Annual Turkish M&A Review 2010 Contents

24

Annual Turkish M&A Review 2010 Corporate Finance January 2011

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Annual Turkish M&A Review 2010 Contents

Annual Turkish M&A Review 2010

Corporate FinanceJanuary 2011

1

Contents

Energy privatizations make their mark 1

Snapshot 3

Privatizations 4

Investor origin 6

Private equity activity 8

Deal rankings 10

Sectoral overview 11

Prospects 12

Deal list (January 1 – December 31) 13

Basis of Presentation

Mergers and acquisitions presented in this report comprise M&A transactions announced between 01.01.2010 and 31.12.2010, including those with on-going legal/closing/financing procedures.

This study does not include; capital market transactions, IPOs, real estate sales, conces-sions based on revenue sharing, intra-group share transfers and transactions of financial institutions within the framework of debt restructuring.

1

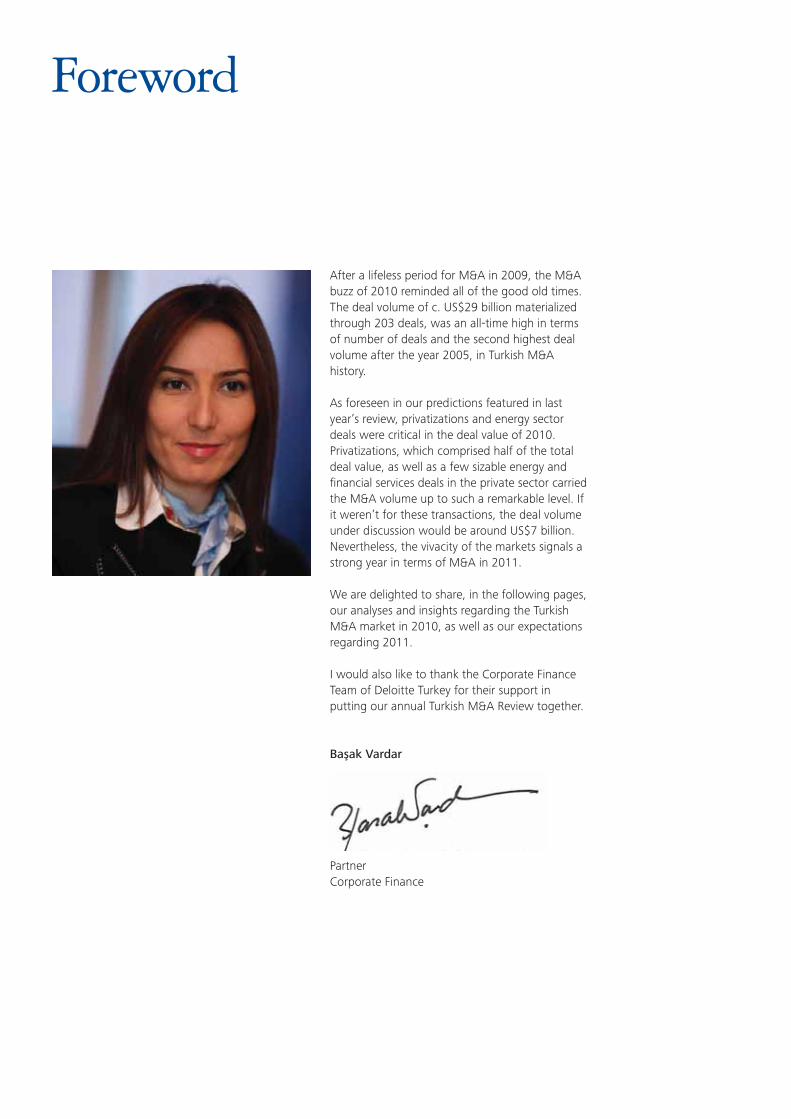

After a lifeless period for M&A in 2009, the M&A buzz of 2010 reminded all of the good old times. The deal volume of c. US$29 billion materialized through 203 deals, was an all-time high in terms of number of deals and the second highest deal volume after the year 2005, in Turkish M&A history.

As foreseen in our predictions featured in last year’s review, privatizations and energy sector deals were critical in the deal value of 2010. Privatizations, which comprised half of the total deal value, as well as a few sizable energy and financial services deals in the private sector carried the M&A volume up to such a remarkable level. If it weren’t for these transactions, the deal volume under discussion would be around US$7 billion. Nevertheless, the vivacity of the markets signals a strong year in terms of M&A in 2011.

We are delighted to share, in the following pages, our analyses and insights regarding the Turkish M&A market in 2010, as well as our expectations regarding 2011.

I would also like to thank the Corporate Finance Team of Deloitte Turkey for their support in putting our annual Turkish M&A Review together.

Başak Vardar

PartnerCorporate Finance

Foreword

1

1

Privatizations, comprised half of the total deal value. The privatizations in the energy sector and a couple of sizable transactions in energy and financial services in the private sector were decisive in the deal volume. 2011 is expected to be a vibrant year in terms of M&A, once again featuring significant privatizations.

Out of 203 transactions in 2010, 119 had a disclosed deal value, adding up to US$25.4 billion. Considering the estimated value of deals with undisclosed values, total M&A volume was around US$29 billion in 2010. (2009 full year c. US$5.8 billion). 2010 was a year of privatizations and secondary sales.

Privatizations made up a considerable part of the deal volume, with 35 transactions having a deal value of US$14.6 billion, which represents half of the total deal value. These transactions were mainly the sale of electricity distribution companies and portfolios of small generation assets. 2010 was the last stop of a long-lasting journey for the privatization of the Turkish electricity distribution companies. Electricty distribution rights for 11 regions were sold off for a total of US$12.3 billion. Additionally, Başkent natural gas distribution company was privatized for US$1.2 billion.

Spanish BBVA’s acquisition of Garanti Bank shares from GE (25%) for a consideration of US$5.8 billion was certainly the deal of the year, which comprised 20% of the total deal value by itself.

Excluding privatizations and the Garanti Bank deal, the total volume of the remainder was only US$8.5 billion, while the average deal size of the remainder was US$50 million, indicating that mid-cap segment hosted the most activity. The number of big-ticket transactions did not exceed the number of fingers on one hand.

Even with a deal value of c. US$10.5 billion (2009 – US$2.2 billion), foreign investors only accounted for 36% of the total deal value. Foreign investors’ contribution to the annual deal volume remained low in 2010 mainly due to Turkish investors’ dominant role in privatizations.

We expect the energized M&A market to keep building up its momentum in 2011.

1. Including estimates for deals with undisclosed values

Energy privatizationsmake their mark

Following the quiet period in 2009, M&A activity in 2010 has soared to rea h the highest number of deals ever and the second highest deal value after the year 2005, in Turkish M&A history. Total M&A volume was around US$29 billion(1)������������ ������� ���� ������two times the deal value and number of last year, respectively.

2

3

Snapshot

Year 2007 2008 2009 2010

Deal Number* 160 169 102 203

Deal Volume* US$19.3 billion US$16.2 billion US$5.8 billion US$29 billion

Privatizations / Share in Total

US$2.3 billion / 12%

US$5.2 billion / 32%

US$1.8 billion / 32%

US$14.6 billion / 50%

Foreign Investors* 70% of deal value 85% of deal value 38% of deal value 36% of deal value

Financial Investors* 13% of deal value 30% of deal value 12% of deal value 3% of deal value

Average Deal Size c. US$120 million c. US$100 million c. US$55 million c. US$140 million***

Largest Deal Value / Share in Total

US$2.7 bn (Oyak Bank) / 14%

US$3.1 bn (Migros Türk) / 19%

US$606 mn (Sugar Factories)** / 10%

US$5.8 bn (Garanti Bank) / 20%

(*) Including estimates for deals with undisclosed values and adjusted for canceled transactions.(**) The legal process regarding the sugar factories is on-going. No adjustments have been made.(***) Excluding privatizations and the Garanti Bank deal, the average deal size of the remainder was US$50 million.

4

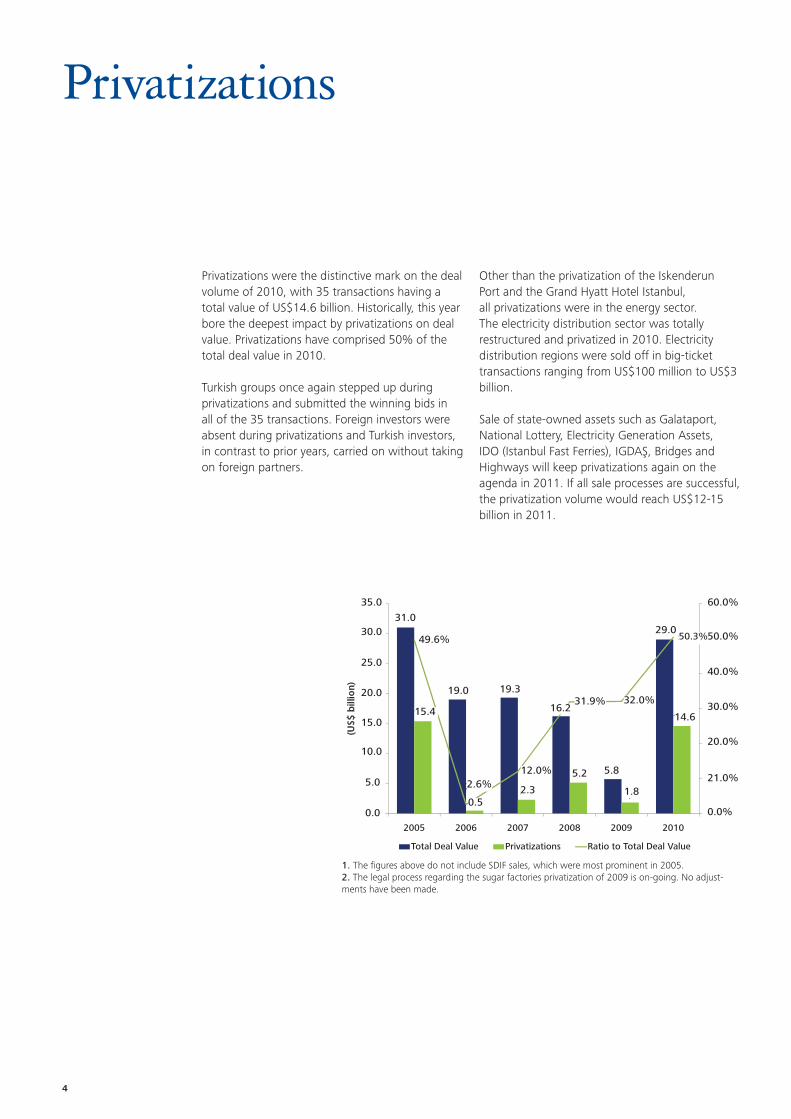

Privatizations

Privatizations were the distinctive mark on the deal volume of 2010, with 35 transactions having a total value of US$14.6 billion. Historically, this year bore the deepest impact by privatizations on deal value. Privatizations have comprised 50% of the total deal value in 2010.

