an economic and financial deconstruction of the commodity ...

313

AN ECONOMIC AND FINANCIAL DECONSTRUCTION OF THE COMMODITY STREAMING BUSINESS MODEL by Daniel Victor DiFilippo A thesis submitted to the Robert M. Buchan Department of Mining In conformity with the requirements for the degree of Master of Applied Science Queen’s University Kingston, Ontario, Canada January 2015 Copyright © Daniel Victor DiFilippo, 2015

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of an economic and financial deconstruction of the commodity ...

AN ECONOMIC AND FINANCIAL DECONSTRUCTION OF THE COMMODITY

STREAMING BUSINESS MODEL

by

Daniel Victor DiFilippo

A thesis submitted to the Robert M. Buchan Department of Mining

In conformity with the requirements for

the degree of Master of Applied Science

Queen’s University

Kingston, Ontario, Canada

January 2015

Copyright © Daniel Victor DiFilippo, 2015

ii

Abstract

The objective of this thesis is to evaluate the viability of the commodity streaming business model, both

as a standalone enterprise and as a financing service for exploration and mining companies. A silver

streaming company, Silver Wheaton, was chosen as the subject of a case study to accomplish this and

nine silver streams that it acquired in its first eight years from 2004-2012 were analysed and evaluated.

Using publicly available technical data, cash flow models were developed for all of the mines and

development projects with which Silver Wheaton made agreements during this time period. Subsets of

these cash flows were isolated to represent the positions of both Silver Wheaton and its operating partners

in each transaction. The Capital Asset Pricing Model and its associated economic metrics were employed

and calculated for all of the isolated stream cash flow models to evaluate the expected financial gain or

loss to each party for every deal.

Cash flow models were developed using two silver price series; one conservative and one bullish price

series. These were compiled through the aggregation of price forecasting data from mining equity

research reports published in the months leading up to each transaction.

It was found that the business model resulted in poor financial outcomes for Silver Wheaton and excellent

financial outcomes for its operating partners in over 50% of the transactions it concluded, when evaluated

at conservative silver prices. Conversely, when evaluated at bullish silver prices it resulted in excellent

financial outcomes for Silver Wheaton and extremely poor financial outcomes for its operating partners in

every instance.

iii

Given that today silver is produced primarily as a by-product to gold and base metals, the business model

has a uniquely large target market when focusing on silver and has been replicated to varying degrees of

success by other companies, both with silver and other commodities. It provides a viable alternative to

traditional financing avenues for exploration and mining companies during all periods of the mining

business cycle and is positioned to grow in significance as a form of mine and project financing.

iv

Acknowledgements

The success of this thesis and associated studies has been achieved with the help and guidance of many

individuals.

Firstly, I would like to thank my two supervisors, Professors Jim Martin and Jeffrey Davidson, for their

invaluable advice, guidance, criticism, and encouragement throughout the development of this thesis’

concept and writing. Special thanks is due to Prof. Davidson for his patience throughout the writing and

re-writing process; without his sound understanding of academic writing I surely would not have

improved this document to a satisfactory calibre.

I would like to thank Dundee Capital Markets and those with whom I worked in Fall 2011: Bob Sangha,

Sandeep Singh, Brad Ralph, and particularly Stanley Iu, Michael Spencer, Alexandra Cowie, and Olga

Ivleva. The experience and guidance I received during my time as a mining investment banking intern

were integral to my understanding of how financial and economic concepts are practically employed

during transactional and enterprise analysis and evaluation in the mining capital markets.

Thank you to my parents, David and Mary Jo, for their constant support and guidance throughout my

schooling and life. Special thanks is due to my father for his interest in Silver Wheaton and its operating

model when I was a young undergraduate student; his fascination with the metal streaming concept

became mine, as well.

Finally, thank you to my fiancée, Catherine. Her love, support, and belief in me and my abilities have

been deeply motivating throughout this academic journey and beyond.

v

Table of Contents

Abstract ......................................................................................................................................................... ii

Acknowledgements ...................................................................................................................................... iv

Table of Contents .......................................................................................................................................... v

List of Figures ............................................................................................................................................ xiv

List of Tables .............................................................................................................................................. xv

List of Abbreviations .............................................................................................................................. xxvii

Chapter 1 ....................................................................................................................................................... 1

Introduction ................................................................................................................................................... 1

Chapter 2 ....................................................................................................................................................... 6

The Silver Streaming Model as exemplified by Silver Wheaton .................................................................. 6

2.1 Problem statement ......................................................................................................................... 9

2.2 Scope ........................................................................................................................................... 10

2.3 Thesis organization ..................................................................................................................... 11

Chapter 3 ..................................................................................................................................................... 14

Basic Concepts in Project Evaluation: A Review of Relevant Concepts and Literature ............................ 14

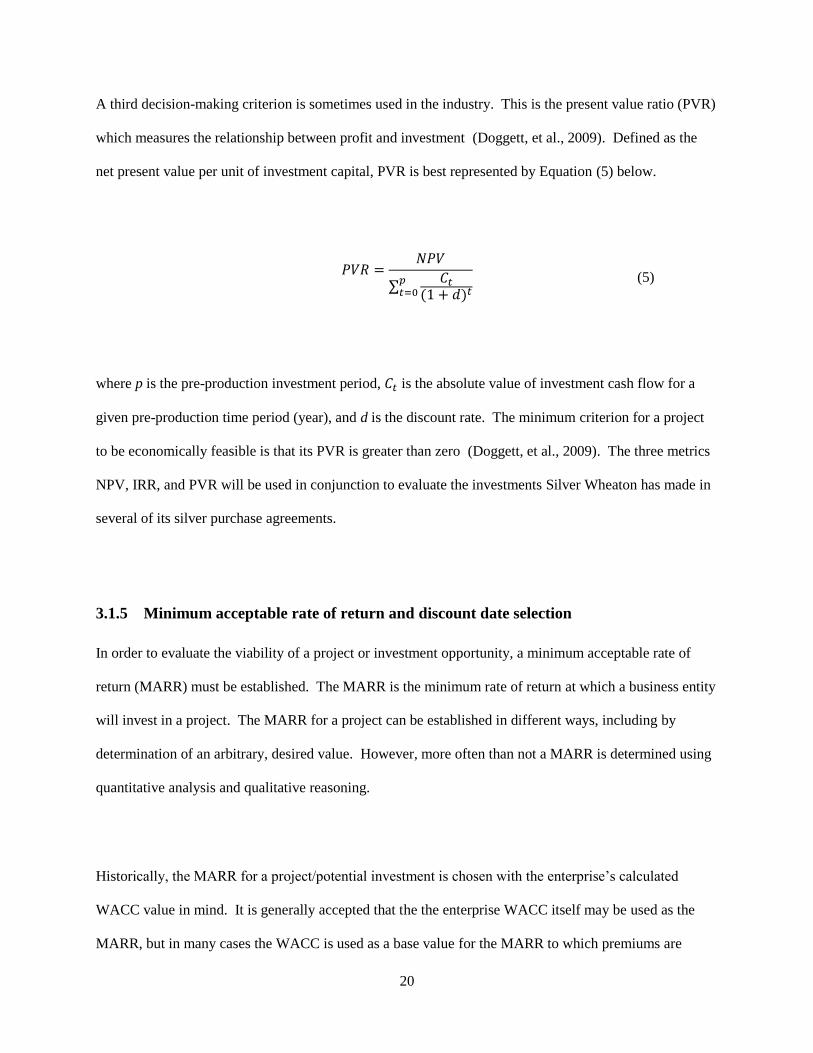

3.1 Basic concepts in project evaluation ........................................................................................... 14

3.1.1 The cash flow concept ......................................................................................................... 14

3.1.2 Discounted cash flows ........................................................................................................ 15

3.1.3 Capital Asset Pricing Model and beta factors ..................................................................... 17

3.1.4 Economic evaluation metrics .............................................................................................. 19

vi

3.1.5 Minimum acceptable rate of return and discount date selection ......................................... 20

3.1.6 Inflation ............................................................................................................................... 22

3.1.7 Consensus price estimate methodology in mining finance ................................................. 23

Chapter 4 ..................................................................................................................................................... 26

Application of Concepts to the Evaluation of the Silver Streaming Business Model ................................. 26

4.1 Methodology and research plan .................................................................................................. 26

4.1.1 Data sources ........................................................................................................................ 26

4.1.2 Case study: Silver Wheaton Corp. and its operating partners ............................................. 27

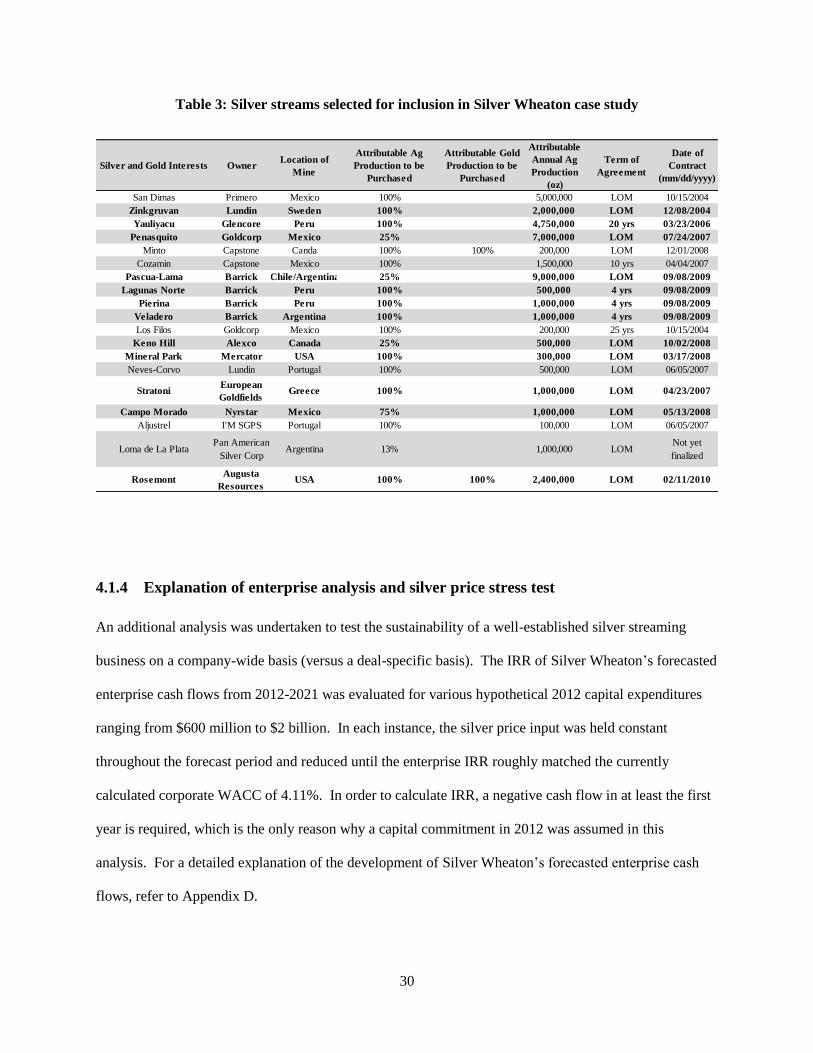

4.1.3 Selection of streams to be evaluated ................................................................................... 28

4.1.4 Explanation of enterprise analysis and silver price stress test ............................................ 30

4.1.5 Analysis of value addition or reduction to development project economics ...................... 31

4.2 Calculation of WACC ................................................................................................................. 31

4.3 Calculation of estimated silver stream cash flows ...................................................................... 33

4.3.1 Calculation of cash flows for mines utilizing silver streams .............................................. 33

4.3.2 Calculation of silver stream cash flows for operating partners ........................................... 36

4.3.3 Calculation of silver stream cash flows for Silver Wheaton ............................................... 36

4.3.4 Treatment of outdated capital and operating cost estimates ............................................... 36

4.3.5 Silver price series used in silver stream cash flow models ................................................. 37

4.4 Limitations and assumptions ....................................................................................................... 39

4.4.1 Sample size ......................................................................................................................... 40

4.4.2 Deterministic cash flow modelling ..................................................................................... 40

vii

4.4.3 Quality of index data used in calculation of corporate WACC ........................................... 41

4.4.4 Calculation method of corporate WACC ............................................................................ 41

4.4.5 Qualitative silver price forecast for 2012+.......................................................................... 41

4.4.6 Escalation of capital and operating costs ............................................................................ 42

4.4.7 Omission of working capital ............................................................................................... 42

4.4.8 Mine closure/ramp-down and metal sales ........................................................................... 42

4.4.9 Treatment of upfront payment ............................................................................................ 43

Chapter 5 ..................................................................................................................................................... 44

Sample Calculation of Discounted Cash Flows for a Silver Stream ........................................................... 44

5.1 Sample calculation of beta and WACC ...................................................................................... 44

5.2 Sample calculation of silver stream cash flow model ................................................................. 51

5.2.1 Calculation of mine cash flow model.................................................................................. 51

5.2.2 Calculation of silver stream cash flows for the stream seller .............................................. 54

5.2.3 Calculation of silver stream cash flows for the stream buyer ............................................. 56

Chapter 6 ..................................................................................................................................................... 57

Commodity and Mining Finance Review ................................................................................................... 57

6.1 Silver commodity review ............................................................................................................ 57

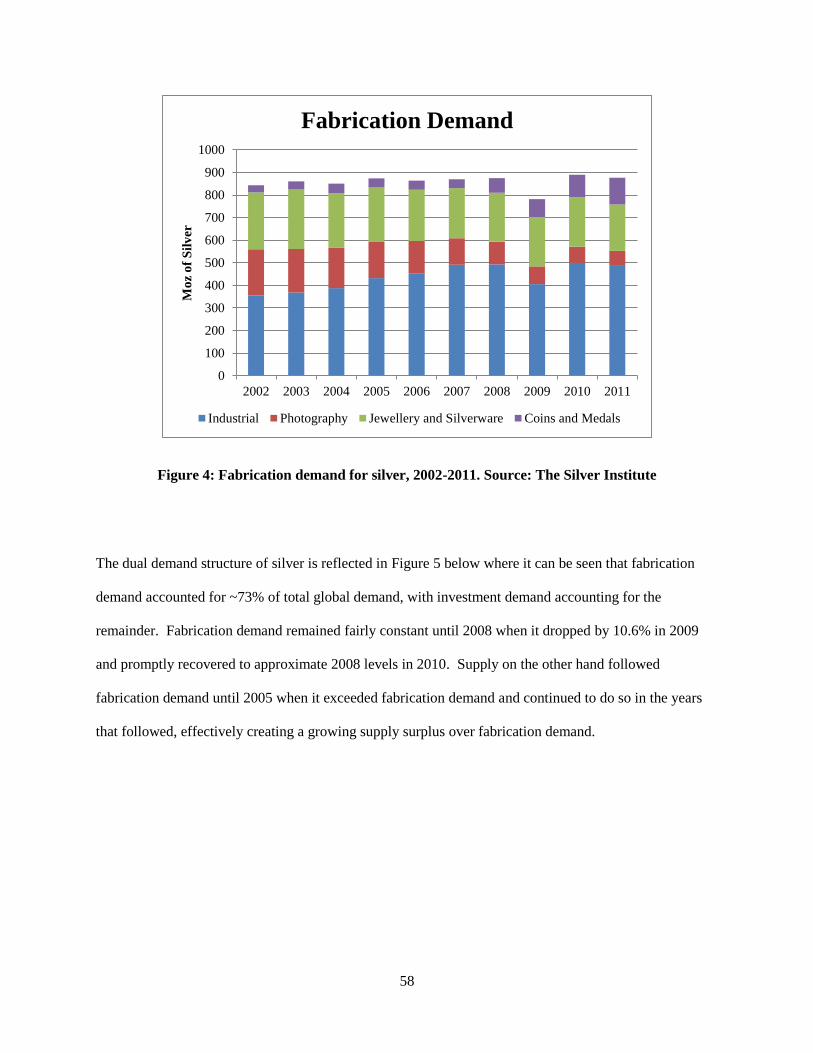

6.1.1 Demand and demand elasticity ........................................................................................... 57

6.1.2 Supply ................................................................................................................................. 63

6.1.3 Relevance to analysis of silver streaming business model .................................................. 65

6.2 Mining finance review ................................................................................................................ 66

viii

Chapter 7 ..................................................................................................................................................... 68

Case Study: Silver Wheaton Perspective .................................................................................................... 68

7.1 Initial financing of Silver Wheaton Corp. ................................................................................... 68

7.2 Results of isolated stream financial analysis ............................................................................... 70

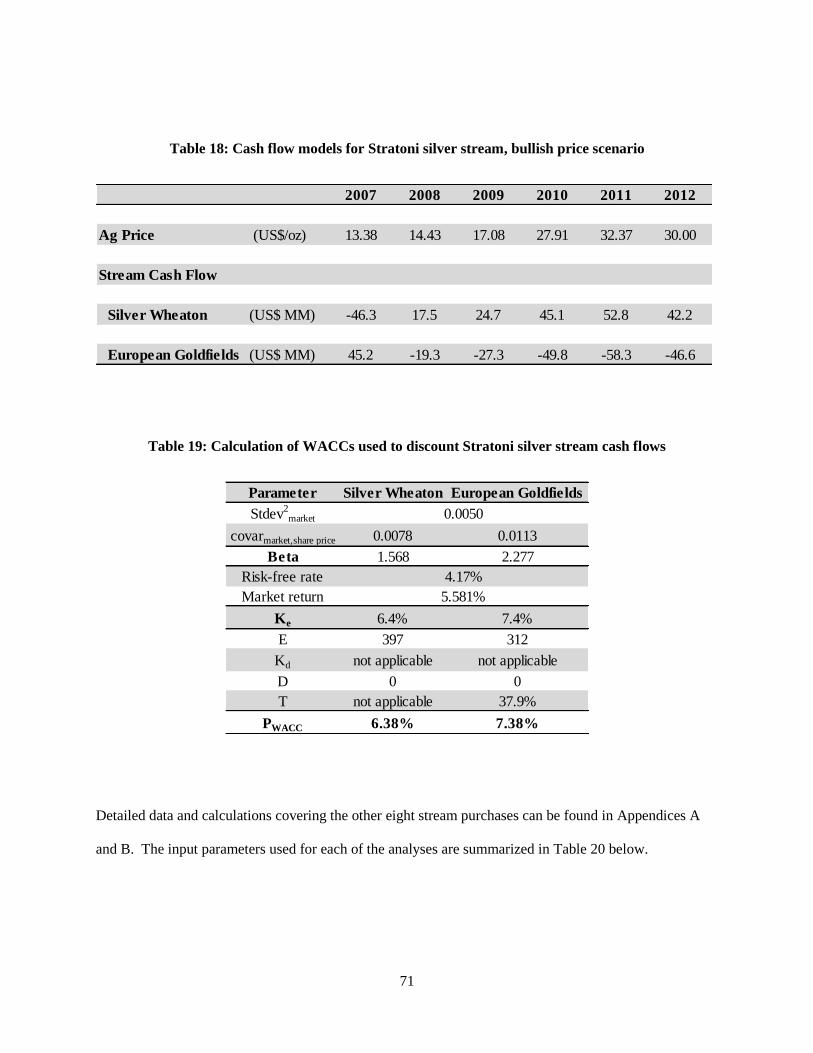

7.2.1 Financial analysis at consensus silver price forecasts ......................................................... 72

7.2.2 Financial analysis at bullish silver price forecasts .............................................................. 74

7.3 Sensitivity analysis ...................................................................................................................... 75

7.4 Estimation of tolerable silver price floors ................................................................................... 80

7.5 Discussion ................................................................................................................................... 82

7.5.1 Base case vs. bullish stream cash flows .............................................................................. 82

7.5.2 Stream life and general comments on portfolio diversity ................................................... 83

7.5.3 Silver purchase agreement terms ........................................................................................ 85

7.5.4 Sustainability of silver streaming business model as an enterprise .................................... 85

7.5.5 Risk mitigation through completion guarantees ................................................................. 85

Chapter 8 ..................................................................................................................................................... 87

Case Study: Silver Wheaton Operating Partner Perspective ....................................................................... 87

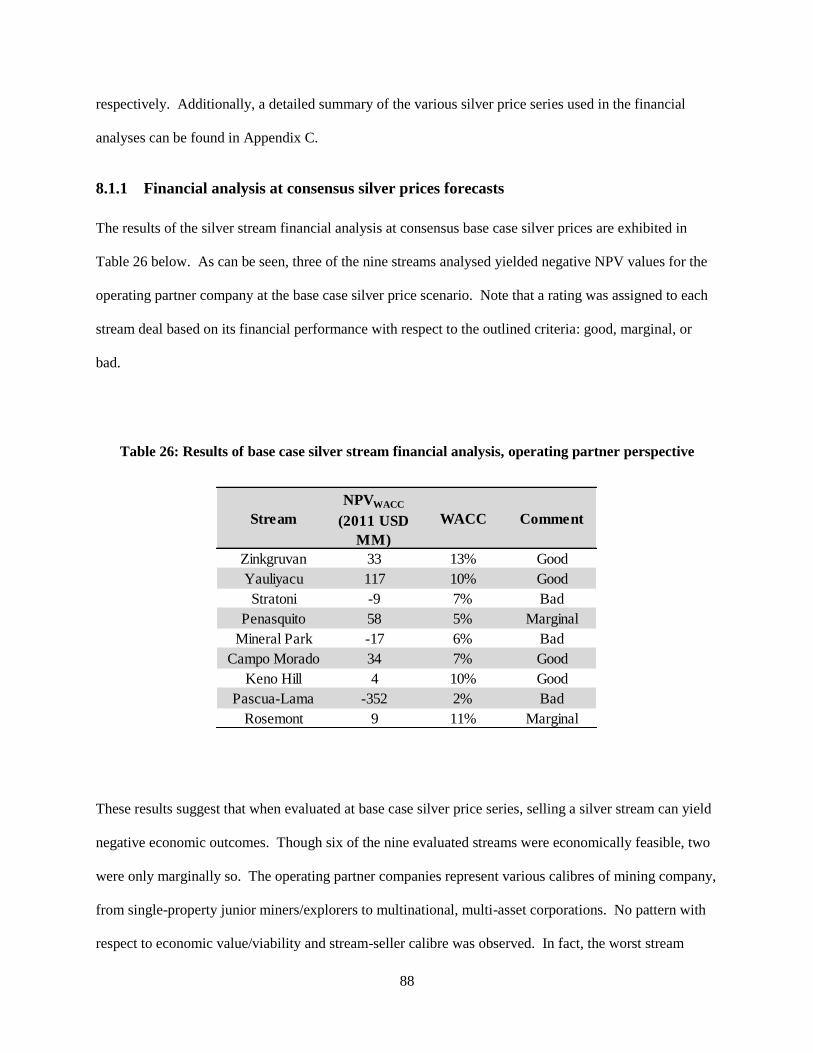

8.1 Results of isolated stream financial analysis ............................................................................... 87

8.1.1 Financial analysis at consensus silver prices forecasts ....................................................... 88

8.1.2 Financial analysis at bullish silver price forecasts .............................................................. 89

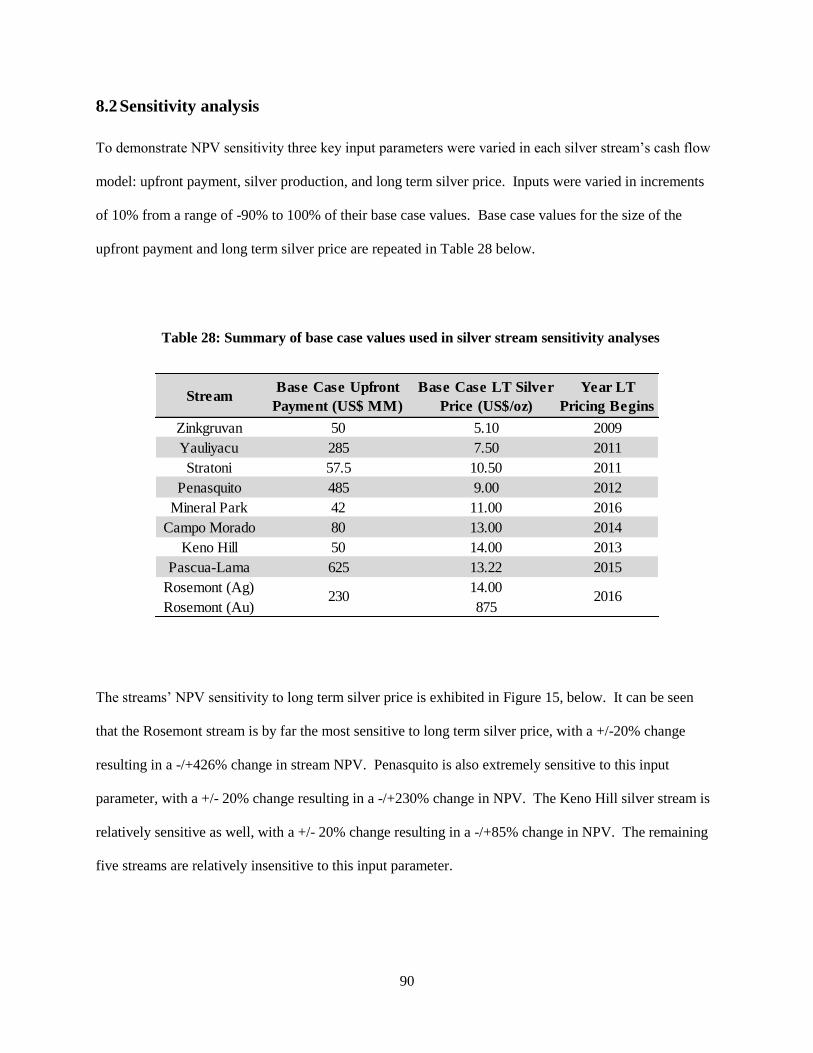

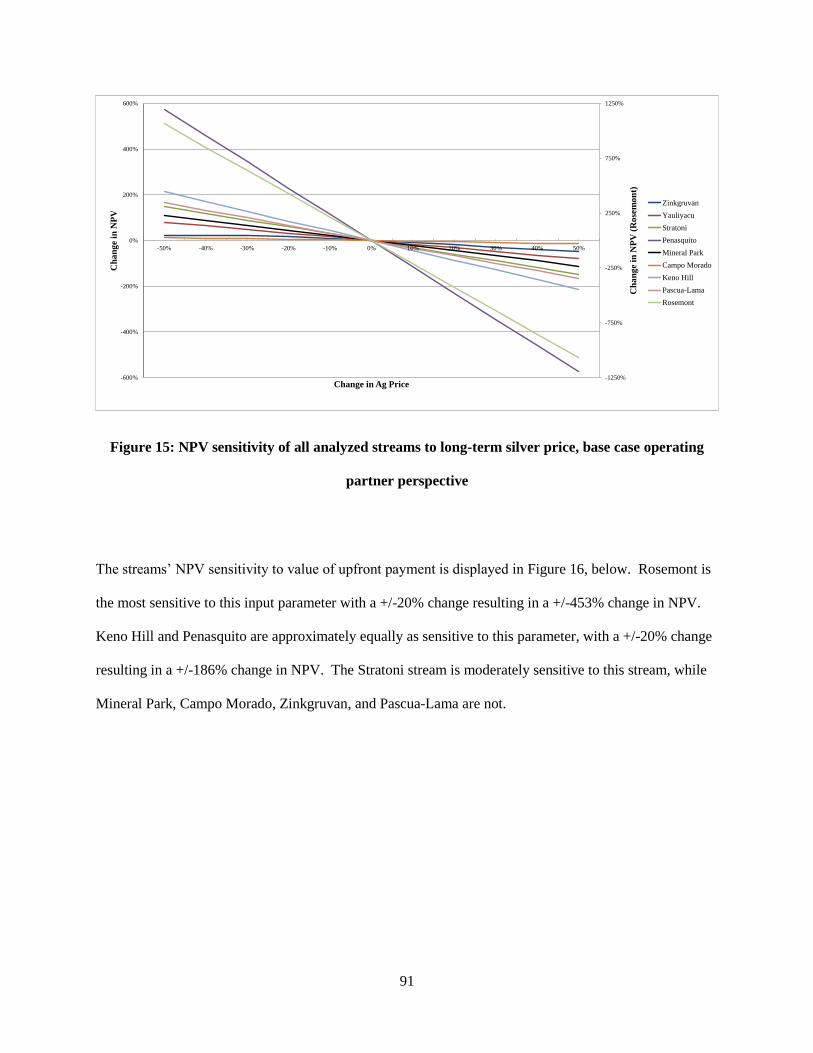

8.2 Sensitivity analysis ...................................................................................................................... 90

8.3 Value of silver streams to development projects ........................................................................ 93

ix

8.4 Internal drivers for opting for stream financing .......................................................................... 95

8.5 Discussion ................................................................................................................................... 98

8.5.1 Isolated stream economics .................................................................................................. 98

8.5.2 Financial sensitivity of streams to operating partners ......................................................... 99

8.5.3 Sustainability of silver streaming business model as a financing service ......................... 100

Chapter 9 ................................................................................................................................................... 101

Comparison of Silver Streaming to Traditional Financing Methods ........................................................ 101

9.1 Debt financing overview ........................................................................................................... 101

9.2 Equity financing overview ........................................................................................................ 102

9.3 Debt and equity financing in mineral exploration and mining.................................................. 103

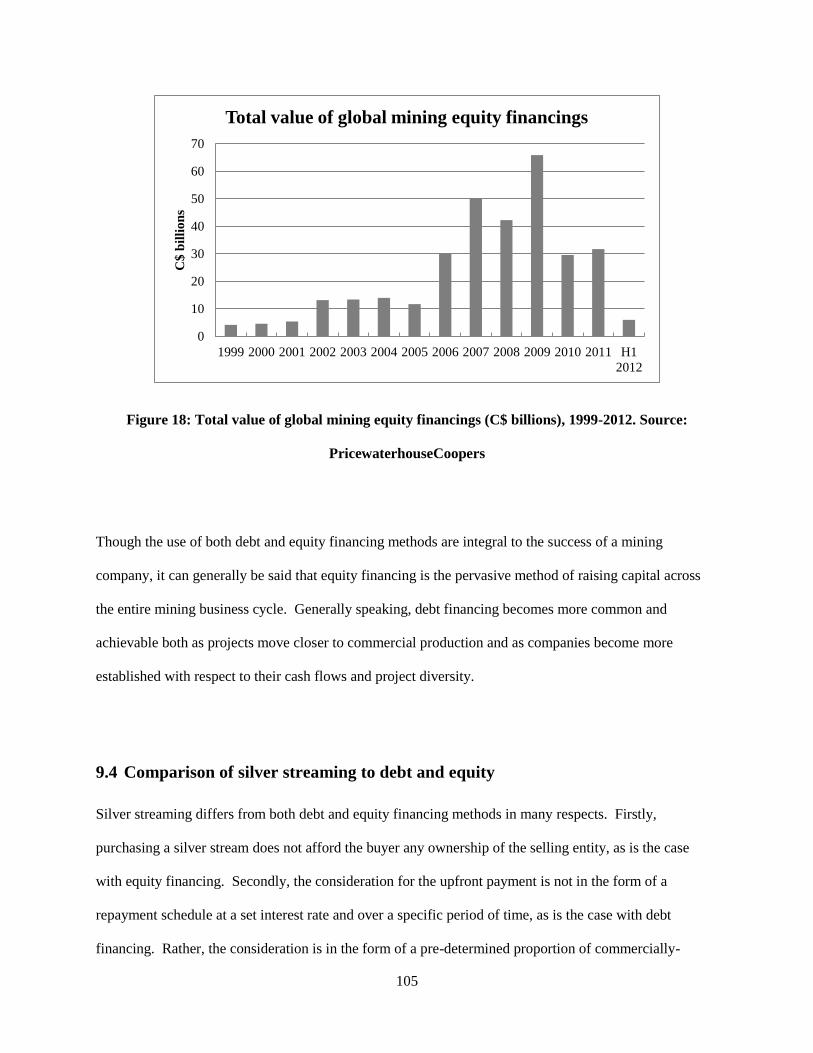

9.4 Comparison of silver streaming to debt and equity .................................................................. 105

Chapter 10 ................................................................................................................................................. 108

Conclusions and Discussions .................................................................................................................... 108

10.1 Summary ................................................................................................................................... 108

10.2 Conclusions and general discussion .......................................................................................... 110

10.2.1 Silver streaming as an enterprise....................................................................................... 110

10.2.2 Silver streaming as a quasi-financing service ................................................................... 111

10.2.3 Disproportionate risk profile of silver streaming .............................................................. 111

10.2.4 Potential to stream commodities other than silver ............................................................ 112

10.3 Conditions for the existence of the silver streaming business model ....................................... 114

10.4 Replication of Silver Wheaton experience and potential for new market entrants ................... 115

x

10.5 Risk elements for the silver streaming business model ............................................................ 116

10.6 Future work and recommendations ........................................................................................... 118

10.6.1 Future work ....................................................................................................................... 118

10.6.2 Recommendations ............................................................................................................. 119

Bibliography ............................................................................................................................................. 121

Appendix A ............................................................................................................................................... 140

Data Used in Beta Factor and WACC Calculations.................................................................................. 140

Silver Wheaton Data ............................................................................................................................. 140

Yauliyacu transaction ........................................................................................................................ 140

Stratoni transaction ........................................................................................................................... 142

Penasquito transaction....................................................................................................................... 145

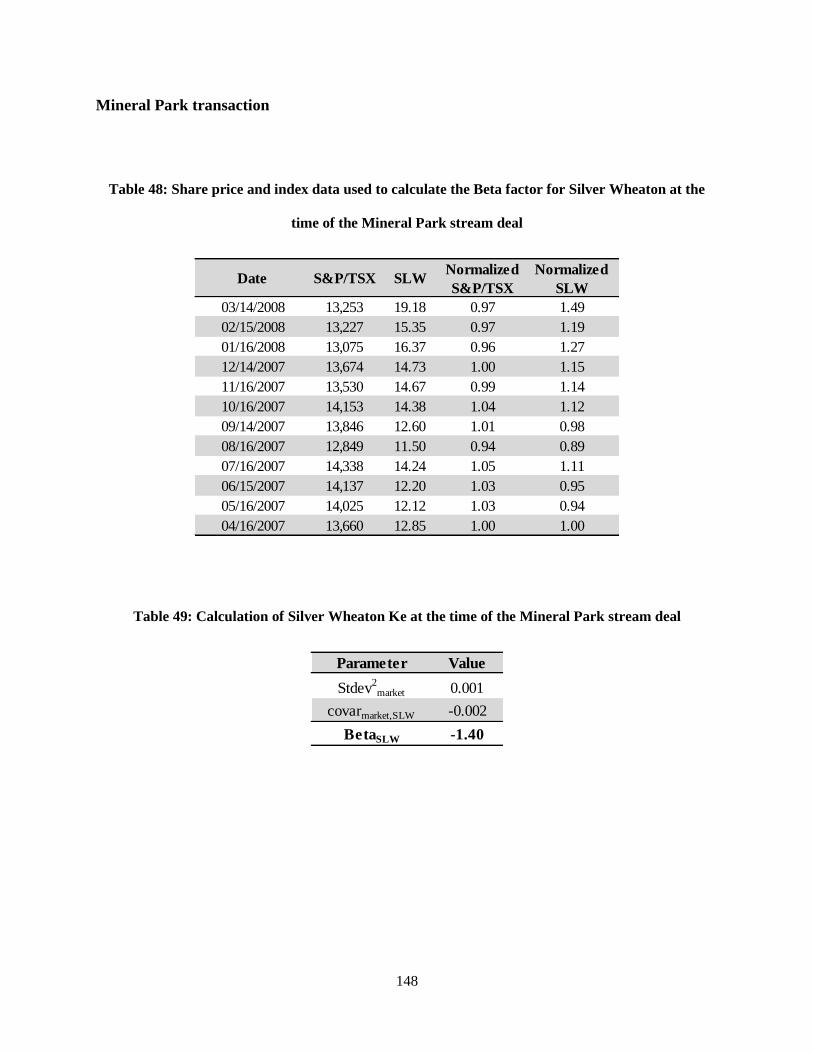

Mineral Park transaction ................................................................................................................... 148

Campo Morado transaction ............................................................................................................... 150

Keno Hill transaction ........................................................................................................................ 152

Pascua-Lama transaction................................................................................................................... 155

Rosemont transaction ........................................................................................................................ 158

Operating Partner Data ......................................................................................................................... 161

Lundin and the Zinkgruvan transaction ............................................................................................ 161

European Goldfields and the Stratoni transaction ............................................................................. 163

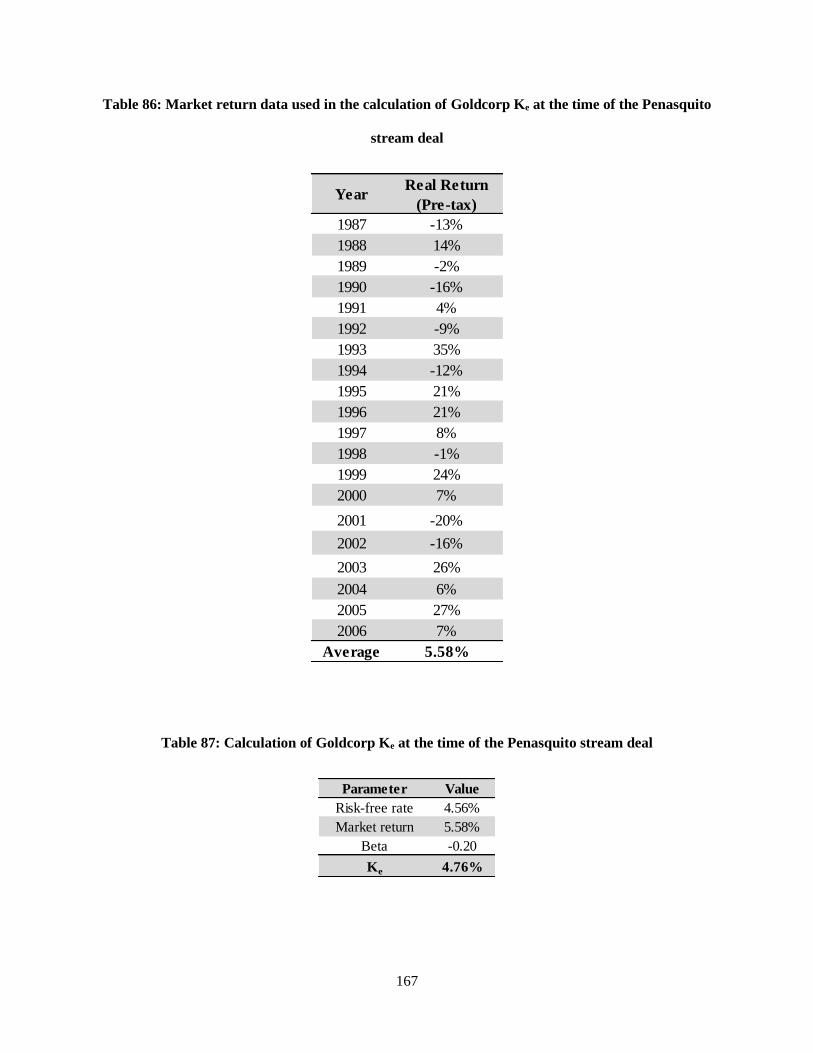

Goldcorp and the Penasquito transaction .......................................................................................... 165

Mercator and the Mineral Park transaction ....................................................................................... 168

xi

Farallon and the Campo Morado transaction .................................................................................... 171

Alexco and the Keno Hill transaction ............................................................................................... 173

Barrick and the Pascua-Lama transaction ......................................................................................... 176

Augusta and the Rosemont transaction ............................................................................................. 178

Appendix B ............................................................................................................................................... 182

Cash Flow Models for Silver Streams and Underlying Mines ................................................................. 182

Zinkgruvan ........................................................................................................................................ 182

Yauliyacu .......................................................................................................................................... 186

Stratoni .............................................................................................................................................. 189

Penasquito ......................................................................................................................................... 193

Mineral Park ...................................................................................................................................... 200

Campo Morado ................................................................................................................................. 205

Keno Hill ........................................................................................................................................... 210

Pascua-Lama ..................................................................................................................................... 216

Rosemont .......................................................................................................................................... 222

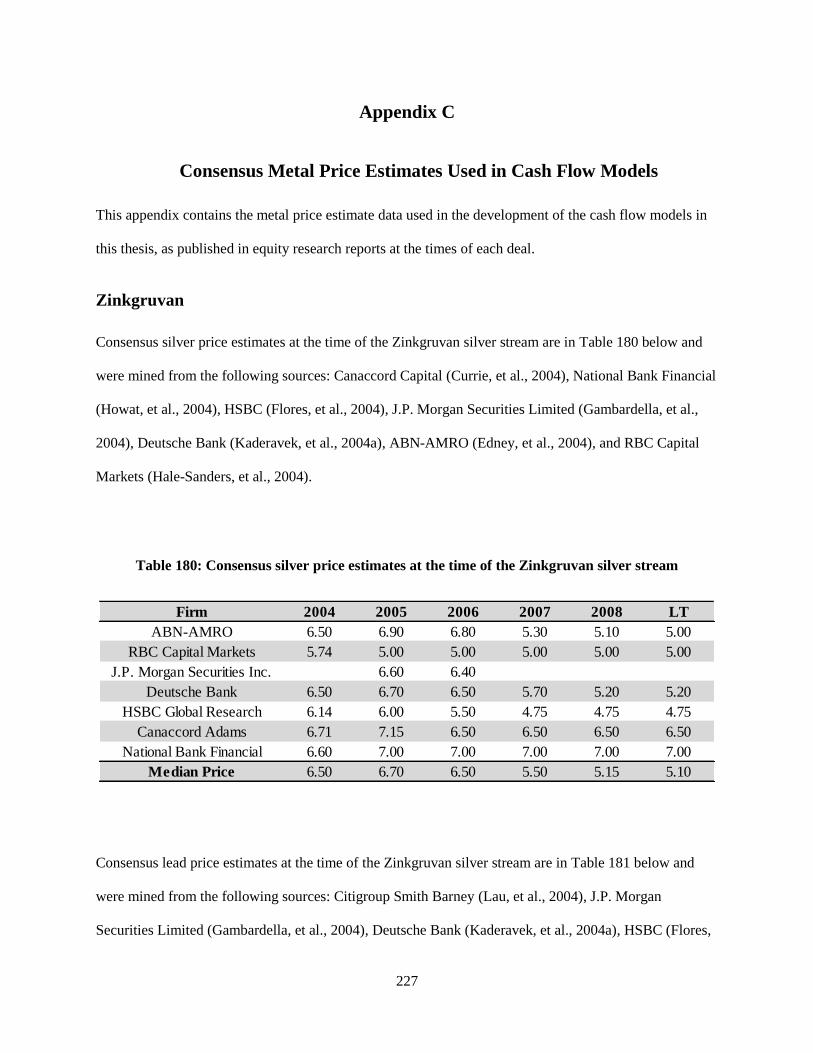

Appendix C ............................................................................................................................................... 227

Consensus Metal Price Estimates Used in Cash Flow Models ................................................................. 227

Zinkgruvan ............................................................................................................................................ 227

Yauliyacu .............................................................................................................................................. 229

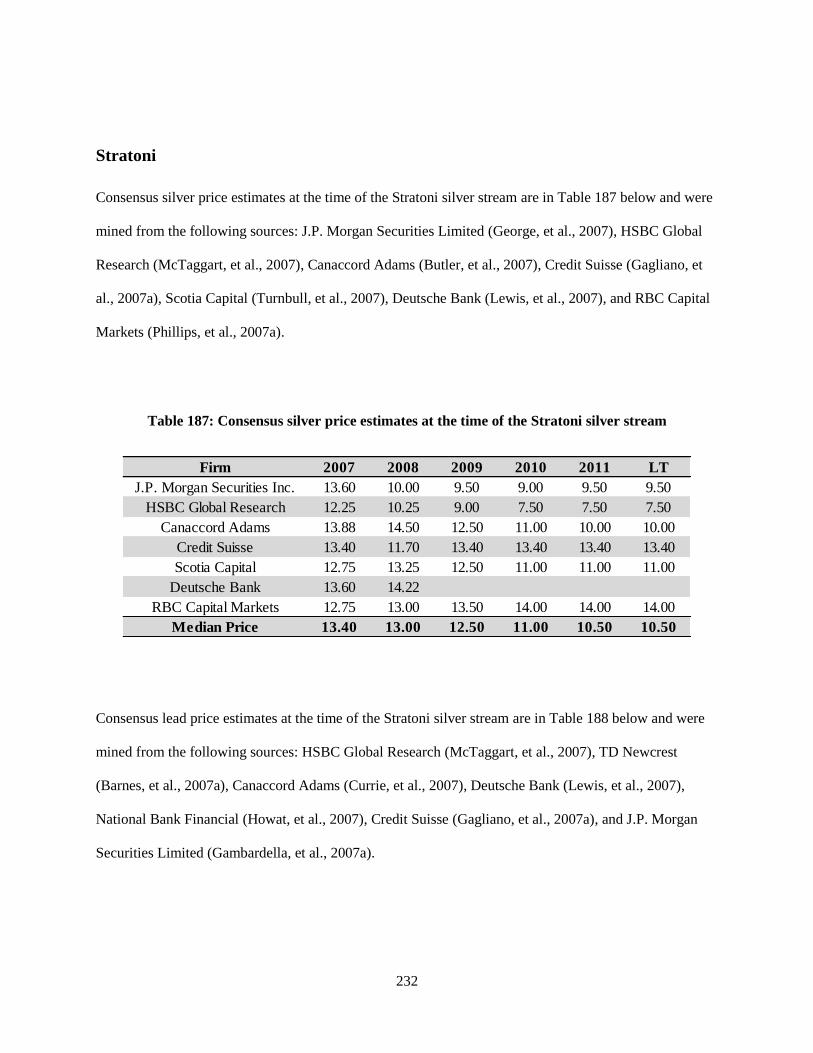

Stratoni .................................................................................................................................................. 232

Penasquito ............................................................................................................................................. 234

xii

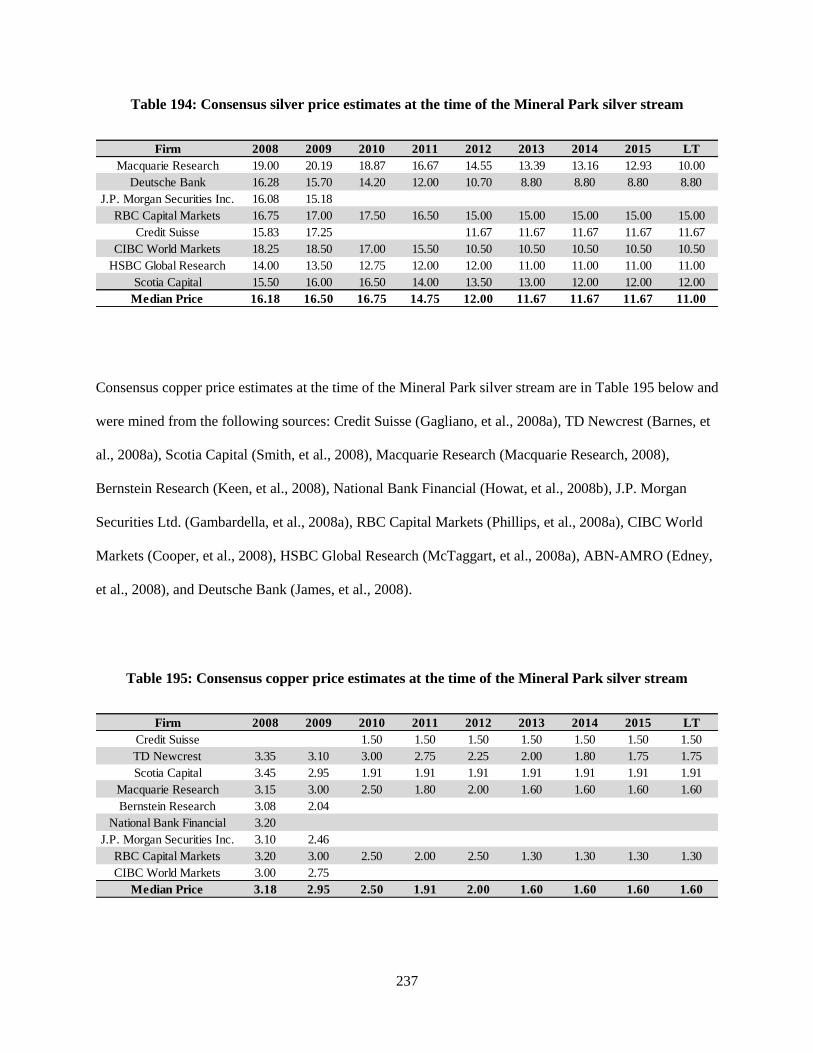

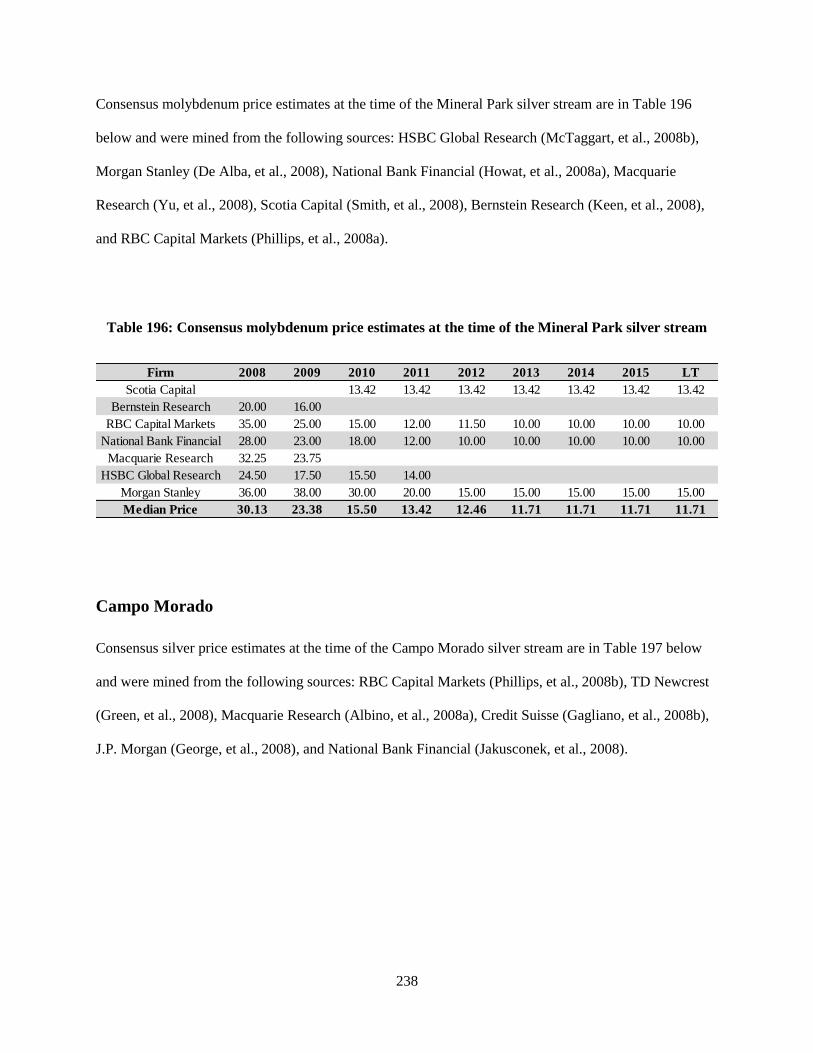

Mineral Park.......................................................................................................................................... 236

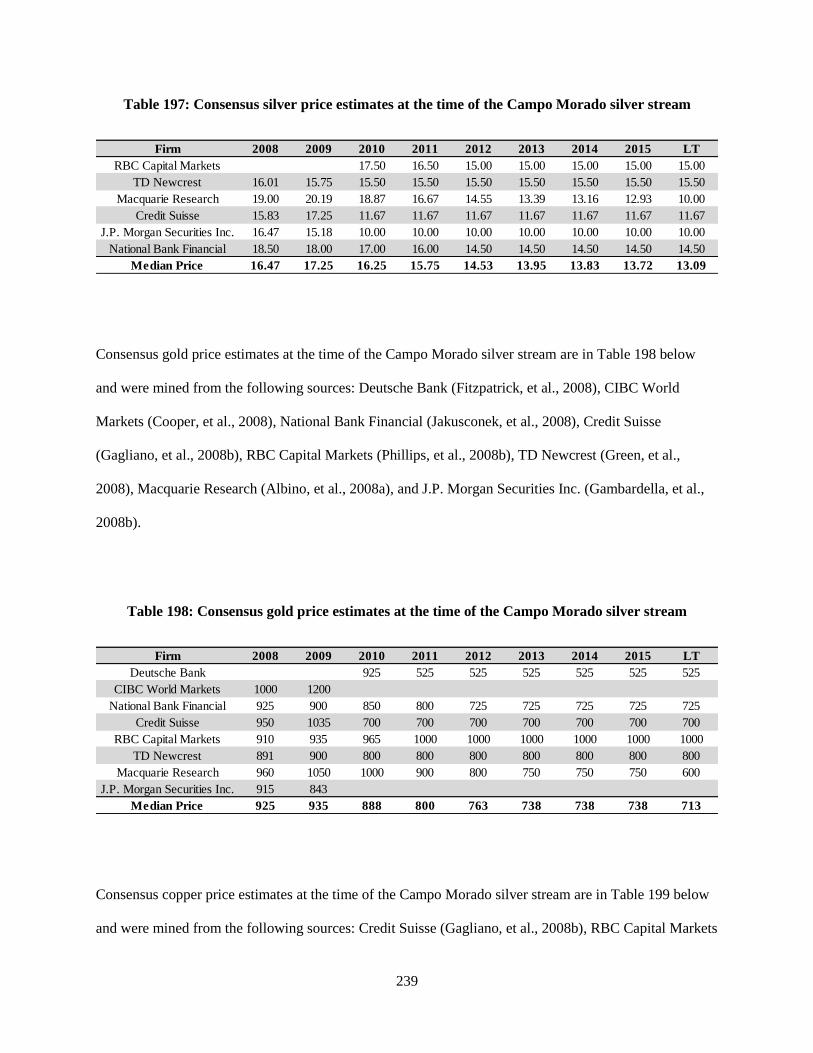

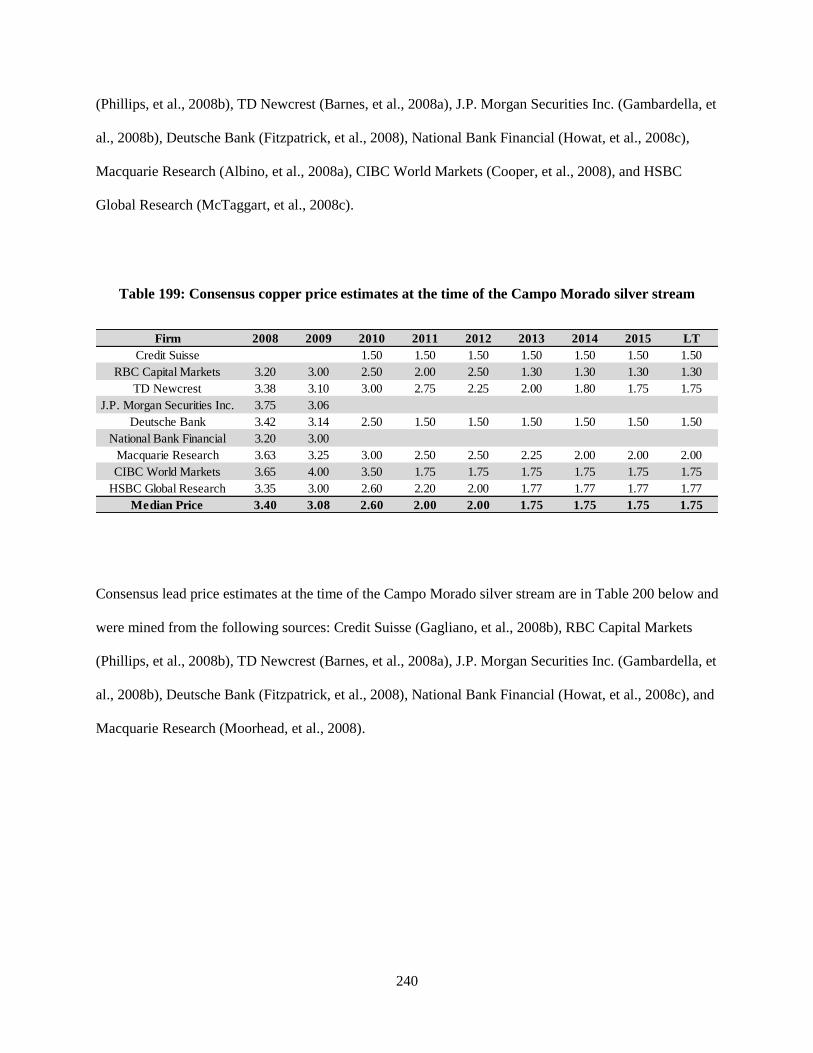

Campo Morado ..................................................................................................................................... 238

