2020 - Pag-IBIG Fund

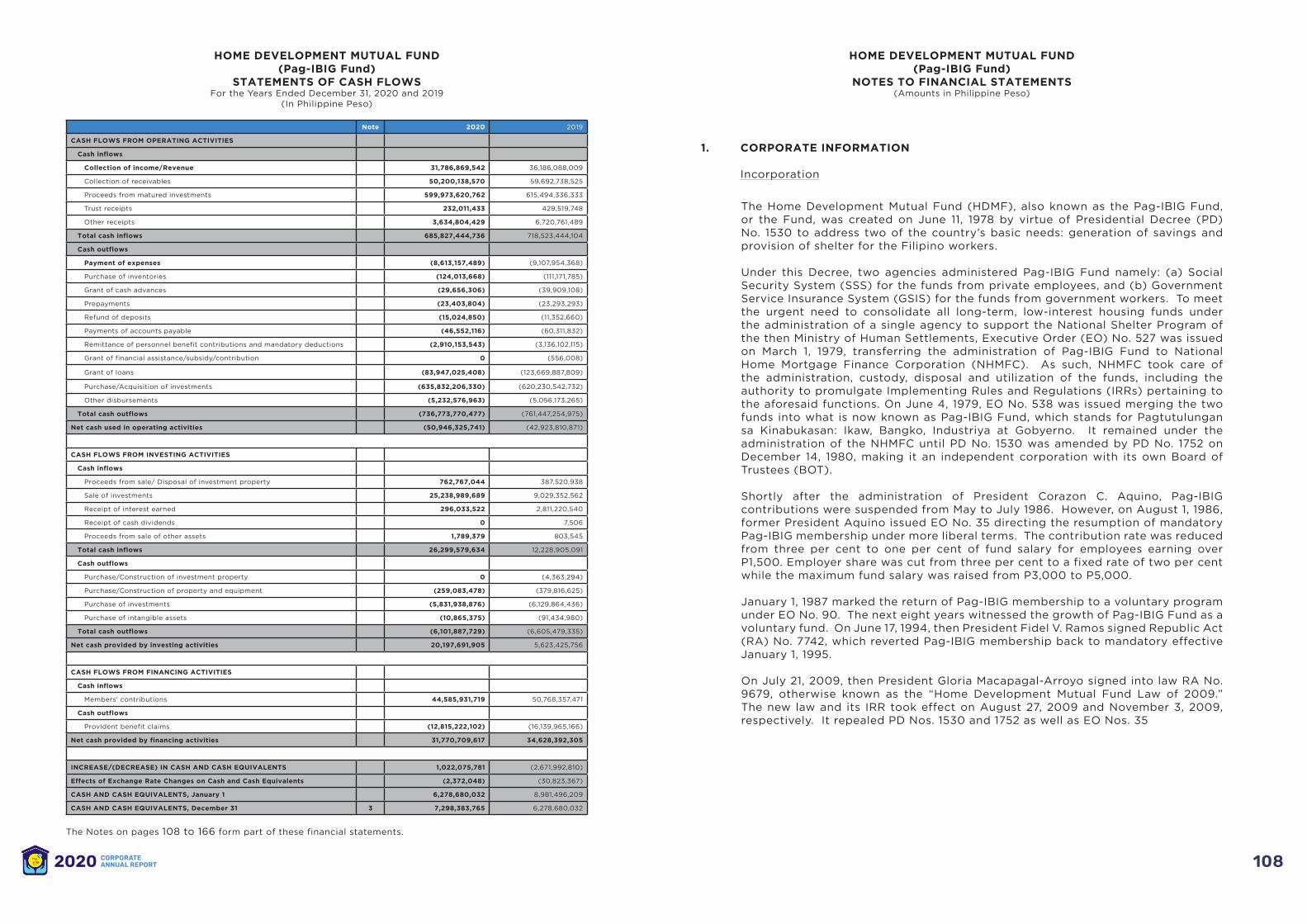

95

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of 2020 - Pag-IBIG Fund

“Kaagapay mo sa Pagbangon Tungo saKinabukasang Puno ng Pag-IBIG”

CORPORATE ANNUAL REPORT

2020

CORPORATE PROFILE

INTRODUCTION

MESSAGES

OPERATIONAL HIGHLIGHTS

Kaagapay mo sa Pagbangon

Tungo sa Kinabukasang Puno ng Pag-IBIG

40 YEARS OF Pag-IBIG FUND

GOVERNANCE REPORT

Pag-IBIG FUND OFFICERS

AT A GLANCE

FINANCIAL STATEMENTS (COA Audited)

DIRECTORY OF UNITS

EDITORIAL BOARD

ACKNOWLEDGMENT

1

3

5

12

25

41

42

66

86

90

159

173

174

COVERAbout the

Pag-IBIG has held the hands of its members and

stakeholders every step of the way throughout

the challenges of the past years, especially in

the year 2020, providing them with security

and guidance through their excellent service.

This highlights how Pag-IBIG did not use the

pandemic as an excuse to take the back seat

when it comes to service, but instead opened

their hearts to serve even better and even more

than in subsequent years, as seen in Pag-IBIG’s

Fund’s 40th Anniversary.

The theme “Kaagapay mo sa Pagbangon Tungo

sa Kinabukasang Puno ng Pag-IBIG” is depicted

in the image of the sunrise, as the sunrise depicts

a new day or in the bigger scale, a brighter future.

The cover for Pag-IBIG’s 2020 Annual Report

encapsulates the overarching values and themes

that were put at the forefront of Pag-IBIG’s

activities for this year––honest love for service

and being a helping hand to its members and

stakeholders.

CONTENTSTable of

vCORPORATEANNUAL REPORT2020

The twin mandates of the Fund are to:

1. Generate savings through membership in an integrated nationwide savings system; and

2. Mobilize the provident funds of its members for housing purposes.

For every Filipino worker to save with Pag-IBIG Fund and to have decent shelter.

To generate more savings from more Filipino workers, to administer a sustainable

Fund with integrity, sound financial principles, and with social responsibility, and to

provide accessible funds for housing of every member.

Corporate Mandate

Vision

Mission

The governing values that will steer the Pag-IBIG Fund in pursuit of its Vision include

Professionalism, Integrity, Excellence, and Service.

To sustain membership growth and retention that would result to a P2 billion annual

increase in member’s savings collection until 2022, and provide affordable home

financing to at least 361,198 low income earners through Socialized and Low-Cost

Housing from 2018 until 2022.

Corporate Values

Corporate Objectives5-Year Plan

PROFILECorporate

2CORPORATEANNUAL REPORT2020

The year 2020 will go down in history as one of the most challenging

and probably one of the most unpredictable years.

It was a year marked with several community quarantines, which

affected everyone’s mobility and forced companies to rethink their

strategies on how to conduct their businesses. It was no different

for Pag-IBIG Fund as every Lingkod Pag-IBIG – from the Board of

Trustees, the Management, to all rank-and-file and allied service

staff adjusted on how to proceed in their usual tasks —from how to

interact with others on a daily basis to how to perform their work

and operate businesses, and how to serve the members even while

protecting themselves against the threat and danger of the virus.

The pandemic forced people to pause, to do most things at home,

and to shift our lives to what is now dubbed as the “new normal.”

Rather than looking at it as a hindrance, the circumstances motivated

Pag-IBIG Fund to better serve its members and stakeholders— their

kaagapay sa pagbangon (reliable partner in recovery). Guided by

its brand of service “Tapat na Serbisyo, Mula sa Puso” (honest

service from the heart), Pag-IBIG Fund offered relevant programs

that allowed members to prioritize and value their own health and

their family’s safety.

Coming from a string of best-ever years, Pag-IBIG Fund saw that for

2020 the measure of accomplishment is not about beating record-

highs but providing assistance for its members and stakeholders

who are experiencing their lows due to the impact of the pandemic --

providing assistance that will enable them to weather the pandemic

and its effects.

Pag-IBIG Fund’s online presence was key in ensuring that its service

would not be compromised or limited. By bringing its services

closer to its members through online platforms, the Fund promoted

accessibility and convenience, while at the same time employing

efficiency by allowing more members to avail of its programs and

services in the comfort of their homes, the safest possible way.

The Pag-IBIG Fund 2020 Corporate Annual Report is a showcase

of the Lingkod Pag-IBIG’s story of Service, Grit, and Resilience,

which empowered the Fund to be more reliable and responsive

to its members’ needs and stakeholders’ requirements tungo sa

kinabukasang puno ng Pag-IBIG (towards a better tomorrow with

Pag-IBIG Fund).

INTRODUCTION

4CORPORATEANNUAL REPORT2020

My warmest greetings to the Home Development Mutual Fund (Pag-IBIG Fund) as it

publishes its 2020 Corporate Annual Report.

I recognize the Pag-IBIG Fund’s strong commitment to uplift the lives of Filipino

workers through its dependable savings and loan programs. Your initiatives to provide

your members with the opportunity to save for their future and build their own home

are truly noteworthy.

Through the agency’s effective fund management, many of our kababayans are able

to access housing, multi-purpose and calamity loans, which lead them towards more

dignified and productive lives. I trust that your accomplishments over the past four

decades will further inspire integrity, accountability and excellence in your endeavors.

As we recover from the COVID-19 pandemic, I hope that you will say unrelenting in

your service to our people, especially to those who are most in need. May you likewise

remain a reliable stakeholder in our pursuit of an inclusive and sustainable future for

the entire nation.

Congratulations and I wish you more success in the years ahead.

RODRIGO ROA DUTERTE

President

Republic of the Philippines

Message from the

PRESIDENT OF THE

PHILIPPINES

6CORPORATEANNUAL REPORT2020

Message from the

CHAIRPERSONOF THE BOARDOF TRUSTEES

The year 2020 will go down in history as one of the most challenging years not just for Pag-IBIG Fund, but for

the entire world. The threat of COVID-19 unraveled a very different world. Truly, the events that transpired in the

last 12 months were far from ordinary.

But while many things changed, one thing remained constant – our commitment to serve our members and

stakeholders, especially during these challenging times. Heeding the call of President Rodrigo Duterte, the

Pag-IBIG Fund Board of Trustees and the Pag-IBIG Fund management approved and implemented numerous

programs to provide aid to fellow Filipinos during the pandemic.

Allow me to list them here.

In mid-March, only a day after the enhanced community quarantine was imposed, we offered our borrowers a

three-month moratorium on their loan payments. Under this moratorium program, more than 320,000 borrowers

were given immediate extended relief on their loan payments. And later, in compliance with ‘Bayanihan to Heal

as One’ laws, we granted automatic grace period on loan payments of more than 4.77 million borrowers under

‘Bayanihan I’ and 3.69 million borrowers later in the year under ‘Bayanihan II.’

We also brought aid to our key stakeholders - in particular, our partner developers - in recognition of their

critical role in realizing our mandate to provide shelter for our members even during these trying times. Thus,

the Pag-IBIG Fund board, on the recommendation of the management, increased the Housing Construction

Financing Line (HCFL) available to our partner developers – from P2 billion to P10 billion. With the HCFL, we

approved 31 housing projects amounting to P2.153 billion in 2020 – ensuring supply of affordable homes while

creating jobs amid the economic slowdown.

We then moved to entice home buyers by reducing the interest rates of our housing loan. The rate for loans

under a three-year repricing period, was reduced to just 5.375% per annum from 6.375% per annum. Meanwhile,

the rate for loans under a one-year repricing period were cut from 5.375% per annum to just 4.985% per annum

– the lowest rate ever offered under our regular housing loan program.

And lastly, after consulting with labor and employer groups, we deferred until 2022 the planned P50 increase of

our members’ monthly contributions, in consideration of the plight of both workers and business owners during

the pandemic.

As they say, when the going get tough, the tough get going. In the midst of the challenges posed by the

pandemic, Pag-IBIG Fund proved that it can continue to respond to the needs of its members and stakeholders

even under unfavorable circumstances.

Allow me also to commend the men and women of Pag-IBIG Fund, who are aptly called Lingkod Pag-IBIG,

whose dedication and commitment to serving you, our members and stakeholders, are the reasons why the

agency was able to achieve all these – despite the many challenges posed by the pandemic.

The theme of the Annual Report for the year 2020 – “Kaagapay mo sa pagbangon, tungo sa kinabukasang

puno ng Pag-IBIG,” rightfully describes the efforts and the accomplishments of your Pag-IBIG Fund during the

extraordinary year.

