Towards dynamic efficiency: Innovation and its implications for antitrust

54

Towards dynamic efficiency: Innovation and its implications for antitrust BY MELISSA A. SCHILLING* _________________________________________________________________ _____________ There is growing consensus that the goal of antitrust enforcement should be to manage for dynamic efficiency, i.e., an appropriate balance between short-run static efficiencies such as reducing costs and maximizing consumer surplus, and the longer term gains that arise from innovation. However, determining how to incorporate innovation into efficiency goals is complicated; innovation typically entails great uncertainty, long time horizons, and interdependencies across projects. This means there are no easy solutions for estimating the welfare impact of any given innovation investment or strategy. We can, however, use what we know about how firms manage the innovation process, including how they choose and value projects and ration their capital to meet their short and long-term needs, to gain insight into how we can best foster firms’ incentives to innovate in ways

Transcript of Towards dynamic efficiency: Innovation and its implications for antitrust

Towards dynamic efficiency:

Innovation and its implications for antitrust

BY MELISSA A. SCHILLING*

_________________________________________________________________

_____________

There is growing consensus that the goal of antitrust enforcement

should be to manage for dynamic efficiency, i.e., an appropriate

balance between short-run static efficiencies such as reducing

costs and maximizing consumer surplus, and the longer term gains

that arise from innovation. However, determining how to

incorporate innovation into efficiency goals is complicated;

innovation typically entails great uncertainty, long time

horizons, and interdependencies across projects. This means there

are no easy solutions for estimating the welfare impact of any

given innovation investment or strategy. We can, however, use

what we know about how firms manage the innovation process,

including how they choose and value projects and ration their

capital to meet their short and long-term needs, to gain insight

into how we can best foster firms’ incentives to innovate in ways

that improve long-run economic welfare. I provide some

illustrative examples for how these insights can be incorporated

into antitrust enforcement.

KEY WORDS: dynamic efficiency, innovation, pharmaceuticals, R&D portfolios,

concentration, mergers, Hatch-Waxman laws

______________________________________________________________________________

*Professor of Management and Organizations at New York

University. Contact at [email protected]

AUTHOR’S NOTE: I wish to thank Noah Brumfield, Albert Foer, and Gregory Gundlach

for their helpful suggestions.

I. THE IMPORTANCE OF INNOVATION AND DYNAMIC EFFICIENCY

Innovation is one of the most powerful drivers of increased human

welfare available to us. Innovation enables the development of

new products, the improvement of processes, and the creation and

improvement of social institutions. Innovation has yielded a

wider range of goods and services to be delivered to people

worldwide. It has made the production of food and other

necessities more efficient, yielded medical treatments that

improve health conditions, and enabled people to travel to and

communicate with almost every part of the world. Innovation can

sometimes result in negative externalities; for example,

production technologies may generate pollution, agricultural and

fishing technologies can result in erosion and depletion of

natural resources, and medical technologies can result in

unanticipated consequences such as antibiotic-resistant strains

of bacteria. However, innovation is, in its purest essence, the

creation and application of new knowledge—knowledge to solve our

problems and pursue our goals.1 Sometimes this knowledge is

applied to problems hastily, without full consideration of the

1 H. A. Simon, Technology and Environment. 19 MANAGEMENT SCI (1973)

consequences and alternatives, but overall it serves us better to

have more knowledge than less.

There is widespread consensus that the goal of antitrust

laws are to promote economic welfare.2 Given the contribution of

innovation to economic welfare, it should be clear that antitrust

laws must pursue dynamic efficiency, that is, an appropriate balance

between short-run static efficiencies such as reducing costs and

maximizing consumer surplus (productive efficiency and allocative efficiency)

with longer term efficiencies that arise from innovation.

