High-resolution continuum-source atomic absorption spectrometry: what can we expect?

Upload

khangminh22Category

view

3download

0

See the last page for disclaimer Page 1 of 9

中

外

运

输

Eq

uit

y R

ese

arc

h

Eq

uit

y R

ese

arc

h R

ep

ort

证

券

研

究

报

告

Co

mp

an

y R

ep

ort

股

票

研

究

公

司

报

告

证

券

研

究

报

告

[Tabl

e_Inf

o1] 消

费

行

业-

酒

店

Co

ns

um

er

Sec

tor-

Ho

tels

[Tab

le_I

nfo2

]

携

程

旅

行

网

Ctr

ip.c

om

In

tern

ati

on

al

(CT

RP

US

)

[Table_Title] Company Report: Ctrip.com International (CTRP US) Noah Hudson

Hudson (86755) 2397 6684

公司报告: 携程旅行网 (CTRP US) [email protected]

2 November 2018

[Table_Summary] Expect Operating Margin to Continue to Climb

预计运营利润率持续攀升

For 3Q18, Ctrip's management guides for revenue YoY growth from

13% to 18% and non-GAAP operating profit in the range of RMB1.8-1.9

bn. In 2Q18, Ctrip's non-GAAP operating profit (excluding share-based

compensation charges) was RMB1.2 bn, flat YoY and 7.1% below Bloomberg

consensus forecast; net revenue was RMB7.3 bn, up 13.3% YoY and on the

lower end of the management's previous growth guidance range; gross

margin fell to 79.9% vs. 82.6% in 2Q17 as Ctrip upgraded service of its

standards; non-GAAP operating margin was 16.5%, down by 2.4 ppt YoY;

net income was RMB2.4 bn, vs. RMB359 mn in 2Q17, largely due to gains

from equity securities fair value change; and excluding share-based

compensation charges and fair value changes of equity securities,

non-GAAP diluted earnings per ADR was RMB1.90, up 27.5% YoY.

We forecast 2018-2020 non-GAAP operating income of RMB4.8 bn,

RMB6.5 bn and RMB8.7 bn, respectively, reflecting 22.0% CAGR. We

forecast 2018-2020 fully diluted earnings per ADR of RMB2.09, RMB4.83

and RMB9.05, respectively.

We lower our target price from US$52.00 to US$38.00 and downgrade to

"Accumulate" investment rating. We expect Ctrip's top-line growth and

market share to continue to grow rapidly as it becomes more profitable over

the medium to long term. In addition, with a large cash balance, we expect

Ctrip to continue to make strategic investments, both in China and

internationally, thereby further expanding its business scale. Our US$38.00

target price is a 19.6% discount to our DCF derived NAV of US$47.43.

携程管理层对 2018 年 3 季度收入同比增长的指引为 13%-18%,对该季度非通用会计准

则下运营利润的指引则为人民币 18-19 亿元。2018 年第 2 季度,携程非通用会计准则下

运营利润(剔除基于股份的薪酬开支)为人民币 12 亿元,与去年同期持平,低于彭博一

致预期 7.1%;净收入为人民币 73 亿元,同比增长 13.3%,达到管理层之前增长预测的低

位水平;毛利率随携程升级其服务标准下降至 79.9%(去年同期为 82.6%);非通用会计

准则下运营利润率为 16.5%,同比下降 2.4 个百分点;得益于权益性证券公允价值变动带

来的收益,公司净利润达到人民币 24 亿元(去年同期为人民币 3.59 亿元);剔除基于股

份的薪酬开支及权益性证券公允价值变动收益,非通用会计准则下稀释后每份 ADR 净利

为人民币 1.90 元,同比上升 27.5%。

我们预计 2018-2020 年非通用会计准则下运营利润将分别为人民币 48、65 和 87 亿元,

年复合增长率为 22.0%。我们预计 2018-2020 年完全稀释后每份 ADR 净利分别为人民币

2.09、4.83 和 9.05 元。

我们将目标价由 52.00 美元下调至 38.00 美元,下调投资评级至“收集”。我们预计随着

携程中长期盈利能力增强,其收入增长及市场份额将持续快速提升。此外,预计持充裕现

金的携程将持续在国内外进行战略投资,进一步扩大其商业规模。我们 38.00 美元的目标

价对于我们用折现现金流方法得出的 47.43 美元的每份 ADR 估值有 19.6%的折让。

[Table_Rank] Rating: Accumulate

Downgraded

评级: 收集 (下调)

[Table_Price] 6-18m TP目标价: US$38.00

Revised from 原目标价: US$52.00

ADR price ADR价格: US$34.880

Stock performance

股价表现

[Table_QuotePic]

(40)

(30)

(20)

(10)

0

10

20

30

Nov-17 Dec-17 Feb-18 Apr-18 May-18 Jul-18 Sep-18 Oct-18

% change

NASDAQ COMP Index CTRIP

Change in ADR Price

ADR 价变动

1 M

1 个月

3 M

3 个月

1 Y

1 年

Abs. % 绝对变动 %

(6.9) (15.1) (24.9)

Rel. % to NASDAQ index 相对纳指变动 %

0.2 (10.3) (35.6)

Avg. ADR price (USD) 平均 ADR 价(美元)

36.8 38.6 44.3

Source: Bloomberg, Guotai Junan International.

