Modernising post-adoption contact - Nuffield Family Justice ...

Upload

khangminh22Category

view

1download

0

A Nuffield Farming Scholarships Trust

Report Award sponsored by

The Trehane Trust

Put a label on it: why the future

of milk is a branded one

Tom Levitt

July 2018

NU

FFIE

LD

U

K

Copyright @ Nuffield Farming Scholarships Trust

ISBN: 978-1-912059-81-2

Published by The Nuffield Farming Scholarships Trust

Southill Farm, Staple Fitzpaine, Taunton, TA3 5SH

Tel: 01460 234012

Email: [email protected]

www.nuffieldscholar.org

NUFFIELD FARMING SCHOLARSHIPS TRUST (UK)

Awarding life changing Scholarships that unlock individual potential and broaden horizons through study and travel overseas, with a view

to developing farming and agricultural industries.

"Leading positive change in agriculture" “Nuffield Farming” study awards give a unique opportunity to stand back from your day-to-day occupation and to research a subject of interest to you. Academic qualifications are not essential, but you will need to persuade the Selection Committee that you have the qualities to make the best use of an opportunity that is given to only a few – approximately 20 each year. Scholarships are open to those who work in farming, food, horticulture, rural and associated industries or are in a position to influence these industries. You must be a resident in the UK. Applicants must be aged between 22 and 45 years (the upper age limit is 45 on 31st July in the year of application). There is no requirement for academic qualifications, but applicants will already be well established in their career and demonstrate a passion for the industry they work in and be three years post tertiary education. Scholarships are not awarded to anyone in full-time education or to further research projects. Full details of the Nuffield Farming Scholarships can be seen on the Trust’s website: www.nuffieldscholar.org. Application forms can be downloaded but only online submission is accepted. Closing date for completed applications is the 31st July each year.

A

Nuffield (UK) Farming

Scholarships Trust

Report

Date of report: September 2018

“Leading positive change in agriculture.

Inspiring passion and potential in people.”

Title Put a label on it: why the future of cow’s milk is a branded one

Scholar Tom Levitt

Sponsor The Trehane Trust

Objectives of

Study Tour

To understand how the market and consumer attitudes to cow’s milk

are changing. And what the sector can do best to adapt.

Countries Visited United States, Netherlands, Sweden, Denmark, Switzerland, Ireland

Messages

• Milk has lost its monopoly on our eating habits • Standardisation has shorn it of value • Public expectations are getting ever harder for farmers to meet • But the market for milk is evolving, not disappearing

• A new approach by entrepreneurs and successful brands can create value in the liquid milk category

• Brands are better at directly appealing and adapting to individual consumer preferences, rather than a generic industry approach to promote milk as a basic food

EXECUTIVE SUMMARY

Despite cow’s milk being consumed by 87% of the population in the UK there are concerns that it is vulnerable to falling out of fashion with a younger generation. It’s the same story in the US where generic marketing tactics like the long-running ‘Got Milk?’ campaign has failed to stop per capita consumption of cow’s milk in the US falling by one-third since the 1970s. In contrast, sales of plant-based ‘milks’ in the US were worth an estimated $2 billion in 2017, accounting for around 10% of the total milk market. Several major dairy companies have already started producing plant-based ‘milks’ or bought into non-cow’s ‘milk’ companies.

The purpose of this study was to understand what constitutes a viable future for the cow’s milk – as opposed to the wider dairy - category. Travelling around major milk consumer markets in North America and Europe and interviewing key stakeholders and consumer experts reveals a sector that has lost its monopoly, with eating habits, lifestyles, innovation and supermarket shelves no longer wedded to milk. Consumers have also long lost their connection to dairy farming and struggle to comprehend the reality of the industry today with bucolic childhood images. The biggest failure with the marketing of milk is how undervalued liquid milk is by the market place. Supermarkets have long used milk as a low margin product or even loss leader and that shows no signs of changing, with Walmart openly talking of being able to cut milk production costs further in the US. This focus on price and standardisation has created a race to the bottom which in turn is holding back innovation. The key recommendation of this report is the importance of investing in the emerging branded market, which accounts for less than 20% of all UK milk sales but is driving growth. The new barista milks, kefir drinks and other drinkable milk products providing a specific taste, health or nutritional benefit are clearly capturing the changing eating habits, interests and lifestyles of consumers. Some are not even marketing themselves as a milk product. If cow’s milk can define its points of difference, the liquid milk category still has a future to be more than an undervalued commodity, even if the word itself becomes redundant. Although some producers have got involved in direct selling, building a successful brand is a significant time and financial commitment. Alternatively, some are collaborating with businesses and entrepreneurs in the supply chain to deliver branded milk products. Dairy producers may prefer to rely on retailers, but retailers have done little, or been unable, to significantly improve the value of milk. And, as they have shown with their heavy promotion of ‘milk’ alternatives, their loyalty is to consumers, not cow’s milk producers. In the long term, dairy producers should be open to seeking partners who have other supply chain skills, expertise and contacts.

CONTENTS EXECUTIVE SUMMARY ..............................................................................................................................

Chapter 1 Personal Introduction ............................................................................................................ 1

Chapter 2 Background to my study subject .......................................................................................... 2

Chapter 3 Research and travel undertaken .......................................................................................... 3

Chapter 4 The dairy sector today .......................................................................................................... 4

Chapter 5 The challenges facing the milk sector ................................................................................... 7

5.1 The value deficit .......................................................................................................................... 7

5.1.1 The fall in value .................................................................................................................... 7

5.1.2 Low retail prices ................................................................................................................... 7

5.1.3 Standardisation and its impact on milk ................................................................................ 8

5.1.4 Market growth for dairy-free ‘milk’ alternatives ................................................................. 8

5.1.5 The failure of generic advertising ......................................................................................... 9

5.1.6 Seeking to regain value ………………………………………………………………………………………………9

5.1.7 New competitors for the dairy sector ................................................................................ 10

5.1.8 Is health a selling point? ...................................................................................................... 10

5.1.9 What’s the place of milk in the diet of today? .................................................................... 11

5.1.10 Who can diversify and add value to milk? ....................................................................... 13

5.1.11 New and emerging competitors to cow’s milk ................................................................ 14

5.2 Innovation and identity ............................................................................................................. 15

5.2.1 Innovation successes ........................................................................................................... 15

5.2.2 Successful barista milk brands..………………………………………………………………………………………15

5.2.3 A new identity for milk ........................................................................................................ 16

5.2.4 The market for flavour and provenance ............................................................................. 17

5.2.5 The success of kefir ……………………………………………………………………………………………………….17

5.2.6 Organic milk success .......................................................................................................... 18

5.2.7 Coca-Cola and Fairlife milk .................................................................................................. 18

5.2.8 The importance of branded milk ......................................................................................... 19

5.2.9 Milk sector still slow on innovation ..................................................................................... 20

5.3 Disconnection and perception ................................................................................................... 21

5.3.1 The dairy sector’s image ...................................................................................................... 21

5.3.2 The Netherlands and the degrading image of dairy..………………………………………………………22

5.3.3 Dutch farmers debate how to change ................................................................................. 22

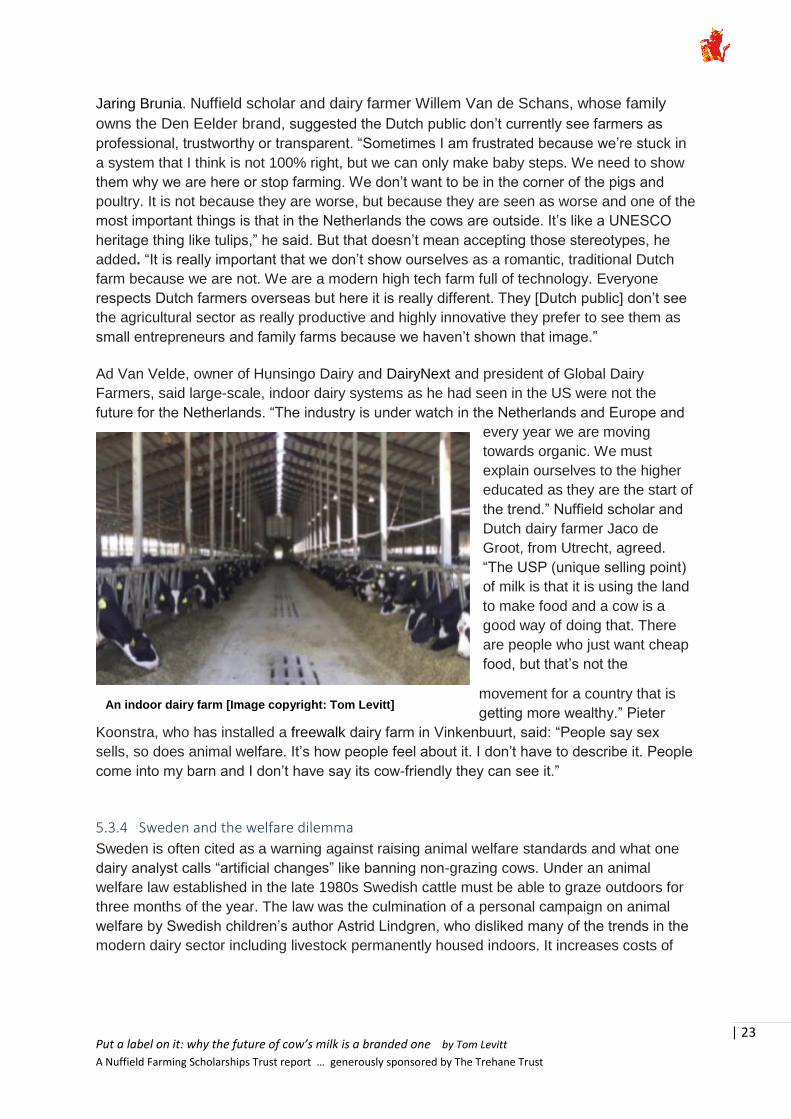

5.3.4 Sweden and the welfare dilemma ...................................................................................... 23

5.3.5 UK public‘s knowledge of reality of dairy today ................................................................. 24

5.3.6 How to re-engage with dairy consumers ............................................................................ 25

Chapter 6 Conclusions ......................................................................................................................... 26

Chapter 7 Recommendations.............................................................................................................. 27

Chapter 8 After my study tour ............................................................................................................ 28

Acknowledgements ............................................................................................................................... 29

DISCLAIMER

The opinions expressed in this report , where not attributed to anyone, are my own and not

necessarily those of the Nuffield Farming Scholarships Trust, or of my sponsor, or of any other

sponsoring body.

