An empirical analysis of the Capital structure of New Zealand Firms

18

An empirical analysis of the Capital structure of New Zealand Firms Ed Vos and Robert Ochoki Nyamori Department of Finance School of Management Studies University of Waikato Private Bag 3105 Hamilton, New Zealand Email [email protected] An Empirical Analysis of the Capital Structure of New Zealand Firms, E Vos and Robert Nyamori, Small Enterprise Research, Vol 5 No 2, 1997, pp29-38.

Transcript of An empirical analysis of the Capital structure of New Zealand Firms

An empirical analysis of the Capital structure of New Zealand

Firms

Ed Vos

and

Robert Ochoki Nyamori

Department of Finance

School of Management Studies

University of Waikato

Private Bag 3105

Hamilton, New Zealand

Email [email protected]

An Empirical Analysis of the Capital Structure of New Zealand Firms, E Vos and Robert Nyamori, Small Enterprise Research, Vol 5 No 2, 1997, pp29-38.

2

An empirical analysis of the Capital structure of New Zealand

Firms

ABSTRACT

While the existence of a difference in capital structure between small and large firms has become

acknowledged, a plethora of explanations have been advanced to explain this difference. We conducted

a mail survey in New Zealand in all sectors to examine these theories. Information on firm

characteristics, the sources of initial and additional finance, the sources of debt currently used and the

ones available and the reasons for accessing these sources was obtained. We find that it is difficult to

offer a single explanation for observed differences in capital structure in New Zealand. Instead, we find

that phenomena that would indicate a finance gap also implying a pecking order framework, control

theory and stages of growth theory, among others. We suggest that efforts towards examining the

financial decision making processes of the small firm may shed more light on this issue.

3

1. Background

Numerous studies have examined the differences in capital structure between small

and large firms (see for example Chittenden (1996); Chu (1996); Reid (1996);

Cowling and Sugden (1995); Chaganti (1995); Holmes and Kent (1990, 91); Ministry

of Commerce (1993, 96); Renfrew (1982)). What is apparent from these studies is that

there are differences in the capital structures of small and large firms. However, there

is little consensus as to the causes of these disparities for a number of explanations

have been advanced.

Some studies of capital structure of New Zealand firms seem to suggest a finance gap

explanation (Coopers and Lybrand (1993)) while more recent evidence points at the

lack of growth ambition (Austin, Fox and Hamilton (1996)). We present evidence

from New Zealand to try and examine some of these explanations. In particular we

have paid attention to how the results are supportive of various explanations of capital

structure of small firms. We suggest, just like Holmes and Kent (1990) that a study of

the financing decisions of the owner managers may provide an avenue for resolving

this impasse.

The paper reports the results of a New Zealand nation-wide survey of businesses from

all sectors. The aim of this research was to study the financial structure of business to

see whether there is a difference between large and small firms. Section two of this

paper provides a review of related literature and develops the questions to be

answered. Section three reports the method while section four provides an analysis of

the results.

2. A Review of Related Literature

The Capital structure of firms

The search for an optimal capital structure of the firm has engaged the minds of

finance academics for a long time. A landmark in this search is the Modigliani and

Miller (1958) study which holds that if taxes and the firms future investment plans are

4

held constant, the firm’s capital structure has no relevance to its value. Subsequent

attempts have relaxed the constraints of tax (Modigliani and Miller (1963)) and

bankruptcy costs (Warner (1977)) but as yet the determination of the optimal capital

structure is elusive (Myers (1984)). A more recent and forceful attempt has been made

by agency theorists who see the optimal capital structure as that point at which agency

costs are minimised and their benefit maximised (Jensen and Meckling (1976), Jensen

(1986)).

The capital structure of the small firm has presented another puzzle altogether. What

is apparent however is that there is a difference in capital structure between large and

small firms. A number of explanations have been advanced to explain these

differences. There are those who advance the view that firms are in a state of

progression from a seed-bed base to maturity. The implication on capital structure is

that each of these phases has different financial requirements and/or constraints.

Among these authors are Vos and Forlong (1997), Reid (1996), Chittenden et al.

(1996), Peterson and Shulman (1987) and Stanworth and Curran (1976).

