Appraisal of the Tin and Tungsten Expansion Project - World ...

185

Report No. 1351-BA Burma Appraisal of the Tin and Tungsten Expansion Project February 8, 1977 Industrial ProjectsDepartment FOR OFFICIALUSE ONLY Document of the World Bank This document hasa restricteddistribution and may be used by recipients only in the performance of their officialduties. Its contentsmay not otherwisebe disclosed without World Bank authorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

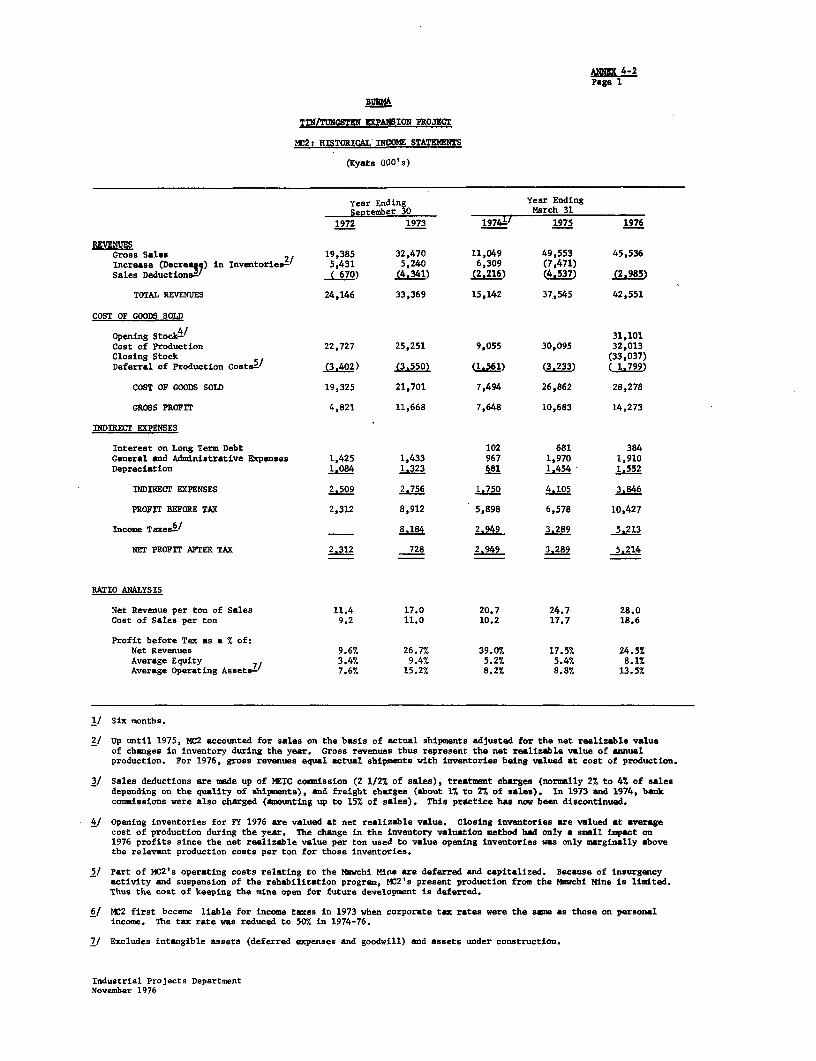

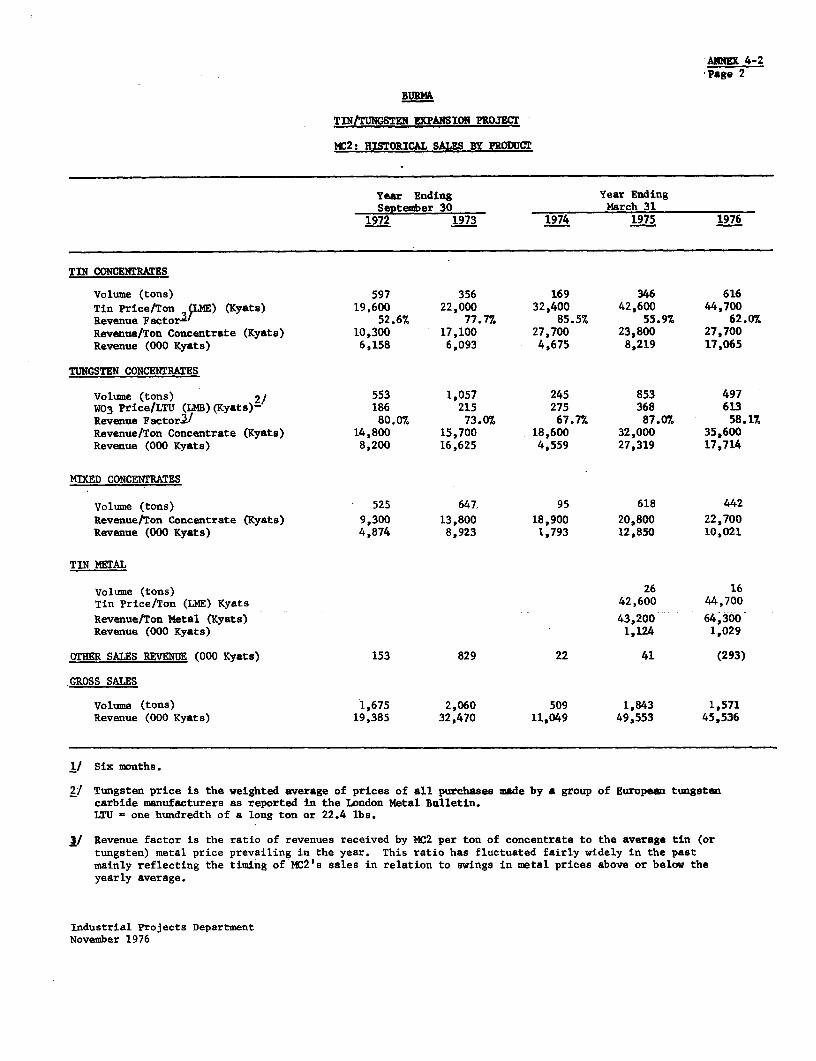

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Appraisal of the Tin and Tungsten Expansion Project - World ...

Report No. 1351-BA

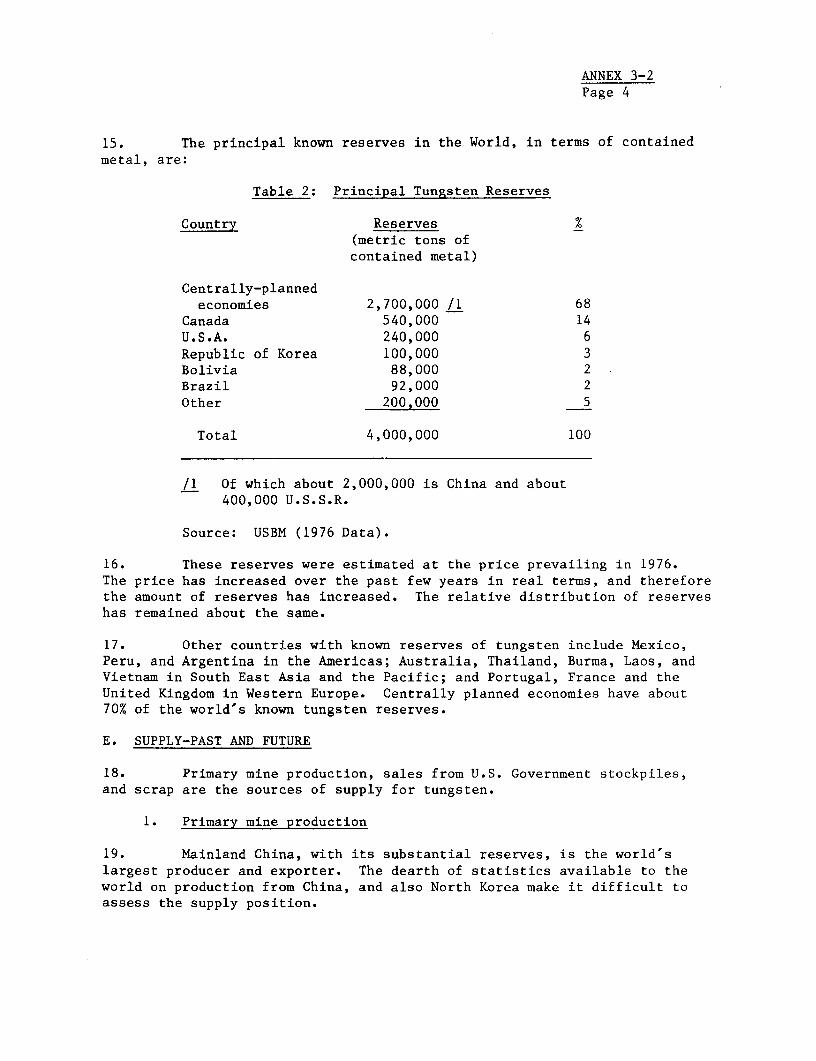

BurmaAppraisal of the Tin andTungsten Expansion ProjectFebruary 8, 1977

Industrial Projects Department

FOR OFFICIAL USE ONLY

Document of the World Bank

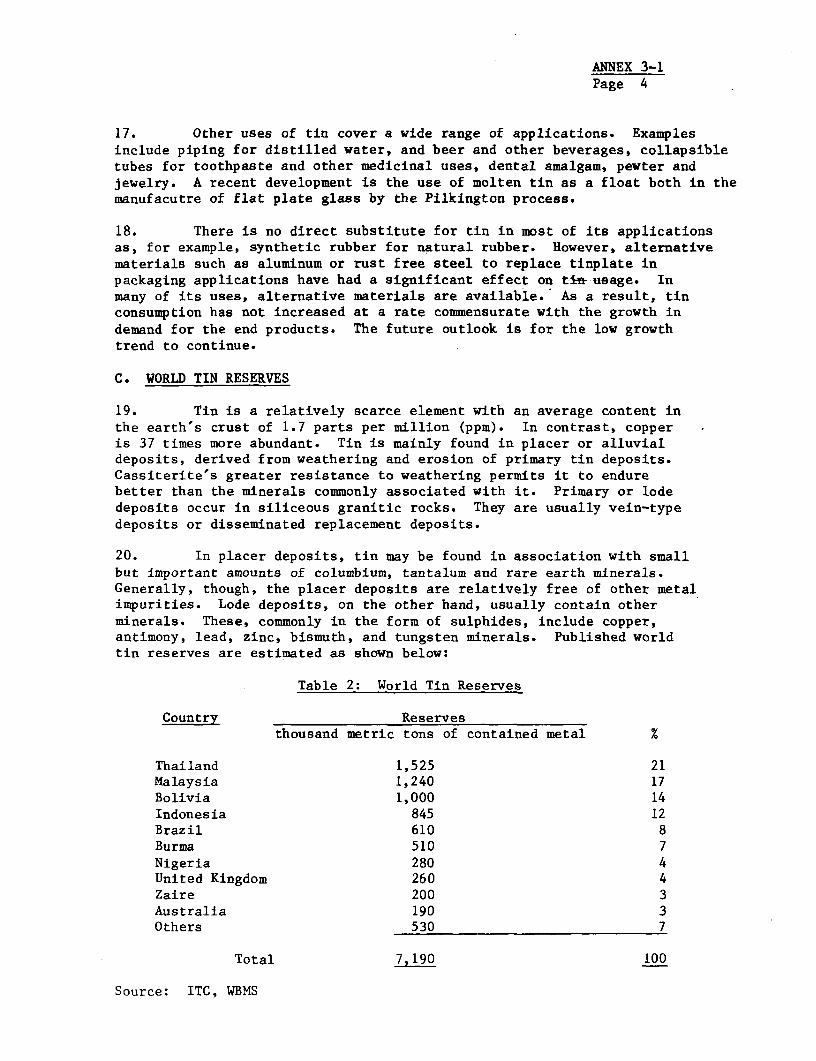

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. Its contents may nototherwise be disclosed without World Bank authorization.

