Q1 2016 - MPM Properties

28

ABU DHABI REAL ESTATE MARKET OVERVIEW Q1 2016 REAL ESTATE SERVICES

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Q1 2016 - MPM Properties

ABU DHABI REAL ESTATE MARKET OVERVIEW

Q1 2016

REAL ESTATE SERVICES

REPORT HIGHLIGHTS Residential

Q1 2016 was characterized by the following trends: 1) Constrained new supply – the addition of only 1,000 new homes 2) Moderation of rental growth – Analysis of the MPM portfolio during Q1 2016 shows 38% of lease renewals were agreed with no increase, 61% showed an increase and 1% had a decline 3) Stable sale prices on the back of subdued transaction activity These trends are expected to continue during the rest of 2016. MPM expects less than 2% housing stock growth in 2016 vs. an average of 4.5% p.a. over the last 7 years. The slowdown of new supply will counter some of the downward pressure on rents, although a marginal correction is expected in the months ahead.

Office

The commercial office market witnessed the addition of approximately 57,000 sqm during Q1 2016, with only 10,000 sqm being speculative, whilst the rest is owner occupied or pre-let. Grade A space rents have increased marginally by 1%, supported by the lack of new supply in this segment. On the contrary rents in Grade B office space have seen a decline of 3%. In terms of office sales

transactional activity has been very low in Q1 2016 given the impact of lower oil prices on the SME segment of market with most companies putting relocation plans on hold.

Retail Sector

There have been no new retail developments completed in Abu Dhabi during the first quarter of 2016 and thus total retail stock in the Capital remains at approximately 2.4 million sqm of GLA. Mall revenues have been under pressure during the first quarter of 2016, with the outlook for the remaining year indicating further softening of consumer spending, leading to increased pressure on revenues.

Hospitality Sector

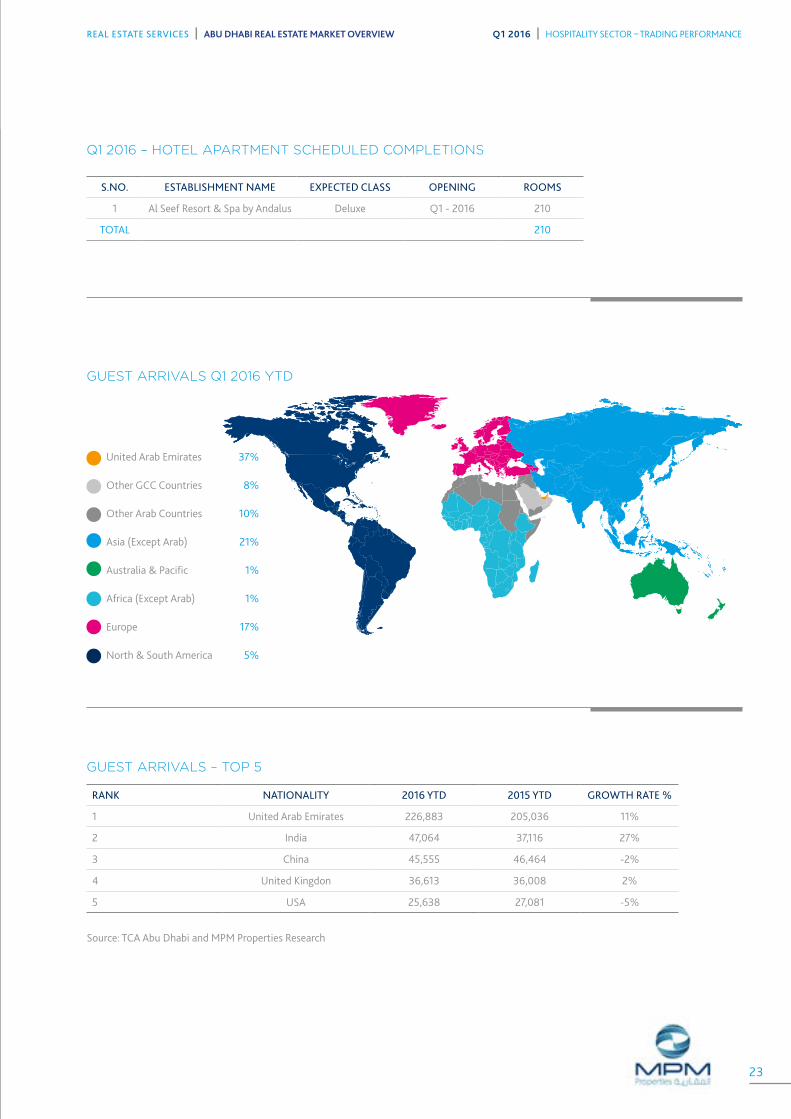

In Q1 2016, only one new hotel (Al Seef Resort) entered the market adding 210 rooms. Supply in the hotel sector is expected to increase by 2,812 keys by the end of 2016. Guest arrivals into Abu Dhabi are up by 10% in Q1 2016 YTD vs. Q1 2015 YTD. This growth came despite a decline in tourist arrivals from key countries of China and USA along with a marginal (2%) increase in arrivals from UK. Total revenue for hotel establishments recorded 9% decrease (AED 1,092 Million), room revenue decreased by 14%, whilst F&B revenue declined 4%.

One of the aims of this report is to aid with improving market transparency by basing our analysis wherever possible on primary transactional evidence derived from our own managed portfolio and from the analysis of our sales and home financing activities. We believe that this adds credibility to the analysis and we hope provides confidence in its reliability.

FOREWORD ADIB Real Estate Services comprises a comprehensive real estate banking and advisory platform providing the full range of professional services from a single provider. Our services include:-

�� Real estate financing�� Strategic development advisory�� Investment advisory�� Asset management�� Project management

�� Valuation�� Agency�� Market research�� Property management�� Facilities management

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ1 2016

2

CONTENTSDemand Drivers 4

Macro Trends 6

Residential Sector 8

Project in Focus 14

Office Sector 16

Retail Sector 20

Hospitality Sector 22

Definitions & Methodology 24

Contact Information 25

Supply - Photo Gallery 26

Development Location Map 28

MPM PROPERTIES FACTS AND FIGURES

TOTAL UAE STAFF PROPERTY MANAGEMENT STAFF ADVISORY STAFF

UNITS UNDER MANAGEMENT

LEASING & SALES STAFF LANDLORD CLIENTS

COMBINED MARKET VALUE OF PROPERTIES VALUED SINCE JANUARY 2012

MORTGAGE VALUATIONS SINCE JANUARY 2012

DEDICATED VALUATION PROFESSIONALS

OCCUPANCY RATE

LARGEST ABU DHABI MAINLAND PORTFOLIO

160+

7,600+

No.1

98.5%20+

30+

90bn

35+

23,500+

95+

1,700

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q1 2016

3

DEMAND DRIVERS – Q1 2016

GOVERNMENT INITIATIVES �� As per February’s Official Gazette, expatriate

tenants in Abu Dhabi will have to pay 3 per cent extra on their rent, as a municipality contract fee. The new charge will be added to monthly electricity and water bills. The collection of this charge is yet to be implemented

�� The Abu Dhabi government is set to hand over 2,048 villas to its citizens across the emirate with 1,463 units in Abu Dhabi, 236 units in Al Ain and 349 in the Western Region. In addition about 4,495 plots will also be distributed to citizens, including 2,432 plots in the Abu Dhabi, 1,713 in Al Ain and 350 in the Western Region

�� The UAE federal government has proposed to raise between AED 80 billion to AED 100 billion through the issue of bonds in the next year, which will allow the UAE to fund the majority of the expected fiscal deficit during 2016. This in turn will reduce the need to draw down on bank deposits or sell assets

�� Abu Dhabi’s mainland areas will have over AED470 million invested in the development of infrastructure projects. The areas cover Musaffah and Mohammad Bin Zayed City, and include the construction of internal roads, parks, sports courts, reservoirs, irrigation networks and pumping stations

KEY EVENTS�� World Future Energy Summit,

18th – 21st January 2016

�� International Water Summit, 16th –19th January 2016

�� Global Forum for Innovation in Agriculture, 16th – 17th February 2016

�� Middle East Drilling Technology Conference & Exhibition, 26th – 28th January 2016

�� Abu Dhabi Pharmacy Conference, 19th – 21st February 2016

�� VIV MEA, 15th – 17th February 2016

�� Global Financial Markets Forum, 2nd – 3rd March 2016

�� Unmanned Systems Exhibition & Conference, 6th – 8th March 2016

�� Abu Dhabi Aviation and Aerospace Week, 6th – 8th March 2016

OIL & GAS�� Q1 2016 began with a sharp decline in oil prices

with levels reaching multi year lows (below $30 per barrel) in early February. However, the prices have rebounded since then, breaching the $40 per barrel mark. Q1 ended with prices above $38 per barrel, representing a 13% surge in March 2016

�� The UAE plans to boost crude output capacity to 3.5 million barrels a day by 2017 from present production levels of approximately 2.98 million barrels per day

�� State oil explorer and power supplier Abu Dhabi National Energy Co (TAQA) has reduced its proposed capital expenditure for the year. The reduction is driven due to low oil prices. The firm, which is 75 per cent owned by the Abu Dhabi government, said it reduced capex by 52 per cent in 2015 and planned a further 42 per cent cut in 2016

4

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ1 2016 | DEMAND DRIVERS

TOURISM INITIATIVES�� As per a new decree, a 4 per cent municipality fee and a AED 15

charge per night per room will be imposed on hotel bills in Abu Dhabi. This will raise hundreds of millions of dirhams in revenue for municipal authorities with fees being collected by the Abu Dhabi Tourism and Culture Authority (TCA) and added to the government budget of the Department of Municipal Affairs

�� ADNEC has signed a deal with INDEX Conferences and Exhibitions to attract more events to Abu Dhabi. The Dubai-based firm will initially bring four new events to Abu Dhabi - Children & Parents World Exhibition, Lifestyle Exhibition, Media Communication & Content World Conference and Atech World Conference and Exhibition this year

�� A delegation from Abu Dhabi including the TCA Abu Dhabi, will attend the World Travel Market Africa 2016 (WTM Africa) in

April to capitalise on the surging growth in South African visitor numbers into the emirate. Since TCA Abu Dhabi opened an office in Johannesburg, South Africa last year to help promote the Emirate as a leisure and business destination, tourist arrivals from South Africa into Abu Dhabi have increased by 50%

�� Etihad Holidays, a unit of Etihad Airways, launched a new campaign offering “guaranteed sunshine or your next holiday for free” for UK visitors staying between May and September. The campaign will apply to every booking that consists of a flight and hotel-inclusive package. Under the offer, the visitors will be eligible for a free holiday if they experience more than 5mm of rain

REAL ESTATE AND CONSTRUCTION - CREATING JOBS�� Aldar Properties has awarded a AED 2 billion ($544.5 million)

construction contract to Arabtec for construction of 1,017 luxury villas in Abu Dhabi. The project is scheduled to be completed towards the end of 2019

