agrlcultufal economlcs : a - AgEcon Search

39

.\ l. | ' Lausalltv anaLvsls ln JJ .lt' agrlcultufal economlcs : a review of theoretical and empirical issues Rakhal SARKER Cabiers d'économie et sociologte ruralet, n" 31-35' 1995

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of agrlcultufal economlcs : a - AgEcon Search

.\ l. | 'Lausalltv anaLvsls lnJJ.lt'

agrlcultufal economlcs : areview of theoretical and

empirical issues

Rakhal SARKER

Cabiers d'économie et sociologte ruralet, n" 31-35' 1995

Rakhal SARKER*

Lanalyse de causalitéen économie agricole:revue des questionsthéoriques ec

empiriques

Mots-clés:causalité de Granger,modèles traditionnelsbivariés, modèles VARnon contralnts,systèmes corntégrés,économie agricole

Caasaliry analysis inagricahualeconomics : a ret ieu oftheoretical and. empiricallSSileS

Key-words:agricaltaral economict,

Granger caasality,unrestricted VAR models,cointegrated systems,

traàitional biuriate models

Résumé - Les travaux de recherche menés en économie agricole comprennent sou-

vent une analyse de causalité. Comme la théorie économique donne peu d'indrca-

rions précises sur ce type de quesrion, Granger a proposé en 1969 une approche sta-

tistique permettant de tester des hypothèses de causalité. Elle a éré largement

utilisée par les économistes agricoles et cet article présente un survol des analyses

qu'ils ont réalisées dans ce domaine depuis les années 70.

Une première partie est consacrée à une brève discussion des relarions encre la causa-

lité au sens de Granger et divers concepts d'exogénéité. Vient ensuite une descrip-

tion des méthodes permettanr de tester des hypothèses de causalicé dans les modèles

rraditionnels VAR bivariés non contraints et dans des systèmes coincégrés. Elle esr

complétée par la présenration critique d'un certain nombre d'applications de ces mé-

thodes en économie agricole. Malgré l'usage très répandu qui en esr fair dans ce do-

maine, les tests de Granger, de Sims (ordinaire et modifié) et de Haugh-Pierce don-nenr des résulrats contradictoires. Leurs résultats sont très sensibles au préfiltrage, à

I'existence de variables manquantes et au choix de Ia longueur des retards. De plus, ilest difficile d'en donner une interprétarion correcte en tetmes de causalité. Alors que

l'utilisation de modèles VAR non contraints permet de résoudre le problème des va-

riables manquantes, les résultats des modèles VAR en niveau peuvent prêter à dis-

cussion, à cause des contraintes d'identification imposées pour l'estimation.

La non-stationarité et I'existence de racines unitaires dans les séries de données peu-

vent aussi être à I'origine de difficultés. Si le modèle VAR comprend des variables

incluant une tendance stochætique et s'il y a une possibilité de coinrégracion, le rest

de \flald utilisé pour tester [a causalité au sens de Granger dans les modèles VAR en

niveau peut ne pas avoir une distribution de probabilité limite, ce qui invalide le

tesr. Si le système comprend des variables non-stationnaires dont certaines Peuventêtre liées par des relations de long terme, la méthode de cointégration permet alors

d'analyser la causalité de Granger d'une façon appropriée. Quelle que soit la métho-

de employée, la plupart des recherches faites sur la causalité en économie agricole a

porté sur I'analyse des prix des produits. Un nombre croissant de travaux s'intéresse

aussi aux effets macroéconomiques sur l'agriculture. Enfin, l'analyse de la causalité

menée à I'aide des systèmes cointégrés a permis Ie réexamen d'un certain nombre de

paradigmes bien établis de l'économie agricole. Compce tenu des avanrages et des

inconvénients des diverses méthodes, l'auteur propose d'uciliser une approche sé-

quentielle basée sur la méthode du maximum de vraisemblance de Johansen pourtester la causalité au sens de Granger dans Ie cas des systèmes cointégrés comprenanc

des variables à tendance stochærique.

Sammary -Tbis paper prwidzs an outraiew of caasality analysis in agricaltaral eco-

nomics. The relationships between Granga caasa/ity and uariols concepts of exogeneity

are discassed. Fotr traditional causality tests deueloped for testing Granga caasality aredtscribed and tbeir applications in agriciltaral economics are critically appraised. Cau-sality analysis in ueclor aatoregressiae and cointegrated systems along with tbeir applica-tions in agricaltaral economics are discussed. lrrupectiae of the nethodology, commodityprice analytis rueiaed nott of the applications of causality analysis in agricultaral econo-

mics. In uiew of the xrengtbs and weah.nessu of different approacltes, a seqilential approa-ch fm nsting Granger caasality basedJohansen's maxirnun likelihood method is suggvs-

ted fm systuns inuoluing aariables witb stocbastic trends and cointegration.

* Department of Agricilnral Economics €t Business, Uniaersity of Gaelph, \ntario, Ca-nada NIG 2V1

,THE concept of causality is central to any scientific inquiry. Al-I though it is a widely used concept in agricultural economics, the

literature on causality does not lack in controversy. Even the meaning ofthe term itself is under dispute (Holland, 1986; Basmann, 1988). 'Whilethe origin of the term 'causality' can be traced back to rhe writings ofAristotle, a renowned Greek philosopher, its meaning has evolved

through time in the writings of prominent philosophers like Locke,

Hume, Mill and Suppes. There is a lack of consistency in the literatureas to how these philosophers defined the term and whether or not it is

measurable in practice. Despite occasional debates among themselves the

philosophers did not produce a precise definition of causality that a ma-jority can accept, nor did they produce an operational definition that is

useful in economic analysis (Granger, 1980; Prioier, 1988)*.

Empirical research in agricultural economics often requires some cau-

sal issues to be resolved. In many occasions, economic theory provides no

precise guidance in this regard. As a consequence, the resolution of var-ious causal issues had been judgemental (Thurman, 1987). Granger(I96Y introduced a statistical approach to confront causal hypothesis rn

economics. According to this approach, a variable X, is said to cause an-

other variable,Y,,if the lagged values of X, provide information useful

for predicting Yr. Notice that this simple notion of causality is firmlyrooted in statistics and has little relation to rhe philosophical notion of"cause and effect". This, however, has not stopped Granger causalitytests from becoming a standard tool in commodity price analysis since

the early 1980s.

A concept closely related to causality is exogeneity. A clear under-standing of the relationship between causality and exogeneity is essential

for the evaluation of causality results and cheir interpretation. Exogen-

eity plays a fundamental role in econometric estimation and statisticalinference. The exogeneity of a variable depends on whether it can be

treated as "given" in a model without loosing information for the pur-pose of research at hand. I on two critical factors: (i)

ihe pa.u-.ters of interest nd (ii) the purpose of the

model, whether it is for s recasting or policy analy-

* I would like to thank four reviewers o[ rhe journal for cheir helpful com-

menrs. I am particularly grateful to the third reviewer whose extensive comments

significantly improved the paper' Any remaining errors are' of course, my resPon-

sibility.

l

R. SARKER

and its dispersion will change. If the conditional relationship between Y,

and X, remains unaffected despite these changes (i.e., if the parameters

of intérest are variant to the structural change), then X, is said to be

super exogenous. While weak exogeneity is essential for conducting sta-

tistical inference, Granger noncausality is required for valid conditionalforecasting. The condition that Y, does not Granger cause X, is neither

necessary nor sufficient for the weak exogeneicy of X,(".

A number of alternative procedures have been developed in the

1970s to conduct Granger causality test in bivariate models. Conflictingcausality resulcs in agricultural economics have been obtained from these

tests. Misspecification inherent in most bivariate causality models along

with conflicting results from alternative causality tests have generated

considerable controversy. The misspecification issue has been addressed

in multivariate vector autoregressive (VAR) models since the mid 1980s.

Impulse responses from these models are used to generate causal infer-

ences. \7hile the introduction of causality analysis in a VAR framework

represents a significant improvement over the traditional causality anal-

ysis in bivariate models, it has been realized in recent years that causal

inferences from VAR models can also be misleading. This is particularlytrue for variables which have stochastic trends in cheir univariate repre-

sentations. Unconstrained VAR modelling with such variables can be

problematic and causality results from such models can be controversial.

It is well known that most economic time series are not stationary intheir levels. That is, both the mean and variance of these series are not

constant over time. The error terms resulting from standard regression

analysis of nonstationary variables do not follow a standard normal dis-tribution even asymptotically. Consequently, rhe conventional statisticaltests such as t. Z. F etc. are not valid. These revelations Ied most recent

studies in agricultural economics to derive causal inferences from cointe-grated or constrained VAR models. Cointegration is a statistical prop-erty which can describe the long-run behaviour of economic time sertes.

The point of departure of cointegration theory is the proposition that ifthe nonstationary variables are integrated oforder one, then it is possiblethat some linear combination of these nonstationary variables are sta-tionary. If this is true, then the variables are called cointegrated. \7hensome economic variables are cointegrared, they cannot move too far

(1)Fo, a more rigorous treatment ofthe concepts ofexogeneity, Granger non-causality and predeterminedness, see Engle et al. (1983) and Ericsson (1992).

CAUSALITY ANALYS/S

apaft from each other in the long-run, although their levels seem tofluctuate widely in the short-run. This property of the cointegrared var-iables fits perfectly with the theoretical notion of a long-run relationshipamong economic variables. Cointegration analysis, therefore, links theconcept of equilibrium relationships among economic variables embed-ded in economic rheory to a statistical model of equilibrium amongrhose variables. As it turns out, in doing so, it provides a theoreticallyconsistent and econometrically more efficient approach to rest causal re-

lationships among economic variables than has been the case with bivar-iate models or with unconstrained VARs.