Chu (1996) adds another dimension to this: the personal attributes of the managers.

They argue that because the needs of business vary over time, firms are not concerned

with an optimal capital structure per se (Chu (1996)). Instead, they are concerned with

a capital structure that meets their evolving financial needs and opportunities, what

they call a flexible capital structure. The capital decision is determined by manager’s

business judgement and risk profile and a concern for maximising the value of the

firm while minimising the cost of capital, given the multiplicity of sources of finance

available. A flexible capital structure takes care of uncertainty. (Also see Barton and

Mathews (1989).)

A popular explanation of the differences in capital structure is given by the finance

gap theory. The Bolton Report (1971), which popularised this view, argued that small

firms suffer from a finance gap. This gap results from the lack of access by small

businesses to appropriate sources of finance because they are more expensive for them

and also because they lack awareness of the various appropriate sources. Thus this gap

is seen as emanating from a cost gap and a knowledge gap. Put differently, the

5

financial structure of small businesses is constrained by their inability to access

appropriate sources of funds. They cannot therefore build an optimal capital structure

that fully exploits their potential and this in turn is bound to limit their contribution to

the overall economy.

It is apparent that there are some differences between the large and the small

businesses in terms of the cost of lending. What is not clear though is what causes this

differential. Some studies have argued that the costs of establishing and maintaining

smaller loans is higher than the larger ones (Johns, Dunlop and Sheehan, 1989,

Levenson 1962). Other studies attribute this to a premium on what is thought to be a

risky sector (Cowling and Sugden 1995, Binks and Ennew 1993, Keasy and Watson

1993). Holmes, Dunstan and Dweyer (1994) was an attempt to see whether this

difference indeed does exist and explain it. Theirs was a test of the hypothesis as to

whether small firms paid more on debt than the larger ones.

Cowling and Sugden (1995) argue that market power of banks is the cause of more

costly lending contracts to the smallest firms; that unlimited (or full) collateral reduces

the role of interest rates in the lending contract; and, that firm size is perceived by

banks to be a good proxy for riskiness. Put differently, the smaller the business the

riskier and therefore the higher the rate of interest charged. The basic argument is that

banks differentiate between firms on the basis of a number of observable

characteristics. It is these characteristics that determine the cost of lending and not

administrative costs as argued by Holmes, Dunstan and Dweyer (1994).

New Zealand Evidence

New Zealand has been characterised as a nation of small business because many of the

enterprises are small (Bollard (1988), and Devlin (1984). Small businesses are also

touted to make a significant contribution to capital accumulation and manufactured

exports (Devlin 1984) and act as a seedbed for innovation and technological

development. Thus the importance of small businesses in the economic development

of New Zealand need not be laboured.

6

Coopers and Lybrand (1993) found that the primary sources of financing for small

firms are founder and family with the banks constituting the dominant external

sources. They concluded that there was limited finance for prospective firms. A

significant weakness of the above study is its focus on the providers of finance to the

exclusion of those seeking the finance. Their conclusions on the sources of capital for

small firms are based on default. There is therefore need to investigate these findings

further by canvassing the views of those who seek finance, hence this study.

Austin, Fox and Hamilton (1996) extended the Coopers and Lybrand study by looking

at sources of capital available to small and medium firms. A major departure of this

study is that it surveyed 265 small businesses, the seekers of finance, unlike the

Coopers and Lybrand (19930 one. They were particularly concerned with three issues:

“to establish what factors are either inhibiting or contributing to the

availability of capital to prospective/start-up or existing small and

medium sized businesses for the purposes of growth and/or restructuring

to exploit opportunities in the market place; to determine whether the

financial markets are innovating at a rate consistent with optimally

meeting the financial needs of small and medium sized businesses. If not,

what factors are affecting the capability of the financial markets to

innovate; and finally, to determine the extent to which managerial

competencies within a firm affect the availability of capital” (p. 5).

Analysis of some of the evidence on finance for small firms in New Zealand suggests

that finance gap theory would explain most differences in the capital structures of

small and large businesses. However, Austin, Fox and Hamilton (1996) do not think

this is the cause. They think that it is the personal attributes of the owners: either

wanting to grow or not, that may explain differences in capital structure. We wish to

test some of the conclusions reached by Coopers and Lybrand (1993) and their

extensions in Austin, Fox and Hamilton (1996). We are encouraged to do so because

the conclusions reached in the earlier studies were not based on a survey of the

seekers but the providers of finance and advisory services.

