INTERNSHIP REPORT ON CREDIT RISK MANAGEMENT OF JANATA BANK LTD

67

INTERNSHIP REPORT ON CREDIT RISK MANAGEMENT OF JANATA BANK LIMITED

-

Upload

dhakauniversity -

Category

Documents

-

view

0 -

download

0

Transcript of INTERNSHIP REPORT ON CREDIT RISK MANAGEMENT OF JANATA BANK LTD

INTERNSHIP REPORT

ON

CREDIT RISK MANAGEMENT OF

JANATA BANK LIMITED

Internship Report On

Credit Risk Management of Janata Bank Limited

Submitted to

Mr. BadruzzamanController of Examinations

National UniversityGazipur-1704

Supervised By

Mohammad Mosharraf HossainAssistant Professor

Department of Business Administration

Dhaka City College

Submitted By

Md. Rezvi BasherNational University Roll No. 1061692

National University Registration No: 1068033Department of Business Administration

Dhaka City College

Date of Submission: March 2nd, 2015

Letter of Transmittal

March 2nd, 2015

Professor Md. Shahjahan KhanPrincipalDhaka City CollegeDhanmondi, Dhaka – 1205

Subject: Submission of Internship Report.

Dear Sir,

This is my pleasure that I have completed my internship report and hereby ready to

submit my report on “Credit Risk Management of Janata Bank Limited”.

According to the instruction I have worked on the actual loan operation & credit

management of JBL. I have really enjoyed the working environment of the Janata

Bank Limited, Kalir Bazar Branch, A.C. Dhar Road, Narayanganj - 1400. I have

tried my best to present all those things that I have experienced over there while

preparing my report.

I have thoroughly enjoyed the overall work during my internship period which is

carrying vast description of practical knowledge. This report along with all kinds of

necessary information regarding the internship is being submitted to you for your

evaluation. I sincerely hope that you will appreciate my effort.

Sincerely yours,

__________________

Md. Rezvi Basher

National University Roll No. 1061692

National University Registration No: 1068033

Department of Business Administration

Dhaka City College

Acknowledgement

I wish to acknowledge the immeasurable grace and profound kindness of almighty

Allah, the supreme ruler of the universe, who enables me to make my report in reality.

I acknowledge my immeasurable gratitude to Mohammad Mosharraf Hossain,

Assistant Professor, Department of Business Administration, for his helpful

supervision, suggestion, guidance and encouragement. In fact, he guided me as my

teacher and motivator to make me understand and conduct a complete report like this

one. I note his contribution with high dignity.

I am also very much grateful to our Coordinator Mr. Md. Shahinur Sobhan and our

Principal Prof. Md. Shahjahan Khan for their scholarly and consecutive suggestions

which were of much assistance to prepare the report.

I sincerely express my deepest gratitude to Department of Business administration

and all the officials of department for their relentless help and caring attitude and to

many others whose names I failed to mention here, I thank you all.

.

Certificate of Supervisor

This is certified that, Md. Rezvi Basher, National University Roll No : 1061692,

Registration No : 1068033, Academic session: 2009-2010, Major in Marketing, is a

regular student of 8th semester (Final Semester) of BBA program, Department of

Business Administration, Dhaka City College, under the National University of

Bangladesh. He has completed an internship program on “Credit Risk Management

of Janata Bank Limited.”. Under my supervision which is fulfillment of partial

requirement of obtaining BBA degree.

I wish his success in all his future endeavors.

____________________

Mohammad Mosharraf Hossain

Assistant Professor

Department of Business Administration

Dhaka City College

Executive Summary

The internship report is based on the credit risk management process of Janata Bank

Ltd. In the beginning of the report the scope, origin, objectives, methodology,

limitations are discussed. The main objective of this report is to present an overview

of credit risk magement activities of Janata Bank Ltd. Primary sources of data are

discussion with the officers and staffs and work experience in different desk. The

secondary data is collected from the annual report, different text books and several

web pages. The scope of this report is limited to the credit risk management activities

of Janata Bank Ltd. In spite of some limitations such as lack of adequate information,

lack of proper experience, I have tried my best to make this report as informative as

possible.

The overview of Janata Bank Ltd. is given in this report. It covers the origin of the

bank, organizational profile and present situation of the bank. The bank is established

in 1971. The bank has various products and services for its customers. It has a huge

number of clients for different types of products. Janata Bank Ltd. also has four

overseas branches. The products and services JBL are also discussed. The values and

philosophies of the bank are discussed in brief too.

In this report the overall credit risk management activities of Janata Bank Ltd. are

discussed. It covers the credit appraisal. Credit sanction for the borrowers. Various

credit documentation procedures followed by the bank. The report also covers credit

administration activities of credit risk administration unit. The report describes

disbursement of the loans and advances in prerequisite ways. It describes the

monitoring and control of individuals’ credits. It explains how the bank manages the

credits and to minimize financial losses. This report describes the classification of

loans. The recovery process implies that a borrower will be treated leagally in case of

failure in repayment of loans.

In the ending, the findings, recommendations and conclusions are discussed. In

findings it is reviewed that the credit officers do not fill up the proposal form properly

in most of the cases. It can be recommended that the bank should concentrate more on

proper documentation of all types of loans. Besides, the documents supporting the

security against the loan have to be verified properly. These recommendations will

reduce the problems of credit risk management of Janata Bank Ltd.

Acronyms

BB Bangladesh Bank

CRG Credit Risk grading

CRM Credit Risk Management

FDR Fixed Deposit Receipt

JBL Janata Bank Limited

L/C Letter of Credit

GM General Manager

DMD Deputy Managing Director

DGM Deputy General Manager

Table of Contents

Serial no.

Particulars Page no.

Letter of Transmittal i

Acknowledgement ii

Certificate of Supervisor iii

Executive Summary iv

Acronyms v

CHAPTER 1 : INTRODUCTION

1.1 Origin of the Report 1

1.2 Objectives of the Report 1

1.3 Methodology of the Report 2

1.4 Scope of the Report 2

1.5 Limitations of the Report 3

CHAPTER 2: OVERVIEW OF THE JANATA BANK LTD.

2.1 Historical Background of Janata Bank Ltd. 4

2.2 Vision of Janata Bank Ltd. 4

2.3 Mission of Janata Bank Ltd. 4

2.4 Main objectives of Janata Bank Ltd. 5

2.5 Business Philosophy of Janata Bank Ltd. 5

2.6 Values of Janata Bank Ltd. 5

2.7 Key Milestones of Janata Bank Ltd. 6

2.8 Services of Janata Bank Ltd. 12

2.9 Branches of Janata Bank Ltd 21

2.10 Organizational Structure of Janata Bank Ltd. 22

2.11 Principal Activities of Janata Bank Ltd. 24

2.12 Present Situation of Janata Bank Ltd. 31

2.13 Future Plans of Janata Bank Ltd. 31

2.14 CSR Activites of Janata Bank Ltd. 32

2.15 Automation and Online Banking of Janata Bank Ltd. 33

2.16 SWOT Analysis of Janata Bank Ltd. 34

CHAPTER 3 CREDIT RISK MANAGEMENT PROCESS OF JANATABANK LTD.

3.1 Credit Processing/Appraisal 37

3.2 Credit Approval/Sanction 38

3.3 Credit Documentation 39

3.4 Credit Administration 39

3.5 Disbursement 40

3.6 Monitoring and Control of Individual Credits 42

3.7 Monitoring the Overall Credit Portfolio (stress testing) 42

3.8 Credit Classification 43

3.9 Classified Loans 44

3.10 Recovery of Loan 47

CHAPTER 4: FINDINGS, RECOMMENDATIONS & CONCLUSION

4.1 Findings of the Report 50

4.2 Recommendations 51

4.3 Conclusion 52

Bibliography 53

List of Tables

NO. Tables Name Page no.

1 Export Trend of Janata Bank Ltd. 14

2 Import Trend of Janata Bank Ltd. 19

3 Branches of Janata Bank ltd. 22

4 Portfolio Wise Investment 26

5 Different products under Rural Credit, Micro Ent. & SP Program 28

6 Industrial Credit 30

7 Loan Classification Systems 45

8 Summary of Loans and Advances with Risk Status 46

CHAPTER - 1INTRODUCTION

1.1 Origin of the Report:

It is said that without theory, practice is blind and without practice theory is

meaningless. An internship is designed to bridge the gap between the theoretical

knowledge and real application. The prime reason of this report is to learn about

credit risk minimization process of a Bank. This report has been prepared based on

one selected listed Bank in Bangladesh, named Janata Bank Limtied. The report has

been prepared based on the information of this bank which has been gathered during

the internship period. The report titled “Credit Risk Management of Janata Bank

Limited”. No knowledge is fully complete unless it is fully supported by events on

ground. Whatever may be the quality of theoretical knowledge, it is not complete

without practical implication on ground. This realization is more pronounced in the

study of Business Administration where experience on ground plays a dominant role.

Internship program is essential for all BBA students because it helps him/her acquit

with real life situation. Bank is a one of the important financial institutions, so I have

selected Janata Bank Limited, which is one of the leading private commercial banks

in Bangladesh. For this reason I have prepared my internship report on Credit Risk

Management of Janata Bank Limited. Throughout the last few years Bangladesh has

been experiencing a rapid and significant change in the banking sector. Not only in

our country, all over the world the dimension of banking has been changing rapidly

due to the technological innovation, globalization and deregulation. Janata Bank Ltd

is a state owned scheduled bank in Bangladesh. It has a vital contribution towards

lending and investment in economy because Janata Bank Ltd. has been participating

in all sectors (from industrial sector to microfinance).

1.2 Objectives of the Report

The main objective of the report is to identify and evaluate the credit risk management

system of Janata bank limited, which includes the following specific objectives:

To know the practices of credit structure of the bank Janata Bank Limited.

To identify the recovery system performed by the bank.

To asses and highlight the legal actions followed by the Branch in terms of credit recovery.

1.3 Methodology of the Report

The report is descriptive in nature. To fulfill the objectives of this report the total

methodology has divided into two major parts. They are:

a) Data Collection Procedure: To conduct the completion of this report data were

collected from both primary & secondary sources.

i. Primary Source:

Personal observation

Desk work in different section, of the bank.

Conversation with bank’s employees.

ii. Secondary Source:

Annual report of Janata Bank Limited

Variety of books, articles & journal related to banking.

Information from the internet.

b) Data Processing & Analysis:

The collected information have then processed & complied with the aid of MS Word

& other computer software. Necessary tables have been prepared on the basis of

collected data. Detail explanations and analysis have also been incorporated in the

report.

1.4 Scope of the Report

Janata bank is the second largest commercial bank in Bangladesh. It has 916 branches

and four overseas branches. It is liked with 1203 foreign correspondents all over the

world. I was assigned to learn practical knowledge from Janata bank Ltd. Here I tried

to learn about how to manage credit risk management, tools of credit risk

management, loan recovery system, facing problems in loan recovery system,

performance of the bank in loan recovery system etc. All things comes under the

theory of credit risk management and finally I would conclude with the critical

evaluation of credit risk management under the guidelines of bank companies act

1991 and a discussion on major findings and recommendations.