The major objective of this paper is to provide an overview of testingcausal hypotheses in agricultural economics and to identifi, potential av-

enues for improvements in causality analysis. The balance of the paper isorganized as follows. The firsr secrion provides a brief exposition of fourtraditional causality tests. The second one concentrates on the applica-tions of traditional causality analysis in agricultural economics and theirlimitations. Section three focuses on causality analysis in VAR models,applications in agriculcural economics and their limitations. Secion fourdeals with nonstationarity, cointegration and causality analysis. This sec-

tion also provides an overview of major agricultural economics applica-tions of causality analysis in cointegrated systems. The limits of causal-

iry analysis in cointegrated systems and possible future directions ofcausality analysis in agricultural economics are also discussed. The finalsection summarizes the main points and concludes the paper.

TRADITIONAL CAUSALITY TESTS: AN EXPOSITION

The staristically testable notion of causality introduced by Granger

led to the development of four major causaliry tests: the Granger test,

the Sims test, rhe modified Sims test and the Haugh-Pierce test. Each ofthese tests investigates three alternative causal hypotheses: (i) Y, causes

X,,cll, (ii) X, causes Y,, or, (iii) there is a feedback relationship between

Y, and X,. The following is a brief exposition of these cests.

The Granger test

The Granger test involves regressing a variable, Y,, on lagged values

of itself and on lagged values of the other variable of interest, X, such

that:

JMY,= co* Z.FiY,r* 2,T,x,-,* e,

j=l ' t=l

9

(l)

R. SARKER

\7here ao is the. intercept, p's and T's arc regression coefficients and

e is the error term('). The assumprion on the error term requires that the

variables are stationary and there is no autocorrelation. The null hypoth-esis that X, does not cause Y,(i.e,, Ho, h = Tz= = Ti = 0) is tested

using an F-test calculated from che residuals of the restricted and unre-stricted forms of eq. (1). The above procedure can be repeated reversingthe roles of Y,and X, to test the null hypothesis thatY, does not cause

X,. These F-tests will also determine if there is any feedback relationshipbetween the two variables. Nore that the Lagrange multiplier (LM) test

can also be used to tesc the above causal hypotheses.

The Sims test

An alternative formulation of Granger causality test was introducedby Sims (1972). Suppose, Y, and X, represent a jointly covariance-sta-

tionary stochastic process. According to Sims, if X causes Y then in theregression of Y on past and future values of X, the future values of X as

a group should have coefficients statistically not different from zero.

Thus, the Sims test is based on the following regression equation:

LP

Y, = ao * 2. g,X,-i + e,j=-LFt 'r

where LF and LP are the lengths of leading and lagged values respec-

tively.

The test of the null hypothesis that Y does not Granger cause X is

equivalent to testing the constraint'. a. = 0, for all j -- -1, -2, ..., -LF.

The joint significance or lack thereof of these future coefficients providesthe basis for the Sims test. The restricted and unrestricted forms of equa-

rion (2) are estimated and the residuals from chese equations are used totest the null hypothesis.

The Modified Sims test

A useful modificarion of the Sims test is proposed by Geweke et al.(1983). The modification involves the inclusion of lagged dependentvariable in the regression to purge serial correlation from the estimatedresiduals. Consequently, there is no need to use an ad hoc quadratic pre-filtering or a generalized least squares (GLS) procedure as suggested bySims (1972). Thus the modified Sims test is based on the followingequatron:

(2) In addition to rhe intercept, ao, one can also include a time trend and sea-sonal dummy variables in equation (l). A time rrend and seasonal dummy vari-ables may also be included in Sims' and modified Sims' tests.

(2)

l0

CAUSALITY ANAtYSl.l

LPP

Y, = ao * E o,X,-, * E FpY,p * e,

t= LF k=r

Here also, the test of the null hypothesis that Y does not cause X is

equivalent to testing the joint significance of the constraints a, = 0, foraIl j = -I, -2, ..., -LF. The residuals from the rescricted and un'restrictedforms of eq. 3 are used to compute an F-statistic to test this hypothesrs.

The Haugh-Pierce test

This test involves a two step procedure; the first step involves esrr-mation of an autoregressive integraced moving ave:: 'ge (ARIMA) modelfor each variable. The residuals from the first step are used to estimatecross-correlation functions in the second stage. The tesr for causalitybetween Y and X is based on the significance of these cross-correlations(Pierce and Haugh, 1978).

Suppose P(B) and L(B) are two previously chosen filters for series Y,and X, respectively, so that, Ut = P(B)Yt,andV,= L(B)X.. There is noserial correlation in eirher of the error terms U, and V,. The causalitypattern between two original series, Y, andX,, can be assessed by cross-

correlating U , and V, such that:

E(U * ,Vr)p,,(k) =

where É is the lag length.

IE(U) , EN2)lt/2

Since both series are white noise, the cross-correlation procedure is

symmetric. Consequently, a single estimate is sufficient to charactenze

causality in both directions. In practice, p,"(k)s are unknown and are es-

timated as residual cross-correlations. Once the residual cross-correla-

tions are estimated, each individual estimate is tested for its statisticalsignificance and only the significant cross-correlations are used to deter-

mine the causal patterns. Finally, the causal hypotheses are tested using

a U-test which has an asymptotic ;' distribution.

Pierce and Haugh (197S) have shown, in terms of linear predictabil-ity, the theoretical equivalence of the above causality testing procedures.

Despite their apparent theoretical equivalence, however, rhese causality

tests have generated inconsistent causal conclusions in empirical appLca-

tions (Conway u al., 1984).

(3)

(4)

ll

R. SARKER

APPLICATIONS & LIMITATIONS OFTRADITIONAL CAUSALITY ANATYSIS

All of the traditional causality tests described above have been used

extensively by agricultural economists since the early 1980s. Commod-ity price analysis experienced a flurry of activity in Granger causalitytesting during the 1980s. For example, 13 out of 16 causality studies

summarized in table 1 investigated some lead-lag relationships berween

various price series. Note chac except for those in Heien (1980), Free-

bairn (1984) and rù(/eersink and Tauer (1991), all causality results re-

ported in table I are derived from bivariate models. In most cases the

lag-lengths are determined arbitrarily. Vhile a wide varrety of prefilter-ing, ranging from simple first differencing to complex ARIMA proce-

dures, has been used to create white noise series, only rn a few cases ithas been empirically verified that such prefiltering did adequarely re-

move serial correlation from che data.

Given rhe variations in lag lengths, model specifications and data

used, it is difficulr co compare causality results from various studies re-

ported in table 1. Clearly, the price transmission and price discoverystudies dominate traditional causality analysis in agricultural economics.

The results are, however, mixed. For example, borh Heien (1980) and

Vard (1982) investigated Granger causality between prices at differentIevels in the food marketing chain with US data. Both found unidirec-tional causality running up the marketing chain from wholesale to retailprices. However, these findings are disputed by Freebairn (1984).

Causality results from international price transmission and prrce

leadership studies are also mixed. For example, while Spriggs et al.(1982) found US wheat prices to lead Canadian wheat prices only dur-ing the commodity boom period of the mid 1970s (1,e., during theI974-76 period), Lee and Cramer (1985) found US wheat prices to lead

all other wheat prices including the Canadian prices since 191 2. ln a bi-variate study ofland rents and land prices Phipps (1984) discovered uni-directional Granger causality from rents to land prices which is consrs-

tent with the present value model of land price determination. However,in a bivariate study of research expenditures and output growth in agri-culture Pardey and Craig (1989) found feedback relationship betweenresearch expenditure and agricultural productivity which is not quireconsistent with the expected theoretical relationship. In rheir study ofthe effects of advertising, Reynolds u al. (I99I) found advertising toGranger cause the sale of both butter and cheese in Canada. Finally, in a

multivariate model Weersink and Tauer (1991) found dairy herd size toGranger cause productivity. They also found unidirectional causalityfrom input and output prices to both herd size and dairy productiviry inthe United States.

I2

CAUSALITY AIIAIYS/S

-Ë P e

=Ëx i* ài-Ëi? È5 efl€îeË,p *Er g*i€€çà= €ji ÉYts3û E E- ;; â Ëg E 3

u_9

éè-E EEYQU.= ,F -

=EE

Ea

E

u .i698

Ë .!P^

q=

! Eooçi-.-g o-Ë.. ..€

-;â-TiÀ < 5

EE p99

'= i E

rc .È\Ë> 9=us9aç biçJ;9.1

rG <-=

=?q€ g éÈ âo== r É : E - ,2;xF-:-Ê iE,Ë E=f,.Ëir ûiÉ sfËÈ3.+ S,€È l,E;3i: É22 e-EEis €-*Ë #58

UË* E; E-g ;c Ei= g::sË e ! e ËÈ i3Z F!È FE;Ë3E ËË Ë*t €^Ë vvz v"u.E;? -EE -;,sE !E -:Ëi s:1ta€ àË à-e b €u à+: àÉ_.;5= aEs Ëiàs *E' =-Ëî =aE3Es 3=+ .3eE+ É4É. 3Èâ 5ËEE

æô{æô

!

NÈæilô

v _!l

E.E

ô

:Èæô

æ-ô3S

û6

E

E

-egil-ôc,

x=Tg*Ë

aà

iâ .e

FO>

æ.Y .X.E E.:::t

ÉFa?^^ç 6

'

E

6

;5

9p-

-q)

-

=U

o

IE

æE

T

;oEÔ<_s

*)

o)S:-ô5oi

<5

p

_t

'ig.àG

I

G

€=

-

z

c

!o

E

r3

U

I

L

(Jlrà0

a

o

Q

,rt-q)

(.,1qJ

C)a

k

a-jc.)

