VILLAGE OF PINGREE GROVE, ILLINOIS

137

VILLAGE OF PINGREE GROVE, ILLINOIS COMPREHENSIVE ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED APRIL 30, 2019

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of VILLAGE OF PINGREE GROVE, ILLINOIS

VILLAGE OF PINGREE GROVE, ILLINOIS

COMPREHENSIVE ANNUAL FINANCIAL REPORT

FOR THE FISCAL YEAR ENDEDAPRIL 30, 2019

VILLAGE OF PINGREE GROVE, ILLINOIS

COMPREHENSIVE ANNUAL FINANCIAL REPORT

FOR THE FISCAL YEAR ENDED APRIL 30, 2019

Prepared by:

Finance Department

VILLAGE OF PINGREE GROVE, ILLINOIS

TABLE OF CONTENTS

12

Letter of Transmittal 3 - 67

INDEPENDENT AUDITORS' REPORT 8 - 9

MANAGEMENT’S DISCUSSION AND ANALYSIS 10 - 21

BASIC FINANCIAL STATEMENTS

Government-Wide Financial StatementsStatement of Net Position 22 - 23Statement of Activities 24 - 25

Fund Financial StatementsBalance Sheet – Governmental Funds 26 - 27Reconciliation of Total Governmental Fund Balance to the

Statement of Net Position – Governmental Activities 28Statement of Revenues, Expenditures and Changes in

Fund Balances – Governmental Funds 29 - 30Reconciliation of the Statement of Revenues, Expenditures and Changes in

Fund Balances to the Statement of Activities 31Statement of Net Position – Proprietary Fund 32 - 33Statement of Revenues, Expenses, and Changes in Net Position – Proprietary Fund 34Statement of Cash Flows – Proprietary Fund 35Statement of Fiduciary Net Position 36

Notes to Financial Statements 37 - 65

REQUIRED SUPPLEMENTARY INFORMATION

Schedule of Employer ContributionsIllinois Municipal Retirement Fund 66

Schedule of Changes in the Employer’s Net Pension Liability

Illinois Municipal Retirement Fund 67 - 68Schedule of Revenues, Expenditures and Changes in Fund Balance – Budget and Actual

General Fund 69

PAGE

INTRODUCTORY SECTION

Principal Officials Organizational Chart

Certificate of Achievement for Excellence in Financial Reporting

FINANCIAL SECTION

VILLAGE OF PINGREE GROVE, ILLINOIS

TABLE OF CONTENTS

OTHER SUPPLEMENTARY INFORMATION

Schedule of Revenues – Budget and Actual – General Fund. 70Schedule of Expenditures – Budget and Actual – General Fund 71 - 76Schedule of Revenues, Expenditures and Changes in Fund Balance – Budget and Actual

Debt Service Fund 77Capital Improvement – Capital Projects Fund 78

Schedule of Expenditures – Budget and Actual

Capital Improvement – Capital Projects Fund 79Schedule of Revenues, Expenditures and Changes in Fund Balance – Budget and Actual

Special Service Area #4 – Capital Projects Fund 80Combining Balance Sheet – Nonmajor Governmental Funds 81Combining Statement of Revenues, Expenditures and Changes in Fund Balance

Nonmajor Governmental Funds 82Schedule of Revenues, Expenditures and Changes in Fund Balance – Budget and Actual

Motor Fuel – Special Revenue Fund 83Schedule of Revenues, Expenditures and Changes in Fund Balance – Budget and Actual

Tax Increment Financing – Bell-Harris – Special Revenue Fund 84Schedule of Revenues, Expenditures and Changes in Fund Balance – Budget and Actual

Special Service Area #9 – Capital Projects Fund 85Schedule of Revenues, Expenses and Changes in Net Position – Budget and Actual

Water and Sewer – Enterprise Fund 86Schedule of Operating Expenses – Budget and Actual

Water and Sewer – Enterprise Fund 87 - 89Combining Statement of Changes in Assets and Liabilities

Special Service Areas – Agency Fund 90Consolidated Year-End Financial Report 91

PAGE

FINANCIAL SECTION – Continued

VILLAGE OF PINGREE GROVE, ILLINOIS

TABLE OF CONTENTS

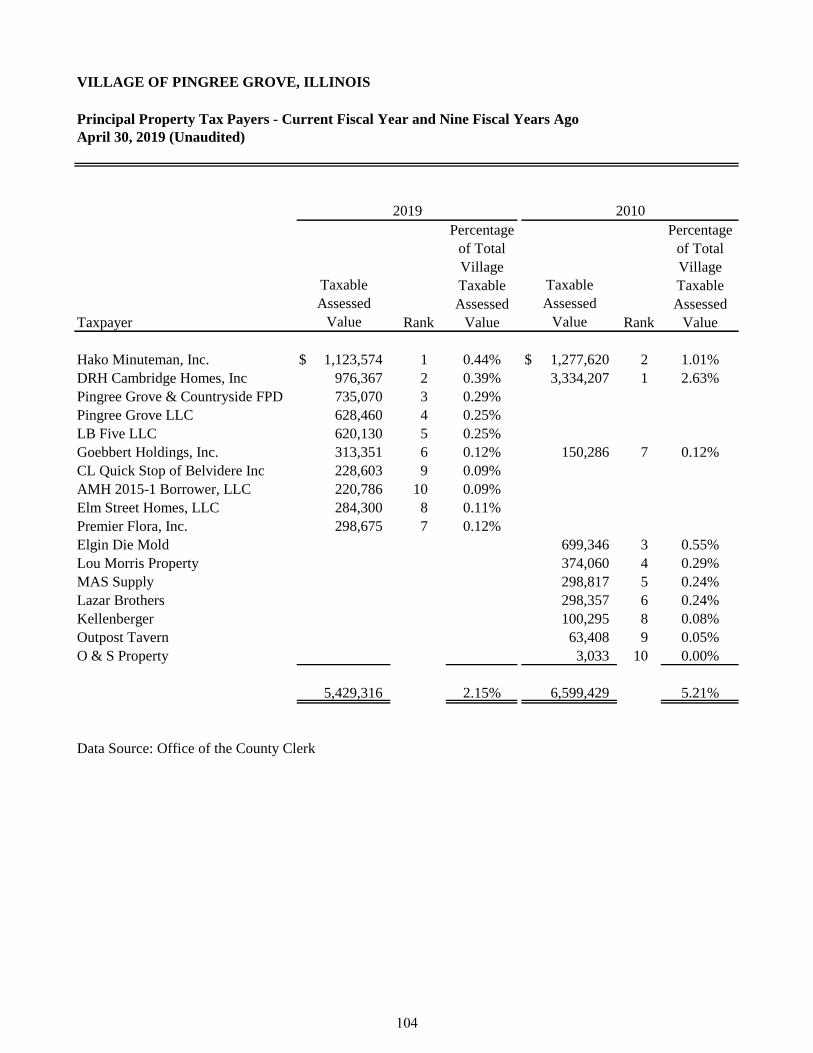

Net Position by Component – Last Ten Fiscal Years 92 - 93Changes in Net Position – Last Ten Fiscal Years 94 - 95Fund Balances of Governmental Funds – Last Ten Fiscal Years 96 - 97Changes in Fund Balances for Governmental Funds – Last Ten Fiscal Years 98 - 99Assessed Value and Actual Value of Taxable Property – Last Ten Fiscal Years 100 - 101Direct and Overlapping Property Tax Rates – Last Ten Fiscal Years 102 - 103Principal Property Tax Payers – Current Fiscal Year and Nine Fiscal Years Ago 104Property Tax Levies and Collections – Last Ten Fiscal Years 105Ratios of Outstanding Debt by Type – Last Ten Fiscal Years 106 - 107Ratios of General Bonded Debt Outstanding – Last Ten Fiscal Years 108Schedule of Direct and Overlapping Governmental Activities Debt 109Schedule of Legal Debt Margin – Last Ten Fiscal Years 110 - 111Pledged-Revenue Coverage – Last Ten Fiscal Years 112Demographic and Economic Statistics – Last Ten Fiscal Years 113Principal Employers – Current Fiscal Year and Nine Fiscal Years Ago 114Full-Time Equivalent Village Government Employees by Function – Last Ten Fiscal Years 115Operating Indicators by Function/Program – Last Ten Fiscal Years 116 - 117Capital Asset Statistics by Function/Program – Last Ten Fiscal Years 118

PAGE

STATISTICAL SECTION (Unaudited)

INTRODUCTORY SECTION

This section includes miscellaneous data regarding the Village of Pingree Grove, Illinois including the List of Principal Officials, Organizational Chart, Transmittal Letter, and Certificate of Achievement for Excellence in Financial Reporting.

