2015 Level II mindmaps (04. FRA)

36

CFA LEVEL II FINANCIAL REPORTING ANALYSIS Copyright (2014), CFA Institute. Reproduced and republished with permission from CFA Institute. All rights reserved

Transcript of 2015 Level II mindmaps (04. FRA)

CFA LEVEL II

FINANCIAL REPORTING ANALYSIS

Copyright (2014), CFA Institute.

Reproduced and republished with permission from CFA Institute. All rights reserved

15.Inventories:Implications

For FS &Ratios

LEASE n=2 years PMT= i= 13%

1. Ordinary annuity PV= 100

Operating lease Financial lease Operating lease Financial leaseYr1 Yr2 Yr1 Yr2 Yr1 Yr2 Yr1 Yr2

Asset 0 0 Asset Asset Lease receivable

Beg. 100 50 Beg. 100 50 Beg. 100 53

(‐)Depr 50 50 (‐)Depr 50 50 (+)Int. rev 13 7

End 50 0 End 50 0 (‐)Receipt 60 60

End 53 0

Liability 0 0 Liability Liability 0 0 Liability 0 0

Beg. 100 53

(+)Int.exp 13 7

(‐)Pmt 60 60

End 53 0

Lease exp 60 60 Depr exp 50 50 Lease rev. 60 60 Int. rev. 13 7

Int. exp 13 7 Depr exp 50 50

63 57 10 10

CF? ‐60 ‐60 CF? ‐13 ‐7 CF? 60 60 CF? 13 7

CF? ‐47 ‐53 CF? 47 53

‐60 ‐60 60 60

Note: if sales‐type lease‐‐>

just add gross profit

2. Annuity due PV= 113

Financial lease Financial leaseYr1 Yr2 Yr1 Yr2

Asset Lease receivable

Beg. 113 56.5 113 60

(‐)Depr 56.5 56.5 (‐)Receipt 60 60

End 56.5 0 Beg 53 0

(+)Int. 7 0

End 60 0

Liability Liability 0 0

113 60

(‐)Pmt 60 60

Beg 53 0

(+)Int. 7 0

End 60 0

Depr exp 56.5 56.5

Int. exp 7 0

63.4 56.5 Int. rev. 7 0

CF? ‐7 0 CF? 7 0

CF? ‐53 ‐60 CF? 53 60

‐60 ‐60 60 60

60

LESSEE LESSOR

LESSEE LESSOR

17.1IntercorporateInvestments

Joint ventures (shared control)

1.Investmentsin financialassets(minoritypassive)

Examples

4. Jointventures

What is a joint venture Shared by 2 investors or moreInvest in foreign markets, special projects, risky ventures

Under IFRS & US GAAP Equity methodin rare cases: Proportionate consolidation

5. SPEand VIE

SPE

Special Purpose Vehiclea legal structure (corporation, partnership, joint venture, trust)

securitizeassets (such assponsor'sreceivables)

remove from sponsor's BSCF in = CFObut if with recourse --> similar tocollaterallized borrowingsFinancial analysts mustadjust CFO & leverage

to isolate assets & liabilities to reduce risk --> reducefinancial cost (previously an OBS --> improve ratios)

VIE

Variable Interest Entity

=SPE+conditions

At risk equity is insufficient tofinance the entity's activities withoutadditional financial support

equityinvestorslacks

decision making rightsobligation to absorb lossesright to receive residualinterest in the SPE

--> must consolidate

QSPE

Qualifying SPE

only hold financial assets(usually receivables)QSPE had totalcontrol of the assetsnot have to consolidate

In the pastUSGAAP permittedIFRS not permit

Now: both USGAAP & IFRS not permit

c. Effects onfinancial ratios

Items

Net income

Equity

Assets & Liabilities

Sales

Ratios

LeverageNet profit marginROEROA

30% 3 Note: PP=BV

TABLE 1: (1/1/2011)

