A Comparative Longitudinal Analysis of Theoretical Perspectives of Interorganizational Relationship...

23

172 Journal of Marketing Vol. 71 (October 2007), 172–194 © 2007, American Marketing Association ISSN: 0022-2429 (print), 1547-7185 (electronic) Robert W. Palmatier, Rajiv P. Dant, & Dhruv Grewal A Comparative Longitudinal Analysis of Theoretical Perspectives of Interorganizational Relationship Performance Four theoretical perspectives currently dominate attempts to understand the drivers of successful interorganizational relationship performance: (1) commitment–trust, (2) dependence, (3) transaction cost economics, and (4) relational norms. Each perspective specifies a different set and distinct causal ordering of focal constructs as the most critical for understanding performance. Using four years of longitudinal data (N = 396), the authors compare the relative efficacy of these four perspectives for driving exchange performance and provide empirical insights into the causal ordering among key interorganizational constructs. The results demonstrate the parallel and equally important roles of commitment–trust and relationship-specific investments as immediate precursors to and key drivers of exchange performance. Building on the insights gleaned from tests of the four frameworks, the authors parsimoniously integrate these perspectives within a single model of interfirm relationship performance consistent with a resource-based view of an exchange. Managers may be able to increase performance by shifting resources from “relationship building” to specific investments targeted toward increasing the efficacy or effectiveness of the relationship itself to improve the relationship’s ability to create value. Moderation analysis indicates that managers may find it productive to allocate more relationship marketing efforts and investments to exchanges in markets with higher levels of uncertainty. Robert W. Palmatier is Evert McCabe Research Fellow and Assistant Pro- fessor of Marketing, Department of Marketing and International Business, University of Washington (e-mail: [email protected]). Rajiv P. Dant is Frank Harvey Distinguished Professor of Marketing, College of Business Administration, University of South Florida (e-mail: rdant@coba. usf.edu).Dhruv Grewal is Toyota Chair of Commerce and Electronic Busi- ness and Professor of Marketing, Babson College (e-mail: dgrewal@ babson.edu). The authors thank the Marketing Science Institute for its financial support of this research. They also thank the anonymous JM reviewers for their constructive comments. To read and contribute to reader and author dialogue on JM, visit http://www.marketingpower.com/jmblog. S uccessful interorganizational relationships are criti- cal to firms’ financial performance because most firms must leverage other organizations’ capabilities and resources to compete effectively. Not only do strong interfirm relationships directly enhance sales and profits (Palmatier et al. 2006), but because of higher levels of cooperation and reduced conflict, they can also improve innovation, expand markets, and reduce costs (Cannon and Homburg 2001; Rindfleisch and Moorman 2001). Mar- keters’ and researchers’ efforts to uncover the drivers of interorganizational relationship performance are well placed because managers can develop strategies to leverage these causal drivers only by understanding the precursors of performance. Thus, a key question is, What are the key dri- vers of interorganizational relationship performance? To investigate this question, researchers usually employ one or more of four theoretical perspectives: (1) commitment– trust, (2) dependence, (3) transaction cost economics, and (4) relational norms (Heide and John 1990; Hibbard, Kumar, and Stern 2001; Morgan and Hunt 1994; Siguaw, Simpson, and Baker 1998). Each of these perspectives suggests different key drivers of exchange performance. For example, Morgan and Hunt (1994, p. 22) propose that commitment and trust, “not power” or dependence, are “key” to promoting “efficiency, productivity, and effectiveness” in interorganizational exchanges; other researchers suggest that the exchange dependence structure determines performance (Bucklin and Sengupta 1993; Hibbard, Kumar, and Stern 2001); and still another school of thought argues for consideration of the direct effect of relational norms (Lusch and Brown 1996; Siguaw, Simpson, and Baker 1998). The perspective based on transaction cost economics (Williamson 1975) proposes that the level of transaction-specific investments and the need to manage opportunism influence governance struc- tures and ultimate exchange performance (Heide and John 1990; Parkhe 1993; Wathne and Heide 2000). Each of these perspectives has received empirical support when tested separately, but the only way to evaluate their relative impact on performance is to compare the effects of each perspec- tive’s focal constructs across a common context (Hunt 2002). Therefore, a comparative analysis of the theoretical perspectives of interorganizational relationship performance is the primary focus of this research. In addition to comparing the relative effects of key per- formance drivers, we address a second important question: How are key performance drivers causally related? Although each perspective promotes different performance

-

Upload

washington -

Category

Documents

-

view

1 -

download

0

Transcript of A Comparative Longitudinal Analysis of Theoretical Perspectives of Interorganizational Relationship...

172Journal of MarketingVol. 71 (October 2007), 172–194

© 2007, American Marketing AssociationISSN: 0022-2429 (print), 1547-7185 (electronic)

Robert W. Palmatier, Rajiv P. Dant, & Dhruv Grewal

A Comparative Longitudinal Analysisof Theoretical Perspectives of

Interorganizational RelationshipPerformance

Four theoretical perspectives currently dominate attempts to understand the drivers of successfulinterorganizational relationship performance: (1) commitment–trust, (2) dependence, (3) transaction costeconomics, and (4) relational norms. Each perspective specifies a different set and distinct causal ordering of focalconstructs as the most critical for understanding performance. Using four years of longitudinal data (N = 396), theauthors compare the relative efficacy of these four perspectives for driving exchange performance and provideempirical insights into the causal ordering among key interorganizational constructs. The results demonstrate theparallel and equally important roles of commitment–trust and relationship-specific investments as immediateprecursors to and key drivers of exchange performance. Building on the insights gleaned from tests of the fourframeworks, the authors parsimoniously integrate these perspectives within a single model of interfirm relationshipperformance consistent with a resource-based view of an exchange. Managers may be able to increaseperformance by shifting resources from “relationship building” to specific investments targeted toward increasingthe efficacy or effectiveness of the relationship itself to improve the relationship’s ability to create value. Moderationanalysis indicates that managers may find it productive to allocate more relationship marketing efforts andinvestments to exchanges in markets with higher levels of uncertainty.

Robert W. Palmatier is Evert McCabe Research Fellow and Assistant Pro-fessor of Marketing, Department of Marketing and International Business,University of Washington (e-mail: [email protected]). Rajiv P.Dant is Frank Harvey Distinguished Professor of Marketing, College ofBusiness Administration, University of South Florida (e-mail: [email protected]). Dhruv Grewal is Toyota Chair of Commerce and Electronic Busi-ness and Professor of Marketing, Babson College (e-mail: [email protected]). The authors thank the Marketing Science Institute for itsfinancial support of this research. They also thank the anonymous JMreviewers for their constructive comments.

To read and contribute to reader and author dialogue on JM, visithttp://www.marketingpower.com/jmblog.

Successful interorganizational relationships are criti-cal to firms’ financial performance because mostfirms must leverage other organizations’ capabilities

and resources to compete effectively. Not only do stronginterfirm relationships directly enhance sales and profits(Palmatier et al. 2006), but because of higher levels ofcooperation and reduced conflict, they can also improveinnovation, expand markets, and reduce costs (Cannon andHomburg 2001; Rindfleisch and Moorman 2001). Mar-keters’ and researchers’ efforts to uncover the drivers ofinterorganizational relationship performance are wellplaced because managers can develop strategies to leveragethese causal drivers only by understanding the precursors ofperformance. Thus, a key question is, What are the key dri-vers of interorganizational relationship performance? Toinvestigate this question, researchers usually employ one ormore of four theoretical perspectives: (1) commitment–

trust, (2) dependence, (3) transaction cost economics, and(4) relational norms (Heide and John 1990; Hibbard,Kumar, and Stern 2001; Morgan and Hunt 1994; Siguaw,Simpson, and Baker 1998).

Each of these perspectives suggests different key driversof exchange performance. For example, Morgan and Hunt(1994, p. 22) propose that commitment and trust, “notpower” or dependence, are “key” to promoting “efficiency,productivity, and effectiveness” in interorganizationalexchanges; other researchers suggest that the exchangedependence structure determines performance (Bucklin andSengupta 1993; Hibbard, Kumar, and Stern 2001); and stillanother school of thought argues for consideration of thedirect effect of relational norms (Lusch and Brown 1996;Siguaw, Simpson, and Baker 1998). The perspective basedon transaction cost economics (Williamson 1975) proposesthat the level of transaction-specific investments and theneed to manage opportunism influence governance struc-tures and ultimate exchange performance (Heide and John1990; Parkhe 1993; Wathne and Heide 2000). Each of theseperspectives has received empirical support when testedseparately, but the only way to evaluate their relative impacton performance is to compare the effects of each perspec-tive’s focal constructs across a common context (Hunt2002). Therefore, a comparative analysis of the theoreticalperspectives of interorganizational relationship performanceis the primary focus of this research.