�� Aldar properties has invested about AED 900 million as part of a AED 3 billion plan to boost their rental portfolio. As a part of these investments Aldar Properties has purchased Daman House, located at the Capital Centre district close to the city’s exhibition centre. The office tower houses the national insurance company Daman on a long term lease. Though the size of the transaction was not revealed, it is estimated to be worth around AED 330 million. Additionally, Aldar has invested AED 410 million in the extension of Al Jimi Mall and will spend AED160 million on construction of Al Mamoura School

�� Construction has commenced on ‘Al Qana’, a leisure oriented, mixed used project being built around the canal near Al Maqta Bridge, admeasuring 150,000 sqm. The project is scheduled to be completed in the second quarter of 2018 and will offer recreation, high-end shopping, and fine dining. The project is being developed under a Build-Operate-Transfer (BOT) arrangement between Al Barakah International Investments and Abu Dhabi Municipality

�� Al Qudra Real Estate has completed the Infrastructure works at their 200,000 sqm Danet Abu Dhabi development. Lighting, power distribution, and water-cooling networks for the master development are now in place

�� Masdar City has outlined a five-year expansion plan that will include the construction of 2,000 homes and a research hub. The completion status of Masdar city master plan will increase to 35 per cent from 5 per cent presently

FREEZONES SIGNING UP NEW TENANTS; FORMING KEY ALLIANCES

�� The Abu Dhabi Global Market Freezone, set up in October 2015, is expecting significant activity this year. They have far received interest from a number of financial services firms to set up businesses within the freezone in Al Maryah Island

�� Dubal Holding, Dubai Investments and Singapore-based industrial group MARS are investing $120 million to build an aluminum rolling

plant in Abu Dhabi’s industrial free zone. The joint venture will be known as Emirates Aluminium Rolling LLC (Emiroll), with plans to manufacture 65,000 tonnes of aluminium coils annually. The plant is anticipated to start production in the third quarter of 2017

5

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q1 2016 | DEMAND DRIVERS

ABU DHABI REAL GDP FORECAST 2014-2018

Source: DED

0%

1%

2%

3%

4%

5%

6%

2013 Avg. 2014-2018

5.2% 5.5%

MACRO TRENDS

REAL GDP GROWTH RATE 2014-2018

Source: DED

0% 3% 6% 9% 12% 15%

Wholesale and retail trade; repairof motor vehicles and motorcycles

Accommodation and foodservice activities

Manufacturing

Transportation and storageand communications

Financial and insurance activities

6.8%

10.0%

10.0%

11.1%

15.0%

Mar

16

96

100

98

102

104

106

CPI Rental Contribution to CPI

Jan

13

Ap

r 13

Ju

l 13

Oct

13

Ap

r 15

Ju

l 15

Oct

15

Jan

14

Ap

r 14

Ju

l 14

Oct

14

Jan

15

Jan

16

Source: DEDSource: DED

Source: SCAD and MPM Properties Research

CPI VS RENTAL CONTRIBUTION TO CPI

REAL GDP GROWTH RATE 2014-2018 ABU DHABI REAL GDP FORECAST 2014-2018

50

60

70

80

Q1

20

16

Q3

20

15

Q1

20

15

Q3

20

14

Q1

20

14

Q3

20

13

Q1

20

13

Q3

20

12

Q1

20

12

Q3

20

11

Q1

20

11

Q3

20

10

Q1

20

10

90

120

150

Q1

20

16

Q1

20

15

Q1

20

14

Q1

20

13

Q1

20

12

Q1

20

11

Q1

20

10

CONSUMER CONFIDENCE INDEX

Source: DED Source: DED

BUSINESS CLIMATE INDEX

6

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ1 2016 | MACRO TRENDS

Dubai realty index Abu Dhabi realty index

400

350

300

250

200

150

100

50

0

Ju

l 0

7

Jan

07

Ju

l 0

8

Jan

08

Ju

l 0

9

Jan

09

Ju

l 10

Jan

10

Ju

l 11

Jan

11

Ju

l 12

Jan

12

Ju

l 13

Jan

13

Ju

l 14

Jan

14

Ju

l 15

Jan

15

Mar

16

Jan

16

Abu Dhabi MurbanCrude Oil

Gold Abu Dhabi Stock Market Index

Dubai Stock Index

0

50

100

150

200

250

300

350

Mar-

16

Dec-1

5

Dec-1

4

Dec-1

3

Dec-1

2

Dec-1

1

Jan

-11

Source: Bloomberg and MPM Properties Research

Source: ADIB Treasury and Bloomberg

Source: ADIB Treasury and Bloomberg

REALTY STOCK INDEX ABU DHABI vs DUBAI

STOCK MARKET vs OIL vs GOLD

FX RATES vs USD PROFIT RATE

FX RATES vs USD

Q1 2016 3mths ago 6mths ago 12mths ago

GBP 1.4226 1.4736 1.5128 1.4818

EUR 1.1175 1.0862 1.1177 1.0731

JPY 113.65 120.22 119.88 120.13

INR 66.55 66.15 65.59 62.50

PKR 104.70 104.73 104.46 101.93

RUB 68.69 72.52 65.36 58.19

CNY 6.5114 6.4937 6.3560 6.1997

HKD 7.7571 7.7507 7.7500 7.7524

QAR 3.6406 3.6419 3.6420 3.6411

AED 3.6725 3.6725 3.6725 3.6725

PROFIT RATES

O/N 3mths ago 6mths ago 12mths ago

GBP 0.4800 0.5881 0.7404 1.0115

EUR -0.3900 -0.2420 -0.1340 -0.0050

USD 0.3745 0.6286 0.9190 1.2312

AED 0.3000 1.0237 1.2790 1.5826

7

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q1 2016 | MACRO TRENDS

MARKET OVERVIEW Q1 2016

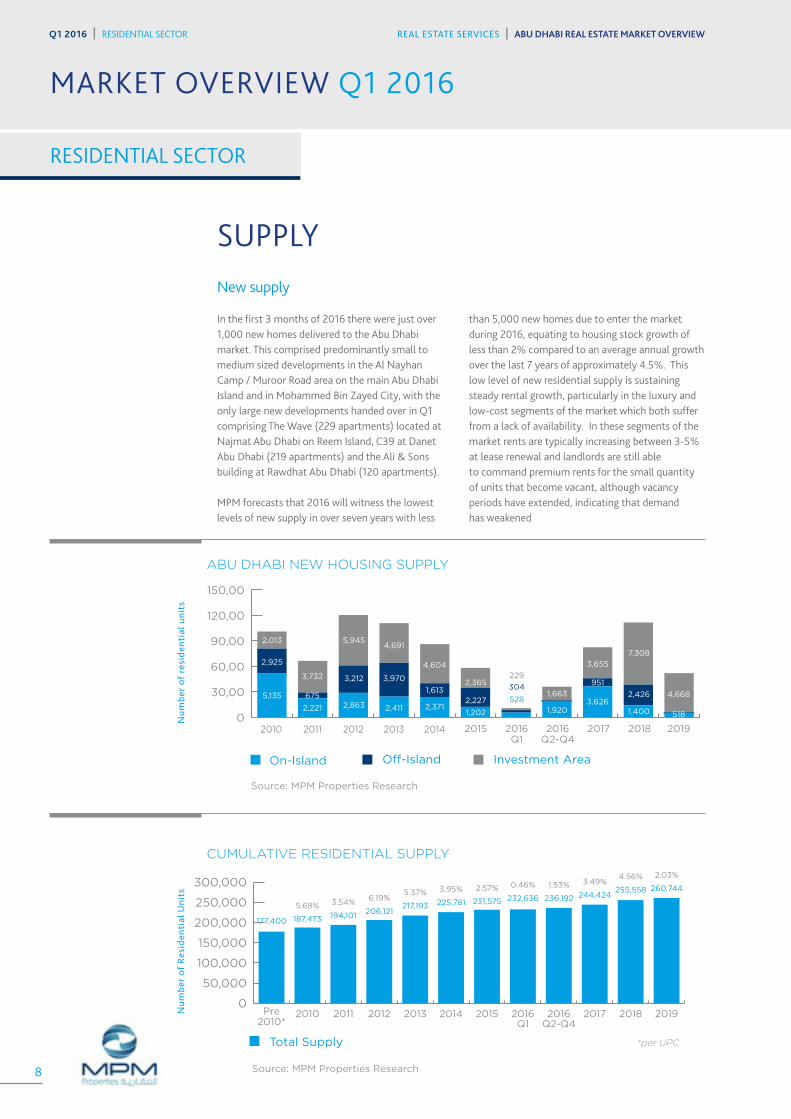

SUPPLY New supply

In the first 3 months of 2016 there were just over 1,000 new homes delivered to the Abu Dhabi market. This comprised predominantly small to medium sized developments in the Al Nayhan Camp / Muroor Road area on the main Abu Dhabi Island and in Mohammed Bin Zayed City, with the only large new developments handed over in Q1 comprising The Wave (229 apartments) located at Najmat Abu Dhabi on Reem Island, C39 at Danet Abu Dhabi (219 apartments) and the Ali & Sons building at Rawdhat Abu Dhabi (120 apartments).

MPM forecasts that 2016 will witness the lowest levels of new supply in over seven years with less

than 5,000 new homes due to enter the market during 2016, equating to housing stock growth of less than 2% compared to an average annual growth over the last 7 years of approximately 4.5%. This low level of new residential supply is sustaining steady rental growth, particularly in the luxury and low-cost segments of the market which both suffer from a lack of availability. In these segments of the market rents are typically increasing between 3-5% at lease renewal and landlords are still able to command premium rents for the small quantity of units that become vacant, although vacancy periods have extended, indicating that demand has weakened

Investment AreaOn-Island Off-Island

2010 2011 2012 2013 2014 2015 2016Q1

2016Q2-Q4

2017 2018 20190

30,00

60,00

90,00

120,00

150,00

5,135

2,925

2,013

2,221

3,732

6752,863

3,212

5,945

2,411

3,970

4,691

2,371

1,613

4,604

3,626

951

3,655

1,202

2,227

2,365

528

304

229

1,920

1,663

1,400

2,426

7,308

518

4,668

Num

ber

of r

esid

enti

al u

nits

Pre2010*

2010 2011 2012 2013 2014 2015 2016Q1

2017 2018 20192016Q2-Q4

Total Supply *per UPC

0

50,000

100,000

150,000

200,000

250,000

300,000

177,400

5.68%

187,473

3.54%

194,101

6.19%

206,121

5.37%

217,193

3.95%

225,781

2.57%

231,575

0.46%

232,636

1.53%

236,192

3.49%

244,424

4.56%

255,558

2.03%

260,744

Num

ber

of R

esid

enti

al U

nits

RESIDENTIAL SECTOR

Source: MPM Properties Research

Source: MPM Properties Research

ABU DHABI NEW HOUSING SUPPLY

CUMULATIVE RESIDENTIAL SUPPLY

8

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ1 2016 | RESIDENTIAL SECTOR

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q1 2016 | RESIDENTIAL SECTOR