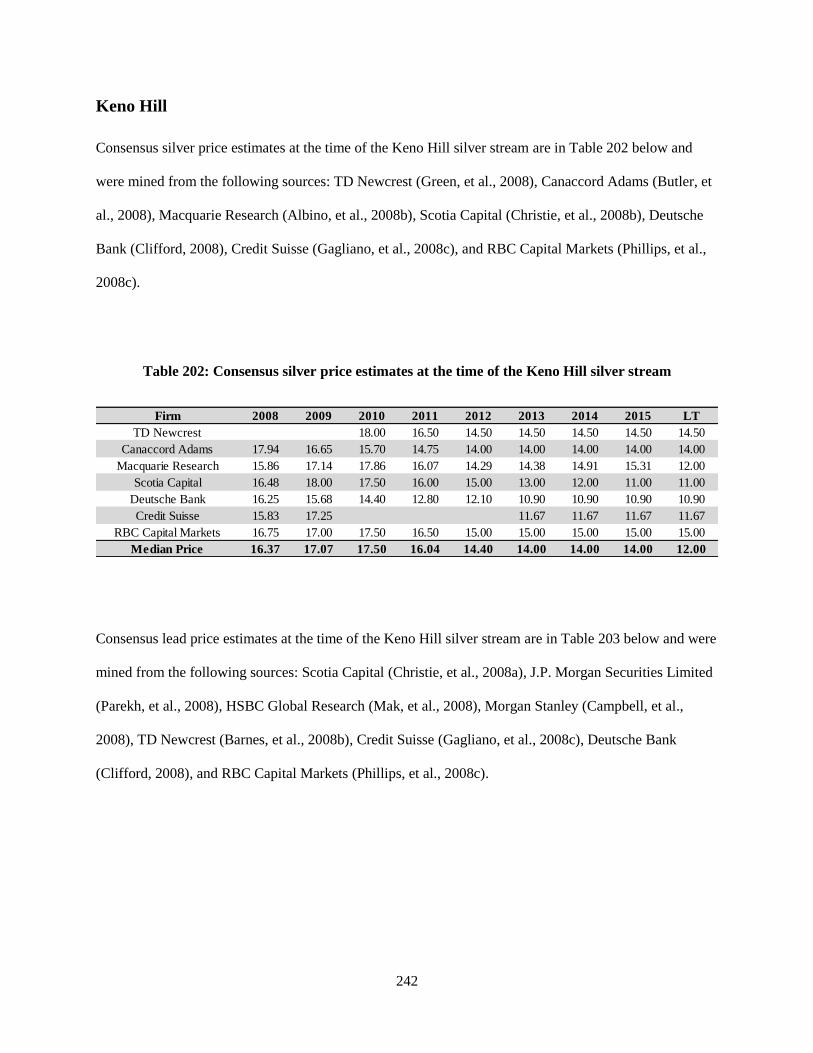

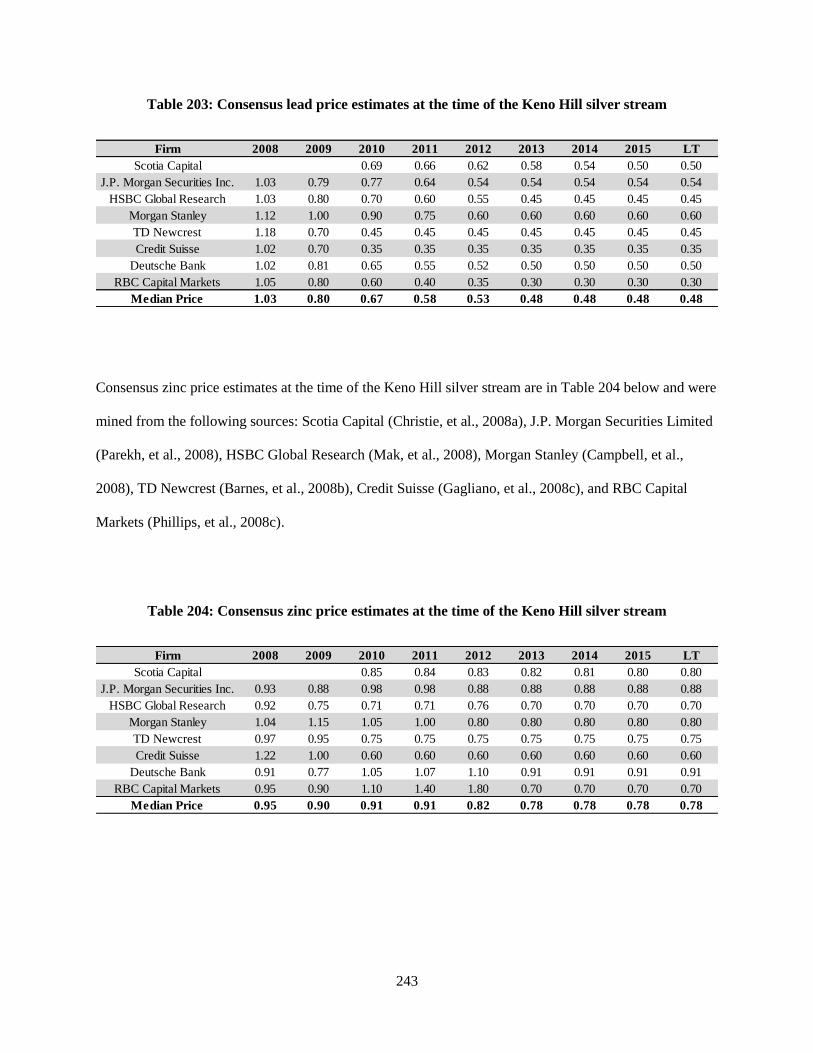

Keno Hill ............................................................................................................................................... 242

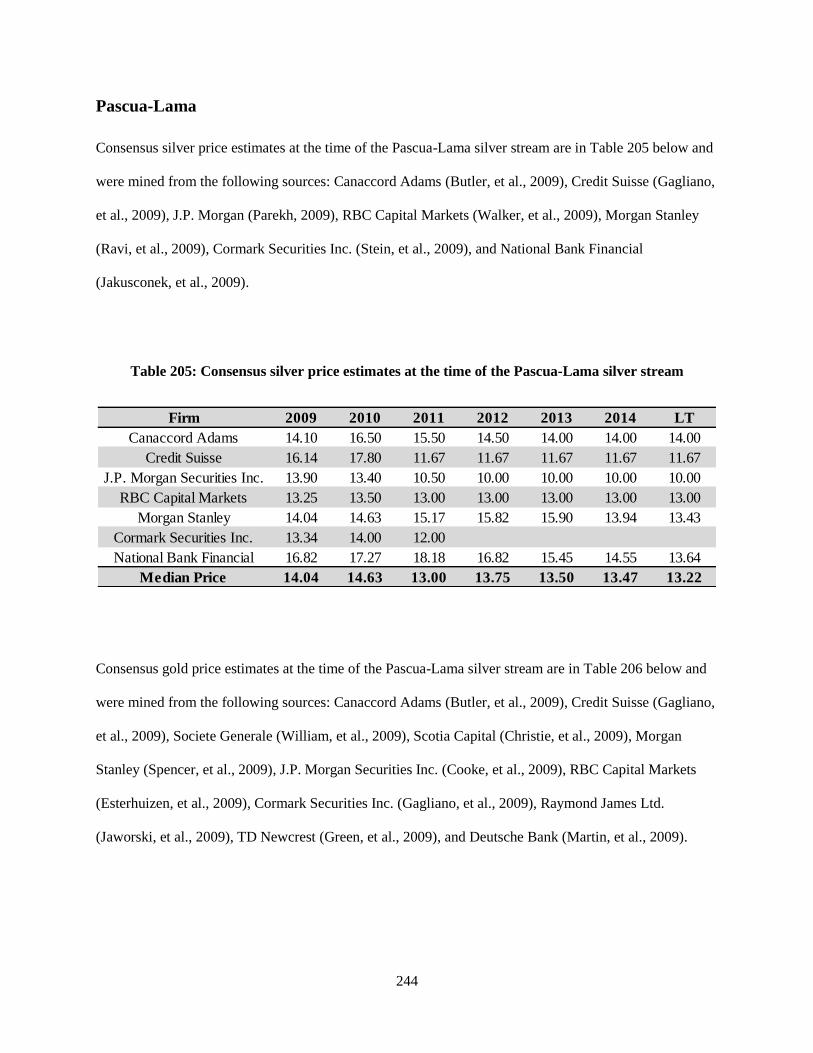

Pascua-Lama ......................................................................................................................................... 244

Rosemont .............................................................................................................................................. 246

Appendix D ............................................................................................................................................... 249

Calculation of Silver Wheaton Stream Cash Flows for 2012, Going Forward ......................................... 249

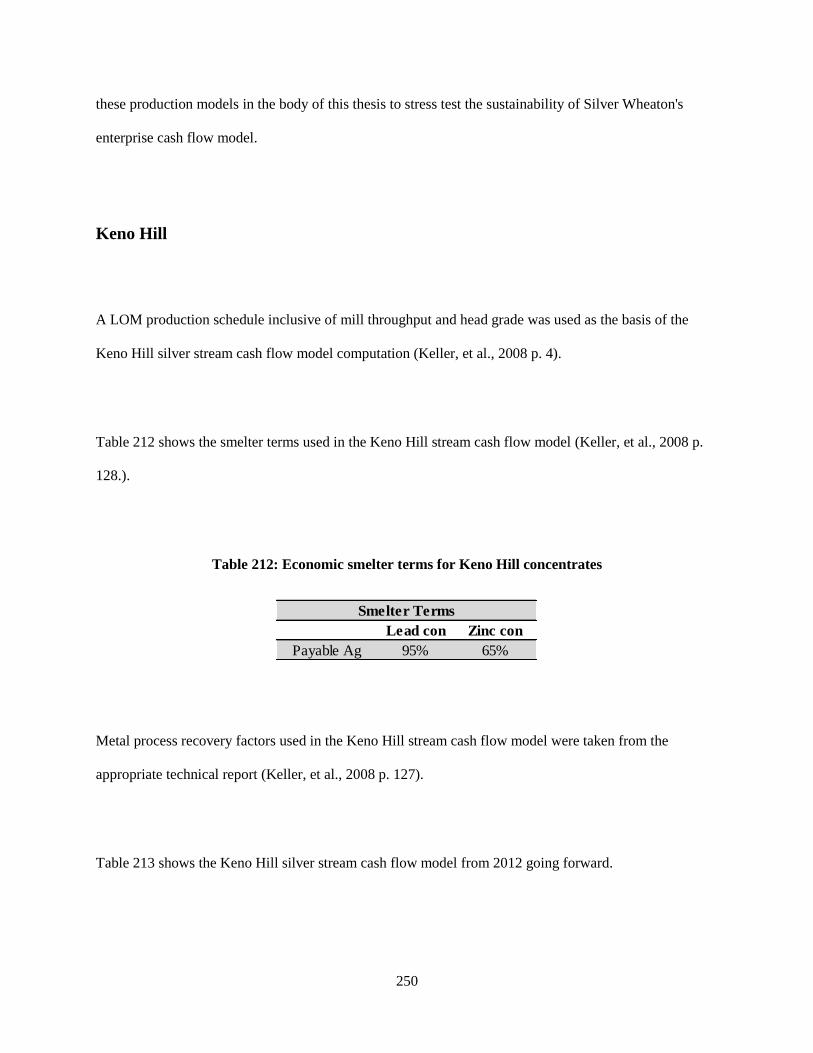

Keno Hill ............................................................................................................................................... 250

Mineral Park.......................................................................................................................................... 251

Zinkgruvan ............................................................................................................................................ 253

San Dimas ............................................................................................................................................. 256

Loma de la Plata.................................................................................................................................... 257

Rosemont .............................................................................................................................................. 259

Yauliyacu .............................................................................................................................................. 261

Cozamin ................................................................................................................................................ 262

Minto ..................................................................................................................................................... 264

Pascua-Lama ......................................................................................................................................... 266

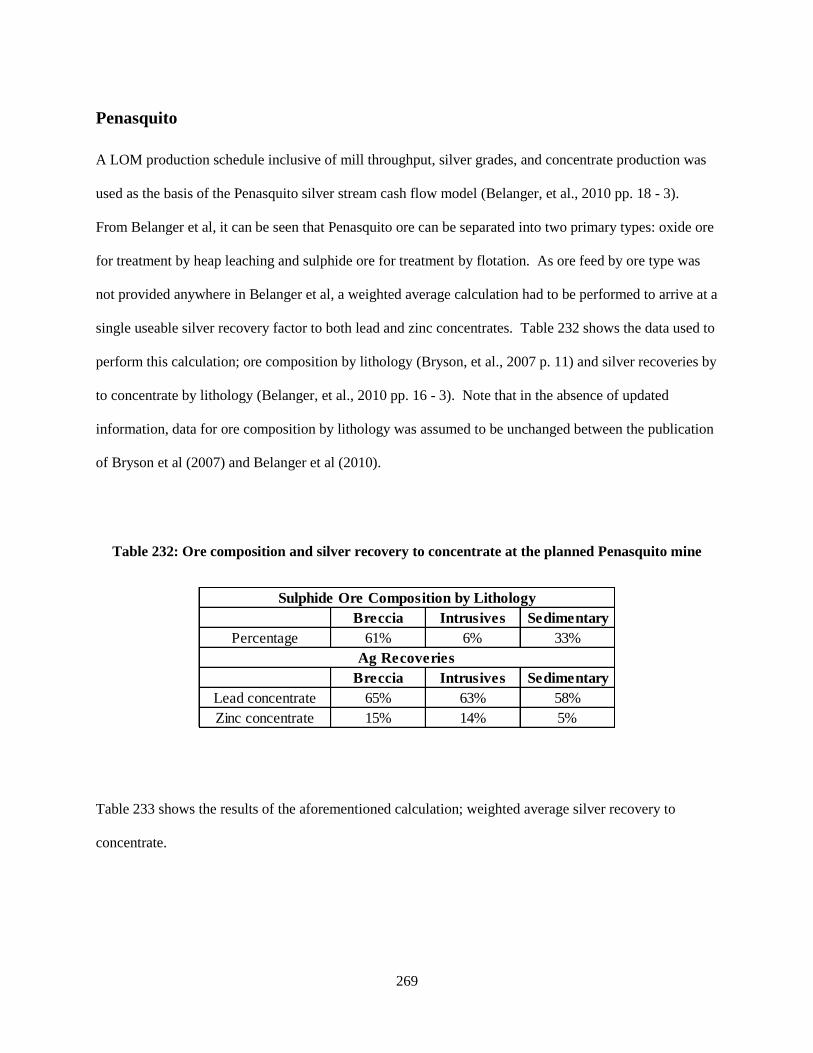

Penasquito ............................................................................................................................................. 269

Stratoni .................................................................................................................................................. 273

Campo Morado ..................................................................................................................................... 273

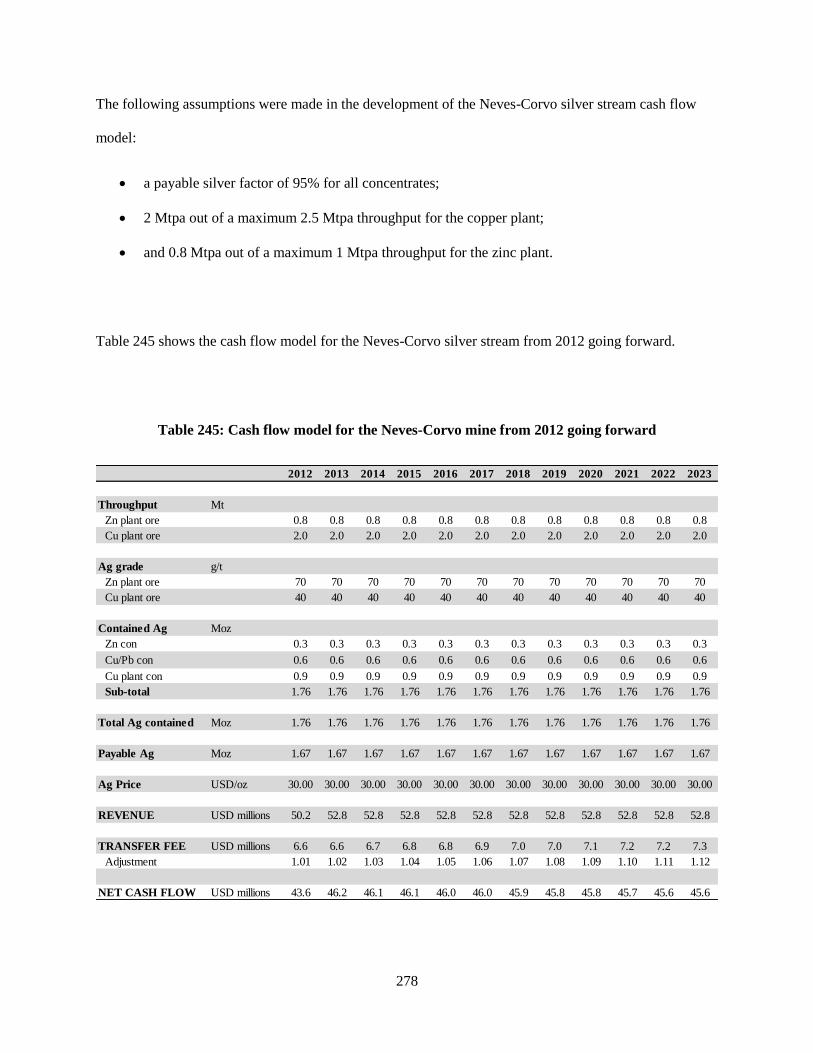

Neves-Corvo ......................................................................................................................................... 277

xiii

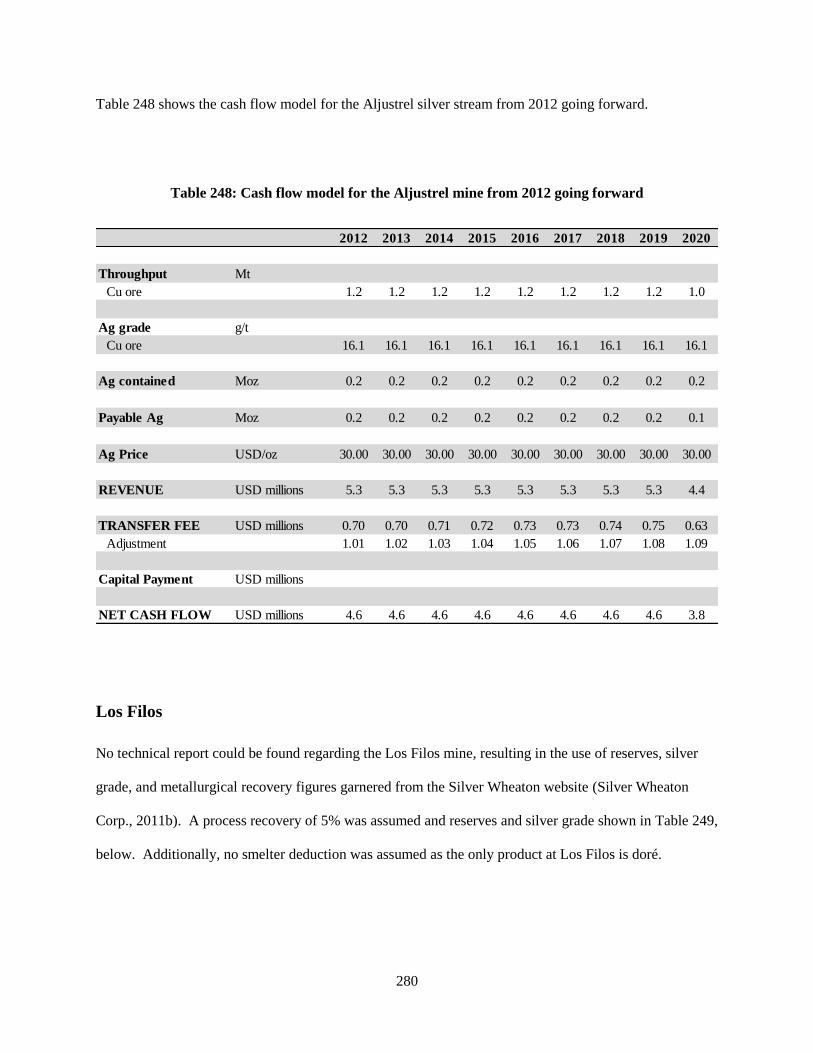

Aljustrel ................................................................................................................................................ 279

Los Filos ............................................................................................................................................... 280

Appendix E ............................................................................................................................................... 282

Pertinent Background Information of Silver Wheaton's Operating Partners ............................................ 282

Lundin Mining .................................................................................................................................. 282

Glencore ............................................................................................................................................ 282

European Goldfields Limited ............................................................................................................ 283

Goldcorp ........................................................................................................................................... 283

Mercator Minerals ............................................................................................................................. 284

Farallon ............................................................................................................................................. 284

Alexco ............................................................................................................................................... 284

Barrick............................................................................................................................................... 285

Augusta ............................................................................................................................................. 285

xiv

List of Figures

Figure 1: Cumulative market capitalization of commodity streaming companies, 2004-2011. Sources:

TSX and SEDAR .......................................................................................................................................... 3

Figure 2: Share price performance of major commodity streaming firms, 2004-2011. Source: TSX .......... 5

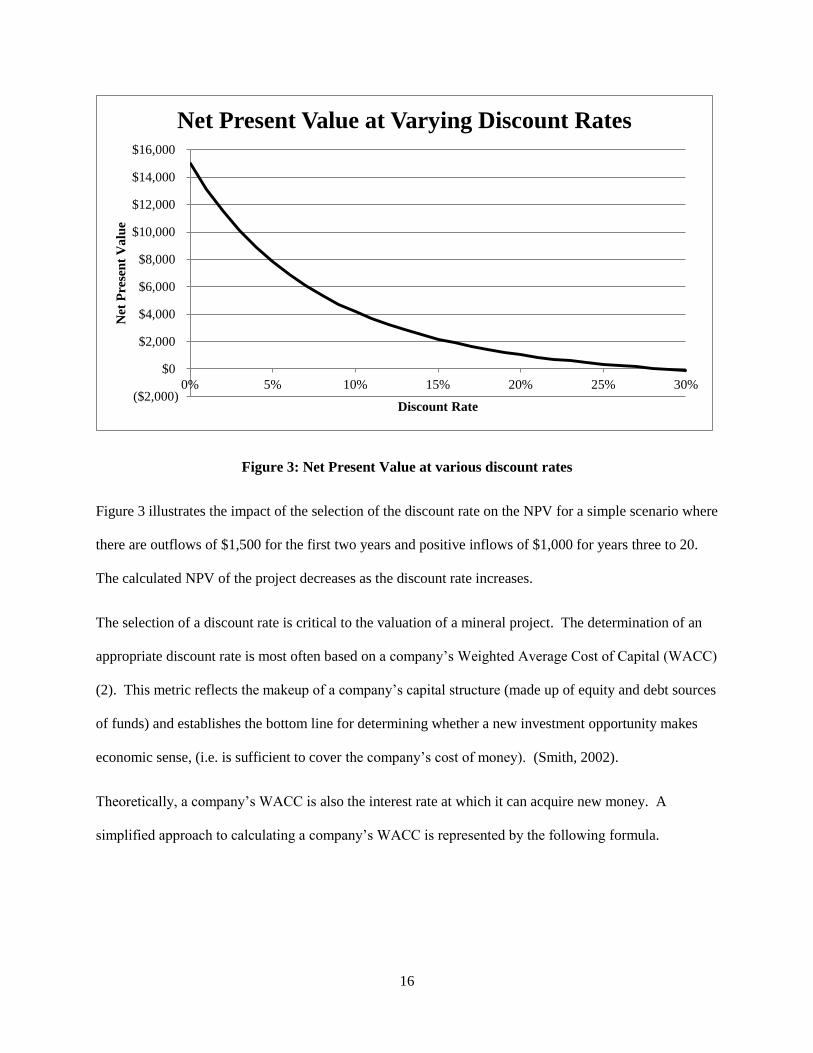

Figure 3: Net Present Value at various discount rates ................................................................................ 16

Figure 4: Fabrication demand for silver, 2002-2011. Source: The Silver Institute .................................... 58

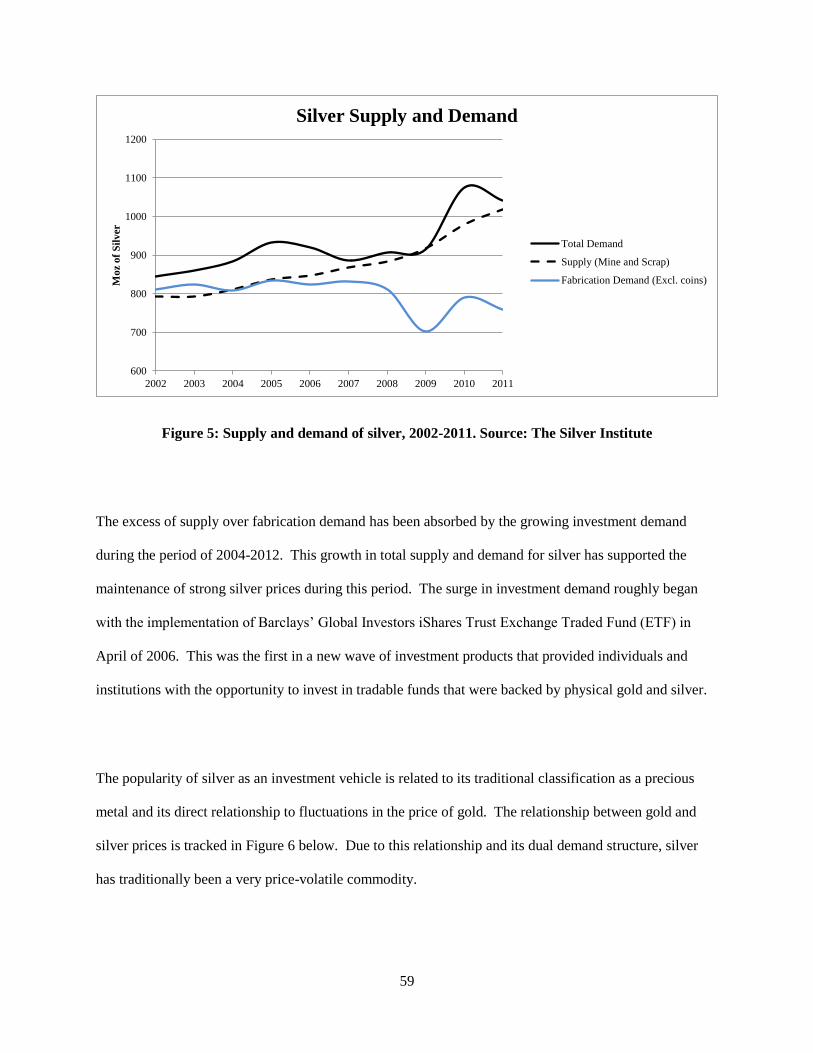

Figure 5: Supply and demand of silver, 2002-2011. Source: The Silver Institute ...................................... 59

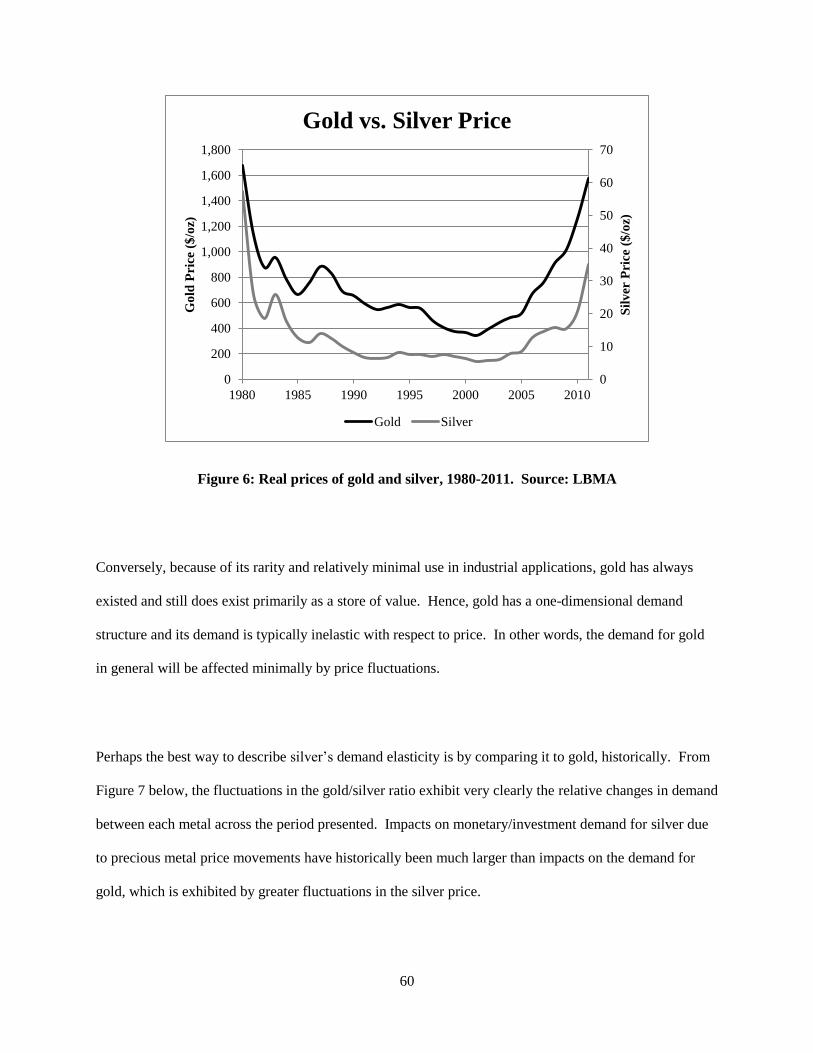

Figure 6: Real prices of gold and silver, 1980-2011. Source: LBMA ....................................................... 60

Figure 7: Gold to silver price ratio from 1980-2011. Source: LBMA ........................................................ 61

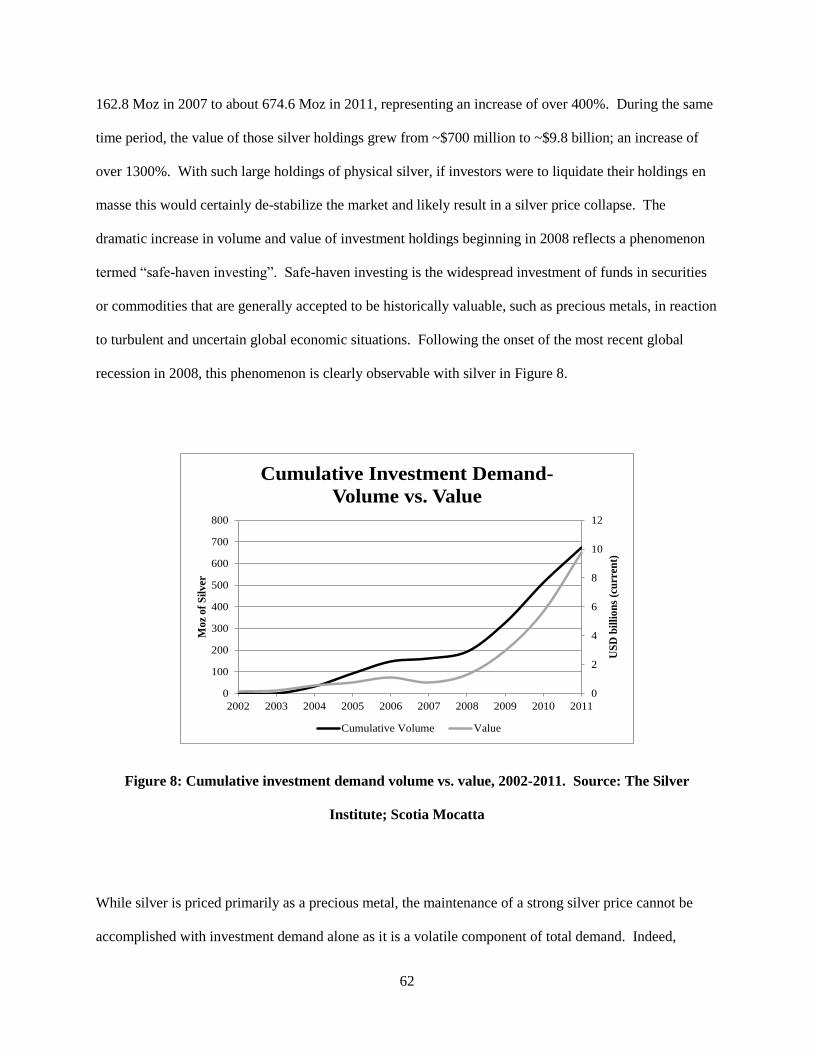

Figure 8: Cumulative investment demand volume vs. value, 2002-2011. Source: The Silver Institute;

Scotia Mocatta ............................................................................................................................................ 62

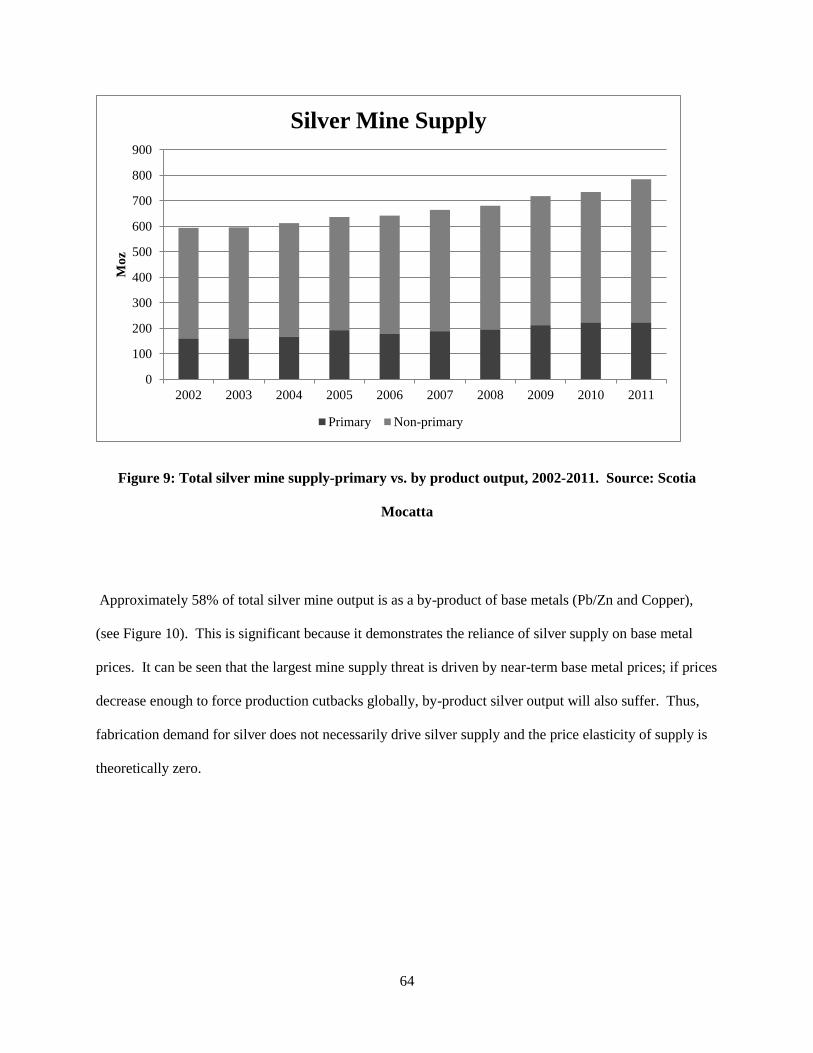

Figure 9: Total silver mine supply-primary vs. by product output, 2002-2011. Source: Scotia Mocatta .. 64

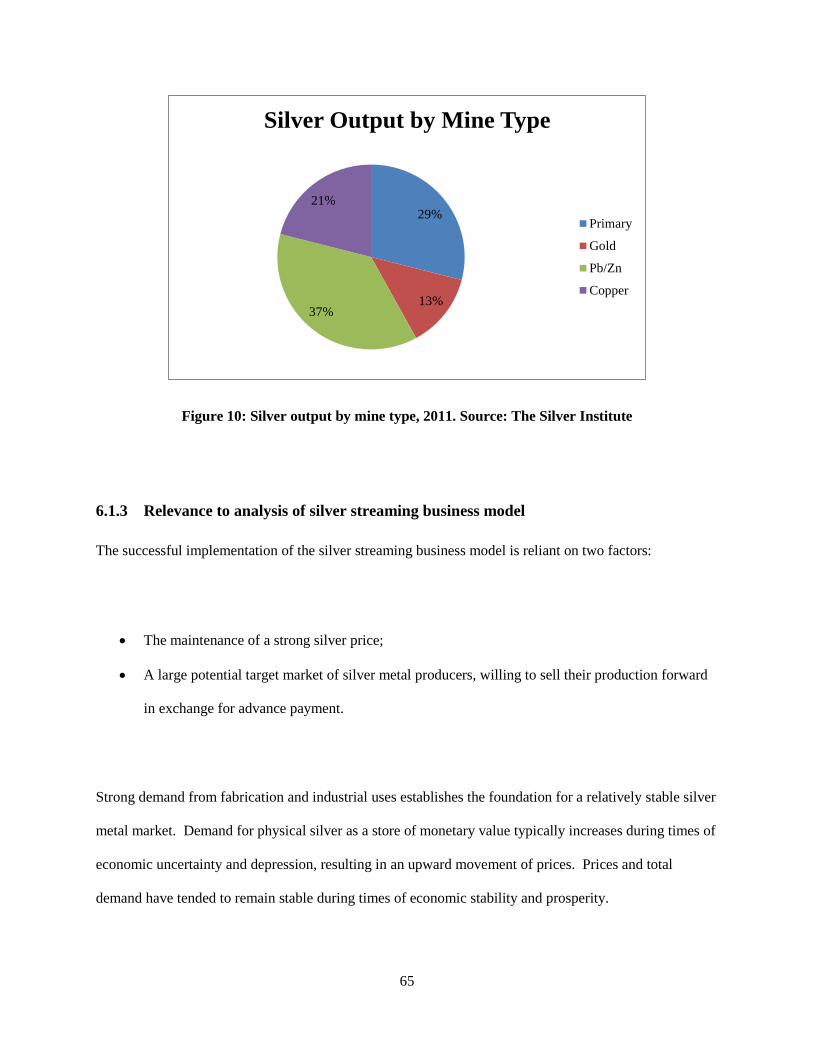

Figure 10: Silver output by mine type, 2011. Source: The Silver Institute................................................. 65

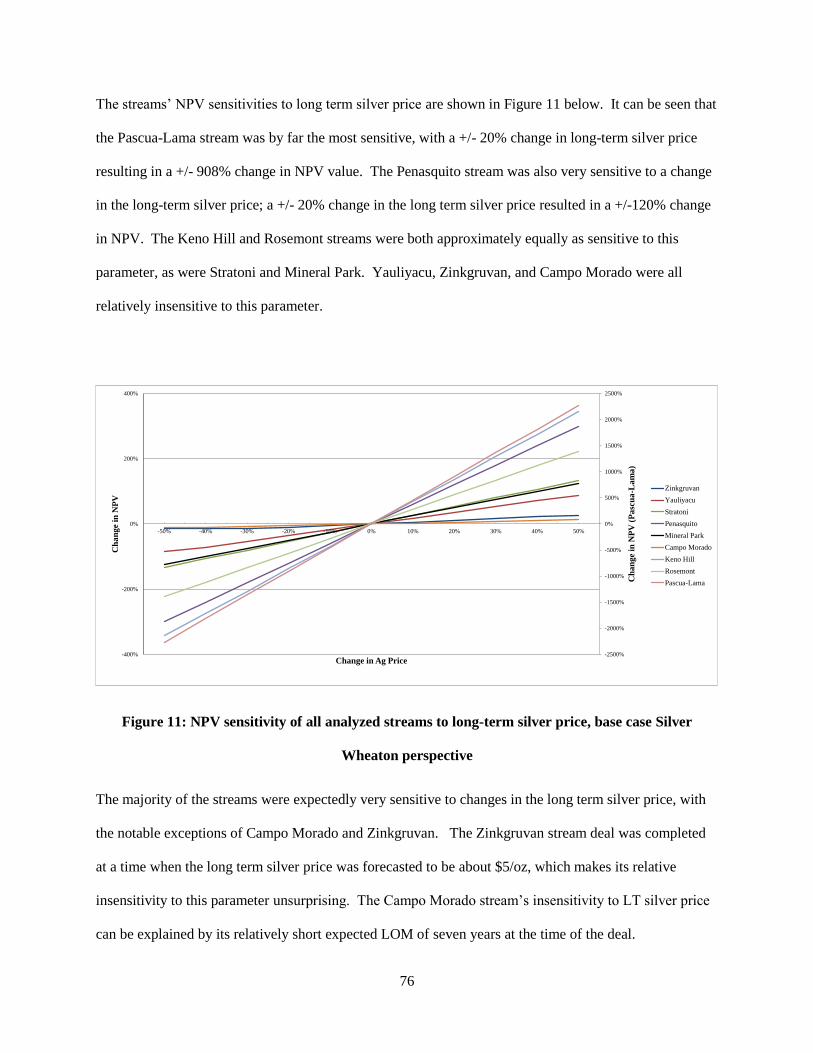

Figure 11: NPV sensitivity of all analyzed streams to long-term silver price, base case Silver Wheaton

perspective .................................................................................................................................................. 76

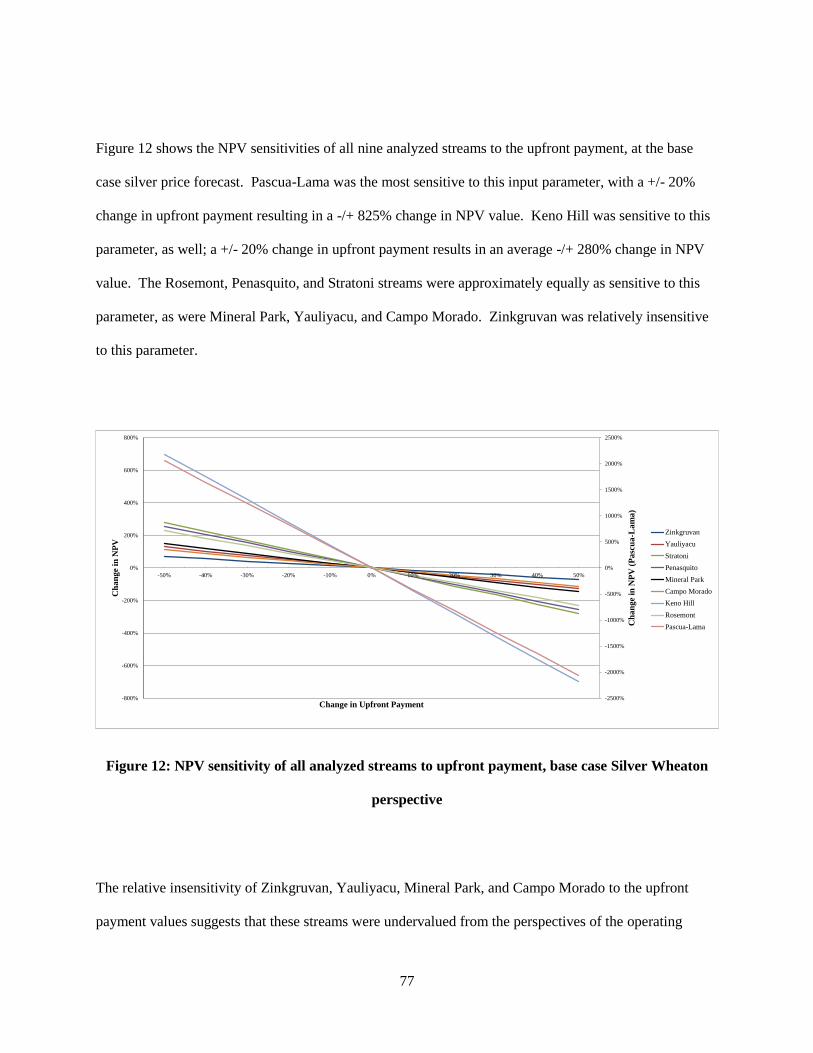

Figure 12: NPV sensitivity of all analyzed streams to upfront payment, base case Silver Wheaton

perspective .................................................................................................................................................. 77

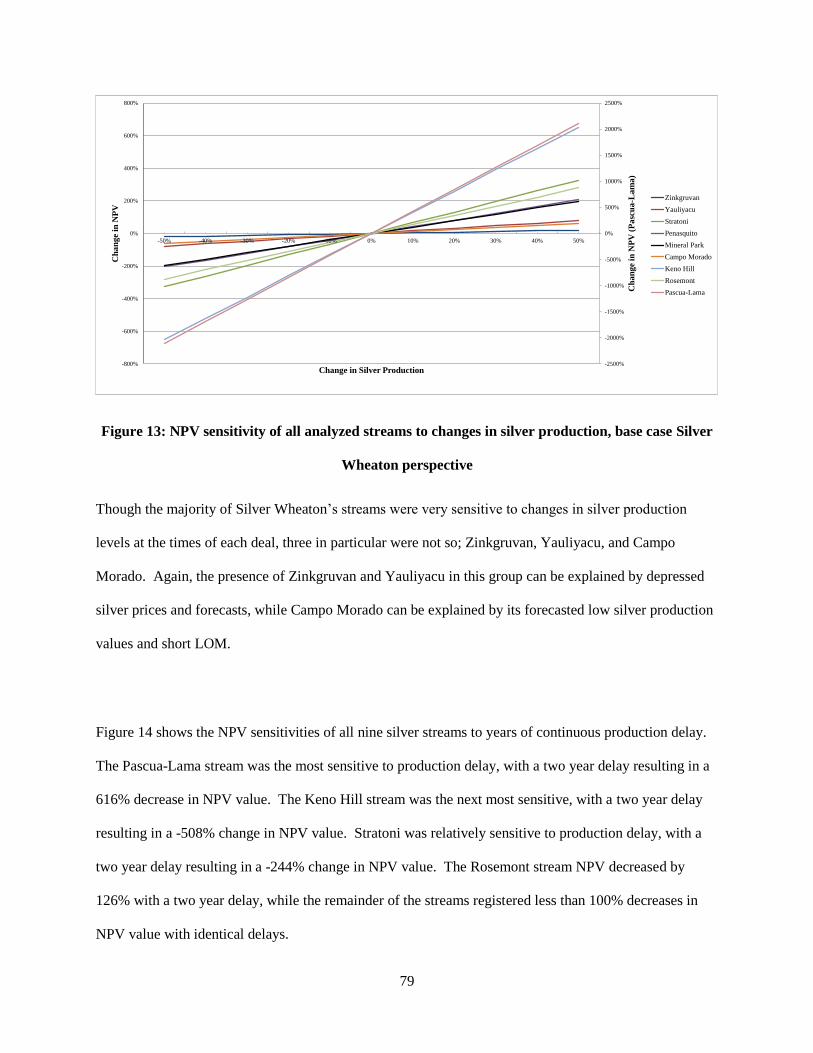

Figure 13: NPV sensitivity of all analyzed streams to changes in silver production, base case Silver

Wheaton perspective ................................................................................................................................... 79

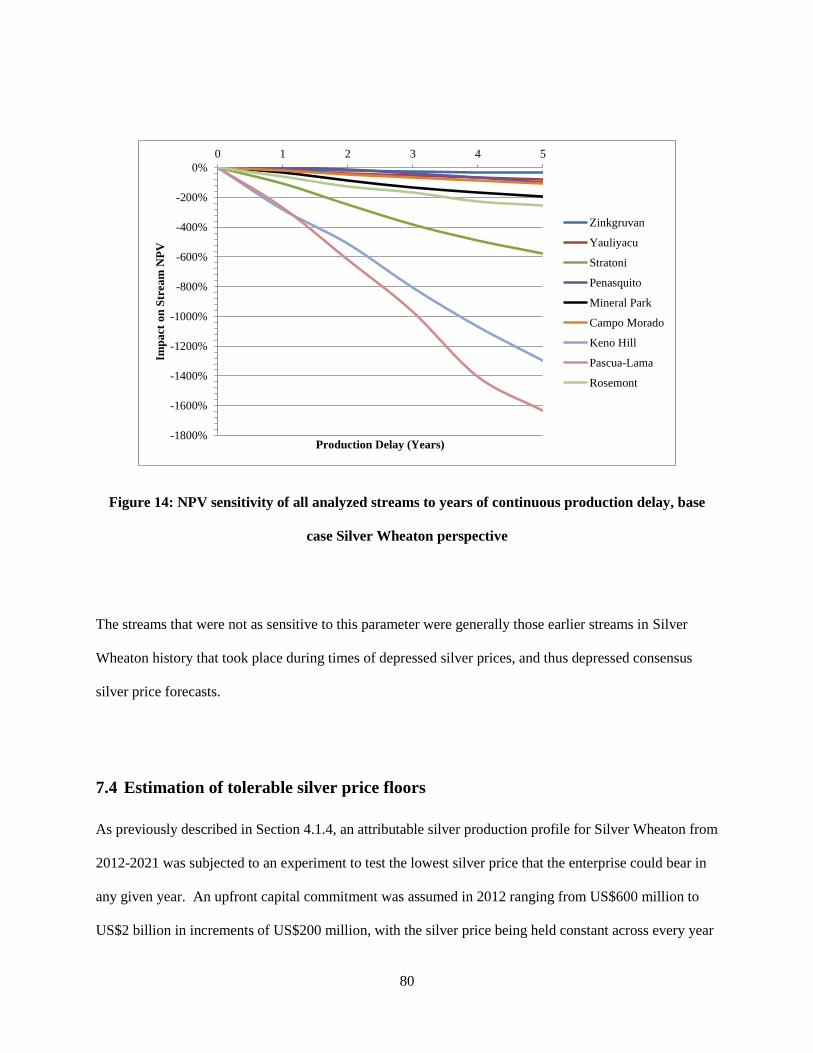

Figure 14: NPV sensitivity of all analyzed streams to years of continuous production delay, base case

Silver Wheaton perspective ........................................................................................................................ 80

Figure 15: NPV sensitivity of all analyzed streams to long-term silver price, base case operating partner

perspective .................................................................................................................................................. 91

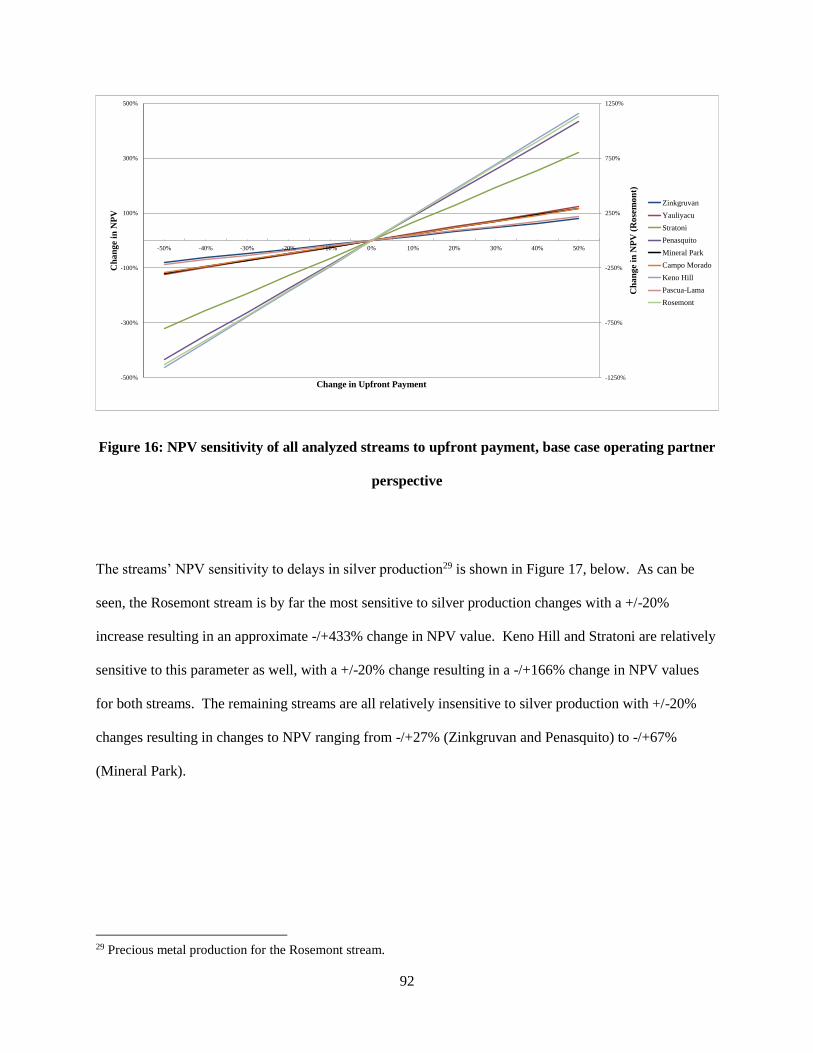

Figure 16: NPV sensitivity of all analyzed streams to upfront payment, base case operating partner

perspective .................................................................................................................................................. 92

xv

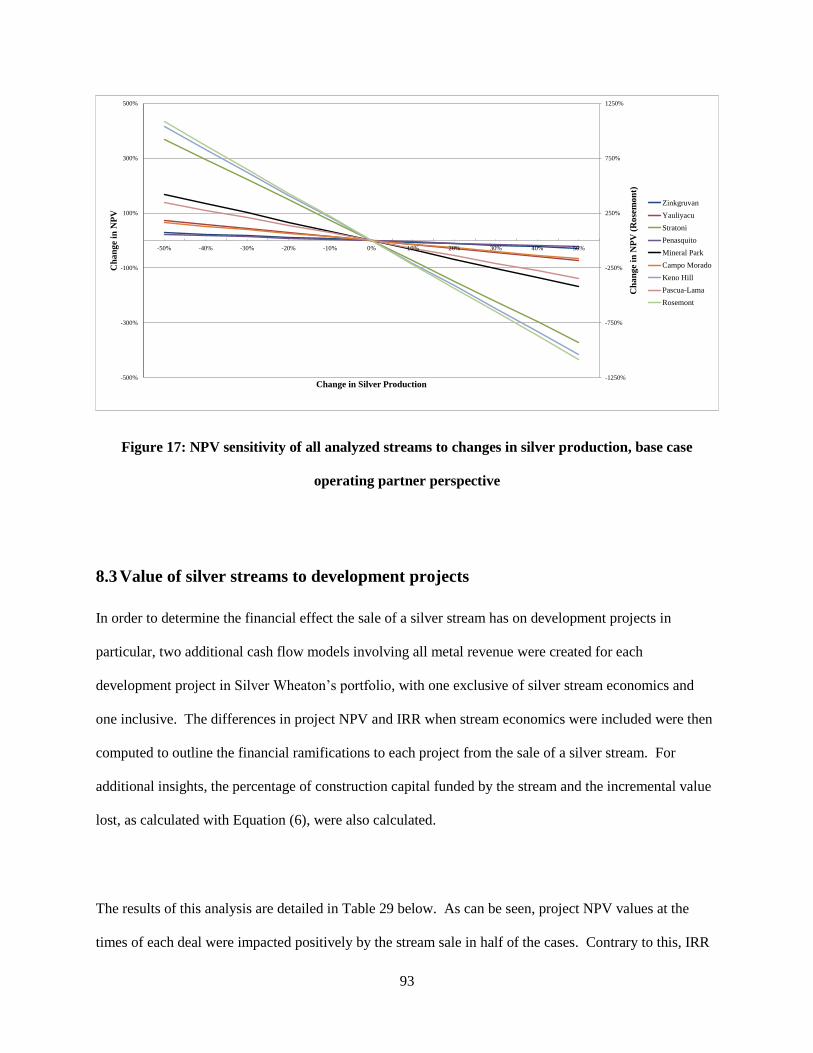

Figure 17: NPV sensitivity of all analyzed streams to changes in silver production, base case operating

partner perspective ...................................................................................................................................... 93

Figure 18: Total value of global mining equity financings (C$ billions), 1999-2012. Source:

PricewaterhouseCoopers ........................................................................................................................... 105

List of Tables

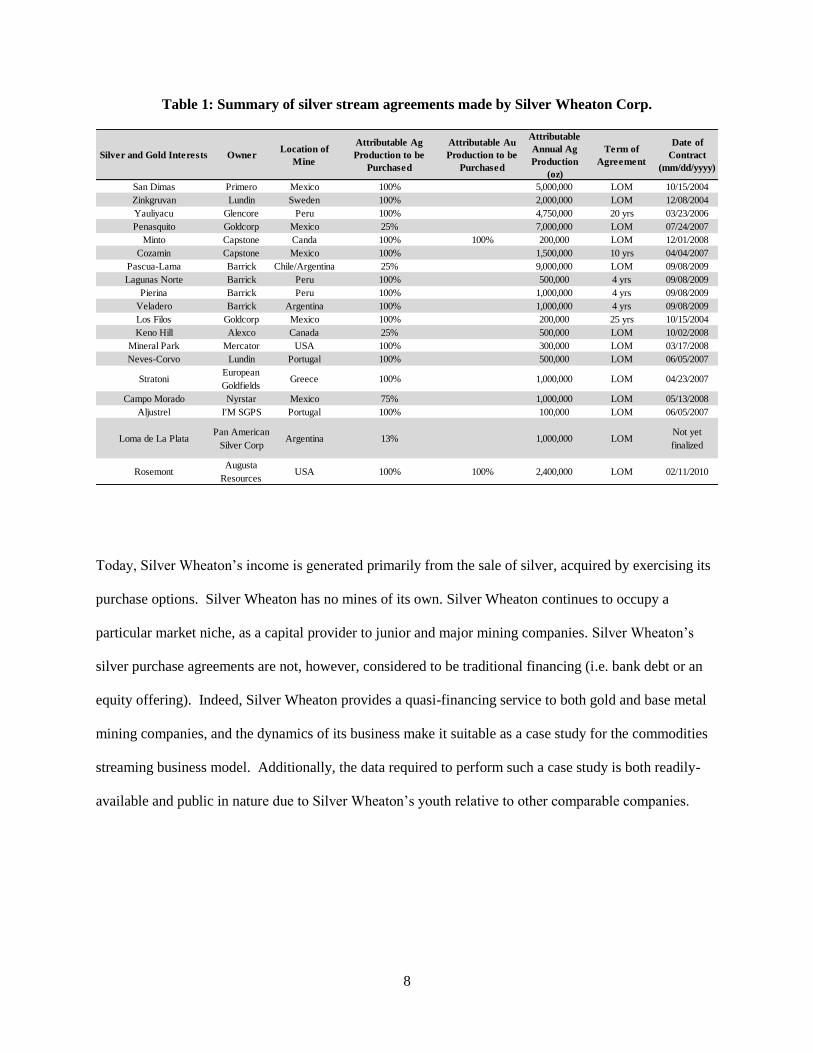

Table 1: Summary of silver stream agreements made by Silver Wheaton Corp. ......................................... 8

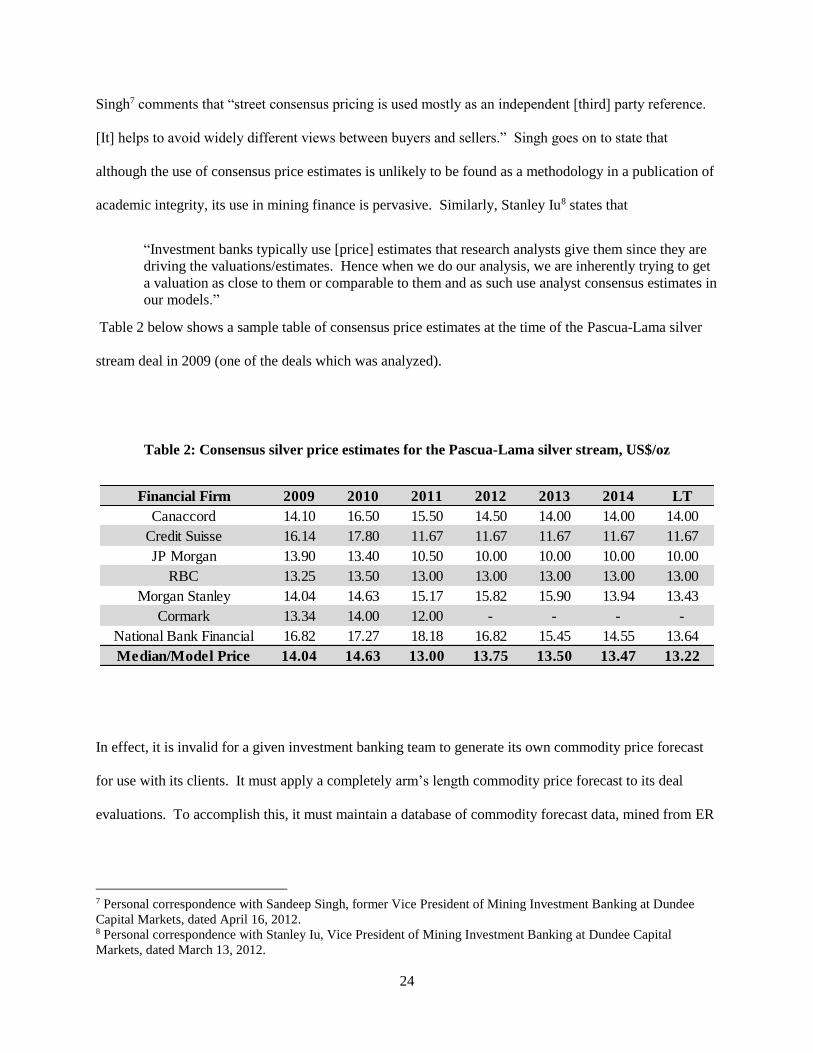

Table 2: Consensus silver price estimates for the Pascua-Lama silver stream, US$/oz ............................. 24

