Bahasa

Halaman

Hukum

Humanising Financial Services

Disclaimer: The contents of this document/information remain the intellectual property of Maybank and no part of this

is to be reproduced or transmitted in any form or by any means, including electronically, photocopying, recording or in

any information storage and retrieval system without the permission in writing from Maybank. The contents of this

document/information are confidential and its circulation and use are restricted.

Financial ResultsFourth Quarter and Full Year FY2020 ended 31 December 202025 February 2021

Investor Presentation

0

Executive Summary 2

4Q & Full Year FY2020 Financial Performance 8

Prospects & Outlook 21

Appendix:

1. Financial Performance 24

2. Community Financial Services 36

3. Global Banking 39

4. Maybank Singapore 42

5. Maybank Indonesia 45

6. Other Segments 48

Table of Contents

Maybank Group FY2020 Overview

2Note: *After proposed dividend and assumption of 85% reinvestment rate.

Flat Income YoY

Net operating income of RM24.76 billion for FY2020, was a result of:

Lower net fund based income of 4.9% as NIM compressed 17bps YoY on steep interest rate cuts across

home markets and Day-1 net modification loss absorbed. Group loans remained flat on reduced business

activities and economic contractions as overseas loans declined, offsetting the 4% loan growth in Malaysia.

Given the slow growth and low-yield environment, we capitalised on unintended opportunities through

bond disposals to mitigate reduced mobility impact on core fees in 2020. This enabled a 12.3% net fee

based income growth, which fortified the Group’s overall income.

1

• Group CASA grew 23.5% supported by growth across all home markets, resulting in Group CASA ratio of

42.8% as at end-Dec’20 (Dec’19: 35.5%). Strong liquidity risk indicators i.e.: Group LCR at 142.0%.

• Total capital and fully loaded CET1 capital ratios at 18.10%* and 14.73%* respectively as at end-Dec’20.

• Final dividend of 38.5 sen per share for FY2020, with an electable portion of 21 sen under the DRP.

Flushed Liquidity

and Robust Capital

Positions

4

Proactive

Provisioning

Loan loss provisioning doubled YoY to RM4.6 billion, with close to 50% of provisioning attributed to

macroeconomic variable adjustments and management overlay for vulnerable borrowers.

Loan loss coverage increased to 106.3% as at end Dec’20 from 77.3% a year earlier, as new impaired loan

formation remained moderate with Group GIL ratio at 2.23% as at end Dec’20 (Dec’19: 2.65%).

Diligent Cost

Management

Given weaker net operating income, the Group emplaced a strategic cost management effort since mid

2020 to ensure:

Close monitoring of discretionary spend but not at the expense of revenue generation. This yielded an

overall cost reduction of 2.7% YoY, resulting in a positive JAWs of 2.8% despite the weak income.

Cost-to-income ratio of 45.4%, marking a historical low in over a decade.

2

3

Maybank2020: FY2020 Achievements in Key Strategic Objectives

3

• Unveiled SME Digital Financing, the first end-to-end digital financing for SMEs in Malaysia with 10-minuteapproval TAT, leveraging on machine learning and a fully-digital application process

• Launched Sama-Sama Lokal, an internally developed platform that was rolled out within 3 weeks, duringMalaysia’s first Movement Control Order in March 2020

The Leading

ASEAN

Wholesale Bank

Linking Asia

• Ranked Top 2 on the ASEAN Local Currency Bonds League Table and Top 3 on the Global Sukuk League Table by Bloomberg

• Executed noteworthy ESG-driven deals such as Malaysia’s Large Scale Solar 3 solar power project financing, and launched Maybank Global Sustainability Equity-i Fund, a Shariah-compliant equity fund adopting ESG factors

The Leading

ASEAN Insurer

• No.1 Bancassurance player in Malaysia with 25% market share in Bancassurance Regular Premiums/ Contribution• Garnered SGD100 million in gross premiums over three months from new customers following Etiqa Singapore’s

new partnership with Singtel

The Global

Leader In Islamic

Finance

• Completed the USD2.5 billion Sovereign Sukuk issuance for the Republic of Indonesia, whereby USD750.0 millionwill be deployed for green projects

• Introduced Malaysia’s first Social Impact Deposit, extending financial relief to those affected by the COVID-19pandemic

The Digital Bank

of Choice

• Most engaging digital banking platform in Malaysia with more than 6 million customers on the Maybank2u app• Processed 13 billion transactions on our digital platforms in Malaysia throughout 2020, of which over 1.1 billion

were monetary transactions worth RM641 billion in value

The Top ASEAN

Community Bank

1

2

3

4

5

Supporting Our Stakeholders Through The Pandemic

• Our business continuity processes were activated even before COVID-19 was declared a pandemic.

4

EMPLOYEES

We seek to keep our employees connected, engaged and productive, while

enabling them to perform for business continuity. Some key initiatives include:

o Declarations and deferment of all events requiring physical attendance.

o Accelerated implementation of flexible work policies.

o Established 24/7 Group Human Capital Staff Emergency Support team.

o Financing assistance for affected employees

o Virtual learning and employee engagement initiatives to promote

mental, physical, emotional and performance fitness.

COMMUNITIES

• Over RM20 million contributed to MERCY Malaysia and the Ministry of Health.

• Raised over RM3 million through crowdfunding initiatives.

• Launched Sama-Sama Lokal to help digitise small local businesses.

• Primary distribution bank for Sukuk Prihatin under PENJANA.

CUSTOMERS

• Provided financial relief and support to affected

customers and clients:

o Feb-Sep 2020: moratorium/payment deferments

and R&R.

o Post-Sep 2020: Repayment Assistance followed by

Targeted Repayment Assistance for specific

borrower groups made available till June 2021.

• Proactive engagement with customers and clients to

offer guidance on options available for financial

assistance.

• Accelerate fully digital financial products and

services to enable daily remote banking with minimal

disruption.

• Physical branches - temporary closures or revised

operating hours when needed, developed EzyQ to

manage queues, regular disinfection exercises,

enforced physical distancing measures and usage of

protective equipment at the counters.

Financing Support for Customers

5

% of Outstanding

Loan Balance^

As at

12/11/20

As at

11/2/21

Mortgage 10.0% 14.6%

Auto Finance 4.1% 6.4%

Unit Trust 4.3% 9.7%

Other Retail Loans 6.3% 1.7%

SME* 23.8% 17.4%

Business Banking* 20.5% 11.2%

Corporate 28.4% 28.2%

Total 14.6% 15.7%

% of Outstanding

Loan Balance^

As at

12/11/20

As at

11/2/21

Mortgage 10.6% 0.8%

SME* 35.6% 26.9%

Business Banking* 40.5% 28.0%

Corporate 7.2% 6.4%

Total 11.3% 6.2%

% of Outstanding

Loan Balance^

As at

10/11/20

As at

11/2/21

Mortgage 17.0% 17.7%

Auto Finance* 16.6% 12.1%

Credit Cards & Personal Loans 10.7% 11.4%

RSME 26.8% 26.3%

SME+ 15.9% 16.6%

Business Banking 15.5% 17.7%

Corporate 25.6% 24.7%

Total 20.8% 20.8%

* Bank-only, not including subsidiaries i.e., WOM and Maybank Finance.

Malaysia Singapore Indonesia

^ Against outstanding total gross loans by each country’s segment @ 31 Oct 2020 & 31 Jan 2021

% of Loans Under Repayment Assistance, Relief and R&R Programmes Against Respective Total Home Market Loans

Malaysia:

• May’20: Automatic moratorium (AM) for all individuals and SMEs effective 1 Apr to 30 Sep’20.

• Aug’20: QoQ reduction as some borrowers opted-out of AM and resumed repayments.

• Nov’20: Reduction as majority of borrowers resumed repayments in Oct with AM expiry. Continued extended relief

support by Maybank, known as Repayment Assistance (RA), provided to impacted individuals and SMEs.

• Feb’21: Captures Targeted Repayment Assistance (TRA) offered to eligible B40 individuals and microenterprise customer

groups, alongside Maybank’s ongoing RA. Both RA and TRA will be made available until 30 June’21.

• Total BNM Special Relief Facility loans disbursed to SMEs was RM1.7 billion as at 11 Feb’21.

Singapore:

• Reduction in Feb’21 as initial moratorium ending Dec’20 expires. Fewer borrowers continue with repayment assistance.

• Provided SGD1.1 billion Government relief loans to 2,134 RSME and Business Banking customers1 as at 11 Feb’21.

Indonesia:

• Initial uptick in 2020 as more borrowers requested restructuring, but has since stabilised in 4Q’20.

