Private Information, Credit Risk and Graph Structure in P2P ...

Upload

khangminh22Category

view

1download

0

A STUDY OF CREDIT RISK MANAGEMENT PRACTICES

OF PUBLIC AND PRIVATE BANKS IN INDIA

Thesis Submitted to the

GOA UNIVERSITY

For the award of the degree of

DOCTOR OF PHILOSOPHY

in

COMMERCE

by

MRS. RESHMA D. PRABHU VERLEKAR

Under the guidance of

PROF. MANOJ S. KAMAT (VVM’s Shree Damodar College Research Centre)

Principal

D.P.M.’s Shree Mallikarjun and Shri Chetan Manju Desai College

Canacona - Goa.

March 2020

I

DEDICATION

This Thesis is dedicated to

Late Shri Datta R. Prabhu Verlekar (Father)

Late Shri Tulshidas V. Kholkar (Father-in-law)

II

DECLARATION

I hereby declare that the thesis titled “A Study of Credit Risk Management

Practices of Public and Private Banks in India” submitted to the Goa

University, Goa for the award of the degree of Doctor of Philosophy in

commerce is an outcome of original and independent research work done by

me during the period 2014 to 2020 under the supervision and guidance of

Prof. Manoj S. Kamat, Principal - Shree Mallikarjun and Shri Chetan Manju

Desai College Canacona - Goa, and also that it has not formed the basis for

award of any degree, diploma, associateship, fellowship or similar title to any

candidate of this or any other University.

Date: ____________ MS. RESHMA D. PRABHU VERLEKAR

Place: Goa University

III

CERTIFICATE

This is to certify that the Ph.D. thesis titled “A Study of Credit Risk

Management Practices of Public and Private Banks in India” is a bonafide

record of the research done by “Ms. Reshma D. Prabhu Verlekar” under my

supervision and guidance, at the Goa Business School - Goa University. This

dissertation or a part thereof has not formed the basis for the award of any

degree, diploma, associateship, fellowship or similar title of this or any other

University.

Date: ______________ Prof. Manoj S. Kamat

Place: Goa University Research Guide

Principal

D.P.M.’s Shree Mallikarjun

and Shri Chetan Manju Desai College

of Arts and Commerce

Canacona - Goa.

IV

ACKNOWLEDGEMENT

It is a genuine pleasure to express my deep sense of gratitude and immeasurable

appreciation to many personalities who are directly and indirectly connected with this

research work.

I am greatly indebted to Professor Manoj S. Kamat, Principal of Shree Mallikarjun and

Shri Chetan Manju Desai College, Canacona - Goa for being my guide and contributing

immensely with his valuable suggestions, advice, motivation, encouragement and

mentoring throughout the course. It is sir’s moral support, valuable guidance, constructive

criticism and ongoing evaluation of my research work, without which it would not have

been possible for me to complete this task. He has been like a lighthouse to steer me

through all the phases of this research work and always encouraged me to present the

research findings with clarity. It was a great privilege and honour to work and study under

his guidance.

My sincere thanks goes to Dr. Sriram Padyala - Faculty of Goa Business School, Goa

University, for tirelessly witnessing my research work, periodically reviewing my progress

as an expert on the Faculty Research Committee and providing me his opinions and advice

throughout my research work.

I wish to express my gratitude to Prof. Dr. Y. V. Reddy, the Registrar of Goa University

for his wholehearted support and advice during the course of this study. I thank Prof. Dr.

K.B. Subhash, the former Dean and Head of Department of Commerce - Goa University

for providing necessary assistance and conducting the research methodology classes for the

research scholars. I am very much pleased to thank Prof. Dr. Anjana Raju – Programme

Director of Research for her valuable suggestions from time to time to improvise my

research work. I am thankful to Prof. Dr. B. Ramesh for his encouragement and

suggestions. I wish to express my gratitude to Dr. Dayanand M. S. - Vice-Dean

(Research), Goa Business School - Goa University for support and encouragement.

V

I am very thankful to the Principal of our college - Dr. Santosh Patkar, Sridora Caculo

College of Commerce & Management Studies, Mapusa for his continuous encouragement

and support. I am indebted to the Management of Saraswat Education Society for

sanctioning my study leave. I am indebted to Teaching , Administrative and Library

staff of our college for their valuable assistance and moral support throughout my research.

I am profoundly thankful to the Principal of my Research Centre, Dr. Prita Mallya -

V.V.M’s Damodar College of Commerce and Economics. I express my gratitude to the

Librarian – Ms. Manasi Rege and the other library staff of research centre for providing

me required source of secondary data. My sincere thanks to teaching and administrative

staff of the research centre for their support and help in the process of my research work.

I am thankful to the Director of Higher Education- Shri Prasad Lolayekar for timely grant

of study leave, which was of immense help in the successful completion of this research.

My special thanks and appreciation also goes to my colleague Mr. Kedar Phadke -

Faculty of National Institute of Construction Management and Research for giving a patient

hearing to my uncounted doubts and willingly helping me out with his abilities in deciding

the right approach towards selecting the statistical tools for my data analysis. His

experience and critical comments have been of immense help to me during my research

work.

My indebtedness is due to, the Librarian of Goa University Dr. Gopakumar V. and the

staff of ARPG section of Goa University for providing necessary assistance. I am thankful

to Dr. Manasvi M. Kamat for her inspiration, assistance and advice.

I am thankful to all the Respondents who contributed to the major part of my research

work by sparing their valuable time and by providing me the required information. I

express my sincere gratitude to the Resource Persons of various workshops.

VI

I am grateful to all the fellow researchers, at the Goa University – Dr. Ujwalah

Hanjunkar, Ms. P.S. Devi, Dr. Meera Mayekar, Dr. Paresh Lingadkar, Dr. Harsha

Talaulikar , Dr. Anjali Sajilal and Mr. Kavir Shirodkar for their support and timely

assistance. My sincere thanks to the faculties of Department of English – Ms. Priyanka

Pednekar and Mr. Merwyn Miranda, Purushottom Walawalkar Higher Secondary School

for the grammar check of my thesis.

I would fail in my duty, if I fall short of thanking and appreciating the valuable sacrifice of

my son Mast. Mehul Kholkar in seeing me achieve my research dream. My wholehearted

gratitude goes to my mother – Smt. Sulekha Prabhu Verlekar and my spouse Mr.

Mahesh Kholkar for supporting me in all the endeavours of my life. Also I express my

thanks to my sibling - Ms. Disha Panandikar for the assistance provided at appropriate

time. I am also indebted to my brother in law, Mr. Siddesh Kenkre for sharing his valuable

expertise in computer skills with me.

Above all, I pay my homage to the Almighty God for giving me the courage, patience and

health as well as surrounding me with people emitting positive vibes.

Reshma Prabhu Verlekar

THANK YOU.

VII

Table of Contents

Title Page

Dedication I

Declaration II

Certificate III

Acknowledgement IV-VI

Table of Contents VII-X

List of Table XI-XVI

List of Abbreviations XVII

Abstract XVIII-XX

Introduction ......................................................................................................................................... 1

1.1. Background of the Study ..................................................................................................... 1

1.2. Statement of Problem .......................................................................................................... 5

1.2.1 Research Questions ..................................................................................................... 7

1.3. Objectives of the Study ....................................................................................................... 9

1.4. Scope of the Study............................................................................................................. 10

1.5. Significance of the Study .................................................................................................. 11

1.6. Organisation of the Study .................................................................................................. 15

Theoretical Foundations and Empirical Literature ..................................................................... 17

2.1 Introduction ....................................................................................................................... 17

2.2 Theoretical Framework ..................................................................................................... 18

2.2.1 Theory Relating to CRMP and Basel III Preparedness ............................................. 18

2.2.2 Bankruptcy Models ................................................................................................... 19

2.3. Empirical Literature .......................................................................................................... 22

2.3.1. Literature on the Determinants of CRMP ................................................................. 22

2.3.2. Literature on Measurement of CRMP ....................................................................... 24

2.3.3. Literature on the Bankruptcy Models ........................................................................ 28

2.3.4. Literature on the Basel III Preparedness and Compliance ........................................ 32

2.4. Research Gap .................................................................................................................... 35

2.4.1 Gaps on Credit Risk Determinants of CRMP ........................................................... 35

2.4.2 Gaps on Measurement of CRMP............................................................................... 36

2.4.3 Gaps on Bankruptcy Models ..................................................................................... 37

2.4.4 Gaps on Basel III Preparedness and Compliance ...................................................... 37

2.5. Summary ........................................................................................................................... 38

VIII

Methodology and Techniques ........................................................................................................ 40

3.1. Introduction ....................................................................................................................... 40

3.2. Data sources ...................................................................................................................... 41

3.2.1 Primary Data ............................................................................................................. 41

3.2.2 Secondary Source ...................................................................................................... 45

3.3. Hypotheses of the study .................................................................................................... 46

3.4. Statistical Tools ................................................................................................................. 50

3.4.1 Principal Component Analysis (PCA) ...................................................................... 50

3.4.2 Reliability Test .......................................................................................................... 50

3.4.3 Descriptive Statistics ................................................................................................. 51

3.4.4 Ratio Analysis ........................................................................................................... 51

3.4.5 Pearson Correlation Coefficient ................................................................................ 51

3.4.6 Parametric Test and Non-parametric Tests ............................................................... 52

3.4.7 Regression Analysis .................................................................................................. 52

3.4.8 Robust Test ................................................................................................................ 54

3.5. Descriptions of Bankruptcy Models .................................................................................. 54

3.5.1 Altman Z-Score Model -1968 ................................................................................... 54

3.5.2 Springate Model - 1978 ............................................................................................. 56

3.5.3 Zmijewski Model (III)-1984 ..................................................................................... 57

