Zenith and the HDTV Challenge - test

41

Zenith and the HDTV Challenge This case was written by Will Mitchell at the University of Michigan’s Business School. “Zenith is committed to establishing an American leadership position in high definition television,” commented the CEO, , Jerry Pearlman, in 1988. High resolution flat tension mask (FTM) color monitors, a technology in which Zenith has uncontested leadership, is a cornerstone in Zenith’s strategic thrust. Now it was February 1993, and the Federal Communications Commission (FCC) had just announced that more tests would be necessary before deciding on the high definition television (HDTV) standard. Japan’s analog system had already been rejected. Europe’s strategy was having a myriad of problems, the most recent being Philip’s announcement to suspend plans to mass produce TV sets compatible to the European Community’s (EC’s) preferred HDTV standard. Ironically, the United States, which abhors formalizing industrial policy, may end up with the most advanced (digital) standard. Japanese and European policy makers worried more about setting a homemade (analog) standard than about achieving a world class (digital) standard. Adopting an advanced standard and doing advanced research does not, however, guarantee significant industry participation. The success of the HDTV industry depends not only on the TV manufacturers, but also on the simultaneous adoption of the new technology by broadcasting stations, program producers and transmission companies. Zenith lost $51.6 million in 1991 and $106 million in 1992, even though operating expenses were cut by $38 million in 1990 and $59 million in 1991. At the same time the company had committed nearly it’s entire display R&D budget to FTM ($65 million over 5 years). In 1989 Zenith teamed up with AT&T, and in 1991 with Scientific Atlanta, to consolidate its position in the emerging HDTV industry. A number of critical questions needed to be answered. Should Zenith’s technological lead in FTM’s be further developed or should Zenith begin developing new technologies? Even if new technologies were pursued for the long run, how could Zenith best capitalize on it’s superior FTM technology today? Would HDTV really be a breakthrough product or would it remain an “amorphous” technology? Were the consumers really “asking” for a clearer picture? Would the Japanese eventually adopt the U.S. standard? Was it pragmatic to assume that the U.S. could really gain an up to five years head start by quickly adopting a digital standard? And should Zenith capitalize on its superior HDTV technology and enter into alliances with leaders in the Japanese electronics industry in order to learn and strengthen its future position in consumer electronics?

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Zenith and the HDTV Challenge - test

Zenith and the HDTV Challenge

This case was written by Will Mitchell at the University of Michigan’s Business School.

“Zenith is committed to establishing an American leadership position in high definitiontelevision,” commented the CEO,, Jerry Pearlman, in 1988. High resolution flat tensionmask (FTM) color monitors, a technology in which Zenith has uncontested leadership,is a cornerstone in Zenith’s strategic thrust.

Now it was February 1993, and the Federal Communications Commission (FCC) hadjust announced that more tests would be necessary before deciding on the highdefinition television (HDTV) standard. Japan’s analog system had already beenrejected. Europe’s strategy was having a myriad of problems, the most recent beingPhilip’s announcement to suspend plans to mass produce TV sets compatible to theEuropean Community’s (EC’s) preferred HDTV standard.

Ironically, the United States, which abhors formalizing industrial policy, may end upwith the most advanced (digital) standard. Japanese and European policy makersworried more about setting a homemade (analog) standard than about achieving aworld class (digital) standard. Adopting an advanced standard and doing advancedresearch does not, however, guarantee significant industry participation. The successof the HDTV industry depends not only on the TV manufacturers, but also on thesimultaneous adoption of the new technology by broadcasting stations, programproducers and transmission companies.

Zenith lost $51.6 million in 1991 and $106 million in 1992, even though operatingexpenses were cut by $38 million in 1990 and $59 million in 1991. At the same timethe company had committed nearly it’s entire display R&D budget to FTM ($65 millionover 5 years). In 1989 Zenith teamed up with AT&T, and in 1991 with ScientificAtlanta, to consolidate its position in the emerging HDTV industry.

A number of critical questions needed to be answered. Should Zenith’s technologicallead in FTM’s be further developed or should Zenith begin developing newtechnologies? Even if new technologies were pursued for the long run, how couldZenith best capitalize on it’s superior FTM technology today? Would HDTV really be abreakthrough product or would it remain an “amorphous” technology? Were theconsumers really “asking” for a clearer picture? Would the Japanese eventually adoptthe U.S. standard? Was it pragmatic to assume that the U.S. could really gain an up tofive years head start by quickly adopting a digital standard? And should Zenithcapitalize on its superior HDTV technology and enter into alliances with leaders in theJapanese electronics industry in order to learn and strengthen its future position inconsumer electronics?

2

HDTV

For the first time in almost fifty years the definition of American television was about tochange with the development of HDTV. Today’s television will be replaced by asystem that offers sharp, clear and larger images with excellent audio and is “smart”like a computer.

Initially, HDTV sets will probably be large screen models. However, HDTV will requirethe integration of a number of technologies: semiconductor, software, multimedia,displays, compression, VCR, compact disc (see Exhibit 1 for details).

The HDTV standards winner would gain the right to royalties on any HDTV set orbroadcasting system using its technology. Dale Cripps, editor of the HDTV newsletter,estimates royalties at $5 a set or about $110 million/year assuming 22 million HDTV’swill be sold at the peak of acceptance. Royalties from broadcasters could amount to afew million more. The head of the Advanced TV Advisory Committee, former FCCChairman Richard Wiley, encouraged contenders to combine forces to move towardthe standard faster. Thus, contestants may be forced to share their bounty.

Electronics Industry and HDTV

In 1992, the consumer electronics industry was waiting for a new growth stimulus. U.S.annual sales of consumer electronics were $33 billion, Japanese sales were $35 billionand European sales were $42 billion. Historically, the industry has been driven bymajor innovations and life cycles of the gramophone (1920s), the radio (1930s), theB/W-TV (1950s), the color TV (1960s), Hi-Fi (1970s) and the VCR (1980s). Recentproduct introductions such as CDs, DAT and 8mm camcorders, however, have notpresented major technological breakthroughs, nor has the trend toward productproliferation refueled sales.

Table 1: World Electronics Industry1

Product 1991 World Sales(in $ billions)

TV Hardware 7.0VCR 3.0Camcorder 3.0TV Advertising 29.0Movies 6.0Video Cassette Rental 14.0Video Games 5.0PC Hardware 50.0PC Software 12.0

3

In 1991, annual sales growth rates of consumer electronics have decreased from 50%to 3.5% with 99% of all Japanese and U.S. households having at least one color TV,80% a VCR and 65% a stereo system. Unfortunately, many fear that the move toHDTV will be far less successful than the move from black and white to color.

In response to lower margins, shorter product life cycles, lower sales growth andcompetition from Taiwan and Korea, the industry has been consolidating. In Japan,Akai was taken over by Mitsubushi and Aiwa became a subcontractor for Sony.Thompson, the French company (82% owned by the state), took over Thorn. MajorGerman manufacturers, Blaupunkt and Telefuken have also been acquired byThompson. Both firms are dependent upon product, process and competenttechnology from Japan. For example, DAT and VCR technology are supplied by JVC,video-disk player technology is supplied by Pioneer and comcorder technology issupplied by Hitachi. Philips, a global electronics firm of Dutch origin, reported a loss of$2.5 billion in 1991.

In 1992, three firms, Sony, Matsushita and Sharp held the strongest position in theemerging HDTV industry. Unlike their weakened world competitors, these companiessustain their R&D spending at more than 6% of sales. As a result, HDTV may be theopportunity for a few Japanese companies to take a major lead in consumerelectronics.

Distribution Trends

During the 1980s, the users of VCR’s and CD players drew annual increases of 15% to20% in sales for retailers. Traditionally, manufacturers have used a two stepdistribution process in which the distributors provide after sales service through partsavailability, advertising support and warehousing. However, this distribution systemhas become too expensive due to shorter product life cycles, lower margins andincreased product variety. Further, as cost reductions in manufacturing have becomemore elusive, producers have focused their attention on distribution costs. Labor, forexample, only accounts for 10% to 20% of manufacturing costs. Thus, manufacturersof late are enforcing minimum order requirements from retailers. Hitachi, for example,requires a $15,000 minimum order.

As a result of their distribution economies and purchasing power vís-a-vísmanufacturers, electronic superstores have replaced small retailers, distributors anddepartment stores. They enjoy large advertising budgets and an assortment of 2,000to 2,500 stock keeping units (SKU) along a large continuum of price points. Inaddition, they receive price discounts for early purchase commitments. In 1991, CircuitCity (a leading U.S. retailer), had sales of $5.5 billion through 200 stores. It dominatedthe metropolitan areas and offered extensive customer service, such as homeinstallation. In 1990, 220 retailers accounted for 70% of total consumer electronicsales in the U.S. Twelve accounts alone represented 65% of Thompson’s sales in theU.S.

4

HDTV and Multimedia Trends

As a digital system, the TV will change from a passive receiver to an integratedinteractive entertainment center. As a telecomputer with multimedia capability, HDTVwill affect electronic products and entertainment markets. While digital HDTV is beingdeveloped, intermediate technologies have arisen. Large monitors with integratedvideo recorders and CD players are a case in point. These intermediary systems arelower in both price and quality. Offering systems at this intermediate stage of industryevolution, however, educates consumers, establishes brand names, developsdistribution systems, influences standards and produces feedback for future HDTVdesigns. Further, alliances in this market might develop standards in software andhardware which might become important in HDTV.