Efficiency as an abstract ideal is relatively clear. It

refers to producing or performing in the best possible way, with

a minimum of waste. In its use in antitrust, however, efficiency

has taken on many more meanings, some of which are very difficult

to define and measure. Productive efficiency refers to production

and distribution at the lowest feasible cost. This definition

adheres most closely to the layman’s definition of efficiency,

though even this definition yields a range of potential outcomes

2 RA POSNER, ANTITRUST LAW ix (2nd edition)(2001).

spanning from maximizing production for a given level of input to

minimizing inputs for a given level of output. Defining

allocative efficiency is more complicated, for it necessitates

assumptions about the type of welfare distribution we deem to be

best. Foer’s description of allocative efficiency as the

allocation of resources to their most valued uses3 corresponds

most closely to what is also known as distributive efficiency, whereby

goods are distributed to those who can gain the most utility from

them.4 Under this utilitarian framework, social welfare is

maximized under perfect economic equality, implying that wealth

should be redistributed from the rich to the poor. The challenge

with such a framework, of course, is that it diminishes the

relationship between action and consequence (which many would

regard as unjust), and consequently reduces the incentives for

economic development and growth (reducing long-term welfare

creation).

3 AA Foer, On the inefficiencies of efficiency as the single-minded goal of antitrust. In this issue of ANTITRUST BULLETIN (2015).

4 AP LERNER, THE ECONOMICS OF CONTROL: PRINCIPLES OF WELFARE ECONOMICS (1944).

Dynamic efficiency is even more complicated. Dynamic

efficiency requires us to take into account the benefits achieved

through research, development, and innovation. This means that

whatever model of welfare optimization we wish to adhere to, we

should be optimizing it over some time frame that extends into

the future, as we do not wish to unduly discount the future for

the sake of the present. In essence, we would like to maximize

the net discounted flow of benefits to total social welfare

(including profit distributions, wages, technological

advancements, etc.) that accrue from now until some time horizon

in the future. However, all of the problems with discounted cash

flow that will be presented later in the paper with respect to

valuing an innovation project apply here also, but are a

magnitude of order greater: The innovation outcomes of

investments and policy decisions are difficult or impossible to

predict, people are heterogeneous in the degree to which they

would value different outcomes, and all the parts of the system

(input costs, technological options, competitors, development of

complements, etc.) are moving. Quantitative approaches to

analyzing the potential dynamic efficiency implications of a firm

strategy should thus be interpreted with extreme caution; they

have the potential to lend an artificial sense of certainty to

something that is, in fact, unknowable. We can, however, use what

we know about innovation, competition, appropriability, and

collaboration to better incorporate dynamic efficiency into

antitrust enforcement.

I will begin here by reviewing what we know about how firms

manage the innovation process, including how they choose and

value projects and ration their capital to meet their short and

long-term needs. This yields several insights into how we can

foster and preserve firms’ incentives to innovate in ways that

best improve long-run economic welfare. I will then provide some

illustrative implications for how these insights can be

incorporated into antitrust enforcement, including, 1. Shifting

from thinking about concentration to thinking about firm size

distributions, 2. Implications of (and for) Hatch-Waxman and

automatic substitution laws in pharmaceuticals, and 3.

Collaboration agreements and merger analysis.

II. THE INNOVATION PROCESS

In a seminal paper on organizational learning, James March

demonstrated the trade-offs between exploration and exploitation:

exploiting local, known solutions is efficient and generates

reliable returns, but offers little hope of creating highly novel

or radical innovation; exploring broader, less familiar domains

increases the variance of outcomes, resulting both in a higher

likelihood of finding no beneficial innovation, and a higher

likelihood of generating breakthrough innovation.5

In general the theoretical and empirical research on

organizational learning has concluded that we need a balance

between exploitation and exploration. If a firm (or economy)

focuses only on exploitation, it may do well in the short run,

but then eventually run out of growth prospects as its existing

technological trajectories mature. It will likely be

technologically leapfrogged by competitors who made longer-term,

riskier bets. On the other hand, a firm (or economy) that invests

only in exploration risks not being able to meet its short term 5 JG March, Exploration and exploitation in organizational learning. 2 ORGANIZATION SCI 71

(1991).