SEC. EDUARDO D. DEL ROSARIODepartment of Human Settlements and Urban Development (DHSUD)

Chairperson, Pag-IBIG Fund Board of Trustees

8CORPORATEANNUAL REPORT2020

Message from the

CHIEF EXECUTIVE OFFICER

ACMAD RIZALDY P. MOTIChief Executive Officer

Pag-IBIG Fund

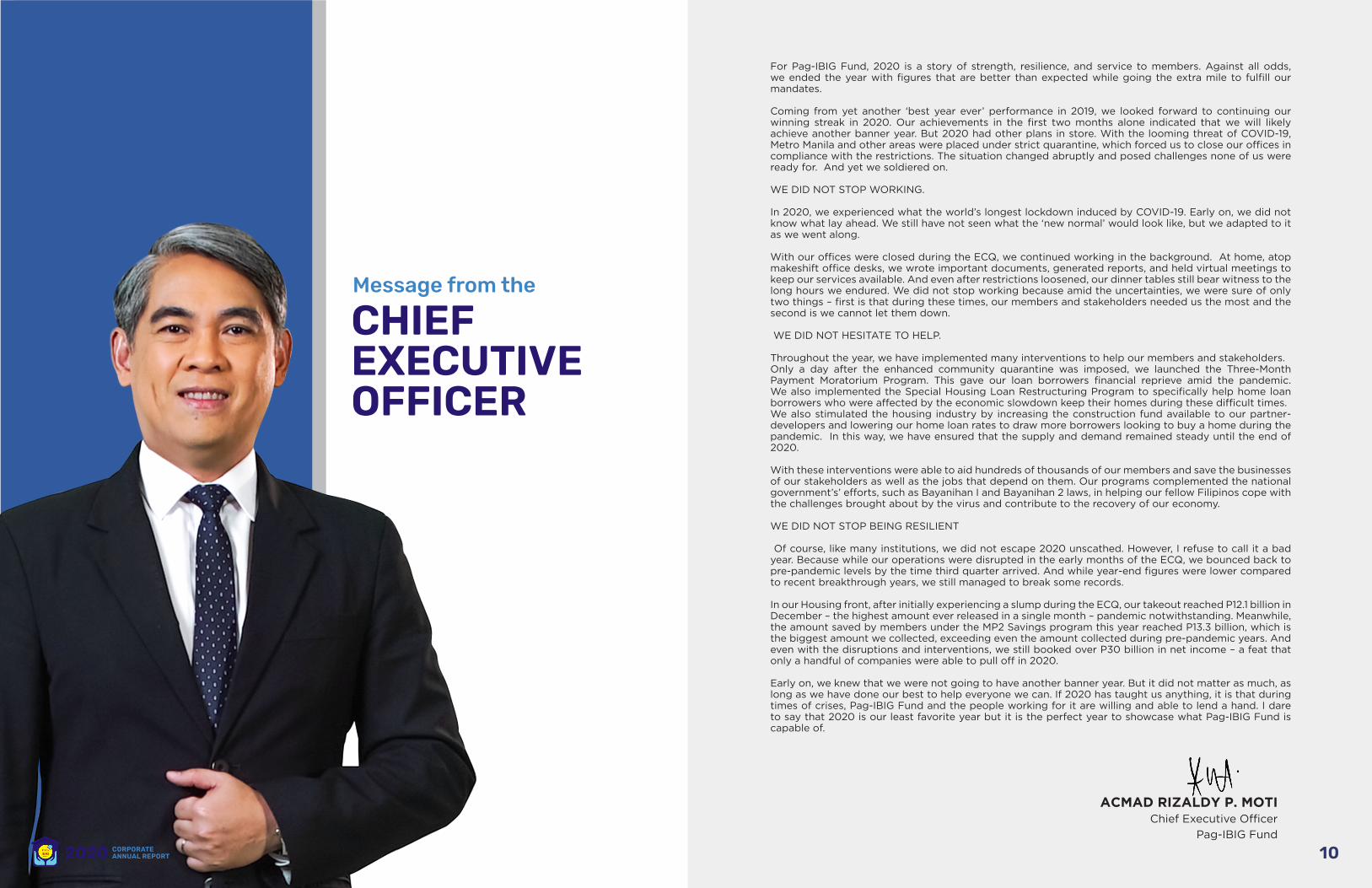

For Pag-IBIG Fund, 2020 is a story of strength, resilience, and service to members. Against all odds, we ended the year with figures that are better than expected while going the extra mile to fulfill our mandates.

Coming from yet another ‘best year ever’ performance in 2019, we looked forward to continuing our winning streak in 2020. Our achievements in the first two months alone indicated that we will likely achieve another banner year. But 2020 had other plans in store. With the looming threat of COVID-19, Metro Manila and other areas were placed under strict quarantine, which forced us to close our offices in compliance with the restrictions. The situation changed abruptly and posed challenges none of us were ready for. And yet we soldiered on.

WE DID NOT STOP WORKING.

In 2020, we experienced what the world’s longest lockdown induced by COVID-19. Early on, we did not know what lay ahead. We still have not seen what the ‘new normal’ would look like, but we adapted to it as we went along.

With our offices were closed during the ECQ, we continued working in the background. At home, atop makeshift office desks, we wrote important documents, generated reports, and held virtual meetings to keep our services available. And even after restrictions loosened, our dinner tables still bear witness to the long hours we endured. We did not stop working because amid the uncertainties, we were sure of only two things – first is that during these times, our members and stakeholders needed us the most and the second is we cannot let them down.

WE DID NOT HESITATE TO HELP.

Throughout the year, we have implemented many interventions to help our members and stakeholders. Only a day after the enhanced community quarantine was imposed, we launched the Three-Month Payment Moratorium Program. This gave our loan borrowers financial reprieve amid the pandemic. We also implemented the Special Housing Loan Restructuring Program to specifically help home loan borrowers who were affected by the economic slowdown keep their homes during these difficult times. We also stimulated the housing industry by increasing the construction fund available to our partner-developers and lowering our home loan rates to draw more borrowers looking to buy a home during the pandemic. In this way, we have ensured that the supply and demand remained steady until the end of 2020.

With these interventions were able to aid hundreds of thousands of our members and save the businesses of our stakeholders as well as the jobs that depend on them. Our programs complemented the national government’s’ efforts, such as Bayanihan I and Bayanihan 2 laws, in helping our fellow Filipinos cope with the challenges brought about by the virus and contribute to the recovery of our economy.

WE DID NOT STOP BEING RESILIENT

Of course, like many institutions, we did not escape 2020 unscathed. However, I refuse to call it a bad year. Because while our operations were disrupted in the early months of the ECQ, we bounced back to pre-pandemic levels by the time third quarter arrived. And while year-end figures were lower compared to recent breakthrough years, we still managed to break some records.

In our Housing front, after initially experiencing a slump during the ECQ, our takeout reached P12.1 billion in December – the highest amount ever released in a single month – pandemic notwithstanding. Meanwhile, the amount saved by members under the MP2 Savings program this year reached P13.3 billion, which is the biggest amount we collected, exceeding even the amount collected during pre-pandemic years. And even with the disruptions and interventions, we still booked over P30 billion in net income – a feat that only a handful of companies were able to pull off in 2020.

Early on, we knew that we were not going to have another banner year. But it did not matter as much, as long as we have done our best to help everyone we can. If 2020 has taught us anything, it is that during times of crises, Pag-IBIG Fund and the people working for it are willing and able to lend a hand. I dare to say that 2020 is our least favorite year but it is the perfect year to showcase what Pag-IBIG Fund is capable of.

10CORPORATEANNUAL REPORT2020

Pag-IBIG Fund has proven to be the Filipino

worker’s reliable partner, especially amid the

challenges brought about by the COVID-19

pandemic in 2020. Its responsiveness to

the needs of its members, as well as its

stakeholders, through relevant programs and

benefits provided and continue to provide

them the means to continuously cope and

recover from the effects of the pandemic.

Indeed, while others may have used the

pandemic as an excuse not to serve, Pag-IBIG

Fund used it as a reason to serve better.

The Filipino Worker’s Reliable Partner

Kaagapay mo sa

PAGBANGON

OPERATIONALHIGHLIGHTS

12CORPORATEANNUAL REPORT2020

A day after the implementation of the Enhanced

Community Quarantine (ECQ) in the National

Capital Region and other parts of the country,

Pag-IBIG Fund immediately offered a 3-month

moratorium on the loan payments of its members.

The program helped alleviate the financial

burden of 283,349 borrowers, whose jobs or

businesses were affected by the pandemic.

This included 177,056 short-term loan borrowers

and 106,293 housing loan borrowers who were

aided through the program.

3-MONTH MORATORIUMON LOAN PAYMENTSA day after the ECQ wasfirst implemented

AUTOMATIC GRANT OF A GRACE PERIOD ON LOAN PAYMENTSUnder the Bayanihan to Heal as One Act R.A. 11469

Pag-IBIG Fund granted an automatic grace

period on all loan payments of 4,774,784

members with housing and short-term loans in

accordance with the Bayanihan to Heal as One

Act (Bayanihan I).

Through this loan payment relief, Pag-IBIG Fund

aided 4,061,559 short-term loan borrowers

and 253,849 housing loan borrowers, enabling

them to allocate their financial resources to

more pressing needs during the early days of the

implementation of the ECQ.

Providing Financial Relief to Filipino Workers Amid the Pandemic

14CORPORATEANNUAL REPORT2020

GRANT OF A 60-DAY GRACE PERIODON LOAN PAYMENTSUnder the Bayanihan to Recover as One Act R.A. 11494

Pag-IBIG Fund granted another grace period in September,

in accordance with the Bayanihan to Recover as One Act, as

it heeded the government’s call to further assist Filipinos in

coping with the financial challenges brought by the pandemic.

A total of 3,648,372 borrowers benefited from the grace

period granted by Pag-IBIG Fund, as it extended the coverage

to not just updated accounts as required by the Act, but also

to accounts which were in arrears of up to nine months.

It also allowed borrowers to pay the accrued interest during

the period of the grace period on a staggered basis, and at any

time during the remaining term of the loan.

Pag-IBIG Fund recognized that a number of its members

who, prior to the pandemic, consistently pay their loans

on time but have now incurred arrears due to the financial

challenges caused by the pandemic.

To aid them in updating their accounts, Pag-IBIG Fund

offered a Special Housing Loan Restructuring Program

to aid its borrowers with unpaid monthly amortizations

of up to 12 months as of August 2020.

By the end of 2020, 76,629 housing loan borrowers

availed of the program, allowing them to update their

accounts, have the penalties on their arrears waived,

and avoid foreclosure or cancellation. These borrowers

were also given the option to resume payment in March

2021, effectively granting them at least three months in

loan payment relief.

SPECIAL HOUSING LOANRESTRUCTURING PROGRAMEnabled borrowers to keep their homeswhile securing better terms on their loans

Providing Financial Relief to Filipino Workers Amid the Pandemic

16CORPORATEANNUAL REPORT2020

SHORT-TERM LOAN PROGRAMImmediate financial assistance that members can count on

VALUING SUSTAINABILITY OVER PROFITABILITYImmediate financial assistance that members can count on

Providing Financial Relief to Filipino Workers Amid the Pandemic

Pag-IBIG Fund made both its Multi-Purpose Loan

(MPL) and Calamity Loan accessible to members

in despite the limitations of the quarantine. This was

made possible by immediately providing for online

filing of applications and submission via dropboxes.

In all, Pag-IBIG Fund released P35.64 billion to

1,735,921 members under its Short-Term Loan

program in 2020.

Amid the numerous payment reprieves provided for

its member-borrowers, Pag-IBIG Fund’s loan payment

collections in year 2020 amounted to P102.82 billion.

This consisted of P56.17 billion from short-term

loan payment collections and P46.65 billion from

housing loan payment collections. By the end of

the year, Pag-IBIG Fund still managed to post a

Performing Loans Ratio (PLR) 87.26% for its housing

loan portfolio.

18CORPORATEANNUAL REPORT2020

After consultations with labor and employer groups,

the Pag-IBIG Fund Board of Trustees approved to

defer by one year the planned increase in monthly

contributions in January 2021. This marked the

35th year that Pag-IBIG Fund has not increased the

amount of the monthly contributions of its members.

The deferment showed Pag-IBIG Fund’s understanding

of the plight of the Filipino worker whose need for

every peso during the pandemic counts.

It also reflected the responsiveness of Pag-IBIG

Fund to the needs of the business community,

easing their financial burden and helping them

maintain their operations amid the health crisis.

DEFERMENT OF THE INCREASEIN MONTHLY CONTRIBUTIONSValuing the voice of its membersand the business community

Providing Financial Relief to Filipino Workers Amid the Pandemic

We know that many of our members and

employers faced financial challenges in the last

few months because of the effects brought about

by the pandemic to the economy. After consulting

with our stakeholders, we will no longer push

through with the increase of the members’ monthly

contributions next year.

“

”Sec. Eduardo D. Del Rosario

Chairperson, Board of Trustees

Pag-IBIG Fund

20CORPORATEANNUAL REPORT2020

Php 10 BILLION HOMECONSTRUCTION FUNDBuild more homes.Help boost the economy.

While the pandemic may have been used by others as an EXCUSE not to serve,Your Lingkod Pag-IBIGused it as a REASON to SERVE BETTER.

Not only did Pag-IBIG decide

to release home loans in the

face of such dark in uncertain

times but they also reach out to

all of us accredited developers

to find solutions to make the

home loan application process

even easier than it was before

the pandemic.

“

”Mr. Kerwin V. Padua

President and CEO,

Lynville Land Development Corporation

Pag-IBIG Fund increased its Housing Construction Financing Line

or HCFL to Php10 billion from Php2 billion, to enable partner

developers to continue the construction and production of socialized

and low-cost housing units.

A total of 31 housing projects worth Php2.153 billion were approved

under the financing line, helping boost housing in the country,

allowing several players in the industry to maintain their operations

and continue providing jobs to Filipinos.

This again showed that Pag-IBIG Fund can be relied upon, not just by

its members, but also by its stakeholders from the housing industry

in providing the needed financial assistance to keep their businesses

afloat during the most difficult times.

Stimulating the Housing Industry while providing Filipino Workers Better Opportunities to Own a Home

22CORPORATEANNUAL REPORT2020

As it ensured the continuous supply of quality and

affordable housing units through its programs

for the housing industry, Pag-IBIG Fund then

offered special promo rates on its housing loan.

This helped Filipino workers secure a home at

even more affordable terms, providing them the

opportunity to own a home where they can be

safe amid the pandemic.

Pag-IBIG Fund’s interest rates, already considered

as among the lowest in the market, were further

reduced by as much as 100 basis points under its

promo rates. From July to December 2020, the

interest rate for a Pag-IBIG Housing Loan stood

To help Filipino workers securea home where they can be safe

PROMO RATES ON THEPag-IBIG HOUSING LOAN

Stimulating the Housing Industry while providing Filipino Workers Better Opportunities to Own a Home

at only 4.985% per annum, from the previous

5.375% rate, under a 1-year repricing period

and only 5.375 per annum, from the previous

6.375% rate, under a 3-year repricing period.

