a multiple case study of school district budget reductions in

252

The Pennsylvania State University The Graduate School EDUCATION BUDGETING DURING A CRISIS: A MULTIPLE CASE STUDY OF SCHOOL DISTRICT BUDGET REDUCTIONS IN CALIFORNIA AND TEXAS DURING THE GREAT RECESSION A Dissertation in Educational Theory and Policy by Jeremy Anderson Ó 2020 Jeremy Anderson Submitted in Partial Fulfillment of the Requirements for the Degree of Doctor of Philosophy December 2020

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of a multiple case study of school district budget reductions in

The Pennsylvania State University

The Graduate School

EDUCATION BUDGETING DURING A CRISIS: A MULTIPLE CASE STUDY OF

SCHOOL DISTRICT BUDGET REDUCTIONS IN CALIFORNIA AND TEXAS

DURING THE GREAT RECESSION

A Dissertation in

Educational Theory and Policy

by

Jeremy Anderson

Ó 2020 Jeremy Anderson

Submitted in Partial Fulfillment of the Requirements

for the Degree of

Doctor of Philosophy

December 2020

ii

The dissertation of Jeremy Anderson was reviewed and approved by the following:

David A. Gamson Associate Professor of Education Educational Theory & Policy Dissertation Advisor Committee Chair

Erica Frankenberg Professor of Education Educational Leadership

Mindy L. Kornhaber Associate Professor of Education Educational Theory & Policy

Kelly Rosinger Assistant Professor of Education Higher Education

Eric Plutzer Professor of Political Science Political Science Kevin Kinser Department Head, Education Policy Studies Professor of Education Higher Education

iii

ABSTRACT

This thesis examines the budget reductions of six high and six low poverty school

districts in California and Texas during the Great Recession. While recent studies have supported

the positive influence of spending on student outcomes, few have looked at what happens when

financial shocks constrain budgets. The study blends the National Center for Education

Statistics’ Common Core of Data school finance survey with a document analysis of publicly

available district budgets, media sources, school board budget presentations, and other district

financial data to highlight the ways that school districts adjusted (or did not adjust) spending

within traditional spending categories. There were four key findings from the analysis of district

data. First, federal aid through the American Reinvestment and Recovery Act proved critical in

addressing school district budget deficits, particularly in higher-poverty school districts. Second,

the loosening of categorical aid in California was a crucial policy decision that helped school

leaders address local budget issues. Third, higher poverty districts in this study became

increasingly reliant on state revenue during the recession, which could harm those districts’

ability to weather future recessions. Finally, inaccurate enrollment and property value projections

led several school districts to overextend their budgets and drain their emergency reserves in the

years leading up to the recession. These districts accumulated a large amount of debt, which

hindered their ability to recover from the recession. The lessons and takeaways from this

research are helpful for policymakers and school leaders for future financial shocks.

iv

TABLE OF CONTENTS

LIST OF FIGURES ....................................................................................................................... vi

LIST OF TABLES ........................................................................................................................ vii ACKNOWLEDGEMENTS ......................................................................................................... viii

Chapter 1 – Introduction ................................................................................................................. 1 Statement of the Problem .......................................................................................................................... 3 Research Questions ................................................................................................................................... 3 Purpose and Significance of the Study ..................................................................................................... 4 Overview of the Dissertation .................................................................................................................... 4

Chapter 2- Literature Review .......................................................................................................... 6 A Brief History of School Finance Research ............................................................................................ 6 Effects of School Finance Reform on Educational Expenditures ............................................................. 9 Effects of School Finance Reform on Achievement (Equity Era) .......................................................... 13 Shifting the Focus: From Equity to Adequacy ....................................................................................... 16

Wave One: Federal Equal Protection Challenges (1954-1973) .......................................................................... 17 Wave Two: State Equal Protection Challenges (1973-1989) ............................................................................. 18 Wave Three: Adequacy and Challenges to State Education Constitution Clause Challenges (1989-Present) .. 19

Different Definitions of "Adequacy" ...................................................................................................... 21 Contemporary Studies in School Finance ............................................................................................... 23

The Types of Expenditures Most Associated with Student Outcomes ............................................................... 25 The Impacts of Additional Instructional Staffing ............................................................................................... 26 Investing More in Existing Instructional Staff ................................................................................................... 27

The 2008 Great Recession and School Funding ..................................................................................... 29 Background on the Great Recession ................................................................................................................... 29 Federal Aid: The American Recovery and Reinvestment Act and the Education Jobs Fund ............................ 30 The Great Recession's Effects on School District Spending .............................................................................. 32 The Great Recession and Student Achievement ................................................................................................. 34

Chapter 3 – School Budgeting and Conceptual Framework ......................................................... 38 The Anatomy of School District Budgets ............................................................................................... 39 Types of Budgets Used in this Study ...................................................................................................... 41 Visualizations of Budget Reductions ...................................................................................................... 46 Conceptual Framework ........................................................................................................................... 49

Chapter 4 – Research Design ........................................................................................................ 53 Introduction and Methodology ............................................................................................................... 53 Multiple-Site Case Study Methodology .................................................................................................. 56 Procedures ............................................................................................................................................... 56

Sample Selection ................................................................................................................................................ 56 Data Collection ................................................................................................................................................... 62 Quantitative Data Source .................................................................................................................................... 62

v

Qualitative Data Sources .................................................................................................................................... 63 Data Analysis .......................................................................................................................................... 64 Threats to Validity .................................................................................................................................. 69

External ............................................................................................................................................................... 69 Internal ................................................................................................................................................................ 70

Chapter 5 – Education Funding Deferred: California ................................................................... 72 Brief Overview of Enrollment in California ........................................................................................... 73 California Sample School Districts ......................................................................................................... 73 Brief History of School Finance in California ........................................................................................ 74 California School Finance Policy During the Great Recession and its Consequences ........................... 80 Analysis and Findings ............................................................................................................................. 86 Conclusion ............................................................................................................................................ 120

Chapter 6- Education Funding Slashed: Texas ........................................................................... 124 Brief Overview of Enrollment in Texas in 2009 .................................................................................. 125 A Brief History of School Finance in Texas ......................................................................................... 126 The Texas School Finance System ....................................................................................................... 127

The Foundation School Program ...................................................................................................................... 128 The Recapture of Local Property Taxes Provision, AKA the “Robin Hood” Provision .................................. 133

The Great Recession in Texas and the Legislative Reaction for School Funding ................................ 134 Texas School Funding Legal Battles 2011-2016 .................................................................................. 138 Analysis and Findings ........................................................................................................................... 144 Conclusion ............................................................................................................................................ 176

Chapter 7 – Conclusion ............................................................................................................... 182 Research Purpose .................................................................................................................................. 182 Summary of Findings ............................................................................................................................ 183

Main Thematic Findings ................................................................................................................................... 188 Implications for Policy and Practice ..................................................................................................... 200 Implications for Future Research .......................................................................................................... 203 Limitations ............................................................................................................................................ 204 Final Words ........................................................................................................................................... 205

References ................................................................................................................................... 210 Appendix A: Original 43 Sample School Districts from California and Texas ......................... 217