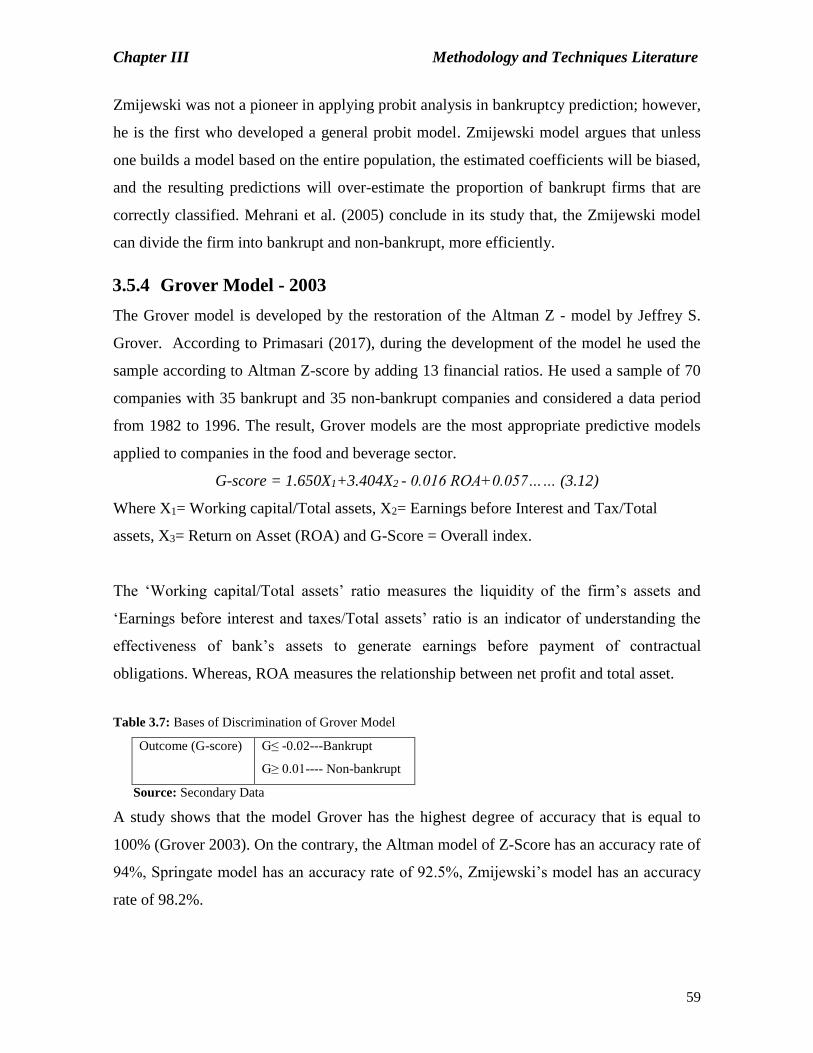

3.5.4 Grover model (IV) -2003 .......................................................................................... 59

Determinants of Credit Risk Management Practices .................................................................. 60

4.1. Introduction ....................................................................................................................... 60

4.2. Theory and Literature ........................................................................................................ 62

4.2.1 Institutional Theory ................................................................................................... 62

4.2.2 Literature Review ...................................................................................................... 62

4.3. Data and Methods.............................................................................................................. 63

4.4. Conceptual Framework of CRMP ..................................................................................... 65

4.4.1 Risk Management Practices (RMP) .......................................................................... 66

4.4.2 Understanding Risk Management (URM) ................................................................ 66

4.4.3 Risk Identification (RI) ............................................................................................. 66

4.4.4 Risk Assessment and Analysis (RAA) ...................................................................... 67

4.4.5 Risk Monitoring and Control (RMC) ........................................................................ 67

4.4.6 Credit Risk Analysis (CRA) ...................................................................................... 67

IX

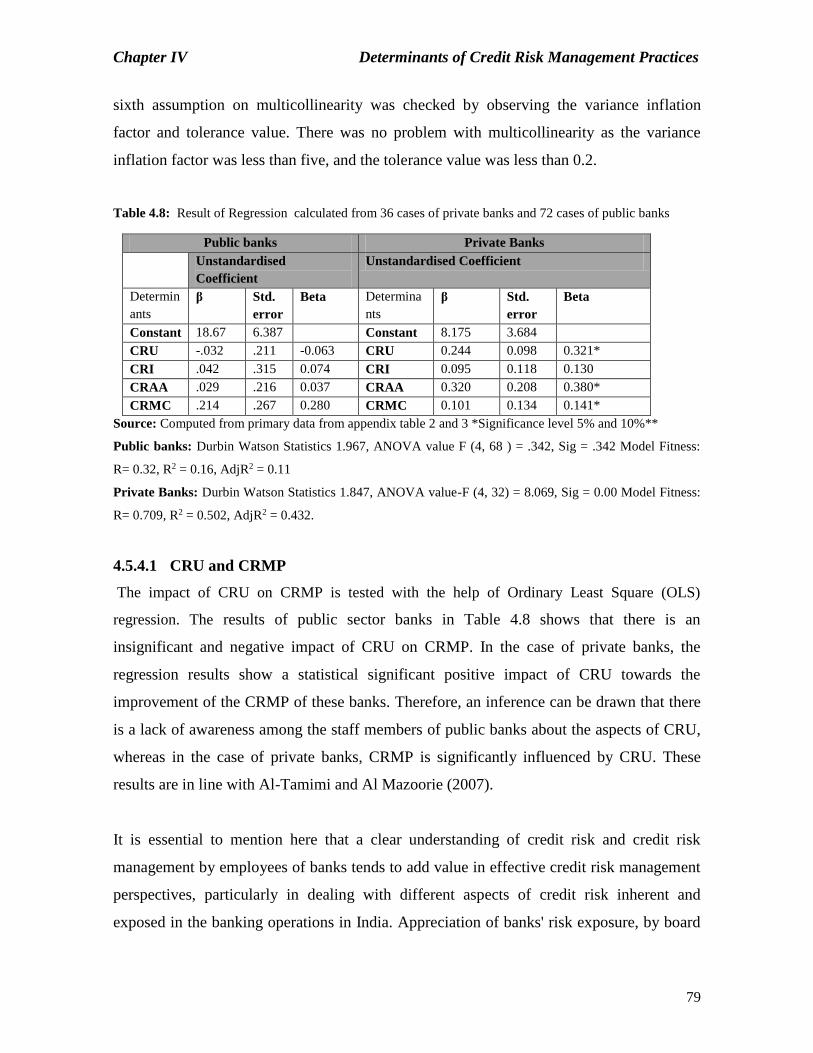

4.5. Results and Discussion ...................................................................................................... 68

4.5.1 Sample Characteristics .............................................................................................. 69

4.5.2 Identification and Classification of Determinants of CRMP .................................... 71

4.5.3 Descriptive Statistics and Correlation Analysis ........................................................ 76

4.5.4 Development of OLS Model ..................................................................................... 77

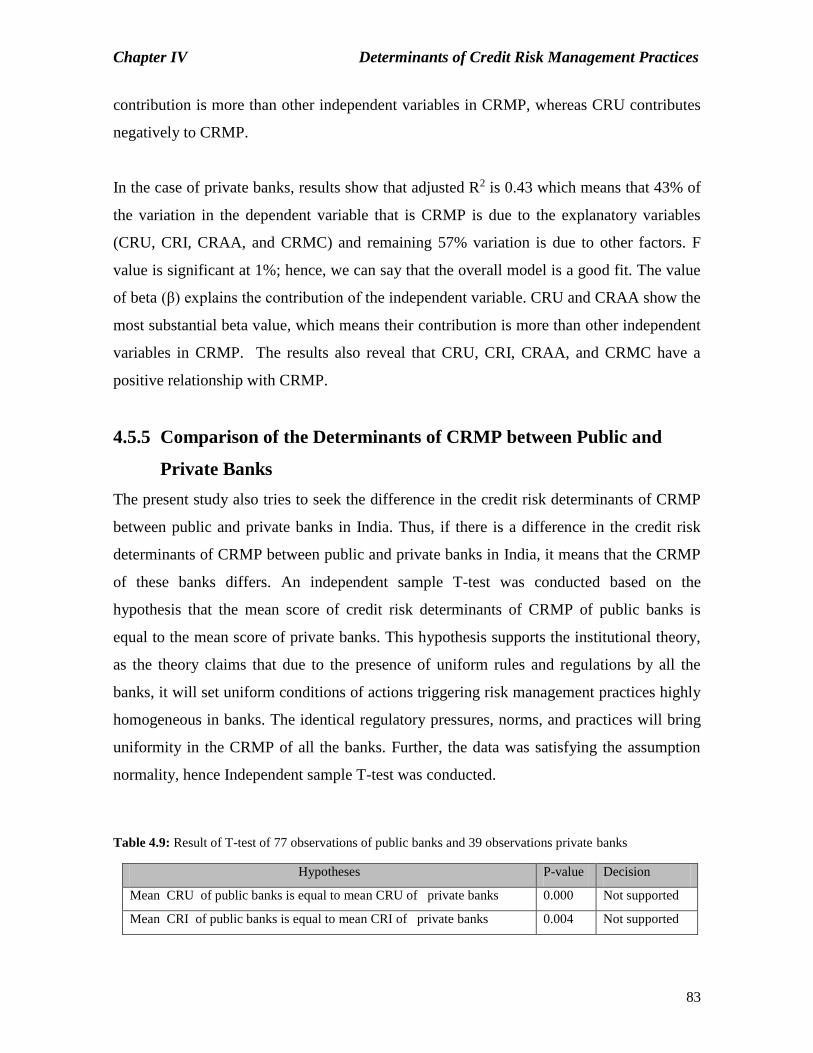

4.5.5 Comparison of the Determinants of CRMP between Public and Private Banks ....... 83

4.6. Summary ........................................................................................................................... 84

Measurement of Credit Risk Management Practices .................................................................. 86

5.1 Introduction ....................................................................................................................... 86

5.2 Literature Review .............................................................................................................. 88

5.3 Data and Methods.............................................................................................................. 90