needs. As Jack Welch, former CEO of GE once famously said, “You

can’t grow long term if you can’t eat short term. Anyone can

manage short. Anyone can manage long. Balancing those two things

is what management is.”6

The synergy between exploration and exploitation strengthens

this point: most breakthrough innovations accrue much of their

ultimate performance and potential for benefiting society through

the myriad incremental improvements that are made to them.7 The

first airplanes or first automobiles, for example, were

interesting novelties, but of little use to most people. It was

the many thousands of improvements that transformed them into the

enormously beneficial means of transportation they are now. Pure

exploration will tend to yield breakthrough discoveries that are

never fully assimilated or made useful; pure exploitation will

tend to yield very little discovery at all. This has important

6 J. A. Byrne, How Jack Welch Runs GE, BUSINESSWEEK, June 8, 1998, at 90. 7 MA SCHILLING, STRATEGIC MANAGEMENT OF TECHNOLOGICAL INNOVATION, 4th ed. (2013); ML

Tushman & P Anderson, Technological discontinuities and organizational environments. 31 ADMINISTRATIVE SCI QUART 439 (1986); P Anderson & ML Tushman, Technological discontinuities and dominant designs: A cyclical model of technological change. 35 ADMINISTRATIVE SCI QUART 604 (1990).

implications for how firms allocate capital to innovation

investments and the importance of R&D portfolios.

A. Capital rationing and the R&D portfolio

Most firms face serious constraints in the capital and other

resources they can generate internally or obtain externally,

forcing them to choose between multiple potentially valuable

projects. Furthermore, innovation is risky – new product

development failure rates are consistently estimated to be over

95% -- and even successful innovations can often take a very long

time to payoff. Firms must thus be very strategic in their

allocation of financial and human resources to innovation

projects. Managers must construct their R&D portfolio in a way

that takes into account projects of different risk, projects with

different payoff horizons, and projects with different kinds of

synergies with the firm’s existing capabilities.

Many firms use a form of capital rationing in formulating

their new product development plans. Under capital rationing, the

firm sets a fixed research and development budget (often some

percentage of the previous year’s sales), and then uses a rank

ordering of possible projects to determine which will be funded.

