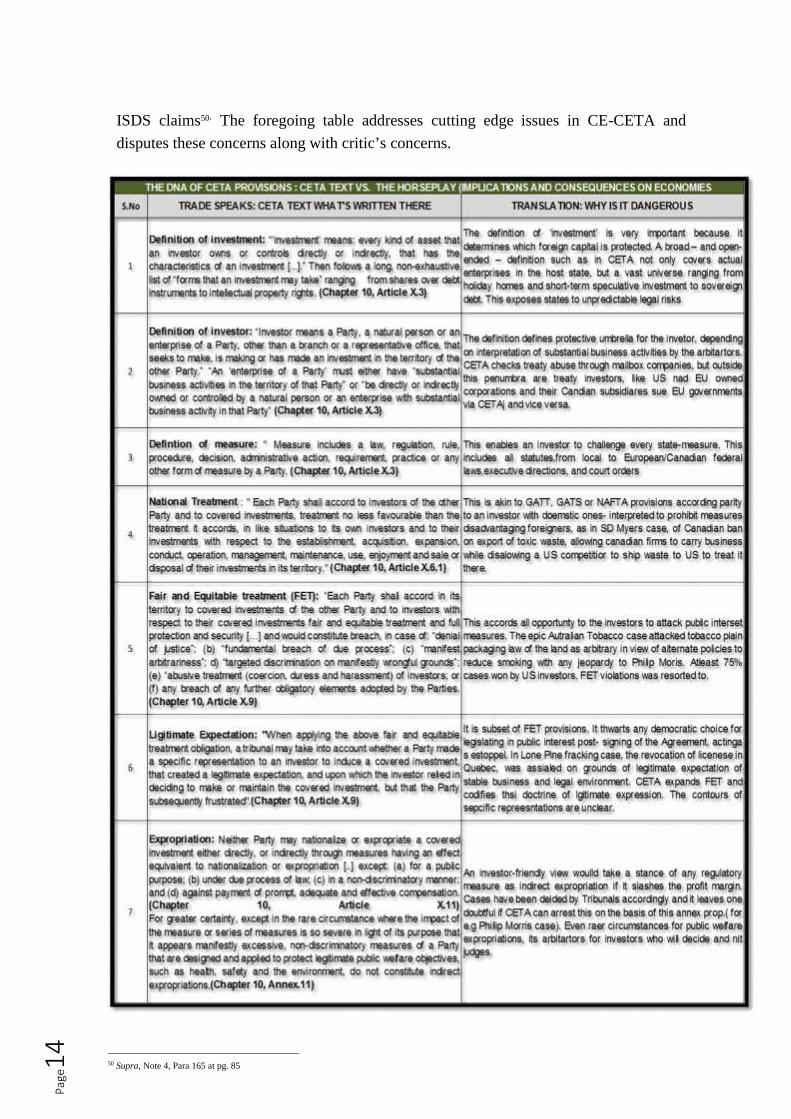

ISDS claims50. The foregoing table addresses cutting edge issues in CE-CETA and

disputes these concerns along with critic’s concerns.

50 Supra, Note 4, Para 165 at pg. 85

Page15

Page16

Incidentally, it would be worth mentioning that Canada signed 7 IIAs besides CE-CETA

in 2014, and that all of them carry four selected aspects of IIAs like protection of health

and safety, labor rights, environment or sustainable goals. However, critics are vehement

in their observation on Eli Lilly NAFTA case where medicinal intellectual property rights

issue related to reformulation of drugs was the issue. The case is still hanging despite

having been disallowed by nine judges in Canadian jurisdiction. Canada wanted it out of

its “investment list”, but EU declined. However, it may be reasonable guessed that EU has

is not US, and perhaps is more mature in their approaching IIAs dispute through ISDS.

Infact, Netherlands despite having 98 IIAs with non-EU developing countries, ran trade

with US without a BIT.

Conclusion:

The ascription of infamy to ISDS is a perception of its use from a protective “shield” to a

strategic, aggressive “sword.”51 Negotiation in international trade and investment law is

not "chill"52 which critics naïvely53misunderstand.