Pag-IBIG Fund approved a total of P36.66

billion in Housing Loans benefitting 32,256

members who now have their own homes

secured under the most affordable terms.

And, by offering these special rates, Pag-IBIG

Fund spurred demand in the housing industry,

thereby helping in the nation’s efforts to get

the economy back on track.

24CORPORATEANNUAL REPORT2020

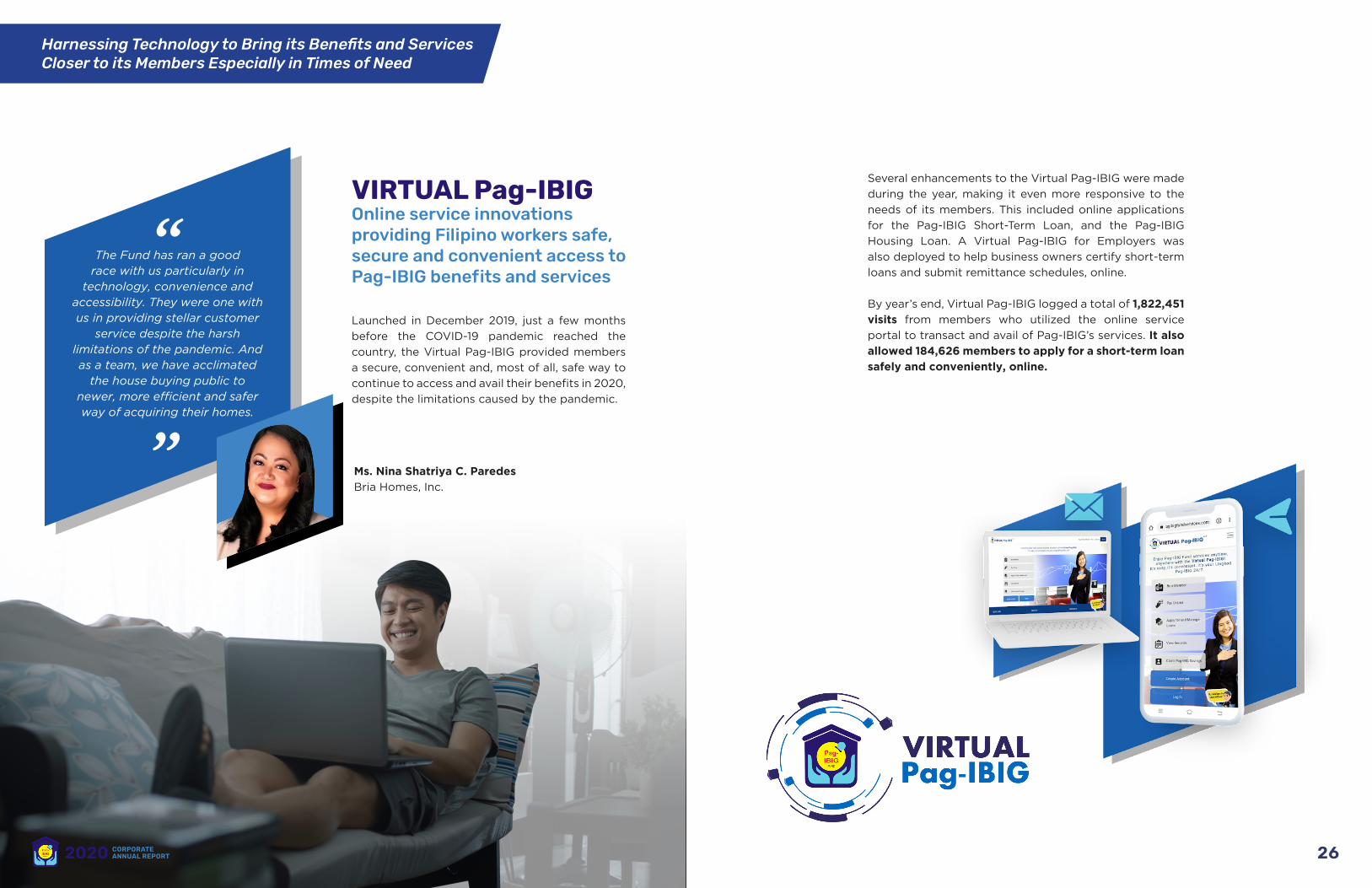

Launched in December 2019, just a few months

before the COVID-19 pandemic reached the

country, the Virtual Pag-IBIG provided members

a secure, convenient and, most of all, safe way to

continue to access and avail their benefits in 2020,

despite the limitations caused by the pandemic.

VIRTUAL Pag-IBIGOnline service innovations providing Filipino workers safe, secure and convenient access to Pag-IBIG benefits and services

Several enhancements to the Virtual Pag-IBIG were made

during the year, making it even more responsive to the

needs of its members. This included online applications

for the Pag-IBIG Short-Term Loan, and the Pag-IBIG

Housing Loan. A Virtual Pag-IBIG for Employers was

also deployed to help business owners certify short-term

loans and submit remittance schedules, online.

By year’s end, Virtual Pag-IBIG logged a total of 1,822,451

visits from members who utilized the online service

portal to transact and avail of Pag-IBIG’s services. It also

allowed 184,626 members to apply for a short-term loan

safely and conveniently, online.

Harnessing Technology to Bring its Benefits and Services Closer to its Members Especially in Times of Need

While the pandemic may have been used by others as an EXCUSE not to serve,Your Lingkod Pag-IBIGused it as a REASON to SERVE BETTER.

The Fund has ran a good race with us particularly in

technology, convenience and accessibility. They were one with us in providing stellar customer

service despite the harsh limitations of the pandemic. And as a team, we have acclimated

the house buying public to newer, more efficient and safer way of acquiring their homes.

“

” Ms. Nina Shatriya C. Paredes

Bria Homes, Inc.

26CORPORATEANNUAL REPORT2020

KEEPING IN TOUCH WITH MEMBERSUNDER THE NEW NORMALUtilizing the internet, social media, teleconferencing platforms to continuereaching out to members and stakeholders

On March 20, just three days after the implementation of

the ECQ in the National Capital Region and other parts

of the country, Pag-IBIG Fund immediately established

an email service to accept applications for its Short-

Term Loans (STL). This provided members the means

to apply for a cash loan during these challenging times,

despite the limitations on mobility brought about by the

quarantine restrictions.

This allowed 37,901 members secure STLs totaling

P716.26 million to address their financial needs. This

email service eventually evolved to the online application

for STL via the Virtual Pag-IBIG.

Harnessing Technology to Bring its Benefits and Services Closer to its Members Especially in Times of Need

Pag-IBIG Fund also increased its presence on social media,

particularly via its official Facebook page, to provide

members and stakeholders information on the agency’s

programs and benefits. It also became a service tool, as

it served and addressed a total of 478,030 messages

sent by members through the Pag-IBIG Fund Facebook

in year 2020.

Through the use of teleconferencing platforms, Pag-IBIG

Fund also continued to reach out to its members and

stakeholders. By the end of the year, it had conducted

7,031 webinars on how to access Pag-IBIG Fund

benefits under the new normal, two virtual events for

key stakeholders and news media, and twelve various

online fora.

28CORPORATEANNUAL REPORT2020

PUNO NG Pag-IBIGTungo sa Kinabukasang

For Pag-IBIG Fund, 2020 was a story of

SERVICE, GRIT, and RESILIENCY.

With its responsive programs and services,

Pag-IBIG Fund radiated hope among members,

as well as stakeholders, empowering them by

providing the means to help rebuild their lives

towards a better tomorrow.

And, while the circumstances of year 2020

hindered Pag-IBIG Fund from continuing its

string of “best-year” evers, the agency rose

above the challenges to play a bigger role in the

lives of its members and stakeholders, serving

them when they needed it most.

Ushering a Better Tomorrow for Filipino Workers

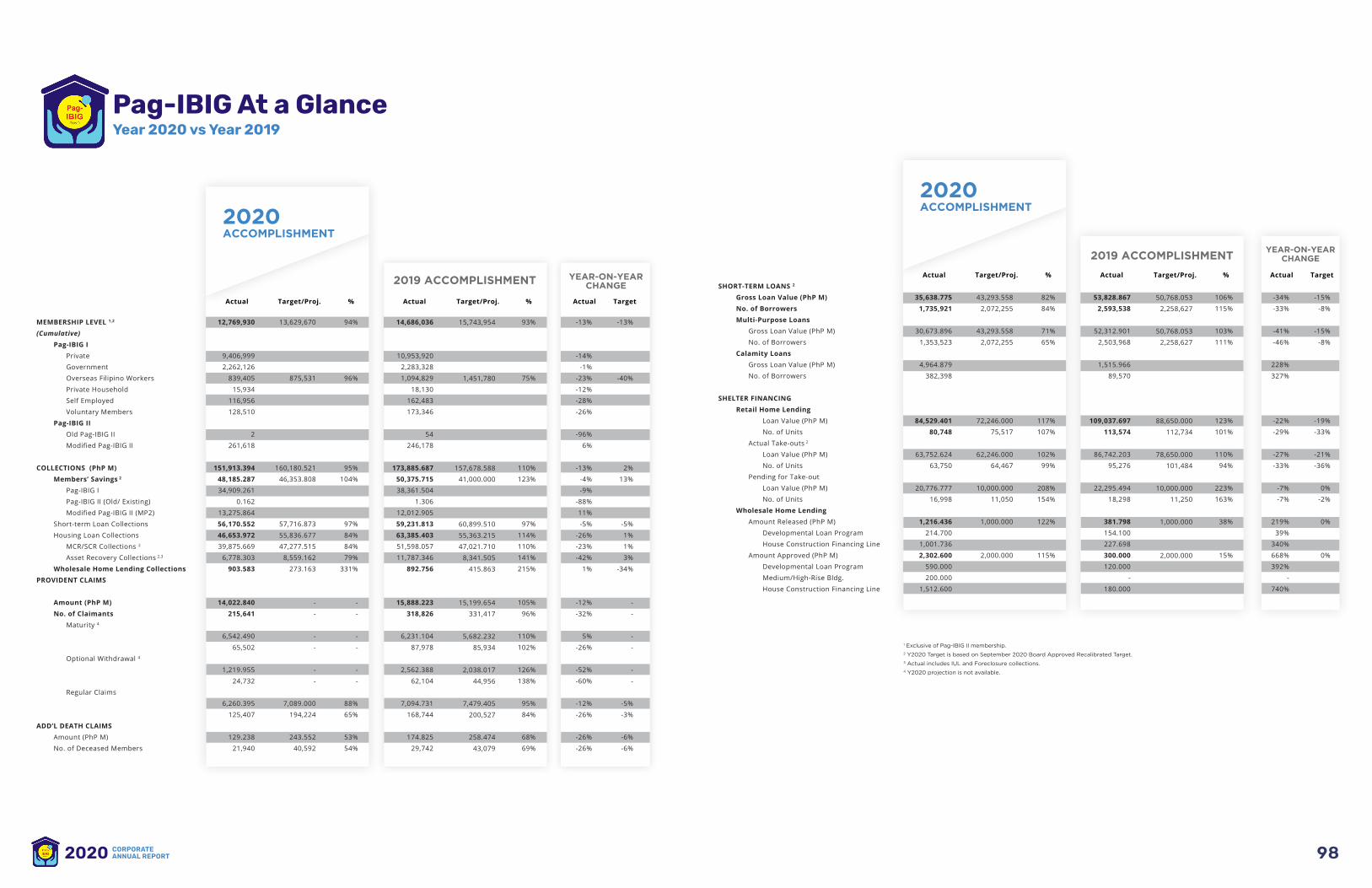

As of December 31, 2020, Pag-IBIG Fund’s active membership

stood at 12.77 million. Active members are those with at least

one monthly membership savings (contribution) with Pag-IBIG

Fund over the past six (6) months for local members and twelve

(12) months for OFWs.

In 2020, notwithstanding the limitations caused by the

pandemic, Pag-IBIG Fund continued serving its members here

and abroad by providing them convenient and safe access to

a secure savings program and a home financing facility to help

uplift their lives, even amid the global pandemic.

CONTINUOUSLY SERVINGFILIPINO WORKERSHere and Abroad

30CORPORATEANNUAL REPORT2020

Despite the financial burden caused

by the COVID-19 pandemic, members

continued to save in Pag-IBIG Fund’s

Regular Savings and Modified Pag-IBIG

2 (MP2) Savings Programs.

In 2020, amid the health and economic

crisis, members collectively saved

P48.2 billion in Pag-IBIG Fund, only 4%

below the record-high P50.4 billion

that members saved in 2019.

SUSTAINED MEMBERS’ SAVINGSAMID THE HEALTH CRISIS

Strong Trust and Unwavering Support from Members and Stakeholders

Of the total amount, P34.9 billion was

collectively saved by members under

its Regular Savings Program.