CONTACT DETAILS

Tom Levitt

Email: [email protected]

Twitter: @tom_levitt

Website: www.tomlevitt.co.uk

Address: 8 Elmwood Avenue, Chester CH2 3RQ

Nuffield Farming Scholars are available to speak to NFU Branches, Agricultural Discussion Groups

and similar organisations

Published by The Nuffield Farming Scholarships Trust

Southill Farmhouse, Staple Fitzpaine, Taunton TA3 5SH

Tel : 01460 234012

email : [email protected]

www.nuffieldscholar.org

Put a label on it: why the future of cow’s milk is a branded one by Tom Levitt

A Nuffield Farming Scholarships Trust report … generously sponsored by The Trehane Trust

| 1

1. Personal Introduction

My farming story started comparatively late in life at the

age of 23. After graduating from York University with a

History degree and then an MA in Journalism at the

University of Central Lancashire, I started out as a

journalist at the Farmers Guardian in 2004. Since then I’ve

worked as an editor and journalist at The Ecologist, CNN

and MSN before, most recently, working at the Guardian

up until last year. It was my early reporting days at

Farmers Guardian that ignited my interest in food and

farming and has since led to my journalism appearing in a

wide variety of publications including Country Life, Earth

Island Journal, The Financial Times, Huffington Post, the

Independent, The New Agriculturalist and Vice media.

Wanting to gain more knowledge and understanding about

our food system, I completed an MSc in Food Policy (with distinction) at City University in

2015. Since then I’ve been a guest lecturer on food at the Centre for Alternative Technology

in Wales, a speaker and chair at the Edinburgh Science Festival, a chair for debates on food

policy issues for The Guardian, and a guest interviewee on BBC Countryfile and BBC Radio

talking about food and farming issues.

I left the Guardian as a full-time staff member in 2017 after relocating outside of London with

my wife and son to Cheshire. After growing up in Cornwall and Lancashire, it was never my

intention to spend so long (more than a decade) in London. Ironically, it was farming that

took me to the city as my reason for re-locating in the first place was to take on a role as a

political reporter for the Preston-based Farmers Guardian. Since leaving London I have been

working as a freelance journalist and researcher for media outlets and industry

organisations. I am also employed as a research associate for the Royal Society of Arts’

RSA Food, Farming and Countryside Commission, developing their communications

strategy up to and beyond its final report in March 2019.

Outside of my paid employment I have taken on voluntary roles as a director for the Oxford

Farming Conference (2019-22) and on the advisory board for the Food Climate Research

Network (FCRN) at Oxford University. I have also run a discussion on the future of dairy for

the Oxford Real Farming Conference.

Tom Levitt, author of this report,

being interviewed on BBC

Countryfile

Put a label on it: why the future of cow’s milk is a branded one by Tom Levitt

A Nuffield Farming Scholarships Trust report … generously sponsored by The Trehane Trust

| 2

2. Background to my study subject

A Nuffield scholarship has long been an ambition of mine since I first heard about them in

the early stages of my journalism career working at Farmers Guardian. But it was not until

2016 that I finally found the right moment in my own career and a subject worthy enough to

merit applying.

The topic I decided upon started out as a series of curiosities: why do we drink milk, why is it

cheaper than water and what will be its place in our diets and farming system in the years

ahead?

As I began my research and travel for the scholarship I quickly realised that we are at a

crossroads in cow’s milk consumption in the long established markets of Europe and North

America. Consumer eating habits and choices are changing and attitudes to dairy farming

are becoming more complex and demanding.

I’ve tried to keep an open mind throughout my travels, looking at the topic from all

perspectives. My report is an attempt to analyse how the cow’s milk category can improve its

consumer perception and value.

I have two important points about the wording used in this report. The use and meaning of

the word milk is rapidly changing among both consumers and the food industry. For the

purpose of clarity when I refer to milk I mean cow’s milk. When I am talking about an

alternative to cow’s milk I will say that i.e. plant-based ‘milk’, which includes soya, almond,

oats and rice-based drinks.

When the food industry refers to the milk category, they invariably mean liquid cow’s milk

including full fat, semi-skimmed and skimmed milk, organic and other specialist branded

liquid milk products. However, they may also now include non-cow’s milk products, such as

goat, sheep or plant-based alternatives, in that category. In addition, they may also be

including drinkable cow’s milk-based products like kefir and ones where cow’s milk only

makes up a proportion of ingredients, i.e. milkshakes, frappuccinos or smoothies.

When I refer to brands, I don’t mean supermarkets’ own-brand range of milks. I mean a

unique product that has been produced by a particular business under a particular name, for

example Bio-tiful Kefir, Graham’s Gold Jersey or Yeo Valley milk.

Put a label on it: why the future of cow’s milk is a branded one by Tom Levitt

A Nuffield Farming Scholarships Trust report … generously sponsored by The Trehane Trust

| 3

3. Research and travel undertaken

I spent eight weeks travelling to the United States, Denmark, Switzerland, Sweden, the

Netherlands, Ireland and the United Kingdom in 2017 and 2018 trying to understand how the

market and consumer attitudes to cow’s milk is changing. These countries were chosen as

representative of mature dairy markets, where consumption of milk was comparatively high,

but where they are facing challenges in terms of producer returns and consumer sales. In

each country I sought to speak with dairy farmers, lobbyists, analysts, manufacturers, retail

firms, major dairy brands and academic researchers. I also sought to speak with

entrepreneurs outside of the dairy sector, to get a broader and more unique perspective on

consumer habits and trends.

Put a label on it: why the future of cow’s milk is a branded one by Tom Levitt

A Nuffield Farming Scholarships Trust report … generously sponsored by The Trehane Trust

| 4

4. The dairy sector today

The global dairy sector is worth more than US$600bn and is forecast to grow at 2.5%

between 2017-22 (Rabobank1). The Asia-Pacific region overtook Western Europe as the

largest dairy consuming region in the world in 2016, with the region forecast to make up two-

thirds of the growth in dairy consumption in volume terms between 2016-2021 (Euromonitor

2.) The growth in Asia-Pacific is being driven by yoghurt and drinking milk products, followed

by cheese (which is starting from a small base). China and India are forecast to be the

largest growth markets, followed by Vietnam, Pakistan, Indonesia and the Philippines.

In the UK, the dairy sector accounted for 17.8% of total agricultural output in the UK (2014),

with the country being the third-largest milk producer in the EU after Germany and France,

and the tenth-largest producer in the world. The total number of dairy farms in the UK is

c.13,000, down from 35,000 in 1995 (Defra 3). The total numbers of dairy cows is 1.9 million,

producing 14.9 billion litres at an average yield of 7,800 litres per cow (2017). The average

herd size is c.140.

The total farmgate value of milk and milk products in the UK was £4.34 billion and the total

value of UK dairy sales was £10.7bn in 2017 ( Kantar4). Around 50% of the milk produced by

UK farmers goes into fluid liquid market (a figure is which compares with 7-16% in rest of

EU). Of the other 50%, one-third goes into producing cheese, 8% into milk powder, 3+% into

yoghurt and 2% into butter and 2% into cream. Sales of whole milk rose by 4% in 2017,

while sales of skimmed milk fell by 4%.

Between 1998 and 2017 the annual sales value of UK dairy exports increased by 134% to

£1.67bn, while export volumes doubled to 1.36m tonnes. The EU remains by far the largest

market for UK dairy, (source: Agriculture and Horticulture Development Board AHDB),

accounting for 92.7% of UK exports in 2017. The value of non-EU exports was £404.7m in

2017, with higher average prices to non-EU markets.

Spending on liquid milk (including non-cow’s milk) in the UK over the past year was at

£3.28bn (up 4%), with spending on cheese at £2.8bn (up 3.5%) and butter at £118m (up

16%)(Kantar5).