In addition to comparing the relative effects of key per-formance drivers, we address a second important question:How are key performance drivers causally related?Although each perspective promotes different performance

Interorganizational Relationship Performance / 173

drivers, interorganizational researchers often take a prag-matic approach and combine theoretical paradigms toexplain performance (Ganesan 1994; Siguaw, Simpson, andBaker 1998). Thus, many studies include similar constructsbut use different causal ordering, depending on the perspec-tives. For example, some researchers suggest thattransaction-specific investments affect performance directly(Heide and John 1990; Parkhe 1993), whereas others arguethat commitment (Anderson and Weitz 1992) or depen-dence (Ganesan 1994) mediates the effect. Moreover, anoverwhelming majority of studies use cross-sectional dataand therefore provide little empirical insight to help resolvenomological differences.

Alternatively, the effect of relational drivers maydepend on external conditions; environmental uncertainty isthe most critical contextual factor (Heide and John 1990;Noordewier, John, and Nevin 1990). This potential contex-tual contingency suggests still another important researchquestion: When does each focal construct have the greatestimpact on exchange performance? We investigate this issueby testing the moderating effect of two types of uncertainty(environmental dynamism and market diversity) on the rela-tionship between focal constructs and performance out-comes across the four theoretical frameworks.

On the basis of the empirical findings, we develop andtest a post hoc framework that integrates the four differentperspectives into a single model of interorganizational rela-tionship performance. The final model is consistent with aresource-based view (RBV) of the exchange and provides aparsimonious theoretical basis for our findings (Dyer 1996;Wernerfelt 1984). Applying RBV theory to an interfirmrelationship parallels strategy research’s focus on firm per-formance (Conner 1991, p. 121) in the sense that the“[RBV] may form the kernel of a unifying paradigm.”

Therefore, our contribution focuses on four researchquestions aimed at enhancing the understanding of interfirmrelationship performance (both financial and relational) byevaluating evidence from 396 interorganizational exchangedyads across four consecutive years. Specifically, we inves-tigate what drives relationship performance, how the driversare causally ordered, when each driver has the greatestimpact, and whether these different drivers can be parsimo-niously integrated into a single, unifying theoretical frame-work. Managers can develop and effectively implementperformance-enhancing strategies only when they under-stand the what, how, and when of the drivers of relationshipperformance. In addition to comparing and synthesizingtheoretical perspectives, we provide a platform for guidingfuture research efforts on interfirm relationships.

Theoretical Perspectives ofInterorganizational Relationship

PerformanceVarious theoretical perspectives from a wide range of disci-plines have been applied to understand interfirm relation-ship performance. Using research from social psychology,sociology, and anthropology, social exchange theory pro-vides a foundation for two prevalent marketing perspectives(Blau 1964; Cook and Emerson 1978). The first, the

commitment–trust perspective (Morgan and Hunt 1994),argues that a party’s commitment to and trust in itsexchange partner determines relationship performance. Thesecond perspective suggests that the dependence or powerstructure among exchange partners drives exchange perfor-mance and the level of interorganizational conflict (Gund-lach and Cadotte 1994; Hibbard, Kumar, and Stern 2001).

Building on early work in social psychology (Thibautand Kelley 1959) and integrating contract law (Macneil1980), researchers have also investigated the importance ofrelational norms (Heide and John 1992; Siguaw, Simpson,and Baker 1998). This perspective suggests that the strengthof relational norms in an exchange affects the level of coop-erative behavior and relationship performance (Cannon,Achrol, and Gundlach 2000).

With its roots in economics (Williamson 1975), trans-action cost economics argues that transaction-specificinvestments and opportunism influence exchange parties’relationship decisions and affect interorganizational perfor-mance (Heide and John 1990; Noordewier, John, and Nevin1990). Although social network theory, game theory, thepolitical economy perspective, the knowledge-based viewof the firm, and analytical modeling represent other theo-retical paradigms used to investigate interorganizationalrelationships, we do not compare these perspectives,because extant marketing research based on them is rela-tively limited (Anderson and Coughlan 2002; Johnson,Sohi, and Grewal 2004; Selnes and Sallis 2003).

Rather, extant interorganizational marketing literaturepredominantly uses (1) commitment–trust, (2) dependence,(3) transaction cost economics, and/or (4) relational normsperspectives to understand interfirm relationship perfor-mance (for a summary, see Table 1). We compare the keydrivers of performance suggested by each framework bydeveloping parallel conceptual models in which the focalperformance drivers serve as immediate precursors ofexchange outcomes. Each theoretical approach defines thefocal or organizing constructs included in its model, buttheir antecedents vary widely across studies and ofteninclude constructs from other perspectives. To mirror theliterature, aid in model comparison, and provide empiricalinsight into the actual causal ordering among constructs, weinclude the same constructs in each model but base thecausal ordering and measurement period on the specificperspective.

More specifically, we measure constructs across foursequential years according to where each construct falls inthe antecedents → mediators → outcomes framework for aspecific perspective. For example, we measure dependencein the commitment–trust model during the first yearbecause that framework models it as an antecedent (Morganand Hunt 1994); in the dependence model, we measure it inthe second year because that perspective considers depen-dence a mediator. In each framework, we measure the con-structs modeled as antecedents in Year 1, mediators in Year2, and outcomes in Years 3 and 4.

Financial metrics provide a universal measure by whichto evaluate different perspectives, whereas other relation-ship performance measures may be linked more closely to aspecific perspective. To provide a “fair” comparison and

174 / Journal of Marketing, October 2007

Theoretical Perspectives

Key PerformanceDrivers

(Focal Constructs)

Commitment–Trust PerspectiveMorgan and Hunt’s (1994, p. 22) classic article builds on social exchange theory (Blau 1964;

Cook and Emerson 1978) and proposes that commitment and trust, not power or depen-dence, are the key focal constructs for understanding interorganizational relationship perfor-mance. Consistent with their relationship marketing focus, they argue that commitment isthe critical precursor to improving financial performance, and commitment and trust areboth important for building strong relationships. These constructs, individually or together,positively influence performance and relational behaviors because customers act positivelytoward and in the best interest of committed, trusted sellers.

Commitment and trust

Dependence PerspectiveBuilding on social exchange theory, marketing researchers (e.g., Bucklin and Sengupta 1993;

Hibbard, Kumar, and Stern 2001) argue that the exchange’s dependence structure is crucialfor understanding interorganizational relationship performance because it determines eachpartner’s ability to influence the other. Many different approaches attempt to capture anexchange’s dependence structure, but partners’ interdependence usually affects perfor-mance positively because partners work to maintain their relationship and avoid destructiveactions, whereas dependence asymmetry undermines the relationship through fewer struc-tural barriers to the use of coercive power.

Interdependence anddependence asymmetry

Transaction Cost Economics PerspectiveTransaction cost analysis, the successor to traditional neoclassical economics (Williamson

1975), can predict interorganizational exchange governance and performance (Heide andJohn 1990; Noordewier, John, and Nevin 1990; Parkhe 1993). Exchanges occur in free mar-kets without relational encumbrances or associated costs (Rindfleisch and Heide 1997),except when specific governance problems exist (e.g., safeguarding specific investmentsfrom opportunism, managing uncertainty). Thus, it suggests that the governance structureand ultimate performance of an exchange are influenced by the level of the exchange part-ners’ specific investments and opportunistic behaviors.

Relationship- (transac-tion-) specific invest-

ments and opportunisticbehaviors

Relational Norms PerspectiveTraceable to Macneil (1980), the relational exchange theory (Kaufmann and Dant 1992)

focuses on contracting norms or shared expectations regarding transactional behavior,ranging from one-time discrete to ongoing relational exchanges. The latter category involvesheightened perceptions of relational norms, which contribute to exchange partners’ strategicability to develop long-term, committed, trusting, value-creating associations that are difficultand costly to imitate. On the basis of this logic, researchers propose that strong relationalnorms positively affect exchange performance (Cannon, Achrol, and Gundlach 2000; Luschand Brown 1996; Siguaw, Simpson, and Baker 1998).