71.9%68.2%

14.6% 15.7%

3.7%10.8% 11.3% 6.2%

14.1%17.7%

20.8% 20.8%

May'20 Aug'20 Nov'20 Feb'21

Malaysia

Singapore

Indonesia

¹ Based on number of accounts

* Includes Special Relief Facility loans

* Includes Government relief loans

24.89k393.40k

819.24k

239.36k

4Q 2019 1Q 2020 2Q 2020 3Q 2020 4Q 2020

1.53 mln1.88 mln

1.59 mln

3.22mln

3.82mln

Continued Growth in Digital Solutions and Platforms

6

• Garnered >100k unique users within 4 days of launch

on 8 Oct, and received a 4.5 star rating on Appstore

• Features intuitive UI/UX, seamless customer

experience, MAE e-wallet, MAE debit card, financial

management control tools and lifestyle applications

(F&B, transportation, entertainment & travel)

QRPay

QR

Pay

Tra

nsa

cti

on

Volu

me

QoQ: 18.7%

YoY: >100%

QoQ: -70.8%

3.955.89 5.10

6.284.28

4Q 2019 1Q 2020 2Q 2020 3Q 2020 4Q 2020

Maybank2u

Moneta

ry T

ransa

cti

on V

alu

e

(RM

bln

/ID

R t

ln/S

GD

bln

)

126.82 132.40 138.97

181.70 187.71

11.18 11.07 12.63 14.88 17.34

QoQ: 3.3%

YoY: 48.0%

QoQ: 16.5%

YoY: 55.0%

QoQ: -31.8%

YoY: 8.3%

Transaction Volume Growth (QoQ):

MY: 9.0% IND: -8.3% SG: 5.0%

34.5542.50

48.73

68.35 71.09

4Q 2019 1Q 2020 2Q 2020 3Q 2020 4Q 2020

Mobile App

QoQ: 4.0%

YoY: >100%

QoQ: 18.0%

YoY: >100%

Transaction Volume Growth (QoQ):

MY: 9.7% IND: -9.1%

Moneta

ry T

ransa

cti

on V

alu

e

(RM

bln

/ID

R t

ln/S

GD

bln

)

5.19 5.92 7.83 9.85 11.62

• SME digital financing: 146% growth QoQ to RM370.5

million in total financing disbursed in 4Q

• Business account STP: 7% growth QoQ in total

accounts created in 4Q, amounting to 27.1k accounts

• Sama-Sama Lokal: Over 4.4k SMEs digitised by year-

end

• Collaboration with ShopeePay for the 11:11

supersale, as well as Shopee and Lazada for the

12:12 mega online sale campaign, contributed

to a QoQ increase in transaction value & volume

by 36X & 38X respectively, to RM99.9 million

from 1.9 million transactions in 4Q

• Ultimate Cashback campaign for Maybank QRPay

drove strong usage in 4Q 2020, charting a 15% &

19% QoQ growth in value & volume respectively,

to RM184 million from 3.8 million transactions.

• Deepamoney with MAE charted a 86% & 50%

growth in value & volume to RM28.7 million

from over 220k transactions for the Send Money

feature during the campaign period against 2019

Launch of

MAE by

Maybank2u

App

Continued

momentum

with SME

solutions

E-commerce

campaigns &

festivities

Note: The QoQ decline in Indonesia’s QRPay transaction volume

was due to stricter movement restrictions imposed during 4QNote: Singapore’s Maybank2u transaction value declined QoQ on

less term deposit placements given lower rates in 4Q.

Executive Summary 2

4Q & Full Year FY2020 Financial Performance 8

Prospects & Outlook 21

Appendix:

1. Financial Performance 24

2. Community Financial Services 36

3. Global Banking 39

4. Maybank Singapore 42

5. Maybank Indonesia 45

6. Other Segments 48

Table of Contents

P&L Summary: FY2020PPOP growth of 2.6% YoY on double-digit fee based income expansion and controlled overheads

8

Note:

* From consolidated Full Year FY2020 Group numbers, Insurance and Takaful accounts for 11.4% of net fund based income and 9.6% of net fee based income

¹ Pre-provisioning operating profit (PPOP) is equivalent to operating profit before impairment losses

² Net Profit is equivalent to profit attributable to equity holders of the Bank

More

details on RM million FY2020 FY2019 YoY4Q

FY2020

3Q

FY2020QoQ

4Q

FY2019YoY

s.26 Net fund based income * 16,650.5 17,514.8 (4.9)% 4,337.5 4,128.3 5.1% 4,518.9 (4.0)%

s.11/

12/26 Net fee based income * 8,112.7 7,226.1 12.3% 1,975.2 1,949.5 1.3% 1,974.0 0.1%

s.24/25 Net operating income 24,763.2 24,740.9 0.1% 6,312.7 6,077.8 3.9% 6,492.9 (2.8)%

s.13 Overhead expenses (11,245.2) (11,561.9) (2.7)% (2,892.4) (2,704.4) 7.0% (2,969.1) (2.6)%

s.25 Pre-provisioning operating profit (PPOP) 1 13,518.0 13,178.9 2.6% 3,420.3 3,373.4 1.4% 3,523.8 (2.9)%

Net impairment losses (5,070.2) (2,323.4) >100% (1,499.3) (805.9) 86.0% (298.9) (>100)%

Operating profit 8,447.8 10,855.5 (22.2)% 1,921.0 2,567.5 (25.2)% 3,224.9 (40.4)%

s.24 Profit before taxation and zakat (PBT) 8,657.0 11,013.9 (21.4)% 1,992.1 2,611.3 (23.7)% 3,263.6 (39.0)%

Net Profit 2 6,481.2 8,198.1 (20.9)% 1,537.4 1,952.4 (21.3)% 2,449.1 (37.2)%

EPS - Basic (sen) 57.7 73.5 (21.5)% 13.7 17.4 (21.2)% 21.8 (37.2)%

22.1 22.6

18.5 16.3

Dec 19 Dec 20

Community Financial Services Global Banking

(10.8)%(10.8)%

+2.2%

200.9 248.0

282.7259.3

81.7 72.9

Dec 19 Dec 20

14.0 19.3

34.3 32.3

Dec 19 Dec 20

CASA FD Others

40.5 45.7

70.4 69.4

Dec 19 Dec 20

(1.4)%

(11.8)%

+23.5%

91.3 71.5

35.536.4

Dec 19 Dec 20

+2.3%

231.3 247.0

82.7 79.6

Dec 19 Dec 20

Net Fund Based Income: FY2020 YoY Trends (1/2)Group deposits grew on CASA growth across home markets, while Group loans remained muted on economic contractions

9

(21.6)%+6.8%

136.0 166.4

133.8 116.3

81.7 72.9

Dec 19 Dec 20

355.7

(8.3)%

108.2523.5 523.7

Dec 19 Dec 20

314.1

40.0

127.0

RM

billion

SG

D b

illion

IDR

tri

llio

n

Gross Loans (YoY)

+4.0% (1.9)% (14.8)% +0.0%

40.7

326.7

RM

billion

RM

billion

SG

D b

illion

IDR

tri

llio

n

Group Deposits (YoY)

29.1% 37.5%38.7% 46.8%35.5% 42.8% 36.5% 39.7%CASA

Ratio:

(13.0)%

+29.8% (5.8)%

565.3 580.2351.5

48.3 51.6 110.9 115.1

+1.2% +6.9% +3.8% +2.6%

+12.9%

RM

billion (3.8)%

Note:

• Industry loans growth for Malaysia is 3.4%, Singapore is -1.2% and Indonesia is -2.7%

• CASA ratio for Group and Malaysia includes investment accounts

• Refer to pages 29-31 for detailed information on loans and deposits growth by country and products.

+22.3%

+37.7%

Group Malaysia Singapore Indonesia

10

Net Fund Based Income: FY2020 (2/2)NIM compressed 17 bps YoY on steep interest rate cuts and net mod loss impact; rebounds 10 bps QoQ in 4Q’20

5 Year Trend

2.27

2.36

2.33

2.27

2.10

FY2016 FY2017 FY2018 FY2019 FY2020

2.13 Without

mod loss

With mod

loss

Net Interest Margin (%)

2.29 2.23

1.96 2.05

2.15

4Q '19 1Q '20 2Q '20 3Q '20 4Q '20

QoQ Trend

Rate cuts in 2020:

125bps OPR cut

3-Mth Sibor reduces 136 bps

125bps cut in Indonesia’s Reference Rate

11

Net Fee Based Income: FY2020 (YoY)Growth driven by MTM derivatives revaluation gains and realised gains on securities’ disposal

7,226

5,730

560 936

8,113

6,495

575 1,043

Total Other Operating Income fromBanking Operations

Fee Income fromIslamic Operations

Net Fee Incomefrom Insurance

FY2019

FY2020

RM million FY2019 FY2020 YoY

Commission, service charges and fees 3,431 3,374 (1.7)%

Investment & trading income 1,685 1,990 18.0%

Unrealised gain/ (losses) on financial assets and investments 1,372 766 (44.1)%

Derivatives and financial liabilities (313) 394 (>100)%

Foreign exchange profit 733 455 (37.9)%

Other income 369 320 (13.4)%

Total Group’s Other Operating Income 7,277 7,299 0.3%

Of which: Other Operating Income from Insurance 1,547 805 (48.0)%

13.3% YoY 2.8% YoY 11.4% YoY 12.3% YoY

Notes using Maybank’s 4Q & Full Year FY2020 Financial Statements:

¹ Group’s ‘Other operating income’ [Note A25] less ‘Other operating income’ from Insurance [Note A40(a)]

² Summation of ‘Other Operating Income’ from Insurance and ‘Net earned insurance premiums’ under Note A40(a) with ‘Net insurance benefits and claims incurred, net fee and commission expenses, change in expense liabilities and taxation

of life and takaful fund’ under Note A26

RM

million

1 2

12

Net Fee Based Income: 4Q FY2020 (QoQ)QoQ growth from higher commission, service charges and fees and unrealised MTM gains on securities

2,380 2,128

187 64

1,808

1,411

109 289

1,949

1,527

160 263

1,975

1,430

119 426

Total Other Operating Income fromBanking Operations

Fee Income fromIslamic Operations

Net Fee Incomefrom Insurance

1Q FY2020

2Q FY2020

3Q FY2020

4Q FY2020

RM million1Q

FY2020

2Q

FY2020

3Q

FY2020

4Q

FY2020QoQ

Commission, service charges and fees 820 693 771 1,089 41.3%

Investment & trading income 769 479 711 30 (95.7)%

Unrealised gain/ (losses) on financial assets and investments (1,352) 1,380 249 489 96.4%