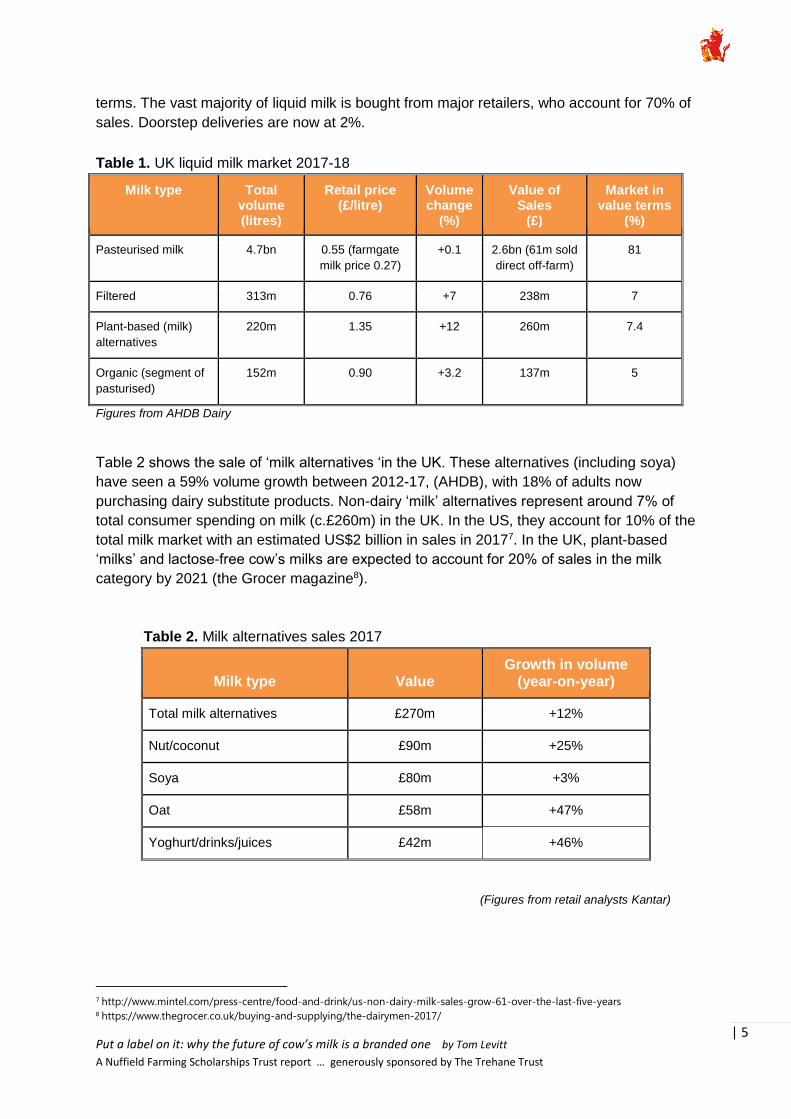

Table 1 shows the market share of the different types of milk. The UK organic dairy sector is

worth £344 million (accounting for almost one-third of the total organic food sales), with Yeo

Valley accounting for 17% of all organic milk sales in 20166. Soy and other ‘milk’ alternatives

account for less than 4% of liquid milk market in volume terms in the UK, but 7% in value

1 https://www.rabobank.com/en/press/search/2018/20180524-rabobank-dare-not-to-dairy-how-the-industry-can-respond-to-

the-rise-of-dairy-free.html 2 http://www.euromonitor.com/succeeding-in-asia-pacific-exploring-the-dairy-market-and-consumer-dynamics/report 3 https://www.gov.uk/government/statistics/agriculture-in-the-united-kingdom-2017 4 http://www.fwi.co.uk/business/fresh-milk-sales-drives-significant-uk-dairy-market-growth.htm 5 https://www.fwi.co.uk/business/fresh-milk-sales-drives-significant-uk-dairy-market-growth 6 http://www.omsco.co.uk/_clientfiles/Omsco Milk Market Report 2017.pdf

Put a label on it: why the future of cow’s milk is a branded one by Tom Levitt

A Nuffield Farming Scholarships Trust report … generously sponsored by The Trehane Trust

| 5

terms. The vast majority of liquid milk is bought from major retailers, who account for 70% of

sales. Doorstep deliveries are now at 2%.

Table 1. UK liquid milk market 2017-18

Milk type Total volume (litres)

Retail price (£/litre)

Volume change

(%)

Value of Sales

(£)

Market in value terms

(%)

Pasteurised milk 4.7bn 0.55 (farmgate

milk price 0.27)

+0.1 2.6bn (61m sold

direct off-farm)

81

Filtered 313m 0.76 +7 238m 7

Plant-based (milk)

alternatives

220m 1.35 +12 260m 7.4

Organic (segment of

pasturised)

152m 0.90 +3.2 137m 5

Figures from AHDB Dairy

Table 2 shows the sale of ‘milk alternatives ‘in the UK. These alternatives (including soya)

have seen a 59% volume growth between 2012-17, (AHDB), with 18% of adults now

purchasing dairy substitute products. Non-dairy ‘milk’ alternatives represent around 7% of

total consumer spending on milk (c.£260m) in the UK. In the US, they account for 10% of the

total milk market with an estimated US$2 billion in sales in 20177. In the UK, plant-based

‘milks’ and lactose-free cow’s milks are expected to account for 20% of sales in the milk

category by 2021 (the Grocer magazine8).

Table 2. Milk alternatives sales 2017

Milk type

Value

Growth in volume (year-on-year)

Total milk alternatives £270m +12%

Nut/coconut £90m +25%

Soya £80m +3%

Oat £58m +47%

Yoghurt/drinks/juices £42m +46%

(Figures from retail analysts Kantar)

7 http://www.mintel.com/press-centre/food-and-drink/us-non-dairy-milk-sales-grow-61-over-the-last-five-years 8 https://www.thegrocer.co.uk/buying-and-supplying/the-dairymen-2017/

Put a label on it: why the future of cow’s milk is a branded one by Tom Levitt

A Nuffield Farming Scholarships Trust report … generously sponsored by The Trehane Trust

| 6

For the future, most of the growth in the dairy sector is forecast to take place outside

Western Europe and North America, where retail sales of milk declined 5% and 3%

respectively between 2012-17. The global sales of dairy alternatives were US$18bn in 2017

(with US$15.6bn in ‘milk’ alternatives) up from US$7bn in 2010 and with an annual growth of

rate of 8% over the past decade (Rabobank) and are predicted to be worth US$22 billion by

20229. Dairy-free ‘milk’ represented 12% of total fluid milk and alternative sales globally in

2017. Only the Middle East and North Africa is expected to see higher growth rates in cow's

milk over ‘milk’ alternatives between 2016-21 (AHDB) with further declines in retail sales

predicted in North America and Western Europe.

9 https://www.rabobank.com/en/press/search/2018/20180524-rabobank-dare-not-to-dairy-how-the-industry-can-respond-to-

the-rise-of-dairy-free.html

Put a label on it: why the future of cow’s milk is a branded one by Tom Levitt

A Nuffield Farming Scholarships Trust report … generously sponsored by The Trehane Trust

| 7

5. The challenges facing the milk sector

5.1 The value deficit

5.1.1 The fall in value

In the mid-1990s the farmgate price for milk was 25p per litre. In 2016, the farmgate price fell

as low as 20p per litre. Over the past year (2017-18) the average price has been 27p.

Spending on milk and milk products, excluding cheese, has fallen in

real terms faster than total spending on food and drink since the

mid-1990s, according to the Defra Family Food survey. The ongoing

price war on conventional milk has been a block on consumers

trading up to higher value milk like organic. In short, people have got

so used to milk being cheap that it requires a big shift to encourage

them to trade up. That shift needs supermarkets to stop using milk as a loss leader to retain

consumer loyalty. “If milk wants higher value it has to change from the top down. The

supermarkets are driving the prices at the moment and giving limited margins to processors.

It needs supermarkets to change how they see and sell it,” said Patrick Denny, RABDF Dairy

Student of the year 2018. The low cost of milk is not the reason for its consumption, said Neil

Hendry, a consultant at the consumer analysts Global Data: “Milk is bought because it’s

ingrained in our DNA not because it is

cheap.”

5.1.2 Low retail prices

The race to the bottom in liquid milk was

accelerated by supermarket price wars

in the 1990s. “The harsh truth is that

consumers are not paying much for milk

today because supermarkets let them

and farmers are stuck with them

[supermarkets] as their access to

market”, said Eddie Andrew, owner of

the Our Cow Molly dairy brand. In the

1980s most milk was still sold in glass

bottles with a head of cream on top.

Today, the doorstep delivery market has

dropped to 2% of total sales, with most

milk sold regionally or nationally from a

smaller number of large processors,

such as Arla, which opened the world's

biggest fresh milk plant in Aylesbury,

Buckinghamshire in 201410. It’s the same story in the US, where Walmart recently

announced its plans to start processing its own milk in a bid to cut costs further, ‘It’s going to

help us provide really high-quality milk at really low prices,’ its vice-president of food is

reported as saying11. As Dean Sommer, from the Centre for Dairy research at the University

10 https://dairy.ahdb.org.uk/market-information/dairy-sales-consumption/liquid-milk-market/#.WzD0cYRKijL 11 https://www.foodbev.com/news/walmart-makes-move-into-dairy-production-with-indiana-plant/

The diversity of milks on offer to consumers in a US

supermarket [image copyright: Tom Levitt]

“Milk is bought because

it’s ingrained in our DNA

not because it is

cheap.”

Put a label on it: why the future of cow’s milk is a branded one by Tom Levitt

A Nuffield Farming Scholarships Trust report … generously sponsored by The Trehane Trust

| 8

of Wisconsin said: “The price of milk is designed to just pay enough to keep a supplier. Most

innovation comes from small players, but the fluid milk sector has no small players left and

the capital entry costs are huge.”

