Security Code Violations, Analysts' Forecast Quality, and Corporate ...

Upload

khangminh22Category

view

1download

0

PT Bank Mandiri (Persero) Tbk1Q 2017Results Presentation

April 25, 2017

Share Information

∆ from: IPO Dec 31, 2016

BMRI 1,662.05% 1.08%

JCI 961.22% 5.12%

-200%

0%

200%

400%

600%

800%

1000%

1200%

1400%

1600%

1800%

Sep

-03

Mar

-04

Sep

-04

Mar

-05

Sep

-05

Mar

-06

Sep

-06

Mar

-07

Sep

-07

Mar

-08

Sep

-08

Mar

-09

Sep

-09

Mar

-10

Sep

-10

Mar

-11

Sep

-11

Mar

-12

Sep

-12

Mar

-13

Sep

-13

Mar

-14

Sep

-14

Mar

-15

Sep

-15

Mar

-16

Sep

-16

Mar

-17

BMRI

JCI

No. of Investor % No. of shares %

I DOMESTIC

1. Government of RI 1 0.01% 14,000,000,000 60.00%

2. Retail 10,487 74.02% 187,122,880 0.80%

3. Employees 1,714 12.10% 10,437,918 0.04%

4. Cooperatives 4 0.03% 363,600 0.00%

5. Foundation 23 0.16% 15,184,145 0.07%

6. Pension Funds 120 0.85% 146,080,764 0.63%

7. Insurance 74 0.52% 524,892,085 2.25%

8. Banks 1 0.01% 150,000 0.00%

9. Corporations 68 0.48% 306,893,169 1.32%

10. Mutual Funds 244 1.72% 501,154,973 2.15%

Total 12,736 89.90% 15,692,279,534 67.25%

II INTERNATIONAL

1. Retail 96 0.68% 1,075,298 0.00%

2. Institutional 1,335 9.42% 7,639,978,501 32.74%

Total 1,431 10.10% 7,641,053,799 32.75%

No. DescriptionBy 31 March 2017

III TOTAL 14,167 100.00% 23,333,333,333 100.00%

2

Table of Contents

Results Overview Page #

Corporate Strategy 3 – 4

Indonesia’s Economic Condition 5

Key Indicators + Financial Highlights 6 – 7

SBU Performance Highlights 8

Bank’s Performance 9 – 11

Loan Performance 12 – 13

ROE, Forex Loan & NIM 14 – 16

Fee-Based & CIR 17 – 18

Wholesale Business 19 – 21

Retail Business 22 – 28

Non-Performing Loan & Restructured Loan 29 – 32

Subsidiaries 33 – 34

Corporate Guidance 35

Additional Information

Operating Performance Highlights

Supporting Materials

Corporate Plan – Realigning Our 2020 Initiatives

Accelerate in Growth Segments

Integrate The GroupDeepen Client Relationship

Indonesia’s Top Financial Institution:Grow above the market, portfolio quality focused, employer of choice in Indonesia

• Become the first choice in consumer

banking, especially in the middle-

income class

• Focus on micro fixed income earners

and asset-backed consumer lending

• Selectively grow SME segment and

productive micro by focusing on asset

quality

Drive subsidiaries’ performance by

increasing synergies within the

Mandiri Group.

Increase distribution network

productivity

Strengthen presence in ASEAN

countries

• Strengthen Bank Mandiri’s position as

the No. 1 Corporate Bank

• Grow in-line with the market in the

Commercial Banking segment

• Offering sector specific solution and

integrated product packages.

Current Achievements (1Q 2017)

Consumer Loans Rp87.3Tn (+18.8% YoY)

Micro Loans Rp52.2Tn (+18.0% YoY)

SME Loans Rp57.5Tn (+2.5% YoY)

Current Achievements (1Q 2017) Current Achievements (1Q 2017)

Corporate Loans Rp235.4Tn (+26.3% YoY)

Wholesale Fee Income Rp2.0Tn (28.1% of wholesale income)

Total income from subsidiaries Rp544Bn (13.3% of EAT)

Average CASA per branch grew by 7.9%

Obtained Singapore Capital Market License

3

2016-2020 Bank Mandiri Corporate Plan– How We Plan To Get There

Focus on Core Business▪ Grow corporate lending above the market growth rate and

deepen relationships with existing clients▪ Increase fee based income & wholesale current accounts

Expanding into Underpenerated Low-Risk Segments

▪ Accelerate consumer lending growth: mortgages, auto loan and salary based loans

▪ Push retail CASA growth through Bank@Work▪ Defend market share in SME

Strengthen The Foundation

▪ Lower cost to income ratio through digitalization and productivity enhancements

▪ Reduce NPL ratio by improving the loan underwriting process▪ Increase utilization and sophistication of data analytics to

enhance insights and cross-selling.

Strategic Initiatives Description

4

5

Inflation Starts to Pick Up

Source : CEIC, Bloomberg

Decreasing inflation gave room to monetary policy easing

Current account balance in 4Q16 was quite stable

4Q16 GDP Growth

3.61

4.75

2

3

4

5

6

7

8

9

10

Mar-1

0

Mar-1

1

Mar-1

2

Mar-1

3

Mar-1

4

Mar-1

5

Mar-1

6

Mar-1

7

Headline inflation (% YoY)

Core inflation (% YoY)

BI Rate

7 Days RR

(10)

(5)

-

5

10

15

(15)

(10)

(5)

-

5

10

15

20

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

4Q16

Capital and Financial AccountCurrent Account (CA)

BoP

4.5

5

5.5

6

6.5

7

4Q

09

2Q

10

4Q

10

2Q

11

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

2Q

16

4Q

16

5.57

3.30

4.94

6.50

6

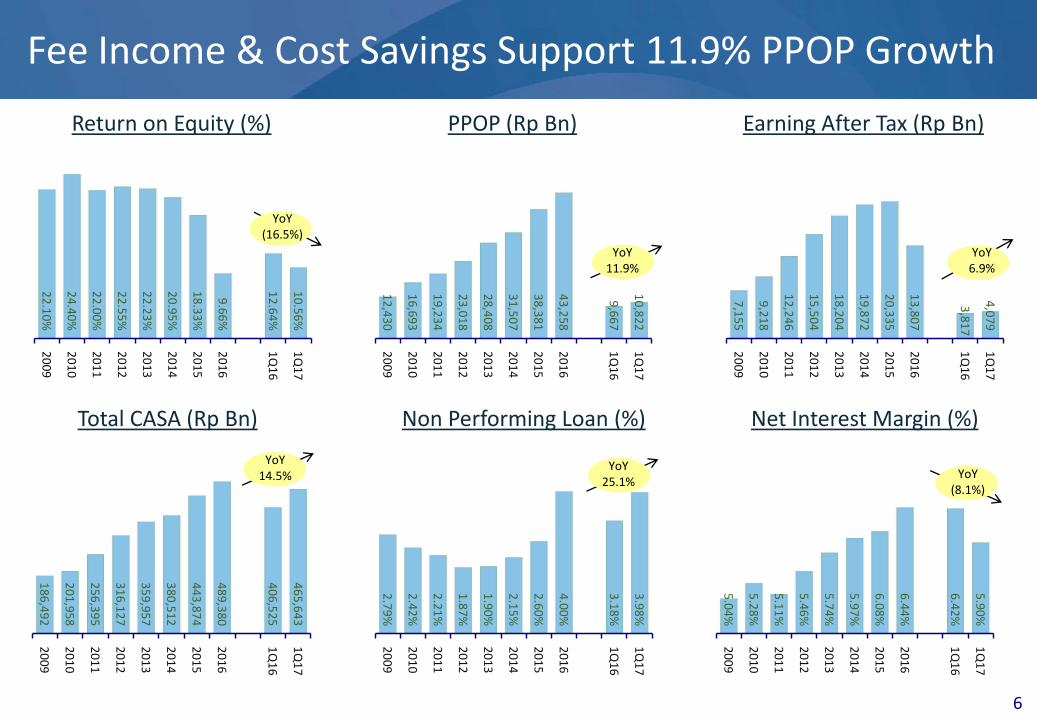

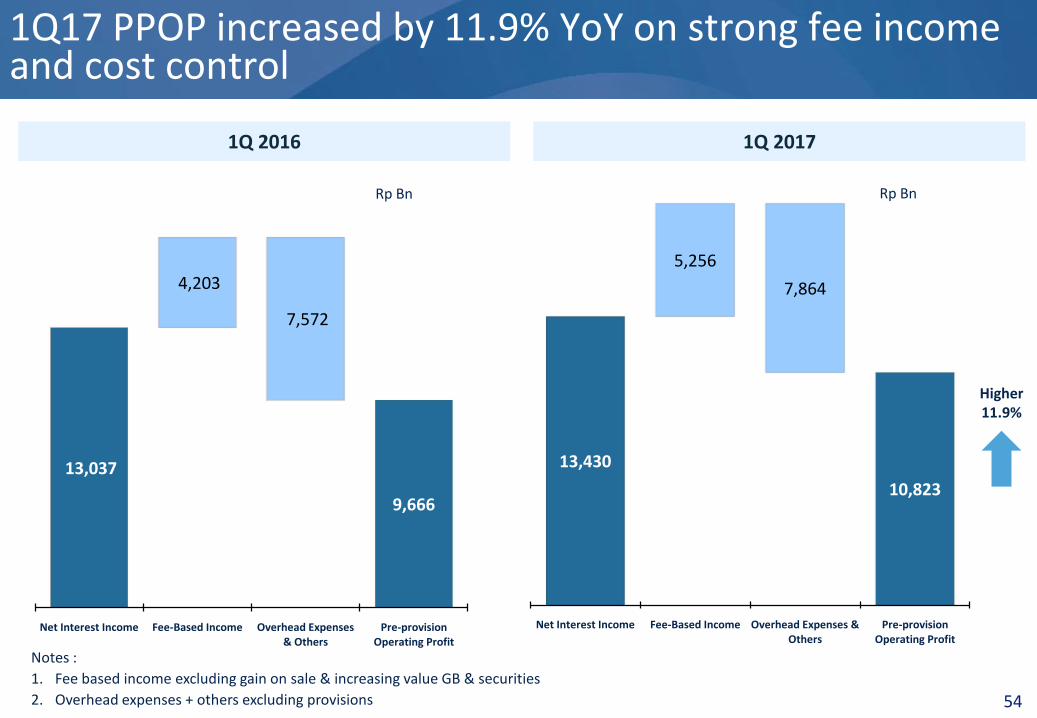

Fee Income & Cost Savings Support 11.9% PPOP Growth

22

.10

%

24

.40

%

22

.00

%

22

.55

%

22

.23

%

20

.95

%

18

.33

%

9.6

6%

12

.64

%

10

.56

%

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

1Q

16

1Q

17

Return on Equity (%)

Total CASA (Rp Bn) Non Performing Loan (%)

18

6,4

92

20

1,9

58

25

6,3

95

31

6,1

27

35

9,9

57

38

0,5

12

44

3,8

74

48

9,3

80

40

6,5

25

46

5,6

43

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

1Q

16

1Q

17

2.7

9%

2.4

2%

2.2

1%

1.8

7%

1.9

0%

2.1

5%

2.6

0%

4.0

0%

3.1

8%

3.9

8%

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

1Q

16

1Q

17

7,1

55

9,2

18

12

,24

6

15

,50

4

18

,20

4

19

,87

2

20

,33

5

13

,80

7

3,8

17

4,0

79

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

1Q

16

1Q

17

Earning After Tax (Rp Bn)

12

,43

0

16

,69

3

19

,23

4

23

,01

8

28

,40

8

31

,50

7

38

,38

1

43

,25

8

9,6

67

10

,82

2

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

1Q

16

1Q

17

PPOP (Rp Bn)