Turkish groups once again stepped up during privatizations and submitted the winning bids in all of the 35 transactions. Foreign investors were absent during privatizations and Turkish investors, in contrast to prior years, carried on without taking on foreign partners.

Other than the privatization of the Iskenderun Port and the Grand Hyatt Hotel Istanbul, all privatizations were in the energy sector. The electricity distribution sector was totally restructured and privatized in 2010. Electricity distribution regions were sold off in big-ticket transactions ranging from US$100 million to US$3 billion.

Sale of state-owned assets such as Galataport, National Lottery, Electricity Generation Assets, IDO (Istanbul Fast Ferries), IGDAŞ, Bridges and Highways will keep privatizations again on the agenda in 2011. If all sale processes are successful, the privatization volume would reach US$12-15 billion in 2011.

31,0

19,0 19,3

16,2

29,0

15,4 14,6

49,6%

31,9% 32,0%

50,3%

30,0%

40,0%

50,0%

60,0%

15,0

20,0

25,0

30,0

35,0

(US$

bill

ion

)

5,8

0,52,3

5,2

1,82,6%

12,0%

0,0%

10,0%

20,0%

0,0

5,0

10,0

2005 2006 2007 2008 2009 2010

Total Deal Value Privatizations Ratio to Total Deal Value

1. The figures above do not include SDIF sales, which were most prominent in 2005.2. The legal process regarding the sugar factories privatization of 2009 is on-going. No adjust-ments have been made.

35.0

31.0

49.6%

19.0 19.331.9%

16.2

5.2

2.30.5

2.6%5.8

14.6

32.0%

60.0%

50.0%

40.0%

30.0%

20.0%

21.0%

0.0%

29.0

1.8

15.4

12.0%

30.0

25.0

20.0

15.0

5.0

0.0

10.0

50.3%

5

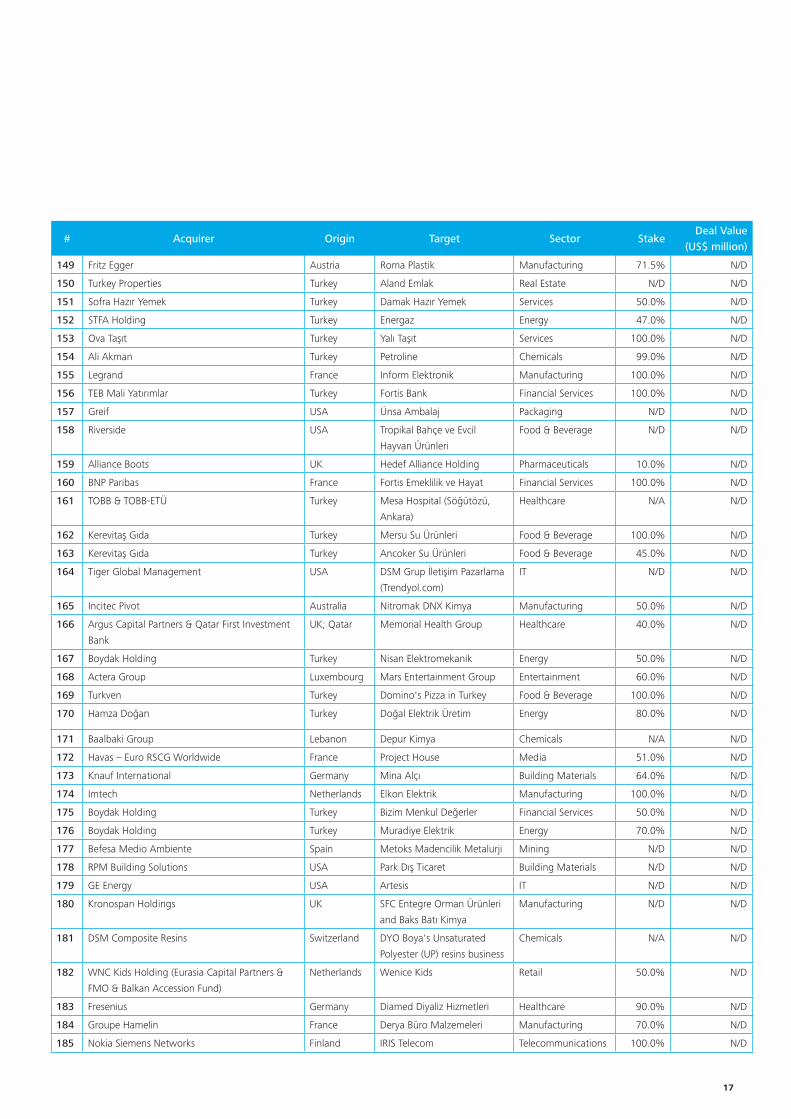

# Acquirer Origin Target Sector StakeDeal Value (US$ million)

1 İşkaya İnşaat San. & MMEKA Makine İthalat Turkey Boğaziçi Elektrik Dağıtım Energy 100.0% 2,990.0

2 Yıldızlar SSS Turkey Toroslar Elektrik Dağıtım Energy 100.0% 2,075.0

3 İşkaya İnşaat San. & MMEKA Makine İthalat Turkey Gediz Elektrik Dağıtım Energy 100.0% 1,920.0

4 MMEKA Makine İthalat Turkey İstanbul Anadolu Yakası Elektrik

Dağıtım (AYEDAŞ)