[Table_Profit] Year End Turnover Net Profit Earnings/ADR Earnings/ADR PER BV/ADR PBR DP ADR Yield ROE

年结 收入 股东净利 每份 ADR 净利 每份ADR净利变

动

市盈率 每份ADR净资产 市净率 每份 ADR 股息 股息率 净资产收益率

12/31 (RMB m) (RMB m) (RMB) (△ %) (x) (RMB) (x) (RMB) (%) (%)

2016A 19,228 (1,431) (3.023) n.a. n.a. 151.134 1.6 0.0 0.0 (2.4)

2017F 26,780 2,142 4.067 n.a. 55.8 159.677 1.4 0.0 0.0 2.7

2018F 30,326 1,417 2.689 (33.9) 85.4 156.460 1.5 0.0 0.0 1.6

2019F 35,125 3,099 5.051 87.9 45.5 150.967 1.5 0.0 0.0 3.4

2020F 40,784 5,802 9.137 80.9 25.1 159.697 1.4 0.0 0.0 6.0

[Table_BaseData] ADR in issue (m) 总 ADR 数 (m) 545.2 Major shareholder 大股东 Baidu (BIDU US) 21.0%

Market cap. (US$ m) 市值 (US$ m) 19,017.2 Free float (%) 自由流通比率 (%) 71.0

3 month average vol. 3 个月平均成交股数 (‘000) 5,416.1 FY18 Net gearing (%) FY18 净负债/股东资金 (%) 36.1

52 Weeks high/low (US$) 52 周高/低 (US$) 51.910 / 29.660 FY18 Est. NAV (US$) FY18 每 ADR 估值(美元) 47.4

Source: the Company, Guotai Junan International.

Co

mp

an

y R

ep

ort

See the last page for disclaimer Page 2 of 9

[Table_RightMar1]

2 N

ove

mb

er

20

18

[Table_RightMar2]

Ctr

ip.c

om

In

tern

atio

na

l 携

程旅

行网

(C

TR

P U

S)

Ctrip.com International (CTRP US)

2Q18 REVIEW

Ctrip's 2Q18 net revenue was RMB7.3 billion, reflecting an increase of 13.3% YoY, which is on the lower end of Ctrip's

management's previous guidance range of 12% to 17% growth. Accommodation reservation revenue was RMB2.8 million,

up 20.8% YoY, primarily driven by an increase in accommodation reservation volume. Ctrip further expanded its total hotel

coverage to close to 1.4 million properties, an increase of 26% YoY. Ctrip's international hotel room night bookings increased by

40% YoY, more than doubling the outbound industry growth pace. Transportation ticketing revenue was RMB3 billion, up just

1% YoY. Ground transportation including train ticketing, bus ticketing and car services continued to grow rapidly. The air

ticketing segment also maintained very strong volume growth momentum across all platforms, but air ticketing revenue growth

was partially offset by the decrease of per air ticket segment revenue. Ctrip has continued to extend its multi-model

transportation offering such as free airport shuttle buses and airport parking vouchers. Package tour revenue was RMB839

million, up 31% YoY primarily driven by increase in volume growth of both organized tours and self-guided tours.

Non-GAAP 2Q18 operating profit (which excludes share-based compensation expense) was RMB1.2 billion, flat YoY

and 7.1% below Bloomberg consensus forecast, while non-GAAP operating profit hit the upper bound of Ctrip’s

management's previous guidance range of RMB1.1 billion to RMB 1.2 billion in 2Q18; this wasn't really a positive surprise since

it has met or exceeded the upper bound of Ctrip’s management's previous guidance range in every quarter at least since 3Q16.

Non-GAAP operating margin was 16.5%, up from 14.4% in the previous quarter but down by 2.4 ppt compared to the same

quarter last year. Gross margin fell to 79.9% compared to 82.6% during 2Q17 as Ctrip upgraded its service standards across its

business.

Excluding share-based compensation charges and fair value changes of equity security investments, 2Q18 non-GAAP

diluted earnings per ADR was RMB1.90, up 27.5% YoY. Net income was RMB2.4 billion compared to RMB359 million for the

same period in 2017 and RMB1.1 billion in the previous quarter, largely due to gains from equity securities measured at fair

value and investing activities. Excluding share-based compensation charges and fair value changes of equity securities

investments, non-GAAP net income was RMB1.1 billion, up 25.4% YoY.

Table-1: Ctrip Results

(% or ppt.)

RMB million 2Q17A 3Q17A 4Q17A 1Q18A 2Q18A

YoY QoQ

Net Revenues 6,459 7,900 6,379 6,731 7,319

13.3% 8.7%

Gross Income 5,334 6,596 5,318 5,487 5,850

9.7% 6.6%

Gross Profit Margin 82.6% 83.5% 83.4% 81.5% 79.9%

(2.7) ppt (1.6) ppt

Operating Income 687 1,359 508 590 724

5.4% 22.7%

Operating Margin 10.6% 17.2% 8.0% 8.8% 9.9%

(0.7) ppt 1.1 ppt

Share Based Compensation Expense (528) (384) (400) (376) (480)

9.1% (27.7%)

Non-GAAP Operating Income 1,215 1,743 908 966 1,204

(0.9%) 24.6%

Non-GAAP Operating Income Margin 18.8% 22.1% 14.2% 14.4% 16.5%

(2.4) ppt 2.1 ppt

Interest Expense (net) (133) (47) 13 158 (47)

64.7% n.a.

Other 397 233 337 397 2,256

468.1% 468.3%

Income Tax Expense (540) (313) (289) (179) (322)

(40.4%) 79.9%

Effective Tax Rate 58.4% 19.9% 38.1% 14.6% 11.8%

(46.5) ppt (2.8) ppt

Income from Affiliates (26) 32 (98) 78 (213)

(719.2%) n.a.

Non-controlling Interest (26) (35) 34 16 (17)

33.5% n.a.

Net Income 359 1,229 504 1,060 2,381

563.2% 124.6%

Net Income Margin 5.6% 15.6% 7.9% 15.7% 32.5%

27.0 ppt 16.8 ppt

Less:

Gain on F.V. Change of Equity Investments 0 0 0 (688) 1,750

n.a. n.a.

Share Based Compensation Expense (528) (384) (400) (376) (480)

9.1% (27.7%)

Non-GAAP Net Income 887 1,613 904 2,124 1,111

25.3% (47.7%)

Non-GAAP Net Income Margin 13.7% 20.4% 14.2% 31.6% 15.2%

1.4 ppt (16.4) ppt

Fully Diluted Earnings per ADR (RMB) 0.65 2.10 0.88 1.81 3.89

501.3% 114.9%

Non-GAAP Fully Diluted Earnings per ADR (RMB) 1.49 2.70 1.56 3.48 1.90

27.5% (45.4%)

Source: the Company, Guotai Junan International.