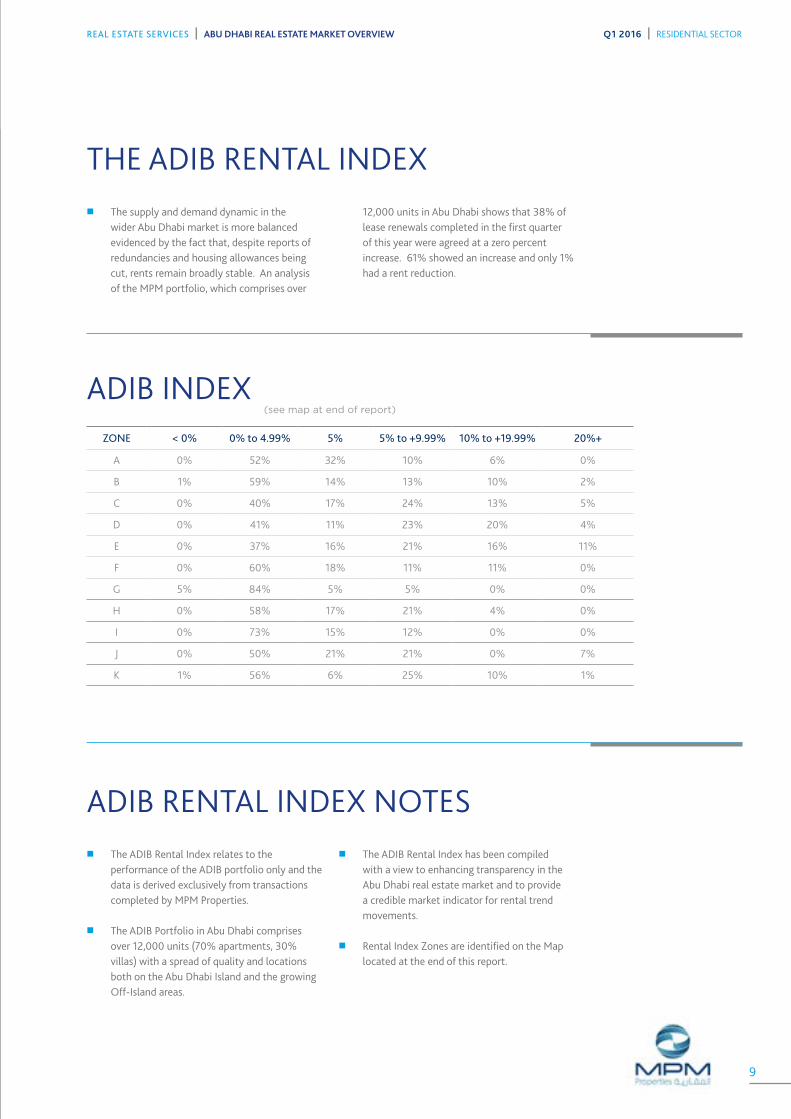

THE ADIB RENTAL INDEX �� The supply and demand dynamic in the

wider Abu Dhabi market is more balanced evidenced by the fact that, despite reports of redundancies and housing allowances being cut, rents remain broadly stable. An analysis of the MPM portfolio, which comprises over

12,000 units in Abu Dhabi shows that 38% of lease renewals completed in the first quarter of this year were agreed at a zero percent increase. 61% showed an increase and only 1% had a rent reduction.

ADIB RENTAL INDEX NOTES �� The ADIB Rental Index relates to the

performance of the ADIB portfolio only and the data is derived exclusively from transactions completed by MPM Properties.

�� The ADIB Portfolio in Abu Dhabi comprises over 12,000 units (70% apartments, 30% villas) with a spread of quality and locations both on the Abu Dhabi Island and the growing Off-Island areas.

�� The ADIB Rental Index has been compiled with a view to enhancing transparency in the Abu Dhabi real estate market and to provide a credible market indicator for rental trend movements.

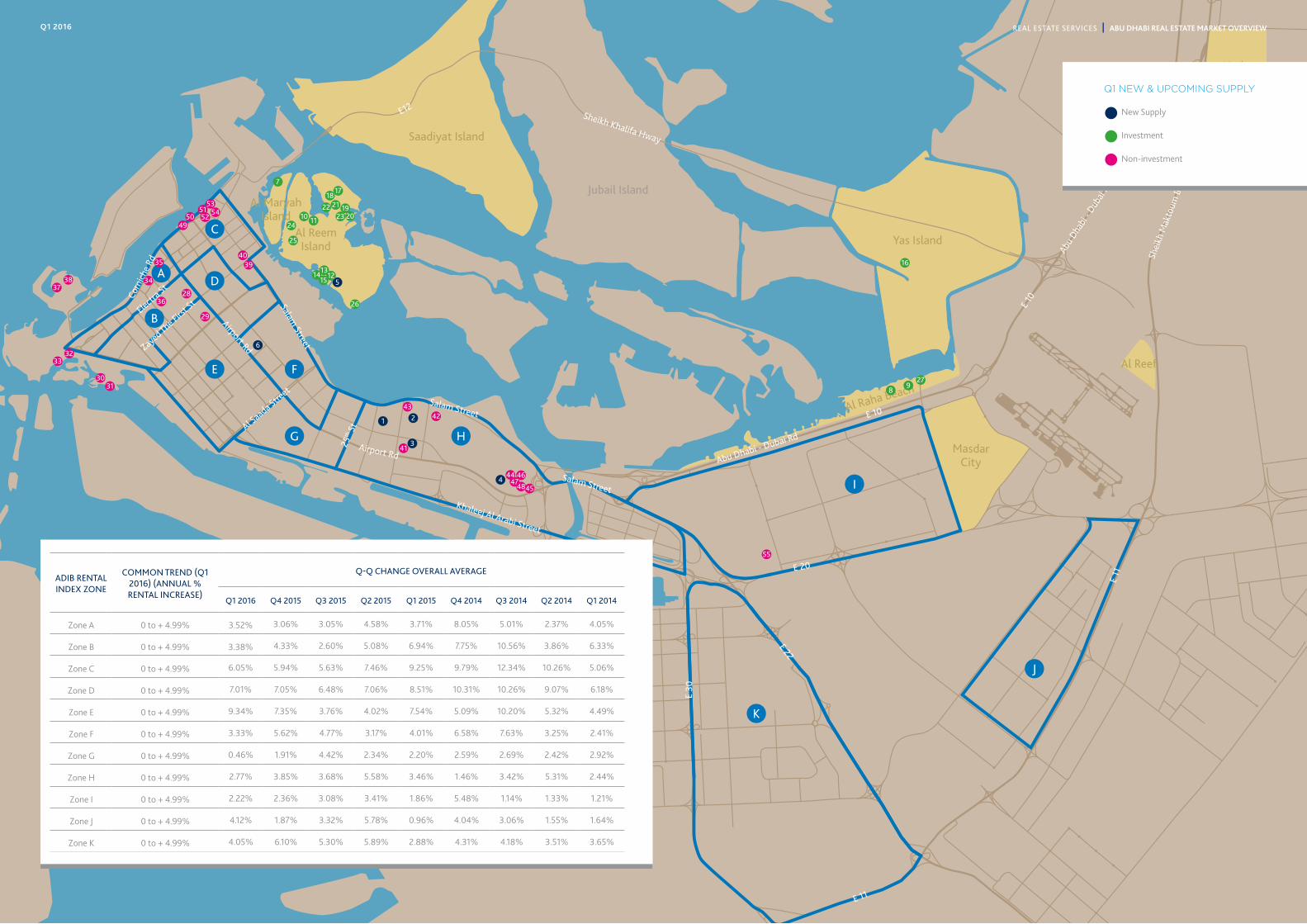

�� Rental Index Zones are identified on the Map located at the end of this report.

ZONE < 0% 0% to 4.99% 5% 5% to +9.99% 10% to +19.99% 20%+

A 0% 52% 32% 10% 6% 0%

B 1% 59% 14% 13% 10% 2%

C 0% 40% 17% 24% 13% 5%

D 0% 41% 11% 23% 20% 4%

E 0% 37% 16% 21% 16% 11%

F 0% 60% 18% 11% 11% 0%

G 5% 84% 5% 5% 0% 0%

H 0% 58% 17% 21% 4% 0%

I 0% 73% 15% 12% 0% 0%

J 0% 50% 21% 21% 0% 7%

K 1% 56% 6% 25% 10% 1%

ADIB INDEX(see map at end of report)

9

APARTMENT SALE PRICES The sales market continues to be characterized by weak sentiment translating into an environment where both buyers and sellers are equally unmotivated to enter the market thus we are seeing low transaction volumes and prices remaining broadly stable. Demand remains focused on small units commanding the highest rental yields, however there are currently few opportunities in the market as vendors continue to hold, collect rental income and wait for the longer term capital appreciation.

Despite some rental declines on Reem Island we have yet to witness any evidence of this impacting sale prices during the first quarter of the year, although a continuation of falling rents will inevitably start to put downward pressure on values to counter the yield erosion.

The first quarter of 2016 witnessed no new projects launched to the market, with developers including

Aldar, TDIC and Bloom all set to announce major new developments at Cityscape in April.

The off-plan sales market in Abu Dhabi has witnessed over 10 new projects launched to the market over the last 18 months, (prior to Cityscape Abu Dhabi April 2016), comprising over 4,500 units. Our research shows that despite more challenging market conditions being experienced in 2015 take up in these new developments has generally been strong with most projects having sold between 60-90% of the inventory released to the market.

Demand has been from both owner occupiers and investors, including bulk investors with the demographic profile of buyers, although varying from project to project is broadly 50% UAE Nationals, 20-30% Arab expats and the remainder spread across Western and Asian expats.

RESIDENTIAL SECTOR

0

500

1,000

1,500

2,000

2,500

Al R

eef

Do

wn

tow

n

Al G

had

eer

Cit

y o

fL

igh

ts

Mari

na

Sq

uare

Sh

am

s

Al Z

ein

a

Al M

un

eera

Gate

Dis

tric

t

Al B

an

dar

SB

R

St.

Reg

is

AE

D/s

q.ft.

