2007 Q1 Sales - Nestlé

17

2007 Q1 Sales - April 2007 1 First Quarter Sales 2007

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of 2007 Q1 Sales - Nestlé

2007 Q1 Sales - April 2007 Name of chairman1

First Quarter Sales 2007

2007 Q1 Sales - April 2007 Name of chairman2

Disclaimer

This presentation contains forward looking statements which reflect Management’s current views and estimates. The forward looking statements involve certain risks and uncertainties that could cause actual results to differ materially from those contained in the forward looking statements. Potential risks and uncertainties include such factors as general economic conditions, foreign exchange fluctuations, competitive product and pricing pressures and regulatory developments.

2007 Q1 Sales - April 2007 Name of chairman3

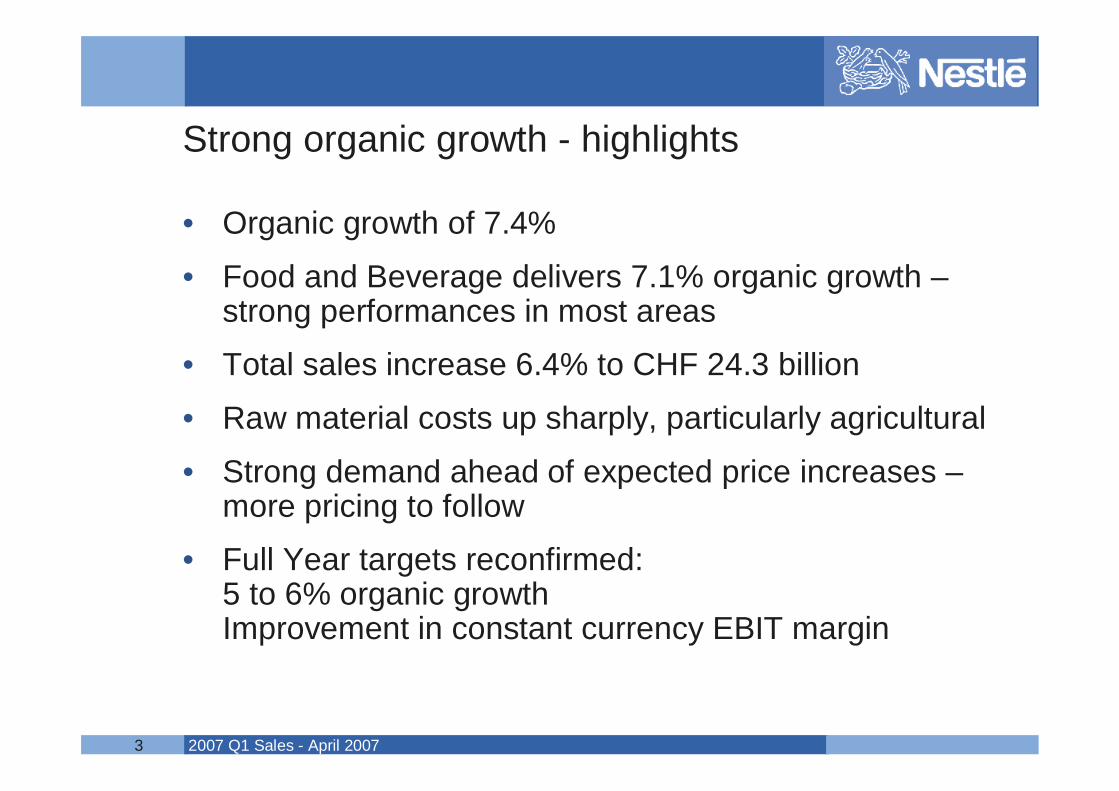

Strong organic growth - highlights

• Organic growth of 7.4%

• Food and Beverage delivers 7.1% organic growth –strong performances in most areas

• Total sales increase 6.4% to CHF 24.3 billion

• Raw material costs up sharply, particularly agricultural

• Strong demand ahead of expected price increases –more pricing to follow

• Full Year targets reconfirmed:5 to 6% organic growthImprovement in constant currency EBIT margin