VILLAGE OF PINGREE GROVE, ILLINOIS

List of Principal Officials April 30, 2019

Title Name Term Expires

Village President Steve Wiedmeyer May, 2019

Trustee Robert Spieker May, 2019

Trustee Charles Pearson May, 2019

Trustee Bernard Thomas May, 2019

Trustee Patricia Dulkoski May, 2021

Trustee Joseph Hirschbein May, 2021

Trustee Amber Kubiak May, 2021

Village Attorney, Dean Frieders

Village Clerk, Dawn R. Grivetti

Finance Director, Karen Plaza

Public Works Director, Pat Doherty

1

VILLAGE OF PINGREE GROVE

ORGANIZATIONAL CHART

PLANNING & ZONING COMMISSION VILLAGE CLERK ATTORNEYLIQUOR COMMISSION FINANCE BUILDING INSPECTOREVENTS COMMITTEE POLICE ENGINEERPARKS COMMITTEE PUBLIC WORKS PLANNER

As of 4/30/2019

ADVISORY COMMISSIONSAND COMMITTEES

RESIDENTS OF PINGREE GROVE

VILLAGE PRESIDENT

BOARD OF TRUSTEES

PROFESSIONALSERVICES

VILLAGEDEPARTMEMTS

2

October 17, 2019 To The Village President, Members of the Village Board of Trustees, and the Citizens of the Village of Pingree Grove: The Comprehensive Annual Financial Report (CAFR) for the Village of Pingree Grove, for the year ending April 30, 2019 is hereby submitted. The CAFR is the management’s annual report to its

taxpayers, governing board, oversight bodies, investors and creditors. Village Management is responsible for all financial transactions for the Village of Pingree Grove and for the contents of this Comprehensive Annual Financial Report. We believe the data, as presented, is accurate in all material aspects and is reported in a manner designed to present fairly the financial position and results of operations of the various funds of the Village. All disclosures necessary to enable the reader to gain an understanding of the Village of Pingree Grove financial activities have been included. The Comprehensive Annual Financial Report consists of the Village’s representations concerning the

finances of the Village. Management assumes full responsibility for the completeness and reliability of all of the information presented in this report. To provide a reasonable basis for making these representations, management has continued to focus on the internal controls that are designed to protect the Village’s assets from loss, theft or misuse and to compile sufficiently reliable information for the

preparation of the Village’s financial statements in conformity with GAAP. Because the cost of a control should not exceed the benefits to be derived, the objective is to provide reasonable, rather than absolute assurance, that the financial statements are free of any material misstatements. Management continues to revise processes, implement internal controls, and establish new financial policies that allow us to successfully address the prior years’ accounting issues and meet the required

deadline for the issuance of this fiscal year’s report. Management asserts that, to the best of our knowledge and belief, this financial report is complete and reliable in all material respects.

3

Fiscal Management

Annually the Village adopts a budget that defines its legal spending authority. In January the Departments are given budgetary information, and in February the departments submit their requests to the Finance Director who prepares a budget by fund, department, function and activity. The budget is presented to the Village Board for review. The Village Board holds a public hearing and makes adjustments to the requested budgeted amounts. The Village’s budget is approved by the Village Board

by May 1st. State statutes require an annual audit by independent Certified Public Accountants. The Village of Pingree Grove selected the accounting firm of Lauterbach & Amen, LLP to conduct the annual audit. The auditor's report on the general-purpose financial statements and combining and individual fund statements and schedules is included in the financial section of this report.

Fiscal Report

Lauterbach & Amen, LLP has concluded that there was a reasonable basis for rendering an unmodified opinion that the Village of Pingree Grove’s financial statements for the fiscal year ended April 30, 2019, are presented fairly, in conformity with GAAP. The independent auditor’s report is located at the front

of the financial section of this report.

GAAP requires that management provide a narrative introduction, overview and analysis to accompany the basic financial statements in the form of Management’s Discussion and Analysis (MD&A). This

letter of transmittal is designed to complement the MD&A and is meant to be read in conjunction with it. The Village’s MD&A can be found immediately following the report of the independent auditors.

ECONOMIC CONDITION AND OUTLOOK

Local Economy

The Village of Pingree Grove was incorporated in 1907. The Village is a non-home rule community governed by a Village President (Mayor) and a six member Board of Trustees, elected for overlapping four-year terms. The Board now appoints a Police Chief, Finance Director, Public Works Director, Attorney, Building Code Official and Engineer. The Village of Pingree Grove is located in Kane County, Illinois and lies approximately 48 miles northwest of the City of Chicago. The Village of Pingree Grove covers an area of approximately 5.35 square miles. Located within commuting distance of Chicago and its suburbs, the Village of Pingree Grove has experienced an increase in equalized assessed valuation as a result of continued new residential construction. During the next fiscal year the growth is expected to continue. According to the 2010 Census, the Village of Pingree Grove has a population of 4,532. It is estimated that the population now exceeds 8,000. This population increase will also impact the need to establish a police pension as defined by state law after the next census in 2020.

4

Data Regarding Major Industry Affecting the Local Economy

The largest employer in Pingree Grove is the Cambridge Lakes Charter School. The major businesses located in the Village of Pingree Grove are: Minuteman International, a manufacturer of industrial cleaning equipment and supplies; Elgin Die Mold, a contract die mold manufacturer; the Cambridge Lakes Community Center; MAS Supply, a manufacturer of custom kitchen cabinets; Kindred at Home, providing home health services; The Outpost, a bar/restaurant; and Lazar Brothers BP Gas and Mini Mart. Economic Condition and Outlook

The Village’s past fiscal year has continued to experience variable economic conditions resulting in no significant increases in anticipated revenue sources. The Village continues to issue new construction building permits at a consistent level. While the Village is pleased with the number of building permits, the Village continues to be fiscally conservative in the revenue projections for next fiscal year due to restrictions in state funding. The increase in building impacts water and sewer services which is causing the Village to review it service rates to ensure these services are self-sustaining. Overall, the Village has maintained a steady course in keeping expenses down and holding at current revenue sources. With increasing population, the Village continues to research revenue enhancements and cost containments in order to meet future obligations of Village operations.

MAJOR INITIATIVES

For the Year

In Fiscal Year 2019, the Village achieved the following goals:

• Annexation of the Pioneer Landing development on Route 47; • 10th Amendment to the Cambridge Lakes Annexation Agreement; • Groundbreaking and construction of the Municipal Center; • Continued commercial development in the Bell Land TIF District.

For the Future

Major projects planned for Fiscal Year 2020 include:

• Construction of road improvements on State Route 72 and Richard J. Brown Boulevard; • Completion of the Municipal Center, June 2019; • Completion of the Water and Sewer Facility Expansion Plan; • Sale redevelopment of the former Village Hall site; • Completion of the Water and Sewer Facility Expansion Plan;

5

6

7

FINANCIAL SECTION

This section includes:

Independent Auditors’ Report

Management’s Discussion and Analysis

Basic Financial Statements

Required Supplementary Information

Other Supplementary Information

INDEPENDENT AUDITORS’ REPORT

This section includes the opinion of the Village’s independent auditing firm.

INDEPENDENT AUDITORS' REPORT

October 17, 2019

The Honorable Village President Members of the Board of Trustees Village of Pingree Grove, Illinois

We have audited the accompanying financial statements of the governmental activities, the business-type activities, each major fund, and the aggregate remaining fund information of the Village of Pingree Grove, Illinois, as of and for the year ended April 30, 2019, and the related notes to the financial statements, which collectively comprise the Village’s basic financial statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the

assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the Village’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Village’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, the business-type activities, each major fund, and the aggregate remaining fund information of the Village of Pingree Grove, Illinois, as of April 30, 2019, and the respective changes in financial position and, where applicable, cash flows thereof for the year then ended in accordance with accounting principles generally accepted in the United States of America.

8

Village of Pingree Grove, Illinois October 17, 2019 Page 2

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the management’s

discussion and analysis as listed in the table of contents and budgetary information reported in the required supplementary information as listed in the table of contents, be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance. Other Information

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the Village of Pingree Grove, Illinois’ basic financial statements. The introductory section, combining and individual fund financial statements and budgetary comparison schedules, and statistical section are presented for purposes of additional analysis and are not a required part of the basic financial statements. The combining and individual fund financial statements and budgetary comparison schedules are the responsibility of management and were derived from and relate directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the combining and individual fund financial statements and budgetary comparison schedules are fairly stated, in all material respects, in relation to the basic financial statements as a whole. The introductory and statistical sections have not been subjected to the auditing procedures applied in the audit of the basic financial statements and, accordingly, we do not express an opinion or provide any assurance on them.