0.0% -1.0% 0.0% 0.0% 2.0% 0.0% -4.0% -2.0% 0.0% -1.0% -8.0%Q-on-Q

0.0% -4.0% -8.0% -7.0% -7.0% -4.0% -4.0% -4.0% 0.0% -7.0% -3.0%Y-on-Y

2,2

50

1,775

1,75

0

1,4

00

1,4

00

1,3

95

1,3

25

1,275

1,15

0

95

0

925

Source: MPM Properties Research

AVERAGE APARTMENT SALES PRICE AED/sq.ft. Q1 2016

10

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ1 2016 | RESIDENTIAL SECTOR

APARTMENT RENTS �� The residential market continues to see rent

increases at lease renewals with the only exception to the common trend witnessed on Reem Island which has seen rents decline on renewals by up to 5% in some developments

�� This is occurring due to this sub-market having had an injection of new supply of over 1,500 units in the second half of last year, (Gate Towers and Hydra Avenue), which are still being absorbed by the market

�� This new supply increased competition for individual expat landlords which are typically

more motivated to reduce rents to attract and retain tenants and thus cover mortgage and service charge payments

�� Rents on new lettings have witnessed a marginal decline quarter-on quarter, highlighting that most high-end developments have reached an affordability ceiling following a period of sustained rental growth. Property managers still have a 10% delta in most towers between the minimum and maximum rents and we anticipate this delta to gradually narrow down during 2016

120

175

220

155

62.5

105

45

105

80

72.5

72.5

70

100

55

195

75

26

5

135

175

26

0

120

155 2

05

115

152.5 2

00

102.5 14

5 177.

5

97.

5 135

190

92.5 13

518

5

87.

511

0 137.

5

115

160

23

5

75 10

5 135

1 BRStudio 2 BR 3 BR No

n-I

nvest

men

tZ

on

e G

rad

e B

No

n Invest

men

tP

rim

e Z

on

e

Al R

eef

Do

wn

tow

n

Sh

am

s

Mari

na

Sq

uare

Gate

Dis

tric

t

Al M

un

eera

Al Z

ein

a

Al B

an

dar

Al G

had

eer

St.

Reg

is

SB

R

-1.4% 1.4% -2.9% -4.0% -0.5% -1.5% 0.5% 1.0% 3.7% -2.4% 2.8%Q-on-Q

-2.0%

-1.0%

0% 11.0% 3.0% 3.0% 4.0% 2.0% 0.0% 3.0% 11.0% -5.0% 7.0%Y-on-Y

Source: MPM Properties Research

AVERAGE APARTMENT ANNUAL RENT Q1 2016

11

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q1 2016 | RESIDENTIAL MARKET PERFORMANCE

VILLA PERFORMANCE: SALES AND RENTS �� Weak demand from buyers resulted in

no sale price movement across most villa communities during Q1 2016. Al Reef villas, Al Raha Gardens and Gold Gardens witnessed a higher proportion of buyer interest with the majority of buyers being end users during the first quarter

�� H1 2016 will witness multiple off-plan villa projects being launched by Aldar, TDIC and

Bloom. These developers are addressing the pent up demand from investors and end users for villas / townhouses between the price band of AED2.5 million to AED5 million

�� Conversely, rental demand for villas over AED300k has slowed during the Q1 2016 with vacancy rates increasing during the first quarter of 2016. We anticipate this trend to continue during the rest of this year

RESIDENTIAL SECTOR

Source: MPM Properties Research

0

100

200

300

400

500

600

105

125

145

140 172.5

185

145

100

115

270

24

0

39

53

60

277.

53

20

45

0

215 23

0 26

5 30

0 35

0

34

0

25

0270

190

29

523

5

237.

5

3 BR2 BR 4 BR 5 BR

Al M

ush

rif

Gard

en

s

Al B

ate

en

Gard

en

s

Blo

om

Gard

en

s

Al R

ah

aG

ard

en

s

Go

lfG

ard

en

s

SB

V(T

ow

nh

om

es)

Hyd

raV

illag

e

Al Z

ein

a

Al R

eef

Al G

had

eer

Source: MPM Properties Research

VILLA AVERAGE ANNUAL RENTS Q1 2016

AED

/sq.

ft.

0

500

1,000

1,500

2,000

Hyd

raV

illag

e

Al R

eef

Al R

ah

aG

ard

en

s

Go

lfG

ard

en

s

Blo

om

Gard

en

s

SB

V

0.0%Q-on-Q

0.0%

-1.79%

-9.24%

0.0%

4.55%

0.0%

0.0%

-1.52%

-2.99%

2.56%

12.36%

0.0%

-2.40%

0.0%

-8.15%Y-on-Y

620815

Al Z

ein

a

1,0001,0501,1501,3751,750

Al G

had

eer

975

AVERAGE VILLA SALES PRICE AED/sq.ft. Q1 2016

12

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ1 2016 | RESIDENTIAL SECTOR

Main island KCA MBZ

Low AverageHigh

0

5

10

15

20

25

16.17

5.4

6

6.7

510.8

10.3

7

23

.0

7.15 15

.07

14.0

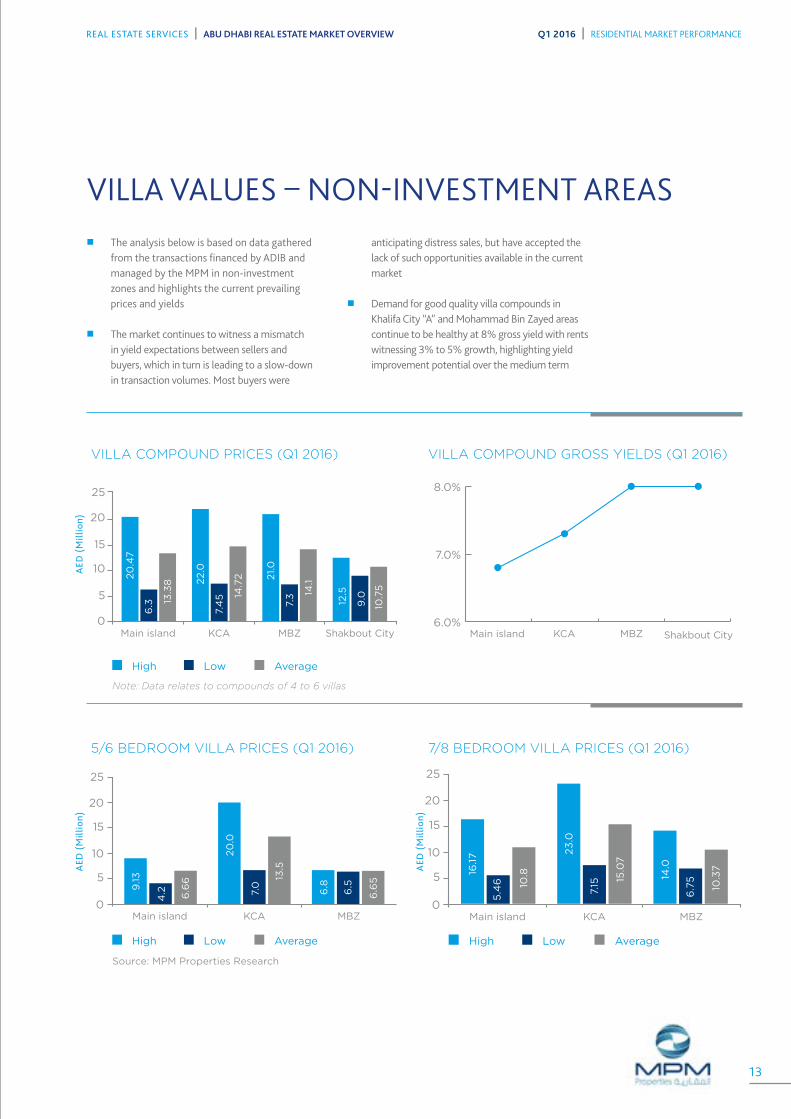

VILLA VALUES – NON-INVESTMENT AREAS�� The analysis below is based on data gathered

from the transactions financed by ADIB and managed by the MPM in non-investment zones and highlights the current prevailing prices and yields

�� The market continues to witness a mismatch in yield expectations between sellers and buyers, which in turn is leading to a slow-down in transaction volumes. Most buyers were

anticipating distress sales, but have accepted the lack of such opportunities available in the current market

�� Demand for good quality villa compounds in Khalifa City “A” and Mohammad Bin Zayed areas continue to be healthy at 8% gross yield with rents witnessing 3% to 5% growth, highlighting yield improvement potential over the medium term

0

5

10

15

20

25

Main island KCA MBZ Shakbout City

Low AverageHigh

20

.47

6.3 13

.38 2

2.0

7.4

5 14.7

2 21.0

7.3 14

.1

12.5

9.0

10.7

5

Main island KCA MBZ

Low AverageHigh

9.13

4.2 6.6

6

20

.0

7.0

13.5

6.8

6.5

6.6

5

0

5

10

15

20

25

6.0%

7.0%

8.0%

Main island KCA MBZ Shakbout City

AED

(M

illio

n)A

ED (

Mill

ion)

AED

(M

illio

n)

VILLA COMPOUND PRICES (Q1 2016)

5/6 BEDROOM VILLA PRICES (Q1 2016)

VILLA COMPOUND GROSS YIELDS (Q1 2016)

7/8 BEDROOM VILLA PRICES (Q1 2016)

Source: MPM Properties Research

Note: Data relates to compounds of 4 to 6 villas

13

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q1 2016 | RESIDENTIAL MARKET PERFORMANCE

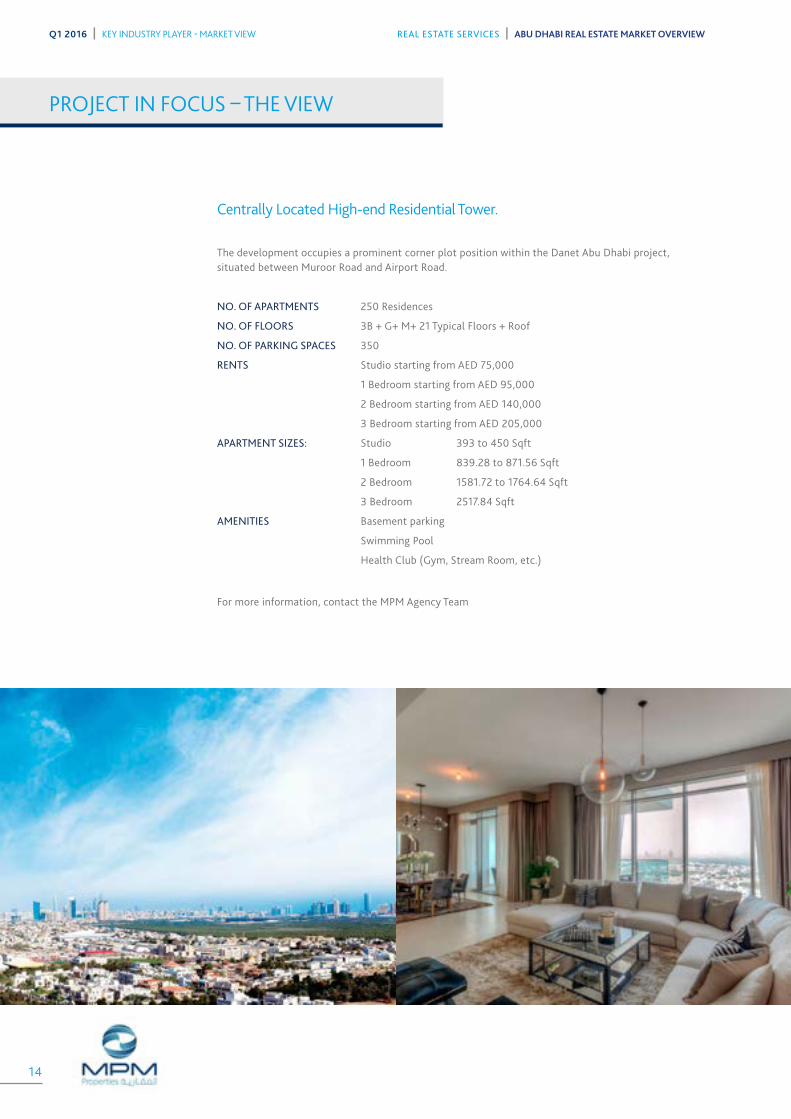

PROJECT IN FOCUS – THE VIEW

Centrally Located High-end Residential Tower.

