Annual Report_2016-17_2017-18.pdf - Civil Bank

204

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Annual Report_2016-17_2017-18.pdf - Civil Bank

l;len a}+s lnld6]8sf];ftf}+ / cf7f}+ jflif{s ;fwf/0f ;ef ;DaGwL

;"rgf

o; a}+ssf] ldlt @)&^÷)!÷)@ ut] a;]sf]] ;+rfns ;ldltsf] @&! cf}+ a}7ssf] lg0f{ofg';f/ a}+ssf] ;ftf}+ / cf7f}+ jflif{s ;fwf/0f ;ef lgDg lnlvt ldlt, :yfg / ;dodf b]xfosf ljifox? pk/ 5nkmn u/L lg0f{o ug{ a:g] ePsf] x'Fbf sDkgL P]g, @)^# sf] bkmf ^& adf]lhd z]o/wgL dxfg'efjx?sf] hfgsf/Lsf] nflu of] ;"rgf k|sflzt ul/Psf] 5 . ;Dk"0f{ z]o/wgL dxfg'efjx?nfO{ pNn]lvt ldlt, :yfg / ;dodf pkl:yltsf] nflu xflb{s cg'/f]w ub{5' . ;ef x'g] ldlt, :yfg / ;do M ;ef x'g] ldlt M @)&^ ;fn a}zfv dlxgf @& ut] -tbg';f/ !) d], @)!( _ z'qmjf/ . :yfg M cd[tef]u, sflnsf:yfg l8NnLahf/, sf7df8f}+;do M ljxfg !!=)) ah] .

jflif{s ;fwf/0f ;efsf] 5nkmnsf] ljifox¿ M -s_ ;fwf/0f k|:tfjx?M != cWoIfHo"sf] k|ltj]bg ;lxt ;+rfns ;ldltsf] jflif{s k|ltj]bg @)&#÷)&$ / @)&$÷)&% kfl/t ug]{ . @= cfly{s jif{ @)&#÷)&$ / @)&$÷)&% sf] n]vfk/LIfssf] k|ltj]bg ;lxtsf] jf;nft, gfkmfgf]S;fg lx;fj tyf gub k|jfx ljj/0f nufotsf ljQLo ljj/0fx?df 5nkmn u/L kfl/t ug]{ . #= sDkgL P]g, @)^# bkmf !!# cg';f/ cfly{s jif{ @)&$÷)&% sf] nflu lgo'Qm n]vfk/LIfs tyf lghsf] kfl/>lds cg'df]bg ug]{ . $= sDkgL P]g, @)^# bkmf !!! cg';f/ cfly{s jif{ @)&%÷)&^ sf] nflu n]vfk/LIfs lgo'Qm ug]{ / lghsf] kfl/>lds lgwf{/0f ug]{ . %= ;+rfns ;ldltn] k|:tfj u/] adf]lhd cfly{s jif{ @)&#÷)&$ sf] d'gfkmfaf6 k|ltz]o/ )=%$Ü sf b/n] x'g cfpg] ?= #,(!,^@,)^(.)^ -cIf/]kL tLg s/f]8 PsfgAa] nfv a};ÝL xhf/ pgG;t/L ?k}ofF 5 k};f dfq_ -s/ k|of]hgsf]_ nflu gub nfef+z ljt/0f ug{ :jLs[t ug]{ . ^= ;+rfns ;ldltn] k|:tfj u/] adf]lhd cfly{s jif{ @)&$÷)&% sf] d'gfkmfaf6 k|ltz]o/ $=)%Ü sf b/n] x'g cfpg] ?=@(,$),)@,)^(.^% -cIf/]kL pGglt; s/f]8 rfnL; nfv b'O{ xhf/ pgfg;Q/L ?k}ofF k};ÝL k};f dfq_ gub nfef+z ljt/0f ug{ :jLs[t ug]{ . &= a}+ssf] ;+:yfks z]o/wgLx?sf] tkm{af6 k|ltlglwTj ug'{x'g] # hgf / ;j{;fwf/0f z]o/wgLx?sf] tkm{af6 k|ltlglwTj ug'{x'g] # hgf u/L hDdf ^ hgf ;+rfnssf] nflu lgjf{rg ug]{ .

-v_ ljz]if k|:tfjx? M != ;+rfns ;ldltn] k|:tfj u/] adf]lhd cfly{s jif{ @)&#÷)&$ sf] d'gfkmfaf6 a}+ssf] r'Qmf k"FhLsf] !)=@%Ü sf b/n] x'g cfpg] ?= &$,$),&(,#!@.)* -cIf/]kL rf}xQ/ s/f]8 rfnL; nfv pgf;L xhf/ tLg ;o af¥x ?k}ofF cf7 k};f dfq_ a/fa/sf] af]g; z]o/ ljt/0f ug{ :jLs[t ug]{ . @= a}+ssf] k|aGwkq tyf lgodfjlndf ;+zf]wgsf] ug]{ . -s_ a}+ssf] k|aGwkq ;+zf]wg ug]{. -s–!_ a}+ssf] p2]Zo k|fKt ug{ ul/g] sfdx? -bkmf %, bkmf % -r_ b]lv -1_ ;Dd_ -s–@_ a}+ssf] hf/L k"FhL tyf r'Qmf k"FhL a[l4 ug]{ -bkmf ^ v / u _ . -s–#_ ;+:yfks z]o/ ljqmL jf lwtf]aGws ;DaGwL Joj:yf -bkmf & u _ .

-v_ a}+ssf] lgodfjnLdf ;+zf]wg ug]{ . -v–!_ ;+:yfksn] lng'kg]{ z]o/ -lgod !)_ . -v–@_ ;+rfns ;ldltsf] u7g, ;+Vof tyf sfo{sfn ;DaGwdf -lgod @& -!,@,#_ . -v–#_ :jtGq ;+rfns lgo'QmL , sfo{sfn tyf of]Uotf ;DaGwdf -lgod @( _ . -v–$_ ;+rfns k'gM lgo'Qm x'g ;Sg] jf g;Sg] ;DaGwdf -lgod #) _ . -v–%_ ;+rfns lgo'QmL ;DjGwL s'g} vf; Joj:yf ug]{ eP ;f] s'/f v'nfpg] -lgod #!_ . -v–^_ ;ldltsf] a}7s ;DaGwL sfo{ljlw -lgod #*-!_ . -v–&_ n]vf k/LIf0f ;DaGwL Joj:yf -lgod $!-!_ . -v–*_ s'g} vf; Joj;fo ug]{ ;DaGwL Joj:yf -lgod $(-#_ .

#= a}+ssf] k|aGwkq tyf lgodfjnLsf] laleGg bkmf tyf lgodx?df /x]sf] æ a}+s tyf ljQLo ;+:yf ;DaGwL P]g, @)^#Æ nfO{ æ a}+s tyf ljQLo ;+:yf ;DaGwL P]g, @)&#Æ u/L ;+zf]wgsf] ug]{ . $= a}+ssf] k|aGwkq tyf lgodfjnLsf] ;+zf]wgsf] ;DaGwdf lgodgsf/L lgsfox?af6, ;+zf]wg, kl/dfh{g tyf yk36 ug{ s'g} lgb]{zg k|fKt ePdf k|fKt lgb]{zg adf]lhd ;f] ;d]t ldnfO{ ;+zf]wg jf kl/dfh{g ;d]tsf ;Dk"0f{ sfo{x? ug{ a}+s ;+rfns ;ldltnfO{ k"0f{ clVtof/L k|bfg ug]{ ;DaGwdf . %= l;len a}+s lnld6]8 / cGo pko'Qm a}+s tyf ljQLo ;+:yfx? Ps cfk;df ufEg]÷ufleg - dh{/ _ jf k|flKt -PlSjlh;g _ ug{÷x'g jf :jb]zL÷ljb]zL /0fgLlts ;fem]bf/Ldf hfg cfjZos ;xdtL / ;Demf}tf nufotsf cfjZos ;Dk"0f{ sfo{x? ug{÷u/fpg ;+rfns ;ldltnfO{ k"0f{ clVtof/L k|bfg ug]{ .

-u_ ljljw k'gZr M ;efdf 5nkmn ul/g] ;~rfns ;ldltsf] jflif{s k|ltj]bg tyf n]vfk/LIfssf] k|ltj]bg ;lxtsf] jf;nft, gfkmf gf]S;fg lx;fa, ;fwf/0f ;ef ;DaGwL hfgsf/L, k|f]S;L kmf/d / k|j]zkq o; a}+ssf] s]Gb|Lo sfof{no ;'Gwf/f, sf7df8f+}df jf a}+ssf] z]o/ /lhi6«f/ l;len Soflk6n dfs]{6 lnld6]8, ;'Gwf/f sf7df8f}+df cfO{ lg/LIf0f ug{ jf k|fKt ug{ ;lsg]5 . ;+lIfKt cfly{s ljj/0f tyf jflif{s k|ltj]bg nufot ;fwf/0f ;efdf k]z x'g] k|:tfjx? a}++ssf] website: www.civilbank.com.np af6 hfgsf/L k|fKt ug'{ x'g ;DalGwt z]o/wgLx?df cg'/f]w 5 .

;~rfns ;ldltsf] cf1fn],lx/f sfhL a:g]t

sDkgL ;lrj

;fwf/0f ;ef;DaGwL yk hfgsf/Lx¿ M!= jflif{s ;fwf/0f ;efnfO{ Wofgdf /fvL ldlt @)&^.)!.!) ut] b]lv ldlt @)&^.)!.@& ut];Dd a}+ssf] z]o/wgL btf{ lstfa aGb /xg]5 . g]kfn :6s PS:fr]~h lnld6]8df ldlt @)&^.)!.)( ut];Dd sf/f]af/ eO{ ldlt @)&^.)!.!& leq o; a}+ssf] z]o/ /lhi6«f/ l;len Soflk6n dfs]{6 lnld6]8, ;'Gwf/f sf7df8f}+df k|fKt z]o/ gfd;f/Lsf] lnvtsf] cfwf/df z]o/wgL btf{ lstfadf sfod z]o/wgLx?n] ;f] ;efdf efu lng, gub nfef+z tyf af]g; z]o/ kfpg]5g\ .

@= k|To]s z]o/wgL dxfg'efjnfO{ z]o/ nfutdf sfod /x]sf] 7]ufgfdf jflif{s k|ltj]bg k'l:tsf k7fOg] 5 . ;efdf pkl:yt x'g] z]o/wgLx¿nfO{ jflif{s k|ltj]bg k'l:tsf ;fy ;+nUg k|j]zkq ;fydf lnO{ cfpg' x'g cg'/f]w 5 . z]o/wgL dxfg'efjn] s'g} sf/0fjz jflif{s k|ltj]bg k'l:tsf gkfpg' ePdf cfˆgf] z]o/ k|df0fkq jf cfˆgf] kl/ro :ki6 x'g] lsl;dsf] kmf]6f] ;lxtsf] s'g} k|df0f jf z]o/ cef}ltsLs/0f u/]sf] vftf (DMAT Account) sf] xsdf lxtu|fxL kl/ro gDa/ (BOID) ;fydf lnO{ ;efdf efu lng cfpg' x'g cg'/f]w 5 .

#= ;ef x'g] lbg ;efdf pkl:yltsf nflu xflh/ k'l:tsf (=)) ah] b]lv @M )) ah] ;Dd v'Nnf /xg]5 . xlh/L hgfpgsf] nflu z]o/wgL dxfg'efjx¿n] cfkm\gf] klrokq jf ;Ssn z]o/ k|df0fkq k]z ug'kg]{ 5 eg] cfkm\gf] z]o/ k|df0fkqx? cef}lts/0f u/fO{ ;Sg'ePsf z]o/wgL dxfg'efjx?sf] xsdf DEMAT vftf gDa/ / ;Ssn cflwsfl/s kl/rokq clgjfo{ ?kdf k|:t't ug'{kg]{5 .

$= z]o/wgLn] cfˆgf] k|ltlglw -k|f]S;L_ lgo'Qm ubf{ cfk'm h'g ;d'xsf] z]o/wgL xf] ;f]xL ;d'xsf] z]o/wgLnfO{ dfq k|f]S;L lbg kfO{g]5 .

%= k|ltlglw -k|f]S;L_ n] dtbfg ug{ kfpg] clwstd xb jf ;Ldf To:tf] z]o/wgLn] lng kfpg] a}+ssf] clwstd z]o/ lx:;fsf] ;LdfeGbf j9L x'g] 5}g .

^= k|ltlglwkq -k|f]S;L kmf/d_ ;ef ;'? x'geGbf sDtLdf &@ 306f cufj} cyf{t ldlt @)&^÷)!÷@$ ut] !!=)) ah] leq ;+:yfkssf] xsdf a}+ssf] s]Gb|Lo sfof{nodf btf{ ul/;Sg' kg]{5 .

&= z]o/wgLn] PseGbf a9L JolQmnfO{ cfˆgf] z]o/ ljefhg u/L jf cGo s'g} lsl;daf6 5'6\ofO{ k|f]S;L lbg kfOg] 5}g . o;/L lbOPsf] k|f]S;L ab/ x'g]5 .

*= Ps hgf z]o/wgLn] PseGbf a9L z]o/wgLnfO{ k|ltlglw -k|f]S;L_ d's// u/]df To:tf] k|ltlglw -k|f]S;L_ :jtM ab/ x'g]5 . t/, klxnf lbPsf] k|ltlglwkq -k|f]S;L kmf/fd_ ab/ u/L kl5 lbO{Psf] k|ltlglwkqnfO{ dfq dfGotf lbg cg'/f]w u/L 5'§} kq ;fy k|ltlglwkq -k|f]S;L kmf/fd_ btf{ ug{ NofPdf eg] 5'§} kq ;fy k|fKt kl5Nnf] k|ltlglwkq -k|f]S;L kmf/fd_ nfO{ dfGotf lbO{g]5 .

(= a'Fbf g+= * adf]lhd lgo'Qm u/]sf] k|ltlglwnfO{ ab/ u/L csf]{ k|ltlglw d's// ug{ rfx]df ;f]sf] lnlvt ;"rgf ;ef x'g' eGbf slDtdf &@ 306f cufj} a}+ssf] s]Gb|Lo sfof{no ;'Gwf/f sf7df08f}df btf{ ul/;Sg' kg]{5 .

!)= k|ltlglw lgo'Qm ul/;s]sf] z]o/wgL, ;efsf] sfd sf/afxL ;'? x'g'eGbf cufj} cfk}m ;efdf pkl:yt eO{ xflh/L k'l:tsfdf b:tvt u/]df To:tf] z]o/wgLn] lbPsf] k|ltlglw kq -k|f]S;L kmf/d_ :jtM ab/ x'g]5 .

!!= a}+ssf] 5fk / sDkgL ;lrjsf] b:tvt ePsf] k|ltlglwkq -k|f]S;L kmf/d_ dfq dfGo x'g]5 .

!@= s'g} ;+ul7t ;+:yf jf sDkgL] z]o/wgLsf] xsdf To:tf ;+ul7t ;+:yf jf sDkgLn] dgf]lgt u/]sf] k|ltlglwn] z]o/jfnfsf] x}l;otn] ;efdf efu lng ;Sg' x'g]5 . o;/L k|ltlglw k7fpFbf a}+snfO{ lnlvt?kdf hfgsf/L lbg'kg]{5 .

!#= gfafns jf czQm z]o/wgLx?sf] tkm{af6 a}+ssf] z]o/ nut lstfadf ;+/Ifssf] ?kdf gfd btf{ ePsf] JolQmn] ;efdf efu lng jf dtbfg ug{ jf k|ltlglw -k|f]S;L _ tf]Sg ;Sg'x'g]5 .

!$= o; a}+ssf] ;~rfns lgj{frg;DaGwL lgb]{lzsf, @)^* sf] k|ltlnlk z]o/wgL dxfg'efjx?n] a}+ssf] s]Gb|Lo sfof{noaf6 ?= !,)))÷– z'Ns lt/L k|fKt ug{ ;Sg'x'g]5 .

!%= pkTosf aflx/ tyf ljb]zdf /xL ;fwf/0f ;efdf :jo+ pkl:yt x'g g;Sg] z]o/wgL dxfg'efjx?n] a}+ssf] j]j;fO6 wwww.civilbank.com.np df /x]sf] k|f]S;L kmf/fdnfO{ 8fpgnf]8 u/L x:tfIf/ u/L Scan Copy k|f]S;L kmf/fd a}ssf] [email protected] df k7fpg ;Sg'x'g]5 .

!^= z]o/wgL dxfg'efjx?nfO{ ;"lrt u/fpg ;lsof];\ eGg] b[li6n] s'g} z]o/wgL dxfg'efjx?nfO{ a}+s ;DaGwL s]xL lh1f;f eP 5nkmnsf] ljifo ;"rL dWo] ljljw lzif{s cGtu{t To:tf] lh1f;f lnlvt ?kdf ;ef x'g'eGbf & -;ft_ lbg cufj} sDkgL ;lrj dfkm{t ;+rfns ;ldltsf] cWoIfnfO{ a'emfpg' x'g cg'/f]w 5 . t/ To:tf lh1f;fnfO{ 5nkmn / kfl/t x'g] k|:tfjsf] ?kdf ;dfj]z ul/g] 5}g .

!&= ;d'x …sÚ / ;d"x …vÚ b'a} ;d"xsf ;+rfnssf] lgjf{rg;DaGwL lj:t[t hfgsf/Lsf] nflu a}+ssf] /lhi6«8{ sfof{no ;'Gwf/f l:yt lgjf{rg clws[sf] sfof{nodf ;Dks{ /fVgx'g cg'/f]w ul/G5 .

!*= lgjf{rg;DaGwL sfo{qmd lgjf{rg clws[tn] tf]s] adf]lhd x'g]5 . lgjf{rg;DaGwL cGo hfgsf/L tyf sfo{qmd;DaGwL ;"rgf ldlt @)&^.)!.!^ ut]sf] lbg a}+ssf] s]Gb|Lo sfof{nosf] ;"rgf kf6Ldf 6fF; ul/g]5 .

