Bahasa

Halaman

Hukum

Corporate Debt Issuance and theHistorical Level of Interest Rates

Christopher B. Barry, Steven C. Mann, Vassil T. Mihov,and Mauricio Rodrı́guez∗

Using a sample that comprises more than 14,000 new issues of corporate debt for the period1970-2001, we examine the relation between debt issues and the level of interest rates relativeto historical levels. Consistent with recent survey evidence, we find that companies issue moredebt, more debt relative to investment spending, and more debt compared to equity when interestrates are low relative to historical rates. The effects continue to hold when we control for othervariables that influence debt issuance and when we account for refinancing.

In the neoclassical theory of investment, a drop in the cost of capital results in increasedinvestment spending. As firms increase their investments, all else equal, they also tend to issuenew debt to finance a portion of those investments. Thus, debt issuance can be a function of thelevel of capital investment by firms. Alternatively, firms may try to time debt issuance if theybelieve that interest rates are advantageous relative to where rates were previously. We define“timing of interest rates” as the practice of issuing debt, relative to financing needs and capitalexpenditures, when interest rates are low compared to historical levels.

We provide evidence that links debt issuance to changes in interest rates relative to their his-torical levels. To distinguish between a timing theory and a more standard neoclassical story,we ask whether firms issue more debt relative to their investment plans (capital expenditures)or relative to equity issuance, following changes in interest rates. We find that past interestrates have prominent effects on the issuance of debt: when current interest rates are low rel-ative to historical levels, firms tend to issue more debt. These effects occur even after weaccount for other factors that can lead to debt issuance, such as capital expenditures, refinancing,firm size and profitability, the level of corporate cash flow, interest rate spreads, and equityvaluation.

Consistent with Graham and Harvey’s (2001) survey evidence that “managers attempt to timeinterest rates by issuing debt when they feel that market interest rates are particularly low,” we

The authors are grateful to Stan Block, Mike Cliff, Michel Dubois, Espen Eckbo, Wayne Ferson, John Graham, RobinGreenwood, Robert Kieschnick, Erik Lie, Steve Lim, Pete Locke, Ehud Ronn, Andy Waisburd, the seminar participantsat the 2004 Winter Finance Workshop, the 2004 European Meetings of the Financial Management Association, the2004 Meetings of the Financial Management Association, the University of Alabama, University of Connecticut, OhioUniversity, and the editor and referees for their helpful comments. We appreciate helpful discussions about corporateborrowing strategies and practices with Tom Hund, CFO, and Linda Hurt, Treasurer, of Burlington Northern Santa Fe.Professors Mann, Mihov, and Rodriguez acknowledge research funding from the Charles Tandy American EnterpriseCenter and the Luther King Capital Management Center for Financial Studies at Texas Christian University.

∗Christopher B. Barry is a Professor of Finance and the Robert and Maria Lowdon Chair in Business Administration,M.J. Neeley School of Business at Texas Christian University, Fort Worth, TX. Steven C. Mann and Vassil T. Mihov areAssociate Professors of Finance, M.J. Neeley School of Business at Texas Christian University, Fort Worth, TX. MauricioRodrı́guez is a Professor of Finance and Real Estate, M.J. Neeley School of Business at Texas Christian University, FortWorth, TX.

Financial Management • Autumn 2008 • pages 413 - 430

414 Financial Management • Autumn 2008

find that the amount of debt issued is substantially higher when interest rates are low relativeto historical levels. We also find that issuance depends not just on the absolute level of interestrates, but also on their recent history. Thus, not only the levels, but also the changes in the levelof interest rates, seem to affect managers’ issuance decisions.

When interest rates are low, there can also be greater incentives to issue equity or to increasethe level of capital expenditures. Therefore, we examine the ratio of debt issuance to the sumof debt and equity issuance, and the ratio of debt issuance to capital expenditures. Both ratiosincrease when interest rates are low relative to recent history.

Since refinancing is natural when interest rates fall and could account for the increased issuancewhen rates are low, we also examine the results after we account for refinancings. We find thatour conclusions continue to hold even when we exclude refinancings.

When we disaggregate the data, we find some evidence that firms with fewer financial con-straints exhibit more evidence of timing debt issues than do more constrained firms. Larger firmsappear to be more able or willing than smaller firms to issue when rates are relatively low. Thesame is true for firms with high, compared to low, free cash flow and for more profitable firmscompared to less profitable firms. Conversely, firms with higher capital expenditures are lesssensitive to the effect of historical rates than are firms with lower capital expenditures.

Managers appear to consider the history of recent interest rates when deciding to issue debt.Regardless of whether or not such considerations actually lower the cost of debt capital, which isa subject of an ongoing debate, they appear to affect corporate financial policy. This observationsuggests that they should be considered more prominently in capital structure investigations.

The paper proceeds as follows. Section I summarizes our data. Section II presents our empiricalresults, and Section III concludes the paper.

I. Data and Sample Characteristics

Our study period is January 1970 to April 2001. For this period we obtain data for new,nonconvertible, public debt issues from Thomson Financial’s Securities Depository Center (SDC)new issues database. There are 85,724 debt issues during this period. We obtain data on the issuedate, the identity, and characteristics of the borrower (such as industry and nationality); andvarious characteristics of the bond issue, such as proceeds in nominal dollars, maturity, yield tomaturity (YTM) at issuance, credit rating, whether the issue is floating or fixed rate, and whetherit is callable or puttable. We adjust the nominal proceeds with the monthly consumer price index(CPI) to obtain proceeds in constant dollars (measured as of January 1, 2001) so that we canmake valid comparisons of the quantities issued across time. We exclude issues by non-US firms,issues outside of the United States, issues by firms in Standard Industrial Classification (SIC)codes 6000-6999 (financial companies) or 9000-9999 (government-related), issues by nonprofitorganizations (such as churches or universities), and issues that are components of derivativeinstruments. Those screens reduce the number of issues with available issuance data to 14,623.

We also obtain study-period data for equity issues in the US public markets from the SDC. Weexclude initial public offers and then apply the same exclusion criteria as described above fordebt issues. After applying these screens, we have 10,209 equity issues.

In addition to data on new issues, we obtain interest rate, inflation, and interest rate spreaddata. We obtain time series of the monthly yields on Treasury and corporate bonds with variousmaturities and on inflation rates, measured from the CPI, from the Federal Reserve Bank of SaintLouis’s FRED database. These include the 90-day Treasury-bill yield (denoted as T-bill 90), the10-year constant maturity Treasury yield, and the Baa corporate yield. We measure the term

Barry, Mann, Mihov, & Rodrı́guez • Corporate Debt Issuance 415

spread as the difference between the 10-year constant maturity Treasury yield and the T-bill 90yield, and we measure the default spread as the difference between the Baa yield and the 10-yearconstant maturity Treasury yield.

We also obtain Compustat data for the issuers. We obtain firm Compustat data for 9,614 ofthe 14,623 issues, or approximately two-thirds of our issuance sample. For some of our tests, weobtain firm-level data on capital expenditures (Compustat data item 128). For each debt-issuingfirm, we aggregate the annual amount of debt issued (from the SDC) and scale it by annual capitalexpenditures. The number of observations in our firm-level tests varies due to the availability ofdifferent data items. We also collect data that characterize (in the aggregate) the stock market,such as the price-earnings ratio and market-to-book value ratio of the S&P 500 index (from CRSPand Compustat).