The development occupies a prominent corner plot position within the Danet Abu Dhabi project, situated between Muroor Road and Airport Road.

NO. OF APARTMENTS 250 Residences

NO. OF FLOORS 3B + G+ M+ 21 Typical Floors + Roof

NO. OF PARKING SPACES 350

RENTS Studio starting from AED 75,000

1 Bedroom starting from AED 95,000

2 Bedroom starting from AED 140,000

3 Bedroom starting from AED 205,000

APARTMENT SIZES: Studio 393 to 450 Sqft

1 Bedroom 839.28 to 871.56 Sqft

2 Bedroom 1581.72 to 1764.64 Sqft

3 Bedroom 2517.84 Sqft

AMENITIES Basement parking

Swimming Pool

Health Club (Gym, Stream Room, etc.)

For more information, contact the MPM Agency Team

14

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ1 2016 | KEY INDUSTRY PLAYER - MARKET VIEW

15

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q1 2016 | KEY INDUSTRY PLAYER - MARKET VIEW

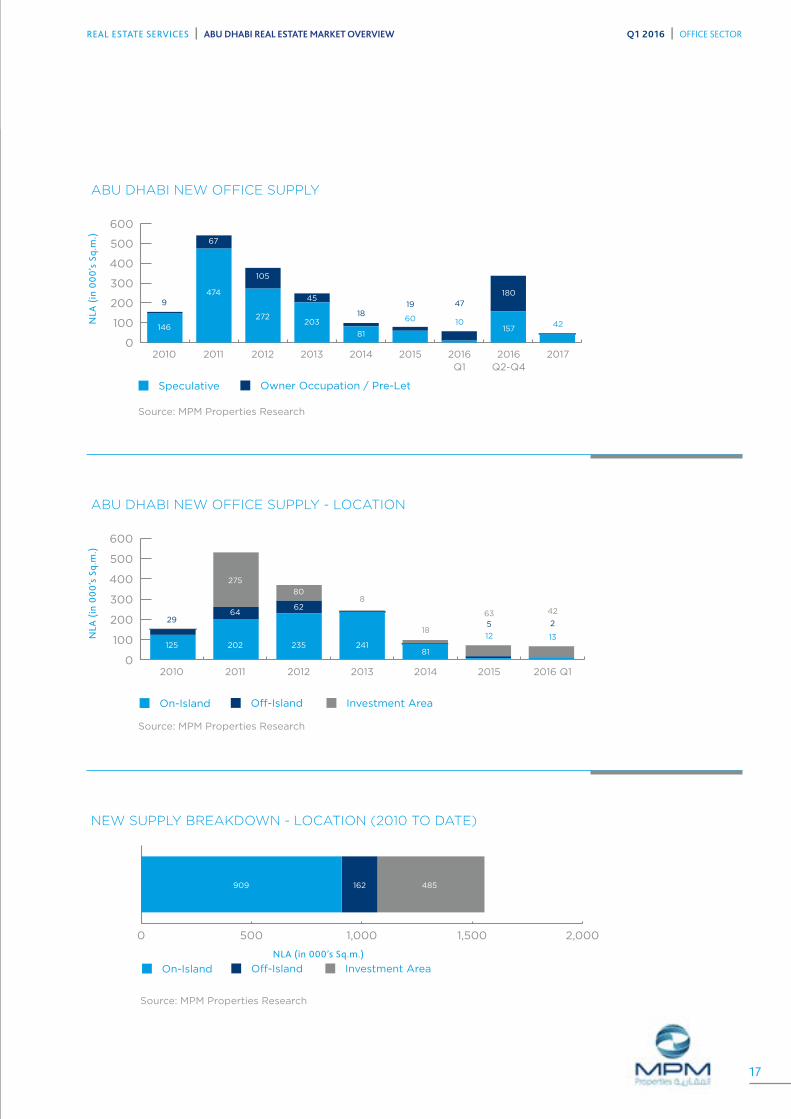

OVERVIEW �� The office market in Abu Dhabi shares a number

of parallels with the residential sector in terms of supply and demand conditions

�� Demand for office space in the Capital has always been driven predominantly by the government sector which has reduced spending on the back of lower oil prices and thus office expansion / relocation plans have been put on hold. However, as with the residential sector new supply is limited which is helping to sustain marginal rental growth levels within the Grade A segment of the market

�� MPM forecasts there will be just over 350,000 sqm of new offices completed by the end of 2016, however this comprises predominantly owner-occupier space including ADNOC HQ & ADIB HQ. The majority of new speculative office space entering the market in 2016 is at City of Lights on Reem Island, with the remaining floors at Addax Tower handed over this quarter and Omega Tower due to complete later in the year

�� Contrary to the shortage of space available in the rest of the office market, and now effectively

operating as its own micro-market, is the Financial Free Zone on Al Maryah Island. Mubadala has released Al Sarab and Al Khatem Towers at ADGM Square which together extend to 98,000 sqm of Grade A space. In addition, Al Maryha Tower, owned by Al Hilal Bank is also now completed adding another 43,700 sqm

�� It is also likely that some companies currently leasing space at ADGM Square, but operating on the Abu Dhabi DED licence, will have to relocate from the free zone due to their onshore business activities, if dual licensing is not possible.

�� The first two global financial institutions that have applied for an ADGM FSRA licence are Macquarie Capital Middle East and Aberdeen Asset Management (UK)

�� Macquarie established offices in ADGM in 2013 whilst Aberdeen’s office in ADGM will be the institution’s first office in the Middle East

MARKET OVERVIEW Q1 2016

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ1 2016 | OFFICE SECTOR

2011 2012 2013 2014 2015 2016Q1

2016Q2-Q4

2017

Running Total New Supply Completed Scheduled New Supply

541

377249 99 79

57337 42

0

1,000

2,000

3,000

4,000

1,9552,495

2,872 3,121 3,220 3,299 3,356 3,693

NLA

(in

00

0’s

Sq.

m.)

ABU DHABI OFFICE SUPPLY (2011-2017)

Source: MPM Properties Research

16

On-Island Off-Island Investment Area

0 500 1,000 1,500 2,000

485162909

0

100

200

300

400

500

600

2010 2011 2012 2013 2014 2015 2016Q1

2016Q2-Q4

2017

Speculative Owner Occupation / Pre-Let

146

9474

67

272

105

203

45

81

1860

19

10

47

157

180

42

On-Island Off-Island Investment Area

0

100

200

300

400

500

600

125 202

64

275

235

62

80

24181

12

563

18

8

13

2

4229

2010 2011 2012 2013 2014 2015 2016 Q1

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q1 2016 | OFFICE SECTOR

NLA

(in

00

0’s

Sq.

m.)

NLA

(in

00

0’s

Sq.

m.)

NLA (in 000’s Sq.m.)

ABU DHABI NEW OFFICE SUPPLY

ABU DHABI NEW OFFICE SUPPLY - LOCATION

NEW SUPPLY BREAKDOWN - LOCATION (2010 TO DATE)

Source: MPM Properties Research

Source: MPM Properties Research

Source: MPM Properties Research

17

Q1 2016

Grade BGrade A S&CGrade A Fitted0

500

1,000

1,500

2,000

1,975

1,650

1,260

2.6% -3.0%0.0%Q-on-Q

6.8% 5%8.2%Y-on-Y

Rent

/ S

q.m

. (A

ED)

Sales Price / Sq.ft.

*as per UPC

Prestige TowerMBZ

Tamouh TowerAddaxThe WaveSky Tower0

300

600

900

1,200

1,500

1,4501,250

1,200 1,175 1,150

0.0% 2.2%4.3% 4.5%0.0%Q-on-Q

-4.9% 6.8%-8.0% 4.5%–Y-on-Y

Sale

s Pr

ice

/ Sq

.ft.

(A

ED)

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q1 2016 | OFFICE SECTOR

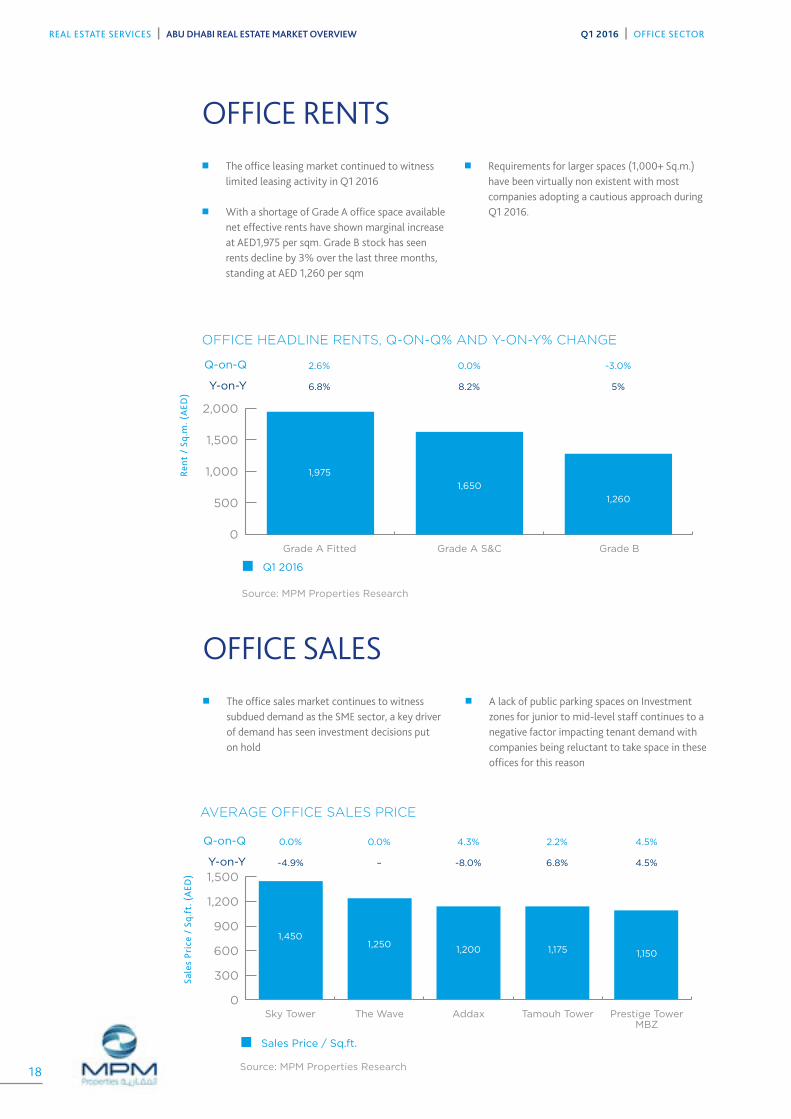

OFFICE RENTS �� The office leasing market continued to witness

limited leasing activity in Q1 2016

�� With a shortage of Grade A office space available net effective rents have shown marginal increase at AED1,975 per sqm. Grade B stock has seen rents decline by 3% over the last three months, standing at AED 1,260 per sqm

�� Requirements for larger spaces (1,000+ Sq.m.) have been virtually non existent with most companies adopting a cautious approach during Q1 2016.

