2 IPCC Group- I Paper - 1 Accounting May - Sauda.com

24

Model Test Paper - 2 IPCC Group- I Paper - 1 Accounting May - 2017 1. (a) M/s Progressive Company Limited has not charged depreciation for the year ended on 31 st March, 2012, in respect of a spare bus purchased during the financial year 2011-12 and kept ready by the company for use as a stand-by , on the ground that, it was not actually used during the year. State your views with reference to Accounting Standard 10 “Property, Plant and Equipment”. Further during the year company made additions to its factory by using its own workforce, at a cost of ` 4,50,000 as wages and materials. The lowest estimate from an outside contractor to carry out the same work was ` 6,00,000. The directors contend that, since they are fully entitled to employ an outside contractor, it is reasonable to debit the Factory Building Account with ` 6,00,000. Comment whether the directors’ contention is right in view of the provisions of Accounting Standard 10? (5 marks) Answer : Provisions: According to AS 10, ‘Property, Plant and Equipment: • Depreciation is a measure of wearing out, consumption or other loss of value of a depreciable asset arising from use, effluxion of time or obsolescence through technology and market changes. • Accordingly, depreciation may arise even when asset has not been used in the current year but was ready for use in that year. • The need for using the stand by bus may not have arisen during the year but that does not imply that the useful life of the bus has not been affected. Therefore, non-provision of depreciation on the ground that the bus was not used during the year is not tenable. • As per AS 10, ‘Property, Plant and Equipment,’ the gross book value of the self constructed fixed asset includes the costs of construction that relate directly to the specific asset and the costs that are attributable to 1.1

-

Upload

khangminh22 -

Category

Documents

-

view

7 -

download

0

Transcript of 2 IPCC Group- I Paper - 1 Accounting May - Sauda.com

Model Test Paper - 2IPCC Group- I

Paper - 1AccountingMay - 2017

1. (a) M/s Progressive Company Limited has not charged depreciation forthe year ended on 31st March, 2012, in respect of a spare buspurchased during the financial year 2011-12 and kept ready by thecompany for use as a stand-by , on the ground that, it was notactually used during the year. State your views with reference toAccounting Standard 10 “Property, Plant and Equipment”.Further during the year company made additions to its factory byusing its own workforce, at a cost of ` 4,50,000 as wages andmaterials. The lowest estimate from an outside contractor to carryout the same work was ` 6,00,000. The directors contend that, sincethey are fully entitled to employ an outside contractor, it isreasonable to debit the Factory Building Account with ` 6,00,000.Comment whether the directors’ contention is right in view of theprovisions of Accounting Standard 10? (5 marks)

Answer :Provisions:According to AS 10, ‘Property, Plant and Equipment:• Depreciation is a measure of wearing out, consumption or other loss of

value of a depreciable asset arising from use, effluxion of time orobsolescence through technology and market changes.

• Accordingly, depreciation may arise even when asset has not been usedin the current year but was ready for use in that year.

• The need for using the stand by bus may not have arisen during the yearbut that does not imply that the useful life of the bus has not beenaffected. Therefore, non-provision of depreciation on the ground that thebus was not used during the year is not tenable.

• As per AS 10, ‘Property, Plant and Equipment,’ the gross book value ofthe self constructed fixed asset includes the costs of construction thatrelate directly to the specific asset and the costs that are attributable to

1.1

1.2 O Solved Scanner IPCC Group- I Paper - 1

the construction activity in general can be allocated to the specific asset.If any internal profit is there it should be eliminated. Saving of ` 1,50,000on account of using its own workforce is an unrealized/internal profit,which should not be capitalized/recorded as per the standard.Analysis and Conclusion:Therefore only ` 4,50,000 should be debited to the factory buildingaccount and not ` 6,00,000.Hence, the contention of the directors of the company to capitalize` 6,00,000 as cost of factory building, on the ground that the companyis fully entitled to employ an outside contractor is not justifiable.

(b) A Ltd. is amalgamating with B Ltd. They are undecided on themethod of accounting to be followed. You are required to advice themanagement of B Ltd. on the method of accounting that can beadopted under AS-14. (5 marks)

Answer :• An amalgamation may be either – an amalgamation in the nature of

merger, or an amalgamation in the nature of purchase.• The selection of method of accounting for amalgamation (pooling of

interests or purchase method) is to be judged after considering theintentions of the both the companies.

• If genuine pooling of all assets, liabilities, shareholders’ interest isintended; separate businesses of both the companies are continued andtheir amalgamation scheme satisfies all the conditions necessary formerger as specified in AS 14 Accounting for Amalgamations, pooling ofinterests method is adopted.

• If B Ltd. or A Ltd. wants to acquire the other company, then purchasemethod needs to be adopted. In that case, the shareholders of theacquired company don’t continue to have proportional share in equity ofthe combined company and the business of the acquired company is notintended to be continued.

• The object of the purchase method is to account for the amalgamationby applying the same principles as are applied in the normal purchaseof assets.

• Thus choice of accounting method depends on the fact whether B Ltd.

Model Test Paper O 1.3

wants to continue its business or not.

(c) In the books of Optic Fiber Ltd., plant and machinery stood at` 6,32,000 on 1.4.2013. However on scrutiny it was found thatmachinery worth ` 1,20,000 was included in the purchases on1.6.2013. On 30.6.2013 the company disposed a machine havingbook value of ` 1,89,000 on 1.4.2013 at ` 1,75,000 in part exchangeof a new machine costing ` 2,56,000. The company chargesdepreciation @ 20% WDV on plant and machinery.You are required to calculate:(i) Depreciation to be charged to P/L(ii) Book value of Plant and Machinery A/c as on 31.3.2014(iii) Loss on exchange of machinery. (5 marks)

Answer :(i) Depreciation to be charged in the Profit and Loss Account

Particulars (`)

Depreciation on old Machinery 31,600

[20% on ` 6,32,000 for 3 months]

Add: Depreciation machinery acquired on 01.06.2013 (` 1,20,000 × 20% ×10/12) 20,000

Depreciation on Machinery after adjustment of Exchange[20% of ` (6,32,000 - 1,89,000 + 2,56,000) for 9 months] 1,04,850

Total Depreciation to be charged in Profit and Loss A/c 1,56,450

(ii) Book Value of Plant and Machinery A/c as on 31.03.2014Particulars (`) (`)

Balances as per books on 01.04.2013 6,32,000

Add: Included in purchases on 01.06.2013 1,20,000

Add: Purchase on 30.06.2013 2,56,000 3,76,000

10,08,000

Less: Book value of Machine sold on

1.4 O Solved Scanner IPCC Group- I Paper - 1

30.06.2013 (1,89,000)