Lauterbach & Amen, LLP LAUTERBACH & AMEN, LLP

9

MANAGEMENT’S DISCUSSION AND ANALYSIS

VILLAGE OF PINGREE GROVE, ILLINOIS Management’s Discussion and Analysis April 30, 2019 Our discussion and analysis of the Village of Pingree Grove’s (Village) financial performance provides an overview of the Village’s financial activities for the fiscal year ended April 30, 2019. Please read it in conjunction with the transmittal letter which begins on page 3 and the Village’s financial statements, which begin on page 22. FINANCIAL HIGHLIGHTS

• The Village’s net position increased as a result of this year’s operations. Net position of the governmental activities increased by $336,098 or 2.0 percent and net position of business-type activities increased by $89,631, or less than one percent.

• During the year, government-wide revenues totaled $6,995,940, while expenses totaled $6,570,211, resulting in an increase to net position of $425,729.

• The Village’s net position totaled $50,957,138 on April 30, 2019, which includes $38,901,794 net investment in capital assets, $1,321,495 subject to external restrictions, and $10,733,849 unrestricted net position that may be used to meet the ongoing obligations to citizens and creditors.

• The General Fund reported a surplus in the current year of $488,927, which includes an

increase in revenues of $189,538 compared to prior year, resulting in ending fund balance of $2,990,564, an increase of 19.5 percent.

USING THIS ANNUAL REPORT This annual report consists of a series of financial statements. The Statement of Net Position and the Statement of Activities (on pages 22 - 25) provide information about the activities of the Village as a whole and present a longer-term view of the Village’s finances. Fund financial statements begin on page 26. For governmental activities, these statements tell how these services were financed in the short term as well as what remains for future spending. Fund financial statements also report the Village’s operations in more detail than the government-wide statements by providing information about the Village’s most significant funds. The remaining statements provide financial information about activities for which the Village acts solely as a trustee or agent for the benefit of those outside of the government. Government-Wide Financial Statements The government-wide financial statements provide readers with a broad overview of the Village’s finances, in a matter similar to a private-sector business. The government wide financial statements can be found on pages 22 - 25 of this report. The Statement of Net Position reports information on all of the Village’s assets/deferred outflows and liabilities/deferred inflows, with the difference between the two reported as net position. Over time, increases or decreases in net position may serve as a useful indicator of whether the financial position of the Village is improving or deteriorating. Consideration of other nonfinancial factors, such as changes in the Village’s property tax base and the condition of the Village’s infrastructure, is needed to assess the overall health of the Village.

10

VILLAGE OF PINGREE GROVE, ILLINOIS Management’s Discussion and Analysis April 30, 2019 USING THIS ANNUAL REPORT – Continued Government-Wide Financial Statements – Continued The Statement of Activities presents information showing how the government’s net position changed during the most recent fiscal year. All changes in net position are reported as soon as the underlying event giving rise to the change occurs, regardless of the timing of related cash flows. Thus, revenues and expenses are reported in this statement for some items that will only result in cash flows in future fiscal periods (e.g., uncollected taxes and earned but unused vacation leave). Both of the government-wide financial statements distinguish functions of the Village that are principally supported by taxes and intergovernmental revenues (governmental activities) from other functions that are intended to recover all or a significant portion of their costs through user fees and charges (business-type activities). The governmental activities of the Village include general government, public safety, and highways and streets. The business-type activities of the Village include water and sewer operations. Fund Financial Statements A fund is a grouping of related accounts that is used to maintain control over resources that have been segregated for specific activities or objectives. The Village, like other local governments, uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. All of the funds of the Village can be divided into three categories: governmental funds, proprietary funds, and fiduciary funds. Governmental Funds Governmental funds are used to account for essentially the same functions reported as governmental activities in the government-wide financial statements. However, governmental fund financial statements focus on near-term inflows and outflows of spendable resources, as well as on balances of spendable resources available at the end of the fiscal year. Such information may be useful in evaluating the Village’s near-term financing requirements.

11

VILLAGE OF PINGREE GROVE, ILLINOIS Management’s Discussion and Analysis April 30, 2019 USING THIS ANNUAL REPORT – Continued Fund Financial Statements – Continued Governmental Funds – Continued Because the focus of governmental funds is narrower than that of the government-wide financial statements, it is useful to compare the information presented for governmental funds with similar information presented for governmental activities in the government-wide financial statements. By doing so, readers may better understand the long-term impact of the government’s near-term financing decisions. Both the governmental fund balance sheet and the governmental fund statement of revenues, expenditures, and changes in fund balances provide a reconciliation to facilitate the comparison between governmental funds and governmental activities. The Village maintains nine individual governmental funds. Information is presented separately in the governmental fund balance sheet and in the governmental fund statement of revenues, expenditures, and changes in fund balances for the General, Debt Service, Capital Improvements, Special Service Area #2, Special Service Area #4, and Special Service Area #7 Funds, all of which are considered major funds. Data from the other three governmental funds are combined into a single, aggregated presentation. Individual fund data for each of these nonmajor governmental funds is provided in the form of combining statements elsewhere in this report. The Village adopts an annual appropriated budget for all of the governmental funds, except the Special Service Area #2 and Special Service Area #7 Funds. A budgetary comparison schedule for the remaining funds has been provided to demonstrate compliance with this budget. The basic governmental fund financial statements can be found on pages 26 - 31 of this report. Proprietary Funds The Village maintains one proprietary fund type: enterprise funds. Enterprise funds are used to report the same functions presented as business-type activities in the government-wide financial statements. The Village utilizes enterprise funds to account for its water and sewer operations. Proprietary fund financial statements provide the same type of information as the government-wide financial statements, only in more detail. The proprietary fund financial statements provide separate information for the Water and Sewer Fund, which is considered to be a major fund of the Village. The basic proprietary fund financial statements can be found on pages 32 - 35 of this report.

12

VILLAGE OF PINGREE GROVE, ILLINOIS Management’s Discussion and Analysis April 30, 2019 USING THIS ANNUAL REPORT – Continued Fiduciary Funds Fiduciary funds are used to account for resources held for the benefit of parties outside the government. Fiduciary funds are not reflected in the government-wide financial statements because the resources of those funds are not available to support the Village’s own programs. The accounting use for fiduciary funds is much like that used for proprietary funds. The basic fiduciary fund financial statements can be found on page 36 of this report. Notes to the Financial Statements The notes provide additional information that is essential to a full understanding of the data provided in the government-wide and fund financial statements. The notes to the financial statements can be found on pages 37 - 65 of this report. Other Information In addition to the basic financial statements and accompanying notes, this report also presents certain required supplementary information concerning the Village’s I.M.R.F. employee pension obligation and the budgetary comparison schedule for the General Fund. Required supplementary information can be found on pages 66 - 69 of this report. The combining statements referred to earlier in connection with non-major governmental funds are presented immediately following the required supplementary information on pensions. Combining and individual fund statements and schedules can be found on pages 70 - 91 of this report.

13

VILLAGE OF PINGREE GROVE, ILLINOIS Management’s Discussion and Analysis April 30, 2019 GOVERNMENT-WIDE FINANCIAL ANALYSIS Net position may serve over time as a useful indicator of a government’s financial position. The following tables show that in the case of the Village, assets/deferred outflows exceeded liabilities/deferred inflows by $50,957,138.

2019 2018 2019 2018 2019 2018

Current and Other Assets $ 7,710,328 10,233,034 6,412,124 5,183,740 14,122,452 15,416,774Capital Assets 15,556,681 12,651,058 28,795,765 30,023,664 44,352,446 42,674,722

Total Assets 23,267,009 22,884,092 35,207,889 35,207,404 58,474,898 58,091,496Deferred Outflows 243,461 165,730 88,347 60,462 331,808 226,192

Total Assets/Deferred Outflows 23,510,470 23,049,822 35,296,236 35,267,866 58,806,706 58,317,688

Long-Term Debt 4,776,817 4,736,285 1,114,917 1,153,226 5,891,734 5,889,511Other Liabilities 788,889 670,592 238,433 233,944 1,027,322 904,536

Total Liabilities 5,565,706 5,406,877 1,353,350 1,387,170 6,919,056 6,794,047Deferred Inflows 918,889 953,168 11,623 39,064 930,512 992,232

Total Liabilities/Deferred Inflows 6,484,595 6,360,045 1,364,973 1,426,234 7,849,568 7,786,279

Net PositionNet Investment in Capital Assets 11,142,977 10,706,664 27,758,817 28,881,481 38,901,794 39,588,145Restricted 1,321,495 1,130,096 - - 1,321,495 1,130,096Unrestricted 4,561,403 4,853,017 6,172,446 4,960,151 10,733,849 9,813,168

Total Net Position 17,025,875 16,689,777 33,931,263 33,841,632 50,957,138 50,531,409

Total

Net PositionGovernmental

ActivitiesBusiness-Type

Activities

A large portion of the Village’s net position, $38,901,794 or 76.3 percent, reflects its investment in capital assets (for example, land, buildings, machinery, and equipment), less any related debt used to acquire those assets that is still outstanding. The Village uses these capital assets to provide services to citizens; consequently, these assets are not available for future spending. Although the Village’s investment in its capital assets is reported net of related debt, it should be noted that the resources needed to repay this debt must be provided from other sources, since the capital assets themselves cannot be used to liquidate these liabilities. An additional portion, $1,321,495 or 2.6 percent, of the Village’s net position represents resources that are subject to external restrictions on how they may be used. The remaining 21.1 percent, or $10,733,849, represents unrestricted net position and may be used to meet the government’s ongoing obligations to citizens and creditors.