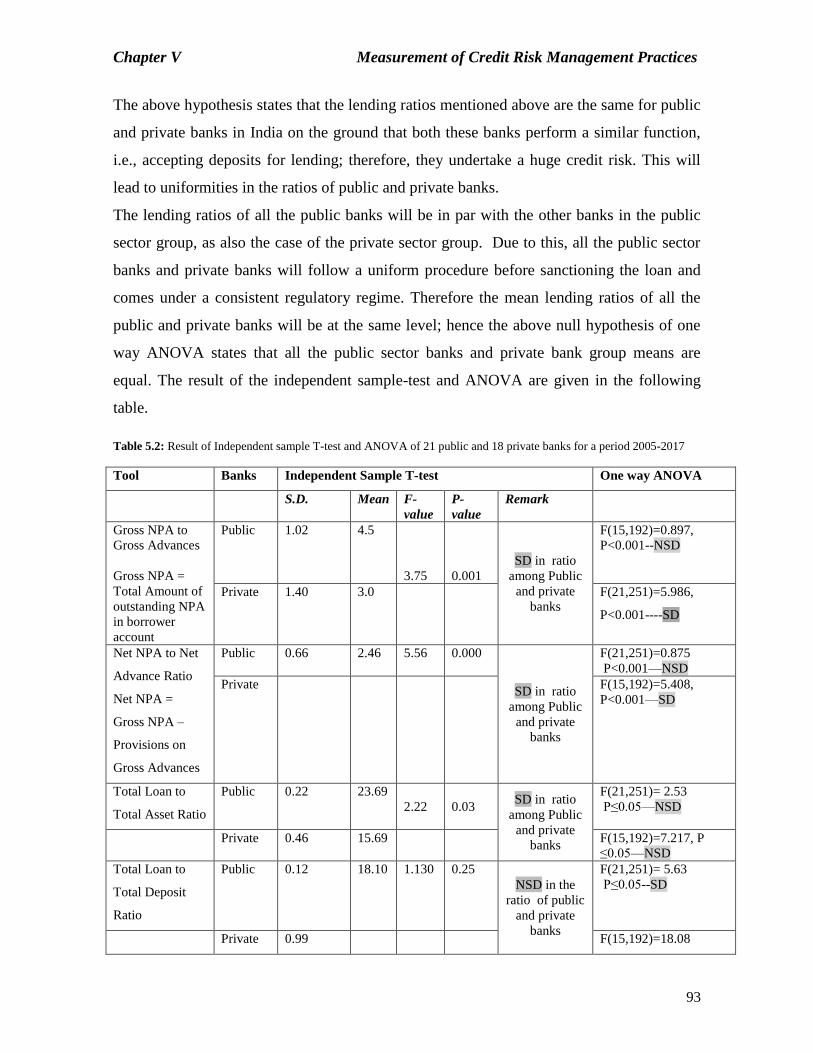

5.4 Result and Discussion ....................................................................................................... 92

5.4.1. Measurement and Comparison of CRMP using the Lending Ratios......................... 92

5.4.2. Measurement and comparison of CRMP using Financial Ratios .............................. 99

5.4.3. Identification of Relationship between Financial Variables ................................... 106

5.5 Summary ......................................................................................................................... 109

Application and Recalibration of Bankruptcy Models in Indian Banking Sector .................. 112

6.1 Introduction ..................................................................................................................... 112

6.1.1. Operational Definitions of Bankruptcy ................................................................... 116

6.2 Review of Literature........................................................................................................ 117

6.2.1 Description of Models ............................................................................................. 120

6.3 Data and Methods............................................................................................................ 121

6.4 Results and discussion ..................................................................................................... 123

6.4.1 An Application of the Altman - 1993 Model (I) ..................................................... 124

6.4.2 An Application of the Springate Model-1978 (II) ................................................... 133

6.4.3 Application of Zmijewski Model - 1984 (III) ......................................................... 142

6.4.4 An Application of Grover Model -2003 (IV) .......................................................... 149

6.4.5 Ranking of Banks as per Bankruptcy Models ......................................................... 155

6.4.6 Comparison of Bankruptcy Score between Public and Private Banks .................... 159

6.5 Summary ......................................................................................................................... 160

Preparedness and Compliance for Basel III Norms in the Indian Banking Sector ................ 163

7.1 Introduction ..................................................................................................................... 163

7.2 Theory and Literature Review ......................................................................................... 166

X

7.2.1. Legal Theory of Finance (LTF)............................................................................... 166

7.2.2. Literature Review .................................................................................................... 166

7.3 Data and Methods............................................................................................................ 168

7.4 Conceptual framework .................................................................................................... 169

7.4.1. Conceptual Framework on Basel III Preparedness ................................................. 170

7.4.2. Operational Definitions (Basel III Compliance) ..................................................... 172

7.5 Results and Discussion .................................................................................................... 173

7.5.1 Basel III Preparedness ............................................................................................. 174

7.5.2 Compliance of Basel III Ratios by an Indian Banks ............................................... 181

7.5.3 Comparison of Capital Ratios of Public and Private Banks .................................... 185

7.6 Summary ......................................................................................................................... 191

Summary and Conclusion ............................................................................................................ 193

8.1 Introduction ..................................................................................................................... 193

8.2 Summary of Major Findings ........................................................................................... 197

8.2.1 Findings from the Determinants of Credit Risk Management Practices ................. 197

8.2.2 Findings from the Measurement of Credit Risk Management Practices ................. 198

8.2.3 Findings from the Application and Recalibration of the Bankruptcy Model .......... 199

8.2.4 Findings from the Preparations and Compliance of Basel III norms ...................... 199

8.3 Conclusion ....................................................................................................................... 201

8.4 Recommendations ........................................................................................................... 202

8.5 Implications of the study ................................................................................................. 205

8.5.1 Managerial Implications .......................................................................................... 205

8.5.2 Theoretical contributions ......................................................................................... 207

8.6 Limitations of the Study……………………………………………………………….208

8.7 Directions for future Research…………………………………………………………209

Bibliography.....................................................................................................................................211

Appendix..........................................................................................................................................223

Publications......................................................................................................................................273

XI

No. List of tables Page no.

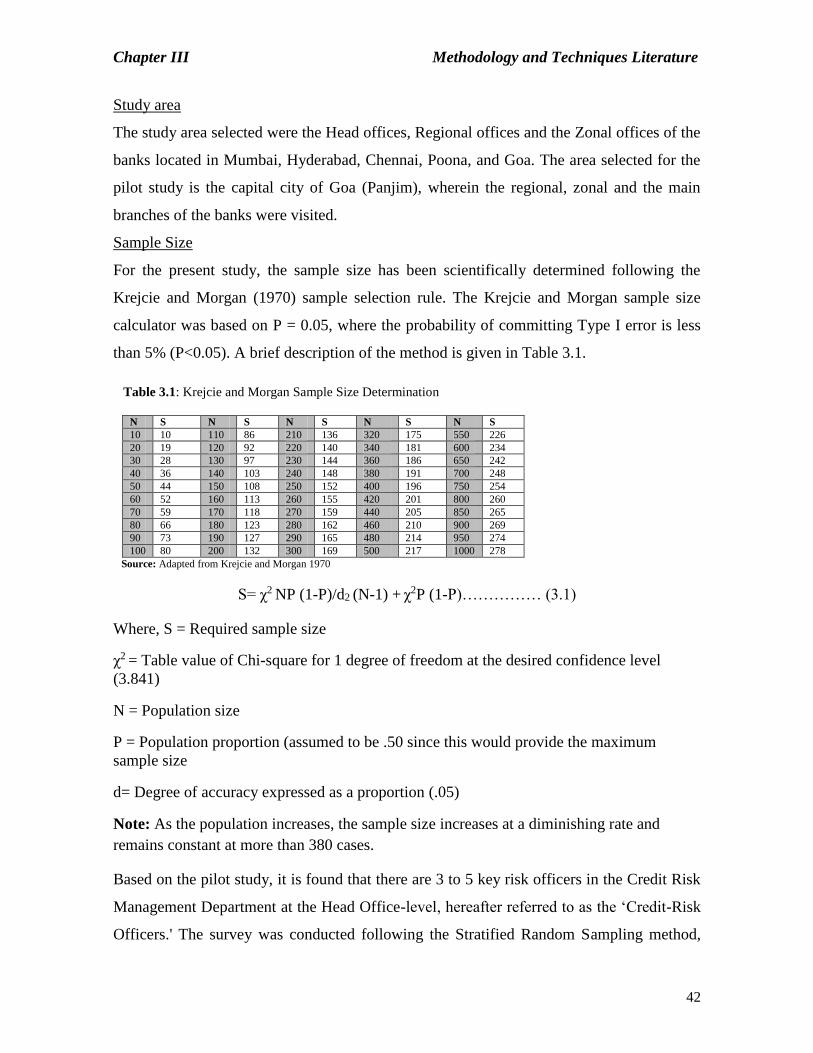

3.1 Krejcie and Morgan Sample Size Determination 42

3.2 Information related to various sections in the questionnaire 43

3.3 CVI score calculated based on nine items from the responses of six

experts

44

3.4 Bases of discrimination of Altman Model 56

3.5 Bases of discrimination of Springate Model 57

3.6 Bases of discrimination of Zmijewski Model 58

3.7 Bases of Discrimination of Grover Model 59

4.1 Results of ranks given for different types of risk based on 116

respondents

68

4.2 The demographic profile of the 116 respondents 69

4.3 Rotated Component Matrix calculated from 31 statements from a

questionnaire

71

4.4 Extraction of the sum of Squared Loadings 72

4.5 Reliability test on 36 statements based on 116 observations 75

4.6 Descriptive Statistics of 39 respondents of private and 77 respondents

of public banks

76

4.7 The Correlation matrix calculated using 39 respondents of private and

77 respondents of public banks

77

4.8 Result of Regression calculated from 36 cases of private banks and

72 cases of public banks

79

4.9 Result of T-test of 77 observations of public banks and 39

observations private banks

83

5.1 Codes to Financial Ratios used by Bankruptcy Models 91

5.2 Result of Independent sample T-test and ANOVA of 21 public and

18 private banks for a period 2005-2017

93

5.3 Result of Independent sample T-test for liquidity analysis of time

series data from year 2005-2017and cross-sectional data of 21 public

and 18 private banks

100

5.4 Result of Independent sample T-test for profitability analysis of time

series data from year 2005-2017and cross-sectional data for 21 public

and 18 private banks

102

5.5 Result of Independent sample T-test for leverage analysis of time

series data from year 2005-2017and cross-sectional data for 21 public

and 18 private banks.

