Vita Flavor Business Plan 01 09 12

20

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of Vita Flavor Business Plan 01 09 12

Cover Page

Table of Contents

1.0Executive Summary2.0Business Overview3.0Market Opportunity4.0Market Solution5.0The Market6.0Management Team7.0Financial Analysis8.0Social Return on Investment9.0Intended Use of GSVC Funding

I. What is VitaFlavor?

VitaFlavor is a line of vitamin-enhanced food seasonings & products that canbe incorporated into every day cooking processes to bring essential vitamins &minerals to people’s diets in the developing world.

VitaFlavor will focus on enhancing products where flavor is the maindifferentiating factor. In addition, VitaFlavor will only focus on productsthat can be packaged into single serving portions to ensure the propernutrient mix is delivered with each product use.

II. What is VitaFlavor’s Vision & Mission?

VitaFlavor believes everyone deserves nutrition. Access to products thatprovide sufficient vitamins & minerals is a fundamental right that should beavailable to adults & children at all income levels. As such, VitaFlavor iscommitted to providing a sustainable solution to nutritional issues for thebillions of people around the world.

III. What Products will VitaFlavor Offer?

During its initial launch, VitaFlavor will offer five distinct product offerings:

1. Rice Flavorings Vitamin enhanced flavoring powders thatcan be incorporated into the rice &grain cooking process.

2. Root Vegetable Flavorings

Vitamin enhanced flavoring powders thatcan be incorporated into the rootvegetable cooking process or

mixed/sprinkled after cooking iscomplete.

3. Soup Flavorings Vitamin enhanced flavoring powders thatcan be used to make a variety of soups &broths.

4. Sauce Mixes Vitamin enhanced flavoring powders thatare used to make sauces used in avariety of dishes.

5. Ramen Noodles Instant ramen noodles that useVitaFlavor soup flavorings as the mainflavoring agent.

As the company grows, VitaFlavor will seek to add new product lines thatfurther its corporate mission and that are driven by customer demand.

IV. Who is the VitaFlavor Team?

1. Michael Kasseris2. Darren Miao3. John Young

V. What is VitaFlavor’s Strategy for Implementing its Vision?

Rather than try to compete directly with existing companies in the market,VitaFlavor will focus its activities on building the ecosystem that willenable the implementation of its vision. Developing a brand that consumerswill associate with delicious yet nutritious food seasonings & product lies atthe core of this strategy. At the same time, VitaFlavor will partner withcompanies across the Fast Moving Consumer Goods (FMCG) industry – includingsuppliers, food manufacturers, distributors and retailers – to provide thegoods & services that will drive this ecosystem.