8,19,000

Less: Depreciation on machinery in use(1,56,450-9,450) (1,47,000)

Book Value as on 31.03.2014 6,72,000

(iii) Loss on exchange of MachineryParticulars (`)

Book value of machinery as on 01.04.2013 1,89,000

Less: Depreciation for 3 months 9,450

WDV as on 30.06.2013 1,79,550

Less: Exchange value 1,75,000

Loss on exchange of machinery 4,550

(d) Sarita Publications publishes a monthly magazine on the 15th ofevery month. It sells advertising space in the magazine toadvertisers on the terms of 80% sale value payable in advance andthe balance within 30 days of the release of the publication. The saleof space for the March 2014 issue was made in February 2014. Themagazine was published on its scheduled date. It received` 2,40,000 on 10.3.2014 and ` 60,000 on 10.4.2014 for the March2014 issue.Discuss in the context of AS 9 the amount of revenue to berecognized and the treatment of the amount received fromadvertisers for the year ending 31.3.2014. What will be the treatmentif the publication is delayed till 2.4.2014? (5 marks)

Answer :According to AS 9, ‘Revenue Recognition’, in a transaction involving therendering of services, performance should be measured either under thecompleted service contract method or under the proportionate completionmethod as the service is performed, whichever relates the revenue to thework accomplished.

Model Test Paper O 1.5

In this case, income accrues when the related advertisement appears beforepublic.

The advertisement service would be considered as performed on the day theadvertisement is seen by public and hence revenue is recognized on thatdate, so in this case, it is 15.03.2014, the date of publication of themagazine.Therefore, ` 3,00,000 (` 2,40,000 + ` 60,000) is recognized as income inMarch, 2014. The terms of payment are not relevant for considering the dateon which revenue is to be recognized. ` 60,000 is treated as amount duefrom advertisers as on 31.03.2014 and ` 2,40,000 will be treated as paymentreceived against the sale.Whereas, if the publication is delayed till 02.04.2014 revenue recognition willalso be delayed till the advertisements get published in the magazine. Insuch case revenue of ` 3,00,000 will be recognized for the year ended31.03.2015 after the magazine is published on 02.04.2014. The amountreceived from sale of advertising space on 10.03.2014 of ` 2,40,000 will beconsidered as an advance from advertisers as on 31.03.2014.

2. On 31st March, 2013 Bose and Sen Ltd. provides to you the followingledger balances after preparing its Profit and Loss Account for the yearended 31st March, 2013:Credit Balances: (`)Equity shares capital, fully paid shares of ` 10 each 70,00,000General Reserve 15,49,100Loan from State Finance Corporation 10,50,000Secured by hypothecation of Plant &Machinery(Repayable within one year ` 2,00,000)Loans: Unsecured (Long term) 8,47,000Sundry Creditors for goods & expenses (Payable within6 months)

14,00,000

Profit & Loss Account 7,00,000Provision for Taxation 3,25,500

1.6 O Solved Scanner IPCC Group- I Paper - 1

Proposed Dividend 4,20,000Provision for Dividend Distribution Tax 71,400

1,33,63,000

Debit Balances: (`)

Calls in arrear 7,000

Land 14,00,000

Buildings 20,50,000

Plant and Machinery 36,75,000

Furniture & Fixture 3,50,000

Stocks: Finished goods 14,00,000

Raw Materials 3,50,000

Sundry Debtors 14,00,000

Advances: Short-term 2,98,900

Cash in hand 2,10,000

Balances with banks 17,29,000

Preliminary Expenses 93,100

Patents & Trade marks 4,00,000

1,33,63,000The following additional information is also provided:(i) 4,20,000 fully paid equity shares were allotted as consideration for

land & buildings.(ii) Cost of Building ` 28,00,000

Cost of Plant & Machinery ` 49,00,000Cost of Furniture & Fixture ` 4,37,500

(iii) Sundry Debtors for ` 3,80,000 are due for more than 6 months.(iv) The amount of Balances with Bank includes ` 18,000 with a bank

which is not a scheduled Bank and the deposits of ` 5 lakhs are fora period of 9 months.

(v) Unsecured loan includes ` 2,00,000 from a Bank and ` 1,00,000from related parties.

Model Test Paper O 1.7

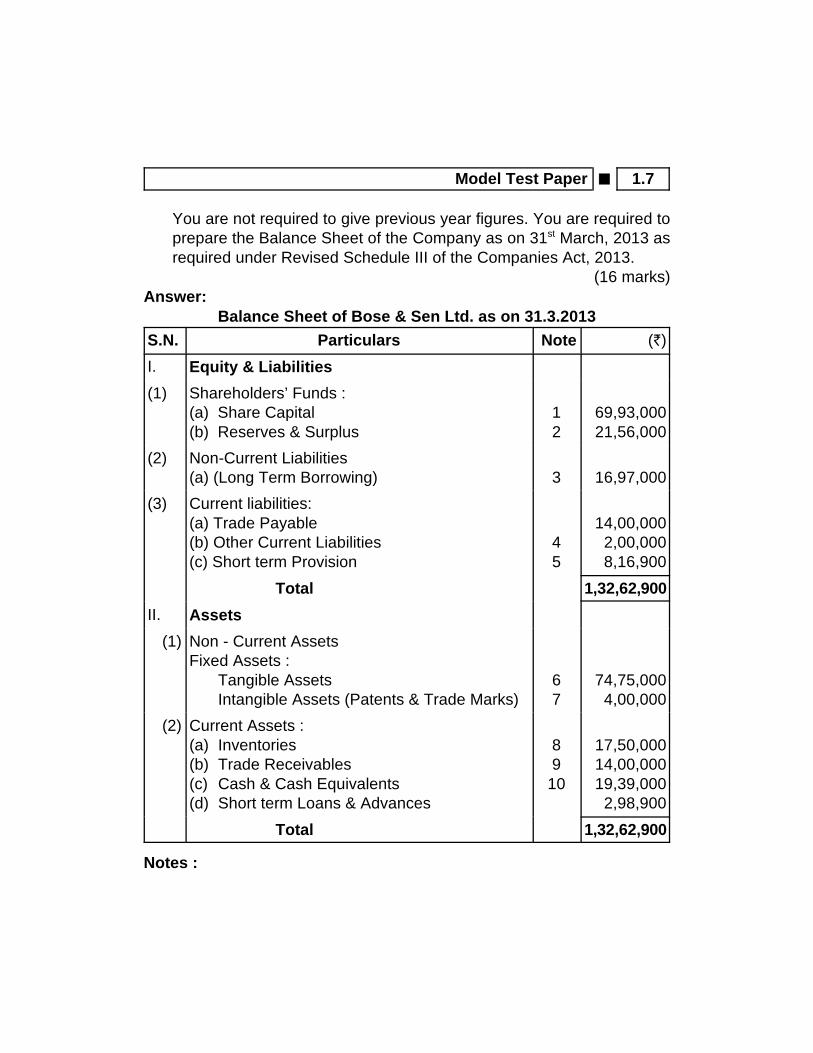

You are not required to give previous year figures. You are required toprepare the Balance Sheet of the Company as on 31st March, 2013 asrequired under Revised Schedule III of the Companies Act, 2013.

