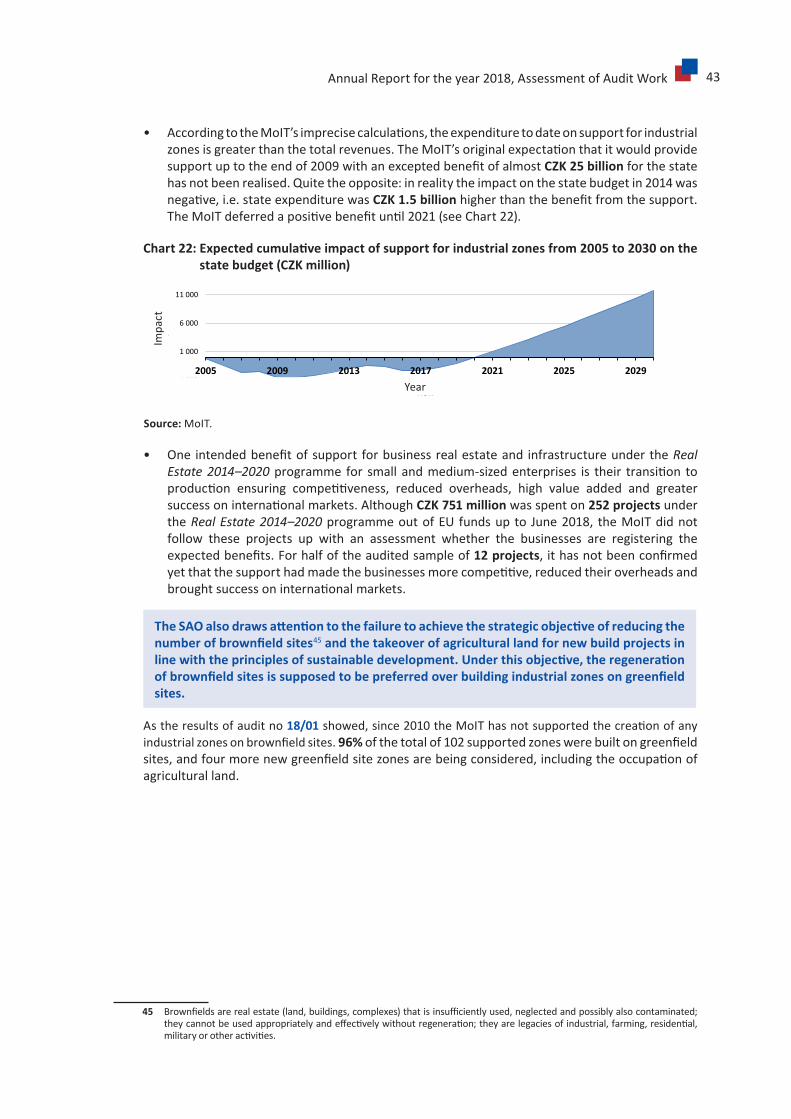

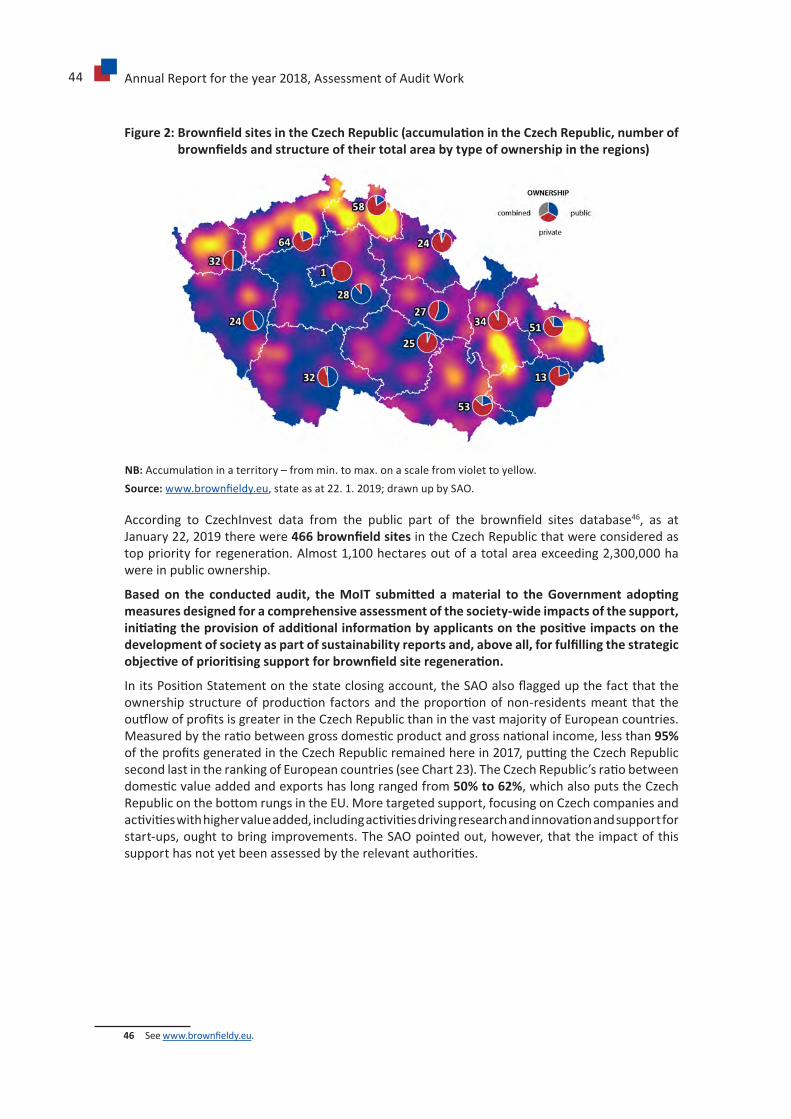

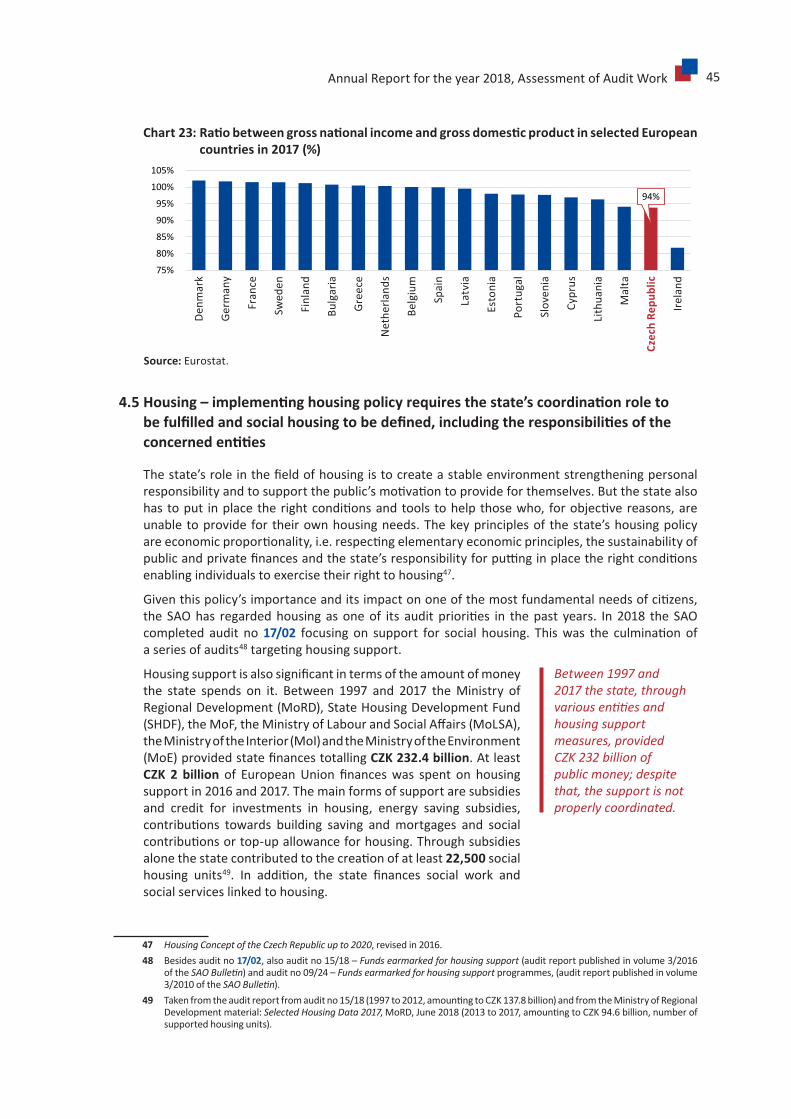

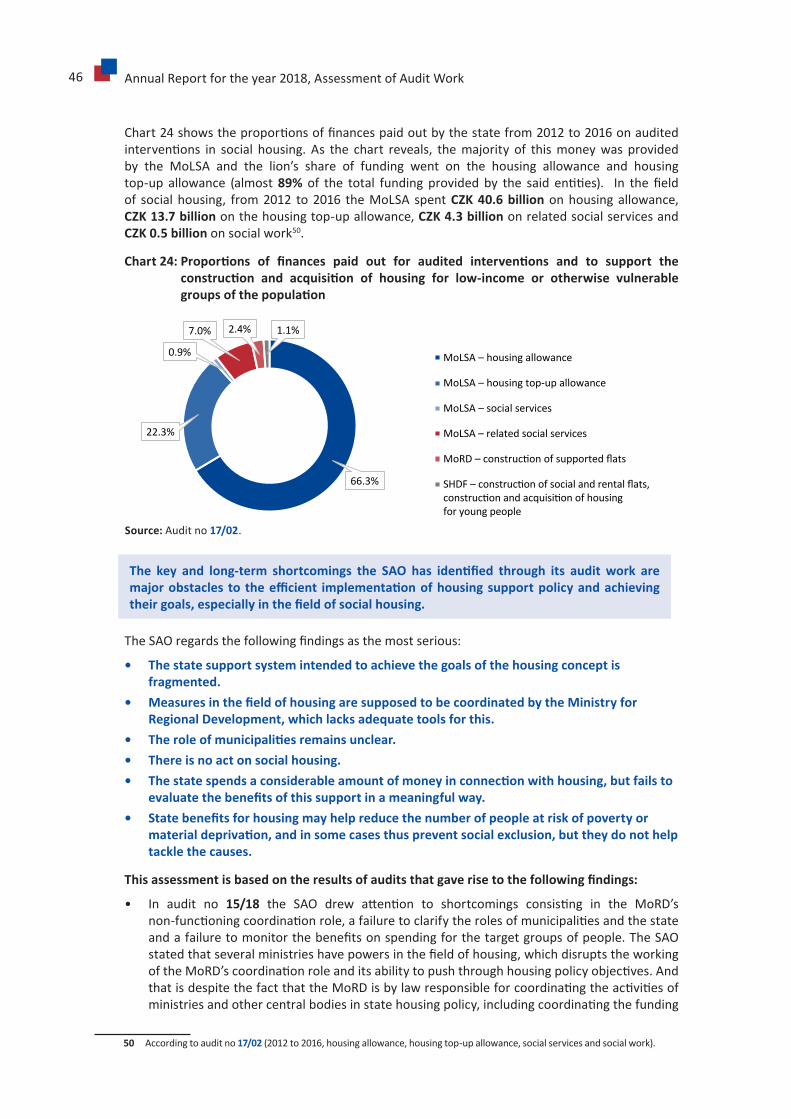

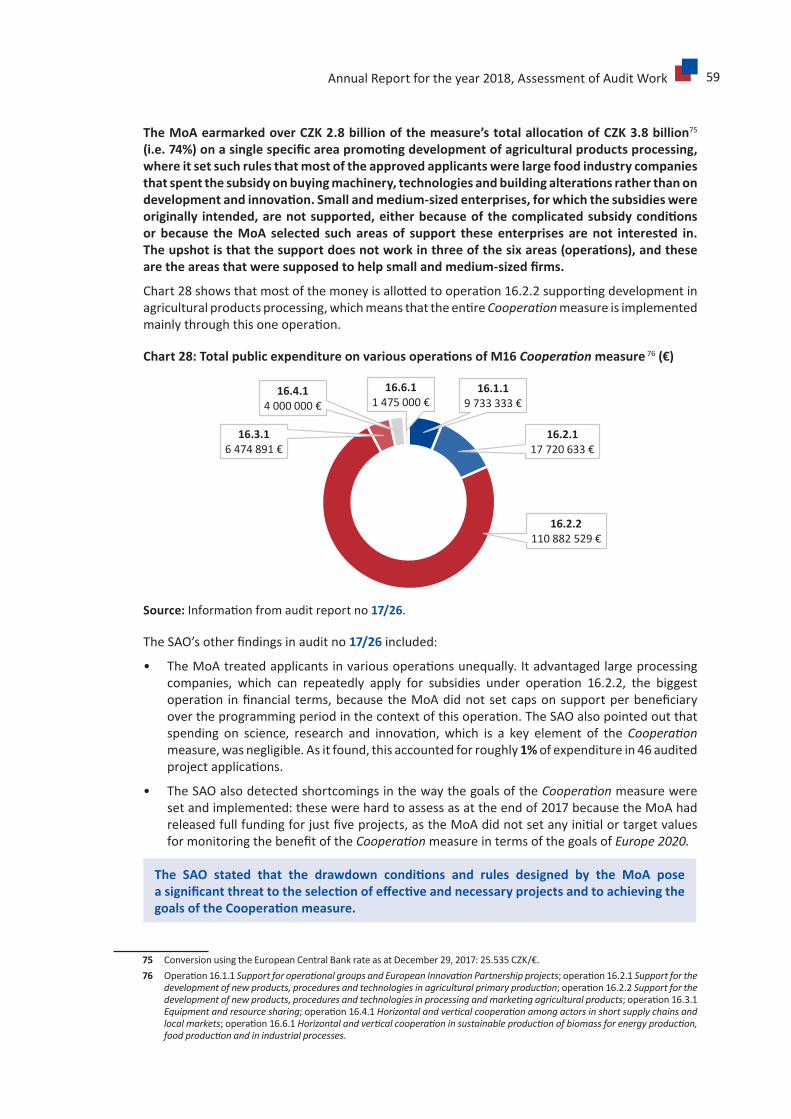

Annual Report for the year 2018 - NKÚ

140

MARCH 2019 ANNUAL REPORT 2018

-

Upload

khangminh22 -

Category

Documents

-

view

5 -

download

0

Transcript of Annual Report for the year 2018 - NKÚ

MARCH 2019

ANNUALREPORT

2018

Czech Republic | Supreme Audit Office | Annual Report 2018

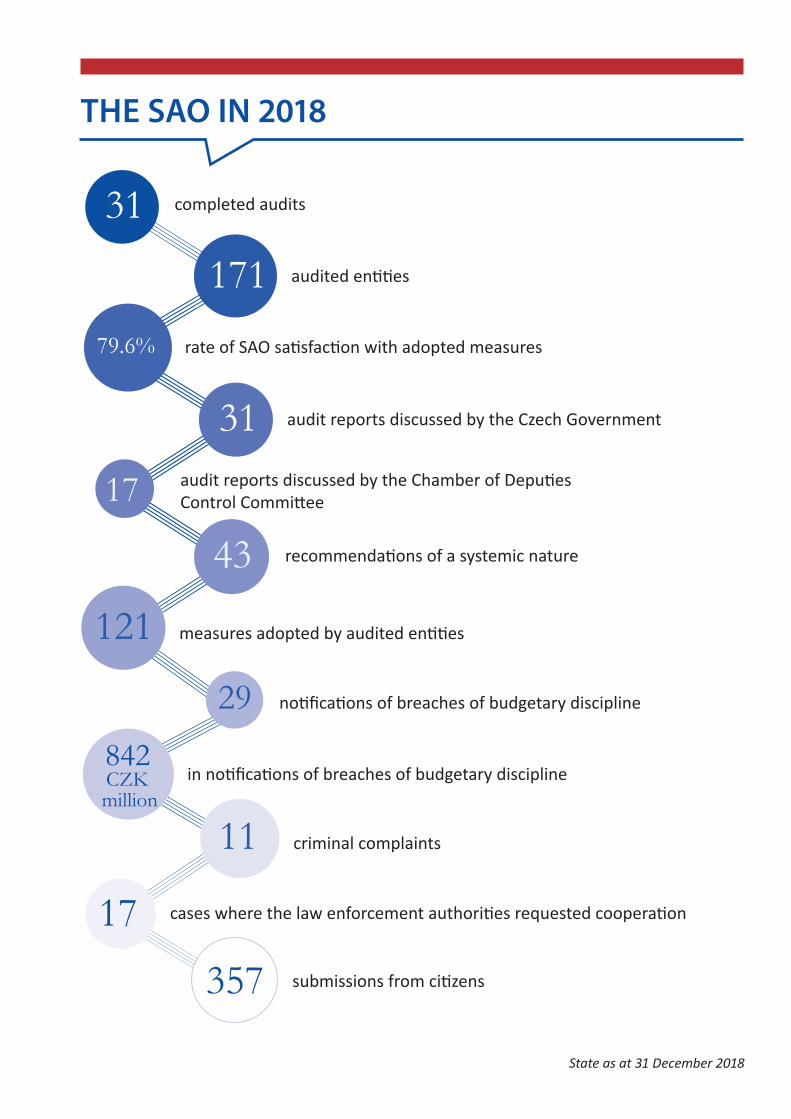

THE SAO IN 2018

31

31

17

17

171

121

79.6%

357

842

43

29

CZK million

completed audits

audited en��es

no�fica�ons of breaches of budgetary discipline

audit reports discussed by the Czech Government

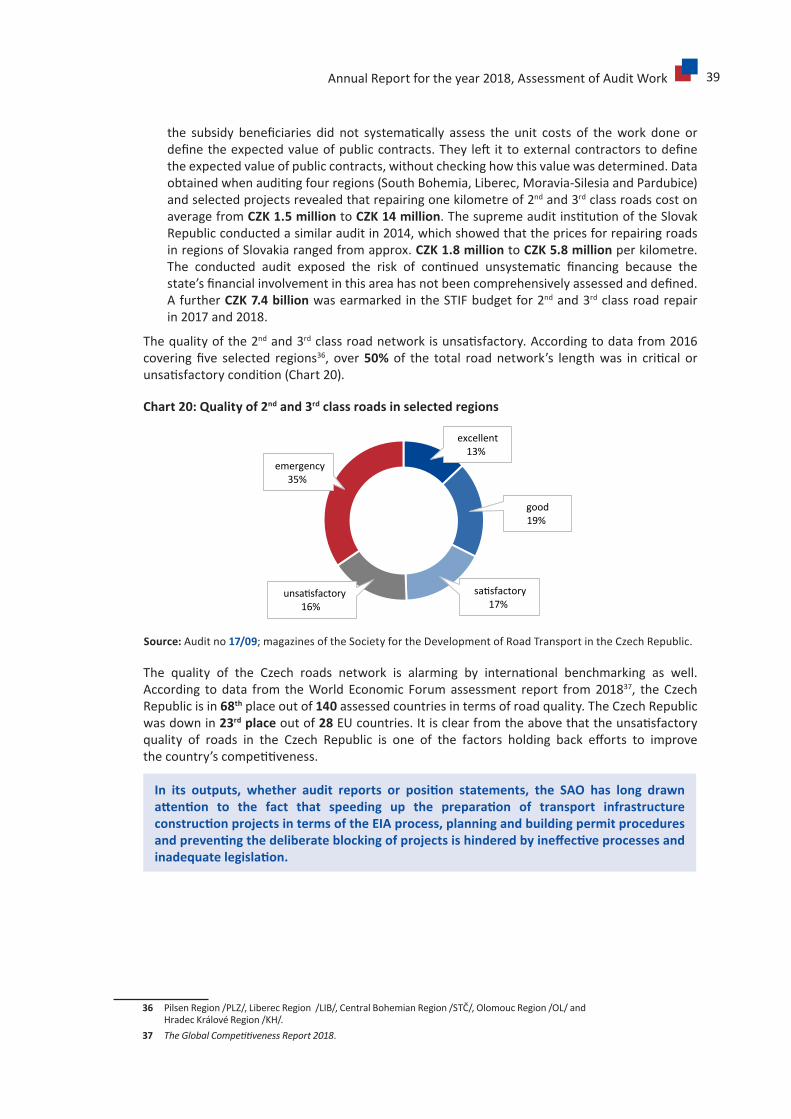

audit reports discussed by the Chamber of Depu�es Control Commi�ee

recommenda�ons of a systemic nature

measures adopted by audited en��es

criminal complaints

submissions from ci�zens

cases where the law enforcement authori�es requested coopera�on

in no�fica�ons of breaches of budgetary discipline

rate of SAO sa�sfac�on with adopted measures

11

State as at 31 December 2018

Annual Report for the year 2018 3

Content

Opening message from the SAO president ............................................................................... 5

I. Status and Powers of the SAO .......................................................................................... 6

1. BasicinformationonthestatusandpowersoftheSAO ......................................................... 6

2. SAOBoard................................................................................................................................ 7

3. SAOmanagement .................................................................................................................... 9

4. MissionandbenefitsoftheSAO’swork ................................................................................ 10

5. Auditplanfor2018 ................................................................................................................ 10

II. Assessment of Audit and Analysis Work in 2018 ............................................................. 12

1. Openingsummary ................................................................................................................. 12

2. Publicfinances ...................................................................................................................... 17

3. Staterevenues ...................................................................................................................... 23

4. Governmentexpenditureareas............................................................................................ 28

4.1 EfficientpublicadministrationandeGovernment ...................................................... 29

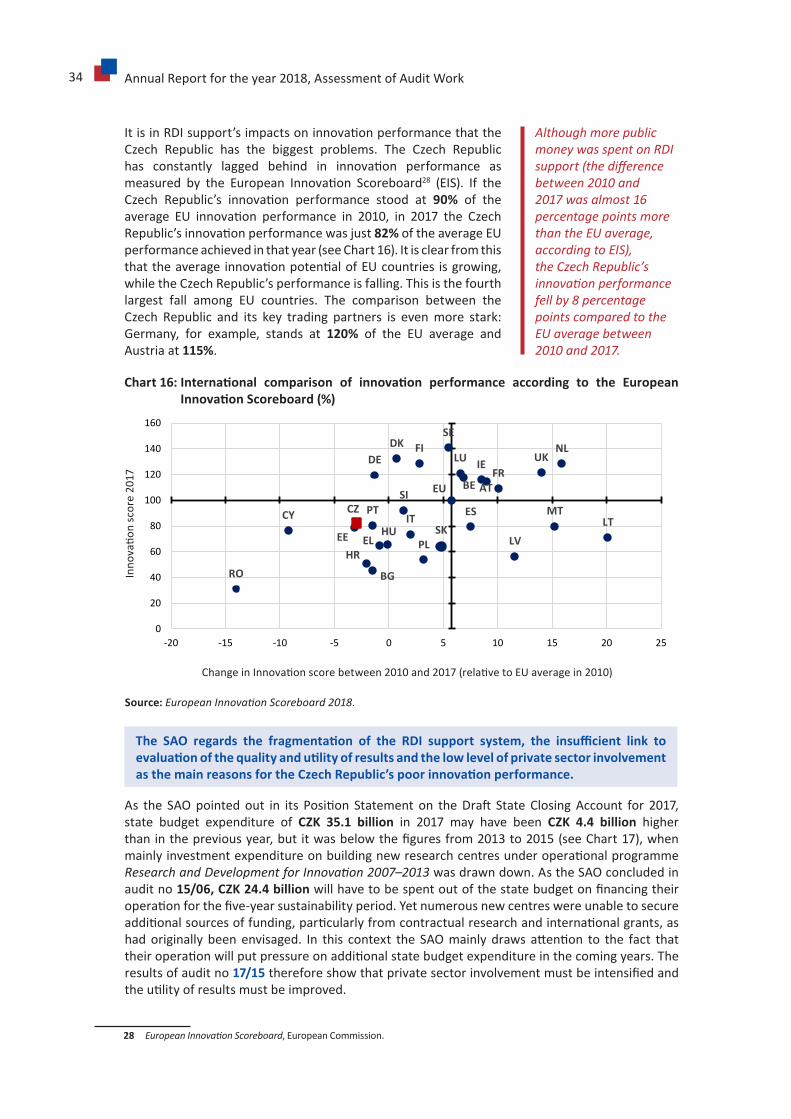

4.2 Research,developmentandinnovation ...................................................................... 32

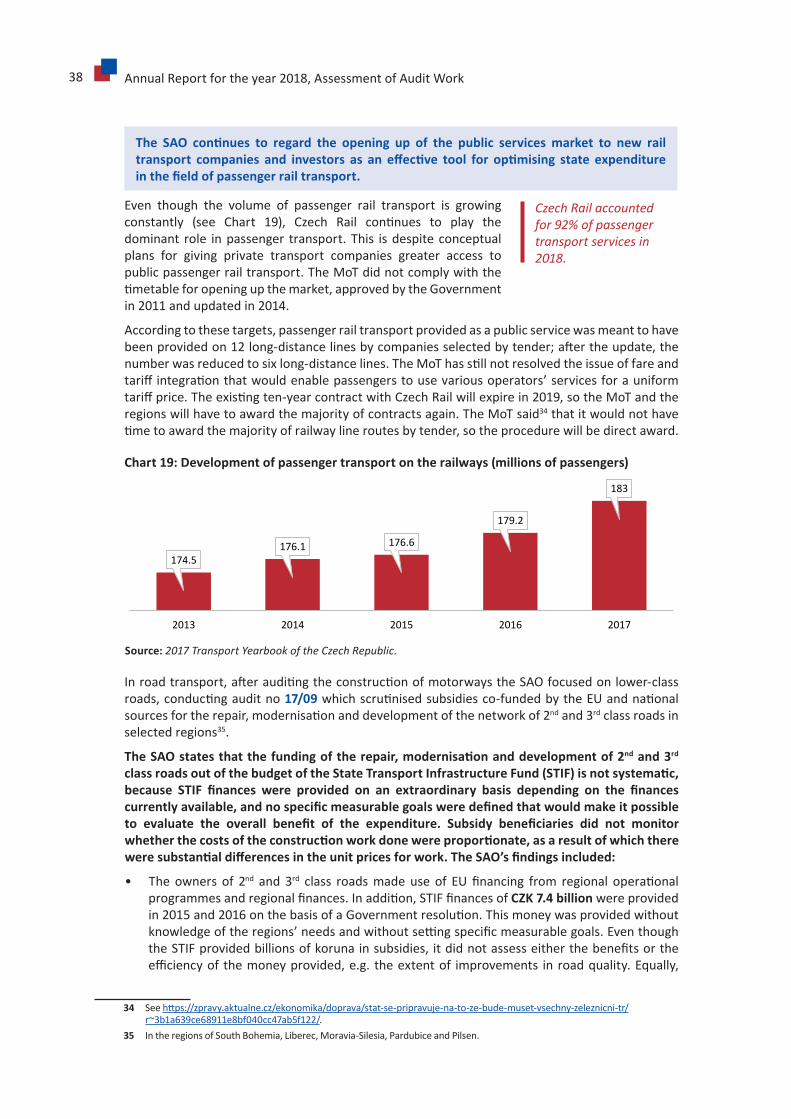

4.3 Transport ..................................................................................................................... 35