5.1.3 Standardisation and its impact on milk

This never-ending fight on price has meant that the vast majority of milk in both the US and

UK is sold in no-frills plastic containers in supermarkets and other retail or wholesale outlets

and homogenised, with the milk fat broken up so that it does not separate from the milk. It’s

a process of standardisation designed to cut costs but has left little room for processors to

invest in packaging, promotion or innovation. What’s more, the use of milk as a loss leader

by supermarkets to boost customer loyalty has meant they have had less interest in

investing in presentation and in-store display. “For too long the aisle has been about three

types of milk. For the average consumer it’s like an industrial aisle of cages of milk. People

pass through fast without spending time. We need to change that,” said Graeme Jack, head

of communications at Müller UK.

The standardisation has also meant dairy processors have had little interest in the distinctive

taste of milk that is either unhomogenised or from different breeds, said Doug Wood, hired

by the Stirlingshire-based Graham’s Family Dairy as the UK’s first milk sommelier. “It’s been

a race to the bottom focused on price and not quality. It’s easy for people to understand it’s

50p, but less easy for them to think it tastes good. They just see it as a glass of white stuff.”

Wood said a new generation of consumers were becoming more concerned about taste in

their food choices, yet many of them don’t realise that milk can and does taste differently.

“We all have preconceived ideas of milk and what it tastes like, so we need to work hard to

break that down and get people to reconsider,” said Wood. For James Baeworlf, who runs

the Sassy Cow dairy farm near Madison, Wisconsin, it’s quite simple: “Milk is poor man’s

food now”. The solution, said both Baeworlf and Dean Sommer, was to premiumise the

market and come up with another product that gets milk out of that cheap commodity box, in

the same way that Coca-Cola is trying to do with its Fairlife brand.

5.1.4 Market growth for dairy-free ‘milk’ alternatives

It’s a case of contrasting fortunes for dairy-free ‘milk’ alternatives, which command a

significant retail premium. They account for just 3.7% of the total sales volume of the milk

category - which includes cow’s milk and plant-based alternatives - but 7.4% of spending in

the category. Although global demand for dairy, which includes cow’s milk, is expected to

grow at 2.5%, demand for plant-based alternatives to milk and other dairy is projected to

grow at 5% (albeit from a lower base) despite the comparatively higher cost to consumers,

according to Rabobank12. The low-growth problem is strongest in Western Europe and North

America. For the UK, the majority of growth in volume terms in the liquid milk market is

taking place in the non-dairy ‘milk’ alternatives category. In 2017-18, pasteurised milk grew

at 0.1%, while plant-based alternatives to cow’s milk, including soya, oat, almond and rice

‘milk’ grew at 12%, according to AHDB. The only exceptions showing higher growth in the

cow’s milk category were filtered (7% growth), lactose-free (10% growth) and organic (3.2%

growth).

12 https://www.rabobank.com/en/press/search/2018/20180524-rabobank-dare-not-to-dairy-how-the-industry-can-respond-

to-the-rise-of-dairy-free.html

Put a label on it: why the future of cow’s milk is a branded one by Tom Levitt

A Nuffield Farming Scholarships Trust report … generously sponsored by The Trehane Trust

| 9

5.1.5 The failure of generic advertising

Until recently, the dairy sector had been focused on the need for generic campaigns to push

milk and dairy consumption to arrest this stagnation. This tactic that failed to arrest a sales

decline in the US13. The AHDB’s recent £1.3m consumer campaign on milk and dairy marks

a change of approach14. It has focused on promoting the taste and enjoyment of dairy to

young people. It’s an attempt to improve the overall brand image of dairy amongst

millennials. It’s distinct from the ‘drink milk for your health’ messaging of yesteryear, however

it has also been unable to prove any uptake in sales15. AHDB’s Rebecca Miah, who heads

up the campaign, said dairy needed to be seen as having more value in the eyes of

consumers. “It’s a hard thing to affect. The premiumisation makes people value things. It

makes people actually think about it. Some dairy companies are doing it and people do trade

up and buy that shiny new thing. A lot of innovation should be on-the-go and convenience

out of home.”

The importance of value was reiterated by Kevin Bellamy, dairy strategist at Rabobank, who

said the main future focus for dairy would be on brands, with companies working hard on

marketing to develop “extra uniqueness” in the marketplace. A former manager at the dairy

company Fonterra explained how: “The key is to follow longer term trends not fashions.

Fashions like frozen yoghurt come and disappear. Trends are clean labels, transparency,

better nutrients, free from

residues. Food is either a staple

or an impulse purchase. The

premiums for impulse purchases

are much higher and it is why

marketing is more important for

those products than for staples

or unbranded products, which

rely more on superior scale or

cost structures.”

5.1.6 Seeking to regain value

Premiumisation is no easy task

when margins for dairy

companies are so tight. “To get

the retailers to pay more is not easy. The retailers’ value milk to get people in stores as it’s in

90% of baskets,” said Müller UK’s head of agriculture Rob Hutchinson. Müller’s aim is to

regain value through changing habits. With morning milk consumption in cereals in decline

that means encouraging consumption of milk on other occasions, particularly snacking which

is already being successfully exploited by dairy alternative products. “It is mayhem for dairy

processors but they have to adapt to the consumer,” said Tetrapak’s dairy marketing

13 https://www.newyorker.com/business/currency/the-end-of-got-milk 14 https://dairy.ahdb.org.uk/consumer-campaign/#.WzTuP4RKijI 15 https://i.pinimg.com/736x/96/3a/19/963a19d7338a0cba7bdc1d1f289d0ea1--advertising-signs-vintage-advertisements.jpg

“The consumption of milk is

evolving, not disappearing”

Products produced by Oatly [Image copyright: Tom Levitt]

Put a label on it: why the future of cow’s milk is a branded one by Tom Levitt

A Nuffield Farming Scholarships Trust report … generously sponsored by The Trehane Trust

| 10

manager Nagrinou Jeim. “The consumption of milk is evolving, not disappearing.

When Starbucks launched in the UK, milk consumption actually went up. I grew up with

cereals and milk but now it’s yoghurt which I didn’t have as a kid. Ten years ago dairy

wouldn’t listen to innovation. They were happy with sales. Now they realise that innovation

and differentiation is key to survival”. The key value trends for dairy in Europe, said Jeim, are

convenience, snacking, on-the-go, healthy balance and local power. “People want a

customised product i.e. lactose-free or added calcium, they want real connection with brands

and they are shopping for breakfast now too so looking for time-reduction solutions.”

5.1.7 New competitors for the dairy sector

In trying to take advantage of new trends and add value, however, the dairy sector faces

many new competitors, including plant-based ‘milk’ alternatives. “It’s not just a fashion. They

are here to stay,” said Thierry Philardeau, head of Nestle’s dairy strategic business unit, who

said the world’s biggest dairy company was open to producing plant or synthetic ‘milk’ and

dairy alternatives. Others have already switched. Danone spent US$10bn buying

Whitewave, Dean Foods bought a stake in Good Karma Foods and Finnish dairy

cooperative Valio launched an oat-based drink and yoghurt called ‘Oddlygood’. Long-time

US dairy manufacturer Elmhurst quit cow’s milk altogether in 2016 blaming low profitability

and reinvented itself as a plant-based ‘milks’ company16. In California, where almond

production reached record levels in 2018, dairy farmers are already hedging their bets by

planting the crop, with almond ‘milk’ accounting for 64% of US ‘milk’ alternative sales1718.

“My father is sticking with dairy, but my brothers are more open. Why are we working so

hard for the profitability they ask when we could grow almonds with less effort and more

money,” said Paul Sousa, a dairy farmer from Modesto and director at Western United

Dairymen who recently planted 35 hectares of almonds.

5.1.8 Is health a selling point?

A big factor behind the rise of alternatives has been health, with the dairy sector continuing

to suffer from decades of dietary advice that animal fats were bad for you, said John Lucey,

director of the Centre for Dairy Research in Madison. “It put a skull and crossbones on the

dairy industry for decades. I don’t think consumers have figured that out yet. Milk is a high

calorie dense material but not a health risk.” This is borne out by UK research commissioned

last year that showed more than one-third of 16-24 year olds are cutting back on dairy, with

60% of them citing health as the reason19. Animal welfare (32%) and impact on the

environment (25%) were the other two. The main health concerns were fat, sugar and

allergy or intolerance. The “mums of the future” are now questioning their need for milk, said

Zoe Kavanagh, chief executive of Ireland’s National Dairy Council. “[Milk] has lost its

monopoly and its nutritional messages are waning,” said Blake Waltrip, US director of A2

Milk.