7

5. Method of Study

An analysis of the above literature has suggested a number of testable propositions

based on a diverse range of theories that attempt to explain the capital structure of

small firms. Some of the propositions we wish to test are:

1. Large firms are more aware of the range of sources of funds available compared

to the small ones.

2. The primary sources of start-up funds for small firms is founder and family

funds. Where additional funds are required, they are obtained from the same

sources and retained earnings. The purpose of the additional funds is to purchase

operating assets for expansion.

3. The primary sources of external funds for the small firms are the banks (not

equity). Where small firms seek external funds, they go for short-term debt

because it least dilutes their control.

To test these hypotheses, we selected a sample of 400 firms from a list of 816 New

Zealand firms with over 100 employees. We obtained the questionnaire used in the

Holmes and Kent (1990, 1991) and, after some slight modifications, mailed it to the

selected sample. We canvassed information on firm characteristics as well as the

initial sources of start-up funds, sources of additional funds, reason for seeking

additional funds and the cost of additional funds. Of the 400 mailed 10 were dead

listings, 11 did not wish to participate in the study and 88 answered the questionnaire,

representing a response rate of about 23%. This was a reasonable response rate given

that prior studies have achieve rates of about 7 to10% (Holmes, Dunstan and Dweyer,

1994).

Of the respondents, 62.5% have been in operation for over 10 years, 9.09% for

between 6-10 years, 4.55% for between 3-5 years, slightly over one percent for 1-3

years and less 12 months. 20.24% did not answer the question. 3.41% of the

respondents had less 50 employees, 9.09% had 50-100, 64.77% had 100-500, 11.36%

had 500-1000, 10.23% had 1000-5000 and only 1.14% were over 5000. 14.77% were

in wholesale, 12.50% in retail, 19.32% in service, 45.45% in manufacturing and

17.05% in other sectors.

8

The initial sample consisted of firms with over 100 employees. However, 11

respondents had employees less 100. These were lumped with firms of employees less

500 because the number will not be representative of the proportion of firms in this

category. This was also to facilitate a more meaningful statistical analysis. The size of

the firms was divided into two categories based on the number of employees: those

with < 500 representing small firms and those with >500 representing the large ones.

This was found to represent a more “normal distribution” than classifications based on

turnover. Classifications on the basis of turnover were found to be highly skewed to

the right and therefore abandoned. Each size category was analysed against the

variables of source of start-up capital, source of additional funding, reason for

additional funding, the sources of debt currently being used and the sources of debt

currently available to the firm. A chi-square test of independence between the

variables was conducted to determine whether the differences between size and the

aforementioned variables was significant at the 95% and 99% confidence levels.

4. Analysis of Results

It is argued that because small firms have little knowledge as to the appropriate

sources of funds. Given that these funds are more expensive for small firms than the

larger ones, the initial source of start-up funds is owners equity, represented by

personal funds and those of friends and family. Coopers and Lybrand (1993) argue

this to be the case in New Zealand. To test this hypothesis, we canvassed answers as

to the sources of initial start-up funds. The results are presented in Table 1.

Personal funds of the owner constituted the source for most small businesses

(46.25%) followed by trading bank finance (35.29%) and other sources (19.12%).

However, there were no significant differences between the two groups in regard to

personal funds of the owner. This is contrary to the findings of Holmes and Kent

(1991), that personal funds constitute the primary source of funds for start-ups.

Perhaps, this may be explained by the stages of growth hypotheses that firms at

different stages access different sources of funds. In this respect then, the large firms

9

were once small and progressed to become large. At their initial stage, they relied on

the personal funds of the owners. That means the firms in the two groups have passed

the small business stage.