ISDS in CETA will balance sustainable development objectives with economic goals due

to shared legal-juridical climate and political and economic principles54 by Canada and

EU (ISDS is essentially within the fold of the negotiating mandate of the Commission55,

as in US-EU TTIP). The cost-benefit risk assessment of ISDS as culled from ISDS

jurisprudence and performance metrics demonstrates this. CE-CETA has "except in rare

circumstances," measures balancing legitimate public welfare objectives, such as public

health, safety, and the environment and general exception clauses and ‘preambular’

language protecting “the human, animal, or plant life or health”. UNCTAD suggests a

four-path action plan56 to address the dynamic of IIA (and ISDS) with sustainability goals.

51 Private Rights, Public Problems, Para 4.1 at pg.16- International School of Sustainable Development at http://www.iisd.org/pdf/trade_citizensguide.pdf,accessed on April 11, 201552 Supra, Note 13 at para 81, pg.4753 International participation is warrants relinquishing sovereignty to international law- S.S. "Wimbledon" United Kingdom, France, Italy & Japan v.Germany [PERMANENT COURT OF INTERNATIONAL JUSTICE, File E. b. II., Docket III.I dated, 17 August 1923]- “The Court declines to see inthe conclusion of any Treaty by which a State undertakes to perform or refrain from performing a particular act an abandonment of its sovereignty. Nodoubt any convention creating an obligation of this kind places a restriction upon the exercise of the sovereign rights of the State, in the sense that itrequires them to be exercised in a certain way. But the right of entering into international engagements is an attribute of State sovereignty.” athttp://www.worldcourts.com/pcij/eng/decisions/ 1923.08.17_wimbledon.htm, accessed on April 11, 201554 It is rather interesting to note that there never was a Netherlands-US BIT, despite the large capital flows between the Netherlands and the US, and theyhave engaged per the n treaty of Friendship, Commerce and Navigation with the US since 1956 that provides with same level of FETs as in current IIAs,including ISDS: 'old' EU Member States, economically similar to the Netherlands have not concluded a BIT with the US- only 9 out of the 28 EU MemberStates have BITs with the US. However, BITs concluded by the Netherlands, ISDS was commonly provided, and it has been an unflinching supporter ofISDS, demonstrated in the explanatory memorandum to the Dutch ratification of ICSID Convention.55 European Commission Memo, 'Member States Endorse EU-US Trade and Investment Negotiations', Brussels, 14 Jun 2013, available at:http://europa.eu/rapid/ press-release_MEMO-13-564_en.htm, accessed on April 11, 2015- “Investment” under para on “Mandate” -…” including investor-to-state dispute settlement, is covered by the negotiating directive. Relevant safeguards are included to avoid any abuse of the system and to safeguard theright to regulate……”56 Supra Note 2, Fig. III.7 at pg. 127