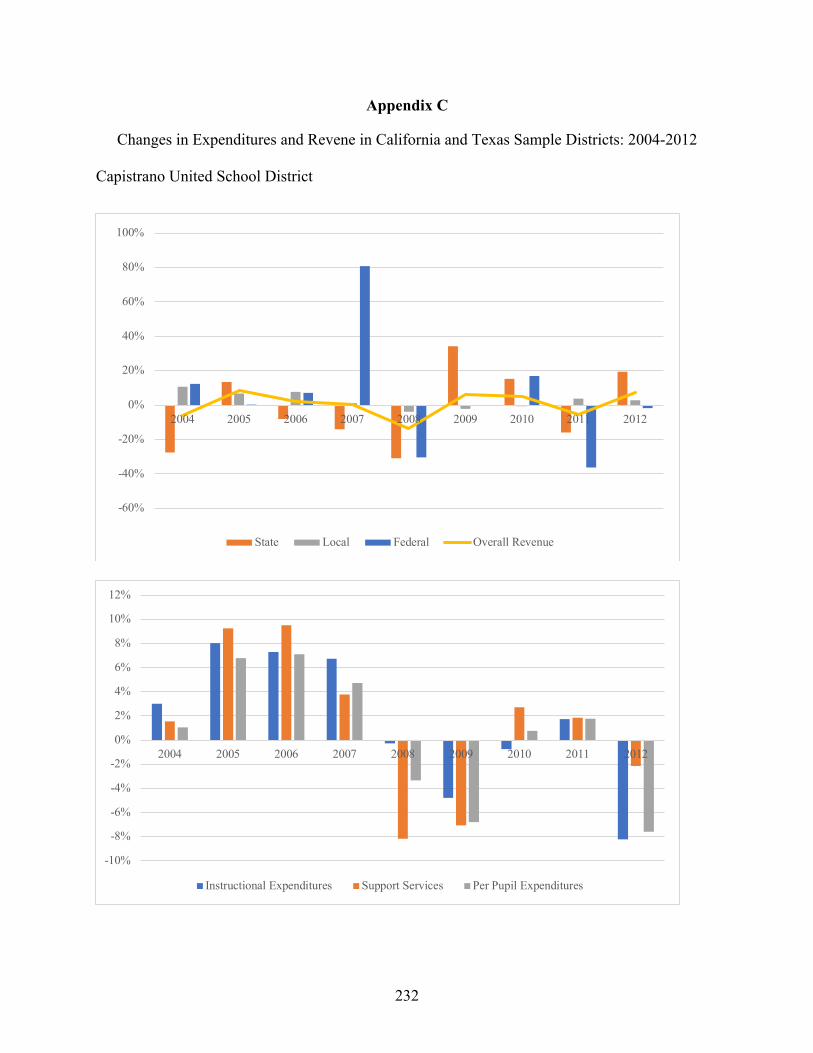

Appendix B: Log of Primary Source Documents from Sample School Districts ....................... 219 Appendix C: Changes in Expenditures and Revene in California and Texas Sample Districts: 2004-2012 ................................................................................................................................... 232

vi

LIST OF FIGURES Figure 2.1: Changes In Average State Expenditures Per Pupil 1977-1992 .................................. 11 Figure 2.2: Differences In Spending Changes And State Revenue Changes Across States 1977-1992............................................................................................................................................... 11 Figure 2.3: Percent Of Students Of Color In High Poverty Schools In The United States, 2010-2016............................................................................................................................................... 35 Figure 3.1: Oakland Unified School District Funding Levels ...................................................... 40 Figure 3.2: Section From Laredo ISD 2008-09 Budget ................................................................ 43 Figure 3.3: Required Components Of A District’s Annual Financial Report In Texas ................ 45 Figure 3.4: Concentric Circle Model Of Budget Reduction Priorities ......................................... 48 Figure 3.5: Budget Reduction Conceptual Framework ................................................................ 51 Figure 5.1: K-12 Expenditures Per Student (In Thousands) ......................................................... 79 Figure 5.2: California State Share Of Total Public K-12 Revenue ............................................... 81 Figure 5.3: Capistrano Unified School District Per Pupil Expenditures Percent Change 2004-2012............................................................................................................................................... 89 Figure 5.4: Percent Change In Instructional And Support Expenditures For Capistrano USD: 2004-2012 ..................................................................................................................................... 90 Figure 5:5 Percent Change In Instructional And Support Expenditures For El Segundo USD: 2004-2012 ..................................................................................................................................... 94 Figure 5.6: Percent Change In Fremont USD Instructional Expenditures And Support Services 2004-2012 ................................................................................................................................... 100 Figure 5.7: Fremont Unified School District Per Pupil Expenditure 2008-2013 ....................... 100 Figure 5.8: Percent Change In Fresno USD Instructional Expenditures And Support Services 2004-2012 ................................................................................................................................... 106 Figure 5.9: Percent Change In Fresno USD Overall Revenue And Revenue Sources: 2004-2012..................................................................................................................................................... 106 Figure 5.10: Percent Change In Stockton USD Revenue Sources: 2004-2012 .......................... 111 Figure 5.11: Percent Change In Instructional Expenditures, Support Services, And Per-Pupil Expenditures 2004-2012 ............................................................................................................. 111 Figure 5.12: Percent Change In Cutler-Orosi Joint USD Revenue Sources: 2003-2012 ........... 116 Figure 5.13: Percent Change In Cutler-Orosi Joint USD Expenditures: 2003-2012 .................. 117 Figure 5.14: Changes In Per Pupil Spending In Cutler-Orosi Joint Unified School District: 2003-2012............................................................................................................................................. 118 Figure 6.1: Sources Of K-12 Revenue In Texas, 2005-2013 ...................................................... 128 Figure 6.2 Texas Economic Stabilization Fund Reserves And Percent To Cap (In Billions) .... 135 Figure 6.3: Average Texas Funding Per Pupil: 2007-2015 ........................................................ 141 Figure 6.4: Percent Enrollment Growth In Hutto Independent School District 2003-2014 ....... 150 Figure 6.5: Changes In Revenue For Hutto ISD: 2004-2012 ..................................................... 154 Figure 6.6: Debt Service Fund Expenditures For Forney ISD 2001-2011 ................................. 160 Figure 6.7: Percent Change In Kingsville ISD Revenue Sources: 2004-2012 ........................... 172 Figure 6.8: Percent Change In Overall Debt For Kingsville ISD, San Antonio ISD, And Laredo ISD: 2007-2013 ........................................................................................................................... 173 Figure 6.9: Percent Change In Kingsville ISD Expenditures: 2003-2012 .................................. 174

vii

LIST OF TABLES

Table 3.1: Continuum for Budget Reduction Categories from Least to Most Impactful For Student Outcomes ......................................................................................................................... 48 Table 4.1: Document Types and Sources ...................................................................................... 55 Table 4.2: Sampling Poverty Quintiles ......................................................................................... 59 Table 5.1: California Sample Districts by Sample Group and CCD Locale Code ....................... 74 Table 5.2: Education Funding Deferrals by the California State Legislation 2008-2012 ............. 82 Table 5.3: List of California Tier 3 Categorical Programs 2009-2010 ......................................... 84 Table 5.4: Program Reductions during the Great Recession in California ................................. 122 Table 6.1: Texas Sample Districts by Sample Group and CCD Locale Code ............................ 126 Table 6.2: Texas School Finance System Maximum Tax Rates by Tier .................................... 130 Table 6.3: Example of Wealthy vs. Property Poor Texas Funding ............................................ 132 Table 6.4: 2011-2012 Texas School Finance Lawsuits and Claimed State Constitutional Infringements .............................................................................................................................. 140 Table 6.5: Program Reductions during the Great Recession in Texas ........................................ 179 Table 7.1: Program Reductions During the Great Recession in California and Texas ............... 186 Table 7.2: Percent Change in Local Revenue Contribution to Overall District Budgets ........... 196

viii

ACKNOWLEDGEMENTS

I want to thank all of my family and friends for supporting me through this process. The

amount of encouragement that you have all given me throughout writing my thesis was

invaluable. To my wife Ashlee, there are not enough words to express my gratitude for the

constant support, late night work sessions, and unrelenting encouragement that you provided

over the past three years. To my parents Ron and Nancy and my sister Renee, thank you for

always picking up the phone and giving me words of motivation to continue in this work. To my

colleagues at Penn State, thank you for always challenging my thinking and giving me moments

of respite from research. I would also like to thank the outstanding faculty and administrative

assistants in the Department of Education Policy Studies at Penn State that I have had the

pleasure to work with over the past five years.

A very special set of thank yous go to my academic advisors and mentors David Gamson

and Erica Frankenberg. They always pushed me and my research far past where I thought I could

go. They asked me the tough questions that always kept me honest and motivated. I want to

thank my other committee members, Mindy Kornhaber, Kelly Rossinger, and Eric Plutzer for

their valuable ideas and feedback. I would also like to thank Gerald LeTendre and Dana Mitra

for their mentorship in the American Journal of Education. Finally, this work was inspired years

ago when I had the privilege to teach at Cornell School District in Pittsburgh and Riverside

Beaver County School District in Ellwood City. I want to thank all of my former colleagues and

students at both of those school districts for lighting my passion for education policy.