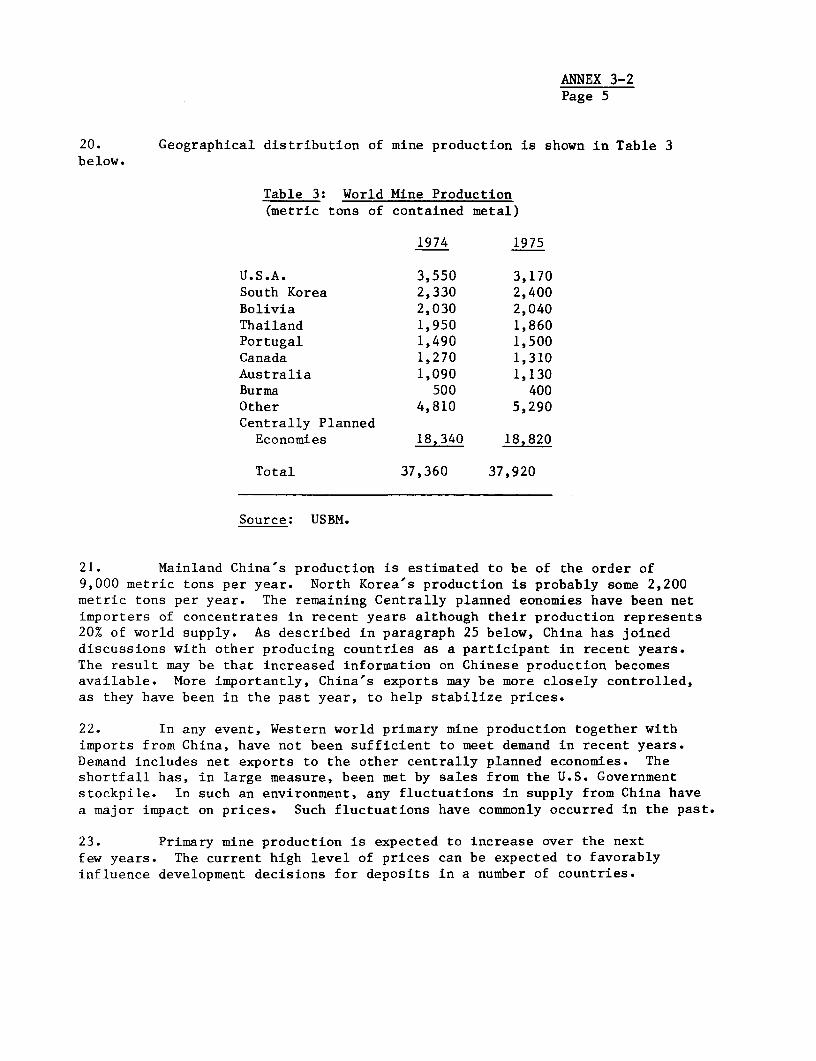

Pub

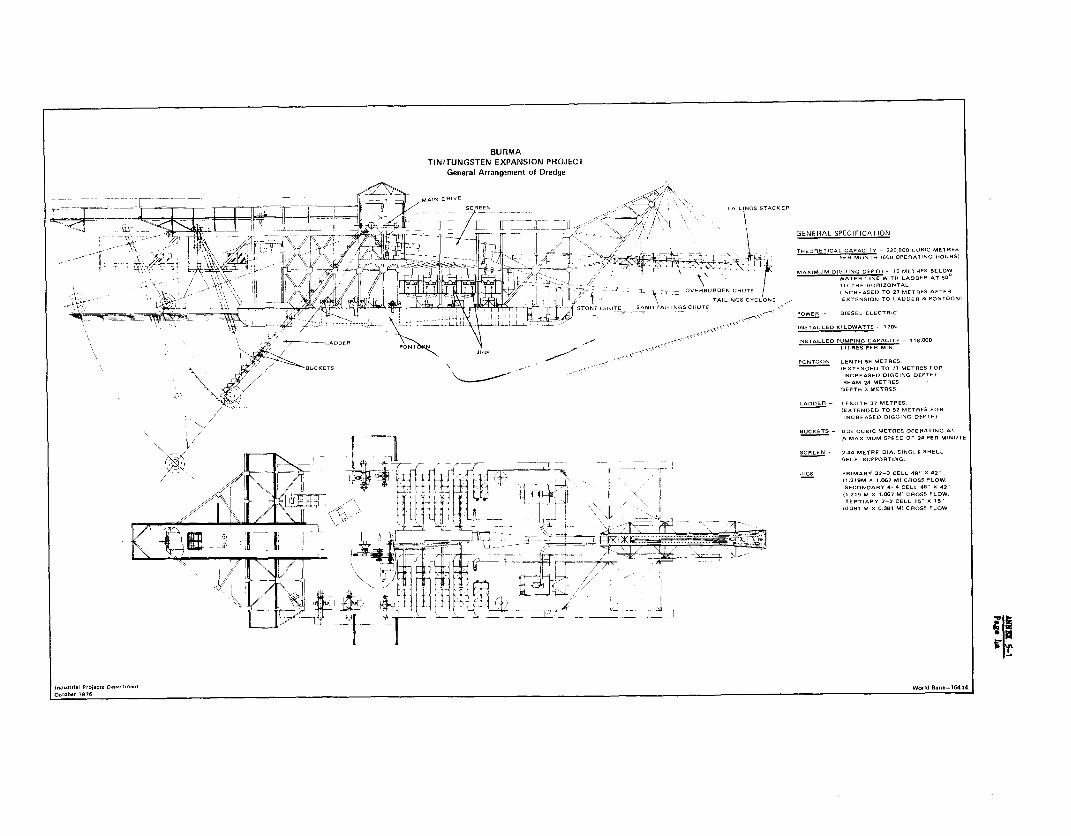

lic D

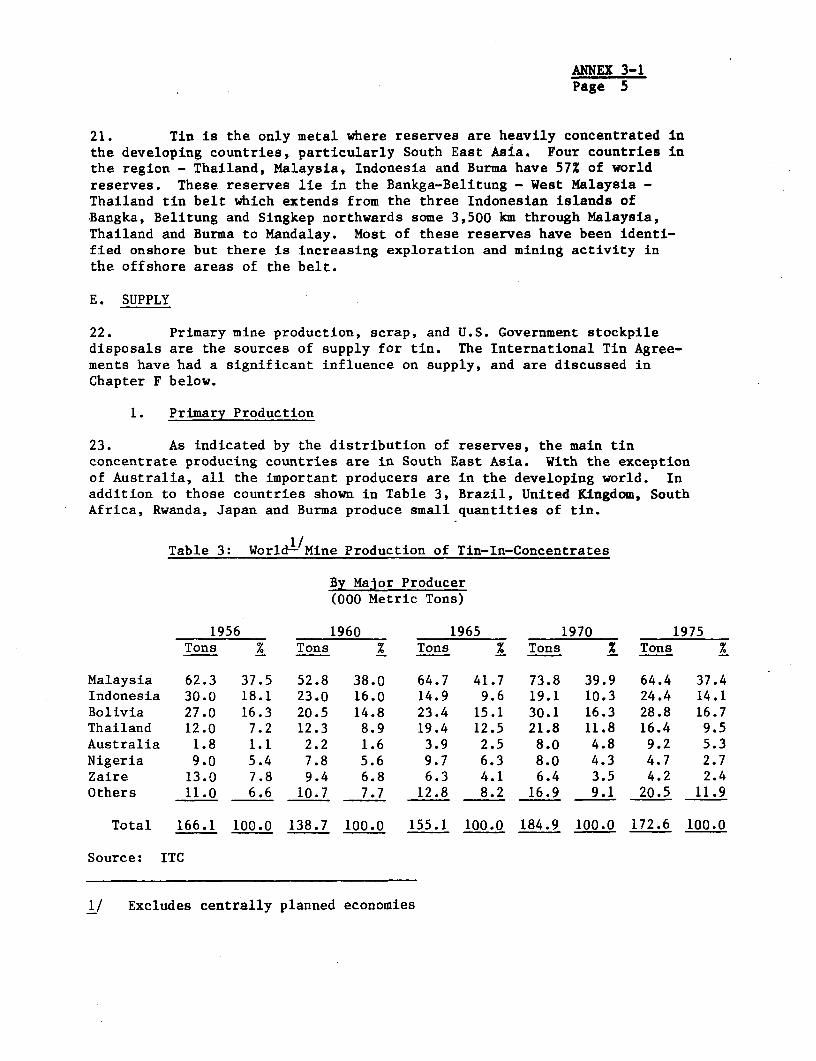

iscl

osur

e A

utho

rized

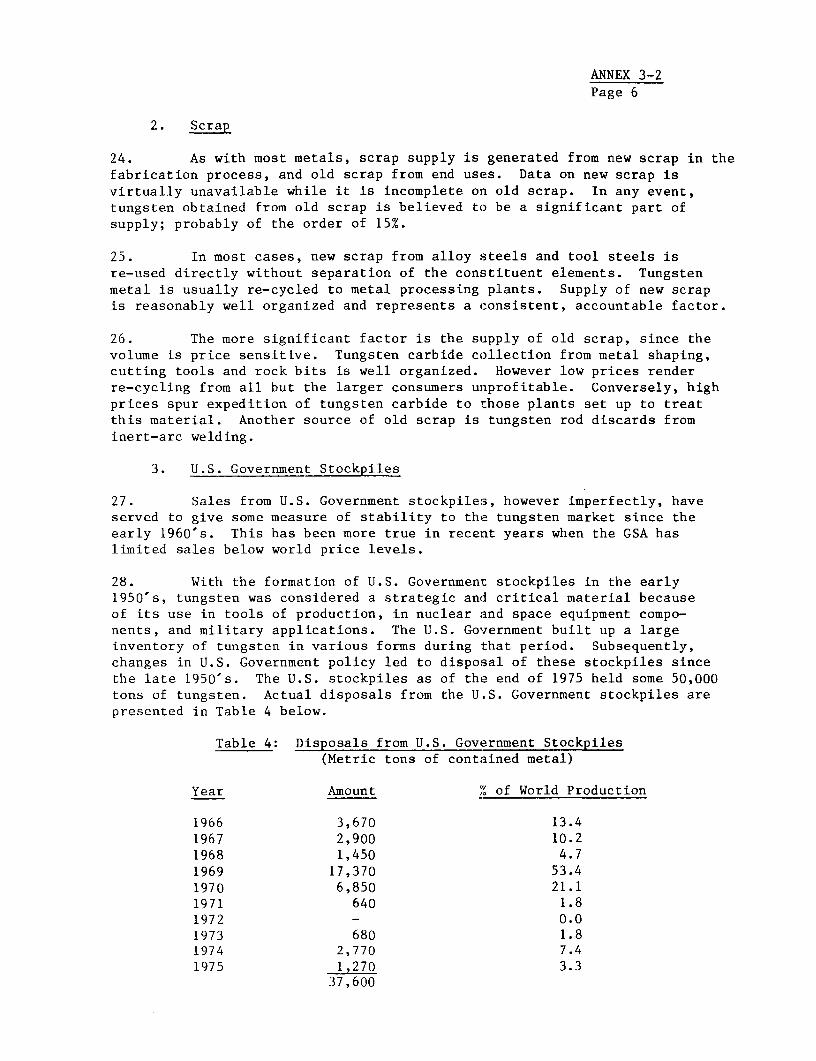

Pub

lic D

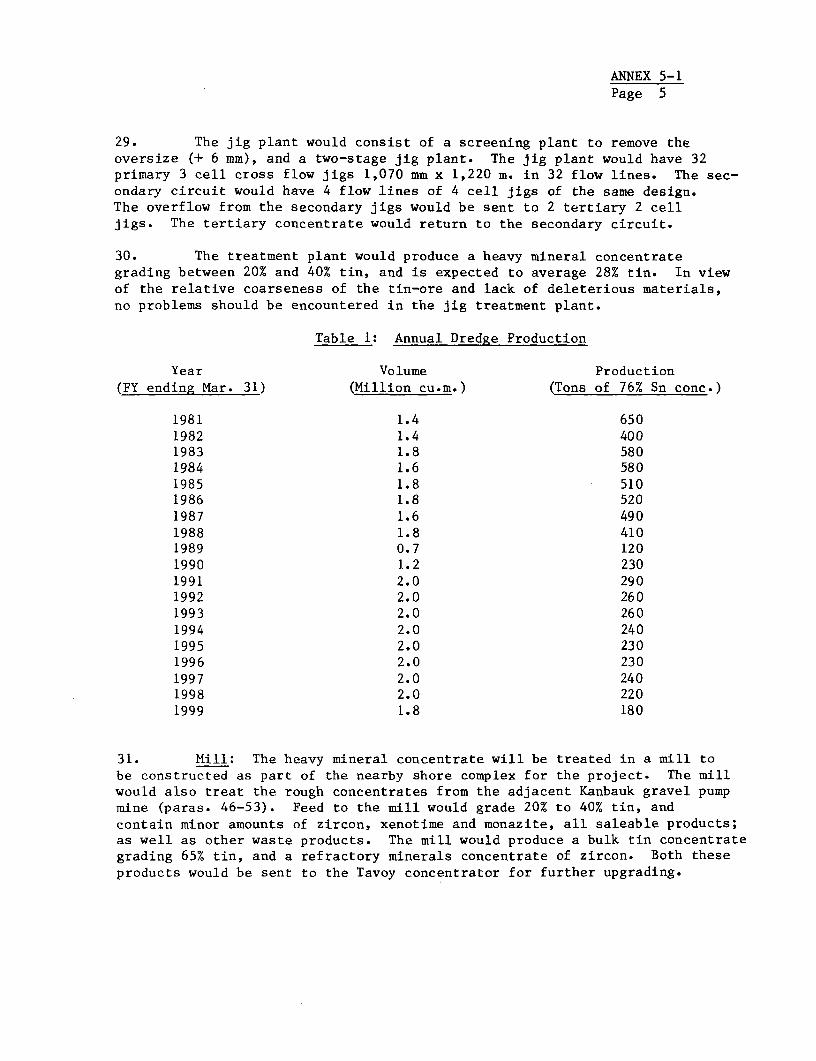

iscl

osur

e A

utho

rized

Pub

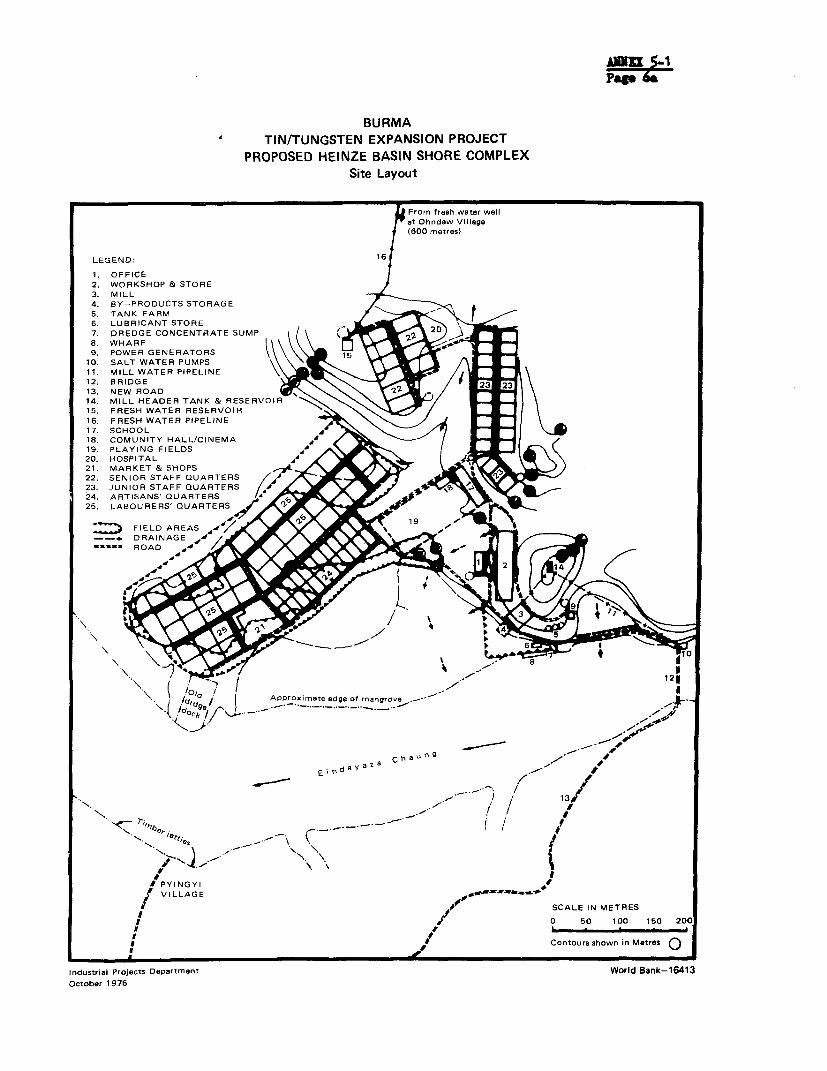

lic D

iscl

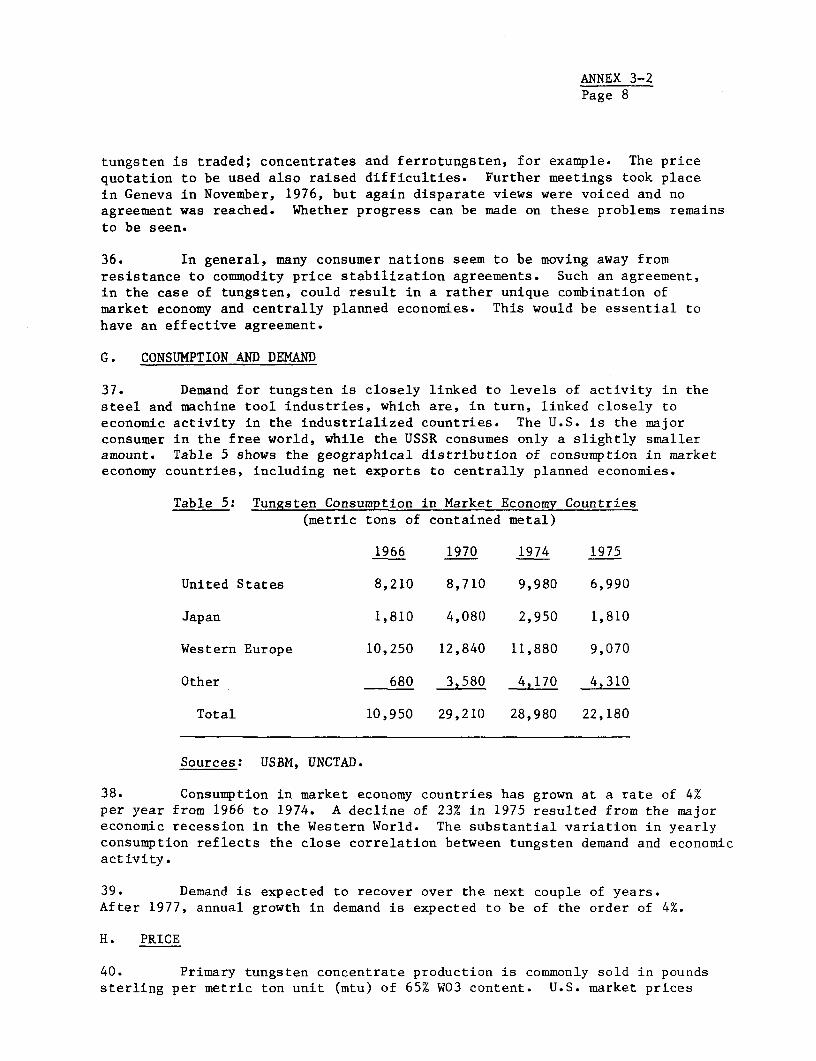

osur

e A

utho

rized

Pub

lic D

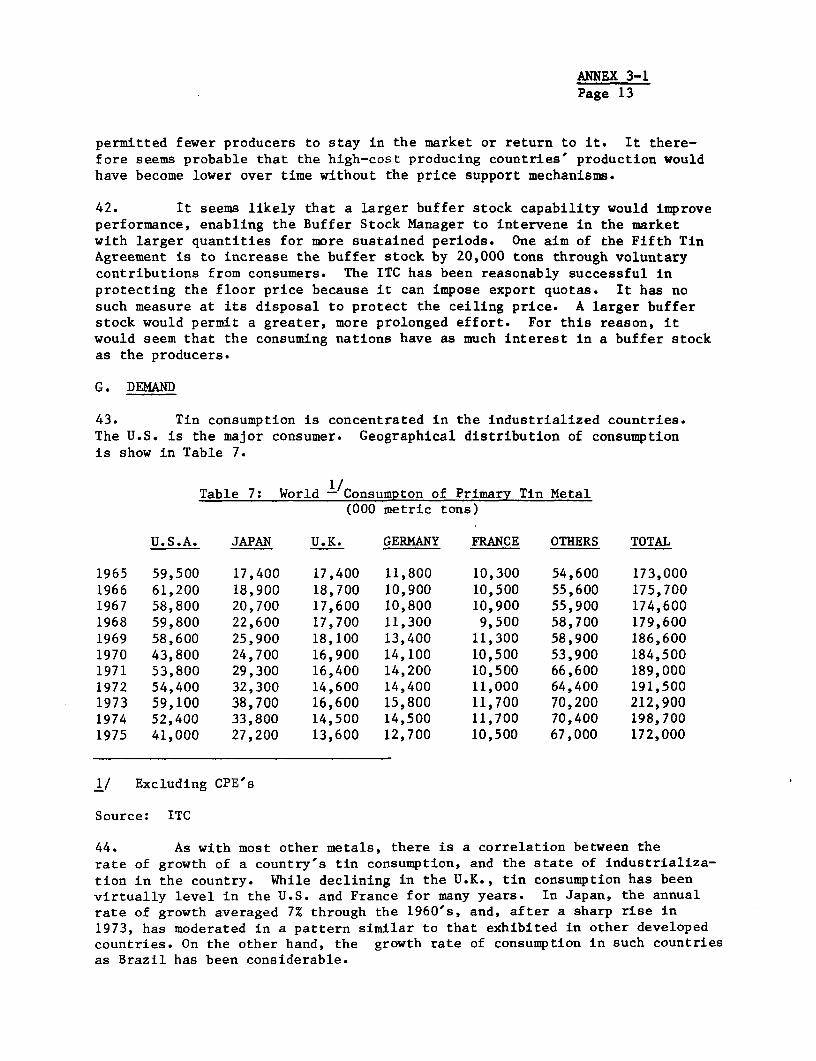

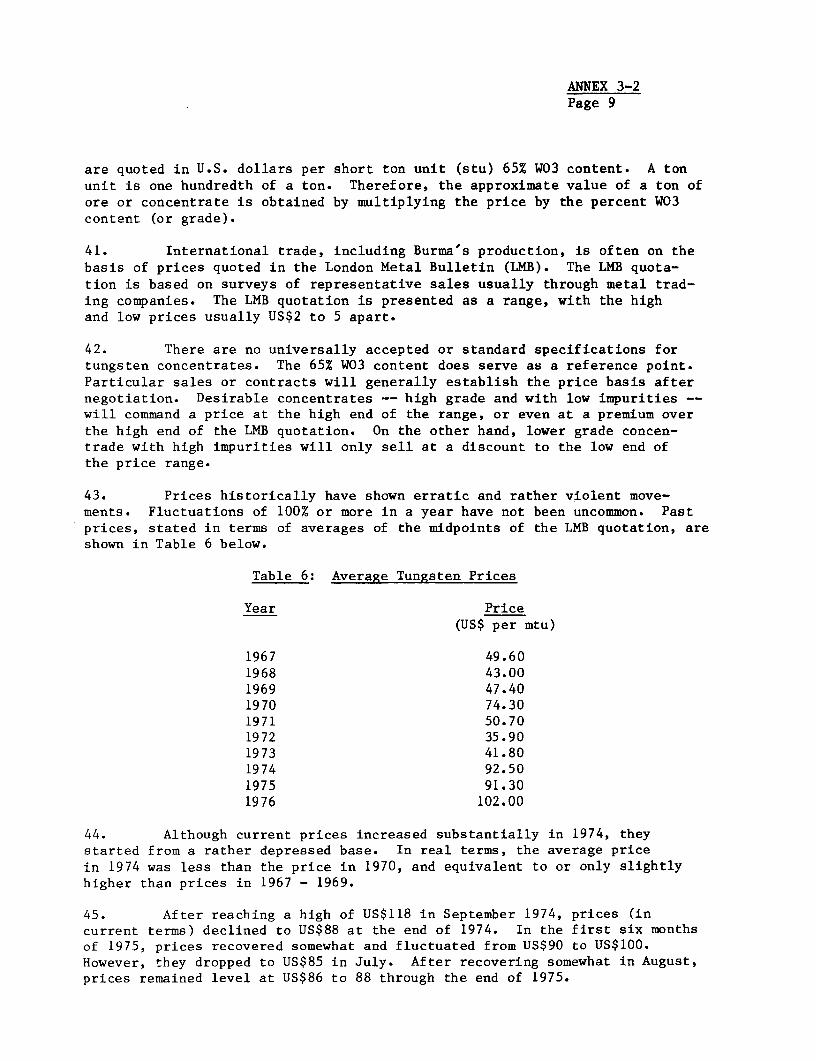

iscl

osur

e A

utho

rized

Pub

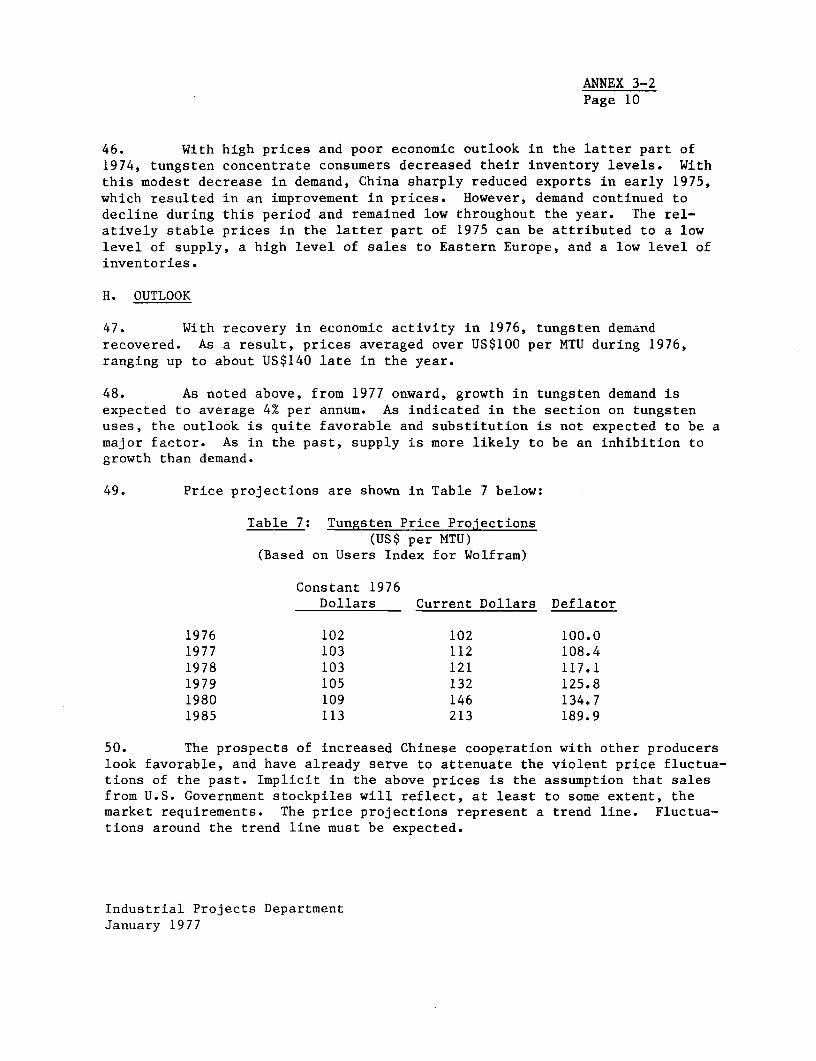

lic D

iscl

osur

e A

utho

rized

Pub

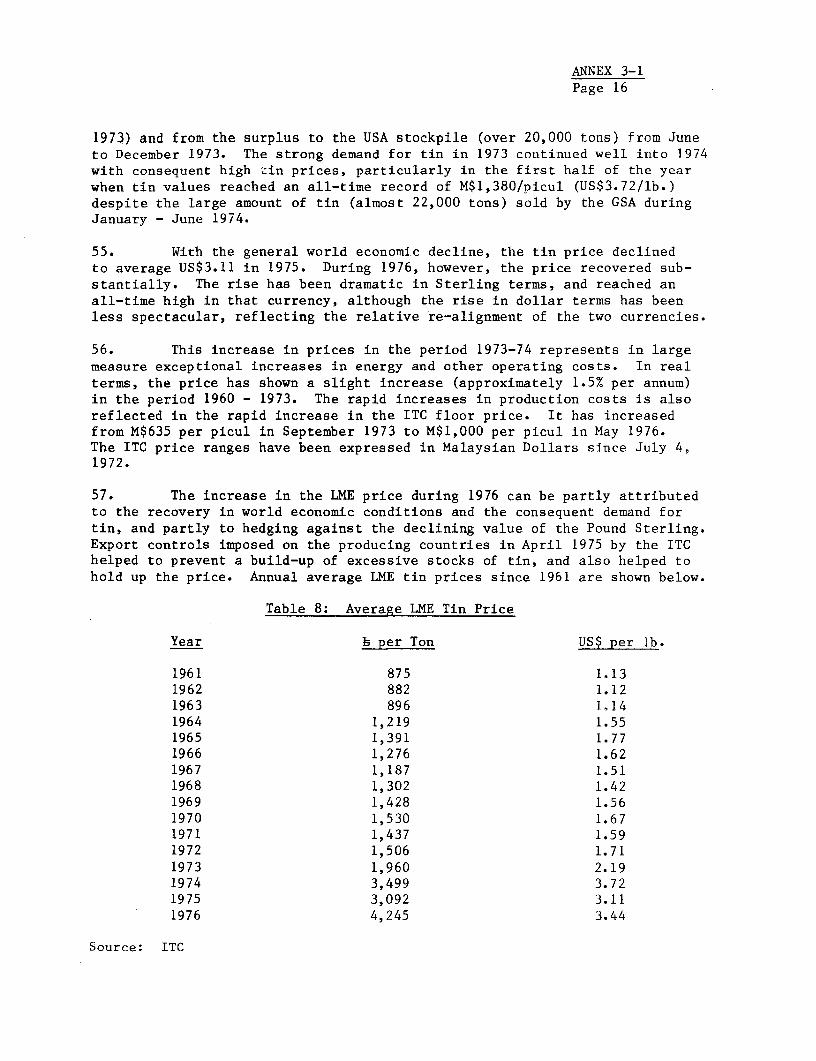

lic D

iscl

osur

e A

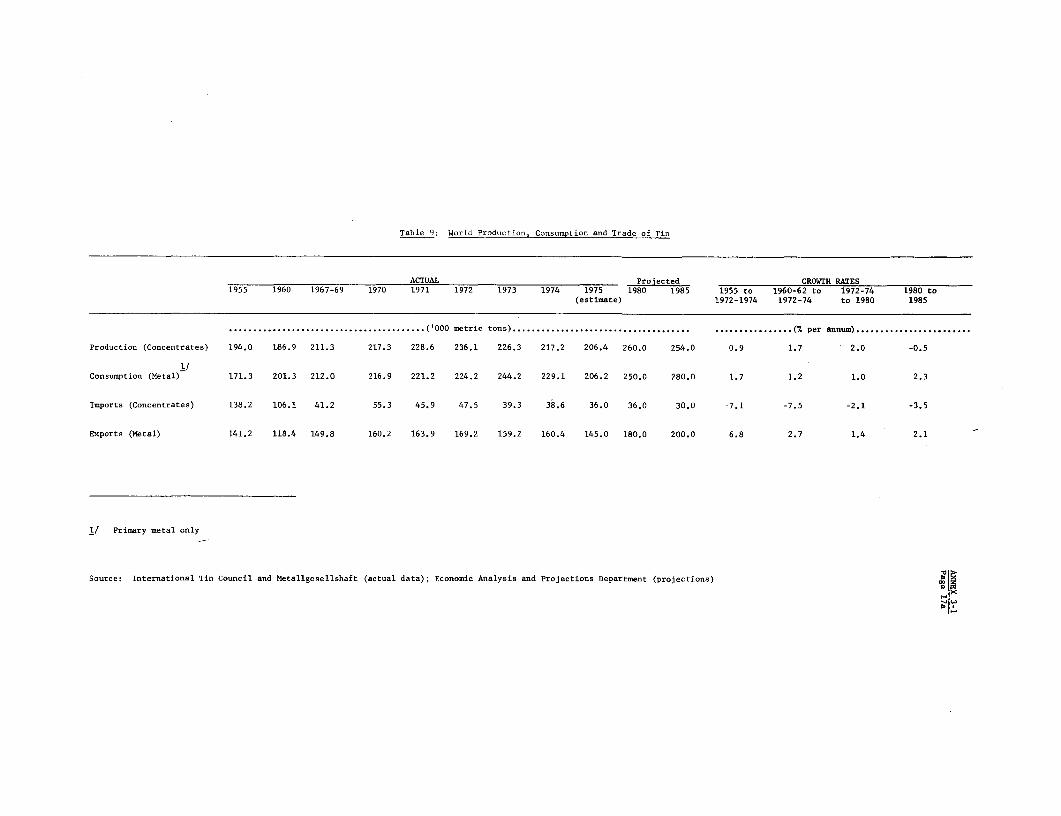

utho

rized

Pub

lic D

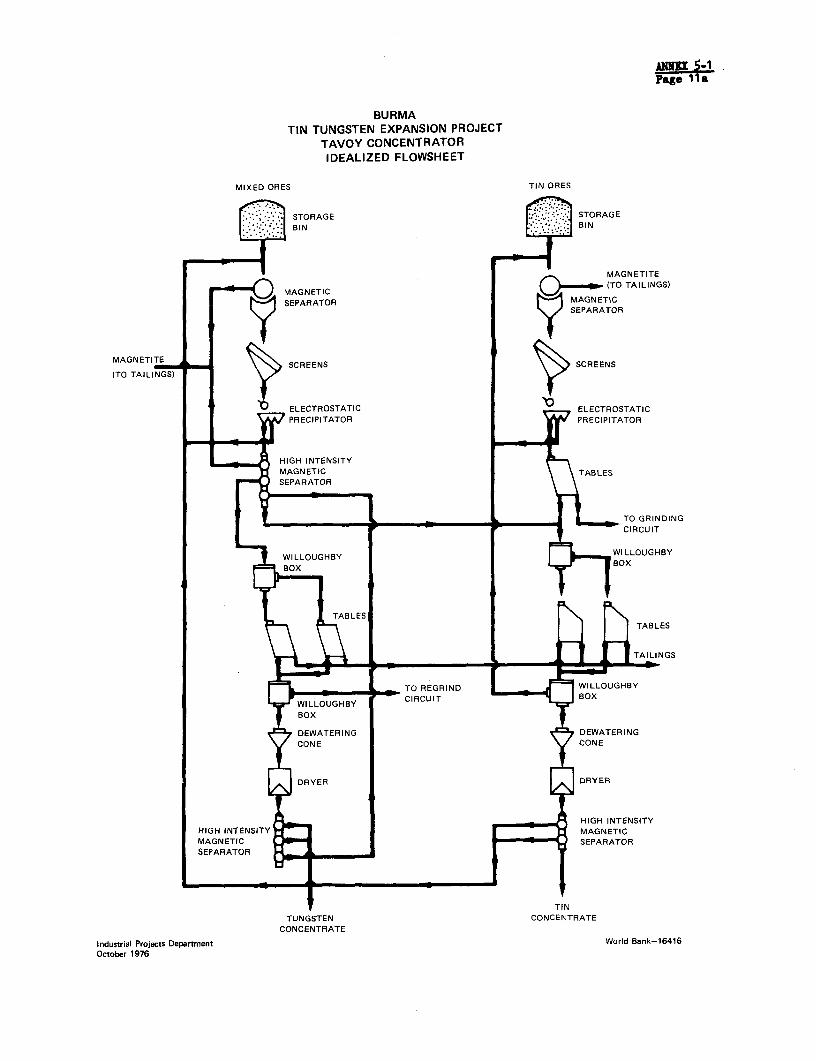

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

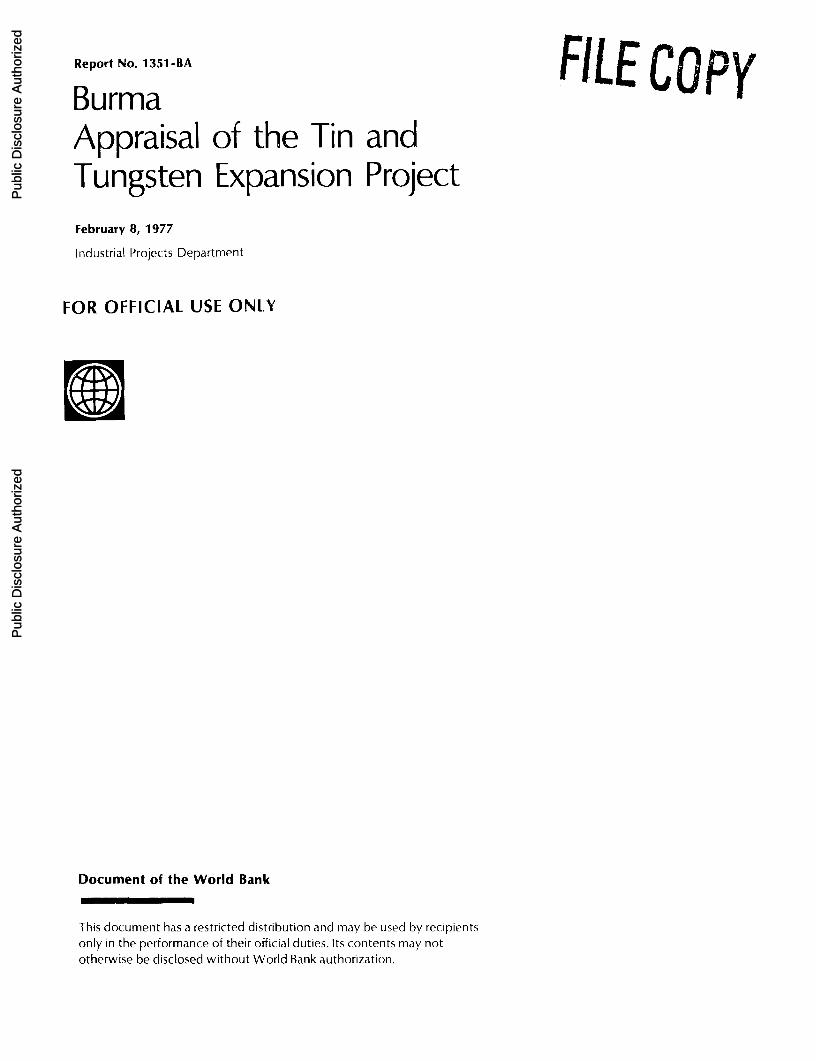

CURRENCY EQUIVALENTS

Except where otherwise indicated, all figures arequoted in Kyats (K) and US Dollars (US$).

