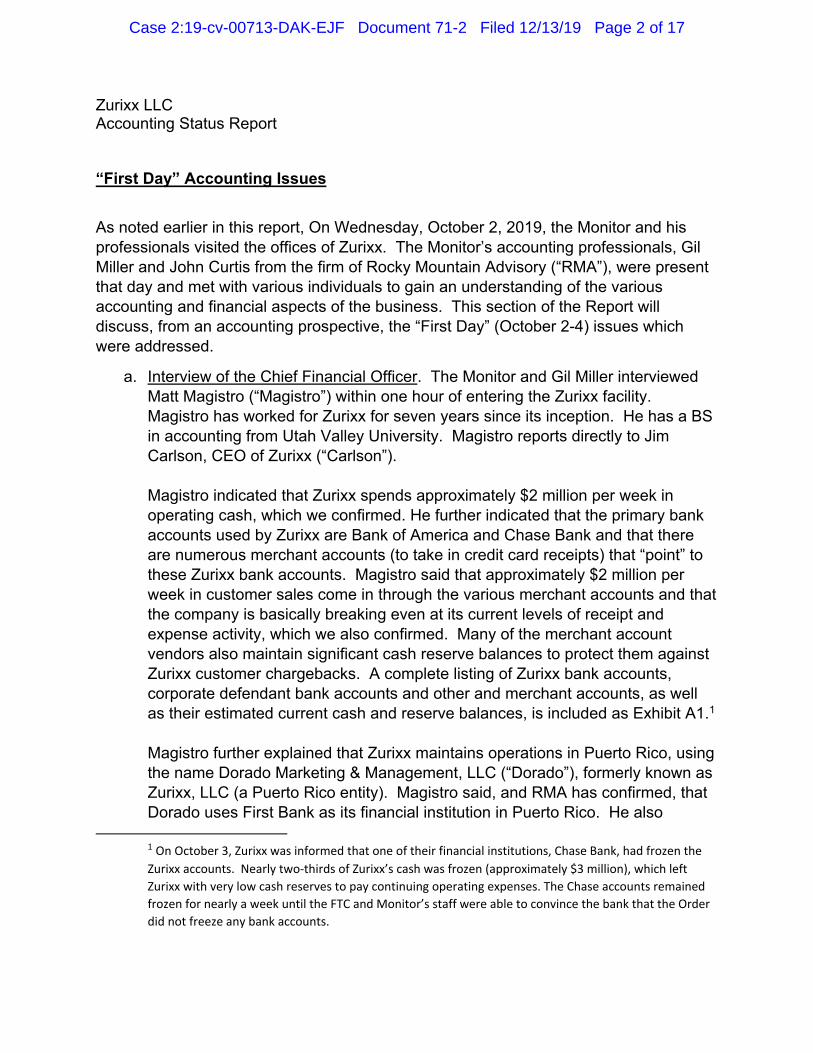

2019-12-13no071 Monitor's Report.pdf - Zurixx

388

Doyle S. Byers, #11440 Cory A. Talbot, #11477 Engels J. Tejeda, #11427 Chelsea J. Davis, #16436 HOLLAND & HART LLP 222 S. Main Street, Suite 2200 Salt Lake City, UT 84101 Telephone: (801) 799-5800 Facsimile: (801) 799-5700 Attorneys for David K. Broadbent as Court- Appointed Receiver UNITED STATES DISTRICT COURT FOR THE DISTRICT OF UTAH, CENTRAL DIVISION FEDERAL TRADE COMMISSION, and UTAH DIVISION OF CONSUMER PROTECTION, Plaintiffs, vs. ZURIXX, LLC, a Utah limited liability company, CARLSON DEVELOPMENT GROUP, LLC, a Utah limited liability company, CJ SEMINAR HOLDINGS, LLC, a Utah limited liability company, ZURIXX FINANCIAL, LLC, a Utah limited liability company, CRISTOPHER A. CANNON, individually and as an officer of ZURIXX, LLC, JAMES M. CARLSON, individually and as an officer of ZURIXX, LLC, and JEFFREY D. SPANGLER, individually and as an officer of ZURIXX, LLC, Defendants. MONITOR’S REPORT Case Number 2:19-cv-00713 Case 2:19-cv-00713-DAK-EJF Document 71 Filed 12/13/19 Page 1 of 21

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of 2019-12-13no071 Monitor's Report.pdf - Zurixx

Doyle S. Byers, #11440 Cory A. Talbot, #11477 Engels J. Tejeda, #11427 Chelsea J. Davis, #16436 HOLLAND & HART LLP 222 S. Main Street, Suite 2200 Salt Lake City, UT 84101 Telephone: (801) 799-5800 Facsimile: (801) 799-5700 Attorneys for David K. Broadbent as Court- Appointed Receiver

UNITED STATES DISTRICT COURT FOR THE DISTRICT OF UTAH, CENTRAL DIVISION

FEDERAL TRADE COMMISSION, and UTAH DIVISION OF CONSUMER PROTECTION, Plaintiffs, vs. ZURIXX, LLC, a Utah limited liability company, CARLSON DEVELOPMENT GROUP, LLC, a Utah limited liability company, CJ SEMINAR HOLDINGS, LLC, a Utah limited liability company, ZURIXX FINANCIAL, LLC, a Utah limited liability company, CRISTOPHER A. CANNON, individually and as an officer of ZURIXX, LLC, JAMES M. CARLSON, individually and as an officer of ZURIXX, LLC, and JEFFREY D. SPANGLER, individually and as an officer of ZURIXX, LLC, Defendants.

MONITOR’S REPORT Case Number 2:19-cv-00713

Case 2:19-cv-00713-DAK-EJF Document 71 Filed 12/13/19 Page 1 of 21

2

On October 1, 2019, the Court entered its Ex Parte Temporary Restraining Order with

Asset Preservation, Appointment of a Temporary Monitor over Corporate Defendants, and Other

Equitable Relief, and Order to Show Cause Why a Preliminary Injunction Should Not Issue (Dkt.

No. 24) (the “Order”). The Order appointed David K. Broadbent as the “temporary monitor for

the Monitored Entities and any of their affiliates, subsidiaries, successors, and assigns, wherever

located,”1 (Order § X), and directed him to submit this Report “prior to the preliminary

injunction show cause hearing set by Section XXII of this Order” with “the Monitor’s findings,

including” the following:

A. The Monitored Entities’ compliance with this Order;

B. An accounting of the Monitored Entities’ financial transactions as they relate to the practices charged in the Complaint or Defendants’ Products;

C. A description of the Monitored Entities’ corporate structures including all parents, subsidiaries (whether wholly or partially owned), divisions (whether incorporated or not), affiliates, branches, charters, joint ventures, partnerships, franchises, operations under assumed names, and all ownership interests of the Monitored Entities.

(Order § XII at 20.)

However, before the Report was submitted, the parties agreed to a Stipulated Preliminary

Injunction (Dkt. No. 54) (the “Injunction”). In light of that stipulation, the Court vacated the

preliminary injunction show cause hearing, (see Dkt. No. 53), thereby eliminating the

1 The Order defined the “Monitored Entities” as the “Corporate Defendants and any other entity that has conducted any business related to the marketing or sale of Defendants’ Products, including receipt of Assets derived from any activity that is subject of the Complaint in this matter, and that the Monitor determines is controlled or owned by any Defendant.” (Order at 7.) The “Corporate Defendants,” in turn, were defined as “Zurixx, LLC, Carlson Development Group, LLC, CJ Seminar Holdings, LLC, and Zurixx Financial, LLC, and each of their subsidiaries, affiliates, successors, and assigns.” (Id. at 6.)

Case 2:19-cv-00713-DAK-EJF Document 71 Filed 12/13/19 Page 2 of 21

3

requirement to file the report discussed above. The Injunction also did away with the role of

temporary monitor and, instead, appointed “David K. Broadbent . . . as receiver over the

Receivership Entities with full powers of an equity receiver.” (Injunction at 17 § XIV.)

Following that appointment, the Court requested that Mr. Broadbent (the “Monitor” or the

“Receiver”)2 submit this Report.

REPORT

I. Summary of the Monitor’s work

The Court entered its Order appointing the Monitor on October 1, 2019. That same day,

the Monitor met with personnel from the FTC and Division to discuss gathering information and

documents from Defendants consistent with the terms of the Order. The next day, the Monitor

and his team went to the headquarters of Zurixx, LLC in Cottonwood Heights, Utah, with law

enforcement and personnel from the FTC and Division. Investigators from the FTC obtained

documents, including electronic documents, and the Monitor and his team obtained documents

and began interviews with personnel from the Monitored Entities.

The Monitor’s team interviewed each of the Individual Defendants, as well as the heads

of Zurixx’s departments and various members of those departments. The Monitor’s team

requested and reviewed a significant number of documents, although many document requests

were unfulfilled at the time the Court appointed Mr. Broadbent as the Receiver. The Monitor’s

team also listened to many recorded sales events put on by the Monitored Entities and to many

2 Unless otherwise noted, defined terms are taken from the Injunction.

Case 2:19-cv-00713-DAK-EJF Document 71 Filed 12/13/19 Page 3 of 21

4

recorded sales calls put on by the Monitored Entities from both before and during the time of the

Monitor’s appointment.

II. The Monitor’s findings

A. Description of the Monitored Entities’ corporate structures

The Court ordered the Monitor to provide “[a] description of the Monitored Entities’

corporate structures including all parents, subsidiaries (whether wholly or partially owned),

divisions (whether incorporated or not), affiliates, branches, charters, joint ventures, partnerships,

franchises, operations under assumed names, and all ownership interests of the Monitored

Entities.” (Order § XII(C) at 20.)

Defendants develop, market, sell, and fulfill “financial education programs” throughout

the United States and Canada. (Zurixx, LLC. United States Transfer Pricing Documentation for

the 2017 Tax Year, attached as Ex. 1, at 8.) These programs start with free two-to-three hour

preview meetings, characterized by the Monitored Entities as “comprehensive educational

seminars,” which are, in fact, events designed to sell consumers, or “students,” access to paid

three-day workshops. Following the workshops, Defendants sell students additional services:

advanced training camps, coaching services, mentoring services, and summits. Defendant Jim

Carlson confirmed that the following generally represents Defendants’ product funnel:

Case 2:19-cv-00713-DAK-EJF Document 71 Filed 12/13/19 Page 4 of 21

5

(Ex. 1 at 13.) Defendants’ programs are tied to, and promoted by, various “celebrities” to provide

real estate, business strategy, entrepreneurship, and coaching and mentoring programs.

The Monitored Entities are comprised of four groups of entities: (1) Zurixx, LLC; (2)

Dorado Marketing & Management, LLC; (3) Brand Management Holdings, LLC and

subsidiaries; and (4) Global Learning Alliance, LLC. As of October 2, 2019, there were

approximately 100 employees of Zurixx, LLC and 20 employees of Dorado Marketing &

Management, LLC. Beyond that, Zurixx, LLC paid several hundred “independent contractors”

over the course of a normal calendar year, which made up about 80% of the Monitored Entities’

payroll.

Turning to the organizational structure, the available ownership information for these

entities was incomplete and, in some instances, inconsistent. That said, the Monitor believes that

these entities are structured as follows:

Preview Workshop

1111 111

Coaching

Mentorship

Advanced camps

Backend support

Case 2:19-cv-00713-DAK-EJF Document 71 Filed 12/13/19 Page 5 of 21

6

Zurixx, LLC3

Zurixx, LLC operates events – preview seminars, workshops, summits, etc. – and

fulfillment in the United States and Canada. It does business under multiple names, including

Flipping Formula Education, Success Path Education, Advanced Real Estate Education, Shark

Academy, Advanced Financial Training, Daymond John Success Formula, Financial Education,

In-Source Connection LLC, Premium Corporate Services, Rules of Renovation, USA Loan

Processing, Premium Financial Training, and Launch Academy.

Zurixx, LLC offered a number of educational programs, which it described as follows:

3 The Receiver is not confident that this chart accurately reflects the corporate structure. The articles of organization for Zurixx Financial, LLC say that Carlson and Carlson Development Group, LLC are the members. Also, there are many missing organizational documents. For instance, the Receiver has no corporate documents for CJ Seminar Holdings, LLC, CAC Investment Holdings, LLC, JSS Investment Holdings, or Carlson Development Group, LLC. Also, according to Carlson, the Sofia Reyes Descendants Trust provided an initial cash investment in the business and is now only a “silent partner.” The Receiver continues to investigate this.