Page17

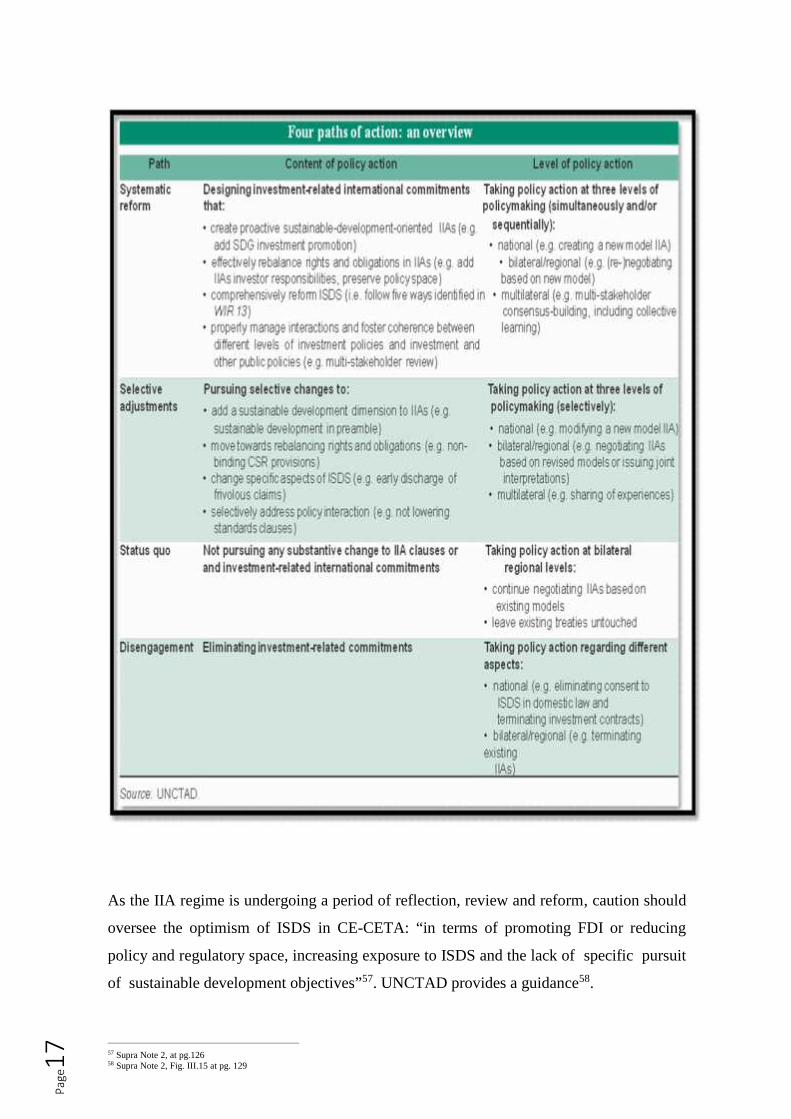

As the IIA regime is undergoing a period of reflection, review and reform, caution should

oversee the optimism of ISDS in CE-CETA: “in terms of promoting FDI or reducing

policy and regulatory space, increasing exposure to ISDS and the lack of specific pursuit

of sustainable development objectives”57. UNCTAD provides a guidance58.

