UNIT 21 CAPITAL INVESTMENT DECISIONS - eGyanKosh

48

UNIT 21 CAPITAL INVESTMENT DECISIONS Structure 2 1.1 Introduction Objectives 2 1.2 Characteristics of Capital Investment 2 1.3 Kinds of Capital Budgeting Decisions 21.3.1 Accept-Reject Decisions 21.3.2 Mutually Exclusive Project Decisions 21.3.3 Capital Rationing Decisions 21.4 Computations in Regard to Future Benefits : CFAT 2 1.5 lllustrative Examples 21.5.1 Single Proposal 21.5.2 Replacement Proposal 21.5.3 Mutually Exclusive Project Proposals 2 1.5.4 Market-based Approximation for Salvage Value 2 1.6 Evaluation TechniquesIApprisal Methods for Capital Budgeting 21.6.1 Traditional Methods 21.6.2 Discounted Cash Flow Techniques 2 1.7 Capital Rationing 21.7.1 The Two-Stage Rocess 21.7.2 Strategic Investments 21.7.3 Period Planning 21.7.4 Project Divisibility 21.8 Risk Analysis 2 1.9 Methods of Incorporating Risk Factors in Capital Budgeting Decisions 21.9.1 Risk-Adjusted Discount Rate Approach 2 1.9.2 Certainty-EquivalentApproach 21.9.3 SensitivityAnalysis 21.9.4 Analysis Based on Probability Distribution of Cash Flows 21.9.5 Decision-Tree Approach 21.10 Summary 2 1.11 Answers to SAQs 21.1 INTRODUCTION "Financial management" is devoted not only to procurement of funds but also on their efficient use with the objective of maximising the owners' wealth. Funds must be allocated both to assets and activities (meaning projects and production to be undertaken). When allocations to assets are to be made, this is referred to as investment decision. In as much as projects, once completed, also create "assets", they too are covered. Investment decisions regarding short-term, or current, assets have been discussed under Unit 20. Long-term, or fixed, assets to be invested upon are covered under Capital Investment Decisions, also designated as capital budgeting (or capital expenditure) decisions and by other designations. Objectives After studying this unit, you should be able to understand risk and return as associated with capital investment decisions, evaluate investment options under both of "accept-reject" criterion and "mutually exclusive choices", ladder out a demand schedule and decide on capital rationing, and analyse project investment opportunitiesin consideration of their risk factors.

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of UNIT 21 CAPITAL INVESTMENT DECISIONS - eGyanKosh

UNIT 21 CAPITAL INVESTMENT DECISIONS

Structure 2 1.1 Introduction

Objectives

2 1.2 Characteristics of Capital Investment

2 1.3 Kinds of Capital Budgeting Decisions 21.3.1 Accept-Reject Decisions 21.3.2 Mutually Exclusive Project Decisions 21.3.3 Capital Rationing Decisions

21.4 Computations in Regard to Future Benefits : CFAT

2 1.5 lllustrative Examples 21.5.1 Single Proposal 21.5.2 Replacement Proposal 21.5.3 Mutually Exclusive Project Proposals 2 1.5.4 Market-based Approximation for Salvage Value

2 1.6 Evaluation TechniquesIApprisal Methods for Capital Budgeting 21.6.1 Traditional Methods 21.6.2 Discounted Cash Flow Techniques

2 1.7 Capital Rationing 21.7.1 The Two-Stage Rocess 21.7.2 Strategic Investments 21.7.3 Period Planning 21.7.4 Project Divisibility

21.8 Risk Analysis

2 1.9 Methods of Incorporating Risk Factors in Capital Budgeting Decisions 21.9.1 Risk-Adjusted Discount Rate Approach 2 1.9.2 Certainty-Equivalent Approach 21.9.3 Sensitivity Analysis 21.9.4 Analysis Based on Probability Distribution of Cash Flows 21.9.5 Decision-Tree Approach

21.10 Summary

2 1.1 1 Answers to SAQs

21.1 INTRODUCTION

"Financial management" is devoted not only to procurement of funds but also on their efficient use with the objective of maximising the owners' wealth. Funds must be allocated both to assets and activities (meaning projects and production to be undertaken). When allocations to assets are to be made, this is referred to as investment decision. In as much as projects, once completed, also create "assets", they too are covered. Investment decisions regarding short-term, or current, assets have been discussed under Unit 20. Long-term, or fixed, assets to be invested upon are covered under Capital Investment Decisions, also designated as capital budgeting (or capital expenditure) decisions and by other designations.

Objectives After studying this unit, you should be able to

understand risk and return as associated with capital investment decisions,

evaluate investment options under both of "accept-reject" criterion and "mutually exclusive choices",

ladder out a demand schedule and decide on capital rationing, and

analyse project investment opportunities in consideration of their risk factors.

Construction Finance Management 21.2 CHARACTERISTICS OF CAPITAL INVESTMENT

A capital investment involves a current cash outlay in anticipation of realising benefits in the future, generally (well) beyond one year. These benefits may be either in the form of increased revenues or reductions in costs -the expenditures are called accordingly as income-expansion, or cost-reduction, expenditures. The cash outlay (as capital expenditure) may go towards addition, disposition, modi'cation, creation and replacement offixed assets. The basic features of capital investment decisions are thus :

(a) . a series of large anticipated benefits;

(b) a relatively high degree of risk; and

(c) a relatively long period over which the returns are likely to be realised.

It must be mentioned that the following descriptions are used synonymously : capital investment decision, capital expenditure decision, capital expenditure management, long-term investment decision, management of fixed assets, capital budgeting decision.

The simplest assumption underlying capital investment decisions is that the required rate of return is given and is the same for all investment projects. This rate of return is designated as the minimum acceptable rate of return (MARR). This assumption presupposes that the selection of any investment project does not alter the L'business-risk companion" of the firm as visualised by the suppliers of capital. Thus, risk, and rate of return are important considerations in capital investment decisions; generally, unless otherwise indicated, risk is held to be constant. Of course, the rate of return may vary with the risk.

Strategic decisions in regard to capital investment may lead to significant changes in the firm's expected profits and in the risks to which these profits will be subjected to. These changes may influence stockholders and creditors to revise their evaluation of the firm.

An investment decision at the right opportunity can boost the profits for quite a few years to come; equally, an ill-advised investment [nay even lead to bankruptcy. Besides this, other impacts on the firm due to any long-term investment may include the following :

(a) Any fixed investment is attended by certain fixed costs in terms of labour, rents, insurance, staff salary, etc. and hence, the break-even points, sales and profits for product ranges would be changed.

(b) Capital investments, once made, are irrecoverable except with losses. There may not be even scrap value in certain cases.

(c) Since funds are blocked on the acquired fixed assets, other investment opportunities may not be financed for want of funds; and thus, besides losses on this asset, potential profits from alternate investments are also lost.

Since future is generally uncertain, there is always an element of risk in estimating the future benefits from an investment. Reliable forecasts of market demands, market share for the firm, consumer preferences, competitors' actions and offers, technological development, changes in economic and potential environment - are the agglomerate of requirements to be carefully looked into. Quantifying the benefits is thus often a "grey" area.

21.3 KINDS OF CAPITAL BUDGETING DECISIONS

In the matter of allocating financial resources to new investment proposals, three types of decisions are basically involved :

(a) Accept-Reject decision;

(b) Mutually exclusive choice decision; and

(c) Capital rationing decision.

21.3.1 Accept-Reject Decisions All proposals which yield a rate of return greater than a certain (pre-establishedlrequired) rate of return, or cost of capital, are acceptable and the rest are rejected. [Note that : "acceptable" is used and not L'accepted' - this is because "acceptance" in the "final sense" may depend on several other considerations following "acceptability". Such considerations include : The line of business thereof being desirable; funds for investment

being available; socio-political influences and mileages that can be acquired thereby; etc.] Capital Investment

One important aspect is that, for acceptance, the project should be independent - i.e, it Decisions

should not be competing with any other project in such a way that the acceptance of one forecloses (or precludes) the possibility of acceptance of another. Ifaccepted, in view of )her considerations also, all so accepted independent projects should be implemented.

Even though f?w proposals in a firm are truly independent, yet, for practical purposes, it is quite reasonable to attribute "independence" in several cases. If a new machine is to be added to improve total production, advertising activity may include information on the prospects of increased production. Yet, the two can be considered as independent proposals - since the proposals arefunctionally different and there is no obvious inviolable dependency between these two proposals. Installing air-conditioning and purchase of fork-lift trucks can be truly independent investment proposals in this manner.

A group of investment proposals may be related to one another in such a way that acceptance of one influences the acceptance of others; like : installing a computer system and purchasing UPS therefor. These are called "dependent" proposals. For purposes of "independence" of projects, such dependent proposals are to be taken together as one independent proposal. .

Another type of relationship between proposals is based on Contingency, i.e. once some initial project is undertaken, other auxiliary investments become feasible; note that the "dependency" is "one-way ", such auxiliary proposals are called "contingent" proposals - since their acceptance is conditional to the acceptance of another proposal. For example, construction of a second floor of a building is contingent on the construction of all lower floors. The pre-requisite proposal is an independent project in such cases.