14

VILLAGE OF PINGREE GROVE, ILLINOIS Management’s Discussion and Analysis April 30, 2019 GOVERNMENT-WIDE FINANCIAL ANALYSIS – Continued

2019 2018 2019 2018 2019 2018

RevenuesProgram Revenues

Charges for ServicesGeneral Government $ 791,650 955,175 - - 791,650 955,175Public Safety 92,826 84,020 - - 92,826 84,020Water and Sewer - - 2,993,840 2,758,873 2,993,840 2,758,873

Capital Grants/Contrib. 115,043 150,535 - - 115,043 150,535General Revenues

Property Taxes 894,047 845,437 - - 894,047 845,437Municipal Utility Taxes 338,301 379,267 - - 338,301 379,267Replacement Taxes 187 156 - - 187 156Use Taxes 140,206 119,847 - - 140,206 119,847Sales Taxes 296,947 200,692 - - 296,947 200,692Income Taxes 468,860 412,411 - - 468,860 412,411Other General Revenues 841,472 713,845 22,561 8,685 864,033 722,530

Total Revenues 3,979,539 3,861,385 3,016,401 2,767,558 6,995,940 6,628,943

ExpensesGeneral Government 1,636,536 1,688,955 - - 1,636,536 1,688,955Public Safety 1,138,318 1,014,855 - - 1,138,318 1,014,855Highways and Streets 774,582 652,691 - - 774,582 652,691Interest on Long-Term Debt 191,773 80,542 - - 191,773 80,542Water and Sewer - - 2,829,002 2,846,133 2,829,002 2,846,133

Total Expenses 3,741,209 3,437,043 2,829,002 2,846,133 6,570,211 6,283,176

Changes in Net Position Prior to Transfers 238,330 424,342 187,399 (78,575) 425,729 345,767

Transfers 97,768 - (97,768) - - -

Change in Net Position 336,098 424,342 89,631 (78,575) 425,729 345,767

Net Position-Beginning 16,689,777 16,265,435 33,841,632 33,920,207 50,531,409 50,185,642

Net Position-Ending 17,025,875 16,689,777 33,931,263 33,841,632 50,957,138 50,531,409

Total

Changes in Net PositionGovernmental

ActivitiesBusiness-Type

Activities

15

VILLAGE OF PINGREE GROVE, ILLINOIS Management’s Discussion and Analysis April 30, 2019 GOVERNMENT-WIDE FINANCIAL ANALYSIS – Continued Net position of the Village’s governmental activities increased by 2.0 percent ($16,689,777 in 2018 compared to $17,025,875 in 2019). Unrestricted net position, the part of net position that can be used to finance day-to-day operations without constraints, totaled $4,561,403 at April 30, 2019. Net position of business-type activities increased by less than one percent ($33,841,632 in 2018 compared to $33,931,263 in 2019). Governmental Activities Revenues for governmental activities totaled $3,979,539, while the cost of all governmental functions totaled $3,741,209. This results in a surplus of $238,330, prior to transfers in of $97,768. The Village saw revenues increase $118,154, or 3.1 percent due to increases in other general revenues and in all of the tax related items, except municipal utility tax. The expenses for governmental activities increased $304,166 or 8.8 percent due to increased expenses in public safety, highways and streets, and interest on long-term debt activities. The following table graphically depicts the major revenue sources of the Village. It depicts very clearly the reliance of charges for services, property taxes, and income taxes to fund governmental activities. It also clearly identifies the less significant percentage the Village receives from municipal utility taxes and sales taxes.

16

VILLAGE OF PINGREE GROVE, ILLINOIS Management’s Discussion and Analysis April 30, 2019 GOVERNMENT-WIDE FINANCIAL ANALYSIS – Continued Governmental Activities – Continued The ‘Expenses and Program Revenues’ Table identifies those governmental functions where program expenses greatly exceed revenues.

Business-Type Activities Business-Type activities posted total revenues of $3,016,401, while the cost of all business-type activities totaled $2,829,002, which includes non-cash depreciation expense of $1,388,365. This results in an increase of $187,399, prior to transfers out of $97,768.

The above graph compares program revenues to expenses for utility operations.

17

VILLAGE OF PINGREE GROVE, ILLINOIS Management’s Discussion and Analysis April 30, 2019 FINANCIAL ANALYSIS OF THE GOVERNMENT’S FUNDS As noted earlier, the Village uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. Governmental Funds The focus of the Village’s governmental funds is to provide information on near-term inflows, outflows, and balances of spendable resources. In particular, unassigned fund balance may serve as a useful measure of a government’s net resources available for spending at the end of the fiscal year. The Village’s governmental funds reported combining ending fund balances of $6,285,960, which is $2,678,015, or 29.9 percent, lower than last year’s total of $8,963,975. Of the $6,285,960 total, $4,923,984, or 78.3 percent, of the fund balance constitutes unrestricted fund balance. The General Fund reported a surplus in fund balance for the year of $488,927, an increase of 19.5 percent. This is due primarily to revenues increasing $189,538 over the prior year, particularly in interest, which increased $140,738. The General Fund is the chief operating fund of the Village. At April 30, 2019, unassigned fund balance in the General Fund was $2,950,083, which represents 98.6 percent of the total fund balance. As a measure of the General Fund’s liquidity, it may be useful to compare unassigned fund balance to total fund expenditures. Unassigned fund balance in the General Fund represents approximately 129.6 percent of total General Fund expenditures. In the prior fiscal year, this percentage was 109.2 percent. The Debt Service Fund reported a deficit for the year of $14,487. The Village created the Debt Service Fund in the current fiscal year. The Capital Improvements Fund reported a deficit for the year of $3,343,854. This was due to the Village spending $3,757,960 in capital related projects in the current fiscal year. The Special Service Area #2, Fund reported a deficit in fund balance of $3,006 as a result of increased expenditures in the special service area. The Special Service Area #4 Funs reported a surplus in fund balance of $122,057 as a result of decreased expenditures in the special service area. The Special Service Area #7 Fund reported a deficit in fund balance of $9,087 as a result of increased expenditures in the special service area.

18

VILLAGE OF PINGREE GROVE, ILLINOIS Management’s Discussion and Analysis April 30, 2019 FINANCIAL ANALYSIS OF THE GOVERNMENT’S FUNDS – Continued Proprietary Funds The Village’s proprietary funds provide the same type of information found in the government-wide financial statements, but in more detail. The Village reports the Water and Sewer as a major proprietary fund, which accounts for all of the operations of the municipal water and sewer system. The spread between purchase and sale rates is intended to finance the operations of the utility system, including labor costs, supplies, and infrastructure maintenance. The Village intends to run the fund at a breakeven rate. Periodically, there will be an annual surplus or draw down due to timing of capital projects. The surplus in the Water and Sewer Fund during the current fiscal year was $89,631. Depreciation expense accounts for $1,388,365 of the total fund’s operating expenses of $2,805,798, or 49.5 percent. GENERAL FUND BUDGETARY HIGHLIGHTS The Village made an amendment to the original budget during the year. The General Fund actual revenues for the year totaled $2,914,472 compared to budgeted revenues of $2,497,363. The Village saw increases in sales taxes, sales tax, and income tax due to the continued modest economic upturn. These increases contributed to the surplus of revenues for the year. The General Fund actual expenditures for the year were $114,999 lower than budgeted ($2,276,663 actual compared to $2,391,662 final budgeted). This was primarily due lower than expected engineering costs in the central services division and in the personnel services in the public safety function.

