Bahasa

Halaman

Hukum

Ann Oper Res (2007) 151:241–267

DOI 10.1007/s10479-006-0118-4

A conditional-SGT-VaR approach with alternativeGARCH models

Turan G. Bali · Panayiotis Theodossiou

Published online: 7 December 2006C© Springer Science + Business Media, LLC 2007

Abstract This paper proposes a conditional technique for the estimation of VaR and expected

shortfall measures based on the skewed generalized t (SGT) distribution. The estimation of

the conditional mean and conditional variance of returns is based on ten popular variations

of the GARCH model. The results indicate that the TS-GARCH and EGARCH models

have the best overall performance. The remaining GARCH specifications, except in a few

cases, produce acceptable results. An unconditional SGT-VaR performs well on an in-sample

evaluation and fails the tests on an out-of-sample evaluation. The latter indicates the need

to incorporate time-varying mean and volatility estimates in the computation of VaR and

expected shortfall measures.

Keywords GARCH models . Skewed generalized t distribution . Conditional value at risk .

Expected shortfall

1 Introduction

Value at Risk (VaR) techniques are widely used to assess the risk exposure of investments.

The VaR for a portfolio is simply an estimate of a specified percentile of the probability

distribution of the portfolio’s returns over a given holding period. The specified percentile

is usually computed for the lower tail of the distribution of returns. For example, a VaR

threshold for the first percentile of daily returns implies that daily loses greater than the VaR

threshold will occur less than 1% of the time.

T. G. Bali (�)Professor of Finance, Department of Economics & Finance, Zicklin School of Business,Baruch College, CUNY, 55 Lexington Avenue, Box B10-225, New York, NY 10010e-mail: Turan [email protected]

P. TheodossiouRutgers University, School of Business,227 Penn Street, Camden, NJ 08102e-mail: [email protected]

Springer

242 Ann Oper Res (2007) 151:241–267

Calculation of portfolio VaR is often based on the variance-covariance approach and

makes the assumption, among other things, that returns follow the normal distribution. Many

researchers show that this assumption is at odds with reality and often leads to misleading VaR

estimates.1 There is substantial empirical evidence showing that the distribution of financial

returns is typically skewed to the left, is peaked around the mean (leptokurtic) and has fat

tails.2 The leptokurtosis is reduced, but not eliminated, when returns are standardized using

time-varying estimates for the means and variances [see Bollerslev, Engle, and Nelson (1994)

and the references therein].

The solutions proposed in the VaR literature to the aforementioned problems are the use of

(a) historical simulation techniques, (b) student’s t , (c) generalized error distribution (GED)

and (d) mixture of two normal distributions. Each of these solutions deals partially with the

issues of skewness and leptokurtosis and cannot fully correct the underestimation of risk

problem.3

This paper proposes a conditional technique for the estimation of VaR measures based on

the skewed generalized t (SGT) distribution of Theodossiou (1998), henceforth called the

conditional-SGT-VaR technique. The SGT provides a flexible tool for modeling the empirical

distribution of financial data exhibiting skewness, leptokurtosis and fat-tails.4 The estimation

of the conditional mean and conditional variance of returns, needed for the implementation

of the technique, is based on several popular variations of the GARCH model. The suitability

of these GARCH models in computing conditional-SGT-VaR measures is also addressed in

the paper.

Although VaR measures constitute a significant advancement over the more traditional

measures mostly based on sensitivities to market variables, their computation can often be a

formidable task in the case of complex portfolios exposed to risks associated with different

risk drivers. Moreover, their computation cannot be split into separate sub-computations

due to the position and risk non-additivity of VaR measures.5 For this reason, Artzner et al.

(1997, 1999) and Delbaen (1998) consider an alternative downside risk measure known as

the “expected shortfall measure.” The latter is simply the conditional expectation of loss of

an investment, given that this loss is beyond the VaR level. This paper also compares the

relative performance of the SGT and normal distributions in constructing expected shortfall

measures of raw and standardized returns.

1 See Longin (2000), McNeil and Frey (2000), Bali (2003), Bali and Neftci (2003), and Seymour and Polakow(2003) among others.2 The fat tails could be attributed to price jumps, the correlations between shocks and changes in volatility,time-varying volatility and other higher order moment dependencies3 Cummins et al. (1990) investigate the use of a four parameter family of probability distributions, the gen-eralized beta of the second kind (GB2), for modeling insurance loss processes, and find that seemingly slightdifferences in modeling the tails can result in large differences in reinsurance premiums and quantiles forthe distribution of total insurance losses. Mittnik and Paolella (2000) and Giot and Laurent (2003) use askewed version of the student-t distribution in calculating VaR. Heikkinen and Kanto (2002) use the symmet-ric student-t density to estimate unconditional value at risk. Jondeau and Rockinger (2003) provide severaleconometric specifications for estimating the conditional volatility, skewness, and kurtosis, which can used tocalculate conditional VaR thresholds.4 The literature on conditional VaR models and their applications to portfolio management is a very large one,e.g., Rockafeller and Uryasev (2000), Krokhmal, Palmquist, and Uryasev (2002), Krokhmal, Uryasev, andZrazhevsky (2002), and Topaloglou, Vladimirou, and Zenios (2002).5 Given a portfolio made of two sub-portfolios, total VaR is not given by the sum of partial VaR’s, with theconsequence that adding a new instrument to a portfolio often make it necessary to re-compute the VaR forthe whole portfolio. For a portfolio depending on multiple risk variables, VaR is not the sum of partial VaR’s.So, for instance, for a convertible bond, VaR is not simply the sum of its interest rate VaR and equity VaR.

Springer

Ann Oper Res (2007) 151:241–267 243

The paper is organized as follows. Section 2 presents discrete time GARCH models.

Section 3 describes the data and presents the estimation results for the GARCH models.

Section 4 presents the Conditional-SGT-VaR approach. Section 5 compares the in-sample

and out-of-sample performance of the conditional-SGT-VaR and conditional-Normal-VaR

measures for the GARCH models. Section 6 provides expected shortfall estimates based on

the SGT and normal distributions. Section 7 concludes the paper.

2 Discrete time GARCH models

Modeling volatility of economic time series has been a popular topic for financial economists

during the past two decades. Engle (1982) developed the Autoregressive Conditional Het-

eroskedasticity (ARCH) model, which was extremely useful in modeling time-varying

volatility of financial data series. Following the introduction of the ARCH model and its

generalization by Bollerslev (1986), there have been numerous refinements of the model

driven by empirical regularities in financial data.6

This paper investigates the suitability of ten variations of the GARCH model in computing

the conditional means and conditional variances for our conditional VaR analysis. The general

form of the GARCH models is as follows:

Rt = α0 + α1 Rt−1 + ut = μt + ut , (1)

g(σt ) = h(σt−1, zt−1, , β0, β1, γ ) + β2g(σt−1,), (2)

g (σt ) = σt , σ2t , or ln (σt ) ,

where μt and σt are the conditional mean and conditional standard deviation of returns Rt

based on the information set �t−1 up to time t−1 and zt = ut /σt .7 The conditional volatility

equations for the various GARCH models are specified as follows:8

AGARCH: Asymmetric GARCH model of Engle (1990)

σ 2t = β0 + β1(γ + σt−1zt−1)2 + β2σ

2t−1, (3)

EGARCH: Exponential GARCH model of Nelson (1991)

ln σ 2t = β0 + β1[|zt−1| − E(|zt−1|)] + β2 ln σ 2

t−1 + γ zt−1, (4)

6 ARCH literature surveys can be found in Bollerslev, Chou, and Kroner (1992), Ding, Granger, and Engle(1993), Bollerslev, Engle, and Nelson (1994), Andersen (1994), Bera, and Higgins (1995), Hentschel (1995),Pagan (1996), Duan (1997), and Bali (2000).7 For simplicity of exposition, we only present GARCH of first order (single-lag) models for both the condi-tional mean and conditional variance specifications. However, in the estimation we considered higher ordermodels as well and explored the possibility of GARCH-in-mean effects.8 One can define the ARCH processes based on the error term, ut , without decomposing ut into standardizedshock, zt , and the conditional volatility, σt . For example, the symmetric GARCH model of Bollerslev (1986)in Eq. (5) can simply be written as σ 2

t = β0 + β1u2t−1 + β2σ

2t−1.