Relational norms (soli-darity, mutuality, and

flexibility)

RBV PerspectiveThe RBV of the firm counters industry structure as the focal unit of analysis for understanding

firm performance; firms that have resources and capabilities that are rare, valuable, and dif-ficult to duplicate or substitute earn superior competitive advantage and performance(Wernerfelt 1984). On the basis of a literature review, Conner (1991) cites the RBV as apotential unifying paradigm, and Dyer (1996) and Jap (1999) extend this framework to inter-firm relationships. The RBV of an interorganizational exchange integrates focal constructsfrom other perspectives by proposing that superior performance occurs when relationshippartners invest time, resources (assets), knowledge, and capabilities into a relationship andthat they build an effective governance structure (Dyer and Singh 1998).

Idiosyncratic assets,resources, and capabili-ties (e.g., relationship-specific investments)and relational gover-

nance mechanism (e.g.,commitment, trust)

TABLE 1Summary of Theoretical Perspectives of Interorganizational Relationship Performance

identify any specific “strengths” among the different per-spectives, we apply both financial and relational outcomemeasures. For financial performance, we consider objectivesales growth measured over two years and overall financialperformance, a composite perceptual measure of sales andprofit growth, and overall profitability. These financial mea-sures focus on the performance of the business-to-businessexchange relationship (e.g., sales of a supplier’s product by

a downstream partner) and do not reflect either partner’soverall performance.

To indicate relationship performance, we use coopera-tion, or the coordinated and complementary actionsbetween exchange partners to achieve mutual goals, andconflict, or the overall level of disagreement and ill willbetween exchange partners (Jap and Ganesan 2000). There-fore, all our conceptual models contain an identical set of

Interorganizational Relationship Performance / 175

outcome measures, as we summarize in Figure 1. Next, weprovide an overview of each theoretical perspective toestablish the nomological net and causal ordering amongthe key constructs driving exchange performance in eachframework.

Commitment–Trust Perspective

The commitment–trust perspective argues that a customer’strust in and/or commitment to a seller is the prime determi-nant of exchange performance (Morgan and Hunt 1994).Commitment is “an enduring desire to maintain a valuedrelationship” (Moorman, Zaltman, and Deshpandé 1992, p.316), and trust is “confidence in an exchange partner’s reli-ability and integrity” that directly and indirectly throughcommitment affects exchange outcomes (Morgan and Hunt1994, p. 23). These constructs, individually or together,positively influence performance and relational behaviorsbecause customers are more likely to act positively towardand in the best interest of committed, trusted sellers (Ander-son and Weitz 1992; Hibbard et al. 2001).

Relationship-specific investments (RSIs) are anexchange partner’s idiosyncratic investments that are spe-cialized to a relationship and not easily recoverable (Gane-san 1994). Customer RSIs positively affect customer com-mitment to a seller (Gilliland and Bello 2002) through theirpositive impact on switching costs, which makes the rela-tionship more important to the customer and increases thecustomer’s desire to maintain the relationship (Andersonand Weitz 1992). Although empirical support is limited,customer RSIs may influence customers’ trust in the sellernegatively because they increase concerns about vulnerabil-ity to unilateral seller actions (Gassenheimer and Manolis2001). The positive effect of seller RSIs on trust depends onthe signal sent to the customer because it can offer “tangibleevidence” that the seller can be “believed” and “cares”about the relationship (Ganesan 1994, p. 5). Seller oppor-tunistic behavior, which has been defined as seeking to sup-port self-interests with guile (Williamson 1975), negativelyinfluences customers’ trust in the seller because it leads cus-tomers to suspect the seller’s benevolence.

Dependence refers to the need to maintain a relationshipto achieve goals; researchers show that both inter-dependence, or the mutual dependence of both partners, anddependence asymmetry, or the imbalance between partners’dependence, are critical to understanding the impact ofdependence in an exchange (Jap and Ganesan 2000).Kumar, Scheer, and Steenkamp (1995) indicate that inter-dependence positively affects commitment and trustthrough a reduction in relationship problems and conver-gence of interests, whereas dependence asymmetry under-mines commitment and trust as partners’ interests divergeand the structural barriers to the coercive use of power fall.

Relational norms have been investigated as both uniquenorms and a composite construct. The most commonlyinvestigated norms are solidarity, or partners’ belief in theimportance of the relationship; mutuality, or the belief thatsuccess is a function of the partner’s success and that part-ners should share benefits and costs; and flexibility, or thewillingness of exchange partners to adapt to new conditions(Cannon, Achrol, and Gundlach 2000; Lusch and Brown

1996). Some researchers argue that specific norms affect aspecific aspect of a relationship (e.g., solidarity → commit-ment, mutuality → trust), but most research employs a com-posite index of norms that positively affect relational bonds(Siguaw, Simpson, and Baker 1998). Finally, communica-tion refers to the amount, frequency, and quality of informa-tion shared between exchange partners and positivelyaffects customers’ trust in and commitment to a seller(Mohr, Fisher, and Nevin 1996).

Dependence Perspective

Dependence has been widely studied as a critical determi-nant of interfirm relationship performance in terms of finan-cial outcomes, cooperation, and conflict, especially in thechannel context (Bucklin and Sengupta 1993; Kumar,Scheer, and Steenkamp 1995). Many aspects of anexchange’s dependence structure appear in the literature,but most research accepts the premise that interdependencepositively affects exchange performance because depen-dence increases both the partners’ desire to maintain therelationship and the level of adaptation they undertake(Hallen, Johanson, and Seyed-Mohamed 1991; Hibbard,Kumar, and Stern 2001). Moreover, dependence asymmetrynegatively influences performance by fostering the coerciveuse of power and reducing willingness to compromise(Gundlach and Cadotte 1994).

As customers invest time and effort to build relationalgovernance structures, they become more dependent ontheir partner because duplicating relational bonds with anew partner would involve additional investments. Thus,commitment and trust in a partner increase interdependence(El-Ansary 1975). As partners commit RSIs, they growmore dependent, and switching threats are less credible(Ganesan 1994; Kim and Frazier 1997). Thus, RSIs shouldaffect interdependence positively. Furthermore, potentialpartners may engage in opportunism, so to find a partner,firms must expend effort and search costs, which increasesdependence on “safe” partners.

Building strong relational norms takes time and effortfrom both exchange partners. Because they are not easilyreplaced, strong relational norms should represent valuable,difficult-to-duplicate assets for both partners and shouldresult in higher interdependence levels. Interdependenceshould also increase as the level of communicationincreases because information typically provides value toeach party and is difficult to replace (Frazier 1983; Mohrand Nevin 1990). Few antecedents of dependence asymme-try appear in the literature, but because RSIs increase a part-ner’s dependence, all else being equal, RSIs by one partnershould increase its relative dependence, leading to a powerimbalance (Kim and Frazier 1997).

Transaction Cost Economics Perspective

The transaction cost perspective (Williamson 1975), whichfocuses on the twin focal constructs of specific investmentsand opportunism to predict governance and exchange per-formance, has received consistent research attention (Heideand John 1990; Wathne and Heide 2000). Empirical studies(Rindfleisch and Heide 1997) have supported the normativeclaim of transaction cost analysis that firms should verti-

176 / Journal of Marketing, October 2007

FIGURE 1Four Theoretical Perspectives of Interorganizational Relationship Performance

Notes: We measured all antecedents in Year 1, mediators in Year 2, and outcomes in Year 3, except for sales growth, which includes Years 3and 4. We modeled exchange age as an antecedent of all mediators and exchange outcomes.

Interorganizational Relationship Performance / 177

cally integrate when confronted with investments in idio-syncratic assets or suspicions of opportunistic behaviors bythe exchange partner. In this sense, RSIs by an exchangepartner simultaneously signal its intent and generate theneed to safeguard investments. Because RSIs representsunk, unredeployable assets in an exchange relationship,parties’ RSIs reduce their motivation to behave opportunis-tically and the credibility of switching threats, which in turnminimizes the partner’s need (and costs) to monitor perfor-mance or safeguard assets. With fewer opportunism con-cerns and lower monitoring and safeguarding costs, theexchange becomes more efficient and more prone to jointaction and includes greater expectations of continuity, all ofwhich contribute to enhanced performance (Heide and John1990; Parkhe 1993; Smith and Barclay 1997). Thus, thetransaction cost perspective suggests that performance isenhanced as the governance structure matches the level ofrelationship uncertainty or ambiguity. Researchers agreethat opportunism has a negative impact on interfirm perfor-mance because it significantly increases the ex post costsassociated with monitoring performance and safeguardinginvestments (Gassenheimer, Davis, and Dahlstrom 1998;Heide and John 1990).