!(= ;fwf/0f ;ef ;DalGw yk hfgsf/Lsf] nflu a}+ssf] s]lGb|o sfof{nosf] kmf]g g+ )!–$@%!)!%, $@%!)*& jf a}+ssf] z]o/ /lhi6«f/sf] sfo{ ug]{ l;len Soflk6n dfs]{6; lnld6]8, ;'Gwf/f sf7df08f}+df ;Dks{ /fVg x'g cg'/f]w 5 .

k|ltlglwkq -k|f]S;L kmf/d_

>L ;~rfns ;ldltl;len a}+s lnld6]8sdnfbL, sf7df08f}+ .

ljifo M k|ltlglw lgo'Qm u/]sf] af/] .

dxfzo,

=========================== lhNnf ========================== g=kf=÷uf=lj=;= j8f g+= ========= a:g] d÷xfdL ========================================================== n]

To; a}+ssf] z]o/wgLsf] x}l;otn] ldlt @)&^÷)!÷@& ut] z'qmaf/sf lbg x'g] ;ftf} / cf7f}+ jflif{s ;fwf/0f ;efdf :jo+ pkl:yt eO{ 5nkmn

tyf lg0f{o k|lqmofdf ;xefuL x'g g;Sg] ePsf]n] pQm ;efdf efu lng tyf dtbfg ug{sf] nflu ========================== lhNnf =================

g=kf=÷uf=lj=;= j8f g+= ===== a:g] To; a}+ssf] z]o/wgL >L ====================================================================== nfO{ d]/f] ÷xfd|f] k|ltlglw

dgf]lgt u/L k7fPsf] 5' ÷5f}+ .

b|i6Ao M k|f]S;L lbFbf lnFbf cfˆgf] ;d'x leq l;ldt /xL lng' lbg' kg]{5 . of] lgj]bg ;fwf/0f ;ef x'g' eGbf sDtLdf &@ 306f cufj} a}+ssf] /lhi68{ sfof{nodf k]z ul/;Sg' kg]{5 .

sDkgL ;lrasf] b:tvta}+ssf] 5fk

k|ltlglwsf]b:tvt Mgfd Mz]o/wgL kl/ro g+= M lxtu|fxL- l8Dof6_ vftf g+=Mldlt M

lgj]bssf]b:tvt Mgfd M7]ufgf M z]o/wgL kl/ro g+= Mlxtu|fxL- l8Dof6_ vftf g+=Mz]o/ ;+Vof Mldlt M

k|j]z –kq

z]o/wgLsf] gfd M =======================================================================================================================================================================================================

z]o/wgL gDa/ / lxtu|fxL kl/ro g+= ============================================================================= z]o/ ;+Vof M ==============================================================

@)&^÷)!÷@& ut] z'qmaf/sf lbg x'g] l;len a}+s lnld6]8sf] ;ftf}+ / cf7f}+ jflif{s ;fwf/0f ;efdf pkl:yt x'g hf/L ul/Psf] k|j]zkq .

z]o/wgLsf] b:tvt M

b|i6Ao M ;ef sIfdf k|j]z ug{ of] k|j]zkq clgjfo{ ?kdf k|:t't ug'{ kg]{5 .

lx/f sfhL a:g]tsDkgL ;lrj

ljifo ;'rL!= cWoIfsf] dGtJo ============================================================================================================================ s

@= ;+rfns ;ldltsf] jflif{s k|ltj]bg ==================================================================================================== u

#= sDkgL P]g @)^# sf] bkmf !)( cg';f/sf] cltl/Qm ljj/0f =================================================================== 5

$= lwtf]kq btf{ tyf lgisfzg lgodfjnL, @)&# sf] lgod @^ sf] pklgod @ ;Fu ;DalGwt cg';"rL !% adf]lhdsf] jflif{s ljj/0f =========================================================== ~f

%= n]vfkl/Ifssf] k|ltj]bg -Plss[t_ cf=j= @)&$÷@)&% ========================================================================= !

^= Plss[t ljQLo cj:yfsf] ljj/0f -jf;nft_ cf=j= @)&$÷@)&% =========================================================== #

&= Plss[t gfkmf gf]S;fg ljj/0f cf=j= @)&$÷@)&% ============================================================================= $

*= Plss[t cGo lj:t[t cfDbfgLsf] ljj/0f cf=j= @)&$÷@)&% ================================================================= %

(= Plss[t OlSj6Ldf ePsf] kl/jt{gsf] ljj/0f cf=j= @)&$÷@)&% =========================================================== ^

!)= Plss[t gub k|jfx ljj/0f cf=j= @)&$÷@)&% ================================================================================= *

!!= n]vf ;DaGwL l6Kk0fLx? tyf k|d'v n]vf gLltx? ================================================================================= (

!@= a}+ssf]] cf=j= @)&$÷@)&% ljQLo ljj/0f k|sfzg ug{ g]kfn /fi6« a}+ssf] :jLs[tL kq ============================== (#

!#= n]vfk/LIfssf] k|ltj]bg cf=j= @)&#÷@)&$ ======================================================================================= (&

!$= jf;nft cf=j= @)&#÷@)&$ =========================================================================================================== ((

!%= gfkmf–gf]S;fg lx;fa cf=j= @)&#÷@)&$ ========================================================================================== !))

!^= gfkmf–gf]S;fg afF8k mfF8 lx;fa cf=j= @)&#÷@)&$ ============================================================================= !)!

!&= OlSj6Ldf ePsf] kl/jt{g;DaGwL ljj/0f cf=j= @)&#÷@)&$ ================================================================ !)@

!*= gub k|jfx ljj/0f cf=j= @)&#÷@)&$ ============================================================================================= !)#

!(= jf;nft / gfkmf–gf]S;fg lx;fasf cg';"rLx¿ cf=j= @)&#÷@)&$ ======================================================= !)$

@)= n]vf;DaGwL dxTjk"0f{ gLltx¿ cf=j= @)&#÷@)&$ ============================================================================= !#%

@!= n]vf;DaGwL l6Kk0fLx¿ cf=j= @)&#÷@)&$ ======================================================================================= !$!

@@= g]kfn /fi6« a+}ssf] kF"hL kof{Kttf ;DaGwL 9fFrf cGt/ut a}+ssf] pb\3f]if0f gLlt (Disclosure policy) cg'?ksf] pb\3f]if0f =cf=j= @)&#÷@)&$ ============================== !%#

@#= n]vfkl/Ifssf] k|ltj]bg -Plss[t_ cf=j= @)&#÷@)&$ ========================================================================= !%(

@$= Plss[t jf;nft gfkmf–gf]S;fg lx;fa tyf cGo ljj/0f cf=j= @)&#÷@)&$ ========================================== !^!

@%= a}+ssf]] cf=j= @)&#÷@)&$ ljQLo ljj/0f k|sfzg ug{ g]kfn /fi6« a}+ssf] :jLs[tL kq =============================== !^*

cWoIf Ho"sf] dGtAo

cf=j= @)&@÷&# sf] df}lb|s gLlt cg';f/ a}+s tyf ljQLo ;+:yfx?sf] k"Flhut cfwf/ ;'b[9 ul/ bL3{sflng ?kdf Joj;fo clej[l¢sf nflu cfjZos kg]{ ;|f]t kl/rfng ug{ tyf ljQLo :yfloTjsf nflu æsÆ ju{sf jfl0fHo a}+sx?sf] xfn sfod /x]sf] Go'gtd r'Qmf kF"hLnfO{ rf/ u'0ffn] j[l¢ u/L a}+ssf] Go'gtd r'Qmf k"FhL ?= * cj{ k'¥ofpg' kg]{ k|fjwfg cg'?k o; a}+sn] cf=j= @)&#÷)&$ df OG6/g]zgn lnlhË P08 kmfOgfG; sDkgL lnld6]8 nfO{ ufEg] tyf o'lgs kmfOgfG; lnld6]8 / xfdf dr]{G6 P08 kmfOgfG; lnld6]8nfO{ k|flKt ug'{sf ;fy} ttkZrft sfod x'g cfpg] r'Qmf k"FhLsf] $) k|ltzt xsk|b z]o/ lgisf;g sfo{ ;DkGg ul/ a}+ssf] k"FhL ?=&,@%,(#,!),#^!.*) -cIf/]kL ;ft cj{ klRr; s/f]8 lqofgAa] nfv bz xhf/ tLg ;o Ps;ÝL ?k}of cl; k};f_ k'¥ofO{;s]sf] / afsL gk'u k"FhL o;} ;fwf/0f ;efdf k]z eP adf]lhdsf] af]gz z]o/af6 k'Ug] Joxf]/f hfgsf/L u/fpg rfxG5' . tyflk cfufld lbgx?df a}+snfO{ cem ;an agfpg tyf k"FhLut lx;fjn] yk dha't agfpgsf] nflu o; a}+sn] cGo a}+s tyf ljQLo ;+:yfnfO{ k|flKt ug]{ jf ufEg] jf pko'Qm ;+:yf;+u l;len a}+s ufleP/ hfg] /0fgLltsf ;fy cufl8 al9/x]sf] hfgsf/L u/fpb5' . ;f] ;DaGwL ljz]if k|:tfjx? cfhsf] ;fwf/0f ;efdf z]o/wgL dxfg'efjx? ;dIf k]z u/]sf] 5' .

o; a}+ssf] ;+rfns ;ldlt z]o/wlgx?sf] clwstd lxt k|lt ;b}j ;r]t /x]sf] ePtf klg v/fa shf{sf] l:yltn] a}+sn] ;f]r] cg'?k k|ult ug{ g;s]sf] x'gfn] z]o/wlgx?nfO{ pRrtd k|ltkmn lbg g;ls/x]sf] cj:yf /x]sf] 5 . shf{ c;'nLnfO{ k|efjsf/L agfpgsf]] nflu s]lGb|o :t/df shf{ c;'nL ljefunfO{ ;jnLs/0f ul/Psf] / ;DalGwt Sn:6/ tyf zfvfx?;Fu ;dGjo ul/ shf{ c;'nL ug]{ sfo{nfO{ ;'b[l9s/0f ug{ a}+s Joj:yfkgnfO{ lgb]{zg lbO{Psf] 5 .

;+rfnsx?nfO{ cfkm\gf] clwsf/, bfloTj tyf st{Jodf k"0f{ ?kdf lhDd]jf/ agfO{Psf] 5 . . ;+:yfut ;'zf;gsf dfkb08x?nfO{ z'Go ;xgzLntfsf] gLlt adf]lhd cIf/; kfngf ub}{ g]kfnsf] ljQLo If]qdf pbfx/0fLo a}+s aGg] xfd|f] nIo xf] . ;+:yfut ;'zf;fgsf] ;'b[9 sfof{Gjog / kfngfaf6 g} :j:Yo / lbuf] k|ltkmn k|fKt ug{ ;lsg] s'/fdf ;+rfns ;ldlt ljZj:t 5 / eljiodf ;f] k|lt ;b}j ;r]t /xg] 5 . d]/f] sfo{Jo:ttf tyf gLltut sf/0fn] ubf{ a}+ssf] ;+rfns ;ldltsf] ;+rfns tyf cWoIf kbaf6 ldlt @)&$ ;fn a}zfv !% ut] b]lv nfu' x'g] ul/ /flhgfdf lbO{ :jLs[t ePtfklg z]o/wlgx?sf] ;'emfj oxfx?s} ljZjf;sf sf/0fn] ldlt @)&$ ;fn kf}if # ut] b]lv k'gM ;+rfns ;ldltsf] cWoIf ;DxfNb} cfPsf] 5' . o; lardf a}+ssf] ;+rfns ;ldltsf] cWoIfsf] e'ldsfnfO{ lhDd]jf/L k'j{s lgjf{x ug'x'g] lgjt{dfg cWoIf >L cDjL/ af]u6LHo"nfO{ xflb{s wGojfb lbg rfxG5' . a}+ssf] lgodfjlndf a}+sdf :jtGq ;+rfns ;d]t u/]/ ( hgf /x]sf] ;+rfns ;ldltsf] Jo:yf ePtfklg a}+s tyf ljQLo ;+:yf ;DaGwL P]g, @)^# nfO{ vf/]h u/L a}+s tyf ljQLo ;+:yf ;DaGwL P]g, @)&# nfu' ePsf] / pQm P]gsf] bkmf !$ sf] pkbkmf -!_ df a}+s tyf ljQLo ;+:yfdf sDtLdf kfFr / a9Ldf ;ft hgf ;+rfnsx? /x]sf] Ps ;+rfns ;ldlt /xg]5 eGg] Joj:yf ePsf] x'gfn] ;fljssf] a}+s tyf ljQLo ;+:yf ;DaGwL P]g, @)^# sf] bkmf !@ sf] pkbkmf -!_ adf]lhd o; a}+ssf] ;+rfns ;ldlt ( hgfsf] x'g] u/L u7g ul/Psf]df gofF P]g nfu' ePkZrft ;f]xL adf]lhd x'g] u/L & hgfsf] ;+rfns ;ldlt u7g ug'{ kg]{ ePsf] x'Fbf ;+:yfks z]o/wgLx?af6 # hgf, ;j{;fwf/0f z]o/wgLx?af6 # hgf / :jtGq ;+rfns ! hgf u/L & hgfsf] ;+rfns ;ldlt u7g u/L a}+s tyf ljQLo ;+:yf ;DaGwL P]g, @)&# sf] bkmf !$ sf] pkbkmf -!_ nfO{ sfof{Gjog ug]{ ;DaGwdf ;+rfns ;ldltdf 5nkmn x'bfF o; a}+ssf] ;+:yfks z]o/wgLx?sf] tkm{jf6 ;+rfns ;ldltdf k|ltlglwTj ug'{x'g] ;+rfns >L l/tf >]i7 / ;+rfns >L ljgf]b nfn >]i7n] cfˆgf] Joj;foLs Jo:ttfsf] sf/0fn] ldlt @)&$ h]7 & ut] b]lv nfu' x'g] u/L l;len a}+s lnld6]8sf] ;+rfns kbdf /xL a}+ssf] ;]jf ug{ ;Sg] cj:yf gePsf] egL ;+rfns kbjf6 lbg' ePsf] /fhLgfdfnfO{ :jLs[t u/]sf] hfgsf/L u/fpb5' . jxfFx?n] o; a}+sdf k'¥ofpg' ePsf] of]ubfgsf] pRr d"NofÍg ub}{ o;} ;ef dfkm{t xflb{s wGojfb lbg rfxG5' . ;fy} a}+ssf] lgodfjnLdf ;+:yfks ;d'xaf6 # hgf, ;j{;fwf/0f ;d'xaf6 # hgf / :jtGq ;+rfns ! hgf u/L & hgfsf] ;+rfns ;ldlt u7g x'g] u/L ;+zf]wgsf] nflu o; ;DDflgt ;fwf/0f ;efdf ;dIf ljz]if k|:tfj k]z ul/Psf] 5 . o; k|:tfjnfO{ cfhsf] ;efn] :jLs[lt k|bfg ug]{ s'/fdf d ljZj:t 5' . ;fy} a}+ssf] ;+rfns ;ldtaf6 cfkm\gf] sfo{ Jo:ttfn] ubf{ ;+rfns kbaf6 /flhgfdf lbg'ePsf >L ldqnfn >]i7 / l;h{gf zfSo tyf sfo{sfn ;dfKt x'g'ePsf :jtGq ;+rfns k|f= 8f= /d]z bfxfnnfO{ jxfFx?n] o; a}+sdf k'¥ofpg' ePsf] of]ubfgsf] pRr sb/ ub}{ o;} ;ef dfkm{t xflb{s wGojfb lbg rfxG5' .

o;sf cnfjf a}+ssf] Joj;fonfO{ lj:tf/ ub}{ hfg] gLlt cg'?k ;fd'lxs nufgL sf]ifsf] :yfkgf k|df0f kq k|fKt ul/;s]sf] hfgsf/L u/fpb} cfufld s]lx ;do leqdf l;len Do'r"cn km08 klg NofO{g] s'/f ;Dk"0f{ z]o/wgL dxfg'efjx?nfO{ cjut u/fpg rfxG5' . a}+ssf] ljQLo cj:yf, ;du| hf]lvd Joj:yfkg, shf{sf]

cfb/0fLo z]o/wgL dxfg'efjx?,

l;len a}+s lnld6]8sf] ;ftf}+ / cf7f}+ jflif{s ;fwf/0f ;efdf xfd|f] lgdGq0ffnfO{ :jLsf/ ul/ pkl:yt cfb/0fLo z]o/wgL dxfg'efjx?, lgodgsf/L lgsfosf k|ltlglwHo"x?, cltlyHo'x?, ko{j]Ifs, kqsf/ ldqx? tyf a}+sdf sfo{/t sd{rf/Lx?nfO{ a}+ssf] ;~rfns ;ldltsf] tkm{af6 / d]/f] JolQmut tkm{af6 ;d]t xflb{s :jfut ub}{ Gofgf] clejfbg JoQm ub{5' . a}+s :yfkgfsf gjf}++ aif{ kf/ ul//xbf;Dd xfdLnfO{ lg/Gt/ ?kdf c;Ld ljZjf; / cflTdo ;xof]usf] nflu a}+s kl/jf/ oxfFx?k|lt xflb{s cfef/ ;d]t k|s6 ub{5f} . ;fy} cfufdL lbgx?df klg oxfFx?sf] ;xof]u / ;b\efj lg/Gt/?kdf /xg]5 eGg] ljZjf; lnPsf] 5' .

z]o/wgL dxfg'efjx?,cf= j= @)&#÷)&$ sf] d'gfkmfaf6 z]o/wgL dxfg'efjx?nfO{ !)=@% k|ltzt af]g; z]o/ / )=%$ k|ltzt gub nfef+z tyf cf=j= @)&$÷)&% sf] d'gfkmfaf6 $=)% k|ltzt gub nfef+z k|:tfj ul/Psf] 5 . o; k|:tfjnfO{ cfhsf] ;efn] kfl/t u/L lbg' x'g cg'/f]w ub{5f}+ . dh{/ tyf PlSjlhzgaf6 k|fKt Soflk6n l/h{e / a}+ssf] d'gfkmfaf6 z]o/wgL dxfg'efjx?nfO{ cf= j= @)&#÷)&$ / )&$÷)&% df s'n !$=*$ k|ltkmn ljt/0f ug{ ;kmn ePsf] 5 .

CIVIL BANK | ANNUAL REPORT 2073 / 2074 & 2074 / 2075

s

u'0f:t/, shf{ c;'nLsf] cj:yf tyf d'gfkmfsf] cj:yfsf] af/]df qmdzM k|ult x'b} u/]sf] s'/f kf/bzL{ ?kdf oxfFx? ;j}nfO{ hfgsf/L ePs} 5 .

a}+sn] OG6/g]zgn lnlhË P08 kmfOgfG; sDkgL lnld6]8nfO{ ufEg] sfo{ ;DkGg ul/ ;s]sf] x'gfn] a}Í tyf ljQLo ;+:yf Ps cfk;df ufEg] ufleg] -dh{/_ tyf k|flKt -PlSjlhzg_ ;DaGwL ljlgodfjnL, @)&# adf]lhd uflePkl5 ;DkGg x'g] klxnf] jflif{s ;fwf/0f ;efaf6 lgjf{rgsf] dfWodaf6 ;+rfns ;ldltsf] k'gu{7g ug'{kg]{ k|fjwfg cg'?k o;} ;fwf/0f ;efn] ;+:yfks ;d'xaf6 # hgf tyf ;j{;fwf/0f ;d'xaf6 # hgf ;+rfnsx? lgjf{lrt÷dgf]lgt ug]{ k|:tfjaf6 a}+sdf of]Uo ;+rfnsx?sf] lgo'lQm x'g]5 eGg] cfzf lnPsf] 5' . gjlgjf{lrt ;+rfnsHo"x?nfO{ ;kmn sfo{sfnsf] clu|d z'esfdgf ;d]t JoQm ub{5' .

a}+sn] xfn;Dd xfl;n u/]sf pknlAwx? tyf ultljlwx?sf af/]df ;+rfns ;ldltsf] jflif{s k|ltj]bgdf lj:t[t ?kdf pNn]v ul/Psf] 5 . ;+rfns ;ldlt, z]o/wgLx?, a}+s Joj:yfkg, sd{rf/L / lgodgsf/L lgsfo tyf cGo ;/f]sf/jfnf aLr ;df~h:otf NofO{ u|fxs ju{nfO{ pRr:t/Lo ;]jf k|bfg ub}{ a}+ssf] ;jf]{kl/ lxtsf nflu sfo{ ug'{ jt{dfg l;len a}+s ;+rfns ;ldltsf] gLlt xf] . o;df ;j} ;/f]sf/jfnfx?nfO{ ;d]6L ;j}sf] ;dfg lxtsf] /Iffn] dfq ;du| a}+ssf] lbuf] ljsf; ;Dej 5 eGg] s'/fdf xfdL ljZj:t 5f} .