'.:

R,.'ÂRKER

3g 3Él ËËfuËËr rEË, ËËËËiË ËËâËàË,

:€a-

TÈ à

'1,ë E->^û^'. -d Tç.-<.: 9

-qx:o.= ri_: Yu g< xg 3oc U<-EÈ E

PU{G

b-è.g>-g

Ë ËË àË; tËsË €c=gâ

;* Ë:sËËâ cË?ta ËËËiË

+È É€ , g;É g**iË€ €=+ €Ë*

Ë€UËÉË Ëài=ËiËËËE ËË+E 5ËË

sèi^;v5A

æôÉ

o

æE9urc^

lc^c66-E :.1 ô:-

E

E

:é

T{<s

Ë€Èb: .= <E '-À P E 5 É€* F E: E t= Ë <3q é'r-i ! :i5 riE€ E =ËE i::r-+E a = à€ I E-29 g 5Ë= €Ë_t:

J,

-

EÉ!

cÈ

ae6ù::>

Ë< E.=J< E E?eP *ir< Ë I

I

oôo

;

æ

=Gô.

z=^.Ëæ\3è z

': c:. Ë;û?.2 ;:

-=9/

=xo-ËY: P-= Y - -:=

gT F !/<ÛHFÈ

v

a

(,

3

(,

j

3-€o.F

rca

E

=z

T

E

Â

a

CAUSALITY ANALYS/S

ËEËËË;cgËËËËËËË;Ë*s1E3ËE;Ëg É:ËËiË ËÉ?i

ar

E

€g-

dgËÉ

c

qo

È:àE

c

I,9ËË

E

=(,lc

<g

ËE

>ii9elCE

Ëa?,-q

.àR-3- E '-

6aF€

i;-UR>=

€ - - *àE ç = E -È:,ë !=È.ùS È -9 -:rc Épiuu-EEc': EE:EF jAËi*€t[€= ËÉË.aË +iÆtrËEÉ3ââ iTî:i ËëàEFËE-eÈe gË:ËF 11-îvxerÈ-væ 5ËREF: EE#EËegEÈà oà=<.,d Fc

TEÈ 90.:

E i=I o.È

JnZ-Ê: i Ècx=c

-ô é.ù jLa-

=

.9 ç *tYç- ! Y

àE U E-oaL

6ôcrét

æôT-

lt

o

=

I

I

o!?

60s

qo

F

a

z

E

I

a

R. SARKER

Although there has been many applicatrons of Granger causality tests

in agricultural economics, it has become clear in recent years that a

number of serious problems are associated with the method (Conway ei

a\.,1984). Causality results are not robust to model specifications. Uni-directional causality between two variables obtained from a bivariate

model can be reversed with the inclusion of a third relevant variable inrorhe model. For example, the one-way causality from rents to land prices

in a bivariate model obtained by Phipps (1984) may change if the model

is expanded to include direct government subsidies to farmers and the

rate of inflation, both of which are expected to influence land prices. AIIcausality results from bivariate models reported in table I are subiect to

this cricicism.

Data transformation or prefiltering, such as simple first differencing,quadratic filtering etc. are essential component of traditional causality

analysis. However, they are not causality preserving (Schwert, 1979).

Since most of the commodity price series are characterized by stochastic

rather than determinisric trends, this aspect of traditronal causaliry test

is especially troublesome. While differencing reduces che effects of sro-

chastic trends it also removes the long-run information from the data.

\7hen long-run information are removed from the data, there is no valid

ground for mounting Granger causality tests in models containing one

or more nonstationary variables (Toda and Phillips, t993) To the extent

data nonstationarity is present, causality results summarized in table Imay also suffer from spurious regression problem identified by Granger

and Newbold (1974).

The choice of appropriate lag-lengths are important for introducingadequate dynamics in the model. The results of traditional causality

tests critically depend on the parameters of the Iagged variables in the

model. Consequently, arbinary choice of lag-lengths may produce mis-leading causal results (Thornton and Batten, 1985; Gupta, 1988). Such

lag selection bias is present in 10 out of 16 studies reported in table l.

The majority of the traditional causality models in agricultural eco-

nomics involves only two variables. Some relevant variables have notbeen included in the analysis. The estimated models are, therefore, miss-pecified. Since there is a tendency for some commodity prices to be cor-related, the estimated parameters of bivariate models can be biased. Such

specification errors may generare misleading causality results. For exam-

ple, Pardey and Craig (1989) investigated causality between research ex-

penditures and output growth in US agriculture with annual data from1910 to 1984. During this period two additional facors, such as theweather and farm programs, must have contributed to the growth of ag-ricultural output in the US. The farm program spending may also be

correlated with research expenditures. Exclusions of these two importantvariables from the model may have generated the somewhat troublingresults reported in Pardey and Craig (1989).

I6

CAUSALITY ANAIYS/S

By construction, the Haugh-Pierce rest has an inherent bias in favour

of the null hyporhesis, excepr in a special case when rhe omitted vari-

ables are uncoirelated with the included ones (sims' 1977)' Moreover'

The above analysis suggesrs thar a number of critical problems are

associated with the traditional causality tests and rhat Granger causality

analysis.

tl

R, SARKER

A second attempr was made by Uri and Lin (1992) to develop a par-ametric test for instantaneous causation. In a bivariate context. thev usedARIMA filters ro obtain white noise series. Insread of cross-corr.lu.,ngthe filtered series as in Haugh-Pierce resr, they regress one series on rhecurrent and lagged values of the orher series and on rhe lagged values ofthe same series. The instantaneous causality from one variable ro anorheris decermined by rhe significance of the coefficient of rhe currenr varuein the regression. uri and Lin used this resr ro examine substiturabilityberween domestically produced beef and beef imporred from the unrtedSrates inJapan while Uri et al. (19%) applied this tesr ro derermine thenature and extent ofspatial market integration for soybeans and soybeanproducs. In addition to the problems associated with the tradiiionalcausality tests in bivariate models, the parametric and nonparamerrictests developed for testing prima facie or insranraneour cuut"iity have afundamental srrucural problem.

Since a lagged time sequence is essential for Granger causality test,the prima facie or instantaneous causality resrs are nor consisrent withGranger's concepr of causality (Granger, 1988). Due to rhese inadequa-cies, the prima facie causality tesr developed by Holmes and Hurron àndthe instantaneous causality rest developed by uri and Lin did nor recervewide applications in agriculrural economics. Causality analysis in agri-cultural economics, however, continues ro flourish in VAR and coinre-grated VAR models. The following sections focus on this literature.

CAUSATITY ANALYSISIN UNRISTRICTED VAR MODELS

vector autoregression (vAR) is a rime-series economerric merhod in-

thro.ugh the sysrem of lags. unlike rraditional strucural models, a vARmodel emphasizes more on empirical regularities and less so on rhe theo-rerical restrictions.

A traditional vAR model wirh a set of É variables can be wrirren as;

r8

CAUSALITY ÂNÂLYS1S

m

A,,Y,=E A,Y,,*n,

\flhere Y, is a (,É x l) vector of observed variables, u, is a (k x 1) vec-

tor of error têrms. The error terms are assumed to have a zero mean and

a diagonal vari Finally, Ao and A)s are (É x É)

matrices of pa c interacrions among the vari-

ables in the m need to be esrimated from the

VAR model.

Premultiplication of equation (1) by the inverse of Ao yields:

,,= irB,Y,-,

+ u, (6)

temporaneously correlated and their variance-covariance matrix is not

diagonal. The model, therefore, needs to be rransformed so that the error

terms are no longer contemporaneously correlated.

Equation (6) can be nary least squares or SUR

and the estimates of B,a . Notice, however, the cru-

cial element of the VAR ne the effects of the shocks

ilt on the observed variables, {. Since.all variables tn the system are

interrelated through lags, it is not possible to disentangle the effects ofshocking one variable on another using the autoregressive (AR) repre-

sentatio; in equation (6). This can be accomplished by inverting the AR

process tn equâtion (6) into a moving ^veru1e

(MA) process. Inversion ofequation (6) yields:

',=2'1,,H,o, Ao'

(t)

(7)=2i--o

r9

R. SARKER

one-rime unit shock in one variable. Note that impulse responses gener-ated from the IRF might be sensitive to rhe ordering of the variables inthe VAR model. The estimares of A;l can also be used to decompose rheforecast-error variance (FEV) for each element of Y, into componenrs at-tributable to innovations in each of the endogenous variables in thesystem.

It is often argued in the context of VAR models that non-zero im-pulse responses indicace the presence of Granger causality, while variancedecompositions yield measures of Granger causal priority. Sims (1982)states :

"A natural mear,ffe of tbe degræ to which Granger caasal priority bolds isthe pacentage of forecast error aariance accounted for by a uariable's own futaredisturbances in a maltiuariate linear autoregressiue nodeL..A aariable tbat is

optimally forecasr from its swn lagged ualuu will baae all its forecast errnr uar-iance accounted for by its own distarbances" (pp. l3l-1?2).

Thus, it has become a standard pracrice in multivariate VAR modelsto infer Granger causality from impulse responses and variance decom-

POSltlons.