(16 marks)Answer:

Balance Sheet of Bose & Sen Ltd. as on 31.3.2013

S.N. Particulars Note (`)

I. Equity & Liabilities

(1) Shareholders’ Funds :(a) Share Capital(b) Reserves & Surplus

12

69,93,00021,56,000

(2) Non-Current Liabilities(a) (Long Term Borrowing) 3 16,97,000

(3) Current liabilities:(a) Trade Payable(b) Other Current Liabilities(c) Short term Provision

45

14,00,0002,00,0008,16,900

Total 1,32,62,900

II. Assets

(1) Non - Current AssetsFixed Assets :

Tangible AssetsIntangible Assets (Patents & Trade Marks)

67

74,75,0004,00,000

(2) Current Assets :(a) Inventories(b) Trade Receivables(c) Cash & Cash Equivalents(d) Short term Loans & Advances

89

10

17,50,00014,00,00019,39,000

2,98,900

Total 1,32,62,900

Notes :

1.8 O Solved Scanner IPCC Group- I Paper - 1

1. Share CapitalIssued, Subscribed & Paid up 70,00,000Less : Calls in arrears (7,000)Total 69,93,000

2. Reserves & SurplusGeneral Reserve 15,49,100Surplus (P & L A/c) 7,00,000Less: Preliminary Expenses (93,100)Total 21,56,000

3. Long term borrowings:Secured

Term LoanLoan from State Financial Corporation 8,50,000(` 10,50,000 - ` 2,00,000)(Secured by hypothecation of Plant and machinery)

UnsecuredBank Loan 2,00,000Loan from related parties 1,00,000Others 5,47,000 8,47,000

Total 16,97,0004. Other Current Liabilities

Loan from State Finance Corporation (Repayable withinone year) 2,00,000

5. Short term provisionsProvision for taxation 3,25,500Proposed dividend 4,20,000Provision for dividend distribution tax 71,400Total 8,16,900

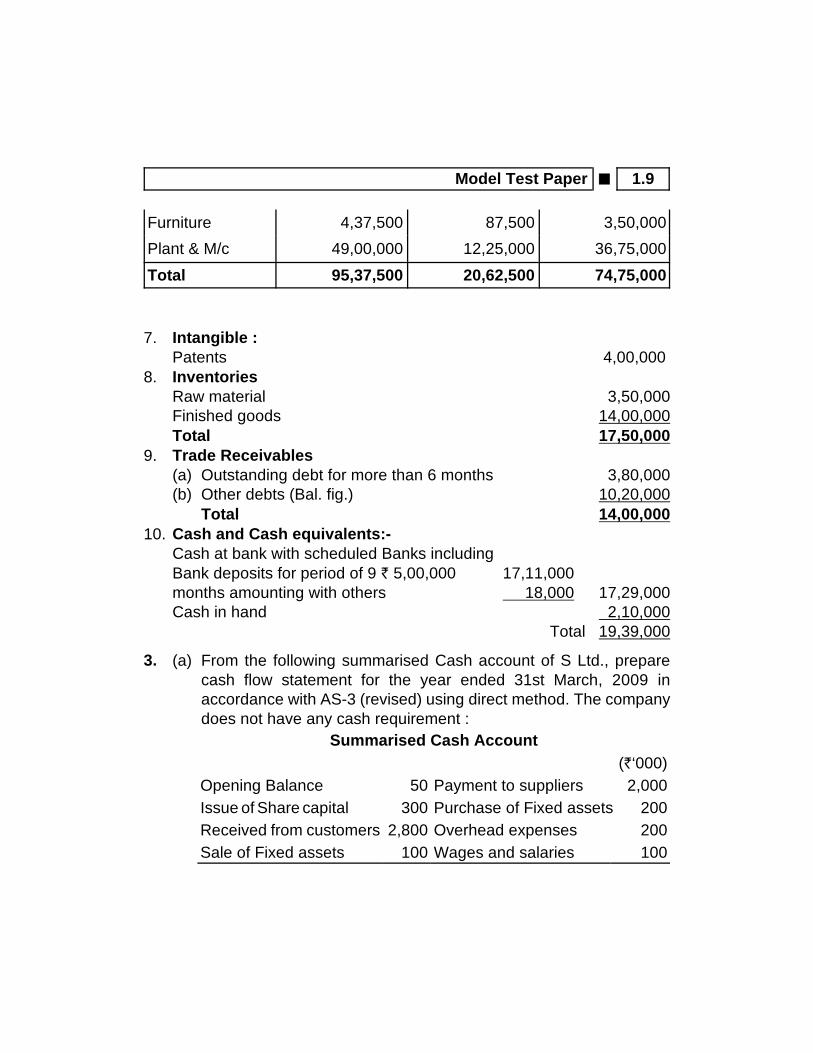

6. Tangible Fixed Assets:Item Closing Balance Depreciation Net

Tangible :

Land 14,00,000 0 14,00,000

Building 28,00,000 7,50,000 20,50,000

Model Test Paper O 1.9

Furniture 4,37,500 87,500 3,50,000

Plant & M/c 49,00,000 12,25,000 36,75,000

Total 95,37,500 20,62,500 74,75,000

7. Intangible :Patents 4,00,000

8. InventoriesRaw material 3,50,000Finished goods 14,00,000Total 17,50,000

9. Trade Receivables(a) Outstanding debt for more than 6 months 3,80,000(b) Other debts (Bal. fig.) 10,20,000

Total 14,00,00010. Cash and Cash equivalents:-

Cash at bank with scheduled Banks includingBank deposits for period of 9 ` 5,00,000 17,11,000months amounting with others 18,000 17,29,000Cash in hand 2,10,000