Chapter 1 – Introduction

"The budget news is worse than we have been anticipating, with the ballooning of the deficit. But every district is different. They all have different reserves. They all have different revenue streams and different priorities. A couple of districts have given raises. Others are looking at

furloughs. Each district's financial picture is very individual." (Harrington, 2011) —Peggy Marshburn, Spokesperson for the Contra Costa County Office of Education

The Great Recession of 2008 was one of the most significant global economic downturns

in a century. The recession lasted 18 months and had powerful adverse effects on the economy

ranging from historical unemployment to a massive decline in household wealth (Rebell &

Wolff, 2011). School districts acutely felt the impact of this fiscal shock through significant

state and local revenue constraints. Nearly 300,000 teachers and other school staff lost their jobs.

The recession wiped out thirteen years of progress in class size reductions and teachers’ salaries

have still not reached pre-recession levels (Evans, Schwab, & Wagner, 2015; Sutcher, Carver-

Thomas, & Darling-Hammond, 2018). The quote that begins this chapter comes from a school

administrator in California. Her sentiment perfectly encapsulates the uncertainty and frustration

that school district leaders worked in during the Great Recession. The recession’s impacts on

school budgeting varied greatly across districts and increased the resource disparities between

high and low poverty school districts. The increase in resource disparity put the importance of

school spending on student outcomes in center stage as state legislatures and school leaders

grappled with how to address ballooning budget deficits.

For decades, the link between spending and student outcomes was contested by

academics, economists, and policymakers. Earlier studies (from the late 1960s through the mid-

1990s) found a weak-to-nonexistent relationship between school spending and academic

achievement (Coleman et al., 1966; Hanushek, 1991; Hanushek & Kimko, 2000). However,

contemporary studies have produced robust evidence to suggest that increases in education

2

spending are connected to improvements in student outcomes. These outcomes include higher

graduation rates, increased years of completed education and higher adult earnings (Card &

Payne, 2002; Jackson, Johson, & Persico, 2015, 2014; Lafortune, Rothstein, & Schanzenbach,

2016).

Today, the overall conversation in educational funding research has mainly moved past

whether spending money matters in education—however, questions of where money should be

spent remain. Recent studies on funding allocation have demonstrated that spending money on

human resources leads to the most significant increases in a range of student outcomes. Such

investments include raising teachers' salaries, investing in after school programs, and lowering

student-to-teacher ratios (Adamson & Darling-Hammond, 2015; B. D. Baker, 2017; Dietrichson,

Bøg, Filges, & Klint Jørgensen, 2017; Dynarski, Hyman, & Schanzenbach, 2011; Figlio, 1997b;

Jackson et al., 2015).

Since research shows that spending money on education matters and since there were

massive cuts to education spending during the Great Recession, what impact did these cuts have

on students? A growing body of research has highlighted early evidence on the Great Recession's

impact on school spending and academic achievement. The findings from these studies suggest

that the recession caused significant decreases in school spending (Bhalla, Chakrabarti, &

Livingston, 2015; Chakrabarti & Livingston, 2013; Evans, Schwab, & Wagner, 2019) and that

those cuts to spending harmed the academic achievement of students in ways that were not

evenly distributed by race and socioeconomic status (Jackson, Wigger, & Xiong, 2018; Shores &

Steinberg, 2017).

3

Statement of the Problem Many education policy researchers and economists have provided valuable findings

showing how state and school district budget reductions during the recession have adversely

affected student outcomes such as academic achievement, prospects for higher education, and

future job attainment. These adverse effects are particularly acute for students in lower-income

communities. However, it is still unclear exactly what types of reductions that school leaders

made at the district level and what role federal, state, and local education finance policies played

in choosing those particular reductions. The choices that policymakers and school leaders made

during the Great Recession are worth examining in more detail because research shows that these

choices exacerbated inequities in funding and student outcomes. The growth in inequity

disproportionately impacted a wide range of academic outcomes for students in higher poverty

school districts. In other words, there is room for additional research into the role of federal,

state, and local funding policy on budgeting decisions during the recession. The findings from

this study complement existing research by providing a more descriptive analysis of district

budget reductions. This thesis also explores how federal, state, and local school funding policies

influenced budgeting decision-making in high and low-poverty districts in two of the country's

largest states, California and Texas.

Research Questions The research questions for this study are:

1. What budget reductions did school leaders in some of California and Texas's highest and

lowest poverty school districts prioritize during the Great Recession?

2. How did budget reductions differ in the highest and lowest poverty school districts in

California and Texas during the Great Recession?

4

3. What state and federal education funding policies were the most influential in school

leaders' budget reduction decisions?

Purpose and Significance of the Study

This dissertation is a multiple case study of twelve school districts, six from California

and six from Texas. I use both primary and secondary data sources to analyze school leaders'

budget reduction decisions in each district. The data includes five years of district expenditures

and revenue from the Common Core’s F-33 school finance survey, school district budgets,

adopted school district budgets, financial audits conducted by third-party accounting firms, debt

transparency reports, local media reports, budget presentations, and other relevant financial

documentation. The goals of this study are to 1) identify what types of reductions school district

leaders such as superintendents, school budget officers, and school boards made during the

recession, 2) document how higher and lower poverty school district leaders made budget

reductions during the recession and to 3) analyze how federal, state, and local school funding

policies impacted the budgeting decisions of school leaders.

Overview of the Dissertation Chapter 2 of this dissertation is a literature review covering the history of school finance

reform in the United States beginning in the 1960s, the evolution of research in school finance,

and the current state of research in school finance. The final section of the chapter discusses

research on how money matters in schools, what types of expenditures matter in schools, and

how the recession impacted school spending and student outcomes. Because school district

budgets make up the bulk of the data analyzed for this study, Chapter 3 provides a concise

overview of a school district budget's anatomy. Chapter 3 continues with a definition of terms in

5

school district budgeting, a budget reduction continuum intended to help school districts make

reductions with the least impact on student learning and educational programming, and this

study's conceptual framework. Chapter 4 presents the methodology of this study, a detailed

description of the sample of school districts from California and Texas, types of data used for the

analysis, and the steps taken in the analysis of the data. Chapters 5 (California) and 6 (Texas)

contain the major findings and analysis from each state. The chapters also contain brief

explanations of each state's school finance system and how the state legislatures in each state

responded to the recession. Finally, Chapter 7 provides an overview of significant findings,

policy implications, and future research recommendations.

One of the main reasons for conducting this study is that there was not, and is not,

enough research on school funding during major fiscal shocks. Though some are more severe

than others, future economic downturns will inevitability occur. The decisions of policymakers

and school leaders from past economic downturns can provide valuable lessons so that we can

avoid negatively impacting students in future crises. As demonstrated in the academic literature,

education funding decisions made during a fiscal shock the size of the Great Recession can

change school spending patterns for decades after the event. The Great Recession was thought to

be a once in a generation economic crisis. However, the country is again in an extraordinary

economic downturn, demonstrating the need for this study and future research. This study

concludes with lessons learned from the districts included in the sample and policy

recommendations for school leaders and policymakers in our current crisis.