57 Supra Note 2, at pg.12658 Supra Note 2, Fig. III.15 at pg. 129

Page18

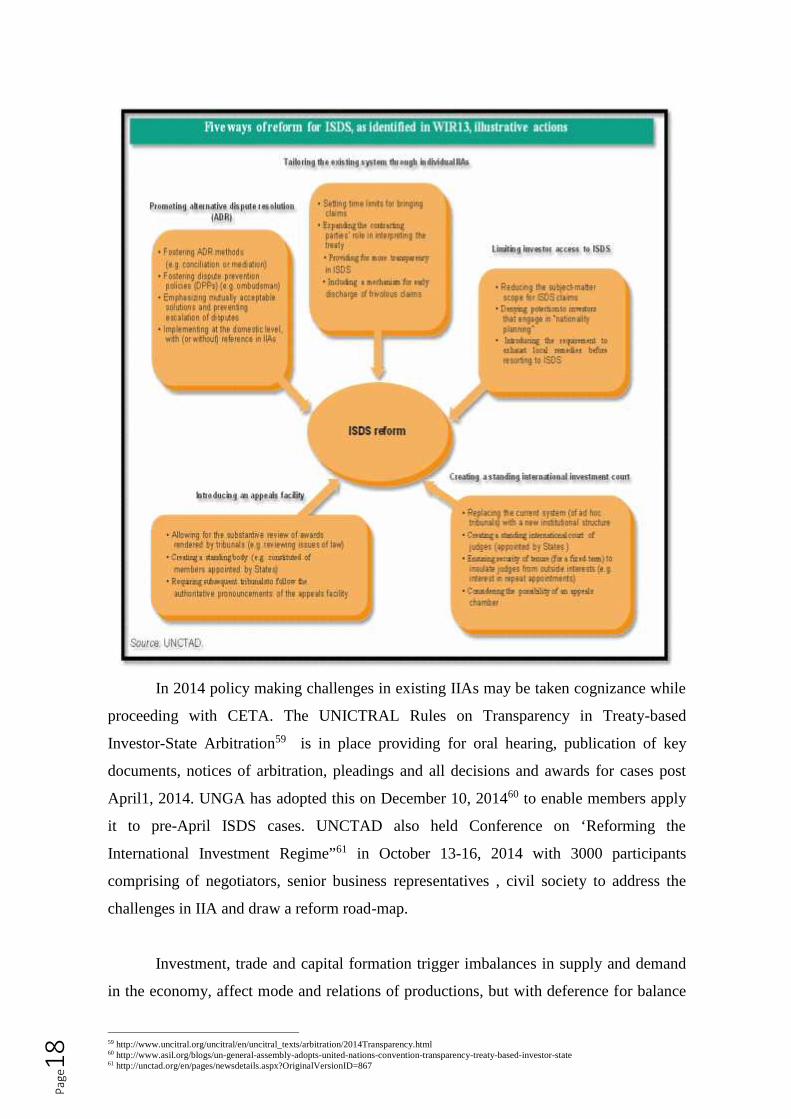

In 2014 policy making challenges in existing IIAs may be taken cognizance while

proceeding with CETA. The UNICTRAL Rules on Transparency in Treaty-based

Investor-State Arbitration59 is in place providing for oral hearing, publication of key

documents, notices of arbitration, pleadings and all decisions and awards for cases post

April1, 2014. UNGA has adopted this on December 10, 201460 to enable members apply

it to pre-April ISDS cases. UNCTAD also held Conference on ‘Reforming the

International Investment Regime”61 in October 13-16, 2014 with 3000 participants

comprising of negotiators, senior business representatives , civil society to address the

challenges in IIA and draw a reform road-map.

Investment, trade and capital formation trigger imbalances in supply and demand

in the economy, affect mode and relations of productions, but with deference for balance

59 http://www.uncitral.org/uncitral/en/uncitral_texts/arbitration/2014Transparency.html60 http://www.asil.org/blogs/un-general-assembly-adopts-united-nations-convention-transparency-treaty-based-investor-state61 http://unctad.org/en/pages/newsdetails.aspx?OriginalVersionID=867

Page19

in political choices disallowing extremities: Friedman’s62 profit maximization doctrine as

business objective on one end and the so-called "fundamentally subversive doctrine"63 of

pure and ethical social responsibility theme on the other. The proportionality doctrine

inherent in the right to regulate in CE-CETA like other ISDS IIAs affords that in

expropriation matters the state first only impacts investments to achieve its legitimate

public policy aims, and secondly fosters credibility that a expropriation (direct or indirect)

does not disproportionately impact a single investor to whom the government made

specific promises64. This regulatory space of the government in public policy stays

sacrosanct and so does the sustainability goals. This is key to success for CE-CETA:

prosper with virtue.

62 Friedman, Milton: The Social Responsibility of Business is to Increase its Profits - The New York Times Magazine, September 13, 1970. Copyright @1970 by The New York Times Company at http://www.colorado.edu/studentgroups/libertarians/issues/friedman-soc-resp-business.htmlaccsesd on March

12, 2015 & course material63 Ibid- quoted in Capitalism and Freedom64 Supra, Note 4, Para 103 at pg. 56

Page20

Bibliography

Statutes

1. Canada–European Union – Comprehensive Economic and Trade Agreement athttp://www. International. gc.ca/trade- agreements-accords-commerciaux/agr-acc/ceta-aecg/index.aspx?lang=eng-, accessed – from March 20 to April 12, 2015

2. North American Free Trade Agreement (NAFTA): http://www.international.gc.ca/trade-agreements-accords-commerciaux/agr-acc/nafta-alena/index.aspx?lang=eng, accessedon April 8, 2015

3. IISD Model International Agreement on Investment: https://www.iisd.org/investment/capacity/ model.aspx, accessed on April 9, 2015

4. The Transatlantic Trade and Investment Partnership http://trade.ec.europa.eu/doclib /press/index. cfm? id=1230#market-access, accessed on April 9, 2015