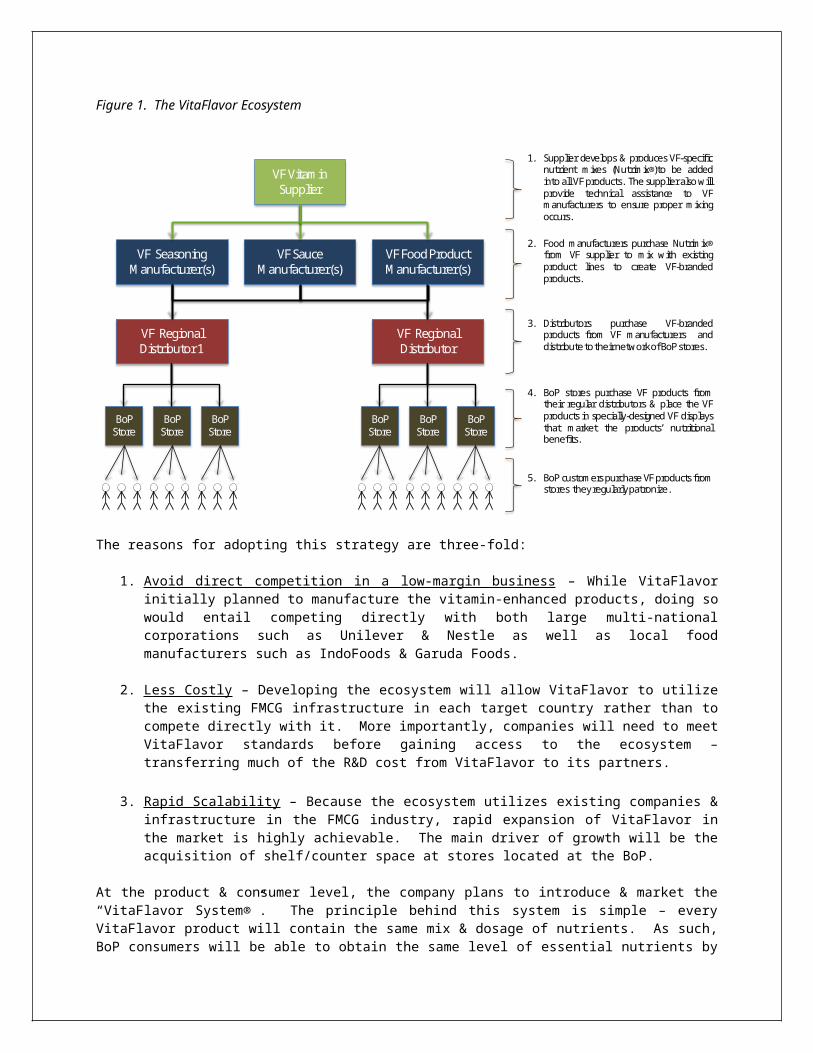

Figure 1. The VitaFlavor Ecosystem

VF Vitam in Supplier

VF Seasoning M anufacturer(s)

VF Sauce M anufacturer(s)

VF Food Product M anufacturer(s)

VF Regional Distributor 1

VF Regional Distributor

BoPStore

BoPStore

BoPStore

BoPStore

BoPStore

BoPStore

1. Supplierdevelops& producesVF-specificnutrient m ixes (Nutrim ix®)to be addedintoallVFproducts.Thesupplieralsowillprovide technical assistance to VFm anufacturers to ensure proper m ixingoccurs.

2. Food m anufacturers purchase Nutrim ix®from VF supplier to m ix with existingproduct lines to create VF-brandedproducts.

3. Distributors purchase VF-brandedproducts from VF m anufacturers anddistributetotheirnetworkofBoPstores.

4. BoP stores purchase VF products fromtheirregulardistributors & place the VFproductsin specially-designed VFdisplaysthat m arket the products’ nutritionalbenefits.

5. BoPcustom erspurchaseVFproductsfromstorestheyregularlypatronize.

The reasons for adopting this strategy are three-fold:

1. Avoid direct competition in a low-margin business – While VitaFlavorinitially planned to manufacture the vitamin-enhanced products, doing sowould entail competing directly with both large multi-nationalcorporations such as Unilever & Nestle as well as local foodmanufacturers such as IndoFoods & Garuda Foods.

2. Less Costly – Developing the ecosystem will allow VitaFlavor to utilizethe existing FMCG infrastructure in each target country rather than tocompete directly with it. More importantly, companies will need to meetVitaFlavor standards before gaining access to the ecosystem –transferring much of the R&D cost from VitaFlavor to its partners.

3. Rapid Scalability – Because the ecosystem utilizes existing companies &infrastructure in the FMCG industry, rapid expansion of VitaFlavor inthe market is highly achievable. The main driver of growth will be theacquisition of shelf/counter space at stores located at the BoP.

At the product & consumer level, the company plans to introduce & market the“VitaFlavor System®”. The principle behind this system is simple – everyVitaFlavor product will contain the same mix & dosage of nutrients. As such,BoP consumers will be able to obtain the same level of essential nutrients by

using at least one VitaFlavor product a day regardless of product type. Thus,a BoP consumer would obtain the same nutritional benefit by using a VitaFlavorrice flavoring one day, a VitaFlavor soup seasoning the next day and eating aVitaFlavor ramen pack the following day. The reasons for developing such asystem are four-fold:

1. Increase nutrient intake – The nutritional impact of VitaFlavor productswill only be realized if BoP consumers ingest its nutrient mix on aconsistent & sustained basis. As such, by offering consumers multipleoptions through which they can obtain this nutrient mix from, VitaFlavorincreases the likelihood that such a behavior will be adopted. Moreimportantly, it addresses product category fatigue issues associatedwith a mono-product strategy as consumers will not be locked into asingle delivery mechanism.

