Bahasa

Halaman

Hukum

China Consumer & Retail Private Equity - 2010 & Beyond

Consumer-Driven Investment Themes

Updated Aug 2010

Presented by K.C.Yoon

Jan 2010 Version 3.0 by KC Yoon

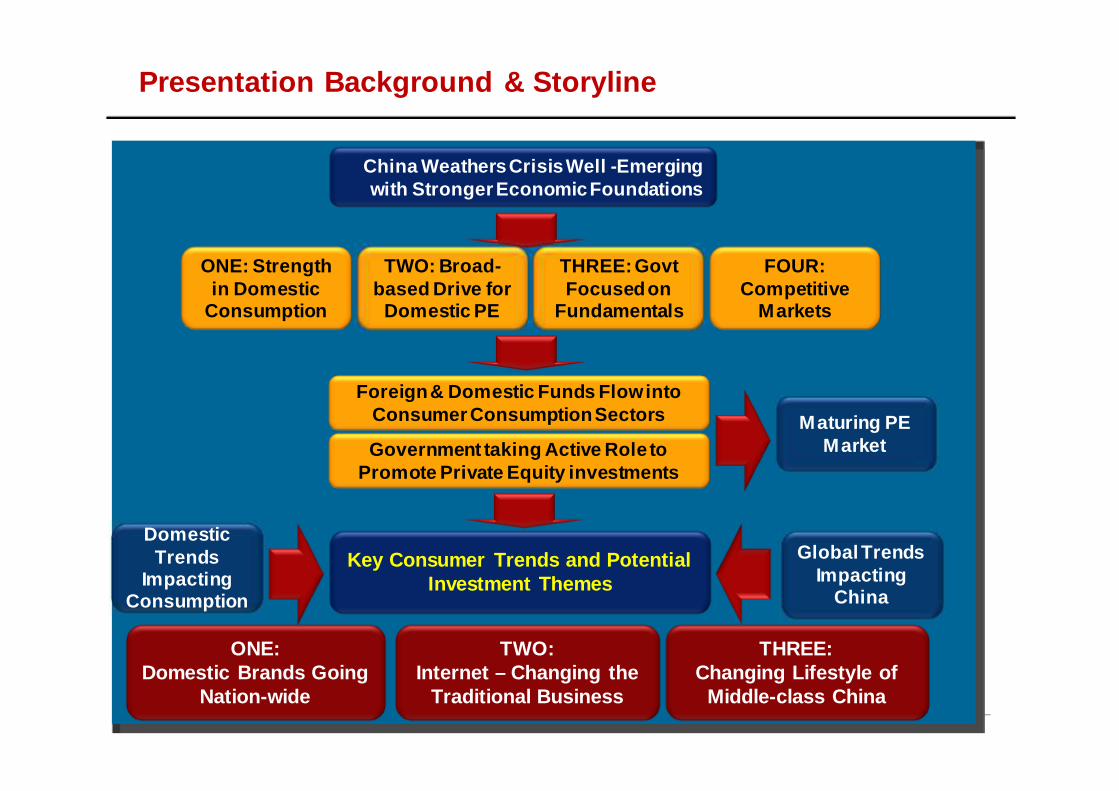

Presentation Background & Storyline

China Weathers Crisis Well -Emerging with Stronger Economic Foundations

Foreign & Domestic Funds Flow into Consumer Consumption Sectors

Key Consumer Trends and Potential Investment Themes

ONE: Domestic Brands Going

Nation-wide

TWO: Internet – Changing the

Traditional Business

ONE: Strength in Domestic

Consumption

TWO: Broad-based Drive for

Domestic PE

THREE: Govt Focused on

Fundamentals

FOUR: Competitive

Markets

Government taking Active Role to Promote Private Equity investments

Maturing PE Market

Global Trends Impacting

China

Domestic Trends

Impacting Consumption

THREE: Changing Lifestyle of

Middle-class China

Jan 2010 Version 3.0 by KC Yoon

China Weathers Crisis Well -Emerging with Stronger Economic Foundations

Foreign & Domestic Funds Flow into Consumer Consumption Sectors

Key Consumer Trends and Potential Investment Themes

ONE: Domestic Brands Going

Nation-wide

TWO: Internet – Changing the

Traditional Business

ONE: Strength in Domestic

Consumption

TWO: Broad-based Drive for

Domestic PE

THREE: Govt Focused on

Fundamentals

FOUR: Competitive

Markets

Government taking Active Role to Promote Private Equity investments

Maturing PE Market

Global Trends Impacting

China

Domestic Trends

Impacting Consumption

THREE: Changing Lifestyle of

Middle-class China

Focus of Today’s Presentation

In 2009: Macro-Factors Driving China’s Consumer Ec onomy

3

Growth of Chinese Middle-Class

Urbanization and Growth of Cities

Growth and Impact of the Internet

> 200 Cities with >1M residents

By2015, >300M lower-middle class; 100M luxury consumers

NOW >300M users;>RMB 120B online consumer sales

Demand for Home-related products and

services

Demand for lifestyle & convenient services

Demand for better healthcare

Over 110 high-consumer potential cities with 34% of GDP

Most widespread media- access middle-

class consumers

Growth of B2C

IKEA continue to open 2 stores/year

Sunning plans a B2C site

Korea SKTelecom to invest RMB500M in

qingxuan its B2C site

