AARTI INDUSTRIES LTD. METROPOLIS HEALTHCARE LTD.

80

Market Overview Prominent Headlines Testimonials Q&A with CIO Mutual Fund Overview Stock Picks Monthly Insight Performance Management Meet Note Economy Review Startup Corner Sector Outlook: Chemical Q3FY20 Result Analysis Technical View Commodity Monthly Round up Book Review World Economic Event Calendar March 2020 BRITANNIA INDUSTRIES LTD. | AARTI INDUSTRIES LTD. METROPOLIS HEALTHCARE LTD. IN SIGHT Q&A WITH CIO Mr. Saurabh Mukherjea, Founder and Chief Investment Officer - Marcellus Investment Managers Viral Markets

-

Upload

khangminh22 -

Category

Documents

-

view

8 -

download

0

Transcript of AARTI INDUSTRIES LTD. METROPOLIS HEALTHCARE LTD.

Market Overview Prominent Headlines Testimonials Q&A with CIO

Mutual Fund Overview Stock Picks Monthly Insight Performance Management Meet Note

Economy Review Startup Corner Sector Outlook: Chemical Q3FY20 Result Analysis

Technical View Commodity Monthly Round up Book Review World Economic Event Calendar

March 2020

BRITANNIA INDUSTRIES LTD. | AARTI INDUSTRIES LTD. METROPOLIS HEALTHCARE LTD.

INSIGHTQ&A WITH CIO Mr. Saurabh Mukherjea, Founder and Chief Investment Officer - Marcellus Investment Managers

ViralMarkets

2March 2020 INSIGHT

INSIDE THIS ISSUE

Marketoverview1 34 Economy

Review

6 Testimo-nials 40 Sector -

Chemical

11 Mutualfund overview

24 Monthlyinsight Recommendation performance

64 Technicalview

69 Book review Value Investing and Behavioral Finance by Parag Parekh

Startupcorner 39

Q&A with CIO- Mr. Saurabh Mukherjea, Founderand Chief Investment Officer - MarcellusInvestment Managers

7 Q3FY20 Result Analysis 46

Stock picks• Britannia Industries

Ltd.• Aarti Industries Ltd.• Metropolis Healthcare

Ltd.

15

Managementmeet note• Phillips Carbon Black

Ltd. 30

Commoditymonthly round up 68

Worldeconomic calendar 72

Testimonial

Prominent headlines February 2020 4PROMINENT

1 March 2020INSIGHT

MarketOVERVIEW

The coronavirus code named as COVID-19 has turned out to be a new scare for the world markets and have beaten previous records of notorious SARS though the positive thing is the mortality rate which is around 2% in comparison to earlier epidemic outbreaks.

2March 2020 INSIGHT

As the number of death toll has already crossed 2,762 worldwide while the total number of infected

people at more than 80,000. What’s concerning for the world markets is the fact that the virus has now spread outside of China and in places such as Italy & Iran which according to WHO doesn’t have any direct links with the epicenter, Hubei province in China. Besides, rate of infecting people in a single day has failed to come down so far. In comparison, SARS which was reported in January 2003, hogged limelight in March 2003 and the attack rate declined some 76 days after shock. By July 2003, WHO declared that the SARS outbreak has been contained. Thus, going by the same, the COVID-19 attack rate is expected to decline sometime in early April. However, what’s concerning is the scale of infections for COVID-19 at this rate of infection compared to SARS which infected ~8100 people and responsible for 774 deaths. The only positive aspect has been the mortality rate which has been at ~3.4% compared to ~9.5% for SARS, although depth, breadth and length of this new coronavirus remains uncertain as of now. According to an article in CNN, a U.S.-Canadian team at Laval University in Quebec projects total coronavirus cases “might reach a cumulative 550,000 cases in Wuhan” alone. Sadly, that is the best-case scenario and in worst-case model projects 4.4 million could be infected by the time the epidemic is over. The researchers warn that COVID-19 “almost certainly cannot be contained and we must prepare for a pandemic.” A 2004 paper by two economists published in Asian Economic Papers (MIT Press) estimated the global economic loss to SARS at $40 billion. One needs to remember that the scale and dependence on the Chinese economy has grown at leaps and bounds. China’s share of World GDP increased from 4% in 2000 to 16% in 2018 and the share of world exports from 2% in 2000 to 11% in 2018. In

2018 alone, 30% of growth in world GDP is contributed by China. These data thus signify that a massive impact on China’s GDP will not spare the World economic growth.

While it is difficult to quantify the losses to the Chinese economy and in turn global economy, inferences could be drawn from SARS over global commodities and economy. Crude oil prices as well food prices softened during the SARS attack, even for COVID-19, global commodity prices have fallen. China’s trade surplus turned negative, albeit only for three months between Jan & March 2003, only to recover in April. GDP growth took a hit in Q2CY2003 (at 9% vs 11% in Q1CY2003), although not a massive extent. The limited impact from SARS have been limited as the same got arrested within a small range of time. Thus, while drawing parallels between SARS and COVID-19, one needs to compare the scale of people infected by COVID-19 vs SARS as well the scale of the Chinese economy in 2003 and now. Thus, the adverse impact could be far reaching and certainly beyond Q1CY20. Besides, economists

have estimated that even after ease of lockdown in March, Chinese economy could experience largest quarterly drop due to simultaneous hit on both supply and demand side of the economy. The only problem is, the virus couldn’t have found a better time to hit, when the world economic growth itself have been soft. US economy has lost steam and have been caught in a shallow range while EU economic growth never really took off after the global financial crisis. With recent slowdown in German economy, the concerns have just been broad-based now. Japan is slowly slipping into recession and despite these developed economies been provided with easy liquidity from their central banks, the whole strategy has been redundant. At the end of the day, balance sheets of these central banks have got stretched and making the monetary policies as a tool to prop economic growth have run its course. In such a scenario, a faltering Chinese economy is the last thing the world policymakers needed. While COVID-19 may not last beyond April and thus a temporary scare, nevertheless, ‘fear factor’ among China’s population is evident and given the export and import dependence on China, production disruption will have a severe impact on world’s supply chain.

As for the economic impact on India, trade balance is expected to be negatively impacted since India has higher import dependence on China comprising of ~14% of total imports. At the same time India has lower export dependency on China since only 5% of Indian exports go to China. Now of total imports, ~32% of the same are oil imports and will benefit with lower oil prices. However, the advantage ends over there and economists are of the view that for the remaining ~68% of imports whether it be inputs or raw materials, it is expected to be priced higher. More, importantly, out of this 68% imports, 14% is accounted

China’s share of World GDP increased from 4% in 2000 to 16% in 2018 and the share of world exports from 2% in 2000 to 11% in 2018. In 2018 alone, 30% of growth in world GDP is contributed by China.

3 March 2020INSIGHT

from china alone and is expected to witness higher prices. Thus, considering that the import volumes are not significantly hampered, trade balance is expected to worsen since the benefits of lower oil & related prices will be overshadowed by inflationary impact on 68% of imports. Similarly, for inflation, 35% of the CPI basket will be moved by the global commodity prices, particularly food articles. In fact, international food prices are also on an uptrend and global food inflation stood at 6.99% in Dec 2019, after 5.97% clocked in November 2019. Thus, either way the trend will be the same. However, categories like Household goods and services & Personal care and effects together accounting for ~8% weight in CPI index would be affected by COVID-19 induced increase in prices of articles. Thus, in a way, core inflation could be impacted more than the general price levels as the prices of electronics and consumer durables could increase.

The Confederation of Indian Industry (CII) estimates that shipping,

pharmaceuticals, automobiles, mobiles, electronics, textiles etc. could be impacted due to prolonged impact. Although there are hopes of factories resuming production, 10% production cut by Hero MotoCorp shows the way things can turn in event of delay in recovery as Indian manufacturing industries will exhaust raw material inventory by

middle of March. The next set of quarterly results for India Inc. could be impacted severely if production doesn’t start as early as March. As for Q3FY20 earnings season, results were broadly in line with expectations. Excluding Tata Motors (due to exceptional loss in Q3FY19), topline growth for Nifty 50 has remained muted (down 0.2% yoy) while EBITDA grew by 5% driven by margin expansion on lower commodity costs and cost cutting exercise by India Inc. Net profit has been higher by 4.7% yoy, lower tax expenses. While the consumer sector has exceeded expectations, automobiles, capital goods and metals have missed expectations, and private banks, NBFC and healthcare have met consensus estimates. All eyes are now on rural recovery post Rabi harvest season to uplift the economic growth engine as higher crop prices and 9.5% increase in Rabi cultivation will result in higher incomes. In a global supply disruption, the inward looking sectors will provide necessary support to the ailing economic growth.

Growing dependence on China

Source: World Bank, Ashika Research

15%

30%

4%

16%

2%

11%

2000 2018 Contribution to GDP growth Share in World GDP China share in world exports

Daily new cases

Source: www.worldometers.info

0

2000

4000

6000

8000

10000

12000

14000

16000

23-J

an

25-J

an

27-J

an

29-J

an

31-J

an

02-F

eb

04-F

eb

06-F

eb

08-F

eb

10-F

eb

12-F

eb

14-F

eb

16-F

eb

18-F

eb

20-F

eb

22-F

eb

24-F

eb

The Confederation of Indian Industry (CII) estimates that shipping, pharmaceuticals, automobiles, mobiles, electronics, textiles etc. could be impacted if the COVID-19 virus scare is prolonged.

Paras BothraPresident - Equity ResearchEmail - [email protected]: +91 22 6611 1700Direct: +91 22 6611 1786Mobile: +91 98203 97061

Reaching for

yield is really

stupid, but it’s

very human, People are

reaching for yield, there’s

no question about that.