Derivatives and financial liabilities 1,063 (412) 179 (436) (>100)%

Foreign exchange profit (52) 197 26 284 >100%

Other income 84 90 100 46 (54.7)%

Total Group’s Other Operating Income 1,333 2,427 2,037 1,502 (26.2)%

Of which: Other Operating Income from Insurance (795) 1,017 510 72 (85.8)%

(25.3)%

46.1%

(41.7)%

(8.7)%

61.9%

(33.7)%

8.2%

(6.3)%

>100%

1.3%

7.8%

(24.0)%

RM

million

1 2

Notes using Maybank’s 4Q & Full Year FY2020 Financial Statements:

¹ Group’s ‘Other operating income’ [Note A25] less ‘Other operating income’ from Insurance [Note A40(a)]

² Summation of ‘Other Operating Income’ from Insurance and ‘Net earned insurance premiums’ under Note A40(a) with ‘Net insurance benefits and claims incurred, net fee and commission expenses, change in expense liabilities and taxation

of life and takaful fund’ under Note A26

13

Overheads: FY2020 (YoY)Cost discipline yielded CIR of 45.4% and positive JAWs of 2.8% for FY2020

Note:

¹ Total cost excludes amortisation of intangible assets for Maybank Indonesia and Maybank Kim Eng

RM million FY2020 FY2019 YoY4Q

FY2020

3Q

FY2020QoQ

4Q

FY2019YoY

Personnel Costs 6,563.2 6,625.0 (0.9)% 1,610.7 1,581.5 1.8% 1,601.5 0.6%

Establishment Costs 1,892.5 1,905.7 (0.7)% 493.5 482.5 2.3% 534.9 (7.7)%

Marketing Expenses 375.1 596.7 (37.1)% 105.8 84.1 25.8% 147.4 (28.2)%

Administration & General

Expenses 2,414.4 2,434.5 (0.8)% 682.4 556.2 22.7% 685.3 (0.4)%

Total 11,245.2 11,561.9 (2.7)% 2,892.4 2,704.4 7.0% 2,969.1 (2.6)%

% FY2020 FY2019 YoY4Q

FY2020

3Q

FY2020QoQ

4Q

FY2019YoY

Total Cost to Income ¹ 45.4 46.7 (1.3) 45.8 44.5 1.3 45.7 0.1

Group JAWS Position 2.8 (3.1) (0.2)

14

Asset Quality (1/2)Proactive recognition of provisioning from MEV adjustments and overlays for vulnerable accounts

77.3% 81.5%90.5% 97.6%

106.3%

90.8% 89.5%99.2%

106.8%115.9%

Loan loss coverage incl.Regulatory Reserve

Loan loss coverage

Allowances for losses on loans

Note:

Loan loss coverage includes ECL for loans at FVOCI as per Note A11(xii) of the Group’s Financial Statements

FY2020 ECL includes:

• ~RM950 million additional

provisioning on MEV adjustments

• ~RM1.2 billion management

overlays for vulnerable borrowers

ECL (RM million) 4Q FY2019 1Q FY2020 2Q FY2020 3Q FY2020 4Q FY2020 FY2019 FY2020

Stage 1, net (218) (133) 102 (63) 330 (766) 236

Stage 2, net (235) 550 906 295 748 (259) 2,499

Stage 3, net 877 598 761 642 155 3,635 2,157

Write-offs 26 19 12 38 26 97 94

Recoveries (107) (73) (41) (115) (168) (430) (398)

Other debts (8) 1 1 8 1 10 11

Total 334 962 1,739 804 1,093 2,287 4,599

Of which, represented by: Group Community Financial Services (GCFS) (216) 1,987

Group Global Banking (GGB) 2,500 2,606

Group Insurance & Takaful (Etiqa) 3 6

Net Charge Off Rate (44) bps (88) bps

15

Asset Quality (2/2)QoQ decline in GIL for Group and Home Markets on slower formation of newly impaired loans

1.95% 1.96% 1.68% 1.57% 1.54%

3.87% 4.04%3.41%

3.36% 3.15%

4.48%4.93%

6.17%5.59%

5.10%

Dec 2019 Mar 2020 Jun 2020 Sep 2020 Dec 2020

Malaysia Singapore Indonesia

GIL Ratio Components Dec 2020 Sep 2020 Jun 2020 Mar 2020 Dec 2019

Non Performing Loans (NPL) 2.02% 1.93% 2.03% 2.20% 2.20%

Restructured & Rescheduled (R&R) 0.05% 0.09% 0.09% 0.06% 0.05%

Performing Loans Impaired Due to

Judgmental/ Obligatory Triggers (IPL)0.16% 0.33% 0.37% 0.45% 0.40%

GIL Ratio 2.23% 2.35% 2.49% 2.71% 2.65%

Group Gross Impaired Loans (GIL) Ratio Composition

GIL Ratio by Home Markets

16

Asset Quality by Line of Business in Home MarketsBusiness lines saw QoQ improvement across home markets; slight QoQ uptick in Malaysia consumer lines

Note:

• In Malaysia, industry GIL ratio for mortgage (purchase of residential property) is 1.2%, 0.8% for auto finance and 1.0% for credit cards.

• In Singapore, industry GIL figure is only available for mortgage, which was 0.5%.

• Maybank Indonesia’s GIL ratios are mapped in accordance to its local regulatory reporting requirements. It has fully adopted IFRS 9 effective 1Q FY2020 reporting.

MBI GIL normalised to include IFRS 9 impact

0.55% 0.64% 0.50% 0.28%0.42%

1.77% 1.88%2.44%

2.35% 1.97%

1.05%1.66%

3.12% 3.11%

2.32%

Dec 19 Mar 20 Jun 20 Sep 20 Dec 20

9.40% 9.63%

7.60% 7.346.84%

1.76% 1.58% 1.89%2.44% 2.29%

6.39%

7.92%

10.30%

8.25%8.83%

Dec 19 Mar 20 Jun 20 Sep 20 Dec 20

Malaysia Singapore Indonesia

Mortgage Auto Finance Credit Cards

Retail SME (RSME) Business Banking (BB) Corporate Banking (CB)

Consumer

Business

0.87% 0.92% 0.85% 0.77%0.90%

0.62% 0.56%0.65% 0.59% 0.54%

2.97%

7.98% 7.16%

5.46%

4.70%5.39%

Dec 19 Mar 20 Jun 20 Sep 20 Dec 20

0.65%

0.71%0.53%

0.40%0.57%

0.09%0.13%

0.27%0.16%

0.11%

0.88%0.98%

2.38%2.22%

1.09%

Dec 19 Mar 20 Jun 20 Sep 20 Dec 20

2.49% 2.37% 2.20% 2.16% 1.89%

8.70% 9.18%

7.43%7.56%

6.83%

4.37% 4.58%3.95% 4.08% 3.95%

Dec 19 Mar 20 Jun 20 Sep 20 Dec 20

2.26% 2.35% 2.02%1.67% 1.55%

2.37% 2.42% 2.23%2.02%

1.75%

4.51%

6.49%8.38%

8.85%

7.66%

Dec 19 Mar 20 Jun 20 Sep 20 Dec 20

30% 29% 41%

Upstream Midstream Downstream

Exposure to Oil & Gas and Real Estate Sectors: 31 December 2020QoQ reduction in Group’s Oil & Gas and Malaysia Real Estate exposure

17

67% 17% 3% 13%

Normal Watchlist Special Mention Account GIL

Group Exposure to Direct & Indirect Oil & Gas Borrowers

Borrowers’ Status:

Segmental Exposure:

Of GIL breakdown:• 69% is from midstream

Maybank Group Malaysia Singapore Indonesia Others

2.48% 1.64% 0.56% 0.05% 0.23%

Note:

Funded-only loans exposure is 2.03% for Group

4.40%3.54% 3.68%

2.87% 2.48%

FY2016 FY2017 FY2018 FY2019 FY2020

5-Year trend (Group exposure):

High Rise Residential,

29.0%

Landed Residential,

15.9%Malls, 9.5%

Offices, 3.7%

Hotels, 6.2%

Others, 35.7%

Real Estate Exposure to

Non-Retail Malaysian Borrowers

RM35.75 bil(or 10.94% of Malaysia

Gross Loans)

Note:

Funded-only loans exposure is 9.63%

‘Others’ include Land, Industrial Buildings & Factories, Other

Residential, Other Commercial and REITs

71% 26% 1% 2%

Normal Watchlist Special Mention Account GIL

Borrowers’ Status:

Of GIL breakdown:

• 41% is from combined exposure to

malls and hotels

• 5% is from high rise residential

Of Watchlist breakdown:

• 31% is from landed residential

• 30% is from combined exposure to

malls, hotels and offices

Note:

Midstream refers to the transportation (i.e. pipeline, rail, barge, oil tanker or truck),

storage and wholesale marketing services of crude or refined petroleum products.

92.4%

95.2%

90.6%

87.8%

90.1%

84.8%86.5%

83.1%

80.3%

83.3%

74.6%76.2%

73.1%70.9%

73.2%

Dec 19 Mar 20 Jun 20 Sep 20 Dec 20

LDR LTF LTFE

141.0% 138.2% 140.5% 146.6% 142.0%

LCR

15.31% 15.58% 14.58%

16.12% 16.34% 15.35%

19.39% 18.64%17.64%

Dec 19 Dec 20 Dec 20

15.73% 15.31% 14.73%

16.49% 16.03% 15.44%

19.39% 18.68% 18.10%

Dec 19 Dec 20 Dec 20

Total Capital Ratio Tier 1 Capital Ratio CET 1 Capital Ratio

After proposed dividend,

assuming 85%

reinvestment rate

Before proposed dividendLiquidity Risk Indicators

18

Strong Liquidity & Capital Positions: 31 December 2020Robust LCR of 142%, while Group CET1 capital ratio at 14.73% (assuming 85% reinvestment rate)

Regulatory Requirements:

• Min. CET 1 Capital Ratio + Capital Conservation Buffer (CCB) is 7.0%, min. Tier 1 Capital

Ratio + CCB is 8.5% and min. Total Capital Ratio + CCB is 10.5%.