Table 3: Silver streams selected for inclusion in Silver Wheaton case study ............................................. 30

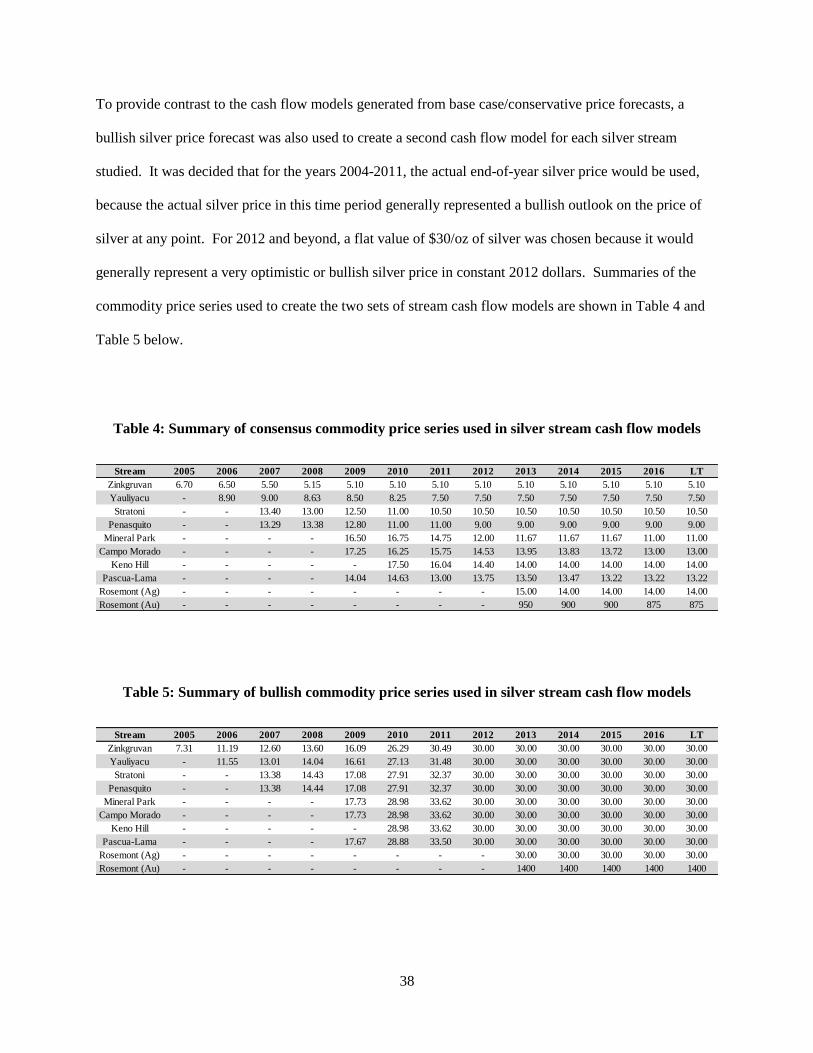

Table 4: Summary of consensus commodity price series used in silver stream cash flow models ............ 38

Table 5: Summary of bullish commodity price series used in silver stream cash flow models .................. 38

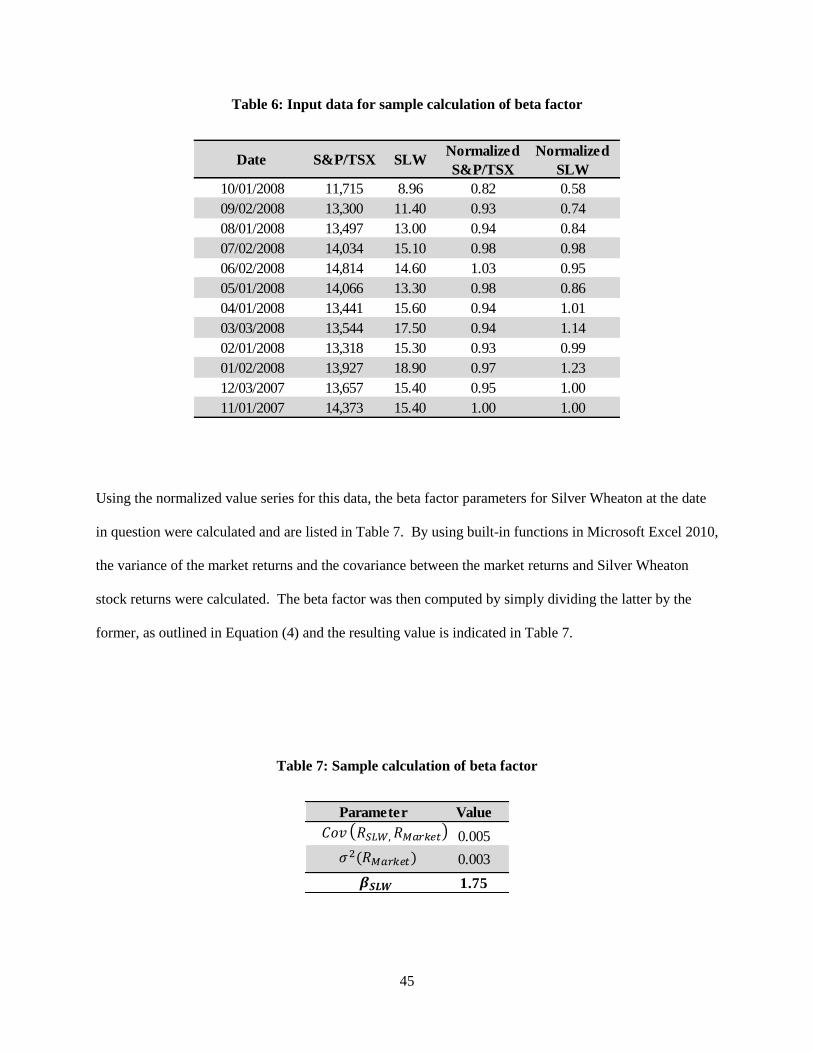

Table 6: Input data for sample calculation of beta factor ............................................................................ 45

Table 7: Sample calculation of beta factor .................................................................................................. 45

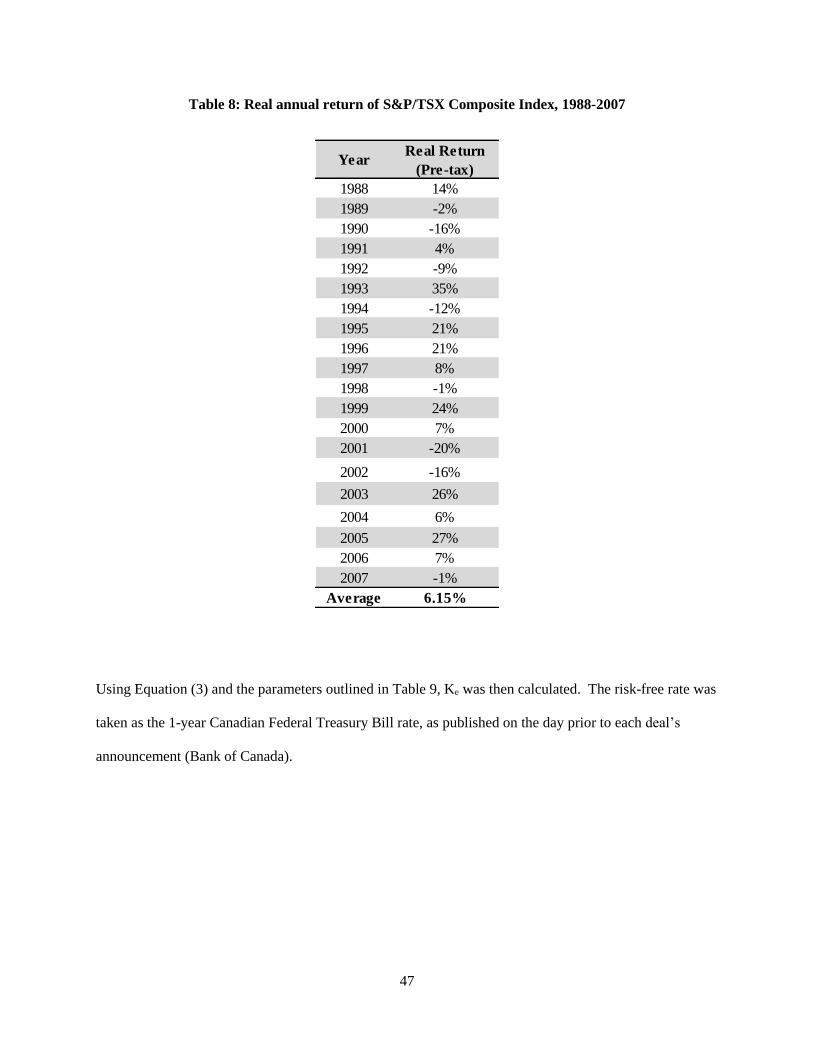

Table 8: Real annual return of S&P/TSX Composite Index, 1988-2007 .................................................... 47

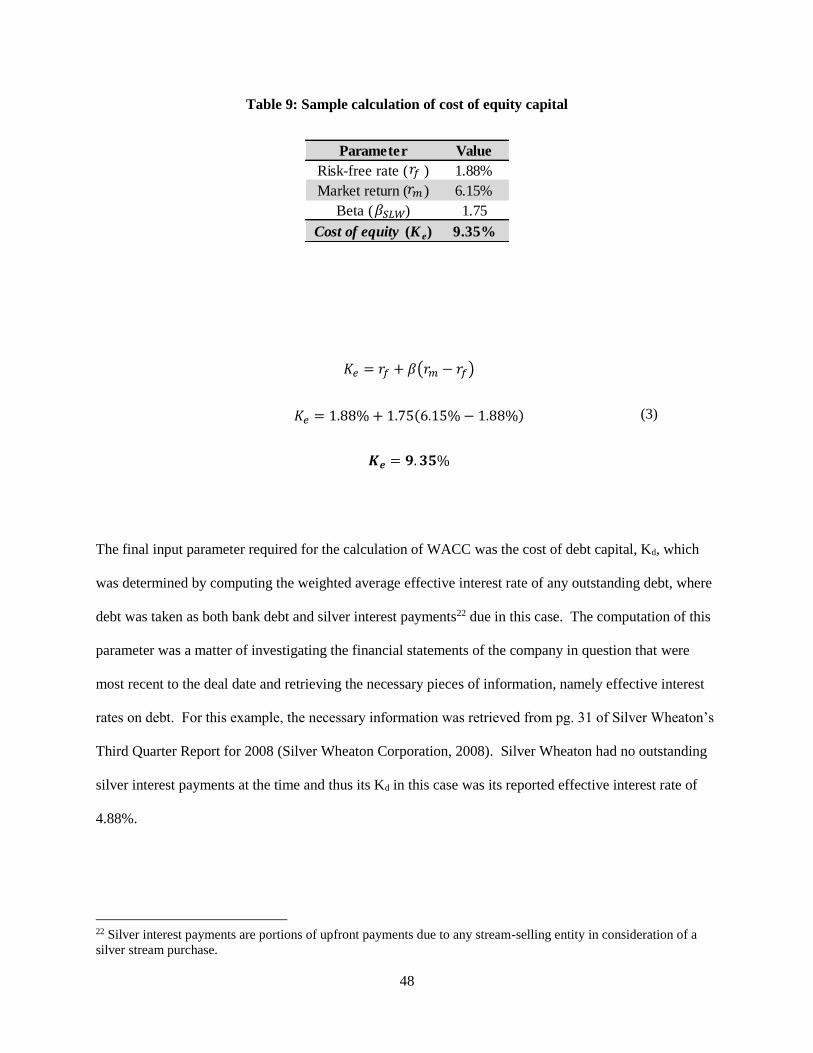

Table 9: Sample calculation of cost of equity capital ................................................................................. 48

Table 10: Sample calculation of WACC ..................................................................................................... 49

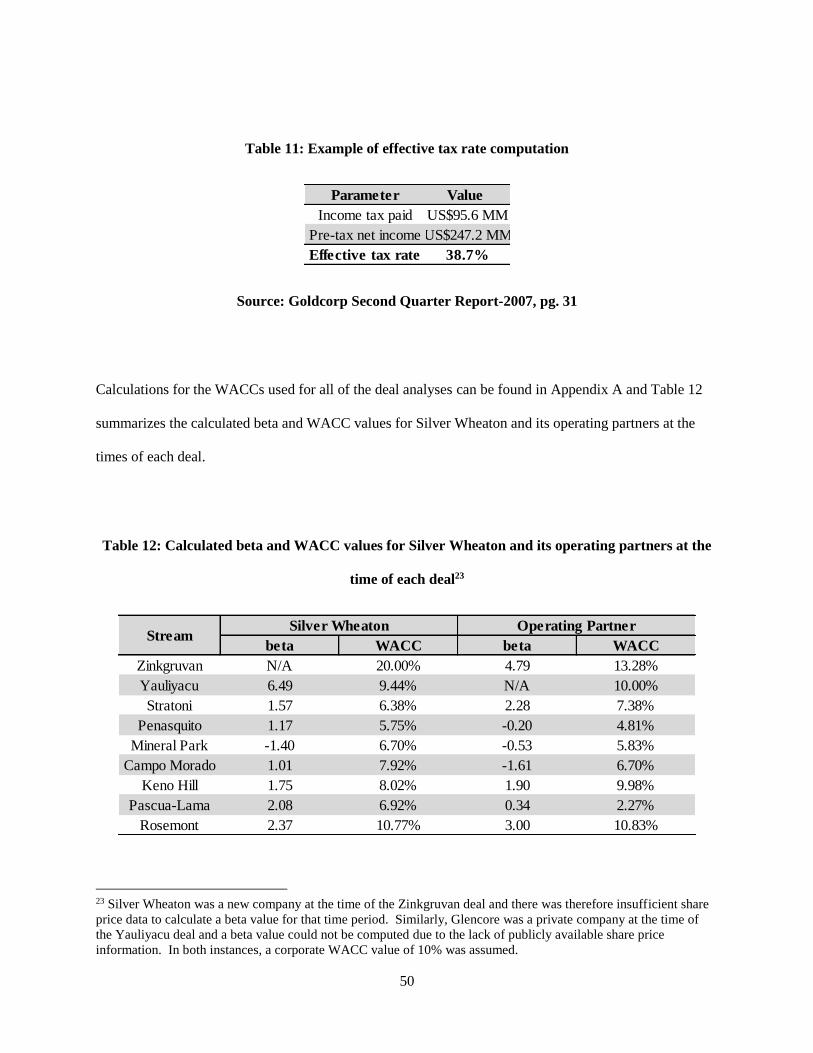

Table 11: Example of effective tax rate computation ................................................................................. 50

Table 12: Calculated beta and WACC values for Silver Wheaton and its operating partners at the time of

each deal ..................................................................................................................................................... 50

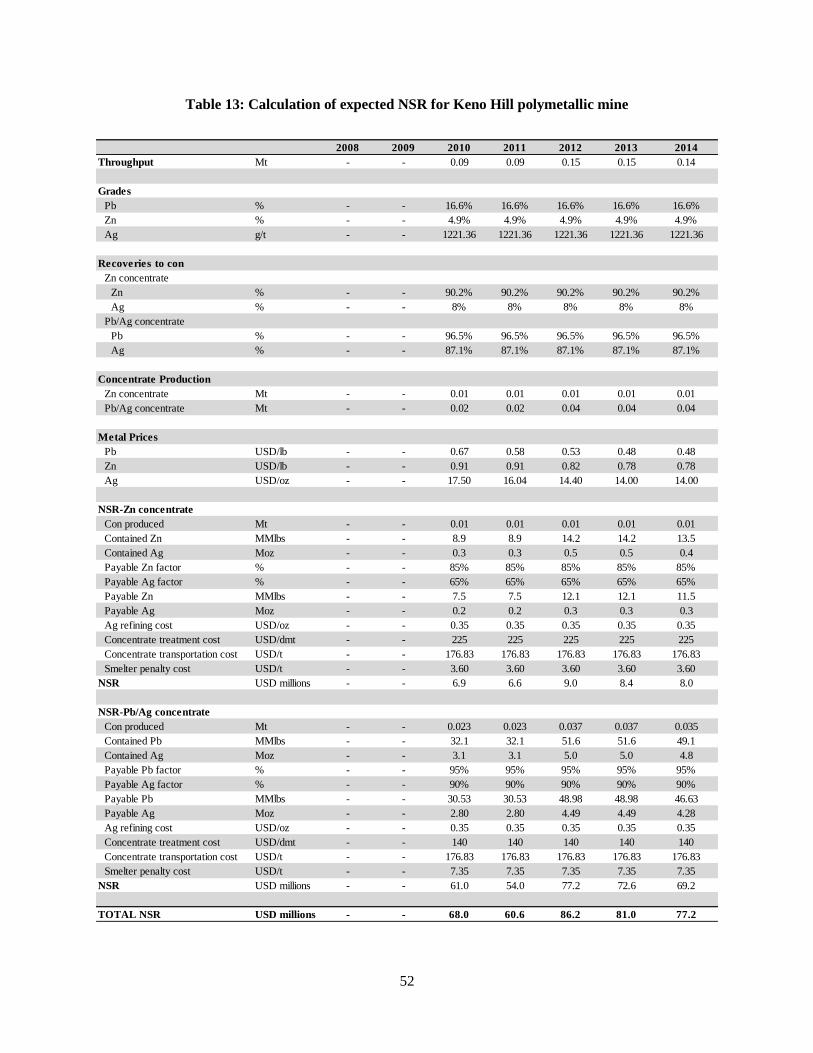

Table 13: Calculation of expected NSR for Keno Hill polymetallic mine ................................................. 52

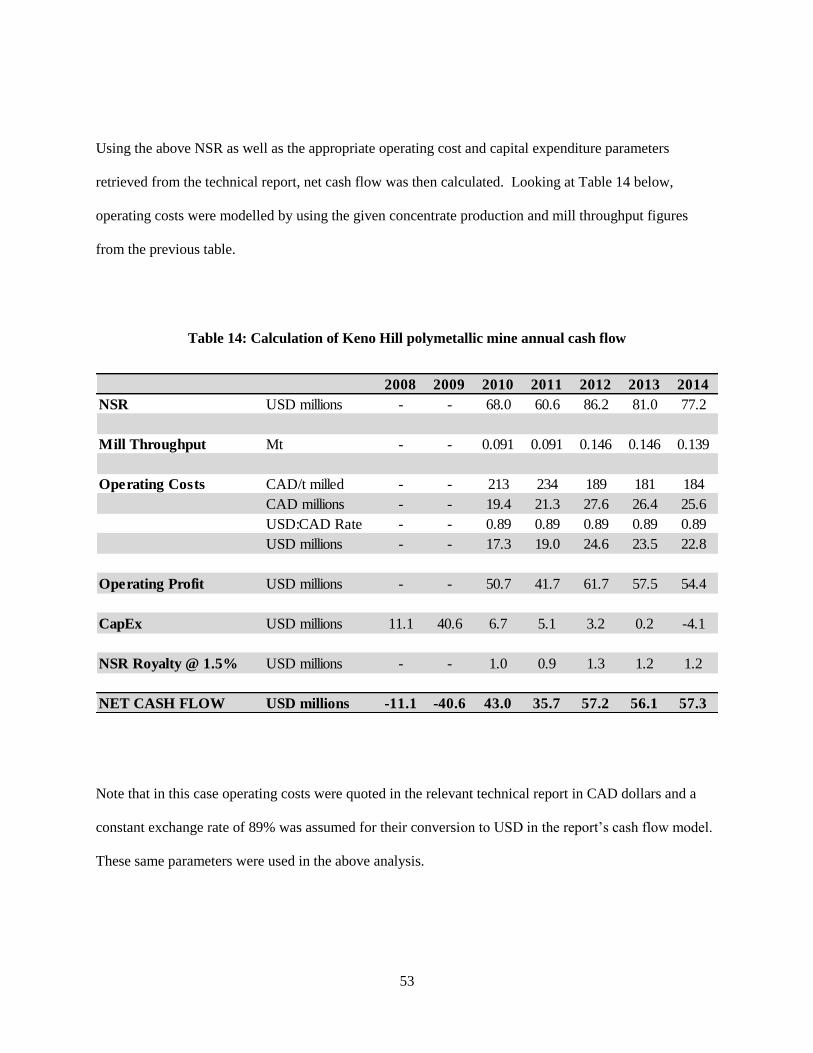

Table 14: Calculation of Keno Hill polymetallic mine annual cash flow ................................................... 53

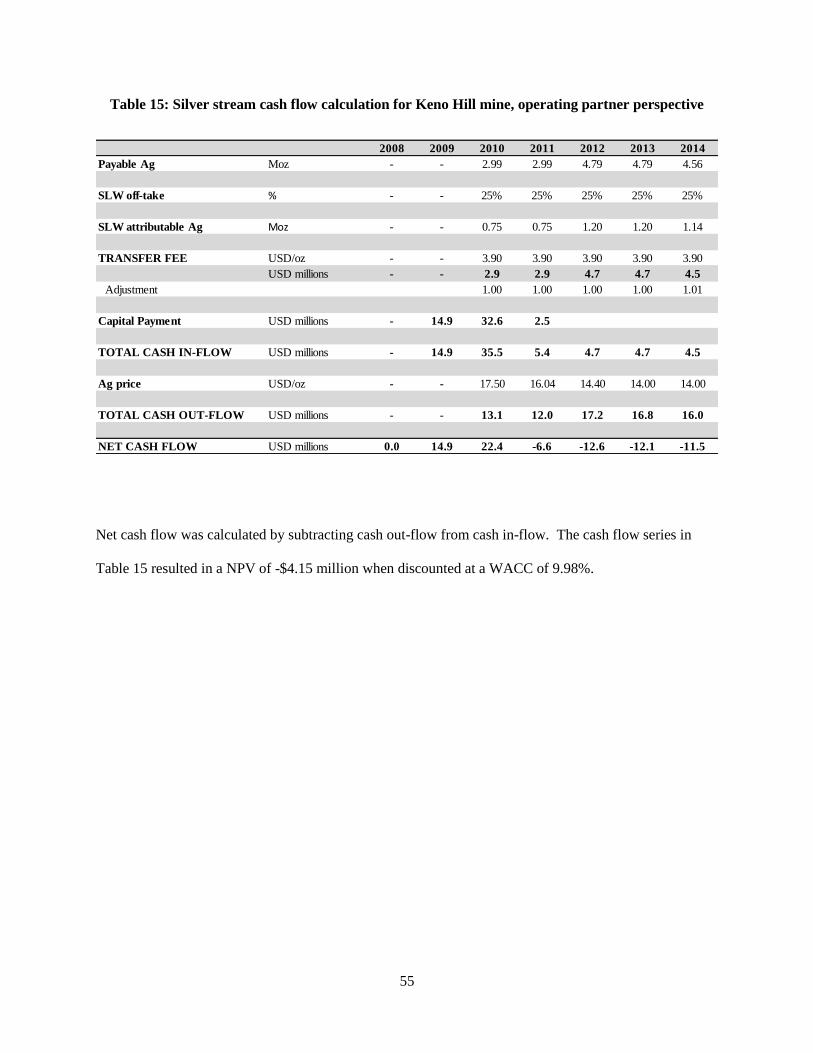

Table 15: Silver stream cash flow calculation for Keno Hill mine, operating partner perspective ............ 55

Table 16: Silver stream cash flow calculation of Keno Hill mine, Silver Wheaton perspective ................ 56

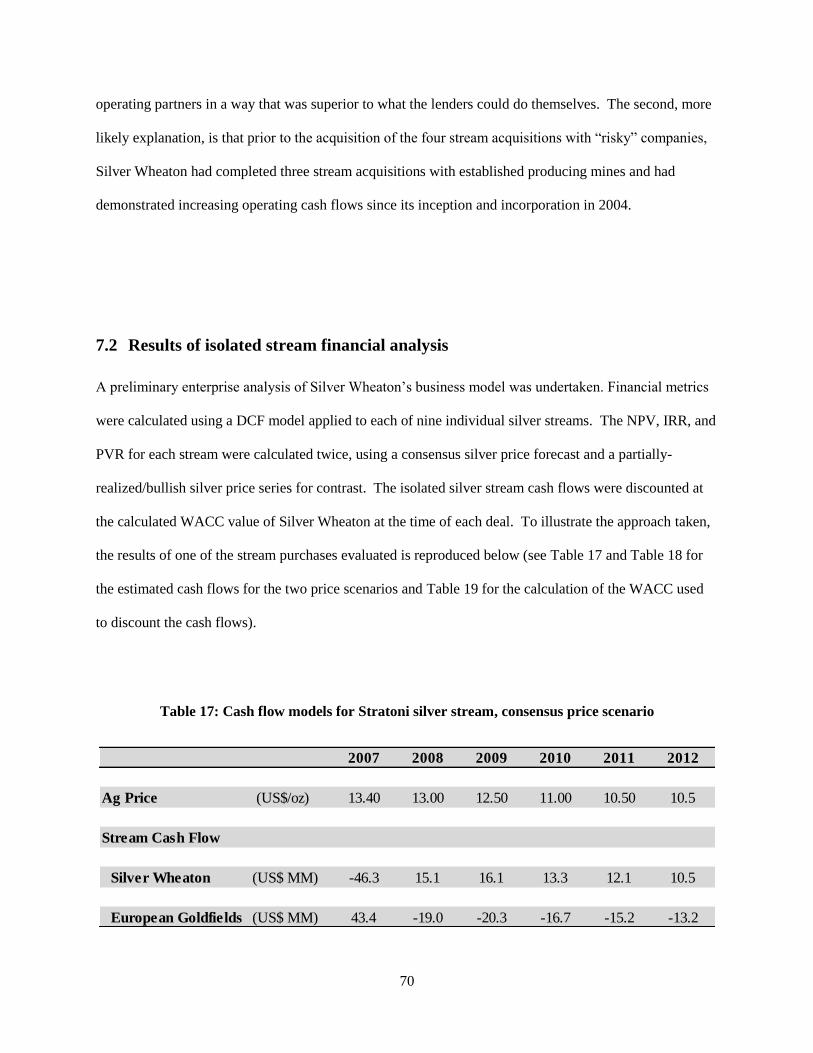

Table 17: Cash flow models for Stratoni silver stream, consensus price scenario ..................................... 70

Table 18: Cash flow models for Stratoni silver stream, bullish price scenario ........................................... 71

xvi

Table 19: Calculation of WACCs used to discount Stratoni silver stream cash flows ............................... 71

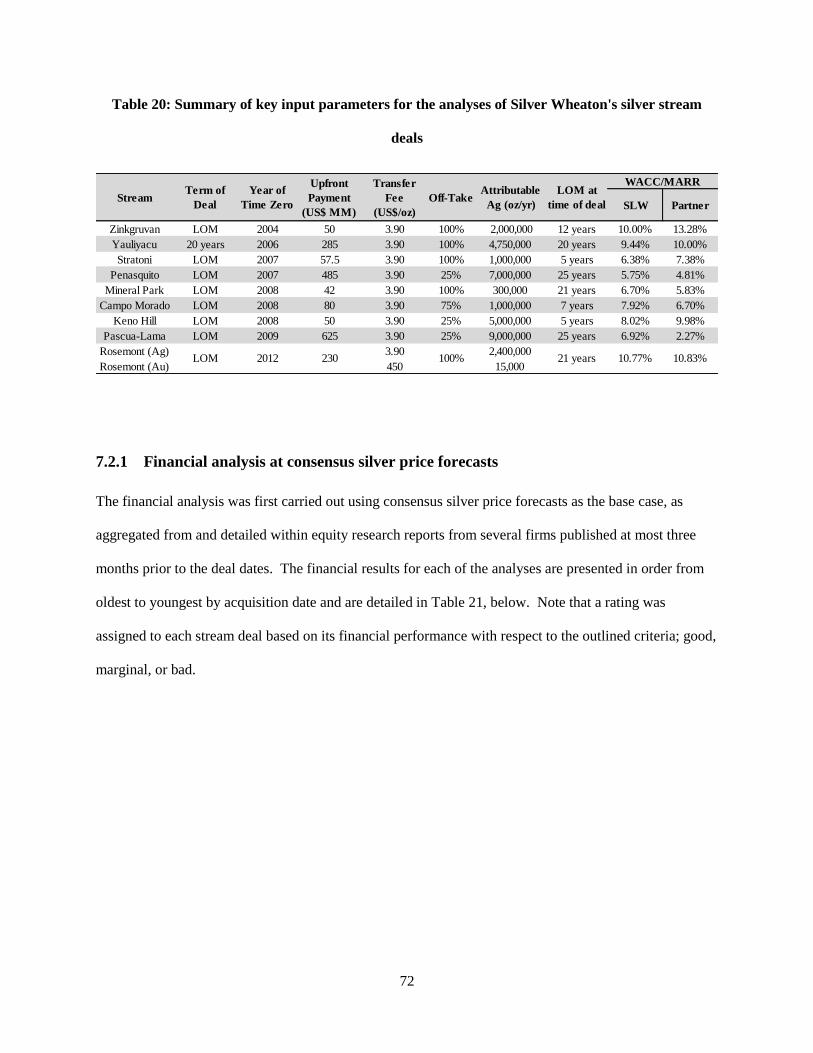

Table 20: Summary of key input parameters for the analyses of Silver Wheaton's silver stream deals ..... 72

Table 21: Results of base case silver stream financial analysis, Silver Wheaton perspective .................... 73

Table 22: Results of bullish silver stream financial analysis, Silver Wheaton perspective ........................ 74

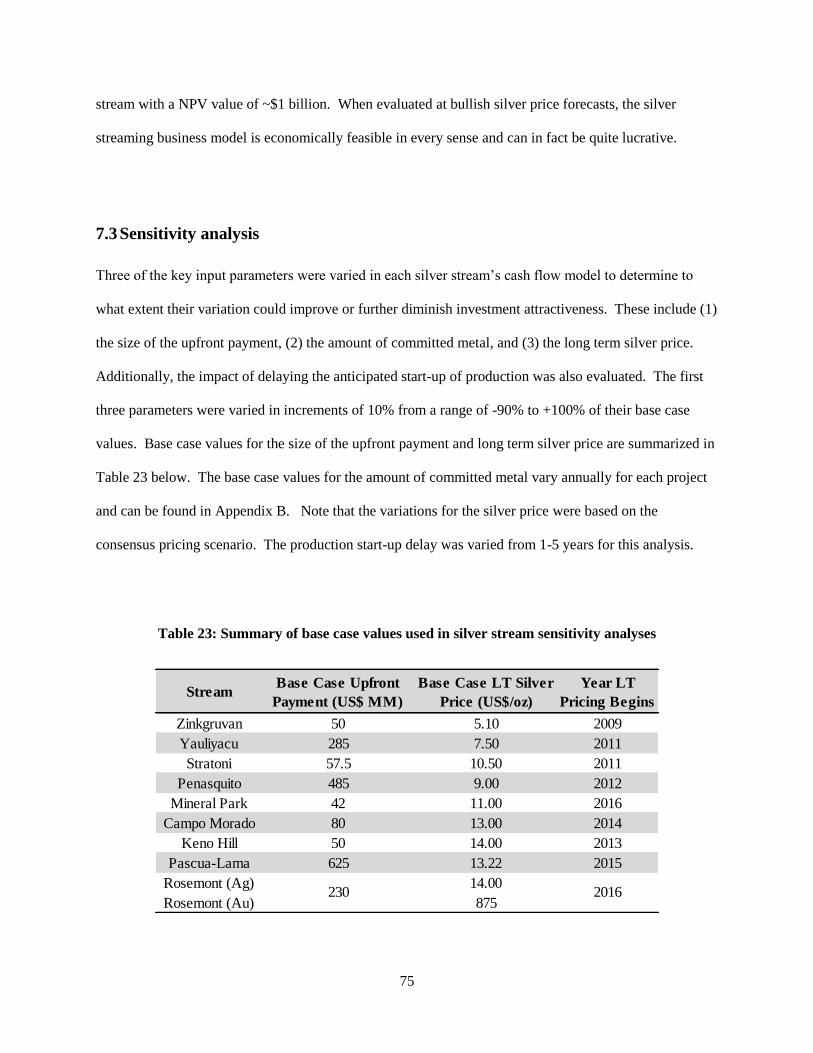

Table 23: Summary of base case values used in silver stream sensitivity analyses .................................... 75

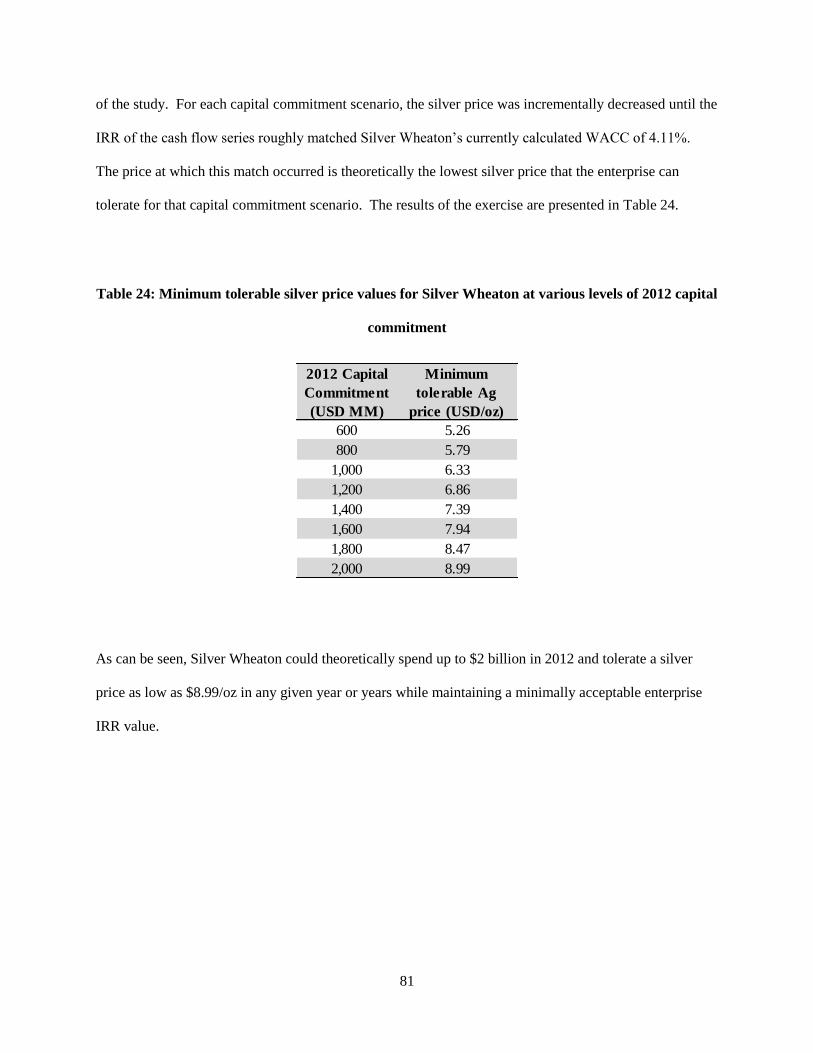

Table 24: Minimum tolerable silver price values for Silver Wheaton at various levels of 2012 capital

commitment ................................................................................................................................................ 81

Table 25: Lives of Silver Wheaton streams at deal times ........................................................................... 84

Table 26: Results of base case silver stream financial analysis, operating partner perspective .................. 88

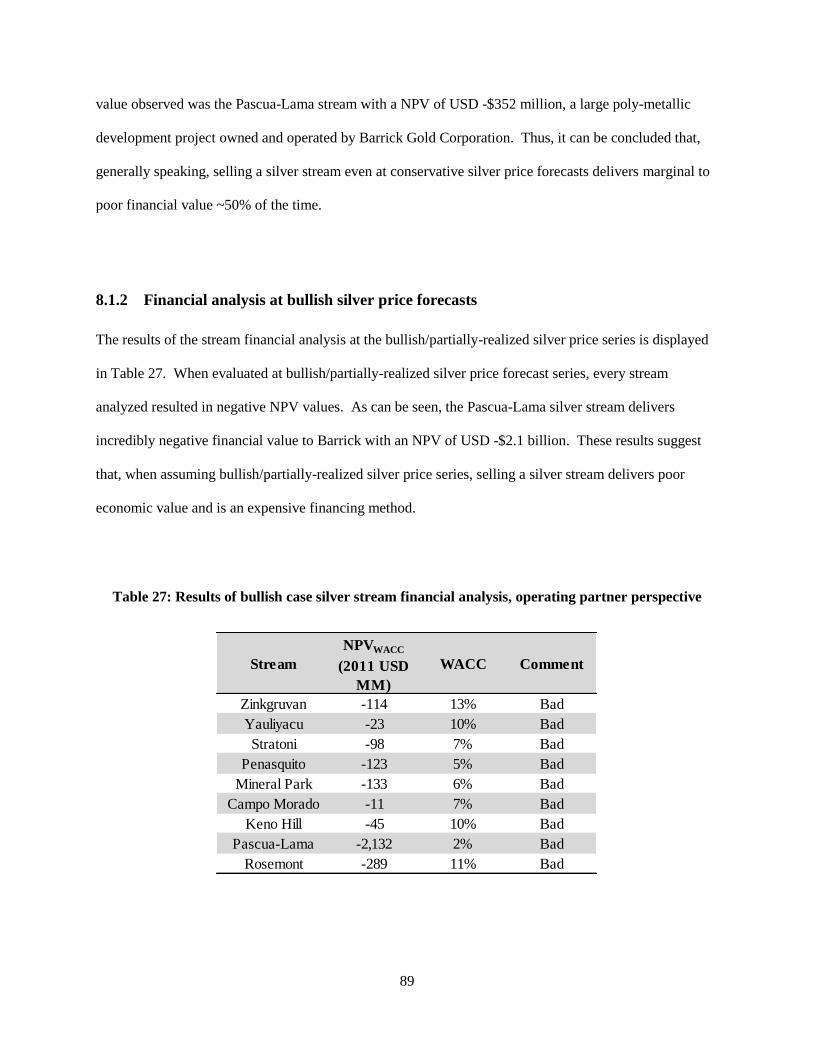

Table 27: Results of bullish case silver stream financial analysis, operating partner perspective .............. 89

Table 28: Summary of base case values used in silver stream sensitivity analyses .................................... 90

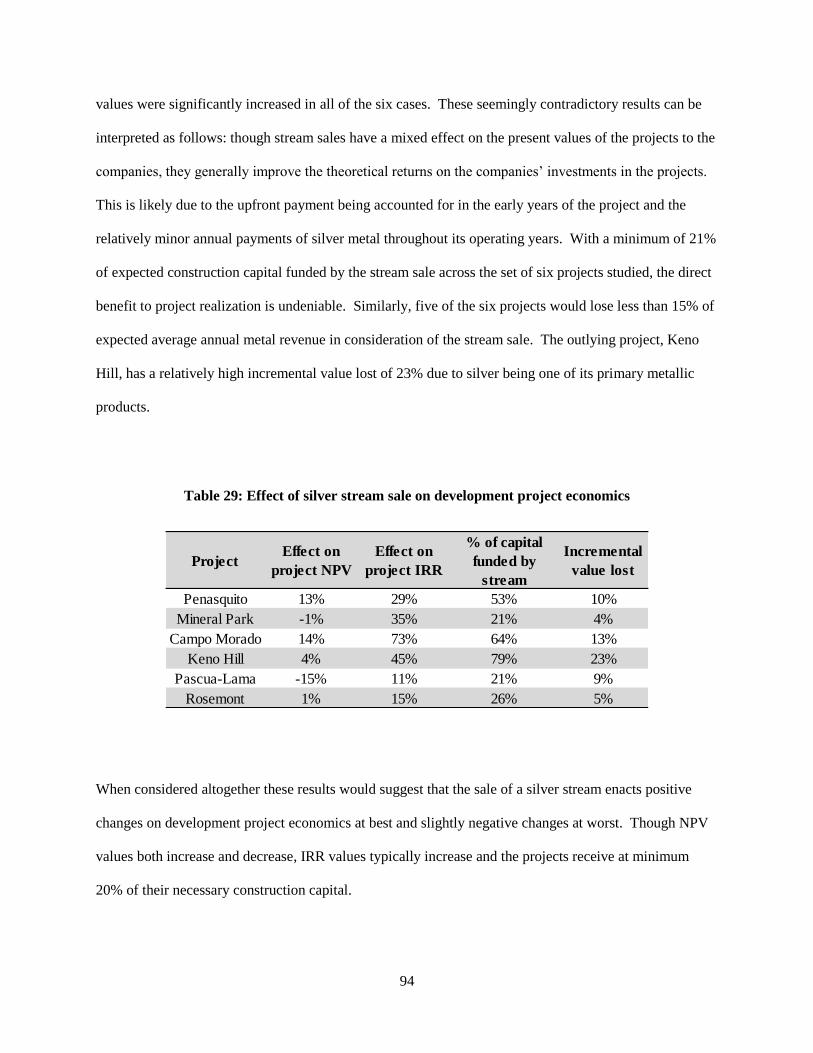

Table 29: Effect of silver stream sale on development project economics ................................................. 94

Table 30: Financings and balance sheet condition of operating partner companies surrounding stream

financings .................................................................................................................................................... 96

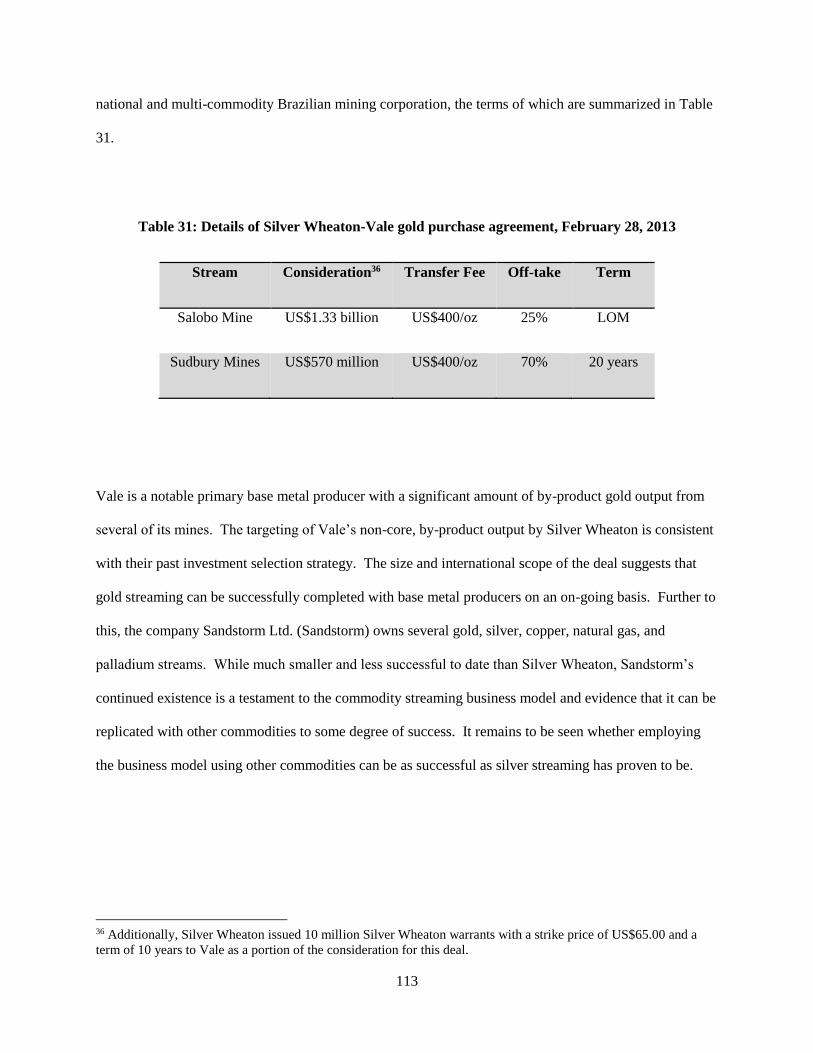

Table 31: Details of Silver Wheaton-Vale gold purchase agreement, February 28, 2013 ........................ 113

Table 32: Share price and index data used to calculate the Beta factor for Silver Wheaton at the time of

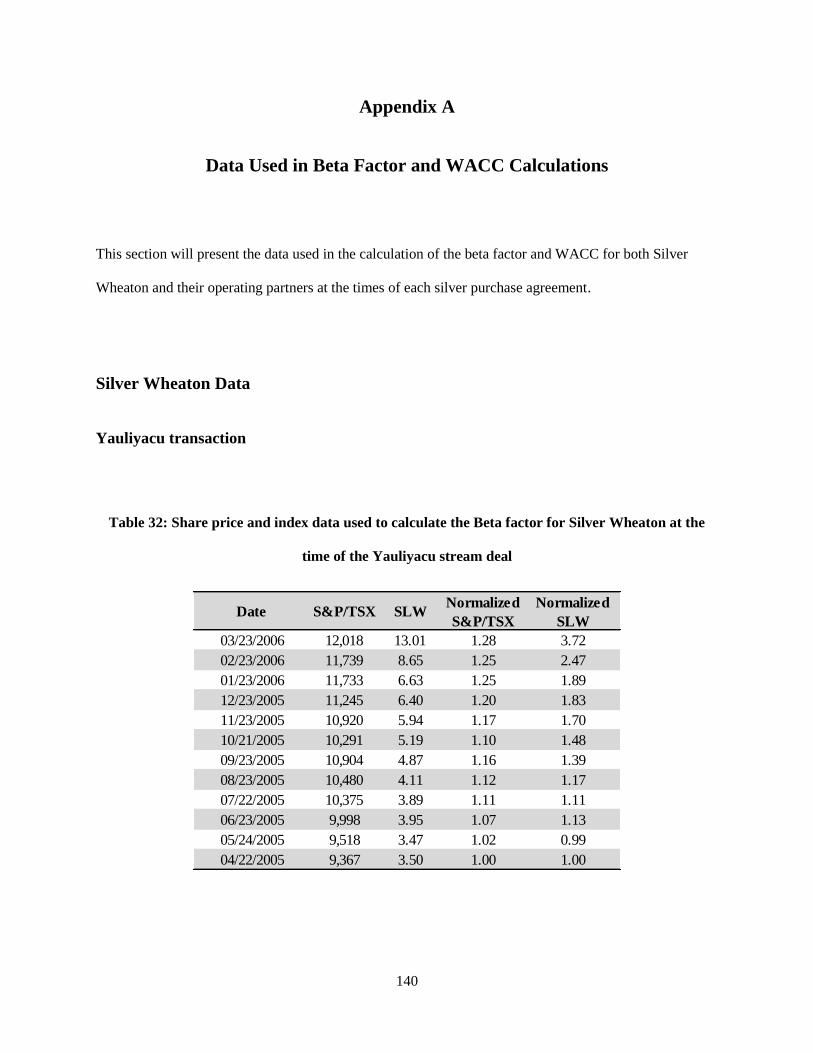

the Yauliyacu stream deal ......................................................................................................................... 140

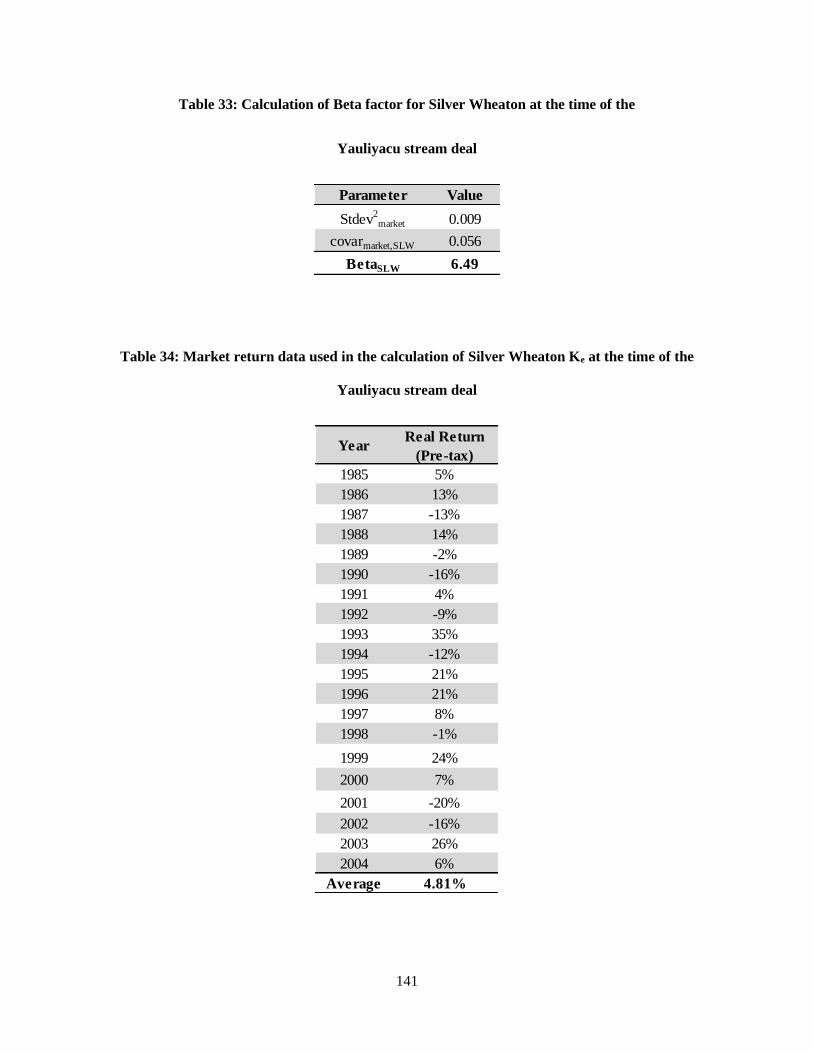

Table 33: Calculation of Beta factor for Silver Wheaton at the time of the ............................................. 141

Table 34: Market return data used in the calculation of Silver Wheaton Ke at the time of the Yauliyacu

stream deal ................................................................................................................................................ 141

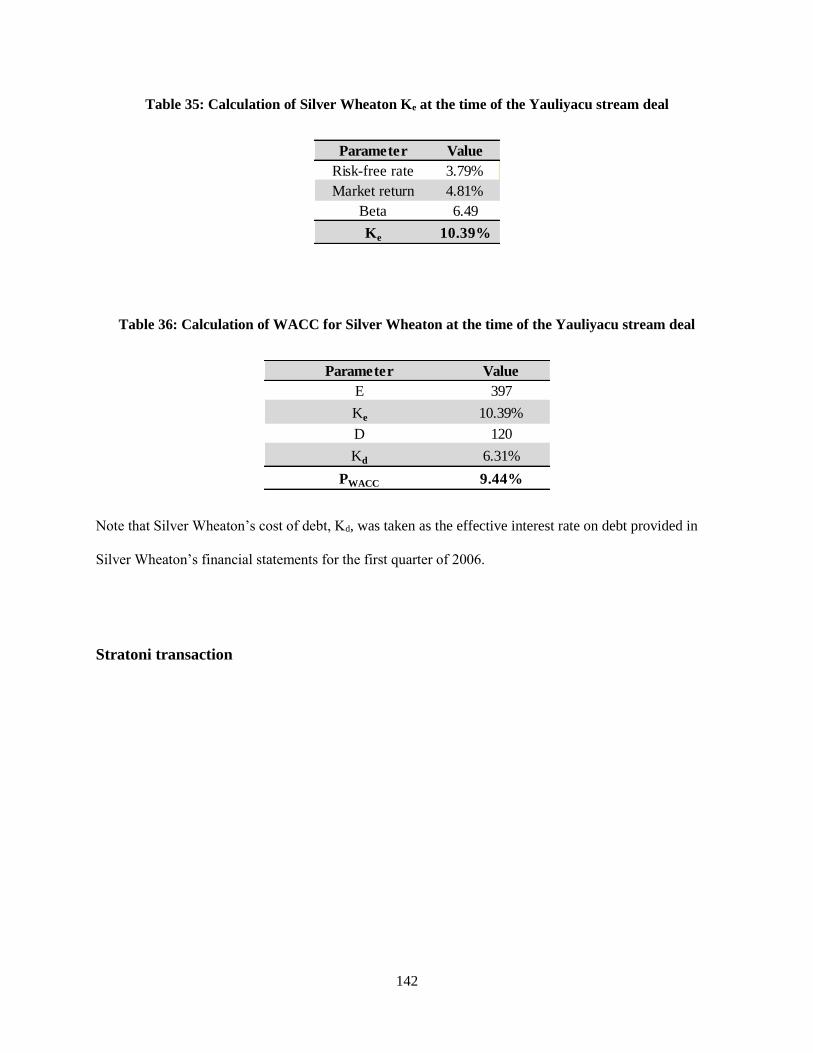

Table 35: Calculation of Silver Wheaton Ke at the time of the Yauliyacu stream deal ............................ 142

Table 36: Calculation of WACC for Silver Wheaton at the time of the Yauliyacu stream deal .............. 142

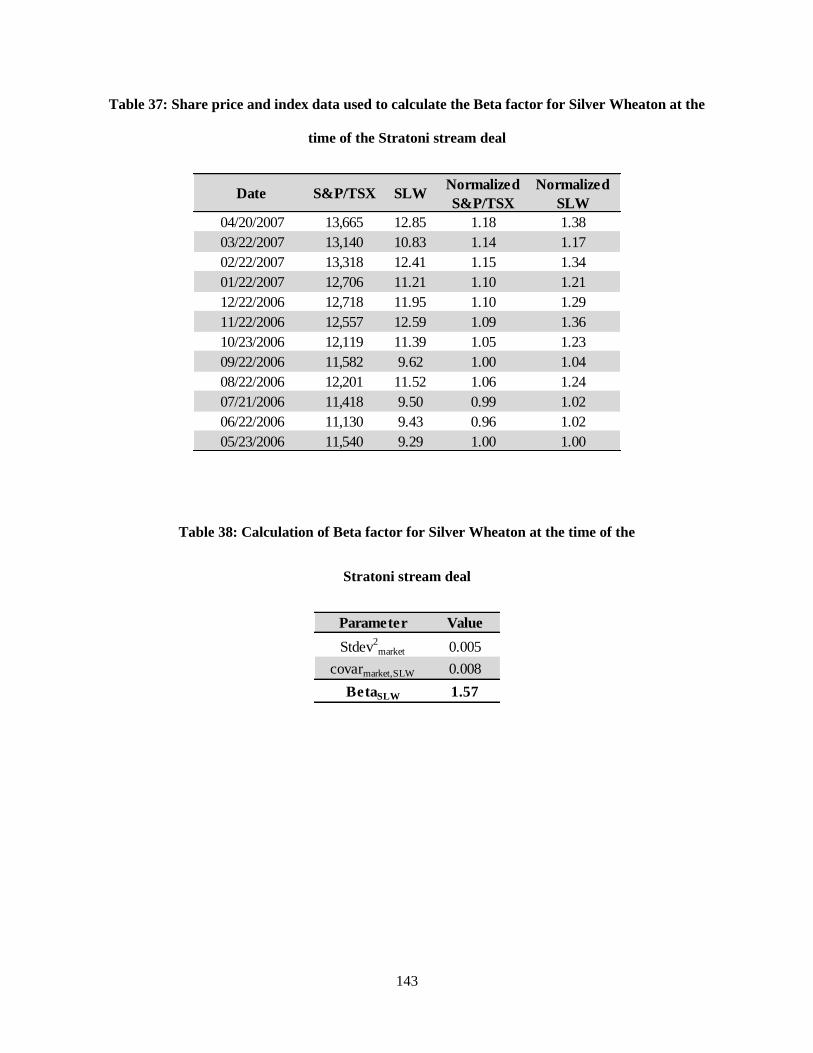

Table 37: Share price and index data used to calculate the Beta factor for Silver Wheaton at the time of

the Stratoni stream deal ............................................................................................................................. 143

Table 38: Calculation of Beta factor for Silver Wheaton at the time of the ............................................. 143

xvii

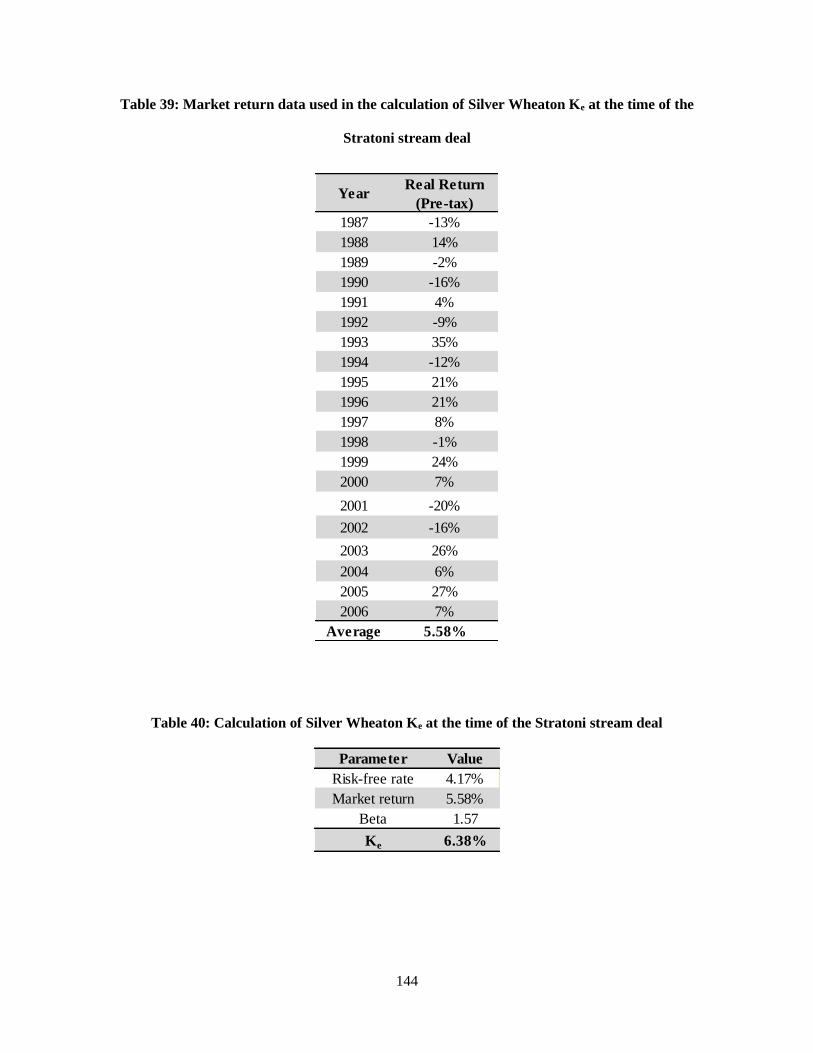

Table 39: Market return data used in the calculation of Silver Wheaton Ke at the time of the Stratoni

stream deal ................................................................................................................................................ 144