Strong relationships cause partners to discount the pos-sibility that their partner will appropriate their idiosyncraticinvestments, and relational bonds increase their willingnessto make RSIs. We expect that interdependence has a posi-tive effect on partners’ RSIs because they are less concernedthat the partner will appropriate them (Heide and John1988). Interdependence should also reduce partners’ ten-dency to behave opportunistically because they do not wantto jeopardize a difficult-to-replace relationship. Conversely,dependence asymmetry should reduce the exchange part-ner’s RSIs because of its concerns about coercive uses ofpower. Consistent with the literature (Parkhe 1993), sellerRSIs suppress sellers’ opportunist behaviors; sellers do notwant to forfeit or undermine their nonrecoverable invest-ments by engaging in relationship-damaging behaviors.

Research also suggests a positive influence of relationalnorms on RSIs, in that strong norms reduce concerns thateither exchange partner will appropriate idiosyncraticinvestments (Heide and John 1992; Noordewier, John, andNevin 1990). Moreover, because relational norms embody apromise of fair play and a mutually beneficial, long-termrelationship, they provide pressure not to behave oppor-tunistically and support RSIs that often pay returns only inthe long run. Transaction cost analysis works on the pre-sumption of bounded rationality (i.e., managers are con-strained by limited cognitive capability and imperfect infor-mation) and thus posits that effective communicationreduces the uncertainties associated with governance-related decisions and concerns of opportunism whileincreasing RSIs (Rindfleisch and Heide 1997).

Relational Norms Perspective

The relational norms perspective, drawn from relationalexchange theory (Kaufmann and Dant 1992; Macneil1980), often appears in conjunction with the commitment–trust perspective to explain the positive influence of rela-tional marketing (Gundlach, Achrol, and Mentzer 1995; Jap

and Ganesan 2000; Siguaw, Simpson, and Baker 1998).Relational exchange theory rests on two key propositions.First, for contracts to function, a set of common contractingnorms must exist (Kaufmann and Dant 1992). Second, incontrast to classical legal theory, which assumes that alltransactions are discrete events, Macneil (1980) argues thattransactions are immersed in the relationships that surroundthem, which may be described in terms of the relationalnorms of the exchange partners. Relational norms positivelyaffect financial results and cooperative behaviors (Cannon,Achrol, and Gundlach 2000; Siguaw, Simpson, and Baker1998) and reduce the level of conflict (Jap and Ganesan2000). Exchanges characterized by high levels of relationalnorms enable exchange partners to respond more effectivelyto environmental contingencies, extend the time horizon forevaluating the outcomes of their relationships, and, ulti-mately, refrain from relationship-damaging behaviors(Kaufmann and Stern 1988). In other words, relationalismplays a significant role in structuring economically efficientexchange relationships under conditions of uncertainty andambiguity and therefore should lead to improved financialperformance (Heide and John 1992).

Commitment and trust promote the emergence of rela-tional norms by fostering behaviors that support bilateralstrategies to accomplish shared goals (Gundlach, Achrol,and Mentzer 1995). Similarly, RSIs positively affect rela-tional perceptions (Bello and Gilliland 1997); idiosyncraticinvestments signify the importance a partner attaches to thepartnership and have a positive impact on switching costs,which makes the relationship more important to theexchange partner and enhances its efforts to maintain it(Anderson and Weitz 1992).

Opportunistic behaviors have a negative impact on theemergence of relational sentiments (Gundlach, Achrol, andMentzer 1995) because perceiving a partner as opportunis-tic undermines extant relational norms and raises thespecter that the exchange partner is not concerned with thewell-being or fairness of the exchange. Interdependenceenhances relational sentiments, in that perceptions ofdependence indicate significant stakes in the relationshipand increase exchange partners’ interest in maintaining therelationship (Ganesan 1994; Lusch and Brown 1996). Con-versely, asymmetric dependence promotes the coercive useof power and undermines relational norms. Communica-tion’s effect on relational sentiments should be positivebecause “communication [is] the glue that holds together achannel of distribution” and helps create an atmosphere ofmutual support and participative decision making (Mohrand Nevin 1990, p. 36).

Moderating Role of Environmental Uncertainty

Interfirm relationships occur within an external environ-ment, so exogenous factors may moderate the effects of thefocal constructs on performance. To provide a more robustcomparison of the different frameworks, we evaluate con-textual effects across theoretical perspectives. Environmen-tal uncertainty, the most frequently studied exogenous fac-tor, plays a key role in interorganizational relationships; thefocal theories attempt to absorb or mitigate the effects ofuncertainty firms face in an exchange (Ganesan 1994;

178 / Journal of Marketing, October 2007

Heide 1994; Noordewier, John, and Nevin 1990). We inves-tigate the moderating role of two sources of uncertainty:environmental dynamism, or the frequency of changes inmarket forces, and market diversity, or the degree of hetero-geneity in the needs and preferences of end customers(Achrol and Stern 1988).

Social and relational exchange theories argue thatrelational-based exchanges outperform transactional-basedexchanges because of their ability to adapt to new condi-tions and to increase confidence in partners’ future actions,which support risk-taking and reciprocity-based behaviors(Cannon and Perreault 1999; Dahlstrom and Nygaard1995). As environmental uncertainty increases, exchangepartners need to adapt and require the enhanced flexibilityand behavioral confidence of relational-based exchanges. Inturn, higher levels of uncertainty should enhance the posi-tive effect of commitment, trust, interdependence, and rela-tional norms on exchange outcomes. Similarly, the abilityof relational bonds to limit conflict should be more impor-tant in turbulent environments because of the higher likeli-hood of disagreements and need for negotiated solutions.

Empirical research, though limited, supports thispremise. For example, Dahlstrom and Nygaard (1995) findpartial support for their argument that as uncertaintyincreases, more formality and rigid structures between part-ners reduce performance. In support of the benefits of flexi-ble, relational-based exchanges, Cannon, Achrol, andGundlach (2000) note that relational norms enhance perfor-mance in high-uncertainty conditions.

Transaction cost economics portrays environmentaluncertainty as debilitating for decision makers’ informationprocessing because of bounded rationality (Rindfleisch andHeide 1997). In an uncertain environment, there is anincreased likelihood that critical information brought to thepartnership can leverage RSIs’ impact on performance. In astable environment, RSIs cannot enhance performance aseffectively by arbitraging a partner’s asymmetric informa-tion because knowledge is homogeneously diffused (Dyer1996). Moreover, partners become valuable resources,increasing cooperation and reducing actions that may leadto conflict. Thus, increases in environmental uncertaintyshould enhance the positive effect of customers’ and sellers’RSIs on exchange outcomes but should reduce the effect onconflict as well as opportunism’s negative effect onexchange outcomes.

Joshi and Stump (1999) find empirical support for theirtransaction cost–based hypothesis that decision-makinguncertainty positively moderates the impact of specificinvestments on cooperation or joint action. Integrating bothrelational and transaction cost perspectives, Noordewier,John, and Nevin (1990) support their premise that relationalgovernance’s effect on performance depends on uncertainty.

Research Method

Sample and Data Collection Procedure

We draw the sample for this research from a longitudinalsurvey of business-to-business relationships between amajor Fortune 500 company (seller) and its local distributor

agents (customers). The business relationships cover vari-ous products, including clothing, hardware, furniture, andappliances, so our sample minimizes any specific product-category effects. The relationships also include diversebusiness functions, such as generating demand, inventory-ing products, selling to consumers, and handling returns.Thus, this setting captures a range of business activities andprovides an excellent context in which to test alternativetheoretical perspectives.

We gathered the data in three successive annual mailsurveys to the manager of each customer firm. The sam-pling frames for the three years were 1651, 1837, and 1965,and the corresponding completed questionnaires receivedwere 984, 1004, and 1089. Thus, the response rates are60%, 55%, and 55%; however, not every customerresponded to all three surveys. Therefore, we base ouranalysis on 396 cases in which the same respondents com-pleted the surveys in all three years, which represents a 24%response rate for the 1651 surveys mailed in Year 1.