4.4 Enterprise .................................................................................................................... 41

4.5 Housing ........................................................................................................................ 45

4.6 Healthcare ................................................................................................................... 49

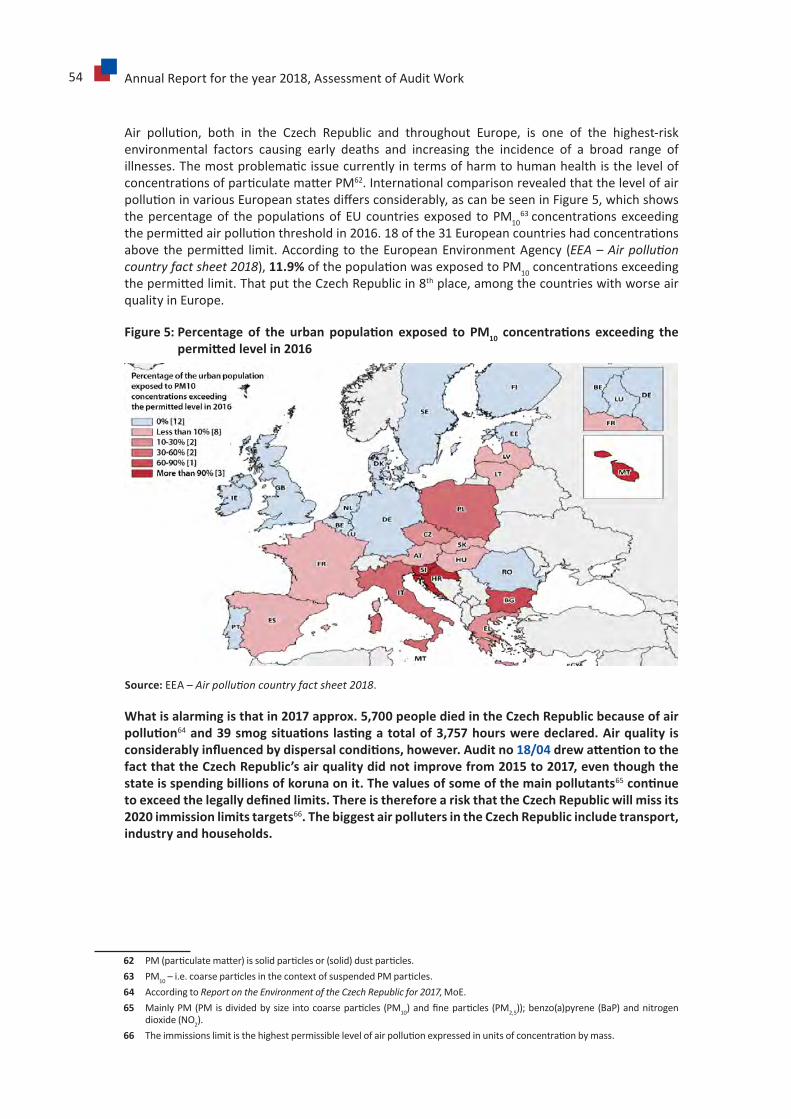

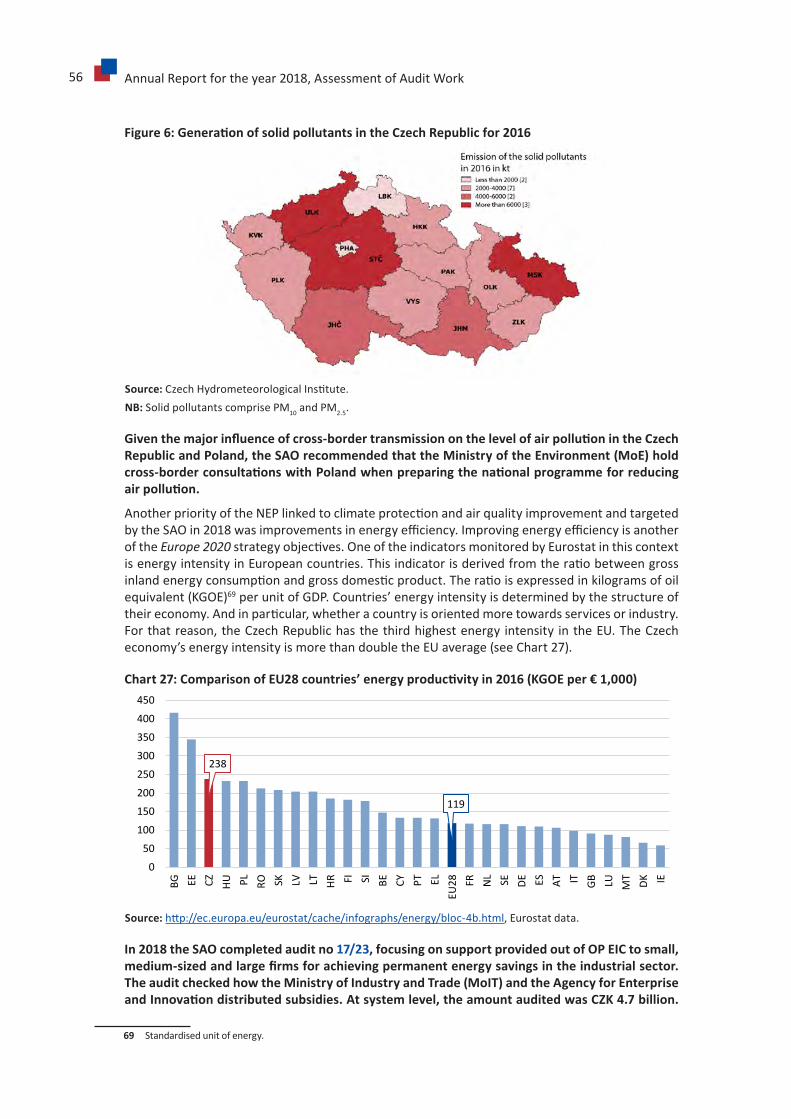

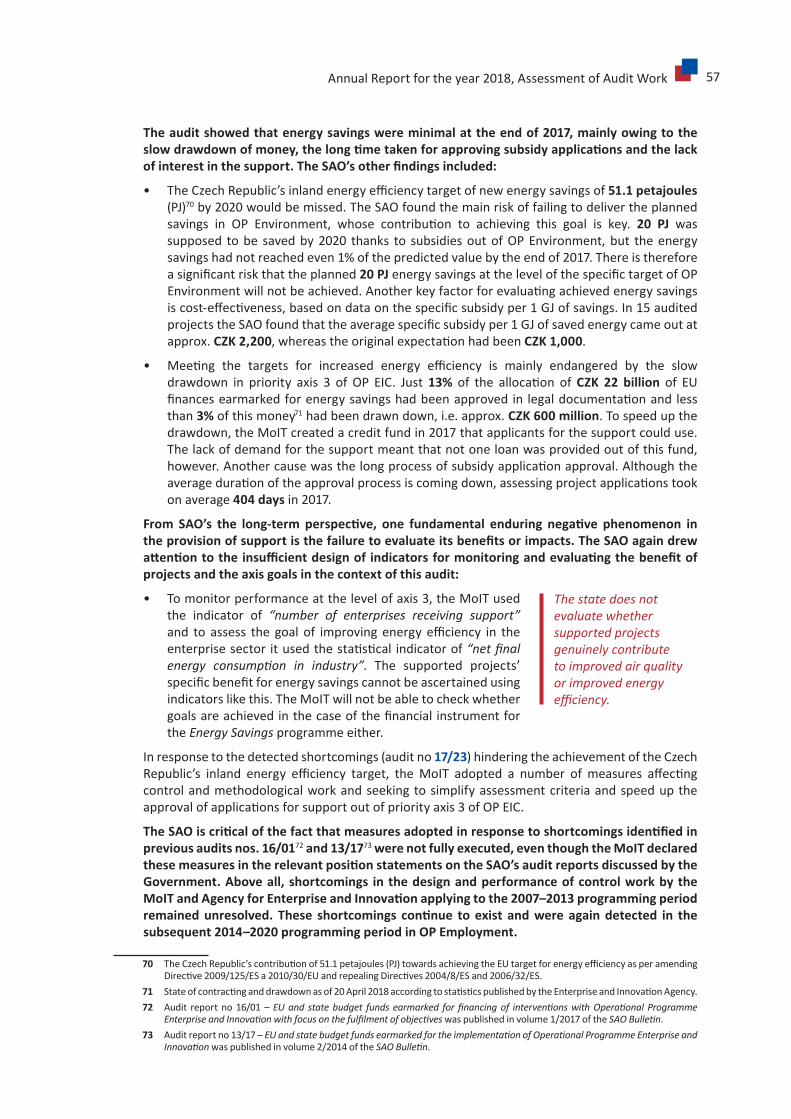

4.7 Environment ................................................................................................................ 53

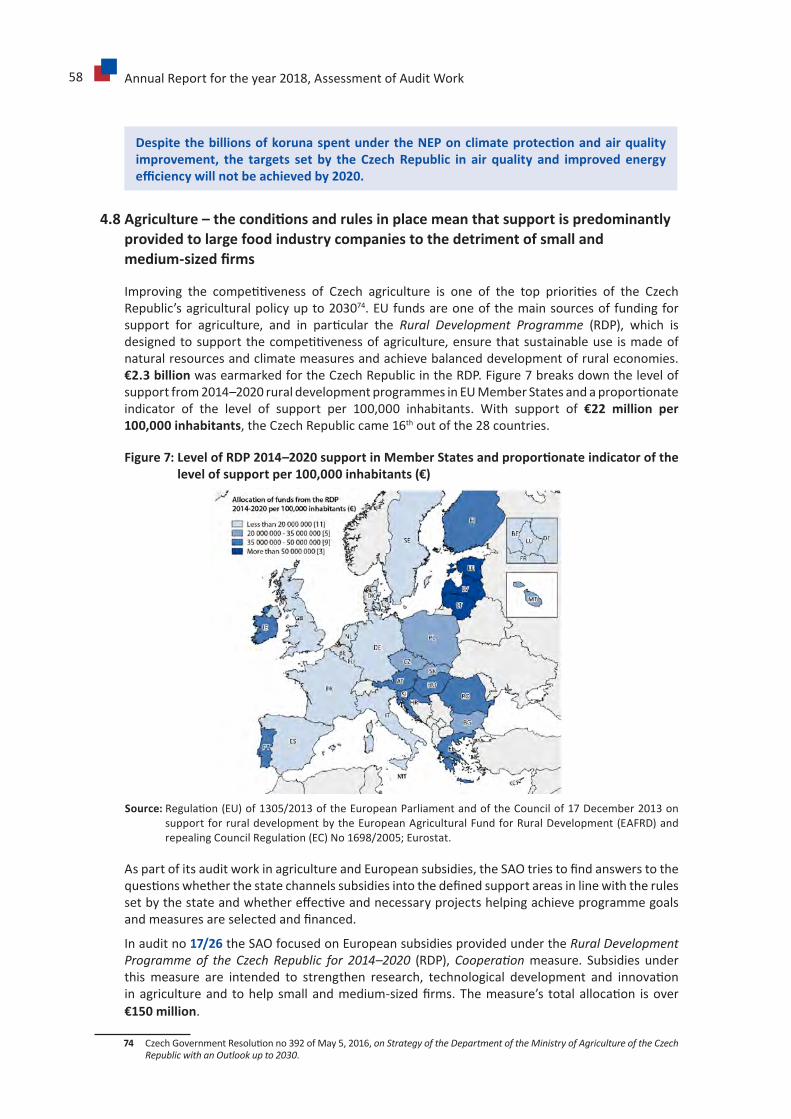

4.8 Agriculture ................................................................................................................... 58

4.9 Education ..................................................................................................................... 60

4.10 Culture ......................................................................................................................... 63

4.11 Defenceandsecurity ................................................................................................... 65

5. Institutionalmanagement .................................................................................................... 69

5.1 Institutions’financialmanagement ............................................................................. 69

5.2 Publicprocurement ..................................................................................................... 75

5.3 ManagementoffundsprovidedtotheCzechRepublicfromabroad ......................... 82

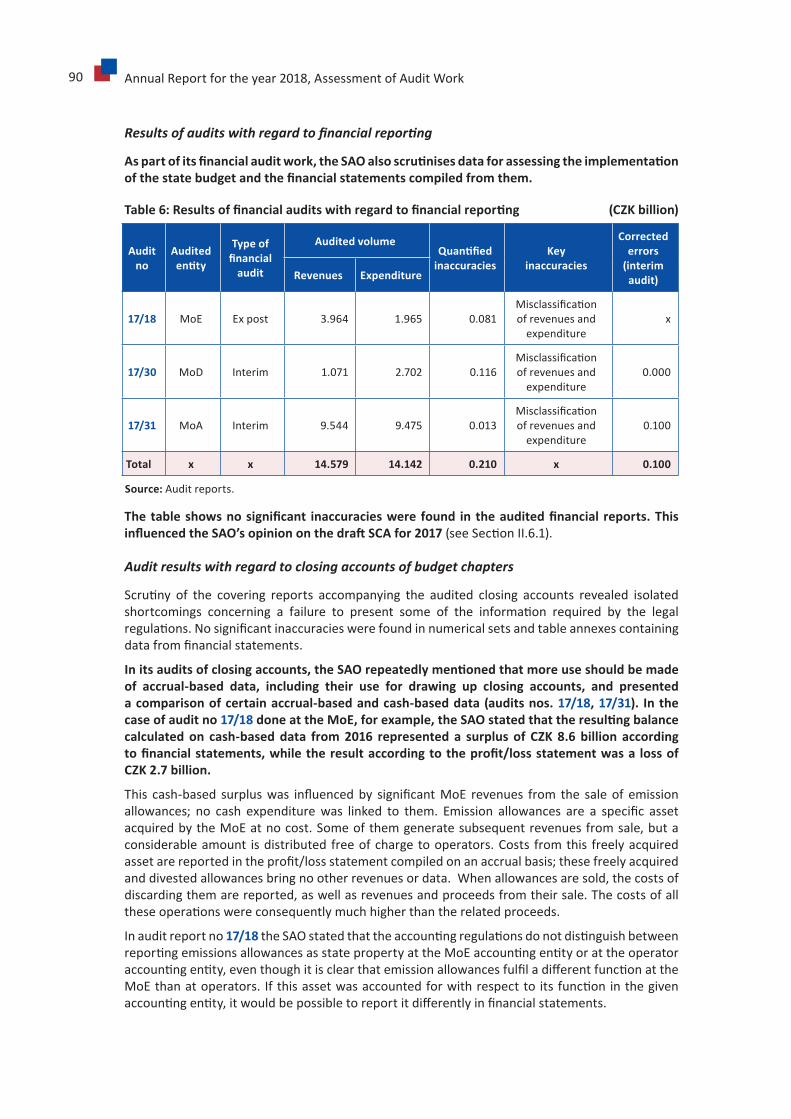

6. SAOopinionsonthestate’sfinancialreporting .................................................................... 87

6.1 OpinionontheDraftStateClosingAccount ............................................................... 87

6.2 Opinionsonthestate’sfinancialreporting .................................................................. 87

6.3 Promotinggoodaccountingandauditpractice ........................................................... 91

III. FinancialEvaluationofAuditWork ................................................................................ 93

1. Overallfinancialevaluationofaudits ................................................................................... 93

2. DischargeofthenotificationdutypursuanttoActno280/2009Coll.,thetaxcode ........... 93

4 Annual Report for the year 2018

IV. AssessmentofOtherActivities ....................................................................................... 94

1. Cooperationwiththecriminaljusticeauthoritiesin2018 .................................................... 94

2. Opinionsondraftlegislationin2018 ..................................................................................... 94

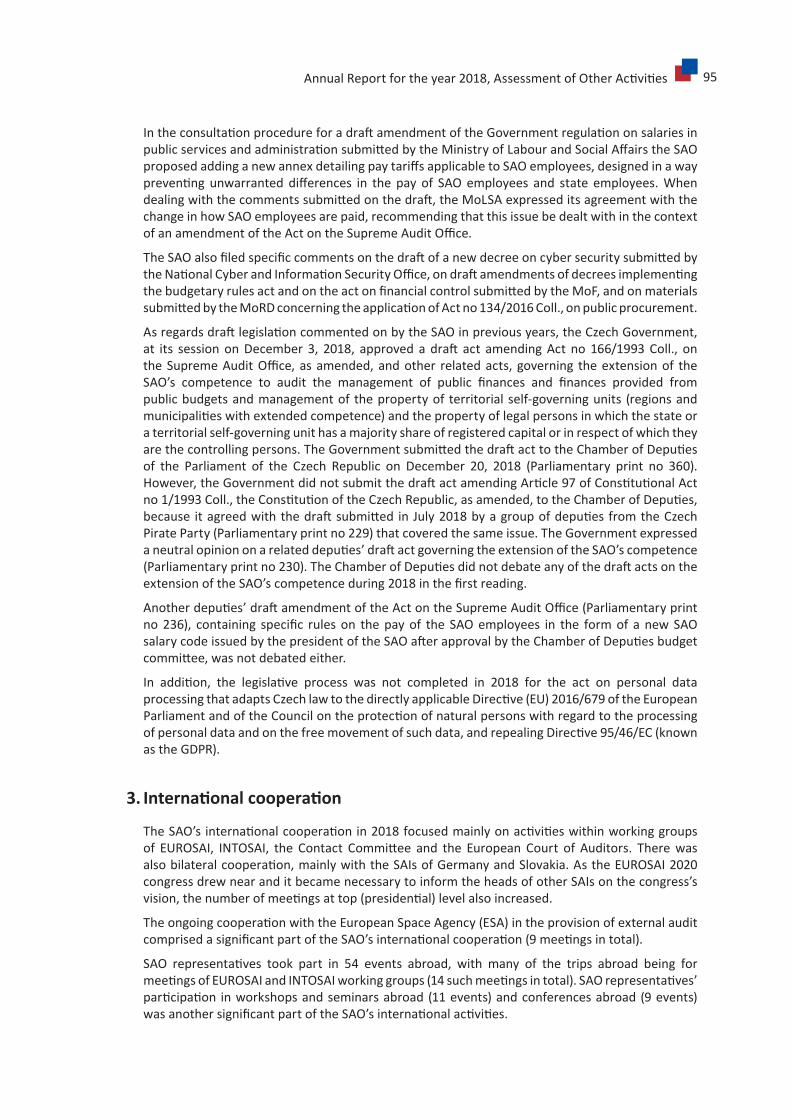

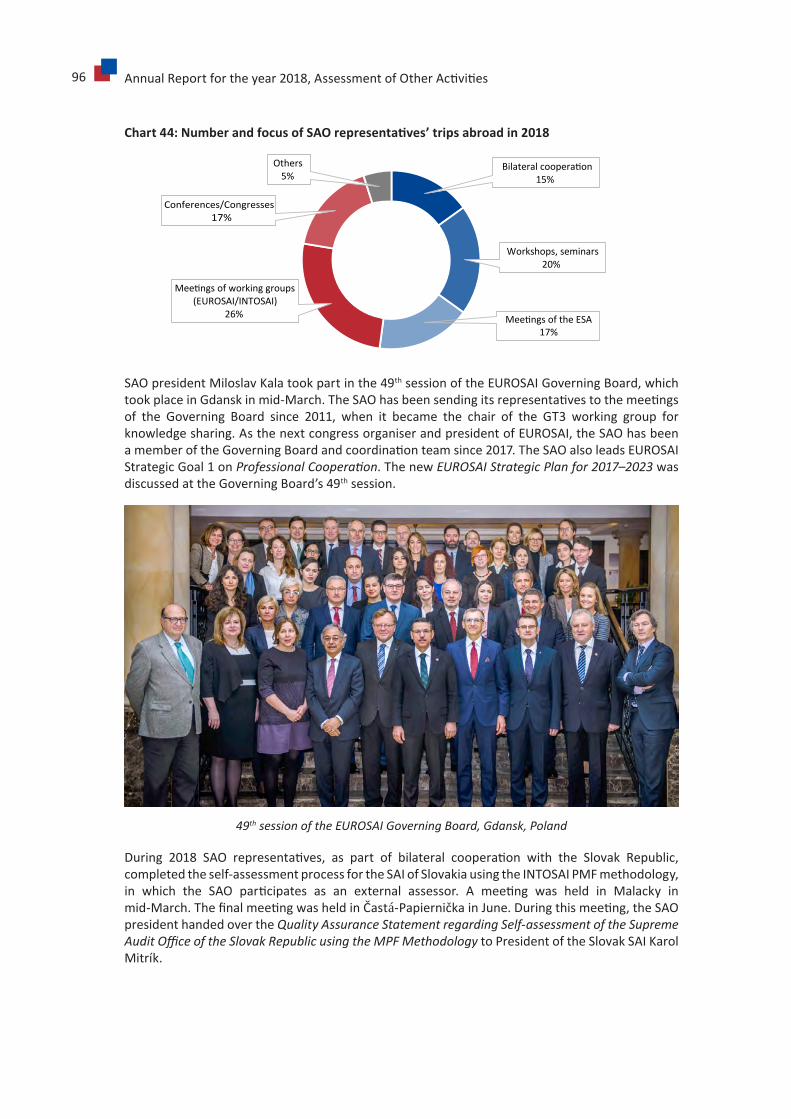

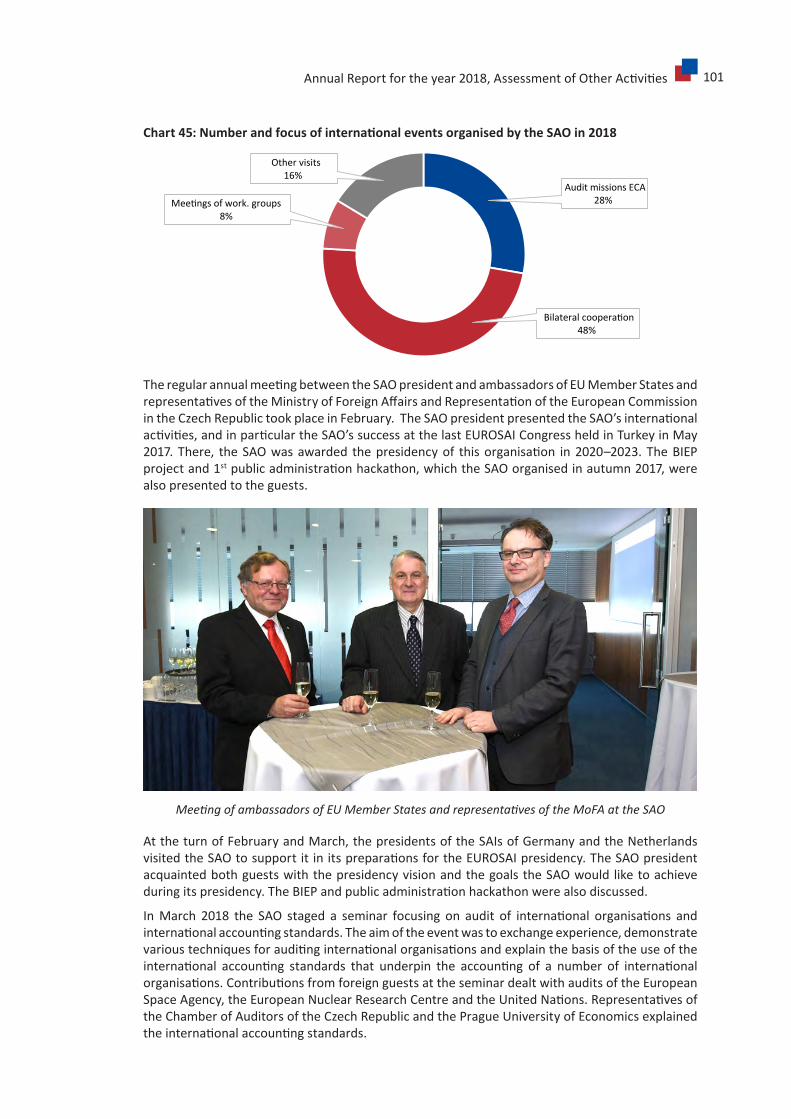

3. Internationalcooperation .................................................................................................... 95

4. TheSAO’sworkinrespectofthepublic .............................................................................. 104

4.1 ProvisionofinformationpursuanttoActno106/1999Coll., onfreeaccesstoinformation..................................................................................... 104

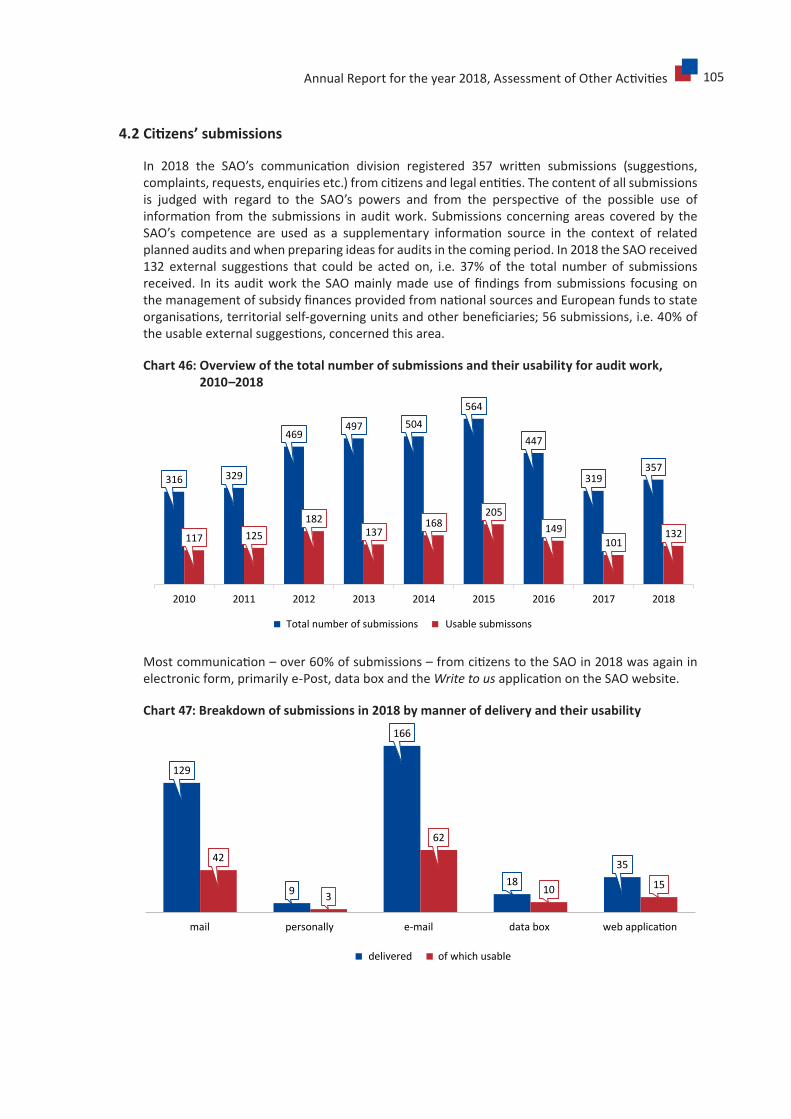

4.2 Citizens’submissions .................................................................................................. 105