32CORPORATEANNUAL REPORT2020

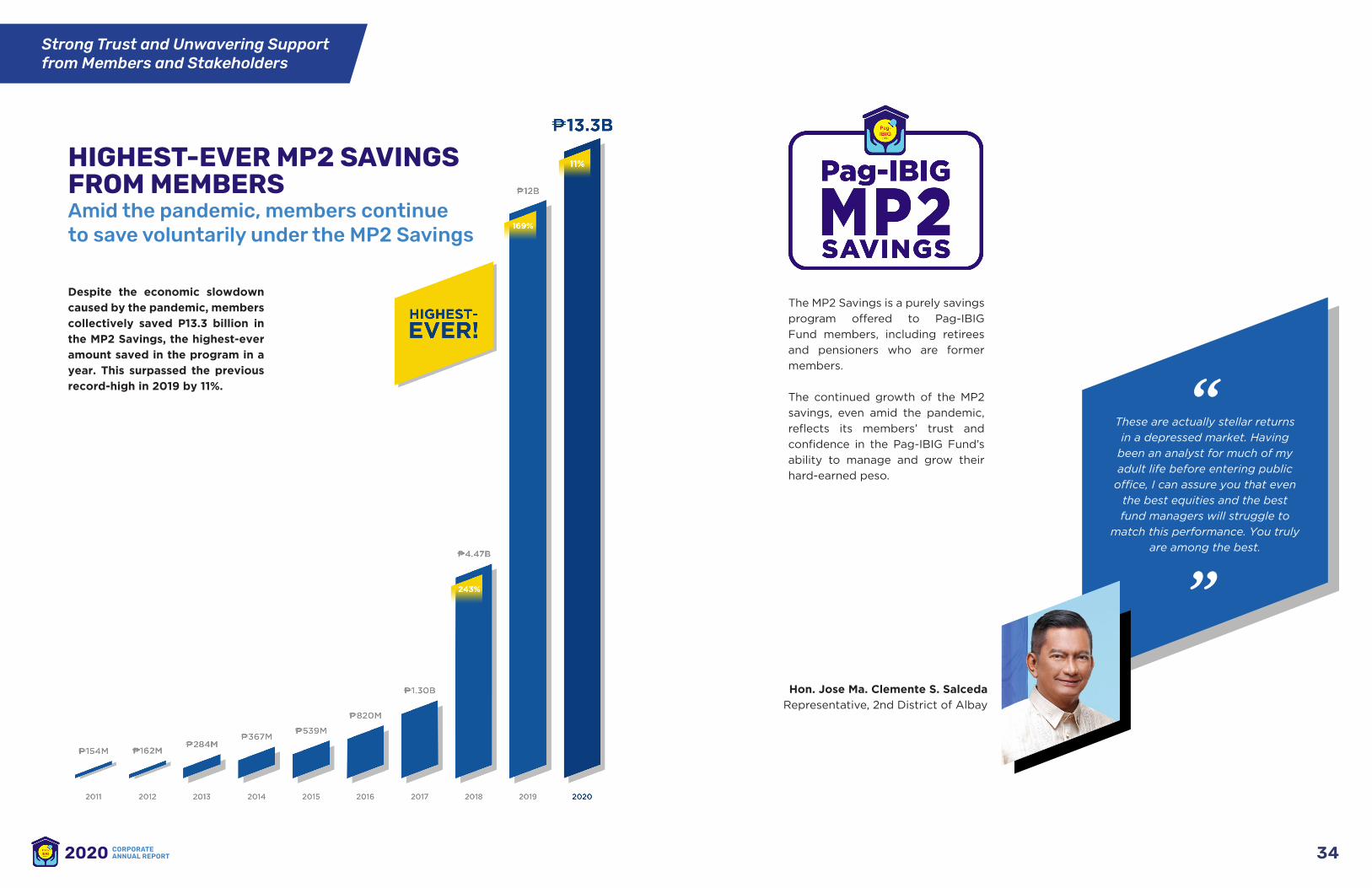

Despite the economic slowdown

caused by the pandemic, members

collectively saved P13.3 billion in

the MP2 Savings, the highest-ever

amount saved in the program in a

year. This surpassed the previous

record-high in 2019 by 11%.

HIGHEST-EVER MP2 SAVINGS FROM MEMBERSAmid the pandemic, members continueto save voluntarily under the MP2 Savings

Strong Trust and Unwavering Support from Members and Stakeholders

The MP2 Savings is a purely savings

program offered to Pag-IBIG

Fund members, including retirees

and pensioners who are former

members.

The continued growth of the MP2

savings, even amid the pandemic,

reflects its members’ trust and

confidence in the Pag-IBIG Fund’s

ability to manage and grow their

hard-earned peso.

While the pandemic may have been used by others as an EXCUSE not to serve,Your Lingkod Pag-IBIGused it as a REASON to SERVE BETTER.

These are actually stellar returns

in a depressed market. Having

been an analyst for much of my

adult life before entering public

office, I can assure you that even

the best equities and the best

fund managers will struggle to

match this performance. You truly

are among the best.

“

”Hon. Jose Ma. Clemente S. Salceda

Representative, 2nd District of Albay

34CORPORATEANNUAL REPORT2020

Pag-IBIG Fund released a total of P63.75 billion

home loans in 2020, which financed the homes

of 63,750 members. Promoting homeownership

during a pandemic was difficult, but Pag-IBIG

Fund rose above this challenge.

By continuing to fulfill this mandate, Pag-IBIG Fund

enables more Filipino workers and their families

fulfill their dream of owning a home come true,

while providing them a safe haven amid the health

crisis.

FULFILLING ITS MANDATE OF PROVIDINGAFFORDABLE HOME FINANCINGHelping Filipino families keep safe in their own homes

Strong Trust and Unwavering Support from Members and Stakeholders

While the pandemic may have been used by others as an EXCUSE not to serve,Your Lingkod Pag-IBIGused it as a REASON to SERVE BETTER.

Our success would not have been possible without the help

of Pag-IBIG Fund. The need for sustainable financing has

been at the core of each of our customers’ decision to purchase

their dream home. The Pag-IBIG Fund has helped us turn these dreams into reality for

thousands of Filipinos.

”Mr. Paolo Giovanni V. Olivares

Vice President for Operations,

Malate Construction and

Development Corporation

“

36CORPORATEANNUAL REPORT2020

Pag-IBIG Fund was poised to achieve

another milestone year in 2020 as the

combined home loan releases in January

and February amounted to P12 billion,

growing 17 percent compared to the same

period in 2019.

But as expected, home loan numbers

started to decline in March when strict

community quarantine measures were

imposed to curb the spread of COVID-19.

Home loan releases dipped to P3.8 billion

in March and P883 million in April.

HIGHEST-EVER HOUSING LOAN AMOUNTRELEASED IN A SINGLE MONTHDisplaying Pag-IBIG Fund’s steadfast resolvein providing Filipino workers a home amid the pandemic

As restrictions were eased, home loan

figures started to recover in as early as

May when disbursements jumped to P1.2

billion and rose even higher to P2.9 billion

in June. Loan releases continued to climb

in the second half of 2020. And by the end

of the third quarter, home loan releases

had already recovered.

And, by December 2020, the Pag-IBIG

Fund released P12.11 billion in home loans

— the highest-ever amount released in a

single month.

38CORPORATEANNUAL REPORT2020

Pag-IBIG Fund continues to offer minimum and low-wage earners its

Affordable Housing Program with a special subsidized home loan interest

rate of 3% per annum, still the lowest in the market.

Pag-IBIG Fund released P7.10 billion for socialized housing loans,

benefitting 16,975 borrowers belonging to the minimum-wage and low-

income sectors. Socialized housing loans represent 27% of the 63,750

units financed by Pag-IBIG Fund in 2020.

With its tax-exempt status under the Corporate Recovery and Tax Incentives

for Enterprises Act (CREATE Act), Pag-IBIG Fund shall continue providing its

Affordable Housing Program to the underserved.

With more than 350 partner-establishments

providing discounts and rewards, the Pag-IBIG

Loyalty Card Plus continues to provide cardholders

an additional means to save.

The card also provides members added convenience,

as it serves as a cash card powered by Asia United

Bank and UnionBank, where they can receive their

Short-Term Loan proceeds, MP2 Savings dividends,

and other benefits.

Its importance was further emphasized during the

health crisis as it allowed cardholders to easily

create a Virtual Pag-IBIG account, enabling them to

enjoy all the services of the agency’s online service

portal 24/7.

UPLIFTING THE LIVES OF THE UNDERSERVEDAffordable housing program for minimum-wage and low-income earners

THE Pag-IBIGLOYALTY CARD PLUSDiscounts, rewards, convenience,and easier access to online services

Strong Trust and Unwavering Support from Members and Stakeholders

40CORPORATEANNUAL REPORT2020

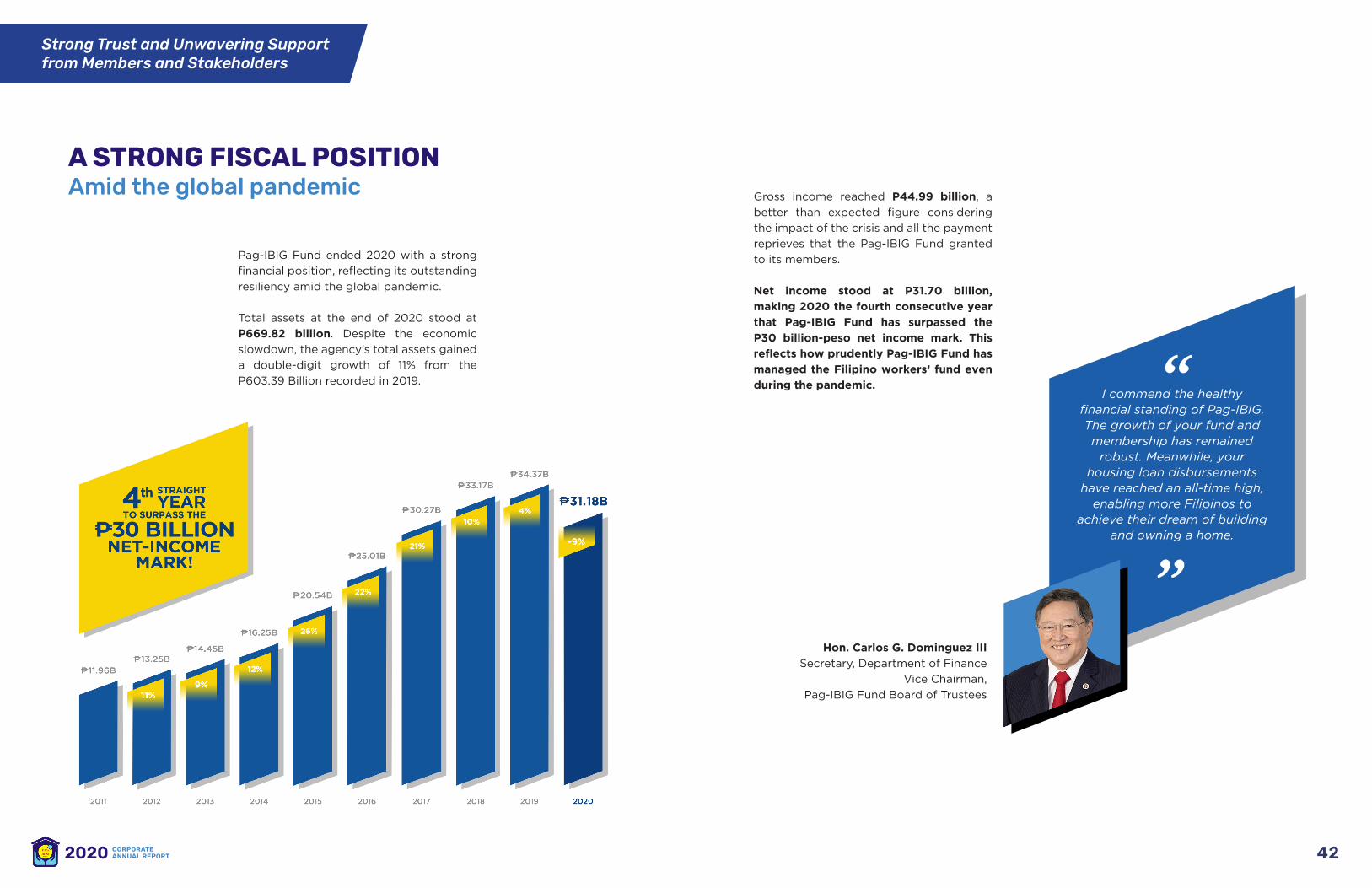

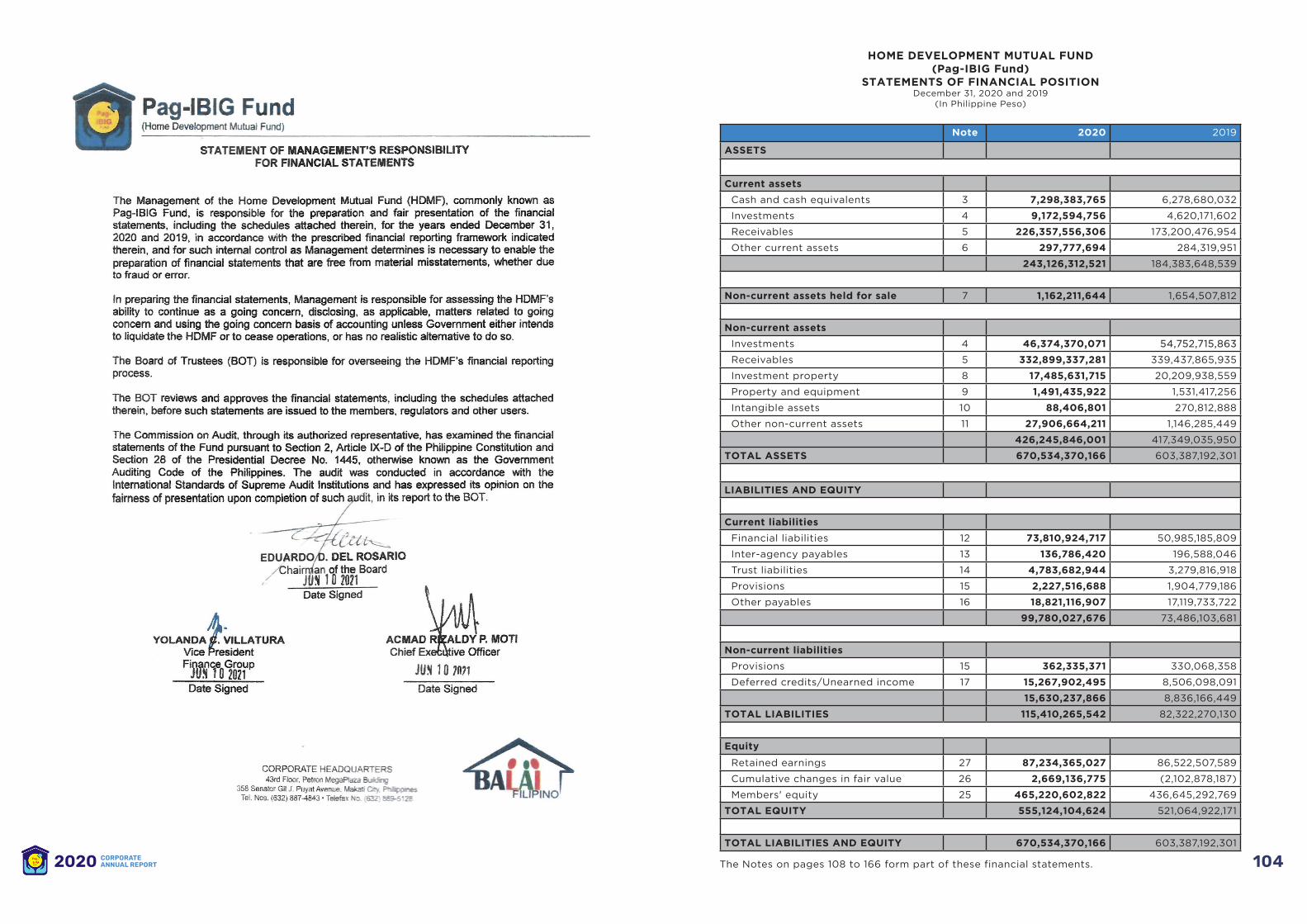

Pag-IBIG Fund ended 2020 with a strong

financial position, reflecting its outstanding

resiliency amid the global pandemic.

