A unified systems perspective of family firm performance: an extension and integration

6

Discussion A unified systems perspective of family firm performance: an extension and integration James J. Chrisman a,b, * , Jess H. Chua b , Reginald Litz b,c a Department of Management and Information Systems, Mississippi State University, Mississippi State, MS 39762-9581, USA b Haskayne School of Business, University of Calgary, Calgary, Alberta, Canada c I.H. Asper School of Business, University of Manitoba, Winnipeg, Manitoba, Canada Abstract This commentary discusses how, by substituting value creation for wealth creation as the defining function of family businesses, we can further extend and integrate the theoretical contributions of Habbershon et al. [J. Bus. Venturing (2003)]. D 2003 Elsevier Inc. All rights reserved. Habbershon et al.’s (2003) article ‘‘A unified systems perspective of family firm performance’’ addresses a fundamental issue in the study of family business—how family involvement and interactions can generate unique resources and capabilities that contribute to the family firm’s ability to create economic rent. The authors’ most important contribution is to draw on systems theory and define the theoretical requirements of inseparability and synergy for these resources and capabilities. This has been overlooked in the literature. A second contribution they make is to move us closer to understanding the essence of the family business. We find ourselves in agreement with many of the premises of the article but believe that the authors have unnecessarily limited the boundaries of their perspective by focusing mainly on wealth creation as the defining function of an enterprising families system. We also believe that further extensions and elaborations should enhance the utility of the theory to the field. We focus our commentary on these areas. 0883-9026/03/$ – see front matter D 2003 Elsevier Inc. All rights reserved. doi:10.1016/S0883-9026(03)00055-7 * Corresponding author. Department of Management and Information Systems, Mississippi State University, Mississippi State, MS 39762-9581, USA. E-mail address: [email protected] (J.J. Chrisman). Journal of Business Venturing 18 (2003) 467–472

-

Upload

independent -

Category

Documents

-

view

3 -

download

0

Transcript of A unified systems perspective of family firm performance: an extension and integration

Journal of Business Venturing 18 (2003) 467–472

Discussion

A unified systems perspective of family firm performance:

an extension and integration

James J. Chrismana,b,*, Jess H. Chuab, Reginald Litzb,c

aDepartment of Management and Information Systems, Mississippi State University, Mississippi State,

MS 39762-9581, USAbHaskayne School of Business, University of Calgary, Calgary, Alberta, Canada

cI.H. Asper School of Business, University of Manitoba, Winnipeg, Manitoba, Canada

Abstract

This commentary discusses how, by substituting value creation for wealth creation as the defining

function of family businesses, we can further extend and integrate the theoretical contributions of

Habbershon et al. [J. Bus. Venturing (2003)].

D 2003 Elsevier Inc. All rights reserved.

Habbershon et al.’s (2003) article ‘‘A unified systems perspective of family firm

performance’’ addresses a fundamental issue in the study of family business—how family

involvement and interactions can generate unique resources and capabilities that contribute to

the family firm’s ability to create economic rent. The authors’ most important contribution is

to draw on systems theory and define the theoretical requirements of inseparability and

synergy for these resources and capabilities. This has been overlooked in the literature. A

second contribution they make is to move us closer to understanding the essence of the family

business.

We find ourselves in agreement with many of the premises of the article but believe that

the authors have unnecessarily limited the boundaries of their perspective by focusing mainly

on wealth creation as the defining function of an enterprising families system. We also believe

that further extensions and elaborations should enhance the utility of the theory to the field.

We focus our commentary on these areas.

0883-9026/03/$ – see front matter D 2003 Elsevier Inc. All rights reserved.

doi:10.1016/S0883-9026(03)00055-7

* Corresponding author. Department of Management and Information Systems, Mississippi State University,

Mississippi State, MS 39762-9581, USA.

E-mail address: [email protected] (J.J. Chrisman).

J.J. Chrisman et al. / Journal of Business Venturing 18 (2003) 467–472468

1. Value creation vs. wealth creation

Habbershon et al. (2003) focus on enterprising family firms—those that pursue wealth

creation as their primary goal. They discuss, and then reject, the use of the broader concept of

value or utility creation, even though that would potentially make their theory applicable to a

much larger population of family firms. In making their decision on the boundary of the

theory, they suggest that the goal of value creation—maximization of the utility function of a

family business social system—is vague, making it difficult to specify a defining function for

the family business system.

