Bahasa

Halaman

Hukum

Research Analyst

Binod ModiContact: 022 4303 4626/9870009382Email: [email protected]

Research Associate:

Girija Shankar RayEmail : [email protected]

1. Cement industry added capacity to the tune of 19mnT in FY20 and despite current pandemic situation, the industry is set to add 25mnT cement capacity in FY21 and 51mnT in next three years.

2. Last two weeks of March are always crucial, as higher billing is done during this period, which was adversely affected by COVID-led nationwide lockdown. Resultantly, cement demand contracted by 1% in FY20.

3. Cement demand is expected to de-grow by 12% in FY21E and likely to rebound by 11.4% and 7.8% in FY22E and FY23E, respectively.

4. Incremental consumption is seen at 20mnT over FY20-FY23E from the base cement consumption of 329mnT in FY20, whereas incremental supply during the period is pegged at 51mnT.

5. Eastern region is expected to add the highest 21mnT capacity (43% of total) followed by 11.5mnT in Western region (23% of total) and 10.5mnT in Central region, while Northern and Southern regions are expected to witness minimal capacity addition (4mnT each).

6. Lower fuel prices are likely to aid the industry to withstand the adverse impact of lower utilization in near-to-medium-term.

7. Strong pricing scenario across regions is likely to aid the companies to report healthy unitary operating performance in 1HFY21E.

8. New capacity addition is not expected to witness very high growth in next decade unlike last decade owing to limited resources. Hence, the demand growth should outpace supply growth in the next decade, in our view.

Outlook & Valuation

Prolonged slowdown in construction activities due to COVID-led disruptions significantly

impacted the cement demand, which is expected to see recovery only in 2HFY21 led by strong

rural demand and pick-up in infrastructure activities. Unlike pre-COVID, net incremental supply

is expected to be 31mnT in next three years. However, we expect the scenario to improve

substantially from FY22E onwards led by revival in demand scenario. Further, the industry is

likely to add only 24mnT of clinker capacity in next three years and thereafter, there is hardly any

capacity addition plan as of now, which bodes well for the cement industry and indicates that

supply glut is likely to wane, going forward. We continue to prefer Northern and Central region

among others due to favourable demand supply situation. We maintain UltraTech as our Top

Pick in large-cap space, while JK Cement, JK Lakshmi Cement, HeidelbergCement India

are our Top Picks in mid-cap space. We prefer Somany Ceramics in tiles Building Materials

space.

Coverage Summary

Company Rating CMP 2 yr %

(Rs) TP (Rs) chg

ACC Ltd BUY 1,388 1,718 24%

Ambuja Cements BUY 219 252 15%

UltraTech Cement BUY 4,035 4,825 20%

Shree Cement BUY 21,513 24,053 12%

Ramco Cements BUY 670 802 20%

India Cements SELL 115 81 -30%

J.K. Cement BUY 1,500 1,711 14%

JK Lakshmi BUY 270 401 49%

Mangalam Cement BUY 197 295 50%

HeidelbergCement BUY 193 226 17%

Sagar Cement BUY 471 619 31%

Kajaria Ceramics SELL 408 384 -6%

Somany Ceramics BUY 133 173 30%

Price Performance

Mkt. Cap. Absolute

Perfromance

Company (Rsbn) 1 M 3 M 12 M

ACC 261 6.6 22.1 (13.0)

Ambuja Cements 435 14.7 28.2 3.2

UltraTech Cement 1,165 5.1 21.2 (4.7)

Shree Cement 776 (1.3) 18.2 10.2

Ramco Cements 158 4.3 26.3 (7.0)

India Cements 36 (1.9) (3.1) 45.8

J.K. Cement 116 8.2 38.3 48.8

JK Lakshmi 32 (3.7) 43.3 (17.0)

Mangalam Cement 5 (1.1) 28.4 (20.3)

HeidelbergCement 44 11.2 31.0 (3.1)

Sagar Cement 10 19.0 68.7 (19.1)

Kajaria Ceramics 65 3.1 34.1 (16.4)

Somany Ceramics 6 17.8 51.7 (55.2)

Key Sectoral Updates:Cement industry to add 51mmT capacity over three yearsCement demand to contract by 12% in FY21E and to grow by 11% in FY22E and 8.5% in FY23ENorthern and Southern regions to witness minimal cement capacity additionCement prices unlikely to see sharp up-tick hereon Cost deflation to offer cushion in case of low utilization Building materials (tiles) segments unlikely to see recovery in medium-term

Click Image for Video Presentation

Cement & Building Materials Sector Update | 18 Aug 2020Institutional Equity Research

Growth Prospects Remain Bright despite Near-term Disruptions

We request for your valuable vote and support

We have made changes to our Recommendation and Target Price. Please refer to Page no. 123 at the end of the report.

Table of Contents

Content Page No.

Executive Summary 1-3

f Channel Check ........................................................................................................................................ 3

f Region-wise Demand Scenario Post COVID-led Lockdown............................................................... 4

f Investment Matrix .................................................................................................................................. 5

f Companies Comparative Analysis ....................................................................................................... 6-7

f Key Charts ............................................................................................................................................... 8

f Change in Ratings & Estimates ............................................................................................................ 9-10

f Key Sectoral Takeaways ........................................................................................................................ 11-14

f Annexure Table ...................................................................................................................................... 15

Company Section 13-79

UltraTech Cement .......................................................................................................................................... 17-24

ACC ................................................................................................................................................................. 25-32

Ambuja Cements .......................................................................................................................................... 33-40

Shree Cement ................................................................................................................................................ 41-48

Ramco Cements ............................................................................................................................................ 49-56

Indian Cements ............................................................................................................................................. 57-64

JK Cement ...................................................................................................................................................... 65-72

JK Lakshmi Cement ....................................................................................................................................... 73-80

HeidelbergCement India .............................................................................................................................. 81-88

Mangalam Cement ....................................................................................................................................... 89-96

Sagar Cement ............................................................................................................................................... 97-104

Kajaria Ceramics ........................................................................................................................................... 105-113

Somany Ceramics ......................................................................................................................................... 114-122

3

Channel Check

f Having seen continued improvement in demand on month-on-month (MoM) basis

in May and June owing to pent-up demand and strong rural traction, the demand

momentum softened in most part of the country in July.

f Notably, demand continued to remain steady in most rural pockets. However, demand

was significantly impacted in urban and semi urban markets due to local lockdown.

Further, workforce availability issues continued to remain a concern despite the

labourers started coming back to several sites. Overall demand still remains at ~60-70%

of normal level. However, non-trade demand continued to suffer with no meaningful

improvement, which resulted in steep price contraction in non-trade segment in Jun’20

and July’20.

f On positive side, the urban demand is expected to recover from current month onwards,

as several real estate developers are trying to finish their near-completion projects,

which were stuck due to COVID-19 pandemic. Further, demand from rural segment is

expected to sustain even in coming months.

f Notably, all Infrastructure projects restarted as of now, but acute shortage of labourers

is impacting the pace of execution. We further note that a large number of infrastructure

projects are seeing just 40-50% of workforce as of now due to exodus of migrant

labourers, who will come back only after monsoon. Hence, the project segment

demand is likely to remain subdued even in 2QFY21.

f With limited availability of drivers/labourers and complete lockdown (shutdown) in

various districts, most cement companies started working on daily plan from logistic

aspects, despite it being an expensive proposition.

f Cement consumption in cities and metros was impacted adversely due to continued

shortage of labourers and its only rural segment demand, which was main demand

driver in 1QFY21.

f Direct transfer of money under Mahatma Gandhi National Rural Employment Guarantee

Act (MGNREGA) and better Rabi yield ensured decent surplus in the hands of rural

population, which is supporting rural economy. Hence, rural demand is expected to

sustain at least for some period of time.

f While proliferation of Work from Home (WFH) trend is a threat for commercial real estate

segment, it can potentially generate better-than-estimated sales volume in residential

space (especially in affordable housing segment), which is likely to arrest any potential

decline in cement demand. As per industry’s sources, urban real estate demand in

India was hovering in the range of ~35-40mnT during pre-COVID. Further, government’s

Pradhan Mantri Awas Yojana (Urban) is expected to get continuous traction, going

ahead.

f Sustainability of steady pricing environment depends upon the demand recovery. In

case, the demand fails to recover, the prices are unlikely to remain at the current levels.

4

Region-wise Demand Scenario Post COVID-led Lockdown

Northern Southern f Pre Unlock 1.0: After allowing the non-essential manufacturing

units to operate from 20th April, the cement industry witnessed very slow progress for want of approval from the local authorities to resume operations at plants. However, demand witnessed recovery in May led by pent-up demand. Non-trade sales, which essentially account for >40%, were significantly impacted due to exodus to migrant labourers from the key states like Delhi, Punjab and Rajasthan.

f Post Unlock 1.0: Demand momentum improved further starting from 1st June mainly supported by increasing movement of inter-state road transport and revival in rural trade demand. Capacity utilization of cement companies reached 60-70% levels in June, which albeit tapered down marginally in July due to monsoon.

f Pre Unlock 1.0: The region, which was already struggling before COVID-19 outbreak, got further hit after lockdown. However, since the beginning of May, the region witnessed decent up-tick in sales volume mainly due to pent-up demand. However, the region witnessed average price improvement to the tune of ~Rs60-70/bag from 20th April to 31st May with which the prices in most pockets surpassed Rs400/bag mark.

f Post Unlock 1.0: Demand scenario improved significantly in June’20 especially in non-metro areas mainly led by sharp up-tick in sales volume for state governments’ funded projects in Andhra Pradesh (AP) and Telangana. Sales volume for select companies reached close to year-ago levels. However, continued lockdown in key cities like Hyderabad, Chennai and Bangalore are still impacting the urban demand. Despite marginal correction, the prices continued to remain steady.

Western Eastern f Pre Unlock 1.0: Demand, which was significantly impacted in

April, witnessed moderate improvement in May. Region witnessed maximum impact of exodus of migrant labourers. A large number of infrastructure projects came to grinding halt with just 10-15% kind of workforce availability in May. As non-trade segment accounts for a large part of cement consumption in the region, it was impacted the most compared to other regions.

f Post Unlock 1.0: While the demand momentum improved on month-on-month comparison in June, shortage of labourers remained a key concern for most projects. Infrastructure projects in cities like Mumbai, Pune and Ahmedabad etc. continued to see just 30-40% workforce availability in June, and the situation worsened in July with heavy downpour. Further, sharp surge in new COVID cases in Maharashtra and lockdown/shutdown imposed by various local authorities also took a toll on demand.

f Pre Unlock 1.0: Demand witnessed a sharp up-tick in May mainly led by pent-up demand and strong recovery in rural segment. The demand in the region is dominated by trade segment. Further, unlike other regions, intensification of COVID-19 was relatively slower in the region, as barring few pockets of West Bengal, most other pockets was under non-containment zone, which also aided the consumption.

f Post Unlock 1.0: Demand continued to remain decent in June, while it got impacted in July due to flood situation in Bihar and other parts of the region. Further, improving cash flows in the hand of farmer and rural population and migrant labourers coming back to their native places resulted in construction/extension of houses, which also aided the demand. Demand in the region is expected to remain firm in ensuing months as well.

Central f Pre Unlock 1.0: Demand in the region has consistently been favourable for last three years. COVID-led lockdown was a temporary blip in

April. However, it improved moderately in May’20 mainly led by pre-monsoon trade demand especially from villages. Further, favourable monsoon, bumper Rabi yields and various government programme to support rural economy led to improvement in rural demand.

f Post Unlock 1.0: Demand in June improved further with the commencement of a number of infrastructure projects. Despite seeing higher COVID cases in select pockets, demand in Uttar Pradesh improved significantly on month-on-month basis in June. However, the demand in Madhya Pradesh is primarily getting support from the rural markets. Notably, the prices continued to remain firm in the region.

5

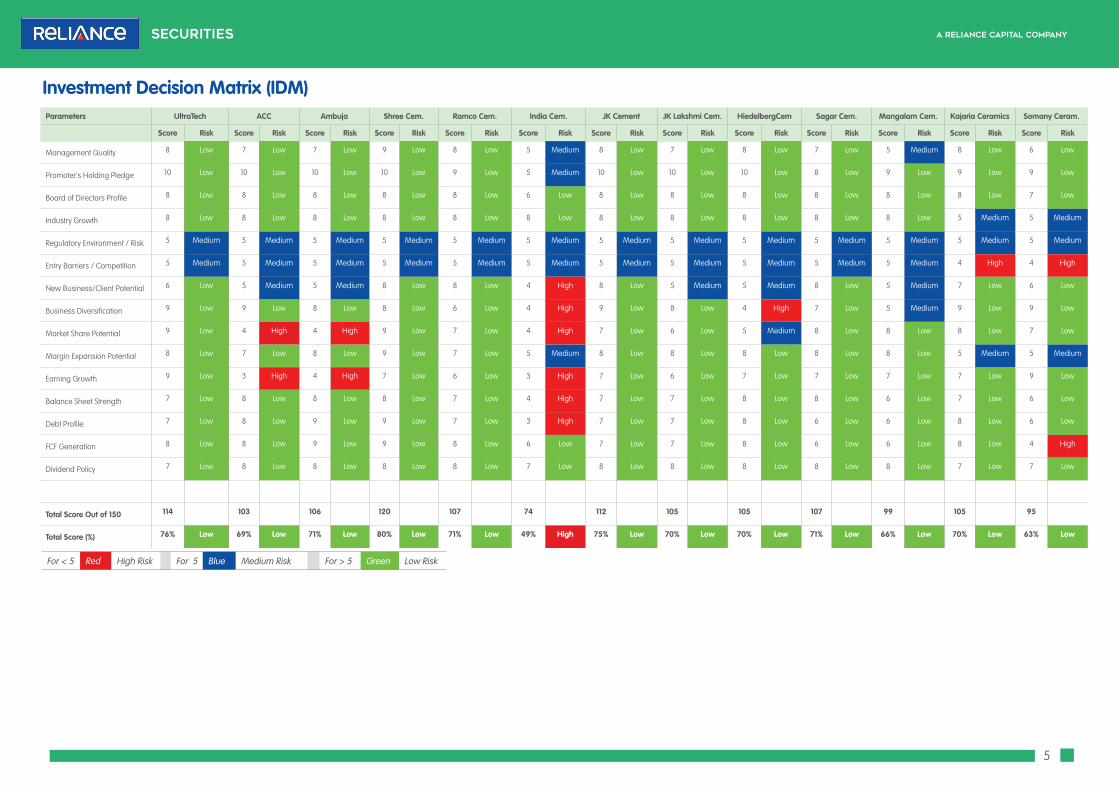

Parameters UltraTech ACC Ambuja Shree Cem. Ramco Cem. India Cem. JK Cement JK Lakshmi Cem. HiedelbergCem Sagar Cem. Mangalam Cem. Kajaria Ceramics Somany Ceram.