Total assets at the end of 2020 stood at

P669.82 billion. Despite the economic

slowdown, the agency’s total assets gained

a double-digit growth of 11% from the

P603.39 Billion recorded in 2019.

A STRONG FISCAL POSITIONAmid the global pandemic

Strong Trust and Unwavering Support from Members and Stakeholders

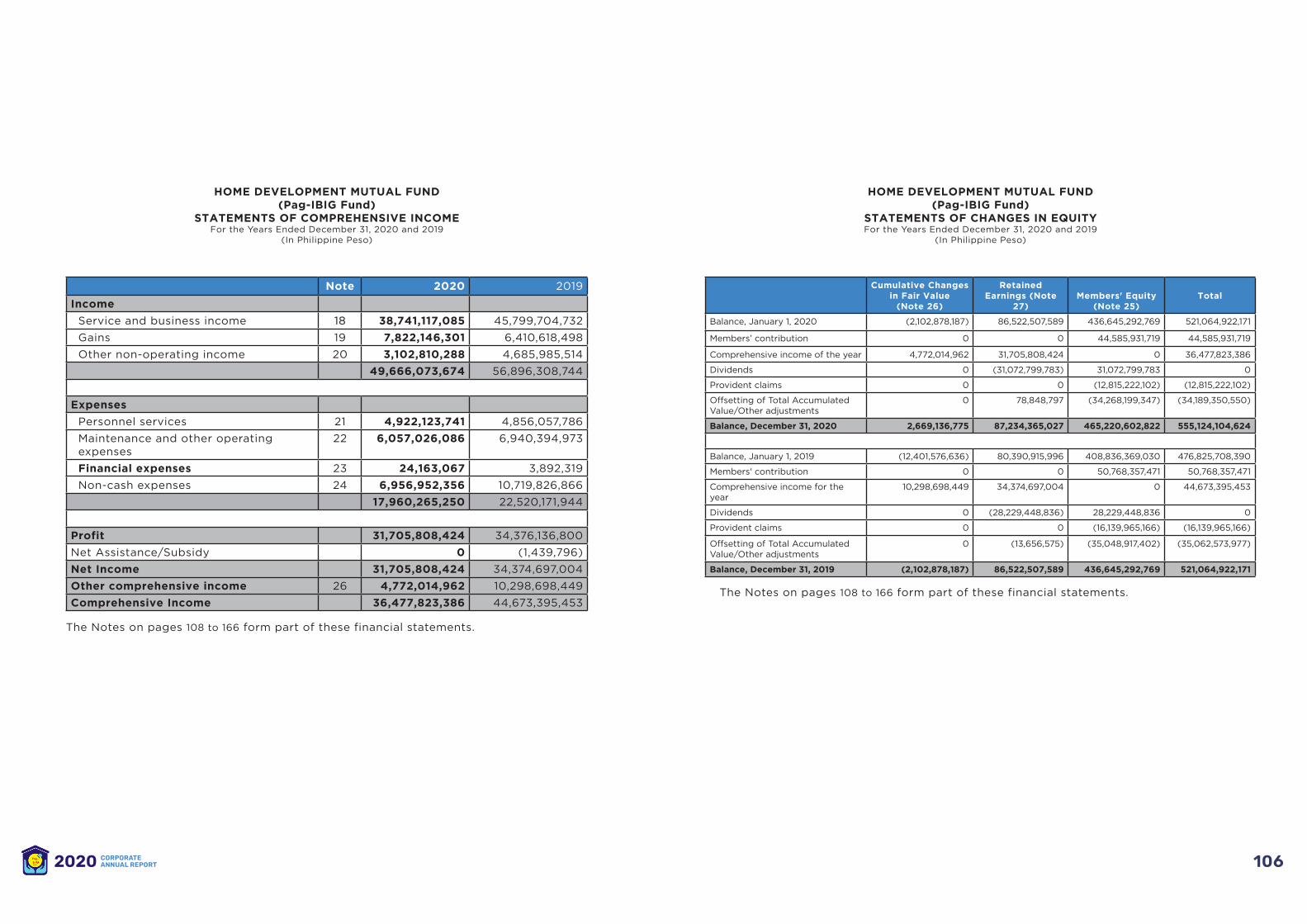

Gross income reached P44.99 billion, a

better than expected figure considering

the impact of the crisis and all the payment

reprieves that the Pag-IBIG Fund granted

to its members.

Net income stood at P31.70 billion,

making 2020 the fourth consecutive year

that Pag-IBIG Fund has surpassed the

P30 billion-peso net income mark. This

reflects how prudently Pag-IBIG Fund has

managed the Filipino workers’ fund even

during the pandemic. While the pandemic may have been used by others as an EXCUSE not to serve,Your Lingkod Pag-IBIGused it as a REASON to SERVE BETTER.

I commend the healthy financial standing of Pag-IBIG. The growth of your fund and membership has remained

robust. Meanwhile, your housing loan disbursements

have reached an all-time high, enabling more Filipinos to

achieve their dream of building and owning a home.

”Hon. Carlos G. Dominguez III

Secretary, Department of Finance

Vice Chairman,

Pag-IBIG Fund Board of Trustees

“

42CORPORATEANNUAL REPORT2020

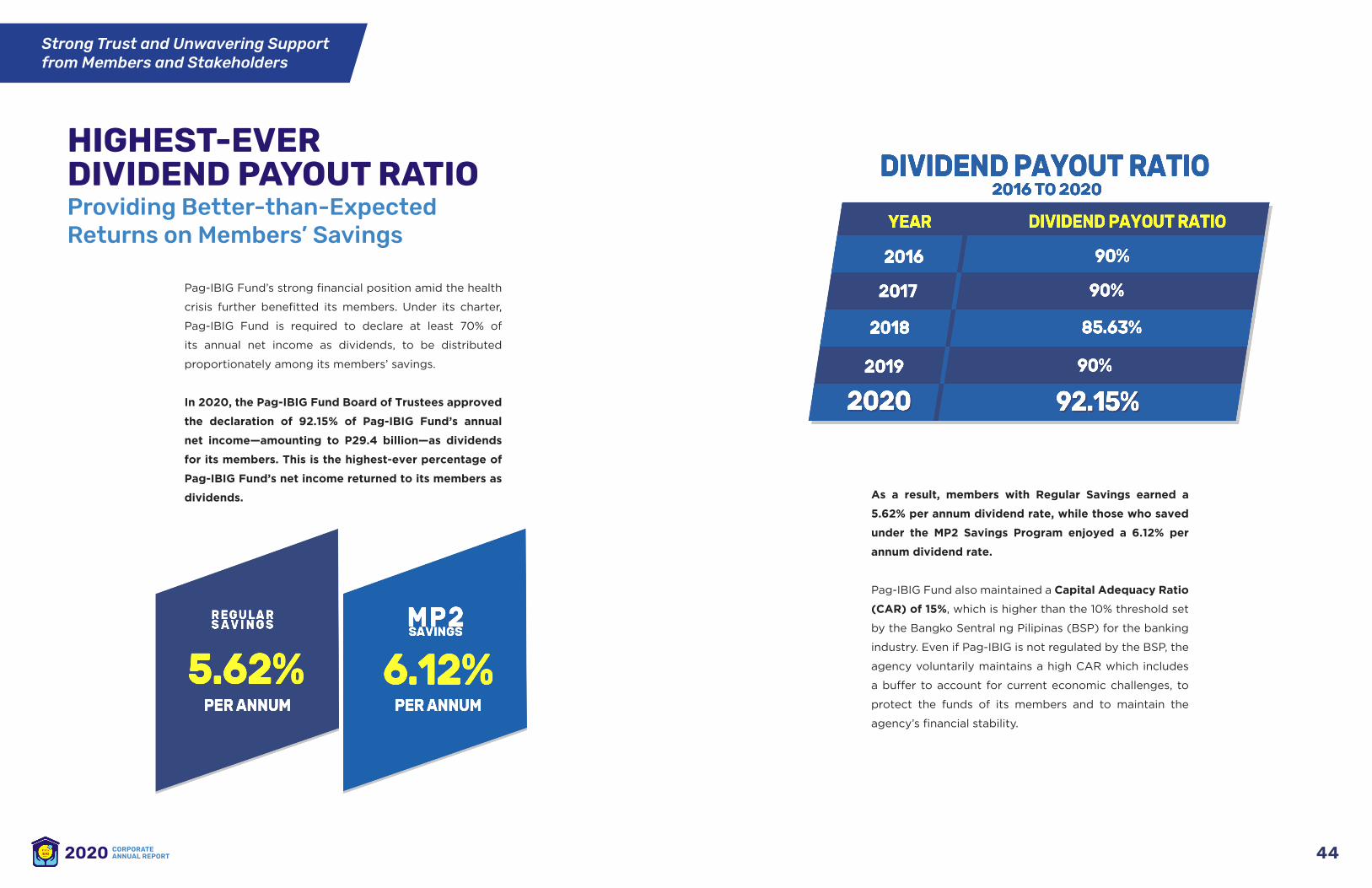

Pag-IBIG Fund’s strong financial position amid the health

crisis further benefitted its members. Under its charter,

Pag-IBIG Fund is required to declare at least 70% of

its annual net income as dividends, to be distributed

proportionately among its members’ savings.

In 2020, the Pag-IBIG Fund Board of Trustees approved

the declaration of 92.15% of Pag-IBIG Fund’s annual

net income—amounting to P29.4 billion—as dividends

for its members. This is the highest-ever percentage of

Pag-IBIG Fund’s net income returned to its members as

dividends.

HIGHEST-EVERDIVIDEND PAYOUT RATIOProviding Better-than-Expected Returns on Members’ Savings

Strong Trust and Unwavering Support from Members and Stakeholders

As a result, members with Regular Savings earned a

5.62% per annum dividend rate, while those who saved

under the MP2 Savings Program enjoyed a 6.12% per

annum dividend rate.

Pag-IBIG Fund also maintained a Capital Adequacy Ratio

(CAR) of 15%, which is higher than the 10% threshold set

by the Bangko Sentral ng Pilipinas (BSP) for the banking

industry. Even if Pag-IBIG is not regulated by the BSP, the

agency voluntarily maintains a high CAR which includes

a buffer to account for current economic challenges, to

protect the funds of its members and to maintain the

agency’s financial stability.

44CORPORATEANNUAL REPORT2020

Since its launch in 2012, Pag-IBIG Fund’s “I Do, I Do! Araw ng Pag-IBIG” has

been helping member-couples from the low-income sector to formalize their

unions.

On February 14, 2020, Pag-IBIG Fund conducted free mass wedding

celebrations in Manila and in eleven other locations nationwide, formalizing

the union of 979 Pag-IBIG Fund member-couples. And to ensure the health

and safety of guests and participants, Pag-IBIG Fund strictly implemented

measures following the recommendations of the Department of Health.

A part of the Pag-IBIG Fund’s corporate social responsibility activities, this

event aims to help Filipino families, especially those in the low-income

sector, recognize the value of savings through Pag-IBIG membership and

thereby gain better access to social benefits.

2020

“I DO, I DO! ARAW NG Pag-IBIG”

Strong Trust and Unwavering Support from Members and Stakeholders

Continuously promoting the valueof savingsamong the underserved

46CORPORATEANNUAL REPORT2020

LINGKOD Pag-IBIG AMID THE PANDEMICTapat na Serbisyo, Mula sa Puso

Strong Trust and Unwavering Support from Members and Stakeholders

Lingkod Pag-IBIG – the name Pag-IBIG Fund

officers and employees are aptly referred to –

remain steadfast in their committed service to the

Filipino worker.

At the heart of each Lingkod Pag-IBIG is the

agency’s core values of Professionalism, Integrity,

Excellence, Commitment and Service – values

which continue to drive them to serve members

and stakeholders, despite the challenges brought

about by the pandemic in their own professional

and personal lives.

In 2020, Pag-IBIG Fund established Anti-

COVID-19 guidelines following the government’s

health and safety protocols so that it can

continue to deliver its Lingkod Pag-IBIG Brand

of Service, “Tapat na Serbisyo, Mula sa Puso”

amid the pandemic, while ensuring the safety of

its own people and the transacting public.

These included the issuance of an office order

on Anti-COVID-19 measures, implementation

of a daily health self-assessment system, and

adherence to the prescribed health and safety

measures of the government which include

social distancing, temperature checks, wearing

of protective masks, frequent sanitation of

both personnel and transacting members in its

branches, and periodic sanitation of its branches

and offices.

48CORPORATEANNUAL REPORT2020

1. Special Award for the Pag-IBIG Fund Website from the Association of Development Financing Institution in Asia and the Pacific (ADFIAP) The Association of Development Financing Institution in Asia and the Pacific (ADFIAP) bestowed a Special Award to the Pag-IBIG Fund under the Best Website, Special Awards Category.

4. Continuous Improvement Recognition Award for the Virtual Pag-IBIG from the ASEAN Social Security Association (ASSA) The ASEAN Social Security Association recognized the Virtual Pag-IBIG with its Continuous Improvement Recognition Award for its visionary and time-to-time integrated developments allowing Pag-IBIG Fund to provide interruption-free and pandemic-ready service, amid the limitations caused by quarantine and safety protocols amid the health crisis.

5. Silver Award for Innovation in Government Services from the Asia-Pacific Stevie Awards The Asia-Pacific Stevie Awards gave a Silver Award to Pag-IBIG Fund, recognizing the Virtual Pag-IBIG as one of the best innovations in government services in the region.

6. Merit Award for the Virtual Pag-IBIG from the Association of Development Financing Institution in Asia and the Pacific (ADFIAP) The Association of Development Financing Institution in Asia and the Pacific (ADFIAP) also gave an Award of Merit for the technological developments made by the agency on its online service portal, Virtual PagIBIG. ADFIAP recognized how Pag-IBIG Fund’s innovation transcended boundaries and brought services closer to members, providing them convenience in accessing Pag-IBIG’s services anytime, anywhere.

2. Bronze Award for Innovationin Government Websites from the Asia-Pacific Stevie Awards The Asia-Pacific Stevie Awards also recognized the Pag-IBIG Fund’s Corporate Website with a Bronze Award under the category, Innovation in Government Websites. The agency’s enhanced corporate website which houses Virtual Pag-IBIG, has been instrumental in providing comprehensive information to members, while providing access to its key services – previously availed only in physical branches – online.

3. Circle of Excellence Award – Most Innovative Company of the Yearfrom the Asia CEO Awards

The Asia CEO Awards included Pag-IBIG Fund under its Circle of Excellence, being one of the Most Innovative Companies of the Year. Cited were its many corporate-wide reforms, led by technological advancements in particular, the Virtual Pag-IBIG.

AWARDS & RECOGNITIONof Pag-IBIG Fund

9th Consecutive Year Unqualified/ Unmodified Opinion (2012-2020)from the Commission on Audit (COA) For the 9th straight year, the Commission on Audit issued Pag-IBIG Fund with an Unmodified Opinion, citing the accurate and fair presentation of its financial statements. An unmodified opinion is the highest audit rating state auditors can give to a government agency.

ISO 9001:2015 Certification Pag-IBIG Fund maintained its ISO 9001:2015 Certification as its services and processes in Housing Loan, Short-Term Loan and Provident Benefit Claims, Membership Registration, and Loans Management and Window I and II Developer-Assisted Process, continued to meet the international standards set by the ISO.

12

34

5

6

50CORPORATEANNUAL REPORT2020

52CORPORATEANNUAL REPORT2020

54CORPORATEANNUAL REPORT2020

GOVERNANCE REPORT

Stakeholder Relationships

Pag-IBIG Fund works for the benefit and welfare of its stakeholders: (a) Pag-IBIG Fund Members, (b) Member-Employers, both Public and Private, (c) Private entities such as Cooperatives, Unions, or Other Similar Organizations, (d) government regulatory agencies (GOCCs and LGUs, GCG, BIR, DHSUD, CoA, etc), (e) the housing industry (i.e., Partner-Developers, (f) Banks and Other Financial Institutions, (g) Trustees, Officers and Employees of the Fund, (h) The Filipino Workers , (i) Non-member buyers of acquired assets, (j) service providers (such as collection partners, telcos, insurance concessionaires, etc), (k) Courts.

a. Pag-IBIG Fund Members

The core of Pag-IBIG Fund’s mandate is to protect and support the welfare of its members.

The Fund’s charter defines its members as “all employees covered by the Social Security System and the Government Service Insurance System, including uniformed members of the Armed Forces of the Philippines, the Bureau of Fire Protection, the Bureau of Jail Management and Penology, and the Philippine National Police”. Filipinos working overseas, and even those employed by foreign-based employers but working in the Philippines are also included. Full-time homemakers may also apply for membership on a voluntary basis, as well as those belonging to the Other Working Group.

In 2020, Pag-IBIG Fund extended support to its members to help address the challenges brought about by the calamities and the COVID-19 pandemic, following guidelines under Circular No. 375.

The Fund announced the availability of its Calamity Loan Program when the Taal Volcano erupted in January. A total of P3.84 billion in calamity loans was released benefiting 301,391 members in the affected areas. Likewise, when Typhoon Rolly hit Luzon, especially the Bicol area, in November, a total of P4.4 billion was made available for an estimated 226,170 affected member-borrowers.

When the threat of COVID-19 forced the government to implement quarantine controls throughout the country in its effort to curb possible infection in March, Pag-IBIG Fund was quick to respond to its members’ predicament.

Both Multi Purpose Loans and Calamity Loans were made available to members in areas where Enhanced Community Quarantine was implemented. This was availed by 151,948 members who collectively borrowed a total of P2.24 billion.

With the government’s issuance of Proclamation Nos. 929 and 922, declaring a State of Calamity and State of Public Health Emergency, Pag-IBIG Fund immediately issued Circular No. 432, granting moratorium on Short-Term Loan (STL) amortization, Housing Loan (HL) amortization/installment payments affected by the management of the COVID-19. A total of 320,406 applications (177,056 STL borrowers and 143, 350 HL borrowers) for moratorium were approved providing relief for borrowers and allowing them to use their funds for more urgent necessities.

In addition, when President Duterte signed into law Republic Act No. 11469 (Bayanihan to Heal as One Act), Pag-IBIG Fund issued Circular No. 433 providing the guidelines on the grant of mandatory 30-day grace period on all loans affected by the Enhanced Community Quarantine (ECQ) and its implementation period (17 March 2020 to 12 April 2020). More than P15 billion in loan amount was deferred for 4.77 million Pag-IBIG Member-borrowers. Of the number, about four million are STL borrowers and 713,225 are HL borrowers. HL borrowers were given further allowance when the ECQ was lifted, as the Fund extended the deadline of HL amortization payment within 30 calendar days through the issuance of Circular No. 435.

56CORPORATEANNUAL REPORT2020

Republic Act No. 11494 (Bayanihan to Recover as One Act) was issued in September 2020 to accelerate the country’s recovery against the pandemic. Pag-IBIG Fund complied with the issuance of Circular No. 438, which again provided a 60-day grace period on STL and HL payments.

Further, the Fund issued Circular No. 439, providing guidelines for the implementation of a Special Housing Loan Restructuring Program, which allowed Pag-IBIG HL borrowers to preserve their properties from foreclosure or cancellation of Contract to Sell/Deed of Conditional Sale (CTS/DCS) by providing them the opportunity to apply for penalty condonation or update, fully pay, or restructure their accounts under affordable and more beneficial terms and conditions. The said program was availed by 85,440 HL borrowers.

With the approval of the Resolution no. 3424, Pag-IBIG Fund also offered special promo rates on housing loans to encourage members to purchase a property despite the pandemic. These rates, which were already considered lowest in the market, were made even lower with the reduction of rates at 4.985% per annum under a 1-year repricing period and 5.375% per annum under a 3-year repricing period for housing loans. The promo rates benefitted a total of 32,256 accounts, amounting to P36.664 billion loan value. Following Resolution No. 3466, Pag-IBIG Fund also extended the coverage of these promo rates to borrowers whose applications were filed with the accredited developers during the promo period, but were not delivered to Pag-IBIG Fund on time due to the limitations caused by the community quarantines.

When the quarantine restrictions were relaxed in June 2020, Pag-IBIG Fund implemented measures to ensure the safety and security of its transacting public. Health screening and contact tracing efforts were installed in the branch entrance. Walk-ins were limited, and only those with face masks and face shields were allowed to go inside. Inside the branches, foot mat and alcohol dispensers were provided for disinfection, while acrylic barriers were mounted in counters to ensure proper distance between the Pag-IBIG front liner and the transacting members.

c. Cooperatives, Unions, or Other Similar Organizations

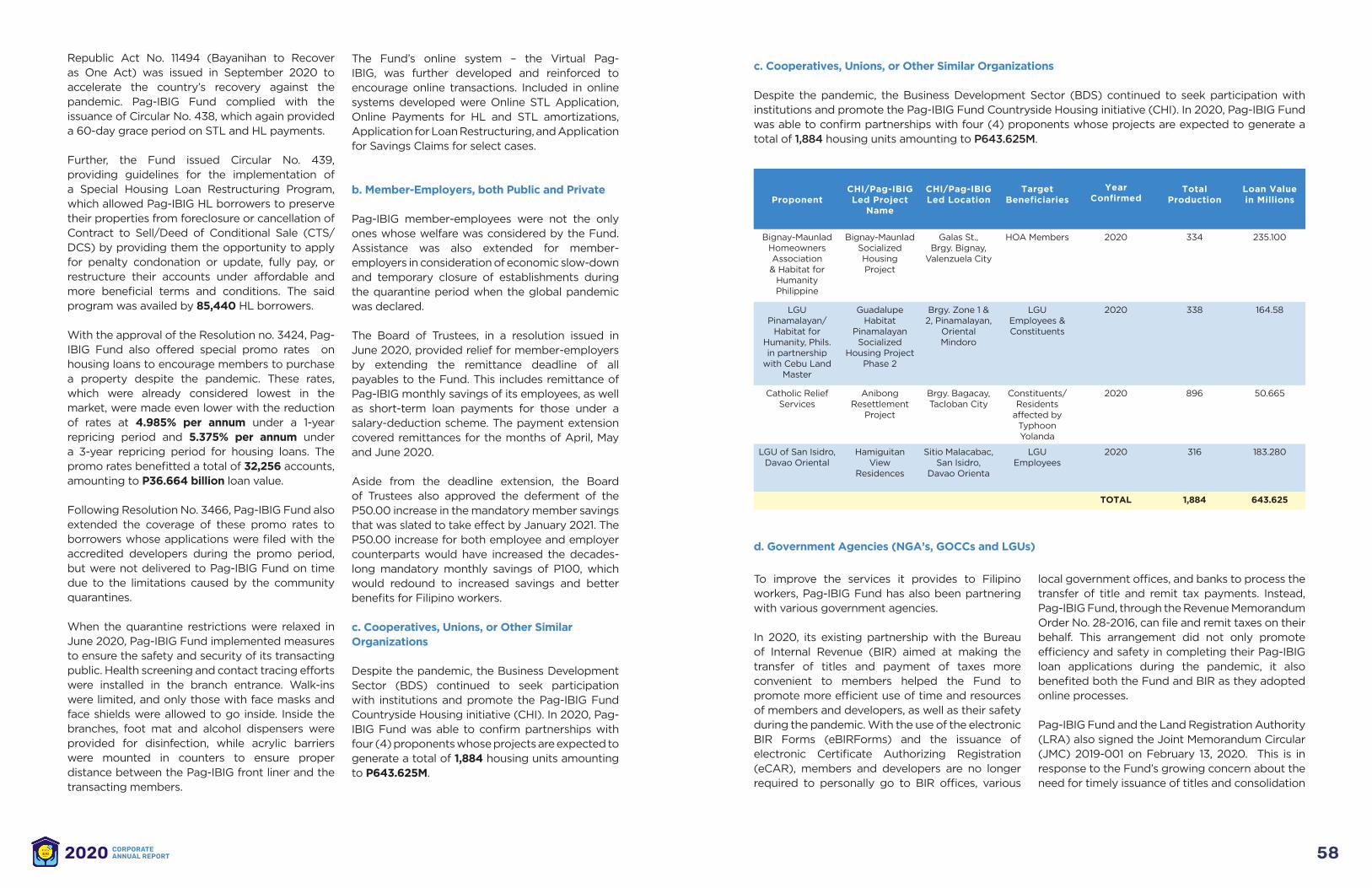

Despite the pandemic, the Business Development Sector (BDS) continued to seek participation with institutions and promote the Pag-IBIG Fund Countryside Housing initiative (CHI). In 2020, Pag-IBIG Fund was able to confirm partnerships with four (4) proponents whose projects are expected to generate a total of 1,884 housing units amounting to P643.625M.

d. Government Agencies (NGA’s, GOCCs and LGUs)

ProponentCHI/Pag-IBIG Led Project

Name

CHI/Pag-IBIG Led Location

Target Beneficiaries

Year Confirmed

Total Production

Loan Value in Millions

Bignay-Maunlad Homeowners Association & Habitat for

Humanity Philippine

Bignay-Maunlad Socialized Housing Project

Galas St., Brgy. Bignay,

Valenzuela City

HOA Members 2020 334 235.100

LGU Pinamalayan/

Habitat for Humanity, Phils.in partnership

with Cebu Land Master

Guadalupe Habitat

Pinamalayan Socialized

Housing Project Phase 2

Brgy. Zone 1 & 2, Pinamalayan,

Oriental Mindoro

LGUEmployees &Constituents

2020 338 164.58

Catholic ReliefServices

Anibong Resettlement

Project

Brgy. Bagacay, Tacloban City

Constituents/Residents

affected by Typhoon Yolanda

2020 896 50.665

LGU of San Isidro, Davao Oriental

Hamiguitan View

Residences

Sitio Malacabac, San Isidro,

Davao Orienta

LGUEmployees

2020 316 183.280

TOTAL 1,884 643.625

The Fund’s online system – the Virtual Pag-IBIG, was further developed and reinforced to encourage online transactions. Included in online systems developed were Online STL Application, Online Payments for HL and STL amortizations, Application for Loan Restructuring, and Application for Savings Claims for select cases.

b. Member-Employers, both Public and Private

Pag-IBIG member-employees were not the only ones whose welfare was considered by the Fund. Assistance was also extended for member-employers in consideration of economic slow-down and temporary closure of establishments during the quarantine period when the global pandemic was declared.