2007 Q1 Sales - April 2007 Name of chairman4

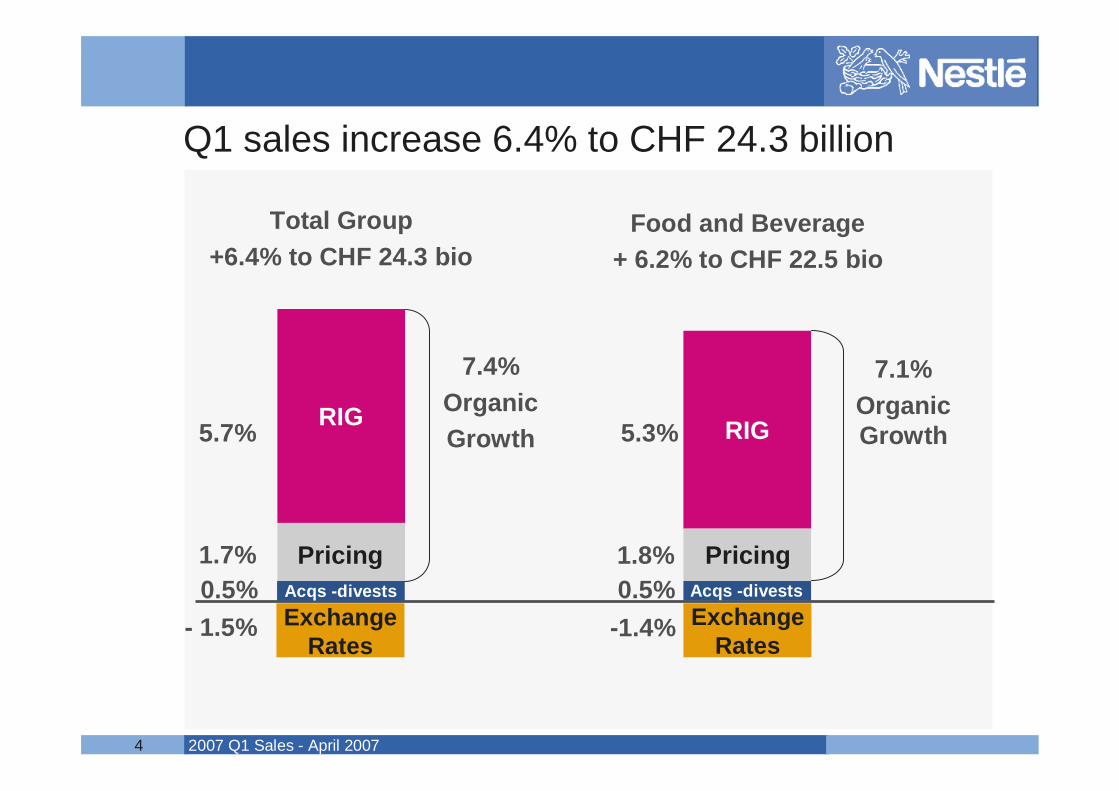

Q1 sales increase 6.4% to CHF 24.3 billion

0.5%Pricing1.7%

5.7%

7.4% OrganicGrowth

Exchange Rates

RIG

- 1.5%Acqs -divests

Total Group+6.4% to CHF 24.3 bio

RIG

Food and Beverage+ 6.2% to CHF 22.5 bio

Pricing

Exchange Rates

Acqs -divests

7.1% OrganicGrowth5.3%

1.8%0.5%

-1.4%

2007 Q1 Sales - April 2007 Name of chairman5

8.7

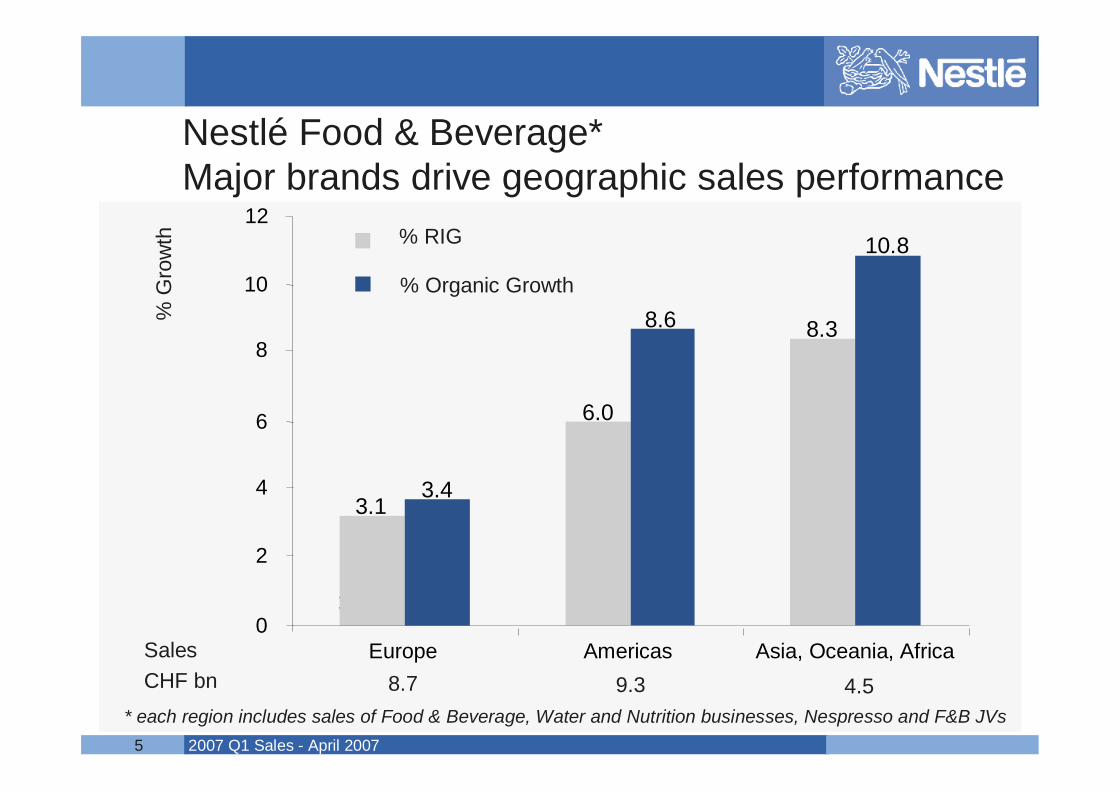

Nestlé Food & Beverage*Major brands drive geographic sales performance

* each region includes sales of Food & Beverage, Water and Nutrition businesses, Nespresso and F&B JVs