Total 19,39,000

3. (a) From the following summarised Cash account of S Ltd., preparecash flow statement for the year ended 31st March, 2009 inaccordance with AS-3 (revised) using direct method. The companydoes not have any cash requirement :

Summarised Cash Account(`‘000)

Opening Balance 50 Payment to suppliers 2,000Issue of Share capital 300 Purchase of Fixed assets 200Received from customers 2,800 Overhead expenses 200Sale of Fixed assets 100 Wages and salaries 100

1.10 O Solved Scanner IPCC Group- I Paper - 1

Tax paid 250Dividend paid 50Bank Loan 300Closing Balance 150

3,250 3,250(8 marks)

Answer :Cash Flow Statement for the year ended 31.3.2009

Particulars(`

In ‘000)Cash flow from Operating ActivitiesCash received from customersLess: Cash paid to suppliers 2,000

Cash paid for overhead expenses 200Cash paid for wages and salaries 100

Less: Income tax paidNet cash generated from Operating ActivitiesCash flow from Investing ActivitiesSales of fixed assets 100Less: Purchase of fixed assets 200Net cash used in Investing ActivitiesCash flow from Financing ActivitiesReceived from issue of share capitalLess: Payment of bank loan 300

Payment of dividend 50Net cash used in Financing ActivitiesNet increase in cash and equivalentsAdd: Cash and equivalents at the beginning of the yearCash and equivalents at the end of the year

2,800

2,300500250

300

350

250

(100)

(50)100 50150

(b) The following particulars relate to Bee Ltd. for the year ended 31stMarch, 2010 :(i) Furniture of book value of ` 15,500 was disposed off for

Model Test Paper O 1.11

` 12,000.(ii) Machinery costing ` 3,10,000 was purchased and ` 20,000 were

spent on its erection.(iii) Fully paid 8% preference shares of the face value of `10,00,000

were redeemed at a premium of 3%. In this connection 60,000equity shares of ` 10 each were issued at a premium of ` 2 pershare. The entire money being received with applications.

(iv) Dividend was paid as follows :On 8% preference shares ` 40,000On equity shares for the year 2009 - 10 `1,10,000

(v) Total sales were ` 32,00,000 out of which cash sales were` 11,50,000.

(vi) Total purchases were ` 8,00,000 including cash purchase of` 60,000.

(vii) Total expenses were ` 12,40,000.(viii) Taxes paid including dividend tax of ` 22,500 were

` 3,30,000.(ix) Cash and cash equivalents as on 31st March, 2010 were

` 1,25,000.You are requested to prepare Cash Flow Statement as per AS-3 forthe year ended 31st March, 2010 after taking into consideration thefollowing also:

On 31st March, 2009 On 31st March, 2010

` `

Sundry debtors 1,50,000 1,47,000

Sundry creditors 78,000 83,000

Unpaid expenses 63,000 55,000(8 marks)

Answer :Cash Flow Statement for the year ended 31st March, 2010

Particulars (`) (`)

l. Cash flow from Operating Activities

1.12 O Solved Scanner IPCC Group- I Paper - 1

Cash receipts from customers (W.N.1)Less : Cash paid to suppliers and paymentfor expenses (W.N.3)Cash generated from operationsIncome tax paid (` 3,30,000 ` 22,500)Net cash from operating activities

ll. Cash flows from Investing ActivitiesSale of furniturePurchase of machineryNet cash used in investing activities

lll. Cash flow from Financing ActivitiesProceeds from issue of equity sharesRedemption of 8% preference sharesDividend paid (` 40,000 + ` 1,10,000)Dividend distribution tax paidNet cash used in financing activities

32,03,000(20,43,000)

11,60,0003,07,500

12,000(3,30,000)

7,20,000(10,30,000)

(1,50,000) (22,500)

8,52,500

(3,18,000)

(4,82,500)

Net increase in cash and cash equivalentsAdd : Cash and cash equivalents as on 31st March, 2009 (Bal. fig.)

52,000 73,000

Cash and cash equivalents as on 31st March, 2010 1,25,000

Working Notes :1. Cash receipt from customers :

Credit sales = Total sales ` 32,00,000 Cash sales ` 11,50,000= ` 20,50,000

Total Debtors AccountParticulars (`) Particulars (`)