1.5 Limitations of the Report

To prepare a report on the topic like this in a short duration is not easy task. In

preparing this report some problems and limitations have encountered which are as

follows:

The main constraint of the study was insufficiency of information, which was

required for the study. But the employees do not provide due to security and

other corporate obligations.

Lack of opportunity to access to internal data.

Due to time limitation, many of the aspects could not be discussed in the

present report.

Since the bank personnel were very busy, they could not give enough time.

Based on secondary data in most cases for preparing this report.

As the data, in most cases, are not in organized way, the bank failed to provide

all information.

Legal action related information was not available.

CHAPTER - 2OVERVIEW OF JANATA BANK

LTD.

2.1 Historical Background of Janata Bank Ltd.

‘Janata’ means ‘People’. So Janata Bank means ‘People’s Bank’. Janata Bank Limited

(JBL) is the 2nd largest state owned commercial bank in Bangladesh. Immediately

after the emergence of Bangladesh in 1971, the erstwhile United Bank Limited and

Union Bank Limited were named as Janata Bank. It was established under the

Bangladesh Bank order 1972. During the privatization process it was incorporated as

a public Limited Company on 21, May 07 vide certificate of incorporation No-

C66933(4425)07. The Bank has taken the over the business of Janata Bank at a

purchase consideration of Tk. 2593.90 million as a going concern through a vendor

agreement signed between the Ministry of Finance of the Peoples’ Republic of

Bangladesh and the Board of Directors on behalf of Janata Bank Limited on 15th

November 2007.

Janata Bank Limited operates through 897 branches including 4 overseas branches at

United Arab Emirates and a subsidiary company named Janata Exchange Company

started in Italy. It is linked to 1202 foreign correspondents all over the world

2.2 Vision of Janata Bank Ltd.

To become the effective largest commercial bank in Bangladesh to support socio-

economic development of the country and to be a leading bank in South Asia.

2.3 Mission of Janata Bank Ltd.

Janata Bank Limited will be an effective commercial bank by maintaining a stable

growth strategy, delivering high quality financial products, providing excellent

customer service through an experienced management team and ensuring good

corporate governance in every step of banking network.

2.4 Main objectives of Janata Bank Ltd.

The main objective of JBL is to provide all types of banking service at the doorsteps

of the people. The bank participates in various social and development programs and

also takes part in implementation of various policies and promises made by the

government.

2.5 Business Philosophy of Janata Bank Ltd.

JANATA Bank Ltd, a full service commercial bank with Local and International

Institutional shareholding, is primarily driven by creating opportunities and pursuing

market niches not traditionally met by conventional banks. Today JANATA Bank is

one of the fastest growing banks in the country to support the planned growth of its

distribution, network and for its various business segments.

The reason JANATA Bank is in business is to build a profitable and socially

responsible financial institution focused on markets and businesses with growth

potential, thereby assisting JANATA and stakeholders build a “just, enlightened,

healthy, democratic and poverty free Bangladesh”. That means to help make

communities and economy of the country stronger and to help people achieve their

dreams as well. They fulfill the purpose by reaching for high standards in everything

we do. For their customers, their shareholders, their associates and their communities

upon, which the future prosperity of their company rests.

2.6 Values of Janata Bank Ltd.

Janata Bank Ltd. holds the following values and will be guided by them as they do

their jobs.

Creating an honest, open and enabling environment.

Have a strong customer focus and relationships based on integrity, superior

service and mutual benefit.

Strive for profit & sound growth.

Work as a team to serve the best interest of their owners.

Relentless in pursuit of business innovation and improvement.

Value and respect people and make decisions based on merit.

Base recognition and reward on performance.

Responsible, trustworthy and law-abiding in all that they do.

2.7 Key Milestones of Janata Bank Ltd.

International Awards

Recently The Bank has been recognized nationally and internationally for its

outstanding performance.

Janata Bank Limited achieves '2013 Performance Excellence Award' by Citi Bank

N.A.

Citi Bank N.A recently recognized Janata Bank Limited with '2013 Performance

Excellence Award'.

The awarding ceremony was held on 11 September, 2013 at the Head Office premise

of the Bank. S M Aminur Rahman, CEO and Managing Director, Janata Bank Ltd.

received the award from Khd. Rashed Maqsood, Managing Director and Citi Country

Officer, Bangladesh. DMDs of the Bank Md. Golam Sarwar, A K M Ashraf Uddin

Khan and Omar Farooque and GMs of the Bank Abdus Salam Azad and Md.

Monjerul Islam and High officials of Citi Bank, N. A. were also present at the

awarding event.

Janata Bank Ltd achieved this award for solidifying leadership in the payment space.

Janata Bank Limited wins 'The Asian Banking & Finance Wholesale Banking Awards

2013 & Retail Banking Awards 2013'

It is a matter of great pleasure for us that Janata Bank Limited has once again been

awarded by Asian Banking and Finance (ABF) Magazine, a concern of Carlton Media

Group (CMG), Singapore. Evaluating Janata Bank Limited's last year's performance

in different fields the magazine has judged JBL winner of three awards in two

following categories:

A. Asian Banking & Finance Wholesale Banking Awards 2013

i. Bangladesh Domestic Project Finance Bank of the Year

ii. Bangladesh Domestic Trade Finance Bank of the Year

B. Asian Banking & Finance Retail Banking Awards 2013

iii. Domestic Retail Bank of the Year Bangladesh

The awarding ceremony was held on 18 July, 2013 in Singapore. Md. Shirajul Islam,

GM(BDMD), Md. Afzalul Bashar, GM(RPD), Sk. Md. Zaminur Rahman,

DGM(MISD) and Md. A.K.M Shamsul Alam AGM(MISD) received the awards on

the podium as representatives of Janata Bank Ltd.

JBL's Position in the Banker's Global Ranking of Banks-2012

"The Banker"- a magazine of Financial Times Group, London ranked JBL in its

Global Ranking of Banks-2012 as follows:

i. Top 5 ROC, Asia pacific- 1st

ii. Top 25 top 1000 ontenders,Tier-1 growth- 4th

iii. Top 1000 Contenders by region, Asia Pacific- 7th

iv. Top 25 top 1000 Contenders, ROC -16th

v. Top 100 of the top 1000 Contenders-23rd

The Banker" selected winning banks based on their overall performance.

Business Asia Most Respected Company Awards-2012

Janata Bank Limited has been awarded 'Business Asia Most Respected Company

Awards-2012' by Business Asia. Business Asia has selected winning banks based on

Overall performance.

Janata Bank Limited wins ‘The Asian Banking & Finance Awards 2012’

It is a matter of great pleasure for us that Janata Bank Limited has once again been

awarded by the Asian Banking and Finance Magazine (ABF), a leading financial

magazine in Asia . For several years the magazine has been recognizing the best

performers in bank business of different countries in Asia with these esteemed

awards. Evaluating Janata Bank Limited's last year's performance in different fields

the magazine has judged JBL winner of two awards in three following categories:

A. The Asian Banking & Finance Wholesale Banking Awards 2012

i. Bangladesh Domestic Project Finance Bank of the Year

ii. Bangladesh Domestic Trade Finance Bank of the Year

B. The Asian Banking & Finance Retail Banking Awards 2012

iii. Domestic Retail Bank of the Year Bangladesh

The awarding ceremony was held on 23 August, 2012 in Singapore . Md. Afzalul

Bashar, General Manager and Md. Mosaddake-Ul-Alam, Company Secretary

received the awards on the podium as representatives of Janata Bank Ltd.

International Award-The Bank of the year-2011 in Bangladesh

Janata Bank Limited has been awarded ‘The Bank of the Year-2011 in

Bangladesh’ by the London based Financial Magazine The Banker of the Financial

Times Group. This is for the sixth time the bank has been awarded ‘The Bank of the

Year’ award. Janata Bank Limited achieved remarkable progress in the year 2010.

ICMAB Best Corporate Award-2011

Janata Bank Limited has been awarded ICMAB Best Corporate Award - 2011 by the

Institute of Cost and Management Accountants of Bangladesh. This Bank secured

first position among the State Owned Commercial Banks in Bangladesh.

International Award -"World's Best Bank Award-2009 in Bangladesh

Janata Bank Limited was awarded Best Bank-Bangladesh in the Global Finance,

World's Best Bank Awards, 2009 by New York based Financial Magazine "Global

Finance". "Global Finance" has selected winning banks based on number of criteria

including growth in Assets, Profitability, Strategic relationships, Customer Service,

Competitive pricing and innovative products.

International Award -"World's Best Bank Award-2008 in Bangladesh

Janata Bank Limited was awarded Best Bank-Bangladesh in the Global Finance,

World's Best Bank Awards, 2008 by New York based Financial Magazine "Global

Finance". "Global Finance" has identified winning banks based on number of criteria

including growth in Assets, Profitability, Strategic relationships, Customer Service,

Competitive pricing and innovative products.

International Award -"World's Best Bank Award-2007 in Bangladesh

Janata Bank Limited was awarded Best Bank-Bangladesh in the Global Finance,

World's Best Bank Awards, 2007 by New York based Financial Magazine "Global

Finance". "Global Finance" has identified winning banks based on number of criteria

including growth in Assets, Profitability, Customer Service, Product innovation and

Advanced Technology.

International Award -"World's Best Bank Award-2006 in Bangladesh

Janata Bank Limited was awarded Best Bank-Bangladesh in the Global Finance,

World's Best Bank Awards, 2006 by New York based Financial Magazine "Global

Finance". "Global Finance" has identified winning banks based on number of criteria

including growth in Assets, Profitability, Customer Service, Product innovation and

Advanced Technology.

International Award –The Bank of the year-2005 in Bangladesh

Janata Bank Limited has been awarded ‘The Bank of the Year-2005 in

Bangladesh’ by the London based Financial Magazine The Banker of the Financial

Times Group. This is for the fifth time the bank has been awarded ‘The Bank of the

Year’. The award has been given considering the growth and performance measure of

the bank.

Janata Bank Limited receives "Asian Banking Awards 2005" on Credit Scheme for

Handicapped People:

The Awards were presented by the Asian Bankers Association (ABA) and Bank

Marketing Association of the Philippines (BMAP) in the Asia Pacific Bankers

Congress (APBC) 2005 on June 17, 2005 in Manila, Philippines.

International Award -The Bank of the Year-2004 in Bangladesh

Janata Bank Limited has been awarded as 'The bank of the year 2004 in Bangladesh'

by the London based Financial Magazine “The Banker of the Financial Times

Group”. This is for the second consecutive year that the Janata Bank Limited has been

awarded 'Bank of the year'. Janata Bank Limited shows a remarkable progress in the

year 2003. Its return on assets was 1.36% and return on investment was 6.47%

respectively. Janata Bank Limited is also emerging as the strong and innovative bank

within the country. The profile of its success is enriched by a package of new

qualitative product lines, prudent liability and assets management and others. Most of

the key financial indicators of the bank showed a very positive improvement at the

year ended December 2003.