Firms might establish this budget on the basis of industry

benchmarks or historical benchmarks of the firm’s own

performance. Firms’ R&D budgets are relatively inelastic to

technological opportunity: most firms have a finite pool of funds

they are able or willing to spend on R&D and they spend this

amount irrespective of the technological developments in their

industries.8

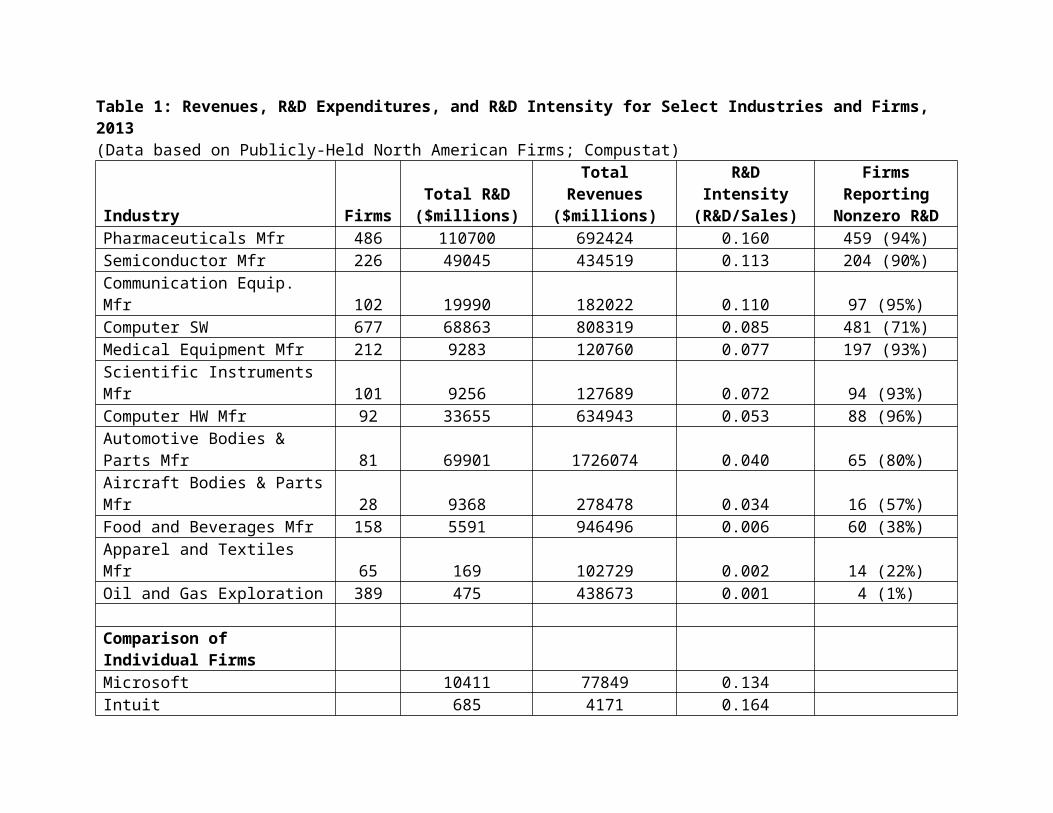

There is, however, considerable variance in spending across

industries and across individual firms within industries. Firms

in the software and pharmaceutical industries, for example, spend

considerably more on R&D than firms in the energy, food, or

automotive industries. Furthermore, some individual firms

significantly outspend their rivals on a percentage of sales

basis (see Table 1).

8 MA SCHILLING, STRATEGIC MANAGEMENT OF TECHNOLOGICAL INNOVATION, 4th ed. (2013); MASchilling, Technology shocks, technological collaboration, and innovation outcomes. ORGANIZATIONSCI (forthcoming).

---------------------Insert Table 1 About

here--------------------------------

Firms also vary significantly in their allocation of R&D

funds across particular kinds of projects. Firms might vary in

their degree of diversification or specialization, for example.

They might also vary in the distribution of risk in their

projects, with some firms choosing mostly lower risk projects,

and others taking on broader range of projects with a multitude

of risk profiles. Google, for example, has an R&D portfolio that

is incredibly diversified both in terms of technological domain

and risk level, with projects ranging from incremental projects

to improve their advertising algorithms to radical projects such

as driverless cars and the Calico project which seeks to cure

aging.

Thinking about the R&D budget as a fixed percentage of sales

also reveals a rather obvious point about firm size: other things

being equal, a large firm can invest significantly more in R&D

than a small firm, permitting it to pursue more projects, or

projects of greater size.9 In general, only large firms will have

large enough R&D budgets to allocate some of their funds to

extremely long-term or risky projects. The development of

fundamentally new technologies, however, often requires such

long-term and risky investment. Consider, for example, the recent

development of ZF-TFs (zinc-finger transcription factors), CRISPR

(clustered regularly interspaced palindromic repeats) or TALEN

(transcriptor activator-like effector nucleases) technologies,

all of which offer the potential for “editing” the genetic code

of a living individual to correct genetically-based diseases

(e.g., cystic fibrosis, sickle cell anemia, Huntington’s, and

many others) or confer genetic resistance to non-genetically-

based diseases (e.g., Sangamo is using a ZF-TF approach to

developing a potential vaccine for HIV). These potential

9 A long historical debate on the advantages of R&D investment by large versus small firms does not conclude that one is superior to the other; rathereach has its strengths. For example, large firms may reap greater economies ofscale in R&D, amass greater learning due to involvement in a greater number ofprojects, and be able to take on projects of greater scale or risk; small firms may be more nimble due to fewer inertia-inducing commitments, may make better choices about projects due to constrained resources, and have higher-powered incentives for employees to innovate due to the potential for more direct risk and profit sharing. See for example WM Cohen, Fifty years of empirical studies of innovative activity and performance. Chapter 4 in the 1 HANDBOOK OF THE ECONOMICS OF INNOVATION, 129 (2010); also ZJ Acs & DB Audretsch, Innovation, market structure, andfirm size. 69 REV ECON STAT, 567 (1987); and TR Zenger & WS Hesterly, The disaggregation of corporations: Selective intervention, high-powered incentives, and molecular units. 8 ORGANIZATION SCI, 209 (1997).

treatment modalities have come about only because of the enormous

amounts of research that have gone into understanding the human

genome, and the ways it might be safely modified. Furthermore,

these gene editing approaches still require years of further

funding to develop effective delivery methods and get through the

process of clinical testing. In the end, they will compete with

each other, and potentially with other modalities developed in

the future. Though these technologies offer huge potential for

easing human suffering, they are clearly extremely risky

investments. How do organizations justify investment in such

risky projects with such a long-term payoff?

