Aims to weather it all - Tata Mutual Fund

28

Aims to weather it all This product is suitable for investors who are seeking*: • Long Term Capital Appreciaon. • An equity scheme that invests predominantly in Indian markets with focus on riding business cycles through dynamic allocaon between various sectors and stocks at different stages of business cycles. *Investors should consult their financial advisors if in doubt about whether the product is suitable for them. NFO Opens: 16th July, 2021 NFO Closes: 30th July, 2021

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Aims to weather it all - Tata Mutual Fund

Aims to weather it all

This product is suitable for investors who are seeking*:• LongTermCapitalAppreciation.• An equity scheme that invests predominantly in Indian markets with

focusonridingbusinesscyclesthroughdynamicallocationbetweenvarioussectorsandstocksatdifferentstagesofbusinesscycles.

*Investors should consult their financial advisors if in doubt about whether the product is suitable for them.

NFO Opens: 16th July, 2021NFO Closes: 30th July, 2021

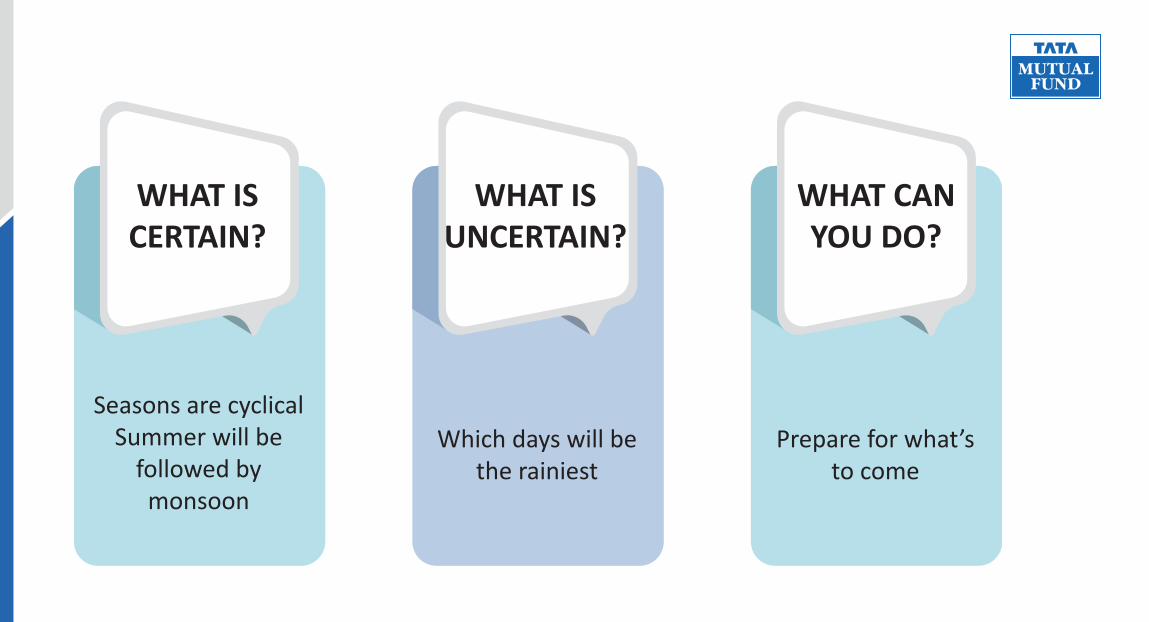

Extreme heat

Rising Humidity

Days getting shorter

Intermittent Thunderstorms DO YOU KNOW WHATS COMING?

WHAT IS CERTAIN?

WHAT IS UNCERTAIN?

WHAT CAN YOU DO?

Seasons are cyclicalSummer will be

followed by monsoon

Which days will be the rainiest

Prepare for what’s to come

I think it’s essential to remember that just about everything is cyclical. There’s little I’m certain of, but these things are true: Cycles always prevail

Howard Marks

BUSINESS CYCLES

The economy goes through a series of stages as it expands and contracts, characterised bydownwardorupwardfluctuationsofGDP.