And that’s stupid and it

has consequences over

time, but it’s very human

- WARREN BUFFETT, chairman and chief exec-

utive officer of Berkshire

Hathaway Inc

I don’t think in the next few months, you will hear of any structural

reforms. We have to realise that the fiscal room available to the government is not very high. It really becomes very difficult to give eco-nomic stimulus - PAWAN GOENKA, Mahindra & Mahindra managing director

India needs pro-busi-ness, not pro-crony policies to take the

country to the goal of USD 5 trillion GDP. Pro-business policies are those that enable fair competition in the coun-try while Pro-crony pol-icies on the other hand just help incumbents and that is something that we have to stay away from in enabling the invisible hands of the market - KRISHNAMURTHY SUBRAMANIAN, Chief Economic Adviser

The economy is heading towards a recovery in the

next fiscal, adding good auto-plays and good private sector banks are a sensible way to play it. Would advise people to leave the high beta names from real estate, steel, construction aside, where there are broader challenges around the balance sheet and governance - SAURABH MUKHERJEA, founder of Marcellus Investment Managers

The government welcomes e-com-merce companies

to work within the framework and laws of the land, promises of a certain number of people benefiting from such companies can’t be at the expense of suffering of many others - PIYUSH GOYAL, Commerce and Industry Minister

Despite near-term challenges, equities are

expected to deliver a return of 10-12 percent CAGR over the next 5-10 years however economic growth could remain muted, impacting topline growth of corporate India. But, weaker crude and continuous inflows from both domestic and foreign investors could provide good support to equity markets - SRINI-VAS RAO RAVURI, PGIM MF

India Inc.’s most important investments in the current decade

would be on skilling soft-ware engineers. “Around 72 percent of new jobs for software engineers are outside the tech industry as the crossover happened in 2017 and forever it’s going to be true - SATYA NADELLA, Microsoft Corp.’s Chief Executive Officer

The impact of

Coronavirus

outbreak will

be felt on global steel

industry for at least two

to three years, as China

is the largest producer

of the alloy. Indian steel

companies should

enhance output, partic-

ularly special steel, to

grab larger global market

share - DHARMENDRA PRADHAN, Union

Minister

The four quarters of 2020 may bring some

gradual improvement in company earnings will be based on four reasons—favourable base, directed measure by the government to iron out sector specific challenges, likelihood of decent rabi season, and full impact of low interest cost… NEELESH SURANA, Mirae Asset Mutual Fund’s Chief Investment Officer

PROMINENT HEADLINES FEBRUARY 2020

4March 2020 INSIGHT

PSUs as a pack look

attractive, dividend

yields of some of

these companies are very

attractive. Price-to-book

multiples have fallen below

one time, in some cases

at 0.5-0.6 times, look very

attractive from buyers’

point of view, but there is

a bit of fear of the supply

overhang - A BALASUBRA-MANIAN, Aditya Birla SL

AMC

India is quite an expen-

sive market now. In the

past, people have been

willing to pay a higher cost

because the economy was

simply one of the fastest

growing in the world and

that has probably slowed

down quite a bit. India

appears to have one of

the strongest prospects

for earnings growth, but

Indian companies tend

to disappoint every year

for the last five years - JIM MCCAFFERTY, joint head

of Asia-Pacific equity

research at Nomura

Value is out of fashion

right now, deeply

out of fashion. Even

Warren Buffett is having

a tough time. Earlier you

used to buy cheap. If you

end up buying cheap,

you were guaranteed to

make money. That’s not

the scene now - RAAM-DEO AGARWAL, MD &

Co-founder, Motilal Oswal

The markets, on an

overall basis look

reasonable right

now. The broader markets

have not done well for

the past two years, but it

seems that the markets

are expanding in terms of

stocks that are now doing

well as compared to very

few movers in recent years

- SAMIR ARORA, founder

and fund manager Helios

Capital

We have seen

NBFCs are get-

ting funded in a

big way, banks have also

started to give them credit.

Hence there is a push

for growth which is very

important for the economy.

So, availability of funds,

lower cost of funds are two

prime drivers of why we

are believing that we are

the cusp for recovery. The

only negative point India’s

growth rate can go off track

if Corona Virus outbreak is

sustained for a longer-term

- S KRISHNAKUMAR, Sundaram Mutual Fund’s

Chief Investment Officer

Coronavirus out-

break in China

provides a good

opportunity to India to

expand trade and follow

an export-driven model -

KRISHNAMURTHY SUBRA-MANIAN, Chief Economic

Advisor

Banks of the future would be extremely different from now, and regulating the distinct segments of these banks would be a chal-lenging task, therefore, an integrated framework for resolution of financial firms operating in India could be expected in the near future as that would add to the resilience of the financial system - SHAKTIKANTA DAS, RBI Governor

Every small business owner has potential in India to become Dhirub-hai Ambani or Bill Gates; entrepreneurial power at grassroots is enormous - MUKESH AMBANI CHAIRMAN, Reliance Industries

5 March 2020INSIGHT

6March 2020 INSIGHT

TESTIMONIALS“INSIGHT” is a absolutely exhaustive and your one-stop-shop for credible public market ideas. The content is thorough, well-researched and action-oriented…

SAKET TODI, Director, Lux Industries

Ashika monthly “INSIGHT” is quite insightful with loads of data and useful information on stocks and mutual funds. I particularly look forward to reading the monthly insight magazine specially the Q&A section with an expert. Keep up the good work…

CHANDRAPRAKASH PADIYAR, Senior Fund Manager, Tata Mutual Fund

I have been reading monthly issue of “INSIGHT”. Good presentation of market statistics and very good list of companies that have been covered…

RAJEEV AGARWAL, Rare Enterprise

Ashika’s monthly “INSIGHT” newsletter is one of the sharpest summaries of financial industry in India with a strong set of industry experts giving their views along with well thought through investment recommendations…

PARAG MEHTA, Director, Edelweiss Alts Investments

Ashika monthly “INSIGHT” is a great research publication with lot of insights on financial market. I always look forward to it and specifically the stock recommendations in it is found worthy of investment.…

Great work!

MAHESH SINGHI, Founder & MD, Singhi Advisors

Ashika monthly “INSIGHT” magazine gives in depth analysis and reasoning of stocks it is recommending to buy. The interviews of various Fund Manager provide their rational of sector and stock selections and broader view of market. It is a must read for all investors…

RAJENDRA KUMAR PARAKH, CFO, Vikram Solar Ltd.

I must that I find “INSIGHT” has good content, is highly informative and nice stock ideas on monthly basis. I am quite impressed with the idea of sharing views of fund manager and management note. I can imagine the hard word behind the output. Keep sending and all the best…

PREM RAJANI, Managing Partner, Rajani Associates

True to its name, “INSIGHT” provides focused, relevant and topical insight into companies, sectors and evolving trends. The easy to read and interesting layout of the content makes it easy to absorb and less mundane. I personally look forward to each publication…

MURZASH MANEKSHANA, Dy Managing Director, MEP Infrastructure Developers Ltd.

I have been reading “INSIGHT” for quite some time and the coverage, analysis and calls made therein have been extremely good. A well-balanced mix of industry knowledge, company research and actionable insights, makes it a great read…

AMOL MIRCHANDANI, Head Business Development, Aries Agro Ltd.

7 March 2020INSIGHT

Q: Do you see any green shoots in our economy at present and whether the economy is going to broad base from here on?

A: There are two different narratives playing out today and these can play out over the next 10 years. The first narrative is companies which have a strong financial position, strong balance sheets & free cashflow generation. These companies are growing at a rapid rate and should be able to continue doing so eg. Titan, Dr. Pathlabs, Asian paints or HDFC Bank, etc,. Across sectors, companies with

a strong financial position, strong balance sheet & strong cash flow generation are not facing significant problems with respect to generating growth. These companies will continue going from strength to strength.

The second parallel narrative is that there are two types of companies which are struggling today and could struggle for the next 10 years. The first type are companies with broken balance sheets, and they could be steel companies, infrastructure companies, NBFCs or manufacturing

companies. Companies with broken balance sheets are now going to struggle in India, with no lenders willing to support the companies. Once upon a time, these companies secured loans with the help of errant politicians. That era is gone and with little or no likelihood of an economic recovery in the horizon, these companies will have a tough time. Second type of companies which are screwed are the ones which are not industry/market leaders. For instance, for a footwear company with ROCE at 15%, there is very little chance of being able to compete with a Relaxo or Bata whose ROCEs are significantly north of their cost of capital. Similarly, for an adhesive company with ROCE of 13-15%, it has very little chance of competing with Pidilite whose ROCE is close to 40%. Second rung or third rung players are typically SMEs whose ROCEs are not above their cost of capital and such firms are going to struggle and gradually they are going to die over the next 10 years. Either they have to sell themselves to the market leader or they have to become outsourcing suppliers to the market leader. This point also pertains to high street retail where on the high street, the kirana stores will gradually die out, the independent restaurants will die out and we will witness the highstreet being dominated by chains whether they are supermarket chains or restaurant chains.

So, what we are going to witness in India over the next 10 years is twin narratives: one of dominance and growth and lasting success of market leading franchises with strong financial strength, balance sheets and strong cash flows. Alongside that we will have the death or demise and bankruptcy of the poorly run entities with weak balance sheets, weak cashflows and subpar ROCEs. These two narratives will play out in parallel and hence at any point of time it will look as if India is booming and at the same point of time it would look like India is bust.

Mr. Saurabh Mukherjea - Founder and Chief Investment Officer - Marcellus Investment Managers

Q&A WITH CIO

8March 2020 INSIGHT

In the next 10 years, the country will end up consolidating in the hands of 50 large, well run companies while everybody else will have a struggle. So, the notion of a broad-based recovery will remain a fantasy. These sorts of socialist notions of broad-based recovery were applicable upto year 2015. Once, the black economy got squeezed out and the ability of the second, third grade franchises to borrow money from the financial system got compromised, broad based recovery became a thing of the past. We will remember this notion of broad-based recovery like we remember the Ambassador car or Fiat car, as relics of a bygone era.

Q: Can you give any kind of anecdotes about the fact that capitalist countries like U.S. might have faced something similar to what we are witnessing at present here in India?

A: We have got in front of us three economic transitions from which we can learn from. For U.S., it will be period between 1880 & 1930s, secondly Japan post world war & thirdly Korea post 1970. Basically, the U.S. economy formalized in the fifty years between 1880 to 1930. The Japanese economy formalized roughly in the forty years after the second world war. The Korean economy formalized in the 22-25 years after 1970. All of these formalizations have been very similar, and India have also entered the same journey. Taking the U.S. as example, there were no supermarkets in America in 1880s at all. By 1930, U.S. had 500,000 supermarkets. As a result, the kirana stores were a thing of the past in USA by 1930.