OFFICE SALES �� The office sales market continues to witness

subdued demand as the SME sector, a key driver of demand has seen investment decisions put on hold

�� A lack of public parking spaces on Investment zones for junior to mid-level staff continues to a negative factor impacting tenant demand with companies being reluctant to take space in these offices for this reason

OFFICE HEADLINE RENTS, Q-ON-Q% AND Y-ON-Y% CHANGE

Source: MPM Properties Research

AVERAGE OFFICE SALES PRICE

Source: MPM Properties Research18

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q1 2016 | OFFICE SECTOR

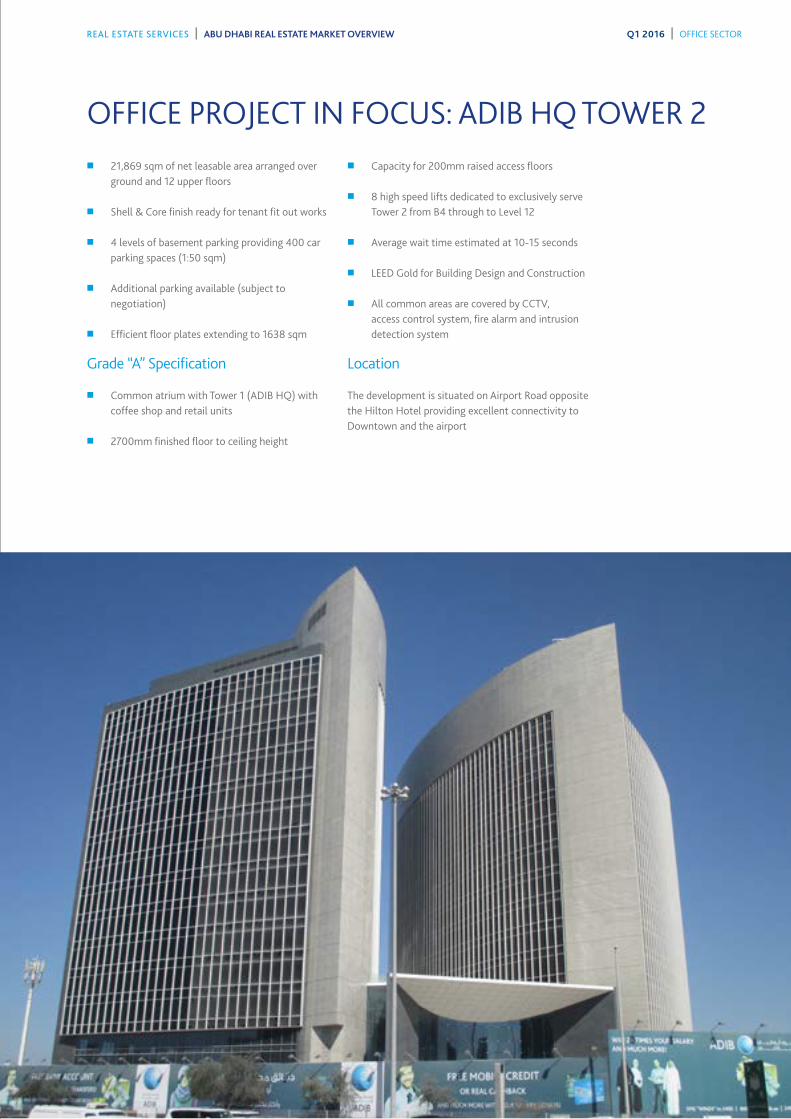

OFFICE PROJECT IN FOCUS: ADIB HQ TOWER 2�� 21,869 sqm of net leasable area arranged over

ground and 12 upper floors

�� Shell & Core finish ready for tenant fit out works

�� 4 levels of basement parking providing 400 car parking spaces (1:50 sqm)

�� Additional parking available (subject to negotiation)

�� Efficient floor plates extending to 1638 sqm

Grade “A” Specification

�� Common atrium with Tower 1 (ADIB HQ) with coffee shop and retail units

�� 2700mm finished floor to ceiling height

�� Capacity for 200mm raised access floors

�� 8 high speed lifts dedicated to exclusively serve Tower 2 from B4 through to Level 12

�� Average wait time estimated at 10-15 seconds

�� LEED Gold for Building Design and Construction

�� All common areas are covered by CCTV, access control system, fire alarm and intrusion detection system

Location

The development is situated on Airport Road opposite the Hilton Hotel providing excellent connectivity to Downtown and the airport

MARKET OVERVIEW Q1 2016

0

500

1,000

1,500

2,000

2,500

3,000

2009 2010 2011 2012 2013 2014 2015 2016Q1

2016Q2-Q4

20182017

Scheduled New Supply Running Total New Supply Completed

28

1,4281,4001,400

259113

185

342 43163

1

53

1,687 1,800 1,985 2,327 2,370 2,3702,533

306

2,586

NLA

(in

00

0’s

) pe

r Sq

.m.

ABU DHABI RETAIL SUPPLY (2009 - 2018+)

Source: MPM Properties Research

OVERVIEW �� There have been no new retail developments

completed in Abu Dhabi during the first quarter of 2016 and thus total retail stock in the Capital remains at approximately 2.4 million sqm of GLA

�� This trend is set to continue over the next two years with no new retail schemes scheduled for delivery until 2018/19, when Maryha Central and Reem Mall are forecast to be completed, which will add over 400,000 sqm of new retail space to the market

�� Mall revenues have been under pressure during the first quarter of 2016, with the outlook for the remaining year indicating further softening of consumer spending, leading to increased pressure on revenues. Property managers will have to carefully balance rent renewal rates, tenant churn rates and provide support to underperforming

retail brands, and maintain overall costs to ensure retail properties retain their attractiveness without significantly impacting the business objectives

�� Looking at the future outlook for retail space in Abu Dhabi from 2017 onwards the GOP and consumer confidence is expected to pick up, yet on-island property will quickly need to prepare for the increasingly competitive environment

�� In this connection some of the existing malls in Abu Dhabi have already started implementing active asset management strategies with the view to repositioning and improving trading performance

�� Online Internet retailing is now generating 1% of a $52+ billion market in the UAE, and expected to grow to 2% by 2020

20

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ1 2016 | RETAIL SECTOR

TAKE-UP & RENTS

The rents quoted above are base rents excluding any turnover provisions and service charges.

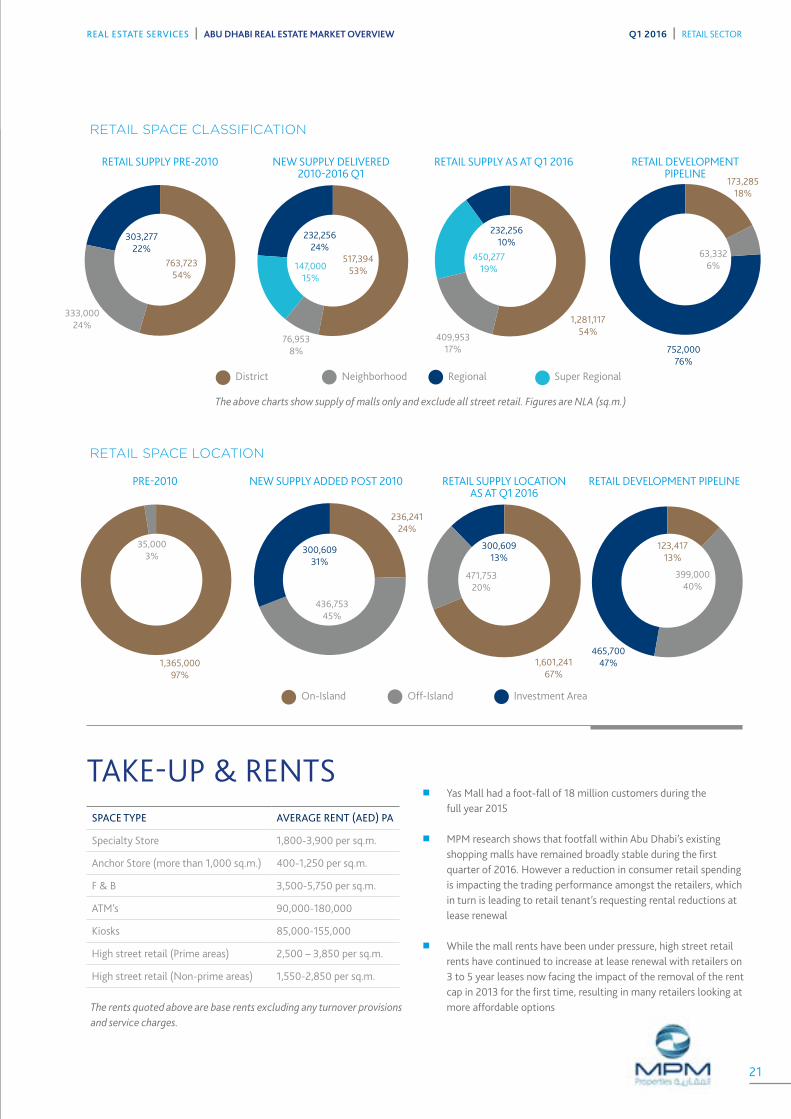

�� Yas Mall had a foot-fall of 18 million customers during the full year 2015

�� MPM research shows that footfall within Abu Dhabi’s existing shopping malls have remained broadly stable during the first quarter of 2016. However a reduction in consumer retail spending is impacting the trading performance amongst the retailers, which in turn is leading to retail tenant’s requesting rental reductions at lease renewal

�� While the mall rents have been under pressure, high street retail rents have continued to increase at lease renewal with retailers on 3 to 5 year leases now facing the impact of the removal of the rent cap in 2013 for the first time, resulting in many retailers looking at more affordable options

SPACE TYPE AVERAGE RENT (AED) PA

Specialty Store 1,800-3,900 per sq.m.

Anchor Store (more than 1,000 sq.m.) 400-1,250 per sq.m.

F & B 3,500-5,750 per sq.m.

