AFM Presentation Latest

17

Capital Structure Decisions Pakistan State Oil

-

Upload

independent -

Category

Documents

-

view

3 -

download

0

Transcript of AFM Presentation Latest

Capital Structure Decisions

Pakistan State Oil

•Pakistan State Oil is the largest oil marketing company in Pakistan.

•The company is engaged in storage, distribution and marketing of POL products.

•As per PARCA PSO has long term credit rating of AA+ & short term credit rating of A1+

•The company is listed on all three stock exchanges of the country i.e. KSE, LSE and ISE

About

Market ShareBlack Oil:

82.1%White Oil:

61.2%

Operating Income 26,109

Million Rupees

Net Income12,871 Million

Rupees

Debt

219,421 Million

Equity 61,888 Million

Shares Outstanding: 217 million

Price per Share:

Rs. 334.88

Financial Highlights – 2013

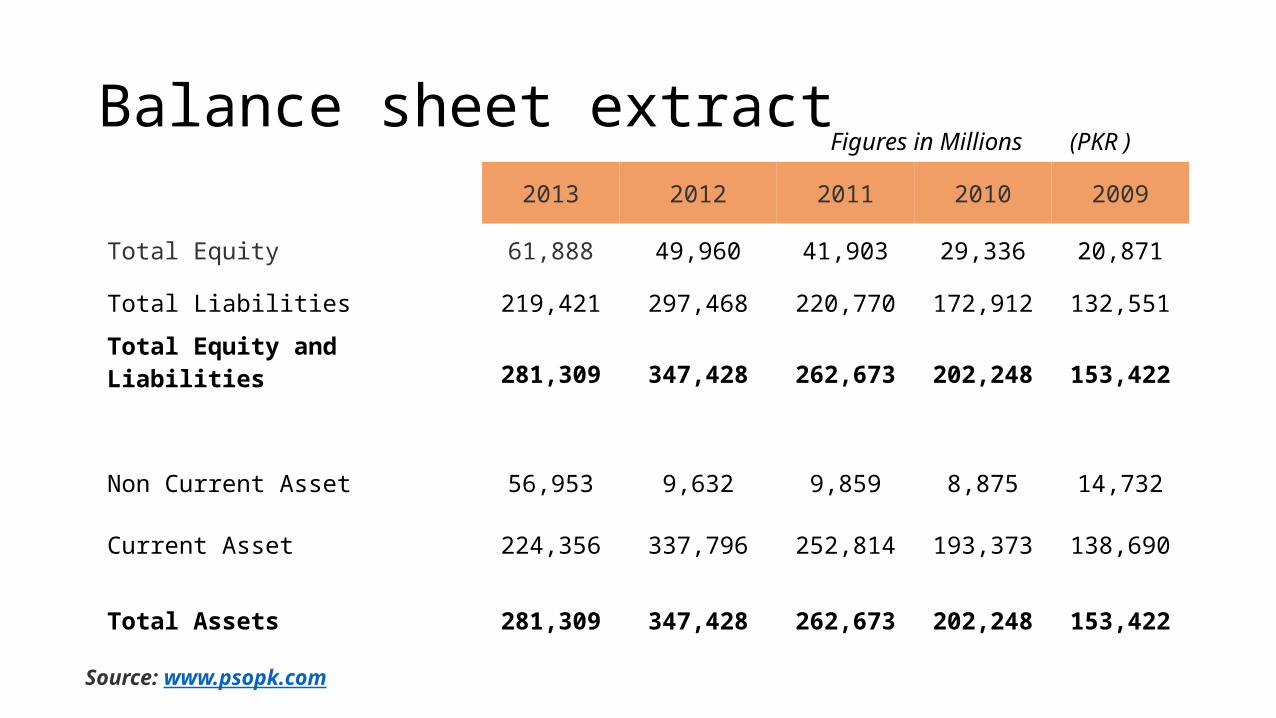

Balance sheet extract

Source: www.psopk.com

Figures in Millions (PKR )

2013 2012 2011 2010 2009

Total Equity 61,888 49,960 41,903 29,336 20,871

Total Liabilities 219,421 297,468 220,770 172,912 132,551Total Equity and Liabilities 281,309 347,428 262,673 202,248 153,422