James M. Carlson

Carlson Development Group, LLC (UT)

Sofia Reyes Descendants Trust

Zurixx Financial, LLC (UT)

Jeffrey D. Spangler

JSS Investment Holdings, LLC

Zurixx, LLC (UT)

Cristopher A. Cannon

CAC Investment Holdings, LLC

CJ Seminar Holdings, LLC

Case 2:19-cv-00713-DAK-EJF Document 71 Filed 12/13/19 Page 6 of 21

7

Success Path Education: This real estate training “workshop teaches participants how to

successfully renovate and ‘flip’ houses by focusing on topics like business planning and goal

setting, asset protection, acquisition funding, and legal entity formation.” (Ex. 1 at 11.) The

program is built around celebrities Tarek El Mousa and Christina Anstead from HGTV’s “Flip or

Flop.”

Daymond John’s Launch Academy: This entrepreneurial workshop is designed to “help[]

prospective entrepreneurs make the transition from an idea to the actual launch of a business,”

and to “teach participants strategies to manage money, position the business, and creat[e] a

legacy.” (Id. at 12.) Daymond John appears as an investor on the ABC reality television show

“Shark Tank.”

The Flipping Formula: This program is similar to Success Path Education in that

“participants learn how to find unlisted properties, which are below market value, obtain

financing, create cash flow, and complete a wholesale real estate transaction in 60 to 90-days.”

The program is a “partnership” with Pete Souhleris and Dave Seymour of the A&E reality TV

show “Flipping Boston.”

Winning the Property War: This educational program provides “flipping and wholesaling

strategies” from Doug Hopkins (of the Discovery Channel series “Property Wars”) and Damon

Line.

Property Bank: Another real estate educational program, Property Bank “teaches

participants how to find growth and wealth opportunities.” The program was created by Mike

Baird (Spike TV’s “Flip Men”) and Greg Herlean (author of “Bank on This”).

Case 2:19-cv-00713-DAK-EJF Document 71 Filed 12/13/19 Page 7 of 21

8

Additional educational programs are associated with other celebrities, such as author and

sales trainer Grant Cardone (10X), Robert Herjabec (“Shark Tank”), and Hillary Farr (HGTV’s

“Love It or List It”).

Dorado Group

By agreement, Dorado Marketing & Management, LLC (“Dorado”) provides services to

Zurixx, LLC, primarily marketing, event management, and celebrity contract management.

Dorado also provides administrative executive support for marketing and events.4

4 Dorado is based in Dorado, Puerto Rico. It appears that the tie to Puerto Rico is based on tax incentives related to Puerto Rico’s Act No. 20 of 2012, as amended, known as the “Export Services Act,” “the Act,” or “Act 20,” which established incentives designed to stimulate the development of a wide variety of ventures in Puerto Rico, including the export of services.

James M. Carlson

Carlson Development Group, LLC(PR)

Sofia Reyes Descendants Trust

Jeffrey D. Spangler

JSS Investment Holdings, LLC

Zurixx Financial, LLC(PR)

SO%

Dorado Marketing & Management, LLC

Cristopher A. Cannon

CAC Investment Holdings, LLC(PR)

Case 2:19-cv-00713-DAK-EJF Document 71 Filed 12/13/19 Page 8 of 21

9

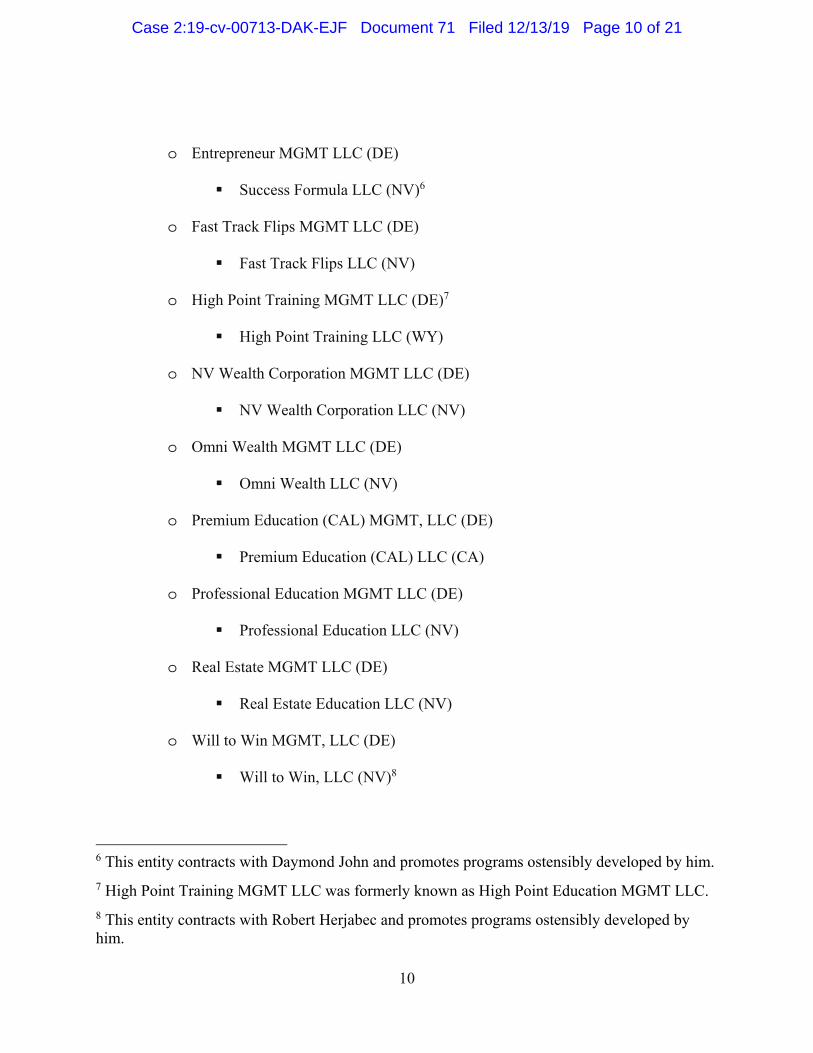

Brand Management Group

Via its network of wholly-owned limited liability companies, Brand Management

Holdings, LLC (“Brand Management”) contracts with the various celebrities who partner with

Zurixx to put on financial education programs. Brand Management’s network is structured such

that the bottom-level company contracts with celebrities and customers. Because the chart is

difficult to read, below is the ownership structure in bullet-point format:

• Brand Management Holdings LLC (DE)5

o Advanced Education (CA) MGMT, LLC (DE)

Advanced Education (CA), LLC (UT)

o Attainable Events MGMT LLC (DE)

Attainable Events LLC (WY)

o Breakthrough Events MGMT LLC (DE)

5 Indicates state of entity organization.

Attalnable EventsllC

James M.Carlson

Carlson Development Group, LLC (UT)

.,,.

Fast Track Flips MGMTLLC

Fast Track Flips LLC

SO%

JeffreyO.Spangler

NV Wealth Corporation MGMTLLC

NV Wealth Corporation LLC

SO%

Cristopher A. Cannon

Case 2:19-cv-00713-DAK-EJF Document 71 Filed 12/13/19 Page 9 of 21

10

o Entrepreneur MGMT LLC (DE)

Success Formula LLC (NV)6

o Fast Track Flips MGMT LLC (DE)

Fast Track Flips LLC (NV)

o High Point Training MGMT LLC (DE)7

High Point Training LLC (WY)

o NV Wealth Corporation MGMT LLC (DE)

NV Wealth Corporation LLC (NV)

o Omni Wealth MGMT LLC (DE)

Omni Wealth LLC (NV)

o Premium Education (CAL) MGMT, LLC (DE)

Premium Education (CAL) LLC (CA)

o Professional Education MGMT LLC (DE)

Professional Education LLC (NV)

o Real Estate MGMT LLC (DE)

Real Estate Education LLC (NV)

o Will to Win MGMT, LLC (DE)

Will to Win, LLC (NV)8

6 This entity contracts with Daymond John and promotes programs ostensibly developed by him. 7 High Point Training MGMT LLC was formerly known as High Point Education MGMT LLC. 8 This entity contracts with Robert Herjabec and promotes programs ostensibly developed by him.

Case 2:19-cv-00713-DAK-EJF Document 71 Filed 12/13/19 Page 10 of 21

11

Defendants’ documents reflect that the following Monitored Entities are “inactive or not

needed”:

• Breakthrough Events Mgmt LLC (DE)

• Breakthrough Events LLC (TX)

• Education Annex MGMT LLC (DE)9

• Education Annex LLC (NV)10

• Misc Real Estate MGMT LLC (DE)

• Zurixx Marketing, LLC (WY)

• Continuing Real Estate Education (WY)11

o According to Carlson, this entity was initially created for contracting with

celebrities Tarek and Christina El Mousa, but is dormant and was never used.

Finally, RE Cash Source is a wholly-owned subsidiary of Zurixx Financial, LLC. It was

created to provide bridge loans for students to purchase rental properties from vendors associated

with Zurixx, LLC’s Las Vegas Summit event. According to Carlson, RE Cash Source generated

significant losses and ceased lending in or about 2014. RE Cash Source does still have some

outstanding loans, but does not function otherwise.

9 This entity appears to have been dissolved as of February 12, 2019. 10 This entity appears to have been dissolved as of February 12, 2019. 11 Continuing Real Estate Education was formerly known as Success Path Education.

Case 2:19-cv-00713-DAK-EJF Document 71 Filed 12/13/19 Page 11 of 21

12

Global Learning Alliance Group

Global Learning Alliance, LLC was purchased to put on large-scale events attended by

celebrities and customers. Citing lack of profitability, Carlson stated that this business was being

shut down at the time of the Monitor’s appointment.

B. Accounting of the Monitored Entities’ financial transactions as they relate to the practices charged in the Complaint or Defendants’ Products

The Receiver retained Rocky Mountain Advisory (“RMA”) as accounting professionals.

RMA prepared an Accounting Status Report as of October 31, 2019. The Accounting Status

Report is submitted with this Report at Exhibit 2.12

C. The Monitored Entities’ compliance with the Order

The Order imposed a variety of restrictions on the Monitored Entities.

1. Compliance with Section I of the Order

The Court enjoined the Monitored Entities and others from engaging in a variety of

business activities in Section One of the Order:

IT IS THEREFORE ORDERED that Defendants, Defendants’ officers, agents, employees, and attorneys, and all other Persons in active concert or participation

12 Several exhibits to the Accounting Status Report contain confidential information, which is redacted for purposes of this filing. However, the Receiver will provide unredacted copies of the Accounting Status Report to the Court and parties.

James M. Carlson Jeffrey D. Spangler

Global Learning Alliance, LLC

JSS Investment Holdings, LLC

Cristopher A. Cannon

CJ Seminar Holdings, LLC

Case 2:19-cv-00713-DAK-EJF Document 71 Filed 12/13/19 Page 12 of 21

13

with them, who receive actual notice of this Order by personal service or otherwise, whether acting directly or indirectly, in connection with the advertising, marketing, promoting, or offering for sale of any goods or services, are temporarily restrained and enjoined from:

A. Making any Earnings Claim, unless the Earnings Claim is truthful and not misleading, and, at the time such claim is made, Defendants: (1) have a reasonable basis for the claim; (2) have in their possession written materials that substantiate the claim; and (3) make the written substantiation available upon request to the consumer, potential purchaser or investor, the Monitor, and Plaintiffs;

B. Misrepresenting or assisting others in misrepresenting, expressly or by implication, that:

1. Consumers who purchase any of Defendants’ Products will receive 100% funding to do real estate deals regardless of their credit;

2. Defendants’ Products allow consumers to make thousands of dollars in profit through real estate investing with little time and effort;

3. Consumers will learn everything they need to know at Defendants’ 3-day workshops to make thousands of dollars in profit through real estate investing;

C. Misrepresenting or assisting others in misrepresenting, expressly or by implication, any other fact material to consumers concerning any good or service, such as: the total costs; any material restrictions, limitations, or conditions; or any material aspect of its performance, efficacy, nature, or central characteristics;

D. Failing to disclose, or disclose adequately, to consumers material aspects of Defendants’ refund policy; and

E. Offering Defendants’ Products for sale without complying with BODA, including filing required information annually with the Division, providing a disclosure statement or prospectus to any prospective purchaser at least 10 business days prior to a purchase, and providing the required warning to purchasers following an earnings representation that: Defendants cannot guarantee earnings or ranges of earning; identifying the number of purchasers who had earned an amount in excess of the amount of their payment; and clarifying what percentage of total purchasers had earned an amount in excess of the amount of their payment.

Case 2:19-cv-00713-DAK-EJF Document 71 Filed 12/13/19 Page 13 of 21

14

(Order § 1 at 8-9.)

The Individual Defendants and employees cooperated with the Monitor in interviews.

Responses to requests for documents, computers, and other materials were frequently delayed,

and numerous requests from the Monitor were outstanding upon appointment of the Receiver.

The Monitor had significant concerns regarding the Monitored Entities’ consumer

protection compliance program. Based on interviews with the Monitored Entities’ personnel, the

Monitor understands that the program uncovered violations of consumer protection laws on a

weekly basis from preview events, workshops, and other consumer presentations. While the

Monitored Entities’ personnel indicated that violators were subject to discipline up to

termination, no information was provided to substantiate the use of the disciplinary system.