President 7-11 to open3-7 stores in Shanghai plans

for 300 stores in 3yrs

China Chain Nepstar drugstar opem/acquire 700

stores 2008, plans 3000

Letao to open largest online toy store in China

Sunning plans 500sqm stores in the rural areas

targetting for 3000

Retailers continue to expand network

In 2009: Key Consumer Trends with Investment Potent ial

+ 1

Growth of Chinese Middle-Class

Urbanization and Growth of Cities

Growth and Impact of the Internet

Govt Stimulus

“City-Living” Consumer Services

Affordable Luxury for the Young Affluent

“Mass Market” + “Good Enough”

Products

Online Consumer Brands

“Knowledge” Services

“Health”+ “Well-being” Services

Large Market

Criteria for Investment

High Growth

Able to Sustain Good

Margins

Defensible Niche

+“GREEN” - Increasingly

important Global trend

3

2010 & Beyond:Same Core Drivers but with New Focal Points

Growth of Chinese Middle-Class

Urbanization and Growth of Cities

Growth and Impact of the Internet

Broader Consumer Base

2nd/3rd Tier Cities New Growth

Areas

Mobile & Ecommerce

Create Market

Pop

ulat

ion

(mill

ions

) fr

om

2007

-202

5 : 6

Ne

w M

ega

city

C

lust

ers

Onl

ine

Sho

ppin

g G

row

th

2007

-201

3 (R

MB

‘00M

)

3

Chengdu Chengdu

Chongqing Chongqing

Shanghai Shanghai Wuhan Wuhan

Guangzhou Guangzhou Shenzhen Shenzhen

Beijing Beijing

Tianjin Tianjin

14.7 14.7 26.8 26.8 Beijing Beijing

17.1 17.1 25.1 25.1 Shanghai Shanghai

12.6 12.6 Tianjin Tianjin

12.4 12.4 Shenzhen Shenzhen

11.9 11.9 Wuhan Wuhan

10.7 10.7 Chongqing Chongqing

10.3 10.3 Chengdu Chengdu

10.1 10.1 Guangzhou Guangzhou

Beijing and Shanghai already

megacities in 2007

Beijing and Shanghai already

megacities in 2007

Chengdu

Chongqing

Shanghai Wuhan

Guangzhou Shenzhen

Beijing

Tianjin

8.2

6.4

7.9

8.6

8.3

8.7

14.7 26.8 Beijing

17.1 25.1 Shanghai

12.6 Tianjin

12.4 Shenzhen

11.9 Wuhan

10.7 Chongqing

10.3 Chengdu

10.1 Guangzhou

Beijing and Shanghai already

megacities in 2007

Source: McKinsey Global Institute CAC model, McKinsey Global Institute analysis

Source: iResearch report 2009

Page 7

Global Trend (1)- Focus on Capturing “Expanding” Middle-class Consumers

Shifting of Global Consumption to Markets

Creating the Largest “Middle-class”