Score Risk Score Risk Score Risk Score Risk Score Risk Score Risk Score Risk Score Risk Score Risk Score Risk Score Risk Score Risk Score Risk

Management Quality 8 Low 7 Low 7 Low 9 Low 8 Low 5 Medium 8 Low 7 Low 8 Low 7 Low 5 Medium 8 Low 6 Low

Promoter's Holding Pledge 10 Low 10 Low 10 Low 10 Low 9 Low 5 Medium 10 Low 10 Low 10 Low 8 Low 9 Low 9 Low 9 Low

Board of Directors Profile 8 Low 8 Low 8 Low 8 Low 8 Low 6 Low 8 Low 8 Low 8 Low 8 Low 8 Low 8 Low 7 Low

Industry Growth 8 Low 8 Low 8 Low 8 Low 8 Low 8 Low 8 Low 8 Low 8 Low 8 Low 8 Low 5 Medium 5 Medium

Regulatory Environment / Risk 5 Medium 5 Medium 5 Medium 5 Medium 5 Medium 5 Medium 5 Medium 5 Medium 5 Medium 5 Medium 5 Medium 5 Medium 5 Medium

Entry Barriers / Competition 5 Medium 5 Medium 5 Medium 5 Medium 5 Medium 5 Medium 5 Medium 5 Medium 5 Medium 5 Medium 5 Medium 4 High 4 High

New Business/Client Potential 6 Low 5 Medium 5 Medium 8 Low 8 Low 4 High 8 Low 5 Medium 5 Medium 8 Low 5 Medium 7 Low 6 Low

Business Diversification 9 Low 9 Low 8 Low 8 Low 6 Low 4 High 9 Low 8 Low 4 High 7 Low 5 Medium 9 Low 9 Low

Market Share Potential 9 Low 4 High 4 High 9 Low 7 Low 4 High 7 Low 6 Low 5 Medium 8 Low 8 Low 8 Low 7 Low

Margin Expansion Potential 8 Low 7 Low 8 Low 9 Low 7 Low 5 Medium 8 Low 8 Low 8 Low 8 Low 8 Low 5 Medium 5 Medium

Earning Growth 9 Low 3 High 4 High 7 Low 6 Low 3 High 7 Low 6 Low 7 Low 7 Low 7 Low 7 Low 9 Low

Balance Sheet Strength 7 Low 8 Low 8 Low 8 Low 7 Low 4 High 7 Low 7 Low 8 Low 8 Low 6 Low 7 Low 6 Low

Debt Profile 7 Low 8 Low 9 Low 9 Low 7 Low 3 High 7 Low 7 Low 8 Low 6 Low 6 Low 8 Low 6 Low

FCF Generation 8 Low 8 Low 9 Low 9 Low 8 Low 6 Low 7 Low 7 Low 8 Low 6 Low 6 Low 8 Low 4 High

Dividend Policy 7 Low 8 Low 8 Low 8 Low 8 Low 7 Low 8 Low 8 Low 8 Low 8 Low 8 Low 7 Low 7 Low

Total Score Out of 150 114 103 106 120 107 74 112 105 105 107 99 105 95

Total Score (%) 76% Low 69% Low 71% Low 80% Low 71% Low 49% High 75% Low 70% Low 70% Low 71% Low 66% Low 70% Low 63% Low

For < 5 Red High Risk For 5 Blue Medium Risk For > 5 Green Low Risk

Investment Decision Matrix (IDM)

6

Parameters Large Cap Cement Companies Key Mid Cap Cement Companies

UltraTech Shree Cement ACC Ambuja Ramco JK Lakshmi JK Cement Heidelberg

Cement Capacity (mnT in FY20) 114.8 44.4 33.1 29.7 19.7 13.2 14.0 6.3

Captive Power (CPP)- MW 934 742 359 417 157 102 126 12

Regional Presence (%)

North 21% 55% 18% 33% 59% 68%

South 18% 7% 30% 84% 21% 9%

East 14% 25% 26% 23% 16% 27%

West 24% 12% 38% 14%

Central 20% 5% 14% 6% 11% 91%

Overseas 3% 9.0%

Capacity Addition in Last Five Years (mnT) 52.3 20.8 2.0 0.9 3.0 4.7 6.5 1.0

Capacity Addition in Next Three Years (mnT) 5.4 6.0 5.9 3.6 3.1 0.0 0.7 0.0

Capacity Utilisation in FY20 73% 62% 87% 81% 57% 86% 61% 75%

Volume CAGR in Last Five Years 12% 9% 4% 2% 7% 9% 6% 2%

FY20 Key Financials (Rs mn)

Volume (mnT) 82.3 24.9 28.9 24.0 11.2 9.2 9.8 4.7

Revenue 4,21,248 1,19,301 1,53,431 1,13,530 52,854 40,435 54,040 21,576

EBITDA 92,836 36,745 20,959 18,340 10,536 6,724 11,217 5,158

EBITDA/tonne (Rs) 1,128 1,446 672 765 940 725 1,146 1,096

APAT 36,985 15,702 13,589 14,255 6,011 2,552 4,004 2,681

Net Debt 1,80,760 30,360 -45,381 -46,584 29,327 10,016 19,889 -907

Free Cash Flow (FCF) -32,481 24,530 17,549 14,994 -11,800 4,489 -746 4,152

OCF Yield (%) 7.4% 4.9% 8.3% 5.9% 4.5% 15.3% 8.0% 10.9%

EV/tonne (US$) 163 254 92 122 131 57 116 88

EV/EBITDA (x) 14.8 21.0 10.8 13.7 18.4 6.7 12.0 8.0

RoCE (%) 10.2% 13.4% 18.1% 9.4% 12.2% 17.5% 16.6% 27.9%

RoE (%) 11.9% 13.9% 12.3% 7.1% 12.8% 14.5% 13.3% 21.6%Source: Company; RSec Research

Companies Comparative Analysis

7

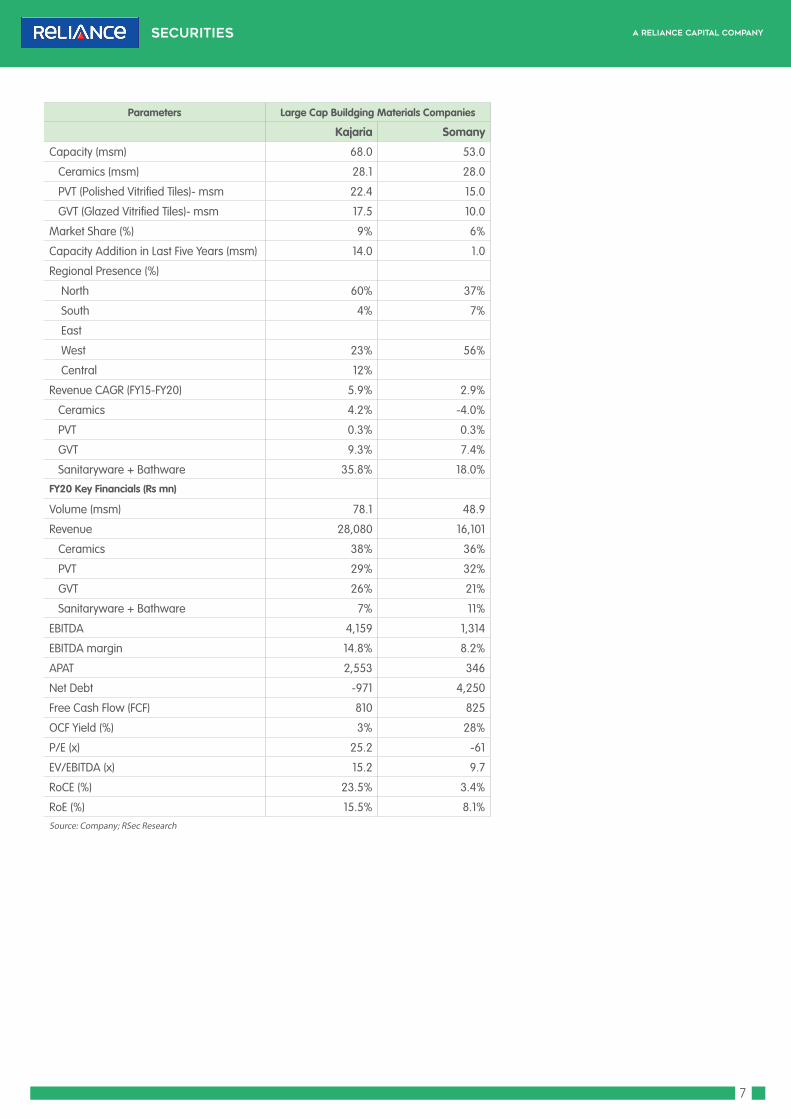

Parameters Large Cap Buildging Materials Companies

Kajaria Somany

Capacity (msm) 68.0 53.0

Ceramics (msm) 28.1 28.0

PVT (Polished Vitrified Tiles)- msm 22.4 15.0

GVT (Glazed Vitrified Tiles)- msm 17.5 10.0

Market Share (%) 9% 6%

Capacity Addition in Last Five Years (msm) 14.0 1.0

Regional Presence (%)

North 60% 37%

South 4% 7%

East

West 23% 56%

Central 12%

Revenue CAGR (FY15-FY20) 5.9% 2.9%

Ceramics 4.2% -4.0%

PVT 0.3% 0.3%

GVT 9.3% 7.4%

Sanitaryware + Bathware 35.8% 18.0%

FY20 Key Financials (Rs mn)

Volume (msm) 78.1 48.9

Revenue 28,080 16,101

Ceramics 38% 36%

PVT 29% 32%

GVT 26% 21%

Sanitaryware + Bathware 7% 11%

EBITDA 4,159 1,314

EBITDA margin 14.8% 8.2%

APAT 2,553 346

Net Debt -971 4,250

Free Cash Flow (FCF) 810 825

OCF Yield (%) 3% 28%

P/E (x) 25.2 -61

EV/EBITDA (x) 15.2 9.7

RoCE (%) 23.5% 3.4%

RoE (%) 15.5% 8.1%Source: Company; RSec Research

8

Sector At a Glance

Key Charts

Exhibit 1: Cement Capacity Over the Years

Source: Industry; RSec Research

Exhibit 2: Capacity Addition

Source: Industry; RSec Research

Exhibit 3: Cement Demand Over the Years

Source: Industry; RSec Research

f Cement capacity, which witnessed over 7% CAGR in last 10 years, is likley to register only 3.4% CAGR over next three years. Hence, demand growth is likley to outpace supply growth in the long-run.

f Industry added 243mnT in last ten years with an annual supply rate of 24mnT.

f Industry would be adding 51mnT in next three years with an annual supply of 17mnT.

f Industry demand has clocked ~5% CAGR over last ten years and we expect this to clock over next three years.

f Industry is likley to see demand contraction of 12% in FY21E due to COVID-led disruption. However, demand is likely to register 9.6% CAGR over FY21E-FY23E.

f Eastern region is expected to see maximum capacity addtion in next three years followed by the Western region.

f Northern and Southern regions are likely to see least capacity addtion over next three years, which offer an edge to these regions.

243281

314341

369408 429 443 455 467 486

511 531 538

0

100

200

300

400

500

600

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

FY21

E

FY22

E

FY23

E

Cement Capacity

206 216 230247 256 271 283 280

298

337 334

293327

352

0

50

100

150

200

250

300

350

400

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

FY21

E

FY22

E

FY23

E

Cement Demand

Exhibit 4: Region-wise capacity addition in next three years

mnT FY21E FY22E FY23E Total

North 1.8 2.0 0.0 3.8

South 1.0 1.8 1.5 4.3

West 5.7 3.9 2.0 11.6

Central 3.5 5.8 1.2 10.5

East 12.0 7.2 2.0 21.2

Total Addition 24.0 20.7 6.7 51.4

Source: Industry; RSec Research

3638

33

27 28

39

21

1511 13

19

2421

7

0

5

10

15

20

25

30

35

40

45FY

10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

FY21

E

FY22

E

FY23

E

New Capaity Addition

9

Change in Ratings & Estimates

We continue to maintain our long-term positive stance on the sector mainly on following grounds.

f New capacity addition is not expected to witness very high growth unlike last ten years here on owing to limited resources. Hence, the demand growth should outpace supply growth in the next decade, in our view.

f A significant Rs102trilliion investment in infrastructure development in next five years under National Infrastructure Pipeline (NIP) is likely to aid cement consumption in ensuing quarters.

f Steady pricing environment is expected to sustain with possibility of demand recovery.

f Continued traction in rural economy augurs well for the cement industry.

f Cost deflation pertaining to benign fuel prices is likely to remain a key tailwind for the sector.