B. Valuing innovation investments

In business schools around the world, students are taught

how to use discounted cash flow methods, and option-based methods

to enable investment valuation. Such quantitative approaches can

help managers to consider the timing of investment and cash

flows, and explore the financial implications of particular what-

if scenarios. They can make the returns of a project seem

unambiguous, and managers often find them very reassuring.

However, this minimization of ambiguity is often illusory;

discounted cash flow estimates are only as accurate as the

original estimates of the profits from the technology, and in

many situations it is extremely difficult to anticipate the

returns of the technology. Furthermore, such methods discriminate

heavily against projects that are long term or risky, and the

methods may fail to capture the strategic importance of the

investment decision. Technology development projects play a

crucial role in building and leveraging firm capabilities, and

creating options for the future. Investments in new core

technologies are investments in the organization’s capabilities

and learning, and they create opportunities for the firm that

might otherwise be unavailable. Thus, standard discounted cash

flow analysis has the potential to severely undervalue a

development project’s contribution to the firm. For example,

Intel’s investment in DRAM technology would have been considered

a total loss by NPV methods (Intel exited the DRAM business after

Japanese competitors drove the price of DRAM to levels Intel

could not match). However, the investment in DRAM technology laid

the foundation for Intel’s ability to develop microprocessors—and

this business has proved to be enormously profitable for Intel.

Options-based methods might offer a better conceptual

framework for innovation investments, yet here too there are

problems in applying the valuation methods literally. Implicit in

the value of options is the assumption that one can acquire or

retain the option for a small price, and then wait for a signal

to determine if the option should be exercised.While this

assumption might hold true for an outside firm investing venture

capital in another firm’s innovation projects, it would be rare

for this assumption to hold for a company investing in its own

development efforts. In the case of a firm undertaking solo new

product development, it may not be possible to secure this option

at a small price; it may require full investment in the

technology before a firm can determine if the technology will be

successful.Furthermore, while the value of a stock is independent

of the call holder’s behavior (that is, the call holder can

simply wait and observe whether the value of the stock rises or

falls), the value of an R&D investment is not independent of the

investor’s behavior. A firm’s degree of investment, its

development capabilities, its complementary assets, and its

strategies can all significantly influence the future returns of

the development project. Therefore, rather than simply waiting

and observing the value of the investment, the investor is an

active driver of the value of the investment.

In practice, innovation investment decisions tend to be

based heavily on qualitative criteria, such as assessments of

what customers are likely to want in the future, and what

projects will best build the firm’s strategic capabilities and

potential for creating a valuable and differentiated position.

Quantitative methods are, in fact, often used to defend or

buttress a decision that has already been made on qualitative

grounds, and it is fortunate for society that this is the case,

as analysis of innovation (and entrepreneurial) investments by

strictly financial means, based on the tools currently available,

would likely result in far less technological development.

C. Innovation portfolios and the investment horizon

As noted previously, many firms manage their R&D investment

as a portfolio, balancing their investment objectives with

respect to risk, timing of payoffs, and breadth of search,

against their current resource position (e.g., cash, man-hours,

capabilities). An example of one well-known portfolio model (the

Aggregate Project Planning Framework) is provided in Figure 1,

with some examples from Toyota’s innovation pipeline as of 2014.

Managers are often exhorted to use such a model because without

such explicit consideration, firms can easily become imbalanced

in their investments, or find that they have many more projects

underway than can be realistically supported.

------------------------Insert Figure 1 About

here---------------------------

The model shown in Figure 1 shows that projects might be

classified into different types based on the amount of product

and process change they require and their expected payoff timing.

