What Should Shipping Expect From China, Japan, & Korea

15

1 What Should Shipping Expect From China, Japan, & Korea June 2014 Julian Proctor, Managing Director & Head of Investment Team, Tiger Group Investments

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of What Should Shipping Expect From China, Japan, & Korea

1

What Should Shipping Expect From China, Japan, & Korea June 2014

Julian Proctor, Managing Director & Head of Investment Team, Tiger Group Investments

2

Country Profile – China

3

China – Shipbuilding

Yards Need Higher Prices

Source: Tiger Internal Estimates

• Building at or below breakeven levels for orders placed in 2012-13

• Banks unwilling to fund refund guarantees on loss making projects

• Subsidy for SOE shipyards for orders placed by SOEs (i.e. COSCO, CSCL,CSG etc.), essentially keeping it all in the family

• Chaotic mix of federal, provincial and municipal state owned, SOE shipyards, Chinese private (1st, 2nd, 3rd , and 4th tier yards), foreign owned yards – almost 3,000 yards

• Simply put, there are too many yards and too many owners willing to take risks

4%4%

4%

4%

3%

3%

3%

3%

2%

2%

68%

Jiangsu New YZJ

Zhejiang Yangfan

Chengxi Shipyd.

Sinopacific Dayang

COSCO Group

Shanghai Waigaoqiao

CIC (Jiangsu)

Weihai Samjin

Fujian Southeast

Jinling Shipyard

Others

Chaotic Mix – Share of Current Orderbook

Note: Based on number of vessels, total: 2,408 vessels

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

2008 2009 2010 2011 2012 2013 Q1 2014 Q2 2014

Capesize Newbuild Price Average Capesize Newbuild Breakeven Price

Note: Calculated breakeven of $55m and then adjusted where by the inflation rate to arrive at approximation

Source: Clarksons

4

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

2008 2009 2010 2011 2012 2013

YZJ COSCORongsheng China Shipbuilding Industra-AGuangzhou Shipyard China CSSC

China – Shipbuilding

Margins Under Pressure Inflationary Pressure TBC

• Inflation starting to bite, productivity not keeping pace

• Many banks not prepared to issue refund guarantees on loss making projects, adding further pressure on yards

• Subsidy program for SOE shipyards for orders placed by SOEs (COSCO, CSG, etc.), keeping it all in the family

-10

-5

0

5

10

15

30

35

40

45

50

55

60

65

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

CPMI (LHS) CPPI (RHS)

Y-o-Y Change Index Value

Source: Bloomberg Source: Bloomberg

5

--

$20bn

$40bn

$60bn

$80bn

$100bn

$120bn

$140bn

2011 2012 2013

RMB Lending In USD Equivalents

--

$2bn

$4bn

$6bn

$8bn

$10bn

2011 2012 2013

USD Lending

China – Ship Finance

Chinese Banks: USD Lending Compared To RMB

• Higher funding costs faced by Chinese banks being passed through to owners (L+350 bps unless very strategic project)

• Banks will negotiate harshly if possible

• Recent hype around leasing companies is a very short-term phenomenon, with banks merely fulfilling their mandate

• Basel 3 will also have a substantial impact

Source: PBOC Note: Converted RMB lending to USD using a fixed exchange rate of 6.3

Hidden Bad Debts: The Nanjing Tanker Saga

• Nanjing Tanker is recent a notable example of the “hidden bad debts” in China’s banking system

• Despite a drastic fall in Operating Profit, lenders were willing to extend new loans to Nanjing Tanker

• Currently unclear how many Chinese shipping companies are likely to encounter a similar fate

Source:Lloyd’s List, Nanjing Tanker filings, Google Finance

23% CAGR

15% CAGR

886

1,468 1,528

1,568 0.2% 0.3%

(8.9%)

(12.8%)

(14.0%)

(12.0%)

(10.0%)

(8.0%)

(6.0%)

(4.0%)

(2.0%)

2.0%

--

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2009 2010 2011 2012

Net Debt (US$m) Operating Profit / Net Debt

6

China – Cargo

Iron-ore Imports

• Increasing end-user demand from Chinese steel Industry

• Demand highly fragmented with the top 10 Chinese steel mills accounting for 35% of crude steel output in 2013

