Councillors P Argyle - Aberdeenshire Council - Committees ...

Australian Journal of Commerce Study ISSN:2203-9422 (Print) ISSN:2203-9430 (Online)

Australian Society for Commerce Industry & Engineering www.scie.org.au

12

Corporate Governance: An Investigation of the Audit

Committees Effectiveness as a Corporate Governance

Mechanism in Nigerian Listed Firms

Simon Ademola Akinteye (Corresponding author)

PhD Candidate, Faculty of Accounting and Finance UGSM-Monarch Business School Switzerland

Flurstrasse 1, P.O.Box 30, CH-6332, Hagendon-Zug, Switzerland [email protected]

+2348180009284; +2348188903250

Prof. Dr. Donald Oxford York

Professor of Leadership, Dean of Student Development and Assistant Dean of Faculty UGSM-Monarch Business School Switzerland

Flurstrasse 1, P.O.Box 30, CH-6332, Hagendon-Zug, Switzerland [email protected]

+1514-267-9815

Prof. Dr. Jefferey Shawn Henderson

Professor of Business Ethics & Dean of Faculty UGSM-Monarch Business School Switzerland

Flurstrasse 1, P.O.Box 30, CH-6332, Hagendon-Zug, Switzerland [email protected]

Abstract

The role of the Audit Committee in corporate governance is significant as one of the major organ through which the Board of Directors exercisies its oversight function on the financial activities of the firm. The Audit Committee is saddled with the responsibility for interacting with both the statutory external auditors and the internal audit function in ensuring quality financial reporting and protection of the financial assets of the firm. To fufil this role requires an effective Audit Committee. This paper examines the effectiveness of the Audit Committee in Nigerian listed firms through a qualitative approach using two stage interviews: in-depth interviews and follow up interviews of the members of the Audit Committee in non-financial listed firms. The results show the existence of ingredients of adequacy, competence and effective Audit Committee. We conclude that the Audit Committee is an effective Corporate Governance Mechanism in Nigerian listed firms. Keywords: Corporate Governance, Corporate Governance Mechanism, Audit Committee, Internal Audit Function, Board of Directors

1. Introduction

Audit Committee is a significant corporate governance mechanism and stands in between the board of directors and the internal audit function (Ramly & Rashid, 2010). The Audit Committee (AC) has the responsibility to strengthen corporate governance by ensuring the production of quality financial statements by the management. It is the key responsibility of the AC to ensure that the financial statements are free of fraud and other irregularities which may impair the status of the enterprise or lead to overstatements of position and subsequent restatements (Klein, 2006). Typically, the AC is responsible for the oversight of the firms’ financial reporting process, internal audit function, internal control structure and the activities of the external auditor (Levitt, 1999). Given these roles and responsibilities of the AC, researchers and practitionals have argued that the AC need to have on its committee, individuals who are qualified, competent, tough-minded, independent and committed for the committee to serve as the most reliable protector of the public interest (Levitt, 1999; Klein, 2006). As such, it is required that the AC must be effective and be seen to be effective through the possession of the ingredients of AC effectiveness. Defond & Jiambalvo (1991) argued that, where the AC is effective, the quality of financial reporting is with less flaws and the corporate governance of the firm is strong (Klein, 2006). Researchers further document that, in firms where the AC is effecive, there were less occurrences

Australian Journal of Commerce Study ISSN:2203-9422 (Print) ISSN:2203-9430 (Online)

Australian Society for Commerce Industry & Engineering www.scie.org.au

13

of earnings restatement (Abbott, Parker, & Peter, 2004). Recent studies on the AC indicates that the AC effectiveness can be examined from three broad categories: the AC size, the Competence of the AC and the Activities of the AC (Srinivasan, 2005; Alkdai & Hanefah, 2012; Davidson, Goodwin-Steward, & Kent, 2005). The competence framework for the AC consists of the presence of at least one financial expert on the AC and the extent to which the AC members have access to training to enhhance their skills in performing their functions (Alkdai & Hanefah, 2012; Klein, 2006). Furthermore, the framework for the activities of the AC include: the use of the AC Charter, involvement of the AC in the development and approval of the IAF annual workplan and the IAF Charter, requency of the AC meetings, and the extent of time devoted at the AC meeting to review the IAF reports and working papers (Oxley, 2007; Abdul-Rayman & Ali, 2006; Bedard, Chtourou, & Courteau, 2004; Xie, Davidson III, & DaDalt, 2003; Dhaliwal, Naiker, & Navissi, 2006). In this paper, we examine the AC effectiveness as a corporate governance mechanism in the firms that are listed on the Nigerian Stock Exchange through qualitative research methods. We utilized two stage interviews: the indepth interviews and the follow up interviews of the members of the AC in Nigerian listed firms to determine the extent to which the AC in Nigerian listed firms possess the charcteristics of effective AC in the lieterature and serve as an effective corporate governance mechanism.

1.1 Research Question

How does the characteristics of the Audit Committee in Nigerian listed firm compared with the literature and contribute to its effectiveness as a Corporate Governance Mechanism?

2. Literature Review

In this section, we review prior studies on the AC effectiveness within the framework of the AC size, Competence of the AC and the Activities of the AC.

2.1 The AC Size

Prior studies on the size of the AC have focused on the number of individual serving on the AC. Researchers believed that the AC should not be made up of too few individuals for its oversight and monitoring effectiveness as a corporate governance mechanism. While prior studies did not fix any ideal numbers of persons to serve on the AC, the Blue Ribbon Committee report of 1999 prescribed a minimum number of three persons to serve on the AC (BRC, 1999). The legal framework for the AC in Nigeria, the Companies and Allied Matters Act 2004 LFN prescribed a maximum number of six persons for the membership of the AC with equal representation of the shareholders and directors (CAMA, 2004). The implication of this statutory provision is that, the AC composition can not be odd number and that the minimum composition is expectedly four persons in Nigerian listed firms. Alkdai & Hanefah (2012) argued that while there is no fixation about the appropriate size of the AC, consideration should be given to the size of the firm and the size of the board of directors in the size of the AC for the firm. Lin, Xiao, & Tang (2008) argued that larger AC may become ineffective, because, more time may be spent on argument resulting in delayed decision making and consequent negative effecton the firm. Furthermore, Alkdai & Hanefah (2012) did not find any relationship between larger soze of the AC and the effectiveness of the AC in Malaysian listed firms. Abdellatiff (2009) argued that larger AC is in a better position to ensure quality financial reporting and good corporate governance. Yang & Krishnan (2005) argued that, larger AC is able to enshrine strong internal controls and benefit from deep knowledge base of the committee. In contrast, Xie, Davidson III, & DaDalt (2003) argued that, the size of the AC has no bearing on its ability to discharge its functions effectively. Thus, the current paper seek to obtain the views of the AC members on the adequacy of the AC size for the effectiveness of the AC in performing its roles.

2.2 Competence of the AC

The framework for evaluating the AC competence revolve round the presence of at least one financial expertise on the AC and the access that non financial expert AC members have to skill enhancing trainings (Alkdai & Hanefah, 2012). Researchers further argued, that the responsibilities with which the AC is sadled by the law and the regulations make it imperative for its members to be equipped with the knowledge and experience in auditing and accounting (Alkdai & Hanefah, 2012). Mat Zain (2005) argued that, the AC members should be familiar with the financial reports including the operational

Australian Journal of Commerce Study ISSN:2203-9422 (Print) ISSN:2203-9430 (Online)

Australian Society for Commerce Industry & Engineering www.scie.org.au

14

activities of the firm to enable the AC carry out its responsibilities in a result oriented manner. Abdul-Rayman & Ali (2006) argued that for the AC to be able to establish the enterprise wide risk management and controls, safeguard the assets and ensure strict adherence to established controls by the management, the AC must be armed with the knowledge and experience in accounting while non finance expert AC members should have access to skill enhancing training to equipp them for their functions. Bedard, Chtourou, & Courteau (2004) document that, when the AC have at least one member with accounting and or auditing experience, there are less occurrence of earnings management. The further document that, the non accounting expert AC members to be given an exposure training in the areas of accountimg and financial statement analysis. Xie, Davidson III, & DaDalt (2003) argued that, the AC with at least one member with accounting or financial background achieve quality financial reporting and less occurrence of earnings management when compared to the AC without member with accounting or finance background. Furthermore, Dhaliwal, Naiker, & Navissi (2006) document higher earnings quality in firms where the AC has at least one member with accounting or finance expertise and lower earnings quality in firms where the AC has no member with accounting or finance expertise. DeFond, Han, & Hu (2005) document positive stock market reaction to an announcement of a finance expertise to the AC, while there was no market reaction to the announcement of a non finance expert to the AC. This suggests that both the market and the investors recognise that the presence of a financial expert on the AC significantly improves the corporate governance of the firm. Chang & Sun (2008) document that the AC with the presence of a finance or accounting expertise is able to significantly constrain any attempts to manipulate accounting earnings by the management. These strong arguments on the need for the AC to have at least one menber with accounting or finance expertice member nothwithstanding, there are few studie which document an insignificant impact of the presence of a finance or accounting expertise on the AC and the ability of the AC to effectively discharge his functions (Klein, 2006; Carcello, Hollingsworth, Klein, & Neal, 2006). This paper therefore, obtained the direct views and comments of the AC members in Nigerian listed firms on the availablity of at least a finance expert on the AC and whether the non finance expert AC members have access to skills enhancing trainings. 2.3 Activities of the AC