19

VILLAGE OF PINGREE GROVE, ILLINOIS Management’s Discussion and Analysis April 30, 2019 CAPITAL ASSETS AND DEBT ADMINISTRATION Capital Assets The Village’s investment in capital assets for its governmental and business type activities as of April 30, 2019, was $44,352,446 (net of accumulated depreciation). This investment in capital assets includes land, construction in progress, buildings, machinery and equipment, water and sewer system improvements, and infrastructure.

2019 2018 2019 2018 2019 2018

Land $ 372,341 372,341 11,834,312 11,834,312 12,206,653 12,206,653Construction in Progress 3,989,075 430,379 57,822 - 4,046,897 430,379Buildings 2,091,393 2,236,838 7,315,704 7,906,191 9,407,097 10,143,029Machinery and Equipment 122,294 146,753 221,257 248,943 343,551 395,696Water Distribution System - - 6,405,469 6,866,783 6,405,469 6,866,783Sewer System - - 2,961,201 3,167,435 2,961,201 3,167,435Infrastructure 8,981,578 9,464,747 - - 8,981,578 9,464,747

Total 15,556,681 12,651,058 28,795,765 30,023,664 44,352,446 42,674,722

Capital Assets - Net of Depreciation

TotalBusiness-typeGovernmental

Activities Activities

There were $3,719,162 of capital asset additions in the current year, which included the following:

Construction in Progress $ 3,616,518 Equipment 102,644

3,719,162

Additional information on the Village’s capital assets can be found in note 3 of this report.

20

VILLAGE OF PINGREE GROVE, ILLINOIS Management’s Discussion and Analysis April 30, 2019 CAPITAL ASSETS AND DEBT ADMINISTRATION – Continued Debt Administration At year-end, the Village had total outstanding debt of $5,450,652. The following is a comparative statement of outstanding debt:

2019 2018 2019 2018 2019 2018

Debt Certificates $ - 1,474,382 - - - 1,474,382General Obligation Bonds 4,342,679 3,030,000 - - 4,342,679 3,030,000Installment Contracts 71,025 92,829 71,025 92,829 142,050 185,658IEPA Loan Payable - - 965,923 1,049,354 965,923 1,049,354

Total 4,413,704 4,597,211 1,036,948 1,142,183 5,450,652 5,739,394

Long-Term Debt Outstanding

TotalBusiness-typeGovernmental

Activities Activities

The Village’s issued general obligation bonds of $1,439,663 in this fiscal year to refund prior year debt issued for capital purchases. State statutes limit the amount of general obligation debt a non-home rule governmental entity may issue to 8.625 percent of its total assessed valuation. The current debt limit for the Village is $18,580,675. Additional information on the Village’s long-term debt can be found in Note 3 of this report. ECONOMIC FACTORS AND NEXT YEAR’S BUDGET AND RATES The Village’s elected and appointed officials considered many factors when setting the fiscal year 2020 budget, including tax rates, and fees that will be charged for its various activities. One of those factors is the economy. The Village is faced with a similar economic environment as many of the other local municipalities are faced with, including inflation, unemployment rates, and a slow residential housing market. REQUESTS FOR INFORMATION This financial report is designed to provide a general overview of the Village of Pingree Grove’s finances for all those with an interest in the government’s finances. Questions concerning any of the information provided in this report or requests for additional information should be directed to Office of the Finance Director, 14N042 Reinking Rd., Pingree Grove, Illinois 60140.

21

• Government-Wide Financial Statements

• Fund Financial Statements

Governmental Funds

Proprietary Fund

Fiduciary Funds

BASIC FINANCIAL STATEMENTS

The basic financial Statements include integrated sets of financial statements as required by the GASB. The setsof statements include:

In addition, the notes to the financial statements are included to provide information that is essential to a user’sunderstanding of the basic financial statements.

VILLAGE OF PINGREE GROVE, ILLINOIS

Statement of Net PositionApril 30, 2019

See Following Page

VILLAGE OF PINGREE GROVE, ILLINOIS

Statement of Net PositionApril 30, 2019

Business-TypeActivities Totals

Current AssetsCash and Investments $ 6,458,810 5,902,077 12,360,887Receivables - Net of Allowances 1,201,006 510,047 1,711,053Due from Other Governments 10,031 - 10,031Prepaids 40,481 - 40,481

Total Current Assets 7,710,328 6,412,124 14,122,452

Noncurrent AssetsCapital Assets

Nondepreciable 4,361,416 11,892,134 16,253,550Depreciable 18,561,923 32,781,086 51,343,009

22,923,339 44,673,220 67,596,559Accumulated Depreciation (7,366,658) (15,877,455) (23,244,113)

Total Noncurrent Assets 15,556,681 28,795,765 44,352,446

Total Assets 23,267,009 35,207,889 58,474,898

Deferred Items - IMRF 243,461 88,347 331,808

Total Assets and Deferred Outflows of Resources 23,510,470 35,296,236 58,806,706

ActivitiesGovernmental

ASSETS

DEFERRED OUTFLOWS OF RESOURCES

The notes to the financial statements are an integral part of this statement.22

Business-TypeActivities Totals

Current LiabilitiesAccounts Payable $ 467,369 112,347 579,716Accrued Salaries Payable 25,854 8,902 34,756Deposits Payable 34,286 - 34,286Deferred Grant 10,000 - 10,000Accrued Interest Payable 46,028 7,258 53,286Current Portion of Long-Term Debt 205,352 109,926 315,278

Total Current Liabilities 788,889 238,433 1,027,322

Noncurrent LiabilitiesCompensated Absences Payable 63,049 8,167 71,216Net Pension Liability - IMRF 489,654 177,686 667,340General Obligation Bonds 4,175,804 - 4,175,804Installment Contract Payable 48,310 48,310 96,620IEPA Loan Payable - 880,754 880,754

Total Noncurrent Liabilities 4,776,817 1,114,917 5,891,734Total Liabilities 5,565,706 1,353,350 6,919,056

Deferred Items - IMRF 32,030 11,623 43,653Property Taxes 886,859 - 886,859

Total Deferred Inflows of Resources 918,889 11,623 930,512Total Liabilities and Deferred Inflows of Resources 6,484,595 1,364,973 7,849,568

Net Investment in Capital Assets 11,142,977 27,758,817 38,901,794Restricted

Property Tax LeviesSpecial Service Areas 432,506 - 432,506Tax Increment Financing 33,768 - 33,768

Highways and Streets 855,221 - 855,221Unrestricted 4,561,403 6,172,446 10,733,849

Total Net Position 17,025,875 33,931,263 50,957,138

NET POSITION

LIABILITIES

GovernmentalActivities

DEFERRED INFLOWS OF RESOURCES

The notes to the financial statements are an integral part of this statement.23

VILLAGE OF PINGREE GROVE, ILLINOIS

Statement of ActivitiesFor the Fiscal Year Ended April 30, 2019

Charges Capitalfor Grants/

Services Contributions

Governmental ActivitiesGeneral Government $ 1,636,536 791,650 - Public Safety 1,138,318 92,826 - Highways and Streets 774,582 - 115,043Interest on Long-Term Debt 191,773 - -

Total Governmental Activities 3,741,209 884,476 115,043

Business-Type ActivitiesWater and Sewer 2,829,002 2,993,840 -

Total Primary Government 6,570,211 3,878,316 115,043

General Revenues Taxes Property Taxes

Municipal Utility Taxes Use Taxes Intergovernmental - Unrestricted Sales Taxes Income Taxes Replacement Taxes Interest Income MiscellaneousTransfers - Internal Activities

Change in Net Position

Net Position - Beginning

Net Position - Ending

Program Revenues

Expenses

The notes to the financial statements are an integral part of this statement.24

Governmental Business-TypeActivities Activities Totals

(844,886) - (844,886)(1,045,492) - (1,045,492)

(659,539) - (659,539)(191,773) - (191,773)

(2,741,690) - (2,741,690)

- 164,838 164,838

(2,741,690) 164,838 (2,576,852)

894,047 - 894,047338,301 - 338,301140,206 - 140,206

296,947 - 296,947468,860 - 468,860

187 - 187265,712 22,561 288,273575,760 - 575,76097,768 (97,768) -

3,077,788 (75,207) 3,002,581

336,098 89,631 425,729

16,689,777 33,841,632 50,531,409

17,025,875 33,931,263 50,957,138

Net (Expenses)/RevenuesPrimary Government

The notes to the financial statements are an integral part of this statement.25

VILLAGE OF PINGREE GROVE, ILLINOIS

Balance Sheet - Governmental Funds

April 30, 2019

DebtService

Cash and Investments $ 2,879,480 - Receivables - Net of Allowances

Taxes 726,025 - Accounts 80,354 -

Due from Other Funds 14,487 - Due from Other Governments - - Prepaids 40,481 -

Total Assets 3,740,827 -

Accounts Payable 197,891 - Accrued Salaries 25,854 - Due to Other Funds - 14,487Deferred Grant - - Deposits Payable 34,286 -