21.3.2 Mutually-Exclusive Project Decisions Mutually exclusive projects are projects that compete mutually (i.e. with others within the "set" of projects under consideration) in such a way that the acceptance of one will exclude the acceptance of all other alternatives. The total set of alternatives are mutually exclusive since only one could be chosen. In this, two major classifications are possible :

(i) Different levels of investment of the same process of expenditure, with each level attributable with different levels of benefit - e.g. providing heat-insulation on the main steam ducts in a central heating system. Here, the process of expenditure is the same - the provision of thermal lagging; but the level of benefit depends on the thickness of insulation provided - the larger the thickness, the smaller the heat loss and hence, the better the heating. The choice of any one thickness of the thermal insulation precludes the (simultaneous) adoption of any other thickness.

(ii) Different instruments1processes of expenditure - each with the same stream of anticipated benefits. Two different machinery - differing in first cost and annual running cost -but yielding the same benefits. In one case, the first cost may be more and the annual running costs may be less; vice-versa for the other. Variations of this aspect of the classification can be of two further categories :

(a) The capital investment may all be done at once; or may be possible in phases : e.g. A 200-bed hospital may be constructed all at one go; or a 100-bed hospital may be first constructed and, after, say, 10 years, expanded to a 200-bed hospital by adding the next 100-bed provisions.

(b) This is almost like under (ii) but the stream of benefits may extend over unequal durations - say, for 10 years with one possible investment, and for 15 years with another alternative. These are called unequal life situations.

Following two important viewpoints must be noted : Firstly, mutually exclusive project decisions are not independent ofthe accept-reject decisions. Each of the projects should be acceptable under the accept-reject criterion. Then, secondly, some technique should be used to determine which of the acceptable ones is the "best"; the acceptance of this "best" alternative automatically eliminates the other alternatives.

21.3.3 Capital Rationing Decisions If sufficient money is available to invest on the acceptable mutually exclusive alternatives of all projects, all such acceptable proposals could, of course, be undertaken for implementation, i.e. all independent "best-alternative" investment proposals each yielding

Construction Management

Finance return (individually) greater than a pre-determined level can be undertaken. However, in real world situations, the capital budget is often limited; and each of these acceptable proposals competes for these limited funds. Then the firm must "ration" the proposals by its own criterion. Generally, the criterion is that the firm allocates funds within (acceptable) projects in such a way as to maximise the long-term returns. (Linear programing formulation is, of course, the best solution methodology in these cases. However, other intuitive or search methods can also be equally effective. Projects are ranked with reference to a chosen criterion, may be, by net present worth (or internal rate or return) in the descending order of profitability. The available funds are then appropriately allocated amongst the ranked projects, considering the rank mainly, but also having an eye to utilise most of the available funds (as an added criterion.)

SAQ 1 (a) What do you understand by "capital investment decisions" or "capital

budgeting (capital expenditure) decisions" ? Explain their basic features, and also, the assumption affecting capital investment decisions.

(b) How is the firm affected by its decisions on long-term investments ?

SAQ 2 From your experience, give example of occasions for the several classes of mutually exclusive investment decisions to be made.

21.4 COMPUTATIONS IN REGARD TO FUTURE BENEFITS : CFAT

Capital budgeting deals with two components, as has been seen : viz. a present investment as a cost; and a stream future returns as benefits. The essential requirement in this instance is therefore the estimation of future benefits accruing from the investment proposal.

Two approaches are available to quantify the benefits, each leading to the same final figures for any future date of accounting. These are called the accounting profit approach and the cash flow approach. An example is used to illustrate. Consider the following data compiled by the accounting profit approach. Recall that "cash flow" is the sum of profit and depreciation generated by operations.

Data and Computation of CFAT*

Sales volume at year-end Rs. 5.60.000

Less cost of goods sold and cash expenses (-) Rs. 3,10,000

Earningshfi t before depreciation Rs. 2,50,000

Less Depreciation

Earnings/Profit before tax

(-) Rs. 90,000

Rs. 1,60,000

Less Tax at 40% (-) Rs. 64,000

(Accounting) Profit (after tax), i.e. net earnings) Rs. 96,000

Add depreciation Rs. 90,000 - *(CFAT) : Cash Flow (After Tax) Rs. 1.86.000

The above is the Accounting Profit Approach.

Computations by cash flow approach would be as follows :

Revenues Rs. 5,60,000 (1

Less cost of goods sold and cash expenses (-) Rs. 3,10,000 (2)

Less Taxes (-) Rs. 64,000 (6)

*(CFAT) : Cash Flow (After Tax) Rs. 1,86,000 (9)

i Not merely for the reason of ease of computation, but also for other reasons (not intended to be discussed here), the cash flow approach of measuring future benefits of the project is superior to the accounting approach. However, the approach to be followed depends on the contexts in the problem to be analysed.

Another aspect to be considered (or, enough to be considered) for capital budgeting relates to the basis on which the cash outflows and cash inflows are to be estimated. The practice to be adopted is incremental analysis. Under this practice, only differences due to the decision in question need be considered. Other factors may be important but not to the decision at hand. For purposes of estimating cash flows in the analysis of investments, only incremental cash flows are taken into account, i.e. those, and only those, cash flows which are directly attributable to the investment. By this reasoning,

1 fixed overhead costs (which remain the same whether the proposal is accepted or I rejected) are not considered except if there is an increase in them due to the new

I proposal. Sunk costs are also excluded.

I We shall illustrate by two examples. I

I Example 21.1 Consider the previous illustration, with the data therein refemng to the production process being semi-mechanical. Let us consider an alternate proposal where an investment of Rs. 2,00,000 on an equipment, to be depreciated by straight line depreciation over the next 8 years, is being considered which will, even as it keeps the sales volume the same, bring down the cost-cum-cash expenses to Rs. 1,80,000 per year over the next 8 years without affecting the other aspects of depreciation. To determine the benefits of this investment, the accounting computations show the following :

Sales volume Rs. 5,60,000 (1)

Less cost and expenses

Less Depreciation Rs. 90,000 + Rs. 25,000

(-) Rs. 1,80,000 (2)

PBT Rs. 2,65,000 ( 5 )

Taxes @ 40% (-) Rs. 1.06,000 (6)

PAT Rs. 1,59,000 (7)

CFAT Rs. 2,74,000 (9)

Incremental CFAT Rs. 88,000 (By excess over previous CFAT)

Hence, the rate of retrun over the investment of Rs. 2,00,000 should be based on annual income of Rs. 88,000 over the next 8 years, i.e. a CRF of 0.44 for 8 years,

I 0.4122 x (1.4122)~ i.e. the ROR will be 41.22%, = 0.44

(1.4122)~ - 1

(Refer to Section 15.4.2). This ROR is, in fact, the IRR.

Example 21.2 Conveyor system K for transporting coarse aggregate will cost Rs. 4.8 lakhs to install and Rs. 1.1 lakh a year to operate. Conveyor system L, based on a different design, but capable of equal performawe, will cost Rs. 2.9 lakhs to install and Rs. 2.0 lakhs a year to operate. Both systems will be written off by straight line depreciation to zero salvage value at the end of 5 years when the project would be completed. Income tax is 35%. Compare the performances to evaluate the indifference rate of return.

Capital Investment Decisions

Construction Finance Solution Management

Let us compute the after-tax net operating disbursements of each of the systems.

Explanation

For system K, the expenses are Rs. 2,06,000; profit will be reduced by the same amount; hence, taxes will be reduced at 35% thereof; i.e. 35% of the expenses will be savings in tax, i.e. post-tax increase in profit, i.e. post-tax net operating

I disbursements will be reduced by this amount of post-tax increase in profit. 1

I

Thus, the post-tax operating disbursements are : Rs. 38,900 per year for system K, !

and Rs. 1,09,700 for system L, i.e. incremental saving by L is Rs. 70,800 per year. 1

Line No.

( 1 )

(2)

(3)

(4)

(5) = (1) - (4)

Detail

Annual operating disbursements

Depreciation expense,

On incremental basis, system K costs Rs. 1.9 lakhs more to install but saves Rs. 70,800 per year in post-tax net operating disbursements for next 5 years. Then,

1

- - - 70.800

the indifference rate of return is given by a 5-.year CRF of = 0.372632; 1.90.000

System K

Rs. 1,10,000

Rs. 96.000

i.e. ROR = 25.103% (Refer to Section 15.4.2). The "indiffera-ice" is explained by the inference, viz. for MARR < 25.103%; CRF decreases, the incremental saving decreases, system K is less preferable to system L; and if MARR > 25.103%, CRF increases, the incremental saving i~creases, system K is more preferable to system L.

--

System L

Rs. 2,00,000

Rs. 58,000

In conclusion, it must be emphasised that the benefits to be considered are incremental after-tax cash flows (being the sum of after-tax profit plus depreciation generated by operations).

Rs. 2,58,000

Rs. 90,300

Rs. 1,09,700

yearly I

Relevant cash outflows will be : Variable expenses on labour and material (being of incremental nature), marginal taxes (being of incremental nature), and cost of investment (relative, in case two mutually exclusive options are available); irrelevant cash outflows are : fixed overhead expenses and sunk costs (since these remain whether or not the investment is made).

Total Annual expense

Tax saving @ 35%

21.4.1 Cash Flows

--

Rs. 2,06,000 I

Ks. 72,100 -

Cash flows (as defined, as incremental after-tax cash flows) can be recorded and illustrated on cash flow diagrams as illustrated in Section 15.3.1 under Unit 15.