6

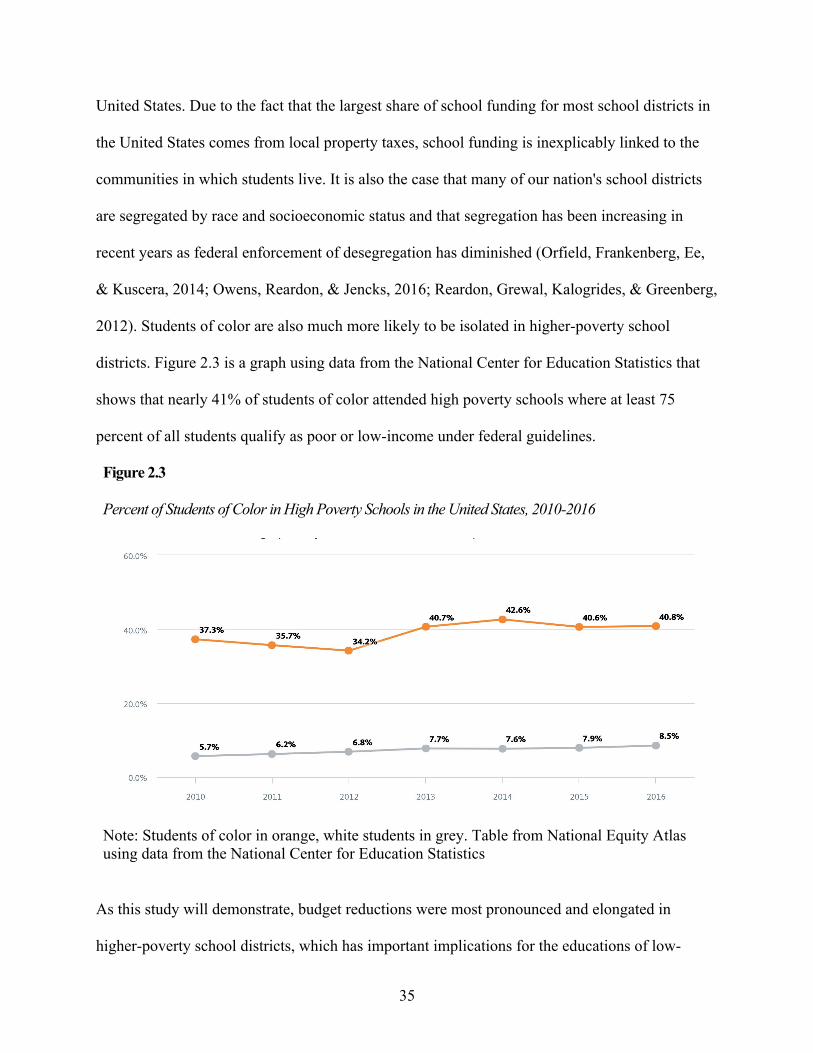

Chapter 2- Literature Review The fiscal impact of the Great Recession on school districts occurred within the context

of a long, contentious history of school finance policy, reform, inequity, inadequacy, and legal

challenges. This context is essential in that it helps to situate the landscape of school finance

before the recession and shows 1) why school district's had such inequitable levels of funding

before the recession 2) how the recession may have impacted school districts in different ways

and 3) why district leaders adjusted budgets in the ways that they did. These are all questions

central to this study. The following literature review incorporates academic and policy literature

from education policy, legal research, and economic literature.

This chapter begins with a history of school finance reform starting in the late-1960s. The

late 60s were a period where numerous influential school finance legal challenges were waged at

both the state and federal level. The decisions from these challenges the ability for states to fund

schools for decades to come and are particularly relevant to the states included in the current

study, California and Texas. Finally, more contemporary literature will be discussed, including

research on how money matters in schools, what types of spending are most consequential for

student outcomes, and school finance literature explicitly related to the Great Recession.

A Brief History of School Finance Research

State supreme courts have heard cases relating to the constitutionality of state education

financing systems in at least 43 different states. There are 16 cases of the state courts overturning

state school finance systems and 20 cases where the system was upheld (Murray, Evans, &

Schwab, 1998). Between 1971-2010, the Supreme Court of the United States heard nearly 70

court cases filed in 28 different states that dealt with the constitutionality of the states' school

financing legislation or formula (Jackson et al., 2015). What is so important about these cases

7

and their rulings, is that they define the boundaries for what school finance reform looked like in

states following the decisions. Importantly, the rulings helped to shape the vocabulary that

school finance reformers and researchers still use in exploring the effects of school finance

reform. The legal interest in financing equity increased substantially after two notable court cases

were heard in the early 1970s, Serrano v. Priest in 1971 and San Antonio Independent School

District v. Rodriguez in 1973 (Card & Payne, 2002; Jackson et al., 2015; Karst, 1973; Murray et

al., 1998; Sutton, 2008; Walter & Sweetland, 2003).

In 1968, a parent in the Los Angeles City School District brought a lawsuit against the

state of California for its method of school funding. The issue most pressing in the case was

"whether substantial inequality in school district capacities to tax and spend means inequality of

educational opportunity" (Karst, 1973). Serrano v. Priest was a series of three cases that

challenged the constitutionality of the system of using local property taxes to fund school

districts under the Equal Protection Clause of the Fourteenth Amendment (Karst, 1973; Kirabo et

al., 2015; Murray et al., 2016; Serrano v. Priest, 1971).

The state court was compelled by the vast disparities in property tax rates across the state.

Wealthy districts, as they still do, were able to gather higher revenue than poorer districts. Poorer

districts to stay afloat taxed their communities at a higher effective rate that did not help local

revenues match those in wealthier districts. The attorneys for Serrano stated that "Beverly Hills

spent more than twice as much per student as Baldwin Park, a low income and property-poor

community twenty-five miles east of Los Angeles. Because of Beverly Hills' far larger tax base,

however, it had a school property tax rate less than half of that of Baldwin Park" (Fischel, 1996).

More specifically, this series of cases raised the issue of "whether substantial inequality in school

8

district capacities to tax and spend means inequality of educational opportunity" (Karst, 1973).

The California Supreme Court ruled that,

We have determined that this funding scheme invidiously discriminates against the poor

because it makes the quality of a child's education a function of the wealth of his parents

and neighbors. Recognizing as we must that the right to an education in our public

schools is a fundamental interest which cannot be conditioned on wealth, we can discern

no compelling state purpose necessitating the present method of financing (Serrano v.

Priest, 1971).

In the years after Serrano, California developed a system of revenue limits and caps that sought

to decrease inequality by allowing lower spending districts to grow spending through state

foundation grants and limit growth in higher spending districts. The goal of the financing system

was to narrow the per-pupil funding gap between lower and higher spending school districts.

Since 1978, California has turned nearly all responsibility for financing schools over to the state

(Karst, 1973; Murray et al., 2016).

San Antonio Independent School District v. Rodriguez (1971) was a similar case to

Serrano in that its' plaintiffs challenged the constitutionality of Texas's school financing system

under the Equal Protection Clause of the Fourteenth Amendment. Texas, like California, relied

heavily on local property taxes to provide funding for schools. As such, more impoverished

Texas communities experienced substantial difficulties in collecting the tax dollars to fund their

schools adequately (Sutton, 2008). Partially due to several new conservative justices appointed

to the United States Supreme Court, the decision in this particular case was to uphold Texas's

school financing system. The court determined that Texas's school financing system did not

"impermissibly interfere with the exercise of a "fundamental" right or liberty…since (education)

9

is not within the limited category of rights recognized by this court as guaranteed by the

Constitution" (San Antonio Independent School District v. Rodriguez, 1973). Also, the court

held that the case as a whole was "an inappropriate case in which to invoke strict scrutiny" (San

Antonio Independent School District v. Rodriguez, 1973). Thus, the school finance system did

not violate the Equal Protection Clause of the Fourteenth Amendment.

The Rodriguez decision created a chilling effect through the school finance reform

movement and, as such, cases slowed. However, around 1989, another wave of state lawsuits

emerged that targeted a different aspect of school funding, statewide funding guarantees.

Claimants, in this second wave of cases, took a different strategy from their predecessors. Instead

of arguing against the constitutionality of the local property tax financing systems, they argued

that levels of statewide funding were too low and inadequate. Since the funding levels were

inadequate, they violated the guarantee that states have in their constitutions to provide an

adequate and "thorough and efficient" education to all students within their states (Sutton, 2008).

Adequacy based lawsuits have met greater court success than equity or equality-based school

financing cases from a decade earlier. Since 1989, two-thirds of the cases that challenged state

funding levels that focused on funding adequacy have won (Sutton, 2008). Courts,

disappointingly, seem more willing to address issues of "adequacy" versus "equity" or "equality,"

which has been instrumental in how school finance research has been framed since the early

1990s.

Effects of School Finance Reform on Educational Expenditures

The critical questions following these court decisions are, did they lead state leaders to

make equitable or adequate changes to their funding systems over time? Are states increasing

revenue per student, and is that translating to increased spending per student at the district level?