Net Interest Margin (%)

5.0

4%

5.2

8%

5.1

1%

5.4

6%

5.7

4%

5.9

7%

6.0

8%

6.4

4%

6.4

2%

5.9

0%

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

1Q

16

1Q

17

YoY11.9%

YoY 6.9%

YoY(16.5%)

YoY14.5%

YoY25.1%

YoY(8.1%)

1Q 2016 1Q 2017 %

Loans Rp 574.7Tn Rp 656.2Tn 14.18%

Gross NPL RatioNet NPL Ratio

3.18%1.16%

3.98%1.33%

25.12%14.46%

Low Cost Funds Ratio[Low Cost Funds (Rp)]

62.1%Rp 406.5 Tn

63.7%Rp 465.6Tn

2.63%14.54%

NIM 6.42% 5.90% (8.13)%

Efficiency Ratio 44.46% 42.68% 3.99%

PPOP Rp 9,667Bn Rp 10,822Bn 11.9%

Earnings After Tax Rp 3,817 Bn Rp 4,079Bn 6.86%

7

Key Financial Highlights

Bank Mandiri’s 1Q 2017 performance showing improvements:

8

Balanced Earnings from All Business Units

519

1,222

194

373

766

603

1,296

253

621

1,117

Micro & Business Banking

Consumer

Commercial

Corporate

Treasury & Markets

1Q '17 1Q '16

Net Interest Income Analysis 1Q 2017 (YTD)

(Rp Bn)

Fee Based Income 1Q 2017 (YTD)

(Rp Bn)

1,1

10

1,1

15

1,1

61 7

31

1Q'17 1Q'16

1,0

24

1,1

36

51

1

47

4

1Q'17 1Q'16

1,0

28

97

2

3,2

24

2,2

92

1Q'17 1Q'16

1,6

13

1,7

08

1,9

94

1,4

66

1Q'17 1Q'16

2,271

1,846

1,5361,610

4,253

3,264

3,607

3,174

Treasury & Markets

Corporate Banking

Commercial Banking

Consumer Banking

Micro & Business Banking

*) Excluding AXA Dividend Rp 612 Bn

*

1,0

94

87

8

18

4

89

1Q'17 1Q'16

1,279

967

Deposits by Product – Consolidated(Rp Tn)

Loans by SBU + Subsidiaries(Rp Tn)

97

.1

12

1.9

15

1.8

18

6.9

21

4.7

20

1.9

20

3.0

20

8.0

22

7.7

20

7.3

21

1.0

21

8.1

24

3.7

22

4.1

24

7.9

24

7.2

27

2.0

25

9.0

9.711.6

12.0

15.3

20.722.1 23.2 22.3

24.723.3 25.4 29.4

28.024.7

25.7 27.030.3

28.5

53

.9

46

.2

67

.3

77

.9

73

.4

67

.2

74

.2

79

.6

78

.9 83

.4

91

.7

90

.7

10

1.2 9

5.4

10

0.2

10

1.2

12

4.4

11

7.6

18.822.2

25.3

36.1

51.143.5 45.0

52.049.1

58.175.8 77.6

70.9

62.4

65.6 61.8

62.7

60.5

10

8.4

14

7.8

14

8.1

15

0.7

17

6.2

17

6.9

19

0.0

20

1.6

22

2.3

22

6.2

22

0.5

21

2.1

20

6.3 2

24

.4

22

7.8

22

9.6

24

2.1

23

8.5

15.1

12.5

17.8

16.1

20.120.0

20.5

27.5

33.7 30.530.5 26.6

26.224.2

24.2 23.6

31.1

26.9

020406080

100120140160180200220240260280300320340360380400420440460480500520540560580600620640660680700720740760780800

4Q

'09

4Q

'10

4Q

'11

4Q

'12

4Q

'13

1Q

'14

2Q

'14

3Q

'14

4Q

'14

1Q

'15

2Q

'15

3Q

'15

4Q

'15

1Q

'16

2Q

'16

3Q

'16

4Q

'16

1Q

'17

FX Time Rp Time

FX Demand Rp Demand

FX Savings Rp Savings

69

.8

93

.1

11

0.9

13

0.2

16

7.9

17

5.8

17

4.5

18

0.6

18

5.0

19

8.8

18

5.2

20

5.0

21

1.4

23

0.3

23

4.7

4.51.4

1.41.8

2.0 1.3 0.8 1.0 0.91.4

1.31.2 1.1

1.1 0.8

49

.1

63

.8

80

.7

10

2.7

11

6.9

14

2.8

14

5.1

14

8.9

14

9.4

16

0.6

15

3.7

15

8.5

16

2.6

16

5.2

15

2.7

23.6

30.7

39.0

47.7

56.6

64.7 65.767.7 69.5

72.373.4

76.178.9

84.8 87.2

17.1

22.7

30.2

38.4

46.5

56.0 55.3 57.9 57.9

60.5

56.1

60.059.8

60.857.5

5.4

7.3

11.8

19.0

27.0

34.6 37.239.7

40.0

42.5

44.2

46.0 46.7

50.652.2

18.8

27.2

40.5

48.9

55.5

54.7 54.357.0 57.9

59.4

60.9

63.9

64.869.3 71.2

020406080

100120140160180200220240260280300320340360380400420440460480500520540560580600620640660680700

4Q

'09

4Q

'10

4Q

'11

4Q

'12

4Q

'13

4Q

'14

1Q

'15

2Q

'15

3Q

'15

4Q

'15

1Q

'16

2Q

'16

3Q

'16

4Q

'16

1Q

'17

Subsidiaries Micro

Small Cons

Comm Int'l

Corp + SAM

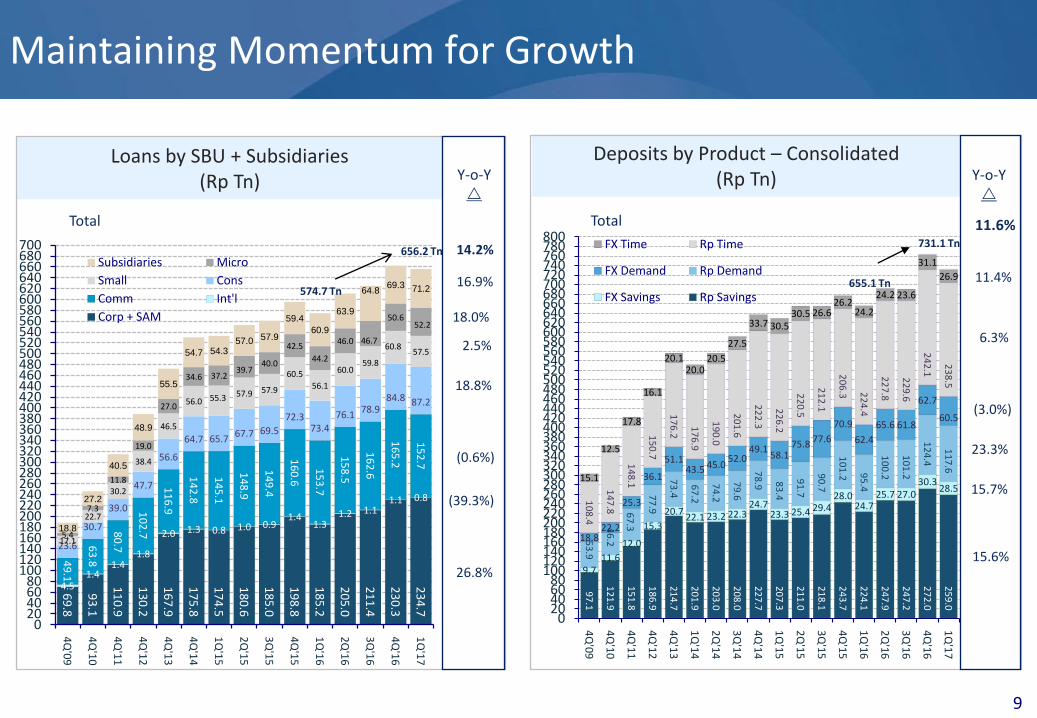

Maintaining Momentum for Growth

Y-o-Y

11.4%

6.3%

(3.0%)

23.3%

15.6%

Y-o-Y

2.5%

(0.6%)

26.8%

(39.3%)15.7%

14.2%656.2 Tn

Total Total

655.1 Tn

731.1 Tn

11.6%

16.9%

9

574.7 Tn

18.8%

18.0%

10

Strong and Liquid Balance Sheet

Assets 1Q 2017 1Q 2016 Liabilities 1Q 2017 1Q 2016

Cash 21,213 18,440 Current Account 178,124 157,769

Current Acc w/ BI & Other Banks 62,665 57,414 Savings 287,519 248,757

Placement w/ BI & Other Banks 73,767 58,048 Time Deposits 265,471 248,538

Advances (Other) 30,376 26,542

Marketable Securities 58,695 45,787 Total Deposits 731,115 655,063

Government Bonds 102,537 98,607

Loans (Gross) 656,211 574,704 Securities Issued 9,026 2,396

Provisions of Loans (34,755) (24,099) Deposits from other banks 33,893 26,332

Net Loans 621,457 550,605 Subordinated Debt 195 3,712

Reverse Repo 2,309 16,339 Borrowings 34,536 33,945

Other Provisions (1,723) (2,312) Other Int. Bearing Liabilities 15,783 14,102

Deferred Tax Assets 5,514 4,318 Non Int. Bearing Liabilities 57,935 53,142

Other Assets 57,499 32,952 Equity incl. Minority Interest 151,824 118,047

Total 1,034,307 906,739 Total 1,034,307 906,739

11

Revenue Growth Driven by Strong Fee Income

Summary P&L (Rp Bn) 1Q 2017 1Q 2016Y-o-Y (%)

4Q 2016Q-o-Q

(%)