Table 40: Calculation of Silver Wheaton Ke at the time of the Stratoni stream deal ............................... 144

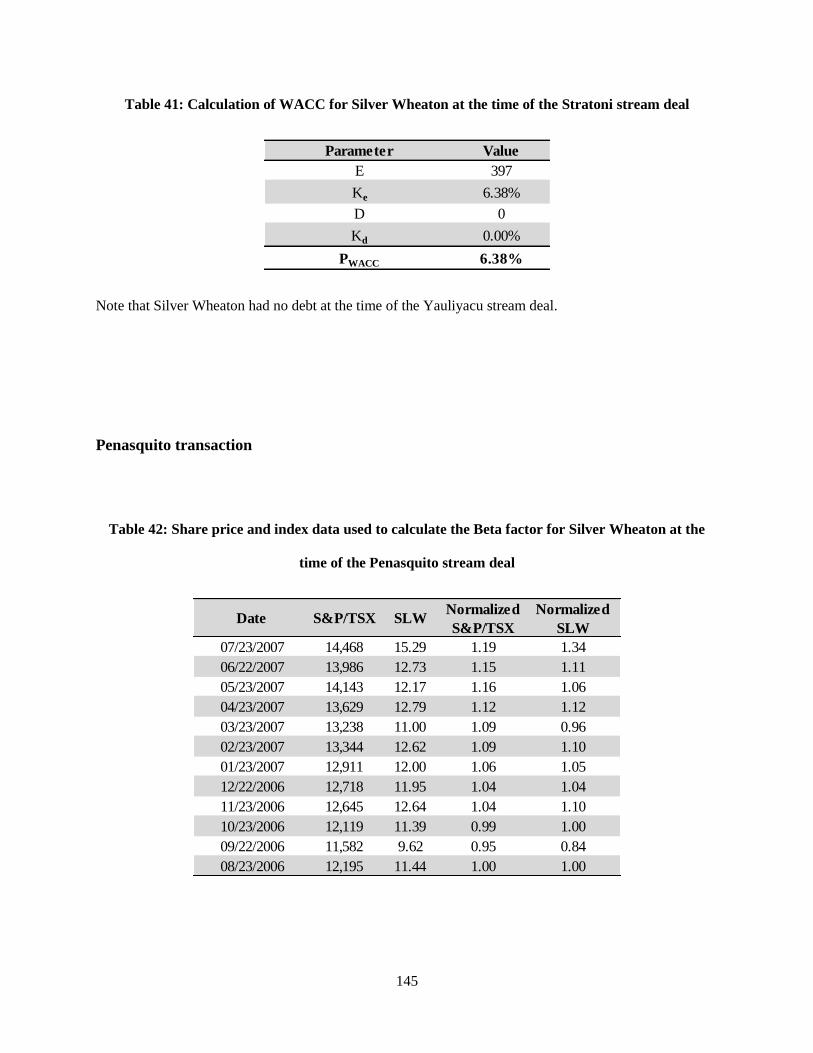

Table 41: Calculation of WACC for Silver Wheaton at the time of the Stratoni stream deal .................. 145

Table 42: Share price and index data used to calculate the Beta factor for Silver Wheaton at the time of

the Penasquito stream deal ........................................................................................................................ 145

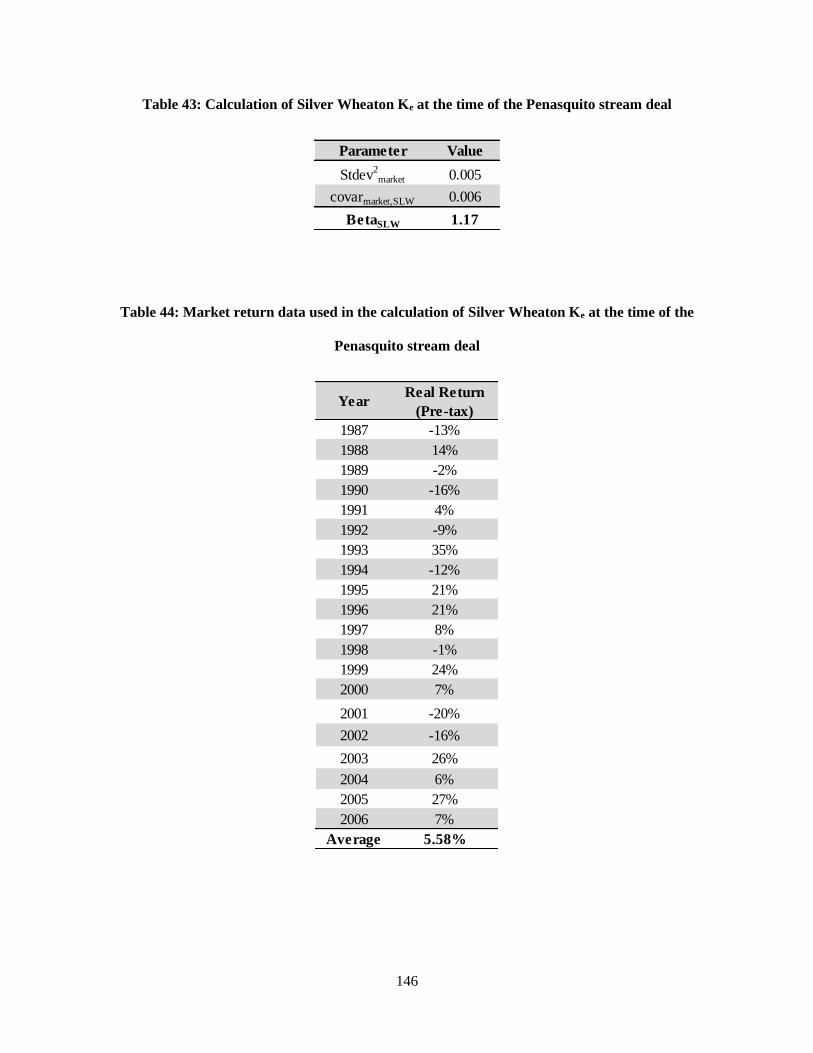

Table 43: Calculation of Silver Wheaton Ke at the time of the Penasquito stream deal ........................... 146

Table 44: Market return data used in the calculation of Silver Wheaton Ke at the time of the Penasquito

stream deal ................................................................................................................................................ 146

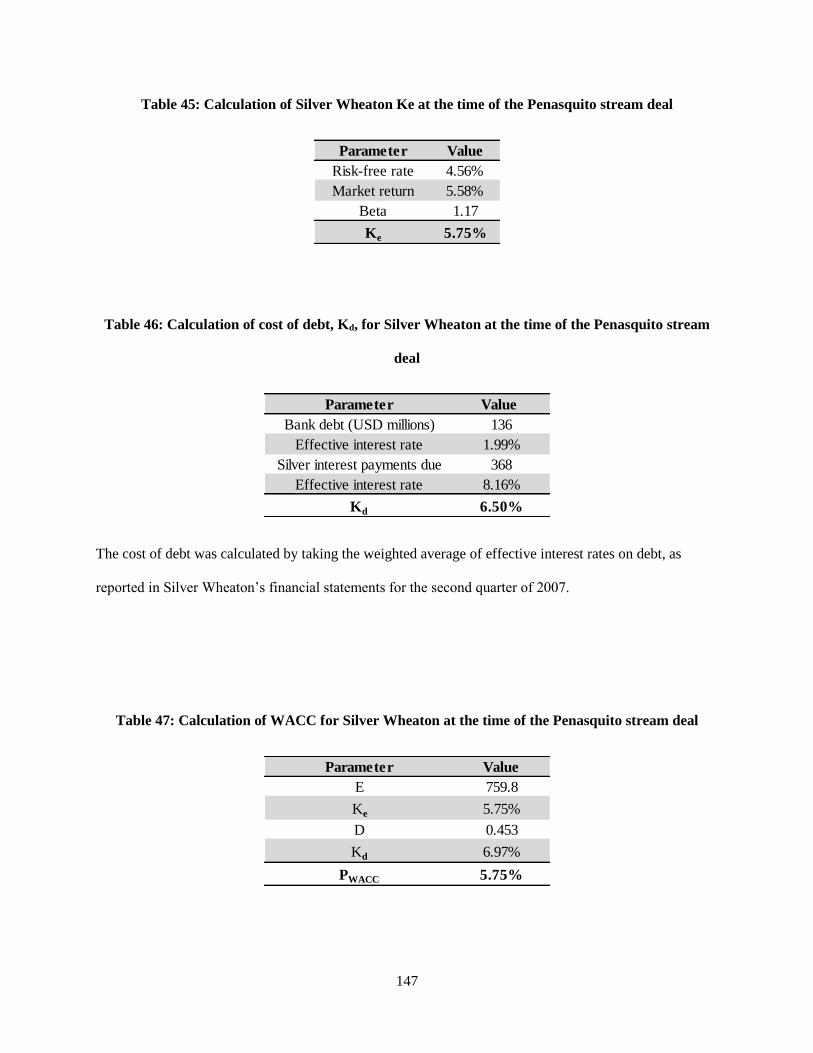

Table 45: Calculation of Silver Wheaton Ke at the time of the Penasquito stream deal .......................... 147

Table 46: Calculation of cost of debt, Kd, for Silver Wheaton at the time of the Penasquito stream deal 147

Table 47: Calculation of WACC for Silver Wheaton at the time of the Penasquito stream deal ............. 147

Table 48: Share price and index data used to calculate the Beta factor for Silver Wheaton at the time of

the Mineral Park stream deal .................................................................................................................... 148

Table 49: Calculation of Silver Wheaton Ke at the time of the Mineral Park stream deal ....................... 148

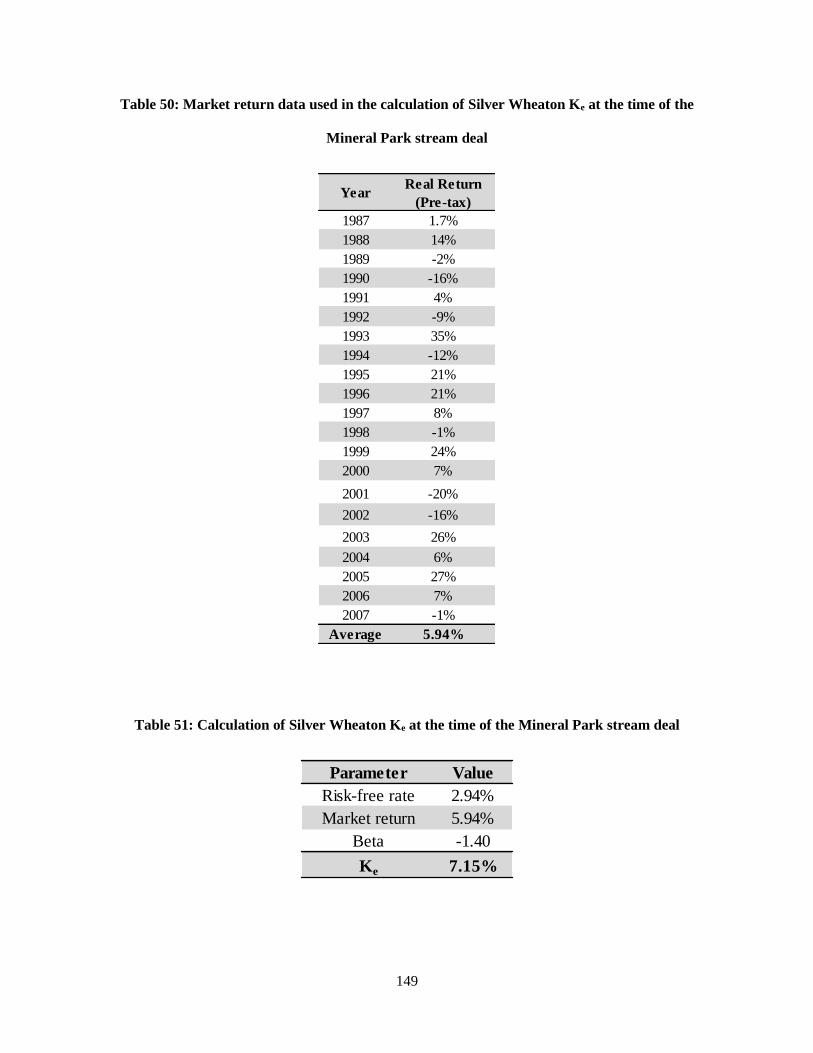

Table 50: Market return data used in the calculation of Silver Wheaton Ke at the time of the Mineral Park

stream deal ................................................................................................................................................ 149

Table 51: Calculation of Silver Wheaton Ke at the time of the Mineral Park stream deal ....................... 149

Table 52: Calculation of WACC for Silver Wheaton at the time of the Mineral Park stream deal .......... 150

Table 53: Share price and index data used to calculate the Beta factor for Silver Wheaton at the time of

the Campo Morado stream deal ................................................................................................................ 150

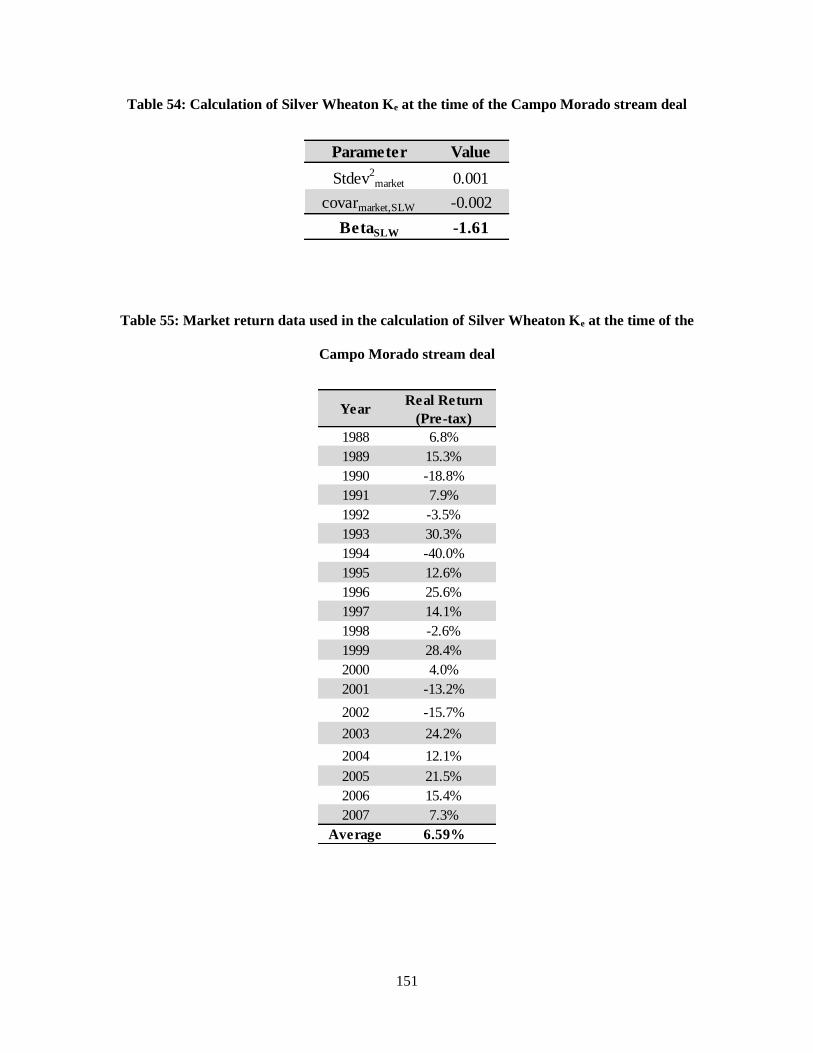

Table 54: Calculation of Silver Wheaton Ke at the time of the Campo Morado stream deal ................... 151

Table 55: Market return data used in the calculation of Silver Wheaton Ke at the time of the Campo

Morado stream deal ................................................................................................................................... 151

Table 56: Calculation of Silver Wheaton Ke at the time of the Campo Morado stream deal ................... 152

Table 57: Calculation of WACC for Silver Wheaton at the time of the Campo Morado stream deal ...... 152

xviii

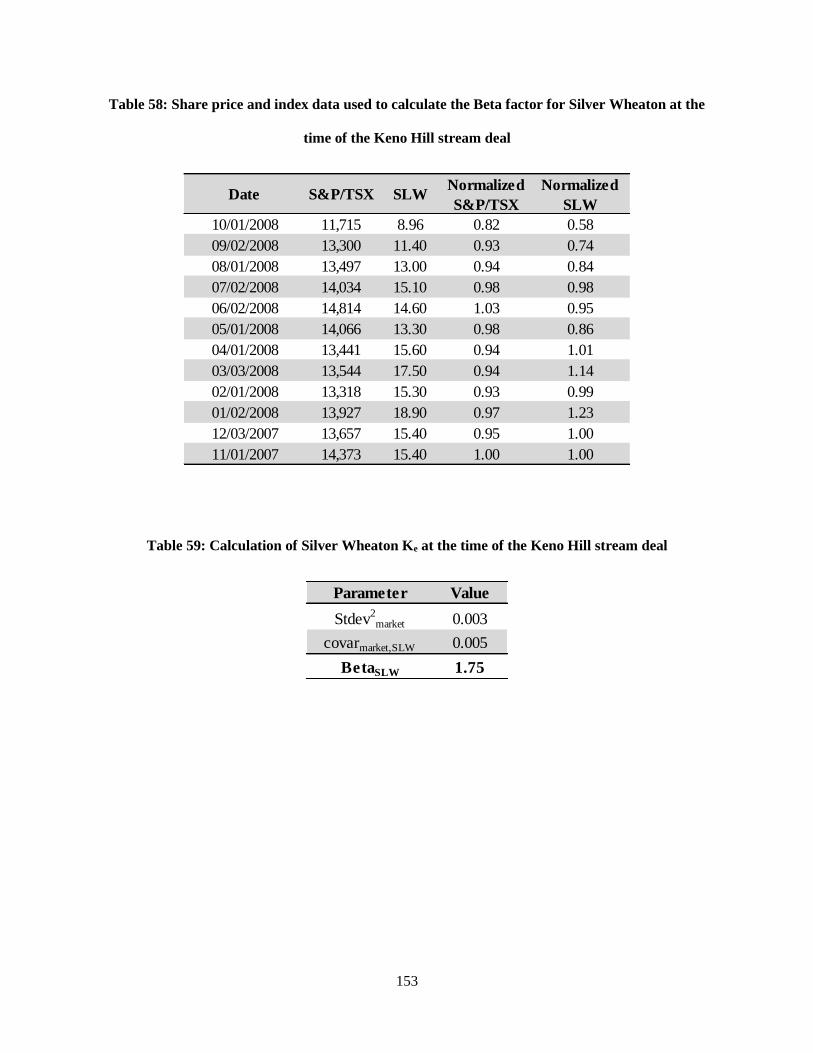

Table 58: Share price and index data used to calculate the Beta factor for Silver Wheaton at the time of

the Keno Hill stream deal ......................................................................................................................... 153

Table 59: Calculation of Silver Wheaton Ke at the time of the Keno Hill stream deal ............................. 153

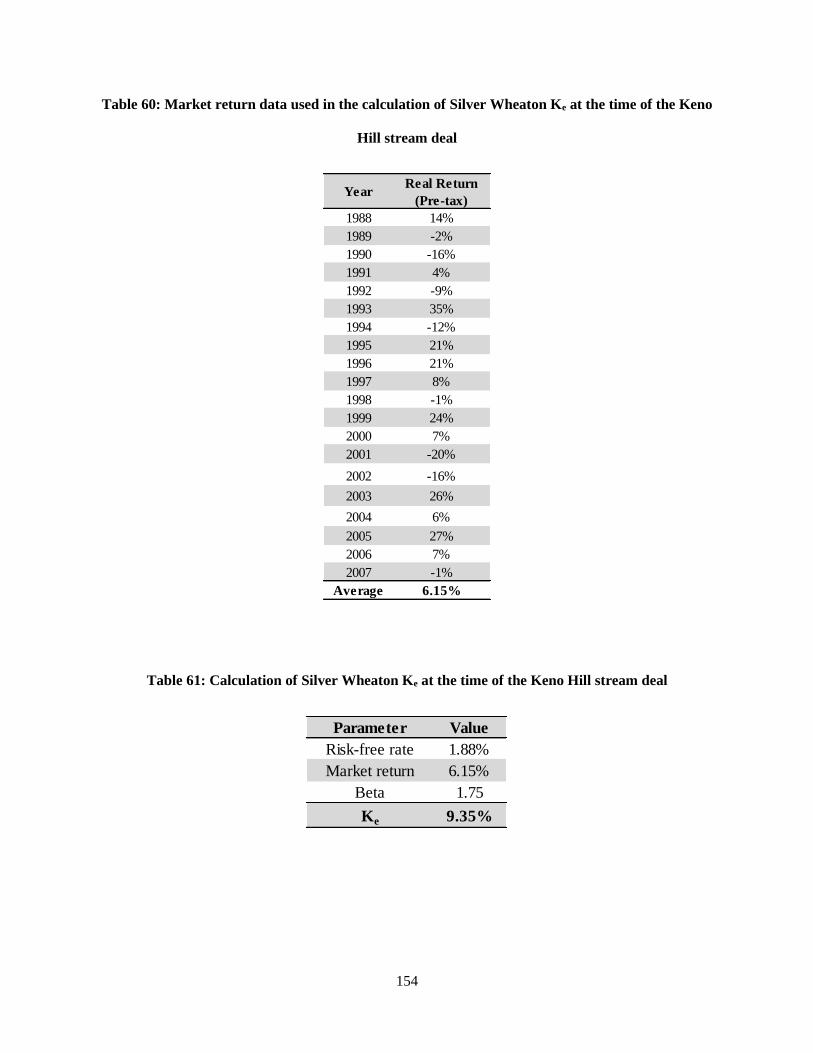

Table 60: Market return data used in the calculation of Silver Wheaton Ke at the time of the Keno Hill

stream deal ................................................................................................................................................ 154

Table 61: Calculation of Silver Wheaton Ke at the time of the Keno Hill stream deal ............................. 154

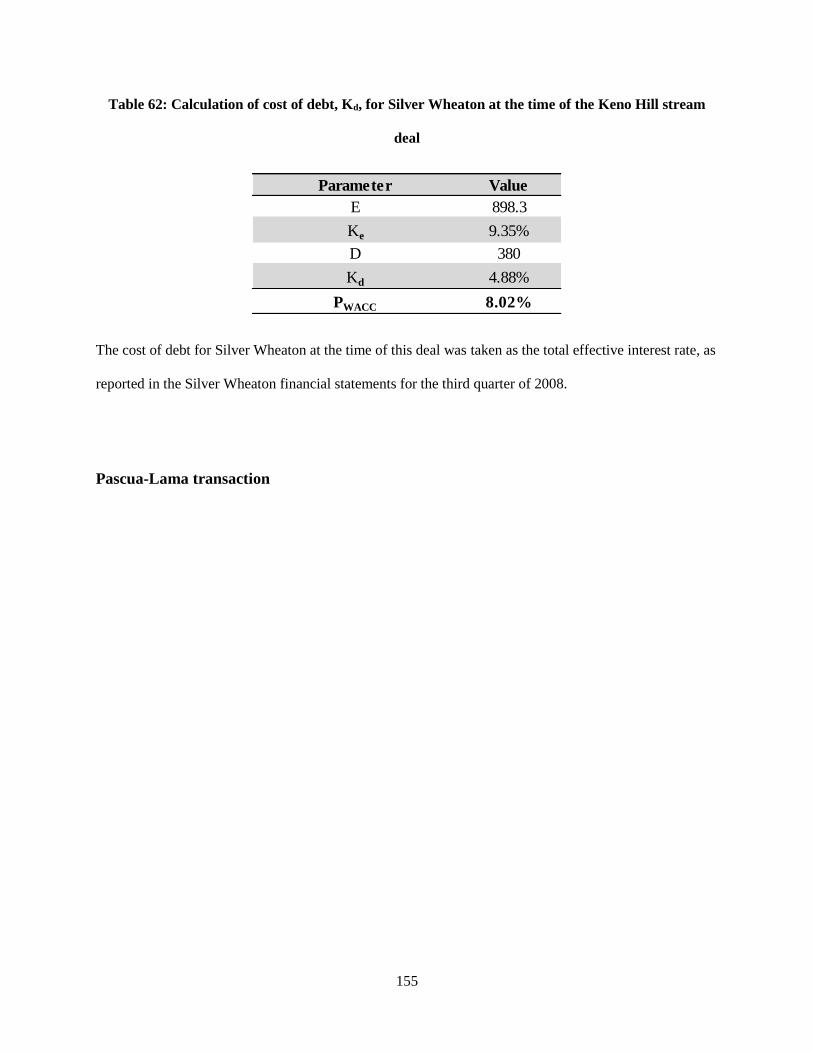

Table 62: Calculation of cost of debt, Kd, for Silver Wheaton at the time of the Keno Hill stream deal . 155

Table 63: Share price and index data used to calculate the Beta factor for Silver Wheaton at the time of

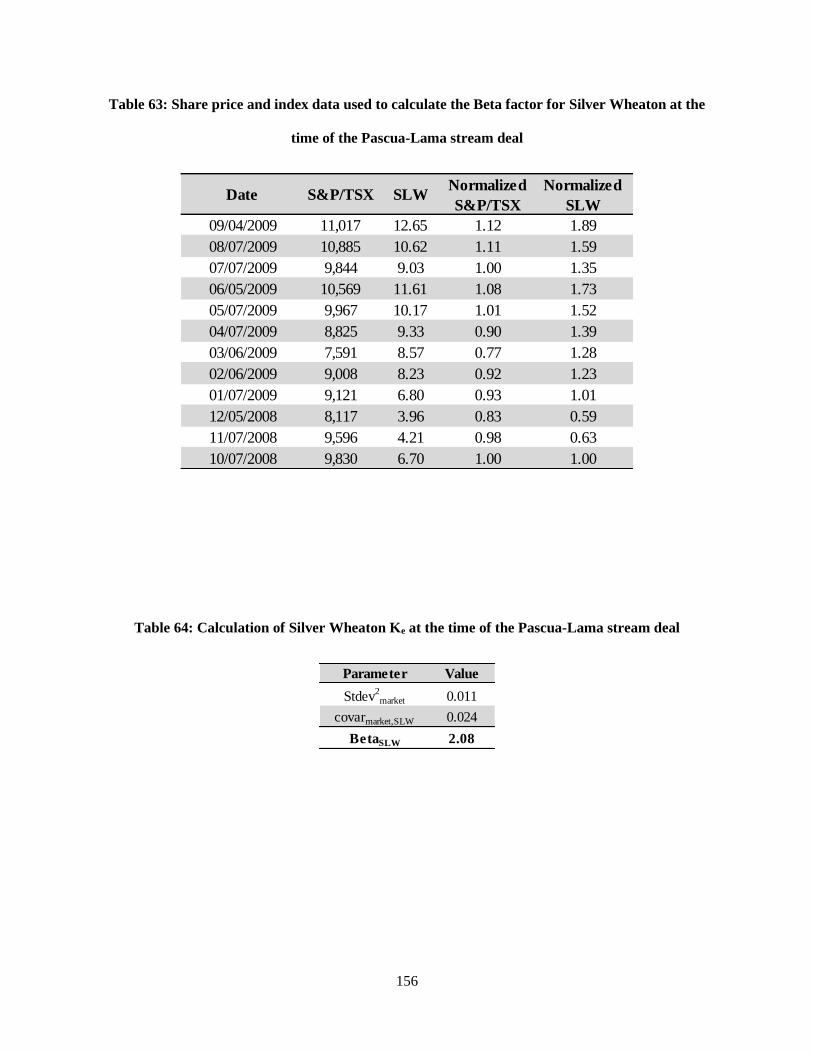

the Pascua-Lama stream deal .................................................................................................................... 156

Table 64: Calculation of Silver Wheaton Ke at the time of the Pascua-Lama stream deal ....................... 156

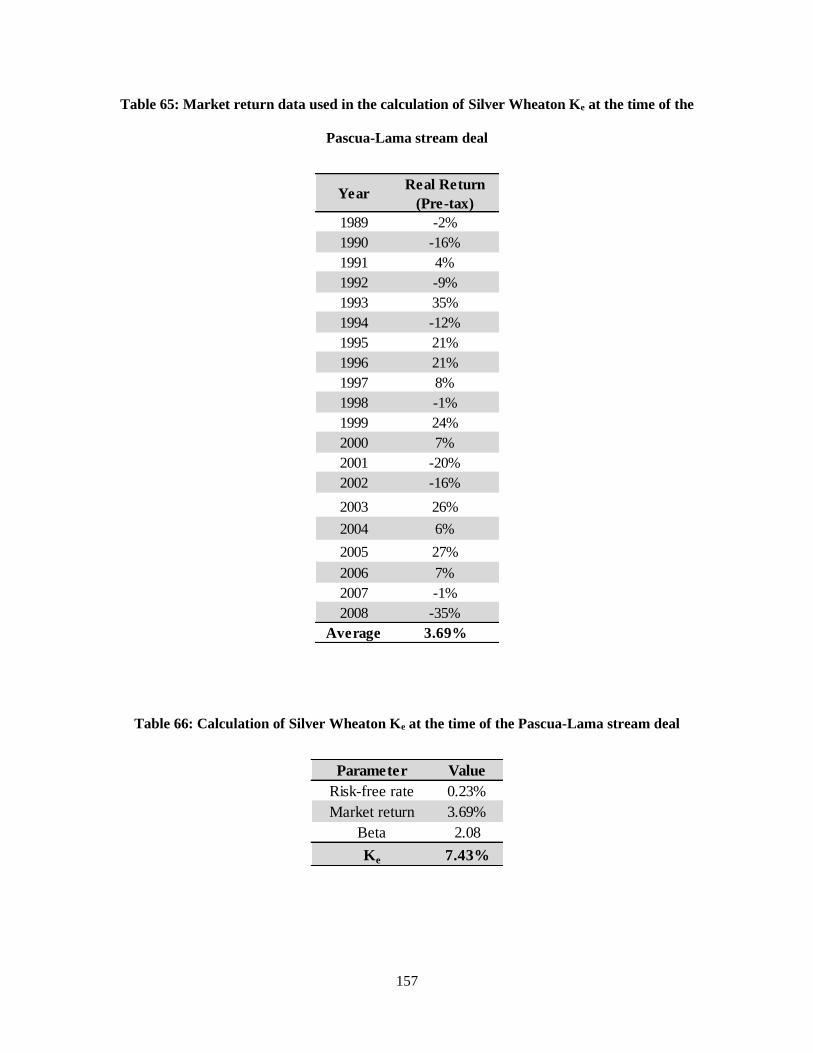

Table 65: Market return data used in the calculation of Silver Wheaton Ke at the time of the Pascua-Lama

stream deal ................................................................................................................................................ 157

Table 66: Calculation of Silver Wheaton Ke at the time of the Pascua-Lama stream deal ....................... 157

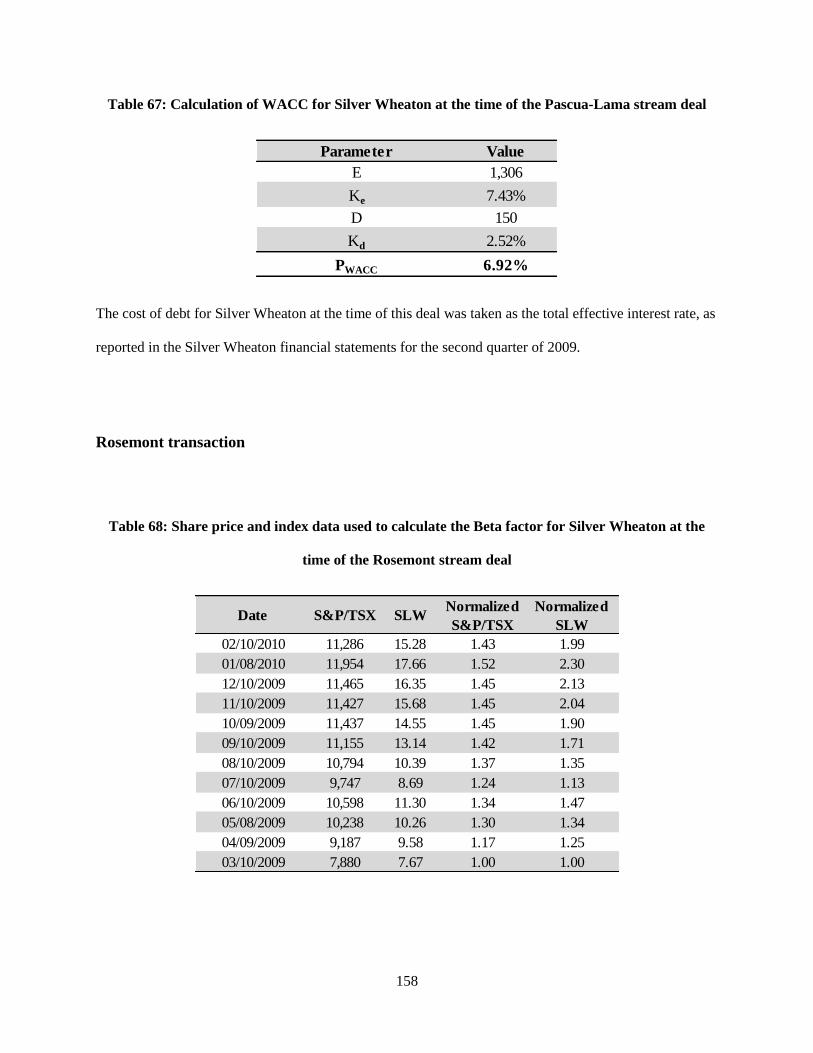

Table 67: Calculation of WACC for Silver Wheaton at the time of the Pascua-Lama stream deal ......... 158

Table 68: Share price and index data used to calculate the Beta factor for Silver Wheaton at the time of

the Rosemont stream deal ......................................................................................................................... 158

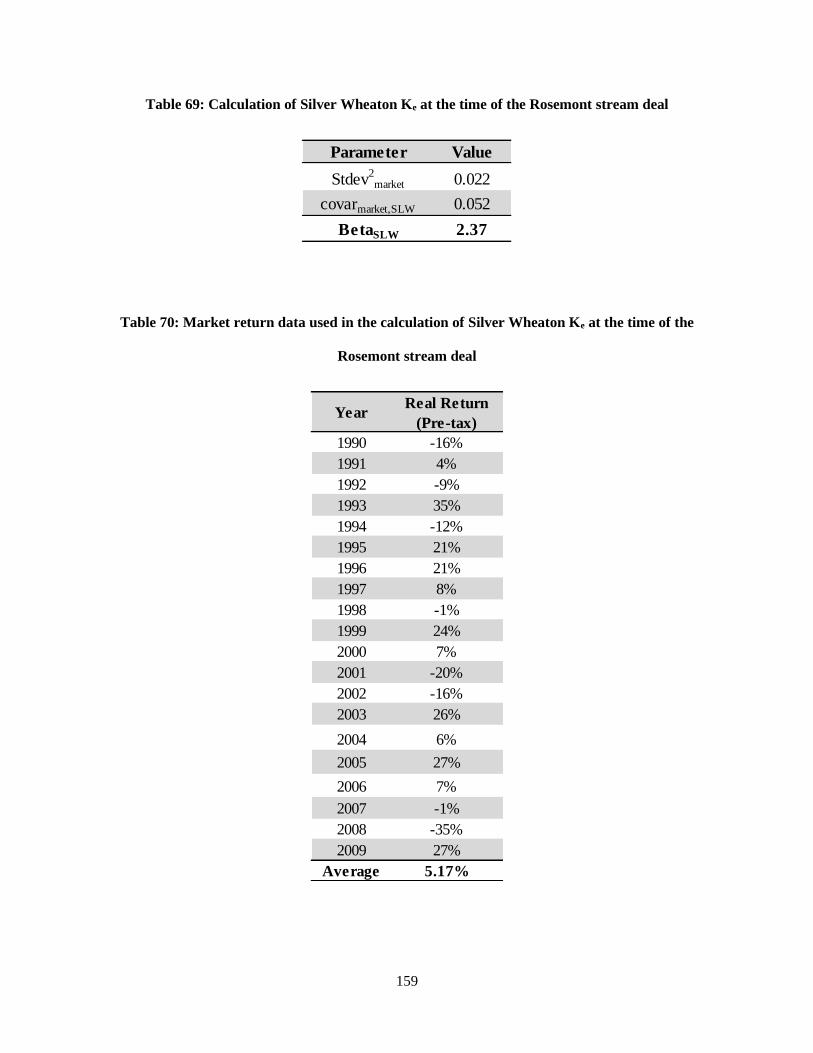

Table 69: Calculation of Silver Wheaton Ke at the time of the Rosemont stream deal ............................ 159

Table 70: Market return data used in the calculation of Silver Wheaton Ke at the time of the Rosemont

stream deal ................................................................................................................................................ 159

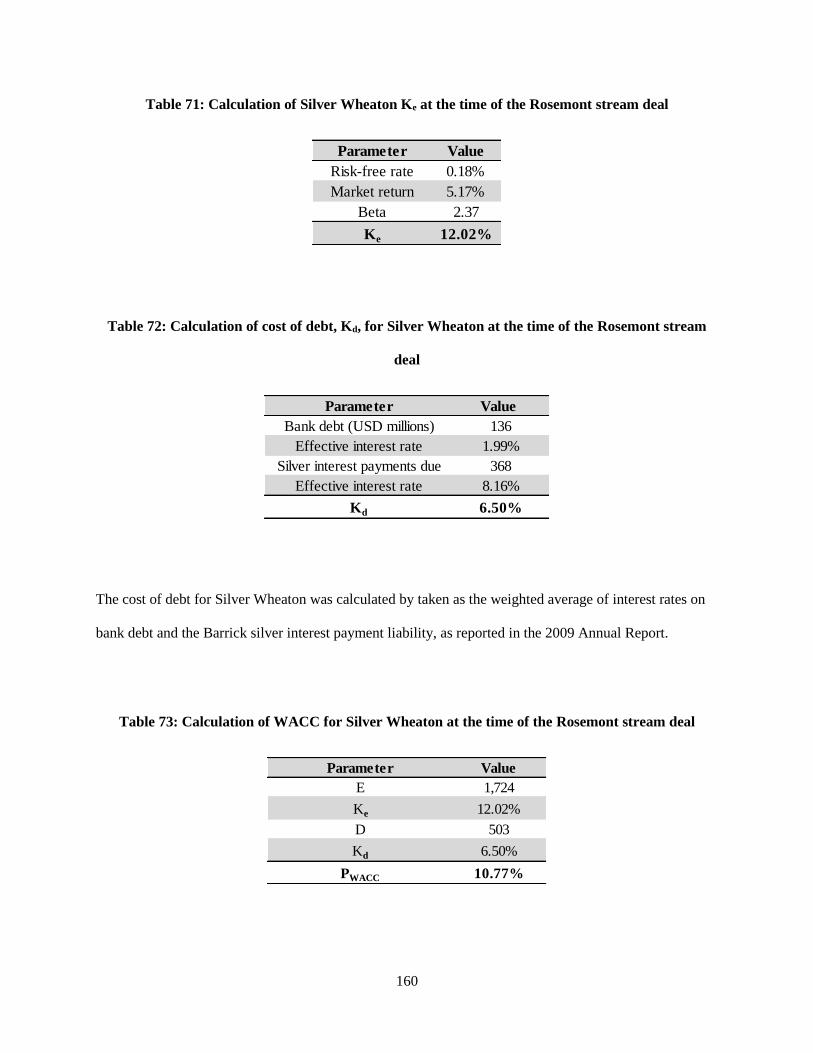

Table 71: Calculation of Silver Wheaton Ke at the time of the Rosemont stream deal ............................ 160

Table 72: Calculation of cost of debt, Kd, for Silver Wheaton at the time of the Rosemont stream deal . 160

Table 73: Calculation of WACC for Silver Wheaton at the time of the Rosemont stream deal ............... 160

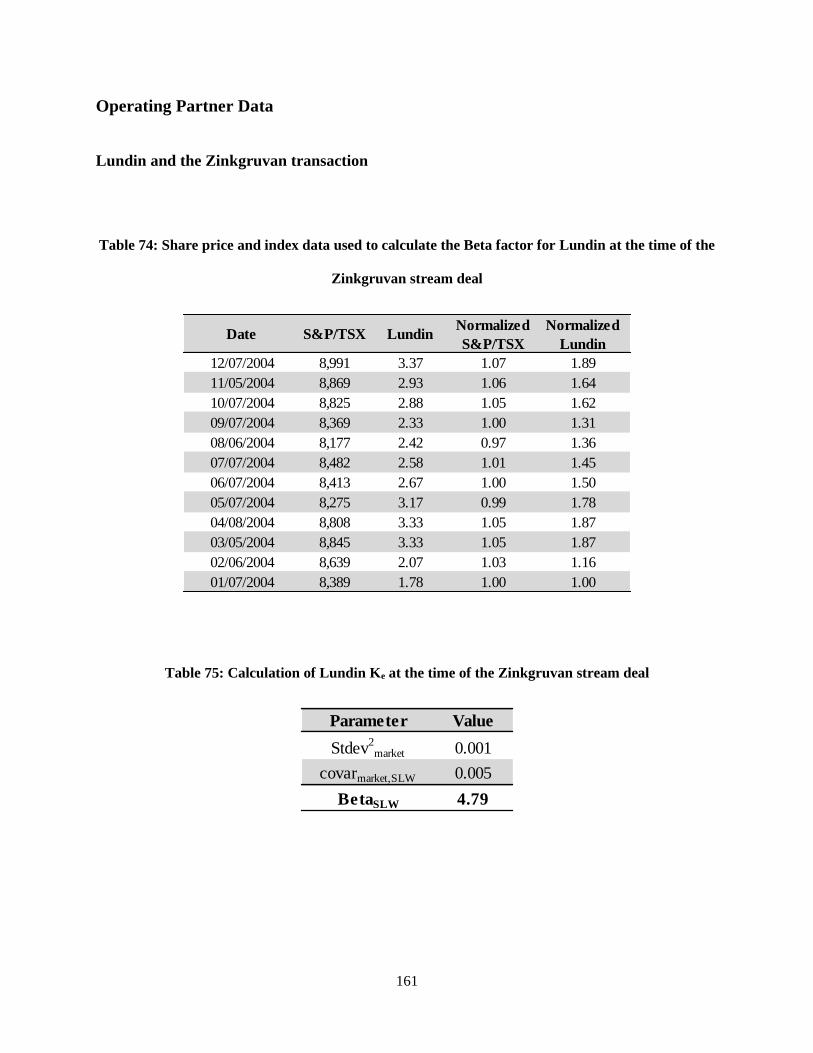

Table 74: Share price and index data used to calculate the Beta factor for Lundin at the time of the

Zinkgruvan stream deal ............................................................................................................................. 161

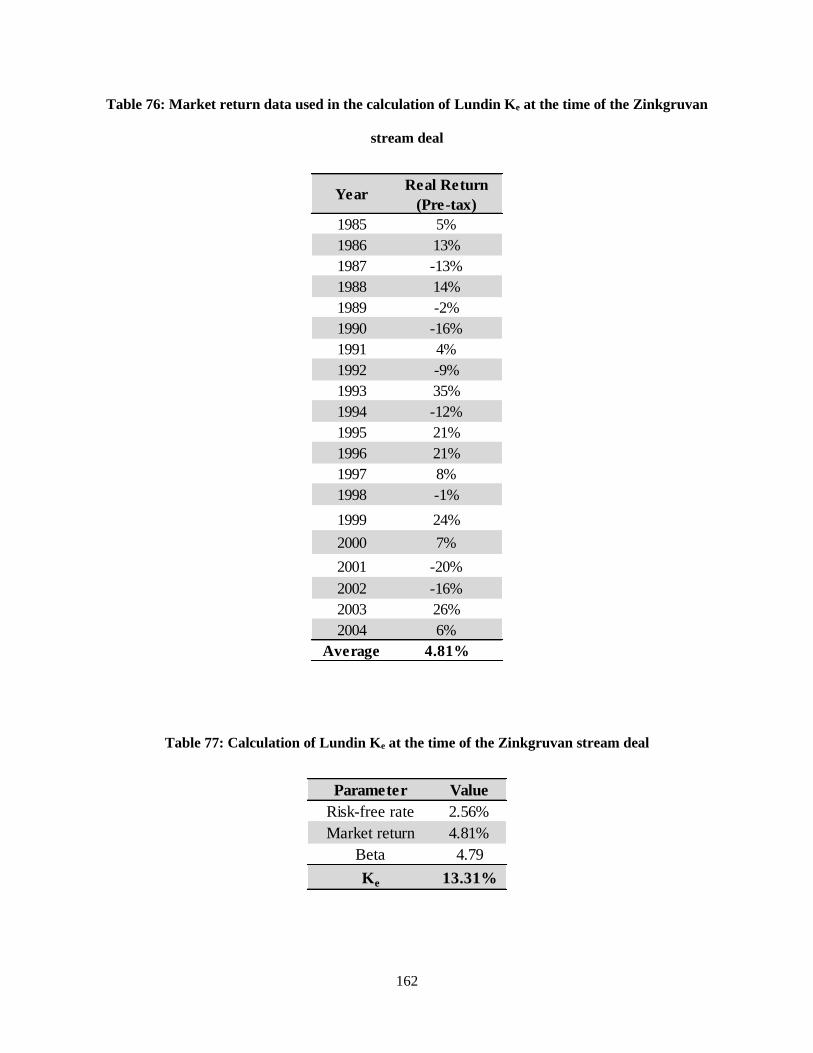

Table 75: Calculation of Lundin Ke at the time of the Zinkgruvan stream deal ....................................... 161

xix

Table 76: Market return data used in the calculation of Lundin Ke at the time of the Zinkgruvan stream

deal ............................................................................................................................................................ 162

Table 77: Calculation of Lundin Ke at the time of the Zinkgruvan stream deal ....................................... 162

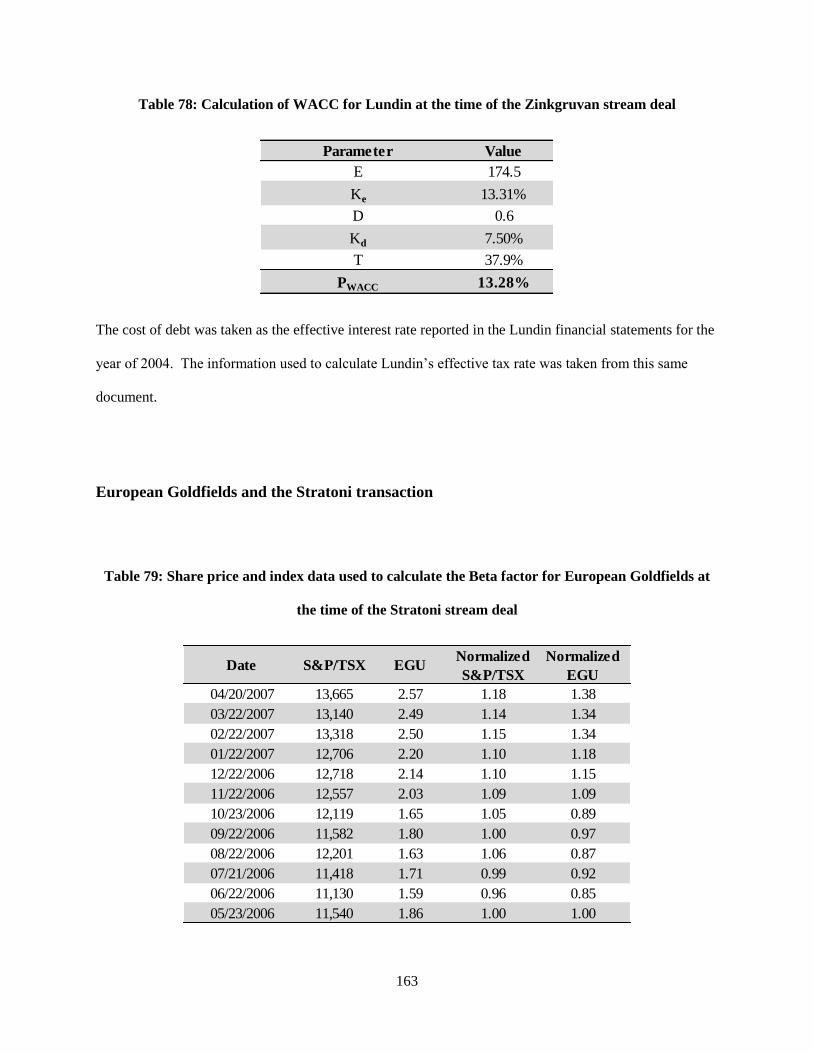

Table 78: Calculation of WACC for Lundin at the time of the Zinkgruvan stream deal .......................... 163

Table 79: Share price and index data used to calculate the Beta factor for European Goldfields at the time

of the Stratoni stream deal ........................................................................................................................ 163

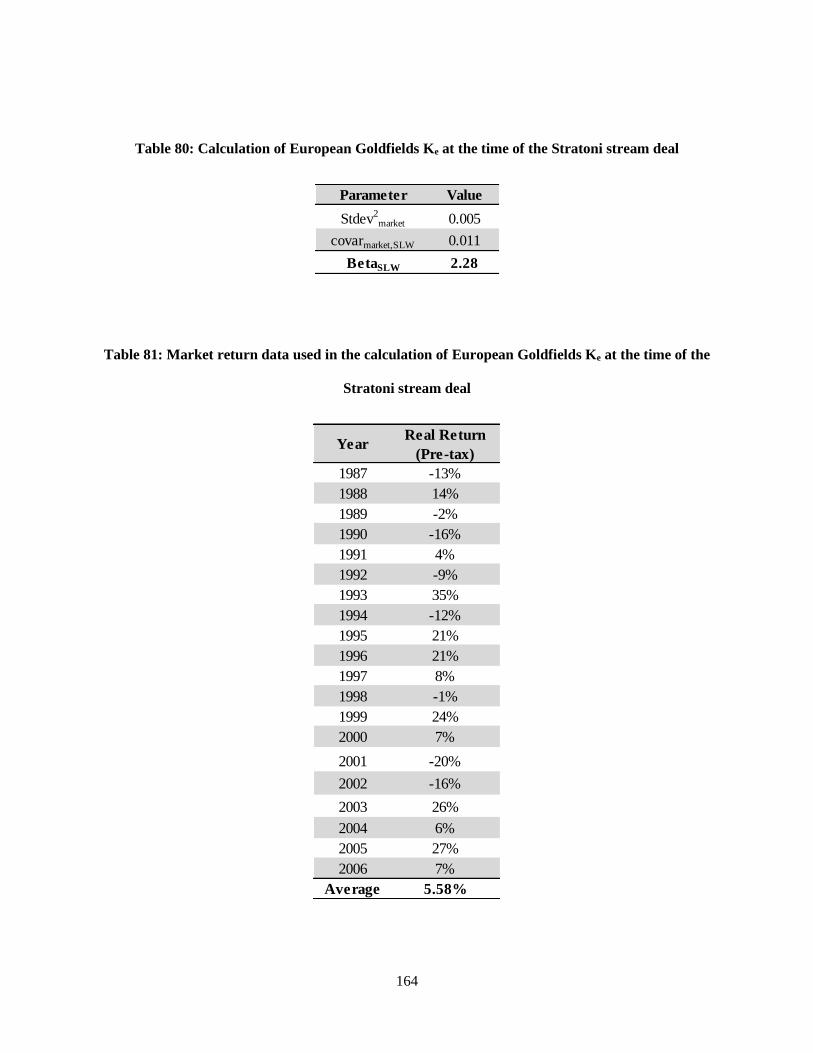

Table 80: Calculation of European Goldfields Ke at the time of the Stratoni stream deal ........................ 164

Table 81: Market return data used in the calculation of European Goldfields Ke at the time of the Stratoni

stream deal ................................................................................................................................................ 164

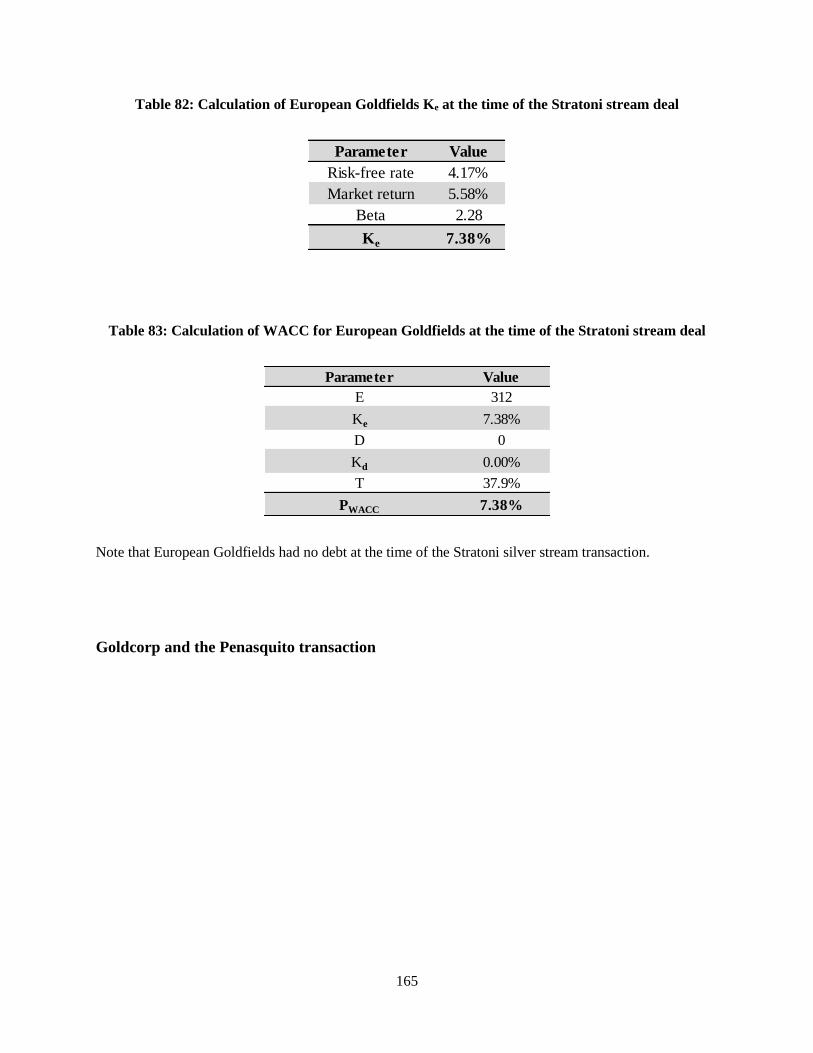

Table 82: Calculation of European Goldfields Ke at the time of the Stratoni stream deal ........................ 165

Table 83: Calculation of WACC for European Goldfields at the time of the Stratoni stream deal .......... 165

Table 84: Share price and index data used to calculate the Beta factor for Goldcorp at the time of the

Penasquito stream deal .............................................................................................................................. 166

Table 85: Calculation of Goldcorp Ke at the time of the Penasquito stream deal ..................................... 166

Table 86: Market return data used in the calculation of Goldcorp Ke at the time of the Penasquito stream

deal ............................................................................................................................................................ 167

Table 87: Calculation of Goldcorp Ke at the time of the Penasquito stream deal ..................................... 167

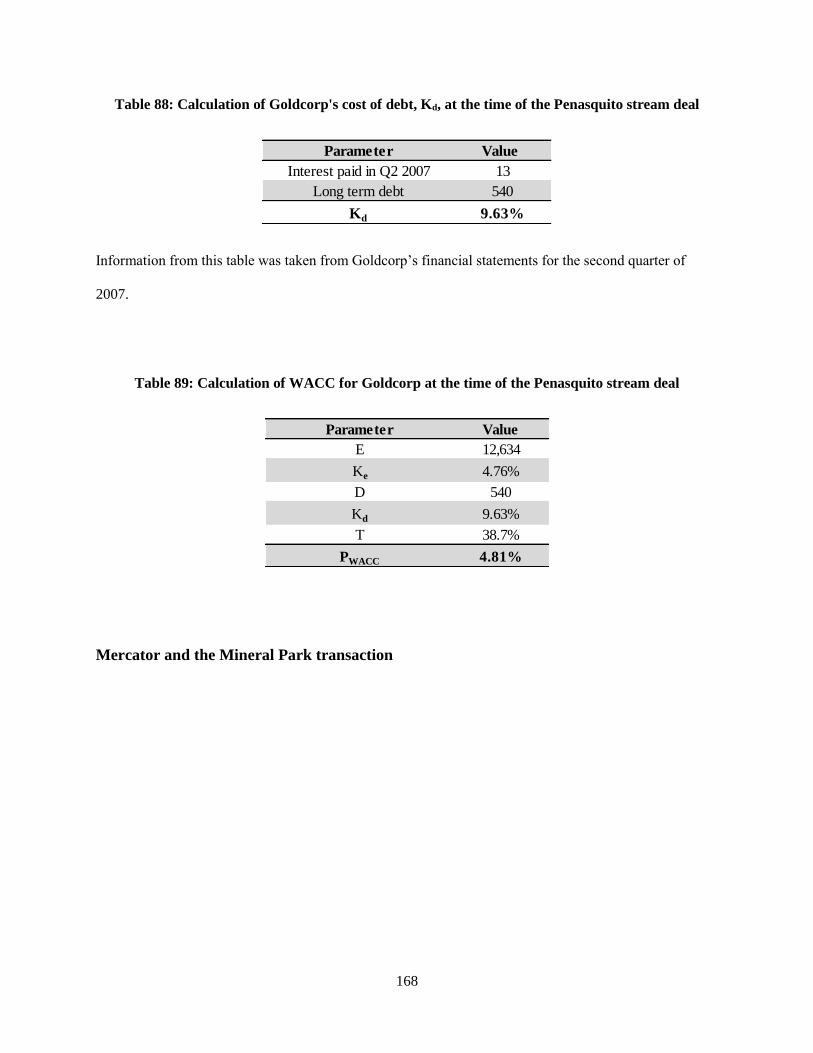

Table 88: Calculation of Goldcorp's cost of debt, Kd, at the time of the Penasquito stream deal ............. 168