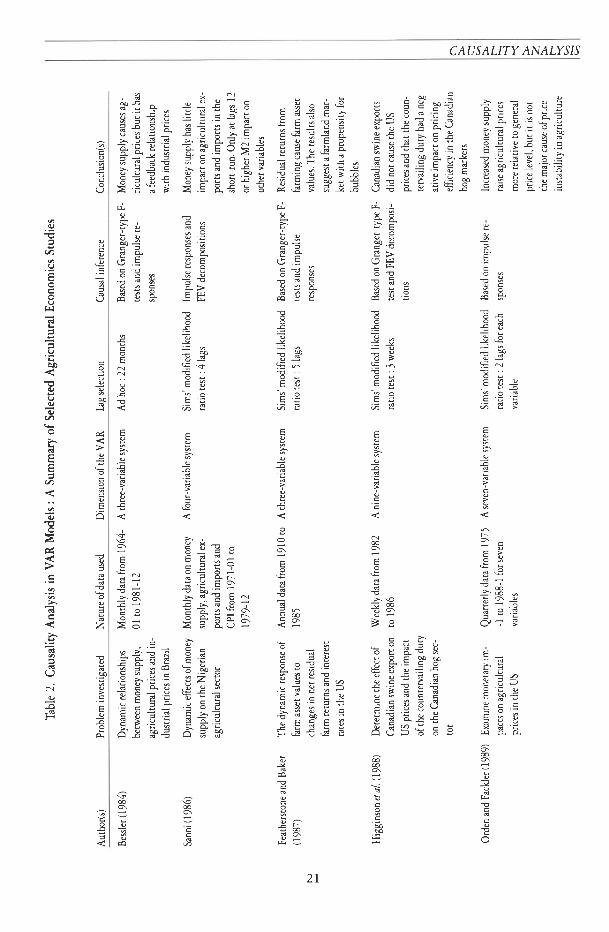

TabIe 2 provides a summary of l0 seleced agncultural economicsstudies which derived causal inferences from unrestricted VAR models.Here also commodity price analysis dominates rhe scene; six out of renstudies deal with dynamic relationships among various commodity orinput prices. Most of the price series used are monrhly and the dimen-sion of the VAR varies from three to eleven. Compared to traditionalGranger causality tests, all bur one study in table 2 used either Sims'modified likelihood ratio tesr or orher empirical merhods ro determrnerhe level of lag truncation. \(hile causal inferences are mostly generatedfrom impulse responses and decomposirion of forecast error variances, afew studies have also used Granger rype F-rest to determine causal or-dering.

Impact of macroeconomic changes, such as changes in money supply,interest rates and taxes on agriculture has been a fertile area of researchsince the mid 1980s. Three studies summarized in table 2 attemDr roinvestigate the causal effects of money supply on agricultural and indus-trial prices. The results are, however, mixed. Using monthly data fromI964-U to l98l-I2 Bessler (1954) found money supply ro cause agri-cultural prices in Braztl. Using quarrerly data from l9]-5-l ro 1988-1,Orden and Fackler (1989) found that money supply is nor the ma;orcause of price instability in US agriculture. Using monthly dara from1970-01 to 1979-12, Sanni (1986) found little evidence of money sup-ply causing agricultural exporrs, imports or price level in Nigeria. Hig-ginson et al. (1988) found in a nine-variable VAR sysrem thai Canadianswine exports ro rhe US did nor cause the US hog prices.

20

CAUSALITY ANALYS/S

g€eËËâËîË-Ë€Ë€Ë sçÈàaË êÉË;ËÉ

3sËË ËiËïEË ËËËËË= ÉËËËieË eÉËiËË

I2ÀE

a?-A

-ç-=Uiq

Çru€;ç?u- !!

Eô

r

ç>o6

È-Tég-;

C/-i S

i =E =Egâs Ë

talË- ÈffËË ilE=

5jË:TËÉgËË,ËîËôæô

ra

ææô-

:r=6Fô

Iæô

æ6

q-l

>=

5€E>9f!

Ëi3

ro

sÀ

ôéZrc€:cègg

EE

çgE';ôù

rE-€à j E Eù - ?.=9^; Up-â? F H,i E î-EÂëEc gY-éY=EÉ e i d.>d n x trr

!

=

SsT..

ba

E

=.s

=

ço90'=4^

: = E.Fd=q:-'Tæ=_xcytsN

E>6V':= açôè +ËEàz;ùv-

- *î= 9-À= : ! :.s71t2 E S;.9 >.9 = 2Z ZËHôf..8y9'E Ê= i EÏ=!;:-* : à

=E U=: Eà=È È.9 E È +.eÀ-E S€ ÀiS

To

=.a' -

ùÈPorc..q9E';

E

!

NæôÈ

s->9--æ1ô

>o

I

E

ôE

-E:æ<:-'

éo

N:é

T

E

E

E

vIô

:æl-ô

o>5

2l

é

.9-a1

L,

p

E

-a

!

a

z

E

€

E

o

Ch

(J

c

Itrlq

9èo

o<t)

>tr

.t)

I

Qcio

R, SARKER

ifugâgËe *ËË € r€a;Ëëts É*Ë:iq.ËËËËEËË-Ë€gâ EËËËÉËÉË = E;ËË ËËàr- Ëâ;EÉ58 6sE Ëf gË îËsÆ Ë eE+EEËEË Ê E=.îË€€ËËËg **E âi'i# Ëi=ËË ggÉ

qoYô

vÈa2 ?

T c'- '_:

=- éO _ 'E

E;E=2aXé

E

j--

E-:àE-Àù^ -s 99 =â- c -b€- F)a-É

à= € s*-i r:Y-ùo o !æ>8; Ëa:=?-^ € |

t iËE i 5=*E;: ù u + ë Ë-i: t: >- g i^i:== E s 9*Ë ùË E r È:p;E È q;* 3F i,": x-ff;i ù F tr Ë-

-â" Ë ù L E -E ".i. A 7 A2 F K ÔP;ËfËËE Àà;E

-=€t=o

Ec

9Fæêa>=

6>èrErcc€?A?=

!;=

6D

Ii.;Eâ

E

6>

Erca?=

rHiue=

!o

=

EEè';

oÈ

'rE.YU;>' 9^o

Erc ,i:r-'4avqÉ 6 9 é--€sE :E-9,39É pËe

OY-E .E -o

:;= 9p E-t-i û<ô= : ç:

l-u.:

3; EggF:

= j u

o.: =64F : È: gpo-

E;À.E

rE

;r

Eé

z

'ô

Ë È- *Ë=c -D-lFd - o Y d-u {-- d x oI { = P giË.;t:'3Â>.:=X-!-

== = a Fe\::tsËi-ô 3

= -Ë S F><ù È Ë.È

::!:

E.= û.eai

>cEo:È

3o

T

Èd

Eè.

Eô

=-E?

€

PoÉg='FS-E-cÉ-bà-*€ Eo E 5ô:"-é€:=- -^ô-= -9 r iù h ec ù U È Ë '=-.= ç.-- d - ê >

=:.c 9/T F=.: y-r ù E,<-àÈ= u Çî p.*ÉT! F'E:ù x F É -!æ}: E€Ë E9

!

ôE

ÈN

àô

*V:* S€se= 4u : xT-Ù-e' c= + :-.ol ::E Ë Ë- EË-=

È

Ë jÈE 3 g Ëi'icEc 9E:!E U.Ë; =3 =UÀËEiË.s"€E

F!

9^

tô

ôô

a

a!

22

U

c

F-.]

;'ô

E

^

!a

T

Ëz

E

.E

c

Ào

o

-

CAUSALITY ANÂLYS/S

Causality analysis in unconstrained VAR models represents a signifi-cant departure from the traditional causality tests in bivariate models. Inmultivariate VAR models one can include past information of many re-

lated variables. This freedom, however, comes at a cost. Firstlg uncon-strained VAR models usually have many parameters relative to the num-ber of data points and one may question the reliability of the estimates.

Vhile economic theory can be used to impose restrictions on the model,in recent empirical studies such restrictions were found to be controver-sial. The controversy arises from the fact that rhe narure of identificationrestrictions imposed on VARs is different than those typically used toidentifi' structural models. Secondly, Dufour and Tessier (199ï have

shown that while there is a duality between the AR and MA character-

izations of Granger noncausality in bivariate models, such duality does

not extend to multivariate systems. Consequently, a different set of re-

strictions are required to test Granger noncausality from moving avelage

coefficients. Without these restriccions inference on Granger noncausal-

iry based on MA coefficients (i.e., based on impulse responses and vari-ance decompositions) can be misleading. All causality results reported intable 2 are subject to this criticism. Thirdly, \7ald tests used for testingGranger causality between subsets of variables may not have asymptoticchi-squared distribution. This is particularly true if the VAR system

contains nonstationary variables (Park and Phillips, 1989; Sims et al.1990). Moreover, the limit theory of \7ald cests involve nuisance param-eters and nonsrandard distributions both of which complicate causal in-ference procedures in unrestricted VAR models. Toda and Phillips(I99, have also shown that without explicit information on the num-ber of cointegrating vectors in the system and the rank of certain subma-

trices in the cointegration space, ic is impossible to determine the appro-priate limit cheory for Granger causality rests. Consequently, they

recommend againsc the empirical use of Granger causality tests in levels

VAR models when there are nonstationarity in the data and the possibil-ity of cointegration. In view of these findings, all causality results intable 2 should be taken with caution.

NONSTATIONARITY, COINTEGRATION ANDCAUSALITY ANATYSIS

It is now well known that most economic time series are characterized

by a unit root nonstationarity in their univariate representation and that

dara nonstationariry complicates Granger causality analysis both in tradi-rional bivariare models and in unrestricted VAR models. \7hen the

system under investigation involves nonstationary variables and there is a

possibility of comovement of some of the variables, cointegration is the

àppropriate methodology to investigate Granger causality. Since cointe-

)z

R. SARKER

gration analysis allows researchers to investigate economic hypotheses in atheoretically consistent and econometrically efficient manner, this ap-

proach has gained enormous popularity in agricultural economics in re-

cent years. The determination of long-run or stable economic relation-ships and subsequent re-examination of some well known hypotheses by

agricultural economists have already generated a healthy debate in the

profession. Even the results from some established theories have been

thrown in doubt. For example, the findings by Phipps (1984) and

Featherstone and Baker (19S7) ofunidirectional causality from returns to

land prices lend empirical support ro the present value model (PVM) ofland price determination. But chree most recent studies have shown,

using cointegration analysis, that other stronger implications of the PVMare soundly rejected by the data (Falk, 1991 ; Clark er al., I993a,b). Simi-larly, the assumption of perfect commodity price arbitrage (popularly

known as the law of one price (LOP)), so crucial in exchange rate and

international trade models, have been brought to question (Ardeni, 1989;Baffes, 199i and Goodwin, 1992). Also, the tradirional measurement ofthe effects of technological change on agricultural production has been

thrown in doubt (see Clark and Youngblood 1992) and significantchanges in econometric modelling of popular relationships in agriculturaleconomics, such as supply response to policy changes, output supply and

input demands etc. are betng sought (see Clark and Spriggs, 1992,Clarkand Coyle, 1994,and Rayner and Cooper, 1994). These are very positive

developmencs essential for the future development of agricultural eco-

nomics research. However, not all of these developments are directly re-

lated to causality analysis. Consequently, only a subset of the cointegra-tion studies is reviewed in this section. These studies have generated

causal inferences bur not always through a formal causality test.