We believe the companies, which are more exposed to Northern and Central regions, are likely to do relatively better due to strong demand supply equilibrium.

Exhibit 5: Change in TP & Rating

Old 1-Yr TP New 2-Yr TP Old Rating New Rating

ACC Ltd 1,310 1,718 BUY BUY

Ambuja Cements 210 252 BUY BUY

UltraTech Cement 4,400 4,825 BUY BUY

Shree Cement 24,050 24,053 BUY BUY

Ramco Cements 600 802 BUY BUY

India Cements 70 81 SELL SELL

J.K. Cement 1,320 1,711 BUY BUY

JK Lakshmi 380 401 BUY BUY

Mangalam Cement 270 295 BUY BUY

HeidelbergCement India 210 226 BUY BUY

Sagar Cement 350 619 BUY BUY

Kajaria Ceramics 400 370 HOLD SELL

Somany Ceramics 180 173 BUY BUYSource: RSec Research ; Note: RSec Research has migrated from one year based Target Price to two years based

Target Price

Exhibit 6: Valuation Table

CMP Reco. Target Price M.Cap EV/tone (US$) EV/EBIDTA (x) RoE (%)

(Rs) (Rs) (Rs bn) FY22E FY23E FY22E FY23E FY22E FY23E

ACC Ltd 1,388 BUY 1,718 261 71 66 10.4 8.7 10 10.1

Ambuja Cements 219 BUY 252 435 97 93 11.8 10.5 6.8 6.9

UltraTech Cement 4,035 BUY 4,825 1,165 142 135 12.6 10.9 12.1 13

Shree Cement 21,513 BUY 24,053 776 210 202 17.6 14.9 13.6 15.3

Ramco Cements 670 BUY 802 158 108 102 13.1 10.9 14.4 15.3

India Cements 115 SELL 81 36 56 53 9.4 7.8 1.9 4.6

J.K. Cement 1,500 BUY 1,711 116 104 98 10 8.1 17.1 18.2

JK Lakshmi 270 BUY 401 32 40 34 4.8 3.9 17 15.9

Mangalam Cement 197 BUY 295 5 25 21 3.8 2.8 12.4 15.9

HeidelbergCement India 193 BUY 226 44 83 76 7.4 6.6 22.4 21.4

Sagar Cement 471 BUY 619 10 56 52 6.2 5 6.3 7.9

Kajaria Ceramics 408 SELL 384 65 13.8 11.5 13 14.3

Somany Ceramics 133 BUY 173 6 6.4 4.6 5.1 11.5

Source: RSec Research

10

Exhibit 7: Change in Estimates

Y/E Mar Old Revised % Change

(Rsmn) FY21E FY22E FY23E FY21E FY22E FY23E FY21E FY22E FY23E

Sales Volume (mnT)

ACC 25.5 27.3 25.0 28.3 30.3 (2.0) 3.7

Ambuja 21.8 24.8 21.8 24.9 25.9 (0.1) 0.4

Shree Cement 22.2 26.7 30.6 23.4 27.7 30.9 5.7 3.8 0.8

Ramco Cements 11.2 13.5 10.4 12 13.5 (7.1) (11.1)

India Cements 10 11.6 8.96 9.97 11.0 (10.4) (14.1)

JK Cement 9 10.1 8 9.6 10.3 (11.1) (5.0)

JK Lakshmi Cem. 8.6 9.9 8.54 9.98 10.37 (0.7) 0.8

HeidelbergCement 4.5 5.1 4.2 4.9 5.2 (6.7) (3.9)

Sagar Cements 3.2 4 2.8 3.4 3.9 (12.2) (16.0)

Mangalam Cement 2.6 2.9 2.3 2.7 3.0 (11.5) (6.9)

Kajaria Ceramics (msm) 77.3 85.8 66.4 79.6 89.2 (14.1) (7.2)

Somany Ceramics (msm) 49.2 54.1 39.1 46.1 51.6 (20.6) (14.8)

Revenue (Rs mn)

ACC 1,36,026 1,46,804 1,35,535 1,52,659 1,65,024 (0.4) 4.0

Ambuja 1,03,520 1,19,844 1,07,547 1,23,382 1,29,739 3.9 3.0

Shree Cement 1,07,785 1,29,572 1,49,106 1,12,594 1,34,036 1,49,884 4.5 3.4 0.5

Ramco Cements 51,654 63,893 52,586 60,759 68,263 1.8 (4.9)

India Cements 48,050 55,987 43,918 48,465 53,578 (8.6) (13.4)

JK Cement 54,885 61,743 51,483 61,589 67,629 (6.2) (0.2)

JK Lakshmi Cem. 38,201 44,435 36,453 43,199 45,375 (4.6) (2.8)

HeidelbergCement 20,520 23,685 19,456 22,752 24,332 (5.2) (3.9)

Sagar Cements 12,155 15,371 12,171 13,776 15,882 0.1 (10.4)

Mangalam Cement 11,702 13,343 10,746 12,797 14,263 (8.2) (4.1)

Kajaria Ceramics 29,437 33,400 24,592 29,865 33,781 (16.5) (10.6)

Somany Ceramics 17,640 19,809 13,236 15,790 17,883 (25.0) (20.3)

EBITDA (Rs mn)

ACC 16,739 18,312 19,359 19,869 22,162 15.7 8.5

Ambuja 16,023 19,688 20,042 22,984 24,384 25.1 16.7

Shree Cement 32,245 40,305 46,970 33,193 41,547 47,086 2.9 3.1 0.2

Ramco Cements 9,632 13,240 12,010 14,123 15,967 24.7 6.7

India Cements 5,995 7,288 6,475 6,884 7,880 8.0 (5.5)

JK Cement 10,887 12,813 10,305 12,851 14,749 (5.3) 0.3

JK Lakshmi Cem. 5,509 6,987 5,614 7,273 7,483 1.9 4.1

HeidelbergCement 4,245 5,152 4,310 5,253 5,394 1.5 2.0

Sagar Cements 1,695 2,357 3,110 2,868 3,301 83.5 21.7

Mangalam Cement 1,510 1,873 1,567 2,028 2,225 3.8 8.3

Kajaria Ceramics 4,268 5,180 2,838 4,460 5,261 (33.5) (13.9)

Somany Ceramics 1,537 1,960 981 1,365 1,829 (36.2) (30.3)

APAT (Rs mn)

ACC 10,558 11,150 13,259 13,159 14,431 25.6 18.0

Ambuja 11,240 13,876 14,246 16,337 17,338 26.7 17.7

Shree Cement 11,352 17,979 24,112 14,883 20,240 25,488 31.1 12.6 5.7

Ramco Cements 3,584 7,944 5,413 8,352 10,150 51.0 5.1

India Cements 475 1,625 546 1,019 2,608 14.9 (37.3)

JK Cement 4,938 6,334 4,672 6,498 8,109 (5.4) 2.6

JK Lakshmi Cem. 1,522 3,070 1,708 3,412 3,710 12.2 11.1

HeidelbergCement 2,432 3,313 2,527 3,306 3,528 3.9 (0.2)

Sagar Cements 197 546 1,131 697 942 474.1 27.6

Mangalam Cement 529 979 451 813 1,198 (14.7) (17.0)

Kajaria Ceramics 2,506 3,160 1,190 2,429 2,944 (52.5) (23.1)

Somany Ceramics 455 766 (36) 260 610 (107.9) (66.0)

Source: RSec Research

11

I. Industry to Add 51mmT Capacity over Next Three YearDespite delay by 3-6 months, capacity expansion plan of companies continues to remain intact. We further note that cement industry added 19mnT capacity in FY20 and despite the current pandemic situation the industry is set to add 25mnT incremental capacity in FY21 and 51mnT in next three years. Hence, the industry will be adding 16-17mnT annual capacity over next three years.

Exhibit 8: A Snapshot of Cement Capacity & Expansion Exhibit 9: Company-wise Capacity Addition

Source: Industry, RSec Research Source: Industry, RSec Research

0

5

10

15

20

25

30

35

40

45

0

100

200

300

400

500

600

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

FY21

E

FY22

E

FY23

E

Installed Cement Capacity Capaccity Addition

mnT FY21E FY22E FY23EAmbuja Cement 1.8Wonder Cement 2Bharathi Cement 1.5Ramco Cements 2JSW Cements 3

Sanghi industries 2 2

JK Cement 2.2Shree Cement 6Birla Corp 3.9 1.2UltraTech 2 3.4Sagar Cements 2.5ACC 5.9

Dalmia Bharat 6 2Star Cement 2Total 24 21 7

II. Demand to Contract by 12% in FY21EDespite slowdown in government’s spending in infrastructure development and absence of any visible revival in private capex, cement demand witnessed steady growth till 9MFY20. However, impact of COVID-19 and lockdown across the nation in Mar’20 significantly impacted the sales volume. Last two weeks of March are always crucial for the companies, as higher billing is done during this period, which was adversely affected by COVID-led nationwide lockdown. Resultantly, cement demand contracted by 1% in FY20.

Exhibit 10: A Snapshot of Demand Growth over the Years

Source: Industry, RSec Research

(15%)

(10%)

(5%)

0%

5%

10%

15%

0

50

100

150

200

250

300

350

400

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

FY21

E

FY22

E

FY23

E

Cement Demand (mnT) Demand Growth (%)

Key Sectoral TakeawaysI. Industry to Add 51mmT Capacity over Next Three YearsII. Demand to Contract by 12% in FY21EIII. Northern & Southern Regions to Witness Least Capacity AdditionIV. Pricing Scenario unlikely to see Sharp Up-tickV. Input Cost Deflation to Aid Operating PerformanceVI. We Continue to Prefer Northern & Central RegionsVII. Building Materials (Tiles) Segment is Unlikely to Recover in Medium-term Term

12

Given almost complete plant shutdown in Apr’20 and lower utilization post resumption of operations subsequently, we expect cement demand to de-grow by 12% in FY21E and likely to rebound by 11.4% and 7.8% in FY22E and FY23E, respectively. Incremental consumption is seen at 20mnT over FY20-FY23E from the base cement consumption of 329mnT in FY20, whereas incremental supply during the period is pegged at 51mnT, which does not bode well for the industry from pricing discipline perspective.

(70)(60)(50)(40)(30)(20)(10)

010203040

FY10 FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

FY21

E

FY22

E

FY23

E

Net Incemental Demand (mnT)

Exhibit 11: Net Incremental Demand (Demand-Supply) over the Years

Source: Industry, RSec Research

III. Northern & Southern Regions to Witness Least Capacity AdditionOut of the estimated 51mnT cement capacity addition over next three years, Northern and Southern regions are expected to add just 4mnT each. While the minimal capacity addition bodes well for both the regions in terms of pricing discipline, Northern region seems to be the most benefitted, as capacity utilization in the region has already surpassed the-industry’s average capacity utilization of 68% in FY20.

Further, Eastern region is expected to add the highest 21mnT capacity (43% of total capacity addition) followed by 11.5mnT in Western region (23% of total addition) and 10.5mnT in Central region. We believe that strong demand growth in these regions during last couple of years encouraged several companies to expand their base in these regions, which led to high capacity addition pipeline.

Exhibit 12: Reigion-Wise Cement Capacity Additon and Outlook

mnT FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20E FY21E FY22E FY23E

North 7.0 3.2 4.5 6.5 11.5 6.6 1.1 3.6 0.0 1.0 1.8 2.0 0.0

South 14.6 14.4 10.0 3.5 7.9 4.6 0.5 2.3 6.2 3.6 1.0 1.8 1.5

West 6.0 4.9 2.7 2.0 5.8 2.3 2.6 1.2 2.0 2.4 5.7 3.9 2.0

Central 7.7 4.5 5.3 9.6 3.0 2.0 0.8 0.0 3.5 6.3 3.5 5.8 1.2

East 2.7 6.2 5.0 6.6 10.3 5.5 9.6 4.1 1.2 5.4 12.0 7.2 2.0

Total Addition 38.0 33.2 27.4 28.1 38.5 21.0 14.5 11.2 12.9 18.7 24.0 20.7 6.7

Source: Industry, RSec Research

Exhibit 13: Region-wise Clinker Capacity Addition and Outlook

mnT FY18 FY19 FY20 FY21E FY22E FY23E

North 65 65 70 74 76 76

South 116 119 123 127 127 128

West 36 36 36 39 42 42

Central 38 41 41 42 45 45

East 44 44 44 46 46 46

Total Addition 299 303 313 328 336 337

Source: Industry, RSec Research

13

IV. Pricing Scenario Unlikely to See Sharp Up-tickWhile demand supply equation does not augur well from the pricing perspective in light of substantial net incremental supply (adjusted with incremental demand) of 31mnT over next three years, we are of the view that the pricing scenario is unlikely to see a sharp up-tick, going forward as sharp increase in supply is mostly limited to Eastern and Central regions. However, we note that recent rebound in the prices, which led all India average prices to historical high in the backdrop of higher fixed cost owing to no operating leverages and logistic bottlenecks, may witness some degree of reversal in subsequent months. Also, onset of monsoon may essentially result in partial roll-back in the prices.

Further, compared to 51mnT of cement capacity addition, the industry will be adding only 24mnT clinker over next three years. Current 313mnT of clinker capacity and 486mnT cement capacity, clearly suggest that there is shortage of clinker in the country. Hence, it will be difficult for several cement companies to operate at 100% utilization level due to clinker constraints. Hence, we believe pricing trend of the industry will not see sharp disruption in case capacity utilization is maintained in the excess of 70% level.