Table 89: Calculation of WACC for Goldcorp at the time of the Penasquito stream deal ....................... 168

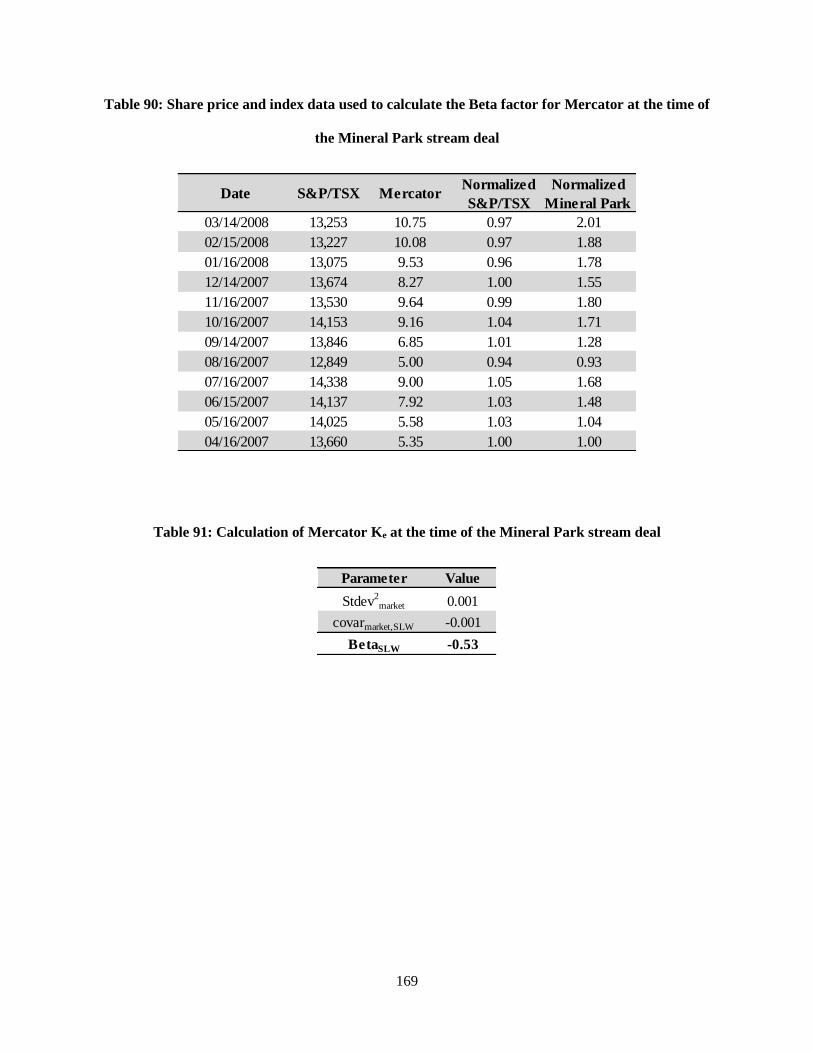

Table 90: Share price and index data used to calculate the Beta factor for Mercator at the time of the

Mineral Park stream deal .......................................................................................................................... 169

Table 91: Calculation of Mercator Ke at the time of the Mineral Park stream deal .................................. 169

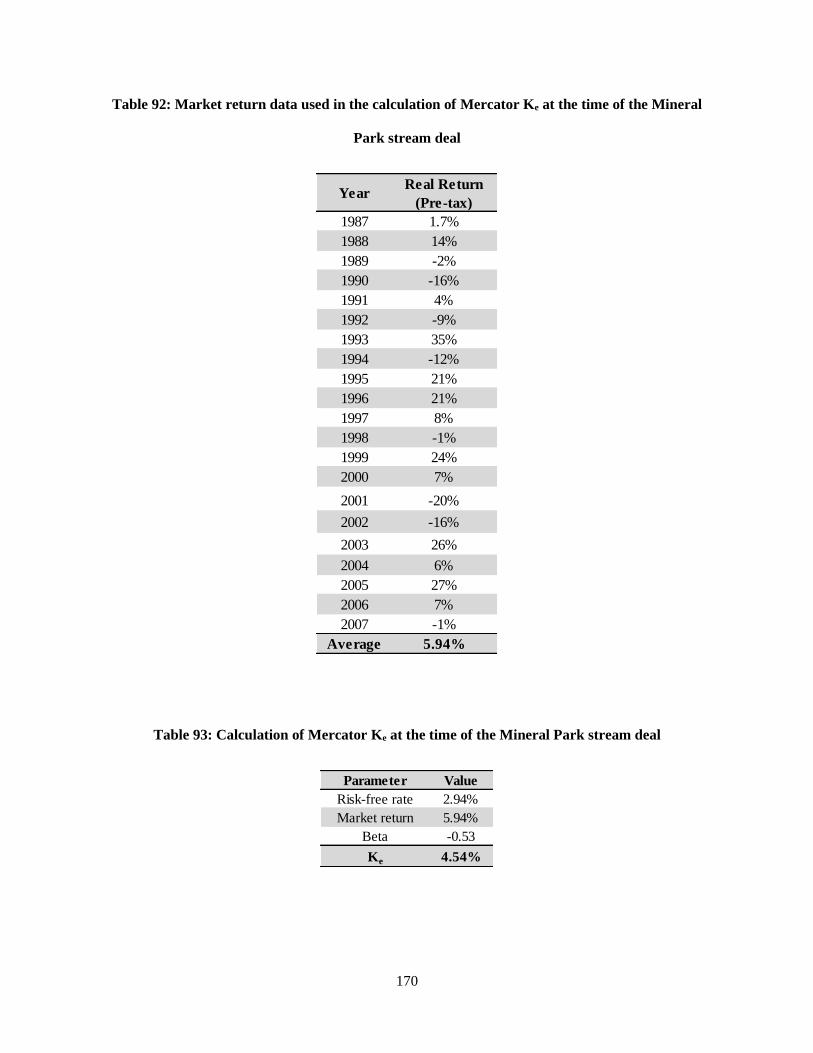

Table 92: Market return data used in the calculation of Mercator Ke at the time of the Mineral Park stream

deal ............................................................................................................................................................ 170

Table 93: Calculation of Mercator Ke at the time of the Mineral Park stream deal .................................. 170

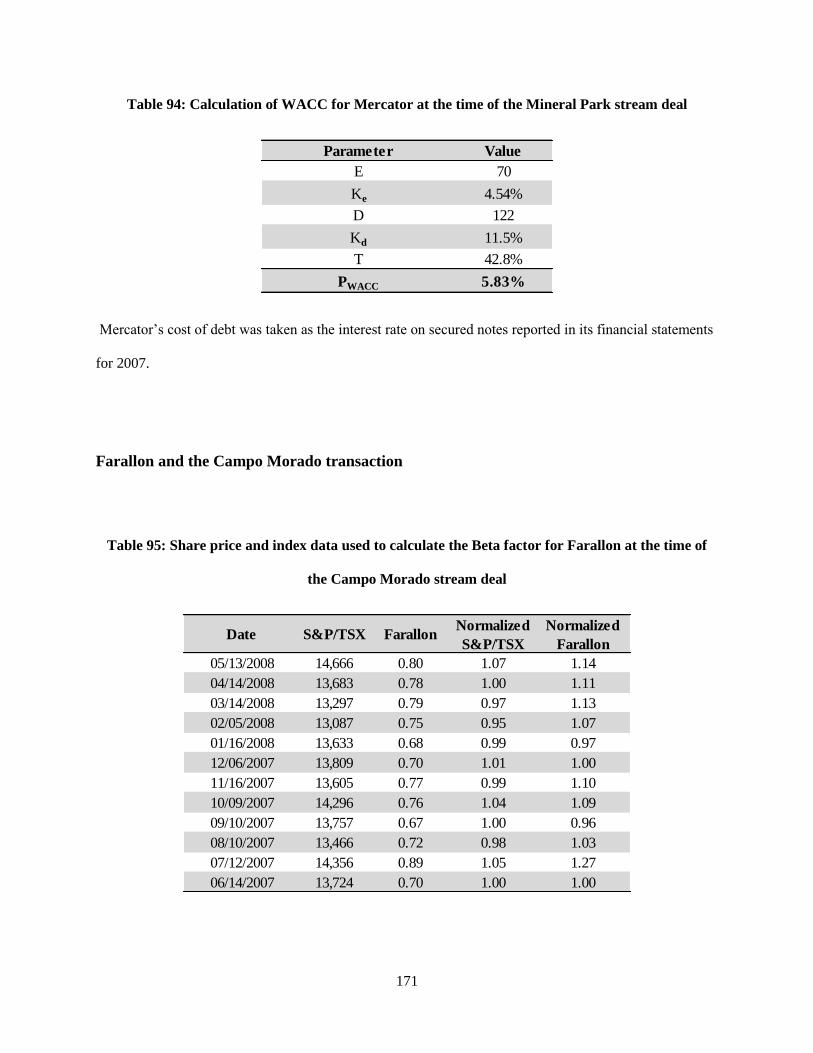

Table 94: Calculation of WACC for Mercator at the time of the Mineral Park stream deal .................... 171

xx

Table 95: Share price and index data used to calculate the Beta factor for Farallon at the time of the

Campo Morado stream deal ...................................................................................................................... 171

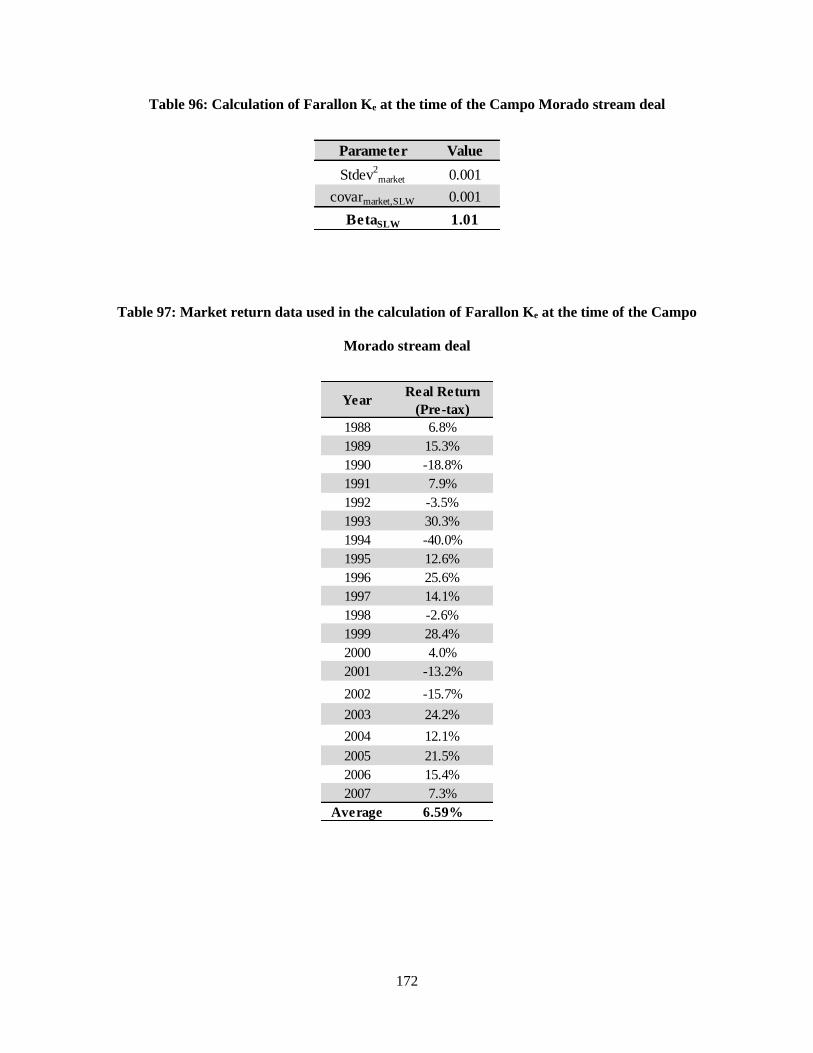

Table 96: Calculation of Farallon Ke at the time of the Campo Morado stream deal ............................... 172

Table 97: Market return data used in the calculation of Farallon Ke at the time of the Campo Morado

stream deal ................................................................................................................................................ 172

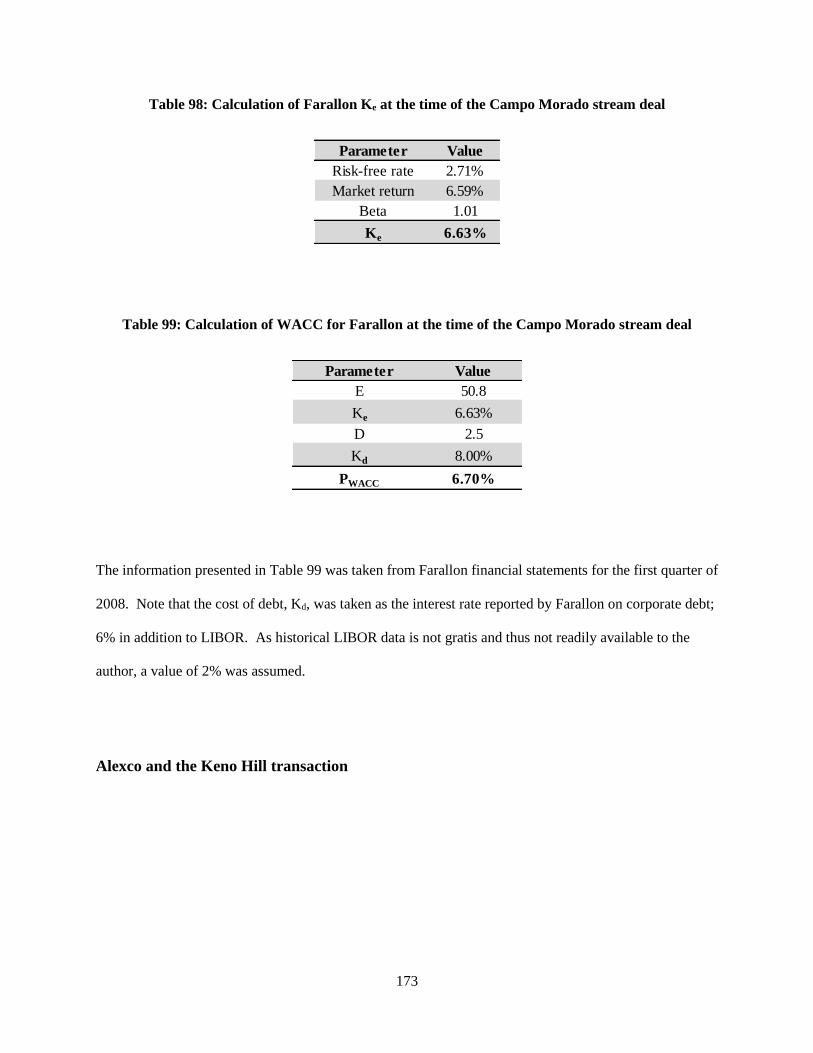

Table 98: Calculation of Farallon Ke at the time of the Campo Morado stream deal ............................... 173

Table 99: Calculation of WACC for Farallon at the time of the Campo Morado stream deal ................. 173

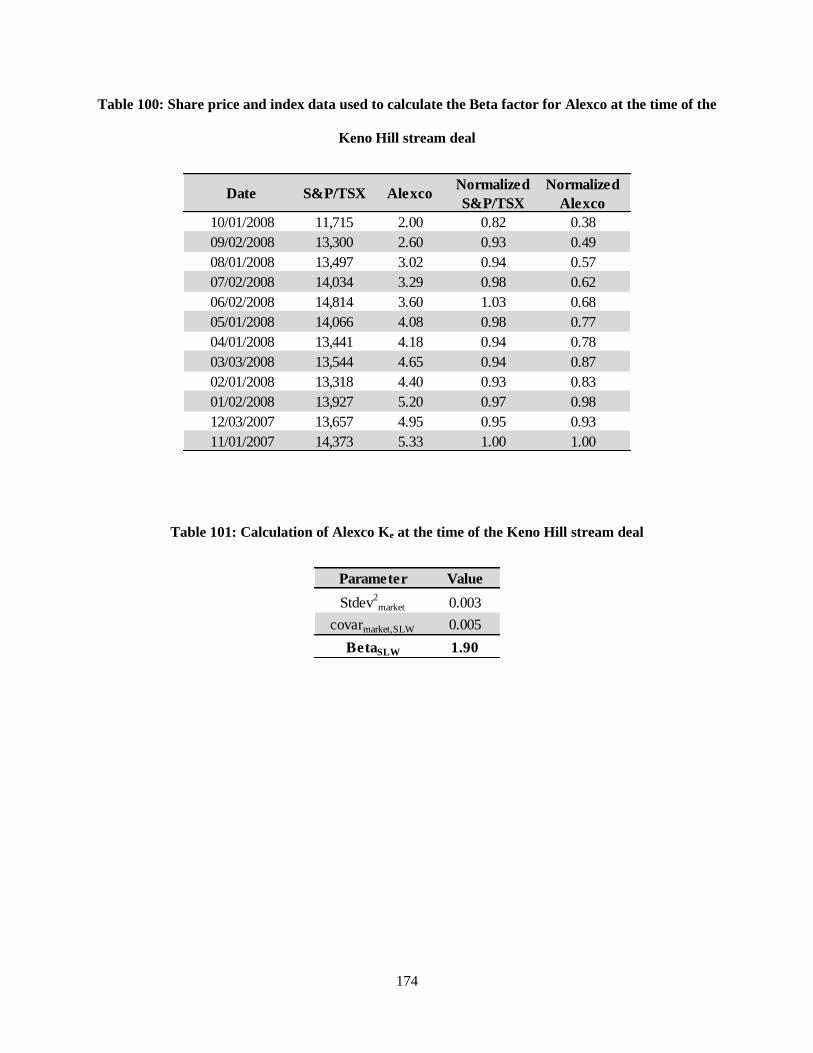

Table 100: Share price and index data used to calculate the Beta factor for Alexco at the time of the Keno

Hill stream deal ......................................................................................................................................... 174

Table 101: Calculation of Alexco Ke at the time of the Keno Hill stream deal ........................................ 174

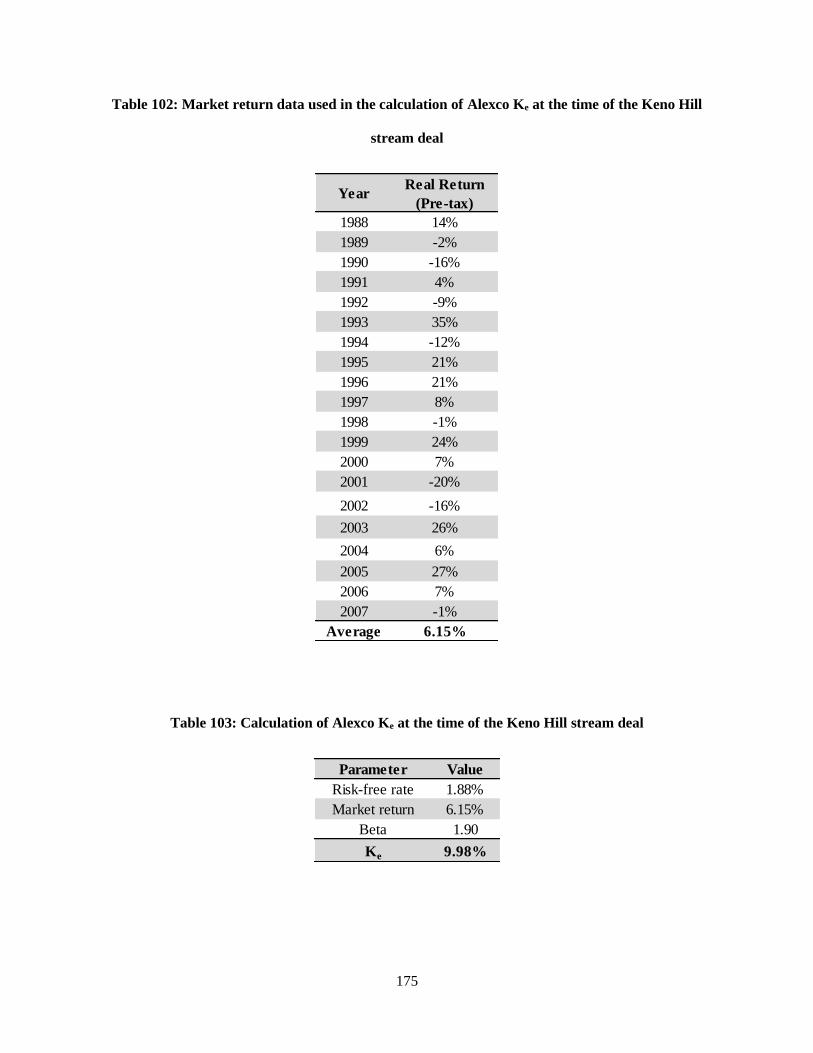

Table 102: Market return data used in the calculation of Alexco Ke at the time of the Keno Hill stream

deal ............................................................................................................................................................ 175

Table 103: Calculation of Alexco Ke at the time of the Keno Hill stream deal ........................................ 175

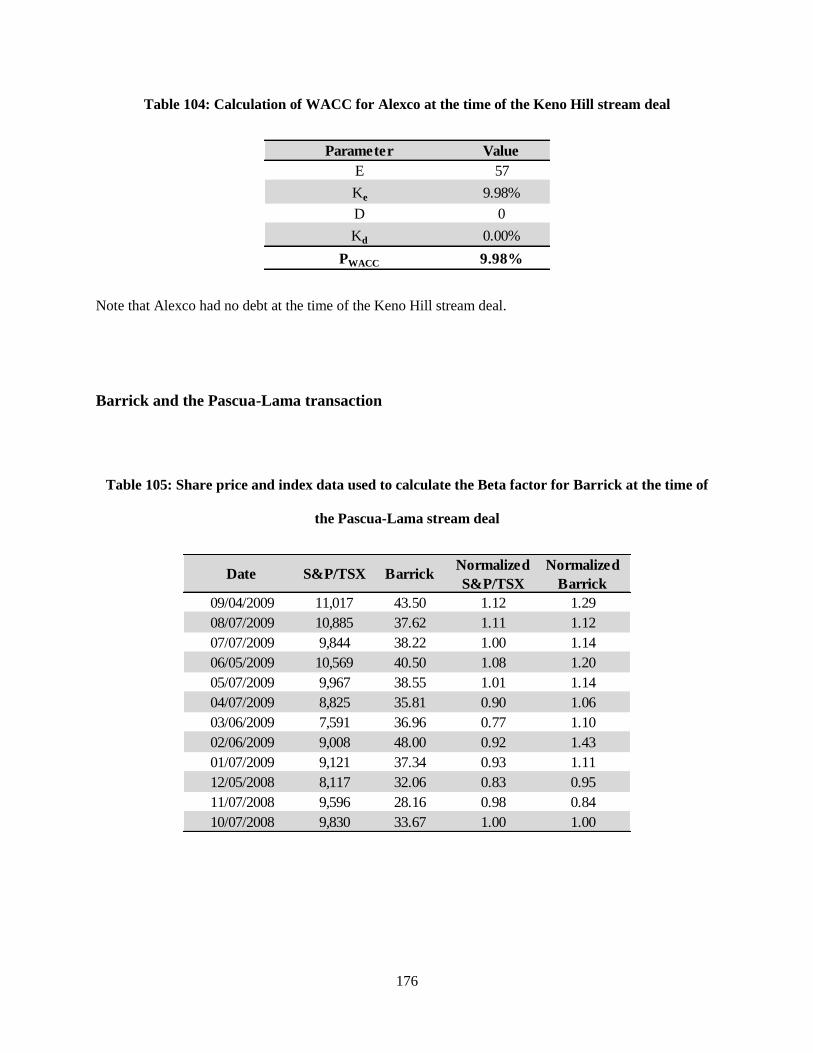

Table 104: Calculation of WACC for Alexco at the time of the Keno Hill stream deal .......................... 176

Table 105: Share price and index data used to calculate the Beta factor for Barrick at the time of the

Pascua-Lama stream deal .......................................................................................................................... 176

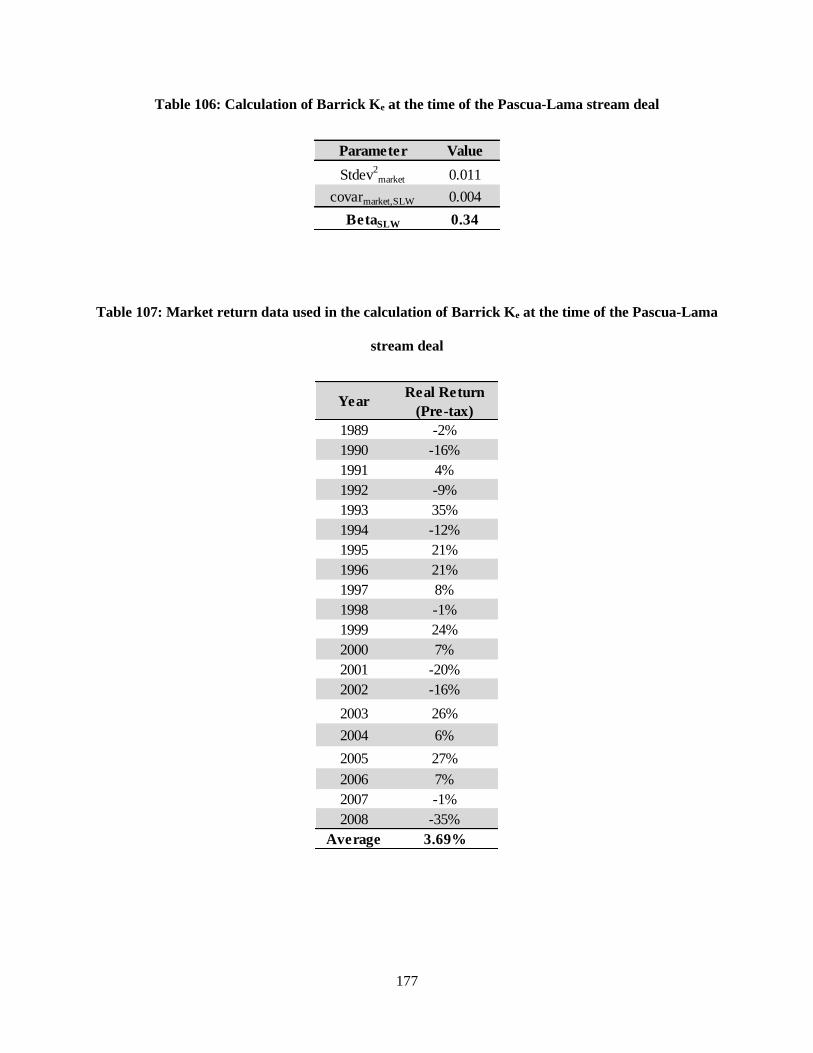

Table 106: Calculation of Barrick Ke at the time of the Pascua-Lama stream deal .................................. 177

Table 107: Market return data used in the calculation of Barrick Ke at the time of the Pascua-Lama stream

deal ............................................................................................................................................................ 177

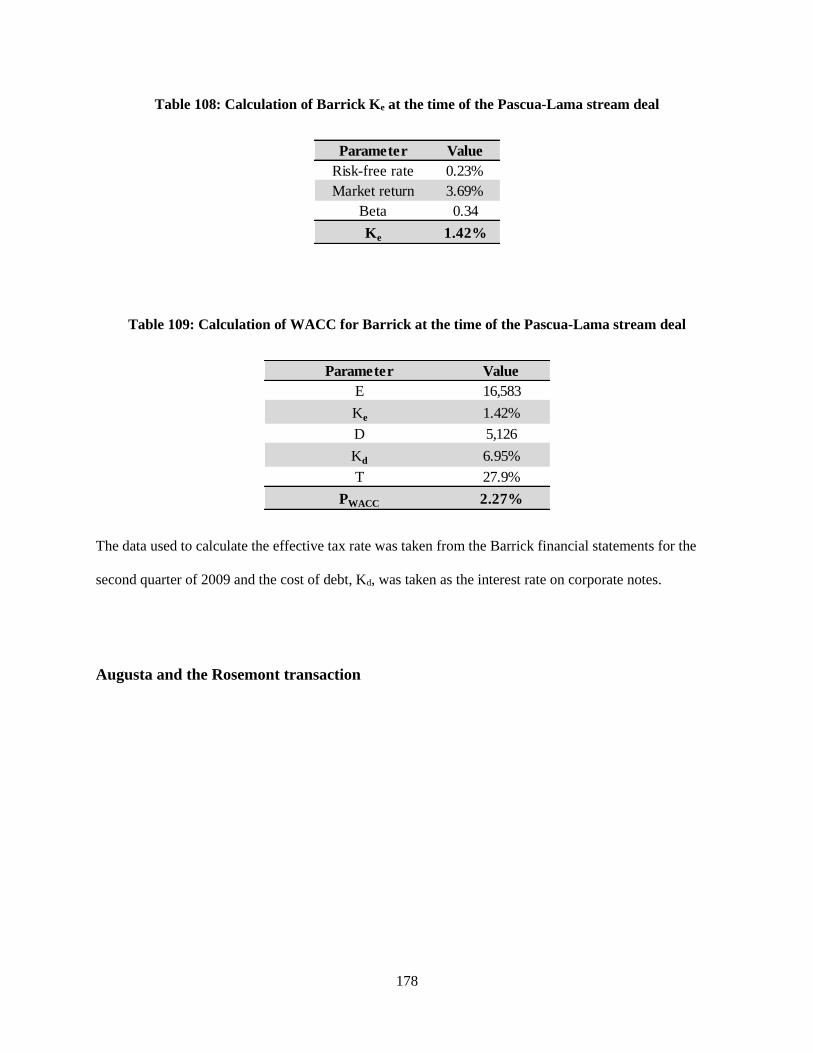

Table 108: Calculation of Barrick Ke at the time of the Pascua-Lama stream deal .................................. 178

Table 109: Calculation of WACC for Barrick at the time of the Pascua-Lama stream deal .................... 178

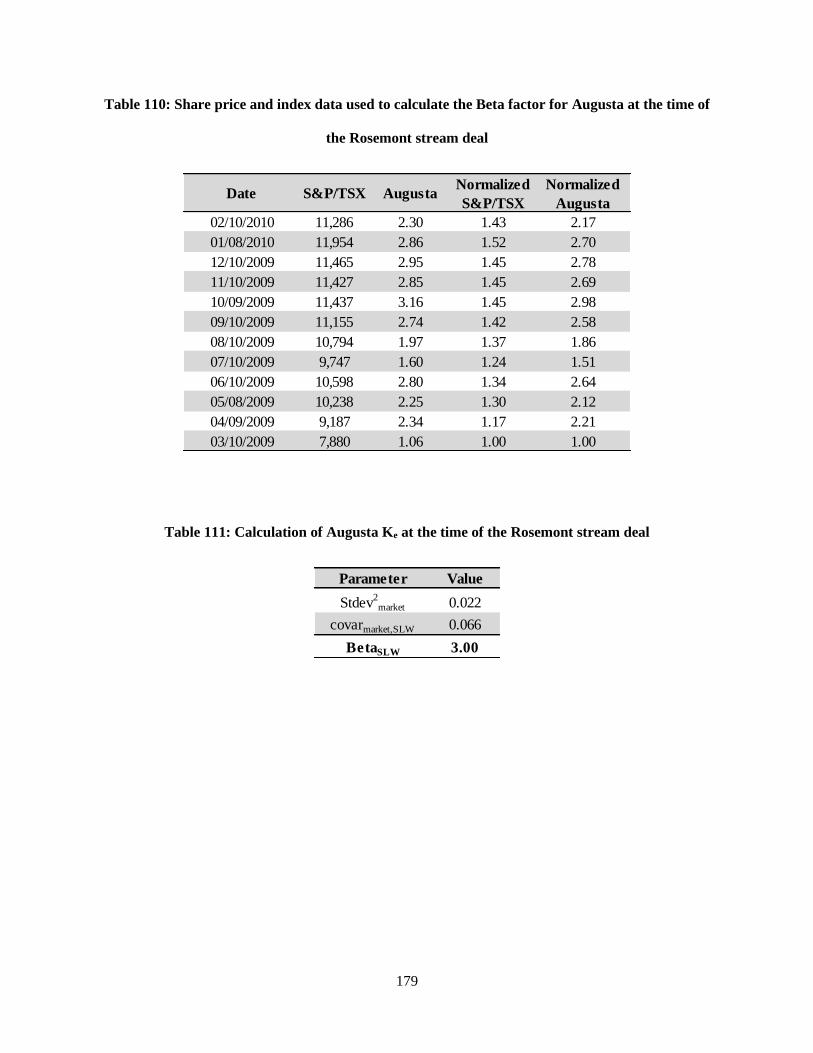

Table 110: Share price and index data used to calculate the Beta factor for Augusta at the time of the

Rosemont stream deal ............................................................................................................................... 179

Table 111: Calculation of Augusta Ke at the time of the Rosemont stream deal ...................................... 179

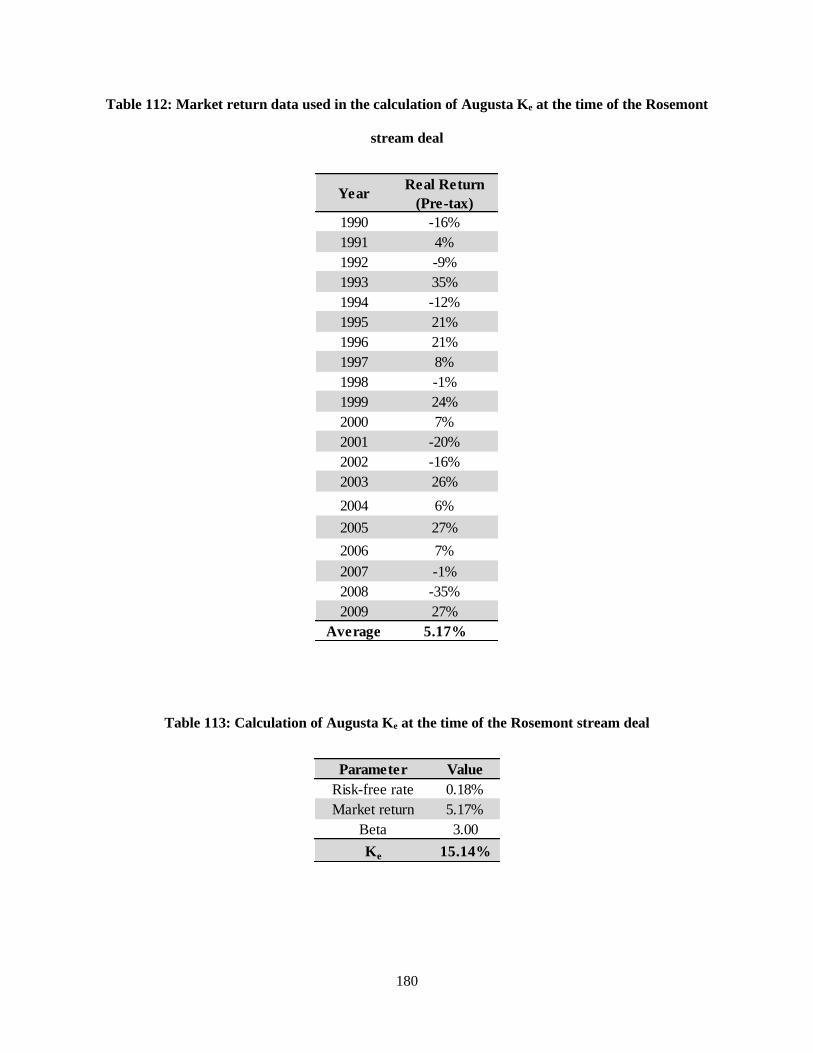

Table 112: Market return data used in the calculation of Augusta Ke at the time of the Rosemont stream

deal ............................................................................................................................................................ 180

xxi

Table 113: Calculation of Augusta Ke at the time of the Rosemont stream deal ...................................... 180

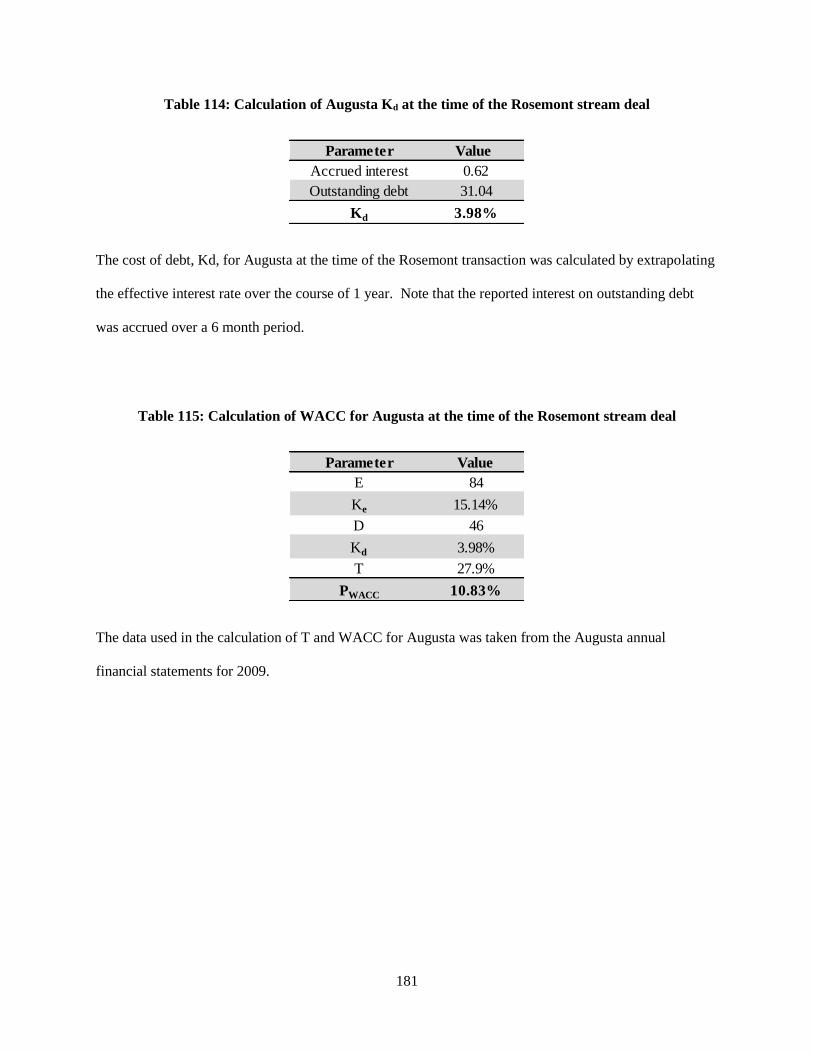

Table 114: Calculation of Augusta Kd at the time of the Rosemont stream deal ...................................... 181

Table 115: Calculation of WACC for Augusta at the time of the Rosemont stream deal ........................ 181

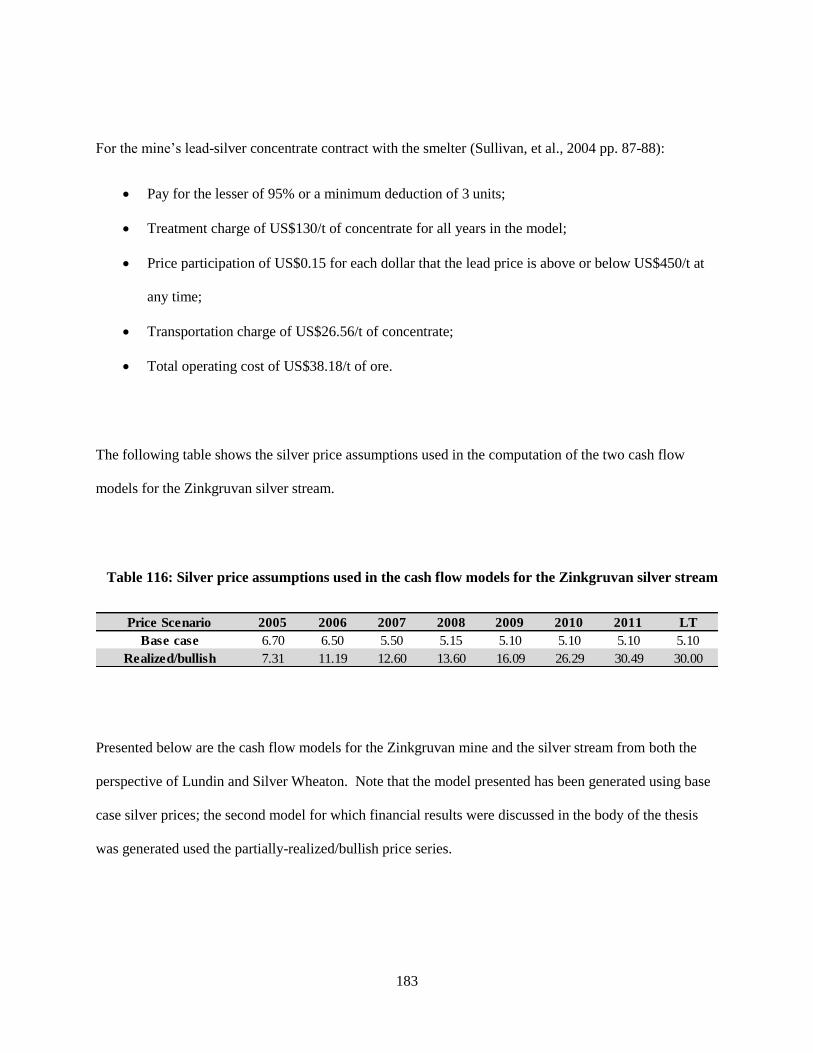

Table 116: Silver price assumptions used in the cash flow models for the Zinkgruvan silver stream ..... 183

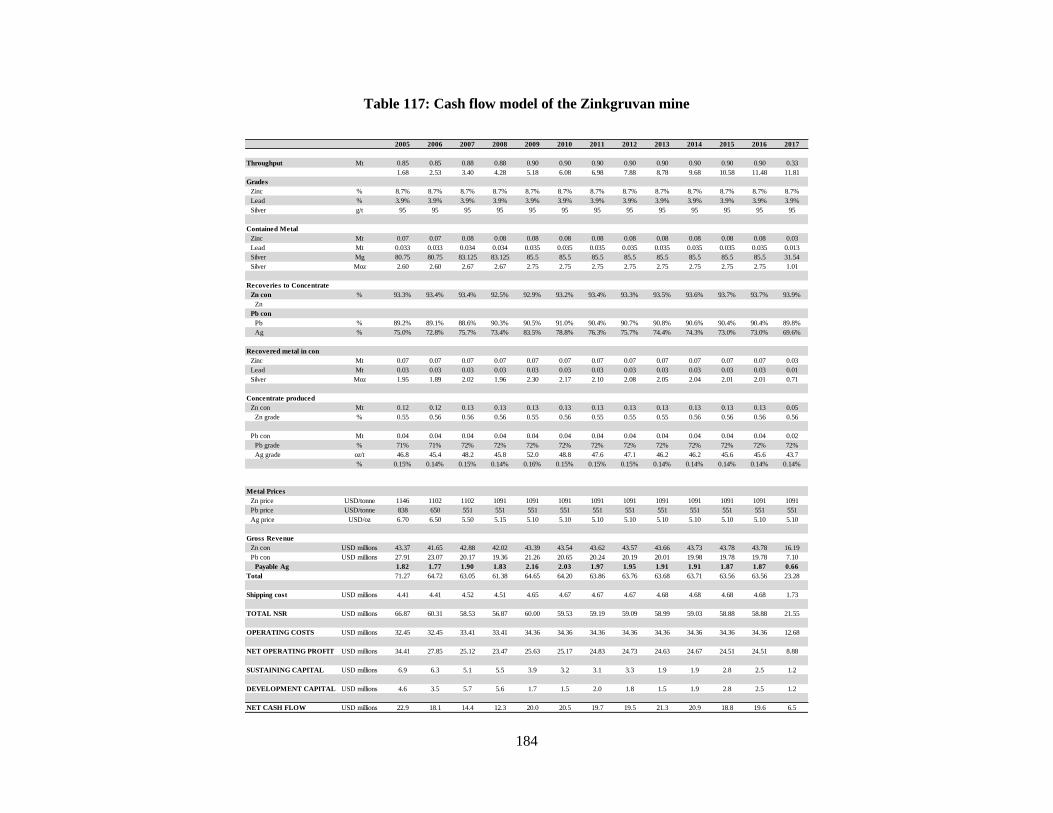

Table 117: Cash flow model of the Zinkgruvan mine .............................................................................. 184

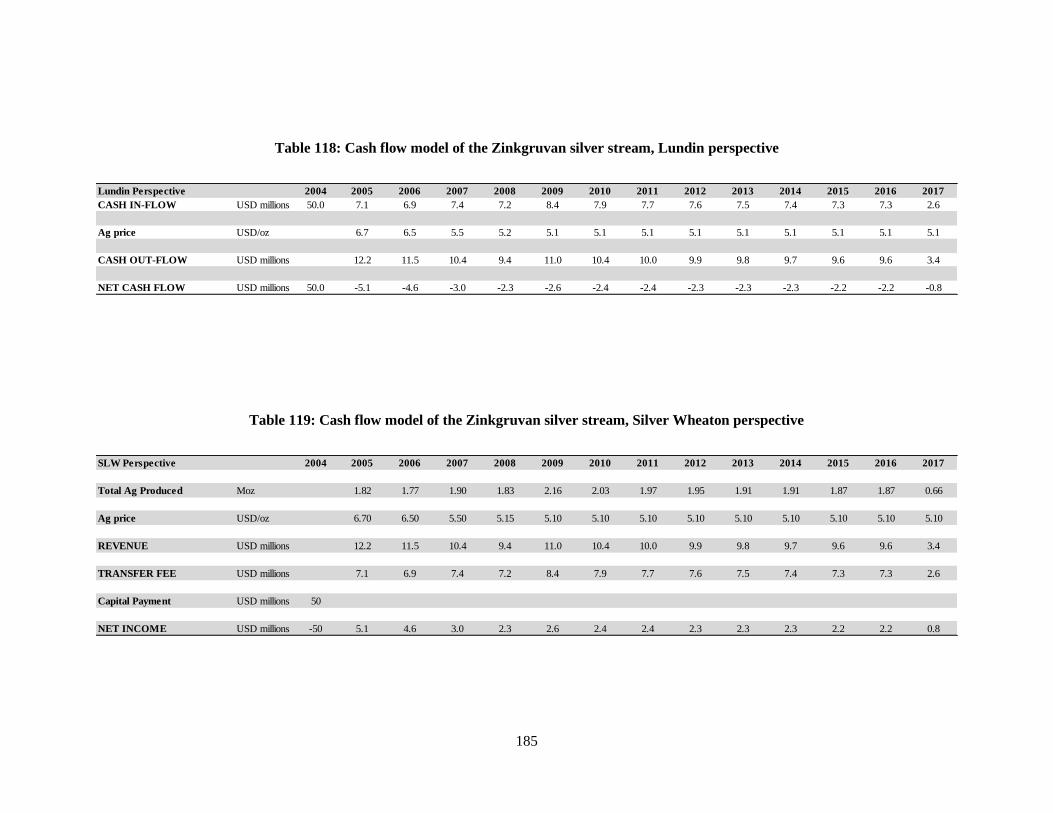

Table 118: Cash flow model of the Zinkgruvan silver stream, Lundin perspective ................................. 185

Table 119: Cash flow model of the Zinkgruvan silver stream, Silver Wheaton perspective .................... 185

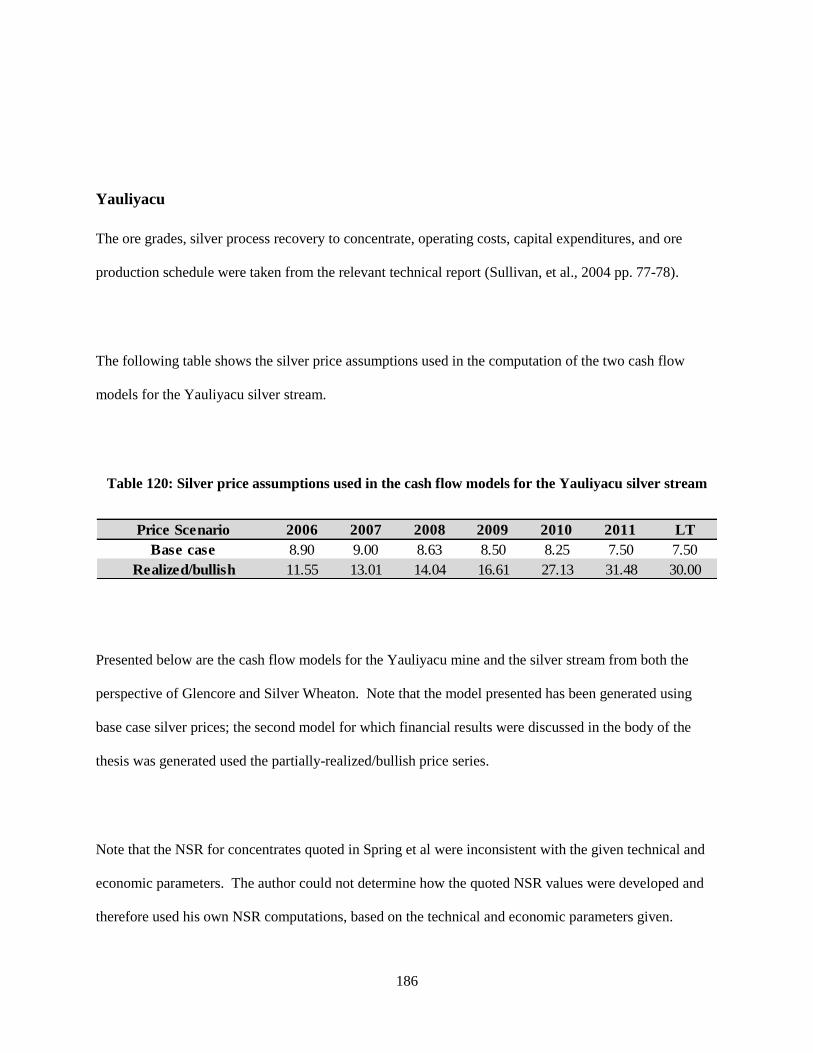

Table 120: Silver price assumptions used in the cash flow models for the Yauliyacu silver stream ........ 186

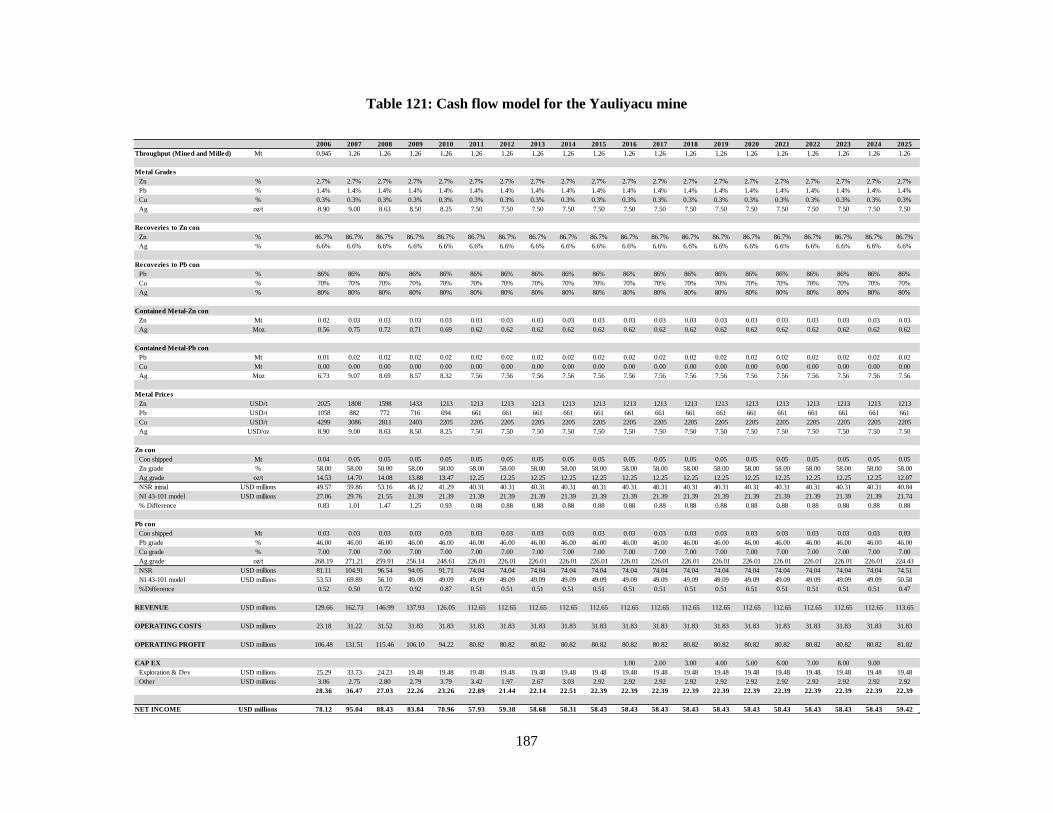

Table 121: Cash flow model for the Yauliyacu mine ............................................................................... 187

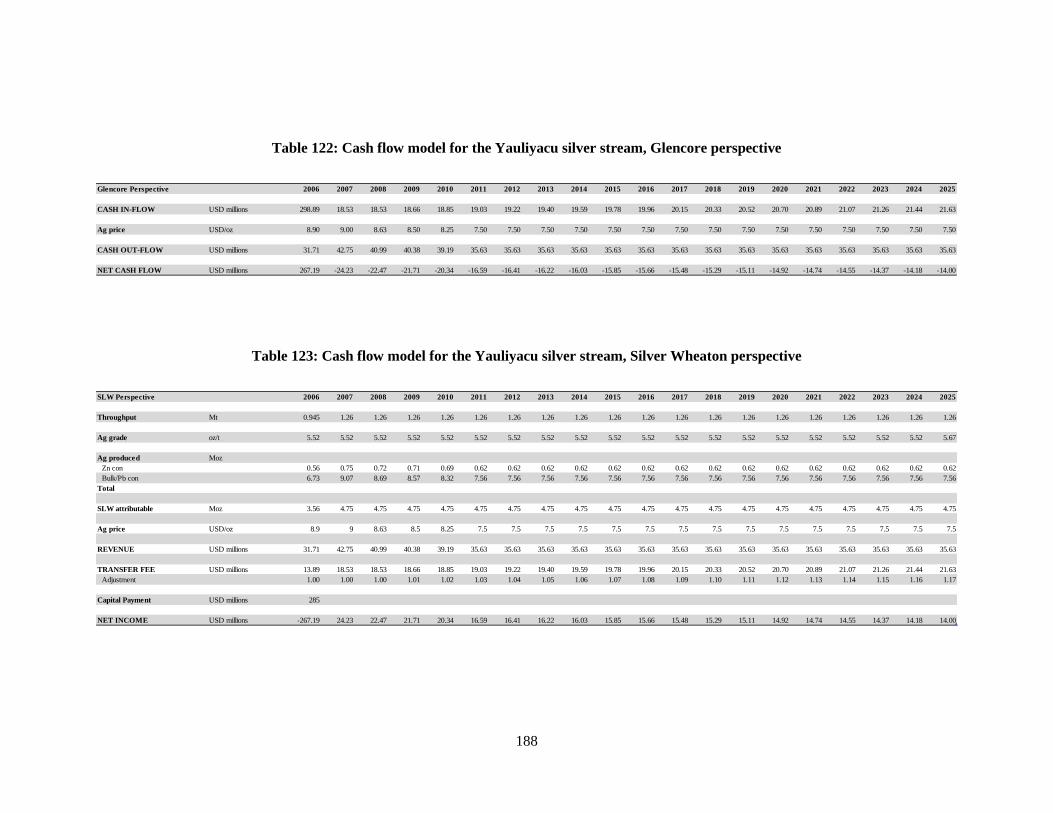

Table 122: Cash flow model for the Yauliyacu silver stream, Glencore perspective ............................... 188

Table 123: Cash flow model for the Yauliyacu silver stream, Silver Wheaton perspective ..................... 188

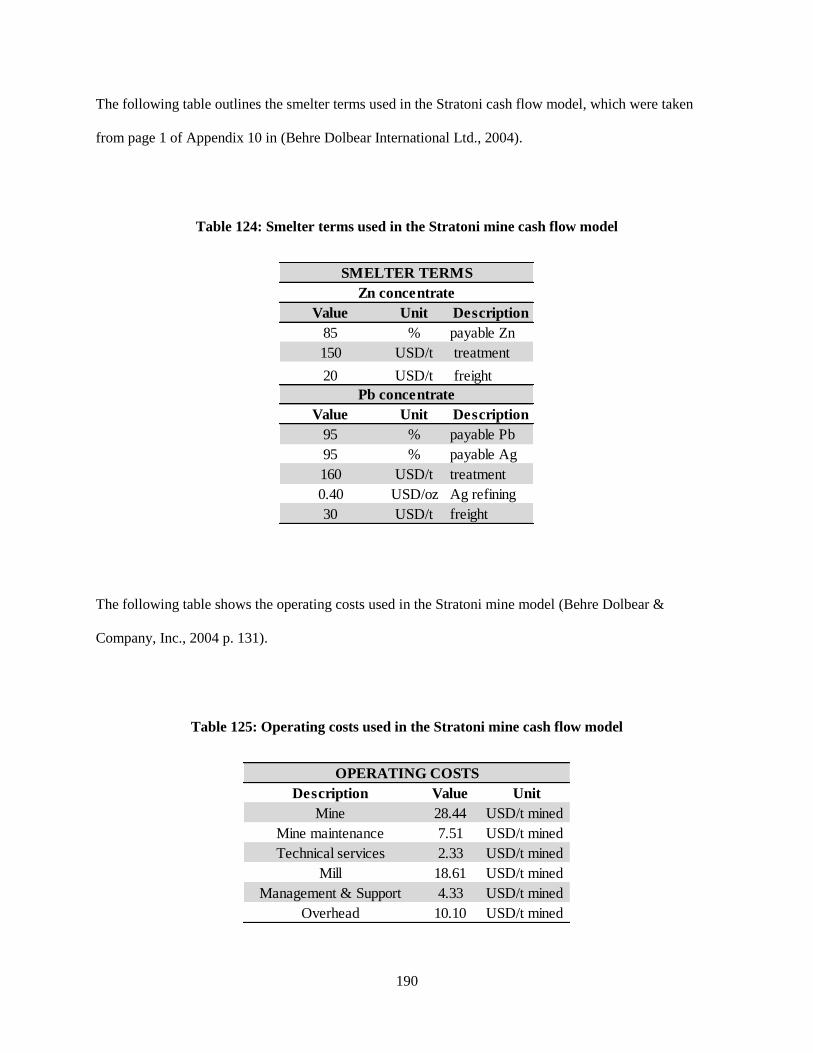

Table 124: Smelter terms used in the Stratoni mine cash flow model ...................................................... 190