16 http://uk.businessinsider.com/dairy-farm-nut-milks-elmhurst-2017-4 17 https://www.bloomberg.com/graphics/2018-thirst-for-almonds/ 18 http://www.mintel.com/press-centre/food-and-drink/us-non-dairy-milk-sales-grow-61-over-the-last-five-years 19 https://www.thegrocer.co.uk/buying-and-supplying/the-dairymen-2017/how-to-sell-dairy-in-the-age-of-scary-expert-

panel/557266.article

Put a label on it: why the future of cow’s milk is a branded one by Tom Levitt

A Nuffield Farming Scholarships Trust report … generously sponsored by The Trehane Trust

| 11

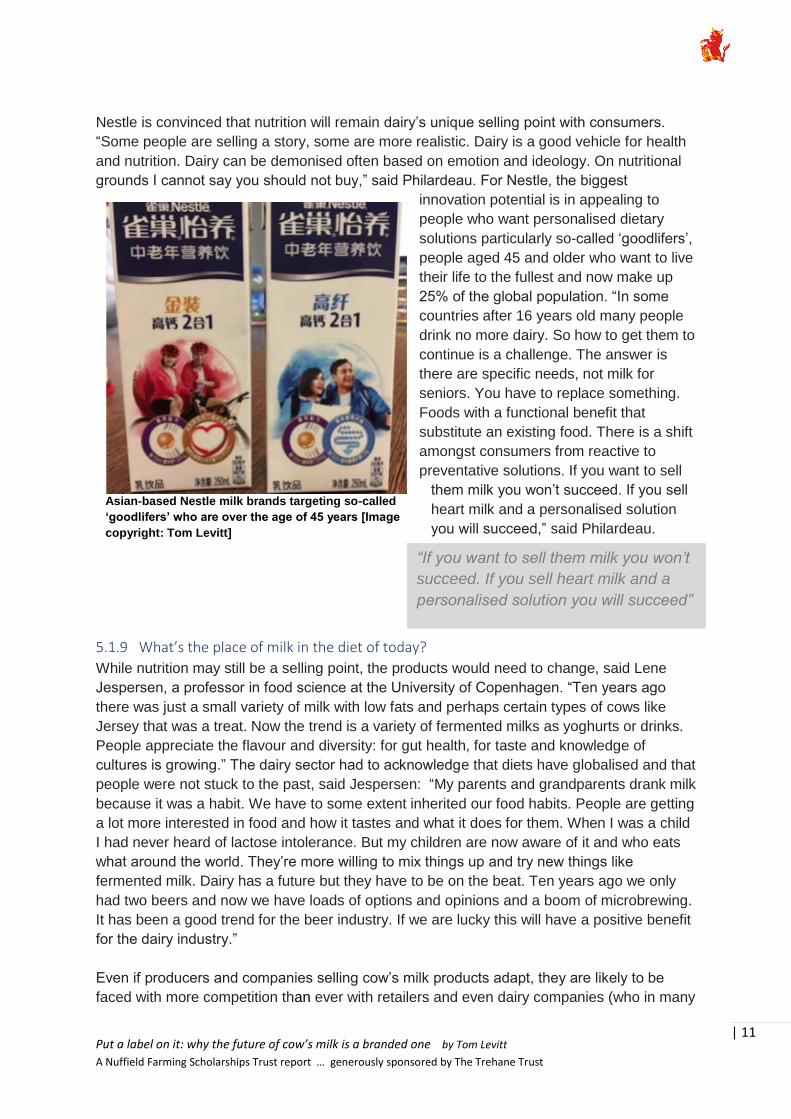

Nestle is convinced that nutrition will remain dairy’s unique selling point with consumers.

“Some people are selling a story, some are more realistic. Dairy is a good vehicle for health

and nutrition. Dairy can be demonised often based on emotion and ideology. On nutritional

grounds I cannot say you should not buy,” said Philardeau. For Nestle, the biggest

innovation potential is in appealing to

people who want personalised dietary

solutions particularly so-called ‘goodlifers’,

people aged 45 and older who want to live

their life to the fullest and now make up

25% of the global population. “In some

countries after 16 years old many people

drink no more dairy. So how to get them to

continue is a challenge. The answer is

there are specific needs, not milk for

seniors. You have to replace something.

Foods with a functional benefit that

substitute an existing food. There is a shift

amongst consumers from reactive to

preventative solutions. If you want to sell

them milk you won’t succeed. If you sell

heart milk and a personalised solution

you will succeed,” said Philardeau.

5.1.9 What’s the place of milk in the diet of today?

While nutrition may still be a selling point, the products would need to change, said Lene

Jespersen, a professor in food science at the University of Copenhagen. “Ten years ago

there was just a small variety of milk with low fats and perhaps certain types of cows like

Jersey that was a treat. Now the trend is a variety of fermented milks as yoghurts or drinks.

People appreciate the flavour and diversity: for gut health, for taste and knowledge of

cultures is growing.” The dairy sector had to acknowledge that diets have globalised and that

people were not stuck to the past, said Jespersen: “My parents and grandparents drank milk

because it was a habit. We have to some extent inherited our food habits. People are getting

a lot more interested in food and how it tastes and what it does for them. When I was a child

I had never heard of lactose intolerance. But my children are now aware of it and who eats

what around the world. They’re more willing to mix things up and try new things like

fermented milk. Dairy has a future but they have to be on the beat. Ten years ago we only

had two beers and now we have loads of options and opinions and a boom of microbrewing.

It has been a good trend for the beer industry. If we are lucky this will have a positive benefit

for the dairy industry.”

Even if producers and companies selling cow’s milk products adapt, they are likely to be

faced with more competition than ever with retailers and even dairy companies (who in many

Asian-based Nestle milk brands targeting so-called

‘goodlifers’ who are over the age of 45 years [Image

copyright: Tom Levitt]

“If you want to sell them milk you won’t

succeed. If you sell heart milk and a

personalised solution you will succeed”

Put a label on it: why the future of cow’s milk is a branded one by Tom Levitt

A Nuffield Farming Scholarships Trust report … generously sponsored by The Trehane Trust

| 12

cases now also own dairy alternative brands) keen to promote ‘milk’ alternatives to

consumers20. “There is a power struggle on the supermarket shelves over placement and

visibility,” said Anna Richert, food advisor at WWF, who said dairy's place, along with meat,

at the centre of our food system and diets was changing. It was no longer seen by everyone

as an essential part of every mealtime, with people switching away, for example, from milk

and cereal for breakfast and trying something different.

But perhaps that re-assessment of dairy could be both fair and beneficial. Milk and dairy has

long had a privileged position in our diets, the shopping basket and fridge. The majority of us

like dairy and consume more of it than we are advised too. The government dietary

recommendations are for dairy to make up 8% of our daily food intake, yet our actual dairy

consumption is estimated to be more than 15%21. In the case of dairy, consumers are now

drinking less fluid milk but eating more dairy products like yoghurt and cheese than they did

40 years ago. That trend away from cow’s milk is expected to continue, but a declining

category for milk products could still return

higher values for producers through the rise of

brands and milk-based products like yoghurt

drinks and smoothies. Cow’s milk can no

longer take its market for granted and must

find new ways to justify its place in people’s

diet. As influential food policy expert Marion

Nestle, a professor of nutrition at New York

University and author of What to Eat, and Food

Politics, said: “In nutrition, there are no

absolutes, only relative statements in the

context of everything else someone eats. I

don’t think the kind of milk or milk at all matters

if the overall diet is reasonable. Everything in

moderation.”

It may, ultimately, be necessary (and

preferable) for the dairy sector in Western

Europe to accept that eating habits are

changing and that the most viable future for

milk producers maybe one where milk and

dairy is more of a premium, rather than

commodity, product. Food analyst Marianne

Smith Edge explained: “The main barriers for Generation Z (born after the mid-1990s)

consuming milk are health concerns about acne, preferring other beverages, not liking the

taste, not liking how it makes them feel and already

drinking enough,” she said. “Consumers are already de-

commodifying the product by switching from cereal and

glasses of milk to smoothies and lattes,” she added.

In Senegal, where a consumer market for dairy is only

20 https://www.alpro.com/uk/faq/detail/why-are-danone-buying-alpro 21 https://www.nhs.uk/live-well/eat-well/the-eatwell-guide/

“Consumers are already de-

commodifying the product by

switching from cereal to

smoothies and lattes”

An advert for keifr milk [Image copyright:

Biotiful Dairy]

Put a label on it: why the future of cow’s milk is a branded one by Tom Levitt

A Nuffield Farming Scholarships Trust report … generously sponsored by The Trehane Trust

| 13

beginning to be established, milk will only ever be sold as a high value product, said Bagoré

Bathily, founder La Laiterie Du Berger, which counts Danone among its investors. “I think

milk is an expensive product if you look at the bigger picture of the planet and our resources.

It needs to be considered a premium product and a pleasure product. We have to go give a

value to our milk, but I don't think we have to push consumption because it seems to be still

an expensive solution.”

5.1.10 Who can diversify and add value to milk?

The task of creating value and de-commodifying milk may not, however, be achieved by

major dairy companies. “We are controlled by companies that want standardisation but we

need diversity in our diets and farming. How can we get off that model that is very

destructive and will be the end of us if we don’t get off it?” said one UK-based dairy farmer to

me. What’s more, the more disconnected dairy producers become from consumers the less

chance they have to highlight the value of what they do on an individual scale, said Roberto

Flore, head of culinary R&D at the Nordic Food Lab at the University of Copenhagen. “It is

easy for the industry to produce a diverse range of products (i.e. 10 different types of milk),

but what is the future of those who cannot do that - a small community of shepherds or dairy

farmers who do not have the capacity to sell their product?”