While we agree that much greater attention to the determinants of economic performance is

needed in family business research, wealth creation is not necessarily the only or even

primary goal of all family firms (Davis and Tagiuri, 1989; Sharma et al., 1997). Furthermore,

as Jensen and Meckling (1994) argue, there does not have to be a loss of economic efficiency

when owner–managers pursue the maximization of a utility function that includes non-

economic goals. In fact, Chrisman and Carroll (1984) have demonstrated that firms that

strategically manage the pursuit of noneconomic goals can actually enhance their economic

performance and produce a systemic, synergistic effect upon wealth creation. Therefore, we

suggest that the authors’ approach can be made more widely applicable, without any loss in

the force of their arguments, by simply recognizing and allowing for the possibility that

family firms will seek to achieve a variety of goals. Transgenerational value creation captures

multiple goals and a purpose that transcends profitability, better than wealth creation that

really represents the means rather than the ends of family enterprise or enterprising families.1

Whether one recognizes noneconomic goals or not, the aspirations and values and social

responsibilities of a business will influence strategy formulation (Andrews, 1980). Put

differently, noneconomic considerations will affect both the unique resources and capabilities

that lead to distinctive familiness and the pursuit of wealth-creating rents, even in enterprising

families, and should be actively incorporated into a theory of family firms.

2. Expanding the scope of the model

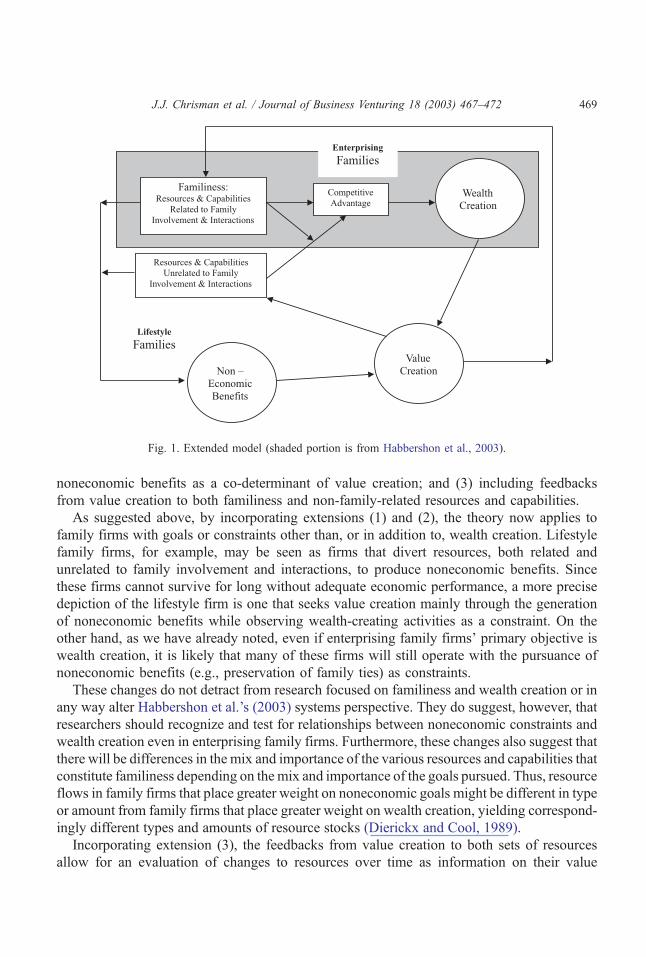

Based on these arguments, Fig. 1 illustrates our extensions to the authors’ perspective. The

shaded portion encompasses the authors’ argument that familiness—resources and capabil-

ities related to family involvement and interactions—leads to a firm’s competitive advantage

that, in turn, creates wealth. Our extensions first show that familiness may contribute both

directly and indirectly through its mediating effects to the development of a competitive

advantage (Dyer and Singh, 1998; Sirmon and Hitt, 2001). More importantly, our extension

consists of (1) substituting value creation for wealth creation as the ultimate goal; (2) adding

1 Thus, it can be argued that wealth creation is, in itself, only a surrogate for the defining purpose of any

organization, family, or otherwise. Drucker (1954, p. 35) summarizes this point of view nicely when he said,

‘‘profitability is not the purpose of business enterprise and business activity, but a limiting factor on it. Profit is not

the explanation, cause or rationale of business behavior and business decisions, but the test of their validity.’’

Fig. 1. Extended model (shaded portion is from Habbershon et al., 2003).