Moreover, the compliance program did not, apparently, cover tele-sales, a significant source of

business for the Monitored Entities. The Monitor was not able to ascertain further details

regarding the compliance program because Defendants took the position that the content was

protected by the attorney-client privilege.

The Monitor’s team listened to many recorded preview events, workshops, and telephone

conversations that pre-dated and post-dated the Monitor’s appointment. In multiple recordings,

Defendants’ personnel touted their programs as leading to “tons of profits, “excellent profits,”

and similar success. Many customer reviews complained that they were not sold the information

promised, but rather sold other products offered by defendants. For instance, one customer

complained that he paid $2,000 to attend a workshop just to be sold another $20,000 product.

Based on the Monitor’s review, it appears that these types of representations were widespread

and consistent.

Case 2:19-cv-00713-DAK-EJF Document 71 Filed 12/13/19 Page 14 of 21

15

2. Compliance with Section II of the Order

The Court enjoined the Monitored Entities and others “from offering, attempting to

enforce, or asserting the validity of, any Review-Limiting Contract Term.” (Order § 2 at 9-10.)

The Monitor is not aware that any of the Monitored Entities have “offer[ed], attempt[ed] to

enforce, or assert[ed] the validity of, any Review-Limiting Contract Term” in violation of the

Order. (Id.) Ongoing litigation regarding Review-Limiting Contract Terms has been stayed as a

result of the Receiver’s appointment.

3. Compliance with Section III of the Order

The Court enjoined the Monitored Entities and others from releasing or benefitting from

certain customer information. (Order § III at 10.) The Monitor is not aware that the Monitored

Entities have released customer information in violation of this Section of the Order. However,

several coaches have reached out to customers for ongoing training, and the Receiver has issued

cease-and-desist letters in response.

4. Compliance with Section IV of the Order

The Court ordered the Monitored Entities and others to preserve records and assets.

(Order § IV at 11-12.) The Monitor is not aware that the Monitored Entities have violated this

Section of the Order.

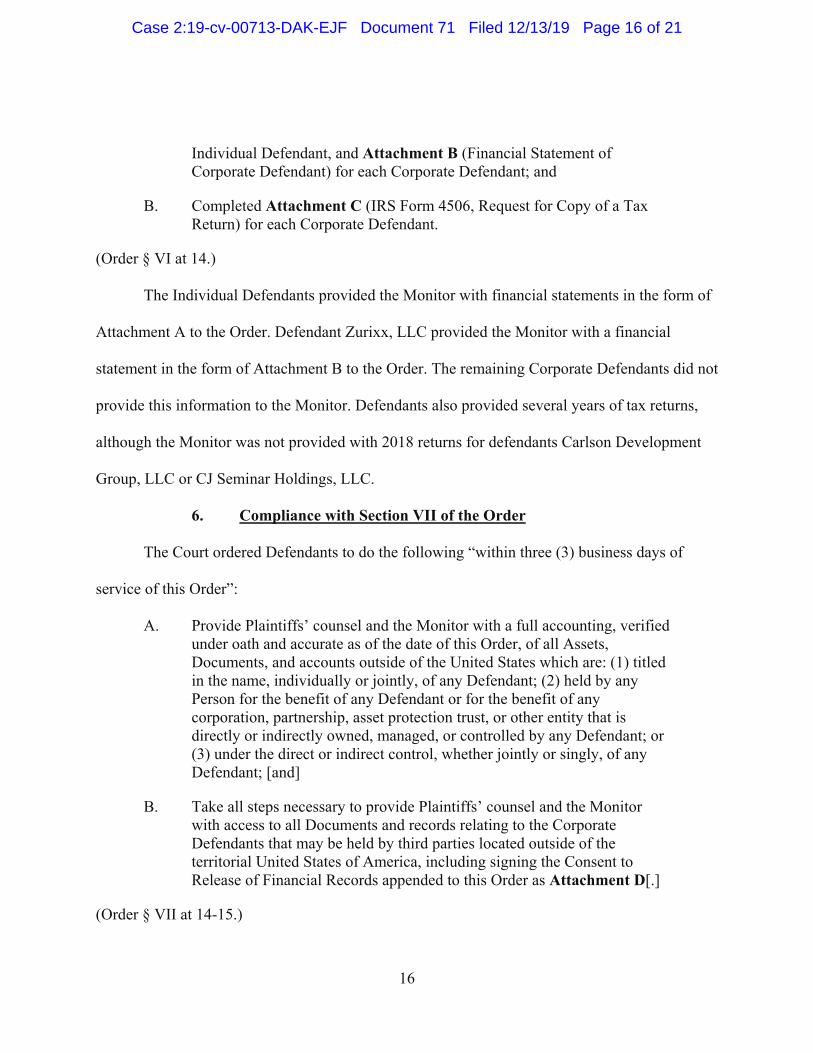

5. Compliance with Section VI of the Order

The Court ordered Defendants to “prepare and deliver to Plaintiffs’ counsel and the

Monitor” the following financial information “within three (3) business days of service of this

Order upon them”:

A. Completed financial statements on the forms attached to this Order as Attachment A (Financial Statement of Individual Defendant) for each

Case 2:19-cv-00713-DAK-EJF Document 71 Filed 12/13/19 Page 15 of 21

16

Individual Defendant, and Attachment B (Financial Statement of Corporate Defendant) for each Corporate Defendant; and

B. Completed Attachment C (IRS Form 4506, Request for Copy of a Tax Return) for each Corporate Defendant.

(Order § VI at 14.)

The Individual Defendants provided the Monitor with financial statements in the form of

Attachment A to the Order. Defendant Zurixx, LLC provided the Monitor with a financial

statement in the form of Attachment B to the Order. The remaining Corporate Defendants did not

provide this information to the Monitor. Defendants also provided several years of tax returns,

although the Monitor was not provided with 2018 returns for defendants Carlson Development

Group, LLC or CJ Seminar Holdings, LLC.

6. Compliance with Section VII of the Order

The Court ordered Defendants to do the following “within three (3) business days of

service of this Order”:

A. Provide Plaintiffs’ counsel and the Monitor with a full accounting, verified under oath and accurate as of the date of this Order, of all Assets, Documents, and accounts outside of the United States which are: (1) titled in the name, individually or jointly, of any Defendant; (2) held by any Person for the benefit of any Defendant or for the benefit of any corporation, partnership, asset protection trust, or other entity that is directly or indirectly owned, managed, or controlled by any Defendant; or (3) under the direct or indirect control, whether jointly or singly, of any Defendant; [and]

B. Take all steps necessary to provide Plaintiffs’ counsel and the Monitor with access to all Documents and records relating to the Corporate Defendants that may be held by third parties located outside of the territorial United States of America, including signing the Consent to Release of Financial Records appended to this Order as Attachment D[.]

(Order § VII at 14-15.)

Case 2:19-cv-00713-DAK-EJF Document 71 Filed 12/13/19 Page 16 of 21

17

Defendants have not complied with Section VII.A. As to Section VII.B, Carlson executed

a Consent to Release Financial Records form, as well as bank statements from a bank in Puerto

Rico. Other than the asset lists and attachments with the other disclosures, no documentation of

assets, documents, and accounts outside of the United States are verified under oath or appear to

be included in the productions that the Receiver has received.

7. Compliance with Section IX of the Order

The Court enjoined the Monitored Entities and others “from creating, operating, or

exercising any control over any business entity, whether newly formed or previously inactive,

including any partnership, limited partnership, joint venture, sole proprietorship, or corporation”

unless the Monitored Entities or others subject to the injunction “first provid[e] Plaintiffs’

counsel and the Monitor with a written statement disclosing: (1) the name of the business entity;

(2) the address and telephone number of the business entity; (3) the names of the business

entity’s officers, directors, principals, managers, and employees; and (4) a detailed description of

the business entity’s intended activities.” (Order § IX at 15.) The Monitor is not aware that the

Monitored Entities have engaged in any activities that would fall within the scope of this Section

of the Order.

8. Compliance with Section XIII of the Order

The Court ordered the Monitored Entities and others to “provide to the Monitor,

immediately upon request, without need of a subpoena or further order, the following” materials:

A. A list of all Assets and accounts of the Monitored Entities, including Assets of the Monitored Entities that are held in any name other than the name of a Monitored Entity, or by any Person other than a Monitored Entity;

Case 2:19-cv-00713-DAK-EJF Document 71 Filed 12/13/19 Page 17 of 21

18

B. A list of all Assets and Documents belonging to other Persons whose interests are under the direction, custody, or control, or in the possession, of the Monitored Entities;

C. A list of all locations where Documents of the Monitored Entities are located, and the means to access such Documents within five (5) hours of the Monitor’s request;

D. Access to all Documents of the Monitored Entities including, but not limited to, books and records of accounts, all financial and accounting records, balance sheets, income statements, bank records (including monthly statements, canceled checks, records of wire transfers, and check registers), client lists, title Documents and other papers that relate to the practices charged in the Complaint or Defendants’ Products;

E. Access to all computers, electronic devices, mobile devices, and machines (onsite or remotely) and any cloud account (including specific method to access account), electronic file in any medium, or other data in whatever form used to conduct the business of the Monitored Entities;

F. Copies of all keys, codes, user names and passwords necessary to gain or to secure access to any Assets or Documents of the Monitored Entities including, but not limited to, access to their business premises, means of communication, accounts, computer systems, or other property; and

G. A list of all agents, employees, independent contractors, officers, attorneys, servants, and those Persons in active concert and participation with the Monitored Entities, or who have been associated or done business with the Monitored Entities since January 1, 2013.

(Order § XIII at 20-21.) The Receiver is not aware that Defendants violated this Section of the

Order.

9. Compliance with Section XIV of the Order

The Court ordered the Monitored Entities and others to cooperate with the Monitor.

(Order § XIV at 21-22.) As stated above, the Individual Defendants and employees cooperated

freely with the Monitor in interviews. Responses to requests for documents, computers, and other

materials were frequently delayed, and numerous requests from the Monitor were outstanding

upon appointment of the Receiver.

Case 2:19-cv-00713-DAK-EJF Document 71 Filed 12/13/19 Page 18 of 21

19

10. Compliance with Section XV of the Order

The Court enjoined the Monitored Entities and others from interfering with the Monitor.

(Order § XV at 22-23.) The Receiver is not aware that Defendants violated this Section of the

Order.

11. Compliance with Section XIV of the Order

The Court ordered the Monitored Entities and others to provide the Monitor with access

to the business premises and records. (Order § XVII at 23-25.) The Receiver is not aware that

Defendants violated this Section of the Order. As stated above, the Individual Defendants and

employees cooperated with the Monitor in interviews. Responses to requests for documents,

computers, and other materials were frequently delayed, and numerous requests from the

Monitor were outstanding upon appointment of the Receiver.

12. Compliance with Section XVIII of the Order

The Court ordered the Monitored Entities and others to distribute copies of the Order as

follows:

Defendants shall immediately provide a copy of this Order to each affiliate, telemarketer, marketer, sales entity, successor, assign, member, officer, director, employee, agent, independent contractor, client, attorney, spouse, subsidiary, division, and representative of any Defendant, and shall, within ten (10) days from the date of entry of this Order, provide Plaintiffs and the Monitor with a sworn statement that this provision of the Order has been satisfied, which statement shall include the names, physical addresses, phone numbers, and email addresses of each such Person who received a copy of the Order.

(Order § XVIII at 25.) On October 11, 2019, counsel for Defendants provided the Monitor with

the Declaration of James M. Carlson, which, in part, provided, “Section XVIII of the [Order] has

been satisfied. A list of the names, physical addresses, phone numbers, and e-mail addresses of

each person or entity to whom the [Order], to the extent reasonably ascertainable, is attached

Case 2:19-cv-00713-DAK-EJF Document 71 Filed 12/13/19 Page 19 of 21

20

hereto as Exhibit A.” (Ex. 3 at 2.) 13 The Monitor does not dispute the assertions in the

Declaration.

Section XVIII of the Order further provides, “Defendants shall not take any action that

would encourage officers, agents, members, directors, employees, salespersons, independent

contractors, attorneys, subsidiaries, affiliates, successors, assigns, or other Persons or entities in

active concert or participation with them to disregard this Order or believe that they are not

bound by its provisions.” (Order § XVIII at 25.) The Monitor is not aware that Defendants have

taken any action in violation of this portion of Section XVIII.

III. Conclusion

The Receiver continues to review information from the Receivership Entities and will

update the Court as his investigation continues.

RESPECTFULLY SUBMITTED this 13th day of December, 2019.