Parent SubsidiaryEquity

methodExplanation

Proportionate consolidation

methodExplanation

Acquisition method (purchase method/

consolidation method)Explanation

Cash 20 9 17 19.7 26A/R+Inventory 28 7 28 30.1 35

Investment in S 3Fixed assets 32 8 32 34.4 40

Total assets 80 24 80 84.2 101

Total liabilities 40 14 40 44.2 54

Common stock 28 6 28 28 28Retained earnings 12 4 12 12 12

Total Equity 40 10 40 40 407 Minority interest

Total liab.&equity 80 24 80 84.2 101

TABLE 2: (31/12/2011)

Parent only

SubsidiaryEquity

methodExplanation

Proportionate consolidation

methodExplanation

Acquisition method (purchase method/

consolidation method)Explanation

Revenues 60 20 60 66 80Expenses -40 -16 -40 -44.8 -56Equity in income of S 1.2

-2.8 Minority interestNet income 20 4 21.2 21.2 21.2Dividend 0 1Retained earnings 20 3

Cash increased due to div from S 0.3 0.3 0.3Investment in S 3.9Accum. Retained Earnings 33.2 33.2 33.2Minority Interest 9.1

Some BS items of Parent for the year ending 31/12/2011

% Purchased of Subsidiary Purchased price

BS before acquisition as at 1/1/2011 BS of Parent after acquisition as at 1/1/2011

IS for the year ending 31/12/2011 IS of Parent for the year ending 31/12/2011

30% Purchased price 4.5 Note: PP=FV>BV

TABLE 3: (1/1/2011) Fixed assets are depreciated SL over: 3 years

Parent SubsidiaryFair Value of Subsi.

Equity method

ExplanationProportionate consolidation

methodExplanation

Acquisition method (purchase method/

consolidation method)Explanation

Cash 20 9 9 15.50 18.20 24.5A/R+Inventory 28 7 7 28 30.1 35

4.5 Investment in SFixed assets 32 8 13 32 35.9 45

Total assets 80 24 29 80 84.2 104.5

Total liabilities 40 14 14 40 44.2 54

Common stock 28 6 28 28 28Retained earnings 12 4 12 12 12

Total Equity 40 10 15 40 40 4010.5 Minority interest

Total liab.&equity 80 24 80 84.2 104.5

TABLE 4: (31/12/2011)

Parent only

SubsidiaryEquity

methodExplanation

Proportionate consolidation

methodExplanation

Acquisition method (purchase method/

consolidation method)Explanation

Revenues 60 20 60 66 80Expenses -40 -16 -40 -44.8 -56

1.2 Equity in income of SAdditional depreciation -0.5 -0.5 -0.5

-2.8 Minority interestNet income 20 4 20.7 20.7 20.7Dividend 0 1Retained earnings 20 3

Investment in S 4.9

% Purchased of Subsidiary

BS before acquisition as at 1/1/2011 BS of Parent after acquisition as at 1/1/2011

IS for the year ending 31/12/2011 IS of Parent for the year ending 31/12/2011

Some BS items of Parent for the year ending 31/12/2011

a. Types ofpost-employmentbenefit plans

Example 1

b. Measuresof a DBpension plan'sliability/asset

c. DBpensioncosts

c. DBpensioncosts(CONT.)

d. Impactof a DBP'sassumptions

e. Adjustmentsfor analyticalpurpose

f. Cash flowinformation

Share-basedcompensation

g. Accountingissues

h.

Stockgrant

Stockoptions

Pension example 1:

Employee: 22 years old, working till 60 years old, lives till 80 years old End of this year --> annual salary 60m Salary growth 5.2611%/year --> last salary before retiring: 400m DB plan: for each year of retirement, pension= 1% (=f) of last salary for number of working years First pension: 61 years old. Last pension: 80 years old Discount rate 10%

PENSION1. PBO (Projected Benefit Obligation) is a Liability; CSC (Current Service Cost) is an expense

22 23 24 60 61 80

Salary: g= 5.2611%

1st yr (23) Discount rate r=10%

2nd yr (24)

22 23 24 60 61 80

60m 400m=last salary f= 1% per working year

CSC=1m 4m 4mPBO=1m

CSC=1.1m 4m 4m2nd yr (24)