In Figure 1, Panel A shows the patterns of the SDC’s monthly debt issuance. Panel B shows theCompustat annual net debt issuance compared to mean monthly Baa yields. Compustat debt datainclude bank debt, which firms could use as a substitute for public debt. We calculate Compustatnet debt issues, which we obtain from the cash flow statement, as data item 111 (issuance oflong-term debt) minus data item 114 (reduction in long-term debt). We measure Compustat grossdebt issuance as data item 111. We use the CPI to convert the dollar amounts into January 2001dollars. For ease of comparison, we divide annual Compustat issuance by 12 to show the averagemonthly issuance. We exclude financial firms and foreign issuers on Compustat.

Both panels in Figure 1 show that debt issuance tends to increase when interest rates drop.When we compare the panels, Panel A shows considerable within-year variations in yields anddebt issuance, thus confirming the benefit of using monthly data to examine timing attempts.The correlation between the annualized SDC debt issuance and annual Compustat net (gross)debt issued is 35% (78%), and the correlation between the annualized SDC debt issuance and theannualized Baa yield series is –54%. In comparison, the correlation between the Baa yield andthe Compustat net (gross) issuance is –18% (–47%).

Table I provides stylized facts about debt issuance and shows yields on issued debt, Treasurybills, and 10-year Treasury securities over the sample period. Measured in January 2001 dollars,the total amount of debt issued in our sample is $2.60 trillion. The largest dollar amount of issuesin a single year is $182 billion in 1993, which coincides with the second largest number of issues(1,049). The year 1993 shows the lowest median level of short-term rates (measured by T-bill90s) and the fourth lowest median level of long-term rates (measured by 10-year Treasuries)across the 32 years of our sample. When we exclude 2001, for which we use only five months ofissuance data, the smallest annual amount raised ($28 billion) and fifth smallest number of issues(221) occur in 1983, when median short-term rates and long-term rates are at their sixth and fifthhighest levels, respectively, across the sample.

Table I shows the ratio of debt issued to the sum of debt and seasoned equity offerings (SEOs).The lowest mean and median values of the ratio occur in 1983, the year that also has the minimumamount of total debt issuance. The highest ratios occur in 1988 and 1989.

Table I also provides an overview of the fraction of issues that were callable or puttable acrosstime. As noted above, we do not report data on callable or puttable debt prior to 1976, since theSDC did not consistently report those features prior to 1976. Overall, about 42% of the issues werecallable. Callability was very common prior to the 1990s, and was used in an average of more than75% of all debt issues. Since 1990, the callability has averaged less than 25% of the debt issues.The year 1981 has the maximum callability level in our sample (88.5%), the same year for whichour data show the maximum yields on debt issues. This finding shows that when the cost of debtis highest, the greatest percentage of callable debt is issued. Callability provides companies withthe ability to reduce the effective maturity of their debt issues at the highest interest rate levels.

416 Financial Management • Autumn 2008

Figure 1. Monthly Debt Issuance Proceeds and Baa Yields: SDC Compared toCompustat

Panel A shows the monthly amounts issued (right axis) for a sample of 14,623 public debt issues by USnonfinancial firms from January 1970 through April 2001. Panel B shows average monthly net debt issueproceeds by US nonfinancial firms from January 1971 through December 2000. We measure dollar amountsin millions of constant (January 2001) dollars. The Baa yields are shown as lines. The proceeds are shownas bars.

Barry, Mann, Mihov, & Rodrı́guez • Corporate Debt Issuance 417T

able

I.C

har

acte

rist

ics

of

Deb

tIs

sues

Thi

sta

ble

repo

rts

the

annu

alch

arac

teri

stic

sof

asa

mpl

eof

14,6

23pu

blic

stra

ight

debt

issu

esan

d10

,209

seas

oned

equi

tyof

fers

(SE

Os)

byU

Sno

nfin

anci

alfi

rms

duri

ngJa

nuar

y19

70-A

pril

2001

repo

rted

byT

hom

son

Fina

ncia

l.A

mou

nts

are

inm

illi

ons

ofco

nsta

nt(J

anua

ry20

01)

doll

ars.

We

calc

ulat

ede

btas

apr

opor

tion

ofto

tali

ssue

sby

usin

gm

onth

lyde

btis

sue

amou

nts

divi

ded

byth

esu

mof

debt

issu

esan

dS

EO

s.“T

-bil

ls”

are

US

Tre

asur

ybi

lls.

Sin

ceth

eS

DC

does

notc

onsi

sten

tlyre

port

data

onca

llab

ilit

y,pu

ttab

ilit

y,an

dca

llan

dpu

tdat

esun

til1

976,

the

sam

ple

peri

odfo

rth

efr

acti

onof

call

able

issu

es,f

ract

ion

ofpu

ttab

leis

sues

,and

effe

ctiv

em

atur

ity

isJa

nuar

y19

76-A

pril

2001

.

Yea

rN

um

ber

Ave

rag

eA

vera

ge

Fra

ctio

nF

ract

ion

Ave

rag

eM

ean

Mea

n(M

edia

n)

of

Deb

tM

on

thly

(Med

ian

)R

atio

of

Issu

eso

fIs

sues

(Med

ian

)Y

ield

(Med

ian

)10

-Yea

rIs

sues

Am

ou

nt

of

Deb

tto

Th

atW

ere

Th

atW

ere

toM

atu

rity

Yie

ldo

f90

-T

reas

ury

of

SD

CT

ota

lMo

nth

lyC

alla

ble

Pu

ttab

leD

ayT

-bill

sC

on

stan

tD

ebt

Issu

eA

mo

un

tM

atu

rity

Rat

eIs

sued

(Deb

t+

SE

Os)

1970

408

86,0

2788

%(8

8%)

N/A

N/A

9.2

(9.1

)6.

39(6

.48)

7.35

(7.3

9)19

7137

375

,002

68%

(64%

)N

/AN

/A7.

9(7

.8)

4.33

(4.3

3)6.

16(6

.13)

1972

268

45,9

3158

%(5

7%)

N/A

N/A

7.5

(7.5

)4.

07(3

.95)

6.21

(6.1

6)19

7318

537

,997

70%

(69%

)N

/AN

/A8.

0(7

.9)

7.03

(7.2

1)6.

84(6

.77)

1974

291

71,3

7288

%(8

8%)

N/A

N/A

9.5

(9.4

)7.

83(7

.84)

7.56

(7.5

6)19

7539

885

,772

80%

(82%

)N

/AN

/A9.

7(9

.5)

5.78

(5.5

6)7.

99(8

.06)

1976

276

54,8

0372

%(7

2%)

0.73

80.

000

8.8

(8.7

)4.

97(4

.96)

7.61

(7.7

4)19

7725

941

,940

73%

(78%

)0.

765

0.00

48.

5(8

.4)

5.27

(5.1

1)7.

42(7

.40)

1978

211

31,7

9972

%(7

2%)

0.83

10.

005

9.7

(9.3

)7.

19(6

.87)

8.41

(8.4

2)19

7920

338

,415

75%

(75%

)0.

877

0.02

510

.8(1

0.5)

10.0

7(9

.50)

9.44

(9.1

5)19

8031

856

,341

65%

(69%

)0.

840

0.00

612

.8(1

2.5)

11.4

3(1

1.81

)11

.46

(11.

49)

1981

261

42,4

0965

%(6

5%)

0.88

50.

011

15.8

(15.

7)14

.03

(14.

72)

13.9

1(1

3.70

)19

8228

738

,715

58%

(61%

)0.

850

0.05

614

.5(1

4.7)

10.6

1(1

1.72

)13

.00

(13.

74)

1983

221

28,5

5039

%(3

6%)

0.82

80.

081

12.5

(12.