Annual (Post-tax) net 1 Rs. 38,900 operating disbursements 1

When considering cash flows, relatively between two mutually exclusive alternatives, care must be taken

(a) if tax life is more than economic life,

(b) on the depreciation methodology adopted,

(c) if there are gains or losses in disposal, and

(d) if expenditure is either expensed or capitalised.

Also (e) carry-forward of losses of set-off against future income must be considered.

If the cash flow of a new investment option is likely to cause changes in the cash-flow in the ongoing operations with an on-hand investment, the mutual effect must be considered as part of the incremental basis of analysis. If changes in overheads occur due to the investment decision, such changes must be considered. How to consider the effect of taxes and depreciation has been already illustrated.

If there are likely to be any changes in the net working capital (i.e. current assets minus current liabilities), due to the investment proposal, this must be considered as part of the initial cash outlav. The recautured amount o f the work in^ cauital at the end o f the uroiect

must be included in the cash inflow in the terminal year. The same applies to any scrap or Capital Investment

salvage value recovered. Increases or decreases in working capital beyond the initial ~ecisions

outlay should be considered as part of the cash outflow in the respective year.

It will particularly be seen that income-expansion capital investment proposals require additional working capital, and cost-reduction capital investment projects help in "releasing out" of the existing working capital. Such increase or decrease should be accordingly added to or subtracted from the initial cash outlay; and the opposite will be appropriately true at the termination of the project.

Any tax benefits due to investment allowance for eligible assets should be considered, generally at the initial year (or zero time) (or, if so indicated, for a limited number of initial years). Investment allowance is granted to encourage capital investment in designated areas to initiate developmental activity and improve employment opportunities in those areas. Also, in the initial cash outlay should be included : cost of land, building, plant, equipment, etc. if then purchased (or allocated by deemed cost), installation cost of plant and equipment, and any costs of royalty, patents, etc.

SAQ 3 (a) What do you understand by cash flow diagram ?

(b) Collect statements on auditedlunaudited results of business given in newspapers by firms and study them in the light of the discussions hereinabove.

21.5 ILLUSTRATIVE EXAMPLES

21.5.1 Single Proposal This example illustrates what is called "cash flows for a single proposal"

Example 21.3

Assume that 5000 units of a product can be sold at cash price of Rs. 20 each. The cash variable expenses to manufacture and sell the product would be Rs. 12.40 per unit, and fixed overheads Rs. 9,000 per year. A machine is to be purchased for the purpose at a cost of Rs. 70,000 and installation would cost Rs. 13,000. The useful life of the machine is 8 years. For working the machine, working capital requirement would increase by Rs. 45,000, the machine will be depreciated by the straight line method to Rs. 6,000 salvage value. The firm is in the 40% tax bracket. 30% investment allowance is allowed in two equal instalments in the initial two years on installation. Develop the cash flows and evaluate the rate of return. Tax-is to be paid in subsequent year.

Solution [Installation cost could be added to purchase cost to t$e first cost as Rs. 83,000 for all purposes. But this has not been done in this illustration for depreciation purposes and investment allowance.]

Sales revenue = Rs. 1,00,000 per year.

Cash operating costs = (5,000 x 12.40) + 9,000 = Rs. 71,000 per year

Net revenue = Rs. 29,000

Initial expenditure = Cost (Rs. 70,000) + Installation (Rs. 13,000) + Working capital extra (Rs. 45,000) = Rs. 1,28,000.

70,000 - 6,000 Annual Depreciation =

8 = Rs.8,000

Profit before tax = Rs. 21,000

Investment allowance, in 1st and 2nd year, each = 15% of Rs. 70,000

= Rs. 10,500.

Construction Nnance I Management

The following tabulation develops the CFAT and costs. - -- --

Tax paid in end of first year is taken as negative, since this would be adjusted in the total taxes payable by the firm considering its other business activities also. Outlays and expenses are shown negative under CFAT. Two entries are made for EOY 8 as described. The structure of CFAT by its three components may be noted. Appropriate tabulation scheme can be developed for each problem context.

The ROR is now calculated by trials (Refer to Section 15.4.2).

EOY Cash flow , ROR= 18% ROR = 15% ROR = 12.5%

1 9 I - 8,400 , ",22::: 1 - 1,894

- 20,190

0.28426

TOTAL

- 2,388

- 9,106

0.34644

TOTAL

- 2.910 1 + 1,717

ROR, by interpolation, is nearly = 12.9%. This ROR is, in fact the IRR (based on CFAT, inclusive of investment).

The problem will rework as under when installation cost is included into first cost of plant and taken thus for depreciation and investment allowance.

Residual value of Rs. 6,000 is also considered notionally as income by sale at WDV at the 8th year.

Sales revenue = Rs. 1,00,000

Cash operating costs = Rs. 71,000

Net revenue = Rs. 29,000

= Rs. 9,625

Profit before tax = Rs. 19.375

Investment allowance in 1st and 2nd year, each = 15% of Rs. 83.000 = Rs. 12.450.

The following tabulation develops CFAT and costs.

1 5 1 Rs. 9.625 Rs. 19,375 1 Rs. 7,750 1 Rs. 21,251 1

EOY

(a)

0

1

2

3

4

1 6 1 Rs. 9,625 1 Rs. 19,375 1 Rs. 7,750 1 Rs. 21.250 (

Tax paid (dl - (el

1 7 1 Rs. 9.625 1 Rs. 19.375 1 Rs. 7.750 1 Rs. 21.250 1

Depreciation + ( 0 - (k) " 1

(0 -

Rs. 9.625

Rs. 9,625

Rs. 9,625

Rs. 9.625

1 8 1 Rs. 9.625 1 Rs. 19.375 1 Rs. 7.750 1 Rs. 21.250 1

Profit before tax, after depreciation

1 s t I - 1 - 1 Rs. 6.000 1

(g) -

Rs. 19.375

Rs. 19,375

Rs. 19,375

Rs. 19,375

Capital Innstment Decisions

(k) -

(-) Rs. 49,80

Rs. 2,770

Rs. 7,750

Rs. 7,750

0) (-) Rs. 1,28,00

Rs. 33,981

Rs. 26.23( 1

Rs. 2 1,251

Rs. 21.250

8

9

-

-

- -

- Rs. 7,750

Rs. 45,000

(-) Rs. 7750

Construction Finance Mnmgement

ROR is calculated by trials (Refer to Section 15.4.2.)

The realised rate of return = 14.237%.

21.5.2 Replacement Proposal This example illustrates what is called "cash flows for Replacement Proposals".

Example 21.4 A firm is currently using a machine which it had purchased 3 years ago for Rs. 85,000 and it has a remaining useful life of 3 years. It is permitted to be depreciated at 20% every year. Over the next three years, the expected cash inflows before depreciation and taxes are : Rs. 40,000; Rs. 35,000 and Rs. 30,000, respectively. However, it can now be sold for Rs. 90,000. But at the end of the sixth year its book value will be the realisable value on sale.

The fm wishes to replace this machine with a new one which would cost Rs. 1,30,000, with a further expenditure of Rs. 20,000 for installation and an additional working capital of Rs. 25,000. The expected cash flows are Rs. 60,000; Rs. 75,000 and Rs. 65,000 in the next three years, respectively. This machine will be depreciated by SLD over 6 years but is expected to fetch only Rs. 20,000 on disposal at the end of the three years of use.

The firm pays 40% tax on income and has to pay 20% as capital gains tax (wherein capital gain will be computed with reference to original purchase cost).

Compute the CFAT on incremental basis for the new machine and evaluate the rate of return. Tax is to be paid in the same year.

A Note :

Before solving the problem, we shall understand a little on capital gains. Here, we have a case where the resale after three years fetches more than the initial

purchase price, and so definitely more than the then book value. If capital gain is to be considered with reference to initial purchase price, it is customary to "index" the initial purchase price for the year of sale. That is if the cost index at year of purchase was, say 110, and the cost index at year of sale was, say, 150,

150 the indexed (price or) cost at the time of sale will be - times the purchase

110 price; and any capital gain shall be with respect to this indexed price. Here, we are not considering this.

Solution

Step I

For the machine now being used since the last three years, the book value at beginning of year, the depreciation through the year, and the book value at the end of year - for the first three years will be as under.

With resale at Rs. 90,000, the overall profit on sale relative to then BKV is Rs. (90,000 - 43,520) = Rs. 46,480, which is considered in two parts : Rs. 41,480 which is w. r. t. (un-indexed) purchase price of Rs. 85,000 plus Rs. 5,000, this being the excess over the purchase price. Accordingly, tax payable on profits on sale is taken as : 40% on ordinary gain of Rs. 41,480 (because 40% of depreciation provision was saved as tax through the three years) plus 20% on capital gain of Rs. 5,000 = Rs. 16,592 + Rs. 1,000 = Rs. 17,592. [However, if all of Rs. 46,480 is considered as capital gain, the tax payable on profits on sale will be 20% of Rs. 46,480 = Rs. 9,296. Taxation procedures may not admit this.] [Also, if indexing is done according to the figures indicated, the indexed cost (at the time of sale) will be

1st year

2nd year

3rd year

150 = Rs. - x 85,000 = Rs. 1,15,909; and a loss on sale of Rs. 25,909 will be

110 recorded, and this would qualify for a reduction in overall tax in the year to the extent of 20% thereof, viz. Rs. 5,182. (But the 40% of depreciation saved as taxes in earlier years has to be paid in lump sum.)] We solve this example with the first stated procedure, viz. tax payable on profits on sale is taken at Rs. 17,592.