cGTodf, a}+snfO{ cfhsf] o; cj:yf;Dd NofO{ k'¥ofpg cgj/t ¿kdf h'l6/xg' ePsf ;+rfns ;fyLx¿, a}+ssf ;+:yfks, z]o/wgL dxfg'efjx?, lgodgsf/L lgsfo, a}+ssf lgIf]kstf{ tyf u|fxsju{x¿, z'e]R5's, ;xof]uL tyf a}+s Joj:yfkgdf /xL dxTjk"0f{ of]ubfg ub}{ cfpg' ePsf k|d'v sfo{sf/L clws[t tyf pxfFsf] g]t[Tjdf /x]sf] Joj:yfkg ;d"x Pj+ ;Dk"0f{ sd{rf/Lx¿af6 k|fKt ;xof]uk|lt xflb{s s[t1tf k|s6 ub}{ o; a}+sn] pT;fxhgs ¿kn] sf/f]af/ lj:tf/ ug'{sf ;fy} ljQLo ahf/df k|ltli7t a}+ssf] ¿kdf klxrfg agfpgsf] nflu cu|;/ e}/x]sf] tYo oxfFx¿nfO{ cjut u/fpb} labf x'g rfxG5' .

wGojfb,

O{= OR5f /fh tfdfË cWoIf

CIVIL BANK | ANNUAL REPORT 2073 / 2074 & 2074 / 2075

v

cfb/0fLo z]o/wgL dxfg'efjx?, o; l;len a}+s lnld6]8sf] ;ftf}+ / cf7f}+ jflif{s ;fwf/0f ;efdf pkl:yt ;Dk"0f{ z]o/wgL dxfg'efjx?, cGo cfdlGqt cltlyx? Pj+ kqsf/ ldqx?nfO{ a}+ssf] ;+rfns ;ldltsf] tkm{af6 tyf d]/f] JolQmut tkm{jf6 cfef/ JoQm ub}{ xflb{s :jfut tyf Gofgf] clejfbg ub{5' . o; ul/dfdo ;efdf d ;+rfns ;ldltsf] tkm{af6 a}+ssf] cf= j= @)&#÷)&$ / @)&$÷)&% sf] ;dLIff cjlwdf ePsf] ;du| sf/f]af/, a}+sn] xfl;n u/]sf] pknAwL / efjL of]hgfx?sf] ljifonfO{ ;d]6]/ sDkgL P]g, @)^#, a}+s tyf ljQLo ;:+yf ;DjGwL P]g, @)&# tyf g]kfn /fi6« a}+ssf] lgb]{zgsf] kl/lw leq /xL of] k|ltj]bg ;+rfns ;ldltsf] tkm{af6 a}+ssf] ;ftf}+ / cf7f}+ jflif{s ;fwf/0f ;efdf 5nkmn tyf kfl/t ug{sf] nflu k]z u/]sf] 5' .

l;len a}+s lnld6]8n] cfly{s jif{ @)&#÷)&$ / @)&$÷)&% sf] ;ldIff cjlwdf u/]sf] sfo{;DkfbgnfO{ lgDgfg';f/ k|:t't ul/Psf] 5 M

-!_ ;ldIff cjlwsf] ;+lIfKt ljQLo emns M

cfly{s jif{ @)&#÷)&$ / @)&$÷)&% df o; a}+ssf] nflu r'gf}ltk"0f{ ;do /xof] . 5f]6f] cGt/fndf t/ntfdf cfPsf] ;+s'rgn] lgIf]k Jofhsf] nfutdf Jofks j[l¢ x'gsf ;fy} shf{ k|jfx ck]Iffs[t sd ePsf]n] v'b Jofh cfDbfgL 36\g k'u]sf] 5 . b]zdf laBdfg /fhgLlts cj:yf, cfly{s r'gf}tL, ;/sf/sf] ljsf; vr{df ePsf] Go"gtf, ljk|]if0f a[l4b/df sdL, >d zlQmsf] knfog cflb h:tf sf/0fx?n] hnljB't / l;d]G6 pBf]u afx]s cGo pTkfbgzLn pBf]ux?sf] :yfkgf / ;+rfng gx'Fbf a}+sx?n] cfkm\gf] nufgL ;d]t cGo If]qdf s]lGb|t ug'{ kg]{ afWotf /xL cfPsf] 5 . g]kfn /fi6« a}+sn] df}lb|s gLlt dfkm{t a}+s tyf ljQLo ;+:yfsf] k"FhL a[l4 ug]{ gLlt cg'?k r'Qmf k"FhL a[l4 ;Fu;Fu} Joj;fo lj:tf/ ug{sf] nflu shf{df u/]sf] a[l4n] shf{sf] Aofhb/ ;ldIff cjlwdf lgs} k|lt:kwL{ x'Fbf xfdL h:tf kl5Nnf] k':tfsf a}+s tyf ljQLo ;+:yfx?nfO{ :yflkt k'/fgf / 7'nf a}+sx?;+u k|lt:kwf{ u/L d'gfkmf cfh{g ug{ lgs} s;/t ug'{ k¥of] . o; sl7g kl/l:yltsf afah'b ;dLIff cjlwdf o; a}+sn] ;Gtf]ifhgs pknlAw xfl;n u/]sf] 5 . a}+ssf] ;ldIff cjlwsf] k|d'v ljQLo ;'rsf+Íx? lgDg adf]lhd /x]sf 5g\ .

-@_ lgIf]k kl/rfng (Deposit Mobilization)

cf=j= @)&#÷)&$ df a}+sn] s"n lgIf]k ?= #$,@#,%@,$@,&&^.– /x]sf]df cf=j= @)&$÷)&% df ?= $),)!,@^,&@,**(.– k'¥ofpg ;kmn ePsf] 5 . h; cGt/ut :jb]zL d'b|fsf] lgIf]k ?= #(,*&,!#,^#,&@& / ljb]zL d'b|fsf] lgIf]]k ?= !$,!#,)(,!^@ /x]sf] 5 . a}+sdf /x]sf] lgIf]knfO{ ljljlws/0f u/L ;fwf/0f jrt lgIf]knfO{ cfslif{t ug{ ljleGg k|sf/sf vftfx? dfkm{t lgIf]k ;+sng ug]{ ul/Psf] 5 . a}+sdf ;fwf/0f jrt lgIf]ksf] c+z a[l4 ug{ cfufdL jif{ klg ljz]if of]hgfsf ;fy lg/Gt/tf lbOg]] 5 . a}+ssf] rNtL art lgIf]ksf] of]ubfg @! k|ltztaf6 a[l4 eO{ @( k|ltzt k'Ubf ;du| lgIf]k !^=** k|ltztn] a[l4 ePsf] 5 .

-#_ shf{ tyf shf{ Joj:yfkg (Credit & Credit Management) a}+sn] shf{ k|jfx ug{ ljz]if ;ts{tf ckgfO{ dfq shf{ k|jfx gLlt adf]lhd >f]tdf g} kof{Kt ;hutf ckgfO{ a}+sdf nfu" ePsf Credit Policy Guidelines, Credit Risk Rating System, Credit Risk Management Framework, Valuation Guidelines Pj+ g]kfn /fi6« a}+sjf6 hf/L ePsf gLlt lgb]{zgx?sf] sfof{Gjog u/L a}+sdf shf{sf] u'0f:t/ pRr /fVg] tkm{ ljz]if ;ts{ /xL sfd ul/Psf] 5 . a}+sn] ;w} em} ljz]if k|yfldstfdf /flv s[lif, ko{6g, hnljw't nufot cGo shf{ nufgL ub}{ cfPsf] 5 . To;}u/L ljkGg ju{ shf{nfO{ klg k|yfldstfdf /fvL g]kfn ;/sf/ / g]kfn /fi6« a}+ssf] gLlt lgb]{zg adf]lhd shf{ lj:tf/ ub}{ cfPsf 5f}+ . cf=j= @)&$÷)&% sf] cfiff9 d;fGtdf ;du| ljQLo If]qdf shf{ a[l4 @@=$! k|ltzt /x]sf]df o; a}+ssf] shf{ #!=&! k|ltztn] a[l4 u/L s'n $)=^& cj{ shf{ nufgL ug{ ;Ifd ePsf] 5 . To afx]s shf{ lj:tf/sf qmddf a}+sn] ljz]if k|yfldstfdf /flv JolQmut lwtf] shf{, z}lIfs shf{, ;jf/L shf{, ;'g rfFbL shf{, z]o/ shf{, d'2lt /l;b shf{, 3/ shf{, zf}o{ zlQm shf{ cflb h:tf pkef]Qmfd'vL shf{ / cGo Jofkf/ shf{x?sf] dfWodaf6 shf{sf] lj:tf/ ul/Psf] 5 .

a}+sn] cy{tGqsf] d"n cfwf/sf] ?kdf /x]sf] s[lif If]q nufot ;fgf] Joj;fox?df ;+nUg 7"nf] ;+Vofdf /x]sf] ljkGg ju{nfO{ nlIft u/L b]zsf ljleGg :yfgx?df n3' a}+lsË (Micro Banking) sfo{qmd / zfvf/lxt ;]jf (Branchless Banking) ;]jf ;+rfngnfO{ lg/Gt/tf k|bfg ul/Psf] 5 .

a}+sn] shf{ nufgLsf] If]qnfO{ ljljlws/0f u/L If]qut shf{ k|jfx of]hgf ( Sectoral Credit Expansion Planning) agfO{ nfu" ul/Psf] 5 . cf=j= @)&$÷)&% sf] cfiff9 d;fGtdf a}+ssf] s'n nufgLsf] s[lif tyf ag If]qdf $=@& k|ltzt, df5f kfngdf )=)! k|ltzt, vfgLdf )=)* k|ltzt, s[lif, ag tyf

l;len a}+s lnld6]8sf];ftf}+ / cf7f} jflif{s ;fwf/0f ;efsf] nflu

;+rfns ;ldltsf] k|ltj]bgcf=j = @)&#÷)&$ / @)&$÷)&%

ljj/0f;fljssf] g]=/f=a} lgb]{lzsf $ adf]lhd NFRS adf]lhd

@)&!÷)&@ @)&@÷)&# @)&#÷)&$ @)&#÷)&$ @)&$÷)&%

;+rfng cfDbfgL 1,043,718 1,239,996 1,423,872 1,639,784 1,850,468

;+rfng vr{ 468,283 510,702 637,551 685,735 992,675

;+rfng d'gfkmf -Joj:yf cl3sf]_ 575,434 729,295 786,321 954,049 857,792

v'b d'gfkmf -s/ kl5sf]_ 230,020 194,228 348,280 1,538,961 629,899

ljj/0f;fljssf] g]=/f=a} lgb]{lzsf $ adf]lhd NFRS adf]lhd

@)&!÷)&@ @)&@÷)&# @)&#÷)&$ @)&#÷)&$ @)&$÷)&%

r'Qmf k"FhL 3,082,779 3,214,793 5,929,301 5,185,222 7,259,310

lgIf]k 26,656,424 31,564,023 34,235,243 34,235,243 40,012,673

shf{ 23,165,580 26,529,053 30,881,205 31,511,144 41,366,703

lgis[o shf{ k|ltzt 3=20 4=49 3=96 3=96 2=63

l:y/ ;DklQ -v'b_ 313,245 262,800 279,164 279,164 296,476

s"n ;DklQ 30,423,585 35,269,450 41,720,922 42,299,417 51,925,229

ljj/0f;fljssf] g]=/f=a} lgb]{lzsf $ adf]lhd NFRS adf]lhd

@)&!÷)&@ @)&@÷)&# @)&#÷)&$ @)&#÷)&$ @)&$÷)&%

v'b d'gfkmf÷s"n cfDbfgL 9=64Ü 7=30Ü 9=93Ü 33=10Ü 12=79Ü

;+rfng vr{÷;+rfng cfDbfgL 44=87Ü 41=19Ü 44=78Ü 41=82Ü 53=64Ü

;DklQdf k|ltkmn 0=76Ü 0=55Ü 0=83Ü 3=64Ü 1=21Ü

Kf|lt z]o/ cfDbfgL 7=46 6=03 5=87 29=68 9.69

:yfoL sd{rf/L 406 404 526 526 685

zfvfx? 41 42 53 53 68

t/ntf (CRR) cg'kft 10=52Ü 8=50Ü 7=13Ü 7=13Ü 6=34Ü

kF"hLsf]if cg'kft 13=65Ü 12=19Ü 18=82Ü 18=82Ü 20=32Ü

-s_ k|d'v pknlAw÷glthf M -v_ k|d'v sf/f]jf/ tyf ;'rsf+Íx? M

-u_ k|d'v ;'rsf+Íx? M

-?=xhf/df_ -?=xhf/df_

CIVIL BANK | ANNUAL REPORT 2073 / 2074 & 2074 / 2075

u

k]o kbfy{df #=%$ k|ltzt, u}/vfB a:t' pTkfbgdf !(=*@ k|ltzt, lgdf{0fdf &=@# k|ltzt ljB't, Uof; / kfgLdf $=*! k|ltzt, wft'sf pTkfbg, d]l;g/L tyf On]S6«f]lgs cf}hf/ tyf h8fgdf )=() k|ltzt, oftfoft, e08f/ / ;+rf/df #=%$ k|ltzt, yf]s tyf v'b|f ljqm]tfdf @@=%! k|ltzt, ljQ, aLdf tyf crn ;DklQdf !@=^$ k|ltzt, ko{6gdf #=#$ k|ltzt, cGo ;]jfx?df $=^% k|ltzt, pkef]Qmf shf{ ^=%( k|ltzt / cGodf ^=)^ k|ltzt shf{ nufgL ul/Psf] 5 . ;dLIff cjlwdf klg ljutdf h:t} 3/hUuf tyf l/on:6]6 If]qdf x'g] nufgLnfO{ l;ldt u/L cToGt} ;+oldt eP/ nufgL ul/Psf]df cfufdL jif{ klg o; gLltnfO{ lg/Gt/tf lbO{g]5 . o;sf ;fy;fy} shf{sf] u'0f:t/ ;'wf/ ub}{ n}hfg] / shf{ lj:tf/ ubf{ pkef]Qmfd'vL shf{, n3'ljQ shf{ / u}/sf]ifdf cfwfl/t shf{ ;'ljwf lj:tf/ ug]{ of]hgfx? sfof{Gjog ul/g]5 .

-$_ dfgj ;+;fwg Joj:yfkg (Human Resource Management)

sd{rf/Lsf] Joj:yfkg / ;]jfdf lg/Gt/tf sfod ug]{ sfo{df ut jif{sf] t'ngfdf ;dLIff jif{df s]xL j9L r'gf}ltk"0f{ /x]sf] 5 . cf=j= @)&$÷)&% sf] cfiff9 d;fGtdf s'n ^*% hgf :yfoL tyf s/f/sf sd{rf/Lx? ljleGg txdf /x]/ a}+ssf] ;]jfdf h'6]sf lyP . k|To]s :yflgo txx?df a}+sx?sf] ;]jf k'¥ofpg] g]kfn ;/sf/sf] gLlt cg'?k g]kfn /fi6« a}+ssf] lgb]{zg cg';f/ a}+sx?n] lta| ?kdf zfvf lj:tf/ u/] ;Fu} bIf sd{rf/Lsf] cefjn] ubf{ cGo a}+sx?n] sd{rf/Lx?nfO{ cfsif{s tnj ;'ljwf ;lxt lgo'Qm ubf{ ;ldIff cjlwdf o; a}+saf6 !#! hgf sd{rf/Lx?n] /flhgfdf u/]sf 5g\ . o;/L a}+sn] u/]sf] cfDbfgL / sd{rf/Lsf] ;]jf ;'ljwfdf ;fd~h:otf sfod ug{ tyf ablnbf] kl/l:ylt tyf Joj;flos lj:tf/ ;+u;+u} bIf sd{rf/Lsf] lgo'lQm / ;]jfdf sfo{/t sd{rf/Lsf] ;]jf lg/Gt/tf lgs} r'gf}ltk"0f{ /x]sf] 5 . sd{rf/Lsf] 5gf}6, ;?jf, j9'jf tyf a[QL ljsf;df a}+sn] kf/bzL{ gLlt agfO{ nfu" u/]sf] 5 .

-%_ zfvf lj:tf/ (Branch Expansion)

a}ssf] xfn s'n zfvf ;+Vof &@ j6f /x]sf] 5 . k|To]s :yfgLo txx?df a}+sx?sf] ;]jf k'¥ofpg] g]kfn ;/sf/sf] gLlt cg'?k g]kfn /fi6« a}+ssf] lgb]{zg cg';f/ o; a}+sn] b'u{ddf !^ j6f zfvf vf]ln;s]sf] 5 . zfvf ;+Vof j[l¢ ;Fu ;Fu} zfvf sfof{nox?nfO{ ;'b[9 / ;Ifd agfpg] gLlt lnO{g]5 . o; jfx]s s'n ^ :yfgaf6 zfvf /lxt a}+lsË tyf ! :yfgdf PS;6]G;g sfpG6/af6 ;]jf ;+rfng ul/Psf] 5 .

-^_ ;+:yfut ;'zf;g (Corporate Governance)

o; a}+sn] ;+:yfut ;'zf;gsf] :t/nfO{ pRrtd ?kdf dxTj lbO{ ;+:yfut ;'zf;gsf] pNn+3gnfO{ z'Go ;xgl;ntf (Zero Tolerance) sf] gLlt cjnDag ub}{ cfPsf]] 5 . g]kfn /fi6« a}+s tyf cGo lgods lgsfox?jf6 ;+:yfut ;'zf;g ;DjGwL hf/L ePsf gLlt lgod tyf o;sf] dd{ / efjgf ;d]tdf a}+ssf] ;+rfns ;ldlt b[9 ;+slNkt 5 . ;+:yfut ;'zf;gsf dfkb08x?nfO{ clwstd k|of]u u/L g]kfnsf] ljQLo If]qdf pbfx/0fLo a}+s aGg] xfd|f] nIo xf] . ;+:yfut ;'zf;gsf] ;'b[9 sfof{Gjog / kfngfaf6 g} :j:y / lbuf] k|ltkmn (Healthy & Sustainable Return) k|fKt ug{ ;lsg] s'/fdf ;+rfns ;ldlt ljZj:t 5 .

;+:yfut ;'zf;g sfof{Gjog ug{sf] nflu a}+sdf ;+rfns ;ldltsf] cnfjf b]xfo adf]lhdsf] ;ldlt tyf pk–;ldltx? u7g ul/Psf] 5 .

;+rfns:t/sf] ;ldltx? M g]kfn /fi6« a}+ssf] lgb]{zg tyf a}+s tyf ljQLo ;+:yf ;DaGwL P]g, @)&# sf] bkmf @^, @&, ^) / ^! sf] Joj:yf cg';f/ ;+rfns ;ldltn] cfkm\gf] hjfkmb]lxdf n]vfk/LIf0f ;ldlt, hf]lvd Aoj:yfkg ;ldlt, dfgj ;+;fwg Aoj:yfkg ;ldlt / ;DklQ z'l¢s/0f lgjf/0f ;ldlt u7g u/]sf] 5 .

-s_ n]vfk/LIf0f ;ldlt (Audit Committee) ;+rfns ;ldltn] u}/ sfo{sf/L ;+rfns >L k|sfz tfonHo"sf] ;+of]hsTjdf ;+rfns >L 3g]Gb| axfb'/ >]i7 ;b:o / cfGtl/s n]vfk/LIf0f ljefusf k|d'v ;b:o ;lrj ePsf] tLg ;b:oLo n]vfk/LIf0f ;ldlt u7g u/]sf] 5 . a}+ssf] cfGtl/s n]vfk/LIf0f u/L ;f]sf] k|ltj]bg n]vfk/LIf0f ;ldltsf] a}7sdf 5nkmn u/L /fo ;'emfj ;+rfns ;ldltdf k]z ug]{ Joj:yf ul/Psf] 5 . o; ;ldltn] a}+s ;+rfns ;ldlt tyf Joj:yfkgnfO{ ;f]em} ;'emfj tyf lgb]{zg klg lbg ;Sg] Joj:yf 5 . cfGtl/s n]vfk/LIf0f ljefunfO{ :jtGq ljefusf] ?kdf :yfkgf ug{sf] nflu cfjZos gLlt lgodx? agfO{ nfu" ul/Psf] 5 . cf=j= @)&#÷)&$ df o; ;ldltsf] !! j6f tyf cf=j= @)&$÷)&% df !! j6f a}7s a;]sf] lyof] . cfGtl/s n]vfk/LIf0f ljefusf] sfo{Ifdtf a[l4 ug{ cfjZos >f]t / ;fwgsf] Joj:yf u/L n]vfk/LIf0f ljefunfO{ cem ;zQm agfpb} nlug]5 .