Sales CHF bn

x.x x.x x.x

3.1

6.0

8.3

3.4

8.6

10.8

0

2

4

6

8

10

12

Europe Americas Asia, Oceania, Africa

% RIG

% Organic Growth

9.3 4.5

% G

row

th

2007 Q1 Sales - April 2007 Name of chairman6

% G

row

th % RIG % Organic Growth

SalesCHF bn

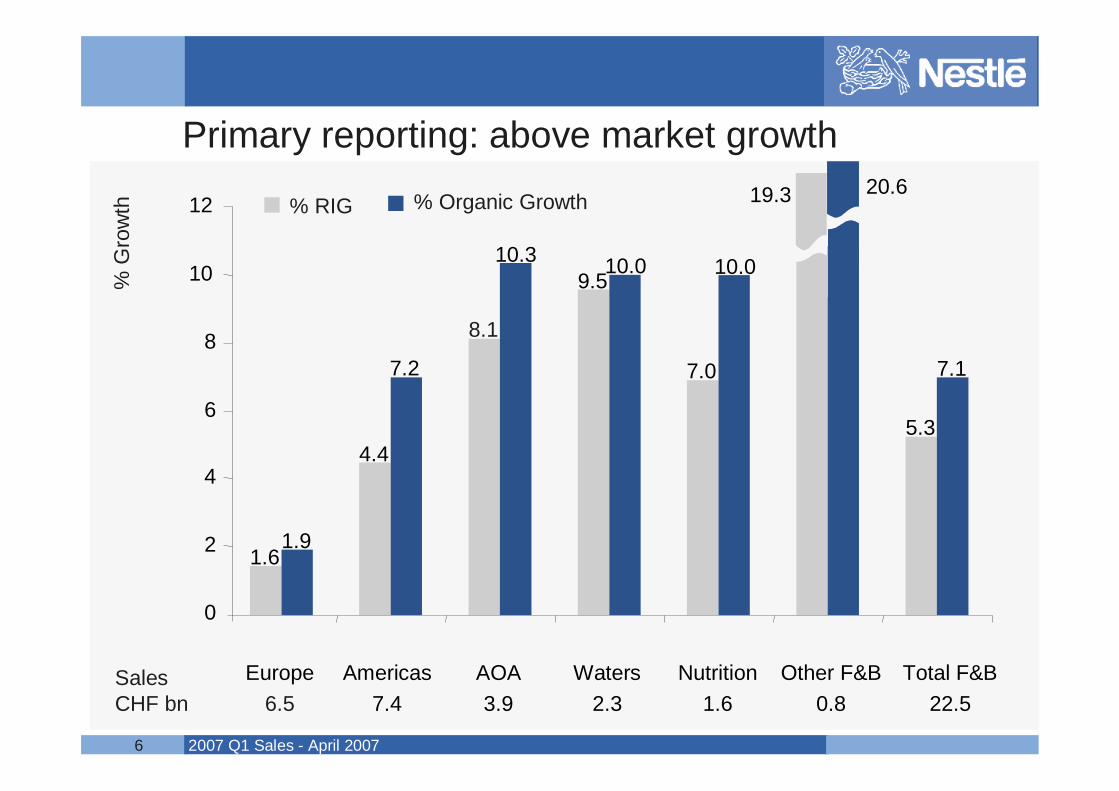

Primary reporting: above market growth

1.6

4.4

8.1

9.5

7.0

19.3

5.3

1.9

7.2

10.3 10.0 10.0

20.6

7.1

Europe6.5

Americas7.4

AOA3.9

Waters2.3

Nutrition1.6

Other F&B0.8

Total F&B22.5

0

2

4

6

8

10

12

2007 Q1 Sales - April 2007 Name of chairman7

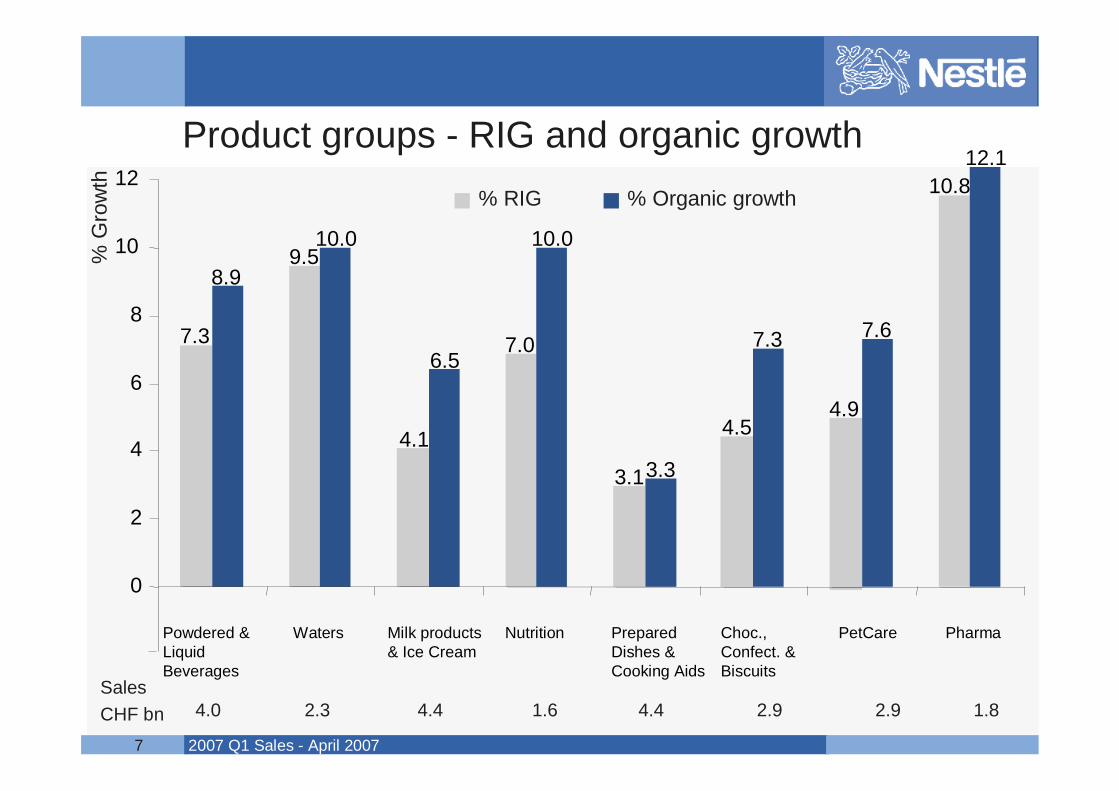

Milk products & Ice Cream

SalesCHF bn