105

5.6 Result of a correlation matrix of 21 public and 18 private banks from 106

XII

2005-2017 taking into account 526 observations

6.1 Description of bankruptcy models 121

6.2 Results of the tested Altman Model on 21 public 18 private and 5

NWB

124

6.3 Altman Model Accuracy rate 125

6.4 Correlation Matrix of Recalibrated Altman Model 126

6.5 Coefficient Test of Recalibrated Altman Model 127

6.6 Results of Recalibrated Altman Model of 21 Public, 18 Private and 2

NWB

128

6.7 Recalibrated Altman Model Accuracy Rate 129

6.8 Result of Independent Sample T-test of Altman and Recalibrated

Altman Model

130

6.9 Bases of discrimination as per Robust Test 130

6.10 Results of tested Robust Test on 39 Indian banks 131

6.11 Comparison of Original and Recalibrated Altman Model with the

Robust test

132

6.12 Results of the applied Springate model on 21 public 18 private and 5

NWB

134

6.13 Model Accuracy Rate of Springate Model 135

6.14 Correlation Matrix of Recalibrated Springate Model 136

6.15 The Coefficient test of Recalibrated Springate Model 137

6.16 Results of Applied Recalibrated Model on 21 Public, 18 Private and 2

NWB

138

6.17 Model Accuracy Rate of Recalibrated Springate Model 139

6.18 Result of Independent Sample T-test of Springate and Recalibrated

Springate Model

140

6.19 Comparison of original and Recalibrated Springate Model with the

Robust test

140

6.20 Result of the tested Zmijewski model on 21 public, 18 private and 2

NWB

142

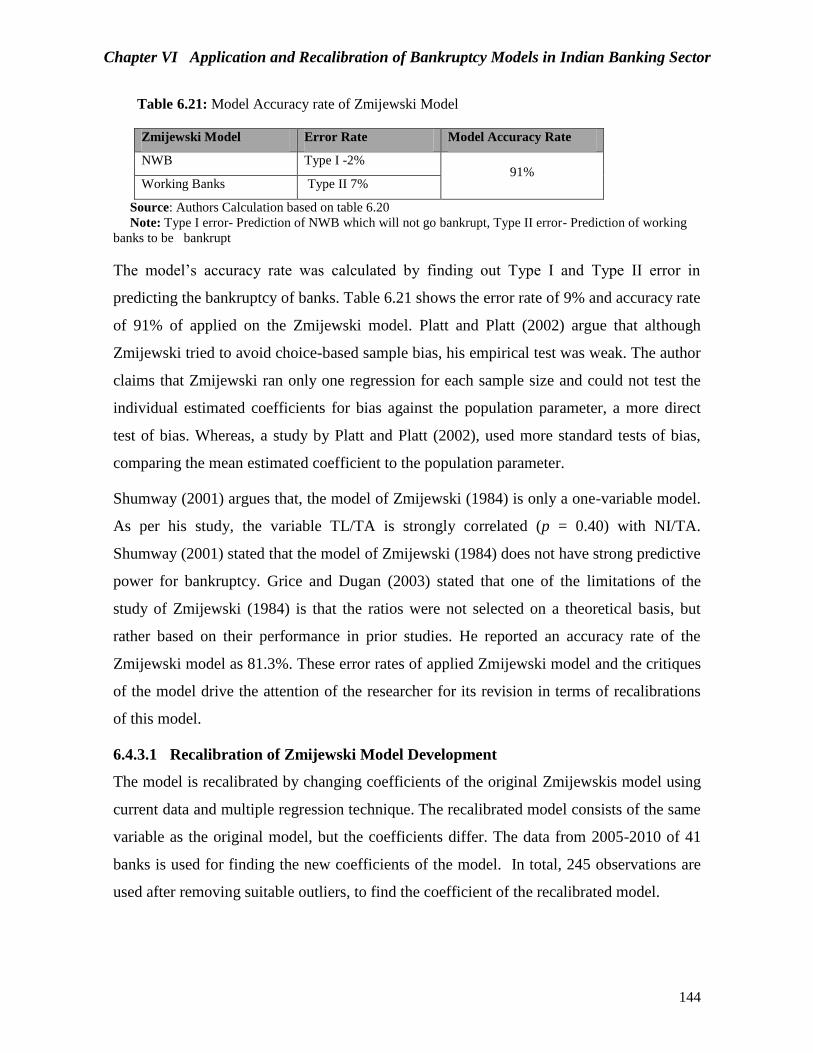

6.21 Model Accuracy rate of Zmijewski Model 144

6.22 Correlation Matrix of Zmijewski Model 145

6.23 Coefficient Test of Zmijewski Model 146

6.24 Result of the tested recalibrated Zmijewski model of 21 Public 18

Private and 2NWB

147

XIII

6.25 Model Accuracy Rate of Recalibrated Zmijewski Model 148

6.26 Result of Independent Sample T-test of Zmijewski and Recalibrated

Zmijewski Model

148

6.27 Results of the Tested Grover model on 21 Public, 18 Private and 5

NWB

149

6.28 Type I and Type II error of Grover Model 150

6.29 Correlation Matrix of Grover model 151

6.30 Results of Coefficient Test of Grover Model 152

6.31 Result of the recalibrated Grover Model of 21 Public, 18 Private and

2 NWB

153

6.32 Model Accuracy rate of Recalibrated Grover Model 154

6.33 Result of Independent Sample T-test of Grover and Recalibrated

Grover Model

155

6.34 Table showing Ranks of banks 156

6.35 Result of Independent Sample T-test in Bankruptcy score of Public

and Private Banks

159

7.1 Reliability test on 27 statements of 116 observations 174

7.2 Descriptive Statistics of 77 respondents of public and 39 respondents

of private banks

175

7.3 Correlation matrix calculated using 77 respondents of public and 39

respondents of private banks

177

7.4 Result of Regression Analysis calculated using 71 respondents of

public and 37 respondents of private banks

177

7.5 Result t-test of 77 observations of public banks and 39 observations

of private banks

180

7.6 Result of one-sample t-test of the capital ratios of 21 public and 18

private banks

181

7.7 Result of Independent sample t-testt on Cross-sectional data of 21

public and18 private banks

185

7.8 Cross-sectional data showing the result of the Paired T-test of 21

public sector banks

188

7.9 Cross sectional data showing the result of Paired T-test of 18 Private

sector banks

189

Annexure Tables

A.1 Questionnaire- Content Validity 223

A.2 Questionnaire in the Pre –PCA stage 227

A.3 Questionnaire in the Post PCA stage 228

A.4 Gross NPA to Gross Advances of 21 Public Banks for the Thirteen 230

XIV

years 2005-2017

A.5 Gross NPA to Gross Advances of 18 Private Banks for Thirteen years

(2005-2017)

231

A.6 Net NPA to Net Advances of 21 Public Banks for the Thirteen years

2005-2017

231

A.7 Net NPA to Net Advances of 18 private Banks for the Thirteen years

2005-2017

232

A.8 Total loan to total Asset of 21 public banks for 13 years for 2005-

2017

233

A.9 Total loan to total Asset of 18 Private Banks for 13 years for 2005-

2017

234

A.10 Total loan to total Deposit of 21 public banks for 13 years for 2005-

2017

234

A.11 Total loan to total Deposit of 18 private banks for 13 years for 2005-

2017

235

A.12 Total loan to Total Equity of 21 public banks for 13 years for 2005-

2017

236

A.13 Total loan to total Equity of 18 private banks for 13 years for 2005-

2017

236

A.14 Provision for NPA to Gross NPA of 21 public banks for 13 years for

2005-2017

237

A.15 Provision for NPA to Gross NPA of 18 Private Banks for 13 years for

2005-2017

238

A.16 NPA to Equity of 21 public banks for 13 years for 2005-2017 238

A.17 NPA to Equity of 21 public banks for 13 years for 2005-2017 239

A.18 CAR of 21 public banks for 13 years for 2005-2017 239

A.19 CAR of 18 private banks for 13 years for 2005-2017 240

A.20 ROA of 21 public banks for 13 years for 2005-2017 241

A.21 ROA of 18 Private Banks for 13 years for 2005-2017 242

A.22 Liquidity Analysis of Indian banks using Proxy L1 (WC/TA) for time

series data from 2005 2017

243

A.23 Liquidity Analysis of Indian banks using Proxy L1 (WC/TA) for

Cross-sectional data from 2005-2017

244

A.24 Liquidity Analysis of Indian banks using Proxy L2 (Current Ratio)

for time series data from 2005-2017

244

A.25 Liquidity Analysis of Indian banks using Proxy L2 (Current Ratio)