10

Finally, if there is an increase in spending, is it equitable across all socioeconomic levels of

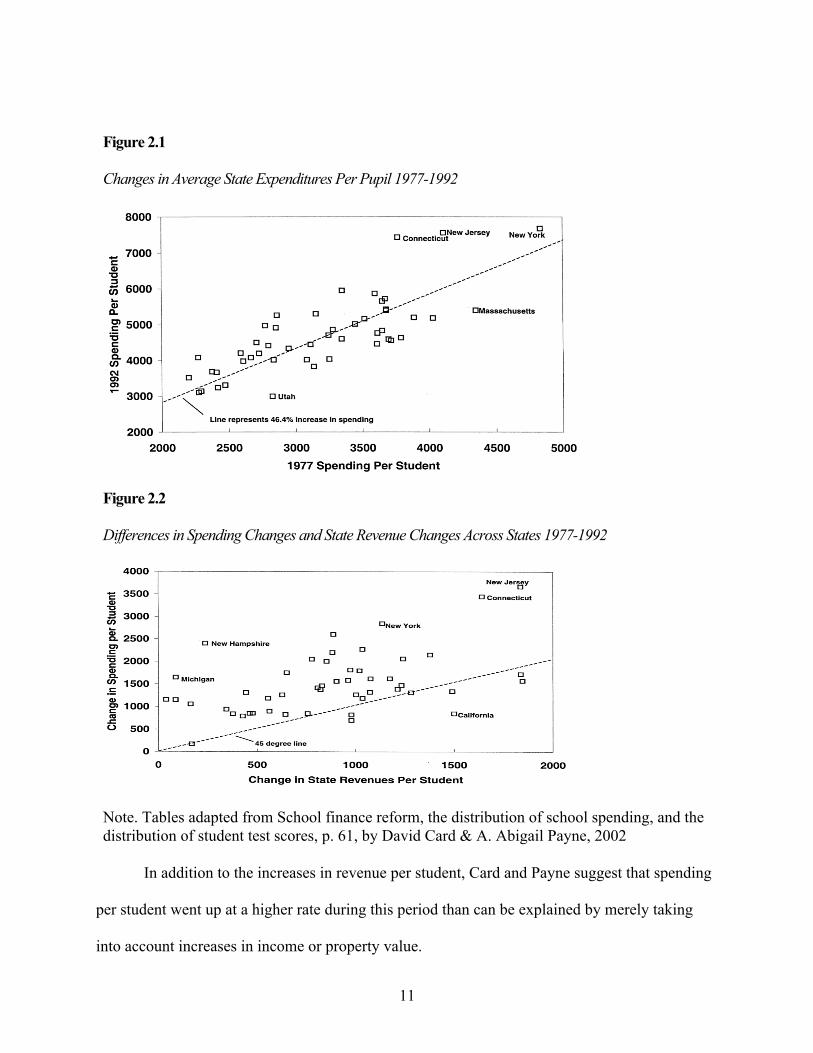

school districts? David Card and A. Abigail Payne conducted a study that examined the effect of

school finance reform decisions during the first and second wave of court cases (1977-1992) on

the levels of school spending across wealthier and poorer districts in over 13,000 school districts

in the United States.

Card and Payne sought to answer whether or not states had reacted to the school finance

reform litigation by changing their funding formulas in a significant way. They separated the

states into three separate categories states with court decisions finding school finance systems

unconstitutional, states with court decisions finding school finance reform systems constitutional,

and states with no court cases by 1992 (Card & Payne, 2002). Between 1977 and 1992, when

many of the first and second waves of court cases took place, state revenue per student in states

with court decisions that found their school finance system unconstitutional increased

substantially more (86%) than in either of the other two groups (46%-49%) (Card & Payne,

2002) suggesting a positive reaction to the court's decision. Changes in expenditure per student

remained relatively constant between the three groups.

11

Figure 2.1 Changes in Average State Expenditures Per Pupil 1977-1992

Figure 2.2 Differences in Spending Changes and State Revenue Changes Across States 1977-1992

Note. Tables adapted from School finance reform, the distribution of school spending, and the distribution of student test scores, p. 61, by David Card & A. Abigail Payne, 2002

In addition to the increases in revenue per student, Card and Payne suggest that spending

per student went up at a higher rate during this period than can be explained by merely taking

into account increases in income or property value.

12

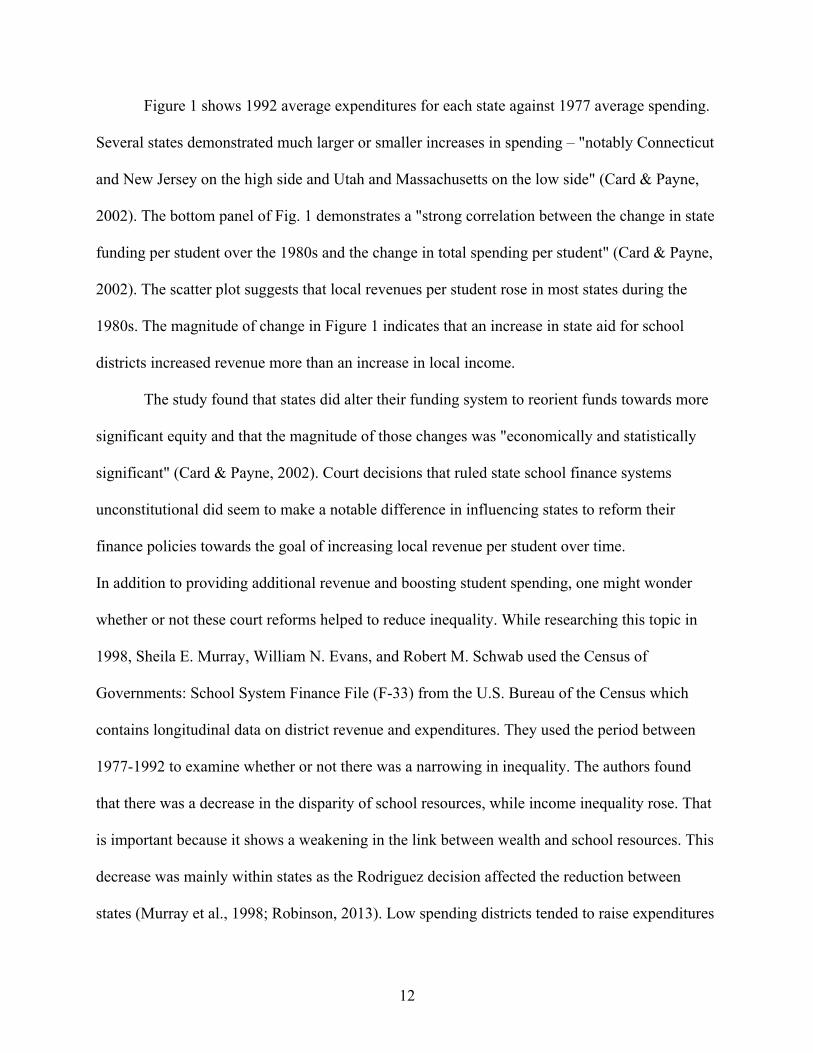

Figure 1 shows 1992 average expenditures for each state against 1977 average spending.

Several states demonstrated much larger or smaller increases in spending – "notably Connecticut

and New Jersey on the high side and Utah and Massachusetts on the low side" (Card & Payne,

2002). The bottom panel of Fig. 1 demonstrates a "strong correlation between the change in state

funding per student over the 1980s and the change in total spending per student" (Card & Payne,

2002). The scatter plot suggests that local revenues per student rose in most states during the

1980s. The magnitude of change in Figure 1 indicates that an increase in state aid for school

districts increased revenue more than an increase in local income.

The study found that states did alter their funding system to reorient funds towards more

significant equity and that the magnitude of those changes was "economically and statistically

significant" (Card & Payne, 2002). Court decisions that ruled state school finance systems

unconstitutional did seem to make a notable difference in influencing states to reform their

finance policies towards the goal of increasing local revenue per student over time.

In addition to providing additional revenue and boosting student spending, one might wonder

whether or not these court reforms helped to reduce inequality. While researching this topic in

1998, Sheila E. Murray, William N. Evans, and Robert M. Schwab used the Census of

Governments: School System Finance File (F-33) from the U.S. Bureau of the Census which

contains longitudinal data on district revenue and expenditures. They used the period between

1977-1992 to examine whether or not there was a narrowing in inequality. The authors found

that there was a decrease in the disparity of school resources, while income inequality rose. That

is important because it shows a weakening in the link between wealth and school resources. This

decrease was mainly within states as the Rodriguez decision affected the reduction between

states (Murray et al., 1998; Robinson, 2013). Low spending districts tended to raise expenditures

13

while already high spending districts remained unchanged following reforms, therefore

increasing state aggregate spending on primary and secondary education (Murray et al., 1998).