The Board of Trustees, in a resolution issued in June 2020, provided relief for member-employers by extending the remittance deadline of all payables to the Fund. This includes remittance of Pag-IBIG monthly savings of its employees, as well as short-term loan payments for those under a salary-deduction scheme. The payment extension covered remittances for the months of April, May and June 2020.

Aside from the deadline extension, the Board of Trustees also approved the deferment of the P50.00 increase in the mandatory member savings that was slated to take effect by January 2021. The P50.00 increase for both employee and employer counterparts would have increased the decades-long mandatory monthly savings of P100, which would redound to increased savings and better benefits for Filipino workers.

c. Cooperatives, Unions, or Other Similar Organizations

Despite the pandemic, the Business Development Sector (BDS) continued to seek participation with institutions and promote the Pag-IBIG Fund Countryside Housing initiative (CHI). In 2020, Pag-IBIG Fund was able to confirm partnerships with four (4) proponents whose projects are expected to generate a total of 1,884 housing units amounting to P643.625M.

To improve the services it provides to Filipino workers, Pag-IBIG Fund has also been partnering with various government agencies.

In 2020, its existing partnership with the Bureau of Internal Revenue (BIR) aimed at making the transfer of titles and payment of taxes more convenient to members helped the Fund to promote more efficient use of time and resources of members and developers, as well as their safety during the pandemic. With the use of the electronic BIR Forms (eBIRForms) and the issuance of electronic Certificate Authorizing Registration (eCAR), members and developers are no longer required to personally go to BIR offices, various

local government offices, and banks to process the transfer of title and remit tax payments. Instead, Pag-IBIG Fund, through the Revenue Memorandum Order No. 28-2016, can file and remit taxes on their behalf. This arrangement did not only promote efficiency and safety in completing their Pag-IBIG loan applications during the pandemic, it also benefited both the Fund and BIR as they adopted online processes.

Pag-IBIG Fund and the Land Registration Authority (LRA) also signed the Joint Memorandum Circular (JMC) 2019-001 on February 13, 2020. This is in response to the Fund’s growing concern about the need for timely issuance of titles and consolidation

58CORPORATEANNUAL REPORT2020

of the properties under the name of the Fund. The JMC was aimed to standardize all the transactions related to the Fund’s housing loan programs, so as to improve the processing time in the issuance of titles and other related documents. Its benefits are as follows:

· Faster delivery of services for both the Fund and the LRA; · Ease of transaction to the Fund’s borrowers and partner developers relative to the issuance of titles and mortgage annotation activities; · Faster way of consolidating properties in the name of the Fund; and · Significant savings for both the agencies

As of December 31, 2020

Regular 3,772

Agency-Hired Contractors 2,942

Job Order Workers 1,701

Allied Services 468

TOTAL 8,883

The pandemic has greatly affected how the Fund prioritized the benefits and activities that will cater to the safety, security, and welfare of its officers and staff.

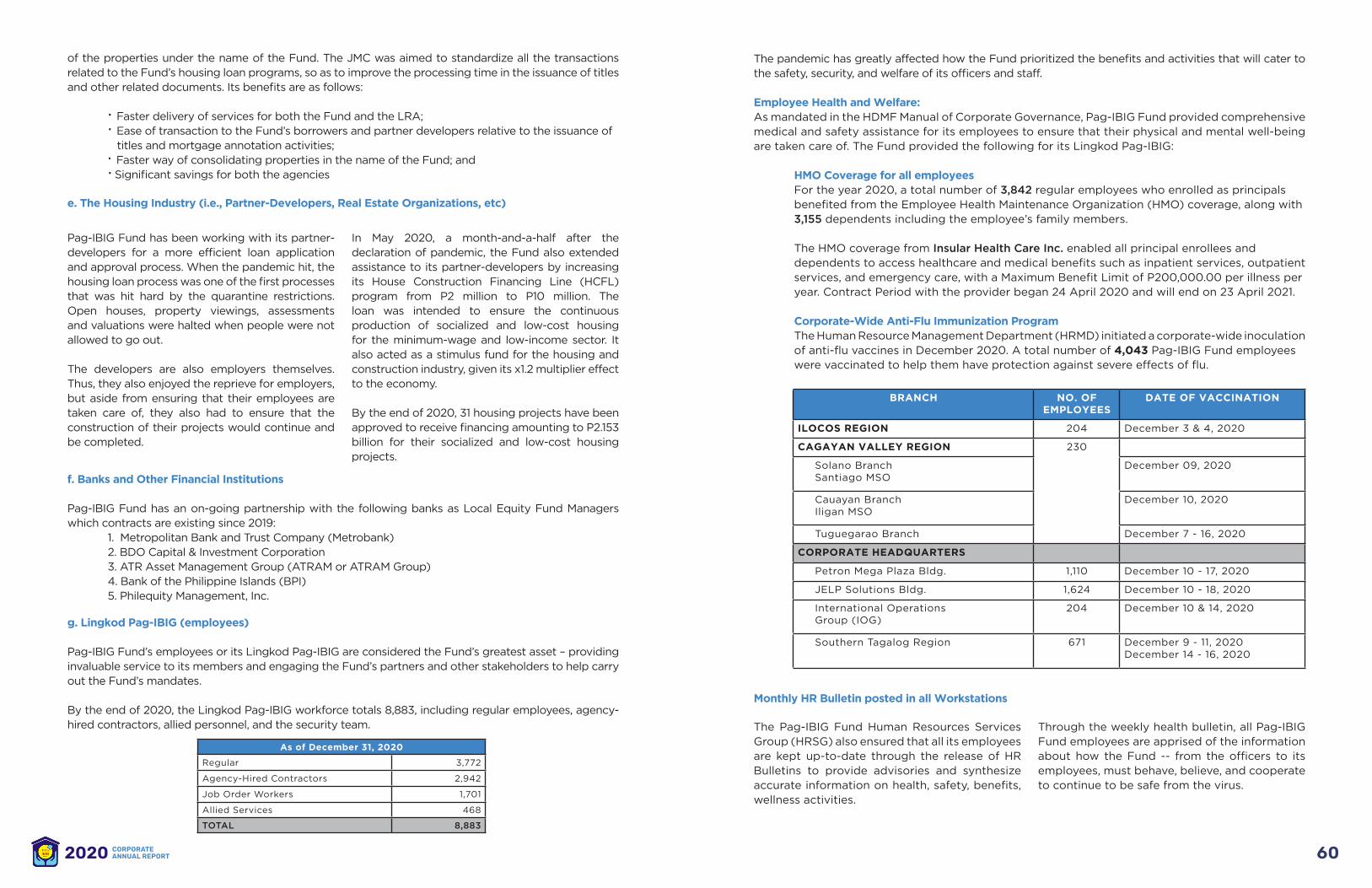

Employee Health and Welfare:As mandated in the HDMF Manual of Corporate Governance, Pag-IBIG Fund provided comprehensive medical and safety assistance for its employees to ensure that their physical and mental well-being are taken care of. The Fund provided the following for its Lingkod Pag-IBIG:

HMO Coverage for all employees For the year 2020, a total number of 3,842 regular employees who enrolled as principals benefited from the Employee Health Maintenance Organization (HMO) coverage, along with 3,155 dependents including the employee’s family members.

The HMO coverage from Insular Health Care Inc. enabled all principal enrollees and dependents to access healthcare and medical benefits such as inpatient services, outpatient services, and emergency care, with a Maximum Benefit Limit of P200,000.00 per illness per year. Contract Period with the provider began 24 April 2020 and will end on 23 April 2021.

Corporate-Wide Anti-Flu Immunization Program The Human Resource Management Department (HRMD) initiated a corporate-wide inoculation of anti-flu vaccines in December 2020. A total number of 4,043 Pag-IBIG Fund employees were vaccinated to help them have protection against severe effects of flu.

Monthly HR Bulletin posted in all Workstations

BRANCH NO. OF EMPLOYEES

DATE OF VACCINATION

ILOCOS REGION 204 December 3 & 4, 2020

CAGAYAN VALLEY REGION 230

Solano Branch Santiago MSO

December 09, 2020

Cauayan Branch Iligan MSO

December 10, 2020

Tuguegarao Branch December 7 - 16, 2020

CORPORATE HEADQUARTERS

Petron Mega Plaza Bldg. 1,110 December 10 - 17, 2020

JELP Solutions Bldg. 1,624 December 10 - 18, 2020

International Operations Group (IOG)

204 December 10 & 14, 2020

Southern Tagalog Region 671 December 9 - 11, 2020December 14 - 16, 2020

e. The Housing Industry (i.e., Partner-Developers, Real Estate Organizations, etc)

Pag-IBIG Fund has been working with its partner-developers for a more efficient loan application and approval process. When the pandemic hit, the housing loan process was one of the first processes that was hit hard by the quarantine restrictions. Open houses, property viewings, assessments and valuations were halted when people were not allowed to go out.

The developers are also employers themselves. Thus, they also enjoyed the reprieve for employers, but aside from ensuring that their employees are taken care of, they also had to ensure that the construction of their projects would continue and be completed.

In May 2020, a month-and-a-half after the declaration of pandemic, the Fund also extended assistance to its partner-developers by increasing its House Construction Financing Line (HCFL) program from P2 million to P10 million. The loan was intended to ensure the continuous production of socialized and low-cost housing for the minimum-wage and low-income sector. It also acted as a stimulus fund for the housing and construction industry, given its x1.2 multiplier effect to the economy.

By the end of 2020, 31 housing projects have been approved to receive financing amounting to P2.153 billion for their socialized and low-cost housing projects.

The Pag-IBIG Fund Human Resources Services Group (HRSG) also ensured that all its employees are kept up-to-date through the release of HR Bulletins to provide advisories and synthesize accurate information on health, safety, benefits, wellness activities.

Through the weekly health bulletin, all Pag-IBIG Fund employees are apprised of the information about how the Fund -- from the officers to its employees, must behave, believe, and cooperate to continue to be safe from the virus.

f. Banks and Other Financial Institutions Pag-IBIG Fund has an on-going partnership with the following banks as Local Equity Fund Managers which contracts are existing since 2019: 1. Metropolitan Bank and Trust Company (Metrobank) 2. BDO Capital & Investment Corporation 3. ATR Asset Management Group (ATRAM or ATRAM Group) 4. Bank of the Philippine Islands (BPI) 5. Philequity Management, Inc.

g. Lingkod Pag-IBIG (employees)

Pag-IBIG Fund’s employees or its Lingkod Pag-IBIG are considered the Fund’s greatest asset – providing invaluable service to its members and engaging the Fund’s partners and other stakeholders to help carry out the Fund’s mandates.

By the end of 2020, the Lingkod Pag-IBIG workforce totals 8,883, including regular employees, agency-hired contractors, allied personnel, and the security team.

60CORPORATEANNUAL REPORT2020

In 2020, 111 HR Bulletins were released by the HRSG, at least once every month.

To ensure that all Lingkod Pag-IBIG are informed, these bulletins were released through email advisories and e-bulletins which launched as start-up in Pag-IBIG-issued computers/workstations.

Briefing and Consultation Sessions with Health Experts

Monthly orientations, briefing sessions, and webinars with the Fund’s Infectious Disease Consultant (Dr. Yasmin Liboro) were also conducted in the months of July to November 2020, benefitting 1,182 participants from different offices and operating units of Pag-IBIG Fund.

In addition to these, more talks and consultations with health experts were made regarding various relevant wellness topics.

COVID-19 Internal Response

As the lead agency in the Philippines for home financing and cash loans, Pag-IBIG Fund’s operations have been affected by the COVID-19 pandemic. From a record-breaking year in 2019, the agency posted a H1 2020 gross income that’s 7.20% lower compared to the previous year.

Amid the pandemic, Pag-IBIG Fund’s top priority is to provide service, while ensuring the safety

Topic Date Conducted

Presenter Numberof Participants

Leptospirosis 17 December 2020

InLife accredited doctor

22

How to maximize the tele consult and the use of my pocket doctor

18 December 2020

Speaker from InLife 23

Maintaining Dental Health in the time of COVID-19

18 December 2020

Dr. Maria Clara Pilar (Issa) Reyes, Pag-IBIG dental consultant

32

2. An Alternative Work Arrangement aligned with the Civil Service Commission is implemented. Employees were divided into teams where one employee would report only thrice a week or less, to the office. Work from home arrangements were also implemented.

3. Door-to-door transportation and temporary shelter (if applicable) for all employees reporting to work was provided.

4. Personal protective equipment or PPEs were given to all workers (face masks, face shields, alcohol, disinfectants, and others) every month.

5. Constant monitoring of health and safety of all employees (through the Fund’s Daily Health Self-Assessment) in coordination with the medical experts, consultants and the agency’s HMO was conducted.

6. Acrylic barriers in all branches to limit physical contact were installed.

7. Offices were sanitized on a weekly basis. 8. All employees received remuneration on time. On top of this, they received loan payment relief in compliance to Philippine laws, RA 11469 and RA 11494 (includes suspension of loan deductions from employees’ payroll).