Product groups - RIG and organic growth% RIG % Organic growth

% G

row

th

7.3

9.5

4.1

7.0

3.1

4.54.9

10.8

8.9

10.0

6.5

10.0

3.3

7.3 7.6

12.1

0

2

4

6

8

10

12

Powdered & Liquid Beverages

Waters Nutrition Prepared Dishes & Cooking Aids

Choc., Confect. & Biscuits

PetCare Pharma

4.0 2.3 4.4 1.6 4.4 2.9 2.9 1.8

2007 Q1 Sales - April 2007 Name of chairman8

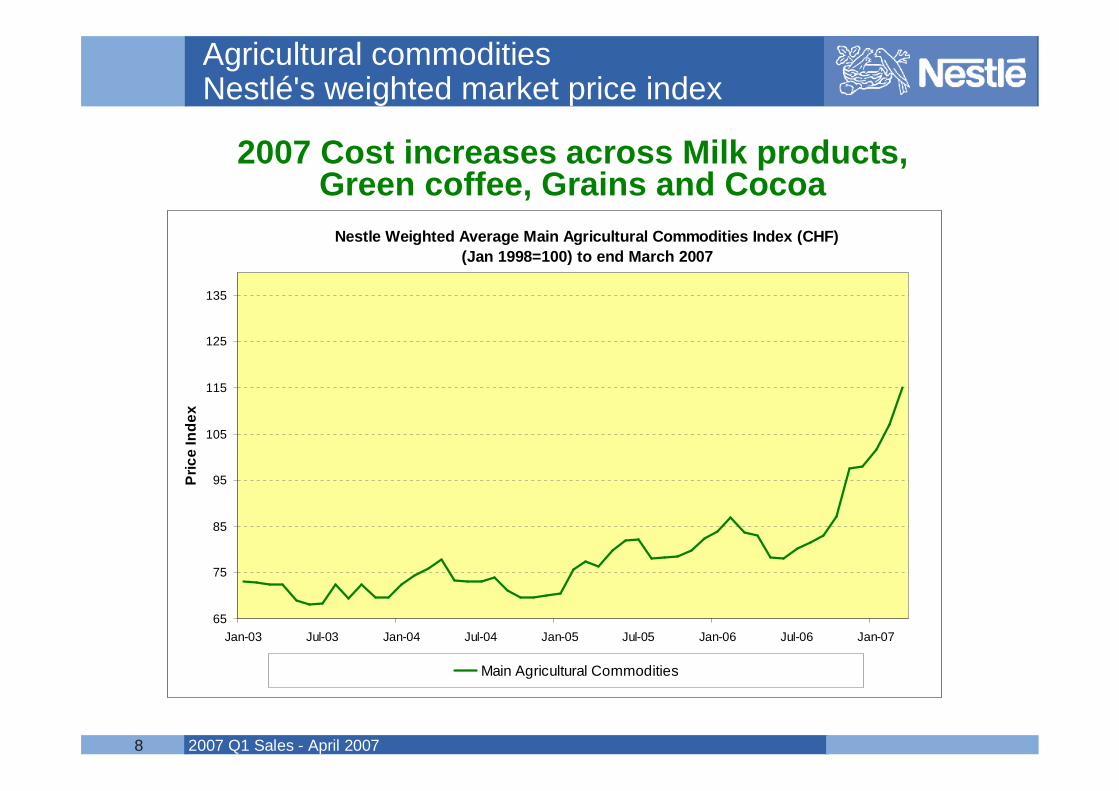

Agricultural commodities Nestlé's weighted market price index

2007 Cost increases across Milk products, Green coffee, Grains and Cocoa

Nestle Weighted Average Main Agricultural Commodities Index (CHF)(Jan 1998=100) to end March 2007