Springer

244 Ann Oper Res (2007) 151:241–267

GARCH: Linear symmetric GARCH model of Bollerslev (1986)

σ 2t = β0 + β1σ

2t−1z2

t−1 + β2σ2t−1, (5)

GJR-GARCH: Threshold GARCH model of Glosten, Jagannathan, and Runkle (1993)

σ 2t = β0 + β1σ

2t−1z2

t−1 + β2σ2t−1 + γ S−

t−1σ2t−1z2

t−1

S−t−1 = 1 for σt−1zt−1 < 0 and S−

t−1 = 0 otherwise, (6)

IGARCH: Integrated GARCH model of Engle and Bollerslev (1986)

σ 2t = β0 + (1 − β2)σ 2

t−1z2t−1 + β2σ

2t−1, (7)

NGARCH: Nonlinear asymmetric GARCH model of Engle and Ng (1993)

σ 2t = β0 + β1σ

2t−1(γ + zt−1)2 + β2σ

2t−1, (8)

QGARCH: Quadratic GARCH model of Sentana (1995)9

σ 2t = β0 + β1σ

2t−1z2

t−1 + β2σ2t−1 + γ σt−1zt−1, (9)

SQR-GARCH: Square-Root GARCH model of Heston and Nandi (1999)10

σ 2t = β0 + β1(γ σt−1 + zt−1)2 + β2σ

2t−1, (10)

TGARCH: Threshold GARCH model of Zakoian (1994)

σt = β0 + β1σt−1|zt−1| + β2σt−1 + γ S−t−1σt−1zt−1

S−t−1 = 1 for σt−1zt−1 < 0 and S−

t−1 = 0 otherwise, (11)

TS-GARCH: The specification proposed by Taylor (1986) and Schwert (1989)

σt = β0 + β1σt−1|zt−1| + β2σt−1, (12)

VGARCH: A version proposed in Engle and Ng (1993)

σ 2t = β0 + β1(γ + zt−1)2 + β2σ

2t−1, (13)

where β0 > 0, 0 ≤ β1 < 1, 0 ≤ β2 < 1 and γ < 0. The conditional volatility parameter γ

allows for asymmetric volatility response to past positive and negative information shocks.

9 In the QGARCH (1,1) model, σ 2t = β0 + β1σ

2t−1z2

t−1 + β2σ2t−1 + γ σt−1zt−1 , positivity of the variance

is achieved when β1, β2 ≥ 0 and γ ≤ 4β0 β1 [Sentana (1995, p. 652)]. To impose these restrictions, one canestimate the likelihood function with the AGARCH model σ 2

t = ρ20 + ρ2

1 (σt−1zt−1 − κ)2 + ρ22σ 2

t−1 , where

β0 = ρ20 + ρ2

1κ2, β1 = ρ21 , β2 = ρ2

2 , and γ = −2ρ21κ . Since both QGARCH and AGARCH models give the

same conditional volatility and VaR estimates, we do not report results from the QGARCH specification.10 Equation (10) converges in the limit to the stochastic variance process of Cox, Ingersoll, and Ross (1985).

Springer

Ann Oper Res (2007) 151:241–267 245

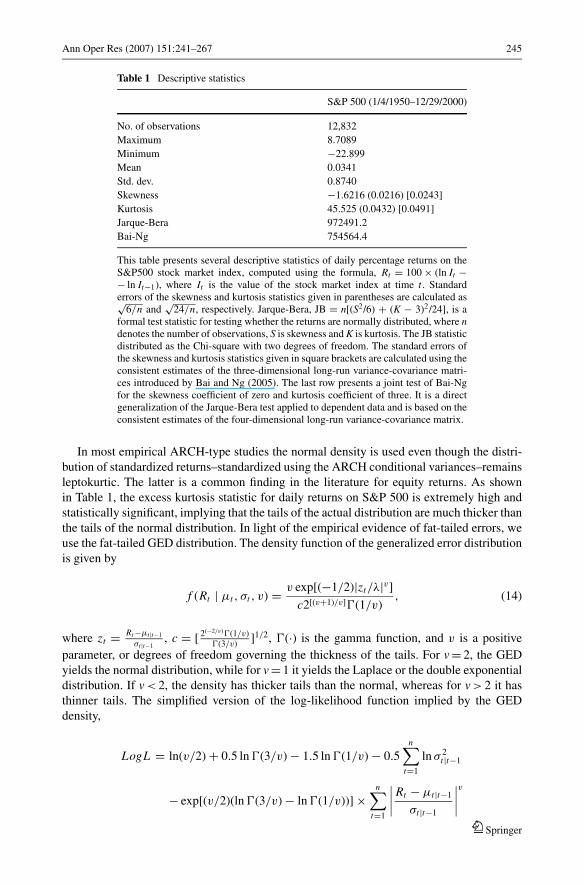

Table 1 Descriptive statistics

S&P 500 (1/4/1950–12/29/2000)

No. of observations 12,832

Maximum 8.7089

Minimum −22.899

Mean 0.0341

Std. dev. 0.8740

Skewness −1.6216 (0.0216) [0.0243]

Kurtosis 45.525 (0.0432) [0.0491]

Jarque-Bera 972491.2

Bai-Ng 754564.4

This table presents several descriptive statistics of daily percentage returns on theS&P500 stock market index, computed using the formula, Rt = 100 × (ln It −− ln It−1), where It is the value of the stock market index at time t . Standarderrors of the skewness and kurtosis statistics given in parentheses are calculated as√

6/n and√

24/n, respectively. Jarque-Bera, JB = n[(S2/6) + (K − 3)2/24], is aformal test statistic for testing whether the returns are normally distributed, where ndenotes the number of observations, S is skewness and K is kurtosis. The JB statisticdistributed as the Chi-square with two degrees of freedom. The standard errors ofthe skewness and kurtosis statistics given in square brackets are calculated using theconsistent estimates of the three-dimensional long-run variance-covariance matri-ces introduced by Bai and Ng (2005). The last row presents a joint test of Bai-Ngfor the skewness coefficient of zero and kurtosis coefficient of three. It is a directgeneralization of the Jarque-Bera test applied to dependent data and is based on theconsistent estimates of the four-dimensional long-run variance-covariance matrix.

In most empirical ARCH-type studies the normal density is used even though the distri-

bution of standardized returns–standardized using the ARCH conditional variances–remains

leptokurtic. The latter is a common finding in the literature for equity returns. As shown

in Table 1, the excess kurtosis statistic for daily returns on S&P 500 is extremely high and

statistically significant, implying that the tails of the actual distribution are much thicker than

the tails of the normal distribution. In light of the empirical evidence of fat-tailed errors, we

use the fat-tailed GED distribution. The density function of the generalized error distribution

is given by

f (Rt | μt , σt , v) = v exp[(−1/2)|zt/λ|v]

c2[(v+1)/v](1/v), (14)

where zt = Rt −μt |t−1

σt |t−1, c = [ 2(−2/v)(1/v)

(3/v)]1/2, (·) is the gamma function, and v is a positive

parameter, or degrees of freedom governing the thickness of the tails. For v = 2, the GED

yields the normal distribution, while for v = 1 it yields the Laplace or the double exponential

distribution. If v < 2, the density has thicker tails than the normal, whereas for v > 2 it has

thinner tails. The simplified version of the log-likelihood function implied by the GED

density,

LogL = ln(v/2) + 0.5 ln (3/v) − 1.5 ln (1/v) − 0.5n∑

t=1

ln σ 2t |t−1

− exp[(v/2)(ln (3/v) − ln (1/v))] ×n∑

t=1

∣∣∣∣ Rt − μt |t−1

σt |t−1

∣∣∣∣vSpringer

246 Ann Oper Res (2007) 151:241–267

yields parameter estimates which are not excessively influenced by extreme observations

that occur with low probability. In addition, the standard errors of the estimated parameters

are robust, allowing for more reliable statistical inference. Another advantage of using the

fat-tailed GED distribution is that one can formally test the empirical validity of existing

models that assume normality.

3 Data and estimation results

The data consist of daily returns on the S&P500 composite index from 1/4/1950 to 12/29/2000

(12832 observations). The computation of the index returns (Rt ) is based on the formula,

Rt = ln(It ) − ln(It−1), where It is the value of the stock market index for period t.11

Table 1 presents several preliminary statistics for the data. The unconditional mean of daily

log-returns is 0.0341% with a standard deviation of 0.87%. The maximum and minimum

values are 8.71% and −22.90%, respectively. The skewness statistic is negative and statis-

tically significant at the 1% level implying that the distribution of daily S&P500 returns is

skewed to the left. The excess kurtosis statistic is very large and significant at the 1% level,

implying that the distribution of returns has much ticker tails than the normal distribution.