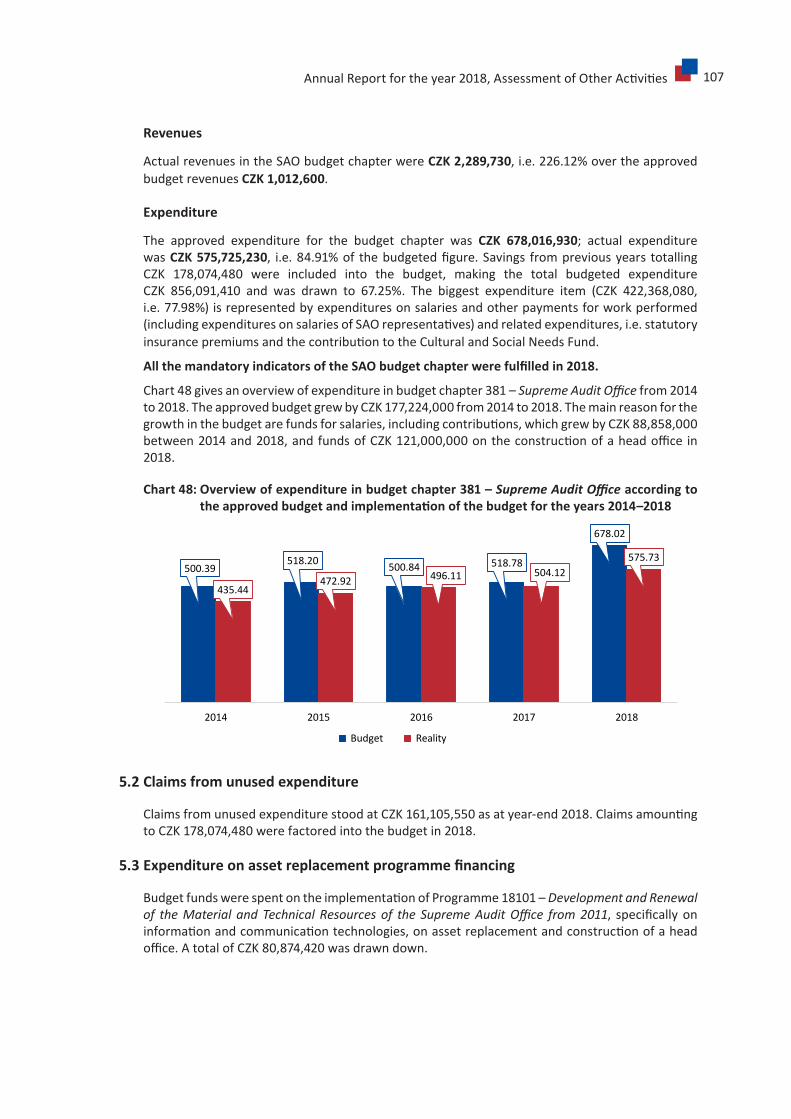

5. ManagementoffinancesallocatedtotheSAObudgetchapterin2018 ............................. 106

5.1 ImplementationofmandatoryindicatorsoftheSAObudgetchapter ...................... 106

5.2 Claimsfromunusedexpenditure ............................................................................... 107

5.3 Expenditureonassetreplacementprogrammefinancing ......................................... 107

5.4 InformationonexternalauditsintheSAO ................................................................. 108

5.5 Mandatoryaudit......................................................................................................... 108

6. Internalaudit ....................................................................................................................... 109

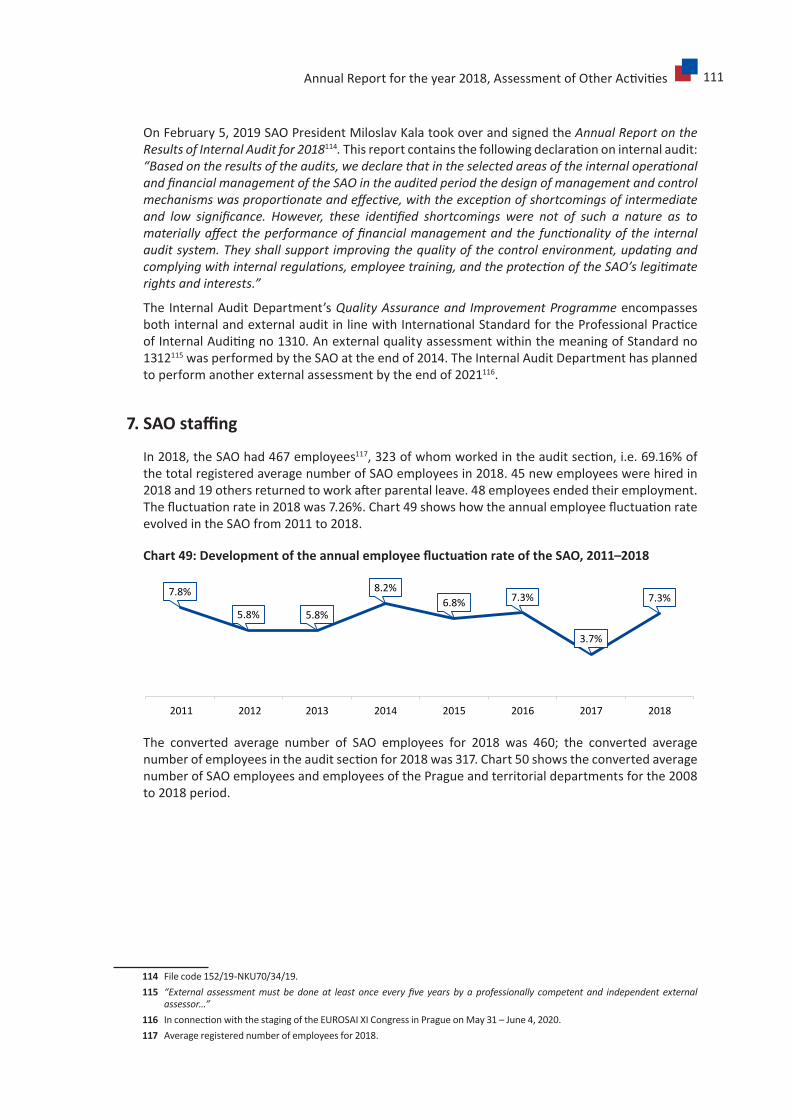

7. SAOstaffing ......................................................................................................................... 111

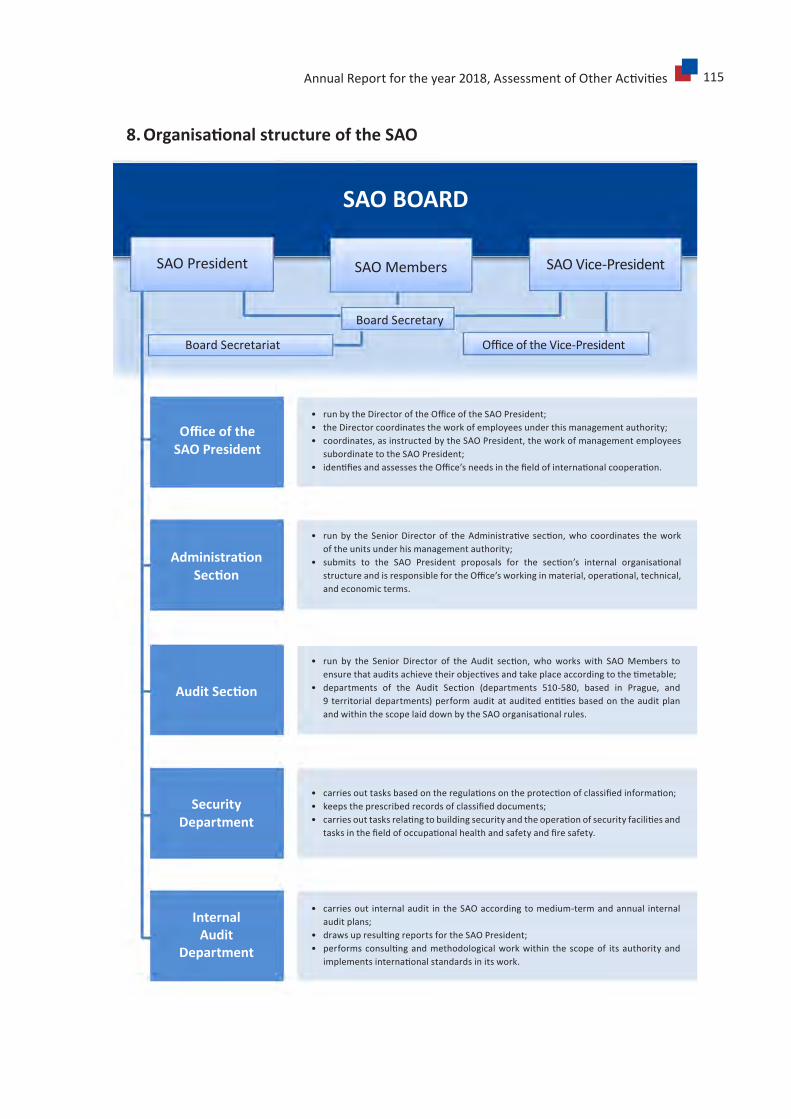

8. OrganisationalstructureoftheSAO ................................................................................... 115

Annexes

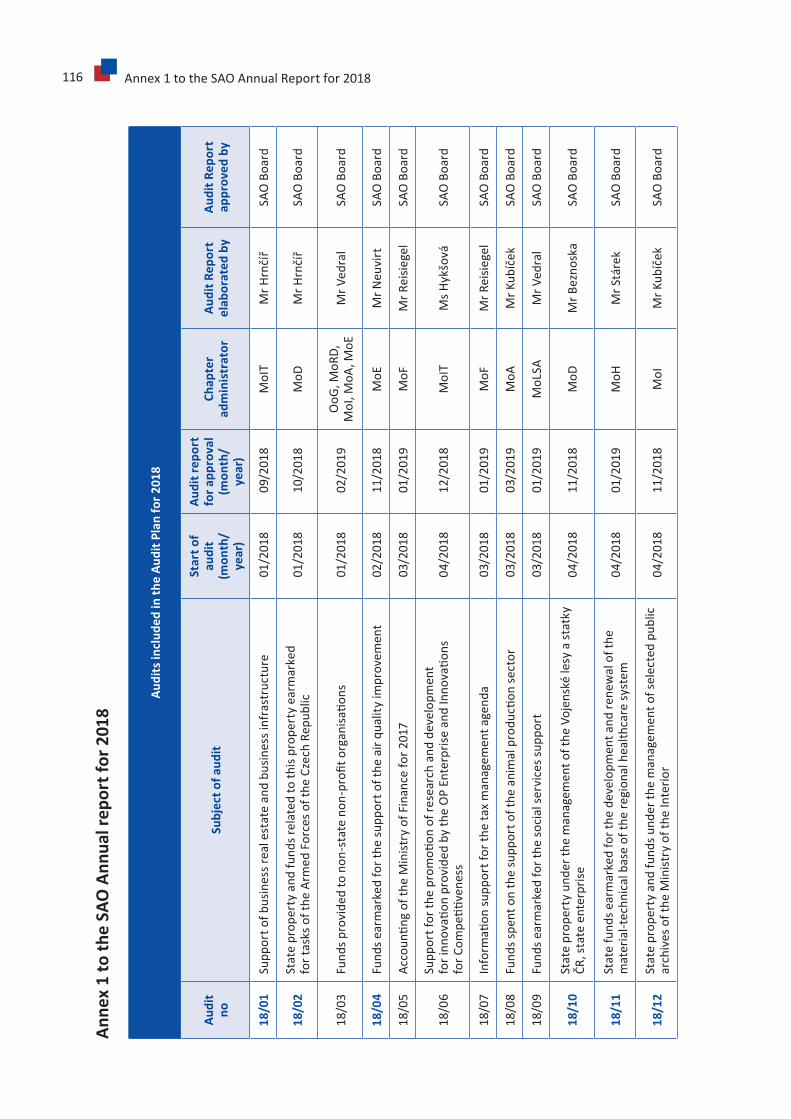

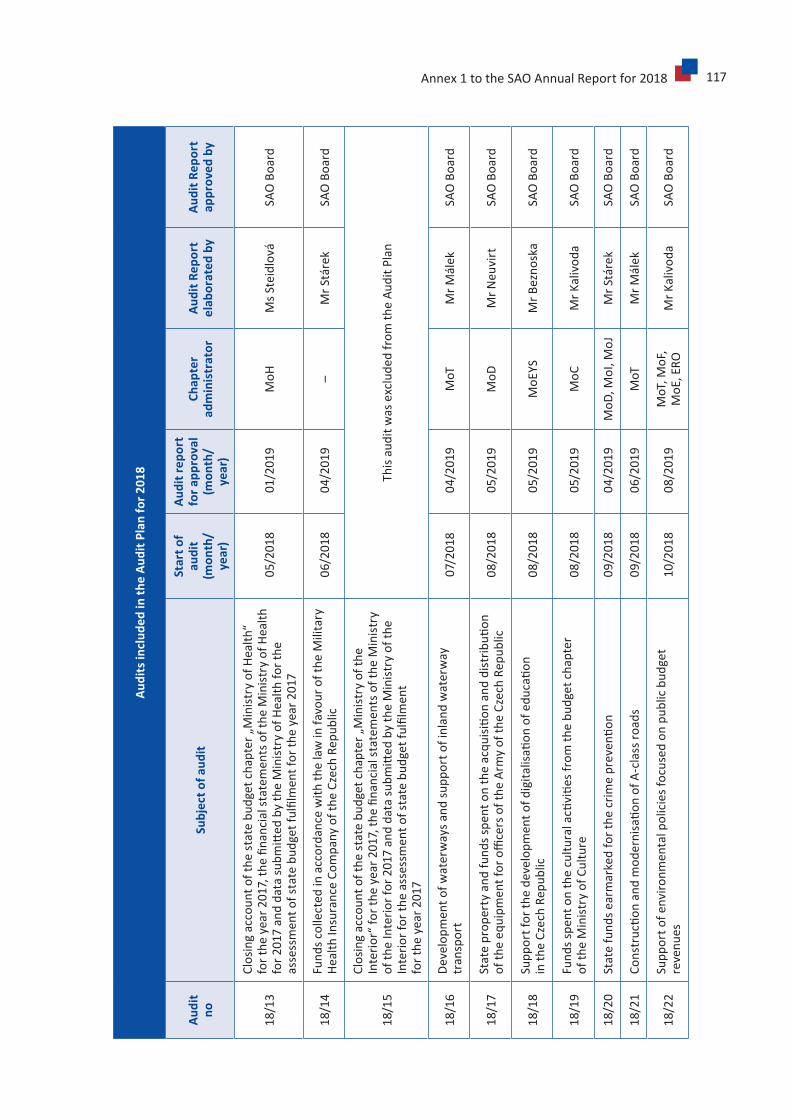

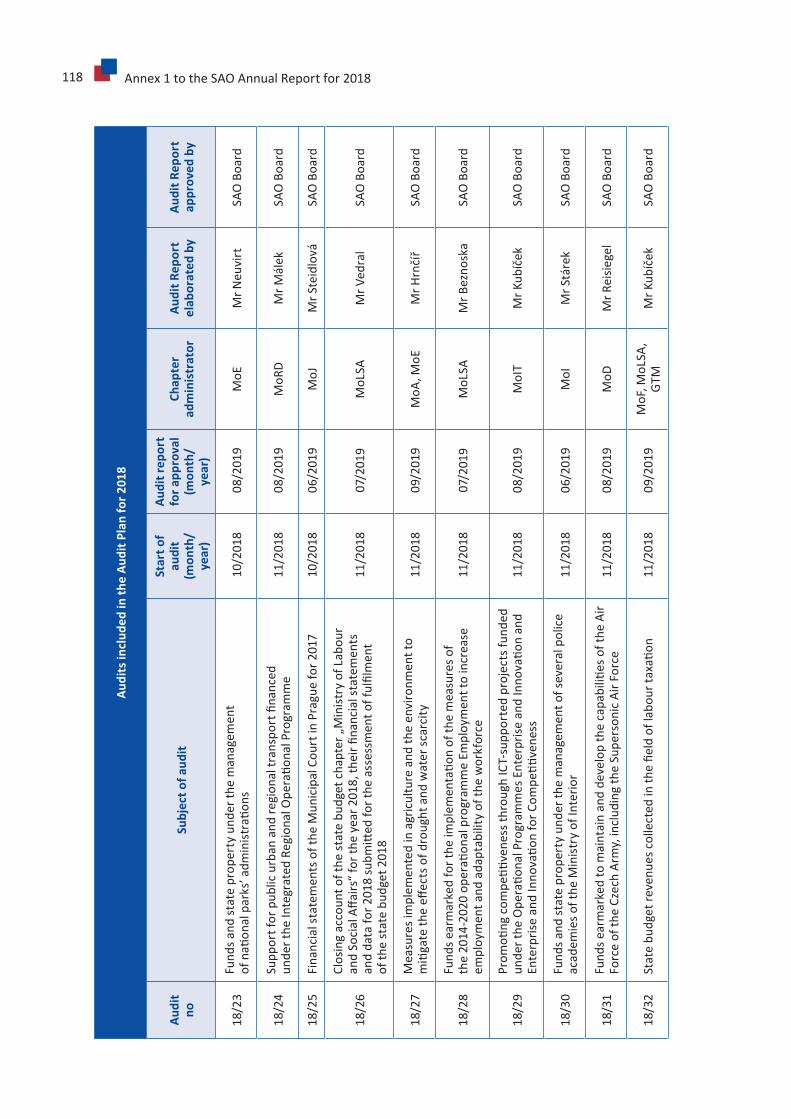

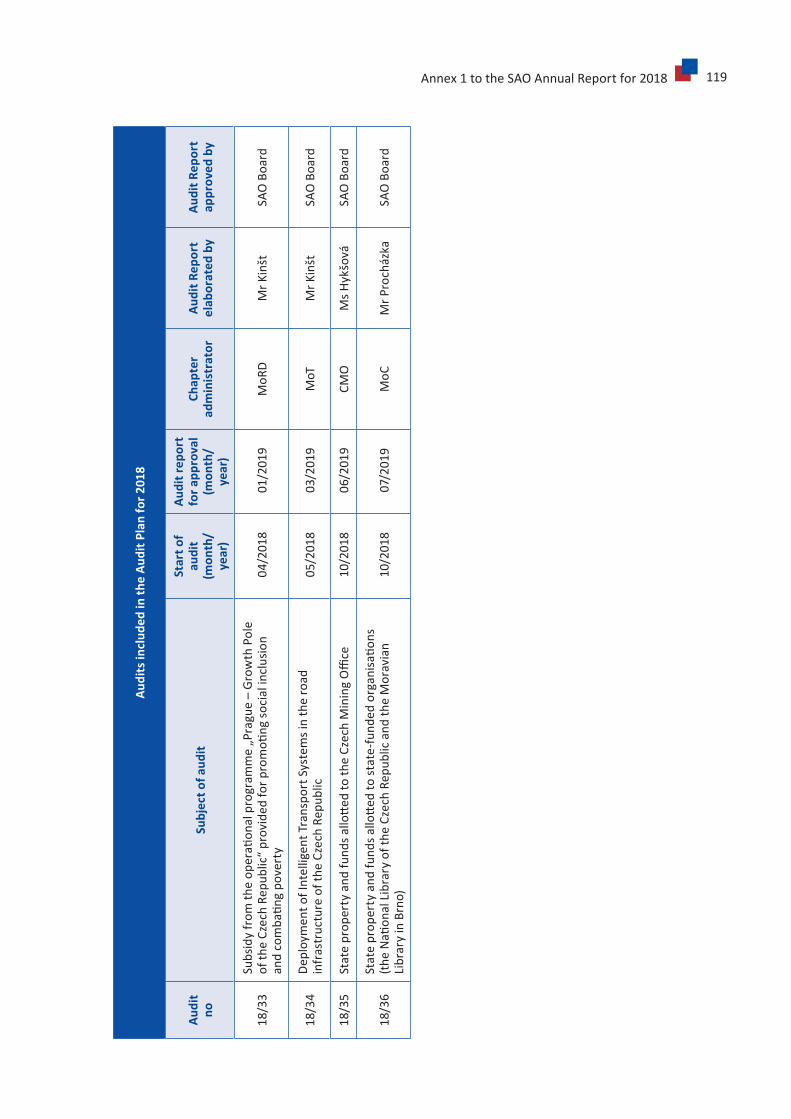

Annex1-AuditsincludedintheAuditPlanfor2018 .................................................................. 116

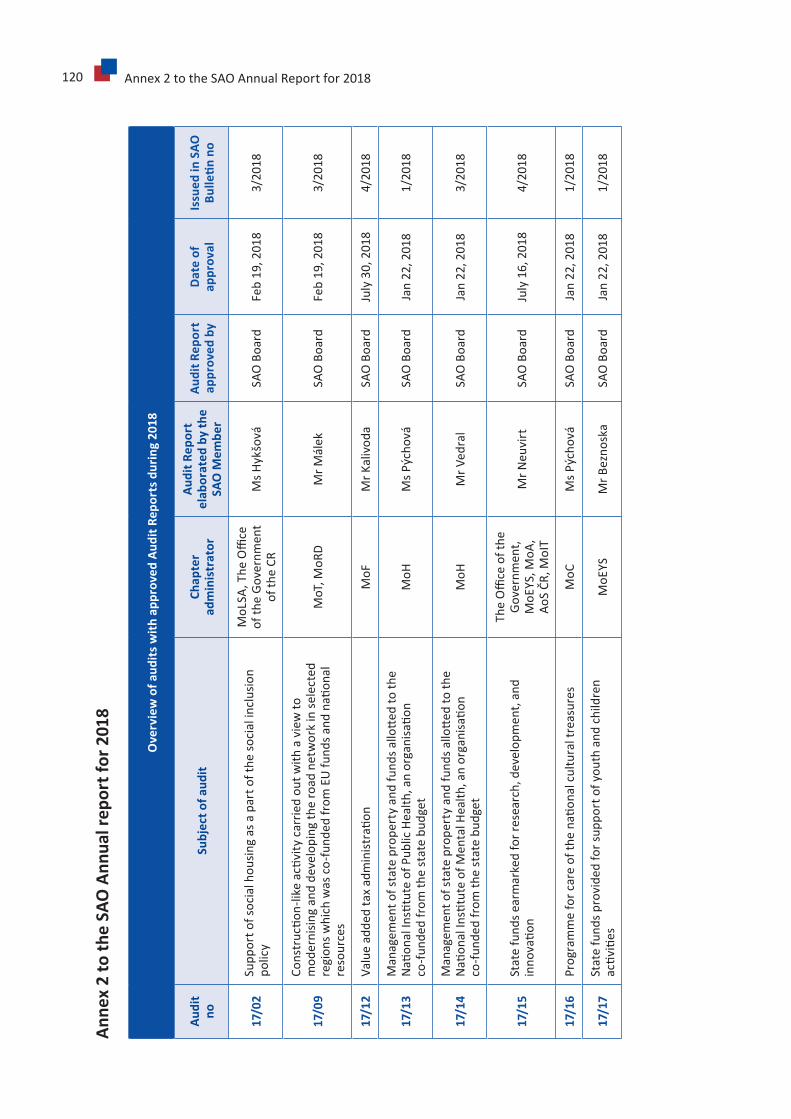

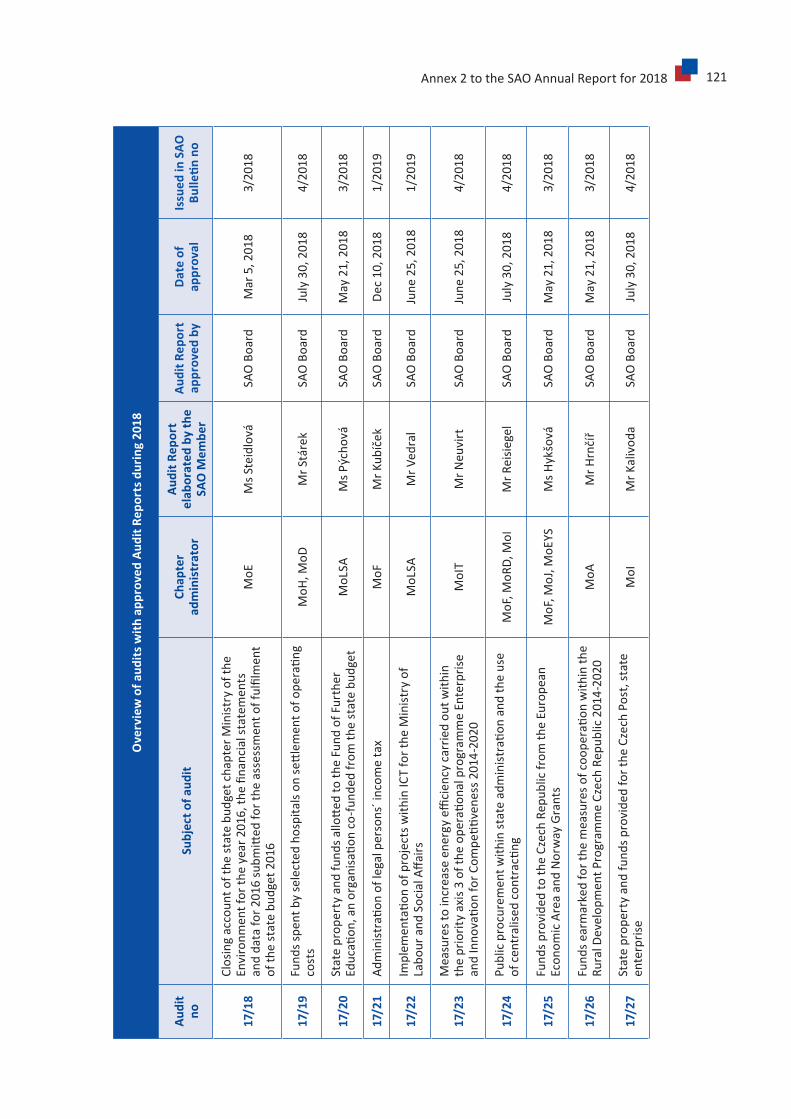

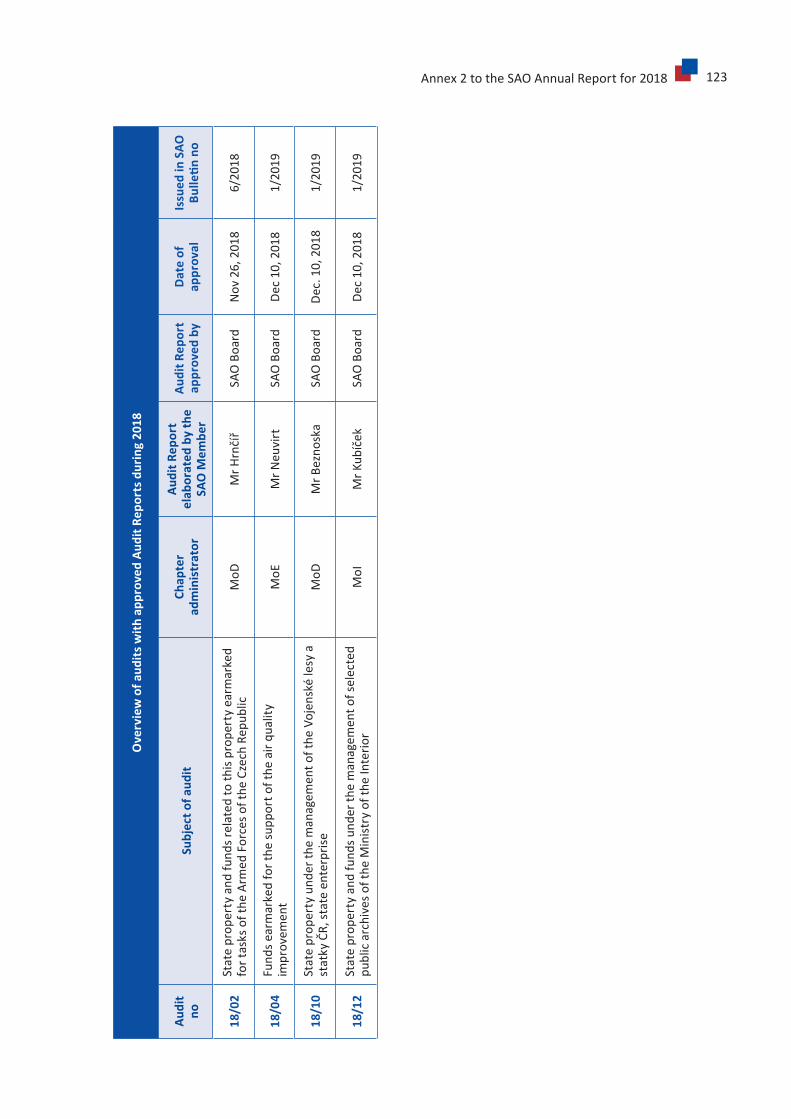

Annex2-OverviewofauditswithapprovedAuditReportsduring2018 ................................... 120