HOLLAND & HART LLP /s/ Cory A. Talbot Doyle S. Byers Cory A. Talbot Engels J. Tejeda Chelsea J. Davis

Attorneys for David K. Broadbent as the Court-appointed Receiver

13 The referenced Exhibit A has not been filed due to privacy concerns.

Case 2:19-cv-00713-DAK-EJF Document 71 Filed 12/13/19 Page 20 of 21

21

INDEX OF EXHIBITS 1 - Transfer Pricing Study, etc. 2 - Accounting Report.

2A1 - Bank Account and Merchant Summary.

2A2 - Org. Chart Zurixx.

2A3 - Owner Distributions.

2A4 - Zurixx UT Office Payroll 10-25-19.

2A5 - Zurixx Weekly AP to Pay 10-18-19 JC Final.

2A6 - Daily Financial Monitoring.

2A7 - AMEXCC.

2A8 - 2019 Staff Payroll – Layoffs.

2A9 - Pro Forma showing new pricing model.

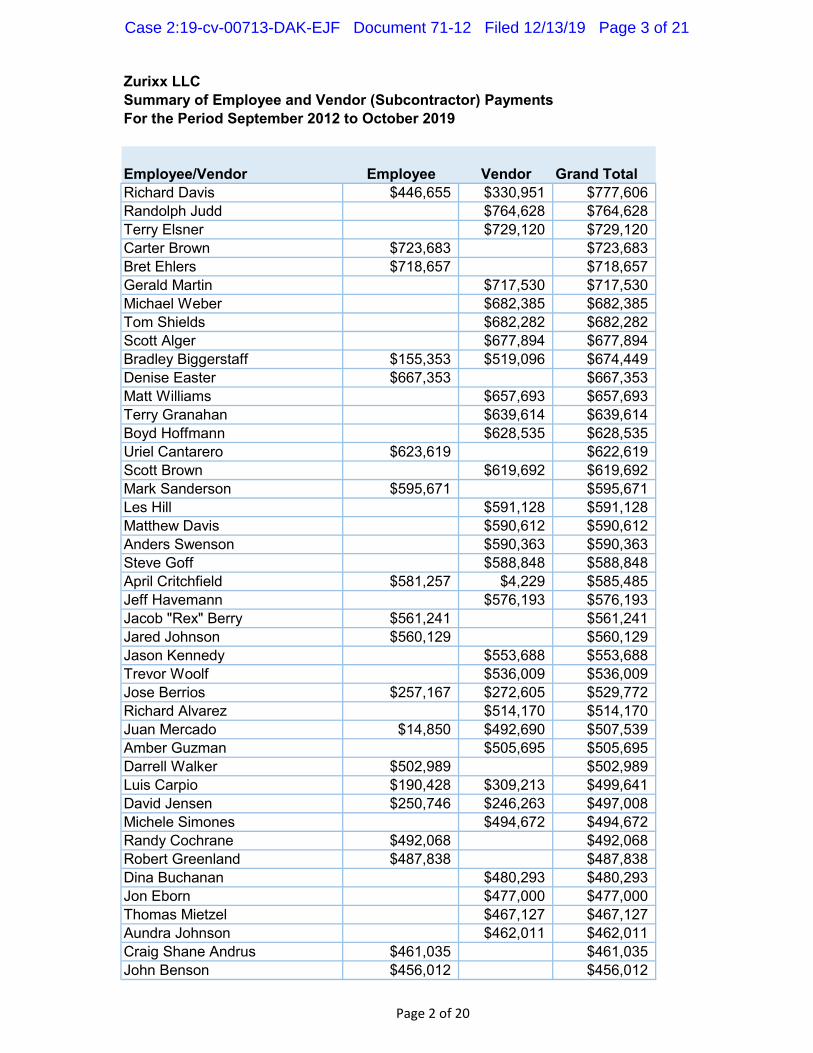

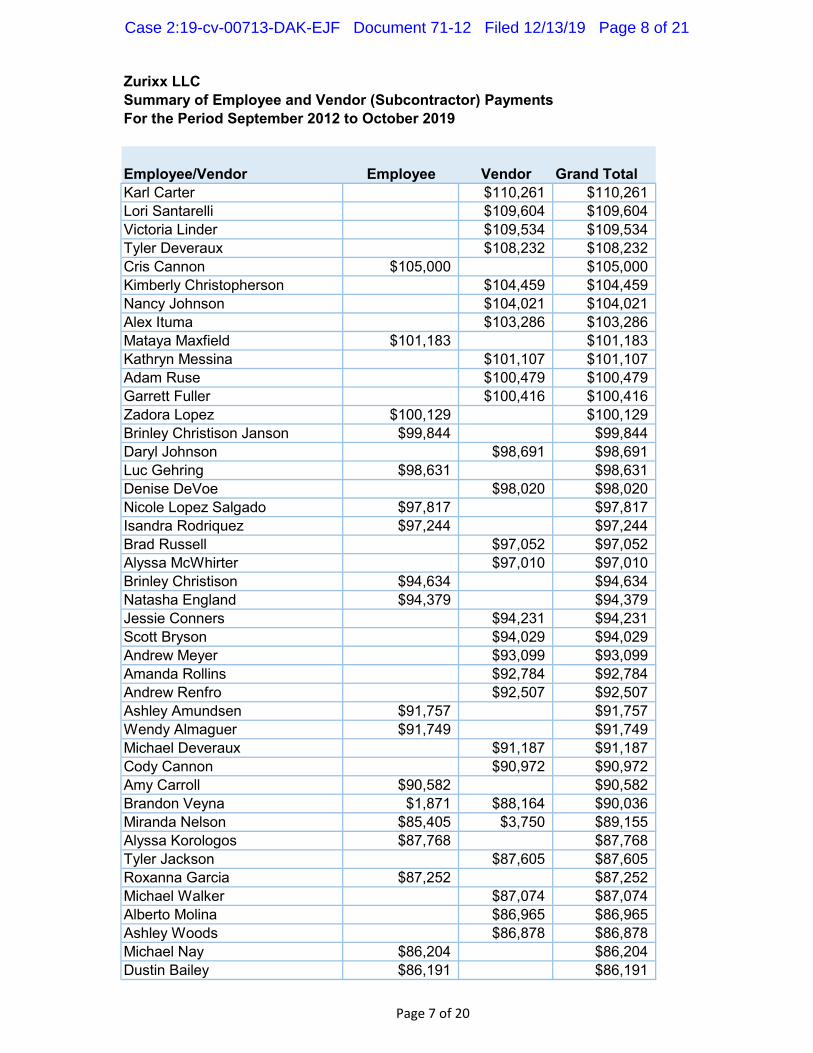

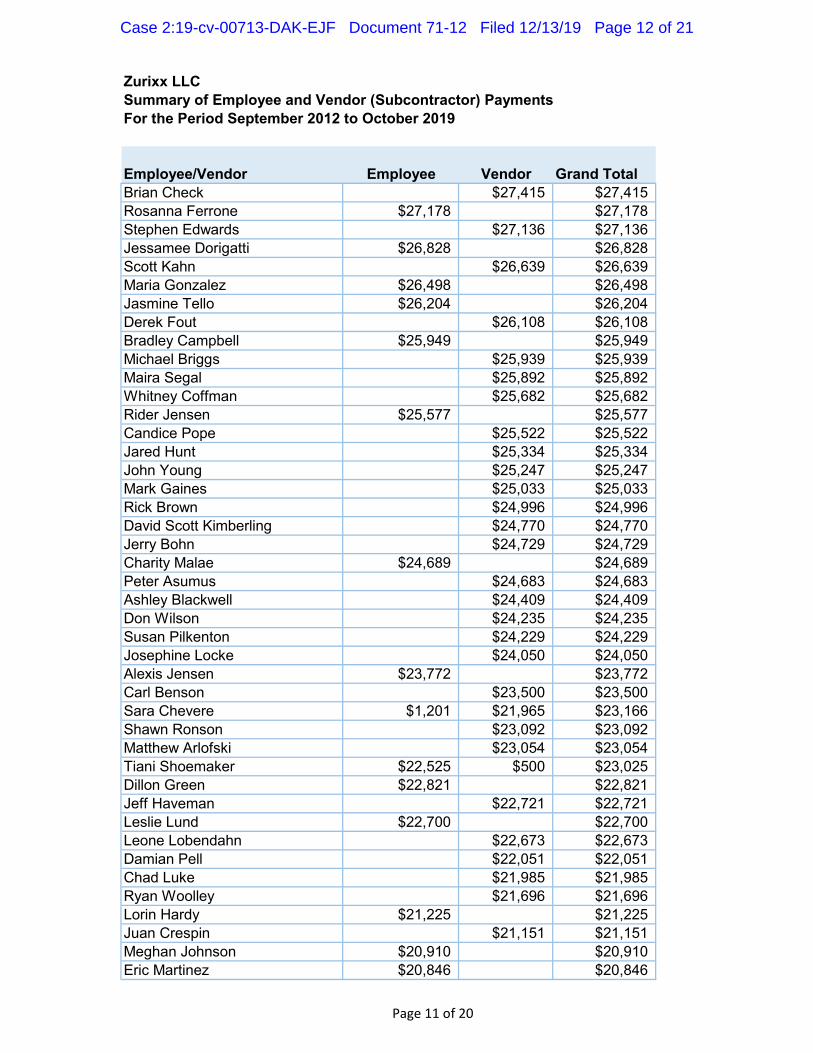

2A10 - Zurixx Employee and Vendor Payment Summary.

2A11 - Summary of Financial Statements.

2A12 - 2018-2017 Zurixx Audit.

2A13 - Carlson Signed Financial Disclosure – Redacted.

2A14 - Cannon Signed Financial Disclosure – Redacted.

2A15 - Spangler Signed Financial Disclosure – Redacted.

2A16 - Zurixx Signed Financial Disclosure – Redacted.

2A17 - Transfer Pricing Study, etc. 3 - Declaration of James M. Carlson.

13639836_v2

Case 2:19-cv-00713-DAK-EJF Document 71 Filed 12/13/19 Page 21 of 21

EXHIBIT “1”

Case 2:19-cv-00713-DAK-EJF Document 71-1 Filed 12/13/19 Page 1 of 85

Zurixx, LLC.

United States Transfer Pricing Documentation

for the 2017 Tax Year

October 2018

ECONOMICS PARTNERS ----LLC ----

Case 2:19-cv-00713-DAK-EJF Document 71-1 Filed 12/13/19 Page 2 of 85

Economics Partners, LLC

www.econpartners.com

Table of Contents

I. Introduction ................................................................................................................................... 5

A. Scope......................................................................................................................................... 5

B. Summary of Analysis and Conclusions .............................................................................. 5

1. Overview of Transaction ................................................................................................. 5

2. Summary of Findings ...................................................................................................... 5

C. Report Structure...................................................................................................................... 6

D. Disclaimers .............................................................................................................................. 7

II. Company Overview ..................................................................................................................... 8

A. Zurixx History......................................................................................................................... 8

B. Zurixx Legal Entity Structure ............................................................................................... 8

C. Zurixx Entities ......................................................................................................................... 9

1. Zurixx, LLC (“Zurixx US”) ............................................................................................. 9

2. Dorado Marketing & Management, LLC (“Dorado”) .............................................. 10

D. Products ................................................................................................................................. 11

1. Success Path Education ................................................................................................. 11

2. Daymond John’s Launch Academy ............................................................................ 12

3. The Flipping Formula .................................................................................................... 12

4. Winning the Property War ........................................................................................... 13

5. Property Bank ................................................................................................................. 13

6. Conclusion ...................................................................................................................... 13

E. Value Chain ........................................................................................................................... 14

F. Competitors ........................................................................................................................... 14

G. Functions, Risks, and Intellectual Property ...................................................................... 15

1. Functions ......................................................................................................................... 15