A computer attached to a HDTV could, for example, customize a movie’s sound track,colors and ultimately the viewing perspective. Furthermore, the high demands thatvideo processing poses on semiconductors has accelerated the rate of semiconductorinnovation benefiting all areas of computing. In 1991, total world semiconductor saleswere $55.5 billion per year. By the end of the decade, the consumer electronics portionof semiconductor sales alone is forecast to reach $48 billion in annual sales.

Japanese HDTV

Initially, Japan led the world by pursuing an analog transmission technology: MUSE(multiple sub-nyquist sampling encoding). This technology—developed in 1965 as ahybrid digital-analog system—is already obsolete according to some analysts.1

HDTV is still relatively expensive in Japan. Sharp has announced a low-end HDTVwhich will cost one million Yen, compared to current HDTVs for Y3-Y5 million. Thisprice reduction has been achieved at the expense of picture quality. Sharp bases itsstrategy on a market forecast that at a price of Y1 million, 16% of all Japanesehouseholds would buy a HDTV set. Given the trend toward large screen TVs in Japan(50% of TV screens are 32-inches or longer), the ministry of Post &Telecommunications (MPT) projects that 40% of all Japanese households will own aHDTV set by the year 2000. This represents a market value of $9.6 billion.2

Sharp’s product introduction was backed by the Japanese broadcasting organization(NHK), which increased HDTV broadcasting from one hour to eight hours in November1991. Sony and Matsushita Electric Industrial have already spent hundreds of millionsof dollars developing manufacturing facilities for HDTV. Based upon historicalevidence of substitutions, the price of HDTV must decrease to within three to fourtimes the price of a color TV, for a mass market to emerge (it took the color TV twelveyears after its introduction to outsell B/W). This would correspond to an installed baseof about $40 billion worldwide by the year 2000.3

5

As of 1992, three main groups were developing the chip set for MUSE. NHK, NEC,Toshiba and Matsushita were able to reduce the number of chips needed for theJapanese HDTV standard, MUSE, to about 100. Fujitsu, Hitachi, Sony and TI workingin tandem, have nearly completed co-development of a thirty chip set for MUSE. LSILogic and Sanyo announced that they intend to reduce the number of chips required toless than ten. Logic-Sanyo were the first to attempt building a chip set with onlyapplication specific integrated circuits (ASIC). Meanwhile, LSI Logic has joinedanother consortium including NEC, Matsushita, Mitsubishi Electric, VLSI Technologyand Sharp, which plan to reduce the number of chips down to 19. In each of theseconsortia, no U.S. firm contributes digital signal processing. TI is responsible fordeveloping frame memory circuits. VLSI is working on color processing and LSI oncircuits for sound processing.

To arouse public interest in HDTV, the Ministry of Post and Telecommunications (MPT)provides Japanese cities with systems through the High Vision Program. The HighVision Center Project was started in 1987 to set up pilot tests in Japanese cities forpublic HDTV theaters and public centers for interactive access to large scaledatabases. The Key Technology Research Center in conjunction with the Ministry ofInternational Trade and Industry (MITI), the MPT and the Ministry of Finance, aresubsidizing development of critical HDTV components. This is achieved through lowinterest loans, extending a 26% permanent tax credit and allowing accelerateddepreciation of assets in the electronic sector.

European HDTV

To counter the threat of Japanese domination of HDTV, the EC has invested nearly $2billion to create a rival system, MAC. MAC has largely been developed by Thompsonand Philips in a public policy vacuum. In December 1991, Thompson announced a$6000 TV which uses an intermediary D2MAC standard. On December 19, 1991, ECTelecommunication Ministers agreed not to force an immediate conversion of currentbroadcasters and satellite channels to MAC. Channels launched after 1994, however,will be required to cane MAC broadcasting equipment.

With the demise of British Satellite Broadcasting, the only European broadcasterscurrently offering D2MAC TV are Canal Plus and Antenne 2, both French companies.Thompson and BIS, a Bosch-Philips joint venture, delivered a thirteen hours per dayHDTV service from the 1992 Winter Olympic Games. The project was funded by theFrench government, the French Telecom and the EC Commission. Without softwareor broadcasters, MAC has been advancing slowly.

The European market is expected to reach $20 billion by the year 2000, with aninstalled base to 500,000 units. By 2004, only 9% of European households will owndigital HDTV sets. Since Europe has a negative trade balance of $35 billion inelectronics, however, European champions like Bull, Thompson, Philips and Siemens

6

may lobby to protect the market. Both Europe and Japan, who support the analogHDTV system would, it seems, eventually adopt the digital system.

United States HDTV

The American electronics industry is losing the war in consumer electronics accordingto a study commissioned by the Department of Commerce and performed by theInternational Trade administration. The study found that Japan has more than doubledthe number of U.S. electronic patents that they have received since the mid 1970s.Further, their patents have been licensed more frequently than those of Americans.4

This report predicts that, at the current pace, Japan will become the world’s numberone electronics producer by the early 1990s. This comes as quite a shock to peoplewho think electronics will be the largest employer by the end of the century. A NationalScience Foundation report on Japanese HDTV research warns that Japan is focusingon the new technology as a catalyst to gain dominance over the semiconductor,computer and telecommunication world markets.

A U.S. firm, ITT Semiconductor, sells more than half of the world's microprocessorsused in conventional TVs for such features as frame within a frame. IIT’s Devoeclaims that many U.S. firms serving niche military markets have the technology tocompete in HDTV, but want to avoid “slugging it out in the marketplace.” Japanesesemiconductor manufacturers were rebuffed when Fujitsu’s proposed purchase ofFairchild Semiconductor was blocked by then U.S. Commerce Secretary MalcolmBaldrige in 1987. Instead, a series of alliances are forming.

Zenith

Zenith’s current strategy is in keeping with the company’s history of parentingstandards. The company invented the remote control in 1956, the FM radio stereotransmission standard in 1968 and the multichannel television stereo (MTS)transmission system in 1986. “There are more fundamental inventions from Zenith intoday’s television than from all the Japanese companies combined,” says James I.Magdid, a senior advisor with Needham & Co., Inc. in New York.5