5)8.

61(8

.70)

11.1

1(1

1.12

)19

8421

639

,433

81%

(82%

)0.

704

0.09

313

.9(1

3.6)

9.52

(9.7

2)12

.44

(12.

42)

1985

386

65,4

5577

%(7

7%)

0.77

20.

044

12.2

(11.

8)7.

48(7

.20)

10.6

2(1

0.35

)19

8670

714

9,31

787

%(8

7%)

0.74

80.

038

9.9

(9.4

)5.

98(5

.95)

7.68

(7.4

4)19

8744

189

,786

87%

(90%

)0.

700

0.05

210

.4(9

.9)

5.78

(5.6

8)8.

38(8

.53)

1988

356

77,6

3892

%(9

3%)

0.80

10.

067

10.8

(10.

0)6.

67(6

.60)

8.85

(8.9

4)19

8934

076

,242

90%

(91%

)0.

644

0.15

910

.7(9

.9)

8.11

(8.0

3)8.

50(8

.24)

1990

293

52,1

6383

%(8

5%)

0.31

40.

041

9.8

(9.8

)7.

49(7

.63)

8.55

(8.5

4)

418 Financial Management • Autumn 2008

Tab

leI.

Ch

arac

teri

stic

so

fD

ebt

Issu

es(C

on

tin

ued

)

Yea

rN

um

ber

Ave

rag

eA

vera

ge

Fra

ctio

nF

ract

ion

Ave

rag

eM

ean

Mea

n(M

edia

n)

of

Deb

tM

on

thly

(Med

ian

)R

atio

of

Issu

eso

fIs

sues

(Med

ian

)Y

ield

(Med

ian

)10

-Yea

rIs

sues

Am

ou

nt

of

Deb

tto

Th

atW

ere

Th

atW

ere

toM

atu

rity

Yie

ldo

f90

-T

reas

ury

of

SD

CT

ota

lMo

nth

lyC

alla

ble

Pu

ttab

leD

ayT

-bill

sC

on

stan

tD

ebt

Issu

eA

mo

un

tM

atu

rity

Rat

eIs

sued

(Deb

t+

SE

Os)

1991

605

100,

033

76%

(75%

)0.

188

0.04

69.

0(9

.0)

5.38

(5.5

2)7.

86(7

.97)

1992

852

151,

290

83%

(83%

)0.

344

0.14

18.

3(8

.1)

3.43

(3.4

3)7.

01(6

.95)

1993

1,04

918

1,64

582

%(8

2%)

0.41

00.

189

7.5

(7.1

)3.

00(3

.01)

5.87

(5.8

9)19

9449

772

,288

74%

(77%

)0.

306

0.21

58.

4(8

.0)

4.25

(4.2

4)7.

08(7

.21)

1995

612

91,9

0968

%(7

0%)

0.19

60.

113

7.7

(7.3

)5.

49(5

.45)

6.58

(6.3

9)19

9673

910

5,41

269

%(6

7%)

0.16

50.

146

7.7

(7.2

)5.

01(5

.01)

6.44

(6.5

2)19

971,

003

110,

239

72%

(73%

)0.

062

0.07

77.

1(6

.9)

5.06

(5.0

5)6.

35(6

.36)

1998

1,15

216

9,73

680

%(7

9%)

0.13

10.

082

6.6

(6.5

)4.

78(4

.96)

5.26

(5.4

8)19

9968

014

6,68

766

%(6

9%)

0.12

80.

063

7.0

(6.9

)4.

64(4

.56)

5.64

(5.8

5)20

0051

812

6,39

762

%(6

6%)

0.25

70.

050

7.9

(7.8

)5.

82(5

.78)

6.03

(6.0

2)20

0121

864

,134

84%

(85%

)0.

349

0.04

16.

9(6

.8)

4.58

(4.6

5)5.

07(5

.12)

All

year

s14

,623

2,60

4,87

774

%(7

7%)

0.41

80.

087

9.0

(8.4

)6.

61(5

.81)

8.15

(7.5

7)

Barry, Mann, Mihov, & Rodrı́guez • Corporate Debt Issuance 419

We also examine the relation between call features and interest rate levels. The correlationsbetween callability and the yields on T-bills, 10-year Treasury bonds, and Baa debt are 61%,69%, and 68%, respectively. We also measure the correlation between the fraction of proceedsthat are callable and interest rate volatility, defined as the standard deviation of the yields onBaa-rated debt over 12, 36, and 60 months prior to issuance. The correlations are 40%, 57%,and 60%, respectively. In unreported multivariate analyses, we regress the fraction of proceedsthat are callable on interest rates, interest rate volatility, time dummies, and control variables. Wethen confirm the positive relation between callables and interest rates and rate volatility and thesecular trend toward a decline in callables.

About 8% of the overall debt issues include put provisions, and a similar percentage of issueshave floating rates (not reported). The period prior to 1989 shows very small percentages ofputtable debt issues. During the peak interest rate year (1981), just over 1% of debt issues includeput options. The year 1994 was a year in which the interest rates of debt issues were at aboutone-half the level for 1981. Thus, the 1994 issues have the maximum percentage of put options(21.5%). Despite the relatively low interest rates during the latter few years of our sample, theyears following 1994 show sharply lessened levels of put options.

II. Interest Rate Levels and Debt Issuance

Many factors affect the decisions by companies to issue new debt and the features they selectfor the debt.1 Graham and Harvey (2001) find that managers are interested in the current levelsof interest rates relative to historical rates. They describe the finding as follows: “We inquirewhether executives attempt to time interest rates by issuing debt when they feel that marketinterest rates are particularly low.” They provide “ . . . moderately strong evidence that firms tryto time the market in this sense.”2 We examine the extent to which debt issues are associatedwith the level of interest rates relative to historical levels, and we account for financing needsand capital expenditures. Graham and Harvey also find that “ . . . market timing is especiallyimportant for large firms,” an item that we examine in addition to other characteristics of issuingfirms. Bancel and Mittoo (2004) find similar results from their survey of European financialmanagers. Other studies that suggest timing considerations might affect debt decisions includeTaggart (1977), Marsh (1982), and Faulkender (2005).

A. Interest Rate Levels and Historical Rates

We construct two measures of historical interest rates. The first measure identifies the decileranking of current interest rates against rates over the previous 10 years. The first decile refersto rates that were below the 10th percentile of average monthly rates in the prior 10 years. Thesecond decile pertains to those rates from the 10th percentile to below the 20th percentile, andso on. Like Graham and Harvey (2001), we also refer to the rates as “low” if they are in one of

1Studies that examine factors related to decisions to issue debt include Fisher (1930), Myers (1977), Myers and Majluf(1984), Diamond (1991), Barclay and Smith (1995), Guedes and Opler (1996), Hoven and Mauer (1996), Jung, Kim, andStulz (1996), Houston and James (1996), Hovakimian, Opler, and Titman (2001), and Brounen, de Jong, and Koedijk(2004), among others.2John Graham explained in private communication with us on this topic that although CFOs in the Graham and Harvey(2001) survey were not explicit about what “particularly low” meant to them, it was his interpretation, based in part onhis conversations with the executives who responded to their survey, that they were referring to current interest ratescompared to their historical levels.

420 Financial Management • Autumn 2008

the bottom three deciles, as “high” if they are in one of the top three deciles, and “medium” forrates in the middle deciles. A given interest rate could be high or low relative to historical rates.For example, each of the 10-year constant maturity Treasury rates from 5% to 9% are relativelylow rates in some periods and relatively high rates in other periods. A manager who faces a 10%cost of new debt might be more willing to issue debt at that rate if it is among the lowest rates inrecent memory.