2. Plan asset (money contribution to trust + investment return) Long term expected return: 15%1st yr (23) Contribute

CSC=1.1m 4m 4mPBO=2xCSC=2.2m=Previous PBO+CSC+Int costInt cost=Discount rate x Previous PBO=0.1m

1mPlan assetCFO

2nd yr (24) (assuming Contribution = 0)Plan asset=1.12m

1m R= 12% (actual return)‐1m

Pension exp=1.00m

= Plan asset ‐ PBO

=CSC + Int cost ‐ E(R)

in IS: E(R)=0.15min OCI: Actuarial loss:‐0.03m

Funded status=‐1.08m

In IS: Pension exp=1.05m

Reporting In BS:USGAAP: Net pension liab: 1.08m; OCI: ‐0.03mIFRS: Net pension liab: 1.05m (no OCI)

3. Plan amendment Year 2: increase f to 2%2 d (24) CSC 2 2 882nd yr (24)

=CSC + Int cost ‐ E(R) +Prior service cost (optional: 10% corridor)

CSC=2.2m 8mPBO=2xCSC=4.4m=Previous PBO+CSC+Int cost+???Int cost=0.1mPrior service cost= 1.1mIn IS: Pension exp=3.25m

8m

4. ABO & VBO Year 2: employee quits2nd yr (24) Last salary 63m

CSC=0.158m 0.632m 0.632mPBO=2xCSC=0.316m=ABOf d /If vested 5 years ‐‐> VBO=1/5xABO=0.063m

Pension example 2:

Expected return on plan assets is 80

Amortization of actuarial loss is 30

Amortization of prior service cost is 10

Calculate

Net periodic benefit expense Economic pension expense

Pension example 3:

Calculate Pension expense and make adjustments for analytical purposes.

Pension example 4:

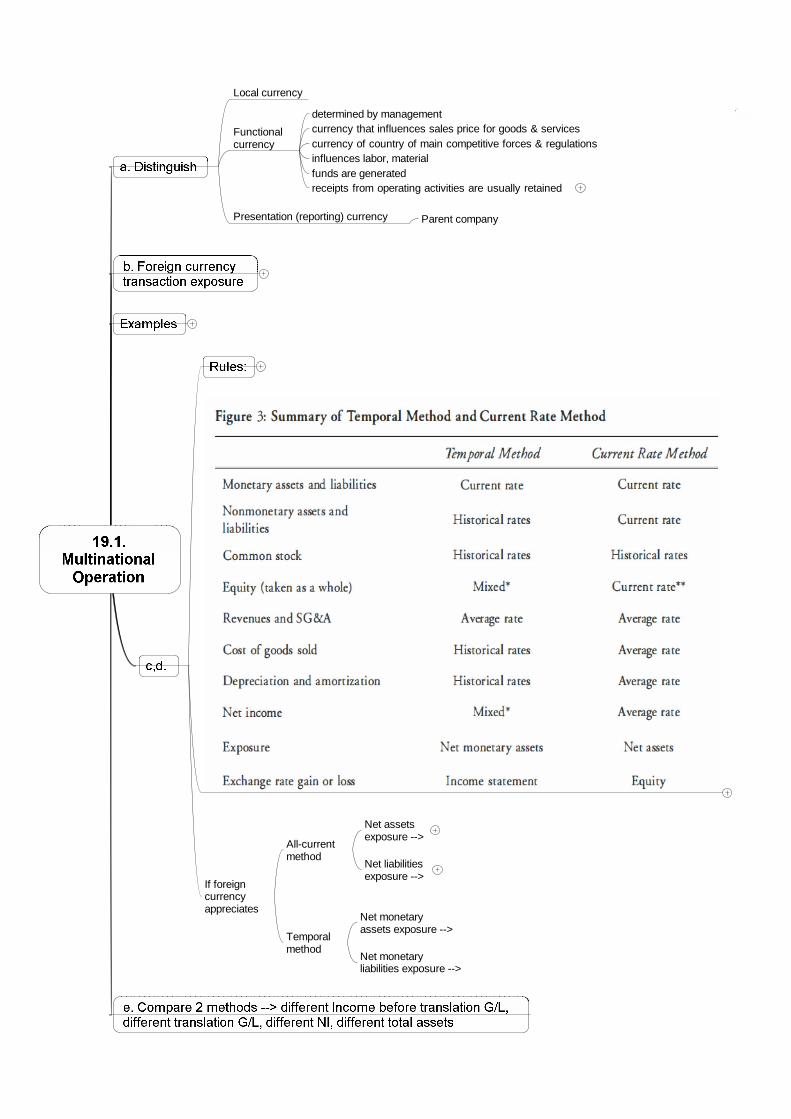

Local currency

Functionalcurrency

determined by managementcurrency that influences sales price for goods & servicescurrency of country of main competitive forces & regulationsinfluences labor, materialfunds are generatedreceipts from operating activities are usually retained

Presentation (reporting) currency Parent company

If foreigncurrencyappreciates

All-currentmethod

Net assetsexposure -->

Net liabilitiesexposure -->

Temporalmethod

Net monetaryassets exposure -->

Net monetaryliabilities exposure -->

19.2.Multinational

Operation

f. Affecting theparent company'sfinancial ratios

g. Subsidiariesoperating inhyperinflationaryeconomies

Analyzing foreign currency disclosure

h. Impact oneffective tax rate

i. Componentsof saleschanges andSustainability

j. Countries of operationaffect financial results

Exchange rate throughout 2010 1.00 Exchange rate at 31‐12‐2011 1.10 Average exchange rate for 2011 0.90

USD VND USD e/r at time ofpurchase/deal

VND All CURRENT VND TEMPORAL

Cash 1,100 1,100 500 550 550A/R ‐ ‐ 400 440 440Inventory ‐ ‐ 600 0.80 660 480

Fixed assets ‐ ‐ 500 1.30 550 650

TOTAL ASSETS 1,100 1,100 2,000 2,200 2,120 ‐

A/P ‐ ‐ 100 110 110Unearned Rev. ‐ ‐ 200 1.25 220 250 Long‐term Liab. ‐ ‐ 400 440 440

Common Equity 1,000 1,000 1,000 1,000 1,000 Retained Earnings 100 100 300 340

TOTAL LIAB.&EQUI 1,100 1,100 2,000

Revenue ‐ ‐ 3,000 2,700 COGS ‐ ‐ (2,000) 0.85 1,700 Depreciation exp. ‐ ‐ (100) 1.30 130 Other exp. ‐ ‐ (700) 630

Net income ‐ ‐ 200 240 INCO

ME STAT

EMEN

TBA

LANCE

SHEET

Year 2011Year 2010

Schweser example (Multinational Operations)

U$/LC 31/12/2008 31/12/2009INCOME STATEMENT 2009

All current method

Current ex/ rate 0.5000 0.4545 LC $ $ ExplanationAverage ex/ rate 0.4762 Revenues 5,000 2,381.00 2,381.00 AverageHistorical ex/ rate COGS 3,300 1,571.46 1,595.22 Historical

For COGS 0.4834 Gross margin 1,700 809.54 785.78 For Depr. Exp. 0.4878 Other expenses ‐400 (190.48) (190.48) AverageFor Fixed assets 0.4881 Depr. Expenses ‐600 (285.72) (292.68) HistoricalFor accum. Depr. 0.4896 302.62 Inc bf remeasureG/LFor end. inventory 0.4762 48.01 Remeasurement G/L

For equity 0.5000 Net Income 700 333.34 350.63

BALANCE SHEETAll current method

BALANCE SHEETAll current method

LC $ LC $ $ E l i

Temporal method

31/12/2008 31/12/2009Temporal method

LC $ LC $ $ ExplanationCash 100 50.00 Cash 100 45.45 45.45 CurrentA/R 500 250.00 A/R 650 295.43 295.43 CurrentInventory 1,000 500.00 Inventory 1,200 545.40 571.44 Historical

Current Assets 1,600 800.00 Current Assets 1,950 886.28 912.32

Fixed Assets 800 400.00 Fixed Assets 1,600 727.20 780.96 HistoricalAccum. Depr. ‐100 (50.00) Accum. Depr. ‐700 (318.15) (342.72) Historical