Co

mp

an

y R

ep

ort

See the last page for disclaimer Page 3 of 9

[Table_RightMar1]

2 N

ove

mb

er

20

18

[Table_RightMar2]

Ctr

ip.c

om

In

tern

atio

na

l 携

程旅

行网

(C

TR

P U

S)

Ctrip.com International (CTRP US)

Ctrip's international air ticketing outperformed during 2Q18. Excluding Skyscanner, with strong growth for both outbound

travel and Trip.com, Ctrip's international air tickets achieved 40% YoY volume growth, around two times faster than the overall

Chinese outbound ticket growth rate. Skyscanner's total revenue growth maintained a healthy rate of approximately 30% YoY,

driven largely by strong traffic growth. Trip.com continued to perform very well, achieving triple-digit growth in air ticket volume

for the seventh consecutive quarter. Ctrip recently launched both local activity and airport transfer services in certain target

markets and plans to expand these product lines into other markets in the months ahead.

Figure-1: Ctrip Revenue Growth Breakdown Figure-2: Ctrip Operating Income Margin

45.6%

46.4%

41.8%

25.9%

10.6%13.3%

0%

10%

20%

30%

40%

50%

60%

1Q17A 2Q17A 3Q17A 4Q17A 1Q18A 2Q18A

Accommodation Transportation TicketingPackaged Tour Corporate TravelTotal

6.8%

10.6%17.2%

8.0%8.8%

9.9%

15.4%

18.8%

22.1%

14.2%14.4%

16.5%

0%

5%

10%

15%

20%

25%

1Q17A 2Q17A 3Q17A 4Q17A 1Q18A 2Q18A

Operating Income Margin

Non-GAAP Operating Income Margin

Source: the Company, Guotai Junan International. Source: the Company, Guotai Junan International.

OUTLOOK & FORECAST REVISIONS

We revise down our forecasts for Ctrip's 2018-2020 net revenue by 2.9%, 9.7% and 16.4%, respectively. For 3Q18,

Ctrip's management guides net revenue growth of 13% YoY to 18% YoY, which is less than our previous forecast. Despite

strong execution from Ctrip, we now revise down our revenue forecasts as we expect revenue growth to slow as a number of

macro indicators point to a slowing economy. We think the recent depreciation of the RMB could negatively impact Ctrip's

outbound air ticketing, which has been one of Ctrip's strongest segments. According to the China National Tourism

Administration, China's domestic tourism revenue was RMB2.45 trillion in 1H18, up 12.5% YoY, reflecting a slowdown in growth

compared to the 15.2% and 15.9% growth rate achieved in 2016 and 2017, respectively. The China Tourism Academy

forecasts domestic tourism revenue to reach RMB5.07 trillion in 2018, an increase of 11%, which if achieved, would be the

slowest growth rate since 2015 when China's domestic tourism revenue increased by 10.5%.

Figure-3: Ctrip Total Net Revenue Figure-4: Ctrip Revenue Breakdown

19.2 26.8 30.8 36.3 42.7

76.5%

39.5%

14.8% 17.9% 17.7%

0%

20%

40%

60%

80%

100%

0

5

10

15

20

25

30

35

40

45

2016A 2017A 2018F 2019F 2020F

Total Net Revenue Growth

RMB mn

35.5%

45.6%

11.2%

2.8%

5.7%

Hotels38.0%

Ticketing40.7%

Packaged-tour

12.3%

Corporate Travel

3.1%

Others6.0%

2018F

2017A

Source: the Company, Guotai Junan International. Source: the Company, Guotai Junan International.

Co

mp

an

y R

ep

ort

See the last page for disclaimer Page 4 of 9

[Table_RightMar1]

2 N

ove

mb

er

20

18

[Table_RightMar2]

Ctr

ip.c

om

In

tern

atio

na

l 携

程旅

行网

(C

TR

P U

S)

Ctrip.com International (CTRP US)

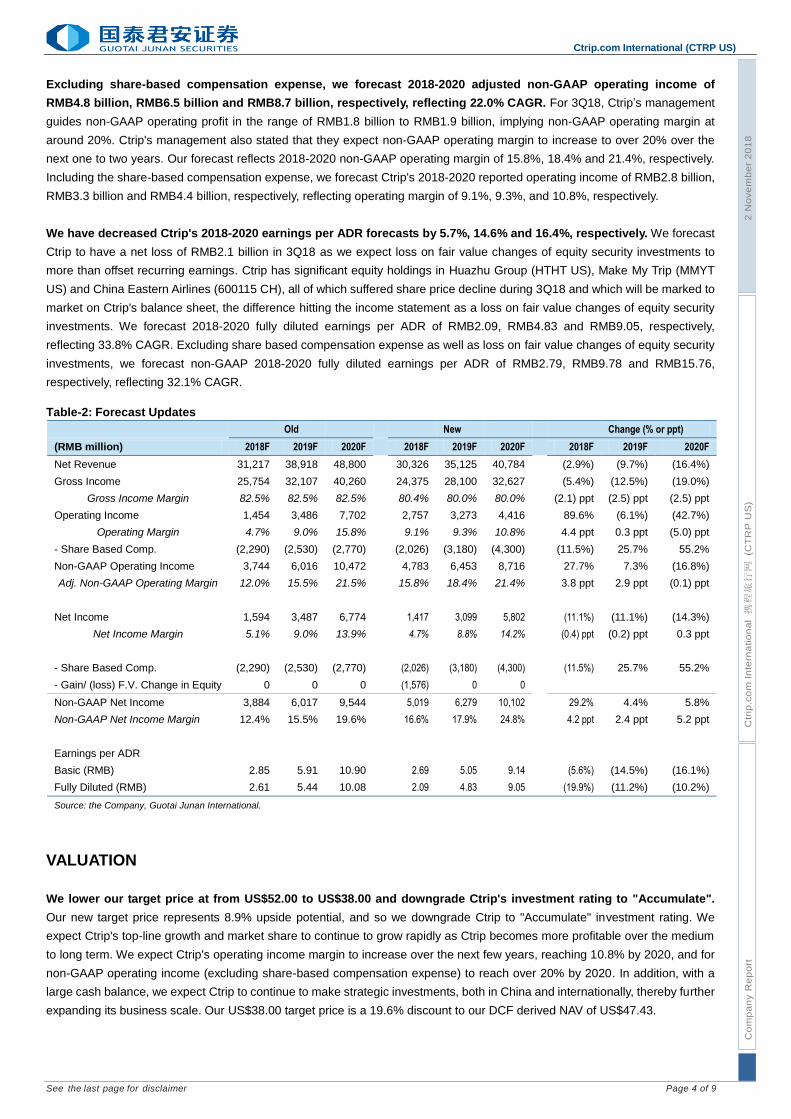

Excluding share-based compensation expense, we forecast 2018-2020 adjusted non-GAAP operating income of