Energy 100.0% 1,813.0

5 MMEKA Makine İthalat Turkey Başkent Doğalgaz Energy 80.0% 1,211.0

6 Park Holding Turkey Akdeniz Elektrik Dağıtım Energy 100.0% 1,165.0

7 Limak Holding Turkey Uludağ Elektrik Dağıtım Energy 100.0% 940.0

8 Aksa Elektrik Turkey Trakya Elektrik Dağıtım Energy 100.0% 622.0

9 Limak Holding Turkey İskenderun Limanı Infrastructure N/A 372.0

10 Kolin İnşaat Turkey Çamlıbel Elektrik Dağıtım Energy 100.0% 258.5

11 Aksa Elektrik Turkey Fırat Elektrik Dağıtım Energy 100.0% 230.3

12 Karavil Dayanıklı Tüketim Malları & Ceylan İnşaat Turkey Dicle Elektrik Dağıtım Energy 100.0% 228.0

13 Doğuş Holding Turkey Grand Hyatt Istanbul Tourism 100.0% 136.8

14 Aksa Elektrik Turkey Vangölü Elektrik Dağıtım Energy 100.0% 100.1

15 Fırat Enerji Üretim Turkey EÜAŞ Portfolio 7 Energy 100.0% 86.4

16 Kayseri ve Civarı Elektrik Turkey EÜAŞ Portfolio 10 Energy 100.0% 69.7

17 Aksu Enerji Turkey EÜAŞ Portfolio 4 Energy 100.0% 56.1

18 Nema Kimya-Espe Consortium Turkey EÜAŞ Portfolio 18 Energy 100.0% 50.1

19 Yiğitler Enerji Turkey Aydın-Pamukören Jeotermal

Sahası

Energy N/A 48.8

20 Nas Enerji Turkey EÜAŞ Portfolio 16 Energy 100.0% 40.8

21 Boydak Enerji Turkey EÜAŞ Portfolio 14 Energy 100.0% 29.1

22 Çelikler İnşaat Turkey Aydın-Sultanhisar Jeotermal

Sahası

Energy N/A 25.6

23 Erdem Consortium (Kipaş Mensucat) Turkey Aydın-Nazilli Jeotermal Sahası Energy N/A 20.5

24 Nema Kimya-Espe Consortium Turkey EÜAŞ Portfolio 3 Energy 100.0% 17.4

25 Kisan İnşaat Turkey EÜAŞ Portfolio 19 Energy 100.0% 14.7

26 Kayseri ve Civarı Elektrik Turkey EÜAŞ Portfolio 13 Energy 100.0% 13.8

27 Seba Consortium Turkey EÜAŞ Portfolio 6 Energy 100.0% 13.5

28 İvme Elektromekanik Turkey EÜAŞ Portfolio 9 Energy 100.0% 7.6

29 Ka-Fnih Enerji Turkey EÜAŞ Portfolio 11 Energy 100.0% 7.0

30 Kent Solar Elektrik Turkey EÜAŞ Portfolio 1 Energy 100.0% 6.6

31 Demistaş Doğu Elektrik Turkey EÜAŞ Portfolio 15 Energy 100.0% 6.6

32 Er-Bu İnşaat Turkey EÜAŞ Portfolio 17 Energy 100.0% 6.4

33 Sarar Giyim Turkey EÜAŞ Portfolio 2 Energy 100.0% 5.8

34 Seba Consortium Turkey EÜAŞ Portfolio 8 Energy 100.0% 5.7

35 Fides Reklam Enerji Turkey EÜAŞ Portfolio 5 Energy 100.0% 2.8

Total 14,596.5

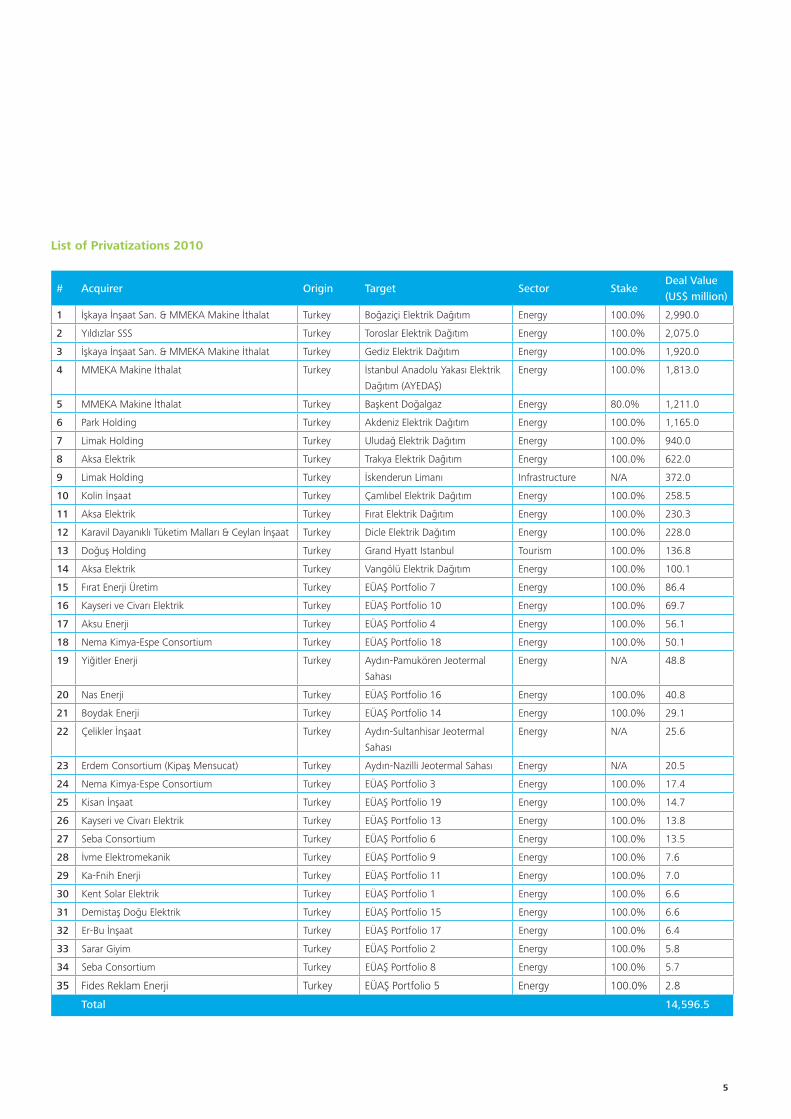

List of Privatizations 2010

6

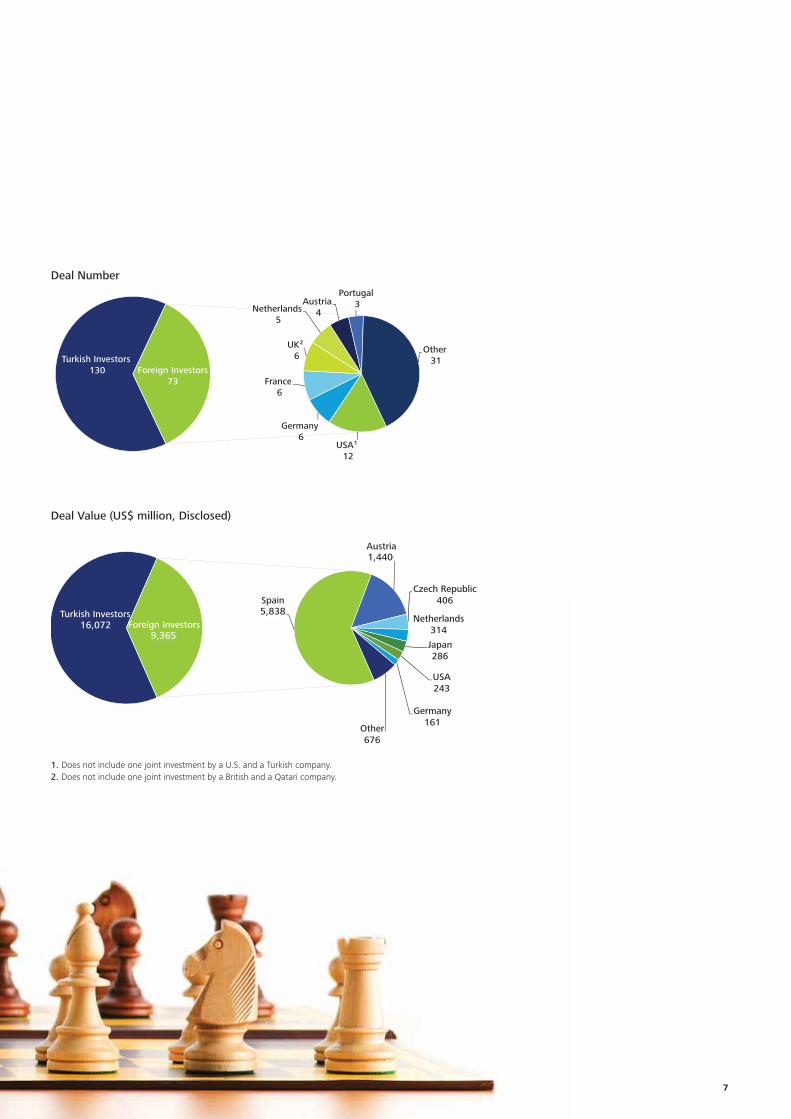

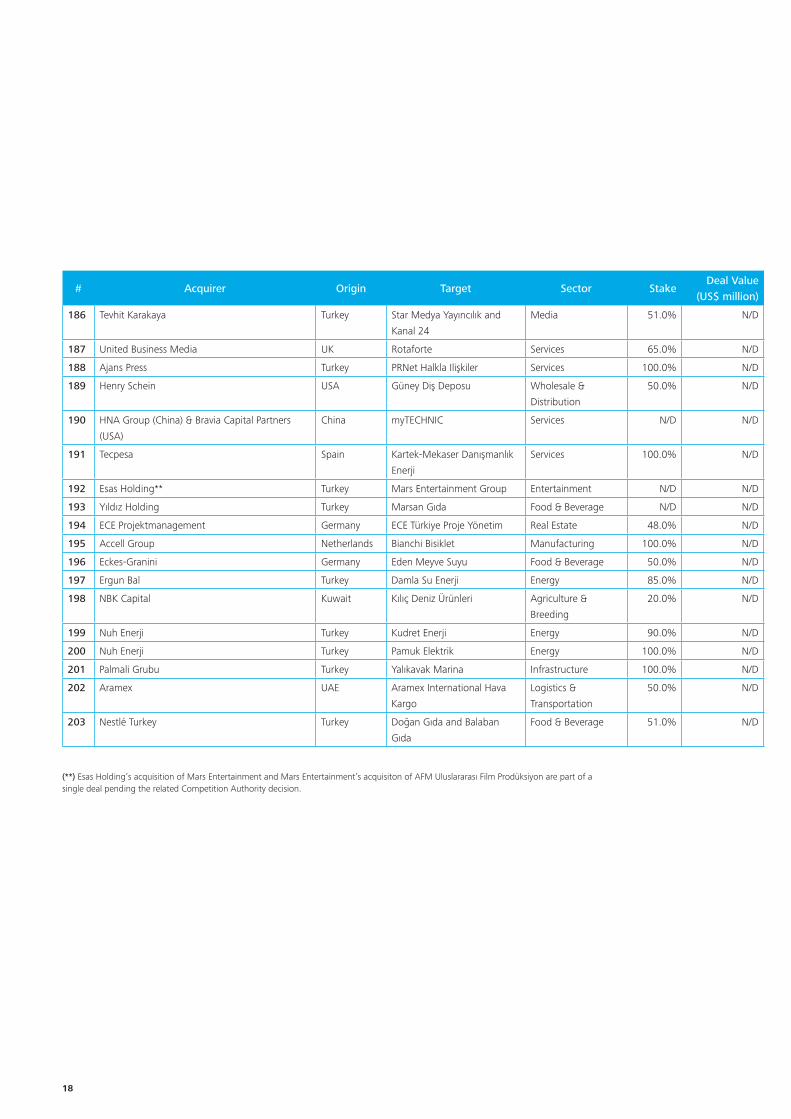

Investor origin

While foreign investors’ interest towards Turkey has gradually increased over the past decade, Turkish investors have truly warmed up to M&A as well. Foreign investors generated a deal volume of c. US$10.5 billion (including estimates) through 73 deals. Foreign investors’ contribution to the total deal volume, which declined in 2009, was low again in 2010 with a level of 36%. The causes of this drop are twofold: Firstly, the global financial crisis hit EU member countries, who are historically the most active buyers in Turkey, relatively harder. Secondly, Turkish investors’ interest towards sizable privatizations was intense. Excluding privatizations, foreign investors’ share in the remaining deal volume was still above 70%, which signals a recovery in their interest in Turkey.

Fervent Turkish investors materialized their new-found fondness of M&A in 2010. Against foreign investors’ 73 transactions in 2010, Turkish investors made 130 acquisitions worth c. US$18.4 billion, including estimates for deals with undisclosed values, US$14.6 billion of which came from privatizations.

45 deals by European investors amounted to a total value of US$9.2 billion (including estimates), thereby comprising 88% of foreign investors’ deal value. Investors from USA, who previously struggled with problems at home, seemed to be in better spirits and re-focused on investing overseas as they concluded the year with 13 deals. On the other hand, the Gulf region completed 9 transactions, half of which were financial investments into the healthcare, food & beverage and breeding sectors. BBVA’s acquisiton of Garanti Bank was the largest deal by a foreign investor, as well as the largest of 2010. Additionally, there were foreign investors who increased their stakes in Turkish subsidiaries (6 deals), as well as a few who sold their stakes and left Turkey (only 3 deals).