To provide a better understanding of the literature, a brief overviewof nonstationarity, cointegration and causality analysis in cointegratedsystems is presented first. Thrs is followed by a review of sixteen agricul-tural economics studies which derived causal inferences from cointe-grated systems. The limits of causality analysis in cointegrated system

and possible future directions of causality analysis are presented in thefinal paragraph of this section.

A set of variables is said to be cointegrated if each variable in the set

has a unit root in its univariate representation, but some linear combi-nation of these variables is starionary (Engle and Granger, 1987). A var-iable X, is said to have a unit root in its autoregressive process if it has

the following autoregressive represen tation :

(l - L)Xt = 0,(t - L)Xrt + ..... + Qo{t- L)X,_o + t, (8)

'Where e is a stationary stochastic process, 2 Qi . l, and L is rhe lag

operator. In general, X, is said to be integrared of order dlor X, - l(d))if it has a stationary representation after differencing d times. Thus, an1(1) variable becomes stationary after firsr differencing. The variance of

24

CAUSALITY ANATYS/S

an 1(l) variable is time dependent; it goes to infinrty as time approaches

infinity. The underlying data generation process (DGP) of an 1(1) vari-

able also has an infinitely long memory. Therefore, a disturbance willhave a permanent effect on the process.

Since rhere is a close correspondence between tests for unit roots and

tests for cointegration and since cointegration is most interesting among

1(l) variables, it is useful to begin the analysis by considering whether ornot the univariate time series have unit roots. In particular, it is neces-

sary to show trepresentarionysls ls to taKe

ature to test

among these tests are the Dickey-Fuller test or augmented Dickey-

Fuller test, Phillips-Perron rest and Kwiatkowski sl al. tesr. The firstthree of these tests investigate the null hypothesis that the series has a

unit root against a stationary around a time trend alternative while the

last one tests the null hypothesis that the series is stationary around a

linear trend against the unir root alternative. Thus, for a given series, ifthe first chree tests are accepted and the last one is rejected, it w9*ldimply that the series is characterized by a unit root nonstationarity(r/-

The unit root tests discussed above implicitly assume that the root

corresponds to a zerc frequency peak in the spectrum and that there are

no other unit roots in the system. Since many economic time series ex-

hibit considerable seasonality, there is a possibility rhat there may be

unit roots at seasonal frequencies as well. If a series is characterized by

seasonal unit roots in addition to a unit root at zero frequency, then sea-

pose by Osborn et al. (1988) are based on the following equation:

ArA Xt= dtDr, + arDr, * dJD), + aoDo, + prAoX,-, + prArX,-o

p

* E, Q,ArAAX,; + u, (9)

\rhere D, is the dummy variable corresponding to the ith quarter.

The t-ratios on p, and É, are used to test seasonal and non-seasonal unit

root hyporher.t. in partiZular, Ho,X,is I(0,1) p.e., there is seasonal unit

(3) The ave beco

ture. So, it Providethis paper. are reteral

s099O), (1992),

')\

R. SARKER

root in Xr) implies that p, = 0 with Fr.0. Simrlarly, Hn,X, is 1(1,0)

fi.e.,rhere is non-seasonal unit root in X,) implies É, = 0 with p, < 0.The alternative hypothesis in either case is: Ho,X, is 1(0,0). Hylleberg el

al. (1990) proposed a set ofalternative tests based on rhe decompositionof seasonal differences to test seasonal and non-seasonal unit roots. Thesetests are complicated but more robust than those developed by Osbornu al. (1988). The critical values for these tests can be obtained fromDickey and Fuller (197Y and from Dickey, Hasza and Fuller (1984)'a).

If the results form above seasonal and non-seasonal unit root tests re-veal that all variables under investigarion have a unit root at zero fre-quency, then the next step is to find out if the variables are cointegratedand how many stable or long-run cointegrating relarionships are there.Six major procedures have been proposed in the literature for testing coin-tegration. These are: (i) the Dickey-Fuller test on cointegrarion regressionresiduals (Engle and Granger, 1987); (ii) the cointegration regressionDurbin-Watson (CRD\V) test (Engle and Granger,l98l); (iii) the Park

/, superfluous variable addition test using the canonical cointegration re-gression (Park, 1990, t992); (iv) the Hansen fully modified regression es-

timator L. test (Hansen, 1992); (v) the dynamic ordinary least squares

procedure developed for testing common trends (Stock and \7arson,1988);and, (vi) the maximum likelihood cointegration approach (|ohan-sen, 1988, 1991). The firsc five tests are based on some variations of re-gression analysis (conventional and modified), while the last one is basedon a VAR model. Also note that the first four tests involve single-equa-tion method while the last rwo involve multiple-equation method ofidenciSring long-run cointegracion relationships. Multiple-equarronmethods are particularly useful for systems involving more rhar one long-run cointegration relationships. One can also impose and test variouscross-equation restrictions in such a method. The Engle-Granger proce-dure has been used extensively in early applications ofcointegration anal-ysis in agricultural economics. Vhile the Engle-Granger procedure offersa simple and attractive test for bivariate models, it does not perform wellin a multivariate situation (Dickey et al., I99D.In light of this result, rhemost recent studies in agricultural economics use Johansen's maximumIikelihood cointegration approach to idenri$, long-run steady srate eco-nomic relationships ()'.

(4) Not. that given rhe large volume o[ theorerical and empirical scudies onunit roots and cointegration, the issue of stochastic seasonaliry atrracced lirrle re-search attention. only a few studies explored seasonal inregration in various mac-roeconomic time series. In studies involvins ceconomics, the issue o[ srochasric seasonallrySince the production, consumption, prices anâities exhibit subsrantial seasonality, researchers in agriculrural economics shouldlook into the issue ofstochastic seasonality more seriously in the future.

(5/ Sin.. rhe approaches developed by Park, Hansen and Srock and Watson didnot yet receive wide acceprance among agricultural economists, no additionalspace is allocared for these resrs in this paper. Derails on rhese tests can be foundin the references cired in this section as well as in Muscarelli and Hurn (1992).

26

CAUSALITY ANATYS/S

The full-system approach developed by Johansen is by far the most

interesting approach for resting cointegration. It is based on the estima-

tion of a VAR system by maximum likelihood method. Johansen's ap-

proach essentially extends the Engle-Granger procedure to a multivari-are context where there may exist more than one cointegrationrelationship among a set of z variables. The maximum likelihood Proce-dure gives estimates of the system's cointegraring vectots and theirweights and these estimates can be used ro test relevant hypotheses

about the structure of cointegrating vectors and their weights. Unlikethe estimates obtained from levels VAR escimation, the maximum like-lihood estimates are symmerrically distributed, median unbiased and

have mixed normal distributions. Consequently, they are better suited

for testing Granger causality among economic variables Çohansen,1992;Toda and Phillips, 1993) rhan those from levels VARs.

Following Johansen (1988, 1991) and Johansen and Juselius (1990,1992), the full-system approach is based on a Éth order unrestricted

VAR representation of X, such that:

X,= It1X6+ ItrX,-r+,.., + frkXr*+ 1t+ @D,+ e, (10)

where X, is including l, and z, and each of these

variables is or 1(1), D, are seasonal dummies, lt,

are pxp ma sapx l vector of constant terms and

€/ are normally identically distributed error terms. Using lag operators

the model in eq. 9 can be reparameterized as:

Y X,= 1t+ \Y X,_r * lzY X,-z+ .... + ln-, Y Xrp,t-ilX,-* (11)

+ (DD,+ e,

rVhere, fi = - I + /tt+ ..... + It,and - II = I - \ . frz--.-..... - ltp;fotalI i = 1,2,...-.., k - L Notice that the reparameterized model in eq. (10)

is a traditional first-difference VAR model except for the term IIX,-..The matrix l-I, which is sometimes called the impact matrix' contains in-

formation about the cointegrating relationships among the variables inthe system. If I1 has a full rank, then X, is a stationary Process. If II has

a zero rank, then the impact matrix is a null matrix and X, is an inre-

is defined as:

21

R. SARKER

Ln(t - À.,) (r2)

Similarly, the maximum eigenvalue statistic for testing H r(r) in H r(r+ l) can be defined as:

-2ln(Q;rlr + l) = - T In(l - tr,tr) (13)

Nocice that the asymptotic distributions of these likelihood ratiotests do not follow the standard cbi-squared distribution. They are dis-tributed as standard Brownian motion which may be considered as a

multivariate version of the Dickey-Fuller distribucion. The critical val-ues for these tesrs are generated through simulations and are reported in

Johansen and Juselius (1990) and in Osterwald-Lenum (1992).

There is a close correspondence between cointegration and error-cor-rection models. If a group of economic variables are cointegrated then,by the Granger's representation theorem, there must exist an error-correction representation of the relevant variables (Engle and Granger,1987). The long-run relationship is a stable steady stare relationship andthe short-run relationships represent deviations around this equilibriumrelationships. Through correcting these short-run errors, the relevant ec-

onomic system approaches its long-run path. Hence, the term error-cor-rection models. Thus, if all variables in a vector stochastic process X, are

1(l) and they are cointegrated, then there exists an error-correction rep-resentation such as:

A(L) (l-L)X,=-yeLr+et (r4)

\X/hËre L is the lag operator, A(L) is a polynomial in L of the form[Ao + prL * FrLt + ....] and t, is a stationary multivariate disturbance.This formulation assumes that A(0) = l, al| elemenrs in A(1) are finireand yi 0. The coinregrating vector is B, where e, = p'X, is 1(0). Because

the series are cointegrared, the error-correction rerm is stationary and thestandard errors of the error-correction models will be consiscent esrr-mates of the true standard errors. Therefore, the standard asymptotic re-

sulcs for parameter estimation and hypothesis testing apply (Engle andGranger, 1987). A properly formulated error-correction model can be

used to test Granger causality among the relevant variables in a system.