-v_ hf]lvd Aoj:yfkg ;ldlt (Risk Management Committee);+rfns ;ldltn] u}/ sfo{sf/L ;+rfns >L ;+ud s]= l;= Ho"sf] ;+of]hsTjdf hf]lvd Aoj:yfkg ;ldlt u7g u/]sf] 5 . ;f] ;ldltsf cGo ;b:ox?df ;+rfns >L k|sfz tfon, k|d'v ;+rfng clws[t / Plss[t hf]lvd Joj:yfkg tyf cg'kfngf ljefusf k|d'v ;b:o ;lrj /xg' ePsf] 5 . a}+ssf] ;du| hf]lvd cj:yfsf] af/]df cWoog tyf d'Nof+sg u/L ;+rfns ;ldltnfO{ /fo l;kmfl/z k]z ug{ hf]lvd Joj:yfkg ;ldlt lqmoflzn 5 . cf=j= @)&#÷)&$ o; ;ldltsf] $ j6f tyf cf=j= @)&$÷)&% df * j6f a}7s a;]sf] lyof] . pNn]lvt a}7saf6 ;+rfns ;ldltnfO{ a}+ssf] shf{ hf]lvd, ;+rfng hf]lvd, t/ntf hf]lvd, ahf/ hf]lvd nufotsf hf]lvd Go"lgs/0fsf] nflu pkof]lu ;'emfj tyf /fox? k|fKt ePsf] lyof] . k|fKt /fo ;'emfjnfO{ tTsfn sfof{Gjog ;d]t ul/Psf] 5 .

-u_ dfgj ;+;fwg Aoj:yfkg ;ldlt (Human Resource Management Committee);+rfns ;ldltn] u}/ sfo{sf/L ;+rfns >L cDaL/ af]u6LHo"sf] ;+of]hsTjdf dfgj ;+;fwg Aoj:yfkg ;ldlt u7g u/]sf] 5 . ;f] ;ldltsf cGo ;b:ox?df ;+rfns >L ;+ud s]= l;= Ho", k|d'v sfo{sf/L clws[t, k|d'v ljQ clws[t ;b:o / dfgj ;+;fwg ljefu k|d'v ;b:o ;lrj /xg' ePsf] 5 . ;ldltn] a}+sdf sd{rf/Lsf] lgo'lQm, ;?jf, a9'jf, a[lQ ljsf;, kb:yfkgf, sfo{;Dkfbg d'Nof+sg, k'/:sf/, ;hfo / >d ;DaGw, kfl/>lds cflbsf] lgoldt ?kn] cWoog u/L pko'Qm gLlt lgdf{0f ug{ ;+rfns ;ldltnfO{ /fo ;'emfj k]z ug]{ u/]sf] . ;fy} o; ;ldltsf] l;kmfl/zdf a}+sdf sd{rf/Lsf] sfo{;Dkfbg d'Nof+sg lgb]{lzsf tyf cGo sd{rf/L;DaGwL gLlt lgodx? lgdf{0f u/L nfu' ul/Psf] 5 .

-3_ ;DkQL z'l¢s/0f lgjf/0f ;ldlt (Assets laundering Prevention Committee)g]kfn /fi6« a}+ssf] Plss[t lgb]{zg @)&$ cg';f/ ;+rfns ;ldltn] u}/ sfo{sf/L ;+rfns >L 3g]Gb| axfb'/ >]i7Ho"sf] ;+of]hsTjdf ;DkQL z'l¢s/0f lgjf/0f ;ldlt u7g u/]sf] 5 . ;f] ;ldltsf cGo ;b:ox?df ;+rfns >L k|sfz tfonHo", PsLs[t hf]lvd Joj:yfkg tyf cg'kfngf ljefu k|d'v ;b:o / k|d'v cg'kfngf OsfO ;b:o ;lrj /xg' ePsf] 5 .

CIVIL BANK | ANNUAL REPORT 2073 / 2074 & 2074 / 2075

#

-&_ ufEg] ufleg]/ k|flKt (Merger/Acquisition)

cf=j= @)&@÷&# sf] df}lb|s gLlt cg';f/ a}+s tyf ljQLo ;+:yfx?sf] k"FhLut cfwf/ ;'b[9 u/L bL3{sflng ljsf;sf nflu cfjZos kg]{ ;|f]t kl/rfng ug{ tyf ljQLo :yfloTjsf nflu a}+s tyf ljQLo ;+:yfx?sf] tTsfn sfod /x]sf] Go'gtd r'Qmf kF'hLnfO{ rf/ u'0ffn] j[l¢ ug'{kg]{ k|fjwfg cg'?k a}+ssf] Go'gtd r'Qmf k"FhL ?= * cj{ k'¥ofpg' kg]{ k|fjwfg cg'?k o; a}+sn] c=j= @)&#÷)&$ leqdf OG6/g]zgn lnlhË P08 kmfOgfG; sDkgL lnld6]8 nfO{ ufEg] tyf o'lgs kmfOgfG; lnld6]8 / xfdf dr]{G6 P08 kmfOgfG; lnld6]8nfO{ k|flKt ug] sfo{ ;DkGg eO;s]sf] ;fy} ;f] ;d]tnfO{ ;d]6]/ $) k|ltzt xsk|b z]o/ lgisf;g sfo{ ;DkGg u/L o; k|ltj]bg tof/ kfbf{sf] ldlt ;Dddf a}+ssf] r'Qmf k"FhL ?= &=@% cj{ k'¥ofO{;s]sf] / afsL gk'u k"FhL o;} ;fwf/0f ;efdf k]z eP adf]lhdsf] k|:tfljt af]gz z]o/af6 k'Ug]5 . cfufld lbgx?df a}+snfO{ cem ;an agfpg tyf k"FhLut lx;fjn] yk dha't agfpgsf] nflu o; a}+sn] cGo pko'Qm a}+s tyf ljQLo ;+:yfx? Ps cfk;df ufEg]÷ufleg - dh{/ _ jf k|flKt -PlSjlh;g _ ug{÷x'g jf :jb]zL÷ljb]zL /0fgLlts ;fem]bf/Ldf hfg cfjZos ;xdtL / ;Demf}tf nufotsf cfjZos ;Dk"0f{ sfo{x? ug{÷u/fpg] ;DaGwL ljz]if k|:tfj o; ;Ddflgt ;efaf6 kfl/t u/L ;f] ;DaGwL cfjZos ;a} sfo{ ug{sf] nflu ;+rfns ;ldltnfO{ clVtof/L k|bfg ug'{ x'g cg'/f]w ul/G5 .

-*_ hf]lvd Aoj:yfkg (Risk Management)

a}+lsË Joj;fodf lglxt hf]lvd, ahf/ hf]lvd, Aofhb/ hf]lvd, ;+rfng hf]lvd, t/ntf hf]lvd nufotsf ;du| a}+lsË hf]lvdx?sf] cfsng Joj;fodf pTkGg x'g] ljljw hf]lvdx?nfO{ Go"lgs/0f ug{ k|0ffnLa4 k|lqmofsf] :yfkgf u/L sfo{ ub}{ cfPsf] 5 . sf/f]af/df x'g] ;du| hf]lvd Go"lgs/0f ug{sf] nflu 5'6\6} Plss[t hf]lvd Joj:yfkg ljefusf] :yfkgf ul/Psf] 5 . o;sf cltl/Qm cg'kfngf ljefu, cfGtl/s n]vfk/LIf0f ljefu, zfvf ;+rfng ljefu, sfg"g ljefu cflb h:tf ;+:yfut ;+/rgfsf] dfWodaf6 Joj;fodf pTkGg x'g] hf]lvdsf] lg/Gt/ cg'udg tyf ;f]sf] Go"lgs/0f ug]{ Joj:yf ul/Psf] 5 .

-(_ l8lh6n a}+lsË (Digital Banking)

l;len a}+s lnld6]8n] gljgtd k|ljlwx?nfO{ cfTd;ft ub}{ a}+ssf b}lgs sfo{x?nfO{ k|ljlw pGd'v agfO{ ;]jf tyf ;'ljwfx?nfO{ l56f] 5l/tf] agfpgsf] nflu l8lh6n a}+lsË ljefusf] :yfkgf ul/Psf] 5 . ;fy} cfufld lbgx?df a}+sn] ug]{ sfo{x?nfO{ :jrflnt (Automation) ub}{ nlug] tyf sfuh /lxt sfo{ ug]{ jftfj/0f agfpg] tkm{ cufl8 al9g]5

-!)_ ljB'tLo a}+lsË (E-banking)

l;len a}+s lnld6]8nfO{ k|ljlwdf cfwfl/t a}+s (IT Driven Bank) sf] ?kdf :yflkt u/fpg Joj:yfkg tyf ;+rfns ;ldlt sl6a4 eO{ nfu]sf] 5 . a}+sn] ;+rfngdf cfPsf] 5f]6f] ;dodf g} MasterCard sf] ;b:otf k|fKt eO{ u|fxsx?nfO{ 8]lj6 sf8{ hf/L u/]sf] 5 . eljiodf qm]l86 sf8{ hf/L ug]{ tkm{ a}+sn] u[xsfo{ k|f/De ul/;s]sf] 5 . 8]lj6 sf8{, OG6/g]6 a}+lsË, SMS Banking, Civil Smart Bank h:tf ;]jf ;+rfngdf lg/Gt/tf lbO{Psf] 5 . ljB'tLo sf/f]af/af6 u|fxsju{df x'g ;Sg] Electronic Fraud sf] hf]lvd Go"lgs/0f ug{sf] nflu ;"rgf k|ljlw ;+/rgfsf] :t/f]GgtL ug]{ sfo{nfO{ lg/Gt/tf lbPsf] 5 . a}+sn] ut cfly{s jif{ b]lv EMV compliance x'g] lrksf8{ hf/L ul/;s]sf] 5 .

a}+ssf zfvfx? tyf Aofkfl/s :yfgx?df ATM d]l;g /fvL ;+rfng ug]{ gLlt cg'?k xfn ;Dddf a}+sn] s'n %$ j6f ATM d]l;gx? h8fg u/L lgIf]kstf{x?nfO{ ;]jf k'¥ofO{ /x]sf] 5 . -!!_ ljk|]if0f sf/f]af/ (Remittance Transaction)

a}+sn] ;+rfngdf NofPsf]] l;len a}+s /]ld6 ;]jfsf] b]z e/df e'QmfgL Ph]G6x? /x]sf] / cGo g]kfndf Vofltk|fKt ljk|]if0f ;]jfx? dlgu|fd, k|e' dlg, cfO{PdO{, ;'ne /]ld6, P;laPn /]ld6, cfO{k], a]i6 /]ld6, OhLlnÍ /]ld6]G;, a'd /]ld6, lxdfn /]ld6, l;l6 PS:k|];, j]i6g{ o'lgog dlg 6«fG;km/ / ljb]zL sDkgLx? dfjfl/8 PS:r]~h b'jO{, cncG;f/L PS:r]~h b'jO{, PlS;; a}+s lnld6]8 ef/tsf] ljk|]if0f e'QmfgL k|ltlglw eO{ cfGtl/s tyf jfXo ljk|]if0f sf/f]af/ ub}{ cfPsf] 5 .

-!@_ ;+:yfut ;fdflhs pQ/bfloTj (Corporate Social Responsibility)

l;len a}+sn] ;+:yfut ;fdflhs pQ/bfloTj sfo{sf] lg/Gt/tfnfO{ ljut em} o; ;ldIff cfly{s jif{df klg lg/Gt/tf lbOPsf] 5 . a}+ssf] ;fgf] ;xof]un] ;dfhdf 7'nf] kl/jt{g gxf]nf t/ To;n] ;dfhsf] nflu ;sf/fTds ;Gb]z k|bfg ug]{ s'/fdf xfdL ljZj:t 5f}+ . ;dLIff cf=j= df lzIff, :jf:Yo, kof{j/0f ;+/If0f, ;+:s[lt ;+/If0f, k|fs[lts ljktdf k/]sf JolQmx?nfO{ ;xof]u ul/Psf] 5 . a}+sn] g]kfn afn ;+u7gdf /x]sf # hgf cgfy afnsx?sf] ;Dk"0f{ vr{ Joxf]g]{ sfo{nfO{ o; jif{ klg lg/Gt/tf lbO{Psf] 5 . o;sf cnfjf a}+sn] rfO{N8 8]enkd]06 ;f];fO{6LnfO{ klg cfly{s ;xof]u u/]sf] 5 . a}sn] k|]d ;fu/ kmfpG8]zg dfkm{t afnaflnsfsf] nflu hn ef]hgsf] nflu cfly{s ;xof]u u/]sf] 5 . a}sn] g]kfn l6=lj= P;f]l;P;gn] u/]sf] l6=lj= ;DalGw ;Dd]ngsf] nflu cfly{s ;xof]u u/]sf] 5 . a}+sn] >L sdnfbL u0f]z lasf; tyf hfqfkj{ ;xof]u ;ldltnfO{ dxk'hfsf] nflu cfly{s ;xof]u k|bfg u/]sf] 5 . ;fy ;fy} a}+sn] jflif{s pT;jsf] cj;/df /Qmbfg, ljlQo ;fIf/tf sfo{qmd tyf ul/j tyf h]x]Gbf/ ljwfyL{x?sf] nflu 5fqj[lt k|bfg ug]{ sfo{ ;DkGg u/]sf] 5 . cfufld lbgx?df ;d]t a}+sn] ;+:yfut ;fdflhs pQ/bfloTj sfo{nfO{ lg/Gt/tf lbO{g]5 .

-!#_ lgis[o shf{sf] Joj:yfkg (Management of Non Performing Loan)

cf=j= @)&#÷)&$ sf] cfiff9 d;fGtdf a}+ssf] lgis[o shf{ cg'kft #=(^ k|ltzt /x]sf]df cf=j= @)&$÷)&% sf] cfiff9 d;fGtdf lgis[o shf{ cg'kft @=^# k|ltzt /x]sf] 5 . cf=j= @)&@÷)&# df of] cg'kft $=$( k|ltzt /x]sf] lyof] . rfn' cly{s jif{sf] bf]>f] q}df;df of] #=%$ k|ltzt x'g cfPsf] 5 . cfb/0fLo z]o/wgL dxfg'efjx? a}+ssf] lgis[o shf{ cg'kft a}+lsË If]qsf cGo a}+ssf] t'ngfdf cem} pRr 5 . shf{ c;'ln tyf lgis[o shf{ 36fpg tyf yk j[l¢ x'g glbgsf] nflu shf{ Jo:yfkg tyf c;'lndf cem k|efjsf/L e"ldsf v]Ng'kg]{ cfjZostf /x]sf] 5 .

CIVIL BANK | ANNUAL REPORT 2073 / 2074 & 2074 / 2075

shf{ c;'nLnfO{ k|efjsf/L agfpgsf]] nflu s]lGb|o :t/df shf{ c;'nL ljefunfO{ ;jnLs/0f ul/Psf] / ;DalGwt Sn:6/ tyf zfvfx?;Fu ;dGjo u/L shf{ c;'nL ug]{ sfo{nfO{ ;'b[l9s/0f ug{ a}+s Joj:yfkgnfO{ lgb]{zg lbO{Psf] 5 . shf{ c;'nLsf] sfo{nfO{ lg/Gt/ ?kdf cufl8 a9fpFb} yk shf{ gf]S;fgL Joj:yf gx'g] tkm{ ;hu /xL lgis[o shf{nfO{ ! k|ltzt leq} /fVg] nIosf ;fy a}+s cufl8 a9]sf] 5 .

-!$_ d'gfkmf tyf nfef+zsf] afF8kmfF8 (Profit and Dividend Distribution) a}+sn] cf=j= @)&@÷)&# sf] t'ngfdf !&^=&^ k|ltztn] ;+rfng d'gfkmf a[l4 u/L shf{ gf]S;fgL Joj:yf tyf s/ kZrft ? #$=*# s/f]8 v'b d'gfkmf, jf;nftdf /x]sf] ;+lrt d'gfkmf / dh{/ tyf PlSjlhzgaf6 cfPsf] Soflk6n l/h{eaf6 z]o/wgL dxfg'efjx?nfO{ r'Qmf k"FhLsf] !)=@%Ü k|ltztsf b/n] x'g cfpg] ?= &$,$),&(,#!@.)* -cIf/]kL rf}xQ/ s/f]8 rfln; nfv pgf;L xhf/ ltg ;o af¥x ?k}of cf7 k};f dfq_ a/fa/sf] af]gz z]o/ tyf )=%$Ü sf b/n] x'g cfpg] ?= #,(!,^@,)^(.)^ -cIf/]kL ltg s/f]8 PsfgAa] nfv a};ÝL xhf/ pgG;t/L ?k}of 5 k};f dfq_ gub nfef+z tyf cf=j= @)&$÷)&% df ;+lrt d'gfkmfaf6 r'Qmf k"FhLsf] $=)%Ü sf b/n] x'g cfpg] ?=@(,$),)@,)^(.^% -cIf/]kL pGglt; s/f]8 rfln; nfv b'O{ xhf/ pgfG;Q/L ?k}of k};ÝL k};f dfq_ gub nfef+z ljt/0f ug]{ k|:tfjnfO{ o; ul/dfdo ;fwf/0f ;efaf6 kfl/t ul/lbg' x'g cg'/f]w ub{5f} . ;fy} af]g; z]o/ ljt/0f ubf{ vl08s[t (Fraction) x'g] z]o/nfO{ ljut jif{df em} z]o/ k"0f{s[t geP;Dd ;DalGwt z]o/wgLs} gfddf /fVg] k|:tfj ul/Psf] 5 .

cGTodf,cGTodf, a}+s ;~rfngsf nflu xfdLnfO{ ;'lDkg' ePsf] uxgtd cleef/fnfO{ OdfGbf/Lk"j{s jxg ug{ sl6j4 /x]sf] Joxf]/f cjut u/fpb} k|ToIf ck|ToIf ?kdf o; a}+ssf] pGgtL tyf k|ultdf of]ubfg k''¥ofpg' x'g] ;Dk"0f{ z]o/wgL dxfg'efjx?, g]kfn /fi6« a}+s, sDkgL /lhi6«f/sf] sfof{no, g]kfn lwtf]kq af]8{, g]kfn :6s PS;r]Gh lnld6]8, g]kfn a}+s;{ ;+3, n]vfk/LIfs, sd{rf/Lx? tyf cfb/0fLo u|fxs dxfg'efjx? nufot ;Dk"0f{ dxfg'efj tyf ;+3 ;+:yfx?nfO{ wGojfb 1fkg ub}{} ;j} kIfaf6 xfn kfO/x]sf] ;befj tyf ;dy{g cfpg] lbgx?df ;d]t lg/Gt/ kfpg] ljZjf; ;lxt a}+ssf] rf}tkmL{ k|ultsf nflu ;b}j k|ltj4 /x]sf] ljZjf; lbnfpg rfxG5f}F .

wGojfb Û

;+rfns ;ldltsf] tkm{af6 O{= OR5f /fh tfdfË

cWoIf

ldlt M @)&^÷)!÷)@

CIVIL BANK | ANNUAL REPORT 2073 / 2074 & 2074 / 2075

r

-!_ ljut jif{sf] sf/f]jf/sf] l;+xfjnf]sg M a}+ssf] ;+rfns ;ldltsf] k|ltj]bgdf o; ;DjGwdf pNn]v ul/Psf] 5 . -@_ /fli6«o tyf cGt/fli6«o kl/l:yltaf6 sDkgLsf] sf/f]jf/nfO{ s'g} c;/ k/]sf] eP ;f] c;/ .