Each Economic Cycle/Business Cycle has 4 phases

GDP

TIME

Recession Recovery Expansion Slowdown

GDP

Time

• FallingActivity• Credit slowdown• ProfitsDecline• Policy eases• Inventories &

Sales fall

•Growthpeaking• Credit growth strong• Profitgrowthpeaks• Policy benign• Inventories & sales

grow, equilibrium reached

• GrowthModerating• Credit Tightens• Earnings under

pressure• Contractionarypolicy• Higher inventories,

lower sales

•Activityrebounds(GDP,Employment)

• Credit begins to grow• Profitsgrowrapidly• Policystillstimulative• Inventories low, sales

improve

Recession Recovery Expansion Slowdown

CHARACTERISTICS OF BUSINESS CYCLES PHASES

Expansion Companies innovate and

produce new products and services.

They create jobs that help individuals build their purchasingpower.

RecessionRecessionsoffer

opportunitiesforbusinessesto reorganize their operationsandrebuildforfuture growth

Recovery The cyclical nature of

economicactivityprovidesbusinesses with the impetus to invest in the present and grow for the future

SlowdownBusinessactivitydeclines

as companies and markets mature

Continuedinnovationsandimprovements have lesser impacts,

Consumer spending slows

WHAT DRIVES THE BUSINESS CYCLE?

Business Conditions

Market Conditions

Macro Conditions

? Are Businesses planning expansion orcuttingcosts?

?What is the

investorsentiment?

?IsInflationrisingor

falling?

? Are factories running at full capacity?

? What is favoured, large or small

companies

? Are people spending onnecessitiesor

luxuries?

?Is credit readily

available?

?Are investors

greedyorfearful?

?Are people able to

findwork?

?Are earnings growing

orcontracting?

?Are investors seeking growthorvalue?

?Monetary policy is accommodativeor

restrictive?