RMB4.8 billion, RMB6.5 billion and RMB8.7 billion, respectively, reflecting 22.0% CAGR. For 3Q18, Ctrip’s management

guides non-GAAP operating profit in the range of RMB1.8 billion to RMB1.9 billion, implying non-GAAP operating margin at

around 20%. Ctrip's management also stated that they expect non-GAAP operating margin to increase to over 20% over the

next one to two years. Our forecast reflects 2018-2020 non-GAAP operating margin of 15.8%, 18.4% and 21.4%, respectively.

Including the share-based compensation expense, we forecast Ctrip's 2018-2020 reported operating income of RMB2.8 billion,

RMB3.3 billion and RMB4.4 billion, respectively, reflecting operating margin of 9.1%, 9.3%, and 10.8%, respectively.

We have decreased Ctrip's 2018-2020 earnings per ADR forecasts by 5.7%, 14.6% and 16.4%, respectively. We forecast

Ctrip to have a net loss of RMB2.1 billion in 3Q18 as we expect loss on fair value changes of equity security investments to

more than offset recurring earnings. Ctrip has significant equity holdings in Huazhu Group (HTHT US), Make My Trip (MMYT

US) and China Eastern Airlines (600115 CH), all of which suffered share price decline during 3Q18 and which will be marked to

market on Ctrip's balance sheet, the difference hitting the income statement as a loss on fair value changes of equity security

investments. We forecast 2018-2020 fully diluted earnings per ADR of RMB2.09, RMB4.83 and RMB9.05, respectively,

reflecting 33.8% CAGR. Excluding share based compensation expense as well as loss on fair value changes of equity security

investments, we forecast non-GAAP 2018-2020 fully diluted earnings per ADR of RMB2.79, RMB9.78 and RMB15.76,

respectively, reflecting 32.1% CAGR.

Table-2: Forecast Updates

Old

New

Change (% or ppt)

(RMB million) 2018F 2019F 2020F

2018F 2019F 2020F

2018F 2019F 2020F

Net Revenue 31,217 38,918 48,800

30,326 35,125 40,784

(2.9%) (9.7%) (16.4%)

Gross Income 25,754 32,107 40,260

24,375 28,100 32,627

(5.4%) (12.5%) (19.0%)

Gross Income Margin 82.5% 82.5% 82.5%

80.4% 80.0% 80.0%

(2.1) ppt (2.5) ppt (2.5) ppt

Operating Income 1,454 3,486 7,702

2,757 3,273 4,416

89.6% (6.1%) (42.7%)

Operating Margin 4.7% 9.0% 15.8%

9.1% 9.3% 10.8%

4.4 ppt 0.3 ppt (5.0) ppt

- Share Based Comp. (2,290) (2,530) (2,770)

(2,026) (3,180) (4,300)

(11.5%) 25.7% 55.2%

Non-GAAP Operating Income 3,744 6,016 10,472

4,783 6,453 8,716

27.7% 7.3% (16.8%)

Adj. Non-GAAP Operating Margin 12.0% 15.5% 21.5%

15.8% 18.4% 21.4%

3.8 ppt 2.9 ppt (0.1) ppt

Net Income 1,594 3,487 6,774

1,417 3,099 5,802

(11.1%) (11.1%) (14.3%)

Net Income Margin 5.1% 9.0% 13.9%

4.7% 8.8% 14.2%

(0.4) ppt (0.2) ppt 0.3 ppt

- Share Based Comp. (2,290) (2,530) (2,770)

(2,026) (3,180) (4,300)

(11.5%) 25.7% 55.2%

- Gain/ (loss) F.V. Change in Equity 0 0 0

(1,576) 0 0

Non-GAAP Net Income 3,884 6,017 9,544

5,019 6,279 10,102

29.2% 4.4% 5.8%

Non-GAAP Net Income Margin 12.4% 15.5% 19.6%

16.6% 17.9% 24.8%

4.2 ppt 2.4 ppt 5.2 ppt

Earnings per ADR

Basic (RMB) 2.85 5.91 10.90

2.69 5.05 9.14

(5.6%) (14.5%) (16.1%)

Fully Diluted (RMB) 2.61 5.44 10.08

2.09 4.83 9.05

(19.9%) (11.2%) (10.2%)

Source: the Company, Guotai Junan International.

VALUATION

We lower our target price at from US$52.00 to US$38.00 and downgrade Ctrip's investment rating to "Accumulate".

Our new target price represents 8.9% upside potential, and so we downgrade Ctrip to "Accumulate" investment rating. We

expect Ctrip's top-line growth and market share to continue to grow rapidly as Ctrip becomes more profitable over the medium

to long term. We expect Ctrip's operating income margin to increase over the next few years, reaching 10.8% by 2020, and for

non-GAAP operating income (excluding share-based compensation expense) to reach over 20% by 2020. In addition, with a

large cash balance, we expect Ctrip to continue to make strategic investments, both in China and internationally, thereby further

expanding its business scale. Our US$38.00 target price is a 19.6% discount to our DCF derived NAV of US$47.43.