Foreign Brands & Investors Making Targeted Entries

Acquisition of Strategic Stakes

Significant Stake in Large Meat

Processor “Yurun” by Goldman Sachs

Blackstone Invests in Agro-Wholesale Market & Logistic

Exchange

Rapid Consumption Growth

Domestic Brands are Gaining Recognition

Fast growth in meat

consumption

Suit Brand “endorsed by Warren

Buffet”

Aggressive & New Market

Global Apparel Groups GAP &

UNIQLO aggressive entry plans

Page 8

Global Trend (2) – As well as Capturing “Emerging” Luxury Consumers

Shifting of Growth to “Emerging” Markets i.e.

China

Increasing Trend of M&A of Luxury Brands

Cash-rich Chinese Companies Seeking Foreign Brands

Acquisition of “Volvo” by

Chinese automaker

Geely

Global Luxury Players seeking to Acquire Domestic Brands/Retailer?

Interest in European

Fashion Brands by Chinese

parties

Foreign Brand Expand/Acquire Chinese operations

Increased Market-entry by Foreign High-end Consumer Brands

Fashion Brands Burberry &

Mango Expands Aggressively

Proliferation of International Fashion & Lifestyle Brands..

Page 9

Domestic Trend – Rapid Rise in “Luxury” Consumers

Growth of Chinese “High Net Worth Individuals”

Values Associated with Luxury Drives Consumption

Chinese Luxury Needs Pervades through their Lifestyle (F&B, Clothes,

Personal care, Living..)

By 2009 China will have over 320,000 HNWI with Total Assets of USD1

trillion; Across 1 st to 3 rd Tier Cities

Source: China Merchant Bank & Bain Report 2009

China Herald 2009

“In 2008, Chinese Domestic Luxury Market was valued at USD8.6 billion” Bain “China to overtake Japan as the world’s 2 nd largest luxury market by 2010”

China Herald 2009

Middle-class Chinese Consumers aspire towards

similar value

China Consumer/Retail Investment Themes for 2010 & Beyond

Domestic Consumer Brands & Retailers Going Nation-wide/Capturing Market Share

to be Market Leaders 1

Products & Services Leveraging on Mobile+Internet to Overcome Traditional

Business Model for Rapid Growth 2

New Needs Created by Changing Lifestyle of Middle-class & Emerging Luxury Needs of

Chinese Consumers 3

Investment Theme Consolidation + M&A to Develop Domestic Market Lead ers

Right Strategy = Winning Fund

Factors Supporting & Driving M&A + Consolidation Market Activities Observed Sectors Impacted

EXPAND RETAIL REACH : Fashion brands, Electronic Good Retailer, Beauty Services seeking Nationwide reach

MULTI-BRAND/PRODUCT/SERVICE PORTFOLIO: Market Leaders building brand portfolio to drive

new revenue growth

FRAGMENTED MARKET SEGMENTS: Segments like Food Processing, Supermarket

Retail, F&B where ,market is large but fragmented

VALUE CHAIN INTEGRATION : M&A of upstream/downstream players to

increase margins & competitiveness eg. Food Processing

FOREIGN INTEREST IN DOMESTIC MARKETS: Foreign MNCs seeking market-entry through

M&A or building strategic stake

Ele

ctro

nic

Re

tail,

Mo

bile

Re

tail,

Su

pe

rma

rket

, C

on

veni

enc

e R

eta

il, F

&B

se

rvic

es, F

MC

G

pro

du

cts,

Fo

od

Pro

cess

ing,

S

po

rtsw

ear

& a

pp

are

l re

tail,

Ed

uca

tion

PE investment in mobile retailerFunTalk to acquire 6 regional distributors to become No.1 distributor/retailer of Mobile phones in China…