2. Create competition among manufacturers – While VitaFlavor manufacturingpartners will enjoy a competitive advantage against their directcompetitors, they will still have to compete against other VitaFlavormanufacturers for the BoP consumer. For example, while the VitaFlavorrice flavoring manufacturer will have a distinct advantage over otherrice flavoring products, the BoP consumer can still choose to use aVitaFlavor soup flavoring to obtain their daily nutrient mix. Thus,manufacturers will still need to provide high-quality and customer-driven products in order to gain market share among the VitaFlavor BoPconsumer base. This competition is an essential part for ensuring thatthe second pillar of VitaFlavor’s strategy – offering products that areflavorful & customer-demanded – is fulfilled.

3. Focus marketing activities – By focusing on the system, VitaFlavor willnot need to market individual products. Instead, by developing consumerconfidence in the VitaFlavor System®, every product introduced into thesystem will benefit from the messaging. As such, VitaFlavor’s marketingresources essentially become fixed costs rather than variable costs thatincrease as new product categories are added. While potentially moreresource-intensive in the short-term, this strategy will allowVitaFlavor to introduce new products at a much lower cost as well ascondition BoP consumers to readily accept new products.

4. Develop brand reputation – In addition, by concentrating VitaFlavor’smarketing on the system rather than individual products, the companyessentially is building its brand as a provider of flavorful &nutritious products among the BoP consumer. More importantly, once thesystem gains widespread acceptance, the company will become less relianton its manufacturers as VitaFlavor brand will become the competitiveadvantage rather than the nutrient mix.

In terms of pricing, VitaFlavor plans to retail its products at a slightpremium in comparison to its competition. The reasons behind this decisionare three-fold:

1. Drive product acceptance – Research has shown that BoP consumers oftenare willing to pay premium prices for products & services that theyperceive as providing value – whether it be antibiotics or baby milkformula. More importantly, research has also shown that BoP consumersoften forgo more effective and cheaper alternatives in favor of premium-price products because of perceived value & effectiveness. Thus, toreinforce VitaFlavor’s messaging that its products contain vitamin-enhancement & avoid the latter scenario, a premium pricing is employed.More importantly, sales at the premium price demonstrate that BoPconsumers understand the nutritional value of VitaFlavor products andare willing to pay for this value.

2. Develop a premium brand image – A premium price will help reinforceVitaFlavor’s message that its products are superior over its competitionas a result of its vitamin-enhancement. In addition, the higher pricingscheme will help differentiate VitaFlavor products at the point of sale.While such a distinction typically is seen as an obstacle to productsales, VitaFlavor’s price differentiation will be supported by point ofsale messaging through its displays & carriers and further enhanced byits community level marketing activities.

3. Create value for the ecosystem – The VitaFlavor ecosystem will flourishonly if it can create monetary value for all of its participants.Retailing Vitaflavor products at a slight premium allows for this valuecreation:

BoP consumers gain access to flavorful, vitamin-enhanced products; Store owners realize higher profits by actively marketing &

selling VitaFlavor products over competitor products; Distributors build stronger relationships with BoP stores by

supplying them with higher margin products demanded by consumers; Manufacturers develop a competitive advantage that allow them to

compete and gain market share against their competitors; VitaFlavor’s Supplier gain to access to new sales channels for

their vitamins that is economically sustainable instead of relianton grants.

In addition, while VitaFlavor’s main goal is to introduce its line of productsto BoP consumers where vitamin deficiency issues are the greatest, the companyalso plans to market its products in retail outlets that serve a higher-incomedemographic. The reasons for this two-pronged distribution strategy are four-fold:

1. Prevent Product Stigmatization – While VitaFlavor’s primary market isthe BoP consumer, the company wants to avoid its product being viewed assomething developed exclusively for the poor. Such a perceptionpotentially could hinder the products’ acceptance if it develops into anegative social stigma.

2. Create an Aspirational Product Image – Research (NEED CITATION) hasshown that BoP consumers purchase products that they perceive are usedby those in higher-income levels – even when those products are not thecheapest options available. For example, BoP consumers – whenpossessing more disposable income – often will purchase better tastingand/or branded food items rather than purchasing more food (NEEDCITATION). As such, VitaFlavor plans to tap into BoP consumers’aspirations to further drive product acceptance by making its productsavailable to higher-income families through traditional retail channels.

3. Obtain Higher Margins – Initial feedback from distributors & retailersin Southeast Asia indicated that interest in VitaFlavor products wentbeyond the BoP consumers (please see Section XX for more details). Moreimportantly, VitaFlavor products likely would realize a higher retailprice point while incurring lower distribution costs given the FMCGinfrastructure for traditional retail channels is well developed. Moreimportantly, the higher margins gained from this sales channel could beused to offset some of the higher costs associated with VitaFlavortargeting the BoP consumer.