Similarly, the Jarque-Bera statistic is also very large and statistically significant, rejecting

the assumption of normality.12

Next we use the Bai and Ng (2005) test for the joint hypothesis that the skewness and

kurtosis coefficients are respectively zero and three. The latter test is a direct generalization

of the aforementioned Jarque-Bera test for data that are serially correlated.13 The Bai and Ng

test statistics, reported in Table 1, reject the null hypothesis at the 1% level of significance.

Panels A and B of Table 2 present the maximum likelihood estimates for the symmetric

and asymmetric GARCH models based on the generalized error and the normal distributions.

The parameters in the conditional mean and conditional variance equations are all statistically

significant at the 1% level. The estimation results reveal the presence of strong conditional

volatility in the S&P500 return series. For example, the symmetric GARCH parameters, β1

and β2, are found to be highly significant and the sum β1 + β2 is close to one. This implies

the existence of strong volatility persistence in stock market returns.

As discussed earlier, for the tail thickness parameter v = 2, the GED density equals the

standard normal density. However, the estimates of v turn out to be highly significant and

less than two for each GARCH model specification. As shown in Panel A of Table 2, the

estimated values for the degrees of freedom parameter v, range between 1.24 and 1.34. A

11 We also examined the DJIA, NASDAQ composite and NYSE stock market indices. Because the qualitativeresults were similar, we present the results for the S&P500 index only. Results on these indices are availableupon request.12 De Ceuster and Trappers (1992) and Peiro (1999) show that the standard test of skewness is not appropriatewhen the series is fat-tailed. For a sample size of 2000 observations, De Ceuster and Trappers (1992) tabulatethat the 95% confidence intervals of the skewness of Student-t distributed observations with a kurtosis of3.5 and 18 are respectively (–0.131; 0.127) and (–0.814; 0.787), i.e., the higher the kurtosis, the larger theconfidence bands of the skewness. Table 3 presents the skewness and kurtosis parameter estimates of SGTand skewed t distributions that give the statistical significance of skewness parameter (λ) after adjusting fortail-thickness of the return distribution.13 Bai and Ng (2005) show that when the data are serially correlated, consistent estimates of three-dimensionallong-run covariance matrices are needed for testing skewness and kurtosis. In the special case of normality,they introduce a joint test for the skewness coefficient of zero and kurtosis coefficient of three based on thefour-dimensional long-run covariance matrix.

Springer

Ann Oper Res (2007) 151:241–267 247

Tabl

e2

Max

imu

mli

kel

iho

od

esti

mat

eso

fth

eG

AR

CH

mo

del

sw

ith

GE

Dan

dn

orm

ald

ensi

ty

Mo

del

sα

0α

1β

0β

1β

2γ

VL

og-L

LR

Pan

elA

.G

ener

aliz

eder

ror

dis

trib

uti

on

AG

AR

CH

0.0

00

34

0.1

23

60

.00

00

00

40

.08

51

0.8

96

9−0

.00

34

41

.33

62

44

87

4.5

01

30

.88

(6.1

72

6)

(14

.42

0)

(2.8

07

6)

(18

.24

7)

(19

6.7

7)

(−1

1.2

68

)(−

50

.62

2)

EG

AR

CH

0.0

00

36

0.1

25

1−0

.35

72

0.1

83

30

.96

24

−0.0

56

71

.24

12

44

87

1.8

31

12

.55

(6.8

47

5)

(15

.59

8)

(−9

.85

20

)(3

1.7

63

)(2

60

.30

)(−

9.9

06

9)

(−5

3.1

75

)

GA

RC

H0

.00

04

70

.12

07

0.0

00

00

10

0.0

86

10

.90

32

0.0

1.3

21

94

48

09

.06

Sy

mm

etri

c

(8.7

48

2)

(14

.23

0)

(8.9

17

9)

(18

.96

7)

(18

8.8

9)

(−5

0.5

06

)

GJR

GA

RC

H0

.00

03

70

.12

43

0.0

00

00

11

0.0

42

30

.89

89

−0.0

90

51

.33

75

44

86

3.6

61

09

.20

(6.8

96

7)

(14

.53

2)

(10

.09

5)

(8.4

39

4)

(19

0.6

5)

(−1

1.7

73

)(−

49

.73

6)

NG

AR

CH

0.0

00

33

0.1

24

80

.00

00

01

10

.08

13

0.8

77

1−0

.60

09

1.3

44

74

48

95

.14

17

0.1

6

(6.0

47

7)

(14

.59

2)

(10

.48

6)

(17

.11

5)

(16

6.8

5)

(−1

1.4

74

)(−

50

.01

9)

SQ

RG

AR

CH

0.0

00

23

0.1

27

50

.00

00

00

30

.00

00

04

0.8

83

9−1

16

.69

1.3

17

54

47

89

.88

21

0.6

8

(4.1

51

2)

(15

.31

7)

(5.9

15

3)

(14

.10

2)

(14

9.5

8)

(−1

3.3

40

)(−

53

.56

4)

TG

AR

CH

0.0

00

34

0.1

28

40

.00

02

72

0.1

54

40

.88

53

−0.0

95

91

.31

54

44

84

5.7

71

52

.04

(6.3

14

0)

(16

.68

8)

(23

.62

5)

(26

.68

3)

(24

6.8

3)

(−1

5.0

67

)(−

50

.71

3)

TS

GA

RC

H0

.00

04

90

.12

66

0.0

00

23

80

.11

15

0.8

86

40

.01

.29

66

44

76

9.7

5S

ym

met

ric

(9.4

78

7)

(16

.54

9)

(22

.51

6)

(24

.91

3)

(23

9.1

9)

(−5

1.2

64

)

VG

AR

CH

0.0

00

20

0.1

26

10

.00

00

00

10

.00

00

04

0.9

35

5−0

.74

78

1.3

11

74

47

80

.17

19

1.2

6

(3.5

94

8)

(15

.15

6)

(9.4

18

3)

(15

.16

5)

(25

1.8

9)

(−1

8.7

83

)(−

54

.76

7)

(Con

tinu

edon

next

page

.)

Springer

248 Ann Oper Res (2007) 151:241–267

Tabl

e2

(Con

tinu

ed).

Mo

del

sα

0α

1β

0β

1β

2γ

Log

-LL

R

Pan

elB

.N

orm

ald

istr

ibu

tio

n

AG

AR

CH

0.0

00

25

0.1

41

10

.00

00

00

90

.09

49

0.8

83

4−0

.00

30

24

44

89

.32

14

7.3

0

(3.9

79

0)

(15

.02

4)

(13

.64

4)

(41

.88

7)

(33

7.7

0)

(−2

1.4

10

)

EG

AR

CH

0.0

00

25

0.1

34

1−0

.38

97

0.1

83

90

.97

42

−0.0

64

34

45

13

.67

31

2.4

9

(4.2

91

9)

(15

.02

9)

(−2

8.8

89

)(5

7.2

06

)(7

68

.96

)(−

30

.59

4)

GA

RC

H0

.00

04

30

.13

71

0.0

00

00

14

0.0

97

50

.88

83

0.0

44

41

5.6

7S

ym

met

ric

(8.1

37

7)

(14

.98

8)

(19

.83

1)

(47

.06

8)

(34

1.9

4)

GJR

GA

RC

H0

.00

02

80

.14

09

0.0

00

00

15

0.0

49

50

.88

66

−0.0

91

94

44

87

.95

14

4.5

6

(4.8

42

6)

(15

.27

8)

(22

.32

6)

(16

.38

0)

(31

5.8

1)

(−2

2.6

08

)

NG

AR

CH

0.0

00

22

0.1

43

10

.00

00

01

50

.08

97

0.8

67

1−0

.54

90

44

52

4.1

82

17

.02

(3.6

47

6)

(15

.42

1)

(23

.12

6)

(34

.89

0)

(30

1.6

0)

(−2

0.6

19

)

SQ

RG

AR

CH

0.0

00

09

0.1

54

00

.00

00

00

30

.00

00

05

0.8

78

4−1

08

.41

44

37

7.6

13

08

.16

(1.5

10

3)