Step 2

BKV at beginning (Rs.)

Rs. 85,000

BKV at beginning (Rs.)

Rs. 68,000

BKV at beginning (Rs.)

Rs. 54,400

Let us then compute what can be called the "effective investment cost" of the "machine which replaces". We should consider, besides the purchase cost, not only installation cost and changes in WC because of this replacing machine, but also the tax-moderated sale proceeds of the existing machine.

Cost of new machine Rs. 1,50,000

Add : Installation cost

Add : Additional WC needed

Depreciation at 20% (Rs.)

Rs. 17,000

Depreciation at 20% (Rs.)

Rs. 13,600

Depreciation at 20% (Rs.)

Rs. 10,880

(+) Rs. 20,000

(+) Rs. 25,000

BKV at end (Its.)

Rs. 68,000

BKV at end (h.1

Rs. 54,400

BKV at end (h)

Rs. 43,520

Less : Sale proceeds of existing machine (-) Rs. 90,000

Add/Subtract : Tax liabilitylsaved in the process of (+) Rs. 17,592 sale of existing machine; Here : Add tax liability

Effective investment wst of newlreplacing machine Rs. 1,22,592

The "effective investment cost" is also called the "notional investment cost". This aspect is crucial in the analysis of "cash flows for Replacement Proposals". This must be considered in the context of "Capital Rationing" also (to be

Construction Nnance Management

discussed later). (While discussing "Capital Rationing", the tax effect is not considered, which implies that the resale value is also not considered. The reason is that, for purposes of "Capital Rationing", all these decisions are just only internal to the company.)

Step 3

Let us now compute the CFAT for the next three years in both options.

For the existing machine, the depreciation chargeable in the next three years is computed by the same methodology as before.

[To check : Rs. 85,000 (1 - 0 .2 )~ = Rs. 22,282.1

For the new equipment, depreciation will be not only on the actual cost paid but on the notional investment cost (inclusive of installation); this latter cost will be

1,50,000 Rs. 15,000. Its depreciation per year will be Rs.

6 = Rs. 25,000 leaving a

residual book value of Rs. 75,000. Its post-tax salvage value will be computed as follows.

Salvage by BKV = Rs. 75000 (1)

(NRV) Net Realisable Value = Rs. ZOO00 (2)

Loss on disposal = Rs. 55000 (3)

Tax saving @ 40?& = Rs. 22000 (4)

Post-tax salvage value = Rs. 42000 (5) = (2) + (4)

Let us now compute CFAT with continuing to use the current equipment (machine) :

(Note that tax has been taken to have been paid in the same year.)

After tax cashflow (existing machine) (All values are in Rs.)

1 First Cost (-) 43.520

Salvage 1 22,282

r I I - 1

3 4 5 6 (CFAT) 27,482 23.785 20.228

Let US now compute CFAT with the new equipment (machine) :

(Note that tax has been taken to have been paid in the same year.)

After tax cashflow (new machine) (All values are in Rs.)

Notional Investment = (-) 1,22.592 (WC included)

Salvage = 42,000 + WC Recovered = 25,000

= 67.000

Figure 21.2

CFAT on Incremental basis for new machine (All values are in Rs.)

Outflow = (-) 79,072 Inflow = 447 18

(Inflows) 18,518 31,215 28,772

Figure 213

Step 4

We can now compute the realised rate of return (which will be the IRR). This works out to be 20.366%.

Capitalising or Expensing

Example 21.5 This example is a variation of the Example 21.4. This considers the effect of considering a major repairing expenditure during the life of an equipment either as a cost on rebuilding, thereby increasing the Book Value or Asset Value which implies Capitalising through depreciation provision in the further years, or as simply reconditioning thereby increasing the M & R (maintenance and repair) costs in the year which implies expensing, i.e. adding to the operational expenses/disbursements during the year.

Consider the Example 21.4 wherein, rather than going in for a replacement, the firm decides to spend Rs. 40.000 on major repairs to make the present machine suitable for continued service on the job for the next three years. At the end of the sixth year its realisable value on sale will remain the same as before, with depreciation continuing at 20% every year. However, over the next three years, the expected cash inflows before depreciation and taxes are : Rs. 56,000; Rs. 48,000, and Rs. 42,000, respectively.

Compute the CFAT for the next three years considering the major repairs expenditure to be (i) capitalised, (ii) expensed.

Capital Investment Lkdsions

Construction Finnna Solution Management

(i) Considering that the major repairs expenditure will be capitalised

The notional investment by considering as rebuilt, i.e. capitalised is computed as follows :

At the end of the third year :

Book Value

Net realisable value

- - Rs. 43,520

- - Rs. 90,000 (A)

Gain, if disposed, - - Rs. 46.480

(Additional to pay) Tax on gain, = Rs. 18,592. (B) if disposed

NRV after tax

Cost to rebuild

- - Rs. 71,408 (C) = (A) - (B)

- - Rs. 40,000

Notional investment = Rs.1,11,408 *

Since we are not actually disposing off, and these computations are only for internal purposes, the ga is not split into two parts.

Since by not selling off, the firm, though it loses a resale value of Rs. 90,000, at the same time, does not have to pay tax to the extent of Rs. 18,592, and hen the after-tax amount foregone by not selling off is only Rs. 7 1,408.

However, the depreciation will now have to be computed on revised book value, viz. the previous residual book value 2111s the cost to rebuild = Rs. 43,: + Rs. 40,000 = Rs. 83,520. Correspondingly, the depreciation chargeable in tl next three years will be computed as under.

Tax-adjusted salvage value will be computed as under :

Realised Salvage - - Rs. 22,282 @)

Book Value - - Rs. 42,762

Loss in realisation - - Rs. 20,480

Tax saving on loss - - Rs. 8,192 (E)

Tax-adjusted Salvage - - Rs. 30,474 (F) = @) + (E)

CFAT from the operations for the next three years is now computed.

Final BKV (RS.1

Rs.66.816

Final BKV (W

Rs. 53.453

Final BKV (W

Rs. 42,762

Depreciation (B.1

Rs. 16,704

Depreciation (Rs.)

Rs. 13,363

Depreciation ( b . 1

Rs. 10.691

4th year

5th year

6th year

Initial BKV (Rs.)

Rs. 83.520

Initial BKV (Rs.1

Rs. 66,816

Initial BKV (b .1

Rs. 53,453

(ii)

Afrer-tax Cash Flow is as follows (noting that there is no change in WC requirements). The IRR is 9.163%.

Fipre 21.4

Considering that the major repairs expenditure will be expensed

The notional investment value after tax after the repairs will be as follows :

Book value = Rs.43.520

Net realisable value

Gain, if disposed,

= Rs.90,000 (A)

= Rs. 46,480

(Addl. to pay) Tax on gain. if disposed = Rs. 18592 (B)

NRV after tax = Rs. 7 1,408 (C) = (A) - (B)

M and R expenses = Rs.40.000

Tax saving on M & R expenses = Rs. 16,000

M and R expenses after tax = Rs.24,000 (G)

Notional investment = Rs. 95,408 @I) = (C) + (G)

Depreciation will now have to be calculated (only) as in Step 3 of Example 21.4. Accordingly, there will be no change in salvage value either.

CFAT from operations for the next three years is now computed.

Afer-tax Cash Flow is as follows; and ZRR is 10.99%. [Note that expense on special repairs is implicitly included in (-) 95,408.1

Fipre 215

The IRR of the relative cash flow (Figure 21.6) works out to be negative; this is seen from the NPV at ROR of zero being Rs. (-) 252. This means that, in this case, capitalising is always a unacceptable proposition compared to expensing, which is verified also by the greater IRR for the expensing alternative.

Construction Finance The relative cash flow by excess in case (i) over in case (ii) will be as follows : Management

(-) 16,000

t I I I I

3 4 5 6

'r T T 2,948 2,560 10,240

Figure 21.6

21.5.3 Mutually Exclusive Project Proposals Example 21.2 has already illustrated this type of problems. It considered uniform annual costs.

We now illustrate another example where we consider annual incomes, and where these are not uniform through the years.