Exhibit 14: All India Average Cement Price Movement Exhibit 15: Average Northern Cement Price Movement

Source: RSec Research Source: RSec Research

Exhibit 16: Average Southern Cement Price Movement Exhibit 17: Average Western Cement Price Movement

Source: RSec Research Source: RSec Research

Exhibit 18: Average Eastern Cement Price Movement Exhibit 19: Average Central Cement Price Movement

Source: RSec Research Source: RSec Research

200

220

240

260

280

300

320

340

Oct

-07

Jul-0

8

Ap

r-09

Jan-

10

Oct

-10

Jul-1

1

Ap

r-12

Jan-

13

Oct

-13

Jul-1

4

Ap

r-15

Jan-

16

Oct

-16

Jul-1

7

Ap

r-18

Jan-

19

Oct

-19

Jul-2

0

200

220

240

260

280

300

320

340

Oct-0

7Ap

r-08

Oct-0

8M

ay-0

9No

v-09

Jun-

10De

c-10

Jun-

11Ja

n-12

Jul-1

2Fe

b-13

Aug-

13Fe

b-14

Sep-

14M

ar-1

5Oc

t-15

Apr-1

6Oc

t-16

May

-17

Nov-

17Ju

n-18

Dec-

18Ju

n-19

Jan-

20Ju

l-20

(Rs)

Price (Rs/bag)

180

230

280

330

380

430

Oct

-07

Apr

-08

Oct

-08

May

-09

Nov

-09

Jun-

10

Dec

-10

Jun-

11

Jan-

12

Jul-1

2

Feb-

13

Aug

-13

Feb-

14

Sep

-14

Mar

-15

Oct

-15

Apr

-16

Oct

-16

May

-17

Nov

-17

Jun-

18

Dec

-18

Jun-

19

Jan-

20

Jul-2

0

(Rs)

Price (Rs/bag)

180

200

220

240

260

280

300

320

340

360

Oct

-07

Apr-0

8O

ct-0

8M

ay-0

9No

v-09

Jun-

10D

ec-1

0Ju

n-11

Jan-

12Ju

l-12

Feb-

13Au

g-13

Feb-

14Se

p-14

Mar

-15

Oct

-15

Apr-1

6O

ct-1

6M

ay-1

7No

v-17

Jun-

18D

ec-1

8Ju

n-19

Jan-

20Ju

l-20

(Rs)

Price (Rs/bag)

200

220

240

260

280

300

320

340

360

Nov-

07M

ay-0

8No

v-08

Jun-

09D

ec-0

9Ju

n-10

Jan-

11Ju

l-11

Jan-

12Au

g-12

Feb-

13Se

p-13

Mar

-14

Sep-

14Ap

r-15

Oct

-15

May

-16

Nov-

16M

ay-1

7D

ec-1

7Ju

n-18

Dec

-18

Jul-1

9Ja

n-20

Jul-2

0

(Rs)

Price (Rs/bag)

200

220

240

260

280

300

320

340

360

Oct

-07

Apr

-08

Oct

-08

May

-09

Nov

-09

Jun-

10

Dec

-10

Jun-

11

Jan-

12

Jul-1

2

Feb-

13

Aug

-13

Feb-

14

Sep

-14

Mar

-15

Oct

-15

Apr

-16

Oct

-16

May

-17

Nov

-17

Jun-

18

Dec

-18

Jun-

19

Jan-

20

Jul-2

0

(Rs)

Price (Rs/bag)

14

V. Input Costs Likely to Remain Benign Given subdued capacity utilization, which resulted in increase in fixed expenditures in the absence of operating leverage, reduction in fuel prices especially domestic and international petcoke prices already aided the companies to arrest sharp deterioration in operating performance. We note that average domestic petcoke price (Reliance petcoke) declined by ~20% YoY and 4% QoQ to Rs6,235/tonne in 1QFY21 (excluding GST). Similarly, the USA petcoke prices fell by 28% YoY and 3% QoQ to US$67 in 1QFY21. However, we note that petcoke prices have increased in last two months, which may negate low fuel price benefits in the ensuing quarters. However, we continue to believe that fuel prices are unlikely to move-up significantly hereon due to bleak outlook of crude prices. Additionally, the prices of other inputs like fly-ash and slag remained broadly flat on sequential comparison during the quarter.

Exhibit 20: Domestic Petcoke price trend (Reliance Petcoke) Exhibit 21: USA Petcoke price trend

Source: RSec Research Source: RSec Research

VI. We Continue to Prefer Northern & Central RegionWe prefer Northern and Central region over other regions mainly due to favourable demand supply equation and resultant favourable pricing environment. While Northern region is expected to see the lowest capacity addition at 4mnT over next three year, estimated capacity utilization to the tune of 80%/86% in FY22E/FY23E offers an edge. Further, imminent clinker constraint in the region offers cushion against any deterioration in pricing scenario. Moreover, Central region is expected to witness 10.5mnT (20% of total supply) capacity addition in next three years. We expect steady demand in the region should get a boost due to pre-election spending in Uttar Pradesh, which is likely to keep utilization level at second best level at 67%/71% in FY22E/FY23E.

VII. Building Materials (Tiles) Segment is Unlikely to Recover in Medium-term Term COVID-led business disruptions aggravated the concerns of the tiles segments, which have been witnessing soft demand for some period of time. Most tiles manufacturers witnessed almost zero production in Apr’20 & May’20, which improved to the extent of 30-40% in Jun’20. Industry demand, which witnessed 4-6% de-growth in FY20, is expected to decline by ~15-25% in FY21E. Average utilization of Morbi players now hovers in the range of ~30-35%. Only 500 players are operating now in Morbi, which were impacted due to ban of coal gasifiers. Given poor demand from real estate and slowdown in private capex, demand revival in this segment is unlikely to happen in the medium-term. We expect revival in sales volume to happen only from 2HFY22E with pick-up real estate sales.

20

40

60

80

100

120

140

Aug-

15

Nov

-15

Feb-

16

May

-16

Aug-

16

Nov

-16

Feb-

17

May

-17

Aug-

17

Nov

-17

Feb-

18

May

-18

Aug-

18

Nov

-18

Feb-

19

May

-19

Aug-

19

Nov

-19

Feb-

20

May

-20

Aug-

20

(US$/tonne)

5,000

5,500

6,000

6,500

7,000

7,500

8,000

8,500

1st A

pr'19

1st M

ay'19

1st J

une'

19

1st J

uly'

19

1st A

ug'19

1st S

ept'1

9

1st O

ct'19

1st N

ov'19

1st D

ec'19

1st J

an'2

0

1st F

eb'2

0

1st M

ar'2

0

1st A

pr'2

0

1st M

ay'2

0

1st J

une'

20

1st J

uly'

20

1st A

ug 2

0

(Rs/tonne)

15

Annexure Table

Exhibit 22: Region wise capacity

(mnT) FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21E FY22E FY23E

North 50 63 68 73 79 90 97 98 102 102 103 105 107 107

% total 21 22 22 21 21 22 23 22 22 22 21 20 20 20

South 92 107 120 130 133 141 146 146 149 155 158 159 161 163

% total 38 38 38 38 36 35 34 33 33 33 33 31 30 30

West 38 43 47 50 52 57 60 62 64 66 68 74 78 80

% total 16 15 15 15 14 14 14 14 14 14 14 14 15 15

East 34 35 39 44 51 61 66 76 80 81 87 99 107 108

% total 14 12 12 13 14 15 15 17 18 17 18 20 20 20

Central 29 33 40 45 55 58 60 61 61 64 70 74 80 81

% total 12 12 13 13 15 14 14 14 13 14 14 14 15 15

Total Capacity 243 281 314 341 369 408 429 443 455 467 486 510 531 538

Source:

Exhibit 23: Region Wise Demand/Consumption Snapshot

Demand (mnT) FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21E FY22E FY23E

North 38.0 40.0 44.0 48.1 51.2 54.2 57.3 57.4 62.5 71.8 73.5 65.1 73.5 79.4

% total 19% 19% 20% 20% 20% 20% 20% 21% 21% 21% 22% 22% 23% 22%

South 61.0 61.0 60.0 62.9 62.7 63.7 64.6 63.9 69.1 77.6 70.2 62.7 68.6 73.0

% total 30% 29% 27% 26% 25% 24% 23% 23% 23% 23% 21% 21% 21% 21%

West 38.0 42.0 47.0 50.6 52.5 55.6 57.5 57.4 53.9 59.0 57.5 48.4 53.9 58.1

% total 19% 20% 21% 21% 21% 21% 20% 21% 18% 18% 17% 17% 17% 16%

East 33.0 35.0 37.0 41.9 44.8 49.6 53.9 52.7 58.1 67.4 70.2 63.9 71.9 79.0

% total 16% 17% 17% 17% 18% 18% 19% 19% 20% 20% 21% 22% 22% 22%

Central 31.0 34.0 36.0 38.2 39.7 42.8 45.1 43.7 49.1 56.3 57.5 50.1 54.9 58.8

% total 15% 16% 16% 16% 16% 16% 16% 16% 17% 17% 17% 17% 17% 17%

Total 201.0 212.0 224.0 241.8 250.8 265.9 278.4 275.0 292.7 332.1 328.9 290.2 322.8 348.3

Export 5.3 4.2 5.5 5.0 5.0 5.0 5.0 5.0 5.0 5.0 5.0 3.0 4.0 4.0

Total Dispatches 206.3 216.2 229.5 246.8 255.8 270.9 283.4 280.0 297.7 337.1 333.9 293.2 326.8 352.3

Source:

Exhibit 24: Region Wise Capacity Utilisation

Regional Utilization FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21E FY22E FY23E

North 94% 81% 82% 84% 83% 76% 75% 74% 78% 82% 83% 72% 80% 86%

South 77% 69% 60% 58% 56% 54% 53% 52% 56% 60% 53% 47% 51% 54%

West 79% 72% 79% 80% 80% 76% 76% 72% 67% 71% 67% 52% 55% 58%

East 85% 86% 79% 80% 74% 68% 68% 58% 61% 70% 68% 54% 57% 61%

Central 103% 97% 88% 82% 70% 72% 73% 70% 79% 85% 79% 66% 67% 71%

Industry Utilization 84.9% 76.9% 73.1% 72.3% 69.2% 66.4% 66.1% 63.1% 65.5% 72.1% 68.7% 57.3% 61.6% 65.5%

Source:

16

COMPANY SECTION

17

Share price (%) 1 mth 3 mth 12 mth

Absolute performance 5.1% 21.2% -4.7%

Relative to Nifty 1% 8% -6%

Shareholding Pattern (%) Mar'20 June'20

Promoter 60 60

Public 40 40

1 Year Stock Price Performance

Note: * CMP as on 17 Aug 2020

Reduction in Debt to Holds the Key

UltraTech CementCement | India

Institutional Equity Research

BUY2 Year Target Price: Rs.4,825

CMP* 4,035

Upside/Downside (%) 20

Bloomberg Ticker UTCEM IN

Market Cap. (Rs bn) 1,165

Free Float (%) 40

Shares O/S (mn) 289Company Update | 18 Aug 2020

1. UltraTech Cement (UTCEM) – which enjoys ~23% market share on pan-India level with dominant presence across regions – is on the firm footing to cash in the secular consumption opportunity for cement due to absence of any meaningful alternatives.

2. With the successful acquisition of Binani’s assets, UTCEM has now got added advantage in terms of new limestone resources in imminent clinker deficit Northern region.

3. While UTCEM has sufficiently built capacity to outpace industry’s growth in next couple of years, it continued to focus on setting up maximum capacity in demand-rich regions. It is likely to commission 0.6mnT each in Dankuni (west bengal) and Pataliputra (Bihar) shortly in FY21 and Phase-II 2mnT cement capacity at Bara is expected to be commissioned in 3QFY21E.

4. Despite acquisition of Century Textile’s cement assets in FY20, UTCEM’s gross debt remained broadly flat on YoY basis at Rs229bn, while net debt to EBITDA and D/E ratio improved from 3x and 0.7x in FY19 to 2x and 0.5x in FY20 led by strong cash flow generation. UTCEM is committed to take it to 1x in FY21.

Impact of COVID-19: Nationwide lockdown resulted in sharp contraction in demand in 1QFY21, which led UTCEM to witness 31% YoY drop sales volume. Going forward, with consistent pick-up in monthly sales volume, we expect 2QFY21 volume to be sequentially better. However, volume momentum is still down by 10-15% compared to pre-COVID period. We expect UTCEM’s sales volume to decline by 12% in FY21E.

Outlook & ValuationConsistent efforts to trim cost along with focus on improvement in RoCE by balance-sheet deleveraging augurs well for UTCEM. Going forward, we expect demand to recover post monsoon followed by pick-up in infrastructure activities led by improved workforce availability. At CMP, the stock trades at attractive levels of 13x/11x EBITDA FY22E/FY23E. Hence, we maintain BUY on UTCEM with a revised 2-Year Target Price of Rs4,825 (13x of EBITDA FY23E).

Key Triggers:Strong market share (23%) in Indian cement industry with dominant presence across

regions

Adequate limestone reserve in imminent clinker deficit region offers an edge

New capacities in high consumption region to result in sustained volume growth

RoCE is set to improve from 11.8% in FY20 to 12.7% FY23E, while free cash flow (FCF) is seen at ~Rs204bn over FY20-FY23E.