Janata Bank Limited receives "Asian Banking Awards 2004" on Financing Program

for Women Entrepreneurship

Financing program for Women Entrepreneurship of Janata Bank Limited has highly

been commended as a Runner-Up in the Micro-Finance Product or Program category

of the Asian Banking awards 2004. The Awards were presented by the Asian Bankers

Association (ABA) and Bank Marketing Association of the Philippines (BMAP) in

the Asia Pacific Bankers Congress (APBC) 2004 on March 26, 2004 in Manila,

Philippines.

Janata Bank Limited gets “The Banker Award-2003”

The Banker, an International Banking Magazine of the Financial Times group in

London has selected Janata Bank Limited as “The Bank of the Year, 2003” among all

other banks in Bangladesh. The Banker’s assessment for award is based on a number

of criteria. Besides core data and results, the criteria include key growth and

performance measures, the use of technology and particular achievement in the past

and overall strategy, it may be mentioned that Janata Bank Limited could achieve the

same award for the year 2001.

International Award-The Bank of the Year-2002

The Banker, a magazine of the London based Financial Times Group of Companies,

has voted Janata Bank Limited as the bank of the year for Bangladesh for 2002. While

making this selection the panel has recognized the efforts made by Janata Bank

Limited in recent times for Improving IT based performances.

International Award-The Bank of the Year-2001

The Banker, a magazine of the London based Financial Times Group of Companies,

has voted Janata Bank Limited as the bank of the year for Bangladesh for 2001. While

making this selection the panel has recognized the efforts made by Janata Bank

Limited in recent times for improving its performances. The bank has also been

included in the listing of top 200 Asian Banks for the year 2001. This listing will be

available to delegates attending the forthcoming IMF/Word Bank meeting in

Washington. The September edition of the Banker will also highlight the recent

achievements of Janata Bank Limited. Besides, a certificate of merit and a bank of

the year logo will be given to Janata Bank Limited for exclusive use on all publicity

and advertising.

It may be noted here that Janata Bank Limited has been working hard in improving

the customer services in recent times by introducing a number of IT-based reform

measures.

2.8 Services of Janata Bank Ltd.

Janata Bank Ltd. offers all the major banking facilities and services to its customers.

The Bank with its network spreading throughout the country has a unique feature of

ploughingback savings from those places and then investing them into different loan

portfolios.

Janata Bank Ltd. with its wide ranging branch network and skilled personnel provides

prompt and personalized services like issuing:

1. Demand Draft

2. Telegraphic Transfer

3. Mail Transfer

4. Pay Order

5. Security Deposit Receipt

6. Transfer of fund by special arrangement

a. Normal transfer

b. Electronic transfer through Ready Cash Card

7. Foreign Remittance Payment

The Bank provides the following Interest facilities:

Current/Savings/STD account status

FDR account status

Advance account status

Loan account status

NRB Accounts

International Banking

Janata Bank Limited has already established a worldwide network and

relationship in international Banking through its 4 (four) overseas branches

and 1239 foreign correspondents.

The bank has earned an excellent business reputation in handling and funding

international trade particularly in boosting export & import of the country.

The bank finances exports within the frame-work of the export policy of the

country.

It is one of the pioneers in promoting back to back Letter of Credit for the

RMG (Ready Made Garments) sectors.

Export Finance

To boost up country's Export, Janata Bank Limited has been providing

different kinds of assistance to exporters. Some of which are as below:-

Providing Pre-Shipment and Post-Shipment Finance, Export Guarantee and

bonding facility etc.

Concessional rate of interest for exports Finance.

Back to Back L/C under bonded Warehouse facility

Sight & Unasked L/C against Firm Contract for import of raw materials.

Sight L/C under EDF

Exporter's Retention Quota A/C both interest bearing and non-interest bearing.

Export incentive Program.

Banking at Export Processing Zone

Scope for establishment of export oriented industry by 100% foreign

investment and by joint-venture

The sole bank to disburse Government Export Promotion Fund against export

of computer software & data entry processing

Undergone to an agreement with Bangladesh Bank to obtain fund from

Government EEF (Equity & Entrepreneurship Fund) to build up entrepreneur's

equity.

Consultancy and advisory services by an expert group of officials.

Special export financing program towards computer software data entry and

service export.

Salient Features:

The salient features of International Banking are:-

A. A Firm or Company having valid ERC, necessary infrastructural and

technical facilities and sufficient skilled man power related computer.

B. Member of BASIS or BCS.

C. Having Computer Literacy or related professional background.

D. Preference to the firm/company having prior experience

E. Satisfactory performance Certificate/Acceptance Letter from Counterpart

abroad.

F. Valid Export Orders are in hand.

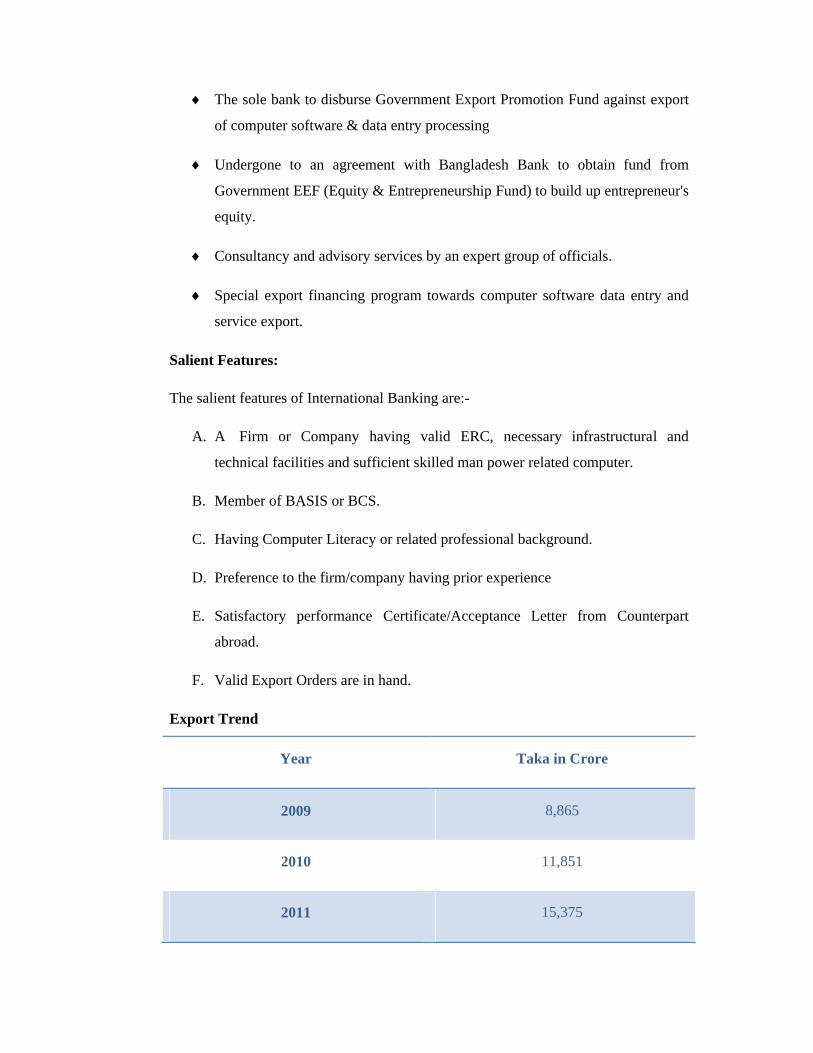

Export Trend

Year Taka in Crore

2009 8,865

2010 11,851

2011 15,375

2012 15,652

2013 15,325

Table 1: Export Trend of Janata Bank Ltd

Source: Janata Bank Limited, Annual Report 2009-2013 (page 21)

Scope of Further Expansion

The Janata Bank Ltd. has the following scopes for further expansion in international

banking:-

Software and data entry

Jewellery

Frozen fish

Dry & dehydrated fish

Processed and semi-processed food fishes and shrimps

Electrical and electronics item

Toys and Luggage

Fashion item

Leather goods

Stationary goods

Diamond cutting and polishing

Orchid

Gift item

Bamboo, Cane and Wooden furniture

Janata Bank Limited also provides the following loans:

Working Capital Loan from EPB under Government Export Promotion Fund

(EPF),

Government Equity and Entrepreneurship Fund from Bangladesh Bank

Working Capital Loan from Epb Under The Government Export Promotion

Fund

The eligibility for obtaining this loan is:-

Limited Company, Partnership or Proprietorship firm having valid ERC and

members of BASIC or BCS.

Commercially & technically viable and profitable as per assessment of EPB.

Latest one among the Entrepreneurs should be computer literate having a

degree or diploma in computer.

Number of programmers will be at least 5 among which at least 3 having

degree or diploma in computer science.

An established computer software firm which has at least 5 PC and necessary

Printers, UPS, IPS, Generator, Voltage Stabilizer etc with LAN and E-

mail/Internet facility.

Salient Features of the above Loan

Minimum loan amount will be 50% of export order or Tk. 2.5 million

whichever is lower,

Export order will remain valid upto one year. Rate of interest @6.00% simple

& service charge @2.5%. In case of default to repay in due time, additional

0.50% service charge will be realized.

Export proceeds to be repatriated through the designated bank i.e. Janata Bank

Limited, Janata Bhaban Corp. Branch.

Loan amount including interest will be adjusted from the export proceeds.

Loan sanctioning authority is EPB and as per their sanction letter Janata

Bhaban Corp. Branch will disburse the loan applying all the formalities as per

MOU made between Janata Bank Limited and EPB.

Government Equity and Entrepreneurship Fund from Bangladesh Bank

Eligibility for obtaining the fund and Salient Features:

New project, registered as Private Limited Company under company Act

1994.

Total project cost including net working capital will not be less than Tk. 15

million.

The project should be viable in consideration of its technical, management &

economical aspect.

Equity participation will be 1/3 of the total project cost, out of which

Bangladesh Bank equity participation will not be more than 49%.

Bank's loan if any and entrepreneurs own contribution to be fully utilized

before utilizing EEF.

The company will issue equal amount of share against EEF in favour of

Peoples Republic of Bangladesh and to be submitted to the concern bank. The

EEF share will be entitled to get dividend as declared by the company or 5%

P.A, whichever is higher,

The entrepreneur will buy back the share within first three years face value

plus 5% P.A.

In case of default to repay the fund due to genuine loss, 90% of the EEF will

be borne by Bangladesh Bank and remaining 10% by the concerned financial

institution.

Financial assistance to boost up export:

Concessional rate of interest.

Export incentive programs

Export Processing Zone facility.

Scope of establishment of export oriented industry by 100% foreign

investment and by joint venture.

Fully fledged infrastructural and logistic support for export i.e. project finance,

working capital, pre-shipment & post-shipment export finance, guarantee,

bonding facility, etc.

Consulting facility by an expert group of officials.

Import Finance

Through quite a good number of Authorized Dealer Branches and 1198 nos. foreign

correspondents world wide Janata Bank Limited has been extending full range import

and relevant finance facilities.

Import Items:

Capit Fuel & Lubricants.al Machineries and Industrial raw materials.

Intermediate goods.

Consumer durable, spare parts and equipments.