65

75

85

95

105

115

125

135

Jan-03 Jul-03 Jan-04 Jul-04 Jan-05 Jul-05 Jan-06 Jul-06 Jan-07

Pric

e In

dex

Main Agricultural Commodities

2007 Q1 Sales - April 2007 Name of chairman9

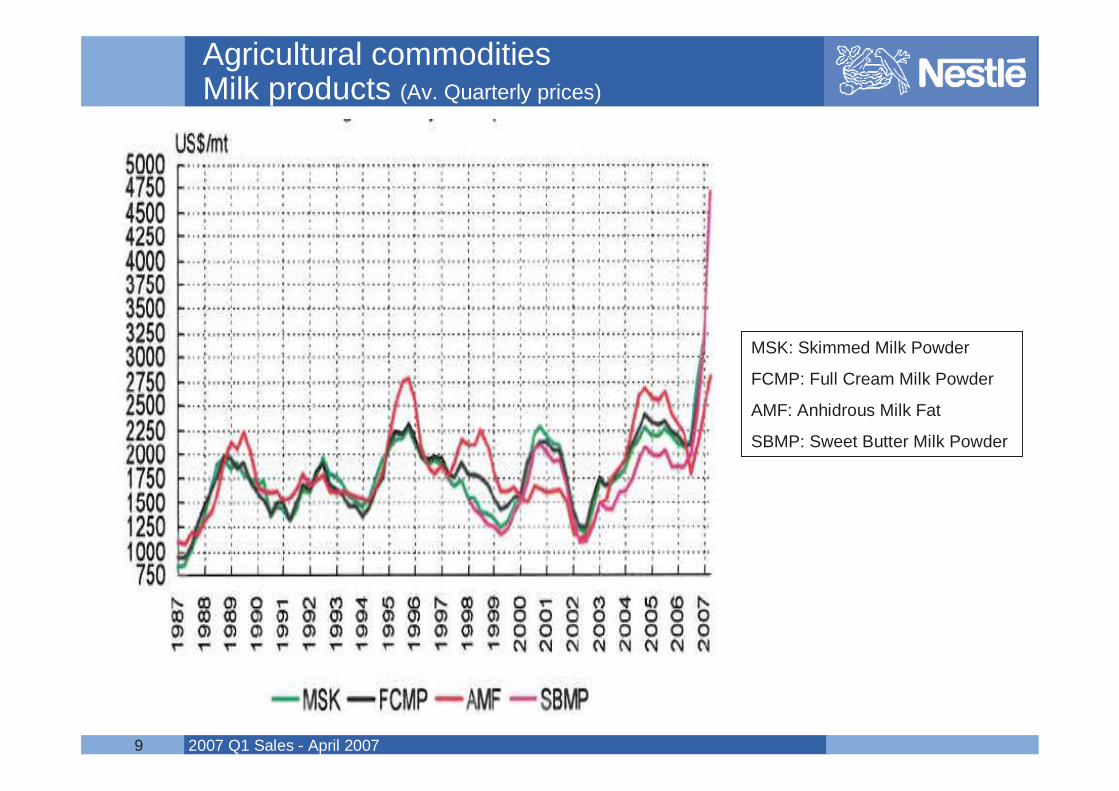

Agricultural commodities Milk products (Av. Quarterly prices)