Our second method of accounting for historical rates is to use the lagged values of interestrates, in addition to their current value.

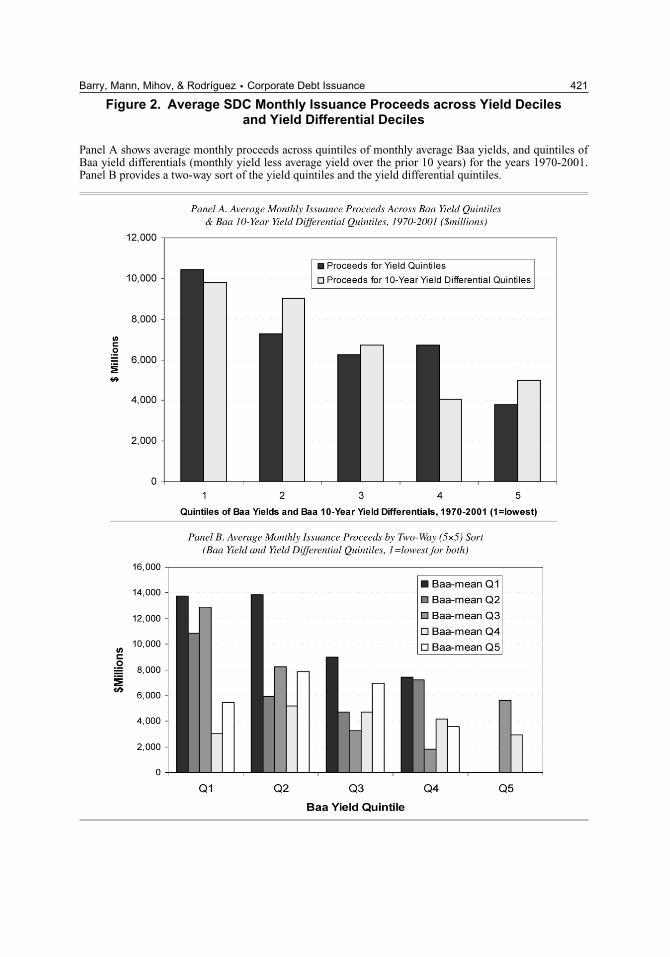

Figure 2 illustrates the point using quintiles of current interest rates relative to historical levels.3

Panel A shows the average monthly SDC debt issue proceeds across quintiles of monthly averageBaa yields. We define 1 as the lowest quintile and 5 as the highest. Clearly, more debt is issuedwhen yields are lower.

Panel A also shows the average monthly proceeds across yield differential quintiles. We identifyyield differential quintiles based on the difference between the current month’s Baa yield and theaverage yield over the prior 10 years. Thus, quintile 1 represents the lowest differential. Moredebt is issued when yields are low as well as when they are low compared to the average yieldover the prior 10 years.

Panel B of Figure 2 illustrates both the level effect (the raw yield level) and the change effect(the deviation from the past 10-year average) by using a two-way sort to compare the averagemonthly proceeds against the quintiles of monthly yields and yield differentials. For example,Panel B shows that the highest amount of debt issues occurs when yields are low and the 10-yearyield differentials are also low. Panel B shows that both the level of the yield and the 10-yearyield differential appear to affect issuance. Proceeds are generally highest in months in whichrates are lower than the prior 10-year average. Thus, Panel B demonstrates a tendency towarddebt issuance when interest rates are low relative to prior levels.

We note that several of the two-way sort categories have no observations. For example, thereare no months in which the yield is at the highest-level quintile and also at the lowest quintileof the 10-year yield differential. Similarly, there are no months with lowest-quintile yields buthighest-quintile 10-year yield differentials.

B. Debt Issuance, Interest Rates, Spreads, and Growth

Table II provides ordinary least squares (OLS) tests that incorporate a number of variables thatmight affect debt issuance. These variables include interest rates (either 10-year constant maturityTreasury rates or Baa rates), rate deciles (relative to historical rates), credit and term spreads,and price-earnings and market-to-book ratios, factors that indicate market growth. In half of theregressions, instead of interest rate deciles, we use five-year and 10-year lagged rates.

We are concerned that debt issuance might occur not because of low rates relative to historicallevels, but because of attractive credit spreads and term spreads. Thus, the regressions in Table IIincorporate such spreads. The term spreads, which we measure as the difference between 90-dayT-bills and 10-year Treasuries, are not significantly associated with debt issuance. Credit spreads,which we measure as the difference between the 10-year constant maturity Treasury rates andBaa rates, are significantly and positively associated with debt issuance. This finding indicateshigher credit spreads during periods of high issuance. The positive association is not consistentwith attempts to time the credit spread, but it is consistent with timing the level of rates. Unlessthe demand to purchase debt issues increases along with the increased supply of debt issues at low

3We thank an anonymous referee for suggesting the figure.

Barry, Mann, Mihov, & Rodrı́guez • Corporate Debt Issuance 421

Figure 2. Average SDC Monthly Issuance Proceeds across Yield Decilesand Yield Differential Deciles

Panel A shows average monthly proceeds across quintiles of monthly average Baa yields, and quintiles ofBaa yield differentials (monthly yield less average yield over the prior 10 years) for the years 1970-2001.Panel B provides a two-way sort of the yield quintiles and the yield differential quintiles.

422 Financial Management • Autumn 2008

Table II. Debt Issued across Relative Rates and Growth Measures

This table presents OLS tests of the monthly amount of debt issued (Panel A), the ratio of debt to secondaryequity offers (SEOs) (Panel B), and the firm-level ratio of the annual amount of debt issued to the annualcapital expenditures (Panel C) as a function of the historical distribution of interest rates, interest rate levels,and control variables. The sample consists of 14,623 public straight debt issues and 10,209 SEOs by USnonfinancial firms during 1970-2001. Amounts are in millions of constant (January 2001) dollars. Wemeasure all independent variables as of the month immediately preceding the month of issuance. Baa isthe Moody’s Seasoned Baa Corporate Bond Yield. The Baa decile is the decile rating of the rate at thetime of issuance among rates over the prior 10 years. We define term spread as the difference betweenthe 10-year Treasury constant maturity rate and the yield on 90-day T-bills. We define credit spread as thedifference between Baa and 10-year Treasury constant maturity rate. Parameter estimates show p-valuesin parentheses. In Panel C, for each firm-year, we calculate the annual amount of debt issued reported byThomson Financial. We then form the ratio of annual amount of debt issued to annual capital expenditures(Compustat item 128). We measure the independent variables as of the end of the year of issuance.