Platform projects, for example, offer fundamental improvements in

the cost, quality, and performance of a technology over preceding

generations. Derivative projects, on the other hand, involve

incremental changes in products and/or processes. A platform

project is designed to serve a core group of consumers, whereas

derivative projects are often modifications of the basic platform

design to appeal to different niches within that core group. For

example, in Figure 1, Toyota’s Prius family of hybrid cars is a

platform that includes the Prius, Prius C, Prius V, and Prius

Plug-In. While all the models are based on the same basic design,

each offers a different combination of features to appeal to

different market segments. Toyota also has a platform project it

calls the Toyota New Global Architecture – a sweeping overhaul of

its powertrain system that will create more commonality of parts

across different engines. At the same time, Toyota is developing

a number of incremental projects -- features such as better

headlights, infra-red rear-view backup cameras, and more, to

enhance the value of its existing cars.

Breakthrough projects may take ten years or more before

resulting in a new product or process, and advanced R&D projects

may not even be tied to one particular commercial objective, but

rather are expected to develop new capabilities that might be

important in the future. Toyota, for example, is working on

advanced R&D and breakthrough projects in its fuel-cell vehicle

lineup, which it began developing in 1996 and is expected to

launch in 2015.

Advanced R&D projects and breakthrough projects often do not

recoup their investments directly; rather they pay off when they

enable later investments in new platforms and derivative

projects. Consider, for example, Boeing’s development of the

Sonic Cruiser. Boeing considered the project to be necessary for

preserving the company’s development capabilities, even though

quantitative analysis suggested that the project would never be

profitable. As noted by Walt Gillette, Boeing’s development

program manager, “If the company doesn’t create a new airplane

every 12 to 15 years, the needed skills and experience will be

gone. Too many of the people who created the last new airplane

will have retired or moved on to other companies, and their

skills and experience will not have been passed on to the next

generation of Boeing employees.”10 Toyota’s FV2, a futuristic

single-person concept car that has no gas pedal or steering wheel

10 L. Gunter, The Need for Speed, BOEING FRONTIERS. Retrieved November 20, 2002,from www.boeing.com/news/frontiers/archive/2002/july/i_ca2.html.

but instead responds to shifts in the user’s body weight, also

falls into this category. The project helps Toyota explore

concepts for future product development but it has no immediate

commercialization objectives.

The preceding suggests that firms in technology-intensive

industries typically have to manage their innovation investments

and products with a long-term lifecycle approach. A firm that

invests heavily in derivative projects that may be immediately

commercialized with little risk may appear to have good returns

on its R&D investment in the short run, but then be unable to

compete when the market shifts to a newer technology. On the

other hand, a firm that invests heavily in advanced R&D or

breakthrough projects may be on the leading edge of technology,

but run into cash flow problems from a lack of revenues generated

from recently commercialized platform or derivative projects. For

the purposes of evaluating dynamic efficiency, this highlights

the importance of evaluating entire research programs rather than

the gains or losses from individual innovation projects.

D. Organizational slack and appropriability mechanisms

It should now be apparent that strong pressure for current

cash flows will tend to induce a firm to focus on derivative

innovation, if any innovation at all. Though innovation is a

powerful competitive lever, it is too simplistic to posit that

more competition will lead to more innovation in an industry. We

must first think about innovation as a distribution over types of

innovation that range from long-term to short-term, and with

varying levels of probability of success. How a firm invests over

that distribution will be influenced by 1) the degree to which it

can spare funds in the present to invest in the future

(“organizational slack”), 2) the risk/return payoff the firm

estimates will arise from its investments, 3) interdependencies

between long-term and short-term projects, and 4) the firm’s

assessment of competitors’ investments and how they are likely to

influence the firm’s future. Firms with healthy margins and/or

large cash reserves can afford to make investments in projects

with longer-term payoff horizons and/or high risk-return

profiles, and are more likely to do so when they perceive

competitors are placing similarly long-term bets. Firms with low

margins and small cash reserves will be forced to focus on a

relatively short payoff horizon of investment, and will not be

able to undertake the riskier projects.