7

Turkish Investors130

France

UK²6

Netherlands5

Austria4

Portugal3

Other31

Foreign Investors73

USA¹12

Germany6

France6

73

Turkish Investors16.072

Spain5.838

Austria1.440

Czech Republic406

Netherlands314

Japan286

Foreign Investors9.365

286

USA243

Germany161

Other676

Deal Number

Deal Value (US$ million, Disclosed)

1. Does not include one joint investment by a U.S. and a Turkish company.2. Does not include one joint investment by a British and a Qatari company.

5,838

1,440

9,36516,072

8

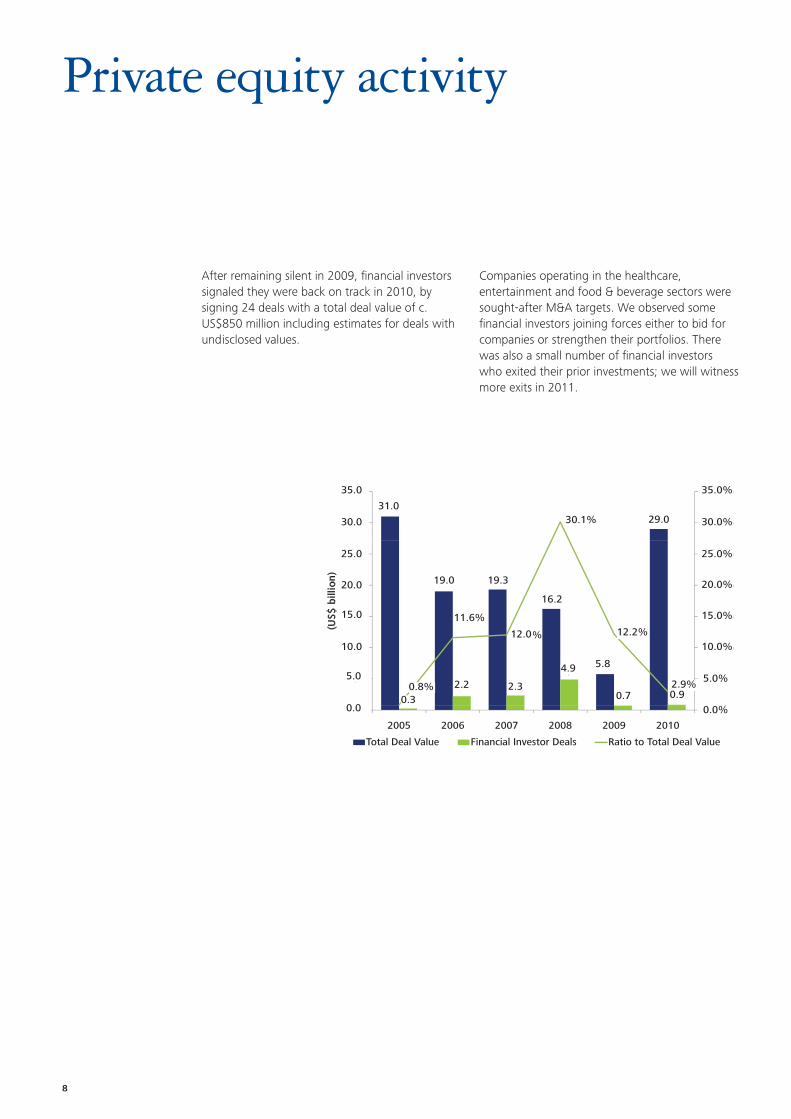

Private equity activity

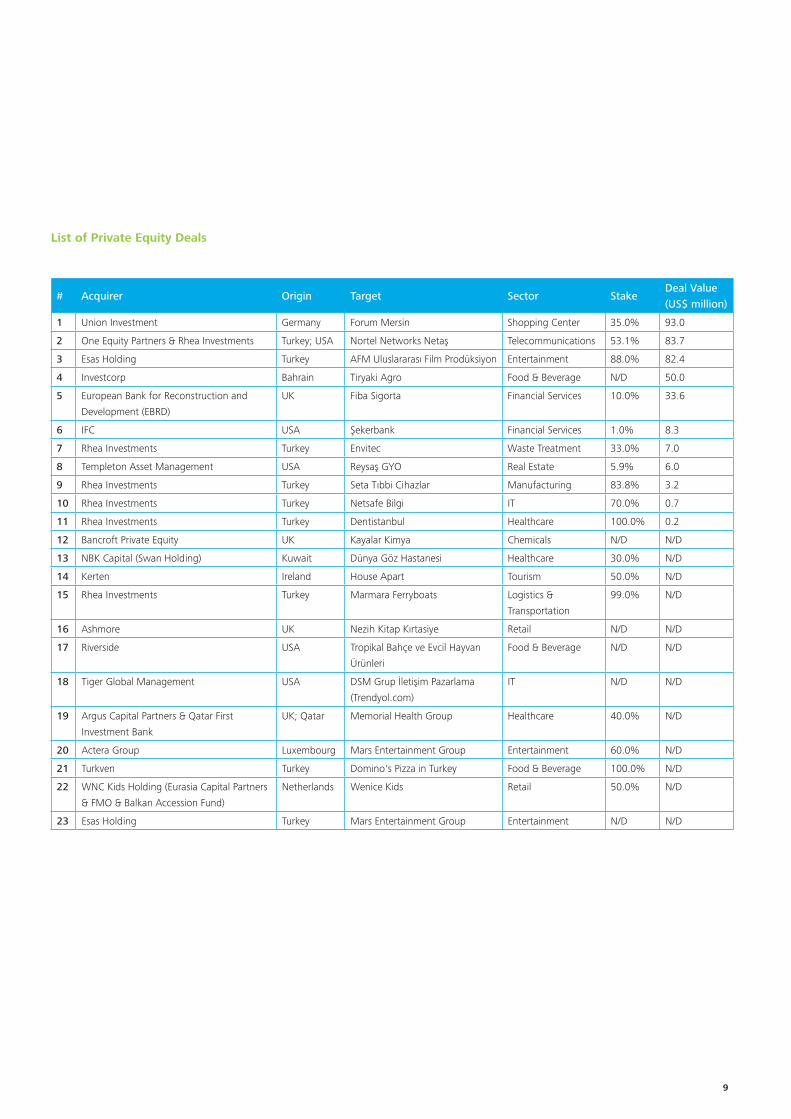

After remaining silent in 2009, financial investors signaled they were back on track in 2010, by signing 24 deals with a total deal value of c. US$850 million including estimates for deals with undisclosed values.

Companies operating in the healthcare, entertainment and food & beverage sectors were sought-after M&A targets. We observed some financial investors joining forces either to bid for companies or strengthen their portfolios. There was also a small number of financial investors who exited their prior investments; we will witness more exits in 2011.

35,0%35,0

31,029,030,1% 30,0%30,0

19 0 19 3 20 0%

25,0%

20 0

25,0

on

)

19,0 19,3

16,2

11,6% 15,0%

20,0%

15,0

20,0

US$

bill

io

5 8

12,0% 12,2%10,0%10,0

(U

5,8

0,32,2 2,3

4,9

0,7 0,90,8% 2,9%

5,0%5,0

0,0%0,0

2005 2006 2007 2008 2009 2010

Total Deal Value Financial Investor Deals Ratio to Total Deal Value

35.0

31.0

19.0

2.3

4.9 5.8

0.72.9%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

29.030.1%

12.2%

0.9

19.3

16.2

12.0

11.6%

2.20.8%0.3

30.0

25.0

20.0

15.0

5.0

0.0

10.0

9

# Acquirer Origin Target Sector StakeDeal Value (US$ million)

1 Union Investment Germany Forum Mersin Shopping Center 35.0% 93.0

2 One Equity Partners & Rhea Investments Turkey; USA Nortel Networks Netaş Telecommunications 53.1% 83.7

3 Esas Holding Turkey AFM Uluslararası Film Prodüksiyon Entertainment 88.0% 82.4

4 Investcorp Bahrain Tiryaki Agro Food & Beverage N/D 50.0

5 European Bank for Reconstruction and

Development (EBRD)

UK Fiba Sigorta Financial Services 10.0% 33.6

6 IFC USA Şekerbank Financial Services 1.0% 8.3

7 Rhea Investments Turkey Envitec Waste Treatment 33.0% 7.0

8 Templeton Asset Management USA Reysaş GYO Real Estate 5.9% 6.0

9 Rhea Investments Turkey Seta Tıbbi Cihazlar Manufacturing 83.8% 3.2

10 Rhea Investments Turkey Netsafe Bilgi IT 70.0% 0.7

11 Rhea Investments Turkey Dentistanbul Healthcare 100.0% 0.2

12 Bancroft Private Equity UK Kayalar Kimya Chemicals N/D N/D

13 NBK Capital (Swan Holding) Kuwait Dünya Göz Hastanesi Healthcare 30.0% N/D

14 Kerten Ireland House Apart Tourism 50.0% N/D

15 Rhea Investments Turkey Marmara Ferryboats Logistics &

Transportation

99.0% N/D

16 Ashmore UK Nezih Kitap Kırtasiye Retail N/D N/D

17 Riverside USA Tropikal Bahçe ve Evcil Hayvan

Ürünleri

Food & Beverage N/D N/D

18 Tiger Global Management USA DSM Grup İletişim Pazarlama

(Trendyol.com)

IT N/D N/D

19 Argus Capital Partners & Qatar First

Investment Bank

UK; Qatar Memorial Health Group Healthcare 40.0% N/D

20 Actera Group Luxembourg Mars Entertainment Group Entertainment 60.0% N/D

21 Turkven Turkey Domino's Pizza in Turkey Food & Beverage 100.0% N/D

22 WNC Kids Holding (Eurasia Capital Partners

& FMO & Balkan Accession Fund)

Netherlands Wenice Kids Retail 50.0% N/D

23 Esas Holding Turkey Mars Entertainment Group Entertainment N/D N/D

List of Private Equity Deals

10

Deal rankings

The largest 5 deals made up c. 51% of the total deal volume in 2010, and the top 10 deals accounted for 69% of the total volume. Privatizations stole the spotlight in the top deals list. As the largest private sector deal, BBVA’s acquisiton of Garanti Bank made up 20% of total deal value in 2010.