Panel A. Amount Issued per Month in 2001 Constant Dollars

Intercept 3,018.4∗∗ (0.033) 5,174.7∗∗∗ (0.000) −250.3 (0.854)Baa decile −360.9∗∗∗ (0.000) −411.0∗∗∗ (0.000)Level of Baa atissuance, %

−257.5∗∗ (0.014) −397.9∗∗∗ (0.000) −550.4∗∗∗ (0.000)

Credit spread 2,336.8∗∗∗ (0.000) 2,754.5∗∗∗ (0.000) 2,471.7∗∗∗ (0.000)Term spread −263.8∗ (0.057) −100.8 (0.497) −278.1∗∗ (0.040)S&P 500 P/E ratio 249.4∗∗∗ (0.000) 241.6∗∗∗ (0.000)S&P 500 market/book ratio 1,179.1∗∗∗ (0.000)Baa lagged 60 months 180.0∗∗ (0.018)Baa lagged 120 months 286.8∗∗∗ (0.000)Adjusted R2 0.48 0.464 0.497Number of observations 375 375 375

Panel B. Proportion of Debt Issued to Total Issues (Debt Plus SEOs)

Intercept 1.115∗∗∗ (0.000) 1.111∗∗∗ (0.000) 0.901∗∗∗ (0.000)Baa decile −0.017∗∗∗ (0.000) −0.018∗∗∗ (0.000)Level of Baa at issuance, % −0.018∗∗∗ (0.000) −0.017∗∗∗ (0.000) −0.030∗∗∗ (0.000)Credit spread 0.031∗ (0.071) 0.024 (0.126) 0.018 (0.280)Term spread −0.004 (0.568) −0.014∗∗ (0.027) −0.003 (0.619)S&P 500 P/E ratio −0.010∗∗∗ (0.000) −0.007∗∗∗ (0.000)S&P 500 market/book ratio −0.070∗∗∗ (0.000)Baa lagged60 months

0.021∗∗∗ (0.000)

Baa lagged120 months

0.003 (0.330)

Adjusted R2 0.114 0.137 0.179Number of observations 375 375 375

Barry, Mann, Mihov, & Rodrı́guez • Corporate Debt Issuance 423

Table II. Debt Issued across Relative Rates and Growth Measures (Continued)

Panel C. Firm-Level Ratio of Debt Issued Divided by Capital Expenditures

Intercept 3.610∗∗∗ (0.000) 3.234∗∗∗ (0.000) 1.149∗∗ (0.031)Baa decile −0.022∗∗∗ (0.000) −0.019∗∗∗ (0.000)Level of Baa atissuance, %

−0.037 (0.391) −0.012 (0.783) −0.156∗∗∗ (0.000)

Credit spread 0.173 (0.216) 0.004 (0.977) −0.251∗ (0.085)Term spread 0.068 (0.133) 0.036 (0.445) 0.127∗∗∗ (0.004)S&P 500 P/E ratio −0.057∗∗∗ (0.000) 0.018 (0.239)S&P 500market/book ratio

−0.245∗∗∗ (0.002)

Baa lagged60 months

0.258∗∗∗ (0.000)

Baa lagged120 months

−0.033 (0.277)

Adjusted R2 0.021 0.020 0.029Number ofobservations

4,314 4,314 4,314

∗∗∗Significant at the 0.01 level.∗∗Significant at the 0.05 level.∗Significant at the 0.10 level.

rates, then during periods of high supply relative to demand, the demand and supply interactionshould lead to lower relative bond prices and thus to higher credit spreads.

A second concern on the apparent relation between issuance and relative interest rates is thatlow relative interest rates might also reflect high contemporaneous levels of corporate growthexpectations. Such a result would be consistent with the neoclassical theory of investment, sinceincreased investment could be a natural part of the growth expectations. To account for thepossibility of such effects, in Table II we include two measures that characterize market-widegrowth expectations, the price-earnings (P/E) ratio, and the market price-to-book value ratio(M/B) for the S&P 500 index.

Even after we incorporate the spread and growth variables, the historical interest rate decilesremain highly significant. The highest levels of debt issuance occur when growth proxies are highand interest rates are historically low. The lowest levels of debt issuance occur when rates arehigh and expected growth is low. Therefore, the effects of relative interest rates on debt issuanceremain even after we account for the effect of expected overall economic growth.

Variation in rates affects issuance in an economically meaningful way. For example, Panel Aof Table I indicates that if the decile rank of the relative rate increases by 1, on average, issuancedecreases by $361 million in a month. For comparison, if the rate itself increases by 1%, theamount issued in a month decreases by $257 million.

In Table II, the panels extend the regressions to utilize historical rate lags instead of the decilesof current rates relative to historical rates. The five- and 10-year lagged rates are positive andsignificant in each regression. The current level of 10-year constant maturity Treasury rates andBaa rates at the time of issuance remain negative and significant. Therefore, whether we measureinterest rates as deciles relative to historical rates or whether we use lagged rates, we see that theysignificantly affect debt issuance.

424 Financial Management • Autumn 2008

In an untabulated analysis (available on request), we also investigate the horizon of relevant ratechanges. We do not have a strict theoretical justification for choosing the 10-year horizon overwhich we calculate the decile ranking of interest rates relative to past rates (our first measure).The relevant horizon should reflect the “memory” of the decision maker for the history of interestrates. For example, one proxy for the length of the decision maker’s “memory” could be the tenureof the CEO or the CFO. Therefore, we examine a model with the current Baa rate and its laggedvalue plus control variables, where the lags range from one year to 20 years. The lagged rate ispositive and significant as early as three years back and as far back as 19 years, with the adjustedR2 and the t-value of the lagged variable maximized at 11 years.

C. Debt Issuance as a Proportion of Total Issuance

An important question is whether the effect is a case of issuing debt to time the interest rates,or if it is a case of raising funds in general. For example, Burch, Christie, and Nanda (2004)specifically examine whether firms time equity offerings. In Panel B of Table II, we examine theissuance of debt and equity and calculate the ratio of debt issued to the sum of debt and equityissued. The equity issues are in the form of SEOs that, like public debt issues, are reported in theSDC. As noted earlier, during the period of our study we find more than 14,000 debt issues and10,000 equity issues. The question is whether the ratio of the amount of debt issued to the totalamount of debt and equity issued increases as interest rates become lower relative to historicallevels. If so, interest rates relative to historical rates do specifically affect debt issuance, not justtotal firm issuance of new funding.

The results in Panel B of Table II demonstrate significantly higher debt-to-total issuance as afunction of lower deciles of current rates relative to historical rates or higher lagged interest rates.The rate deciles remain highly significant, as do the five-year lagged rates, although the 10-yearlagged rates do not. The results hold whether we use 10-year Treasuries or Baa rates. The levelsof interest rates also continue to hold strongly.

Thus, even if more attractive economic conditions do attract equity issuance, the amount ofdebt issuance relative to the total of debt and equity issuance is still greater when interest ratesare lower relative to historical rates. These results remain consistent with the survey results inGraham and Harvey (2001).

D. Debt Timing and Capital Expenditures

When interest rates decline to relatively low levels, the net present value of some capitalinvestment projects may become positive because of the lower discount rate. Thus, what weobserve may not be debt timing per se, but the result of firms issuing debt because of increasedopportunities for capital spending.

We measure debt issuance relative to capital expenditures and examine the impact of changesin rates on this ratio. We obtain data on capital expenditures from Compustat (item 128). Foreach firm-year within our SDC sample for which the capital expenditure data are available fromCompustat, we calculate the annual amount of SDC debt issued and divide it by the annual amountof capital expenditures. We exclude the extreme top 1% of the observations, limiting the ratio toa range of 0 to 38.4. The resulting sample size is 4,313 firm-years. We then regress the ratio ofthe quantity of debt issued divided by capital expenditures of each of the issuing firms on theinterest rate level, interest rate deciles, or lagged interest rates, and control measures.

Panel C in Table II presents the results of regressions with a dependent variable equal tothe quantity of debt issued divided by capital expenditures of the issuing firms. The historicaldecile ranks of current interest rates are strongly associated with the ratio of debt issued to

Barry, Mann, Mihov, & Rodrı́guez • Corporate Debt Issuance 425

capital expenditures. The lagged historical rates with a five-year lag remain significant, and, asin Panel B, the 10-year lags are not significant. Unlike the previous tests, the current level ofinterest rates (as opposed to its historical decile) does not remain significant when we include thehistorical rate deciles, but they do remain significant when we use lagged historical rates instead.