For Flore, value for dairy producers would come from re-connecting consumers with the

traditional farming in their locality. “Milk production is an activity based in defined

geographical areas. Food production trends don’t favour Sardinia or rural Wales with high

production costs and transport costs to markets. Milk is still 1,000 of different realities around

the world. We need to be careful to preserve the local tradition and not just promoting

something for getting more money for the industry. If we just think about feeding cows and

pumping milk and not all the process

around that gives you the milk then

the system cracks. We need to talk

about the value of culture and what

we have learnt over a millennia. A

farm of the future should be a little

more entrepreneurial - not just one

that is producing but one that is

producing ideas/thoughts and a farm

that is delivering experience.” Not

everyone is convinced. “Selling

direct is not the answer if you are

competing against dairy companies

with big budgets,” said Anna

Carlsson, co-owner of Skogsgard

dairy farm in Southern Sweden,

which has sold its own produce in the

past. “It was nice to find consumers,

but it was hard to live on them.”

Animal-free milk developed by US-based Perfect Day

[Image copyright: Perfect Day]

Put a label on it: why the future of cow’s milk is a branded one by Tom Levitt

A Nuffield Farming Scholarships Trust report … generously sponsored by The Trehane Trust

| 14

5.1.11 New and emerging competitors to cow’s milk

Aside from plant-based ‘milk’ alternatives, the other challenger lurking in the near future is

synthetic milk. Through a combination of yeast, cow DNA and plant nutrients, the

Californian-based start-up Perfect Day (whose investors include one of Asia’s richest men Li

Ka Shing) claims to have created a product identical in taste and nutritional value to cow’s

milk, but without the use of an animal22. To make the animal-free cow’s milk, Perfect Day

insert cow DNA – which is readily available thanks to decades of research by the dairy

industry – into yeast and add sugar to create milk proteins through fermentation. These milk

proteins are then combined with sugar, fats and nutrients to create the final product.

Although comparisons have been made with lab-grown meat, Perfect Day co-founder Ryan

Pandya said they are not using novel technology. “Many people initially go ‘oh is this like lab

or test-tube milk’, but that’s wrong. There are no test tubes in our fermentation process, it’s

just like brewing craft beer. The meat folks are trying to invent technology that doesn’t exist

today, but our milk is made through techniques in use for more than three decades.” The

company has raised almost US$25 million in financial backing already and said dairy

companies are interested in bringing their product to market. “The assumption was that we’d

be hated by the dairy industry, but it’s actually the opposite. They see us as the long-term

solution to problems they didn’t even know were solvable,” said Pandya.

Another US-based company, Impossible Foods, which is producing four million of its

imitation meat-free burgers a month, has said it wants to target dairy next. “[Before

becoming a vegan] I loved putting milk in my coffee and cereal, but plant-based milks don’t

work for me so far,” said founder Pat Brown. “No-one is trying very hard to deliver the full

experience of what consumers value from milk. We don’t want to follow the course of soya

and almond milk. We’re after 100% of the market, not a niche of people avoiding meat or

being health conscious.” While some say the dairy sector can see off synthetic alternatives

by focusing on dairy’s “lack of processing” and “quality

of nutrients”, others are less convinced. Any assumption

that the consumer would prefer a ‘natural’ alternative

would be misplaced said Hans Van Trijp, a professor of

marketing and consumer behaviour at Wageningen

University: “In the end milk is just a bit of protein and

water with a nice profile, but maybe we can mimic that. If you can extract protein from grass

why would you give it to a cow first? Whether people are up for this is unclear. How natural

is it to get milk from cows kept inside all-day? A lot will depend on how we define natural and

health. I think we realise there will be a divide in society and in people between going all

natural or processed. Only a small group is committed to one way or another. It is a sign of a

level of pragmatism.”

22 https://www.dairyreporter.com/Article/2016/08/22/Perfect-Day-vegan-animal-free-milk-a-gamechanger

“In the end milk is just a bit of

protein and water with a nice

profile, but maybe we can

mimic that”

Put a label on it: why the future of cow’s milk is a branded one by Tom Levitt

A Nuffield Farming Scholarships Trust report … generously sponsored by The Trehane Trust

| 15

5.2 Innovation and identity

5.2.1 Innovation successes

One of the biggest innovation successes in drinks involving milk over the past decade has

been the rising consumption of coffee, led by high street chains Costa and Starbucks. An

estimated 9.5 million cups of coffee a day are consumed in cafes, bars and restaurants23. It

is a market popular with the consumers aged 35 and under who say they are most likely to

be cutting back on dairy, according to survey data released by consumer research firm

Kantar Worldpanel last year. While older people are more likely to buy instant coffee for

home consumption, younger consumers use a coffee machines at home or visit coffee

shops. Millennials (aged 20-37) contributed to 50% of all the coffee consumed in coffee

shops, bars or restaurants.

So far the dairy sector has largely failed to profit from consumer’s love affair with coffee and

willingness to pay upwards of £2.50 for a latte. Only more recently has there been attempts

to promote specialist milk for coffee and

capitalise on the willingness of coffee shops

to pay a premium for good-quality milk with

provenance. Milk can affect the taste and

texture of coffee, depending on the type

used, said Jeremy Challender, of Prufrocks

Coffee “The biggest influence is fat content.

With full-fat milk, you will get a creamy,

sweet, melt-in-your-mouth texture. This is

down to the milk’s fat globules, which coat

the tongue and inhibit the taste of the coffee.

What this really amounts to is less bitterness

and less acidity. Good for making a rich,

sweet, creamy, delicious drink, but bad if

you like it fruity.” The other milk ingredient

that matters is protein, he said. The level of

protein in cow’s milk (it’s not always found in

non-dairy alternatives) is essential in

creating tiny bubbles, or micro foam, during

heating.

5.2.2 Successful barista milk brands

A large proportion of specialist coffee shops

are now choosing a specific brand of milk

and sticking to it, but former barista Shaun Young went a step further in 2016 and set up his

own brand, The Estate Dairy, sourcing milk via direct contracts with dairy farmers. “With a

bespoke herd we can adjust the cows’ diet and conditions to make sure that everything is

tailored to producing the milk wanted by cafes,” said Young. After just two years, he is selling

85,000 litres of milk a week across 500 outlets in London. Another successful barista milk

brand is Brades Farm barista milk, which won its founders the British Farming Awards Dairy

23 https://www.newfoodmagazine.com/news/66042/british-coffee-consumption/

Specialist milk for coffee brand The Estate Dairy

[Image copyright: The Estate Dairy]

Put a label on it: why the future of cow’s milk is a branded one by Tom Levitt

A Nuffield Farming Scholarships Trust report … generously sponsored by The Trehane Trust

| 16

Innovator of the Year award in 2017. Both brands are able to sell their non-organic milk at a

market premium. As well as selling to food service outlets, The Estate Dairy is also selling its

milk at retail for £1.80 a litre in a few select stores in London, together with a premium

chocolate milk drink, produced in partnership with a specialist chocolate brand. Co-founder

Shaun Young said he had been inspired by the success of Lewis Road Creamery in New

Zealand, which achieved sales of US$40m in its first year of selling flavoured milk brand.

“We are trying to pioneer something different and raise the quality and perception of milk by

getting cafes to stand behind it and be more passionate about the milk they sell.” Young said

presentation and packaging was key to making a dairy product stand out and get noticed by

customers. “Our milk bottle looks different to a conventional one you find in the supermarket.

“We buy the labels reverse facing so when it is sat in a coffee bar it’s facing the customer.

We use a clear material which looks quite bespoke. It is a niche thing but by doing these

small things, it makes a difference.”

5.2.3 A new identity for milk

New brands like these can help create an identity for

milk it currently lacks, said Netherlands-based Bas

Groot, who became known as the world’s first milk

sommelier back in 201524. “Milk has a bad reputation

because it has none. Differentiation can help create more identity in dairy. In the future you

could have normal milk during the week like cheap wine and then on the weekend you can

buy special bread and milk and have and enjoy it with friends. A lot of people are not

consuming a product because it is healthy or because they like it, but because it fits their

identity. The drink is an expression of who they are or want to be.” Groot said differentiation

can come through breed-specific milk, animal welfare, A2, free-range milk, regional or even

cow-specific milk i.e. from Bella39, homogenised. “All these storylines create identity and a

product cannot have too much identity,” he said. Groot said adding value will become even

more important for dairy, as consumption per capita in Europe is likely to fall. “The

consensus in the future will be to eat and drink less dairy which is a good thing. Feeding the

world we have to consume less animal protein. That makes it more important to focus on

quality not volume.” But, he warned, changing ingrained cultural habits like buying milk

cheaply was “the biggest and most difficult thing to do”.

Re-inventing milk in the eyes of consumers - and creating identity - will be no quick fix. It is

also about much more than pumping out images of cows and green fields, with modern-day

consumers demanding much more, said investigative food journalist Joanna Blythman. For

Nick Barnard, founder of the Rude Health food brand, milk needs to go back to the product

itself: “It is called the white stuff because it has lost connection with consumers. It is mixed

from multiple farms and homogenised. We are in this blighted phase of misunderstanding

dairy. We need to understand the value of dairy and the innovation in non-dairy," he said.

“Milk has no name and nothing unique. It’s valueless. We're fighting against a generation

that see milk as white, not creamy or uncoloured. The only choice people have is the colour

of the cap. Farmers need to look in their own fridges and become consumers as well as

producers. A generation force-fed in schools have given it up and a generation on fat-free

wouldn't notice if they replaced it as it’s tasteless.”