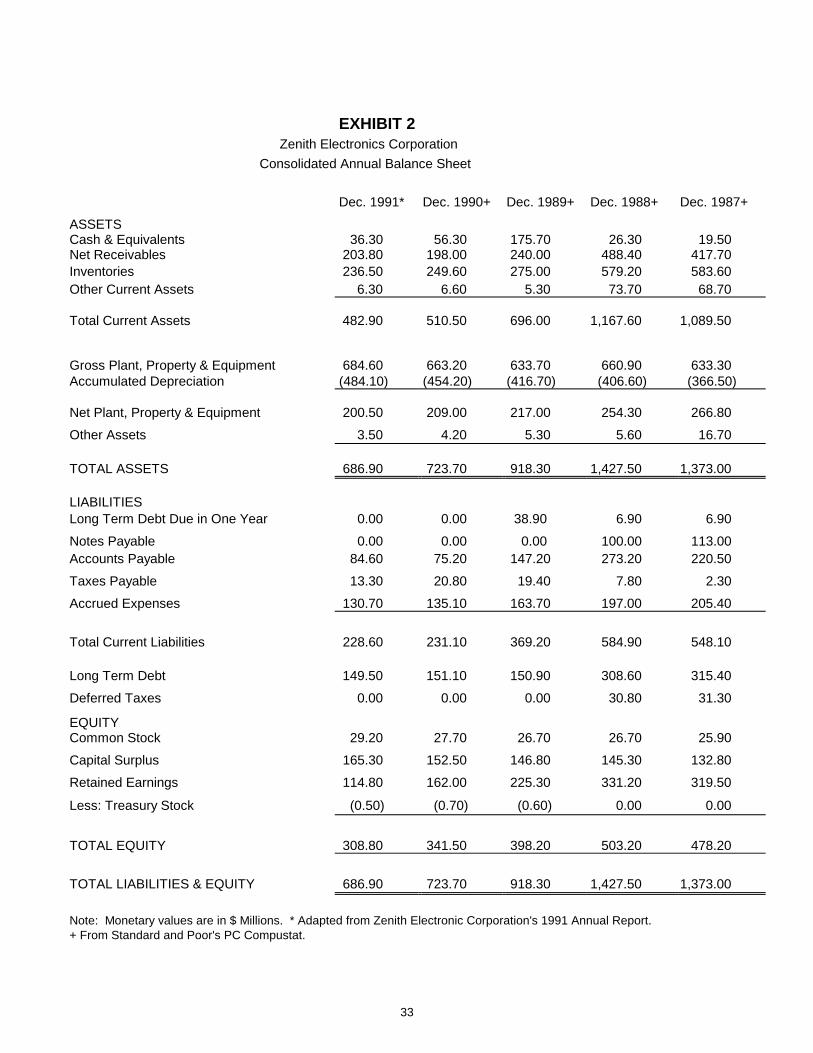

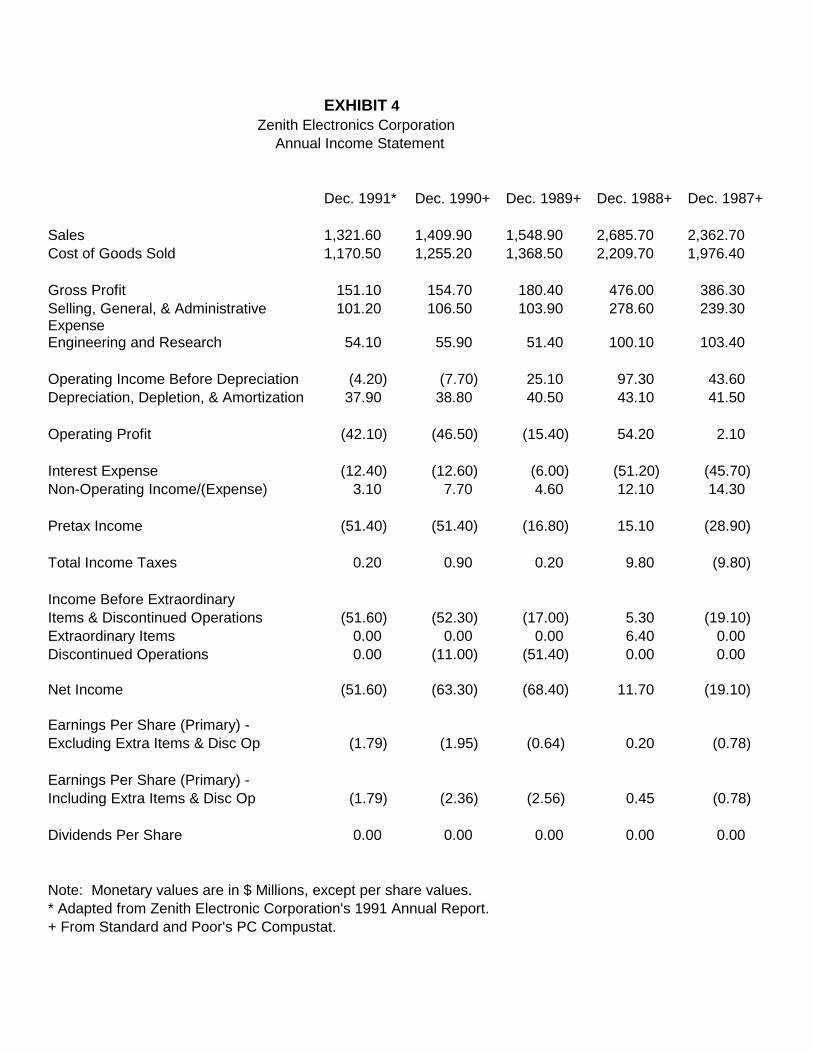

Since 1988, Zenith has phased out or cut back operations in several key (non-highresolution) products. Total nonvideo products accounted for only $78 million in sales in1991, down from $136 million in 1989. (See Exhibits 2–6.) In 1991, Zenith reducedcapacity in magnetics production as well as announcing plans to phase out automotiveelectronics, low end color computer monitors and monochrome monitors. In 1990,power supply and other electronic component production was restructured anddownsized worldwide. Finally, in a major move in 1989, Zenith sold its computerproducts division to France’s Groupe Bull.

7

Computer products accounted for over half of Zenith’s sales in 1988 and was its onlyprofitable division. The $450 million that Zenith received from the sale allowed it tosignificantly reduce debt and focus more R&D spending on their FTM and HDTVtechnologies. These actions improved their balance sheet, but the market value of thecompany still continued to decline through December, 1990, reducing Zenith’s marketvalue to nearly half its book value at one point. By March of 1992, however, themarket value had rebounded to about 75% of book. (See Exhibits 2-6.)

In addition to product line phase-outs, Zenith has rationalized operations worldwide.Because of the price competitive nature of consumer electronics, cost sensitiveproducers have chosen Mexico for its low labor costs and “the perceived benefits ofthe possible (North American) free trade pact.” The number of workers at theSpringfield, Missouri plant was reduced by 75% in March, 1992 when TV assemblywas consolidated in Mexico. This plant is scheduled to be shut down sometime in late1993.6 Zenith predicts that “virtually all of its television production will be located inMexico” by the end of 1993. “The cost savings of Mexican production, where hourlywages are only about a tenth of those in the U.S., have proved too critical to pass upfor loss-making Zenith.” Jerry Pearlman predicts that Zenith’s costs would be $400million higher if it were not for their Mexican operations.

Following these restructurings, Zenith operates in two major segments: consumerelectronics and components. Consumer electronics accounts for 85% of total sales,with color TV representing 75% of these sales. Approximately $100 million sales incolor picture tubes are derived from OEMs. Component products include powersupplies and low resolution displays.

During all this cost cutting, Zenith increased R&D spending on HDTV and FTMscreens. Through 1991, Zenith had spent $25 million to develop the DSC-HDTVsystem. This is a fraction of the $1 billion spent by Japanese firms to develop whatmany consider to be an inferior standard. Zenith has had similar success with ashoestring budget for FTM monitors.

What remains to be seen is if Zenith can capitalize on its technology and create amanufacturing base capable of supporting demand for HDTV. Zenith’s current CRTmanufacturing facility is a 40-year old cookie factory that was converted to CRT screenmanufacturing in 1967. The spaces are small and cramped, while the factory lacks themodern systems that typify today’s high-tech manufacturing. For instance, there areno automated materials handling systems so the workers must lift bulky CRT screenson and off a conveyor belt. Similarly, workers must manually perform the exactingoperation of mating the shadow mask with the phosphorous coated screen. Yet, for alltheir apparently antiquated work habits, in 1992, Zenith workers—running three shifts aday—turned out 3.6 million picture tubes a year. Working with aging equipment andtechniques, they still manage to manufacture a picture tube in 22 hours. Matsushita, inTroy, Ohio, does it in just under 24 hours at a new, well-equipped plant.

8

Since current CRT plants are at capacity, Zenith needs to develop new manufacturingplants to supply an increased demand spurred by HDTV. These plants will probablybe located in Mexico. A more fundamental question is whether Zenith should sink moremoney into CRT manufacturing when investment is needed for future technologies.

Not everyone associated with Zenith is excited about the high resolution standard. InMarch 1991, Sal Giordano, owner of Nycor, a New Jersey based holding company and8% shareholder of Zenith, sent proxies to all Zenith shareholders asking them to votefor the Nycor nominees for the ten member Zenith board. The letter indicated Nycor’sdissatisfaction with current management strategy and outlined their plan to turn thecompany around. “The most serious problem at Zenith has been and continues to bemanagement’s lack of a clear strategic plan. Though Zenith management hastrumpeted the existence of a long term strategy for the company, to date they havefailed to articulate to stockholders any plan which explains how Zenith will return toprofitability.7 In an effort to fend off this attack, Zenith issued $15 million in commonstock (a 5% interest) to Korea’s Goldstar. Goldstar and Zenith have been workingtogether on several trade and technology agreements. Nycor candidates weredefeated two to one at the shareholders meeting, giving a strong vote of confidence forcurrent management’s strategic direction. (See Exhibit 9.)

Zenith and AT&T

Since Zenith did not have capabilities in digital compression and semiconductors tobring its system from the drawing board to the lab, the company teamed with AT&T in1989 to develop the Digital Spectrum Compatible (DSC-HDTV) system. Under thisagreement, AT&T Bell Laboratories develops video compression and AT&TMicroelectronics develops semiconductors. The DSC-HDTV system has unique digitaltransmission properties, based on technologies developed by Zenith, to preventinterference with standard TV signals and to transmit snow-free, ghost-free picturesand compact-disc quality audio.

AT&T and Zenith have become extrememly successful bringing the HDTV systemtogether. As noted by Paine Webber analyst Jack Grubman, AT&T uses compressiontechnology in its core long-distance business. “They know how to do it better thananybody, if they can transfer that to another application, so much the better.”8 Inaddition to technology transfer, Zenith’s $25 million investment in DSC-HDTV “hasbeen more than matched by the substantial investments of (their) HDTV partners,particularly AT&T.”9 Over a thirty-nine month span, this partnership was able todevelop and improve Zenith’s paper system into a working prototype.

Harris Allied Broadcast Division and Hewlett Packard (HP) announced plans in 1993 todevelop broadcast equipment for the DSC-HDTV system and to license DSC-HDTVtechnology if the FCC adopts the Zenith-AT&T system. Harris would support the rapiddeployment of HDTV modulation and transmitting equipment to broadcasters followingFCC adoption of the new broadcast standard. Likewise, HP would develop HDTV

9

encoders (the electronic systems used by broadcasters to process and compresssignals).

In 1993 the digital HDTV Grand Alliance was formed. It merges technologies from thethree groups that had developed all-digital HDTV systems for consideration as the U.S.standard: Zenith and AT&T, General Instrument Corporation and the MassachusettsInstitute of Technology, and a consortium composed of Thomson ConsumerElectronics, Philips Consumer Electronics and the David Sarnoff Research Center.Zenith and the other Alliance members are pooling their resources, skills andtechnologies to create a “best of the best” solution for the HDTV system beingproposed to the FCC. The system elements for digital video compression, transport,scanning formats and audio all were selected by the Grand Alliance in October 1993.

In early 1994, after extensive competitive laboratory testing, the Grand Allianceselected Zenith’s VSB (vestigial sideband) technology as its terrestrial broadcast andcable HDTV transmission subsystem. The 8-VSB system assures broad HDTVcoverage area, minimizes interference with existing analog broadcasts and providesimmunity from interference into the digital signal.