The results of Panel C in Table II further illustrate that debt timing, based on the current ratesrelative to historical rates, remains significant and is not caused merely by the need for capitalexpenditures. This evidence of timing is a noteworthy result, since the neoclassical theory ofinvestment suggests increased capital expenditures when the cost of capital is low. Although in-creased expenditures do occur, they do not fully account for the quantity of debt issued. To accountfor the potential impact of interest rate persistence, we re-estimate the regressions in Table IIby using a first-order autoregressive error model. The autoregressive results produce lower re-gression R2 and lower t-values for the independent variables. However, the overall inferences onthe relation between issuance and historical rates are consistent with those we find when we useOLS, in that the coefficients and the significance of the relative rate variables remain qualitativelysimilar. For example, in the first model specification in Panel A of Table II, the coefficient on theBaa decile variable changes from –360.91, with a t-value of –5.30 and a p-value less than 0.0001,to –284.62 with a t-value of –2.89 and a p-value of 0.004. The R2 of the autoregressive model is0.56 (including the autoregressive term), and 0.29 for the original regressors, compared to 0.48in the original model. When we use second- or third-order autoregressive models, the variableremains significant and has a coefficient of similar magnitude.

E. Debt Timing, Refinancing, and Net Stock Issuance

The timing of debt issuance relative to historical rates can be influenced by the desire torefinance expensive existing debt. Therefore, we examine the robustness of the interest ratetiming results with respect to the use of the proceeds. We also study the effects of net stockrepurchases compared to net stock issuance, since repurchases could represent another type ofrefinancing. If firms issue new debt to retire expensive existing debt, then that decision mightbe driven entirely by the potential for reducing the cost of existing debt rather than for theissuance of further debt. Therefore, we divide our sample into subsets of firms that are net issuersof debt compared to firms that apparently use the proceeds to refinance existing debt. Sinceshare repurchases can also be a form of refinancing, we break the samples into those with debtrefinancing that do or do not make net share repurchases.

We calculate the net issuance of debt for each firm in each fiscal year as the difference betweenthe amount of debt issued (Compustat item 111) and the amount of debt retired (Compustatitem 114). We then divide firms into a net issuers subsample if the difference is positive, anda refinancing subsample if the difference is 0 or negative. We present our results in Panel A ofTable III.

Panel A of Table III documents the significant effects of relative interest rates in both therefinancing subsample and the net issuers subsample. Refinancing is strongly associated with therelative levels of interest rates compared to historical levels (measured, again, by low, medium,or high deciles). Nevertheless, even when there is no refinancing, there continues to be a sig-nificant association between debt issuance and the historical decile levels of current interestrates.

We further split the net issuers into firms that use some of the proceeds for refinancing andfirms whose net debt increases by more than the amount of the public debt issued, indicatingthat in addition to issuing public debt, those firms borrow from other sources. Once again,although it appears that there is more timing by the firms that use at least part of the proceeds for

426 Financial Management • Autumn 2008

Table III. Timing of Net Issues versus Refinancings

The table presents comparisons of the timing of net debt issues and debt refinancings. Panels A and B showthe monthly amount of debt issued across historical interest rate deciles and use of proceeds. The amountissued is in millions of constant (January 2001) dollars. “Low” indicates that the Baa rate falls into the lowestthree deciles of relative rates in the preceding 10 years. “Medium” indicates that the rate falls into decilesfour to seven. “High” indicates that the rate falls into the highest three deciles. We use Compustat data toclassify issues as debt refinancings if the net amount of debt by the firm for the fiscal year is negative, andotherwise classify issues as net debt issues. Among the net debt issues, we classify those cases in which thenet debt was lower than the annual amount issued as “some refinancing.” We use Compustat data to furtherclassify debt issues by net stock repurchasers if the net amount of stock issued by the firm for the fiscal yearis negative, and otherwise classify issues as net stock issuers. We present in parentheses t-statistics for thetest that the mean in category “Low” is equal to the mean in category “High.”

Panel A. Net Debt Issues Compared to Refinancings

Relative Category of the Baa Rate Debt Net Debt Issuers, Net DebtRefinancing Some Refinancing Issuers

Low 1,396.7 2,876.0 1,424.7Medium 504.2 1,654.5 1,245.2High 92.1 1,082.5 564.9t-test: Low compared to high (11.57)∗∗∗ (10.02)∗∗∗ (7.93)∗∗∗

Panel B. Net Debt and Stock Issues Compared to Refinancings

Relative Category Debt Net Debt Issuers, Net Debtof the Baa Rate Refinancing Some Refinancing Issuers

Negative Positive Negative Positive Negative PositiveStock Stock Stock Stock Stock Stock

Issuance Issuance Issuance Issuance Issuance Issuance

Low 848.7 418.1 1,542.6 1,098.43 734.6 519.1Medium 264.8 183.1 861.0 698.0 719.9 464.9High 38.2 48.4 320.3 733.7 175.1 380.3t-test: Low compared to high (10.83)∗∗∗ (7.87)∗∗∗ (12.76)∗∗∗ (3.41)∗∗∗ (7.80)∗∗∗ (2.51)∗∗

∗∗∗Significant at the 0.01 level.∗∗Significant at the 0.05 level.∗Significant at the 0.10 level.

refinancing, there continues to be significant timing by the firms that use all of their proceeds asnew financing. Therefore, consistent with the evidence discussed earlier, the results continue toshow that whether or not refinancing is a part of their debt issuance decision, managers tend toissue more debt when interest rates are at low levels relative to historical rates.

We also break each of the three debt samples into subsamples with positive or negative netstock issuance. We calculate the net issuance of common and preferred stock for each firm ineach fiscal year as the difference between the amount of stock issued (Compustat item 108) andthe amount of stock repurchased (Compustat item 115). The results from this further subsamplingare presented in Panel B of Table III. Our results for historically based debt timing remain robustacross the stock issuance categories. In all cases, the evidence supports the hypothesis that theamount of debt issuance depends on where interest rates are relative to historical levels.

We also perform multivariate regressions, using the same structure and the same explanatoryvariables as those reported in Table II. In these regressions we redefine the dependent variable

Barry, Mann, Mihov, & Rodrı́guez • Corporate Debt Issuance 427

to be the aggregate monthly ratio of net debt to the sum of net debt and equity issued. Thisspecification requires the assumption that annual net equity issuance and net debt issuance areevenly distributed across the months of the fiscal year. We define net long-term debt issuanceas the minimum of either the total annual SDC debt issues or the increase in (annually reported)Compustat debt, thus eliminating all potential refinancing from the sample. We allocate eachfirm’s net annual debt increase to months by using each firm’s monthly proportion of its annualissuance. We then allocate net equity issuance, which is available only annually, to months byassuming that the issuance of net equity during the year is on the same monthly schedule as debtissuance.

The untabulated results (available on request) strongly support the results in Table II. Whencurrent rates are low relative to historical rates, companies issue a significantly higher proportionof net debt compared to net equity. For example, for the specification that uses the level of the Baayield, the Baa decile, the credit spread, the term spread, and the S&P 500 P/E ratio as dependentvariables, the adjusted R2 is 0.074, and the coefficient on the Baa decile is –0.006 with a t-valueof 2.97, and a p-value of 0.003. The results are similar for the rest of the specifications.

F. Corporate Characteristics, Debt Issuance, and Interest Rates

Graham and Harvey (2001) report that managers of larger firms tend to attempt interest ratetiming more than do the managers of smaller firms. There can be other characteristics of firmsthat also influence the tendency to time debt issuance based on relative interest rates. For example,firms with greater financial flexibility may be better able to time their issuance than can firms thatare financially constrained, either due to lower cash flows or large investment intensity.