Jurisprudence

1. Al-Kharafi V. Libya- http://www.italaw.com/sites/default/files/case-documents .pdf &http://unctad.org/en/publicationslibrary/webdiaep cb2014d3_en.pdf - AlKharafi v.s Libya2. Crompton (Chemtura) Corp. v. Government of Canada-http://www.international.gc.ca/trade-agreements-accords-commerciaux/topics-domaines/disp-diff/crompton.aspx?lang=eng3. Ethyl Corporation v. the Government of Canada- http://www.international.gc.ca/trade-agreements-accords-commerciaux/topics-domaines/disp-diff/ethyl.aspx?lang=eng;4. Eli Lilly and Company v. Government of Canada-http://www.international.gc.ca/trade-agreements-accords-commerciaux/topics-domaines/disp-diff/eli.aspx?lang=eng-5. Global Financial Disruptions and Related Cases – Lamm, B. Carolyn, Heelbeck.R.E, SakaOnur, Rosenburg D- http://primefinancedisputes.org/wp-content/uploads and Supra Note47 at 66. John R. Andre v. Government of Canada- http://www.international.gc.ca/trade-agreements-accords-commerciaux/topics-domaines/disp-diff/JohnR_Andre.aspx?lang=eng7. Lone Pine case Notice of Arbitration- http://www.international.gc.ca/trade-agreements-accords-commerciaux/assets/pdfs/disp-diff/lone-02.pdf8. Mobil Investments Inc. v. Government of Canada- http://www.international.gc.ca/trade-agreements-accords-commerciaux/topics-domaines/disp-diff/mobil.aspx?lang=eng9. S.D. Myers Inc. v. Government of Canada- http://www.international.gc.ca/trade-agreements-accords-commerciaux/topics-domaines/disp-diff/SDM.aspx?lang=eng

10. Pope & Talbot Inc. v. Government of Canada- http://www.international.gc.ca/trade-agreements-accords-commerciaux/topics-domaines/disp-diff/pope.aspx?lang=eng

Page21

11. Windstream Energy LLC v. Government of Canada- http://www.international.gc.ca/trade-agreements-accords-commerciaux/topics-domaines/disp-diff/windstream.aspx?lang=eng

12. http://blog.martindale.com/slovak-bank-shareholder-file-arbitration-against-greece-over-

debt restructure

13. Micula Brother & Ors. V. Romania: http://www.italaw.com/sites/default/files/case-documents/italaw3036.pdf-case-t-64614-micula-v-commission-state-aids-and-international-dispute-settlement-systems/

14. Piero Foresti, Laura de Carli & Others v. The Republic of South Africa, ICSID Case No.ARB(AF)/07/01 - http://www.italaw.com/cases/446

15. Vattenfall AB, Vattenfall Europe AG, Vattenfall Europe Generation AG v. FederalRepublic of Germany, ICSID Case No. ARB/09/6 (formerly Vattenfall AB, VattenfallEurope AG, Vattenfall Europe Generation AG & Co. KG v. The Federal Republic ofGermany) - http://www.italaw.com/cases/1148

16. Veolia Propreté v. Arab Republic of Egypt, ICSID Case No. ARB/12/15-http://www.italaw.com/cases/2101

17. https://www.citizen.org/documents/oxy-v-ecuador-memo.pdf- Occidental PetroleumCorporation and Occidental Exploration and Production Company v. The Republic ofEcuador

18. S.S. "Wimbledon" United Kingdom, France, Italy & Japan v. Germany [PERMANENT

COURT OF INTERNATIONAL JUSTICE, File E. b. II., Docket III.I dated, 17 August

1923]

Books

1. World Investment Report- United Nations Conference on Trade and DevelopmentInvesting in the SDGs: An Action Plan - at http://unctad.org/en /Publications Library/wir2014 _en.pdf, accessed on March 28, 2015-

2. The Impact of Investor-State-Dispute Settlement (ISDS) in the Transatlantic Trade andInvestment Partnership, Study prepared for the Minister for Foreign Trade andDevelopment Cooperation, Ministry of Foreign Affairs, The Netherlands, 24/06/2014 (seeP127, para 283) http://www.rijksoverheid.nl/documenten-en-publicaties/rapporten/2014/06/24/the-impact-of-investor-state-dispute-settlement-isds-in-the-ttip.html accessed on April 8, 2015

3. Soto de Hernando- The Mystery of Capital- Why capitalism triumphs in the West and failseverywhere else- Black Swan book- ed. 2001

4. Gaukrodger, D. and K. Gordon (2012), "Investor-State Dispute Settlement: A ScopingPaper for the Investment Policy Community", OECD Working Papers on InternationalInvestment, 2012/03, OECD Publishing (see P17- 19) http://www.oecd-ilibrary.org/docserver/download/ 5k46b1r85j6f.pdf?expire accessed on April 8, 2015-

Page22

“Investor claimants range from individuals with quite limited international experience (e.g.an association of retirees) to major multinational enterprises with tens of thousands ofemployees and global operations”.