K 1.00 = US$0.15K 6.65 = US$1.00

ABBRIVIATIONS AND ACRONYMS

CIDA Canadian International Development AssociationDGSE Directorate of Geological Survey and Mineral ExplorationGovernment Government of the Socialist Republic of the Union of BurmaKfW Kreditanstalt fur WiederaufbauITC International Tin CouncilLMB London Metal BulletinLME London Metal ExchangeLTPY Long tons per yearMC2, the Corporation No. 2 Mining Corporation (formerly Myanma Tin Tungsten

Corporation - MTTC)MDC Mineral Development CorporationMEB Myanma Economic BankIMEIC Myanma Export Import CorporationMMDC Myanma Mineral Development CorporationHOC Myanma Oil Corporation1'PY Metric tons per yearPTA Primary Tungsten AssociationUBB Union Bank of BurmaUGCF Union Government Consolidated FundUNCTAD United Nations Conference on Trade and DevelopmentUNDP United Nations Development ProgramUSBM US Bureau of MinesWBMS World Bureau of Metal Statistics

WEIGHTS AND MEASURES

1 Hectare = 2.47 acres1 Kilometer (km) = 0.62 miles1 Long Ton (LT) = 2,240 pounds1 Long Ton Unit (LTU) = 1% of a long ton or 22.4 pounds1 Meter (m) = 39.3 inches1 Metric Ton (MT) = 2,205 pounds1 Metric Ton Unit (MTU)= 1% of a metric ton, or 22.05 pounds1 Picul (Pikul) = 133.33 pounds

FISCAL YEAR

April 1 - March 31

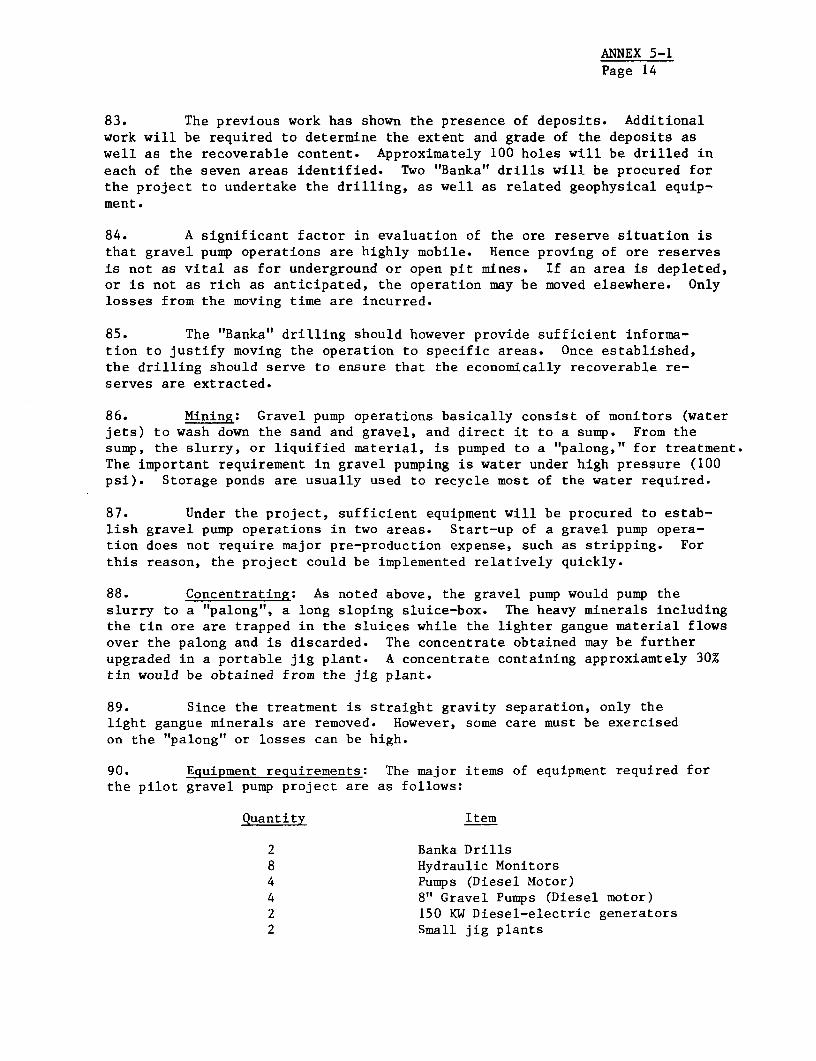

Industrial Projects DepartmentFebruary 1977

FOR OFFICIAL USE ONLYBURMA

APPRAISAL OF THE TIN AND TUNGSTEN EXPANSION PROJECT

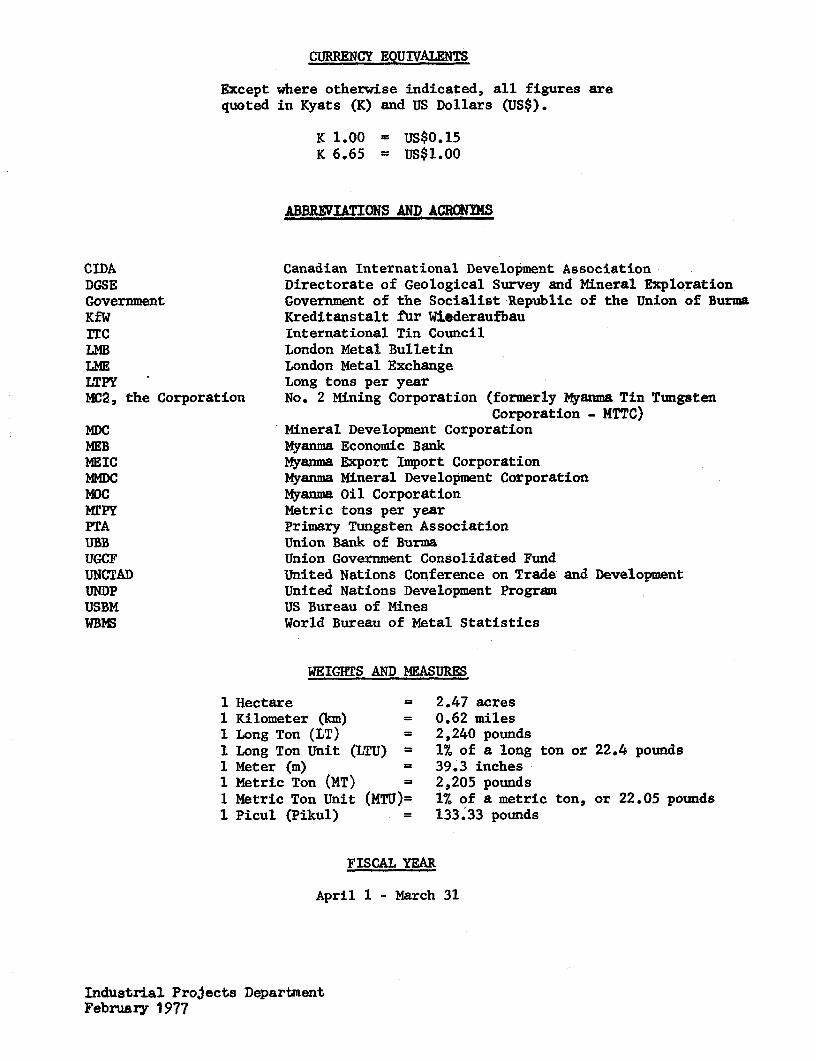

TABLE OF CONTENTS

Page No.

SUMMARY AND CONCLUSIONS . ........................... . . . . . i-iii

I. INTRODUCTION ........................................ ............... 1

II. THE MINERAL SECTOR .. * * * * * * * ................................... ... 1

A. Present Position and Recent Trends ................ . 1B. Impact on the Economy .......oe .... o........ ....... 2C. Structure .. .. *......... ....... o ............ ....... 3D. Legislation and Operational Guidelines

for the Sector ...... ....................... 3E. Mineral Potential and Exploration 4........... a... 4F. Planned Sector Investment and Needs ............... 4

III. THE MARKET .................. o.o. ..................... 6

A. The International Tin Market ....................... 6

1. International Demand and Supply ......0 ........ 62. International Tin Agreements .................. 73. Price Structure and Projections 8............. 84. Marketing Arrangements ..... ................... 8

B. The International Tungsten Market ... .. ........... 9

1. International Demand and Supply ............... 92. Price Structure and Projections ............... 103. Marketing Arrangements ...... ..............

IV. THE CORPORATION ........................................... 1

A. Operations ......... o ......................................... .o. 11

1. Mining Facilities and Output .................. 112. Production Costs ... ............................. 12

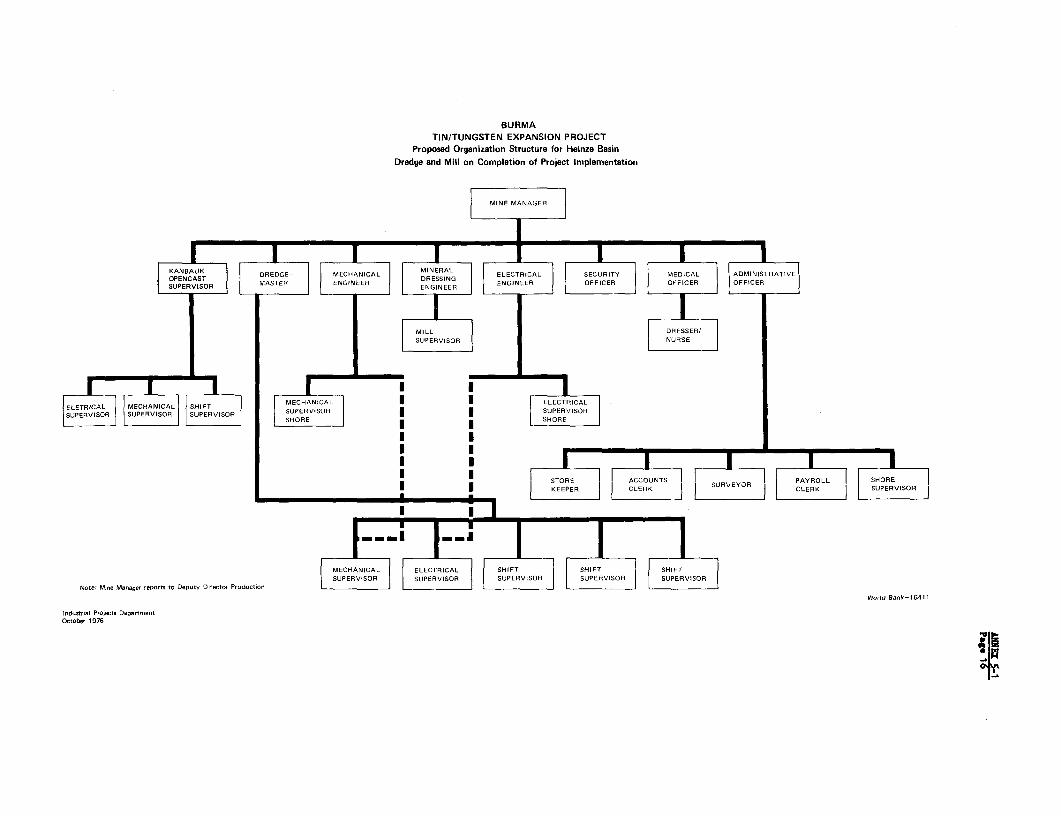

B. Past Performance and Financial Condition ........... 12C. Organization and Management .................... *.... 15D. Accounts and Audit ..... . ............................ 16E. Ore Reserves ... ............... ............ ..... ... 16

This report was prepared by Messrs. H.E. Wackman, R. Rodger, and S. Greigof the Industrial Projects Department and Mr. A. Freyman (Consultant).

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

-2-

Page No.

V. THE PROJECT ............... .... ......**. **.......... 16

A. Technical Description . ..................... 17

1. Heinze Basin Dredging Project and Concentrator. 172. Central Concentrator at Tavoy ................. 183. Gravel Pump Mining Project .................. 194. Technical Assistance ................. *...... 195. Other Expansion Plans.. 206. Sector Study ......... 20

B. Environmental Aspects ......... .. . ..... .......... 20C. Capital Costs........ 20D. Financing Plan . ... 22

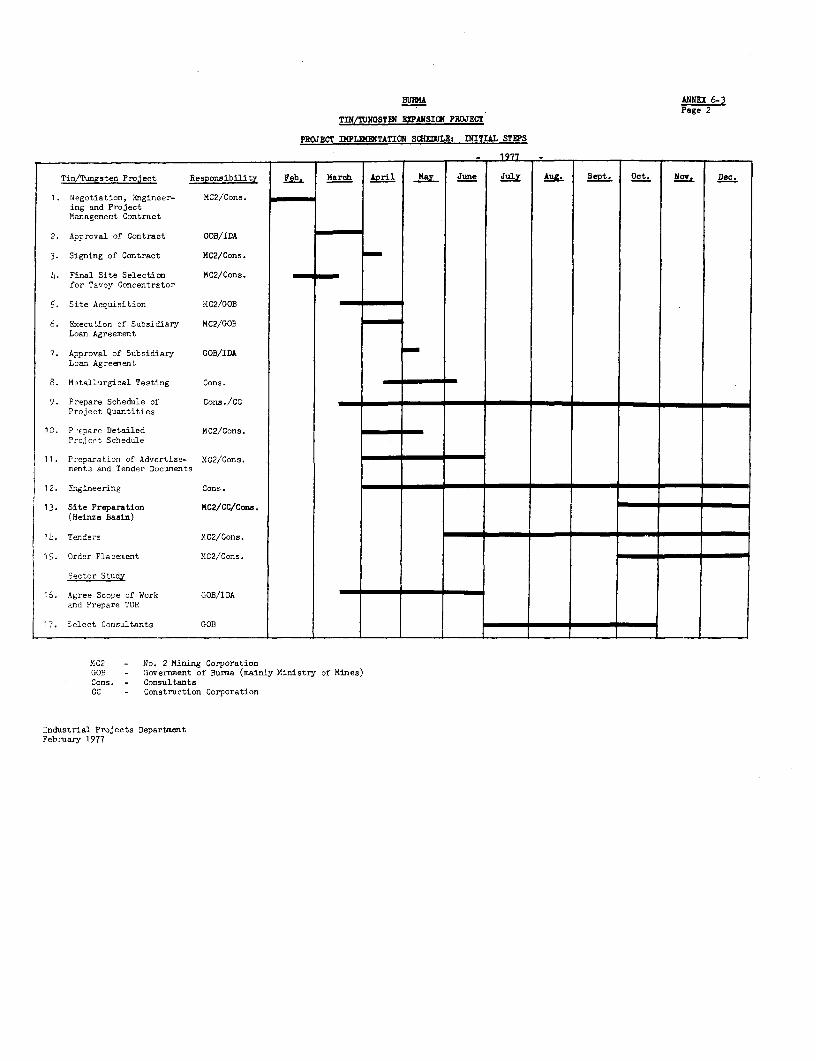

VI. PROJECT IMPLEMENTATION... .o. ...... 23

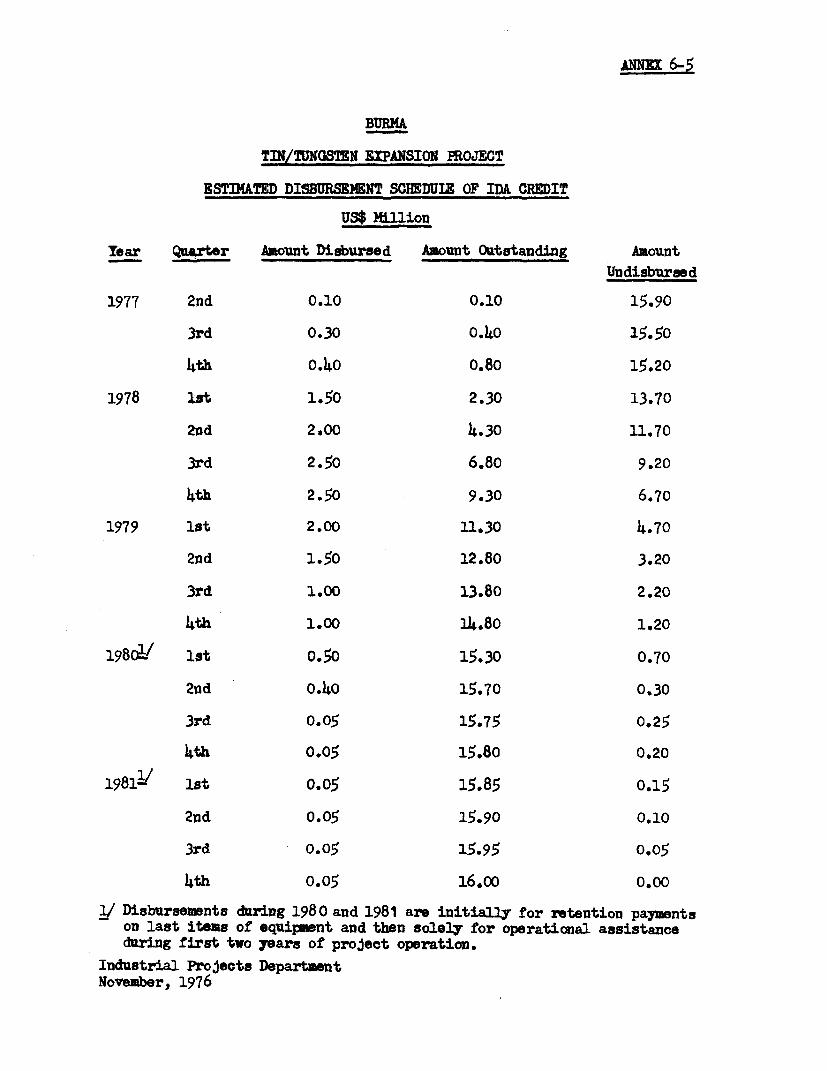

A. Project Organization and Management 23B. Project Schedule ... ............. .............. 23C. Procurement ... o ......... ............ ...... .. 23D. Allocation and Disbursement of IDA Credit .......... 24

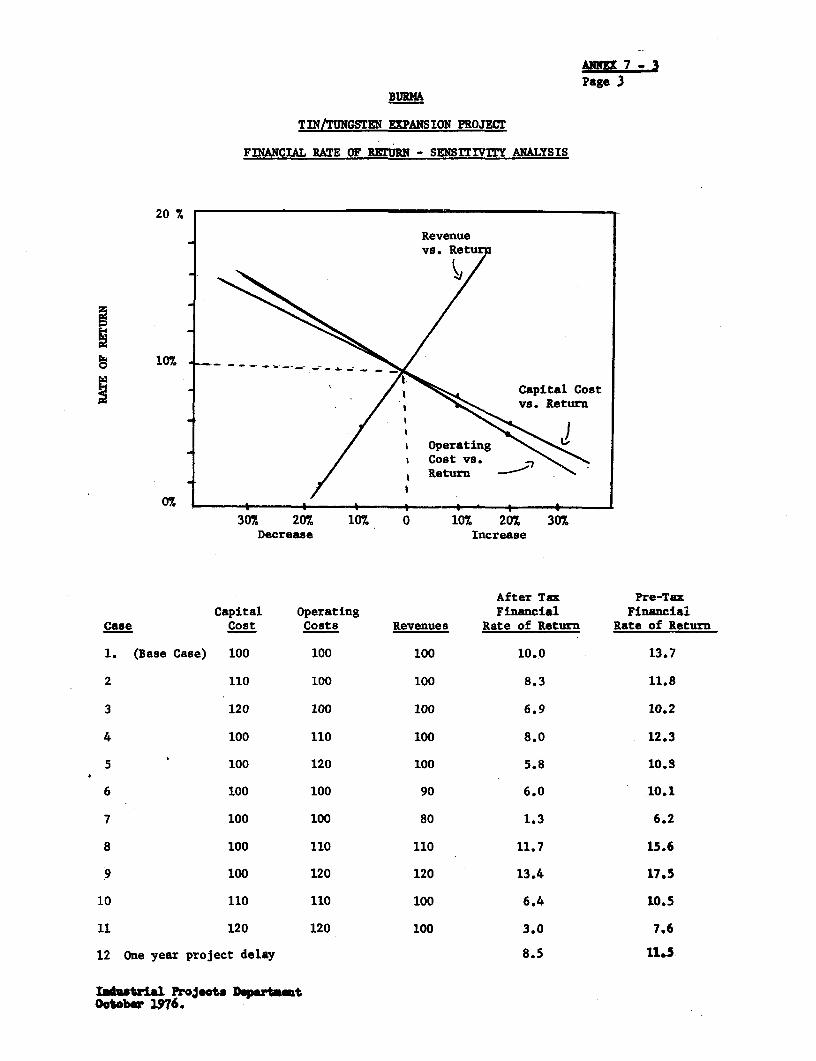

VII. FINANCIAL ANALYSIS ... ....... ...... ...... ... 24

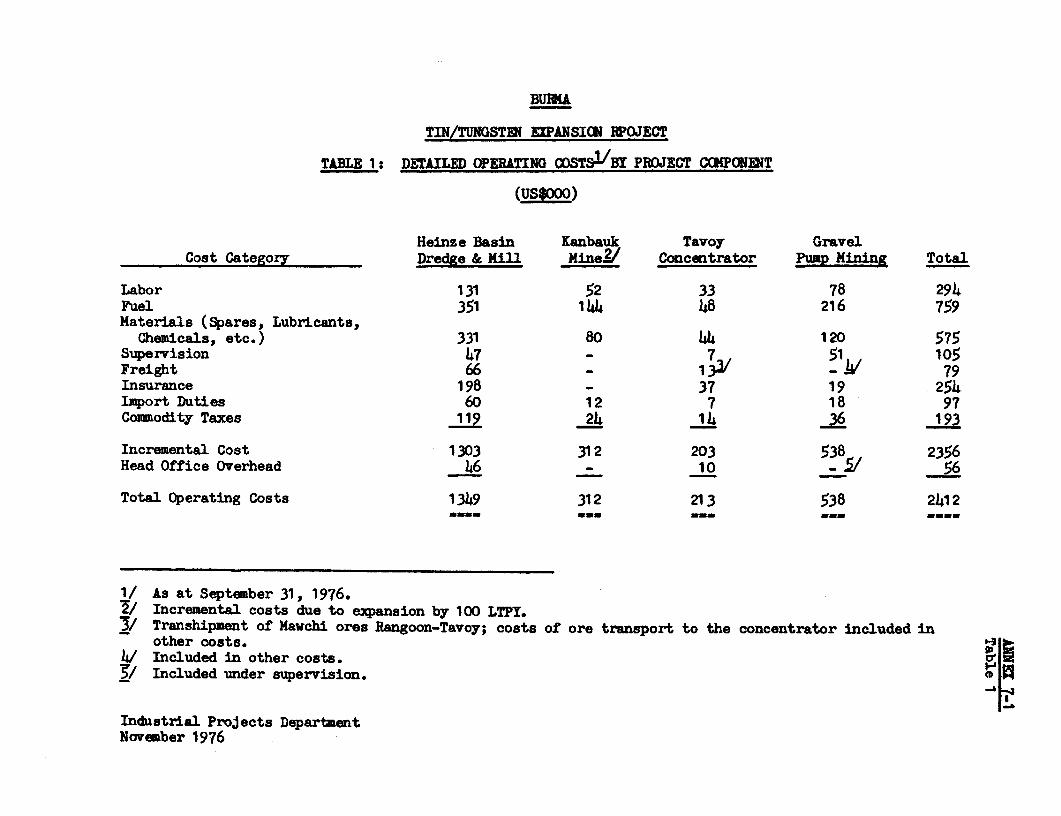

A. Project Operating Costs and Revenues .24

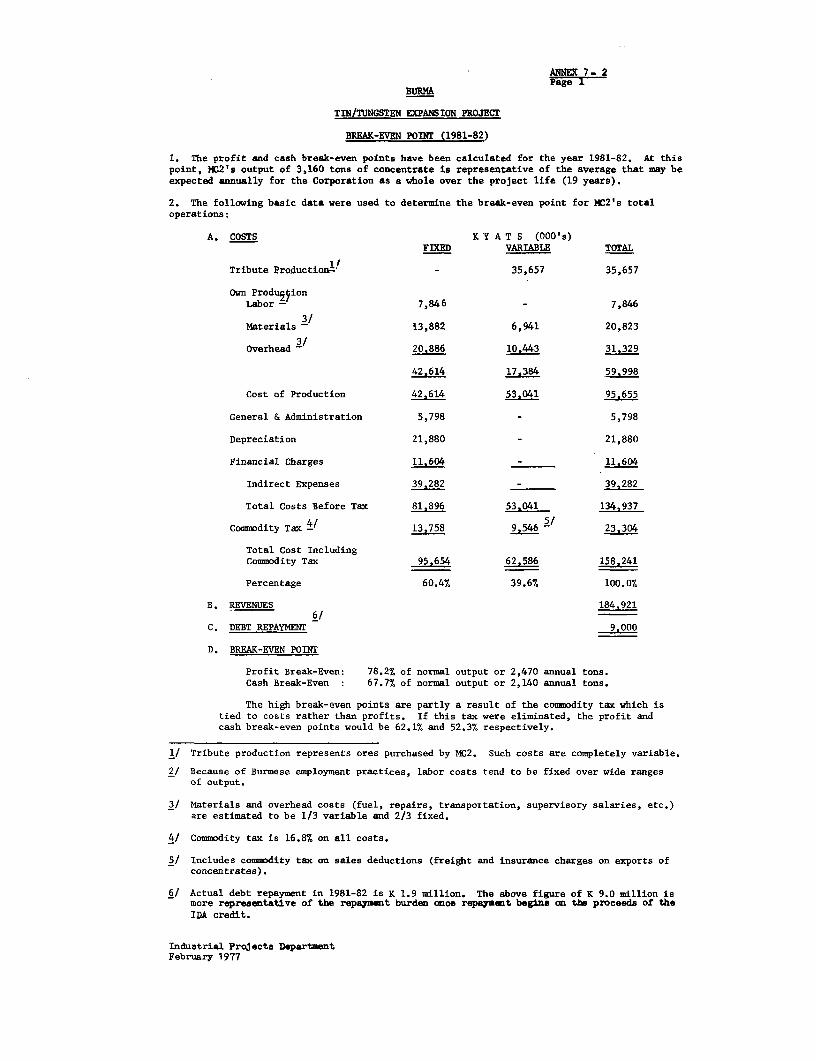

B. Financial Rate of Return 24C. Break-Even Point ........ . 25D. Overall Profitability .......... 25E. Financial Position and Covenants ...... 26F. Major Risks ....... ........................... 28

VIII. ECONOMIC JUSTIFICATION ......... . ........ ............... 28

A. Economic Rate of Return ............................ 28B. Foreign Exchange and Other Benefits .... o .......... 29

IX. AGREEMENTS...... ......... 29

ANNEXES

1 Glossary of Technical Terms

2 The Burmese Mineral Sector

3-1 The Tin Market3-2 The Tungsten Market

- 3-

4-1 Description of Operations4-2 Historical Financial Statements4-3 Organization and Management

5-1 Description of the Project5-2 Capital Costs

6-1 Project Organization and Management6-2 Terms of Reference for Consultants6-3 Project Schedule6-4 Allocation of IDA Credit6-5 Disbursement Schedule

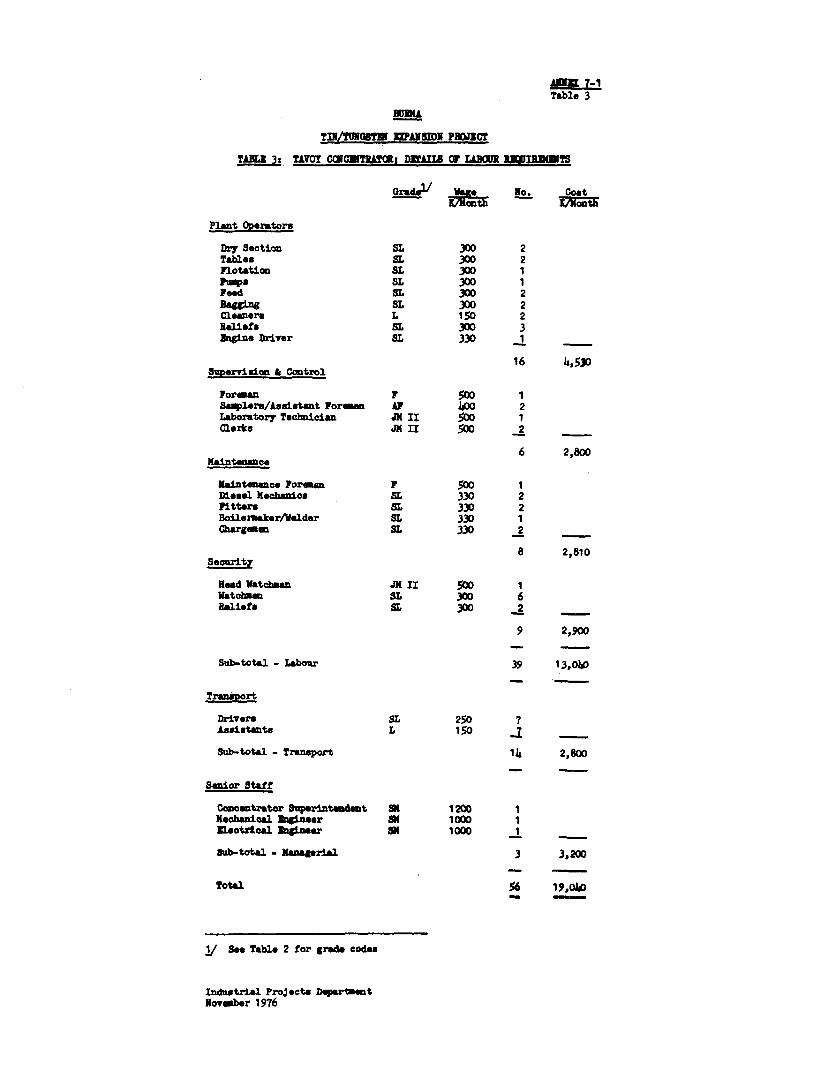

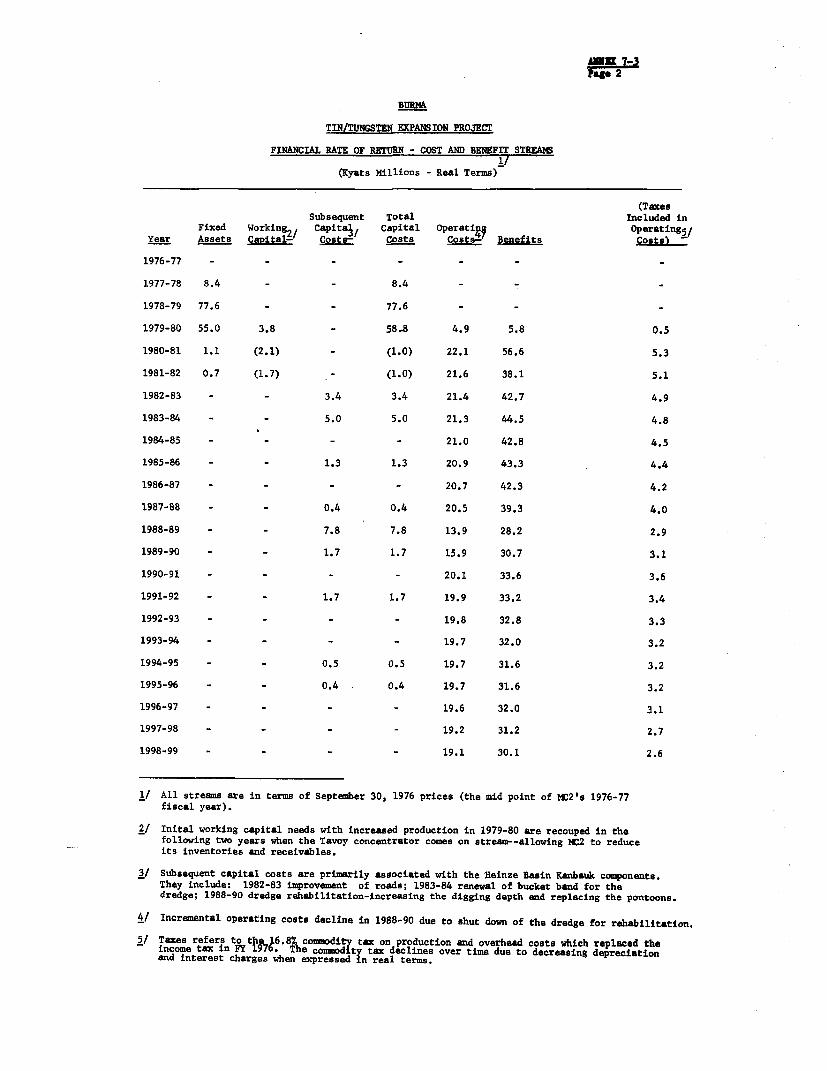

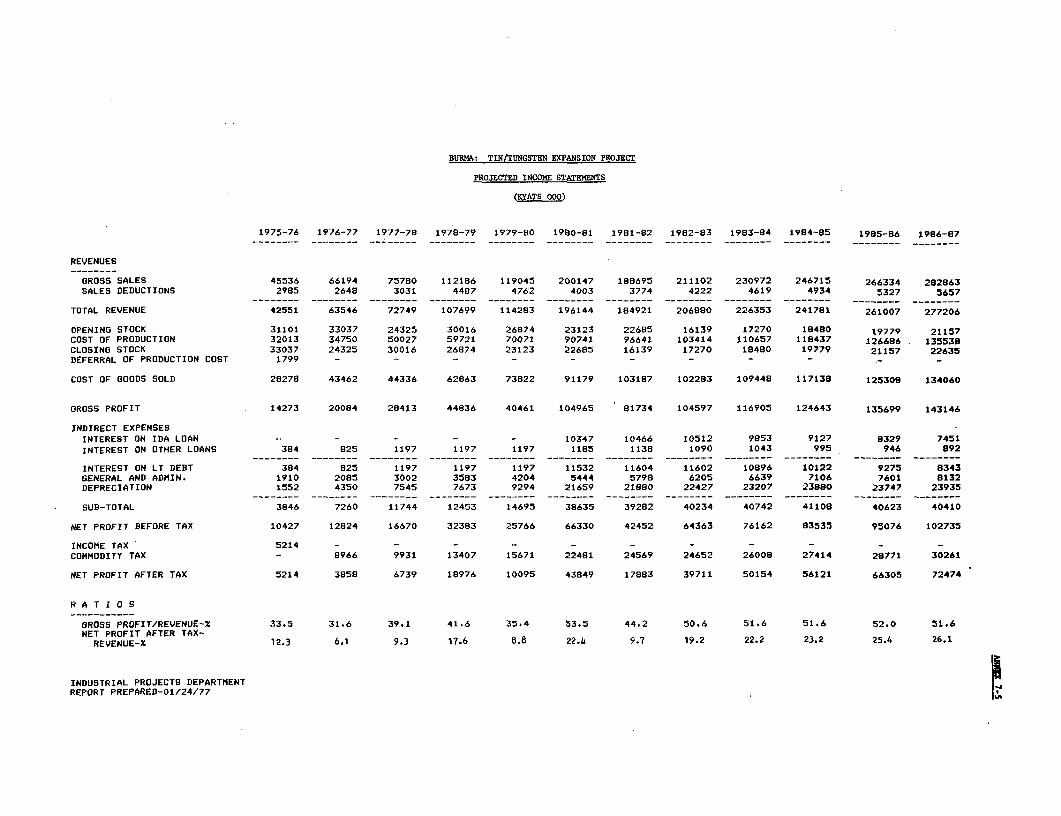

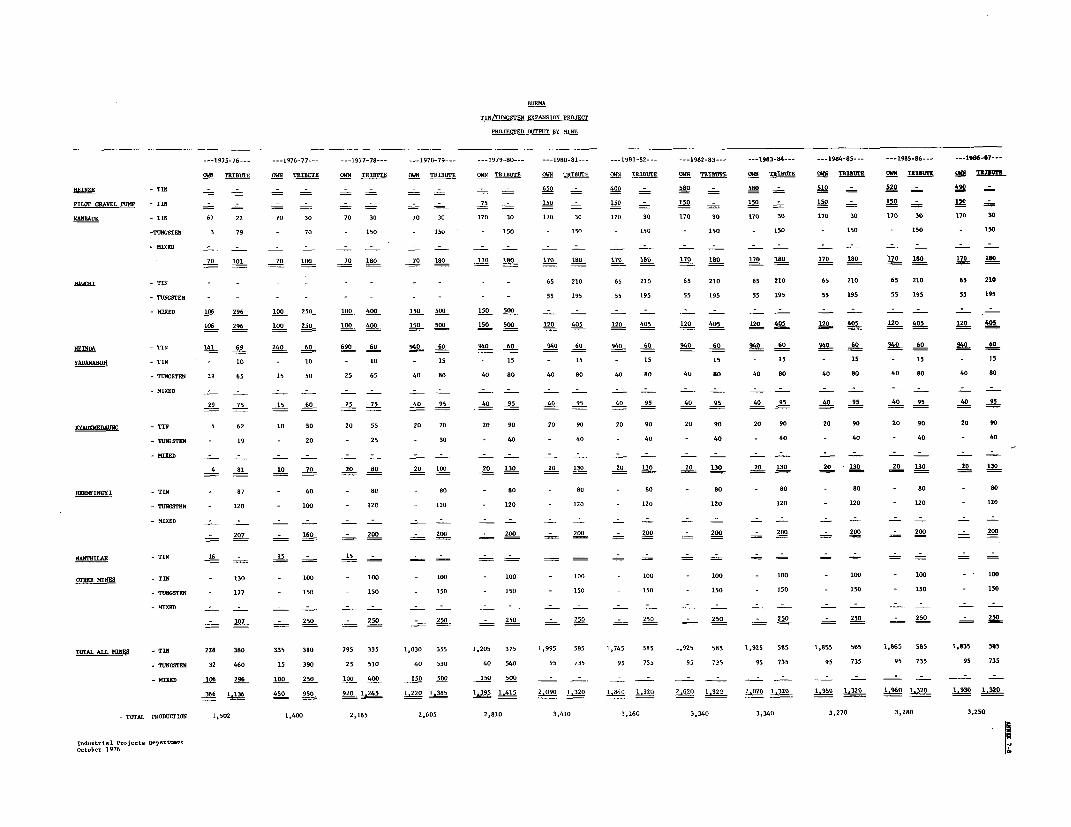

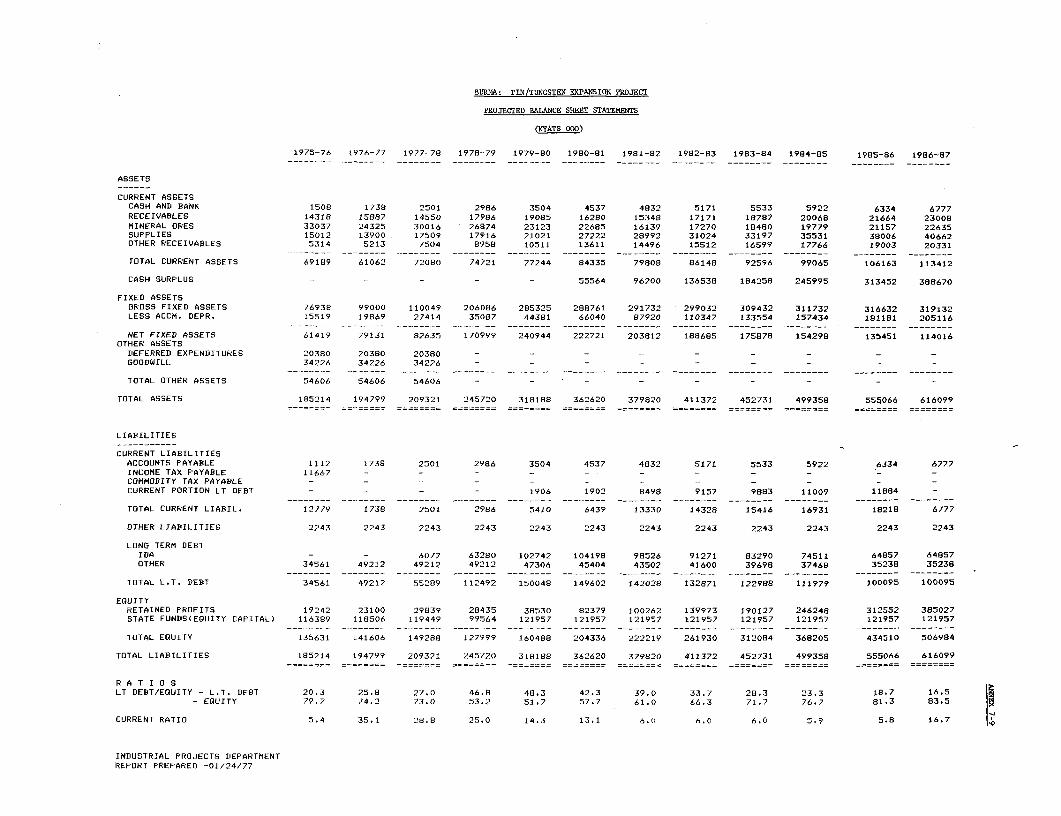

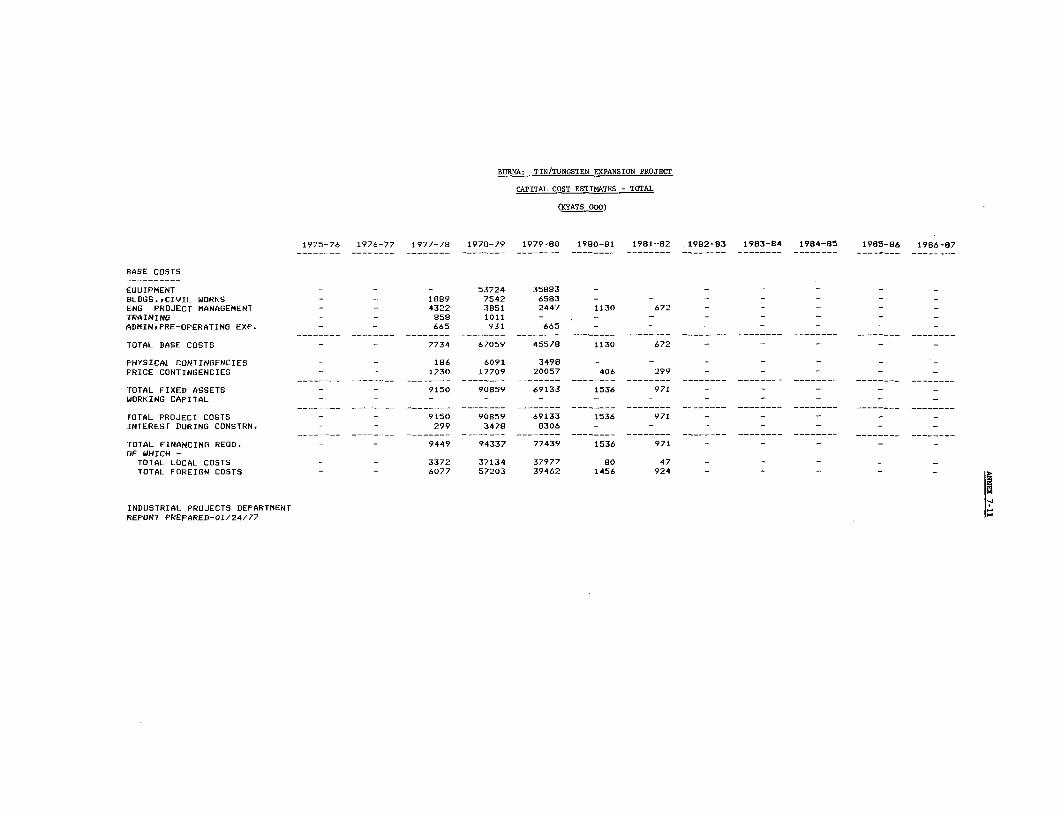

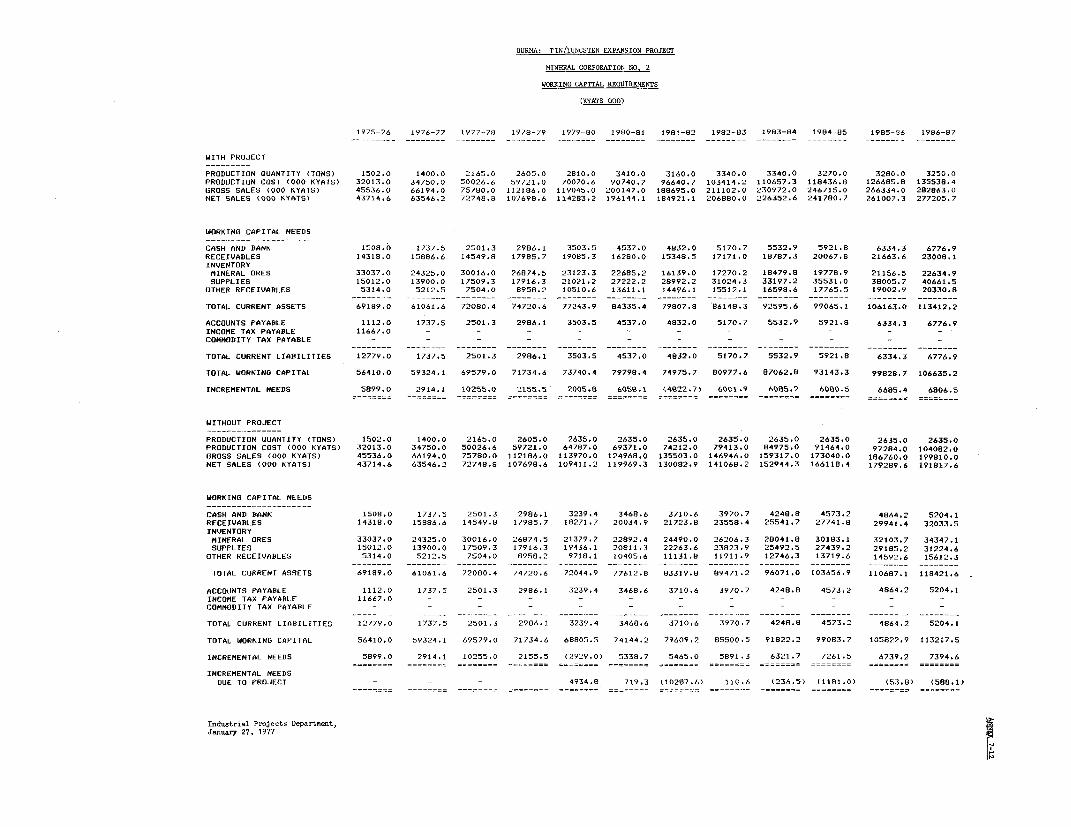

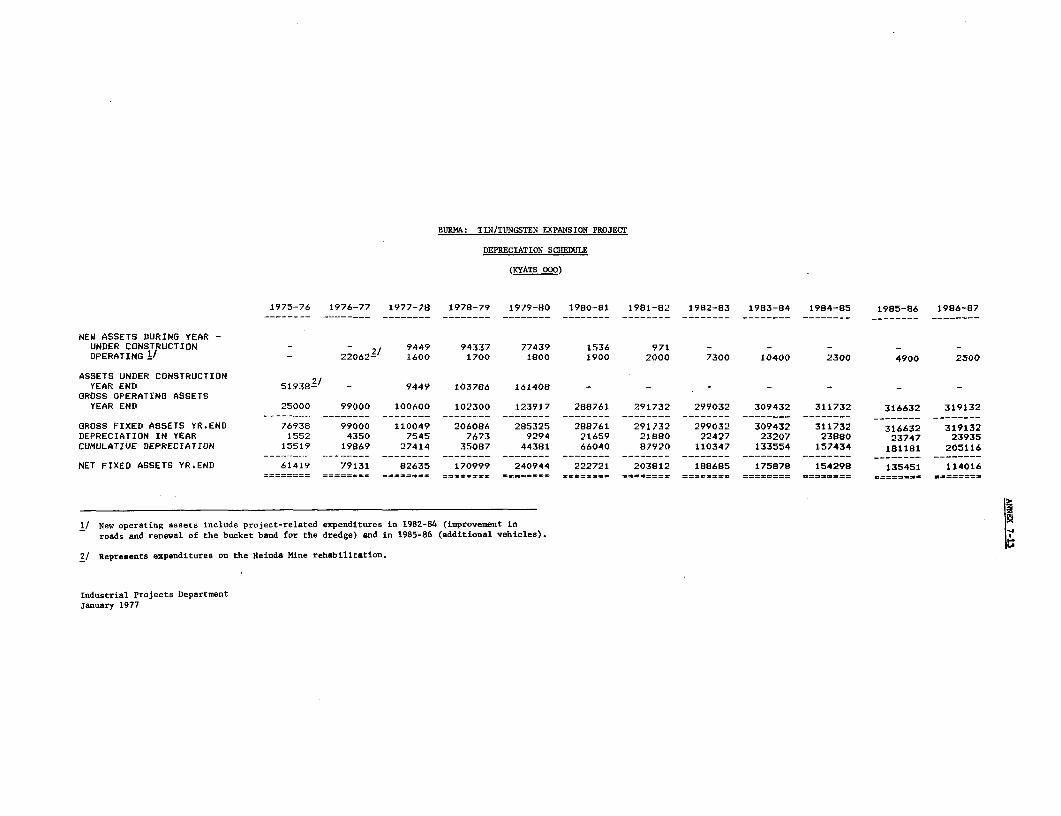

7-1 Detailed Operating Costs7-2 Breakeven Point7-3 Financial Rate of Return and Sensitivity Analysis7-4 Assumptions Used in Financial Projections7-5 Projected Income Statements7-6 Projected Sales7-7 Projected Production Costs7-8 Projected Output by Mine7-9 Projected Balance Sheets7-10 Projected Sources and Applications of Funds7-11 Capital Cost Estimates7-12 Working Capital Requirements7-13 Depreciation Schedule7-14 Debt Repayment Schedule

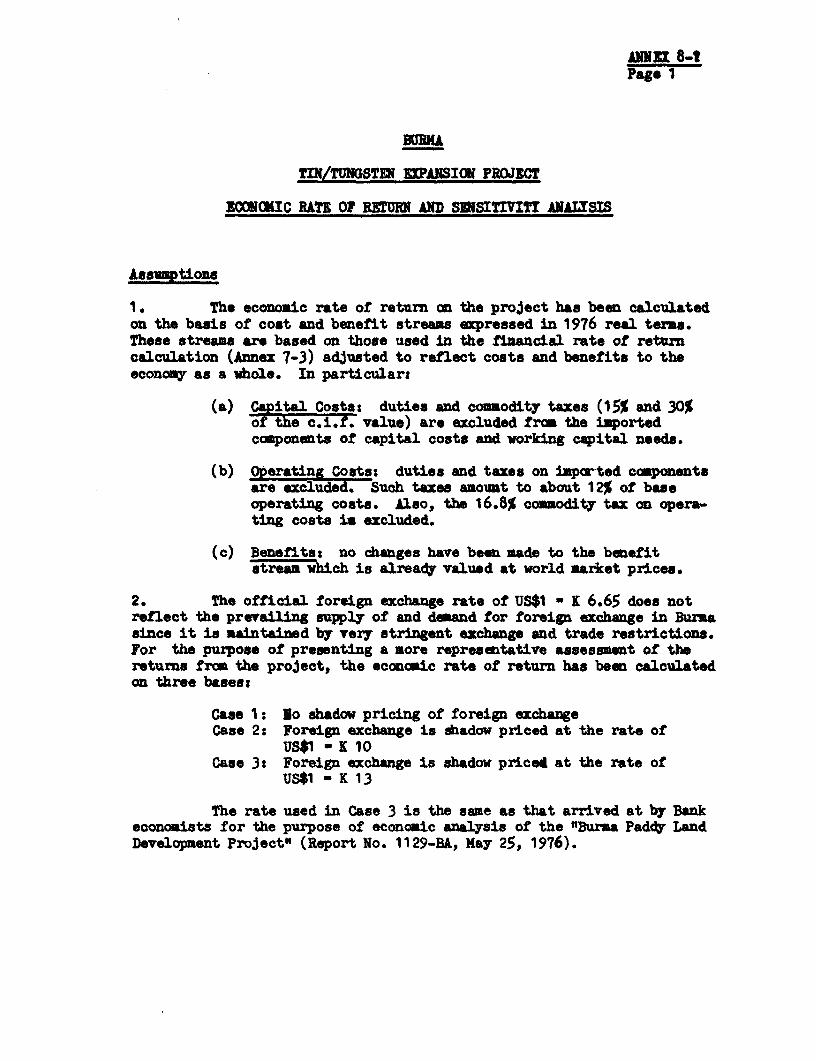

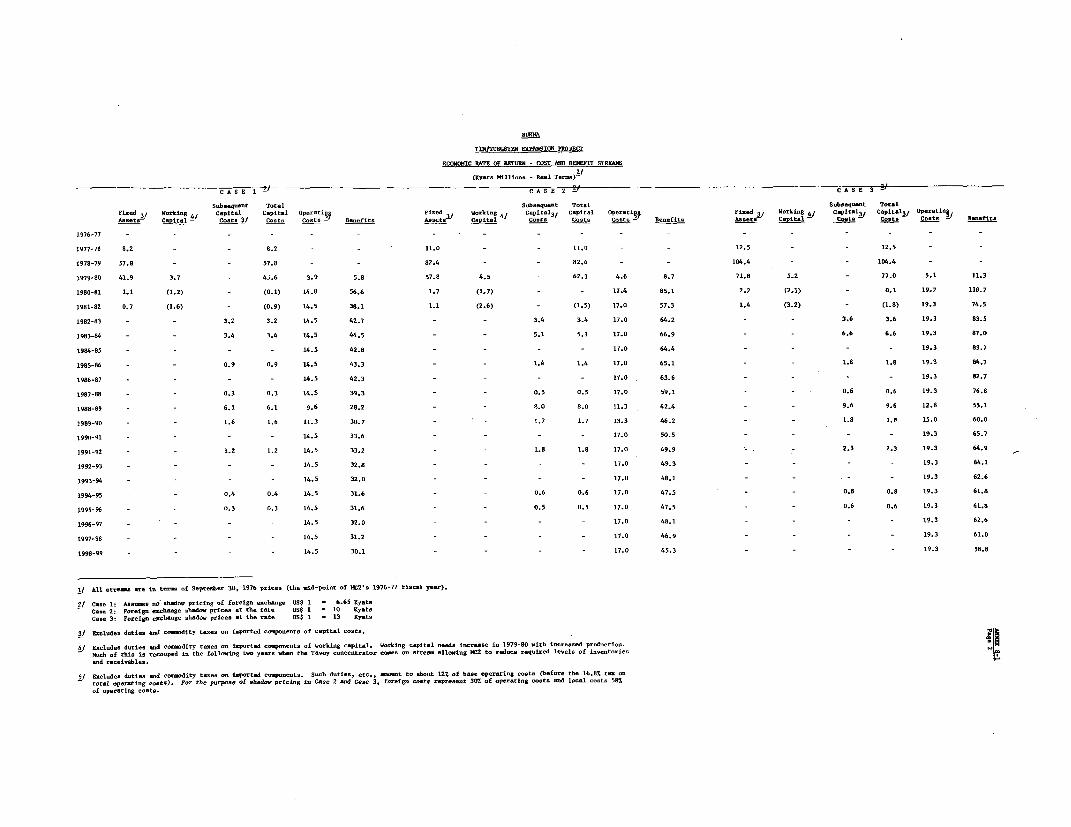

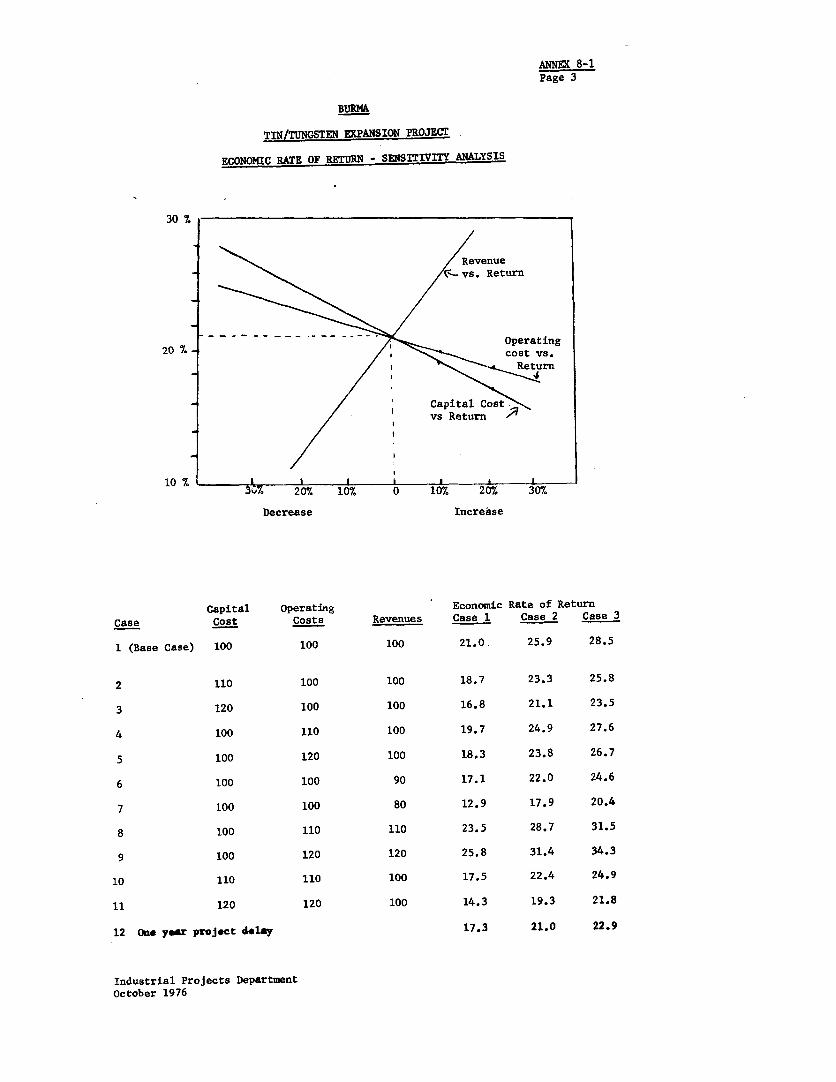

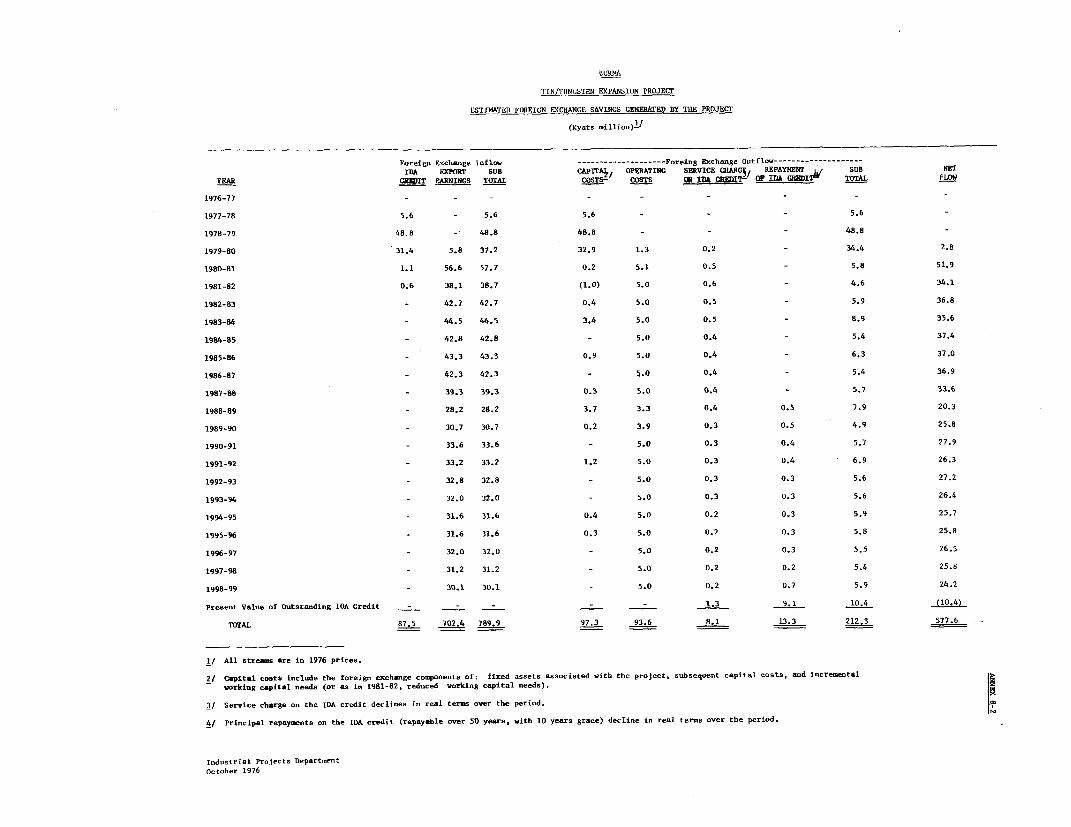

8-1 Economic Rate of Return and Sensitivity Analysis8-2 Estimated Foreign Exchange Savings

MAPS

IBRD 12322 - Main Mining Centers and DepositsIBRD 12524 - Tenasserim Division

BURMA

APPRAISAL OF THE TIN AND TUNGSTEN EXPANSION PROJECT

SUMMARY AND CONCLUSIONS

i. The Government of Burma and the No. 2 Mining Corporation (formerlythe Myanma Tin Tungsten Corporation) have requested a US$16 million creditfor a project to reintroduce dredging to the tin mining industry of Burma.The project would include a dredge and associated beneficiation and infra-structural facilities, gravel pump mining equipment, and a central concen-trating plant designed to upgrade tin and tungsten ores from various mines.The project is located about 300 km south east of Rangoon in the TenasserimDivision of Burma. Output of tin concentrates (about 75% tin) would be ex-panded by about 800 long tons per year (LTPY) and the improved upgradingfacilities would produce better quality, higher grade tin and tungsten con-centrates than are presently produced, thus making them more marketableand able to bring higher prices. Also included in the project is a study ofthe future development of the mineral sector, with a view to the identifica-tion of further projects. Financing requirements for the project are estimatedat about US$28 million.

ii. Burma's mineral sector has considerable potential for expansion,but it has experienced a long period of decline due to war damaged facili-ties, nationalization of private mining interests, a lack of technical ex-pertise and investment capital, and the smuggling of mineral products, anactivity made attractive by the distorted exchange rate for the Burmesekyat. Nearly all of the sector's output is exported, and although foreignexchange revenue for minerals presently constitutes only about 7% of totalexport earnings, it has significant potential for expansion, particularlyin tin, tungsten, copper, lead, zinc, gems, jade and antimony.

iii. At present, no foreign investment is allowed in mining. Therehas, however, been increased sector activity in recent years, particular-ly with technical assistance from Germany, Japan and the UNDP. Numerousstudies have been done but few projects have as yet entered the executionstage. The best prospects include the proposed tin and tungsten expansion,and development of the existing Bawdwin lead/zinc/silver mine, which isthe country's largest mining operation, but which has serious operatingand financial difficulties. Large projects are difficult to put togetherdue to the lack of project preparation experience in the country, the prob-lem of obtaining sufficient funds given the shortage of domestic resources,and the reluctance of the Government to come to firm agreements on projectpriorities, financing sources, and the extent and nature of foreign partici-pation. Otler problems affecting investment in the sector are insurgencyactivities in certain parts of the country, the above-noted distorted ex-change rate for the kyat, and the high tax levels which have recently beenintroduced on imported equipment and production. Projects which may have veryattractive returns to the economy tend to be somewhat marginal financially, asituation which could act against stimulating the interest of prospective

- ii -

financing institutions, and which could lead to a misallocation of resourcesin the economy.

iv. There are five mining corporations; they are all Government ownedand operate under a system of highly centralized financial and managerialcontrol, with all policy decisions being made at the level of the Ministerof Mines or the Economic Committee of the Council of Ministers. There havebeen some recent measures to extend more autonomy and responsibility to thecorporations but steps to put these intentions into practice will likely beslow and cautious, since both the Government and the corporations are soaccustomed to close control that it will likely be some time before muchautonomous behavior results.

v. The No. 2 Mining Corporation is the best prospect for IDA partici-pation in the mining sector at this time. Its senior staff are technicallycompetent and experienced in tin mining. The Corporation has adequateproven reserves for further expansion and it is in a financially sound posi-tion. Furthermore, its operating costs are in the lower range of inter-national tin and tungsten mining costs and should continue to be at a competi-tive level even after some capital intensive mechanization, which is a pre-requisite for obtaining a higher value product. The technology being used inthe project represents a degree of modernization appropriate to the Burmesesituation, and will be introduced in conjunction with a reasonable level ofoutside technical assistance. With the start-up during 1977 of a KfW-financed expansion of one of its major tin mines, the Corporation is expectedto be in a strong position to continue its expansion with the IDA-financedproject.

vi. It is expected that tin demand will show modest growth, supply/demand will be in reasonable balance, and that there will be continuanceof a modest long term upward trend in real tin prices. International TinCouncil buffer stock operations should also, in the future, moderate interna-tional price fluctuations, especially on the downside. Demand for tungstenis expected to continue strong and the price outlook is good. Prices maywell be more stable in the future, with some prospects for producer coopera-tion on stabilizing prices. Even with the proposed expansion, Burma willstill be a very minor supplier to the international markets for both tin andtungsten. With the improved product quality that will result from the project,the country should be able to market its concentrates readily.

vii. The project is not overly complex, and is based on feasibilitystudies which incorporate Malaysian experience under very similar operatingconditions and with very similar ores. Although the Corporation is inex-perienced in dredging and the operation of more modern facilities, theinvolvement of experienced consultants throughout the project, and opera-tional supervision for a minimum of two years after start-up should mini-mize the technical risk. Also included in the project will be overseastraining of the key Burmese technicians. Ore reserve estimates are conser-vative, and operating assumptions make due allowance for Burmese conditions.

- iii -

The project execution time is fairly short (about 3 years with the gravel pumpmining components perhaps coming on-stream sooner), and all facilities areexpected to be in operation by early 1980.

viii. The project will be financed by the proposed IDA credit (US$16.0million), the Corporation's internal cash generation (US$5.8 million), andGovernment funds (US$6.0 million) to be provided either in the form of equityor debt. The credit will finance the c.i.f. value of imported equipment andmachinery and the foreign exchange costs of the consultancy assistance, butno local expenditures, which will all be covered by Government/Corporationresources. All imported goods will be subjected to international competi-tive bidding, except for some small items of highly specialized equipment,estimated to total about US$1.0 million, for which international shoppingwill be used.

ix. The financial situation of the Corporation is projected to be soundboth during and after project execution, although the financial rate of re-turn is expected to be only 10% after the commodity tax on production value(13.7% before the tax). These low returns are due to the very high taxburden, the distorted exchange rate, and lower grade reserves which will beencountered by the dredge in the later years of operation. Nevertheless, theeconomic rate of return is estimated at 21%. Net foreign exchange benefits tothe economy are projected to average US$4.6 annually (in real terms) over theproject life and substantial additional revenues will accrue to the Governmentthrough import and production taxes and from interest on the on-lending of thecredit proceeds. Wider economic benefits will result through some increasedemployment, the technical training involved, and the inclusion of infrastruc-tural facilities in the project. Overall, the project will represent asubstantial forward step in the rehabilitation of Burma's tin industry, andmake a valuable contribution towards reversing the long downward trend in thesector, which has the potential for a greatly expanded contribution to Burma'seconomic development.

x. The risks of this project are basically threefold and acceptable.First, the Corporation is inexperienced in dredging and the more modernconcentrating operations to be introduced and certain weaknesses exist inproject implementation management; these are intended to be overcome by theprovision of experienced assistance in these areas. Secondly, tin and tungstenprices could be lower than projected. Offsetting this risk is the influenceof the International Tin Council, the prospects of increased cooperationamong tungsten producers, and the important fact that the Corporation isa producer of both tin and tungsten whose prices do not necessarily followidentical trends and have good long term prospects. Thirdly, potentialinsurgency activities present some risk, but these have been kept undercontrol in the area and the nearby KfW project has not been affected adversely.

xi. Based on the agreements summarized in Chapter IX of this report, theproject is suitable for an IDA credit to the Government of Burma of US$16million equivalent, with onlending to the No. 2 Mining Corporation of US$15.8million equivalent for a period of 15 years, including 5 years grace, at 10%interest per annum, and US$0.2 million equivalent used by the Government tofinance the mineral sector study.

I. INTRODUCTION

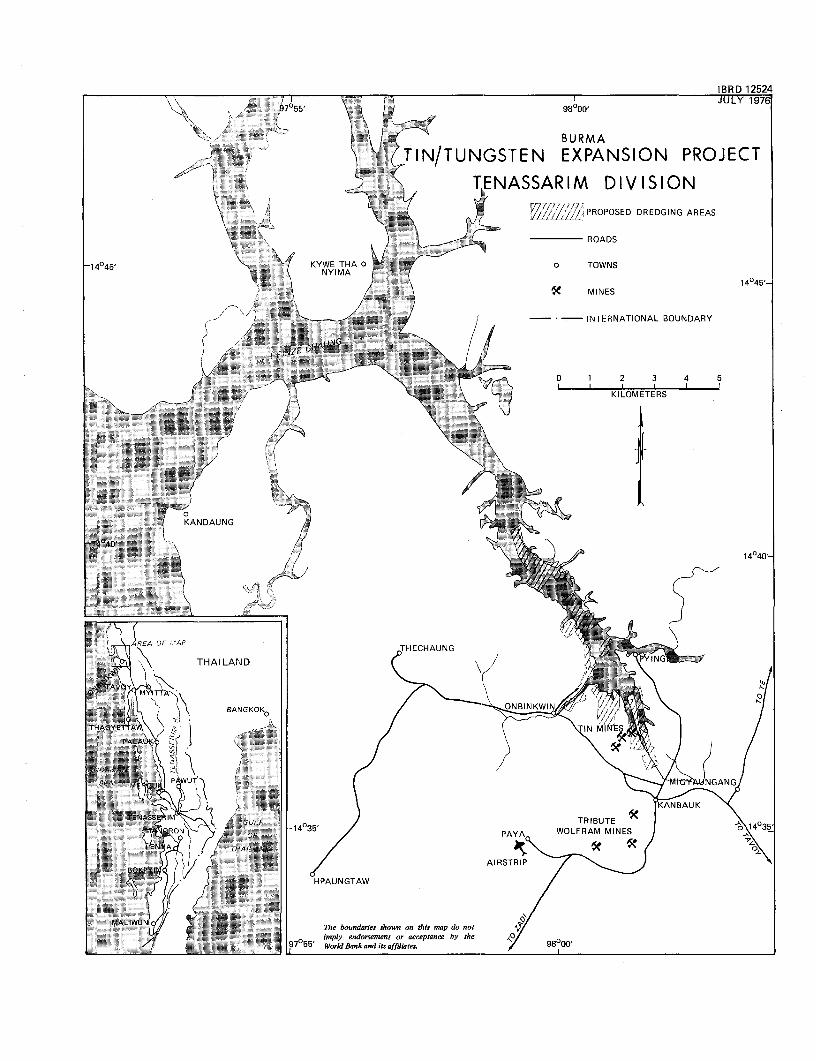

1.01 The Government of Burma and No. 2 Mining Corporation (MC2), theGovernment-owned tin and tungsten mining company, have asked IDA for a creditof US$16 million equivalent, US$15.8 million equivalent of which would financethe foreign exchange costs of a project to expand production of tin concen-trates by 800 long tons per year (LTPY). The remaining US$0.2 million is fora study of the future development of the mineral sector. The tin/tungstenproject, which is estimated to require financing of US$27.6 million equivalent,is located in the Tenasserim Division of Burma (Map IBRD 12322) about 300km. south east of Rangoon.

1.02 The project was appraised in Burma in March and August 1976 bymissions consisting respectively of Messrs. H.E. Wackman (Chief) andR. Rodger of the Industrial Projects Department and Mr. A. Freyman (Con-sultant), and Messrs. Wackman and Greig (Industrial Projects). A glossaryof technical terms is contained in Annex 1.

II. THE MINERAL SECTOR

A. Present Position and Recent Trends

2.01 Based on official statistics (below and Annex 2), Burma's mineralproduction is presently less than one-tenth of pre-World War II levels. Whileinclusion of smuggling activities in the figures would increase reported pro-duction in recent years by perhaps as much as 40%, the long-term sectoraldecline is obvious.

Production of Major Minerals in Burma

(000's long tons)

FY 1939 FY 1962 FY 1971 FY 1975 FY 1976

Tin Concentrates 5.4 0.9 0.5 0.5 0.6Tungsten Concentrates N/A /a 1.5 0.3 0.6 0.5Tin/Tungsten MixedConcentrates 5.6 N/A /a 0.4 0.4 0.4

Silver (million ounces) 6.2 1.4 0.8 0.4 0.2Refined Lead 77.0 16.6 8.7 4.9 2.4Zinc Concentrates 61.7 14.2 7.0 5.1 4.4

/a Not available.

2.02 Burma holds a very minor position in the world production andtrade of mineral products although nearly all of its non-fuel mineral outputis exported. It currently accounts for less than 1% of world tin production,about 1.5% of world tungsten production, and under 0.2% for zinc, lead andsilver.

-2-

2.03 Despite considerable potential for development, much of the mineralsector remains in the decimated state which resulted from the War. No signi-ficant new mines have been opened for 40 years, reflecting the progressiveGovernment take-over of private activities (especially during the 1950'sand 60's), which are now limited to illegal mining and tribute mining 1/ oftin and tungsten by small groups of individuals. Overall, the Governmenthas emphasized investment in other sectors which, combined with the shortageof foreign exchange, has left the mining sector with poor and outmoded plantand spare parts shortages which hamper operations. Other factors contributingto the decline of mining in Burma include: the lack of experience in projectpreparation and execution; extensive insurgency activities in large areas ofthe country where minerals can be produced; labor shortages at some mines dueto low wages and more attractive alternatives including illegal mining andtrade; and a distorted exchange rate for the kyat which is partly responsiblefor the financial weakness of mining corporations, results in marginal finan-cial returns for most new projects, and encourages diversion of a significantproportion of sector output into illegal trading. The Bank is discussing withthe Burmese authorities steps, including price adjustment, by which theillegal flow of tin and tungsten can be directed to official purchasers.

2.04 Government policy does not allow direct foreign or private partici-pation in development of the sector -- an exception has been the recent adventof joint ventures in petroleum exploration involving foreign oil companies.In the non-petroleum mining sector, however, foreign participation has beenlimited to bilateral and multilateral technical assistance and financial aid.This has picked up in recent years and should result in a reversal of mining'slong-term downtrend. Agencies which have been particularly active are: KfWof Germany, Metals Mining Agency of Japan, UNDP, Canadian International De-velopment Association (CIDA) and, with the proposed project, IDA. While areasonable degree of technical competence exists at various levels in thesector's institutions, management abilities are limited by a lack of innova-tion and initiative. Substantial projects in the sector could not be ade-quately prepared and implemented without extensive outside technical assis-tance in addition to the essential outside financial resources.

B. Impact on the Economy

2.05 While the mineral sector in Burma contributes slightly over 1% ofGDP and less than 1% of official employment, mineral exports average about7% of total export value. Domestic consumption of the metallic mineralsproduced is negligible. There are no substantial smelting, refining orother value-adding facilities other than an antiquated lead/zinc smelter.Despite the relatively low level of employment (about 28,000 workers), thesector provides employment opportunities in areas of the country where theseare often limited. Although there is little scope to increase the relativeimpact of the sector on employment, the opportunity for increased foreignexchange earnings from expanded sector output is substantial (para 2.15).

1/ Tribute miners are independent individuals who work tin/tungsten depositsunder the loose supervision of MC2's staff, and sell their production tothe Corporation. Part of their output is undoubtedly smuggled out, however.

-3-

C. Structure

2.06 A small number of government corporations, which are essentiallypart of the Ministry of Mines, are responsible for all official productionof minerals. These include: the Myanma Bawdwin Corporation (now No. 1 MiningCorporation or MCI) responsible for lead, zinc and silver production, with.50%-60% of sector output; the Myanma Tin Tungsten Corporation (No. 2 MiningCorporation), responsible for tin and tungsten production with 30%-40% ofsector output; the Myanma Mineral Development Corporation (No. 3 MiningCorporation), responsible for production of antimony and coal and the de-velopment of copper deposits; the Industrial Minerals Corporation (No. 4Mining Corporation), responsible for production of limestone, gypsum andother non-metallic products; and the Gem and Jade Corporation, responsiblefor production and marketing of jade, rubies, pearls and other gems.

2.07 There are two main supporting entities within the Ministry: TheDepartment of Geological Survey and Mineral Exploration (DGSE), responsiblefor exploration and geological studies; and the Department of Planning andWorks Inspection, responsible for mine inspection, safety, planning andstatistics. The Myanma Oil Corporation (MOC) is charged with oil and gasexploration and production. The Myanma Export Import Corporation (MEIC), apart of the Ministry of Trade, was responsible for all export sales ofmetallic products until late 1976, but this function has now been vested in aMinerals Marketing Committee which is jointly administered by the threemetal producing corporations; i.e. Mining Corporations Nos. 1, 2, and 3.

2.08 Although called corporations, their status as separate legal enti-ties is vague and they have extremely limited autonomous power. There areno shares or similar instruments, ownership is by the people, and effectivelycontrol is vested in the State. In the past, all revenues have gone to theUnion Government Consolidated Fund (UGCF), with operating and capital expendi-tures being drawn from the Fund under extremely rigid budgets approved by theGovernment. Overall, the corporations have had little effective control overtheir financial resources and the UGCF has been the sole source of financeother than a few bilateral credits on-lent through the Union Bank of Burma.The responsibilities and powers of the mining corporations have been purelyoperational and all policy decisions have been taken by the Minister of Minesor the Economic Committee of the Council of Ministers. Some liberalization ofthis highly centralized management and financial control is envisaged undernew guidelines described below.

D. Legislation and Operational Guidelines for the Sector

2.09 When the agency formerly responsible for all mining activities inBurma (the Mineral Development Corporation) was subdivided in 1972, legisla-tion was approved for each new corporation, outlining its powers and respon-sibilities. In MC2's case (the entity responsible for executing the proposedproject), this was contained in the Myanma Tin Tungsten Corporation Act of1974. In May 1975, "Standard Guidelines for the Operation of State EconomicEnterprisest' were issued by the Ministry of Planning and Finance. Underthese guidelines, more autonomy and financial responsibility is intended torest with the corporations and new fiscal and financial measures are being

-4-

introduced. While the system of annual budgets is to be maintained, the UGCFfund has been discontinued. Corporations now have their own bank accountsand will meet operating expenditures out of their own receipts.

2.10 Part of net cash generation can now remain with the corporations tooffset a portion of fixed and working capital needs. Capital expenditureswill no longer be met through interest-free budgetary allocations; necessaryfunds must be borrowed from the newly-formed Myanma Economic Bank. Eachenterprise is set an annual operating ratio target (defined as the ratio ofoperating expenditures to revenues) to be used as one of the bases for the newemployees' bonus system. Producing corporations also now have more influenceover their own marketing (para 4.15). There will also supposedly be morerecognition of foreign exchange earners in the allocation of the country'sscarce foreign exchange resources. The changes are being introduced cautiously.Although implementation commenced in April 1976, the Government and theCorporations are so accustomed to close control that it will likely be sometime before much autonomous behavior results.

E. Mineral Potential and Exploration

2.11 Burma has a highly varied and favorable mineral endowment whichjustifies a strong effort in mapping and exploration. There have beennumerous foreign technical assistance missions in this respect adding tothe resources assessment from the pre-War Geological Survey of India workand post-War work by the DGSE and forerunner organizations.

2.12 Due to insurgency problems, however, large tracts of the countuyhave not been geologically mapped or prospected in any detail, and geologicalmissions are assigned only "secure" areas for exploration. A systematic in-ventory of mineral reserves which would certainly aid sector developmentstrategy thus has not been developed. The priorities for exploration aretin/tungsten, lead/zinc, copper and nickel, a ranking consistent with theexploitable potential of Burma's known mineralization. Known reserves alonehave an estimated potential export value of some US$1.5 billion at presentmineral prices.

F. Planned Sector Investment and Needs

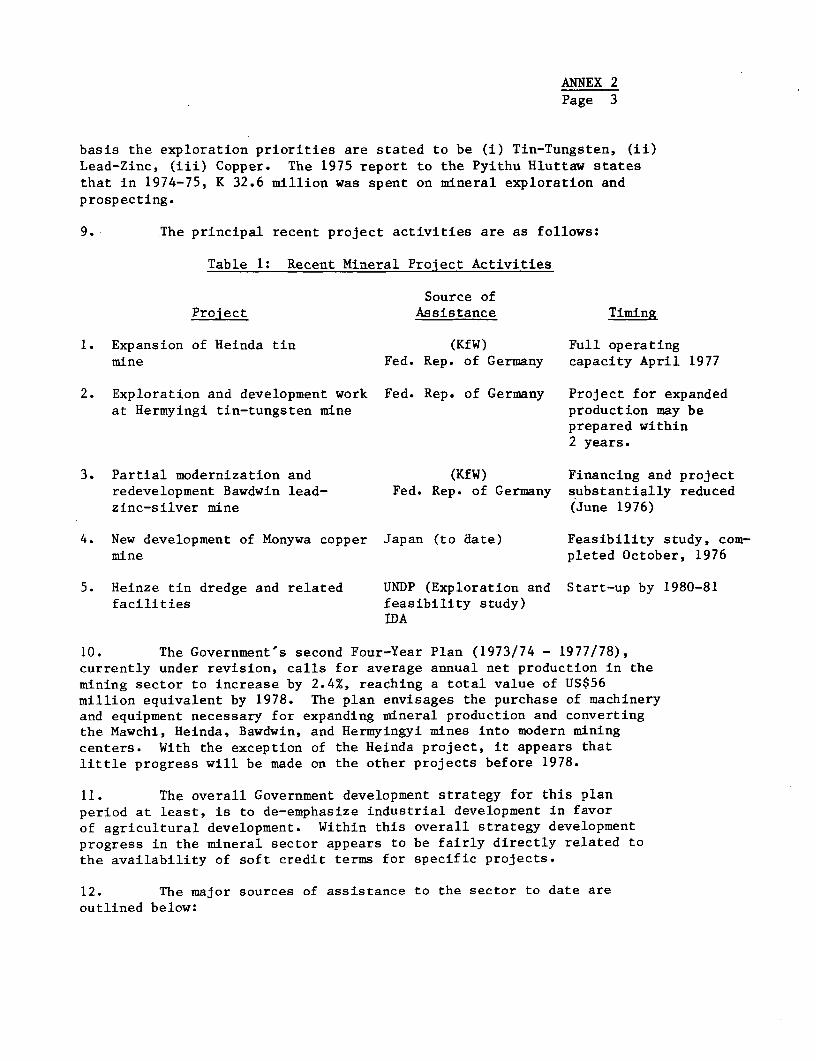

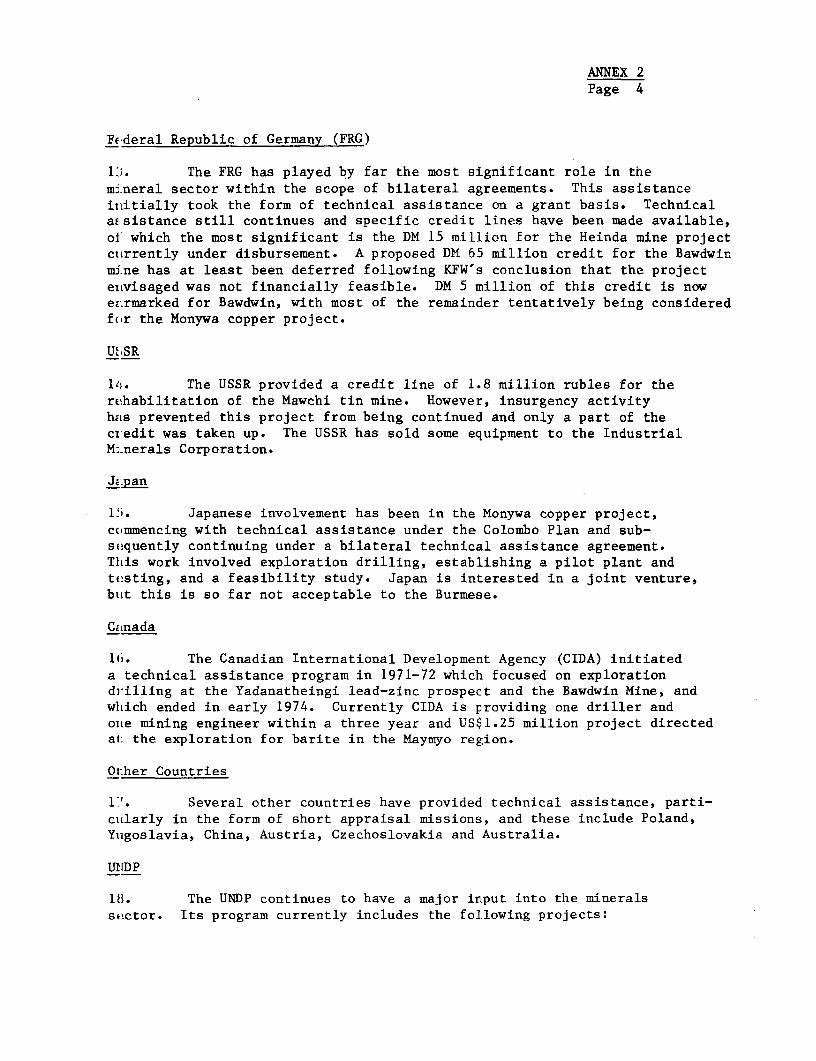

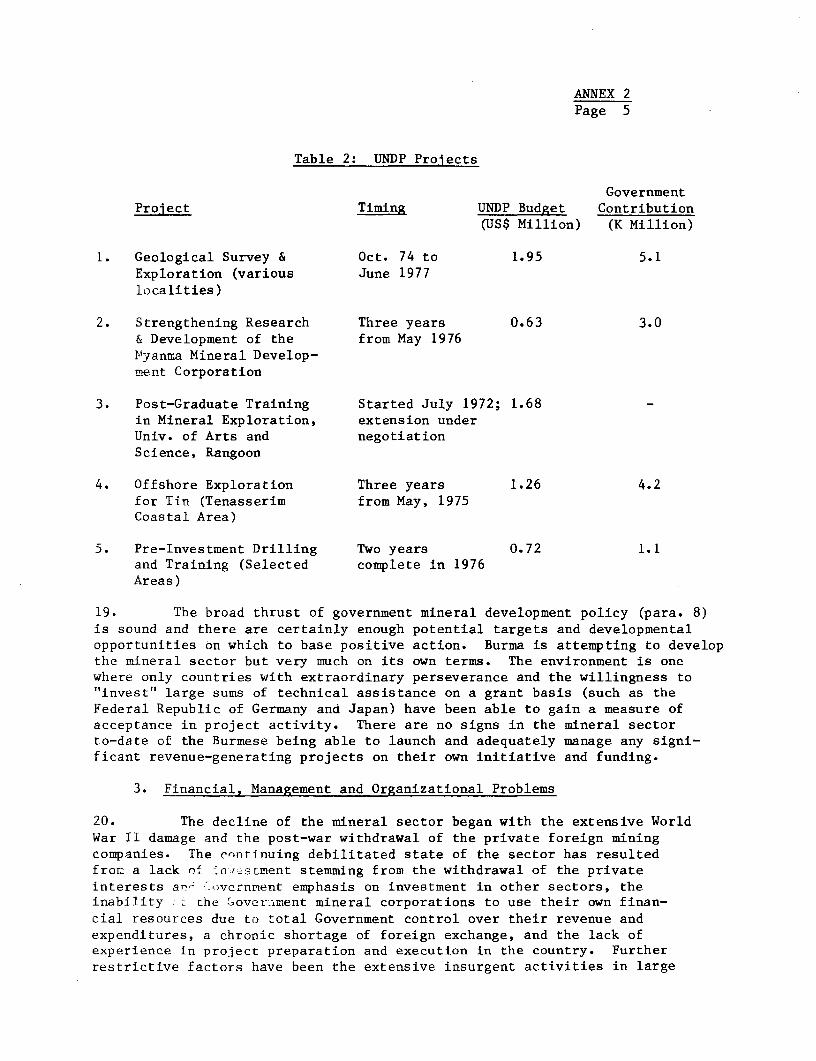

2.13 Given mining's potential for augmenting Burma's foreign exchangeearnings, the Government has given high priority to the sector and recentpolicy has opened the way for external technical assistance and finance.Significant contributions have come from the Federal Republic of Germany(Heinda Tin Mine Expansion, exploration and geological work in tin and lead/zinc, and appraisal of a project at the Bawdwin mine); Japan (appraisal of acopper mining and concentrator project at Monywa); and the UNDP (a number ofprojects in exploration, feasibility studies and training). A number of othercountries have also provided technical assistance, but apart from the Heindaexpansion, no significant new development has resulted so far.