AT&T has become particularly aggressive in the last few years in its bid to excel insemiconductors, an increasingly important element within the communicationsindustry. AT&T’s Bell Labs was a pioneer in the software industry and developed boththe C language and the UNIX operating systems to meet in-house softwaredevelopment needs. Large internal demand for semiconductors has made AT&T theworld’s largest producer of standard cells, with annual sales of about $250 million.Purchasing the world’s third largest standard cell producer, NCR, propelled AT&T evenfurther into the lead. In 1992, AT&T had eleven manufacturing plants and twelvedesign centers for semiconductors. Despite AT&T’s large internal market, theirpenetration into external markets has been limited.

Antitrust concerns initially hampered AT&T’s ability to compete in the computerindustry. In 1985, AT&T finally entered the merchant semiconductor industry but withlittle success. Two years later, over fifty middle and senior level managers withextensive industry experience were brought in to revitalize AT&T’s semiconductorinitiative. AT&T is developing semiconductors not only for HDTV, but also for videoconferencing, cellular telephones and network computing.

GoldStar and Scientific Atlanta

Support for Zenith’s DSC-HDTV has also come from GoldStar and Scientific Atlanta.In addition to GoldStar’s $15 million capital investment in Zenith stock, GoldStar hasentered into a licensing agreement to market Zenith’s FTM screens for televisions inKorea. The agreement calls for GoldStar to pay a fee to Zenith for each TV CRT, ontop of a substantial up-front fee. The deal allows Zenith to expand its technologies topreviously untapped overseas markets.

10

In late 1992, Zenith and GoldStar announced the joint development of a digital high-definition VCR for home use. The new digital HD-VCR, developed for the DSC-HDTVsystem, is designed to record HDTV signals on standard Super-VHS videocassettes.The HD-VCR also would be able to record and play back programs in today’s TVformat using standard VHS tapes.

Scientific Atlanta is a technological leader in satellite and cable transmission oftelevision signals. In December 1991, Scientific Atlanta pledged its support for theDSC-HDTV system as the U.S. standard. Under agreements developed with Zenithand AT&T, Scientific Atlanta develop the transmission and conditional access systemsand equipment necessary to allow secure satellite transmission of the DSC-HDTVsignal to make HDTV programming available to all markets and to support a timelymarket introduction.

In addition to satellite signals, Zenith and Scientific Atlanta announced that under aseparate agreement they have developed a common transmission structure forcarrying the Zenith/AT&T digital HDTV signal and Scientific Atlanta's digitallycompressed conventional TV signal through cable plants to the home. This willcombine Scientific Atlanta’s Vector Quantization digital compression system forconventional TV signals with Zenith’s four level vestigial sideband modulationtechnology for cable transmission. Similarly, Scientific Atlanta will utilize a commontransmission structure in the satellite system for carrying the DSC-HDTV digital signaland for Scientific Atlanta’s digitally compressed conventional TV signals.

Hence, both the HDTV signal and the Vector Quantization digital compression signalwill have end-to-end transmission capability over satellite and down the cable to thehome. Programmers and cable operators will benefit from the flexibility and costadvantages. The U.S. consumer will share in these benefits not only because oftransmission efficiencies, but also because the same high definition television set tunerwill accept HDTV signals off the air or down the cable, resulting in lower cost TV setsand cable boxes. By combining forces (with AT&T and Scientific Atlanta) on digitalcompression and transmission, Zenith will be able to bring high performance, low costdigital video to the cable industry, and at the same time lay a compatible transmissionfoundation for the smooth adoption of HDTV.

HDTV Technology

HDTV systems mandate the integration of various technologies, from the productionand transmission of programs, to the television terminal at the user’s home. There aremany emerging technologies capable of achieving the requirements of HDTV. Withrapid development of high resolution displays, compression technologies, DSP chipsand VLSI capabilities the arena is wide open when considering which technology wouldultimately be dominant (see Exhibit 1 for details). Following is a brief description ofeach parameter.

11

High Resolution Displays

High resolution displays are much more than just a component of HDTV systems. AsRobert Duboc of Coloray puts it, “Displays become the tail that wags the dog.”10 Withinthe HDTV industry, the high resolution display is the single most expensive componentand the component that most effects image quality as perceived by the viewer.Outside of the HDTV industry, high resolution displays are already used for everythingfrom computer screens to car consoles. The defense, airline, space and medicalimaging industries have employed high resolution displays for years. Sales areexpected to reach $9.3 billion by 1996, 40% of which will be in consumer electronicswith the balance in computers.

High resolution displays for HDTV must be defined with numerous parameters.Resolution is quantified as the number of horizontal strings of dots (scanning lines) thatfill a screen (frame) and the rate by which new screens appear (refresh rate). Screendimensions are stated as the ratio of the screen's width to height (aspect ratio).

There are various technologies in the development stage that provide improved clarityand contrast from that of the traditional CRT terminal (see Exhibit 1 for details). In1992, Zenith had the lead in flat tension monitors (FTMs), but considering the researchbeing put into this area and the options available, the future is highly uncertain withregards to which technology will emerge most effective, yet economically viable.

Software Availability

An important variable in determining HDTV demand will be the availability of software.HDTV broadcast equipment will require a large initial investment by broadcasters not tomention larger camera crews (up to 3 times as large) since flaws are magnified. Someof these extra costs are mitigated by decreased production costs realized byeliminating film.

A study by the Transition Scenarios Group of the Advanced TV Advisory committeehas determined that broadcasters in large markets will be ready to broadcast HDTVwithin eighteen months of a standard. Smaller broadcasters will, however, be at adisadvantage due to capital demands for new equipment. A TV station might have topay between $12 million and $22 million to convert to HDTV. The average price of aTV station sold between 1987 and 1990 was only $19.7 million. HDTV stations mightalso service a smaller area causing perhaps a 20% decline in revenues.

To alleviate conversion costs, Zenith-AT&T have developed a simple up-conversionprocess that will allow local TV stations to convert their existing NTSC equipment toZenith’s DSC-HDTV format. Through a two-step process the conventional NTSCsignal is stepped up to a high definition format compatible with DSC-HDTV. “With aminimal investment, TV stations would be able to move to high definition signal and theup-converted locally produced signal.”11

12

The FCC has given away HDTV licenses to 1700 stations to encourage investment bythe existing broadcasters in HDTV. There will be no competition for HDTV licenses.The value of these licenses is estimated at $1 billion. Alfred Sikes, chairman of theFCC, states that “it's not a give away, it’s a transition from one format (of broadcasting)to another.”12 Two months before the license announcement was made, 100broadcasters petitioned the FCC to require cable to carry HDTV to ensure an adequateaudience to justify investment. It is feared that without fresh competition, existingbroadcasters will cling to the NTSC standard. Public demand for HDTV is likely tomaterialize mainly in response to broad program selection. Studios will be hesitant toproduce programs in two standards until broadcasters are able to transmit HDTV.

HDTV & Semiconductors

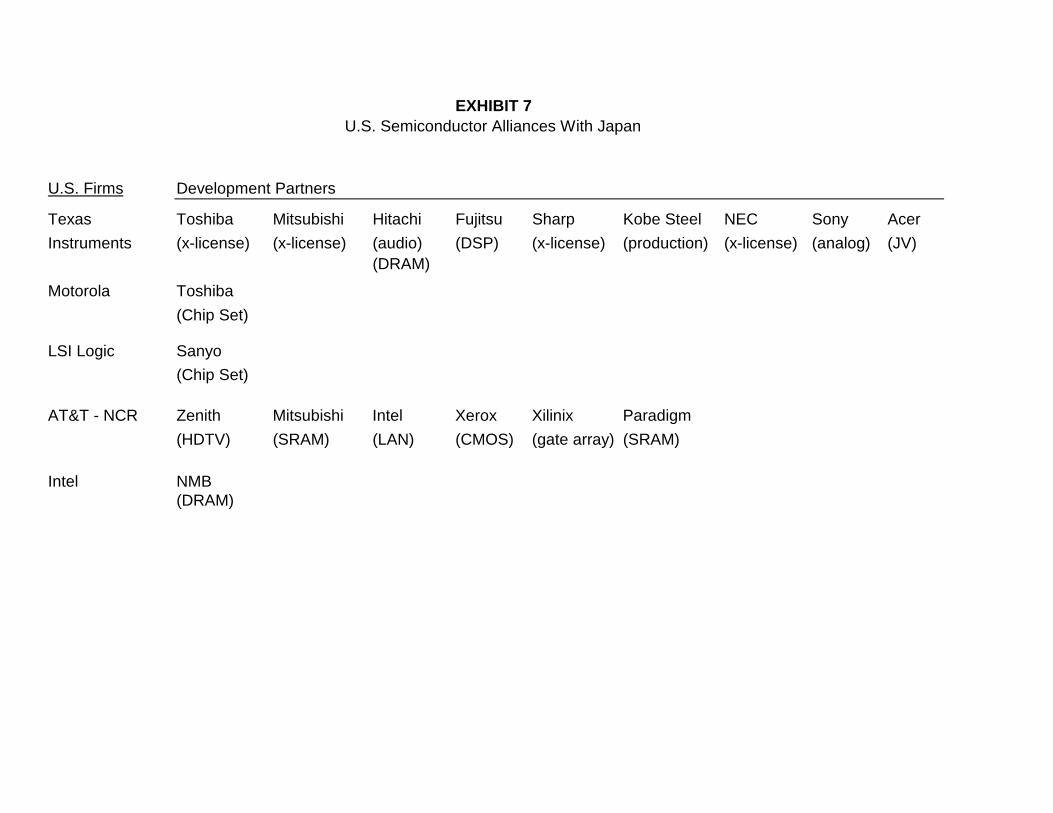

HDTV represents a major boost to the semiconductor industry. Not only will HDTVsuse large quantities of semiconductors internally but they will stimulate sales ofcomplimentary semiconductors for applications ranging from multimedia tophotography. (See Exhibits 7 and 8 for related information on the semiconductorindustry.)