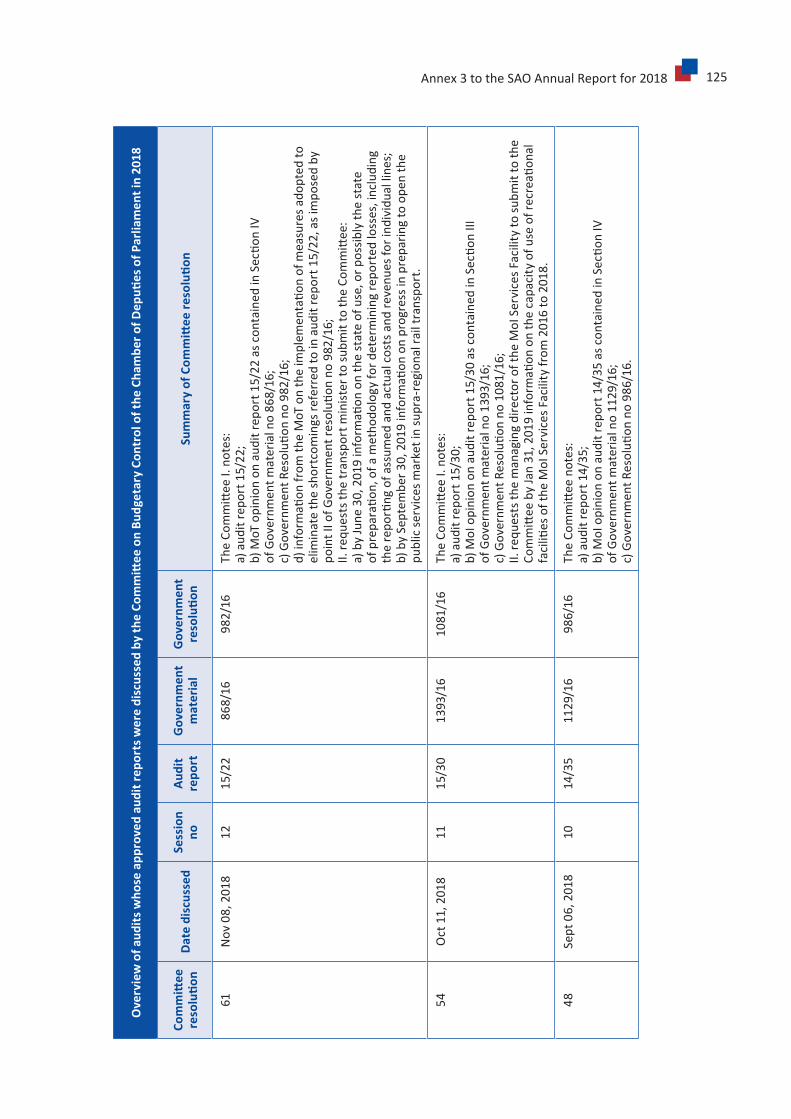

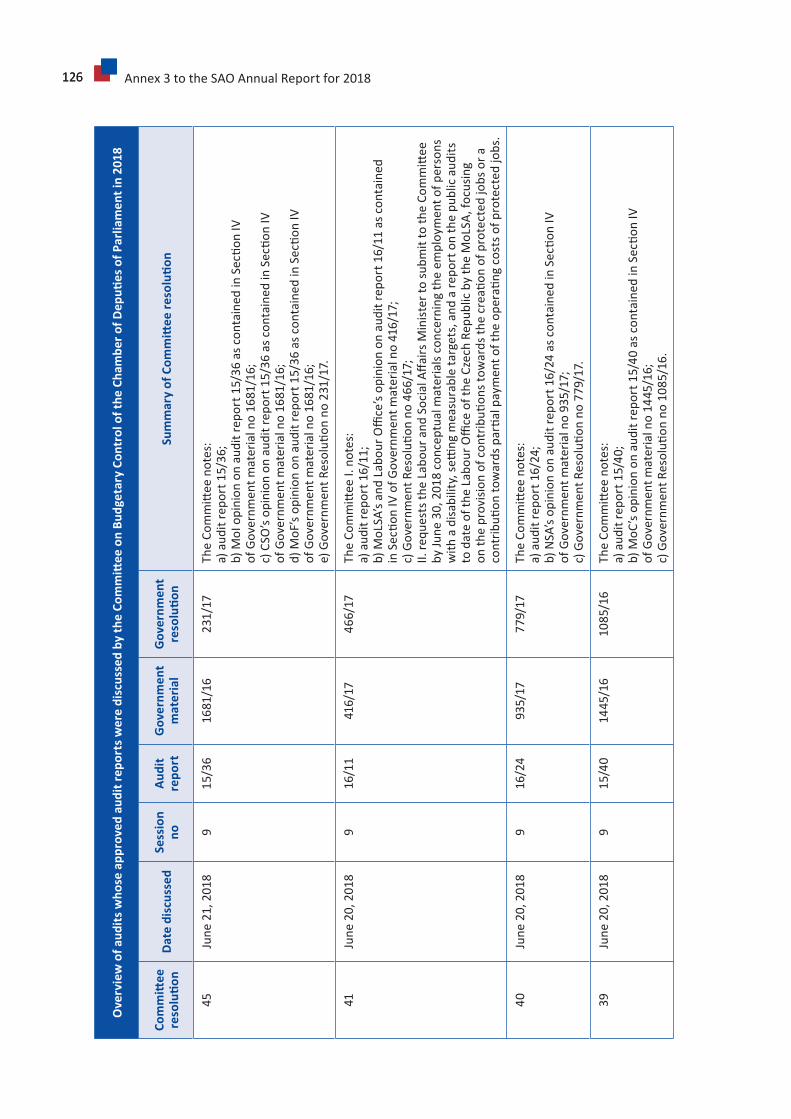

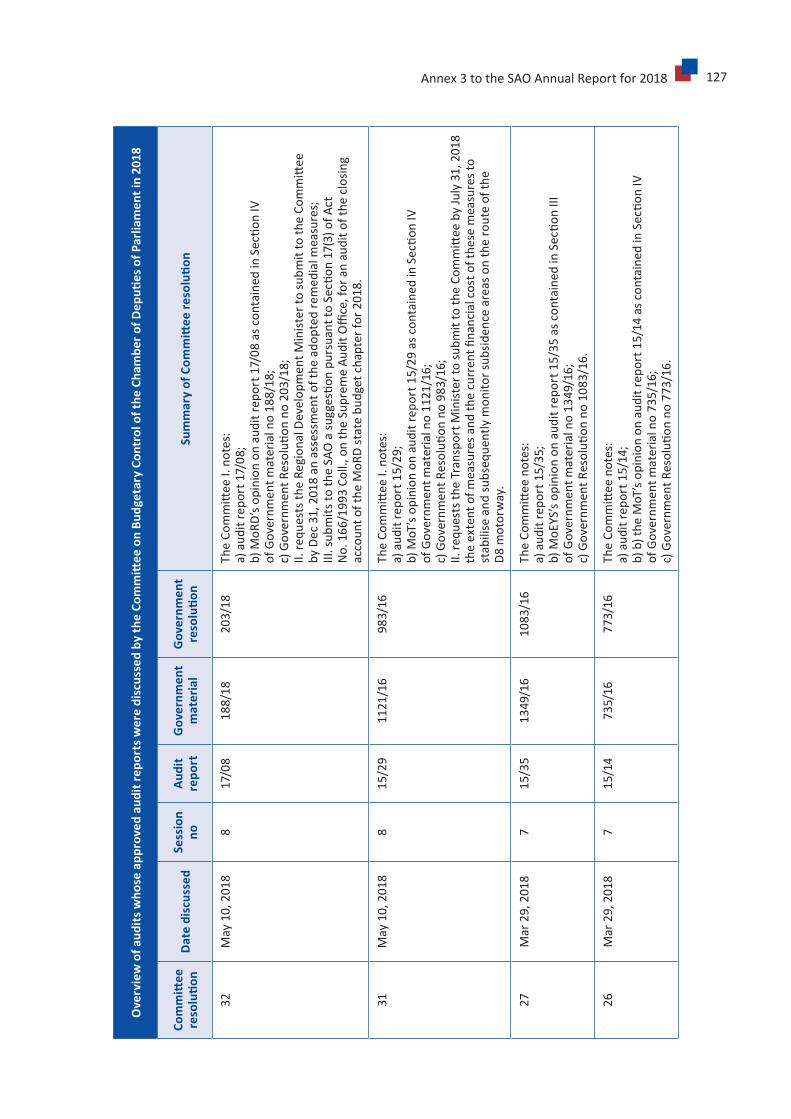

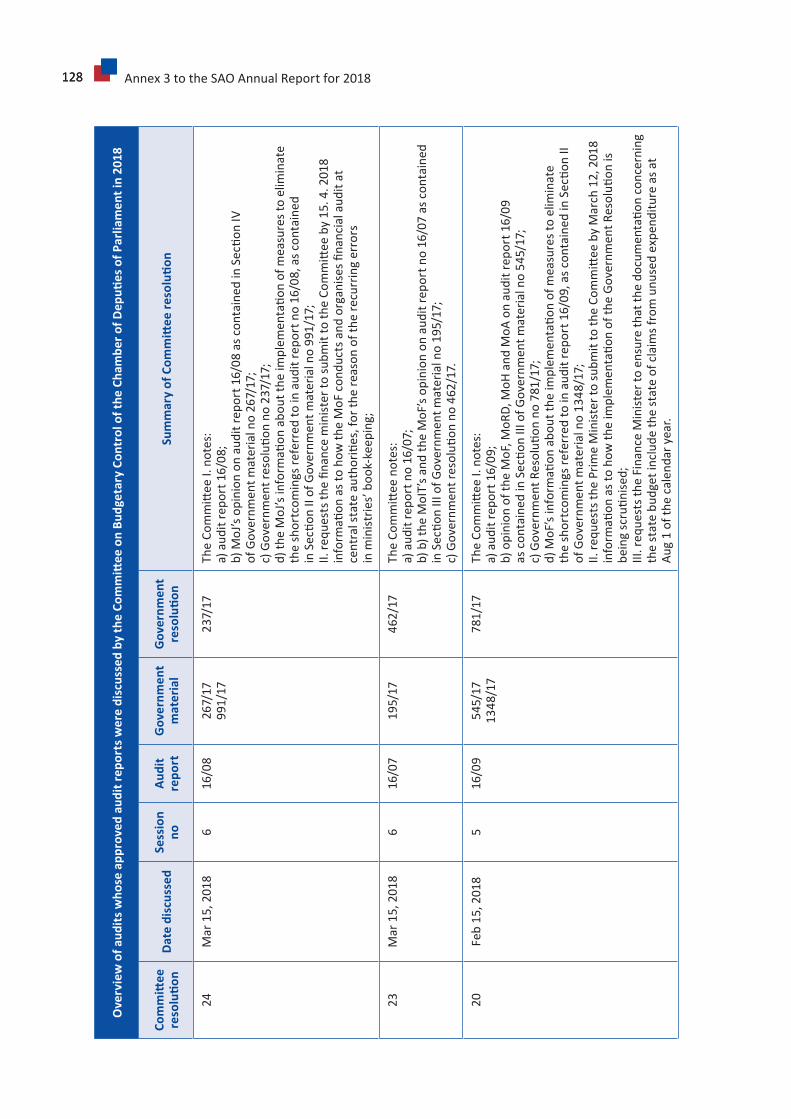

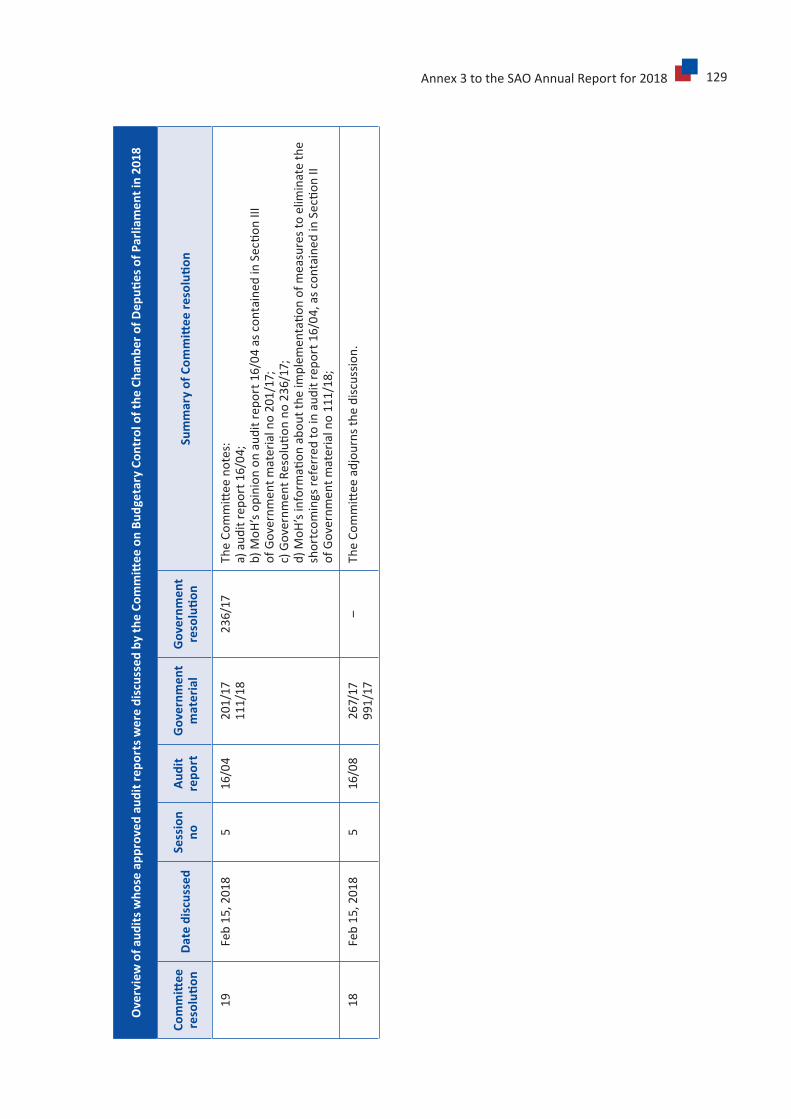

Annex3-Overviewofauditswhoseapprovedauditreportswerediscussed bytheCommitteeonBudgetaryControloftheChamber ofDeputiesofParliamentin2018................................................................................ 124

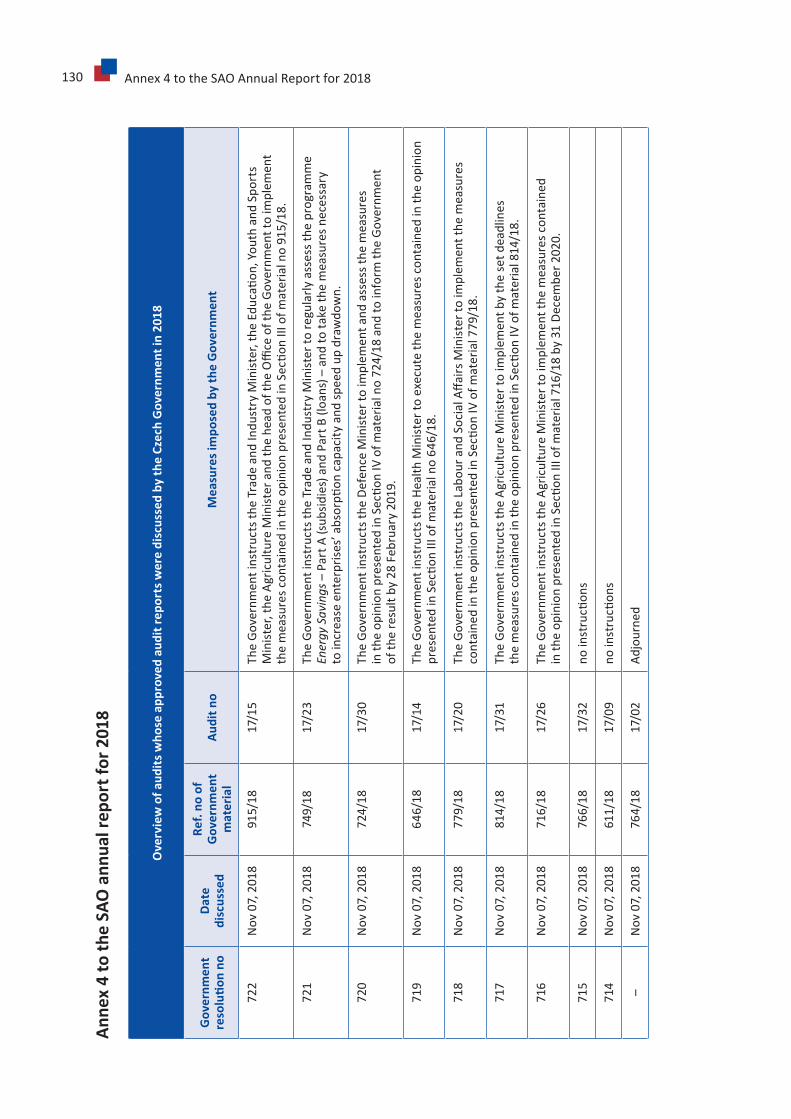

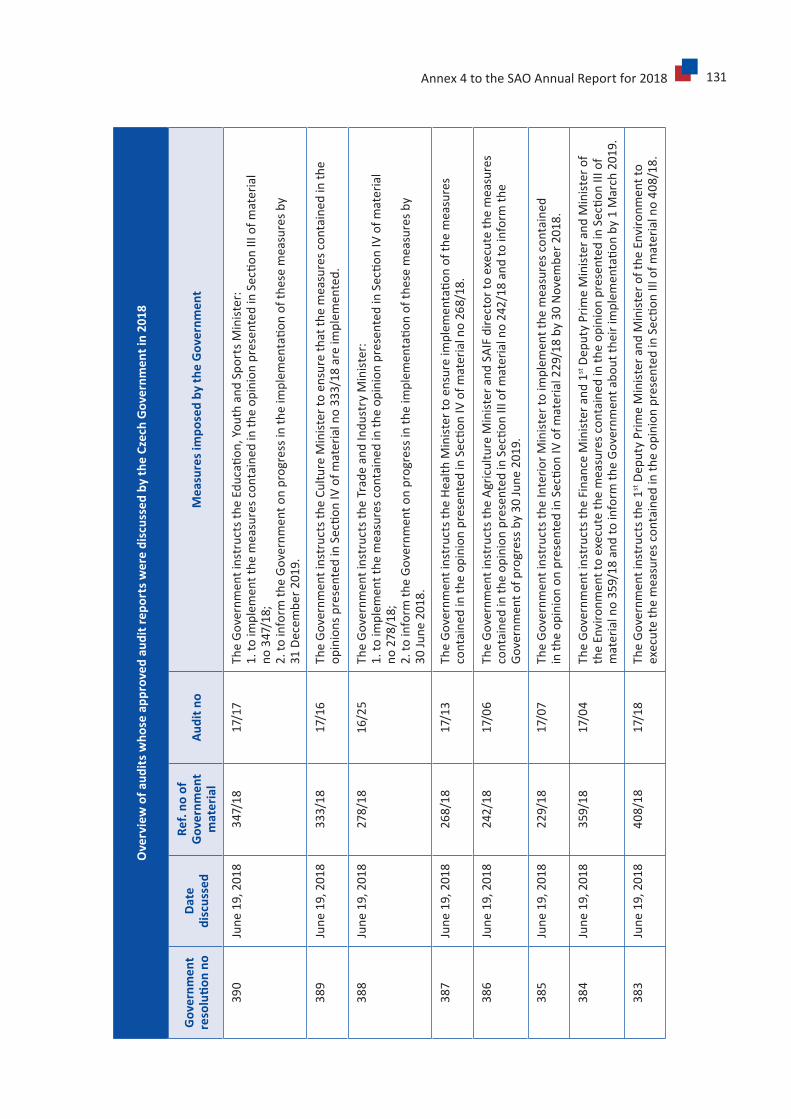

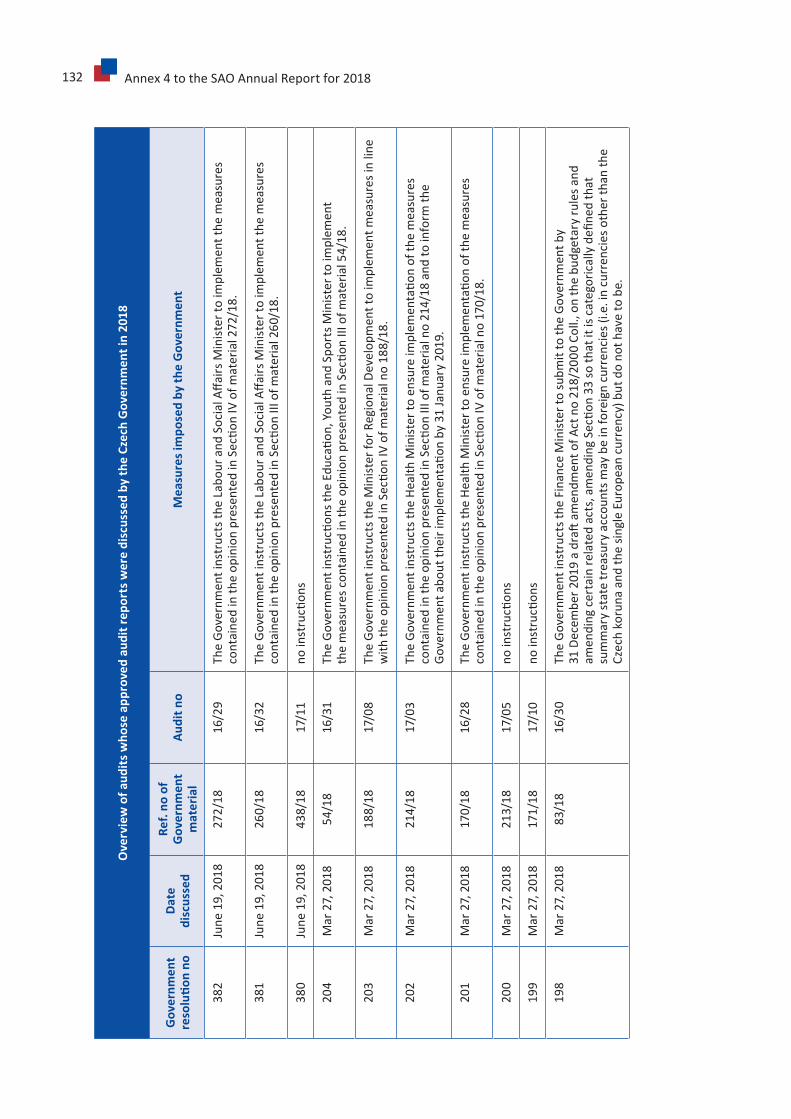

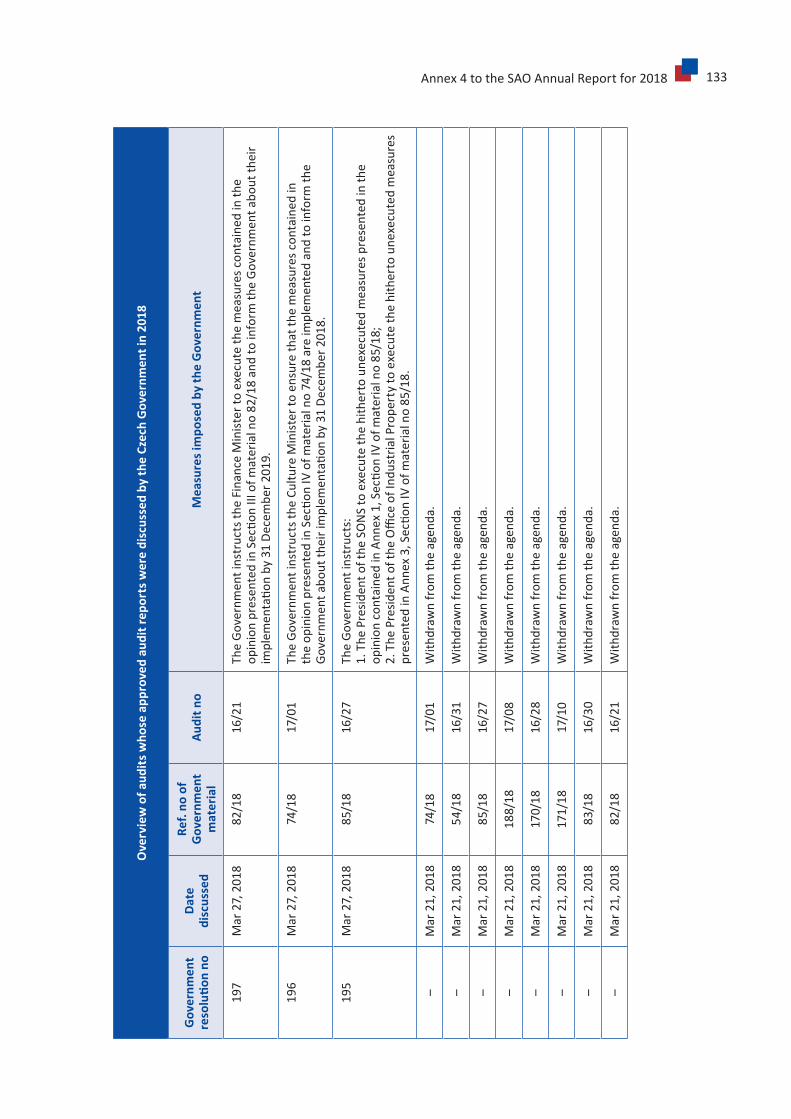

Annex4-Overviewofauditswhoseapprovedauditreportswerediscussed bytheCzechGovernmentin2018 ............................................................................... 130

Listofabbreviations ..................................................................................................................... 134

Annual Report for the year 2018 5

Opening message from the SAO president

Dearreaders,

inadditiontoitsstandarddutiesatnationallevel,theSupremeAuditOfficewasfullyengagedininternationalactivitiesin2018.WehavebeenchosenbyEUROSAI,theinternationalorganisationof50auditinstitutions,tobethenextpresidencycountry.Thatmeansthatwearepreparingthe2020EUROSAICongressinPrague,ahighlyimportantandprestigiousinternationaleventatwhichwewilltakeovertheorganisation’spresidencyforthecomingthreeyears.