It is well understood that organizational slack permits the

organization to make investments in projects other than those

required by short-term optimization, enhancing greater

experimentation and risk taking.11 More generally, scarcity of

resources required for survival will narrow the scope (both

breadth of activities and length of time horizon) of that to

which an individual or firm will attend; excess resources (or

“slack”) permit (though do not necessarily induce) the individual

or firm to broaden the scope of that in which they can plan and

invest.12 Notably, this suggests that the presence or lack of

organizational slack should also directly influence investment in

activities related to environmental sustainability, employee

welfare, and long-term social welfare more generally.

11 RM CYERT & JG MARCH, A BEHAVIORAL THEORY OF THE FIRM (1964); N Nohria & R Gulati, Is slack good or bad for innovation? 39 ACADEMY OF MANAGEMENT J. 1245 (1996).

12 This is consistent with Perelman’s observation that in a stagnant or contracting economy, businesses tend to focus on cutting costs, while in a growing economy, firms focus on investment for the future (M PERELMAN, RAILROADING ECONOMICS: THE CREATION OF THE FREE MARKET MYTHOLOGY 2006)

It should also be apparent that firms cannot afford to make

large investments in innovation if the results of their efforts

can be readily expropriated by others. Without some form of

appropriability mechanism that enables the firm to capture the

returns of their innovations, they will have neither resources

nor incentive to invest in innovation projects. Consider, for

example, the pharmaceutical industry. Drug development is hugely

expensive and has a very high failure rate. Most studies indicate

that it costs at least $1.5 billion and a decade of research to

bring a new FDA-approved pharmaceutical product to market.13 As a

result, on average, branded pharmaceutical companies spend a much

larger portion of their revenues on R&D than firms in most other

industries, as previously shown in table 1. The statistics on

drug development costs are, in fact, an understatement because

they do not fully account for the costs of the many failed drugs

that are abandoned earlier in the development process. In the

pharmaceutical industry, only one out of every 5,000 compounds

tested makes it to the pharmacist’s shelf, and only one-third of

13 See Joseph A. DiMasi & Henry G. Grabowski, The Costs of Biopharmaceutical R&D: Is Biotech Different?, 28 MANAGERIAL & DECISION ECON. 469 (2007).

those will be successful enough to recoup the investment in

researching and developing the original 5,000 compounds (see

Figure 2).14

--------------------Insert Figure 2 about

here-------------------------

Accounting for investment in failed drug efforts suggests

that the cost of drug development is much higher than is

typically reported. A study of R&D spending and new drug

approvals published in Forbes in 2012, for example, found that

firms spent over $6 billion per approved drug (see Table3

below).15 16 A firm’s incentive to make such long-term, high cost,

and high risk investments is directly related to the strength of

appropriability mechanisms that will enable them to recoup their

14 Pharmaceutical Industry, 2008, STANDARD & POOR’S INDUSTRY SURVEYS. See also H Grabowski, J Vernon & JA DiMasi, Returns on research and development for 1990s new drug introductions, PHARMACOECONOMICS (2002); Innovation.org, Drug Discovery and Development: Understanding the R&D Process, Washington, DC: PhRMA, (February 2007), available athttp://www.innovation.org/drug_discovery/objects/pdf/RD_Brochure.pdf.

15 M Herper, The truly staggering costs of inventing new drugs. FORBES, February 10th , 2012.

16 According to a study by the Manhattan Institute for Policy Research, the majority of the drug development expense is due to the extremely costly and time-consuming process of clinical trials: if analysis is limited to drugsthat are ultimately approved by the FDA, phase III clinical trials representedover 90% of the total cost of development. (Project FDA Report, MANHATTAN INSTITUTE FOR POLICY RESEARCH, No. 5 April 2012)

costs.17 One study concluded that about 65% of pharmaceutical

inventions would not have been introduced into the market absent

patent protection.18

-----------------------Insert Table 3 About

here---------------------------

III. IMPLICATIONS FOR MANAGING FOR DYNAMIC EFFICIENCY

The fact that innovation typically entails great

uncertainty, long time horizons, and interdependencies across

projects, means that there are no easy solutions for estimating

the welfare impact of any given innovation investment or

strategy. We can, however, use what we know about the innovation

process to improve how we manage for dynamic efficiency in

antitrust enforcement. I will provide three examples below: 1.