(17

.53

6)

(8.7

48

6)

(36

.98

1)

(38

6.6

0)

(−3

0.5

65

)

TG

AR

CH

0.0

00

26

0.1

52

20

.00

03

88

0.1

73

50

.85

81

−0.0

98

34

44

33

.02

19

2.2

2

(4.7

61

1)

(22

.71

9)

(39

.56

8)

(64

.62

9)

(41

6.2

6)

(−2

9.3

87

)

TS

GA

RC

H0

.00

05

00

.15

50

0.0

00

34

20

.13

27

0.8

58

30

.04

43

36

.91

Sy

mm

etri

c

(9.9

42

8)

(23

.16

0)

(36

.51

0)

(70

.95

2)

(40

4.7

1)

VG

AR

CH

0.0

00

05

0.1

48

20

.00

00

00

10

.00

00

05

0.9

27

4−0

.64

52

44

35

3.0

62

59

.06

(0.8

66

0)

(16

.65

3)

(10

.78

2)

(44

.89

6)

(45

7.6

2)

(−3

7.2

51

)

Pan

elA

and

Bp

rese

nt

the

max

imu

mli

kel

iho

od

esti

mat

eso

fth

eG

AR

CH

mo

del

sw

ith

GE

Dan

dN

orm

ald

ensi

ty.T

he

asy

mp

toti

ct-

stat

isti

csar

esh

own

inp

aren

thes

es.T

he

t-st

atis

tics

fro

mte

stin

gw

het

her

v=

2(i

.e.,

wh

eth

erth

ere

turn

sfo

llow

an

orm

ald

istr

ibu

tio

n)

are

giv

enin

par

enth

eses

un

der

v.L

og-L

isth

em

axim

ized

log

-lik

elih

oo

dva

lue.

LR

isth

elo

g-l

ikel

ihood

rati

ote

stst

atis

tics

for

the

null

hypoth

esis

of

sym

met

ric

GA

RC

Hm

odel

s,i.

e.,γ

=0

.

Springer

Ann Oper Res (2007) 151:241–267 249

comparison of the maximized log-likelihood values of the GED and normal log-likelihood

specifications for each GARCH model indicates that v is statistically different from two. The

latter implies that the distribution of daily (standardized) returns is leptokurtic relative to the

normal distribution. Moreover, the results suggest that the double exponential or Laplace

with v = 1 is a more appropriate than the normal density function. An intuitive understanding

can be gained by realizing that for the normal distribution (v = 2) the degree of kurtosis is

equal to 3, while for the double exponential or Laplace distribution (v = 1) the degree of

kurtosis is equal to 6.

A notable point in Table 2 is that the asymmetry parameter γ of the conditional volatility

equations is highly significant. This parameter allows for an asymmetric volatility response

in the diffusion function to past positive and negative information shocks. It is found to be

negative for all volatility models implying that negative shocks exert larger impact on stock

market volatility than positive shocks of the same magnitude. This finding may be the result

of the leverage or the initial margin requirements, e.g., Hardouvelis and Theodossiou (2002).

The presence of asymmetry in return volatility is further evaluated using a likelihood ratio

(LR) based on the sample log-likelihood functions of the asymmetric and symmetric GARCH

models. Specifically, LR = −2(LogL∗–LogL), where LogL

∗and LogL are respectively the

maximized log-likelihood values under the null hypothesis of γ = 0 and the alternative

hypothesis of γ 0. The LR statistic follows the χ2(1) distribution with one degree of freedom.

The LR statistics in Table 2 are well above the critical value, reconfirming the presence of

asymmetric volatility in the return series.

4 A conditional value at risk approach

The discrete time version of the geometric Brownian motion governing financial price move-

ments is:

Rt = ln (Pt+�t ) − ln (Pt ) = μ∗�t + zσ ∗√�t, (15)

where μ∗ and σ ∗ are the annualized mean and standard deviation of Rt , �t is the length of time

between two successive prices and �Wt = z√

�t is a discrete approximation of the Wiener

process. The latter term has mean zero, variance �t and follows the normal distribution.14

In the case of time-varying mean and variance, the above equation can be modified to reflect

these dependencies as:

Rt = μ∗t �t + zσ ∗

t

√�t, (16)

where μ∗t and σ ∗

t are annualized measures of conditional mean and conditional standard

deviation of the log-return Rt . This paper employs daily data, thus the length of time �treflects that of a trading day and is approximately equal to 1/252. For simplicity, the above

equation can be rewritten as

Rt = μt + zσt , (17)

14 The method presented here can also be applied to profits and losses generated by portfolios of financialassets.

Springer

250 Ann Oper Res (2007) 151:241–267

where μt = μ∗t �t and σt = σ ∗

t

√�t are respectively the conditional mean and conditional

standard deviation of daily returns. Note that the standardized return z = (Rt −μt )/σ t pre-

serves the properties of zero mean and unit variance.

There is substantial empirical evidence showing that the distributions of returns of fi-

nancial assets are typically skewed to the left and peaked around the mode and, have fat

tails. The fat tails suggest that extreme outcomes happen much more frequently than would

be predicted by the normal distribution. Similarly, the distribution of standardized returns,

although normalized, follows a similar pattern.

The conditional threshold for Rt at a given coverage probabilityø, denoted by θ t , is obtained

from the solution of the following cumulative distribution of returns,

Pr(Rt ≤ θt | �t−1) ≡∫ θt

−∞f (Rt | �t−1)d Rt = φ, (18)

where Pr(·) denotes the probability and f (Rt | �t−1) is the conditional probability density

function for Rt .

The above probability function can be written in terms of the standardized returns as

follows:

Pr (Rt ≤ θt | �t−1) = Pr

(Rt − μt

σt≤ θt − μt

σt

∣∣∣∣ �t−1

)= Pr

(z ≤ a = θt − μt

σt

)=

∫ a

−∞f (z) dz = φ, (19)

where the density f(z) and the threshold a associated with the coverage probability φ do not

depend on the information set �t−1. The latter is a byproduct of the assumption that the series

of standardized returns z is identically and independently distributed. The latter assumption

is consistent with empirical evidence related to the GARCH models for stock returns.

The skewed generalized t (SGT) probability density function for the standardized residuals

is:

f = C

(1 + |z + δ|k

((n + 1) | k)(1 + sign(z + δ)λ)kθ k

)− n+1k

(20)

where

C = .5 k

(n + 1

k

)− 1k

B

(n

k,

1

k

)−1

θ−1,

θ = 1/√

g − ρ2,

δ = ρθ,

ρ = 2λB

(n

k,

1

k

)−1 (n + 1

k

) 1k

B

(n − 1

k,

2

k

),

Springer

Ann Oper Res (2007) 151:241–267 251

Table 3 Maximum likelihood estimates of alternative distribution functions

Distribution μ σ λ k N Log-L

SGT 0.00036 0.008501 −0.02455 1.60084 5.2113 43948.62

(4.8204)∗∗ (86.631)∗∗ (−2.2302)∗ (26.421)∗∗ (12.791)∗∗

Generalized t 0.00045 0.00853 0 1.62115 5.0227 43948.21

(7.2617)∗∗ (83.557)∗∗ (26.168)∗∗ (13.063)∗∗

Skewed t 0.00099 0.00875 −0.02647 2 3.6890 43938.56

(3.7824)∗∗ (60.960)∗∗ (−2.1958)∗ (27.569)∗∗

Symmetirc t 0.00044 0.00875 0 2 3.6889 43936.32

(7.0147)∗∗ (61.074)∗∗ (27.608)∗∗

Normal 0.00034 0.00874 0 2 ——- 42611.27

(4.2735)∗∗ (733.25)∗∗

This table presents the parameter estimates of the SGT, Generalized t , Skewed t , Symmetric t , and Normaldistributions. The results are based on the daily raw returns on the S&P 500 composite index spanning theperiod 1/4/1950–12/29/2000 (12832 observations). Asymptotic t−statistics are given in parentheses. Log-L isthe maximized log-likelihood value. ∗,∗∗ denote significance at the 5% and 1% level, respectively.

and

g = (1 + 3λ2

)B

(n

k,

1

k

)−1 (n + 1

k

) 2k

B

(n − 2

k,

3

k

).