Research Analyst

Binod ModiContact: 022 4303 4626/9870009382Email: [email protected]

Research Associate:

Girija Shankar RayEmail : [email protected]

Key Financials (Rs mn) FY19 FY20 FY21E FY22E FY23E Sales 416,088 421,248 383,534 440,316 487,235EBITDA 73,469 92,836 87,478 99,621 109,249APAT 24,767 36,985 34,603 46,020 53,899EPS (Rs) 90.2 128.1 119.9 159.4 186.7DPS (Rs) 10.5 13.0 13.0 15.0 15.0P/E (x) 44.7 31.5 33.7 25.3 21.6P/B (x) 3.3 3.0 2.8 2.5 2.3

EV/EBITDA (x) 18.2 14.5 14.9 12.6 10.9

RoE (%) 10.0 11.9 10.2 12.1 13.0Divi. Yield (%) 0.3 0.3 0.3 0.4 0.4

Source: Company, RSec Research

TOP PICK in Large-cap

2,500

3,000

3,500

4,000

4,500

5,000

Jul-

19

Aug

-19

Sep-

19

Oct

-19

Nov

-19

Dec

-19

Jan-

20

Feb-

20

Mar

-20

Apr

-20

May

-20

Jun-

20

Jul-

20

18

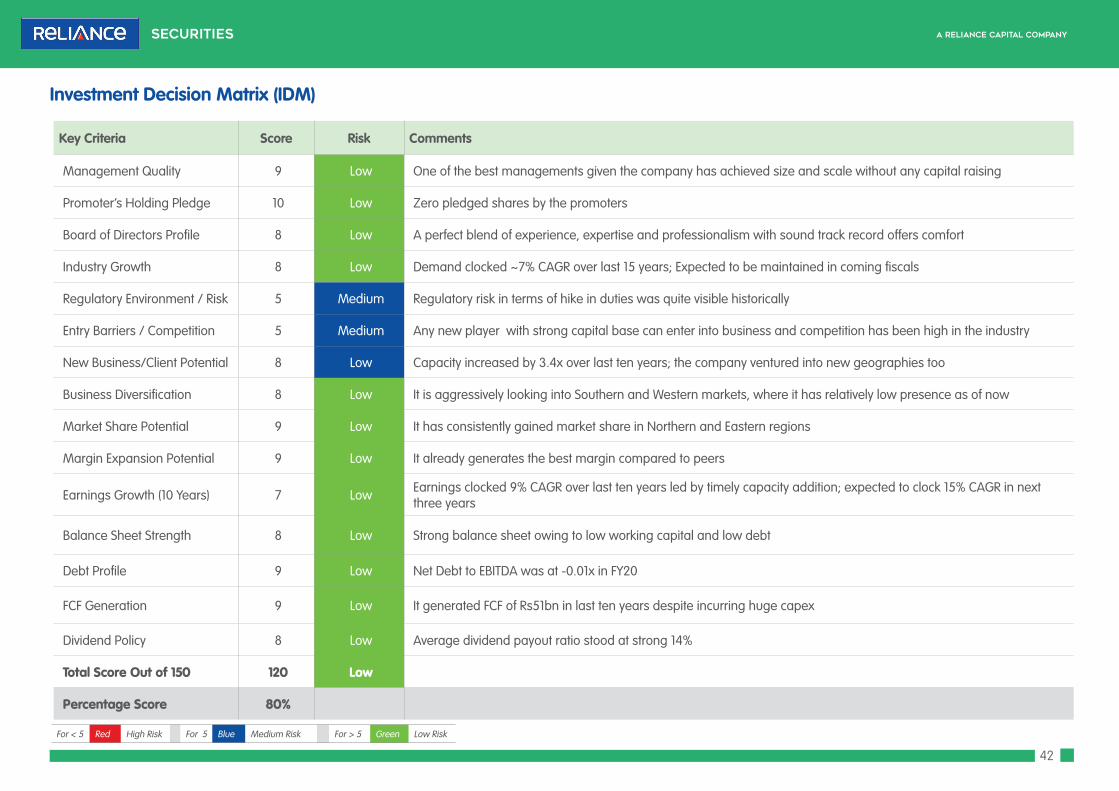

Key Criteria Score Risk Comments

Management Quality 8 Low The management has displayed remarkable quality over the years in terms of maintaining industry leadership

Promoter’s Holding Pledge 10 Low Zero pledged shares, despite the promoter group has varied interest in other businesses as well

Board of Directors Profile 8 Low A perfect blend of experience, expertise and professionalism with sound track record offers comfort

Industry Growth 8 Low Demand clocked ~7% demand CAGR over last 15 years; expected to be maintained in coming fiscals

Regulatory Environment / Risk 5 Medium Regulatory risk in terms of hike in duties was quite visible historically

Entry Barriers / Competition 5 Medium Any new player with strong capital base can enter into business and competition has been high in the industry

New Business/Client Potential 6 Low Strong brand equity always helps to get more customers

Business Diversification 9 Low It has presence across all geographies in India and has presence overseas also

Market Share Potential 9 Low Necessary resources are in place to maintain market share

Margin Expansion Potential 8 Low Working on various measures to contain opex further

Earnings Growth (10 Years) 9 Low Earnings clocked 18% CAGR in 10 year; expected to clock 13% CAGR in next three years

Balance Sheet Strength 7 Low Despite doing back-to-back acquisition, its balance sheet remains resilient and strong

Debt Profile 7 Low Net Debt to EBITDA ratio stood at 2x in FY20, which is likely to witness further improvement in FY21

FCF Generation 8 Low It generated FCF of Rs218bn in last ten years (which is the best) despite doing huge capex

Dividend Policy 7 Low Average dividend payout ratio stood at 9%

Total Score Out of 150 114 Low

Percentage Score 76%

Investment Decision Matrix (IDM)

For < 5 Red High Risk For 5 Blue Medium Risk For > 5 Green Low Risk

19

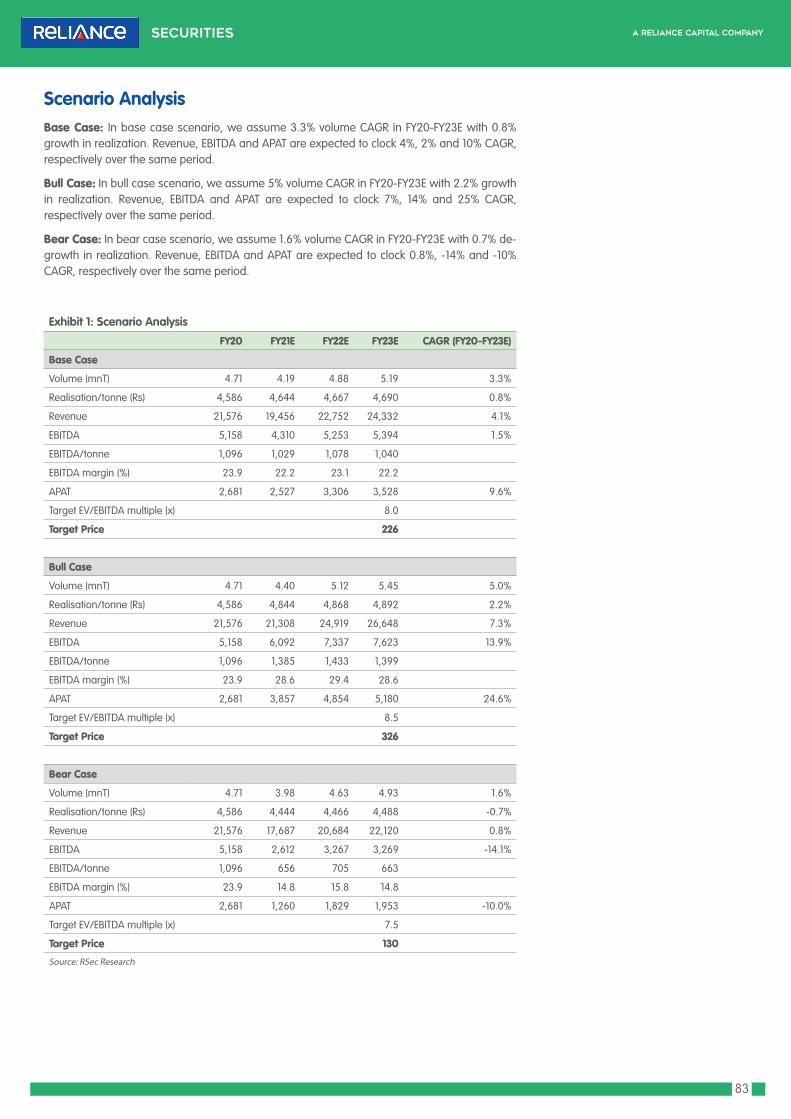

Exhibit 1: Scenario Analysis

FY20 FY21E FY22E FY23E CAGR (FY20-FY23E)

Base Case

Volume (mnT) 82.3 72.4 83.6 91.9 8.3%

Realization/tonne (Rs) 4,721 4,877 4,871 4,920 0.3%

Revenue 421,248 383,534 440,316 487,235 8.3%

EBITDA 92,836 87,478 99,621 109,249 7.7%

EBITDA/tonne 1,128 1,209 1,192 1,189

EBITDA margin (%) 22.0 22.8 22.6 22.4

APAT 36,985 34,603 46,020 53,899 15.9%

Target EV/EBITDA multiple (x) 13.0

Target Price 4,825

Bull Case

Volume (mnT) 82.3 76.2 91.6 105.2 11.3%

Realization/tonne (Rs) 4,721 5,026 5,021 5,121 0.6%

Revenue 421,248 397,286 473,523 567,622 12.6%

EBITDA 92,836 87,851 104,178 143,661 17.8%

EBITDA/tonne 1,128 1,153 1,138 1,366

EBITDA margin (%) 22.0 22.1 22.0 25.3

APAT 36,985 36,059 49,430 79,650 30.2%

Target EV/EBITDA multiple (x) 13.5

Target Price 6,464

Bear Case

Volume (mnT) 82.3 70.2 77.8 81.7 5.2%

Realization/tonne (Rs) 4,721 4,726 4,721 4,674 -0.4%

Revenue 421,248 368,230 406,676 411,274 3.8%

EBITDA 92,836 81,176 88,722 75,185 -2.5%

EBITDA/tonne 1,128 1,157 1,141 921

EBITDA margin (%) 22.0 22.0 21.8 18.3

APAT 36,985 31,064 37,864 28,409 -2.9%

Target EV/EBITDA multiple (x) 12.5

Target Price 3,178

Source: RSec Research

Scenario AnalysisBase Case: In base case scenario, we assume 8.3% volume CAGR in FY21E-FY23E with 0.3% growth in realization. Revenue, EBITDA and APAT are expected to clock 8.3%, 7.7% and 16% CAGR, respectively over the same period.

Bull Case: In bull case scenario, we assume 11.3% volume CAGR in FY21E-FY23E with 0.6% growth in realization. Revenue, EBITDA and APAT CAGR are expected to clock 12.6%, 17.8% and 30% CAGR, respectively over the same period.

Bear Case: In bear case scenario, we assume 11.3% volume CAGR in FY21E-FY23E with 0.6% growth in realization. Revenue, EBITDA and APAT CAGR are estimated at 3.8%, -2.5% and -2.9%, respectively over the same period.

20

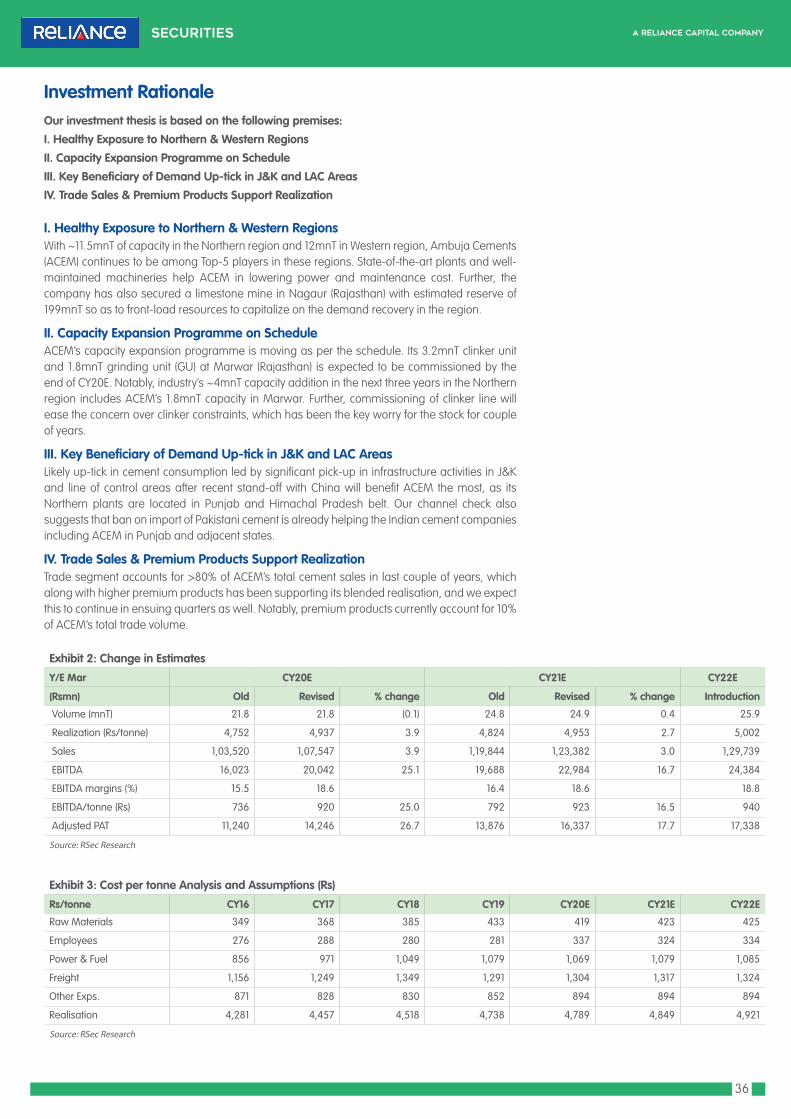

I. Leadership Status Bodes WellUTCEM – which enjoys ~23% market share on pan-India level with dominant presence across regions – is on the firm footing to cash in the secular consumption opportunity for cement due to absence of any meaningful alternatives. With the acquisition of Century Cement’s assets, UTCEM has crossed the 100mnT-mark in domestic cement industry, which is unmatched. Surprisingly, capacity utilization of Century’s assets improved to 83% in 4QFY20 (from 55% in 3QFY20) despite COVID-led disruptions. Its EBITDA/tonne is expected to improve to Rs800-900/tonne in FY21E from Rs575 in 4QFY20 with 100% brand conversion. Going forward, we expect UTCEM’s volume to clock 4% CAGR through FY20-FY23E and 13% over FY21E-FY23E.