Net fixed assets 700 350.00 Net fixed assets 900 409.05 438.24

Total assets 2,300 1,150.00 Total assets 2,850 1,295.33 1,350.56

Accounts payable 400 200.00 Accounts payable 500 227.25 227.25 CurrentCurrent debt 100 50.00 Current debt 200 90.90 90.90 CurrentLong term debt 1,300 650.00 Long term debt 950 431.78 431.78 CurrentTotal liabilities 1,800 900.00 Total liabilities 1,650 749.93 749.93

Common stock 400 200.00 Common stock 400 181.80 200.00 HistoricalRetained earnings 100 50.00 Retained earnings 800 363.60 400.63 Plug number

???Total equity 500 250.00 Total equity 1,200 545.40 600.63

FRA2‐ Multinational operations‐ Eg.3

1234567

891011

12

13

141516171819202122

A B C D E

Adjustments for inflation under IFRS

Price indicesDec. 31. 2006 100Dec. 31. 2007 150Average for 2007 125

INCOME STATEMENT2007

Adjustment factor

Inflation adjusted

Revenues 15,000 1.20 18,000Expenses ‐12,000 1.20 ‐14,400Net purchasing power G/L 6,900

Net Income 3,000 10,500

BALANCE SHEET 2006 2007Adjustment

factorInflation adjusted

Cash 5,000 8,000 8,000Supplies 25,000 25,000 1.50 37,500

Total assets 30,000 33,000 45,500

Accounts payable 20,000 20,000 20,000Common stock 10,000 10,000 1.50 15,000Retained earnings 0 3,000 10,500

Total liab.& equity 30,000 33,000 45,500

20.1.EvaluatingFinancialReporting

Quality

FR qualityReportingquality

= info is

f. Earningsquality

3 conditions

Conceptualframework

Answer 2questions

is FR GAAP compliant& Decision-useful

High quality earnings?

ContinuumFrom highest tolowest FR quality

Arisefrom

Measurement& Timing

aggressive vs. conservativeaffecting multiple FS elements

ClassificationExamplesaffecting one FS element only

Biasedaccounting

Misstateprofitability

Mechanism

RevenueChannel stuffingBill & holdOutright fake sales

Lessor use of finance lease_____ operating revenue, _____ non operating expense_____ IS gain, ______ OCI loss

Warning signs

high revenue growthA/R growth > Sales growthHigh customer returnsCFO < EBITFinal quarter surprisesInconsistency in operating classificationAggressive accounting assumptionsExecutive compensation tied to financial results

Misstateassets/liabilities

Mechanism

Inappropriate models (useful life...)Reclassification from current to non-currentOver/Understate allowances and reservesUnderstate identifiable assets(overstate GW) in acquisition

Warning signs

Inconsistency in model inputs forvaluation of assets vs liabilitiesAllowances & reserves differfrom peers & fluctuateHigh GW / Total assetsUse of SPELarge fluctuations in DTA, DTLLarge OBS liabilities

OverstateCFO

MechanismManage activitiesto affect CFO

e.g.: Stretching payables

Misclassify CFI as CFO

Warning signs

A/P increases while Inventory & A/R decreaseCapitalized expenditures (deduct CFI)Sale and leaseback of assetsBank overdraft increases

Business combinations-acquisition method

buy target with high CFO --> increase CFO (pay by stocks or CFI)

reason foracquiring may be

hiding accountingirregularities

buy targets with dissimilar operations orwith less publicly available information

Both acquiring and target firms have incentives topursue aggressive accounting to inflate stock priceOverstate GW (understate value of identifiable net assets

GAAP accounting butnot economic reality e.g..: Enron was able to avoid consolidation of SPEs

Restructuring provisions & Impairment losses

7 steps

Understand company, industry, accounting principlesUnderstate mgmt (compensation & independence)Areas of accounting vulnerable to subjectivityCompare cross-sectional & time series FS & ratiosCheck for warning signsCheck for shifting of profits or rev. among multiple business linesUse quantitative tools to evaluate the likelihood of misreporting

Quantitativetools

TheBeneishmodel

M-score

8 variables

DSRI =

GMI =

AQI =

SGI =

DEPI =

SGAI =

Accruals =

LEVI =

Cut-off value

Limitationsrely on accounting datacompanies aware --> game the measures--> reducing predictive power