In the capital intensive semiconductor industry, large up-front capital expenditureshave encouraged increased consolidation. The investment in R&D and manufacturingfor 16 bit dynamic random access memory (DRAM), for example, exceeds $1 billion. Itis estimated that companies have to produce at least 5 million DRAM chips per monthto recoup their initial investment. As a response to high investment and short lifecycles, companies specialize in one stage of the R&D process or in a particularproduct. Toshiba, for example, supplies memory chips to Motorola and Motorolareciprocates with microprocessors. Further, Toshiba transfers production technologyto Siemens.

HDTV looks like it will transform to digital the last high volume analog consumerelectronics segment, TV. Analog refers to information represented in wave form anddigital refers to information represented in numeric form. Sound and image naturallyoccur in wave form, thus digital systems must first translate waves into numbers andlater recreate the waves based upon the numeric descriptors. Digital HDTV systemshave many advantages over analog including less distortion and more flexibility. Themajor disadvantage of a digital system is the incredible volume of numbers that mustbe processed to relay HDTV images.

One second of HDTV data requires one billion binary (0s and 1s) numbers of code. Toput the volume of numbers to be processed into perspective, it would requireappproximately 360 personal computers with standard 40 megabyte hard drives tostore a two hour HDTV program uncompressed. Secondly, in terms of broadcastingbandwidth, uncompressed digital HDTV would require 100 times the signal capacityavailable on current 6 MHz band width channels. The solution lies in compressing thesignals before transmission. This solves the bandwidth problem as well as reduces the

13

volume of numbers that must be processed, but increases the number of operationsthat must be performed on each signal, thereby developing the need for parallelprocessing and digital speed processing (DSP) chips. It should be noted that theincreased resolution and aspect ratio of HDTV would still surpass the current channelcapacity by a factor of four or five times even if we use conventional analog signals.

Digital HDTV was long thought unfeasible because it would require the processingpower of a super computer. Recent semiconductor advances in video compression(VC), digital speed processing (DSP), digital to analog converters (DAC) and very largescale integration (VLSI) make it highly likely, however, that a digital standard for HDTVwill be implemented in the U.S. in the next few years.

Video Compression

General Instruments announced that it had found a way to compress HDTV signals toa manageable size in June 1990, two days prior to the deadline set by the FTC forstandards proposals. Three other consortiums, Zenith-AT&T, M.I.T. and Philips-Sarnoff (the Grand Alliance) soon announced competing digital standards. The digitalvideo compression strategies that have been devised involve several components,including coding options, quadrature modulation, motion compensation and errorcorrection (see Exhibit 1 for details). Together, these compression techniques allow anHDTV signal to be compressed by a ratio of approximately 100:1.

Digital Signal Processing

Compression reduces the HDTV signal size to a manageable 1.2 MB/second but itvastly increases the number of operations that must be performed on each signal. Itmust be encoded, compressed, decompressed and debugged. During the encodingprocess, a series of compressions must take place sequentially. Each compression, inturn incorporates the results of multiple calculations for such compensatory measuresas motion correction. These calculations may take place in parallel. The sameprocess occurs in decoding followed by an elaborate debugging process. Thus,broadcast HDTV is constrained not only by bandwidth, but also by affordableprocessing power. Digital speed processing (DSP) chips promise to deliver the mostappropriate computing power for the least price. This is achieved by their multi-taskingcapability that allows them to perform several applications simultaneously, such asplaying music and receiving faxes.

Several semiconductor manufacturers have already introduced high performanceDSPs for HDTV image processing. National Semiconductor has introduced a 50 MHzDSP capable of 100 million instructions per second (MIPS). AT&T Microelectronicshas already produced a DSP for HDTV and is currently working on a DSP capable of10,000 MIPS. Due to its ties with Bell Labs, AT&T has unique strength in algorithm

14

design. In 1990, AT&T achieved a 10% market share in the $300 million DSP market,which is expected to grow to $4 billion by the end of 1996.

Digital Analog Converters

DACs are required to ultimately translate the digital signal back to an analog signal todrive the speakers and the display. Fully integrated and temperature tolerant 12 bitDACs have only been available a few years at low cost, further increasing the priceperformance ratio of HDTV.

Very Large Scale Integration

Considering the vast increase in the number of chips required for processing HDTVdata, VLSI along with faster DSPs, will be important catalysts for reducing HDTV costs.Initial systems required about 2000 chips, arranged on what has been likened toshelves in a refrigerator. Thus, semiconductor components currently comprise 33% ofHDTV costs. Miniaturization advancements in both manufacturing and design willdrastically lower the number of chips required for HDTV. Faster processors will beable to perform more tasks per frame, further reducing the number of chips required.Fewer and smaller chips translate to a greater HDTV price-performance ratio.

Trade Lobbies

Various trade associations, directly or indirectly effected by the emerging HDTVindustry, independently lobby to safeguard and promote their interests.

Semiconductor Equipment and Materials International represents firms that buildthe machine tools for primary HRDs. Their main goal is thus to develop a U.S.manufacturing base for HRD. Their lobby efforts focus on the Defense AdvancedResearch Project Administration (DARPA) funding for HRD, and only indirectly onHDTV.

The American Electronics Association (AEA) concluded in 1989 that the Japanesewould use HDTV technology to overtake the U.S. in semiconductors.13 Further, theyfelt that losing in HDTV could jeopardize the U.S. electronics industry. To ease thetransition, AEA recommended moving to EDTV (enhanced) as an intermediate stepbefore going to HDTV. This concept is supported by the Advanced TV Researchconsortia, however the FCC has made it clear that they will not accept a piecemealstandard.

A study commissioned by the AEA in 1990 recommended a $500 million governmentloan program and another $500 million in loan guarantees to support U.S. HDTVresearch. AEA spokeswoman Sue Wirth notes that this study has never been formallyadapted by the AEA. The AEA’s lobbying activity supports the component technologies

15

that produce HDTV. In fiscal year 1993, the AEA lobbied for $75 million from DARPAand an additional $5 million from other organizations. Further, the AEA hasestablished an Industry-Government Advisory Board to encourage domestic electronicmanufacturing.

The National Academy of Sciences recommended in March 1992 that a new self-funding Civilian Technology Corporation (CTC) be created. The CTC would promoteHRD technologies, notably HRDs and microelectronics. Funding would be provided bya onetime $5 billion appropriation, with the rest of the financing coming from licensingfees and patents. Senator Hollings, Democrat from South Carolina and chairman of theSenate Commerce Committee endorses the CTC. This is considerably more than the$100 million effort from which Sematech was founded.14

The National Association of Broadcasters (NAB) made the mistake of inaction withaid stereo and they do not want to repeat this mistake with either digital audio (DAB) orHDTV. This group has moved to protect industry interests by successfully lobbying theFCC to reserve unused spectrum for HDTV. The NAB questions if the FCC proposed15 year conversion period from NTSC to HDTV is realistic.

Government Lobbies

The U. S. does not have a comprehensive national policy addressing the basicresearch, commercialization or manufacture of the electronics industry. By default,defense concerns and a myriad of special interest constructs serve as public policy.Throughout the cold war the federal government supported basic research withdefense applications. DARPA coordinated the mainstream of this effort.15

HRD in particular has been targeted by DARPA. The agency has financed R&Dprojects for such companies as Texas Instruments, Projectivision, Photonics, Ovonic,Norden Systems, MRS Technology, Microelectronics and Computer Technology Corp.,Tektronix, Sarnoff Research Center and Zenith.

Legislative Branch

Trade Barriers: The 1988 Trade Act allowed the U.S. to target unfair traders andimpose retaliatory measures, the retaliatory provision is commonly known as Super301. In 1992, the Bush Administration threatened to use it against Japan, and it iscredited with opening Japanese lumber, semiconductor and super computer markets.In 1990, the Super 301 clause was removed (vís-a-vís Japan) and replaced with theStructural Impediments Initiative (SII).16 This move was considered a “serious tacticalmistake” by Senator John Danforth (R-MO), the ranking Republican on the SenateCommerce, Science and Technology Committee and a key author of the bill.

In August 1991, the FTC levied a 63% duty on LCD displays from Japan whichcomprised 97% of the U.S. supply. A group of small U.S. producers filed a petition

16

under the Tariff Act of 1930 asking for tariff protection, alleging that the Japanesemanufacturers were selling screens at below fair market value.

Since this tariff does not apply to finished products, such as laptop computers,manufacturers have been forced offshore. In 1991, IBM and Apple petitioned theCommerce Department to set up a foreign trade subzone for imported JapaneseAMLCDs, to avoid paying the 63% tariffs. An approved foreign trade zone would allowfirms that manufacture in the zone to import parts duty-free for assembly.

Antitrust Policy: One option is to relax antitrust enforcement on domestic competitors,relevant market is defined globally and antitrust enforcement is based on world share.This assumes that domestic firms will become stronger, however it does not assurereciprocal access to foreign markets. Another path is to export U.S. antitrust policy toensure that foreign markets encourage new entrants. Policies are tempered to localeconomies, attacking vertical monopolies (e.g., the Japanese Kierstu), as well as totraditional horizontal monopolies.