Table 125: Operating costs used in the Stratoni mine cash flow model ................................................... 190

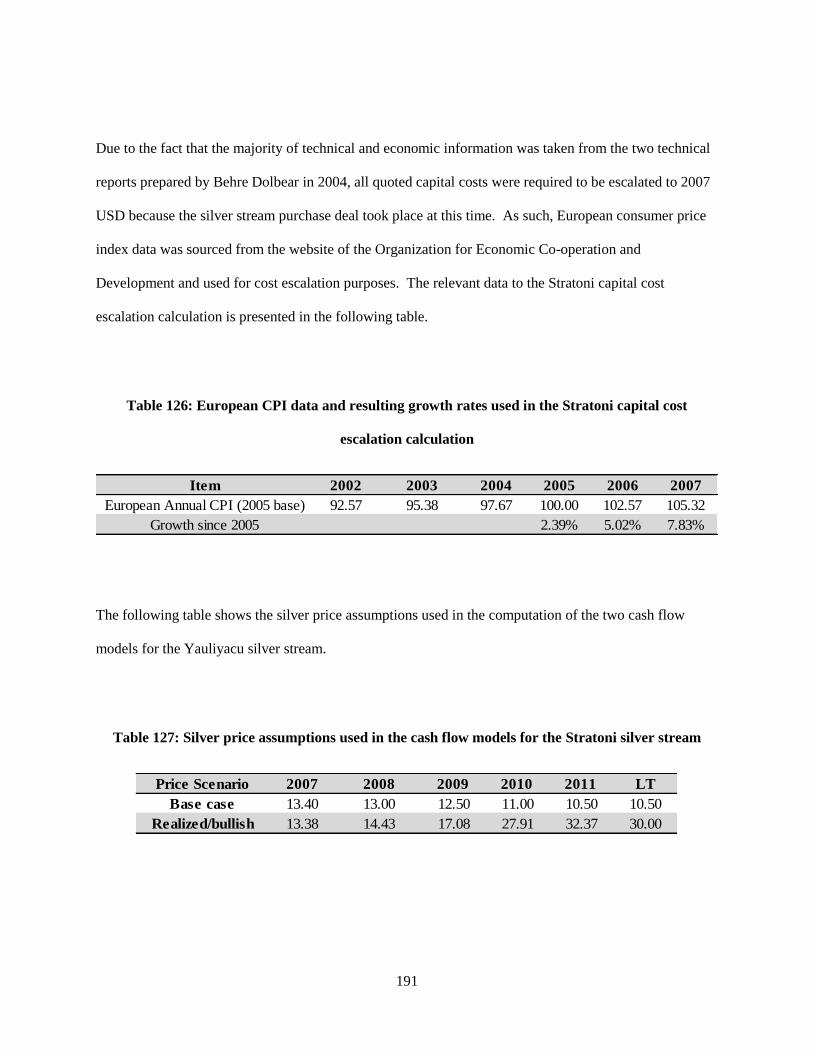

Table 126: European CPI data and resulting growth rates used in the Stratoni capital cost escalation

calculation ................................................................................................................................................. 191

Table 127: Silver price assumptions used in the cash flow models for the Stratoni silver stream ........... 191

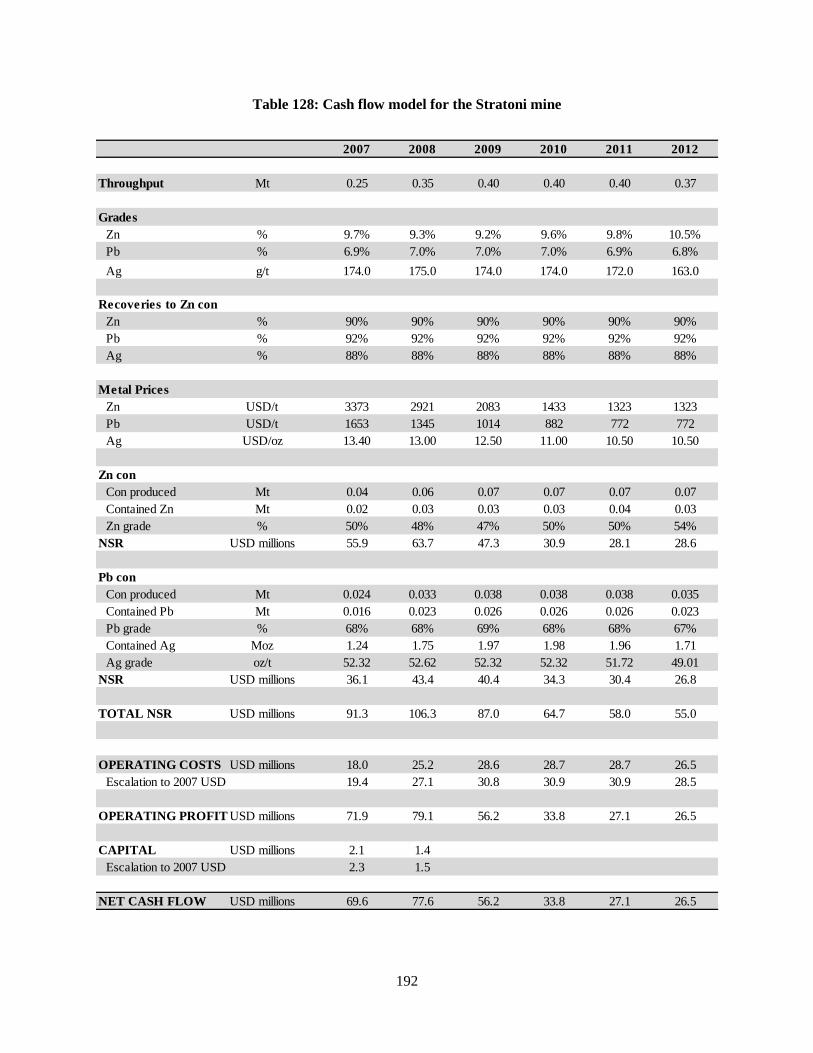

Table 128: Cash flow model for the Stratoni mine ................................................................................... 192

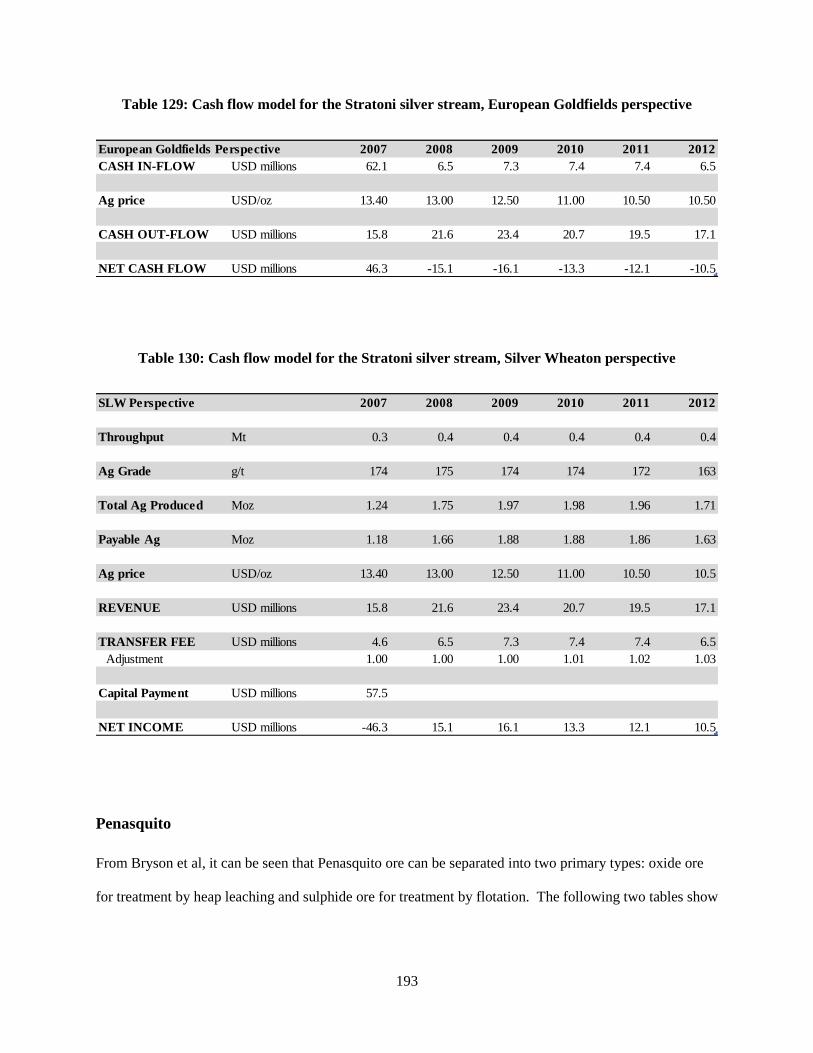

Table 129: Cash flow model for the Stratoni silver stream, European Goldfields perspective ................ 193

Table 130: Cash flow model for the Stratoni silver stream, Silver Wheaton perspective ........................ 193

Table 131: Penasquito sulphide ore composition by lithology ................................................................. 194

Table 132: Metal process recovery factors by lithology for Penasquito sulphide ore .............................. 194

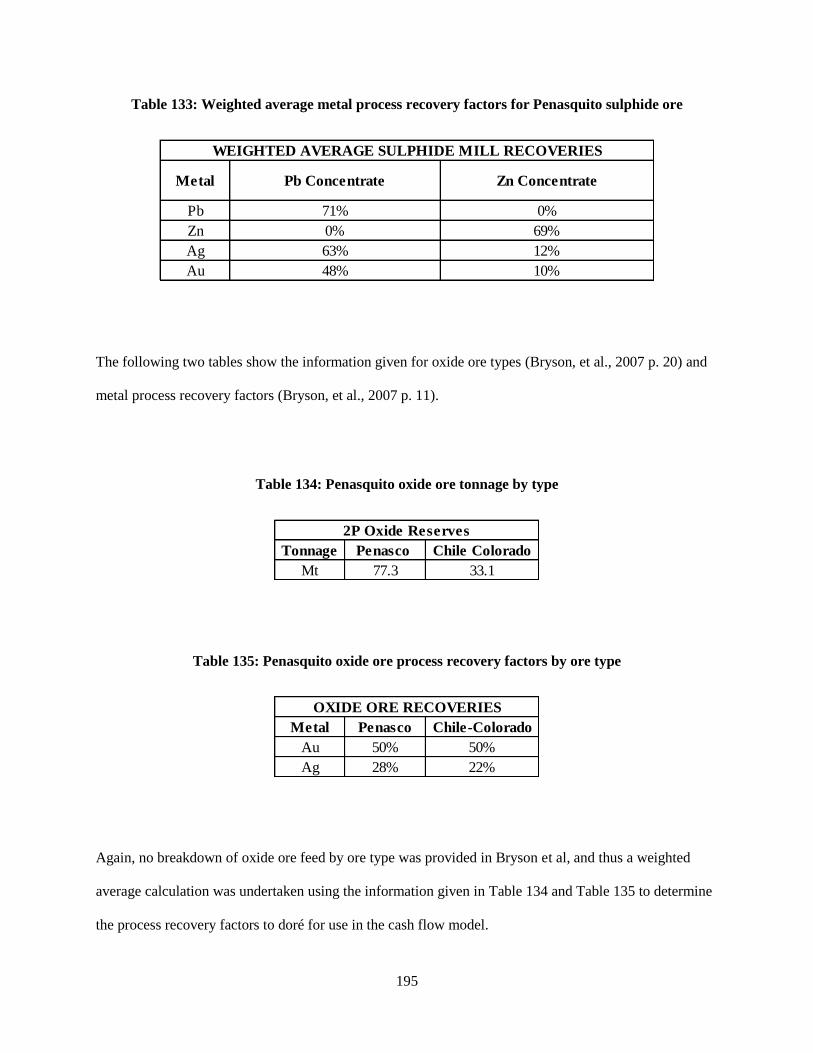

Table 133: Weighted average metal process recovery factors for Penasquito sulphide ore ..................... 195

Table 134: Penasquito oxide ore tonnage by type .................................................................................... 195

Table 135: Penasquito oxide ore process recovery factors by ore type .................................................... 195

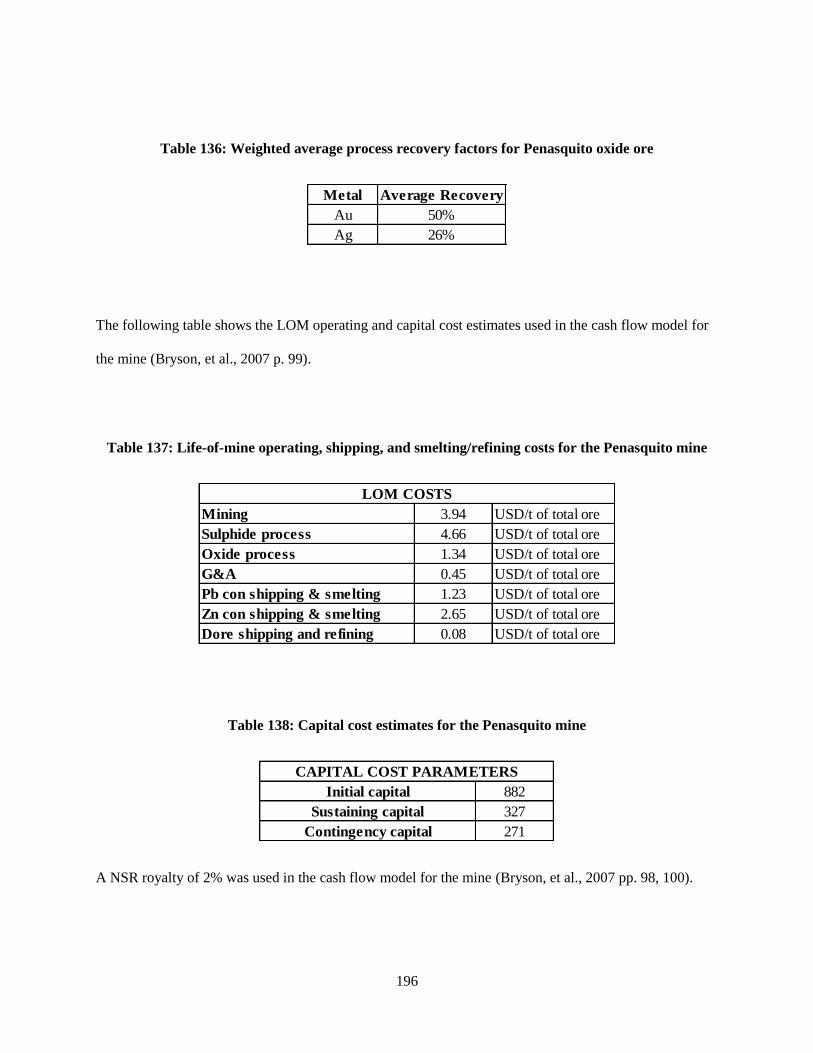

Table 136: Weighted average process recovery factors for Penasquito oxide ore .................................... 196

Table 137: Life-of-mine operating, shipping, and smelting/refining costs for the Penasquito mine ........ 196

xxii

Table 138: Capital cost estimates for the Penasquito mine ....................................................................... 196

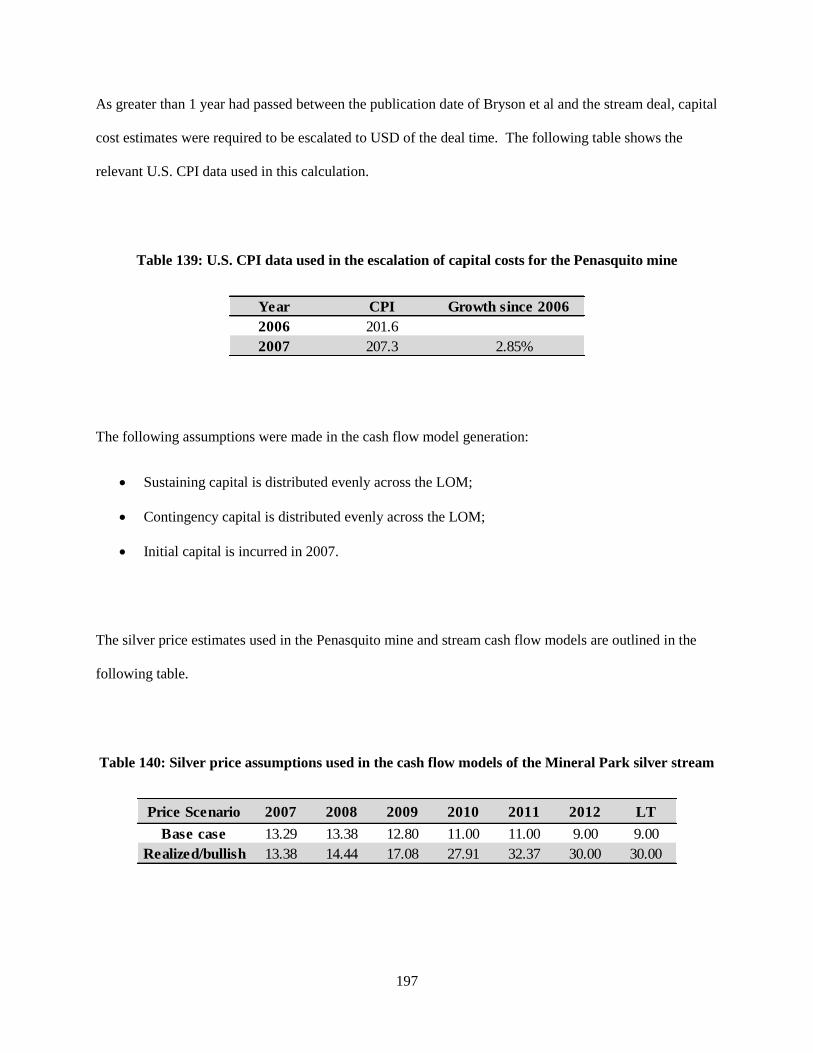

Table 139: U.S. CPI data used in the escalation of capital costs for the Penasquito mine ....................... 197

Table 140: Silver price assumptions used in the cash flow models of the Mineral Park silver stream .... 197

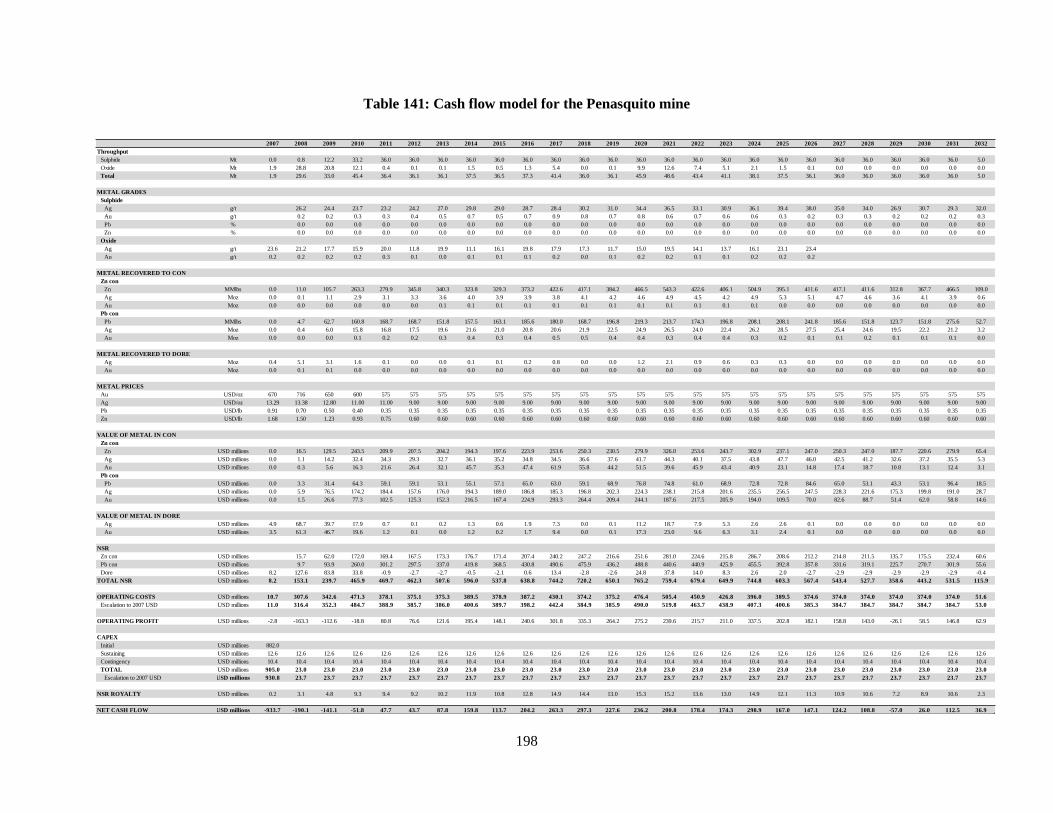

Table 141: Cash flow model for the Penasquito mine .............................................................................. 198

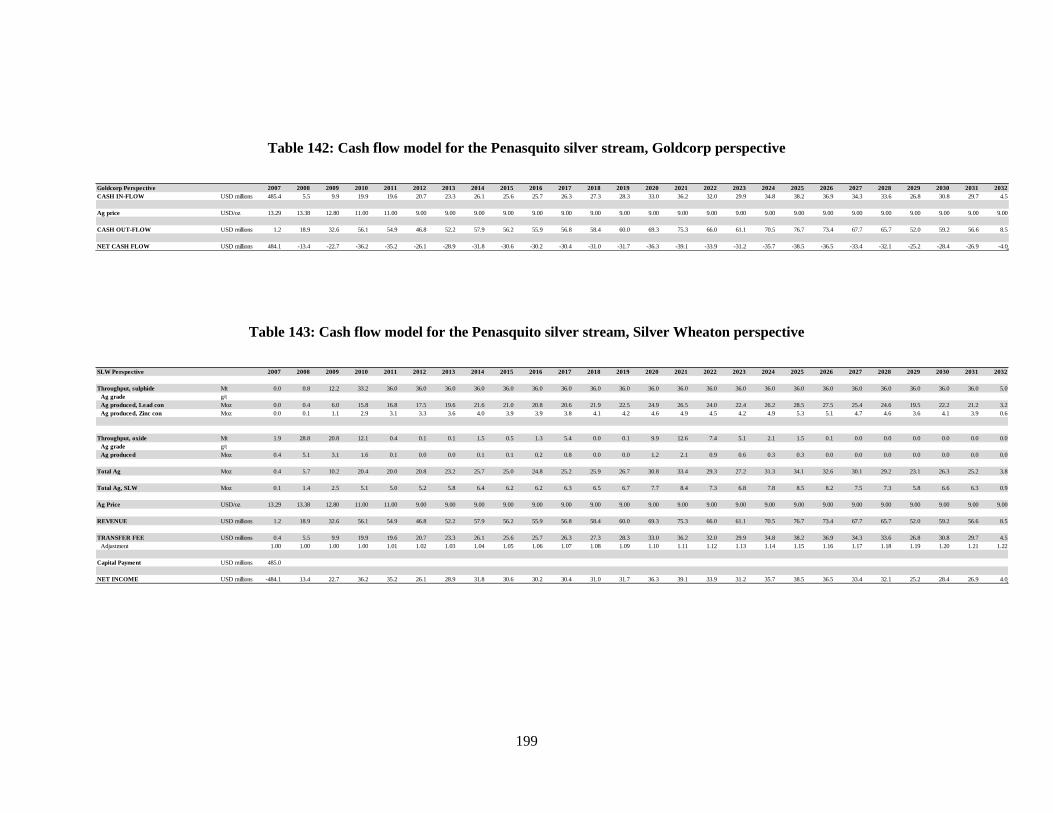

Table 142: Cash flow model for the Penasquito silver stream, Goldcorp perspective ............................. 199

Table 143: Cash flow model for the Penasquito silver stream, Silver Wheaton perspective.................... 199

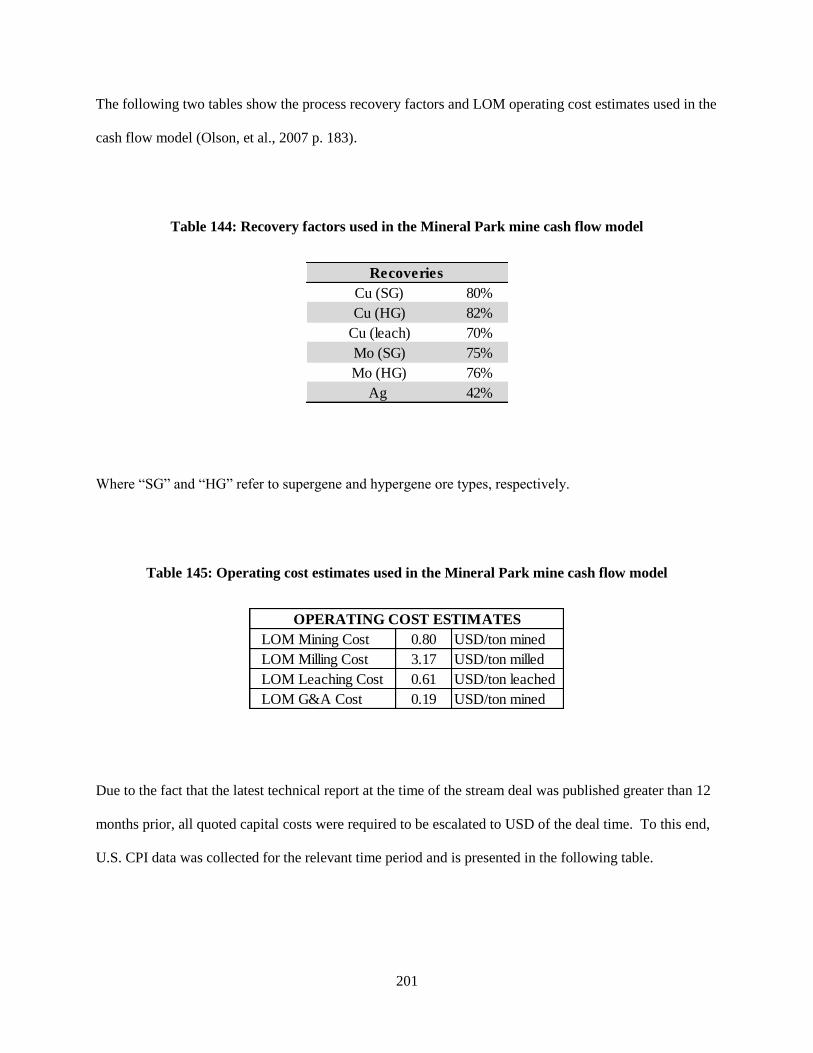

Table 144: Recovery factors used in the Mineral Park mine cash flow model ......................................... 201

Table 145: Operating cost estimates used in the Mineral Park mine cash flow model ............................. 201

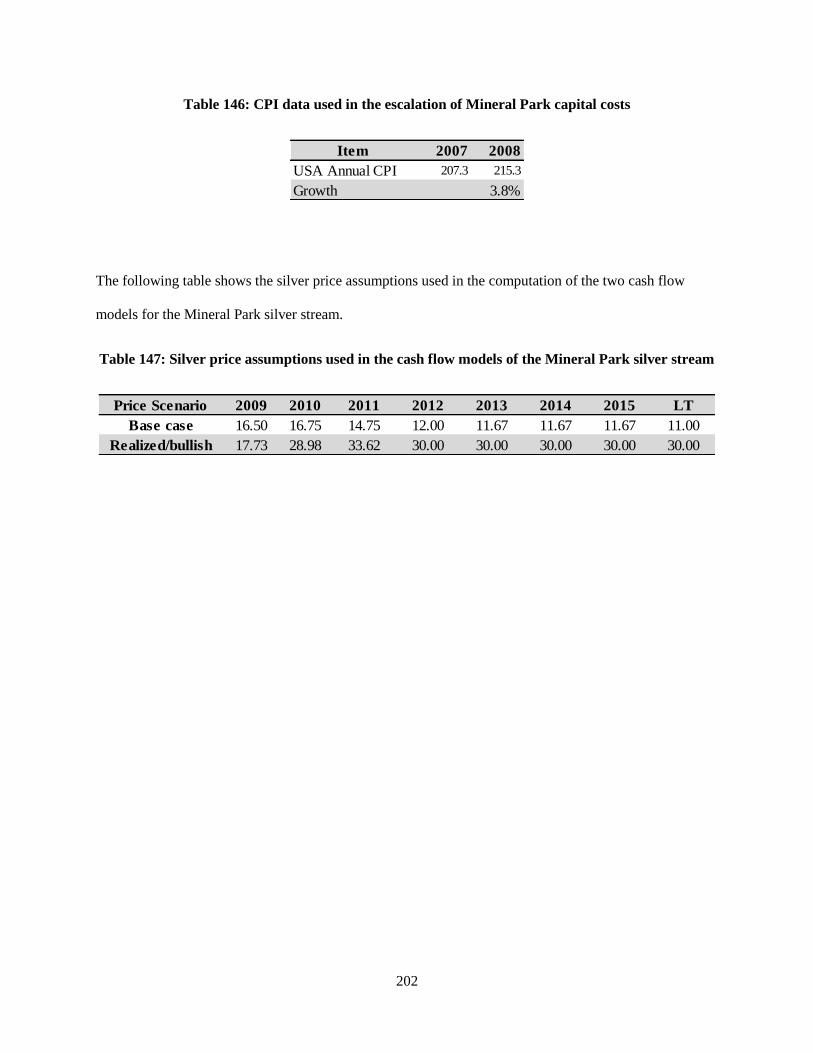

Table 146: CPI data used in the escalation of Mineral Park capital costs ................................................ 202

Table 147: Silver price assumptions used in the cash flow models of the Mineral Park silver stream .... 202

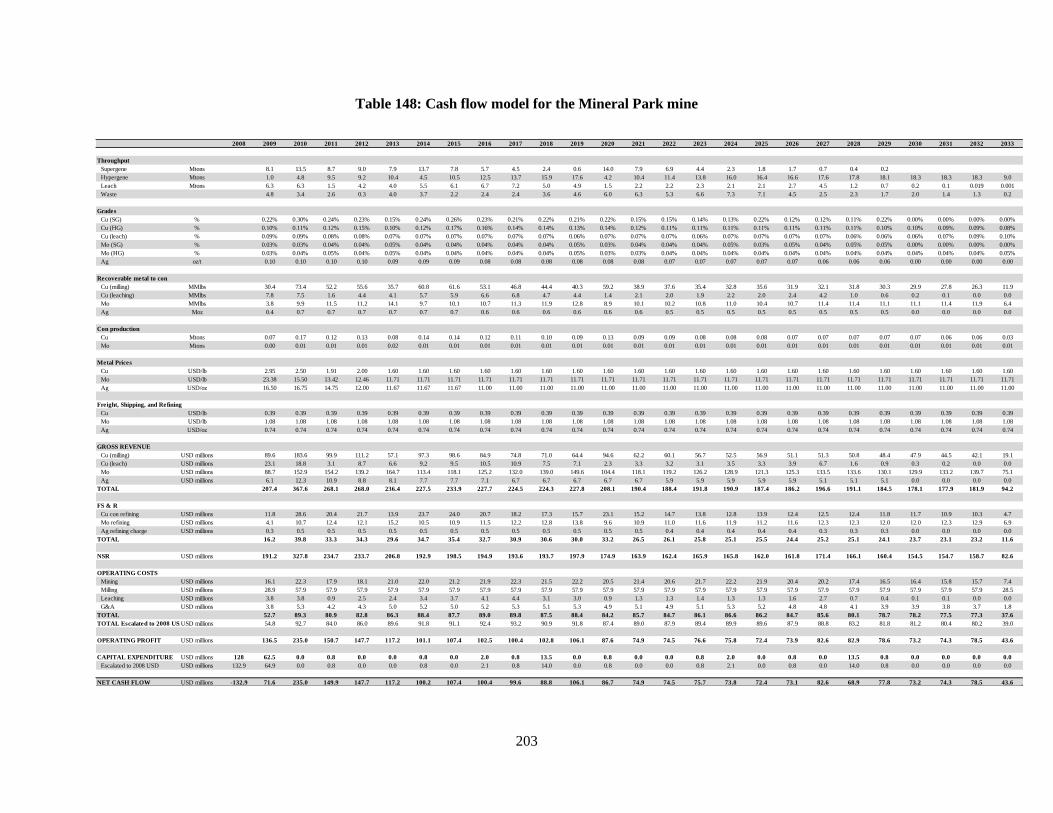

Table 148: Cash flow model for the Mineral Park mine ........................................................................... 203

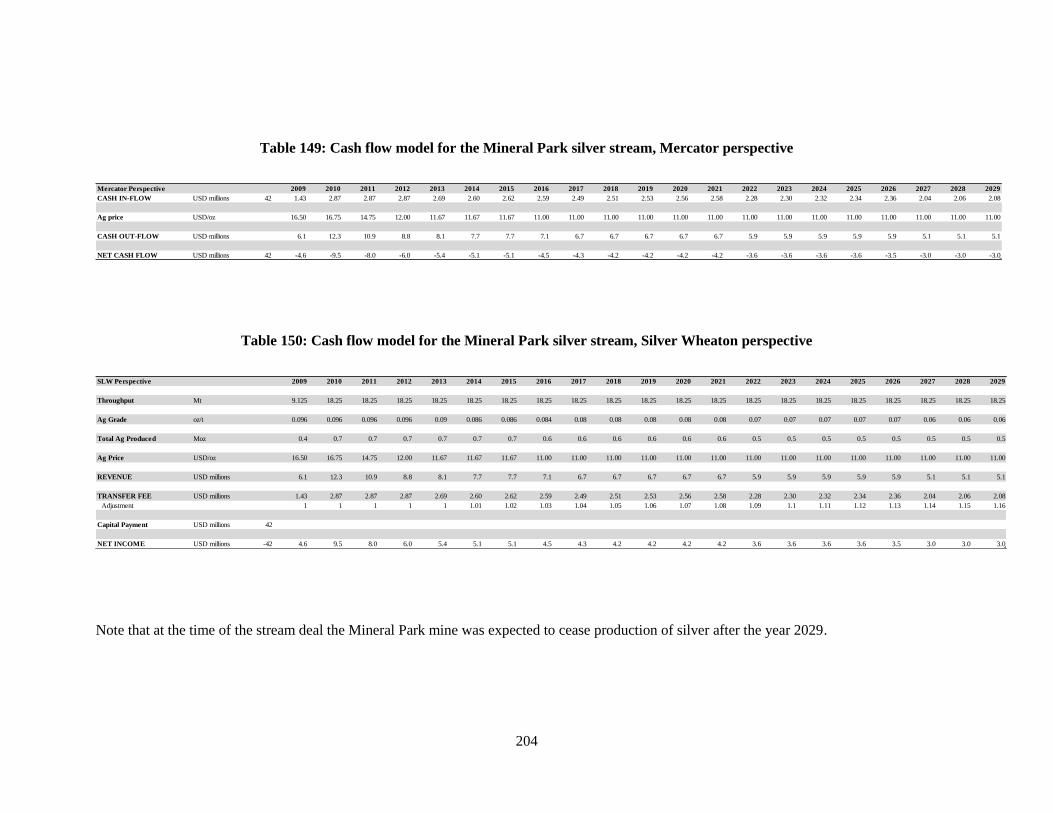

Table 149: Cash flow model for the Mineral Park silver stream, Mercator perspective .......................... 204

Table 150: Cash flow model for the Mineral Park silver stream, Silver Wheaton perspective ................ 204

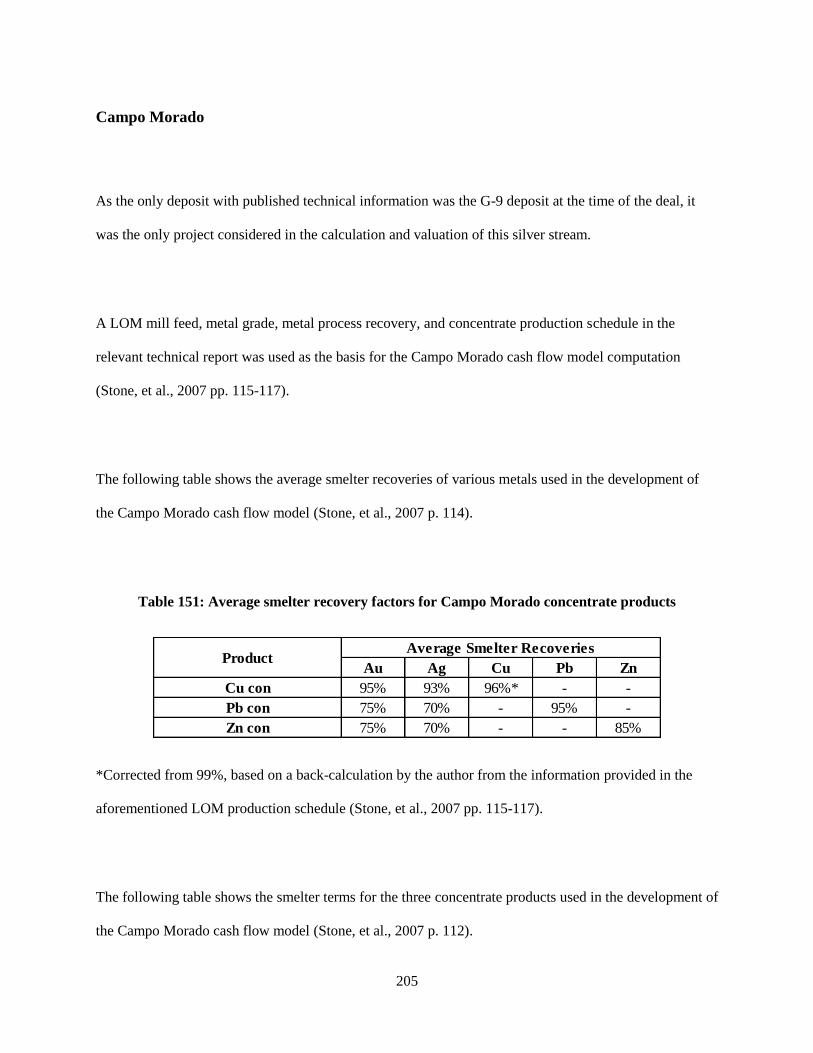

Table 151: Average smelter recovery factors for Campo Morado concentrate products ......................... 205

Table 152: Metal refining costs for the Campo Morado project ............................................................... 206

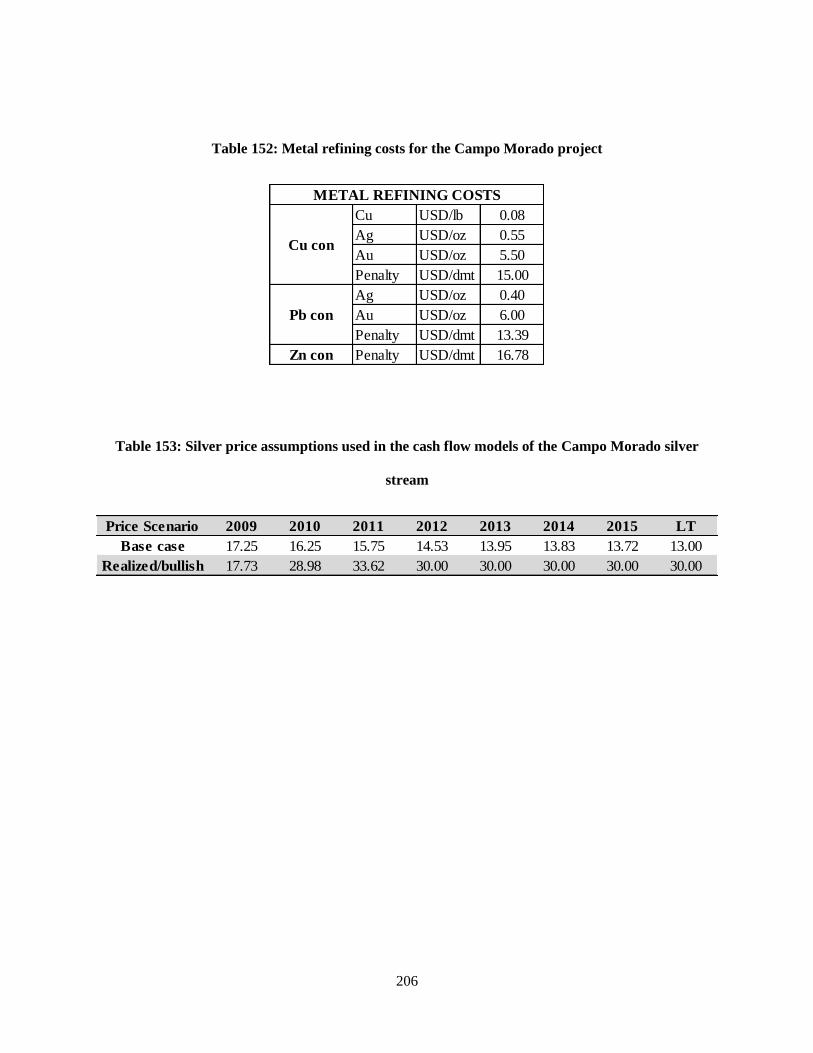

Table 153: Silver price assumptions used in the cash flow models of the Campo Morado silver stream 206

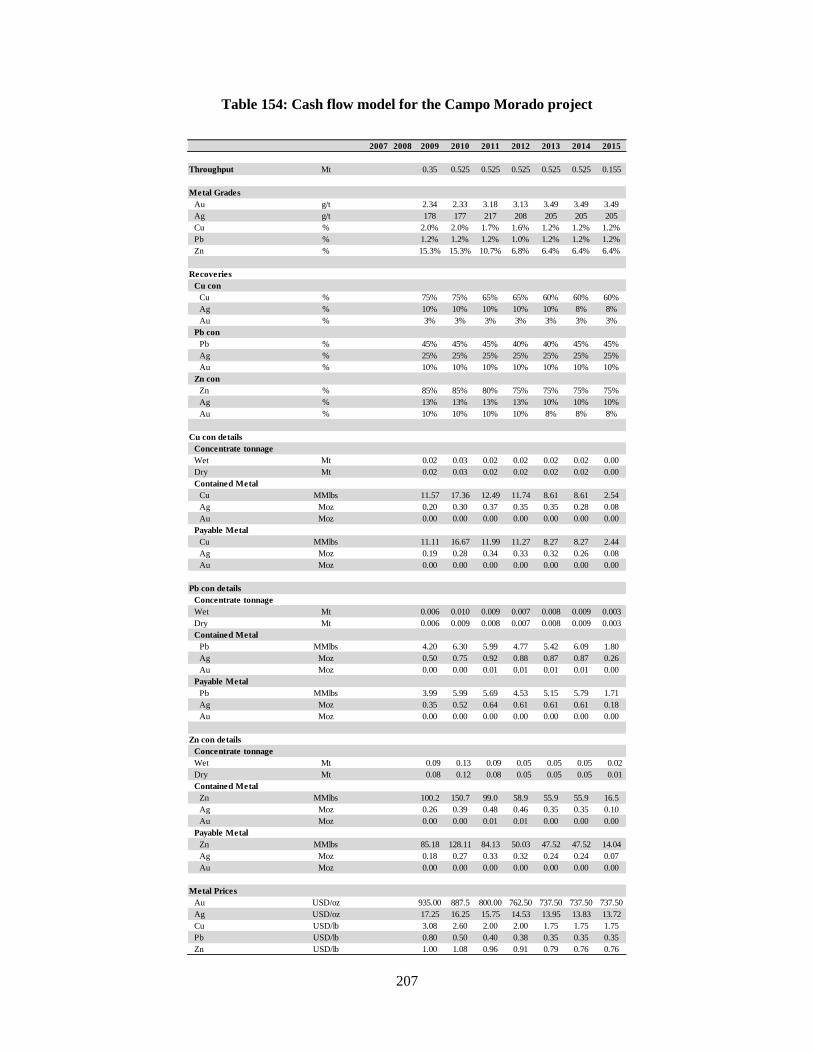

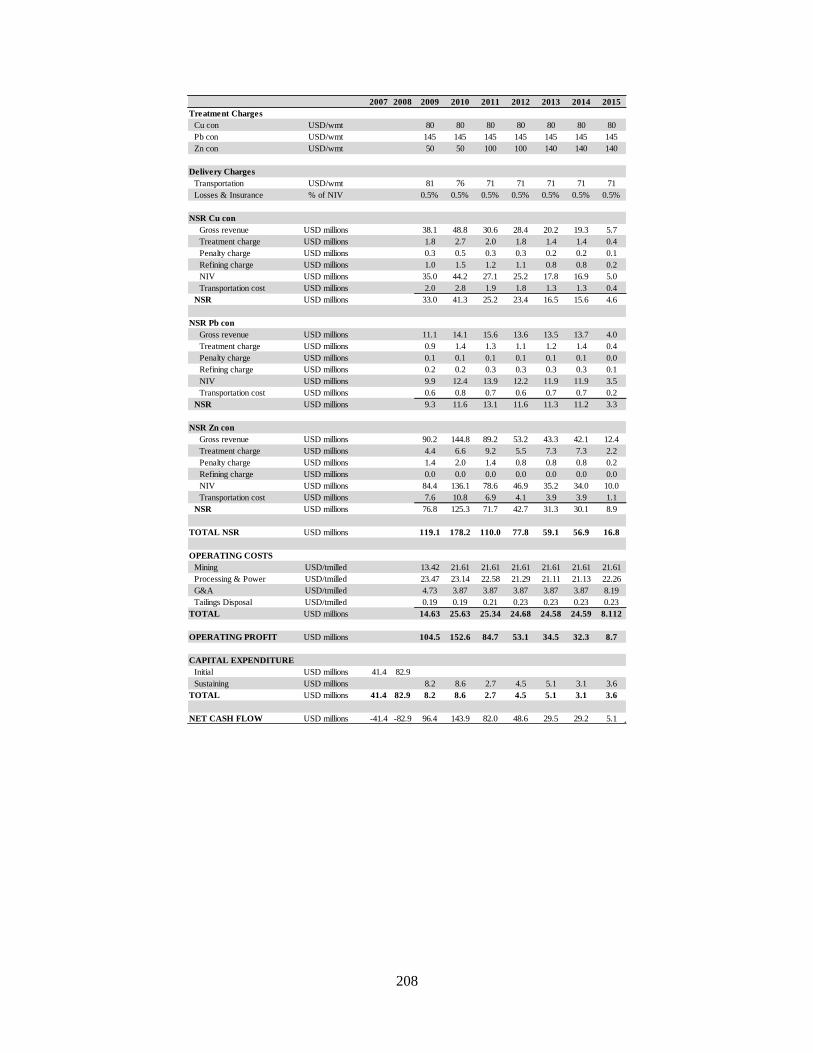

Table 154: Cash flow model for the Campo Morado project ................................................................... 207

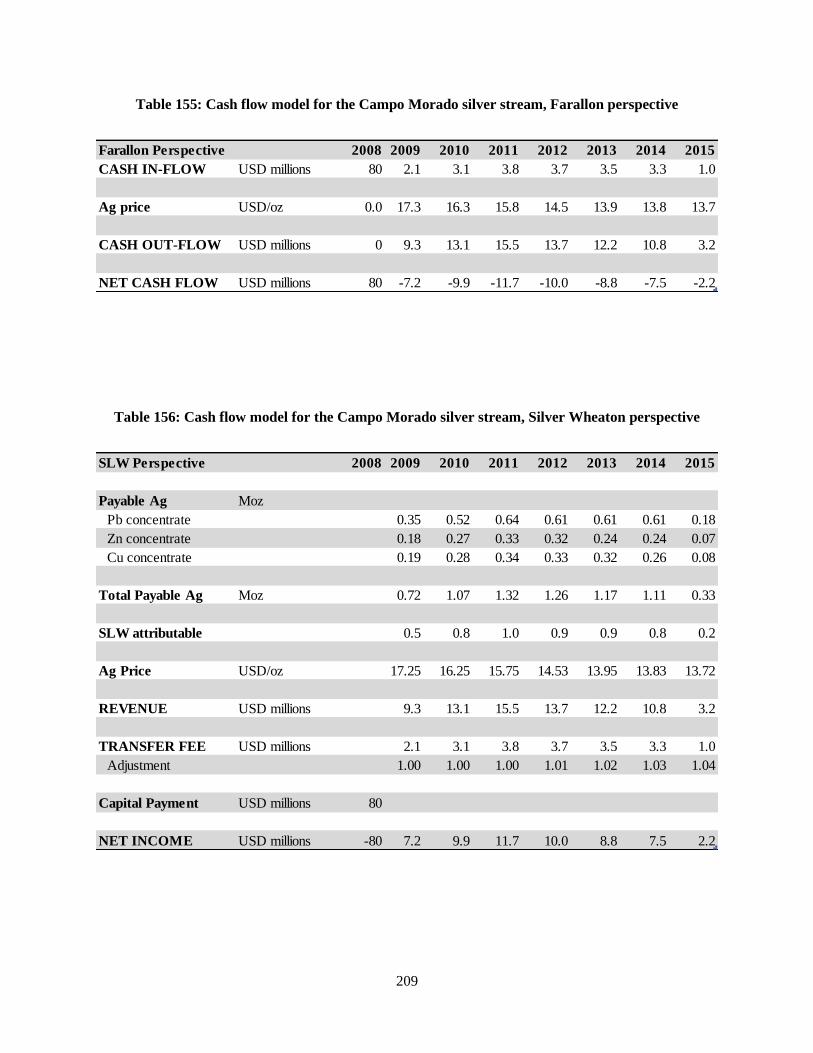

Table 155: Cash flow model for the Campo Morado silver stream, Farallon perspective........................ 209

Table 156: Cash flow model for the Campo Morado silver stream, Silver Wheaton perspective ............ 209

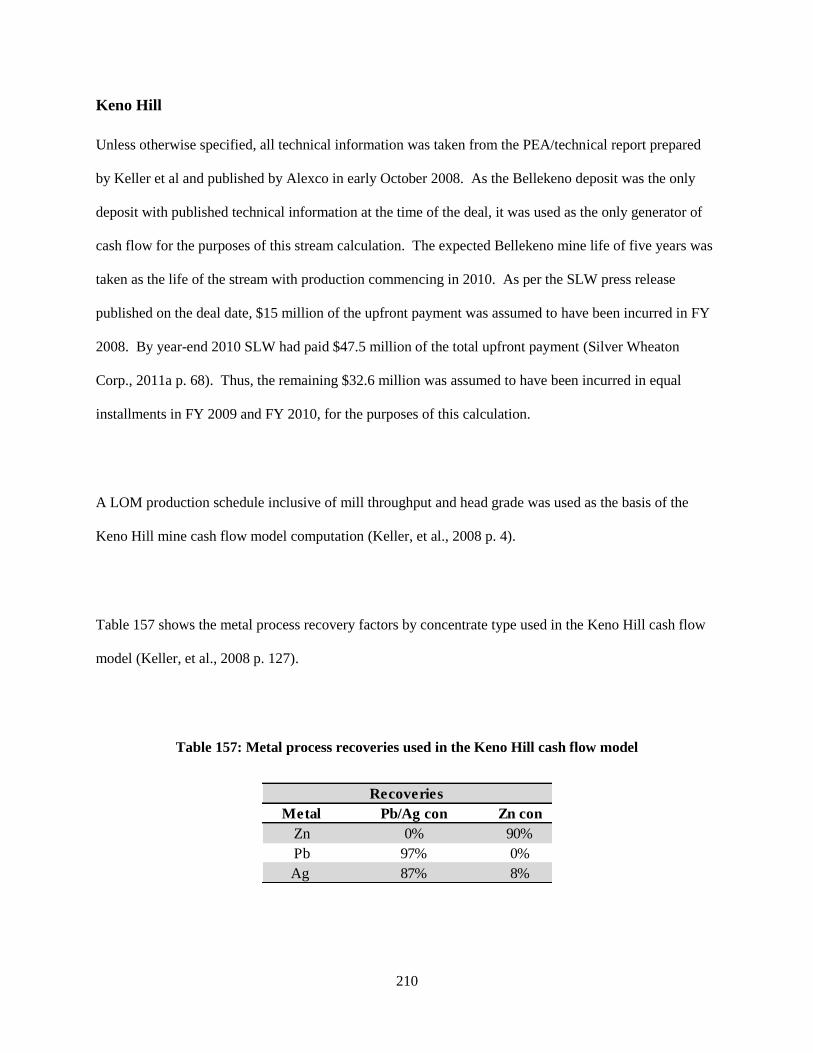

Table 157: Metal process recoveries used in the Keno Hill cash flow model .......................................... 210

Table 158: Smelter terms for the Keno Hill mine ..................................................................................... 211

Table 159: Operating cost estimates for the Keno Hill mine .................................................................... 211

Table 160: Estimated metal penalties for the Keno Hill mine concentrate products ................................ 212

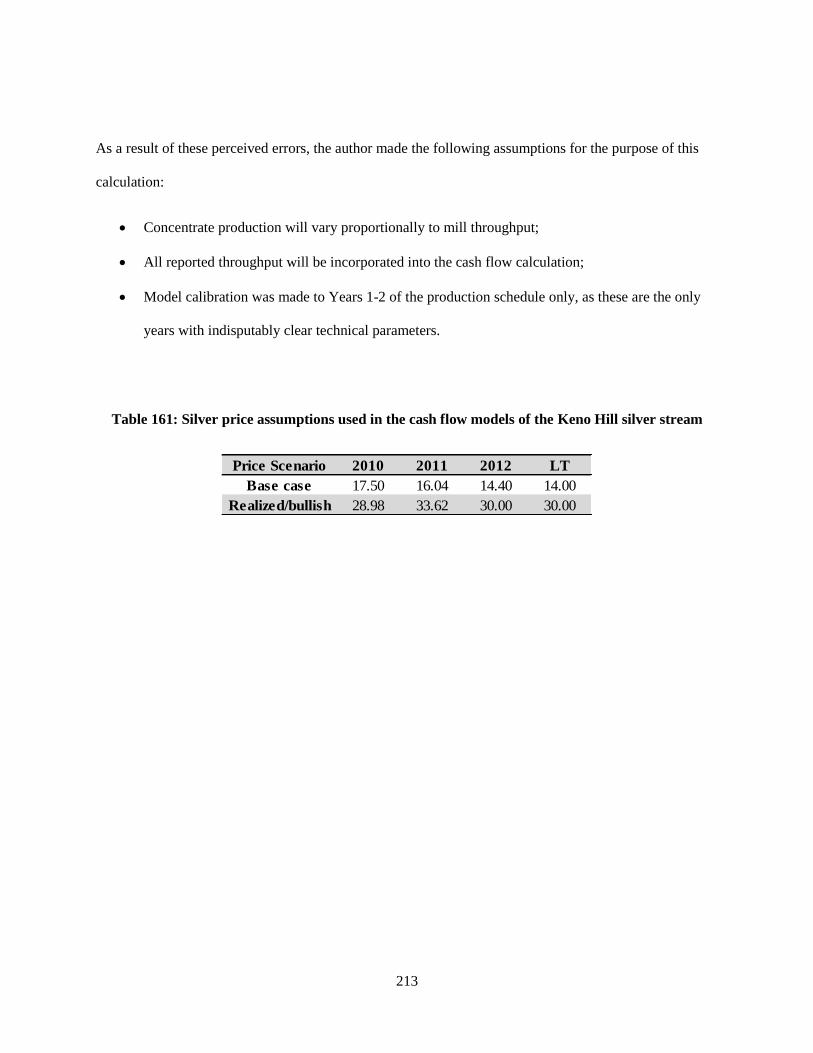

Table 161: Silver price assumptions used in the cash flow models of the Keno Hill silver stream ......... 213

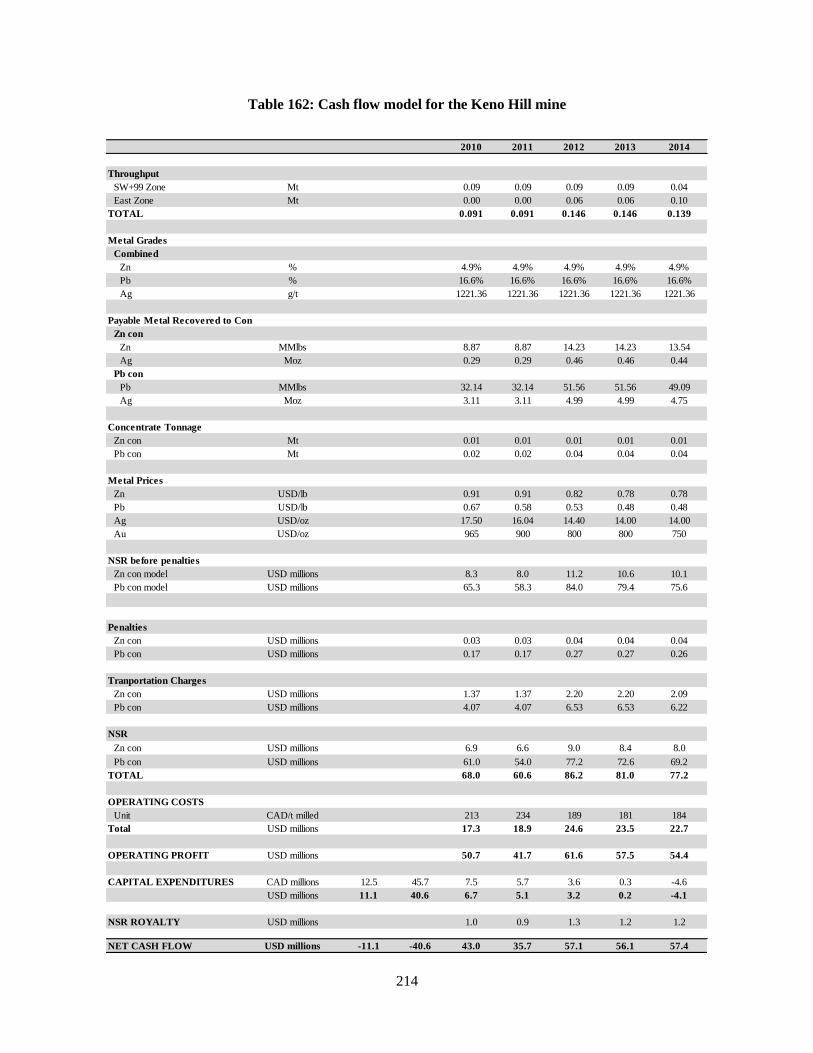

Table 162: Cash flow model for the Keno Hill mine ................................................................................ 214