Co

mp

an

y R

ep

ort

See the last page for disclaimer Page 5 of 9

[Table_RightMar1]

2 N

ove

mb

er

20

18

[Table_RightMar2]

Ctr

ip.c

om

In

tern

atio

na

l 携

程旅

行网

(C

TR

P U

S)

Ctrip.com International (CTRP US)

Figure-5: Ctrip 2-Year Historical Forward P/E

(non-GAAP)

Figure-6: Ctrip 1-Year Historical Forward P/E

(non-GAAP)

10

20

30

40

50

60

Nov/16 Oct/17 Oct/18

BEst P/E Ratio (Next 4 Quarters)

Mean

+1 ST. DEV.

-1 ST. DEV.

20

25

30

35

40

45

50

BEst P/E Ratio (Next 4 Quarters)Mean +1 ST. DEV. -1 ST. DEV.

Source: Bloomberg. Note*: "Forward" valuations are based on the next four quarters earnings forecasts.

Source: Bloomberg. Note*: "Forward" valuations are based on the next four quarters earnings forecasts.

Table-3: Peers Comparison

Company Stock

Cncy Last Mkt. Cap PE (Adjusted)

PE (GAAP) ROE(%) PB

Code price US$ mil 18F 19F 20F

18F 19F 20F 18F 18F

USA - Listed

Ctrip.Com-Adr CTRP US USD 34.880 19,017 27.4 21.6 17.6 363.7 35.2 114.2 5.0 1.5

Booking Holdings BKNG US USD 1,896.090 90,011 21.1 18.7 16.6 41.8 38.6 68.3 38.5 7.6

Tripadvisor Inc TRIP US USD 53.290 7,330 37.3 33.4 27.6 34.1 35.0 39.6 10.8 5.1

Makemytrip Ltd MMYT US USD 26.580 2,711 n.a. n.a. n.a. n.a. n.a. 237.3 (14.7) 1.0

Expedia Inc EXPE US USD 127.620 19,012 22.8 19.4 16.7 38.5 19.9 49.4 16.7 4.4

Travelzoo Inc TZOO US USD 8.490 103 26.5 23.6 n.a. n.a. 10.4 6.5 n.a. n.a.

Tuniu Corp-Adr TOUR US USD 6.520 846 n.a. 73.3 42.3 n.a. n.a. n.a. (7.5) 2.5

Simple Average 27.0 31.7 24.2 119.5 27.8 85.9 8.1 3.7

Weighted Average 23.1 20.4 17.5 86.1 35.3 73.8 28.1 6.0

Source: Bloomberg, Guotai Junan International

Table-4: DCF Analysis

DCF Assumptions Calculation Perpetual growth rate 3.0%

PV Free Cash Flows to the Firm (RMB mn) 165,237

PV Terminal Value (RMB mn) 75,120

Risk free rate 2.31%

Enterprise Value (RMB mn) 240,357

Adjusted Beta 1.20

- Debt (RMB mn) 49,398

Market risk premium 10.9%

- Minority Interest -7.0%

Cost of Equity 15.4%

+ Cash & Equivalents (RMB mn) 18,344

Total NAV (RMB mn) 207,424

Borrowing interest rate 4.0%

Effective tax rate 26.0%

ADR Outstanding (fully diluted, as at end of 2018, mn) 634

Cost of Debt 3.0%

NAV per ADR (RMB) 327.2

US$:RMB 6.90

E/ (D+E) 66%

NAV per ADR (US$) 47.43

D/ (D+E) 30%

WACC 11.0%

Source: Bloomberg, Guotai Junan International.

Table-5: Target Price Valuation

FY17A

FY18F FY19F FY20F

Earnings per ADR (RMB GAAP) 4.07 2.69 5.046 9.115

Earnings per ADR (US$ GAAP) 0.63 0.39 0.73 1.32

PER (GAAP) based on Target Price 60.8 97.5 52.0 28.8

Source: the Company, Guotai Junan International.

Co

mp

an

y R

ep

ort

See the last page for disclaimer Page 6 of 9

[Table_RightMar1]

2 N

ove

mb

er

20

18

[Table_RightMar2]

Ctr

ip.c

om

In

tern

atio

na

l 携

程旅

行网

(C

TR

P U

S)

Ctrip.com International (CTRP US)

Financial Statements and Ratios

[Table_IncomeStatement] Income Statement

Year end 31 Dec (RMB m) 2016A 2017A 2018F 2019F 2020F

Total revenue 19,228 26,780 30,326 35,125 40,784

Cost of revenues (4,730) (4,678) (5,950) (7,025) (8,157)

Gross profit 14,499 22,101 24,375 28,100 32,627

Product development (7,687) (8,259) (9,519) (11,143) (12,869)

SG&A (8,380) (10,917) (12,099) (13,685) (15,343)

Operating profit (1,568) 2,926 2,757 3,273 4,416

Interest income (expense) (165) (299) 43 (994) (66)

Other income (27) 879 (35) 0 0

Income from affiliates 602 (65) (235) 200 200

Profit before tax (1,158) 3,441 2,530 2,479 4,549

Income tax (478) (1,281) (1,014) 619 1,136

Profit after tax (1,636) 2,161 1,516 3,098 5,686

Non-controlling interest 206 (19) (99) 1 117

Shareholders' profit / loss (1,431) 2,142 1,417 3,099 5,802

Non-GAAP net profit 2,129 3,976 5,019 6,279 10,102

Basic EPADR (3.023) 4.067 2.689 5.051 9.137

Diluted EPADR (3.023) 3.777 2.091 4.828 9.050

[Table_CashFlowStatement] Cash Flow Statement

Year end 31 Dec (RMB m) 2016A 2017F 2018F 2019F 2020F

Net profit (1,636) 2,161 1,516 3,098 5,686

Share based compensation 3,560 1,834 2,026 3,180 4,300

Equity in gain of affiliates (602) 65 235 (200) (200)

D&A 719 883 168 168 168

Deferred income tax & other (177) (72) (69) 42 77

Change in working capital 3,410 2,197 3,771 3,840 4,642

Cash from operating activities

5,273 7,069 7,647 10,128 14,673

Purchases of PP&E (683) (471) (741) (995) (1,249)

Cash paid for investments (5,408) (1,541) (3,759) (3,759) (3,759)

Change in short-term invest. (5,935) (13,936) (5,048) (1,894) (1,894)

Others (7,799) 716 (1,966) (1,845) (1,845)

Cash from investing activities

(19,825) (15,232) (11,515) (8,493) (8,747)

Short term loan proceeds 1,980 2,137 3,170 (6,240) 8,407

Issuance of convertibles 6,545 0 692 (888) (888)

Others 3,765 5,882 162 251 188

Cash from financing activities

12,290 8,019 4,024 (6,877) 7,707

Cash at beg of year 19,216 18,435 18,243 18,352 13,062

Net changes in cash (2,263) (144) 156 (5,242) 13,633

Effect of for-ex 1,482 (47) (47) (47) (47)

Cash at end of year 18,435 18,243 18,352 13,062 26,648

Source: the Company, Guotai Junan International.