IDENTIFYING A PHASE

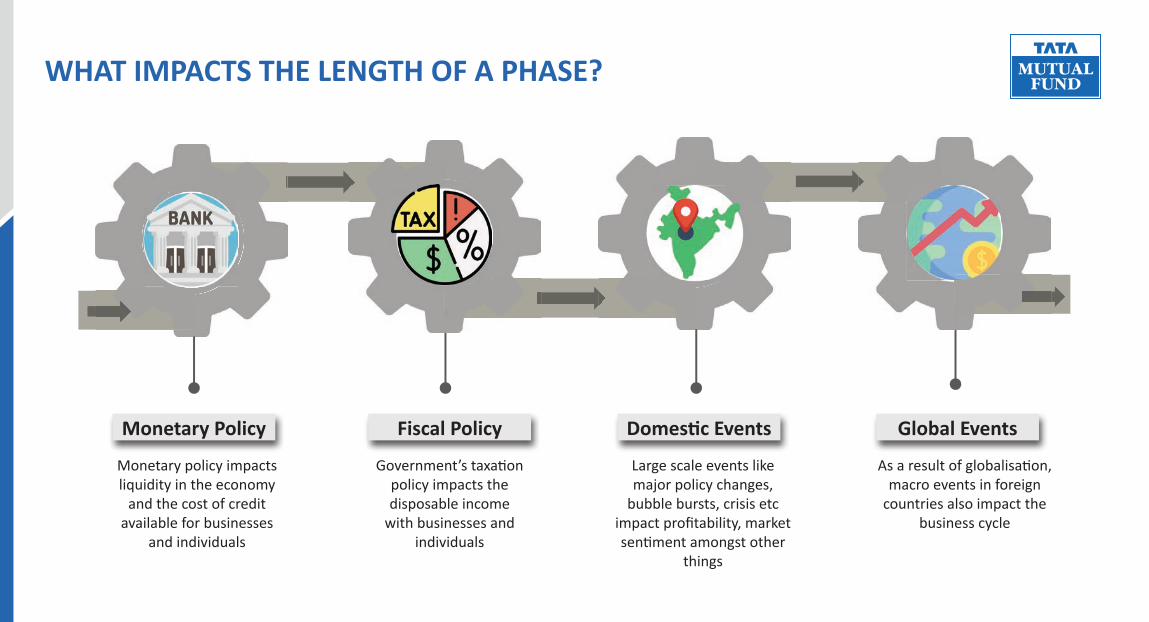

Monetary Policy Fiscal Policy Domestic Events Global Events

Monetary policy impacts liquidity in the economy

and the cost of credit available for businesses

and individuals

Government’staxationpolicy impacts the disposable income

with businesses and individuals

Large scale events like major policy changes,

bubble bursts, crisis etc impactprofitability,marketsentimentamongstother

things

Asaresultofglobalisation,macro events in foreign

countries also impact the business cycle

WHAT IMPACTS THE LENGTH OF A PHASE?

BUSINESS CYCLE INVESTING

BUSINESS CYCLE INVESTING

Eachphaseinthebusinesscyclepresentsuniqueinvestmentopportunities.Incorporatingbusinesscycles theme into investments helps make the most of the current economic environment

Recovery & ExpansionInvestor Sentiment: Increased Risk AppetiteInvestmentsthataremoresensitivetofastereconomic growth and business activity willlikelyoutperform.

Stocks of midsize and small companies, aswellasemerginlgmarketequities

Younger, growth-oriented firms andindustries

Generally referred to as Cyclical Stocks

Slowdown & RecessionInvestor Sentiment: Fearful and Cautious

Defensive investments and those that aresensitivetofallinginterestrateshavegreaterpotentialtooutperform

Stocks of larger and stable companies

Businesses that experience steady consumer demand even during economic slowdowns

Generally referred to as Defensive Stocks

Cyclical stocks• Directrelationshiptotheeconomy

• Companiesthatmakeorselldiscretionaryitems and services that are in demand when the economy is doing well

• These are stocks which do well during phasesofincreasedconsumptionandhigh employment

• CapitalGoods,Industrialsandotherhighcapex sectors tend to perform well during economic upcycle

Defensive stocks

• Defensive/Structural growth Stocks outperform the market when economic growth slows

• They produce or distribute goods and services we always need

• Characterisedbylowpenetrationi.elongrunway for growth, strong balance sheet androbustESGtrackrecord

CYCLICALS VS DEFENSIVES

Predominantly Large Cap

• Utilities

• Pharma

• FMCG

Diversified across Market Cap

• Auto

• Metals & Mining

• Large Financials

• InformationTechnology

More Mid & Small Cap• Financialsincl.

NBFCs• Real estate• Consumer

Discretionary• CapitalGoods&

Industrials

Predominantly Diversified & Bottom-up stock picking• Utilities• Pharma• FMCG• IT services

Recession Recovery Expansion Slowdown

GDP

TimeSectors/industriesmentionedaboveisforillustrationpurposeonlyanditmayormaynotformpartofactualportfolioofTataBusinessCycleFund.Theoreticallythesesectors/segmentsareexpectedtoperformwell,actualperformancemaybeimpactedbyotherexternalfactorsandmaynotalignwiththeaboverepresentation