• Consolidation to drive economies of scale

• The leading driver in world trade, but the Chinese have a hard time to gauge

• Conflicts between the objectives of SOEs

Source: Clarksons, Xinhua Financial Network News

Capesize TC & Spot Rates $/day

• 2014 Chinese Iron ore imports are forecasted to be ~2x the level seen in 2008, but yet rates remain 4x lower

• China continues to play the arbitrage game between domestic supplies, Brazil and Australia

• Strategic government objective to transport 60% of seaborne oil imports through local shipping companies

$/ton

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

2008 2009 2010 2011 2012 2013 2014

$0$5

$10$15$20$25$30$35$40$45

Tubarao Beilun, Bao Hay Point Qingdao

2009 2010 2011 2012 2013 H2 2014

436

615 603665

724795

897

0MT

100MT

200MT

300MT

400MT

500MT

600MT

700MT

800MT

900MT

1,000MT

2008 2009 2010 2011 2012 2013 2014 (f)

Source: Clarksons

Source: Clarksons

7

Country Profile – Korea

8

Korea – Shipbuilding

• Korean yards still some of the best in the world

• Outsourcing substantial amounts of steel work to China

• Yards slots are taken right up till H1 2016

Korean Yards Forward Deliveries Rising Korean Won (Won to USD)

• Rising Won a big concern for Korean yards

• Potential exposure to offshore industry

Source: Clarksons, Bloomberg

$0.0006

$0.0007

$0.0007

$0.0008

$0.0008

$0.0009

$0.0009

$0.0010

$0.0010

$0.0011

$0.0011

06/04 06/05 06/06 06/07 06/08 06/09 06/10 06/11 06/12 06/13 06/14

0

20

40

60

80

100

120

140

160

180

200

Hyundai Group

Daewoo STX SPP Sungdong Daehan Samsung H.I.

Dae Sun

2014 2015 2016 2017

Note: total orderbook stands at 1,043 vessels Source: Clarksons Source: Bloomberg

9

$9bn

$10bn

$14bn

$17bn

--

2

4

6

8

10

12

14

16

18

2010 2011 2012 2013

25% CAGR

Korea – Ship Finance

• Korea Exim Bank appears to be the largest Korean lender to the shipping industry

• Relatively small players, except for government agencies

• Export credit agencies remain open, as evidenced by the 25% CAGR in Korea Exim Bank’s shipping loan portfolio since 2010

• Decline in CDS prices for Korea Exim Bank debt suggests improved credit environment for Korean government agencies

• Significantly lower government bond yields likely to encourage Korean insurers and pension funds to seek higher yielding assets

Korea Exim Bank – Shipping Loan Portfolio ($bn) Improving Credit Environment

Note: Based on available reporting

Korea Exim Bank – CDS Prices (2009 – 2014 YTD)

Korean Government – 10-Year Bond Yields (June 2009 – 2014 YTD)

2.5%3.0%3.5%4.0%4.5%5.0%5.5%6.0%

06/09 06/10 06/11 06/12 06/13 06/14

Source: Petrofin Research

Source: Bloomberg

10

Country Profile – Japan

11

Japan – Shipbuilding

Resurgent Japan- Share of Global Orderbook Japanese Orderbook By Type

24%

21%20%

18% 18%

22%

0%

5%

10%

15%

20%

25%

2008 2009 2010 2011 2012 2013

63%

3%

9%

1%

2%

4%

18%

Bulk

Container

Chem & Oil

Tankers

LNG

LPG

Other

• A reorganized and consolidated industry

• Focused on the production of certain types of vessels depending on yard

• Weakening Yen making prices more attractive

• Older work force still an issue- several yards have visa programs to import Chinese workers

• Ability to do new designs, but scope to accommodate change is limited

• Potential big change is willingness to take USD contracts, even though Japan was already a large part of the world economy

Weakening Yen Helping (Yen to USD)

¥70

¥75

¥80

¥85

¥90

¥95

¥100

¥105

2009 2010 2011 2012 2013 2014

Note: Based on number of vessels, total: 907 vessels Note: Based on annual Japanese orderbook DWT and Global orderbook DWT Source: Clarksons Source: Clarksons

Source: Bloomberg

12

$0

$10

$20

$30

$40

$50

$60

2010 2011 2012 2013

BTMU SMBC JBIC

Japan – Ship Finance

Japanese Banks - Shipping Loan Portfolios ($bn)

Source: JBIC Annual Report, Petrofin Research

• Japanese banks mostly focused on domestic owners, who are financed in Japanese Yen