-s_ cGt/fli6«o kl/l:ylt

;g\ @)!* df ljZj cy{tGq #=& k|ltztn] j[l4 ePsf]df ;g\ @)!( df #=% k|ltztn] j[l4 x'g] cGt/fli6«o d'b|fsf]ifsf] k|If]k0f 5 . ljsl;t d'n'sx?sf] cy{tGq ;g\ @)!* df @=# k|ltztn] j[l4 ePsf]df ;g\ @)!( df @ k|ltztn] j[l4 x'g] cGt/fli6«o d'b|fsf]ifsf] k|If]k0f 5 .

pbLodfg tyf ljsf;zLn cy{tGq ;g\ @)!* df $=^ k|ltztn] j[l4 ePsf]df ;g\ @)!( df $=% k|ltztn] a9\g] cGt/fli6«o d'b|fsf]ifsf] k|If]k0f 5 . rLgsf] cy{tGq ;g\ @)!* df ^=^ k|ltztn] j[l4 ePsf]df ;g\ @)!( df ^=@ k|ltzt / ef/tLo cy{tGq ;g\ @)!* df &=# k|ltztn] j[l4 ePsf]df ;g\ @)!( df &=% k|ltztn] lj:tf/ x'g] sf]ifsf] k|If]k0f 5 .

ljsl;t cy{tGqx?df pkef]Qmf d'b|:kmLlt ;g\ @)!* df @=) k|ltzt /x]sf]df ;g\ @)!( df !=& k|ltzt x'g] cGt/fli6«o d'b|fsf]ifsf] k|If]k0f 5 . pbLodfg tyf ljsf;zLn cy{tGqx?df pkef]Qmf d'b|:kmLlt ;g\ @)!* sf] $=( k|ltztsf] t'ngfdf ;g\ @)!( df %=! k|ltzt /xg] sf]ifsf] k|If]k0f 5 .

->f]t M cfly{s jif{ @)&%÷&^ sf] df}lb|s gLltsf] bf];|f] q}dfl;s ;dLIff, g]kfn /fi6« a}+s_

-v_ /fli6«o kl/l:ylt

g]kfn ;/sf/n] cfly{s jif{ @)&%÷&^ sf] ah]6df * k|ltzt cfly{s j[l4sf] nIo lnPsf] lyof] . xfn} ;fj{hlgs s]lGb|o tYofÍ ljefusf] /fli6«o n]vf tYofÍ cg';f/ cfly{s jif{ @)&%÷&^ df oyfy{ s'n ufx{:Yo pTkfbg %=( k|ltztn] j[l4 x'g] cg'dfg /x]sf]5 .

cfly{s jif{ @)&$÷&% sf] df}lb|s gLltn] jflif{s cf};t pkef]Qmf d'b|f:kmLlt ^=% k|ltztsf] ;Ldfleq /fVg] nIo lnPsf] lyof] . rfn' cfly{s jif{sf] 5 dlxgfdf cf};t d'b|f:kmLlt b/ $=@ k|ltzt /x]sf] 5 -tflnsf !_ . jflif{s ljGb'ut cfwf/df @)&% k';df o:tf] d'b|f:kmLlt $=^ k|ltzt /x]sf] 5 . cg's'n df};d, Go"g cGt/fli6«o d'b|fl:kmlt / cfk"lt{ Joj:yfkgdf cfPsf] ;'wf/ nufotsf sf/0f d'b|fl:kmlt lgolGqt g} /x]sf] 5 .

@)&% kf}if d;fGtdf @* jfl0fHo a}+s, ## ljsf; a}+s, @$ ljQ sDkgL / &@ n3'ljQ ljQLo ;+:yfx?;+rfngdf /x]sf 5g\ eg] oL ;+:yfx?sf] zfvf ;+Vof $,%(! k'u]sf] 5 .

@)&% kf}if d;fGtdf a}+s tyf ljQLo ;+:yfx?sf] r'Qmf k'FhL ?= @(% ca{ *( s/f]8 k'u]sf] 5 .

@)&% c;f/df jfl0fHo a}+sx¿sf efl/t cf};t shf{ b/ !@=@( k|ltzt /x]sf]df @)&% kf}ifdf !@=@* k|ltzt /x]sf] 5 . To;}u/L, @)&% c;f/df jfl0fHo a}+sx?sf] efl/t cf};t lgIf]k b/ ^=$( k|ltzt /x]sf]df @)&% kf}ifdf ^=&@ k|ltzt /x]sf] 5 .

jfl0fHo a}+sx?n] @)&% c;f/ d;fGt ;Dd s[lif If]qdf !) k|ltzt, pmhf{df % k|ltzt, ko{6g If]qdf % k|ltzt / afFsL cGo k|fyldstf k|fKt If]qdf u/L cfˆgf] s'n shf{sf] Go"gtd @% k|ltzt shf{ clgjfo{ ?kdf k|jfx ug'{kg]{ Joj:yf ul/Psf]df @)&% kf}if d;fGt;Dddf s[lif If]qdf (=(# k|ltzt, pmhf{df $=@! k|ltzt, ko{6g If]qdf $=$) k|ltzt u/L s'n !*=%$ k|ltzt shf{ k|jfx u/]sf 5g\ . @)&% c;f/df jfl0fHo a}+sx?sf] cf};t lgliqmo

shf{ cg'kft !=^ k|ltzt /x]sf]df @)&% kf}ifdf !=&% k|ltzt /x]sf] 5 .

- >f]t M cfly{s jif{ @)&%÷&^ sf] df}lb|s gLltsf] bf];|f] q}dfl;s ;dLIff / dfl;s a}+lsË tyf ljQLo tYofÍ k|ltj]bg, g]kfn /fi6« a}+s _

-#_ k|ltj]bg tof/ ePsf] ldlt;Dd rfn" jif{sf] pknlAw / eljiodf ug'{ kg]{ s'/fsf] ;DaGwdf ;~rfns ;ldltsf] wf/0ff M

-s_ rfn' cfly{s jif{sf] bf]>f] qodf; cGt/ut k|ltj]bg tof/ kfbf{;Dddf a}+ssf] sf/f]af/sf] l:ylt b]xfo adf]lhd /x]sf] 5 .

ljj/0f @)&%÷)&^ kf}if d;fGtr'Qmf k'FhL 7,25,93,10

lgIf]k 43,08,45,86

shf{ 43,55,06,37

t/ntf (CRR) cg'kft 4=81Ü

kF'hLsf]if cg'kft 19=86Ü

lgis[o shf{ cg'kft 3=54Ü

cfwf/ b/ (Base Rate) 11=31Ü

sDkgL P]g, @)^# sf] bkmf !)( sf] pkbkmf $ adf]lhdsf] ljj/0f

-v_ a}+ssf] pGglt k|ultsf] nflu eljiodf ug'{ kg]{ sfo{sf] ;DaGwdf ;+rfns ;ldltsf] wf/0ff M

lgIf]ksf] cf};t Jofhb/df sdL Nofpgsf nflu CASA lgIf]k a9fpgsf] nflu gofF of]hgfx? th'{df u/L sfof{Gjog ug]{ / JolQmut lgIf]kstf{x?sf] cfwf/ j[l¢ ub}{ ;+:yfut lgIf]k tkm{sf] lge{/tf sd ub}{ n}hfg] . a}+ssf] Joj;fo lj:tf/sf] nflu zfvfsf] ;+hfn qmlds ?kdf lj:tf/ ub}{ nfg] . shf{sf] u'0f:t/df ;'wf/ ub}{ n}hfg] tyf a}+sn] cfkm\gf] nufgLnfO{ cy{Joj:yfsf] tNnf] tx;Dd k'¥ofpgsf] nflu pkef]Qmf shf{ tyf n3'ljQ shf{nfO{ k|fyldstf lbO{ ;fgf tyf demf}nf shf{ tyf lgIf]kdf hf]8 lbO{ 7f]; /0fgLltsf ;fy sfo{ ug]{ . a}+snfO{ k"FhLut, zfvf ;+hfn, u|fxs ;+Vof cflbsf] b[li6sf]0faf6 ;'b[9 agfO{ k|lt:kwL{ a}+ssf] ?kdf :yflkt ug{sf] nflu cGo pko'Qm a}+s tyf ljQLo ;+:yfx?nfO{ o; l;len a}+sdf ufEg] jf k|flKt ug]{ sfo{nfO{ lg/Gt/tf lbg] . ljk|]if0f ;]jfsf] kx'Fr lj:tf/ ug{ l;len a}+s /]ld6sf Ph]06 tyf sfp06/x? yk ug]{ . cfw'lgs a}+lsË ;]jfsf ;a} k|ljlwx? k|of]u u/L a}+lsË ;]jfsf] nflu Technology Driven Bank sf] ?kdf :yflkt ug]{ . a}+ssf] hf]lvd Joj:yfkgnfO{ yk ;'b[9Ls/0f ub}{ nlug] / sf/f]af/;+u ;DalGwt ljljw hf]lvd Go"lgs/0f ug{sf] nflu cfjZos k"j{ ;ts{tfx? ckgfpg] . clws]Gb|Lt hf]lvd sd ug{ Pj+ jhf/ ljljlws/0f ug{ a}+sn] ;fgf tyf demf}nf k|s[ltsf] Joj;fodf nufgL ug]{ p2]Zon] SME Banking nfO{ lj:tf/ ul/g]5 . a}+sn] lk5l8Psf] tyf u|fld0f If]qsf hgtfnfO{ nlIft u/L ;+rfngdf NofPsf] Micro Banking sfo{qmdnfO{ cem lj:tf/ ub}{ nlug]5 . a}+ssf] Brand lj:tf/ ug{sf] nflu lj1fkg tyf Jofkf/ k|j¢gsf nflu gofF gofF /0fgLlt agfO cuf8L a9g] . Jofkf/sf gofF gofF If]qx?sf] klxrfg ug]{ tyf u|fxs ;]jfnfO{ cem k|efjsf/L agfpb} nlug]5 . sd{rf/LnfO{ bIftf clej[l¢ ug{sf] nflu lgoldt tflnd lbO{g]5 a}+ssf] xfnsf] v/fa shf{nfO{ k|efjsf/L ?kdf Joj:yfkg ul/g]5 . o; jfx]ssf ;~rfns ;ldltsf] cGo wf/0ffx? ;~rfns ;ldltsf] k|ltj]bgdf pNn]v ul/Psf] 5 .

=

=

=

=

=

=

=

=

=

=

=

==

CIVIL BANK | ANNUAL REPORT 2073 / 2074 & 2074 / 2075

%

? xhf/df

*

* g]kfn /fi6« a}+saf6 kfl/t eO{;s]sf] cf=j= @)&#÷@)&$ sf] af]g; z]o/ jflif{s ;fwf/0f ;efaf6 kfl/t eP kZrft r'Qmf k"FhL ? * cj{ k'Ug] .

-$_ sDkgLsf] cf}Bf]lus jf Jofj;flos ;DaGw Mu|fxssf cfoft lgof{t tyf cGt/f{li6«o sf/f]af/nfO{ ;xhtf k|bfg ug{ cGt/fli6«o :t/df /fd|f] ;+hfn / /fd|f] ljQLo cj:yf ePsf a}+s tyf ljQLo ;+:yf;+u ;DjGw :yfkgf ug{'kg]{ x'G5 . To;sf cltl/Qm ljb]zdf /x]sf g]kfnLx?nfO{ ;xh ?kdf ljk|]if0f dfkm{t /sd k7fpgsf] nflu ;d]t ljleGg cGt/fli6«o:t/df /fd|f] ;+hfn ePsf /]ld6fG; tyf PS;r]Gh sDkgLx?;+u ;d]t ;DjGw :yfkgf ug{'kg]{ x'G5 . ;f] cg'?k a}+sn] ef/tsf] Standard Chartered Bank, Axis Bank tyf HDFC Bank, a]nfotsf] Standard Chartered Bank UK, hd{gLsf] Commerz Bank, cd]l/sfsf] Standard Chartered Bank, Habib American Bank, c:6]«lnofsf] National Australia Bank h:tf a}+sx?;+u Correspondent Banking ;DaGw :yfkgf u/L sf/f]af/ u/L cfPsf] 5 . ljk|]if0f ;DjlGw sf/f]jf/ ug{ Western Union Money Transfer nufotsf cGt/fli6«o sDkgLx?;+u ;DaGw :yfkgf u/L sf/f]af/ u/L cfPsf] 5 .o;sf ;fy} OG6/g]zgn lnlhË P08 kmfO{gfG; sDkgL lnld6]8 o; a}+sdf uflePl5 pQm ;+:yfsf] ljb]zL nufgL stf{ KDB Capital Korea ;+u a}+ssf] ;DaGw :yfkgf ePsf] 5 .

-%_ ;~rfns ;ldltdf ePsf] x]/km]/ / ;f]sf] sf/0f M

a}+s tyf ljQLo ;+:yf ;DaGwL P]g, @)^# sf] bkmf !@ sf] pkbkmf -!_ adf]lhd o; a}+ssf] ;+rfns ;ldlt ( hgfsf] x'g] u/L u7g ul/Psf]df gofF P]g nfu' ePkZrft ;f]xL adf]lhd x'g] u/L & hgfsf] ;+rfns ;ldlt u7g ug'{ kg]{ ePsf] x'Fbf ;+:yfks z]o/wgLx?af6 # hgf, ;j{;fwf/0f z]o/wgLx?af6 # hgf / :jtGq ;+rfns ! hgf u/L & hgfsf] ;+rfns ;ldlt u7g u/L a}+s tyf ljQLo ;+:yf ;DaGwL P]g, @)&# sf] bkmf !$ sf] pkbkmf -!_ nfO{ sfof{Gjog ug{sf] nflu o; a}+ssf] ;+:yfks z]o/wgLx?sf] tkm{jf6 ;+rfns ;ldltdf k|ltlglwTj ug'{x'g] ;+rfns >L l/tf >]i7 Ho" / ;+rfns >L ljgf]b nfn >]i7 Ho"n] cfˆgf] Joj;foLs Jo:ttfsf] sf/0fn] ldlt @)&$ h]7 & ut] b]lv nfu' x'g] u/L /flhgfdf lbg'ePsf] 5 . ;fy} cfkm\gf] sfo{ Jo:ttfn] ubf{ ;+rfns kbaf6 >L ldqnfn >]i7 Ho" / ;[h{gf zfSo Ho"n] /flhgfdf lbg'ePsf] 5 . ;[h{gf zfSo -tfdfË_ Ho"n] /flhgfdf lbP kZrft l/Qm ;+rfns kbdf a}+s tyf ljQLo ;+:yf ;DaGwL P]g, @)&# sf] bkmf !$ sf] pkbkmf @ sf] k|ltjGwfTds jfSof+z tyf a}+ssf] lgodfjnLsf] lgod @& sf] pklgod -$_ adf]lhd afFsL cjlwsf] nflu ;+:yfks >L O{= OR5f /fh tfdfË Ho"nfO{ ;+rfns kbdf lgo'Qm ug]{ lg0f{o ;+rfns ;ldltsf] @#@ cf}+ a}7saf6 ePsf] hfgsf/L u/fpb} ;f] lg0f{onfO{ o;} ;Ddflgt ;efaf6 cg'df]bg ul/lbg x'g cg'/f]w ub{5' . :jtGq ;+rfns k|f= 8f= /d]z bfxfn Ho"sf] sfo{sfn ;dfKt ePsf]n] ldlt @)&%.)#.@( df a;]sf] a}7s g+= @%! sf] lg0f{o cg';f/ :jtGq ;+rfns kbdf >L eLdfgGb 9'ªufgf Ho"nfO{ lgo'Qm ul/Psf] hfgsf/L u/fpb5f} . ;fy} >L clDa/ af]u6LHo"n] ;+rfns kbdf oyfjt /xg] ul/ a}+ssf] cWoIf kbaf6 k]z ug'{ ePsf] /flhgfdf :jLs[t ePsf]n] @)&$ ;fn kf}if # ut] a;]sf] ;+rfns ;ldltsf] @## cf}+ a}7saf6 O{= OR5f /fh tfdfË Ho"nfO{ cWoIf rog ul/Psf] 5 . t];|f] ;fwf/0f ;efaf6 ;j{;fwf/0f z]o/wlgx?sf] tkm{af6 k|ltlglwTj ;+rfns ;ldltdf k|ltlglwTj ul//xg'ePsf ;+rfnsx? >L 3g]Gb|axfb'/ >]i7 tyf >L ;+ud s]=;L= Ho"sf] kbfjlw kf}if d;fGtdf ;dfKt x'g] ePsf]df a}+ssf] ;+rfns ;ldltdf ;j{;fwf/0f ;d"xsf] k|ltlgwTj ug]{ ;+rfns gx'g] cj:yf /xg] ePsf] sf/0fn] ubf{ a}+s tyf ljQLo ;+:yf ;DaGwL P]g, @)&# sf] bkmf !$ sf] pkbkmf @ -v_ sf] k|ltjGwfTds jfSof+z adf]lhd cfufdL ;fwf/0f ;ef geP;Ddsf] nflu ;+rfns kbdf >L 3g]Gb|axfb'/ >]i7 tyf >L ;+ud s]=;L=Ho"nfO{ k'gM lgo'lQm u/L ;+rfns kbdf lg/Gt/tf lbg] lg0f{o ;+rfns ;ldltsf] @#$ cf}+ a}7saf6 ePsf] hfgsf/L u/fpb} ;f] lg0f{onfO{ o;} ;Ddflgt ;efaf6 cg'df]bg ul/lbg x'g cg'/f]w ub{5' . a}+ssf] ;+rfns ;ldlt ( hgfsf] x'g] u/L u7g ul/Psf]df a}+s tyf ljQLo ;+:yf ;DaGwL P]g, @)&# sf] bkmf !$ sf] pkbkmf -!_ nfO{ sfof{Gjog ug{sf] nflu ;+rfns ;ldltsf] lg0f{oaf6 ;+:yfks z]o/wgLx?af6 # hgf, ;j{;fwf/0f z]o/wgLx?af6 # hgf / ljz]if1 ;+rfns ! hgf u/L & hgfsf] ;+rfns ;ldlt u7g ug]{ lg0f{o eP cg'?k o; ;fwf/0f ;efaf6 lgodfjnLdf ;+zf]wg k|:tfj k]z ul/Psf] 5 ;fy} a}+s tyf ljQLo ;+:yf ;DaGwL P]g, @)&# nfO{ cfwf/ dfgL ;+rfns

;ldltn] u/]sf] lg0f{o cg'?k ;+rfnsx?sf] lgjf{rg o;} ;fwf/0f ;efaf6 ;DkGg u/L k"0f{ ;+rfns ;ldlt aGg]5 . a}+sdf xfn 5 hgfsf] ;+rfns ;ldlt /x]sf] 5 .