We assess possible nonresponse bias in three ways.First, we conduct tests comparing early and late respon-dents for all three waves in terms of archival sales data,demographic information, and study constructs. The resultsindicate that early versus late respondents constitute thesame population (p > .05). Second, we compare the retainedsample of 396 with respondents excluded from the analysisbecause of their failure to complete surveys in all threeyears—588 in the first year, 608 in the second, and 693 inthe third—across the study constructs using a series of mul-tivariate analyses of variance and univariate analyses. Theseresults are not significant (p > .05). Third, we compare therespondent pools in each year with the total samplingframes (e.g., 984 compared with 1651 in Year 1). Again, wefind no significant differences (p > .05). The relatively highresponse rates and the results of these three tests suggestthat nonresponse bias is not a concern.

Measures

We base our reflective measures on extant literature that hasundergone prior psychometric scrutiny and adapt them to fitthe context of our investigation. In all three years, we useidentical measurement items; in the Appendix, we presentthe full battery of scales employed, item loadings, and prin-cipal literature sources.

For the measures of financial outcomes, we use a per-ceptual format reported by customers and average salesgrowth for Years 2–4 that the seller provided for each cus-tomer. Consistent with the literature (e.g., Cannon, Achrol,and Gundlach 2000; Gundlach, Achrol, and Mentzer 1995),we conceptualize relational norms as a composite constructusing three items generated by averaging the items used tomeasure each of three specific norms (solidarity, mutuality,and flexibility). We verify the reliability of the scales foreach norm and then average them to form the relationalnorm indicators in the measurement and structural models.

Following Jap and Ganesan (2000), we operationalizeinterdependence as the product of the customer’s depen-dence on the seller and its perception of the seller’s depen-dence on it, whereas dependence asymmetry is the seller’sdependence less the customer’s dependence. Note that other

Interorganizational Relationship Performance / 179

operationalizations of dependence structure can be found inthe literature (e.g., Ganesan 1994; Kumar, Scheer, andSteenkamp 1995). Exchange age, a control variable, servesas an antecedent for all mediators and outcomes.

Measurement Models

We estimate separate confirmatory measurement models forall latent constructs captured in each of the three data col-lection efforts (Years 1, 2, and 3). Thus, the first measure-ment model pertains to data collected in Year 1, includingall antecedent and mediator constructs; the second dupli-cates this approach with Year 2 data; and the third modelincludes the three customer-reported latent outcome con-structs measured during Year 3. Each item’s loading isrestricted to its a priori construct, and each construct is cor-related with all other constructs. The measurement fitindexes for the first, second, and third models are as fol-lows: Year 1: χ2

(395) = 656.8, p < .01; comparative fit index(CFI) = .96; Tucker–Lewis index (TLI) = .95; and rootmean square error of approximation (RSMEA) = .04; Year2: χ2

(395) = 695.6, p < .01; CFI = .96; TLI = .95; andRSMEA = .04; Year 3: χ2

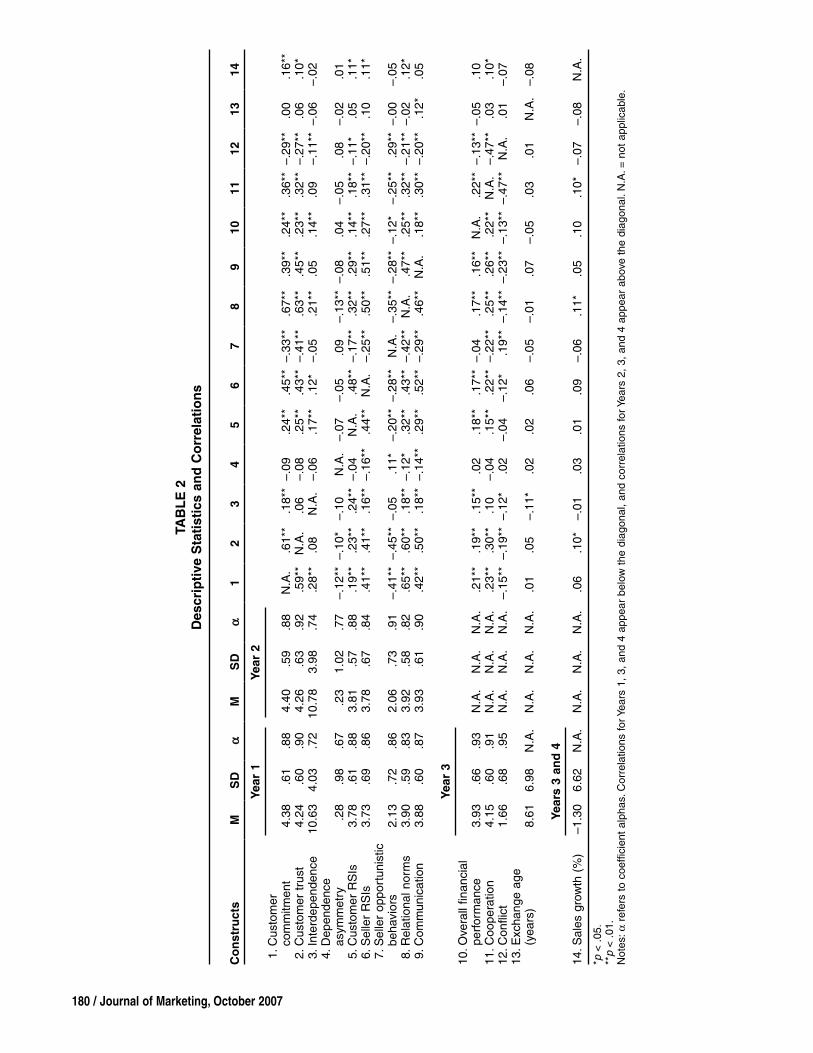

(24) = 34.5, p < .01; CFI = .99;TLI = .99; and RSMEA = .03. Thus, the fit indexes for allthree models are acceptable. All factor loadings are signifi-cant and in the predicted direction (p < .001), in support ofconvergent validity. Finally, all latent constructs’ compositereliabilities are .67 or greater, indicating internal reliability.We provide the descriptive statistics and correlations for allmeasures in Table 2.

We confirm discriminant validity by comparing twonested models for each pair of latent constructs for eachmeasurement year in which we either allow the correlationbetween two constructs to be free or restrict the correlationto 1. Discriminant validity is supported; the chi-square sta-tistic is significantly lower (p < .05) in the unconstrainedmodel than in the constrained model for all constructs. Wefind additional support for discriminant validity by verify-ing that the average variance extracted by each latent con-struct is greater than its shared variance (intercorrelation2)with other constructs. On the basis of these tests, we con-clude that our measures are valid and reliable.

Analysis and ResultsWe test our conceptual models using structural path model-ing with maximum likelihood criteria. We evaluate the maineffects among key interfirm constructs according to thenomological framework suggested by each theoretical per-spective (Figure 1) and perform mediation tests for thedirect effect of each antecedent on each outcome variable.These tests provide key insights into the causal orderingamong constructs and the primary drivers of performance.We report the results of proposed main effects in Table 3.On the basis of the results across these four models, we pro-pose and test a fifth post hoc integrative model. The fitindexes across the five structural models are relatively sta-ble, ranging from χ2

(762 to 766) = 1144.8 to 1209.3, p < .01;CFI = .96 (all models); TLI = .95–.96; and RSMEA = .04(all models), all of which indicate acceptable fit.

1Chi-square difference test statistics are available for all media-tion tests on request.

Results: Commitment–Trust Perspective

As we show in Table 3, building customer trust (β = .53, p <.01), increasing interdependence (β = .12, p < .01), andbuilding stronger dyadic relational norms (β = .27, p < .01)lead to higher levels of customer commitment. CustomerRSIs, dependence asymmetry, and communication are notsignificantly related to commitment. Customers trust sellersthat make RSIs (β = .21, p < .01) and those involved inexchanges with high levels of relational norms (β = .23, p <.01) and communication (β = .22, p < .01). The premise thatcustomers that make RSIs are concerned that they will beheld hostage by these investments is supported by theirlower levels of trust in the seller (β = –.10, p < .05). As weexpected, seller opportunistic behaviors (β = –.13, p < .05)undermine customers’ trust in the seller. However, neitherinterdependence nor dependence asymmetry has a signifi-cant influence on customer trust.

Commitment has a strong effect on all four outcomes:sales growth (β = .18, p < .01), overall financial perfor-mance (β = .18, p < .01), cooperation (β = .30, p < .01), andconflict (β = –.21, p < .01). Similarly, trust has a directimpact, in addition to its indirect impact, on cooperation(β = .14, p < .05) and conflict (β = –.14, p < .05), but itsdirect impact on sales growth and overall financial perfor-mance is not significant. The exchange age control variablehas a negative effect on sales growth (β = –.08, p < .05),indicating that new partners grow faster than long-termpartners.

