PE Report 1213 p2

10

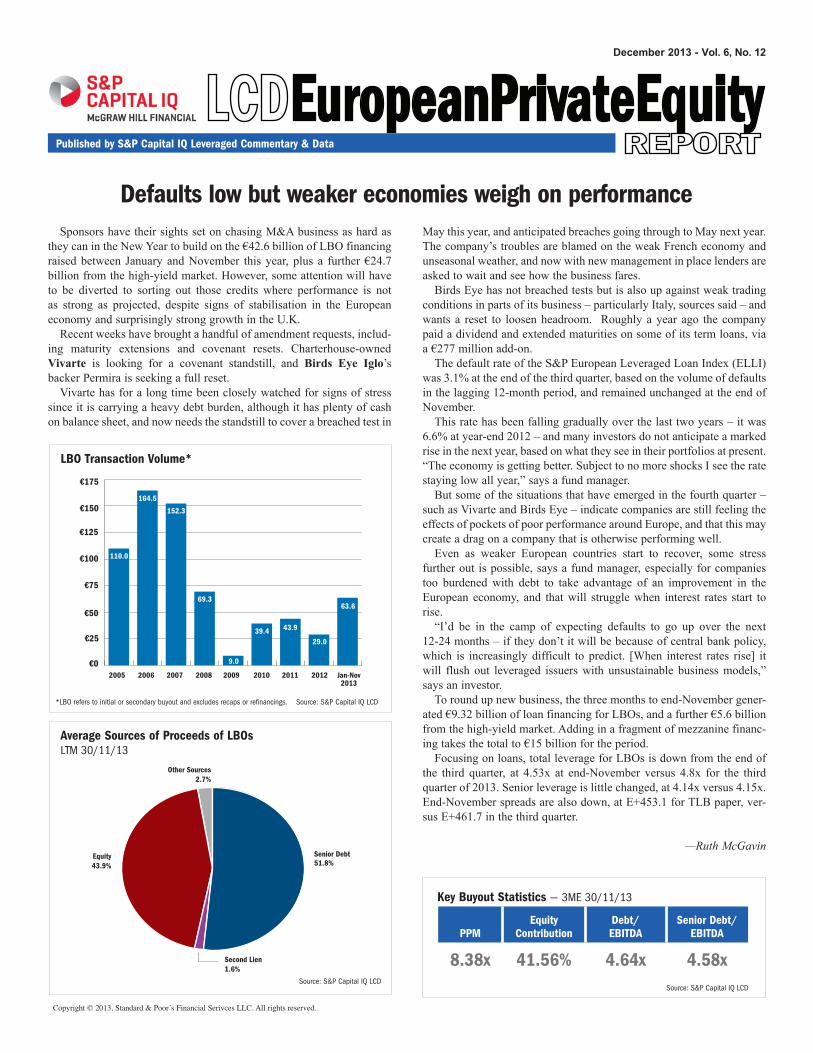

Published by S&P Capital IQ Leveraged Commentary & Data Sponsors have their sights set on chasing M&A business as hard as they can in the New Year to build on the €42.6 billion of LBO financing raised between January and November this year, plus a further €24.7 billion from the high-yield market. However, some attention will have to be diverted to sorting out those credits where performance is not as strong as projected, despite signs of stabilisation in the European economy and surprisingly strong growth in the U.K. Recent weeks have brought a handful of amendment requests, includ- ing maturity extensions and covenant resets. Charterhouse-owned Vivarte is looking for a covenant standstill, and Birds Eye Iglo’s backer Permira is seeking a full reset. Vivarte has for a long time been closely watched for signs of stress since it is carrying a heavy debt burden, although it has plenty of cash on balance sheet, and now needs the standstill to cover a breached test in May this year, and anticipated breaches going through to May next year. The company’s troubles are blamed on the weak French economy and unseasonal weather, and now with new management in place lenders are asked to wait and see how the business fares. Birds Eye has not breached tests but is also up against weak trading conditions in parts of its business – particularly Italy, sources said – and wants a reset to loosen headroom. Roughly a year ago the company paid a dividend and extended maturities on some of its term loans, via a €277 million add-on. The default rate of the S&P European Leveraged Loan Index (ELLI) was 3.1% at the end of the third quarter, based on the volume of defaults in the lagging 12-month period, and remained unchanged at the end of November. This rate has been falling gradually over the last two years – it was 6.6% at year-end 2012 – and many investors do not anticipate a marked rise in the next year, based on what they see in their portfolios at present. “The economy is getting better. Subject to no more shocks I see the rate staying low all year,” says a fund manager. But some of the situations that have emerged in the fourth quarter – such as Vivarte and Birds Eye – indicate companies are still feeling the effects of pockets of poor performance around Europe, and that this may create a drag on a company that is otherwise performing well. Even as weaker European countries start to recover, some stress further out is possible, says a fund manager, especially for companies too burdened with debt to take advantage of an improvement in the European economy, and that will struggle when interest rates start to rise. “I’d be in the camp of expecting defaults to go up over the next 12-24 months – if they don’t it will be because of central bank policy, which is increasingly difficult to predict. [When interest rates rise] it will flush out leveraged issuers with unsustainable business models,” says an investor. To round up new business, the three months to end-November gener- ated €9.32 billion of loan financing for LBOs, and a further €5.6 billion from the high-yield market. Adding in a fragment of mezzanine financ- ing takes the total to €15 billion for the period. Focusing on loans, total leverage for LBOs is down from the end of the third quarter, at 4.53x at end-November versus 4.8x for the third quarter of 2013. Senior leverage is little changed, at 4.14x versus 4.15x. End-November spreads are also down, at E+453.1 for TLB paper, ver- sus E+461.7 in the third quarter. —Ruth McGavin Defaults low but weaker economies weigh on performance Key Buyout Statistics — 3ME 30/11/13 PPM Equity Contribution Debt/ EBITDA Senior Debt/ EBITDA 8.38x 41.56% 4.64x 4.58x Equity 43.9% Other Sources 2.7% Senior Debt 51.8% Second Lien 1.6% Average Sources of Proceeds of LBOs LTM 30/11/13 €0 €25 €50 €75 €100 €125 €150 €175 2007 2011 2012 Jan-Nov 2013 2010 2009 2005 2006 2008 164.5 152.3 110.0 69.3 39.4 43.9 29.0 63.6 9.0 LBO Transaction Volume* LCD EuropeanPrivateEquity REPORT December 2013 - Vol. 6, No. 12 Copyright © 2013, Standard & Poor’s Financial Serivces LLC. All rights reserved. *LBO refers to initial or secondary buyout and excludes recaps or refinancings. Source: S&P Capital IQ LCD Source: S&P Capital IQ LCD Source: S&P Capital IQ LCD

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of PE Report 1213 p2

Published by S&P Capital IQ Leveraged Commentary & Data

Sponsors have their sights set on chasing M&A business as hard as they can in the New Year to build on the €42.6 billion of LBO financing raised between January and November this year, plus a further €24.7 billion from the high-yield market. However, some attention will have to be diverted to sorting out those credits where performance is not as strong as projected, despite signs of stabilisation in the European economy and surprisingly strong growth in the U.K.