λ is a skewness parameter obeying the constraint |λ| < 1, n and k are positive kurtosis

parameters, sign is the sign function, B(·) is the beta function and δ is the Pearson’s skewness

and mode of f(z). The SGT parameters are obtained from the maximization of the sample

log-likelihood function

L =T∑

t=1

ln f (zt | n, k, λ), (21)

with respect to n, k, and λ; see Theodossiou (1998) for the estimation details.

The SGT nests several well-known distributions. Specifically, it gives for λ = 0 the

generalized-t of McDonald and Newey (1988), for k = 2 the skewed t of Hansen (1994),

for n = ∞ the skewed generalized error distribution, for n = ∞ and λ = 0 the generalized

error distribution or power exponential distribution of Subbotin (1923) [used by Box and

Tiao (1962) and Nelson (1991)], for n = ∞, λ = 0 and k = 1 the Laplace or double expo-

nential distribution, for n = ∞, λ = 0 and k = 2 the normal distribution and for n = ∞, λ = 0

and k = ∞ the uniform distribution [see Hansen, McDonald, and Theodossiou (2001) for a

comprehensive survey on the skewed fat-tailed distributions].

Table 3 presents the parameter estimates of the SGT of Theodossiou (1998), the gener-

alized t of McDonald and Newey (1988), the skewed t of Hansen (1994), the symmetric

standardized t of Bollerslev (1987), and the normal distribution. The LR test results indicate

rejection of the skewed t , symmetric t and normal distributions in favor of the SGT. The gen-

eralized t of McDonald and Newey cannot be rejected based on the maximized log-likelihood

values.15

15 For the SGT and normal distributions, we calculated the Kolmogorov-Smirnov (KS) statistic for testing thenull hypothesis that the data follow the corresponding distribution function. The KS statistic of 0.06393 for

Springer

252 Ann Oper Res (2007) 151:241–267

Table 4 presents the estimated SGT parameters for the standardized returns of the GARCH

models. Observe that in all cases, the parameter n is close to six indicating significant fat tails

for the empirical distribution of standardized returns. The parameter k has values close to those

of the normal distribution (i.e., two) indicating no peakness for the empirical distribution.

The skewness parameter is negative and statistically significant for all models indicating that

the distribution of standardized returns is skewed to the left. The LR-Normal ratio for testing

the null hypothesis of normality of standardized returns against that of the SGT is large and

highly significant rejecting the null hypothesis of normality.

Given the probability density function of standardized returns f(z), the threshold a can be

easily obtained from the solution of the equation

∫ a

−∞f (z) dz = φ. (22)

That is, by finding the numerical value of a that equalizes the area under f(z) to the coverage

probability φ . In the case of traditional VaR analysis (normal distribution), the value of the

threshold for φ = 1% is constant and equal a = −2.326.16 However, in the more general case

of the SGT, the value of a is a function of the skewness and kurtosis parameters λ, k and n.

Given the estimated threshold a, the conditional (time-varying) threshold for the returns

can be computed using the equation

θt = μt + aσt , (23)

where the values of μt and σ t are based on anyone of the AR(1)-GARCH models presented

previously. This equation is used to compute the conditional 1-day VaR thresholds and

evaluate the performance and suitability of the GARCH models, considered in the paper, and

the conditional-SGT-VaR technique.17,18

the normal distribution indicates rejection of the null hypothesis at the 1% level, whereas the KS statistic of0.00928 for SGT suggests that the index return data follow the SGT distribution.16 The values of a for the normal distribution associated with the 0.5%, 1%, 1.5%, 2%, 2.5%, and 5% VaRtails are 2.5758, 2.326, 2.1701, 2.0536, 1.960, and 1.645, respectively.17 We should note that the conditional mean-volatility models given in Eqs. (1)–(13) are estimated in a firststep and the tail distributions in a second step because of the absence of SGT-GARCH computer programs.Currently, we do not have the estimation technology for SGT-GARCH models. However, to check the ro-bustness of our findings, we use alternative distributions in the first step estimation. For example, our tablespresent results based on the generalized error distribution (GED). At an earlier stage of the study, we alsouse the skewed generalized error distribution (SGED) of Theodossiou (2001), the generalized t distributionof McDonald and Newey (1988), and the skewed t distribution of Hansen (1994) in the first step estimation.Using the standardized returns obtained from the SGED, generalized t and Skewed t distributions, we calculatethe VaR measures based on the SGT density. The results turn out to be very similar to those reported in ourtables. This indicates that the second step estimation (i.e., estimation of tail distributions) is more crucial toVaR calculations.18 Engle and Manganelli (2004) introduce a conditional autoregressive VaR model based on the quintileregression approach. Wu and Xiao (2002) present a comprehensive analysis of several left-tail measures usingthe ARCH quintile regression approach.

Springer

Ann Oper Res (2007) 151:241–267 253

Tabl

e4

Par

amet

eres

tim

ates

of

the

SG

Td

istr

ibu

tio

nfo

rth

est

and

ard

ized

retu

rns

of

GA

RC

HM

od

els

AG

AR

CH

EG

AR

CH

GA

RC

HG

JRG

AR

CH

NG

AR

CH

SQ

RG

AR

CH

TG

AR

CH

TS

GA

RC

HV

GA

RC

HU

nco

nd

itio

nal

k2

.03

50

2.2

23

61

.95

73

2.0

10

82

.04

98

1.9

71

72

.07

78

1.9

84

01

.97

03

1.6

20

4

(26

.34

)∗∗

(24

.57

)∗∗

(26

.23

)∗∗

(26

.23

)∗∗

(26

.24

)∗∗

(26

.52

)∗∗

(25

.67

)∗∗

(25

.76

)∗∗

(26

.63

)∗∗

(26

.04

)∗∗

λ−0

.03

58

−0.0

26

6−0

.04

19

−0.0

40

5−0

.03

76

−0.0

28

5−0

.03

51

−0.0

37

3−0

.02

80

−0.0

24

7

(−2

.79

)∗∗

(−2

.01

)∗∗

(−3

.34

)∗∗

(−3

.17

)∗∗

(−2

.92

)∗∗

(−2

.26

)∗∗

(−2

.72

)∗∗

(−2

.96

)∗∗

(−2

.22

)∗∗

(−2

.22

)∗∗

n6

.52

23

5.8

19

46

.71

32

6.6

53

26

.54

28

6.6

11

36

.13

16

6.3

54

26

.55

88

5.0

36

0

(13

.59

)∗∗

(14

.21

)∗∗

(12

.44

)∗∗

(13

.08

)∗∗

(13

.56

)∗∗

(13

.01

)∗∗

(13

.99

)∗∗

(12

.78

)∗∗

(13

.19

)∗∗

(12

.94

)∗∗

S−0

.11

30

−0.0

84

7−0

.13

53

−0.1

27

3−0

.11

72

−0.0

92

5−0

.11

47

−0.1

24

5−0

.09

16

−0.1

38

6

K5

.29

31

5.6

02

35

.35

92

5.2

50

25

.23

46

5.3

92

55

.58

78

5.6

18

95

.44

50

12

.07

5

Log

-L−1

78

45

.54

−17

60

8.7

8−1

78

39

.65

−17

85

1.5

7−1

78

54

.07

−17

82

5.2

9−1

77

96

.02

−17

78

3.2

3−1

78

14

.49

−15

13

7.4

3

LR

-GE

D1

76

.86

∗∗2

02

.06

∗∗1

51

.86

∗∗1

67

.46

∗∗1

78

.20

∗∗1

60

.82

∗∗1

85

.78

∗∗1

57

.10

∗∗1

65

.42

∗∗4

56

2.8

2∗∗

LR

-No

rmal

97

0.9

0∗∗

87

1.0

8∗∗

94

6.0

5∗∗

93

4.6

2∗∗

94

0.1

8∗∗

99

2.3

0∗∗

10

11

.48

∗∗9

99

.42

∗∗1

03

1.6

8∗∗

70

71

.58

∗∗

Th

ista

ble

pre

sen

tsth

ep

aram

eter

esti

mat

esfo

rth

esk

ewed

gen

eral

ized

t(S

GT

)d

istr

ibu

tio

nu

sin

gth

est

and

ard

ized

retu

rns

of

allG

AR

CH

mo

del

s.T

he

stan

dar

diz

edre

turn

sar

eo

bta

ined

fro

mth

eG

ED

-AR

(1)-

GA

RC

Hsp

ecifi

cati

on

s.P

aren

thes

esin

clu

de

the

asy

mp

toti

ct-

stat

isti

csfo

rth

ep

aram

eter

so

ffa

t-ta

ils

n,le

pto

ku

rto

sis

kan

dsk

ewn

ess

λ.