for Cross-sectional data from 2005-2017

245

A.26 Profitability Analysis of Indian banks using Proxy P1 (EBIT/TA) for

time series data from 2005-2017, N=273

244

A.27 Profitability Analysis of Indian banks using Proxy P1 (EBIT/TA) for

Cross-sectional data from 2005-2017

246

XV

A.28 Profitability Analysis of Indian banks using Proxy P2 (ROA) for time

series data from 2005-2017, N=273

246

A.29 Profitability Analysis of Indian banks using Proxy P2 (ROA) for

Cross-sectional data from 2005-2017

247

A.30 Profitability Analysis of Indian banks using Proxy P3 (PBIT/CL) for

time series data from 2005-2017

248

A.31 Profitability Analysis of Indian banks using Proxy P3 (PBIT/CL) for

Cross-sectional data from 2005-2017

248

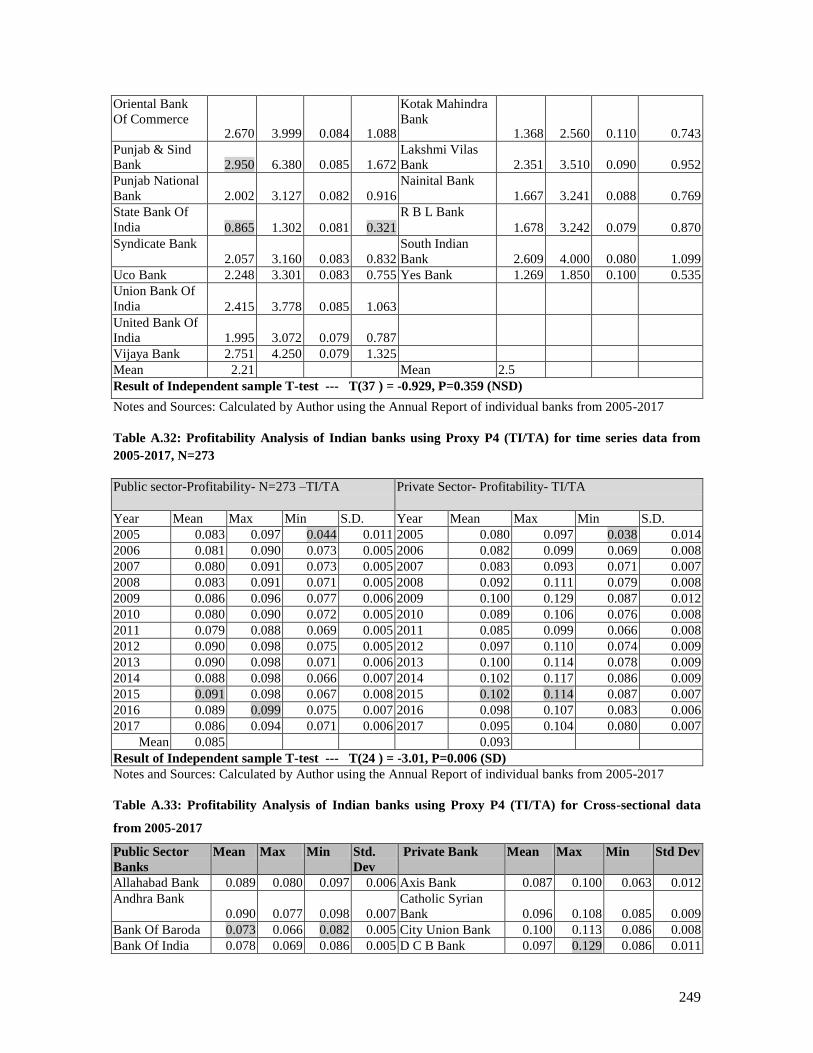

A.32 Profitability Analysis of Indian banks using Proxy P4 (TI/TA) for

time series data from 2005-2017

249

A.33 Profitability Analysis of Indian banks using Proxy P4 (TI/TA) for

Cross-sectional data from 2005-2017

249

A.34 Leverage Analysis of Indian banks using Proxy LV1 (RE/TA) for

time series data from 2005-2017

250

A.35 Leverage Analysis of Indian banks using Proxy LV1 (RE/TA) for

Cross-sectional data from 2005-2017

251

A.36 Leverage Analysis of Indian banks using Proxy LV2 (MVE/TL) for

time series data from 2005-2017,

251

A.37 Leverage Analysis of Indian banks using Proxy LV2 (MVE/TL) for

Cross-sectional data from 2005-2017

252

A.38 Leverage Analysis of Indian banks using Proxy LV3 (TD/TA) for

time series data from 2005-2017

253

A.39 Leverage Analysis of Indian banks using Proxy LV3 (TD/TA) for

Cross-sectional data from 2005-2017

253

A.40 Result of Altman Z-score of 21 public banks for 2005-2017 254

A.41 Result of Altman Z- score of 18 Private Banks for 2005-2017 255

A.42 Result of Altman Z-score of five NWB from 2005-2013 255

A.43 Result of Springate Model of 21 public banks for 2005-2017 255

A.44 Result of Springate Model of 18 private banks for 2005-2017 256

A.45 Result of Springate Model NWB banks from 2005-2014 257

A.46 Result of Zmijewski model for 21 public banks from 2005-2017 257

A.47 Result of Zmijewski model for18 Private banks from 2005-2017 258

A.48 Results of Zmijewski Model for NWB from 2005-2014 258

A.49 Result of Grover model of 21 Public Sector banks from 2005-2017 259

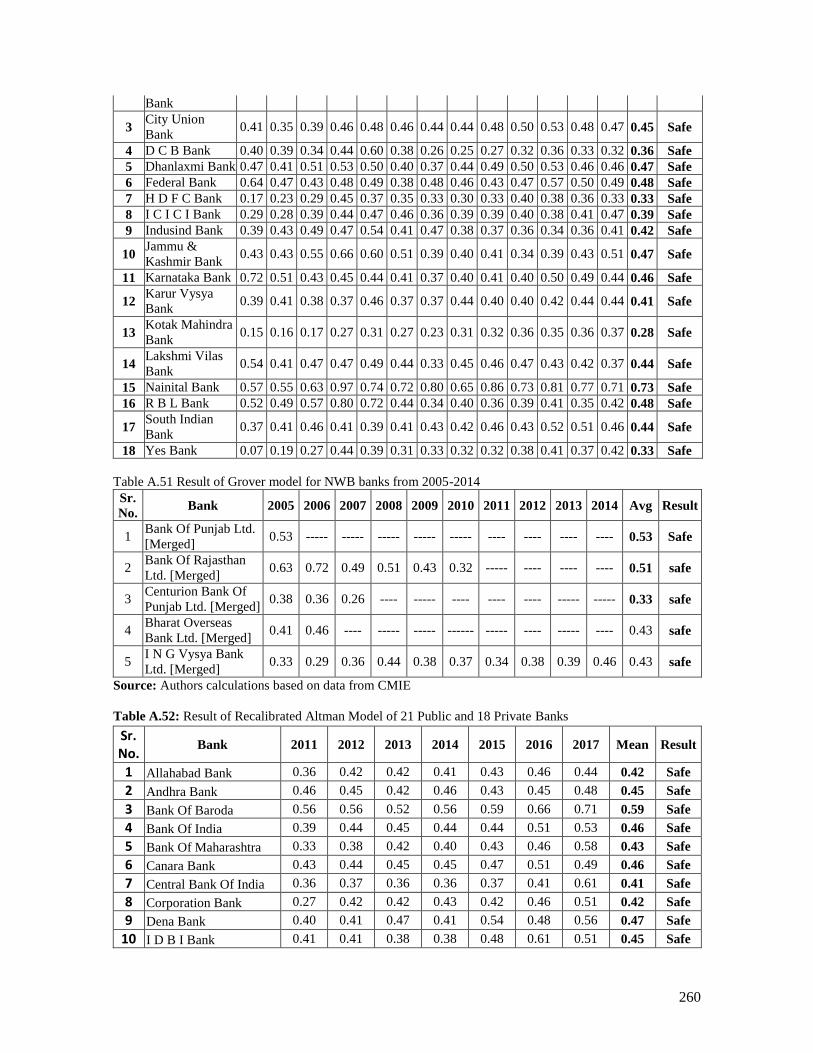

A.50 Result of Grover model for 18 Private Banks from 2005-2017 259

A.51 Result of Grover model for NWB banks from 2005-2014 260

A.52 Result of Recalibrated Altman Model of 21 Public and 18 Private

Banks

260

XVI

A.53 Result of Recalibrated Springate Model of 21 Public and 18 Private

Banks

261

A.54 Result of Recalibrated Zmijewski Model of 21 Public and 18 Private

Banks

262

A.55 Result of Recalibrated Grover Model of 21 Public and 18 Private

Banks

263

A.56 Questionnaire (Part 2): Preparedness in Basel III Implementation 264

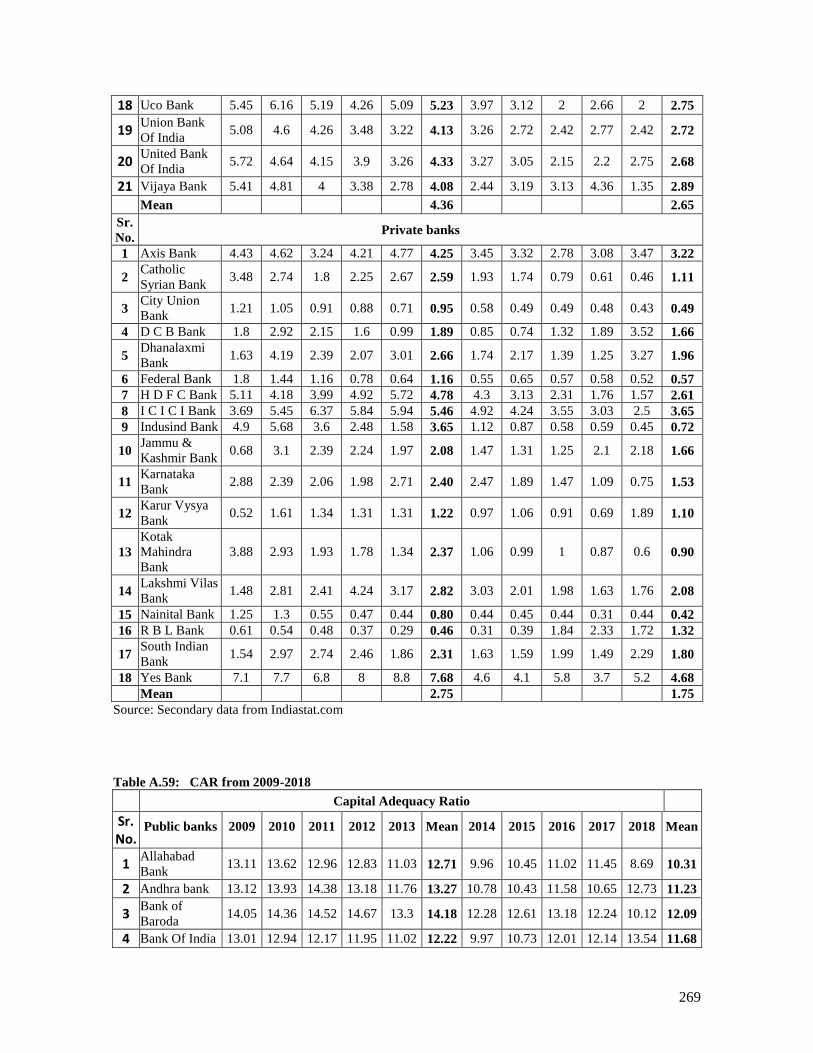

A.57 Result of Tier I Capital Ratio from 2009-2018 267

A.58 Result of Tier II Capital Ratio from 2009-2018 268

A.59 Result of CAR from 2009-2018 269

A.60 Result of Leverage Ratio from 2009-2018 271

XVII

List of Abbreviations

AB Anticipated Benefit NPA Non-Performing Asset

AC Anticipated Cost NSFR Net Stable Funding Ratio

AI Anticipated Impact NWB Non - Working Banks

AR Availability of Resources OLS Ordinary Least Square

BP Basel III Preparedness PBIT/TA

Profit before Interest and Tax to

Total Asset (PBIT/TA)

CA/CL

Current assets / Current

Liabilities PBT/CL

Profit Before Tax to Current

Liabilities

CAR Capital Adequacy Ratio PCA Principal Component Analysis

CCB Capital Conservation Buffer RAA Risk Assessment Analysis

CCCB Counter Cyclical Capital Buffer RBI Reserve Bank of India

CRA Credit Risk Analysis RE/TA Retained Earnings to Total Asset

CRAA Credit Risk Assessment and

Analysis

RI Risk Identification

CRI Credit Risk Identification RMC Risk Monitoring Control

CRMC Credit Risk Monitoring Control RMP Risk Management Practices

CRMP Credit Risk Management

Practices ROA Return on Asset

CRU Credit Risk Understanding RWA Risk Weighted Assets

EBIT/CL

Earnings Before Interest and

Tax/Current Liability SEBI

Security Exchange Board of

India

EBIT/TA

Earnings Before Interest and Tax

to Total Asset TD/TA Total Deposit to Total Asset

EC Expected Challenge TI/TA Total Income / Total Asset,

FD Financial Distress TL Tolerance Level

LCR Liquidity Coverage Ratio TL/TA Total liabilities / Total Assets

LR Leverage Ratio URM Understanding Risk Management

MVE/TA

Market Value of Equity to Total

Asset VIF Variable Impact Factor

NI/TA Net Income / Total Assets WC/TA Working Capital to Total Asset

XVIII

ABSTRACT

Credit Risk is a significant threat for banks as the value of any organisation is measured by

its creditworthiness. Given the above, effective Credit Risk Management Practice (CRMP)

needs to be followed by banks to reduce this risk. The CRMP of public and private sector

banks in the Indian banking sector significantly differs as shown by past studies. In the

spirit of these studies, the present research assesses and compares the CRMP of the public

and the private banks in India, to check the extent and magnitude of variations. It is crucial

to study the lending and financial ratios of the banks as piling of NPAs adversely affects the

financial performance of the banks. Therefore the present study measures and compares the

credit risk management practices of public and private banks using lending ratio and

financial ratios.