[Table_BalanceSheet] Balance Sheet

Year end 31 Dec (RMB m) 2016A 2017A 2018F 2019F 2020F PP&E 5,592 5,616 6,191 7,021 8,105 Investments 20,533 25,574 27,008 28,442 29,876 Goodwill 56,015 56,246 58,571 60,896 63,221 Intangible assets 13,925 13,750 13,900 14,050 14,199 Others 2,438 1,636 1,726 1,638 1,514 Total non-current assets 98,502 102,822 107,397 112,047 116,916 Cash & cash equivalents 18,435 18,243 18,352 13,062 26,648 Restricted cash 1,744 1,749 2,500 3,251 4,002 Short-term investments 14,113 28,130 33,178 35,072 36,966 Accounts receivable, net 4,625 4,559 7,278 8,430 9,788 Prepayments & other 6,995 6,546 7,413 8,586 9,969 Total current assets 45,911 59,227 68,721 68,402 87,374 Total assets 144,414 162,048 176,117 180,448 204,290 Short term borrowings 6,887 16,316 19,486 13,246 21,653 Accounts payable 7,279 7,459 11,221 12,996 15,090 Salary and welfare payable 2,508 3,465 3,923 4,544 5,277 Advances from customers 8,191 7,868 9,915 12,393 15,492 Others 5,430 7,052 7,914 8,981 10,218 Total current liabilities 30,295 42,160 52,459 52,161 67,730 Convertible note 34,651 29,220 29,912 29,024 28,136 Other long-term liabilities 3,947 4,195 4,443 4,691 4,939 Total non-current liabilities 38,598 33,416 34,355 33,715 33,075 Total liabilities 68,893 75,575 86,814 85,876 100,804 Total shareholders' equity 71,537 84,694 87,425 92,593 101,407 Minority interest 3,984 1,779 1,879 1,979 2,079 Total equity 75,521 86,473 89,304 94,572 103,486

[Table_FinancialRatio] Financial Ratios

2016A 2017A 2018F 2019F 2020F Gross margin 75.4% 82.5% 80.4% 80.0% 80.0% Operating margin -8.2% 10.9% 9.1% 9.3% 10.8% Net income margin -4.0% 12.2% 3.6% 6.6% 8.5% Non-GAAP net profit margin 11.1% 14.8% 16.6% 17.9% 24.8% Asset turnover (x) 0.1 0.2 0.2 0.2 0.2 ROA -1.1% 1.4% 0.8% 1.7% 3.0% Assets/equity (x) 2.3 2.0 2.0 2.0 2.0 ROE -2.4% 2.7% 1.6% 3.4% 6.0% Net gearing 39.5% 34.9% 36.1% 32.5% 23.9% Current ratio (x) 1.5 1.4 1.3 1.3 1.3 Debt/equity 55.0% 52.7% 55.3% 44.7% 48.1%

Co

mp

an

y R

ep

ort

See the last page for disclaimer Page 7 of 9

[Table_RightMar1]

2 N

ove

mb

er

20

18

[Table_RightMar2]

Ctr

ip.c

om

In

tern

atio

na

l 携

程旅

行网

(C

TR

P U

S)

Ctrip.com International (CTRP US)