San

dK

are

the

esti

mat

edsk

ewn

ess

and

ku

rto

sis

stat

isti

cso

fst

and

ard

ized

retu

rns.

Log

-Lis

the

max

imiz

edlo

g-l

ikel

iho

od

valu

eo

fth

eS

GT

den

sity

.L

R-N

orm

al(L

R-G

ED

)is

the

likel

ihood

rati

ost

atis

tic

from

test

ing

the

null

hypoth

esis

that

the

seri

esfo

llow

the

Norm

al(G

ED

)dis

trib

uti

on

agai

nst

the

SG

Tsp

ecifi

cati

on

.∗,∗

∗d

eno

tesi

gn

ifica

nce

atth

e5

%an

d1

%le

vel

s,re

spec

tivel

y.

Springer

254 Ann Oper Res (2007) 151:241–267

5 Risk measurement performance of conditional VaR models

In this section, we evaluate the in-sample and out-of-sample risk measurement performance

of conditional value at risk models based on the unconditional and conditional coverage test

statistics.

5.1 Evaluation of alternative GARCH-SGT-VaR specifications

Table 5 presents statistics on the VaR thresholds (a) of all models for the coverage probabilities

(φ) 0.5%, 1%, 1.5%, 2%, 2.5% and 5% using the entire sample. Specifically, columns 2 to

10 present statistics for the nine conditional GARCH-SGT-VaR models and the last column

presents the statistics for the unconditional-SGT-VaR model based on the standardized returns

computed using the unconditional model, i.e., constant mean and constant standard deviation

of returns.

The first row for each coverage probability presents the estimated thresholds of the ten

models. The second row presents the actual and expected (in parentheses) number of stan-

dardized returns (observations) that fall below each threshold. The third row presents the

log-likelihood ratio (LR) for testing the null hypothesis that the actual and the expected num-

ber of observations falling below each threshold are statistically the same. This is computed

using the formula

L R = 2[τ ln(τ/(φN )) + (N − τ ) ln((N − τ )/(N − φN ))], (24)

where N is the number of sample observations, φ is the coverage probability, φN is the

expected number andτ is the number of sample observations that falls below the threshold

a.19 Kupiec (1995) indicates that the LR statistic is uniformly the most powerful statistic for

a given sample and has an asymptotic chi-square distribution with one degree of freedom,

χ2(1). 20

For example, at φ = 1% the estimated threshold for the EGARCH standardized returns is

−2.5857. The expected number of observations that falls below the threshold a = −2.5857

is 128.32 (i.e., 1% of 12832 observations) and the actual number of observations is 122. The

LR statistic for evaluating the performance of the EGARCH model at φ = 1% is

L R = 2[122 ln(122/128.32) + (12,832 − 122) ln ((12,832 − 122)/

(12,832 − 128.32))] = 0.3197.

This LR statistic is statistically insignificant and indicates that the expected and actual number

of observations falling below the aforementioned threshold is statistically the same. The latter

implies that the estimated EGARCH-SGT-VaR threshold provides a good assessment of the

risk exposure of a portfolio mimicking the S&P500 index.

The conditional threshold θt could be computed easily from Eq. (23) by substituting the

estimates for the conditional mean and conditional standard deviation of returns. For example,

assuming that the conditional mean is 0.05% and the conditional standard deviation is 1.2%,

the risk exposure of the institution on a single day will be θt = μt +aσ t = 0.05% −2.5857

19 Assuming that the VaR measures are accurate, the variableτ can be modeled as independent draws form abinomial distribution, see Kupiec (1995).20 The critical value of χ2(1) at the 5% level is 3.841 and at the 1% level is 6.635.

Springer

Ann Oper Res (2007) 151:241–267 255

Tabl

e5

In-s

amp

lep

erfo

rman

ceo

fS

GT

dis

trib

uti

on

wit

hal

tern

ativ

eG

AR

CH

mo

del

sfo

rti

me-

vary

ing

VaR

thre

sho

lds

VaR

AG

AR

CH

EG

AR

CH

GA

RC

HG

JRG

AR

CH

NG

AR

CH

SQ

RG

AR

CH

TG

AR

CH

TS

GA

RC

HV

GA

RC

HU

nco

nd

itio

nal

0.5

%−3

.03

83

−3.0

25

6−3

.09

52

−3.0

56

8−3

.03

37

−3.0

31

3−3

.04

37

−3.0

92

9−3

.02

74

−2.8

07

1

N(0

.5%

)6

1(6

4)

57

(64

)6

0(6

4)

59

(64

)6

1(6

4)

56

(64

)5

9(6

4)

63

(64

)5

4(6

4)

55

(64

)

LR

0.1

60

.83

0.2

80

.43

0.1

61

.09

0.4

30

.02

1.7

11

.38

1%

−2.5

90

4−2

.58

57

−2.6

39

0−2

.60

79

−2.5

88

0−2

.58

05

−2.5

87

7−2

.63

09

−2.5

74

8−2

.30

64

N(1

%)

11

2(1

28

)1

22

(12

8)

11

8(1

28

)1

14

(12

8)

11

4(1

28

)1

07

(12

8)

11

7(1

28

)1

20

(12

8)

10

9(1

28

)1

13

(12

8)

LR

2.1

90

.32

0.8

61

.67

1.6

73

.79

1.0

40

.55

3.0

91

.92

1.5

%−2

.33

88

−2.3

41

2−2

.38

23

−2.3

55

2−2

.33

75

−2.3

27

1−2

.33

30

−2.3

72

3−2

.32

06

−2.0

33

8

N(1

.5%

)1

72

(19

2)

18

4(1

92

)1

73

(19

2)

17

0(1

92

)1

79

(19

2)

17

2(1

92

)1

66

(19

2)

18

0(1

92

)1

69

(19

2)

17

8(1

92

)

LR

2.2

90

.38

2.0

72

.77

0.9

82

.29

3.8

7∗

0.8

43

.02

1.1

3

2%

−2.1

63

9−2

.17

23

−2.2

03

7−2

.17

94

−2.1

63

2−2

.15

09

−2.1

56

6−2

.19

29

−2.1

44

0−1

.84

85

N(2

%)

23

4(2

57

)2

53

(25

7)

24

5(2

57

)2

37

(25

7)

23

5(2

57

)2

38

(25

7)

24

5(2

57

)2

43

(25

7)

24

0(2

57

)2

46

(25

7)

LR

2.0

90

.05

0.5

41

.57

1.9

11

.41

0.5

40

.75

1.1

20

.45

2.5

%−2

.02

98

−2.0

43

2−2

.06

67

−2.0

44

6−2

.02

96

−2.0

15

7−2

.02

17

−2.0

55

7−2

.00

86

−1.7

09

1

N(2

.5%

)3

29

(32

1)

31

7(3

21

)3

27

(32

1)

31

9(3

21

)3

19

(32

1)

30

2(3

21

)3

13

(32

1)

32

4(3

21

)3

02

(32

1)

31

9(3

21

)

LR

0.2

20

.05

0.1

20

.01

0.0

11

.15

0.1

90

.03

1.1

50

.01

5%

−1.6

17

7−1

.64

92

−1.6

45

9−1

.62

99

−1.6

18

8−1

.60

09

−1.6

09

2−1

.63

55

−1.5

93

2−1

.29

64

N(5

%)

64

3(6

42

)6

49

(64

2)

64

7(6

42

)6

41

(64

2)

64

7(6

42

)6

54

(64

2)

65

2(6

42

)6

54

(64

2)

66

3(6

42

)6

63

(64

2)

LR

0.0

00

.09

0.0

50

.00

0.0

50

.25

0.1

80

.25

0.7

50

.75

Aver

age

6.5

3%

3.9

5%

5.2

1%

6.4

6%

5.3

9%

9.0

8%

6.4

4%

3.7

2%

9.7

1%

6.8

7%

MA

%E

Th

ista

ble

pre

sen

tsst

atis

tics

on

the

in-s

amp

lep

erfo

rman

ceo

fS

GT

Dis

trib

uti

on

wit

hA

lter

nat

ive

GA

RC

Hm

od

els

for

tim

e-va

ryin

gV

aRth

resh

old

s.T

he

resu

lts

are

bas

edo

nth

est

and

ard

ized

retu

rns

on

S&

P5

00

span

nin

gth

ep

erio

d1

/4/1

95

0to

12

/29

/20

00

(12

83

2o

bse

rvat

ion

s).T

he

firs

tle

vel

of

nu

mb

ers

atea

chro

war

eth

ees

tim

ated

VaR

thre

sho

lds.