• 1.0% D-SIB Buffer effective 31 January 2021

• Pending finalisation of Countercyclical Capital Buffer (0%-2.5%)

Note: 1) BNM’s minimum LCR requirement is 100%2) LTF is gross loans divided by (deposits + borrowings +

subdebt) while LTFE’s denominator is (deposits +

borrowings + subdebt + equity + capital securities)

3) LDR, LTF & LTFE excludes loans to banks and FIs

Group

Bank

11

28 3222.5 24

2420 23 25

25

13.5

44

32

36

33

3133 30

3232 32

39

38.5

FY10 FY11 FP11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20

Final

Interim

19

Dividend: FY2020Single-tier final dividend of 38.5 sen per share, of which 21 sen is electable under the Dividend Reinvestment Plan

76.5% 74.9% 79.9% 74.7% 71.9% 78.5% 76.3% 78.1% 78.5% 77.3%87.8% 91.2%

Dividend (sen), Payout Ratio (%) and Cash Component (%)

Dividend

Payout Ratio

Cash Component

of Total Dividend

Effective Cash

Dividend Paid Out

from Net Profit

60.4% 61.4% 26.2% 17.2% 17.0% 19.0% 22.0% 29.0% 23.2% 28.6% 57.2% 47.1% 87.8%

Note:

* Actual Reinvestment Rate for Dividend Reinvestment Plan. The reinvestment rate for Final Dividend FY2020 is pending the execution of the 20th DRP.

+ The Final Dividend for FY2017, Interim and Second Interim Dividend (reclassification from Final Dividend) for FY2019 were fully in cash.

# The Net Dividend is 28.5 sen of which 15 sen is single-tier dividend. Maybank adopted the single-tier dividend regime with effect from FY2012.

• Effective Cash Dividend Paid Out for FY2020 is based on the actual reinvestment rate for Interim Dividend FY2020 and an 85% reinvestment rate assumption for Final Dividend FY2020.

27% 13% 11% 12% 20% 25% 19% 27%67% 53%

100%

34%

39.3%

FY08 FY09 FY10 FY11 FP11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20

85.9%*

85.7%*

88.2%*85.9%*

88.5%*91.1%*

86.1%*

88.6%*

82.6%*

84.0%*

83.7%*

87.5%*

89.1%*

83.5%* 85.7%* 84.0%*

+

81.7%*

+

+

#

55.060.0

36.0

65.0

53.557.0

54.0 52.055.0

57.0

64.0

87.4%*

52.0

Executive Summary 2

4Q & Full Year FY2020 Financial Performance 8

Prospects & Outlook 21

Appendix:

1. Financial Performance 24

2. Community Financial Services 36

3. Global Banking 39

4. Maybank Singapore 42

5. Maybank Indonesia 45

6. Other Segments 48

Table of Contents

21

Market Outlook2021 industry outlook for our home markets

Key Indicators

Indonesia

• GDP: 4.5% (2021F) vs -5.4% (2020)

• System loan: 5% to 7% (2021F) vs -1.2% (2020)

• 3M SIBOR: 0.40% (2021F) vs 0.41% (2020)

• USD/SGD: 1.28 (2021F) vs 1.32 (2020)

• Inflation average: 0.8% (2021F) vs -0.2% (2020)

• GDP: 5.3% (2021F) vs -2.1% (2020)

• System loan: 4.5% (2021F) vs -2.7% (2020)

• Reference Rate: 3.50% (2021F) vs 3.75% (2020)

• USD/IDR: 14,176 (2021F) vs 14,105 (2020)

• Inflation average: 2.4% (2021F) vs 2.0% (2020)

Singapore

• GDP: 5.1% (2021F) vs -5.6% (2020)

• System loan: 3.8% (2021F) vs 3.4% (2020)

• OPR: 1.75% (2021F) vs 1.75% (2020)

• USD/MYR: 3.90 (2021F) vs 4.02 (2020)

• Inflation average: 2.6% (2021F) vs -1.2% (2020)Malaysia

Outlook

• Vaccine deployment will help restore domestic mobility

and revive consumer spending and investments, while

accommodative monetary policy to extend, with the 25

bps rate cut in February 2021.

• Loans growth expected to improve from mild pick-up in

credit demand amid the prolonged pandemic, with working

capital recovering faster than investment.

• U-shaped recovery is expected as tourism-related and

consumer-facing services sectors take longer to normalise.

Budget 2021 remains expansionary, but with a smaller

fiscal deficit as support measures taper.

• Loan growth may see a turnaround, especially as

economies emerge from lockdowns, but could be tempered

by continued border closures. Deposit growth may taper,

given low interest rates and improving economic activity.

• Economic recovery expected to be gradual and uneven

amid pandemic containment measures that include re-

imposition of Movement Control Order and declaration of

emergency, as well as rollout of COVID-19 vaccines.

• Loan growth is expected to gather momentum, in line with

economic recovery, while NIM should improve as deposits

fully re-price, barring further OPR cuts.

Maybank Performance OutlookGroup guidance for FY2021

22

Operating EnvironmentGroup’s Key Priorities and Guidance

• Leverage fee-based income opportunities in wealth management, global

markets, investment banking, asset management and insurance.

• Accelerate product rollouts on our digital platform to increase market

penetration and generate fee-based revenues. The global economy is expected to

rebound in 2021 following the

development and deployment of

COVID-19 vaccines to achieve herd

immunity. However, the recovery

across different economies will

remain uneven.

Our home markets are expected to

see economic growth this year on

the back of accommodative

monetary policies and

expansionary fiscal policies.

Rates are expected to remain

stable in our home markets, taking

into consideration the recent 25

bps rate cut in Indonesia.

• Capital and liquidity conservation will remain a key focus given lingering

uncertainty in the environment.

• Continued prioritisation of CASA growth across the home markets, in view

of low rate environment. Group NIM expected to remain flat YoY.

• Maintaining disciplined cost management with Group CIR expected to range

between 46% and 47%.

• Reimagining workplace and work arrangements to enhance productivity

and efficiencies as we embrace the new normal.

• Remain cautious on potential asset quality slippages given uncertainty over

economic recovery trajectory for some key markets.

• As such, net credit charge off to remain elevated albeit slightly lower YoY

at potentially 70 to 80 bps for FY21.

• Group ROE guidance of ~9% in FY21, on continued soft income environment

and elevated provisioning.

• Maintaining our 40-60% dividend payout policy rate to reward shareholders,

whilst maintaining capital resiliency.

Income Growth

Continued

Productivity

Drive

Sustainable

Shareholder

Returns

Balance Sheet

Management

Asset Quality

Management

Executive Summary 2

4Q & Full Year FY2020 Financial Performance 8

Prospects & Outlook 21

Appendix:

1. Financial Performance 24

2. Community Financial Services 36

3. Global Banking 39

4. Maybank Singapore 42

5. Maybank Indonesia 45

6. Other Segments 48

Table of Contents

83.7%

6.7%

7.7% 1.9%

Malaysia Singapore Indonesia Others

86.4%

0.7%

6.0% 6.9%

62.8%

24.1%

5.9%7.2%

International & Malaysia Portfolio Mix FY2020

24

Overseas:

16.3%Overseas:

37.2%

65.5%

17.2%

11.1%

6.2%

Net Operating Income Profit Before Tax

FY2020

Gross Loans *

Overseas:

34.5%

(Jan 20 – Dec 20)

RM8.66

billionRM523.7

billion

RM24.76

billion

60.5%24.4%

7.1%8.0%Overseas:

13.6%Overseas:

39.5%

61.8%18.7%

12.1%

7.4%

FY2019

Overseas:

38.2%

(Jan 19 – Dec 19)

RM11.01

billionRM523.5

billion

RM24.74

billion

Note:

* Net of unwinding interest and effective interest rate

Segmental Performance of Businesses: FY2020 (1/2)

25

13,179

6,249 6,457

74 12 972

13,518

5,654 6,847

518 34 1,017

Total Group CommunityFinancial Services

Group Corporate Banking& Global Markets

Group Investment Banking Group Asset Management Group Insurance& Takaful

FY2019 FY2020

24,741

13,792

8,341

1,144 125 1,923

24,763

12,914

8,747

1,528 144

1,982

Total Group CommunityFinancial Services

Group Corporate Banking& Global Markets

Group Investment Banking Group Asset Management Group Insurance& Takaful

FY2019 FY2020

Net Operating Income

+0.1%

RM

million

PPOP

(6.4)% +4.9%

Group Global Banking +13.1%

Group Global Banking +8.4%

FY2019: 9,611 FY2020: 10,419

FY2019: 6,544 FY2020: 7,398

RM

million

+6.0% (9.5)%

+33.5% +14.8% +3.0%

+2.6%

+>100% +>100% +4.7%

Note:

Net income & PPOP for Group includes “Head Office & Others” expenditure of RM585.7 million for FY2019 and RM551.5 million for FY2020.

17,515

10,408

5,261

260 1 1,287

16,651

9,900

5,409

243 2 1,260

Total Group CommunityFinancial Services

Group Corporate Banking &Global Markets

Group Investment Banking Group Asset Management Group Insurance& Takaful

FY2019 FY2020

Segmental Performance of Businesses: FY2020 (2/2)

26

7,226

3,384 3,081

884 124

636

8,113

3,014 3,338

1,285

142 721

Total Group CommunityFinancial Services

Group Corporate Banking& Global Markets

Group Investment Banking Group Asset Management Group Insurance& Takaful

FY2019 FY2020

Net Fund Based Income

Group Global Banking +2.4%

Net Fee Based Income

(6.4)% +>100% (4.9)% +2.8% (2.1)%

FY2019: 5,522 FY2020: 5,655

Group Global Banking +16.5%

FY2019: 4,090 FY2020: 4,764

+8.3% (10.9)%

RM

million

RM

million

+12.3%

(4.9)%

+45.3% +13.9% +13.3%

Note:

Net fund based income includes “Head Office & Others” income of RM298.2 million for FY2019 and expenditure of RM164.8 million for FY2020.