Recent weeks have brought a handful of amendment requests, includ-ing maturity extensions and covenant resets. Charterhouse-owned Vivarte is looking for a covenant standstill, and Birds Eye Iglo’s backer Permira is seeking a full reset.

Vivarte has for a long time been closely watched for signs of stress since it is carrying a heavy debt burden, although it has plenty of cash on balance sheet, and now needs the standstill to cover a breached test in

May this year, and anticipated breaches going through to May next year. The company’s troubles are blamed on the weak French economy and unseasonal weather, and now with new management in place lenders are asked to wait and see how the business fares.

Birds Eye has not breached tests but is also up against weak trading conditions in parts of its business – particularly Italy, sources said – and wants a reset to loosen headroom. Roughly a year ago the company paid a dividend and extended maturities on some of its term loans, via a €277 million add-on.

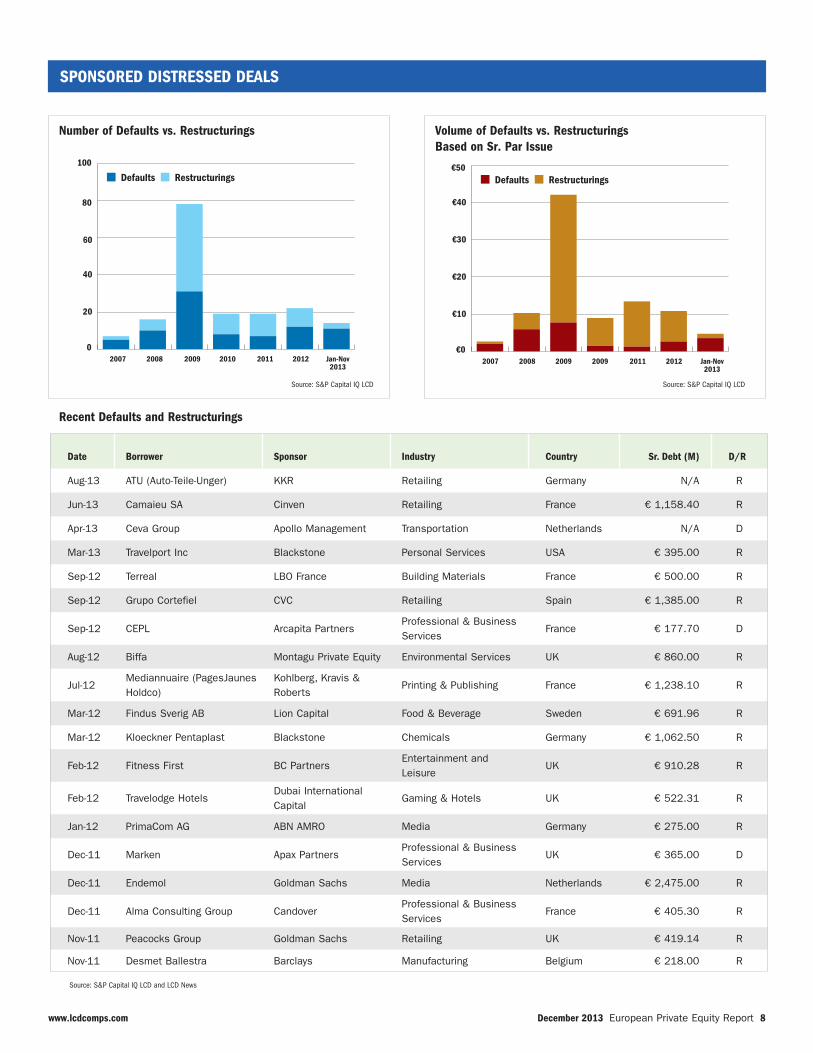

The default rate of the S&P European Leveraged Loan Index (ELLI) was 3.1% at the end of the third quarter, based on the volume of defaults in the lagging 12-month period, and remained unchanged at the end of November.

This rate has been falling gradually over the last two years – it was 6.6% at year-end 2012 – and many investors do not anticipate a marked rise in the next year, based on what they see in their portfolios at present. “The economy is getting better. Subject to no more shocks I see the rate staying low all year,” says a fund manager.

But some of the situations that have emerged in the fourth quarter – such as Vivarte and Birds Eye – indicate companies are still feeling the effects of pockets of poor performance around Europe, and that this may create a drag on a company that is otherwise performing well.

Even as weaker European countries start to recover, some stress further out is possible, says a fund manager, especially for companies too burdened with debt to take advantage of an improvement in the European economy, and that will struggle when interest rates start to rise.

“I’d be in the camp of expecting defaults to go up over the next 12-24 months – if they don’t it will be because of central bank policy, which is increasingly difficult to predict. [When interest rates rise] it will flush out leveraged issuers with unsustainable business models,” says an investor.

To round up new business, the three months to end-November gener-ated €9.32 billion of loan financing for LBOs, and a further €5.6 billion from the high-yield market. Adding in a fragment of mezzanine financ-ing takes the total to €15 billion for the period.

Focusing on loans, total leverage for LBOs is down from the end of the third quarter, at 4.53x at end-November versus 4.8x for the third quarter of 2013. Senior leverage is little changed, at 4.14x versus 4.15x. End-November spreads are also down, at E+453.1 for TLB paper, ver-sus E+461.7 in the third quarter.

—Ruth McGavin

Defaults low but weaker economies weigh on performance

Key Buyout Statistics — 3ME 30/11/13

PPMEquity

ContributionDebt/ EBITDA

Senior Debt/EBITDA

8.38x 41.56% 4.64x 4.58x

Equity43.9%

Other Sources2.7%

Senior Debt51.8%

Second Lien1.6%

Average Sources of Proceeds of LBOsLTM 30/11/13

€0

€25

€50

€75

€100

€125

€150

€175

2007 2011 2012 Jan-Nov2013

201020092005 2006 2008

164.5

152.3

110.0

69.3

39.4 43.9

29.0

63.6

9.0

LBO Transaction Volume*

LCDEuropeanPrivateEquityREPORT

December 2013 - Vol. 6, No. 12

Copyright © 2013, Standard & Poor’s Financial Serivces LLC. All rights reserved.