Interest Income 19,443 18,308 6.2% 19,825 -1.9%

Interest Expense 6,627 5,976 10.9% 6,656 -0.4%

Net Interest Income 12,816 12,331 3.9% 13,168 -2.7%

Net Premium Income 614 706 -13.1% 357 72.0%

Net Interest Income & Premium Income 13,430 13,037 3.0% 13,525 -0.7%

Other Non Interest Income

* Other Fees and Commissions 2,996 2,531 18.4% 3,202 -6.4%

* Foreign Exchange Gains - Net 653 417 56.7% 631 3.6%

* Gain fr. sale & Incr. in Val & Sale of Bonds 262 203 29.0% 90 192.0%

* Others 1,345 1,052 27.9% 1,899 -29.2%

Total Non Interest Income 5,256 4,203 25.1% 5,822 -9.7%

Total Operating Income 18,686 17,240 8.4% 19,347 -3.4%

Provisions, Net (5,401) (4,596) 17.5% (8,734) -38.2%

Personnel Expenses (3,498) (3,406) 2.7% (3,435) 1.8%

G&A Expenses (3,401) (3,305) 2.9% (3,517) -3.3%

Loss from decr. in value of Sec & Gov Bonds - - -

Other Expenses (965) (862) 12.0% (1,011) -4.5%

Total Expense (7,864) (7,572) 3.9% (7,963) -1.2%

Profit from Operations 5,421 5,071 6.9% 2,651 104.5%

Non Operating Income (24) (5) 391.4% (17) 39.4%

Net Income Before Tax 5,397 5,066 6.5% 2,634 104.9%

Net Income After Tax 4,079 3,817 6.9% 1,793 127.4%

12

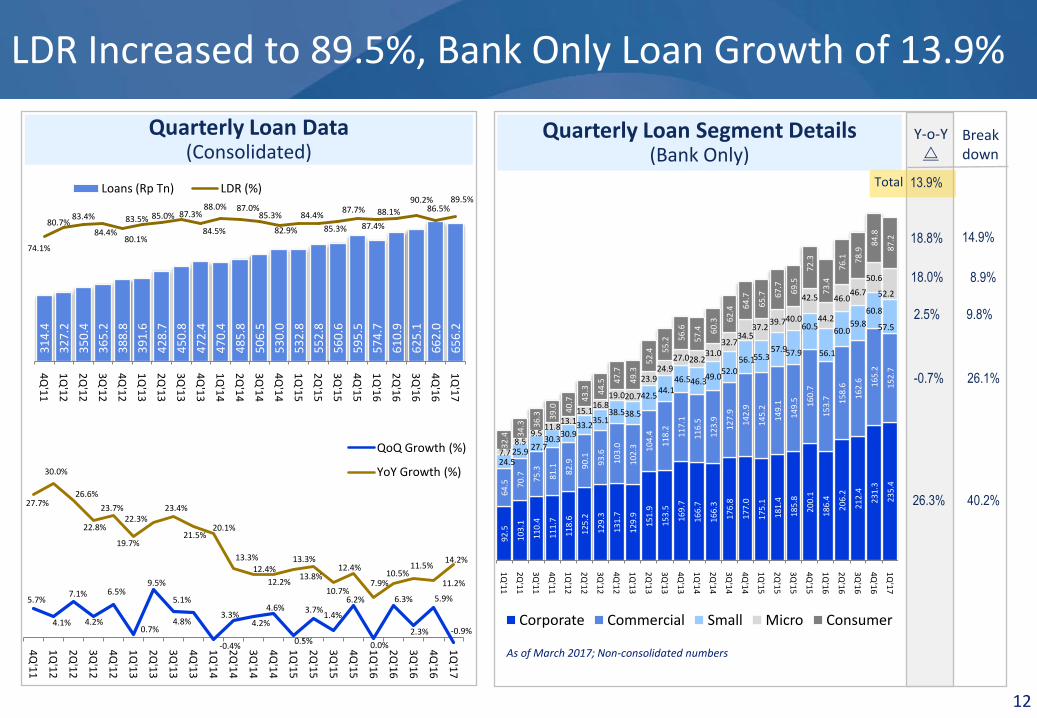

LDR Increased to 89.5%, Bank Only Loan Growth of 13.9%

92.

5

103.

1

110

.4

111

.7

118.

6

125.

2

12

9.3

13

1.7

129.

9

15

1.9

153.

5

16

9.7

16

6.7

166.

3

176.

8

177.

0

175

.1

18

1.4

185.

8

200

.1

186.

4

206.

2

212.

4

231.

3

23

5.4

64

.5 70.7 75

.3

81.1

82.9 90

.1

93.6

103

.0

102.

3 10

4.4

118.

2

117

.1

116

.5

123.

9

127

.9

14

2.9

14

5.2

149.

1

149.

5 16

0.7

153.

7 158.

6

162

.6 16

5.2

15

2.7

24.525.9

27.730.3

30.933.2

35.138.538.5

42.544.1

46.546.349.0

52.056.155.3

57.957.9

60.5

56.1

60.059.8

60.8

57.5

7.78.5

9.511.8

13.115.1

16.819.020.7

23.924.9

27.028.231.0

32.734.5

37.239.740.0

42.5

44.2

46.046.7

50.6

52.2

32.

4 34

.3 36.3 39.

0

40.7 4

3.3

44.

5 47.7

49.3

52.4 55

.2 56.

6

57

.4 60.

3 62.

4 64

.7

65.

7 67.

7

69

.5

72.

3

73

.4

76

.1 78.

9

84

.8

87.

2

1Q'1

1

2Q'1

1

3Q'1

1

4Q'1

1

1Q'1

2

2Q'1

2

3Q'1

2

4Q'1

2

1Q'1

3

2Q'1

3

3Q'1

3

4Q'1

3

1Q'1

4

2Q'1

4

3Q'1

4

4Q'1

4

1Q'1

5

2Q'1

5

3Q'1

5

4Q'1

5

1Q'1

6

2Q'1

6

3Q'1

6

4Q'16

1Q'17

Corporate Commercial Small Micro Consumer

Quarterly Loan Segment Details(Bank Only)

Y-o-Y

18.8%

18.0%

2.5%

-0.7%

26.3%

13.9%Total

14.9%

8.9%

9.8%

26.1%

40.2%

Breakdown

As of March 2017; Non-consolidated numbers

31

4.4

32

7.2

35

0.4

36

5.2

38

8.8

39

1.6

42

8.7

45

0.8

47

2.4

47

0.4

48

5.8

50

6.5

53

0.0

53

2.8

55

2.8

56

0.6

59

5.5

57

4.7

61

0.9

62

5.1

66

2.0

65

6.2

74.1%

80.7%83.4%

84.4%80.1%

83.5% 85.0% 87.3%

84.5%

88.0% 87.0%85.3%

82.9%

84.4%

85.3%

87.7%

87.4%

88.1%

90.2%86.5%

89.5%

4Q

'11

1Q

'12

2Q

'12

3Q

'12

4Q

'12

1Q

'13

2Q

'13

3Q

'13

4Q

'13

1Q

'14

2Q

'14

3Q

'14

4Q

'14

1Q

'15

2Q

'15

3Q

'15

4Q

'15

1Q

'16

2Q

'16

3Q

'16

4Q

'16

1Q

'17

Loans (Rp Tn) LDR (%)

5.7%

4.1%

7.1%

4.2%

6.5%

0.7%

9.5%

5.1%

4.8%

-0.4%

3.3%4.2%

4.6%

0.5%

3.7%1.4%

6.2%

0.0%

6.3%

2.3%

5.9%

-0.9%

27.7%

30.0%

26.6%

22.8%

23.7%

19.7%

22.3%23.4%

21.5%20.1%

13.3%

12.4%

12.2%

13.3%

13.8%

10.7%

12.4%

7.9%10.5%

11.5%

11.2%

14.2%

4Q

'11

1Q

'12

2Q

'12

3Q

'12

4Q

'12

1Q

'13

2Q

'13

3Q

'13

4Q

'13

1Q

'14

2Q

'14

3Q

'14

4Q

'14

1Q

'15

2Q

'15

3Q

'15

4Q

'15

1Q

'16

2Q

'16

3Q

'16

4Q

'16

1Q

'17

QoQ Growth (%)

YoY Growth (%)

Quarterly Loan Data(Consolidated)

13

Rp 164.12 Tn in Loans Disbursed in 1Q 2017

592.67

164.12123.87

32.90 10.870.87 3.22

585.05

4Q'16 Disburs. Install. Payment Pay-off FX Impact Write-Offs

1Q '17

Loan Movement– 1Q 2017 Bank-OnlyRp Tn

Loan Disbursement by Segment – 1Q 2017 Bank-OnlyRp Tn

129.67

13.21

6.119.12

6.02

164.12

Corporate Commercial Small Micro Consumer Total

14

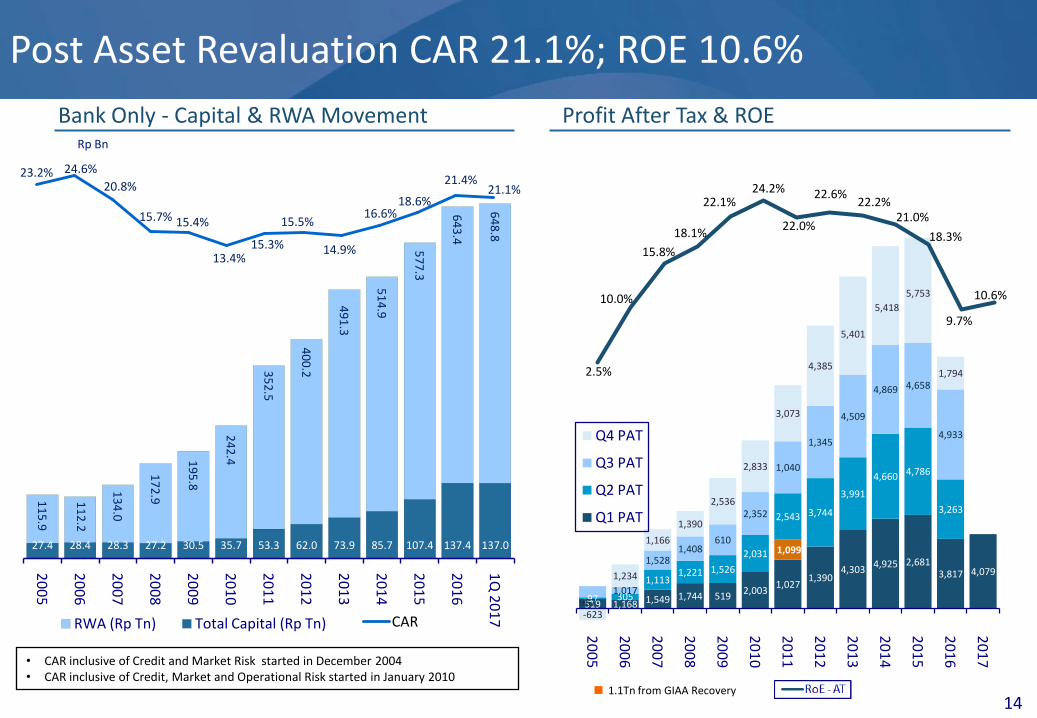

Post Asset Revaluation CAR 21.1%; ROE 10.6%

11

5.9

11

2.2

13

4.0

17

2.9

19

5.8

24

2.4

35

2.5

40

0.2

49

1.3

51

4.9

57

7.3

64

3.4

64

8.8

27.4 28.4 28.3 27.2 30.5 35.7 53.3 62.0 73.9 85.7 107.4 137.4 137.0

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

1Q

20

17

RWA (Rp Tn) Total Capital (Rp Tn)

Rp Bn

Bank Only - Capital & RWA Movement Profit After Tax & ROE

• CAR inclusive of Credit and Market Risk started in December 2004• CAR inclusive of Credit, Market and Operational Risk started in January 2010

1.1Tn from GIAA Recovery

23.2% 24.6%

20.8%

15.7% 15.4%

13.4%15.3%

15.5%

14.9%

16.6%18.6%

21.4%21.1%

CAR519 1,168 1,549 1,744 519

2,0031,027

1,390 4,303

4,925 2,681 3,817 4,079

1,099

97 305

1,1131,221 1,526

2,031

2,543 3,744

3,991

4,660 4,786

3,263

967 1,017

1,528 1,408

610

2,352

1,040

1,345

4,509

4,869 4,658

4,933

-623

1,234

1,166

1,390

2,536

2,833

3,073

4,385

5,401

5,418

5,753

1,794

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Q4 PAT

Q3 PAT

Q2 PAT

Q1 PAT

2.5%

10.0%

15.8%

18.1%

22.1%24.2%

22.0%

22.6%22.2%

21.0%

18.3%

9.7%

10.6%

38

.60

41

.87

44

.44

40

.35

41

.88

45

.47

45

.73

49

.62

48

.17

53

.29

59

.79

67

.75

62

.22

62

.95

72

.24

75

.38

73

.52

76

.90

78

.52

87

.79

83

.85

86

.55

77

.72

87

.85

89

.14

82.9%

91.5%

89.0%

75.8%

76.0%

76.2%75.4%

76.4%

68.0%

65.1% 64.3%

69.0%

72.0%

71.3%

74.2%73.2%

66.8%

61.1%61.0%

73.1%

80.3% 79.2%

72.6%

74.3%

80.8%

50%

55%

60%

65%

70%

75%

80%

85%

90%

95%

100%

Mar 1

1

Jun

e 11

Sep 1

1

Dec 1

1

Mar 1

2

Jun

12

Sep 1

2

Dec 1

2

Mar 1

3

Jun

13

Sep 1

3

Dec 1

3

Mar 1

4

Jun

e 14

Sep 1

4

Dec 1

4

Mar 1

5

Jun

15

Sep 1

5

Dec 1

5

Mar 1

6

Jun

16

Sep 1

6

Dec 1

6

Mar 1

7

20

30

40

50

60

70

80

90

100

Loan FX LDR FX

Prudent Management of FX Balance Sheet

USD Bn

Rp TnBreakdown of FX lending (Bank-Only)1Q ’17 (Total USD 6.69 Bn)