How did America formalize between 1880-1930? First came the railroads, then came the Telegraph, then came the road network, then came the motor car. These various things networked the U.S. economy and created an integrated whole. We are going through a very similar process

in India. 10 years ago, we had barely 4-5 million broadband users and now we have 100 times that number. Airline traffic grows at 20% per annum in our country. Road network has more than doubled in the last 15 years. The number of mobile phone voice users actually exceeds the population. We are thus linking up what was either to a fragmented economy and on top of that we have now full throttle GST implementation by Govt. which clearly needs the tax revenues which GST can bring. When you integrate a fragmented economy, you create national giants. In the American context, all the famous FMCG brands that we know about in the likes of Heinz, Kellogg’s, Coca Cola, Wrigley’s, Pillsbury were born in 1880-1930 era. Till 1880, there were lot of ketchup makers in U.S., however in the next 50 years, Heinz captured the sauce & ketchup industry and the smaller players either shut down or sold themselves to Heinz

or became outsourced suppliers to Heinz and Heinz ended up on all the supermarket shelves by 1930.

Basically, in a non-networked economy, every village by itself is a mini economy and thus every village has a cereal maker or ketchup maker or a biscuit maker. However, once the economy is well linked/networked, those local cereal makers, biscuit makers or ketchup makers end up consolidating. In the process of consolidation, the most efficient company with the best cashflows, best return on capital ends up dominating. We are going through that identical process in India. The story of development in any country is the rise of around 50 really well-run high-quality corporates who pull towards themselves the country’s cashflow into their balance sheets and then use it to fuel development. That is the story of economic growth the world over and we have to live with that regardless of the fact whether anybody likes it or not.

Q: Are the moats getting broadened for companies such as Pidilite, Britannia or Hindustan Unilever? For an investor how do they see that these changes are taking place.

A: The Govt. has expedited two sets of legal changes, two sets of tax changes which are allowing dominant cash generating market leaders to pull away from the rest. First change was the announcement back in September 2019 of a 15% tax rate if you set up a new subsidiary and a new plant inside the subsidiary. In our country, we have 25 monopolists whose return on capital is ~45%. Assuming that cost of capital is 15% it means that every year these companies are throwing out 30% of capital employed as free cashflow. This in turn means that every three years, these companies are returning to their investors the entire capital invested in the business. We are talking about giant companies here - the likes of Britannia, ITC, Nestle, Marico, Pidilite. If the same free

The U.S. economy formalized in the fifty years between 1880 to 1930. The Japanese economy formalized roughly in the forty years after the second world war. The Korean economy formalized in the 22-25 years after 1970. All of these formalizations have been very similar, and India have also entered the same journey.

9 March 2020INSIGHT

cashflow is reinvested back into the business, every three to five years, the size of the franchise doubles. Now, if we consider the Finance Minister’s new tax regime, the market leaders which doubles their franchise sizes in every three years or more conservatively even five years, will end up paying lower effective tax rate as its doubles capacity. However, this is not possible for competitors who do not generate enough free cashflow to grow their capacity. And given the state of the country, banks are not going to finance doubling of capacity. Hence, five years down the line, market leaders’ effective tax rate will be much lower at 17-18% compared to 25% for inefficient competitors. This 7% tax rate differential is huge. The laggard competitor will either get sold to the market leader or become an outsourced manufacturer to the market leader or might wind up. This lower tax rate of 15% for setting up new manufacturing facilities is a potent weapon in the hands of market leaders.

Next is GST, which is also a very powerful weapon for the market leading franchises. Based on rough estimates, ~30 crore Indians – i.e. around half of our workforce - work in retail/logistics sector. Most of these people haven’t paid tax before and now they are forced to pay GST, which has squeezed their profit margins from 12-14% earlier to ~3%. Thus, these shops are facing a working capital crunch to buy the next consignment of manufactured products from the wholesaler. These retailers will also not get easy finance from high street banks since most of them don’t possess three years of financial statements. The easy option to get finance earlier was through NBFC channel, which is also running dry. Thus, the only option left for the retailers is to get financing from manufacturers. Here again there would be two possibilities, one, where the market leader given its financial strength and firepower will find it easy to convince banks to finance its

channels at ~8% with no-recourse to market leader’s balance sheet while the laggard competitor which doesn’t have the financial strength & stature can only manage financing of its dealers at ~12-15% with recourse to its balance sheet. Thus, on the high street there are two types of retailers, one that of market leaders with low cost, abundant financing and other one of the laggard with high cost, limited financing. The high street will thus polarize in favour of market leader and its products have better chances of sitting on shelves of supermarket stores due to its competitive deals which are unlikely to be provided by laggards.

This process of manufacturing consolidation and retail consolidation is already happening in India and at bewildering speed. This process will result in economic polarizing in the hands of 50 market leading franchises who will end up becoming giants over the next 10 years and the moats around these are also very powerful – one is GST and the other is the lower corporate tax rate. These two are the irreversible government

created moats for market leading franchises. The only thing that is pending is land law reforms sine the 2013 land acquisition Act has resulted in acquisition of land at four times of market price. If the Govt. liberalizes the Act, there will be frenzy of land acquisition by the market leaders. This could speed up the formalization process in India and what America achieved in 50 years (1880-1930) could arguably be achieved by India in 15 years.

Q: These businesses with strong brands, moats and high return of capital, these are consistent businesses which are also not hit hard by recessions, there are however businesses which are cyclical in nature, like for e.g. metals or chemicals or agribusinesses. How do an investor deal with these kinds of businesses?

A: If we focus on non CCP (consistent compounders) businesses which don’t have stable, sustainable, recurring cashflows, there are two types of non-CCP businesses. Most of them don’t have the ability to generate free cashflow at all whether it be in an economic boom or bust whether it be steel, real estate, power, infrastructure companies etc,. If a business has not been able to generate free cashflows in last 12 years, then the value of business is either zero or close to zero. It is highly unlikely that these companies which couldn’t generate free cashflow in last 12 years, will be able to do so in future. For these non-free cashflow companies which makes up 35 of the Nifty 50 list, their enterprise value is the value of debt only since value of equity is zero and the banks would own these. Post IBC-NCLT, banks are ending up owning these companies and shareholders are irrelevant logically, financially and practically.

The second type of non-CCP companies which are interesting to look at is the auto sector. Six out of ten years, the ROCE of auto majors like Maruti, Hero Motocorp

If a business has not been able to generate free cashflows in last 12 years, then the value of business is either zero or close to zero. It is highly unlikely that these companies which couldn’t generate free cashflow in last 12 years, will be able to do so in future.

10March 2020 INSIGHT

will be 25% plus, well above the cost of capital and generating free cashflow. They will re-invest that free cashflow in new plants, new models and over 10 years may clock ~12-13% EPS growth. With these sorts of companies where there are genuine moats, there is genuine ability to create free cashflow, but the problem is they can’t do it every single year. They do it in 6-7 years out of 10 and 3-4 years they won’t be able to generate free cashflow. For these sorts of companies, there is a style of cyclical investing which might work. There is merit in saying that once an economic downturn has progressed for 2-3 years; one should look at buying best of these sort of franchises. Auto companies, Genset manufacturers, T&D companies would fall into this bracket. Note however, that CCP is barely 1% of the Indian stock market, and out of the remaining 99%, only 1/10th falls into this sort of non-CCP companies (i.e. cyclical companies) and hence are worth considering. 90% of Indian stock market falls into the category of non-CCP, non-free cash flow generating franchices (regardless of the state of the economy) and hence are inherently worthless and to be avoided at all cost. Unfortunately, the majority of Indian large cap portfolios are made up of such companies where there is no underlying free cashflow generation whatsoever.

Q: Where do you see the real tailwinds in years to come. Sectors or themes worth considering?

A: Formalization is an epic tailwind for the Indian markets. For a company with strong cashflow, strong balance sheet and deep moats, India is a glass half full and there is ocean of opportunities to fill up that glass. If on the other hand, you are running a weak franchise with weak moats, weak competitive standing and have historically survived by gettinh PSU banks to provide loans

and/or by doing tax evasion, you are clearly faced with challenging circumstance and a very weak future. Such franchises will have to probably sell their businesses.

Q: What’s your view on the new age businesses which are platform based and have network effect, low marginal cost of acquiring new customers and there is scale? The ROEs could be ever expanding for these kinds of businesses and cash generation could be large.

A: Asian Paints is actually one such business given its dealer network, IT system, collection of data. That’s why decade upon decade, Asian Paints’ profit margins and ROCEs keep climbing because they are using a virtuous cycle of network effects to deepen their data moats, to deepen their collection of market data. Better collection of market data is giving them accurate forecasting of demand at the dealer level and better forecasting of data is giving them lower working capital cycles. This is giving them higher ROCEs that is allowing them to be even more competitive which is resulting

in better collection of data. So Asian Paints is a very good example of network effects.

Similarly, Dr. Lal PathLabs is also a very good example of using information technology and using the effect of virtuous cycles to locate franchises in optimal fashion. So, what Google and Amazon have done globally, our Indian giants are doing it locally. HDFC Bank’s CASA network has very similar dynamics - the CASA network feeds on itself, it creates network economics and gives HDFC Bank the lowest cost of funds after SBI, thus enabling HDFC Bank to earn NIMs of 4.2-4.3% with almost no NPA cost. So, the theory expounded is perfect. The skill in successful investing is to see the application of the theory, not just in America but back closer home in India in world class franchises which have been built under our very nose and which are growing like a rocket as India formalizes its economy.

Q: Majority of these businesses with strong moats, strong financials and free cashflow generation looks to be quite expensive. Are there pockets of investing avenues which are not that expensive?

A: The way to understand whether a company is expensive or not is to use DCF becuase P/E multiple doesn’t take you very far. Nestle’s P/E multiple twenty years ago was identical to what it is today. The stock has given 20% compounded return in the intervening period. Asian Paints’ P/E multiple 20 years ago was identical to what it is today, the stock has delivered 100 times. HDFC Bank’s P/B 10 years ago was what it is today, the stock has given 12 times. There is no link in Indian large cap, midcap, small cap between P/E and subsequent returns. If people out there look at P/E and invest, they are not going to make very much money in India.

Disclaimer: Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Formalization is an epic tailwind for the Indian markets. For a company with strong cashflow, strong balance sheet and deep moats, India is a glass half full and there is ocean of opportunities to fill up that glass.

11 March 2020INSIGHT

Consistent Compounders is a PMS strategy launched by Marcellus Investment Managers in December 2018 to invest in a concentrated portfolio of heavily moated companies which can drive healthy earnings growth over long periods of time.

The Portfolio construction involves two stage process: 1) a filter based approach to create an investible universe of 30-35 stocks; 2) in-depth bottom-up research of such companies in the universe to assess sustainable competitive moats to build a portfolio of 10-20 stocks that deliver healthy compounded earnings growth over long periods of time.

Such a portfolio is monitored for sustainability of moats on a continuous basis through extensive primary research. Repeating the filters annually helps keep the investible universe updated and also such a universe is continuously researched for developing or strengthening of moats to augment the portfolio.

Strategy:The Filter Based Approach creates a list of stocks using a twin-filter criterion of double-digit YoY revenue growth and return on capital being in excess of cost of capital, each year for 10 years in a row. Next a portfolio of such stocks each year are created and taken each of these annual iterations of portfolios for the subsequent 10 years (without any churn).

Unique DNA of these companies: By “filtering in” companies with a history of very consistent fundamentals over very long time periods, the portfolio is skewed towards companies with a DNA built around relentlessly

deepening their competitive moats despite disruptive changes taking place both inside as well as outside the organization. More often than not, such DNA sustains over the subsequent 5-10 years investment horizon of the filter-based approach.

Power of compounding: Holding a portfolio of stocks untouched for 10 years allows the power of compounding to play out, such that the portfolio becomes dominated by the winning stocks while losing stocks keep declining to eventually become inconsequential.

Avoiding the pitfalls of psychology and reducing transaction costs: Being patient with a portfolio helps cut out ‘noise’ of trying to time entry / exit decisions. With no churn, this filter-based approach also reduces transaction costs. Consider two data points: (a) In a portfolio with 70% churn (average churn of large cap mutual funds), 20bps broking cost and 30bps impact cost, churn reduces the terminal value of the portfolio (after 10 years) by 10% (i.e. a drag of 120bps on the 10-year CAGR); and (b) deferring the 10% long term capital gains tax payable on the portfolio by 10 years enhances the terminal value of the portfolio by 8% (i.e. 100bps increase in the 10-year CAGR) vs a portfolio where capital gains are paid each year.

The above deep-dive stock-specific research help generate outperformance of 4-5% per annum over and above these filter-based portfolios which is achieved via 3 factors:

1. Portfolio concentration:

2. Ignorable consistency in historical fundamentals

3. Excusable blips in historical fundamentals are forgiven

Mutual Fund Overview MARCELLUS PMS STRATEGY - CONSISTENT COMPOUNDERS

12March 2020 INSIGHT

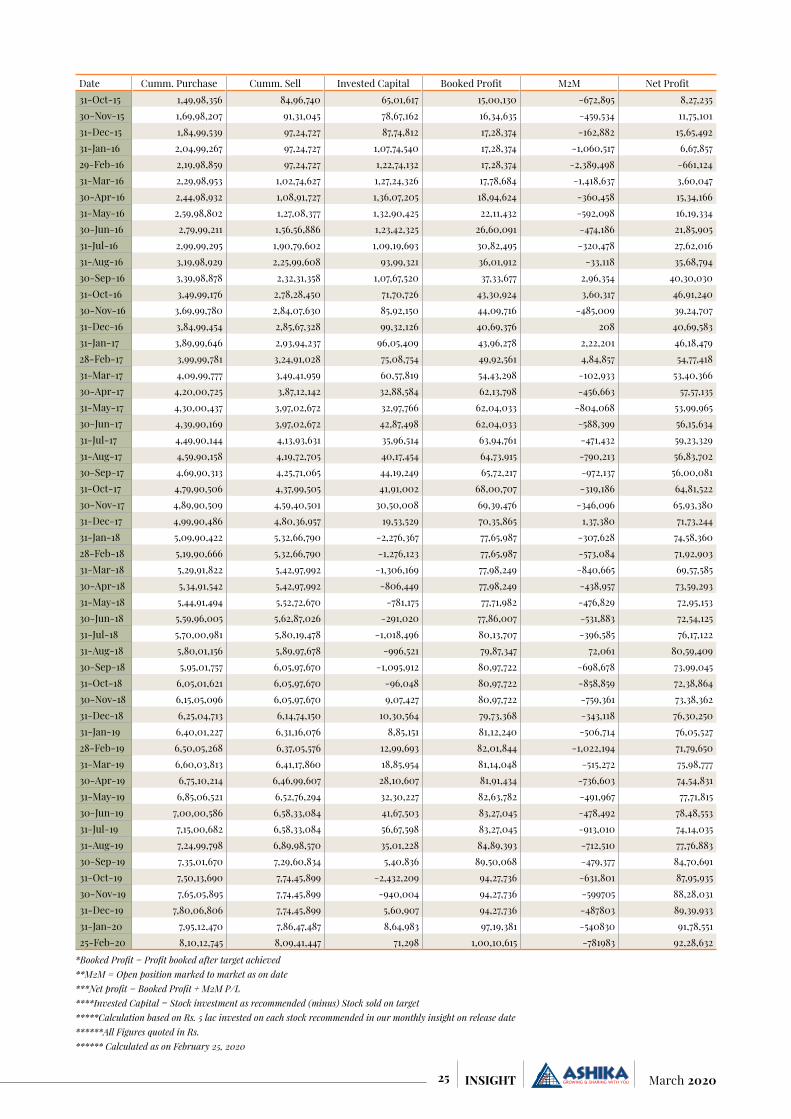

Ashika Mutual Fund Recommendation Alpha GenerationMonth of Recom

Fund Name Benchmark NAV as on 24.02.2020

1 Year Return

(%)

3 Year Return

(%)

5 Year Return

(%)

Mar-19 Mirae Asset Large Cap Fund NIFTY 200 53.4 12.78 11.41 10.24

Apr-19 SBI Focused Equity Fund S&P BSE 500 160.72 24.95 15.87 11.8

May-19 Invesco India Small Cap Fund S&P BSE 250 SmallCap TRI 12.12 27.41 - -

Jun-19 ICICI Prudential Multi Asset Fund Nifty 50 Total Return (70) 268.29 7.17 5.92 6.72

Jul-19 ICICI Prudential Asset Allocator Fund CRISIL Hybrid 50+50 Moderate Index

58.78 9.54 9.47 8.73

Aug-19 Reliance MultiCap Fund S&P BSE 500 98.36 7.94 8.94 5

Sep-19 Canara Robeco Emerging Equities Fund Nifty Large midcap 250 TRI 103.5 18.64 12.44 12.27

Oct-19 LIC MF large & Mid Cap Fund Nifty Large midcap 250 TRI 16.73 21.59 11.72

Nov-19 ITI Multi Cap Fund Nifty 500 TRI 11.13 - - -

Dec-19 Parag parikh Long Term Equity Fund Nifty 500 TRI 28.81 16.66 13.69 12.2

Jan-20 DSP Dynamic Asset Allocation Fund CRISIL Hybrid 35+65 Aggressive 16.48 11.41 7.47 7.4

Feb-20 Invesco India Growth opportunities Fund S&P BSE 250 Large Midcap 65:35 TRI

36.99 16.41 12.65 9.37

Note: All data are as on Jan 31, 2020; NAV are as on Feb 24, 2020, Source: Factsheet, Value Research

ALL DATA BELONGS TO 02/24/2020NAV AUM

(Rs Cr)3 M 6 M 1 Yr 3 Yr 5 Yr Since

Inception Return

Sharpe Ratio

Exp. Ratio

SBI - Large & Midcap Fund Reg (G) 239.17 2978 6.62 17.96 16.42 10.30 8.97 13.92 0.53 2.2Invesco - India Growth Opportunities Fund (G) 36.99 2447 3.30 14.38 16.50 12.65 9.37 10.99 0.66 2.04Kotak - Equity Opportunities Fund (G) 131.75 3188 5.82 17.35 19.47 10.29 9.65 18.11 0.54 2.02LIC - Large & Mid Cap Fund - Reg (G) 16.74 639 6.44 18.10 21.72 11.72 0.00 10.85 0.51 2.5Sundaram - Large and Mid Cap Fund (G) 37.57 1110 2.75 16.82 17.66 12.02 10.57 10.73 0.61 2.19

Large & Mid Cap Fund

Performance: The filter-based portfolio delivers returns of 20-30%

p.a. and 8-12% outperformance relative to the Sensex.

The volatility of returns of such portfolios, for holding periods longer than 3 years, is similar to that of a Government Bond

Returns here (both for our portfolio and for the Sensex) are on a Total Shareholder Return basis i.e. all dividends are included in the returns.

Fee Structure:Marcellus offers Consistent Compounders Portfolio with zero fixed fees

The Consistent Compounders PMS comes with ZERO entry load/exit load and with no lock-in. Clients can choose any of the following fee structures:

1. a fixed fees model (2% p.a. fixed fees + zero performance fees) or

2. a variable fees model (zero fixed fees + performance fees of 20% profit share above a hurdle of 8%, no catch-up)

3. a hybrid model (1% p.a. fixed fees + performance fees of 15% profit share above a hurdle of 12%, no catch-up).

Minimum investment: Rs. 50 lakhs

Source: Bloomberg. Note: Only the Consistent Compounder Portfolios which have finished their 10 year run have been shown. Note: These are total shareholder returns.

13 March 2020INSIGHT

Value FundALL DATA BELONGS TO 02/24/2020

NAV AUM (Rs Cr)

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

SBI - Contra Fund Reg (G) 103.12 1367 0.76 9.32 2.11 2.37 2.66 17.06 0.02 2.34UTI - Value Opportunities Fund (G) 65.71 4634 4.86 16.69 15.44 9.12 5.47 13.70 0.45 1.78Nippon India - Value Fund (G) 75.51 3114 2.07 12.98 12.16 8.89 7.23 14.70 0.35 2Kotak - India EQ Contra Fund (G) 55.55 900 2.53 12.36 12.52 11.96 8.60 12.47 0.69 2.32Invesco - India Contra Fund (G) 50.95 4751 5.57 16.46 14.86 12.20 10.05 13.48 0.56 1.93

Focus Fund

Axis - Focused 25 Fund Reg (G) 31.7 9627 5.28 17.84 25.20 15.93 11.89 16.14 0.83 1.85

Mirae - Asset Focused Fund Reg (G) 11.77 2701 1.03 15.28 0.00 0.00 0.00 21.32 - 1.97

SBI - Focused Equity Fund Reg (G) 160.73 7694 6.52 20.56 25.11 15.87 11.80 19.62 0.82 2.03

Motilal Oswal - Focused 25 Reg (G) 24.4 1220 3.55 17.61 22.49 10.38 8.35 13.92 0.49 2.22

Sundaram - Select Focus Reg (G) 194.75 1074 2.50 12.57 18.04 13.21 8.18 18.36 0.76 2.18

ELSS Fund

Mirae - Asset Tax Saver Fund Reg (G) 18.98 3293 1.62 13.47 16.61 13.70 0.00 16.65 0.8 2.05

Kotak - Tax Saver Scheme (G) 48 1155 5.06 15.61 18.31 9.93 8.74 11.62 0.53 2.49

Motilal Oswal - Long Term Equity Fund Reg (G) 19.2 1725 5.09 19.41 21.02 10.70 12.96 13.66 0.56 2.12

DSP - Tax Saver Fund Reg Fund (G) 51.59 6381 1.63 12.59 17.68 9.33 9.91 13.34 0.41 1.96

SBI - Long Term Equity Fund Reg (G) 143.69 7582 0.50 11.25 6.89 5.49 4.62 15.20 0.2 1.97

Multi Cap Fund

Parag Parikh - Long Term Equity Fund Reg (G) 27.71 2784 5.25 13.61 15.83 12.94 11.51 16.20 0.85 2.02

SBI - M Multicap Fund Reg (G) 51.49 8760 2.09 11.35 14.82 9.33 9.96 12.07 0.5 2.01

Kotak - Standard Multicap Fund (G) 37.57 30546 2.16 12.82 15.82 10.49 9.96 13.30 0.56 1.63

ICICI Pru - Multicap Fund Reg (G) 291.26 5197 (0.39) 8.32 7.09 6.60 7.65 14.19 0.33 2.24

DSP - Equity Fund Reg (G) 45.28 3502 8.35 20.96 27.62 12.90 9.72 12.60 0.54 2.07

Small Cap Fund

Invesco - India Smallcap Fund Reg (G) 12.12 522 14.77 31.17 27.58 0.00 0.00 15.00 - 2.54

SBI - Small Cap Fund Reg (G) 57.05 3493 6.10 19.66 19.40 13.30 13.95 18.10 0.54 2.26

Axis - Small Cap Fund Reg (G) 34.97 2084 11.51 24.05 35.07 14.82 12.56 22.21 0.75 2.04

Kotak - Smallcap Fund (G) 79.15 1592 11.31 24.89 22.22 6.42 8.93 14.78 0.23 2.15

ICICI Pru - Smallcap Fund Reg (G) 27.33 1030 9.23 19.50 25.83 5.61 5.61 8.47 0.16 2.43

Thematic/Sectoral Fund

Franklin - Build India Fund (G) 40.13 1208 (3.03) 7.01 6.31 4.48 6.82 13.96 0.19 2.51

ICICI Pru - Banking & Financial Services Fund Reg (G)

68.14 3615 0.71 15.00 17.69 11.29 12.49 18.13 0.54 2.12

Kotak - Pioneer Fund (G) 10.41 717 3.55 0.00 0.00 0.00 0.00 11.21 - 2.73

Sundaram - Services Fund (G) 13.5 1304 10.58 27.19 31.65 0.00 0.00 22.28 - 2.37

Aditya Birla SL - Digital India Fund Reg (G) 58.63 440 9.59 10.98 11.13 17.94 9.88 6.95 1.04 2.52

Blance/BAF Fund

SBI - Equity Hybrid Fund Reg (G) 148.92 32585 3.87 12.84 18.50 11.78 9.40 15.32 0.71 1.72

Sundaram - Equity Hybrid Fund Reg (G) 98.83 1876 3.77 12.91 15.86 10.58 8.28 12.64 0.61 2.21

ICICI Pru - Balanced Advantage Fund Reg (G) 37.98 28853 1.31 8.95 12.00 8.57 8.42 10.55 0.71 1.75

Kotak - Balanced Advantage Fund Reg (G) 11.29 3719 1.69 8.55 12.77 0.00 0.00 7.79 - 2.15

Aditya Birla SL - Balanced Advantage Fund (G)

55.43 2736 0.69 7.86 10.13 5.94 8.07 9.00 0.25 2.04

14March 2020 INSIGHT

Arbitrage Fund

Aditya Birla SL - Arbitrage Fund Reg (G) 20 5769 1.27 2.73 6.28 5.98 6.27 6.76 0.4 0.85

ICICI Pru - Equity Arbitrage Fund Reg (G) 25.73 13739 1.22 2.59 6.05 5.95 6.30 7.45 0.29 0.93

Kotak - Equity Arbitrage Fund (G) 27.85 17856 1.25 2.68 6.20 6.15 6.39 7.37 0.66 0.98

Nippon India - Arbitrage Fund (G) 19.99 10497 1.23 2.64 6.20 6.23 6.49 7.63 0.69 1.08

SBI - Arbitrage Opp Fund Reg (G) 25.38 5253 1.29 2.60 6.28 6.01 6.18 7.25 0.31 0.91

Index Fund

HDFC - Index Fund-NIFTY 50 Plan - (G) 108.03 1064 (0.76) 9.20 10.42 10.73 7.13 14.20 0.58 0.3

ICICI Pru - Nifty Next 50 Index Fund Reg (G) 24.88 618 0.01 10.64 7.67 5.13 7.74 9.83 0.15 0.85

HDFC - Index Fund - Sensex Plan 358.66 722 (0.14) 9.81 13.17 12.57 7.87 14.67 0.71 0.3

SBI - Nifty Index Fund Reg (G) 101.64 514 (0.91) 8.96 9.94 10.29 6.59 14.25 0.55 0.69

ICICI Pru - Nifty Index Fund Reg (G) 114.65 517 (0.77) 9.24 10.30 10.14 6.63 14.61 0.54 0.45

Dynamic/Multi Assets

Invesco - India Dynamic Equity Fund (G) 30.58 870 0.57 27.44 (28/02/2019)

1.97 8.52 11.36 4.39 0.34 2.16

ICICI Pru - Asset Allocator Fund (FOF) (G) 58.79 6941 1.47 53.6284 (27/02/2019)

1.23 6.51 9.60 9.46 0.91 1.36

DSP - Dynamic Asset Allocation Reg (G) 16.49 1224 1.23 14.813 (28/02/2019)

2.97 9.04 11.48 7.72 0.51 2.41

SBI - Dynamic Asset Allocation Fund (G) 13.55 664 0.90 13.0557 (22/08/2019)

(0.67) 3.54 3.44 3.49 0.51 2.02

Disclaimer: Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

SolutionsNAV AUM Mod

Duration (in Yrs)

AMP (IN Yrs )

3 M 6 M 1 Yr 2 Yr Sharpe Ratio

Exp. Ratio

ICICI Pru - Retirement Fund Pure Debt Plan (G)

11.18 370 - 10 (27/02/2019)

3.01 5.07 11.79 0.00 - 2.07

Aditya Birla SL - Retirement Fund 30s Plan (G)

10.42 129 - 9.061 (22/08/2019)

1.96 14.33 4.18 0.00 - 2.65

HDFC - Retirement Savings Fund Hybrid Equity Reg (G)

17.39 387 0.68 15.736 (26/02/2019)

2.74 9.86 10.72 4.67 0.45 2.73

Aditya Birla SL - Bal Bhavishya Yojna Wealth Plan (G)

10.82 230 - 9.45 (22/08/2019)

1.88 13.89 8.20 0.00 - 2.6

Axis - Childrens Gift Fund Reg (G) 14.56 470 0.63 12.4304 (25/02/2019)

3.37 12.30 18.08 7.98 0.55 2.44

Equity Savings FundALL DATA BELONGS TO 02/24/2020

NAV AUM (Rs Cr)

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

HDFC - Equity Savings Fund (G) 37.33 4168 (0.07) 3.90 5.67 5.59 7.58 8.92 0.14 1.97

ICICI Pru - Equity Savings Fund (G) 14.78 1553 1.86 6.79 11.21 7.19 7.59 7.82 0.6 1.39

Kotak - Equity Savings Fund Reg (G) 15.03 1804 1.56 6.27 8.67 7.74 7.39 7.78 0.59 2.1

Axis - Equity Saver Fund Reg (G) 13.65 820 2.25 6.81 10.35 8.68 0.00 7.02 0.51 2.32

SBI - Equity Savings Fund Reg (G) 13.75 1567 1.88 7.82 10.04 6.45 0.00 6.86 0.23 1.7

15 March 2020INSIGHT

STOCK PICKS

Britannia Industries Ltd.CMP: Rs 2,962 Rating: BUY Target: Rs 3,400

Company InformationBSE Code 500825NSE Code BRITANNIABloomberg Code BRIT INISIN INE216A01030Market Cap (Rs. Cr) 71,455Outstanding shares(Cr) 24.052-wk Hi/Lo (Rs.) 3583.75 / 2300Avg. daily volume (1yr. on NSE) 4,83,971Face Value(Rs.) 1Book Value 165.8

Investment RationaleNew product launchesBritannia Industries Ltd. (BIL) continues to remain committed in launching new products which are futuristic and highly differentiated in nature, targeting various markets at the same time. The recent new launches (contribute ~3% to overall revenue) performed well, finding strong acceptance in most markets. The company is also focusing on fine tuning the existing brands and then scaling its launches. As is evident from the cake business which saw a relaunch of bar, veg and tiffin cakes and introduction of new formats like swiss rolls, layer cakes, brownies and muffils. During Q4, the company is expected to come up with four new launches – Treat Burst, Treat Stars, Whole Wheat Marie and Milk Bikis Choco Cream. Further, BIL plans to fine tune its products in new cate-gories like Croissants (national roll out in next 3-4 months), Salty Snacks (national roll out in 6 months) once demand pick up is visible. Wafers is doing well and BIL is already a No. 3 brand with a 10% market share.

However, the wafers market segment is highly fragmented and largely operates in trade promotions, but BIL has differentiated by giving freebies to ensure it creates a Pull brand than being a Push brand. In bread, the company continued its focus toward driving profitable growth while dairy business profitability was impacted due to significant upsurge in milk prices. Several additional investments led growth initiatives such as investments in the value added dairy segment, Chitpita JV (Greek company) for manufacturing and selling long life filled croissants has been gaining result. Hence some new launches have already started to yield result (~2.5% of revenue) and for some category extension will help the company to increase its market share going ahead.

Distribution reach to drive growthBritannia Industries is one of the companies with the lowest depen-dency on the wholesale channel for its domestic business. Increased direct reach and lower dependence

on wholesale channels have benefited BIL in last three years. Britan-nia’s direct distribution reach increased by 2.9x to 21.7 lakh outlets in last 5 years and total distribution reach currently stands at 55 lakh outlet increased from 36 lakh outlets 5 years ago. Hence the gap with market leader has narrowed down to 8 lacs during the quarter. Rural distribution (preferred dealers) has grown to 21,000 villages at end of Dec-2019 compared to 18,000 in Mar-2019. Company wit-nessed unprecedented gain in market share in all rural states, especially the Hindi belt, as it continues to strengthen its distribution network. Management targets to cross 6 mn outlets mark over the next three years to expand its distribution network.

Prudent cost management helps margin expansionBritannia has taken various cost saving measures in the past few years which help the company to considerably improve the margin from 11.0% in FY15 to 15.9% in 9MFY20. The margin expansion was primarily

Promoters 50.6%

DII 13.6%

FII 15.8%Others 20.0%

Share holding pattern as on Dec 2019

16March 2020 INSIGHT

attributable to cost efficiencies achieved through management initiatives such as use of renewable energy, rainwater harvesting and commodity hedging. Recent food inflation shot up cost of raw mate-rials (mainly dairy up 42% YoY), but company’s contract of raw materials, strong cost cutting measures and waste deduction techniques pro-pelled EBITDA margins. Management is also eyeing vertical integration such as in-house sourcing of whey for biscuit. Moreover, the company plans to reduce its dependency on third-party manufacturers and wants to focus on in-house capacity. Right now, the in-house to outsourced offerings ratio stands at 55:45, which will be 65:35 by FY20, as envisaged by the company. Further, the manage-ment indicated that the focus is going to be on driving revenue growth rather than volume growth and that it would go for a price hike to offset the inflation in raw material prices. Management expects to implement price increases selectively and con-tinues to target cost savings at 2.1% of revenue. Company is confident to expand margins moderately led by its relentless focus on cost saving initiatives, premiumization drive and scale benefits

Venture into new geographyManagement has plans to enter one new geography every year. It entered Nepal in FY19 and has ~17-18% market share. With in-house manufacturing, management expects Britannia’s Nepal business is likely to see margin expansion of ~600bps owing to no import duty. The company is expected to increase capacity in

Nepal form current capacity of 600tonnes to 1,200 tonnes with small investment. Overall capex in Nepal is pegged at ~Rs. 55 cr, which management estimates to yield ~Rs. 100- 150 cr revenue in three years on p.a. basis. The company has large part of its international business in the Middle East, where it has two overseas manufacturing units in Dubai and Oman. It is looking to create a hub-and-spoke model to get into more and more markets like Myanmar and the African continent. The company is presently considering entry in tougher market like Bangla-desh which is characterized by many players.

Q3FY20 Result AnalysisCompany continued to report decent

growth in all front in Q3FY20. Consolidated revenues grew by 3.8% YoY at Rs. 2936 cr marked by volume growth of 3% YoY on the back of domestic slump in urban and rural demand. According to management, about half of growth was contributed by

its base business, with new innova-tion and new categories contributing 1% each to the topline. Its increased efforts on reducing trade inventory and rising freshness alsohad some impact on volumes. The Company has shown increase in its operating profits by 11.1% YoY to Rs. 502 cr while Operating Profit margin increased by 94 bps on YoY basis to 16.8%. Opera-tional margins surprised positively on back of moderate RM inflation (due to forward cover on key RMs) and enhanced focus on cost saving initiatives (partly aided by flat A&P spends). PBT stood at Rs. 497 crore, up by 6.8% YoY. Net Profit of the company has increased by 22.9% YoY to Rs. 370 cr while Net Profit margin increased by 181 basis points for Q3 on YoY basis to 12.4%. Net Profit growth aided by corporate tax rate reduction as tax decline by 23.2% to Rs. 127 cr.

Key Risks Rising competitive intensity

especially from large organized / unorganised regional players can potentially result in volume pressures Rise in the raw material prices

like wheat, flour, RPO, milk without commensurate hike in product prices can lead to pressure on the gross margins. Prolonged slowdown particularly in

rural areas, will lead to slowing of the category growth rates.

ValuationBritannia is the leader in the biscuit category in terms of value. Despite the challenging environment the company managed to continuously improve its market share. Major pos-itive for Q3FY20 was EBITDA margin expansion in spite of inflation in key raw materials prices. Cover on input prices and company’s cost saving initiatives with flat advertisement expenses helped in expansion in EBITDA margin. BIL initiatives of new launches and innovations, distribu-tion expansion (reducing gap with market leader) and judicious pricing (to be competitive in the market) will lead to better growth than peers. Improving product mix (premium growing faster than value category), moderate competitive intensity, modest price hike (to offset raw material inflation) and sharp focus

Britannia Industries Ltd. Price Chart

0 200 400 600 800 1,000 1,200 1,400 1,600 1,800 2,000

2200

2400

2600

2800

3000

3200

3400

3600

Feb-

18

Apr-

18

Jun-

18

Aug-

18

Oct

-18

Dec

-18

Feb-

19

Apr-

19

Jun-

19

Aug-

19

Oct

-19

Dec

-19

Total Traded Quantity Britannia

Despite the challenging environment the company managed to continuously improve its market share. Major positive for Q3FY20 was EBITDA margin expansion in spite of inflation in key raw materials prices.

17 March 2020INSIGHT

on cost optimization (cost savings target for the current year is 2.1% of revenue) should continue to support operating margin trend. Recovery in the biscuit category’s growth and a scale-up in performances of new products and adjacencies (including dairy and bakery businesses) would help Britannia record better earnings

in the near to medium term. Going forward, it is expected that company’s thrust on distribution expansion and category expansion with pre-miumization to drive growth. While judicious pricing and strategic input buying with cost saving measures will help in better margins. Considering government rural initiatives, we

are optimistic of bouncing back of demand in few quarters time. Hence, we hold positive view on the scrip and recommend BUY with a target price of Rs. 3400 from 12 - 18 months investment perspective. Currently, the scrip is valued at P/E multiple of 44x on FY21E Bloomberg consensus EPS of Rs 67.3.

Valuation charts

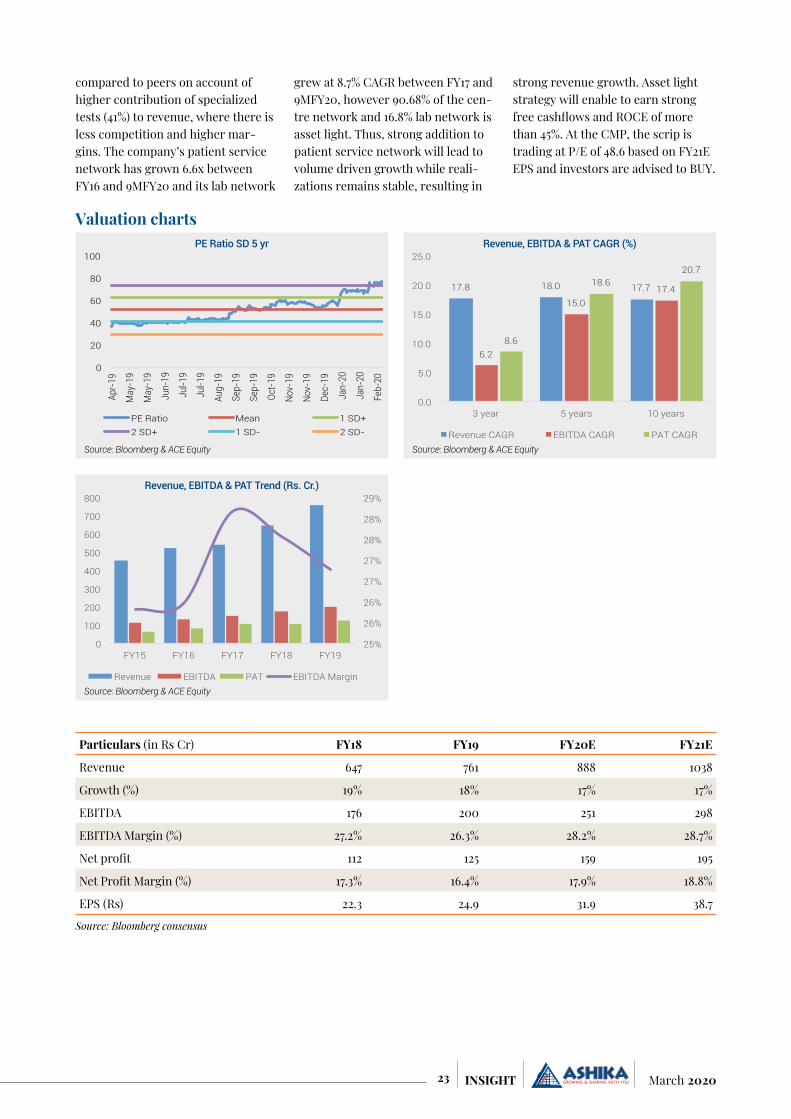

Particulars (in Rs Cr) FY19 FY20E FY21E FY22ENet Sales 11054.7 11784.3 13045.2 14519.3Growth (%) 11.5 6.6 10.7 11.3EBITDA 1733.4 1873.7 2126.4 2424.7EBITDA Margin (%) 15.7 15.9 16.3 16.7Net profit 1156.4 1402.3 1617.6 1858.5Net Profit Margin (%) 10.5 11.9 12.4 12.8EPS (Rs) 48.2 58.3 67.3 77.3

Consensus Estimate: Bloomberg, Ashika Research

PE Band

Source: Bloomberg & ACE Equity

0

1000

2000

3000

4000

5000

Apr-1

5 Au

g-15

De

c-15

Ap

r-16

Aug-

16

Dec-

16

Apr-1

7 Au

g-17

De

c-17

Ap

r-18

Aug-

18

Dec-

18

Apr-1

9 Au

g-19

De

c-19

Ap

r-20

Aug-

20

Dec-

20

Price 35x 40x 45x 50x 55x

Revenue, EBITDA & PAT CAGR (%)

Source: Bloomberg & ACE Equity

10.5 8.9

12.7

16.5 19.0

30.1

14.4 13.8

30.8

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

3 year 5 years 10 years

Revenue CAGR EBITDA CAGR PAT CAGR

P/E Median

Source: Bloomberg & ACE Equity0x 10x 20x 30x 40x 50x 60x

8 Years

5 Years

3 Years

PE Ratio SD 5 yr

Source: Bloomberg & ACE Equity

30

40

50

60

70

80

90

Jan-

15

May-

15

Sep-

15

Jan-

16

May-

16

Sep-

16

Jan-

17

May-

17

Sep-

17

Jan-

18

May-

18

Sep-

18

Jan-

19

May-

19

Sep-

19

Jan-

20

PE Ratio Mean 1 SD+ 2 SD+ 1 SD- 2 SD-

Revenue, EBITDA & PAT Trend (Rs. Cr.)

Source: Bloomberg & ACE Equity

10%

11%

12%

13%

14%

15%

16%

0

2,000

4,000

6,000

8,000

10,000

12,000

FY15 FY16 FY17 FY18 FY19

Revenue EBITDA PAT EBITDA Margin

18March 2020 INSIGHT

STOCK PICKS

Aarti Industries Ltd.CMP: Rs 980 Rating: BUY Target: Rs 1,177

Company InformationBSE Code 524208NSE Code AARTIINDBloomberg Code ARTO INISIN INE769A01020Market Cap (Rs. Cr) 17,041Outstanding shares (Cr) 17.42 52-wk Hi/Lo (Rs.) 1071.0/676.8Avg. daily volume (1yr. on NSE) 128,260 Face Value (Rs.) 5Book Value (Rs) 169.0

Company profileIncorporated in 1984, Aarti Industries ltd. is a leading specialty chemicals company in Benzene based deriva-tives with integrated operations and high level of cost optimization. Aarti operates in two division, specialty chemical account 84% of total revenue and pharma contributes 16% of turnover. Company’s pharma operations include APIs, intermedi-ates and Xanthene derivatives. It has 11 plants for specialty chemicals and 4 for pharma (2 USFDA and 2 WHO/GMP). Further, another 2 projects are coming at Dahej SEZ and setting up 4th R&D center at Navi Mumbai.

Investment RationaleLargest benzene derivatives producerAarti Industries is the largest pro-ducer of benzene derivatives in India and leading manufacturer globally. Globally, it has strong market share with most of its products having market share in the range of 25-40%. Further, 75% of its specialty chemical products are commanding a position in Top-4 in their respective catego-ries. Aarti is the third largest player globally in chlorination, fourth in the world in nitration, globally second in ammonolysis, second largest in the world in hydrogenation, and is the first and only player in India

to commercialize manufacturing of flouro compounds via Halex chemistry. It has a diversified product portfolio with relative low dependency on individual products. Company’s top 5 products contrib-ute nearly 39% of the consolidated revenue, while the top 10 products contribute 58% of revenue. It has also a diversified customer base across North America, Europe, Japan, China and RoW and no single company/customer accounts for more than 5% of consolidated revenue. Aarti’s top 10 customers contribute 27% of consolidated revenue while top 20 contribute 38% of revenue. Company is also focusing on innova-tion in order to effectively utilize its

Promoters 48.3%

FIIs 7.5%

DII 16.7%Others 27.6%

Share holding pattern as on Dec 2019

19 March 2020INSIGHT

by-products and generate additional revenue. Diversified product portfo-lio and customers help the company to mitigate the concentration risk from business model.

Focus on moving up the value chainAarti industries has a integrated business model and management continued its focus in moving up the value chain yielded positively for the company. Company has presence in both the chains (Simple & Advance) and sells 30% commoditized and 70% in the complex. Advanced products have higher gross margins (USD 800-1000 per tonne vs USD 400-600 per tonne) compared to simple products which help the company to sustain healthy margins. However, in simple product division the market size is much bigger than advanced. Aarti has strong market share of around 50-70% in complex segment, while 30-40% market share in simple category. First mover advantage and scale benefits help the company to be the low cost of producer compared to standalone players. Aarti’s presence across the value chain with scale is a key moat for the company.

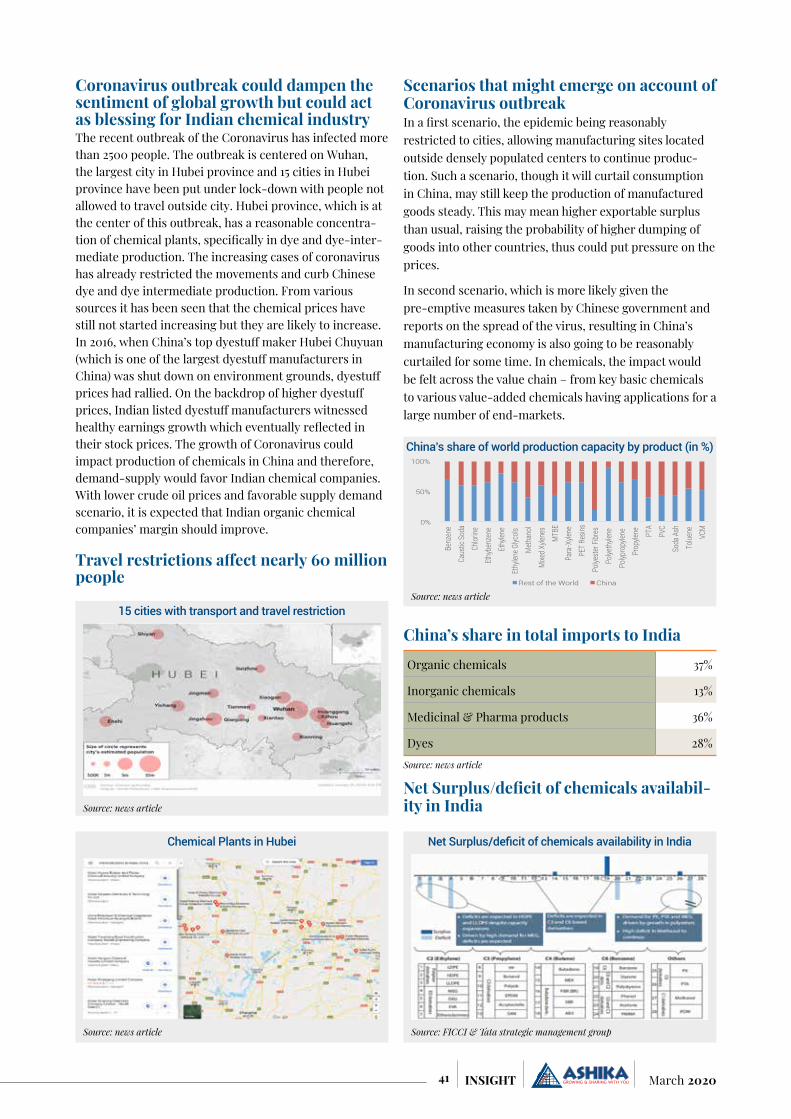

Coronavirus epidemic throws opportunity for chemical sectorThe recent outbreak of coronavirus in China which infected around 77,000 people and death toll of around 2,500, lockdown the manufacturing activities in the mainland. China is one of the largest chemical manufac-turers globally, shutting down their plants amid threat of coronavirus and that benefit the Indian integrated

chemical companies like Aarti indus-tries. For integrated chemical man-ufacturers such as Aarti Industries, it could mean new opportunities because of the growing preference for India as an alternative reliable supplier of chemicals. Over the years, supply chain disruptions in China due to operational hazards, environ-mental compliance issues and higher cost of operations have made the case for this likely shift. A 5-10% business shift to India can actually more than double the opportunity size for many chemical companies. As per man-agement, its chemical business is not dependent on imports from China as its operation is fully backward integrated. Overall, coronavirus outbreak in China is a positive for its specialty chemical business as far as demand and prices are concerned. As per the management, due to corona-

virus company’s market share will improve as it has been getting more orders from their existing custom-ers. Management also conveyed that more impact would start coming in from March onwards and company will have carry-for-ward orders

for a month or so. Thus, most of the impact will come from March onwards. Due to ongoing supply disruption from China led by environmental issues and followed by coronavirus epidemic, global innovators and generic companies are establishing alternative source for a steady and assured supply of intermediates. India on the other hand is a known alternative hub for chemicals and stands to bag a multi-year exports opportunity. Against this backdrop, Aarti Indus-tries is well-poised to cash out the growing opportunities because of its market leadership and strong global presence.