INVESTING IN DIFFERENT PHASES

2008-09 2010-12 2013-17 2018-19 2020-21

Auto: 14.05%

IT: 10.70%

Pharma: 8.93%

Realty: -45.64%

Consumer Disc: -16.57%

Industrials: -16.36%

Realty: -17.42%

Metal: -13.36%

Utilities: -11.78%

Realty: 3.83%

Metal: 5.62%

Utilities: 7.38%

Auto: -16.76%

Metal: -16.33%

Industrials: -13.34%

Realty: 11.82%

FMCG: 10.09%

Financial Services: 9.84%

FMCG: 28.61%

Pharma: 17.21%

Auto: 15.70%

Consumer Disc: 20.79%

Auto: 18.15%

Financial Services: 14.91%

Financial Services: 18.53%

IT: 16.59%

FMCG: 3.67%

Metal: 50.53%

Pharma: 48.27%

IT: 47.04%

Recession Recovery Expansion Slowdown Double-dip + Recovery

Time

Source:MFI,Indices:NiftyFinancialServices,NiftyIT,NiftyPharma,S&PBSEAUTO,S&PBSECG,S&PBSEConsumerDiscGoods&Services,S&PBSEFMCG,S&PBSEIndustrials,S&PBSEMETAL,S&PBSERealty,S&PBSEUtilities.Phasesclassifiedonthebasisofalignmentofeconomicindicators(Inflation,InterestRate,CapacityUtilisation,GDPAnnualGrowthRate)withtheoreticallyexpectedtrendsinbusinesscyclesphases

GDP

TOP SECTORS

BOTTOM SECTORS

SECTOR PERFORMANCES

Overthelastdecade,Businesscycleshavebecomeshorter and harder to predict.Thisisresultofa number of factors:

Increasingly dynamic and responsive monetary policy

Activeimpetusorrestrictionsthroughgovernment policy

Impactofdomesticmacrovariables, ie, policy changes,

industry crisis etc

Impact of global macro variables, ie, global crisis, foreign interest rates etc

THE CHALLENGE

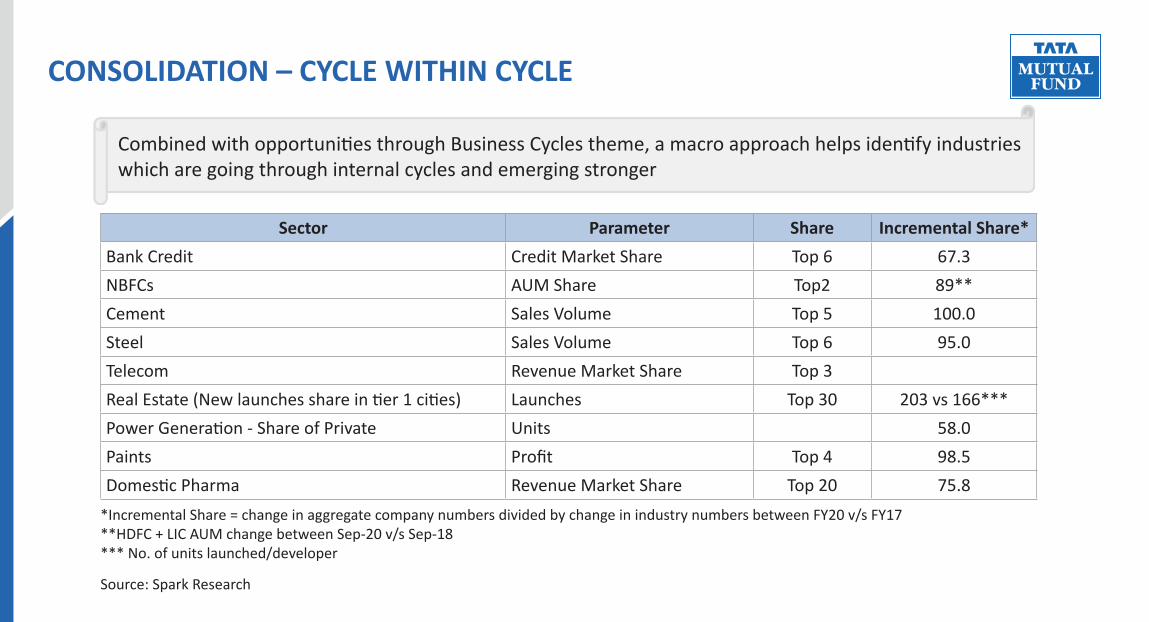

CombinedwithopportunitiesthroughBusinessCyclestheme,amacroapproachhelpsidentifyindustrieswhich are going through internal cycles and emerging stronger