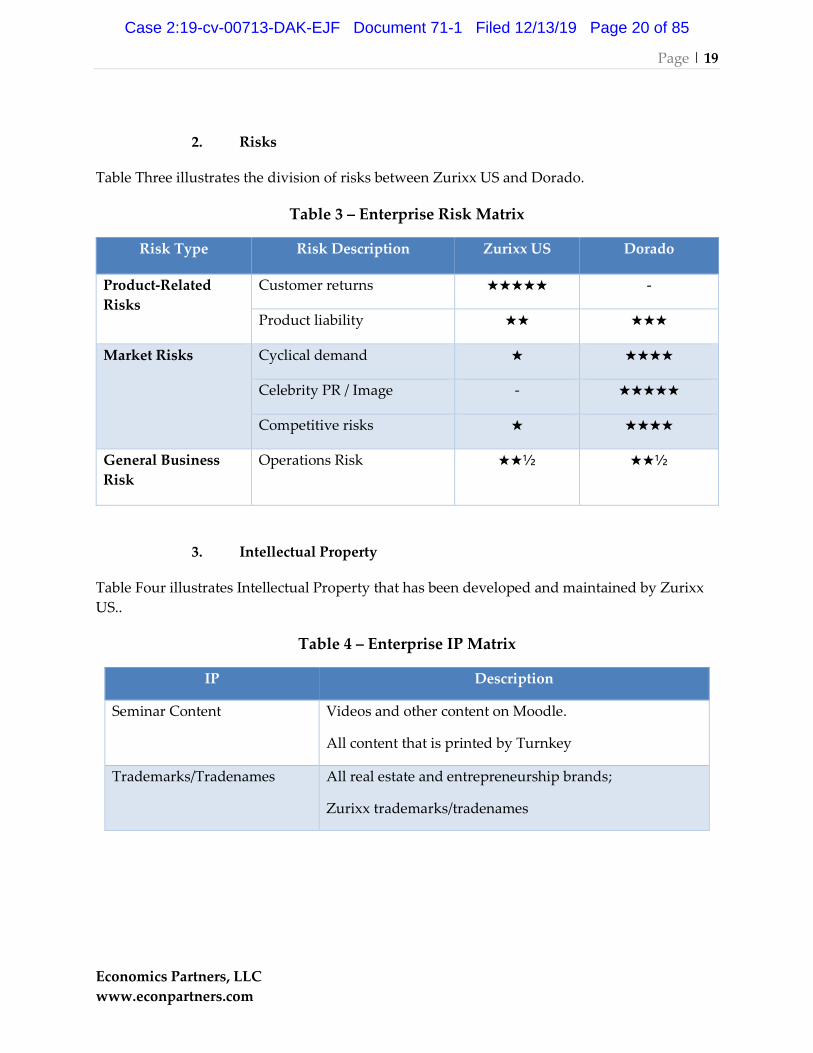

2. Risks ................................................................................................................................. 19

3. Intellectual Property ...................................................................................................... 19

III. Industry Background .................................................................................................................. 20

A. Education and Training Services Industry ....................................................................... 20

1. Industry Overview ......................................................................................................... 20

2. Performance .................................................................................................................... 20

3. Competition .................................................................................................................... 21

B. Sales and Marketing Industry Overview .......................................................................... 21

1. Industry Overview ......................................................................................................... 21

2. Performance .................................................................................................................... 21

3. Competition .................................................................................................................... 21

IV. Functional Analysis .................................................................................................................... 23

A. Introduction ........................................................................................................................... 23

B. Overview of Transaction ..................................................................................................... 24

C. Functions Performed ............................................................................................................ 24

Case 2:19-cv-00713-DAK-EJF Document 71-1 Filed 12/13/19 Page 3 of 85

Economics Partners, LLC

www.econpartners.com

1. Accounting and Finance ............................................................................................... 24

2. Celebrity Relationships ................................................................................................. 25

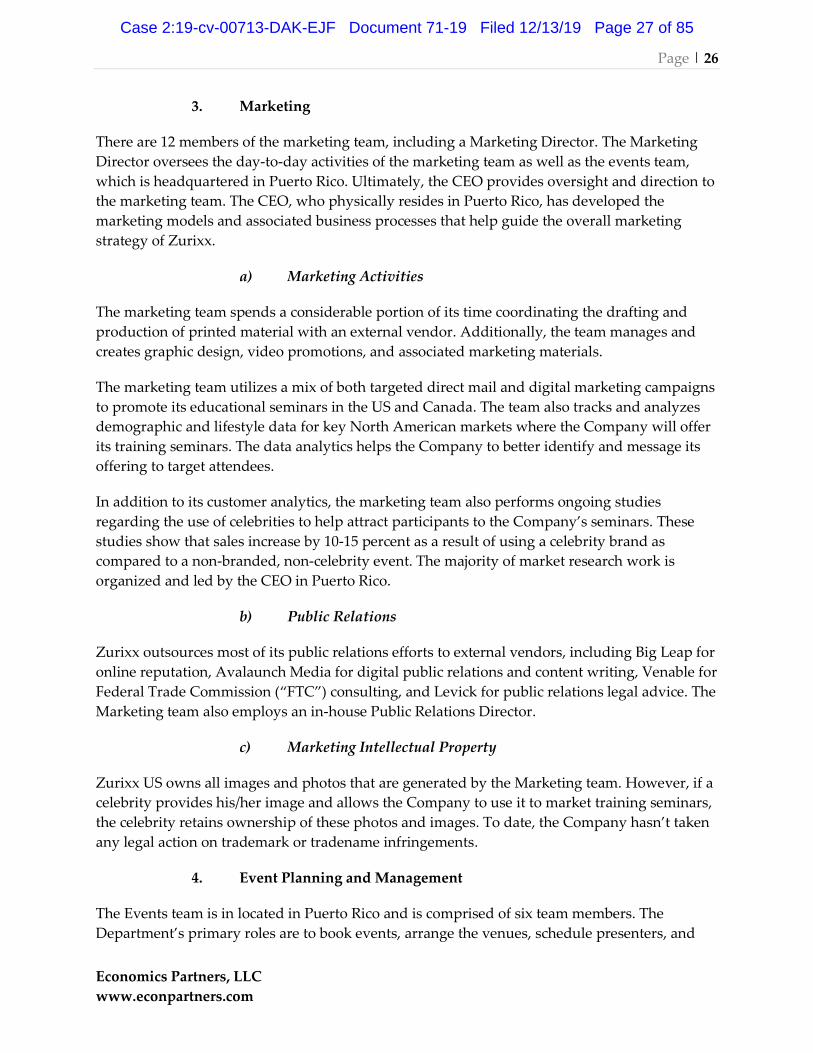

3. Marketing ........................................................................................................................ 26

4. Event Planning and Management ............................................................................... 26

5. Sales Support .................................................................................................................. 27

6. Information Technology ............................................................................................... 28

7. Customer Support .......................................................................................................... 30

8. Sales.................................................................................................................................. 32

9. Coaching and Educational Content............................................................................. 33

10. Intercompany Agreements and Financing ................................................................. 34

D. Conclusion ............................................................................................................................. 35

V. Regulatory Overview ................................................................................................................. 36

A. U.S. Transfer Pricing Regulations ...................................................................................... 36

B. The Arm’s Length Principle ................................................................................................ 36

C. Best Method Rule ................................................................................................................. 37

D. Choice of Methodology ....................................................................................................... 38

E. Methods Available and Additional Considerations for Services Transactions ........... 38

1. Overview ......................................................................................................................... 38

2. Benefit Test ...................................................................................................................... 39

3. Methods Available for Services Transactions ............................................................ 40

F. Methods Available for Tangible Goods Transactions ..................................................... 42

1. Comparable Uncontrolled Price Method ................................................................... 42

2. Cost Plus Method ........................................................................................................... 42

3. Resale Price Method ...................................................................................................... 43

4. Comparable Profits Method ......................................................................................... 43

5. Profit Split Method ........................................................................................................ 44

6. Unspecified Methods ..................................................................................................... 44

VI. Economic Analysis ...................................................................................................................... 45

A. Executive Management Fees – North America Search ................................................... 45

1. Selection of the Tested Party ........................................................................................ 45

2. Selection of Years for Comparison .............................................................................. 45

3. Selection of Profit Level Indicator ............................................................................... 46

4. Selection of North American Comparable Companies ............................................ 46

5. Results of the CPM Analysis ........................................................................................ 47

6. Implementation .............................................................................................................. 47

B. Registration Fees ................................................................................................................... 47

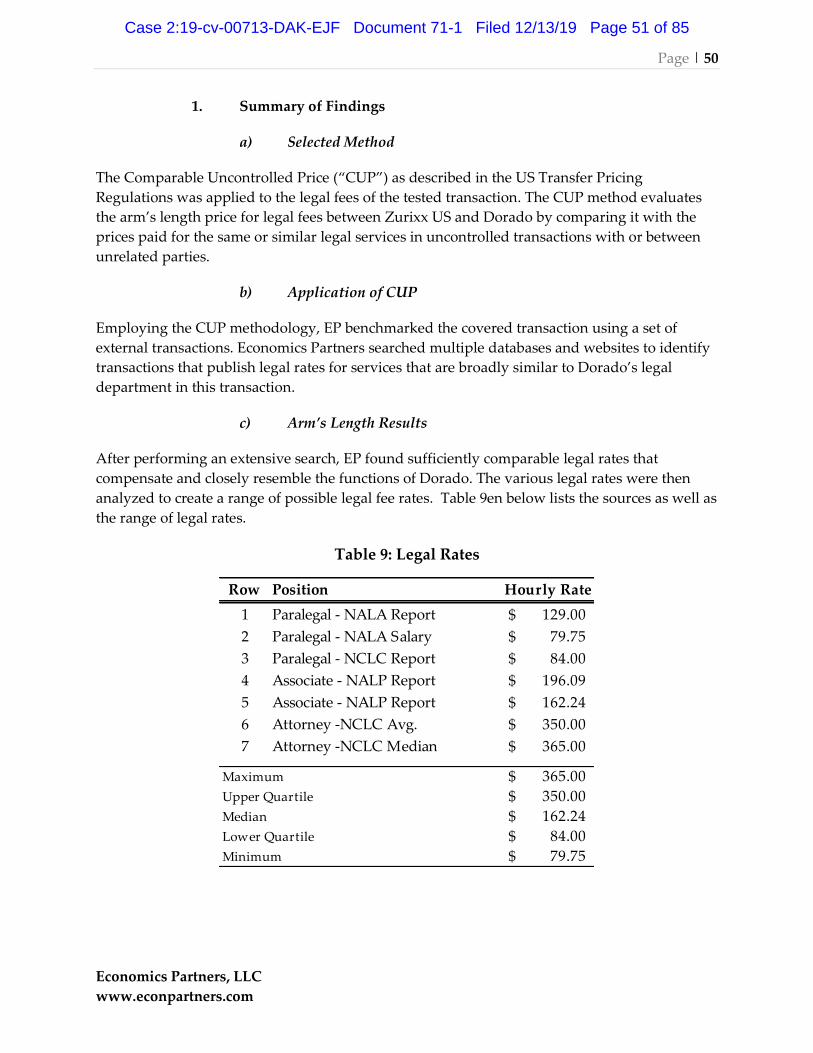

1. Summary of Findings .................................................................................................... 48

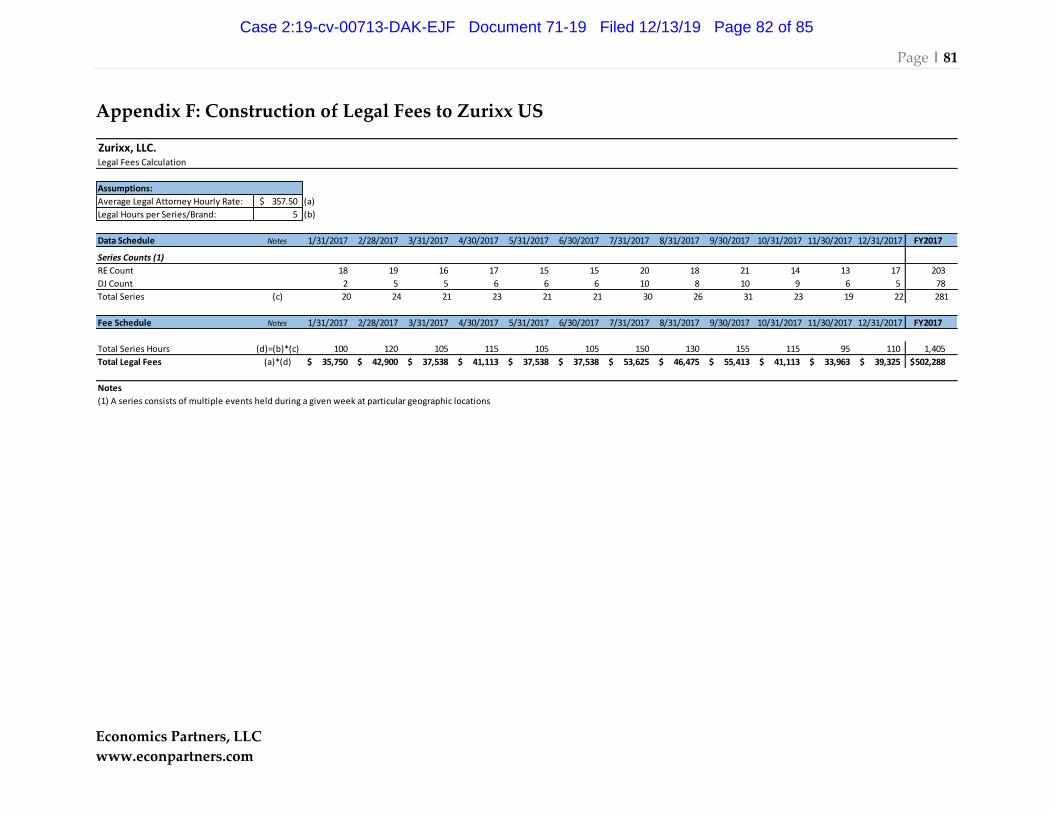

C. Legal Fees .............................................................................................................................. 49