Prior studies on the activities of the AC have examined this subject within a framework of five components parts which revolve around: the availability of the AC Charter (IIA, 2009; Briotta Jnr, Gazzaway, Colson, & Shridha, 2010), approval of the IAF Annual Workplan by the AC (Briotta Jnr, Gazzaway, Colson, & Shridha, 2010; Turley & Zaman, 2004; Mat-Zain & Subramaniam, 2007), the frequency and the degree of effectiveness of the AC meetings (BRC, 1999; Coonger, Finegold, & Lawler III, 1998; Yang & Krishnan, 2005; Zhou & Chen, 2004; Menon & Williams, 1994), approval of the IAF Charter (IIA, 2009b; Briotta Jnr, Gazzaway, Colson, & Shridha, 2010; Beasley, Hermanson, & Neal, 2009; IIA, 2009), and the frequency and extent of the AC review of the IAF reports and working papers (Beasley, Hermanson, & Neal, 2009; IIA, 2009). An effective AC meetings should discuss such issues as: the AC Charter which guides the operationalization of the AC; the IAF annual workplan (which is the annual roadmap for the activities of the IAF); the IAF Charter; the reports of IAF and the IAF Working Paper. Menon & Williams (1994) argued that, the effectiveness of the AC is measured by the frequency and the regularity of its meetings. They further argued that, the AC which meet regularly will be able to set the pace for the IAF activities, discuss the IAF reports, discuss and approve the IAF annual plans, consider and approve the IAF Charter, and review the working papers of the IAF (Menon & Williams, 1994). Xie, Davidson III, & DaDalt (2003) document that the AC that meets regularly is able to monitor the activities of the management and constrain managerial tendencies to manage accounting earnings. Coonger, Finegold, & Lawler III (1998) document that a regular and frequent meetings improve the functionality of the AC, put the AC in full control of the financial activities of the firm and ensure quality financial reporting. Vafeas (2000) document that, regular meeting of the AC can improve operating performance and quality of earnings. Furthermore, Zhou & Chen (2004) document that, the frequency and regularity of the AC meetings is a significant factor in the AC effectiveness. They further argued that the AC that meets regularly is able to constrain managerial opportunistic tendencies and are more effective corporate governance mechanism. This paper, therefore, invetigates the activities of the AC in Nigerian listed firms within the framework discussed in this section.

3. Research Methodology

Australian Journal of Commerce Study ISSN:2203-9422 (Print) ISSN:2203-9430 (Online)

Australian Society for Commerce Industry & Engineering www.scie.org.au

15

The research methodology of this paper is a qualitative method by way of phenomenological study.

3.1 Research Instrument

The research instrument for this paper is a questionnaire divided into two parts as presented in Appendix A. The first part of the questionnaire is the participant profile. This is designed to recognize the role of the Audit Committee (AC) as a corporate governance mechanism. The objective is to capture the gender, the job title, academic and professional qualification, years of experience, age range, place of birth, religious and philosophical upbringing. We are of the view that these features as important because they can influence the responses of the participant and the degree of their comprehension of corporate governance issues. The second part is the research questionnaires. This comprises Eight open ended questions designed with the aim of gaining deeper understanding of the CG-AC independence. We pre-tested the research instrument through the test-re-test method. This was done through the the administration of the questionnaire on a sample of chartered accountants practitioners, practicing auditors and accounting and finance professionals in academia with internal consistency and reliability measured by Pearson Product Moment Correlation of 0.98 indicating that the research instrument is effective and consistent in capturing the relevant data for the research . The use of the open ended questionnaire is justified as it enables the respondents to answer the question in their own words and in their normal style of speaking. Furthermore, yhis approach is brings out clearly the hidden meanings and beliefs that are personally held by each of the respondents and eliminate the bias which can result by imposing the external thoughts, feelings and beliefs on the research participants (Zikmund, 2003; Cresswell & Miller, 2000)

3.2 Data Collection Techniques

The data collection technique was as face to face recorded two staged interviews: the initial and follow up interviews. The initial interviews and follow up interviews were conducted in Lagos between the July and October 2014. At the initial stage, we contacted fifteen Audit Committee members representing fifteen companies and ten NSE sector classifications through the emails and telephone and were sent the electronic copies of the introductory letters, consent forms and research subject approval forms. In the end, only five individuals representing five organizations and five sectors participated in the initial interviews while three individuals representing three organizations participated in the follow up interviews. Each individual was initially given 2 weeks to confirm their willingness to participate in the research. However, because of low response rate, we gave additional 2 weeks. Where there was no response afterwards, the participants were removed from the process. The reasn for the removal from the process is due to the voluntary nature of the participants required and the need to complete the research within a reasonable time frame. The final sample of the Audit Committee represents those who responded to the email, communicated their willingness to participate in the research and showed consideration for the research timeframe. The final sample is adequate for research saturation. Researchers held that, a long interview with 2 to 10 participants is sufficient to form saturation in phenomenological studies

(Cresswell & Miller, 2000)

We collected the data in face-to-face interviews using a Samsun GT-S762 recording device. Furthermore, we transcribed the recorded interviews through a play-replay method. Thereafter, we forwarded the transcribed copy of the interviews to each of the participants for them to individually confirm that the transcribed copy represents the expression of each of the participants. Where the participant made amendments, these were done and sent back for agreement by the participants. Thus, before we commenced the data analysis, we obtained written confirmation from each of the participants on the contents of the interviews. We followed the same procedure for the follow up interviews.

3.3 Data Distillation

The responses from the participants were broadly categorized into two parts. The participants’ profile and the characteristics survey. Eight (8) classification categories originated from the characteristics survey. Thereafter, we coded and allocated the eight (8) categories to tally charts and tables to express the results as indicated in section 4 below. We believed that this method provides enhanced understanding of the phenomenon of study and deepens the understanding of the subject matter of the research (Sommer & Simmer, 1991; Vogt, 2007). The details of the data is presented in the next section.

Australian Journal of Commerce Study ISSN:2203-9422 (Print) ISSN:2203-9430 (Online)

Australian Society for Commerce Industry & Engineering www.scie.org.au

16

4. Data Presentation

In this section, we presented the data in two parts. In section 4.0, we presented the data on the research participants profile. In sections 4.1-4.8, we presented the data on the characteristics survey. 4.1 Research Participants Profile

In Appendix A, the research participant, each CG-ACs was asked specific questions relating to the the individual profile, we document the responses provided by each CG-AC in Table 4.1 below:

TABLE 4.1

PARTICIPANTS PROFILE- AUDIT COMMITTEE

CG-AC-I CG-AC-2 CG-AC-3 CG-AC-4 CG-AC-5 Gender Male Male Male Male Male Title ACM/NED ACM/NED ACM/NED ACM/NED ACM/ED Qualification PhD, CISA,

CISM CISSP

Bsc, MBA, FCA BSc-Comp-Sc CISA,CISSP, CCNA,CPU, CHFI, CEH, MCP

Bsc. Econs, FCA

BSc, FCA, FCTI

Year Appointed

2006 2005 2007 2006 2007

Age Range 45-50 years 40-45 years 40-45 years 45-50 years 40-45 years Birth Place Oyo Ondo Oyo Osun Oyo Nationality Nigerian Nigerian Nigerian Nigerian Nigerian Religion Philosophy

Christianity Christianity Islam Christianity Islam

LEGEND 1. corporate governance # Audit Committee #= CORPGOV#AC# 2. Audit Committee Member= ACM 3. Non Executive Director=NED 4. Doctor of Philosophy PhD 5.Certified Systems Information Auditor= CISA 6. Certified Information System Manager=CISM 7.Certified Information System Security Professional= CISSP 8. Bachelors of Science Degree = BSc 9. Master of Business Administration = MBA 10. Fellow of the Institute of Chartered Accountants of Nigeria 11. Executive Director= ED

12. Certified Cisco Network Administrator=CCNA 13. Certified Postilion User= CPU 14.Certified Hacker and Forensic Investigator=CHFI 15. Certified Ethical Hacker = CEH 16. Microsoft Certified Professional= MCP 17. Fellow, Chartered Taxation Institute of Nigeria= FCTI 18. Bachelors of Science Degree in Economics =BSc. Econs

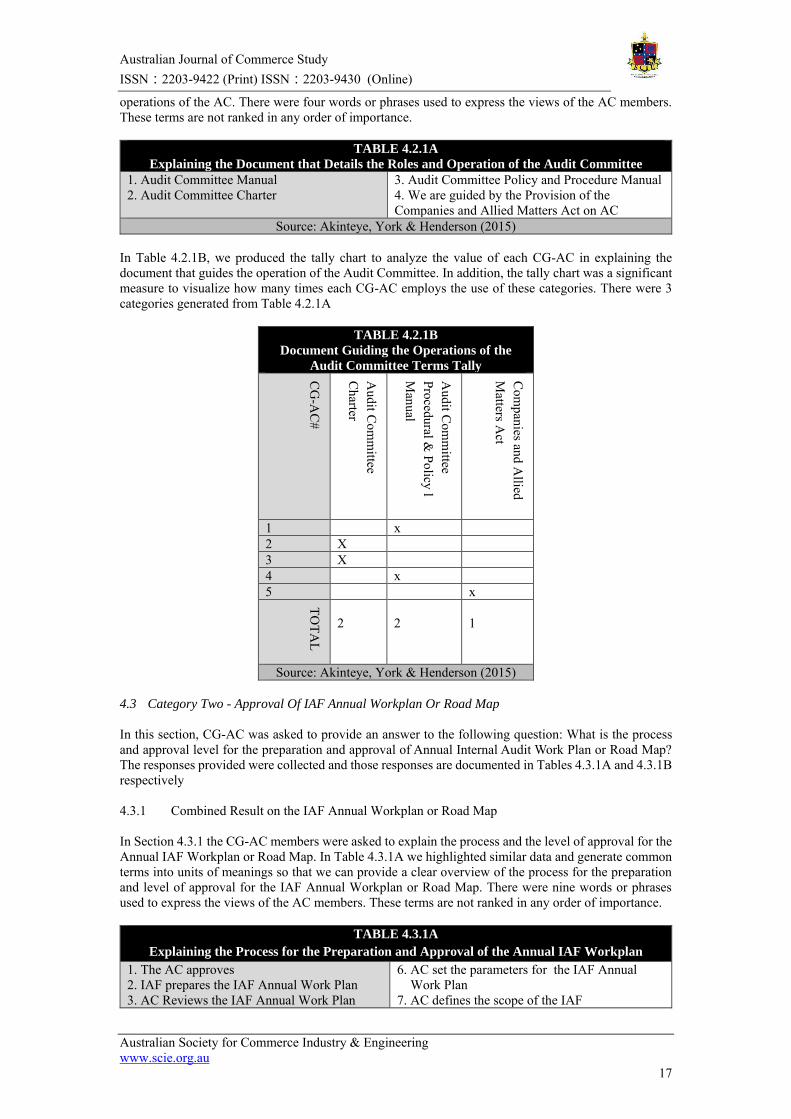

Source: Akinteye, York & Henderson (2015) 4.2 Category One- Audit Committee Charter