5. Private Rights, Public Problems, Para 4.1 at pg.16- International School of SustainableDevelopment at http://www.iisd.org/pdf/trade_citizensguide.pdf, accessed on April 11,2015

6. Introduction- IISD Model International Agreement on Investment for SustainableDevelopment, April, 2005 at http://www.italaw.com/documents/ investment_ model_ int_agreement.pdf

Articles

1. Being Virtuous and Prosperous: SRI’s Conflicting Goals- Richardson, J. Benjamin andCragg, Wes - course reading; also at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1463936-; also course material

2. Friedman, Milton: The Social Responsibility of Business is to Increase its Profits - TheNew York Times Magazine, September 13, 1970. Copyright @ 1970 by The New YorkTimes Company at http://www.colorado.edu/studentgroups /libertarians/issues/friedman-soc-resp-business.htmlaccsesd on March 12, 2015

3. Recent Trends in IIAs and ISDS- IIA Issue Note No.1, February, 2015 athttp://unctad.org/en/PublicationsLibrary/webdiaepcb2015d1_en.pdf accessed on April 5,20151

4.. Investor-to-State Dispute Settlement (ISDS) Some facts and figures- EuropeanCommission at http://trade.ec.europa.eu/doclib/docs/2015/ January/ tradoc_153046.pdf,accessed on April 8, 2015

5.. The Economist, Feb.27, 2014Reading “Capital”: Introduction; course material –

6. Arlidge, John- I'm doing 'God's work'. Meet Mr. Goldman Sachs- the Sunday Timespublished: 8 November 2009 – at http://www.thesundaytimes. co.uk/ sto/news/worl d_news/article 189615.ece; and also course material

7. Rubin Richard- “U.S. Companies Are Stashing $2.1 Trillion Overseas to Avoid Taxes”- athttp://www.bloomberg.com/news/articles/2015-03-04/ accessed on March 8,015, also on myFacebook post

8. Towards an EU-US trade deal: European Commission at http://trade.ec.europa.eu/doclib/ docs/ 2015/January /tradoc_ 153046. pdf accessed on April 9, 2015 atpg.9

9. European Commission Memo, 'Member States Endorse EU-US Trade and InvestmentNegotiations', Brussels, 14 Jun 2013, available at: http://europa.eu/rapid/ press-release_MEMO-13-564_en.htm, accessed on April 11, 2015- “Investment” under para on“Mandate” -…” including investor-to-state dispute settlement, is covered by the negotiating

Page23

directive. Relevant safeguards are included to avoid any abuse of the system and tosafeguard the right to regulate……”10. London Principles of Sustainable Finance (2002)-

http://www.cityoflondon.gov.uk/services/environmentand-planning/sustainability/Documents/ pdfs/ SUS_lonprinciples.pdf (accessed on April 12, 2015);11. United Nations Principles for Responsible Investment(UNPRI-2006)- athttp://www.unpri.org/about-pri/the-six-principles/ accessed on April 12, 2015;12. Equator Principles( 2003)- at http://www.equator-principles.com/ accessed on April 12,2015.13. Expropriations- - at http://en.wikipedia.org/wiki/Expropriation;14. Fair and Equitable Treatment (FET) –“FAIR AND EQUITABLE TREATMENT -UNCTAD Series on Issues in International Investment Agreements II athttp://unctad.org/en/Docs/ unctaddiaeia2011d5_en.p df, accessed on April 15, 2015;15. National Treatment-National Treatment- UNCTAD Series on Issues in InternationalInvestment Agreements at http://unctad.org/en/pages/PublicationArchive.aspx?publicationid= 340 II , accessed on April 12, 2015

-16. http://www.uncitral.org/uncitral/en/uncitral_texts/arbitration/2014Transparency.html17. http://www.asil.org/blogs/un-general-assembly-adopts-united-nations-convention-transparency-treaty-based-investor-state18. http://unctad.org/en/pages/newsdetails.aspx?OriginalVersionID=867