0.03

0.03

0.13

0.15

0.31

0.41

0.58

0.77

0.77

1.26

2.25

Oth

Constr

Utilities

Bus Serv

Trans

Agri

Trading

Mining

Soc Serv

Oil & Gas

Mfg

% (YoY)

23%

34%

1%

0%

-12%

-36%

-1%

-33%

307%

-56%

-71%

FX Loans & LDR (Bank-Only)

15

16

Q1 Consolidated NIM of 5.9%

5.3

3%

5.8

4%

5.4

4%

5.1

9%

5.5

4%

5.8

4%

5.6

7%

5.5

0%

5.3

4%

5.7

1%

6.0

8%

5.9

4%

5.9

0%

5.8

4%

5.9

2%

5.4

1%

5.7

9%

5.7

4%

6.7

4%

6.2

8%

6.0

0%

7.0

6%

6.0

3%

5.6

9%

4Q

'09

4Q

'10

4Q

'11

1Q

'12

2Q

'12

3Q

'12

4Q

'12

1Q

'13

2Q

'13

3Q

'13

4Q

'13

1Q

'14

2Q

'14

3Q

'14

4Q

'14

*

1Q

'15

2Q

'15

3Q

'15

4Q

'15

**

1Q

'16

2Q

'16

3Q

'16

**

4Q

'16

1Q

'17

NIM

9.49.6

8.78.2 8.1

8.4

8.2 8.1 7.8

8.39.0 9.1 9.2 9.6 9.6

9.1 9.2 9.2 9.8 9.3 9.110.0

9.0

8.6

4.33.8

3.4

3.22.8 2.7 2.7 2.8 2.6

2.8 3.1 3.3

3.53.9 3.8 3.9

3.6 3.73.3

3.2

3.3

3.1 3.0 2.9

Yield on Assets (%)Cost of Funds (%)

6.47.2

5.3

4.9 5.1

4.4

4.5 4.5

6.6

4.2 4.3 4.4

6.4

4.64.6

13.3

3.84.3

1.50.7

0.60.7 0.7 0.8 0.7 0.7 0.9 1.1 0.8 0.7 0.7 1.0 1.0 1.2 1.3 1.3

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

4Q

'09

4Q

'10

4Q

'11

4Q

'12

4Q

'13

1Q

'14

2Q

'14

3Q

'14

4Q

'14

1Q

'15

2Q

'15

3Q

'15

4Q

'15

1Q

'16

2Q

'16

3Q

'16

4Q

'16

1Q

'17

12.6 12.5 12.5

11.3 11.8 11.8

12.012.4 12.2

12.1

12.2 12.2

12.1 11.911.3

11.3 11.3 10.8

6.7 6.5

4.1 4.0

5.3 5.45.9 5.7 6.0

6.4 6.4 6.7 6.9 7.06.6 6.7 6.8

6.6

4.74.2 3.9

3.03.7 3.9

4.14.6 4.4 4.5

4.3 4.33.8 3.7 3.6

3.5 3.4 3.3

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Avg Loan Yield Avg Bond Yield Avg COF

* Starting on 4Q2014, we back out the LPS premium from the interest expense** 4Q 15 / 3Q16, If we adjust the interest income from RGM, NIM would be 6.5% / 6.0% , YoA would be 9.5% / 8.9%, Average FX Loan Yield 4.2% / 4.2%

17

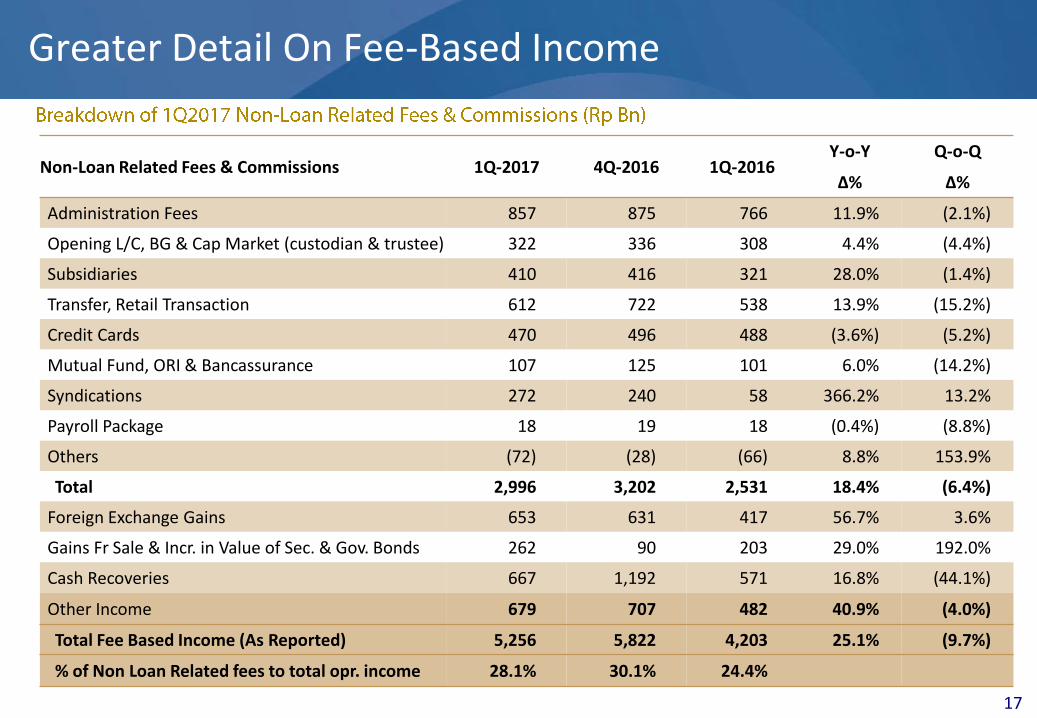

Greater Detail On Fee-Based Income

Non-Loan Related Fees & Commissions 1Q-2017 4Q-2016 1Q-2016Y-o-Y Q-o-Q

Δ% Δ%

Administration Fees 857 875 766 11.9% (2.1%)

Opening L/C, BG & Cap Market (custodian & trustee) 322 336 308 4.4% (4.4%)

Subsidiaries 410 416 321 28.0% (1.4%)

Transfer, Retail Transaction 612 722 538 13.9% (15.2%)

Credit Cards 470 496 488 (3.6%) (5.2%)

Mutual Fund, ORI & Bancassurance 107 125 101 6.0% (14.2%)

Syndications 272 240 58 366.2% 13.2%

Payroll Package 18 19 18 (0.4%) (8.8%)

Others (72) (28) (66) 8.8% 153.9%

Total 2,996 3,202 2,531 18.4% (6.4%)

Foreign Exchange Gains 653 631 417 56.7% 3.6%

Gains Fr Sale & Incr. in Value of Sec. & Gov. Bonds 262 90 203 29.0% 192.0%

Cash Recoveries 667 1,192 571 16.8% (44.1%)

Other Income 679 707 482 40.9% (4.0%)

Total Fee Based Income (As Reported) 5,256 5,822 4,203 25.1% (9.7%)

% of Non Loan Related fees to total opr. income 28.1% 30.1% 24.4%

18

1Q 17 Cost to Income Ratio of 42.7%

1,5

24

1,5

10

1,8

83

2,1

07

1,6

14

2,0

04

2,0

71

2,5

65

2,0

34

2,3

22

2,3

75

3,1

67

2,3

09

2,6

93

2,9

58

3,4

88

2,5

74

3,1

73

3,3

22

3,7

30

3,3

05

3,6

40

3,4

97

3,5

17

3,4

01

1,5

47

1,6

31

1,6

71

1,9

03

1,8

65

1,9

39

1,8

69

2,3

72

2,0

42

2,3

36

2,6

79

2,3

74

2,6

26

2,6

62

2,7

52

2,8

07

2,9

20

3,1

09

2,9

03

3,4

44

3,4

06

3,4

88

3,2

90

3,4

35

3,4

98

1Q

'11

2Q

'11

3Q

'11

4Q

'11

1Q

'12

2Q

'12

3Q

'12

4Q

'12

1Q

'13

2Q

'13

3Q

'13

4Q

'13

1Q

'14

2Q

'14

3Q

'14

4Q

'14

1Q

'15

2Q

'15

3Q

'15

4Q

'15

1Q

'16

2Q

'16

3Q

'16

4Q

'16

1Q

'17

G&A Expenses Personnel Expenses

Breakdown of 1Q 2017 Operating ExpensesQuarterly Consolidated Operating Expenses & CIR

(Rp Bn) (Rp Bn)

32.4%

37.3%

39.0%41.6%

44.0%43.2%

42.7%

51.3%

41.1%

43.1%

42.5%

48.4%

41.8%

43.2%46.6%

44.4%

44.4% 45.2%

40.1%

42.7%44.5%

46.0%

38.5%41.3%

42.7%

CIR (%)

Q1 2017 Q4 2016 Q1 2016Growth

QoQ YoY

Personnel Expenses

Base Salary 934 882 879 5.9% 6.3%

Other Allowances 1,618 1,542 1,635 4.9% (1.1%)

Post Empl. Benefits 83 54 96 55.7% (13.6%)

Training 60 177 81 (66.0%) (25.8%)

Subsidiaries 802 780 714 2.9% 12.3%

Total Personnel Expenses 3,498 3,435 3,406 1.8% 2.7%

G&A Expenses

IT & telecoms 585 573 540 2.1% 8.3%

Occupancy Related 663 839 595 (20.9%) 11.4%

Promo & Sponsor 235 386 293 (39.2%) (19.7%)

Transport & Travel 152 189 150 (19.7%) 1.2%

Goods, Prof. Svcs. & Oth. 453 668 437 (32.2%) 3.7%

Employee Related 605 622 579 (2.8%) 4.5%

Subsidiaries 709 240 711 195.6% (0.3%)

Total G&A Expenses 3,401 3,517 3,305 (3.3%) 2.9%

Other Expenses 965 1,011 862 (4.5%) 12.0%

Total Operating Expenses 7,864 7,963 7,572 (1.2%) 3.9%

19

Top 10 Industries in Corporate Lending Expansion1Q ’17 – 1Q’16 (Total Rp49.09 Tn)

Rp Bn2,365

2,859

3,161

3,461

4,611

4,806

5,004

6,630

8,450

12,659

Mfg-NonM

Mfg-Chem

Mining-Metal Ore

Bus Serv

Mining-Oil & Gas

Trad-Exp

Roads & Bridge

Trad-Ret

Mfg-F&B

Electricity

%

110%

44%

169%

94%

215%

43%

28%

52%

20%

89%Rp Bn

Top 10 Industries in Commercial Lending Contraction1Q ’17 – 1Q ’16 (Total –Rp1.02 Tn)

-324

-428

-509

-650

-690

-734

-941

-1,167

-1,294

-2,885

Mfg-Wood

SocServ-Health

Mfg-Text

Mining-Oil & Gas

Trad-Exp

Mining-Coal

Plantations

Trad-Distr

Mfg-P&P

4 Wheels-Vehicles

%

-62%

-26%

-6%

-6%

-16%

-27%

-17%

-7%

-39%

-16%

Diversifying our Strength in Wholesale Lending…

20

Wholesale Transactions Driving CASA

74

52

,41

44

,06

66

,15

37

,78

41

0,9

43

11

,89

91

2,9

32

13

,62

91

3,8

73

14

,10

51

4,3

97

14

,67

61

5,1

01

15

,56

51

6,2

00

16

,85

31

7,5

92

18

,53

1

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

Cash Management Users

24

86

77

1,1

78

2,2

01

2,6

57

3,5

98

3,9

89

4,4

84

4,8

32

5,1

23

5,2

66

5,3

84

5,7

04

7,0

85

7,3

92

7,5

63

8,4

39

4Q

10

4Q

11

4Q

12

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

Average # of Cash Management Tx(000), total 25.3 Mn transactions in

1Q 2017*

*) Excluding Mandiri Transaction System

Wholesale CASA Deposits(Rp Bn)

58

,05

5

62

,25

7

61

,69

1

53

,60

4

74

,11

6

89

,95

9

74

,33

4

73

,19

2

14

0,2

78

14

9,3

51

12

6,4

30

14

2,4

87

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

1Q

16

1Q

17

12.7% YoY Growth

21

Strong Pickup in Forex, As Trade Transactions Remain Slow

Forex

34

42

63

61

56

41

46

11 14

281,153

310,512322,795

399,500 379,730

348,436

433,929

106,291114,186

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

Dec 10 Dec 11 Dec 12 Dec 13 Dec 14 Dec 15 Dec 16 Mar 16 Mar 17

Value (USD Bn) # of Trx

Wholesale Remittance

70

94

12

1

13

5

14

6

12

6

90

22 28

435,866 448,219

599,909 651,241

739,046 730,011

399,585

125,510 137,920

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

Dec 10 Dec 11 Dec 12 Dec 13 Dec 14 Dec 15 Dec 16 Mar 16 Mar 17

Value (USD Mn) # of Trx

*) Excluding Mandiri Transaction System

Mandiri Cash Management*

54

9

81

8

1,5

19

2,2

31

3,1

20

3,7

78

4,5

49

91

4

1,3

04

2,503 7,668

13,676 24,543

44,184

61,599

82,075

17,869

25,316

(25,000)

(5,000)

15,000

35,000

55,000

75,000

95,000

-

500.0

1,000.0

1,500.0

2,000.0

2,500.0

3,000.0

3,500.0

4,000.0

4,500.0

5,000.0

Dec 10 Dec 11 Dec 12 Dec 13 Dec 14 Dec 15 Dec 16 Mar 16 Mar 17

Value (Rp Tn) # of Trx (000)

Trade Transactions : Export, Import, Domestic

85

11

0

12

5

13

3

13

7

12

7

10

7

23

31

495,813 510,916 517,251 520,948

509,207 468,870

406,669

101,017 105,974

-

100,000

200,000

300,000

400,000

500,000

600,000

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

Dec 10 Dec 11 Dec 12 Dec 13 Dec 14 Dec 15 Dec 16 Mar 16 Mar 17

Value (USD Bn) # of Trx

22

Retail Deposits Increased by 13.4% Year on Year

13

2.7

14

0.6

14

6.1

16

5.0

15

7.5

16

6.8

17

6.3

19

0.9

17

9.0

18

0.8

18

4.7

20

2.6

18

2.5

18

6.0

18

8.0

20

9.8

19

3.0

21

4.8

21

2.1

23

3.5

22

0.5

12.712.813.0

13.714.715.6

18.420.7

21.022.021.8

24.0

22.223.224.3

23.121.1

21.723.1

26.024.5

14.615.416.1

18.617.0

16.7

28.6

33.029.733.634.4

40.2

33.536.425.0

31.9

29.0

29.930.5

36.532.9

4.3 4.3

10.711.4

12.111.913.1

13.0

12.814.4

7.8

7.6

6.9

6.5 6.8

9.0

9.3

71.670.3

71.5

71.472.1

70.7

80.2

84.588.4

100.1108.3

120.0

119.2116.0

110.0

110.3

112.2

115.5116.9

120.0

119.5

5.05.0 5.1

5.04.7

4.6

6.4

7.06.3

7.07.2

9.5

9.0 7.8

7.7

7.4

6.9

6.8 7.0

10.711.7

0

20

40

60

80

100

120

140

160

180

200

220

240

260

280

300

320

340

360

380

400

420

440

460

480

1Q

'12

2Q

'12

3Q

'12

4Q

'12

1Q

'13

2Q

'13

3Q

'13

4Q

'13

1Q

'14

2Q

'14

3Q

'14

4Q

'14

1Q

'15

2Q

'15

3Q

'15

4Q

'15

1Q

'16

2Q

'16

3Q

'16

4Q

'16

1Q

'17

Rp Savings Deposits FX Savings Deposits Rp Demand Deposits

FX Demand Deposits Rp Time Deposits FX Time Deposits

Retail Deposit Analysis – Bank Only

2.2%1.7%

2.0% 2.0% 2.0% 2.0% 2.1% 1.9% 2.1% 2.1% 2.1% 2.0% 1.8% 1.9% 2.1%2.3%

2.1%1.5% 1.5% 1.6% 1.5% 1.5% 1.4% 1.3% 1.2% 1.2% 1.2% 1.3% 1.1% 1.1% 1.1% 1.1%

6.3%

5.1%

6.6%7.0%

7.3%

8.3%7.9% 7.8%

7.4% 7.5% 7.2%6.9% 6.7% 6.6% 6.4% 6.2%

0%

5%

10%

4Q

'11

4Q

'12

4Q

'13

1Q

'14

2Q

'14

3Q

'14

4Q

'14

1Q

'15

2Q

'15

3Q

'15

4Q

'15

1Q

'16

2Q

'16

3Q

'16

4Q

'16

1Q

'17

Rp DD

Rp Savings

Rp TD

Average Quarterly Deposit Costs (%)

0.1% 0.2% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3%0.4%

0.2%

0.3%

0.6%0.7% 0.8%

0.7%0.8%

0.6%0.8%

1.2% 1.2% 1.1%1.3%

1.8%

1.2%

0.8%

0.6% 0.5%

0.5% 0.6% 0.6%0.7%

0.0%

0.5%

1.0%

1.5%

2.0%

4Q

'11

4Q

'12

4Q

'13

1Q

'14

2Q

'14

3Q

'14

4Q

'14

1Q

'15

2Q

'15

3Q

'15

4Q

'15

1Q

'16

2Q

'16

3Q

'16

4Q

'16

1Q

'17

FX DD FX TD

66.5%69.6%

70.1%

72.5%

71.6%

73.0% 73.7% 71.9%69.9%

68.8%

68.4%66.2%

67.7% 67.6%

69.8%

67.7%

69.1%

68.8%

70.0%

68.6%

CASA as % of total deposits

44,21052,195

7,985

1Q2016 Growth 1Q2017

23

63

,32

3

66

,85

1

73

,32

4

81

,04

6

84

,67

5

91

,50

4

96

,26

8

10

5,1

92

10

8,4

34

11

8,7

88

12

3,8

33

13

0,1

58

13

1,8

57

14

0,1

89

14

6,7

44

15

5,3

38

15

8,1

73

16

5,3

04

16

7,4

29

17

5,2

11

17

3,7

39

18

2,1

90

18

5,3

35

19

6,1

94

19

6,9

09

28.6%

27.6%28.3%

29.6%

29.8%

30.2%30.9%

31.8% 31.7%

31.3% 31.2%

31.8%

32.6% 32.7%33.1% 33.3%

32.7%

33.8%33.1% 33.1%

33.7%

20%

22%

24%

26%

28%

30%

32%

34%

30,00040,00050,00060,00070,00080,00090,000

100,000110,000120,000130,000140,000150,000160,000170,000180,000190,000200,000210,000220,000230,000

1Q

20

11

2Q

20

11

3Q

20

11

4Q

20

11

1Q

20

12

2Q

20

12

3Q

20

12

4Q

20

12

1Q

20

13

2Q

20

13

3Q

20

13

4Q

20

13

1Q

20

14

2Q

20

14

3Q

20

14

4Q

20

14

1Q

20

15

2Q

20

15

3Q

20

15

4Q

20

15

1Q

20

16

2Q

20

16

3Q

20

16

4Q

20

16

1Q

20

17

Retail to Total Loans

Consumer and Micro Are Key Retail Growth Drivers

Retail to Total Loans

Micro Credit Business Banking Consumer

(Rp Bn)

Business Banking

56,108 57,508

1,401

1Q2016 Growth 1Q2017

YoY2.5%

(Rp Bn)

Micro Credit

YoY18.1%

(Rp Bn)

73,41387,206

13,794

1Q2016 Growth 1Q2017

YoY18.8%

Consumer

Strong Microfinance Growth

24

20

0

30

0

50

2

68

7

89

8

99

4

1,0

84

1,0

85

60

0

80

0

80

0

87

8

92

8

1,0

27

1,1

27

1,4

27

1,7

18

1,7

17

10

15

2

48

0

71

0

76

0

75

1

70

6

65

3

61

2

61

1 6

10 10

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

1Q

17

Branch Unit Kiosk Cash Outlet

Customers (000)Network # Of New Customers

73

,56

6

79

,50

0

76

,32

5

94

,85

5

74

,03

7

11

0,0

00

1

21

,00

7

14

6,3

59

1

26

,50

9

14

0,0

64

1

31

,71

5

14

7,8

25

1

38

,74

7

16

0,6

20

1

36

,19

6

16

2,1

81

1

40

,88

6

16

7,1

45

1

58

,90

9

16

2,7

38

1

34

,50

1

13

8,5

00

9

7,1

64

1

27

,82

8

13

0,2

27

1

46

,32

3

11

7,5

65

1

17

,97

1

11

6,4

40

1Q

'10

2Q

'10

3Q

'10

4Q

'10

1Q

'11

2Q

'11

3Q

'11

4Q

'11

1Q

'12

2Q

'12

3Q

'12

4Q

'12

1Q

'13

2Q

'13

3Q

'13

4Q

'13

1Q

'14

2Q

'14

3Q

'14

4Q

'14

1Q

'15

2Q

'15

3Q

'15

4Q

'15

1Q

'16

2Q

'16

3Q

'16

4Q

1'6

1Q

1'7

271

430

562

694

815

889

1,009

1,112

1,2081,195

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

1Q

17

25

…as well as Consumer Lending, which Rose 18.8% Y-o-Y as Mortgages Grew 12.3%

14

,26

8

15

,52

3

16

,46

6

17

,77

9

18

,76

4

20

,11

3

20

,91

9

22

,81

8

24

,09

2

26

,13

5

27

,35

7

26

,99

5

26

,69

0

26

,50

5

26

,34

7

26

,49

5

26

,20

7

26

,34

0

26

,36

9

26

,83

2

26

,86

9

27

,65

1

28

,00

1

29

,99

4

30

,17

2

3,9

64

3,9

79

3,9

49

3,8

87

3,7

77

3,6

79

3,5

71

3,4

71

3,3

65

3,3

12

3,2

40

3,1

81

3,1

72

3,1

98

3,2

40

3,3

10

3,3

26

3,4

32

3,5

34

3,7

39

3,8

92

4,3

13

4,9

14

5,8

81

6,2

46

6,3

98

6,7

08

6,8

61

6,9

95

7,1

43

7,4

12

7,7

53

8,2

06

8,3

86

8,9

58

9,3

74

9,7

81

10

,03

0

10

,64

2

11

,25

3

11

,88

0

12

,20

1

12

,83

8

13

,40

8

14

,10

3

14

,49

7

15

,27

9

16

,16

0

17

,44

1

17

,98

6

3,5

75

3,7

61

3,9

10

4,2

96

4,2

45

4,4

92

4,5

90

5,0

35

5,0

25

5,1

95

5,3

03

5,6

20

5,5

57

6,8

55

7,5

68

8,2

88

8,3

43

8,7

51

8,6

83

8,9

70

8,7

68

8,7

61

8,6

74

9,1

28

9,0

48

3,4

54

3,4

92

4,2

00

5,1

15

5,8

29

6,5

93

6,6

09

7,2

09

7,4

86

7,9

05

9,0

13

10

,21

8

11

,08

3

12

,26

0

13

,27

1

13

,98

3

14

,89

0

15

,63

0

16

,64

1

17

,60

8

18

,34

4

18

,98

1

20

,00

1

21

,12

4

22

,55

5

698 791

873 928

964 1,016

1,037

1,010 966 927

904 809 840

805 765

750 683 733

892 998 1,043

1,091 1,133

1,194 1,199

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

65,000

70,000

75,000

80,000

85,000

90,000

95,000

100,000

1Q

'11

2Q

'11

3Q

'11

4Q

'11

1Q

'12

2Q

'12

3Q

'12

4Q

'12

1Q

'13

2Q

'13

3Q

'13

4Q

'13

1Q

'14

2Q

'14

3Q

'14

4Q

'14

1Q

'15

2Q

'15

3Q

'15

4Q

'15

1Q

'16

2Q

'16

3Q

'16

4Q

'16

1Q

'17

Other

Auto

Credit Cards

Payroll Loans

Home Equity Loans

Mortgages

Loan TypeGrowth (%)

Y-o-Y Q-o-Q

Other 14.97% 0.47%

Auto Loans 22.96% 6.77%

Credit Cards 3.20% -0.88%

Payroll Loans 24.07% 3.12%

Home Equity Loans 60.49% 6.21%

Mortgages 12.29% 0.59%

Total Consumer 18.79% 2.88%

Quarterly Consumer Lending Balances by Type Consumer Lending Growth by Type

Rp 87.2 Tn

*Auto & Motorcycle Loans channeled or executed through finance companies = Rp 10.1 Tn in our Commercial Portfolio

26

Transaction Capabilities Growth Driven By Mobile Banking Transaction Volume

Quarterly Transaction Value (Rp Tn) Quarterly Users (Mn)

95.5

122.2

147.7 153.8

170.0

179.3

191.2 192.6

208.1 210.0

241.5

245.0

236.8

252.7

238.0

248.3

271.2

2.1 3.5 4.1 5.0 6.6 8.3 10.5

17.6 28.3 35.7

38.9 53.0 55.3

68.9

67.8

84.0 85.2

7.1 14.0

18.1 23.5 26.8

29.4 33.3 33.3

34.5 46.7

32.6

36.1

36.5

35.5

40.0 37.3

0

20

40

60

80

100

120

140

160

180

200

220

240

260

280

4Q

'09

4Q

'10

1Q

'11

2Q

'11

3Q

'11

4Q

'11

1Q

'12

2Q

'12

3Q

'12

4Q

'12

1Q

'13

2Q

'13

3Q

'13

4Q

'13

1Q

'14

2Q

'14

3Q

'14

4Q

'14

1Q

'15

2Q

'15

3Q

'15

4Q

'15

1Q

'16

2Q

'16

3Q

'16

4Q

'16

1Q

'17

ATM

Mobile Banking

Internet Banking

7.7

8.6 8.2

9.2

10.0

10.6

11.1 11.6

11.8 12.4

12.6

12.6

13.6 13.8

14.1 14.4

3.2

4.7 4.9 5.3

5.6 5.8

6.1 6.3

6.5 6.7 6.8 6.9 7.0 7.1 7.3 7.4

1.2 1.0 1.1 1.2 1.3 1.4 1.5 1.6 1.7

1.8 1.9 2.0 2.1

2.1 2.2

0

2

4

6

8

10

12

14

4Q

'09

4Q

'10

1Q

'11

2Q

'11

3Q

'11

4Q

'11

1Q

'12

2Q

'12

3Q

'12

4Q

'12

1Q

'13

2Q

'13

3Q

'13

4Q

'13

1Q

'14

2Q

'14

3Q

'14

4Q

'14

1Q

'15

2Q

'15

3Q

'15

4Q

'15

1Q

'16

2Q

'16

3Q

'16

4Q

'16

1Q

'17

Debit Cards

Mobile Banking

Internet Banking

Quarterly Transaction Volume (Mn)

142

157

184

189

212 218

233 235

246 249

268

293 295

287

309

291

306 313

39

36 44

41 43 41 39 44

51

53

47 48

50

46

49

45

48

46

12 18

23 26 32 31 34

57

70

113

172

196

190

254 258

295

311

17

42

55

78 85

67 76

81 89

117

102

117

131

138 149

156

154

0

25

50

75

100

125

150

175

200

225

250

275

300

325

4Q

'09

4Q

'10

1Q

'11

2Q

'11

3Q

'11

4Q

'11

1Q

'12

2Q

'12

3Q

'12

4Q

'12

1Q

'13

2Q

'13

3Q

'13

4Q

'13

1Q

'14

2Q

'14

3

Q '1

44

Q '1

41

Q '1

52

Q '1

53

Q '1

54

Q '1

51

Q '1

62

Q '1

63

Q '1

64

Q '1

61

Q '1

7

ATM

Branch

Mobile Banking

Internet Banking

27

Retail Payment System Gaining Traction

Fee Income from e-channel Tx (Rp Bn)

200.3 258.2 315.2 347.6 414.7 604.3 711.7 758.2

196.5 285.7

318.6 382.0

490.3

663.4

765.2

249.3

313.9361.8

437.5

489.2

683.3

742.7

268.5

312.8

464.4

512.9

664.8

771.0

862.6

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Q4 Q3 Q2 Q1

6.5% YoY

Growth

Numbers of EDC

23,690 27,611

33,732

47,127

92,903

180,532

230,352

270,352

286,861

236,711

239,312

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

1Q

17

Volume Mandiri BusinessSaving Account (Rp Tn)

17.7

34.7

59.4

85.8

102.3

108.5

120.6

93.1

110.8

20

10

20

11

20

12

20

13

20

14

20

15

20

16

1Q

'16

1Q

'17

19.0%YoY

Growth

18

,52

8

25

,85

7

32

,27

3

42

,58

2

47

,30

4

53

,12

4

57

,44

7

73

,66

6

79

,97

0

88

,01

3

79

,17

3

89

,38

9

89

,90

6

11

8,3

89

10

5,7

81

12

6,8

57

12

6,5

45

11,535

13,542 15,312 15,971

17,802

18,216 22,570

24,676 26,441

28,122 27,591

29,040 29,967

40,285

34,251 37,059

39,025

1Q '13

2Q '13

3Q '13

4Q '13

1Q '14

2Q '14

3Q '14

4Q '14

1Q '15

2Q '15

3Q '15

4Q '15

1Q '16

2Q '16

3Q '16

4Q '16

1Q '17

Transaction Value (Rp Bn) # of Active Users

28

Making Inroads into SME and Retail Payments

Fiesta Point Program

A program to get points based on savings average balance and # of transactions through e-channel or branch, so that customer has the opportunity to earn immediate prizes.

Mandiri Belanja Untung Program

Prizes for buyers who do the transactions in the merchant (as a participants), or using Mandiri EDC. For sellers, they have the opportunity to be included into the national lucky draw.

Belanja Hoki/ Dagang Hoki Program

Co-promotion with the ITC Group for the merchants and the buyers who transact in ITC using Mandiri Debit and also a reward program for the building management.

# MTB Transaction & Volume

20

1,1

06

21

2,8

44

26

1,9

35

26

5,4

23

27

2,2

12

29

0,0

19

30

6,8

31

34

9,8

68

29

9,4

17

32

2,5

87

30

8,8

32

34

8,0

59

26

7,1

95

33

4,9

12

32

2,3

77

38

2,1

04

34

0,2

88

9,235

10,601

11,385

12,616

12,773

14,068

14,508

16,052

15,996 17,444

17,101

18,373 20,186 20,187

18,974

20,357 20,329

-

3,000

6,000

9,000

12,000

15,000

18,000

21,000

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

1Q

'13

2Q

'13

3Q

'13

4Q

'13

1Q

'14

2Q

'14

3Q

'14

4Q

'14

1Q

'15

2Q

'15

3Q

'15

4Q

'15

1Q

'16

2Q

'16

3Q

'16

4Q

'16

1Q

'17

# of Volume # of Transactions (000)

# MIB Transaction Value & Users

# SME Business w/ Mandiri Acc

543,972

643,334

789,300 845,073 851,069 853,539

2012 2013 2014 2015 2016 1Q17

29

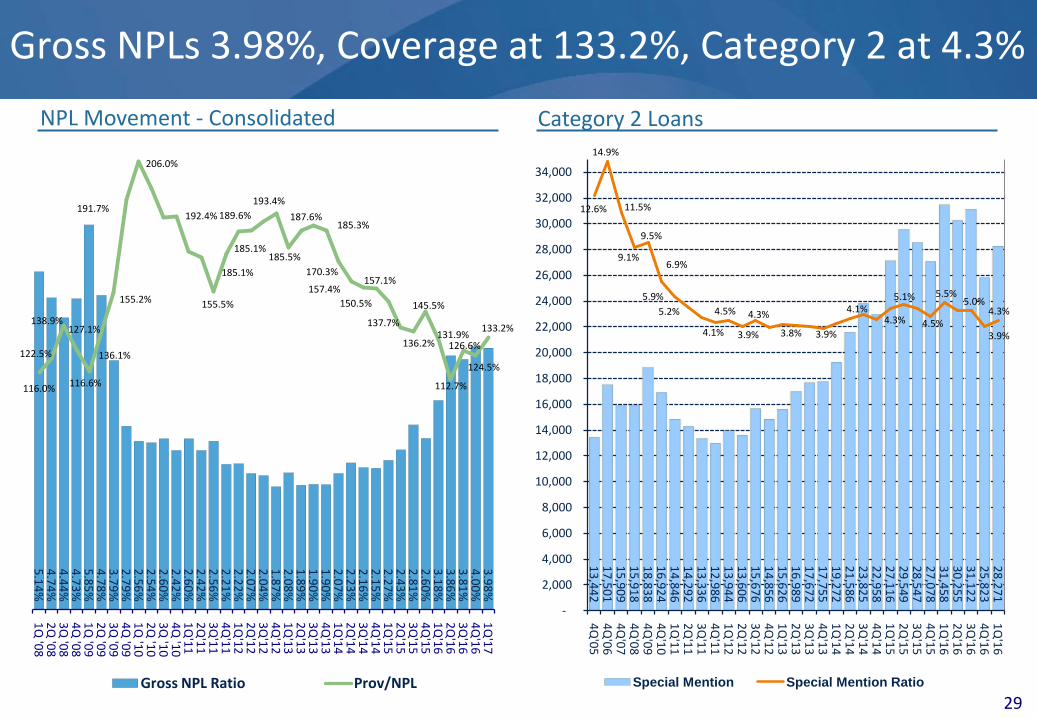

Gross NPLs 3.98%, Coverage at 133.2%, Category 2 at 4.3%

13

,44

2

17

,50

1

15

,90

9

15

,91

8

18

,83

8

16

,92

4

14

,84

6

14

,29

2

13

,33

6

12

,98

6

13

,94

4

13

,60

6

15

,67

6

14

,85

6

15

,62

6

16

,98

9

17

,67

2

17

,75

5

19

,27

2

21

,58

6

23

,82

5

22

,95

8

27

,11

6

29

,54

9

28

,54

7

27

,07

8

31

,45

8

30

,25

5

31

,12

2

25

,82

3

28

,27

1

12.6%

14.9%

11.5%

9.1%

9.5%

6.9%

5.9%

5.2% 4.5%

4.1%

4.3%

3.9% 3.8% 3.9%

4.1%4.3%

5.1%

4.5%

5.5%5.0%

3.9%

4.3%

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

22,000

24,000

26,000

28,000

30,000

32,000

34,000

4Q

'05

4Q

'06

4Q

'07

4Q

'08

4Q

'09

4Q

'10

1Q

'11

2Q

'11

3Q

'11

4Q

'11

1Q

'12

2Q

'12

3Q

'12

4Q

'12

1Q

'13

2Q

'13

3Q

'13

4Q

'13

1Q

'14

2Q

'14

3Q

'14

4Q

'14

1Q

'15

2Q

'15

3Q

'15

4Q

'15

1Q

'16

2Q

'16

3Q

'16

4Q

'16

1Q

'16

Special Mention Special Mention Ratio

NPL Movement - Consolidated

5.1

4%

4.7

4%

4.4

4%

4.7

3%

5.8

5%

4.7

8%

3.7

9%

2.7

9%

2.5

6%

2.5

4%

2.6

0%

2.4

2%

2.6

0%

2.4

2%

2.5

6%

2.2

1%

2.2

2%

2.0

7%

2.0

4%

1.8

7%

2.0

8%

1.8

9%

1.9

0%

1.9

0%

2.0

7%

2.2

3%

2.1

6%

2.1

5%

2.2

7%

2.4

3%

2.8

1%

2.6

0%

3.1

8%

3.8

6%

3.8

1%

4.0

0%

3.9

8%

116.0%

122.5%

138.9%127.1%

116.6%

136.1%

155.2%

206.0%

191.7%192.4%

155.5%

185.1%

185.1%

189.6%

193.4%

185.5%

187.6%185.3%

170.3%

157.4%157.1%

150.5%

137.7%

136.2%

145.5%

131.9%

112.7%

126.6%

124.5%

133.2%

1Q

'08

2Q

'08

3Q

'08

4Q

'08

1Q

'09

2Q

'09

3Q

'09

4Q

'09

1Q

'10

2Q

'10

3Q

'10

4Q

'10

1Q

'11

2Q

'11

3Q

'11

4Q

'11

1Q

'12

2Q

'12

3Q

'12

4Q

'12

1Q

'13

2Q

'13

3Q

'13

4Q

'13

1Q

'14

2Q

'14

3Q

'14

4Q

'14

1Q

'15

2Q

'15

3Q

'15

4Q

'15

1Q

'16

2Q

'16

3Q

'16

4Q

'16

1Q

'17

Gross NPL Ratio Prov/NPL

Category 2 Loans

30

Non-Performing Loans by Segment

Movement by Customer Segment (Rp Bn)Non-Performing Loan Movements (Rp Tn) – Bank-Only

* Excluding loans to other banks

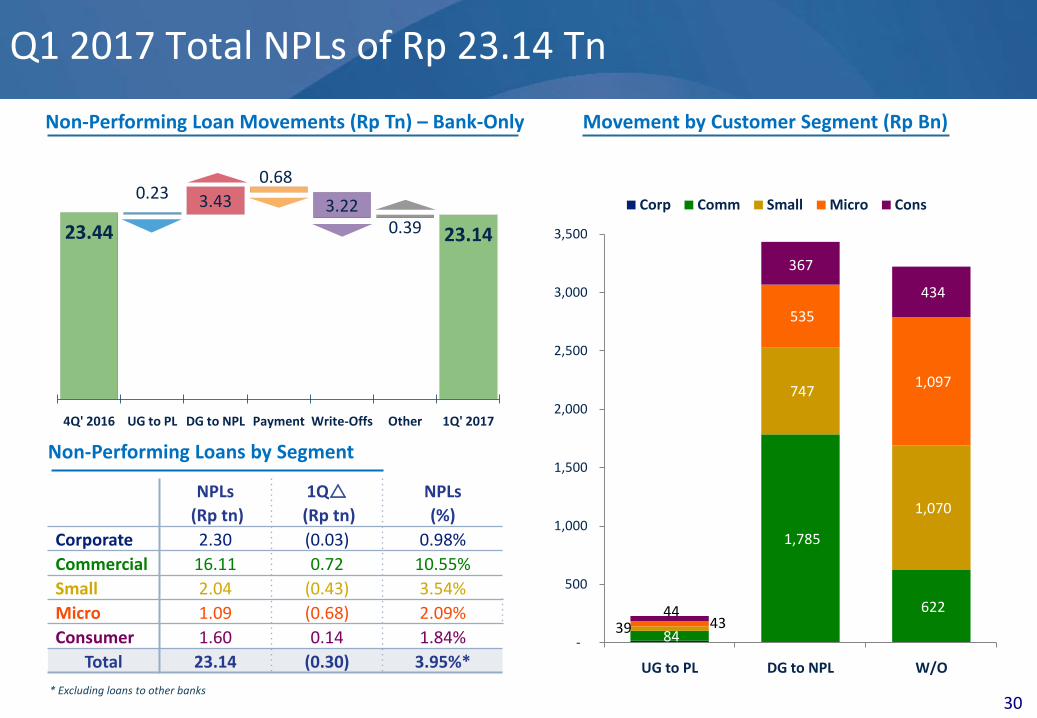

Q1 2017 Total NPLs of Rp 23.14 Tn

23.44

0.23 3.43

0.68

3.220.39 23.14

4Q' 2016 UG to PL DG to NPL Payment Write-Offs Other 1Q' 2017

84

1,785

622

39

747

1,070

43

535

1,097

44

367

434

-

500

1,000

1,500

2,000

2,500

3,000

3,500

UG to PL DG to NPL W/O

Corp Comm Small Micro Cons

NPLs 1Q NPLs

(Rp tn) (Rp tn) (%)

Corporate 2.30 (0.03) 0.98%

Commercial 16.11 0.72 10.55%

Small 2.04 (0.43) 3.54%

Micro 1.09 (0.68) 2.09%

Consumer 1.60 0.14 1.84%

Total 23.14 (0.30) 3.95%*

31

Total Loans originated since 2005

Net Upgrades(%)/Downgrades(%)# 1Q 2016 Details

LoanBackground

1Q’17Balance(Rp Bn)