Growth backed by strong capexAarti industries growth story has been backed by capacity expansions and introduction of value-added products. Company embarked an ambitious capex plan to the tune of Rs 2100-2400 over FY19-21 compared to Rs 2740 over FY09-18. Company’s capex including investments towards long-term multi year deals, capacity expansions in hydrogenation and NCB, de-bottlenecking and expan-sions in various specialty chemicals, API and pharma intermediates and setting up new R&D center in Navi Mumbai. Management have positive visibility of long-term demand for their products, as a result they have continued to drive capital expenditure as per plan, spending Rs 830 crore in the first 9MFY20 and expects to close FY20 within guided range of Rs 1,000-2,000 crore. As per management, all its key projects including the expansion of chlorina-tion capacity, investments underlying various long-term contracts, etc. are on track and will be commissioned as per scheduled timelines. Timely, commissioning of all the capacities will support the long-term growth of the company.

Key Risks Any unfavorable movement in raw

material prices and resultant spike in working capital could adversely impact the margins of the company Any delay in commissioning

the new capacities and lower than expected offtake could hurt

Aarti Industries ltd 3 Year Price Chart

100 200 300 400 500 600 700 800 900

1000 1100

Feb-

17

Apr

-17

Jun-

17

Aug

-17

Oct

-17

Dec

-17

Feb-

18

Apr

-18

Jun-

18

Aug

-18

Oct

-18

Dec

-18

Feb-

19

Apr

-19

Jun-

19

Aug

-19

Oct

-19

Dec

-19

Aarti industries has a integrated business model and management continued its focus in moving up the value chain yielded positively for the company.

20March 2020 INSIGHT

company’s long-term revenue growth.

ValuationAarti is leading integrated specialty chemical manufacturer globally with strong product pipeline. Manage-ment’s continuous focus on increas-ing contribution from downstream products of chemical business and scaling presence in non-commod-itized segments at 75% are the most encouraging developments from business perspective. Further, com-pany’s diversified product portfolio and low dependency on single clients mitigate the concentration risks.

The coronavirus epidemic in China disrupted the supply chain of global chemical sector, resulting in shortage of raw materials. Aarti being an integrated specialty chemical and API manufacturer is going to benefit from acute supply shortage of key chemical ingredients on wake of coronavirus epidemic in China as far as demand and prices are con-cerned. Management have positive view on the long-term demand for their products, thus will continue to drive capex plan which will further underpin its long-term revenue growth visibility. In pharma business, margins are expanding as company

started to derive higher contribution from supplies to regulated markets and improve the product mix to more value addition. Also, Pharma capacity expansions are continuing which will drive deeper penetration in some key therapies such as antihypertensive, cardiovascular, oncology, corticoste-riods, etc. Overall, we believe, Aarti is on right track to achieve humongous growth in coming 2 to 3 years. Thus, we recommend our investors to BUY the scrip with target of Rs 1,177 from 12 months investment perspective. At current price, the scrip is valued at P/E multiple of 24.5 on Bloomberg consensus EPS of Rs 39.9.

Valuation charts

Particulars (in Rs Cr) FY18 FY19 FY20E FY21E

Revenue 3,759.3 4,659.5 4,629.0 5,602.7

Growth (%) 20.7% 23.9% -0.7% 21.0%

EBITDA 691.4 963.0 1,016.8 1,243.1

EBITDA Margin (%) 18.4% 20.7% 22.0% 22.2%

Net profit 328.6 490.6 561.1 694.4

Net Profit Margin (%) 8.7% 10.5% 12.1% 12.4%

EPS (Rs) 20.2 28.3 32.3 39.9

Source: Bloomberg consensus

PE Band - Aarti Industries Ltd.

Source: Bloomberg & ACE Equity

0.00

200.00

400.00

600.00

800.00

1000.00

1200.00

1400.00

01-Apr-15 01-Apr-16 01-Apr-17 01-Apr-18 01-Apr-19

Price 10x 15x 20x 25x 30x

Revenue, EBITDA & PAT CAGR

Source: Bloomberg & ACE Equity

12% 12%

16% 15%

19% 19% 18%

25% 24%

10 Years 5 Years 3 Years

Revenue CAGR (%) EBITDA CAGR PAT CAGR

Revenue, EBITDA & PAT trend

Source: Bloomberg & ACE Equity

2,908

2,956

3,115

3,759

4,659

466

566

652

691 96

3

206

256

315

329 491

0%

5%

10%

15%

20%

0

1,000

2,000

3,000

4,000

5,000

FY15 FY16 FY17 FY18 FY19

Revenue (Rs crs) EBITDA (Rs crs)

PAT (Rs crs) EBITDA Margins (%)

P/E Median

Source: Bloomberg & ACE Equity

29.5x

25.0x

17.4x

0.0x 5.0x 10.0x 15.0x 20.0x 25.0x 30.0x 35.0x

3 Years

5 Years

8 Years

21 March 2020INSIGHT

STOCK PICKS

Metropolis Healthcare Ltd.CMP: Rs 1,880 Rating: BUY Target: Rs 2,200

Company InformationBSE Code 542650NSE Code METROPOLISBloomberg Code METROHL INISIN INE112L01020Market Cap (Rs. Cr) 9,341Outstanding shares (Cr) 5.0252-wk Hi/Lo (Rs.) 1950/907Avg. daily volume (1yr. on NSE) 82,040Face Value(Rs.) 2Book Value (Rs) 97.98

Investment RationaleFormalization driven industry growthThe industry is expected to grow at 15% p.a. between FY19 & FY22, driven by population above 60 years old accounting for majority of healthcare spend. Besides, rising awareness, rising income and urbanization leads to preference for shifting trend from unorganized pro-viders to organized providers in the diagnostics market. There is

plenty of room for growth of orga-nized players since 80% of the market is catered by un-organized players. Favorable government incentives like tax breaks towards preventive testing could further add to volume growth. Besides, organized players could easily pass on price hikes of ~0.5% p.a to cover medical cost inflation despite increasing scrutiny from the regulators and government. In short, formalization in the industry will lead to market share gains of 5-7 major diagnostic chains at the cost of small

regional players or standalone labs.

Volume driven growth on increased B2C focusMETROHL organic growth strategy has been driven by consolidating its position in its 5 focus cities (Mumbai, Bengaluru, Chennai, Surat and Pune), accounting for 54% of revenue. It is focusing on increasing its sales contribution from the B2C channel (currently 43%) through increase in its collection centers and lab net-works. The B2C contribution in focus

Promoters 57.41%

DIIs 5.85%

FIIs 16.58%Others 34.98%

Share holding pattern as on Dec 2019

22March 2020 INSIGHT

cities of METROHL has increased from 43% in FY16 to 55% by 9MFY20 and is further targeted to reach 65%. The company’s patient service network has grown 6.6x between FY16 and 9MFY20 and its lab network grew at 8.7% CAGR between FY17 and 9MFY20. This growth in B2C network has enabled the company to clock 12.8% CAGR in number of patient vis-its and 9% CAGR in number of tests between FY17 & FY19. For 9MFY20, number of patients has grown at 15.5% yoy (after 15.6% yoy growth in FY19) and no. of tests at 19.3% yoy. Earlier, growth for tests as well as patient visits for METROHL used to lag peers. The growth in FY19 & FY20 have been after company invested heavily in infrastructure together with expansion of test offerings which is paying off. METROHL’s B2C segment has thus registered 22% sales CAGR over FY16-19 and the company is focusing on increasing its B2C contribution further through (a) aggressive network expansion (b) strengthen Metropolis brand (c) building awareness amongst doctors for quality & service differentiators (d) focus on customer experience & improvement. Besides, since 79% of the existing Individual patients touch points added during FY2017-19, it is a young network. According to the company, average retail centre matures in five years thus enabling short and midterm future growth as the young network matures.

Premium realization compared to peersMETROHL’s realizations are at premium compared to peers due to its evolving mix of B2C segment and higher contribution of specialized tests (41%) to revenue. According to the company, there are few players in the specialized test segment as market demands high accuracy and quality parameters, thus leading to lower competition and high margins on low volumes. This is in contrast to semi-specialized tests where there is intense competition. Revenue per patient has grown at a CAGR of 7.3% and revenue per test at a CAGR of 7.9% between FY16 and FY19, while realization has remained

flat for peers. Government’s intention to lower healthcare costs could be a major deterrent for METROHL to increase reali-zation further, however increas-ing contribution of international business could support the cause.

Asset-light business modelMETROHL works on an asset-light model and 90.68% of the centre network and 16.8% lab network is asset light. Major addition in the labs in FY19 and 9MFY20 is through lab on lease model which is asset light with no capital requirement. It is working on the hub & spoke model and expanding its third-party collection centers (currently 66% of its collec-tion centers are third party). The company aims to establish strategic partnerships with 3rd Party Patient Service Centers in India, Africa and Middle East to boost geographic reach. Thus, leveraging on the existing infrastructure, METROHL will expand customer base as well as profitability matrix. Being asset-light, has helped the company to generate ROCE of more than 45% in last three years.

Key Risks Government putting a cap on prices

of medical tests

Intensifying competition in orga-nized space

Decline in realizations.

ValuationMetropolis Healthcare (METROHL) is a dominant player in West India providing extensive coverage of tests and quality services. The industry is expected to grow at 15% p.a. between FY19 & FY22 driven by senior citizens, urbanization, growing awareness & rising income to bring a shift in preference towards organized play-ers from inorganized players. The industry is highly fragmented thus leading to bountiful opportunities for growth for organized players and thus gain market share. METROHL has successfully increased its presence in B2C channel thus raising its contribution in total sales through consolidating its presence in focused cities. This has resulted in nearly 16% growth in number of patients in FY19 as well as in 9MFY20, against 8-9% CAGR earlier. Besides, the company earns strong realizations

Metropolis Healthcare share price chart

800

1000

1200

1400

1600

1800

2000

Apr

-19

May

-19

May

-19

Jun-

19

Jul-

19

Jul-

19

Aug

-19

Sep

-19

Sep

-19

Oct

-19

Nov

-19

Dec

-19

Dec

-19

Jan-

20

Feb-

20

Feb-

20