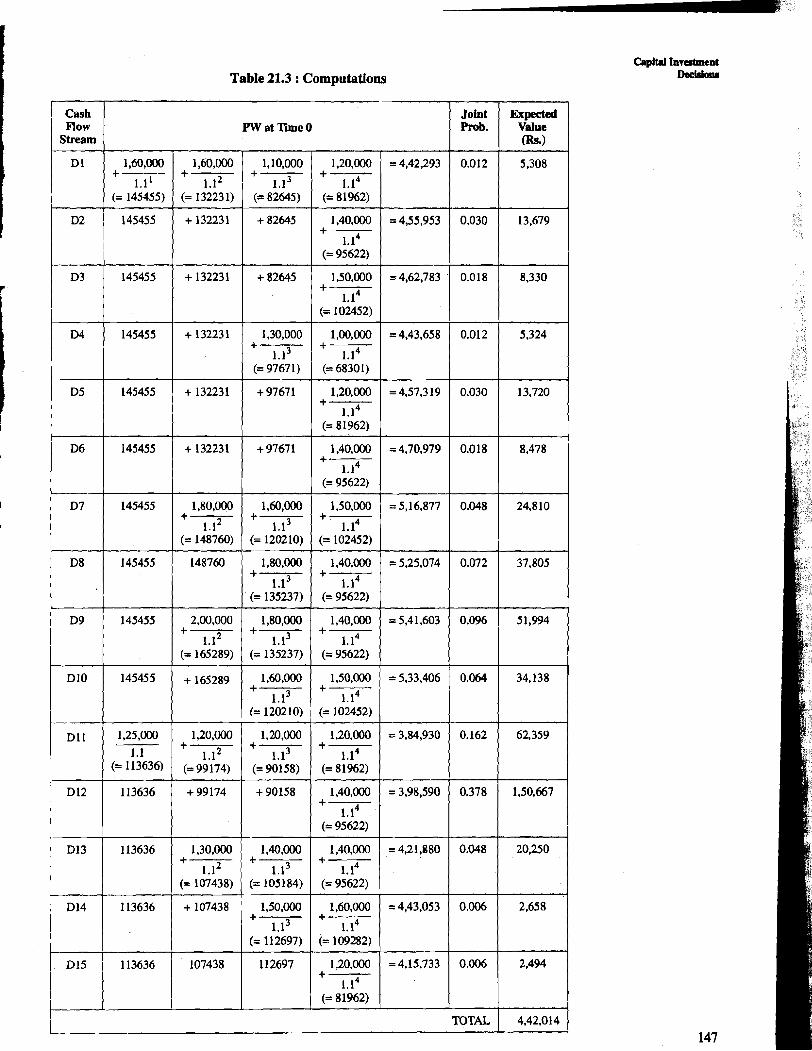

Example 21.6 Cash flows without depreciation and taxes for two mutually exclusive project proposals are as under. Project I is written down by sum-of-year's digit method to 10% of first cost. Project I1 is written down to 15% of first cost by uniform rate on declining balance method. The firm's tax rate is 35%. Determine the CFAT for both projects and the incremental CFAT of project I1 over project I. Comment on the results.

Initial CFBDT, Rs. Cost, Rs.

Year 1 Year 2 Year 3 Year4 Year5

Project 1 2,20,000 74,000 63,000 62,000 55,000 50.000

Project11 3,80,000 1,30,000 1,10,000 85,000 65,000 60,000

Solution Depreciation for Project I through the years will be in the proportions

5 : 4 : 3 : 2 : 1 , i . e . 5 ,4 ,3 ,2 ,1

15 (90% of first cost), i.e. Rs. 66,000, Rs. 52,800,

Rs. 39,600, Rs. 26,400 and Rs. 13,200.

Depreciation for Project I1 will be by the rate = [l - (0.15)ln] = 0.315745.

We now list down the depreciation and residual BKV through the years.

Year 0 - 1 1 - 2 2 - 3 3 - 4 4 - 5

Initial BKV, Rs. 3,80,000 2,60,017 1,77,918 1,21,741 83,302

Dept, Rs. 1,19,983 82,099 56.177 38,439 26,302

To check : BKV at the end of 5th year = Rs. 57,000, which is 15% of Rs. 3,80,000. This is correct.

We can now tabulate the computations for both the projects. All values are in Rs.

Capital Investment

-

- 1,60.000 55,294 40,805 20,752 - 1,164 18,482

Comments

Individually, each project has NPV > 0 for ROR = 0%. Hence, both have positive NPV's for some range of ROR higher than zero. However, the above incremental CFAT has NPV < 0 for ROR = 0%. Hence, for all ROR values, Project I1 is inferior to Project I in terms of profitability.

The same conclusion may be checked by comparison of the IRRs of the two projects. IRR of Project I works out to be : 7.65% (with a NPV of + Rs. 16) as seen below. All values are in Rupees.

EOY 0 1 2 3 4 5

Cash - 2.20,000., 7 1,200 59,430 54,160 44,990 37,120 flow

k

j PWF 1.00000 0.92894 0.86292 0.80160 0.74464 0.69172

' ~ ~ ~ 2 . 1 M 0 0 66,140 51,283 43.415 33,501 25,677

By summation of last row values, NPV = + Rs. 16.

IRR of Project I1 works out to be : 2.195% (with NPV = + Rs. 2). The detailed computations are as under. All Values are in Rupees.

. . . .- . --

flow

PWF 1.00000 0.97852 0.95750 0.93694 0.91081 0.89712 -

PW - 3,80,000 1.23.777 95,9?5 ' 70,188 40,180 49,882

By summation of last row values, NPV = + Rs. 2.

21.5.4 Market-based Approximation for Salvage Value It is difficult to estimate the salvage value of fixed assets (we restrict to other than buildings and land). Several factors influence the possible salvage value, like technological status and innovations, wear and tear, demand pattern changes, inflation, and so on and even urgency to sell or buy. Yet, a seemingly rational method is to compare for similar equipment in the market both as recent past purchase and as available for salvage. It is better illustrated through an example as under.

Example 21.7

A firm is planning to purchase a new machine for a possible use over the next 8 years; and its present market cost is Rs. 2.4 lakhs. The cost of a similar new machine purchased by the same firm or by firms in the peer group 3 years before is Rs. 1 .!2 lakhs. Also, the present market price of a similar machine which has been used far ? years is Rs. 0.6 lakh. It is desired to estimate the possible salvage value of the machine now bought for Rs. 2 lakhs at the end of its 8 years of service.

Construction Finance Solution Manegement

Rate of growth of purchase cost,

Possible purchase price of a similar new machine 7 years before,

2.4 --- - - Rs. 1.39 lakhs. (1 .08117

Rate of decline of book value is given by 1.39 (I - y)7 = 0.6;

i.e. y = 0.1131.

Hence, possible salvage value of the present purchase cost of Rs. 2.4 lakhs after 8 years = 2.4 (1 - 0.1 13 1)* = 0.9188 lakh, say, Rs. 0.92 l a b .

It is seen that we essentially develop two ratios, viz. rate of growth of purchase cost and rate of decline of book value. As an interim step, we hindcast the possible purchase price of a comparable machine whose present salvage value and age are known from market enquiries. Notwithstanding all this, it should be appreciated that in the initial year, often, the depreciation is much more and it declines thereafter and in the terminal years it is again severe, in general.

SAQ 4 Rework all the examples (Example 21.3 to Example 21.7) given in Section 21.5 with increased values (by 10%) of costs/disbursements, all other features remaining unaltered.

21.6 EVALUATION TECHNIQUESIAPPRISAL METHODS FOR CAPITAL BUDGETING

Whereas apprisal is generally referring to enquiring into the worthwhileness of a prospective capital investment, evaluation refers to rigorously checking for the realised worthwhileness after the investment has been made; however, evaluation is just used to refer to enquiring into the worthwhileness both before and after the investment has been made. In this study, both terms are used interchangeably for both pre-, and post-, investment computations for the economic costs and benefits of any capital investments.

Though time value of money has to be taken into account in all cases, yet what are called Traditional methods do not consider the time value of money. As has been mentioned in Sections 15.3 and 15.4, finding the time-adjusted value as at an earlier instant is called "discounting" and as at a later instant is called "compounding". Based on this, methods based on adjusting for time-based values of costs and benefits are generally called Discounted Cash Flow Techniques.

Traditional methods include Pay Back Period method; and Average Rate of Return method. Discounted Cash Flow Technique include : Net Present Value method; Internal Rate of Return method; Annual Equivalent method; Net Terminal Value method; Benefit Cost Ratios or Profitability Indices. Of these, NPV, IRR, AE and BCR methods have already been dealt with in Unit 15 and in the earlier sections in this unit. If rather than finding the NPV at the initial date of the project, the cumulative inflow duly (i.e. even admitting variable rates of interest over the years) compounded, as at the terminal date of the project be computed, and then discounted to the zero-date, that becomes the NTV method. This needs additional information on how the cash flows are to be compounded or made cumulative at the terminal date through interest rates for reinvestment. This is not discussed further in this study. However, some important points regarding the methods already dealt with will also be brought forth herein.

21.6.1 Traditional Methods Pay Back Period (PBP) Method

Payback, or payout, period is the length of time required to recover the first cost of an investment from the net cash inflow produced by that investment for an interest rate equal to zero. If Fo is the first cost of the investment and if F, is the net cash flow in period t, then the payback period is that value of n that satisfies the following equation :

n

Fo + F, = zero t = 1

If F, is constant for all t, then it is the ratio of the initial fixed investment over the annual cash flow (taken numerically and not algebraically). And, the Pay Back Period (PBP) can include fractions of years also. Thus, if the initial cash outlay was Rs. 2,00,000 and the net cash flow in each year was Rs. 48,000, then the PBP

2,00,000 1 is

48,000 = 4- years. If F,'s are unequal over the several t's sequential

6 summation of F,'s are made starting from the first year and fractions interpolated if necessary. Thus, if F,'s were Rs. 25,000; Rs. 45,000; Rs. 65,000; Rs. 35,000; Rs. 40,000; Rs. 25,000 in six successive years, first to sixth, respectively, PBP is' through the fifth year, since the first four years would pay back Rs. 1,70,000 and the first five years would pay back Rs. 2,10,000. Considering pro-rata, PBP would

3 be four years plus three-fourth of the fifth year, i.e. 4- years. 4

If the PBP calculated is less than a-pre-stipulated (maximum) acceptable period, the proposal is accepted; if not, rejected. If the desired PBP was 3 years the above proposal would have been rejected; if desired PBP was 5 years, the proposal would have been accepted. In that case, it matters nothing whether there was any cash flow on sixth year or any later year. This failure to consider the cash flows after the PBP is one main drawback of this method. Moreover, even if the above F,'s had been reordered in the sequence : Rs. 65,000; Rs. 45,000; Rs. 35,000; Rs. 25,000; and then followed by Rs. 40,000 and Rs. 25,000; the PBP would have

3 remained at 4- years. But, obviously, any sane investor would prefer this latter 4

stream of F,'s compared to the former stream, since longer amounts are recovered in earlier years in this latter stream. This is yet another drawback of this method, viz. it does not take into account the magnitude or timing of the cash flows during the PBP; it considers only the recovery as a whole. Additionally, salvage value too is neglected in this method; but this statement can be considered as included in the previous statement that it mattered nothing if there was any cash inflow beyond the PB P.

When ranking mutually exclusive projects, the shorter the PBP of a project, the higher its rank, i.e. it is listed at the top.

By the PBP method, projects with large cash inflow in the latter part of their lives may be rejected in favour of less profitable projects which happen to generate a larger proportion of their cash inflows in the earlier part of their lives. Yet, the advantage is based on the fact that the later the cash flow, the more uncertain its quantum. Also, under politically unstable situations, this method is good enough to assure to oneself of an early return of the investment. The same is true if the firm is under a liquidity crunch; then it must get back its cash outlays as early as possible.

Average Rate of Return (ARR) Method It is also called the Accounting Rate of Return method since it is based on accounting information rather than cash flow. It is the ratio of the average annual profits afer taxes to the average investment in the project. The numerator of this .ratio is just the arithmatic average of the after-tax profits taken year-by-year over the project's life. The average investment in the denominator; on the assumption of straight line depreciation, will be given by :

1 [Net working capital + - (Initial cost - Salvage) + Salvage]. 2

Capital Investment De&iOlM

Construction Finance Management

The following example illustrates the computations :

Let the instaliation cost of new machine be Rs. 2,50,000; its service life 6 years; depreciation by straight line method; salvage after 6 years, Rs. 40,000; and the working capital needed, Rs. 80,000. Then its average investment will be :

Ks'2910'0001, i.e. Rs. 2,25,000. 1 Rs. 80,000 + Rs. 40,000 + L 1

Let the year-by-year estimated income after depreciation and taxes be : Rs. 40,000; Rs. 45,000; Rs. 65,000; Rs. 50,000; Rs. 40,000 and Rs. 30,000, respectively, through the six years. The annual average after-tax income is the arithmatic average of these values, i.e. Rs. 40,000 per year (for 6 years). By this, the

Acceptance of the project is subject to the ARR being no less than a pre-stipulated value which is called the minimum required rate of return or the cut-off rate. If the cut-off rate (also called hurdle rate) prescribed was 2096, the above proposal would be rejected; but if the cut-off was prescribed at 15%; the same proposal would be accepted. Among accepted projects, they may be ranked in the decreasing order of ARR.

This method is easy to calculate compared to the DCF methods. It also considers the benefits received over the entire project life, unlike the PBP method. Like PBP, ARR method also does not take time value of money into account, nor the timings of the incomes. The ARR does not differentiate between the sizes (or quanta) of investment needed; it only takes the ratio of profits to investment (both on average basis); this is not helpful for capital rationing decisions. When a replacement will be considered, ARR method does not resort to incremental cash flow computations. Its main drawback, in short, is that is based on accounting income rather than upon cash flows besides neglecting the timings of the individual incomes. [Note that cash flow includes depreciation.]

21.6.2 Discounted Cash Flow Techniques DCF techniques for capital budgeting consider both the magnitude and the timing of the cash flows in each period covering the project's whole life. All the methods are pinned on the cashflows being discounted at a certain rate which may be the "cost of capital" or which may be compared with the "cost of capital ". "Cost of capital" is the minimum discount rate that must be earned on a project so as to leave the firm's market value unchanged. As said earlier, the NPVand IRR methods are the two main techniques; and BCR, net terminal value and annual equivalent methods are but variations out of these two main techniques. The difference between these two techniques, and very important this difference is. I ' - . I ~ NPV technique depends on the time instant to which the cashflows are discounted (for dny adopted rate of return); but, in the IRR method, once the IRR is evaluated at an instant of time, it is independent of the time instantfor its evaluation; i.e. IRR will remain the same for all time instants for a given cash flow stream. For the same reason, additionally, IRR is indifferent to how ambiguous items are considered, viz. items that may qualify to be viewed either as part of benefits or part of costs - i.e. whether an item, depending on the view taken, either adds to the benefit or diminishes the cost; or, alternatively whether an item, adds to the cost or diminishes the benefit. If rebate on income tax is given against payment 01 insurance premia, the rebate can be taken as an increase in benefit or decrease in cost. If money has to be spent in rehabilitating displaced persons from a project site. it can be considered as a decrease in benefit or an increase in cost.

Net Present Value (NPV) Method

All the cash flow stream components are discounted to an instant defined as "present " and the net sum (i.e. considering whether the component is a cost item or a benefit item) of such discounted values is the NPV at that instant. Generally, the zero-date of the project is taken as "present" instant. The discounting must be done at a specified rate of interest. Detailed computations have already been illustrated in several contexts both in Unit 15 and in this unit. It is but necessary that benefits are in terms of CFAT.

A project is accepted if NPV > 0; and rejected otherwise. This method is very useful in choosing between mutually exclusive projects, particularly if all the

projects have the same duration or life. Most importantly, this method of project Capital Investment

(or asset) selection helps in maximisation of shareholders' wealth. If the NPV is ~ecisions

zero, the return on investment is just equal to the rate of return expected or required by the investors. If NPV > 0, the return would be higher than expected by the investors; and then share prices would increase. Thus, this method stands out as theoretically correct for selection of investment projects. Its one difficulty lies in the selection of the correct discounting rate. With any change in this rate, the NPV will change and the relative acceptability of the project will change. The cost of capital to be used as the discounting rate is often difficult to estimate (due to several complications involved). Care must be taken when the outlays on different projects are different; since, generally, a larger outlay is needed for a larger NPV; going merely by the NPV should not go with being unmindful of the needed outlay to be made. When projects are of different lives, a larger NPV with a longer duration project implies locking up the investment for a longer rime; and this may preclude the choice of any shorter duration projects if these msy have lesser NPV.

Internal Rate of Return (IRR) Method

The Concepts

This technique is also known by other names : yield on investment, marginal efficiency (or productivity) of capital, (the) rate of return. The IRR for an investment proposal is the discount rate that equates the present value of the expected cash outflows with the present value of the expected cash lnflows; i.e. the NPV as at the instant of evaluation is zero. For this reason, the IRR is described as the rate of return that the project earns; and hence, the name as yield on investment.

Since zero net value, if discounted or compounded to any earlier or later instant, respectively, will yet remain zero (no matter what the interest rate - IRR just being one of the multitude of rates of return possible), the estimated IRR is the same for all instants of evaluation.

If there is any item of cash flow that is not clearly classifiable as either benefit or cost, this non-clarity does not affect the magnitude of IRR as seen herewith. IRR requires (B) - (C) (in absolute values of B's and C's) to be zero. Let the ambiguous item within all items considered be called A. Then, it either affects B as (B +A) without affecting C or it can affect C as (C -A) without affecting B. In either case, this leaves the net effect on ( B - C) to be the same, being either [(B +A) - C] or [B - (C -A)]. The same argument holds if it affects B as (B -A) without affecting C or affects C as (C + A) without affecting B, in either case leaving only (B - C ) as either [(B -A) - or [B - (C + A)], these being of the same magnitude.

IRR vs NPV

When compared with the NPV method, the basis of the discount factor is different in both cases. In the NPV method, the discount rate is the required rate of return and is pre-determined, usually at the value of the cost of capital, thus, its determinants are external to the investment proposal being considered. The IRR method is based on the facts (and figures) internal to the proposal; and hence, the description "internal" for this rate of return.

When adopting the IRR method for evaluation of a project, acceptance of the project depends on the derived IRR being greater than the required rTtc of return, also called the cut-off, or hurdle, rate.

Multiple Values of IRR The computation of IRR has repeatedly been illustrated in Unit 15 (Accounting for Construction) and in this unit. Mathematically considered, the IRR can be unique (single) (real positive) value only when there is only one change of sign in the cash flow stream, generally, a single initial cash outflow, followed by a series of cash inflows. If there are more than one changes of sign, again when mathematically considered, the IRR can have multiple real positive values depending on the number of changes of sign in the cash flow stream. The following illustrations help in understanding this concept.

(a) The cash flow stream, - 875 at time 0, + 600 at time 1, and + 700 at time 2. has its IRR as ;0.075%, as seen by the NPV = - 875 + 461.27 + 413.73 = ZERO. [The other IRR will be - 161.5%.]

construction Finrnee (b) Consider the cash flow stream as given in Figure 2 1.7. Management

+ 1.00.000 + 40.320 + 2.87.7 12

Figure 21.7

In this, the interest-less cash-out is Rs. 3,96,800, and cash-in is Rs. 4,28,032, indicating a notional profit of 7.871 %. However, it caq be shown that, given the two changes of sign (between times 0 and 1, and between times 2 and 3) there are two IRR values, these being 8% and 80%. [The details to prove these values can be worked out on the lines as in the above illustration (a).] [Also, as a fourth-order equation, the other two IRR] values are [- 220 f 20 n ] %, which can be verified by application on to the cash flow stream.]

(c) Consider the cash flow stream as given in Figure 2 1.8.

Figure 216

With two changes of signs, both roots of the second order equation in this instance will be real positive numbers. These are 108, and 30%. which can be verified by application into the cash flow stream.

(d) Consider the cash flow stream as given in Figure 2 1.9. + 1.00,000 + 4,78,250

Figure 21.9

With 3 changes sign in this third order equation, all the three roots will be real positive, these being the three IRR values of lo%, 25% and 45%.

The question of which of the multiple IRR values is the relevant one in project apprisal is not dealt with in this study; but suffice it to say that the lowest value is the possible one to be considered in the context of economic and financial apprisal and not the higher values.

Relevance and Utility of IRR as a Criterion for Project Selection The IRR method considers time value of money and also the total cash inflows and cash outflows. It is more easily understood and appreciated : vide : Project X generates 18% against the minimum acceptable rate of return, or cost of capital, of 12% - is a statement better understood than; Project X has net present value of Rs. 18,275 when evaluated at 12% rate of return. This concept reinforces the other advantage in using IRR, viz. IRR concept is independent of cost of capital concept. Also, the wealth maximisation objective of any firm is immediately impressed upon by the statement that IRR is 18% against cost of capital which is 12%. Problems arise in case of existence of multiple IRR's. In such situations, either the lowest IRR value is recognised, or better still, the dual rates of return concept is employed wherein having discounted the later-time cash flows starting from the last one at MARR by one time step at a time, thus going towards the

initial time till only one change of sign is left in the discounted, truncated situations. This has been explained and illustrated in Unit 15. Another illustration follows.

Example 21.8 Consider the following cash flow stream :

Let the MARR be 14%. By discounting one step at a time, with this rate, the effective cash flow at different EOY's from the terminal end are :

Time, EOY

Cash Flow, Rs.

Now the 14% discounted-truncated cash flow has only one change of sign and reads as :

0

- 5000

This has an IRR of 17.2%. This result is quoted as : Given the original cash flow stream with a desired rate of return of 14%, IRR (as a dual rate of return) is 17.2%. [In fact, out of the five possible IRR's that can be developed mathematically for the originally given cash flow, one of the real positive IRR values will be between 14% and 17.2%; in fact, it is : 16.315%.]

T i e , EOY

Cash Flow, Rs.

If the IRR exceeds the cost of capital, share prices tend to rise and this naturally leads to the maximisation of the shareholders' wealth. However, this cannot be an absolute statement and it can be misleading. This is illustrated as follows. Consider a cash flow stream R which is : [- 2880 at time 0; + 2000 at time 1; and + 2000 at time 21. Its IRR = 25%. Consider another cash flow stream S (R and S being mutually exclusive) which is : [- 6875 at time 0; + 4500 at time 1; and + 4500 at time 21. Its IRR = 20%. If MARR is 15%, the NPV of R is 371.4 units; and NPV of S is 440.7 units. Clearly S, though with lesser IRR, yet maximises the shareholders' wealth better than R at the given cut-off or hurdle rate of 15%. This anamoly in the relative ranking by IRR vs by NPV arises because of the very definition of IRR. IRR is concerned (internally) with the yield, o r return, on investment and not on the total yield (in quantity terms) out of the investment. This is explained by considering the incremental situation of S over R : This is : [- 3995 at time 0; + 2500 at time 1; and + 2500 at time 21. This has an IRR of 16.359%. In other words, increasing from R to S does not continue to yield 25% on the increments but yields only 16.359% on the increments. Continuing with the discussions, it is clear that when faced with mutually exclusive projects (each, of course, having a positive NPV), the more the NPV, the better the effect on shareholders' wealth; but the same cannot be said in terms of relative magnitudes of IRR's. A further important point must be emphasised. It is seen that the increment from R to S has on IRR more than the MARR (16.359% > 15%); this means that, in terms of MARR, the firm gets the profits (in terms of NPV) associated with the smaller outlay of R, plus a profit (relative to and better than the MARR) even on the incremental outlay of S, if S is chosen in preference to R. Thus, incremental IRR approach would give the same rankings as NPV approach between mutually exclusive projects.

1

+ 2500

[The aspect of reinvestment assumption in the matter of IRR is not discussed here.]

0

- 5000

[What is called the size-disparity problem in the matter of IRR has amply been discussed above in the discussion on Projects R and S. The "Time-Disparity Problem" is not discussed here, except to say that, again, the cost of capital, and hence, NPV is the criterion for ranking among mutually exclusive projects.]

2

+ 3100

CnpW Investment Deddom

1

+ 2500

3

- 2000

2

+ 3100

4

+ 3000

3

+ 982.56

5 6

- 2000 + 2800

Construction Finance Benetit-Cost Ratio (BCK) or k'rutitahility Index (PI) Management

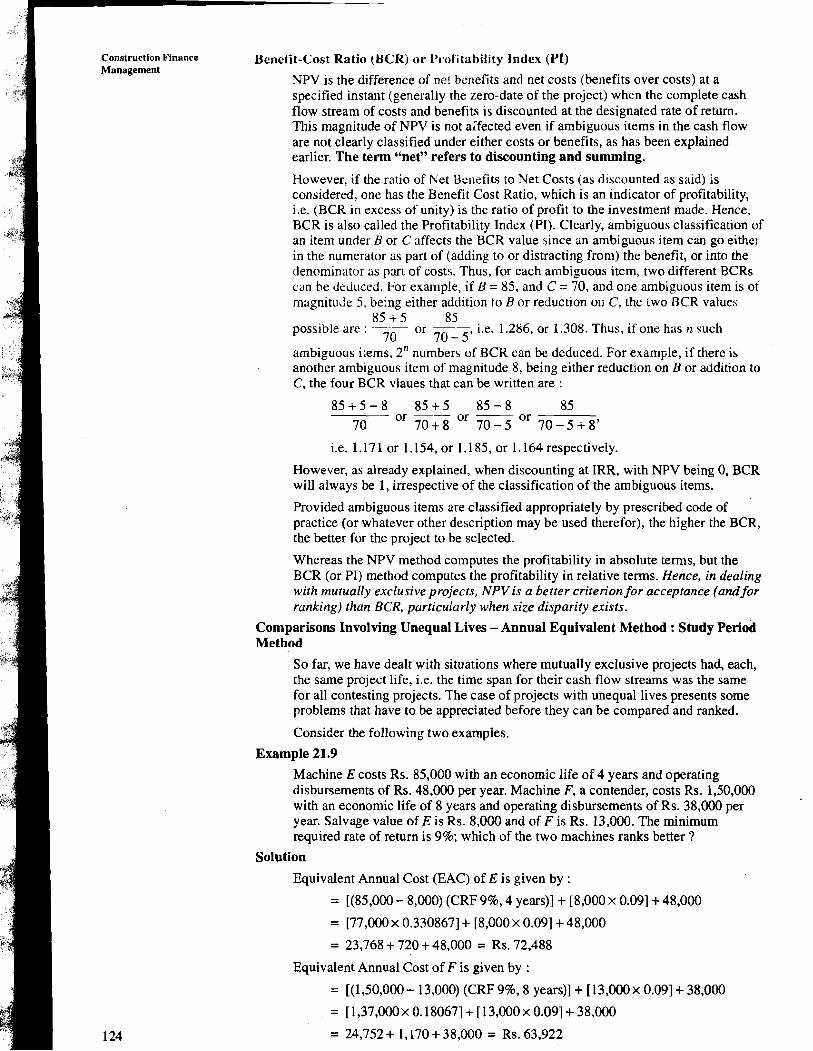

NPV is the difference of net benefits and net costs (benefits over costs) at a specified instant (generally the zero-date of the project) when the complete cash flow stream of costs and benefits is discounted at the designated rate of return. This magnitude of NPV is not alfected even if ambiguous items in the cash flow are not clearly classified under either costs or benefits, as has been explained earlier. The term "net" refers to discounting and summing.

However, if the ratio of Net Benefits to Net Costs (as discounted as said) is considered, one has the Benefit Cost Ratio, which is an indicator of profitability, i.e. (BCR in excess of unity) is the ratio of profit to the investment made. Hence, BCR is also called the Profitability Index (PI). Clearly, ambiguous classification of an item under B or C affects the BCR value since an ambiguous item can go either in the numerator as part of (adding to or distracting from) the benefit, or into the denominator 3s part of costs. Thus, for each ambiguous item, two different BCRs can he deduced. For example, if B = 85, and C = 70, and one ambiguous item is of ~nagnitudc 5, being either addition to B or reduction on C, the two BCR values

85 + 5 85 possible arc :

70 or --, i.e. 1.286, or 1.308. Thus, if one has n such

7 0 - 5 ambiguous items, 2" numbers of BCR can be deduced. For example, if there is another ambiguous item of magnitude 8, being either reduction on B or addition to C, the four BCR vlaues that can be written are :

i.e. 1.171 or 1.154, or 1.1 85, or 1.164 respectively.

However, as already explained, when discounting at IRR, with NPV being 0, BCR will always be 1, irrespective of the classification of the ambiguous items.