Average deal size in 2010 was c. US$140 million (c. US$55 million in 2009). Excluding privatizations and the Garanti Bank deal, the average deal size of the remainder fell to US$50 million (c. US$35 million in 2009), indicating that mid-cap segment deals continue to dominate the Turkish M&A scene. On the other hand, valuations have shown signs of recovery and signal a return to pre-crisis levels in 2011.

Acquirer Target Stake AcquiredDeal Value(US$ million)

Banco Bilbao Vizcaya Argentaria Türkiye Garanti Bankası 24.9% 5,837.8

İşkaya İnşaat San. & MMEKA Makine İthalat

Boğaziçi Elektrik Dağıtım 100.0% 2,990.0

Yıldızlar SSS Toroslar Elektrik Dağıtım 100.0% 2,075.0

İşkaya İnşaat San. & MMEKA Makine İthalat

Gediz Elektrik Dağıtım 100.0% 1,920.0

MMEKA Makine İthalat İstanbul Anadolu Yakası Elektrik Dağıtım (AYEDAŞ)

100.0% 1,813.0

Top 5 Deals

11

Sectoral overview

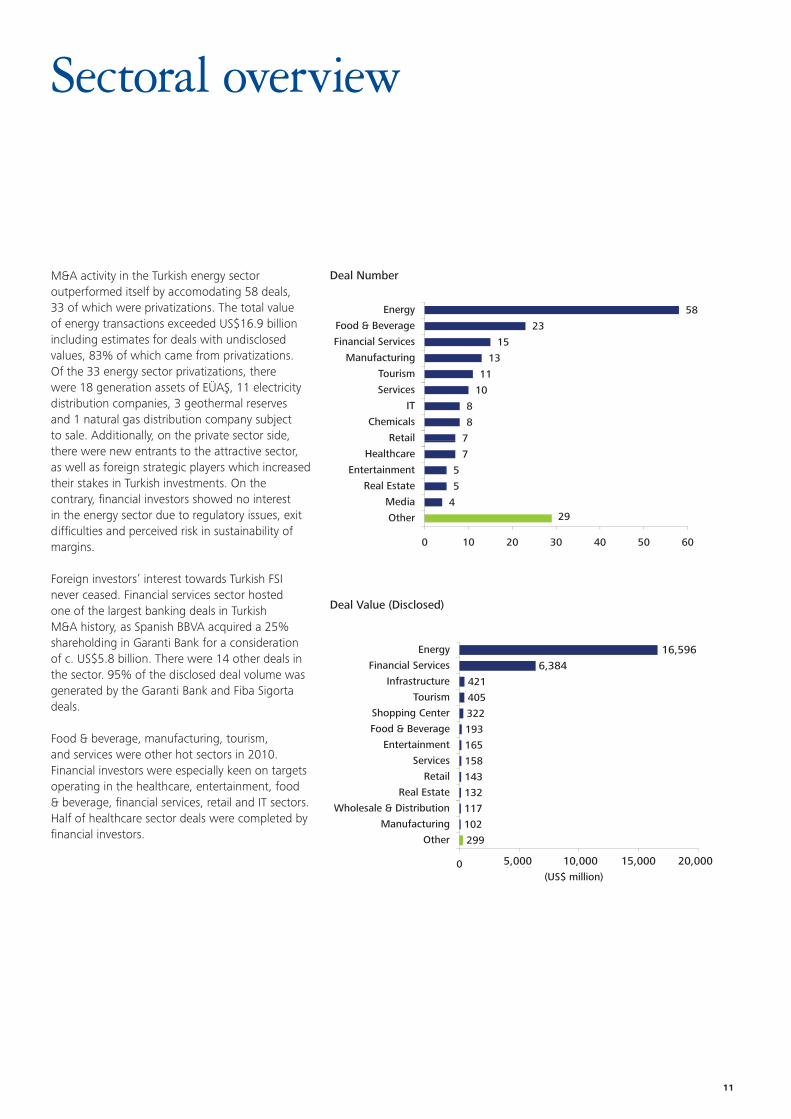

M&A activity in the Turkish energy sector outperformed itself by accomodating 58 deals, 33 of which were privatizations. The total value of energy transactions exceeded US$16.9 billion including estimates for deals with undisclosed values, 83% of which came from privatizations. Of the 33 energy sector privatizations, there were 18 generation assets of EÜAŞ, 11 electricity distribution companies, 3 geothermal reserves and 1 natural gas distribution company subject to sale. Additionally, on the private sector side, there were new entrants to the attractive sector, as well as foreign strategic players which increased their stakes in Turkish investments. On the contrary, financial investors showed no interest in the energy sector due to regulatory issues, exit difficulties and perceived risk in sustainability of margins.

Foreign investors’ interest towards Turkish FSI never ceased. Financial services sector hosted one of the largest banking deals in Turkish M&A history, as Spanish BBVA acquired a 25% shareholding in Garanti Bank for a consideration of c. US$5.8 billion. There were 14 other deals in the sector. 95% of the disclosed deal volume was generated by the Garanti Bank and Fiba Sigorta deals.

Food & beverage, manufacturing, tourism, and services were other hot sectors in 2010. Financial investors were especially keen on targets operating in the healthcare, entertainment, food & beverage, financial services, retail and IT sectors. Half of healthcare sector deals were completed by financial investors.

Deal Number

Deal Value (Disclosed)

7

8

8

10

11

13

15

23

58

Retail

Chemicals

IT

Services

Tourism

Manufacturing

Financial Services

Food & Beverage

Energy

29 4

5

5

7

7

0 10 20 30 40 50 60

Other

Media

Real Estate

Entertainment

Healthcare

Retail

143

158

165

193

322

405

421

6.384

16.596

Retail

Services

Entertainment

Food & Beverage

Shopping Center

Tourism

Infrastructure

Financial Services

Energy

299

102

117

132

0 5.000 10.000 15.000 20.000

Other

Manufacturing

Wholesale & Distribution

Real Estate

(US$ million)

5,000

6,38416,596

10,000 15,000 20,000

12

Prospects

As foreseen in last year’s review, 2010 was indeed a year of gradual recovery in the financial markets. Domestic and foreign investors, as well as Turkish sellers were able to act more confidently as their perception regarding the future was altered for the better.

As 2011 begins, we observe that all investors have begun to view Turkey as a country they must invest in, rather than a country they consider investment-worthy. Today, for the first time, the upcoming general election is not perceived as a potential risk by investors. While investors foster a heart-felt belief in the growth potential of Turkey; they also closely monitor macro indicators such as the current account deficit, budget deficit, per capita borrowing and the value of the Turkish Lira. Expectations regarding the economy and the credit rating upgrade are also positive influences, supporting investors’ perception. As a result of all, we expect a high volume of M&A in 2011.

Nonetheless, given a successful privatization program in 2011, a significant portion of the deal volume in 2011 would come from privatizations again. State-owned assets such as IDO (Istanbul Fast Ferries), IGDAŞ, Electricity Generation Assets, Sugar Factories, Bridges and Highways, Galataport and National Lottery are all subject to sale.

Foreign investors’ appetite towards Turkey is expected to increase in 2011, leading them to re-claim a higher stake in the deal volume.

Energy, healthcare, pharmaceuticals, retail, media, education and automotive parts will be sectors hosting significant activity.

Private equity firms will invest much more in 2011. Furthermore, we will see more exits.

The investment enthusiasm towards Turkey will hike up valuations, driving multiples back to pre-crisis levels.

Provided that privatizations are run successfully, we expect the deal volume in 2011 to exceed the US$20 billion level.