MSK: Skimmed Milk Powder

FCMP: Full Cream Milk Powder

AMF: Anhidrous Milk Fat

SBMP: Sweet Butter Milk Powder

2007 Q1 Sales - April 2007 Name of chairman10

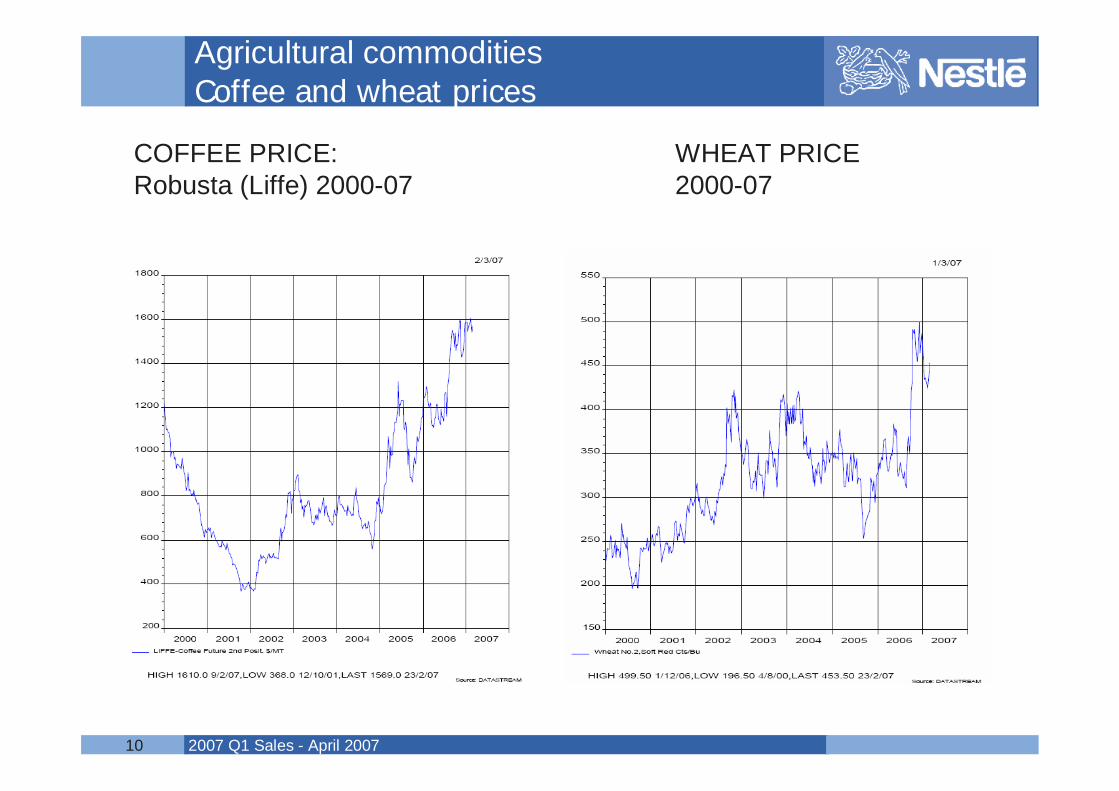

COFFEE PRICE: Robusta (Liffe) 2000-07

WHEAT PRICE 2000-07

Agricultural commodities Coffee and wheat prices

2007 Q1 Sales - April 2007 Name of chairman11

Conclusion: The Nestlé Model reconfirmed

• Organic growth ahead of market, driven by key brands

• Further pricing to come; likely to dampen demand

• The Nestlé Model reconfirmed for 2007: 5-6% organic growth targetImprovement in constant currency EBIT margin

• Transformation to Nutrition, Health & Wellness is accelerating