J.J. Chrisman et al. / Journal of Business Venturing 18 (2003) 467–472 469

noneconomic benefits as a co-determinant of value creation; and (3) including feedbacks

from value creation to both familiness and non-family-related resources and capabilities.

As suggested above, by incorporating extensions (1) and (2), the theory now applies to

family firms with goals or constraints other than, or in addition to, wealth creation. Lifestyle

family firms, for example, may be seen as firms that divert resources, both related and

unrelated to family involvement and interactions, to produce noneconomic benefits. Since

these firms cannot survive for long without adequate economic performance, a more precise

depiction of the lifestyle firm is one that seeks value creation mainly through the generation

of noneconomic benefits while observing wealth-creating activities as a constraint. On the

other hand, as we have already noted, even if enterprising family firms’ primary objective is

wealth creation, it is likely that many of these firms will still operate with the pursuance of

noneconomic benefits (e.g., preservation of family ties) as constraints.

These changes do not detract from research focused on familiness and wealth creation or in

any way alter Habbershon et al.’s (2003) systems perspective. They do suggest, however, that

researchers should recognize and test for relationships between noneconomic constraints and

wealth creation even in enterprising family firms. Furthermore, these changes also suggest that

there will be differences in the mix and importance of the various resources and capabilities that

constitute familiness depending on themix and importance of the goals pursued. Thus, resource

flows in family firms that place greater weight on noneconomic goals might be different in type

or amount from family firms that place greater weight on wealth creation, yielding correspond-

ingly different types and amounts of resource stocks (Dierickx and Cool, 1989).

Incorporating extension (3), the feedbacks from value creation to both sets of resources

allow for an evaluation of changes to resources over time as information on their value

J.J. Chrisman et al. / Journal of Business Venturing 18 (2003) 467–472470

creation properties becomes better known, or as a firm changes its goals. Thus, if family

involvement and interactions do not contribute to value creation through either greater wealth

or noneconomic benefits, the family may decide to alter its level of involvement, change its

business strategy, or dispose of the business altogether.

In summary, we agree with Habbershon et al. (2003) that there is a need for a strategic

management approach to family business management (Sharma et al., 1997). Where we differ

is in our relative belief on the importance of incorporating all of the factors that might affect

strategy formulation and implementation. Because a family in business will consist of a

confluence of aspirations and beliefs on how the business should be managed, the strategic

management approach we advocate recognizes the power, legitimacy, and urgency of all

stakeholders (Mitchell et al., 1997) as they vie for recognition when formulating the goals and

strategies in a family business. We call these human processes the ‘‘politics of value

determination’’ in family firms. This concept is entirely consistent with the two concepts

of transgenerational intentionality and the familial coalition’s vision that was used by Chua et

al. (1999) to develop a theoretical definition of family firms and the systems perspective

proposed by Habbershon et al. (2003). Furthermore, it is these processes that will influence

whether familiness becomes distinctive or constrictive (Habbershon and Williams, 1999).

Thus, this modification extends the scope of theory, enhancing its descriptive as well as

prescriptive potential without altering its conceptual foundations or empirical possibilities.

3. Integrating the essence of a family business into the theory

The family business literature has long struggled with a definition of family business and

rightly so since the definition will determine the boundaries and nature of the inquiries made

about such organizations. Early researchers concentrated on the components of family in-

volvement: ownership, governance, management, and succession within the family. Recently,

researchers have come to realize that these components of family involvement do not determine

whether a firm is a family firm; instead, they are merely surrogate measures of the essence of a

family firm. If a firm with these components lacks the essential features, it is not a family firm.

Litz (1995) suggests that the essence is intention, various authors (e.g., Shanker and

Astrachan, 1996) propose vision, and Chua et al. (1999) have argued that behavior should be

added. Habbershon et al. (2003) contribute another part with their characterization of

familiness as unique, inseparable, and synergistic resources and capabilities arising from

family involvement and interactions. These four parts are not mutually exclusive; in fact, they

are complementary and may be combined to form an integrated theory of family business.