In this section, CG-AC was asked to provide an answer to the following question: What does your Audit Committee has in place detailing the roles of the individual members of the Audit Committee and guiding the conduct of the AC business? The responses provided were collected and those responses are documented in Tables 4.2.1A and 4.2.1B respectively 4.2.1 Combined Result on Audit Committee Charter In Section 4.2.1, the CG-AC members were asked to explain the instrument or document which defines the role of each individual member of the committee and stipulate how the business of the AC should be conducted at their meetings. In Table 4.2.1A we highlighted similar data and generate common terms into units of meanings so that we can provide a clear overview of the document guiding the conduct and

Australian Journal of Commerce Study ISSN:2203-9422 (Print) ISSN:2203-9430 (Online)

Australian Society for Commerce Industry & Engineering www.scie.org.au

17

operations of the AC. There were four words or phrases used to express the views of the AC members. These terms are not ranked in any order of importance.

TABLE 4.2.1A

Explaining the Document that Details the Roles and Operation of the Audit Committee

1. Audit Committee Manual 2. Audit Committee Charter

3. Audit Committee Policy and Procedure Manual 4. We are guided by the Provision of the Companies and Allied Matters Act on AC

Source: Akinteye, York & Henderson (2015) In Table 4.2.1B, we produced the tally chart to analyze the value of each CG-AC in explaining the document that guides the operation of the Audit Committee. In addition, the tally chart was a significant measure to visualize how many times each CG-AC employs the use of these categories. There were 3 categories generated from Table 4.2.1A

4.3 Category Two - Approval Of IAF Annual Workplan Or Road Map

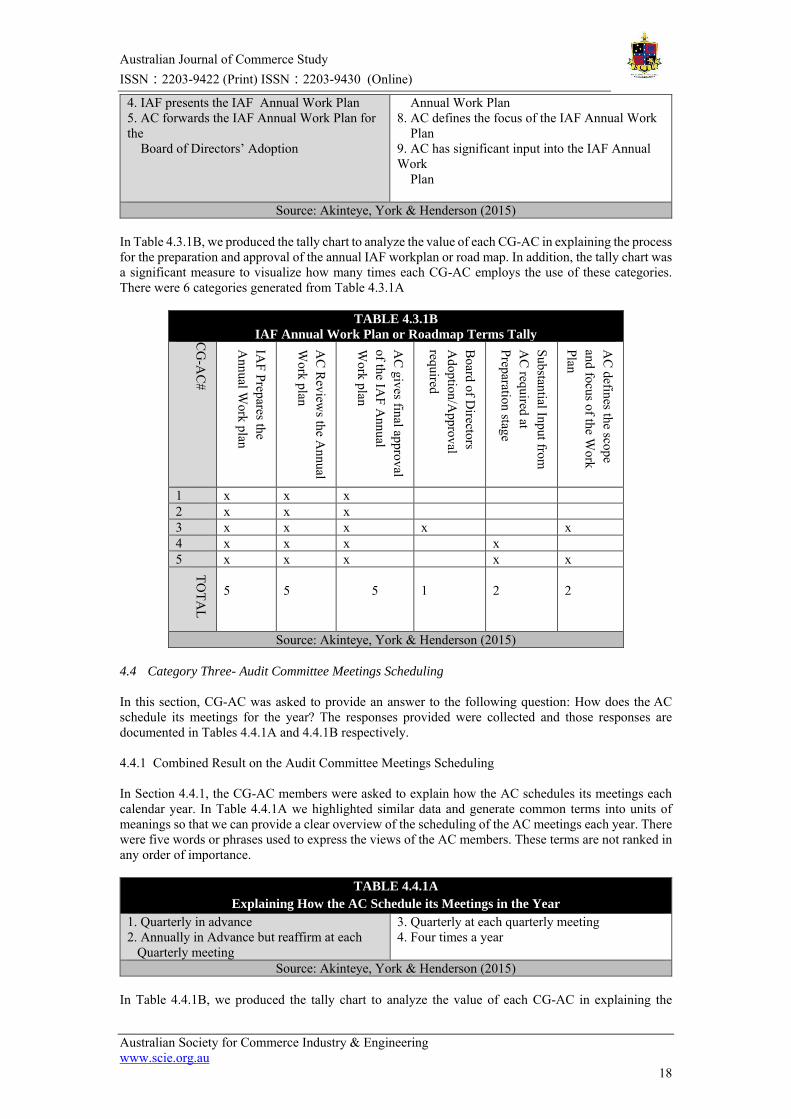

In this section, CG-AC was asked to provide an answer to the following question: What is the process and approval level for the preparation and approval of Annual Internal Audit Work Plan or Road Map? The responses provided were collected and those responses are documented in Tables 4.3.1A and 4.3.1B respectively 4.3.1 Combined Result on the IAF Annual Workplan or Road Map In Section 4.3.1 the CG-AC members were asked to explain the process and the level of approval for the Annual IAF Workplan or Road Map. In Table 4.3.1A we highlighted similar data and generate common terms into units of meanings so that we can provide a clear overview of the process for the preparation and level of approval for the IAF Annual Workplan or Road Map. There were nine words or phrases used to express the views of the AC members. These terms are not ranked in any order of importance.

TABLE 4.3.1A

Explaining the Process for the Preparation and Approval of the Annual IAF Workplan

1. The AC approves 2. IAF prepares the IAF Annual Work Plan 3. AC Reviews the IAF Annual Work Plan

6. AC set the parameters for the IAF Annual Work Plan 7. AC defines the scope of the IAF

TABLE 4.2.1B

Document Guiding the Operations of the

Audit Committee Terms Tally

CG

-AC

#

Audit C

omm

ittee C

harter

Audit C

omm

ittee Procedural &

Policy l M

anual

Com

panies and Allied

Matters A

ct

1 x 2 X 3 X 4 x 5 x

TOTA

L

2

2

1

Source: Akinteye, York & Henderson (2015)

Australian Journal of Commerce Study ISSN:2203-9422 (Print) ISSN:2203-9430 (Online)

Australian Society for Commerce Industry & Engineering www.scie.org.au

18

4. IAF presents the IAF Annual Work Plan 5. AC forwards the IAF Annual Work Plan for the Board of Directors’ Adoption

Annual Work Plan 8. AC defines the focus of the IAF Annual Work Plan 9. AC has significant input into the IAF Annual Work Plan

Source: Akinteye, York & Henderson (2015) In Table 4.3.1B, we produced the tally chart to analyze the value of each CG-AC in explaining the process for the preparation and approval of the annual IAF workplan or road map. In addition, the tally chart was a significant measure to visualize how many times each CG-AC employs the use of these categories. There were 6 categories generated from Table 4.3.1A

TABLE 4.3.1B

IAF Annual Work Plan or Roadmap Terms Tally CG

-AC

#

IAF Prepares the

Annual W

ork plan

AC

Review

s the Annual

Work plan

AC

gives final approval of the IA

F Annual

Work plan

Board of D

irectors A

doption/Approval

required

Substantial Input from

AC

required at Preparation stage

AC

defines the scope and focus of the W

ork Plan

1 x x x 2 x x x 3 x x x x x 4 x x x x 5 x x x x x

TOTA

L 5

5

5

1

2

2

Source: Akinteye, York & Henderson (2015)

4.4 Category Three- Audit Committee Meetings Scheduling

In this section, CG-AC was asked to provide an answer to the following question: How does the AC schedule its meetings for the year? The responses provided were collected and those responses are documented in Tables 4.4.1A and 4.4.1B respectively. 4.4.1 Combined Result on the Audit Committee Meetings Scheduling In Section 4.4.1, the CG-AC members were asked to explain how the AC schedules its meetings each calendar year. In Table 4.4.1A we highlighted similar data and generate common terms into units of meanings so that we can provide a clear overview of the scheduling of the AC meetings each year. There were five words or phrases used to express the views of the AC members. These terms are not ranked in any order of importance.