VI. What will be VitaFlavor’s Core Operations?

To build the ecosystem, VitaFlavor will focus its operations on several key aspects of the FMCG market:

1. Developing awareness & demand among consumers – Developing & increasingconsumer demand for VitaFlavor products will drive the growth of theecosystem. VitaFlavor has an inherent advantage in this area as itsproducts will be identical with its competitors’ products from a flavorand usage perspective. As such, the vitamin-enhancement component ofVitaFlavor products will be a clear & distinguishing feature in themarket. More importantly, the purpose behind all of VitaFlavor products– improving the health of families & individuals through betternutrition – is one that appeals to consumers. As multiple marketresearch studies have indicated (NEED CITATION – Cone Roper Report?, IEGSponsorship Report?), given the choice between two identical products,consumers overwhelmingly prefer products associated with a positivesocial cause.

To develop awareness of VitaFlavor products, the company initially willfocus on two main channels:

Community-level marketing – The focus of these activities will be toeducate the BoP consumers about the importance of nutrition, propernutrient intake & the types of products available in the market thatmeet recommended nutrient standards. VitaFlavor will develop thecontent and messaging for the activities but will look to activelypartner with NGOs and MFIs at the community-level to deliver theinformation. However, the company is also prepared to engage indirect community interaction if no suitable partner can be found intargeted areas.

In-store marketing – In conjunction with its community marketingactivities, VitaFlavor will develop in-store displays and productcarriers to differentiate its products at the point of sale. Thedisplays & carriers will have brief messages about the nutritionalimpact of VitaFlavor products as well as collateral pieces that BoPconsumers can take to learn more about benefits VitaFlavor products.Distinct VitaFlavor packaging will ensure that BoP consumers cantrust that all products on the display & carriers are actualVitaFlavor products. In addition, the VitaFlavor displays & carriersdesign will be compact enough to fit in any store size and moreimportantly, to be placed in prominent locations. The ideal locationfor the VitaFlavor displays & carriers will be at the front of thestore either on or alongside the counter which the store owner sitsbehind as this placement will allow for maximum exposure and foottraffic.

Figure 2. VitaFlavor Store Display Concept

Figure 3. Mock-up of VitaFlavor Store Display

Delicious & Nutritious Flavorings & FoodsUse Once a Day for 100% of Essential Vitamins & Minerals

Figure 4. Mock-up of VitaFlavor Display at a Filipino Sari-Sari Store

Figure 5. Mock-up of VitaFlavor Display at Indonesian Warung Store

2. Building & Maintaining the VitaFlavor brand – Establishing VitaFlavor asa trusted brand that offers flavorful, vitamin-enhanced products iscritical to the proposed ecosystem. To accomplish this goal, VitaFlavorwill develop a standardized marketing system & monitoring regime thatwill ensure consistency across all of its product offerings including:

Standardized packaging – All Vitaflavor products will be packagedin such a way that BoP consumers will instantly recognize them asbeing part of the VitaFlavor family. Packaging standards willcover such things as logo placement, product information &packaging color. These standards will apply to all VitaFlavorproducts regardless of the manufacturer. To ensure consistency,VitaFlavor will either sell the packaging to be used bymanufacturers directly or work with manufacturers to re-designtheir packaging to meet VitaFlavor standards.

Supplier Auditing – VitaFlavor will obtain independentverification of the efficacy & usage properties of vitamin mix

provided by its supplier. In addition, VitaFlavor will workclosely with its supplier to develop new vitamin mixes (VitaFlavorVitamin Mix®)as product expansion & usage occurs.

Manufacturing Auditing – VitaFlavor initially will partner withits vitamin supplier in assisting its food manufacturers integrateVitaFlavor Vitamin Mix® into its existing production processes.This initial assistance is to ensure that all products producedfor VitaFlavor will contain the proper mix & dosage of vitamins.The company will then conduct periodic manufacturing audits &product samplings to ensure that its manufacturers consistentlyadhere to VitaFlavor standards.

Retailer Auditing –VitaFlavor will periodically visit BoP storesto ensure its carriers & displays are being used properly as wellas to check the availability of its product in the market. Inaddition, these retailer audits will allow VitaFlavor to solicitfeedback directly from store owners & customers to identify whatadditional marketing activities are needed to support productsales as well as to inform new product development.