Committee Work: Many measures have gained limited support within Congress. Forexample, the American Trade Preeminence Act contained provisions for suspendingantitrust, a $400 million research provision to create a commission to study HDTV, thehi-tech industry capital costs and to evaluate a new cabinet post for technology policy,passed the House Science, Space and Technology Comrnittee by a vote of 49-0 inMarch 1990. The primary author of the bill was Congressman Don Edwards (D-CA),the antitrust provisions were written by Congressman Tom Campbell (R-CA). Houseleader Richard Gephardt (D-MO) favored a “managerial industrial policy” to restoreAmerican competitiveness. Toward this goal he, together with Senator John Glenn (D-OH), supported the formation of a civilian DARPA. Congressman Edward Markey (D-MA) chairman of the House Subcommittee on Telecommunications and Finance(which has jurisdiction over the FCC) proposed federal funding of HDTV research inFebruary 1990. In 1992, none of these initiatives had received the necessary supportand funding, so HDS is funded primarily through defense associated grants.

Information Gathering: Within Washington, various agencies have been establishedto filter information for an informed legislative decision. The Congress Office ofTechnology Assessment was created to assist legislators in determining the potentialof new technologies. The office is administered through the Commerce Departmentand congressional direction comes from the House Committee on Science, Space andTechnology. In June 1990, James Curlin, program manager for Telecommunicationand Computing Technologies, issued a report concluding that development of a HDTVindustry could reverse the erosion of leadership in many electronic technologies.

Research Costs: Various proposals have been introduced to lower the cost ofresearch by a reduction in the capital gains tax, by encouraging tax free savings plansand by formally changing the mission of DARPA. Federal Labs would be allowed tocommercialize their research through licensing agreements. Currently Federal labs

17

employs 18% of the scientists in the U.S. Thus, they enjoy a large portion of thegovernment’s $65 billion annual research budget.

Tax Considerations: Many observers have asked for a reconsideration of section 861of the IRS code. This section requires that companies allocate a certain portion oftheir R&D to foreign income, thus creating an incentive to move R&D operationsoffshore.

Executive Branch

The Bush Administration talked about “moving more toward an investment on appliedR&D at the margin” and emphasizing support of “high performance computing...batterytechnology...[and] ...magnetic levitation.”17 The American Technology PreeminenceAct avoided a veto only after a $10 million loan program to help companies' researchof commercial applications was deleted. Further, the two year old AdvancedTechnology program (ATP), which funds small and medium sized companies engagedin fundamental research, is expected to spend $45.8 million in grants in the early1990s. A 38% increase is sought for the ATP in fiscal 1993.

The Bush Administration considered HDTV to be the seed of industrial policy andopposed support for a technology with such a direct product outcome. Administrationofficials often risk their careers when they take too bold a position on industrial policy.For example, Craig Fields, a former DARPA director, lost his job over HDTV. Thisdismissal drew a strong reaction, particularly from Senator Al Gore (D-TN), chairman ofthe Senate Commerce, Science and Technology Committee. In response to industrialpolicy allegations, the HDTV concept was renamed High Definition Systems (HDS) toemphasize the much wider applications of the technology. In addition, CongressmenMel Levine (D-CA) and Don Ritter (R-PA) co-chairs of the Congressional HDTVCaucus changed its’ name to the Congressional High Technology Caucus.

Within the executive branch, various agencies exist to monitor technologicaldevelopments. In the Commerce Department, the Technology Administration isresponsible for analyzing and removing barriers to technology commercialization. Thisdepartment consists of the Office of Technological Assessment and the NationalInstitutes of Standards. The President’s Council of advisors on Science andTechnology helps inform the Office of Science and Technology on policy, which in turnreviews the research and development budgets of the Department of Energy,Commerce, Interior and the National Science Foundation. These reviews areforwarded to the Office of Management and Budget. The National Science Board setspolicy for the National Science Foundation. In the Defense Department most of theactivity takes place in DARPA, although there is a civilian run agency, the Office ofResearch and Advanced Technology, that is responsible for the guidance, policy andoversight of the Science and Technology Program.

18

Regulatory Environment

The Federal Communications Commission’s (FCC) has among other charters, thegoal of protecting consumer investment. This surfaced over forty years ago when theFCC mandated that color TV’s be backward integrated with black and white sets. TheFCC currently stipulates that the HDTV standard be compatible with current TVtransmission.

Zenith wants to set a fixed time after adoption of the HDTV standard to terminateNTSC. Such a date should be at least seven years after adoption of the standard. Toprotect consumer investments, Zenith argues that HDTV must be scalable (throughconverters) to accommodate resolution on the 13-inch to 20-inch sets. Zenith forecastsa 1% penetration one year after the adoption of the HDTV standard. Additionallobbying by Zenith includes a proposed foreign excise tax. The company recommendsthat those sets with a domestic content of 50% or more, enjoy reduced licensing fees.

The competition for a transmission standard will be judged by the Advanced TVAdvisory Committee composed of colliding interests including: chief executives fromTV manufacturers, broadcasters, cable TV companies and suppliers. The Committeewill finish testing and recommend a system to the FCC in early 1993. Digital systemproposals are now being tested at the Advanced Television Test Center (ATTC).These tests and those of analog proposals will be presented to the FCC. A standardshould be chosen by mid-1993.

Industry Players

Sony lost about $160 million in 1991. Thus, it cut its capital expenditures by $500million in 1992. Together with Fujitsu, Hitachi and TI, Sony has been co-developing achips set for the MUSE decoder. The chips set, which reduced the number of devicesin the decoder from 150 to 30, and the cost to less than $1500, has been available incommercial volumes since April 1991.

Sony is the leading developer of professional HDTV equipment. In July, 1992, Sonyintroduced a 32-inch HDTV in Japan incorporating a full-specification MUSE decoder.In April 1993, Sony also introduced in Japan a low-priced, basic feature 32-inch model.Both of these units are capable of receiving HD broadcasts and are equipped forlinkage to HD laserdisc players and other HD equipment that will be sold in the future.In 1994, Sony introduced in Japan a 28-inch model equipped with a newly developedfull-specification MUSE decoder, at a price lower than that of any of Sony’s existingmodels.

In digital video editing systems, Sony’s D-2 standard has been adopted by 5000broadcasters worldwide. Sony also works on HDTV optical videodisk systems with atwo hour playing time. In 1992, Apple and Sony set up General Magic, a venturewhich will develop multimedia players. Additionally, Hitachi, Sony and Matsushita co-

19

developed an analog, uncompressed base-band VCR format for recording HDTVsignals and for playing back prerecorded tapes. They plan to make this formatcompatible with other HDTV products. Since Sony and Matsushita had been rivals inthe VCR format, this announcement surprised industry analysts.18 Sony alsodeveloped HDTV equipment for use in car production at Ford’s plants in England.

Hitachi introduced a HDTV with a 46-inch screen, the largest for HDTV sets targetingconsumers. In 1991, the company had an output of 1000 AMLCDs per month, only10% of the quantity promised to OEMs.

Toshiba and Applied Materials will jointly develop LCD technology based on chemicalvapor deposition. Also, Toshiba produces the TFS-800 system which can store andretrieve 240 HDTV pictures. In 1991, Toshiba introduced a $26,000 HDTV system anda professional HDTV camera with 2 million pixels. Furthermore, the companycommitted itself to reducing the price of an 11-inch AMLCD to $385 by the end of1995. Display technologies, a 50-50 joint venture between IBM and Toshiba, beganfull scale production of TFT-LCDs in November 1991. Investment by both companiesin the joint venture totaled $1.2 billion. As an alliance partner with Motorola, Toshiba isinvolved in the development of chips for the MUSE decoder.

In the field of industrial HDTV equipment, Toshiba developed the world’s first 3/4 inchdigital, high-definition VCR, which is based on a universal digital high-definitionrecording format jointly developed with Broadcast Television Systems GmbH (BTS).

Toshiba is currently cooperating with Scientific Atlanta to develop a digital set-topconverter for Time Warner Cable’s experimental full-service, interactive home videonetwork in Orland, Florida. In 1994, Toshiba also supplied HDTV systems to theWarner Brothers Studio Store in New York City.

Sharp has marketed a receiver since March 1992 for $8,000, 25% of the price ofexisting HDTV sets. The set has a 36-inch picture tube with 1,125 scanning lines, ascreen with 16:9 aspect ratio and uses a Muse NTSC converter. Sharp also introduceda 16.5-inch color LCD which handles 1.2 million pixels, allowing the use of computergraphics and multimedia. With a 1991 production capacity of 200,000 passivemonochrome LCDs per month, and 10,000 color LCDs a year, Sharp is the marketleader in HRD technology. Sharp hopes to decrease the cost of a 10-inch AMLCDdown to $400 by the year 1995. In February 1992, Apple and Sharp set up analliance. Both companies will develop a notebook with video and sound capability withSharp supplying color AMLCDs.

Matsushita, in 1991, demonstrated a 15-inch amorphous silicon, thin film transistorAMLCD which displays 16.7 million colors. Together with NHK, the companydeveloped a VCR for professional broadcast studios. With Dai Nippon Printing andOki, Matsushita will develop a 55-inch gas plasma panel TV screen. Further, thecompany entered into an agreement with Gain Technology to develop object orientedmultimedia software.