1. Summary of Findings .................................................................................................... 50

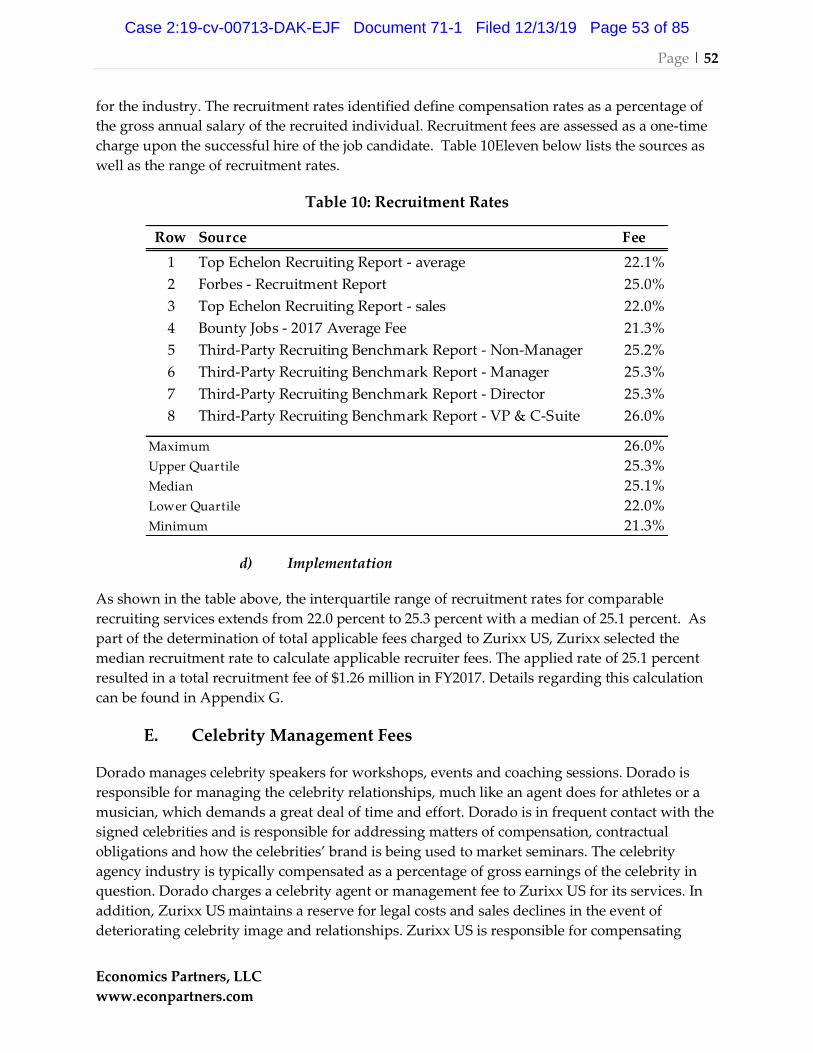

D. Workshop Recruitment Fees ............................................................................................... 51

1. Summary of Findings .................................................................................................... 51

E. Celebrity Management Fees ................................................................................................ 52

1. Summary of Findings .................................................................................................... 53

Case 2:19-cv-00713-DAK-EJF Document 71-1 Filed 12/13/19 Page 4 of 85

Economics Partners, LLC

www.econpartners.com

VII. Conclusion ................................................................................................................................... 54

A. Overview of Transaction ..................................................................................................... 54

B. Summary of Findings........................................................................................................... 54

1. Executive Management Fees ........................................................................................ 54

2. Registration Fees ............................................................................................................ 54

3. Legal Fees ........................................................................................................................ 54

4. Workshop Recruitment Fees ........................................................................................ 54

5. Celebrity Management Fees ......................................................................................... 55

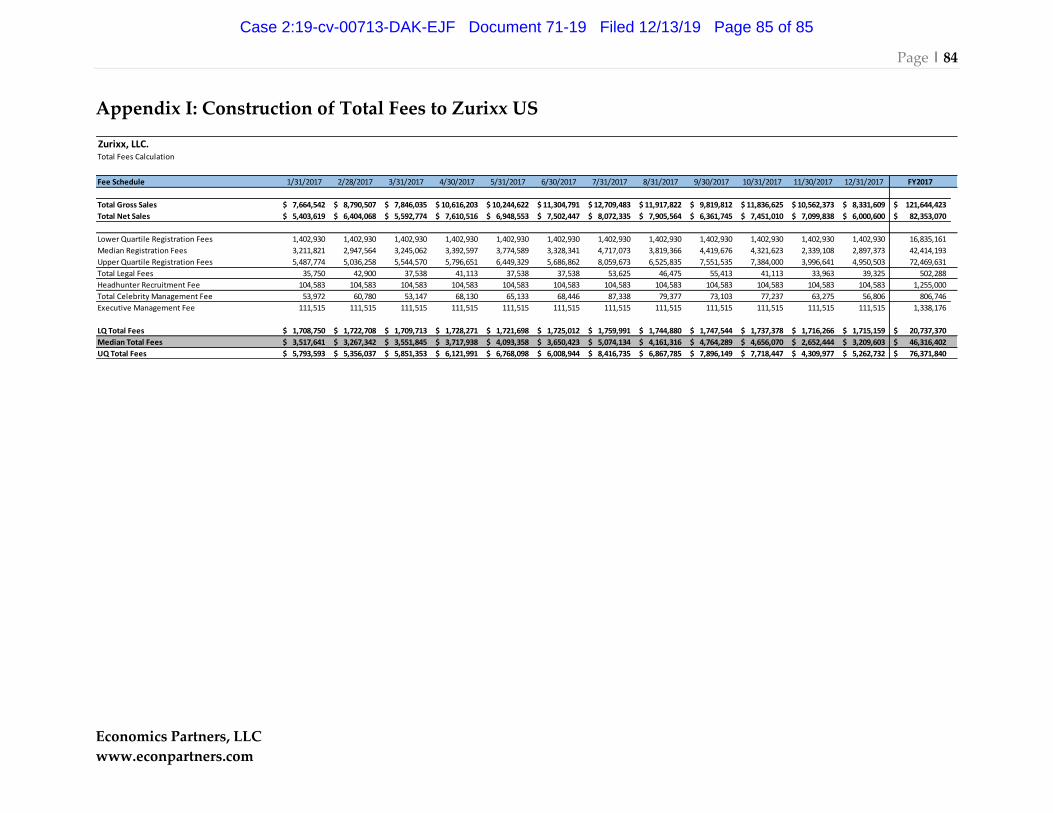

6. Total Fees ......................................................................................................................... 55

Appendix A: Comparable Company Business Descriptions ............................................................. 56

A. North American Comparable Company Business Descriptions ................................... 56

Appendix B: Comparable Company Financials .................................................................................. 60

A. North American Comparable Company Financials ........................................................ 60

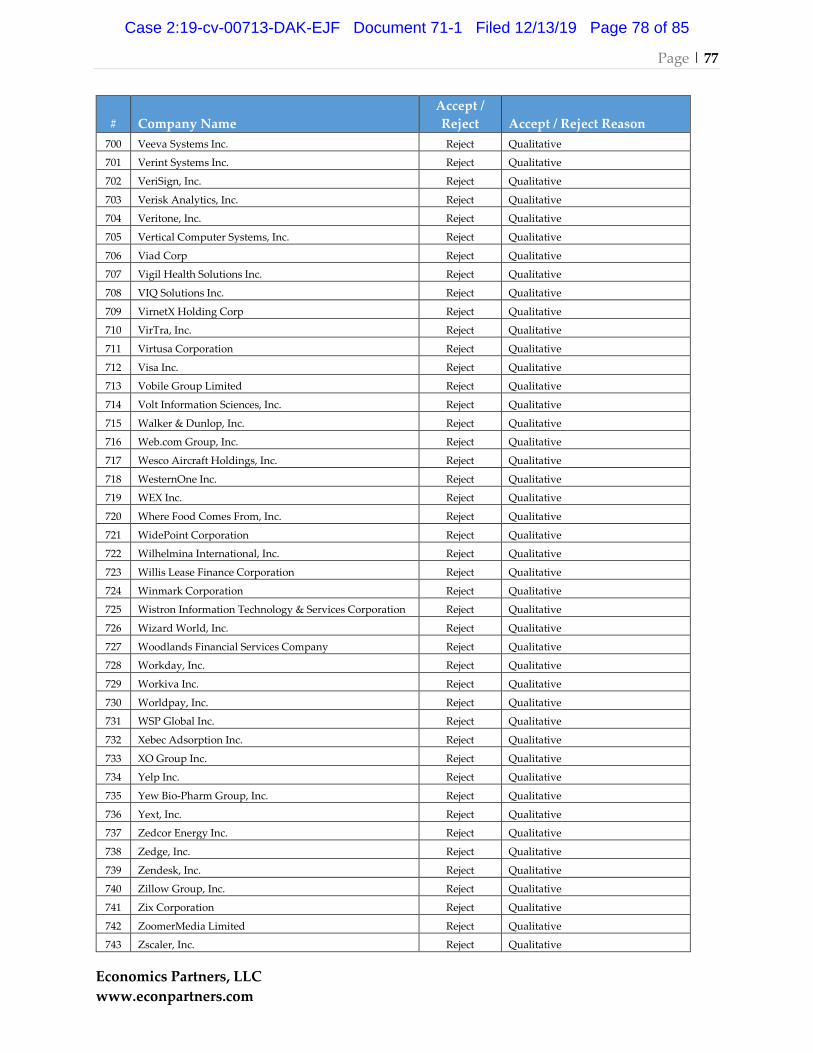

Appendix C: Accept / Reject Matrices ................................................................................................... 61

A. North American Comparables – Qualitative Rejections ................................................. 61

Appendix D: Construction of Executive Management Fees to Zurixx US ...................................... 79

Appendix E: Construction of Registration Fees to Zurixx US ........................................................... 80

Appendix F: Construction of Legal Fees to Zurixx US ....................................................................... 81

Appendix G: Construction of Workshop Recruitment Fees to Zurixx US ...................................... 82

Appendix H: Construction of Celebrity Management Fees to Zurixx US ....................................... 83

Appendix I: Construction of Total Fees to Zurixx US ........................................................................ 84

Case 2:19-cv-00713-DAK-EJF Document 71-1 Filed 12/13/19 Page 5 of 85

Page | 5

Economics Partners, LLC

www.econpartners.com

I. Introduction

A. Scope

Zurixx, LLC (“Zurixx” or “Company”) engaged Economics Partners, LLC (“Economics

Partners” or “EP”) to analyze certain intercompany transactions and prepare a US transfer

pricing planning study for the fiscal year ended December 31, 2017.

Zurixx develops, promotes, sells, and fulfills financial education programs throughout the

United States and Canada by partnering with well-known financial celebrities to provide real

estate, business, entrepreneurship, and coaching and mentoring programs to consumers.

The analyses described in this report have been conducted in accordance with Section 482 of the

U.S. Internal Revenue Code1 and the Regulations2 thereunder (“Section 482” or the “US

Regulations”). The underlying principle of the Regulations is the arm’s length standard. In

general, a controlled transaction meets the arm’s length standard if the results of the transaction

are consistent with the results that would have been realized had uncontrolled taxpayers

engaged in a comparable transaction under comparable, but uncontrolled, circumstances.

B. Summary of Analysis and Conclusions

1. Overview of Transaction

The intercompany transaction at issue in this report is the provision of certain sales and

executive management services from Dorado Marketing & Management, LLC (“Dorado”) to

Zurixx, LLC (“Zurixx US”). As described in the Functional Analysis section, Dorado provides

sales and executive management services for Zurixx US. During FY 2017, Dorado charged sales

and executive management services fees of $21.14 million to Zurixx US in consideration of these

services.

2. Summary of Findings

a) Selected Method

The Unspecified Method, as described in the US Transfer Pricing Regulations, was applied to

the tested transaction. From the standpoint of Section 482, a method that is unspecified in that it

is not the CUP method, the cost-plus method, the resale price method, the CPM method, or the

1 References in this report to the “Code,” or to particular provisions of the “Code,” refer to the Internal Revenue Code of 1986 (26 U.S.C. § 1 et seq.), as amended, as in effect for the fiscal year ended December 31, 2014. 2 References in this report to the “Regulations,” or to particular provisions of the “Regulations,” refer to the Treasury Regulations (Title 26, Code of Federal Regulations), as amended, as in effect for the fiscal year ended December 31, 2014.