Net fee based income includes “Head Office & Others” expenditure of RM883.8 million for FY2019 and RM386.7 million for FY2020.

P&L Summary: QoQ

27

RM million4Q

FY2020

3Q

FY2020

2Q

FY2020

1Q

FY2020

Net fund based income 4,337.5 4,128.3 3,840.3 4,344.5

Net fee based income 1,975.2 1,949.5 1,808.3 2,379.7

Net operating income 6,312.7 6,077.8 5,648.5 6,724.2

Overhead expenses (2,892.4) (2,704.4) (2,706.3) (2,942.0)

Personnel Costs 1,610.7 1,581.5 1,644.0 1,727.0

Establishment Costs 493.5 482.5 458.4 458.0

Marketing Expenses 105.8 84.1 76.5 108.7

Administration & General Expenses 682.4 556.2 527.4 648.3

Pre-provisioning operating profit (PPOP)1 3,420.3 3.373.4 2,942.2 3,782.2

Net impairment losses (1,499.3) (805.9) (1,740.7) (1,024.3)

Operating profit 1,921.0 2,567.5 1,201.5 2,757.9

Profit before taxation and zakat (PBT) 1,992.1 2,611.3 1,255.7 2,797.8

Net Profit 2 1,537.4 1,952.4 941.7 2,049.7

EPS - Basic (sen) 13.7 17.4 8.4 18.2

Note:

¹ Pre-provisioning operating profit (PPOP) is equivalent to operating profit before impairment losses

² Net Profit is equivalent to profit attributable to equity holders of the Bank

Income Statement for Insurance and Takaful Business

28

RM million FY2020 FY2019 YoY 4Q FY2020 3Q FY2020 2Q FY2020 1Q FY2020 QoQ

Net interest income 1,260.1 1,286.2 (2.0)% 318.0 310.7 315.9 315.4 2.4%

Net earned premiums 9,458.9 6,760.6 39.9% 2,782.8 2,990.3 1,740.9 1,944.9 (6.9)%

Other operating income 804.6 1,546.8 (48.0)% 72.4 509.9 1,016.9 (794.7) (85.8)%

Total operating income 11,523.5 9,593.6 20.1% 3,173.3 3,810.9 3,073.7 1,465.7 (16.7)%

Net insurance benefits & claims incurred, net fee &

commission expenses, change in expense liabilities and

life & takaful fund tax

(9,559.6) (7,683.6) 24.4% (2,527.2) (3,344.5) (2,519.9) (1,168.0) (24.4)%

Net operating income 1,963.9 1,910.0 2.8% 646.1 466.4 553.8 297.6 38.5%

Overhead expenses (932.7) (930.1) 0.3% (245.7) (224.8) (222.2) (240.1) 9.3%

PPOP 1,031.2 979.9 5.2% 400.4 241.6 331.6 57.6 65.7%

Net impairment losses (21.2) (35.0) (39.4)% 0.6 (9.0) (6.1) (6.8) (>100)%

Operating profit 1,010.0 944.9 6.9% 401.0 232.6 325.6 50.8 72.4%

RM million FY2020 FY2019 YoY 4Q FY2020 3Q FY2020 2Q FY2020 1Q FY2020 QoQ

Net insurance benefits & claims incurred, net fee &

commission expenses, change in expense liabilities and

life & takaful fund tax

(9,559.6) (7,683.6) 24.4% (2,527.2) (3,344.5) (2,519.9) (1,168.0) (24.4)%

Less: intercompany elimination 338.8 312.3 8.5% 98.3 107.7 50.6 82.2 (8.7)%

Total net insurance benefits & claims incurred, net fee

& commission expenses, change in expense liabilities

and life & takaful fund tax

(9,220.8) (7,371.3) 25.1% (2,428.9) (3,236.9) (2,469.2) (1,085.8) (25.0)%

Reconciliation of net insurance benefits & claims incurred, net fee & commission expenses, change in expense liabilities and life & takaful

fund tax

Group Gross Loans Growth: 31 December 2020

29

% of

Portfolio

31 Dec

2020

30 Sep

2020QoQ

30 Jun

2020

31 Mar

2020

31 Dec

2019YoY

Group Gross Loans 523.7 521.8 0.4% 520.2 518.4 523.5 0.0%

Malaysia (RM billion) 62% 326.7 324.2 0.8% 316.1 314.3 314.1 4.0%

Community Financial Services (reported) 76% 247.0 243.2 1.6% 234.6 231.7 231.3 6.8%

Community Financial Services (rebased)¹ 76% 247.0 243.2 1.6% 234.6 231.7 231.0 6.9%

Global Banking (reported) 24% 79.6 80.8 (1.5)% 81.0 82.4 82.7 (3.8)%

Global Banking (rebased)¹ 24% 79.6 80.8 (1.5)% 81.0 82.4 82.9 (4.1)%

International (RM billion) 36% 189.9 189.8 0.1% 198.1 199.1 203.0 (6.4)%

Singapore (SGD billion) 64% 40.0 38.6 3.6% 38.9 40.2 40.7 (1.9)%

Community Financial Services 58% 22.6 21.9 3.3% 21.8 21.9 22.1 2.2%

Global Banking 42% 16.3 16.4 (0.9)% 17.0 18.2 18.5 (11.8)%

Indonesia (IDR trillion) 16% 108.2 112.7 (4.0)% 119.5 128.1 127.0 (14.8)%

Community Financial Services 66% 71.5 74.6 (4.0)% 80.9 88.6 91.3 (21.6)%

Global Banking 34% 36.4 37.9 (4.0)% 38.4 39.3 35.5 2.3%

Other markets (RM billion) 20% 37.6 41.3 (8.8)% 42.7 43.6 41.7 (9.8)%

Investment banking (RM billion) 2% 7.1 7.8 (9.7)% 6.0 5.0 6.4 9.8%

Note:

¹ Rebased loan growth figures are based on adjusted 31 December 2019 position in line with migration of client accounts, effective 1 January 2020

Malaysia Loans Growth: 31 December 2020

30

RM billion% of

Portfolio

31 Dec

2020

30 Sep

2020QoQ

30 Jun

2020

31 Mar

2020

31 Dec

2019YoY

Community Financial Services (reported) 76% 247.0 243.2 1.6% 234.6 231.7 231.3 6.8%

Community Financial Services (rebased)¹ 76% 247.0 243.2 1.6% 234.6 231.7 231.0 6.9%

Consumer 61% 199.2 196.4 1.5% 189.3 187.9 186.9 6.6%

Total Mortgage 33% 108.1 105.6 2.3% 102.4 100.5 97.7 10.6%

Auto Finance 16% 52.8 52.3 1.1% 49.4 49.4 49.6 6.5%

Credit Cards 2% 7.1 7.1 (0.2)% 6.7 7.2 7.8 (9.0)%

Unit Trust 9% 29.2 29.2 0.0% 28.7 28.5 29.5 (1.1)%

Other Retail Loans 1% 2.1 2.2 (5.6)% 2.2 2.3 2.3 (10.4)%

Business Banking + SME (reported) 15% 47.8 46.8 2.1% 45.3 43.8 44.4 7.6%

Business Banking + SME (rebased)¹ 15% 47.8 46.8 2.1% 45.3 43.8 44.1 8.2%

SME (reported) 7% 21.7 20.9 3.9% 20.0 19.0 19.1 13.9%

SME (rebased)¹ 7% 21.7 20.9 3.9% 20.0 19.0 18.8 15.9%

Business Banking (reported) 8% 26.0 25.9 0.6% 25.2 24.8 25.3 2.8%

Business Banking (rebased)¹ 8% 26.0 25.9 0.6% 25.2 24.8 25.4 2.6%

Global Banking (Corporate) (reported) 24% 79.6 80.8 (1.5)% 81.0 82.4 82.7 (3.8)%

Global Banking (Corporate) (rebased)¹ 24% 79.6 80.8 (1.5)% 81.0 82.4 82.9 (4.1)%

Total Malaysia 326.7 324.2 0.8% 316.1 314.3 314.1 4.0% Note:

¹ Rebased loan growth figures are based on adjusted 31 December 2019 position in line with migration of client accounts, effective 1 January 2020

Group Deposits Growth: 31 December 2020

31

% of

Portfolio

31 Dec

2020

30 Sep

2020QoQ

30 Jun

2020

31 Mar

2020

31 Dec

2019YoY

Group Gross Deposits 580.2 593.2 (2.2)% 573.3 543.8 565.3 2.6%

Malaysia (RM billion) 61% 355.7 367.8 (3.3)% 355.4 336.7 351.5 1.2%

Savings Deposits 16% 56.8 56.0 1.4% 54.5 48.8 45.0 26.2%

Current Accounts 31% 109.6 117.1 (6.4)% 103.0 97.8 91.0 20.4%

Fixed Deposits 33% 116.3 125.7 (7.4)% 125.2 129.9 133.8 (13.0)%

Others 20% 72.9 69.0 5.7% 72.7 60.2 81.7 (10.8)%

International 39% 225.6 226.8 (0.5)% 219.3 210.0 214.7 5.1%

Singapore (SGD billion) 69% 51.6 52.5 (1.6)% 48.8 47.2 48.3 6.9%

Savings Deposits 17% 8.6 8.3 4.3% 8.9 7.8 7.9 8.8%

Current Accounts 21% 10.7 9.6 11.9% 7.7 6.6 6.1 75.2%

Fixed Deposits 62% 32.3 34.6 (6.7)% 32.2 32.8 34.3 (5.8)%

Indonesia (IDR trillion) 15% 115.1 116.7 (1.3)% 105.9 117.4 110.9 3.8%

Savings Deposits 19% 21.2 21.3 (0.7)% 21.5 21.9 21.0 1.1%

Current Accounts 21% 24.5 24.8 (1.3)% 20.8 21.7 19.5 25.6%

Fixed Deposits 60% 69.4 70.5 (1.6)% 63.7 73.7 70.4 (1.4)%

92.4%95.2%

90.6%87.8% 90.1%

35.5%38.4% 40.2% 42.1% 42.8%

33.2%35.1%

37.3%39.1%

39.6%

Dec 19 Mar 20 Jun 20 Sep 20 Dec 20

LDR CASA CASA (without IA)