To Balance b/dTo Credit sales

1,50,00020,50,000

By Cash/Bank (Bal. fig.)By Balance c/d

20,53,0001,47,000

22,00,000 22,00,000Total sale receipts = ` 20,53,000 + ` 11,50,000 = ` 32,03,000

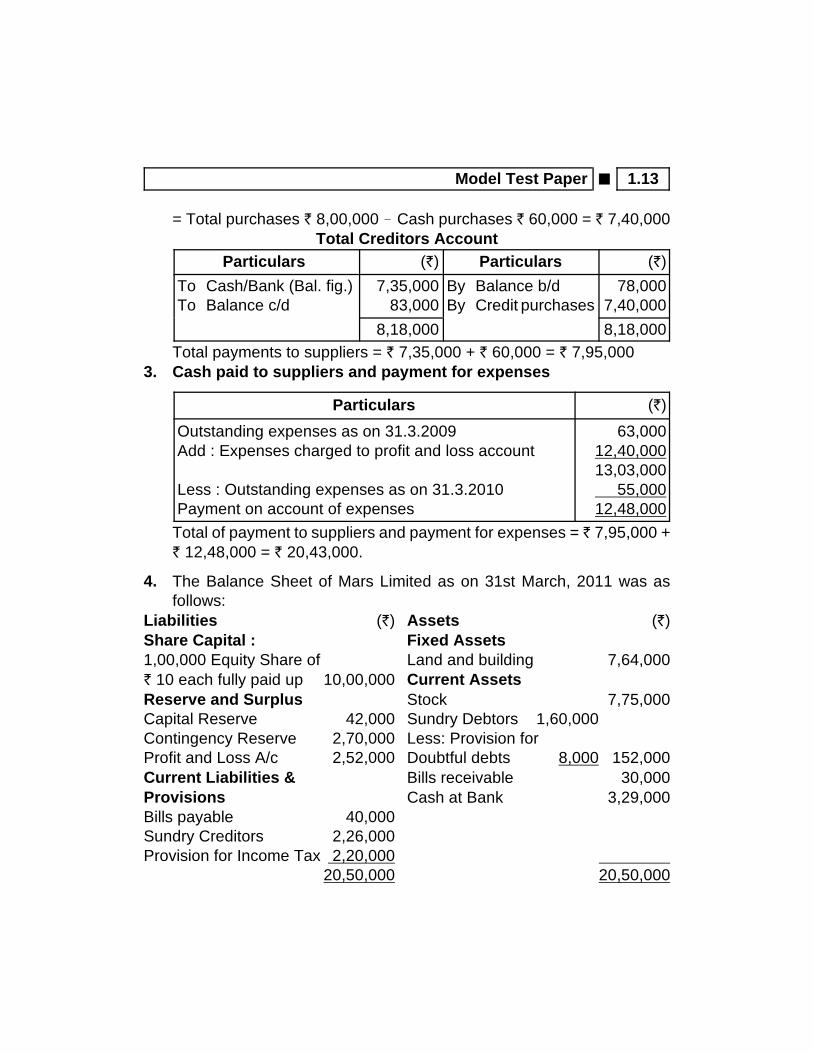

2. Cash payment to suppliers :Credit Purchases

Model Test Paper O 1.13

= Total purchases ` 8,00,000 Cash purchases ` 60,000 = ` 7,40,000Total Creditors Account

Particulars (`) Particulars (`)

To Cash/Bank (Bal. fig.)To Balance c/d

7,35,00083,000

By Balance b/dBy Credit purchases

78,0007,40,000

8,18,000 8,18,000Total payments to suppliers = ` 7,35,000 + ` 60,000 = ` 7,95,000

3. Cash paid to suppliers and payment for expenses

Particulars (`)

Outstanding expenses as on 31.3.2009Add : Expenses charged to profit and loss account

Less : Outstanding expenses as on 31.3.2010Payment on account of expenses

63,00012,40,00013,03,000 55,00012,48,000

Total of payment to suppliers and payment for expenses = ` 7,95,000 +` 12,48,000 = ` 20,43,000.

4. The Balance Sheet of Mars Limited as on 31st March, 2011 was asfollows:

Liabilities (`) Assets (`)Share Capital : Fixed Assets1,00,000 Equity Share of Land and building 7,64,000` 10 each fully paid up 10,00,000 Current AssetsReserve and Surplus Stock 7,75,000Capital Reserve 42,000 Sundry Debtors 1,60,000Contingency Reserve 2,70,000 Less: Provision forProfit and Loss A/c 2,52,000 Doubtful debts 8,000 152,000Current Liabilities & Bills receivable 30,000Provisions Cash at Bank 3,29,000Bills payable 40,000Sundry Creditors 2,26,000Provision for Income Tax 2,20,000

20,50,000 20,50,000

1.14 O Solved Scanner IPCC Group- I Paper - 1

On 1st April, 2011 Jupiter Limited agreed to absorb Mars Limited on thefollowing terms and conditions :1. Jupiter Limited will take over the assets at the following values :

Land and building ` 10,80,000Stock ` 7,70,000Bills receivable ` 30,000

2. Purchase consideration will be settled by Jupiter Ltd. as under :4,100 fully paid 10% preference shares of ` 100 will be issued andthe balance will be settled by issuing equity shares of ` 10 each at` 8 paid up.

3. Liquidation expenses are to be reimbursed by Jupiter Ltd. to theextent of ` 5,000.

4. Sundry debtors realised ` 1,50,000. Bills payable were settled for` 38,000.Income Tax authorities fixed the taxation liability at ` 2,22,000 andthe same was paid.

5. Creditors were finally settled with the cash remaining after meetingliquidation expenses amounting to ` 8,000.

You are required to :(i) Calculate the number of equity shares and preference shares to be

allotted by Jupiter limited in discharge of purchase consideration.(ii) Prepare the Realisation A/c. Bank Account, Equity Shareholders

Account and Jupiter Limited's Account in the books of Mars Ltd.(16 marks)

Answer:(i) Calculation of No. of Shares to be allotted

Particulars Amount (`)

Land and buildingInventories (Stock)Bills receivableTotalAmount discharged by issue of preference shares

10,80,0007,70,000

30,00018,80,0004,10,000

Model Test Paper O 1.15

Number of preference shares to be issued (4,10,000/100)Amount discharged by issue of equity shares (` 18,80,000 - 4,10,000)Number of equity shares to be issued (` 14,70,000/8)

4,100 shares14,70,0001,83,750

shares

(ii) Ledger Accounts in the books of Mars LimitedRealization A/c

Particulars Amount(`)

Particulars Amount(`)

To Land and buildingTo Inventories (stock)To Sundry debtorsTo Bills receivableTo Bank A/c (Liquidation

expenses)To Bank A/c (bills payable)To Bank A/c (income tax)To Bank A/c (Sundry creditors)To Profit transferred to equity

shareholders A/c

7,64,0007,75,0001,60,000

30,0003,000

38,0002,22,0002,16,000

3,16,000

By Provision for doubtful debtsBy Bills payableBy Trade PayablesBy Provision for taxationBy Jupiter Ltd. (Purchase

consideration)By Bank A/c (Sundry debtors)

8,00040,000

2,26,0002,20,000

18,80,0001,50,000

25,24,000 25,24,000

Bank A/cParticulars Amount

(`)Particulars Amount

(`)

To Balance b/dTo R e a l i z a t i o n A / c

(payment received fromdebtors)

To Jupiter Ltd. (Liquidationexpenses)

3,29,000

1,50,000

5,000

By Realization A/c (Liquidationexpenses)

By Jupiter Ltd.By Bills payableBy Income TaxBy Sundry creditors (Bal. fig)