Non Current Asset 56,953 9,632 9,859 8,875 14,732

Current Asset 224,356 337,796 252,814 193,373 138,690

Total Assets 281,309 347,428 262,673 202,248 153,422

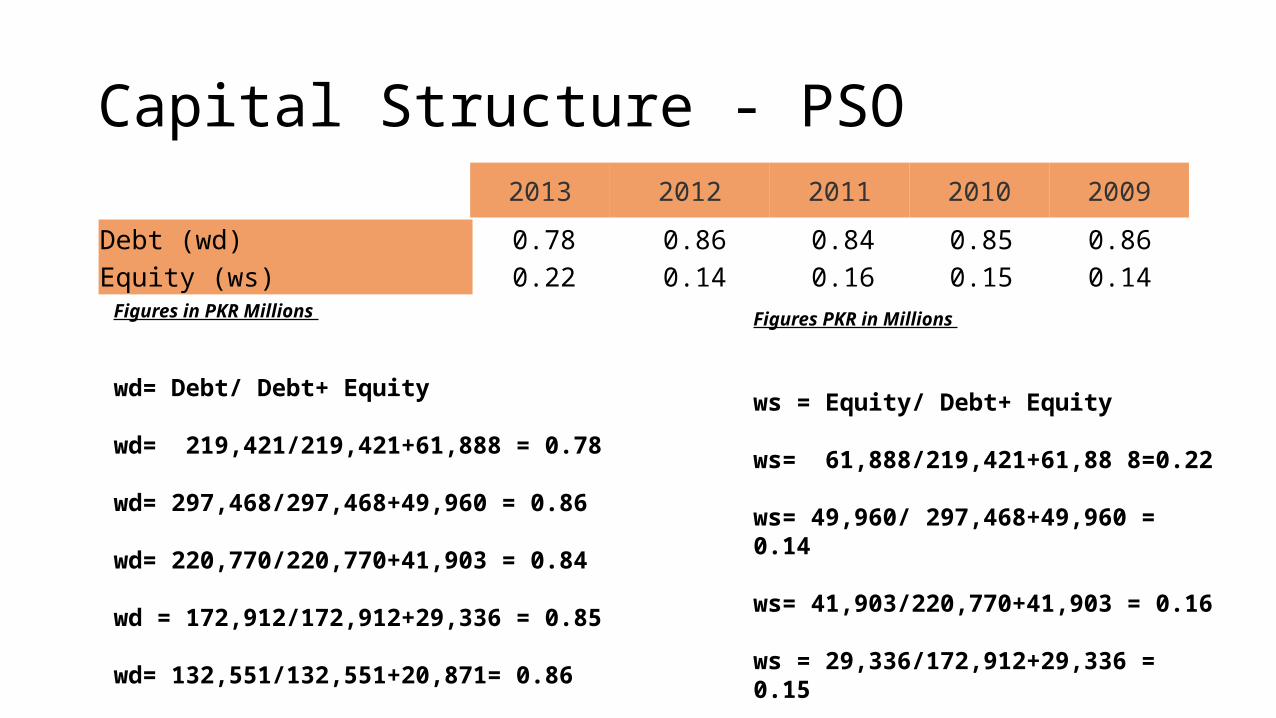

Capital Structure –PSO (2009-2013)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%78%

86% 84% 85% 86%

22%14% 16% 15% 14%

DebtEquity

Capital Structure - PSO

Debt (wd) 0.78 0.86 0.84 0.85 0.86Equity (ws) 0.22 0.14 0.16 0.15 0.14

2013 2012 2011 2010 2009

Figures in PKR Millions

wd= Debt/ Debt+ Equity

wd= 219,421/219,421+61,888 = 0.78

wd= 297,468/297,468+49,960 = 0.86

wd= 220,770/220,770+41,903 = 0.84

wd = 172,912/172,912+29,336 = 0.85

wd= 132,551/132,551+20,871= 0.86

Figures PKR in Millions

ws = Equity/ Debt+ Equity

ws= 61,888/219,421+61,88 8=0.22

ws= 49,960/ 297,468+49,960 = 0.14

ws= 41,903/220,770+41,903 = 0.16

ws = 29,336/172,912+29,336 = 0.15

ws= 20,871/132,551+20,871 = 0.14

1.Growth Rate: g = retention rate x ROE

2013 2012 2011 2010ROE 0.2029 0.1813 0.3527 0.3085Dividend Pay out Ratio 0.1377 0.142 0.116 0.1516Retention Rate= (1- Dividend payout ratio)(Calculated) 0.862 0.858 0.884 0.848

For 2012:

G= (RR x ROE)G = 0.1813 x 0.858

For 2011:

G= (RR x ROE)G = 0357 x 0.884

For 2010:

G= (RR x ROE)G = 0.3085 x 0.848

For 2013:

G= (RR x ROE)G = 0.2029 x 0.862

Growth Rate % 17.5% 15.6% 31.2% 26.2%

Source: www.psopk.com

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

17.5 15.6

31.226.2

2013 2012 2011 2010

Growth Rate (%)

Ks= D1/Po +g= 5/334.8 + 0.175

KS= = 0.1899= 18.99%

2013Ks= D1/Po +g

= 5.5/270.77 + 0.156

KS= 0.1759= 17.59%

2012

Ks= D1/Po +g= 10/313.8 + 0.312

KS= 0.3437=34.7%

2011Ks= D1/Po +g

= 8/342.95 + 0.262

KS= 0.2581=25.81%

2010

2. RATE OF RETURN OF EQUITY ( DISCOUNTED CASH FLOW METHOD)

2013 2012 2011 2010 2009Price of share (Rs.) 334.88 270.77 313.8 342.95 428.79Dividend (Rs.) 5 5.5 10 8 5

Source: www.psopk.com

0

50000000

100000000

150000000

200000000

250000000

300000000

350000000

2013 2012 2011 2010 2009

283574809

318761079

252625634.165724

192974515.475351

153735365.809017

Value of the Firm PKR (‘000)