*LBO refers to initial or secondary buyout and excludes recaps or refinancings. Source: S&P Capital IQ LCD

Source: S&P Capital IQ LCD Source: S&P Capital IQ LCD

December 2013 European Private Equity Report 2www.lcdcomps.com

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

7.0x

2007 2011 2012 Jan-Nov2013

201020092005 2006 2008

First Lien/EBITDA Second Lien/EBITDA Other Debt/EBITDA

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

2007 2011 2012 Jan-Nov2013

201020092005 2006 2008

Debt/EBITDA Equity/EBITDA Other/EBITDA

€0

€25

€50

€75

€100

€125

€150

€175

2007 2011 2012 Jan-Nov2013

201020092005 2006 2008

Buyouts Other Sponsored Deals

0%

10%

20%

30%

40%

50%

60%

2007 2011 2012 Jan-Nov2013

201020092005 2006 2008

Retained Equity/Vendor Financing

Equi

ty a

s a

Perc

enta

ge o

f Tot

al S

ourc

es

Contributed Equity

Industry Diversification

Country Diversification

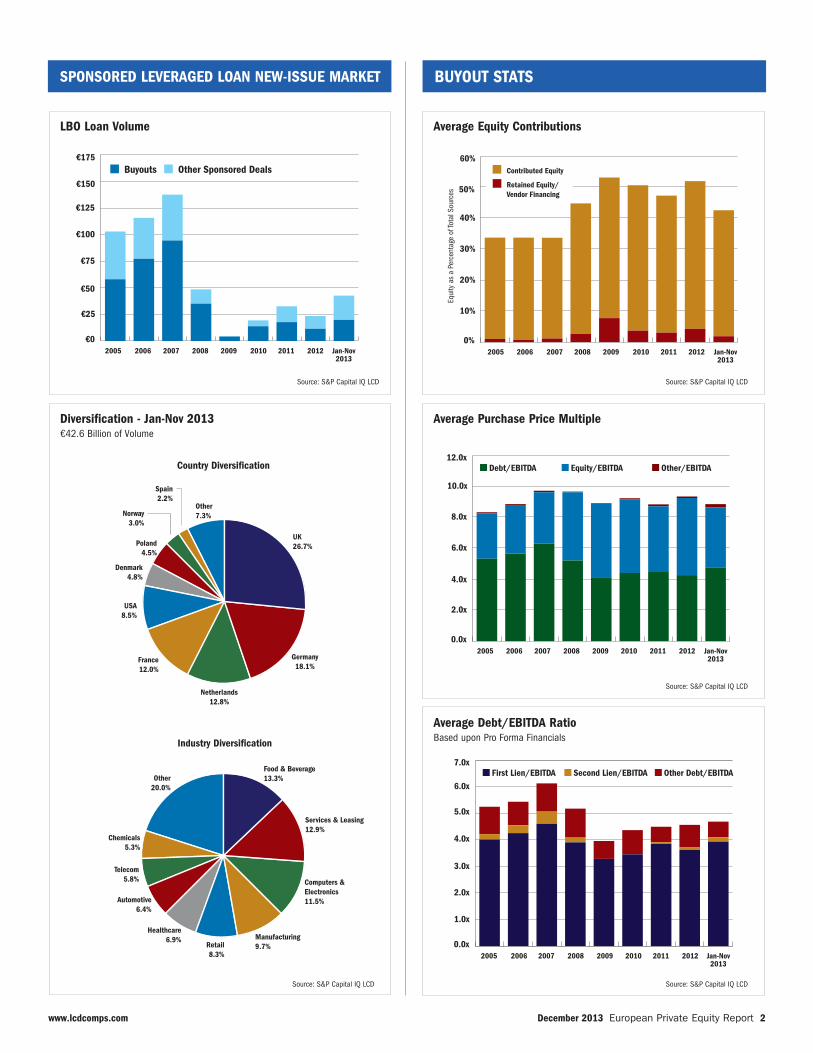

Average Debt/EBITDA RatioBased upon Pro Forma Financials

Diversification - Jan-Nov 2013€42.6 Billion of Volume

Average Purchase Price Multiple

LBO Loan Volume Average Equity Contributions

SPONSORED LEVERAGED LOAN NEW-ISSUE MARKET BUYOUT STATS

UK26.7%

Netherlands12.8%

Norway3.0%

Denmark4.8%

France12.0%

Germany18.1%

USA8.5%

Poland4.5%

Spain2.2%

Other7.3%

Chemicals5.3%

Food & Beverage13.3%

Manufacturing9.7%

Healthcare6.9%

Retail8.3%

Computers & Electronics11.5%

Services & Leasing12.9%

Telecom5.8%

Automotive6.4%

Other20.0%

Source: S&P Capital IQ LCD Source: S&P Capital IQ LCD

Source: S&P Capital IQ LCD

Source: S&P Capital IQ LCD Source: S&P Capital IQ LCD

December 2013 European Private Equity Report 3www.lcdcomps.com

PRIVATE EQUITY FUNDING

LTM

Sponsor Share

CVC 7.94%

Carlyle Group 7.94%

Bain Capital 6.35%

Kohlberg, Kravis & Roberts 4.76%

EQT Partners 3.17%

Advent International 3.17%

BC Partners 3.17%

Cinven Ltd 3.17%

Bridgepoint Capital 3.17%

Teachers' Private Capital 3.17%

Permira 3.17%

Charterhouse Equity Partners 3.17%

PAI Management 3.17%

Joh. A. Benckiser 1.59%

3i plc 1.59%

Golden Gate Capital 1.59%

Insight Ventures 1.59%

Clayton, Dubilier & Rice 1.59%

Silver Lake Partners 1.59%

Pamplona Capital Management 1.59%

Last 3 Years

Sponsor Share

Carlyle Group 5.59%

CVC 5.03%

Advent International 4.47%

AXA Equity 4.47%

Bain Capital 4.47%

BC Partners 3.35%

Cinven Ltd 3.35%

Charterhouse Equity Partners 3.35%

Kohlberg, Kravis & Roberts 3.35%

Bridgepoint Capital 3.35%

EQT Partners 2.79%

3i plc 2.79%

Nordic Capital 2.23%

PAI Management 2.23%

Blackstone Group 1.68%

Apax Partners 1.68%

Permira 1.68%

Altor Equity Partners 1.68%

LBO France Gestion 1.68%

Clayton, Dubilier & Rice 1.12%

€0B

€30B

€60B

€90B

€120B

€150B

2008 2009 2010 2011 2012 Jan-Nov2013

0

90

180

270

360

450

207 169

391

255

201154

65.7

111.2

Aggr

egat

e Co

mm

itmen

ts

Number of Funds Raised

44.550.2

64.9

73.8

€0B

€50B

€100B

€150B

€200B

€250B

2011 2012 Jan-Nov2013

20102009200820072006

Europe Focused Fundraising Private Equity Dry Powder in Europe

Source: PreqinSource: Preqin

Note: The analysis reflects sponsors related to buyouts (initial and secondary) only and is based all sponsors named on a transaction. Share is based upon transaction count.