II. Abundant Limestone Resource – AdvantageIn a scenario of looming higher limestone cost due to exorbitant higher price in new auction of mines, the companies having rich limestone resources are considered to be the winners in future. Notably, with the successful acquisition of Binani’s assets, UTCEM has now got added advantage in terms of new limestone resources in imminent clinker deficit Northern region.

III. Capacity Expansion in High Consumption RegionsWhile UTCEM has sufficiently built capacity to outpace industry’s growth in next couple of years, it continued to focus on putting maximum capacity in demand-rich regions. It is likely to commission 0.6mnT each in Dankuni (west bengal) and Pataliputra (Bihar) shortly in FY21 and Phase-II 2mnT cement capacity at Bara is expected to be commissioned in 3QFY21E. Further, clinker unit (2.3mnT) at Dalla (Uttar Pradesh) is expected to be commissioned in Mar’21. However, 2.2mnT Split Grinding Unit (SGU) in Cuttack (Odisha) is expected to come on stream in FY22E.

IV. Acquisitions Well-Absorbed in Balance-sheet; Now Focus on Improving RoCEDespite acquisition of Century Textile’s cement assets in FY20, UTCEM’s gross debt remained broadly flat on YoY basis at Rs229bn in FY20, while net debt to EBITDA and D/E ratio improved from 3x and 0.7x in FY19 to 2x and 0.5x in FY20 led by strong cash flow generation. UTCEM is committed to take it to 1x in FY21. We foresee its RoCE to improve from 11.8% in FY20 to 12.7% FY23E, while free cash flow (FCF) is seen at ~Rs204bn over FY20-FY23E.

Exhibit 2: Cost per tonne Analysis and Assumptions (Rs)

Rs/tonne FY17 FY18 FY19 FY20 FY21E FY22E FY23E

Raw Materials 802 836 762 767 797 805 805

Employees 282 286 240 305 349 332 332

Power & Fuel 782 1,001 984 1,029 987 1,007 1,017

Freight 1,165 1,155 1,033 1,181 1,205 1,193 1,193

Other Exps. 740 646 552 708 736 721 721

Realisation 4,186 3,965 4,465 4,721 4,790 4,796 4,843

Source: RSec Research

Investment RationaleOur investment thesis is based on the following premises:I. Leadership Status Bodes WellII. Abundant Limestone Resource – AdvantageIII. Capacity Expansion in High Consumption RegionsIV. Acquisitions Well-Absorbed in Balance-sheet; Now Focus on Improving RoCE

21

Exhibit 3: EBITDA & Target Price Exhibit 4: EV/EBITDA 1yr Fwd

Source: RSec Research Source: RSec Research

Exhibit 5: Price Sensitivity Analysis EBITDA (Rs bn) Growth (%) Fwd EV/EBITDA (x) 11 12 13 14 15FY17 (-3) 46.3 29.8 1,812 1,972 2,133 2,292 2,453

FY18 (-2) 61.5 32.8 22.4 1,812 2,024 2,238 2,450 2,663

FY19 (-1) 73.5 19.6 18.7 2,000 2,255 2,510 2,764 3,019

FY20 (Base year) 92.8 26.4 14.8 2,910 3,232 3,555 3,875 4,197

FY21E (year 1) 87.5 -5.8 15.7 2,853 3,156 3,460 3,762 4,065

FY22E (Year 2) 99.6 13.9 13.8 3,488 3,833 4,180 4,524 4,869

FY23E (Year 3) 109.2 9.7 12.6 4,067 4,445 4,825 5,202 5,581

Source: Company, RSec Research

Key Risks f Further slowdown in demand scenario.

f A steep contraction in prices.

f A sharp increase in input and fuel cost.

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Mar

-13

Jul-1

3

Nov

-13

Mar

-14

Jul-1

4

Nov

-14

Mar

-15

Jul-1

5

Nov

-15

Mar

-16

Jul-1

6

Nov

-16

Mar

-17

Jul-1

7

Nov

-17

Mar

-18

Jul-1

8

Nov

-18

Mar

-19

Jul-1

9

Nov

-19

Mar

-20

Jul-2

0

12x

13x

14x

15x

16x

2,133 2,2382,510

3,555 3,460

4,825

46.3

61.5

73.5

92.887.5

109.2

0

20

40

60

80

100

120

0

1,000

2,000

3,000

4,000

5,000

6,000

FY17 (-3) FY18 (-2) FY19 (-1) FY20 (Base year)

FY21E (year 1)

FY23E (Year 3)

Target Price (Rs) EBITDA (Rs bn)

22

Exhibit 7: Revenue Trend Exhibit 8: EBITDA Trend

Source: Company, RSec Research Source: Company, RSec Research

Exhibit 9: PAT Trend Exhibit 10: ROCE vs. RoE

Source: Company, RSec Research Source: Company, RSec Research

Exhibit 6: Volume (mt)

Source: Industry, RSec Research

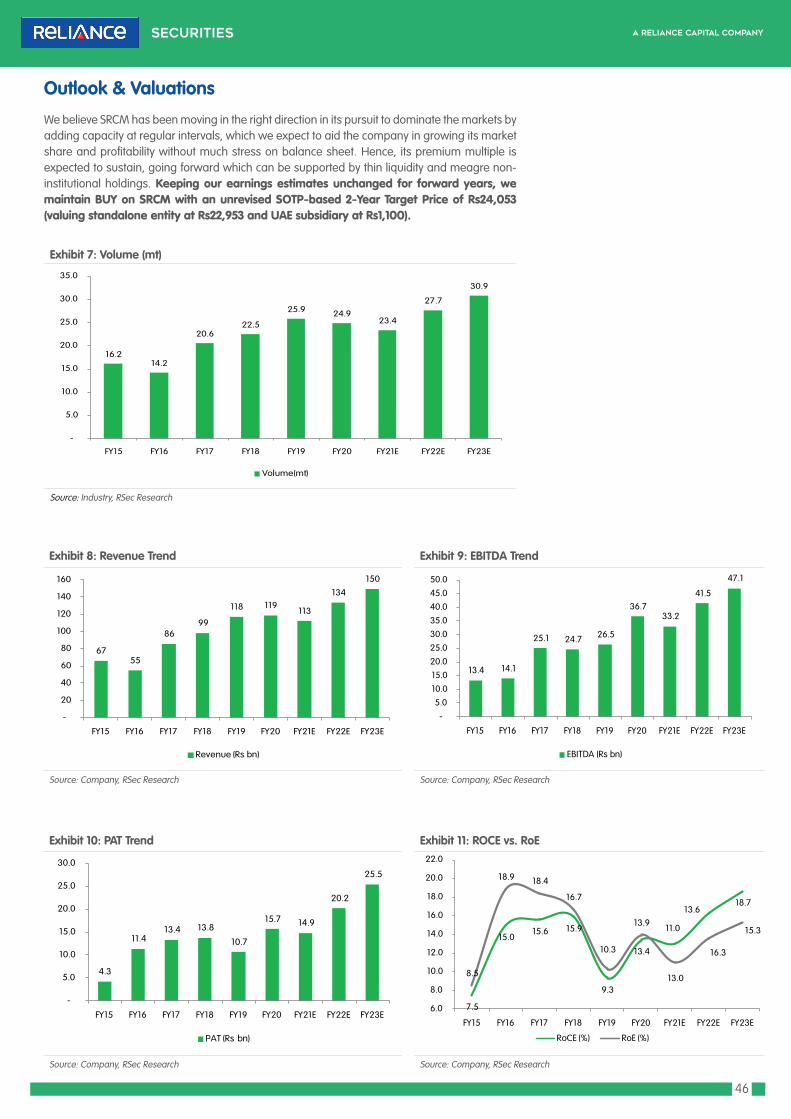

Outlook & Valuations

Consistent efforts to trim cost along with focus on improvement in RoCE by balance-sheet deleveraging augurs well for UTCEM. Going forward, we expect demand to recover post monsoon followed by pick-up in infrastructure activities led by improved workforce availability. At CMP, the stock trades at attractive levels of 13x/11x EBITDA FY22E/FY23E. Hence, we maintain BUY on UTCEM with a revised 2-Year Target Price of Rs4,825 (13x of EBITDA FY23E).

46.1 49.3 50.2

63.3

85.7 82.3

72.4

83.6

91.9

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

FY15 FY16 FY17 FY18 FY19 FY20 FY21E FY22E FY23E

Volume(mt)

227 237 239

310

416 421 381

439 485

-

100

200

300

400

500

600

FY15 FY16 FY17 FY18 FY19 FY20 FY21E FY22E FY23E

Revenue (Rs bn)

39 46 50

61

73

93 87

100 109

-

20

40

60

80

100

120

FY15 FY16 FY17 FY18 FY19 FY20 FY21E FY22E FY23E

EBITDA (Rs bn)

20 24

26 25 25

37 35

46

54

-

10

20

30

40

50

60

FY15 FY16 FY17 FY18 FY19 FY20 FY21E FY22E FY23E

PAT (Rs bn)

14.1 13.6

14.5

12.2

8.2

10.2

8.5

10.4

11.0

11.2 11.7 11.5

8.9

10.0

11.9

10.2

12.1

13.0

7

8

9

10

11

12

13

14

15

FY15 FY16 FY17 FY18 FY19 FY20 FY21E FY22E FY23E

RoCE (%) RoE (%)