3,000

5,00038,000

2,22,0002,16,000

1.16 O Solved Scanner IPCC Group- I Paper - 1

4,84,000 4,84,000

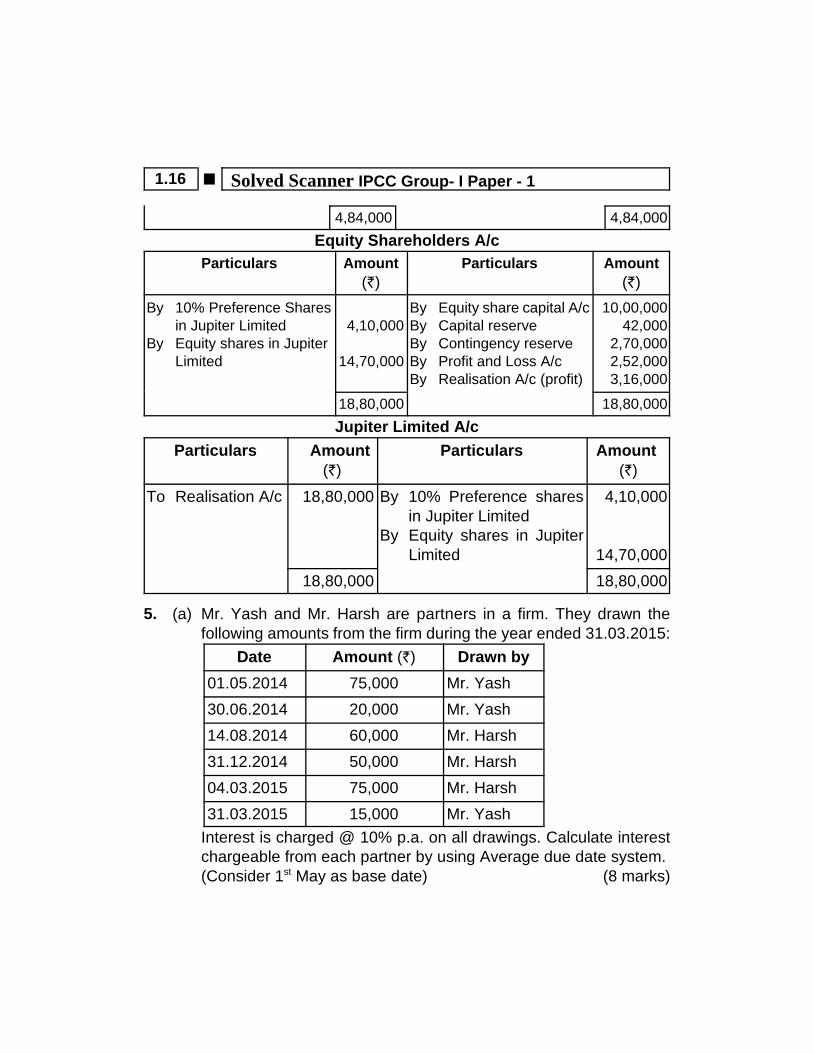

Equity Shareholders A/cParticulars Amount

(`)Particulars Amount

(`)

By 10% Preference Sharesin Jupiter Limited

By Equity shares in JupiterLimited

4,10,000

14,70,000

By Equity share capital A/cBy Capital reserveBy Contingency reserveBy Profit and Loss A/cBy Realisation A/c (profit)

10,00,00042,000

2,70,0002,52,000

3,16,000

18,80,000 18,80,000

Jupiter Limited A/c

Particulars Amount(`)

Particulars Amount(`)

To Realisation A/c 18,80,000 By 10% Preference sharesin Jupiter Limited

By Equity shares in JupiterLimited

4,10,000

14,70,000

18,80,000 18,80,000

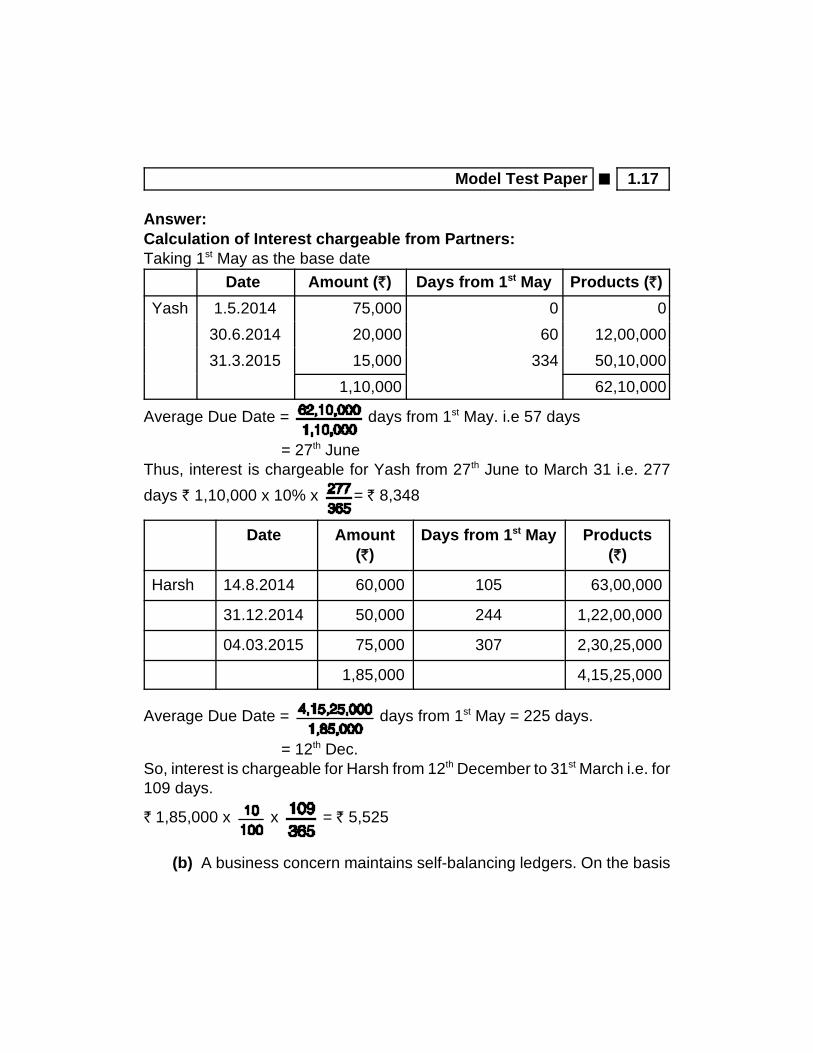

5. (a) Mr. Yash and Mr. Harsh are partners in a firm. They drawn thefollowing amounts from the firm during the year ended 31.03.2015:

Date Amount (`) Drawn by

01.05.2014 75,000 Mr. Yash

30.06.2014 20,000 Mr. Yash

14.08.2014 60,000 Mr. Harsh

31.12.2014 50,000 Mr. Harsh

04.03.2015 75,000 Mr. Harsh

31.03.2015 15,000 Mr. Yash

Interest is charged @ 10% p.a. on all drawings. Calculate interestchargeable from each partner by using Average due date system.(Consider 1st May as base date) (8 marks)

Model Test Paper O 1.17

Answer:Calculation of Interest chargeable from Partners:Taking 1st May as the base date

Date Amount (`) Days from 1st May Products (`)

Yash 1.5.2014 75,000 0 0

30.6.2014 20,000 60 12,00,000

31.3.2015 15,000 334 50,10,000

1,10,000 62,10,000

Average Due Date = days from 1st May. i.e 57 days

= 27th JuneThus, interest is chargeable for Yash from 27th June to March 31 i.e. 277

days ` 1,10,000 x 10% x = ` 8,348

Date Amount(`)

Days from 1st May Products(`)

Harsh 14.8.2014 60,000 105 63,00,000

31.12.2014 50,000 244 1,22,00,000

04.03.2015 75,000 307 2,30,25,000

1,85,000 4,15,25,000

Average Due Date = days from 1st May = 225 days.