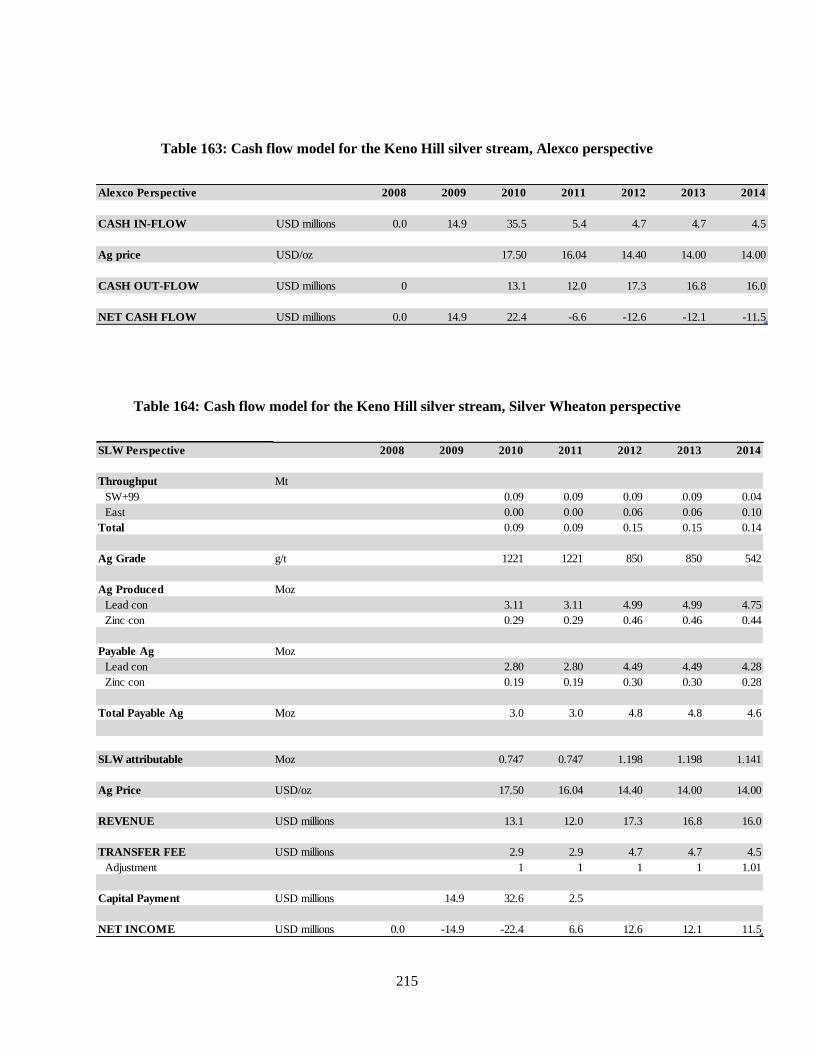

Table 163: Cash flow model for the Keno Hill silver stream, Alexco perspective ................................... 215

xxiii

Table 164: Cash flow model for the Keno Hill silver stream, Silver Wheaton perspective ..................... 215

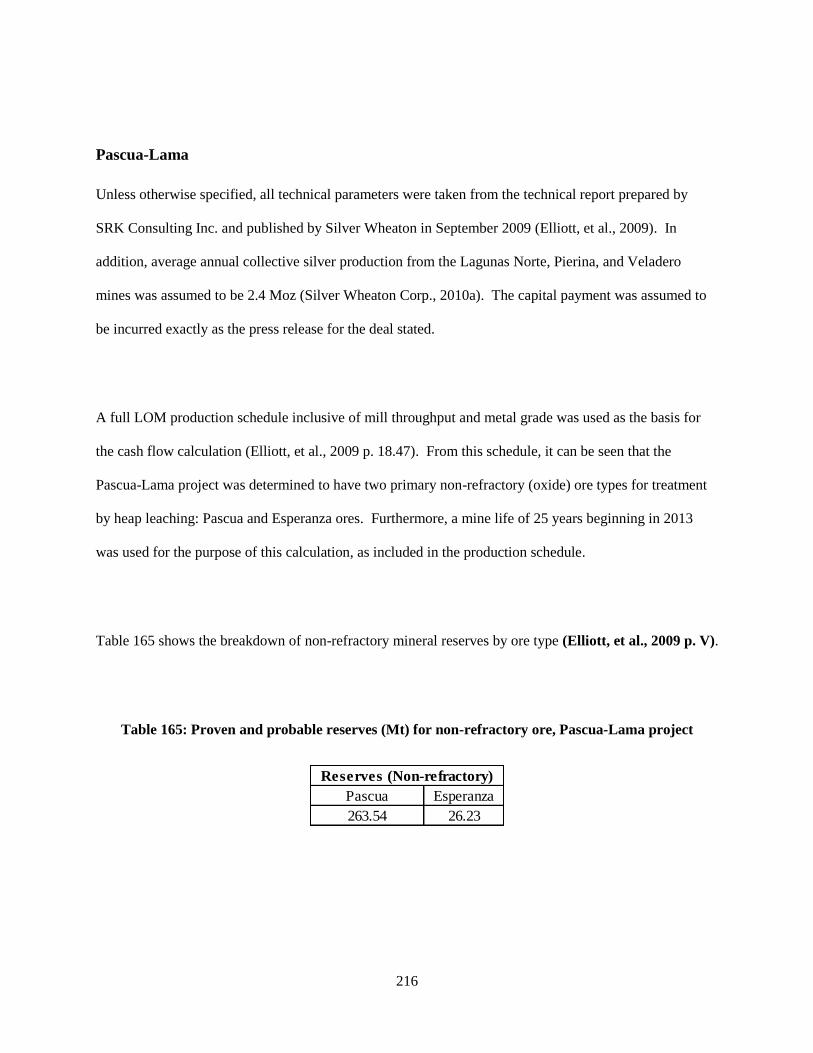

Table 165: Proven and probable reserves (Mt) for non-refractory ore, Pascua-Lama project .................. 216

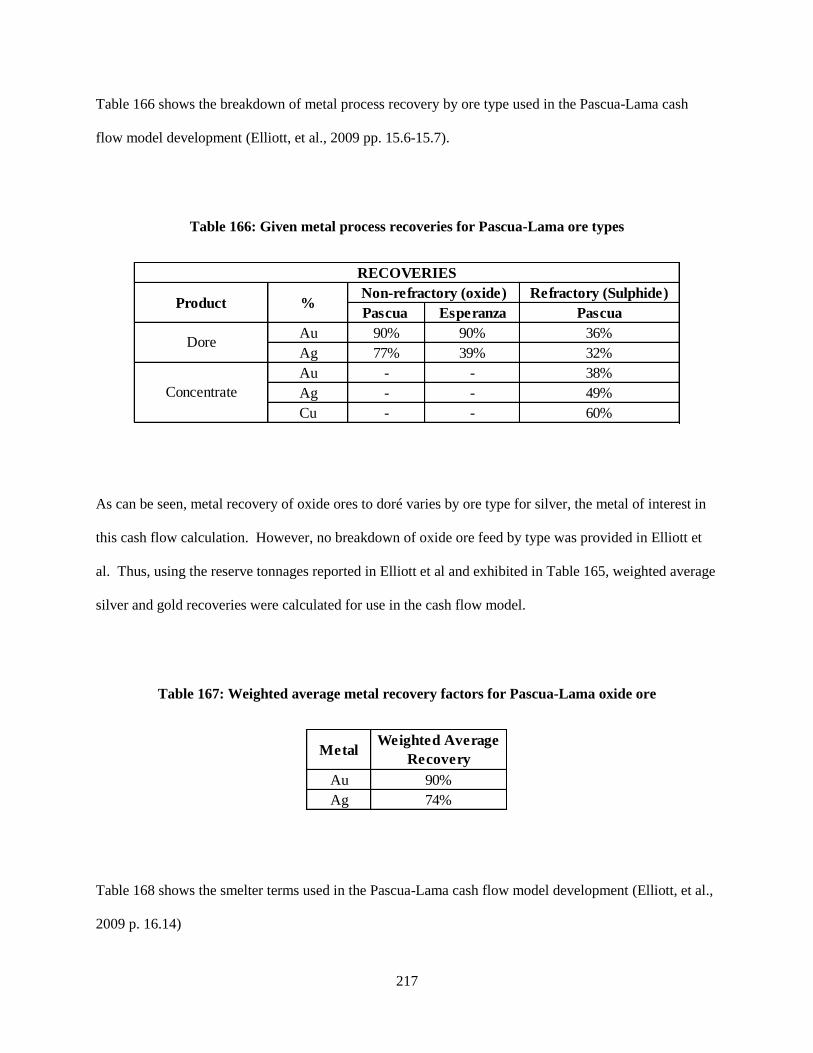

Table 166: Given metal process recoveries for Pascua-Lama ore types ................................................... 217

Table 167: Weighted average metal recovery factors for Pascua-Lama oxide ore ................................... 217

Table 168: Estimated smelter terms for Pascua-Lama concentrate at the time of the stream deal with

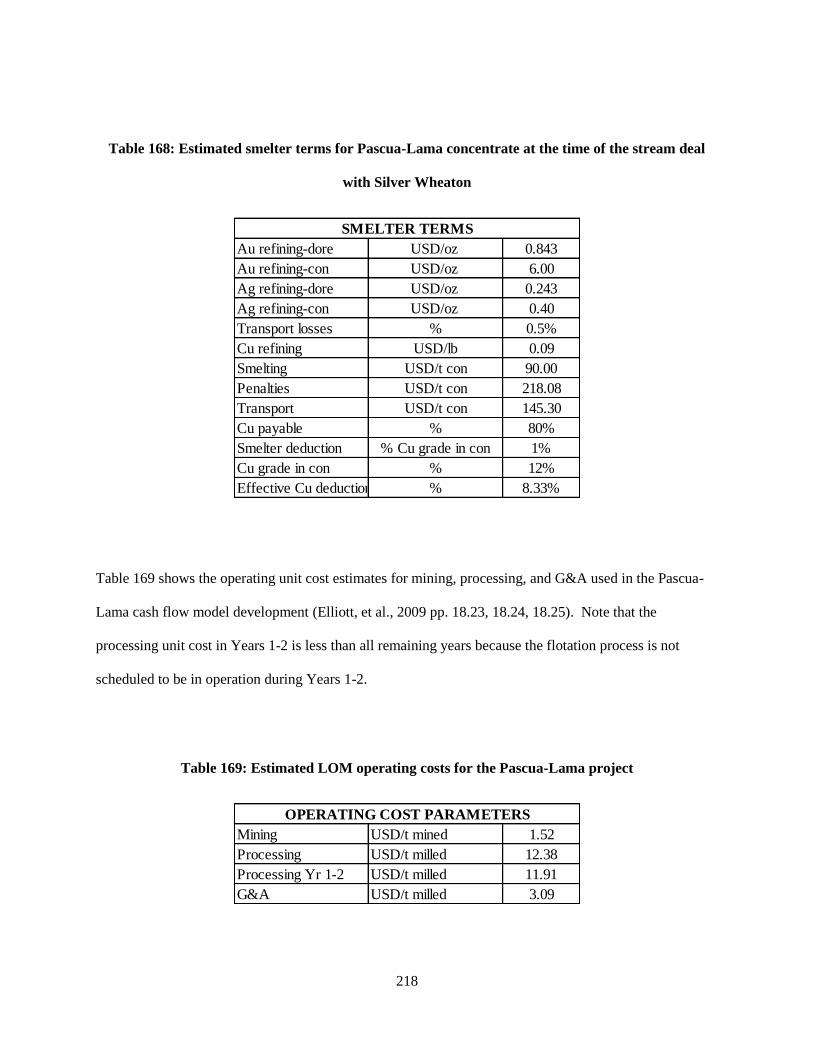

Silver Wheaton.......................................................................................................................................... 218

Table 169: Estimated LOM operating costs for the Pascua-Lama project ............................................... 218

Table 170: Silver price assumptions used in the cash flow models of the Pascua-Lama silver stream .... 219

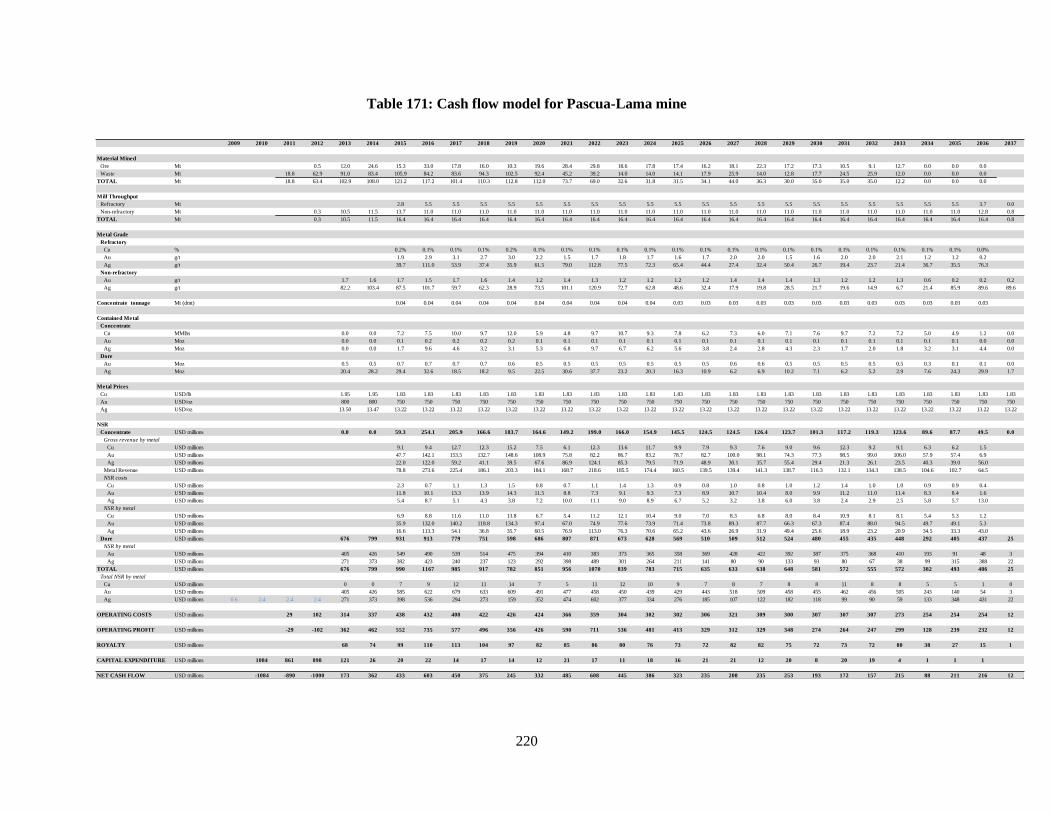

Table 171: Cash flow model for Pascua-Lama mine ................................................................................ 220

Table 172: Cash flow model for Pascua-Lama silver stream, Barrick perspective .................................. 221

Table 173: Cash flow model for Pascua-Lama silver stream, Silver Wheaton perspective ..................... 221

Table 174: Smelter terms for the Rosemont project ................................................................................. 223

Table 175: Expected LOM operating costs for the Rosemont project ...................................................... 223

Table 176: Metal price assumptions used in the Rosemont mine and precious metals stream cash flow

calculations ............................................................................................................................................... 224

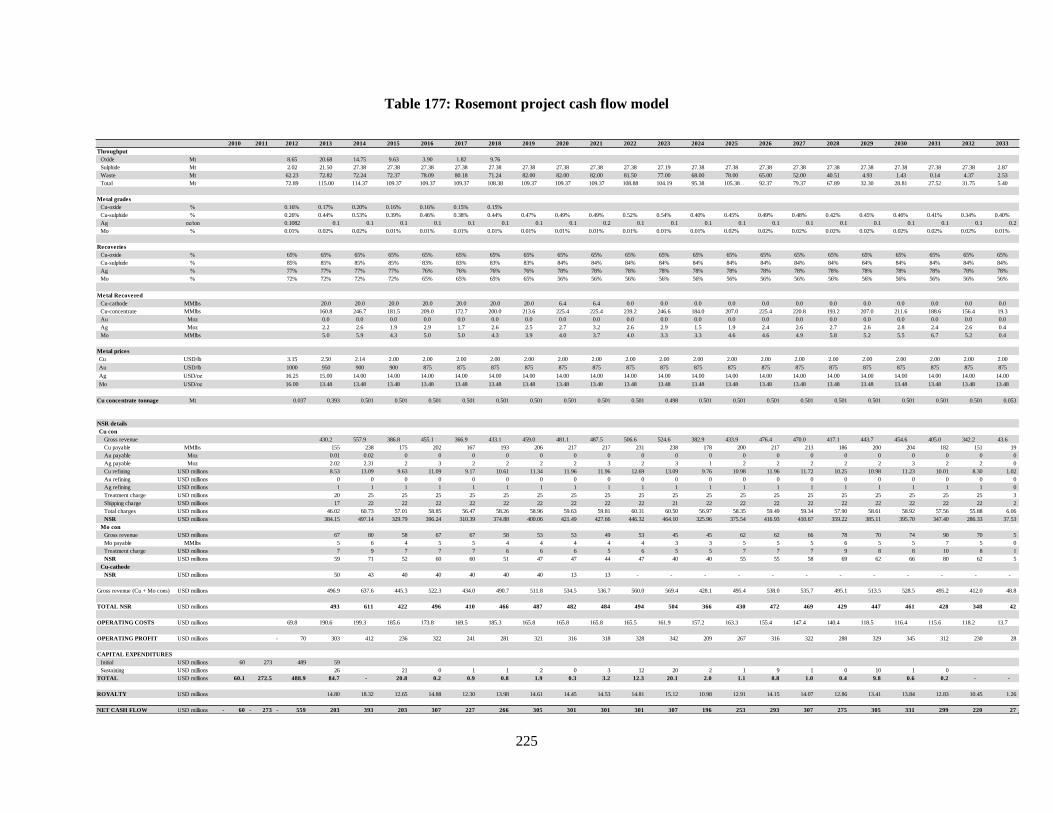

Table 177: Rosemont project cash flow model ......................................................................................... 225

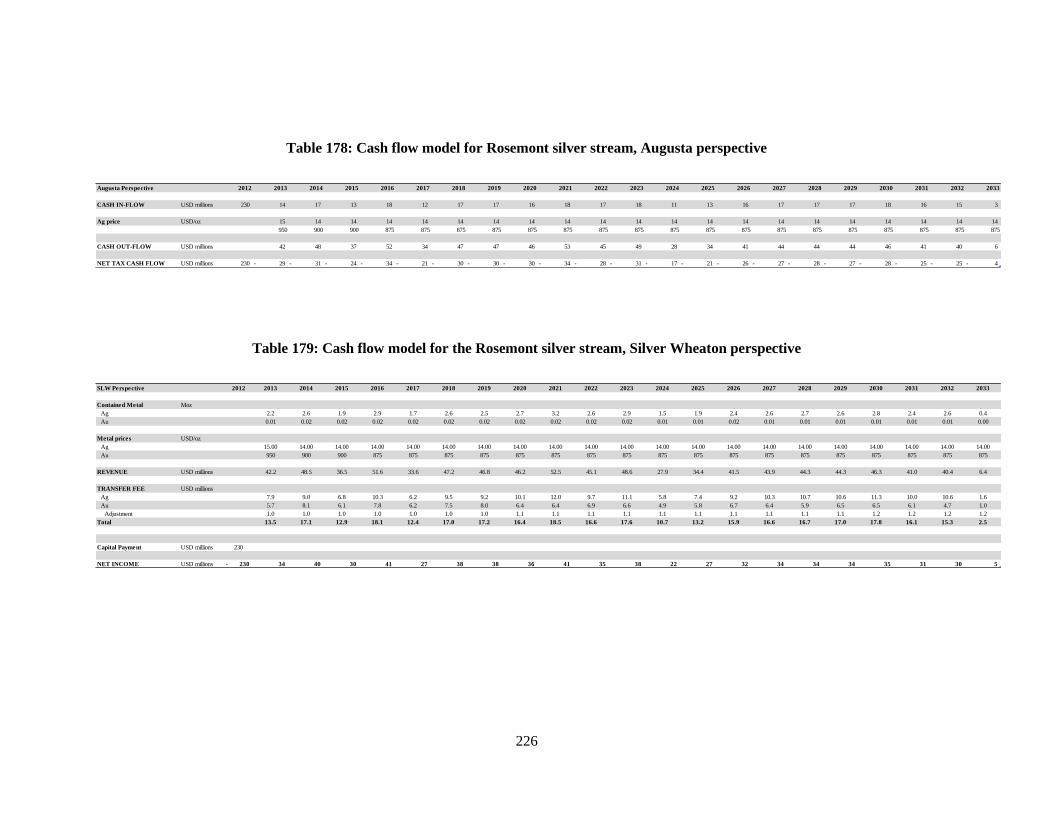

Table 178: Cash flow model for Rosemont silver stream, Augusta perspective ...................................... 226

Table 179: Cash flow model for the Rosemont silver stream, Silver Wheaton perspective ..................... 226

Table 180: Consensus silver price estimates at the time of the Zinkgruvan silver stream........................ 227

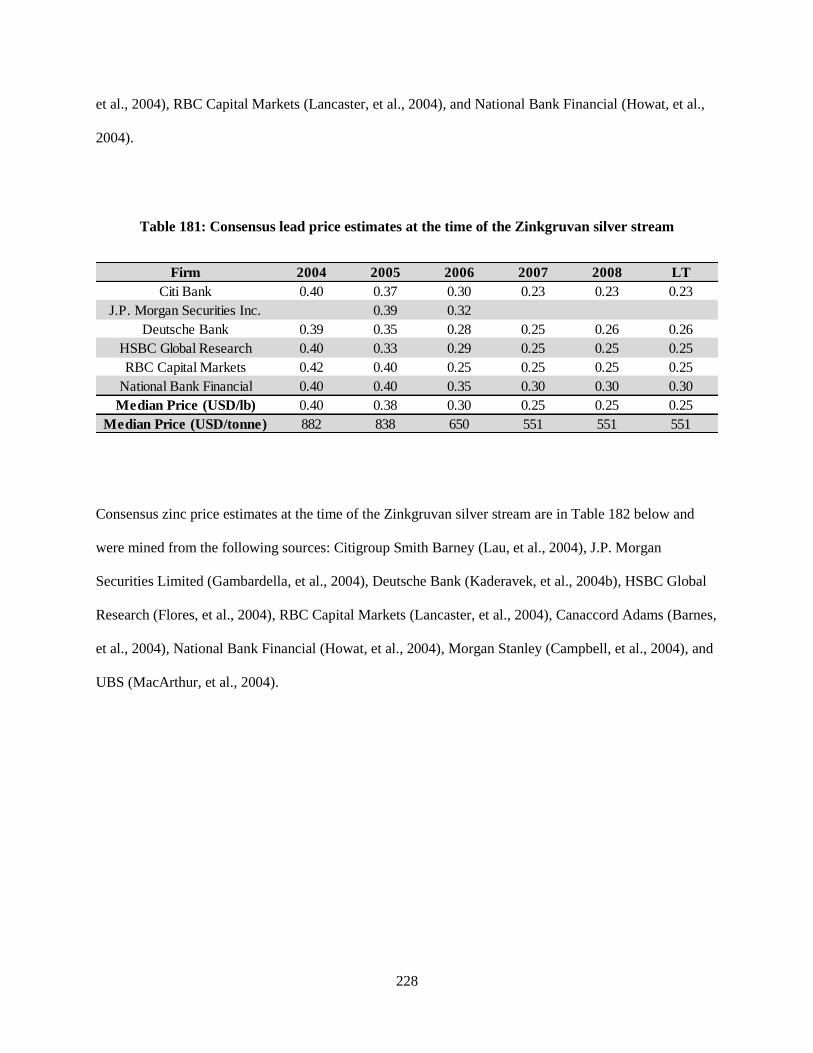

Table 181: Consensus lead price estimates at the time of the Zinkgruvan silver stream .......................... 228

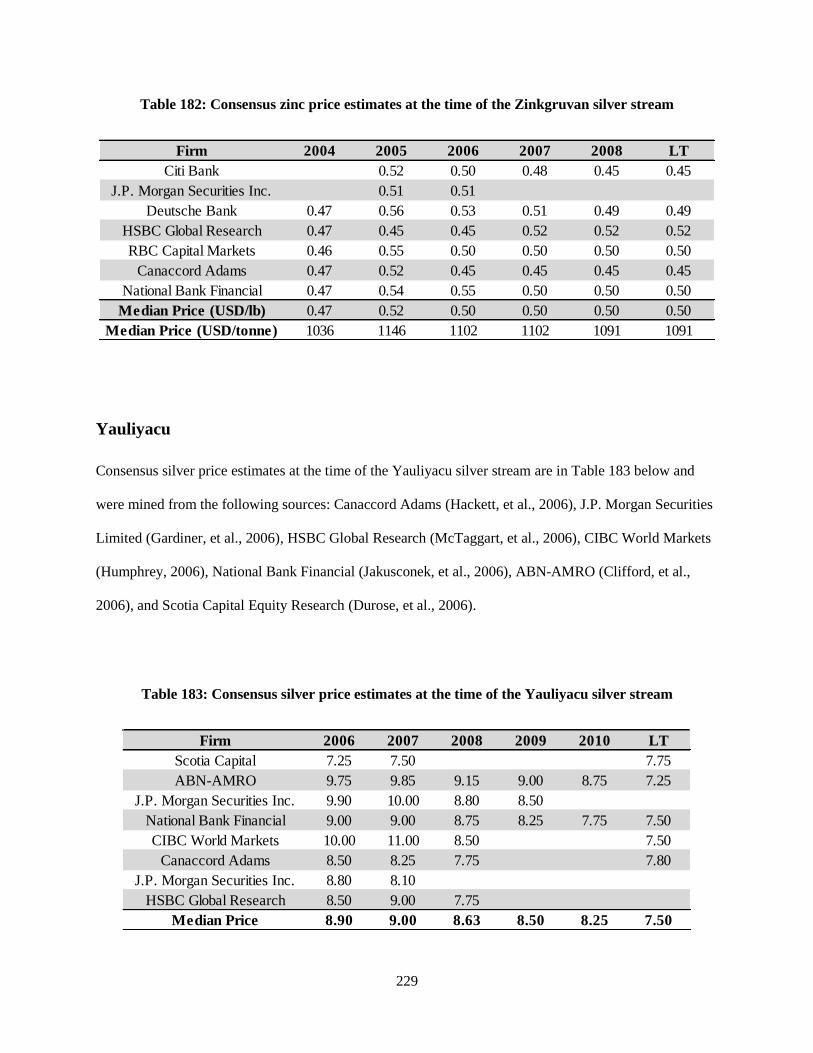

Table 182: Consensus zinc price estimates at the time of the Zinkgruvan silver stream .......................... 229

Table 183: Consensus silver price estimates at the time of the Yauliyacu silver stream .......................... 229

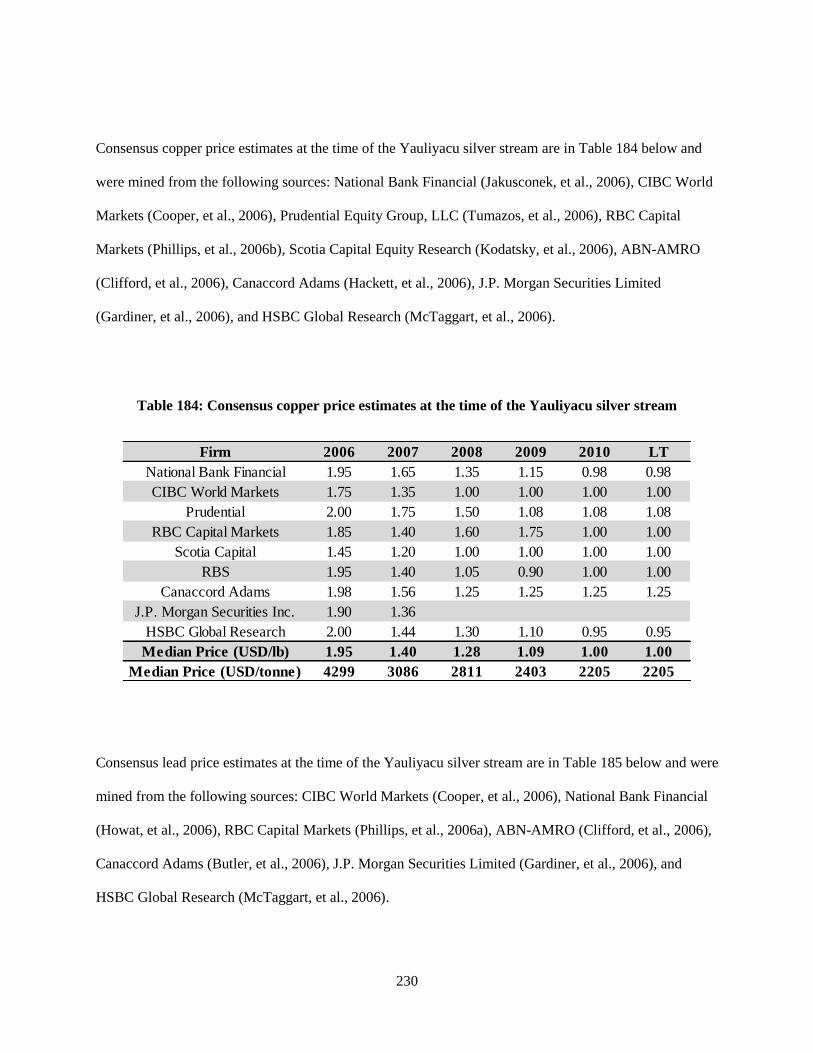

Table 184: Consensus copper price estimates at the time of the Yauliyacu silver stream ........................ 230

Table 185: Consensus lead price estimates at the time of the Yauliyacu silver stream ............................ 231

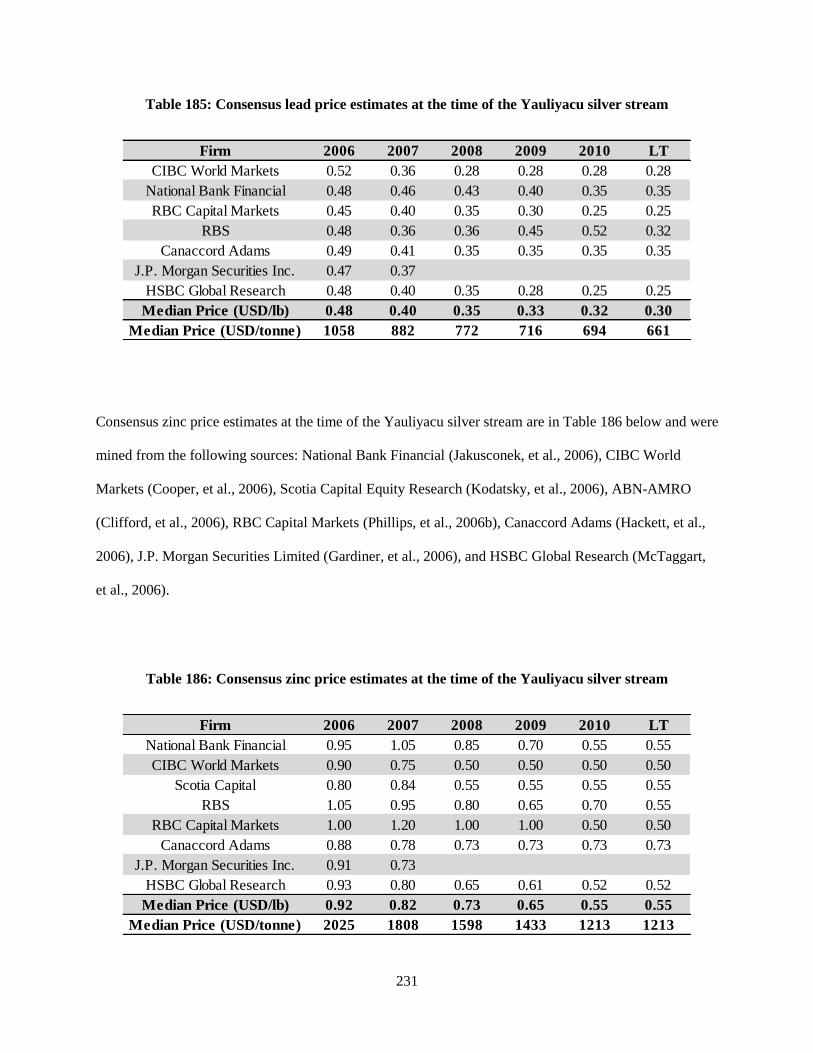

Table 186: Consensus zinc price estimates at the time of the Yauliyacu silver stream ............................ 231

Table 187: Consensus silver price estimates at the time of the Stratoni silver stream ............................. 232

xxiv

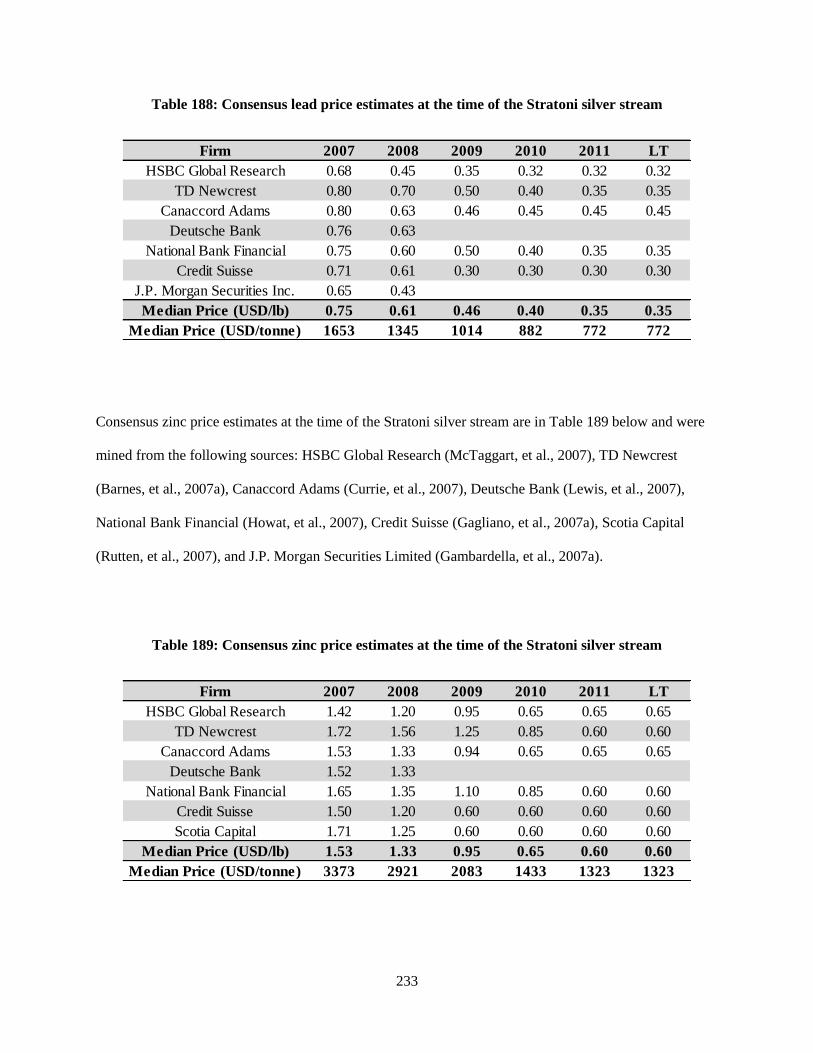

Table 188: Consensus lead price estimates at the time of the Stratoni silver stream ................................ 233

Table 189: Consensus zinc price estimates at the time of the Stratoni silver stream ................................ 233

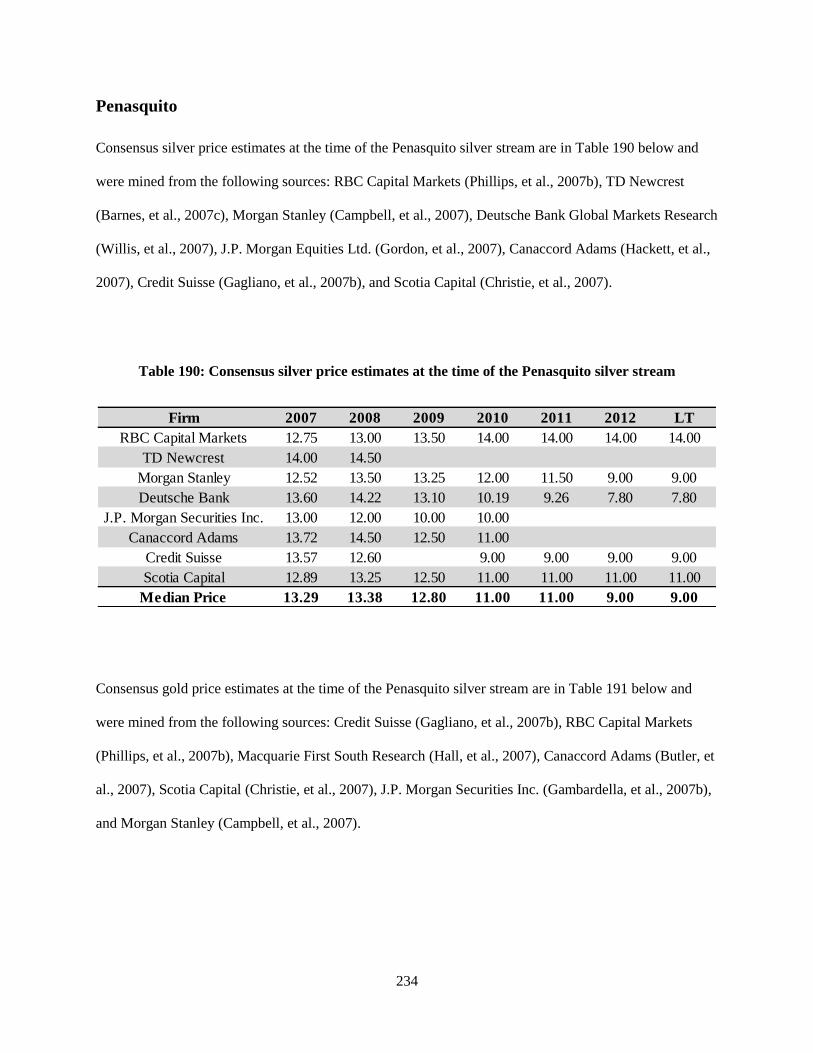

Table 190: Consensus silver price estimates at the time of the Penasquito silver stream ......................... 234

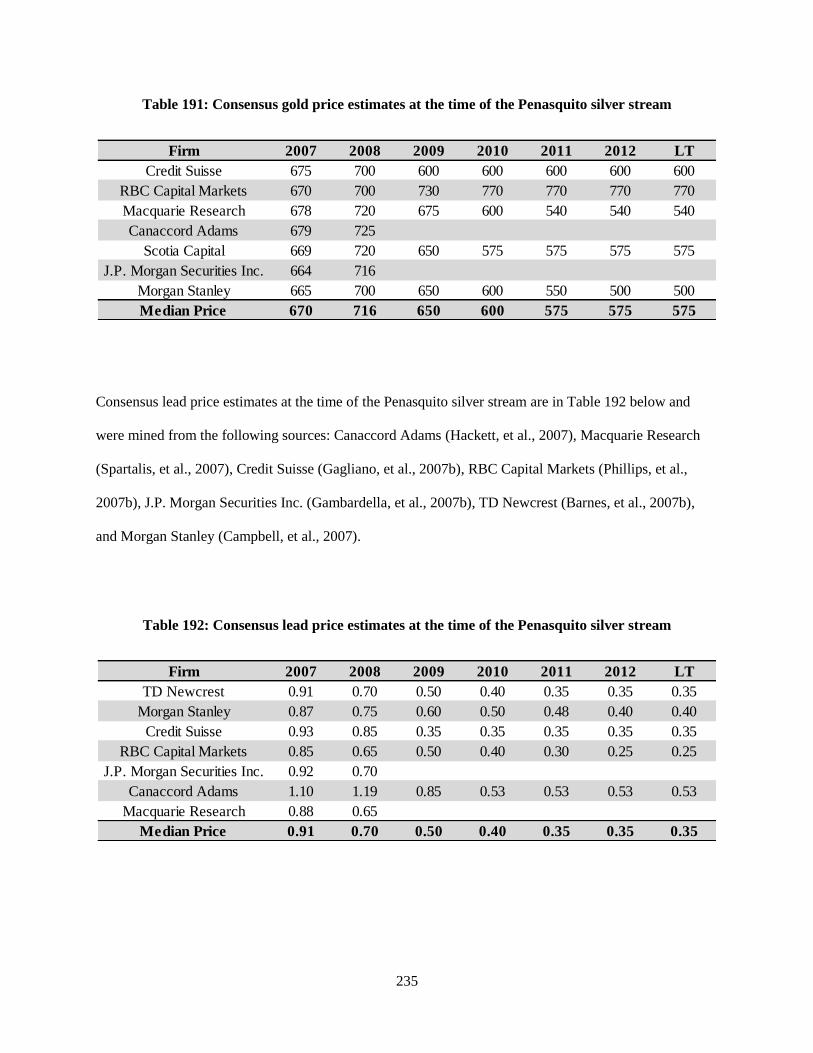

Table 191: Consensus gold price estimates at the time of the Penasquito silver stream .......................... 235

Table 192: Consensus lead price estimates at the time of the Penasquito silver stream ........................... 235

Table 193: Consensus zinc price estimates at the time of the Penasquito silver stream ........................... 236

Table 194: Consensus silver price estimates at the time of the Mineral Park silver stream ..................... 237

Table 195: Consensus copper price estimates at the time of the Mineral Park silver stream ................... 237

Table 196: Consensus molybdenum price estimates at the time of the Mineral Park silver stream ......... 238

Table 197: Consensus silver price estimates at the time of the Campo Morado silver stream ................. 239

Table 198: Consensus gold price estimates at the time of the Campo Morado silver stream ................... 239

Table 199: Consensus copper price estimates at the time of the Campo Morado silver stream ............... 240

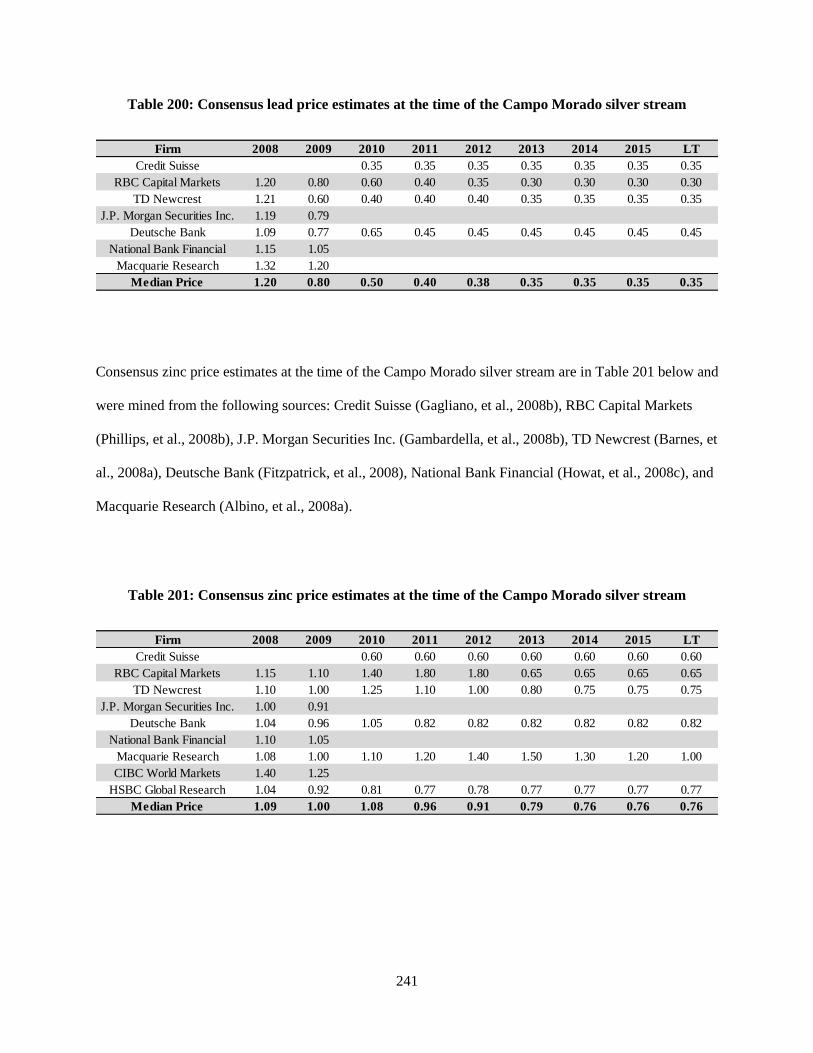

Table 200: Consensus lead price estimates at the time of the Campo Morado silver stream ................... 241

Table 201: Consensus zinc price estimates at the time of the Campo Morado silver stream ................... 241

Table 202: Consensus silver price estimates at the time of the Keno Hill silver stream .......................... 242

Table 203: Consensus lead price estimates at the time of the Keno Hill silver stream............................. 243

Table 204: Consensus zinc price estimates at the time of the Keno Hill silver stream............................. 243

Table 205: Consensus silver price estimates at the time of the Pascua-Lama silver stream ..................... 244

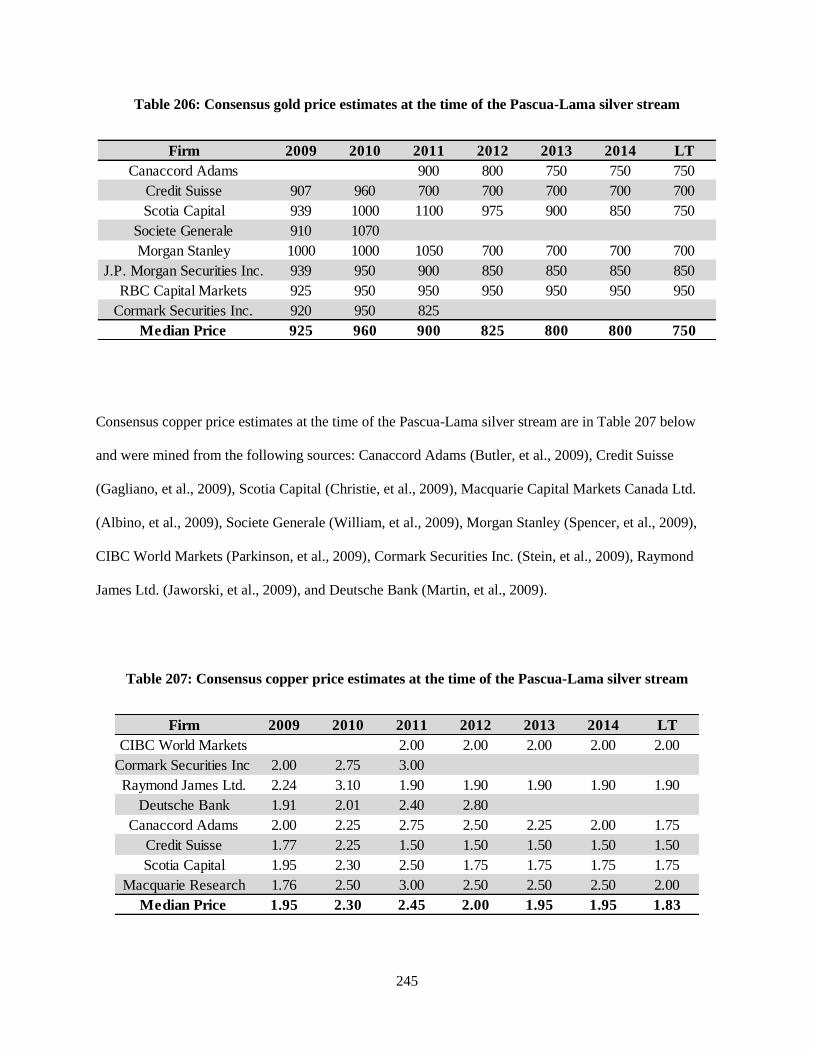

Table 206: Consensus gold price estimates at the time of the Pascua-Lama silver stream ...................... 245

Table 207: Consensus copper price estimates at the time of the Pascua-Lama silver stream ................... 245

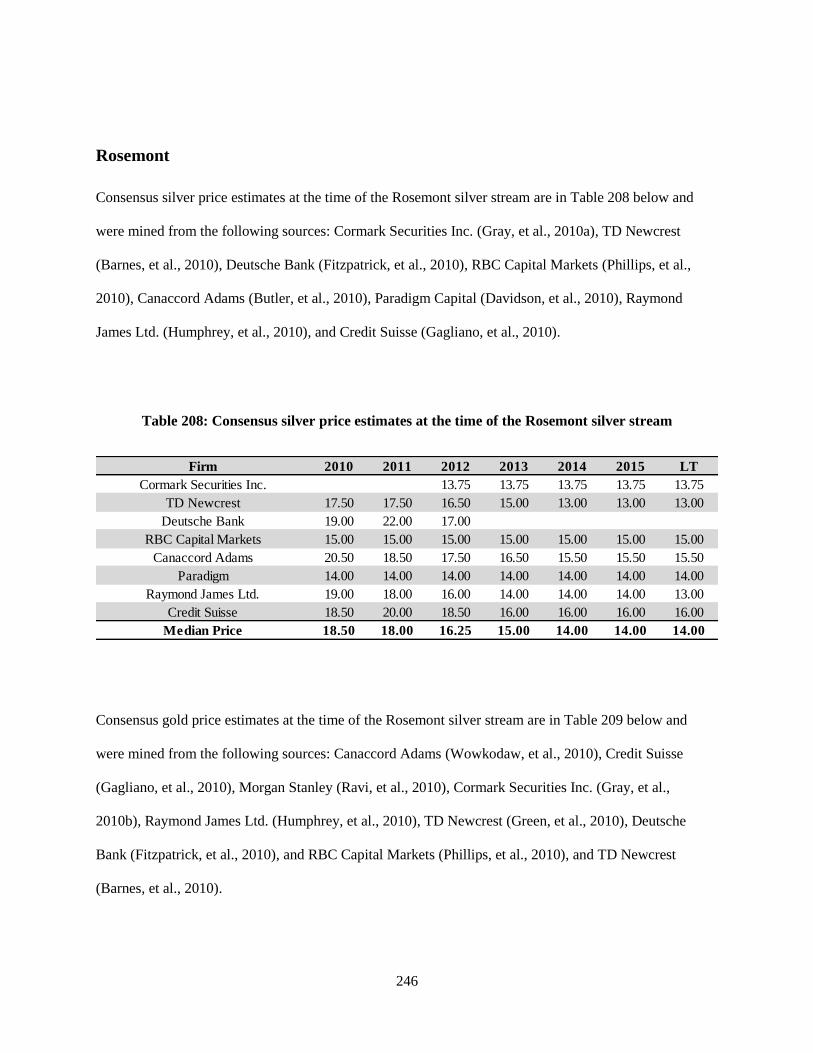

Table 208: Consensus silver price estimates at the time of the Rosemont silver stream .......................... 246

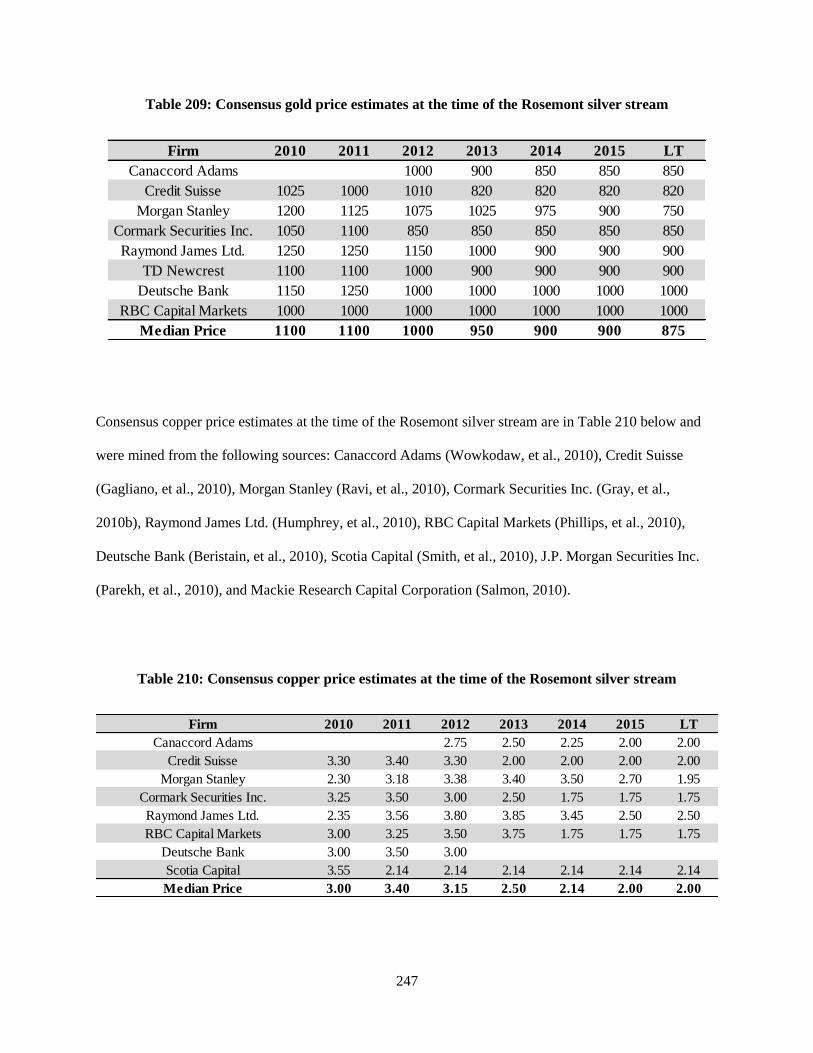

Table 209: Consensus gold price estimates at the time of the Rosemont silver stream ............................ 247

Table 210: Consensus copper price estimates at the time of the Rosemont silver stream ........................ 247

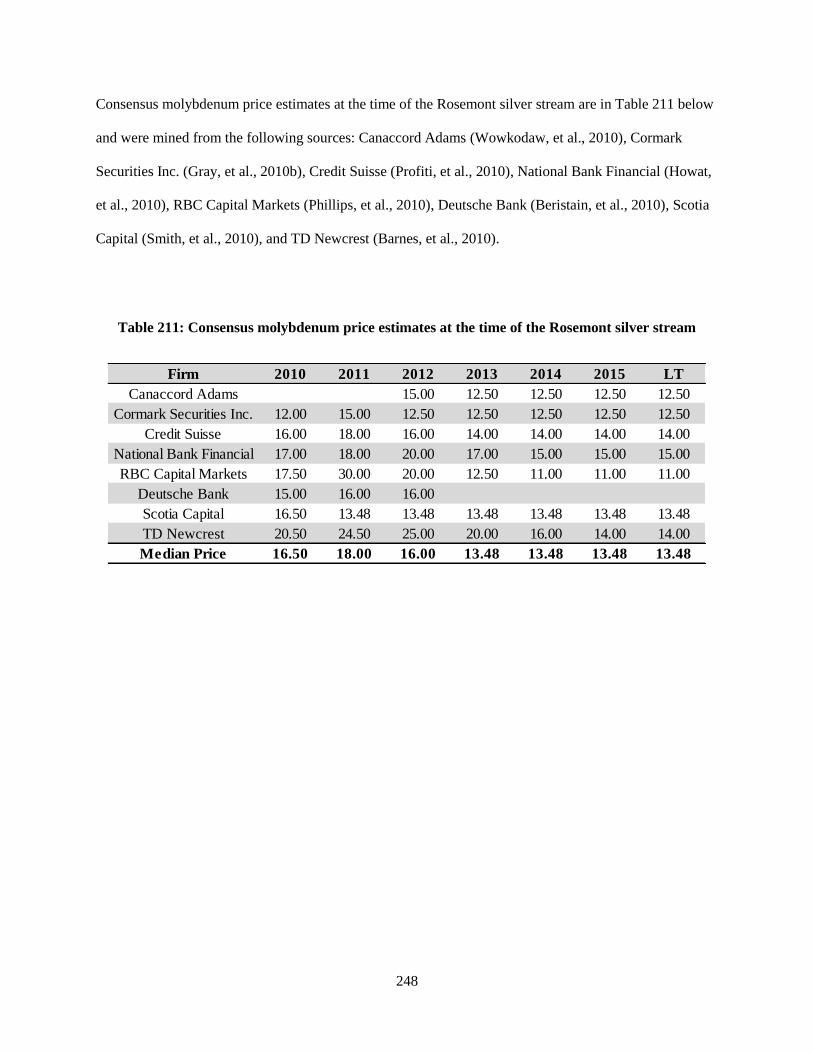

Table 211: Consensus molybdenum price estimates at the time of the Rosemont silver stream .............. 248

Table 212: Economic smelter terms for Keno Hill concentrates .............................................................. 250

