A financial history of the Metropolitan Railway, 1853–1933

110

A financial history of the Metropolitan Railway, 1853–1933 By Tony Sheward © Tony Sheward 2019

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of A financial history of the Metropolitan Railway, 1853–1933

A financial history of the Metropolitan Railway, 1853–1933

By

Tony Sheward

© Tony Sheward 2019

1

A FINANCIAL HISTORY OF THE METROPOLITAN RAILWAY

1853-1933

1. Introduction

Although the literature covering numerous aspects of the history of the Metropolitan

Railway (MR) is extensive, there is no one work which deals with the financial

performance of the company in a comprehensive way over its complete 80-year history.

This is not to denigrate what has been written. For instance, Alan Jacksoni gives many

financial statistics in the chapters of his book, including a two-page examination of the

financial history of the company. Similarly, Barker and Robbins two volume History of

London Transportii only includes a limited amount of financial information about the MR.

Nevertheless, these works have been invaluable sources for the historical background to

the figures. A History of the Metropolitan Railway & Metrolandiii published in 2018 by

Irene Hawkes does not contain any new material on financial matters. Mention should

also be made of Douglas Rose’s Diagrammatical Historyiv, which has been a useful

source of reference for the opening of the MR’s stations. This article takes as its basis the

annual reportsv of the MR and the Railway Returnsvi and attempts to chart the financial

history of the MR in a continuous way over its life starting with the act of incorporation

for the North Metropolitan Railway in August 1853 (name changed to the MR in 1854)

and ending with its absorption by the London Passenger Transport Board (LPTB) in July

1933.

The importance of presenting a financial history of the MR may not be readily apparent,

given the prominence of its other achievements. The original investors and those that

followed relied on the company to make regular reports indicating how capital works

were progressing and whether the resulting revenue stream was capable of adequately

rewarding the investors in its loans and shares. This was, of course, an ongoing process as

the company as the company expanded and new tranches of capital were required. The

confidence of the investors in the MR was key to its progress. The directors and managers

of the MR of course also needed a regular stream of financial information to fulfil their

roles.

Later on, the various booms and busts in railway development led the government to

move away from its normal laissez faire approach to commerce and industry and in the

Regulation of the Railways Act 1868 (the 1868 Act) specify the formats that railway

companies were to use in their reports to shareholders and to the Board of Trade. This

went considerably beyond the requirements for joint stock companies in general and

remained so for the rest of the MR’s existence, supplemented by the Railway Companies

(Accounts and Returns) Act 1911 (the 1911 Act) and the Railway Companies (Accounts

and Returns) Order 1928 (the 1928 Order). In the late Victorian period concern grew

about the level of railway charges and whether they were exploiting their monopoly

position in inland transport. The Railway Commission established by the Regulation of

the Railways Act 1873 to investigate complaints of malpractice and its later incarnations

were able to rely on the reporting formats specified by the above legislation as part of the

evidence for their work. By the same token, the company and the shareholders could

2

point to the accounts to refute accusations of excess profits. The accounts for 1913 were

to have an important role in calculating an adequate return for the railway companies

following takeover by the Railway Executive Committee in World War I and forming the

basis for rates and charges under the Railways Act 1921. Last but not least, the MR’s

accounts in the years before 1933 provided part of the justification for the compensation

to shareholders on the takeover by the LPTB.

Presenting the financial information in a consistent way is difficult, because of the

changes in financial reporting over the 80 years, as outlined by Tony Shewardvii. The

period 1868-1912 was governed by the 1868 Act and an attempt has been made to present

the figures for the years 1853-67 in a similar fashion. The period 1913-33 was governed

by the 1911 Act, with minor changes made the 1928 Order. Again, an attempt has been

made to provide some consistency between the pre and post 1913 periods. The period of

government control during and immediately after World War I saw some of the

information being withheld for security purposes. The published accounts of the MR

complied with the government regulations, but private and confidential accounts were

produced for the Board members, which contained a full set of schedules. Copies of

these, apart from 1921, are in TNA. Thus, there are gaps for 1921 in the graphs and tables

below.

To aid understanding of the figures, Appendix 1 gives an overview of capital financing

structure and Appendix 2 of running powers, leased lines and joint lines.

Although up to 1912, the annual reports were prepared in two half yearly tranches, the

information in this article is presented by calendar year for ease of understanding and

comparison.

Where possible, the narrative tries to provide explanations for the most significant

figures. However, the annual reports often do not make it clear what exactly has been

happening. The quality of financial information provided to shareholders has improved

radically since 1933, but the pace of change has accelerated considerably since the issue

of the first Statement of Standard Accounting Practice in 1971 and the formation of the

Financial Reporting Council in 1990. Even as late as the 1930s directors of limited

companies were very paternalistic in their attitude to shareholders and expected them to

have faith in their judgement and not question their decisions.

2. An Overview

Before looking in detail at the figures for the 80 years concerned, it is useful to take a

bird’s eye view of what happened to the MR during that period. The following graphs are

set out in Graphs A-F:

A. Total Receipts from Passenger and Freight Trains

B. Number of Passengers

C. Total Capital Receipts

D. Net Revenue before Interest on Debentures and Loans, and Dividends

E. Percentage Dividend on Ordinary Stock and Surplus Land Stock

3

F. Percentage Return on Capital versus Return on Government Long Term Debt and

Consumer Prices Index

In Graphs A and B, the figures for 1921 have been estimated, because the accounts for

that year are incomplete.

The monetary figures are as reported in the accounts, but of course inflation over the

period distorts the picture. The Bank of England’s inflation calculator gives some

indication of the impact that it has had. The figures below show the purchasing power of

£1 in 2018 pounds at ten-year intervals during the MR’s history and for 1932 its last full

year of operations:

Year Equivalent in 2018 Pounds

£

1863 123.42

1873 106.81

1883 119.44

1893 126.23

1903 119.44

1913 113.35

1923 59.40

1932 68.57

1933 70.30

Between 1863 and 1913, the overall impact of inflation was relatively modest with £1 in

1963 having purchasing power of £123.42 in 2018 pounds and £1 in 1913 £113.35. This

was not a smooth progression due to the economic booms and slumps during that period.

However, inflation was much more rapid during World War I and the years immediately

afterwards with £1 in 1923 having a purchasing power of £59.40 in 2018 pounds. By

1933, there had been some deflation as a result of the Great Depression and £1 in 1933

had purchasing power of £70.30 in 2018 pounds (£68.57 in 1932 the last full year of

operations).

As reported, the MR’s total receipts from passenger and freight trains rose from £102k in

1863 to £1.454m in 1932. Even if the two figures were converted to 2018 pounds using

the above inflation rates, this would still be a huge increase. There was not, of course, a

steady increase over the whole period, as explained below, and receipts peaked at

£1,950m in 1924, the year of the British Empire Exhibition at Wembley. The number of

passengers carried rose from 9.455m in 1863 to 119.664m in 1932, an increase of more

than 11½ times. As with receipts, the peak year was 1924 with 154.184m.

At the beginning of 1863, the money that had been received into the capital account

amounted to £1.342m and by 30 June 1933, the last day of the MR’s independent

existence, this had risen to £22.713m. As this money was received in numerous tranches

spread over the years concerned, it would be misleading to apply the above inflation rates

to these two amounts. In crude terms, it would have cost over £165m in 2018 pounds to

4

complete the opening stretch of line and conceivably several billions of pounds to

complete the network as it was in 1933.

The MR developed a good reputation for servicing the various components of its capital

and Graph D shows the money that was left after net revenue from operations, other

receipts and other expenditures for payments to these components. From 1887, this

includes the amount allocated by the Surplus Lands Committee for dividends on the

Surplus Land Stock (see explanation of this below in the section covering 1885-92). The

net revenue started as £72k in 1863 and rose to £875k in 1932, as with total receipts a

huge increase. Again, 1924 was the peak year at £980m. In terms of dividends on its

consolidated ordinary stock, the MR was always able to pay a dividend even in the most

difficult years. Even in the worst years, 1907-08, a dividend of ½ per cent was paid. The

highest payments of 7 per cent were paid in the years 1865-68 in special circumstances,

which are explained below. Thereafter, it was only possible to pay 5 per cent in good

years. Dividends on Surplus Land Stock were also paid in all years and, apart from small

fluctuations in individual years, rose gradually from 2½ per cent in 1887 to 3⅞ per cent in

1932. Graph E shows the percentage dividend paid on both categories of ordinary stock.

Graph E, the percentage return on capital (the net revenue in Graph D as a percentage of

the capital receipts in Graph C), gives a better indication of what sort of investment the

MR was for its stock holders. For much of its life, the return was above 4 per cent and

above 5 per cent in good years like 1924. Apart from the years 1919-20 in the post-World

War I boom, the MR’s return on capital was normally enough to provide protection

against inflation. Before 1913, the MR’s return on capital generally provided a small

margin above the return on long term government bonds. Thereafter, it was only in the

years 1923-25 and 1928-30 that the MR’s return on capital exceeded the return on long

term government bonds.

3. The Pre-Operational Period

The capital authorised and created for the initial 3¾ route miles was £1.533m consisting

of £1.150m in shares and £0.383m in loans, including adjustments to the original 1853

Act. By the end of 1861, a further £0.666m amount had been authorised and created for a

¾ mile extension to Moorgate, consisting of £0.5m in shares and £0.166m in loans. By

the time construction of the initial mileage had been completed at the end of 1862 some

£1.342m had been received into the capital account.