Effects of School Finance Reform on Achievement (Equity Era) In 1966 James Coleman released his influential report, Equality of Educational

Opportunity. This report influenced a new wave of arguments surrounding school finance reform

when it found little to no effect of resource-based education policy on the nation's schools

(Coleman et al., 1966). These arguments have centered around whether or not school finance

policy has/or can have an effect on student outcomes and closing gaps between richer and poorer

school districts. Education is in the position of having to compete with other public services such

as healthcare, retirement, corrections, etc. for public monies (Walter & Sweetland, 2003). As

such, it has to assert its significance in a politically resonant way to public officials. The way it is

most often argued is on the grounds of student performance. There is a significant body of work

within the field of education on school finance reform and student performance. The findings

from these works are equivocal, nuanced, and varied.

Finding a direct correlation between school funding and student performance has proven

difficult for researchers (Downes & Figlio, 1997; Robinson, 2013; Walter & Sweetland, 2003).

While education research has produced differing results on the effects of school finance reform

on student outcomes, there have been compelling studies in the field of economics. Economics

seems a natural fit for studying education finance reform as education is one of the more

significant components of government spending in the United States, accounting for 7.3% of

GDP across federal, state, and local expenditures (Jackson et al., 2015).

In the previous section, findings were presented that found that states react to school

finance reform cases by increasing revenue to students, which results in higher spending per

14

student. Another major question in school funding has been whether or not an increase in school

resources has had an impact on student performance. Eric Hanushek conducted a meta-analysis

of 377 studies that looked at the effects of different inputs (teacher-pupil ration, teacher salary,

expenditure per pupil, etc.) on student performance. Hanushek chose to use many kinds of

indicators representing student performance, such as standardized tests, dropout rates, college

performance, etc. In his meta-analysis, he found that while school resources had increased,

student achievement had remained either unchanged or decreased slightly (Hanushek, 1996).

"The vast majority of parameter estimates are statistically insignificant" (Hanushek, 1996).

Therefore, Hanushek asserted that it was not the amount of resources we put into schools, but

how those resources are used that effect student achievement. Hanushek found that "today the

existing knowledge base does not ensure that any added funds will, on average, be spent wisely.

That is true even if some schools may spend their funds wisely" (Hanushek, 1996).

There has been significant pushback on Hanushek’s findings that increased education

funding did not impact student achievement. Larry Hedges and Rob Greenwald offer criticisms

of the method and model that Eric Hanushek uses in his meta-analysis of the data. Hedges and

Greenwald point out that several prominent changes happened in education between the years of

1970-1995 (the years that Hanushek had concentrated on) including an expansion in the level

and comprehensiveness of education and a decline in the overall social capital (Bourdieu, 1986)

available for lower-income families (Hedges & Greenwald, 1996). When segments of the

population experience erosion in their social capital, they can be trapped in a cycle of inequality

that reproduces itself across generations (Bourdieu, 1986). As lower-income communities have

been demonstrated to have connections to lower spending school districts (Downes & Figlio,

1997; Jackson et al., 2015), the concern surrounding the loss of social capital has substantial

15

implications for the educational opportunity of students. Hedges and Greenwald argue that the

decline in social capital occurred due to the rising levels of poverty that disproportionately

impacted communities of color in the late 1980s and early 1990s. They also look at data from the

National Assessment of Educational Progress (NAEP) to assess how much student achievement

had decreased in relation to the expansion of level and comprehensiveness of education and

decline in social capital. After evaluating the data, they conclude that the relatively stable levels

of academic achievement, despite increased wealth disparity, was evidence for the positive effect

of increases in school expenditures.

Too often, the overarching discussion on the effects of school finance reform becomes

dichotomous. Either money matters for students or money does not matter. However, most of the

findings on these issues are much more complicated. Thomas Downes and David Figlio looked

at the imposition of expenditure limits on local governments and whether those limits affected

student performance on standardized test scores. Downes and Figlio argued that previous

research treated the effects of policy changes as purely exogenous events. Previous studies

treated finance reform as an entirely homogenous event. In reality, school finance reforms are

wide-ranging and affect different states in different ways. Some states have been forced to

assume finance reform under court-order while others do so in processes that originate from their

legislature. Downes and Figlio account for these variations by categorizing reform as court-

mandated or legislative. They then categorize on a separate level of pro-spending and anti-

spending. Downes and Figlio used individual-level data from two cohorts of high school seniors,

"one that attended school in an era before any recent substantial changes in school finance policy

occurred, and another that spent most (or all) of their academic careers in schools subject to tax

16

limits or school finance reforms" to study the effects of those reforms on academic achievement

(Downes & Figlio, 1997).

The findings from Downes & Figlio's study found, "economically and statistically

significant evidence" (Downes & Figlio, 1997) to suggest that tax limits decreased math scores,

but had virtually no impact on reading scores. More importantly, tax limits disproportionately

affect already low-spending school districts. These districts tended to be low income with higher

percentages of students of color. Therefore, tax limits were "increasing inequality in educational

opportunity and outcomes" (Downes & Figlio, 1997). When examining the effects of court-

mandated and legislatively induced school finance reform, these reforms have led on average to

increased student performance. The research presented so far has studied school finance reform

using datasets compiled during significant portions of what is known as the "equity era" of

school finance reform. Since 1989, the focus of school finance reform literature pivoted to the

"adequacy era." The next section presents a brief history of the adequacy era.

Shifting the Focus: From Equity to Adequacy Scholars who study the school finance reform movement have traditionally broken it into

three distinct "waves" (Card & Payne, 2002; Jackson et al., 2014; Koski & Reich, 2006;

Lafortune et al., 2016). The legal approach of plaintiffs’ court challenges (both at the federal and

state level) to states’ school financing systems define each of the three waves. Wave one and

wave two were both concentrated on the concept of "equity." The equity movement concentrated

on inputs to the school system. More specifically, it focused on equalizing per-pupil expenditures

across school districts (Heise, 1995; Mcmillan, 1998). Wave three of school finance reform

shifted the framing of court claims from "equity" to "adequacy." This shift proved to be more

17

legally successful and had significant implications for the types of policies states adopted to

address their educational attainment gaps (Card & Payne, 2002; Lafortune et al., 2016).

Wave One: Federal Equal Protection Challenges (1954-1973) Wave one of the school finance reform movement is tightly intertwined with the

desegregation movement initiated, in part, by the U.S. Supreme Court's Brown v. Board of

Education decision in 1954. Though the ruling fell short of declaring education as a fundamental

human right, the language of the decision emphasized the societal importance of education by

writing that "education is perhaps the most important function of state and local

governments…the great expenditures… demonstrate the importance of education to our

democratic society" (Heise, 1995). The fight to desegregate schools began to incorporate the

battle to equalize school spending across school districts. These new court cases based their

inequity claims in the Equal Protection Clause of the 14th amendment to the U.S. Constitution.

An example of this justification is present in the Serrano v. Priest cases. In 1968, a parent in the

Los Angeles City School District brought a lawsuit against California for its method of school

funding. The issue most pressing in the case was "whether substantial inequality in school

district capacities to tax and spend means inequality of educational opportunity" (Karst, 1973).

In 1971, with a 6-1 vote, the California Supreme Court ruled that California's funding scheme

did violate the equal protection clause of the state constitution.

The U.S. Supreme Court halted the early progress in the federal equity movement with

San Antonio v. Rodriguez in 1973. The court ruled that education was not a fundamental right as

it was not included in the Bill of Rights. Therefore, disparities in school funding could not be

held to be unconstitutional. This decision effectively halted school funding equity challenges at

the federal level. Despite this setback, Justice Marshall included wording in his dissent that left

18

the door open for state challenges to education funding, "nothing in the Court's decision today

should inhibit further review of state educational funding schemes under state constitutional

provisions" (Dayton & Dupre, 2006).

Wave Two: State Equal Protection Challenges (1973-1989)

Wave two of school finance reform began very shortly after the Rodriguez decision in

1973. This wave is similar to wave one in that it focuses on equity and closing gaps in per-pupil

expenditures. However, it departs from the first wave in that challenges from this wave

concentrate on equal protection clauses within individual state constitutions (Heise, 1995;

Mcmillan, 1998).