23

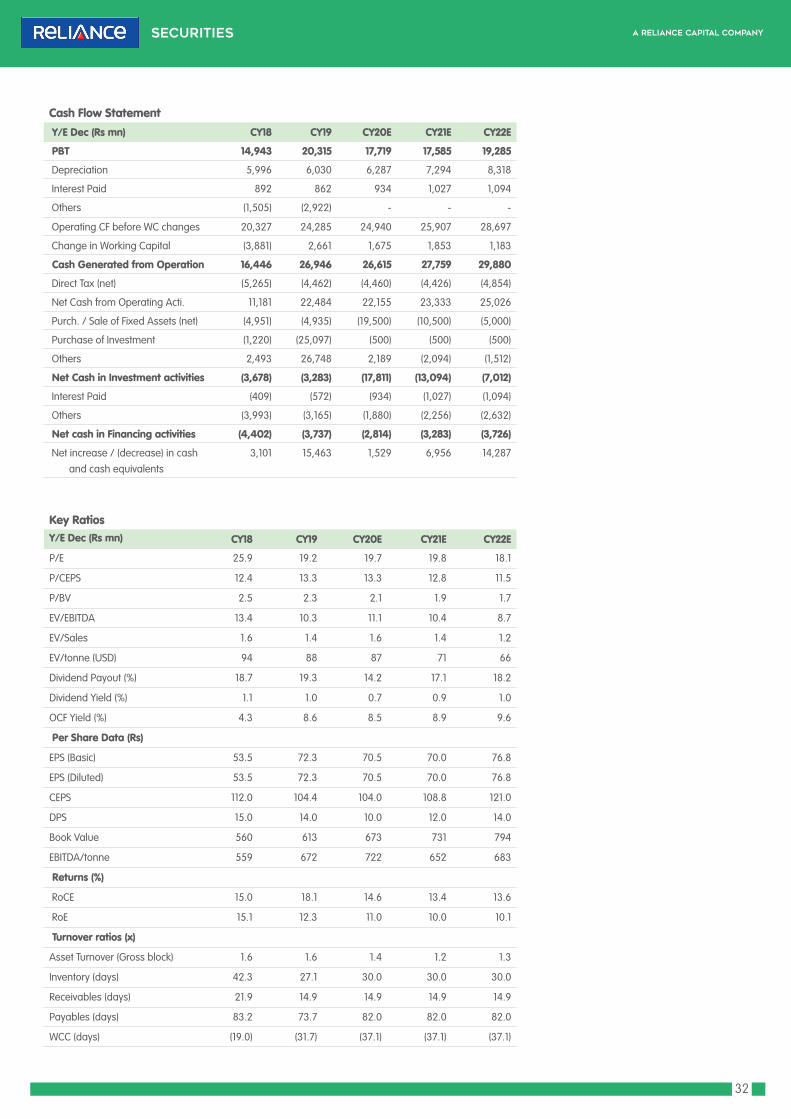

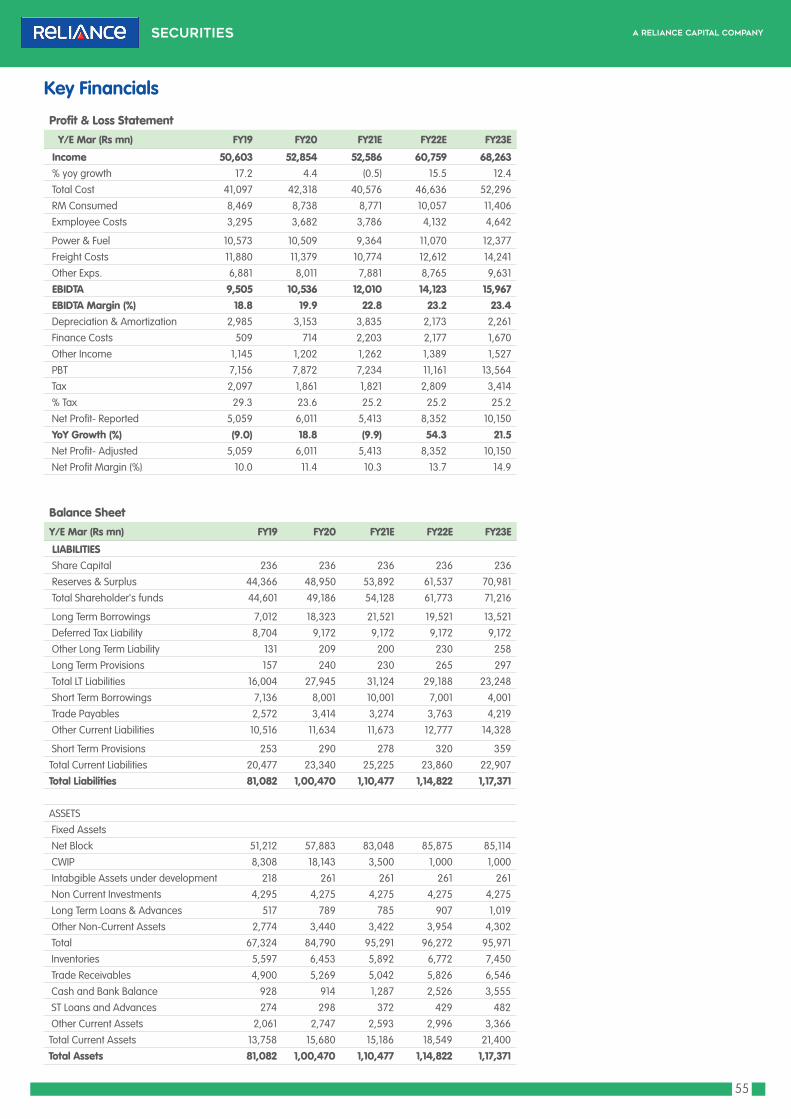

Profit & Loss StatementY/E Mar (Rs mn) FY19 FY20 FY21E FY22E FY23E

Net Sales 4,16,088 4,21,248 3,83,534 4,40,316 4,87,235 Total Cost 3,42,619 3,28,413 2,96,056 3,40,695 3,77,986

Cost of Materials 69,831 63,131 57,712 67,339 74,763

Employee 22,911 25,094 25,596 28,156 30,971

Power & Fuel 94,361 84,679 71,456 84,200 93,484

Freight & Forwarding 1,03,145 97,254 88,051 1,00,704 1,11,807

Others 52,371 58,255 53,242 60,296 66,960

EBIDTA 73,469 92,836 87,478 99,621 1,09,249 EBIDTA Margin (%) 17.7% 22.0% 22.8% 22.6% 22.4%

Depreciation and Amortisation 24,507 27,022 28,124 28,978 29,716

Interest 17,779 19,857 17,478 15,798 14,560

Other Income 4,634 6,478 5,959 6,675 7,075

Excrptional items (1,139) - (1,574) - -

PBT 34,679 52,435 46,262 61,519 72,048 Tax 10,681 (5,682) 11,639 15,479 18,130

% Tax 31% -11% 25% 25% 25%

Net Profit 23,998 58,117 34,623 46,040 53,919 APAT 24,767 36,985 34,603 46,020 53,899

Net Profit Margin (%) 6% 9% 9% 10% 11%

Balance SheetY/E Mar (Rs mn) FY19 FY20 FY21E FY22E FY23E

Share Capital 2,746 2,886 2,886 2,886 2,886

Reserves & Surplus 3,34,760 3,88,268 4,19,120 4,60,810 5,10,379

Total Shareholder's funds 3,37,506 3,91,155 4,22,006 4,63,696 5,13,266

Long Term Borrowings 2,06,504 1,73,675 1,53,675 1,33,675 1,13,675

Deferred Tax Liabilities (net) 64,114 49,120 49,120 49,120 49,120

Other LT Liabilities and Prov. 1,917 13,114 11,947 13,704 15,156

Total NC Liabilities 2,72,535 2,35,909 2,14,742 1,96,499 1,77,951

Short Term Borrowings 36,684 39,851 38,851 37,851 36,851

Trade Payables 31,597 35,014 31,880 36,599 40,499

Other Curren Liabilities and Prov. 87,052 91,442 85,615 94,388 1,01,638

Total Current Liabilities 1,55,333 1,66,308 1,56,345 1,68,839 1,78,988

TOTAL LIABILITIES 7,65,374 7,93,371 7,93,092 8,29,034 8,70,205

Gross Block 5,71,584 5,99,345 6,19,345 6,36,345 6,51,345

Less: Accumulated Depreciation 67,371 92,046 1,20,170 1,49,148 1,78,864

Net Block 5,04,213 5,07,299 4,99,175 4,87,198 4,72,481

CWIP 11,486 9,095 4,095 4,095 4,095

Goodwill 62,233 62,525 62,525 62,525 62,525

Intangible Assets under development

47 101 101 101 101

Non Current Investment 14,048 16,850 17,050 17,250 17,450

Other NC Assets 43,804 47,428 46,991 53,525 58,923

Total Non-Current Assets 6,35,832 6,43,298 6,29,937 6,24,693 6,15,576

Inventories 40,990 41,483 37,769 43,361 47,981

Investments 15,165 42,437 52,437 67,437 92,437

Trade Receivables 27,870 22,383 20,379 23,396 25,889

Cash and Bank 7,397 5,392 16,665 30,518 45,617

Other Current Assets 38,121 38,379 35,906 39,629 42,705

Total Current Assets 1,29,542 1,50,074 1,63,156 2,04,341 2,54,629

Total Assets 7,65,374 7,93,371 7,93,092 8,29,034 8,70,205

Key Financials

24

Cash Flow StatementY/E Mar (Rs mn) FY19 FY20 FY21E FY22E FY23E

PBT 34,685 52,423 46,242 61,499 72,028

Adjustments for: Depreciation and Obsolescence 24,507 27,022 28,124 28,978 29,716

Interest & Dividend Income (1,188) (1,422) - - -

Interest Expense 17,779 19,857 17,478 15,798 14,560

Others (2,168) (4,447) - - -

Operating Profit Before WC Changes 73,615 93,432 91,844 1,06,275 1,16,304

Net change in WC (6,957) 4,503 (1,502) (3,615) (2,987)

Tax Paid (7,101) (8,914) (11,639) (15,479) (18,130)

Net Cash from Operating activities 59,557 89,020 78,703 87,181 95,187

Purchase of fixed assets (net) (15,959) (16,272) (15,000) (17,000) (15,000)

(Purchase)/Proceeds of Investment 27,667 (26,907) (10,200) (15,200) (25,200)

Others (570) 1,086 - - -

Net Cash from Investing activities 11,138 (42,094) (25,200) (32,200) (40,200) Proceeds from Issue of Share Capital 52 27 - - -

Purchase of Treasury Shares(net) (812) (31) - - -

Proceeds / (Repayment) of Loans (Net) (46,482) (27,164) (21,000) (21,000) (21,000)

Others (20,312) (22,744) (21,230) (20,128) (18,889)

Net Cash from Financing activities (67,553) (49,911) (42,230) (41,128) (39,889) Opening Cash & Bank Balance 771.9 4,412.4 1,465.3 12,737.9 26,591.4

Net Increase or decrease in Cash 3,142 (2,985) 11,273 13,854 15,099

Cash & Cash Equiv. transferred from UNCL 385.2 - - - -

Cash and Cash Equivalents transferred from Century Cement Division

123.9 - - - -

Effect of Exchange rate fluctuation on Cash and Cash Equivalents

4.5 37.5 - - -

Closing Cash & Bank 4,427 1,465 12,738 26,591 41,690

Key RatiosY/E Mar (Rs mn) FY19 FY20 FY21E FY22E FY23E

P/E 44.7 31.5 33.7 25.3 21.6

P/CEPS 22.8 13.7 18.6 15.5 13.9

P/BV 3.3 3.0 2.8 2.5 2.3

EV/EBIDTA 18.2 14.5 14.9 12.6 10.9

EV/Sales 3.2 3.2 3.4 2.8 2.4

EV/tonne (USD) 186 160 152 142 135

Dividend Payout (%) 11.6 10.1 10.8 9.4 8.0

Dividend Yield (%) 0.3 0.3 0.3 0.4 0.4

Per Share Data (Rs)EPS (Basic) 90.2 128.1 119.9 159.4 186.7

CEPS 176.6 295.0 217.4 259.9 289.8

DPS 10.5 13.0 13.0 15.0 15.0

Book Value 1,229 1,355 1,462 1,607 1,778

EBIDTA/tone 857.6 1,127.6 1,208.8 1,191.6 1,188.7

Returns (%)RoCE 8.2 10.2 8.5 10.4 11.0

RoE 10.0 11.9 10.2 12.1 13.0

Turnover ratios (x) Asset Turnover 0.7 0.7 0.6 0.7 0.7

Inventory (days) 36 36 36 36 36

Receivables (days) 24 19 19 19 19

Payables (days) 28 30 30 30 30

WCC (days) 33 25 25 25 25

25

Share price (%) 1 mth 3 mth 12 mth

Absolute performance 6.6% 22.1% -13.0%

Relative to Nifty 2.5% 9.3% -14.1%

Shareholding Pattern (%) Mar'20 June'20

Promoter 54.5 54.5

Public 45.5 45.5

1 Year Stock Price Performance

Note: * CMP as on 17 Aug 2020

Upcoming Capacities to Ensure Growth Sustainability

Key Financials (Rs mn) CY18 CY19 CY20E CY21E CY22ESales 144,775 153,431 135,535 152,659 165,024EBITDA 17,208 20,959 19,359 19,869 22,162APAT 10,060 13,589 13,259 13,159 14,431EPS (Rs) 53.5 72.3 70.5 70.0 76.8DPS (Rs) 15.0 14.0 10.0 12.0 14.0P/E (x) 25.9 19.2 19.7 19.8 18.1P/B (x) 2.5 2.3 2.1 1.9 1.7

EV/EBIDTA (x) 13.4 10.3 11.1 10.4 8.7

RoE (%) 15.1 12.3 11.0 10.0 10.1Div. Yield (%) 1.1 1.0 0.7 0.9 1.0

Source: Company, RSec Research

ACCCement | India

Institutional Equity Research

BUY2 Year Target Price: Rs.1,718

CMP* 1,388

Upside/Downside (%) 24

Bloomberg Ticker ACC IN

Market Cap. (Rs bn) 261

Free Float (%) 46

Shares O/S (mn) 188Company Update | 18 Aug 2020

1. ACC continues to enjoy strong brand equity especially in the trade segment with sound distribution reach in rural India. Pan-India distribution network comprising of >50,000 dealers/distributors has been the prime growth driver for the company.

2. It continues to remain placed amongst the Top-5 cement companies across regions barring the Northern markets.

3. With ongoing capacity expansion of 5.9mnT in strong demand potential markets, the concern over capacity constraint appears to have subsided. Further, we understand ACC's all units in Uttar Pradesh and Jharkhand enjoy fiscal incentives.

4. Its revenue from value-added products and services (VAPS) grew by 36% YoY and 52% YoY in CY18 and CY19, respectively. Further, premium products (~5 brands) volume now accounts for ~15-20% of its total volume. Moreover, foray into adhesive business with different range of products has already started aiding its margin.

Impact of COVID-19: ACC’s volume was impacted significantly in June quarter mainly led by

sharp contraction in construction activities post lockdown. In line with the industry, ACC has also

witnessed improvement on MoM sales volume in May’20 and Jun’20. It is likely to see better

sequential volume in 3QCY20. However, we estimate its volume to drop by ~13% in CY20.

Outlook & ValuationWhile ACC has been a laggard due to higher cost of production, it has been continuously

undertaking measures to reduce its operating cost. Going forward, we believe a healthy demand

outlook in the Eastern and Central regions will aid the company to get traction in volume and

profitability in post COVID-19 scenario. The stock has been trading at a discount to other pan-

India peers due to higher cost of production, which we expect to shrink in the ensuing period.

Increasing EBITDA estimate by 4% each for CY20E and CY21E to factor in lower fuel prices and recent improvement in realization, we maintain BUY on ACC with a revised 2-Year Target Price of Rs1,718 (11.5x of CY22 EBITDA).