Total Liabilities 258,031 14,487

Property Taxes 492,232 - Total Liabilities and Deferred Inflows of Resources 750,263 14,487

Nonspendable 40,481 - Restricted - - Committed - - Unassigned 2,950,083 (14,487)

Total Fund Balances 2,990,564 (14,487)

Total Liabilities, Deferred Inflows of Resources and Fund Balances 3,740,827 -

FUND BALANCES

General

ASSETS

LIABILITIES

DEFERRED INFLOWS OF RESOURCES

The notes to the financial statements are an integral part of this statement.26

Special Special SpecialCapital Service Service Service

Improvements Area No. 2 Area No. 4 Area No. 7 Nonmajor Totals

2,250,636 8,065 377,782 8,970 933,877 6,458,810

- - 349,056 - 45,571 1,120,652- - - - - 80,354- - - - - 14,487- - - - 10,031 10,031- - - - - 40,481

2,250,636 8,065 726,838 8,970 989,479 7,724,815

252,248 - 5,398 - 11,832 467,369- - - - - 25,854- - - - - 14,487

10,000 - - - - 10,000- - - - - 34,286

262,248 - 5,398 - 11,832 551,996

- - 349,056 - 45,571 886,859262,248 - 354,454 - 57,403 1,438,855

- - - - - 40,481- 8,065 372,384 8,970 932,076 1,321,495

1,988,388 - - - - 1,988,388- - - - - 2,935,596

1,988,388 8,065 372,384 8,970 932,076 6,285,960

2,250,636 8,065 726,838 8,970 989,479 7,724,815

Capital Projects

The notes to the financial statements are an integral part of this statement.27

VILLAGE OF PINGREE GROVE, ILLINOIS

Reconciliation of Total Governmental Fund Balance to

Net Position of Governmental Activities

April 30, 2019

Total Governmental Fund Balances $ 6,285,960

Amounts reported for governmental activities in the Statement of Net Positionare different because:

Capital assets used in governmental activities are not financialresources and therefore, are not reported in the funds. 15,556,681

Deferred outflows (inflows) of resources related to the pensions not reportedin the funds.

Deferred Items - IMRF 211,431

Long-term liabilities are not due and payable in the currentperiod and therefore are not reported in the funds.

Compensated Absences Payable (78,811)Net Pension Liability - IMRF (489,654)General Obligation Bonds Payable (4,342,679)Installment Contracts Payable (71,025)Accrued Interest Payable (46,028)

Net Position of Governmental Activities 17,025,875

The notes to the financial statements are an integral part of this statement.28

VILLAGE OF PINGREE GROVE, ILLINOIS

Statement of Revenues, Expenditures and Changes in Fund Balances - Governmental Funds

For the Fiscal Year Ended April 30, 2019

See Following Page

VILLAGE OF PINGREE GROVE, ILLINOIS

Statement of Revenues, Expenditures and Changes in Fund Balances - Governmental Funds

For the Fiscal Year Ended April 30, 2019

Debt Service

RevenuesTaxes $ 925,438 - Intergovernmental 785,186 -

678,529 - Fines and Forfeits 73,846 - Charges for Services 113,121 - Interest 202,072 - Miscellaneous 136,280 -

Total Revenues 2,914,472 -

ExpendituresCurrent

General Government 1,020,359 - Public Safety 1,072,862 - Highways and Streets 183,442 -

Capital Outlay - - Debt Service

Principal Retirement - 190,194Interest and Fiscal Charges - 156,609

Total Expenditures 2,276,663 346,803

Excess (Deficiency) of RevenuesOver (Under) Expenditures 637,809 (346,803)

Other Financing Sources (Uses)Disposal of Capital Assets - Debt Issuance - 1,439,663Payment to Escrow Agent - (1,417,463)Transfers In - 310,116Transfers Out (148,882) -

(148,882) 332,316

Net Change in Fund Balances 488,927 (14,487)

Fund Balances - Beginning 2,501,637 -

Fund Balances - Ending 2,990,564 (14,487)

General

Licenses and Permits

The notes to the financial statements are an integral part of this statement.29

Special Special SpecialCapital Service Service Service

Improvements Area No. 2 Area No. 4 Area No. 7 Nonmajor Totals

- - 357,240 - 89,664 1,372,342- - - - 115,043 900,229- - - - - 678,529- - - - - 73,846- - - - - 113,121

42,665 199 - 181 20,595 265,712400,000 20,230 - 19,250 - 575,760442,665 20,429 357,240 19,431 225,302 3,979,539

- 23,435 235,183 28,518 55,593 1,363,088- - - - - 1,072,862- - - - 26,202 209,644

3,757,960 - - - 62,072 3,820,032

21,804 - - - - 211,9983,289 - - - - 159,898

3,783,053 23,435 235,183 28,518 143,867 6,837,522

(3,340,388) (3,006) 122,057 (9,087) 81,435 (2,857,983)

60,000 - - - - 60,000- - - - - 1,439,663- - - - - (1,417,463)

100,000 - - - - 410,116(163,466) - - - - (312,348)

(3,466) - - - - 179,968

(3,343,854) (3,006) 122,057 (9,087) 81,435 (2,678,015)

5,332,242 11,071 250,327 18,057 850,641 8,963,975

1,988,388 8,065 372,384 8,970 932,076 6,285,960

Capital Projects

The notes to the financial statements are an integral part of this statement.30

VILLAGE OF PINGREE GROVE, ILLINOIS

Reconciliation of the Statement of Revenues, Expenditures and Changes in Fund Balances of

Governmental Funds to the Statement of Activities

For the Fiscal Year Ended April 30, 2019

Net Change in Fund Balances - Total Governmental Funds $ (2,678,015)

Amounts reported for governmental activities in the Statement of Activitiesare different because:

Governmental funds report capital outlays as expenditures. However, in theStatement of Activities the cost of those assets is allocated over their estimateduseful lives and reported as depreciation expense.

Capital Outlays 3,558,696Depreciation Expense (653,073)

The net effect of deferred outflows (inflows) of resources related to the pensionsnot reported in the funds.

Change in Deferred Items - IMRF 152,778

The issuance of long-term debt provides current financial resources togovernmental funds, while the repayment of the principal on long-termdebt consumes the current financial resources of the governmental funds.

(Additions) to Compensated Absences Payable (15,447)(Additions) to Net Pension Liability - IMRF (186,764)Issuance of Debt (1,439,663)Retirement of Debt 1,623,170

Changes to accrued interest on long-term debt in the Statement of Activitiesdoes not require the use of current financial resources and, therefore, are notreported as expenditures in the governmental funds. (25,584)

Changes in Net Position of Governmental Activities 336,098

The notes to the financial statements are an integral part of this statement.31

VILLAGE OF PINGREE GROVE, ILLINOIS

Statement of Net Position - Proprietary Fund - Business-Type Activities - Enterprise Fund

April 30, 2019

See Following Page

VILLAGE OF PINGREE GROVE, ILLINOIS

Statement of Net Position - Proprietary Fund - Business-Type Activities - Enterprise FundApril 30, 2019

Current AssetsCash and Investments $ 5,902,077Receivables - Net of Allowances

Accounts 510,047Total Current Assets 6,412,124

Noncurrent AssetsCapital Assets

Nondepreciable 11,892,134Depreciable 32,781,086Accumulated Depreciation (15,877,455)

Total Noncurrent Assets 28,795,765

Total Assets 35,207,889

Deferred Items - IMRF 88,347

Total Assets and Deferred Outflows of Resources 35,296,236

Sewer

Waterand

ASSETS

DEFERRED OUTFLOWS OF RESOURCES

The notes to the financial statements are an integral part of this statement.32

Current LiabilitiesAccounts Payable $ 112,347Accrued Salaries Payable 8,902Accrued Interest Payable 7,258Compensated Absences Payable 2,042Installment Contract Payable 22,715IEPA Loan Payable 85,169

Total Current Liabilities 238,433

Noncurrent LiabilitiesCompensated Absences Payable 8,167Net Pension Liability - IMRF 177,686Installment Contract Payable 48,310IEPA Loan Payable 880,754

Total Noncurrent Liabilities 1,114,917

Total Liabilities 1,353,350

Deferred Inflows - IMRF 11,623

Total Liabilities and Deferred Inflows of Resources 1,364,973

Net Investment in Capital Assets 27,758,817Unrestricted 6,172,446

Total Net Position 33,931,263

NET POSITION

LIABILITIES

DEFERRED INFLOWS OF RESOURCES

Waterand

Sewer

The notes to the financial statements are an integral part of this statement.33

VILLAGE OF PINGREE GROVE, ILLINOIS

Statement of Revenues, Expenses and Changes in

Net Position - Business-Type Activities - Enterprise Fund

For the Fiscal Year Ended April 30, 2019

Operating RevenuesCharges for Services $ 2,986,665Miscellaneous 7,175

Total Operating Revenues 2,993,840

Operating ExpensesOperations

Water 600,999Sewer 682,612Capital Maintenance 133,822

Depreciation 1,388,365Total Operating Expenses 2,805,798

Operating Income 188,042

Nonoperating Revenues (Expenses)Interest Income 22,561Interest and Fiscal Charges (23,204)

(643)

Income Before Transfers 187,399

Transfers Out (97,768)

Change in Net Position 89,631

Net Position - Beginning 33,841,632

Net Position - Ending 33,931,263

Waterand

Sewer

The notes to the financial statements are an integral part of this statement.34

VILLAGE OF PINGREE GROVE, ILLINOIS

Statement of Cash Flows - Proprietary Fund - Business-Type Activities - Enterprise Fund

For the Fiscal Year Ended April 30, 2019

Cash Flows from Operating ActivitiesReceipts from Customers and Users $ 2,912,889Payments to Suppliers (1,041,864)Payments to Employees (331,595)

1,539,430

Cash Flows from Noncapital Financing ActivitiesTransfers Out (97,768)

Cash Flows from Capital and Related Financing ActivitiesPurchase of Capital Assets (160,466)Retirement of Debt (105,235)Interest Expense (23,204)

(288,905)

Cash Flows from Investing ActivitiesInterest Income 22,561

Net Change in Cash and Cash Equivalents 1,175,318

Cash and Cash Equivalents - Beginning 4,726,759

Cash and Cash Equivalents - Ending 5,902,077

Reconciliation of Operating Income to Net Cash Provided (Used) by Operating ActivitiesOperating Income (Loss) 188,042Adjustments to Reconcile Operating Income

Income to Net Cash Provided by(Used in) Operating Activities:

Depreciation 1,388,365(Increase) Decrease in Current Assets (80,951)Increase (Decrease) in Current Liabilities 43,974

Net Cash Provided by Operating Activities 1,539,430

Waterand

Sewer

The notes to the financial statements are an integral part of this statement.35

VILLAGE OF PINGREE GROVE, ILLINOIS

Statement of Fiduciary Net PositionApril 30, 2019

Cash and Cash Equivalents $ 2,907,809

LIABILITIES

Due to Bondholders 2,907,809

ASSETS

Agency

The notes to the financial statements are an integral part of this statement.36

VILLAGE OF PINGREE GROVE, ILLINOIS

Notes to the Financial Statements April 30, 2019

NOTE 1 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The Village of Pingree Grove (the Village), Illinois, is a municipal corporation governed by an elected president and six-member Board of Trustees. The Village’s major operations include police safety, highway and street, maintenance and reconstruction, economic development, public improvements, water and sewer services and general administrative services.

The government-wide financial statements are prepared in accordance with generally accepted accounting principles (GAAP). The Governmental Accounting Standards Board (GASB) is responsible for establishing GAAP for state and local governments through its pronouncements (Statements and Interpretations). The more significant of the Village’s accounting policies established in GAAP and used by the Village are described below.

REPORTING ENTITY

In determining the financial reporting entity, the Village complies with the provisions of GASB Statement No. 61, “The Financial Reporting Omnibus – an Amendment of GASB Statements No. 14 and No. 34,” and includes all component units that have a significant operational or financial relationship with the Village. Based upon the criteria set forth in the GASB Statement No. 61, there are no component units included in the reporting entity.

BASIS OF PRESENTATION

Government-Wide Statements

The Village’s basic financial statements include both government-wide (reporting the Village as a whole) and fund financial statements (reporting the Village’s major funds). Both the government-wide and fund financial statements categorize primary activities as either governmental or business-type. The Village’s police safety, economic development, highway and street maintenance and reconstruction, public improvements, and general administrative services are classified as governmental activities. The Village’s water and sewer services are classified as business-type activities.

In the government-wide Statement of Net Position, both the governmental and business-type activities columns are: (a) presented on a consolidated basis by column, and (b) reported on a full accrual, economic resource basis, which recognizes all long-term assets/deferred outflows and receivables as well as long-term debt/deferred inflows and obligations. The Village’s net position is reported in three parts: net investment in capital assets; restricted; and unrestricted. The Village first utilizes restricted resources to finance qualifying activities.

37

VILLAGE OF PINGREE GROVE, ILLINOIS

Notes to the Financial Statements April 30, 2019

NOTE 1 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES – Continued

BASIS OF PRESENTATION – Continued

Government-Wide Statements – Continued

The government-wide Statement of Activities reports both the gross and net cost of each of the Village’s functions and business-type activities (general government, highways and streets, etc.). The functions are supported by general government revenues (property, sales and use taxes, certain intergovernmental revenues, fines, permits and charges, etc.).

The Statement of Activities reduces gross expenses (including depreciation) by related program revenues, which include 1) changes to customers or applicants who purchase, use or directly benefit from goods, services or privileges provided by a given function or segment and 2) grants and contributions that are restricted to meeting the operational or capital requirements of a particular function or segment.

The net costs (by function or business-type activity) are normally covered by general revenue (property tax, sales tax, intergovernmental revenues, interest income, etc.).

The Village allocates indirect costs to the proprietary funds for personnel who perform administrative services for those funds, along with other indirect costs deemed necessary for their operations, but are paid through the General Fund.

This government-wide focus concentrates on the sustainability of the Village as an entity and the change in the Village’s net position resulting from the current year’s activities.

Fund Financial Statements

The financial transactions of the Village are reported in individual funds in the fund financial statements. Each fund is accounted for by providing a separate set of self-balancing accounts that comprises its assets/deferred outflows, liabilities/deferred inflows, fund equity, revenues and expenditures/expenses. Funds are organized into three major categories: governmental, proprietary, and fiduciary. The emphasis in fund financial statements is on the major funds in either the governmental or business-type activities categories. Nonmajor funds by category are summarized into a single column.

GASB Statement No. 34 sets forth minimum criteria (percentage of the assets/deferred outflows, liabilities/deferred inflows, revenues or expenditures/expenses of either fund category or the governmental and enterprise combined) for the determination of major funds. The Village electively added funds, as major funds, which either had debt outstanding or specific community focus. The nonmajor funds are combined in a single column in the fund financial statements.

A fund is considered major if it is the primary operating fund of the Village or meets the following criteria:

38

VILLAGE OF PINGREE GROVE, ILLINOIS Notes to the Financial Statements April 30, 2019 NOTE 1 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES – Continued BASIS OF PRESENTATION – Continued Fund Financial Statements – Continued

Total assets/deferred outflows, liabilities/deferred inflows, revenues, or expenditures/expenses of that individual governmental or enterprise fund are at least 10 percent of the corresponding total for all funds of that category or type; and Total assets/deferred outflows, liabilities/deferred inflows, revenues, or expenditures/expenses of the individual governmental fund or enterprise fund are at least 5 percent of the corresponding total for all governmental and enterprise funds combined.

The various funds are reported by generic classification within the financial statements. The following fund types are used by the Village: Governmental Funds The focus of the governmental funds’ measurement (in the fund statements) is upon determination of financial position and changes in financial position (sources, uses, and balances of financial resources) rather than upon net income. The following is a description of the governmental funds of the Village: General Fund is the general operating fund of the Village. It is used to account for all financial resources except those required to be accounted for in another fund. The General Fund is a major fund. Debt service funds are used to account for the accumulation of funds for the periodic payment of principal and interest on general long-term debt. The Debt Service Fund is treated as a major fund and records all of the Village’s general obligation and tax increment financing debt activity. Special revenue funds are used to account for the proceeds of specific revenue sources that are legally restricted to expenditures for specified purposes. The Village maintains one nonmajor special revenue fund. Capital projects funds are used to account for financial resources to be used for the acquisition or construction of major capital facilities. The Village maintains six capital projects funds. The Special Service Area No. 2 Fund, the Special Service Area No. 4 Fund, and the Special Service Area No. 7 Fund are major funds and are used to account for the proceeds of the Special Service Area bonds and the related capital outlays. The Capital Improvements Fund is a major fund and used to account for the proceeds of bonds and expenditures restricted for capital improvements. Proprietary Funds The focus of proprietary fund measurement is upon determination of operating income, changes in net position, financial position, and cash flows. The generally accepted accounting principles applicable are those similar to businesses in the private sector. The following is a description of the proprietary fund of the Village:

39

VILLAGE OF PINGREE GROVE, ILLINOIS

Notes to the Financial Statements April 30, 2019

NOTE 1 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES – Continued

BASIS OF PRESENTATION – Continued

Fund Financial Statements – Continued

Proprietary Funds – Continued

Enterprise funds are required to account for operations for which a fee is charged to external users for goods or services and the activity (a) is financed with debt that is solely secured by a pledge of the net revenues, (b) has third party requirements that the cost of providing services, including capital costs, be recovered with fees and charges or (c) establishes fees and charges based on a pricing policy designed to recover similar costs. The Water and Sewer Fund, a major fund, accounts for the provision of water and sewer services to the residents of the Village. All activities necessary to provide such services are accounted for in this fund, including but not limited to, administration, operations, maintenance, repair, financing and billing and collection.

Fiduciary Funds

Fiduciary funds are used to report assets held in a trustee or agency capacity for others and therefore are not available to support Village programs. The reporting focus is on net position and changes in net position and is reported using accounting principles similar to proprietary funds.

Agency funds are used to account for assets held by the Village in a purely custodial capacity. The Village maintains two Special Service Area Funds which are used to accumulate monies for the payment of special assessment bonds and vouchers of various amounts, which are due upon call for payment, with financing provided by an annual assessment upon the benefiting property owners. The Special Service Area Funds accumulate monies for the payment of bank loans, the proceeds of which were used to finance improvements. Financing is provided by an annual property tax levy upon the benefiting property owners.

The agency funds are presented in the fiduciary fund financial statements. Since by definition these assets are being held for the benefit of a third party (other local governments, private parties, pension participants, etc.) and cannot be used to address activities or obligations of the Village, these funds are not incorporated into the government-wide statements.

MEASUREMENT FOCUS AND BASIS OF ACCOUNTING

Measurement focus is a term used to describe “which” transactions are recorded within the various financial statements. Basis of accounting refers to “when” transactions are recorded regardless of the measurement focus applied.

On the government-wide Statement of Net Position and the Statement of Activities, both governmental and business-type activities are presented using the economic resources measurement focus as defined below.

40

VILLAGE OF PINGREE GROVE, ILLINOIS

Notes to the Financial Statements April 30, 2019

NOTE 1 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES – Continued

MEASUREMENT FOCUS AND BASIS OF ACCOUNTING – Continued

Measurement Focus

In the fund financial statements, the “current financial resources” measurement focus or the “economic resources” measurement focus is used as appropriate.

All governmental funds utilize a “current financial resources” measurement focus. Only current financial assets/deferred outflows and liabilities/deferred inflows are generally included on their balance sheets. Their operating statements present sources and uses of available spendable financial resources during a given period. These funds use fund balance as their measure of available spendable financial resources at the end of the period.

All proprietary funds utilize an “economic resources” measurement focus. The accounting objectives of this measurement focus are the determination of operating income, changes in net position (or cost recovery), financial position, and cash flows. All assets/deferred outflows and liabilities/deferred inflows (whether current or noncurrent) associated with their activities are reported. Proprietary fund equity is classified as net position.

Agency funds are not involved in the measurement of results of operations; therefore, measurement focus is not applicable to them.

Basis of Accounting

In the government-wide Statement of Net Position and Statement of Activities, both governmental and business-type activities are presented using the accrual basis of accounting. Under the accrual basis of accounting, revenues are recognized when earned and expenses are recorded when the liability/deferred inflow is incurred or economic asset used. Revenues, expenses, gains, losses, assets/deferred outflows, and liabilities/deferred inflows resulting from exchange and exchange-like transactions are recognized when the exchange takes place.

In the fund financial statements, governmental funds are presented on the modified accrual basis of accounting. Under this modified accrual basis of accounting, revenues are recognized when “measurable and available.” Measurable means knowing or being able to reasonably estimate the amount. Available means collectible within the current period or within sixty days after year-end. The Village recognizes property taxes when they become both measurable and available in accordance with GASB Codification Section P70. A sixty-day availability period is used for revenue recognition for all other governmental fund revenues. Expenditures (including capital outlay) are recorded when the related fund liability is incurred, except for general obligation bond principal and interest which are recognized when due.

41

VILLAGE OF PINGREE GROVE, ILLINOIS

Notes to the Financial Statements April 30, 2019

NOTE 1 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES – Continued

MEASUREMENT FOCUS AND BASIS OF ACCOUNTING – Continued

Basis of Accounting – Continued

In applying the susceptible to accrual concept under the modified accrual basis, those revenues susceptible to accrual are property taxes, sales and use taxes, franchise taxes, licenses, interest revenue, and charges for services. All other revenues are not susceptible to accrual because generally they are not measurable until received in cash.

All proprietary and agency funds utilize the accrual basis of accounting. Under the accrual basis of accounting, revenues are recognized when earned and expenses are recorded when the liability is incurred or economic asset used.

Proprietary funds distinguish operating revenues and expenses from nonoperating items. Operating revenues and expenses generally result from providing services and producing and delivering goods in connection with a proprietary fund’s principal ongoing operations. The principal operating revenues of the Village’s enterprise funds, are charges to customers for sales and services. The Village also recognizes as operating revenue the portion of tap fees intended to recover the cost of connecting new customers to the system. Operating expenses for enterprise funds include the cost of sales and services, administrative expenses, and depreciation on capital assets. All revenues and expenses not meeting this definition are reported as nonoperating revenues and expenses.

ASSETS/DEFERRED OUTFLOWS, LIABILITIES/DEFERRED INFLOWS, AND NET POSITION OR EQUITY

Cash and Investments

Cash and cash equivalents on the Statement of Net Position are considered to be cash on hand, demand deposits, cash with fiscal agent. For the purpose of the proprietary funds “Statement of Cash Flows,” cash and cash equivalents are considered to be cash on hand, demand deposits, cash with fiscal agent, and all highly liquid investments with an original maturity of three months or less.

Investments are generally reported at fair value. Short-term investments are reported at cost, which approximates fair value. For investments, the Village categorizes its fair value measurements within the fair value hierarchy established by generally accepted accounting principles. The hierarchy is based on the valuation inputs used to measure the fair value of the asset. Level 1 inputs are quoted prices in active markets for identical assets; Level 2 inputs are significant other observable inputs; Level 3 inputs are significant unobservable inputs. All of the Village’s investments are in 2a7-like investment pools that are measured at the net asset value per share determined by the pool.

42

VILLAGE OF PINGREE GROVE, ILLINOIS

Notes to the Financial Statements April 30, 2019

NOTE 1 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES – Continued

ASSETS/DEFERRED OUTFLOWS, LIABILITIES/DEFERRED INFLOWS, AND NET POSITION OR EQUITY – Continued

Receivables

In the government-wide financial statements, receivables consist of all revenues earned at year-end and not yet received. Allowances for uncollectible accounts receivable are based upon historical trends and the periodic aging of accounts receivable. Major receivables balances for governmental activities include property taxes, sales and use taxes, franchise taxes, and grants. Business-type activities report water and sewer charges as their major receivables.

Interfund Receivables, Payables and Activity

Interfund activity is reported as loans, services provided, reimbursements or transfers. Loans are reported as interfund receivables and payables as appropriate and are subject to elimination upon consolidation. Services provided, deemed to be at market or near market rates, are treated as revenues and expenditures/expenses. Reimbursements occur when one fund incurs a cost, charges the appropriate benefiting fund and reduces its related cost as a reimbursement. All other interfund transactions are treated as transfers. Transfers between governmental or proprietary funds are netted as part of the reconciliation to the government-wide financial statements.

Prepaids

Prepaids are valued at cost, which approximates market, using the first-in/first-out (FIFO) method. The costs of governmental fund-type prepaids are recorded as expenditures when consumed rather than when purchased. Certain payments to vendors reflect costs applicable to future accounting periods and are recorded as prepaids in both the government-wide and fund financial statements.

Capital Assets

Capital assets purchased or acquired with an original cost of $50,000 or more are reported at historical cost or estimated historical cost. Contributed assets are reported at acquisition value as of the date received. Additions, improvements and other capital outlays that significantly extend the useful life of an asset are capitalized. Other costs incurred for repairs and maintenance are expensed as incurred.

The accounting and financial reporting treatment applied to a fund is determined by its measurement focus. General capital assets are long-lived assets of the Village as a whole. Infrastructure such as streets, traffic signals and signs are capitalized. The valuation basis for general capital assets are historical cost, or where historical cost is not available, estimated historical cost based on replacement costs.

43