3. Attracting local operators – The VitaFlavor ecosystem cannot be built iflocal manufacturers, distributors and retailers cannot be secured.Individually, each stakeholder has no incentive in the development ofthe ecosystem. As such, VitaFlavor must be the institution thatidentifies local partners that share the company’s vision. Moreimportantly, the company must act as the central coordinating body thatconnects the various groups with one another that will lead to thedevelopment of the VitaFlavor ecosystem.

4. Understanding the BoP consumer – Ultimately, VitaFlavor seeks to delivervitamin-enhanced products that fit with existing preferences, desires &behavior among the BoP consumer. As such, gaining insight into consumerflavor preferences, cooking behaviors, consumption habits and personalaspirations will be critical in developing a line of demand-drivenproducts. More importantly, this information will help VitaFlavordecide which types of food manufacturers it will need to partner with aswell inform its marketing activities needed including packaging,messaging and advertising.

VII. How will VitaFlavor be Structured?

VitaFlavor plans to establish a franchise-like model for its operations with the majority of field operations handled by in-country operators. In addition, the company plans to adopt a hybrid system of operations at the global level with a for-profit entity handling the traditional franchisor

responsibilities and a non-profit entity handling much of the BoP consumer education & social impact assessment activities:

Figure 6. VitaFlavor Company Structure

The reasons for developing VitaFlavor as a franchise model are five-fold:

1. Secure local operators – Given that developing economies – particularlythose in Southeast Asia – are the primary markets for VitaFlavorproducts, local knowledge of market conditions will be essential to thecompany’s success. Franchising at all levels of operations allowsVitaFlavor to gain this expertise more cheaply & efficiently than if itcentralized all operations. Local operators – particularly those at thecountry level – will have a better understanding of local marketconditions & which stakeholders to partner with in developing thecountry’s VitaFlavor ecosystem. More importantly, regulatory, cultural& language issues become less of an issue when operating under thisstructure.

2. Links incentives to VitaFlavor ecosystem – By granting franchises at thecountry, manufacturer, distributor & retail levels, each stakeholder hasa financial interest in growing the VitaFlavor ecosystem. Not only dotheir profits increase as the ecosystem increases, but also their accessto the ecosystem is tied directly to their performance. Like allfranchisors, VitaFlavor will revoke the franchise licenses of all under-performers and award them to local operators that can meet the company’sstandards.

3. Significantly reduces both start-up & operating costs – Awardingfranchise licenses removes significant costs as VitaFlavor does not needto build actual operations in the field – in particular themanufacturing & distribution networks. Instead, these expenses areborne by the franchisees – most of whom will have such operations inplace. In addition, franchisees are motivated to continually increaseefficiency & reduce expenses in their area of the ecosystem as itdirectly affects their profit margins. Thus, the primary expense forVitaFlavor will be monitoring & auditing the ecosystem – a verymanageable expense compared to the planned scope of operations.

4. Allows for rapid scalability – The franchise model allows the company toleverage a country’s existing FMCG infrastructure by making them a partof the VitaFlavor ecosystem. As such, growing the operations ofVitaFlavor is mainly limited by the company’s ability to identify &partner with local operators as opposed to building entire networks.Given that the FMCG industry is quite developed in VitaFlavor’s initialtarget markets, the opportunity to rapidly grow the company’s operationsexists.

5. Creates competition to access the ecosystem – By limiting the number offranchise licenses awarded in a particular country, local operators mustcompete with one another to become part of the VitaFlavor ecosystem.Competition is essential – particularly among food manufacturerfranchisees as only one license will be awarded per food category. Thisaspect will help ensure manufacturers meet VitaFlavor’s product quality& consistency standards in order to maintain its franchise license.

In terms of establishing two separate for-profit & non-profit entities, thereasons for such a structure are three-fold:

1. Creates clear decision-making & personnel responsibilities – VitaFlavorwill only improve the nutritional lives of children & families if thecompany succeeds as a business. Clearly delineating VitaFlavor’sbusiness activities from its social activities enables efficientdecision-making and allows each entity to focus on their area ofresponsibility. In addition, operating a profitable venture oftenrequires a different set of skills and mindset than running a socially-focused foundation. As such, separate entities allow each organizationto recruit the most talented individuals that can effectively worktogether.