TABLE 4.4.1A

Explaining How the AC Schedule its Meetings in the Year

1. Quarterly in advance 2. Annually in Advance but reaffirm at each Quarterly meeting

3. Quarterly at each quarterly meeting 4. Four times a year

Source: Akinteye, York & Henderson (2015) In Table 4.4.1B, we produced the tally chart to analyze the value of each CG-AC in explaining the

Australian Journal of Commerce Study ISSN:2203-9422 (Print) ISSN:2203-9430 (Online)

Australian Society for Commerce Industry & Engineering www.scie.org.au

19

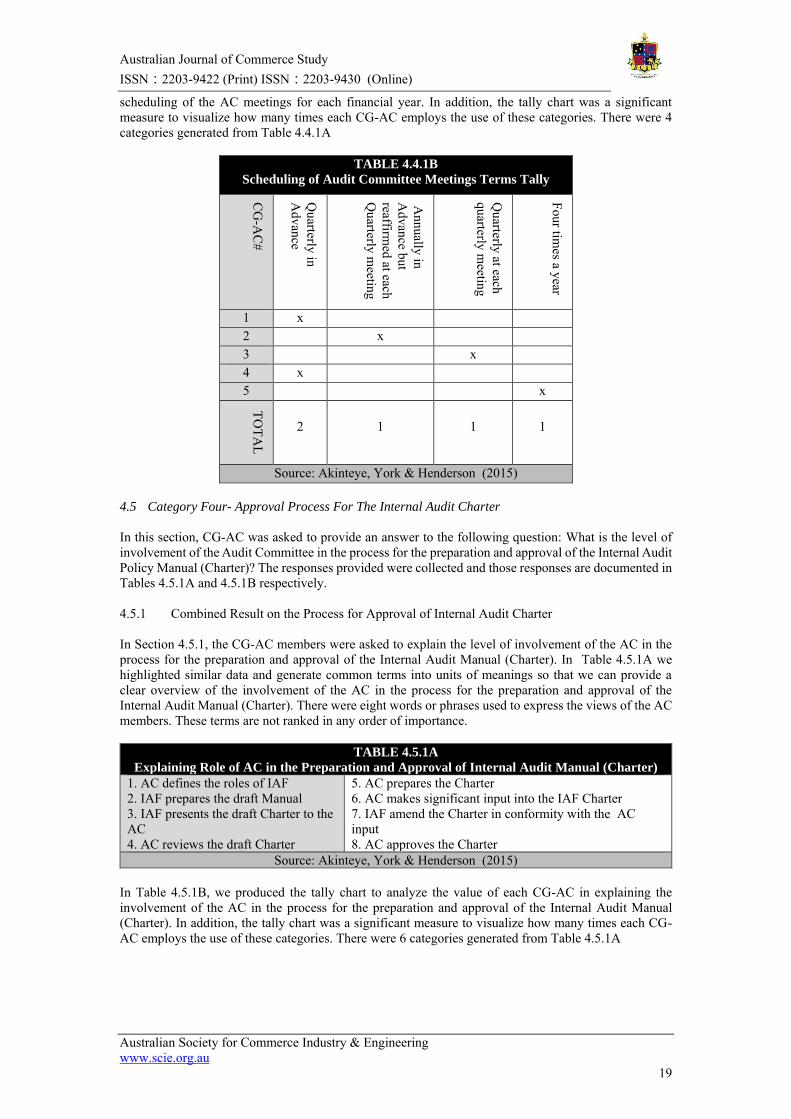

scheduling of the AC meetings for each financial year. In addition, the tally chart was a significant measure to visualize how many times each CG-AC employs the use of these categories. There were 4 categories generated from Table 4.4.1A

TABLE 4.4.1B

Scheduling of Audit Committee Meetings Terms Tally

CG

-AC

#

Quarterly in

Advance

Annually in

Advance but

reaffirmed at each

Quarterly m

eeting Q

uarterly at each quarterly m

eeting

Four times a year

1 x 2 x 3 x 4 x 5 x

TOTA

L

2

1

1

1

Source: Akinteye, York & Henderson (2015)

4.5 Category Four- Approval Process For The Internal Audit Charter

In this section, CG-AC was asked to provide an answer to the following question: What is the level of involvement of the Audit Committee in the process for the preparation and approval of the Internal Audit Policy Manual (Charter)? The responses provided were collected and those responses are documented in Tables 4.5.1A and 4.5.1B respectively. 4.5.1 Combined Result on the Process for Approval of Internal Audit Charter In Section 4.5.1, the CG-AC members were asked to explain the level of involvement of the AC in the process for the preparation and approval of the Internal Audit Manual (Charter). In Table 4.5.1A we highlighted similar data and generate common terms into units of meanings so that we can provide a clear overview of the involvement of the AC in the process for the preparation and approval of the Internal Audit Manual (Charter). There were eight words or phrases used to express the views of the AC members. These terms are not ranked in any order of importance.

TABLE 4.5.1A

Explaining Role of AC in the Preparation and Approval of Internal Audit Manual (Charter)

1. AC defines the roles of IAF 2. IAF prepares the draft Manual 3. IAF presents the draft Charter to the AC 4. AC reviews the draft Charter

5. AC prepares the Charter 6. AC makes significant input into the IAF Charter 7. IAF amend the Charter in conformity with the AC input 8. AC approves the Charter

Source: Akinteye, York & Henderson (2015) In Table 4.5.1B, we produced the tally chart to analyze the value of each CG-AC in explaining the involvement of the AC in the process for the preparation and approval of the Internal Audit Manual (Charter). In addition, the tally chart was a significant measure to visualize how many times each CG-AC employs the use of these categories. There were 6 categories generated from Table 4.5.1A

Australian Journal of Commerce Study ISSN:2203-9422 (Print) ISSN:2203-9430 (Online)

Australian Society for Commerce Industry & Engineering www.scie.org.au

20

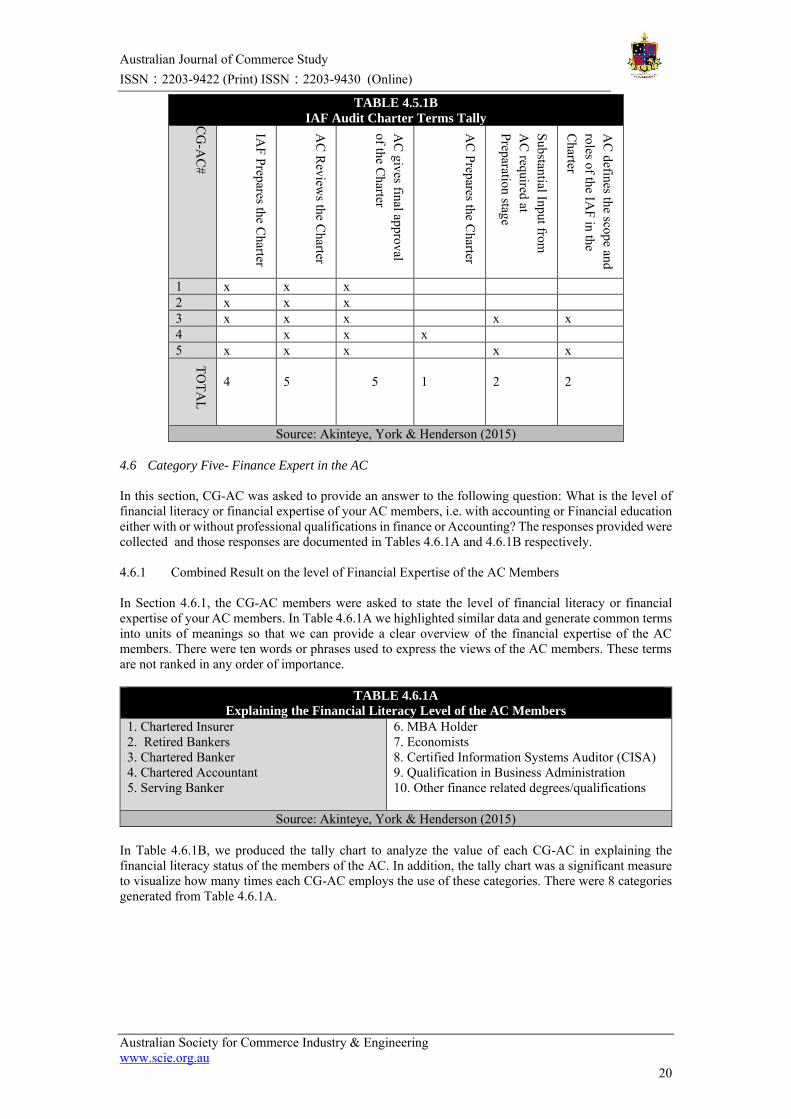

TABLE 4.5.1B

IAF Audit Charter Terms Tally CG

-AC

#

IAF Prepares the C

harter

AC

Review

s the Charter

AC

gives final approval of the C

harter

AC

Prepares the Charter

Substantial Input from

AC

required at Preparation stage

AC

defines the scope and roles of the IA

F in the C

harter

1 x x x 2 x x x 3 x x x x x 4 x x x 5 x x x x x

TOTA

L

4

5

5

1

2

2

Source: Akinteye, York & Henderson (2015)

4.6 Category Five- Finance Expert in the AC

In this section, CG-AC was asked to provide an answer to the following question: What is the level of financial literacy or financial expertise of your AC members, i.e. with accounting or Financial education either with or without professional qualifications in finance or Accounting? The responses provided were collected and those responses are documented in Tables 4.6.1A and 4.6.1B respectively. 4.6.1 Combined Result on the level of Financial Expertise of the AC Members In Section 4.6.1, the CG-AC members were asked to state the level of financial literacy or financial expertise of your AC members. In Table 4.6.1A we highlighted similar data and generate common terms into units of meanings so that we can provide a clear overview of the financial expertise of the AC members. There were ten words or phrases used to express the views of the AC members. These terms are not ranked in any order of importance.

TABLE 4.6.1A

Explaining the Financial Literacy Level of the AC Members

1. Chartered Insurer 2. Retired Bankers 3. Chartered Banker 4. Chartered Accountant 5. Serving Banker

6. MBA Holder 7. Economists 8. Certified Information Systems Auditor (CISA) 9. Qualification in Business Administration 10. Other finance related degrees/qualifications

Source: Akinteye, York & Henderson (2015) In Table 4.6.1B, we produced the tally chart to analyze the value of each CG-AC in explaining the financial literacy status of the members of the AC. In addition, the tally chart was a significant measure to visualize how many times each CG-AC employs the use of these categories. There were 8 categories generated from Table 4.6.1A.

Australian Journal of Commerce Study ISSN:2203-9422 (Print) ISSN:2203-9430 (Online)

Australian Society for Commerce Industry & Engineering www.scie.org.au

21

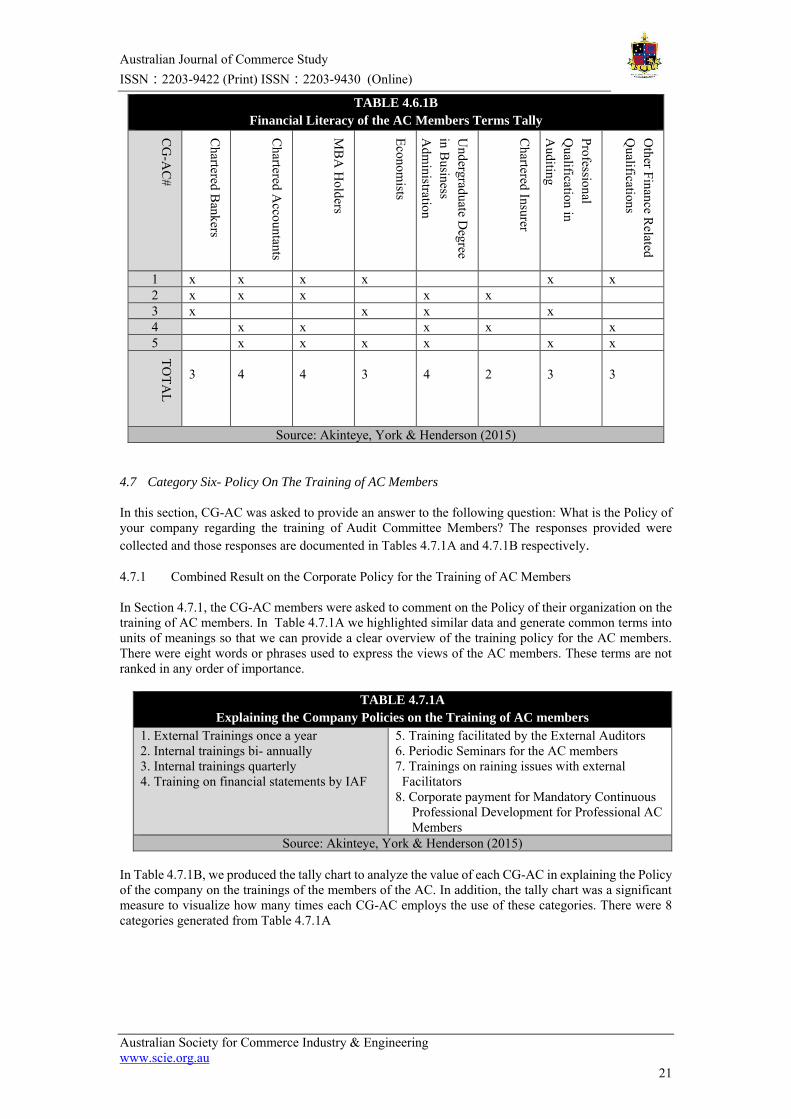

TABLE 4.6.1B

Financial Literacy of the AC Members Terms Tally

CG

-AC

#

Chartered B

ankers

Chartered A

ccountants

MB

A H

olders

Economists

Undergraduate D

egree in B

usiness A

dministration

Chartered Insurer

Professional Q

ualification in A

uditing

Other Finance R

elated Q

ualifications

1 x x x x x x 2 x x x x x 3 x x x x 4 x x x x x 5 x x x x x x

TOTA

L

3

4

4

3

4

2

3

3

Source: Akinteye, York & Henderson (2015)

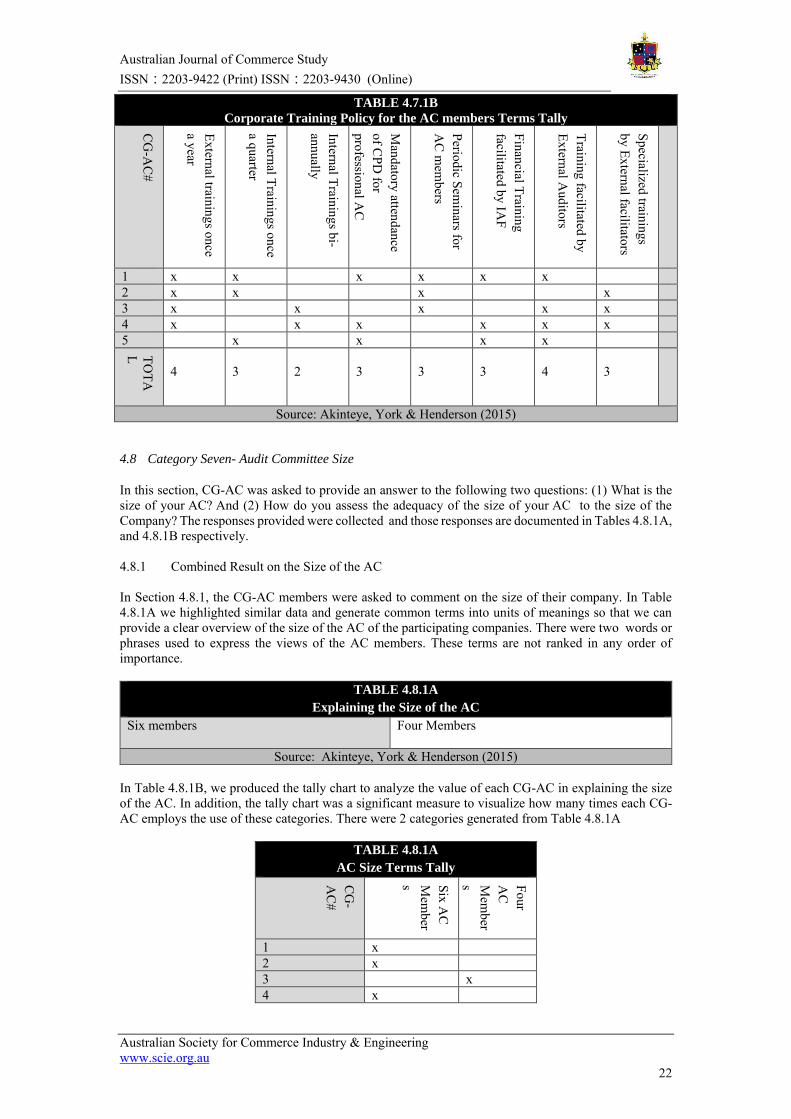

4.7 Category Six- Policy On The Training of AC Members

In this section, CG-AC was asked to provide an answer to the following question: What is the Policy of your company regarding the training of Audit Committee Members? The responses provided were collected and those responses are documented in Tables 4.7.1A and 4.7.1B respectively. 4.7.1 Combined Result on the Corporate Policy for the Training of AC Members In Section 4.7.1, the CG-AC members were asked to comment on the Policy of their organization on the training of AC members. In Table 4.7.1A we highlighted similar data and generate common terms into units of meanings so that we can provide a clear overview of the training policy for the AC members. There were eight words or phrases used to express the views of the AC members. These terms are not ranked in any order of importance.

TABLE 4.7.1A

Explaining the Company Policies on the Training of AC members

1. External Trainings once a year 2. Internal trainings bi- annually 3. Internal trainings quarterly 4. Training on financial statements by IAF

5. Training facilitated by the External Auditors 6. Periodic Seminars for the AC members 7. Trainings on raining issues with external Facilitators 8. Corporate payment for Mandatory Continuous Professional Development for Professional AC Members

Source: Akinteye, York & Henderson (2015) In Table 4.7.1B, we produced the tally chart to analyze the value of each CG-AC in explaining the Policy of the company on the trainings of the members of the AC. In addition, the tally chart was a significant measure to visualize how many times each CG-AC employs the use of these categories. There were 8 categories generated from Table 4.7.1A

Australian Journal of Commerce Study ISSN:2203-9422 (Print) ISSN:2203-9430 (Online)

Australian Society for Commerce Industry & Engineering www.scie.org.au

22

TABLE 4.7.1B

Corporate Training Policy for the AC members Terms Tally

CG

-AC

#

External trainings once a year

Internal Trainings once a quarter

Internal Trainings bi-annually

Mandatory attendance

of CPD

for professional A

C

mem

bers

Periodic Seminars for

AC

mem

bers

Financial Training facilitated by IA

F

Training facilitated by External A

uditors

Specialized trainings by External facilitators

1 x x x x x x 2 x x x x 3 x x x x x 4 x x x x x x 5 x x x x

TOTA

L 4

3

2

3

3

3

4

3

Source: Akinteye, York & Henderson (2015)

4.8 Category Seven- Audit Committee Size

In this section, CG-AC was asked to provide an answer to the following two questions: (1) What is the size of your AC? And (2) How do you assess the adequacy of the size of your AC to the size of the Company? The responses provided were collected and those responses are documented in Tables 4.8.1A, and 4.8.1B respectively. 4.8.1 Combined Result on the Size of the AC In Section 4.8.1, the CG-AC members were asked to comment on the size of their company. In Table 4.8.1A we highlighted similar data and generate common terms into units of meanings so that we can provide a clear overview of the size of the AC of the participating companies. There were two words or phrases used to express the views of the AC members. These terms are not ranked in any order of importance.

TABLE 4.8.1A

Explaining the Size of the AC

Six members Four Members

Source: Akinteye, York & Henderson (2015) In Table 4.8.1B, we produced the tally chart to analyze the value of each CG-AC in explaining the size of the AC. In addition, the tally chart was a significant measure to visualize how many times each CG-AC employs the use of these categories. There were 2 categories generated from Table 4.8.1A

TABLE 4.8.1A

AC Size Terms Tally

CG

-A

C#

Six AC

M

ember

s Four A

C

Mem

bers

1 x 2 x 3 x 4 x

Australian Journal of Commerce Study ISSN:2203-9422 (Print) ISSN:2203-9430 (Online)

Australian Society for Commerce Industry & Engineering www.scie.org.au

23

5 x Source: Akinteye, York & Henderson (2015)

4.8.2 Combined Result on the Adequacy of the AC Size In Section 4.8.2, the CG-AC members were asked to comment on the adequacy size of their company. In Table 4.8.2A we highlighted similar data and generate common terms into units of meanings so that we can provide a clear overview of the adequacy of the size of the AC of the participating companies. There were eleven words or phrases used to express the views of the AC members. These terms are not ranked in any order of importance.

TABLE 4.8.2A

Explaining the Adequacy of the Size of the AC

1. CAMA 2004 limit level reached 2. The optimum level attained 3. Desire to increase the size, but reached a maximum by the Law 4. Adequate 5. Sufficient for good governance 6. Proportional to business size

7. The company size is commensurate with the AC size 8. AC Size suit company’s operations 9. Future expansion may call for more AC member 10. Suitable 11. Highly okay

Source: Akinteye, York & Henderson (2015) In Table 4.8.2B, we produced the tally chart to analyze the value of each CG-AC in explaining the adequacy of the present size of AC. In addition, the tally chart was a significant measure to visualize how many times each CG-AC employs the use of these categories. There were 7 categories generated from Table 4.8.2A

TABLE 4.8.2B

The Adequacy of Size of Audit Committee Terms Tally

CG

-AC

#

Adequate

Sufficient for good governance

Optim

um level

reached

Maxim

um provided

by the Law is

reached

Com

pany Size C

omm

ensurate with

AC

size

Future expansion m

ay lead to more A

C

AC

size limited by

CA

MA

2004LFN

1 x x x x 2 X x x 3 X x x 4 X x x x 5 X x x x

TOTA

L

4

2

3

3

3

1

2

Source: Akinteye, York & Henderson (2015)

4.9 Category Eight-Audit Committees Review of IAF Reports

In this section, CG-AC was asked to provide an answer to the following question: How often does the Audit Committee review Internal Audit Report at the Committee meetings? The responses provided were collected and those responses are documented in Tables 4.9.1A and 4.9.1B respectively.

4.9.1 Combined Result on the Frequency of AC Review of the IAF Reports

Australian Journal of Commerce Study ISSN:2203-9422 (Print) ISSN:2203-9430 (Online)

Australian Society for Commerce Industry & Engineering www.scie.org.au

24

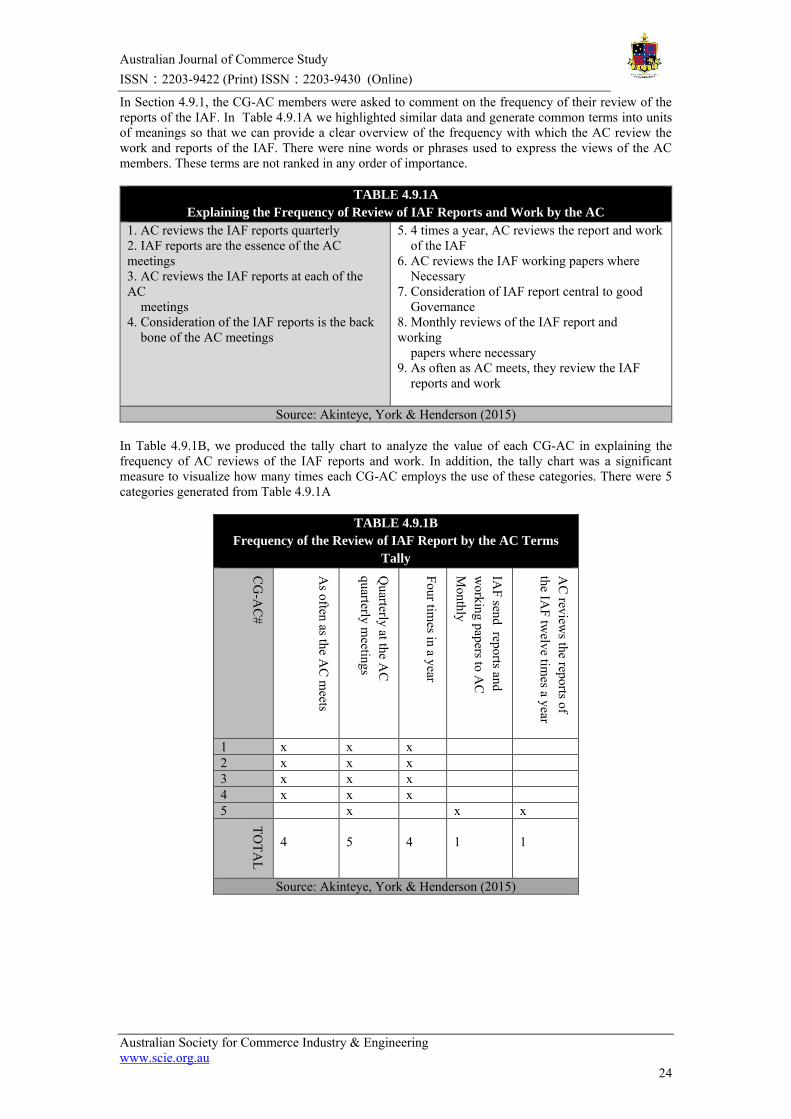

In Section 4.9.1, the CG-AC members were asked to comment on the frequency of their review of the reports of the IAF. In Table 4.9.1A we highlighted similar data and generate common terms into units of meanings so that we can provide a clear overview of the frequency with which the AC review the work and reports of the IAF. There were nine words or phrases used to express the views of the AC members. These terms are not ranked in any order of importance.

TABLE 4.9.1A

Explaining the Frequency of Review of IAF Reports and Work by the AC

1. AC reviews the IAF reports quarterly 2. IAF reports are the essence of the AC meetings 3. AC reviews the IAF reports at each of the AC meetings 4. Consideration of the IAF reports is the back bone of the AC meetings

5. 4 times a year, AC reviews the report and work of the IAF 6. AC reviews the IAF working papers where Necessary 7. Consideration of IAF report central to good Governance 8. Monthly reviews of the IAF report and working papers where necessary 9. As often as AC meets, they review the IAF reports and work

Source: Akinteye, York & Henderson (2015) In Table 4.9.1B, we produced the tally chart to analyze the value of each CG-AC in explaining the frequency of AC reviews of the IAF reports and work. In addition, the tally chart was a significant measure to visualize how many times each CG-AC employs the use of these categories. There were 5 categories generated from Table 4.9.1A

TABLE 4.9.1B

Frequency of the Review of IAF Report by the AC Terms

Tally

CG

-AC

#

As often as the A

C m

eets

Quarterly at the A

C

quarterly meetings

Four times in a year

IAF send reports and

working papers to A

C

Monthly

AC

reviews the reports of

the IAF tw

elve times a year

1 x x x 2 x x x 3 x x x 4 x x x 5 x x x

TOTA

L

4

5

4

1

1

Source: Akinteye, York & Henderson (2015)

Australian Journal of Commerce Study ISSN:2203-9422 (Print) ISSN:2203-9430 (Online)

Australian Society for Commerce Industry & Engineering www.scie.org.au

25

5. Discussions of Findings and Conclusion

As discussed in section 2 in the literature review, the AC plays a crucial role in ensuring good corporate governance of a firm (Ramly & Rashid, 2010). To fulfil this role, the AC must possess the ingredient of effectiveness. As discussed in the literature review, the indices of the AC effectiveness are: the size of the AC, the competence of the AC and the activities of the AC (Abdellatiff, 2009; Alkdai & Hanefah, 2012; Bedard, Chtourou, & Courteau, 2004; Menon & Williams, 1994; Mat Zain, 2005). In the qualitative research, we captured the indicators of the AC size (Tables 4.7.1A , 4.7.1B, 4.7.2A and 4.7.2B), the competence of the AC (Tables 4.1, 4.6.1A, 4.6.1B,4.7.1A and 4.6.1B), and, the activities of the AC (Tables 4.2.1A, 4.2.1B, 4.3.1A, 4.3.1B, 4.4.1A, 4.4.1B, 4.5.1A, 4.5.1B, 4.9.1A and 4.9.1B). In the following sections, we will discuss the findings of the present research in relation to each of the three frameworks of effective AC as a corporate governance mechanism. 5.1 Size of the AC

In Tables 4.8.1A, 4.8.1B, 4.8.2A and 4.8.2B, we captured qualitative data on the size of the AC. The tally chart in Table 4.8.1B indicates that 80% of the firms in our sample (80% of the AC respondents) have six members in their AC while 20% of the firms in our sample (20% of AC respondents) have four members in their AC. The tally chart presented in Table 4.8.2B aided our understanding of the adequacy of the AC size for optimal performance of their role as a corporate governance mechanism. The data shows that 80% of the Ac respondents stated that the size of the AC in their firm is adequate for optimal efficiency, 40% of the AC respondents stated that the AC size is sufficient for sound corporate governance, 60% of the AC respondents stated that the size of their AC is at optimal level and maximum allowed by the law and commensurate with the size of the firm, while only 20% expressed the possibility of additional AC members if their firm grow beyond the capacity of the existing four AC members. On the basis of the evidence from the data obtained, we document that the size of the AC in Nigerian listed firms is adequate, optimal for effective supervision and monitoring of the activities of the management and consistent with the prior studies (Alkdai & Hanefah, 2012; BRC, 1999; Menon & Williams, 1994). Thus, we found conclusive evidence to argue that the size of the AC in Nigerian firm is adequate and optimal and that the AC is thus an effective corporate governance mechanism. 5.2 Competence of the AC

As discussed in the literature review, the framework for the competence of the AC centers around the presence of at least one financial expert on the AC and the access of the non financial expert AC members to skill enhancing training to aid their effectiveness in their supervisory roles (Carcello, Hollingsworth, Klein, & Neal, 2006; Dhaliwal, Naiker, & Navissi, 2006). In Tables 4.1, 4.6.1A, 4.6.1B, 4.7.1A and 4.7.1B, we captured the indicator of the AC competence. The findings of this paper on these indicators are discussed in the next subsections. 5.2.1 Presence of Financial Expert on the AC In Table 4.1, we captured the qualitative data on the profile of the members of the AC in our sample. All the AC members, respondents (100% of research participants) possess at least a qualification in finance, auditing or accounting. The data revealed that 60% of the AC respondents are Chartered Accountants and with a Bachelors degree either in Accounting or Economics. Furthermore, 60% of the AC members have an MBA Degree, 40% have Certifications in Auditing, while 20% have advanced degree at the doctoral level (PhD level). In Table 4.6.1A and 4.6.1B, we captured the qualitative data on the financial literacy level of the AC members. We obtained that all the firms in our sample (100% of the AC respondents) have at least a member with financial expertise on their AC. Furthermore, 60% of the sampled firm have Chartered Bankers on their AC, 80% of the sampled firm have at least a chartered accountant on their AC, 80% of the sampled firm have AC members with an MBA Degree, 60% have AC members with Undergraduate Degree in Economics, 80% have AC members with Undergraduate Degree in Business Administration, 40% have AC members that a chartered insurers, 60% have AC members with professional certification in auditing while 60% have AC members with other finance related qualifications. These details indicate that the AC in Nigerian listed firms is equipped with individuals that have a high level of financial literacy, which is a prime requirement for the AC to be able to competently perform its functions and serve as an effective corporate governance mechanism (Carcello, Hollingsworth, Klein, & Neal, 2006; Srinivasan, 2005; Dhaliwal, Naiker, & Navissi, 2006) Thus, we document conclusive evidenceis argue that the AC in Nigerian listed firms are competent and are

Australian Journal of Commerce Study ISSN:2203-9422 (Print) ISSN:2203-9430 (Online)

Australian Society for Commerce Industry & Engineering www.scie.org.au

26

effective corporate governance mechanism. 5.2.2 Training of the AC Members In Table 4.7.1A, and 4.7.1B, we captured qualitative data on the policy of the firms on the training of the AC members. The data showed that all the firms in our sample (100% of the AC respondents) have policy to train the AC members on financial statements and on the other financial activities of the of the firm to enhance the skills of non finance expert members of the AC for effective performance of their responsibilities. Further analysis of the data showed that 80% of the Ac respondents attends external training once a year, 60% of the AC respondents attends internal training once a qurter, 40% of the AC respondents attends internal training bi-annually, 60% of the AC respondents further attends the mandatory CPD of their regulatory professional body, 60% of the AC respondents attends periodic seminars for the AC members, 60% of the AC respondents attends the financial training sessions facilitated by the IAF, 80% of the AC respondents attends financial training facilitated by the Statutory External Auditors to their firms, while 60% attended other specialized trainings facilitated by external trainers or facilitators.These details furnished us with the evidence that the AC members (finance and non finance experts) have access to skills enhancing trainings in financial and non financial matters which are aimed at enhancing the competence with which the AC discharcges its responsibilities in a manner consistent to the prior studies on this subject (Carcello, Hollingsworth, Klein, & Neal, 2006; Dhaliwal, Naiker, & Navissi, 2006) . Thus, we document conclusive evidence that the AC in Nigerian listed firms possesses the ingredients of competence and as such, an effective corporate governance mechanism. 5.3 Activities of the AC

As discussed in the literature review, the framework for assessment of the effectiveness of the activities of the AC as a corporate governance mechanism can be categorized into five: the availability of the AC Charter to define the roles and responsibilities of the AC (qualitative data captured in Table 4.2.1A and 4.2.1B), the degree of involvement of the AC in the preparation and approval of the annual workplan of the IAF ( qualitative data captured in Table 4.3.1A and 4.3.1B), the frequency and regularity of the AC meetings ( qualitative data captured in Table 4.4.1A and 4.4.1B), the extent of the AC authority over the preparation and approval of the IAF Charter ( qualitative data captured in Table 4.5.1A and 4.5.1B), and, the regularity of the AC review of the IAF reports and working papers ( qualitative data captured in Table 4.9.1A and 4.9.1B). In the following sections, we will discuss the findings of this paper on each of these indices of the activities of the AC as a corporate governance mechanism with particular reference to Nigerian listed firms. 5.3.1 The AC Charter The AC Charter is the equivalence of the Constitution of a Sovereign State. The AC Charter represents the policy document that guides and defines the role and activities of the AC (IIA, 2009; Briotta Jnr, Gazzaway, Colson, & Shridha, 2010). It is expected that the AC will have in place a Charter that guides its operationalisations to be able to function as an effective corporate governance mechanism (Briotta Jnr, Gazzaway, Colson, & Shridha, 2010). In Tables 4.2,1A and 4.2.1B, we captured qualitative data on the status of AC Charter with respect to Nigerian listed firms. We obtained that all but one firm in our sampled firms (80% of AC respondents) has in place an AC Charter or its equivalent AC Handbook Policy Manual that guides the AC. We further obtained that 20% of our sampled firms (20% of AC respondents) have no AC Charter or its equivalent AC Handbook Policy Manual in place, but are guided by the provision of the Nigerian Companies and Allied matters Act 2004. These details indicate that although not all the AC has in place and AC Charter or its equivalent AC handbook Policy Manual, the majority of the listed firms (80% of the sampled firms) has in place an AC Charter. This represents a gap that the market regulators, the Nigerian Stock Exchange (NSE) and the Securities and Exchange Commission (SEC) need to address so that the firms listed on the Nigerian Stock Exchange can migrate toward 100% attainment. 5.3.2 The Involvement of the AC in the Approval of the Annual Work Plan of the IAF The involvement of the AC in the review and approval of the Annual Work Plan of the IAF is a cardinal requirement of an effective AC (Briotta Jnr, Gazzaway, Colson, & Shridha, 2010; IIA, 2009; Turley & Zaman, 2004; Mat-Zain & Subramaniam, 2007). In Table 4.3.1A and 4.3.1B, we captured qualitative data on the involvement of the AC in the process for the preparation and approval of the IAF Annual

Australian Journal of Commerce Study ISSN:2203-9422 (Print) ISSN:2203-9430 (Online)

Australian Society for Commerce Industry & Engineering www.scie.org.au

27

Work Plan. The tally chart shows that in all the sampled firms (100% of the AC respondents), the IAF prepares the annual workplan, while the AC reviews, amend where necessary the annual work plan submitted to it by the IAF for consideration and subsequently give the final approval. In 40% of the sample firms, the AC defines the scope and focus of the annual work plan, while in 40% of the sampled firms, the IAF annual workplan receives substantial input from the AC at the preparation stage. In 20% of the sampled firms, the approved IAF workplan is forwarded to the Board of Directors for ratification or adoption. The details presented in this section indicate that the activities of the AC in relation to the approval of the Annual Work Plan of the IAF are consistent with literature and document a conclusive evidence that the AC is an effective corporate governance mechanism. 5.3.3 The AC Meetings The frequency and regularity of the AC meeting are a factor in assessing how effective the AC functions as a corporate governance mechanism (Menon & Williams, 1994; Coonger, Finegold, & Lawler III, 1998; Zhou & Chen, 2004). In Table 4.4.1A and 4.4.1B, we captured qualitative data on the frequency and regularity of the AC meetings. The tally charts in Table 4.4.1B indicate that the AC in all the sampled firms (100% of AC respondents) holds quarterly meetings and have their meetings well schedule in advance to make it possible for all the AC members to be present at the meetings. In 40% of the sampled firms, the AC meetings are scheduled quarterly in advance, in 20% of the firm, the AC meetings are scheduled annually in advance but reaffirmed at each quarterly meeting. The data further show that in 40% of the sampled firms, the AC meeting is scheduled at each quarterly meeting which is four times in a year. This finding is consistent with existing literature on the frequency of AC meetings for effective oversight as a corporate governance mechanism (BRC, 1999; Menon & Williams, 1994; Yang & Krishnan, 2005). Thus, we document conclusive evidence to argue that the AC is an effective corporate governance mechanism in Nigerian listed firms. 5.3.4 The Role of the AC in the Approval of the IAF Charter The IAF Charter is a Policy Framework that defines the power, scope, responsibilities and expectations from the IAF (IIA, 2009b). As the organ of corporate governance with the oversight responsibilities for the IAF, an effective AC should have the responsibility for the preparation or review and approval of the IAF Charter (Briotta Jnr, Gazzaway, Colson, & Shridha, 2010; IIA, 2009; Beasley, Hermanson, & Neal, 2009). In Tables 4.5.1A and 4.5.1B, we captured qualitative data on the degree of the AC involvement with the preparation or review and approval of the IAF Charter. The tally chart in Table 4.5.1B indicates that in all the sampled firms (100% of AC respondents), the AC is involved in the review of the IAF Charter. The data further show that in all the sampled firms (100% of the AC respondents), the AC gives the final approval for the IAF Charter. Further analysis of the data indicates that in 20% of the sampled firms (20% of AC respondents), the AC prepares the IAF Charter, while in 40% of the sampled firms, the AC, defines the scope and focus of the IAF in the Charter, and, in 40% of the sampled firms, the AC, there is substantial input from the AC at the preparation stage of the IAF Charter. The findings of this paper on the role of the AC in the approval of the IAF Charter is consistent with existing literature for an effective AC (Beasley, Hermanson, & Neal, 2009; IIA, 2009; Briotta Jnr, Gazzaway, Colson, & Shridha, 2010). Thus, this provides further conclusive evidence to argue that the AC is an effective corporate governance mechanism in the Nigerian listed firm. 5.3.5 The AC Review of the IAF Reports and Working Papers The IAF reports represent the output from the oversight functions of the IAF within the purview of the approved IAF Charter and the IAF Annual Workplan by the AC (IIA, 2009; Beasley, Hermanson, & Neal, 2009). It is expected that an effective AC will thoroughly review the IAF reports and working papers at each of its quarterly meetings for effective oversights of the management (IIA, 2009; Beasley, Hermanson, & Neal, 2009). In Tables 4.9.1A and 4.9.1B, we captured qualitative data on the frequency of the AC review of the IAF reports and working papers. In Table 4.9.1B, the tally chart shows that in all our sampled firms (100% of AC respondents), the AC does consider, discuss and review the IAF reports and working papers at its quarterly meetings. Furthermore, 80% of the AC respondents stated that, the IAF reports and working papers are considered as often as the AC meets while 20% of the AC respondents stated that the IAF reports and working papers are dispatched to the AC members on a monthly basis for their reviews and further discussions at the quarterly AC meetings. This finding indicates that, consistent with the existing literature, the AC is effectively discharging its oversight responsibilities over the activities of the firm as represented by the its regular reviews of the activities of

Australian Journal of Commerce Study ISSN:2203-9422 (Print) ISSN:2203-9430 (Online)

Australian Society for Commerce Industry & Engineering www.scie.org.au

28

the IAF. Thus, we document conclusive evidence that the AC is an effective corporate governance mechanism in Nigerian listed firms. In summary, the discussions of the findings of this paper in sections 5.3.1 - section 5.3.5 provides sufficient evidence that the activities of the AC in Nigerian listed firms are consistent with existing literature on the expected activities of an effective AC. Thus, we argue that the activities of the AC in Nigerian listed firms provide conclusive evidence that the AC is an effective corporate governance mechanism in Nigerian listed firms. In conclusion, this paper examines the effectiveness of the AC as a corporate governance mechanism in Nigerian listed firms. Using a tow staged interviews: the indepth interviews and follow up interviews of the Ac members in the listed firms, we found conclusive evidence that the size of the AC is adequate for the effective discharge of its functions as a corporate governance mechanism. Furthermore, we document conclusive evidence that the AC of Nigerian listed firms possesses the ingredients of competence required of an effective corporate governance mechanism. Also, we document conclusive evidence that the activities of the AC are consistent with the existing literature on the activities of an effective AC. Thus, overall, we found conclusive evidence to argue that the AC is an effective corporate governance mechanism in Nigeria listed firms. This paper makes an original contribution to the existing literature in the field of corporate governance. It is believed that this paper would be of interest to corporate governance actors such as the Board of Directors, the Audit Committees, the investor community, the shareholders and other stakeholders. This paper would also be of interest to the Nigerian Stock Exchange, the Securities and Exchange Commission, the institutions charged with the task of ensuring sound corporate governance in Nigerian listed firms. This paper would also be of interest to scholars in the field of corporate governance and the academic community. It is expected that this paper will trigger further research in this field in other jurisdictions and Stock Exchanges. It is suggested that future research should qualitatively examine the independence of the AC as a corporate governance mechanism in Nigerian listed firms using qualitative indicators of AC independence.

References

Abbott, L., Parker, S., & Peter, G. (2004). Audit Committee Characteristics and Restatements.

Auditing: A Journal of Practice and Theory, 23 (1), 69-87.

Abdellatiff, A. E. (2009). Corporate Governance Mechanism and Asymmetric Information: An

Application on the UK Capital Market. UK: University of Surrey: PhD Thesis. Retrieved

September 28, 2014, from http://epubs.surrey.ac.uk/681/1/fulltext.pdf

Abdul-Rayman, R., & Ali, F. H. (2006). Audit Committee, Culture and Earnings Management:

Malysian Evidence. Managerial Auditing Journal, 783-804.

Alkdai, H. K., & Hanefah, M. M. (2012). Audit Committee and Earnings Management in Malaysian

Sharia-Compliant COmpanies. Business and Management Reviews, 2 (2), 52-61.

Beasley, M., Hermanson, D., & Neal, T. (2009). The Audit Committee Oversight Process. Journal of

Contemporary Accounting Research, 26 (1), 65-122.

Bedard, J., Chtourou, S. M., & Courteau, L. (2004). The Effect of Audit Committee Expertise,

Independence and Activity on Aggressive Earnings Management. Auditing: A Journal of

Practice and Theory, 23, 55-79.

BRC. (1999). Report and Recommendation of Blue Ribbon Committee on Improving the Effectiveness

of Corporate Audit Committees. New York, USA: New York Stock Exchange.

Briotta Jnr, L., Gazzaway, T., Colson, R., & Shridha, R. (2010). The Audit Committee Handbook (2nd

Ed.). New Jessey, USA: John Willey & Sons.

CAMA. (2004). Companies and ALlied Matters Act Law of the Federal Republic of Nigeria. Abuja:

Attorney General of the Federation.

Australian Journal of Commerce Study ISSN:2203-9422 (Print) ISSN:2203-9430 (Online)

Australian Society for Commerce Industry & Engineering www.scie.org.au

29

Carcello, J., Hollingsworth, C., Klein, A., & Neal, T. (2006). Audit Committee Financial Expertise,

Competing Corporate Governance Mechanisms, and Earnings Management. Working Paper,

1-53. Retrieved September 23, 2014, from http://hdl.handle.net/2451/27455

Chang, J.-C., & Sun, H.-L. (2008). The Relation Between Earnings Informativeness, Earnings

Management and Corporate Governance in the Pre and Post-SOX Periods. Working Paper,

1-48.

Coonger, J., Finegold, D., & Lawler III, E. (1998). Appreciating Boardroom Performance. Harvard

Business Review, 76, 136-148.

Cresswell, J., & Miller, D. (2000). Determining Valididty in Qualitative Inquiry. Theory Into Practice,

39(3), 121-131.

Davidson, R., Goodwin-Steward, J., & Kent, P. (2005). Internal Governance Structure and Earnings

Management. Journal of Accounting and Finance, 45, 241-267.

Defond, M., & Jiambalvo, J. (1991). Incidences and Circumstances of Accounting Errors. The

Accounting Reviews, 66, 643-655.

DeFond, M., Han, R., & Hu, X. (2005). Does the Market Value Financial Expertise on Audit

Committee Boards of Directors. Journal of Accounting Research, 43(2), 153-194.

Dhaliwal, D., Naiker, V., & Navissi, F. (2006). Financial Expertise, Corporate Governance and

Accruals Quality:An Emprirical Analysis. Working Paper, 1-52. Retrieved September 1, 2014,

from http://ssrn.com/abstract=906690

IIA. (2009). The Audit Committee: Internal Audit Oversight. Institute of Internal Auditors, 1-8.

IIA. (2009b). Definition of Internal Audit Code of Ethics: International Standards for the Professional

Practice of Internal Auditing. Institute of Internal Auditing.

Klein, A. (2006). Audit Committee, Board of Directors Characteristics and Earnings Management.

Journal of Accounting and Economics, 33, 375-400.

Levitt, A. (1999). The Numbers Game. New York, New York, USA. Retrieved October 22, 2014, from

http:www.sec.gov/news/speech/speecharchive/1998/spch220.txt

Lin, J., Xiao, J., & Tang, Q. L. (2008). The Roles, Responsibilities and Characteristics of Audit

Committee in China. Accounting, Auditing and Accountability Journal, 21(5), 721-751.

Mat Zain, M. (2005). The Impact of Audit Committees on Internal Audit Contribution to Financial

Statements Audit and Audit Fees: Perception of Malysian Internal Auditors. Australia:

Griffith University-PhD Thesis.

Mat-Zain, M., & Subramaniam, N. (2007). The Relationship Between Audit Committee and Internal

Audit Function. Journal of Accounting Research, 230-245.

Menon, K., & Williams, J. D. (1994). The Use of Audit Committee for Monitoring. Journal of

Accounting and Public Policy, 33, 121-139.

Oxley, M. (2007). The Sarbanes-Oxley Act of 2002-Restoring Investors Confidence. Current Issues in

Auditing, C1-C2.

Ramly, Z., & Rashid, H. M. (2010). Critical Review of Literature on Corporate Governance and the

Cost of Capital: The Value Creation Perspective. African Journal of Business Management,

2198-2204.

Sommer, B., & Simmer, R. (1991). A Practical Guide to Behavioural Research: Tools and Techniques.

New York: Oxford University Press.

Australian Journal of Commerce Study ISSN:2203-9422 (Print) ISSN:2203-9430 (Online)

Australian Society for Commerce Industry & Engineering www.scie.org.au

30

Srinivasan, S. (2005). Consequence of Financial Reporting Failure for Outside Directors: Evidence

from Accounting Restatements and Audit Committee Members. Journal of Accounting

Research, 43(2), 291-334.

Turley, S., & Zaman, M. (2004). The Corporate Governance Effect of Audit Committee. Journal of

Management and Governance, 8, 304-332.

Vafeas, N. (2000). Board Structure and Informativeness of Earnings. Journal of Accounting and Public

Policy, 19(2), 139-160.

Vogt, P. (2007). Qualitative Research Methods for Professionals. Califonia: Sage Publications.

Xie, B., Davidson III, W., & DaDalt, P. (2003). Earnings Management and Corporate Governance:

The Role of Board and the Audit Committee. Journal of Corporate Governance, 9(3), 295-

316.

Yang, J., & Krishnan, J. (2005). Audit Committee and Quarterly Earnings Management. International

Journal of Auditing, 9(3), 201-219. doi:10.1111/j.1099-1123.205.00278.x.

Zhou, J., & Chen, K. (2004). Audit Committee, Board Characteristics and Earnings Management by

Commercial Banks. Proceedings at 2004 American Accounting Association Annual Meeting

and 2005 European Accounting Association Annual Conference (pp. 1-35). New York:

American Accounting Association.

Zikmund, W. (2003). Business Research Methods. Indiana: Thompson/ South-Western.

Appendix A

PART A- Participant Profile

1. Gender: 2. Title: 3. Career Level in the Company: Manager/Senior Manager/AGM/DGM/GM 4. Years with the Company: 5. Age Range: 6. Place of Birth: 7. Religious or Philosophical upbringing:

PART B- Characteristics Survey

1. What does your Audit Committee has in place detailing the roles of the individual members of the Audit Committee and guiding the conduct of the AC business?

2. What is the process and approval level for the preparation and approval of Annual Internal Audit Work Plan or Road Map?

3. How does the AC schedule its meetings for the year? 4. What is the level of involvement of the Audit Committee in the process for the preparation

and approval of the Internal Audit Policy Manual (Charter)? 5. What is the level of financial literacy or financial expertise of your AC members , i.e. with

accounting or Financial education either with or without professional qualifications in finance or Accounting?

6. What is the Policy of your company regarding the training of Audit Committee Membe 7. What is the size of your AC? and (2) How do you assess the adequacy of the size of your

AC to the size of the Company? 8. How often does the Audit Committee review Internal Audit Report at the Committee

meetings? Source: Akinteye, York & Henderson (2014)

Copyright © 2022 FDOKUMEN