= 12th Dec.So, interest is chargeable for Harsh from 12th December to 31st March i.e. for109 days.

` 1,85,000 x x = ` 5,525

(b) A business concern maintains self-balancing ledgers. On the basis

1.18 O Solved Scanner IPCC Group- I Paper - 1

of following information, prepare General Ledger AdjustmentAccount in Debtors Ledger for the month of April, 2012:

`Debit balances in Debtors Ledger on 01-04-2012 3,58,200Credit balances in Debtors Ledger on 01-04-2012 9,400Transactions during the month of April, 2012 are:Total Sales (including Cash Sales, ` 1,00,000) 20,95,400Sales Returns 33,100Cash received from credit customers 17,25,700Bills Receivable received from customers 95,000Bills Receivable dishonoured 7,500Cash paid to customers for returns 6,000Transfers to Creditors Ledger 16,000Credit balances in Debtors Ledger on 30-04-2012 9,800

(5 marks)Answer:

General Ledger Adjustment Account in Debtors LedgerDate Particulars (`) Date Particulars (`)

1.4.20121.4.2012

to30.4.2012

30.4.2012

To Balance b/dTo Debtors ledger

adjustment A/c:Cash receivedSales ReturnsBills receivable

receivedTransfer tocreditors ledger

To Balance c/d(bal. fig.)

9,400

17,25,70033,100

95,000

16,000

4,97,700

1.4.20121.4.2012

to30.4.2012

By Balance b/dBy Debtors ledger

adjustment A/c:Credit salesCash paid forreturnsBills receivabledishonoured

By Balance c/d

3,58,200

19,95,400

6,000

7,500 9,800

23,76,900 23,76,900

6. The following is the Receipt and Payment Account of Park View Club inrespect of the year ended 31st March 2011.

Receipts Amount Payment Amount

` `

Model Test Paper O 1.19

To Balance b/d 1,02,500 By Salaries 2,08,000

To subscriptions : By Stationery 40,000

2008-09 4,500 By Rent 60,000

2009-10 2,11,000 By Telephone Exp. 10,000

2010-11 7,500 2,23,000 By Investment 1,25,000

To Profit on sports meet 1,55,000 By Sundry Expenses 92,500

To Income from investment 1,00,000 By Balance c/d 45,000

5,80,500 5,80,500

Additional information :1. There are 450 members each paying an annual subscription of ` 500.

On 1st April, 2010, outstanding subscription was ` 5,000.2. There was an outstanding telephone bill for ` 3,500 on 31st March, 2011.3. Outstanding sundry expenses as on 31st March, 2010 totaled ` 7,000.4. Stock of stationery :

On 31st March, 2010 ` 5,000On 31st March, 2011 ` 9,000

5. On 31st March, 2010 building stood in the books at ` 10,00,000 and itwas subject to depreciation @ 5% per annum.

6. Investment on 31st March, 2010 stood at ` 20,00,000.7. On 31st March, 2011, income accrued on the investments purchased

during the year amounted to ` 3,750.Prepare an Income and Expenditure Account for the year ended 31st March,2011 and the Balance Sheet as at that date. (16 marks)Answer :

Park View ClubIncome and Expenditure A/c

for the year ending on 31st March 2011

Expenditure Amount(`)

Income Amount (`)

To SalariesTo Stationery consumed (W.N.3)To Rent

2,08,00036,00060,000

By Subscriptions (W.N.2)By Profit on sports meetBy Income on investments 1,00,000

2,25,0001,55,000

1.20 O Solved Scanner IPCC Group- I Paper - 1

To Telephone expenses 10,000 Add: Outstanding on 31.311 3,500To Sundry expenses 92,500

Less: Outstanding on 31.3.10 (7,000)To Depreciation of buildingTo Surplus (excess of income over expenditure)

13,500

85,50050,000

30,750

Add: Income accrued 3,750 1,03,750

4,83,750 4,83,750

Balance Sheet as at 31st March 2011Liabilities Amount

(`)Assets Amount

(`)

Capital fund (W.N.1) 31,05,500Add: Surplus 30,750Subscriptions received in advanceOutstanding telephone bills

31,36,2507,5003,500

Outstanding subscriptionsInvestment(20,00,000 + 1,25,000) 21,25,000Add: Interest accrued on investments 3,750Building 10,00,000Less: Depreciation (50,000)Stock of stationeryCash balance

14,500

21,28,750

9,50,0009,000

45,000

31,47,250 31,47,250

Working Notes:(1) Balance Sheet as at 31st March 2010

Liabilities Amount(`)

Assets Amount(`)

Outstanding sundryexpensesCapital fund (Bal. fig)

7,00031,05,500

BuildingInvestmentsStock of stationeryCash balanceOutstanding subscriptions

10,00,00020,00,000

5,0001,02,500

5,000

31,12,500 31,12,500

Model Test Paper O 1.21

(2) Calculation of subscriptions accrued during the yearSubscription A/c

Particulars Amount(`)

Particulars Amount(`)

To Outstanding Subscriptions (as on 1.4.10)To Income & Expenditure A/cTo Subscriptions received in advance for 2011-12

5,0002,25,000

7,500

By Cash A/cBy Outstanding subscriptions(as on 31.3.11) (Bal. fig)

2,23,000

14,500

2,37,500 2,37,500

(3) Calculation of Stationery consumed during the year.(`)

Stock of stationery as on 31 March, 2010 5,000Add: Purchased during the year 2010-11 40,000

45,000Less: Stock of stationery as on 31st March, 2011 (9,000) Stationery consumed 36,000

7. (a) An amount of ` 9,90,000 was incurred on a contract work upto 31-3-2010. Certificates have been received to date to the value of` 12,00,000 against which ` 10,80,000 has been received in cash.The cost of work done but not certified amounted to ` 22,500. It isestimated that by spending an additional amount of ` 60,000(including provision for contingencies) the work can be completed inall respects in another two months. The agreed contract price ofwork is ` 12,50,000. Compute a conservative estimate of the profitto be taken to the Profit and Loss Account as per AS-7. (4 marks)

Answer :Computation of Estimated Profit as per AS 7

Particulars (`)

Expenditure incurred upto 31.3.2010Estimated additional expenses (including provision forcontingency)

9,90,000

60,000

1.22 O Solved Scanner IPCC Group- I Paper - 1

Estimated cost (A)Contract price (B)Total estimated profit [(B-A)]Percentage of completion (9,90,000/10,50,000) × 100

10,50,00012,50,000 2,00,000

94.29%

Computation of estimate of the profit to be taken to Profit and Loss Account:

= Total estimated profit ×

= 2,00,000 × = 1,88,571

Provision:According to AS 7, ‘Construction Contracts’, when the outcome of aconstruction contract can be estimated reliably, contract revenue andcontract costs associated with the construction contract should berecognised as revenue and expenses respectively by reference to stage ofcompletion of the contract activity at the reporting date.Analysis and Conclusion: Therefore estimated profit amounting ` 1,88,571should be recognised as revenue in the statement of profit and loss.