Case 2:19-cv-00713-DAK-EJF Document 71-1 Filed 12/13/19 Page 6 of 85

Page | 6

Economics Partners, LLC

www.econpartners.com

profit split method and can be applied if it provides the most reliable measure of an arm’s

length result under the principles of the best method rule. Unspecified methods take into

account the general principle that “information be provided on the prices or profits that the

controlled taxpayer could have realized by choosing a realistic alternative to the controlled

transaction.”3

b) Application of the Unspecified Method

Using an unspecified method, EP benchmarked the covered transaction against a combination

of similar internal comparable transactions and comparable external uncontrolled prices and

transactions. These comparable prices and transactions were used to derive a benchmark of fees

representative of arm’s length compensation.

c) Unspecified Method Result

• Using the unspecified method described above, EP calculated Dorado’s median

estimated service fees to total approximately $46.32 million in FY 2017.

d) Intercompany Results

• In FY 2017, Dorado charged approximately $21.14 million in sales and executive

management fees. This result falls outside the benchmarked fee calculation because of a

stressed celebrity brand, specifically Tarek and Christina El Moussa. During FY 2017,

Tarek and Christina announced plans to divorce which negatively impacted their public

image and brand. Zurixx’s Success Path Education seminar is aggressively promoted by

Tarek and Christina and suffered substantial losses as a result. Due to these unforeseen

economic hardships, Zurixx US was only charged $21.14 million. The fee charged is

below the estimated median fee of $46.32 million and is considered arm’s-length.

C. Report Structure

The remainder of this report proceeds as follows.

Section II provides a high-level overview of Zurixx International LLC.

Section III provides an overview of the industry in which Zurixx operates.

Section IV provides a functional analysis of the intercompany transaction.

Section V provides an overview of the relevant transfer pricing regulations applicable to the

intercompany transaction under review.

Section VI describes the transaction and puts forth our analysis.

3 Treas. Reg. §1.482-3(e)(1)

Case 2:19-cv-00713-DAK-EJF Document 71-1 Filed 12/13/19 Page 7 of 85

Page | 7

Economics Partners, LLC

www.econpartners.com

Section VII summarizes our conclusions.

D. Disclaimers

In preparing this report, we have relied on the information and data provided by Zurixx

personnel, including both written documents and information obtained orally in meetings and

interviews. We have also relied on information available from public, financial, and industry

sources.

We have not independently validated or audited this information. Accordingly, we do not

express an opinion or any other form of assurance thereon. The conclusions set forth in this

report are dependent upon such information being complete and accurate in all material

respects. If the actual facts were to be different from the facts set forth in this report, our

analysis and conclusions might be different.

The applicable law and regulations upon which this report is based is subject to change and re-

interpretation from time to time, and some or all such changes and re-interpretations may have

retroactive effect. In addition, the application of the applicable law and regulations to the facts

and circumstances of the inter-company transactions reviewed in this report may be subject to

examination and adjustment by the local taxing authorities, which are generally empowered to

exercise significant discretion in conducting examinations and proposing adjustments to

transfer pricing results, which may include the assertion of penalties. The conclusions set forth

in this report are not binding on the local taxing authorities, and there can be no assurance that

upon examination the local taxing authorities will accept, in whole or in part, such conclusions.

Case 2:19-cv-00713-DAK-EJF Document 71-1 Filed 12/13/19 Page 8 of 85

Page | 8

Economics Partners, LLC

www.econpartners.com

II. Company Overview4

Zurixx develops, promotes, sells, and fulfills financial education programs throughout the

United States and Canada by partnering with well-known financial celebrities to provide real

estate, business strategy, entrepreneurship, and coaching and mentoring programs to

consumers. The Company utilizes a multi-phase educational process to equip students with

tools, knowledge and resources that help them be financially successful.

A. Zurixx History

In 2012 Jeff Spangler (President, U.S.) and Chris Cannon (President, P.R.) formed Zurixx with

Jim Carlson (CEO). All three founders had previous experience in the industry and were able to

leverage previous celebrity relationships, employees, and industry “know-how” to launch the

Zurixx business. Since founding the business, Zurixx’s management team has focused on

managing business fundamentals including detailed weekly financial statement reports, weekly

cash-flow forecast as well as other Key Performance Indicators (“KPI”). The Zurixx

management team recognizes that many of its competitors, both current and former, lack a

similar focus which frequently leads liquidation issues that often end up in bankruptcy. This

data-driven approach has become a competitive advantage for Zurixx and is one of the most

important factors in the Company’s on-going success.

B. Zurixx Legal Entity Structure

Figure 1 below shows the Zurixx legal structure as of December 31, 2017.

4 This section was adapted from the Zurixx website and discussions with Zurixx management.

Case 2:19-cv-00713-DAK-EJF Document 71-1 Filed 12/13/19 Page 9 of 85

Page | 9

Economics Partners, LLC

www.econpartners.com

Figure 1: Zurixx Legal Entity Structure

C. Zurixx Entities

1. Zurixx, LLC (“Zurixx US”)

Zurixx US is a Utah limited liability company, which began operations in February 2012.

Zurixx US’s main operations are located in Cottonwood Heights, Utah. Zurixx US follows a

calendar year and keeps it books and records in U.S. dollars as its functional currency. Zurixx

US is treated as a partnership for U.S. federal income tax purposes.

Case 2:19-cv-00713-DAK-EJF Document 71-1 Filed 12/13/19 Page 10 of 85

Page | 10

Economics Partners, LLC

www.econpartners.com

2. Dorado Marketing & Management, LLC (“Dorado”)

a) Overview

Dorado’s primary function is marketing, event management, and celebrity contract

management celebrity management. However, Dorado also provides administrative executive

support for marketing and events (see the Marketing and Events Management sections). All

Dorado employees are residents of Puerto Rico. The Zurixx Group management headquarters

are located in Dorado, Puerto Rico. Operations for Dorado began in January 2015. Dorado

follows a calendar year and keeps its books and records in U.S. dollars as its functional

currency.

Dorado has elected to be treated as a corporation for both U.S. federal and Puerto Rican tax

purposes. The Commonwealth of Puerto Rico is a United States territory, not a state.

Consequently, U.S. federal income taxes do not apply generally to income generated by Puerto

Rico corporations as they are treated as foreign corporations not generally subject to U.S. federal

corporate tax rates.

On January 17, 2012, Puerto Rico enacted Act No. 20 of 2012, as amended, known as the “Export

Services Act,” “the Act,” or “Act 20,” to offer the necessary elements for the creation of a world-

class international service center. The Act establishes a legal framework of incentives designed

to stimulate the development of a wide variety of ventures, including the export of services.

Additionally, this law promotes investments in research and development and initiatives from

the academic and private sectors by granting credits and exemptions for these activities.

Further, the Act helps to decrease operational and energy spending for companies moving to

the island to help their operations remain profitable and efficient.

The Act provides tax exemptions and tax credits to businesses engaged in eligible activities in

Puerto Rico. To qualify for Act 20 benefits, a business prepares an application that includes

details about the services it will provide at its Puerto Rican entity including details regarding

employee headcount, wages, projected revenues from providing the services and other similar

financial information required on the Act 20 application.5

5 The Act provides benefits for services provided from Puerto Rico to outside markets. Eligible activities to receive benefits under the Act are services in the following areas: i) research and development; ii) advertising and public relations; iii) economic, scientific, environmental, technological, managerial, marketing, human resources, engineering, information systems, auditing, and consulting services; iv) consulting services for any trade or business; v) commercial art and graphic services; vi) production of engineering and architectural plans and designs, and related services; vii) professional services such as legal, tax, and accounting services; viii) centralized managerial services, including, but no limited to, strategic direction, planning and budgeting, provided by regional headquarters or a headquarters company engaged in the business of providing such services; ix) services performed by electronic data processing centers; x) development of licensee computer software; xi) telecommunications voice and data

Case 2:19-cv-00713-DAK-EJF Document 71-1 Filed 12/13/19 Page 11 of 85

Page | 11

Economics Partners, LLC

www.econpartners.com

The business submits its completed application to the Office of Industrial Tax Exemption of

Puerto Rico. The decree issued by the Puerto Rican government provides full detail of tax rates

and conditions mandated by the Act and is considered a contract between the Government of

Puerto Rico and the service provider. Dorado filed its application in August 2014 and obtained

its tax exemption decree in January 20156.

Dorado is not subject to any taxes (e.g., dividend tax, tollgate tax etc.) with exception to local

corporate and municipal taxes on its income from its eligible activities in Puerto Rico. Dorado is

also subject to Puerto Rico’s fixed income tax rate established in the tax decree.

D. Products

Zurixx markets and sells workshops and events, online content as well as coaching sessions

focused on teaching students how to invest in real estate and how to become a successful

entrepreneur. The Zurixx target customer is between 35 and 55 years old and is looking for a

way to earn extra money apart from a typical full-time job. Zurixx plans to launch a stock

market education program in 2018 to further expand its educational offerings. While product

lines (i.e., real estate and entrepreneurship) don’t change very often, the brands (i.e., celebrity

endorsements) under the product line umbrellas frequently change to align with market

preferences and interests.

Zurixx has developed certain educational programs branded as the following:

1. Success Path Education

Success Path Education is a real estate training workshop that is built around the “know-how”

and persona of Tarek and Christina El Mousa. This workshop teaches participants how to

successfully renovate and “flip” houses by focusing on topics like business planning and goal

setting, asset protection, acquisition funding, and legal entity formation. Specifically, the

Success Path workshops teach participants the following subjects:

• How to launch a real estate business and generate a profit by flipping, buying

and holding, and wholesaling homes;

• How to find unlisted properties using nontraditional techniques;

• How to utilize participants credit, retirement savings, hard money lenders,

gap funding, and traditional mortgages to fund real estate transactions; and,

between persons located outside of Puerto Rico; xii) call centers; xiii) shared service centers; xiv) medical, hospital, and laboratories services; xv) investment banking and other financial services, including but not limited to asset management, alternative investments, management of activities related to private capital investment, management of coverage funds or high-risk funds, management of pools of capital, trust management that serves to convert different groups of assets into securities, and escrow account management services; and xvi) any other service designated by the Secretary of the Department of Economic Development and Commerce of Puerto Rico.

6 A copies of Zurixx’s Act 20 application and decree are available upon request.

Case 2:19-cv-00713-DAK-EJF Document 71-1 Filed 12/13/19 Page 12 of 85

Page | 12

Economics Partners, LLC

www.econpartners.com

• How to generate income through wholesale real estate transactions and,

connecting with real estate investors for a finder’s fee.

Participants receive a starter kit including an MP3 player and a compact disc featuring 50 Ways

to Find Your Next Flip.

2. Daymond John’s Launch Academy

The Launch Academy helps participants achieve their goals of becoming a successful

entrepreneur. This workshop focuses on helping prospective entrepreneurs make the transition

from an idea to the actual launch of a business. Further, the workshops teach participants

strategies to manage money, position the business, and creating a legacy. Launch Academy

was introduced to the market during the third quarter of 2015. The topics covered during the

training include the following:

• Validating the business concept;

• Moving toward a product launch with greater speed;

• Engaging with potential customers and transforming them into buyers; and,

• Positioning leaders to efficiently build the business.

The skills obtained during the workshop include mastering the components of a business

presentation, business planning and goal setting, marketing strategy and research, social media

and networking tools, funding acquisitions, and advertising and media. All attendees receive a

starter kit including an MP3 player and Daymond John’s eBooks, Stepping Up for Success and

Perfecting Your Pitch.

3. The Flipping Formula

Pete Souhleris and Dave Seymour built a successful house-flipping business on a formula they

created. Pete and Dave, in partnership with Zurixx, have turned their formula into an

educational program that has helped people start their own successful real estate businesses.

Similar to Success Path, participants learn how to find unlisted properties, which are below

market value, obtain financing, create cash flow, and complete a wholesale real estate

transaction in 60 to 90-days. Participants receive a starter kit including the Ripe or Rotten? DVD

on how to evaluate properties, the Zero to Hero DVD, the Flipping Formula eBook, and the 24

Ways to Profit eBook.

The Flipping Formula helps participants determine the profitability of their prospective

purchases. The formula starts with surveying three months of sales data for comparable

properties within a mile and a two-and-a-half-mile radius. Once a probable post-flip listing

price is determined, the program employs a Maximum Offer for Ownership (“MOFO”)

formula. The formula starts with the post-flip listing price and subtracts an ideal profit

(generally 20 percent to account for the unexpected), an allotment for fees like commissions and

closing costs, and the cost of construction, which is carefully determined after reviewing bids

Case 2:19-cv-00713-DAK-EJF Document 71-1 Filed 12/13/19 Page 13 of 85

Page | 13

Economics Partners, LLC

www.econpartners.com

from multiple contractors. The formula also incorporates what design trends and products are

important to adding value.