Consumer goods : Food & Food Grains, Baby food, Petroleum, CDSO

(Crude Degummed Soya bean Oil), CPO (Crude Palm Olin) Oilseeds, Cement

Clinker, Construction Materials, Fertilizer, Chemicals and many other goods

permissible by Import by Import Policy of the country.

Facilities Offered:

Opening of L/C at competitive/ reasonable margin and commission

Interest at concession rate on import finance to the prime customers & interest rebate

facilities.

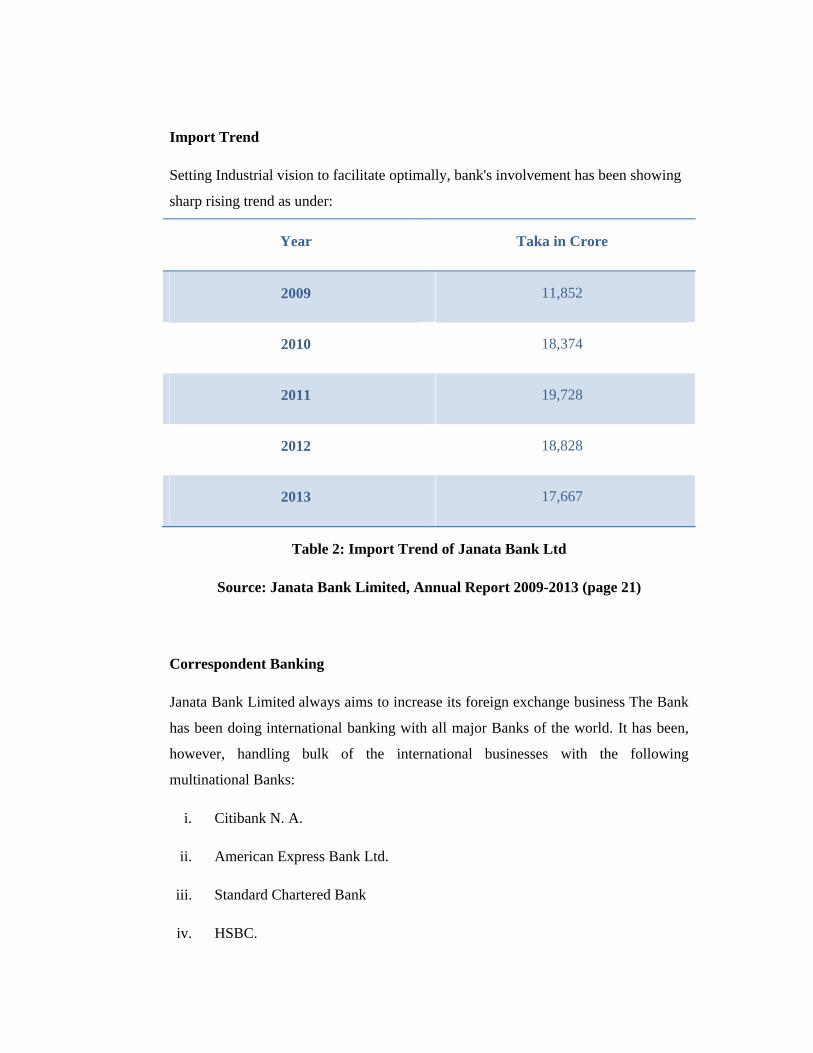

Import Trend

Setting Industrial vision to facilitate optimally, bank's involvement has been showing

sharp rising trend as under:

Year Taka in Crore

2009 11,852

2010 18,374

2011 19,728

2012 18,828

2013 17,667

Table 2: Import Trend of Janata Bank Ltd

Source: Janata Bank Limited, Annual Report 2009-2013 (page 21)

Correspondent Banking

Janata Bank Limited always aims to increase its foreign exchange business The Bank

has been doing international banking with all major Banks of the world. It has been,

however, handling bulk of the international businesses with the following

multinational Banks:

i. Citibank N. A.

ii. American Express Bank Ltd.

iii. Standard Chartered Bank

iv. HSBC.

v. The Chase Manhattan Bank

Utility Services of Janata Bank Ltd.

Besides normal banking operation, Janata Bank Limited offers special services to a

large number of clients/agencies throughout the country. Under the network of utility

service, customers of different govt. organizations, corporate bodies, local bodies,

educational institutions, students, etc are continuously getting benefits from the Bank.

Janata Bank Limited's utility services are:

Bills Collection:

a. Gas bills of Titas, Bakhrabad and Jalalabad Gas Transmission and

Distribution Companies.

b. Electricity bills of Dhaka Electricity Supply Authority, Dhaka Electricity

Company, Bangladesh Power Development Board and Rural Electrification

Board.

c. Telephone bills of Telegraph and Telephone Board.

d. Water/Sewerage bills of Water and Sewerage Authority.

e. Municipal holding tax of City Corporation/Municipalities.

f. A pilot scheme is underway to provide personalized services to our clients.

Payments made on behalf of Govt. to:

a. Non- Govt. teachers salaries

b. Girl Students scholarship/stipend & Primary Student Stipend.

c. Army pension

d. Widows , divorcees and destitute Women Allowances

e. Old-age Allowances

f. Food procurement Bills

Issuance of Television License: The only Bank providing this service in Bangladesh.

2.9 Branches of Janata Bank Ltd.

There are 897 branches of Janata Bank Limited in home and abroad. Among them

450 branches are situated in urban areas including four foreign branches and 443

branches are in rural areas. And all foreign branches are situated in United Arab

Emirates.

Division Urban Rural Zone Total

Dhaka 171 91 262

Chittagong 100 102 202

Rajshahi 53 93 146

Sylhet 22 37 59

Khulna 52 59 111

Barisal 22 19 41

Rangpur 30 42 72

Overseas 4 0 4

Total 454 443 897

Table 3: Branches of Janata Bank Ltd

Source: Janata Bank Limited, Annual Report 2009-2013 (page 109)

2.10 Organizational Structure of Janata Bank Ltd.

Like every other business organization, the foremost duty of the top management is to

makes all the major decisions of Janata Bank. The boards of directors are being at the

topmost level of organizational structure plays an important role in policy formulation

and successful execution, but it is not a direct concern of the day-day operations of the

bank. The duty was delegated to the management committee. The board mainly sets

the objectives and policies of the bank. The management consists of one chairman,

eleven directors, one CEO & MD and one company secretary. Mid and lower level

employees get the direction and instruction from the Board of Directors about the

tasks they have to meet. The chief executive provides the guideline to the managers

and employees, but bears the responsibility for

be attained.

Graph

Organogram of Janata Bank Ltd.

and employees, but bears the responsibility for determining how tasks and goals are to

Graph 1: Organogram of Janata Bank Ltd.

Organogram of Janata Bank Ltd.

Chairman

Managing Director

General Manager

Deputy General Manager

Assistant General Manager

Senior Principal Officer

Principal Officer

Senior Officer

Officer

Sub Accountant

Senior Clerk

determining how tasks and goals are to

Board of Directors

Chairman of the Board of Directors

Professor Dr. Abul Barkat

Members of the Board of Directors

Dr. Jamaluddin Ahmed, FCA

Mr. Md. Emdadul Hoque

Mr. Nagibul Islam Dipu

Dr. R M Debnath

Syed Bazlul Karim, B.P.M.

Prof. Mohammad Moinuddin

Mr. Md. Abu Naser

Mrs. Sangita Ahmed

Prof. Dr. Nitai Chandra Nag

Mr. A.K.M Kamrul Islam, FCA

Mr. Md. Mahabubur Rahman Hiron

Mr. S M Aminur Rahman, CEO & Managing Director

2.11 Principal Activities of Janata Bank Ltd.

Janata Bank Ltd. is the second largest commercial bank in Bangladesh. The aim of the

bank is to actively participate in the socio-economic development of the nation by

operating a commercially sound banking system. It provides credit to deserving

borrowers and at the same time, protects depositor’s interest.

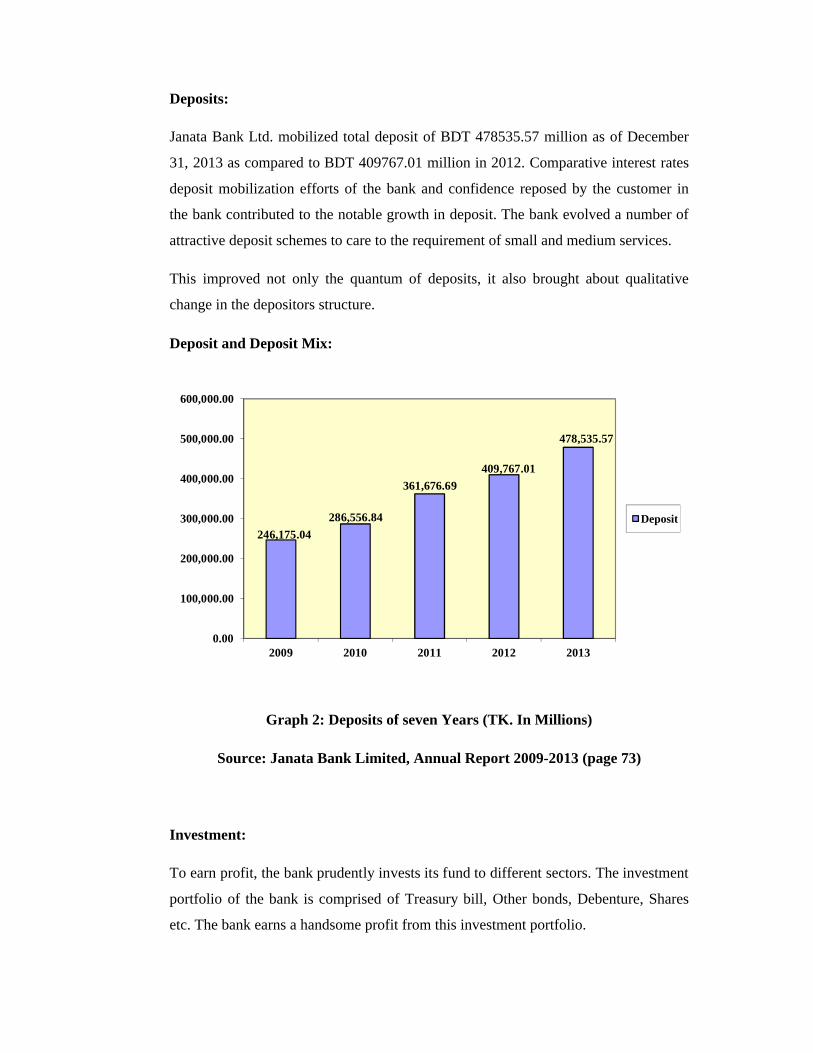

Deposits:

Janata Bank Ltd. mobilized total deposit of BDT 478535.57 million as of December

31, 2013 as compared to BDT 409767.01 million in 2012. Comparative interest rates

deposit mobilization efforts of the bank and confidence reposed by the customer in

the bank contributed to the notable growth in deposit. The bank evolved a number of

attractive deposit schemes to care to the requirement of small and medium services.

This improved not only the quantum of deposits, it also brought about qualitative

change in the depositors structure.