-^_ sf/f]af/nfO{ c;/ kfg]{ d'Vo s'/fx¿ M

/fi6«Lo k"FhL lgdf{0fdf l;ldttf, ljk]|if0fdf sdL, ;/sf/L vr{df lg/Gt/tfsf] cefjn] lgIf]k kl/rfngdf cefj tyf cl:y/tf . a}+saf6 k|bfg ul/g] shf{ tyf u}x| sf]ifdf cfwfl/t ;]jfx? pknAw u/fpbf x'g ;Sg] hf]lvdx? . t/ntfdf x'g] ptf/ r9fj tyf ;f]sf] sf/0faf6 ;Dklt / bfloTj tyf lgIf]k tyf shf{sf] Jofhb/ Joj:yfkgdf r'gf}ltx? . oyf;dodf shf{ c;'nL geO{ pTkGg x'g] hf]lvdx¿ . ljb]lz ljlgdo sf/f]jf/ ubf{ ljlgdo b/df x'g] kl/jt{gaf6 x'g ;Sg] ;+efljt hf]lvdx? . /fi6«sf] cfly{s, df}lb|s tyf ljQLo gLlt kl/jt{gaf6 x'g ;Sg] ;+efljt hf]lvdx? . kF"lh ahf/df cfpg ;Sg] ptf/ r9fjaf6 x'g ;Sg] ;+efljt hf]lvdx? . cGt/f{li6«o ahf/df x'g] dGbLaf6 g]kfnL ahf/df kg{ ;Sg] c;/af6 x'g ;Sg] cfly{s hf]lvdx¿ . ljleGg k|fs[lts k|sf]kaf6 >[hgf x'g;Sg] hf]lvdx? . lta|t/ a}+lsË k|lt:kwf{sf] sf/0fn] shf{ tyf nufgLsf] bfo/f ;fF3'l/P/ nufgLstf{x?nfO{ lg/Gt/ k|ltkmn k|bfg ul//xg] r'gf}lt . j}slNks nufgLsf] If]qx?sf] cefj .

-&_ n]vfk/LIf0f k|ltj]bgdf s'g} s}lkmot pNn]v ePsf] eP ;f] pk/ ;~rfns ;ldltsf] k|lts[of M

;ldIff cfly{s jif{sf] n]vfk/LIf0f k|ltj]bgdf ;f/e't s}lkmot gePsf] . a}+ssf] lgoldt a}+lsË sf/f]jf/sf] l;nl;nfdf x'g] ;fdfGo s}lkmot -l6Kk0fL_ x? pk/ ;~rfns ;ldltsf] Wofgfsif{0f ePsf] / ;'wf/fTds sbdx? rfNg / eljiodf gbf]xf]l/g] Joj:yf ldnfpg a}+s Joj:yfkgnfO{ lgb]{zg ;d]t lbO{Psf] 5 .

-*_ nfef+z afF8kmfF8 ug{ l;kmfl/; ul/Psf] /sd Mcf=j= @)&#÷)&$ sf] d'gfkmfaf6 xsk|b z]o/ ;d]t ul/ sfod x'g cfPsf] xfnsf] r'Qmf k"FhL ?=&,@%,(#,!),#^!.*) -cIf/]kL ;ft cj{ klRr; s/f]8 lqofgAa] nfv bz xhf/ tLg ;o Ps;ÝL ?k}of cl; k};f dfq_ sf] !)=@%Ü sf b/n] x'g cfpg] ?= &$,$),&(,#!@.)* -cIf/]kL rf}xQ/ s/f]8 rfln; nfv pgf;L xhf/ tLg ;o af¥x ?k}of cf7 k};f dfq_ a/fa/sf] af]gz z]o/ / s/ k|of]hgsf] nflu )=%$Ü sf b/n] x'g cfpg] ?= #,(!,^@,)^(.)^ -cIf/]kL tLg s/f]8 PsfgAa] nfv a};ÝL xhf/ pgG;t/L ?k}of 5 k};f dfq_ gub nfef+z tyf cf=j=@)&$÷)&% df r'Qmf k"FhLsf] $=)%Ü sf b/n] x'g cfpg] ?=@(,$),)@,)^(.^% -cIf/]kL pGglt; s/f]8 rfln; nfv b'O{ xhf/ pgfG;Q/L ?k}of k};ÝL k};f dfq_ gub nfef+z lbg] k|:tfj ul/Psf] 5 .

-(_ z]o/ hkmt ePsf] eP hkmt ePsf] z]o/ ;+Vof, To:tf] z]o/sf] clÍt d"No, To:tf] z]o/ hkmt x'g'eGbf cufj} ;f]afkt sDkgLn] k|fKt u/]sf] hDdf /sd / To:tf] z]o/ hkmt ePkl5 ;f] z]o/ laqmL u/L sDkgLn] k|fKt u/]sf] /sd tyf hkmt ePsf] z]o/afkt /sd lkmtf{ u/]sf] eP ;f]sf] ljj/0f M ;ldIff cjlwdf s'g} z]o/ hkmt ul/Psf] 5}g .

-!)_ ljut cfly{s jif{df sDkgL / o;sf] ;xfos sDkgLsf] sf/f]af/sf] k|ult / ;f] cfly{s jif{sf] cGtdf /x]sf] l:yltsf] k'g/fjnf]sg M;ldIff cjlwdf g} a}+sn] l;len Soflk6n dfs]{6 lnld6]8sf] %@=*$ k|ltzt z]o/ vl/b u/L ;xfos sDkgLsf] ?kdf ;+rfng ub}{ cfPsf] 5 . cf= j= @)&#÷)&$ sf] d'gfkmfaf6 pQm ;xfos sDkgLn] @% k|ltzt jf]gz z]o/ tyf !=@% k|ltzt gub nfef+z tyf cf= j= @)&$÷)&% sf] d'gfkmfaf6 *=$@ k|ltzt gub nfef+z ljt/0f u/]sf] lyof] . o;sf cnfjf OG6/g]zgn

=

=

=

=

=

=

=

=

=

=

=

CIVIL BANK | ANNUAL REPORT 2073 / 2074 & 2074 / 2075

h

lnlhË P08 kmfOgfG; sDkgL lnld6]8;+usf] dh{/ kZrft cfOPnPkml;cf] dfO{qmf] kmfO{gfG; lnld6]8sf] gfd kl/jt{g ul/ l;len n3'ljQ ljQLo ;+:yfsf] gfdaf6 o; a}+ssf] ;xfos sDkgLsf] ?kdf ;+rfng x'b} cfPsf] 5 . cf= j= @)&#÷)&$ sf] d'gfkmfaf6 l;len n3'ljQ ljQLo ;+:yfn] $=% k|ltzt jf]gz z]o/ tyf )=@#^*$ k|ltzt gub nfef+z tyf cf= j= @)&$÷)&% sf] d'gfkmfaf6 l;len n3'ljQ ljQLo ;+:yfn] $=)) k|ltzt jf]gz z]o/ tyf #=*( k|ltzt gub nfef+z ljt/0f u/]sf] lyof] .

-!!_ sDkgL tyf To;sf] ;xfos sDkgLn] cfly{s jif{df ;DkGg u/]sf] k|d'v sf/f]af/x? / ;f] cjlwdf sDkgLsf] sf/f]af/df cfPsf] s'g} dxTjk"0f{ kl/jt{g M a}+sn] ;ldIff cjlwdf u/]sf] sf/f]af/x? dfly pNn]v eO;s]sf] .

-!@_ ljut cfly{s jif{df sDkgLsf] cfwf/e"t z]o/wgLx?n] sDkgLnfO{ pknAw u/fPsf] hfgsf/LM cfwf/e"t z]o/wgLx?n] s'g} hfgsf/L pknAw gu/fPsf] .

-!#_ ljut cfly{s jif{df sDkgLsf ;~rfns tyf kbflwsf/Lx?n] lnPsf] z]o/sf] :jfldTjsf] ljj/0f / sDkgLsf] z]o/ sf/f]af/df lghx? ;+nUg /x]sf] eP ;f] ;DaGwdf lghx?af6 sDkgLn] k|fKt u/]sf] hfgsf/L Mo; a}+ssf lgDg ;+rfnsx?sf] b]xfo adf]lhd z]o/ :jfldTj sfod /x]sf] / a}+ssf cGo kbflwsf/Lx?n] sd{rf/L z]o/ cGt/ut k|fylds z]o/ hf/L ubf{ z]o/ wf/0f u/]sf] t/ z]o/ sf/f]af/df ;+nUg ePsf] s'g} hfgsf/L a}+snfO{ k|fKt gePsf] .

-!$_ljut cfly{s jif{df sDkgL;Fu ;DalGwt ;Demf}tfx?df s'g} ;~rfns tyf lghsf] glhssf] gft]bf/sf] JolQmut :jfy{sf] af/]df pknAw u/fOPsf] hfgsf/Lsf] Joxf]/fM s]xL gePsf] .

-!%_ sDkgLn] cfˆgf] z]o/ cfkm}n] vl/b u/]sf] eP To;/L cfˆgf] z]o/ vl/b ug'{sf] sf/0f, To:tf] z]o/sf] ;+Vof / clÍt d"No tyf To;/L z]o/ vl/b u/]afkt sDkgLn] e'QmfgL u/]sf] /sd Ma}+sn] ;ldIff cjlwdf cfˆgf] z]o/ cfkm}n] v/Lb u/]sf] 5}g .

-!^_ cfGtl/s lgoGq0f k|0ffnL eP jf gePsf] / ePsf] eP ;f]sf] lj:t[t ljj/0f M

;+rfns ;ldltn] g]kfn /fi6« a}+ssf] Plss[t lgb]{zg , a}+s tyf ljQLo ;+:yf ;DaGwL P]g tyf sDkgL P]gsf] clwgdf /xL n]vfk/LIf0f ;ldlt, hf]lvd Joj:yfkg ;ldlt, dfgj ;+;fwg Aoj:yfkg ;ldlt tyf ;Dklt z'¢Ls/0f lgjf/0f ;DaGwL ;ldlt u7g ul/Psf] 5 . ;ldltx?n] ;do ;dodf a}7s a;L lgb]{zgdf ePsf Joj:yfx?sf] cfwf/df sfd tyf lhDd]jf/L k'/f ub{5g . a}+sdf cfGtl/s lgoGq0f k|0ffnL Joj:yf adf]lhd a}+ssf] n]vfk/LIf0f ;ldltsf] dftxtdf cfGtl/s n]vfk/LIf0f ljefusf] Joj:yf /x]sf] 5 . o; ljefun] n]vfk/LIf0f u/L ;ldlt ;dIf cfˆgf] k|ltj]bg k]z ub{5 . ;fy} shf{ tyf sfg"gL hf]lvdx? Go"lgs/0f ug]{ p2]Zon] hf]lvd lgoGq0f (Risk Control) tyf sfg"g ljefusf] k|ToIf ;+nUgtfdf shf{ k|zf]wg sfo{ ug]{ k|aGw ul/Psf] 5 . a}+sdf 5'§} cg'kfngf ljefu (Compliance Department) sf] Joj:yf ePsf]n] ;f] ljefujf6 lgoldt cg'kfngfsf] cg'udg ug]{ ul/Psf] 5 . ;fy} a}+ssf ;Dk"0f{ x/lx;fj cTofw'lgs sDKo'6/ ;km\6j]o/sf] dfWodjf6 ;+rfng ug]{ ul/Psf] 5 .

-!&_ ljut cfly{s jif{sf] s'n Joj:yfkg vr{sf] ljj/0f Mcf=j= @)&#÷)&$ tyf @)&$÷)&% df ePsf] s"n Joj:yfkg vr{sf] ljj/0f lgDgfg';f/ /x]sf] 5 M–

ljj/0f cf=j= @)&#÷)&$ cf=j= @)&$÷)&%sd{rf/L vr{ ?= #^,#!,(!,%(@ ?= %%,*$,!#,@##sfof{no ;~rfng vr{ ?= #@,@%,$#,&#% ?= $#,$@,^@,@^)s'n Joj:yfkg vr{ ?= ^*,%&,#%,#@& ?= ((,@^,&%,$(#

-!*_ n]vfk/LIf0f ;ldltsf ;b:ox?sf] gfdfjnL, lghx?n] k|fKt u/]sf] kfl/>lds, eQf tyf ;'ljwf, ;f] ;ldltn] u/]sf] sfd sf/afxLsf] ljj/0f / ;f] ;ldltn] s'g} ;'emfj lbPsf] eP ;f]sf] ljj/0f Ma}+ssf] n]vfk/LIf0f ;ldltsf ;b:ox? lgDg adf]lhd /x]sf] 5s_ >L k|sfz tfon – ;+rfns – ;+of]hs v_ >L 3g]Gb| axfb'/ >]i7 – ;+rfns – ;b:o u_ cfGtl/s n]vfk/LIf0f ljefu k|d'v – ;b:o ;lrj

n]vfk/LIf0f ;ldltsf ;+rfns ;b:onfO{ a}7s eQf ;+rfns ;ldltsf] a}7sdf pkl:yt ePjfkt k|bfg ul/g] eQf a/fa/sf] eQf k|bfg ul/Psf] / cGo s'g} ;'ljwf k|bfg ul/Psf] 5}g .

-!(_ ;~rfns, k|aGw ;~rfns, sfo{sf/L k|d'v, sDkgLsf cfwf/e"t z]o/wgL jf lghsf] glhssf gft]bf/ jf lgh ;+nUg /x]sf] kmd{, sDkgL jf ;+u7Lt ;+:yfn] sDkgLnfO{ s'g} /sd a'emfpg afFsL eP ;f] s'/f M gePsf] .

-@)_ ;~rfns, k|aGw ;~rfns, sfo{sf/L k|d'v tyf kbflwsf/Lx?nfO{ e'QmfgL ul/Psf] kfl/>lds, eQf tyf ;'ljwfsf] /sd M k|jGw ;+rfns kb gePsf] . ;+rfnsx?n] ;+rfns ;ldltsf] j}7sdf pkl:yt eP afkt k|lt a}7s ;+rfns ;ldltsf cWoIfn] ?=!),)))÷– / ;+rfnsx?n] ?= *,)))÷– a}7s eQf k|bfg ug]{ ul/Psf]5 . sfo{sf/L k|d'v tyf cGo sfo{sf/L kbflwsf/L÷Joj:yfksx¿sf] cfly{s jif{ @)&#÷&$ / @)&$÷&% sf] jflif{s tnj, eQf ;'ljwfx¿ M cfly{s jif{ @)&#÷&$

qm=;+= ljj/0f k|d'v sfo{sf/L clws[t cGo sfo{sf/L kbflwsf/L ÷Joj:yfks

!= tna !,)),*),))).)) #,((,@&,@*$.*%@= eQf $#,@),))).)) @,@^,@^,(@^.&@#= bz} vr{ !@,)),))).)) $!,##,*((.))$= ;+ro sf]if !),)*,))).)) #(,(@,&@*.%)%= af]gz uf8L ;'ljwf, rfns,

df]jfO{n vr{, aLdf, P]g adf]lhd af]g;

uf8L ;'ljwf, rfns, df]jfO{n vr{, aLdf,

cfjf; shf{, ;fdflhs shf{, P]g adf]lhd af]g;

cfly{s jif{ @)&$÷&%

qm=;+= ljj/0f k|d'v sfo{sf/L clws[t cGo sfo{sf/L kbflwsf/L ÷Joj:yfks

!= tna ^*,!(,)@#.$$ $,^),#&,)$$.#$@= eQf @*,@),!%).)) @,^!,(^,*&$.*@#= bz} vr{ &,^&,()).)) $%,$@,*@).$!$= ;+ro sf]if ^,*!,()@.#$ $^,)#,&)$.$%%= af]gz uf8L ;'ljwf, rfns,

df]jfO{n vr,{ aLdf, P]g adf]lhd af]g;

uf8L ;'ljwf, rfns, df]jfO{n vr{, aLdf,

cfjf; shf{, ;fdflhs shf{, P]g adf]lhd af]g;

-@!_ z]o/wgLx?n] a'lemlng afFsL /x]sf] nfef+zsf] /sd M cfly{s jif{ @)&#÷)&$ ;Dddf z]o/wgLx?n] ?= $,(%,$(,#^( gub nfef+; /sd a'lemlng af+sL /x]sf]df cfly{s jif{ @)&#÷)&$ sf] cfiff9 d;fGtdf ;f] /sd ?= $,@),*),#*( /x]sf] 5 . -of] /sd ;fljssf] kz'klt 8]enkd]06 a}+s, pBd ljsf; a}+s, PlS;; 8]enkd]06 a}+s, l;len dr]{G6 ljQLo ;+:yf lnld6]8, OG6/g]zgn lnlhË P08 kmfOgfG; sDkgL lnld6]8, o'lgs kmfO{gfG; lnld6]8 tyf xfdf dr]{G6 kmfO{gfG; lnld6]8n] 3f]if0ff u/]sf] nfef+z ;d]t xf] _ .

-@@_ bkmf !$! adf]lhd ;DklQ vl/b jf laqmL u/]sf] s'/fsf] ljj/0f M ;ldIff cjlwdf a}+lsË sf/f]af/sf] nflu cfjZos ;DklQ afx]s cGo ;DklQx? vl/b jf ljqmL gePsf] .

-@#_ bkmf !&% adf]lhd ;Da4 sDkgLaLr ePsf] sf/f]af/sf] ljj/0f M ;ldIff cjlw;Dd o; a}+ssf] ;xfos sDkgL;+u ePsf] sf/f]af/sf] ljj/0f ;DalGwt cg';"rLdf pNn]v ul/Psf] 5 .

=

=

;+rfnssf] gfd, y/ kb z]o/ ;d'x hDdf lsQf

O{= O{R5f /fh tfdfË cWoIf -;+:yfks z]o/wgL ;d"x_;+:yfks 23,89,939

;j{;fwf/)f 4,06,894

>L cDaL/ af]u6L ;+rfns -;+:yfks z]o/wgL ;d"x_;+:yfks 1,54,641

;j{;fwf/0f 35,830

>L k|sfz tfon ;+rfns -;+:yfks z]o/wgL ;d"x_;+:yfks 3,16,309

;j{;fwf/)f 53,853>L 3g]Gb| axfb'/ >]i7 ;+rfns -;j{;fwf/)f z]o/wgL ;d"x_ ;j{;fwf/)f 837>L ;+ud s]=;L= ;+rfns -;j{;fwf/)f z]o/wgL ;d"x_ ;j{;fwf/)f 663>L eLdfgGb 9'ªufgf :jtGq ;~rfns ;j{;fwf/)f 251

CIVIL BANK | ANNUAL REPORT 2073 / 2074 & 2074 / 2075

em

lwtf]kq btf{ tyf lgisfzg lgodfjnL, @)&# sf] lgod @^ sf] pklgod @ ;+u ;DalGwtcg';"rL—!% adf]lhdsf] jflif{s ljj/0f

!= ;~rfns ;ldltsf] k|ltj]bg M aflif{s k|ltj]bgsf] ;DalGwt zLif{s cGtu{t /flvPsf] .

@= n]vfk/LIfssf] k|ltj]bg M aflif{s k|ltj]bgsf] ;DalGwt zLif{s cGtu{t /flvPsf] .

#= n]vfk/LIf0f ePsf] ljQLo ljj/0fM aflif{s k|ltj]bgsf] ;DalGwt lzif{s cGtu{t /flvPsf] .

$= sfg'gL sf/jfxL ;DaGwL ljj/0f M

s_ q}dfl;s cjlwdf ;+ul7t ;+:yfn] jf ;+:yfsf] lj?4 s'g} d'2f bfo/ ePsf] eP Mcfly{s jif{ @)&#÷&$ / @)&$÷&% df a}+sn] jf a}+ssf] lj?4 a}lsË sf/f]jf/sf] l;nl;nfdf qmdz @^ / #* j6f d'4f ljleGg cbfntx?df ljrf/flwg /x]sf] 5 .

v_ ;+ul7t ;+:yfsf] ;+:yfks jf ;+rfnsn] jf ;+:yfks jf ;+rfnssf] lj?4 k|rlnt lgodsf] cj1f jf kmf}Hfbf/L ck/fw u/]sf] ;DaGwdf s'g} d'2f bfo/ u/]sf] jf ePsf] eP M o; ;DjGwdf a}+snfO{ s'g} hfgsf/L k|fKt gePsf] .

u_ s'g} ;+:yfks jf ;~rfns lj?4 cfly{s ck/fw u/]sf] ;DaGwdf s'g} d'2f bfo/ ePsf] eP M o; ;DjGwdf a}+snfO{ s'g} hfgsf/L k|fKt gePsf] .