2. Expands funding base to reduce business costs – By adopting a hybridoperational model, VitaFlavor can access foundation & NGO funding tosupport parts of its nutrition education & community awarenessactivities. More importantly, it transfers a significant expense ofcreating the VitaFlavor ecosystem from the for-profit venture to the

nonprofit entity. As a result, scaling up the operations of the for-profit entity become less costly over time.

3. Replicates model of successful social enterprises – A hybrid model ofoperations has been adopted successfully by a range of socialenterprises both domestically & internationally. VitaFlavor intends toadopt the practices & operational strategies pioneered by theseinstitutions including Pioneer Human Services in Seattle, Hapinoy in thePhilippines and PT Ruma in Indonesia (likely will need to add a shortdescription of each organization in the Appendices).

VIII. What are the Economics of the VitaFlavor Model?

Figure 7. VitaFlavor Economic Model

IX. What Sustainable Competitive Advantages Will VitaFlavor’s Strategy Create?

1. The VitaFlavor Brand – By promoting the VitaFlavor System® overindividual products, the company is conditioning consumers to look forthe VitaFlavor brand as evidence of vitamin-enhancement rather than theproduct ingredients themselves. By making VitaFlavor synonymous withflavorful & nutritious products, competitors cannot simply vitaminenhance their existing product lines as they will lack the VitaFlavor

endorsement that BoP consumers will expect before adopting suchproducts.

2. The VitaFlavor Ecosystem – The ecosystem which VitaFlavor is creating isa closed one. Gaining access to the system will be strictly controlledby the company and any company wishing to become a part of it will needto meet standards established by VitaFlavor. Secondly, because theecosystem supports multiple product categories, competitors would not beable to compete on product-by-product basis without building a similarsupporting ecosystem. More importantly, VitaFlavor’s structure createsan ecosystem of local operators with a vested financial interest in thenetwork’s success. Replicating such an ecosystem would be costly bothin terms of resources & time – even for a conglomerate such as Unileveror Nestle. In addition, brand managers in such organizations would havelittle incentive in developing such an ecosystem it became anoverarching strategic initiative for the company.

3. VitaFlavor Scalability of Operations – VitaFlavor’s strategy is based onstealth marketing and a rapid scaling of operations – similar to the oneJollibee implemented to become the top fast food chain in thePhilippines and followed similarly by Mang Inasal (CITATION NEEDED).VitaFlavor understands that in order to thrive in the highly competitiveFMCG industry it must be able to saturate the market before one of thelarger players is able to respond. Once VitaFlavor has achieved scale,it will be difficult for competitors to replicate as the company’s brand& network will represent significant obstacles. As such, VitaFlavor’sstrategy is designed with the purpose of reaching this scale as quicklyas possible.

X. Why does VitaFlavor Believe its Strategy will be Successful?

VitaFlavor’s strategy is based on addressing specific pain points felt bystakeholders in the company’s operations. Because of this focus, VitaFlavorpartners have a significant financial & operational interest in helping thecompany succeed. More importantly, VitaFlavor does not need to rely onfinding partners that share the same social vision for developing itsecosystem – although such alignment is highly preferred by the company.

Table 1. Stakeholder Pain Points Addressed by VitaFlavor

XI. What are the Major Assumptions & Risks Underlying this Strategy?

1. Adding VitaFlavor Vitamin Mixes into existing food products is toocostly or operationally complex.

2. Customers are not willing to pay a premium for VitaFlavor products.3. Obtaining regulatory approval for VitaFlavor products may prove time-

consuming.4. Customer acceptance of VitaFlavor products is low – leading to intake

levels below what is needed to improve nutritional health.5. VitaFlavor is unable to partner with sufficient distributors to reach a

large number of BoP stores.

XII. What has VitaFlavor Achieved to Date?

1. Product Developmenta. DSMb. Chilean Cold Packerc. VitaFlavor Prototyped. Other Achievements

2. Market Developmenta. Trip to Philippinesb. Trip to Indonesia

3. VitaFlavor Ecosystem (Pilot)

a. Vitamin Supplier: DSMb. Country Franchisee

i. Indonesia – Darrenii. Philippines – Michael

c. Franchise Food Manufactureri. Indonesia – TBD (Work with John, Sampoerna,etc.?)ii. Philippines – TBD (Work with Hapinoy?)

d. Franchise Retaileri. Indonesia – Sampoerna Foundationii. Philippines – Hapinoy

e. Franchise Distributori. Indonesia – TBD (John Young?)ii. Philippines – TBD (Kopiko distributor)

XIII. What are the Next Steps for VitaFlavor?

Given the positive market feedback that VitaFlavor received from stakeholdersduring its Asia trip in 2011, the company plans to undertake a 2-phase pilotproject in 2012. The goal of the pilot is two-fold:

1. To validate customer assumptions regarding taste preferences &product usage, the ability to create a meaningful VitaFlavor brandand to determine what educational & marketing activities thecompany will need to undertake.