Sector Parameter Share Incremental Share*Bank Credit Credit Market Share Top 6 67.3NBFCs AUM Share Top2 89**Cement Sales Volume Top 5 100.0Steel Sales Volume Top 6 95.0Telecom Revenue Market Share Top3RealEstate(Newlaunchesshareintier1cities) Launches Top30 203vs166***PowerGeneration-ShareofPrivate Units 58.0Paints Profit Top 4 98.5DomesticPharma Revenue Market Share Top 20 75.8

*Incremental Share = change in aggregate company numbers divided by change in industry numbers between FY20 v/s FY17**HDFC+LICAUMchangebetweenSep-20v/sSep-18***No.ofunitslaunched/developer

Source: Spark Research

CONSOLIDATION – CYCLE WITHIN CYCLE

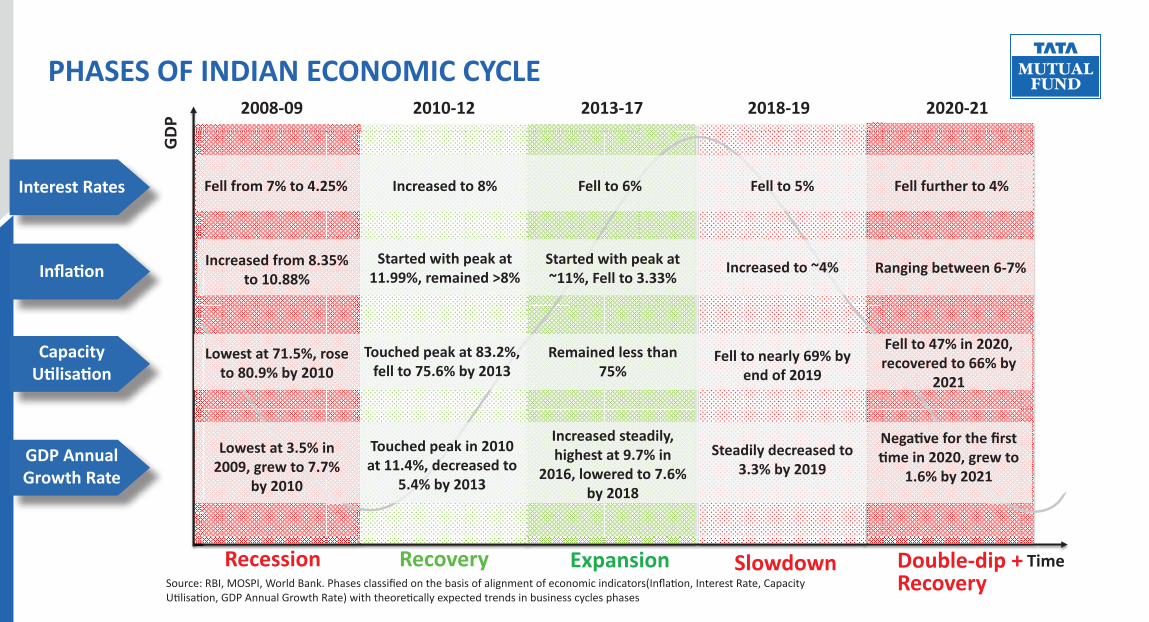

WHERE ARE WE NOW?

Interest Rates

Inflation

Capacity Utilisation

GDP Annual Growth Rate

PHASES OF INDIAN ECONOMIC CYCLE2008-09 2010-12 2013-17 2018-19 2020-21

Time

GDP

Recession Recovery Expansion Slowdown Double-dip + RecoverySource:RBI,MOSPI,WorldBank.Phasesclassifiedonthebasisofalignmentofeconomicindicators(Inflation,InterestRate,Capacity

Utilisation,GDPAnnualGrowthRate)withtheoreticallyexpectedtrendsinbusinesscyclesphases