• Organisational transformation enabling markets to focus on profitable growth

• Nestlé is opportunity rich - innovation for growth and mix; scale for growth and efficiencies

2007 Q1 Sales - April 2007 Name of chairman12

Questions & answers

2007 Q1 Sales - April 2007 Name of chairman13

We plan to deliver the Nestlé Model annually over the next 10 years

5-6% organic growth Sustainable improvement in EBIT

Improving trend in Return on Invested Capital

2007 Q1 Sales - April 2007 Name of chairman14

First Quarter Sales 2007

2007 Q1 Sales - April 2007 Name of chairman15

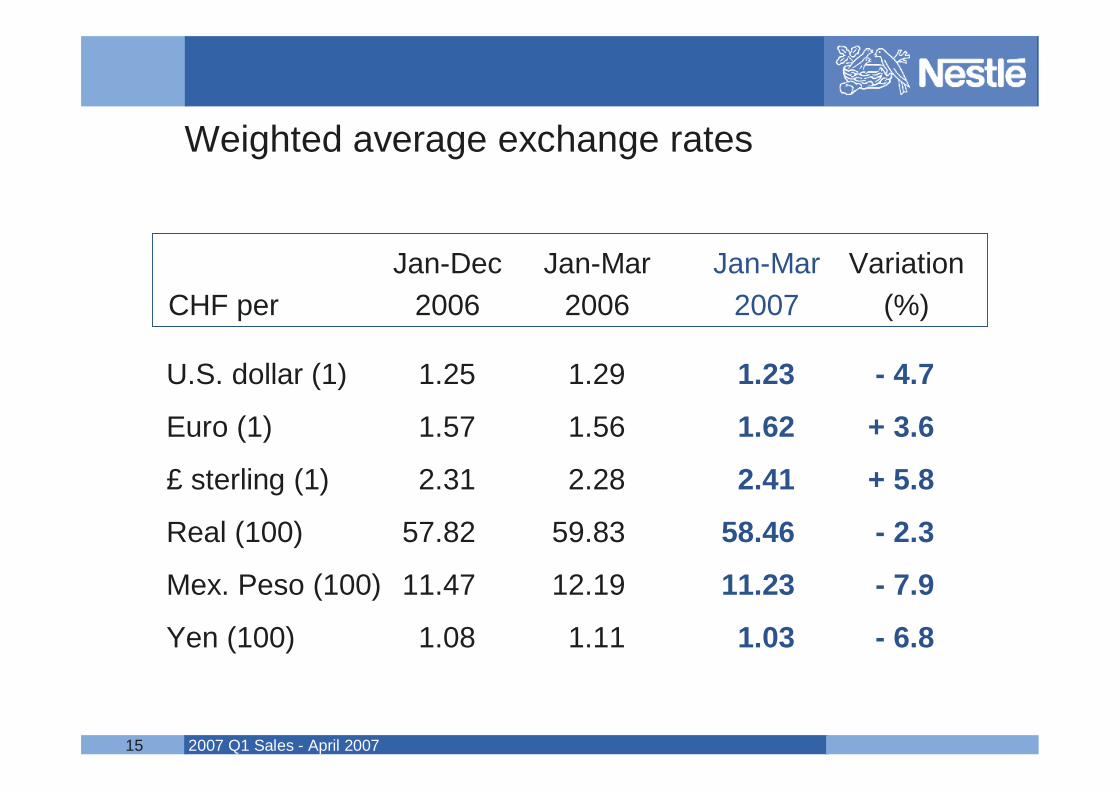

Weighted average exchange rates

Jan-Dec Jan-Mar Jan-Mar VariationCHF per 2006 2006 2007 (%)