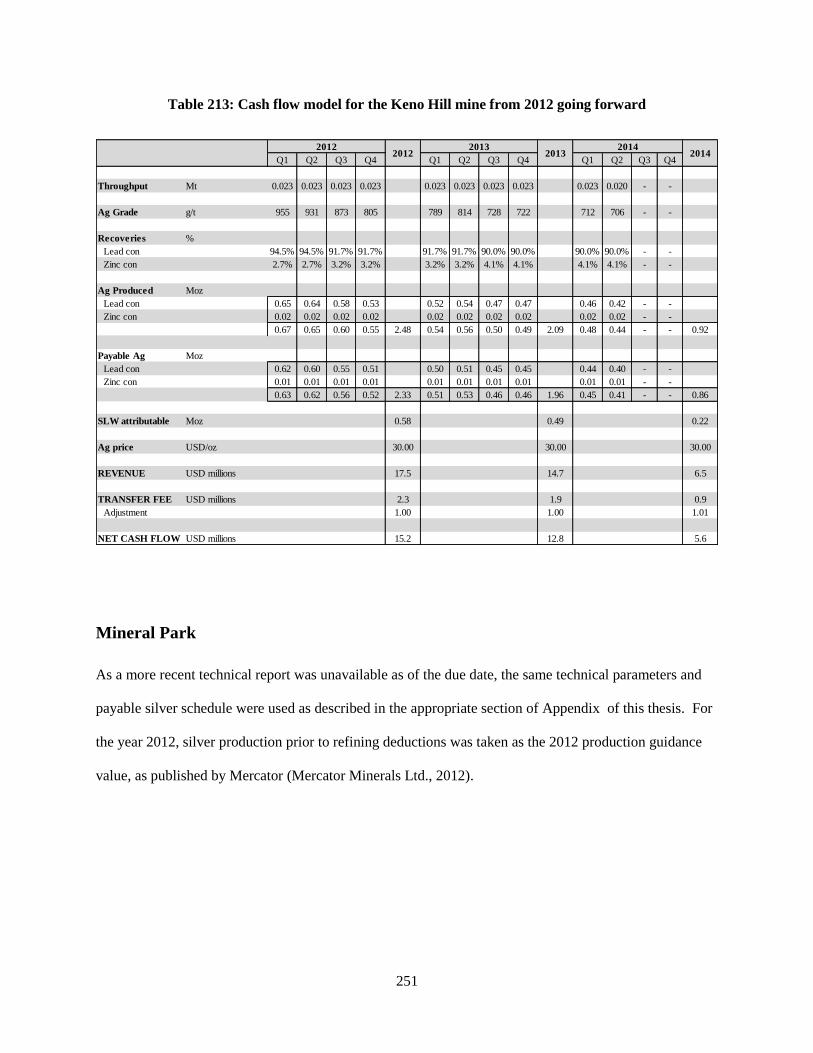

Table 213: Cash flow model for the Keno Hill mine from 2012 going forward ...................................... 251

xxv

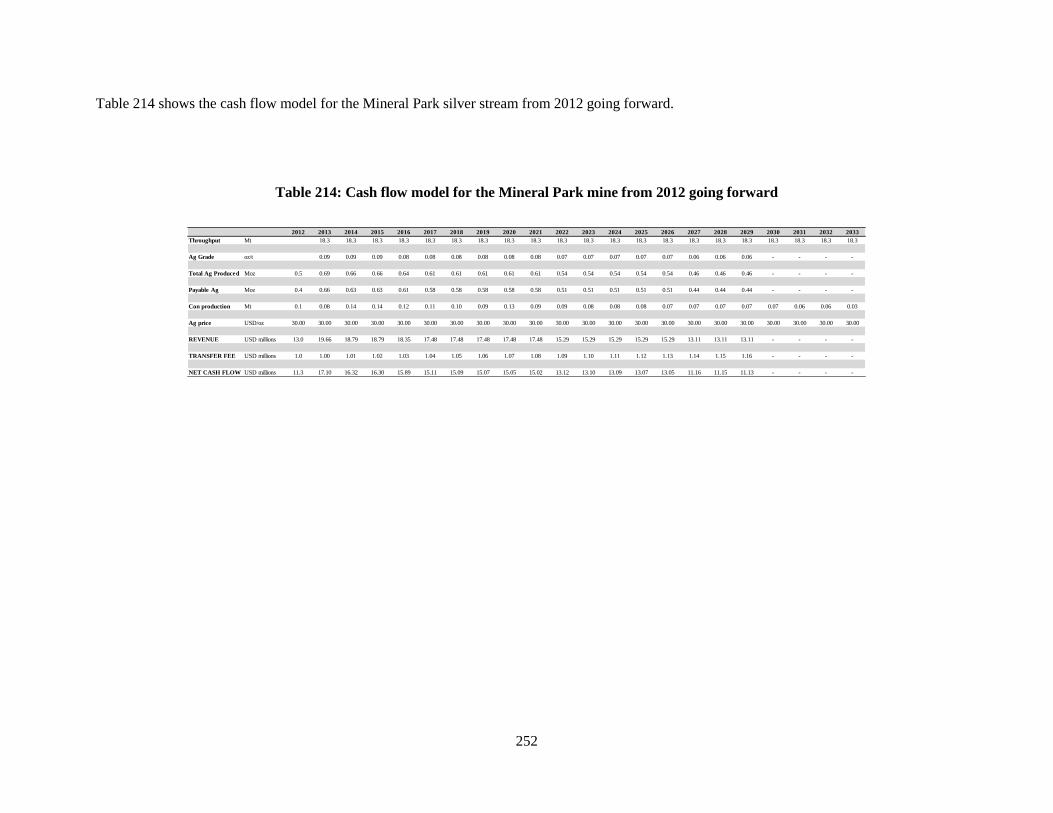

Table 214: Cash flow model for the Mineral Park mine from 2012 going forward ................................. 252

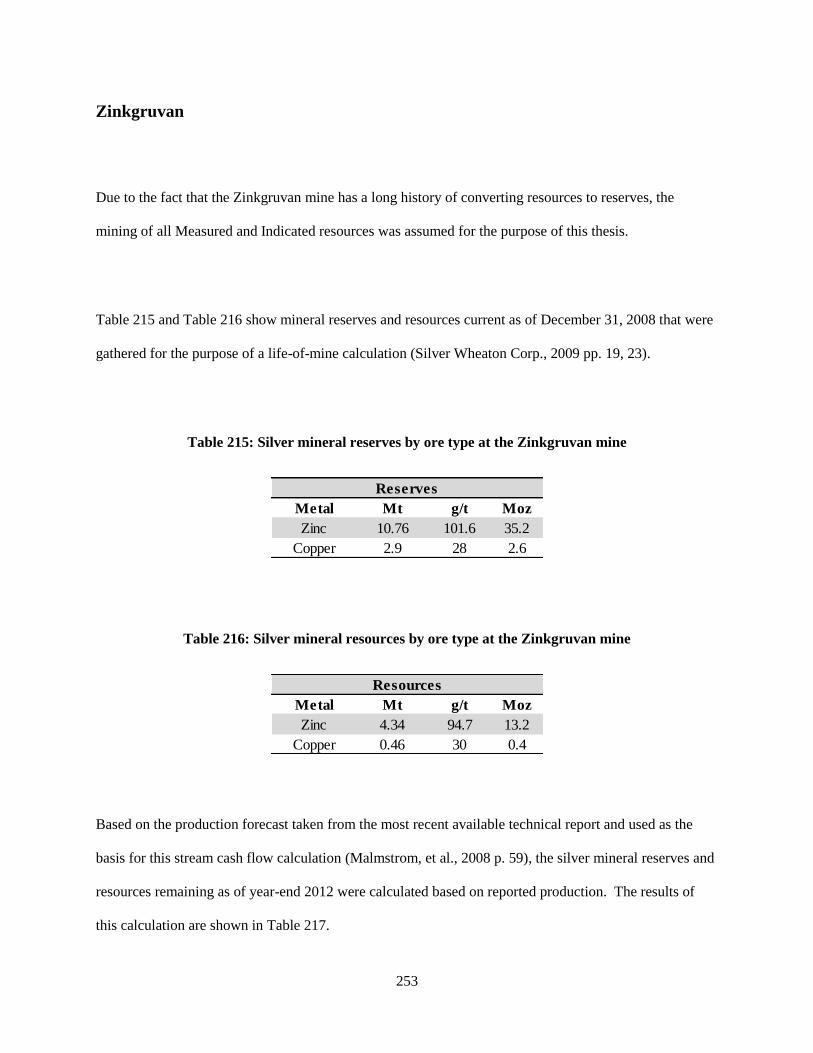

Table 215: Silver mineral reserves by ore type at the Zinkgruvan mine .................................................. 253

Table 216: Silver mineral resources by ore type at the Zinkgruvan mine ................................................ 253

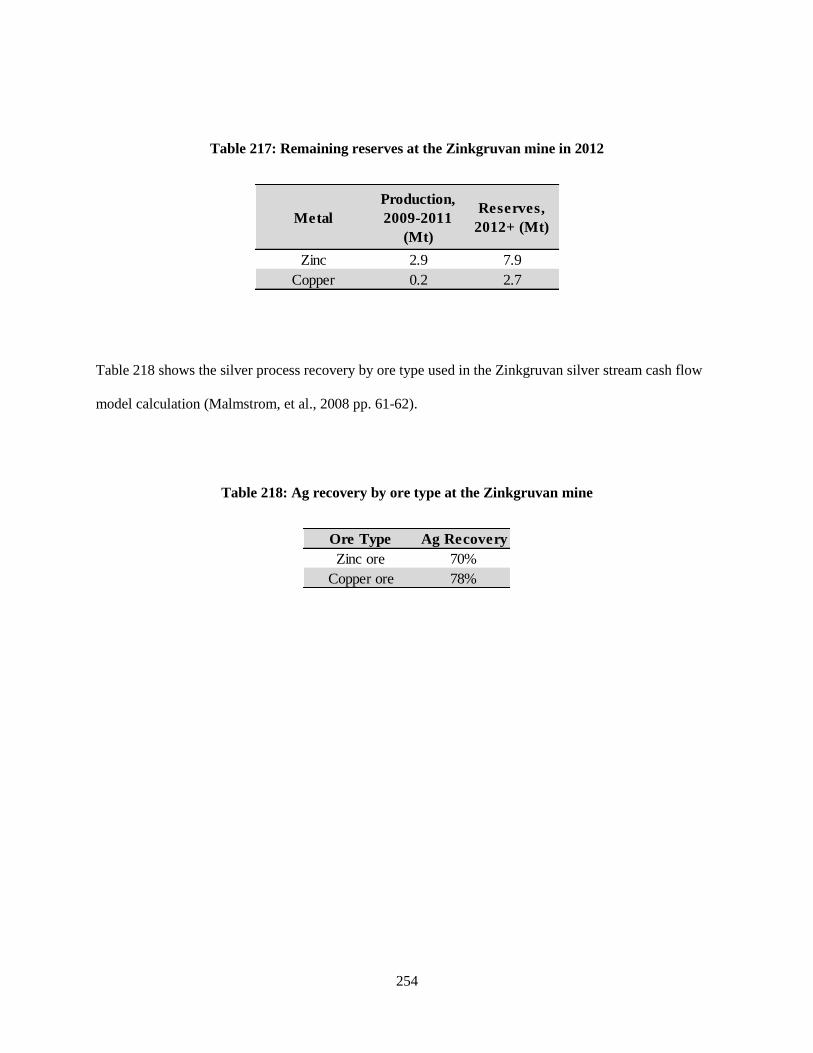

Table 217: Remaining reserves at the Zinkgruvan mine in 2012 ............................................................. 254

Table 218: Ag recovery by ore type at the Zinkgruvan mine ................................................................... 254

Table 219: Cash flow model for Zinkgruvan mine from 2012 going forward ......................................... 255

Table 220: Cash flow model for the San Dimas mine from 2012 going forward ..................................... 256

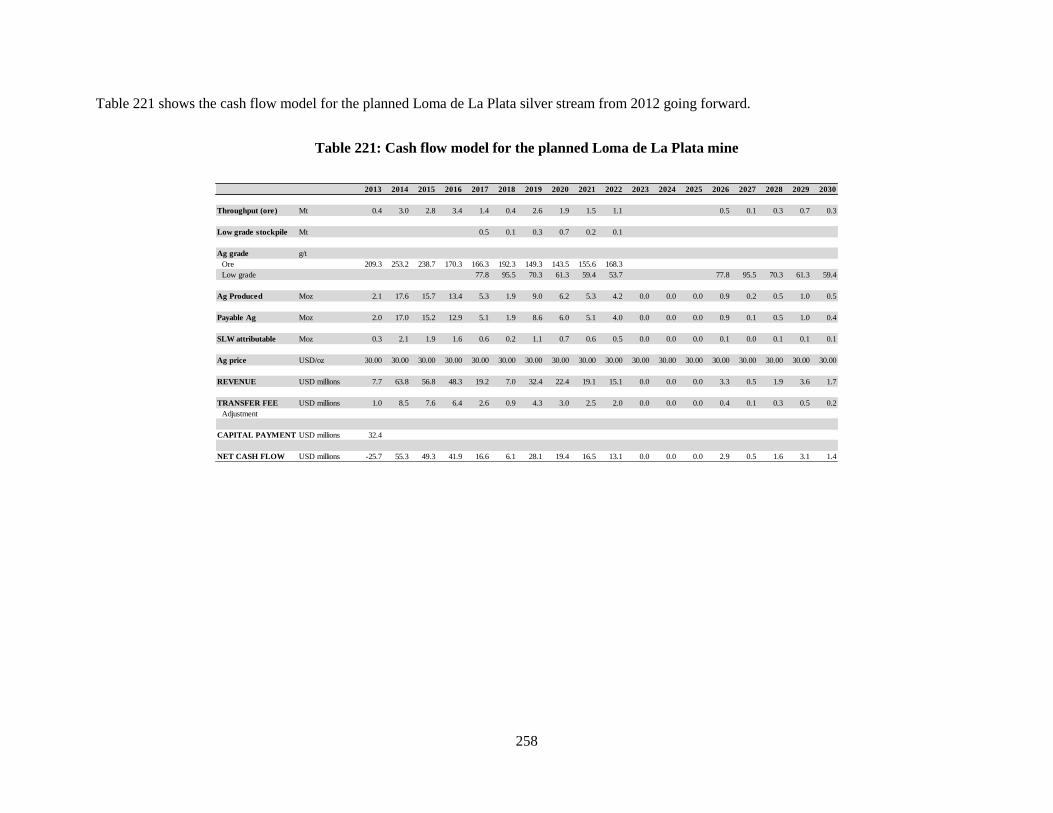

Table 221: Cash flow model for the planned Loma de La Plata mine ...................................................... 258

Table 222: Economic smelter terms for the Rosemont mine .................................................................... 259

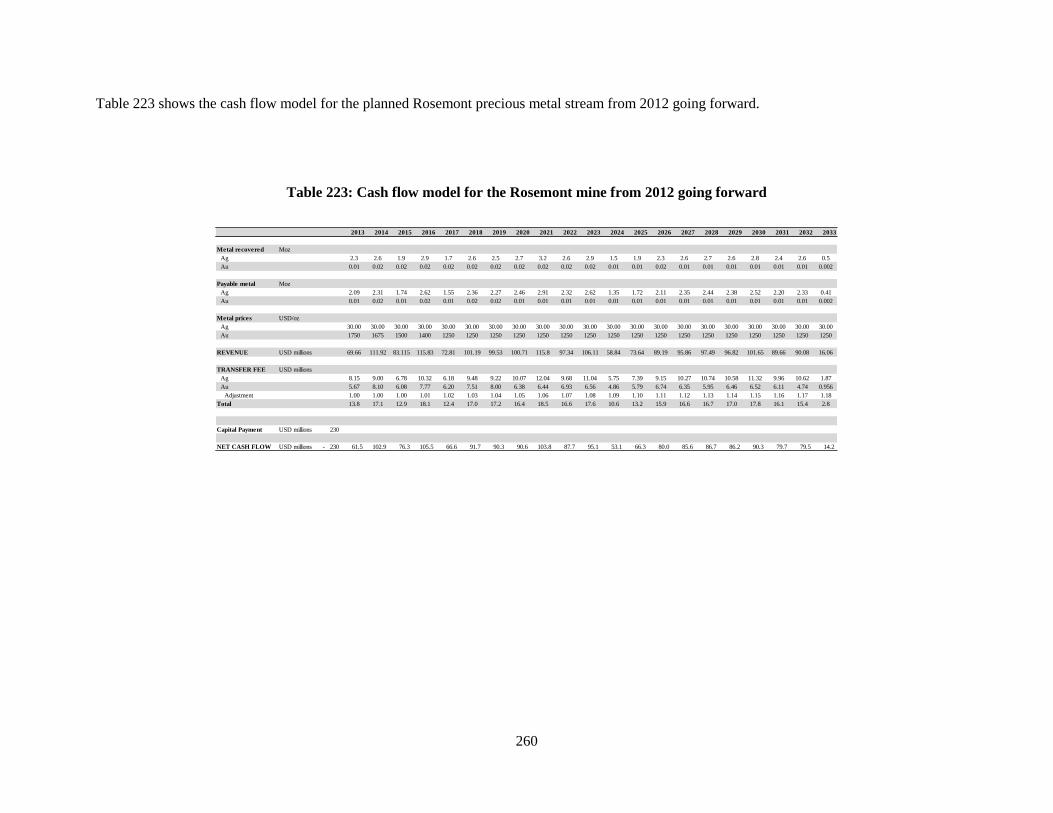

Table 223: Cash flow model for the Rosemont mine from 2012 going forward ...................................... 260

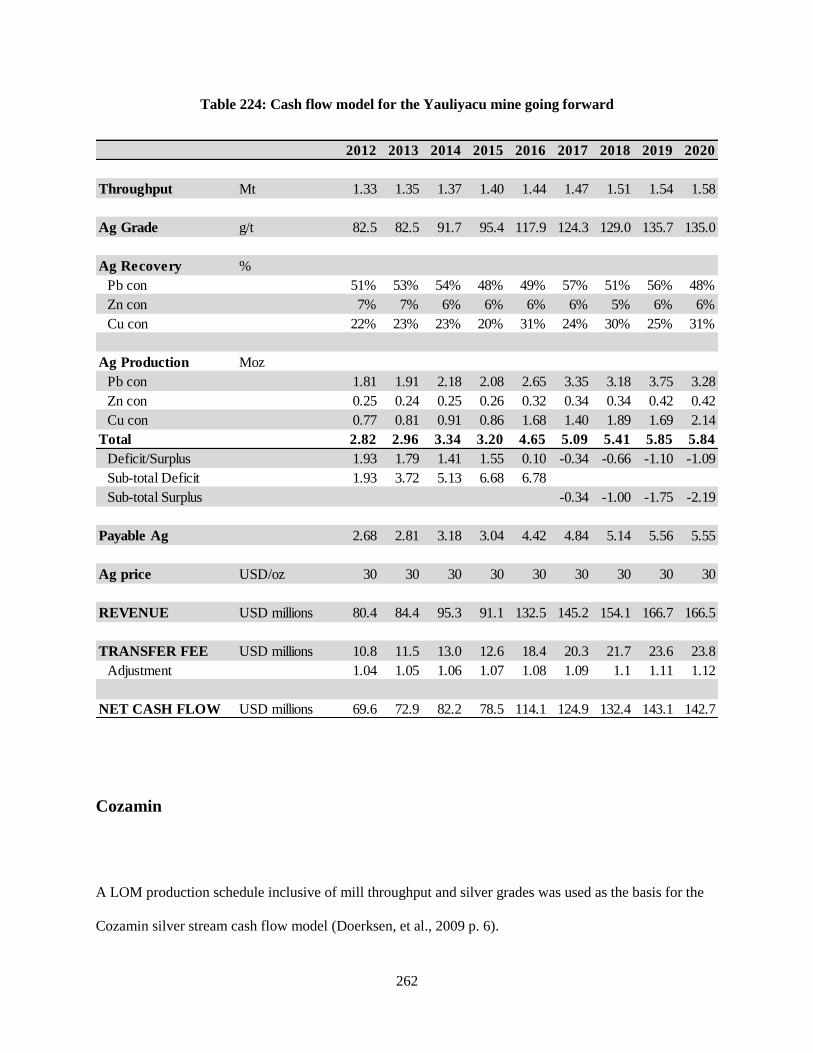

Table 224: Cash flow model for the Yauliyacu mine going forward........................................................ 262

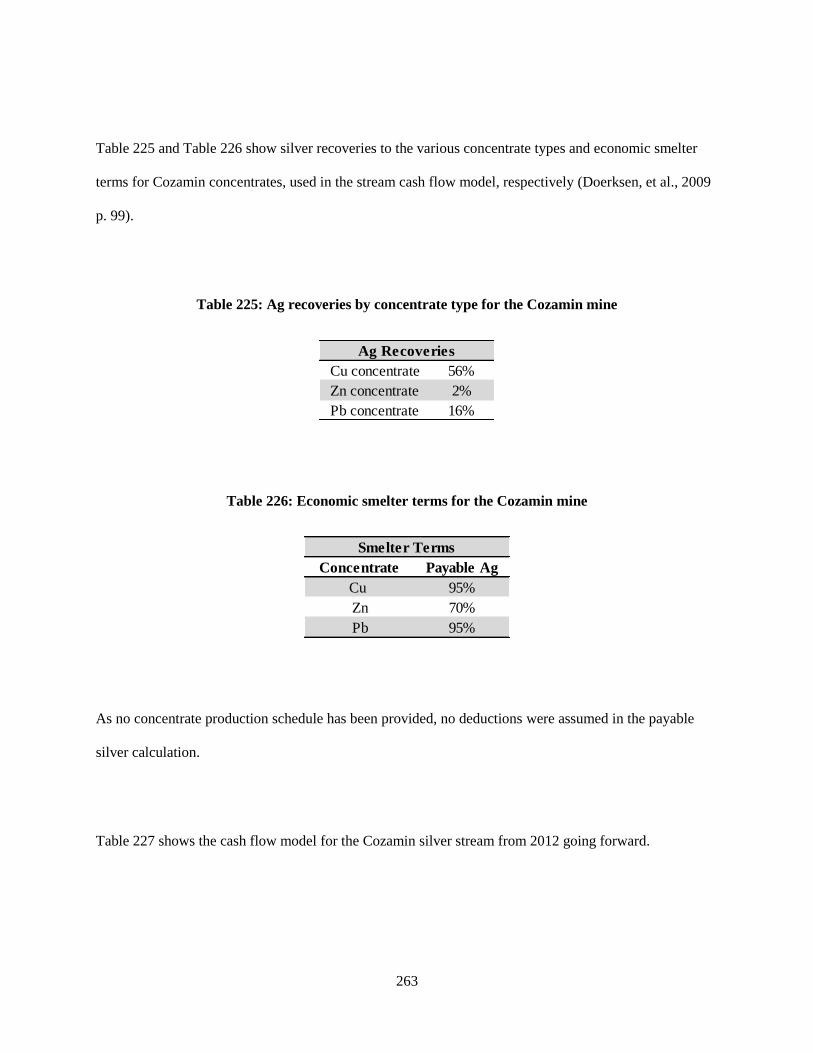

Table 225: Ag recoveries by concentrate type for the Cozamin mine ...................................................... 263

Table 226: Economic smelter terms for the Cozamin mine ...................................................................... 263

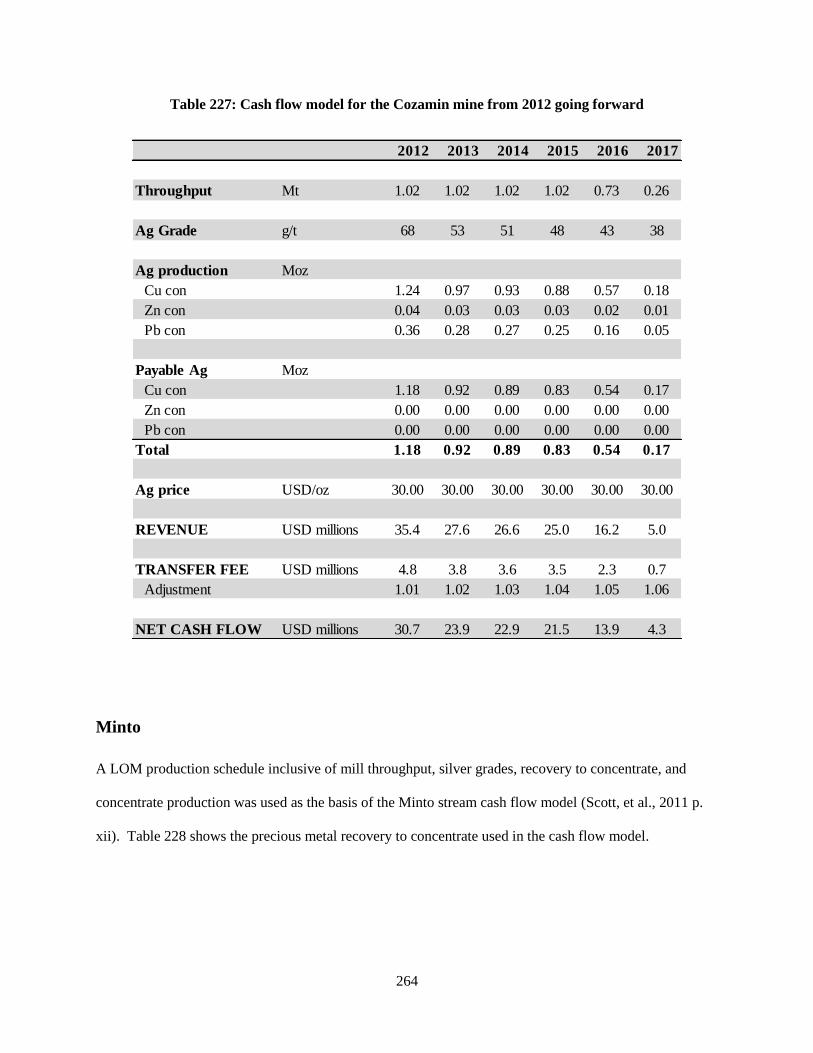

Table 227: Cash flow model for the Cozamin mine from 2012 going forward ........................................ 264

Table 228: Metal recovery to concentrate for the Minto mine ................................................................. 265

Table 229: Economic smelter terms for the Minto mine concentrate ....................................................... 265

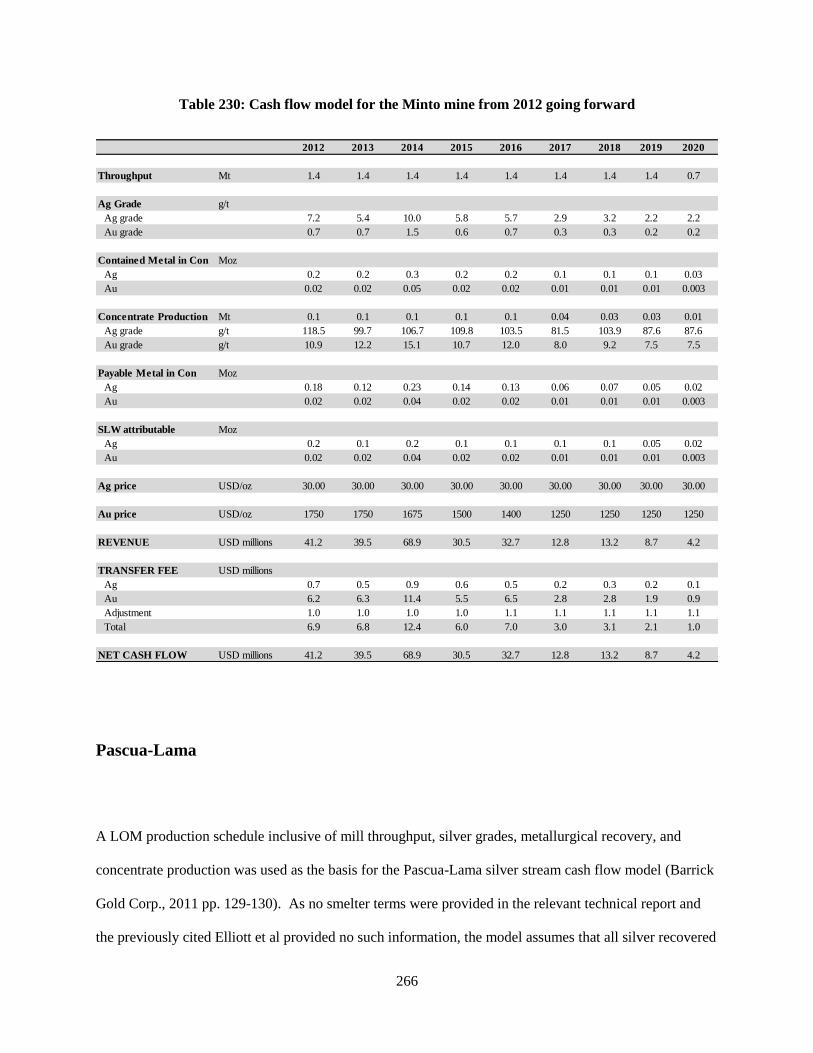

Table 230: Cash flow model for the Minto mine from 2012 going forward ............................................ 266

Table 231: Cash flow model for the planned Pascua-Lama mine from 2012 going forward ................... 268

Table 232: Ore composition and silver recovery to concentrate at the planned Penasquito mine ............ 269

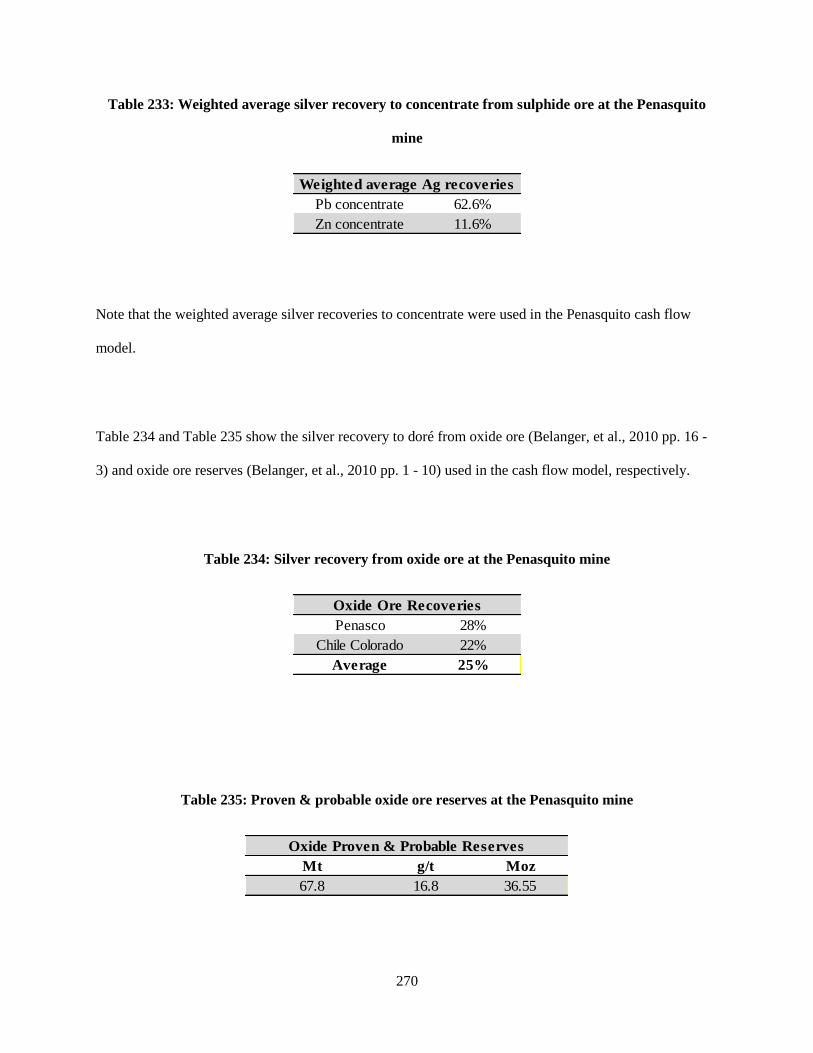

Table 233: Weighted average silver recovery to concentrate from sulphide ore at the Penasquito mine . 270

Table 234: Silver recovery from oxide ore at the Penasquito mine .......................................................... 270

Table 235: Proven & probable oxide ore reserves at the Penasquito mine ............................................... 270

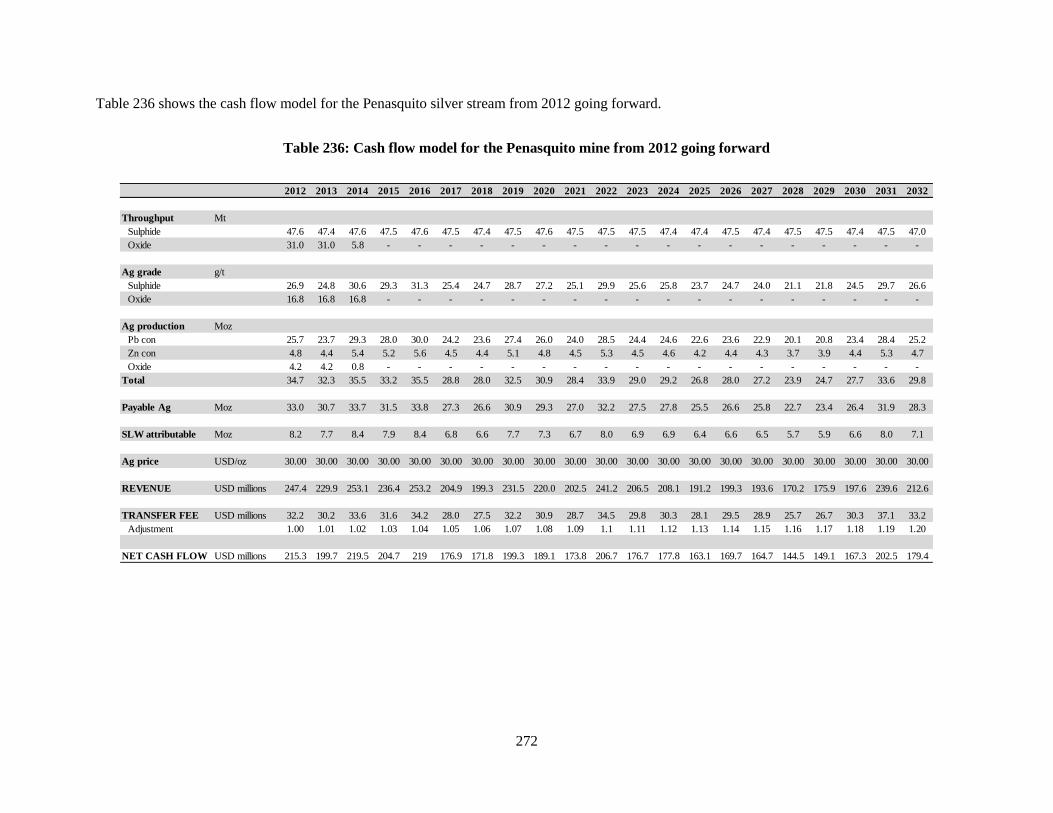

Table 236: Cash flow model for the Penasquito mine from 2012 going forward ..................................... 272

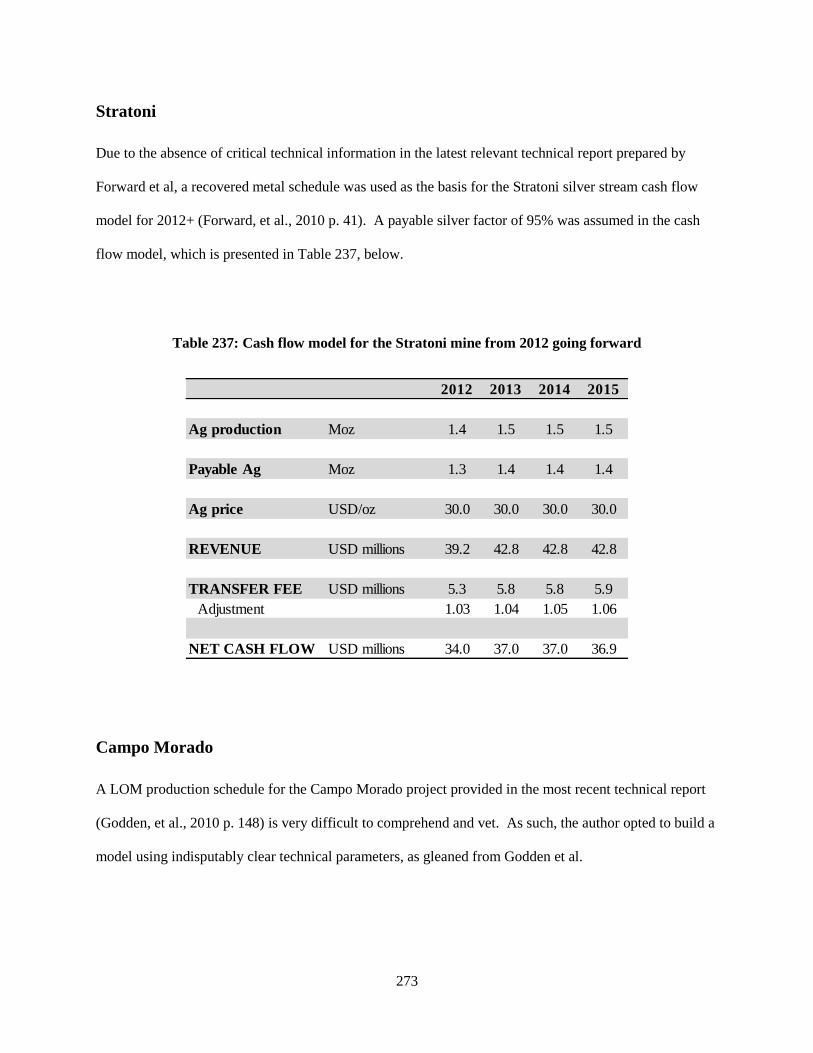

Table 237: Cash flow model for the Stratoni mine from 2012 going forward .......................................... 273

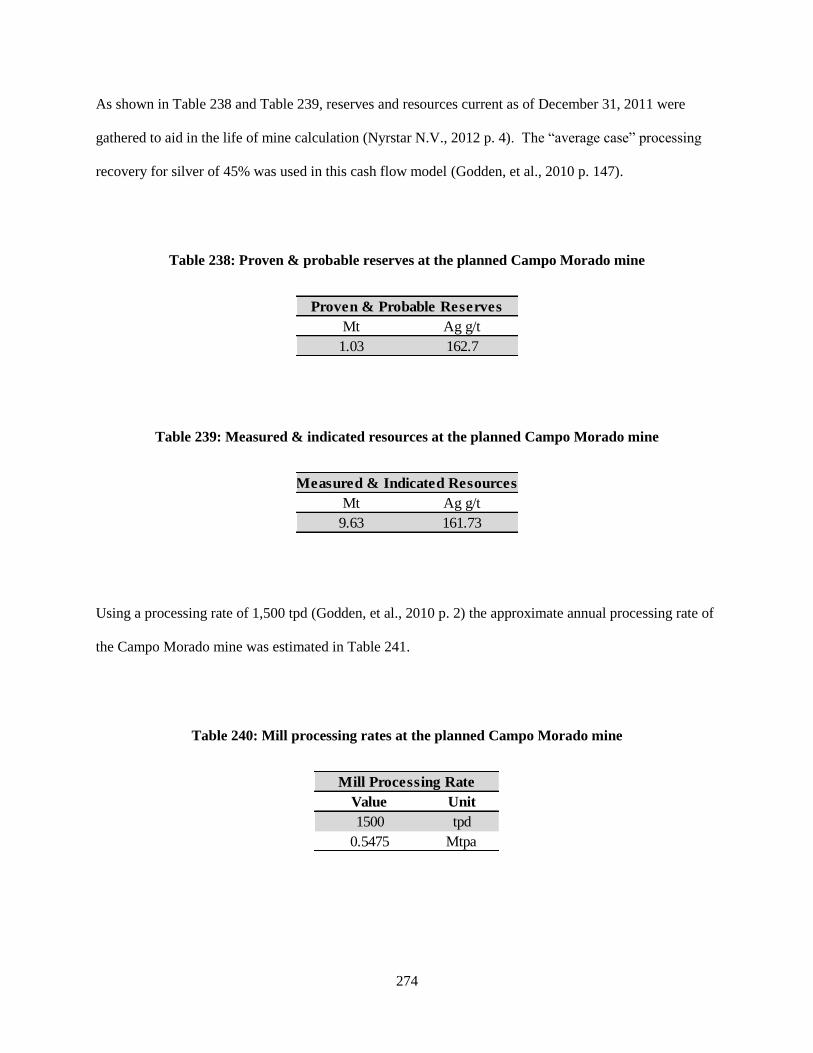

Table 238: Proven & probable reserves at the planned Campo Morado mine ......................................... 274

Table 239: Measured & indicated resources at the planned Campo Morado mine .................................. 274

xxvi

Table 240: Mill processing rates at the planned Campo Morado mine .................................................... 274

Table 241: Approximate LOM calculation for the planned Campo Morado mine ................................... 275

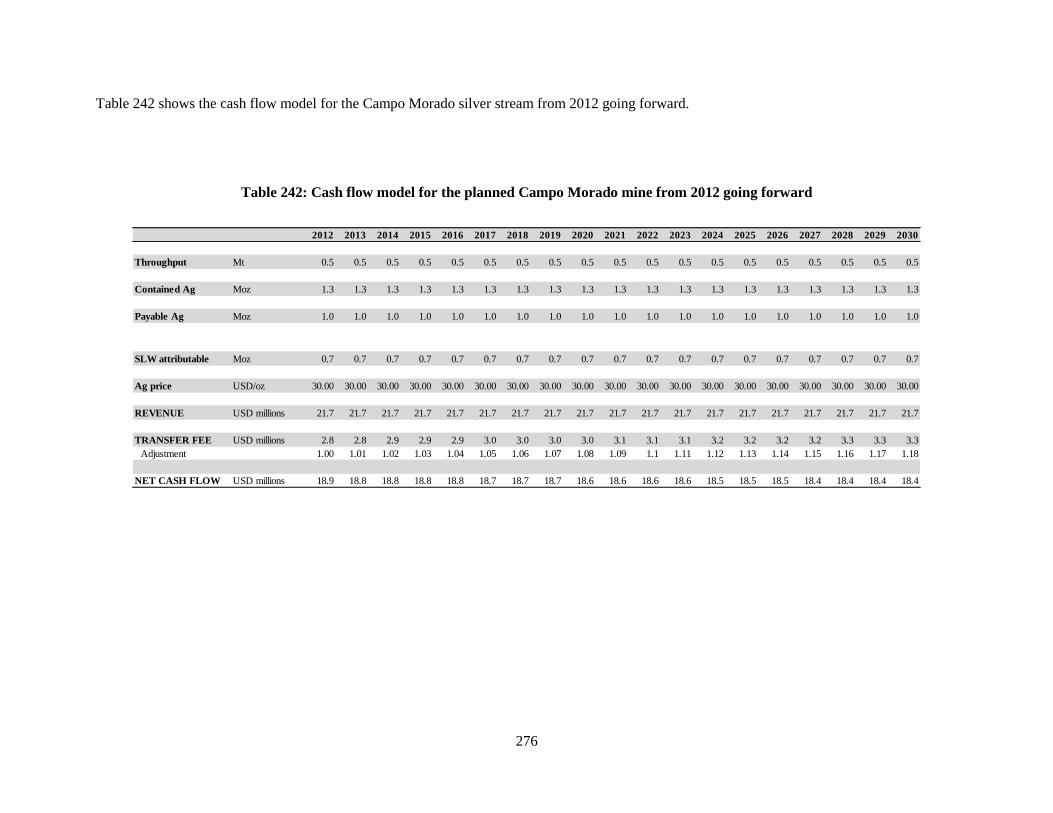

Table 242: Cash flow model for the planned Campo Morado mine from 2012 going forward ............... 276

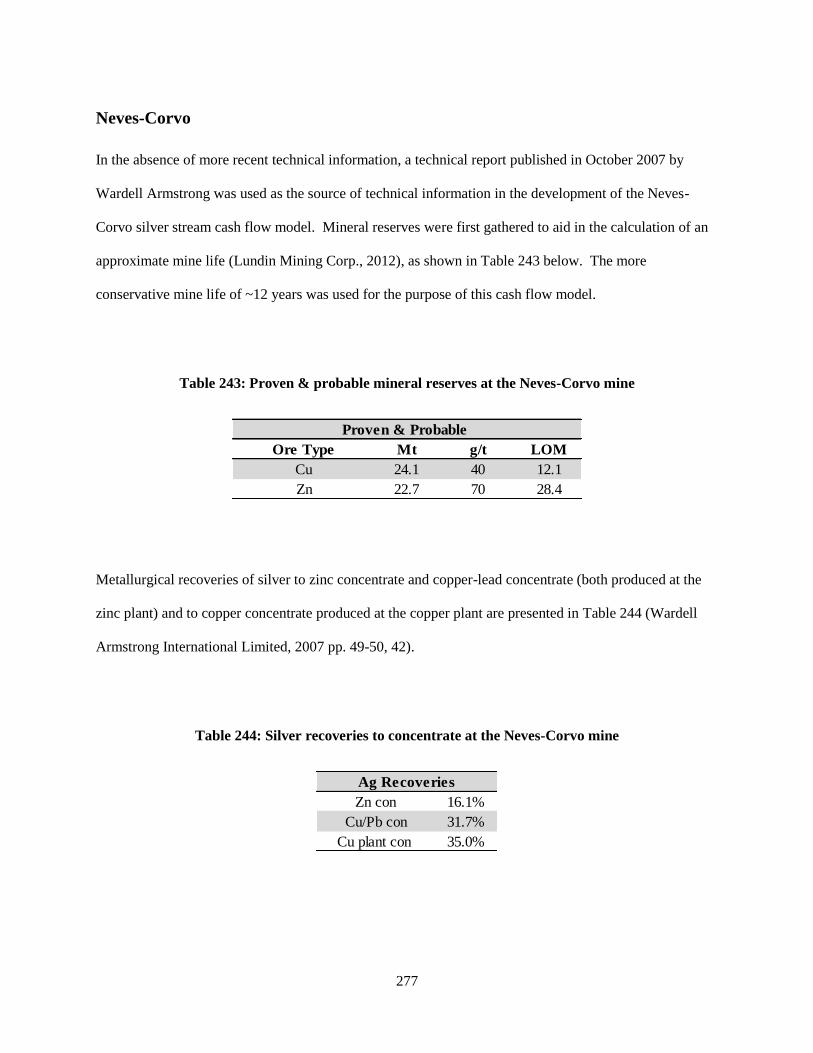

Table 243: Proven & probable mineral reserves at the Neves-Corvo mine .............................................. 277

Table 244: Silver recoveries to concentrate at the Neves-Corvo mine ..................................................... 277

Table 245: Cash flow model for the Neves-Corvo mine from 2012 going forward ................................. 278

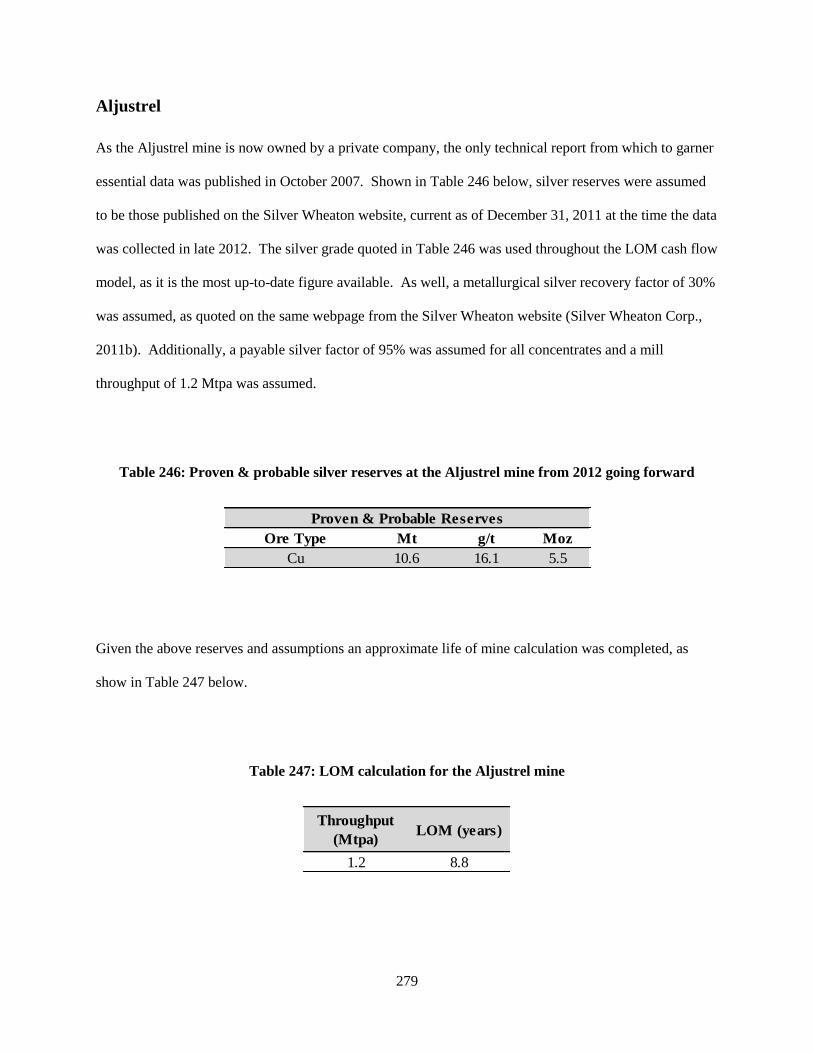

Table 246: Proven & probable silver reserves at the Aljustrel mine from 2012 going forward ............... 279

Table 247: LOM calculation for the Aljustrel mine.................................................................................. 279

Table 248: Cash flow model for the Aljustrel mine from 2012 going forward ........................................ 280

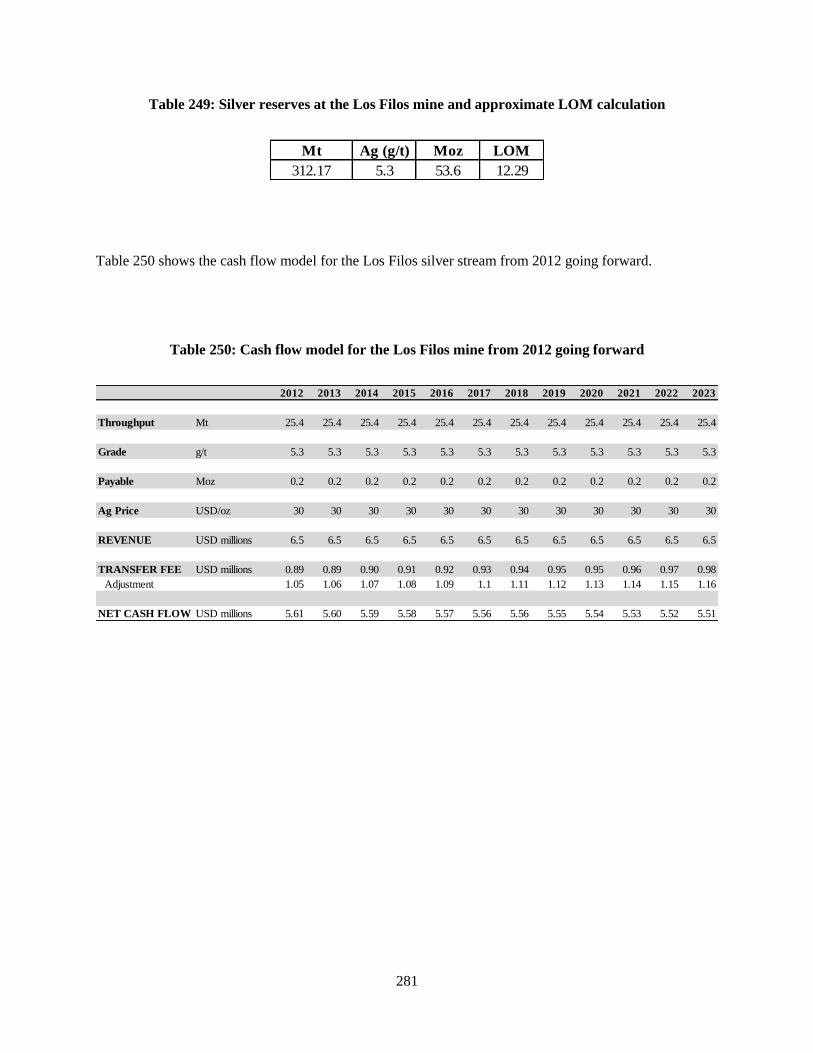

Table 249: Silver reserves at the Los Filos mine and approximate LOM calculation .............................. 281

Table 250: Cash flow model for the Los Filos mine from 2012 going forward ....................................... 281

xxvii

List of Abbreviations

CAD: Canadian dollars. Currency used in Canada.

CPI: Consumer Price Index.

ETF: exchange-traded fund, a financial security whose value is derived from and meant to replicate that

of an index or physical commodity.

ER: equity research.

FX rate: foreign exchange rate.

FY: fiscal year for a public corporation, generally defined as January 1st to December 31st of a given year.

FYE: fiscal year end. Final day of a defined fiscal year for a public corporation, usually December 31st

of a given year.

H1 or H2: first or second half of a fiscal year, respectively. Refers to the first or last 6 month period of a

fiscal year and typically defined as January 1st to June 30th or July 1st to December 31st, respectively.

IRR: internal rate of return.

LOM: life of mine.

MARR: minimum acceptable rate of return or hurdle rate.

NPV: net present value

NI 43-101: National Instrument 43-101, Standards of Disclosure for Mineral Projects. A code of

guidelines and standards for the reporting of technical and financial data relating to a mineral project that

is owned and operated by a publicly traded corporation in Canada.

NSR: net smelter return.

Operating partner: referred to as OP.

xxviii

PVR: present value ratio.

First, second, third, or fourth quarter of a fiscal year: referred to as Q1, Q2, Q3, and Q4, respectively,

followed by the fiscal year in question (e.g Q1 2010). Generally refers to the following defined periods:

January 1st to March 31st (Q1), April 1st to June 30th (Q2), July 1st to September 30th (Q3), and October 1st

to December 31st (Q4).

SEDAR: System for Electronic Document Analysis and Retrieval. Repository of publicly available

information and data issued by publicly traded corporations in Canada.

SLW: Silver Wheaton Corporation.

TSX: Toronto Stock Exchange. The largest stock exchange in Canada, which lists and trades the largest

proportion of the world’s public mining companies.

TSXV: TSX Venture Exchange. A stock exchange that primarily lists and trades junior companies whose

market capitalization and assets are too small to be listed on the TSX.

USD: United States Dollars. Currency used in the United States of America.

WACC: weighted average cost of capital.

1

Chapter 1

Introduction

“Royalty streaming” or “commodity streaming” is a business model that was first employed by Franco-

Nevada Mining Corporation in 1986. It has become an increasingly important and significant form of

alternate mine financing as well as an accepted and particularly successful method of doing business.

Within the last decade, several companies have emerged whose sole business focus is “commodity

streaming”, with their source of income being the sale of product or receipt of royalties resulting from

these deals. This business model is now being used within both the hard rock mining and hydrocarbon

extraction industries.

The commodity streaming model is simple in nature. A “commodity stream” is effectively an option to

purchase a fixed percentage or volume of a commodity that may be produced in the future from an

exploration property or that is currently being produced by an operating mine. The streaming company

(streaming firm or stream buyer) strikes a deal (commodity stream or commodity purchase agreement)

with a mining/energy exploration or extraction company (miner, operating partner, or stream seller)

exploring for or mining the commodity of interest. The deal always involves an upfront cash payment to

the miner or stream seller which is advanced by the stream buyer. These advance payments have ranged

from the tens to hundreds of millions of dollars. In exchange for advancing money, the stream buyer

receives the right to purchase a percentage of the miner’s production from a particular operation over a set

term and at a pre-established price. The term typically extends over the commercial life of the operation,

and the price ultimately paid to the stream seller or miner (referred to as the “transfer price”) is the lesser

of a pre-established fixed price (e.g. $3.90/oz of silver) or the prevailing spot market price of the

commodity at the time that the option to purchase is exercised. A streaming firm’s operating income is

2

then the difference between the market price of the commodity at the time of sale and the transfer fee it

paid to acquire the commodity, which will either be lower or equal to the market price at the time of

transfer of ownership.

Alternatively, some companies involved in the streaming business have chosen to take a royalty position

or “royalty stream” on all or some of the mine/project’s future profit, instead of holding an option to

purchase the physical commodity at a fixed price. For example, Franco-Nevada Corp. and Royal Gold

Inc. derive the majority of their revenues not from streaming, but from royalties. The royalty, a fixed

percentage, is applied to net revenues, usually the Net Smelter Return (NSR) and would be paid out on an

incremental basis (i.e. semi-annually or annually), although this is not always the case. It is this type of

streaming that Franco-Nevada first employed as a main aspect of its business model in the mid-1980s. It

is worth noting that royalty streams and commodity streams are distinct and separate deal types; the

streaming market was dominated by the former until the early 2000s when the latter began to gain in

popularity.

Prior to the early 2000s, there existed only a few companies engaged in royalty/commodity streaming

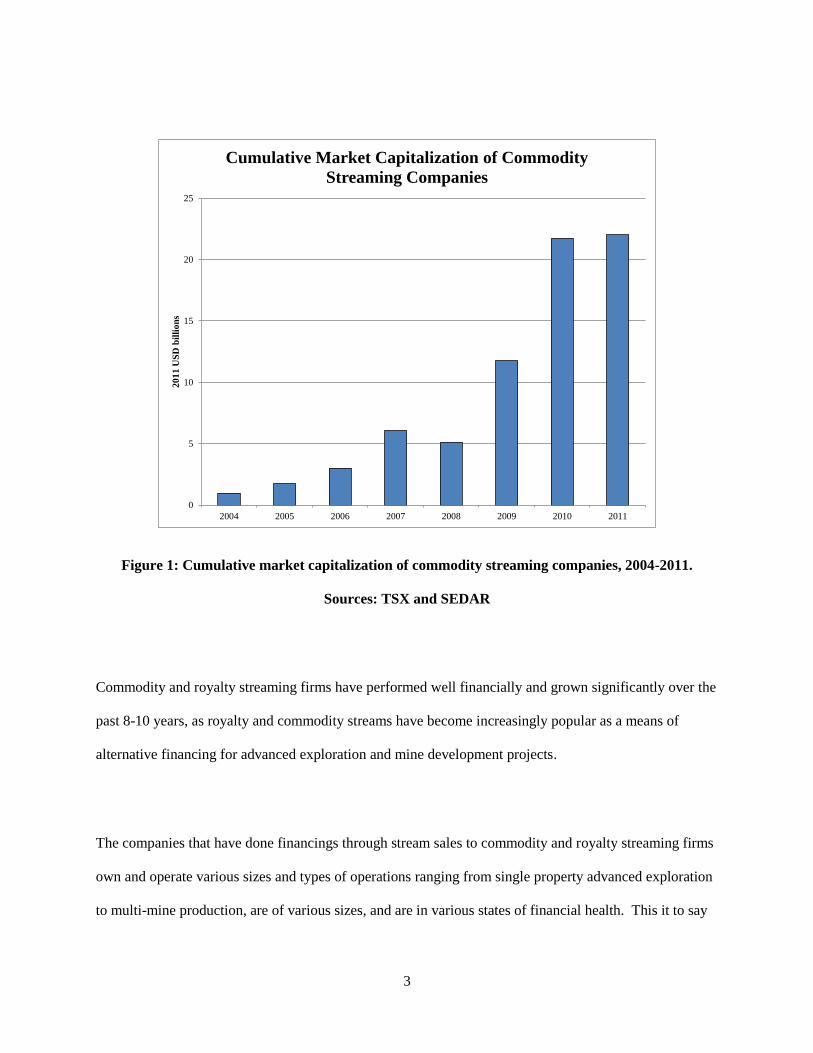

activities, Franco-Nevada being chief among them (Careaga, 2012). From the years 2004-2012, the

quantity and value of royalty/commodity streaming firms1 and the deals they completed increased

significantly. For illustrative purposes, the cumulative market capitalization of the four major streaming

firms2 from 2004-2011 is presented in Figure 1.

1 Defined as a business entity whose only source of revenue is through royalty and/or commodity streams on hard

rock mining or hydrocarbon extraction operations. 2 Franco-Nevada Corp., Royal Gold Inc, Sandstorm Gold Ltd, and Silver Wheaton Corp.

3

Figure 1: Cumulative market capitalization of commodity streaming companies, 2004-2011.

Sources: TSX and SEDAR

Commodity and royalty streaming firms have performed well financially and grown significantly over the

past 8-10 years, as royalty and commodity streams have become increasingly popular as a means of

alternative financing for advanced exploration and mine development projects.

The companies that have done financings through stream sales to commodity and royalty streaming firms

own and operate various sizes and types of operations ranging from single property advanced exploration

to multi-mine production, are of various sizes, and are in various states of financial health. This it to say

0

5

10

15

20

25

2004 2005 2006 2007 2008 2009 2010 2011

20

11

US

D b

illi

on

s

Cumulative Market Capitalization of Commodity

Streaming Companies

4

that mining and energy companies of all types have sought stream and royalty financing over the past

decade and there is no single profile that describes companies seeking these types of financing.