Our office’s 3C – Comparison, Cooperation and Communication projectmetwith success. Theidea is quite simple.We live in a dynamically evolvingworld facing new threats, ranging fromthesustainabilityoflifeonourplanet,globalwarming,andenergy,waterandfoodshortagestofundamentalchangesinsociety,ageingpopulationand,say,thesearchforsourcesoffundingforpublicservices.

Every country has to wrestle with these issues, and the role of courts of auditors and auditinstitutions is no longer limited to coming upwith answers at the national level.Wewant tofind examples of good practice in countries tackling similar problems;wewant to showwhatresultsthesecountriesachievedandhowtheyachievedthem–inshort,everythingwecandrawinspirationfrom.Sharingthisinformationandthesepracticesproducesafundamentalchangeinthequalityofthemessagessupremeauditinstitutionstransmittosociety.Andthatisourpriority–ensuringourresultsareasusefulaspossible.

The SupremeAuditOffice’s annual report contains a number of such comparisons. Unlike theprivate sector,which adaptsdynamically to change, thepublic sector lags significantlybehind.In2018theWorldEconomicForumrankedtheCzechRepublic’scompetitiveness29th out of 140 assessedcountries,but intermsofpublicsectorperformancetheCzechRepublicwasdown in97thplace,behindcountrieslikeMoldova,UkraineorRomania.

Thiscomparisonisawarningtothepublicsectorthatthepublicadministrationisnotpreparedfordynamicchangesinsocietyandtheadjustmentsithasmadetodateareoftenmerelycosmetic.

Adapting to dynamic changes is difficult at any time. The first step towards finding a solutionis recognising the gravity of the situation. Realising that we have a cumbersome state that isincapableofcompletingthemotorwaynetwork.Astate thathas failed to respondto thebarkbeetlecalamity.Astatewherethegapbetweenthecentreandtheperipheryiswidening.Astatewithashortageofaffordablehousing.Andthatthisisthecasedespitethelargesumsofmoneythatareoftenspentontheseareas.

Let’s takea lookatourcloseneighboursormoredistantcountriestoseehowtheyfacetheseandotherchallenges,andhowtheydealwiththem.Governmentregulation,itsneedandeffect,shouldbeevaluated;thelegalframeworkanditseffectivenessindisputeresolutionneedstobeexamined; andGovernment interventions should be designedwith respect to the cost-benefitratio.

Let’smakeourstatemoredynamicandeffective.

Miloslav Kala, SAO president

6 AnnualReportfortheyear2018,StatusandPowersoftheSAO

I. Status and Powers of the SAO

1.BasicinformationonthestatusandpowersoftheSAO

TheexistenceoftheSupremeAuditOffice(SAO)isrooteddirectlyintheConstitutionoftheCzechRepublic,whichguaranteesitsindependencefromthelegislative,executiveandjudicialpowers.TheSAOthusrepresentsoneoftheindispensableelementsofparliamentarydemocracy.

More detailed rules on the status, powers, organisational structure andwork of the SAO arecontainedinActno166/1993Coll.,ontheSupremeAuditOffice(theSAOAct).UnderthisAct,theSAOmainlyscrutinisesthemanagementofstatepropertyandfinancescollectedbylawinfavouroflegalpersons,theimplementationofrevenueandexpenditureitemsofthestatebudgetandthemanagementoffundsprovidedtotheCzechRepublicfromabroad.

The SAObodies are the President andVice-President, the Board, Senates and theDisciplinaryChamber. In the interest of ensuring objectivity in the assessment of audit findings and infundamentalquestionsconcerningtheSAO’sauditpowers,theSAOBoardandsenatesdecideascollectivebodies.

TheSAO’sindependenceguaranteesthatitisnotinfluencedbythelegislature,theexecutiveorthejudiciarywhenplanning,preparingandconductingauditwork.Besidesinstitutionalindependence,theSAOhasappropriatefinancialautonomyaswell.ThedecisivebodyinthisareaistheChamberofDeputies,whichapprovesthestatebudget,includingtheSupremeAuditOfficebudgetheading.

ThebasisfortheSAO’sauditworkisitsauditplan.AfterbeingapprovedbytheSAOBoard,theauditplanisputbeforetheSAOpresident;itispresentedtotheCzechParliamentandGovernmentfortheirinformationandpublishedintheSAO Bulletin.Auditworkresultsinauditreports,whichsummariseandassessauditfindings.AuditreportsareapprovedbytheBoardortheappropriatesenatesoftheSAO.

Under its defined powers the SAO performs audits in linewith its audit standards,which arebasedontheinternationalstandardsofsupremeauditinstitutions.TheSAOperformscompliance,financialandperformanceaudits.

TheSAO’scomplianceauditscheckwhethertheauditedactivitiescomplywiththelawandreviewthesubstantialandformalcorrectnessoftheauditedactivitiesinthescopenecessaryforachievingtheauditgoals.

The SAO’sfinancial audits checkwhether theauditedentities’financial statements give a trueandfairviewofthesubjectofaccountinginaccordancewiththelaw.ThistypeofauditisatoolforverifyingtheaccuracyofinformationthatispresentedintheclosingaccountsofstatebudgetheadingsandwhichtheSAOuseswhenformulatingitsopinionsonthedraftStateClosingAccount.

TheSAO’sperformanceauditsassesstheeffectiveness,efficiencyandeconomyoftheuseofstatebudgetfinances,statepropertyorotherfinancestheSAOauditsinlinewithitspowers.

AnnualReportfortheyear2018,StatusandPowersoftheSAO 7

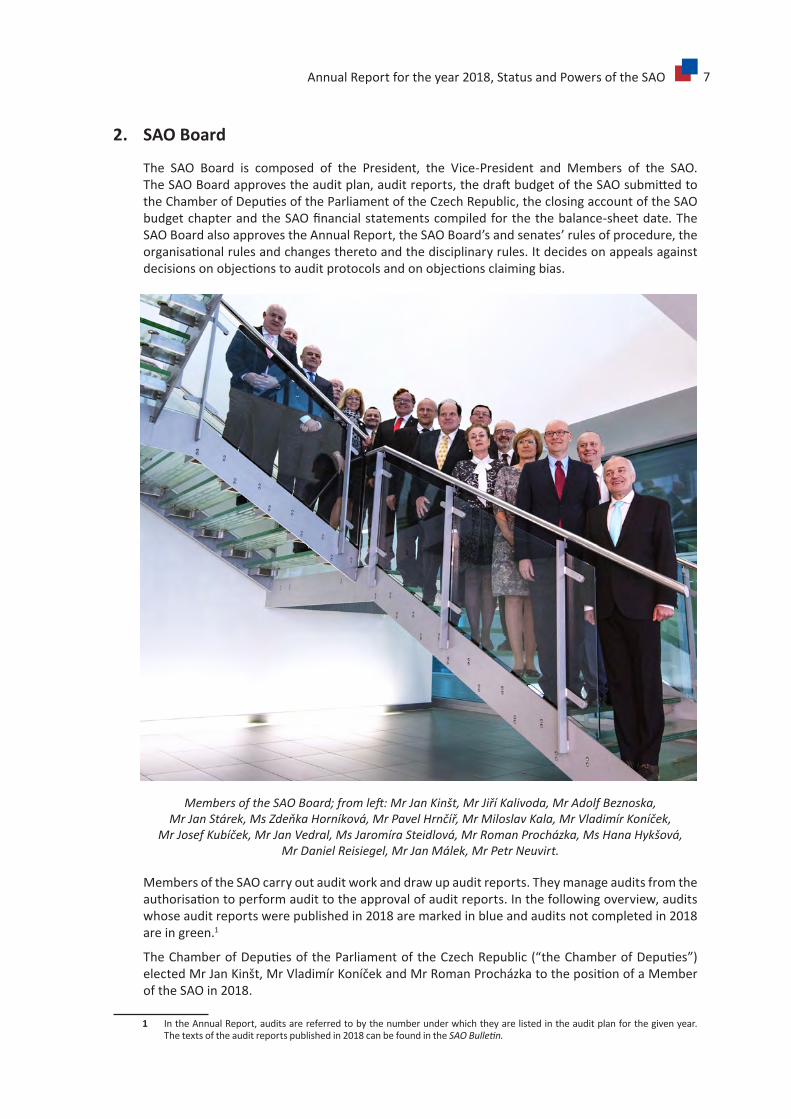

2. SAO Board

The SAO Board is composed of the President, the Vice-President and Members of the SAO.TheSAOBoardapprovestheauditplan,auditreports,thedraftbudgetoftheSAOsubmittedtotheChamberofDeputiesoftheParliamentoftheCzechRepublic,theclosingaccountoftheSAObudgetchapterandtheSAOfinancialstatementscompiledforthethebalance-sheetdate.TheSAOBoardalsoapprovestheAnnualReport,theSAOBoard’sandsenates’rulesofprocedure,theorganisationalrulesandchangestheretoandthedisciplinaryrules.Itdecidesonappealsagainstdecisionsonobjectionstoauditprotocolsandonobjectionsclaimingbias.

Members of the SAO Board; from left: Mr Jan Kinšt, Mr Jiří Kalivoda, Mr Adolf Beznoska, Mr Jan Stárek, Ms Zdeňka Horníková, Mr Pavel Hrnčíř, Mr Miloslav Kala, Mr Vladimír Koníček,

Mr Josef Kubíček, Mr Jan Vedral, Ms Jaromíra Steidlová, Mr Roman Procházka, Ms Hana Hykšová, Mr Daniel Reisiegel, Mr Jan Málek, Mr Petr Neuvirt.

MembersoftheSAOcarryoutauditworkanddrawupauditreports.Theymanageauditsfromtheauthorisationtoperformaudittotheapprovalofauditreports.Inthefollowingoverview,auditswhoseauditreportswerepublishedin2018aremarkedinblueandauditsnotcompletedin2018areingreen.1

TheChamberofDeputiesoftheParliamentoftheCzechRepublic(“theChamberofDeputies”)electedMrJanKinšt,MrVladimírKoníčekandMrRomanProcházkatothepositionofaMemberoftheSAOin2018.

1 IntheAnnualReport,auditsarereferredtobythenumberunderwhichtheyarelistedintheauditplanforthegivenyear.Thetextsoftheauditreportspublishedin2018canbefoundintheSAO Bulletin.

8 AnnualReportfortheyear2018,StatusandPowersoftheSAO

Table 1: Overview of audits conducted in 2018

SAOMember Membersince

NumberofauditsmanagedbytheSAO

Memberupto theendof2018

AuditsmanagedbytheSAOMemberin2018

Completed Notcompleted

MrJiříAdámek Apr 25, 2001 46 17/3217/33 –

MrAdolfBeznoska Mar 14,2017 4 17/1718/10

18/1818/28

MrPavelHrnčíř Dec 11, 2009 2217/2618/0118/02

18/27

MsHanaHykšová Feb13,2014 12 17/0217/25

18/0618/35

MrJiříKalivoda Sept17,1993 70 17/1217/27

18/1918/22

MrJanKinšt Jan25,2018 3 – 18/3318/34

MrVladimírKoníček Dec 4, 2018 0 – –

MrJosefKubíček Jun10,2014 13 17/2118/12

18/0818/2918/32

MrJanMálek Jun21,2016 817/0917/3517/36

18/1618/2118/24

MrPetrNeuvirt Dec 21, 2010 2917/1517/2318/04

18/1718/23

MrRomanProcházka Jan25,2018 1 – 18/36

MsHanaPýchová Oct24,2014 817/1317/1617/20

–

MrDanielReisiegel Apr 30, 2010 25 17/2417/34

18/0518/0718/31

MrJanStárek Jun4,2015 9 17/1917/29

18/1118/1418/2018/30

MsJaromíraSteidlová Nov16,2006 2817/1817/31

18/15*

18/1318/25

MrJanVedral Apr 25, 2001 5517/1417/2217/30

18/0318/0918/26

*Auditno18/15wasremovedfromtheauditplanbySAOBoardResolutionno4/VI/2018ofMay21,2018.

AnnualReportfortheyear2018,StatusandPowersoftheSAO 9

3. SAO management

TheSAOmanagementconsistsofemployeesdirectlysubordinatetotheSAOPresident.ThesearetheSeniorDirectorof theAuditSection, theSeniorDirectorof theAdministrativeSection, theDirectoroftheSAOPresident’soffice,theBoardsecretary,theDirectoroftheSecurityDepartmentandtheDirectoroftheInternalAuditDepartment.

From left: Mr Radek Haubert, Senior Director of the Administrative Section; Ms Alena Fidlerová, Secretary of the SAO Board; Ms Zdeňka Horníková, SAO Vice-President;

Mr Miloslav Kala, SAO President; Ms Zuzana Čandová, Director of the President’s Office; Ms Jana Ermlová, Director of the Security Department; Ms Ladislava Slancová, Director of the Internal

Audit Department; Mr Stanislav Koucký, Senior Director of the Audit Section.

10 AnnualReportfortheyear2018,StatusandPowersoftheSAO

4. MissionandbenefitsoftheSAO’swork

TheSAOcontinuestobealong-termreliableandtrustworthypartnerandproviderofindependentandobjectivefeedbackonthefunctioningoftheCzechRepublic.TheSAO’smission2istoprovideobjectiveinformationonthestate’smanagementofpublicfundsandproperty.ThisinformationisnotjustimportanttotheSAO’skeypartners,i.e.theCzechParliamentandtheCzechGovernmentas the bodies responsible for the correct control and management of public funds: it is alsonecessaryforthegeneralpublicandthefunctioningofexternalcontrolassuch.

Inlinewithitsstrategy,theSAOfocusesmainlyonthoseareasthatpresentariskintermsoftheCzechRepublic’s currentand futuredevelopmentandcompetitiveness.Outputs in the formofauditreports,statementontheimplementationofthestatebudget,opinionsonthestateclosingaccountsandotheroutputsoftheSAO’sworkprovideinformationonthelegality,effectiveness,economyand efficiencyof public spending. The SAO’s objective, targeted and comprehensiblereportsandrecommendationsleadtotheremedyofshortcomingsandtoapositiveshiftinthemanagementofpublicfundsandproperty,withthepromotionofgoodpracticeinthatfield.

Themost importantbenefitsoftheSAO’sworkincludemakingtheconcernedbodieseliminateidentified shortcomings andmaking the responsible authorities adopt systemicmeasures. Theresults of audits also have an important preventive effect on other entities not targeted by aparticular audit, encouraging them toavoid similarmanagementand control errors, aswell asimprovingaccountabilityinpublicadministrationandtheenforceabilityofthelawingeneral.Thatis linkedtotheresultsoftheSAO’sworkinthefieldofassessingtheworkingof legislationandmaking legislativerecommendations.Lastbutnot least,andalthoughit isnottheprimarygoalofauditwork,theSAOdeliversakeyimpactintheformofcarryingoutitsobligationtoreportincaseswhereitidentifiesabreachofbudgetarydisciplineorfactsindicatingcommissionofacrime.

5. Audit plan for 2018

TheSAOauditplan,whichisthefundamentalbasisfortheperformanceofauditwork,determinesthefocusandtimingofauditsinthebudgetaryyear.ItisakeytoolforexercisingtheSAO’sauditpowersinlinewiththeSAOAct.TheSAO’sauditplaniscompiledindependentlyinlinewiththeSAO’spowersguaranteedbytheConstitutionoftheCzechRepublic.TheSAO’sindependenceisalso

2 TheSAO’smissionispartoftheStrategy of the Supreme Audit Office for 2018–2022.

AnnualReportfortheyear2018,StatusandPowersoftheSAO 11

exercisedinaccordancewiththebestpracticeofauditworkdonebysupremeauditinstitutionsinlinewiththekeyprinciplesofINTOSAI3.TheConstitutionoftheCzechRepublic,theSAOActandinternationalpracticearethefundamentalpillarsunderpinningtheexerciseofitspowers.

WhencompilingtheauditplantheSAOfocusesmainlyonthoseareasthatareimportantforthelivesofcitizens,theefficiencyofpublicadministrationandtheCzechRepublic’scompetitivenessininternationalcomparison.Forthatreason,theSAOmainlyappliesarisk-basedapproachwithaviewtoidentifyingrealrisksinareaswherethereisalikelihoodthattheprinciplesofeffectiveness,efficiencyandeconomywillnotberespectedorthelawwillbeviolated.TheSAO’sultimategoalisnotmerelytofindshortcomingsinthestate’sfinancialmanagement:aboveall,itistoimprovefinancialmanagementintherelevantareasbasedonmeasurestoremedytheshortcomings.

This endeavourplayed a central role in the compilationof the audit plan for 2018. The auditsincludedinthe2018auditplanwerebasedlargelyonsuggestionsarisingoutoftheSAO’sownindependentmonitoringandanalysiswork.Theplanalso featured twoauditsdesignedon thebasisofexternalinstigationsfromtheChamberofDeputiesandtheSenateofParliamentoftheCzechRepublic.

ProblemareastargetedbytheSAO’s2018auditplanincluded:

• staterevenuesfromthetaxationoflabourandenvironmentalpolicy;• thedigitisationoftaxproceedings;• statesupportforenterprise,researchandinnovation;• developmentoftheroadsandwaterwaysinfrastructureandsupportforregionaltransport;• investmentandmanagementofpropertyinthedefencesector;• statesupportforthenon-profitsectorandthefightagainstpoverty;• statesupportinsocialservicesandyouthemployment;• statesupportinthefieldofairqualityandmeasurestomitigatetheimpactofdrought;• managementofpublichealthinsurancefinances;• statesupportforregionalhealthcare;• digitalisationofeducationinschools;• statesupportforagriculturalproduction;• statesupportinthefieldofcrimeprevention;• reliability of financial information through which institutions are accountable for state

budgetfinancesmanagement.

Anumberofthesetopicsarepartofthelong-termstrategicareasoftheSAO’sauditwork.TheyarealsokeyareasofGovernmentpolicy.

Theauditplanfor2018wasapprovedbytheSAOBoardatits23October2017session.32auditswereapprovedintotal.During2018oneauditwascancelledandfourotherauditswereadded,makingatotalof35 audits.

Anoverviewof theaudits included in the2018auditplan,and their specific focusandtiming,ispresented inAnnex1.Theauditswerecommenced in sequenceduring theyear in linewiththetimetable.Depending on the start time and audit duration, the planned completiondates(i.e.approvaloftheaudits’auditreports)arein2018and2019.

3 The Mexico Declaration on SAI IndependenceapprovedbytheXIXCongressoftheInternationalOrganisationofSupremeAuditInstitutionsinMexicoin2007;ISSAI10.

12 AnnualReportfortheyear2018,AssessmentofAuditWork

25

4

11 10

18

hospodaření se státním majetkem a finančními prostředky vybíranými na základě zákona ve prospěch právnických osobs výjimkou prostředků vybíraných obcemi nebo kraji v jejich samostatné působnos�státního závěrečného účtu

plnění státního rozpočtu

hospodaření s prostředky poskytnutými České republice ze zahraničí a s prosředky, za něž převzal záruky stát

zadávání státních (veřejných) zakázek

II. Assessment of Audit and Analysis Work in 2018

1. Opening summary

Theassessmentofauditandanalysisworkpresentedinthissectionisbasedmainlyontheresultsofauditsthatwerecompletedin2018whentheirauditreportswereapprovedbytheSAOBoard.In addition, the assessment draws on findings from the SAO’s statements on the Draft StateClosingAccount for2017(“SCAstatement”or“SCApositionstatement”)andonthereportoneconomicdevelopmentand the implementationof theCzech statebudget for thefirsthalf of2018,informationfromEU Report 2018 andotherfindingsfromtheSAO’sanalysisandmonitoringwork.

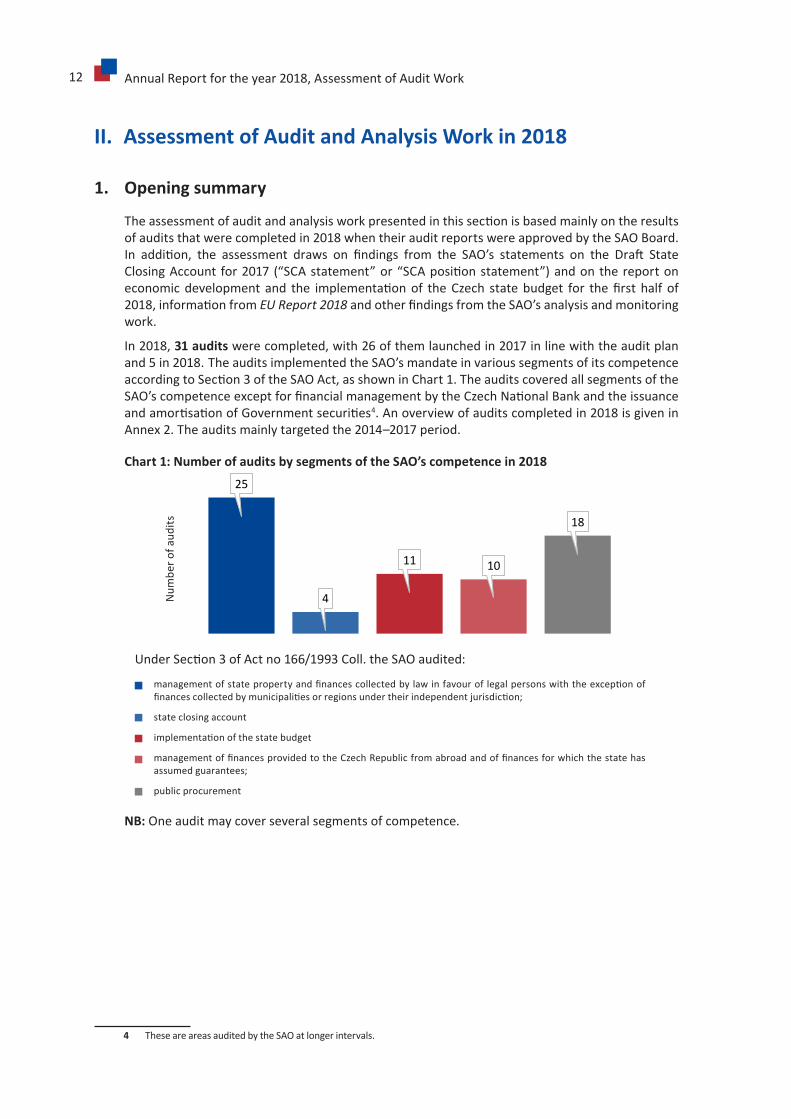

In 2018, 31 auditswerecompleted,with26ofthemlaunchedin2017inlinewiththeauditplanand5in2018. TheauditsimplementedtheSAO’smandateinvarioussegmentsofitscompetenceaccordingtoSection3oftheSAOAct,asshowninChart1.TheauditscoveredallsegmentsoftheSAO’scompetenceexceptforfinancialmanagementbytheCzechNationalBankandtheissuanceandamortisationofGovernmentsecurities4.Anoverviewofauditscompletedin2018isgiveninAnnex2.Theauditsmainlytargetedthe2014–2017period.

Chart1:NumberofauditsbysegmentsoftheSAO’scompetencein2018

NB:Oneauditmaycoverseveralsegmentsofcompetence.

4 TheseareareasauditedbytheSAOatlongerintervals.

managementofstatepropertyandfinancescollectedbylawinfavourof legalpersonswiththeexceptionoffinancescollectedbymunicipalitiesorregionsundertheirindependentjurisdiction;

stateclosingaccount

implementationofthestatebudget

managementoffinancesprovidedtotheCzechRepublicfromabroadandoffinancesforwhichthestatehasassumedguarantees;

publicprocurement

UnderSection3ofActno166/1993Coll.theSAOaudited:

Num

bero

faud

its

AnnualReportfortheyear2018,AssessmentofAuditWork 13

Thecompletedauditsscrutinisedpropertyandfundsat171auditedentitiesinlinewiththefocusandgoalsoftheaudits.TheauditedfinancesandpropertyofthestatewasworthCZK 114 billion. Insystemicterms,theauditscoveredstatefinancesandpropertyamountingtoCZK 1,216 billion. 29notificationsofabreachofbudgetarydisciplinewithafinancialvalueofatleastCZK 842 million and11criminalcomplaintswerefiled(asdetailedinSectionIII).

171 auditedentities

31 completed audits

43 recommendationsofasystemicnature

17 auditreportsdiscussedbytheChamberofDeputiesControlCommittee

121 measuresadoptedbyauditedentities

31 audit reports discussed by the Czech Government

79.6% rateofSAOsatisfactionwithadoptedmeasures

CZK 842 million innotificationsofbreachesofbudgetarydiscipline

11 criminal complaints

TheSAOregardsthediscussionofauditreportswithkeypartners intheCzechParliamentandGovernmentascrucialforpromotingtheresultsofaudits.TheChamberofDeputiesCommitteeonBudgetaryControldiscussed17auditreportsin2018.TheGovernment’sdiscussionofauditreportswaskey.Havingdiscussed31auditreportsandtheidentifiedshortcomingsandsystemicrecommendations,theGovernmentimposed121correctivemeasures,whichtheSAOjudgedtobefullyorpartiallysatisfactoryfortheshortcomingsorrecommendations.Ifeffectivelyimplemented,thesemeasuresshouldhelpimprovethestate’sfinancialmanagementinthegivenareas.TheSAOcanthusdeclarethatthedegreeofsatisfactionwiththeadoptedmeasuresasevaluatedbytheSAOwasalmost80%.

TheaboveshowsthattheSAOscrutinisedasignificantportionofpublicfundsin2018anddeliveredsignificantbenefits,bothfinancialandnon-financial.However,itismainlythetangibleresultsoftheSAO’sauditandanalysisworkprovidingvaluableobjectiveinformationonthestate’sfinancialmanagement that liebehind thefigurespresentedabove.Every suchoutput shouldbeagoodopportunitytoputthingsrightwherevertherearedeficiencies.