9. A Flu vaccination program was conducted for all employees in December 2020.

10. Weekly emails and reminders were sent from the Human Resources team and the CEO of Pag-IBIG Fund on safety reminders, guidelines, and recent updates about COVID-19. Assessment) in coordination with the medical experts, consultants and the agency’s HMO was conducted.

With all these efforts, Pag-IBIG Fund was able to remain in service of its members and stakeholders, while putting the health and welfare of its people first. Pag-IBIG Fund stands by its promise as the government agency you can truly count on in these difficult times.

of its people together with their families. Top executives of Pag-IBIG Fund knew that to fulfill its mandates and serve its members, its people must be taken care of above anything else. Hence, the agency initiated its own COVID-19 interventions to help its employees become well-informed, responsible and safe from the pandemic.

With this, the Pag-IBIG launched the following initiatives:

1. A four-part Office Order which states Pag-IBIG Fund’s Anti-COVID response was developed, disseminated, and implemented; grounded on the outputs of intensive research, discussions, and consultations with medical professionals, ensuring that every move to fight cross- infection in the office is science and evidence-based.

Employee Training The Pag-IBIG Fund Human Resources Development Department was able to facilitate the conduct of 94 training programs, for the benefit of a total of 4,438 participants.

Before the imposition of community quarantine restrictions in Metro Manila, 7 face-to-face trainings were conducted in January to March with 271 attendees. When minimum health standards were implemented to curb the spread of the COVID-19, Pag-IBIG Fund utilized the online platform as an alternative

medium to deliver these trainings. From the end of March 2020 to December 2020, 87 webinar sessions were conducted for the benefit of 4,167participants from various Pag-IBIG Fund offices and operating units nationwide.

The list and photo documentation of Employee Trainings conducted in 2020 can be accessed via the Pag-IBIG Fund Corporate Website > Employee Welfare > Trainings. (https://pagibigfund.gov.ph/EmployeeWelfare_Trainings_2020.html)

62CORPORATEANNUAL REPORT2020

h. The Filipino Workers

In 2020, Pag-IBIG Fund implemented a number of interventions to cover inactive or non-registered members of the workforce. These include the following programs/ plans: 1. Increasing Membership Level targets to achieve its goal of generating more Pag-IBIG Fund members; 2. Setting target on reactivating OFW members; 3. Rolling out of Lingkod Pag-IBIG on wheels; and 4. Establishment of offices in key areas (at least in every province and every major city

Stakeholder Communications

Corporate Social Responsibilityand Sustainability Development

Pag-IBIG Fund provides various channels, which the members can use to bring up their concerns and requests.

The Pag-IBIG Fund Corporate Website (www.pagibigfund.gov.ph) provides all the information about Pag-IBIG Fund, its programs, and services.

The Pag-IBIG Fund Contact Center (+632) 8724-4244) is a 24/7 call center facility, which the members may call for to inquire about their accounts, follow-up their loans, or simply to get an answer for their queries. With the pandemic, the Contact Center operations were reduced to within office hours, to comply with government guidelines and restrictions.

Pag-IBIG Fund also has a Chat facility in its website to provide members with the option to talk to a Lingkod Pag-IBIG employee real-time.

Members who prefer to engage Pag-IBIG Fund through writing may do so via Email ([email protected]). Inquiries, requests, or even complaints may be coursed through this facility. Depending on the member’s need, a Lingkod Pag-IBIG or a member of the Customer Service Audit Team will conduct a review of the request or complaint.

Members may also visit and follow Pag-IBIG Fund’s official Facebook page (https://www.facebook.com/PagIBIGFundOfficialPage/) and leave a direct message in the Messenger for their concerns

Pag-IBIG Fund also put up a Member Services Helpline https://www.pagibigfund.gov.ph/ helpline.html which was set-up to help resolve issues, problems, and delays in the processing of the member’s Multi-Purpose Loan or Provident Savings Claims.

The Fund’s contact points are accessible and available 24/7 for its stakeholders.

Virtual Events

The Pag-IBIG Fund also ensures that all relevant stakeholders are kept updated on the undertakings and state of the agency especially amid the pandemic through the conduct of the Pag-IBIG Fund Virtual Events spearheaded by its Public and Media Affairs Department.

In 2020, events like the Virtual Stakeholders’ Accomplishment Report (vStAR), Developers’ Technical Forum, Employers’ Virtual Forum, and Fund Coordinators’ Virtual Forum were conducted to engage partner-developers, employers, fund coordinators, and service partners, on the latest updates in the Fund’s programs and services.

Internal events like the Virtual State of the Fund Address (vSOFA) were also conducted per quarter to inform all Lingkod Pag-IBIG on how the different clusters (Member Services, Home Lending Operations, Support Services, and Corporate-Wide) performed for the year being.

Aside from its stakeholders’ welfare, Pag-IBIG Fund is also concerned with social responsibility and sustainability. Incorporated in its business processes and member servicing is the conscious effort to consider environmental protection and preservation, and public accountability.

Pag-IBIG Fund conducted the following activities related to its CSR program:

The Pag-IBIG Fund Home Lending Operations Cluster, in partnership with Lio Tourism Estate, organized a clean-up drive at Lio Beach and

Damilatan Beach in El Nido, Palawan last 30 January 2020 to promote recycling and waste reduction. Most of the trash collected were cigarette butts, candy/snacks/chips wrappers, plastic bags, ropes, straw, glass bottles and pet bottles, wood/planks, wires, nylon cords, and diapers. The garbage collected was brought to a recycling facility also located in El Nido.

Pag-IBIG Fund provides a section in the website for its CSR activities. (https://www.pagibigfund.gov.ph/EmployeeWelfare_CSR_2020.html)

Compliance to Ethical and Good Governance Standards

Pag-IBIG Fund strictly adheres to the provisions of RA No. 6173 or the Code of Conduct and Ethical Standards for Public Officials and Employees. Recognizing that public office is public trust, the HDMF Manual of Corporate Governance was developed, which provides the guidelines and ethical standards that a Lingkod Pag-IBIG must hold for himself while serving its stakeholders.

The Fund’s Code of Conduct is cascaded to each Lingkod Pag-IBIG during on-boarding for new hires. Employees are reminded of the ethical standards through regular emails dispatched by the Office of the CEO or the Human Resources Group.

A copy of the HDMF Manual of Corporate Governance is also uploaded in the Employee’s portal.

Among the provisions in the HDMF MCG is adherence to the No Gift Policy and No Noon Break.

In instances when a Lingkod Pag-IBIG is suspected or assumed to be in violation of the ethical standards, Pag-IBIG Fund formed a committee that will address such concerns. Adapting GCG’s Whistle-blowing Policy, Pag-IBIG Fund also implemented procedures that will allow witnesses to lodge complaints against illegal (including corruption) or unethical behavior. Whistle-blower reports may be sent to [email protected]. Reports submitted are treated with confidentiality.

The logo should not be intentionally cropped. Use Pag-IBIG Fund flag from CTB materials (similar to DHSUD style).

64CORPORATEANNUAL REPORT2020

SEC. EDUARDO D. DEL ROSARIODepartment of Human Settlements and Urban Development (DHSUD) Chairperson, Pag-IBIG Fund Board of Trustees

Retired Major General Eduardo D. del Rosario, Filipino, 64 years old, was appointed as Chairperson

of the (now-defunct) Housing and Urban Development Coordinating Council (HUDCC) on 12 July

2017 and as ad interim Secretary of the newly created Department of Human Settlements and Urban

Development (DHSUD) on 04 January 2020. On November 19, 2020, he was officially confirmed by

the Commission on Appointments (CA) to spearhead the department.

As HUDCC Chairperson, and now Secretary of Human Settlements and Urban Development,

Secretary del Rosario also sits as Chairperson of the 11-member Pag-IBIG Fund Board of Trustees.

He also serves as the Chairperson of key shelter agencies such as the National Housing Authority,

National Home Mortgage Finance Corporation, Social Housing Finance Corporation.

Secretary del Rosario served the military for nearly 37 years, until his compulsory retirement in

November 2012. He has occupied key positions in the Philippine military, which include serving as

General Officer-in-Charge of the Southern Luzon Command, Commander of the 2nd Infantry Division

of the Philippine Army, among others. He also headed “Task Force Kalihim” in August 2012, which

successfully conducted the search and retrieval operations for the remains of the late Department of

Interior and Local Government (DILG) Secretary Jesse M. Robredo from a plane wreckage under the

sea near the Province of Masbate. He received the Bakas Parangal ng Kabayanihan for accomplishing

this mission.

After his retirement from the military, Secretary del Rosario was appointed as the Administrator

of the Office of Civil Defense, while concurrently serving as the Executive Director of the National

Disaster Risk Reduction and Management Council (NDRRMC) from February 2013 to May 2014. On

30 June 2016, he was appointed as Undersecretary for Civil, Veterans and Retiree Affairs of the

Department of National Defense, a position he held until his appointment to HUDCC.

Secretary del Rosario also serves as head of “Task Force Bangon Marawi”, mandated to oversee the

rebuilding and rehabilitation of Marawi City.

Secretary del Rosario took up Bachelor of Science in Mechanical Engineering in Adamson University

before joining the Philippine Military Academy. He was a member of the 1980 Class Mapitagan,

graduating with a bachelor’s degree in Military Science. He holds a master’s degree in Public

Administration from the Philippine Christian University in 2012, and a master’s degree in Business

Administration from the Ateneo Graduate School of Business in 1994.

Secretary del Rosario has attended seminars on public governance and orientations about the key

shelter agencies’ operations.

Pag-IBIG FundBOARD OF TRUSTEES

66CORPORATEANNUAL REPORT2020

Finance chief and economist Carlos G. Dominguez III, Filipino, 75 years old, was appointed as

Secretary of the Department of Finance (DoF), and de facto Vice Chairperson of the Pag-IBIG Board

of Trustees on 30 June 2016.

As Finance Secretary, he also serves as Chairperson of the Land Bank of the Philippines (LBP), the

Philippine Deposit Insurance Corporation (PDIC), Philippine Guarantee Corporation, and is a member

of the Monetary Board of the Bangko Sentral ng Pilipinas (BSP).

Sec. Dominguez has over 40 years of experience in both the government and the private sector. He

began his career in government service in 1986 when he served at the helm of the Ministry of Natural

Resources, and then with the Department of Agriculture in 1987. He left government service in 1989

and held top executive posts and chairmanship in the private sector, most notably as Chairperson and

President of Philippine Airlines (1993 - 1995), and the Philippine Tobacco Flue-Curing and Redrying

Corporation (1992 - 2016). His family also owns the prestigious Marco Polo Hotel in Davao City.

He returned to public service in 2016 as Finance Secretary to support his childhood friend and

classmate President Rodrigo Roa Duterte.

Sec. Dominguez graduated from the Ateneo de Manila University with a bachelor’s degree in

Economics (1965), and a master’s degree in Business Administration (1969). In 1982, he completed

the Executive Management Program offered by Stanford University’s Graduate School of Business.

Chief Executive Officer Acmad Rizaldy P. Moti, Filipino, 46 years old, was appointed as head of Pag-

IBIG Fund on 17 May 2017.

After graduating from the University of the Philippines in 1995, CEO Moti began his professional

career as a faculty member in his alma mater. In November 1998, he started his career as a banker

with Asia United Bank (AUB), leaving a couple of years later to launch the web development start-

up agency, 25by8, where he manned its daily operations. He went back to AUB in 2006, and then

became the Vice President for Chinatrust (Philippines) Commercial Bank Corporation, where he

managed the Software Development and Maintenance Group.

He joined Pag-IBIG Fund as Senior Vice President for the Information Technology Services Sector in 2008, where he led the foundation of Pag-IBIG Fund’s integrated and innovative computer systems of today. He was then tasked to lead the agency’s Home Lending Operations Cluster in 2011, where he then initiated policy reforms to improve Pag-IBIG Fund’s Housing Loan programs. In March 2017, he was assigned as the agency’s officer-in-charge until he was appointed as Pag-IBIG Fund Chief Executive Officer by President Rodrigo Duterte in May 2017.

Under his leadership, Pag-IBIG Fund achieved consecutive banner years, with the agency achievingrecord-highs in housing loan releases, members’ savings collections, dividend rates on members’ savings, performing loans, net income, and customer satisfaction ratings.

He continues to lead Pag-IBIG Fund amid the pandemic, through the implementation of responsiveprograms and in delivering the Lingkod Pag-IBIG brand of service: Tapat na Serbisyo, Mula sa Puso – to aid members, stakeholders and the nation cope and move forward in its journey to recovery.

CEO Moti is a Computer Science degree holder from the University of the Philippines, obtaining a bachelor’s degree in 1995 and has completed all academic requirements towards a master’s degree in 2000.

He attended the virtual Advanced Corporate Governance Program (20 November 2020 & 28 January 2021), and also attended trainings on Equity Portfolio Management and Corporate Governance Orientation Program for Government Owned and Controlled Corporations (GOCCs) last 2019 and 2018, respectively.

SEC. CARLOS G. DOMINGUEZ IIIDepartment of Finance (DOF) Vice Chairperson, Pag-IBIG Fund Board of Trustees

ACMAD RIZALDY P. MOTIChief Executive Officer, Pag-IBIG Fund (HDMF)

68CORPORATEANNUAL REPORT2020

Sec. Wendel E. Avisado, Filipino, 67 years old, was appointed as the Secretary for the Department of

Budget and Management on 05 August 2019.

Sec. Avisado has an established career in public service, notable for his leadership and innovation.

He was the Regional Director of the Department of Interior and Local Government (DILG) - Region

XI, from April 1986 to December 1992, and then for Region XII after until March 1993.

He left government service in March 1993 to become the Vice President for Legal and External

Affairs ofthe JVA Management Corporation – a position he held until June 1998, and would assume