Since possessing the resources, intention, and vision without the proper behavior does not

make a firm a family firm and such behavior is impossible without the other three parts, the

four parts are inseparable. Thus, we propose that the essence of a family firm consists of:

1. Intention to maintain family control of the dominant coalition;

2. Unique, inseparable, and synergistic resources and capabilities arising from family

involvement and interactions;

J.J. Chrisman et al. / Journal of Business Venturing 18 (2003) 467–472 471

3. A vision held by the family for transgenerational value creation; and

4. Pursuance of such a vision.

Having now proposed the factors that make up the essence of a family firm, and by

substituting value creation for wealth creation, we may restate Habbershon et al.’s (2003)

defining function of a family business system as the systemic vision of the familial coalition

that generates distinctive familiness for transgenerational value creation. From there we can

derive a set of lawlike generalizations with the empirical content and nomic necessity

required of a theory (Priem and Butler, 2001). Thus, holding all else equal:

1. The familiness of a family business will depend upon the vision established by the

dominant coalition of family stakeholders through a political process of value

determination (Chua et al., 1999; Habbershon et al., 2003).

2. The familiness (distinctive or constrictive) of the family business will determine whether

a family firm creates value for the dominant coalition of family stakeholders (Habbershon

et al., 2003).

3. The types of, and extent to which, value is created for the dominant coalition of family

stakeholders will determine whether a family business system grows, changes, or is

abandoned over time and across generations.

We believe the third proposition is necessary to complete the systems perspective proposed

by the authors. Whereas the first statement specifies the process of intentionality among

family members and the second specifies the vehicle by which intentions might be realized,

the final statement closes the loop by providing a specific feedback mechanism between

performance and intentionality.

4. Conclusion

In conclusion, the article by Habbershon et al. (2003) takes an important step toward a

theory of transgenerational wealth creation by family firms. We argued that with some

extensions it can be made applicable to all family firms. Furthermore, we attempted to show

that by integrating the concepts of intentionality, vision, behavior, and familiness, there

appears to be an opportunity to develop a theory of the family firm (cf. Conner, 1991) from

these beginnings.

References

Andrews, K.R., 1980. The Concept of Corporate Strategy. Irwin, Homewood, IL.

Chrisman, J.J., Carroll, A.B., 1984. Corporate responsibility-reconciling economic and social goals. Sloan Man-

age. Rev. 25 (2), 59–65.

Chua, J.H., Chrisman, J.J., Sharma, P., 1999. Defining the family business by behavior. Entrep. Theory Pract. 23

(4), 19–39.

J.J. Chrisman et al. / Journal of Business Venturing 18 (2003) 467–472472

Conner, K.R., 1991. A historical comparison of resource-based theory and five schools of thought within indus-

trial organization economics: do we have a new theory of the firm? J. Manage. 17, 121–154.

Davis, J.A., Tagiuri, R., 1989. The influence of life-stage on father–son work relationships in family companies.

Fam. Bus. Rev. 2, 47–74.

Dierickx, I., Cool, K., 1989. Asset stock, accumulation and sustainability of competitive advantage. Manage. Sci.

35, 1504–1511.

Drucker, P.F., 1954. The Practice of Management. Harper & Row, New York.

Dyer, J.H., Singh, H., 1998. The relational view: cooperative strategy and sources of interorganizational com-

petitive advantage. Acad. Manage. Rev. 23, 660–679.

Habbershon, T.G., Williams, M., 1999. A resource-based framework for assessing the strategic advantages of

family firms. Fam. Bus. Rev. 12, 1–25.

Habbershon, T.G., Williams, M., MacMillan, I.C., 2003. A unified systems perspective of family firm perform-

ance. J. Bus. Venturing (this issue).

Jensen, M.C., Meckling, W.H., 1994. The nature of man. J. Appl. Corp. Finance 7 (2), 4–19.

Litz, R., 1995. The family business: toward definitional clarity. Fam. Bus. Rev. 8, 71–81.

Mitchell, R.K., Agle, B.R., Wood, D.J., 1997. Toward a theory of stakeholder identification and salience: defining

the principle of who and what really counts. Acad. Manage. Rev. 22, 853–886.

Priem, R.L., Butler, J.E., 2001. Is the resource-based ‘‘view’’ a useful perspective for strategic management

research? Acad. Manage. Rev. 26, 22–40.

Shanker, M.C., Astrachan, J.H., 1996. Myths and realities: family businesses’ contributions to the US economy.

Fam. Bus. Rev. 9, 107–123.

Sharma, P., Chrisman, J.J., Chua, J.H., 1997. Strategic management of the family business: past research and

future challenges. Fam. Bus. Rev. 10, 1–35.

Sirmon, D., Hitt, M., 2001. Creating wealth in family firms through managing resources. Presented at Theories of

Family Enterprise: Establishing a Paradigm for the Field. First Annual Conference of Enterprising Families,

Edmonton, AB.