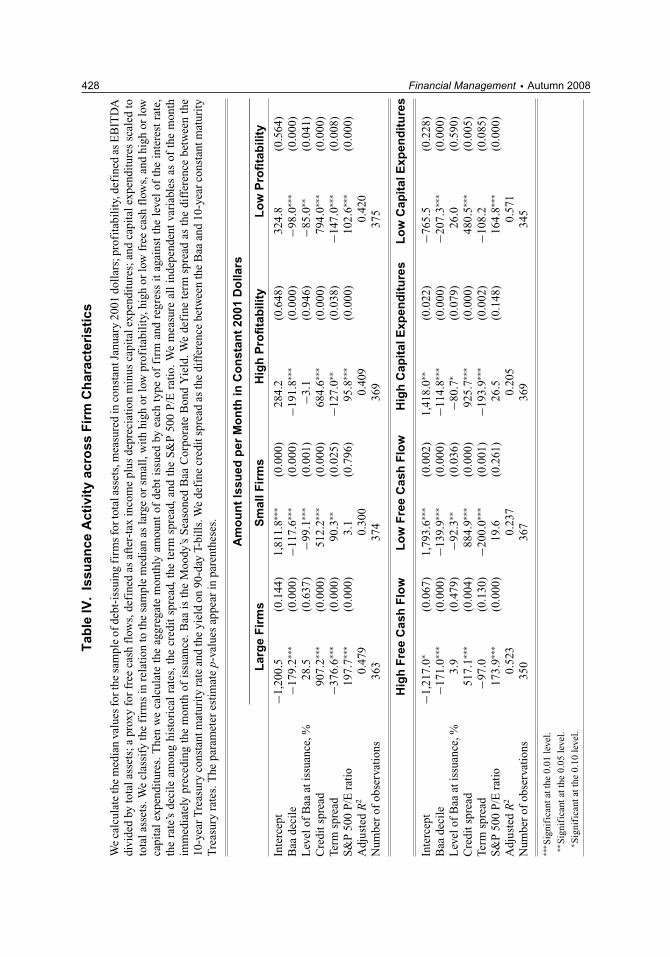

In Table IV we consider the effects of corporate profitability, the amount of free cash flow afterfunding investments (scaled by total assets), and the intensity of capital expenditures upon thetendency to issue debt. Table IV presents regression results based on the comparisons of largefirms compared to small firms, highly profitable firms compared to less profitable firms, firmswith high free cash flow compared to firms with low free cash flow, and firms with high capitalexpenditures compared to firms with low capital expenditures. In each of the paired subsamples,we break the samples into the upper and lower half of firms relative to the median of the variableof interest.

The results in Table IV show that for all the cases we examine, the level of interest ratesmeasured as deciles based on historical rates is consistently significant in determining debtissuance. Small firms and large firms both issue more debt when the rate decile is lower. The ratecoefficient is more negative for larger firms, indicating that larger firms are more able or willingto issue when rates are relatively low. Highly profitable firms and less profitable firms all issuemore debt when rates are historically lower, although, like the results for larger firms, the moreprofitable firms show stronger negative coefficients than do the less profitable firms. The samepattern holds for firms with high compared to low free cash flow. Conversely, firms with highercapital expenditures are less responsive to where interest rates are relative to historical rates thanare firms with lower capital expenditures.

We test for the differences in coefficients across firm types. We pool the subsamples to combinefirm types and add interactive variables consisting of each dependent variable multiplied by adummy variable for the firm type. We then examine the significance of the coefficients on theinteractive terms.

The coefficient for the large firm dummy (set equal to 1 for large firms) times the Baa decilevariable is –109.3 with a t-value of –2.64 and p-value of 0.009. Thus, issuance of debt by largefirms is more sensitive to the relative level of interest than is small firm issuance. The coefficient

428 Financial Management • Autumn 2008T

able

IV.

Issu

ance

Act

ivit

yac

ross

Fir

mC

har

acte

rist

ics

We

calc

ulat

eth

em

edia

nva

lues

fort

hesa

mpl

eof

debt

-iss

uing

firm

sfo

rtot

alas

sets

,mea

sure

din

cons

tant

Janu

ary

2001

doll

ars;

prof

itab

ilit

y,de

fine

das

EB

ITD

Adi

vide

dby

tota

lass

ets;

apr

oxy

for

free

cash

flow

s,de

fine

das

afte

r-ta

xin

com

epl

usde

prec

iati

onm

inus

capi

tale

xpen

ditu

res;

and

capi

tale

xpen

ditu

res

scal

edto

tota

lass

ets.

We

clas

sify

the

firm

sin

rela

tion

toth

esa

mpl

em

edia

nas

larg

eor

smal

l,w

ith

high

orlo

wpr

ofit

abil

ity,

high

orlo

wfr

eeca

shfl

ows,

and

high

orlo

wca

pita

lex

pend

itur

es.T

hen

we

calc

ulat

eth

eag

greg

ate

mon

thly

amou

ntof

debt

issu

edby

each

type

offi

rman

dre

gres

sit

agai

nst

the

leve

lof

the

inte

rest

rate

,th

era

te’s

deci

leam

ong

hist

oric

alra

tes,

the

cred

itsp

read

,th

ete

rmsp

read

,an

dth

eS

&P

500

P/E

rati

o.W

em

easu

real

lin

depe

nden

tva

riab

les

asof

the

mon

thim

med

iate

lypr

eced

ing

the

mon

thof

issu

ance

.Baa

isth

eM

oody

’sS

easo

ned

Baa

Cor

pora

teB

ond

Yie

ld.W

ede

fine

term

spre

adas

the

diff

eren

cebe

twee

nth

e10

-yea

rT

reas

ury

cons

tant

mat

urit

yra

tean

dth

eyi

eld

on90

-day

T-bi

lls.

We

defi

necr

edit

spre

adas

the

diff

eren

cebe

twee

nth

eB

aaan

d10

-yea

rco

nsta

ntm

atur

ity

Tre

asur

yra

tes.

The

para

met

eres

tim

ate

p-va

lues

appe

arin

pare

nthe

ses.

Am

ou

nt

Issu

edp

erM

on

thin

Co

nst

ant

2001

Do

llars

Lar

ge

Fir

ms

Sm

allF

irm

sH

igh

Pro

fita

bili

tyL

ow

Pro

fita

bili

ty

Inte

rcep

t−1

,200

.5(0

.144

)1,

811.

8∗∗∗

(0.0

00)

284.

2(0

.648

)32

4.8

(0.5

64)

Baa

deci

le−1

79.2

∗∗∗

(0.0

00)

−117

.6∗∗

∗(0

.000

)−1

91.8

∗∗∗

(0.0

00)

−98.

0∗∗∗

(0.0

00)

Lev

elof

Baa

atis

suan

ce,%

28.5

(0.6

37)

−99.

1∗∗∗

(0.0

01)

−3.1

(0.9

46)

−85.

0∗∗(0

.041

)C

redi

tspr

ead

907.

2∗∗∗

(0.0

00)

512.

2∗∗∗

(0.0

00)

684.

6∗∗∗

(0.0

00)

794.

0∗∗∗

(0.0

00)

Term

spre

ad−3

76.6

∗∗∗

(0.0

00)

90.3

∗∗(0

.025

)−1

27.0

∗∗(0

.038

)−1

47.0

∗∗∗

(0.0

08)

S&

P50

0P

/Era

tio

197.