20

Sanyo developed an HDTV system with a 400-inch screen and 4.5 million pixels basedon the MUSE transmission system. Together with LSI Logic, Sanyo is developing achip set for the Japanese HDTV system that should reduce the number of chips fromthe current 46 to 10. Ownership of the chip design will be held jointly by both firms.Under the agreement, the chips would be manufactured in Japan by LSI Logic’saffiliate, Nihon Semiconductor.

Philips, in 1992, was awarded $41.7 million in R&D subsidies for liquid crystal displays(LCD) research under the European EUREKA and JESSI programs. The company willconvert a factory to flat panel production by early 1993. Philips is seeking otherEuropean partners for its LCD project. Thompson, however, had already decided todevelop and manufacture LCDs in its own Grenoble facility. Philips announced its firstHDTV sets in the D2-MAC standard for 1994. Despite $2.5 billion provisions forrestructuring expenses, Philips has committed more than $2 billion to R&D. Much ofthese research efforts will go into digital compact cassettes, CD-I and HDTV. Togetherwith Thompson and AEG, Philips is establishing a research consortium to developLCDs based on ferroelectric technology. This new technology is expected to havehigher manufacturing yields than AMLCDs.

Apple, in response to a decrease in net income of 40% in FY 1991, plans to diversifyinto the consumer electronics industry. Mr. Sculley, the CEO, envisions designing the“Paradigm 3 TV scalable, interactive and personalized.” In addition to accessing thehardware skills from Sony and Sharp, Apple set up a joint venture with IBM (Taligent)to develop software standards and file formats for multimedia applications. Sony andPhilips support this venture. The future of the IBM-Apple relationship is uncertain.Many expect an Apple-Sony relationship to be better suited to Apple’s diversificationplans.

Coloray received financing for the development by Micron Technology, a companythat produces memory chips. Micron, with $450 million sales in 1991, will also buildthe pilot plant. Coloray expects to commercialize 10 inch diagonal displays forcomputers by 1994.

Microelectronics and Technology Corporation, a member of the InternationalElectronics Devices Association, established a consortium of U.S. companies involvedin field-emitter CRT technology. The consortium includes Optical Imaging Systems(OIS), Cherry Display Products, Electro Plasma Inc., Magnascreen Planar Systems,Plasmaco Inc. and Tektronix. In 1991, the consortium received $15 million; $7.5million from its own members, and $7.5 million from the Advanced TechnologyProgram. The research program will cover automated inspection and repairtechnologies in flat panel manufacturing. Under a DARPA contract, MCC alsodevelops displays based on field emission technology. The first commercial screensfrom MCC is expected around 1995.

Photonics Technology has developed 19-inch displays for the U.S. military. Thefirm’s proprietary technology handles 262,000 colors and achieves flicker-free imaging

21

with wide-angle viewing. The company was part of a group that lobbied for 4.6%antidumping duties levied by the Commerce Department on Sharp and Toshiba.Photonics has been supplying 60-inch monochrome screens to the military for$100,000 each. In 1992, only approximately fifteen screens were produced per year.Photonics estimates that the cost of production could fall to as low as $1,000 each ifmass produced.

Planar Systems received a $2.5 million contract from DARPA for research andmanufacturing in its thin film electroluminescent (EL)technology. Since its merger withFinnish Finlux Display Electronics, Planar has become the largest maker of ELtechnology in the world. The company expects to begin pilot production of 8-inch VGApanels in late 1993. Further, Planar will develop EL displays for DEC workstations.Like Photonics, the company successfully lobbied for antidumping duties.

In-Focus had 1991 revenues of $37 million. Additionally, Compaq paid In-Focus$650.000 for the rights to use its Stacked PMLCD technology. In-Focus is working onreducing, by threefold, the response time. Since In-Focus imports passive LCD glassscreens from Japan, in 1991 it joined Compaq in lobbying against the 62% dutiesimposed on imported LCDs. The company announced it would pursue licensingoptions in military, instrumentation and medical computers.

Tektronix has been selected to carry out research for military applications for its PALCtechnology under a DARPA contract.

22

Footnotes

1 Interactive Video: Industry Report, Morgan Stanley & Co., Inc. January, 1992.2 Variations on a Theme. The Economist, April 11, 1991, p. 54.3 Electronic Business, August 20, 1990, p. 30.4 The New York Times, June 9, 1990, p. 31. “Report Warns of Decline of U.S.

Electronics Industry” by Clyde H. Farnsworth.5 Burrows, Peter, Robert Haavind and Garrett DeYoung. Zenith’s HDTV strategy:

“Made in the USA.” December 15, 1991.6. Durr, Barbara. Financial Times. “Zenith Heads South of the Border.” December 6,

1991.7 From Zenith Proxy sent by Nycor, Inc. March 25, 1991.8 Quote printed in BC Cycle Financial Report. “Zenith Heats Up HDTV race with AT&T

Venture” by Joanne Kelly. December 17, 1990.9 From Zenith’s statement to shareholders in response to the Nycor proxy written by

company Chairman Jerry Pearlman. Other partners in HDTV besides AT&T includeGoldStar and Scientific Atlanta.

10 Harbert, Tammi. HDTV holds promise and peril for EEs; Development may produceenhanced displays, but could cost EE jobs. EDN Copyright 1991 Information AccessCompany; Cahners Publishing Co. 1991. March 7. 1991. Vol. 36: No. 5; Pg. 23.

11 From Backgrounder Report for Winter/Spring 1992 provided by Zenith ElectronicsCorporation.

12 “FCC to Grant O vner of Every TV Station Another License Free.” Bob Davis. WallStreet Journal. March 18, 1992.

13 “America’s Billion Dollar Boob Tube Battle.” Economist (UK). Vol. 311, Is.: 7604, pp.67-68. May 27, 1989.

14 Sematech is a Government-Industry corporation dedicated to advancing chiptechnology.

15 DARPA’s fiscal 1993 budget is approximately $40 billion, total government researchoutlays for fiscals 1993 are approximately $65 billion. 1980 government researchoutlays approximately $31 billion, $15 billion in defense, $16 billion civilian. Source:Office of Management and Budget Historical Tables, HJ2052.A2 U58 pg 178.

16 The SII is a dialogue between Japan and the United States to open Japanesemarkets to foreign goods. The dialogue focuses on closed supply relationships notedin the Japanese economy.

17 Budget Director Richard Dannan, Hearing of the Senate Governrnent AffairsCommittee, Fiscal 1993 Budget Management Issues, in response to a question fromSenator Kohl.

23

18 “Japanese Electronic Firms agree to Consumer VTR Format forHDTV.” Video Technology News. July 1991, p. 8.

19 “Flat out in Japan.” The Economist. February 1, 1992, p. 79.20 “Sharp’s Long Range Gamble on its Innovation Machine.” Business Week. April 29,1991, pp. 84-85.

24

EXHIBIT 1Technology Details

HDTV & Compression

One second of HDTV signal requires approximately one billion binary (0s and 1s)numbers of code or a gigabit. Bits are arranged in groups of eight called bytes. Thus,a gigabit equals 120 megabytes. Microprocessors perform operations on one or morebytes at a time (a word) depending upon the width of the data path measured in bits.Within the Intel chip family, the 8088 processes 8 bit words, the 80286:16 bit words,the 80386: 32 bit words and the i860:64 bit words. One or more instructions areperformed on these words per clock cycles measured in thousandths of a second ormegahertz (MHz). Overall chip performance is measured in millions of instructions persecond (MIPS).

The digital video compression strategies that have been devised involve severalcomponents, including coding options, quadrature modulation, motion compensationand error correction. Together, these compression techniques allow an HDTV signalto be compressed by a ratio of 100:1.

Coding refers to the numeric description of pixels. At the most basic level, codingtransforms continuous waves into discrete numbers (quantization). Quantization isachieved by dividing waves into nonoverlapping subranges and assigning discretenumbers to each subrange. Coding can also reduce the number of signals that mustbe processed and transmitted by taking advantage of pixel redundancies.Redundancy occurs both within a frame and across time.

At any one time, large blocks of pixels, such as the sky, have little variance. Thus,Ioterpolative Coding can send a subset of pixel infonnation upon which can beextrapolated during decoding to recreate a close approximation of the original pixels.Transform Coding involves transforming pixel intensity into frequency coefficients forblocks of pixels. Adaptive Transform Coding changes the transformation process asa function of either picture statistics or as a function of subjective quality requirements.

Across moderate- to low-action frames, most pixels change in a predictable manner.Differential Pulse Code Modulation (DPCM) takes advantage of evolutionarychanges by using past trends to predict future changes. A decoder is able to make theexact same predictions. Thus, only the common prediction error must be transmitted.

Quadrature Modulation allows two distinct signals to be broadcast over the samefrequency by insuring that the two signals are 90 degrees out of phase. Quadrature iscurrently used in the NTSC standard to transmit chrominance (color) information.

Motion Compensation can correct for the distortions introduced by compression toolssuch as interlace scanning. As discussed under HRD, scouting provides a 2:1compression ratio, but it distorts moving objects. Motion estimation algorithms extract

25

three-dimensional motion parameters from a sequence of two-dimensional images.These motion parameters, in turn, can be used to compensate for the distortions thatmotion introduces to compression.

Error Correction involves detecting faulty bits in a word of information and formingnew bits. It is essential that transmission errors be corrected due to the magnifyingeffect of decompression and the lingering effect of differential transmission. Thecorrected bits are interpolated from the preceding and/or following words. ForwardError Correction (FEC) can correct for as much as 33% error in a word by storing asequence of words upon which to make predictions.