TheSAO’sfindingspoint to the followingkey strengthsandweaknesses in the state’sfinancialmanagementinthepreviousperiod:

Strengths

+ State budget surplus in 2018 + Favourable economic growth in the Czech Republic + Low rate of unemployment, pay growth in private and public sectors + FallingGovernmentdebtandsmallershareofgrossdomesticproduct + Significantincreaseinstatebudgettaxrevenuesasaconsequenceofpositive

economic growth factors + Year-on-year increase in state budget investment expenditure + Faster drawdown of revenues and expenditure from the EU/FM budget for the 2014+

programming period + CzechRepublicfulfilledthefinancialindicatorfordrawdownofEuropeansubsidies

for 2018

14 AnnualReportfortheyear2018,AssessmentofAuditWork

Weaknesses

– Planningastatebudgetdeficitatatimeofeconomicgrowthandpoorquality ofthebudgetingprocess

– Soaringstatecurrentexpenditureandrelatedriskofunsustainablepublicfinances in the future

– Taxadministration‘sinsufficientpreparednessforthegrowthine-commerce – Insufficienttaxstreamliningandsimplificationfortaxpayers – Fragmentationoftheresearch,developmentandinnovationsupportsystem;

CzechRepublic‘sresultslagbehindbyinternationalbenchmarking – Slowexecutionofstrategicinvestmentsinroadsinfrastructureandinsufficientprogress

inspeedingupauthorisationprocessesforconstructionprojects – UneconomicalspendingonMoLSAinformationsystemsandcontinuingdependency

on suppliers – FailuretoimplementmeasurestoimproveairqualityandachievetheCzechRepublic‘s

energyefficiencytargets – StructureandvolumeofrealestatedonotcorrespondtotheCzecharmy‘sneedsand

puts a needless burden on the state budget – Littleuseofcentralisedprocurementinstateadministrationtocutcostsandreduce

paperwork – Failuretomakeuseofpublicprocurement‘spotentialtodeliversavingsinpurchasing

byuniversityhospitalsandnon-transparentuseoffinancialbonuses – Supportforlargefoodindustryfirmstothedetrimentofsmallandmedium-sized

agricultural enterprises – Absenceofmeaningfulevaluationoftheeffectivenessofsupportforindustrialzones

andcompetitivenessofsmallandmedium-sizedenterprises – Poordesignofthehousingsupportsystem;poorcoordinationofhousingsupporttools

andincreaseinsociallyexcludedlocalities – Unsystemicfundingofrepair,modernisationanddevelopmentof2ndand3rdclassroads;

statesubsidiesdeliverinsufficientimprovementsinroadquality – Statesubsidieshavelittleimpactontheconditionofrailrollingstock;failuretocomply

withthetimetableforopeningupthepublicrailtransportmarket,asatoolforoptimisingstate expenditure

– Insufficientuseofaccountinginformationonmanagementofstatebudgetfinances,whichsubstantiallyreducesthebenefitsofaccountingreform

Favourable economic growth and state budget results in 2018.

The 2018 results showed that the Czech Republic was doing well. The period of economic growthwasreflectedinpositivemacroeconomicdatalinked,forexample,togrowthingrossdomesticproduct(GDP)andinfinalhouseholdconsumption,fallingunemploymentandafallinGovernmentdebt as aproportionofGDP. Thehighdomestic consumptionwasdrivenbypaygrowthintheprivateandpublicsectorsandbyincreasingpublicsectoractivity,reflectedin rising state revenues, especially tax revenues and revenues from social security insurance payments.

Thestateachievedapositiveresultintheimplementationofthestatebudgetin2018,withtheoriginallyplannedstatebudgetdeficitofCZK 50 billion becomingaCZK 2.9 billion surplus.Besidesthepreviouspositiveinfluencesmentioned, increasedrevenuesfromtheEU/FMbudget,betterdrawdownoffinancesforprojectsfundedoutofoperationalprogrammesandbetterdrawdown

AnnualReportfortheyear2018,AssessmentofAuditWork 15

ofinvestmentfinancesalsoplayedarole.Despitethepositiveyear-on-yearincreaseininvestmentspending in2018,however, its share in totalbudgetexpenditure continues to fall shortof thevaluesfromtheperiodoftheeconomiccrisis.TheswifterutilisationofEU/FMbudgetfundsattheendoftheyearneverthelessremainsslightlybelowtheEUaverage.

Long-termsystemicobstaclesendangerthefuturesustainabilityofpublicfinances.

The excellent macroeconomic and state budget developments have long concealed systemic obstacles, however, which will impactontheCzechRepublic’sfutureresultsandcompetitiveness.The favourable state budget results for 2018 are no guarantee of healthypublicfinancesinthelongerterm.TheSAOhaspointedoutthatcurrentexpenditureisrisingandlittleprogresshasbeenmade towards both strategic investments and important reforms – these still largely exist on paper in conceptual or strategicdocumentsinsteadofbeingputintoeffect. Othernegativefactorsincludeinefficienciesinthestate’sfinancialmanagementandthepoorperformanceofstateadministrationincertainfields.

In 2018 the Czech Government was also warned about the long-term sustainability of publicfinances by theNational Budget Council,which regards the discrepancies between legislation,futuredemographicdevelopmentsandthedeferringofpensionreformasthechiefrisk.

AccordingtotheforecastfortheCzechRepublic’spopulationfrom2018to21005,therewillbe2.1millionpeopleagedover65inthecountryin2020and2.4millionin2030.

Aboveall,thestatehasfailedtomakeuseoftheperiodofeconomicgrowthtodrawupabudgetthatisatleastbalancedandtakesintoaccounttheprinciplesofeconomiccycles.Atthesametime,implementationofthestatebudgetishighlydependentoneconomicgrowthandunderestimatestheriskofincreasedcurrentormandatoryGovernmentspending.Thecompilationofthebudgetcontinues to be affected by inaccuracies, most notably the underestimation of revenues andfailuretorealiseexpenditure.Thatwasagainconfirmedbythepronounceddifferencesbetweentheapprovedbudgetandtheactualresults.AlthoughstatebudgetrevenuesincreasedbyalmostCZK 270 billion between 2014 and 2018, the planned state budget deficit decreased by justCZK 62 billion inthattime.ThedifferencebetweentheapprovedbudgetandrealitywasalmostCZK 53 billion in2018.AnothernegativeisthattheCZK 86.5 billion year-on-yearincreaseinstatebudgetcurrentexpenditureexceededtheCZK 84.8 billion increaseintaxrevenues,whichposesarisktothesustainabilityofstatebudgetfinancesinfuture.

Important reforms and strategic goals, e.g. simplifying taxes, streamlining tax administration for taxpayers, opening up thepublic rail transport market, developing the roads infrastructure, digitisation of public administration, improving air quality,achievingenergysavingsandsupportingsmallandmedium-sizedenterprise, are being deferred.

Oneexampleofthisintransportinfrastructureisthefactthatthemotorways network grewby less than 4 km in 2018. Significantprogresswasnotachievedinthestreamliningoftaxadministrationfor taxpayers: the act on income tax was not simplified, andcompaniesintheCzechRepublichavetospendconsiderablymoretimeonfulfillingtheirtaxobligations.

5 Published by the Czech Statistical Office in November 2018; https://www.czso.cz/csu/czso/projekce-obyvatelstva-ceske-republiky-2018-2100.

In 2018 state budget current expenditure grew by more than CZK 86 billion, which outstripped the CZK 85 billion growth in state budget tax revenues.

Companies in the Czech Republic have to spend 40% more time on fulfilling their tax obligations than the EU and European Free Trade Association average.

16 AnnualReportfortheyear2018,AssessmentofAuditWork

The poor quality of management and control by the responsible authorities hindersthe achievement of the goals of numerous state policies.

Thestate’sfinancialmanagementalsofailedtomovetowardsgoodpracticeinotherareaslinkedtothestandardofmanagementandcontrolbytheresponsibleauthorities.Theupshotisthatinanumberofareasstateadministrationisnoteffectiveatfulfillingthestate’sindispensableroleinmeetingsocialneeds.

Management and control errors in general are linked to a failure to take responsibility for effective,efficientandeconomicalmanagementofpublicfunds.Formalism,neglectofduties,growingbureaucracy,inefficientprocesses,inertiaand,inanumberofcases,afailuretoadoptmeasurestoremedyshortcomingsidentifiedbypreviousSAOauditspersist.Theunsatisfactorydesignoftheauditedentities’internalcontrolsystemsisoftenanotherreasonforthis.

Inadditiontotheabove,theSAOrepeatedlyfindsthat incertainareastherightconditionsfortheeffectiveworkingofGovernmentpoliciesarenot inplace.Thefundamentalproblemshereincludefragmentation,unclearpowersandresponsibilitiesof theconcernedbodies (e.g. in thesystemofsupportforresearch,developmentandinnovation);theabsenceofeffectivelegislationin certain areas (e.g. in support for social housing); haphazard or non-systematic approaches(e.g.tofinancingtherepair,modernisationanddevelopmentof2ndand3rdclassroads);andaboveall,inconclusiveassessmentoftheeffectiveness,efficiencyandeconomyofspendingintermsofresultsandbenefits(e.g.insupportforbusinessrealestateandinfrastructure).

Herewecangiveoneexamplefromthefieldofhousingsupport:EventhoughthestatespentoverCZK 230 billion onhousingsupportover20years, thestate’sevaluationof thebenefitsof thissupportprovideslittlemeaningfulinformation.Thesocialhousingsupportsystemisfragmented,withunclearlydefinedpowersandresponsibilitiesforthevariousbodies,includingmunicipalities,and the MoRD, as the ministry responsible for this policy, does not have the right tools tocoordinatethevariousbodies’measures.Theupshotisthatinsteadofaddressingthecausesitistheconsequencesthataredealtwith,sincethenumberofexcludedlocalitiesandthenumberofpeoplelivinginthemhaveincreasedmarkedly.

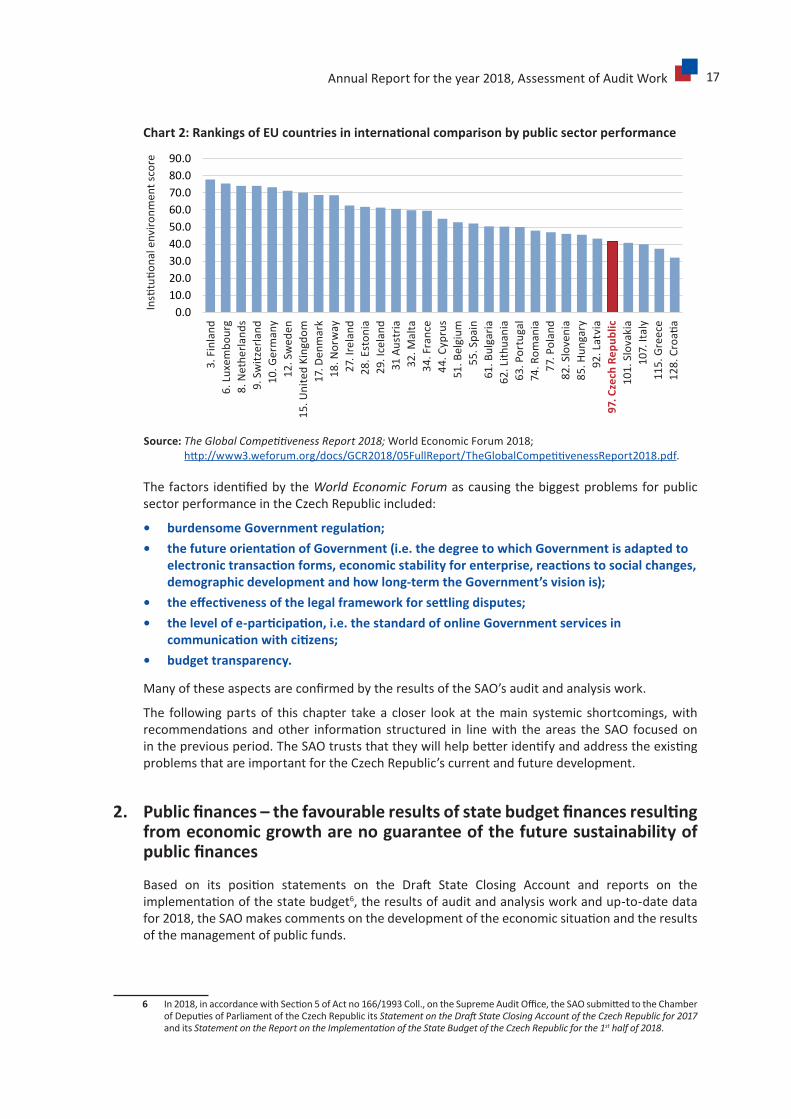

The performance of the Czech Republic’s public sector lags far behind in internationalcomparisonandhindersthecountry’soverallcompetitiveness.

ItisevidentthatthepoorperformanceofpublicadministrationrestrictstheCzechRepublic’soverall competitiveness. And that is confirmed by international comparison. According tothe regular ranking of countries’ competitiveness by the World Economic Forum’s Global Competitiveness Index (GCI),theCzechRepublicdidnotdotoobadlyin2018,comingin29th out of140assessedcountries,an improvementof threeplacesoverthepreviousyear’s ranking.However,publicsectorperformancehadanegativeimpactoncompetitiveness.Accordingtothe public sector performance indicator that is part of the overall GCI, the Czech Republic was down in 97th place. The Czech Republic is in 24th place out of the 28 EU countries (seechartno2).

AnnualReportfortheyear2018,AssessmentofAuditWork 17

Chart2:RankingsofEUcountriesininternationalcomparisonbypublicsectorperformance

0.010.020.030.040.050.060.070.080.090.0

ídeřtsorp ohlánoicutitsnI eletazaku atondoH

Source: The Global Competitiveness Report 2018; WorldEconomicForum2018; http://www3.weforum.org/docs/GCR2018/05FullReport/TheGlobalCompetitivenessReport2018.pdf.

Thefactors identifiedbytheWorld Economic Forum ascausingthebiggestproblemsforpublicsectorperformanceintheCzechRepublicincluded:

• burdensomeGovernmentregulation;• thefutureorientationofGovernment(i.e.thedegreetowhichGovernmentisadaptedto

electronictransactionforms,economicstabilityforenterprise,reactionstosocialchanges,demographicdevelopmentandhowlong-termtheGovernment’svisionis);

• theeffectivenessofthelegalframeworkforsettlingdisputes;• thelevelofe-participation,i.e.thestandardofonlineGovernmentservicesin

communicationwithcitizens;• budget transparency.

ManyoftheseaspectsareconfirmedbytheresultsoftheSAO’sauditandanalysiswork.

The followingpartsof this chapter takea closer lookat themain systemic shortcomings,withrecommendationsandother information structured in linewith theareas theSAO focusedoninthepreviousperiod.TheSAOtruststhattheywillhelpbetteridentifyandaddresstheexistingproblemsthatareimportantfortheCzechRepublic’scurrentandfuturedevelopment.

2. Publicfinances–thefavourableresultsofstatebudgetfinancesresultingfrom economic growth are no guarantee of the future sustainability of publicfinances

Based on its position statements on the Draft State Closing Account and reports on theimplementationofthestatebudget6,theresultsofauditandanalysisworkandup-to-datedatafor2018,theSAOmakescommentsonthedevelopmentoftheeconomicsituationandtheresultsofthemanagementofpublicfunds.

6 In2018,inaccordancewithSection5ofActno166/1993Coll.,ontheSupremeAuditOffice,theSAOsubmittedtotheChamberofDeputiesofParliamentoftheCzechRepublicitsStatement on the Draft State Closing Account of the Czech Republic for 2017 anditsStatement on the Report on the Implementation of the State Budget of the Czech Republic for the 1st half of 2018.

Insti

tutio

nalenv

ironm

entscore

3.Finland

6.Luxem

bourg

8.Nethe

rland

s9.Switz

erland

10. G

erm

any

12. Swed

en

1 5.U

nitedKing

dom

17.D

enmark

18.N

orway

27.Ireland

28. E

ston

ia29

.Iceland

31 A

ustr

ia32

. Mal

ta34

.France

44. C

ypru

s51

.Belgium

55.Spa

in61

.Bulgaria

62. L

ithua

nia

63.P

ortugal

74. R

oman

ia77.P

olan

d82

.Slovenia

85.H

ungary

92.Latvia

97. C

zech

Rep

ublic

101.Slovakia

107.

Ital

y11

5. G

reec

e12

8.Croati

a

18 AnnualReportfortheyear2018,AssessmentofAuditWork

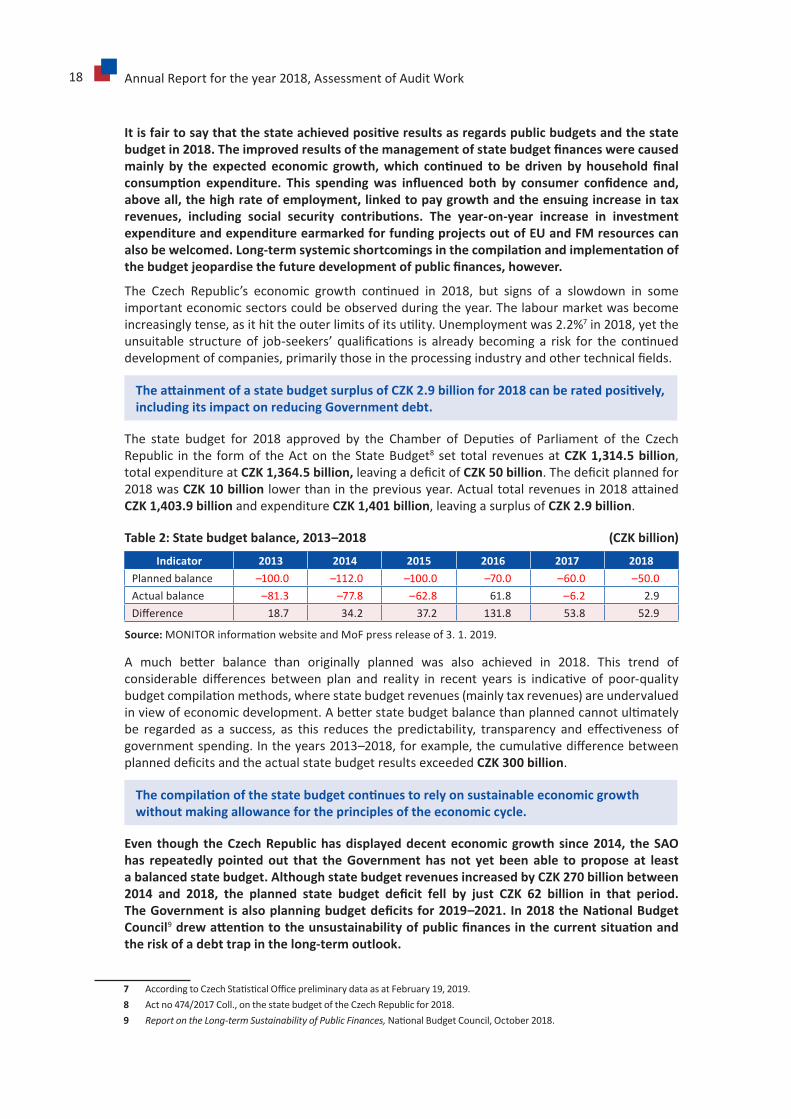

Itisfairtosaythatthestateachievedpositiveresultsasregardspublicbudgetsandthestatebudgetin2018.Theimprovedresultsofthemanagementofstatebudgetfinanceswerecausedmainly by the expected economic growth,which continued to be driven by household finalconsumption expenditure. This spendingwas influenced both by consumer confidence and,above all, the high rate of employment, linked to pay growth and the ensuing increase in tax revenues, including social security contributions. The year-on-year increase in investmentexpenditureandexpenditureearmarkedforfundingprojectsoutofEUandFMresourcescanalsobewelcomed.Long-termsystemicshortcomingsinthecompilationandimplementationofthebudgetjeopardisethefuturedevelopmentofpublicfinances,however.

The Czech Republic’s economic growth continued in 2018, but signs of a slowdown in someimportanteconomicsectorscouldbeobservedduringtheyear.Thelabourmarketwasbecomeincreasinglytense,asithittheouterlimitsofitsutility.Unemploymentwas2.2%7 in 2018, yet the unsuitable structureof job-seekers’ qualifications is alreadybecoming a risk for the continueddevelopmentofcompanies,primarilythoseintheprocessingindustryandothertechnicalfields.

TheattainmentofastatebudgetsurplusofCZK2.9billionfor2018canberatedpositively,including its impact on reducing Government debt.

The state budget for 2018 approved by the Chamber of Deputies of Parliament of the CzechRepublic in the formof theActon theStateBudget8 set total revenuesatCZK 1,314.5 billion, totalexpenditureatCZK 1,364.5 billion,leavingadeficitofCZK 50 billion.Thedeficitplannedfor2018wasCZK 10 billion lowerthaninthepreviousyear.Actualtotalrevenuesin2018attainedCZK 1,403.9 billionandexpenditureCZK 1,401 billion,leavingasurplusofCZK 2.9 billion.

Table2:Statebudgetbalance,2013–2018 (CZKbillion)

Indicator 2013 2014 2015 2016 2017 2018Plannedbalance –100.0 –112.0 –100.0 –70.0 –60.0 –50.0Actualbalance –81.3 –77.8 –62.8 61.8 –6.2 2.9Difference 18.7 34.2 37.2 131.8 53.8 52.9

Source:MONITORinformationwebsiteandMoFpressreleaseof3.1.2019.

A much better balance than originally planned was also achieved in 2018. This trend ofconsiderable differences between plan and reality in recent years is indicative of poor-qualitybudgetcompilationmethods,wherestatebudgetrevenues(mainlytaxrevenues)areundervaluedinviewofeconomicdevelopment.Abetterstatebudgetbalancethanplannedcannotultimatelybe regarded as a success, as this reduces the predictability, transparency and effectiveness ofgovernmentspending.Intheyears2013–2018,forexample,thecumulativedifferencebetweenplanneddeficitsandtheactualstatebudgetresultsexceededCZK 300 billion.

Thecompilationofthestatebudgetcontinuestorelyonsustainableeconomicgrowthwithout making allowance for the principles of the economic cycle.

Even though the Czech Republic has displayed decent economic growth since 2014, the SAO has repeatedly pointed out that the Government has not yet been able to propose at least a balanced state budget. Although state budget revenues increased by CZK 270 billion between 2014 and 2018, the planned state budget deficit fell by just CZK 62 billion in that period.TheGovernment isalsoplanningbudgetdeficitsfor2019–2021. In2018theNationalBudgetCouncil9drewattentiontotheunsustainabilityofpublicfinancesinthecurrentsituationandthe risk of a debt trap in the long-term outlook.

7 AccordingtoCzechStatisticalOfficepreliminarydataasatFebruary19,2019.8 Actno474/2017Coll.,onthestatebudgetoftheCzechRepublicfor2018.9 Report on the Long-term Sustainability of Public Finances, NationalBudgetCouncil,October2018.

AnnualReportfortheyear2018,AssessmentofAuditWork 19

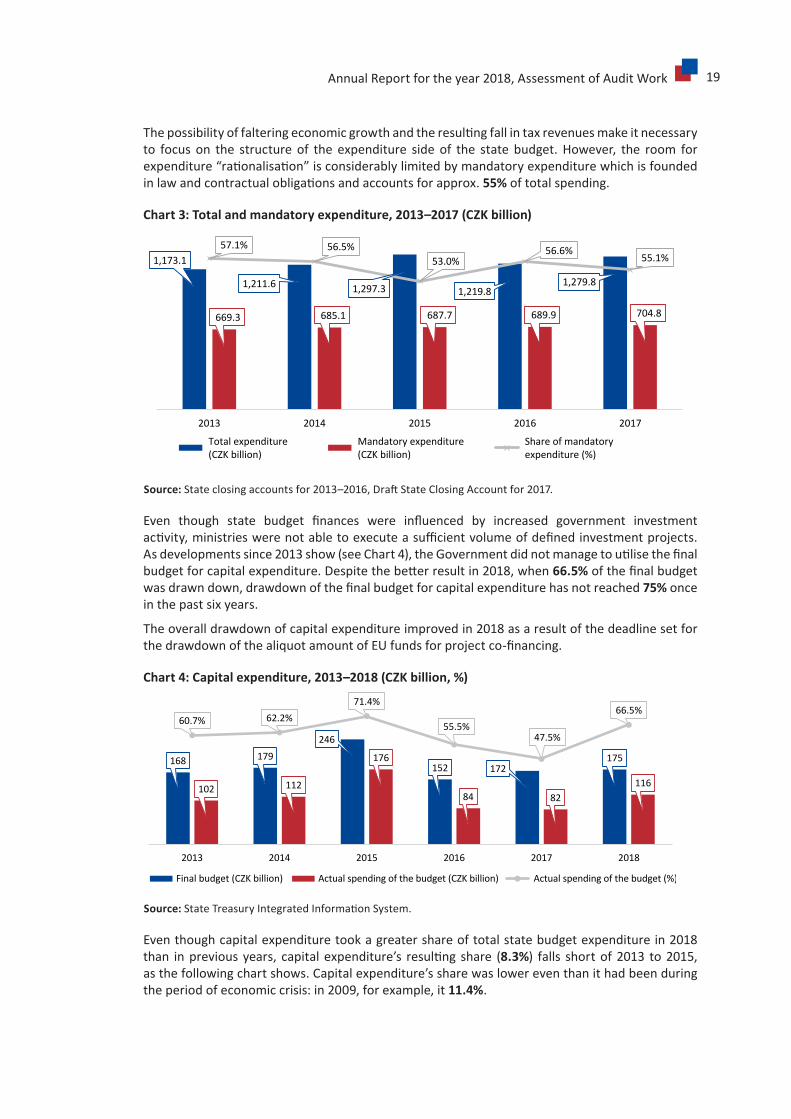

Thepossibilityoffalteringeconomicgrowthandtheresultingfallintaxrevenuesmakeitnecessaryto focus on the structure of the expenditure side of the state budget.However, the room forexpenditure“rationalisation”isconsiderablylimitedbymandatoryexpenditurewhichisfoundedinlawandcontractualobligationsandaccountsforapprox.55% oftotalspending.

Chart3:Totalandmandatoryexpenditure,2013–2017(CZKbillion)

1,173.1

1,211.6 1,297.3 1,219.81,279.8

669.3 685.1 687.7 689.9 704.8

57.1% 56.5%53.0%

56.6%55.1%

2013 2014 2015 2016 2017

Total expenditure (CZK billion)

Mandatory expenditure (CZK billion)

Share of mandatory expenditure (%)

Number of audits

Source:Stateclosingaccountsfor2013–2016,DraftStateClosingAccountfor2017.

Even though state budget finances were influenced by increased government investmentactivity,ministrieswerenotabletoexecuteasufficientvolumeofdefinedinvestmentprojects.Asdevelopmentssince2013show(seeChart4),theGovernmentdidnotmanagetoutilisethefinalbudgetforcapitalexpenditure.Despitethebetterresultin2018,when66.5% ofthefinalbudgetwasdrawndown,drawdownofthefinalbudgetforcapitalexpenditurehasnotreached75% once inthepastsixyears.

Theoveralldrawdownofcapitalexpenditureimprovedin2018asaresultofthedeadlinesetforthedrawdownofthealiquotamountofEUfundsforprojectco-financing.

Chart4:Capitalexpenditure,2013–2018(CZKbillion,%)

168 179

246

152 172175

102 112

176

84 82116

60.7% 62.2%71.4%

55.5%47.5%

66.5%

2013 2014 2015 2016 2017 2018

Final budget (CZK billion) Actual spending of the budget (CZK billion) Actual spending of the budget (%)

Source:StateTreasuryIntegratedInformationSystem.