84.3% 85.2%79.9%

73.5% 77.4%

29.1% 30.5% 34.0% 34.0% 37.5%

Dec 19 Mar 20 Jun 20 Sep 20 Dec 20

LDR and CASA Ratio

32

Indonesia

Malaysia

90.0% 93.9% 89.4% 88.7% 92.5%

38.7%43.6% 44.3% 47.1% 46.8%

34.9%38.2% 39.7% 42.3% 41.7%

Dec 19 Mar 20 Jun 20 Sep 20 Dec 20

Singapore

Group

111.3% 106.3% 109.9%

94.1% 91.5%

36.5% 37.2% 39.9% 39.5% 39.7%

94.1%89.7% 94.2%

80.7% 79.3%

Dec 19 Mar 20 Jun 20 Sep 20 Dec 20

LDR (Bank Level)

Note:

• Group and Indonesia LDR excludes loans to banks and FIs

• Group and Malaysia LDR include investment accounts totaling RM23.84 billion for 31 Dec 2020, RM23.48 billion for 30 Sep 2020, RM22.54 billion for 30 Jun 2020, RM24.50 billion for 31 Mar 2020, RM20.74 billion

for 31 Dec 2019.

523.5 521.8 523.7

Dec 19 Sep 20 Dec 20

Borrowings, 5%

Capital Instruments, 2%

Customer Funding, 77%

FI Deposits, 5%

Equity, 11%

310.3 315.0 326.8

27.3 26.2

33.2

42.9 43.4

43.6

Operational RWA Market RWA

Credit RWA Gross Loans

RWA Optimisation and Funding Management

33

USD, 36%

RM, 28%

JPY, 12%

HKD, 7%

IDR, 6%

THB, 3%AUD, 2%SGD, 2%

Others, 4%

Funding Breakdown

Note:

• Customer Funding comprises Deposits from Customers & Investment Accounts of Customers.

By maturity:

≤ 1 Year 27%

> 1 Year 73%

Borrowings and

Capital Instruments

by Currency

Group Gross Loans & Group RWA

RM

bill

ion

Growth (%) YoY QoQ

Group Gross Loans 0.0% 0.4%

Total Group RWA 6.1% 4.9%

- Group Credit RWA 5.3% 3.7%

380.4 384.6

403.6

RM752.4

billion

RM49.9

billion

Key Operating Ratios

34

% FY2020 FY2019 YoY4Q

FY2020

3Q

FY2020QoQ

2Q

FY2020

1Q

FY2020

4Q

FY2019YoY

Return on Equity 4 8.1 10.9 (2.8)% 7.7 9.7 (2.0)% 4.7 10.6 13.0 (5.3)%

Net Interest Margin 4 (bps) 2.10 2.27 (17) bps 2.15 2.05 10 bps 1.96 2.23 2.29 (14) bps

Fee to Income Ratio 32.8 29.2 3.6% 31.3 32.1 (0.8)% 32.0 35.4 30.4 0.9%

Loans-to-Deposit Ratio 1 90.1 92.4 (2.3)% 90.1 87.8 2.3% 90.6 95.2 92.4 (2.3)%

Cost to Income Ratio 2 45.4 46.7 (1.3)% 45.8 44.5 1.3% 47.9 43.7 45.7 0.1%

Asset Quality

Gross Impaired Loans Ratio 2.23 2.65 (42) bps 2.23 2.35 (12) bps 2.49 2.71 2.65 (42) bps

Loans Loss Coverage 106.3 77.3 29.0% 106.3 97.6 8.7% 90.5 81.5 77.3 29.0%

Net Charge Off Rate 4 (bps) (88) (44) (44) bps (84) (61) (23) bps (133) (73) (26) (58) bps

Capital Adequacy 3

CET1 Capital Ratio 14.73 14.58 15 bps 14.73 15.28 (55) bps 15.43 14.79 14.58 15 bps

Total Capital Ratio 18.10 18.23 (13) bps 18.10 18.89 (79) bps 19.04 18.50 18.23 (13) bps

Note:1 LDR excludes loans to banks and FIs.2 Total cost excludes amortisation of intangibles for Maybank Indonesia and Maybank Kim Eng.3 The capital ratios are based on an assumption of 85% reinvestment rate for periods relating to dividends under DRP, and based on full cash payment of dividends for period without DRP.4 Quarterly positions of Return on Equity, Net Interest Margin and Net Charge Off Rate are on an annualised basis

Executive Summary 2

4Q & Full Year FY2020 Financial Performance 8

Prospects & Outlook 21

Appendix:

1. Financial Performance 24

2. Community Financial Services 36

3. Global Banking 39

4. Maybank Singapore 42

5. Maybank Indonesia 45

6. Other Segments 48

Table of Contents

36

Community Financial Services: Overview of Market Share for Malaysia

Note:

* Refers to housing, shophouse and other mortgage loans

** Credit cards market share refer to receivables for commercial banks

*** Total bank deposits inclusive of investment asset (“IA”)∑ Industry number from ABM

^ Without IA. With IA, the market share as at Dec’20 for Total Core Retail Deposits , Retail CASA, Retail

Savings, Demand Deposits and Retail Fixed Deposits are 17.9%, 26.6%, 28.1%, 23.9% and 13.8%

respectively (against MBB retail IA)

^^ Excluding non-financial transactions as per BNM guidelines

Loans

Total consumer (Household) 17.7% 17.8% 17.9% 18.1% 18.1%

Auto (Hire Purchase + Block Discounting + Floor Stocking) 29.6% 29.7% 30.3% 30.4% 30.4%

Total mortgage * 14.0% 14.2% 14.3% 14.4% 14.5%

Credit cards ** 18.6% 18.6% 18.5% 19.3% 19.3%

Unit trust 48.5% 49.8% 49.7% 49.2% 48.9%

Deposits

Total deposits *** 17.8% 17.5% 17.6% 17.4% 17.1%

Total core retail deposits ^ 16.5% 16.9% 17.4% 17.5% 17.6%

Retail CASA ^ 24.3% 25.3% 25.7% 25.3% 25.2%

Retail savings ^ 27.8% 28.1% 28.7% 28.4% 28.0%

Demand deposits ^ 18.2% 19.9% 19.8% 19.3% 19.7%

Retail fixed deposits ^ 12.8% 12.7% 12.9% 13.0% 13.0%

Channels

Internet banking - Subscriber base 39.6% 39.1% 40.3% 39.9% 39.5%

Mobile banking - Subscriber base 31.3% 32.6% 31.9% 31.4% 30.9%

Internet banking - Transaction Volume ^^ 51.0% 50.5% 50.1% 50.0% 49.8%

Mobile banking - Transaction Volume 63.0% 62.9% 62.7% 61.9% 60.7%

Branch network ∑ 19.4% 19.4% 19.4% 19.4% 19.3%

Dec-20Sep-20Mar-20Dec-19Market share Jun-20

Community Financial Services: Overview of Malaysia Portfolio

37

215.5234.5 239.4

Dec 19 Sep 20 Dec 20

6.01

6.75

Dec 19 Dec 20

3.764.80

Dec 19 Dec 20

138.9 153.3 154.7

65.4 66.3 69.0

Dec 19 Sep 20 Dec 20

Consumer BB + RSME

204.3 219.6

Wealth Management segment’s TFA grew 11.1% YoY

to RM239.4 billion

Total CFS loans on an upward trend of 6.8% YoY and

1.6% QoQ

+1.9% QoQ

Total CFS deposits increased by 9.5% YoY driven by CASA

growth of 22.6%

+9.5% YoY

Maybank2u 1-month active users grew 12.5% YoY driven by

mobile users growth

186.9 196.4 199.2

44.4 46.8 47.8

Dec 19 Sep 20 Dec 20

Consumer BB + RSME

247.0

+1.6% QoQ

+6.8% YoY

+11.1% YoY

+2.1% QoQ

+27.6% YoY

+12.5% YoY

M2u 1-month active users

of which Mobile 1-month

active users

231.3 243.2223.8

Note:

• TFA: Total Financial Assets (Deposits, Investments, Financing & Protection).

• TFA for total Individual customers (excl. NPL) amounted to RM357.8 billion as at Dec’20,

RM352.8 billion as at Sep’20 and RM327.7 billion as at Dec’19.