%= ;+ul7t ;+:yfsf] z]o/ sf/f]jf/ tyf k|ultsf] ljZn]if0f M

s_ lwtf]kq ahf/df ePsf] ;+ul7t ;+:yfsf] z]o/sf] sf/f]af/ ;DaGwdf Joj:yfkgsf] wf/0ff M g]kfn lwtf]kq jf]8{sf] /]vb]vdf lwtf]kqahf/df v'Nnf ahf/n] lgwf{/0f u/] cg'?k sf/f]af/ x'g] x'+bf a}+s Joj:yfkg t6:y 5 .

v_ ut jif{sf] k|To]s q}dfl;s cjlwdf ;+ul7t ;+:yfsf] z]o/sf] clwstd, Go"gtd / clGtd d"Nosf ;fy} s'n sf/f]af/ z]o/ ;+Vof / sf/f]af/ lbg M ut cfly{s aif{df z]o/sf] clwstd, Go"gtd, clGtd d"No, sf/f]af/ ;+Vof / sf/f]jf/ ePsf] lbgsf] ljj/0f -g]kfn :6s PS;r]Gh lnld6]8sf] j]e;fO6 cg';f/_ lgDg adf]lhd /x]sf] 5 M

cf= j= @)&#÷)&$

cf= j= @)&#÷)&$

^= ;d:of tyf r'gf}tLx? M

-!_ cfGtl/s ;d:of / r'gf}tL M

-s_ zfvf lj:tf/ tyf a9\bf] d'b|fl:kmltsf sf/0f ;+rfng vr{df a[l4 .-v_ zfvf lj:tf/ tyf gofF ;]jf z'? ug{sf] nflu cfjZos bIf hgzlQmsf] cefj .-u_ Aofhb/ cGt/ sd ug'kg]{ . -3_ lgis[o shf{sf] k|ltzt 36fpg' kg]{ . -ª_ ;j{;fwf/0fsf] lgIf]ksf] c+z a9fO{ lgIf]k nfut sd ug'{ kg]{ . -r_ bIf sd{rf/Lx? knfog x'gaf6 /f]Sg' kg]{ .

-@_ jfXo r'gf}tLx? M

-s_ a}+s tyf ljQLo ;+:yfx?sf] ;+Vofdf ePsf] j[l4n] l;h{gf u/]sf] k|lt:kwf{ .-v_ l;ldt nufgL If]qdf ePsf] k|lt:kwf{ .-u_ t/ntfdf x'g] ptf/ r9fj tyf ;f]sf] sf/0faf6 ;Dklt / bfloTj tyf lgIf]k tyf shf{sf] Jofhb/ Joj:yfkgdf r'gf}ltx? . -3_ nufgL d}qL jftfj/0fsf] ;d:of . -ª_ ;/sf/sf] k"FhLut vr{df ePsf] sld / Go"g t/ntf .

&= ;+:yfut ;'zf;g M

-s_ ;+:yfut ;'zf;gsf] pNn+3gnfO{ z'Go ;xglzntfsf] gLltnfO{ lg/Gt/tf lbOb} cfPsf] 5 . a}+ssf] nufgLstf{ z]o/wgLx?, ;j{;fwf/0f lgIf]kstf{x?, sd{rf/L, C0fL nufot ;Da4 ;j} ;/f]sf/jfnfx?sf] lxtsf] ;+/If0fdf ljz]if k|fyldstf lbb} cfPsf] 5 .

-v_ k|rlnt g]kfn sfg"g, g]kfn /fi6« a}+s nufotsf lgodgsf/L lgsfoaf6 hf/L ePsf lgb]{zg kl/kqx? Pj+ a}+ssf] gLlt lgodx?sf] cIf/;M kl/kfngf ub}{ cfPsf] 5 .

-u_ a}+ssf] cg'kfngf ljefu (Compliance Department) / cfGtl/s n]vfk/LIf0f ljefu (Internal Audit) sf] u7g ul/ ;f] dfkm{t ;+:yfut ;'zf;g kl/kfngfsf] k|Tofe'lt tyf ;f]sf] k|efjsfl/tfsf] cg'udg, lg/LIf0f tyf k/LIf0f u/L cfGtl/s lgoGq0f k|0ffnLnfO{ ;'b[9 ul/Psf] 5 .

-3_ ;+rfns ;ldltsf] k|To]s a}7sdf ljutdf ePsf] lg0f{osf] sfof{Gjog / a}+ssf] sf/f]af/sf] cj:yfsf] af/]df a}+s Joj:yfkgaf6 hfgsf/L lnO{ cfjZostf cg';f/ a}+ssf] lxtdf sfo{ ug{ Joj:yfkgnfO{ lgb]{zg lbg] u/]sf] . qm=;+= ljj/0f klxnf] q}df; bf]>f]

q}df;Tf]>f] q}df;

rf}yf] q}df;

! clwstd d"No

dh{/ k|lqmofdf

/x]sf]n] sf/f]af/

gePsf] .

369 316 276

@ Go"gtd d"No 233 198 235

# clGtd d"No 252 280 246

$ sf/f]jf/ ;+Vof 8,796 6,436 4,073

% sf/f]af/ lbg 51 59 57

qm=;+= ljj/0f klxnf] q}df; bf]>f] q}df;

Tf]>f] q}df;

rf}yf] q}df;

! clwstd d"No 272 250 179 176

@ Go"gtd d"No 219 177 140 141

# clGtd d"No 232 180 151 153

$ sf/f]jf/ ;+Vof 3,954 4,835 3,581 4,594

% sf/f]af/ lbg 56 57 56 63

CIVIL BANK | ANNUAL REPORT 2073 / 2074 & 2074 / 2075

k"FhL tyf bfloTj k|If]lkt @)&$÷)&%n]vfkl/If0f kZrft

@)&$÷)&%km/s km/s k|ltztdf km/s x'gfsf sf/0fx?

z]o/ k"FhL 8,000,279 7,259,310 -740,968_ -10=21_

hu]8f tyf sf]ifx? 1,012,240 2,590,605 1,578,365 60=93

lgodgsf/L ;dfof]hg sf]ifsf] yk, Pqm'on cfwf/df hgfOPsf] Jofh cfdbfgL, aLdf+lss d'NofÍgdf cfPsf] km/sn], ljQLo ;Dkltsf] km]o/ Eofn' u0fgf ePsf] kl/jt{g,:yUg s/ bfloTjdf cfPsf] km/s

lgoGq0f gx'g] :jfy{ ” ” ” ”

C0fkq tyf a08 ” ” ” ”

ltg{ afFsL shf{ ;fk6L 476,130 1,308,424 832,294 63=61 cGt/ a+}s ;fk6Ldf ePsf] a[l4n]

lgIf]k bfloTj 42,638,426 40,012,673 -2,625,753_ -6=56_

e'QmfgL lbg' kg]{ lanx? 26,894 69,270 42,376 61=18 uf|xs tyf ;fx'x?sf] r]s÷ 8fkm\t dfuy{df x'gfn]

k|:tfljt tyf e'QmfgL lbg afFsL nfef+z 800,028 ” -800,028_ -100=00_NFRS adf]lhdsf] ljQLo ljj/0fdf jflif{s ;fwf/0f ;efaf6 kfl/t geP;Dd jf;tnftdf nfef+zsf] lx;fa ;dfj]z gu/Lx'gfn]

cfos/ bfloTj -v'b_ 455,681 ” -455,681_ -100=00_ clu|d cfos/g} kof{Kt ePsf] sf/0f

cGo bfloTj 594,473 684,947 90,474 13=21

s"n k"FhL tyf bfloTj 54,004,151 51,925,229 -2,078,922_ -4=00_

;DklQ k|If]lkt @)&$÷)&%n]vfkl/If0f kZrft

@)&$÷)&%km/s km/s k|ltztdf km/s x'gfsf sf/0fx?

gub df}Hbft 1,419,085 1,193,699 -225,385_ -18=88_

g]kfn /fi6" a}+sdf /x]sf] df}Hbft 4,966,796 2,178,890 -2,787,906_ -127=95_ cfjZos ljQLo Joj:yfkg

a}s ÷laQLo ;+:yfdf /x]sf] df}Hbft 1,261,408 1,804,377 542,968 30=09 cfjZos ljQLo Joj:yfkg

dfu tyf cNk ;"rgfdf k|fKt x'g] /sd 236,514 ” -236,514_ -100_

nufgL 7,573,211 5,647,089 -1,926,122_ -34=11_ nufgL of]Uo /sdsf] cefjsf sf/0f

shf{ ;fk6 tyf lan vl/b 37,151,054 40,122,944 2,971,890 7=41

l:y/ ;DklQ 329,414 296,476 -32,938_ -11=11_

u}/ a}+ls+Í ;DklQ -v'b_ ” ” ” ”

cGo ;DklQ 1,066,669 681,754 -384,914_ -56=46_ ljljw cf;fdLx?df ePsf] kl/jt{g

s"n ;DklQ 54,004,151 51,925,229 -2,078,922_ -4=00_

*= ljj/0fkqdf k|If]k0f ul/Psf / n]vfk/LIf0f ePsf] ljj/0fx?df aL; k|ltzt jf ;f] eGbf a9L km/s ;DaGwL ljj/0fM

;Dklt bfloTj lx;fj

gfkmf gf]S;fg lx;fj

? xhf/df

? xhf/df

ljj/0f k|If]lkt @)&$÷)&%n]vfkl/If0f kZrft

@)&$÷)&%km/s km/s k|ltztdf sf/0f

Jofh cfDbfgL 3,934,618 4,441,858 507,240 11=42

Jofh vr{ 2,242,505 3,033,461 790,956 26=07 Jofhb/sf] sf/0f

v'b Aofh cfDbfgL 1,692,113 1,408,397 -283,715_ -20=14_

sldzg tyf l8:sfp06 144,759 102,456 -42,303_ -41=29_ shf{ tyf cGo a}+lsË ;'ljwfdf ePsf] sdLn]

cGo ;+rfng cfDbfgL 148,599 165,230 16,631 10=07

;6xL 36a9 cfDbfgL 128,839 168,932 40,093 23=73 8]/Le]l6esf] sf/f]af/df a[l4x'gfn]

s'n ;+rfng cfDbfgL 2,114,310 1,845,016 -269,294_ -14=60_

sd{rf/L vr{ 412,812 468,888 56,077 11=96

cGo ;+rfng vr{ 382,805 434,262 51,458 11=85

;6xL 36a9 gf]]S;fg ” ” ” ”

;Defljt gf]S;gL Aoa:yf cl3sf] ;+rfng d'gfkmf 1,318,694 941,865 -376,829_ -40=01_

;Defljt gf]S;fgL -59,306_ -8,818_ 50,488 -572=57_ v/fa shf{df ePsf] sdLn]

;+rfng d'gfkmf÷-gf]S;fg_ 1,259,388 933,048 -326,341_ -34=98_

u}/ ;+rfng cfDbfgL÷-gf]S;fg_ 11,442 686 -10,756_ -1,568=31_

;Defljt gf]S;fgL Aoa:yfaf6 lkmtf{ 400,000 134,649 -265,351_ -197=07_ shf{ c;'nLsf] sf/0f

lgoldt sf/f]jf/af6 ePsf] d'gfkmf 1,670,830 1,068,383 -602,448_ -56=39_

c;fdfGo sf/f]jf/af6 ePsf] d'gfkmf÷-vr{_ ” -83,608_ -83,608_ 100=00 v/fa shf{sf] ckn]vg tyf ckn]lvt shf{sf] c;'nLsf] v'b

;Dk"0f{ sf/f]jf/ ;dfj]z kl5sf] v'b gfkmf 1,670,830 984,774 -686,056_ -69=67_

sd{rf/L af]g; Joj:yf 151,894 89,525 -62,369_ -69=67_ ;Grfng cfDbfgLdf ePsf] sdLn]

cfos/ Aoa:yf 455,681 265,350 -190,331_ -71=73_

v'b d'gfkmf÷-gf]]S;fg_ 1,063,257 629,899 -433,357_ -68=80_

CIVIL BANK | ANNUAL REPORT 2073 / 2074 & 2074 / 2075

^

l;len a}+s lnld6]8k|aGwkqdf ;+zf]wg, @)&%

tLg dxn]bkmf xfnsf] Joj:yf ;+zf]lwt Joj:yf ;+zf]wg ug'{kg]{ sf/0f

bkmf %

o; a}+sn] bkmf $ adf]lhdsf] p2]Zo k|fKt ug{ sDkgL P]g,@)^# sf] bkmf !* sf] pkbkmf -!_ sf] v08 -3_ / a}+s tyf ljQLo ;++:yf ;DaGwL P]g, @)^# sf] bkmf $& sf] pkbkmf -!_ adf]lhd æsÆ ju{sf] Ohfhtkq k|fKt ;+:yfsf] ¿kdf /xg] u/L ;f] P]g, sDkgL sfg"g tyf cGo k|rlnt sfg"gsf] cwLgdf /xL b]xfo adf]lhdsf sfo{x¿ ug{ ;Sg]5 M–

o; a}+sn] bkmf $ adf]lhdsf] p2]Zo k|fKt ug{ sDkgL P]g,@)^# sf] bkmf !* sf] pkbkmf -!_ sf] v08 -3_ / a}+s tyf ljQLo ;++:yf ;DaGwL P]g, @)&# sf] bkmf $( sf] pkbkmf -!_ adf]lhd æsÆ ju{sf] a}+ssf] ¿kdf /xg] u/L ;f] P]g, sDkgL sfg"g tyf cGo k|rlnt sfg"gsf] cwLgdf /xL b]xfo adf]lhdsf sfo{x¿ ug{ ;Sg] M–

a}+s tyf ljQLo ;+:yf ;DaGwL P]g, @)&# sf] bkmf $( -!_ cg';f/ ldnfg ug{ .

% su

bkmf % sf] -r_ b]lv -1_ ;Dd

gePsf]

-r_ Jofh jf ljgf Jofhdf lgIf]k :jLsf/ ug]{ tyf To:tf] lgIf]ksf] e'QmfgL lbg],

-5_ g]kfn /fi6« a}+sn] tf]lslbP adf]lhd ljleGg k|sf/sf shf{ lbg],

-h_ k|rlnt sfg"g tyf g]kfn /fi6« a}+sn] lbPsf] lgb]{zgsf] cwLgdf /xL ljb]zL ljlgdo sf/f]jf/ ug]{,

-em_ xfo/kr]{h, xfOkf]lys]zg, lnlhË, xfpl;Ë tyf ;]jf Joj;fosf] nflu shf{ lbg],

-`_ g]kfn /fi6« a}+sn] lbPsf] lgb]{zgsf] cwLgdf /xL dr]{06 a}+lsË sf/f]jf/ ug]{

-6_ cGo a}+s jf ljQLo ;+:yfx?;Fu ldnL ;xljQLos/0fsf] cfwf/df lwtf] ljefhg -kf/Lkf;'_ ug]{ u/L cfk;df ePsf] ;Demf}tf cg';f/ ;+o'Qm ?kdf shf{ lbg], lbnfpg] Joj:yf ug]{,

-7_ :jb]zL jf ljb]zL a}+s jf ljQLo ;+:yfsf] hdfgtdf shf{ lbg],

-8_ cfˆgf] u|fxssf] tk{maf6 hdfgtkq hf/L ug]{ / ;f] afkt u|fxs;Fu cfjZos zt{ u/fpg], ;'/If0f lng], lghsf] rn crn ;DklQ lwtf] aGws lng] jf t];|f] JolQmsf] h]yf hdfgt lng],

-9_ k|tLtkq, k|lt1fkq, ljlgdokq, r]s, ofq'r]s, 8«fˆ6 jf cGo ljQLo pks/0f lgZsfzg ug]{, :jLsf/ ug]{, e'QmfgL lbg], l8:sfp06 ug]{ jf v/Lb ljqmL ug]{,

-su_ ;DalGwt lgsfosf] :jLs[lt lng'kg]{ eP ;f] ;d]t lnO{ a}+s cfkm} jf ;xfos sDkGL dfkm{t z]o/ bnfn (Share Broker) ;DaGwL sfo{ ug]{ ,

-r_ Aofh jf lagf Aofhdf lgIf]k :jLsf/ ug]{ jf ljleGg ljQLo pks/0f dfkm{t lgIf]k kl/rfng ug]{ / ltgsf] e'QmfgL lbg],

-5_ ljB'tLo pks/0f jf ;fwgsf] dfWodaf6 lgIf]k :jLsf/ ug{], e'QmfgL lbg], n]gb]g ug]{, dWo:ytfsf] sfd ug]{ / /sdfGt/ ug]{,

-h_ xfo/ kr]{h, lnlhË, xfplhË, clwljsif{ nufotsf shf{ lbg],

-em_ kl/of]hgf tyf xfOkf]lys]zg lwtf] /fvL] shf{ lbg] Pj+ ;xljQLos/0fsf] cfwf/df lwtf] ljefhg -kf/L kf;'_ ug]{ u/L cfk;df ePsf] ;Demf}tf cg';f/ ;+o'Qm ?kdf shf{ lbg] lbnfpg] Joj:yf ug]{,

-`_ ljb]zL a}+s jf ljQLo ;+:yfsf] hdfgtdf shf{ lbg],

-6_ cfk"m sxfF klxn] g} lwtf] /lx;s]sf] rn crn ;DklQsf] d"Non] vfd];Ddsf] /sd shf{ lbg] jf cGo a}+s jf ljQLo ;+:yfdf lwtf] /lx;s]sf] rn crn ;DklQsf] k'gM lwtf]df To;sf] d"Non] vfd];Ddsf] /sd shf{ lbg],

-7_ cfˆgf] u|fxssf] tk{maf6 hdfgtkq hf/L ug]{ / ;f] afkt u|fxs;Fu cfjZos zt{ u/fpg], lghsf] rn crn ;DklQ lwtf]aGws lng] jf t];|f] JolQmsf] h]yf hdfgt lng] / lwtf]aGws, ;'/If0fdf lnPsf] ;DklQ k|fKt ug]{, wf/0f ug]{ tyf ;f] ;DaGwL cGo sf/f]af/ ug]{,

z]o/ a|f]s/]h ;DaGwL sfo{ ug{ gofF Joj:yf yk ug'{kg]{ ePsf]n] .

a}+s tyf ljQLo ;+:yf ;DaGwL P]g, @)&# n] æsÆ ju{sf] a}+sn] ug{ ;Sg] egL tf]s]sf] sf/f]jf/ ;d]tnfO{ ;dfof]hg u/L ldnfg ug{ .