• Hit hard by the Japanese Yen and global shipping crisis. Major banks only just looking at shipping again

• Particular focus on LNG and offshore sector

3-Year CAGR: 58.8%

3-Year CAGR: 0.0%

3-Year CAGR: (4.1%)

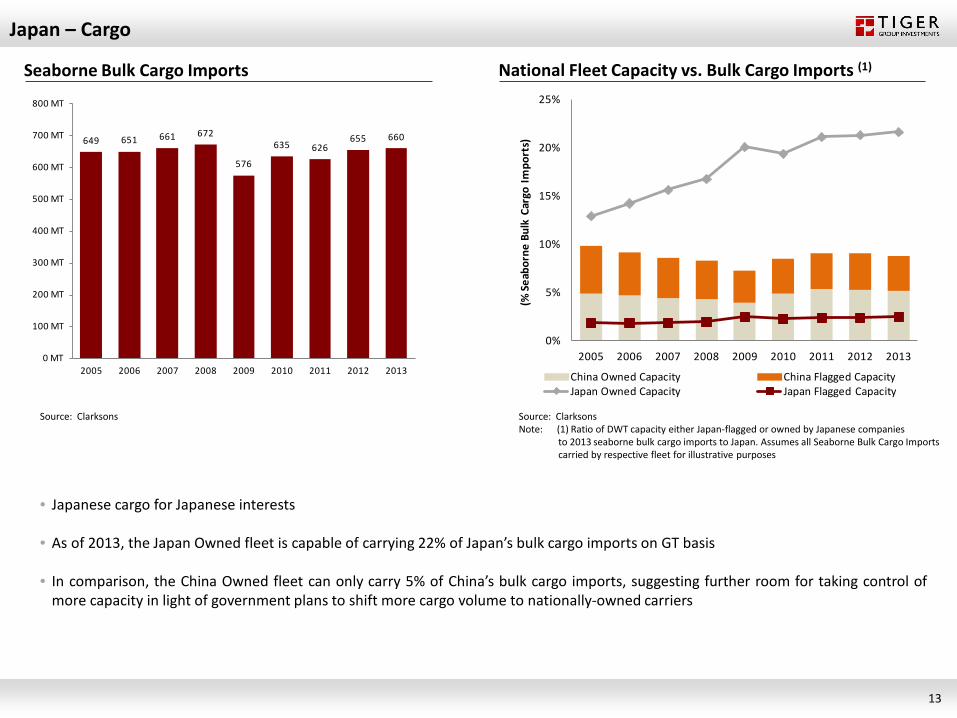

13

Japan – Cargo

Seaborne Bulk Cargo Imports

Source: Clarksons

649 651 661 672

576

635 626655 660

0 MT

100 MT

200 MT

300 MT

400 MT

500 MT

600 MT

700 MT

800 MT

2005 2006 2007 2008 2009 2010 2011 2012 2013

0%

5%

10%

15%

20%

25%

2005 2006 2007 2008 2009 2010 2011 2012 2013

(% Se

abor

ne B

ulk

Carg

o Im

port

s)

China Owned Capacity China Flagged CapacityJapan Owned Capacity Japan Flagged Capacity

• Japanese cargo for Japanese interests

• As of 2013, the Japan Owned fleet is capable of carrying 22% of Japan’s bulk cargo imports on GT basis

• In comparison, the China Owned fleet can only carry 5% of China’s bulk cargo imports, suggesting further room for taking control of more capacity in light of government plans to shift more cargo volume to nationally-owned carriers

Source: Clarksons Note: (1) Ratio of DWT capacity either Japan-flagged or owned by Japanese companies to 2013 seaborne bulk cargo imports to Japan. Assumes all Seaborne Bulk Cargo Imports carried by respective fleet for illustrative purposes

National Fleet Capacity vs. Bulk Cargo Imports (1)

14

Concluding Remarks

15

Concluding remarks

• National economic agendas and foreign policy will drive larger fleets and stronger capabilities in ship yard production particularly in Japan and China

• Currency movements from the Big 3 will have the largest consequences on their shipwoning and yard footprints, especially given their addiction to local currency debt; Korea and Japan exposed if China decides to unexepected depreciate RMB to support growth in next years

• Foreign shipowners will find it harder to compete for Asian cargo given implicit national cargo policy, whilst select Asian shipowners will continues to benefit from superior access to low cost capital, subsidies and often policy driven goals – resulting in substantial competition to international owners