RM

billion

RM

billion

RM

billion

RM

billion

Executive Summary 2

4Q & Full Year FY2020 Financial Performance 8

Prospects & Outlook 21

Appendix:

1. Financial Performance 24

2. Community Financial Services 36

3. Global Banking 39

4. Maybank Singapore 42

5. Maybank Indonesia 45

6. Other Segments 48

Table of Contents

10.8

25.1

46.7

9.8

21.6

49.3

9.9

21.2

48.4

Dec 20 Sep 20 Dec 19

51.1 52.9 63.2 60.7 65.2

52.5 51.454.0 59.3 54.0

60.0 55.157.2 58.5 60.6

20.7 24.2

23.828.3 28.08.5 5.9

5.97.3 7.4

Dec 19 Mar 20 Jun 20 Sep 20 Dec 20

Govt. Securities - Domestic Govt. Securities - Foreign

PDS/Corp Bonds - Domestic PDS/Corp Bonds - Foreign

Others

Global Banking: Overview of Malaysia Corporate Banking and Group Securities Portfolio

39

Note:

- ‘Term Loan’ includes foreign currency denominated accounts, while ‘Trade Finance and Others’ is

combined with ‘Overdraft’

- Trade Finance market share as at Dec’20 is 21.8%

Total Corporate Banking loans in Malaysia decreased 3.8%

YoY to RM79.6 billion

RM billion

Term Loan

Short Term

Revolving

Credit

Trade

Finance

and Others

+3.6% YoY

Group Securities Portfolio¹ grew 11.6% YoY

Note:

¹ Group Securities Portfolio is inclusive of Financial assets designated upon initial

recognition (part of FVTPL)

+11.6% YoY

192.8189.5

204.1214.1 215.2

RM

billion

(15.3)% YoY

(8.7)% YoY

Global Banking: Overview of Group Investment Banking Portfolio

40

FY2020 Fee-based Income for MalaysiaFY2020 Total Income Breakdown by Country

FY2020 Brokerage Market Share by Country

Country Rank Market ShareTrading Value

(USD billion)

Malaysia 5 8.8% 46.3

Singapore 11 3.8% 20.6

Thailand 2 6.3% 60.1

Indonesia 6 4.7% 14.8

Philippines 9 4.0% 2.9

Hong Kong Tier 3 0.1% 10.2

Vietnam >10 2.6% 4.0

Note:

¹ Maybank Kim Eng represents the combined business of Maybank IB and business segments under Maybank Kim Eng Holdings.

Malaysia52%

Singapore23%

Indonesia5%

Philippines1%

Thailand12%

HongKong3%

Others4%

RM1,528.1

million

Arranger's Fees23%

Underwriting & Placements

Fees7%

Brokerage Fee47%

Agency/Guarantee Fees4%

Advisory Fee4%

Other Fee Income

15%

Executive Summary 2

4Q & Full Year FY2020 Financial Performance 8

Prospects & Outlook 21

Appendix:

1. Financial Performance 24

2. Community Financial Services 36

3. Global Banking 39

4. Maybank Singapore 42

5. Maybank Indonesia 45

6. Other Segments 48

Table of Contents

Maybank Singapore: P&L Summary

42

Income of SGD977 million was 14.1% lower YoY largely due to lower fund based income but partially offset by fee based income growth.

Fund based income decline of 27.1% was largely impacted from lower interest rates and slower lending activities, leading to a lower loans to deposit ratio in

recent quarters.

NOII growth was aided by gains on investment sales as well as wealth management and credit related fees, which picked up significantly over the last quarter

following the easing of activities from the lockdown in Singapore.

Overheads of SGD466 million was marginally higher YoY largely due to the additional BCP related expenses incurred during the year.

Profit before taxation of SGD184 million was significantly higher due to a reduction in impairment losses YoY. Notwithstanding, additional management overlay

allowance were provided during the year to take on the impact from the weakening of MEVs amid the pandemic.

SGD million FY2020 FY2019 YoY 4Q FY2020 3Q FY2020 QoQ

Net fund based income 555.17 761.13 (27.1)% 125.54 116.40 7.9%

Net fee based income 421.57 376.39 12.0% 131.27 100.38 30.8%

Net income 976.74 1,137.52 (14.1)% 256.81 216.78 18.5%

Overhead expenses (465.69) (454.76) 2.4% (117.44) (111.57) 5.3%

Operating profit 511.05 682.76 (25.1)% 139.37 105.21 32.5%

Profit/ (Loss) before taxation 183.66 8.41 >100% 80.30 17.53 >100%

7.9 8.3 8.6

6.1 9.6 10.7

34.3 34.6 32.3

Dec 19 Sep 20 Dec 20

Time Deposits

Demand Deposits

Savings

43

Maybank Singapore: Overview of Loans and Deposits Portfolio

5.3 8.2 9.1

15.918.2 16.4

8.89.7 10.2

18.3 16.5 16.0

Dec 19 Sep 20 Dec 20

Consumer - TimeDeposits

Consumer CASA

Business TimeDeposits

Business CASA

51.6

Diversified Loan Portfolio

-3.9% -5.6%-9.1%

-7.8% -1.9%

4.2% 8.3%2.1%

-0.2% -1.2%

Dec 19 Mar 20 Jun 20 Sep 20 Dec 20

Maybank Singapore Growth Industry Growth

Consumer

50.7%

Corporate

49.3%

Consumer deposits increased to 50.7% of total deposits

CASA Ratio: 37.5%

SG

D b

illion

CASA ratio higher at 37.5% from 29.1% in December 2019, on

expanded demand deposits, from both corporates and individuals.

Business deposits expanded SGD4.3 billion YoY, contributed mainly by demand

deposits.

Consumer CASA deposits grew, while fixed deposits declined.

52.548.3

Maybank Singapore’s loans portfolio saw a decline due to slowdown

in business activities, in line with the industry

+6.9% YoY

SG

D b

illion

% YoY change

SGD Billion% of

Portfolio

31 Dec

2020

30 Sep

2020QoQ

31 Dec

2019YoY

CFS 58% 22.6 21.9 3.3% 22.1 2.2%

Consumer 42% 16.4 15.8 4.0% 16.0 2.5%

Housing Loan 28% 11.0 10.5 5.1% 10.6 3.9%

Auto Loan 6% 2.3 2.3 1.1% 2.4 (5.4)%

Cards 1% 0.3 0.3 6.7% 0.4 (14.9)%

Others 7% 2.8 2.7 1.9% 2.6 6.9%

Non-Individuals 16% 6.2 6.1 1.6% 6.1 1.6%

RSME 4% 1.7 1.7 4.0% 1.5 18.0%

Business Banking 8% 3.2 3.2 1.5% 3.2 1.7%

Others 4% 1.3 1.3 (1.1)% 1.5 (14.7)%

Global Banking 42% 16.3 16.4 (0.9)% 18.5 (11.8)%

Total 100% 40.0 38.6 3.6% 40.7 (1.9)%

Executive Summary 2

4Q & Full Year FY2020 Financial Performance 8

Prospects & Outlook 21

Appendix:

1. Financial Performance 24

2. Community Financial Services 36

3. Global Banking 39

4. Maybank Singapore 42

5. Maybank Indonesia 45

6. Other Segments 48

Table of Contents

Maybank Indonesia: P&L Summary

45

IDR billion FY2020 FY2019 YoY4Q

FY2020

3Q

FY2020QoQ

Net Fund Based income 7,260 8,168 (11.1)% 1,647 1,677 (1.8)%

Net Fee Based income 2,379 2,587 (8.0)% 650 546 18.9%

Net income 9,639 10,755 (10.4)% 2,297 2,223 3.3%

Overhead expenses (5,713) (6,397) (10.7)% (1,295) (1,381) (6.2)%

Personnel (2,536) (2,571) (1.3)% (596) (622) (4.3)%

General and Administrative (3,176) (3,826) (17.0)% (699) (758) (7.8)%

Operating profit 3,927 4,358 (9.9)% 1,001 842 18.9%

Provisions Expenses (2,076) (1,781) 16.5% (630) (435) 44.8%

Non Operating Income/(Expense) (32) 22 (>100)% (6) (19) (66.7)%

Profit Before Tax and Non-Controlling Interest 1,819 2,599 (30.0)% 365 388 (5.9)%

Tax and Non-Controlling Interest (552) (757) (27.0)% (198) (99) >100%

Profit After Tax and Non-Controlling Interest 1,266 1,843 (31.3)% 167 289 (42.2)%

EPS - Basic (IDR) 16.62 24.18 (31.3)% 2.20 3.80 (42.2)%

Maybank Indonesia: Financial Ratios and Loans Portfolio Breakdown

46

Key Operating Ratios Loans Portfolio Breakdown

Key Operating Ratio Dec-20 Sep-20 Dec-19 YoY

Profitability & Efficiency

Return On Assets 1.04% 1.11% 1.45% (0.40)%

Return On Equity (Tier 1) 5.13% 6.00% 7.73% (2.60)%

Net Interest Margin 4.55% 4.69% 5.07% (0.51)%

Cost to Income Ratio 59.26% 60.16% 59.48% (0.22)%

Asset Quality

NPL - Gross 4.00% 4.34% 3.33% 0.67%

Liquidity & Capital Adequacy

LCR 212.63% 184.60% 146.49% 66.14%

CET1 22.80% 21.85% 19.54% 3.26%

CAR 24.31% 23.47% 21.38% 2.94%

IDR Trillion% of

Portfolio

31 Dec

2020

30 Sep

2020QoQ

31 Dec

2019YoY

CFS 67% 70.8 73.9 (4.1)% 90.5 (21.7)%

CFS Retail 32% 34.0 35.1 (3.1)% 42.2 (19.3)%

Auto Loan 16% 16.8 18.0 (6.8)% 23.5 (28.5)%

Mortgage 13% 14.0 14.0 0.3% 15.0 (6.4)%

CC + Personal Loan 3% 2.7 2.6 3.2% 3.2 (17.6)%

Other loans 0% 0.5 0.5 3.8% 0.4 13.1%

CFS Non-Retail 35% 36.8 38.7 (5.1)% 48.3 (23.8)%

Business Banking 17% 17.7 19.0 (6.7)% 25.3 (30.0)%

SME+ 4% 4.0 4.2 (5.8)% 5.1 (21.7)%

RSME 14% 15.1 15.6 (2.9)% 17.9 (15.7)%

Global Banking 33% 34.5 35.6 (3.1)% 32.1 7.4%

Total 105.3 109.4 (3.8)% 122.6 (14.1)%

Note: Maybank Indonesia’s loans breakdown is mapped in accordance to its local

regulatory reporting requirements.^ LCR is disclosed on a quarter-end basis

Executive Summary 2

4Q & Full Year FY2020 Financial Performance 8

Prospects & Outlook 21

Appendix:

1. Financial Performance 24

2. Community Financial Services 36

3. Global Banking 39

4. Maybank Singapore 42

5. Maybank Indonesia 45

6. Other Segments 48

Table of Contents

RM million FY2020 FY2019 YoY

Total Income 5,357.1 5,103.0 5.0%

Profit Before Tax 2,328.2 3,800.4 (38.7%)

Financing & Advances 220,230.5 206,714.2 6.5%

Deposits & Investment Account: 202,392.8 191,887.5 5.5%

Deposits from Customers 178,552.0 171,149.8 4.3%

Investment Account 23,840.8 20,737.7 15.0%

Maybank Islamic, 62.6%

Maybank Conventional,

Malaysia, 37.4%

Islamic Banking: Performance Overview

48

Group Islamic Banking Financial Performance

Maybank Islamic: Key Financial Ratios

Key Financial Ratios FY2020 FY2019

Total Capital Ratio (TCR) 18.06% 18.55%

Net Profit Margin (YTD) 1.73% 1.75%

Cost to Income Ratio (CIR) 33.4% 36.3%

Direct FDR1 95.3% 96.1%

Note:

¹ Direct Financing to Deposits Ratio (FDR) comprising gross financing against deposit and Unrestricted

Investment Account (exc. RPSIA assets and liabilities)

Maybank Islamic: Total Gross Financing grew to RM206.7 billion

Note: Figures are as per latest segmentation breakdown

Year Contribution

Dec 2019 60.7%

Mar 2020 61.3%

Jun 2020 61.7%

Sep 2020 62.2%

Dec 2020 62.6%

Maybank Islamic Contribution to Maybank Malaysia Loans

and Financing as at December 2020

36.7

54.2

42.2

7.9

30.4

20.7

41.7

61.5

45.7

7.7

30.7

19.4

AITAB Mortgage Term Financing Others (CFS) Term Financing Others (GB)

Dec-19

Dec-20

8%

RM

billion

1%

(6)%

CFS:11% GB: (2)%

(3)%

14%

14%

Islamic Banking: Market Share

49

Key Products Dec 20 Dec 19

Automobile Financing 48.5% 47.7%

Home 26.9% 26.3%

Term financing 27.4% 28.6%

Maybank Islamic ranks No.1 by Asset Market Share in Malaysia

Market Share by Product (Malaysia) Maybank Islamic Market Share

31.1% 30.9% 30.7% 30.8% 30.8%

27.8% 27.6% 27.9%28.9%

27.0%

Dec 19 Mar 20 Jun 20 Sep 20 Dec 20

Financing Deposits & Investment Accounts

MalaysiaAsset Market Share

Sep 20Rank

Maybank Islamic 30% 1

CIMB Islamic 13% 2

RHB Islamic 9% 3

Source: Latest BNM Monthly Statistical Bulletin

Sukuk League Table Ranking December 2020

Source : Latest BNM Monthly Statistical Bulletin

Source: BloombergSource: Respective Bank’s Financial Statements

Global Sukuk League

Table Ranking

Market

Share (%)

Amount

(USD million)Issues

#3 Maybank 8.46% 5,328 151

MYR Sukuk League

Table Ranking

Market

Share (%)

Amount

(USD million)Issues

#1 Maybank 27.99% 5,024 148

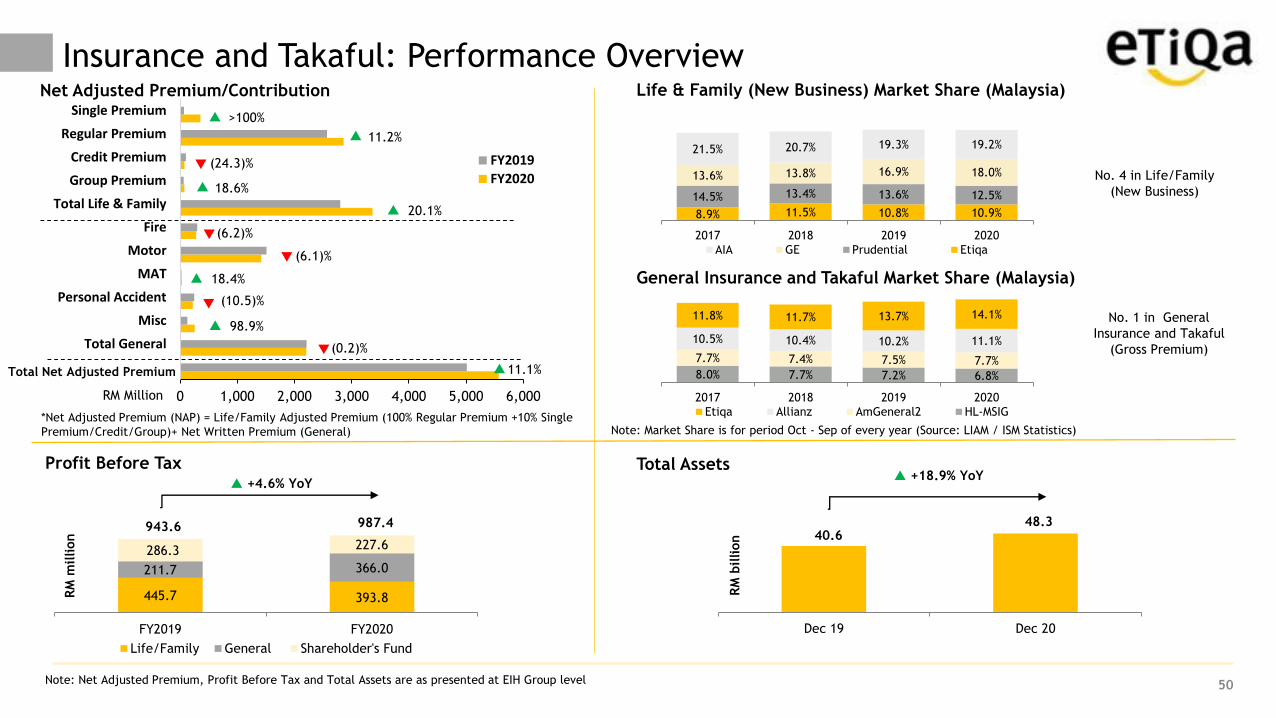

Profit Before Tax

Insurance and Takaful: Performance Overview

50

Total Assets

Net Adjusted Premium/Contribution Life & Family (New Business) Market Share (Malaysia)

No. 1 in General

Insurance and Takaful

(Gross Premium)

General Insurance and Takaful Market Share (Malaysia)

Note: Market Share is for period Oct - Sep of every year (Source: LIAM / ISM Statistics)

No. 4 in Life/Family

(New Business)

*Net Adjusted Premium (NAP) = Life/Family Adjusted Premium (100% Regular Premium +10% Single

Premium/Credit/Group)+ Net Written Premium (General)

Note: Net Adjusted Premium, Profit Before Tax and Total Assets are as presented at EIH Group level

445.7 393.8

211.7 366.0

286.3 227.6

FY2019 FY2020

Life/Family General Shareholder's Fund

+4.6% YoY

943.6 987.4

RM

million 40.6

48.3

Dec 19 Dec 20

+18.9% YoY

RM

billion

8.9% 11.5% 10.8% 10.9%

14.5% 13.4% 13.6% 12.5%

13.6% 13.8% 16.9% 18.0%

21.5% 20.7% 19.3% 19.2%

2017 2018 2019 2020

AIA GE Prudential Etiqa

8.0% 7.7% 7.2% 6.8%

7.7% 7.4% 7.5% 7.7%

10.5% 10.4% 10.2% 11.1%

11.8% 11.7% 13.7% 14.1%

2017 2018 2019 2020

Etiqa Allianz AmGeneral2 HL-MSIG

0 1,000 2,000 3,000 4,000 5,000 6,000

Total General

Misc

Personal Accident

MAT

Motor

Fire

Total Life & Family

Group Premium

Credit Premium

Regular Premium

Single Premium

RM Million

FY2019

FY2020

>100%

11.2%

(24.3)%

18.6%

20.1%

(6.2)%

(6.1)%

(10.5)%

18.4%

98.9%

(0.2)%

11.1%Total Net Adjusted Premium

Humanising Financial Services

MALAYAN BANKING BERHAD14th Floor, Menara Maybank100, Jalan Tun Perak50050 Kuala Lumpur, MalaysiaTel : (6)03-2070 8833

www.maybank.com

Disclaimer. This presentation has been prepared by Malayan Banking Berhad (the “Company”) for information purposes only and does not purport to contain all the information that

may be required to evaluate the Company or its financial position. No representation or warranty, express or implied, is given by or on behalf of the Company as to the accuracy or

completeness of the information or opinions contained in this presentation.

The presentation does not constitute or form part of an offer, solicitation or invitation of any offer, to buy or subscribe for any securities, nor should it or any part of it form the basis

of, or be relied in any connection with, any contract, investment decision or commitment whatsoever.

The Company does not accept any liability whatsoever for any loss howsoever arising from any use of this presentation or their contents or otherwise arising in connection therewith.

Top Related

Copyright © 2022 FDOKUMEN