(1) very substantial disposal - Investor Relations - TodayIR.com

211

THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION 13 June 2013 If you are in any doubt as to any aspect of this circular or as to the action to be taken, you should consult your licensed securities dealer or registered institution in securities, bank manager, solicitor, professional accountant or other professional advisers. If you have sold or transferred all your shares in Xiwang Sugar Holdings Company Limited (the “Company”), you should at once hand this circular and the accompanying form of proxy to the purchaser(s) or transferee(s) or to the bank, the licensed securities dealer or registered institution in securities or other agent through whom the sale or the transfer was effected for transmission to the purchaser(s) or the transferee(s). Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this circular, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this circular. * (Incorporated in Bermuda with limited liability) (Stock Code: 2088) (1) VERY SUBSTANTIAL DISPOSAL; (2) CONNECTED TRANSACTION; AND (3) PROPOSED CONDITIONAL SPECIAL DIVIDEND OF HK$0.75 PER SHARE AND CONVERTIBLE PREFERENCE SHARE Financial adviser to the Company SOMERLEY LIMITED Independent financial adviser to the Independent Board Committee and the Independent Shareholders Shenyin Wanguo Capital (H.K.) Limited A letter from the Board is set out on pages 6 to 49 of this circular. A letter from the Independent Board Committee containing its recommendation to the Independent Shareholders is set out on page 50 of this circular. A letter from Shenyin Wanguo Capital (H.K.) Limited containing its advice to the Independent Board Committee and the Independent Shareholders is set out on pages 51 to 78 of this circular. A notice convening the SGM to be held at Boardroom 3-4, Mezzanine Floor, Renaissance Hong Kong Harbour View Hotel, No. 1 Harbour Road, Wanchai, Hong Kong on Saturday, 29 June 2013 at 11:00 a.m. is set out on pages SGM–1 to SGM–3 of this circular. Whether or not you are able to attend the meeting, you are requested to complete the accompanying form of proxy in accordance with the instructions printed thereon and return the same to the office of the Company’s branch share registrar in Hong Kong, Tricor Investor Services Limited, at 26/F., Tesbury Centre, 28 Queen’s Road East, Wanchai, Hong Kong, as soon as possible and in any event not less than 48 hours before the appointed time for holding the meeting or any adjournment thereof (as the case may be). Completion and return of the form of proxy will not preclude you from attending and voting in person at the meeting or any adjournment thereof (as the case may be) if you so wish. * For identification purpose only

-

Upload

khangminh22 -

Category

Documents

-

view

5 -

download

0

Transcript of (1) very substantial disposal - Investor Relations - TodayIR.com

THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION

13 June 2013

If you are in any doubt as to any aspect of this circular or as to the action to be taken, you should consult your licensed securities dealer or registered institution in securities, bank manager, solicitor, professional accountant or other professional advisers.

If you have sold or transferred all your shares in Xiwang Sugar Holdings Company Limited (the “Company”), you should at once hand this circular and the accompanying form of proxy to the purchaser(s) or transferee(s) or to the bank, the licensed securities dealer or registered institution in securities or other agent through whom the sale or the transfer was effected for transmission to the purchaser(s) or the transferee(s).

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this circular, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this circular.

*

(Incorporated in Bermuda with limited liability)(Stock Code: 2088)

(1) VERY SUBSTANTIAL DISPOSAL;(2) CONNECTED TRANSACTION;

AND (3) PROPOSED CONDITIONAL SPECIAL DIVIDEND OF HK$0.75 PER SHARE

AND CONVERTIBLE PREFERENCE SHARE

Financial adviser to the Company

SOMERLEY LIMITED

Independent financial adviser to the Independent Board Committee and the Independent Shareholders

Shenyin Wanguo Capital (H.K.) Limited

A letter from the Board is set out on pages 6 to 49 of this circular. A letter from the Independent Board Committee containing its recommendation to the Independent Shareholders is set out on page 50 of this circular.

A letter from Shenyin Wanguo Capital (H.K.) Limited containing its advice to the Independent Board Committee and the Independent Shareholders is set out on pages 51 to 78 of this circular. A notice convening the SGM to be held at Boardroom 3-4, Mezzanine Floor, Renaissance Hong Kong Harbour View Hotel, No. 1 Harbour Road, Wanchai, Hong Kong on Saturday, 29 June 2013 at 11:00 a.m. is set out on pages SGM–1 to SGM–3 of this circular. Whether or not you are able to attend the meeting, you are requested to complete the accompanying form of proxy in accordance with the instructions printed thereon and return the same to the office of the Company’s branch share registrar in Hong Kong, Tricor Investor Services Limited, at 26/F., Tesbury Centre, 28 Queen’s Road East, Wanchai, Hong Kong, as soon as possible and in any event not less than 48 hours before the appointed time for holding the meeting or any adjournment thereof (as the case may be). Completion and return of the form of proxy will not preclude you from attending and voting in person at the meeting or any adjournment thereof (as the case may be) if you so wish.

* For identification purpose only

R14.63(2)(b)R14A.58(3)(b)

R14.58(1)R14A.59(1)

App1B(1)

R13.51A

CONTENTS

Pages

Definition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Expected timetable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Letter from the Board . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Letter from the Independent Board Committee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

Letter from Shenyin Wanguo . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

Appendix I – Financial information of the Group . . . . . . . . . . . . . . . . . . . . . . . . . . . . . I – 1

Appendix II – Accountant’s report on the Group . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II – 1

Appendix III – Management discussion and analysis on the Remaining Group . . . . . . . III – 1

Appendix IV – Unaudited pro forma financial information of the Remaining Group . . IV – 1

Appendix V – Property valuation report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . V – 1

Appendix VI – Valuation report on machinery and equipment . . . . . . . . . . . . . . . . . . . . VI – 1

Appendix VII – General information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . VII – 1

Notice of SGM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . SGM – 1

DEFINITION

1

In this circular, unless the context requires otherwise, the following terms have the following

meanings:

“Agreement” the conditional sale and purchase agreement dated 21 May 2013

entered into between the Purchaser and the Company in relation to

the Disposal

“associate(s)” has the same meaning as defined in the Listing Rules

“Board” the board of the Directors

“Business Day” a day (other than a Saturday, Sunday and any day on which a

tropical cyclone warning no. 8 or above is hoisted or on which a

“black” rainstorm warning is hoisted between 9:00 a.m. and 5:00

p.m.) on which licensed banks are generally open for business in

Hong Kong throughout their normal business hours

“BVI” the British Virgin Islands

“Company” Xiwang Sugar Holdings Company Limited, a company incorporated

in Bermuda with limited liability and the issued Shares of which

are listed on the Main Board of the Stock Exchange

“Completion” completion of the Disposal

“connected person” has the same meaning as defined in the Listing Rules

“Consideration” the consideration of RMB661 million for the disposal of the

Sale Share and the consideration of RMB1,435 million for the

assignment of the Sale Loans payable by the Purchaser to the

Company pursuant to the Agreement

“CPS(s)” the convertible preference share(s) with par value of HK$0.1 each

in the issued share capital of the Company

“CPS Holder(s)” holder(s) of CPSs

“Director(s)” the director(s) of the Company

“Disposal” the proposed disposal of the entire issued share capital of the

Disposal Company, and assignment of the Sale Loans pursuant to

the terms and conditions of the Agreement

“Disposal Company” Master Team International Limited, a company incorporated in

BVI with its entire issued share capital held by the Company as at

the date of the Agreement

DEFINITION

2

“Disposal Group” the Disposal Company and its subsidiaries comprising (i) Winning

China Limited, a company incorporated in Hong Kong; (ii)山東西王糖業有限公司(Shandong Xiwang Sugar Industry Company Limited), a company incorporated in the PRC; and (iii)西王糖業

(北京)有限公司(Xiwang Sugar (Beijing) Co., Ltd.), a company incorporated in the PRC, being all of the subsidiaries of the Company that engage in the corn processing business as at the Latest Practicable Date (excluding a subsidiary of the Remaining Group which also engages in the export trading business)

“Dividend Payment Date” the date on which the Proposed Special Dividend and the Preferred Distribution will be paid to Ordinary Shareholders and CPS Holders whose names are registered on the register of members of the Company on the Record Date, and is currently expected to be on or around 23 July 2013

“Group” the Company and its subsidiaries

“HKFRS” Hong Kong Financial Reporting Standards

“Hong Kong” the Hong Kong Special Administrative Region of the PRC

“Independent Board Committee” independent committee of the Board comprising Mr. Shi Wei Chen, Mr. Wong Kai Ming and Mr. Wang An, all being independent non-executive Directors

“Independent Shareholders” Ordinary Shareholders other than the Purchaser and its associates

“Independent Valuer” Grant Sherman Appraisal Limited, an independent professional valuer appointed by the Company for the Disposal

“Last Trading Day” 7 May 2013, being the last trading day of the Shares before the release of the Company’s announcement dated 21 May 2013 in relation to, among other things, the Disposal, the Proposed Special Dividend and the Preferred Distribution

“Latest Practicable Date” 7 June 2013, being the latest practicable date prior to printing of this circular for ascertaining certain information contained in this circular

“Listing Rules” the Rules Governing the Listing of Securities on the Stock Exchange

“Ordinary Shareholder(s)” holder(s) of the Shares

“PRC” the People’s Republic of China and, for the purpose of this circular, excluding Hong Kong, Macao Special Administrative Region of the People’s Republic of China and Taiwan

DEFINITION

3

“Preferred Distribution” the distribution of RMB0.01 for each CPS for the financial year

ended 31 December 2012

“Previous Acquisition” the acquisition of the property development business in the PRC

as detailed in the Company’s circular dated 11 December 2012

“Promissory Note A” the promissory note in the principal amount of RMB901,734,114

to be issued by the Purchaser in favour of the Company for partial

settlement of the Consideration at Completion

“Promissory Note B” the promissory note in the principal amount being half of the

Remaining Balance to be issued by the Purchaser in favour

of the Company for partial settlement of the Consideration at

Completion

“Promissory Notes” Promissory Note A and Promissory Note B

“Proposed Special Dividend” the proposed conditional distribution of special dividend of

HK$0.75 per Share and CPS

“PwC” PricewaterhouseCoopers, Certified Public Accountants

“Record Date” the date for determining the entitlements of the Shareholders to

the Proposed Special Dividend and the Preferred Distribution

which is fixed at 10 July 2013

“Remaining Group” the Group after Completion

“Sale Loans” various unsecured and non-interest bearing loans owed by each

of the Disposal Company, Winning China Limited, a company

incorporated in Hong Kong, and 山東西王糖業有限公司(Shandong Xiwang Sugar Industry Company Limited), a company

incorporated in the PRC, in currencies of HK$ and RMB to the

Company as set out in the Agreement and the Unpaid Dividend

“Sale Share” the entire issued share capital of the Disposal Company, which

was one share with par value of US$1 as at the date of the

Agreement

“SFO” the Securities and Futures Ordinance (Chapter 571 of the laws of Hong Kong) as amended, supplemented or otherwise from time to time

“SGM” the special general meeting of the Company to be convened for

the purpose of considering and, if thought fit, approving the

Agreement, the transactions contemplated thereunder and the

Proposed Special Dividend

DEFINITION

4

“Share(s)” the ordinary share(s) with par value of HK$0.1 each in the issued

share capital of the Company

“Shareholders” Ordinary Shareholders and CPS Holders

“Shenyin Wanguo” Shenyin Wanguo Capital (H.K.) Limited, a licensed corporation

to carry on type 1 (dealing in securities), type 4 (advising on

securities) and type 6 (advising on corporate finance) regulated

activities under the SFO; and the independent financial adviser

appointed to advise the Independent Board Committee and the

Independent Shareholders in respect of the Agreement, the

transactions contemplated thereunder and the Proposed Special

Dividend

“Stock Exchange” The Stock Exchange of Hong Kong Limited

“Unpaid Dividend” the dividend declared but unpaid by the Disposal Group to the

Company

“Xiwang Investment” Xiwang Investment Company Limited, a company incorporated in

or “Purchaser” the BVI, a controlling shareholder of the Company and is a

wholly-owned subsidiary of Xiwang Holdings Limited. Xiwang

Holdings Limited is owned as to 64.36% by Mr. Wang Yong,

being chairman of the Board and an executive Director of the

Company

“Xiwang Special Steel” Xiwang Special Steel Company Limited (stock code: 1266), a

company incorporated in Hong Kong with limited liability and the

issued shares of which are listed on the Main Board of the Stock

Exchange

“HK$” Hong Kong dollar(s), the lawful currency of Hong Kong

“RMB” Renminbi, the lawful currency of the PRC

“US$” United States dollar(s), the lawful currency of the United States of

America

“sq.m” square metre(s)

“%” per cent

The English translations of the Chinese names are included in this circular for identification

purpose only and should not be regarded as their official English translation. In the event of any

inconsistency, the Chinese name prevails.

For the purpose of illustration, the exchange rate between Renminbi and Hong Kong dollars

provided in this circular is RMB1 = HK$1.2512 (unless otherwise stated). The provision of such exchange

rates does not mean that Hong Kong dollars could be converted into Renminbi based on such exchange

rate.

EXPECTED TIMETABLE

5

Set out below is the expected timetable in relation to the Disposal, the Proposed Special Dividend

and the Preferred Distribution. Shareholders should note that the timetable is indicative only and subject

to change depending on, among other things, results of the SGM and date of Completion. The Company will notify the Shareholders on any change to the expected timetable as and when appropriate.

2013

Latest time for return of proxy forms for the SGM . . . . . . . . . . . . . . . . . . . . . . . . . 11:00 a.m. on 27 June

SGM to be held . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11:00 a.m. on 29 June

Announcement of results of the SGM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 July

Last day of dealings in Shares and CPSs on a cum-entitlement basis . . . . . . . . . . . . . . . . . . . . . . . . . 3 July

First day of dealings in Shares and CPSs on an ex-entitlement basis . . . . . . . . . . . . . . . . . . . . . . . . . 4 July

Latest time for lodging transfer of Shares and

CPSs for registration in order to be qualified

for the Proposed Special Dividend and/or

the Preferred Distribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4:30 p.m. on 5 July

Closure of the register of members of the Company

for determining the entitlements to the Proposed

Special Dividend and/or the Preferred Distribution . . . . . . . . . . 8 July to 10 July (both dates inclusive)

Record Date . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10 July

Register of members of the Company re-opens . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11 July

Expected date of despatch of the cheque for the

Proposed Special Dividend and/or the

Preferred Distribution to the Shareholders

(i.e. the Dividend Payment Date) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . on or around 23 July

Notes:

1. The payment of the Proposed Special Dividend is subject to the approval of the Independent Shareholders having been obtained and Completion having taken place. The payment of the Preferred Distribution is also subject to Completion having taken place.

2. Cheques for the Proposed Special Dividend and/or the Preferred Distribution will be sent to Shareholders by ordinary post at their own risk to their registered addresses.

3. All references in this circular to times and dates are references to Hong Kong times and dates.

LETTER FROM THE BOARD

6

*

(Incorporated in Bermuda with limited liability)(Stock Code: 2088)

Executive Directors: Registered Office:Mr. Wang Yong (Chairman) Clarendon HouseMr. Wang Di 2 Church StreetMr. Wang Fangming Hamilton HM 11Dr. Li Wei BermudaMr. Han Zhong Principal place of business Non-execuitve Director: in Hong Kong:Mr. Sun Xinhu Unit 2110, 21/F Harbour CentreIndependent non-executive Directors: 25 Harbour RoadMr. Shi Wei Chen WanchaiMr. Wong Kai Ming Hong KongMr. Wang An 13 June 2013

To the Ordinary Shareholders and, for information only, the CPS Holders

Dear Sir or Madam,

(1) VERY SUBSTANTIAL DISPOSAL;(2) CONNECTED TRANSACTION;

AND (3) PROPOSED CONDITIONAL SPECIAL DIVIDEND OF HK$0.75 PER SHARE

AND CONVERTIBLE PREFERENCE SHARE

INTRODUCTION

On 21 May 2013, the Company (as the vendor) entered into the Agreement pursuant to which

Xiwang Investment (as the Purchaser) has conditionally agreed to acquire, and the Company (as the

vendor) has conditionally agreed to (1) sell the Sale Share, being the entire issued share capital of the

Disposal Company; and (2) assign to the Purchaser all interests, benefits and rights of the Sale Loans. The

consideration for the disposal of the Sale Share shall be RMB661 million and the consideration for the

assignment of the Sale Loans shall be RMB1,435 million.

R14.63(1)R14A.58(1)

R2.14

R14.60(1)

* For identification purpose only

LETTER FROM THE BOARD

7

The Disposal Company is an investment holding company wholly and beneficially owned by the

Company as at the Latest Practicable Date. The Disposal Group is principally engaged in corn processing

business with a focus on the production of starch sugars and corn co-products in the PRC, and the

distribution and the sale of such products within and outside the PRC.

The Board proposes a special dividend of HK$0.75 per Share and per CPS to be distributed to the

Shareholders whose names are registered on the register of members of the Company on the Record Date,

subject to the approval of the Independent Shareholders having been obtained and Completion having

taken place. The Board has resolved, subject to Completion taking place, to pay the Preferred Distribution

of RMB0.01 in Hong Kong dollars at the exchange rate of RMB1.00 = HK$1.2512 to the CPS Holders on

the Dividend Payment Date.

As the relevant percentage ratios applicable to the Company exceed 75%, the Disposal constitutes

a very substantial disposal for the Company under the Listing Rules. Since the Purchaser is a connected

person of the Company, the Disposal also constitutes a connected transaction for the Company, and is

subject to reporting, announcement and the Independent Shareholders’ approval at the SGM.

The Independent Board Committee comprising all of the three independent non-executive

Directors, namely Mr. Shi Wei Chen, Mr. Wong Kai Ming and Mr. Wang An, has been constituted to

advise the Independent Shareholders as regards the terms of the Agreement, the transactions contemplated

thereunder and the Proposed Special Dividend. Shenyin Wanguo has been appointed as the independent

financial adviser to advise the Independent Board Committee and the Independent Shareholders in this

regard.

The purpose of this circular is to provide you with, among other things, (a) information on the

Disposal; (b) the letter of advice from Shenyin Wanguo to the Independent Board Committee and the

Independent Shareholders; (c) the recommendation from the Independent Board Committee to the

Independent Shareholders; (d) the financial information of the Group; (e) the accountant’s report on the

Group; (f) the unaudited pro forma financial information of the Remaining Group; (g) valuation reports

in respect of property, machinery and equipment of the Disposal Group; (h) a notice of the SGM; and (i)

other information required under the Listing Rules.

THE AGREEMENT

Date: 21 May 2013

The Vendor: The Company

The Purchaser: Xiwang Investment

The Purchaser is principally engaged in investment holding and is a controlling shareholder of each

of the Company and Xiwang Special Steel which is listed on the Main Board of the Stock Exchange. As

at the Latest Practicable Date, the Purchaser was a wholly-owned subsidiary of Xiwang Holdings Limited,

which was owned as to approximately 64.36% by Mr. Wang Yong, the chairman and an executive

Director of the Company. The Purchaser and its associates did not engage in any property development

business in the PRC as at the Latest Practicable Date. Accordingly, it is expected that Mr. Wang Yong,

R14.58(3)R14A.59(2)(a)

R14A.59(2)(d)

R14.58(2)R14A.59(2)(a),(e),(f)

LETTER FROM THE BOARD

8

the Purchaser and their respective associates will not have an interest in a business (other than through

holding the interest in the Company) which competes, or is likely to compete, either directly or indirectly,

with the Remaining Group after Completion.

Assets to be disposed of

Pursuant to the Agreement, the Purchaser has conditionally agreed to acquire, and the Company

has conditionally agreed to (1) sell the Sale Share, being the entire issued share capital of the Disposal

Company; and (2) assign to the Purchaser all interests, benefits and rights of the Sale Loans. The Disposal

Group is principally engaged in corn processing business with a focus on the production of starch sugars

and corn co-products in the PRC, and the distribution and the sale of such products within and outside the

PRC.

The Company has injected capital into the Disposal Group for the development of the Disposal

Group’s business by way of equity investment and loans. As at 31 March 2013, the Company advanced

loans in an aggregate amount of approximately RMB1,710.1 million to the Disposal Group. The Company

had not advanced additional loan to the Disposal Group in the period between 31 March 2013 and the

Latest Practicable Date. During the period from 31 March 2013 and up to the Latest Practicable Date, the

Disposal Group repaid an amount of approximately RMB255,000 to the Company, with the outstanding

loans amounted to approximately RMB1,709.9 million. All the loans are unsecured, non-interest bearing

with no fixed repayment term and remained outstanding as at the Latest Practicable Date. The Disposal

Company previously declared payment of dividend to the Company and such dividend remained unpaid

as at the Latest Practicable Date. As at the Latest Practicable Date, the Unpaid Dividend amounted

to approximately RMB222.0 million. Based on the above, the Sale Loans amounted to approximately

RMB1,931.9 million (being the sum of loans owed by the Disposal Group to the Company and the Unpaid

Dividend) as at the Latest Practicable Date. Based on the accountant’s report on the Group in Appendix

II to this circular, as at 31 March 2013, the Disposal Group recorded total current assets of approximately

RMB2,646.2 million (including amount due from the Remaining Group of approximately RMB366.5

million to remain outstanding upon Completion) and total current liabilities of approximately RMB4,536.8

million (including the loans advanced by the Remaining Group to the Disposal Group of approximately

RMB1,710.1 million and the Unpaid Dividend of approximately RMB222.0 million as at 31 March 2013).

Setting aside the loans owed by the Disposal Group to the Company and the Unpaid Dividend, the net

current assets of the Disposal Group were approximately RMB41.5 million as at 31 March 2013. As at

31 March 2013, the Disposal Group recorded cash and cash equivalents (excluding restricted cash) in the

amount of approximately RMB263.8 million, and its short-term external loans amounted to approximately

RMB1,725.7 million. For the three months ended 31 March 2013 and the year ended 31 December

2012, the Disposal Group incurred losses after income tax expense of approximately RMB16.3 million

and RMB21.8 million respectively. Based on the current financial position of the Disposal Group, the

Directors are of the view that it is unlikely that the Disposal Group will be able to repay the Sale Loans to

the Company in full in the near future.

Upon Completion, the Group will cease to have any interest in the Disposal Company and the

Disposal Group will cease to be subsidiaries of the Company.

R14.60(2)R14A.59(2)(b)

R14.58(6)

R14.60(6)R14.66(6)(a)R14A.59(16)

LETTER FROM THE BOARD

9

Consideration

The consideration for the disposal of the Sale Share shall be RMB661 million and consideration

for the assignment of the Sale Loans shall be RMB1,435 million. The total consideration was determined

after arm’s length negotiations between the Purchaser and the Company having taken into account (i)

the audited net assets value of the Disposal Group of approximately RMB1,020.8 million as at 31 March

2013; (ii) losses of the Disposal Group for the year ended 31 December 2012 and the three months ended

31 March 2013 (as detailed in the section headed “Information on the Disposal Group” below); and (iii)

the independent valuation of the property, machinery and equipment of the Disposal Group (including

indicative market value of certain properties pending registration of legal titles as set out in the property

valuation report contained in Appendix V to this circular) as at 30 April 2013.

The Consideration will be payable by the Purchaser to the Company in the following manner:

(a) offset against the amount payable to the Purchaser by the Company for early repayment of

the promissory note in the principal amount of RMB308 million issued by the Company

in favour of Xiwang Investment on 31 December 2012 to satisfy the consideration for the

Previous Acquisition, together with interests accrued up to the date of Completion (the

interests accrued amounted to approximately RMB1.9 million as at 31 March 2013);

(b) issue of Promissory Note A by the Purchaser to the Company upon Completion in the

principal amount of RMB901,734,114 (which is equivalent to the Purchaser’s aggregate

entitlements to the Proposed Special Dividend and the Preferred Distribution based on the

Shares and the CPSs held by the Purchaser as at the Latest Practicable Date and details of

Promissory Note A are set out in the section headed “Principal terms of the Promissory

Notes” below); and

(c) as to the remaining balance after deducting items (a) and (b) above (the “Remaining

Balance”):

(i) 50% of it will be payable by the Purchaser to the Company in cash upon Completion;

and

(ii) 50% of it will be settled by issue of Promissory Note B by the Purchaser to the

Company upon Completion.

For illustration purpose only, if Completion had taken place on 31 March 2013, whereupon

the Consideration had been settled by the issuance of Promissory Note A in the principal amount

of RMB901,734,114 and offsetting the amount payable to the Purchaser by the Company for

early repayment of the promissory note in the principal amount of RMB308 million issued by

the Company in favour of the Purchaser on 31 December 2012 (together with interest accrued

thereon for the period up to 31 March 2013 in the amount of approximately RMB1.9 million), the

Remaining Balance would have been RMB884,365,886.

Details of Promissory Note B are set out in the section headed “Principal terms of the

Promissory Notes” below.

R14.58(4)R14A.59(2)(c)

R14.58(5)

R14.58(6)

LETTER FROM THE BOARD

10

The Independent Valuer performed an independent valuation in respect of the property, machinery

and equipment of the Disposal Group. Based on (a) the market value of such property, machinery and

equipment as at 30 April 2013 as appraised by the Independent Valuer; (b) the value of such construction

in progress which did not form part of the independent valuation but recorded in financial statements of

the Disposal Group; and (c) indicative market value of certain properties pending registration of legal

titles as set out in the property valuation report contained in Appendix V to this circular, the value of

property, machinery and equipment of the Disposal Group amounted to approximately RMB2,774.7

million, which represented a deficit of approximately RMB131.2 million to the carrying amount of the

property, plant and equipment and land use rights of approximately RMB2,905.9 million as at 31 March

2013. The value of the construction in progress could not be reflected by the independent valuation

but such value, representing the costs incurred and prepayments made for construction of fixed assets

mainly for the corn warehouse, was recorded in the financial statements of the Disposal Group. As the

construction of the related fixed assets had not yet been completed and no ownership titles had been

obtained, the Independent Valuer cannot include this amount of construction in progress in the valuation

reports. Details of the valuation deficit of approximately RMB131.2 million are as follows:

RMB million RMB million

Market value of property of the Disposal Group as at 30 April 2013 1,180.1

Market value of the machinery and equipment of the Disposal Group

as at 30 April 2013 1,495.4

Indicative market value of certain properties pending registration

of legal titles 55.4

Construction in progress not included in the valuation

but recorded in financial statements of the Disposal Group 43.8 2,774.7

Net book value of the property, plant and equipment

as at 31 March 2013 2,638.9

Net book value of the land use rights as at 31 March 2013 267.0 2,905.9

Valuation deficit taken into account in determining

the Consideration (131.2)

The Directors and the Purchaser have taken into account the aforesaid valuation deficit

of approximately RMB131.2 million when determining the Consideration. Further details of the

independent valuation are set out in the property valuation report and the valuation report on machinery

and equipment, both issued by the Independent Valuer, contained in Appendix V and Appendix VI

respectively to this circular.

As (a) it is a condition precedent that the Sale Loans will be the only outstanding liability owed

by the Disposal Group to the Remaining Group; (b) the Company does not intend to make any further

advances to the Disposal Group; and (c) the Disposal Group does not intend to make any repayment to

the Company, the total aggregate of the Sale Loans of approximately RMB1,931.9 million will not be

further adjusted. Accordingly, no adjustment to the consideration for the assignment of the Sale Loans of

RMB1,435 million is anticipated. On this basis, the Directors consider that it is fair and reasonable for not

having an adjustment mechanism in relation to the consideration for the assignment of the Sale Loans.

R14.58(6)

LETTER FROM THE BOARD

11

Set out below are the assets and liabilities of the Disposal Group as at 31 March 2013 extracted

from the disclosure above and note 33 to the financial information in the accountant’s report on the Group

set out in Appendix II to this circular:

RMB million

Non-current assets 2,911.5

Amount due from the Remaining Group 366.5

Unrestricted cash 263.8

Other current assets 2,015.8

Amount due to the Company (1,710.1)

Unpaid Dividend (222.0)

Borrowings (1,725.7)

Other current liabilities (879.0)

Net assets 1,020.8

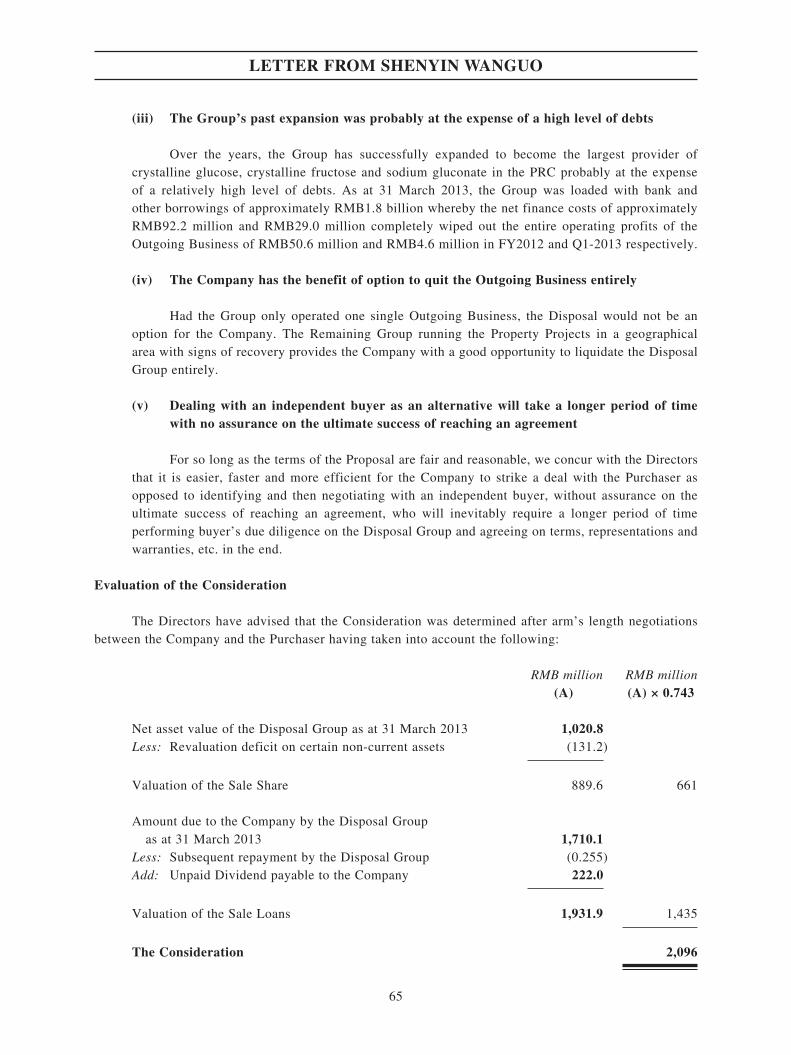

Based on (a) the sum of (i) the audited net asset value of the Disposal Group as at 31 March 2013

of approximately RMB1,020.8 million; (ii) the aggregate amount of loans owed by the Disposal Group

to the Company of approximately RMB1,709.9 million as at the Latest Practicable Date; (iii) the Unpaid

Dividend of approximately RMB222.0 million as at the Latest Practicable Date; and (iv) the valuation

deficit of approximately RMB131.2 million; and (b) the total Consideration of RMB2,096 million, the

historical price to book multiple (“PBR”) for the Disposal is approximately 0.743 times.

The determination of the Consideration is illustrated as below:

RMB million RMB million

(A) (A) × 0.743

Audited net asset value of the Disposal Group as at 31 March 2013 1,020.8

Less: Valuation deficit (131.2)

Valuation of the Sale Share 889.6 661

Aggregate amount of loans owed by the Disposal Group

to the Company as at 31 March 2013 1,710.1

Less: Subsequent repayment by the Disposal Group (0.255)

Add: Unpaid Dividend 222.0

Valuation of the Sale Loans 1,931.9 1,435

The Consideration 2,096

LETTER FROM THE BOARD

12

When determining the Consideration, the Directors have made reference to, among other things,

the PBR of other Hong Kong listed companies, namely Global Sweeteners Holdings Limited (stock code:

3889) (“Global Sweeteners”) and China Starch Holdings Limited (stock code: 3838) (“China Starch”)

(the “Comparable Companies”). Global Sweeteners is principally engaged in the production and sale

of corn refined products and corn sweeteners, categorised into upstream and downstream products. The

principal activities of China Starch include, among other things, the manufacture and sale of cornstarch

and ancillary corn-refined products.

Based on the market capitalisation of Global Sweeteners of approximately HK$947.1 million as at

the Latest Practicable Date and audited net assets attributable to equity holders as at 31 December 2012

of approximately HK$2,329.7 million, the historical PBR of Global Sweeteners was approximately 0.41

times. Based on the market capitalisation of China Starch of approximately HK$1,282.5 million as at

the Latest Practicable Date and audited net assets attributable to equity holders as at 31 December 2012

of approximately RMB1,844.8 million (equivalent to approximately HK$2,308.2 million), the historical

PBR of China Starch was approximately 0.56 times. In addition, based on the market capitalisation of

approximately HK$746.3 million (equivalent to approximately RMB596.5 million) of the Company

as at the Last Trading Day and audited net assets attributable to equity holders of the Company of

approximately RMB2,776.1 million (equivalent to approximately HK$3,473.5 million) as at 31 March

2013, the historical PBR of the Company was approximately 0.21 times.

The historical PBR represented by the Consideration for the Disposal is higher than the historical

PBR of the Comparable Companies and the historical PBR of the Company of approximately 0.21 times.

The Consideration of RMB2,096 million represents about 3.5 times and 1.6 times of the market

capitalisation of the Company as at the Last Trading Day and the Latest Practicable Date respectively.

Accordingly, the Disposal provides the Company with an opportunity to unlock the value of the Disposal

Group which is considered by the Directors to be in the interests of the Company and the Shareholders as

a whole.

On this basis, together with the unlikelihood of full repayment of the Sale Loans by the Disposal

Group as set out in the sub-section headed “Assets to be disposed of” above, the Directors consider that

the Consideration is fair and reasonable.

Conditions precedent

Completion is conditional upon the following conditions being satisfied (or waived where

applicable):

(a) the Company having obtained the Independent Shareholders’ approval of (i) the Agreement

and the transactions contemplated thereunder; and (ii) the Proposed Special Dividend in

accordance with the requirements under the Listing Rules;

(b) save for the Sale Loans, all other liabilities owed by the Disposal Group to the Remaining

Group having been fully repaid; and there being no outstanding guarantee or security granted

by any member of the Remaining Group in favour of any third party to secure any liability or

obligation of any member of the Disposal Group;

R14A.58(2)

R14A.58(2)

LETTER FROM THE BOARD

13

(c) the Purchaser having obtained all necessary consent, approval, permission and/or waiver for

the Agreement and the transactions contemplated thereunder;

(d) the representations and warranties given by the Company being materially true and accurate;

and

(e) the representations and warranties given by the Purchaser being materially true and accurate.

The Company may in its sole discretion decide to waive any of conditions (c) and (e) above,

and the Purchaser may in its sole discretion decide to waive condition (d) above. Neither parties may

waive conditions (a) and (b) above. If any of the conditions is not fulfilled (or waived where applicable)

on or before 30 June 2013 or such later date as may be agreed by the Purchaser and the Company, the

Agreement will lapse but the rights of a party in respect of the other’s antecedent breach of the Agreement

will not be affected. As at the Latest Practicable Date, none of the conditions precedent have been fulfilled

(or waived where applicable).

Completion

Completion shall take place on the third Business Day after the fulfilment (or waiver where

applicable) of the conditions precedent set out in the Agreement, or such other date as the Company and

the Purchaser may agree in writing.

PRINCIPAL TERMS OF THE PROMISSORY NOTES

Under the Agreement, the Promissory Notes will be issued by the Purchaser to the Company for

partial settlement of the total Consideration. The principal terms of the Promissory Notes are as follows:

Promissory Note A

Principal amount: RMB901,734,114

Maturity: the Dividend Payment Date

The Promissory Note A is unsecured and non-interest bearing.

Pursuant to the Agreement, the Purchaser has agreed and irrevocably authorised the Company to

fully offset the amount of the Purchaser’s aggregate entitlement to the Proposed Special Dividend and

the Preferred Distribution against the equivalent amount payable to the Company by the Purchaser under

Promissory Note A. The Purchaser has undertaken to the Company under the Agreement that it will not

sell, transfer, dispose of or otherwise reduce its holding in, the Shares or CPSs held by it, nor will it

convert any of its CPSs into Shares for the period between the date of the Agreement and the Record Date.

Pursuant to the Agreement, the exchange rate of RMB1.00 = HK$1.2512 will be used to determine

the Purchaser’s entitlement to the Proposed Special Dividend and the Preferred Distribution to offset the

amount payable by the Purchaser to the Company under Promissory Note A.

LETTER FROM THE BOARD

14

Further details with respect to the Proposed Special Dividend and the Preferred Distribution are set

out in the section headed “Proposed conditional special dividend” below.

Promissory Note B

Principal amount: half of the Remaining Balance (as defined in the sub-section headed

“Consideration” under the section headed “The Agreement” above)

Interest: interest shall accrue at the interest rate of 2.5% per annum for the period between the date of issue of Promissory Note B and the maturity date, or where applicable, the date of early repayment

Maturity: six months from the date of issue or 31 December 2013 whichever is the earlier

Security: a first fixed charge over such number of shares held by the Purchaser in Xiwang Special Steel which represents 75% of the issued share capital of Xiwang Special Steel (the “Charged Shares”). As at the Latest Practicable Date, the Charged Shares constitute 1,500 million shares in Xiwang Special Steel. This security will only be given upon the issue of Promissory Note B (i.e. upon Completion).

In addition, Mr. Wang Yong, an executive Director, will issue a letter of financial support to the Company prior to Completion undertaking that he will, among other things, at the request of the Purchaser, assist the Purchaser to obtain the required funding so that the Purchaser can fulfill its repayment obligation under Promissory Note B.

For illustration purpose only, if Completion had taken place on 31 March 2013, whereupon the Consideration had been settled by the issuance of Promissory Note A in the principal amount of RMB901,734,114 and offsetting the amount payable to the Purchaser by the Company for early repayment of the promissory note in the principal amount of RMB308 million issued by the Company in favour of the Purchaser on 31 December 2012 (together with interest accrued thereon for the period up to 31 March 2013 in the amount of approximately RMB1.9 million), the principal amount of Promissory Note B would have been RMB442,182,943.

Based on the market capitalisation of the Charged Shares of HK$1,335 million (equivalent to approximately RMB1,067.0 million) as at the Latest Practicable Date, together with the abovementioned letter of financial support of Mr. Wang Yong, the Directors consider that the Company’s exposure under Promissory Note B is safeguarded.

When negotiating the Consideration and terms of the Agreement, in view of such large amount of half of the Remaining Balance, the Purchaser indicated that more time will be required to make available such funding and accordingly the arrangement of a promissory note was proposed. It is stated in the sub-section headed “(C) Benefits to the Group and the Shareholders” under the section headed “Background to, reasons for and benefits of the Disposal” below that the earliest time for the Remaining

Group to participate in the bidding mechanism to acquire the land use rights for the Yintaishan corn

cultural project and Qinghe project is estimated to be around end of 2013 or early 2014. In view of (i)

the security available under Promissory Note B; (ii) the letter of financial support to be issued by Mr. Wang Yong; (iii) the timing for funding the Yintaishan corn cultural project and Qinghe project; and

R14.58(9)R14A.59(12)

LETTER FROM THE BOARD

15

(iv) the Consideration for the Disposal representing a higher historical PBR as compared to that of the Comparable Companies as at the Latest Practicable Date, the Directors, balancing on all relevant factors, consider that this arrangement is in the interests of the Company and the Shareholders as a whole.

In addition, when considering the interest rate of 2.5% per annum for Promissory Note B, the Directors took into account the fact that such interest rate is the same as that under the promissory note in the principal amount of RMB308 million issued by the Company in favour of the Purchaser in the Previous Acquisition, which was unsecured. Pursuant to the terms of the Agreement, the Charged Shares will be offered as security. On this basis, together with the fact that the Consideration for the Disposal represents a higher historical PBR as compared to that of the Comparable Companies as at the Latest Practicable Date, the Directors consider that the interest rate for Promissory Note B is fair and reasonable.

INFORMATION ON THE DISPOSAL GROUP

The Disposal Company is an investment holding company wholly and was beneficially owned

by the Company as at the Latest Practicable Date. The Disposal Group is principally engaged in corn

processing business with a focus on the production of starch sugars and corn co-products in the PRC, and

the distribution and the sale of such products within and outside the PRC.

Financial information

Based on the accountant’s report on the Group in Appendix II to this circular, for the three

months ended 31 March 2013, the Disposal Group recorded audited loss before and after taxation of

approximately RMB15.2 million and RMB16.3 million respectively. Based on the accountant’s report

on the Group in Appendix II to this circular, for the year ended 31 December 2012, the Disposal Group

recorded audited loss before and after taxation of approximately RMB27.2 million and RMB21.8 million

respectively. For the year ended 31 December 2011, the Disposal Group recorded audited profit before

and after taxation of approximately RMB239.7 million and RMB206.4 million respectively. The audited

profit/loss before and after taxation of the Disposal Group for the years ended 31 December 2011 and

2012 are different from the audited segmental profit/loss before and after taxation as stated in the 2012

annual report of the Company. The difference is mainly attributable to the fact that the segmental figures

for the corn processing business as set out in the Company’s 2012 annual report are composed of three

components: (1) the Disposal Group; (2) the Company’s subsidiary for the Remaining Group’s export

trading business; and (3) expenses incurred by the Group companies outside the Disposal Group allocated

to the corn processing business segment. As at 31 March 2013, the audited net asset value of the Disposal

Group amounted to approximately RMB1,020.8 million. Save for the loans advanced by the Company

to the Disposal Group and the Unpaid Dividend, there were also other intercompany balances between

the Disposal Group and the Remaining Group. It is expected that, except for the amount payable by the

Remaining Group to the Disposal Group of approximately RMB366.5 million to remain outstanding upon

Completion, all other intercompany balances between the Disposal Group and the Remaining Group

will be settled before Completion. The amount payable by the Remaining Group to the Disposal Group

in an amount of approximately RMB366.5 million represents the advance by the Disposal Group to the

Remaining Group to settle certain borrowings of the Remaining Group. In the course of negotiation

of terms of the Disposal, the Company intended to offset such amount payable against the Sale Loans.

However, the Company’s PRC legal advisers advised the Company that relevant PRC laws and regulations

on foreign exchange restricted the offset. The Company also considered to repay the amount payable at

R14.58(7)

LETTER FROM THE BOARD

16

discount after Completion. However, the repayment at discount would attract PRC tax under Corporate

Income Tax Law (中華人民共和國企業所得稅法). During the negotiation of terms of the Disposal with the Purchaser, the Company bargained for a higher consideration for the Sale Share and the Sale Loans

with an implied PBR represented by the Consideration to be higher than the historical PBR of both of

the Comparable Companies and the Company as at the date of the Agreement. The Purchaser finally

accepted the Company’s bargain to pay a total Consideration of RMB2,096 million (which is considered

by the Directors to be fair and reasonable as explained in the sub-section headed “Consideration” in the

section headed “The Agreement” above). On this basis, the Company agreed to settle the amount payable

in full after Completion, and considers that this arrangement is in the interests of the Company and the

Shareholders as a whole.

It is stated in the 2012 annual report of the Company that the corn processing business (including

starch sugars segment and corn co-products segment) recorded audited segmental assets and liabilities of

approximately RMB5,157.5 million and RMB2,462.0 million respectively as at 31 December 2012, with

a segmental net assets value of approximately RMB2,695.5 million. The difference between the audited

net assets value of the Disposal Group of approximately RMB1,020.8 million as at 31 March 2013 and the

net assets value of the corn processing business of approximately RMB2,695.5 million as at 31 December

2012 was mainly due to the elimination of the loans advanced by the Company to the Disposal Group

and the Unpaid Dividend. The loans advanced by the Company to the Disposal Group and the Unpaid

Dividend were intra-group balances and were not included in the segmental net assets value of the corn

processing business for the purpose of disclosure in the 2012 annual report of the Company. As a result,

the segmental net assets value of the corn processing business was grossed up by the loans advanced to

the Disposal Group of approximately RMB1,710.1 million and the Unpaid Dividend of approximately

RMB222.0 million as at 31 March 2013. The difference was also attributable to the fact that (a) the net

liabilities of the Company’s subsidiary for the Remaining Group’s export trading business, which does not

form part of the Disposal Group, were included in the segmental net assets value of the corn processing

business of the Group; and (b) the Disposal Group recorded net loss of approximately RMB16.3 million

for the three months ended 31 March 2013.

Further details of financial information of the Disposal Group are set out in the accountant’s report

on the Group issued by PwC contained in Appendix II to this circular.

INDEPENDENT VALUATION

(1) Valuation methodology and assumptions

The Company understands from the Independent Valuer that in assessing the value of machinery

and equipment of the Disposal Group, both market approach and depreciated replacement cost approach

have been used.

LETTER FROM THE BOARD

17

Set out below are the summarised market values of the machinery and equipment as appraised by

the Independent Valuer.

Item

Unaudited net book

value as at 30 April 2013

Fair marketvalue as at

30 April 2013

No. of production lines Capacity Use

No. of years used by the Group Status

(RMB’000) (RMB’000)

Corn starch production line

448,550 325,293 4 Annual capacity of 1,630,000 tonnes

Production of corn starch

1 to 8 In use

Maltodextrin production line

26,761 24,478 2 Annual capacity of 120,000 tonnes

Production of maltodextrin

1 In use

Dehydration production line

7,679 6,193 1 Efficiency of 52,500 gigawatts per hour

Dehydration 1 In use

Starch sugars production line

786,717 771,793 6 Annual capacity of 850,000 tonnes

Production of starch sugars

1 to 12 In use

Sodium gluconate production line

256,909 252,035 1 Annual capacity of 130,000 tonnes

Production of sodium gluconate

4 In use

Others 49,872 42,714

Production equipment

1,576,488 1,422,506

Electronic equipment

4,779 4,415

Other equipment

58,746 54,369

Motor vehicles 7,650 7,783

Installation and other

6,368 6,368

Total: 1,654,031 1,495,441

The Independent Valuer has conducted physical inspection of the machinery and equipment to

assess their physical condition such as whether the assets are kept in a reasonable condition and there is

any physical obsolescence, wear or tear.

LETTER FROM THE BOARD

18

The Company has discussed with the Independent Valuer regarding the valuation methodologies considered in the valuation and noted the reasons for not applying the income capitalization approach as explained by the Independent Valuer, details of which are set out in the valuation report on machinery and equipment contained in Appendix VI to this circular. The Company has also made reference to the valuation report on machinery as set out in the Company’s circular dated 2 March 2012. Vigers Appraisal & Consulting Limited were appointed to value certain plant and equipment to be acquired by the Group at that time. It was disclosed in the valuation report issued by Vigers Appraisal & Consulting Limited that the income approach was not adopted as it was extremely difficult to segregate an earning and expenses stream attributable only to specific piece of asset. Based on the above, the Company considers that the basis for not applying the income capitalization approach by the Independent Valuer is not unreasonable.

Market approach is employed in the valuation of the machinery and equipment for which there is a known used market. Under the market approach, the value of the appraised machinery and equipment is estimated through analysis of recent sales of comparable items. The Independent Valuer obtains the price information of the second hand machinery and equipment from second hand equipment traders and agencies. After obtaining the second hand price information, the Independent Valuer compares the differences between the subject machinery and equipment, and the comparable machinery and equipment in terms of, among other things, (a) used life; (b) capacity; (c) maintenance/condition observed during site inspection; (d) technology of the machinery and equipment; and (e) manufacturer. The Independent Valuer then determines an adjustment rate with reference to these factors and in accordance with its professional knowledge and experiences. The Independent Valuer advises that market approach is mainly employed for valuing motor vehicles and office equipment.

Due to the nature of the machinery and equipment, and in the limited known market based on comparables sales, the market approach cannot be used by the Independent Valuer for valuing majority of machinery and equipment. Therefore, a majority of machinery and equipment have been valued using the depreciated replacement cost approach, which takes into account the current cost of replacement/reproduction of the machinery and equipment less deductions for physical deterioration and all relevant forms of obsolescence and optimisation, but without provision for overtime, bonuses for labour, or premiums for materials or equipment.

Under the depreciated replacement cost approach, the Independent Valuer searches the market information of the machinery and equipment from the first hand market. After that, transportation expenses, insurance, commissioning (testing) costs and installation costs are added.

Market information relating to the machinery and equipment is obtained by the Independent Valuer from the following sources:

(a) Manufacturers, wholesalers or dealers: the Independent Valuer directly communicates with manufacturers, wholesalers and dealers for direct and reliable information of the new machinery and equipment of similar models such as quotations and listed prices;

(b) Business-related/industry websites: the Independent Valuer obtains recommended selling price and/or benchmark price information; and

(c) Reference magazines/books.

LETTER FROM THE BOARD

19

Following the determination of current cost of replacement/reproduction of the machinery and

equipment, the Independent Valuer assesses the amount of deductions for physical deterioration and

all relevant forms of obsolescence and optimization. Such assessment is made based on professional

judgment of the Independent Valuer taking into account, among other things, the following matters:

(a) Manufacturers: equipment made by some well-known manufacturers are more durable than

those manufactured by small producers;

(b) Maintenance policy: enquiring the maintenance policy of the Company, such as the

frequency of maintenance and inspection checking work and the qualification of engineers

involved;

(c) Physical conditions of the machinery and equipment observed during the physical inspection

by the Independent Valuer; and

(d) The period of machinery and equipment having been used and the typical useful life of

assets similar to subject machinery and equipment. The useful lives of the machinery

and equipment are in the range of 5 to 15 years, where production equipment, electronic

equipment, other equipment and motor vehicles have a useful life of 15 years, 5 years, 5

years and 8 to 10 years respectively. The useful life of assets is comparable to the useful life

of fixed assets as set out in the Company’s 2012 annual report.

As advised by the Independent Valuer, the Independent Valuer collects market information only

from reputable sources in order to ensure the accuracy. Moreover, cross checking has been made by the

Independent Valuer against its internal database and industry knowledge.

The Company is informed by the Independent Valuer that the market approach and depreciated

replacement cost approach are commonly adopted in valuing machinery and equipment.

The Company understands that the person in charge for the machinery and equipment valuation is

an Accredited Senior Appraiser (Business Valuation) of the American Society of Appraisers who has over

25 years’ experience in the valuation of intangible assets and plant and machinery. Moreover, the other

person involved in preparation of the machinery and equipment valuation report is an associate member

of Hong Kong Institution of Engineers, a member of Society of Automobile Engineer and an associate

member of the Institution of Mechanical Engineers, and has over 19 years’ experience in the valuation of

plant and machinery.

Further details of valuation methodology, basis of assumption and qualifications of the personnel of

the Independent Valuer responsible for preparation of the machinery and equipment valuation report are

set out in the valuation report on machinery and equipment contained in Appendix VI to this circular.

Based on the above, the Directors consider that the Independent Valuer’s valuation methodology

and basis of assumption in appraising the fair market value of machinery and equipment are fair and

reasonable.

LETTER FROM THE BOARD

20

(2) Valuation deficits

The valuation deficits of approximately RMB131.2 million represent the difference between

(1) the carrying amount of the property, plant and equipment and land use rights of approximately

RMB2,905.9 million as at 31 March 2013; and (2) the aggregate value of approximately RMB2,774.7

million representing (a) the market value on the property, machinery and equipment of the Disposal

Group appraised by the Independent Valuer; (b) the value of construction in progress recorded in financial

statements of the Disposal Group but such value could not be reflected in the independent valuation; and

(c) indicative market value of the properties of the Disposal Group pending registration of legal titles on

which the Independent Valuer has ascribed no commercial value.

The aforesaid difference is mainly due to the differences between valuation methodology and

accounting policies of the Group. According to the accounting policies of the Group, property, plant

and equipment are stated at historical cost less depreciation and impairment loss, if any. Historical cost

includes expenditure that is directly attributable to the acquisition of the items.

The Group acquired a brand new production line of starch with an expected annual capacity of

600,000 tonnes last year. The Group has conducted trial run and testing to fine tune the production line

before commencing commercial production. Total net expenses of approximately RMB118.3 million were

incurred by the Group during the trial run and testing period. Pursuant to the accounting policies of the

Group, the amount of approximately RMB118.3 million was capitalised as fixed assets in the financial

statements of the Group. The net book value of these net expenses amounted to approximately RMB116.4

million as at 31 March 2013.

As advised by the Independent Valuer, due to the nature of the machinery and equipment, and in

the limited known market based on comparable sales, the market approach is not the most appropriate

approach in this valuation. Therefore, a majority of the machinery and equipment have been valued using

the depreciated replacement cost approach, which takes into account the current cost of replacement/

reproduction of the machinery and equipment less deductions for physical deterioration and all relevant

forms of obsolescence and optimisation, but without provision for overtime, bonuses for labour, or

premiums for materials or equipment. Market approach is adopted by the Independent Valuer for the

equipment which is comparatively easy to be disposed of in the market, such as motor vehicles and office

equipment, etc. Therefore, both cost and market approaches are adopted in the course of valuation. It is

stated in the property valuation report contained in Appendix V to this circular that as the nature of the

buildings and structures of the Disposal Group cannot be valued on the basis of market value, they have

therefore been valued on the basis of their depreciated replacement costs. The depreciated replacement

cost approach considers the current cost of replacement (reproduction) of the buildings and improvements

less deductions for physical deterioration and all relevant forms of obsolescence and optimisation.

Under the depreciated replacement cost approach and market approach, the expenses for the trial

run and testing with a net book value of approximately RMB116.4 million as at 31 March 2013 will not be

taken into account in the course of the independent valuation.

LETTER FROM THE BOARD

21

(3) Comparison of target assets valuation

The assets acquired for the corn processing business as detailed in the Company’s circular dated 2

March 2012 in relation to the acquisition of certain target assets, including the aforesaid starch production

line and certain land and properties, were also included in the assets of the Disposal Group. As disclosed

in the Company’s circular dated 2 March 2012, the valuation of the target assets as at 31 December 2011

was approximately RMB852.2 million (which includes the capital value (after completion) of property

under construction (the “Property Under Construction”) and estimated cost of construction-in-progress of

machinery and equipment).

The consideration payable by the Company for the target assets was RMB825 million.

In the course of valuation, the Independent Valuer performed, among other things, the following

work:

(a) collecting the relevant information checklist of the assets to be appraised from the Company

and review the items on the checklist;

(b) conducting physical inspection of the target assets to assess their physical condition such as

whether the assets are kept in a reasonable condition and there is any physical obsolescence,

wear or tear;

(c) discussing with the Company to understand the maintenance arrangements and policies on

the target assets;

(d) obtaining evidence for the purchase cost of target assets, such as gathering information from

the suppliers and internet, etc;

(e) assessing the useful life and remaining useful life of the target assets by reference to, among

other things, (i) physical conditions of target assets observed during physical inspection; (ii)

the period of target assets having been used; and (iii) typical useful life of assets similar to

target assets; and

(f) estimating the replacement/reproduction costs for target assets by conducting extensive

research on replacement/reproduction costs for particular assets in public domain, such

as local suppliers and contractors, for fee quotation. In order to ensure the accuracy, the

Independent Valuer collects market information only from reputable sources.

Construction of target assets (including the Property Under Construction) has been completed

and target assets have been in use by the Company for corn processing. In assessing the market value at

existing state of the target assets as of 30 April 2013, the Independent Valuer has adopted the depreciated

replacement cost approach and market approach in respect of buildings, structures, machinery and

equipment.

Moreover, the machinery and equipment under the target assets include assets which are designed

for specific use so as to meet special needs of particular industry. Accordingly, the Independent Valuer

has also considered the original purchase cost (i.e. original book value) in the course of valuation.

LETTER FROM THE BOARD

22

The Independent Valuer has concluded that the market value (in existing state) of target assets,

which included the Property Under Construction as part of group I of property interest as set out in

Appendix V to this circular, as at 30 April 2013 was approximately RMB757.2 million, representing a

difference of approximately RMB95 million as compared to the capital value after completion of target

assets as at 31 December 2011 of approximately RMB852.2 million.

As advised by the Independent Valuer, the above difference in value of the target assets is mainly

attributable to the following reasons:

(a) Amount of amortisation and depreciation of target assets

The capital value after completion of target assets as set out in the circular of the Company

dated 2 March 2012 takes into account the amortisation and depreciation amount up to 31

December 2011 for existing assets but not for those assets under construction.

On the other hand, amortisation and depreciation amounts have to be deducted in arriving

at the market value (in existing state) of target assets as of 30 April 2013 because all target

assets have been in use by the Company. Aggregate amount of amortisation and depreciation of

approximately RMB54.0 million for the period from the respective dates of target assets recorded

as assets of the Company to 30 April 2013 have been determined by the Independent Valuer by

reference to their respective estimated remaining useful life.

(b) Purchase cost booked as original book value of target assets

The consideration paid by the Company for the target assets was RMB825 million.

According to the accounting policies of the Group, target assets were recorded at RMB825 million

as their original book value instead of the capital value (after completion) of approximately

RMB852.2 million.

As stated above, the Independent Valuer has also made reference to the original purchase

cost (i.e. original book value) of target assets in the course of valuation. This has resulted in a

variance of approximately RMB27.2 million (852.2 – 825).

(c) Change of physical conditions and others

It is stated above that the depreciated replacement cost approach takes into account the

current cost of replacement/reproduction of the machinery and equipment less deductions for

physical deterioration and all relevant forms of obsolescence and optimisation, but without

provision for overtime, bonuses for labour, or premiums for materials or equipment. Moreover,

change of physical conditions and other factors have also been considered by the Independent

Valuer in the course of valuation. All of these contribute to the difference.

LETTER FROM THE BOARD

23

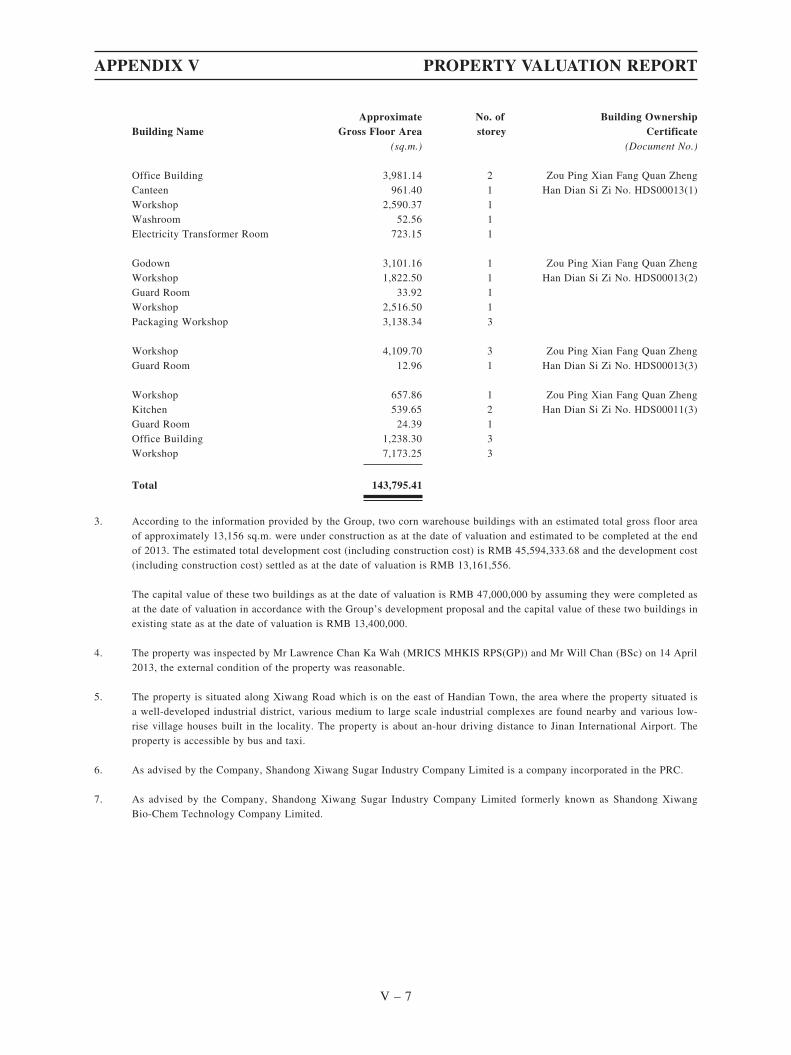

(4) Certain assets pending registration of legal titles

As set out in the Company’s circular dated 2 March 2012, Shandong Xiwang Sugar Industry

Company Limited (formerly known as Shandong Xiwang Bio-chem Technology Co., Ltd.) acquired

certain properties from Shandong Xiwang Pharmaceutical Company Limited (presently known as Xiwang

Pharmaceutical Company Limited). As disclosed in the valuation report on land and property as contained

therein, the title documents of these properties were registered under the name of Shandong Xiwang

Pharmaceutical Company Limited who is entitled to occupy, transfer, lease and mortgage the property,

and therefore the independent valuer could assign market value to the properties. As set out in the property

valuation report of the Disposal Group contained in Appendix V to this circular, Shandong Xiwang

Pharmaceutical Company Limited (not a member of the Disposal Group) is the current registered owner

of the property. As such, the Independent Valuer has ascribed no commercial value to these properties due

to the absence of the State-owned Land Use Certificates and Building Ownership Certificates registered

under the name of Shandong Xiwang Sugar Industry Company Limited (a member of the Disposal Group).

However, for indicative purpose, such properties were valued as at the date of valuation at approximately

RMB55.4 million assuming that the relevant certificates had been registered under the name of Shandong

Xiwang Sugar Industry Company Limited. As advised by the Company’s PRC legal advisers, there are

no material legal impediments for Shandong Xiwang Sugar Industry Company Limited to complete the

transfer registrations and obtain the title documents in respect of these properties. When determining

the total consideration for the Disposal, the Company and the Purchaser have taken into account such

indicative market value. On this basis, the Directors consider that the Shareholders’ interests have

not been adversely affected by the issues on the legal title of properties of the Disposal Group in the

determination of the terms of the Disposal. As the Disposal involves the proposed disposal of the Sale

Share and the Sale Loans only and not the properties concerned, and Completion is not conditional on

the availability of the State-owned Land Use Certificates and Building Ownership Certificates registered

in the names of members of the Disposal Group, the Disposal will not be affected by the absence of title

documents for these properties.

HISTORICAL RESULTS OF THE GROUP FROM 2006 TO 2012

The Group has principally been engaging in corn processing business with a focus on the

production of starch sugars and corn co-products in the PRC, and the distribution and the sale of such

products within and outside the PRC since its listing on the Stock Exchange in December 2005. In view of

the deteriorating results of the corn processing business, the Group has been participating in the property

development business since late 2012.

R14.58(2)

R14A.59(2)(a)

LETTER FROM THE BOARD

24

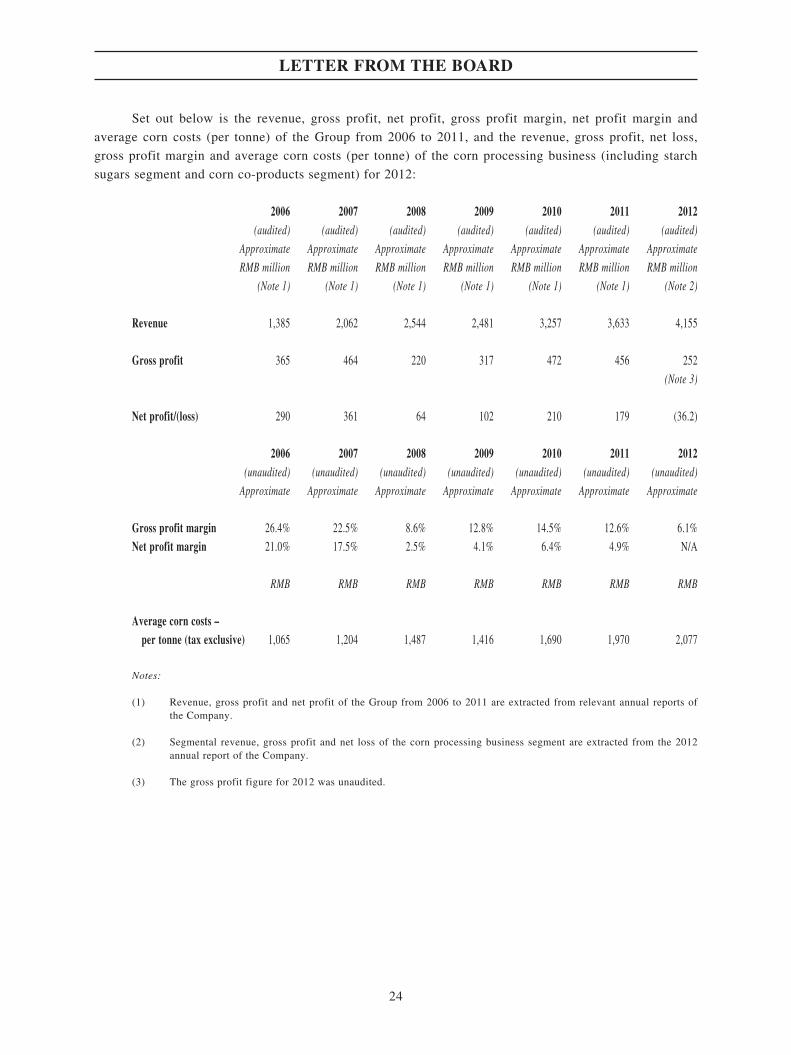

Set out below is the revenue, gross profit, net profit, gross profit margin, net profit margin and

average corn costs (per tonne) of the Group from 2006 to 2011, and the revenue, gross profit, net loss,

gross profit margin and average corn costs (per tonne) of the corn processing business (including starch

sugars segment and corn co-products segment) for 2012:

2006 2007 2008 2009 2010 2011 2012 (audited) (audited) (audited) (audited) (audited) (audited) (audited)

Approximate Approximate Approximate Approximate Approximate Approximate Approximate

RMB million RMB million RMB million RMB million RMB million RMB million RMB million

(Note 1) (Note 1) (Note 1) (Note 1) (Note 1) (Note 1) (Note 2)

Revenue 1,385 2,062 2,544 2,481 3,257 3,633 4,155

Gross profit 365 464 220 317 472 456 252

(Note 3)

Net profit/(loss) 290 361 64 102 210 179 (36.2)

2006 2007 2008 2009 2010 2011 2012 (unaudited) (unaudited) (unaudited) (unaudited) (unaudited) (unaudited) (unaudited)

Approximate Approximate Approximate Approximate Approximate Approximate Approximate

Gross profit margin 26.4% 22.5% 8.6% 12.8% 14.5% 12.6% 6.1%

Net profit margin 21.0% 17.5% 2.5% 4.1% 6.4% 4.9% N/A

RMB RMB RMB RMB RMB RMB RMB

Average corn costs – per tonne (tax exclusive) 1,065 1,204 1,487 1,416 1,690 1,970 2,077

Notes:

(1) Revenue, gross profit and net profit of the Group from 2006 to 2011 are extracted from relevant annual reports of the Company.

(2) Segmental revenue, gross profit and net loss of the corn processing business segment are extracted from the 2012 annual report of the Company.

(3) The gross profit figure for 2012 was unaudited.

LETTER FROM THE BOARD

25

(A) Measures adopted by the Board to promote the business of the Group

The Board has been committed to promote the business of the Group so as to enhance the return to

the Shareholders. In response to this, the Board has adopted the following measures since listing:

(1) Production capacity expansion

Following listing, the Group has applied part of the net proceeds to expand the production

capacity. The Group completed its crystalline glucose production capacity expansion at the

beginning of 2007 and raised the designed annual capacity from 250,000 tonnes to 800,000 tonnes.

The designed annual capacity of starch paste also increased from 400,000 tonnes to 1,000,000

tonnes. After such expansion, the Group’s designed annual capacity of corn processing was

1,500,000 tonnes. As the production capacity of corn starch reached its limit and corn starch is

an intermediate raw material for processing into the Group’s downstream products, the Group

acquired, among other things, a new production line of starch with an annual designed capacity

of 600,000 tonnes and an existing production line of starch with an annual designed capacity of

150,000 tonnes in 2012. The production expansion allowed the Group to capture the business

opportunities in the market, and further benefit from economy of scale which can improve the

production efficiency. It also allowed the Group to produce sufficient amount of products to serve

large customers who purchase large amount of starch sugars and corn co-products from the Group.

All of these result in recognition of the Group’s brand name in the market thus increasing market

shares.

(2) Development of higher value-added product to improve product mix

The Group regards its research and development capability as one of the key elements in

fostering the Group’s market position and promoting the Group’s future development. Accordingly,

the Group continues to dedicate its resource and effort in research and development so as to

develop higher value-added product to improve product mix. Supported by the Group’s research

and development team, the Group has successfully developed crystalline fructose.

Fructose is the sweetest sugar among all the natural sugars, therefore the amount to be used

and hence the calorie value in food is largely reduced. In addition, the fruity fragrance of fructose