13

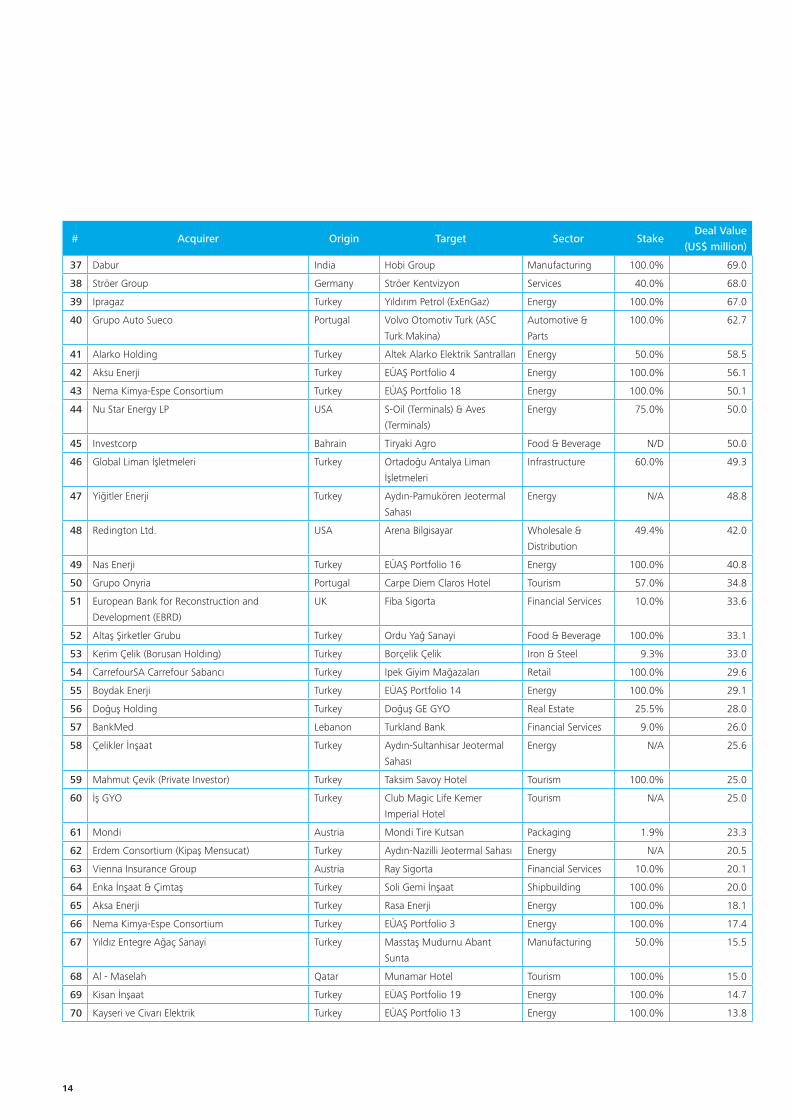

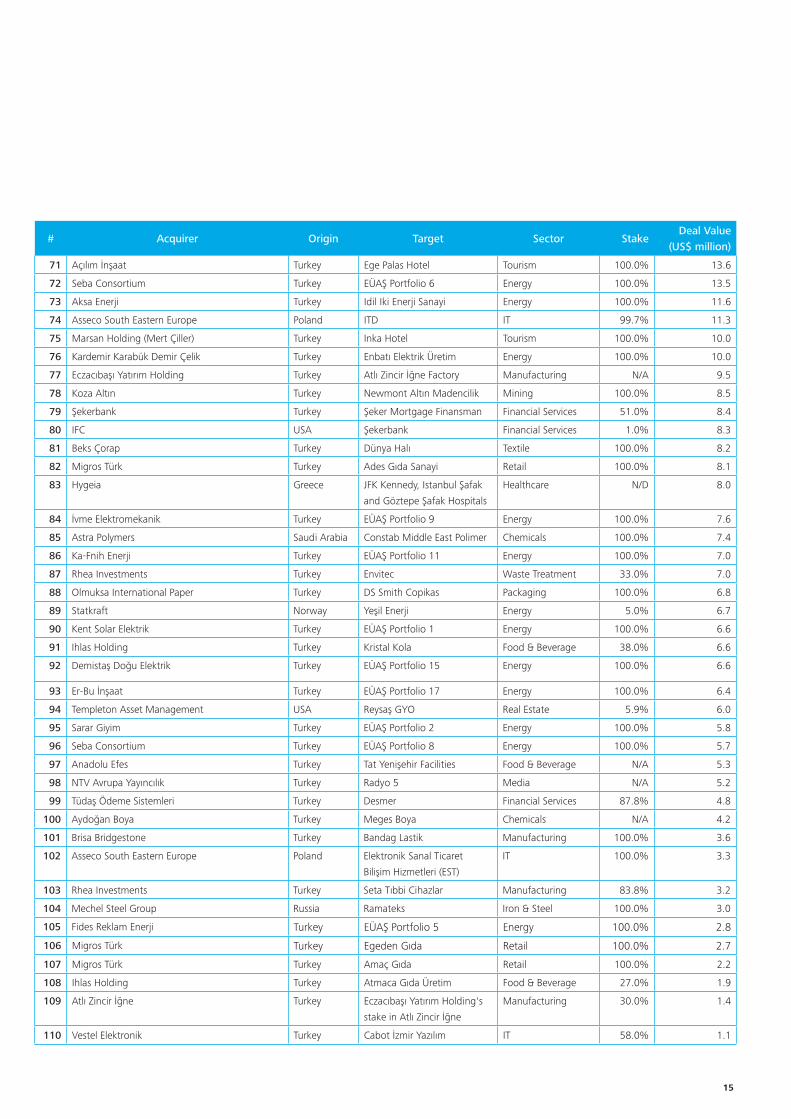

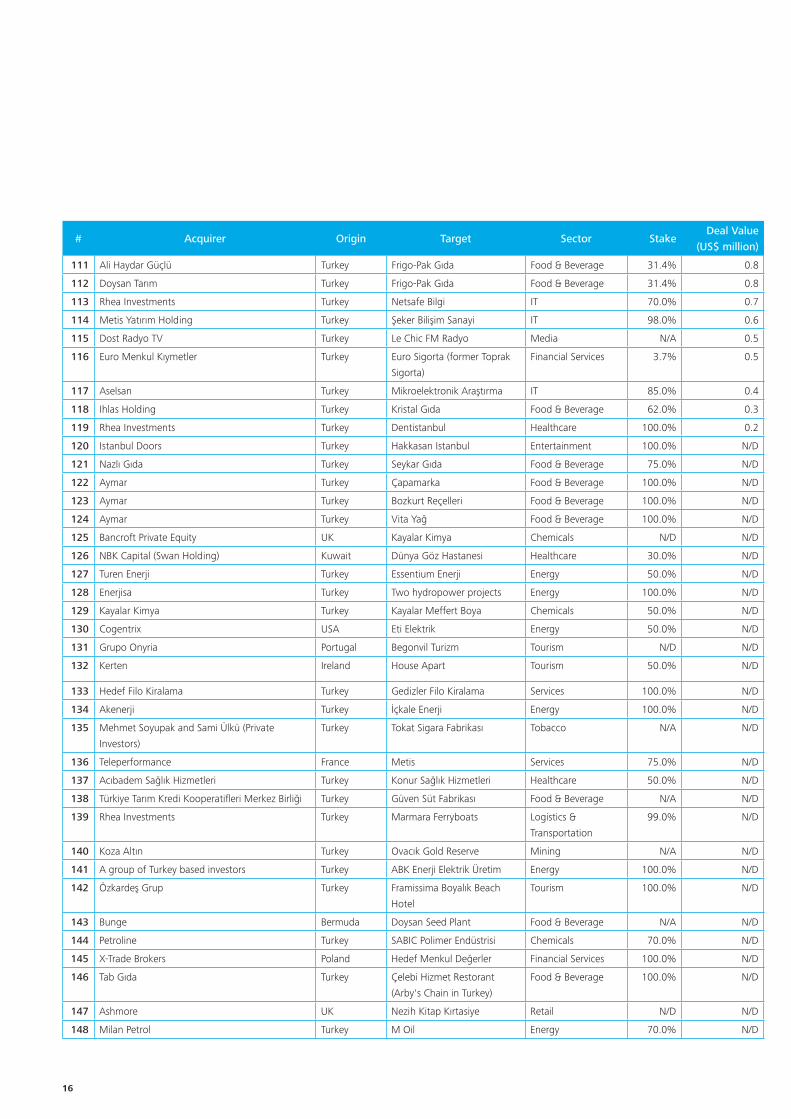

Deal list (January 1 – December 31)

# Acquirer Origin Target Sector StakeDeal Value

(US$ million)

1 Banco Bilbao Vizcaya Argentaria Spain Türkiye Garanti Bankası Financial Services 24.9% 5,837.8

2 İşkaya İnşaat San. & MMEKA Makine İthalat* Turkey Boğaziçi Elektrik Dağıtım Energy 100.0% 2,990.0

3 Yıldızlar SSS Turkey Toroslar Elektrik Dağıtım Energy 100.0% 2,075.0

4 İşkaya İnşaat San. & MMEKA Makine İthalat* Turkey Gediz Elektrik Dağıtım Energy 100.0% 1,920.0

5 MMEKA Makine İthalat Turkey İstanbul Anadolu Yakası

Elektrik Dağıtım (AYEDAŞ)

Energy 100.0% 1,813.0

6 OMV Austria Petrol Ofisi Energy 54.2% 1,397.1

7 MMEKA Makine İthalat Turkey Başkent Doğalgaz Energy 80.0% 1,211.0

8 Park Holding Turkey Akdeniz Elektrik Dağıtım Energy 100.0% 1,165.0

9 Limak Holding Turkey Uludağ Elektrik Dağıtım Energy 100.0% 940.0

10 Aksa Elektrik* Turkey Trakya Elektrik Dağıtım Energy 100.0% 622.0

11 Energo-Pro Czech

Republic

Aralık HEPP, Hamzalı HEPP &

Reşadiye Cascade

Energy 100.0% 405.9

12 Limak Holding Turkey İskenderun Limanı Infrastructure N/A 372.0

13 Sompo Japan Insurance Japan Fiba Sigorta Financial Services 93.4% 286.4

14 Kolin İnşaat Turkey Çamlıbel Elektrik Dağıtım Energy 100.0% 258.5

15 SGM Enerji Turkey Bis Enerji Energy 50.0% 250.0

16 Aksa Elektrik Turkey Fırat Elektrik Dağıtım Energy 100.0% 230.3

17 Corio Netherlands Bursa Anatolium Shopping Center 100.0% 229.0

18 Karavil Dayanıklı Tüketim Malları & Ceylan İnşaat Turkey Dicle Elektrik Dağıtım Energy 100.0% 228.0

19 Turk Tur Turkey Marmaris Imperial, Bodrum

Imperial and Belek Waterworld

Tourism N/A 145.0

20 Doğuş Holding Turkey Grand Hyatt Istanbul Tourism 100.0% 136.8

21 AES USA Entek Elektrik Energy 49.6% 136.5

22 Kamil Engin Yeşil Turkey Ceylan Giyim Retail 92.0% 100.8

23 Aksa Elektrik Turkey Vangölü Elektrik Dağıtım Energy 100.0% 100.1

24 Akfen Holding Turkey Akfen GYO Real Estate 32.5% 97.8

25 TransAtlantic Worldwide Canada Zorlu Petrogas and Amity Oil

International

Energy 100.0% 96.5

26 Dosu Maya Turkey Akmaya Food & Beverage 100.0% 94.0

27 Union Investment Germany Forum Mersin Shopping Center 35.0% 93.0

28 Groupe Cheque Dejeuner France Multinet Kurumsal Hizmetler Services 100.0% 90.0

29 Fırat Enerji Üretim Turkey EÜAŞ Portfolio 7 Energy 100.0% 86.4

30 Credit Europe Bank N.V. Netherlands Millenium Bank Financial Services 95.0% 85.0

31 One Equity Partners & Rhea Investments Turkey; USA Nortel Networks Netaş Telecommunications 53.1% 83.7

32 Esas Holding Turkey AFM Uluslararası Film

Prodüksiyon

Entertainment 88.0% 82.4

33 Mars Entertainment Group** Turkey AFM Uluslararası Film

Prodüksiyon

Entertainment 88.0% 82.4

34 Luxottica Group Italy Luxottica Gözlük Wholesale &

Distribution

35.2% 75.3

35 Fortis Finansal Kiralama Turkey TEB Finansal Kiralama Financial Services 90.0% 72.9

36 Kayseri ve Civarı Elektrik Turkey EÜAŞ Portfolio 10 Energy 100.0% 69.7

(*) The acquirer might change in either one of the Boğaziçi, Gediz and Trakya electricity distribution privatizations pending the related Competition Authority decision.(**) Esas Holding’s acquisition of Mars Entertainment and Mars Entertainment’s acquisiton of AFM Uluslararası Film Prodüksiyon are part of a single deal pending the related Competition Authority decision.