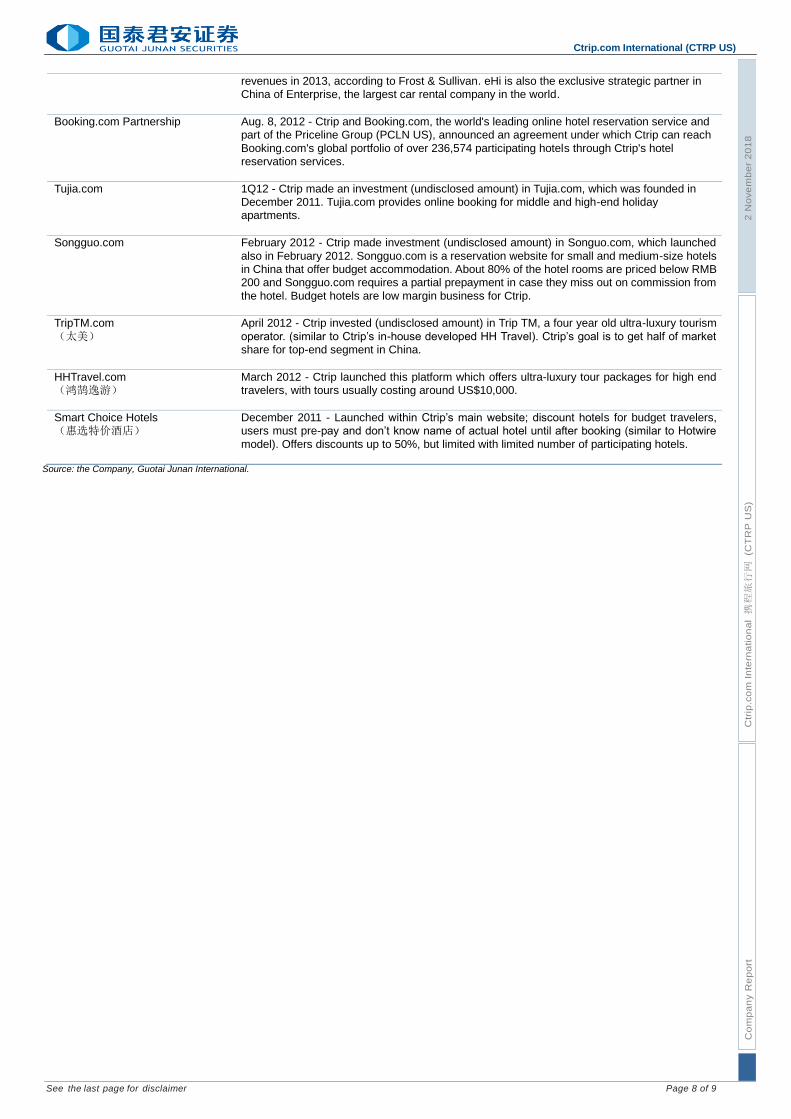

APPENDIX: Ctrip - Projects & Partnerships

Project / Investment Description

Skyscanner Holdings Ltd. Dec. 2016 - Ctrip acquired Skyscanner Holdings Limited ("Skyscanner"), a leading global travel

search site headquartered in Edinburgh, the United Kingdom. The acquisition valued Skyscanner at £1.4 billion. Skyscanner's management team will continue to manage Skyscanner's operations independently as part of the Ctrip group. With the investment in

Skyscanner, Ctrip aims to improve its global travel services, especially the international air ticketing business. Skyscanner ranks as one of the top online travel brands serving 60 mn monthly active users and is available in over 30 languages.

Qunar (QUNR US) Jan. 12, 2016 - Ctrip announced investment of US$1.3 billion in cash and issued 5.4 mn shares

as investment in several non-U.S. investment entities, which acquired a significant minority stake of Qunar (QUNR US). Combined with Ctrip's Oct. 2015 investment in Qunar, this gives Ctrip effective control of Qunar and nearly all of Qunar's economic interest, although Qunar will

remain listed on the NASDAQ. Ctrip began consolidating Qunar's results starting from Jan. 2016.

MakeMyTrip Ltd. (MMYT US) Jan. 7, 2016 - Ctrip invested US$180 mn in MakeMyTrip Ltd. (MMYT US), India's largest online travel company, via convertible bonds. MakeMyTrip has also granted Ctrip permission to acquire MakeMyTrip shares in the open market, so that combined with shares convertible under

the convertible bonds, Ctrip may own up to 26.6% of MakeMyTrip's outstanding shares. One MakeMyTrip director is appointed by Ctrip.

Qunar (QUNR US) - Baidu (BIDU US) share swap

Oct. 26, 2015 - share swap deal whereby Ctrip held approximately 45% interest in Qunar (QUNR US) and Baidu (BIDU US) held approximately 25% interest in Ctrip Four Ctrip

representatives, namely, Ctrip's Chairman, CEO, Co-president and COO were appointed to Qunar's board of directors. Two representatives of Baidu (Chairman/CEO and a vice president) were appointed to Ctrip's board of directors.

eLong (LONG US) May 22, 2015 - Ctrip announced that it acquired 37.6% equity stake of eLong (LONG US) with a total purchase price of approximately US$ 400 mn. Ctrip will obtained one seat on eLong’s

board of directors. The two companies continue to run as two separate operations, each maintaining their own brands and platforms.

Travel Fusion Jan. 2015 - Ctrip invested in Travel Fusion, a leading online travel company for low-cost carriers. Company expected this strategic relationship to not only help international travel

business, but also enhance the efficiency and effectiveness of Company’s IT systems by leveraging Travel Fusion's advanced technology.

Beijing Joint Wisdom Information Technology Co., Ltd. (Joint Wisdom)

1Q15 - Ctrip established Joint Wisdom by merging several key subsidiaries, including Brandwisdom.cn with Ctrip Beijing China Software Hotel Information System Co., Ltd. Joint Wisdom has integrated big data and cloud-based technology in three segments: software,

information stream and data intelligence products. With the combined strength, Joint Wisdom provides the full set of property management system solutions to cover about 60,000 hotels in China, ranging from hostels to high star ones.

eHi Auto Services (EHIC US)

(一嗨租车)

Jan. 21, 2015, Ctrip and eHi expand their business relationship. Ctrip has integrated eHi's

chauffeured car services, including airport pick-up and drop-off and other business transportation services, into its corporate and individual service offerings. Ctrip also features and promotes eHi's services on its various channels.

“Young” Mobile Application 2Q14 - Ctrip launched a new mobile app called Young that offers special features tailor-made to college students.

LY.com (Tongcheng) Ctrip invested US$200 mn to become the second largest shareholder (about a 30% stake) of

Tongcheng Network Technology Share Co., Ltd., a leading local attraction ticket service provider that operates LY.com. The investment is classified as an affiliate under the equity method.

Tuniu.com (TOUR US) Ctrip bought US$15 mn worth of Tuniu.com shares as an anchor investor in Tuniu.com’s IPO. Tuniu.com specializes in China’s leisure package tour business and launched its IPO on the

NASDAQ on May 9, 2014.

cn.toursforfun.com (途风)

Dec. 2013 - Ctrip acquired cn.toursforfun.com, an online travel supplier focused on overseas tours and vacation packages and daytrips for Chinese travelers in the United States.

Yongche.com (易到用车)

Dec. 2013 - Ctrip made investment in Beijing-based Dongfang Cheyun, operator of online car rental platform Yongche.com, which offers car rental, high-end chauffeur mobile booking, and mobile taxi booking services.

eHi Auto Services (EHIC US)

(一嗨租车)

Dec. 2013 - Ctrip bought slightly less than 20% interest in eHi, classified as an available for sale

financial investment. Ctrip became eHi’s designated and preferred business partner and integrated access to eHi's online reservation system in its Ctrip Travel mobile application. eHi is China's No. 1 car services provider and No. 2 car rentals provider in terms of market share by

Co

mp

an

y R

ep

ort

See the last page for disclaimer Page 8 of 9

[Table_RightMar1]

2 N

ove

mb

er

20

18

[Table_RightMar2]

Ctr

ip.c

om

In

tern

atio

na

l 携

程旅

行网

(C

TR

P U

S)

Ctrip.com International (CTRP US)

revenues in 2013, according to Frost & Sullivan. eHi is also the exclusive strategic partner in China of Enterprise, the largest car rental company in the world.