Robinson v. Cahill was a 1973 challenge to New Jersey's education funding system

decided by the New Jersey State Supreme Court. The court struck down the state's school

finance system, ruling that it did not meet the state's constitutional requirements. The foundation

for the court's decision was based upon New Jersey's state constitution's guarantee of a "thorough

and efficient" school system (Heise, 1995). This decision sparked a new groundswell of

education funding challenges based on state constitutional education clauses.

Every state in the United States contains a clause in its constitution that includes a form

of educational obligation (Parker, 2016). The wording of these clauses is often vague and open to

wide interpretation. Litigators during the second and third wave of school finance reform used

these clauses to make the case that states were falling short of their constitutional obligations to

educate their children. In wave two, legal challenges argued that states were falling short by

allowing significant gaps in per-pupil expenditures. This wave was useful in redirecting school

finance challenges from the federal to the state level. This redirection led to a majority of

victories early on but questions of local control and a rejection of the concept of equity as

19

"lacking the simplicity and unquestioned normativity that gave it its initial appeal" (Enrich,

1995) ended this wave. Equity could not stand as a concept, at the state level, because it

demanded equity or equalization in "other important variables that also influence educational

opportunity" (Heise, 1995). In short, equity, as a concept, was ruled to be too broad and

politically unpalatable in the late 1980s.

Wave Three: Adequacy and Challenges to State Education Constitution Clause Challenges (1989-Present)

In 1989, the Kentucky Supreme Court ushered in a third wave of school finance reform

with Rose v. Council for Better Education (Card & Payne, 2002; Jackson et al., 2015; Koski &

Reich, 2006; Lafortune et al., 2016). The argument, in this case brought by 66 Kentucky school

districts, concerned the states' clause to provide an "efficient system" of public schools. The

court wrote that the state's school finance system was "underfunded and inadequate; … fraught

with inequalities and inequities; … and … not uniform across the districts in educational

opportunities" (Rose v. Council for Better Education, Inc., 790 S.W.2d 186, Ky. 1989). The

court went on to say that, "each child, every child,…must be provided with an equal educational

opportunity to have an adequate education" (Lafortune et al., 2016). The wording in the court's

decision was highly consequential because it fundamentally shifted the emphasis of school

finance reform literature, legal and academic, from equity to adequacy. This change moved the

focus of school funding from purely school inputs (raw expenditure equalization) to outputs or

parity of outcomes for all students. The court’s ruling went so far as to outline seven areas in

which students should have an adequate education1.

1 These areas of adequacy included (1) oral and written communication skills; (2) knowledge of social, economic, and political systems; (3) knowledge of governmental processes; (4) knowledge of mental and physical wellness; (5) grounding in the arts; (6) adequate training for life work; and (7) sufficient academic and vocational training to compete with students in surrounding states (Heise, 1995).

20

Despite the court’s guidance, adequacy is still a difficult concept to define, but scholars

point to a few reasons why it has continued to be more legally successful than its equity

counterpart. First, equity often challenged the concept of local control that is so engrained in the

United States' idea of schooling. States would likely have to centralize school funding to achieve

equity. This is an unpopular concept amongst school districts who covet ground-level control of

their districts. Adequacy can attempt to avoid the issue of local control while holding states

accountable for their education obligations within their constitutions. Second, adequacy gained

momentum because it came on the heels of increasing accountability standards. Accountability

standards were popularized after the Reagan administration released A Nation at Risk in 1983

and continued through all presidential administrations that followed (Card & Payne, 2002; Heise,

1995; Lafortune et al., 2016; Mcmillan, 1998).

The result of Rose v. Council for Better Education was swift legislative reform of the

entire Kentucky school system in the form of the Kentucky Education Reform Act of 1990

(KERA). The act contained provisions for a new funding structure to help narrow the vast

financial disparities between school districts. A policy analysis of KERA in 2003 by Melissa

Clark found that that the act did, "substantially increase funding to lower-income districts…and

these increased revenues from the state were not offset by decreases in spending at the local

level" (Clark, 2003). Also, of importance, most of the redirected funding went towards

increasing teacher salaries. In regards to student achievement, Clark found mixed results. Clark

used ACT scores as her metric of academic performance, which admittedly could be somewhat

limiting in its scope. KERA moderately contributed to improvements in ACT scores for black

students relative to students in Tennessee.

21

Different Definitions of "Adequacy"

The definition of funding adequacy is not uniform from state to state. However, there are

common characteristics of adequacy, and it is operationalized in academic literature. How states

define what it means to provide an adequate education helps to guide how state legislatures and

state departments of education allocate resources to school districts.

In the 1989 Rose ruling, the Kentucky Supreme Court ruled that seven areas had to be

addressed to argue that children were receiving an adequate education. These seven areas were,

(1) oral and written communication skills; (2) knowledge of social, economic, and political

systems; (3) knowledge of governmental processes; (4) knowledge of mental and physical

wellness; (5) grounding in the arts; (6) adequate training for life work; and (7) sufficient

academic and vocational training to compete with students in surrounding states (Heise, 1995).

As a result, the Kentucky legislature, in KERA, intended to address these seven areas through

policy. This policy was a "sweeping overhaul of the Kentucky legislative system…that addressed

funding, curriculum, and governance" (Clark, 2003). KERA presented the earliest framework for

how policy could be designed to address the needs of adequacy.

William Clune attempted to define adequacy reform in 1992. He laid out a three-point

plan to address adequacy decisions in Kentucky, New Jersey, and Texas. His three-point plan

blended concepts from both adequacy and equity and included, (1) a base program of substantial

equality of spending for ninety-five percent of a state's students (maintained at that level of

equalization from year to year); (2) compensatory aid calculated to produce substantial

educational gains for children affected by poverty (for example, about $1000 per pupil); and (3)

a set of performance-oriented policies designed to improve the impact of educational resources

on student achievement (Koski & Reich, 2006).

22

William Koski and Rob Reich (2006) explore the concept of adequacy in a more holistic

manner. They break conceptions of adequacy into two groups: adequacy as a state constitutional

standard and adequacy as a remedy. Adequacy, as a state legal standard refers to how "state

education clause jurisprudence" has developed and influenced standards for adequacy. These

standards include

(1) those that articulate a vague and broad qualitative standard aimed at furthering the

state's interest in producing civic-minded and economically productive students but

provide little guidance to policymakers; (2) those that identify specific, though abstract,

capacities and skills that all children should receive from public education to serve both

the state's and the students' individual interests and then order the legislature to provide

the resources that would permit children to obtain those capacities and resources; and (3)

those that tie adequacy to state educational content standards, which define with a high

degree of specificity what all children should know and be able to do (Koski & Reich,

2006).

Adequacy as a remedy deals more with remedial court orders. These are both broader

definitions than those espoused by KERA. Koski and Reich define this conception of adequacy

in terms of the general remedies of courts:

(1) the mere declaration that the current system is unconstitutional and a directive to the

legislature to develop a new system in line with the court's constitutional standard, (2) the

directive that the state legislature determine the cost of an adequate education and an

order that such funding be provided (an inputs standard that may be tied to outcomes), (3)

the specific directive that the state provide a certain type of educational programming for

certain children and schools (an inputs standard), and (4) the order that the state shall

23

ensure that students achieve a certain outcome without dictating the specific inputs (an

outcomes standard) (Koski & Reich, 2006).

Both of these definitions demonstrate an expansion of the notion of adequacy. Phrases in the

above quotes such as "achieve a certain outcome," "educational content standards," and

"capacities and skills that children should receive" emphasize the output focus by states and help

to define adequacy-based school finance literature.

Contemporary Studies in School Finance

Over time, scholars in both education policy and economics have applied a more

comprehensive array of methodologies and approaches to study the central question of whether

school funding matters in ways that range from academic achievement to broader adult

outcomes. This new array of studies offers a much different picture than earlier studies in the

1970s, 80s, and 90s. They push back on the notion that was popularized by schools such as Eric

Hanushek as they find a positive relationship between school spending and student outcomes.

This section highlights a few of the more contemporary, critical studies to the school finance

literature on whether school finance policy makes a difference to students. Additionally,

literature will be discussed that address how money matters. Or to reframe that question, what

types of expenditures make a difference in students’ education?