Since ineffective CRMP may result in the bankruptcy of banks, the prediction of

bankruptcy by applying the bankruptcy model in the Indian banking context plays a

significant role. Due to some criticism of the models and the error rates that occurred in the

application of the model in present study, the current study aims at recalibration of the

applied models. Effective CRMP is possible due to precise control exercised by regulations

and supervision (Basel III norms). These controls pose challenges to bankers, which drives

the attention of bankers towards adequate preparedness needed for Basel III

implementation. Therefore the present study assesses the level of preparedness and

compliance of Basel III norms by public and private sector banks.

The present study used Principal Component Analysis (PCA) to determine the factors

influencing Credit Risk management Practices (CRMP) of banks. Descriptive statistics

were used to provide a summary of variables (CRMP determinants and Basel III

dimensions). In ratio analysis, lending and financial ratios were used to measure the credit

risk. Pearson’s Correlation Coefficient is used to find the relationship between financial

variables such as liquidity, profitability and leverage. An independent sample t-test is

conducted to compare the difference in credit risk determinants of CRMP, lending and

XIX

financial ratios, bankruptcy scores, Basel III preparedness and the Tier I, Tier II and CAR

between public and private banks in India. The test of ANOVA, along with a post hoc test

is conducted to find which bank reveals a statistically significant difference in the group.

One sample t-test and paired t-test was used on Basel III ratios. The robust test is conducted

to measure the financial health of the bank in the year 2017.

Regression Analysis such as, Ordinary Least Square (OLS) regression is used to determine

the statistical impact of the credit risk determinants on CRMP. Multiple linear regression is

used to measure the factors influencing the impact of the Basel III preparedness. Present

study applied Altman Z-score, Springate, Grover, and Zmijewski's model for assessing the

bankruptcy risk and also recalibrated these models by changing its coefficients through

multiple linear regression analysis.

In measuring the impact of the credit risk determinants on their respective CRMP for

public and private banks, regression results reveals that explanatory variable Credit Risk

Understanding and Credit Risk Assessment and Analysis (CRAA) among the four

components are most influential in the contribution of CRMP of private banks. The

regression model fits the data well for private banks compared to public banks in India. The

results of the Independent sample t-test show a significant difference in the credit risk

determinants between public and private banks.

In measuring the CRMP using lending ratios, it is observed that the certain lending ratios

are high in case of public banks. In measuring the CRMP using financial ratios, the result

states that both public and private banks experience low liquidity ratios and the leverage

ratios are lower for public banks and higher for private banks. The profitability ratios of

private banks show a fluctuating trend, and public banks show a decreasing trend.

The risk of bankruptcy of public and private banks was analysed by applying four

bankruptcy models. It is found that the results are not appropriate in case of two models.

The ranking results as per bankruptcy models shows that Bank of Baroda and Nainital Bank

XX

are in the first position (most efficient, and credit-risk safe) among public and private bank

respectively.

In measuring the statistical impact of factors of Basel III Preparedness, the regression

results shows that the factor ‘Anticipated Benefit’ is the most crucial followed by

‘Anticipated Impact’ in Basel III preparedness. The result of one-sample t-test shows that

private sector banks commenced disclosure towards compliance (minimum common equity

Tier I) ratio from 2018 while the public sector banks started compliance from 2014. The

private as well as public banks showed higher compliance of the Tier 1 capital ratio and

capital adequacy ratio, compared to a limit prescribed by Basel III norms.

Based on these findings, a broad conclusion can be drawn that private banks are generally

more efficient in terms of following credit risk management practices. The lending ratios

are low for private banks, indicating a better financial position. The bankruptcy study

concludes that the recalibrated Altman and the Grover model perform better than the

original model. In contrast, the original Springate and the Zmijewski model showed

improved accuracy over the recalibrated model. Further, it can be concluded that Indian

banks are well prepared to implement Basel III norms, as the Basel III ratios are maintained

by the public and private banks are at a much higher level than prescribed by RBI.

The study contributes to the literature in terms of the determination of credit risk

determinants of CRMP using the Principal Component Analysis (PCA) technique and

recalibration of bankruptcy models. The uniformity assumption of Institutional theory does

not apply in our study on account of differences in the understanding among employees on

the different aspects of credit risk and in the assessment and monitoring and control policies

of credit risk followed by the public and private banks in India. The private banks show a

negative relationship of factor, ‘Anticipated Cost’ with Basel III preparedness. These

results support the Legal Theory of Finance.

Chapter I Introduction

1

Chapter I

Introduction

1.1. Background of the Study

The health of a nation’s economy is largely dependent on a sound financial system. The

financial system provides necessary funds for the nation’s growth and development. In the

financial system, the banking sector occupies the most important position as it holds the

savings of the public provides a means of payment for goods and services and finances the

growth of business. The banks also play a major role in planning and implementing a

country’s financial policy (Itanisa 2016). Thus, a banking sector needs to be strong and

resilient for the strong economy of nation.

The word bank is derived from the French word banco or "bancus" or banc which means a

bench (Jhingan, 2001). The early Jews in Lombardy conducted the banking business by

sitting on benches. The banking is as old as the authentic history and the origins of modern

commercial banking are traceable in ancient times. According to Shekhar and Shekhar

(2008), in ancient Greece around 2000 B.C., the famous temple of Ephesus was used as

depositories for people’s surplus fund and these temples were the centres of money lending

transactions. The Priest of these temples acted as financial agent.

The period of banking reforms began in the year 1992, which provided a basis for looking

into the future of the Indian banking system (Kumar, 2014). During the last two decades,

there have been several reforms at the global and national levels that had an impact on the

operating environment of the banks. These reforms are in the form of, the introduction of

new players, new institutions, and new instruments. The introduction of new financial

products and services and the huge strides in technology and communication have brought

significant changes in the working of banks (Mallya 2012). These changes are gradual

liberalization of Indian banking, deregulation of interest rate, global competition, new

financial reforms, virtual banking, diversification of activities, retail character of banking,

liberalization of Foreign Direct Investment (FDI), active role of banks in upliftment of

Chapter I Introduction

2

socio-economic development of the country, implementation of new Basel requirement

etc. Given these above growing complexities in the bank’s business and the dynamic

operating environment, has led the banks to face a new or higher risk.

Risk is understood as “anything that can create hurdles in the way of achievement of certain

goals”. Therefore, the requirement of the risk management perceives a paramount

importance for the banks. According to Rao and Rentala (2012) the dynamic operating

environment of banks, have pushed the risk management to the forefront of the financial

landscape.

Risk management is understood as “adopting a practice of identifying the potential risk in

advance, analysing them and taking precautionary steps to reduce the risk”. Risk

management is significant because, today’s banks run its operation with two goals in mind

i.e. to generate profit and to stay in the business (Marision 2005), In other words, although

avoiding failure is the principal reason for managing risk but financial institution also have

broader objective of maximizing Risk Adjusted Rate of Return on Capital (RAROC).

According to Rao and Rentala (2012), the importance of risk management in banks is

because of their effect on the financial crisis and determining its role in the survival growth

and profitability of the bank. The risk management provides reasonable assurance of

achieving firm’s goals, compliance with applicable laws and regulations. It also helps in

encouragement of specific investment and decreasing the earnings volatility.

The risk management in banks witnessed a substantial change, due to emergence of

regulations evolved from the global financial crisis. As per these regulations the banks

need to retain higher standards for capital, leverage, liquidity, funding requirements and

risk reporting (Phillipe 2015). Although a variety of regulatory and supervisory authorities

have set norms for managing risk, still it remains a challenge for banks, as managing risk

depends on bank’s ability and stability. The process of risk management is complex and

difficult due to absence of risk culture in many banks. As the bank moved into a new high

powered world of financial operations and trading, with a new risk, there is a need for the

more sophisticated and versatile instrument for risk assessment, monitoring and controlling

risk exposure (Nandi and Chaudhary, 2011). The banks are expected to perform risk

management practice by designing effective risk management policies, designing a

Chapter I Introduction

3

procedure for identification and assessment of risk etc. Indian banking industry requires a

combination of new technologies, better processes of credit and risk appraisal, treasury

management, product diversification, internal control and external regulation for better risk

management (Adamson 2012).

Banks face three types of risk i.e. credit risk, market risk, and operational risk. Among

these risks, credit risk is the most important because it has a substantial effect on the return

on investment of the banks. According to Ngoroge and Ngahu (2017) Credit risk is a

significant threat for the banks as the value of any organization is measured by its

creditworthiness. Given the above, effective Credit Risk Management Practice (CRMP)

needs to be followed by banks to reduce this risk. The CRMP assumes establishing a

suitable credit risk management environment by identifying, measuring and managing

credit risk and covers all aspects such as identification of credit risk, understanding what

determines it and its measurement using various tools. The CRMP of public and private

sector banks in the Indian banking sector significantly differ as shown by the studies of

Thiagarajan (2011), Goel and Rekhi (2013), Kattel (2016) and Pourkeiki (2016). In the

spirit of these studies, the present research assesses and compares the CRMP of the public

and the private banks in India, to check the extent and magnitude of variations.