ATM’s 90,000-180,000

Kiosks 85,000-155,000

High street retail (Prime areas) 2,500 – 3,850 per sq.m.

High street retail (Non-prime areas) 1,550-2,850 per sq.m.

District Neighborhood Regional Super Regional

On-Island Off-Island Investment Area

763,72354%

1,365,000 97%

333,000 24%

35,000 3%

303,27722%

517,39453%147,000

15%

1,281,117 54%409,953

17%

232,256 10%

450,277 19%

752,000 76%

236,241 24%

76,9538%

436,75345%

232,256 24%

300,60931%

RETAIL SUPPLY PRE-2010

PRE-2010

NEW SUPPLY DELIVERED 2010-2016 Q1

NEW SUPPLY ADDED POST 2010

The above charts show supply of malls only and exclude all street retail. Figures are NLA (sq.m.)

RETAIL SUPPLY LOCATION AS AT Q1 2016

1,601,241 67%

471,75320%

300,60913%

RETAIL DEVELOPMENT PIPELINE

RETAIL SUPPLY AS AT Q1 2016

173,285 18%

63,332 6%

465,70047%

123,41713%

RETAIL DEVELOPMENT PIPELINE

399,00040%

RETAIL SPACE CLASSIFICATION

RETAIL SPACE LOCATION

21

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q1 2016 | RETAIL SECTOR

MARKET OVERVIEW Q1 2016

ARR RevPAR Occupancy

100%

90%

80%

70%

60%

50%

40%

30%

20%

Jan

13

Ju

l

Jan

14

Ju

l

Jan

15

Ju

l

Jan

16

Mar

0

100

200

300

400

500

600

700

800

Ave

rage

roo

m r

ate

HOTEL ESTABLISHMENT PERFORMANCEHISTORICAL TRADING PERFORMANCE 2010-2016

Source: TCA Abu Dhabi and MPM Properties Research

In Q1 2016, only one new hotel (Al Seef Resort) entered the market adding 210 rooms.

Supply in the hotel sector is expected to increase by 2,853 keys by the end of 2016. New hotels scheduled for completion this year include Four Seasons, Marriott, Grand Millennium Bab Al Qasr Hotel and Emirates Pearl.

Abu Dhabi Tourism and Culture Authority and Miral have announced that the $1 billion Warner Brothers theme park on Yas Island will open in 2018,which along with the Louvre on Saadiyat Island will act as a major tourism driver.

Num

ber

of r

oom

s

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Pre 2009

2009 2010 2011 20132012 2014 2015 2016Q1

2016Q2-Q4

2017+

Scheduled New Supply Running Total New Supply Completed

5,3742,397

2,6462,653

2,3122,805

1,835 2132,599

3,357

8,278 8,27813,652 16,049 18,695 21,348

23,66026,465 28,300 28,513

31,112

ABU DHABI HOTEL ROOM SUPPLY (2009 - 2017+)

Source: MPM Properties Research

22

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ1 2016 | HOSPITALITY SECTOR – TRADING PERFORMANCE

Q1 2016 – HOTEL APARTMENT SCHEDULED COMPLETIONS

GUEST ARRIVALS – TOP 5

GUEST ARRIVALS Q1 2016 YTD

S.NO. ESTABLISHMENT NAME EXPECTED CLASS OPENING ROOMS

1 Al Seef Resort & Spa by Andalus Deluxe Q1 - 2016 210

TOTAL 210

RANK NATIONALITY 2016 YTD 2015 YTD GROWTH RATE %

1 United Arab Emirates 226,883 205,036 11%

2 India 47,064 37,116 27%

3 China 45,555 46,464 -2%

4 United Kingdon 36,613 36,008 2%

5 USA 25,638 27,081 -5%

United Arab Emirates 37%

Other GCC Countries 8%

Other Arab Countries 10%

Asia (Except Arab) 21%

Australia & Pacific 1%

Africa (Except Arab) 1%

Europe 17%

North & South America 5%

Source: TCA Abu Dhabi and MPM Properties Research

23

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q1 2016 | HOSPITALITY SECTOR – TRADING PERFORMANCE

DEFINITIONS & METHODOLOGY

RESEARCH STUDY AREA

The geographic extent of the study area covers the key districts in Dubai.

RESIDENTIAL

New residential developments are classified as delivered and thus entered into the new supply category when they are made available for occupation. This is verified via a combination of site inspections and discussion with the developer and hence our supply numbers do take into consideration the phased release of large projects.

Rental and sales trend analysis is based on transactional data derived from the MPM Properties Agency team and data sourced from developers and owners.

OFFICES

New office developments are classified as delivered and thus entered into the new supply category when they are available for tenant fit-outs.

Given the general lack of transparency in the local market rents quoted are headline rents, thus exclude any rent free period of other financial incentives that may have been negotiated between

the parties. The rents quoted are also exclusive of service charges.

RETAIL

New retail developments are classified as delivered and thus entered into the new supply category when the first units are open and trading.

Our classification of malls is based on our own assessment having regard to size and the catchment area which the mall typically penetrates.

HOSPITALITY

New hotels are classified as delivered and thus entered into the new supply category when they are opened and trading. All trading performance data is provided by DTCM.

FUTURE SUPPLY PROJECTIONS

Our future supply projections across all sectors are based on a combination of regular site inspections and discussions with developers.

BESPOKE CLIENT RESEARCH ADDING VALUE TO YOUR PROPERTY INTERESTSThe ADIB Real Estate Services team covers all sectors of the real estate market. We provide bespoke market research to our valued clients to meet their specific requirements.

We provide reports, information and presentations derived from primary market data that directly assist our clients to save or make money from real estate and shape strategies to enhance value.

DISCLAIMER:

The information contained in this report has been obtained from and is based upon sources that MPM Properties believes to be reliable, however, no warranty or representation, expressed or implied, is made to the accuracy or completeness of the information contained herein, and same is submitted subject to errors, omissions, change of price, rental or other conditions, withdrawal without notice, and to any special listing conditions imposed by our principals. MPM Properties will not be held responsible for any third-party contributions. All opinions and estimates included in this report constitute MPM Properties, as of the date of this report and are subject

to change without notice. Figures contained in this report are derived from a basket of locations highlighted in this report and therefore represent a snapshot of the Dubai market. Due care and attention has been used in the preparation of forecast information. However, actual results may vary from forecasts and any variation may be materially positive or negative. Forecasts, by their very nature, involve risk and uncertainty because they relate to future events and circumstances which are beyond MPM Properties’ control. For a full in-depth study of the market, please contact MPM Properties team.

24

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ1 2016 | DEFINITIONS & METHODOLOGY

A collaborative team providing our integrated services

PAUL MAISFIELD BSC (HONS) MRICS CEO T: +971 (0)2 610 0545 M: +971 (0)50 660 9437 [email protected]

YOUSEF AL ZAROONI Regional Head – Al Ain T: +971 (0)3 708 8636 M: +971 (0)50 600 1002 [email protected]

ABDULLAH SAID AL KUWEITI Business Development Director T: +971 (0)2 610 1554 M: +971 (0)50 623 5854 [email protected]

PRADEEP FERNANDES MRICS Advisory & Valuation Manager T: +971 (0)2 510 0663 M: +971 (0)55 961 3626 [email protected]

SAMUEL MORRIS BSC (HONS) FRICSDirector of Valuation & Regional Head - Dubai T: +971 (0)4 371 9466 M: +971 (0)50 107 1704 [email protected]

WAHIDA KARAMA Head of Property Operations T: +971 (02) 610 0435 M: +971 (0)50 765 7679 [email protected]

FRANK O’DWYER MBA (Hons); BEng.COO T: +971 (0)2 610 0402 M: +971 (0)50 812 1070 [email protected]

DOMINIC BARLOW Head of Retail, Hospitality & Leisure T: +971 (0)2 510 0655 M: +971 (0)56 288 1458 [email protected]

JUBRAN AL HASHMI Head of Property Services T: +971 (0)2 610 0232 M: +971 (0)50 122 0041 [email protected]

VAIBHAV SHARMA MCOM; MDBA Director of Strategic Advisory and Research T: +971 (0)2 412 8914 M: +971 (0)50 660 9295 [email protected]

ALI ABDULLAH ABDUL RAHMAN Acting Regional Head – Northern Emirates T: 971 (0)6 597 2514 M: +971 (0)50 656 2486 [email protected]

MOHAMED AL ZOUBI Head of Development Advisory BSc Civil Engineering T: +971 (0)2 610 0564 M: +971 (0)50 310 3570 [email protected]

KHALED CHAHAL Director of Agency – Abu Dhabi T: +971 (0)2 412 8402 M: +971 (0)50 110 2929 [email protected]

JASON FIELDEN BSC (HONS) MRICS Valuation Manager - Abu Dhabi T: +971 (0)2 510 0653 M: +971 (0)56 244 7696 [email protected]