David Card and Abigail Payne (2002) evaluated the effect of spending equalization

policy on SAT scores from 1980-2001. They found that "in the aftermath of negative court

decisions states tend to increase the relative funding available to lower-income districts" (Card &

Payne, 2002). For every additional dollar of state aid to a school district, there was a 30-65 cent

increase in spending in that district. For student achievement, the authors find a modest effect.

When comparing students from lower-income vs. higher-income districts, they find SAT scores

24

close by about five percent. This study of student outcomes from the adequacy era suggested

modest, but positive relationships between these policies and increases in per-pupil expenditures

and academic achievement.

C. Kirabo Jackson, Rucker C. Johnson, and Claudia Persico (2015) used the timing of the

passage of court-mandated reforms and their associated type of funding formula change, as an

exogenous factor on school spending. They then compare the adult outcomes of cohorts that

were differentially exposed to school finance reforms, depending on place and year of birth. The

authors then take this approach a step further by measuring the effects of financial on completed

years of education, future wages, and annual rates of poverty (Jackson et al., 2015). The authors

argue that past studies (such as Hanushek (1996) or Coleman (1966)) focused more narrowly on

test scores and may have missed the long-term effects of the reforms on students. This study

found only minor positive effects for children from affluent families. The authors found that a

10% increase in per-pupil spending each year for all 12 years of public school was associated

with 0.43 additional years of completed education, 9.5% higher earnings, and a 6.8 percentage-

point reduction in the annual incidence of adult poverty for children from low income

communities (Jackson et al., 2015). These findings point to the real impact of school finance

reform not only on student achievement but long-term outcomes concerning students. The effect

of the reforms are predominantly felt by students in need who reside in lower spending school

districts.

Julien Lafortune, Jesse Rothstein, and Diane Whitmore Schanzenbach further explored

the contribution of adequacy era reforms on student outcomes. They used representative samples

from the National Assessment of Educational Progress and the random timing of exogenous

events to evaluate changes in absolute and relative spending as well as achievement in low-

25

income school districts. For changes in relative expenditures the authors find "sharp, sustained

increases in both relative and absolute funding for low-income districts" (Lafortune et al., 2016).

A question might be raised to whether low-income districts were actually receiving increases in

revenue or if state policy had slowed the growth of higher-income districts, somewhat obscuring

the actual net gain to lower-income districts. Importantly, states were not accomplishing this by

"leveling down" spending for education; they adopted a more progressive financing policy that

increased funding to lower-income districts at a faster rate. Academic achievement was a more

mixed result. Finance reforms, "reduced achievement gaps between high- and low-income school

districts but did not have detectable effects on resource or achievement gaps between high- and

low-income (or white and black) students" (Lafortune et al., 2016). The results of studies such as

Card & Payne and Lafortune, Rothstein, and Schanzenbach indicate a relationship between

finance reform policy in the adequacy era and changes in the racial and socioeconomic gaps of

student outcomes.

The Types of Expenditures Most Associated with Student Outcomes Research demonstrates that money matters for improving not only the academic

achievement of all students (particularly students in lower-income school districts) but also for a

host of outcomes in the adult lives of students. Money is not a panacea to educational and social

ills. Still, funding is directly associated with the resources necessary to educate students and,

therefore, does impact nearly all aspects of student learning. Given this premise, where should

money be spent to provide the most significant impact on the quality of student outcomes,

particularly students of color and students from lower-income districts? Many educational

interventions that research has demonstrated positively impact student outcomes are in some way

tied into having greater access to funding and resources. This question has seen an increase in

26

attention in the past two decades with most research pointing to the importance of human

resources and expenditures connected to human resources (B. D. Baker, 2017; Dietrichson et al.,

2017; Jackson et al., 2015) through additional staffing and investing in existing staff.

The Impacts of Additional Instructional Staffing Investing more money into human resources is shown in school finance literature to be

one of the more effective spending choices a district can make, especially for students in lower-

income communities. One of the more comprehensive studies that explores this question is by

Jens Dietrichson et al. (2017). They conducted a meta-analysis on academic interventions for

elementary and middle school students from low-income communities. The researchers included

101 studies conducted between 2000 to 2014 from OECD and EU countries. All of the studies

used a treatment-control design and measured achievement by standardized tests in mathematics

and reading. The analysis found that the most significant effect sizes on achievement came from

interventions that included tutoring, small-group instruction, and coaching/mentoring of teachers

(Dietrichson et al., 2017). While the effect sizes were not large enough to completely close the

achievement gaps in math and reading between low and high-income students, the authors

contend that resources directed to more human resources could go a long way towards reducing

that gap (Dietrichson et al., 2017).

The findings of Dietrichson et al. are mainly consistent with Jackson, Johnson, and

Persico (2015) in that they demonstrate the significant impact of investing in human resources as

an effective way to improve student outcomes. Jackson, Johnson, and Persico's study reveals

additional types of human resources and instructional expenditures that were associated with

improved student outcomes beyond Dietrichson's meta-analysis. The author's findings on the

educational effects of increased spending were discussed previously in this literature review,

27

however, another crucial result had to do with how school leaders spent the money. Increased

spending was associated with reductions in student-to-teacher ratios, increases in teacher

salaries, and longer school years (Jackson et al., 2015). Dietrichson et al. 's and Jackson et al. 's

research find that spending that is directly focused on student instruction (i.e. hiring more

teachers, raising teachers’ salaries, tutoring, smaller class sizes, longer school years) lead to the

most significant gains in student outcomes.

A common result of additional staff is smaller class sizes. The positive impact of smaller

class sizes on student outcomes is demonstrated by a large body of research. Students who are

exposed to smaller class sizes at younger ages have long and lasting positive educational effects

(B. D. Baker, 2017; Finn, Gerber, Achilles, & Boyd-Zaharias, 2001; Konstantopoulos & Chung,

2009; Krueger & Whitmore, 2001). A 2011 study on the effects of class size by Susan Dynarski

et al. used data from the Project STAR experiment in Tennessee to examine college enrollment

and degree completion income and racial gaps. Project STAR (Student/Teacher Achievement

Ratio) was an experiment funded by the Tennessee legislature in 1986 that randomly assigned

different class sizes to children in kindergarten through third grade (Dynarski et al., 2011). The

authors find that assignment to a smaller class size increased the probability of attending college,

on average, by 2.7 percentage points. This number was double for African American students.

For students enrolled in the poorest third of schools in the study, there was a 7.3 percentage point

effect and shifted students toward higher-earning fields such as those in science, technology,

engineering, math (STEM), business, and economics.

Investing More in Existing Instructional Staff An alternate path school districts may choose to add additional staff is to invest more

funding in their existing staff. Competitive wages, especially concerning the economy in which a

28

school district operates, have proven to attract higher-quality teachers. Higher teacher salaries

have been found to attract more highly qualified teachers (Figlio, 1997b), that are more likely to

stay in the district in which they were employed (Ondrich, Pas, & Yinger, 2008). A teaching staff

this is highly qualified and stable is positively associated with student outcomes (Loeb & Page,

2000).

If wage competitiveness is associated with the attainment of higher-quality teachers and

better student outcomes, does the inverse hold? Does investing less in wage competitiveness and

teacher quality negatively impact student outcomes? Research suggests that this is the case.

Studies have found that restricting school personnel expenditures can lead to more inexperienced

teachers, which negatively affects student outcomes and that this effect is not evenly distributed

among school districts (Adamson & Darling-Hammond, 2015; Figlio, 1997a; Figlio & Rueben,

2001). This effect has important equity implications. In a wide-ranging study on the inequity in

the distribution of qualified teachers in California and New York, Adamson and Darling-

Hammond (2015) found that districts with lower salaries often served students with higher needs,

offered more unsatisfactory working conditions, hired teachers with lower qualifications, and

experienced higher turnover (Adamson & Darling-Hammond, 2015). They additionally found

that school districts in California and New York that had the highest proportion of students of

color and low-income students had twice as many uncredentialled and inexperienced teachers as

school districts that had the lowest proportions.

Adamson and Darling-Hammond went further to examine the inequitable distribution of

well-qualified teachers' effects on student achievement. If lower-income schools with students

with greater educational need don't have the funding necessary to attract the quality of teachers

that may benefit their students, the outcomes of those students are negatively impacted. While

29

these studies looked tax limits and tax revolts the central premise, that funding reduction

negatively impacts student outcomes, holds for other instances of budget reduction necessity