Table 1: Primary source of start-up funds

Percentage of responses (%)

Sources of funds < 500 >500 Total Respo*

Personal funds of owner 42.65 35 40.91

Finance company 0** 10** 2.27

Merchant bank funds 1.47 0 1.14

Government grant 2.94 5 3.41

Trading bank finance 35.29 40 36.36

Friends and family 1.47 0 1.14

Informal investors 0 0 0

Other sources 19.12 20 19.32

*Percentages do not total 100% as more than one response for each category was possible

**Significant at 0.10 level of confidence

There was a significant difference in the percentage of firms using finance company

sources for start-up: more large firms use this source than the small ones. This may

result from the fact that this source targets only the large enterprises (Arthur Andersen

(1995)), which may be supportive of finance gap theory.

The second most important source of finance for small firms is trading bank finance

(35.29% for small and 40% for large). There is however no significant difference

between the two groups. There is no significant difference between the two groups in

regard to merchant bank funds, government grants, trading bank finance, friends and

family, informal investors and other. What is apparent however is that the large firms

lead the small ones on most forms of debt they have accessed except the personal

funds of the owner, which partly supports the hypothesis of personal funds being the

primary source of the initial start. On the other hand, it may suggest the abundance of

financial sources open to the large firms compared to the small ones, which supports

the finance gap hypothesis. What is also apparent is that small firms have accessed

more sources than the larger firms. This may imply that large firms can obtain their

funds in a few places given their market power (Cowling and Sugden, (1995)) while

10

small firms have to struggle to get enough by approaching a multiplicity of sources

(Fraser 1995).

A key component of the finance gap is the knowledge gap, which means that small

firms do not have access to appropriate sources of funds because they lack knowledge

of them (McMahon et al. (1995)). Large firms are aware of the range of sources of

finance available compared to the small ones. We asked what the current sources of

debt were. Table 2 shows the results of analysis of the sources of debt for all the firms

in the sample.

The results show a significant difference between the large and the small in regard to

trading bank overdraft. Generally, 72% of the firms of the small firms and 45% of the

large ones currently use trading bank overdraft. The fact that the differences are

significant may be explained by control theory, that is, small firms generally use

family and friends sources, and when compelled to seek external funds, go for short-

term funds which do not compel them to share decision making with external

constituents. On the other hand, this may be due to the fact that smaller businesses

perceive debt to be the more appropriate source of finance than equity (Coopers and

Lybrand (1993)), a case of finance gap. This also partly answers the hypothesis that

small firms go for short-term debt, which does not dilute their control. However, for

supplier credit, the other short-term credit, there are no differences between the large

and the small, although again a greater percentage of small firms (26.47%) access this

source compared to the large (20%).

A look at Table 2 shows that the traditional forms of debt such as trade bank loans,

trade bank overdraft and trade credit are used more than the other sources such as

merchant banks and finance banks. This may be due to the undeveloped nature of

these facilities (Coopers and Lybrand (1993)). What is also apparent is that the

percentage of large firms using “other sources” is higher than for small firms. This

other sources could be the ones open to the larger firms and not the small ones such as

offshore borrowing and the capital market. There is a significant difference in usage

of finance company term loans and finance company lease, which vindicates the

hypothesis that the large firms are generally more aware of these facilities compared

11

to the small ones. On the other hand, this may show not awareness, but the fact that

these sources are not open to the small firms (Arthur Andersen (1995)). It may also

show lack of preference of these sources by management (Myers (1984)).

Table 2: Sources of debt currently used

Percentage of responses (%)

Sources < 500 >500 Total

Trading (Supplier credit) 26.47 20 25

Trading Bank overdraft 72.06*** 45*** 65.91

Trading bank term loan 41.18 40 40.91

Trading bank lease 4.41 0 3.41

Finance company term loan 1.47** 10** 3.41

Finance company lease 4.41** 15** 6.82

Finance company other 1.47 0 1.14

Merchant bank overdraft 0 0 0

Merchant bank term loan 5.88 5 5.68

Merchant bank Lease 0 0 0

Merchant bank other 2.94 0 2.27

Other source 23.53 30 25

*Percentages do not total to 100% as more than one response for each category was possible

**Significant χ2 statistic at .05 level of confidence

***Significant χ2 statistic at .01 level of confidence

There is no significant difference in debt in current use of trading bank term loan,

trading bank lease, finance company other, merchant bank overdraft, merchant bank

term loan, merchant bank lease and other source between the two groups.