Th

ese

con

dle

vel

of

nu

mb

ers

giv

eth

eac

tual

cou

nts

and

the

exp

ecte

dco

un

tsin

par

enth

eses

(or

the

nu

mb

ero

fo

bse

rvat

ion

sfa

llin

gin

the

0.5

%,1

%,1

.5%

,2%

,2.5

%,a

nd

5%

tail

so

fth

ere

turn

dis

trib

uti

on

).T

he

thir

dle

vel

of

nu

mb

ers

are

the

corr

esp

on

din

gli

kel

iho

od

rati

o(L

R)

stat

isti

cs.

Aver

age

MA

%E

isth

eav

erag

em

ean

abso

lute

per

cen

tag

eer

ror

bas

edo

nth

eac

tual

and

exp

ecte

dco

un

ts.

∗,∗∗

den

ote

sig

nifi

can

ceat

the

5%

and

1%

level

s,re

spec

tivel

y.

Springer

256 Ann Oper Res (2007) 151:241–267

(1.2%) = −3.0528%. That is, on 100 million dollars investment the VaR amount would be

about 3.0528 million dollars.

The LR test statistic is embodied in the market risk amendment (MRA), which requires

commercial banks with significant trading activities to set aside capital to cover the market

risk exposure in their trading accounts. Under the MRA, banks report their VaR estimates to

the regulators, who observe when actual portfolio losses exceed these estimates. Rejection

of the null hypothesis implies that computed VaR estimates are not accurate enough.

The last row of Table 5 gives the average mean absolute percentage errors (MA%E) based

on the actual and expected counts. This is computed as:

MA%E = 1

6

6∑i=1

(τi − φi N

φi N

)(25)

where τ i and φi N are the actual and expected number of observations that fall below the

threshold for the coverage probabilities φ i = 0.5%, 1%, 1.5%, 2%, 2.5% and 5% and i = 1,

2, . . . ,6. Equation (25) measures the relative performance of conditional-SGT-VaR measures

for each GARCH model.

According to the LR statistics, all GARCH-SGT and unconditional-SGT models produce

accurate VaR estimates for the aforementioned coverage probabilities (tail probabilities).

The only exception is the VaR estimate for the TGARCH model at the 1.5% tail probability.

Based on the MA%E statistic, the TS-GARCH has the best overall performance, followed

closely by the EGARCH model. The GARCH and NGARCH model also exhibit good per-

formance. Among the ten GARCH models considered, the performance of the VGARCH

and SQRGARCH models is the worst.

Table 6 presents the same statistics based on a rolling-window holdout sample (out-

of-sample) procedure. This is necessary because in practice portfolio managers obtain VaR

estimates based on past data and subsequently use these estimates to assess the risks associated

with current and future movements of their portfolios’ value. Hence, a true assessment of

VaR’s performance should be based on their out-of-sample rather than estimation sample

(in-sample).

To measure the out-of-sample performance of the conditional-SGT-VaR measures, we pro-

ceed as follows: A 10-year rolling sample, starting 1/4/1950, is used to estimate conditional-

SGT-VaR measures and a 1-year holdout sample (year subsequent to the estimation) to

evaluate their performance. Specifically, the first rolling (estimation) sample includes the

returns for the years 1950 to 1959 (2,514 returns) and the first holdout sample includes the

returns for the year 1960. The estimated VaR thresholds (based on rolling sample) are then

used to compute the number of returns in the 1960 holdout sample falling in the 0.5%, 1%,

1.5%, 2%, 2.5%, and 5% tails of each estimated probability distribution. Next, the estimation

sample is rolled forward by removing the returns for the year 1950 and adding the returns for

the year 1960. Consequently, the new holdout sample includes the returns for the year 1961.

The new estimated VaR thresholds are then used to compute the number of returns in the new

holdout sample falling in the aforementioned tails. The procedure continues until the sample

is exhausted. Given that the returns on S&P500 span the period 1/4/1950 to 12/29/2000,

the 10-year rolling estimation procedure yields a total holdout sample of 41 years or 10302

observations.

The results of Table 6 are quite similar to those of Table 5. The only exceptions are the

results for the VGARCH for the coverage probabilities of 2.5% and 5% and the unconditional

VaR at all coverage probabilities. Based on the MA%E statistics, the TS-GARCH has the

Springer

Ann Oper Res (2007) 151:241–267 257

Tabl

e6

Ou

t-o

f-sa

mp

lep

erfo

rman

ceo

fS

GT

dis

trib

uti

on

wit

hal

tern

ativ

eG

AR

CH

mo

del

sfo

rti

me-

vary

ing

VaR

thre

sho

lds

VaR

AG

AR

CH

EG

AR

CH

GA

RC

HG

JRG

AR

CH

NG

AR

CH

SQ

RG

AR

CH

TG

AR

CH

TS

GA

RC

HV

GA

RC

HU

nco

nd

itio

nal

0.5

%−2

.94

75

−2.9

54

6−3

.02

37

−2.9

76

6−2

.94

50

−2.9

11

9−2

.94

47

−3.0

12

2−2

.91

28

−2.6

44

2

N(0

.5%

)4

8(5

1)

55

(51

)4

9(5

1)

46

(51

)4

6(5

1)

56

(51

)5

4(5

1)

53

(51

)5

1(5

1)

67

(51

)

LR

0.2

60

.22

0.1

30

.63

0.6

30

.37

0.1

10

.04

0.0

14

.23

∗

1%

−2.5

26

6−2

.53

51

−2.5

89

2−2

.55

15

−2.5

25

3−2

.49

14

−2.5

18

3−2

.57

46

−2.4

89

8−2

.18

45

N(1

%)

99

(10

3)

10

2(1

03

)1

00

(10

3)

97

(10

3)

10

1(1

03

)1

08

(10

3)

10

1(1

03

)1

04

(10

3)

10

3(1

03

)1

33

(10

3)

LR

0.1

70

.01

0.1

00

.38

0.0

50

.22

0.0

50

.01

0.0

07

.98

∗∗

1.5

%−2

.28

86

−2.3

00

8−2

.34

36

−2.3

11

0−2

.28

79

−2.2

54

0−2

.27

85

−2.3

28

2−2

.25

11

−1.9

33

8

N(1

.5%

)1

46

(15

4)

15

1(1

54

)1

45

(15

4)

15

0(1

54

)1

51

(15

4)

15

9(1

54

)1

41

(15

4)

14

7(1

54

)1

56

(15

4)

20

4(1

54

)

LR

0.5

10

.09

0.6

40

.15

0.0

90

.12

1.2

80

.40

0.0

11

4.4

6∗∗

2%

−2.1

22

4−2

.13

85

−2.1

72

1−2

.14

30

−2.1

22

0−2

.08

83

−2.1

11

5−2

.15

67

−2.0

84

7−1

.76

32

N(2

%)

21

6(2

06

)2

15

(20

6)

20

6(2

06

)2

05

(20

6)

20

8(2

06

)2

38

(20

6)

21

2(2

06

)2

02

(20

6)

23

2(2

06

)2

66

(20

6)

LR

0.4

50

.36

0.0

00

.01

0.0

14

.72

∗0

.16

0.0

93

.13

16

.13

∗∗

2.5

%−1

.99

45

−2.0

14

2−2

.04

03

−2.0

13

7−1

.99

44

−1.9

61

0−1

.98

33

−2.0

25

1−1

.95

69

−1.6

34

7

N(2

.5%

)2

67

(25

7)

26

5(2

57

)2

71

(25

7)

27

0(2

57

)2

66

(25

7)

30

2(2

57

)2

66

(25

7)

26

7(2

57

)2

97

(25

7)

33

7(2

57

)

LR

0.3

20

.20

0.6

70

.57

0.2

67

.32

∗∗0

.26

0.3

25

.79

∗2

2.6

9∗∗

5%

−1.5

99

0−1

.63

27

−1.6

33

2−1

.61

40

−1.5

99

5−1

.56

79

−1.5

88

3−1

.62

01

−1.5

62

4−1

.25

27

N(5

%)