Fell from 7% to 4.25%

Increased from 8.35% to 10.88%

Lowest at 71.5%, rose to 80.9% by 2010

Lowest at 3.5% in 2009, grew to 7.7%

by 2010

Increased to 8%

Started with peak at 11.99%, remained >8%

Touched peak at 83.2%, fell to 75.6% by 2013

Touched peak in 2010 at 11.4%, decreased to

5.4% by 2013

Fell to 5%

Increased to ~4%

Fell to nearly 69% by end of 2019

Steadily decreased to 3.3% by 2019

Fell further to 4%

Ranging between 6-7%

Fell to 47% in 2020, recovered to 66% by

2021

Negative for the first time in 2020, grew to

1.6% by 2021

Fell to 6%

Started with peak at ~11%, Fell to 3.33%

Remained less than 75%

Increased steadily, highest at 9.7% in

2016, lowered to 7.6% by 2018

0

2

4

6

8

10

12

2015 2016 2017 2018 2019 2020

Credit Increased

Crash Cleanse

Cure Covid

• Highly leveraged corporates

• Increased lending and NPAs

• Weaker Banking System

• Multiplecompanyspecificevents of bankruptcy & defaults were excesses of the past

Source: RBI

• Banks provision coverage ratio–70%to80%

• Deleveragingcycleofcorporates

CYCLE OF CREDIT Graph - NPLs

• RBI introduced AQR• NBFCs saw an opportunity

and expanded their loan book• High rates, low growth-

Corporatesfounditdifficulttoservice debt

• Lockdowns impaired businesses• Banks raised capital• Structural cost cuts• High commodity prices

improvescashflows

CRAZY SOWS SEEDS OF CALM

GREEN SHOOTS

Deleveraging Wage Growth

ConsumptionBanks

Highcashflowsleadingtobalancesheetcleansing.Creatingagroundforfreshinvestmentcycleinnext1-2 years

As economic growth is picking up, companiesarereinstatingsalarycutsintroduced at the start of FY21

Most consumer companies were able to recover and secure higher sales

New bad loans are tapering, and older bad loans are well provided for

Source:Companies,KotakInstitutionalEquities

Company Debt Reduced in FY21 Debt added in FY08A 1,996 23,909B 9,124 1,560C 974 7,963D 15,625 (752)E 31,389 28,699Illustrationusingsteelcompanies

Provisionsforbadloans-Provisioncoverageratio(%)

020406080

100

Public Bank A Old PrivateBank A

New PrivateBank A

Small FinanceBank A

2018201920202021

-40-20

02040

ConsumerStaples

DiversifiedFinancials

Metals andMining

Real Estate Total (allsectors)

Employee Expenses (YoY Growth %)

4QFY201QFY212QFY213QFY214QFY21

20

-40-20

0204060

Staples CompanyA

Staples CompanyB

Discre�onaryCompany A

Discre�onaryCompany B

QoQ Volume Growth of Consumer Companies

4QFY19 4QFY20 4QFY21

Aims to weather it all

Aim

Economic Trends

Focus on Sector Calls

Stock Selection

Todeploythebusinesscycleapproachtoinvestingtoidentifyeconomictrendsandinvestinsectorsand stocks that are likely to outperform

Investingaspertheeconomicconditions–CyclicalsduringExpansionandDefensivesduringContraction

ExpansionBuy either the sector leaders or Companies

benefittingdisproportionatelyfromthesectoraltailwinds during economic & business cycles

Extent of leverage to the cycle Marketcapagnostic Management record

ContractionInvest in companies from sectors which provide

cushion during downcycles

INVESTMENT APPROACH

Thesizeoftheportfoliowillvarydependingonthecycle.Inacontractionarycycle,wemayhave more stocks compared to an expansionary cycle

The business cycle theme may allow for a more aggressive stance in terms of sector over/under weight compared to other diversifiedfunds

With no constraint on market cap allocation,thesplitwillbepurelybased on the business cycle phase, with focus on segments most likely to do well

Thechurnintheportfoliowilldepend on how quickly the cycles areturning.Suddenupswingsordownswings may cause higher churn

Portfolio SizeSector Allocation

Portfolio ChurnMarket Cap Allocation

FUND CHARACTERISTICS

01 02

.