Booking.com Partnership Aug. 8, 2012 - Ctrip and Booking.com, the world's leading online hotel reservation service and part of the Priceline Group (PCLN US), announced an agreement under which Ctrip can reach

Booking.com's global portfolio of over 236,574 participating hotels through Ctrip's hotel reservation services.

Tujia.com 1Q12 - Ctrip made an investment (undisclosed amount) in Tujia.com, which was founded in December 2011. Tujia.com provides online booking for middle and high-end holiday apartments.

Songguo.com February 2012 - Ctrip made investment (undisclosed amount) in Songuo.com, which launched

also in February 2012. Songguo.com is a reservation website for small and medium-size hotels in China that offer budget accommodation. About 80% of the hotel rooms are priced below RMB 200 and Songguo.com requires a partial prepayment in case they miss out on commission from

the hotel. Budget hotels are low margin business for Ctrip.

TripTM.com

(太美)

April 2012 - Ctrip invested (undisclosed amount) in Trip TM, a four year old ultra-luxury tourism

operator. (similar to Ctrip’s in-house developed HH Travel). Ctrip’s goal is to get half of market share for top-end segment in China.

HHTravel.com (鸿鹄逸游)

March 2012 - Ctrip launched this platform which offers ultra-luxury tour packages for high end travelers, with tours usually costing around US$10,000.

Smart Choice Hotels (惠选特价酒店)

December 2011 - Launched within Ctrip’s main website; discount hotels for budget travelers, users must pre-pay and don’t know name of actual hotel until after booking (similar to Hotwire

model). Offers discounts up to 50%, but limited with limited number of participating hotels.

Source: the Company, Guotai Junan International.

Co

mp

an

y R

ep

ort

See the last page for disclaimer Page 9 of 9

[Table_RightMar1]

2 N

ove

mb

er

20

18

[Table_RightMar2]

Ctr

ip.c

om

In

tern

atio

na

l 携

程旅

行网

(C

TR

P U

S)

Ctrip.com International (CTRP US)

[Table_CompanyRatingDefinition] Company Rating Definition

The Benchmark: NASDAQ Composite Index

Time Horizon: 6 to 18 months

Rating Definition

Buy Relative Performance>15%; or the fundamental outlook of the company or sector is favorable.

Accumulate Relative Performance is 5% to 15%; or the fundamental outlook of the company or sector is favorable.

Neutral Relative Performance is -5% to 5%; or the fundamental outlook of the company or sector is neutral.

Reduce Relative Performance is -5% to -15%; or the fundamental outlook of the company or sector is unfavorable.

Sell Relative Performance <-15%; or the fundamental outlook of the company or sector is unfavorable.

[Table_IndustryRatingDefinition] Sector Rating Definition

The Benchmark: NASDAQ Composite Index

Time Horizon: 6 to 18 months

Rating Definition

Outperform Relative Performance>5%; or the fundamental outlook of the sector is favorable.

Neutral Relative Performance is -5% to 5%; or the fundamental outlook of the sector is neutral.

Underperform Relative Performance<-5%; Or the fundamental outlook of the sector is unfavorable.

[Table_DISCLOSUREOFINTERESTS] DISCLOSURE OF INTERESTS

(1) The Analysts and their associates do not serve as an officer of the issuer mentioned in this Research Report. (2) The Analysts and their associates do not have any financial interests in relation to the issuer mentioned in this Research Report. (3) Except for KAISA GROUP (01638 HK), GUOTAI JUNAN I (01788 HK),BINHAI INVESTMENT (02886 HK),VALUE A SHARE (03095

HK), CAM SCSMALLCAP (03157 HK), MR CSI300 ETF-R (CNY) (83127 HK), Guotai Junan and its group companies do not hold equal to or more than 1% of the market capitalization of the issuer mentioned in this Research Report.

(4) Guotai Junan and its group companies have not had investment banking relationships with the issuer mentioned in this Research Report within the preceding 12 months.

(5) Guotai Junan and its group companies are not making a market in the securities in respect of the issuer mentioned in this Research Report.

(6) Guotai Junan and its group companies have not employed an individual serving as an officer of the issuer mentioned in this Research Report. There is no officer of the issuer mentioned in this Research Report associated with Guotai Junan and its group companies.

DISCLAIMER This Research Report does not constitute an invitation or offer to acquire, purchase or subscribe for securities by Guotai Junan Securities (Hong Kong) Limited ("Guotai Junan"). Guotai Junan and its group companies may do business that relates to companies covered in research reports, including investment banking, investment services, etc. (for example, the placing agent, lead manager, sponsor, underwriter or invest proprietarily). Any opinions expressed in this report may differ or be contrary to opinions or investment strategies expressed orally or in written form by sales persons, dealers and other professional executives of Guotai Junan group of companies. Any opinions expressed in this report may differ or be contrary to opinions or investment decisions made by the asset management and investment banking groups of Guotai Junan. Though best effort has been made to ensure the accuracy of the information and data contained in this Research Report, Guotai Junan does not guarantee the accuracy and completeness of the information and data herein. This Research Report may contain some forward-looking estimates and forecasts derived from the assumptions of the future political and economic conditions with inherently unpredictable and mutable situation, so uncertainty may contain. Investors should understand and comprehend the investment objectives and its related risks, and where necessary consult their own financial advisers prior to any investment decision. This Research Report is not directed at, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any jurisdiction where such distribution, publication, availability or use would be contrary to applicable law or regulation or which would subject Guotai Junan and its group companies to any registration or licensing requirement within such jurisdiction. © 2018 Guotai Junan Securities (Hong Kong) Limited. All Rights Reserved. 27/F., Low Block, Grand Millennium Plaza, 181 Queen’s Road Central, Hong Kong. Tel.: (852) 2509-9118 Fax: (852) 2509-7793 Website: www.gtja.com.hk

Copyright © 2022 FDOKUMEN