The MR opened to the public on 10 January 1963 and at that point £1.329m had been

spent, probably the bulk on the initial 3¾ mile route, as the Moorgate extension would not

be opened until late 1865. Construction had only taken about three years following the

award of the first contracts in December 1859. An analysis of this expenditure is shown

below:

5

Table 1

Analysis of Pre-Operational Capital Expenditure

Pre 1860 1860 1861 1862 Total

£ £ £ £ £

Land Purchase 13,125 215,550 170,565 213,309 612,549

Construction 136,840 234,703 276,100 647,643

Parliamentary Expenses 31,036 6,574 3,627 589 41,826

Interest 4,466 6,047 2,836 13,246 26,595

Sale of Surplus Materials (24,262) (24,262)

Other 13,293 5,290 6,256 106 24,945

Total 61,920 370,301 417,987 479,088 1,329,296

It was not until the end of 1859 that all the necessary support to finance the project was in

place. Not unnaturally, the bulk of the expenditure was related to the acts of parliament from

1853. The costs of constructing the permanent way and stations took nearly 49 per cent of the

total cost, but land purchase at just over 46 per cent took nearly as much. The New Road (the

current Marylebone Road, Euston Road and Pentonville Road) under which the railway ran

for much of its length then represented the effective northern boundary of the London built

up area and even then, property prices were expensive.

4. Operations Prior to the Chairmanship of Sir Edward Watkin 1863-72

Sir Edwin Watkin was voted in as chairman of the MR on 7 August 1872 and in October,

following the appointment of three directors from the Manchester area, was able to exercise

effective control over the board. Up to 1872, the MR had seen its role as a railway serving

central London and some of the then suburbs such as Hammersmith. Thereafter, the MR

began to see its role as wider player in the railway industry, in particular linking up with

Watkin’s interests in the Manchester Sheffield & Lincolnshire Railway (MSLR) and the

South Eastern Railway (SER) and in the process expanding its lines into areas outside

London such as Harrow, which was then a separate town surrounded by countryside. For

convenience, the whole of 1872 has been treated as part of the pre-Watkin period.

Operations in 1863 related purely to the initial route between Paddington and Farringdon, but

this was gradually to change as additional capital expenditure expanded the line. The projects

directly controlled by the MR with completion dates were:

Eastern extension Farringdon to Moorgate 1865

City widened lines Farringdon to Moorgate 1866

City widened lines Kings Cross to Farringdon 1868

Western extension Paddington to South Kensington 1868

Projects involving other companies that were completed during the period were:

Junction with the Great Northern Railway (GNR) at Kings Cross 1863

6

Connection with the Hammersmith & City Railway (H&CR), separate company with

MR participation, 1865

West facing junction with the London Chatham & Dover Railway (LCDR) at

Farringdon 1866

Baker Street to Swiss Cottage by the Metropolitan & St John’s Wood Railway

(M&SJWR), separate company with MR participation, 1868

Junction with the Midland Railway (MidR) at St Pancras 1868

Connection with the London & South Western Railway (LSWR) at Hammersmith

1870

East facing junction with the LCDR at Farringdon 1871

The increases in capital authorised and created and the amount received into the capital

account over the period were as follows:

31 December 1862 31 December 1872 Increase

£m £m £m

Capital Authorised & Created

Shares 1.650 5.950 4.300

Loans 0.549 1.867 1.318

Total 2.199 7.817 5.618

Amount Received into Capital Account

Shares 0.906 5.802 4.896

Loans 0.423 1.951 1.528

Miscellaneous 0.013 (13)

Total 1.342 7.753 6.411

Until the 1868 Act, railway companies were not required to distinguish between capital

expenditure on lines under construction and those open for traffic in their accounts and, even

then, there was no requirement to split the expenditure within these two categories into

individual projects. By the end of 1872 the total spent on capital account was £7.640m made

up of:

£m

Lines in the course of construction 0.632

Lines open for traffic 6.678

Working stock 0.269

Subscriptions to other railways 0.100

Other (0.039)

Total 7.640

7

The capital expenditure on the Moorgate to Aldgate extension and on the other extensions

and widening 1863-1872, including miscellaneous capital works on the lines already opened,

was made up as follows:

8

Table 2

Analysis of Capital Expenditure 1863-72

1863 1864 1865 1866 1867 1868 1869 1870 1871 1872 Total

£ £ £ £ £ £ £ £ £ £ £

Moorgate - Aldgate

Under Construction

Land Purchase 109,957 84,709 132,182 82,839 45,875 455,562

Construction of Way

& Stations

119,208 2,250 121,458

Law & Parliamentary 8,048 400 1,150 9,598

Interest 19,295 19,295

Miscellaneous 23,084 1,265 1,938 (51) 26,236

260,297 107,919 134,120 82,788 47,025 632,149

Lines Open for

Traffic

Land Purchase 233,165 490,878 720,538 641,156 495,419 234,377 131,083 202,715 79,435 94,445 3,323,211

Construction of Way

& Stations 55,019 144,319 313,953 492,371 440,745 165,708 171,394 19,874 81,646 21,468 1,906,497

Law & Parliamentary 6,734 3,071 42,467 1,278 8,145 5,686 4,754 117 3,388 75,640

Interest 14,558 6,493 14,543 15,264 25,687 24,487 101,032

Miscellaneous (42,600) (14,693) (57,293)

309,476 644,761 1,091,501 1,150,069 969,996 424,572 265,563 212,650 161,198 119,301 5,349,087

Working Stock 28,172 52,545 20,815 32,025 11,462 48,102 42,557 32,367 1,209 112 269,366

Subscriptions to

Other Railways

78,000 22,000 100,000

Credits from Surplus

Land

(66,421) (66,421)

Other 3,397 1,800 2,104 2,799 3,146 13,591 26,837

Total 341,045 699,106 1,114,420 1,184,893 1,062,604 754,971 429,630 379,137 245,195 100,017 6,311,018

9

When looking at the cost of the lines 1863-72, other than the Moorgate to Aldgate extension,

compared with that of the original section, it is noticeable that land purchase took up a much

larger proportion of the total, 62 per cent versus 46 per cent. Correspondingly, the cost of the

way and stations was 36 per cent compared to 49 per cent. Part of the reason was the

proximity of some of the work to the City of London, particularly the extension from

Farringdon to Moorgate and the City Widened Lines. The peak of expenditure in the years

1865-66 also relates to those projects. There was a flurry of expenditure on working stock in

the years 1863-64, as a result the breakdown of the initial arrangement with the Great

Western Railway (GWR) for the provision of stock for the initial 3¾ miles and to provide

extra, when the MR began to run its own trains on the line to Hammersmith, where new

stations were provided at Latimer Road, Royal Oak and Westbourne Park by the end of the

period. Expenditure on working stock peaked again in 1868, when trains began to use the

extension from Paddington to South Kensington. All the 44 locomotives purchased during the

period were of the A class. The total investment of £100k in the M&SJWR was made in the

years 1867-68. On the Moorgate to Aldgate extension land purchase rose to 72 per cent of the

total, with the cost of the way and stations falling to 19 per cent.

Presentation of the revenue account for the years 1863-68 is limited, because a standard

analysis of income and expenditure only came in with the implementation of the 1868 Act.

Although the new format was introduced for the accounts for the second half of 1868, those

for the first half were not reworked, so 1869 was the first complete year in the new format.

Table 3 below provides the detail that is available:

Table 3

Revenue Account 1863-68

1863 1864 1865 1866 1867 1868

£ £ £ £ £ £

Total Receipts 75,168 116,491 141,513 210,242 233,180 290,672

Expenditure

Maintenance of Way, Works

& Stations 1,663 5,489 8,633 12,298 10,584 10,702

Locomotive Power 6,237 11,079 18,717 31,497 33,441 29,655

General Charges 7,324 20,648 18,888 27,919 28,107 35,635

Compensation 3,395 2,348

Rates, Taxes & Government

Duty 3,407 8,498 9,266 12,845 14,145 23,369

Other 1 2 2 399 4,161

Sub Total 18,631 45,715 55,506 84,561 90,071 105,870

Revenue Balance 56,537 70,776 86,007 125,681 143,109 184,802

The year 1863 is not comparable with the other years, as the GWR operated the service on

behalf of the MR for part of the year. Both revenue and expenditure grew rapidly as the

system expanded. Table 4 gives the revenue account for the years 1869-72:

10

Table 4

Revenue Account 1869-72

1869 1870 1871 1872

£ £ £ £

Total Receipts

Passenger Trains 367,687 373,008 381,623 385,109

Freight Trains 6,395 12,363 14,444 16,281

Other 61,945 67,409 67,181 42,625

Sub Total 436,027 452,780 463,248 444,015

Expenditure

Maintenance of Way, Works &

Stations 15,723 19,973 18,273 20,075

Locomotive Power 53,567 57,628 54,234 42,207

Carriage & Wagon Repairs 8,295 9,185 9,526 9,381

Traffic Expenses 57,748 61,443 61,505 51,767

General Charges 15,359 16,308 15,463 18,385

Law Charges 2,117 2,709 2,535 15,624

Compensation 12,803 6,554 4,560 17,699

Rates, Taxes & Government Duty 30,480 30,111 28,309 26,015

Other 5,056 2,470 4,467 12,619

Sub Total 201,148 206,381 198,872 213,772

Allowance for Working Other Cos

Trains 36,568 52,891 48,684 21,495

Revenue Balance 271,447 299,290 313,060 251,738

Although sub totalling of traffic revenue by passenger and freight trains was not introduced

until the 1911 Act, for convenience, passenger train revenue is taken to include mails,

parcels, horses and carriages and goods train revenue to include merchandise, livestock and

minerals. It can be seen that even in 1872 freight train revenue was fairly insignificant

compared to passenger train revenue. The largest regular item in other revenue was rents for

such items as parts of stations, refreshment rooms, advertising and properties not considered

as surplus land. In 1869-71, there were also credits for the redemption of preference shares,

which should more properly have been dealt with in the net revenue account or appropriation

account.

As might be expected, the heaviest items of expenditure were associated with providing

locomotive power and the organisation of traffic. Compensation and law charges tended to be

variable, dependent on incidents causing loss or injury. The allowances for working other

companies’ trains were costs recoverable for running trains on behalf of other companies,

both on its own system and on other companies’ lines such as the H&CR and the

Metropolitan District Railway (MDR).