Deposit and Deposit Mix:

Graph 2: Deposits of seven Years (TK. In Millions)

Source: Janata Bank Limited, Annual Report 2009-2013 (page 73)

Investment:

To earn profit, the bank prudently invests its fund to different sectors. The investment

portfolio of the bank is comprised of Treasury bill, Other bonds, Debenture, Shares

etc. The bank earns a handsome profit from this investment portfolio.

246,175.04

286,556.84

361,676.69

409,767.01

478,535.57

0.00

100,000.00

200,000.00

300,000.00

400,000.00

500,000.00

600,000.00

2009 2010 2011 2012 2013

Deposit

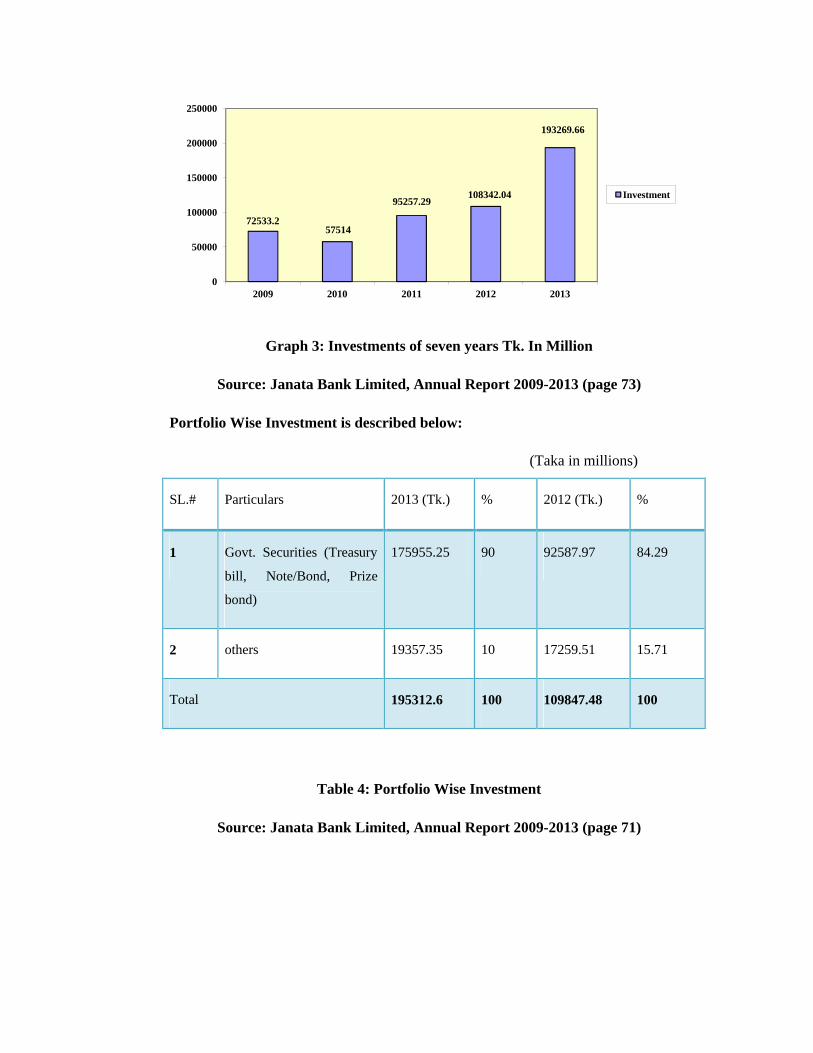

Graph 3: Investments of seven years Tk. In Million

Source: Janata Bank Limited, Annual Report 2009-2013 (page 73)

Portfolio Wise Investment is described below:

(Taka in millions)

SL.# Particulars 2013 (Tk.) % 2012 (Tk.) %

1 Govt. Securities (Treasury

bill, Note/Bond, Prize

bond)

175955.25 90 92587.97 84.29

2 others 19357.35 10 17259.51 15.71

Total 195312.6 100 109847.48 100

Table 4: Portfolio Wise Investment

Source: Janata Bank Limited, Annual Report 2009-2013 (page 71)

72533.257514

95257.29108342.04

193269.66

0

50000

100000

150000

200000

250000

2009 2010 2011 2012 2013

Investment

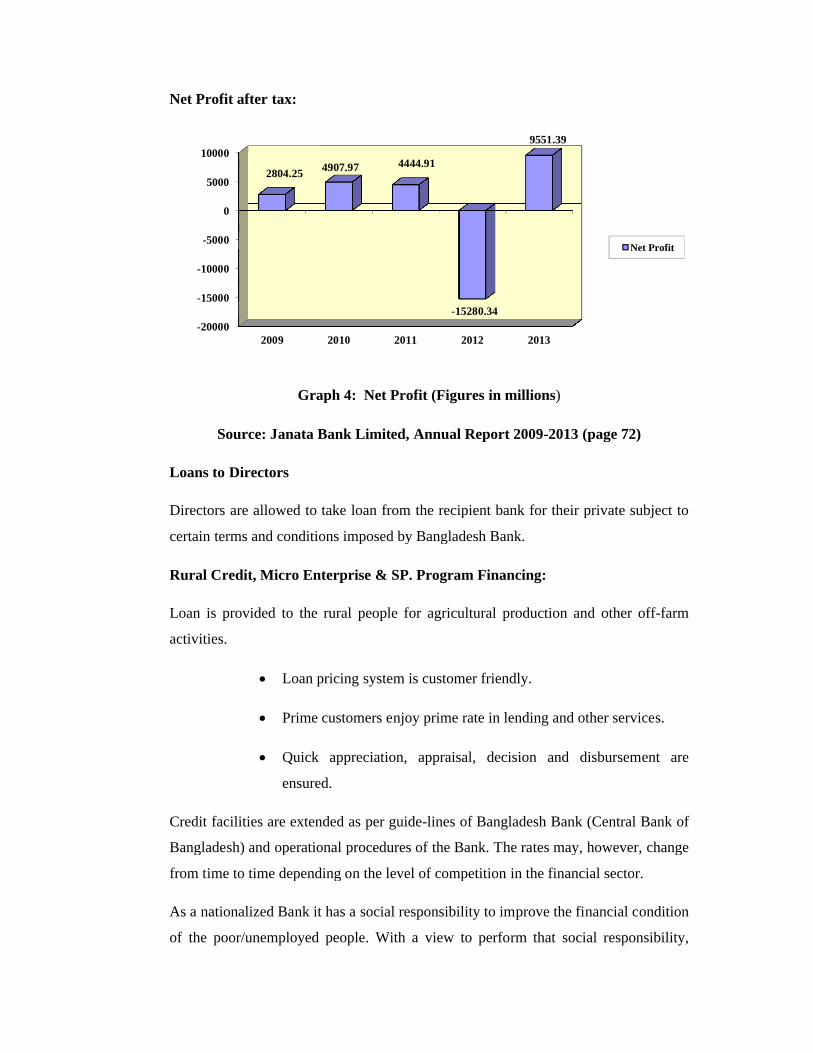

Net Profit after tax:

Graph

Source: Janata Bank Limited, Annual Report 2009

Loans to Directors

Directors are allowed to take loan from the recipient bank for their private subject to

certain terms and conditions imposed by Bangladesh Bank.

Rural Credit, Micro Enterprise

Loan is provided to the rural people for agricultural production and other off

activities.

Loan pricing system is customer friendly.

Prime customers enjoy prime rate in lending and other services.

Quick apprec

ensured.

Credit facilities are extended as per guide

Bangladesh) and operational procedures of the Bank. The rates may, however, change

from time to time depending o

As a nationalized Bank it has a social responsibility to improve the financial condition

of the poor/unemployed people. With a view to perform that social responsibility,

-20000

-15000

-10000

-5000

0

5000

10000

2009

2804.25

Graph 4: Net Profit (Figures in millions)

Source: Janata Bank Limited, Annual Report 2009-2013 (page 72)

Directors are allowed to take loan from the recipient bank for their private subject to

certain terms and conditions imposed by Bangladesh Bank.

Micro Enterprise & SP. Program Financing:

Loan is provided to the rural people for agricultural production and other off

Loan pricing system is customer friendly.

Prime customers enjoy prime rate in lending and other services.

Quick appreciation, appraisal, decision and disbursement are

ensured.

Credit facilities are extended as per guide-lines of Bangladesh Bank (Central Bank of

Bangladesh) and operational procedures of the Bank. The rates may, however, change

from time to time depending on the level of competition in the financial sector.

As a nationalized Bank it has a social responsibility to improve the financial condition

of the poor/unemployed people. With a view to perform that social responsibility,

2010 2011 2012 2013

4907.97 4444.91

-15280.34

9551.39

(page 72)

Directors are allowed to take loan from the recipient bank for their private subject to

Loan is provided to the rural people for agricultural production and other off-farm

Prime customers enjoy prime rate in lending and other services.

iation, appraisal, decision and disbursement are

lines of Bangladesh Bank (Central Bank of

Bangladesh) and operational procedures of the Bank. The rates may, however, change

n the level of competition in the financial sector.

As a nationalized Bank it has a social responsibility to improve the financial condition

of the poor/unemployed people. With a view to perform that social responsibility,

Net Profit

Bank has initiated rural credit program since 1974. Now under this rural portfolio

there are 34 products.

Information related to important products under this program are shown below:

Different Products under the Program

(Taka in millions)

Sl. No. Name of Products No. of LoansOutstanding

on Dec, 2013%

1 Cyber-cafe loan 13 2.70 0.01

2 Credit for forestry/horticulture nursery 751 32.90 0.13

3 Credit program for employees 78,368 3814.20 14.82

4 Financing “ women entrepreneurship” 267 86.92 o.34

5 Financing goat and sheep farming 11,370 154.70 0.60

6 Gharoa project 3,812 148.80 0.58

7 Crop loan program 3,46,528 1130.20 44.79

8 Doctor’s loan 66 24.96 0.10

9 Small business Dev. Loan 161 28.63 0.11

10 Credit for disable people 113 2.59 0.01

11 Consumer’s credit 1,069 90.80 0.36

12 Agro-based project/industry 1,567 1080.90 4.20

13 Fisheries &Shrimp Culture Credit 321 260.30 1.01

14 Agricultural & irrigation equipment 229 26.90 0.11

15 Others 1,40,699 8450.20 32.83

Total 5,85,328 25744.70 100.00

Table 5: Different products under Rural Credit, Micro Ent. & SP Program

Source: www.janatabank-bd.com/jb15.htm

SME Financing Scheme

Small and Medium Enterprise (SME) Financing Scheme has been introduced to assist

new or experienced entrepreneurs to invest in small and medium scale industries.

Small business development loan, Gharoaproject, credit for

forestry/Horticulture/Nursery, crop loan project all are designed for this purpose.

Light engineering, cottage industry, handy craft, CNG station, power loom, garments

accessories etc. are considered as thrust segment under this sector. The Bank

disbursed TK.25, 500 million in SME sector during the year 2013.

Doctors’ Credit Scheme

Doctors’ credit scheme is designed to facilitate financing to fresh medical graduates

and established physicians to acquire medical equipment’s and set up clinics and

hospitals. Total loan outstanding in 2013 was Tk12.96 million. The no. of loans was

66.