An ineffective CRMP may result in the bankruptcy of banks therefore, the prediction of

bankruptcy may help stakeholders to obscure themselves from the risks arising there from.

There are many models available for bank failure predictions. Literature survey shows that

the majority of international bank failure prediction employs the Altman-Z score model,

Grover model, Springate model and Zmijewski model. The present research aims to apply

all these models in the Indian banking context. Some critics of the above mentioned models

opine that when the original model is applied to a more recent sample, its predictive power

may be deficient and the risk of bankruptcy may be over predicted. Due to this fact, the

present study aims at the recalibration of the above models and compares the results from

the recalibrated and the original model, to judge its accuracy.

The effective CRMP is possible due to precise control by authorities in terms of regulations

and supervision. The concern regarding credit risk management at an international level

Chapter I Introduction

4

began in 1974, with the creation of the committee for regulation and supervision of banking

practices known as the Basel Committee on Banking Supervision (BCBS). Due to this

concern, the formal framework for bank’s capital structure was evolved in 1988 with an

introduction of Basel I. Basel I primarily focused on credit risk and appropriate Risk

Weighted Asset (RWA). The RBI implemented Basel I in the year 1992 in India. Basel I

was criticized for its rigidity of the "One Size Fit" approach and the absence of risk

sensitivity in capital requirements (Jayadev 2013). Due to these deficiencies in Basel I

accord, the BCBS introduced Basel II. Basel II is a much more comprehensive framework

of banking supervision when compared to Basel I (Sarma 2007). It was built on three

mutually reinforcing pillars such as Minimum Capital Requirements (Pillar1), Supervisory

Review (Pillar 2) and Market discipline (Pillar 3). Basel II was criticized for not

considering the liquidity and leverage risk in capital regulation and also failed to address

the systemic risk (Jayadev 2013). It was also criticized for its inability to prevent the

financial crisis; hence in response to the 2007-09 global financial crisis, BCBS issued Basel

III norms.

Basel III focused on four vital banking parameters viz. capital, leverage, funding, and

liquidity. Basel III introduced different aspects to control risk such as Counter Cyclical

Capital Buffers (CCCB), Capital Conservation Buffer (CCB), Leverage Ratio (LR),

Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR). Basel III poses

several challenges to the bankers; risk managers, finance managers, and Basel III program

managers are under pressure to implement Basel III. The key challenges for these managers

will be deciding how best to implement a solution that allows them to comply with Basel

III (Whitepaper). These challenges drive the attention of bankers towards the adequate

preparedness needed for Basel III implementation. This prompts the present study to assess

the level of preparedness by public and private sector banks of Basel III norms.

India should transit to Basel III because of several reasons. By far the most important

reason is that, as India integrates with the rest of the world, as increasingly Indian banks go

abroad and foreign banks come on to our shores, we cannot afford to have a regulatory

deviation from global standards. Also, as per RBI guidelines, Basel III need to be

Chapter I Introduction

5

implemented in phases, due to this Basel III is not implemented fully by some of the banks.

This drives the attention of the researcher, to study the compliance of Basel III.

1.2. Statement of Problem

Over the current years, there has been an increased number of credit-related problems in the

banks due to increased Non-Performing Assets (NPAs). Moreover, the piling of NPAs of

public and private banks adversely affects the profitability, liquidity and leverage position

of banks. It is a worrying fact that public sector banks report higher NPAs than the private

banks. This NPA problem may be the result of ineffective CRMP. The result of ineffective

CRMP may lead to the breakdown of the whole banking system (Ishitiq 2015).

The other problem that guides this study is that recognising of exact determinants of CRMP

is difficult given the different factors that govern CRMP in different countries. The factors

applicable in some context/nations may not apply to Indian banks due to the difference in

the economic background and the Central Bank’s policies of the country.

The credit risk management is also a significant challenge for an Indian banking system due

to the constant heat of competition that banks face from foreign banks. This fact compels

the banks to look into its profitability, liquidity and leverage position, as the financial

position is positively affected by these three variables, or one is achieved at the cost of

others. Since the available literature state an inverse relationship between liquidity and

profitability and also between profitability and leverage, an effort is made to judge the

relation in the Indian context.

In today's era, the most common problems of the Indian banking sector are bank frauds and

hike in NPAs leading the banks towards state of bankruptcy. The stakeholders are

concerned about forecasting the likelihood of financial distress to respond before the event

takes place. Thus a variety of scoring models that can predict the bank failure have been

developed. Further, although the scoring model is one of the powerful tools used for

bankruptcy prediction, it also has its loopholes. Some authors question the model’s capacity

for sound default detection and argue that the bankruptcy prediction model is less accurate

Chapter I Introduction

6

when it is applied to a different environment, period and industry as compared to the reason

for which it was initially devised. The problem is that the prediction models used in this

research might have been for other industries rather than banking or may be outdated. Thus

the models may not provide credible results under all conditions and may need some kind

of calibration. This may lead to another problem. There may be a difference in the

predictive ability in the original and the recalibrated model, as a result both these models

may not match with each other due to change in coefficients. This demands a need for

comparing the results of both the models with the robust test, to decide the accuracy of the

models followed.

Furthermore, due to the above loopholes in the models, the reliability of the model is

doubtful; hence using a single model may not give a perfect result. Therefore, more than

one model needs to be used to predict bankruptcy. According to Kleinert (2014), single

bankruptcy prediction model faces limitations and use of multiple bankruptcy prediction

models improved the prediction accuracy.

The Basel III implementations need proper preparations as it involves huge cost and

resources in terms of capital, manpower and technology. Further, Basel III preparations are

affected by several factors i.e. Anticipated Benefit (AB), Anticipated Cost (Anticipated

Cost), Anticipated Impact (AI), Expected Challenge (EC), Availability of Resources (AR),

Education Level (EL) etc. Thus, there is a need to find the most significant factors

influencing its preparedness. The other research problem is related to compliance of Basel

III implementation by Indian banks. RBI has given the transitional schedule for

implementation of these new norms from the year 2013-2019. In this schedule, the

minimum requirement for Basel III ratios (CAR, Tier I, Tier II, leverage and liquidity ratio)

required to be followed by individual banks are prescribed by RBI. A reference to annual

reports show that some of the banks have recently moved towards Basel guidelines and are

still following standard approaches, but still many do not follow the expected advanced

approaches. This explains the need to study the compliance of Basel III norms in the Indian

context.

Chapter I Introduction

7

The other research problem is related to the pre and post-implementation phase of Basel III.

Capital ratios of the banks differ in the pre and post-implementation phase of Basel III.

Capital ratios of the banks need to be enhanced in the post-implementation of Basel III in

order to meet the higher requirements. Therefore the present study assesses Basel III ratios

in these two phases.

1.2.1 Research Questions

The research question underlying this study is recognizing the exact determinants of

CRMP. These determinants are not standard and as per the literature review it is observed

that, the factors governing the CRMP differs from country to country. In the past, some of

the studies undertaken in one country have used three determinants whereas some other

studies have used five determinants in other country. Thus, determinants applicable in other

context or country may not apply to the Indian banks. Therefore, the research question

addressing the above issue states, what are the determinants of Credit Risk Management

Practices in India? These different determinants have certain impact on the CRMP as per

the reviews of past studies. Therefore, a further question arises as, what is the impact of

these determinants on the CRMP?

The primary function of public and private banks is accepting deposits for lending. In

performing a lending function, both these banks undertake a heavy credit risk. Also, these

banks follow an equivalent procedure and safety precautions before sanctioning a loan and

are on equal foot of bearing the credit risk. Considering this fact, it is understood that there

is uniformity in the risk management practices among the public and private banks.

However it is a worrying fact that, public sector banks report higher NPAs than the private

banks. This triggers the researcher to find an answer to a research question such as, whether

there is a difference in the credit risk determinants of CRMP between public and private

banks?

Financial performance indicators such as, liquidity, profitability and leverage measured

through financial ratios helps public and private banks in knowing its financial position to

manage its credit risk. The financial position of both these banks may not be uniform as the

pattern and extent of liquidity, profitability and leverage differs between public and private

banks due to their nature of operations. Therefore, the research question arises, whether

Chapter I Introduction

8

there is significant difference in the financial ratios between the public and private banks?

The research gap from the literature review highlights the fact that the relationship between

liquidity profitability and leverage has been studied in other countries, but very few similar

studies have been carried out in the Indian banking sector. Therefore, the research question

arises to find - Whether there exists a particular trend and relations among liquidity,

profitability and leverage of Indian banks?

A study on lending ratio helps to understand the lending and NPA position of the banks.

As per the studies of Goel and Rekhi (2013) and kattel (2016) the credit risk management

practices of public and private banks differ. This difference in the CRMP may be on

account of various factors and one amongst them may be lending ratios. Due to this, a

question arises, whether there is a significant difference in the lending ratios between public

and private banks?

The bankruptcy models applied in the present study were originally developed at a different

time period, with different samples and were affected by the country’s economic

environment. Therefore the predictive power of these models may differ. Thus the question

arises as to how accurate are the bankruptcy models? If the predictive power of the model is

affected after its application to the Indian banking sector, the next question arises as to,

whether there is a need for the recalibration of these models to suit the current economic

environment and our specific regulatory environment of the country? After recalibration

and application of these models to the Indian banking sector, the study tries to answer the

question –Which financial distress model is accurate to predict bankruptcy of banks?

The financial position of the bank is assessed using bankruptcy score. Based on these

bankruptcy scores which Indian banks could be ranked as the best, and the worst? Lastly,

based on these scores, it further tries to answer a question whether there is significant

difference in the bankruptcy score of public and private banks?

It is crucial for the Indian banks to have good preparations for the Basel III implementation

in order to meet international standards. Therefore the question arises as to verify, whether

the Indian banks are prepared for the implementation of Basel III norms? The Basel III

preparations are affected by several factors as per the studies of Al- Tamimi (2008) and

Chapter I Introduction

9

Kapoor and Kaur (2015), with this raises the question as to, what are the significant factors

contributing towards Basel III preparedness? The Basel III preparations of public and

private banks may differ due to their nature of operation, availability of resources, etc.

Thus, further question arises whether there is statistical difference in the Basel III

preparations of public and private banks?