4. Winning the Property War

Doug Hopkins and Damon Line have decades of professional real estate experience and have

put together their flipping and wholesaling strategies into an educational program called

Winning the Property War. This seminar trains real estate agents and investors to: 1) learn to

flip, renovate, and wholesale houses; 2) obtain key real estate information; and, 3) position the

participants to become full-time real estate investors.

5. Property Bank

Mike Baird from Spike TV’s Flip Men and Greg Herlean, best-selling author of Bank on This,

have created the Property Bank real estate training system. This educational system teaches

participants how to find growth and wealth opportunities.

6. Conclusion

Many of the previously described products follow a “product funnel” that seek to steadily

engage customers with additional advanced trainings and products. Figure 2 below illustrates

the product sale funnel that customers typically engage in.

Figure 2: Zurixx Product Funnel

Preview Workshop

Coaching

Mentorship

Advanced camps

Backend supportFree Paid

Case 2:19-cv-00713-DAK-EJF Document 71-1 Filed 12/13/19 Page 14 of 85

Page | 14

Economics Partners, LLC

www.econpartners.com

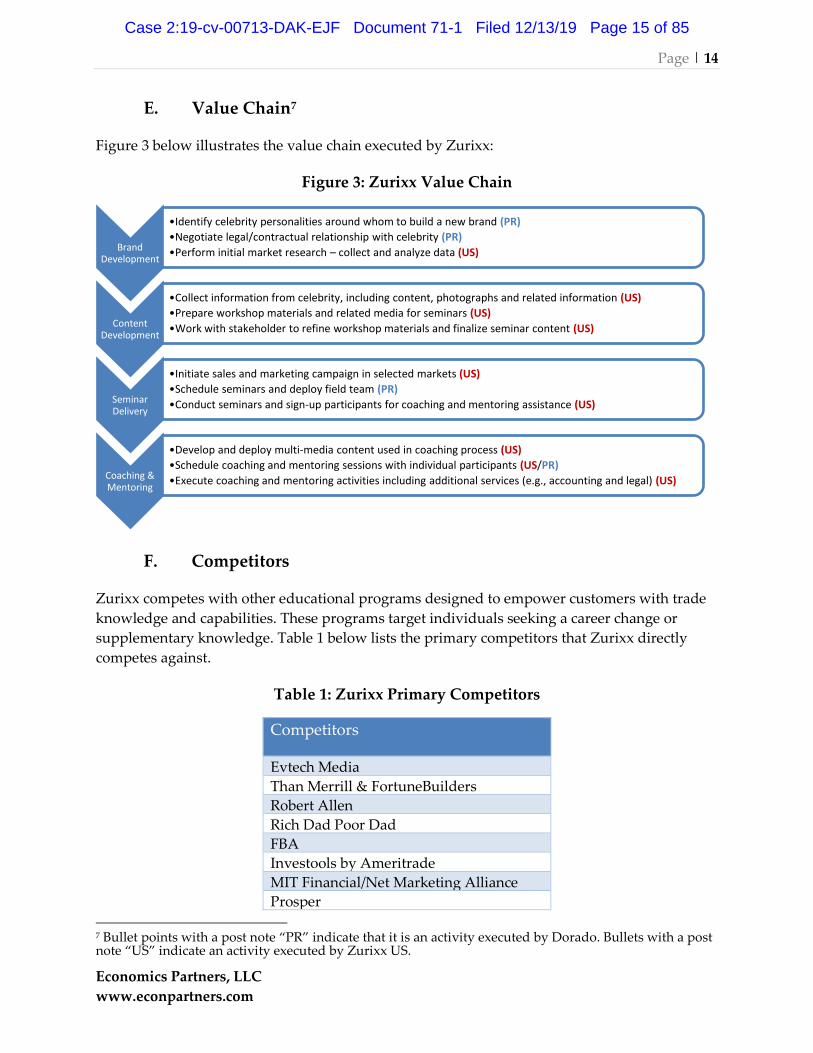

E. Value Chain7

Figure 3 below illustrates the value chain executed by Zurixx:

Figure 3: Zurixx Value Chain

F. Competitors

Zurixx competes with other educational programs designed to empower customers with trade

knowledge and capabilities. These programs target individuals seeking a career change or

supplementary knowledge. Table 1 below lists the primary competitors that Zurixx directly

competes against.

Table 1: Zurixx Primary Competitors

Competitors

Evtech Media

Than Merrill & FortuneBuilders

Robert Allen

Rich Dad Poor Dad

FBA

Investools by Ameritrade

MIT Financial/Net Marketing Alliance

Prosper

7 Bullet points with a post note “PR” indicate that it is an activity executed by Dorado. Bullets with a post note “US” indicate an activity executed by Zurixx US.

Brand Development

•Identify celebrity personalities around whom to build a new brand (PR)

•Negotiate legal/contractual relationship with celebrity (PR)

•Perform initial market research – collect and analyze data (US)

Content Development

•Collect information from celebrity, including content, photographs and related information (US)

•Prepare workshop materials and related media for seminars (US)

•Work with stakeholder to refine workshop materials and finalize seminar content (US)

Seminar Delivery

•Initiate sales and marketing campaign in selected markets (US)

•Schedule seminars and deploy field team (PR)

•Conduct seminars and sign-up participants for coaching and mentoring assistance (US)

Coaching & Mentoring

•Develop and deploy multi-media content used in coaching process (US)

•Schedule coaching and mentoring sessions with individual participants (US/PR)

•Execute coaching and mentoring activities including additional services (e.g., accounting and legal) (US)

Case 2:19-cv-00713-DAK-EJF Document 71-1 Filed 12/13/19 Page 15 of 85

Page | 15

Economics Partners, LLC

www.econpartners.com

Competitors

Armando Montelongo

The Learning Annex

Scott McGileray

Grant Cardone

G. Functions, Risks, and Intellectual Property

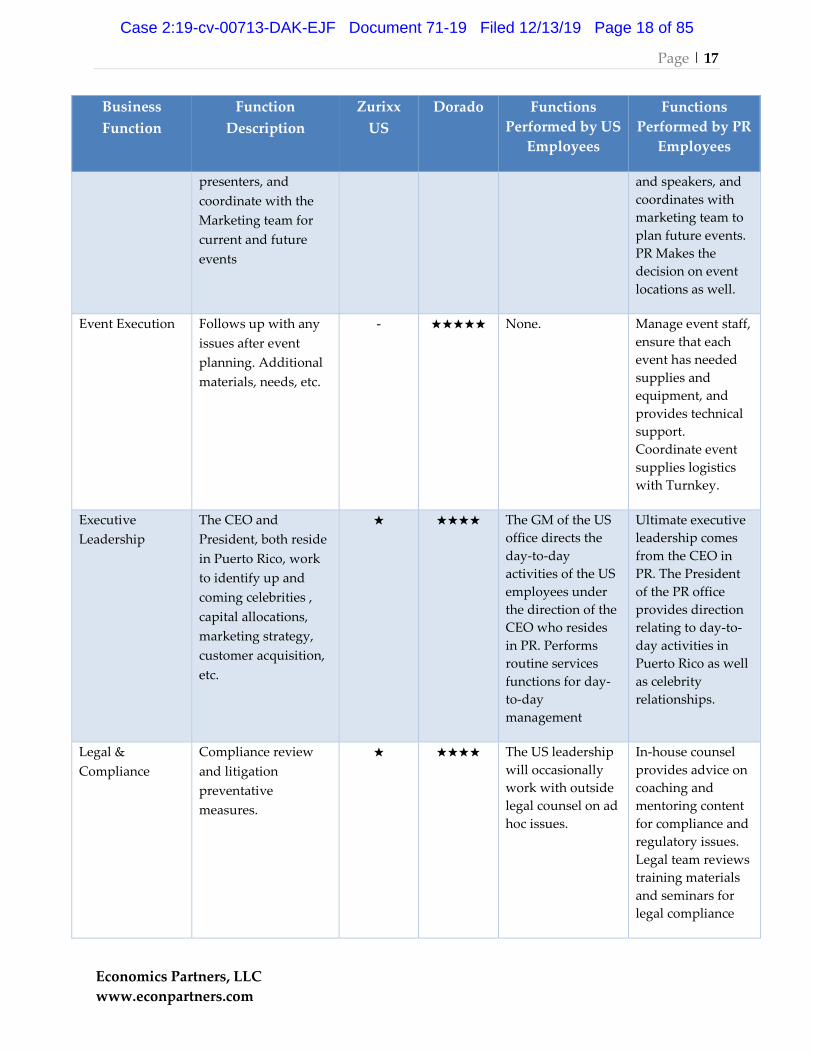

1. Functions

Table Two illustrates the division of functions between Zurixx US and Dorado. Differing levels

of functional involvement between Zurixx US and Dorado are determined and represented

using stars in the table below. For example, Accounting & Finance functions are primarily

controlled and performed by Zurixx US through financial statement preparation, cash

management, etc. Dorado performs limited Accounting & Finance functions, such as payroll

processing, which merit an overall weighting of four to one stars. Weightings between Zurixx

US and Dorado sum to equal five stars. A detailed analysis of Company functions and

responsibilities will be described further in succeeding sections within the report.

Table 2 – Division of Functions Between US and Puerto Rico

Business

Function

Function

Description

Zurixx

US

Dorado Functions

Performed by US

Employees

Functions

Performed by PR

Employees

Accounting &

Finance

Corporate finances,

financial statement

preparation, cash

management, payroll,

financial planning

and analysis, and

corporate

expenditures.

★★★★ ★ Corporate finances,

financial statement

preparation, cash

management,

payroll, FP&A, and

corporate

expenditures.

Limited assistance

in payroll

processing.

Celebrity

Management

Identify and manage

up and coming

celebrities who have

developed a brand to

promote company

products and services

- ★★★★★ None. PR performs initial

acquisition of

celebrity

relationships as

well as maintains

oversight of

relationships

management.

Case 2:19-cv-00713-DAK-EJF Document 71-1 Filed 12/13/19 Page 16 of 85

Page | 16

Economics Partners, LLC

www.econpartners.com

Business

Function

Function

Description

Zurixx

US

Dorado Functions

Performed by US

Employees

Functions

Performed by PR

Employees

Coaching &

Mentoring

Manage the coaching

relationship and the

material provided on

the online educational

platform

★★★★★ - Manage coaching

relationships and

develop

educational

material and online

content.

None. (see legal

functions for some

functions

associated with

educational

material)

Customer Service Inbound

communication from

seminar participants

and attendee

registrants. Outbound

communication with

attendees and

registrants who did

not attend.

★★★ ★★ Functions shared

equally between

the US and PR.

Functions include

inbound, outbound

and ad hoc

customer support.

Exceptions for US-

only functions

include contract

compliance and

high-level direction

and approval.

Functions shared

equally between

the US and PR.

Functions include

inbound, outbound

and ad hoc

customer support.

Content &

Graphic Design

Creates designs and

scopes the market in

order to incorporate

Celebrity image into

the developing brand.

★★ ★★★ Marketing team

performs routine

functions to design

content around

brands. US

executes CEO

strategy and how

seminar materials

relate to products

High level

direction from CEO

who resides in PR.

Strategy and

content execution is

performed in PR

and strategy is

disseminated to the

US.

IT Infrastructure

& Software

Development

Manages both

hardware and

software technology

solutions for the

Company

★★★★★ - Hardware and

software

infrastructure,

software

development, help

desk support, and

data storage.

None.

Event Planning Book events, arrange

venues, schedule

- ★★★★★ None. PR organizes,

books all events,

schedule venues

Case 2:19-cv-00713-DAK-EJF Document 71-1 Filed 12/13/19 Page 17 of 85

Page | 17

Economics Partners, LLC

www.econpartners.com

Business

Function

Function

Description

Zurixx

US

Dorado Functions

Performed by US

Employees

Functions

Performed by PR

Employees

presenters, and

coordinate with the

Marketing team for

current and future

events

and speakers, and

coordinates with

marketing team to

plan future events.

PR Makes the

decision on event

locations as well.

Event Execution Follows up with any

issues after event

planning. Additional

materials, needs, etc.

- ★★★★★ None. Manage event staff,

ensure that each

event has needed

supplies and

equipment, and

provides technical

support.

Coordinate event

supplies logistics

with Turnkey.

Executive

Leadership

The CEO and

President, both reside

in Puerto Rico, work

to identify up and

coming celebrities ,

capital allocations,

marketing strategy,

customer acquisition,

etc.

★ ★★★★ The GM of the US

office directs the

day-to-day

activities of the US

employees under

the direction of the

CEO who resides

in PR. Performs

routine services

functions for day-

to-day

management

Ultimate executive

leadership comes

from the CEO in

PR. The President

of the PR office

provides direction

relating to day-to-

day activities in

Puerto Rico as well

as celebrity

relationships.

Legal &

Compliance

Compliance review

and litigation

preventative