Table 3 provides a summary of sixreen seleced agricultural econom-ics studies which derived some causal inferences from coinregration anal-ysis. Once again, commodity price movemencs received rhe highest re-search attention. This is perhaps due to che fact that owing to spill overeffeccs of supply and demand shocks and macroeconomic shocks, com-modity prices exhibit a rendency of moving together and that the theoryof cointegration offers a theory and dara consisrent approach ro formal-ize the idea of comovemenrs in commodiry prices. Eleven out of sixteenstudies reported in table 3 involve identification of some causal relation-ships among commodity prices.

p

-2Iu(Q;H, Hr) = -7,J.,

28

CAUSALITY ANALYS/S

iÊ€ii;Ês ËiËiÉËËË

ÉâiËgÉËËËËËËëËËà--ô

>È9rccB

yv

l-I ; =}QEJ

1A=+P:;;9t;.:=à *EÈ

T

!

È!

ôU;>5

a;76.F -:.= q

9rt?Co2Y

.à9h

^2È E.: Ex ->; ç=-Xi^"ç:?r!tr:ÈËëeO E àco=EFÉË É;

o

Ëà

-ô

cÈ.E

{

-{

_s

T

8T

éËù-si.E ô

>3=Â>-

aÀ

rE

;^g1

.E

'i

r

'-

3o *-ôI- cPE=-:a\

G'4:f*.2 iË.ùùx ù: o=>eas ; È c ;ù-æù:N : E ô h

îl€orù: -:^-^> !r.+ EÂ=

èooô{ad

rl

rcP :r-

l6

-rc

=ô-ç"

ÔÈr>

'+É-f ËgÈ'e::,^lJcqÈ-.4?Z.iër c Er 3ô s=+;9 ù é {c s^"< x- t t ta:1'â: E È E - ii EEE elù: (i E F P > ê :. v,:--u : I -; i ^tr âF E i: È È -

;SEgE ôî+,Ë [B

oX-

o.:;i_c .' -Y

==c:i= s sz

T

€o

-6ô

=tq!> =

É-

i'>;o 999 Ë -€;:!3o6^=€.c = =É 9c ;. -: : ts,Y.r.=r

'i "è: E 3

âæ3-

29

èE

a

U

.9

.-a

L)

o

U

o

È.1

!

?

Â

o

a

6k

U!ào

q.)

Uq)

OJ(t)

>-li

(t)

q)

(t)

!èo(.)

I

6

>.

G

Iôa

R. SARKER

E; Ér a ? 4=xùÉcËY x'= E p:-!-6

s E-- ç ç.S.==.ZTq9ixcos.Y È v_s€i ir= o'E Fé Y L X- Se à hF^è E

='6

E

.=j

â2Âtt

ÉË;Ét rtgË eFiEË i?ËggË É; ++= +?Ëë iË +iËËuÈE Ë ËË 3!

'

_Ê g Ë E 3 € Fâ g Ë EË Ë

!É.;E

-o

cÈ.=

.sè

.àc

ç9ou-9 .l

bE

a=

!o

ÇruE.

tr';

gËgËËa,ËgEÊ3ËË,àËâËÊâ

E8E":;ÉË> €É-= X=6*O.E E

€ -'Ec -J

;o

E

-!

6X

ôo{

Eo

T8E

.-GcE-b;

,.+é2ùE.s;

!j

èÀÀ

rI

{a

'-E

'.; c

'= o-i .:<t

éT

æE

oa?ç,: -6.ô !Es<sô.i

o iô-:?

s < e>E ,r

_ll ."?

a-= ?

'èE>! -rc

: ËEx:c

N

ô

E

E

z -E *.E i-EïËÈ Ë*i; i;ËgçE ':EEi ËË:EjE Ëts E 3-*E F .e c F ë

-.*ËÈi 3EéËs ËËÈE

ôô

È;

È

N

ô

è

ôô

J

30

-(J

.g

a(-)

(,

J

ù

€

Ejo

o

CAUSALITY ANAIYS/.'

gi;ëgËgrâg€gËËËËËËgiÉigiâê€i

t_>-e

v,Att

5 ç i3 c=;€9 2-É.q 3 à rc - {r7EÈ=.EÊ Ë+'.i ËF ? = 4=.i ç Êi;Ë.9 s: hu r'-,55 ÉË vË Ë s Ë;EE;,5 : +E e, Ê * 5;'E â âË; ËÉ ËT Ë 5,8È É 8'Ë g; d *.s*=sËsË*ËËËË,=ËËs

ôô

cN

ôôôô{a

>l

ôô

v

(J

!ô6

S

è

(J

3Ào.

ô

.!-do

È

p

=;Z-r+=:E Ë Ë:*;&-- q U àô c;È Âô E-rù9-=.trçA'- " g ç - =rÀi:=oE-+Ê uÉ?I:E>E*!Dé:.! X-

=-6ÈE aËÈ 59

À,9çOFgE=5-.> +z_9 tr|1qJ -1 -tr:ÈôËpF-P ioË:ê E *A

e:az,i,atûd€:: = 9^'c ! E:as u s*ËÈ E-a È F c pé---:EÊ :EF3

_--lts 9!.: ù 99: :fçË:i €:EE

-ô!+

E-

-6F

p

!Ev-..çgts;ôù

5È ._.ë "tr" x =ô= - .â j ËEr=. ,?FiE -E:E sSE; È:

*?t -Ëô= -ËFi6 -Ëôëi: 3;= ;E€; 3;E"É Ets Egs-r gl€â€ à8ëâ eEEàr a8t

Es,EE

c:

!ô

E

=ô-€Sv

çgt-

-6e,;étr Y4 E q

o--È è EEçÉÀ 5 9

FE E :*,i-- E .c èYFqouy+^zY E=â-e = *i

==ô-ôad_s!EsEÛE-E

û

è

3r

-

U

.9

(J

'-

o(J

ocai

!

Ejo

Eoa

R. SARKER

L:o9

ë: E F u Ë26>,::^-

=^r = : o L

û= < ;oT 9é = 6 à_E o'=

- c ô e eYEeZ=3!E;ç 3.9

? 2.9 Ë E gô<E-Ë"€E

q)-

U=Ëë . E:cÉ:p:3:=v= È=cbE E : g s: Ë Ë {rF: I â; q i c 3Ë: U : E o !r .9 d.s È-E E E æ ;::-3 €z?i, <É = E::Æ E

Ë E: E Ë E *=Ê€€ËoÈ;i5E :=E;;9 ;'È È à= 9 È ..- - -Ê&€ ô È a Ë = 9E E

cùÉ'= : o9=FO

=:{-.= 9 U ygô- :E! EE Ù Y

i È È i E+y .: r Y o "b È = H-e€Éi: Ëo: di H E

x 5Ed tr9!d .= vu 5Ec-v!! --rc q

(l i: : =tq__

v É .- o

H j=r= è

gU-?a:

=ts-: ù:àP ëCOEts

a

(,€c

*ggËg, ggËË€iË

ËËËiËEâ*

:

-o<-9

qo

<s

E9Ësô -< ç_'-ù-4UF-: F'Ë eE È F-ë srEç EO Ëx o€D 9pi U Fc F<;": sG

âô3

.s

tsÈSE;T !.: ûYÈ_C." ù"É +ç-M:.:OEè

ÀË E_g

a

=Q.vs3\

.Q O

T!

<L.-F\9!Z

ooôUæ

32

U

.9:aU

.;

J

'-

è

E

E

!-

oa

CAUSALITY ANALYS/S

At least one test (the ADF test) has been employed in each of these

studies to investigate data nonstationariry. In most cases, Sims' modifiedIikelihood ratio rest has been used to determine the appropriate lag'Iength. Nine srudies used the Engle-Granger approach to determine co-

integrated relationships while the others used the maximum likelihoodapproach itself or in conjunction with other approaches. Three studies

investigated the long-run validity of the law of one price and produced

mixed results. Ardeni (1989) found that the LOP does not hold forinternationally traded primary commodities. However, findings fromtwo more recent studies, Baffes (1991) and Goodwin (1992), contradicrArdeni's results. The transportation costs seem to be responsible for thiscontradiction. Investigating the formation of land prices in cointegratedsystems, both Falk (199I) and Clark u al, (1993b) found that the re-

stricrions implied by the simple present value model of land prices are

not data consistent. Clark et al. also found weak empirical support forcapitalization of government subsidies into land values in Saskatchewan.'Money is not veil in the long-run' is the message from studies by Rob-

ertson and Orden (1990) and Choe and Koo (199r. Similarly, Sarker

099, found that the bilateral exchange rate has a significant positive

effect on Canadian lumber exports to the US in the long-run. Four stud-

ies investigated the nature and degree of market integration producingmixed results. Regional livestock markets in the US are found not to be

spatially integrated by Goodwin and Schroeder (1991b) while Zanias

09%) found lack of integration in the EC agricultural product markets.

Diakosawas (199t) also report less than full integration between Aus-

tralian and US beef prices. In contrast, Srlvapulle and Jayasuriya (1994)

found the regional rice markets in the Philippines to be well integrated

in the long-run with Manila as the dominant market.