MOST ACTIVE SPONSORS - TOP 20

Source: S&P Capital IQ LCD

December 2013 European Private Equity Report 4www.lcdcomps.com

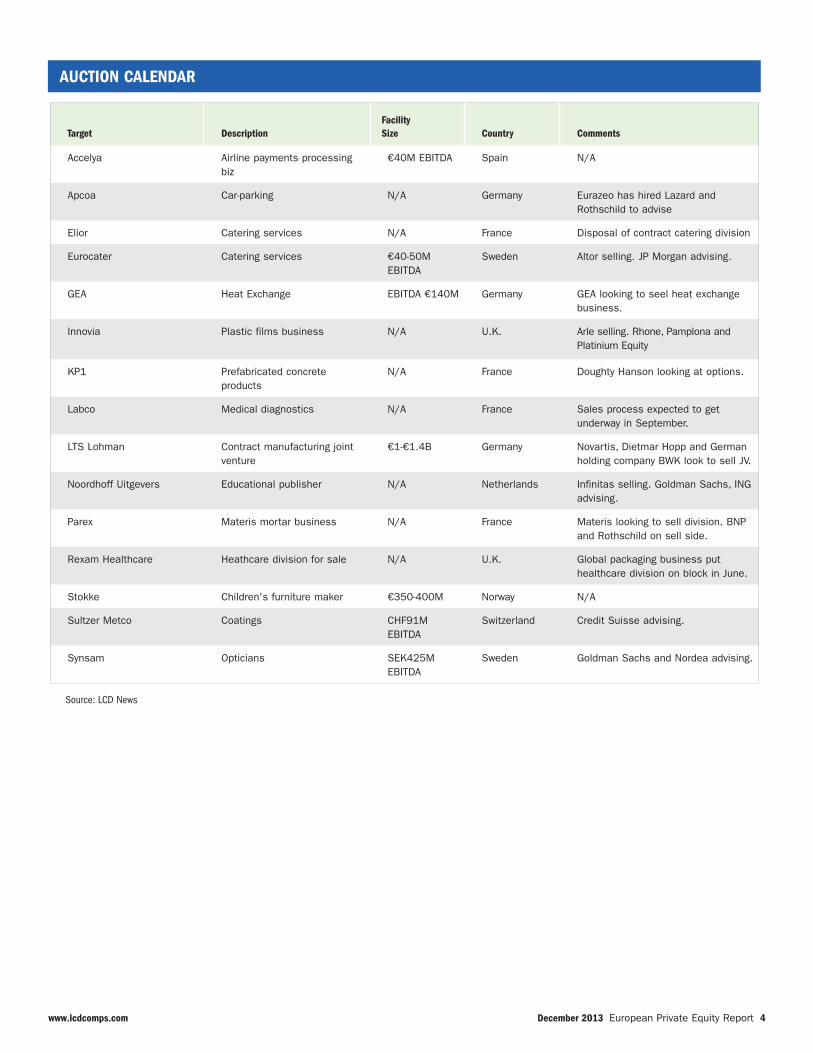

AUCTION CALENDAR

Source: LCD News

Target DescriptionFacility Size Country Comments

Accelya Airline payments processing biz

€40M EBITDA Spain N/A

Apcoa Car-parking N/A Germany Eurazeo has hired Lazard and Rothschild to advise

Elior Catering services N/A France Disposal of contract catering division

Eurocater Catering services €40-50M EBITDA

Sweden Altor selling. JP Morgan advising.

GEA Heat Exchange EBITDA €140M Germany GEA looking to seel heat exchange business.

Innovia Plastic films business N/A U.K. Arle selling. Rhone, Pamplona and Platinium Equity

KP1 Prefabricated concrete products

N/A France Doughty Hanson looking at options.

Labco Medical diagnostics N/A France Sales process expected to get underway in September.

LTS Lohman Contract manufacturing joint venture

€1-€1.4B Germany Novartis, Dietmar Hopp and German holding company BWK look to sell JV.

Noordhoff Uitgevers Educational publisher N/A Netherlands Infinitas selling. Goldman Sachs, ING advising.

Parex Materis mortar business N/A France Materis looking to sell division. BNP and Rothschild on sell side.

Rexam Healthcare Heathcare division for sale N/A U.K. Global packaging business put healthcare division on block in June.

Stokke Children's furniture maker €350-400M Norway N/A

Sultzer Metco Coatings CHF91M EBITDA

Switzerland Credit Suisse advising.

Synsam Opticians SEK425M EBITDA

Sweden Goldman Sachs and Nordea advising.