Altmanmodel

Z-score

Discriminant analysis

5 variables

Net WC/ Total assets

Retained earnings / total assets

EBIT/ Total assets

Pshare / BV liab

Sales / Total assets

Limitationsrely on accounting datasingle period static

consider life cycleindustry norms

CFObe high --> cover CAPEX, debt repmt, divsustainable sourceslow volatility

Checkunusual itemsrevenue qualitystrategic provisioning

Companies may include proformaincome (excl non recurring)

check reconciliation from proformaincome to reported income

Formula:to gauge earnings persistence

Accruals

Non discretionary occur as part of normal business

Discretionary

from non-normal transactionsor accounting choicessometimes used to manipulate earningsindicator:residualsfromregressionmodel with:

total accruals as Y variablefactors that give rise tonormal accruals as Xvariables, e.g:

Red flag when: Net income > 0 but CFO <0

Otherindicators

Repeatedly meet or barely beat consensus estimates

Externalindicators

Enforcement actions by regulatory authorities (SEC)Restatements

Extreme earnings --> not continue forever but revert back to normal level

Accruals increase --> mean reversion faster

Revenuerecognitionissues

Concern both Quantity & Quality

6 steps

Understand the basicsEvaluate & question ageing A/RCash vs accrualsCompare financial with physical dataEvaluate rev. trend and compare with peersCheck for related party transactions

Expensecapitalization

3 stepsUnderstand the basicsTrend and comparative analysisCheck for related party transactions

Completeness check for OBSTake-or-pay contracts --> shouldrecord obligations (penalty pmt)Operating lease --> should capitalize

concern when equity methods for subsidiaries with close to 50% ownership

Unbiasedmeasurement Subjectivity in

measuring(pension, investment, GW, inventory, PP&E impairments)

Clearpresentation

discretion in choosing to present as a single-line item or groupedclear presentation (FS+footnotes+supplementarydisclosures) --> allow comparison

FS, Auditor's report, footnotes, MD&A, financial pressSEC form "NT" (unable to file required reports timely)

BENEISH MODEL – M SCORE

Days Sales Receivable Index (DSRI) is: DSRI = (Net Receivablest / Salest) / Net Receivablest-1 / Salest-1) Gross Margin Index (GMI) is: GMI = [(Salest-1 - COGSt-1) / Salest-1] / [(Salest - COGSt) / Salest] Asset Quality Index (AQI) is: AQI = [1 - (Current Assetst + PP&Et + Securitiest) / Total Assetst] / [1 - ((Current Assetst-1 + PP&Et-

1 + Securitiest-1) / Total Assetst-1)] Sales Growth Index (SGI) is: SGI = Salest / Salest-1 Depreciation Index (DEPI) is: DEPI = (Depreciationt-1/ (PP&Et-1 + Depreciationt-1)) / (Depreciationt / (PP&Et + Depreciationt)) SG&A Expense Index (SGAI) is: SGAI = (SG&A Expenset / Salest) / (SG&A Expenset-1 / Salest-1) Leverage index (LVGI) is: LVGI = [(Current Liabilitiest + Total Long Term Debtt) / Total Assetst] / [(Current Liabilitiest-1 + Total Long Term Debtt-1) / Total Assetst-1] Total Accruals to Total Assets (TATA) is: TATA = (Income from Continuing Operationst - Cash Flows from Operationst) / Total Assetst

Beneish M-Score

1

234567891011121314151617181920212223242526272829303132333435363738

A B C D E F G H I J

Beneish M-Scorehttp://investexcel.net

Parameters GlossaryYear 2008 2009 SGA Selling, General and Administrative ExpensesNet Sales 93823 93685 CA Current AssetsCost of Goods 52155 49193 DSRI Days Sales in Receivables IndexNet Receivables 1174 1373 GMI Gross Margin IndexCurrent Assets 73717 67991 AQI Asset Quality IndexProperty, Plant and Equipment 2532 2058 SGI Sales Growth IndexDepreciation 1696 1716 DEPI Depreciation IndexTotal Assets 86291 84832 SGAI Sales, General and Administrative Expenses IndexSGA Expense 32426 33013 LVGI Leverage IndexNet Income 5741 9888 TATA Total Accruals to Total AssetsCash Flow from Operations 8416 2877Current Liabilities 26297 26275Long-term Debt 1232 1470