To fully comprehend the extent of awareness of the opportunities open for borrowing,

we asked what types of debt are available to the firm if required. Table 3 shows the

results of this analysis. Generally, a majority of the firms listed the traditional forms of

debt such as trading bank overdraft, trading bank loan, and trading bank term lease in

that order. There is a fairly high level of awareness of other forms of financing such as

finance lease, finance term loan and merchant bank loan. Awareness of other forms of

debt is there but is low. Suffice it to say that the differences in awareness as measured

by the percentage of firms does not appear to be large. An explanation for this could

be that the financial market has become more sophisticated and has made conscious

efforts to increase their portfolio of small firms (Austin, Fox and Hamilton 1996) but

since this is a recent development, it has yet to permeate to all. There is a significant

difference in the level of merchant bank overdraft with small firms showing more

12

awareness than the large ones. This may also be supportive of the hypothesis that

small firms prefer short-term funding which does not dilute their control.

Table 3: Types of debt available to the business if required

Percentage of responses (%)

Source <500 >500 Total Respo*

Trading bank overdraft 85.29 85 85.23

Trading bank term lease 20.59 10 18.18

Finance company term lease 17.65 15 17.05

Merchant bank overdraft 14.71** 0** 11.36

Government grant 4.41 5 4.55

Trading bank term loan 71.64 55 67.82

Finance company term loan 19.12 15 18.18

Merchant bank loan 14.93 5 12.64

Merchant bank overdraft 7.35 5 6.82

Other source 16.18 15 15.91

*Percentages do not total to 100% as more than one response for each category was possible

**Significant χ2 statistic at .05 level of confidence

A key omission of the Holmes and Kent (1991) study was their failure to solicit the

reasons for the preference of the sources of funds currently used. We felt that this

would shed light on the motivations for using certain sources and not others. We

asked the respondents why they preferred the forms of debt they are currently using.

The results are reported in Table 4. Generally, only a few of the firms have made

decisions based on lack of awareness. Three of the respondents said they took this

form of debt because it was “available”. Given that other sources were also available,

this may show lack of awareness of the full range of funding available and lack of

interest in investigating. Information has a cost and funding preferences do not compel

them to investigate a case supportive of the pecking order hypothesis. These however

are in the minority. Majority of the firms chose their sources based on cost assessment

(32.35%) for small and 40 for large. The convenience and flexibility of the form of

debt was considered important, with (23.53%) of the small and 10% of the large

stating this.

Table 4: Reason for choosing the sources of debt currently in use

Percentage of respondents (%)

Reason <500 >500 Total Respo*

Lower cost 32.35 40 34.09

13

Relationship with the bank 7.35 10 7.95

Convenient and flexible 23.53 10 20.45

Corporate policy 10.29 0 7.95

Additional facilities 2.94 5 3.41

Only one willing to lend

amounts required

1.47 0 1.14

Diversify debt portfolio 2.94 0 2.27

Good terms 1.47 0 1.14

Available 4.41 0 3.41

Fits need requirements 11.76 0 9.09

*Percentages do not total to 100% as more than one response for each category was possible

Generally, small firms seem to have a plethora of reasons why they preferred their

chosen source, probably indicative of the importance of the finance decision for the

small firm given the difficulties of obtaining the finance. Generally, the implication

would be that firms made rational, conscious decisions in regard to source of debt

having considered the range available. This is consistent with pleas for a cost focus in

analysis of capital structure (Chittenden et al. (1996), Chu (1996), Hutchinson

(1995)). Minimising cost of borrowing is also consistent with refusing to cede control

of the firm (Hutchinson (1995)), and the pecking order hypothesis. However, there are

no significant differences between the large and the small in regard to the reasons for

their decisions.

It has been suggested that because small firms generally lack knowledge of

appropriate sources of finance, and that the sources they approach are generally more

expensive for them than for the larger firms, additional funding would come from

family and friends and retained earnings. We asked what the sources of additional

funding were and the results are reported in Table 4. The results are significant in

respect of “other sources”. Generally, large firms use “other sources” of funds which

may not be available to the small firms. Smaller firms may not raise money in the

stock exchange, a facility open to the large listed firms.

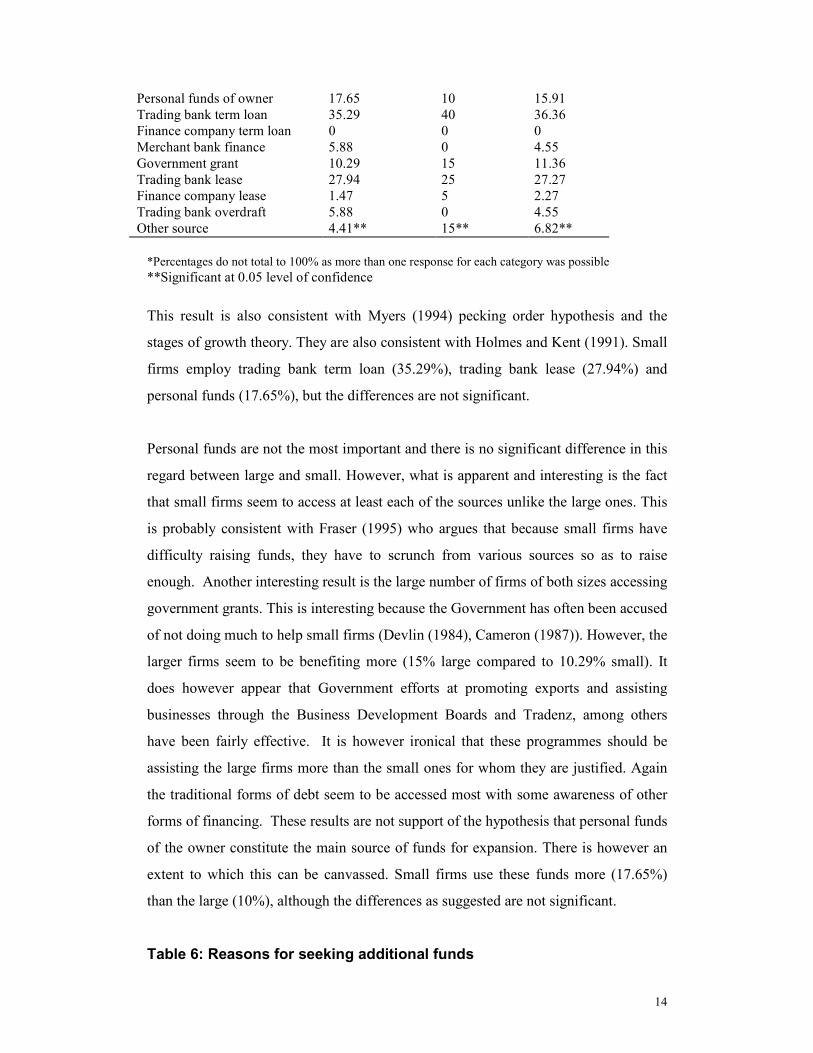

Table 5: Sources of additional funding

Percentage of responses (%)

Sources <500 >500 Total

Respo*

14

Personal funds of owner 17.65 10 15.91

Trading bank term loan 35.29 40 36.36

Finance company term loan 0 0 0

Merchant bank finance 5.88 0 4.55

Government grant 10.29 15 11.36

Trading bank lease 27.94 25 27.27

Finance company lease 1.47 5 2.27

Trading bank overdraft 5.88 0 4.55

Other source 4.41** 15** 6.82**

*Percentages do not total to 100% as more than one response for each category was possible

**Significant at 0.05 level of confidence

This result is also consistent with Myers (1994) pecking order hypothesis and the

stages of growth theory. They are also consistent with Holmes and Kent (1991). Small

firms employ trading bank term loan (35.29%), trading bank lease (27.94%) and

personal funds (17.65%), but the differences are not significant.