As indicated earlier, only a few studies summarized in rable 3 derived

causal inferences from properly formulated error-correction models. Thisis a major limitation for most causality results currently available from

cointegrated systems. Moreover, not all error-correction models can gen-

erate meaningful 'Wald tests with sound statistical basis for testinguslng's andrables

etrot-

correction models, Toda and Phillips (199, suggest cesting rank condi-

tions for the estimated cointegrating matrix and the associated loading

matrix empirically before formularing the error-correction model. This

amounrs to a sequential testing procedure. Notice that some size distor-

tion causality test in ertor-correc-

cion s because of its sequential na-

ture fr rank conditions, formulate

the ausalitY). Even with size dis-

rortion and loss of power, however, the sequenCial causality tests based

33

R, SARKER

on Johansen-type error-correction model were found to outperform the

conventional tests in simulations (Toda and Phillips, 1994). k is to be

emphasized here that none of the sudies reported in table 3 followedsuch a sequential approach to test Granger causality.

Based on the preceding discussion the following suggestions can be

offered concerning the future direction of causality analysis in agricultu-ral economics. First, use economic theory to determine relevant variables

to be included in the model. Second, test for the presence ofseasonal and

non-seasonal stochasric trends in the univariate process of each variablein rhe system under investigation. Third, if the variables are found tohave unit root nonstationarity, test for the existence of cointegration rn

the sysrem using the full-system cointegration approach developed by

Johansen. Fourth, if there is no long-run relationship among the vari-ables then reparameterize rhe model as a firsr difference-VAR and per-form causality tests based on the autoregressive parameters estimatedfrom the reparameterized model. In this case, the \7ald test has an

asymptotic cbi-squared distribution and hence, the critical values of chi-

squared can be employed. Fifth, if cointegration is detected, then deter-mine the number of cointegrating vectors, veri$, the rank conditionsand formulate a Johansen-type error-correction model (ECM). Finally,test Granger noncausality hypotheses based on the estimated parameters

of this error-correction model. It is to be emphasized here that the se-

quential inference procedures for testing causality involve some un-known dynamics at each stage. One has to select lag-lengrh for testingunit roots and cointegration. Very recently, Gonzalo (1994) has shownthat Johansen's method performs better when the model is overparamet-erized than when it is underparamecerized. Based on this result, one

should use Akaike's FPE criterion to select optimal lag-lengrhs. This cri-terion is known for its tendencv to overDarameterize a model.

CONCLUDING REMARKS

Testing causal hypotheses is central to empirical research in agricul-tural economics. The four alternative causality tests, the Granger test,the Sims test, rhe modified Sims test and the Haugh-Pierce tesr, havebeen developed based on the statistically testable norion of causality in-croduced by Granger (1969). Vhile these tests received wide applica-tions in agricultural economics, they have also generated conflicting cau-sal results in bivariate models and led ro a number of conrroversies. Anattempt to improve causality analysis by developing a nonparamernccausality test did not fare well. However, rhe use of Granger causalitytest in agricultural economics continued to flourish in unrestricred VARmodels and in cointegrared systems. This paper provides an overview ofthe literature on Granger causality testing in agricultural economics. Iroutlines the methodology of tescing causal hypothesis in traditional bi-

1+

CAUSALITY ANALYSI.Î

variate models, unrestricted VAR models and in cointegrated systems.

Selected applications of each of these methodologies in agricultural eco-

nomics are reviewed and their limitatrons are critically assessed. Poten-

tial avenues for improvement in causality analysis are also discussed.

Irrespective of the methodology, most applications of Granger causal-

ity tests in agricultural economics concentrate on commodity price anal-

ysis. The apparent comovement of various commodity prices may partlyexplain such concentration of research efforts. Effects of the macroecon-

omy on agriculture have also been investigated by an increasing number

of researchers using levels VARs and cointegrated models. A number ofestablished paradigms in agricultural economics, such as the LOP, land

price formation, measurement of technological change etc., ate being re-

examined using causality analysis in coinregrated systems.

A number of crucial problems are associated with the rraditionalGranger causality tests. The results from traditional bivariate causality

models are particularly sensirive to prefiltering, omitted variables and

the choice of lag-lengths. The most important limitation of the tradi-tional bivariate models is that they lack an explicit cheoretical structure.

This makes it difficult to give proper interpretation to the causality re-

sults. S7hile causality analysis in unconstrained VARs represents a sig-

nificant departure from the traditional causality tests, causal results from

unconstrained levels VARs can also be controversial. The controversy can

arise from the identification restrictions imposed on a VAR model dur-ing estimation or from data nonstationarity. If a VAR model includes

variables with stochastic trends and there is a possibility of cointegra-

tion, the \?ald test used to test for Granger causality in VAR models

may not have a limiting distribution and so, there is no valid basis formounting Granger causality tests. Consequently, the causality test

breaks down. To the extent data nonstationarity is present in exiscingVAR models, the causality results can be dubious.

\7hen the system under investigation involves nonstationary vari-ables and there is a possibility of long-run relationships among them,

cointegration is the appropriate methodology to investigate Granger

causaliry. Most recent studies in agricultural economics seem to have ac-

knowledged this and derive causal inference from cointegrated systems.

However, not in all cases causal inferences are generated from a properly

proach will provide a useful guidance to future causality analysis in ag-

ricultural economics.

3t

R. SARKER

RIFERINCES

AnoEur (P.G.), 1989 - Does the law of one price really hold for com-modity prices? American Joarnal of Agricaltaral Economics, 71,pp.66r-669.

Besure (R.4.), and Brssrsn (D.4.), 1990 - The corn-egg price trans-mission mechanism. Sorthnn Joarnal of Agricultaral Economics 22,

Pp.79-86.

Bnrnrs g.), l99l - The law of one price still holds. American Joarnal ofAgricultural Economict, I 3, pp. 1264-127 3.

Bnsu,rNN (R.L.), 1988 - Causality tests and observationally equivalentrelationships of econometric models. Journal of Econometricr, )9,pp.69-104.

BrssrEn (D.4.), and ScHnnoEn (L.F.), 1980 - Relarionships betweentwo quotes for eggs. American Joarnal of Agricultural Economics, 62,pp.767-771.

Bpssrnn (D.4.), 1984 - Relative prices and money: a vector autore-gression on Brazilian data. AmuicanJoarnal of Agricaltaral Econom-

ics,66, pp.2530.

BraNx (S.C.), l98i - Using causality and supply response models rn

interpreting foreign agricultural policies. Agribusinas : An Intana-tionalJournal, 1, pp. 177-18).

Boyo (M.S.) and BnonsrN (B.rV.), 1986 - Dynamrc price relation-ships for US and EC corn gluten feed and related markets. Euro-pean Reuiew of Agricultural Economics,13, pp. 199-217.

BnonsEN (B.Iù(/.), CHavns (J.P.) and GnaNr (\f.), 1984 - Dynamic re-

lationships of rice import prices in Europe. European Reuiew of Ag-ricultural Economics, I 1, pp. 29-43.

CHor (Y.C.) and Koo (\7.W.), 1993 - Monetary impacts on prices inthe short and long-run: further results for the United States.Joar-nal of Agricultural and Resource Economics,18, pp. 2ll-224.

Cranr (f.S.), KrErN (K.K.) and TuoupsoN (S.J.), 1993 - Are subsi-dies capitalized inro land values ? Some time series evidence fromSaskatchewan. Canadian Joarnal of Agricultural Economics, 41,pp.155-168.

Crnn< (f.S.), FurroN (M.), and Scorr (J.T.), 19% - The inconsis-tency of land values, land rents, and capitalization formulas. Ame-rican Journal of Agricultaral Economics , 7 5 , pp. 147 -ltt .

36

CAUSALITY ÂNALYS/S

Cr,rnx (f .S.) and Coyre (8.), 1994 - Çemmsnts on neoclassical pro-duction theory and testing in agriculture. Canadian Joarnal ofAgricultural Economics, 42, pP. 19-27

Cranx Ç.S.) ,tNo Spntc'cs (J),1992 - Policy implications in multi-

product acrcage response systems. Jotrnal of Poliry Modtling, 14,pp.183-i98.

Cr,rnx (J.S.) and Yourvcarooo (C.E.), 1992 - Estimating dualitymodels with biased technological change: a time series approach.

American Journal of Agricultural Econornics, 7 4, pp. )52-36I.

Couwav (R.), Sw,t',rv (P.), Y,tNacne (f.) and Von Zun MusHrrN(P.), 1984 - The impossibility of causality testing. AgriculturalEconomics Research,36, pp. l-I9.

Coorrv (T.F.), and Lr Rov (S.F.), 198i - A theoretical macroeconom-

ics: a critique.Joarnal of Monetary Economics,16, pp. 2$-308.

Dtaxos,qwas (D.), I99t - How integrated are world beef markers?

The case of Australian and US beef markets . Agricultaral Econonics,

12, pp. 37 -53.

Drcxnv (D.4.), J,rNsrN (D.\f.) and TsonNroN (D.L.), I99l - A

primer on cointegration with an application to money and in-come. The Fedrral Reserue Banh of St. Loais,J3, pp. 58-78.

Drcxrv (D.), and FurrEn (W.),I979. Distributron of the estimators for

autoregressive time series with a unit root. Journal of the Amerian

Statistical Association, T 4, pp. 427 -41.

DrcrEv (D.), Hasze (H.P.) and FunEn (\ùf.4.), 1984 - Testing for

unit roots in seasonal time series.rlournal of Anaican Statistical As'

sociation,79, pp. )55-361 .

DoaN (T.), LrrrrnunN (R.), and Srus (C.4.), 1984 - Forecasting and

conditional projection using realistic prior distribution. Econometric

Reuiew,3, pp. 1-100.

Dornoo (1.J.), JENxrNsoN (T.) and Sosvnr,r-Rrvrno (S.), 1990 - Co-

integiation and unit roots. Journal of Economic Surueys, 4, pp' 249-)14

Dnrns (M.4.), and UNr.uvrun (LJ.), 1990 - Influence of trade policies

on price integration in the world beef market. Agricaltural Econo-

mics,4, pp.73-89.