03

Withthedurationofbusiness cycles

shortened, the need for a fund that changes with change in

cycle has arisen

Overthelastfewyears, the impact of sectorallocationshasbeen greater on alpha generationversusstock

levelallocations.

A fund that adapts to changes is needed because:

• Markets are at fair valuations

• Macro challenges posedbyinflationandbondyieldsgoingup.

SHORTER BUSINESS CYCLES

IMPACT OF SECTOR ALLOCATIONS

MARKET CONDITIONS

WHY NOW?

ASSET ALLOCATION OF THE FUND

Instruments Indicative allocations (% of net assets)

Risk Profile

Minimum Maximum High/Medium/LowEquity and equity related instruments selected on the basis of business cycle 80 100 HighOtherEquity&EquityrelatedInstruments 0 20 Medium to HighDebtandmoneymarketinstruments&GoldETF 0 20 Low to MediumUnitsissuedbyREITs&InvITs. 0 10 Medium to High

• Investments in Foreign Securities(to theextentof 20%of net assets) shall be subject to the investment restrictionsspecifiedbySEBI/RBIfromtimetotime.ThefundmanagerswillconsiderallrelevantriskbeforemakinganyinvestmentinForeignSecurities.

• Further,theportfoliooftheSchemewillbeconstructedinaccordancewiththeinvestmentrestrictionsspecifiedundertheRegulationswhichwouldhelpinmitigatingcertainrisksrelatingtoinvestmentsinsecuritiesmarket.

• TheSchememay invest inequityderivatives instruments to theextentpermittedunderand inaccordancewith theapplicableRegulations

Scheme Name Tata Business Cycle Fund

NFO Dates NFO Opens: 16th July 2021

NFO Closes: 30thJuly2021

Investment Objective Togeneratelong-termcapitalappreciationbyinvestingwithfocusonridingbusinesscyclesthroughallocationbetweensectorsandstocksatdifferentstagesofbusinesscycles.

However,thereisnoassuranceorguaranteethattheinvestmentobjectiveoftheSchemewillbeachieved.Theschemedoesnotassureorguaranteeanyreturns.

Type of Scheme Anopen-endedequityschemefollowingbusinesscyclesbasedinvestingtheme.

Fund Manager RahulSingh,VenkatSamala(OverseasInvestment)andMurthyNagarajan(DebtPortfolio)

Benchmark Nifty500TRI

Min. Investment Amount Minimum subscription amount:Rs5,000/-andinmultipleofRe.1/-thereafter.

Additional Purchase: Rs.1000/-&inmultiplesofRe.1/-thereafter.

Load Structure Entry Load:N.A.

Exit Load:Redemption/Switch-out/SWP/STPonorbeforeexpiryof365daysfromthedateofallotment:Ifthewithdrawalamountorswitchedoutamountisnotmorethan12%oftheoriginalcostofinvestment-NIL

Redemption/Switch-out/SWP/STPonorbeforeexpiryof365daysfromthedateofallotment:Ifthewithdrawalamountorswitchedoutamountismorethan12%oftheoriginalcostofinvestment-1%ofapplicableNAV

Redemption/Switch-out/SWP/STPafterexpiryof365daysfromthedateofallotment-NIL

FUND DETAILS

This product is suitable for investors who are seeking*:

• LongTermCapitalAppreciation.

• An equity scheme that invests predominantly in Indian markets with focusonridingbusinesscyclesthroughdynamicallocationbetweenvarioussectorsandstocksatdifferentstagesofbusinesscycles.

*Investors should consult their financial advisors if in doubt about whether the product is suitable for them

Thank you

Mutual Fund Investments are subject to market risks, read all scheme related documents carefully

Call: (022) 6282 7777 (Mon to Sat 9:00 am to 5:30 pm) | SMS: TMF to 57575 | www.tatamutualfund.com