Basel III implementation poses a variety of challenges in terms of enhanced capital

requirements, design of comprehensive liquidity management framework, data acquisition

and software and hardware development. Therefore, some of the banks may not follow

these norms due to cost factor thus the question arises as to Whether Indian banks comply

with the minimum requirements of Basel norms stipulated by the RBI? The post

implementation period of Basel III requires banks to maintain higher capital to meet the

norms. Therefore, the question arises as to what is the difference in the Basel III ratios of

banks in the pre and post-implementation phase of Basel III? and whether banks have

followed required capital requirements in the pre and post-implementation phase of Basel

III?

1.3. Objectives of the Study

Following are the four objectives o this study:

1. To identify the factors (determinants) affecting the credit risk management

practices, measure its individual impact and compare them between public and

private banks.

2. To measure and compare the credit risk management practices of public and private

banks using lending ratios and financial ratios.

3. To analyse the risk of bankruptcy of public and private banks using the bankruptcy

models, judge their accuracy and rank the banks based on its score.

4. To assess the preparedness and compliance of the Basel III accord of public and

private banks in India.

Chapter I Introduction

10

1.4. Scope of the Study

The present study has been undertaken primarily to examine the CRMP of public and

private banks in India. Banks face three types of risk – Credit risk, Market Risk and

Operational risk. Among these risks credit risk is the most important one, because it has a

substantial effect on the return on investment of the bank. Therefore, present study is

restricted to credit risk, ignoring the other risk. There are different methods to measure

CRMP, however, the present study covers two methods i.e. credit risk measurement tools

and identifying determinants of credit risk.

The current study covers banks from two categories public sector banks and private banks.

There are 27 public sector banks in India, consisting of 19 Nationalised banks , six State

Bank group, Industrial Development Bank of India (IDBI) and Bhartiya Mahila Bank. The

present study covers 19 nationalized banks, State Bank of India and IDBI bank making it

twenty one public sector banks. There are 29 private banks (old and new private sector

banks) operating in the country, however the present study covers 18 private banks. The

type and the number of banks are selected based on the availability of data and the

consequences of time constraints.

Present study assesses the risk of bankruptcy of public and private banks using bankruptcy

models. There are many models available for bank failure predictions such as Standard and

Moody’s financial ratios, Beaver model, Altman Z- score model, Ohlson’s model CAMEL

model, Grover Model, Springate Model, Neural Network and Zmijewskis Model to predict

the health of the bank. Among these models, the present study focuses on the most

frequently used model in past studies. These models are the Altman-Z score model, Grover

model, Springate model, and Zmijewski model.

The accuracy of these models could be judged based on various factors; however present

study covers Type I and Type II errors, robust test and the ranks given to the individual

banks. The secondary data for the bankruptcy study is collected for thirteen years period

from the year 2004-5 to 2016-17. The data period consists of two phases, the pre-

implementation and the post-implementation phase of Basel II and Basel III norms. This is

the period where the Basel committee put norms on the banks and the effect of all these

Chapter I Introduction

11

norms is reflected in the financial statements of the banks, which are more reliable and will

reduce measurement errors.

Although a study concerning Basel III norms covers many aspects such as impact,

challenges, cost- benefit analysis etc, however, due to time and resource constraints present

study is limited to the assessment of the preparedness and compliance of Basel III norms

between select public and private banks in India.

A vast and intensive study is possible with respect to full compliance of these norms by the

Indian banking sector, but based on the data availability and time factor, present study,

focuses on compliance of Basel III ratios (Minimum Common Equity Tier I capital, Tier I

capital, Tier II capital, Capital Adequacy Ratio and leverage ratios). The other ratios such

as Liquidity ratio and Net Stable Funding ratio is not covered due to lack of data in the

annual statements.

1.5. Significance of the Study

The credit risk is a significant threat for banks as it has a direct impact on the profitability

of the bank. A study by Ishitiq (2015) found a positive relationship between the

performance and risk management. This relationship throws light on the paramount

rationale of management of credit risk. A study by Rehman (2016) states that credit risk

management is getting more attention, especially after the credit crunch of 2007-2009.

According to Ngoroge and Ngahu (2017) effective risk management can bring far reaching

benefits to all organisations, whether large or small, public or private sector. Therefore

efficient CRMP is one of the vital strategy bank needs to make by diverting its resources

for the growth and survival of banking business. This strategy of CRMP can give many

advantages to the financial institution in terms of financial performance, competitive

advantage, optimum utilisation of resources, improved service delivery, growth and

survival, reduced waste and developing policies for regulatory bodies.

The information about CRMP will assist in developing policies for regulatory bodies.

According to Onyano (2010) policy makers in the financial industry will use this study in

understanding the extent to which the banking industry is exposed to credit risks. This will

Chapter I Introduction

12

guide them in designing the best practices for the financial institution to manage credit risk.

The findings will further enhance the managers understanding of the key systems that will

improve the banks performance. Proper CRMP is also important because Ishitiq (2015)

found in its study that, there is positive relationship between the performance and risk

management. In addition to the regulatory requirement, the CRMP is valuable and relevant

in order to increase the value of the firm (Ishitiq 2015).The value of financial institution is

judged based on its financial performance. The credit risk management is found to be one

of the determinants of returns of banks stock (Hussain and Ajmi, 2012). Thus the credit risk

management will maximize the banks risk adjusted rate of return by adjusting credit risk

exposure within acceptable limit.

It is crucial to study the lending and financial ratios of the banks as piling NPAs adversely

affects the financial performance of the banks. A study on measurement of credit risk using

lending and financial ratios is significant to managers, investors, creditors, government and

regulators. Managers can depend on these ratios to have the right choice in the decision-

making process and efficiently adopt new policies and a new management system. These

ratios help the investors to predict the future situation, earning capacity of their invested

companies and the safety of their investments. The ratio analysis assist the creditors in

knowing the ability of a company to pay off its debt and the company's potential in the

future to keep lending it. The ratios aid government to compare individual bank with the

industry ratio to provide financial support for the weaker banks and could help the bank

regulators to evaluate and compare banks performance.

The bank health needs attention because banking is a business entity that collects funds

from the public in the form of savings and Chanel’s to the community in the form of credit.

This process attaches the risk that the borrower may default on his application. This

uncertain economic environment during recent years has stressed the importance

bankruptcy prediction. In such a condition it becomes necessary to assess the financial state

of the banks using distress prediction model to estimate the business risk. This study will

help the banks to understand its financial position much in advance and to avoid financial

distress.

Chapter I Introduction

13

A proper prediction of bank bankruptcies is significant as the financial sector is very crucial

for a growing economy, and any variations in its performance can affect the economy either

way (Chaudhary and Nandi, 2011). The bankruptcy information is useful to the

management to undertake precautions and essential to the auditor to report on the viability

of the firm. Investors are interested in the bankruptcy model to avoid the risk of loss from

an unsuccessful investment, and the lenders are interested in taking decisions on the

granting of loans to the bank. The government agency has an interest in seeing the signs of

bankruptcy to provide support for its revival. Score value calculated using models is useful

to banks to demand loans from RBI or any other funding agency as per Pradhan (2014).

Thus the financial health of banks can help each beneficiary and it can be applied in a wide

variety of situations. Bankruptcy study will provide information on variables that will

influence the health of a bank (Stingar and Warstuti 2014). In total, if bankruptcy could be

predicted with reasonable accuracy ahead of time banks could better protect their business

and could take action to minimize risk and loss of business perhaps even prevent

bankruptcy (Ramage and Pongstal 2004).

The progress report on the implementation of Basel III regulatory framework (2013)

reflects that RBI has taken the steps for convergence of the International Basel standards

and the Indian banks need to transit to Basel III because of several reasons. The most

important reason being, the Indian banks make it presence in the world and foreign banks

come on to our shores. Hence the Indian banks cannot afford to have a regulatory deviation

from global standards. Considering this fact, preparedness of Indian banks for the

implementation of Basel III norms assumes a high level of significance. Further, it is also

significant because it poses a variety of challenges to the banks. These challenges drive

them to develop technological infrastructure and human resources to cope up with risk

environment.

A major challenge for the Indian banks is the implementation of regulations as per the

transitional schedule specified by RBI. In the post-implementation period of Basel III

norms, the banks need to infuse an additional capital, to maintain quantity, quality,

consistency, and transparency of capital as per set norms. According to Athira and Shanti

(2014), banks require additional capital of 5 lakh crores and further the public sector banks

Chapter I Introduction

14

require common equity of 1.4 - 1.5 trillion to meet Basel III requirements. Apart from this,

Basel III norms require banks to follow the Capital Conservation Buffer and Counter

Cyclical Capital Buffer for the better risk management framework. All these stipulations

trigger the banks to enhance their capital base by balancing the profitability aspects of

banks. These facts trigger the significance of Basel III preparations.

Due to the above challenges, RBI introduced phase in arrangement for the implementation

of Basel III norms from 2013-14 to 2018-19, which will also align full implementation of

Basel III in India closer to the internationally agreed date of January 1, 2019. Thus, all

banks are proceeding at their own pace for meeting the Basel III requirements. Therefore, a

study on the compliance of Basel III norms as per the transitional schedule specified by

RBI perceives paramount importance.

The evolution of Basel III norms has taken place due to the impact of the financial crisis in

2008. This crisis affected the U.S. economy and other economies very badly as the capital

was dried up during this crisis. However, the impact of the same was less on the Indian

economy, maybe due to the better capital position of the Indian banks in this period. This

period was known as the pre-implementation period of the Basel III norms and in this

period the capital position of the Indian banks was sufficient to face the financial crisis. The

post-implementation period of Basel III norms shows an improvement in the minimum core

capital stipulations. Thus there is difference in the capital ratios in the pre and post-

implementation period of Basel III norms. Therefore, a comparative study on the Basel III

capital ratios of the public and private banks in the pre-implementation phase and also in

the post-implementation phase achieves due importance.

The present study is also significant as it makes valuable contribution to the current

academic literature in the area of banking and also proposes methodologies as well as

practical additions to the key area. Furthermore, it will act as a source of reference and

background for other research in this area plus findings will stimulate the future research.

Chapter I Introduction

15

1.6. Organisation of the Study

Our study titled “A Study of Credit Risk Management Practices of Public and Private

Banks in India” is organized into eight chapters, and is arranged as follows:

Chapter I: Introduction: This chapter throws light on the background of the study,

statement of the problem, research questions, objectives of the study, scope of the study,

significance of the study, and organization of the study.

Chapter II: Theoretical Foundations and Empirical Literature: This chapter explores

exhaustive and comprehensive literature on Credit Risk management Practices (CRMP),