Personal funds are not the most important and there is no significant difference in this

regard between large and small. However, what is apparent and interesting is the fact

that small firms seem to access at least each of the sources unlike the large ones. This

is probably consistent with Fraser (1995) who argues that because small firms have

difficulty raising funds, they have to scrunch from various sources so as to raise

enough. Another interesting result is the large number of firms of both sizes accessing

government grants. This is interesting because the Government has often been accused

of not doing much to help small firms (Devlin (1984), Cameron (1987)). However, the

larger firms seem to be benefiting more (15% large compared to 10.29% small). It

does however appear that Government efforts at promoting exports and assisting

businesses through the Business Development Boards and Tradenz, among others

have been fairly effective. It is however ironical that these programmes should be

assisting the large firms more than the small ones for whom they are justified. Again

the traditional forms of debt seem to be accessed most with some awareness of other

forms of financing. These results are not support of the hypothesis that personal funds

of the owner constitute the main source of funds for expansion. There is however an

extent to which this can be canvassed. Small firms use these funds more (17.65%)

than the large (10%), although the differences as suggested are not significant.

Table 6: Reasons for seeking additional funds

15

Percentage of responses (%)

Reason < 500 >500 Total

Increase level of current assets 19.12 20 19.32

Prevent liquidity problem 8.82 5 7.95

Replace existing assets 16.18 20 17.05

Purchase fixed assets for

diversification

10.29 15 11.36

Purchase fixed assets for

expansion

33.82 50 37.50

0ther reasons 7.46*** 25*** 11.49

*Percentages do not total to 100% as more than one response for each category was possible

**Significant at 0.05 level of confidence

***Significant at the 0.01 confidence level

The literature on pecking order hypothesis (POH) suggests that firms operate under a

constrained pecking order resulting from external funds being more expensive than

internal ones and management therefore preferring internal equity. It further argues

that the main reason for additional funds is to purchase operating assets for expansion.

To test this hypothesis, we asked what the reasons were for seeking additional funds.

The results are reported in Table 6.

The difference between large firms and small ones regarding other reasons is

significant at 99% confidence level. This implies that large firms have other reasons

for seeking additional finance than the small ones and may be supportive of the POH.

On the other hand, there is no significant difference between small and large firms in

regard to the other reasons for seeking additional funds, which fails to support the

pecking order hypothesis. However, the results may be indicative of the relative

homogeneity of the sample in terms of the stage of growth. This implies that most of

the firms are at the same stage of growth and, therefore, the reason for seeking

additional funds are homogenous. If the stage of growth is to be measured by age, this

contention may be supported for majority of the firms (62.5%) are in the 10+ age

group while a meagre 16% occupy the remaining age groups with 21% not responding

(see Table 7).

Table 7: The age of the firms in the sample

Age Count Percent

Less 12 Months 1 1.14

16

1-3 Years 1 1.14

3-5 Years 4 4.55

6-10 Years 8 9.09

Over 10 Years 55 62.5

No answer 19 21.59

Total 88 100

5. Conclusion

We have examined New Zealand evidence in order to explain the different capital

structures between small and the large firms. What has emerged from this study is that

there are a number of differences in financing between small and large firms.

Obviously, this is bound to result to differences in capital structure. We found

significant differences between the large and the small firms in the sourcing of finance

company funds for start-up, implying greater awareness on the part of large than small

firms. There was a significant difference in sources of debt currently used in regard to

trading bank overdraft and finance company sources. We also found significant

differences in types of debt available to the firm for merchant bank overdraft. There

were significant differences in the source of additional funding in regard to “other

sources” and for “other reasons” for seeking this source. These results are generally

supportive of a finance gap theory. However, an interesting thing is that other

frameworks, such as the pecking order framework, stages of growth theory and

control theory could very well explain the results. Holmes and Kent (1991) had

suggested an investigation of the funding preferences of managers. We attempted to

do this by asking for the reasons for sourcing the additional funds. What emerges is

that small firms, just like the large, make conscious attempts at minimising costs,

consistent with, yet again both theories identified here. It does appear to us that this

line of research should be pursued, although this may entail the use of a methodology

that more closely pays attention to human intentionally in decision making. We mean

a field study probably based on case studies.

17

REFERENCES

Arthur Andersen (1994), Access to finance and business advice. Te Puni Kokiri,

Wellington.

Barton S. L. and Mathews C. H., (1989), “Small firm financing: Implications from a

strategic management perspective”. Journal of Small Business

Management. Vol 27(1): 1-7, Jan.

Bollard A., (1988), Small Business in New Zealand. Allen and Unwin: Port

NicholsonPress: Wellington.