14

# Acquirer Origin Target Sector StakeDeal Value

(US$ million)

37 Dabur India Hobi Group Manufacturing 100.0% 69.0

38 Ströer Group Germany Ströer Kentvizyon Services 40.0% 68.0

39 Ipragaz Turkey Yıldırım Petrol (ExEnGaz) Energy 100.0% 67.0

40 Grupo Auto Sueco Portugal Volvo Otomotiv Turk (ASC

Turk Makina)

Automotive &

Parts

100.0% 62.7

41 Alarko Holding Turkey Altek Alarko Elektrik Santralları Energy 50.0% 58.5

42 Aksu Enerji Turkey EÜAŞ Portfolio 4 Energy 100.0% 56.1

43 Nema Kimya-Espe Consortium Turkey EÜAŞ Portfolio 18 Energy 100.0% 50.1

44 Nu Star Energy LP USA S-Oil (Terminals) & Aves

(Terminals)

Energy 75.0% 50.0

45 Investcorp Bahrain Tiryaki Agro Food & Beverage N/D 50.0

46 Global Liman İşletmeleri Turkey Ortadoğu Antalya Liman

İşletmeleri

Infrastructure 60.0% 49.3

47 Yiğitler Enerji Turkey Aydın-Pamukören Jeotermal

Sahası

Energy N/A 48.8

48 Redington Ltd. USA Arena Bilgisayar Wholesale &

Distribution

49.4% 42.0

49 Nas Enerji Turkey EÜAŞ Portfolio 16 Energy 100.0% 40.8

50 Grupo Onyria Portugal Carpe Diem Claros Hotel Tourism 57.0% 34.8

51 European Bank for Reconstruction and

Development (EBRD)

UK Fiba Sigorta Financial Services 10.0% 33.6

52 Altaş Şirketler Grubu Turkey Ordu Yağ Sanayi Food & Beverage 100.0% 33.1

53 Kerim Çelik (Borusan Holding) Turkey Borçelik Çelik Iron & Steel 9.3% 33.0

54 CarrefourSA Carrefour Sabancı Turkey Ipek Giyim Mağazaları Retail 100.0% 29.6

55 Boydak Enerji Turkey EÜAŞ Portfolio 14 Energy 100.0% 29.1

56 Doğuş Holding Turkey Doğuş GE GYO Real Estate 25.5% 28.0

57 BankMed Lebanon Turkland Bank Financial Services 9.0% 26.0

58 Çelikler İnşaat Turkey Aydın-Sultanhisar Jeotermal

Sahası

Energy N/A 25.6

59 Mahmut Çevik (Private Investor) Turkey Taksim Savoy Hotel Tourism 100.0% 25.0

60 İş GYO Turkey Club Magic Life Kemer

Imperial Hotel

Tourism N/A 25.0

61 Mondi Austria Mondi Tire Kutsan Packaging 1.9% 23.3

62 Erdem Consortium (Kipaş Mensucat) Turkey Aydın-Nazilli Jeotermal Sahası Energy N/A 20.5

63 Vienna Insurance Group Austria Ray Sigorta Financial Services 10.0% 20.1

64 Enka İnşaat & Çimtaş Turkey Soli Gemi İnşaat Shipbuilding 100.0% 20.0

65 Aksa Enerji Turkey Rasa Enerji Energy 100.0% 18.1

66 Nema Kimya-Espe Consortium Turkey EÜAŞ Portfolio 3 Energy 100.0% 17.4

67 Yıldız Entegre Ağaç Sanayi Turkey Masstaş Mudurnu Abant

Sunta

Manufacturing 50.0% 15.5

68 Al - Maselah Qatar Munamar Hotel Tourism 100.0% 15.0

69 Kisan İnşaat Turkey EÜAŞ Portfolio 19 Energy 100.0% 14.7

70 Kayseri ve Civarı Elektrik Turkey EÜAŞ Portfolio 13 Energy 100.0% 13.8

15

# Acquirer Origin Target Sector StakeDeal Value

(US$ million)

71 Açılım İnşaat Turkey Ege Palas Hotel Tourism 100.0% 13.6

72 Seba Consortium Turkey EÜAŞ Portfolio 6 Energy 100.0% 13.5

73 Aksa Enerji Turkey Idil Iki Enerji Sanayi Energy 100.0% 11.6

74 Asseco South Eastern Europe Poland ITD IT 99.7% 11.3

75 Marsan Holding (Mert Çiller) Turkey Inka Hotel Tourism 100.0% 10.0

76 Kardemir Karabük Demir Çelik Turkey Enbatı Elektrik Üretim Energy 100.0% 10.0

77 Eczacıbaşı Yatırım Holding Turkey Atlı Zincir İğne Factory Manufacturing N/A 9.5

78 Koza Altın Turkey Newmont Altın Madencilik Mining 100.0% 8.5

79 Şekerbank Turkey Şeker Mortgage Finansman Financial Services 51.0% 8.4

80 IFC USA Şekerbank Financial Services 1.0% 8.3

81 Beks Çorap Turkey Dünya Halı Textile 100.0% 8.2

82 Migros Türk Turkey Ades Gıda Sanayi Retail 100.0% 8.1

83 Hygeia Greece JFK Kennedy, Istanbul Şafak

and Göztepe Şafak Hospitals

Healthcare N/D 8.0

84 İvme Elektromekanik Turkey EÜAŞ Portfolio 9 Energy 100.0% 7.6

85 Astra Polymers Saudi Arabia Constab Middle East Polimer Chemicals 100.0% 7.4

86 Ka-Fnih Enerji Turkey EÜAŞ Portfolio 11 Energy 100.0% 7.0

87 Rhea Investments Turkey Envitec Waste Treatment 33.0% 7.0

88 Olmuksa International Paper Turkey DS Smith Copikas Packaging 100.0% 6.8

89 Statkraft Norway Yeşil Enerji Energy 5.0% 6.7

90 Kent Solar Elektrik Turkey EÜAŞ Portfolio 1 Energy 100.0% 6.6

91 Ihlas Holding Turkey Kristal Kola Food & Beverage 38.0% 6.6

92 Demistaş Doğu Elektrik Turkey EÜAŞ Portfolio 15 Energy 100.0% 6.6

93 Er-Bu İnşaat Turkey EÜAŞ Portfolio 17 Energy 100.0% 6.4

94 Templeton Asset Management USA Reysaş GYO Real Estate 5.9% 6.0

95 Sarar Giyim Turkey EÜAŞ Portfolio 2 Energy 100.0% 5.8

96 Seba Consortium Turkey EÜAŞ Portfolio 8 Energy 100.0% 5.7

97 Anadolu Efes Turkey Tat Yenişehir Facilities Food & Beverage N/A 5.3

98 NTV Avrupa Yayıncılık Turkey Radyo 5 Media N/A 5.2

99 Tüdaş Ödeme Sistemleri Turkey Desmer Financial Services 87.8% 4.8

100 Aydoğan Boya Turkey Meges Boya Chemicals N/A 4.2

101 Brisa Bridgestone Turkey Bandag Lastik Manufacturing 100.0% 3.6

102 Asseco South Eastern Europe Poland Elektronik Sanal Ticaret

Bilişim Hizmetleri (EST)

IT 100.0% 3.3

103 Rhea Investments Turkey Seta Tıbbi Cihazlar Manufacturing 83.8% 3.2

104 Mechel Steel Group Russia Ramateks Iron & Steel 100.0% 3.0

105 Fides Reklam Enerji Turkey EÜAŞ Portfolio 5 Energy 100.0% 2.8

106 Migros Türk Turkey Egeden Gıda Retail 100.0% 2.7

107 Migros Türk Turkey Amaç Gıda Retail 100.0% 2.2

108 Ihlas Holding Turkey Atmaca Gıda Üretim Food & Beverage 27.0% 1.9

109 Atlı Zincir İğne Turkey Eczacıbaşı Yatırım Holding's

stake in Atlı Zincir İğne

Manufacturing 30.0% 1.4

110 Vestel Elektronik Turkey Cabot İzmir Yazılım IT 58.0% 1.1

16

# Acquirer Origin Target Sector StakeDeal Value

(US$ million)

111 Ali Haydar Güçlü Turkey Frigo-Pak Gıda Food & Beverage 31.4% 0.8

112 Doysan Tarım Turkey Frigo-Pak Gıda Food & Beverage 31.4% 0.8

113 Rhea Investments Turkey Netsafe Bilgi IT 70.0% 0.7

114 Metis Yatırım Holding Turkey Şeker Bilişim Sanayi IT 98.0% 0.6

115 Dost Radyo TV Turkey Le Chic FM Radyo Media N/A 0.5

116 Euro Menkul Kıymetler Turkey Euro Sigorta (former Toprak

Sigorta)