Derived VariablesOther L/T Assets [TA-(CA+PPE)] 10042 14783DSRI 0.854 =(C8/C6)/(D8/D6)GMI 1.069 =((D6-D7)/D6)/((C6-C7)/C6)AQI 0.668 =(C20/C12)/(D20/D12)SGI 1.001 =C6/D6DEPI 1.134 =(D11/(D11+D10))/(C11/(C11+C10))SGAI 0.981 =(C13/C6)/(D13/D6)TATA -0.031 =(C14-C15)/C12LVGI 0.975 =((C17+C16)/C12)/((D17+D16)/D12)

M-score5 variable model -3.16 if M > -2.22, firm is likely to be a manipulator8 variable model -2.83

Notes5 variable equation M = -6.065+ .823 DSRI + .906 GMI + .593 AQI + .717 SGI + .107 DEPI8 variable equation M = -4.84 + .920 DSRI + .528 GMI + .404 AQI + .892 SGI + .115 DEPI -.172 SGAI + 4.679 Accrual to TA - .327 Leverage

Altman Z-Scorehttp://investexcel.net

PARAMETERSIncome statementNet sales 200Operating income 10Balance sheetCurrent assets 95Total assets 150Current liabilities 80Total liabilities 125Retained earnings 25Public companiesMarket value of equity 300Private companiesBook value of equity 200

CALCUATIONS Z Z1 Z2Factor Public Private General

Mfg Mfg UseWorking capital/Total assets X1 0.1 1.2 0.717 6.56Retained earning /Total assets X2 0.16667 1.4 0.847 3.26EBIT/Total assets X3 0.06667 3.3 3.107 6.72Market value of equity/Total liabilities X4 2.4 0.6

Book value of equity/Total liabilities X4A 1.6 0.42 1.05Net sales/Total assets X5 1.33333 1 0.998

Z-Score 3.35 2.42 3.33

LEGENDFinancially sound if greater than 2.99 2.9 2.6Caution required if between 2.77 - 2.99Likely to go bankrupt within 2 years if between 1.8 - 2.7Likelihood of bankruptcy is high if below 1.88 1.23 1.1Average for nonbankrupt companies 5.02 4.14 7.7Average for bankrupt companies -0.29 0.15 4.06

Primary purpose: identify potential outcomes, good or bad, that could affect an investment decision

Dupont Formula:

As reported Figure 3

Stand-alone basis: -->remove equity income Figure 4

Common size BS Figure 5

Divide by total LT capital Figure 6

Working capital ratios Figure 7

By Business segmentsGeographic segments

Figure 8,9,10

Accrual ratios & CF/Operating income

Figure 11-15

standalone value ofparent, P/E multiple

Figure 16

Eliminate operating lease

Eliminate QSPE

Figure 17

1 | P a g e

FRA LEVEL II INTEGRATION OF FS ANALYSIS TECHNIQUES Focus 1: Sources of earnings & ROE

2 | P a g e

Focus 2: Asset base

Focus 3: Capital structure

3 | P a g e

Focus 4: Capital allocation decisions

4 | P a g e

5 | P a g e

Focus 5: Earnings quality & CF analysis

6 | P a g e

7 | P a g e

Focus 6: Market value decomposition

Eg.: Market cap of parent = $137b, Market cap of associate = EUR 60b, Average e/r = $1.4/EUR. Ownership = 30%. Implied (stand-alone) value of parent (without associates) =?

Implied (stand-alone) P/E = ?

8 | P a g e

Focus 7: OBS financing Operating lease pmt = $2.4m/ year, n=5 years, r=10% => PV of lease pmts = Make adjustments:

Focus 8: Anticipating changes in accounting standards Eliminate operating lease treatment (USGAAP) USGAAP & IFRS convergence Prohibit QSPE: