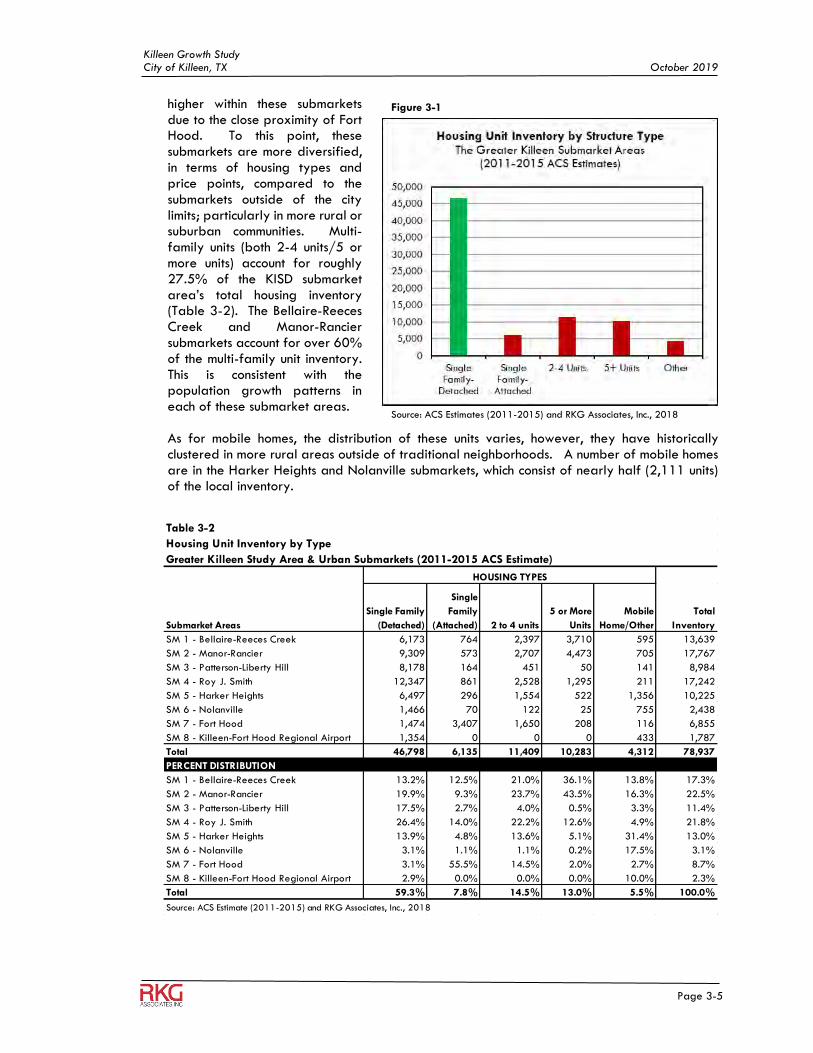

Bahasa

Halaman

Hukum

KILLEEN GROWTH STUDY

KILLEEN, TEXAS

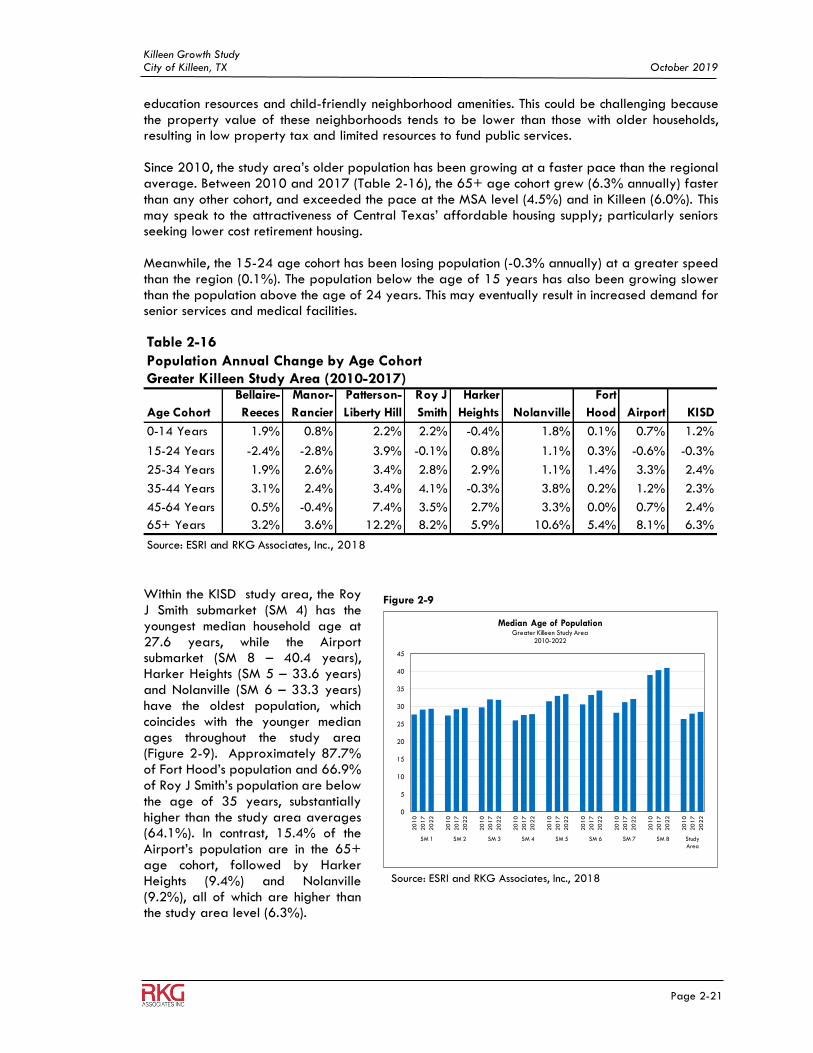

Prepared by:

RKG Associates, Inc. Economic, Planning and Real Estate Consultants

300 Montgomery Street

Suite 203

Alexandria, VA 22314

Tel: (703) 739-0965

www.rkgassociates.com

October 2019

Killeen Growth Study Killeen, Texas

October 2019

Prepared for:

One Santa Fe Plaza

Killeen, TX 76541

Contact: Jennifer Hetzel [email protected] Tel: 254.526.9551 killeenchamber.com

Special Thanks:

Prepared by:

Economic, Planning and Real Estate Consultants

300 Montgomery Street, Suite 203

Alexandria, VA 22314

Tel: 703.739.0965

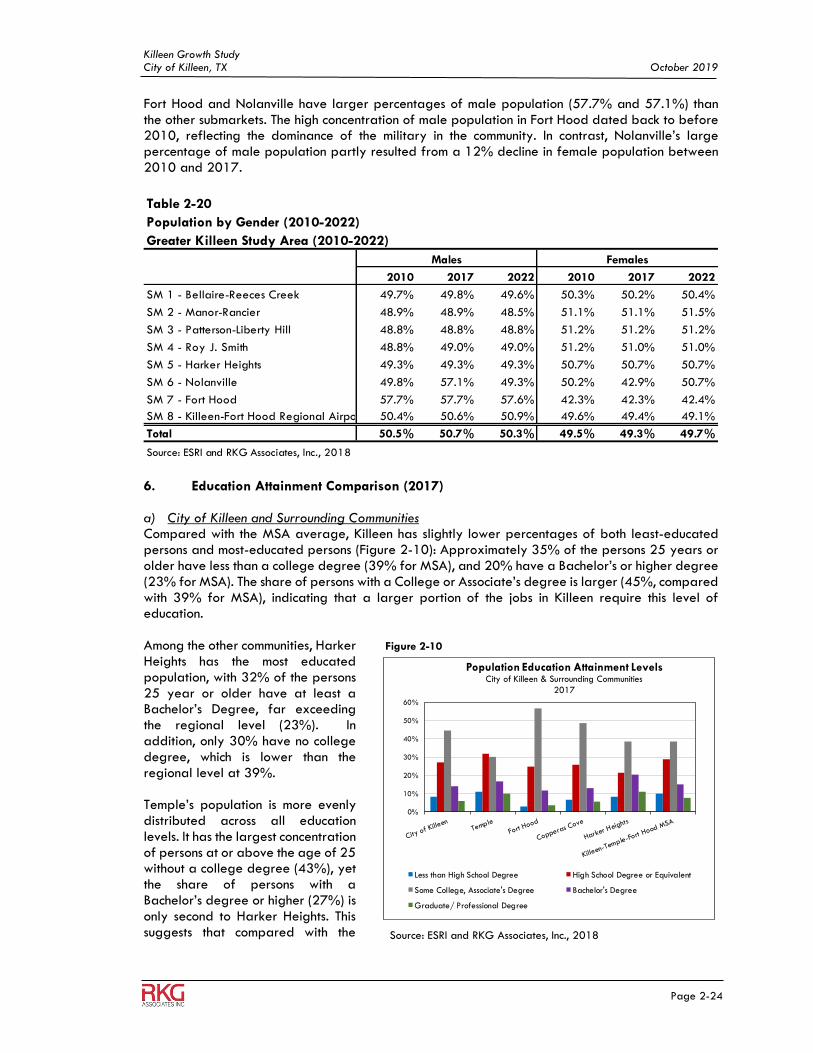

rkgassociates.com

i

Table of Contents

Chapter 1 EXECUTIVE SUMMARY

A. Purpose of the Study ................................................................................................................ 1-1 B. Overview of Growth Study ..................................................................................................... 1-1 C. Executive Summary ................................................................................................................... 1-2

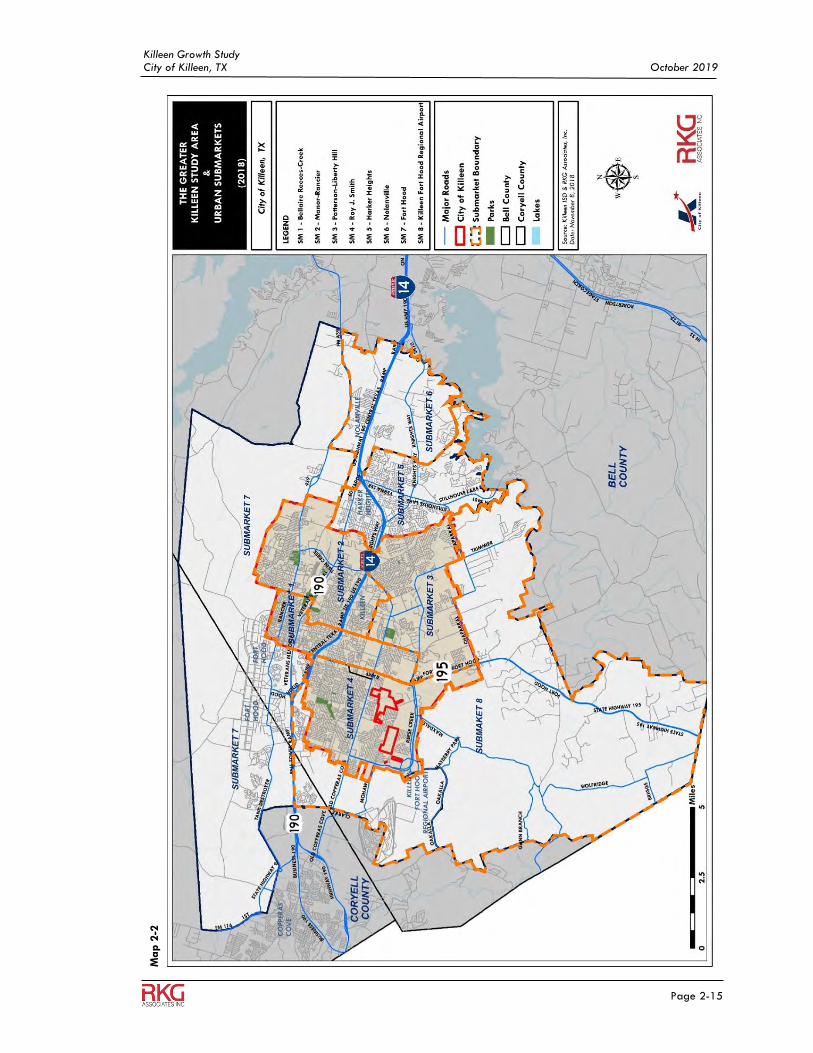

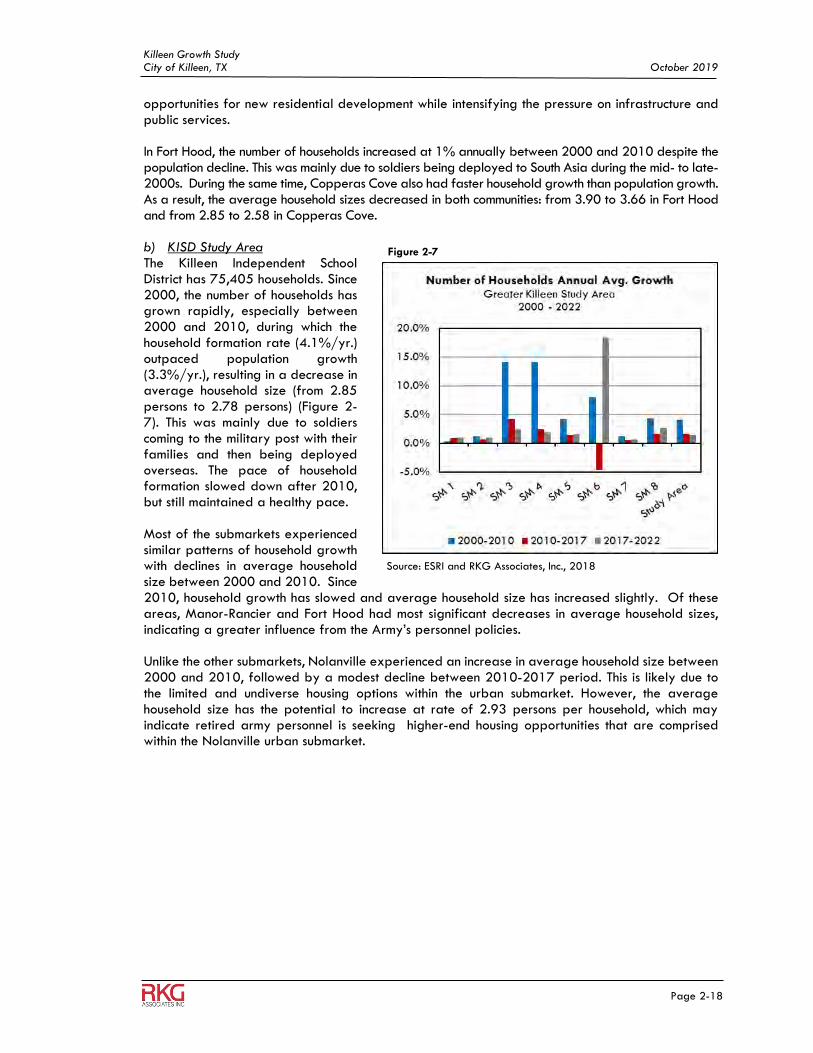

Chapter 2 DEMOGRAPHIC TRENDS AND ANALYSIS A. Introduction ................................................................................................................................ 2-1 B. Regional Demographic Trends and Existing Conditions ................................................... 2-1 C. City of Killeen, Surrounding Communities and KISD Submarket Trends (2010-2s) .. 2-13 D. Demographic Characteristics and Trends .......................................................................... 2-14 E. Implications ............................................................................................................................. 2-36

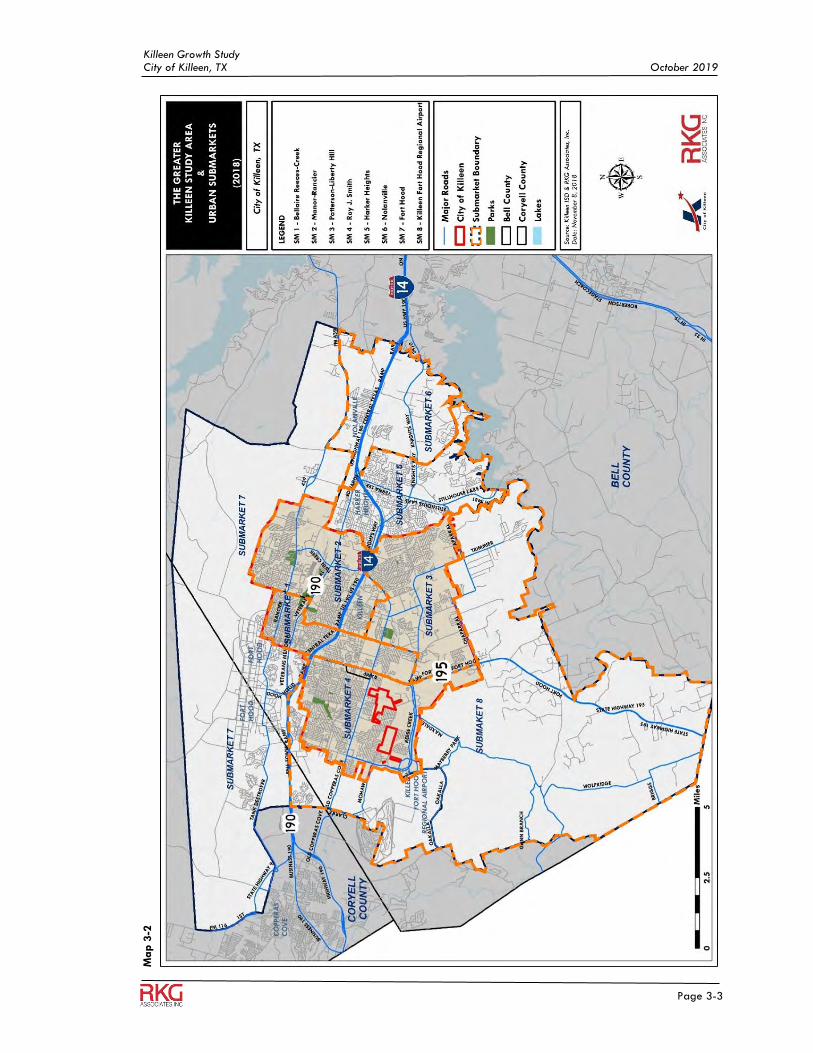

Chapter 3 REGIONAL HOUSING ANALYSIS A. Introduction ................................................................................................................................ 3-1 B. Methodology ......................................................................................................................... 3-1 C. Regional and Submarket Housing Characteristics ............................................................. 3-4 D. Implications .............................................................................................................................. 3-15

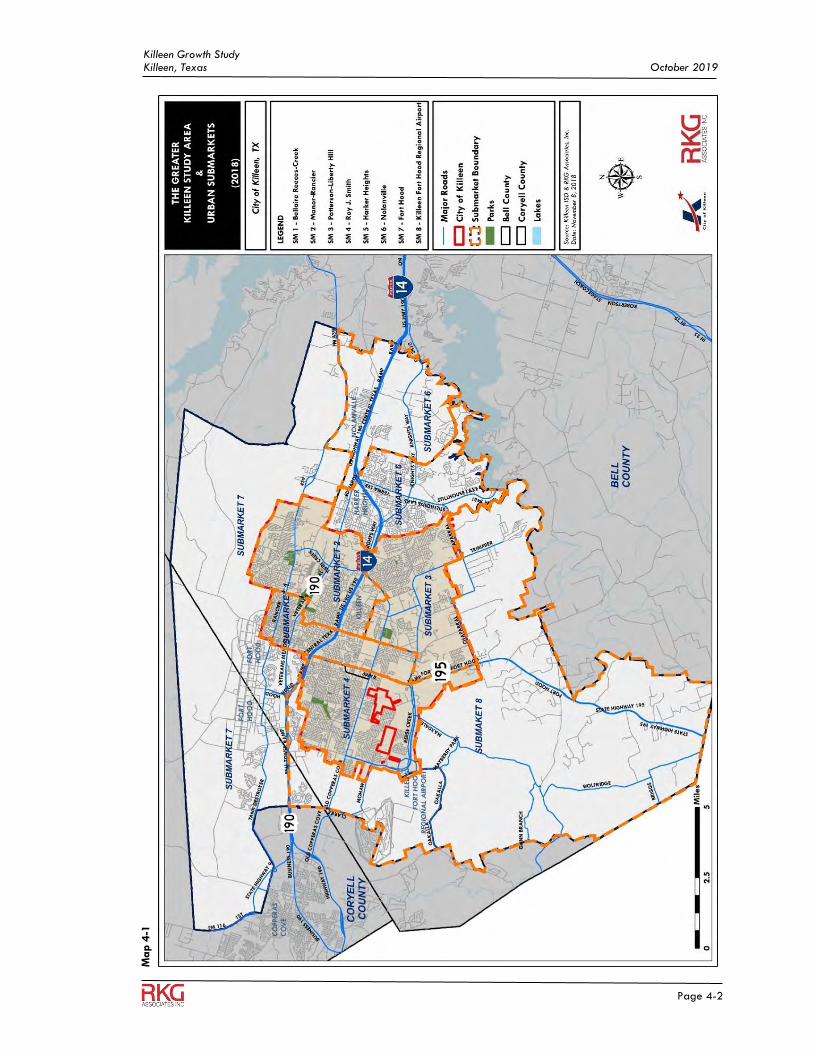

Chapter 4 DEVELOPMENT TRENDS ANALYSIS A. Introduction ............................................................................................................................... 4-1 B. Methodology ............................................................................................................................ 4-1 C. Regional Development Trends ............................................................................................... 4-1 D. Greater Killeen/KISD Urban Submarket Development Activity (2007-2017........... 4-10 E. Implications ............................................................................................................................. 4-12 F. Appendix Tables and Maps - Development Trends ...................................................... 4-14 Chapter 5 KISD GROWTH PROJECTIONS A. Introduction ................................................................................................................................ 5-1 B. Methodology and Date Sources ........................................................................................... 5-1 C. Population Growth Projections by Submarket ................................................................... 5-1 D. KISD Employment Growth Projections by Submarket ....................................................... 5-6 E. Implications ................................................................................................................................. 5-8 Chapter 6 FISCAL IMPACT ANALYSIS A. Introduction ................................................................................................................................ 6-1 B. Methodology and Data Sources ............................................................................................ 6-1 C. Fiscal Impact Analysis .............................................................................................................. 6-1 D. Implications .............................................................................................................................. 6-24

Killeen Growth Study City of Killeen, TX October 2019

Page 1-1

1 EXECUTIVE SUMMARY

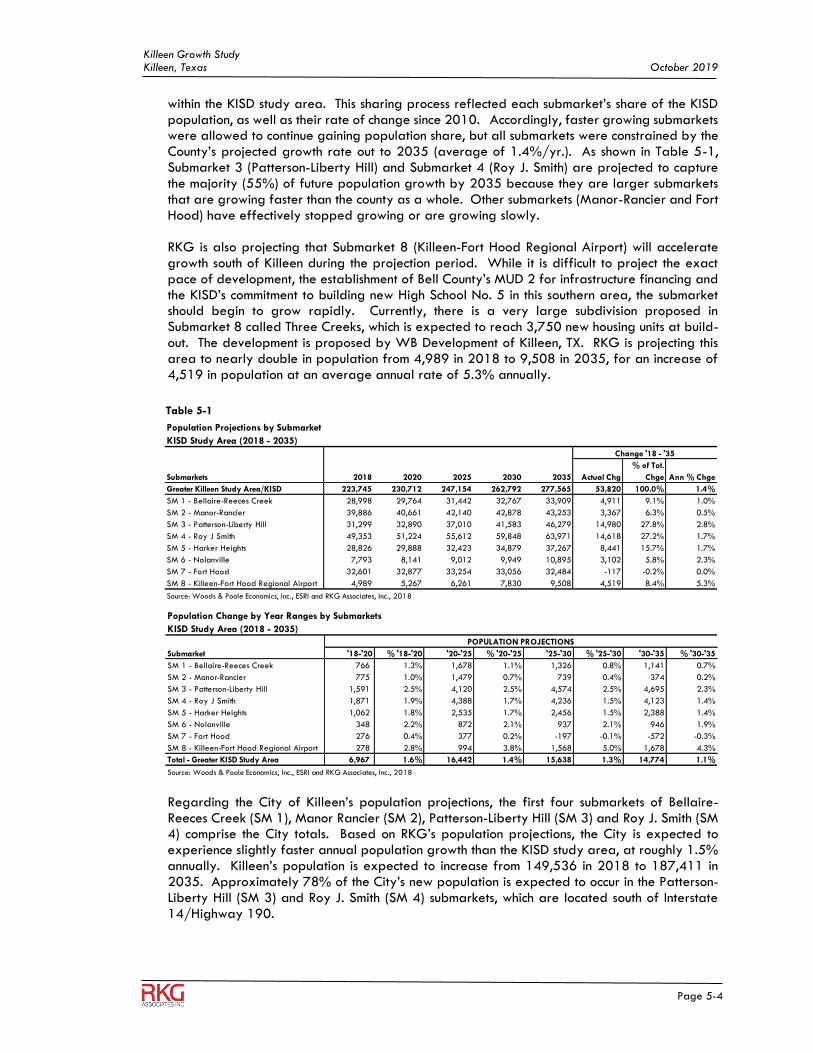

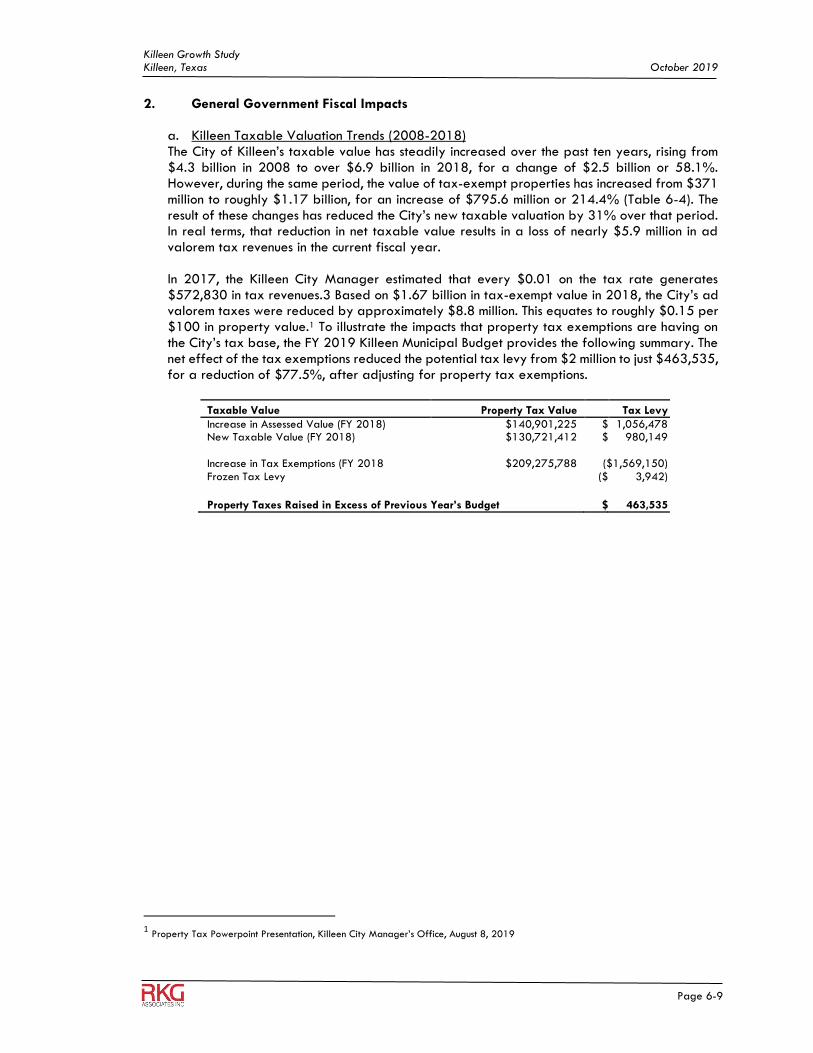

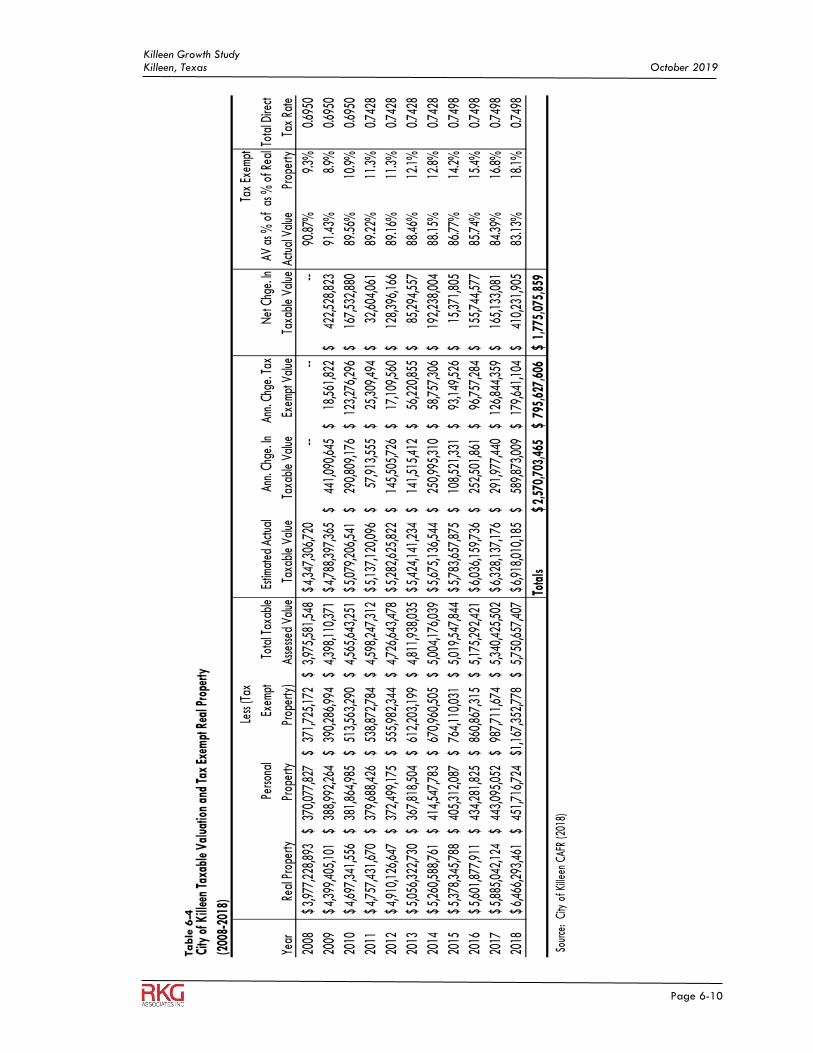

A. PURPOSE OF THE STUDY The Killeen Growth Study was commissioned by the Greater Killeen Chamber of Commerce, in cooperation with the Killeen Independent School District and the City of Killeen. This study was originally conceived in order to understand demographic and growth characteristics of the region in order to better plan for the education and municipal service needs of the community in the face of rapid population growth. Since the year 2000, the soldier population at Fort Hood has ranged from 41,250 in 2000 to a peak of 53,831 in 2008 and then dropped to 37,053 in 2019 – a decline of 16,778 Soldiers since 2008 and 3,293 since 2000. During the same period of time, overall total population for the Killeen-Temple-Fort Hood Metropolitan Statistical Area (MSA), which includes Bell, Coryell, and Lampasas Counties, increased substantially but at varying rates. There is some evidence that this runs counter to historical trends. Historically, enrollments in the Killeen Independent School District have been closely proportionate to the number of active duty Soldiers assigned to Fort Hood. In recent years, the number of enrollments in KISD has continued to increase while the number of active duty Soldiers has decreased. This means that the recent population growth is not directly attributable to the military population as shown in the data over this period. Communities geographically closest to Fort Hood traditionally experienced growth rates comparable to the military population of Fort Hood. However, the local communities recently have grown while the military population has dropped. The Greater Killeen Chamber of Commerce (GKCC) sought the services of a professional economic consultant to facilitate the development of a Growth Analysis that will guide the GKCC and partner entities. GKCC represents a collaboration between the Chamber and Killeen Economic Development Corporation, City of Killeen, Killeen Independent School District, Heart of Texas Defense Alliance and Workforce Solutions of Central Texas. These organizations were focused on obtaining a better understanding of these regional dynamics in order to assist local leaders with short-and-long-term strategic planning and policy implementation.

B. OVERVIEW OF GROWTH STUDY This report provides a detailed understanding of the demographic and market factors that have shaped growth in the City of Killeen and the Killeen Independent School District over the past several decades. The chapters are arranged in the following order:

Chapter 1 – Introduction Chapter 2 – Demographic Trends Analysis Chapter 3 – Regional Housing Analysis Chapter 4 – Development Trend Analysis Chapter 5 – KISD Growth Projections Chapter 6 – Fiscal Impact Analysis

Killeen Growth Study City of Killeen, TX October 2019

Page 1-2

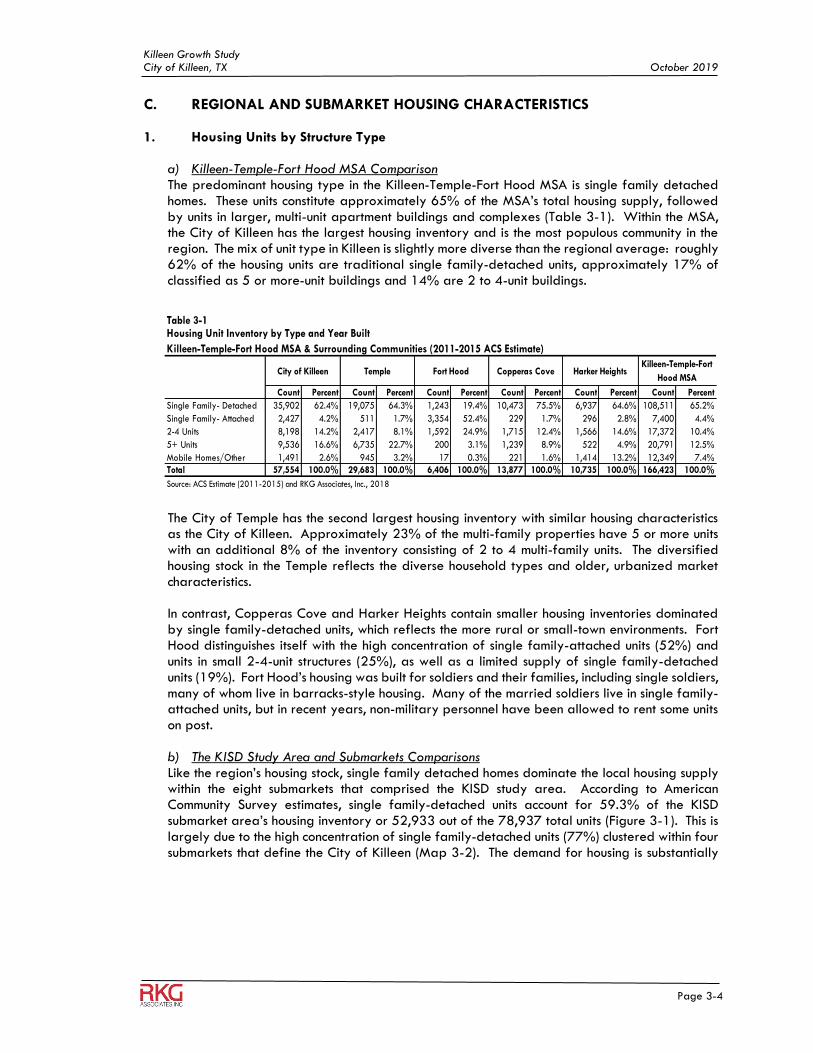

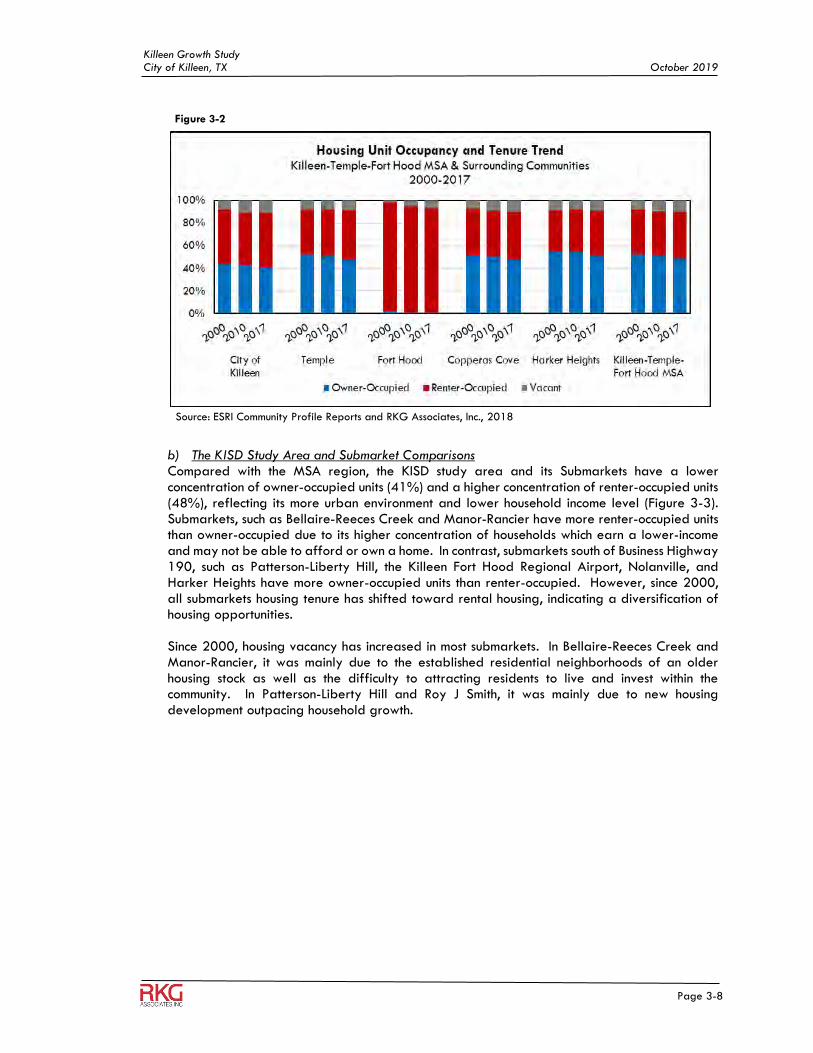

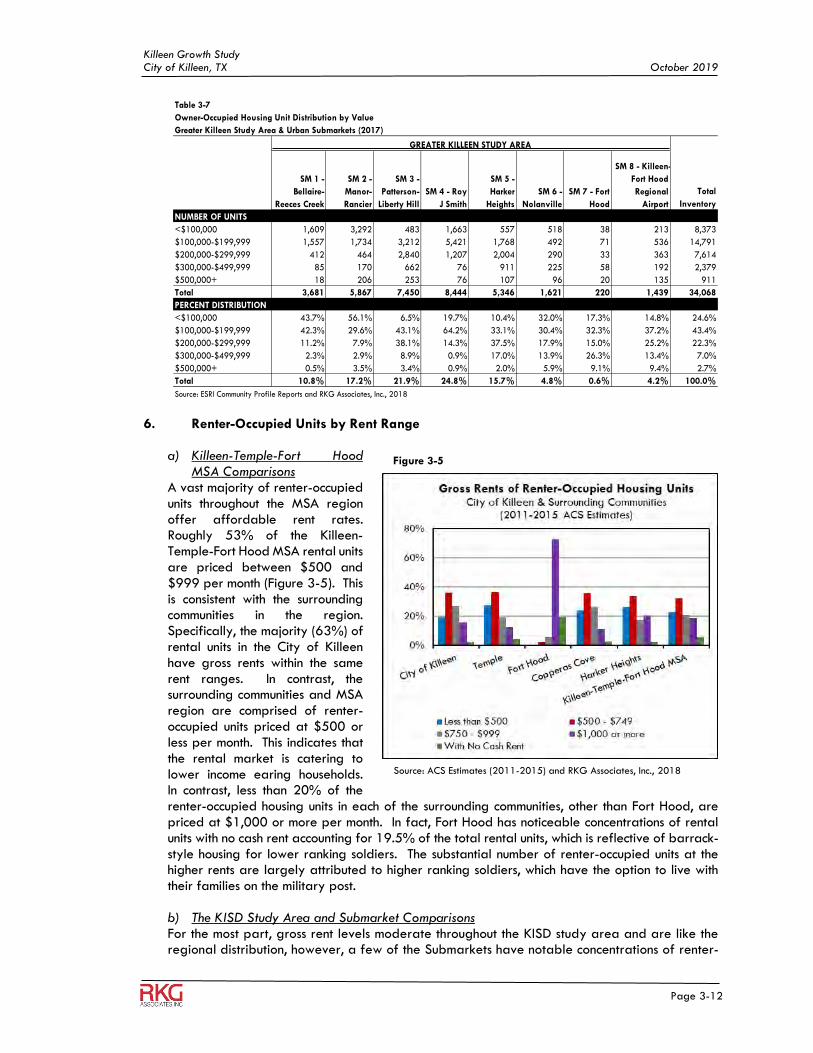

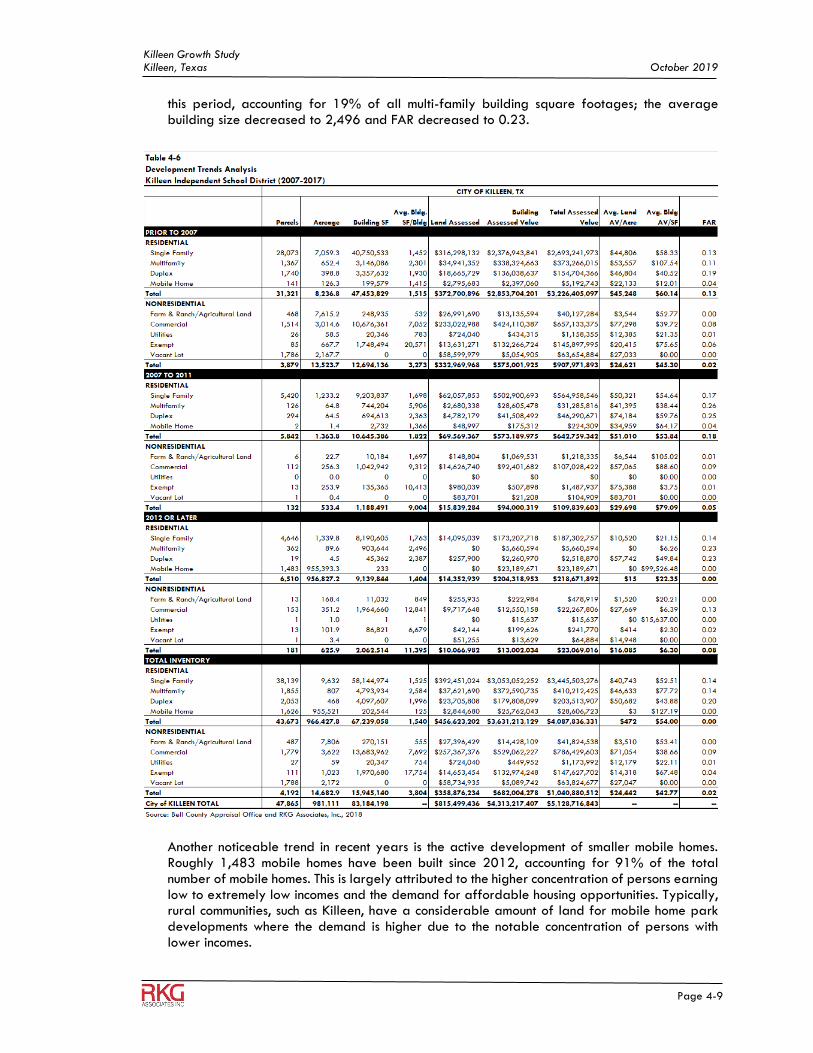

C. EXECUTIVE SUMMARY 1. Demographic Trends Analysis a) Regional Overview RKG analyzed the demographic trends and conditions for both the region and the Greater/KISD study area. This analysis focused mainly on the population trends, indicators, and conditions for the 50-year period between 1970-2017. To complete the population trend analysis, RKG used data obtained from Woods & Poole Economics, Inc and ESRI. Between 2000-2010, all three counties in the Killeen-Temple-Fort Hood MSA experienced population growth. Additionally, since 2010, the age group with the largest growth rate in all three counties was seniors (65+ years old). This is part of a national trend of the country getting older as “Baby Boomers” hit retirement age. Also, due to immigrants migrating to the region since 1970, the MSA has experienced a 12% annual increase in the Hispanic population. Part of the region population increase can be attributed to a disproportionate rate of natural births over deaths, which far outpace the state average. In fact, natural population change resulted in nearly 30,000 net new population in Bell County between 2011 and 2017. This is a significant driver of population change, which is evidence in the area’s younger population base and increased enrollment trends in the KISD school district. In addition, movements of military personnel and their families from other locations of the country, and their desire to remain in the region after separating or retiring from the military has resulted in population increases. Finally, over the past 15 years, the rising cost of living in California has made Texas a popular destination for Californians looking for both housing affordability and employment. Based on migration data, it can be shown that the state continues to attract large numbers of people from higher cost regions of the Country. With the US entering conflicts in both Iraq and Afghanistan in the early 2000s, Bell County experienced population growth in the 0-14 age group, young adult population (19-34 years old), and older adult population (45-54-year-old). The older adult population could be attributable to family members of soldiers moving to the region to support military spouses and children left behind. Even though annual growth has slowed down slightly as Fort Hood’s solider levels have decreased, Bell County has remained an attractive place for both soldiers and young adults that want to establish their family. Coryell County experienced much of its population growth during the 1970-1980 period. Similar to Bell County, Coryell experienced population growth during the early 2000s. Since then, it has experienced a decline in school age population. This decline is likely due to the families migrating to Killeen and other communities within the region. Lampasas County is the smallest county by population and has the largest percentage of seniors. The county has struggled to attract young families, which can be reflected in the fact that it has the oldest workforce of any county in the region. Additionally, Lampasas County has a large concentration of senior care facilities. The City of Killeen has experienced the most population, growth compared to the other surrounding communities in the region. Killeen experienced rapid population growth between 2000-2010, which slowed slightly after 2010 but still outpaced any other surrounding community. While Killeen experienced changes in its population it also experienced changes in the age of its residents. During the study period (2000-2017), the senior population grew enough for the median age of the population to rise. However, Killeen still has the youngest population within the region. Killeen was able to maintain a comparable young population due to its growth in the 0-14 and 34-44 age cohorts. Growth in these age cohorts shows the large concentration of young families and

Killeen Growth Study City of Killeen, TX October 2019

Page 1-3

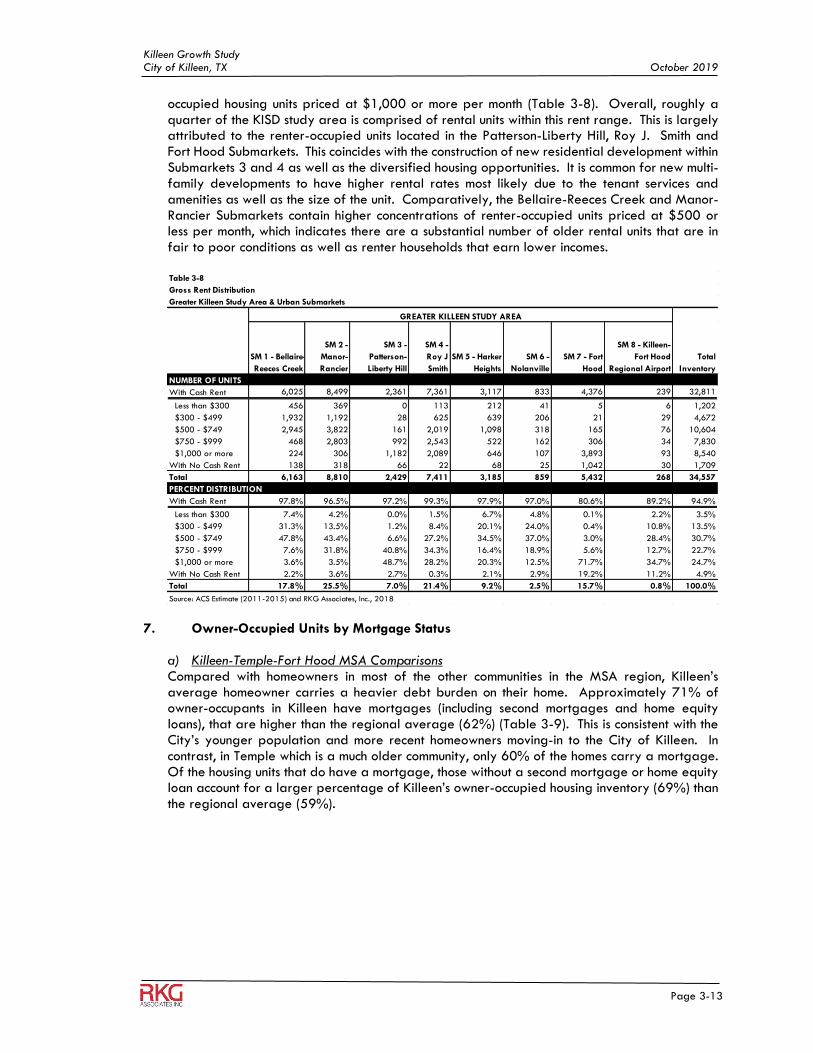

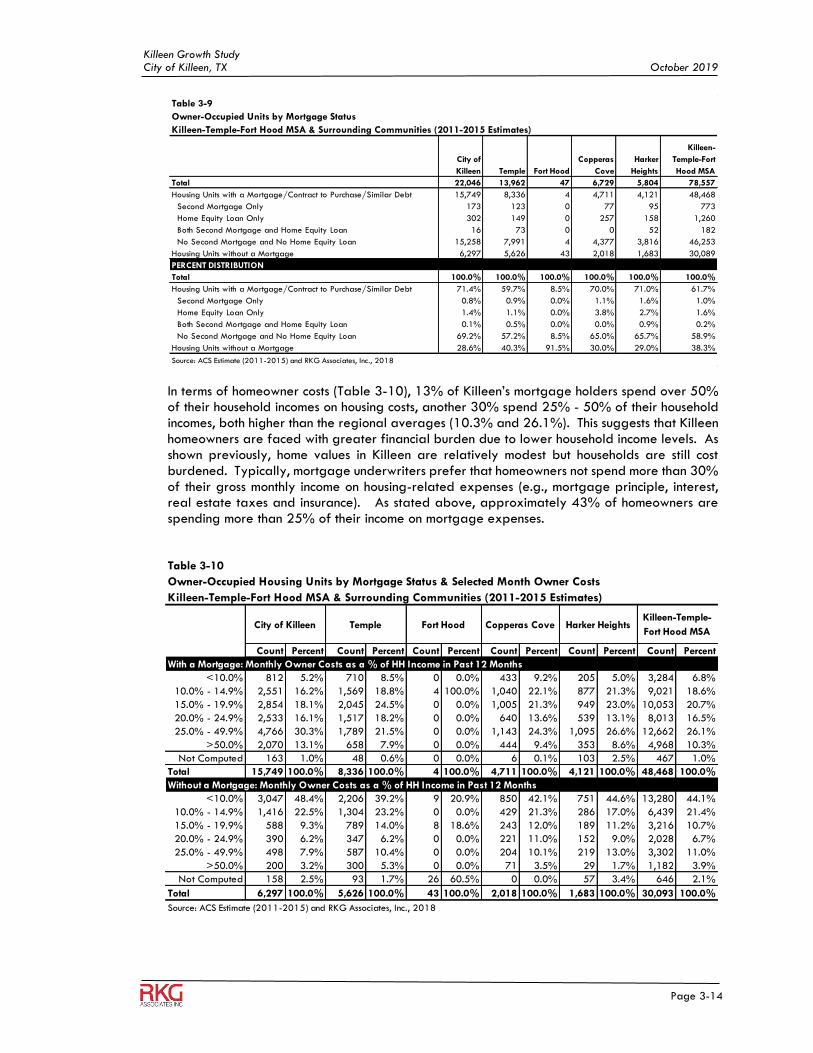

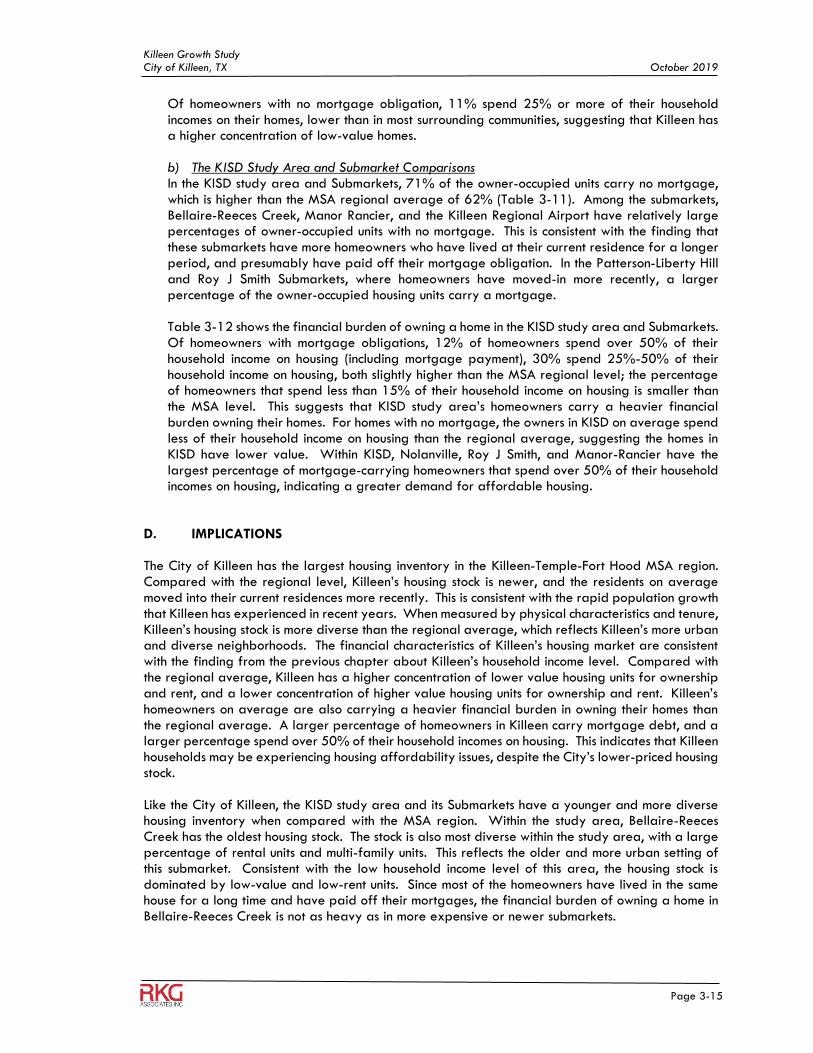

school aged children. This is likely due to Killeen’s affordable and diverse housing market compared to other communities. Temple is the second largest population center in the region and the most diverse economically. The population of Temple is the oldest within the region, primarily made up of the 45-64 and 65+ age cohorts. Because of this aging population, Temple is home to many 1-person households and senior care facilities. Temple’s economy is built upon a high concentration of both least-educated and most-educated persons. This can be reflected in Temple’s housing market, which has a mix of both high-value and low-value homes. Fort Hood, unsurprisingly, is most directly affected by changes at the post. Fort Hood is home to both the youngest population and highest concentration of person in group quarters within the region. This community’s education levels reflect a military installation with a large percentage of residents that have achieved mid-level educational attainment. b) KISD As the region has grown in population, the Roy J Smith and Patterson-Liberty Hill submarkets have been the recipients of most of this new population. The growth in these two submarkets reflects the demand from families seeking the best educational offerings. Also, these areas are attractive to recently separated and retired military, who want to stay in the region and are looking for places to raise their families. This is directly reflected in the large increases in school-aged children within these two submarkets. Both submarkets now share an educated workforce, as compared to other parts of the study area. Because of the pace of growth in these two submarkets, the demand for municipal services, commercial offerings and basic infrastructure has put fiscal stress on City, KISD and County. Previously developed submarkets like Bellaire-Reeces Creek and Manor-Rancier experienced slight population growth during the study period. Both areas are aging at a slower pace, due to their lack of senior living options. These submarkets also have low educational attainment levels, which also reflects in lower median household incomes. The other submarkets - Harker Heights, Nolanville, and Killeen/Fort Hood Regional Airport – exhibit their own unique characteristics. Harker Heights has a higher than average median household income, which matches its higher valued housing market and the population’s higher education attainment levels. Nolanville did not experience growth in children or young adult cohorts because of the lack of job opportunities and affordable housing. The Killeen/Fort Hood Regional Airport submarket has a higher than average household income levels, while having below average educational attainment levels. In the future, this submarket is positioned to grow rapidly. 2. Regional Housing Analysis RKG analyzed the residential market for both the region and the Greater/KISD study area. This analysis focused mainly on the market trends, indicators, and conditions for both for-sale and for-rent housing markets for the 10-year period between 2007-2017. RKG utilized Killeen Independent School District (KISD), U.S. Census, and the 2011-2015 American Community Survey data for this analysis. The City of Killeen and Temple have the largest inventory of housing within the region. The City of Killeen’s population has grown rapidly, this has allowed for significant new housing to be built. This population growth is reflected by the fact that 33% of all housing was built in the city between the years of 2000 and 2009. Since Fort Hood’s most recent expansion phase did not include the construction of housing units, areas outside the installation took on much of the housing demand. Compared to Temple, Killeen has a larger concentration of lower value housing units for ownership and rent. Furthermore, residents of Killeen more often carry mortgage debt and spend over 50%

Killeen Growth Study City of Killeen, TX October 2019

Page 1-4

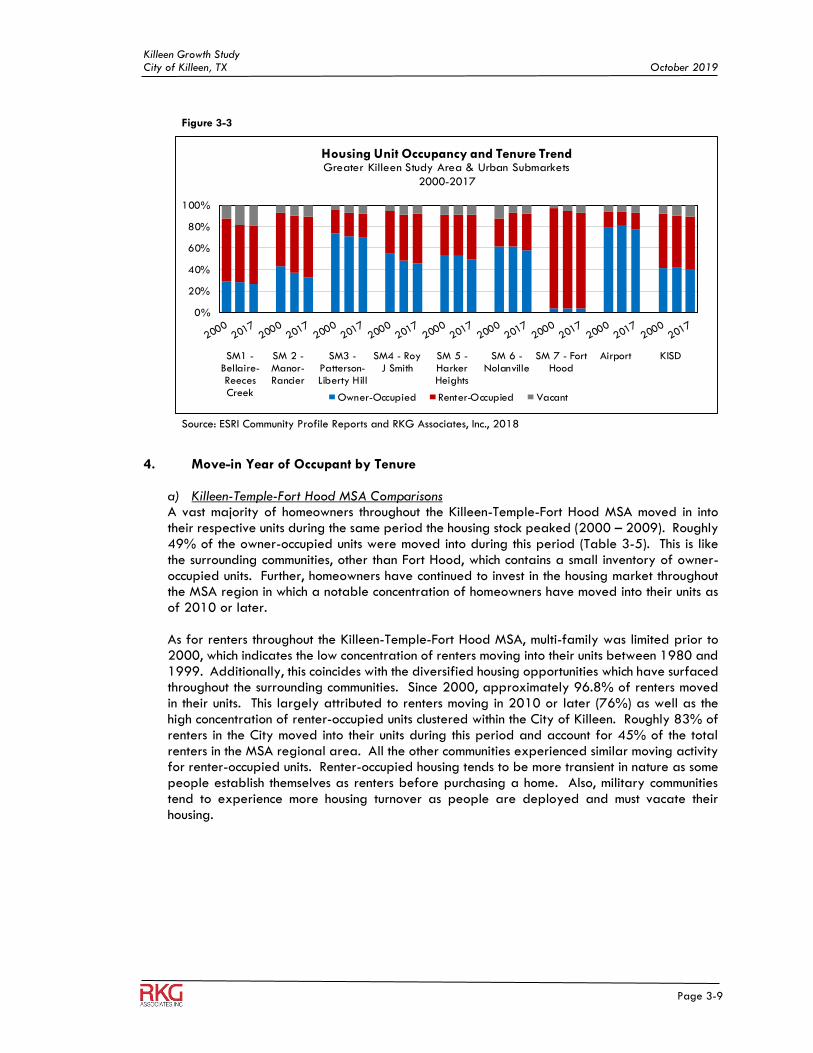

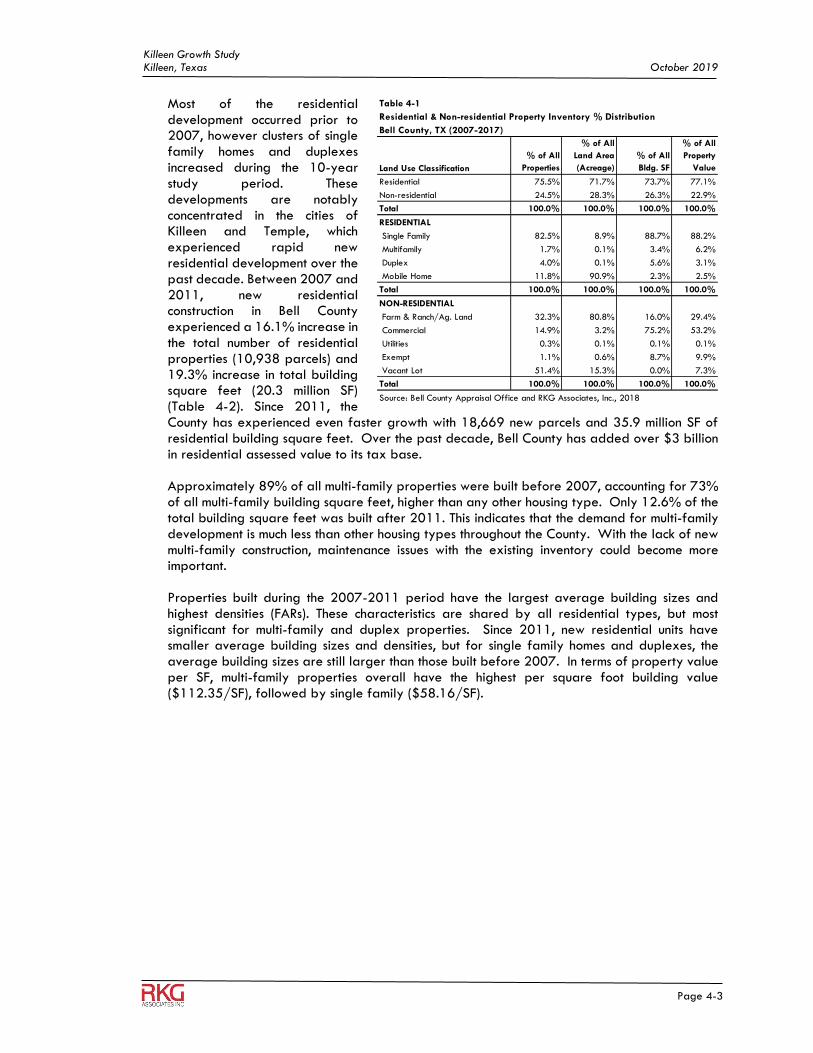

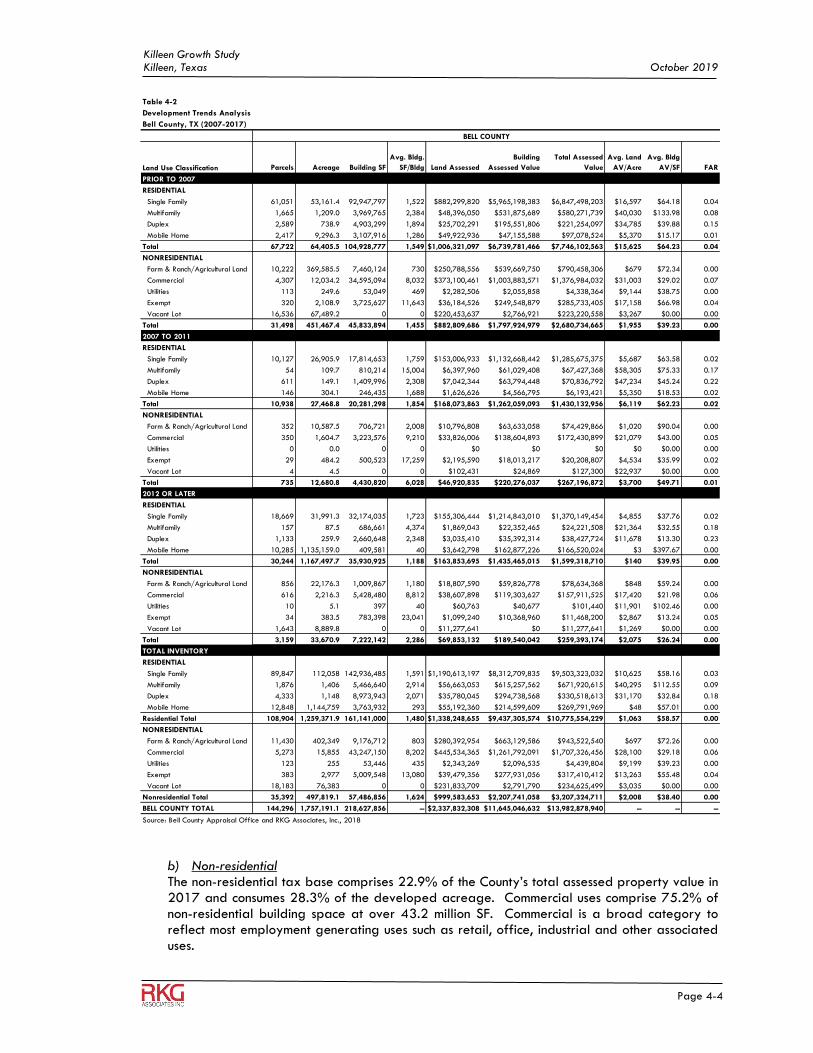

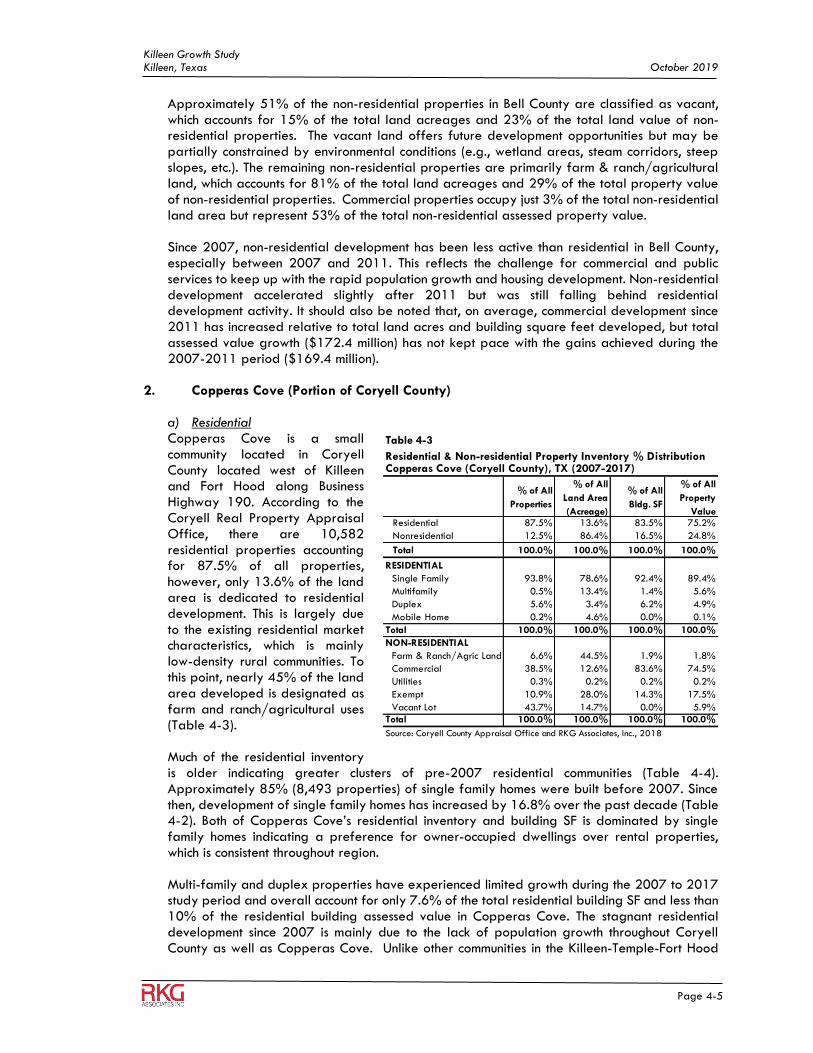

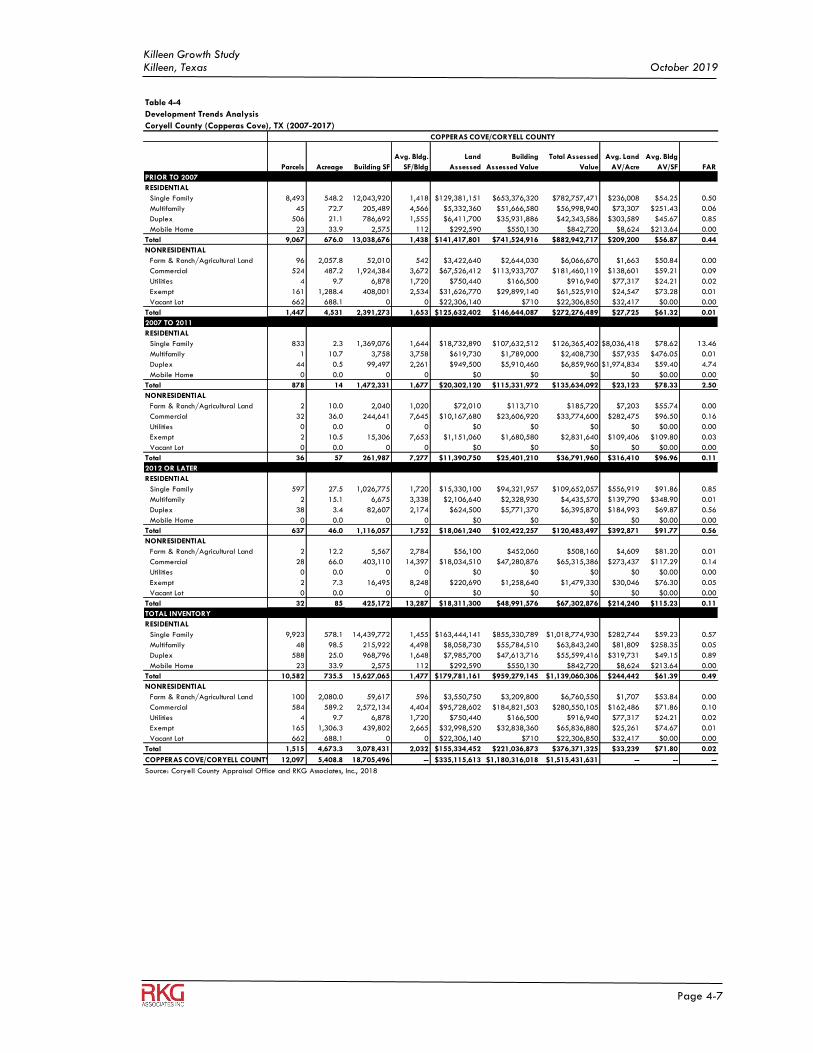

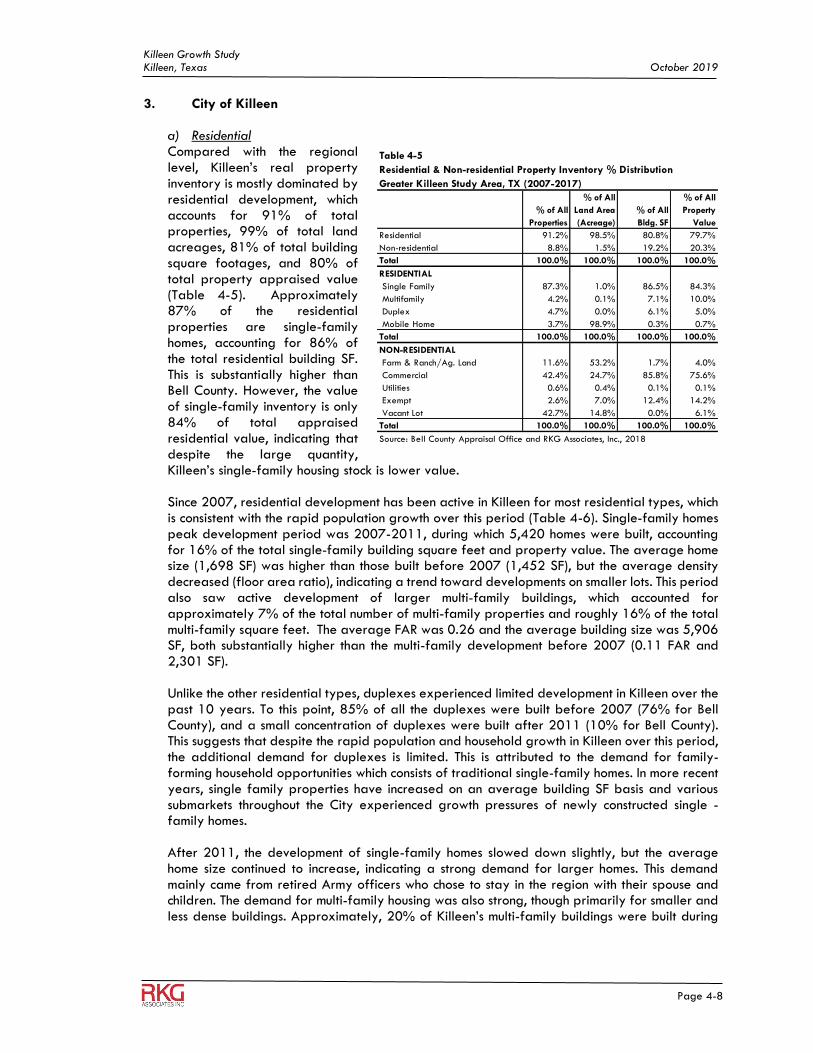

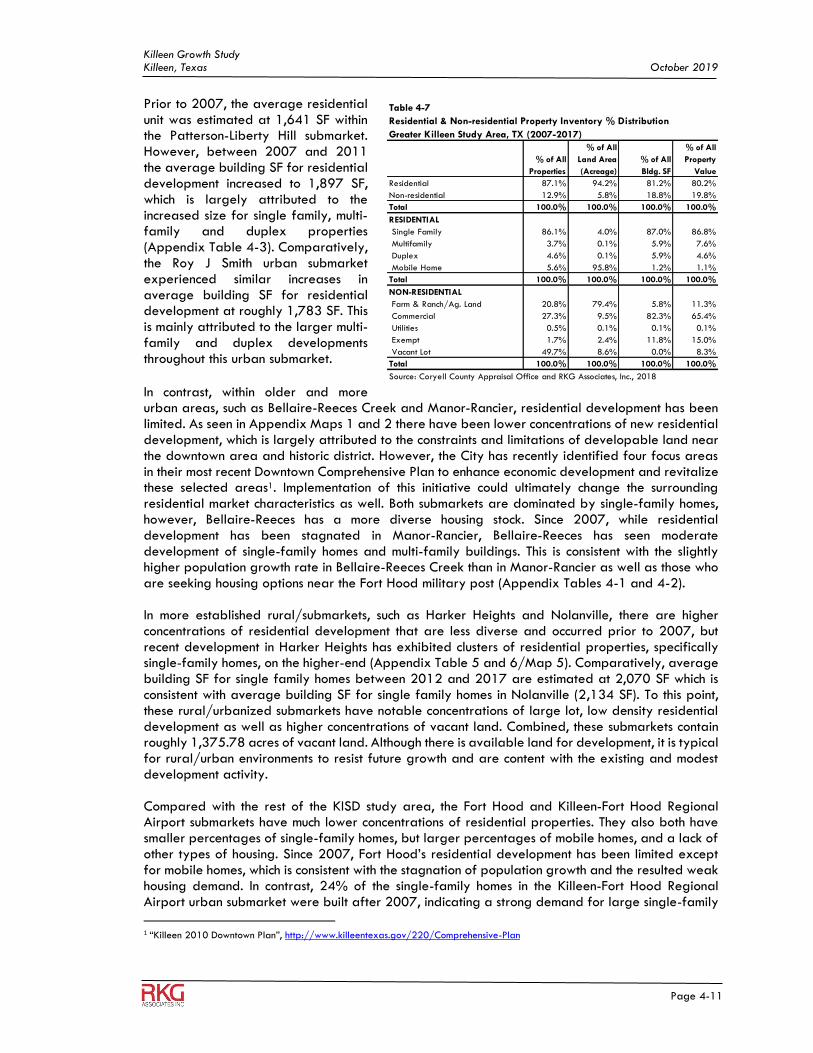

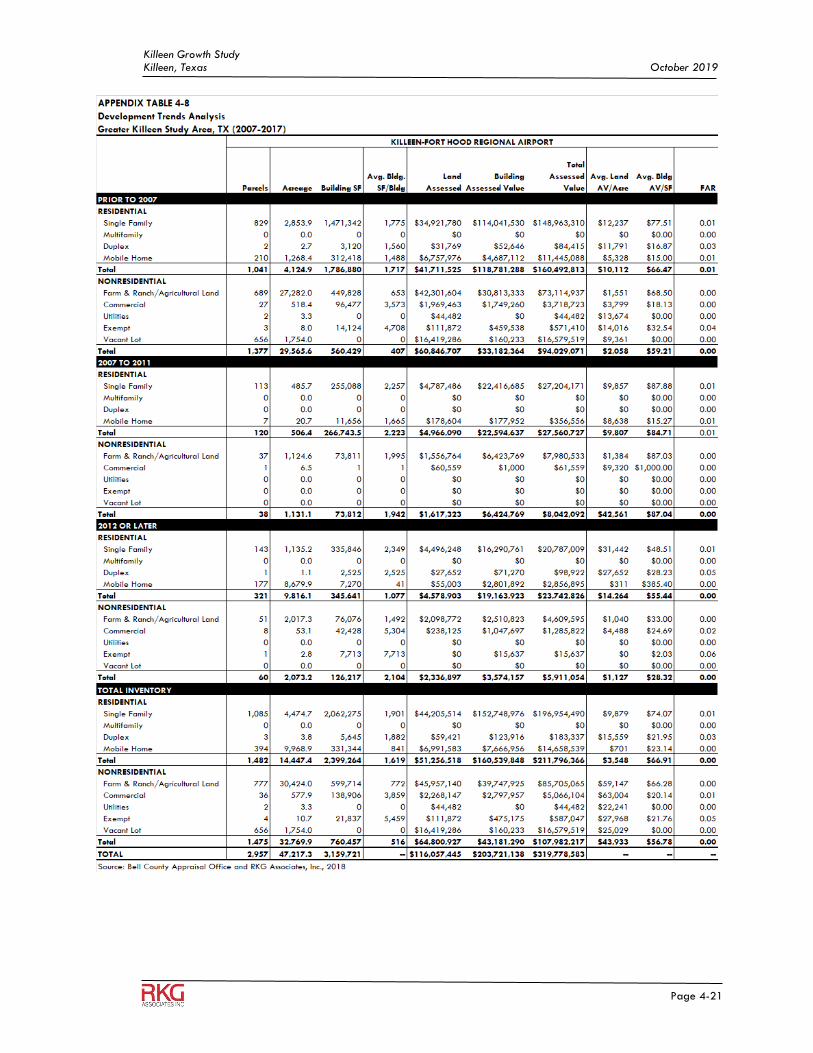

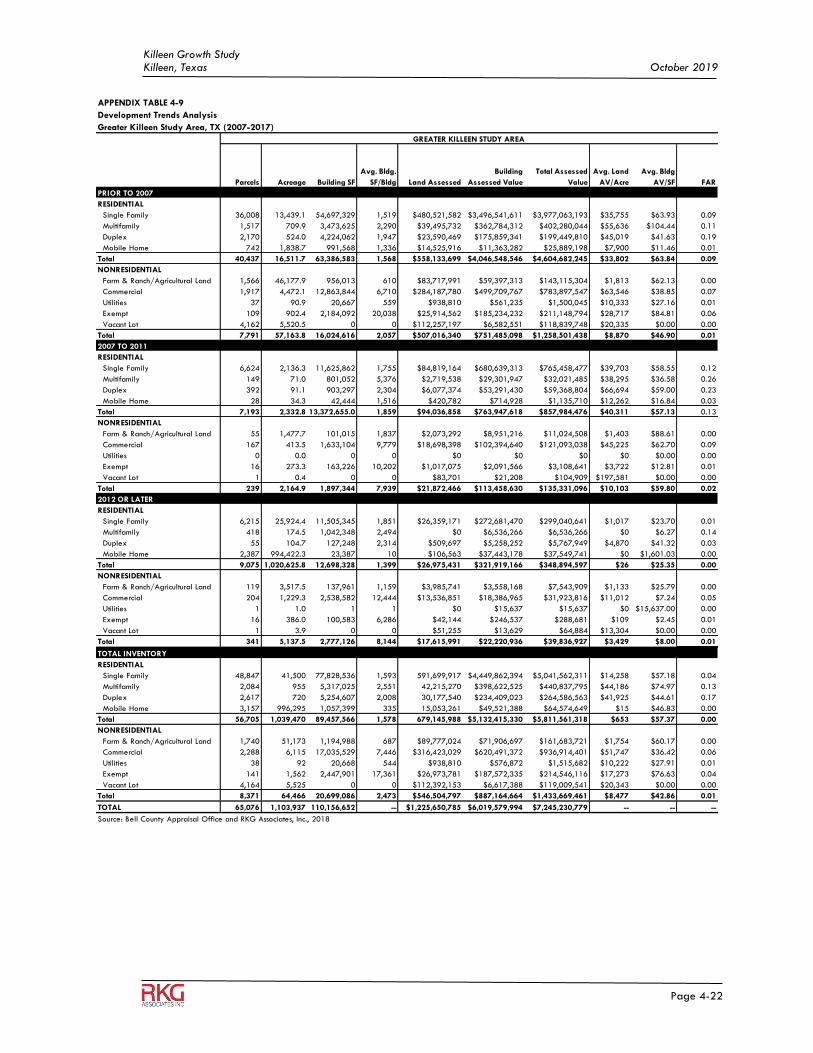

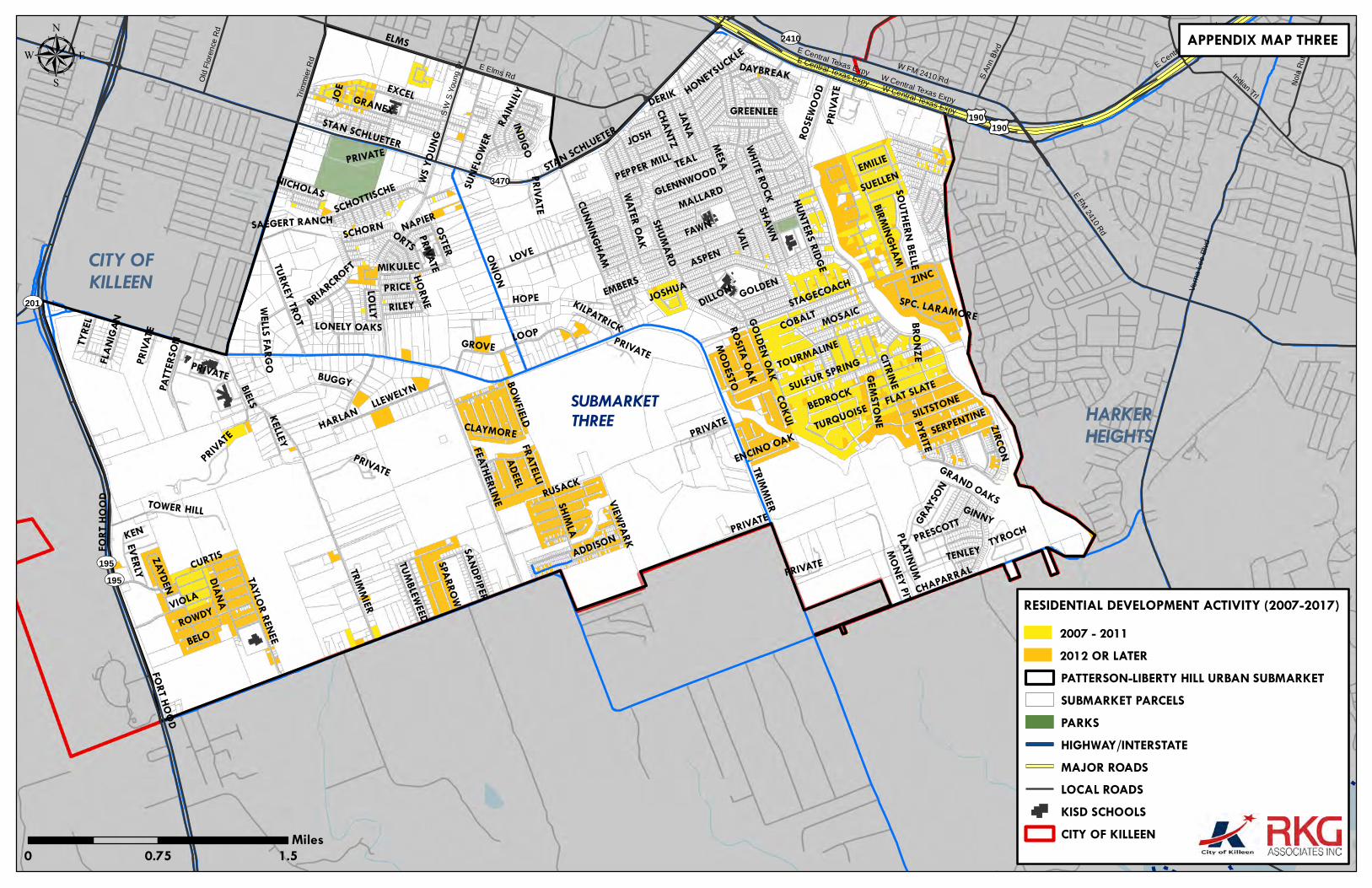

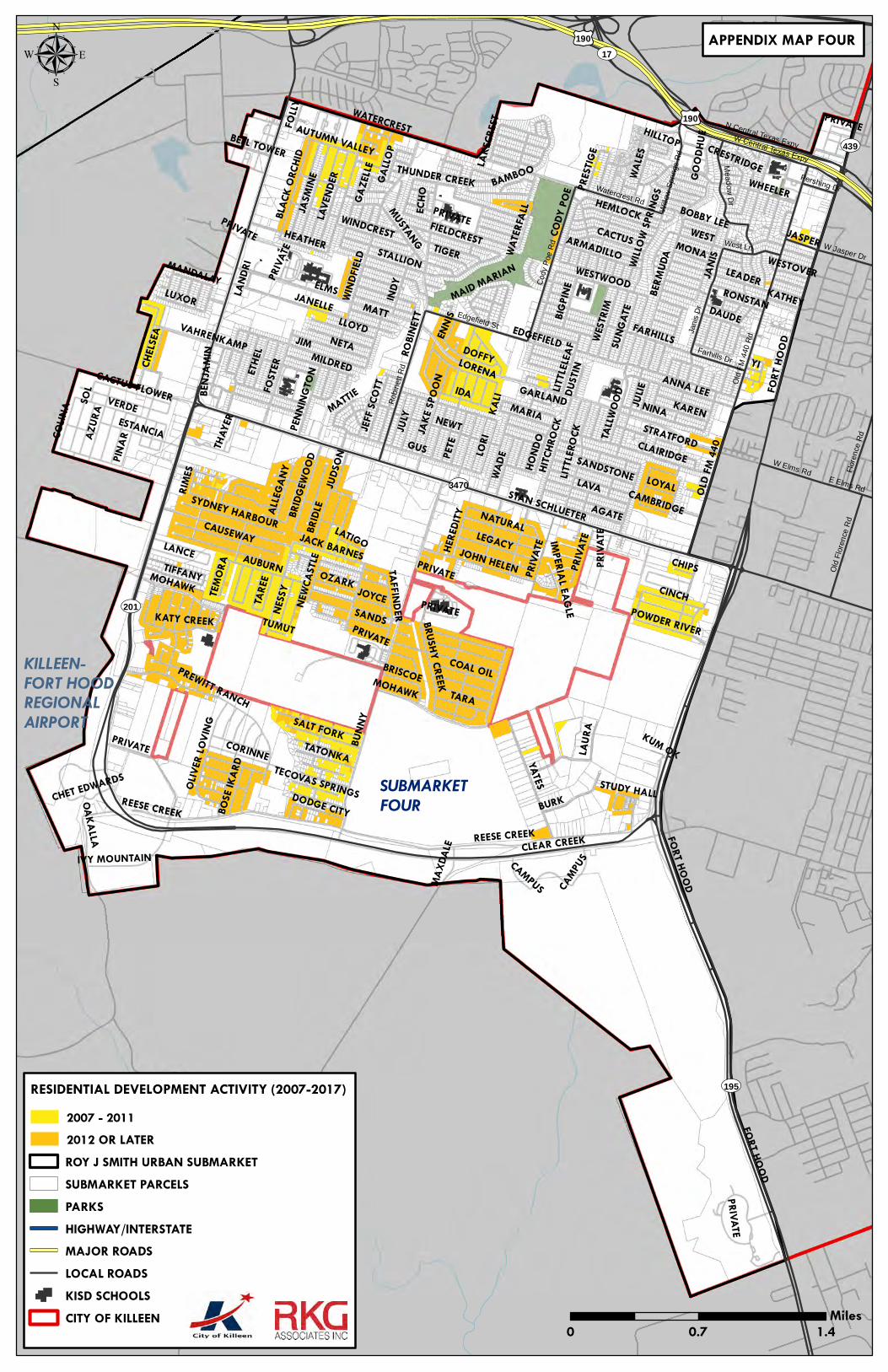

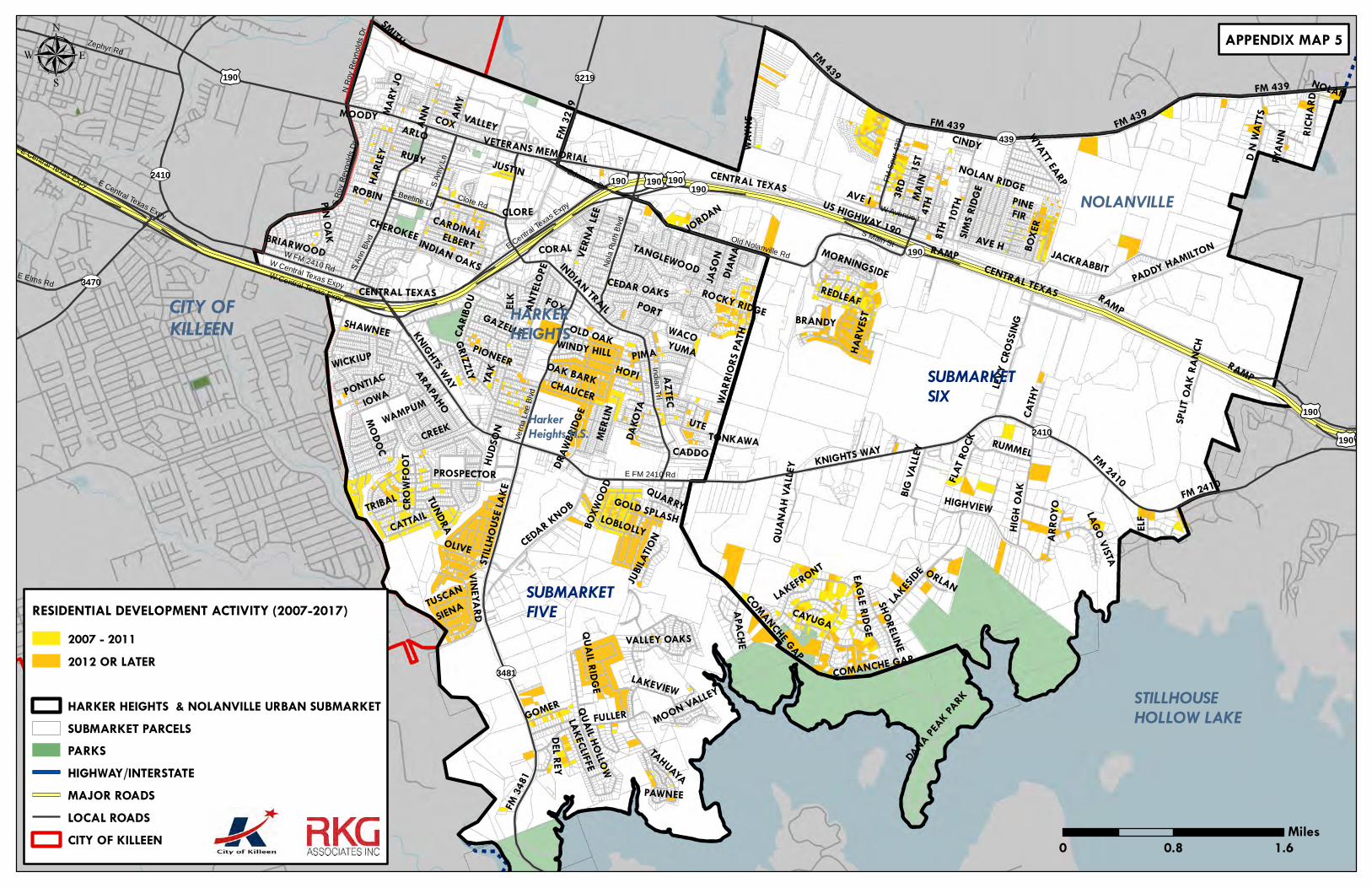

of their household income on housing. This often indicates that residents are experiencing housing affordability issues, despite its comparatively affordable housing market. All submarkets within the Greater Killeen Study Area have a housing stock that is a majority single family detached homes. Housing demand is concentrated within the submarkets that make up the City of Killeen (submarkets 1-4) due to the services offered in the city and their proximity to Fort Hood. These submarkets are more diverse both in type and price compared to the rest of the study area. The population growth that occurred between 2000 and 2009 in the submarkets of Patterson-Liberty Hill and Roy J Smith, allowed for much of the new housing units to be developed there. Most of Patterson-Liberty Hill’s resident population moved into their homes after 2000, whereas Roy J Smith, with its more diverse rent level and housing stock have a much larger percentage of long-term residents. Over the past two decades, the region has shifted from owner-occupied centric to renter-occupied. This has increased the level of moving activity within the study area. Of the 32,000-total renter-occupied units, approximately 80% of renters moved in 2010 or later. a) Owner Occupied Within the Greater Killeen Study Area’s owner-occupied housing market, 75% of homes are valued under $200,000. These houses are mainly concentrated in the Bellaire-Reeces Creek, Manor-Rancier, and Roy J Smith submarkets. Conversely, areas with large lots and suburban features like Patterson-Liberty Hill and Harker Heights submarkets have higher concentrations of homes values above $300,000. Harker Heights has been able to attract new high income-households by building large custom-built homes and rental units. Additionally, as seniors downsize, they have looked at this submarket to rent because of the vibrant long-established neighborhoods. Compared to the metro area, homeowners within the study area spend more of their household income on housing. This is most evident in submarkets like Roy J Smith, Manor-Rancier, and Nolanville, which have significant homeowners spending over 50% of their incomes on housing. In areas such as Bellaire-Reece Creek which have older houses and longer resident tenures, homeowners do not experience the same housing cost burden because they have likely paid off their mortgages. b) Renter-Occupied As the study area has grown over the past 20 years, it has experienced an increase in the amount of rental housing in all submarkets. Within the study area, 48% of units are renter occupied. This rental population is mostly concentrated in the Bellaire-Reeces Creek and Manor-Rancier submarkets, which now account for 60% of multi-family unit inventory. This is consistent with the makeup of the population moving into these areas which are dominated by 1-person and 2-person households. Patterson-Liberty Hill, Roy J Smith, and Fort Hood have the most expensive rental markets, with gross rents near $1000 per month. This is likely due to the new multifamily developments happening in those submarkets. Bellaire-Reece Creek and Manor-Rancier with their older rental housing stock have the most affordable rental housing. These submarkets offer gross rents closer to $500 or below. 3. Development Trend Analysis RKG analyzed the residential and non-residential development activity for both the region and the Greater/KISD study area. This analysis focused mainly on the development trends for the 10-year period between 2007-2017. RKG utilized assessment records for each county analyzed in this study. a) Regional Trends- Residential Bell County’s residential market accounts for 72% of all land acreage within the county. The county’s housing mix is dominated by single family housing. Due to the population growth between 2007 and 2011, Bell County added 10,938 parcels or 20.3 Million SF of residential housing. Additionally,

Killeen Growth Study City of Killeen, TX October 2019

Page 1-5

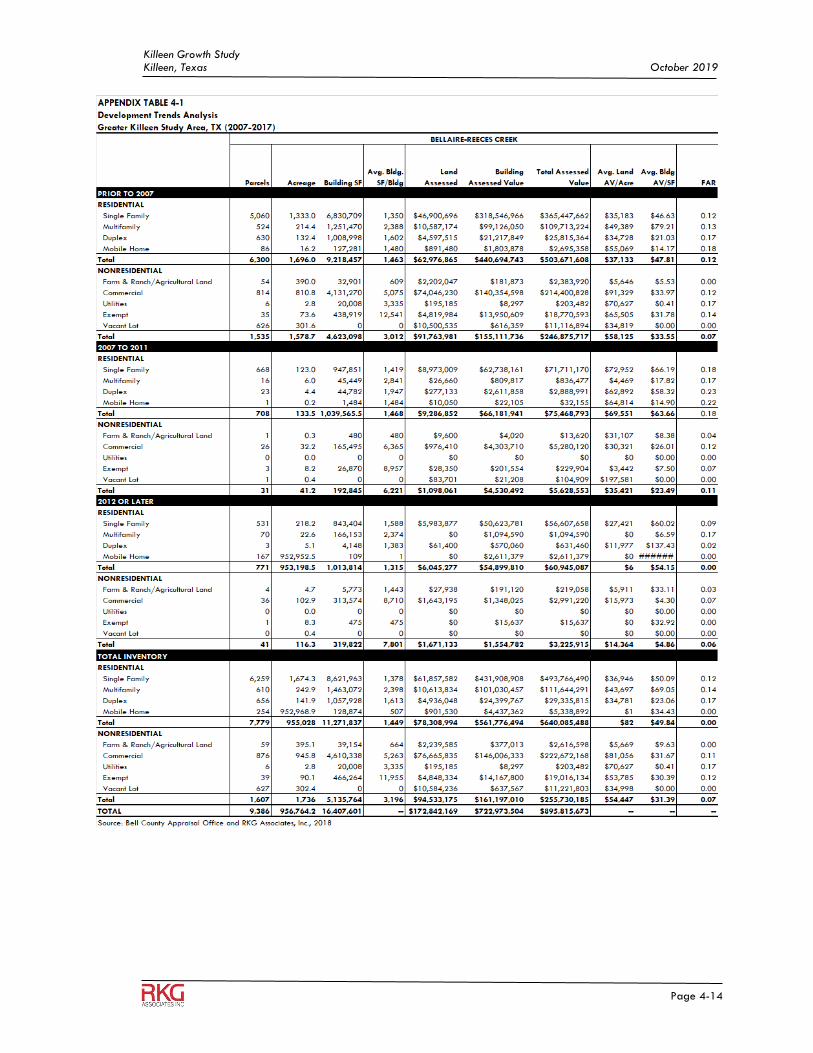

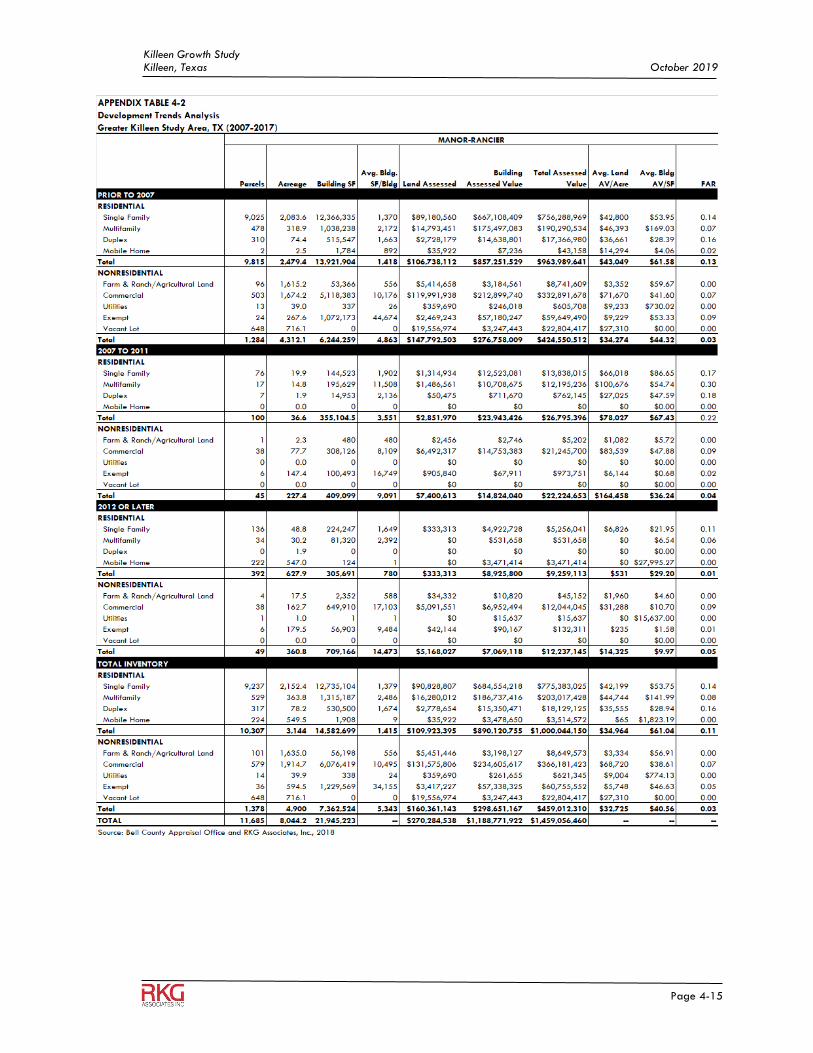

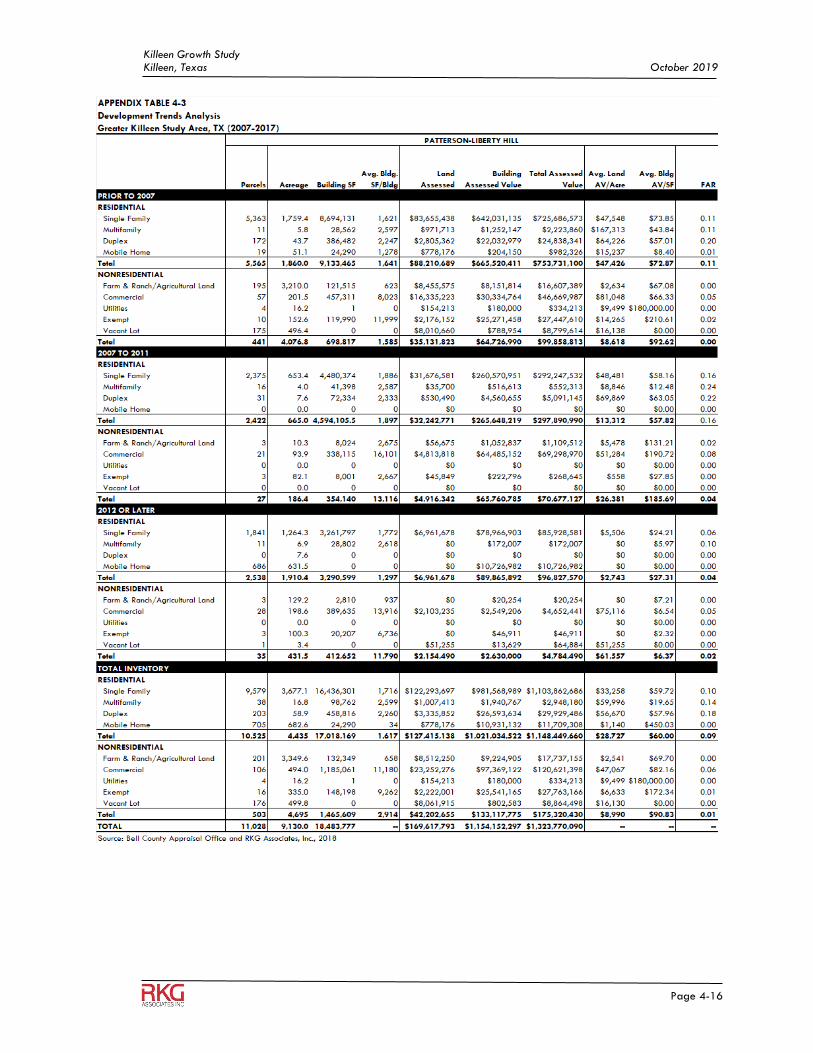

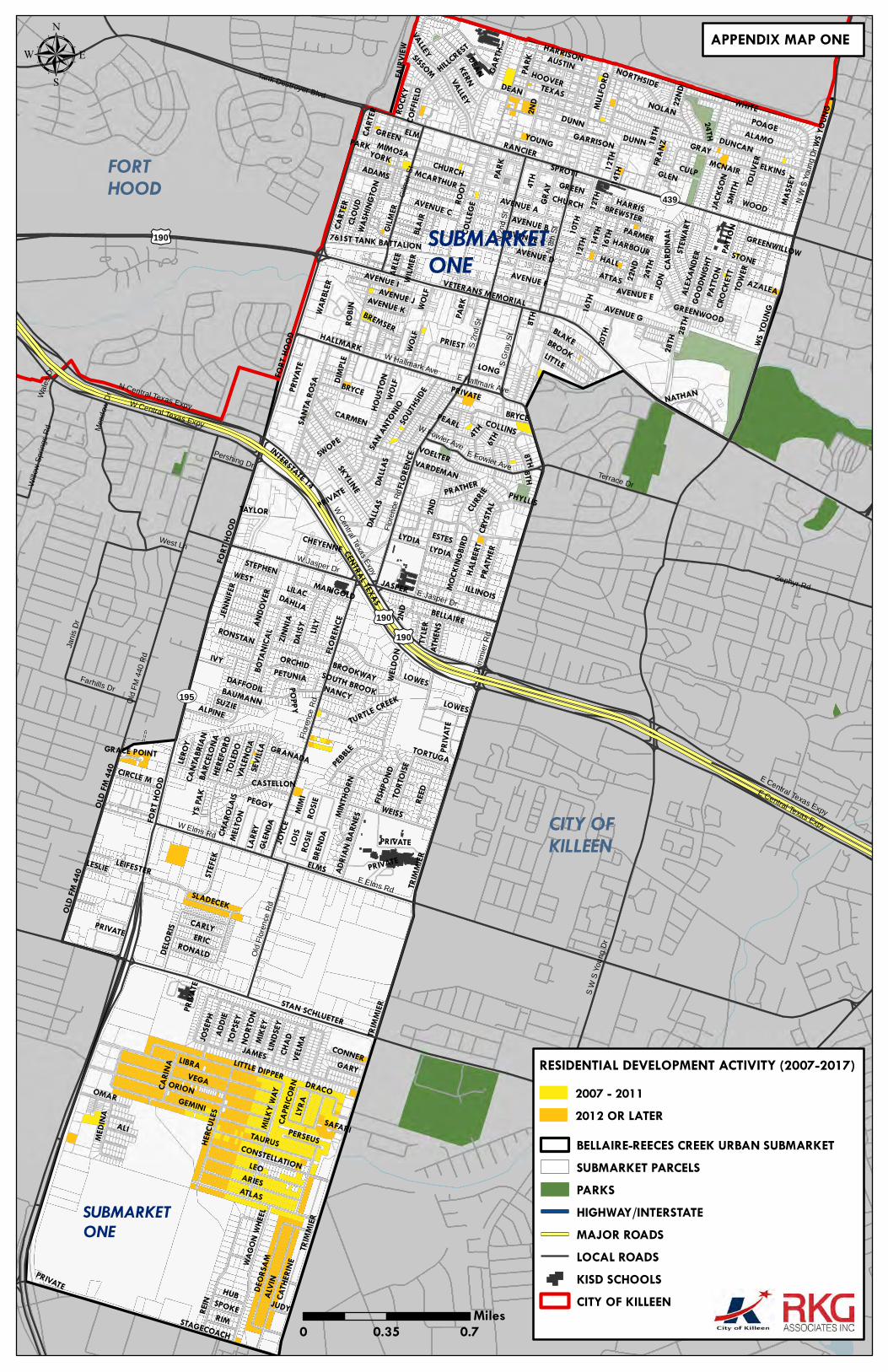

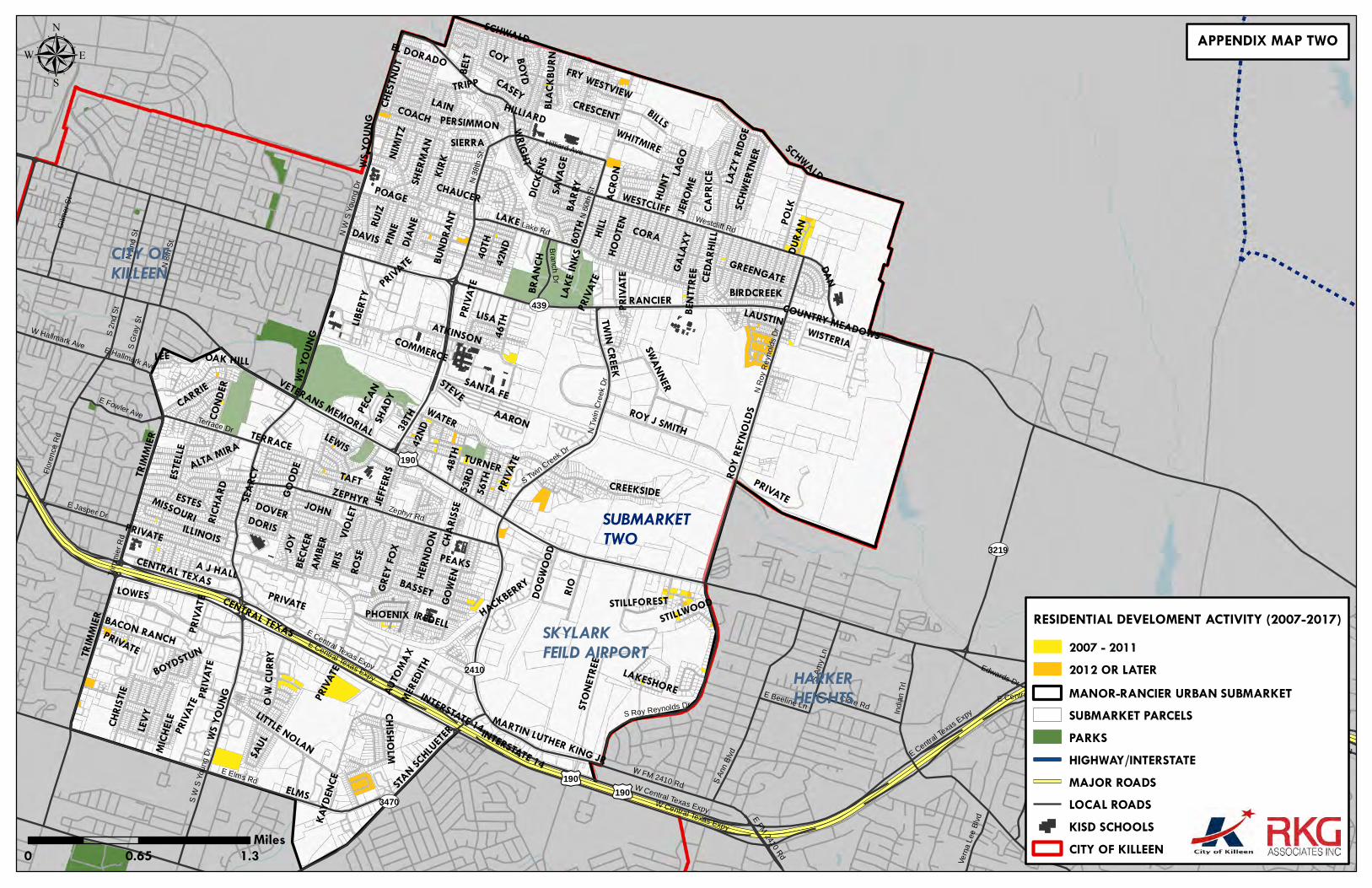

since 2011, the county has exceeded that growth with 18,669 new parcels and 35.9 million SF of residential housing. The 2007-2011 development phased produced larger square footages and higher square feet building value compared to the 2012-2017 phase for both single family and multi-family housing, which reflects a higher demand for less expensive housing. Copperas Cove is a low-density, rural community located in Coryell County. This community has not experienced the same population growth as other areas in the study area. Because of this, 85% of all single-family homes were built before 2007. The development that has occurred over the study period (2007-2017) has been focused on single family housing. These new are substantially larger and of higher value than those built previously in this community. This displays a demand for higher-end housing compared to previous development phases. As the City of Killeen has experienced robust population growth, its residential development market produced different types of housing choices. Between 2007 and 2011, developers invested heavily in the city’s single-family housing market. Because much of the population growth came from families with children, duplexes were not a housing type that developers focused on during this period. Additionally, the city did see a large buildup of multi-family inventory. Since 2011, 20% of the city’s multi-family properties were built, as more non-family households came to the region. b) KISD Trends- Residential Due to the significant population growth in both Patterson-Liberty Hill and Roy J Smith, these submarkets have been the most active from a residential development perspective. Patterson-Liberty Hill added 4,216 residential properties between 2007 and 2017. Roy J Smith saw growth in the multi-family segment of the residential market. Additionally, both submarkets saw demand for higher-end housing increase, evident by the larger average residential unit square footage. The submarkets of Bellaire-Reeces Creek and Manor-Rancier have not experienced the same residential development due to their lack of developable land. However, because of the proximity to the Fort Hood military post, Bellaire-Reeces Creek has experienced modest residential development of both single family and multi-family buildings. The Fort Hood submarket has only seen residential growth in mobile homes during the study period, which coincides with the lack of population of growth. Killeen-Fort Hood Regional Airport submarket has experienced strong demand for large single-family house since 2007, as homeowners have used this submarket to build high-value housing. c) Non-Residential Within Bell County, only 3% of all non-residential land is currently occupied by commercial properties. Most of the non-residential land within the county is vacant or farmland. In terms of development, the non-residential market has not kept pace with the residential market during the study period. With the large increase in population and a significant amount of vacant land, non-residential developments should be viable to meet commercial and public service needs. The City of Killeen non-residential market has also not kept pace with its residential market. The City of Killeen’s non-residential market added an additional 3 million SF of commercial space during the study period. The city also has a large amount of vacant commercial lots, that could be assembled to eventually meet the commercial needs of a now larger population. Within the Greater Killeen/KISD study area, most of the non-residential properties are in older submarkets like Bellaire-Reeces Creek and Manor-Rancier. These two submarkets attract workers, shoppers, and patrons from other surrounding submarkets because of their concentrated downtowns. Though Bellaire-Reeces Creek has experienced population growth, it has not experienced commiserate growth in non-residential development. Because of that many, needs for both commercial and public services within this submarket are not being met. As the residential population

Killeen Growth Study City of Killeen, TX October 2019

Page 1-6

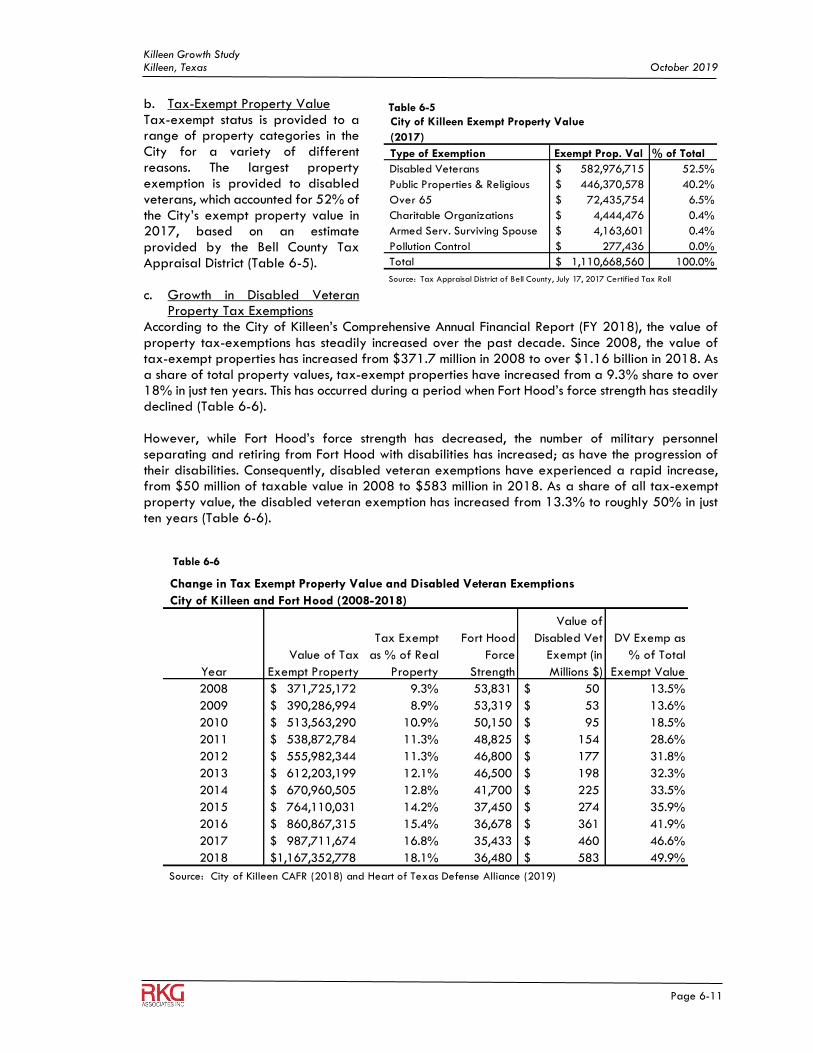

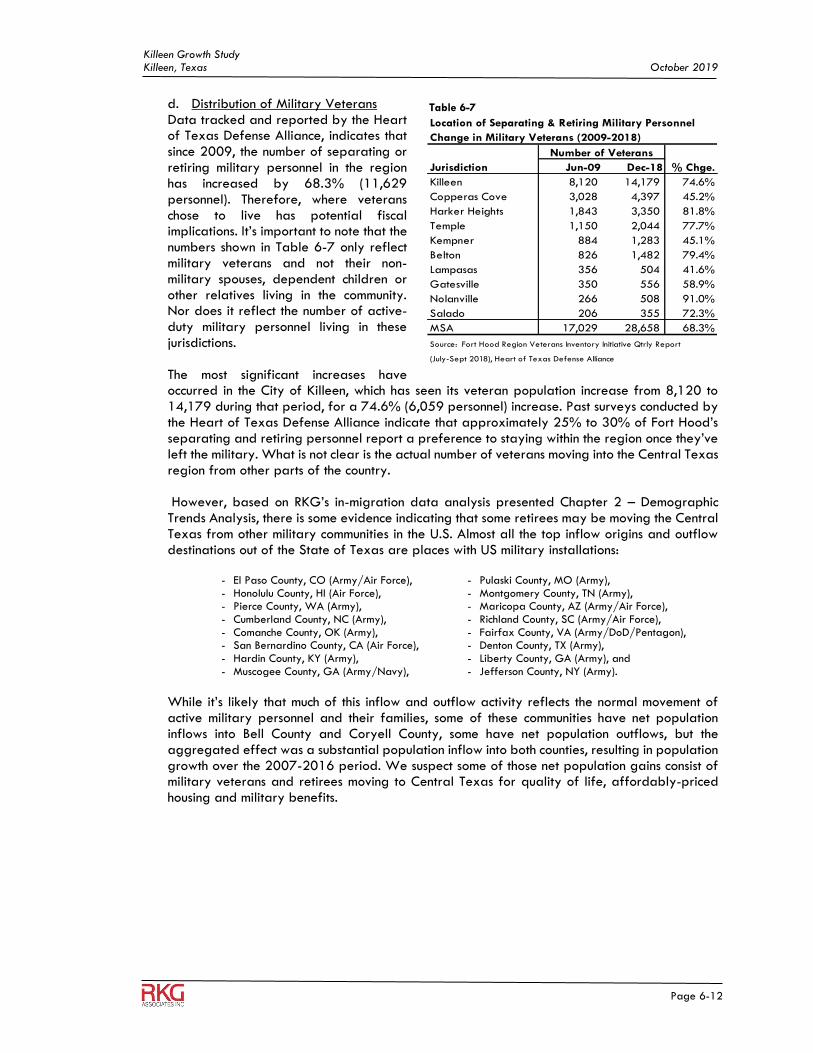

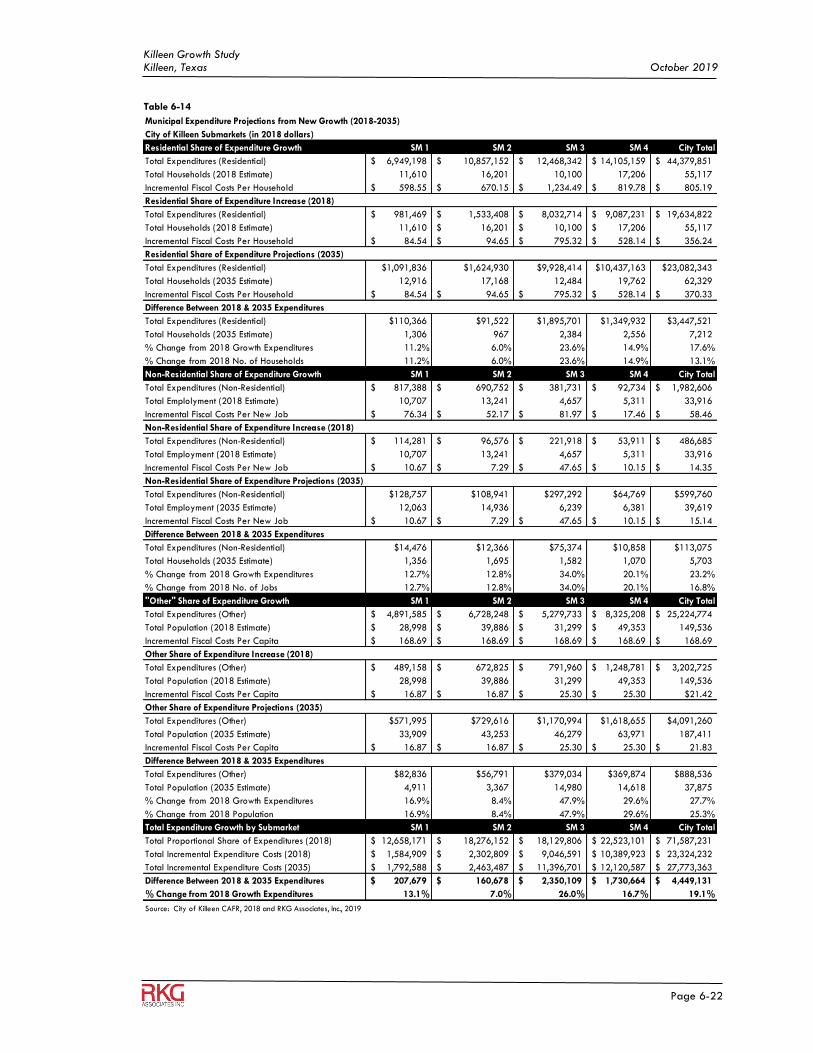

has grown in the Patterson-Liberty Hill and Roy J Smith submarkets, new non-residential properties have begun to be developed to support these new population centers. As the population is expected to continue to grow in these two submarkets, government officials and developers should focus their attention on making sure the commercial and public services needs are being addressed. 4. KISD Growth Projections This section details the results of a growth analysis that projected population and employment growth from 2018 to 2035. RKG Associate focused their analysis on the Killeen Independent School District (KISD) study area. a) Population The major shift in the region over the past 20 years is the lessening of dependence on the Fort Hood soldier population. Fort Hood’s population peaked in 2008, yet the Killeen-Temple-Fort Hood Metropolitan area (MSA) continued to grow its population at 1.9% annually. Additionally, as the military population has deceased, student enrollment within the KISD increased during this time period. A majority of this growth will occur in the Patterson-Liberty Hill and Roy J Smith submarkets. This will be a continuation of the population growth that both submarkets have experienced over recent years. Over the next 17 years, Bell County is projected to have an annual population growth rate of 1.4%. Based on these projections, the population of people between the ages of 20-54 is expected to grow by 54% over this period. This is critical to the region, as these ages contribute significantly to both the labor force and family-forming households. Additionally, like the national trend, the county is expected to see significant annual increases in the number of people aged 75 and older. b) Employment RKG projected the employment makeup of the KISD study area from 2018 to 2035 by using the 2018 employment figures for each submarket. Total employment is projected to increase at 0.9% annually, which is slower than the projected population growth. This new employment will cluster in the fast-growing and traditional employment hubs that have the infrastructure and population needed to support them. Since 2010, 80% of commercial development within the KISD happened in the City of Killeen. Traditional employment hubs such as Bellaire-Reeces Creek and Manor-Rancier will continue to be attractive to employers. Additionally, areas south of I-14 like Patterson-Liberty Hill and Roy J Smith, which have experienced significant population and employment growth this decade will also continue to be attractive to employers and commercial developers. 5. Fiscal Impact Analysis This chapter analyzes the fiscal impact of the growth projections detailed in Chapter 5-KISD Growth Projections. The purpose of this chapter is to give insight to both the City of Killeen and KISD on how the expected growth will impact their financial operations over the next 17 years. a) General Government Fiscal Impact As the City of Killeen has grown, its taxable property value experienced a 58% increase. However, the value of tax-exempt properties that are located within the city increased by 214%. In real terms, the City has lost nearly $5.9 million in ad valorem tax revenues in the current fiscal year. Within the City, disabled veterans take up the largest share of tax-exempt property value. This number has continued to increase even as Fort Hood’s force strength has declined. This reflects the rapid increase in veterans retiring within the region. The City of Killeen has experienced the most substantial growth in veteran population regionally. Military veterans and retirees from other parts

Killeen Growth Study City of Killeen, TX October 2019

Page 1-7

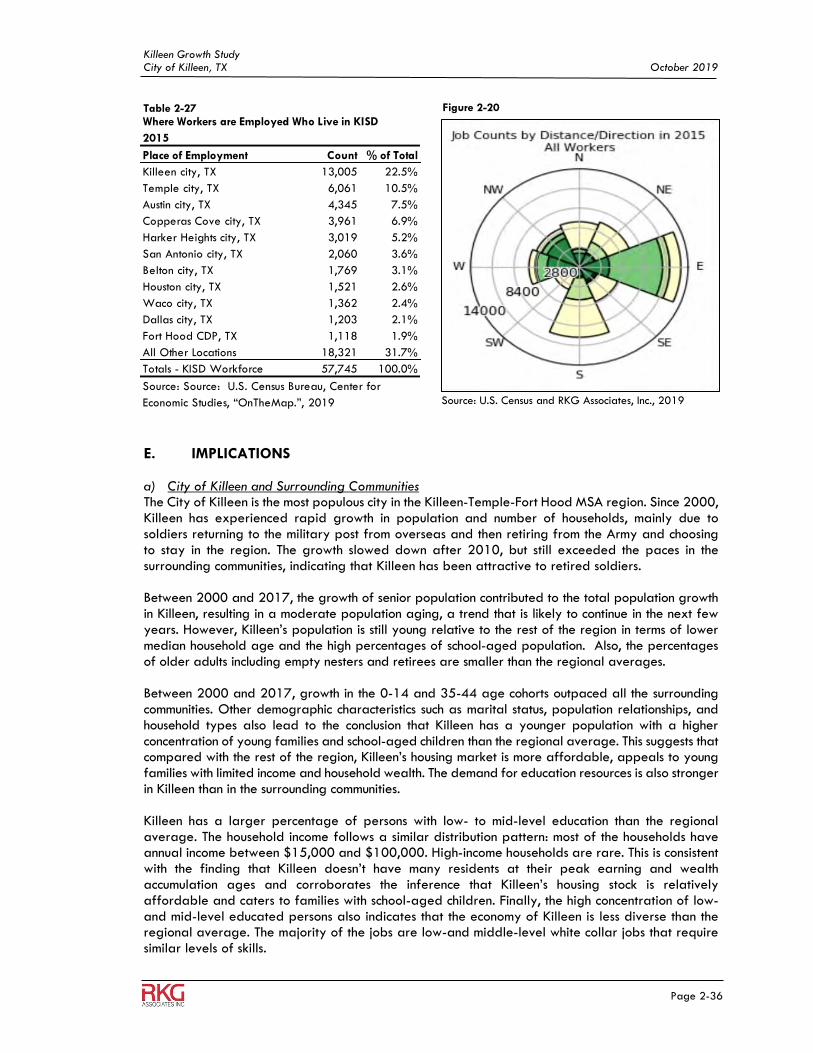

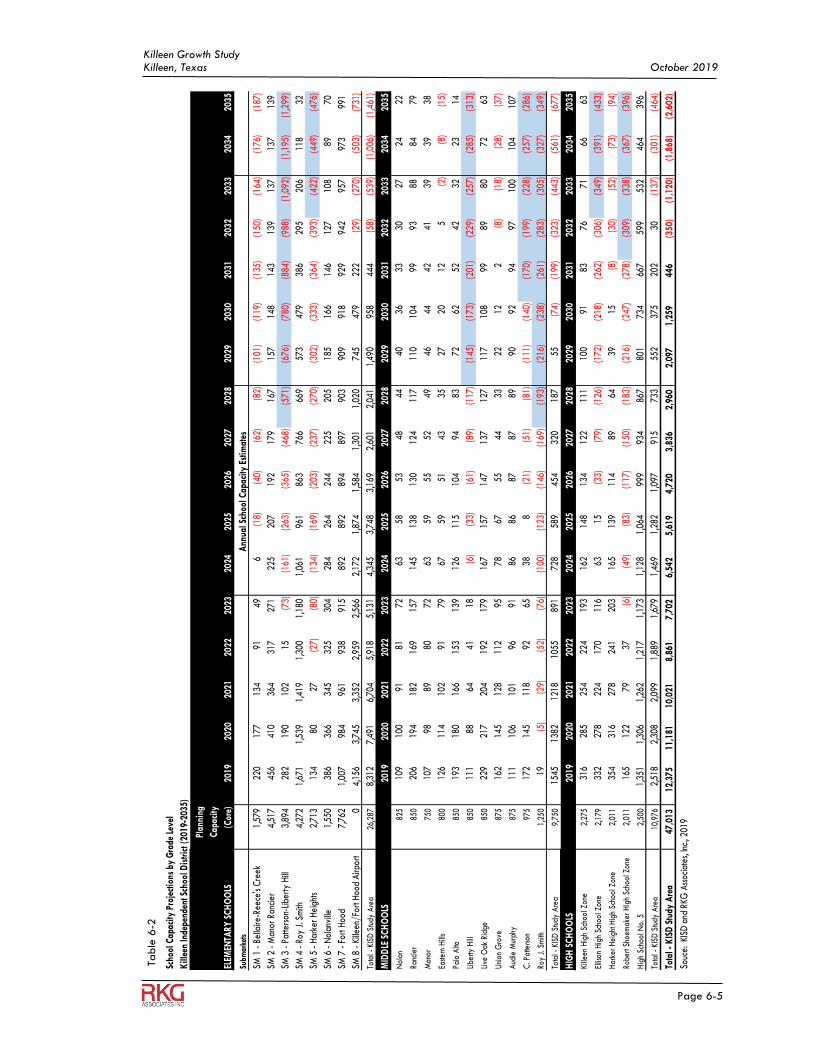

of the country are moving to this region because of the quality of life, affordable housing, and military benefits. As the region is expected to grow in population over the next 17 years, it will need to build new residential and non-residential properties to accommodate that growth. Based on a model created by RKG, Bell County is expected to add an additional $1.7 billion (2018 dollars) in new residential assessed value during this study period. The largest portion of this growth will occur during the 2020-2025 period. Fast-growing submarkets such as Patterson-Liberty Hill and Roy J Smith will be the areas that have the largest residential property value growth. On the non-residential side, with estimated job growth of less than 1% each year, the KISD study area is projected to add 3.6 million SF of new building space to accommodate over 7,000 new jobs. Due to the new development within both the KISD and the City of Killeen, both entities are expected to annually average an additional $12 million and $5 million respectively, in new property tax revenues. The City of Killeen, over the 17-year projection period, with the new retail and hotel offerings, would collect $28.4 million in new sales tax and $5.8 million in hotel occupancy tax. This money will help offset the new expenditures needed to accommodate this growth. RKG created a model to investigate the impact of municipal expenditures based on the expected growth in each submarket. Based on growth projections, an additional $4.5 million dollars will be spent in 2035 on municipal expenditures. As Patterson-Liberty Hill and Roy J. Smith are expected to account for much of the growth within the city, the model allocates most of the future expenditure changes to those submarkets. b) KISD RKG obtained detailed school attendance data for all schools within the KISD to project future school facility needs for each submarket. Overall, from 2019 to 2035, the KISD is projected to add 25% more students based on the 2019 enrollment figures. A majority of these new students will be enrolled in elementary schools. Most of this growth will occur in the submarkets of Patterson-Liberty Hill, Roy J Smith, and Harker Heights. It will be necessary for KISD to monitor these expected growth submarkets closely to have time to plan for the services needed. Taking into account the already planned new school construction and consolidations, RKG projects the following building additions to the school district:

• Year 2028 – New elementary school in the fast-growing Patterson-Liberty Hill submarket

• Year 2030 – New middle schools for Patterson-Liberty Hill and Roy J. Smith submarkets

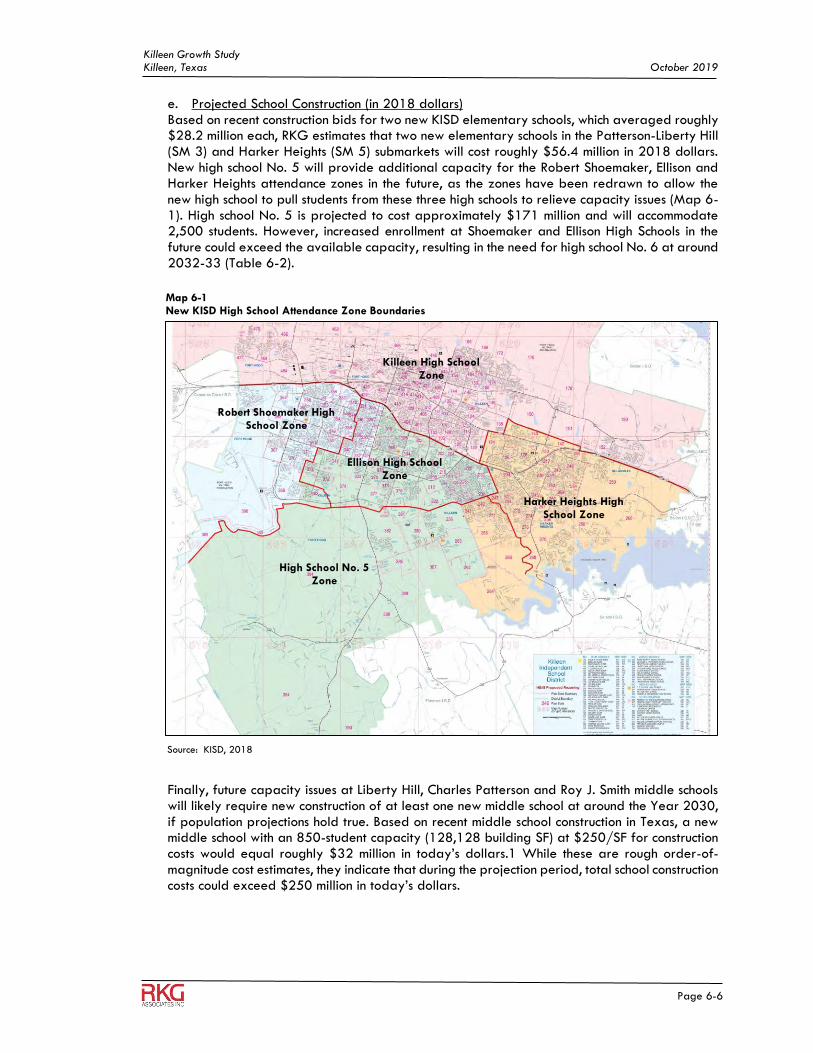

• Year 2031- Robert J. Shoemaker High School is projected to exceed its capacity. New High school (No. 5) would pool students from Robert Shoemaker, Ellison, and Harker Heights attendance zones.

• Year 2033- Ellison High School is projected to exceed its capacity. New High School (No. 6) is projected to be needed to accommodate this growth.

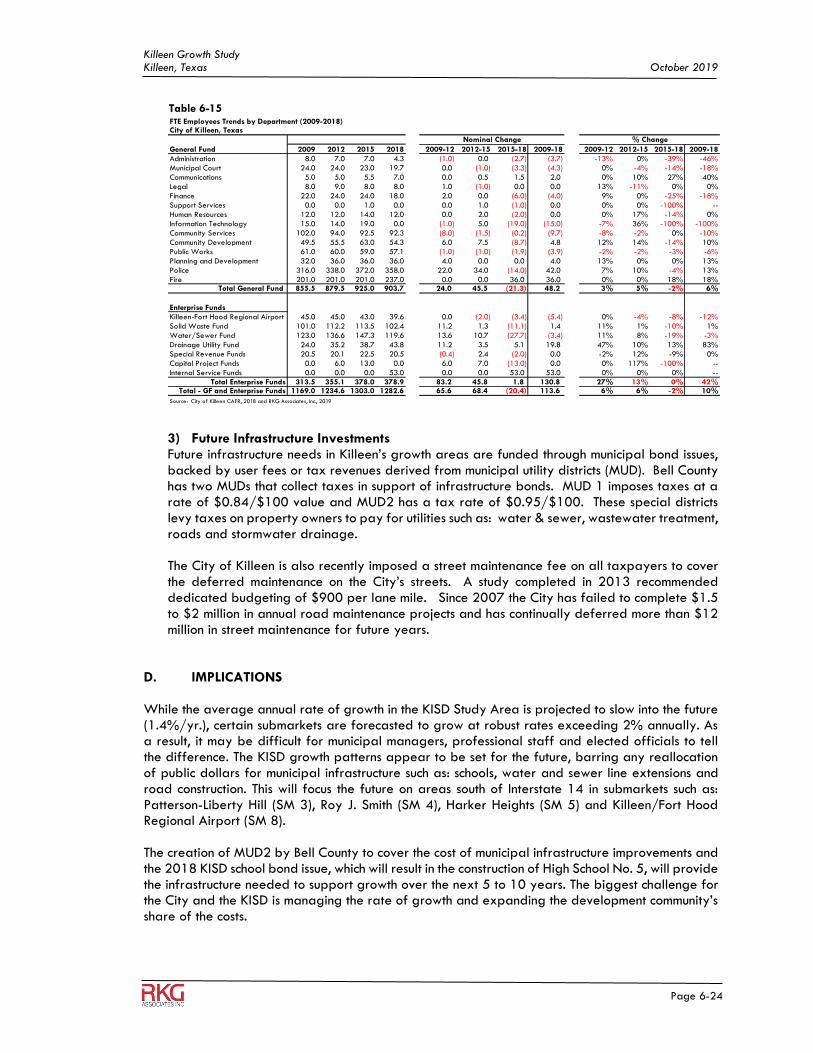

These projected new schools based on recent school construction in Texas could exceed $250 million in today’s dollars. Additionally, based on these projections, KISD will have to hire roughly 775 new teachers (or 45 new staff per year) to accommodate this growth. Finally, KISD receives up to $50 million in Federal Impact Aid because of its high population of federally-connected students. As the number of federally-connected students has dropped over the past 10 years, KISD is expected to go below the federal threshold to receive this aid. Going below the federal threshold could be detrimental to KISD as they could lose up to $20 million from its operating budget.

Killeen Growth Study City of Killeen, TX October 2019

Page 2-1

2 DEMOGRAPHIC TRENDS ANALYSIS

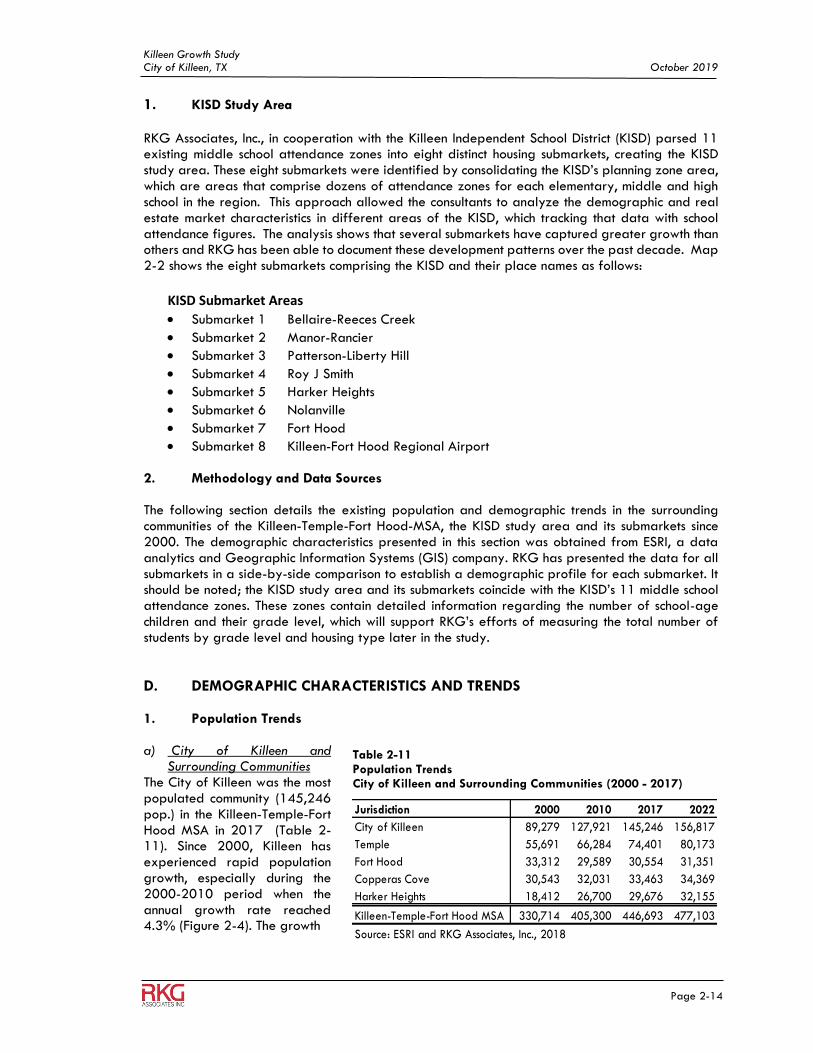

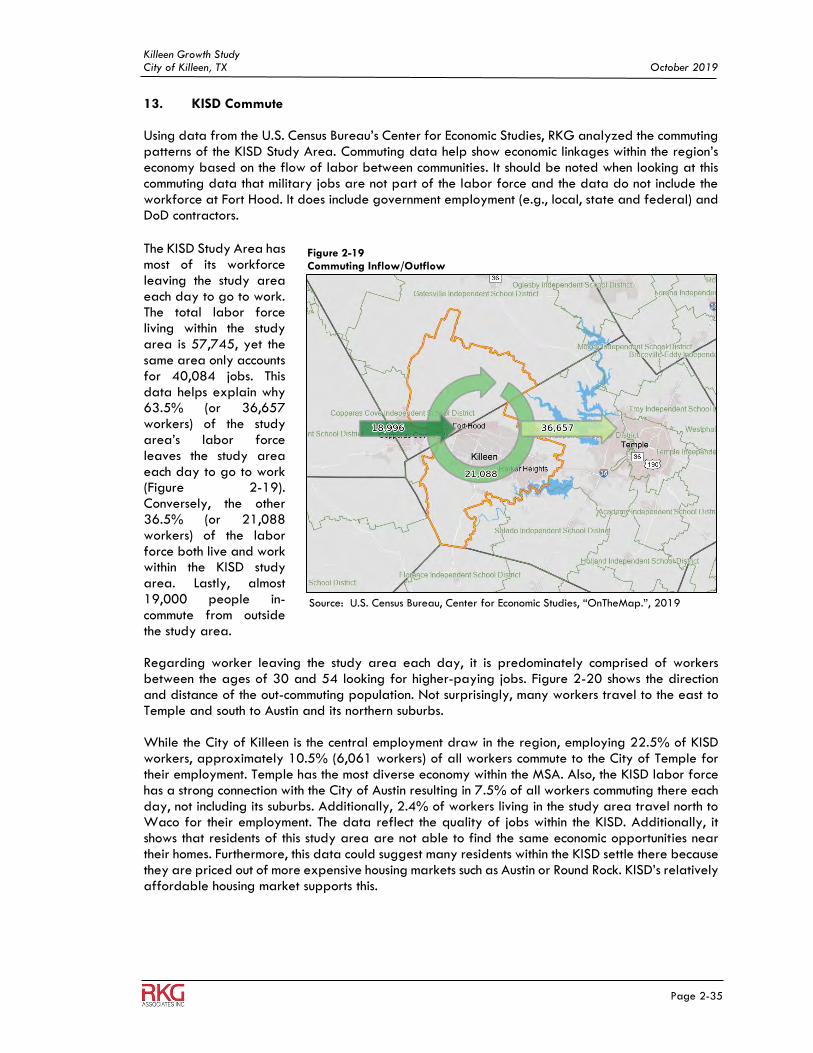

A. INTRODUCTION The City of Killeen is in Bell County, which is the principal city in the Killeen-Temple-Fort Hood Metropolitan Statistical Area (MSA). Additionally, Killeen is directly adjacent to Fort Hood, one of the country’s largest military installations. The city and region’s economy are largely dependent on the activities of Fort Hood, with its 36,000 military personnel and their dependents. Over the past seventeen years, Fort Hood’s population has experienced significant fluctuations depending on the nation’s war-fighting posture around the world. During the same period, the total population of the Killeen-Temple-Fort Hood MSA, which includes Bell, Coryell, and Lampasas Counties, increased substantially but at varying rates of growth. However, there is some evidence that this runs counter to historical trends. Historically, regional population changes have mirrored changes at Fort Hood, however, since 2010 there has been a divergence from historical trends. Primarily, the region’s population has continued to rise while Fort Hood’s population behind the fence has declined. Likewise, student enrollment in the Killeen Independent School District (KISD) has also risen sharply outside the installation while student enrollment has declined on post. The Greater Killeen Chamber of Commerce (GKCC) retained RKG Associates, Inc. to provide a regional demographic and economic analysis to better understand the drivers of population, school enrollment and development growth in the region; particularly in the City of Killeen and the KISD region. It is hoped that the results of this analysis will help local leaders and elected officials plan for this new and emerging future. In order to complete this analysis, RKG examined a variety of housing/development activity, economic and demographic factors shaping the surrounding Killeen-Temple-Fort Hood MSA, the City of Killeen and the KISD study area. To identify local population and development trends, RKG broke the KISD service area into eight separate submarkets. Four of the eight submarkets comprise the City of Killeen’s municipal boundaries. The other four submarkets comprise the smaller towns and suburban areas that are located within the Killeen Independent School District (KISD) boundaries. The results of this analysis are essential for understanding the future growth opportunities that exist in the KISD area.

B. REGIONAL DEMOGRAPHIC TRENDS & EXISTING CONDITIONS

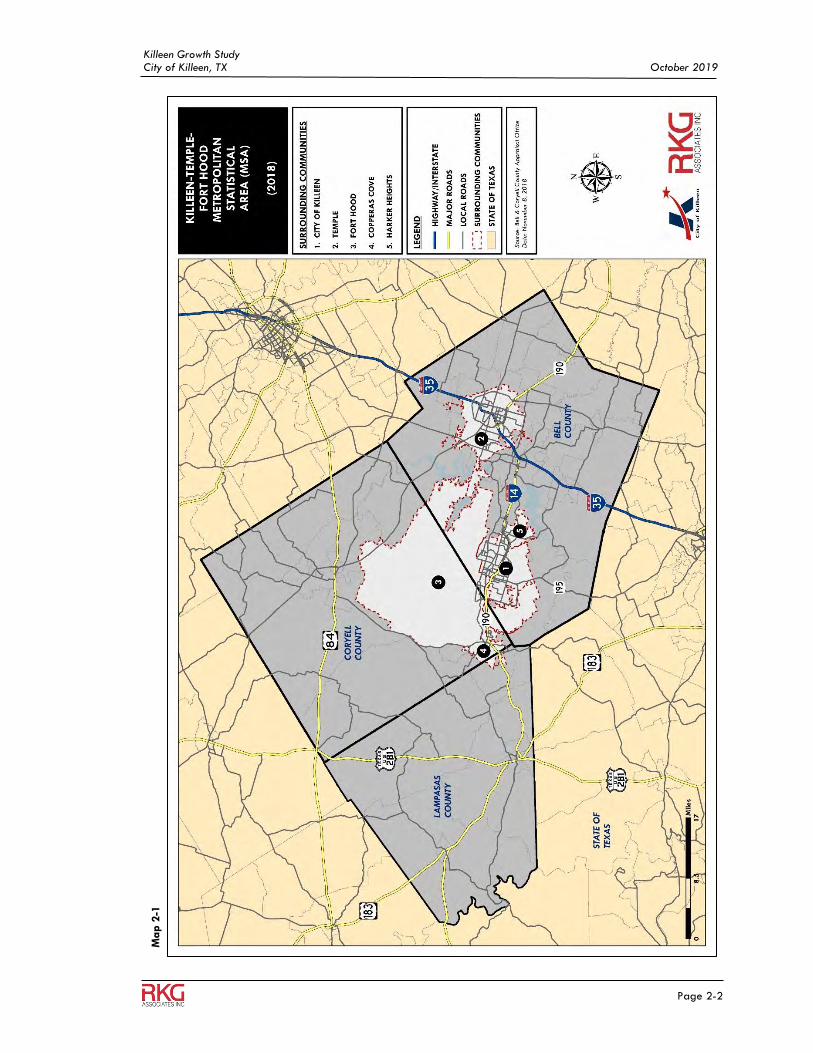

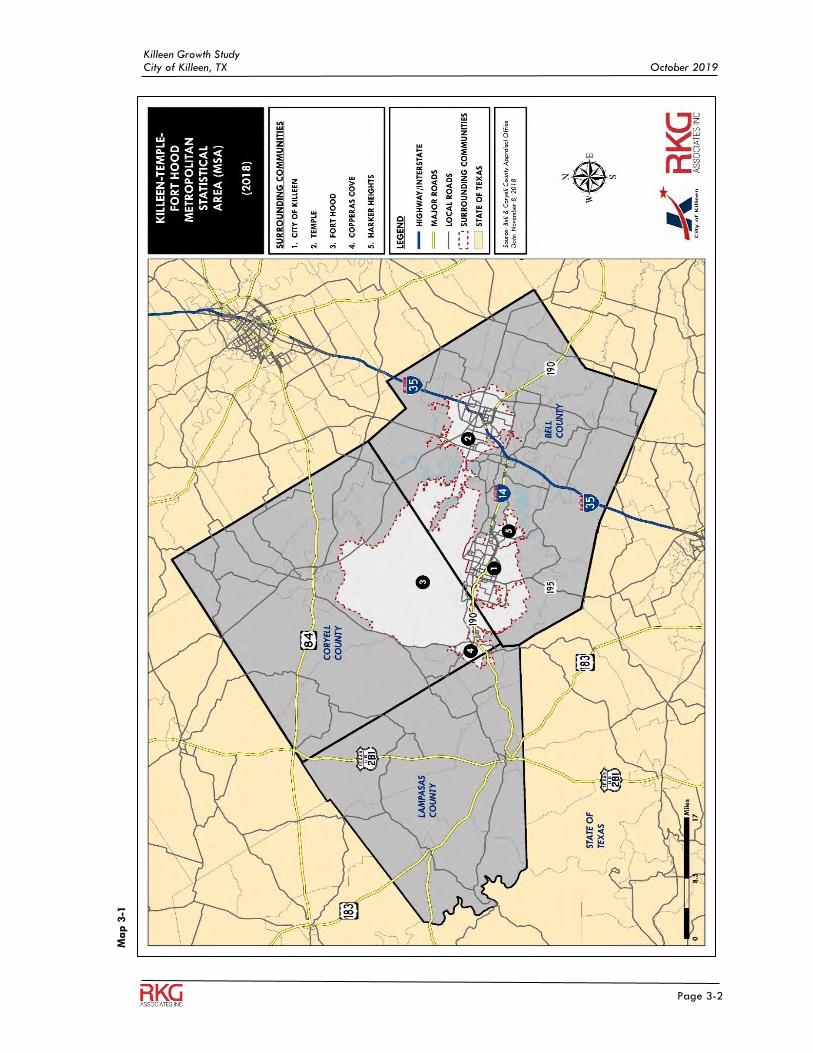

1. Methodology and Data Sources This section quantifies and compares the counties within the Killeen-Temple-Fort Hood MSA that compete against the City of Killeen for new residents and jobs. RKG analyzed nearly 50-year population trends (1970-2017) for the following counties that comprise the Killeen-Temple-Fort Hood MSA, which include: (1) Bell County, (2) Coryell County, (3) Lampasas County (Map 2-1). To complete the population trend analysis the consultant used data obtained from Woods & Poole Economics, Inc., a national data analytics firm.

Killeen Growth Study City of Killeen, TX October 2019

Page 2-2

Ma

p 2

-1

Killeen Growth Study City of Killeen, TX October 2019

Page 2-3

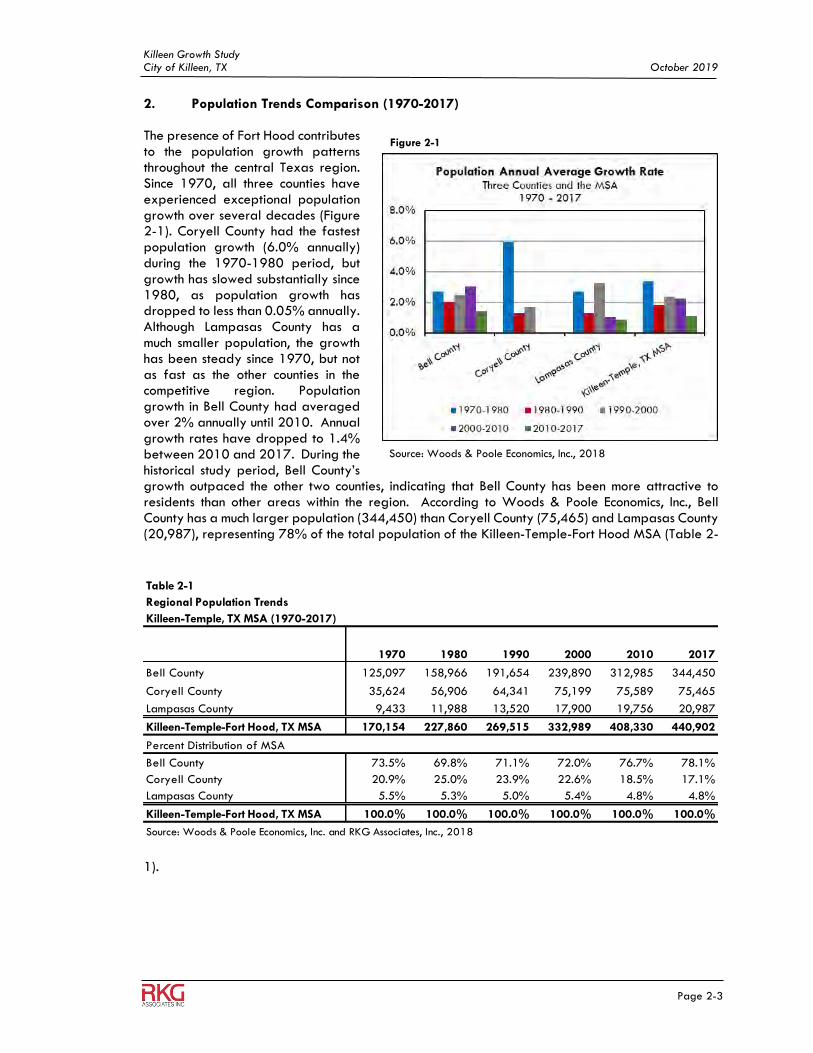

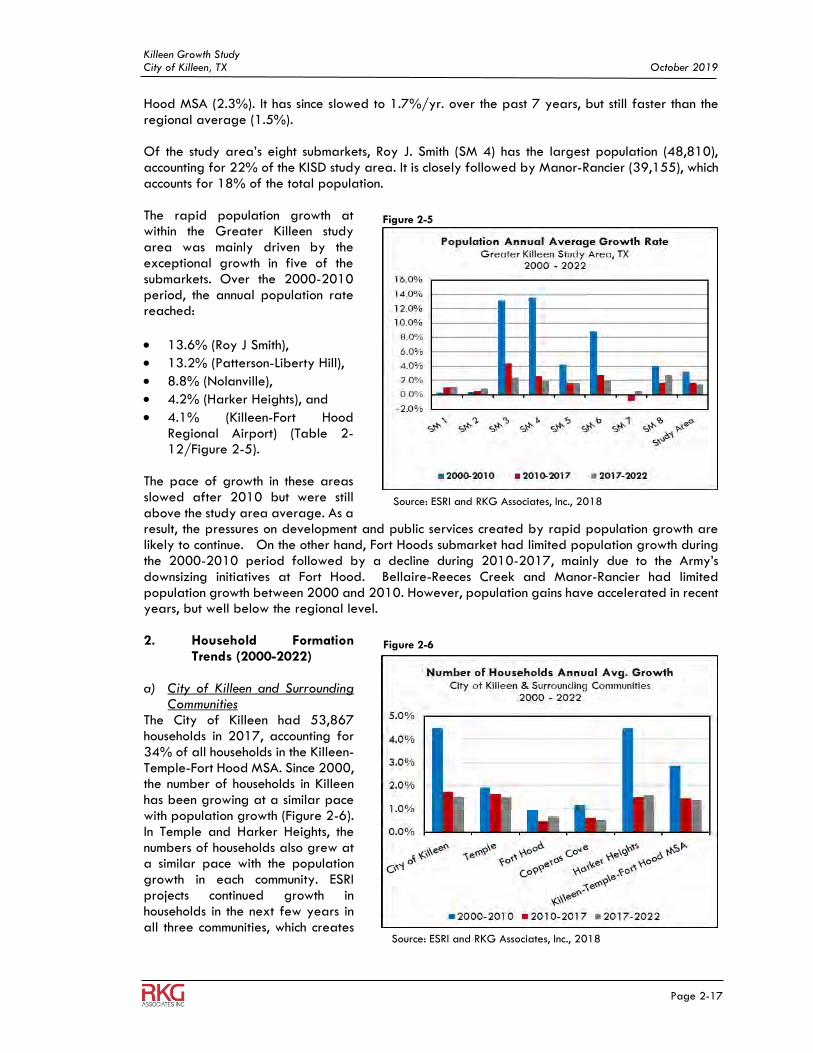

2. Population Trends Comparison (1970-2017) The presence of Fort Hood contributes to the population growth patterns throughout the central Texas region. Since 1970, all three counties have experienced exceptional population growth over several decades (Figure 2-1). Coryell County had the fastest population growth (6.0% annually) during the 1970-1980 period, but growth has slowed substantially since 1980, as population growth has dropped to less than 0.05% annually. Although Lampasas County has a much smaller population, the growth has been steady since 1970, but not as fast as the other counties in the competitive region. Population growth in Bell County had averaged over 2% annually until 2010. Annual growth rates have dropped to 1.4% between 2010 and 2017. During the historical study period, Bell County’s growth outpaced the other two counties, indicating that Bell County has been more attractive to residents than other areas within the region. According to Woods & Poole Economics, Inc., Bell County has a much larger population (344,450) than Coryell County (75,465) and Lampasas County (20,987), representing 78% of the total population of the Killeen-Temple-Fort Hood MSA (Table 2-

1).

Figure 2-1

Source: Woods & Poole Economics, Inc., 2018

Table 2-1

Regional Population Trends

Killeen-Temple, TX MSA (1970-2017)

1970 1980 1990 2000 2010 2017

Bell County 125,097 158,966 191,654 239,890 312,985 344,450

Coryell County 35,624 56,906 64,341 75,199 75,589 75,465

Lampasas County 9,433 11,988 13,520 17,900 19,756 20,987

Killeen-Temple-Fort Hood, TX MSA 170,154 227,860 269,515 332,989 408,330 440,902

Percent Distribution of MSA

Bell County 73.5% 69.8% 71.1% 72.0% 76.7% 78.1%

Coryell County 20.9% 25.0% 23.9% 22.6% 18.5% 17.1%

Lampasas County 5.5% 5.3% 5.0% 5.4% 4.8% 4.8%

Killeen-Temple-Fort Hood, TX MSA 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Source: Woods & Poole Economics, Inc. and RKG Associates, Inc., 2018

Killeen Growth Study City of Killeen, TX October 2019

Page 2-4

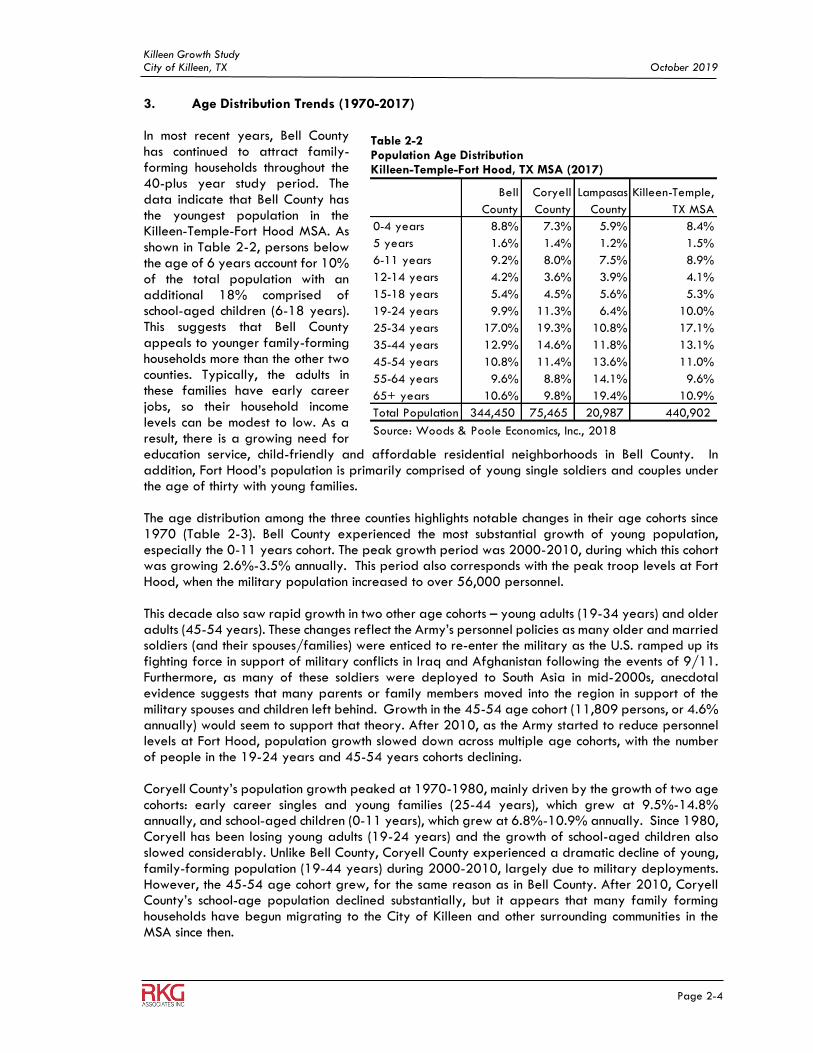

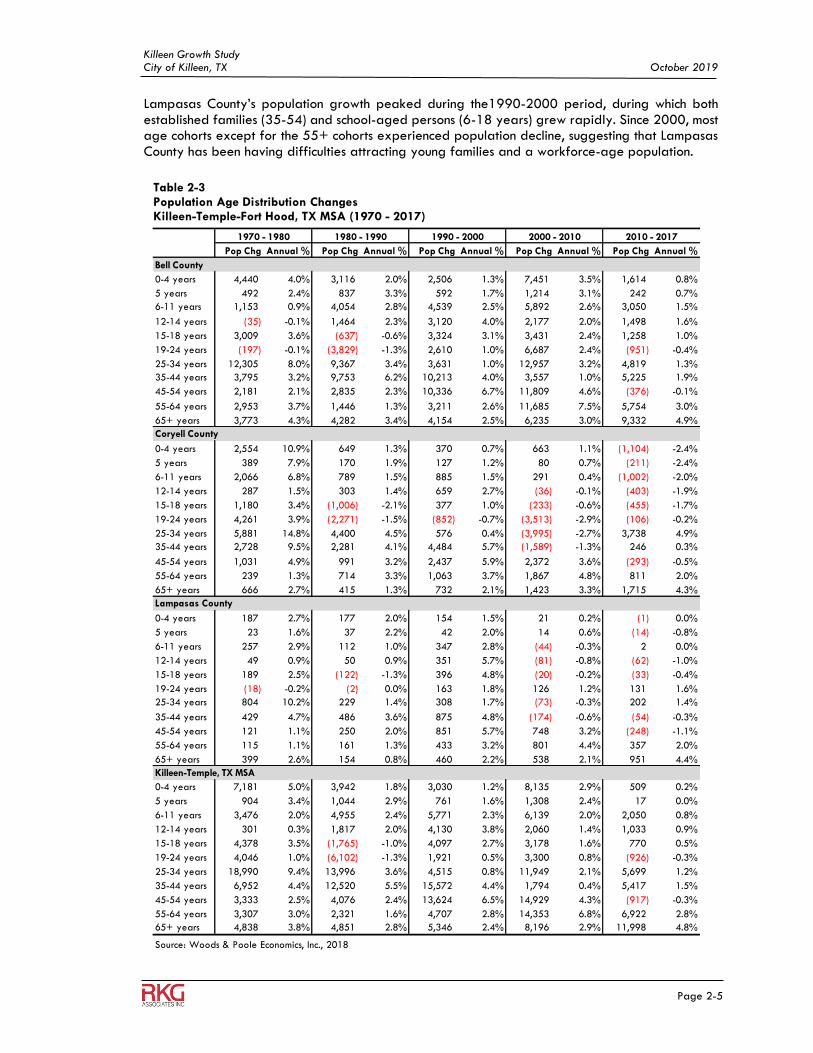

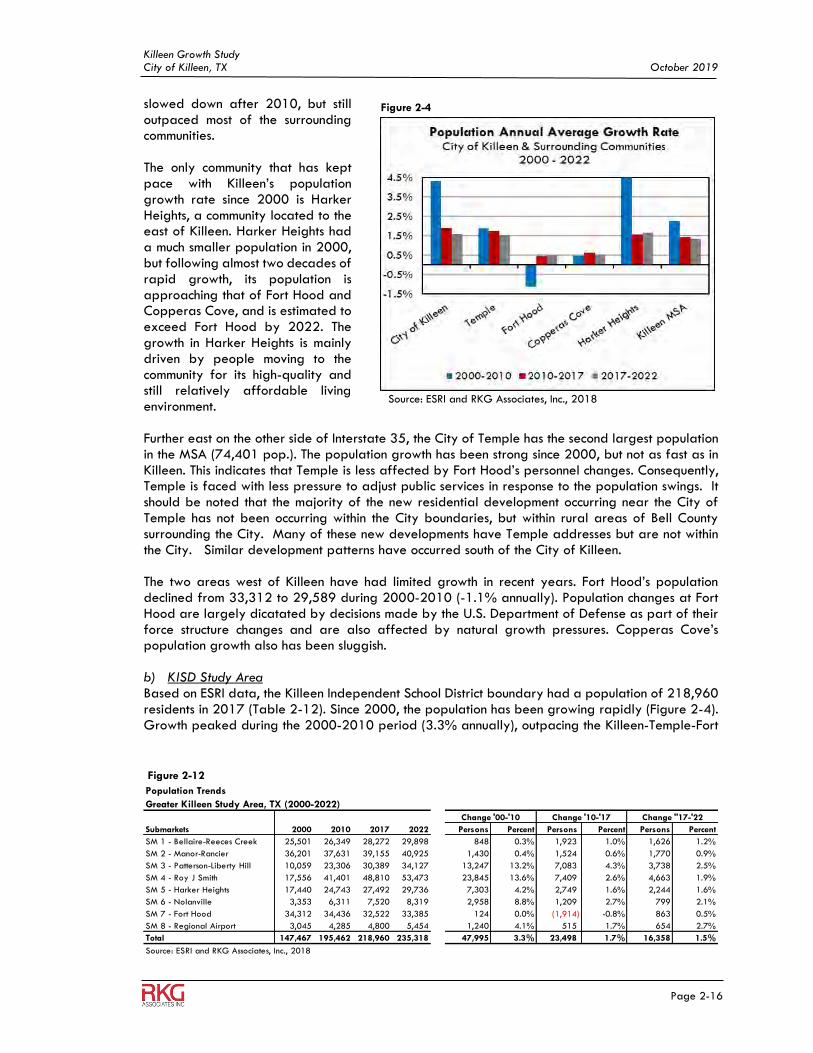

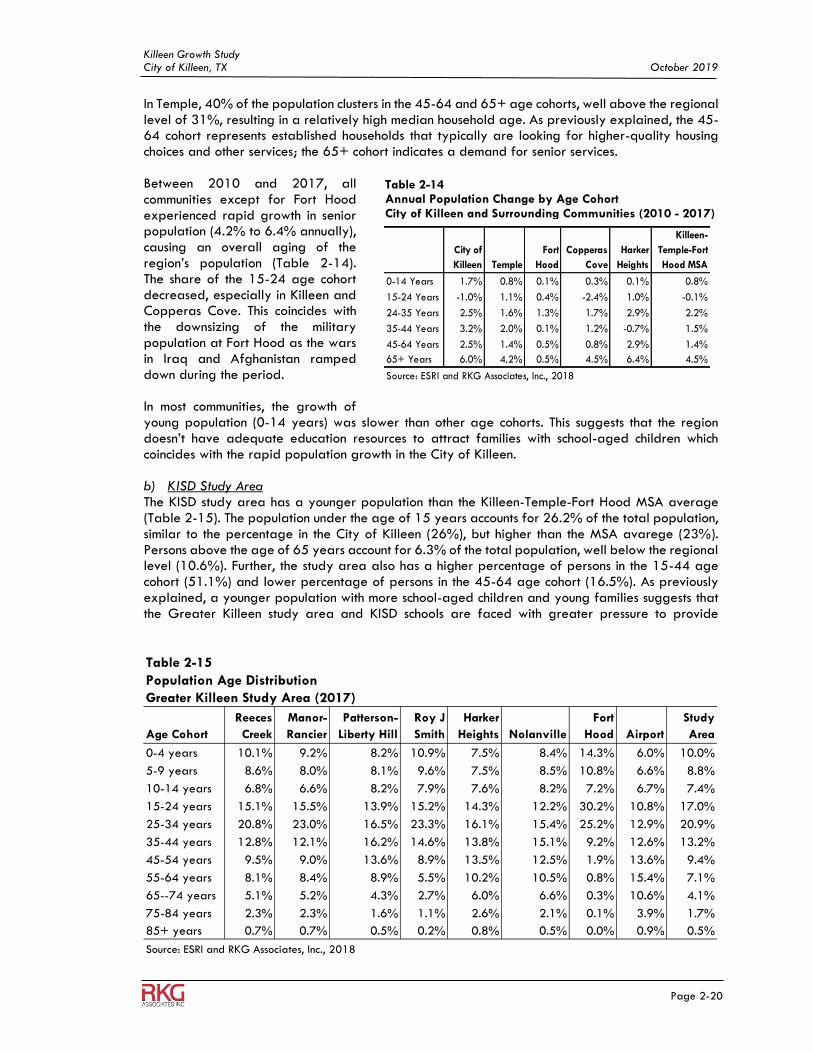

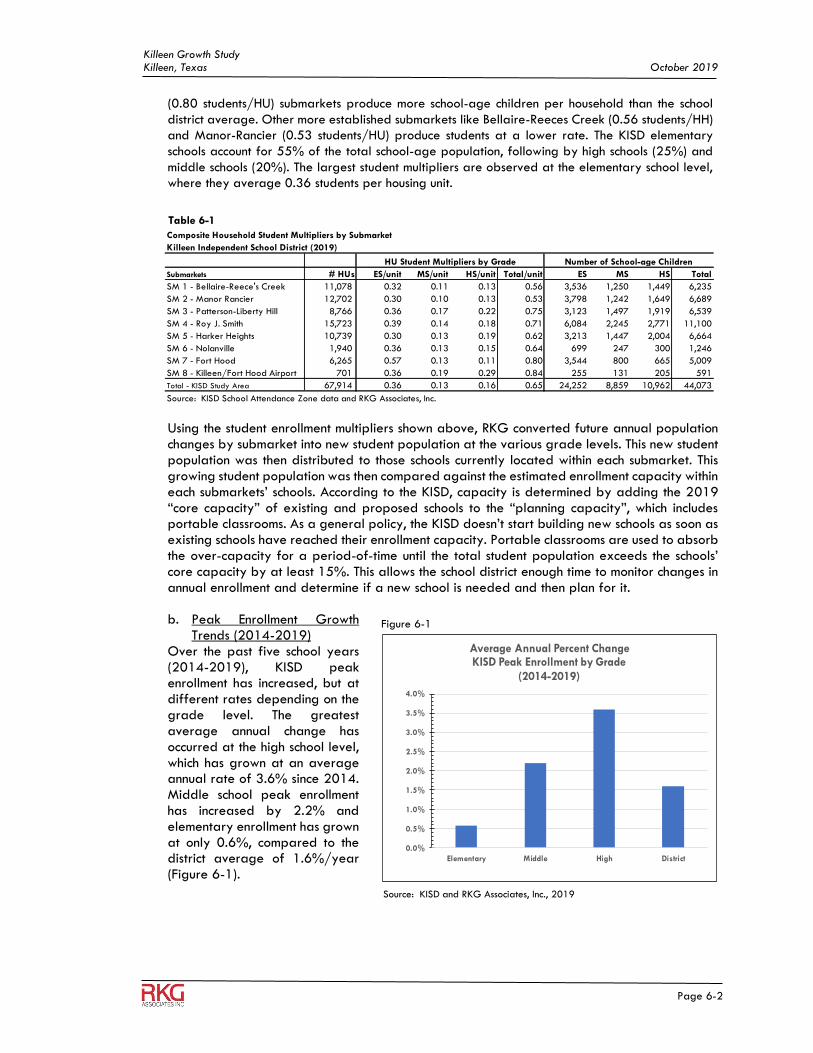

3. Age Distribution Trends (1970-2017) In most recent years, Bell County has continued to attract family-forming households throughout the 40-plus year study period. The data indicate that Bell County has the youngest population in the Killeen-Temple-Fort Hood MSA. As shown in Table 2-2, persons below the age of 6 years account for 10% of the total population with an additional 18% comprised of school-aged children (6-18 years). This suggests that Bell County appeals to younger family-forming households more than the other two counties. Typically, the adults in these families have early career jobs, so their household income levels can be modest to low. As a result, there is a growing need for education service, child-friendly and affordable residential neighborhoods in Bell County. In addition, Fort Hood’s population is primarily comprised of young single soldiers and couples under the age of thirty with young families. The age distribution among the three counties highlights notable changes in their age cohorts since 1970 (Table 2-3). Bell County experienced the most substantial growth of young population, especially the 0-11 years cohort. The peak growth period was 2000-2010, during which this cohort was growing 2.6%-3.5% annually. This period also corresponds with the peak troop levels at Fort Hood, when the military population increased to over 56,000 personnel. This decade also saw rapid growth in two other age cohorts – young adults (19-34 years) and older adults (45-54 years). These changes reflect the Army’s personnel policies as many older and married soldiers (and their spouses/families) were enticed to re-enter the military as the U.S. ramped up its fighting force in support of military conflicts in Iraq and Afghanistan following the events of 9/11. Furthermore, as many of these soldiers were deployed to South Asia in mid-2000s, anecdotal evidence suggests that many parents or family members moved into the region in support of the military spouses and children left behind. Growth in the 45-54 age cohort (11,809 persons, or 4.6% annually) would seem to support that theory. After 2010, as the Army started to reduce personnel levels at Fort Hood, population growth slowed down across multiple age cohorts, with the number of people in the 19-24 years and 45-54 years cohorts declining. Coryell County’s population growth peaked at 1970-1980, mainly driven by the growth of two age cohorts: early career singles and young families (25-44 years), which grew at 9.5%-14.8% annually, and school-aged children (0-11 years), which grew at 6.8%-10.9% annually. Since 1980, Coryell has been losing young adults (19-24 years) and the growth of school-aged children also slowed considerably. Unlike Bell County, Coryell County experienced a dramatic decline of young, family-forming population (19-44 years) during 2000-2010, largely due to military deployments. However, the 45-54 age cohort grew, for the same reason as in Bell County. After 2010, Coryell County’s school-age population declined substantially, but it appears that many family forming households have begun migrating to the City of Killeen and other surrounding communities in the MSA since then.

Table 2-2 Population Age Distribution Killeen-Temple-Fort Hood, TX MSA (2017)

Bell

County

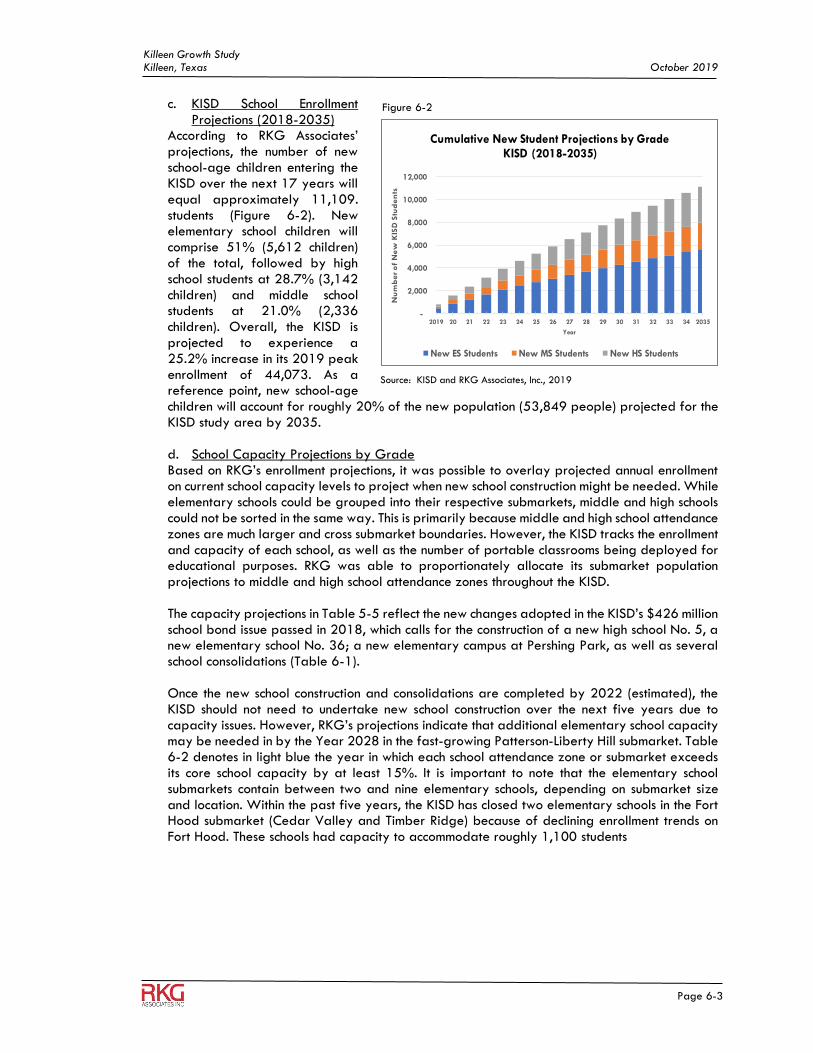

Coryell

County

Lampasas

County

Killeen-Temple,

TX MSA

0-4 years 8.8% 7.3% 5.9% 8.4%

5 years 1.6% 1.4% 1.2% 1.5%

6-11 years 9.2% 8.0% 7.5% 8.9%

12-14 years 4.2% 3.6% 3.9% 4.1%

15-18 years 5.4% 4.5% 5.6% 5.3%

19-24 years 9.9% 11.3% 6.4% 10.0%

25-34 years 17.0% 19.3% 10.8% 17.1%

35-44 years 12.9% 14.6% 11.8% 13.1%

45-54 years 10.8% 11.4% 13.6% 11.0%

55-64 years 9.6% 8.8% 14.1% 9.6%

65+ years 10.6% 9.8% 19.4% 10.9%

Total Population 344,450 75,465 20,987 440,902

Source: Woods & Poole Economics, Inc., 2018

Killeen Growth Study City of Killeen, TX October 2019

Page 2-5

Lampasas County’s population growth peaked during the1990-2000 period, during which both established families (35-54) and school-aged persons (6-18 years) grew rapidly. Since 2000, most age cohorts except for the 55+ cohorts experienced population decline, suggesting that Lampasas County has been having difficulties attracting young families and a workforce-age population.

Table 2-3 Population Age Distribution Changes Killeen-Temple-Fort Hood, TX MSA (1970 - 2017)

Pop Chg Annual % Pop Chg Annual % Pop Chg Annual % Pop Chg Annual % Pop Chg Annual %

Bell County

0-4 years 4,440 4.0% 3,116 2.0% 2,506 1.3% 7,451 3.5% 1,614 0.8%

5 years 492 2.4% 837 3.3% 592 1.7% 1,214 3.1% 242 0.7%

6-11 years 1,153 0.9% 4,054 2.8% 4,539 2.5% 5,892 2.6% 3,050 1.5%

12-14 years (35) -0.1% 1,464 2.3% 3,120 4.0% 2,177 2.0% 1,498 1.6%

15-18 years 3,009 3.6% (637) -0.6% 3,324 3.1% 3,431 2.4% 1,258 1.0%

19-24 years (197) -0.1% (3,829) -1.3% 2,610 1.0% 6,687 2.4% (951) -0.4%

25-34 years 12,305 8.0% 9,367 3.4% 3,631 1.0% 12,957 3.2% 4,819 1.3%

35-44 years 3,795 3.2% 9,753 6.2% 10,213 4.0% 3,557 1.0% 5,225 1.9%

45-54 years 2,181 2.1% 2,835 2.3% 10,336 6.7% 11,809 4.6% (376) -0.1%

55-64 years 2,953 3.7% 1,446 1.3% 3,211 2.6% 11,685 7.5% 5,754 3.0%

65+ years 3,773 4.3% 4,282 3.4% 4,154 2.5% 6,235 3.0% 9,332 4.9%

Coryell County

0-4 years 2,554 10.9% 649 1.3% 370 0.7% 663 1.1% (1,104) -2.4%

5 years 389 7.9% 170 1.9% 127 1.2% 80 0.7% (211) -2.4%

6-11 years 2,066 6.8% 789 1.5% 885 1.5% 291 0.4% (1,002) -2.0%

12-14 years 287 1.5% 303 1.4% 659 2.7% (36) -0.1% (403) -1.9%

15-18 years 1,180 3.4% (1,006) -2.1% 377 1.0% (233) -0.6% (455) -1.7%

19-24 years 4,261 3.9% (2,271) -1.5% (852) -0.7% (3,513) -2.9% (106) -0.2%

25-34 years 5,881 14.8% 4,400 4.5% 576 0.4% (3,995) -2.7% 3,738 4.9%

35-44 years 2,728 9.5% 2,281 4.1% 4,484 5.7% (1,589) -1.3% 246 0.3%

45-54 years 1,031 4.9% 991 3.2% 2,437 5.9% 2,372 3.6% (293) -0.5%

55-64 years 239 1.3% 714 3.3% 1,063 3.7% 1,867 4.8% 811 2.0%

65+ years 666 2.7% 415 1.3% 732 2.1% 1,423 3.3% 1,715 4.3%

Lampasas County

0-4 years 187 2.7% 177 2.0% 154 1.5% 21 0.2% (1) 0.0%

5 years 23 1.6% 37 2.2% 42 2.0% 14 0.6% (14) -0.8%

6-11 years 257 2.9% 112 1.0% 347 2.8% (44) -0.3% 2 0.0%

12-14 years 49 0.9% 50 0.9% 351 5.7% (81) -0.8% (62) -1.0%

15-18 years 189 2.5% (122) -1.3% 396 4.8% (20) -0.2% (33) -0.4%

19-24 years (18) -0.2% (2) 0.0% 163 1.8% 126 1.2% 131 1.6%

25-34 years 804 10.2% 229 1.4% 308 1.7% (73) -0.3% 202 1.4%

35-44 years 429 4.7% 486 3.6% 875 4.8% (174) -0.6% (54) -0.3%

45-54 years 121 1.1% 250 2.0% 851 5.7% 748 3.2% (248) -1.1%

55-64 years 115 1.1% 161 1.3% 433 3.2% 801 4.4% 357 2.0%

65+ years 399 2.6% 154 0.8% 460 2.2% 538 2.1% 951 4.4%

Killeen-Temple, TX MSA

0-4 years 7,181 5.0% 3,942 1.8% 3,030 1.2% 8,135 2.9% 509 0.2%

5 years 904 3.4% 1,044 2.9% 761 1.6% 1,308 2.4% 17 0.0%

6-11 years 3,476 2.0% 4,955 2.4% 5,771 2.3% 6,139 2.0% 2,050 0.8%

12-14 years 301 0.3% 1,817 2.0% 4,130 3.8% 2,060 1.4% 1,033 0.9%

15-18 years 4,378 3.5% (1,765) -1.0% 4,097 2.7% 3,178 1.6% 770 0.5%

19-24 years 4,046 1.0% (6,102) -1.3% 1,921 0.5% 3,300 0.8% (926) -0.3%

25-34 years 18,990 9.4% 13,996 3.6% 4,515 0.8% 11,949 2.1% 5,699 1.2%

35-44 years 6,952 4.4% 12,520 5.5% 15,572 4.4% 1,794 0.4% 5,417 1.5%

45-54 years 3,333 2.5% 4,076 2.4% 13,624 6.5% 14,929 4.3% (917) -0.3%

55-64 years 3,307 3.0% 2,321 1.6% 4,707 2.8% 14,353 6.8% 6,922 2.8%

65+ years 4,838 3.8% 4,851 2.8% 5,346 2.4% 8,196 2.9% 11,998 4.8%

Source: Woods & Poole Economics, Inc., 2018

1990 - 2000 2000 - 2010 2010 - 20171970 - 1980 1980 - 1990

Killeen Growth Study City of Killeen, TX October 2019

Page 2-6

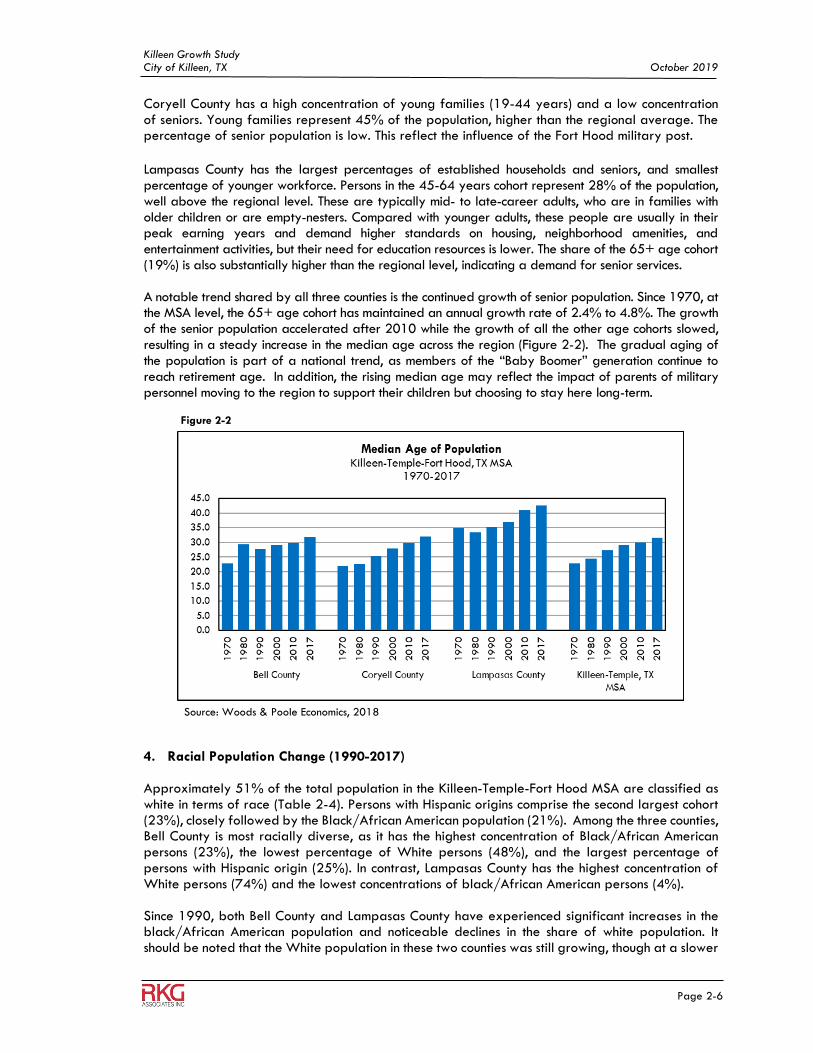

Coryell County has a high concentration of young families (19-44 years) and a low concentration of seniors. Young families represent 45% of the population, higher than the regional average. The percentage of senior population is low. This reflect the influence of the Fort Hood military post. Lampasas County has the largest percentages of established households and seniors, and smallest percentage of younger workforce. Persons in the 45-64 years cohort represent 28% of the population, well above the regional level. These are typically mid- to late-career adults, who are in families with older children or are empty-nesters. Compared with younger adults, these people are usually in their peak earning years and demand higher standards on housing, neighborhood amenities, and entertainment activities, but their need for education resources is lower. The share of the 65+ age cohort (19%) is also substantially higher than the regional level, indicating a demand for senior services. A notable trend shared by all three counties is the continued growth of senior population. Since 1970, at the MSA level, the 65+ age cohort has maintained an annual growth rate of 2.4% to 4.8%. The growth of the senior population accelerated after 2010 while the growth of all the other age cohorts slowed, resulting in a steady increase in the median age across the region (Figure 2-2). The gradual aging of the population is part of a national trend, as members of the “Baby Boomer” generation continue to reach retirement age. In addition, the rising median age may reflect the impact of parents of military personnel moving to the region to support their children but choosing to stay here long-term.

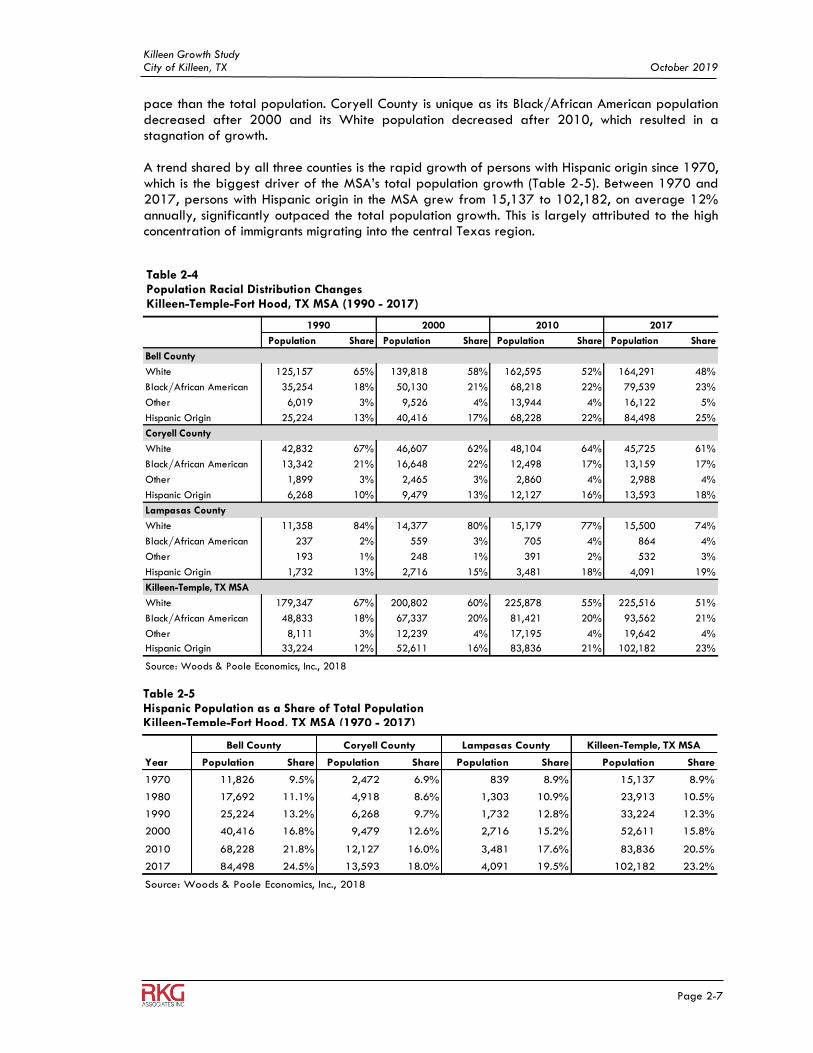

4. Racial Population Change (1990-2017) Approximately 51% of the total population in the Killeen-Temple-Fort Hood MSA are classified as white in terms of race (Table 2-4). Persons with Hispanic origins comprise the second largest cohort (23%), closely followed by the Black/African American population (21%). Among the three counties, Bell County is most racially diverse, as it has the highest concentration of Black/African American persons (23%), the lowest percentage of White persons (48%), and the largest percentage of persons with Hispanic origin (25%). In contrast, Lampasas County has the highest concentration of White persons (74%) and the lowest concentrations of black/African American persons (4%). Since 1990, both Bell County and Lampasas County have experienced significant increases in the black/African American population and noticeable declines in the share of white population. It should be noted that the White population in these two counties was still growing, though at a slower

Figure 2-2

Source: Woods & Poole Economics, 2018

Killeen Growth Study City of Killeen, TX October 2019

Page 2-7

pace than the total population. Coryell County is unique as its Black/African American population decreased after 2000 and its White population decreased after 2010, which resulted in a stagnation of growth. A trend shared by all three counties is the rapid growth of persons with Hispanic origin since 1970, which is the biggest driver of the MSA’s total population growth (Table 2-5). Between 1970 and 2017, persons with Hispanic origin in the MSA grew from 15,137 to 102,182, on average 12% annually, significantly outpaced the total population growth. This is largely attributed to the high concentration of immigrants migrating into the central Texas region.

Table 2-4 Population Racial Distribution Changes Killeen-Temple-Fort Hood, TX MSA (1990 - 2017)

Population Share Population Share Population Share Population Share

Bell County

White 125,157 65% 139,818 58% 162,595 52% 164,291 48%

Black/African American 35,254 18% 50,130 21% 68,218 22% 79,539 23%

Other 6,019 3% 9,526 4% 13,944 4% 16,122 5%

Hispanic Origin 25,224 13% 40,416 17% 68,228 22% 84,498 25%

Coryell County

White 42,832 67% 46,607 62% 48,104 64% 45,725 61%

Black/African American 13,342 21% 16,648 22% 12,498 17% 13,159 17%

Other 1,899 3% 2,465 3% 2,860 4% 2,988 4%

Hispanic Origin 6,268 10% 9,479 13% 12,127 16% 13,593 18%

Lampasas County

White 11,358 84% 14,377 80% 15,179 77% 15,500 74%

Black/African American 237 2% 559 3% 705 4% 864 4%

Other 193 1% 248 1% 391 2% 532 3%

Hispanic Origin 1,732 13% 2,716 15% 3,481 18% 4,091 19%

Killeen-Temple, TX MSA

White 179,347 67% 200,802 60% 225,878 55% 225,516 51%

Black/African American 48,833 18% 67,337 20% 81,421 20% 93,562 21%

Other 8,111 3% 12,239 4% 17,195 4% 19,642 4%

Hispanic Origin 33,224 12% 52,611 16% 83,836 21% 102,182 23%

Source: Woods & Poole Economics, Inc., 2018

1990 2000 2010 2017

Table 2-5 Hispanic Population as a Share of Total Population Killeen-Temple-Fort Hood, TX MSA (1970 - 2017)

Year Population Share Population Share Population Share Population Share

1970 11,826 9.5% 2,472 6.9% 839 8.9% 15,137 8.9%

1980 17,692 11.1% 4,918 8.6% 1,303 10.9% 23,913 10.5%

1990 25,224 13.2% 6,268 9.7% 1,732 12.8% 33,224 12.3%

2000 40,416 16.8% 9,479 12.6% 2,716 15.2% 52,611 15.8%

2010 68,228 21.8% 12,127 16.0% 3,481 17.6% 83,836 20.5%

2017 84,498 24.5% 13,593 18.0% 4,091 19.5% 102,182 23.2%

Source: Woods & Poole Economics, Inc., 2018

Coryell County Lampasas County Killeen-Temple, TX MSABell County

Killeen Growth Study City of Killeen, TX October 2019

Page 2-8

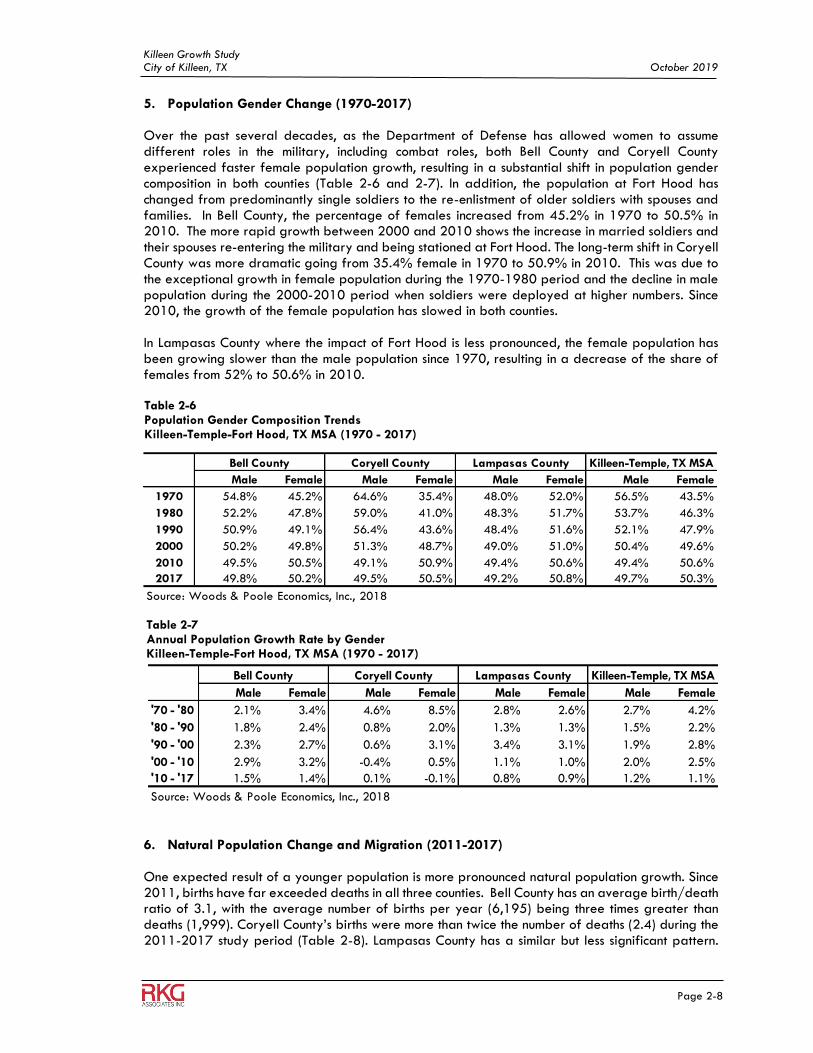

5. Population Gender Change (1970-2017) Over the past several decades, as the Department of Defense has allowed women to assume different roles in the military, including combat roles, both Bell County and Coryell County experienced faster female population growth, resulting in a substantial shift in population gender composition in both counties (Table 2-6 and 2-7). In addition, the population at Fort Hood has changed from predominantly single soldiers to the re-enlistment of older soldiers with spouses and families. In Bell County, the percentage of females increased from 45.2% in 1970 to 50.5% in 2010. The more rapid growth between 2000 and 2010 shows the increase in married soldiers and their spouses re-entering the military and being stationed at Fort Hood. The long-term shift in Coryell County was more dramatic going from 35.4% female in 1970 to 50.9% in 2010. This was due to the exceptional growth in female population during the 1970-1980 period and the decline in male population during the 2000-2010 period when soldiers were deployed at higher numbers. Since 2010, the growth of the female population has slowed in both counties. In Lampasas County where the impact of Fort Hood is less pronounced, the female population has been growing slower than the male population since 1970, resulting in a decrease of the share of females from 52% to 50.6% in 2010.

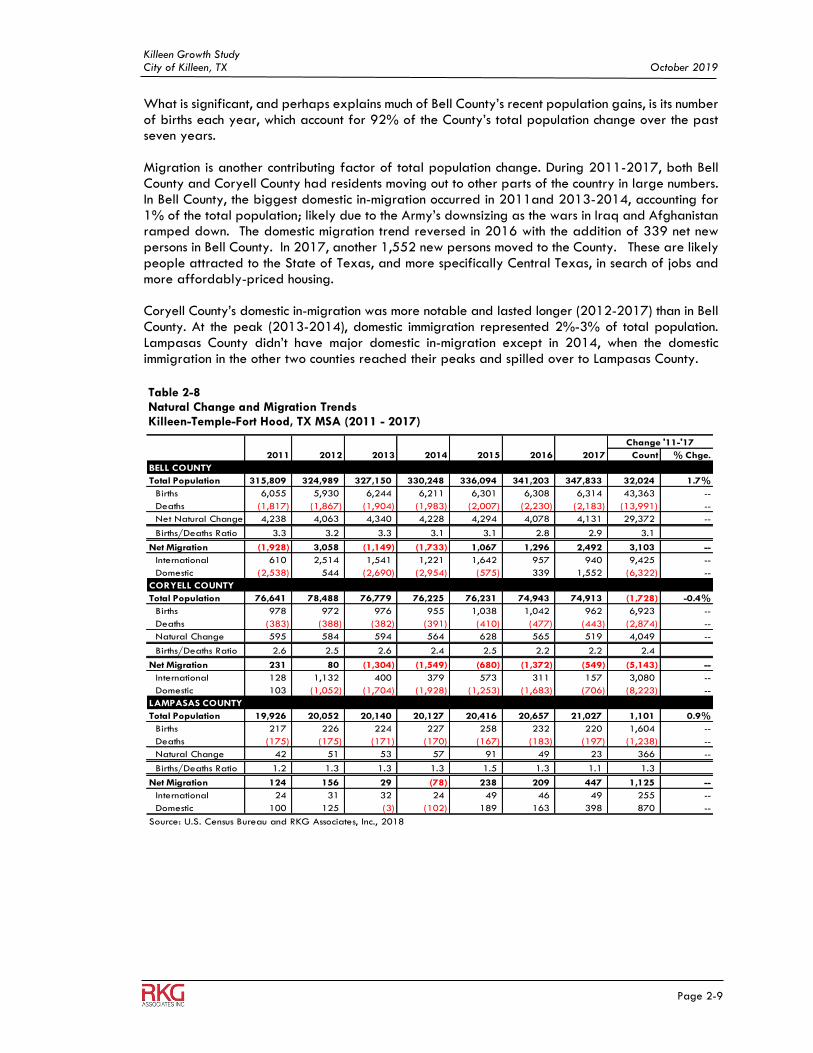

6. Natural Population Change and Migration (2011-2017) One expected result of a younger population is more pronounced natural population growth. Since 2011, births have far exceeded deaths in all three counties. Bell County has an average birth/death ratio of 3.1, with the average number of births per year (6,195) being three times greater than deaths (1,999). Coryell County’s births were more than twice the number of deaths (2.4) during the 2011-2017 study period (Table 2-8). Lampasas County has a similar but less significant pattern.

Table 2-6 Population Gender Composition Trends Killeen-Temple-Fort Hood, TX MSA (1970 - 2017)

Male Female Male Female Male Female Male Female

1970 54.8% 45.2% 64.6% 35.4% 48.0% 52.0% 56.5% 43.5%

1980 52.2% 47.8% 59.0% 41.0% 48.3% 51.7% 53.7% 46.3%

1990 50.9% 49.1% 56.4% 43.6% 48.4% 51.6% 52.1% 47.9%

2000 50.2% 49.8% 51.3% 48.7% 49.0% 51.0% 50.4% 49.6%

2010 49.5% 50.5% 49.1% 50.9% 49.4% 50.6% 49.4% 50.6%

2017 49.8% 50.2% 49.5% 50.5% 49.2% 50.8% 49.7% 50.3%

Source: Woods & Poole Economics, Inc., 2018

Bell County Coryell County Lampasas County Killeen-Temple, TX MSA

Male Female Male Female Male Female Male Female

'70 - '80 2.1% 3.4% 4.6% 8.5% 2.8% 2.6% 2.7% 4.2%

'80 - '90 1.8% 2.4% 0.8% 2.0% 1.3% 1.3% 1.5% 2.2%

'90 - '00 2.3% 2.7% 0.6% 3.1% 3.4% 3.1% 1.9% 2.8%

'00 - '10 2.9% 3.2% -0.4% 0.5% 1.1% 1.0% 2.0% 2.5%

'10 - '17 1.5% 1.4% 0.1% -0.1% 0.8% 0.9% 1.2% 1.1%

Source: Woods & Poole Economics, Inc., 2018

Bell County Coryell County Lampasas County Killeen-Temple, TX MSA

Table 2-7 Annual Population Growth Rate by Gender Killeen-Temple-Fort Hood, TX MSA (1970 - 2017)

Killeen Growth Study City of Killeen, TX October 2019

Page 2-9

What is significant, and perhaps explains much of Bell County’s recent population gains, is its number of births each year, which account for 92% of the County’s total population change over the past seven years. Migration is another contributing factor of total population change. During 2011-2017, both Bell County and Coryell County had residents moving out to other parts of the country in large numbers. In Bell County, the biggest domestic in-migration occurred in 2011and 2013-2014, accounting for 1% of the total population; likely due to the Army’s downsizing as the wars in Iraq and Afghanistan ramped down. The domestic migration trend reversed in 2016 with the addition of 339 net new persons in Bell County. In 2017, another 1,552 new persons moved to the County. These are likely people attracted to the State of Texas, and more specifically Central Texas, in search of jobs and more affordably-priced housing. Coryell County’s domestic in-migration was more notable and lasted longer (2012-2017) than in Bell County. At the peak (2013-2014), domestic immigration represented 2%-3% of total population. Lampasas County didn’t have major domestic in-migration except in 2014, when the domestic immigration in the other two counties reached their peaks and spilled over to Lampasas County.

Table 2-8 Natural Change and Migration Trends Killeen-Temple-Fort Hood, TX MSA (2011 - 2017)

2011 2012 2013 2014 2015 2016 2017 Count % Chge.

BELL COUNTY

Total Population 315,809 324,989 327,150 330,248 336,094 341,203 347,833 32,024 1.7%

Births 6,055 5,930 6,244 6,211 6,301 6,308 6,314 43,363 --

Deaths (1,817) (1,867) (1,904) (1,983) (2,007) (2,230) (2,183) (13,991) --

Net Natural Change 4,238 4,063 4,340 4,228 4,294 4,078 4,131 29,372 --

Births/Deaths Ratio 3.3 3.2 3.3 3.1 3.1 2.8 2.9 3.1

Net Migration (1,928) 3,058 (1,149) (1,733) 1,067 1,296 2,492 3,103 --

International 610 2,514 1,541 1,221 1,642 957 940 9,425 --

Domestic (2,538) 544 (2,690) (2,954) (575) 339 1,552 (6,322) --

CORYELL COUNTY

Total Population 76,641 78,488 76,779 76,225 76,231 74,943 74,913 (1,728) -0.4%

Births 978 972 976 955 1,038 1,042 962 6,923 --

Deaths (383) (388) (382) (391) (410) (477) (443) (2,874) --

Natural Change 595 584 594 564 628 565 519 4,049 --

Births/Deaths Ratio 2.6 2.5 2.6 2.4 2.5 2.2 2.2 2.4

Net Migration 231 80 (1,304) (1,549) (680) (1,372) (549) (5,143) --

International 128 1,132 400 379 573 311 157 3,080 --

Domestic 103 (1,052) (1,704) (1,928) (1,253) (1,683) (706) (8,223) --

LAMPASAS COUNTY

Total Population 19,926 20,052 20,140 20,127 20,416 20,657 21,027 1,101 0.9%

Births 217 226 224 227 258 232 220 1,604 --

Deaths (175) (175) (171) (170) (167) (183) (197) (1,238) --

Natural Change 42 51 53 57 91 49 23 366 --

Births/Deaths Ratio 1.2 1.3 1.3 1.3 1.5 1.3 1.1 1.3

Net Migration 124 156 29 (78) 238 209 447 1,125 --

International 24 31 32 24 49 46 49 255 --

Domestic 100 125 (3) (102) 189 163 398 870 --

Source: U.S. Census Bureau and RKG Associates, Inc., 2018

Change '11-'17

Killeen Growth Study City of Killeen, TX October 2019

Page 2-10

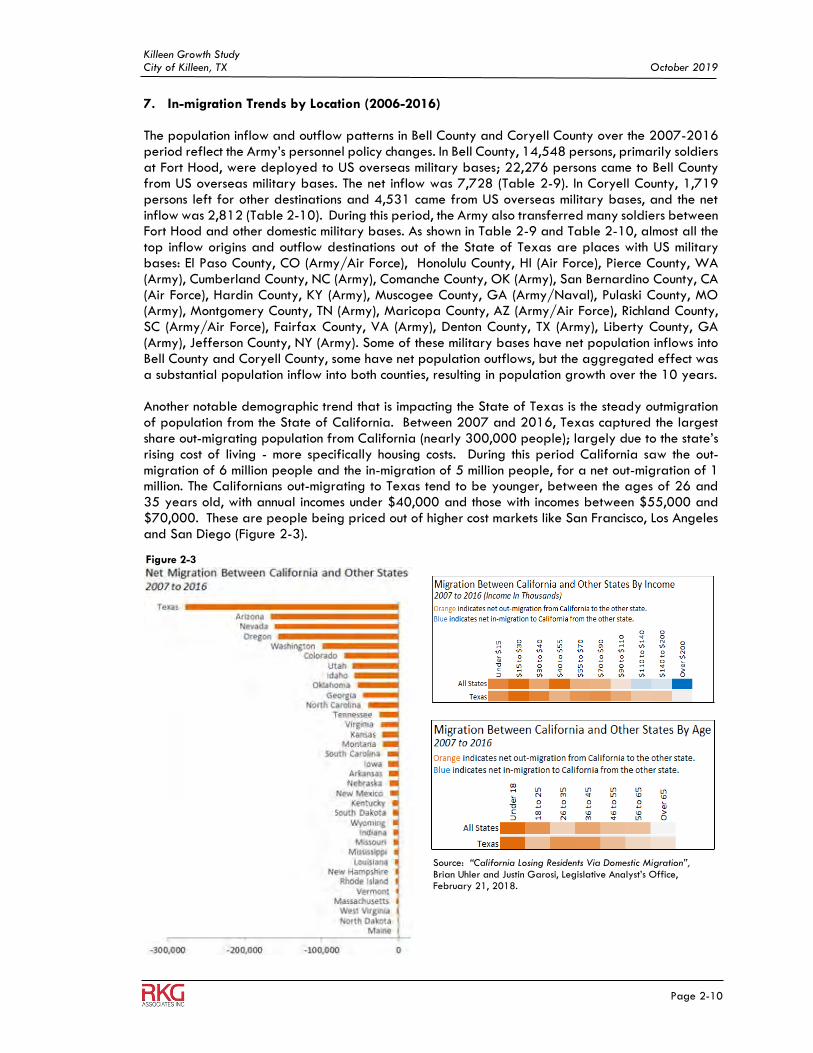

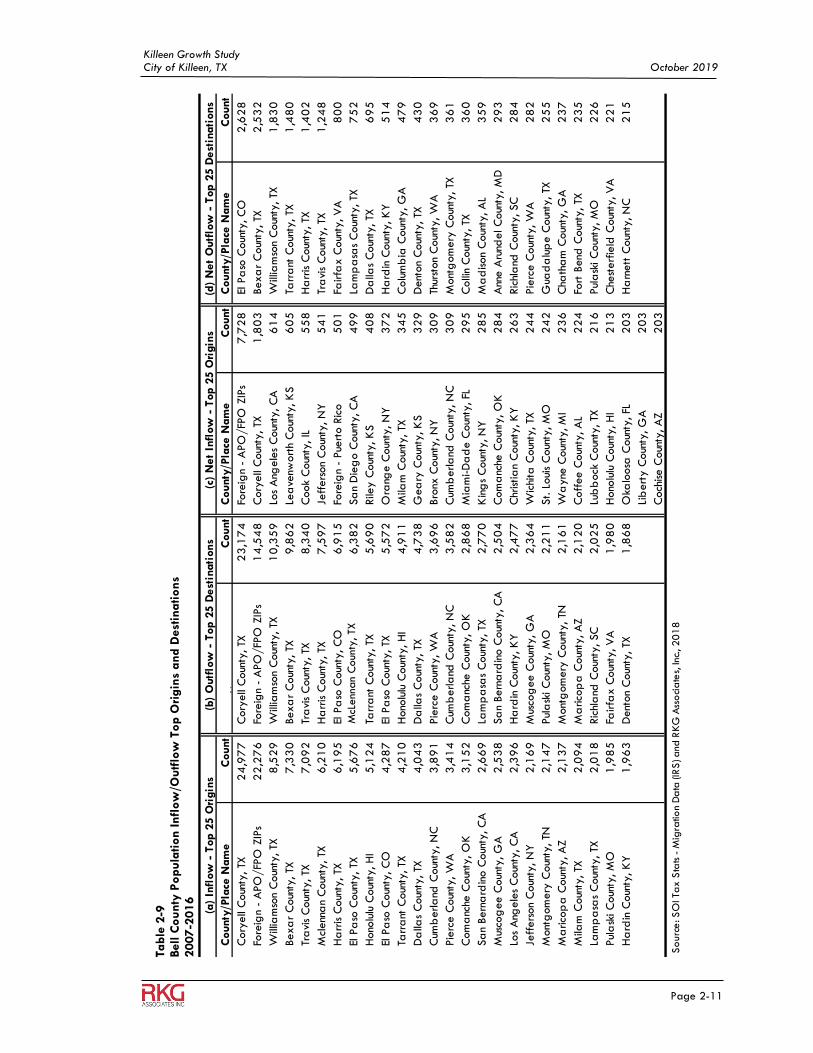

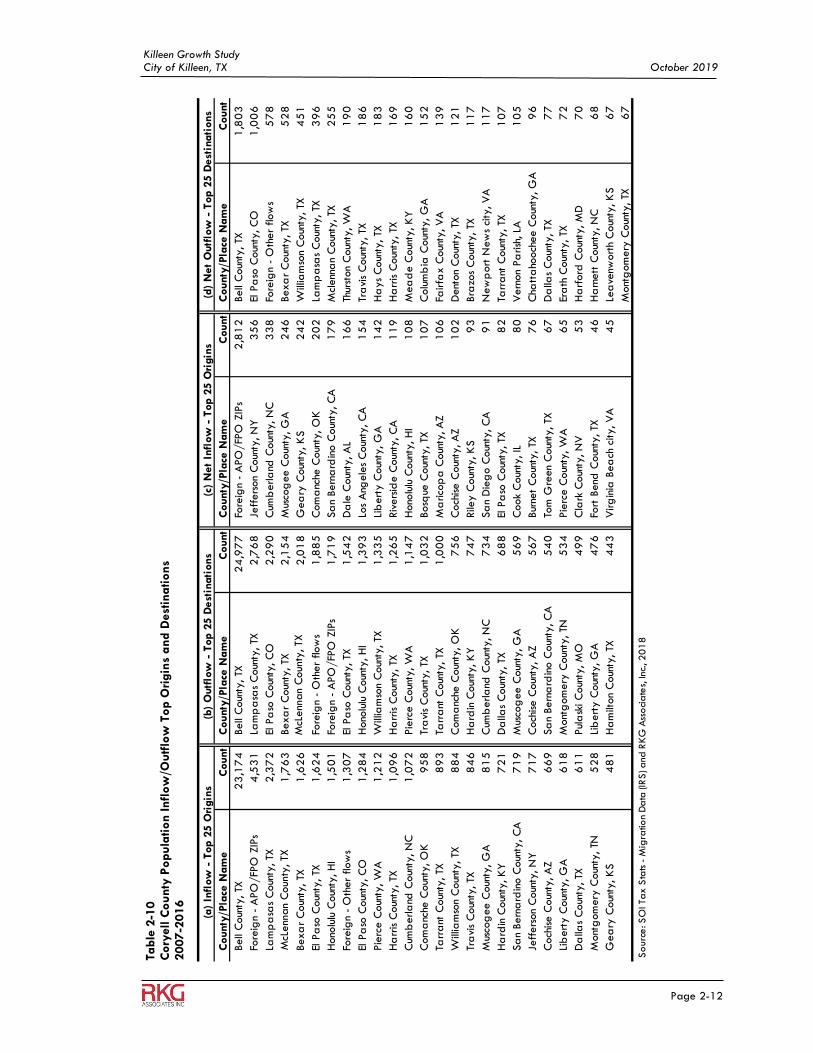

7. In-migration Trends by Location (2006-2016) The population inflow and outflow patterns in Bell County and Coryell County over the 2007-2016 period reflect the Army’s personnel policy changes. In Bell County, 14,548 persons, primarily soldiers at Fort Hood, were deployed to US overseas military bases; 22,276 persons came to Bell County from US overseas military bases. The net inflow was 7,728 (Table 2-9). In Coryell County, 1,719 persons left for other destinations and 4,531 came from US overseas military bases, and the net inflow was 2,812 (Table 2-10). During this period, the Army also transferred many soldiers between Fort Hood and other domestic military bases. As shown in Table 2-9 and Table 2-10, almost all the top inflow origins and outflow destinations out of the State of Texas are places with US military bases: El Paso County, CO (Army/Air Force), Honolulu County, HI (Air Force), Pierce County, WA (Army), Cumberland County, NC (Army), Comanche County, OK (Army), San Bernardino County, CA (Air Force), Hardin County, KY (Army), Muscogee County, GA (Army/Naval), Pulaski County, MO (Army), Montgomery County, TN (Army), Maricopa County, AZ (Army/Air Force), Richland County, SC (Army/Air Force), Fairfax County, VA (Army), Denton County, TX (Army), Liberty County, GA (Army), Jefferson County, NY (Army). Some of these military bases have net population inflows into Bell County and Coryell County, some have net population outflows, but the aggregated effect was a substantial population inflow into both counties, resulting in population growth over the 10 years. Another notable demographic trend that is impacting the State of Texas is the steady outmigration of population from the State of California. Between 2007 and 2016, Texas captured the largest share out-migrating population from California (nearly 300,000 people); largely due to the state’s rising cost of living - more specifically housing costs. During this period California saw the out-migration of 6 million people and the in-migration of 5 million people, for a net out-migration of 1 million. The Californians out-migrating to Texas tend to be younger, between the ages of 26 and 35 years old, with annual incomes under $40,000 and those with incomes between $55,000 and $70,000. These are people being priced out of higher cost markets like San Francisco, Los Angeles and San Diego (Figure 2-3).

Source: “California Losing Residents Via Domestic Migration”, Brian Uhler and Justin Garosi, Legislative Analyst’s Office, February 21, 2018.

Figure 2-3

Killeen Growth Study City of Killeen, TX October 2019

Page 2-11

T

able

2-9

Bell C

ounty

Po

pula

tion I

nfl

ow

/Outf

low

To

p O

rigin

s and D

est

inations

2007-2

016

County

/Pla

ce N

am

eC

ount

County

/Pla

ce N

am

eC

ount

County

/Pla

ce N

am

eC

ount

County

/Pla

ce N

am

eC

ount

Cory

ell

Coun

ty, TX

24

,97

7

Cory

ell

Coun

ty, TX

23

,17

4

Fore

ign

- A

PO

/FP

O Z

IPs

7,7

28

El P

aso

Coun

ty, C

O2

,62

8

Fore

ign

- A

PO

/FP

O Z

IPs

22

,27

6

Fore

ign

- A

PO

/FP

O Z

IPs

14

,54

8

Cory

ell

Coun

ty, TX

1,8

03

Bexa

r C

oun

ty, TX

2,5

32

Will

iam

son

Coun

ty, TX

8,5

29

Will

iam

son

Coun

ty, TX

10

,35

9

Los

Ang

ele

s C

oun

ty, C

A6

14

W

illia

mso

n C

oun

ty, TX

1,8

30

Bexa

r C

oun

ty, TX

7,3

30

Bexa

r C

oun

ty, TX

9,8

62

Lea

venw

ort

h C

oun

ty, K

S6

05

Ta

rra

nt C

oun

ty, TX

1,4

80

Tra

vis

Coun

ty, TX

7,0

92

Tra

vis

Coun

ty, TX

8,3

40

Cook

Coun

ty, IL

55

8

Ha

rris C

oun

ty, TX

1,4

02

Mcl

enn

an

Coun

ty, TX

6,2

10

Ha

rris C

oun

ty, TX

7,5

97

Jeff

ers

on

Coun

ty, N

Y5

41

Tr

avi

s C

oun

ty, TX

1,2

48

Ha

rris C

oun

ty, TX

6,1

95

El P

aso

Coun

ty, C

O6

,91

5

Fo

reig

n -

Pue

rto R

ico

50

1

Fairfa

x C

oun

ty, V

A8

00

El P

aso

Coun

ty, TX

5,6

76

Mcl

enn

an

Coun

ty, TX

6,3

82

Sa

n D

ieg

o C

oun

ty, C

A4

99

La

mp

asa

s C

oun

ty, TX

75

2

Hono

lulu

Coun

ty, H

I5

,12

4

Ta

rra

nt C

oun

ty, TX

5,6

90

Rile

y C

oun

ty, K

S4

08

D

alla

s C

oun

ty, TX

69

5

El P

aso

Coun

ty, C

O4

,28

7

El

Pa

so C

oun

ty, TX

5,5

72

Ora

nge C

oun

ty, N

Y3

72

H

ard

in C

oun

ty, K

Y5

14

Tarr

ant

Coun

ty, TX

4,2

10

Hono

lulu

Coun

ty, H

I4

,91

1

M

ilam

Coun

ty, TX

34

5

Colu

mb

ia C

oun

ty, G

A4

79

Da

llas

Coun

ty, TX

4,0

43

Da

llas

Coun

ty, TX

4,7

38

Gea

ry C

oun

ty, K

S3

29

D

ent

on

Coun

ty, TX

43

0

Cum

berla

nd C

oun

ty, N

C3

,89

1

Pie

rce C

oun

ty, W

A3

,69

6

Bro

nx C

oun

ty, N

Y3

09

Th

urst

on

Coun

ty, W

A3

69

Pie

rce C

oun

ty, W

A3

,41

4

C

umb

erla

nd C

oun

ty, N

C3

,58

2

C

umb

erla

nd C

oun

ty, N

C3

09

M

ont

gom

ery

Coun

ty, TX

36

1

Com

anc

he C

oun

ty, O

K3

,15

2

C

om

anc

he C

oun

ty, O

K2

,86

8

M

iam

i-D

ad

e C

oun

ty, FL

29

5

Colli

n C

oun

ty, TX

36

0

Sa

n Bern

ard

ino C

oun

ty, C

A2

,66

9

La

mp

asa

s C

oun

ty, TX

2,7

70

Kin

gs

Coun

ty, N

Y2

85

M

ad

ison

Coun

ty, A

L3

59

Mus

cog

ee C

oun

ty, G

A2

,53

8

Sa

n Bern

ard

ino C

oun

ty, C

A2

,50

4

C

om

anc

he C

oun

ty, O

K2

84

A

nne A

rund

el C

oun

ty, M

D2

93

Los

Ang

ele

s C

oun

ty, C

A2

,39

6

H

ard

in C

oun

ty, K

Y2

,47

7

C

hristia

n C

oun

ty, K

Y2

63

Ric

hla

nd C

oun

ty, SC

28

4

Jeff

ers

on

Coun

ty, N

Y2

,16

9

M

usco

gee C

oun

ty, G

A2

,36

4

W

ichi

ta C

oun

ty, TX

24

4

Pie

rce C

oun

ty, W

A2

82

Mont

gom

ery

Coun

ty, TN

2,1

47

Pul

ask

i C

oun

ty, M

O2

,21

1

St. L

oui

s C

oun

ty, M

O2

42

G

uad

alu

pe C

oun

ty, TX

25

5

Ma

rico

pa

Coun

ty, A

Z2

,13

7

M

ont

gom

ery

Coun

ty, TN

2,1

61

Wa

yne

Coun

ty, M

I2

36

C

hath

am

Coun

ty, G

A2

37

Mila

m C

oun

ty, TX

2,0

94

Ma

rico

pa

Coun

ty, A

Z2

,12

0

C

off

ee C

oun

ty, A

L2

24

Fo

rt B

end

Coun

ty, TX

23

5

Lam

pa

sas

Coun

ty, TX

2,0

18

Ric

hla

nd C

oun

ty, SC

2,0

25

Lub

bock

Coun

ty, TX

21

6

Pul

ask

i C

oun

ty, M

O2

26

Pul

ask

i C

oun

ty, M

O1

,98

5

Fa

irfa

x C

oun

ty, V

A1

,98

0

H

ono

lulu

Coun

ty, H

I2

13

C

hest

erf

ield

Coun

ty, V

A2

21

Ha

rdin

Coun

ty, K

Y1

,96

3

D

ent

on

Coun

ty, TX

1,8

68

Oka

loosa

Coun

ty, FL

20

3

Ha

rnett

Coun

ty, N

C2

15

Lib

ert

y C

oun

ty, G

A2

03

Coch

ise C

oun

ty, A

Z2

03

Sourc

e: SO

I Tax S

tats -

Mig

ration D

ata

(IR

S) a

nd

RK

G A

ssoci

ate

s, Inc., 20

18

(a)

Infl

ow

- T

op 2

5 O

rigin

s(b

) O

utf

low

- T

op 2

5 D

est

inati

ons

(c)

Net

Infl

ow

- T

op 2

5 O

rigin

s(d

) N

et

Outf

low

- T

op 2

5 D

est

inati

ons

McL

enn

an

Coun

ty, TX

Killeen Growth Study City of Killeen, TX October 2019

Page 2-12

Table

2-1

0

Cory

ell C

ounty

Po

pula

tion Infl

ow

/Outf

low

To

p O

rigin

s an

d D

est

inations

2007-2

016

County

/Pla

ce N

am

eC

ount

County

/Pla

ce N

am

eC

ount

County

/Pla

ce N

am

eC

ount

County

/Pla

ce N

am

eC

ount

Bell

Coun

ty, TX

23

,17

4

Bell

Coun

ty, TX

24

,97

7

Fo

reig

n -

APO

/FP

O Z

IPs

2,8

12

Bell

Coun

ty, TX

1,8

03

Fore

ign

- A

PO

/FP

O Z

IPs

4,5

31

La

mp

asa

s C

oun

ty, TX

2,7

68

Je

ffers

on

Coun

ty, N

Y3

56

El

Pa

so C

oun

ty, C

O1

,00

6

Lam

pa

sas

Coun

ty, TX

2,3

72

El

Pa

so C

oun

ty, C

O2

,29

0

Cum

berla

nd C

oun

ty, N

C3

38

Fo

reig

n -

Oth

er

flow

s5

78

Mcl

enn

an

Coun

ty, TX

1,7

63

Bexa

r C

oun

ty, TX

2,1

54

M

usco

gee C

oun

ty, G

A2

46

Bexa

r C

oun

ty, TX

52

8

Bexa

r C

oun

ty, TX

1,6

26

M

clenn

an

Coun

ty, TX

2,0

18

G

ea

ry C

oun

ty, K

S2

42

W

illia

mso

n C

oun

ty, TX

45

1

El P

aso

Coun

ty, TX

1,6

24

Fo

reig

n -

Oth

er

flow

s1

,88

5

Com

anc

he C

oun

ty, O

K2

02

La

mp

asa

s C

oun

ty, TX

39

6

Hono

lulu

Coun

ty, H

I1

,50

1

Fore

ign

- A

PO

/FP

O Z

IPs

1,7

19

Sa

n Bern

ard

ino C

oun

ty, C

A1

79

M

clenn

an

Coun

ty, TX

25

5

Fore

ign

- O

ther

flow

s1

,30

7

El P

aso

Coun

ty, TX

1,5

42

D

ale

Coun

ty, A

L1

66

Th

urst

on

Coun

ty, W

A1

90

El P

aso

Coun

ty, C

O1

,28

4

Hono

lulu

Coun

ty, H

I1

,39

3

Los

Ang

ele

s C

oun

ty, C

A1

54

Tr

avi

s C

oun

ty, TX

18

6

Pie

rce C

oun

ty, W

A1

,21

2

Will

iam

son

Coun

ty, TX

1,3

35

Li

bert

y C

oun

ty, G

A1

42

H

ays

Coun

ty, TX

18

3

Ha

rris C

oun

ty, TX

1,0

96

H

arr

is C

oun

ty, TX

1,2

65

Riv

ers

ide C

oun

ty, C

A1

19

H

arr

is C

oun

ty, TX

16

9

Cum

berla

nd C

oun

ty, N

C1

,07

2

Pie

rce C

oun

ty, W

A1

,14

7

Hono

lulu

Coun

ty, H

I1

08

M

ea

de C

oun

ty, K

Y1

60

Com

anc

he C

oun

ty, O

K9

58

Tr

avi

s C

oun

ty, TX

1,0

32

Bosq

ue C

oun

ty, TX

10

7

Colu

mb

ia C

oun

ty, G

A1

52

Tarr

ant

Coun

ty, TX

89

3

Tarr

ant

Coun

ty, TX

1,0

00

M

arico

pa

Coun

ty, A

Z1

06

Fa

irfa

x C

oun

ty, V

A1

39

Will

iam

son

Coun

ty, TX

88

4

Com

anc

he C

oun

ty, O

K7

56

C

och

ise C

oun

ty, A

Z1

02

D

ent

on

Coun

ty, TX

12

1

Tra

vis

Coun

ty, TX

84

6

Ha

rdin

Coun

ty, K

Y7

47

Rile

y C

oun

ty, K

S9

3

Bra

zos

Coun

ty, TX

11

7

Mus

cog

ee C

oun

ty, G

A8

15

C

umb

erla

nd C

oun

ty, N

C7

34

Sa

n D

ieg

o C

oun

ty, C

A9

1

N

ew

port

New

s ci

ty, V

A1

17

Ha

rdin

Coun

ty, K

Y7

21

D

alla

s C

oun

ty, TX

68

8

El P

aso

Coun

ty, TX

82

Tarr

ant

Coun

ty, TX

10

7

Sa

n Bern

ard

ino C

oun

ty, C

A7

19

M

usco

gee C

oun

ty, G

A5

69

C

ook

Coun

ty, IL

80

Vern

on

Pa

rish

, LA

10

5

Jeff

ers

on

Coun

ty, N

Y7

17

C

och

ise C

oun

ty, A

Z5

67

Bur

net

Coun

ty, TX

76

Cha

tta

hooch

ee C

oun

ty, G

A9

6

Coch

ise C

oun

ty, A

Z6

69

Sa

n Bern

ard

ino C

oun

ty, C

A5

40

To

m G

reen

Coun

ty, TX

67

Da

llas

Coun

ty, TX

77

Lib

ert

y C

oun

ty, G

A6

18

M

ont

gom

ery

Coun

ty, TN

53

4

Pie

rce C

oun

ty, W

A6

5

Er

ath

Coun

ty, TX

72

Da

llas

Coun

ty, TX

61

1

Pul

ask

i C

oun

ty, M

O4

99

C

lark

Coun

ty, N

V5

3

H

arf

ord

Coun

ty, M

D7

0

Mont

gom

ery

Coun

ty, TN

52

8

Lib

ert

y C

oun

ty, G

A4

76

Fo

rt B

end

Coun

ty, TX

46

Ha

rnett

Coun

ty, N

C6

8

Gea

ry C

oun

ty, K

S4

81

H

am

ilton

Coun

ty, TX

44

3

Virg

inia

Bea

ch c

ity, V

A4

5

Le

ave

nwort

h C

oun

ty, K

S6

7

Mont

gom

ery

Coun

ty, TX

67

Sourc

e: SO

I Tax S

tats -

Mig

ration D

ata

(IR

S) a

nd

RK

G A

ssoci

ate

s, Inc., 20

18

(a)

Infl

ow

- T

op 2

5 O

rigin

s(b

) O

utf

low

- T

op 2

5 D

est

inati

ons

(c)

Net

Infl

ow

- T

op 2

5 O

rigin

s(d

) N

et

Outf

low

- T

op 2

5 D

est

inati

ons

McL

enn

an

Coun

ty, TX

McL

enn

an

Coun

ty, TX

Killeen Growth Study City of Killeen, TX October 2019

Page 2-13

8. Implication of Regional Population Trends In the Killeen-Temple-Fort Hood MSA region, all the three counties have experienced rapid population growth since 1970. However, the differences between the three counties reflect the impacts of the Army’s changing force structure. Bell County, which has the largest population, has maintained the most consistent pace of growth, suggesting that it has been attractive to residents and still relatively affordable for middle income households. The percentage of school-aged children is particularly high, indicating a strong demand for education resources and family-oriented neighborhood amenities. Still, the changes in the population’s age cohorts and gender composition reflect the influence of the military post. The population of children, young adults and older adults grew substantially between 1990 and 2000, as many married soldiers and their spouses entered the military and were stationed at Fort Hood. The increase of older adults continued into mid- to late-2000s, when the parents of some soldiers who were deployed overseas moved here to support their children. Since 1970, as the Army allowed women to assume expanded roles in the military, the share of female population started to increase. Coryell County has a smaller population than Bell County, but since most of Fort Hood’s land area falls into Coryell County, the impacts of the Army appeared to be more direct. First, the expansion of the military post between 1970 and 1980 led to 6% annually population growth. In the mid- and late-2000s, as soldiers were deployed overseas in large numbers, the total population stagnated, and the population of young adults and middle-aged adults declined substantially. However, the population of older adults increased, for the same reason as in Bell County. After 2010, as the Army downsized, Coryell County’s total population declined. The shift in the population’s gender composition has been more dramatic in Coryell County than in Bell County: between 1970 and 2017, Coryell County changed from 34.4% female to 50.5% female. During the 2007-2016 period, both Bell County and Coryell County had substantial population migrations to and from US domestic and overseas military bases. The net effect was an inflow of population, which contributed to increased population gains in both counties. Lampasas County has the smallest population and has been less affected by the Army than the other two counties. Its population is older than the MSA average, with a lower percentage of school-aged children, a higher percentage of persons in senior career facilities and in established households, and a higher percentage of seniors/retirees. This suggests that the housing and neighborhood qualities as well as home values in Lampasas are higher than in Bell County and Coryell County. Senior facilities are also more available in Lampasas. Despite the differences, the three counties share two common demographic trends in terms of median age and racial diversity in population. The diversification in population is largely attributed to affordable living options that have surfaced throughout the Killeen-Temple-Fort Hood MSA., which will be discussed in detail in the next chapter.