Women Entrepreneurs Development Scheme

Women Entrepreneurs Development Scheme has been introduced to encourage

women in doing business. Under this scheme, the bank finances the small and cottage

industry projects sponsored by women. Total loan outstanding in 2013 was Tk. 43.92

million. The no. of loans was 267.

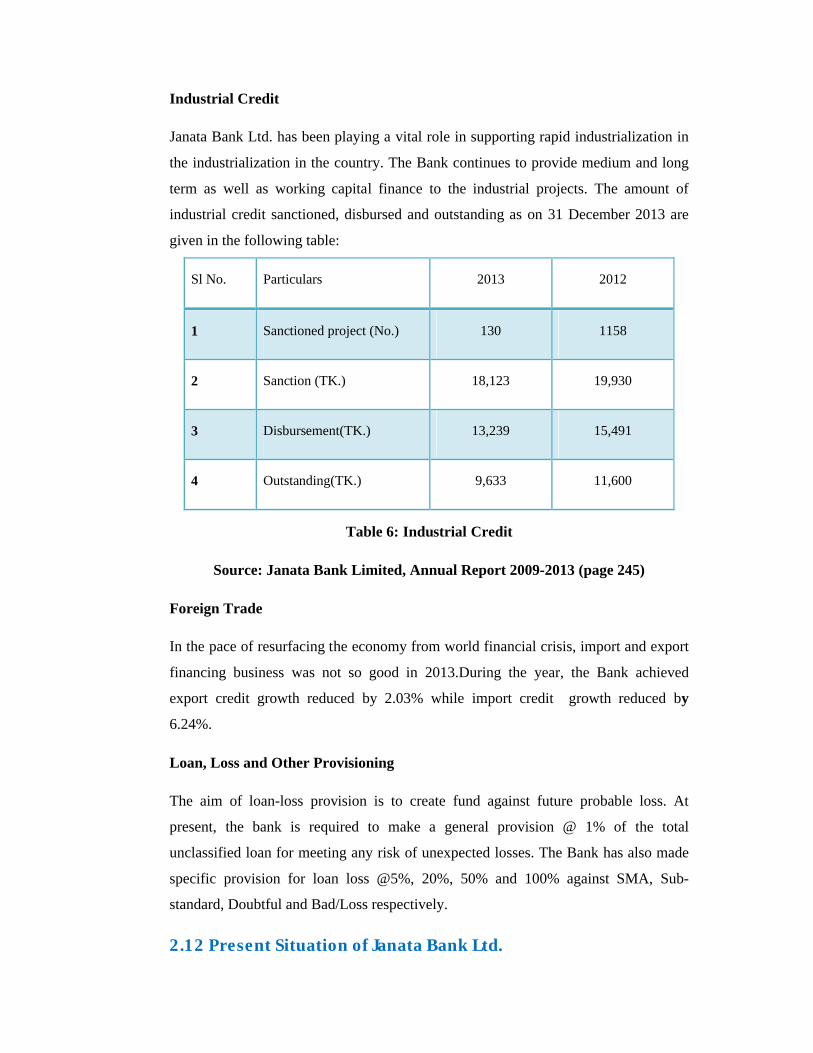

Industrial Credit

Janata Bank Ltd. has been playing a vital role in supporting rapid industrialization in

the industrialization in the country. The Bank continues to provide medium and long

term as well as working capital finance to the industrial projects. The amount of

industrial credit sanctioned, disbursed and outstanding as on 31 December 2013 are

given in the following table:

Sl No. Particulars 2013 2012

1 Sanctioned project (No.) 130 1158

2 Sanction (TK.) 18,123 19,930

3 Disbursement(TK.) 13,239 15,491

4 Outstanding(TK.) 9,633 11,600

Table 6: Industrial Credit

Source: Janata Bank Limited, Annual Report 2009-2013 (page 245)

Foreign Trade

In the pace of resurfacing the economy from world financial crisis, import and export

financing business was not so good in 2013.During the year, the Bank achieved

export credit growth reduced by 2.03% while import credit growth reduced by

6.24%.

Loan, Loss and Other Provisioning

The aim of loan-loss provision is to create fund against future probable loss. At

present, the bank is required to make a general provision @ 1% of the total

unclassified loan for meeting any risk of unexpected losses. The Bank has also made

specific provision for loan loss @5%, 20%, 50% and 100% against SMA, Sub-

standard, Doubtful and Bad/Loss respectively.

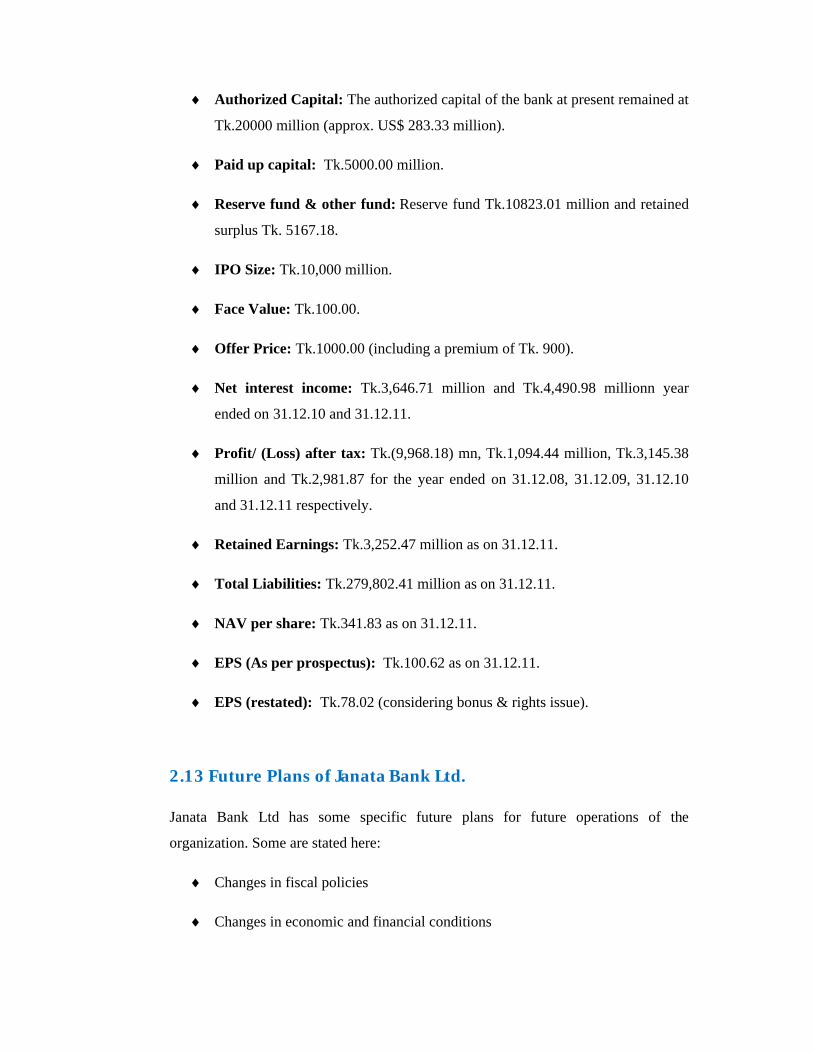

2.12 Present Situation of Janata Bank Ltd.

Authorized Capital: The authorized capital of the bank at present remained at

Tk.20000 million (approx. US$ 283.33 million).

Paid up capital: Tk.5000.00 million.

Reserve fund & other fund: Reserve fund Tk.10823.01 million and retained

surplus Tk. 5167.18.

IPO Size: Tk.10,000 million.

Face Value: Tk.100.00.

Offer Price: Tk.1000.00 (including a premium of Tk. 900).

Net interest income: Tk.3,646.71 million and Tk.4,490.98 millionn year

ended on 31.12.10 and 31.12.11.

Profit/ (Loss) after tax: Tk.(9,968.18) mn, Tk.1,094.44 million, Tk.3,145.38

million and Tk.2,981.87 for the year ended on 31.12.08, 31.12.09, 31.12.10

and 31.12.11 respectively.

Retained Earnings: Tk.3,252.47 million as on 31.12.11.

Total Liabilities: Tk.279,802.41 million as on 31.12.11.

NAV per share: Tk.341.83 as on 31.12.11.

EPS (As per prospectus): Tk.100.62 as on 31.12.11.

EPS (restated): Tk.78.02 (considering bonus & rights issue).

2.13 Future Plans of Janata Bank Ltd.

Janata Bank Ltd has some specific future plans for future operations of the

organization. Some are stated here:

Changes in fiscal policies

Changes in economic and financial conditions

Changes in regulatory guidelines

Changes in accounting standards

Changes in corporate tax structure

Changes in legislation and regulation of VAT on banking services

Volatility of interest rate

Instability in capital market

Volatility in money market

Changes in socio-economic condition arise from natural calamity and political

disturbance

Adverse impact of inflationary pressure

Increases of business competitor

Fluctuation of exchange rate

Increase of provision requirements.

2.14 CSR Activities of Janata Bank Ltd.

Since inception, Janata Bank is playing a leading role in CSR (Corporate Social

Responsibilities) activities among the state owned commercial banks. Janata Bank

Limited distributed BDT 113.38 million in the year 2012 and BDT 292.20 million in

2013 as assistance to different sectors comprising down trodden people. Number of

beneficiaries in 2013 is 3995. Among the recipients, health care and education have

been considered as thrust sectors. Information technology has also been emphasized.

Janata Bank Limited can boast of being the pioneer in publishing an extra ordinary

directory comprising the life stories and other necessary information of 626 valiant

Freedom Fighters who have been conferred different titles for their heroic

contributions in the liberation war under the title ‘Ekattorer Birjoddader

Obishworonya Jibongatha- Khetabprapto Muktijodda Sommanona Smarakgrantho’ in

the year 2013. Grandeur reception with Crest and financial grants has been provided

in the honor of titled freedom fighters at 10 towns all over the country including

Dhaka. Preparation of a list of insolvent freedom fighters who took part directly in the

liberation war is under way through the network of branches to provide them financial

support. These freedom fighters will be given assistance from CSR Fund as far as

possible. It may be mentioned that education, poverty alleviation, history of libaration

war, arts and culture has been given sufficient importance in the case of assistance

from this fund.

2.15 Automation and Online Banking of Janata Bank Ltd.

JBL is keen to reap the benefits of modern technology in banking. In keeping with the

Government’s ‘Digital Bangladesh’ policy for technological development, the bank as

undertaken pragmatic work plan to computerize the branches and implement online

banking system. Real time online banking activities had already started in 42 branches

using deposit, advance and local remittance modules by the real time centralized

online core banking system (CBS) software TEMENOS -24 (T24). Live operation in

all inland branches (893) of the bank are conducted using off – line systems. JB

cheque payment and JB cash deposit system through cheque have been developed in

all inland branches (893) by its own software. Speedy foreign remittance system has

been implemented in all inland branches. As a result, it is now possible to send money

from abroad within fastest possible time which hed increase the flow of remittance.