2.14 The Government's near-term development strategy is to: rehabili-tate old tin tungsten mines and the Bawdwin lead/zinc/silver mine; exploit

-5-

the Monywa copper deposit; commence tin dredging at Heinze Basin (the projecthere considered) and carry out a number of smaller projects in antimony,gemstones and tin/tungsten. These priorities are sound but realization islikely to be slow due to shortcomings in project preparation and executionabilities, the limited foreign exchange resources that can be attracted, andthe limited local funds available. The distorted exchange rate for the kyatcompounds the above difficulties. For example, following a recent appraisal,a bilateral institution decided to scale down drastically its financing of alimited modernization project at Bawdwin, partly for security reasons, butalso due to its poor financial return. In addition, both Monywa and HeinzeBasin are financially marginal projects even though reasonable shadow-pricingof foreign exchange costs and benefits produces very attractive economicreturns. For significant redevelopment of the sector to take place some meansof augmenting the foreign exchange revenues of export-oriented projects andinstitutions may have to be found.

2.15 Despite the above-mentioned difficulties, the sector has the poten-tial t6 approach an export level of US$35 million (1976 prices) by FY 1981,from US$19 million in FY1974, assuming the envisaged expansion and productquality improvement in tin/tungsten, tighter security over gem production,improved gem marketing procedures, and some expansion in antimony. By themid-80's, exports could approach US$100 million annually assuming two majorprojects like Monywa or Bawdwin are executed, or one of these is done inparallel with minor improvements in, for example, tin/tungsten, gem stones,jade, or antimony. Growth of this latter magnitude is not conditional onnew mineral discoveries but would require sector investment of at leastUS$200 million (1976 prices) over the next 5-10 years combined with tech-nical assistance for project preparation, execution and early operation.Potential would be substantially greater if illegal exports could be broughtinto the official sector and more active foreign participation were allowed.

2.16 While the development impact of larger sized projects is greater,execution could overtax Burma's limited financial, technical and managerialresources and require a level of outside technical participation which wouldbe unacceptable to the Government. The Government intends to push for imple-mentation of a number of projects, both large and small, but the limitationsoutlined may force it to be very selective in those chosen for advancement.Also, despite the expressed interest of certain bilateral financing sources,the Government has been slow in pushing potential projects to the executionstage.

2.17 The Bank's role in sectoral development could be threefold. Firstpriority should be in financing specific projects such as the proposed tin/tungsten expansion, thereby establishing a record of successful experience inthe sector. Second, the Bank can, through consultants, help to identify andselect development priorities from the longer term alternatives. Part(US$200,000 equivalent) of the proposed credit will be used for this purpose(para. 5.16). Third, the Bank could act as a catalyst for other sources offinance to enable larger projects to be undertaken, quite possibly underjoint/parallel financing arrangements. The newly-formed Aid Group for Burmais expected to serve as a useful coordinating mechanism in this respect.

-6-

III. THE MARKFT

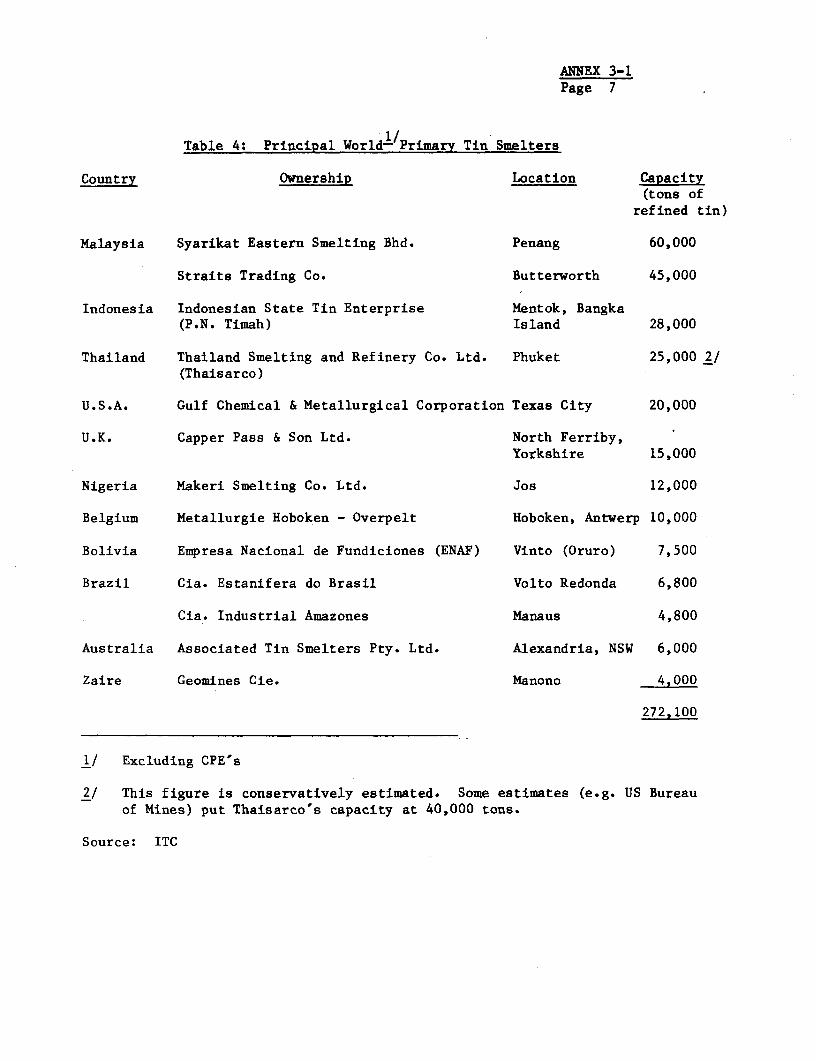

3.01 The international markets -or tin and tungsten, including mineralreserves, uses, and past and future trends in production, consumption andprices are described in detail in AunL-xes 3-1 and 3-2 respectively.

A. The International Tin Market

1. International Demand and Supply

3.02 Demand: Tin is a malleable and ductile white metal primarilyused in improving the properties of other materials. About 95% of tin con-sumed is in metallic form, with developed countries accounting for 75Z ofworld consumption. Tinplate and solders are the most important outletsfor tin metals, accounting for about 47% and 23% of all tin consumed inindustrialized countries. Between 1955 and 1972-74, consumption of tin grewat 1.7% per annum. This low rate of growth reflects, in part, the substi-tution of tinplate in cans by tin-free steel and aluminum. Also, technicalinnovations have reduced the amount of tin contained in tinplate. Of theother important end-uses, solder expanded quite slowly in the post-war period,while the use of tin in bronze and brass declined sharply.

3.03 Future demand will continue to depend to a large extent on tinplatefor containers. In developed countries, it is expected that the containerindustry will continue to grow steadily, but technological substitutionwill allow only a modest growth in tin use. In developing and centrallyplanned economies, the substitution effect will be more moderate and tindemand growth should be proportionately greater. Overall, world demandis projected to increase at only 1.5% per annum between 1972-74 and 1985,and will likely be below this trend rate until the late 1970's. There-after, the effect of lower real prices (para 3.06) should stimulate demandgrowth.

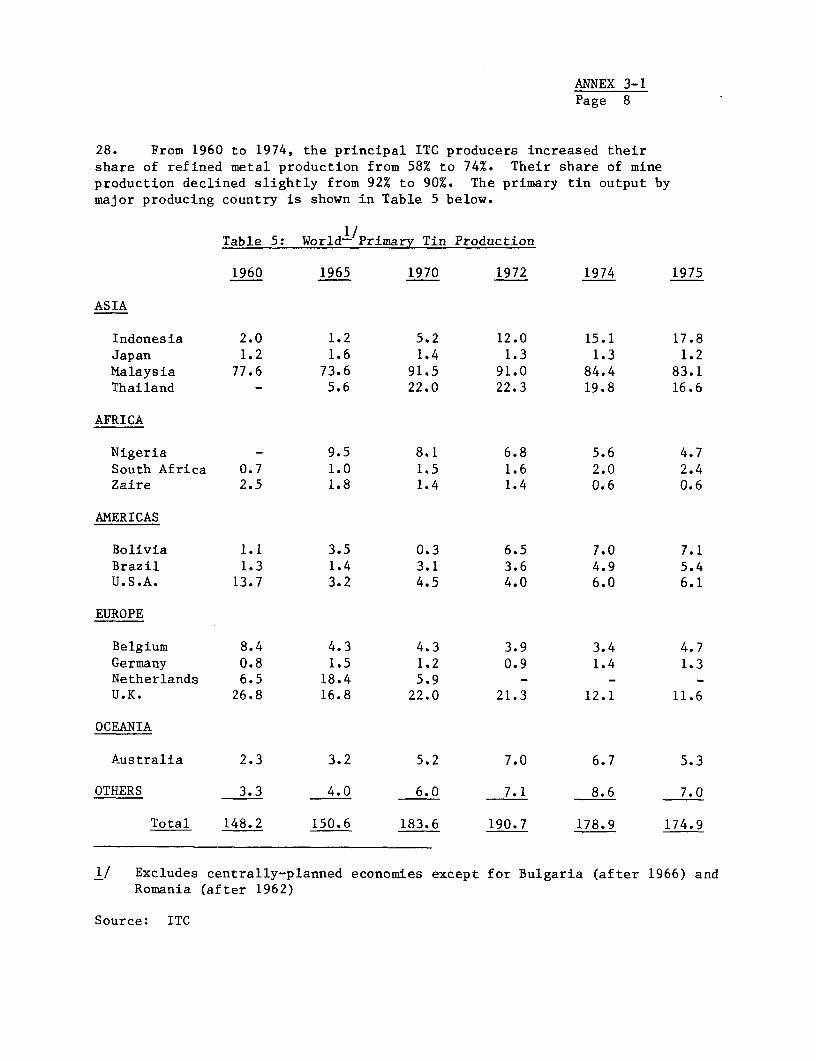

3.04 Supply: Tin is mainly found in placer or alluvial deposits, derivedfrom the weathering and erosion of primary tin ores. Over 90% of global re-serves are concentrated in developing countries, which account for about 75%of world production. Malaysia has remained the dominant producer, with 37% ofworld mine production of 173,000 tons in 1975 (excluding centrally plannedeconomies). Bolivia, Indonesia and Thailand are the other major producers,with 17%, 14% and 10% of mine production respectively in 1975. South-EastAsian production is almost entirely from alluvial mines, employing dredging,gravel pump mining and other hydraulic mining methods, but Bolivian produc-tion is mostly from high-cost hard rock underground mines. In the past, tinsupply has been affected by sales from the U.S. Government stockpile, whichis presently equivalent to about one year's world consumption. In addition,scrap represents a significant portion of supply, especially in the U.S.where old scrap accounts for 15% of tin supply.

3.05 As Malaysian reserves are gradually being depleted, that country'soutput is expected to decline as a proportion of world production, withThailand, Indonesia, Australia and Brazil increasing their share accord-ingly. As for Burma, even with the planned increase in official output

-7-

over the next five years, it will still account for only 1% of world supply.Moreover, the output associated with the project will amount to only 1/4 of1% of world supply and 10% of the annual incremental world' consumption atthe time the project comes on stream.

3.06 Historically, tin production has followed (with a certain lag)movements in real prices. Based on the relatively high prices of the pastthree years, tin production is forecast to increase at an annual rate of2.0% from the 1972-74 base through 1980. This, combined with slow demandgrowth, could result in a supply surplus in the late 1970's and a consequentdecline in real prices at that time. Beyond 1980, demand growth is expectedto outstrip supply (which can be assumed to decline slightly in response tothe decline in real prices) with possible tin shortages developing by themid-1980's, as shown below.

World /a Production and Consumption of Tin Metal

Average Actual Projected Growth Rates1960-62 1972-74 1981to to to

1960-62 1972-74 1980 1985 1972-74 1980 1985

(000's metric tons) (% per annum)

Production 186.9 226.5 260.0 254.0 1.7 2.0 -0.5Consumption 201.3 232.5 250.0 280.0 1.2 1.0 2.3Surplus (Deficit) (14.4) (6.0) 10.0 (26.0)

/a Including estimates for Centrally Planned Economies.

2. International Tin Agreements

3.07 The Fifth International Tin Agreement came into force July 1,1976, under the auspices of the International Tin Council, seated in London.This event was particularly significant as the U.S. is included for the firsttime, thereby increasing the proportion of world consumption represented byconsuming members to over 90%--it had only been 66% during the Fourth Agree-ment (1971-76). Tin producing members produce 90% of world tin output.For the time being, Burma has elected not to become a member of the ITC.Since the country represents such a small proportion of world output, non-membership has not had in the past and is not expected in future to have amaterial impact on its ability to sell its production, even in periods ofover-supply. The Bank has informed ITC of its consideration of the project.

3.08 Through the ITC buffer stock, and with the cooperation of theproducing countries in the control of exports, the amplitude of potentiallyviolent price fluctuations in the world tin price is reduced. The presentbuffer stock ceiling price is about US$3.93 per lb. and the floor price aboutUS$3.19 per lb. The Buffer Stock Manager must always sell tin when the marketprice reaches the ceiling and always buy when it reaches the floor. Theseactivities probably had an effect in lessening the impact of the recent worldeconomic decline on international tin prices. For the future, it is expected

-8-

that ITC buffer stock and export control operations will continue to have amoderating influence on tin price fluctuations, and, particularly in downmarkets, in defending floor prices.

3. Price Structure and Projections

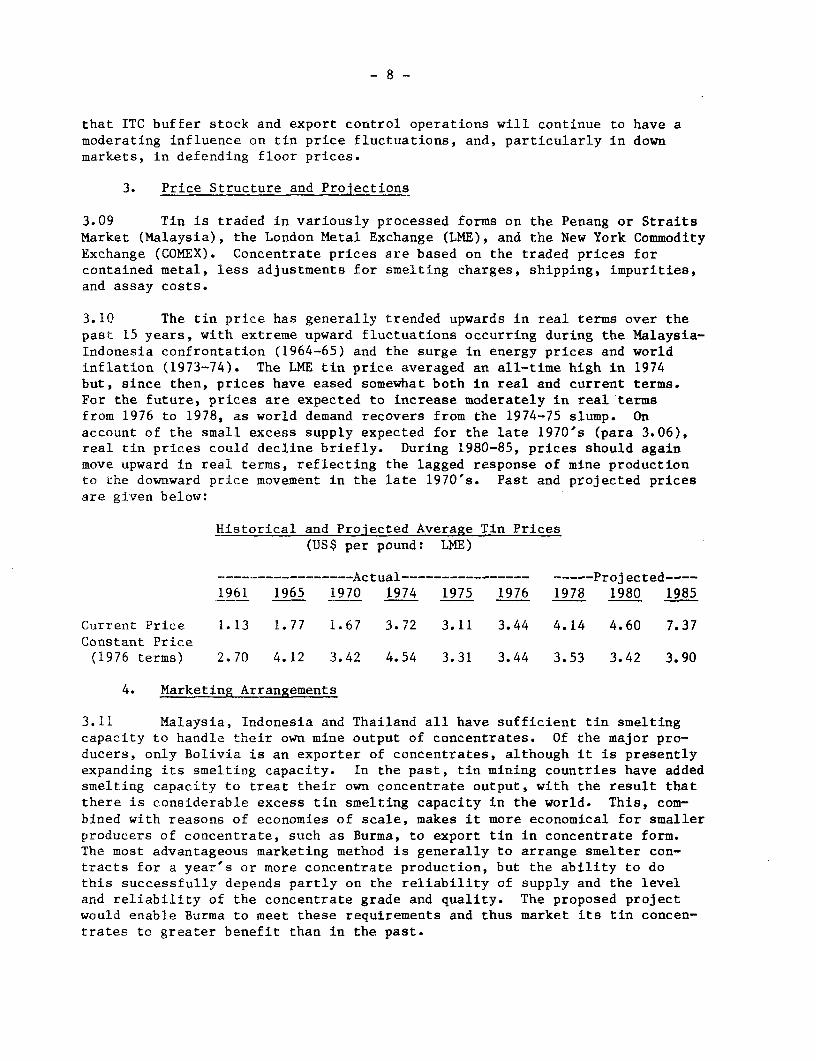

3.09 Tin is traded in variously processed forms on the Penang or StraitsMarket (Malaysia), the London Metal Exchange (LME), and the New York CommodityExchange (COMEX). Concentrate prices are based on the traded prices forcontained metal, less adjustments for smelting charges, shipping, impurities,and assay costs.

3.10 The tin price has generally trended upwards in real terms over thepast 15 years, with extreme upward fluctuations occurring during the Malaysia-Indonesia confrontation (1964-65) and the surge in energy prices and worldinflation (1973-74). The LME tin price averaged an all-time high in 1974but, since then, prices have eased somewhat both in real and current terms.For the future, prices are expected to increase moderately in real termsfrom 1976 to 1978, as world demand recovers from the 1974-75 slump. Onaccount of the small excess supply expected for the late 1970's (para 3.06),real tin prices could decline briefly. During 1980-85, prices should againmove upward in real terms, reflecting the lagged response of mine productionto the downward price movement in the late 1970's. Past and projected pricesare given below:

Historical and Projected Average Tin Prices(US$ per pound: LME)

…-------------…Actual---------------- ---- Projected----1961 1965 1970 1974 1975 1976 1978 1980 1985

Current Price 1.13 1.77 1.67 3.72 3.11 3.44 4.14 4.60 7.37Constant Price(1976 terms) 2.70 4.12 3.42 4.54 3.31 3.44 3.53 3.42 3.90

4. Marketing Arrangements

3.11 Malaysia, Indonesia and Thailand all have sufficient tin smeltingcapacity to handle their own mine output of concentrates. Of the major pro-ducers, only Bolivia is an exporter of concentrates, although it is presentlyexpanding its smelting capacity. In the past, tin mining countries have addedsmelting capacity to treat their own concentrate output, with the result thatthere is considerable excess tin smelting capacity in the world. This, com-bined with reasons of economies of scale, makes it more economical for smallerproducers of concentrate, such as Burma, to export tin in concentrate form.The most advantageous marketing method is generally to arrange smelter con-tracts for a year's or more concentrate production, but the ability to dothis successfully depends partly on the reliability of supply and the leveland reliability of the concentrate grade and quality. The proposed projectwould enable Burma to meet these requirements and thus market its tin concen-trates to greater benefit than in the past.

-9

B. The International TunRsten Market

1. International Demand and Supply

3.12 Demand: Tungsten is a heavy, hard, heat and corrosion resistantmetal, with the highest melting point and tensile strength of all metals.It also has good electrical and thermal conductivity and a low thermal ex-pansion coefficient. Tungsten's major uses are in carbide form (e.g. 45%of U.S. consumption) for machine tool cutting edges, dies, rock bits, ballpoint pen tips, gas turbine blades, and tire studs. In steel alloy form (25%of U.S. consumption), it is used primarily in metal working (drilling andcutting), grader blades, rock crusher jaws, and teeth for excavators. Otherapplications include: tungsten alloys for incandescent lamp filaments andelectrical contact points, and tungsten chemicals for textile dyes, paintsand pigments, and glass manufacture.

3.13 Demand is closely linked to levels of activity in the steel andmachine tool industries. The U.S., Japan, and Western Europe account for80% to 90% of tungsten consumption outside the centrally-planned economies.Despite wide fluctuations (e.g. a 23% decline in 1975 consumption) withchanges in economic activity, world consumption has grown at about 4% perannum from 1966 to 1974. Demand is expected to recover over the nextcouple of years, with the 4% growth rate to resume, given the low substi-tutability of the metal in its major applications, even at higher prices.

3.14 SupPly: Tungsten mainly occurs in nature as wolframite or schee-lite, and is commonly found in association with other metals such as tin,molybdenum, copper, and bismuth. Most of it is mined in hard rock under-ground mines, but some is also obtained by alluvial methods in conjunctionwith tin mining, as is the case in Burma.

3.15 The centrally-planned economies account for about half of worldtungsten production of 38,000 tons and hold about 70% of known reserves.The People's Republic of China accounts for about half of world reservesand produces about 25% of world supply. Among the non-centrally plannedeconomies, the leading producers are the U.S., South Korea, Bolivia,Thailand, Portugal, Canada and Australia.

3.16 Production in market-economy countries, together with importsfrom China, has not been sufficient to meet demand in recent years. Theshortfall has largely been met by sales from the U.S. Government stockpile,where disposals over the past ten years, though fluctuating widely, haveaveraged 12% of annual world production with a peak of 53% in 1969. Underthese circumstances, fluctuations in supply from China can and have had amajor impact on price. Recently, price levels have stabilized at fairly highlevels, partly due to some attempts at increased cooperation between producers,with China's support. Expansion of mine production should result. New orexpanded mines are being developed in the U.S., Australia and Turkey, andthere are possibilities in other countries, including Bolivia, Canada, and inthe longer term, in Burma. While data is incomplete, old scrap probablyaccounts for 15% of annual tungsten supply.

3.17 Producers' Association: In recent years, an ad hoc committeeon tungsten under the United Nations Conference on Trade and Development

- 10 -

(UNCTAD) has become more active, with some movement toward an internationalagreement aimed at stabilizing prices. To this end, the Primary TungstenAssociation (PTA) was formed in 1975, involving producing companies fromPeru, Portugal, Australia, France and Bolivia. Significantly, China was aparticipant in multilateral government meetings on tungsten held in Boliviain 1975 and is participating on the UNCTAD tungsten committee, which last metin Geneva in November, 1976. The UNCTAD commitee members hold disparate viewson the approach to stabilization measures. Obstacles to some form of finalagreement revolve around the fact that tungsten is traded in several forms, aswell as the need to achieve consensus between market and centrally-plannedeconomies.

2. Price Structure and Projections

3.18 International trade is often on the basis of prices quoted in theLondon Metal Bulletin (LMB). The LMB publishes a tungsten ore-users indexwhich is a weighted average of the prices of all purchases made by a groupof European tungsten carbide manufacturers. The LMB quotations are givenfor wolfram and scheelite (65% W03 and 70% W03 respectively). It also pub-lishes price ranges based on surveys of representative sales usually throughmetal trading companies. This is widely used as a basis for spot sales orlonger-term contracts. Production is commonly sold in pounds sterling permetric ton unit (MTU) or U.S. dollars per short ton unit (STU) of 65% W03content. The approximate value of a ton of ore or concentrate is obtainedby multiplying the price per ton unit by the percent W03 content (or grade).A ton unit is one hundredth of a ton.

3.19 Prices historically have shown erratic movements with fluctua-tions of 100% or more in a year not uncommon. Overall, however, the trendin real prices has been upwards reaching a peak in 1970 (see below). Withhigh prices and poor economic conditions in the latter part of 1974, con-sumers of tungsten reduced their inventory levels. In response, China cutback exports sharply thereby maintaining prices. Even at present levels,real prices are well below those reached in 1970 and equivalent to thoseprevailing in 1967-69.