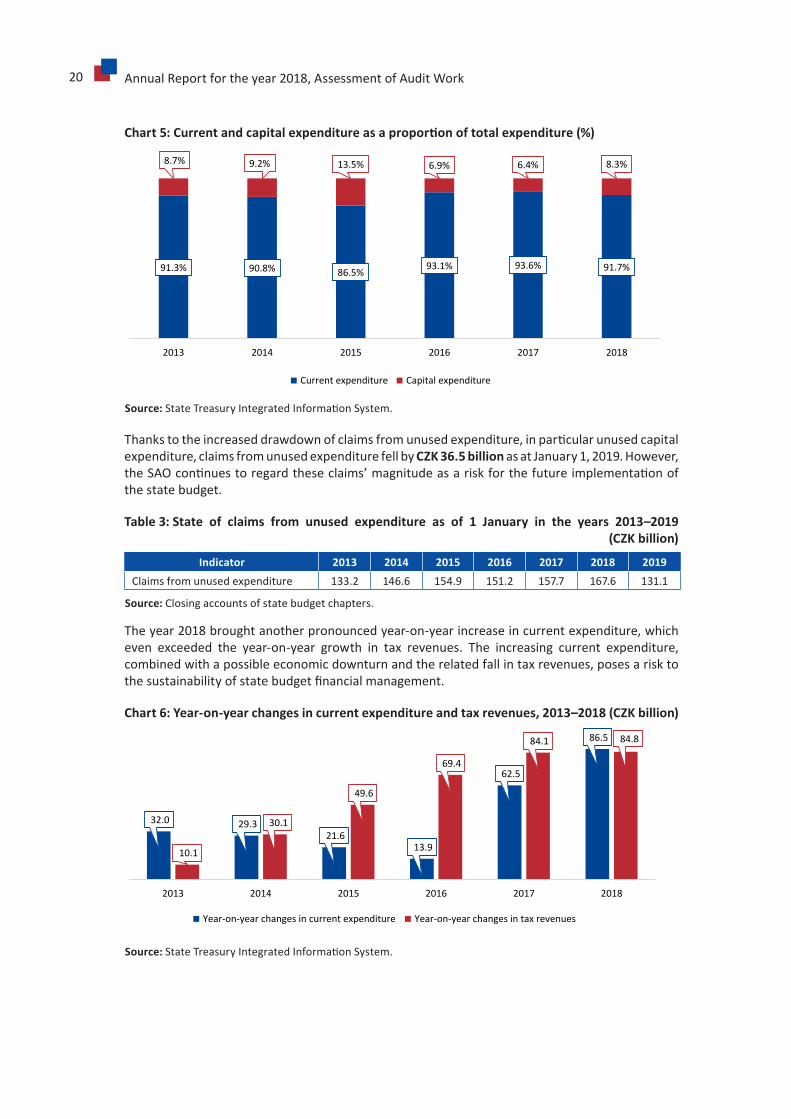

Eventhoughcapitalexpendituretookagreatershareoftotalstatebudgetexpenditurein2018than inpreviousyears, capitalexpenditure’s resulting share (8.3%) falls shortof2013 to2015,asthefollowingchartshows.Capitalexpenditure’ssharewaslowereventhanithadbeenduringtheperiodofeconomiccrisis:in2009,forexample,it11.4%.

20 AnnualReportfortheyear2018,AssessmentofAuditWork

Chart5:Currentandcapitalexpenditureasaproportionoftotalexpenditure(%)

91.3% 90.8% 86.5% 93.1% 93.6% 91.7%

8.7% 9.2% 13.5% 6.9% 6.4% 8.3%

2013 2014 2015 2016 2017 2018

Current expenditure Capital expenditure

Source:StateTreasuryIntegratedInformationSystem.

Thankstotheincreaseddrawdownofclaimsfromunusedexpenditure,inparticularunusedcapitalexpenditure,claimsfromunusedexpenditurefellbyCZK 36.5 billion asatJanuary1,2019.However,theSAOcontinuestoregardtheseclaims’magnitudeasariskforthefutureimplementationofthestatebudget.

Table 3: State of claims from unused expenditure as of 1 January in the years 2013–2019 (CZKbillion)

Indicator 2013 2014 2015 2016 2017 2018 2019Claimsfromunusedexpenditure 133.2 146.6 154.9 151.2 157.7 167.6 131.1

Source:Closingaccountsofstatebudgetchapters.

Theyear2018broughtanotherpronouncedyear-on-yearincreaseincurrentexpenditure,whicheven exceeded the year-on-year growth in tax revenues. The increasing current expenditure,combinedwithapossibleeconomicdownturnandtherelatedfallintaxrevenues,posesarisktothesustainabilityofstatebudgetfinancialmanagement.

Chart6:Year-on-yearchangesincurrentexpenditureandtaxrevenues,2013–2018(CZKbillion)

32.0 29.3 21.6

13.9

62.5

86.5

10.1

30.1

49.6

69.4

84.1 84.8

2013 2014 2015 2016 2017 2018

Year-on-year changes in current expenditure Year-on-year changes in tax revenues

Source:StateTreasuryIntegratedInformationSystem.

AnnualReportfortheyear2018,AssessmentofAuditWork 21

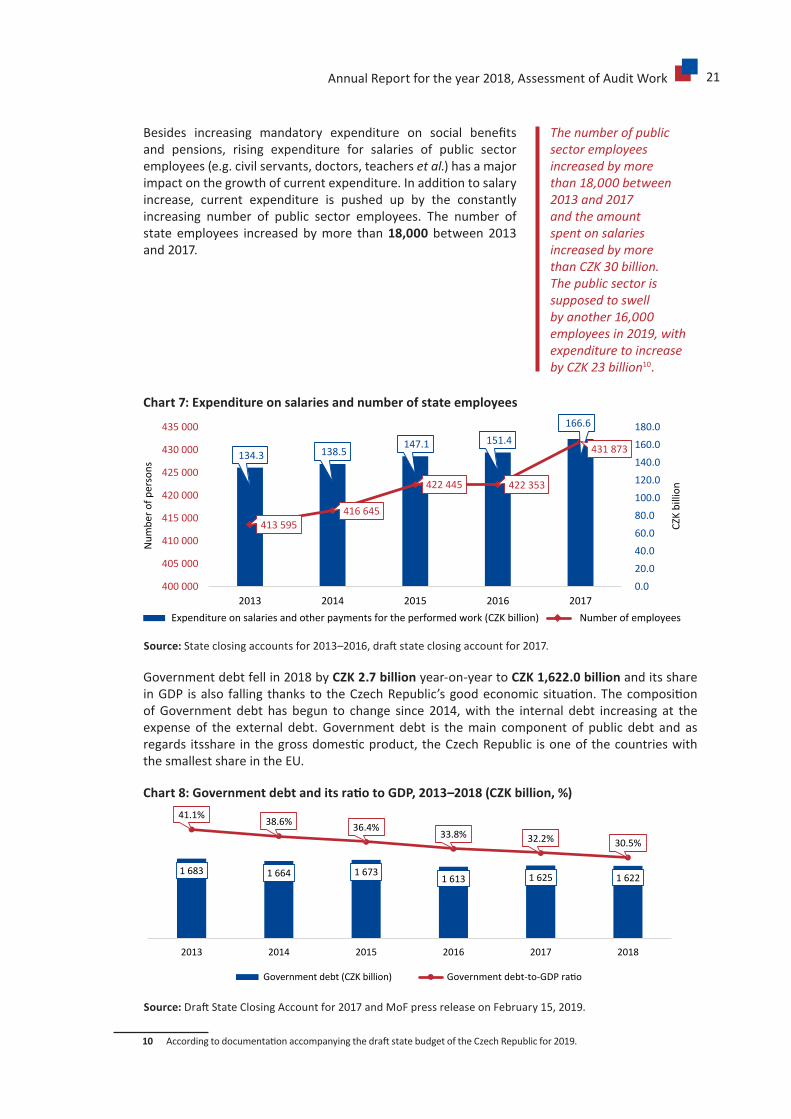

Besides increasing mandatory expenditure on social benefitsand pensions, rising expenditure for salaries of public sectoremployees(e.g.civilservants,doctors,teacherset al.)hasamajorimpactonthegrowthofcurrentexpenditure.Inadditiontosalaryincrease, current expenditure is pushed up by the constantlyincreasing number of public sector employees. The number ofstate employees increasedbymore than18,000 between2013and2017.10

Chart 7: Expenditure on salaries and number of state employees

134.3 138.5147.1 151.4

166.6

413 595416 645

422 445 422 353

431 873

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

400 000

405 000

410 000

415 000

420 000

425 000

430 000

435 000

2013 2014 2015 2016 2017

CZK

billi

on

Num

ber o

f per

sons

Expenditure on salaries and other payments for the performed work (CZK billion) Number of employees

Source:Stateclosingaccountsfor2013–2016,draftstateclosingaccountfor2017.

Governmentdebtfellin2018byCZK 2.7 billion year-on-yeartoCZK 1,622.0 billionanditsshareinGDP isalso falling thanks to theCzechRepublic’sgoodeconomicsituation.ThecompositionofGovernment debt has begun to change since 2014,with the internal debt increasing at theexpenseof the external debt.Government debt is themain component of public debt and asregards itsshare inthegrossdomesticproduct,theCzechRepublic isoneofthecountrieswiththesmallestshareintheEU.

Chart8:GovernmentdebtanditsratiotoGDP,2013–2018(CZKbillion,%)

1 683 1 664 1 6731 613 1 625 1 622

41.1% 38.6% 36.4%33.8% 32.2% 30.5%

2013 2014 2015 2016 2017 2018

Government debt (CZK billion) Government debt-to-GDP ra�o

Source:DraftStateClosingAccountfor2017andMoFpressreleaseonFebruary15,2019.

10 AccordingtodocumentationaccompanyingthedraftstatebudgetoftheCzechRepublicfor2019.

The number of public sector employees increased by more than 18,000 between 2013 and 2017 and the amount spent on salaries increased by more than CZK 30 billion. The public sector is supposed to swell by another 16,000 employees in 2019, with expenditure to increase by CZK 23 billion10.

22 AnnualReportfortheyear2018,AssessmentofAuditWork

Certainnegativefactorsthatpresentsignificantriskstohealthyandsustainablepublicfinancesastheprincipalobjectivesofbudgetaryresponsibilityhaveforlongimpactedonthemanagementofstatebudgetfinances.Thefollowingfactorsareparticularlyserious:

• failuretomakeuseofthepotentialofeconomicgrowthforputtinginplacetherightconditionsforthelong-termsustainabilityofpublicfinancesmakingallowancefortherulesoftheeconomiccycle;

• budgetcompilationmethodsthatresultinmarkeddifferencesbetweenplannedandactualrevenuesandexpenditure and undermine the predictability, transparency andeffectivenessofthemanagementofpublicfunds;

• the lack of a link between budget expenditure and performance indicators and measurable policy goals so that they are binding on the administrators of budget chapters;thatleadstoareductionin the budgetary responsibility of budget chapters´ administrators for the transparency, effectiveness,efficiencyandeconomyofthemanagementofpublicfunds;

• thepersistinginabilityofbudgetchapters´administratorstodrawdownplannedexpenditureforprogrammeandprojectfundinginconsequenceofprojects’andprocurementprocedures’insufficientpreparation,includinginefficientprocessesandineffectivelegislation;

• the lack of emphasis on responsible budgetary policy – the high dependency of budget implementationoneconomicgrowthandtheunderestimationoftherisksofthegrowthincurrentexpenditure(e.g.owingtopopulationageing,increaseinthenumberofpublicsectoremployees)andotherplannedexpenditure(e.g.discounts)withoutsecuringsources of funding.

In2018theSAOconductedoneaudittouchingonriskstothestatebudgetlinkedtoguaranteesprovided by the state11. Audit no 17/34 scrutinised whether the Ministry of Finance (MoF)proceededaccording to the lawwhenestablishing,keeping recordsofand implementingstateguaranteesandwhethertherulesformanagingreceivablesfromimplementedstateguaranteesaresetandfollowedinawayminimisingtherisksofstatebudgetlosses.TheSAO’skeyfindingswere:

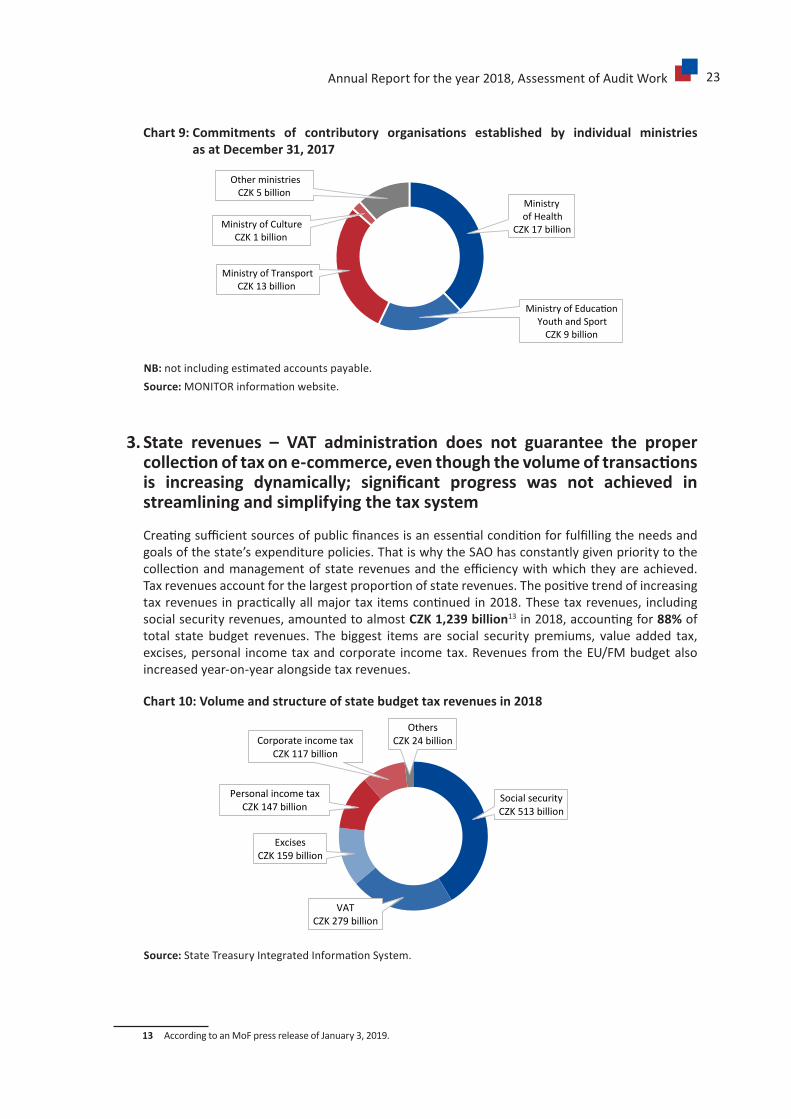

• Attheendof2016theMoFregisteredguaranteesworthCZK 439 billion. In the years 2013 to2016thestatebudgetfinancesspent inconnectionwithstateguaranteesandcollateralamountedtoCZK 13.6 billion. In2017thestateofguaranteesfellsharplybyCZK 190 billion, largelybecauseofthereductionoftheguaranteeprovidedtotheCzechNationalBankforthesaleofInvestičníapoštovníbanka.Consequently,stateguaranteesamountedtoCZK 248 billion atyear-end2017.TheSAOidentifiedcertainminorshortcomingsintherecordingandreportingof stateguaranteesand theirdisclosure in thestateclosingaccount.Theauditalso found,however,thatinformationonthesizeofcommitmentsofcontributoryorganisationsforwhichthestateisliableunderthetermsofActno218/2000Coll.12 isnotpartofthestateclosingaccountorevenoftheclosingaccountsoftherelevantstatebudgetchapters.Accordingtoacalculationbytheauditteam,thesecommitmentsincreasedby42%between2014and2016toreachapprox.CZK 34 billionandconstituteapotentialriskforthestatebudgetiftheyhavetobecovered.TheSAOthereforerecommendseliminatingthisshortcominginthelegislationandmakingitobligatorytoprovideinformationaboutthesizeofthistypeofcommitment.Commitmentsofthestate’scontributoryorganisationsreachedalmostCZK 45 billionbytheendof2017;seeChart9,brokendownbyGovernmentdepartment.

11 Bymeansofguaranteesthestateassumestheobligationtopay,incertainsituations,thefinancialcommitmentofaspecificdebtorthestatedecidedtostandsuretyfor.Thesearestandardguarantees,mostcommonlyforCzechRailandtheRailTrackAdministration,andnon-standardguarantees,whichincludeguaranteeslinkedtothesaleofInvestičníapoštovníbanka,orstateguaranteeslinkedtoexportinsuranceandfinancing.

12 ActNo.218/2000Coll.,onthebudgetaryrulesandamendingcertainrelatedacts(thebudgetaryrules).

The state is planning state budget deficits in the coming years as well. A state budget deficit of CZK 40 billion is planned for 2019. The same deficit is envisaged for 2020 and 2021.

The state plans to spend CZK 6 billion on transport discounts for seniors and students in 2019.

AnnualReportfortheyear2018,AssessmentofAuditWork 23

Chart9:Commitments of contributory organisations established by individual ministries as at December 31, 2017

Ministryof Health

CZK 17 billion

Ministry of Educa�onYouth and Sport

CZK 9 billion

Ministry of TransportCZK 13 billion

Ministry of CultureCZK 1 billion

Other ministriesCZK 5 billion

NB:notincludingestimatedaccountspayable.Source:MONITORinformationwebsite.

3.State revenues – VAT administration does not guarantee the propercollectionoftaxone-commerce,eventhoughthevolumeoftransactionsis increasing dynamically; significant progress was not achieved instreamlining and simplifying the tax system

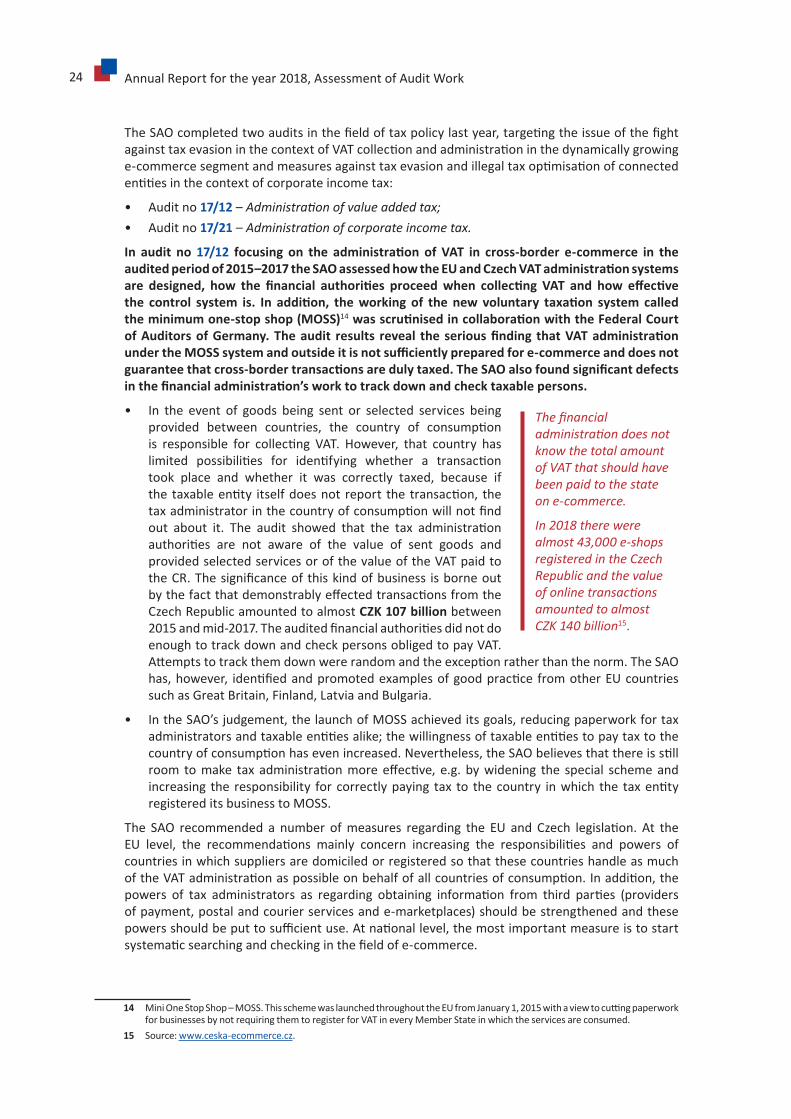

Creatingsufficientsourcesofpublicfinancesisanessentialconditionforfulfillingtheneedsandgoalsofthestate’sexpenditurepolicies.ThatiswhytheSAOhasconstantlygivenprioritytothecollectionandmanagementofstaterevenuesandtheefficiencywithwhichtheyareachieved.Taxrevenuesaccountforthelargestproportionofstaterevenues.Thepositivetrendofincreasingtaxrevenues inpracticallyallmajortax itemscontinued in2018.Thesetaxrevenues, includingsocialsecurityrevenues,amountedtoalmostCZK 1,239 billion13 in2018,accountingfor88% of total state budget revenues. The biggest items are social security premiums, value added tax,excises,personal incometaxandcorporate incometax.RevenuesfromtheEU/FMbudgetalsoincreasedyear-on-yearalongsidetaxrevenues.

Chart 10: Volume and structure of state budget tax revenues in 2018

Social security CZK 513 billion

VAT CZK 279 billion

ExcisesCZK 159 billion

Personal income tax CZK 147 billion

Corporate income taxCZK 117 billion

Others CZK 24 billion

Source:StateTreasuryIntegratedInformationSystem.

13 AccordingtoanMoFpressreleaseofJanuary3,2019.

24 AnnualReportfortheyear2018,AssessmentofAuditWork

TheSAOcompletedtwoauditsinthefieldoftaxpolicylastyear,targetingtheissueofthefightagainsttaxevasioninthecontextofVATcollectionandadministrationinthedynamicallygrowinge-commercesegmentandmeasuresagainsttaxevasionandillegaltaxoptimisationofconnectedentitiesinthecontextofcorporateincometax:

• Auditno17/12–Administration of value added tax; • Auditno17/21 –Administration of corporate income tax.

In audit no 17/12 focusing on the administration of VAT in cross-border e-commerce in theauditedperiodof2015–2017theSAOassessedhowtheEUandCzechVATadministrationsystemsare designed, how the financial authorities proceedwhen collecting VAT and how effectivethe control system is. In addition, theworking of the new voluntary taxation system calledtheminimumone-stopshop(MOSS)14wasscrutinisedincollaborationwiththeFederalCourtofAuditorsofGermany.Theaudit results reveal the seriousfinding thatVATadministrationundertheMOSSsystemandoutsideitisnotsufficientlypreparedfore-commerceanddoesnotguaranteethatcross-bordertransactionsaredulytaxed.TheSAOalsofoundsignificantdefectsinthefinancialadministration’sworktotrackdownandchecktaxablepersons.

• In the event of goods being sent or selected services beingprovided between countries, the country of consumptionis responsible for collecting VAT. However, that country haslimited possibilities for identifying whether a transactiontook place and whether it was correctly taxed, because ifthe taxableentity itselfdoesnot report the transaction, thetaxadministratorinthecountryofconsumptionwillnotfindout about it. The audit showed that the tax administrationauthorities are not aware of the value of sent goods andprovidedselectedservicesorofthevalueoftheVATpaidtotheCR.Thesignificanceofthiskindofbusiness isborneoutbythefactthatdemonstrablyeffectedtransactionsfromtheCzechRepublicamountedtoalmostCZK 107 billion between2015andmid-2017.TheauditedfinancialauthoritiesdidnotdoenoughtotrackdownandcheckpersonsobligedtopayVAT.Attemptstotrackthemdownwererandomandtheexceptionratherthanthenorm.TheSAOhas,however, identifiedandpromotedexamplesofgoodpractice fromotherEUcountriessuchasGreatBritain,Finland,LatviaandBulgaria. 15

• IntheSAO’sjudgement,thelaunchofMOSSachieveditsgoals,reducingpaperworkfortaxadministratorsandtaxableentitiesalike;thewillingnessoftaxableentitiestopaytaxtothecountryofconsumptionhasevenincreased.Nevertheless,theSAObelievesthatthereisstillroom tomake tax administrationmoreeffective, e.g. bywidening the special schemeandincreasing the responsibility for correctlypaying tax to thecountry inwhich the taxentityregistereditsbusinesstoMOSS.

The SAO recommended a number ofmeasures regarding the EU and Czech legislation. At theEU level, the recommendations mainly concern increasing the responsibilities and powers ofcountriesinwhichsuppliersaredomiciledorregisteredsothatthesecountrieshandleasmuchoftheVATadministrationaspossibleonbehalfofallcountriesofconsumption.Inaddition,thepowers of tax administrators as regarding obtaining information from third parties (providersofpayment,postalandcourierservicesande-marketplaces)shouldbestrengthenedandthesepowersshouldbeputtosufficientuse.Atnationallevel,themostimportantmeasureistostartsystematicsearchingandcheckinginthefieldofe-commerce.

14 MiniOneStopShop–MOSS.ThisschemewaslaunchedthroughouttheEUfromJanuary1,2015withaviewtocuttingpaperworkforbusinessesbynotrequiringthemtoregisterforVATineveryMemberStateinwhichtheservicesareconsumed.

15 Source:www.ceska-ecommerce.cz.

The financial administration does not know the total amount of VAT that should have been paid to the state on e-commerce.

In 2018 there were almost 43,000 e-shops registered in the Czech Republic and the value of online transactions amounted to almost CZK 140 billion15.

AnnualReportfortheyear2018,AssessmentofAuditWork 25

Based on the results of the SAO audit, the Czech tax administration will start activelysearchingforentitiesnotfulfillingtheirtaxobligationsanddeclaredanumberofmeasuresto improve e-commerce VAT administration. The European Court of Auditors has alsoturneditsattentiontothisissue.TheimplementationoftheMOSSschemeisincreasinglyimportantafteritwasextendedtothesendingofgoodsinthe2019–2021period.

TheMoFandtheGeneralFinancialDirectorate(GFD)bothagreedwiththeSAO’sprincipalfindingsandadoptedordeclaredtheadoptionofanumberofmeasuresto improvetheadministrationofVATinthefieldofe-commerce,e.g.theestablishmentofanewunittotrackdowntaxpayerswhoarenot fulfillingthestatutoryconditions forVATregistration.TomakecontrolworkmoreeffectiveaftertheMOSSschemeisextended,theadministrationoftaxeswillnotbedonebytheFinancialOfficefortheSouthMoravianRegionfortheentireCzechRepublic,butthiswillbedoneby the appropriate local financial offices. The CustomsAdministration is prepared for changesaffectingimportsofsmallconsignmentsthatwilltakeplaceinconnectionwiththeadoptionofthe“e-commerceVATpackage”fromJanuary1,2021.

In audit no 17/21theSAOtargetedtheadministrationofcorporateincometax.AfterVATandsocial security premiums, corporate income tax is the third largest revenue for public budgets. Thetotaltaxcollectedintheauditedperiodof2013–2016wasCZK565billion.TheSAOidentifiedillegal taxoptimisation in international transactionsbetweenentities connected in termsofpersonnel and capital as the greatest risk.