(b) A trader intends to take a loss of profit policy with indemnity periodof 6 months, however, he could not decide the policy amount. Fromthe following details, suggest the policy amount :

`Turnover in last financial year 4,50,000Standing charges in last financial year 90,000Net profit earned in last year was 10% of turnover and the sametrend expected in subsequent year.Increase in turnover expected 25%To achieve additional sales, trader has to incur additionalexpenditure of ` 31,250. (4 marks)

Answer :(a) Computation of Gross Profit

Model Test Paper O 1.23

Gross Profit =

= = 30%

(b) Computation of policy amount to cover loss of profitParticulars (`)

Turnover in the last financial yearAdd : 25% increase in turnover

Gross profit on increased turnover (5,62,500 × 30%)Add : Additional standing charges

4,50,0001,12,5005,62,5001,68,750

31,250

Policy Amount 2,00,000Therefore, the trader should go in for a loss of profit policy of ` 2,00,000.

(c) What are the advantages of outsourcing the accounting functions?(4 marks)

Answer :Advantages of outsourcing the accounting functions :1. The organisation is able to save time to Concentrate in core area of

business.2. Organisation is able to utilise expertise of the third party.3. Storage and maintenance cost of the data is in the hands of professional

people.4. The proposition often proves to be economical as the firm is not affected

when any employee of Accounting Department leaves the organisation.

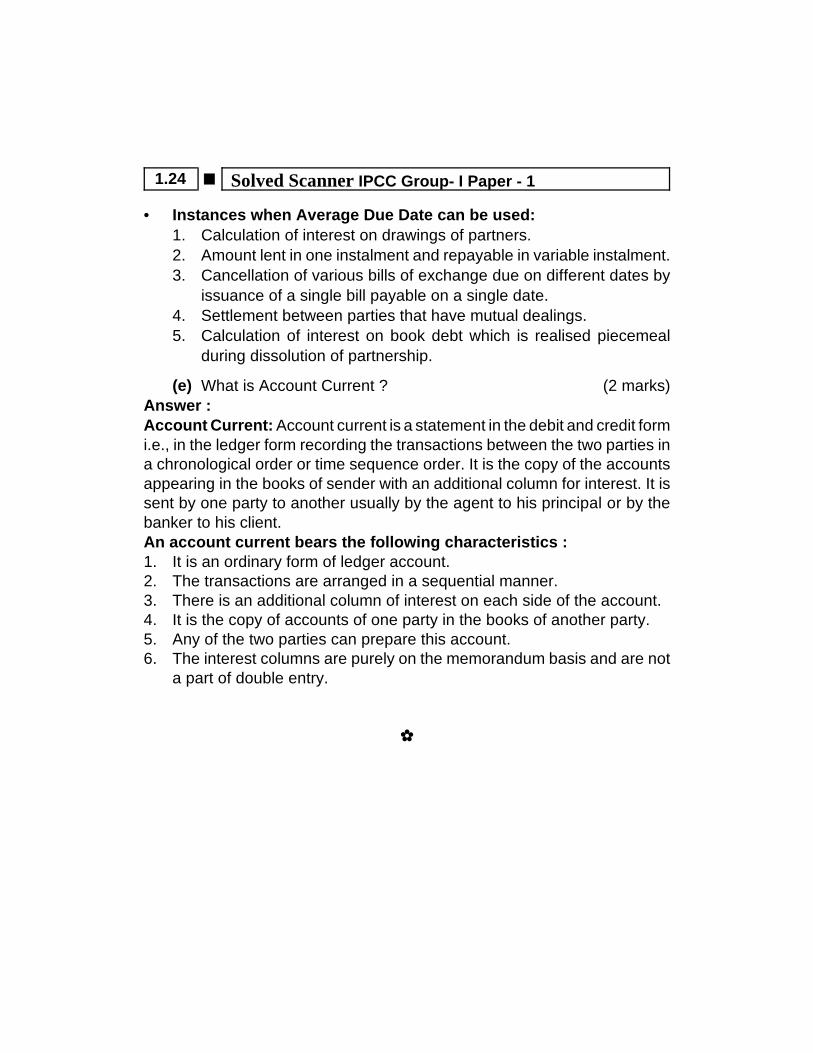

(d) Define Average Due Date. List out the various instances whenAverage Due Date can be used. (4 marks)

Answer:Meaning of Average Due date:Average Due Date is weighted Average of given any number of dates withequal or unequal amounts. It is a single equivalent date for those differentdates, hence anything to be measured from those respective dates can bealternatively measured from this Average Due Date.

1.24 O Solved Scanner IPCC Group- I Paper - 1

• Instances when Average Due Date can be used:1. Calculation of interest on drawings of partners.2. Amount lent in one instalment and repayable in variable instalment.3. Cancellation of various bills of exchange due on different dates by

issuance of a single bill payable on a single date.4. Settlement between parties that have mutual dealings.5. Calculation of interest on book debt which is realised piecemeal

during dissolution of partnership.

(e) What is Account Current ? (2 marks)Answer :Account Current: Account current is a statement in the debit and credit formi.e., in the ledger form recording the transactions between the two parties ina chronological order or time sequence order. It is the copy of the accountsappearing in the books of sender with an additional column for interest. It issent by one party to another usually by the agent to his principal or by thebanker to his client.An account current bears the following characteristics :1. It is an ordinary form of ledger account.2. The transactions are arranged in a sequential manner.3. There is an additional column of interest on each side of the account.4. It is the copy of accounts of one party in the books of another party.5. Any of the two parties can prepare this account.6. The interest columns are purely on the memorandum basis and are not

a part of double entry.