Key Triggers:Strong brand equity in trade segment with sound distribution reach in rural India

Capacity expansion of 5.9mnT in strong demand potential markets

Value-added products and services to witness strong traction

Healthy demand outlook in Eastern and Central regions to drive volume and profitability

Research Analyst

Binod ModiContact: 022 4303 4626/9870009382Email: [email protected]

Research Associate:

Girija Shankar RayEmail : [email protected]

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

Jul-

19

Aug

-19

Sep-

19

Oct

-19

Nov

-19

Dec

-19

Jan-

20

Feb-

20

Mar

-20

Apr

-20

May

-20

Jun-

20

Jul-

20

26

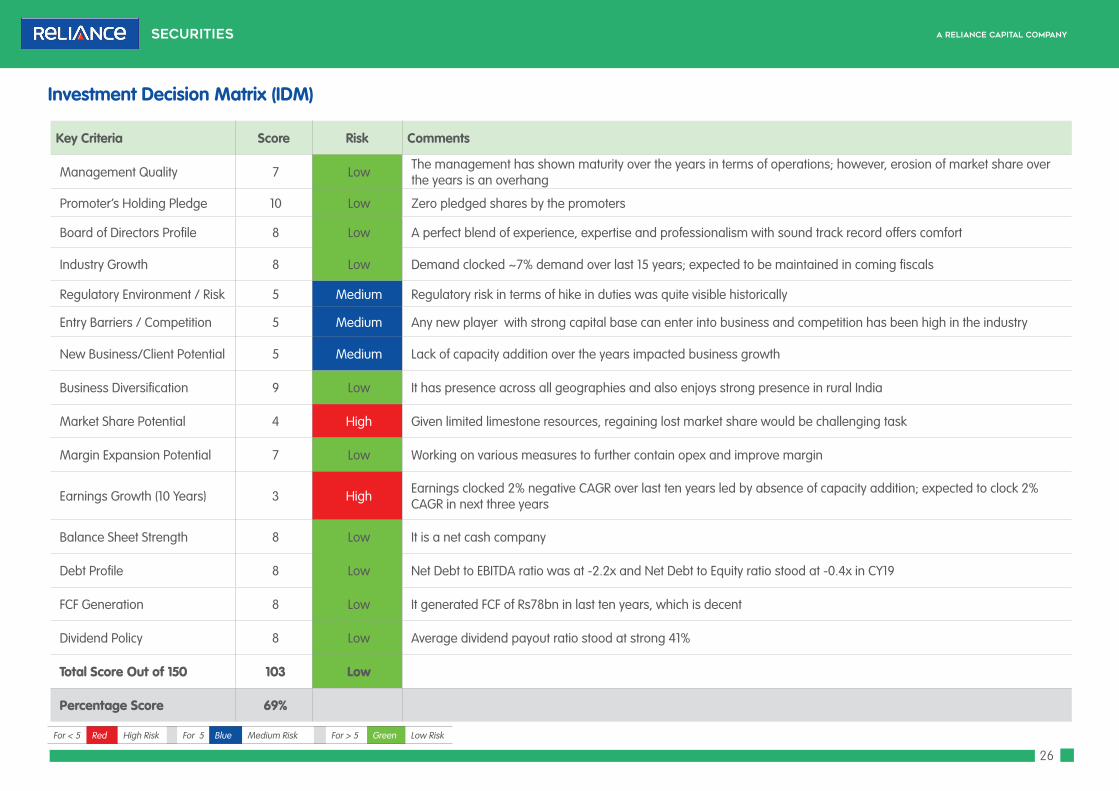

Key Criteria Score Risk Comments

Management Quality 7 Low The management has shown maturity over the years in terms of operations; however, erosion of market share over the years is an overhang

Promoter’s Holding Pledge 10 Low Zero pledged shares by the promoters

Board of Directors Profile 8 Low A perfect blend of experience, expertise and professionalism with sound track record offers comfort

Industry Growth 8 Low Demand clocked ~7% demand over last 15 years; expected to be maintained in coming fiscals

Regulatory Environment / Risk 5 Medium Regulatory risk in terms of hike in duties was quite visible historically

Entry Barriers / Competition 5 Medium Any new player with strong capital base can enter into business and competition has been high in the industry

New Business/Client Potential 5 Medium Lack of capacity addition over the years impacted business growth

Business Diversification 9 Low It has presence across all geographies and also enjoys strong presence in rural India

Market Share Potential 4 High Given limited limestone resources, regaining lost market share would be challenging task

Margin Expansion Potential 7 Low Working on various measures to further contain opex and improve margin

Earnings Growth (10 Years) 3 High Earnings clocked 2% negative CAGR over last ten years led by absence of capacity addition; expected to clock 2% CAGR in next three years

Balance Sheet Strength 8 Low It is a net cash company

Debt Profile 8 Low Net Debt to EBITDA ratio was at -2.2x and Net Debt to Equity ratio stood at -0.4x in CY19

FCF Generation 8 Low It generated FCF of Rs78bn in last ten years, which is decent

Dividend Policy 8 Low Average dividend payout ratio stood at strong 41%

Total Score Out of 150 103 Low

Percentage Score 69%

Investment Decision Matrix (IDM)

For < 5 Red High Risk For 5 Blue Medium Risk For > 5 Green Low Risk

27

Exhibit 1: Scenario Analysis

CY19 CY20E CY21E CY22E CAGR (CY20E-CY22E)

Base Case

Volume (mnT) 28.9 25.0 28.3 30.3 10.1%

Realization/tonne (Rs) 4,171 4,206 4,279 4,279 0.9%

Revenue 153,431 135,535 152,659 165,024 10.3%

EBITDA 20,959 19,359 19,869 22,162 7.0%

EBITDA/tonne 672 722 652 683

EBITDA margin (%) 13.7 14.3 13.0 13.4

APAT 13,589 13,259 13,159 14,431 4.3%

Target EV/EBITDA multiple (x) 11.5

Target Price 1,718

Bull Case

Volume (mnT) 28.9 25.6 29.9 33.2 14.0%

Realization/tonne (Rs) 4,171 4,939 5,080 5,207 2.7%

Revenue 153,431 139,210 165,888 187,256 16.0%

EBITDA 20,959 20,523 25,481 30,823 22.6%

EBITDA/tonne 672 751 804 884

EBITDA margin (%) 13.7 14.7 15.4 16.5

APAT 13,589 14,115 17,305 20,822 21.5%

Target EV/EBITDA multiple (x) 12.0

Target Price 2,291

Bear Case

Volume (mnT) 28.9 24.6 27.2 27.7 6.0%

Realization/tonne (Rs) 4,862 4,871 4,759 4,736 -1.4%

Revenue 153,431 132,937 143,088 145,428 4.6%

EBITDA 20,959 18,400 15,851 14,685 -10.7%

EBITDA/tonne 672 694 532 478

EBITDA margin (%) 13.7 13.8 11.1 10.1

APAT 13,589 12,552 10,191 8,916 -15.7%

Target EV/EBITDA multiple (x) 11.0

Target Price 1,227

Source: RSec Research

Scenario AnalysisBase Case: In base case scenario, we assume 10% volume CAGR over CY20E-CY22E with 0.9% growth in realization. Revenue, EBITDA and APAT are expected to clock 10%, 7% and 4% CAGR, respectively over the same period.

Bull Case: In bull case scenario, we assume 14% volume CAGR over CY20E-CY22E with 2.7% growth in realization. Revenue, EBITDA and APAT are expected to clock 16%, 23% and 22% CAGR, respectively over the same period.

Bear Case: In bear case scenario, we assume 6% volume CAGR over CY20E-CY22E with 1.4% de-growth in realization. Revenue, EBITDA and APAT are expected to clock 5%, -11% and -16% CAGR, respectively over the same period.

28

I. Strong Brand Equity & Healthy Rural PresenceACC – being one of the oldest cement manufacturers in India – enjoys strong brand equity especially in the trade segment with sound distribution reach in rural India. While the company has been losing its market share with no meaningful capacity addition, its strong distribution network comprising of >50,000 dealers/distributors has been the prime growth driver. Notably, ACC continues to remain placed amongst the Top-5 cement companies across regions barring the Northern markets.

II. Capacity Expansion Moving SatisfactorilyCapacity constraints have been the major cause of concern for ACC for last couple of years despite healthy balance sheet. With ongoing capacity expansion of 5.9mnT in strong demand potential markets, the said concern appears to have subsided. Further, we understand that all units in Uttar Pradesh and Jharkhand enjoy fiscal incentives, as per the policy of respective state governments. Though ACC has not secured any limestone mine in last four years, we believe it is still having abundant limestone reserves in Southern and Eastern units for next leg of expansion.

III. Value-added Premium Products & Services Augur WellACC’s blended realization growth has been surpassing industry’s average for last couple of quarters on the back of focus on VAPS. Its VAPS revenue grew by 36% YoY and 52% YoY in CY18 and CY19, respectively. Further, premium products volume now accounts for ~15-20% of its total volume. Currently, ACC has ~5 different premium brands. Further, foray into adhesive business with different range of products has already started aiding its margin. We believe continued traction in premium products segment is likely to enable ACC to enjoy better pricing at blended level, going ahead.

Exhibit 2: Change in Estimates

Y/E Mar CY20E CY21E CY22E

(Rsmn) Old Revised % change Old Revised % change Introduction

Volume (mnT) 25.5 25.0 (2.0) 27.3 28.3 3.9 30.3

Realization (Rs/tonne) 4,822 4,904 1.7 4,888 4,900 0.3 4,974

Sales (Rs mn) 1,36,026 1,35,535 (0.4) 1,46,804 1,52,659 4.0 1,65,024

EBITDA (Rs mn) 16,739 19,359 15.7 18,312 19,869 8.5 22,162

EBITDA/tonne (Rs) 604 722 19.4 621 652 4.9 683

APAT (Rs mn) 10,558 13,259 25.6 11,150 13,159 18.0 14,431

EPS (Rs) 56.2 70.5 25.6 59.3 70.0 18.0 76.8

Source: RSec Research

Exhibit 3: Cost per tonne Analysis and Assumptions (Rs)

Rs/tonne CY16 CY17 CY18 CY19 CY20E CY21E CY22E

Raw Materials 1,006 1,040 1,080 1,087 1,086 1,123 1,131

Employees 328 312 311 299 320 310 319

Power & Fuel 938 1,036 1,057 1,084 1,067 1,078 1,089

Freight 1,155 1,317 1,414 1,401 1,415 1,430 1,444

Other Exps. 712 635 635 713 758 744 729

Realisation 4,379 4,565 4,672 4,862 4,904 4,900 4,974

Source: RSec Research

Investment RationaleOur investment thesis is based on the following premises:

f Strong Brand Equity & Healthy Rural Presence

f Capacity Expansion Moving Satisfactorily

f Value-added Premium Products & Services Augur Well

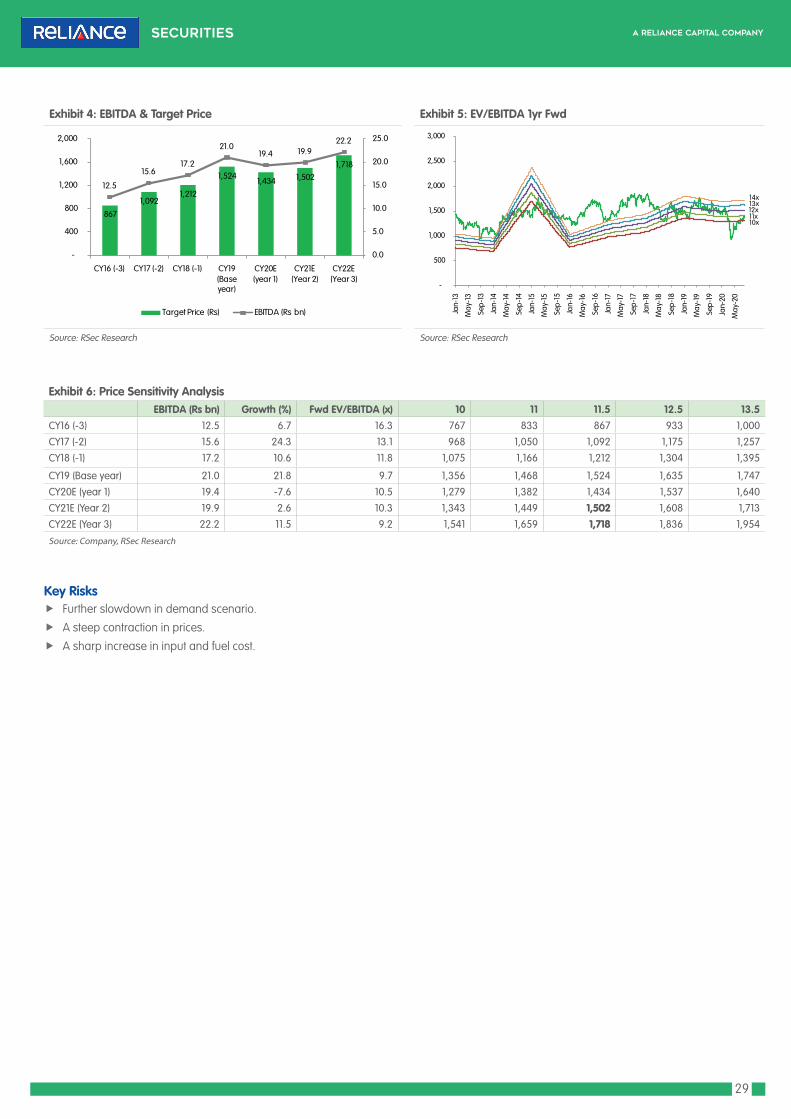

29

Exhibit 6: Price Sensitivity Analysis EBITDA (Rs bn) Growth (%) Fwd EV/EBITDA (x) 10 11 11.5 12.5 13.5CY16 (-3) 12.5 6.7 16.3 767 833 867 933 1,000

CY17 (-2) 15.6 24.3 13.1 968 1,050 1,092 1,175 1,257

CY18 (-1) 17.2 10.6 11.8 1,075 1,166 1,212 1,304 1,395

CY19 (Base year) 21.0 21.8 9.7 1,356 1,468 1,524 1,635 1,747

CY20E (year 1) 19.4 -7.6 10.5 1,279 1,382 1,434 1,537 1,640

CY21E (Year 2) 19.9 2.6 10.3 1,343 1,449 1,502 1,608 1,713

CY22E (Year 3) 22.2 11.5 9.2 1,541 1,659 1,718 1,836 1,954

Source: Company, RSec Research

Key Risks f Further slowdown in demand scenario.

f A steep contraction in prices.

f A sharp increase in input and fuel cost.

Exhibit 4: EBITDA & Target Price Exhibit 5: EV/EBITDA 1yr Fwd

Source: RSec Research Source: RSec Research

867

1,092 1,212

1,524 1,434 1,502

1,718

12.5

15.617.2

21.019.4 19.9

22.2

0.0

5.0

10.0

15.0

20.0

25.0

-

400

800

1,200

1,600

2,000