• One risk area identified in tax administration in the auditedperiodwastransferprices,ortransactionscarriedoutbetweenentitiesconnectedinpersonnelorcapitaltermsathomeandabroad. Corporate income tax is not harmonised in the EU,whichenablestaxpayerstoperformundesirableoptimisationviaconnectedentitiesabroadortaxhavens.TheEUhasadoptedseveral directives concerning international informationexchange and laying down rules to combat tax avoidancepractices.Becauseofthelengthylegislativeprocess,theCzechRepublic implemented the EU directive governing tools fordetectingillegaltaxoptimisationintonationallegislationafteradelayofseveralmonths,andthensuccessfullytookpartininternationalinformationexchange.Asregardstheimpactofinformationexchange,theGFDquantifiedtheproceedsintheauditedperiodatCZK 103 million indirecttaxes(i.e.corporateincometaxandpersonalincometax).TheSAOalsostatedthattheFinancialAdministrationoftheCzechRepublicdidnotreacttotheriskofabuseofkorunabondsingoodtime,asitstartedtocheckthetaxationofkorunabonds issued in2012as lateasin2017,i.e.fiveyearslater,andonlydidsoinresponsetoinformationfromthemediaorfromthepublicorinformationarising out of sessions of the budgetary committee of theChamberofDeputiesofParliamentoftheCR.Asaresult,thethree-yearstatuteoflimitationsforimposingtaxhadexpiredforatleast15taxpayers.

Thefightagainsttaxevasion,makingtaxcollectionmoreeffectiveandcuttingpaperworkfortaxpayers have long ranked among the Government’s key priorities in tax policy16. For that reason, the SAO has long monitored and evaluated the effectiveness and costliness of tax collectionandofmeasureslinkedtopreventinganddetectingtaxevasionandstreamliningtaxadministrationfortaxpayers.

16 Seee.g.nationalreformprogrammesoftheCzechRepublicfor2016to2018.

The statistics on the results of the financial administration’s control work were overstated in 2015 and 2016. For 2015 the GFD stated that additional tax of almost CZK 1.8 billion was levied on the basis of its checks. After appeals that were filed by the entities but were not factored into the financial administration statistics, the figure was in fact CZK 850 million. A similar thing happened in 2016, when the GFD again published a figure of CZK 1.8 billion, while the reality was just under CZK 1.1 billion.

26 AnnualReportfortheyear2018,AssessmentofAuditWork

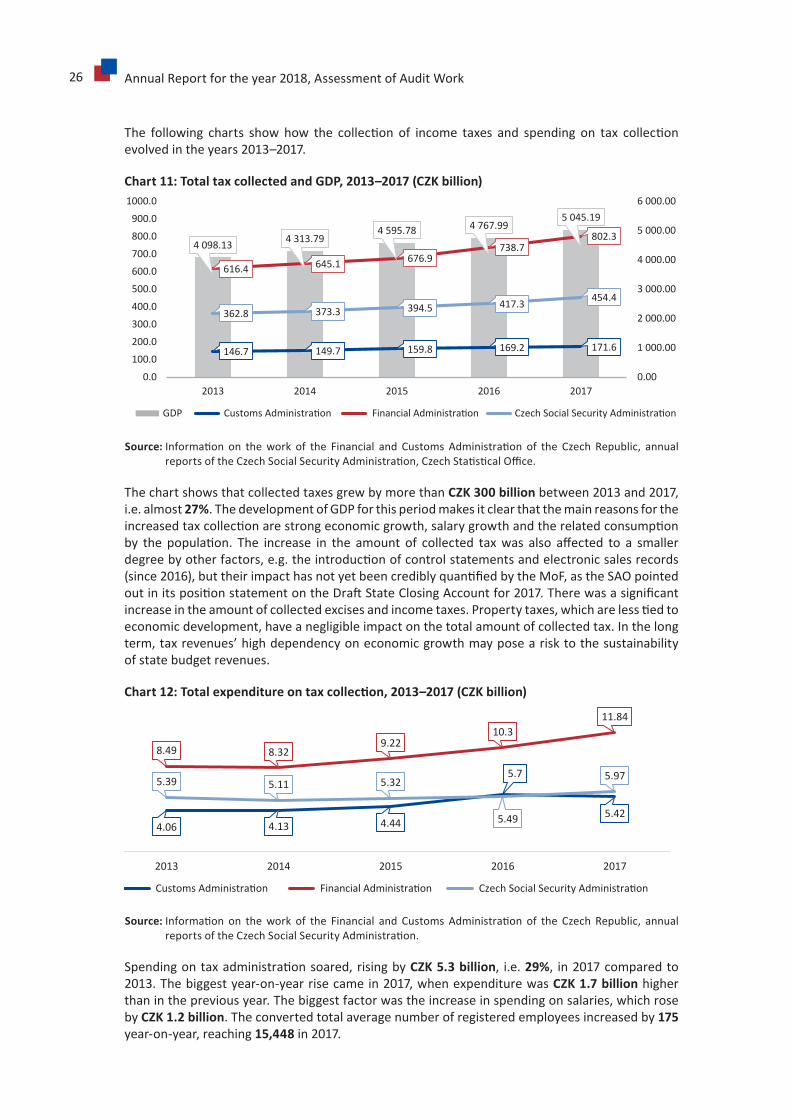

The following charts showhow the collection of income taxes and spending on tax collectionevolvedintheyears2013–2017.

Chart11:TotaltaxcollectedandGDP,2013–2017(CZKbillion)

4 098.13 4 313.794 595.78 4 767.99

5 045.19

146.7 149.7 159.8 169.2 171.6

616.4 645.1 676.9738.7

802.3

362.8 373.3 394.5 417.3 454.4

0.00

1 000.00

2 000.00

3 000.00

4 000.00

5 000.00

6 000.00

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

1000.0

2013 2014 2015 2016 2017

GDP Customs Administra�on Financial Administra�on Czech Social Security Administra�on

Source:Information on thework of the Financial and Customs Administration of the Czech Republic, annualreportsoftheCzechSocialSecurityAdministration,CzechStatisticalOffice.

ThechartshowsthatcollectedtaxesgrewbymorethanCZK 300 billion between2013and2017,i.e. almost 27%.ThedevelopmentofGDPforthisperiodmakesitclearthatthemainreasonsfortheincreasedtaxcollectionarestrongeconomicgrowth,salarygrowthandtherelatedconsumptionby the population. The increase in the amount of collected taxwas also affected to a smallerdegreebyotherfactors,e.g.theintroductionofcontrolstatementsandelectronicsalesrecords(since2016),buttheirimpacthasnotyetbeencrediblyquantifiedbytheMoF,astheSAOpointedoutinitspositionstatementontheDraftStateClosingAccountfor2017.Therewasasignificantincreaseintheamountofcollectedexcisesandincometaxes.Propertytaxes,whicharelesstiedtoeconomicdevelopment,haveanegligibleimpactonthetotalamountofcollectedtax.Inthelongterm,taxrevenues’highdependencyoneconomicgrowthmayposearisktothesustainabilityofstatebudgetrevenues.

Chart12:Totalexpenditureontaxcollection,2013–2017(CZKbillion)

4.06 4.13 4.44

5.7

5.42

8.49 8.329.22

10.311.84

5.39 5.11 5.32

5.49

5.97

2013 2014 2015 2016 2017

Customs Administra�on Financial Administra�on Czech Social Security Administra�on

Source:Information on thework of the Financial and Customs Administration of the Czech Republic, annualreportsoftheCzechSocialSecurityAdministration.

Spendingontaxadministrationsoared,risingbyCZK 5.3 billion, i.e. 29%, in2017comparedto2013.Thebiggestyear-on-yearrisecamein2017,whenexpenditurewasCZK 1.7 billion higherthaninthepreviousyear.Thebiggestfactorwastheincreaseinspendingonsalaries,whichrosebyCZK 1.2 billion.Theconvertedtotalaveragenumberofregisteredemployeesincreasedby175 year-on-year,reaching15,448 in 2017.

AnnualReportfortheyear2018,AssessmentofAuditWork 27

A comparison of total tax revenues and expenditure in the years 2013–2017 reveals that expenditureincreasedatafasterratethanrevenues,whichshowsthattaxadministration’scost-effectivenessdeclined.Atthesametime,themagnitudeoftaxrevenueswaslargelydrivenbythepositiveeconomicsituationandgrowinghouseholdconsumption.

InrecentyearstheCzechRepublichasalsofocusedonintroducingmeasures to fight tax evasion, especially in the VAT field. Thedevelopmentofthetaxburdenindicatesthatthesemeasures,suchascontrolstatements,hadapositiveimpactprimarilyoncompliancewith the regulations andon the fulfilmentof obligationsbyVATpayers,i.e.apreventiveeffect.Thatsaid,significantprogresshasnotbeenmadetowardsreducingtheadministrativeburdenlinkedto theadministrationandpaymentof taxes.Quite theopposite:somemeasuresintroducedtofighttaxevasionhavebroughtextrapaperworkbothfortaxpayersandtaxadministrators.Eventhoughcontrol statements, for example, are fully electronic, the timespentonadministrativeworkhasincreasedforVATpayers.

According to theTime to comply indicator,which is regularly assessedby theWorldBank andPricewaterhouseCoopers(PwC)andmeasurestheamountoftimerequiredbytaxpayerstofulfiltheirtaxobligations,230 hours hadtobespentonfulfillingtaxobligationsintheCzechRepublicin2017,whichcontinuedtobefarmorethantheEUandEFTAaverage(161 hours);seeChart13.FirmsintheCzechRepublichavetospend53 hours oncorporateincometax;75 hours ontaxesonlabour(i.e.personalincometax,includingmandatorysocialcontributionsforemployees);and102 hours onconsumptiontaxes(correspondingtoVATandexcises)17.Theintroductionofcontrolstatements in2016, forexample, addeda further14 hours18 to thetime required to fulfilVATobligations.

Chart13:Timerequiredtocomplywithtaxobligationstothestate inEUandEFTAcountries in2017(hours)

50 52 55 63 79 82 90 99 105 119 122 123 131 132 136 139 139 140 148 161 163 169192 193 206 218 230 235 238 243

277

334

453

Corporate tax Income tax Consump�on tax

Nizo

zem

sko

Source: pwc.com/gx/en/services/tax/publications/paying-taxes-2019/explorer-tool.html.

So far, thenecessaryprogress in cuttingpaperwork for taxpayers, simplifying taxes andmakingtaxadministrationmoreuser-friendlyfortaxpayershasnotbeenachieved.

17 Seehttps://www.pwc.com/gx/en/services/tax/publications/paying-taxes-2019/explorer-tool.html.18 AccordingtothePaying Taxes 2018 report;TheWorldBankGroupandPwC2017.

Esto

nia

SanMarino

Luxembo

urg

Switz

erland

Norway

Ireland

F inlan

dLi

thua

nia

UnitedKing

dom

Nethe

rland

sSw

eden

Cy

prus

Au

stria

De

nmark

Belgium

Fran

ce

Mal

ta

Icelan

dSp

ain

EUand

EFTA

Rom

ania

Latvia

Slov

akia

Gre

ece

Croa

tia

Ger

man

y CzechRe

public

Slov

enia

Italy

Po

rtug

al

H ung

ary

P oland

Bu

lgaria

No real progress was made in terms of reducing taxpayers’ administrative burden when complying with tax obligations. Firms in the Czech Republic have to spend more than 40% more time on tax compliance than the average for EU/EFTA countries.

28 AnnualReportfortheyear2018,AssessmentofAuditWork

TheMoF,forexample,agreedwiththeconclusionsofauditreportno16/2119 that the personal incometaxsystemisconfusingandcomplicated,withnumerousexemptionsandformsofrelief.That makes tax administrationmore complicated and increases the administrative burden ontaxpayers,withoutmakingthecollectionofthistaxmoreeffective.TheMoFpledgedtoprepareabrandnew income taxactandaMOJE daně (My taxes) website that shouldmakeelectroniccommunicationwiththeauthoritiesmoreeffective.AccordingtotheMoF,theMy taxes projectshoulddeliverasimplertaxsystem.Inadditiontothenewincometaxesact,thissimplertaxsystemshouldincludeself-assessment,individualisationandanelectronicwebsitefortaxadministration.

TheMoFhadalreadyannouncedthisprojectinresponsetotheresultsofauditno15/1720,linkedto the collapse of the Single CollectionPoints (SCP) project thatwas supposed to simplify thecollectionandadministrationoftaxesandinsurancepremiums.

Asthenewincometaxesactunderpreparationhasnotyetenteredthelegislativeprocessandthe My taxesprojectstillawaitsimplementation,improvementscannotbeexpectedinthenearfuture.

4. Government expenditure areas – achieving the goals of Government policies is hindered by recurring management and control errors

ThefollowingpartsoftheannualreportaredevotedtotheresultsoftheSAO’sauditandanalysisworkinthemainexpenditureareasofGovernmentpoliciescoveredbytheSAOlastyear.

They include a summary of the SAO’s significant findings concerning both the achievement ofpolicy goals and shortcomingsandany recommendations intended tohelppolicymakers applygoodpracticeandbettermanagementofpublicspendingwherevernecessary.Thefindingsshouldalso functionas objective assurance for the general public in termsofwhere the state standsinvariousareasandwherechange isnecessary toensure taxpayers’money is spentcorrectly.Inotherwords,toensurethatthestateisabletodeliverthenecessaryvalueforitscitizensinlinewiththeobjectiverequirementsandthustofulfilitsindispensableroleaswellaspossible.Andadditionally,toensurethatthestate’sinterventionscontributetoimprovingthecountry’sglobalcompetitiveness.Attainingmaximumvalueformoneyisanecessarypreconditionofthat.

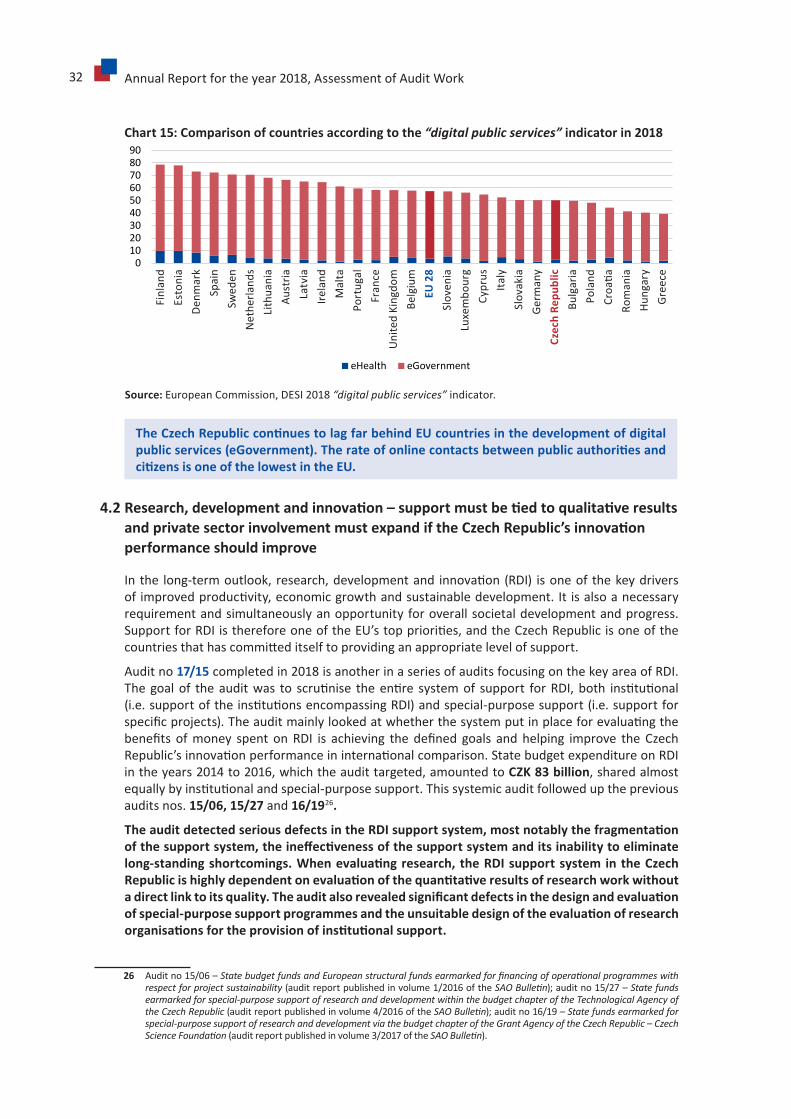

According to the results presented in the following passages, broken down by policy areas,thesystemformanagementandcontrolofpublicfundsdidnotalwaysensurethatpublicspendingwascompliantwiththelegalregulations,effective,efficientandeconomical.

If we are to summarise the similar and recurring types of management and control shortcomings as the reasons for the state not always being able to achieve policy goals in the manner described above, the main systemic shortcomings include:

• theabsenceofeffectivelegislation (auditno17/02inthefieldofsupportforsocialhousing);

• ahaphazardandunsystematicapproach (e.g.auditno17/09inthefieldoffundingtherepair,modernisationanddevelopmentof2ndand3rdclassroads);

• fragmentation,authorities’unclearpowersandresponsibilities (e.g.auditno17/15 in the systemofsupportforresearch,developmentandinnovation);

• failuretoassesstheeffectiveness,efficiencyandeconomyinprovidingsupport asregardstheresultsandbenefitsofthesupport(e.g.auditno18/01 inthefieldofsupportforbusinessrealestate);

19 Auditreportno16/21–Income tax administration and the impacts of legislative amendments on state budget revenueswaspublishedinvolume4/2017ofthe SAO Bulletin.

20 Auditreportno15/17–Funds spent on measures related to streamlining of tax and insurance collection and administration, mainly within the project “Setup of Single Collection Point for state budget revenues” was published in volume 4/2016 of the SAO Bulletin.

AnnualReportfortheyear2018,AssessmentofAuditWork 29

• unequal treatment of applicants for support and lack of transparency when awardingsubsidies (e.g. audit no 17/26 in support under the Rural Development Programme andprioritisinglargefirmsoversmallandmedium-sizedenterprise);

• poor preparation of projects and delays in programme implementation (audit no 17/16 in the Programme of Care for National Cultural Treasures);

• failuretomakeuseofacompetitiveenvironmentwhenawardingcontractstoachievecostsavings (auditno17/33inthefieldofcostsofrailwaylevel-crossingsafety);

• insufficient control work and failure to implement measures to remedy shortcomings (e.g.auditno17/22inthefieldofICTprojectsforthedisbursementofsocialbenefits).

4.1EfficientpublicadministrationandeGovernment–notimplementingmeasurestosolveICTdevelopmentproblemsmakesthedigitisationofpublicadministrationmuchmoreexpensive;theCzechRepubliccontinuestolagfarbehindindevelopingonline state services

In2018theSAOfollowedupthefindingsithadmadeinpreviousyearswhenauditinginformationtechnologiesandthedigitisationofpublicadministration.InitsauditworktheSAOmainlyfocusesonprojectsandinformationsystemsthatareviewedashigh-risk.Andnotjusthigh-riskfromtheSAO’spointofview,butbecauseoftheirsocialramifications.

It has become clear that there has been a long-term failure to solve the problems associated with informationandcommunicationtechnologies,sotheyremainamajorcauseofuneconomicalandinefficientspending.

Persistingproblems in the expansionof thedigitisationof public administration includehaphazardmanagementof ICTresources, insufficientstaffingcapacitiesanddependencyon external ICT contractors.

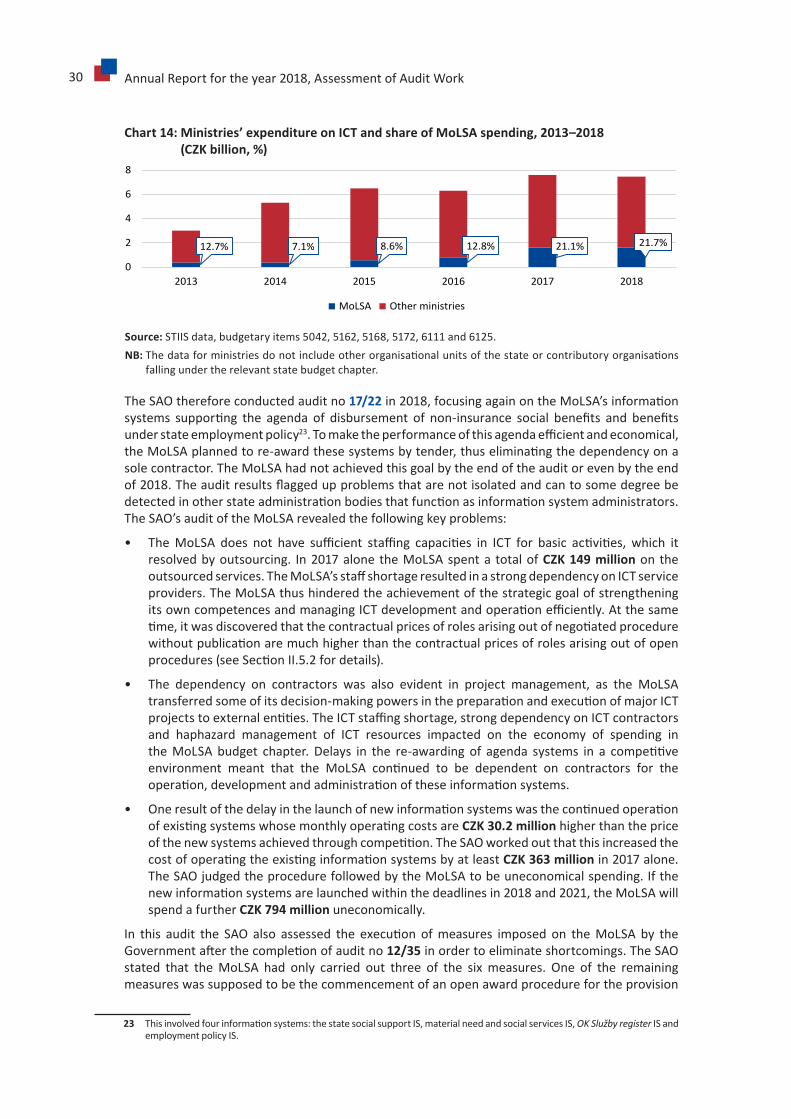

ThesefactorshaveanimpactontheamountthestatehastospendonICTeveryyear.Datafromthe State Treasury Integrated Information System (STIIS)revealthatdepartmentsspentatotalofCZK 12.6 billion21 in2018.Totalexpendituremaybehigher,though,asthisfiguredidnotincludebudgetaryitemsthatmaycompriseotherrelatedspendingthanmerelydirectexpenditureonICT.

ThroughregularandsystematicmonitoringandriskanalysistheSAOidentifiedenduringandgraveproblemsinthefieldoftheMoLSA’sinformationsystemsthathadalreadybeencoveredbyauditno 12/3522.ThedatainChart14showthattheMoLSAhaslongfailedtocutspendingonICT–spendinghasrisensharplyeveryyearsince2014.In2018,whenitwasfourtimeshigherthanin2013,expenditureonICTexceededCZK 1.6 billion,accountingforover21% ofallministries’totalspendingonICT,whichamountedtoCZK 7.5 billion in 2018.

21 Selectionofbudgetitems5042,5162,5168,5172,6111,6125.22 Auditno12/35–Establishment of the Labour Office of the Czech Republic and management of state budget’s and the EU’s

property and funds related to the establishment and activity of this office and to preparation and implementation of projects in the area of welfare disbursement information systems(auditreportpublishedinvolume3/2013oftheSAO Bulletin).

30 AnnualReportfortheyear2018,AssessmentofAuditWork

Chart14:Ministries’expenditureonICTandshareofMoLSAspending,2013–2018 (CZKbillion,%)

12.7 % 7.1 % 8.6 % 12.8 % 21.1 % 21.7 %

0

2

4

6

8

2013 2014 2015 2016 2017 2018

MoLSA Other ministries

Source:STIISdata,budgetaryitems5042,5162,5168,5172,6111and6125.NB:Thedataforministriesdonotincludeotherorganisationalunitsofthestateorcontributoryorganisations

fallingundertherelevantstatebudgetchapter.

TheSAOthereforeconductedauditno17/22 in2018,focusingagainontheMoLSA’sinformationsystems supporting the agenda of disbursement of non-insurance social benefits and benefitsunderstateemploymentpolicy23.Tomaketheperformanceofthisagendaefficientandeconomical,theMoLSAplannedtore-awardthesesystemsbytender,thuseliminatingthedependencyonasolecontractor.TheMoLSAhadnotachievedthisgoalbytheendoftheauditorevenbytheendof2018.Theauditresultsflaggedupproblemsthatarenotisolatedandcantosomedegreebedetectedinotherstateadministrationbodiesthatfunctionasinformationsystemadministrators.TheSAO’sauditoftheMoLSArevealedthefollowingkeyproblems:

• TheMoLSA does not have sufficient staffing capacities in ICT for basic activities, which itresolvedbyoutsourcing. In2017alonetheMoLSAspenta totalofCZK 149 million on the outsourcedservices.TheMoLSA’sstaffshortageresultedinastrongdependencyonICTserviceproviders.TheMoLSAthushinderedtheachievementofthestrategicgoalofstrengtheningitsowncompetencesandmanagingICTdevelopmentandoperationefficiently.Atthesametime,itwasdiscoveredthatthecontractualpricesofrolesarisingoutofnegotiatedprocedurewithoutpublicationaremuchhigherthanthecontractualpricesofrolesarisingoutofopenprocedures(seeSectionII.5.2fordetails).

• The dependency on contractors was also evident in project management, as the MoLSAtransferredsomeofitsdecision-makingpowersinthepreparationandexecutionofmajorICTprojectstoexternalentities.TheICTstaffingshortage,strongdependencyonICTcontractorsand haphazard management of ICT resources impacted on the economy of spending intheMoLSAbudget chapter.Delays in the re-awarding of agenda systems in a competitiveenvironment meant that the MoLSA continued to be dependent on contractors for theoperation,developmentandadministrationoftheseinformationsystems.

• OneresultofthedelayinthelaunchofnewinformationsystemswasthecontinuedoperationofexistingsystemswhosemonthlyoperatingcostsareCZK 30.2 million higherthanthepriceofthenewsystemsachievedthroughcompetition.TheSAOworkedoutthatthisincreasedthecostofoperatingtheexistinginformationsystemsbyatleastCZK 363 million in 2017 alone. TheSAOjudgedtheprocedurefollowedbytheMoLSAtobeuneconomicalspending.Ifthenewinformationsystemsarelaunchedwithinthedeadlinesin2018and2021,theMoLSAwillspendafurtherCZK 794 million uneconomically.

In this audit the SAO also assessed the execution ofmeasures imposed on theMoLSA by theGovernmentafterthecompletionofauditno12/35 inordertoeliminateshortcomings.TheSAOstated that theMoLSA had only carried out three of the sixmeasures. One of the remainingmeasureswassupposedtobethecommencementofanopenawardprocedurefortheprovision

23 Thisinvolvedfourinformationsystems:thestatesocialsupportIS,materialneedandsocialservicesIS,OK Služby registerISandemploymentpolicyIS.

AnnualReportfortheyear2018,AssessmentofAuditWork 31