DnoNNE (Y.) and TRvERa (C.), 1990 - Shom-run dynamics of feed in-

gredient prices facing the EC: a causal analysis. Agricaltaral Econo-

nics,4, pp. 3tI-364.

R. SÂRKER

Duroun (l-M.), and TEssrrn (D.), 1993 - On the relationship betweenimpulse response analysis, innovation accounting and Grangercausalicy. Economics Letters,42, pp. 321333.

ENcrE (R.F.), HrNonv (D.F.), and RrcunnD (1.F.), 198) - Exogeneity.Econometrica, 11, pp. 211-304.

ENcrE (R.) and Gn,tNcrn (C.), 1987 - Cointegration and error correc-tion: representation, estimation and testing. Econonetrica, 55,pp.25r-276.

EnrcssoN (N.R.;, 1992 - Cointegration, exogeneiry, and policy analy-sis: an overview. Journal of Poliry Modeling,14, pp. 2tl-280.

Fnrx (B.), l99l - Formally tesring the present value model of farm-Iand prices. American Joarnal of Agricultural Economics,73, pp. l-10.

FERrnEnsroNr (4.M.) and BnrEn (T.G.), 1987 - An examination offarm secror real asset dynamics: 1910-85. AmaicanJournal of Agri-cultural Economics, 69, pp. 532-146.

FnErsarnN (].\f.), 1984 - Farm and retail food prices. Rwiau of Mar-kuing and Agricultual Economics, 52, pp. 1 l-90.

GrwErE Ç.), Mrssl (R.) and Dnrr (\7.), 1983 - Comparing alterna-tive tests of causality in temporal system: analytical results andexperimental evidence. rl ourna I of Econometrics, 2I, pp. 16I -194.

Grrnnnr (C.L.), 1986 - Professor Hendry's econometric methodology.1xford Bulletin of Economics and Statistics, 48, pp. 281-307 .

GoNz,rro g.), 1994 - Five alternative methods of estimaring long-runequilibrium relationships. Journal of Econometrics, 60, pp. 203-233.

GooowrN (B.K.), 1992 - Multivariate cointegration test and the lawof One Price in international wheat market. Reuiew of AgricultaralEconomics, 14, pp. ll7 -124.

Gooowrtt (8.K.), and Scsnororn (T.C.), l99la - Price dynamics ininternational wheat markets. Canadian Journal of Agricultural Eco-

nonics, 39, pp. 2)7 -254.

Gooowrr.r (B.K.) and ScrnoroEn (T.C.), 1991b - Cointegration restsand spatial price linkages in regional cattle markers. Anerican

Joarnal of Agricultural Economics,73, pp. 452-464.

Gn,rNcEn (C.!fJ.), 1988 - Some recent developmenrs in a concept ofcausalicy. Journal of Econometrics, 39, pp. I99-2lL

GnnNcrn (C.'ùfJ.), 1980 - Testing for causality: a personal viewpoint.Journal of Econonic Dynanics and Control, 2, pp. 329-352.

38

CAUSALITY ANALYS/S

GRnNcrn (C.\f.J.), 1969 - Investigating causal relations by econo-

metric models and cross-spectral methods. Econometrica, 3J ,

pp 424-4)8.

GnaNcEn (C.Iùry.) and Nrwsoro (P.), l9l4 - Spurious regression ineconometrics. Joarnal of Econometrics,2, pp. l2l-130.

GnaNr ('ù/.R.), NcrNca (4.\7.), BnonsrN (B \Y.) and Cunv,rs Ç-P.),1983 - Grain price interrelationshtps. Agricultural Economics Re-

search, 35, pp. 1-9.

Guprn (S.), 1988 - Profits, investment, and causality: an examinatton

of alternative paradigms. Soutbrn Economic Joarnal, 1), pP. 9-20-

Hnu-Rr,t (D.), M,qcnaDo (F.) and Rapsot'TANIKIS (G.),1992 - Cointe-

gration analysis and the determination of land prices. Joarnal ofAgricaltural Econonics, 43, pp 28-18.

H,qNsrN (B.8.), 1992 - Tests of parameter instability in regressions

with I(1) process. Journal of Economic and Basiness Statistics, 10,

pp.32r-))5.

HrrrN (D.M.), 1980 - Markup pricing in a dynamic model of the food

industry. American Jozrnal of Agricultaral Econonics,62, pp. 10-18.

HrccrNsoN (N.), Hn'x/xrNs (M.)and Aoauowlcz (W.), 1988 - Pric-

rng relationships in rnterdependent North American hog markets:

thË impact of iounteruailing duty. Canadian Joarnal of AgricilturalEconomics, 36, pp. i0l -5 1 8.

Horrnuo (P.\f.), 1986 - Statistics and causal inference. Joarnal of tbe

Amaican Statistkal Association, 8i, pp. 945-960.

HornEs (J'M.) and Hurrou (P'A'), 1988 - A functional form' distri-bution free alternative to parametric analysis of Granger causal

models. Adaanca in Econonenics, 7, pp. 2ll-225.

Horurs Ç.M.)and HurroN (P.4.), 1990 - Small sample properties ofthe Multiple-Rank F test with lagged dependent variables' Eco-

nomic Letters, )3, Pp. 3))-3)9.

Hor (P.4.), 1991 - An application of a new

lity to livestock markets. Canadian JournalJ9, PP. 481-49L

Hvlrrsrnc (S.), Er.rcrE (R.F.), Gn'aNcrn (C.\ilJ.) and Yoo (B'S'),

l99O - Seasonal integration and cointegration. Joarnal of Econo-

metrics, 44, pp. 2lt-238.

JounusEN (S.), 1992 - Testing weak.exogeneity and t-h:gldtt-of coin-"

,rgr^rLon in UK money âemand dara. Jonrnal of Poliry Moùling,

14, pp. 313-3)4.

39

R. S,ARKER

JoHaNsrN (S.), 1991 - Estimation and hypothesis testing of cointegra-tion vectors in Gaussian vector autoregressive models. Economelrica,

59, pp. 15t1-1180.

JoHnusrN (S.), 1988 - Statistical analysis of cointegration vectors.

Joarnal of Economic Dynamics and Control, 12,pp. 2)l-254.

JounusrN (S.) and Juserrus (K.), 1990 - Maximum likelihood estima-tion and inference on coinregrarion - with applications to the de-mand for money. 0*f*d Bulletin of Economics and Statistics, 52,pp. 169-210.

JoH.a,usrN (S.), and Jusruus (K.), 1992 - Testing srrucrural hyporhe-ses in a multivariate cointegrarion analysis of the PPP and theUIP for UK. Journal of Econometrics, 53, pp. 211-244.

KwrRrxo,oqsxl (D.), Psrrups (P.C.B.), Scnrtllor (P.) and SrrrN (Y.),1992 - Testing the null hypothesis of stationarily against rhe al-ternative of a unit root: how sure are we that economic time serieshave a unit root? Joarnal of Econometrics,54, pp. 1i9-178.

Lanur (B.) and Kan (A.), 1993 - S7orld price variability versus pro-tectionism in agriculture: a causaliry analysis. Rwiew of Economics

and Statistics,Jl, pp. 342-)46.

L,rnur (8.), 1991 - Farm input, farm ourpur and retail food prices: a

cointegration analysis. Canadian Joarnal of Agricaltural Economict,

19, pp.)35-)55.

Lrr (E.), and Cnauen (G.), 198i - Causal relationships among worldwheat prices. Agribusinus: An lnternationalJoarnal, l, pp. 89-91.

LINc (R.F.), 1982 - Review of correlation and causation by David A.Kenny. Journal of the Anaican Statistical Association, TT, pp. 489-49r.

Lru (D.J.), CsuNc (PJ.) and MryrRs (\f.H.), 1993 - The impact ofdomestic and foreign macroeconomic variables on US mear ex-ports. Agricultural and Resource Econmnics Rniew,22, pp.210-221.

Muscnrnu (V.4.) and HunN (S.), 1992 - Cointegrarion and dynamictime series models. Joarnal of Econonic SaruEs, 6, pp. l-43.

Onoeu (D.), and Fncxun (P.L.), 1989 - Identifring monerary impacrson agricultural prices in VAR models. Anaican Journal of Agrical-taral Economics, Tl, pp. 495-502.

OssonN (D.R.), CHur (4.P.), Surru (P.) and BrncurNnarr (C.R.),1988 - Seasonality and the order of integration for consumprion.}xfad Balletin of Econonics and Statistics, j0, pp. j6l31j.

40

CAUSALITY ANALYS/S

OsrrRwaro-LrNuu (M.), 1992 - A note with quantiles of the asymp-totic distribution of the maximum likelihood }xfad Balletin ofEconomics and Statistics,14, pp. 461-411.

Pnnorv (P.G.) and Cnarc (8.), 1989 - Causal relationships between

public sector agricultural research expenditures and outpvt. Ame-

rican Journal of Agricultural Economics, 7 I, pp. 9-I9.

Panr Ç.Y.), 1990 - Testing for cointegration through variable addi-tion. ln: FnoMsv and Ruools. eds.. Studia in Economelric Thenry,

New York, JAI Press.

P,rnx (|.Y.), 1992 - Canonical cointegration regressions. Econometric Re-

uiew, 60, pp. 119-14).

Panx Ç.Y.), and PHrI-lrps (P.C.B.), 1989 - Statistical inference in re-

gression with integrated processes: part II. Economeîric Theory, 5,

pp.9i-131.

PHnrps (P.C.B.) and Prnnou (P.), 1988 - Testing for a unit root intime series. Biometriha, Tl, pp. 335-346.

Pnrps (T.T.), 1984 - Land prices and farm-based returns. American

Joarnal of Agricaltural Economics,66, pp. 422-429-

Prsncr (D.), and Hnucn (L.), 1978 - Causality in temporal systems:

characterization and a survey. Joarnal of Econometria, 5, pp- 265-

293.

Pnrotrn (DJ.), 1988 - Causal relationships and replicability.Joarnal of