25

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q1 2016

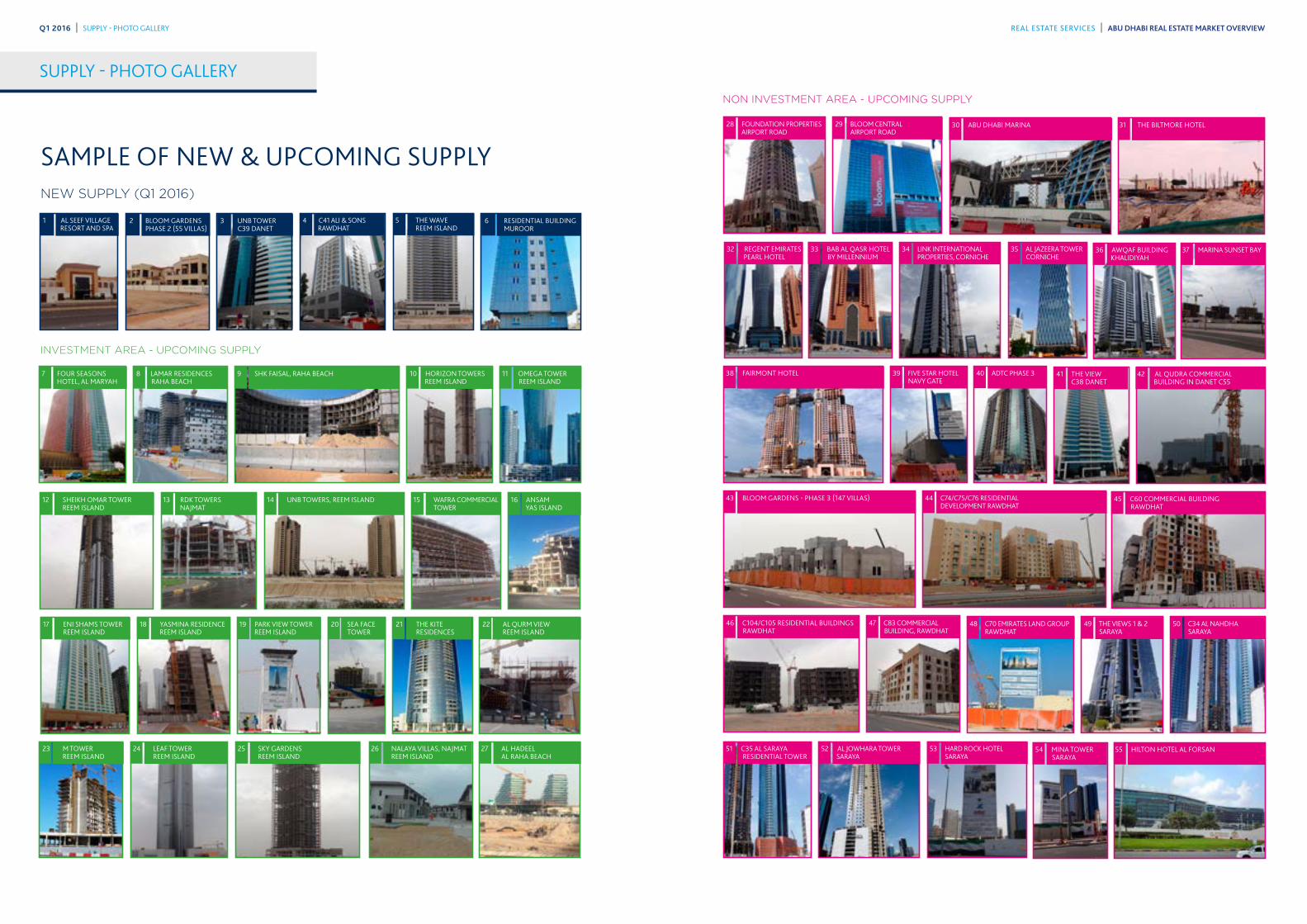

SUPPLY - PHOTO GALLERY

SAMPLE OF NEW & UPCOMING SUPPLYNEW SUPPLY (Q1 2016)

INVESTMENT AREA - UPCOMING SUPPLY

2 BLOOM GARDENS PHASE 2 (55 VILLAS)

6 RESIDENTIAL BUILDING MUROOR

3 UNB TOWER C39 DANET

NON INVESTMENT AREA - UPCOMING SUPPLY

17 ENI SHAMS TOWER REEM ISLAND

18 YASMINA RESIDENCE REEM ISLAND

28 FOUNDATION PROPERTIES AIRPORT ROAD

39 FIVE STAR HOTEL NAVY GATE

52 AL JOWHARA TOWER SARAYA

44 C74/C75/C76 RESIDENTIAL DEVELOPMENT RAWDHAT

47 C83 COMMERCIAL BUILDING, RAWDHAT

34 LINK INTERNATIONAL PROPERTIES, CORNICHE

29 BLOOM CENTRAL AIRPORT ROAD

40 ADTC PHASE 3

53 HARD ROCK HOTEL SARAYA

48 C70 EMIRATES LAND GROUP RAWDHAT

49 THE VIEWS 1 & 2 SARAYA

50 C34 AL NAHDHA SARAYA

35 AL JAZEERA TOWER CORNICHE

31 THE BILTMORE HOTEL

42 AL QUDRA COMMERCIAL BUILDING IN DANET C55

55 HILTON HOTEL AL FORSAN

37 MARINA SUNSET BAY

30 ABU DHABI MARINA

41 THE VIEW C38 DANET

54 MINA TOWER SARAYA

45 C60 COMMERCIAL BUILDING RAWDHAT

36 AWQAF BUILDING KHALIDIYAH

32 REGENT EMIRATES PEARL HOTEL

38 FAIRMONT HOTEL

51 C35 AL SARAYA RESIDENTIAL TOWER

43 BLOOM GARDENS - PHASE 3 (147 VILLAS)

46 C104/C105 RESIDENTIAL BUILDINGS RAWDHAT

33 BAB AL QASR HOTEL BY MILLENNIUM

24 LEAF TOWER REEM ISLAND

25 SKY GARDENS REEM ISLAND

26 NALAYA VILLAS, NAJMAT REEM ISLAND

27 AL HADEEL AL RAHA BEACH

7 FOUR SEASONS HOTEL, AL MARYAH

8 LAMAR RESIDENCES RAHA BEACH

11 OMEGA TOWER REEM ISLAND

12 SHEIKH OMAR TOWER REEM ISLAND

13 RDK TOWERS NAJMAT

14 UNB TOWERS, REEM ISLAND 15 WAFRA COMMERCIAL TOWER

16 ANSAM YAS ISLAND

19 PARK VIEW TOWER REEM ISLAND

20 SEA FACE TOWER

21 THE KITE RESIDENCES

22 AL QURM VIEW REEM ISLAND

23 M TOWER REEM ISLAND

1 AL SEEF VILLAGE RESORT AND SPA

9 SHK FAISAL, RAHA BEACH 10 HORIZON TOWERS REEM ISLAND

4 C41 ALI & SONS RAWDHAT

5 THE WAVE REEM ISLAND

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ1 2016 | SUPPLY - PHOTO GALLERY

Residential

Offices

Retail

Hotels

Residential

Offices

Retail

Hotels

Q2 2014 NEW SUPPLY UNDER CONSTRUCTION

Jubail Island

Al ReemIsland

Al MaryahIsland

Al Raha Beach

MasdarCity

Saadiyat Island

Yas Island

HydraVillage

Al Reef

B

D

E F

G H

K

I

J

A

C

Salam Street

Khaleej Al Arabi Street

Airport Rd

Airport Rd

E 20

E 20

E 22

E 30

Corn

iche

Rd

Electra St

Zayed The First S

t

E12

Al Saada Stre

et

25th S

t

Salam Street

Salam Street

Sheikh Khalifa Hway

Abu D

habi

- Dub

ai Rd

Abu Dhabi - Dubai Rd

E 10

Shei

kh M

akto

um B

in R

ashi

d Rd

E 11

E 11

E 11

E 10

6

5

4

7

89

27

11 2322

10

1514 12

1316

1920

21

1718

25

24

4039

34

3130

3233

3837

35

3628

29

26

413

4243

21

454847

44 46

4950

5153

5254

55

New Supply

Investment

Non-investment

Q1 NEW & UPCOMING SUPPLY

ADIB RENTAL INDEX ZONE

COMMON TREND (Q1 2016) (ANNUAL % RENTAL INCREASE)

Q-Q CHANGE OVERALL AVERAGE

Q1 2016 Q4 2015 Q3 2015 Q2 2015 Q1 2015 Q4 2014 Q3 2014 Q2 2014 Q1 2014

Zone A 0 to + 4.99% 3.52% 3.06% 3.05% 4.58% 3.71% 8.05% 5.01% 2.37% 4.05%

Zone B 0 to + 4.99% 3.38% 4.33% 2.60% 5.08% 6.94% 7.75% 10.56% 3.86% 6.33%

Zone C 0 to + 4.99% 6.05% 5.94% 5.63% 7.46% 9.25% 9.79% 12.34% 10.26% 5.06%

Zone D 0 to + 4.99% 7.01% 7.05% 6.48% 7.06% 8.51% 10.31% 10.26% 9.07% 6.18%

Zone E 0 to + 4.99% 9.34% 7.35% 3.76% 4.02% 7.54% 5.09% 10.20% 5.32% 4.49%

Zone F 0 to + 4.99% 3.33% 5.62% 4.77% 3.17% 4.01% 6.58% 7.63% 3.25% 2.41%

Zone G 0 to + 4.99% 0.46% 1.91% 4.42% 2.34% 2.20% 2.59% 2.69% 2.42% 2.92%

Zone H 0 to + 4.99% 2.77% 3.85% 3.68% 5.58% 3.46% 1.46% 3.42% 5.31% 2.44%

Zone I 0 to + 4.99% 2.22% 2.36% 3.08% 3.41% 1.86% 5.48% 1.14% 1.33% 1.21%

Zone J 0 to + 4.99% 4.12% 1.87% 3.32% 5.78% 0.96% 4.04% 3.06% 1.55% 1.64%

Zone K 0 to + 4.99% 4.05% 6.10% 5.30% 5.89% 2.88% 4.31% 4.18% 3.51% 3.65%

Q1 2016 REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW

INTEGRATED SERVICES COVERING THE FULL PROPERTY LIFECYCLE

Property Management

Investment Advisory

Project Management and ESCROW

Research & Strategic AdvisoryAgency (Sales & Leasing)

Valuation

PAUL MAISFIELD BSC (HONS) MRICS CEO T: +971 (0)2 610 0545 M: +971 (0)50 660 9437 [email protected]

VAIBHAV SHARMA MCOM; MDBA Director of Strategic Advisory and Research T: +971 (0)2 412 8914 M: +971 (0)50 660 9295 [email protected]

ABU DHABI HEAD OFFICE 6th Floor, Al Wahda Tower P.O Box 114686 Abu Dhabi

Tel. +971 2 610 0252Fax. +971 2 610 0514 www.mpmproperties.ae

DUBAI OFFICE Office 004 - Level 100 Arenco Tower, Dubai Internet City Dubai

Tel. +971 (0)4 371 9462

AL AIN OFFICE 201-204 ADIB Ladies Branch Building Oud Touba Street Al Ain

Tel. +971 (0)3 703 9521

SHARJAH OFFICE AL Ikhlas Tower AL Khan Shajrah

Tel. +971 (0)6 597 2555

Enhancing value for individual & institutional property owners:

�� Prompt leasing & debt collection

�� Effectively market & lease vacant units

�� Physical & technical maintenance of asset

�� Maintain tenant satisfaction

�� Timely lease renewals

�� Manage risk, insurance & litigation

�� Protect your interests and enhance value

Complete Project Management services at planning & construction stage:

�� Engineering Review & Scheduling

�� Cost Estimate & Procurement

�� Project Monitoring

�� Cost Control & Accounting

�� Assist with Permits & Licensing

�� Ensure appropriate fund movement for Escrow based on Project Assessment

Aiding developers and investors to maximize value:

�� Investment Advisory & Due Diligence

�� Investment Management

�� Disposal Strategy

�� Portfolio Review & Optimization

�� Deal Structuring & Capital Sourcing

�� Investment Sale

We work with developers, commercial tenants, retailers and individuals, offering:

�� Launch Strategy

�� Project Launch Handling

�� Project Marketing Events

�� Acquisitions

�� Leasing

�� Sales

We cover all sectors, including residential, commercial, industrial, retail, and land.

Bankable studies for your real estate and business needs:

�� Highest & Best Use

�� Market & Financial Feasibility

�� Development Strategy

�� Market Research

�� Corporate Real Estate Strategy

�� Master-plan and design review

Valuation reports for:

�� Mortgage & Loan Security

�� Securing Project Funding

�� Internal Accounting

�� Mergers & Acquisitions

�� Investment appraisal

�� Litigation

�� Inheritance

We cover all asset classes. Our reports are in compliance with the International Valuation Standards (IVS) and the RICS Professional Valuation Standards.