2. To validate business model assumptions regarding the proposedeconomic model, supply chain management and implementation ofVitaFlavor’s educational & marketing activities.

The findings of the pilot project will be critical to the company’s businessdevelopment activities as it will prove to partners that the VitaFlavorEcosystem is a viable initiative. As such, the design of the pilot project isalso critical as it will need to meet the market research standards of thepartners VitaFlavor is looking to attract – namely those of local foodmanufacturers & distributors.

Pilot Phase Key Objectives Key Action Item sPhaseI: Validate Customer Assumptions

1. Understand customer taste & usage preferences

2. Test VitaFlavorbrand concept3. Determ ine educational &

marketing needs

1. Conduct in-field market research of BoPcustom ers withlocal partner

2. Identify local food manufacturers & distributors

Phase II: Validate BusinessM odel Assumptions

1. Trial educational & marketing activities

2. Identifykey supply chain managem ent issues

3. Refinerevenuemodel

1. Develop educational & marketing activities with local partner.

2. Begin production, distribution & sales to BoPclients through local partner sales channels.

Phase 1: Validating Customer Assumptions

The first phase of the VitaFlavor pilot project will consist of customer and BoP store owner interviews & focus groups. The number of interviews & focus groups to be conducted will be determined by acceptable by potential VitaFlavor

Stakeholder

Key Topics Key Information Sought

I. BoP Customers

1. Product Usage

How often do consumers use the types of products that VitaFlavor is planning to enrich?

For each product type:o What food dishes do they incorporate the

flavoring / seasoning?o What is the preferred method for

incorporating the flavoring / seasoning?o How do consumers measure how much

flavoring / seasoning to add to the dishes?

2. Flavor Preference

For each product type, what are the preferred flavors used by consumers?

3. VitaFlavor Brand Concept

What brands do BoP consumers trust & why? How can VitaFlavor prove to consumers that its

products deliver the promised nutrients? Would a VitaFlavor POS display be appealing to

consumers?o How should the VitaFlavor display be

designed to make it more appealing?

4. EducationalActivities

What is the level of understanding regarding nutrition among BoP consumers?

o What do families currently do to obtain nutritious food for their families?

o What practices to consumers currently engage in that they consider healthy / nutritious?

Do BoP consumers understand the health contentof the foods & seasonings they consume?

o What sources of information do they access to learn about the nutritional content of their food?

D

5. Marketing Activities

How do consumers choose which type of flavoring / seasoning to purchase?

o Priceo Flavoro Consistencyo Ease-of-useo Brand recognition

How do consumers hear of new products?o Word of moutho Advertisements (TV, radio, print, etc.)o Point of sale displays

What are the most important factors that persuade a consumer to a new product?

o Word of moutho Celebrity endorsemento Government seal of approval

How important is flavor variety for consumers to use at least one VitaFlavor product per day?

II. BoP Store Owners

1. VitaFlavor Brand Concept

2. Flavor Preference

Customer

1. Understanding Customer Taste & Product Usage Preferences2. Testing VitaFlavor Brand Concept3. Determining Marketing & Educational Activitie

4. Indonesia:5.

Phase 2: Large-scale product testing to validate distribution & customer demand assumptions

1. Indonesia: Sampoerna2. Philippines: Hapinoy

Phase 2: Large scale to test distribution, 3. Phase 2

4. Pilot Project to Test Initial Assumptionsi. Indonesia – MICRA, Sampoerna Foundation, Mercy Corps, World

Vision Indonesiaii. Philippines – ASEI, Hapinoy

5. Expanding Teami. Recruit another MBA student with Food Industry/Franchise

Operational Experience

6. Darren move to Indonesia

7. Michael move to Philippines

XIV. What Resources does VitaFlavor Need Moving Forward?

1. Resources Needed in next 6 months