December 2013 European Private Equity Report 5www.lcdcomps.com

0.0

1.0

2.0

3.0

4.0

2007 2010 2011 2012 Nov-1320092006 2008

2013

20202014

2015

2016

2017

2018

2019

80

84

88

92

96

1Q13 4Q134Q11 1Q12 2Q12 3Q12 4Q12 2Q13 3Q13

Average Bid Weighted Average Bid

0%

20%

40%

60%

80%

100%

20092008 2010 2011 2012 Jan-Nov2013

BB B CCC/CC Others NR

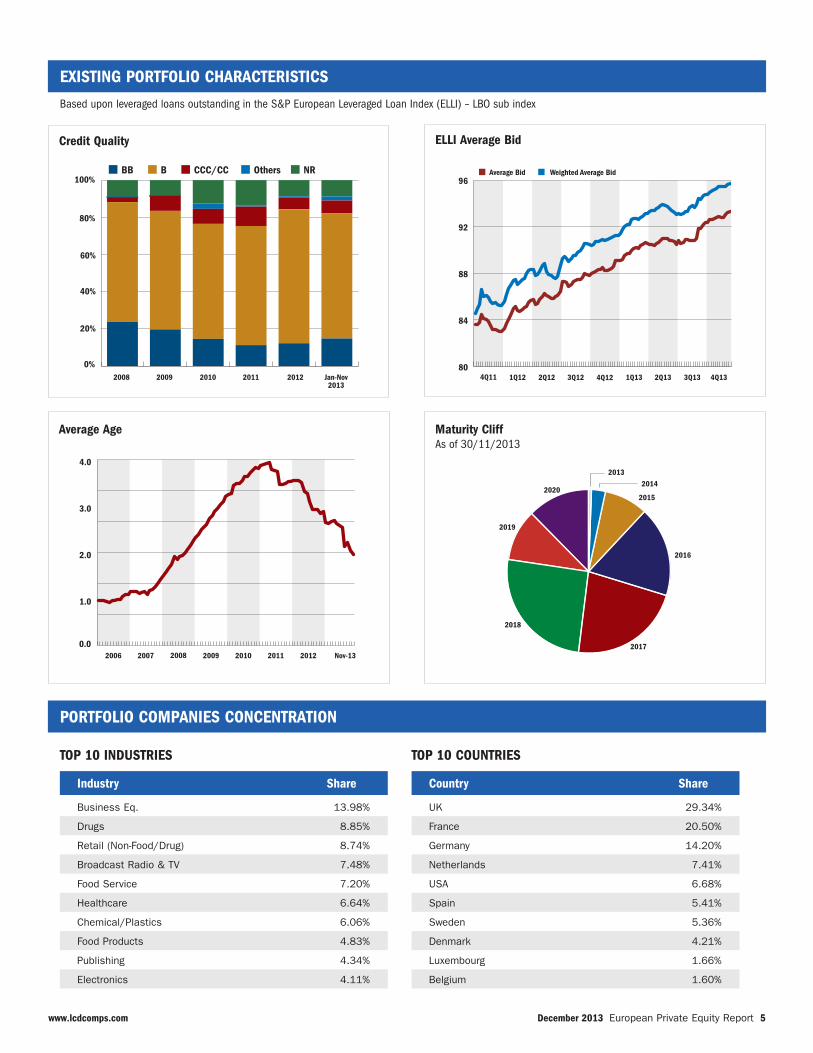

Average Age Maturity CliffAs of 30/11/2013

ELLI Average BidCredit Quality

EXISTING PORTFOLIO CHARACTERISTICS

PORTFOLIO COMPANIES CONCENTRATION

TOP 10 INDUSTRIES

Industry Share

Business Eq. 13.98%

Drugs 8.85%

Retail (Non-Food/Drug) 8.74%

Broadcast Radio & TV 7.48%

Food Service 7.20%

Healthcare 6.64%

Chemical/Plastics 6.06%

Food Products 4.83%

Publishing 4.34%

Electronics 4.11%

TOP 10 COUNTRIES

Country Share

UK 29.34%

France 20.50%

Germany 14.20%

Netherlands 7.41%

USA 6.68%

Spain 5.41%

Sweden 5.36%

Denmark 4.21%

Luxembourg 1.66%

Belgium 1.60%

Based upon leveraged loans outstanding in the S&P European Leveraged Loan Index (ELLI) – LBO sub index

December 2013 European Private Equity Report 6www.lcdcomps.com

0%

20%

40%

60%

80%

100%

20092008 2010 2011 2012 Jan-Nov2013

Re�nancing Recapitalization IPO Sec. LBO Other

0

10

20

30

40

50

60

70

Mon

ths

2008 2009 2010 2011 2012 Jan-Nov2013

Full Repayment of Sponsored Deals Average Time to Repayment

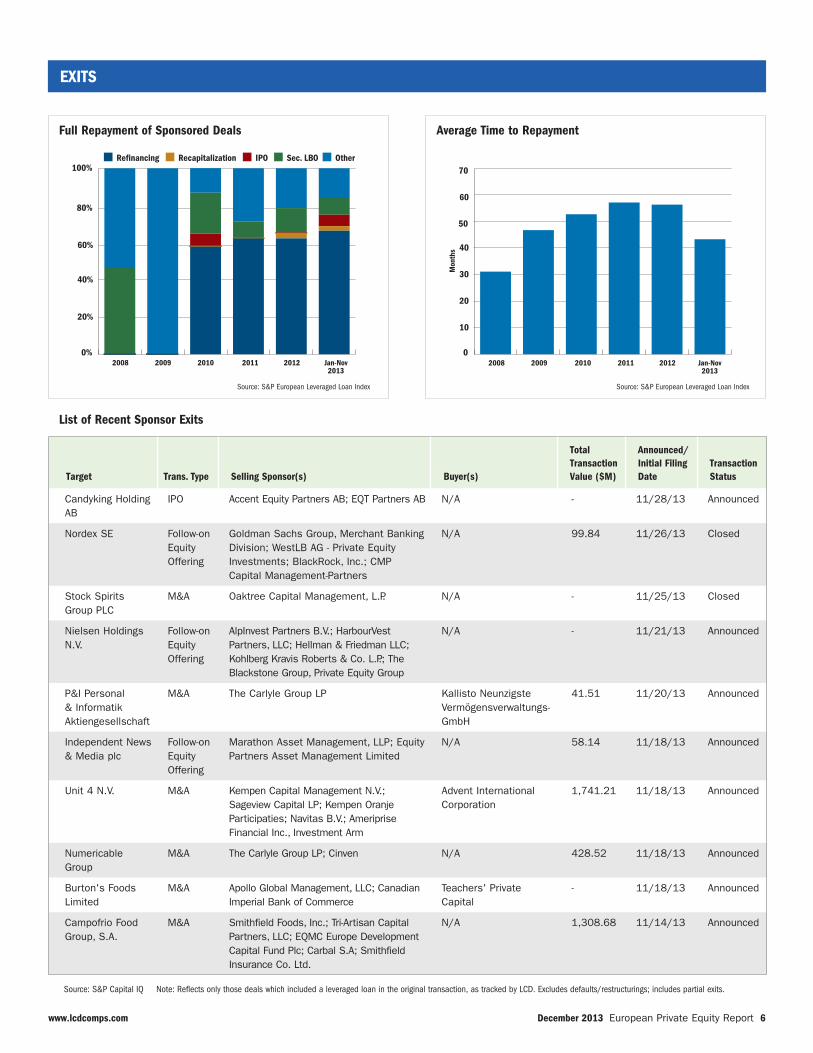

List of Recent Sponsor Exits

EXITS

Source: S&P Capital IQ Note: Reflects only those deals which included a leveraged loan in the original transaction, as tracked by LCD. Excludes defaults/restructurings; includes partial exits.

Source: S&P European Leveraged Loan Index Source: S&P European Leveraged Loan Index

Target Trans. Type Selling Sponsor(s) Buyer(s)

Total Transaction Value ($M)

Announced/Initial Filing Date

Transaction Status

Candyking Holding AB

IPO Accent Equity Partners AB; EQT Partners AB N/A - 11/28/13 Announced

Nordex SE Follow-on Equity Offering

Goldman Sachs Group, Merchant Banking Division; WestLB AG - Private Equity Investments; BlackRock, Inc.; CMP Capital Management-Partners

N/A 99.84 11/26/13 Closed

Stock Spirits Group PLC

M&A Oaktree Capital Management, L.P. N/A - 11/25/13 Closed

Nielsen Holdings N.V.

Follow-on Equity Offering

AlpInvest Partners B.V.; HarbourVest Partners, LLC; Hellman & Friedman LLC; Kohlberg Kravis Roberts & Co. L.P.; The Blackstone Group, Private Equity Group

N/A - 11/21/13 Announced

P&I Personal & Informatik Aktiengesellschaft

M&A The Carlyle Group LP Kallisto Neunzigste Vermögensverwaltungs-GmbH

41.51 11/20/13 Announced

Independent News & Media plc

Follow-on Equity Offering

Marathon Asset Management, LLP; Equity Partners Asset Management Limited

N/A 58.14 11/18/13 Announced

Unit 4 N.V. M&A Kempen Capital Management N.V.; Sageview Capital LP; Kempen Oranje Participaties; Navitas B.V.; Ameriprise Financial Inc., Investment Arm

Advent International Corporation

1,741.21 11/18/13 Announced

Numericable Group

M&A The Carlyle Group LP; Cinven N/A 428.52 11/18/13 Announced

Burton's Foods Limited

M&A Apollo Global Management, LLC; Canadian Imperial Bank of Commerce

Teachers' Private Capital

- 11/18/13 Announced

Campofrio Food Group, S.A.

M&A Smithfield Foods, Inc.; Tri-Artisan Capital Partners, LLC; EQMC Europe Development Capital Fund Plc; Carbal S.A; Smithfield Insurance Co. Ltd.