To understand whether the effect of the antecedents onoutcomes is fully mediated by each perspective’s focal con-structs and to generate insight into the causal orderingamong the constructs, we perform a series of mediationtests for each antecedent on each outcome by comparingtwo nested models: the proposed full mediation model anda partial mediation model with an additional path from anantecedent to an outcome. If the new model provides signif-icantly better fit, the antecedent’s effect on the outcome isnot fully mediated by the proposed focal constructs.1 Ourtests demonstrate that only customer and seller RSIs are notfully mediated by commitment and trust. Moreover, wecompare mediation results across the four theoretical mod-els and derive key insights into causal ordering. For exam-ple, neither trust’s nor commitment’s effect on outcomes isfully mediated when they serve as antecedents in othermodels. This finding provides additional support for therole of commitment and trust in driving performance. Thatis, commitment and trust mediate all constructs except forRSIs, and no other perspective mediates their effect on out-comes; therefore, commitment and trust are immediate pre-cursors to exchange performance.

Results: Dependence Perspective

As customers’ commitment (β = .20, p < .05) increases, asthey make more RSIs (β = .15, p < .05), and as they havehigher levels of relational norms (β = .18, p < .05), the levelof interdependence increases. Contrary to our expectations,

180 / Journal of Marketing, October 2007

Co

nst

ruct

sM

SD

ααM

SD

αα1

23

45

67

89

1011

1213

14

Year

1Ye

ar 2

1.C

usto

mer

co

mm

itmen

t4.

38.6

1.8

84.

40.5

9.8

8N

.A.

.61*

*.1

8**

–.09

**.2

4**

.45*

*–.

33**

.67*

*.3

9**

.24*

*.3

6**

–.29

**.0

0**

.16*

*2.

Cus

tom

er t

rust

4.24

.60

.90

4.26

.63

.92

.59*

*N

.A.

.06*

*–.

08**

.25*

*.4

3**

–.41

**.6

3**

.45*

*.2

3**

.32*

*–.

27**

.06*

*.1

0**

3.In

terd

epen

denc

e10

.63

4.03

.72

10.7

83.

98.7

4.2

8**

.08*

*N

.A.

–.06

**.1

7**

.12*

*–.

05**

.21*

*.0

5**

.14*

*.0

9**

–.11

**–.

06**

–.02

**4.

Dep

ende

nce

asym

met

ry.2

8.9

8.6

7.2

31.

02.7

7–.

12**

–.10

**–.

10**

N.A

.–.

07**

–.05

**.0

9**

–.13

**–.

08**

.04*

*–.

05**

.08*

*–.

02**

.01*

*5.

Cus

tom

er R

SIs

3.78

.61

.88

3.81

.57

.88

.19*

*.2

3**

.24*

*–.

04**

N.A

.–.

48**

–.17

**.3

2**

.29*

*.1

4**

.18*

*–.

11**

.05*

*.1

1**

6.S

elle

r R

SIs

3.73

.69

.86

3.78

.67

.84

.41*

*.4

1**

.16*

*–.

16**

.44*

*N

.A.

–.25

**.5

0**

.51*

*.2

7**

.31*

*–.

20**

.10*

*.1

1**

7.S

elle

r op

port

unis

tic

beha

vior

s2.

13.7

2.8

62.

06.7

3 .9

1–.

41**

–.45

**–.

05**

.11*

*–.

20**

–.28

**N

.A.

–.35

**–.

28**

–.12

**–.

25**

0.29

**–.

00**

–.05

**8.

Rel

atio

nal n

orm

s3.

90.5

9.8

33.

92.5

8.8

2.6

5**

.60*

*.1

8**

–.12

**.3

2**

.43*

*–.

42**

N.A

..4

7**

.25*

*.3

2**

–.21

**–.

02**

.12*

*9.

Com

mun

icat

ion

3.88

.60

.87

3.93

.61

.90

.42*

*.5

0**

.18*

*–.

14**

.29*

*.5

2**

–.29

**.4

6**

N.A

..1

8**

.30*

*–.

20**

.12*

*.0

5**

Year

310

.Ove

rall

finan

cial

pe

rfor

man

ce3.

93.6

6.9

3N

.A.

N.A

.N

.A.

.21*

*.1

9**

.15*

*.0

2**

.18*

*.1

7**

–.04

**.1

7**

.16*

*N

.A.

.22*

*–.

13**

–.05

**.1

0**

11.C

oope

ratio

n4.

15.6

0.9

1N

.A.

N.A

.N

.A.

.23*

*.3

0**

.10*

*–.

04**

.15*

*.2

2**

–.22

**.2

5**

.26*

*.2

2**

N.A

.–.

47**

.03*

*.1

0**

12.C

onfli

ct1.

66.6

8.9

5N

.A.

N.A

.N

.A.

–.15

**–.

19**

–.12

**.0

2**

–.04

**–.

12**

.19*

*–.

14**

–.23

**–.

13**

–.47

**N

.A.

.01*

*–.

07**

13.E

xcha

nge

age

(yea

rs)

8.61

6.98

N.A

.N

.A.

N.A

.N

.A.

.01*

*.0

5**

–.11

**.0

2**

.02*

*.0

6**

–.05

**–.

01**

.07*

*–.

05**

.03*

*.0

1**

N.A

.–.

08**

Year

s 3

and

4

14.S

ales

gro

wth

(%

)–1

.30

6.62

N.A

.N

.A.

N.A

.N

.A.

.06*

*.1

0**

–.01

**.0

3**

.01*

*.0

9**

–.06

**.1

1**

.05*

*.1

0**

.10*

*–.

07**

–.08

**N

.A.

TAB

LE

2D

escr

ipti

ve S

tati

stic

s an

d C

orr

elat

ion

s

*p<

.05

.**

p<

.01

.N

otes

:αre

fers

to

coef

ficie

nt a

lpha

s.C

orre

latio

ns fo

r Yea

rs 1

, 3,

and

4 a

ppea

r be

low

the

dia

gona

l, an

d co

rrel

atio

ns fo

r Yea

rs 2

, 3,

and

4 a

ppea

r ab

ove

the

diag

onal

.N.A

.= n

ot a

pplic

able

.

Interorganizational Relationship Performance / 181

TAB

LE

3R

esu

lts:

Mai

n E

ffec

ts

An

tece

den

ts →

Med

iato

rsββ

t-V

alu

eM

edia

tors

→O

utc

om

esββ

t-V

alu

e

Co

mm

itm

ent–

Tru

st P

ersp

ecti

veC

usto

mer

tru

st →

cust

omer

com

mitm

ent

.53

9.85

**C

usto

mer

com

mitm

ent

→sa

les

grow

th.1

82.

38**

Cus

tom

er R

SIs

→cu

stom

er c

omm

itmen

t–.

07–1

.54

Cus

tom

er c

omm

itmen

t →

over

all f

inan

cial

per

form

ance

.18

2.33

**In

terd

epen

denc

e →

cust

omer

com

mitm

ent

.12

2.40

**C

usto

mer

com

mitm

ent

→co

oper

atio

n.3

03.

94**

Dep

ende

nce

asym

met

ry →

cust

omer

com

mitm

ent

.02

.31

Cus

tom

er c

omm

itmen

t →

conf

lict

–.21

–2.8

0**

Rel

atio

nal n

orm

s →

cust

omer

com

mitm

ent

.27

4.67

**C

omm

unic

atio

n →

cust

omer

com

mitm

ent

.04

.65

Cus

tom

er t

rust

→sa

les

grow

th–.

01–.

16C

usto

mer

RS

Is →

cust

omer

tru

st–.

10–1

.74*

Cus

tom

er t

rust

→ov

eral

l fin

anci

al p

erfo

rman

ce.1

21.

61S

elle

r R

SIs

→cu

stom

er t

rust

.21

2.82

**C

usto

mer

tru

st →

coop

erat

ion

.14

1.90

*S

elle

r op

port

unis

tic b

ehav

iors

→cu

stom

er t

rust

–.13

–2.3

0*C

usto

mer

tru

st →

conf

lict

–.14

–1.8

7*In

terd

epen

denc

e →

cust

omer

tru

st.0

2.2

8D

epen

denc

e as

ymm

etry

→cu

stom

er t

rust

.05

.84

Rel

atio

nal n

orm

s →

cust

omer

tru

st.2

33.