Tsingtao acquisiition ofJi’an brewery to consolidate Shandong market

1

Acquisition of 14% stake in Chinese shoe retailer to fund domestic expansion

Ctrip’s strategic 9.5% stake in Home Inns

PE Investments into several Chinese dairy companies

Potential Investment Targets

Leading regional brands in cosmetics, personal care, Food &

drinks, fashion wear, etc

Leading Niche Domestic Brands with Strengths in

Growing 2nd /3rd Tier Markets

Regional Retailers/ Services with Strong

2nd /3rd Tier Distribution Network

Strong Brands with Nationwide Potential currently limited by distribution reach

• Dabao domestic personal care brand acquired by P&G for USD300M

• “Yurun” processed ham generating strong sales

Supermarkets in inner cities, restaurant & food service chains,

etc

•Fujian-based supermarket retail chain dominates 2 nd/3rd tier cities and operates at higher-then industry margins

• KungFu Catering invested by leading VCs

Larger well-established brands or global brands that has potential to

be national market leader

• Burberry – franchised operations in China acquired by parent brand recognizing strong market potential • Ladies shoe brand retailer with strong product but growth cpr to industry peers limited by lack of expansion funds

1

Investment Theme 2 : Technology Led Growth of New Business Niches

Right Strategy = Winning Fund

Factors Supporting & Driving Growth Market Activities Observed Sectors Impacted

EXPANDING BRAND REACH TO 2 nd & 3 rd TIER CITIES:

Global luxury brands have successfully created awareness online

IMPACT OF SOCIAL INTERNET :

Peer Interaction & social networks have been used to build brand and product knowldge

IMPROVING TRANSACTION INFRASTRUCTURE: Good Customer online experience due to efficient payment & low cost door-to-door

delivery system

SHIFT IN VALUE PROPOSITION : Online travel has captured major & significant

market share

CREATE NEW CONSUMER RETAIL CHANNEL : Fashion Retail Online experiencing rapid growth

& TV shopping

Ele

ctro

nic

Re

tail,

Mo

bile

, fa

shio

n (

esp

eci

ally

clo

thin

g) re

tail,

tra

vel

inte

rne

t B

2C

/;C2

C s

erv

ices

Explosive growth seen in online retail (eg.clothing in2009 valued at RMB2.4 billion or 9.7% of total clothing retail) VANCL founded in 2007 & invested by VCs SAIF, IDG is leader with 24% market share

2

Lancome pioneered online beauty community “Lancome Beauty Rose” capturing 4M subscribers

Potential Investment Targets

New Business Models Resulting Technology & Change in Value Proposition

+ Create New Market Niche

New Retail Channels with Nationwide Reach +

Ability to Rapidly Build Brand at Low Cost

• Hunan TV & Taobao launching TV Home shopping channel to target lucrative & growing market

• Online Jewellery Retailer with offline retail POS for customer service

•

Sales of China’s TV Shopping will reach RMB 20billion in 2008

Innovative Retail ers Leveraging New Media (internet/mobile/digital TV) – Pure

online or “offline”+ “online”

• Mobile content download retail service as a result of growth of mobile users and obstacle to access conte nt

Propriety Customer Interface + Attractive

Retail Kiosks + Professional Service

Mobile Content Providers

Mobile Operators/

Mobile Retailers

In

nova

tive

Bus

ines

s M

odel

s in

M

obile

+ I

nter

net S

pace

2

• Innovative “group buying” sites driving consumers to bulk buy for high discounts

Investment Theme 3 : Changing “Middle-Class” & “Luxury” Consumer Lifesty le

Right Strategy = Winning Fund

Factors Supporting & Driving Growth Market Activities Observed Sectors Impacted

ENJOY GREATER LEISURE & ENTERTAINMENT : Luxury Travel Services, Niche Luxury Hotels &

Holiday Resorts

SPENDING ON CHILDREN NEEDS: Affordability to spend on “single” child esp

educationi.e. Special K1-12 Schools, Learning Products & Services

FOCUS ON SELF-IMPROVEMENT & PERSONAL IMAGE:

Consumer-focused services from beauty-care, Adult education, Sports Coaching, etc

DEMAND FOR STATUS : Membership Exclusive Social Clubs & Services, Fashion Apparel & Accessories, Premium Food

FOCUS ON HEALTHY LIFESTYLE : Demand for healthcare products/services,

Sports Services, Health Food

He

alth

care

De

vice

s +

Se

rvic

es,

”Hea

lth” F

oo

d,

Ph

arm

a R

eta

il,E

duca

tion

Se

rvic

es,

Me

dia

&

En

tert

ain

men

t, T

rave

l S

erv

ices

, Lu

xury

Ho

tesl

&

Re

sort

s

Pearson acquisition of China’s WSI- leading English learning school

Sequoia’s investment into China’s leading animation company as demand for cartoon/animation content grows

3

Swiss Luxury Travel Group acquisition of strategic 10% stake in Chinese travel service company ET-China Intl.

Legend Capital investment into hair accessory retail with unique service model

Potential Investment Targets

Niche- Luxury Domestic Branded

Products & Services for Status

Sports, Health & Medical Related Products & Services + Retail Service Chains

Domestic Fashion Designer Brands & Beauty Care

services

• Family-focused Chinese history-based themed retail/entertainment venues;

• Regional cuisine themed Food service

Family Resorts & Parks; Themed F&B Chains

Sports & Spa Services; Health Food Supplements & Health Products; Medical Services;

Beauty care & Spa Chains

• Home-grown fashion design houses

• Exclusive Members Social Club

• Family-use home healthcare check-up devices

• Health Supplements • Massage & Fitness Products

• Fitness, Yoga & Sports Coaching Services

• Specialist Medical Services, Hospitals, etc

3

Lifestyle & Entertainment

Services & Retail Chains

Spotlight on Emerging Agro-Food Sub-Sectors (1)

Expenditure on Food still accounts >25% of Spend even in High Income Households

WHY? Chinese Agro-industry the Next Biggest Concer n of the Govt (1)Raise rural income(2) Drives overall consumption

Huge Market with Favorable Consumer Behavior Changes

A.T. Kearney (2007) estimates that the

growing middle class spends an increasing amount on food, with annual sales of

branded food products expected to grow from US $150 billion to US $650 billion by

2017.

Chinese Consumers Willingness for New Taste : DataMonitor’s Survey shows 44% vs 30% for

Global Consumers

Higher Income Consumers Pay for Premium Food :

DataMonitor’s Survey shows 67% of surveyed had purchased Premium Food in last 6 months

Data from DataMonitor’s survey in July 2009

Spotlight on Emerging Agro-Food Sub-Sectors (2)

Life Cycle of Food & Beverage Products in China

DBS Vickers Report 2010

Chocolate

Bakery

Icecream

Wine

Milk

Processed Meat

Sun-Rise Fast- Growth Decelerating Matured

Juice

Bottled Water

Instant Noodles

Beer

15X 17X 5X 4X 8X 5X 3X 2X 1X 1X

20% 20% 25% 30% 30% 25% 35% 40% 75% 80%

Per Capita Consumption

JPN/CHN Multiple

Penetration in China

Spotlight on Emerging Agro-Food Sub-Sectors (3)

Branded Premium Food (Organic, Safe,

GREEN)

Premium Food Products

• Fresh fruits like strawberry, blackberry and their by-products i.e. juices • Baked food & snacks • Premium Beef

TCM-related Health/Nutraceutical

Products

Agro-Food Industry-Focused Support

Services

USD9BN NUTRACEUTICAL MARKET OPPORTUNITY

• China largest worldwide producer of

nutraceutical ingredients; and expected to surpass the US as largest consumer by 2013

• Over 3,000 manufacturers of nutraceutical products in China, with an annual production value of over $6.3 billion

• Sales in China are expected US$8.8 billion in 2009, with CAGR of 15.2%

China produces 80% of the World’s Ginseng and Dominates most other key TCM herbs

Key Services

• National Cold Chain Logistics Service • Food Distribution Services with nationwide reach • Wholesale & Market Making Services

Page 20

Contact :

K.C Yoon Mobile: +86 18675573803 Email : [email protected] Skype: kcyoon07

Linkedin: http://cn.linkedin.com/in/kcyoon

Thank you THE END

Copyright © 2022 FDOKUMEN