54

9(5

15

)5

41

(51

5)

54

5(5

15

)5

53

(51

5)

54

7(5

15

)5

85

(51

5)

54

7(5

15

)5

46

(51

5)

58

6(5

15

)6

39

(51

5)

LR

2.1

91

.27

1.7

02

.75

1.9

49

.36

∗∗1

.94

1.8

29

.62

∗∗2

8.8

3∗∗

Aver

age

5.0

5%

3.8

8%

3.9

9%

5.1

9%

4.0

6%

10

.76

%4

.82

%3

.55

%7

.21

%2

9.5

5%

MA

%E

Th

ista

ble

pre

sen

tsst

atis

tics

on

the

ou

t-o

f-sa

mp

lep

erfo

rman

ceo

fS

GT

Dis

trib

uti

on

wit

hA

lter

nat

ive

GA

RC

Hm

od

els

for

tim

e-va

ryin

gV

aRth

resh

old

s.T

he

resu

lts

are

bas

edo

nth

est

and

ard

ized

retu

rns

on

S&

P5

00

and

the

tota

lo

ut-

of-

sam

ple

per

iod

1/4

/19

60

to1

2/2

9/2

00

0(1

03

02

ob

serv

atio

ns)

.T

he

firs

tle

vel

of

nu

mb

ers

atea

chro

war

eth

eav

erag

ees

tim

ated

VaR

thre

sho

lds.

Th

ese

con

dle

vel

of

nu

mb

ers

giv

eth

eav

erag

eac

tual

cou

nts

and

the

exp

ecte

dco

un

tsin

par

enth

eses

(or

the

nu

mb

ero

fo

bse

rvat

ion

sfa

llin

gin

the

0.5

%,1

%,1

.5%

,2

%,2

.5%

,an

d5

%ta

ils

of

the

retu

rnd

istr

ibu

tio

n).

Th

eth

ird

level

of

nu

mb

ers

are

the

corr

esp

on

din

gli

kel

iho

od

rati

o(L

R)

stat

isti

cs.A

ver

age

MA

%E

isth

eav

erag

em

ean

abso

lute

per

cen

tag

eer

ror

bas

edo

nth

eac

tual

and

exp

ecte

dco

un

ts.

∗,∗∗

den

ote

sig

nifi

can

ceat

the

5%

and

1%

level

s,re

spec

tivel

y.

Springer

258 Ann Oper Res (2007) 151:241–267

best overall performance, followed very closely by the EGARCH, GARCH and NGARCH

models. Again, the VGARCH and SQRGARCH perform the worst. The fact that the uncon-

ditional VaR model performs poorly is indicative of the need to use VaR models that account

for time-varying mean and standard deviation of returns.

5.2 Evaluation of alternative GARCH-normal-VaR specifications

Table 7 presents statistics on the in-sample performance of Normal distribution with alter-

native GARCH models for estimating time-varying VaR thresholds. Specifically, columns

2 to 10 show statistics for the nine conditional GARCH-Normal-VaR models and the last

column displays the statistics for the Integrated GARCH (IGARCH) specification which is

very close to the RiskMetrics model.

In its most simple form, the RiskMetrics model is equivalent to the IGARCH model with

normally distributed errors, σ 2t = β0 + (1 − β2)σ 2

t−1z2t−1 + β2σ

2t−1, where the intercept β0 is

restricted at zero and the autoregressive parameter β2 is set at a pre-specified value λ and

the coefficient of σ 2t−1z2

t−1 is equal to 1 – λ. In the original RiskMetrics specification, λ is

assumed to be 0.94 for daily data and the error process is assumed to follow a normal density,

ut = σt zt , where zt is i.i.d. N(0,1) and σ 2t is defined as:

σ 2t = (1 − λ)u2

t−1 + λσ 2t−1 (26)

In this paper, we prefer to estimate a slightly generalized version of the RiskMetrics model

and thus do not restrict β0 at zero.

According to the LR statistics in Table 7, all the GARCH models with normal density

produce inaccurate VaR estimates for the 0.5%, 1%, and 1.5% loss probability levels. In

fact, the GARCH and IGARCH models yield acceptably accurate VaR measures only for the

5% loss probability level. Based on the MA%E statistics, the performance of the GARCH-

Normal and IGARCH-Normal (RiskMetrics) models turns out to be worse than the alternative

volatility specifications. The results in Tables 5 and 7 indicate that among the ten GARCH

models considered in the paper, the conditional SGT distribution performs much better than

the conditional Normal distribution.

Table 8 presents the same statistics based on a rolling-window holdout sample (out-of-

sample) procedure. The procedure used to evaluate the performance of conditional-SGT-

VaR measures is utilized to determine the out-of-sample performance of the conditional-

Normal-VaR measures. Specifically, we use a 10-year rolling sample, starting 1/4/1950, to

estimate conditional-SGT-VaR measures and a 1-year holdout sample (year subsequent to

the estimation) to evaluate their performance. The results in Table 8 are quite similar to those

of Table 7. Based on the LR and MA%E statistics, the asymmetric GARCH models have

slightly better performance than the GARCH-Normal and IGARCH-Normal (RiskMetrics)

specifications. However, comparing Tables 6 and 8 provides strong evidence that the out-of-

sample performance of the conditional SGT distribution is superior to the conditional Normal

distribution.

5.3 Conditional coverage test

As discussed by Christoffersen (1998), VaR estimates can be viewed as interval forecasts of

the lower tail of the return distribution. Interval forecasts can be evaluated conditionally and

Springer

Ann Oper Res (2007) 151:241–267 259

Tabl

e7

In-s

amp

lep

erfo

rman

ceo

fn

orm

ald

istr

ibu

tio

nw

ith

alte

rnat

ive

GA

RC

Hm

od

els

for

tim

e-va

ryin

gV

aRth

resh

old

s

VaR

AG

AR

CH

EG

AR

CH

GA

RC

HG

JRG

AR

CH

NG

AR

CH

SQ

RG

AR

CH

TG

AR

CH

TS

GA

RC

HV

GA

RC

HIG

AR

CH

0.5

%−2

.57

40

−2.5

75

7−2

.59

92

−2.5

79

9−2

.57

12

−2.5

51

4−2

.57

36

−2.6

02

7−2

.54

40

−2.5

55

3

N(0

.5%

)1

10

(64

)1

14

(64

)1

25

(64

)1

13

(64

)1

08

(64

)1

05

(64

)1

13

(64

)1

25

(64

)1

04

(64

)1

23

(64

)

LR

27

.10

∗∗3

1.5

9∗∗

45

.36

∗∗3

0.4

4∗∗

24

.97

∗∗2

1.9

1∗∗

30

.44

∗∗4

5.3

6∗∗

20

.92

∗∗4

2.7

1∗∗

1%

−2.3

24

2−2

.32

58

−2.3

49

6−2

.33

02

−2.3

21

5−2

.30

19

−2.3

24

3−2

.35

35

−2.2

94

5−2

.30

99

N(1

%)

16

0(1

28

)1

66

(12

8)

17

6(1

28

)1

66

(12

8)

16

6(1

28

)1

67

(12

8)

17

1(1

28

)1

81

(12

8)

16

2(1

28

)1

77

(12

8)

LR

7.3

4∗∗

10

.24

∗∗1

6.0

5∗∗

10

.24

∗∗1

0.2

4∗∗

10

.77

∗∗1

3.0

0∗∗

19

.39

∗∗8

.25

∗∗1

6.7

0∗∗

1.5

%−2

.16

83

−2.1

69

9−2

.19

37

−2.1

74

3−2

.16

56

−2.1

46

1−2

.16

87

−2.1

98

0−2

.13

53

−2.1

56

8

N(1

.5%

)2

21

(19

2)

22

2(1

92

)2

33

(19

2)

22

7(1

92

)2

22

(19

2)

22

8(1

92

)2

26

(19

2)

23

5(1

92

)2

20

(19

2)

23

4(1

92

)

LR

4.1

0∗

4.3

9∗

8.1

3∗∗

5.9

6∗

4.3

9∗

6.3

0∗

5.6

2∗

8.9

3∗∗

3.8

4∗

8.5

2∗∗

2%

−2.0

51

8−2

.05

33

−2.0

77

3−2

.05