44**

Com

mun

icat

ion

→cu

stom

er t

rust

.22

3.17

**R

2 :cu

stom

er c

omm

itmen

t=

.54

, tr

ust

= .

33,

sale

s gr

owth

= .

04,

over

all f

inan

cial

per

form

ance

= .

08,

coop

erat

ion

= .

17,

and

conf

lict

= .

11

Dep

end

ence

Per

spec

tive

Cus

tom

er c

omm

itmen

t →

inte

rdep

ende

nce

.20

2.02

*In

terd

epen

denc

e →

sale

s gr

owth

–.02

–.36

Cus

tom

er t

rust

→in

terd

epen

denc

e–.

26–2

.67*

*In

terd

epen

denc

e →

over

all f

inan

cial

per

form

ance

.16

2.74

**C

usto

mer

RS

Is →

inte

rdep

ende

nce

.15

2.08

*In

terd

epen

denc

e →

coop

erat

ion

.10

1.72

*S

elle

r R

SIs

→in

terd

epen

denc

e–.

11–1

.21

Inte

rdep

ende

nce

→co

nflic

t–.

11–1

.91*

Sel

ler

oppo

rtun

istic

beh

avio

rs →

inte

rdep

ende

nce

.18

2.48

**R

elat

iona

l nor

ms

→in

terd

epen

denc

e.1

81.

83*

Dep

ende

nce

asym

met

ry →

sale

s gr

owth

.00

.72

Com

mun

icat

ion

→in

terd

epen

denc

e.1

21.

43D

epen

denc

e as

ymm

etry

→ov

eral

l fin

anci

al p

erfo

rman

ce.0

5.8

1C

usto

mer

RS

Is →

depe

nden

ce a

sym

met

ry–.

07–.

96D

epen

denc

e as

ymm

etry

→co

oper

atio

n–.

07–1

.11

Sel

ler

RS

Is →

depe

nden

ce a

sym

met

ry–.

10–1

.27

Dep

ende

nce

asym

met

ry →

conf

lict

.11

1.87

*R

2 :in

terd

epen

denc

e=

.11

, de

pend

ence

asy

mm

etry

= .

02,

sale

s gr

owth

= .

01,

over

all f

inan

cial

per

form

ance

= .

03,

coop

erat

ion

= .

02,

and

conf

lict

= .

03

Tran

sact

ion

Co

st E

con

om

ics

Per

spec

tive

Cus

tom

er c

omm

itmen

t →

cust

omer

RS

Is.0

3.3

4C

usto

mer

RS

Is →

sale

s gr

owth

.12

2.36

**C

usto

mer

tru

st →

cust

omer

RS

Is.1

01.

14C

usto

mer

RS

Is →

over

all f

inan

cial

per

form

ance

.01

.11

Inte

rdep

ende

nce

→cu

stom

er R

SIs

.13

2.77

**C

usto

mer

RS

Is →

coop

erat

ion

.03

.67

Dep

ende

nce

asym

met

ry →

cust

omer

RS

Is.0

2.2

8C

usto

mer

RS

Is →

conf

lict

.01

.14

Rel

atio

nal n

orm

s →

cust

omer

RS

Is.0

0–.

01C

omm

unic

atio

n →

cust

omer

RS

Is.0

81.

12S

elle

r op

port

unis

tic b

ehav

iors

→sa

les

grow

th–.

00–.

04S

elle

r R

SIs

→se

ller

oppo

rtun

istic

beh

avio

rs–.

18–2

.92*

*S

elle

r op

port

unis

tic b

ehav

iors

→ov

eral

l fin

anci

al p

erfo

rman

ce–.

03–.

61In

terd

epen

denc

e →

selle

r op

port

unis

tic b

ehav

iors

–.04

–.68

Sel

ler

oppo

rtun

istic

beh

avio

rs →

coop

erat

ion

–.17

–3.0

0**

Dep

ende

nce

asym

met

ry →

selle

r op

port

unis

tic b

ehav

iors

–.01

–.17

Sel

ler

oppo

rtun

istic

beh

avio

rs →

conf

lict

.26

4.76

**R

elat

iona

l nor

ms

→se

ller

oppo

rtun

istic

beh

avio

rs–.

24–3

.90*

*C

omm

unic

atio

n →

selle

r op

port

unis

tic b

ehav

iors

–.08

–1.1

5S

elle

r R

SIs

→sa

les

grow

th.0

81.

31In

terd

epen

denc

e →

selle

r R

SIs

.08

1.41

Sel

ler

RS

Is →

over

all f

inan

cial

per

form

ance

.32

5.37

**D

epen

denc

e as

ymm

etry

→se

ller

RS

Is.0

1.1

7S

elle

r R

SIs

→co

oper

atio

n.3

05.

14**

Rel

atio

nal n

orm

s →

selle

r R

SIs

.19

2.96

**S

elle

r R

SIs

→co

nflic

t–.

16–2

.85*

*C

omm

unic

atio

n →

selle

r R

SIs

.29

4.33

**R

2 :cu

stom

er R

SIs

= .

07,

oppo

rtun

istic

beh

avio

rs=

.17

, se

ller

RS

Is=

.21

, sa

les

grow

th=

.03

, ov

eral

l fin

anci

al p

erfo

rman

ce=

.11

, co

oper

atio

n=

.15

, an

d co

nflic

t=

.12

182 / Journal of Marketing, October 2007

Rel

atio

nal

No

rms

Per

spec

tive

Cus

tom

er c

omm

itmen

t →

rela

tiona

l nor

ms

.24

3.20

**R

elat

iona

l nor

ms

→sa

les

grow

th.1

22.

36**

Cus

tom

er t

rust

→re

latio

nal n

orm

s.2

32.

99**

Rel

atio

nal n

orm

s →

over

all f

inan

cial

per

form

ance

.27

4.90

**C

usto

mer

RS

Is →

rela

tiona

l nor

ms

.05

.88

Rel

atio

nal n

orm

s →

coop

erat

ion

.37

6.54

**S

elle

r R

SIs

→re

latio

nal n

orm

s.0

81.

10R

elat

iona

l nor

ms

→co

nflic

t–.

25–4

.52*

*S

elle

r op

port

unis

tic b

ehav

iors

→re

latio

nal n

orm

s–.

07–1

.25

Inte

rdep

ende

nce

→re

latio

nal n

orm

s.0

81.

43D

epen

denc

e as

ymm

etry

→re

latio

nal n

orm

s.0

2.3

5C

omm

unic

atio

n →

rela

tiona

l nor

ms

.05

.76

R2 :

rela

tiona

l nor

ms

= .

35,

sale

s gr

owth

= .

02,

over

all f

inan

cial

per

form

ance

= .

07,

coop

erat

ion

= .

14,

and

conf

lict

= .

06

*p<

.05

(on

e-si

ded)

.**

p<

.01

(on

e-si

ded)

.N

otes

:βre

pres

ents

the

sta

ndar

dize

d pa

th c

oeffi

cien

t.

TAB

LE

3C

on

tin

ued

An

tece

den

ts →→

Med

iato

rsββ

t-V

alu

eM

edia

tors

→→O

utc

om

esββ

t-V

alu

e

Interorganizational Relationship Performance / 183

customer trust negatively (β = –.26, p < .01) and oppor-tunism positively (β = .18, p < .01) affect interdependence.The customer’s evaluation of the seller’s reliability and self-interest may affect interdependence perceptions, in that ifthe seller sincerely stands by its word, the customer expectsit to help minimize losses if the relationship were to end. Atrusted, nonopportunistic seller is more likely to follow theletter and spirit of a contract regarding notification and ter-mination payments, which would make the loss of the rela-tionship less costly (lowering interdependence), whereas aless trusted, more opportunistic seller may provide a rela-tively lower level of transitional support. We offer this con-jecture in the spirit of novel thinking; other conjectures areequally plausible.

Seller RSIs and communication are not significantlyrelated to customer interdependence. Similarly, neither cus-tomer RSIs nor seller RSIs have a significant impact ondependence asymmetry. Interdependence has a positiveinfluence on overall financial performance (β = .16, p < .01)and cooperation (β = .10, p < .05) and a negative influenceon conflict (β = –.11, p < .01). Unbalanced relationshipsexperience higher levels of conflict, but dependence asym-metry does not influence any of the other three outcomes.Exchange age has a negative effect on sales growth (β =–.04, p < .05).