1Q2015

2Q2015

3Q2015

4Q2015

1Q2016

2Q2016

3Q2016

4Q2016

1Q2017

DG to NPL%

UG toPL%

Corporate 229,872 - 0.11 0.38 0.24 0.13 0.24 - 0.32 0.14 - 0.14

Commercial 148,210 0.13 0.95 0.83 0.77 1.97 3.02 0.16 3.87 1.13 1.18 0.06

Small 55,178 1.29 1.17 1.24 0.54 1.31 1.50 1.36 0.63 1.20 1.26 0.07

Micro 52,175 1.25 1.37 1.50 1.08 1.37 1.45 1.35 0.84 0.94 1.03 0.08

Consumer 87,070 0.28 0.23 0.25 0.17 0.32 0.21 0.30 0.17 0.37 0.42 0.05

Total 572,505 0.33 0.60 0.68 0.31 0.94 1.28 0.35 1.36 0.49 0.59 0.09

1Q17 Net Downgrades of 0.49% On Loans Originated since 2005

# % downgrades and upgrades are quarterly % figures

32

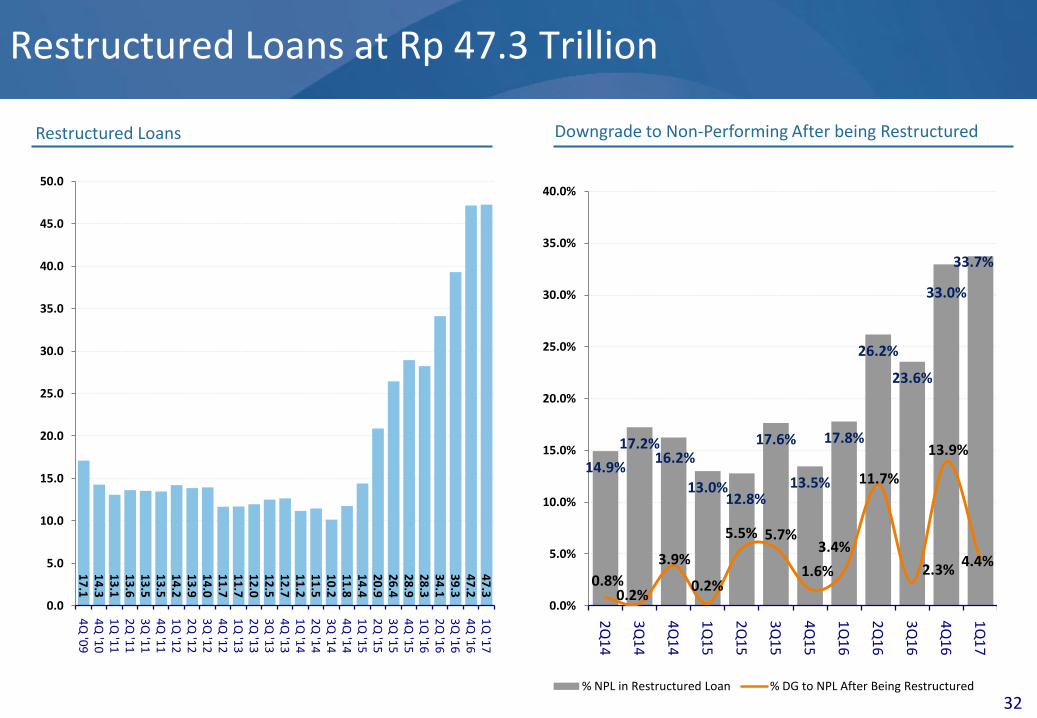

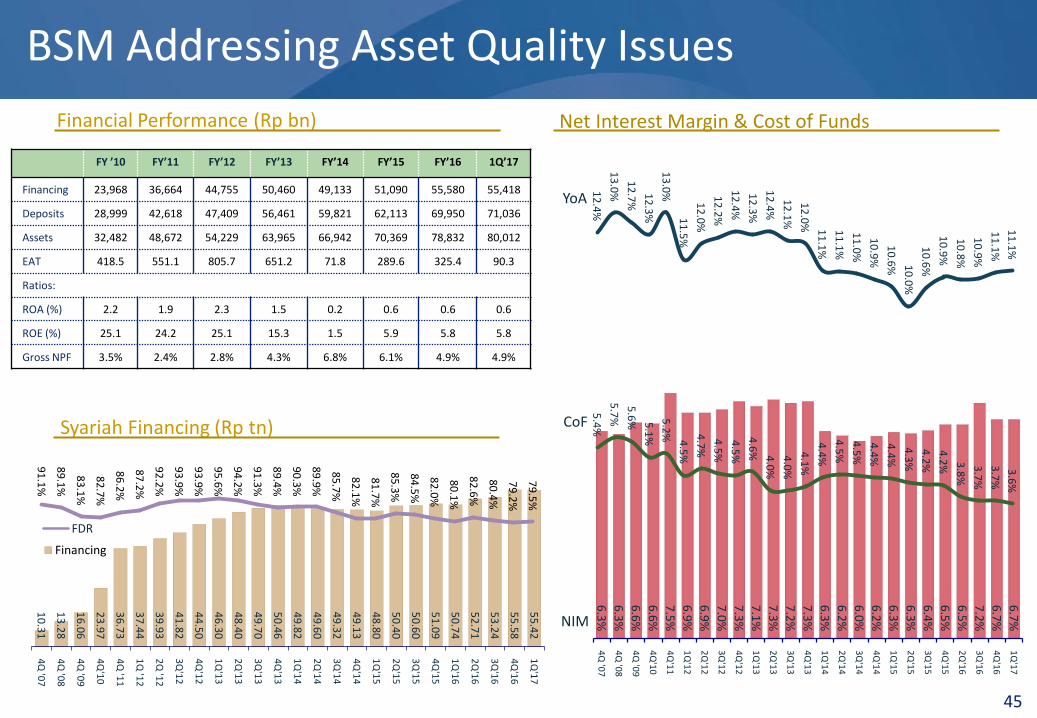

Restructured Loans

17

.1

14

.3

13

.1

13

.6

13

.5

13

.5

14

.2

13

.9

14

.0

11

.7

11

.7

12

.0

12

.5

12

.7

11

.2

11

.5

10

.2

11

.8

14

.4

20

.9

26

.4

28

.9

28

.3

34

.1

39

.3

47

.2

47

.3

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

4Q

'09

4Q

'10

1Q

'11

2Q

'11

3Q

'11

4Q

'11

1Q

'12

2Q

'12

3Q

'12

4Q

'12

1Q

'13

2Q

'13

3Q

'13

4Q

'13

1Q

'14

2Q

'14

3Q

'14

4Q

'14

1Q

'15

2Q

'15

3Q

'15

4Q

'15

1Q

'16

2Q

'16

3Q

'16

4Q

'16

1Q

'17

Restructured Loans at Rp 47.3 Trillion

Downgrade to Non-Performing After being Restructured

14.9%

17.2%16.2%

13.0%12.8%

17.6%

13.5%

17.8%

26.2%

23.6%

33.0%

33.7%

0.8%0.2%

3.9%

0.2%

5.5% 5.7%

1.6%

3.4%

11.7%

2.3%

13.9%

4.4%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

% NPL in Restructured Loan % DG to NPL After Being Restructured

33

Enhancing Synergies & Value from Subsidiaries

Total Assets

Rp80.0Tn

Bond Trading Volume

Rp18.1Tn

Total Assets

Rp26.3Tn

Total Loans

Rp6.2Tn

Total Financing

Rp4.6Tn

Total Financing

Rp55.4Tn

Equity & FI Underwriting

Rp2.7Tn

Annual FYP

Rp0.8Tn

Net Interest Margin

6.6%

Net Interest Margin

2.9%

Total Deposits

Rp71.0Tn

Equity Trading Volume

Rp42.9Tn

ROA

4.7%

ROA

2.1%

ROA

2.6%

ROE

5.8%

ROE

7.4%

ROE

56.6%

ROE

11.1%

ROE

14.0%

• Remains the leader in syariah financing

• Capital injection program over 3 years

• Cross-selling syariahproducts to Mandiri customers

• Expansion of business to fully utilize current capital base

• Cross-sell capital market services to broad range of Mandiri customers

• Refocus business toward higher fee income

• Providing end-to-end bank assurance business

• Continue to build cross-sell opportunities in various segments

• Bancassurance products to complete our suite of consumer offerings

• Enhancing operating model

• Improving risk management systems and IT

• Improving productivity

• Penetrate Bank Mandiri’s network and customer base to develop the multifinance segment with a strong focus on new 4 wheel vehicles.

Investment BankingSyariah Banking Insurance Niche Banking Multi-Finance

AXA Mandiri Financial Services Performance

34

17

1

18

3

23

7

25

5

25

8

23

4

26

2

25

9

29

8

27

0

26

9

25

6

34

8

29

7

31

6

30

8

36

0

27

4

24

7

38

7

33

1

28

0

26

2

43

4

30

0

1Q

'11

2Q

'11

3Q

'11

4Q

'11

1Q

'12

2Q

'12

3Q

'12

4Q

'12

1Q

'13

2Q

'13

3Q

'13

4Q

'13

1Q

'14

2Q

'14

3Q

'14

4Q

'14

1Q

'15

2Q

'15

3Q

'15

4Q

'15

1Q

'16

2Q

'16

3Q

'16

4Q

'16

1Q

'17

Net Profit After Tax (Rp Bn)Annual First Year Premium (AFYP) (Rp Bn) # of Policy Holders (‘000)

82

0

74

2

76

9

94

6

79

6

89

2

71

2

66

7

69

5

85

0

72

6

77

4

61

1

83

2

87

4

64

8

64

8

81

6

71

9

89

3

76

0

66

8

59

1

1,0

46

7

56

1Q

'11

2Q

'11

3Q

'11

4Q

'11

1Q

'12

2Q

'12

3Q

'12

4Q

'12

1Q

'13

2Q

'13

3Q

'13

4Q

'13

1Q

'14

2Q

'14

3Q

'14

4Q

'14

1Q

'15

2Q

'15

3Q

'15

4Q

'15

1Q

'16

2Q

'16

3Q

'16

4Q

'16

1Q

'17

1,6

03

1

,63

9

1,6

95

1

,74

4

1,7

91

1

,85

9

1,8

78

1

,91

9

1,9

67

2

,03

3

2,1

23

2

,21

7

2,3

54

2

,47

9

2,6

57

2

,96

2

3,1

62

3

,36

0

3,4

65

3

,71

0

3,8

32

3

,96

1

3,9

39

4

,10

1

3,9

30

1Q

'11

2Q

'11

3Q

'11

4Q

'11

1Q

'12

2Q

'12

3Q

'12

4Q

'12

1Q

'13

2Q

'13

3Q

'13

4Q

'13

1Q

'14

2Q

'14

3Q

'14

4Q

'14

1Q

'15

2Q

'15

3Q

'15

4Q

'15

1Q

'16

2Q

'16

3Q

'16

4Q

'16

1Q

'17

(0.5%) YoYGrowth

(9.3%) YoYGrowth

2.6% YoYGrowth

35

Bank Mandiri’s 2017 Corporate Guidance

2017 Target 2017 Realization

Gross Loan Growth (YoY) 11.0% - 13.0% 14.2%

Low Cost Deposits Rp 537.0 Tn Rp 465.6 Tn

Net Interest Margins 5.7% - 5.8% 5.9%

Efficiency Ratio 43.0% 42.7%

Gross NPLs 3.5% - 4.0% 3.98%

Cost of Credit 2.5% - 2.7% 3.32%

# of New ATMs 197 233

# of New EDCs 10,000 2,601

# of New Micro Network 34 (1)

# of New Conventional Branches 16 2

37

Corporate Banking:Generating Strong Asset Spread

Performance to Date: 1Q2017 (Rp Bn) Strategies for 2017

1. Focusing on Anchor Clients and penetrating through using of Transaction Banking

2. Account Plan implementation for top 76 Corporate Banking Customers.

3. Provide ‘one stop service’ solutions for customer’s transactions and create new business process to accelerate the execution of Account Plan including effective and responsive Complaint Handling.

4. Strengthen business alliance with Mandiri InHealth & Mandiri DPLK to ease corporate customers to manage their needs in health insurance & pension fund / severance

1,110

1,161

621 177

2,71556

2,771

38

InHealth – Opportunity to Increase Fee Income and Contribute to the Insurance Portfolio

Leveraging our institutional, corporate, & commercial customers

Providing solutions through our banking products to InHealth healthcare provider

Cross-selling Mandiri products to InHealth members

We have over 700 institutional, 300 corporate, and 1,700commercial customers with the potential to become membersof InHealth

• InHealth has 6,870 healthcare providers and recorded overRp 297 Bn in claims year to date 2017

• Bank Mandiri will leverage the hospital network as InHealth’spartner to increase transactions through enhanced cashmanagement products

• Bank Mandiri also will provide retail packaged products forall the doctors as InHealth’s partner

InHealth earned premium payments of Rp 398 Bn in 2017 yearto date from clients. Going forward, Bank Mandiri willencourage the use of cash management products throughBank Mandiri’s distribution channels and cross sell otherproducts to over 1.4 Mn InHealth members.

69

2,8

31

1,0

23

,22

8

1,1

75

,24

0

1,1

18

,20

6

1,1

41

,89

6

1,0

87

,31

3

94

0,6

96

1,2

47

,33

4

1,3

55

,22

9

5,501 6,242 6,314 6,262 6,094

6,189

7,072 7,018 6,870

-

2,000

4,000

6,000

8,000

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

2009 2010 2011 2012 2013 2014 2015 2016 1Q17

Total Member # of Providers

36 78 47 107 120 203 155 163 42 52

203

811

1,073 1,203

1,410 1,400 1,432

1,620

323 453

0

50

100

150

200

250

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2009 2010 2011 2012 2013 2014 2015 2016 1Q16 1Q17

Profit (Rp Bn) GWP (Rp Bn)

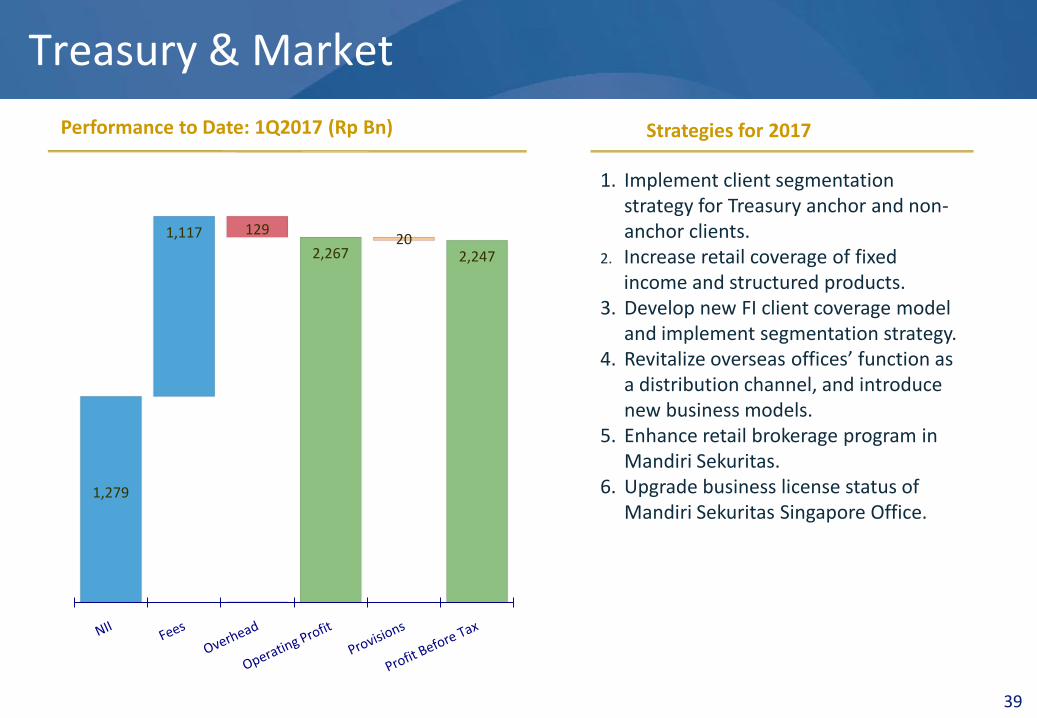

39

1. Implement client segmentation strategy for Treasury anchor and non-anchor clients.

2. Increase retail coverage of fixed income and structured products.

3. Develop new FI client coverage model and implement segmentation strategy.

4. Revitalize overseas offices’ function as a distribution channel, and introduce new business models.

5. Enhance retail brokerage program in Mandiri Sekuritas.

6. Upgrade business license status of Mandiri Sekuritas Singapore Office.

Treasury & Market

Performance to Date: 1Q2017 (Rp Bn) Strategies for 2017

1,279

1,117 129

2,26720

2,247

Mandiri Sekuritas’ financial performance

(Rp Bn)

40

Q1 2017 Q1 2016Y-o-Y

(%)

Revenues 185 154 20%

• Investment Banking 18 28 -37%

• Capital Market 70 64 9%

• Proprietary 10 17 -44%

• Investment Mgt 87 44 97%

Operating Expenses 161 117 38%

Earnings After Tax 19 26 -26%