Provided ambiguous items are classified appropriately by prescribed code of practice (or whatever other description may be used therefor), the higher the BCR, the better for the project to be selected.

Whereas the NPV method computes the profitability in absolute terms, but the BCR (or PI) method computes the profitability in relative terms. Hence, in dealing with mutually exclusive projects, NPV is a better criterion for acceptance (and for ranking) than BCR, particularly when size disparity exists.

Comparisons Involving Unequal Lives - Annual Equivalent Method : Study Period Method

So far, we have dealt with situations where mutually exclusive projects had, each, the same project life, i.e. the time span for their cash flow streams was the same for all contesting projects. The case of projects with unequal lives presents some problems that have to be appreciated before they can be compared and ranked.

Consider the following two examples.

Example 21.9

Machine E costs Rs. 85,000 with an economic life of 4 years and operating disbursements of Rs. 48,000 per year. Machine F, a contender, costs Rs. 1,50,000 with an economic life of 8 years and operating disbursements of Rs. 38,000 per year. Salvage value of E is Rs. 8,000 and of F is Rs. 13,000. The minimum required rate of return is 9%; which of the two machines ranks better ?

Solution

Equivalent Annual Cost (EAC) of E is given by :

= [(85,000 - 8,000) (CRF 9%, 4 years)] + [8,000 x 0.091 + 48,000

= [77,000 x 0.3308671 + [8,000 x 0.091 + 48,000

= 23,768 + 720 + 48,000 = Rs. 72,488

Equivalent Annual Cost of F is given by :

= [(1,50,000 - 13,000) (CRF 9%, 8 years)] + [13,000 x 0.091 + 38,000

= [1,37,OOOx 0.180671 + [13,000 x 0.091 + 38,000

= 24,752+ 1,170+ 38,000 = Rs. 63,922

i Should we then call that F has an advantage of Rs. 8,566 per year over E ? May be it is so, but what about the EAC of F at a total value of Rs. 63,922 during the 5th to

i 8th years, both inclusive ? This seems to be acceptable if we assume that during the 5th to 8th year, both inclusive, an exactly equivalent machine E follows the present machine E, which will then need an EAC during this extended period exactly equal to that of the earlier E.

Accordingly, it is reasonable to adopt the above method of comparison based on Equivalent Annual Values (costs in this case). If machines E and F had lives, say, 4 and 7 years respectively, we may argue on the same times that machine E repeats itself over 7 times in 28 years commonly with machine F repeating itself over 4 times in the same 28 years (i.e. the least common multiple of the lives of the individual machines). In other words, disregarding all possible events which might occur after the time duration of shortest life alternative is the method to be adopted. This, therefore, is called the Study Period Method.

We may justify, the study period approach by the following argument also. That EAC of machine E as Rs. 72,488 stands. Regarding machine F, the investment cost and the salvage, which pertain to the entire life period must be prorated for the period of comparison, which is the shorter of the two lives of the machines E and F, this being the life of E, viz. 4 years in this problem. This prorating is'based on the dictum : Having distributed the EAC over the life of F, we collect the costs belonging to the 4-year study period by the following concept.

In the term (1,50,000- 13,000) x (CRF 9%, 8 years), considering the first four years only, the prorated present worth will be by multiplying this amount by USPWF (9%, 4 years), and taking its equivalent annual value over the 4 years will be by multiplying further by CRF (996, 4 years); noting that USPWF and CRF are mutually reciprocals, the term (1,50,000- 13,000), x (CRF 9%, 8 years), remains unaltered. [Likewise a possible second term 113,000 x SFF 9%, 8 years] too remains unaltered even after prorating for the first 4 years and then redistributing over the same 4 years.] Thus, on prorating basis too, the study period method is justified.

The case of unequal expenses through the years is simply to be handled by first getting the Net Present Equivalent cost by discounting individual yearly costs and summating these discounted values; and then distributing this sum as annuities through the years, i.e. by multiplying by the CRF. For example, if the operating disbursements in the 4 years were, respectively, Rs. 44,000; Rs. 47,000; Rs. 50,000 and Rs. 53,000, then, this part of the EAC would be computed as follows :

= [(44,000 x SPPWF 9%, 1 year) + (47,000 x SPPWF 9%. 2 years) + (50,000 x SPPWF 9%,3 years) + (53,000 SPPWF 9%, 4 years)] x (CRF 9%, 4 years)

= [(44,000x 0.91743) + (47,000~ 0.84168) + (47,000~ 0.77218) + (53,000 x 0.70843)] x 0.30867

= [40,367 + 39,559 + 3,6292 + 37,5471 x 0.30867 = Rs. 47,463

Example 21.10 Project A has an initial outlay of Rs. 18,000, with a service life of 2 years through which the yearly CFAT values are Rs. 14,000 and Rs. 12,800, respectively, with zero salvage value. Project B has an initial outlay of Rs. 35,000, with a service life of 4 years through which the yearly CFAT values are Rs. 14,000; Rs. 16,000; Rs. 12,800 and Rs. 10,800, respectively, with zero salvage value. The required rate of return is 10%.

Which of the two projects ranks better ?

Solution Project A

Present worth of the CFAT values

= (14,000 x 0.90909) + (12,800 x 0.82645) = Rs. 23,306

NPV = - 18,000 + 23,306 = + 5,306

EA Benefit = [5,306 x (CRF 10%. 2 years)]

= 5,306 x 0.57619 = Rs. 3,057

Capital Investment Decisions

Construction Nnance Management

Project B

Present worth of all the CFAT values

= Rs. 42,944

NPV = - 35,000 + 42,944 = + 7944

EA Benefit = [7,944 x (CRF 10%. 4 years)]

= 7,944 x 0.3 1547 = Rs. 2,506

Project A ranks better than Project B.

Investment Proposals for Income-Expansion and for Cost-Reduction In Example 21.9, we prefer F to E since the EAC is less for F. In Example 21.10, we prefer A to B since the EAB is more for A. Thus, for invesmentproposals for generating incomes, expansion of income is the criterion for choice; and for investment proposals for contributing towards the costs, reduction in cost is the criterion for choice.

It is generally premised that a cost-reduction expenditure does not affect the gross income. Of course, there can be instances of combined cost-reduction and income-expansion expenditures. For an income-expansion expenditure, the increase in income must be more than the increase in expenditure.

Also, cost-reduction alternatives are mutually exclusive; but mutual exclusivity is not always true of multiple income-exp~nsion alternatives.

Following example illustrates a combined cost-reduction cum income-expansion expenditure.

Example 21.11 Two processes are available for stone crushing at a quany site. One has a first cost of Rs. 4,00,000 with an annual operating cost of Rs. 1,28,000. The other would cost Rs. 5,60,000 with an annual operating cost of Rs. 1,35,000. The second process will also sort the crushed stone and hence, it is expected that annually an extra Rs. 55,000 is realised in profits. The life of equipment in each of the processes is 11 years with zero salvage value. The minimum required rate of return is 10%. Is the extra expenditure in the second process approvable ?

Solution Equivalent Annual Cost (EAC) of the first process is

= [4,00,000x (CRF lo%, 11 years)] + 1,28,000

= (4,00,000x 0.15396) + 1,28,000 = Rs. 1,89,584

Equivalent Annual Cost (EAC) of the second process is

= [5,60,000x (CRF lo%, 11 years)] + 1,35,000- 55,000

= (5,60,000 x 0.15396) + 1,35,000 - 55,000 = Rs. 1,66,218

The extra investment is approvable since EAC is reduced, when considering inclusive of income expansion.

Here, the first process goes relatively for cost reduction; but, because of the extra profits, the second process involves income-expansion. Rather than straightaway tending to chose the first process for cost-reduction purposes, we have to consider the opportunity for income-expansion also if taking to the second process.

A Note We had so far considered that the equipment (or the project) will be used for as long as it will be economically alive even allowing (conceptually) for continuing with like replacements into a long future (as discussed in explaining the study period method).

However, in some instances, the length of service required may be short and known. In such instances, we use this period for capital recovery on the investment cost net of salvage and allow for the interest liability on the salvage.

The following example illustrates this.

Example 21.12 A battery-operated fork-lift costs Rs. 1,70,000 and will have an operating cost of Rs. 40,000 per year and a salvage value of Rs. 65,000. A diesel-operated fork-lift capable of performing the same tasks costs Rs. 1.10.000 with operating cost of Rs. 70,000 per year and a salvage value of Rs. 25,000. The construction job on which the equipment will be needed is likely to be completed in 2 years. The minimum required rate of return is 11%. Which alternative is preferable ?

Solution Annual cost of battery-operated fork-lift is

= [(I ,70,000 - 65,000) x (CRF 11%. 2 years)] + (65,000 x 0.11) + 40,000

= (1,05,000~ 0.57619) + 7,150+ 40,000 = Rs. 1,07,650

Annual cost of diesel-operated fork-lift is

= [(1,10,000- 25,000) x (CRF 11%. 2 years)] + (25,000~ 0.11) + 70,000

= (85,000 x 0.57619) + 2,750 + 70,000 = Rs. 1,21,726

The battery-operated fork-lift is the preferable alternative.

SAQ 5 Rework all the examples (Example 2 1.9 to Example 2 1.12) with costs decreased by 10% and benefits increased by 5%.

21.7 CAPITAL RATIONING