24 https://www.bbc.co.uk/programmes/b06j0wf5

“We are trying to pioneer

something different and raise

the quality and perception of

milk”

Put a label on it: why the future of cow’s milk is a branded one by Tom Levitt

A Nuffield Farming Scholarships Trust report … generously sponsored by The Trehane Trust

| 17

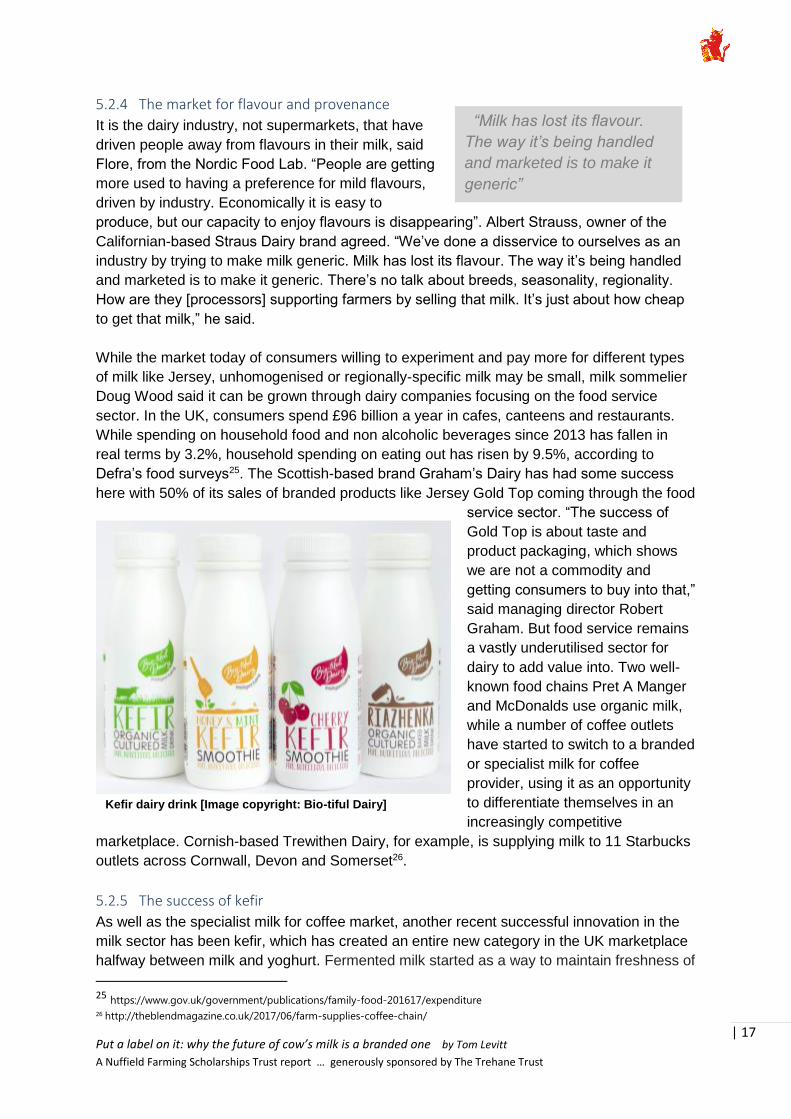

5.2.4 The market for flavour and provenance

It is the dairy industry, not supermarkets, that have

driven people away from flavours in their milk, said

Flore, from the Nordic Food Lab. “People are getting

more used to having a preference for mild flavours,

driven by industry. Economically it is easy to

produce, but our capacity to enjoy flavours is disappearing”. Albert Strauss, owner of the

Californian-based Straus Dairy brand agreed. “We’ve done a disservice to ourselves as an

industry by trying to make milk generic. Milk has lost its flavour. The way it’s being handled

and marketed is to make it generic. There’s no talk about breeds, seasonality, regionality.

How are they [processors] supporting farmers by selling that milk. It’s just about how cheap

to get that milk,” he said.

While the market today of consumers willing to experiment and pay more for different types

of milk like Jersey, unhomogenised or regionally-specific milk may be small, milk sommelier

Doug Wood said it can be grown through dairy companies focusing on the food service

sector. In the UK, consumers spend £96 billion a year in cafes, canteens and restaurants.

While spending on household food and non alcoholic beverages since 2013 has fallen in

real terms by 3.2%, household spending on eating out has risen by 9.5%, according to

Defra’s food surveys25. The Scottish-based brand Graham’s Dairy has had some success

here with 50% of its sales of branded products like Jersey Gold Top coming through the food

service sector. “The success of

Gold Top is about taste and

product packaging, which shows

we are not a commodity and

getting consumers to buy into that,”

said managing director Robert

Graham. But food service remains

a vastly underutilised sector for

dairy to add value into. Two well-

known food chains Pret A Manger

and McDonalds use organic milk,

while a number of coffee outlets

have started to switch to a branded

or specialist milk for coffee

provider, using it as an opportunity

to differentiate themselves in an

increasingly competitive

marketplace. Cornish-based Trewithen Dairy, for example, is supplying milk to 11 Starbucks

outlets across Cornwall, Devon and Somerset26.

5.2.5 The success of kefir

As well as the specialist milk for coffee market, another recent successful innovation in the

milk sector has been kefir, which has created an entire new category in the UK marketplace

halfway between milk and yoghurt. Fermented milk started as a way to maintain freshness of

25 https://www.gov.uk/government/publications/family-food-201617/expenditure 26 http://theblendmagazine.co.uk/2017/06/farm-supplies-coffee-chain/

“Milk has lost its flavour.

The way it’s being handled

and marketed is to make it

generic”

Kefir dairy drink [Image copyright: Bio-tiful Dairy]

Put a label on it: why the future of cow’s milk is a branded one by Tom Levitt

A Nuffield Farming Scholarships Trust report … generously sponsored by The Trehane Trust

| 18

milk and is created by adding a live kefir culture (bacteria and yeast) to the milk. It is touted

as providing various health benefits although the NHS has said there’s little evidence yet to

support the health claims27. The UK-based brand Bio-tiful Dairy was started in 2012 by

former Russian skater Natasha Bowes, and is sold by the Co-op, Sainsburys and Waitrose.

It sources its milk from two dairy farm suppliers Berkeley Farm Dairy in Wiltshire, which

provides its organic range, and Blackmore Vale Dairy in South Downs. Its Strawberry &

Grapefruit Kefir Smoothie won Best Dairy Drink at the World Beverage Innovation Awards in

2017. It is currently selling 80,000 bottles a week at £1.60 for the 250ml sized unit, but a new

bottling line could now increase capacity to 16 million bottles a year.

Bowes said: “I grew up on kefir. It was a fundamental part of diet in Russia at breakfast, as a

snack or before bed. A fantastic meal supplement. I am mildly lactose intolerant. It is

naturally low in lactose as the culture eats up the lactose enzymes so I don’t have a

problem. I realised it was a scalable opportunity in the UK and beneficial for people. It does

not matter how much money you throw at it, it must taste good. I knew I was ahead of the

curve on trends on gut health and that the market would come to us.” Bowes said kefir

appeals to slimming women, exactly the consumer most likely to be avoiding dairy. “That’s

the big market. It’s great nutrition and an important recovery food. It is between a food and a

drink. I have a rule that if someone wants to leave, it is counter-productive to stop them

leaving. Let them find their way back if they want to. You can’t force people. We make

choices for good reasons. The reason I think kefir is a good product is that it’s good for

everyone.”

5.2.6 Organic milk success

One category which has already had success in adding value in dairy has been organic.

Organic dairy sales made up 29% of the total organic food and drink market, with total sales

of £344 million in 201728. This growth led to the recent deal between the dairy cooperative

Arla and the well-known organic dairy brand Yeo Valley (which has adapted its farming

system to improve public perception of the brand). “Our ambition is to encourage customers

to trade up from standard to organic milk, butter and cheese, driving overall growth for

organic across dairy categories,” Arla has said. The company accepts that most people still

see milk as an ingredient rather than a product in its own right. “It’s cereal with milk and

coffee with milk and not the other way round,” said Ash Amirahmadi, UK managing director

at Arla Foods UK. Its approach has been to continue to push new added value brands like its

longer lasting Cravendale and lactofree brands and newer additions like Protein Milk, Skyr

drink and a Starbucks-branded ready-to-drink coffee. The idea, said Arla’s head of

innovation Sven Thormahlen, is to “follow our consumers where they go, which at the

moment is consuming more food and drink out of the home, not somewhere where dairy has

traditionally exploited”.

5.2.7 Coca-Cola and Fairlife milk

Innovation in dairy can and is being led by companies from outside the category too. Coca-

Cola was one of those to realise the opportunity for dairy to steal market share from

carbonated drinks under fire over sugar content. It launched the Fairlife brand in the US in

27 https://www.nhs.uk/conditions/probiotics/ 28 http://www.omsco.co.uk/_clientfiles/Omsco Milk Market Report 2017.pdf

Put a label on it: why the future of cow’s milk is a branded one by Tom Levitt

A Nuffield Farming Scholarships Trust report … generously sponsored by The Trehane Trust

| 19

2014 and is now expanding to Canada29. It sells itself as a nutritional product with less fat

and added protein and calcium. “Milk is the perfect candidate to innovate because it starts as

a superfood before you add anything. What we’re doing is making better what is already

there,” said Anders Porter, head of communications at Fairlife. “We are targeting parents

who do shopping. The idea is that before you send the kids off to school you add Fairlife to

what you already do i.e. cereal or smoothie. We’re giving you the fuel to live your life to the

fullest.”

Porter said milk was long overdue a

re-invention. “Milk has still to

overcome the home tag. The dairy

industry was not listening to what

the consumers wanted. It’s wasted

lots of advancements in the

beverage sector i.e. a juice

company now has something with a

protein source, or water with added

ingredients. Even coffee has

reinvented itself as people wanted a

bit more. Dairy has done nothing.

Just sat and waited. We saw an

opportunity to take what milk has

and make it better.” This point was

echoed by a director from The

Boulder Food Group, an early-stage

investment fund, who pointed to

Kabacha and Coconut water, two

categories that were almost non-existent five years ago but now worth US$1bn and $3bn

respectively in the US-alone. “Trends can move much quicker today with the internet and are

easier to launch and scale,” he said, “The key considerations for us [when investing in a

brand] is sourcing, transparency and understanding the story.”

5.2.8 The importance of branded milk

Although the vast majority of milk is sold as a low-value product, there are signs of retailers

being keen to promote and stock higher value brands which bring added returns for

supermarkets. Just like the food service sector, retailers are keen to differentiate themselves

and be first movers on a trend. That can benefit dairy. Sainsburys took a punt on kefir milk,

Asda started stocking free-range branded milk and Morrisons did For Farmers Milk. All of the

UK’s retailers also stock a range of milkshakes and coffee and milk drink brands, with the

sales value of coffee drinks up 38% in 2017, according to Kantar. "This is paying dividends

for the milk sector as a whole with branded milk now driving growth in the liquid milk

category, with value sales up 4.4% and volumes up 52% in 2017, compared with a +1.1%

increase in the value of sales and a -1.2% decline in volume for own label milk, according to

Kantar30. “Brands is where milk needs to be if it wants to be successful with the next

29 https://www.foodbev.com/news/coca-cola-to-build-66m-dairy-facility-in-ontario-canada/ 30 https://www.thegrocer.co.uk/buying-and-supplying/the-dairymen-2017/how-to-sell-dairy-in-the-age-of-scary-expert-

panel/557266.article

US-based Fairlife’s milk drink [Image copyright: Fairlife]

Put a label on it: why the future of cow’s milk is a branded one by Tom Levitt

A Nuffield Farming Scholarships Trust report … generously sponsored by The Trehane Trust

| 20

generation of consumers”, said food futurologist Dr Morgaine Gaye: “People get caught up in

trends that are so powerful they pull along without them realising. Brands are like a religion,

people follow them.”

5.2.9 Milk sector still slow on innovation

Despite these moves, the milk sector still lags behind

innovation, said Sainsburys head of agriculture Beth

Hart. “Everyday we’re getting approached by a new

product as an alternative to milk. The sector is full of

bright entrepreneurs who I wish would come to dairy

too. Milk has not changed, but the category has. We

believe it is customers changing their diets, the social status of saying you drink almond

‘milk’, that is all impacting milk. Who is taking milk and innovating with it? The innovation is in

non-dairy. You look at the premium they can add for non-dairy. Milk is viewed as a

commodity. It’s almost too cheap to be a superfood. How do we add value back into milk?

Only through innovation,” she said. Zoe Kavanagh from Ireland’s National Dairy Council

(NDC) agreed. “The fundamental challenge to the sector is that we’re in a high volume, low

margin industry so the investment back has always been poor. We’ve been unable to invest

to respond. We need an innovation agenda. Every dairy company needs to capitalise on the

functional benefit of dairy.” It also needs to recognise the shift to convenience and rise in the

numbers of smaller households and people living and working longer in the UK, said a

former dairy manager for The Co-op: “Eating is a less formal occasion now. People want

immediacy. A key driver for milk is going to be new product development brands like milk in

pouches, flavoured and iced coffee, not local brands.”

“It’s almost too cheap to be

a superfood. How do we add

value back into milk? Only

through innovation”

Put a label on it: why the future of cow’s milk is a branded one by Tom Levitt

A Nuffield Farming Scholarships Trust report … generously sponsored by The Trehane Trust

| 21

5.3 Disconnection and perception

5.3.1 The dairy sector’s image

The dairy sector’s public image in media, marketing and product branding has long been tied

to bucolic images of cows in green fields. Coca-Cola could not stop itself using idyllic images

when describing its new Fairlife-branded milk’s traceability from ‘grass to glass’. It makes the

claim despite admitting that the cows it sources milk from are not fed or even kept on grass

and the final product is sold in a plastic carton, not an old-fashioned glass bottle31. But, such

images are also tying the hands of dairy producers. “Some farms have a very good

ecological footprint, but the public does not like the way they run the farm,” said Trienke

Elshof, chair at LTO Noord and dairy farmer in the province of Friesland in the Netherlands.

“People want to see a cow outside. We are not doing anything illegal but society does not

accept the way we treat our animals. For us it is clear that we have to change our mindsets,

but we have to balance getting a profit and getting

accepted by society.”

This objective is only made harder by consumer

behaviour, said Hans Van Trijp, a professor of marketing

and consumer behaviour at Wageningen University. “We

nurture a nostalgic image of dairy farming that we know can’t be true but we want to believe

it’s true. People don’t want to know the truth. We don’t want to be reminded of our hypocrisy.

As long as there is choice, you go

for price over social benefit. We

are not good at putting aside our

personal self-interest. It’s a

dilemma for farmers, but the

industry has to make sure the

sensitive issues do not exist.” Put

simply, said Kees de Koning,

manager of Wageningen’s Dairy

Campus: “They want one thing as

citizens and make another decision

as consumers.” Navigating the

“disneyfication of farming”, as

Anna Carlsson, who runs the

Skogsgard dairy farm in Sweden

calls it, is almost impossible. “Who

should have a worst night’s sleep

the farmer or the consumer who buys cheap milk and food?”

5.3.2 The Netherlands and the degrading image of dairy

Of all the places I visited, it was the Netherlands where navigating the public perception

tightrope seemed most challenging. With its comparatively large livestock sector, including

31 https://fairlife.com/our-promise/our-farms/

Dutch dairy farmer Pieter Koonstra [Image copyright: Tom

Levitt]

“We nurture a nostalgic

image of dairy farming that

we know can’t be true but we

want to believe it’s true”

Put a label on it: why the future of cow’s milk is a branded one by Tom Levitt

A Nuffield Farming Scholarships Trust report … generously sponsored by The Trehane Trust

| 22

1.6 million dairy cows, the Netherlands is the fifth largest dairy exporter in the world.

Although the image of the sector is in the Dutch dairy industry’s own words, ‘inextricably

linked to a characteristic landscape of fields dotted with cows and windmills', in reality it is a

modern sector seeing the growing use of technologies such as automatic milking systems

and a rising number of continuously housed systems (around 25% of farms do not give their

cows access to pasture for at least part of the day during the year)3233. In recent years the

sector has suffered bad publicity with reports of farms being unable to handle excess cow

manure and, in a small number of cases, the illegal dumping of manure3435. Environmental

groups have started to actively campaign against the sector, with WWF Netherlands now

calling for a 40% cut in cow numbers in the country. “A long-term reduction of 40% will

enable the Netherlands to comply with the EU’s Nitrates Directive without needing

derogation, will support the climate targets in 2030 and will have positive effects on the other

environmental and biodiversity challenges,” said WWF’s head of agriculture Natasja

Oerlemans.

The image of the dairy sector in the country had been degrading in the last few years, one

Dutch industry analyst told me, who was concerned about dairy being seen as part of the

intensive livestock sector. “The image of cows and pasture is still a great one [but] the farms

that quit are mostly pasture and the ones who make

big investments are indoors,” he said. Martin Scholten,

director of animal science at Wageningen, agreed:

“Dairy farms have an advantage over other sectors as

they are more transparent. Public perception is better

with cows that live for years not months. But they have

to keep it. Pasture is a trade-off for animal welfare. It’s

about us wanting to have a better feeling in the countryside.”

It’s likely to be a delicate balancing act for the sector going forward admitted Professor Van

Trijp: “If you were to redesign the Netherlands and were not tied to the status quo, would you

do it again?” said Professor Van Trijp. “The answer is probably not.” The response of the

Dutch Farmers’ Union has been to set a goal for 80% of cows to be out on pasture. Critics

say it’s a marketing con with just a small percentage of their lifetime likely to be spent

outdoors under most systems and that more attention should be spent on overall welfare

targets. Yet, Friesland Campina (and others) is taking no risks and is paying farmers who

allow their cows to graze for part of the year an extra €1,50 per 100kg of milk produced. “As

long as we make enough progress on getting more herds outdoor grazing, improve calf

welfare and lower our greenhouse gas footprint then we don’t think the Government will

legislate against us,” said a spokesperson for the company.

5.3.3 Dutch farmers debate how to change

Many of those I spoke to in the Netherlands said they have no choice but to adapt in order to

maintain a so-called ‘social licence to operate’. “People are not against farmers in the

Netherlands, they are against the system. Farmers are the victims too,” said dairy farmer

32 http://www.zuivelnl.org/wp-content/uploads/2016/09/Dutch-dairy-in-figures-2015.pdf 33 http://library.wur.nl/WebQuery/wurpubs/441879 34 https://www.nrc.nl/nieuws/2017/11/10/het-mestcomplot-a1580703 35 http://www.clo.nl/indicatoren/nl052811-mestproductie-bij-gebruiksnormen-bedrijven-met-overproductie

“Dairy farms have an

advantage over other sectors

as they are more