7∗∗∗

(0.0

00)

3.1

(0.7

96)

95.8

∗∗∗

(0.0

00)

102.

6∗∗∗

(0.0

00)

Adj

uste

dR

20.

479

0.30

00.

409

0.42

0N

umbe

rof

obse

rvat

ions

363

374

369

375

Hig

hF

ree

Cas

hF

low

Lo

wF

ree

Cas

hF

low

Hig

hC

apit

alE

xpen

dit

ure

sL

ow

Cap

ital

Exp

end

itu

res

Inte

rcep

t−1

,217

.0∗

(0.0

67)

1,79

3.6∗∗

∗(0

.002

)1,

418.

0∗∗(0

.022

)−7

65.5

(0.2

28)

Baa

deci

le−1

71.0

∗∗∗

(0.0

00)

−139

.9∗∗

∗(0

.000

)−1

14.8

∗∗∗

(0.0

00)

−207

.3∗∗

∗(0

.000

)L

evel

ofB

aaat

issu

ance

,%3.

9(0

.479

)−9

2.3∗∗

(0.0

36)

−80.

7∗(0

.079

)26

.0(0

.590

)C

redi

tspr

ead

517.

1∗∗∗

(0.0

04)

884.

9∗∗∗

(0.0

00)

925.

7∗∗∗

(0.0

00)

480.

5∗∗∗

(0.0

05)

Term

spre

ad−9

7.0

(0.1

30)

−200

.0∗∗

∗(0

.001

)−1

93.9

∗∗∗

(0.0

02)

−108

.2(0

.085

)S

&P

500

P/E

rati

o17

3.9∗∗

∗(0

.000

)19

.6(0

.261

)26

.5(0

.148

)16

4.8∗∗

∗(0

.000

)A

djus

ted

R2

0.52

30.

237

0.20

50.

571

Num

ber

ofob

serv

atio

ns35

036

736

934

5

∗∗∗ S

igni

fica

ntat

the

0.01

leve

l.∗∗

Sig

nifi

cant

atth

e0.

05le

vel.

∗ Sig

nifi

cant

atth

e0.

10le

vel.

Barry, Mann, Mihov, & Rodrı́guez • Corporate Debt Issuance 429

for the more profitable firm dummy (set equal to 1 for more profitable firms) times the Baadecile variable is –94.5 with a t-value of –2.47 and p-value of 0.014. This result shows that moreprofitable firms exhibit more timing than do less profitable firms. The coefficient for the highercapital expenditure firm dummy (set equal to 1 for high capital expenditure firms) times the Baadecile variable is 124.3 with a t-value of 3.01 and a p-value of 0.003, showing that firms withhigher capital expenditures exhibit less timing than do firms with lower capital expenditures.Finally, the coefficient for the greater free cash flow firm dummy (set equal to 1 for high free cashflow firms) times the Baa decile variable is –75.3 with a t-value of 1.82 and a p-value of 0.069,showing that firms with higher free cash flow exhibit more timing than do firms with lower freecash flow. Thus, it appears that larger firms and firms with less financial constraints are morelikely to attempt to time debt markets.

III. Conclusion

We examine whether the timing of debt issuance is affected by the current level of interest ratesrelative to historical rates, after we have accounted for total financing and capital expenditures.While controlling for other factors that affect the issuance decision, we examine empiricallywhether corporate managers time the issuance of external debt with respect to interest rates. Wefind that debt issuance activity is very much affected by the level of interest rates relative tohistorical rates.

Our results on debt issuance are consistent with the survey results on debt timing in Grahamand Harvey (2001) and Bancel and Mittoo (2004). Like these two studies, our results indicatethat financial managers try to issue debt when rates are “particularly low” if the interpretation of“particularly low” is low relative to previous levels. We show that debt issuance, measured by totalamount issued and number of issues of new debt, relates to the relative level of interest rates incomparison to their historical values over the prior 10 years and/or by the lagged historical levels.Our evidence indicates that debt issuance as a proportion of total capital issuance (includingequity) reflects timing effects, and that debt issuance relative to capital expenditures also reflectstiming.

We find strong evidence that the amount of debt issued and the number of debt issues arerelated, both to the absolute level of interest rates and to their levels relative to historical rates.After controlling for other market conditions or corporate characteristics that can affect issuance,we find that the firms in our sample issue significantly higher amounts of long-term debt whenlong-term interest rates are low in either absolute or relative terms.

When interest rates decline, companies tend to refinance past debt that is eligible for refinanc-ing. Therefore, we also consider the effects of refinancing transactions on debt issuance related tolevels of interest rates. We find that refinancing is more common in our sample when interest ratesare at low levels relative to their history. Even when we focus on the non-refinancing transactions,we still find that debt issuance is significantly greater when relative interest rate levels are low.Thus, debt timing is not merely driven by refinancing.�

References

Bancel, F. and U. Mittoo, 2004, “Cross-Country Determinants of Capital Structure Choice: A Survey ofEuropean Firms,” Financial Management 33, 103-132.

430 Financial Management • Autumn 2008

Barclay, M. and C. Smith, 1995, “The Maturity Structure of Corporate Debt,” Journal of Finance 50,609-632.

Brounen, D., A. de Jong, and K. Koedijk, 2004, “Corporate Finance in Europe: Confronting Theory withPractice,” Financial Management 33, 71-101.

Burch, T., W. Christie, and V. Nanda, 2004, “Do Firms Time Equity Offerings? Evidence from the 1930sand 1940s,” Financial Management 33, 5-23.

Diamond, D. W., 1991, “Debt Maturity Structure and Liquidity Risk,” Quarterly Journal of Economics 33,341-368.

Faulkender, M., 2005, “Hedging or Market Timing? Selecting the Interest Rate Exposure of CorporateDebt,” Journal of Finance 60, 931-962.

Fisher, I., 1930, The Theory of Interest, as Determined by Impatience to Spend Income and Opportunity toInvest It, New York, NY, Macmillan.

Graham, J. and C. Harvey, 2001, “The Theory and Practice of Corporate Finance: Evidence from the Field,”Journal of Financial Economics 60, 187-243.

Guedes, J. and T. Opler, 1996, “The Determinants of Maturity of Corporate Debt Issues,” Journal of Finance51, 1809-1833.

Houston, J. and C. James, 1996, “Bank Information Monopolies and the Mix of Private and Public DebtClaims,” Journal of Finance 51, 1863-1889.

Hovakimian, A., T. Opler, and S. Titman, 2001, “The Debt-Equity Choice,” Journal of Financial andQuantitative Analysis 36, 1-24.

Hoven, S. M. and D. C. Mauer, 1996, “The Determinants of Corporate Debt Maturity Structure,” Journalof Business 69, 279-312.

Jung, K., Y. Kim, and R. M. Stulz, 1996, “Timing, Investment Opportunities, Managerial Discretion, andthe Securities Issue Decision,” Journal of Financial Economics 42, 159-185.

Marsh, P., 1982, “The Choice between Equity and Debt: An Empirical Study,” Journal of Finance 37,121-144.

Myers, S.C., 1977, “Determinants of Corporate Borrowing,” Journal of Financial Economics 5, 147-175.

Myers, S.C. and N.S. Majluf, 1984, “Corporate Financing and Investment Decisions When Firms HaveInformation That Investors Do Not Have,” Journal of Financial Economics 13, 187-221.

Taggart, R.A., Jr., 1977, “A Model of Corporate Financing Decisions,” Journal of Finance 32, 1467-1484.

Top Related

Copyright © 2022 FDOKUMEN