Proposed Compression Standards

General Instrument proposed fitting a digital HDTV signal into a 6 MHz channel byfirst using a Transform Coding algorithm. The signal is further compressed by onlysending the difference between the predicted signal and the actual signal using DPCM.To increase the accuracy of predicted signals, Motion Compensation is used toforecast movements. Lastly, the chrominance is averaged in groups of 4 pixels by 2pixels while the luminance (brightness) is broadcast for each individual pixel.Chrominance is broadcast at a relatively lower resolution due to the eye’s relativelygreater sensitivity to luminance.

Zenith-AT&T (DSC-HDTV) have also developed a compression algorithm thatsqueezes an HDTV signal into a bandwidth of 6 MHz. Again, DPCM is used tobroadcast only the discrepancy between the new image and the predicted image. Thedifference between the two algorithms lies largely in their prediction accuracy. TheDSC-HDTV algorithm forecasts movements in the form of vectors by trackingluminance. Luminance moving in blocks across frames is translated into vectors usinga hierarchical block-matching motion estimator. Before transmission, the signal iscompressed a second time using Transformation Coding. Since luminance andchrominance are encoded separately, the signals must be synchronized, as well aserror corrected by the decoder.

Philips-Sarnoff’s Advanced Digital Television (ADTV) adopts the collection ofcompression methods outlined by the Moving Pictures Expert Group (MPEG), acommittee of the International Standards Organization. The methods include motionestimation, motion-compensated predictive coding, adaptive Transform Coding,quantization and variable-length coding-decoding. A prioritization layer determineshow the various compression methods interact so that the most important video data istransmitted with the greatest reliability. MPEG promises the least distortion, but it alsobroadcasts the lowest resolution of the four proposed digital standards (1050 linesinterlaced).

MIT’s American Television Alliance System (ATVA) also adapts the compressionstrategy to the circumstance. When there is little to moderate motion, the difference

26

between predictions and actual images are compressed (DPCM). To increase theaccuracy of predictions, motion estimation and compensation techniques are used.When there is significant motion or scene changes, DPCM compression is disabledand the image frame is encoded in bands of 8 pixels by 8 pixels. A weighted averagebased on luminance and chrominance determines which bands are most importantand thus first compressed. The process continues until the band width is saturatedwith compressed data.

Screen Measurements

Refreshing may occur every other line (interlaced) or every single line (non-interlaced).Keeping the scanning frequency constant, interlacing doubles the number of lines andthus doubles the resolution. Though resolution increases, image quality decreasessince the screen is displaying simultaneously two consecutive frames out ofsynchronization by 1/30th of a second. Motion is thus blurred and jagged edges result.The traditional standard (NTSC) calls for interlacing, while the Zenith/AT&T HDTVstandard proposes non-interlacing.

The scanning frequency is measured in megahertz (MHz). NTSC is broadcast at59.94 MHz, which translate to thirty interlaced frames per second. The Zenith/AT&THDTV standard also proposes broadcasting at 59.94 MHz, but in a non-interlacedformat that corresponds to sixty frames per second.

A line consists of a string of colored dots known as pixels. Each individual pixel isuniform in color and shade. When arranged as a tightly packed mosaic, however,these monotone pixels form pictures of all colors and shades. How seamless thepixels blend together is directly proportional to the resolution and inversely proportionalto the screen size. NTSC consists of 525 inter-laced lines per frame. HDTV proposalsstandards that range from 700 non-interlaced lines to 1575 interlaced lines per frame.

Lastly, the NTSC aspect ratio calls for the screen width to be 4/3rds as long as thescreen height. This near square proportion was adopted largely to add stability to thecathode ray tubes (CRT) first used as screens. A CRT’s contains a vacuum in a largeglass tube. The more cylindrical the tube, the lower the stress introduced by thevacuum. The Zenith/AT&T HDTV standard is modeled after the 35mm film or cinemaformat, which has a width 16/9ths as long as the height. Though HDTV screens willinitially be made from CRTs, improved technology will allow adequate stability in therectangular format.

Attaining HDTV resolution is a trivial task for today’s CRT technology. The challlenge inHRD lies in improving a screen’s production cost, color fidelity, image contrast, viewingangle and physical size. The 90-year old CRT technology is likely to be eclipsed in themedium run with alternate HRD technologies currently under development. By the endof the decade, several flat screen technologies are expected to out perform CRTs inevery respect, except perhaps price.

27

Cathode Ray Tube

CRTs have been the standard display technology from the birth of television to thebirth of the HDTV. Modern advances in CRT technology can compensate for most ofthe inherent drawbacks of small CRT displays, however, large CRT displays are likelyto remain awkward due to their depth and weight.

CRTs consist of a large glass cone (tube) with an electron gun (cathode) on the narrowend and a coating of phosphor dots on the inside of the broad flat end (screen). Theelectron gun emits electrons (rays) which are attracted to the positively chargedscreen. The phospors on the screen emit colored light when they are excited by theelectrons. The sides of the cone contain electron coils (yoke) which channel the flowof electrons into vertical and horizontal lines by virtue of the magnetic field which theycreate.

Color CRTs require three electron guns. Each excites a distinct phosphor dot in acluster. The cluster of phosphor dots, representing the three primary colors, form apixel (the intersection of a vertical and horizontal line). To insure that an electron rayhits only the intended primary color within a cluster, a sheet of metal in front of thescreen full of minute holes (shadow mask)absorb errant rays.

Traditionally, CRT color saturation and contrast have been limited by the amount ofelectron energy the shadow mask could absorb. To improve saturation and contrast, apolarizing filter can be applied to the screen. This filter, however, reduces the lightintensity producing a dimming effect. Increasing the intensity of the electron beamcompensates for the dimming effect, but the increased errant energy expands themetal show mask causing image distortion. Zenith has solved this problem inmoderate size screens by placing the shadow mask under such high tension that theheat fails to distort the holes. Zenith continues to expand this technology to ever largerscreen sizes.

Another CRT weakness that Zenith has been able to overcome in smaller screens isthe traditional curvature of CRT screens. Hemispherical screens restrict the angle ofview and increase the problem of glare. Screens are curved along the circumferenceof the electron beam to insure that the cross section of the rays remain circular and infocus from the center to the edge of the screen. Zenith has overcome these difficultiesin smaller screens bv adjusting the ray focal length as it scans across the screen andaltering the distance between dot clusters. Other manufacturers have been able toflatten their screens using similar technology, but Zenith remains in the lead in bothsize and degree of flatness.

Despite these advances, CRTs remain prohibitively heavy and bulky. The larger thescreen, the further back the electron gun must be placed and the thicker the glass tubemust become for strength. If the gun is not recessed, the beam must be moved

28

through larger angles exacerbating ray distortions. As the glass tube becomes largerand less cylindrical, it must be made thicker to avoid breakage. Thus, a 3 x 5 footscreen, a likely format for HDTV, would weigh approximately 800 lbs. The neck of itstube would be too long to fit though the door of a home.

CRTs are also toxic. The radiation emitted by CRTs are suspected of adverselyaffecting health. This is of growing concern, especially to people who work aroundcomputer displays all day. The flicker caused by the sweeping beam of electrons isalso suspected of aggravating the sight of computer operators over extended periodsof time. Lastly, the radiated tube and phosphor are too toxic for landfills.

To date, Zenith has been unable to apply its flat tension mask (FTM) technology toscreens above 34-inches in diameter, and then only at high cost. Thus, initial HDTVscreens will be limited in size and quality by CRT flaws. Zenith’s CEO Jerry Pearlmanmay well be correct in his prediction that “Over the next 10 years, the CRT is going tobe the most cost-effective display, and by far the most cost-effective high definitiondisplay.”

Projection System

A current alternative to CRTs is a projection system which basically folds a projectedimage via a mirror. The image is first created by any of a number of technologies,including CRT-Liquid Crystal Display (LCD) or a lightvalve. The image is then bouncedoff a mirror and projected onto the back of the viewing screen. These systems havethe advantage of a large flat screen, but the disadvantages of poor image contrast anda lack of brightness. Hughes Aircraft and Hughes Electronics have traditionallyproduced projection systems with the highest contrast and brightness, but at very highcost. A lower cost system is expected for HDTV.

Field Emission Display

Several companies are developing a radical variation on the CRT theme called FieldEmission Display (FED). Instead of the rays from one electron gun exciting millions ofpixel dots, ten to one hundred microscopic electron guns (emitter tips) illuminate eachindividual pixel dot. Thus, several emitter tips per pixel can be defective withoutcompromising the quality of the screen.

The emitter tips are mounted on the intersections of row and column electrodes whichdrive the cluster of electron guns. The electrodes in turn are mounted on a thin baseplate. Parallel to the base plate, is the face plate which is coated on the inside withdots of phosphor in cluster formation to form pixels. The entire sandwich is only a fewmillimeters in depth.

29

The advantages of FED over CRT are numerous. FED screens are perfectly flat andvery thin. They also require much less energy, reducing unwanted radiation, loweringpower consumption and reducing heat buildup. The fault tolerance built in throughemitter tip redundancy increases yields, decreasing production costs. Thedisadvantage is that the largest FED produced to date is only six inches in diameter.

Microscopic cathodes were developed by Capp Spindt at SRI International in the late1960s. LETI Labs in France advanced the technology in 1983 by producing the firstvideo screen with the cathodes. Spindt left SRI in 1989 to develop FED screens in hisown firm, Coloray.

Active Matrix Liquid Crystal Display