U.S. dollar (1) 1.25 1.29 1.23 - 4.7

Euro (1) 1.57 1.56 1.62 + 3.6

£ sterling (1) 2.31 2.28 2.41 + 5.8

Real (100) 57.82 59.83 58.46 - 2.3

Mex. Peso (100) 11.47 12.19 11.23 - 7.9

Yen (100) 1.08 1.11 1.03 - 6.8

2007 Q1 Sales - April 2007 Name of chairman16

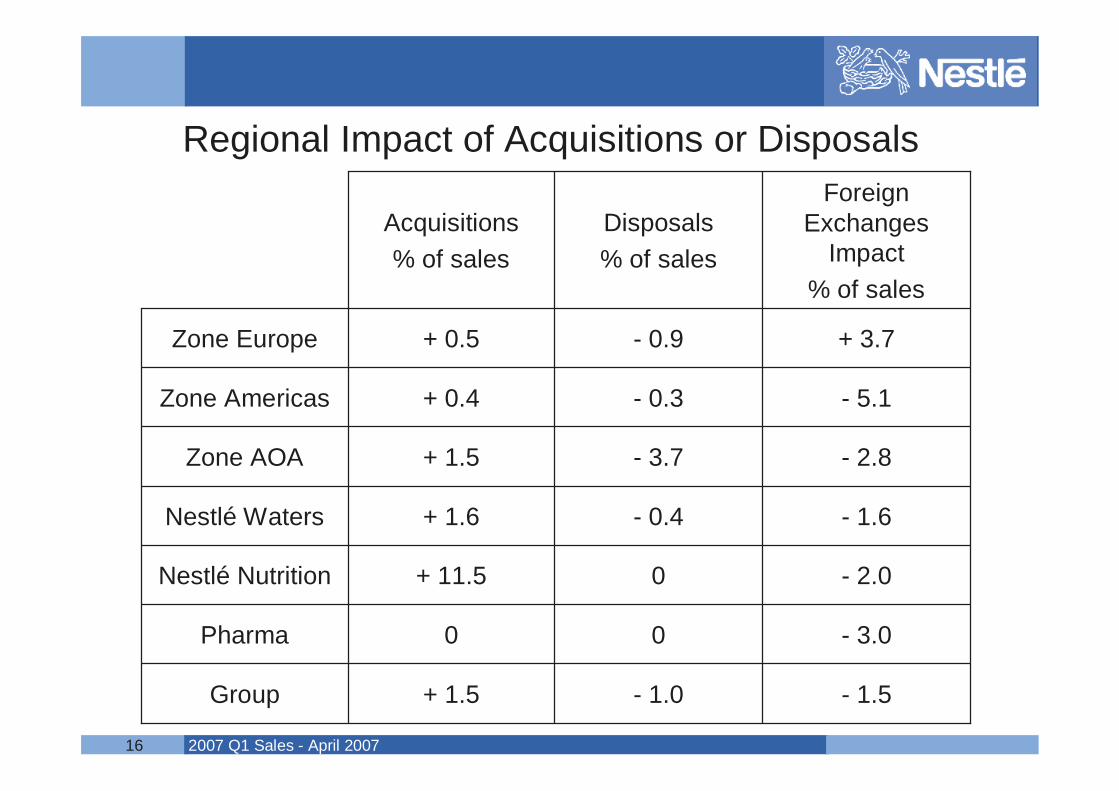

Regional Impact of Acquisitions or Disposals

- 1.5

- 3.0

- 2.0

- 1.6

- 2.8

- 5.1

+ 3.7

ForeignExchanges

Impact% of sales

- 1.0+ 1.5Group

00Pharma

0+ 11.5Nestlé Nutrition

- 0.4+ 1.6Nestlé Waters

- 3.7+ 1.5Zone AOA

- 0.3+ 0.4Zone Americas

- 0.9+ 0.5Zone Europe

Disposals% of sales

Acquisitions% of sales

2007 Q1 Sales - April 2007 Name of chairman17

First Quarter Sales 2007