N/A 1,308.68 11/14/13 Announced

December 2013 European Private Equity Report 7www.lcdcomps.com

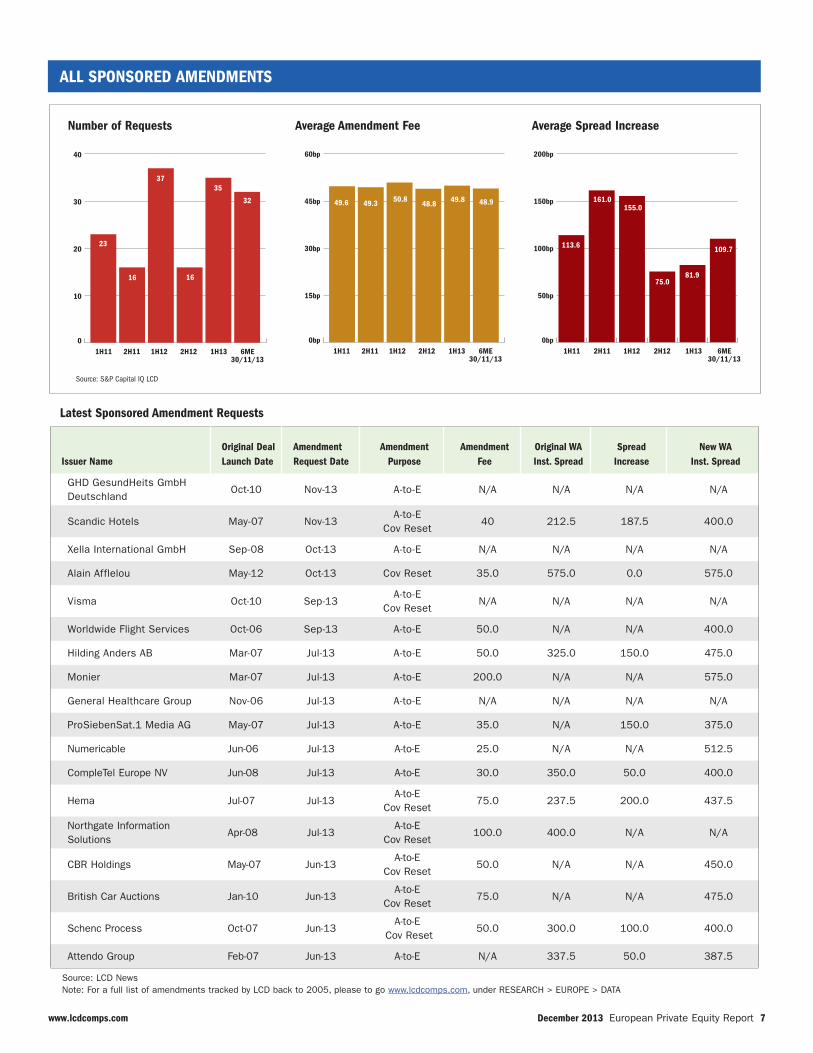

ALL SPONSORED AMENDMENTS

0

10

20

30

40

0bp

15bp

30bp

45bp

60bp

0bp

50bp

100bp

150bp

200bp

2H11 1H121H11 2H12 6ME30/11/13

23

16

3537

23

1H13 2H11 1H121H11 2H12 6ME30/11/13

1H13 2H11 1H121H11 2H12 6ME30/11/13

1H13

16

50.848.8 49.849.6 49.3 155.0

75.081.9

113.6

161.032 48.9

109.7

0

10

20

30

40

0bp

15bp

30bp

45bp

60bp

0bp

50bp

100bp

150bp

200bp

2H11 1H121H11 2H12 6ME30/11/13

23

16

3537

23

1H13 2H11 1H121H11 2H12 6ME30/11/13

1H13 2H11 1H121H11 2H12 6ME30/11/13

1H13

16

50.848.8 49.849.6 49.3 155.0

75.081.9

113.6

161.032 48.9

109.7

0

10

20

30

40

0bp

15bp

30bp

45bp

60bp

0bp

50bp

100bp

150bp

200bp

2H11 1H121H11 2H12 6ME30/11/13

23

16

3537

23

1H13 2H11 1H121H11 2H12 6ME30/11/13

1H13 2H11 1H121H11 2H12 6ME30/11/13

1H13

16

50.848.8 49.849.6 49.3 155.0

75.081.9

113.6

161.032 48.9

109.7

Number of Requests

Latest Sponsored Amendment Requests

Average Amendment Fee Average Spread Increase

Issuer NameOriginal Deal Launch Date

Amendment Request Date

Amendment Purpose

Amendment Fee

Original WA Inst. Spread

Spread Increase

New WA Inst. Spread

GHD GesundHeits GmbH Deutschland

Oct-10 Nov-13 A-to-E N/A N/A N/A N/A

Scandic Hotels May-07 Nov-13A-to-E

Cov Reset40 212.5 187.5 400.0

Xella International GmbH Sep-08 Oct-13 A-to-E N/A N/A N/A N/A

Alain Afflelou May-12 Oct-13 Cov Reset 35.0 575.0 0.0 575.0

Visma Oct-10 Sep-13A-to-E

Cov ResetN/A N/A N/A N/A

Worldwide Flight Services Oct-06 Sep-13 A-to-E 50.0 N/A N/A 400.0

Hilding Anders AB Mar-07 Jul-13 A-to-E 50.0 325.0 150.0 475.0

Monier Mar-07 Jul-13 A-to-E 200.0 N/A N/A 575.0

General Healthcare Group Nov-06 Jul-13 A-to-E N/A N/A N/A N/A

ProSiebenSat.1 Media AG May-07 Jul-13 A-to-E 35.0 N/A 150.0 375.0

Numericable Jun-06 Jul-13 A-to-E 25.0 N/A N/A 512.5

CompleTel Europe NV Jun-08 Jul-13 A-to-E 30.0 350.0 50.0 400.0

Hema Jul-07 Jul-13A-to-E

Cov Reset75.0 237.5 200.0 437.5

Northgate Information Solutions

Apr-08 Jul-13A-to-E

Cov Reset100.0 400.0 N/A N/A

CBR Holdings May-07 Jun-13A-to-E

Cov Reset50.0 N/A N/A 450.0

British Car Auctions Jan-10 Jun-13A-to-E

Cov Reset75.0 N/A N/A 475.0

Schenc Process Oct-07 Jun-13A-to-E

Cov Reset50.0 300.0 100.0 400.0

Attendo Group Feb-07 Jun-13 A-to-E N/A 337.5 50.0 387.5

Source: LCD News Note: For a full list of amendments tracked by LCD back to 2005, please to go www.lcdcomps.com, under RESEARCH > EUROPE > DATA

Source: S&P Capital IQ LCD

December 2013 European Private Equity Report 8www.lcdcomps.com

0

20

40

60

80

100

2007 2011 2012 Jan-Nov2013

201020092008

Defaults Restructurings

€0

€10

€20

€30

€40

€50

2007 2011 2012 Jan-Nov2013

200920092008

Defaults Restructurings

Number of Defaults vs. Restructurings Volume of Defaults vs. RestructuringsBased on Sr. Par Issue

SPONSORED DISTRESSED DEALS

Recent Defaults and Restructurings

Date Borrower Sponsor Industry Country Sr. Debt (M) D/R

Aug-13 ATU (Auto-Teile-Unger) KKR Retailing Germany N/A R

Jun-13 Camaieu SA Cinven Retailing France € 1,158.40 R

Apr-13 Ceva Group Apollo Management Transportation Netherlands N/A D

Mar-13 Travelport Inc Blackstone Personal Services USA € 395.00 R

Sep-12 Terreal LBO France Building Materials France € 500.00 R

Sep-12 Grupo Cortefiel CVC Retailing Spain € 1,385.00 R

Sep-12 CEPL Arcapita PartnersProfessional & Business Services

France € 177.70 D

Aug-12 Biffa Montagu Private Equity Environmental Services UK € 860.00 R

Jul-12Mediannuaire (PagesJaunes Holdco)

Kohlberg, Kravis & Roberts

Printing & Publishing France € 1,238.10 R

Mar-12 Findus Sverig AB Lion Capital Food & Beverage Sweden € 691.96 R

Mar-12 Kloeckner Pentaplast Blackstone Chemicals Germany € 1,062.50 R

Feb-12 Fitness First BC PartnersEntertainment and Leisure

UK € 910.28 R

Feb-12 Travelodge HotelsDubai International Capital

Gaming & Hotels UK € 522.31 R

Jan-12 PrimaCom AG ABN AMRO Media Germany € 275.00 R

Dec-11 Marken Apax PartnersProfessional & Business Services

UK € 365.00 D

Dec-11 Endemol Goldman Sachs Media Netherlands € 2,475.00 R

Dec-11 Alma Consulting Group CandoverProfessional & Business Services

France € 405.30 R

Nov-11 Peacocks Group Goldman Sachs Retailing UK € 419.14 R

Nov-11 Desmet Ballestra Barclays Manufacturing Belgium € 218.00 R

Source: S&P Capital IQ LCD

Source: S&P Capital IQ LCD and LCD News

Source: S&P Capital IQ LCD

December 2013 European Private Equity Report 9www.lcdcomps.com

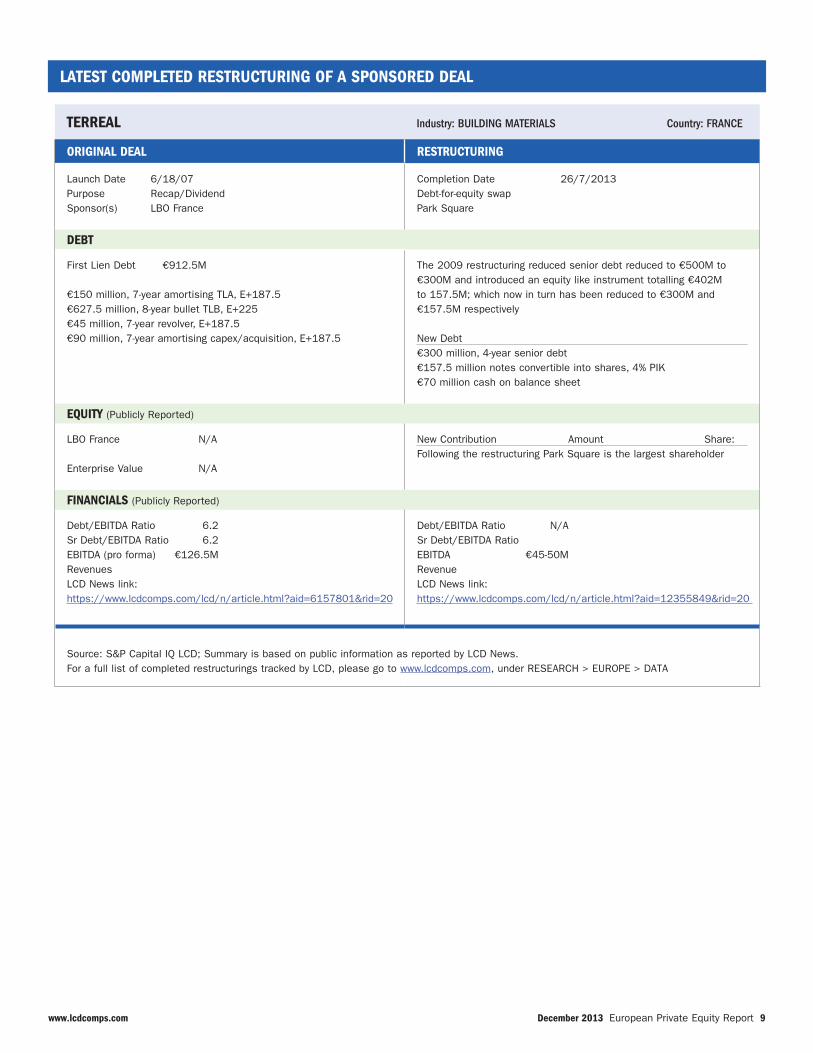

LATEST COMPLETED RESTRUCTURING OF A SPONSORED DEAL

TERREAL Industry: BUILDING MATERIALS Country: FRANCE

ORIGINAL DEAL RESTRUCTURING

Launch Date 6/18/07Purpose Recap/DividendSponsor(s) LBO France

Completion Date 26/7/2013Debt-for-equity swapPark Square

DEBT

First Lien Debt €912.5M €150 million, 7-year amortising TLA, E+187.5€627.5 million, 8-year bullet TLB, E+225€45 million, 7-year revolver, E+187.5€90 million, 7-year amortising capex/acquisition, E+187.5

The 2009 restructuring reduced senior debt reduced to €500M to €300M and introduced an equity like instrument totalling €402M to 157.5M; which now in turn has been reduced to €300M and €157.5M respectively

New Debt€300 million, 4-year senior debt€157.5 million notes convertible into shares, 4% PIK€70 million cash on balance sheet

EQUITY (Publicly Reported)

LBO France N/A Enterprise Value N/A

New Contribution Amount Share:Following the restructuring Park Square is the largest shareholder

FINANCIALS (Publicly Reported)

Debt/EBITDA Ratio 6.2Sr Debt/EBITDA Ratio 6.2EBITDA (pro forma) €126.5MRevenuesLCD News link:https://www.lcdcomps.com/lcd/n/article.html?aid=6157801&rid=20

Debt/EBITDA Ratio N/ASr Debt/EBITDA RatioEBITDA €45-50MRevenueLCD News link:https://www.lcdcomps.com/lcd/n/article.html?aid=12355849&rid=20

Source: S&P Capital IQ LCD; Summary is based on public information as reported by LCD News.For a full list of completed restructurings tracked by LCD, please go to www.lcdcomps.com, under RESEARCH > EUROPE > DATA

December 2013 European Private Equity Report 10www.lcdcomps.com

S&P Capital IQ Leveraged Commentary & Data www.lcdcomps.com • [email protected] Water Street, 43rd Floor • New York, New York 10041 New York - Tel: (212) 438-2701 • Fax: (212) 438-270220 Canada Square, Canary Wharf, London E14 5LH, United Kingdom London - Tel: +44-20-7176-3997 • Fax: +44-20-7176-7245

LCD Global ResearchSteven Miller, Managing Director, (212) 438-2715, [email protected] Polenberg, Vice President, (212) 438-2717, [email protected] Lukatsky, Associate Director, (212) 438-2709, [email protected] Levy, Senior Index Manager, (212) 438-2714, [email protected] Huynh, Senior Analyst, (212) 438-5202, [email protected] Lempert, Senior Analyst, (212) 438-2712, [email protected] McGrane, Senior Analyst, (212) 438-5837, [email protected] O’Keefe, Senior Analyst, (212) 438-5511, [email protected] Shmulenson, Senior Analyst, (212) 438-5605, [email protected] Tulli, Senior Analyst, (212) 438-1970, [email protected] Dowling, Analyst, [email protected] Ishkanian, Senior Analyst, (212) 438-3034, [email protected] Sharif, Analyst, 44 (0)20 7176 6025, [email protected] Weiss, Analyst, (212) 438-0296, [email protected] Yip, Analyst, (212) 438-1695, [email protected]

LCD News Christopher Donnelly, Vice President, (212) 438-5094, [email protected] Fuller, Director, (212) 438-2050, [email protected] Kantin, Director, (212) 438-4097, [email protected] Atkins, Associate Director, (212) 438-1961, [email protected] Husband, Associate Director, 44 (0)20 7176 3928, [email protected] Thompson, Associate Director, (312) 233-7054, [email protected] Zimmerman, Associate Director, (646) 415 8143, [email protected] Bringardner, Associate, (212) 438-7258, [email protected] Cox, Associate, 44 (0)20 7176 3995, [email protected] Fujimoto, Associate, 44 (0)20 7176 3966, [email protected] Hemingway, Associate, (212) 438-0192, [email protected] Iyer, Associate, (212) 438-2726, [email protected] Kellerhals, Associate, (212) 438-7783, [email protected] Latour, Associate, (212) 438-1858, [email protected] McGavin, Associate, 44 (0)20 7176 3924, [email protected] Millar, Associate, 44 (0)20 7176 3926, [email protected]

AdministrationRuth Yang Van de Castle, Vice President, (212) 438-2722, [email protected] Lecour, Administrative Assistant, (212) 438-2711, [email protected]

Performance Optimization ProgramJeffrey Reichert, Vice President, (212) 438-3299, [email protected] Szymczak, Director, (212) 438-7608, [email protected] Thollesson, Director, (212) 438-3297, [email protected] Chopra, Associate Director, (212) 438-2059, [email protected] Wnuck, Associate Director, (212) 438-9310, [email protected] Kim, Associate, (212) 438-7467, [email protected] Novatny, Associate, (212) 438-2725, [email protected] Shahi, Associate, (212) 438-7453, [email protected] Silva, Associate, (212) 438-5066, [email protected] Polanco, Database Developer, (212) 438-3231, [email protected] Woyma, Database Developer, (212) 438-5840, [email protected]

Marketing/SalesMarc Auerbach, Vice President, (212) 438-2703, [email protected] D’Souza, Director, (212) 438-2708, [email protected] Gupte, Director, 44 (0)20 7176 7235, [email protected] Maria Cini, Sales Manager, 44 (0)20 7176 3997, [email protected] Greaves, Sales Associate, (212) 438-2292, [email protected] Dookie, Administrative Assistant, (212) 438-2705, [email protected]

TechnologyTim Cross, Vice President, (212) 438-2724, [email protected] Challi, Director, (212) 438-2721, [email protected] Richardson, Associate, (212) 438-1986, [email protected] Grullon,Senior Systems Analyst, (212) 438-0211, [email protected] Lifton, Senior Systems Analyst, (212) 438-2713, [email protected] Lu, Senior Systems Analyst, (212) 438-2718, [email protected]

Copy EditingBrian Manning, Copy Editor Manager, (212) 438-1462, [email protected] Jones, Senior Copy Editor, (212) 438-2704, [email protected] Matthes, Senior Copy Editor, (212) 438-3592, [email protected] Baron, Copy Editor, (212) 438-4816, [email protected] Poole, Copy Editor, 44 (0)20 7176 3933, [email protected]

LCD European Private Equity Report is a publication of S&P Capital IQ LCD. Copyright © 2013 Standard & Poor’s Financial Services LLC. LCD has obtained data from sources believed to be accurate, but it does not guarantee their accuracy.