Customers are notified through mobile messages as soon as they receive foreign

remittance. 93 branches (each district has at least 1 branch) of Janata Bank Limited

are operating the payment system of electronic Government procurement. tenderer

registration fee / renewal fee, tender document fee and other fees of tender (tender

security, performance security) are collected under this service. On the other hand,

expansion of online banking activities will be gradually expanded among the

remaining branches. As part of these expansion activities, central data centre (CDC)

& disaster recovery site (DRS) is going to be modernized and made more powerful

progressively. Apart from inland branches, four foreign branches (Abu Dhabi, Dubai,

Sharjah, Al - Ain) are conducting online core banking activities.

2.16 SWOT Analysis of Janata Bank Ltd.

SWOT analysis refers to analysis of strengths, weaknesses, opportunities and threats

of an organization. For all of these, SWOT analysis is considered as an important tool

for making changes in the strategic management of an organization.

2.13.1 Strengths of Janata Bank Ltd.

Top Management consisting efficient management group.

Company Reputation with positive image in the banking industry.

Many Branches to satisfy customer needs.

Various Products and Services for clients.

2.13.2 Weaknesses of Janata Bank Ltd.

Heavily depended on head office for decision making.

Absence of upgraded website.

Low remuneration package.

Low promotional campaign.

Not fully computerized.

2.13.3 Opportunities of Janata Bank Ltd.

Product line proliferation for introducing more branches

Introducing special corporate scheme

Developing new products and services.

2.13.4 Threats of Janata Bank Ltd.

The default risks of all terms of loan have to be minimizing in order to sustain in

the financial market. Because default risk leads the organization towards to

bankrupt.

The low compensation package of the employees from mid-level to lower level

position threats the employee motivation.

Some commercial/ foreign as well as private banks.

Customer awareness of pricing and services.

CHAPTER - 3CREDIT RISK MANAGEMENT PROCESS OF JANATA BANK

LIMITED

Credit Risk Management Process

The Credit Risk Management Division is vital for the efficient functioning of JBL. It

critically scrutinizes the credit proposals from risk weighted point of view before

sanctioning approvals ensuring a high quality credit portfolio. The goal of credit risk

management is to maximize a bank's risk-adjusted rate of return by maintaining credit

risk exposure within acceptable parameters. Banks need to manage the credit risk

inherent in the entire portfolio as well as the risk in individual credits or transactions.

The credit risk management process of Janata Bank Ltd. covers the following tasks:

Credit Processing/Appraisal

Credit Approval/Sanction

Credit Documentation

Credit Administration

Disbursement

Monitoring and Control of Individual Credits

Monitoring the Overall Credit Portfolio (stress testing)

Credit Classification

Disbursement of Loan

Classified Loans

Recovery of Loan

3.1 Credit Processing/Appraisal

Credit processing is the stage where all required information on credit is gathered and

applications are screened. Credit application forms should be sufficiently detailed to

permit gathering of all information needed for credit assessment at the outset. In this

connection, financial institutions should have a checklist to ensure that all required

information is, in fact, collected. Financial institutions should set out pre-qualification

screening criteria, which would act as a guide for their officers to determine the types

of credit that are acceptable. For instance, the criteria may include rejecting

applications from blacklisted customers. These criteria would help institutions avoid

processing and screening applications that would be later rejected. The next stage to

credit screening is credit appraisal where the financial institution assesses the

customer’s ability to meet his obligations. Institutions should establish well designed

credit appraisal criteria to ensure that facilities are granted only to creditworthy

customers who can make repayments from reasonably determinable sources of cash

flow on a timely basis.

As a general rule, the appraisal criteria will focus on:

amount and purpose of facilities and sources of repayment;

integrity and reputation of the applicant as well as his legal capacity to

assume the credit obligation;

risk profile of the borrower and the sensitivity of the applicable industry

sector to economic fluctuations;

physical inspection of the borrower’s business premises as well as the

facility that is the subject of the proposed financing;

current and forecast operating environment of the borrower;

management capacity of corporate customers.

3.2 Credit Approval/Sanction

A financial institution must have in place written

process and the approval authorities of individuals or committees as well as the basis

of those decisions. Approval authorities should be sanctioned by the board of

directors. Approval authorities will cover new credit app

credits, and changes in terms and conditions of previously approved credits,

particularly credit restructuring, all of which should be fully documented and

recorded. Prudent credit practice requires that persons empowered with

approval authority should not also have the customer relationship responsibility.

Depending on the size of the financial institution, it should develop a corps of credit

risk specialists who have high level expertise and experience and demonstra

judgment in assessing, approving and managing credit risk. An accountability regime

should beestablished for the decision

trail of decisions taken, with proper identification of individuals/committees involv

All this must be properly documented.

Graph 5: Net Profit (Figures in millions)

Source: Credit Risk Management Guideline, Bangladesh Bank (page 18)

Credit Approval/Sanction

A financial institution must have in place written guidelines on the credit approval

process and the approval authorities of individuals or committees as well as the basis

of those decisions. Approval authorities should be sanctioned by the board of

directors. Approval authorities will cover new credit approvals, renewals of existing

credits, and changes in terms and conditions of previously approved credits,

particularly credit restructuring, all of which should be fully documented and

recorded. Prudent credit practice requires that persons empowered with

approval authority should not also have the customer relationship responsibility.

Depending on the size of the financial institution, it should develop a corps of credit

risk specialists who have high level expertise and experience and demonstra

judgment in assessing, approving and managing credit risk. An accountability regime

should beestablished for the decision-making process, accompanied by a clear audit

trail of decisions taken, with proper identification of individuals/committees involv

All this must be properly documented.

Graph 5: Net Profit (Figures in millions)

Source: Credit Risk Management Guideline, Bangladesh Bank (page 18)

guidelines on the credit approval

process and the approval authorities of individuals or committees as well as the basis

of those decisions. Approval authorities should be sanctioned by the board of

rovals, renewals of existing

credits, and changes in terms and conditions of previously approved credits,

particularly credit restructuring, all of which should be fully documented and

recorded. Prudent credit practice requires that persons empowered with the credit

approval authority should not also have the customer relationship responsibility.

Depending on the size of the financial institution, it should develop a corps of credit

risk specialists who have high level expertise and experience and demonstrated

judgment in assessing, approving and managing credit risk. An accountability regime

making process, accompanied by a clear audit

trail of decisions taken, with proper identification of individuals/committees involved.

Source: Credit Risk Management Guideline, Bangladesh Bank (page 18)

3.3 Credit Documentation

Documentation is an essential part of the credit process and is required for each phase

of the credit cycle, including credit application, credit analysis, credit approval, credit

monitoring, and collateral valuation, and impairment recognition, foreclosure of

impaired loan and realization of security. The format of credit files must be

standardized and files neatly maintained with an appropriate system of cross-indexing

to facilitate review and follow up.

The Bangladesh Bank will pay particular attention to the quality of files and the

systems in place for their maintenance. Documentation establishes the relationship

between the financial institution and the borrower and forms the basis for any legal

action in a court of law. Institutions must ensure that contractual agreements with

their borrowers are vetted by their legal advisers.

For security reasons, financial institutions should consider keeping only the copies of

critical documents (i.e., those of legal value, facility letters, and signed loan

agreements) in credit files while retaining the originals in more secure custody. Credit

files should also be stored in fire-proof cabinets and should not be removed from the

institution's premises.

Financial institutions should maintain a checklist that can show that all their policies

and procedures ranging from receiving the credit application to the disbursement of

funds have been complied with. The checklist should also include the identity of

individual(s) and/or committee(s) involved in the decision-making process.

3.4 Credit Administration

The Credit Administration function is critical in ensuring that proper documentation

and approvals are in place prior to the disbursement of loan facilities. For this reason,

it is essential that the functions of Credit Administration be strictly segregated from

Relationship Management/Marketing in order to avoid the possibility of controls

being compromised or issues not being highlighted at the appropriate level.

A financial institution’s credit administration function should, as a minimum, ensure

that:

Credit Administration procedures should be in place to ensure the

following. credit files are neatly organized, cross-indexed, and their

removal from the premises is not permitted;

the borrower has registered the required insurance policy in favor of the

bank and is regularly paying the premiums;

credit facilities are disbursed only after all the contractual terms and

conditions have been met and all the required documents have been

received;

collateral value is regularly monitored;

the borrower is making timely repayments on interest, principal and any

agreed to fees and commissions;

the established policies and procedures as well as relevant laws and

regulations are complied with; and

On-site inspection visits of the borrower’s business are regularly

conducted and assessments documented.

3.5 Disbursement

Once the credit is approved, the customer should be advised of the terms and

conditions of the credit by wa5y of a letter of offer. The duplicate of this letter should

be duly signed and returned to the institution by the customer. The facility

disbursement process should start only upon receipt of this letter and should involve,

inter alia, the completion of formalities regarding documentation, the registration of

collateral, insurance cover in the institution’s favor and the vetting of documents by a

legal expert. Under no circumstances shall funds be released prior to compliance with

pre-disbursement conditions and approval by the relevant authorities in the financial

institution.

Graph 6: Credit Disbursement Process

Source: Credit Risk Management Guideline, Bangladesh Bank (page 20)

Getting Credit Information

Information Collection

Analyzing these Information

Lending Risk Analysis

Proposal Analysis

Collateral Evaluation

Final Decision about the Project

Proper Supervision of the Project

Documentation on the Loan

Creation of Charges for Securing Loan

3.6 Monitoring and Control of Individual Credits

To safeguard financial institutions against potential losses, problem facilities need to

be identified early. A proper credit monitoring system will provide the basis for taking

prompt corrective actions when warning signs point to deterioration in the financial

health of the borrower. Examples of such warning signs include unauthorized

drawings, arrears in capital and interest and deterioration in the borrower’s operating

environment. Financial institutions must have a system in place to formally review

the status of the credit and the financial health of the borrower at least once a year.

More frequent reviews (e.g at least quarterly) should be carried out of large credits,

problem credits or when the operating environment of the customer is undergoing

significant changes.

In broad terms, the monitoring activity of the institution will ensure that:

funds advanced are used only for the purpose stated in the customer’s

credit application;

financial condition of a borrower is regularly tracked and management

advised in a timely fashion;

collateral coverage is regularly assessed and related to the borrower’s

financial health;

The institution’s internal risk ratings reflect the current condition of the

customer.

3.7 Monitoring the Overall Credit Portfolio (stress testing)

An important element of sound credit risk management is analyzing what could

potentially go wrong with individual credits and the overall credit portfolio if

conditions/environment in which borrowers operate change significantly. The results

of this analysis should then be factored into the assessment of the adequacy of

provisioning and capital of the institution. Such stress analysis can reveal previously

undetected areas of potential credit risk exposure that could arise in times of crisis.

Possible scenarios that financial institutions should consider in carrying out stress

testing include:

Significant economic or industry sector downturns;

Adverse market-risk events; and

Unfavorable liquidity conditions.

Financial institutions should have industry profiles in respect of all industries where

they have significant exposures. Such profiles must be reviewed /updated every year.

Each stress test should be followed by a contingency plan as regards recommended

corrective actions. Senior management must regularly review the results of stress tests

and contingency plans. The results must serve as an important input into a review of

credit risk management framework and setting limits and provisioning levels.