3.20 With recovery in world economic activity in 1976, tungsten demandhas been increasing during the year. As a result, prices can be expected tomaintain their level of the last two years, or increase slightly. Over thelonger term, the prospects of increased Chinese cooperation with other pro-ducers look favorable, and would serve to attenuate the violent price fluc-tuations of the past. This assumes that sales from U.S. Government stock-piles will roughly reflect market requirements. The long term price trendis thus projected to be slightly upward in real terms as illustrated below:

Historical and Projected Average Tungsten Prices(US$ per MTU: LMB)

Actual Projected1961 1965 1967 1970 1972 1975 1976 1978 1980 1985

Current Price 16.9 28.8 49.6 74.3 35.9 91.3 102.0 121.0 146.3 213.2Constant Price(1976 terms) 40.3 67.0 112.0 151.9 63.5 97.2 102.0 103.3 108.6 112.9

- 11 -

3. Marketing Arrangements

3.21 The volume of trade in tungsten is small, and there is no univer-sally acknowledged marketing system as there is for many other metals. Fur-thermore, there is no real trade in tungsten metal itself but rather invarious forms such as concentrates or carbides. Concentrates are mainlybought and sold through brokers or metal trading firms, and small supplierssuch as Burma generally market their concentrates on a negotiated basis foreach sale to metal trading companies. Even Chinese sales and purchases bymajor consumers are done substantially through traders. However, providedthat reliable supply, quality and grade can be maintained, there is somescope for longer-term contract sales of tungsten concentrate, as for tin.

IV. THE CORPORATION

A. Operations

1. Mining Facilities and Output

4.01 No. 2 Mining Corporation (MC2) conducts mining operations in twoseparate parts of the country -- the Tenasserim Division in extreme south-eastern Burma (major mines: Heinda, Hermyingyi, and Kanbauk), and the Mawchiarea northeast of Rangoon (Mawchi Mine). Overall, MC2 operates 7 mines witha number of scattered smaller sites being worked exclusively by tributeminers. Primitive concentrating facilities exist at 6 mines and additionalupgrading plants are located at Rangoon and Tavoy (Annex 4-1). Over 75% ofthe concentrates produced by MC2 are purchased from tributers. These concen-trates generally contain a minimum 65% tin-ore/wolfram and are further upgradedby MC2 before sale.

4.02 Production is well below what it was many years ago and has beendeclining further in recent years. The causes have been the same as for therest of the mineral sector (para 2.03), i.e. war damage, ousting of privateoperations, deterioration of plant and infrastructure, shortage of spares andcapital, and increased leakage of tributor output through smuggling. Thetable below illustrates the trend in recent years:

MC2: Historical Production of Concentrates(Long Tons)

FY 1972 FY 1973 FY 1974/- FY 1975 FY 1976

Tin Concentrates 643 514 230 529 608Tungsten Concentrates 815 817 335 603 492Mixed Concentrates 652 635 168 387 402

Total 2,110 1,966 733 1,519 1,502

Of which tribute production 1,668 1,633 578 1,258 1,136

/a Six months, due to change in year-end from September 30 to March 31.

- 12 -

4.03 Mining methods vary from location to location and comprise gravelpumping, underground, and ground sluicing operations. Most of the mines arein alluvial-type deposits, the main exceptions being the hard rock under-ground operations at Mawchi and Hermyingyi, which are the principal sourcesof the tungsten ores. Concentrating facilities are generally primitiveand in poor running order, both at the mine sites and at two small upgradingplants in Tavoy and Rangoon. As a result, most of MC2's concentrates arelow grade, and contain high levels of impurities, thus reducing their salesvalue. Mixed tin/tungsten ores, such as those from Mawchi, are not separatedand recoveries are poor. Outmoded facilities also contribute to MC2's highproduct inventories. Products often flow from mines to concentrators inTavoy and back to utilize available wet and dry upgrading facilities and thusbring the products to a more marketable state.

4.04 Mines in the Tenasserim Division are connected to Tavoy by road.In the wet season, sections become impassable for days due to flooding,and even during favorable weather, delays arise due to the necessity oforganizing military escorts for security reasons. Concentrates are shippedfrom Tavoy to Rangoon by boat and then exported. Mawchi and Rangoon, on theother hand, are connected by both rail and road but because of the securitysituation, the most direct route cannot be taken.

4.05 Infrastructural facilities, such as power and water supply at themines, are generally poor and unreliable. Water shortages in the dry seasonand frequent power shut-downs hamper production, with generating and pumpingfacilities both suffering from shortages of spare parts and maintenance mate-rials.

2. Production Costs

4.06 Production costs for tin and tungsten concentrate vary by mine, butare generally somewhat below levels in other countries, reflecting the highlylabor intensive low-wage aspects of Burmese mining, with depreciation andfinancial charges well below those of more modern or mechanized operationselsewhere. Moderately more capital intensive production methods are warran-ted, even if total costs per ton mined are increased, in order to ensure thatoutput can be more closely controlled, and to prevent deposits from beinginefficiently and harmfully exploited by the haphazard high-grading operationsof the tribute miners.

B. Past Performance and Financial Condition

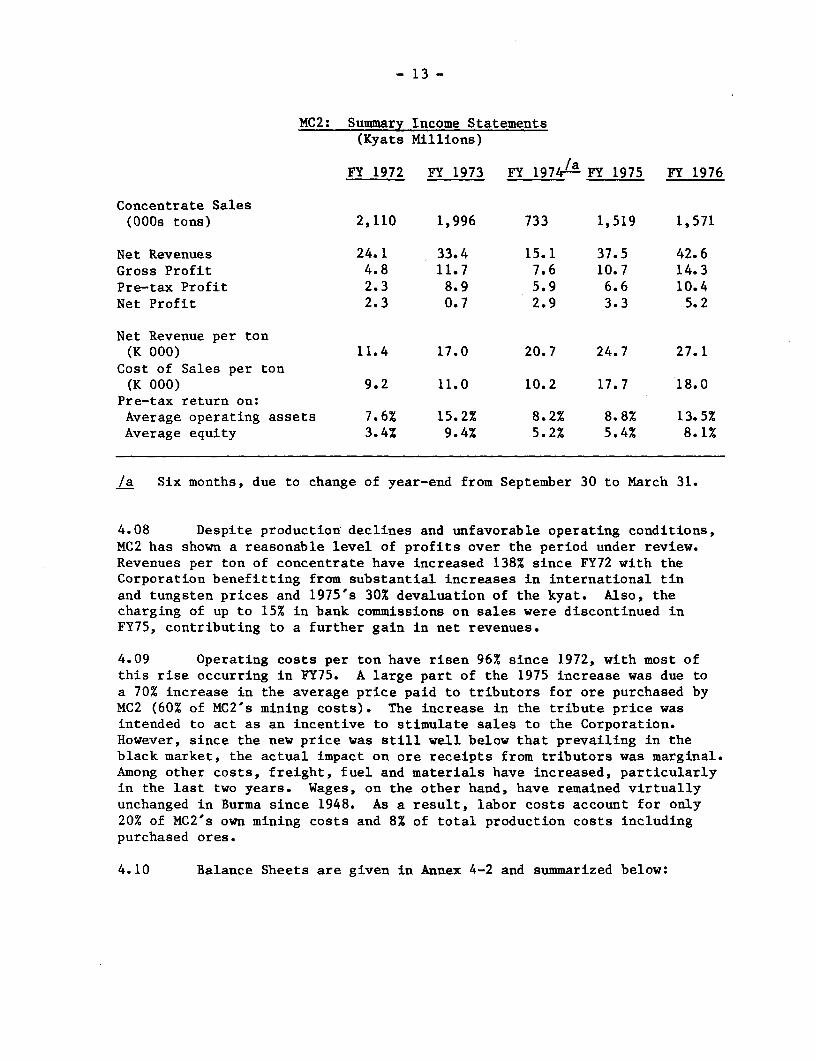

4.07 MC2's income statements for 1972-1976 are summarized below fromAnnex 4-2:

- 13 -

MC2: Summary Income Statements(Kyats Millions)

/aFY 1972 FY 1973 FY 1974/- FY 1975 FY 1976

Concentrate Sales(000s tons) 2,110 1,996 733 1,519 1,571

Net Revenues 24.1 33.4 15.1 37.5 42.6Gross Profit 4.8 11.7 7.6 10.7 14.3Pre-tax Profit 2.3 8.9 5.9 6.6 10.4Net Profit 2.3 0.7 2.9 3.3 5.2

Net Revenue per ton(K 000) 11.4 17.0 20.7 24.7 27.1

Cost of Sales per ton(K 000) 9.2 11.0 10.2 17.7 18.0

Pre-tax return on:Average operating assets 7.6% 15.2% 8.2% 8.8% 13.5%Average equity 3.4% 9.4% 5.2% 5.4% 8.1%

/a Six months, due to change of year-end from September 30 to March 31.

4.08 Despite production declines and unfavorable operating conditions,MC2 has shown a reasonable level of profits over the period under review.Revenues per ton of concentrate have increased 138% since FY72 with theCorporation benefitting from substantial increases in international tinand tungsten prices and 1975's 30% devaluation of the kyat. Also, thecharging of up to 15% in bank commissions on sales were discontinued inFY75, contributing to a further gain in net revenues.

4.09 Operating costs per ton have risen 96% since 1972, with most ofthis rise occurring in FY75. A large part of the 1975 increase was due toa 70% increase in the average price paid to tributors for ore purchased byMC2 (60% of MC2's mining costs). The increase in the tribute price wasintended to act as an incentive to stimulate sales to the Corporation.However, since the new price was still well below that prevailing in theblack market, the actual impact on ore receipts from tributors was marginal.Among other costs, freight, fuel and materials have increased, particularlyin the last two years. Wages, on the other hand, have remained virtuallyunchanged in Burma since 1948. As a result, labor costs account for only20% of MC2's own mining costs and 8% of total production costs includingpurchased ores.

4.10 Balance Sheets are given in Annex 4-2 and summarized below:

- 14 -

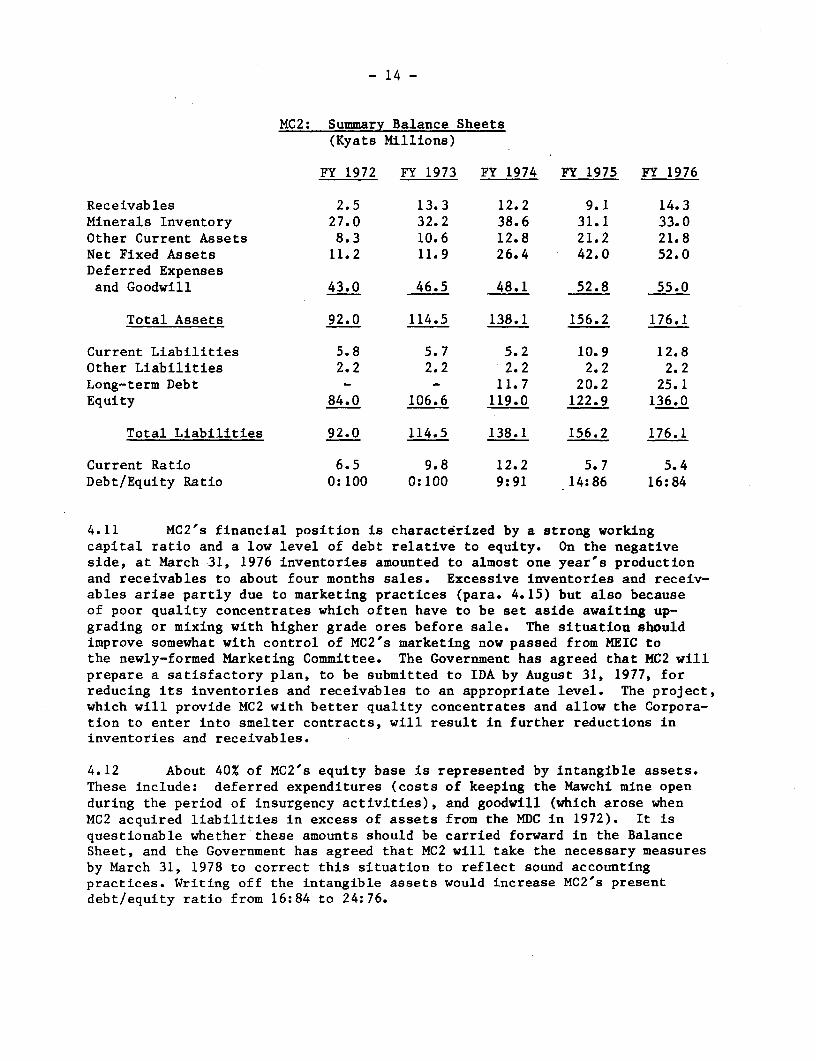

MC2: Summary Balance Sheets(Kyats Millions)

FY 1972 FY 1973 FY 1974 FY 1975 FY 1976

Receivables 2.5 13.3 12.2 9.1 14.3Minerals Inventory 27.0 32.2 38.6 31.1 33.0Other Current Assets 8.3 10.6 12.8 21.2 21.8Net Fixed Assets 11.2 11.9 26.4 42.0 52.0Deferred Expensesand Goodwill 43.0 46.5 48.1 52.8 55.0

Total Assets 92.0 114.5 138.1 156.2 176.1

Current Liabilities 5.8 5.7 5.2 10.9 12.8Other Liabilities 2.2 2.2 2.2 2.2 2.2Long-term Debt - - 11.7 20.2 25.1Equity 84.0 106.6 119.0 122.9 136.0

Total Liabilities 92.0 114.5 138.1 156.2 176.1

Current Ratio 6.5 9.8 12.2 5.7 5.4Debt/Equity Ratio 0:100 0:100 9:91 14:86 16:84

4.11 MC2's financial position is characterized by a strong workingcapital ratio and a low level of debt relative to equity. On the negativeside, at March 31, 1976 inventories amounted to almost one year's productionand receivables to about four months sales. Excessive inventories and receiv-ables arise partly due to marketing practices (para. 4.15) but also becauseof poor quality concentrates which often have to be set aside awaiting up-grading or mixing with higher grade ores before sale. The situation shouldimprove somewhat with control of MC2's marketing now passed from MEIC tothe newly-formed Marketing Committee. The Government has agreed that MC2 willprepare a satisfactory plan, to be submitted to IDA by August 31, 1977, forreducing its inventories and receivables to an appropriate level. The project,which will provide MC2 with better quality concentrates and allow the Corpora-tion to enter into smelter contracts, will result in further reductions ininventories and receivables.

4.12 About 40% of MC2's equity base is represented by intangible assets.These include: deferred expenditures (costs of keeping the Mawchi mine openduring the period of insurgency activities), and goodwill (which arose whenMC2 acquired liabilities in excess of assets from the MDC in 1972). It isquestionable whether these amounts should be carried forward in the BalanceSheet, and the Government has agreed that MC2 will take the necessary measuresby March 31, 1978 to correct this situation to reflect sound accountingpractices. Writing off the intangible assets would increase MC2's presentdebt/equity ratio from 16:84 to 24:76.

- 15 -

C. Organization and Management

4.13 Like other state organizations in Burma, all policy decisionsand many managerial functions have been outside MC2's immediate control.Decisions on production plans, marketing, investment, employment, wages,and financing are decided mainly at the level of the Minister or the EconomicCommittee of the Council of Ministers. The Managing Director of MC2 isappointed by the Government to carry out plans set by the Ministry of Minesand to supervise the day-to-day operations of the Corporation. Reportingto him are four Directors (Administration, Production, Planning and Projecting,and Engineering) and a Chief Accounts Officer (Annex 4-3). It is the Gov-ernment's intention to transfer more managerial and financial autonomy tothe various state economic enterprises through newly-formed ManagementCommittees. This, however, will be a gradual, cautious process. In MC2'scase, the Committee includes: the Managing Director, the Director of Produc-tion, the Chief Accounts Officer and two members representing the work-ers, one of whom is the Director of Administration. All are competent people,with good technical qualifications and many years experience in the industry,but with little management experience other than in a highly centralizeddecision-making environment.

4.14 MC2 employs about 2,700 persons, including 73 officers. Wagelevels are low, being equivalent to US$15 per month for laborers, US$70-150per month for engineers and geologists, and US$200 per month for top manage-ment. In some cases, inadequate wages have resulted in high rates of turnoverand absenteeism at MC2's mine sites, especially where other opportunities suchas tribute mining or illegal trade exist. A recently-established bonussystem and a cost-of-living allowance may help to relieve growing dissatis-faction in the face of rising prices. Overstaffing exists at some locations,largely due to output declines not being fully reflected in a reduction orrelocation of manpower, e.g. at Mawchi mine. The Government has agreed thatMC2 will prepare a manpower plan, with the assistance of the project consul-tants, which will include steps to establish employee levels consistent withchanges in output and profitability at its various operating locations. Alsoincluded in the plan, to be submitted to IDA by December 31, 1977, willbe a system of bonuses, incentive schemes and special allowances to augmentwages where appropriate.

4.15 As noted above, MC2's activities are presently limited to produc-tion; exploration, geological work, and, until recently, marketing, beingcarried out by other agencies within the Ministry of Mines. MC2 has nowgained closer control over marketing operations with this function transferredfrom the MEIC to the Minerals Marketing Committee in late 1976. The Committeeis jointly administered by representatives from the three metal producingcorporations. Also, with respect to tin/tungsten, MEIC's Sales Manager forthese metals (a highly competent individual) has assumed a key role in themanagement of the Committee. Principal advantages of the new arrangementsare: elimination of the excessive 2-1/2% MEIC sales commission; and scope toreduce MC2's high inventories and receivables, which have been partly causedby inefficient MEIC practices and the problems of inter-Ministry communi-cations. The marketing policies of the Committee have yet to be finalized,but the Government has agreed that the Committee will be granted authority totake appropriate measures to improve marketing efficiency, including entering

- 16 -

into long-term smelter contracts where appropriate. This should be facilitatedby the proposed project, with production expanded and quality and quantity ofsupply more reliable.

D. Accounts and Audit

4.16 MC2's accounting records are well maintained and contain reason-able detail on the Corporation's costs, revenues, production, inventories,and other financial and operational data. Apart from the annual accountsand monthly statements of production, cash receipts and expenditures, how-ever, management does not receive adequate information for effective opera-tional or financial control. The terms of reference for the consultantsretained for the project (para. 5.14) will include assistance in improvingthe Corporation's management information systems and its financial planningcapabilities.

4.17 The State Audit Office is the only official audit service availablein Burma, and has been used satisfactorily in other IDA projects in thecountry. In MC2's case (like that of many other state corporations in Burma),audits have been several years behind, but at the request of IDA, MC2 hassubmitted audited financial statements for FY76. The Government has agreedthat MC2 will submit audited accounts to IDA within five months of the closeof each fiscal year, and quarterly financial statements within 60 days.

E. Ore Reserves

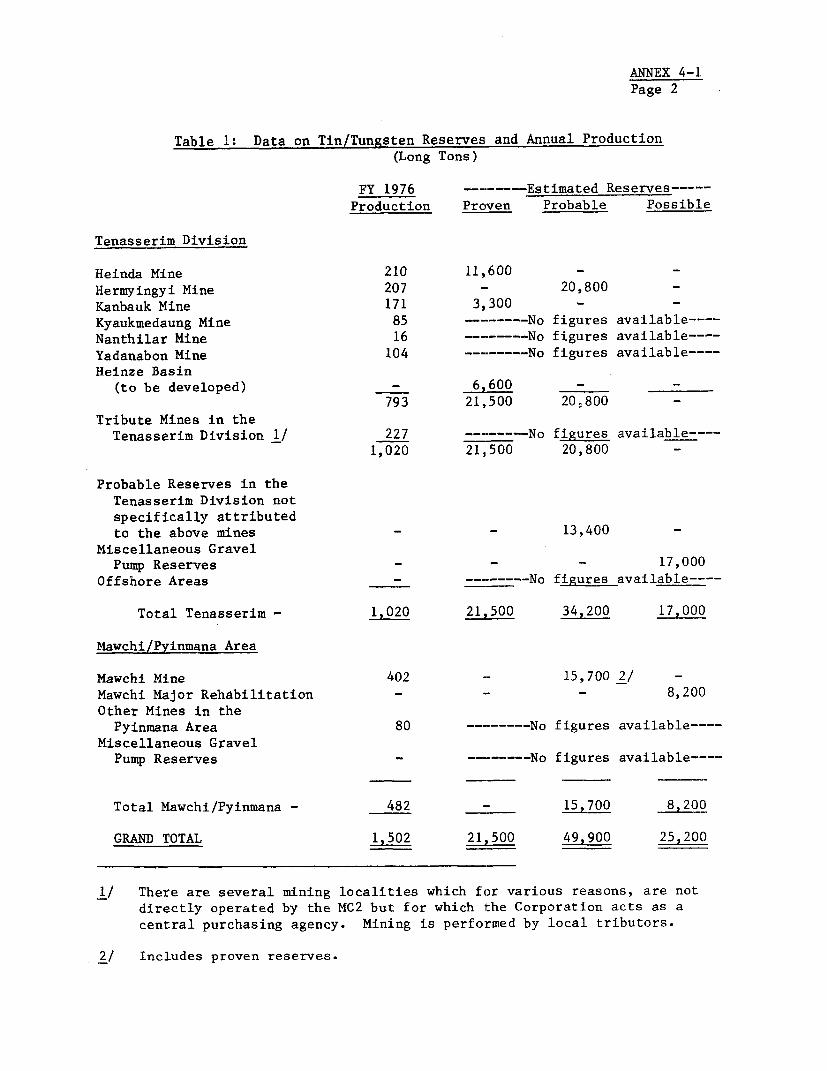

4.18 Sufficient ore reserves exist in the present areas of operationto produce at least 67,000 tons of tin concentrates and 30,000 tons of tungstenconcentrates. Of these 97,000 tons, only about 22,000 have been proved --sufficient for 15 years' production at present mining rates. These totals areunderstated, however, as they do not reflect recent real price increases,particularly for tungsten. For those mining sites scheduled for developmentas part of the proposed project (Heinze Basin, Kanbauk and various gravel pumpreserves), there are sufficient proved reserves for at least 15 years operationat the expanded rates of production. Proven reserves at the Heinda mine,where increased output will commence during 1977 following completion ofthe KfW-financed project, are only sufficient for 11 years. Conversion ofprobable and possible reserves to proved status, for these and other tin!tungsten deposits in Burma, is expected to be easily accomplished with modestamounts of further exploration and expenditures.

V. THE PROJECT

5.01 The project consists of the following components: (a) dredgingand related concentrating and infrastructural facilities (including a townshipwith housing and community facilities) at Heinze Basin (300 km S.E. of Rangoon)to produce about 650 LTPY of tin concentrate by FY81 (Map IBRD 12524), andimprovements to gravel pump operations at Kanbauk close to the Heinze Basin,increasing tin concentrate production by about 100 LTPY by FY81; (b) a newtin/tungsten concentrating and upgrading plant at Tavoy, 80 km south of Heinze

- 17 -

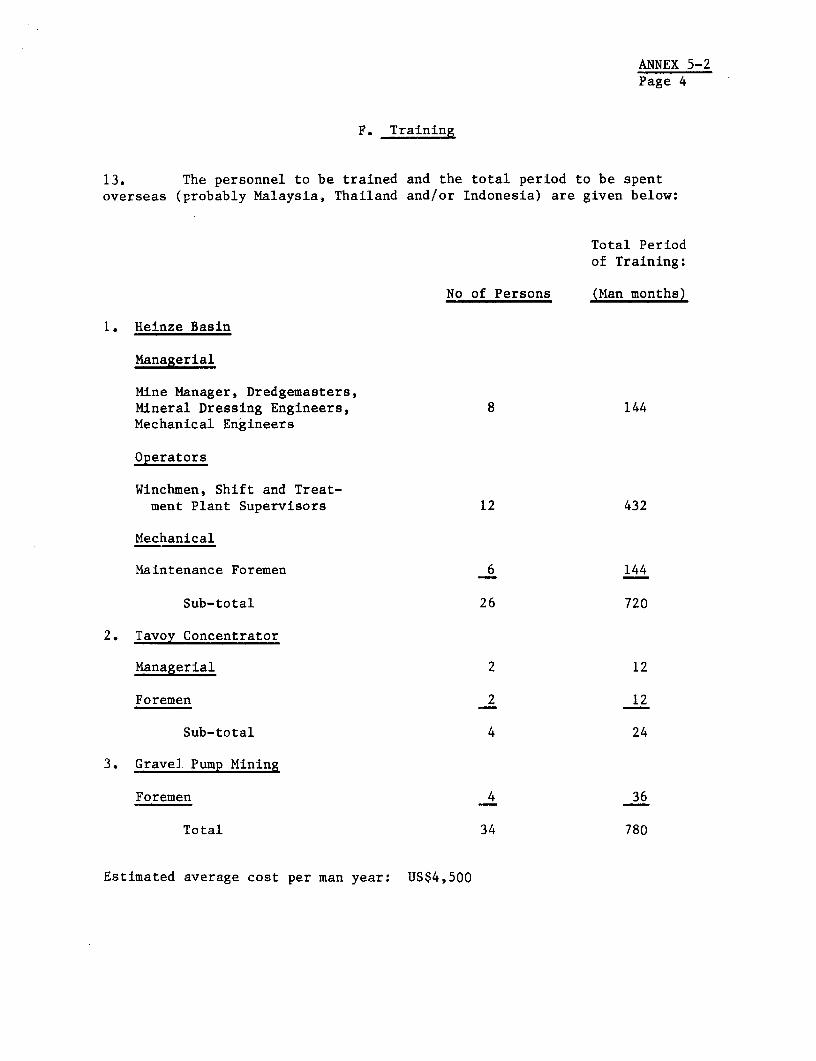

Bas., to separate mixed concentrates and improve the grade and quality of tinand tungsten concentrates produced by the Corporation; (c) equipment for newgravel pump mining operations near Tavoy to produce about 150 LTPY of tinconcentrates by FY81; and (d) technical assistance for training of key tech-nicians, engineering,project management, procurement, start-up, and theinitial operation of the project, plus assistance in improving the Corporation'soperating and financial controls, preparing a manpower plan (para. 4.14) andpreparing a study of exporting concentrates directly from Tavoy. In particular,the provision of consultants experienced in dredging and concentration oftin/ tungsten ores is to compensate for MC2's unfamiliarity in these areas.A more detailed description of the tin/tungsten project is given in Annex5-1. In addition, US$200,000 equivalent of the proposd credit will be used fora study of the future development of the mineral sector (para. 5.16).

A. Technical Description

1. Heinze Basin Dredging Project and Concentrator

5.02 The dredging would take place in a 25 km long southern sectionof the Heinze Basin, access to which is by sea or by surfaced road fromTavoy or Ye (both within 60 km of the project area). Sea access is limitedduring the monsoon season, and road access is also somewhat limited due to5-ton load limits on bridges and 13 km of unsurfaced road between the Basinand Tavoy. The project can be planned around these restrictions and theGovernment has agreed that the unsurfaced road will be improved to an all-weather condition no later than December 31, 1979, i.e., before projectstart-up.

5.03 A portion of the Basin was dredged prior to World War II and inter-mittent dredging was carried out west of the Basin up to 1952. A UNDP-fi-nanced program (1972-75) undertook extensive borings in the Basin and afeasibility study was completed by the Malaysian consulting firm, Osborneand Chappel, in mid-1975. Recoverable concentrate is conservatively esti-mated at 6,640 tons, sufficient for 19 years at the proposed rate of mining.In the initial years, production will average 550 tons of concentrate perannum, and after the tenth year will decline to about 250 tons per annum,as lower grade ores are worked.

5.04 Careful study was done by the consultants to determine the optimumdredge size based on both operational and economic factors. The dredge se-lected will be a conventional bucket ladder dredge with a jig treatmentplant on board. The dredge would be capable of digging to a depth of 16m. during the first 8 years of operation. Its pontoon and ladder wouldthen be extended to increase digging depth to 27 m. The dredging sequencehas been selected to maximize the present value of the cash flow. Annualproduction is estimated at 1.4 million cu. m. of ore in the early years(reflecting operator inexperience and dredging conditions), increasing to2.0 million cu. m. after the tenth year. These production estimates are51% and 74% of theoretical dredge capacity, respectively.