Mediation tests demonstrate that all antecedents havedirect effects on the outcome variables (i.e., no antecedentsare fully mediated), though in the commitment–trust andtransaction cost perspectives, dependence constructs arefully mediated. Therefore, we posit that interdependenceand dependence asymmetry are not immediate precursors toperformance, and the dependence structure of exchangepartners represents a structural characteristic of anexchange that may provide an important context for otherproximate performance drivers.

Results: Transaction Cost Economics Perspective

As interdependence increases, customers make larger RSIs(β = .13, p < .01). None of the other antecedents of cus-tomer RSIs are significant. Seller opportunism drops as aresult of strong relational norms (β = –.24, p < .01) and highseller RSIs (–.18, p < .01). Similarly, seller RSIs are influ-enced positively by relational norms (β = .19, p < .01) andcommunication (β = .29, p < .01) but are unaffected bydependence. Customer RSIs have a positive effect only onsales growth (β = .12, p < .01), whereas seller opportunisticbehavior affects both relationship outcomes, underminingcooperation (β = –.17, p < .01) and increasing conflict (β =.26, p < .01), but has no effect on financial outcomes. Thus,opportunistic behaviors do not appear to influence financialoutcomes directly but rather indirectly through their impacton relational behaviors. Seller RSIs have significant effectson three outcomes: They improve overall financial perfor-mance (β = .32, p < .01) and cooperation (β = .30, p < .01)and decrease the level of conflict (β = –.16, p < .01).Exchange age has a positive effect on seller RSIs (β = .11,p < .05) but a negative effect on sales growth (β = –.10, p <.05) and financial performance (β = –.09, p < .05).

Mediation tests demonstrate that commitment, trust,relational norms, and communication are not fully mediated

in the transaction cost perspective, and customer and sellerRSIs have direct effects on outcomes (i.e., not fully medi-ated) when tested in the three other perspectives. Thus,RSIs have a direct effect on outcomes across all models, sothey should be considered immediate precursors ofexchange outcomes. The failure of this perspective to medi-ate fully the effect of the relational constructs on outcomessupports the view that transaction cost economics cannotcapture the relational aspect of an exchange.

Results: Relational Norms Perspective

Of the eight antecedents tested, only customer commitment(β = .24, p < .01) and trust (β = .23, p < .01) have signifi-cant effects on the level of relational norms. It is especiallysurprising that opportunistic behaviors and communicationdo not influence relational norms, but we posit that thisfinding may be due to the time lapse in our longitudinaldata; one year between antecedent and mediator measuresmay be relatively short compared with the time needed formeaningful changes in norms. Relational norms have strongeffects on all four outcomes: sales growth (β = .12, p < .01),financial performance (β = .27, p < .01), cooperation (β =.37, p < .01), and conflict (β = –.25, p < .01).

Relational norms fail to mediate fully commitment,trust, customer and seller RSIs, and communication, butthey fully mediate dependence measures and opportunisticbehaviors. The results from the other models’ mediationtests show that relational norms are fully mediated in thecommitment–trust perspective. In addition, only two of theeight antecedents of relational norms are significant in thismodel, whereas norms are significantly related to five of thesix focal constructs across the other models. Therefore, weposit that relational norms provide an important backdropfor other focal performance drivers but are not an immedi-ate precursor of exchange performance themselves.

Results: Moderating Role of EnvironmentalUncertainty

To evaluate whether environmental dynamism or marketdiversity moderates the effects of the focal constructs onoutcomes across perspectives, we use multigroup structuralmodel analysis and examine moderation effects on the basisof a median split (N = 198 in both groups). We use a chi-square difference test to compare models in which we con-strain all structural paths to be equal across the two groupsversus an unconstrained model in which we allow the pathbeing tested to vary. If the free model has a significantlylower chi-square than the constrained model, the path ismoderated. We perform an analysis for the effects of allmediators on each of the four outcomes for both environ-mental dynamism and market diversity across the four per-spectives and summarize the results in Table 4.

Compelling evidence shows the enhanced impact ofstrong interfirm relationships (commitment, trust, and rela-tional norms) on overall financial performance and cooper-ation as environmental uncertainty increases. Commit-ment’s impact on overall financial performance (Δχ2

(1) =5.7, p < .05) and cooperation (Δχ2

(1) = 7.4, p < .01) is sig-nificantly moderated by environmental dynamism, whereascommitment’s impact on cooperation (Δχ2

(1) = 11.2, p <

184 / Journal of Marketing, October 2007

*p<

.05

.**

p<

.01

.N

otes

:βre

pres

ents

the

sta

ndar

dize

d pa

th c

oeffi

cien

t fo

r th

at g

roup

, an

d Δχ

2re

pres

ents

the

diff

eren

ce in

χ2

betw

een

the

cons

trai

ned

and

the

free

mod

els

for

the

path

bei

ng t

este

d w

ith 1

deg

ree

of f

reed

om.

Env

iro

nm

enta

l Dyn

amis

mM

arke

t D

iver

sity

Med

iato

rs →

Ou

tco

mes

ββo

f L

ow

Gro

up

ββo

f H

igh

Gro

up

ΔΔχχ2

(1 d

.f.)

ββo

f L

ow

G

rou

pββ

of

Hig

h

Gro

up

ΔΔχχ2

(1 d

.f.)

Co

mm

itm

ent–

Tru

st P

ersp

ecti

veC

usto

mer

com

mitm

ent

→sa

les

grow

th.1

5.1

8*.1

.18*

.18*

.0C

usto

mer

com

mitm

ent

→ov

eral

l fin

anci

al p

erfo

rman

ce.0

5.3

0**

5.7*

.08

.27*

*3.

0C

usto

mer

com

mitm

ent

→co

oper

atio

n.2

0*.4

3**

7.4*

*.1

7*.4

6**

11.2

**C

usto

mer

com

mitm

ent

→co

nflic

t–.

30**

–.22

**1.

7–.

20**

–.29

**.6

Cus

tom

er t

rust

→sa

les

grow

th–.

07.0

51.

3.0

1–.

03.1

Cus

tom

er t

rust

→ov

eral

l fin

anci

al p

erfo

rman

ce–.

08.2

7**

12.3

**–.

02.2

1**

4.6*

Cus

tom

er t

rust

→co

oper

atio

n.0

1.2

2**

6.3*

*.0

2.2

7**

7.6*

*C

usto

mer

tru

st →

conf

lict

–.23

**–.

044.

6*–.

09–.

19*

.9

Dep

end

ence

Per

spec

tive

Inte

rdep

ende

nce

→sa

les

grow

th.0

3–.

08.9

–.03

–.02

.0In

terd

epen

denc

e →

over

all f

inan

cial

per

form

ance

.16*

.15*

.1–.

05.2

9**

6.1*

*In

terd

epen

denc

e →

coop

erat

ion

.11

.11

.1.0

6.1

3*.3

Inte

rdep

ende

nce

→co

nflic

t–.

06–.

18*

.5–.

12–.

11.3

Dep

ende

nce

asym

met

ry →

sale

s gr

owth

–.10

.07

2.2

–.10

.10

3.2

Dep

ende

nce

asym

met

ry →

over

all f

inan

cial

per

form

ance

.05

.05

.0–.

08.1

5*3.

9*D

epen

denc

e as

ymm

etry

→co

oper

atio

n–.

11–.

06.2

–.07

–.08

.0D

epen

denc

e as

ymm

etry

→co

nflic

t.1

8**

.06

2.4

.15*

.10

.5

Tran

sact

ion

Co

st E

con

om

ics

Per

spec

tive

Cus

tom

er R

SIs

→sa

les

grow

th.0

6.1

2.3

.00

.23*

*4.

6*C

usto

mer

RS

Is →

over

all f

inan

cial

per

form

ance

–.06

.05

1.3

–.04

.02

.4C

usto

mer

RS

Is →

coop

erat

ion

.02

.10

.8.0

4–.

01.3

Cus

tom

er R

SIs

→co

nflic

t.0

1–.

05.3

.02

.00

.0S

elle

r op

port

unis

tic b

ehav

iors

→sa

les

grow

th.0

6–.

03.8

.05

–.03

.6S

elle

r op

port

unis

tic b

ehav

iors

→ov

eral

l fin

anci

al p

erfo

rman

ce.0

3–.

101.

6–.

01–.

09.4

Sel

ler

oppo

rtun

istic

beh

avio

rs →

coop

erat

ion

–.21

**–.

15*

.3–.

13*

–.26

**1.

0S