3.8 Credit Classification

It is required for the board of directors of a financial institution to “establish credit

risk management policy, and credit impairment recognition and measurement policy,

the associated internal controls, documentation processes and information systems;”

Credit classification process grades individual credits in terms of the expected degree

of recoverability. Financial institutions must have in place the processes and controls

to implement the board approved policies, which will, in turn, be in accord with the

proposed guideline. They should have appropriate criteria for credit provisioning and

write off. International Accounting Standard 39 requires that financial institutions

shall, in addition to individual credit provisioning, assess credit impairment and

ensuing provisioning on a credit portfolio basis. Financial institutions must, therefore,

establish appropriate systems and processes to identify credits with similar

characteristics in order to assess the degree of their recoverability on a portfolio basis.

Financial institutions should establish appropriate systems and controls to ensure that

collateral continues to be legally valid and enforceable and its net realizable value is

properly determined. This is particularly important for any delinquent credits, before

netting off the collateral’s value against the outstanding amount of the credit for

determining provision. As to any guarantees given in support of credits, financial

institutions must establish procedures for verifying periodically the net worth of the

guarantor.

3.9 Classified Loans

Banks are financial service firm, producing and selling professional management of

the public’s funds as well as performing many other roles in the economy. But now-

a-days commercial banks are not performing their activities smoothly for a large

burden of default loan. Every year Janata Bank distributes thousand crore taka among

individuals, organizations etc. but a large sum of these distributed fund cannot be

recovered in due time. The Bank has to classify this loan.

Signs for Classification

First and foremost requirement for any and all credit managers is to identify a

problem credit in its earlier stages by recognizing the signs of deterioration. Such

signs include but not limited to the following:

Non-payment of interest or principal or both on due dates or past dues beyond

a reasonable period or recurring past dues.

In case of Overdraft no movement in the account beyond a reasonable period.

Deterioration in financial condition of the client, as gathered from client’s

latest financial statement.

A shortfall in collateral coverage, particularly if the collateral was a key factor

in the decision-making.

Death or withdraw of key-owners or management personnel.

Company filing for bankruptcy or voluntary dissolution.

Adverse market report about the company itself or its principal owners.

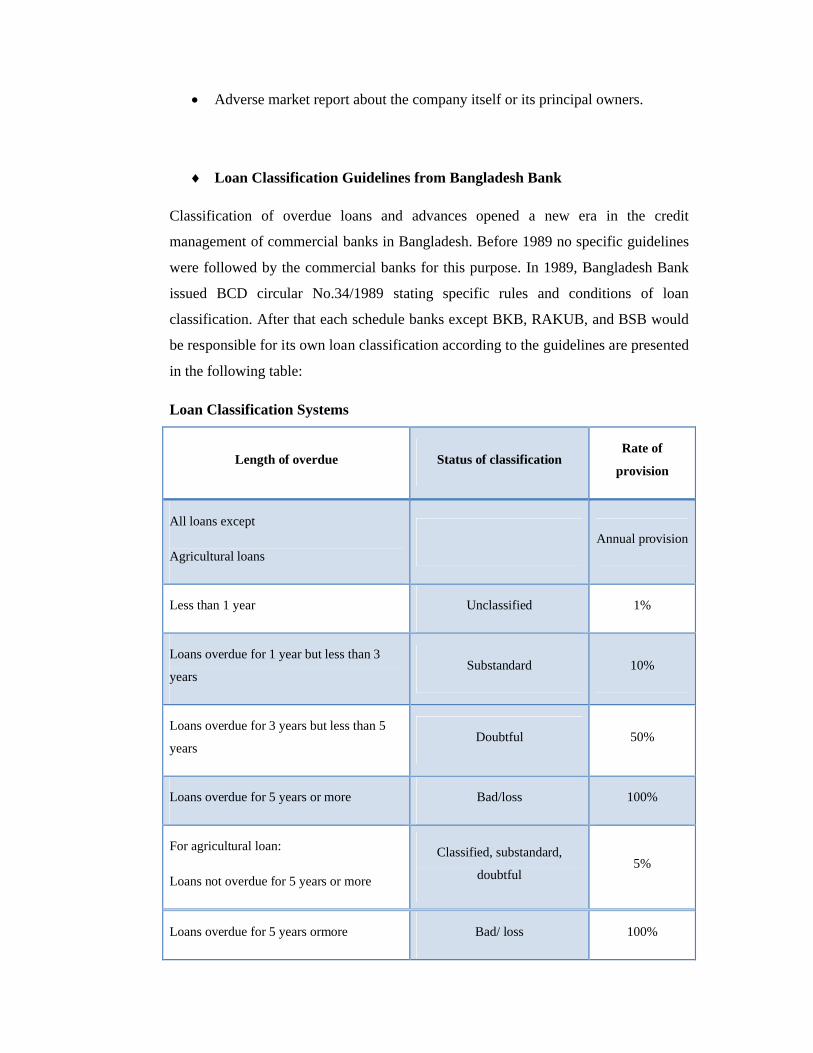

Loan Classification Guidelines from Bangladesh Bank

Classification of overdue loans and advances opened a new era in the credit

management of commercial banks in Bangladesh. Before 1989 no specific guidelines

were followed by the commercial banks for this purpose. In 1989, Bangladesh Bank

issued BCD circular No.34/1989 stating specific rules and conditions of loan

classification. After that each schedule banks except BKB, RAKUB, and BSB would

be responsible for its own loan classification according to the guidelines are presented

in the following table:

Loan Classification Systems

Length of overdue Status of classificationRate of

provision

All loans except

Agricultural loansAnnual provision

Less than 1 year Unclassified 1%

Loans overdue for 1 year but less than 3

yearsSubstandard 10%

Loans overdue for 3 years but less than 5

yearsDoubtful 50%

Loans overdue for 5 years or more Bad/loss 100%

For agricultural loan:

Loans not overdue for 5 years or more

Classified, substandard,

doubtful5%

Loans overdue for 5 years ormore Bad/ loss 100%

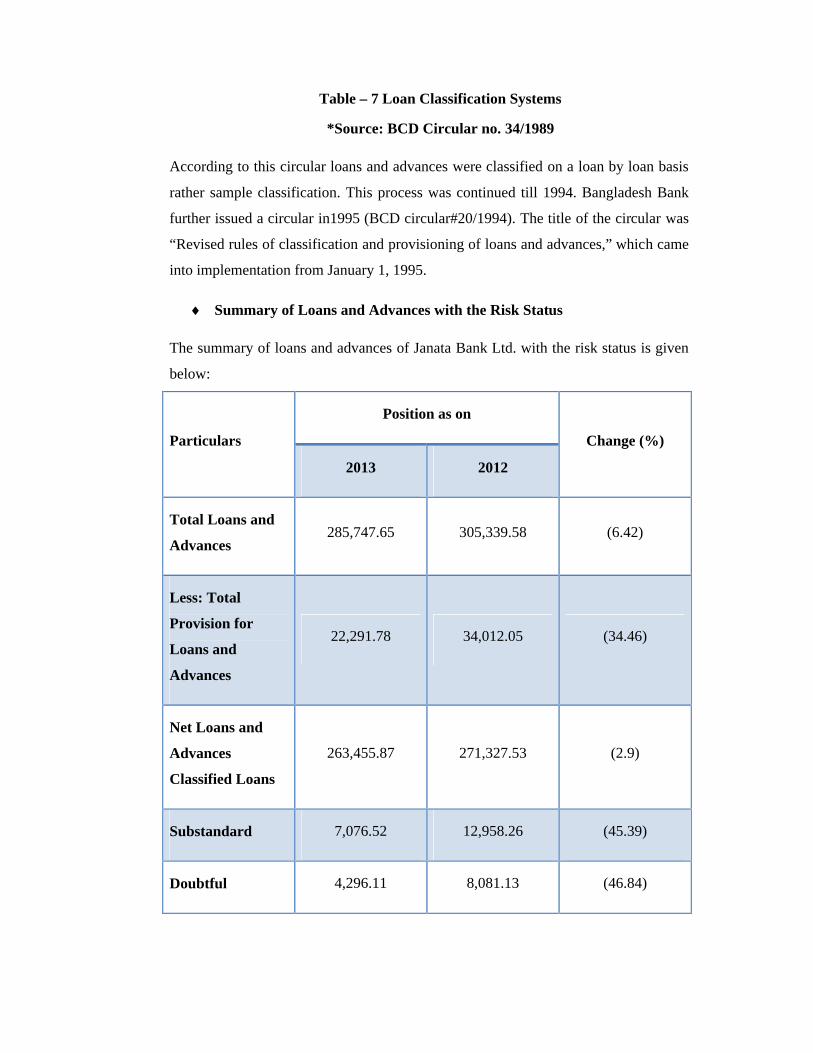

Table – 7 Loan Classification Systems

*Source: BCD Circular no. 34/1989

According to this circular loans and advances were classified on a loan by loan basis

rather sample classification. This process was continued till 1994. Bangladesh Bank

further issued a circular in1995 (BCD circular#20/1994). The title of the circular was

“Revised rules of classification and provisioning of loans and advances,” which came

into implementation from January 1, 1995.

Summary of Loans and Advances with the Risk Status

The summary of loans and advances of Janata Bank Ltd. with the risk status is given

below:

Particulars

Position as on

Change (%)

2013 2012

Total Loans and

Advances285,747.65 305,339.58 (6.42)

Less: Total

Provision for

Loans and

Advances

22,291.78 34,012.05 (34.46)

Net Loans and

Advances

Classified Loans

263,455.87 271,327.53 (2.9)

Substandard 7,076.52 12,958.26 (45.39)

Doubtful 4,296.11 8,081.13 (46.84)

Bad/Loss 20,394.23 32,162.3 (36.59)

Total Classified

Loans and

Advances

31,766.86 53,201 (40.29)

Classified loans as

percent of total

loans

Substandard 2.48% 4.24% (1.77)

Doubtful 1.50% 2.65% (1.14)

Bad/Loss 7.14% 10.53% (3.4)

Total 11.12% 17.42% (6.31)

Net Classified

Loans31,766.86 53,201.69 (40.29)

Net Classified

Loans as % of

Total Loans

11.12% 17.42% (6.30)

Table 8: Summary of Loans and Advances with the Risk Status

Source: Janata Bank Limited, Annual Report 2009-2013 (page 119)

3.10 Recovery of Loan

The Recovery procedure of Janata Bank is the ultimate combination of time, effort of

money. It follows several procedural steps to recover the lending amount, which is

joint effort of Bank, society and legal institutions. There are several programs taken

by the bank to recover the disbursed loans. They are discussed hereafter.

Programs for Loan Recovery

When Janata Bank sanctions loans and advances to its customers, they clearly state

the repayment pattern in the loan agreement. But some credit holders do not pay their

credit in due period. The nationalized and private sector commercial banks have to

face this sort of problems. This situation is especially severe in Janata Bank. To

overcome the problem of overdue loan, the bank needs to take some particular loan

recovery programs. They are:

Establishing credit supervision and monitoring cell in the bank

Re-structuring the loan sanctioning and distributing policy of the bank