5.05 The dredge's jig plant would produce a concentrate grading 20-40%tin which would then be transported by barge to the nearby shore-based mill.After upgrading there, concentrate grading 65% tin would be transported byroad or sea to Tavoy for further processing.

- 18 -

5.06 The flowsheet for the Heinze Basin mill would include screening,magnetic scalping, classifying, and Wilfey table treatment. The concen-trate would pass through a fresh water wash and, after drying, be treated onhigh-intensity magnetic separators to separate refractory minerals. Themill flowsheet has been thoroughly tested by the consultants. The ore typeis quite common in south-east Asia, the flowsheet is conventional, and theequipment proposed is standard and widely used in alluvial tin concentrators.

5.07 Due to the remote location of the Heinze Basin and the lack ofexisting infrastructure, the project will require extensive support facili-ties including: water craft (tugboat, work boat, personnel boats, barges);power (diesel generators for the dredge and shore complex); wells for watersupply; and workshops, offices, and a warehouse. Social infrastructure wouldinclude: a 237-home townsite, school, community hall/cinema, hospital, mar-ket, playfield, and electrical, water, and sanitary facilities.

5.08 Production of tin concentrates at the nearby Kanbauk gravel pumpmines is expected to increase by about 100 LTPY (from the current 200 LTPY)as a result of better maintenance and operational supervision associated withthe Heinze dredging and concentrating complex and improved power and watersupply. Only a very small amount of additional direct investment at Kanbaukwould be involved. Concentrates from Kanbauk would be further upgraded at theHeinze Basin mill and the Tavoy concentrator. Recoverable ore reserves atKanbauk are estimated at 3,400 tons, sufficient for 10 years operation at theprojected rate of output.

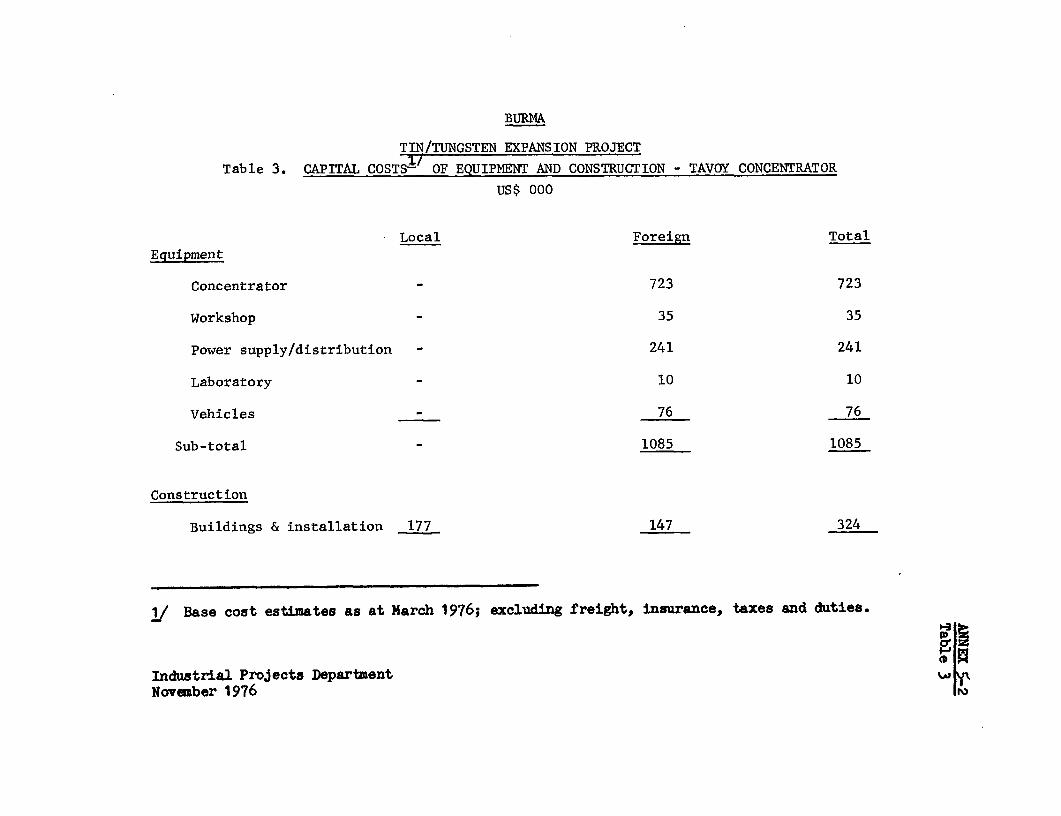

2. Central Concentrator at Tavoy

5.09 As a result of antiquated and inefficient concentrating facilities(Annex 4-1), much of MC2's output is of a low and unreliable grade (averagingabout 69% for tin concentrates and 64% for tungsten), high in impurities andsells at a substantial discount below standard prices. Based on a proposalby the Corporation, IDA commissioned a study of various alternative new con-centrating facilities to determine the best location and a preliminary flowsheet for the selected alternative. This was carried out by Osborne andChappel of Malaysia and their final report was produced in July 1976.

5.10 The selection of a large centralized concentrator located in Tavoyis based on its favorable economic return, and the ability of a Tavoy loca-tion to provide the focus for improved operational control of the Corpora-tion's mines in the Tenasserim Division. As the concentrator would treata variety of ores, including mixed concentrates from Mawchi, the flowsheetinvolves a number of circuits including: crushing, screening, electrostaticprecipitation, wet gravity separation on tables, cleaning in Willoughby boxes,drying and high intensity magnetic separation. In addition to producing highquality wolfram and tin concentrates, the concentrator would produce a numberof byproducts, but incremental revenues from these will be small. Testingdone by the consultants was sufficient to determine the basic flowsheet butfurther metallurgical testing will be required to finalize concentratordesign. A preliminary study has been conducted by the Corporation to identifyspecific possible sites for the concentrator. The final site will be chosenwith the assistance of the project consultants and the site acquired as acondition of credit effectiveness.

- 19 -

5.11 Overall, the concentrator will produce 3,000 - 4,000 LTPY of concen-trates (grading 75% for tin concentrates and 67% for tungsten) on a single-shift basis, with ample flexibility for increasing its capacity and modifyingits flowsheet as other mines are developed in the area. Infrastructuralfacilities for the concentrator include: water supply from nearby wells orthe Tavoy river, electric power (two 345 kw diesel generators), and transport(five six-ton trucks - concentrates from various mines in the area are presentlydelivered to Tavoy by local buses).

5.12 The Government has agreed that the terms of reference of the projectconsultants will include assistance to MC2 in the improvement of the export ofconcentrates. This will include study of the feasibility and desirability ofdirect export of the Corporation's products from Tavoy to smelters in Malaysiaor Thailand, without the inefficient and time-consuming process of shipment toRangoon as presently practised. The expanded output of concentrates in thearea should provide sufficient incentive for vessels to stop at Tavoy, and,since concentrates would be trans-shipped from lighter vessels, minimalinfrastructure would be required.

3. Gravel Pump Mining Project

5.13 Although knowledge of reserves is patchy, there are a number oftin and tungsten-rich deposits in the Tenasserim Division which are idealfor gravel pump operations. This process consists of monitors (water jets)to wash down sand and gravel to a sump. From the sump, the slurry of liqui-fied material is pumped to a palong (sluice box) for treatment. Equipmentwould be acquired to establish gravel pump operations at one or two loca-tions. Since major production preparation, such as extensive stripping, wouldnot be necessary, this component of the project could be implemented relativelyquickly. Equipment needed (drills, hydraulic monitors, pumps, diesel generator,and jig plants) is highly mobile and expensive infrastructural facilities arenot required. In addition to yielding about 150 LTPY of tin concentrates, theproject, under consultant supervision, will provide valuable training.

4. Technical Assistance

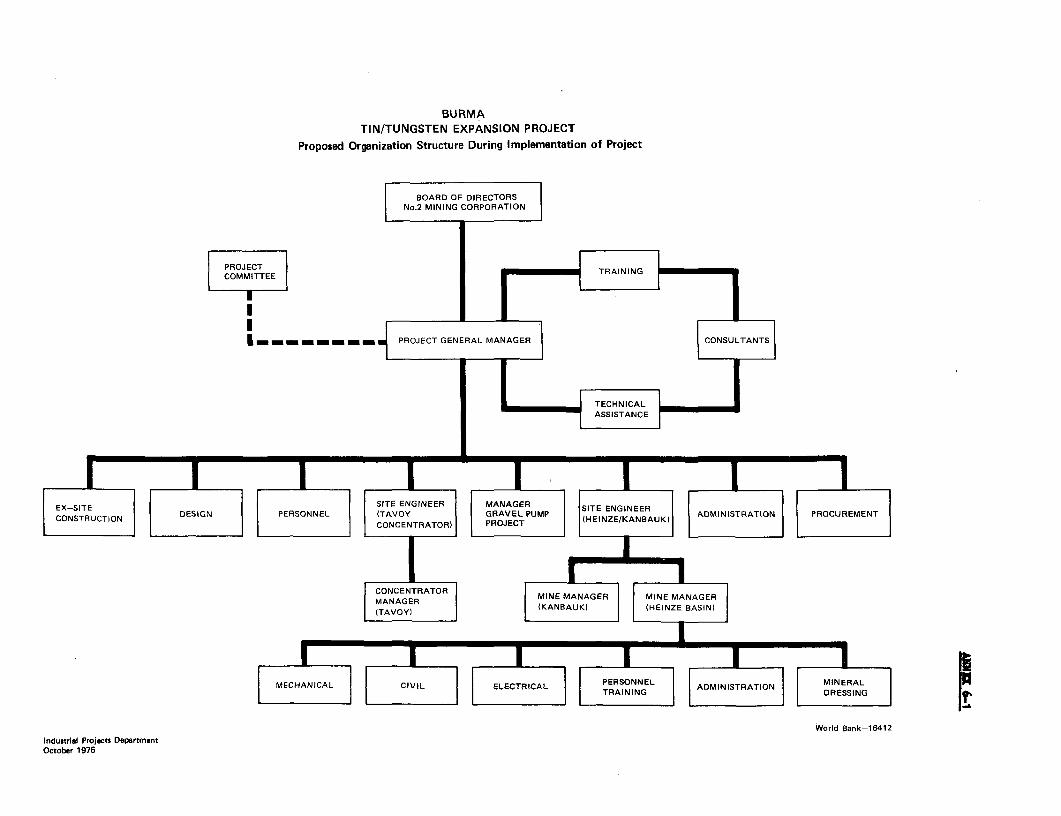

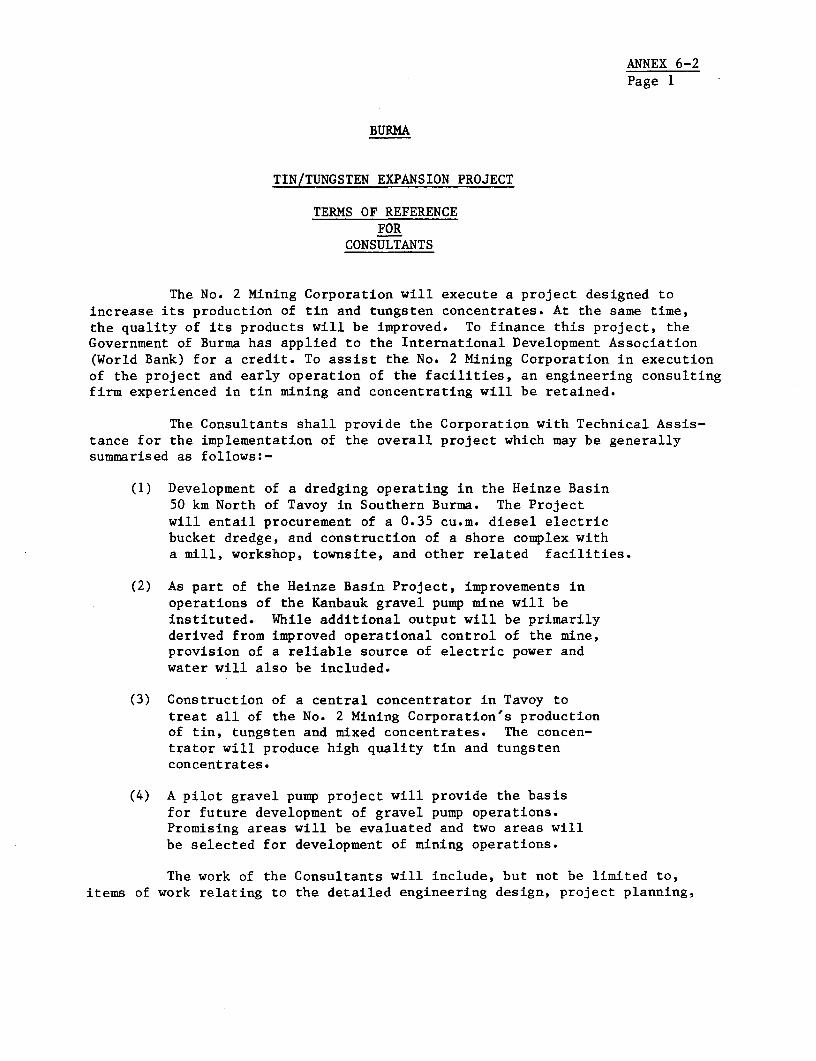

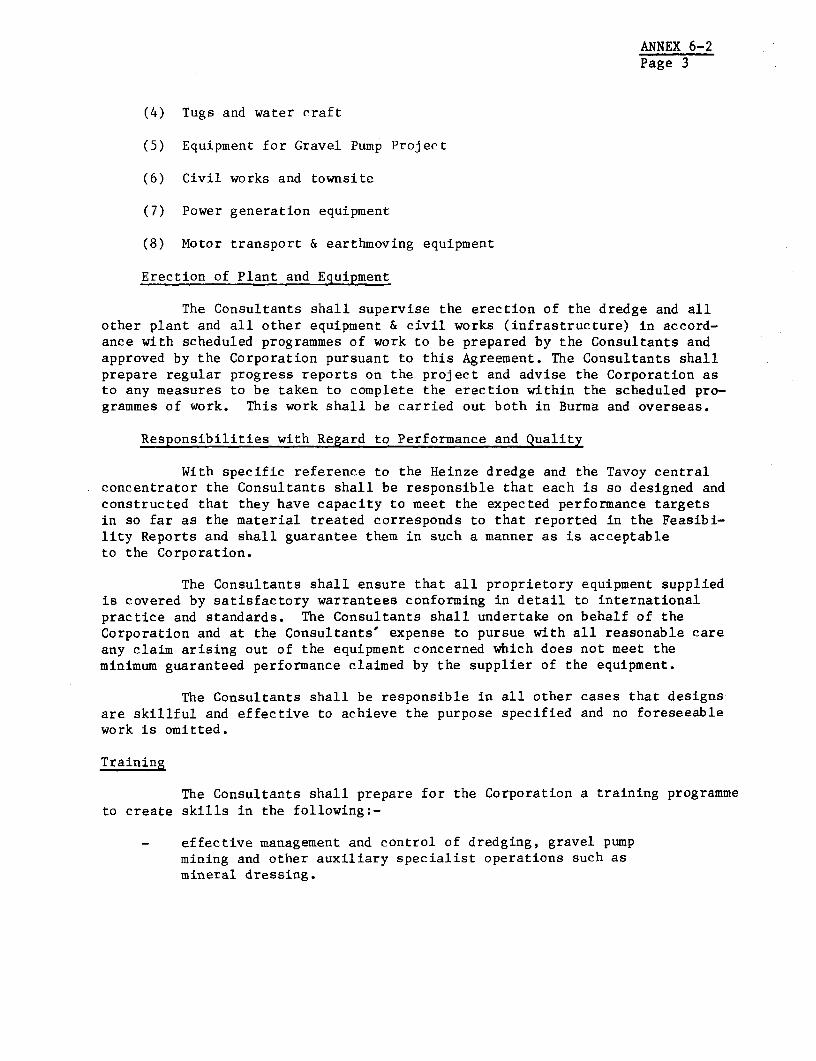

5.14 MC2's inexperience in the operation of other than simple miningand concentrating activities necessitates fairly extensive outside technicalassistance by consultants experienced in the design and operation of dredg-ing, mining, and concentrating facilities. The Government has agreed that theCorporation will retain consultants, to be financed from the proposed credit,and on terms of reference satisfactory to IDA, to assist with project engineer-ing, project management, overseas training of key technicians, procurement,and to supervise and assist during the start-up of the facilities and duringat least the first two years of their operation (with IDA to be consultedbefore the termination or reduction of this operational assistance). Theconsultants will also assist in the development of physical, cost, and finan-cial control systems to improve MC2's overall operational effectiveness,assist with export improvements (para. 5.12), and help prepare a manpower plan(para. 4.14). Draft terms of reference (Annex 6-2) have been discussed withthe Corporation. Osborne and Chappel, the Malaysian consulting firm which didthe project feasibility studies, has been selected for this assistance. Theemployment of the consultants is a condition of credit effectiveness. The

- 20 -

estimated cost for engineering services and other consulting assistance isUS$1.9 million, of which about US$0.5 million would be technical assistance,spread over a five-year period. The average cost per man-year is estimated tobe US$84,000 including all travel, overhead, and associated expenses.

5. Other Expansion Plans

5.15 Significant future expansion of production is envisaged by MC2and three major mine rehabilitation programs, in addition to the project, arein the pipeline. The Heinda mine is being expanded with the help of KfWfinancing through a new open-pit system and a new concentrating mill whichshould increase annual production by 800 LTPY of tin concentrates, withproduction scheduled to start during 1977. At Hermyingyi, explorationwork assisted by German technical aid is being carried out with a view toproving adequate reserves on which to base a project. This could add another500 LTPY of tin/tungsten concentrates by the early to mid-eighties. AtMawchi, a USSR-financed rehabiltation program to increase output by 1,000 LTPYof tin was suspended in 1973. This could be resumed if insurgency problemswere brought under control and new financing found. The timing of this isuncertain, but there have been recent indications that the security situationmay be inproving. In order to ensure sufficient managerial attention is givento the proposed IDA project, the Government has agreed that the Corporationwill not embark on any major new investments (over US$1 million equivalent peryear) without prior IDA approval.

6. Sector Study

5.16 The Government has agreed that it will employ consultants acceptableto the Association with satisfactory terms of reference, to assist in carryingout a study of the future development of the mineral sector. This would helpthe Government to establish sector priorities and to identify suitable develop-ment projects. The scope of the study should be agreed by June 30, 1977. TheGovernment has agreed to employ the consultants by December 31, 1977, and tocommence the study within three months. The study's recommendations willbe reviewed with IDA and implementation steps agreed. Part of the credit(US$200,000 equivalent) will be used to finance the work, with the Ministry ofMines as executing agency.

B. Environmental Aspects

5.17 As the project operations involve physical, rather than chemicalprocesses, no harmful pollutants will result. Dredge tailings will be deposi-ted back into the Basin, but in the same form as the naturally occurringmaterials. Concentrator tailings will be disposed of on land and shou'ld notraise any environmental problems. Dredging operations will create some minordisruption of fishing activities in the Basin, but these are not economicallysignificant to the local population. Moreover, the area affected at any onetime will be confined to a small part of the Basin.

C. Capital Costs

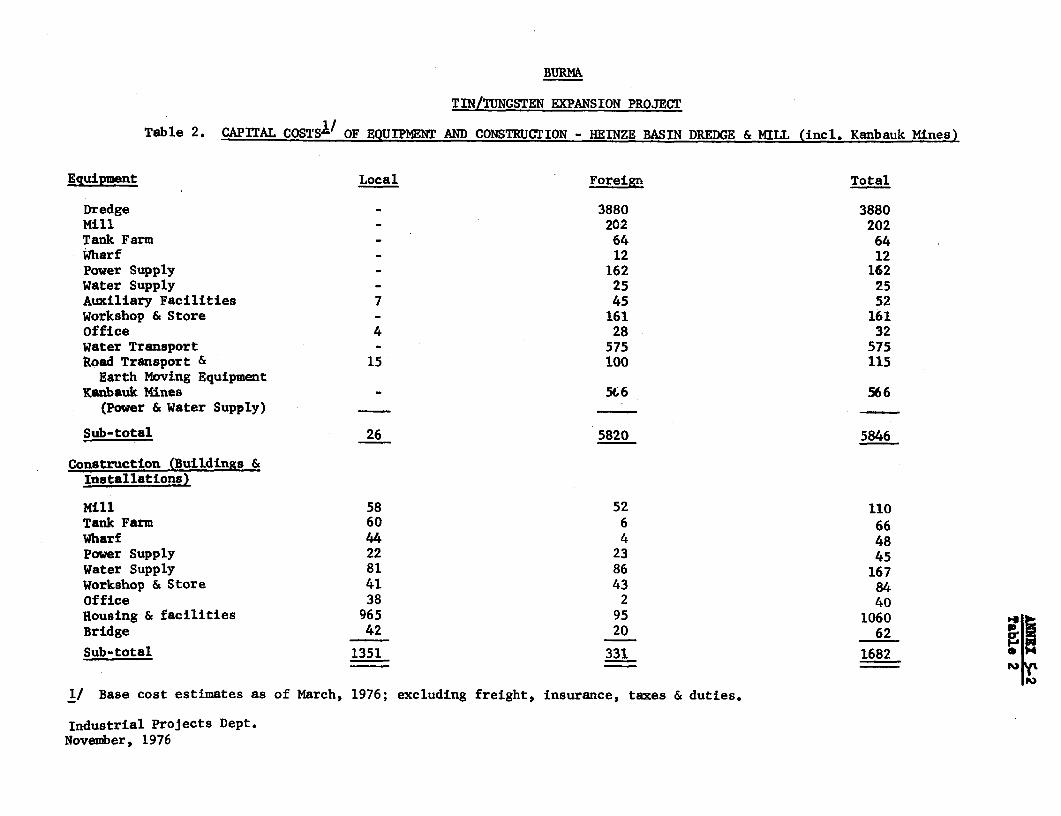

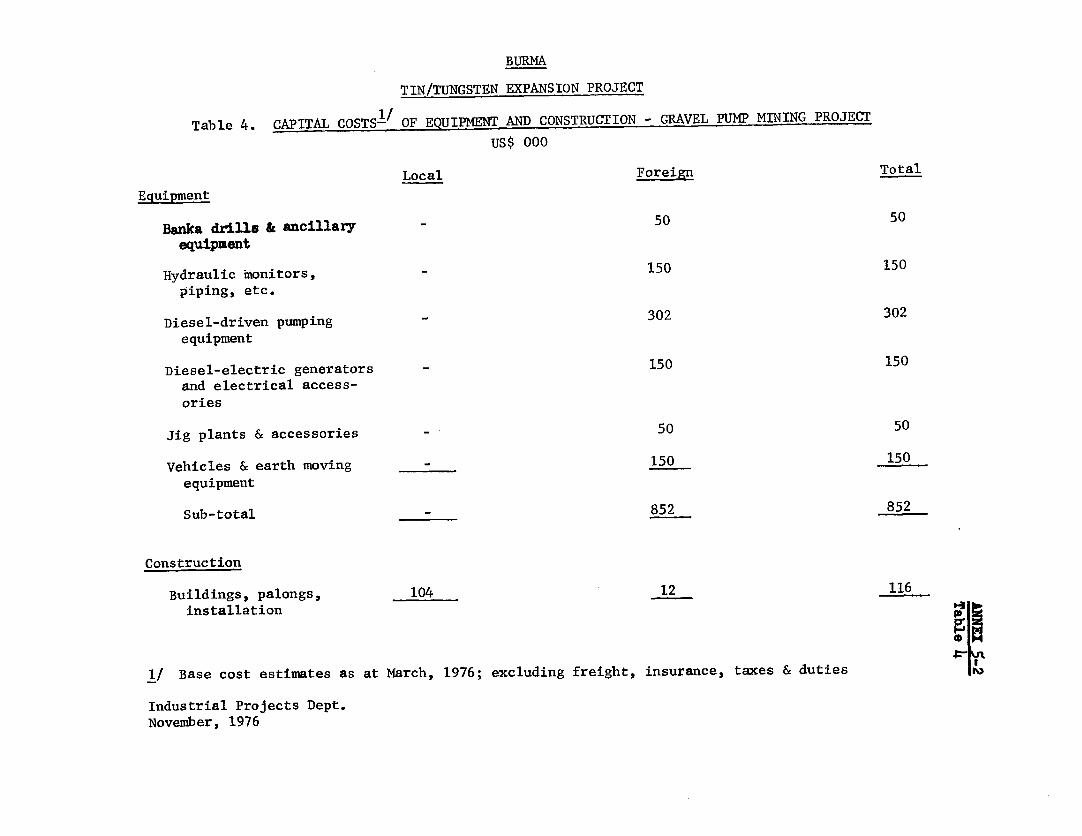

5.18 Project cost, excluding interest during construction and incrementalworking capital, is estimated at US$26.0 million equivalent, of which US$18.9

- 21 -

million would be for the dredging, concentrating and related facilities atHeinze Basin (including Kanbauk); US$3.7 million for the central concentratorat Tavoy, US$2.7 million for the gravel pump mining pilot project, US$0.5million for technical assistance additional to the engineering and projectmanagement included in other project components, and US$0.2 million for thesector study. Total financing requirements are estimated at US$27.8 million;these costs are detailed in Annex 5-2 and summarized below:

Summary of Capital Costs

Local Foreign Total Local Foreign Total %---- Kyats Millions ----- ------US$ Millions-----

Equipment /a 28.8 60.8 89.6 4.4 9.1 13.5 52Construction andCivil Works /a 12.6 3.4 16.0 1.9 0.5 2.4 9Engineering andProject Management 0.8 11.6 12.4 0.1 1.8 1.9 7

Training - 1.9 1.9 - 0.3 0.3 1Administration andPre-Production 2.3 - 2.3 0.3 - 0.3 1Sector Study - 1.3 1.3 - 0.2 0.2 1

Total Base Cost 44.5 79.0 123.5 6.7 11.9 18.6 71PhysicalContingencies 4.0 5.7 9.7 0.6 0.9 1.5 6Price Contingencies 18.0 21.7 39.7 2.7 3.2 5.9 23

Project Cost 66.5 106.4 172.9 10.0 16.0 26.0 100Incremental Work-ing Capital /b - - - - - -

Interest DuringConstruction 12.1 - 12.1 1.8 - 1.8Total Financ-ing Required 78.6 106.4 185.0 11.8 16.0 27.8

Taxes and Dutiesin Project Costs (39.8) (-) (39.8) (6.0) () (6.0) (23)

/a Includes freight, insurance, duties and commodity taxes. Spares for equip-ment are included in equipment costs.

/b No incremental working capital needs are shown for the project since im-provements in product quality and marketing efficiency will permit a re-duction in receivables and inventories sufficient to offset the addi-tional requirements that would otherwise result from increased output.

5.19 All base costs reflect March 31, 1976 prices. Estimates have been pre-pared in great detail by the consultants, based on their extensive experiencein Malaysia, and supplemented by budget quotations from suppliers. Estimatesfor civil construction and infrastructure are based on quotations from theConstruction Corporation of the Burmese Ministry of Works, and were foundby the consultants to be reasonably in line with their Malaysian experience.Duties and taxes amount to 23% of capital costs. In addition to normal

- 22 -