The net revenue & appropriation account 1863-72 is shown below:

11

Table 5

Net Revenue & Appropriation Account 1863-72

1863 1864 1865 1866 1867 1868 1869 1870 1871 1872

£ £ £ £ £ £ £ £ £ £

Receipts

B/Fwd Balance 1,312 7,778 1,709 7,999 6,999 4,167 2,043 98 2,065

Balance Revenue Account 56,537 70,776 86,007 125,681 143,109 184,802 271,447 299,290 313,060 251,738

Rents Received 5,191

Dividends Received 1,250 2,323 1,720 2,810 2,346

Bank & General Interest 2,241 22,793 39,917 10,526 5,600 2,880 981 1,487

Lands Committee 15,000

Other 12,635 15,976 8,368 24,215 72,535 125,131 26,728

71,413 110,857 142,070 162,131 229,243 321,062 304,665 303,053 316,949 277,827

Expenditure

Interest on Debentures & Loans 16,864 15,880 12,750 20,220 20,220 31,485 75,129 76,780 83,682 85,365

Other 125 28,558 21,629 20,267 28,601

16,864 15,880 12,750 20,220 20,220 31,610 103,687 98,409 103,949 113,966

Transfer to Special Account 18,830

Balance Available for Dividends 54,549 94,977 129,320 141,911 209,023 289,452 200,978 204,644 213,000 145,031

Preference Stocks 10,861 15,000 15,000 15,000 19,024 38,999 50,935 74,274 80,663 84,906

Extension/Preferred Ordinary Stocks 57,000 77,604 49,556 3,146 3,450 1,974

Consolidated Ordinary Stock 42,376 72,199 112,611 118,912 126,000 167,696 97,464 126,864 126,375 58,151

Deferred Ordinary Stock 986 980 262 447

53,237 87,199 127,611 133,912 202,024 285,285 198,935 204,546 210,935 145,031

Balance C/Fwd 1,312 7,778 1,709 7,999 6,999 4,167 2,043 98 2,065 0

% on Consolidated Ordinary Stock 5% 6% 7% 7% 7% 7% 4% 3¼% 3⅛% 1½%

12

As the accounts were prepared for half yearly periods, dividends were also declared for each

half year. The dividend percentage for each year has been calculated by taking a simple

average of the two percentages, ignoring any changes in ordinary share capital during the

year. Between 1865 and 1868 the holders of the consolidated ordinary stock had been paid a

regular dividend of 7%, despite the economic disruption which followed the Overend Gurney

bank failure in 1866. By 1868, shareholder unease began to grow about the management of

the Chairman, John Parson, and a court action was taken by a holder of Extension Preferred

Ordinary Shares, Frederick Bloxham, alleging that the proceeds of the share offering had not

been properly used for capital purposes. The case went against the company. A further court

case was started in 1869 by shareholder Enoch Salisbury alleging that the 7 per cent dividend

payment in 1868 had only been possible as a result of suspicious receipt of £42,600 from a

contractor, John Kelk. Restrained from including this credit, the Board tried to include an

interest credit in respect of unremunerative surplus lands, which resulted in a further court

case, where the Court of Chancery in 1870 found the directors guilty of breach of trust.

Moves to remove Parson and his fellow directors then began, leading to a Committee of

Investigation and an examination of the books by accountants, Price, Hoyland & Waterhouse.

Numerous errors and omissions were found, as well as misallocation between capital and

revenue. New accounting systems and annual audits were introduced.

The figures in Tables 4 and 5 are taken from the accounts as originally published, as there is

not a complete record of the revised versions. Because of problems described above,

meaningful analysis would be difficult. However, it should be mentioned that the interest and

dividends on debentures, loans and preference shares rose from £28k in 1863 to £170k in

1872, as a result of the capital raised to expand the MR network. This figure is important

because it is the burden of fixed charges, which needs to be satisfied before any payment to

the ordinary shareholders can be made.

5. The Early Years of Sir Edward Watkin’s Chairmanship 1873-77

As indicated above, the MR in 1872 had serious financial problems. Of necessity, the first

priority of Watkins chairmanship was to overcome these and put the company back in a

stable position. Despite his connections with the MSLR and the SER, any plans that he may

have had for the MR to co-operate with these railways had per force to be to be put on the

back burner. In any event, the previous management had obtained powers to extend the MR

beyond Moorgate to Bishopsgate (Liverpool Street) and ultimately under Watkin further

powers were obtained to extend to Aldgate. These extensions were to be the priority after

1872. In addition to this, there was pressure from the Metropolitan Board of Works and the

City of London authorities to complete the Inner Circle, which required some

accommodation with the MDR, which was not financially strong enough to extend its line

eastwards from Mansion House. Because the relations between Watkin and the MDR

chairman, James Forbes, were difficult, it would not be until 1879 that the two railways were

able to obtain parliamentary authority for a joint scheme to complete the Inner Circle. Two

years earlier, the MR had obtained powers to extend from Aldgate to Tower Hill. This section

looks at the MR’s financial performance 1873-77, before the final push to complete the Inner

Circle began. The year 1877 was a unique year for the MR in that there were no lines under

construction.

13

Operations between 1873 and 1877 remained as before, with the extensions to Liverpool

Street and Aldgate opening in 1875 and 1876 respectively. However. The MR did start a

service to Richmond from the beginning of 1877 via the H&CR and the LSWR.

The increases in capital authorised and created and the amount received into the capital

account over the period were as follows:

31 December 1872 31 December 1877 Increase

£m £m £m

Capital Authorised & Created

Shares 5.950 5.950

Loans 1.867 2.474 0.607

Total 7.817 8.424 0.607

Amount Received into Capital Account

Shares 5.802 5.835 0.033

Loans 1.951 2.400 0.449

Premiums 0.020 0.020

Total 7.753 8.255 0.501

The increase of capital authorised and created of £0.607m was primarily related to the

extension from Moorgate to Aldgate, although a small amount was for purchase of H&CR

debentures.

The total spent on capital account by the end of 1877 was £8.337m made up of:

£m

Lines open for traffic 7.859

Working stock 0.264

Subscriptions to other railways

- M&SJWR 0.200

- H&CR 0.018

Other (0.004)

Total 8.337

The capital expenditure 1873-77 was made up of the following:

14

Table 6

Analysis of Capital Expenditure 1873-77

1873 1874 1875 1876 1877 Total

£ £ £ £ £ £

Moorgate - Aldgate

Under Construction

Land Purchase 50,723 120,620 43,294 61,201 275,838

Construction of Way

& Stations 13,300 58,778 35,194 20,604 127,876

Law & Parliamentary 1,947 2,510 2,279 994 7,730

65,970 181,908 80,767 82,799 411,444

Lines Open for Traffic

Land Purchase 150,764 56,936 17,110 36,229 64,934 325,973

Construction of Way &

Stations 2,452 7,616 5,019 73,881 29,029 117,997

Law & Parliamentary 31,836 2,509 2,605 2,244 3,805 42,999

185,052 67,061 24,734 112,354 97,768 486,969

Sub Total Lines 251,022 248,969 105,501 195,153 97,768 898,413

Working Stock (4,818) (813) 884 (4,747)

Subscription

(M&SJWR)

99,335 665 100,000

Subscription (H&CR) 11,000 7,575 18,575

Credits Surplus Land (100,000) (121,555) (8,841) (61,701) (16,806) (308,903)

Other 40,000 40,000

Total 146,204 167,414 195,182 146,001 88,537 743,338

15

The Moorgate to Aldgate extension was completed during the period. The total cost was

£1.044m, including the £0.632m spent prior to 1873. As noted above in relation to the early

development of the MR, the high cost of land dwarfed the cost of constructing the railway

infrastructure. However, the benefit from the sale of surplus land did help to reduce the

overall capital spend, amounting to £0.309m in 1873-77. This had its origins in MR Acts of

1862 and 1868, which enabled the company to grant building leases of superfluous land and

to purchase and hold property not required for the construction of the railway. This was

further refined in the MR Act of 1873, which allowed the company to retain any

superfluous lands, whenever acquired, including those acquired in the future. To take

advantage of these powers, the company merely had to believe that such lands may be

hereafter necessary for the widening of the railway, stations or sidings.

As can also be seen, the MR began to take up shares and debentures in sister railways, the

M&SJWR and the H&CR. The £40k item of other expenditure in 1874 related to the bonus

payable on redemption of redeemable preference shares.

Table 7 gives the revenue account for the period 1873-77:

16

Table 7

Revenue Account 1873-1877

1873 1874 1875 1876 1877

£ £ £ £ £

Total Receipts

Passenger Trains 390,318 392,605 423,512 450,566 464,777

Freight Trains 18,065 18,945 24,852 25,226 26,050

Other 30,119 30,138 31,360 32,148 33,431

Sub Total 438,502 441,688 479,724 507,940 524,258

Total Expenditure Maintenance of Way, Works &

Stations 22,490 22,968 21,684 22,936 24,192

Locomotive Power 48,166 47,017 41,536 40,466 41,125

Carriage & Wagon Repairs 9,425 9,977 9,687 10,245 10,504

Traffic Expenses 48,464 51,542 54,852 58,604 60,202

General Charges 18,527 19,562 24,377 24,307 22,994

Law Charges 3,825 2,092 1,623 3,257 3,885

Compensation 4,223 1,461 786 6,676 2,418

Rates, Taxes & Government Duty 26,354 28,084 30,703 31,232 30,260

Other 18,747 14,354 12,155 11,098 10,904

Sub Total 200,221 197,057 197,403 208,821 206,484

Allowance for Working Other Cos

Trains 15,165 15,622 15,996 16,310 16,930

Revenue Balance 253,446 260,253 298,317 315,429 334,704

Whereas total receipts had tended to plateau in the years 1869-72, growth resumed in 1873

and those in 1877 were 18 per cent higher than in 1872. Although freight train revenues in

1877 still only accounted for 5 per cent of the total, that percentage had been rising slowly

during the period. Rents still accounted for the bulk of the other revenues. Compared to

revenues, total expenditure in 1877 was about £7k lower than in 1872, in part as a result of

the tighter financial controls exercised since the problems experienced up to 1872. Traffic

expenses increased proportionately more than the other categories, whereas locomotive

power costs tended to fall. The allowances for working other companies’ trains, which had

peaked at £53k in 1870, stabilised at around £16k per annum.

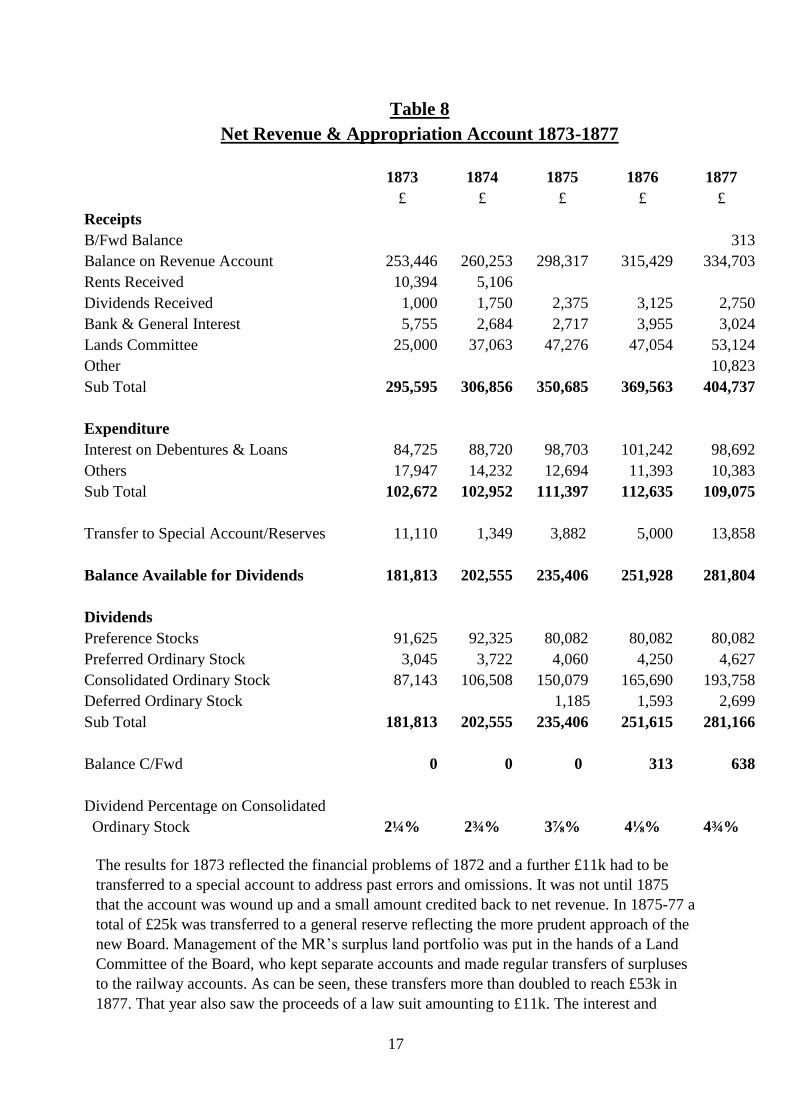

The Net Revenue & Appropriation Account 1873-77 is shown below:

17

Table 8

Net Revenue & Appropriation Account 1873-1877

1873 1874 1875 1876 1877

£ £ £ £ £

Receipts

B/Fwd Balance 313

Balance on Revenue Account 253,446 260,253 298,317 315,429 334,703

Rents Received 10,394 5,106

Dividends Received 1,000 1,750 2,375 3,125 2,750

Bank & General Interest 5,755 2,684 2,717 3,955 3,024

Lands Committee 25,000 37,063 47,276 47,054 53,124

Other 10,823

Sub Total 295,595 306,856 350,685 369,563 404,737

Expenditure

Interest on Debentures & Loans 84,725 88,720 98,703 101,242 98,692

Others 17,947 14,232 12,694 11,393 10,383

Sub Total 102,672 102,952 111,397 112,635 109,075

Transfer to Special Account/Reserves 11,110 1,349 3,882 5,000 13,858

Balance Available for Dividends 181,813 202,555 235,406 251,928 281,804

Dividends

Preference Stocks 91,625 92,325 80,082 80,082 80,082

Preferred Ordinary Stock 3,045 3,722 4,060 4,250 4,627

Consolidated Ordinary Stock 87,143 106,508 150,079 165,690 193,758

Deferred Ordinary Stock 1,185 1,593 2,699

Sub Total 181,813 202,555 235,406 251,615 281,166

Balance C/Fwd 0 0 0 313 638

Dividend Percentage on Consolidated

Ordinary Stock 2¼% 2¾% 3⅞% 4⅛% 4¾%

The results for 1873 reflected the financial problems of 1872 and a further £11k had to be

transferred to a special account to address past errors and omissions. It was not until 1875

that the account was wound up and a small amount credited back to net revenue. In 1875-77 a

total of £25k was transferred to a general reserve reflecting the more prudent approach of the

new Board. Management of the MR’s surplus land portfolio was put in the hands of a Land

Committee of the Board, who kept separate accounts and made regular transfers of surpluses

to the railway accounts. As can be seen, these transfers more than doubled to reach £53k in

1877. That year also saw the proceeds of a law suit amounting to £11k. The interest and

18

dividends on debentures, loans and preference shares rose from £170k in 1872 to £179k in

1877. The preferred ordinary shareholders received their 6 per cent during the period and it

was possible for the holders of consolidated ordinary stock see their dividends rise from a

low of 2¼ per cent in 1873 to 4¾ per cent in 1877. The deferred ordinary stock holders had

not received a dividend since 1871 and this was resumed at 1¾ per cent in 1875 rising to 3½

per cent in 1877.

6. Reaching Out Beyond the Inner Circle 1878-84

By 1877, the finances of the MR had been well stabilised by the Watkin regime. In the

following years, it became possible to consider extending the system both to the north west

and south east. To the north west, the MR had been involved with the M&SJWR since 1864

and by 1868 had invested £100k in the company’s preference stock. The 2¼ mile single line

to Swiss Cottage was completed in 1868 and was worked from the start by the MR. Although

the financial results of the line were not encouraging, as early as 1874 Watkin indicated his

desire to shareholders that the MR should connect with Northampton and Birmingham and

many other important townsviii. However, reaching a deal for the MR to take over the

M&SJWR proved tortuous and it was not until 1882 that the company was fully absorbed. In

the meantime powers had been granted to extend the line to Kingsbury (now Neasden) and

double the original section. A further extension from Kingsbury to Harrow was granted to the

MR and M&SJWR jointly. Watkin also had his eyes on a route to the north of Harrow and

had joined the board of the Aylesbury & Buckingham Railway (A&BR) in 1875. By Acts of

1880 and 1881, the MR obtained powers to extend firstly from Harrow to Rickmansworth

and then to Aylesbury and Chesham. From 1880, the MR was operating trains to Harrow and

by 1884 construction work to the north was under way.

To the south east, it was apparent that a link with the SER’s line at New Cross would need to

cross the Thames using the East London Railway (ELR), which had opened in 1876, and that

there would need to be a link off the Inner Circle to reach that railway. As mentioned above,

powers to complete the Inner Circle, including a link to the ELR, were not granted until 1879.

It would take until 1884 for all the work to be completed and MR trains were able to run

through to New Cross. An Act of 1882 modified the original powers to link the Inner Circle

to the ELR and set up a Joint Committee to run the latter consisting of the MR, MDR,

London Brighton & South Coast Railway (LBSCR), LCDR and SER.

The increases in capital authorised and created and the amount received into the capital

account over the period were as follows:

19

31 December 1877 31 December 1884 Increase

£m £m £m

Capital Authorised & Created

Shares 5.950 8.684 2.734

Loans 2.474 3.184 0.710

Total 8.424 11.868 3.444

Amount Received into Capital Account

Shares 5.835 7.883 2.048

Loans 2.400 3.036 0.636

Premiums/(Discounts) 0.020 (0.010) (0.030)

Total 8.255 10.909 2.654

The increase of £3.444m in capital authorised and created was related to the expansion

described above, including the acquisition of the M&SJWR. At the eastern end there was

direct expenditure on the Aldgate to Minories (Tower Hill) extension and the Aldgate North

Curve, as well as contributions to the City Lines & Extensions Joint Committee (CL&EJC).

The total amount spent on capital account by the end of 1884 was £10.915m made up of:

£m

Lines under construction 1.550

Lines open for traffic 8.956

Working stock 0.369

Subscriptions to other railways 0.040

Total 10.915

The capital expenditure 1878-84 was made up of the following:

20

Table 9 Part 1

Analysis of Capital Expenditure 1878-84

1878 1879 1880 1881 1882 1883 1884 Total

£ £ £ £ £ £ £ £

Lines Under

Construction

St John’s Wood -

Kingsbury

Land Purchase 210,667 15,332 22,564 9,410 257,973

Construction of Way

& Stations 21,341 122,482 32,709 44,612 221,144

232,008 137,814 55,273 54,022 479,117

Kingsbury -

Harrow

Land Purchase 32,358 15,015 7,821 55,094

Construction of Way

& Stations

37,500 54,844 4,355 96,699

69,758 69,859 12,176 151,793

Harrow-Aylesbury

Land Purchase 726 10,026 17,520 46,023 18,487 92,782

Construction of Way

& Stations

29,259 29,259

Law & Parliamentary 402 402

726 10,026 17,922 46,023 47,746 122,443

Neasden Depot 45,685 45,685

Hendon Extension 20,264 20,264

Sub Total North

West

232,008 207,572 125,858 121,909 17,922 46,023 68,010 819,302

21

Table 9 Part 2

Analysis of Capital Expenditure 1878-84

1878 1879 1880 1881 1882 1883 1884 Total

£ £ £ £ £ £ £ £

Lines Under

Construction

B/Fwd North West 232,008 207,572 125,858 121,909 17,922 46,023 68,010 819,302

Minories Extension

Land Purchase 34,338 40,822 43,004 110,981 132,745 1,407 363,297

Construction of Way

& Stations

19,620 102,499 2,520 124,639

34,338 40,822 43,004 130,601 235,244 3,927 487,936

Aldgate North

Curve

Land Purchase 58,297 58,297

Construction of Way

& Stations

44,196 12,500 56,696

44,196 70,797 114,993

City Lines &

Extensions

550 550

Sub Total

South East

34,338 41,372 43,004 130,601 235,244 48,123 70,797 603,479

Sub Total Under

Construction

266,346 248,944 168,862 252,510 253,166 94,146 138,807 1,422,781

22

Table 9 Part 3

Analysis of Capital Expenditure 1878-84

1878 1879 1880 1881 1882 1883 1884 Total

£ £ £ £ £ £ £ £

B/Fwd Lines Under

Construction 266,346 248,944 168,862 252,510 253,166 94,146 138,807 1,422,781

Lines Open for

Traffic

Land Purchase 17,920 9,013 7,418 1,099 108,039 7,130 5,418 156,037

Construction of Way

& Stations 2,548 629 176 3,556 92,162 19,618 10,390 129,079

Law & Parliamentary 1,983 1,573 1,725 2,454 2,307 2,565 4,052 16,659

Other 4,286 4,286

22,451 11,215 9,319 7,109 202,508 29,313 24,146 306,061

Sub Total Lines 288,797 260,159 178,181 259,619 455,674 123,459 162,953 1,728,842

Working Stock (72) 5,658 31,414 5,391 2,374 16,792 44,217 105,774

Purchase of

M&SJWR

133,170 141,822 274,992

Subscription H&CR 12,925 8,000 500 21,425

Subscription

CL&EJC

478,500 413,500 212,575 1,104,575

Credits Surplus Land (45,000) (6,729) (19,447) (12,007) (5,000) (19,000) (107,583)

Credits from City

Authorities

(300,000) (300,000)

Credit from MDR (250,000) (250,000)

Total 256,250 259,088 198,148 253,503 1,064,718 695,573 (149,255) 2,578,025

23

It is perhaps surprising that the expenditure on the Aldgate North curve, the Minories

extension and the CL&EJC was shown under lines under construction in the accounts for the

half year to 30 December 1884, when services had started from 6 October. However, the

transfer of the cost to lines open for traffic took place in the accounts for the following half

year. What stands out is the huge cost of completing the last few miles of the Inner Circle and

the extension to the ELR, particularly for the land, compared to the cost of extending the old

M&SJWR out to Harrow; for roughly two miles compared to seven miles. For the Minories

extension of less than a mile, land at £0.363m took up near three quarters of the cost, whereas

from Kingsbury to Harrow, about 3½ miles, the cost of the land at £55k was less than the cost

of construction and only made up 36 per cent of the total. Although the cost of the MR’s

contribution to the CL&EJC is shown as £1.105m, the net cost was actually £0.805m because

of a £0.300m contribution from the City Board of Works and Commissioner for Sewers for

improvements enabled by the construction of the railway. The MR also received £0.250m

from the MDR for its extension to Minories, which was to become part of the line controlled

by the CL&EJC, but this was credited separately from the cost.

Included in other works under construction was £20k for a projected extension from West

Hampstead to Hendon that was never to be built. Credits from sales of surplus land of

£0.108m during the period helped to offset the cost of the capital projects. Working stock

increased by £0.106m over the period 1878-84 to total £0.369m at the end of 1884. The

increase took place in two main tranches, one around 1880 when the extension to Harrow was

completed and another around 1884 for the new ELR and Inner Circle services, and included

22 class B locomotives. In 1882, the MR finally acquired the M&SJWR and had to pay a

further £0.275m over and above its cumulative investment of £0.200m. The MR’s investment

in the H&CR more than doubled in the period to £40k.

Table 10 gives the revenue account for the period 1878-84:

24

Table 10

Revenue Account 1878-1884

1878 1879 1880 1881 1882 1883 1884

£ £ £ £ £ £ £

Total Receipts

Passenger Trains 467,561 478,189 497,126 520,762 527,294 573,350 572,596

Freight Trains 27,311 28,015 29,087 31,015 29,705 30,418 31,155

Other 33,381 33,079 33,167 35,331 35,347 36,073 35,851

Sub Total 528,253 539,283 559,380 587,108 592,346 639,841 639,602

Total Expenditure Maintenance of Way, Works

& Stations 24,309 23,771 25,635 25,727 25,899 27,407 26,336

Locomotive Power 44,497 44,712 49,844 53,628 55,551 58,084 66,794

Carriage & Wagon Repairs 11,088 12,139 12,892 14,063 19,081 20,868 22,567

Traffic Expenses 59,990 62,055 65,316 68,262 63,025 67,170 70,624

General Charges 23,575 23,296 23,753 23,197 25,862 24,956 25,192

Law Charges 3,221 2,392 2,086 2,803 6,513 4,260 5,461

Compensation 2,156 1,574 1,040 2,885 1,041 303 1,762

Rates, Taxes & Government

Duty 29,994 31,694 31,841 38,661 40,848 41,358 36,920

Other 9,670 9,385 10,840 13,179 10,350 10,494 11,551

Sub Total 208,500 211,018 223,247 242,405 248,170 254,900 267,207

Allowance for Working

Other Cos Trains 22,158 21,709 23,374 23,561 23,838 14,333 16,374

Revenue Balance 341,911 349,974 359,507 368,264 368,014 399,274 388,769

25

Total receipts grew by 22 per cent on their 1877 level to reach £0.640m in 1884. As might be

expected, most of the growth took place in the years 1879-80, when the extension from Swiss

Cottage to Harrow came into operation. The completion of the Inner Circle and the connection to

the ELR came too late to impact on the revenues for 1884. Although the extension to Harrow made

provision for freight traffic, revenue from freight grew more slowly than that from passengers.

Revenue from rents increased by about £2k per annum over the period.

Total expenditures rose by 29 percent on their 1877 level to reach £0.267m in 1884. Allowances for

working other companies’ trains were marginally lower in 1884 than they had been in 1877,

although they had increased up to 1882. Once the M&SJWR was acquired, there were no receipts

for operating its trains. The overall effect was that the revenue balance, which had been 64 per cent

of total revenues in 1877, fell to 61 per cent in 1884. The categories of cost which had the largest

proportionate increase were locomotive power and carriage & wagon repairs.

The net revenue & appropriation account for the period 1878-84 was as follows:

26

Table 11

Net Revenue & Appropriation Account 1878-84

1878 1879 1880 1881 1882 1883 1884

£ £ £ £ £ £ £

Receipts

B/Fwd Balance 638 502 5,949 4,155 1,217 717 2,019

Balance Revenue Account 341,911 349,974 359,507 368,264 368,014 399,274 388,769

Dividends Received 3,000 2,750 2,750 2,750 3,758

Bank & General Interest 90 1,260 1,510 4,031 1,600 1,600 4,509

Lands Committee 56,625 60,137 63,505 63,121 65,297 67,591 67,284

Other 1,171 6,500 5,461

403,435 414,623 433,221 442,321 446,386 469,182 468,042

Expenditure

Interest on Debentures & Loans 99,641 103,521 104,361 103,692 106,116 115,322 120,900

Other 10,042 9,903 12,955 11,463 9,146 13,513 8,932

109,683 113,424 117,316 115,155 115,262 128,835 129,832

Transfer to/(from) Reserve 1,500 3,500 15,000 24,199 (23,566)

Balance Available for Dividends 292,252 297,699 300,905 302,967 331,124 340,347 361,776

Preference Stocks 80,082 80,082 80,082 80,082 96,738 103,408 108,408

Preferred Ordinary Stocks 4,628 4,628 4,778 4,984 4,996 4,996 4,996

Consolidated Ordinary Stock 203,956 203,956 208,706 213,342 225,342 226,592 235,967

Deferred Ordinary Stock 3,084 3,084 3,184 3,342 3,331 3,332 3,330

291,750 291,750 296,750 301,750 330,407 338,328 352,701

Balance C/Fwd 502 5,949 4,155 1,217 717 2,019 9,075

% on Consolidated Ordinary Stock 5% 5% 5% 5% 5% 5% 5%

27

As can be seen, revenue from the Lands Committee continued to make an important contribution to

the funds available to pay interest charges and dividends. The annual total rose from £53k in 1877

to £67k in 1884. Other receipts included a profit related to the sale of electric telegraph equipment

in 1882 and the first share of profits from the CL&EJC in 1884. The interest and dividends on

debentures, loans and preference shares rose from about £179k in 1877 to nearly £229k in 1884,

reflecting the additional capital raised for the various extensions. A reorganisation of preference

stocks took place in 1881, when all previous issues at 5 per cent were replaced by 4 per cent

perpetual preference stock. Throughout the period, the dividends on preferred ordinary stock,

consolidated ordinary stock and deferred ordinary stock were maintained at 6 per cent, 5 per cent

and 4 per cent respectively. Whereas transfers to the general reserves totalling £44k were made in

the years 1878-81, none were made in the following two years and a transfer of £24k was made

from the reserves in 1884.

7. The Drive to the North West Reaches its Zenith 1885-1892

In 1884 the MR had already begun work to extend beyond Harrow to Aylesbury. The first seven

miles to Rickmansworth had been authorised by parliament first and were opened to traffic in 1887.

Although Aylesbury was the principal target, the line from Rickmansworth was ultimately to be

built in two stages. The first stage was to Chesham, which was not in the original powers and

required a further act in 1885. A double track of 5 miles was to be laid to Chalfont &Latimer with

the intention of going on to Aylesbury and a further 2½ miles of single-track branch to Chesham.

Watkin looked upon the latter as a possible route to join the LNWR at Tring. The line between

Rickmansworth and Chesham was completed in 1889. The final 16¼ miles to Aylesbury was

completed in 1892. In parallel with this extension, the MR had obtained powers under an act of

1890 to acquire the A&BR, which were exercised in 1891. The existing A&BR single line between

Aylesbury and Verney Junction would give the MR just over 50 route miles from Baker Street.

However, the MR initially could only operate as far as a temporary station in Aylesbury, until a

dispute with the GWR about powers to use the joint station in the town had been settled. It would

not be until 1894 that refurbishment of the joint station was completed, and the MR could run

through trains to Verney Junction. Nevertheless, by 1892 the MR had largely fulfilled the role that

Watkin had envisaged for it to the north west of London. Although it still had improvement works

to carry out after 1892, the focus would shift to what would become the Great Central Railway

(GCR) London Extension.

By contrast, the eastern end of the MR system had reached a stable position. It was able to run

through trains to connect with the SER at New Cross and use the station at Whitechapel as a

terminus. It would be the MDRix in conjunction with the independent Whitechapel & Bow Railway

and London Tilbury & Southend Railway (LT&SR) that would drive further eastern expansion.

An important development during this period was a further reorganisation of the MR’s management

of its surplus lands. Watkin had been uneasy for some time that profits from the surplus lands had

been unduly inflating the results of its railway operations and complicating its competitive position

vis a vis other railways. By an act of 1885, the ordinary stock of the company was split into two

portions. New surplus land shares with a value of £2.641m were issued to stock holders at a rate of

£1 for every £2 of consolidated ordinary stock. The effect on the net revenue account and the

28

appropriation account is covered below. At the same time, there was a reorganisation of capital,

which extinguished both the existing preferred and deferred ordinary shares.

The increases in capital authorised and created and the amount received into the capital account

over the period were as follows:

31 December 1884 31 December 1892 Increase

£m £m £m

Capital Authorised & Created

Shares 8.684 9.292 0.608

Loans 3.184 3.383 0.199

Total 11.868 12.675 0.807

Amount Received into Capital Account

Shares 7.883 8.100 0.217

Loans 3.036 3.310 0.274

Premiums/(Discounts) (0.010) (0.005) 0.005

Total 10.909 11.405 0.496

The increase in capital authorised and created of £807m was related to the expansion described

above, including the acquisition of the A&BR. The total amount spent on capital account by the end

of 1892 was £11.438m made up of:

£m

Lines open for traffic 8.338

Working stock 0.419

Subscriptions to other railways 0.040

Surplus Land Stock 2.641

Total 11.438

The capital expenditure 1885-92 was made up of the following:

29

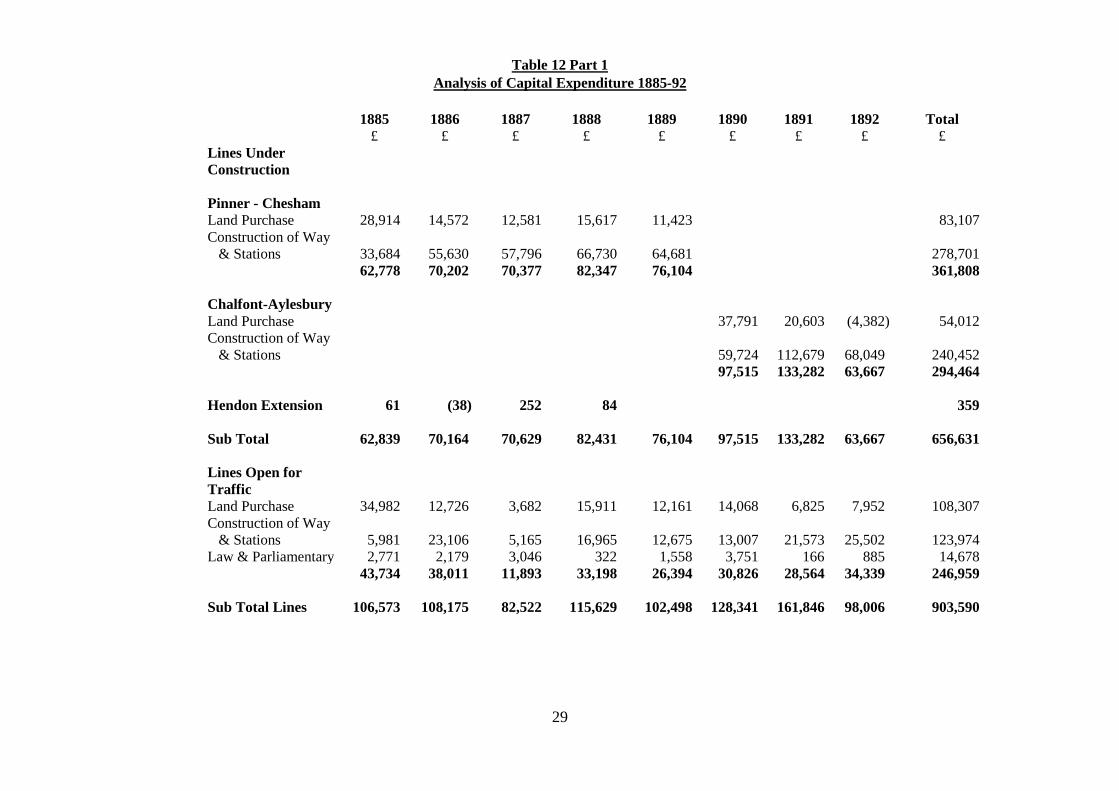

Table 12 Part 1

Analysis of Capital Expenditure 1885-92

1885 1886 1887 1888 1889 1890 1891 1892 Total

£ £ £ £ £ £ £ £ £

Lines Under

Construction

Pinner - Chesham

Land Purchase 28,914 14,572 12,581 15,617 11,423 83,107

Construction of Way

& Stations 33,684 55,630 57,796 66,730 64,681 278,701

62,778 70,202 70,377 82,347 76,104 361,808

Chalfont-Aylesbury

Land Purchase 37,791 20,603 (4,382) 54,012

Construction of Way

& Stations

59,724 112,679 68,049 240,452

97,515 133,282 63,667 294,464

Hendon Extension 61 (38) 252 84 359

Sub Total 62,839 70,164 70,629 82,431 76,104 97,515 133,282 63,667 656,631

Lines Open for

Traffic

Land Purchase 34,982 12,726 3,682 15,911 12,161 14,068 6,825 7,952 108,307

Construction of Way

& Stations 5,981 23,106 5,165 16,965 12,675 13,007 21,573 25,502 123,974

Law & Parliamentary 2,771 2,179 3,046 322 1,558 3,751 166 885 14,678

43,734 38,011 11,893 33,198 26,394 30,826 28,564 34,339 246,959

Sub Total Lines 106,573 108,175 82,522 115,629 102,498 128,341 161,846 98,006 903,590

30

Table 12 Part 2

Analysis of Capital Expenditure 1885-92

1885 1886 1887 1888 1889 1890 1891 1892 Total

£ £ £ £ £ £ £ £ £

Sub Total Lines

B/Fwd

106,573 108,175 82,522 115,629 102,498 128,341 161,846 98,006 903,590

Working Stock 4,890 824 3,316 130 8,950 1,232 12,530 17,476 49,348

Subscription CL&EJC 22,143 (7,285) 12,837 (97,626) (23,980) 1,590 4,201 (13,725) (101,845)

Purchase of A&BR 100,663 100,663

Credits Surplus Land (71,594) (913) (9,000) (81,507)

Transfer of Aylesbury

& Rickmansworth

line to the A&RR

(347,714) (347,714)

Total 62,012 100,801 98,675 18,133 78,468 131,163 178,577 (145,294) 522,535

31

As mentioned above, the Minories Extension and the Aldgate North Curve schemes, which had

been completed by 1884, were transferred to lines open for traffic in 1885. Apart from a small

amount spent on the Hendon Extension, before it was finally abandoned in 1889, the only line

under construction was that from Harrow to Aylesbury, including the Chesham branch. In total, this

28¾ mile route cost £778k, including £122k spent before 1885, of which only 30 per cent related to

the cost of the land. The line from Rickmansworth to Aylesbury and Chesham was authorised by

two Acts in 1885. One covered only the Chesham branch and was an exclusively MR project. The

other provided for a separate Aylesbury & Rickmansworth Railway (A&RR), which was to be built

for it by the MR. An amount of £348k spent by the MR on the Aylesbury & Rickmansworth line

was transferred to the A&RR in 1892. This included the amount designated in the accounts for

work on the Chalfont to Aylesbury section plus part of that for work on Pinner to Chesham section.

Also, in 1892, the MR acquired the A&BR at a cost of £101k and its proprietors were paid in the

form of MR 3 per cent preference shares at a lower rate than the 4 per cent preference shares

already in existence and indicating the weak financial state of the A&BR.

The MR had regular capital transactions with the CL&EJC during the period. There were several

large credits particularly in 1888, 1889 and 1892, which mainly related to surplus lands being sold.

In fact, over the years 1885-92 the MR received a net amount of £102k from the CL&EJC. The MR

also had receipts from the sale of surplus lands on its own account during the period amounting to

£82k, particularly in 1885, when the work at the eastern end of the system had been completed. The

MR’s investment in the H&CR remained static at £40k. Working stock increased by £49k during

the period to a total of £419k, as the various stages of the route to Aylesbury were opened. This

included four class C locomotives and “Jubilee” stock carriages.

Table 13 gives the revenue account for the period 1885-92:

32

Table 13

Revenue Account 1885-1892

1885 1886 1887 1888 1889 1890 1891 1892

£ £ £ £ £ £ £ £

Total Receipts

Passenger Trains 561,244 584,953 558,650 575,908 590,394 601,895 628,214 633,954

Freight Trains 30,737 31,316 31,012 33,857 36,702 40,393 42,080 43,135

Other 36,458 37,281 37,767 38,204 39,610 38,561 38,729 38,778

Sub Total 628,439 653,550 627,429 647,969 666,706 680,849 709,023 715,867

Total Expenditure Maintenance of Way, Works &

Stations 25,467 27,451 27,667 28,653 30,824 29,256 29,951 31,470

Locomotive Power 76,051 75,906 77,910 79,240 84,667 85,680 85,606 87,215

Carriage & Wagon Repairs 25,599 25,828 25,471 26,034 26,980 25,769 26,789 27,394

Traffic Expenses 71,198 72,433 72,771 73,737 77,352 79,042 81,468 86,718

General Charges 26,389 27,769 29,165 28,165 29,302 28,770 28,676 29,443

Law Charges 5,253 4,704 3,025 3,047 2,930 2,959 4,337 5,682

Compensation 1,390 3,091 690 2,596 394 947 3,094 1,130

Rates, Taxes & Government Duty 37,971 40,168 40,826 38,485 41,771 42,872 46,818 45,187

Other 10,935 12,898 11,534 11,787 12,089 11,700 12,219 12,028

Sub Total 280,253 290,248 289,059 291,744 306,309 306,995 318,958 326,267

Allowance for Working Other Cos

Trains 21,032 23,519 26,000 24,756 22,142 21,303 21,727 22,374

Revenue Balance 369,218 386,821 364,370 380,981 382,539 395,157 411,792 411,974

33

Total receipts grew by 12 per cent on their 1884 level to reach £0.716m in 1892. Most of the

increase took place from 1889 onwards, when the extension from Rickmansworth to Chesham was

opened. Revenue from freight traffic grew by 38 per cent from its 1884 level at last reflecting the

impact of the facilities, which the MR had built for it from Finchley Road northwards. Revenue

from rents increased by about £3k per annum over the period.

Total expenditures rose by 22 per cent on their 1884 level to reach £0.326m in 1892. Allowances

from for working other companies trains rose from £16k in 1884 to £22k in 1892, although they

had reached £26k in 1887. The increases were the result of the reorganisation of services following

the completion of the Inner Circle and the introduction of through services to the ELR. The

proportions of the various expenditure categories making up the total remained largely similar

between 1884 and 1892. Locomotive power showed the largest relative increase and other (mainly

charges from other companies working MR trains) the largest relative decrease.

The net revenue & appropriation account for the period 1885-92 was as follows:

34

Table 14

Net Revenue & Appropriation Account 1885-92

1885 1886 1887 1888 1889 1890 1891 1892

£ £ £ £ £ £ £ £

Receipts

B/Fwd Balance 9,075 14,909 52,527 21,228 21,811 14,012 9,592 10,943

Balance Revenue Account 369,218 386,821 364,370 380,981 382,539 395,157 411,792 411,974

Bank & General Interest 7,217 3,199 7,873 8,908 6,493 5,914 9,139 6,723

Railway Estates Revenue 70,528 70,839 39,339 6,891 7,027 8,610 8,310 9,154

CL&EJC 27,274 15,096 18,438 17,395 16,886 14,755 17,784 15,849

Other 36,381

Sub Total 483,312 527,245 482,547 435,403 434,756 438,448 456,617 454,643

Expenditure

Interest on Debentures & Loans 121,875 121,822 123,481 128,059 128,044 129,333 131,458 131,544

Other 15,185 14,743 14,762 13,879 14,443 14,664 15,652 13,728

Sub Total 137,060 136,565 138,243 141,938 142,487 143,997 147,110 145,272

Transfer to/(from) Reserve

Balance Available for Dividends 346,252 390,680 344,304 293,465 292,269 294,451 309,507 309,371

Preference Stocks 113,408 113,408 118,405 126,404 126,404 126,404 126,904 127,904

Preferred Ordinary Stocks 4,996 4,996

Consolidated Ordinary Stock 211,273 217,876 204,671 145,250 151,853 158,455 171,660 171,660

Deferred Ordinary Stock 1,666 1,873

Sub Total 331,343 338,153 323,076 271,654 278,257 284,859 298,564 299,564

Balance C/Fwd 14,909 52,527 21,228 21,811 14,012 9,592 10,943 9,807

% on Consolidated Ordinary

Stock

4% 4¼% 3⅞% 2¾% 2⅞% 3% 3¼% 3¼%

Surplus Lands Dividend 33,011 66,022 66,022 66,022 66,022 69,324

% on Surplus Lands Stock 2½% 2½% 2½%

2½%

2½%

2⅝%

35

The change involving the issue of Surplus Land Stock took place in the second half of 1887.

Whereas prior to that time the net revenue account had received transfers from the Lands

Committee of tens of thousands of pounds per annum reaching £71k in 1886, thereafter the Surplus

Lands Committee kept separate accounts for the properties represented by the Surplus Lands Stock.

At the end of each accounting period the Committee made an allocation of its net revenue to

provide a dividend on this stock. The MR still had land transactions relating to properties required

for railway purposes, but by 1892 the revenue income from these was below £10k in each year.

Revenue income from the CL&EJC was £27k in 1885, its first full year but settled down thereafter

to a range of £15k to £18k per annum. The interest and dividends on debentures, loans and

preference shares rose from £229k in 1884 to £259k in 1892, as additions to capital were made for

the extension to Aylesbury and to acquire the A&BR. In 1886, the last full year before the new

Surplus Land Stock was issued, a dividend of 4¼ per cent was paid on the consolidated ordinary

stock. Thereafter, the rate fell to a low of 2¾ per cent in 1888 but recovered to 3¼ per cent in 1891-

92. However, the Surplus Land Stock paid a regular dividend of 2½ per cent in 1887-91 with 2⅝

per cent in 1892. There were no transfers to/from the reserves in the period 1885-92.

8. The Coming of the Great Central 1893-1900

One of Watkin’s motives in becoming Chairman of the MR was to facilitate the development of the

MSLR (name changed to the GCR in 1897) and enable it to serve London. When the MSLR

obtained parliamentary authority for its London extension in 1893, the scheme approved, including

amendments approved in 1896, comprised the following:

- a wholly owned line from Annesley near Nottingham to a junction with the MR just

north of Quainton Road on its Aylesbury-Verney Junction line

- joint use of the MR’s line from Quainton Road to Harrow South junction

- exclusive use of a pair of tracks to built by the MR from Harrow South junction to

Canfield Place near Finchley Road alongside its existing tracks

- a wholly owned line from Canfield Place to a new terminus at Marylebone

Much of the MR’s activity in the period 1893-1900 was related to bringing these plans into effect

and, although the GCR started through running to Marylebone in 1899, the last section of the new

tracks just south of Harrow was not completed until 1900. Watkin was not able to steer the plans

through as Chairman, as ill health caused him to step down in 1894 and John Bell, already General

Manager, took over the chairmanship role as well. One offshoot of the MR’s work in preparing for

the GCR was that it agreed to lease the 6½ mile Brill Tramway, which ran west from Quainton

Road station.

It might have been expected that Bell would not have the close relationship with the GCR that had

been possible because of Watkins’s involvement with both companies. In fact, Bell’s relationship

with William Pollitt, the GCR’s general manager, was particularly combative, because they had

rivals when both working for the MSLR. The matter of most importance was the GCR’s concern

about the suitability of the route that Watkin had devised between Quainton Road and Harrow. The

MR had originally engineered it for local stopping and freight services, not for express passenger

services. The gradients and curves in places were not suitable for high speeds and there was no

provision for additional platforms and freight loops to enable overtaking. During this period, Pollitt

36

started negotiations with the GWR to use their Birmingham cut off line between Northolt and

Ashenden, which would enable GCR trains to approach Marylebone via a short link between

Northolt and Neasden. Powers for this were granted by parliament in 1898. This left the MR with a

sizeable grievance about the traffic from the GCR which would be lost. A settlement of this dispute

would not be resolved until 1904.

The increases in capital authorised and created and the amount received into the capital account

over the period were as follows:

31 December 1892 31 December 1900 Increase

£m £m £m

Capital Authorised & Created

Shares 9.292 9.492 0.200

Loans 3.383 3.566 0.183

Total 12.675 13.058 0.383

Amount Received into Capital Account

Shares 8.100 9.050 0.950

Loans 3.310 3.310 -

Premiums/(Discounts) (0.005) 0.004 0.009

Total 11.405 12.364 0.959

The increase since the end of 1892 in capital authorised and created of £383m was primarily related

to the works needed to accommodate the GCR. The total amount spent on capital account by the

end of 1900 was £12.731m made up of:

£m

Lines under construction 0.041

Lines open for traffic 9.466

Working stock 0.543

Subscriptions to other railways 0.040

Surplus Land Stock 2.641

Total 12.731

The capital expenditure 1893-1900 was made up of the following:

37

Table 15 Part 1

Analysis of Capital Expenditure 1893-1900

1893 1894 1895 1896 1897 1898 1899 1900 Total

£ £ £ £ £ £ £ £ £

Lines Under

Construction

Finchley Road -

Harrow Widening

Land Purchase 4,240 67,558 18,899 11,789 209 102,695

Construction of Way

& Stations 750 28,471 97,865 85,946 15,525 14,162 242,719

Law & Parliamentary 1,423 135 1,558

6,413 96,164 116,764 97,735 15,734 14,162 346,972

Lines Open for Traffic

Land Purchase 6,088 8,119 11,082 6,966 4,203 (635) 407 17,030 53,260

Construction of Way

& Stations 33,266 17,855 90,749 52,673 14,760 50,347 67,464 51,628 378,742

Law & Parliamentary 37 2,182 2,120 2,932 (1) 531 7,801

39,354 25,974 101,868 61,821 21,083 52,644 67,870 69,189

439,803

Sub Total Lines 39,354 25,974 108,281 157,985 137,847 150,379 83,604 83,351 786,775