Bolton J. E., (1971), Small firms: report of the committee of inquiry on small firms.

Cmnd. 4811. HMSO: London.

Chaganti R., et al. (1995), “Predictors of capital structure in small ventures”.

Entrepreneurship: Theory and Practice. 20(2): 7-18.

Chittenden F., et al. (1996), “Small firm growth, access to capital markets and

financial structure: Review of issues and empirical investigation”.

Small Business Economics, 8(1): 59-67.

Chu F. J., (1996), “Optimal capital structure revisisted”. Bankers Magazine (BZE),

179(5): 9-13.

Cowling M. and Sugden R., (1995), “Small firm lending contracts: Do banks

differentiate between firms?” Journal of Small Business Finance.

4(1): 87-98.

Devlin H. M., (1984), “Government assistance programmes for small businesses in

New Zealand”. Paper presented at the International Council for

Small Businesses. Chicago, USA. 10-12 June.

Devlin H. M., (1977), Needs and problems of small business: Some research findings.

Occassional Paper No. 15, Dept of Business, Massey University.

Dunstan K, Dwyer D. and Holmes S.,(1992), “The small business funding debate: An

empirical review”, Paper to the International Research

Symposium on Small firm Finance, Baylor University, Texas.

Fraser J. A., (1996), “Capital steps”. Inc. (INO), 18(2): 42-47.

Fox M.A. and Walker G. R., (1994), “Sources of funding for small and medium sound

companies in New Zealand”. New Zealand Law Journal. Nov:

421-425.

Holmes S. and Kent P., (1991) “An empirical analysis of the financial structure of

small and large Australian manufacturing enterprises”. The

Journal of Small Business Finance. 1(2): 141-54.

Holmes S and Kent P. (1990) “An empirical analysis of the financial structure of

small and large Australian manufacturing enterprises”. Paper

presented to the 5th National Small Business Research

Conference, Toowoomba, Queensland.

Holmes S., Dunstan K., and Dweyer D., (1994), “The cost of debt for small firms:

Evidence from Australia”. Journal of Small Busines Management.

32(1): 27-35.

Hutchinson R. W., (1995), “The capital structure and investment decisions of the

small owner-managed firm: Some exploratory issues”. Small

Business Economics, 7(3): 231-239. June.

18

Jensen M.C., and Meckling W. H., (1976), “Theory of the firm: Managerial

behaviour, agency costs and ownership structure”. Journal of

Financial Economics, 3(4): 305-360.

Levenson , A. (1962), “Interest rates and cost differentials in bank lending to small

and large businesses”. Review of Economics and Statistics. 4692:

190-198.

McMahon R. G. P., et al., (1993), Small enterprise financial management. Harcourt

Brace: Sydney.

Modigliani F.,and Miller M., (1958), “The cost of corporation finance and the theory

of investment”. American Economic Review. 486: 261-297.

Modigliani F.,and Miller M., (1963), “Corporate income taxes and the cost of capital:

A correction”. American Economic Review, 53: 433-443.

Myers S., (1984), “The capital structure puzzle”. Journal of Finance. July: 575-592.

Coopers and Lybrand, (1993), “Factors affecting the supply of capital for company

growth”. Ministry of Commerce, New Zealand Government,

Wellington.

Peterseon R. and Shulman J., (1987), “Capital structure of growing small firms: a 12

Country study on becoming bankeable”. International Small

Business Journal, 5(4): 10-22.

Reid G. C., (1996), “Financial structure and the growing small firm: Theortical

underpinning and current evidence”. Small Business Economics,

8(1): 1-7.

Renfrew K., (1982), “The adequacy of finance for small business in Australia”, in W.

Dunlop and w. Sheehan (eds.), Small Business Research Series

No.11, Institute of Industrial Economics, Newcastle, pp103-8.

Stanworth J and Curran H., (1976), “Growth and the small firm: An alternative view”.

Journal of Management Studies, 13(2): 95-110.

Warner S., (1977), “Bankruptcy costs: Some evidence”. Journal of Finance, 32: 337-

348.

Vos E. And Forlong C., (1997), “The agency advantage of debt over the lifecycle of

the firm.” Journal of Small Business Finance.