Vf = (EBIT-I)(1-T) + DebtKs

=(26,109-7,591)(1-

0.342) + 219,4210.1899

= Rs. 283 Bn

Vf = (EBIT-I)(1-T)+ Debt

Ks

=(17,313-1,165)(1-

0.338) + 297,4680.1759

= Rs. 318 Bn

2013 2012

Value of Firm 2013 2012 2011 2010 2009

Revenue (PKR) 1,294,503,000 1,199,927,907 974,917,064 877,173,254 719,282,176Operating Income /EBIT (PKR) 26,109,000 17,313,296 25,217,134 21,233,413 (6,353,344)

Interest Expense (PKR) 7,591,156 11,658,928 11,903,162 9,882,010 6,232,056Profit / (Loss) before Tax (PKR) 19,089,000 13,674,000 17,974,000 17,963,000 (11,357,000)

Profit / (Loss) after Tax (PKR) 12,558,000 9,056,000 14,779,000 9,050,000 (6,699,000)

Tax Paid (PKR) 6,531,000 4,618,000 3,195,000 8,913,000 (4,658,000)

Tax Rate (calculate) 34.2% 33.8% 17.8% 49.6% 41.0%Source: www.psopk.com

Figures in PKR ‘000

Value of Firm

2009

Vf = (EBIT-I)(1-T) + DebtKs

=(-6,3535-6,232)(1-

0.410)+

132,551-0.35

= Rs. 153 Bn

Vf = (EBIT-I)(1-T) + DebtKs

=(25,217-1,190)(1-

0.178)+

172,9120.3437

= Rs. 252 Bn

2011Vf = (EBIT-I)(1-T) + DebtKs

=(21,233-9,882)(1-

0.496)+

220,7700.2851

= Rs. 192 Bn

2010

Recommended Capital Structure Structure1: Debt : Equity 70%:30%Working:Beta (2013)= 1.1*Rd (SBP source) = 10.50% (August 2014)Beta Unleveraged

BL = BU [ 1+ (1-T)D/S]

1.1 =Bu [ 1+ (1-0.342)(78%/22%)]

Bu= 0.33

Beta Leveraged NewBL = BU [ 1+ (1-T)D/S]

=0.33[1+(1-.342)(.70/.30)]

=0.8366Ks = Rrf + RPM (B)

=13% + 6% (.8366)

= 18.012%

Vf = (EBIT)(1-T)WACC

= (26,109)(1-0.342)0.1020

= Rs. 168 Bn

WACC = wdrd(1-T) + wsks

=(0.7*0.105)(1-0.342) +(0.3)(0.18012)

=10.20%Sources of Beta• http://markets.ft.com/research/Markets/Tearsheets/Financials?s=PSO:KAR

• http://www.reuters.com/finance/stocks/overview?symbol=PSO.KA

• http://investorguide360.com/wp-content/uploads/2013/04/PSO-Detailed-Report.pdf

Sources of Market Risk Premium and Risk Free Rate:•www.sbp.com.org.pk(Data source: Reuters)•http://investorguide360.com/latest-economic-news/pakistan-state-oil-a-bumpy-ride-to-new-highs-research-of-the-day-by-bma-research/•http://investorguide360.com/wp-content/uploads/2014/03/FS-Research2.pdf

Structure2: Debt : Equity 88%:12%Working:Beta (2013 )= 1.1Rd (SBP source) = 10.50% (2014)Beta Unleveraged

BL = BU [ 1+ (1-T)D/S]

1.1 =Bu [ 1+ (1-0.342)(78%/22%)]

Bu= 0.33

Beta Leveraged NewBL = BU [ 1+ (1-T)D/S]

=0.33[1+(1-.342)(.88/.12)]

=1.19856Ks =Rrf + RPM (B)

=13% + 6% (1.19856)=20.19%

Vf = (EBIT)(1-T)WACC

=(26,109-7,591)(1-

0.342)0.084

= Rs. 204 Bn

WACC = wd rd(1-T) + ws ks

=(0.88*0.105)(1-0.342) + (0.12)(0.2019)

=8.40%

Recommended Capital Structure

70% : ... 88% :... 78%:...265270275280285290295300305310315

287

311

283

Comparisons Capital Structures & Values of the Firm (Billion PKR)

Question and Answers Session

Thank You !

ReferencesPSO’s Financial reports 2009 – 2013 • www.psopk.comSources of Beta• http://markets.ft.com/research/Markets/Tearsheets/Financials?s=PSO:KAR• http://www.reuters.com/finance/stocks/overview?symbol=PSO.KA• http://investorguide360.com/wp-content/uploads/2013/04/PSO-Detailed-Report.pdfSources of Market Risk Premium and Risk Free Rate• www.sbp.com.org.pk(Data source: Reuters)• http://investorguide360.com/latest-economic-news/pakistan-state-oil-a-bumpy-ride-to-new-highs-research-of-the-day-by-bma-research/

• http://investorguide360.com/wp-content/uploads/2014/03/FS-Research2.pdfSource of Interest Rate • www.sbp.org.pk