Working Stock 10,380 2,998 11,329 12,451 8,553 29,990 6,544 42,069 124,314

Subscriptions to

CL&EJC 1,025 (125) 7,550 1,000 8,233 (500) 17,183

Purchase of the A&RR 365,051

365,051

Total 415,810 28,847 127,160 170,436 147,400 188,602 89,648 125,420 1,293,323

38

Table 15 Part 2

Analysis of Capital Expenditure 1893-1900

1893 1894 1895 1896 1897 1898 1899 1900 Total

£ £ £ £ £ £ £ £ £

Included in Lines Open

for Traffic

Aylesbury – Verney Jct

Widening

Land Purchase 4,756 7,754 1,817 2,804 17,131

Construction of Way &

Stations

698 71,520 41,558 5,322 119,098

5,454 79,274 43,375 8,126 136,229

39

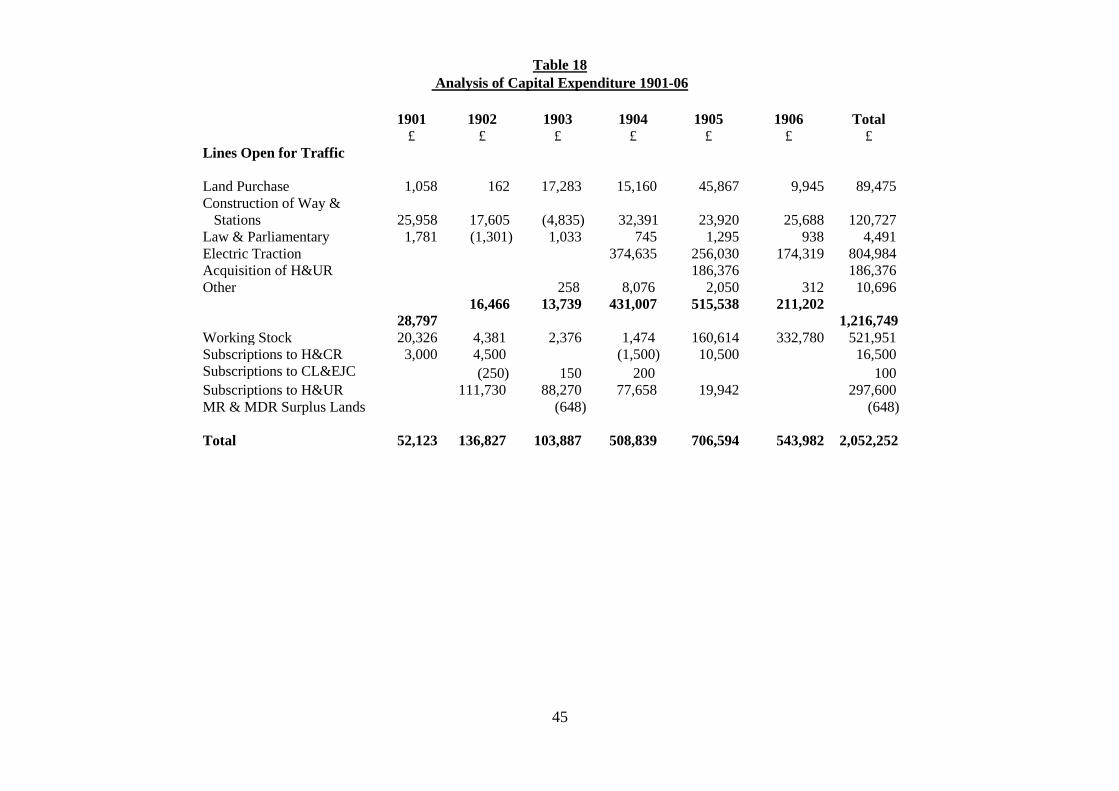

The widening between Finchley Road and Harrow was shown under lines under construction,

because it was a completely new a pair of tracks alongside the original. A new station was opened

at Wembley Park in 1894. The original concept in the MSLR’s 1895 Act was that the company

would have exclusive use of two tracks between Canfield Place and Wembley Park. However, the

MR decided to extend the quadrupling through to Harrow on its own initiative and by an Act of

1896 the MSLR was granted exclusive use of two tracks on this additional stretch. The total cost of

the Finchley Road to Harrow widening was £347k of which 30 per cent was for the land. By the

end of 1900, the GCR was able to run trains over the whole length of the new pair of tracks, but the

part of the bridge over the LNWR main line at Northwick Park being rebuilt for the MR’s existing

tracks was not completed until 1901 and the MR had to share the new tracks for a short period. It

was thus that the expenditure on the new pair of tracks was classified as lines under construction at

the end of the period.

The doubling of the original single track between Aylesbury and Verney Junction, which included a

new station at Waddesdon, was treated as part of work on lines open for traffic and is shown as a

memo total at the foot of the table. A total of £136k was spent on the doubling between Aylesbury

and Verney Junction, with only 13 per cent for the additional land.

The £124k spent on working stock during the period included six D class locomotives and most of

the six E class locomotives, as well as new bogie passenger stock made by Ashbury Railway

Carriage & Iron Co. Some of these Ashbury carriages remained in service on the Chesham branch

until electrification in 1960. This new equipment was primarily required for the MR’s expanding

traffic north of Harrow, including freight. Similarly, the expenditure on lines open for traffic

included additional freight facilities at a number of stations. A further £17k was advanced to the

CL&EC during the period. The A&RR was purchased by the MR in 1893 for a sum of £365k in

1893.

Table 16 gives the revenue account for the period 1893-1900:

40

Table 16

Revenue Account 1893-1900

1893 1894 1895 1896 1897 1898 1899 1900

£ £ £ £ £ £ £ £

Total Receipts

Passenger Trains 626,629 637,777 644,783 666,027 694,843 689,219 718,496 705,419

Freight Trains 41,433 51,072 55,184 67,728 83,871 100,167 98,843 117,884

Other 38,945 43,070 43,799 44,072 44,647 43,148 43,376 43,721

Sub Total 707,007 731,919 743,766 777,827 823,361 832,534 860,715 867,024

Total Expenditure

Maintenance of Way, Works &

Stations 34,884 38,464 37,669 37,535 41,070 42,206 51,834 58,055

Locomotive Power 88,060 80,540 82,600 85,278 96,423 103,515 105,761 121,622

Carriage & Wagon Repairs 28,162 26,884 26,704 28,405 28,994 29,645 31,112 33,075

Traffic Expenses 81,631 81,024 84,456 85,755 91,810 95,626 100,253 97,072

General Charges 29,612 28,835 27,606 28,203 29,933 31,230 33,430 33,571

Law Charges 3,817 3,395 3,319 4,394 3,883 5,373 4,070 4,237

Compensation 740 1,237 1,036 454 495 545 950 574

Rates, Taxes & Government Duty 46,028 47,539 49,617 51,437 50,934 47,904 50,067 52,495

Other 12,761 13,209 13,322 14,005 16,036 15,433 16,038 15,862

Sub Total 325,695 321,127 326,329 335,466 359,578 371,477 393,515 416,563

Allowance for Working Other Cos

Trains 23,334 5,568 4,165 3,467 3,792 2,944 5,494 3,014

Revenue Balance 404,646 416,360 421,602 445,828 467,575 464,001 472,694 453,475

41

The opening of the Aylesbury Extension had quite a positive effect on total receipts, which

increased by 21 per cent on their 1892 level to reach £0.867m in 1900. The extent of the increase is

partially disguised by the opening of the Central London Railway (CLR) to the public at the end of

July 1900. The MR and the MDR, its fellow operator of the Inner Circle, no longer had a monopoly

of under-ground rail traffic in the capital and now had a rival which used cleaner electric traction.

Taking receipts from passengers only i e excluding other items carried by passenger trains such as

parcels and horses, the 1899 total of £0.702m fell to £0.629m in 1901, a reduction of 10 per cent.

Fortunately, the MR’s efforts to stimulate freight traffic had begun to bear fruit and total receipts

from freight trains rose from £43k in 1892 to £118k in 1900, by nearly one and three quarters.

Other receipts, mainly rents, rose modestly from £39k to £44k.

Total expenditures rose by 28 per cent from their 1892 level to reach £0.417m in 1900. Allowances

for working other companies’ trains, which had reached a peak in of £23k in 1893 fell substantially

thereafter and did not exceed £6k per annum for the rest of the period. This was principally because

of a change in the operating arrangements for the H&CR. Previously the MR had provided almost

all of the trains, but the GWR now started to provide its half of the services. The proportions of the

various expenditure categories making up the total did show a significant movement between 1892

and 1900, with locomotive power and maintenance of the infrastructure increasing from 26.7 to

29.2 per cent and 9.6 to 13.9 per cent respectively. By contrast, traffic expenses fell from 26.6 to

23.3 per cent. The longer route mileage and the wider spacing of stations at the outer end probably

help to explain these movements.

The net revenue & appropriation account for the period 1893-1900 was as follows:

42

Table 17

Net Revenue & Appropriation Account 1893-1900

1893 1894 1895 1896 1897 1898 1899 1900

£ £ £ £ £ £ £ £

Receipts

B/Fwd Balance 9,807 1,493 10,787 12,145 14,130 17,133 17,281 18,341

Balance Revenue Account 404,646 416,360 421,602 445,828 467,575 466,001 472,694 453,475

Bank & General Interest 5,551 3,857 3,794 4,245 6,323 6,143 3,759 1,600

Railway Estates Revenue 8,874 8,739 9,182 9,777 9,171 10,741 11,361 11,483

CL&EJC 14,276 15,998 15,516 13,899 14,105 15,192 14,898 15,065

Other 8,438 13,549

Sub Total 443,154 446,447 460,881 485,894 511,304 523,648 533,642 499,964

Expenditure

Interest on Debentures & Loans 131,544 131,544 131,544 131,544 131,544 131,544 131,544 131,544

Other 14,485 14,586 15,134 15,729 15,029 15,786 15,702 19,138

Sub Total 146,029 146,130 146,678 147,273 146,573 147,330 147,246 150,682

Transfer to/(from) Reserve 3,000

Balance Available for Dividends 297,125 300,317 314,203 338,621 364,731 373,318 386,396 349,282

Preference Stocks 143,779 144,280 146,905 149,530 149,530 149,531 149,529 149,529

Consolidated Ordinary Stock 151,853 145,250 155,153 174,961 198,068 206,506 218,526 179,120

Sub Total 295,632 289,530 302,058 324,491 347,598 356,037 368,055 328,649

Balance C/Fwd 1,493 10,787 12,145 14,130 17,133 17,281 18,341 20,633

% on Consolidated Ordinary

Stock

2⅞%

2¾% 215/16% 35/16% 3¾% 3¾% 313/16% 3⅛%

Surplus Lands Dividend 69,324 69,324 69,324 69,324 72,626 70,975 72,626 70,975

% on Surplus Land Stock 2⅝% 2⅝% 2⅝% 2⅝% 2¾% 211/16% 2¾% 211/16%

43

Railway Estates revenue, which had reached £9k in 1892 rose gradually during the period to over

£11k in 1900. Revenue from the CL&EJC, which had nearly reached £16k in 1892, never exceeded

that level during the period and fell below £14k in 1896. In 1898-99 £22k in interest was credited in