Financial Services 3.7% 0.5

117 Aselsan Turkey Mikroelektronik Araştırma IT 85.0% 0.4

118 Ihlas Holding Turkey Kristal Gıda Food & Beverage 62.0% 0.3

119 Rhea Investments Turkey Dentistanbul Healthcare 100.0% 0.2

120 Istanbul Doors Turkey Hakkasan Istanbul Entertainment 100.0% N/D

121 Nazlı Gıda Turkey Seykar Gıda Food & Beverage 75.0% N/D

122 Aymar Turkey Çapamarka Food & Beverage 100.0% N/D

123 Aymar Turkey Bozkurt Reçelleri Food & Beverage 100.0% N/D

124 Aymar Turkey Vita Yağ Food & Beverage 100.0% N/D

125 Bancroft Private Equity UK Kayalar Kimya Chemicals N/D N/D

126 NBK Capital (Swan Holding) Kuwait Dünya Göz Hastanesi Healthcare 30.0% N/D

127 Turen Enerji Turkey Essentium Enerji Energy 50.0% N/D

128 Enerjisa Turkey Two hydropower projects Energy 100.0% N/D

129 Kayalar Kimya Turkey Kayalar Meffert Boya Chemicals 50.0% N/D

130 Cogentrix USA Eti Elektrik Energy 50.0% N/D

131 Grupo Onyria Portugal Begonvil Turizm Tourism N/D N/D

132 Kerten Ireland House Apart Tourism 50.0% N/D

133 Hedef Filo Kiralama Turkey Gedizler Filo Kiralama Services 100.0% N/D

134 Akenerji Turkey İçkale Enerji Energy 100.0% N/D

135 Mehmet Soyupak and Sami Ülkü (Private

Investors)

Turkey Tokat Sigara Fabrikası Tobacco N/A N/D

136 Teleperformance France Metis Services 75.0% N/D

137 Acıbadem Sağlık Hizmetleri Turkey Konur Sağlık Hizmetleri Healthcare 50.0% N/D

138 Türkiye Tarım Kredi Kooperatifleri Merkez Birliği Turkey Güven Süt Fabrikası Food & Beverage N/A N/D

139 Rhea Investments Turkey Marmara Ferryboats Logistics &

Transportation

99.0% N/D

140 Koza Altın Turkey Ovacık Gold Reserve Mining N/A N/D

141 A group of Turkey based investors Turkey ABK Enerji Elektrik Üretim Energy 100.0% N/D

142 Özkardeş Grup Turkey Framissima Boyalık Beach

Hotel

Tourism 100.0% N/D

143 Bunge Bermuda Doysan Seed Plant Food & Beverage N/A N/D

144 Petroline Turkey SABIC Polimer Endüstrisi Chemicals 70.0% N/D

145 X-Trade Brokers Poland Hedef Menkul Değerler Financial Services 100.0% N/D

146 Tab Gıda Turkey Çelebi Hizmet Restorant

(Arby's Chain in Turkey)

Food & Beverage 100.0% N/D

147 Ashmore UK Nezih Kitap Kırtasiye Retail N/D N/D

148 Milan Petrol Turkey M Oil Energy 70.0% N/D

17

# Acquirer Origin Target Sector StakeDeal Value

(US$ million)

149 Fritz Egger Austria Roma Plastik Manufacturing 71.5% N/D

150 Turkey Properties Turkey Aland Emlak Real Estate N/D N/D

151 Sofra Hazır Yemek Turkey Damak Hazır Yemek Services 50.0% N/D

152 STFA Holding Turkey Energaz Energy 47.0% N/D

153 Ova Taşıt Turkey Yalı Taşıt Services 100.0% N/D

154 Ali Akman Turkey Petroline Chemicals 99.0% N/D

155 Legrand France Inform Elektronik Manufacturing 100.0% N/D

156 TEB Mali Yatırımlar Turkey Fortis Bank Financial Services 100.0% N/D

157 Greif USA Ünsa Ambalaj Packaging N/D N/D

158 Riverside USA Tropikal Bahçe ve Evcil

Hayvan Ürünleri

Food & Beverage N/D N/D

159 Alliance Boots UK Hedef Alliance Holding Pharmaceuticals 10.0% N/D

160 BNP Paribas France Fortis Emeklilik ve Hayat Financial Services 100.0% N/D

161 TOBB & TOBB-ETÜ Turkey Mesa Hospital (Söğütözü,

Ankara)

Healthcare N/A N/D

162 Kerevitaş Gıda Turkey Mersu Su Ürünleri Food & Beverage 100.0% N/D

163 Kerevitaş Gıda Turkey Ancoker Su Ürünleri Food & Beverage 45.0% N/D

164 Tiger Global Management USA DSM Grup İletişim Pazarlama

(Trendyol.com)

IT N/D N/D

165 Incitec Pivot Australia Nitromak DNX Kimya Manufacturing 50.0% N/D

166 Argus Capital Partners & Qatar First Investment

Bank

UK; Qatar Memorial Health Group Healthcare 40.0% N/D

167 Boydak Holding Turkey Nisan Elektromekanik Energy 50.0% N/D

168 Actera Group Luxembourg Mars Entertainment Group Entertainment 60.0% N/D

169 Turkven Turkey Domino's Pizza in Turkey Food & Beverage 100.0% N/D

170 Hamza Doğan Turkey Doğal Elektrik Üretim Energy 80.0% N/D

171 Baalbaki Group Lebanon Depur Kimya Chemicals N/A N/D

172 Havas – Euro RSCG Worldwide France Project House Media 51.0% N/D

173 Knauf International Germany Mina Alçı Building Materials 64.0% N/D

174 Imtech Netherlands Elkon Elektrik Manufacturing 100.0% N/D

175 Boydak Holding Turkey Bizim Menkul Değerler Financial Services 50.0% N/D

176 Boydak Holding Turkey Muradiye Elektrik Energy 70.0% N/D

177 Befesa Medio Ambiente Spain Metoks Madencilik Metalurji Mining N/D N/D

178 RPM Building Solutions USA Park Dış Ticaret Building Materials N/D N/D

179 GE Energy USA Artesis IT N/D N/D

180 Kronospan Holdings UK SFC Entegre Orman Ürünleri

and Baks Batı Kimya

Manufacturing N/D N/D

181 DSM Composite Resins Switzerland DYO Boya's Unsaturated

Polyester (UP) resins business

Chemicals N/A N/D

182 WNC Kids Holding (Eurasia Capital Partners &

FMO & Balkan Accession Fund)

Netherlands Wenice Kids Retail 50.0% N/D

183 Fresenius Germany Diamed Diyaliz Hizmetleri Healthcare 90.0% N/D

184 Groupe Hamelin France Derya Büro Malzemeleri Manufacturing 70.0% N/D

185 Nokia Siemens Networks Finland IRIS Telecom Telecommunications 100.0% N/D

18

# Acquirer Origin Target Sector StakeDeal Value

(US$ million)

186 Tevhit Karakaya Turkey Star Medya Yayıncılık and

Kanal 24

Media 51.0% N/D

187 United Business Media UK Rotaforte Services 65.0% N/D

188 Ajans Press Turkey PRNet Halkla Ilişkiler Services 100.0% N/D

189 Henry Schein USA Güney Diş Deposu Wholesale &

Distribution

50.0% N/D

190 HNA Group (China) & Bravia Capital Partners

(USA)

China myTECHNIC Services N/D N/D

191 Tecpesa Spain Kartek-Mekaser Danışmanlık

Enerji

Services 100.0% N/D

192 Esas Holding** Turkey Mars Entertainment Group Entertainment N/D N/D

193 Yıldız Holding Turkey Marsan Gıda Food & Beverage N/D N/D

194 ECE Projektmanagement Germany ECE Türkiye Proje Yönetim Real Estate 48.0% N/D

195 Accell Group Netherlands Bianchi Bisiklet Manufacturing 100.0% N/D

196 Eckes-Granini Germany Eden Meyve Suyu Food & Beverage 50.0% N/D

197 Ergun Bal Turkey Damla Su Enerji Energy 85.0% N/D

198 NBK Capital Kuwait Kılıç Deniz Ürünleri Agriculture &

Breeding

20.0% N/D

199 Nuh Enerji Turkey Kudret Enerji Energy 90.0% N/D

200 Nuh Enerji Turkey Pamuk Elektrik Energy 100.0% N/D

201 Palmali Grubu Turkey Yalıkavak Marina Infrastructure 100.0% N/D

202 Aramex UAE Aramex International Hava

Kargo

Logistics &

Transportation

50.0% N/D

203 Nestlé Turkey Turkey Doğan Gıda and Balaban

Gıda

Food & Beverage 51.0% N/D

(**) Esas Holding’s acquisition of Mars Entertainment and Mars Entertainment’s acquisiton of AFM Uluslararası Film Prodüksiyon are part of a single deal pending the related Competition Authority decision.

19

This publication contains general information only and is not intended to be comprehensive nor to provide specific accounting, business, financial, investment, legal, tax or other professional advice or services. This publication is not a substitute for such professional advice or services, and it should not be acted on or relied upon or used as a basis for any decision or action that may affect you or your business. Before making any decision or taking any action that may affect you or your business, you should consult a qualified professional advisor. Whilst every effort has been made to ensure the accuracy of the information contained in this publication, this can not be guaranteed, and neither Deloitte Touche Tohmatsu nor any related entity shall have any liability to any person or entity that relies on the information contained in this publication. Any such reliance is solely at the user’s risk.

20

For more information about M&A advisory services from Deloitte Turkey, contact:

Başak [email protected]+ 90 212 366 63 71

DRT Kurumsal Finans Danışmanlık Hizmetleri A.Ş.

Sun PlazaMaslak Mah. Bilim Sok. No:534398 Şişli, İstanbulTel: 90 (212) 366 60 00Fax: 90 (212) 366 60 30

Armada İş MerkeziA Blok Kat:7 No:806510, Söğütözü, AnkaraTel: 90 (312) 295 47 00Fax: 90 (312) 295 47 47

Punta Plaza1456 Sok. No:10/1Kat:12 Daire: 14 – 15Alsancak, İzmirTel: 90 (232) 464 70 64Fax: 90 (232) 464 71 94

www.deloitte.com.trwww.verginet.netwww.denetimnet.net

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 140 countries, Deloitte brings world-class capabilities and deep local expertise to help clients succeed wherever they operate. Deloitte's approximately 170,000 professionals are committed to becoming the standard of excellence.

Deloitte's professionals are unified by a collaborative culture that fosters integrity, outstanding value to markets and clients, commitment to each other, and strength from cultural diversity. They enjoy an environment of continuous learning, challenging experiences, and enriching career opportunities. Deloitte's professionals are dedicated to strengthening corporate responsibility, building public trust, and making a positive impact in their communities.

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms.

©2011 Deloitte Turkey. Member of Deloitte Touche Tohmatsu Limited