CIVIL BANK | ANNUAL REPORT 2073 / 2074 & 2074 / 2075

&

-0f_ g]kfn /fi6« a}+sn] lbPsf] lgb]{zgsf] cwLgdf /xL 6]lnkmf]g, 6]n]S;, ˆofS;, sDKo"6/, jf DofUg]l6s 6]k jf cGo To:t} k|sf/sf ljB'tLo pks/0f jf ;fwgsf] dfWodaf6 lgIf]k lng], e'QmfgL lbg], /sdfGt/ ug]{ ,

-t_ g]kfn /fi6« a}+sn] lbPsf] lgb]{zgsf] cwLgdf /xL qm]l86 sf8{, 8]lj6 sf8{, rfh{ sf8{ nufotsf cGo ljQLo pks/0fx? hf/L ug]{, :jLsf/ ug]{ / ;f] ;DjGwL sfo{ ug{ Ph]G6 lgo'Qm ug]{ ,

-y_ cfkm'n] kTofPsf] JolQmnfO{ ;+rfns ;ldltn] lgwf{/0f u/]sf] gLlt lgod cGtu{t /xL clwljsif{ (Overdraft) shf{ lbg],

-b_ c6f]d]6]8 6]n/ d]l;g / Sof; l8:k]lG;Ë d]l;gsf] dfWodaf6 lgIf]k lng], e'QmfgL lbg] / shf{ lbg],

-w_ cfkm"sxfF klxn] g} lwtf] /xL;s]sf] rn crn ;DklQsf] d"Non] vfd];Ddsf] /sd lgodfg';f/ k'gM Ps}k6s jf k6sk6s u/L shf{ lbg] jf cGo a}+s jf ljQLo ;+:yfdf lwtf] /lx;s]sf] rncrn ;DklQsf] k'gM lwtf]df To;sf] d"Non] vfd];Ddsf] /sd lgodfg';f/ k'gM Ps}k6s jf k6sk6s u/L shf{ lbg],

-g_ g]kfn /fi6« a}+sn] tf]s]sf] zt{df ;f] a}+ssf] Ph]06 e} g]kfn ;/sf/sf] tkm{af6 ;/sf/L sf/f]jf/ nufot cGo sf/f]jf/ ug]{ ,

-k_ g]kfn /fHoleq jf ljb]zdf ljlgdokq, r]s jf cGo ljQLo pks/0fåf/f /sd k7fpg] jf rnfg ug]{, ;'g, rfFbL, z]o/, l8j]~r/, a08 cflb vl/b ljqmL ug]{ / z]o/sf] nfef+z tyf k|lt1fkq, l8j]~r/, a08 cflbsf] Jofh c;"n pk/ ug]{,

-km_ u|fxssf] lgldQ sldzg Ph]06 eO{ z]o/, l8j]~r/ jf ;'/If0fsf] lhDdf lng], vl/b ljqmL ul/lbg], z]o/sf] nfef+z, l8j]~r/ jf ;'/If0fsf] Jofh cflb p7fO lbg] / ;f]sf] nfef+z, d'gfkmf jf Aofh g]kfn /fHoleq jf ljb]zdf ;d]t k7fpg],

-a_ ;]km l8kf]lh6 eN6sf] Joj:yf ug]{,

-e_ g]kfn ;/sf/ jf g]kfn /fi6« a}+sn] hf/L u/]sf] C0fkq vl/b ljqmL ug]{ jf ;sf/ ug]{,

-8_ cfjZostf cg';f/ /fi6« a}+saf6 k'gs{hf{{ lng] jf cGo a}+s jf ljQLo ;+:yfaf6 shf{ lng] lbg],

-9_ kl/of]hgfsf] k|a4{gsf] nflu g]kfn ;/sf/ jf cGo :jb]zL jf ljb]zL lgsfo dfkm{t k|fKt ePsf] /sdaf6 shf{ k|jfx ug]{ jf shf{ Joj:yfkg ug]{,

-0f_ k|rlnt shf{ ckn]vg ljlgodfjnLsf] cwLgdf /xL shf{ ckn]vg ug{],

-t_ k"FhLsf]if k'/f ug{] k|of]hgsf nflu z]o/, l8a]~r/, C0fkq cflb hf/L ug{],

-y_ k|tLtkq, ljlgdokq, k|lt1fkq, r]s, ofq' r]s, 8«fˆ6 jf cGo ljQLo pks/0f lgisfzg ug]{, :jLsf/ ug]{, e'QmfgL lbg], l8:sfp06 ug]{ jf vl/b laqmL ug]{,

-b_ ljB'tLo sf/f]af/sf nflu l8lh6n jf sf8{ nufotsf ljQLo pks/0f hf/L ug]{, :jLsf/ ug]{, Joj:yfkg ug]{ / ;f] ;DaGwL sfo{ ug{ Ph]06 lgo'Qm ug]{,

-w_ k|rlnt sfg"gsf] cwLgdf /xL ljb]zL ljlgdo sf/f]af/ ug]{,

-g_ /fi6« a}+sn] tf]s]sf] ;Ldf, zt{ jf lgb]{zg adf]lhd ;/sf/L sf/f]af/ ug]{]{,

-k_ g]kfn ;/sf/ jf /fi6« a}+sn] hf/L u/]sf] C0fkq vl/b–laqmL ug]{ jf ;sf/ ug]{,

-km_ g]kfnleq jf ljb]zdf ljlgdokq, r]s jf cGo ljQLo pks/0fåf/f /sd k7fpg] jf rnfg ug]{, ljb]zaf6 ljk|]if0f k|fKt ug{] / ;f] sf] e'QmfgL ug{],

-a_ u|fxssf] lgldQ sldzg Ph]06 eO{ z]o/, l8a]~r/ jf ;'/If0fsf] lhDdf lng], vl/b–laqmL ul/lbg], z]o/sf] nfef+z, l8a]~r/ jf ;'/If0fsf] Aofh cflb p7fO{ lbg] / ;f]sf] nfef+z, d'gfkmf jf Aofh g]kfnleq jf ljb]zdf k7fpg], u|fxssf] nflu ;]km l8kf]lh6 eN6sf] Joj:yf ug]{,

-e_ jf;nft aflx/sf] sf/f]af/ ug]{,

-d_ ljkGg ju{, Go"g cfo ePsf] kl/jf/, b}jL k|sf]k kLl8t tyf d'n'ssf s'g} If]qsf afl;Gbfsf] cfly{s pTyfgsf] nflu JolQmut jf ;fd'lxs hdfgLdf /fi6« a}+sn] tf]s] adf]lhdsf] /sd;Dd shf{ lbg],

CIVIL BANK | ANNUAL REPORT 2073 / 2074 & 2074 / 2075

*

-d_ g]kfn /fi6« a}+sn] tf]lslbPsf] zt{df jf;nft aflx/sf] sf/f]jf/ ug]{,

-o_ ljkGg ju{, Go"g cfo ePsf kl/jf/, b}jL k|sf]k kLl8t tyf d'n'ssf s'g} If]qsf afl;Gbfsf]] cfly{s pTyfgsf] nflu JolQmut jf ;fd"lxs hdfgLdf g]kfn /fi6« a}+sn] tf]s] adf]lhdsf] /sd;Dd shf{ lbg],

-/_ cfk"m tyf cGo s'g} a}+s tyf ljQLo ;+:yfaf6 shf{ lng] C0fL jf u|fxssf] ljj/0f, ;"rgf jf hfgsf/L g]kfn /fi6« a}+s jf s'g} cGo a}+s jf ljQLo ;+:yf jLr lng] lbg],

-n_ cGo s'g} a}+s tyf ljQLo ;+:yfaf6 cfˆgf] u|fxsnfO{ shf{ pknAw u/fpg hdfgL a:g],

-j_ g]kfn /fi6« a}+sn] tf]lslbPsf] ;Ldf leq /xL z]o/, l8j]~r/, a08, C0fkq, artkq jf cGo ljQLo pks/0fsf] dfWodaf6 k"FhL kl/rfng ug]{,

-z_ cfjZostfg';f/ g]kfn /fi6« a}+saf6 k'g{shf{ lng] jf cGo a}+s tyf ljQLo ;+:yfnfO{ shf{ lng] lbg],

-if_ kl/of]hgfsf] k|j4{gsf nflu g]kfn ;/sf/ jf cGo :jb]zL jf ljb]zL lgsfoaf6 k|fKt ePsf] /sd shf{sf] ?kdf k|jfx ug]{ jf shf{ Joj:yfkg ug]{,

-;_ kl/of]hgf :yfkgf, ;+rfng / d"NofÍg ;DaGwL cWoog, cg';Gwfg, ;e]{If0f ug]{, u/fpg] tyf tflnd, k/fdz{ / cGo hfgsf/L pknAw u/fpg],

-x_ ;+rfns ;ldltn] agfPsf] ljlgodsf] cwLgdf /xL shf{ ckn]vg ug]{,

-If_ s'g} JolQm jf ;+:yfnfO{ shf{ lb+bf jf lgh;Fu s'g} sf/f]jf/ ubf{ cfˆgf] lxtsf] ;+/If0fsf nflu cfjZostf cg';f/ zt{ u/fpg],

-q_ cfˆgf] hfoh]yfsf] plrt k|jGw jf las|L ug]{ / cfˆgf] rn crn, hfoh]yf lwtf] /fvL shf{ lng]

-1_ g]kfn /fi6« a}+sn] ;do ;dodf tf]s]sf cGo sfd ug]{ .

-o_ cfk"m tyf cGo a}+s jf ljQLo ;+:yfaf6 shf{ lng] jf s'g} k|sf/sf] ;'ljwf lng] C0fL jf u|fxssf] ljj/0f, ;"rgf jf hfgsf/L /fi6« a}+s, ;DalGwt lgsfo jf cGo a}+s jf ljQLo ;+:yfaLr lng] lbg],

-/_ ;'g, rFfbL vl/b–laqmL ug]{,-n_ kl/of]hgf :yfkgf, ;~rfng / d"NofÍg ;DaGwL cWoog, cg';Gwfg, ;j]{If0f ug]{ u/fpg] tyf tfnLd, k/fdz{ / cGo hfgsf/L pknAw u/fpg],

-j_ o; P]g / k|rlnt sfg"g adf]lhd cfˆgf] :jfldTjdf cfpg] ;a} k|sf/sf hfoh]yfsf] plrt Joj:yfkg tyf laqmL ug]{,

-z_ k|rlnt sfg"g adf]lhd b'O{ jf b'O{eGbf a9L JolQmx?aLr x'g] s'g} sfo{ afkt ltg'{ a'emfpg' jf lng' kg]{ /sd pQm sfd ePkl5 e'QmfgL lng] lbg] Joj:yf ug{ b'O{ kIfsf] ;xdltdf hdfgL a:g],

-if_ cGo s'g} a}+s tyf ljQLo ;+:yfaf6 cfˆgf] u|fxsnfO{ shf{ pknAw u/fpg hdfgL a:g],

-;_ g]kfn /fi6« a}|sn] tf]lslbPsf] ;Ldfleq /xL z]o/, l8a]~r/, a08, C0fkq, artkq jf cGo ljQLo pks/0fsf] dfWodaf6 k"FhL kl/rfng ug]{,

-x_ s'g} JolQm jf ;+:yfnfO{ shf{ lbFbf jf lgh;Fu s'g} sf/]af/ ubf{ cfˆgf] lxtsf] ;+/If0fsf nflu cfjZostf cg'';f/ zt{ u/fpg],

-If_ g]kfn /fi6« a}+sn] tf]lslbP adf]lhd shf{ lbg],

-q_ ;DalGwt lgsfosf] :jLs[lt lng'kg]{ eP ;f] ;d]t lnO cfjZostf cg';f/ af]g; z]o/ jf xsk|b z]o/ hf/L ug]{ ,

-1_ /fi6« a}+sn] tf]s]sf] cGo sfd ug]{

CIVIL BANK | ANNUAL REPORT 2073 / 2074 & 2074 / 2075

(

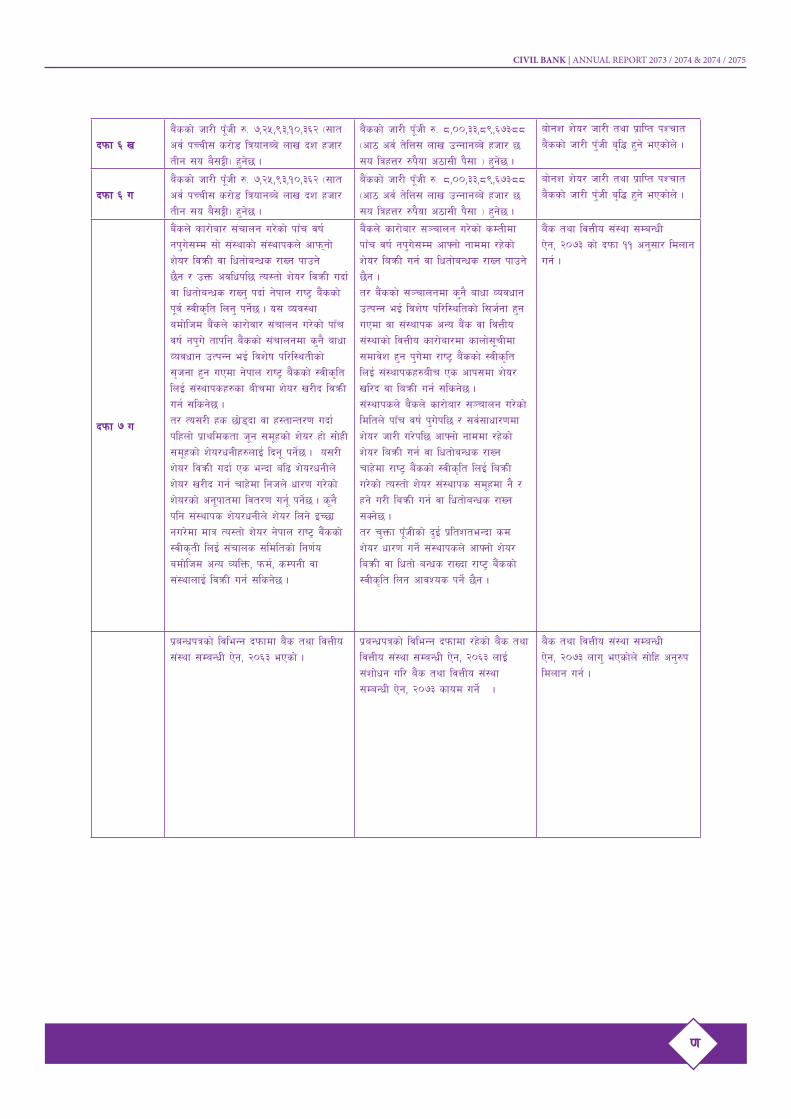

bkmf ^ v a}+ssf] hf/L k"FhL ?= 7,25,93,10,362 -;ft cj{ kRrL; s/f]8 lqofgAa] nfv bz xhf/ tLg ;o a};¶L_ x'g]5 .

a}+ssf] hf/L k"FhL ?= 8,00,33,89,673=88 -cf7 cj{ t]lQ; nfv pGgfgAa] xhf/ 5 ;o lqxQ/ ?k}of c7f;L k};f _ x'g]5 .

Aff]gz z]o/ hf/L tyf k|flKt kZrft a}+ssf] hf/L k'FhL a[l4 x'g] ePsf]n] .

bkmf ^ ua}+ssf] hf/L k"FhL ?= 7,25,93,10,362 -;ft cj{ kRrL; s/f]8 lqofgAa] nfv bz xhf/ tLg ;o a};¶L_ x'g]5 .

a}+ssf] hf/L k"FhL ?= *,00,33,89,673=88 -cf7 cj{ t]lQ; nfv pGgfgAa] xhf/ 5 ;o lqxQ/ ?k}of c7f;L k};f _ x'g]5 .

Aff]gz z]o/ hf/L tyf k|flKt kZrft a}+ssf] hf/L k'FhL a[l4 x'g] ePsf]n] .

bkmf & u

a}+sn] sf/f]af/ ;+rfng u/]sf] kfFr jif{ gk'u];Dd ;f] ;+:yfsf] ;+:yfksn] cfkm\gf] z]o/ ljqmL jf lwtf]aGws /fVg kfpg] 5}g / pQm cjlwkl5 To:tf] z]o/ ljqmL ubf{ jf lwtf]aGws /fVg' kbf{ g]kfn /fi6« a}+ssf] k"j{ :jLs[lt lng' kg]{5 . o; Joj:yf adf]lhd a}+sn] sf/f]jf/ ;+rfng u/]sf] kfFr jif{ gk'u] tfklg a}+ssf] ;+rfngdf s'g} afwf Jojwfg pTkGg eO{ ljz]if kl/l:ytLsf] ;[hgf x'g uPdf g]kfn /fi6« a}+ssf] :jLs[lt lnO{ ;+:yfksx?sf aLrdf z]o/ v/Lb ljqmL ug{ ;lsg]5 . t/ To;/L xs 5f]8\bf jf x:tfGt/0f ubf{ klxnf] k|fyldstf h"g ;d"xsf] z]o/ xf] ;f]xL ;d"xsf] z]o/wgLx?nfO{ lbg" kg]{5 . o;/L z]o/ ljqmL ubf{ Ps eGbf al9 z]o/wgLn] z]o/ v/Lb ug{ rfx]df lghn] wf/0f u/]sf] z]o/sf] cg"kftdf ljt/0f ug"{ kg]{5 . s"g} klg ;+:yfks z]o/wgLn] z]o/ lng] OR5f gu/]df dfq To:tf] z]o/ g]kfn /fi6« a}+ssf] :jLs[tL lnO{ ;+rfns ;ldltsf] lg0f{o adf]lhd cGo JolQm, kmd{, sDkgL jf ;+:yfnfO{ ljqmL ug{ ;lsg]5 .

a}+sn] sf/f]af/ ;~rfng u/]sf] sDtLdf kfFr jif{ gk'u];Dd cfˆgf] gfddf /x]sf] z]o/ laqmL ug{ jf lwtf]aGws /fVg kfpg] 5}g . t/ a}+ssf] ;~rfngdf s'g} afwf Jojwfg pTkGg eO{ ljz]if kl/l:yltsf] l;h{gf x'g uPdf jf ;+:yfks cGo a}+s jf ljQLo ;+:yfsf] ljQLo sf/f]af/df sfnf];"rLdf ;dfj]z x'g k'u]df /fi6« a}+ssf] :jLs[lt lnO{ ;+:yfksx?aLr Ps cfk;df z]o/ vl/b jf laqmL ug{ ;lsg]5 . ;+:yfksn] a}+sn] sf/f]af/ ;~rfng u/]sf] ldltn] kfFr jif{ k'u]kl5 / ;j{;fwf/0fdf z]o/ hf/L u/]kl5 cfˆgf] gfddf /x]sf] z]o/ laqmL ug{ jf lwtf]aGws /fVg rfx]df /fi6« a}+ssf] :jLs[lt lnO{ laqmL u/]sf] To:tf] z]o/ ;+:yfks ;d"xdf g} /xg] u/L laqmL ug{ jf lwtf]aGws /fVg ;Sg]5 . t/ r'Qmf k"FhLsf] b'O{ k|ltzteGbf sd z]o/ wf/0f ug{] ;+:yfksn] cfˆgf] z]o/ laqmL jf lwtf] aGws /fVbf /fi6« a}+ssf] :jLs[lt lng cfjZos kg{] 5}g .

a}+s tyf ljQLo ;+:yf ;DaGwL P]g, @)&# sf] bkmf !! cg';f/ ldnfg ug{ .

k|aGwkqsf] ljleGg bkmfdf a}+s tyf ljQLo ;+:yf ;DaGwL P]g, @)^# ePsf] .

k|aGwkqsf] ljleGg bkmfdf /x]sf] a}+s tyf ljQLo ;+:yf ;DaGwL P]g, @)^# nfO{ ;+zf]wg ul/ a}+s tyf ljQLo ;+:yf ;DaGwL P]g, @)&# sfod ug]{ .

a}+s tyf ljQLo ;+:yf ;DaGwL P]g, @)&# nfu' ePsf]n] ;f]lx cg'?k ldnfg ug{ .

CIVIL BANK | ANNUAL REPORT 2073 / 2074 & 2074 / 2075

)f

lgodfjnLsf] ;DalGwt lgod