Shifting from thinking about concentration to thinking about firm17 See H. Grabowski, H. Patents, innovation and access to new pharmaceuticals. 5 J.

INTERNATIONAL ECON LAW, 849 (2012); Henry G. Grabowski & John M. Vernon, Effective Patent Life in Pharmaceuticals, 19 INT’L J. TECH. MGMT. 98 (2000) (pharmaceutical industry particularly sensitive to patent incentives); Bronwyn H. Hall & Dietmar Harhoff, Recent Research on the Economics of Patents, 4 ANN. REV. ECON. 541 (2012) (describing a survey that found that patents effectively increase innovation primarily in the pharmaceutical industry); B.N. Roin, Unpatentable Drugs and the Standards of Patentability, 87 TEX. L. REV. 503 (2008) (describing the pharmaceutical industry’s unique dependence on patent protection to spur research and development investment).

18 Edwin Mansfield, Patents and Innovation: An Empirical Study, 32 MGMT. SCI. 173 tbl.1 (1986).

size distributions, 2. Implications of (and for) Hatch-Waxman and

automatic substitution laws in pharmaceuticals, and 3.

Collaboration agreements and merger analysis.

A. Firm size distributions versus concentration

In the preceding, I described three fundamentally new

medical technologies being developed for editing the human genome

in situ, CRISPRs, TALENs, and ZF-TFs. It is worth noting that the

advances in these technologies have been due to a synergistic

combination of efforts among university scientists, small-to-

medium sized biotechnology firms, and large pharmaceutical firms.

For example, though early research into zinc fingers was

primarily conducted in university labs by small teams of

researchers, a U.S. based biotechnology firm called Sangamo (with

$24 million in revenues in 2013), has been responsible for many

of its advances into potential gene therapy treatments, and

developed ZF-TF applications for hemophilia, Huntington’s, HIV,

and more. Sangamo, in turn, signed a collaboration and licensing

agreement with the much larger Shire, a UK-based pharmaceutical

firm (with nearly $5 billion in revenues in 2013). Under the

agreement, Shire will be responsible for clinical testing and

commercialization of the hemophilia related products. This value

chain of drug development and commercialization aptly illustrates

a key point of this article: different kinds of organizations

have different incentives and capabilities to perform different

kinds of innovation, and we need different kinds of innovation to sustain

optimal technological advance.

For most industries, there is no single optimal size of firm

for maximizing innovation -- most industries require a

distribution of firm sizes. There are some types of projects and

innovation activities that only large firms can realistically

pursue. Microsoft spent about $500 million developing the Xbox

game console, spent another $500 million advertising it, and then

had to be able to sustain losses while it sold the console at a

loss until it recouped profits through game royalties. Toyota

spent about $1 billion developing the Prius – about average for

the cost of developing a new car. Boeing spent $32 billion

creating the 787 Dreamliner. Clearly these innovations could not

have been developed by small firms. However, in each of these

industries, small and/or new firms also keep the pressure on

large players by investing in different kinds of projects: Ouya

and MOJO, for example, released microconsoles for video gaming

based on Android software for a small fraction of the development

cost of a regular console; Tesla woke up the auto industry with

its surprisingly successful development of an electric vehicle

based on 18650 lithium-ion batteries (the type used in laptops);

and Terrafugia hopes to disrupt commercial aircraft manufacturing

with its breakthrough flying car. Many of these start-ups will

not survive, but they foster innovation and competition by

bringing fundamentally new ideas into their industries.

The previous suggests that rather than focusing simply on

market concentration, greater empirical research should attempt

to identify the characteristics of productive distributions for

different kinds of industries. Work has begun to emerge that

examines the distribution of firm sizes in industries, and

generally concludes that most industries exhibit a power law

distribution 19in firm sizes, though industries vary considerably

19 A power law is a function where one quantity varies as a power of another, e.g, f(x) = axk. Many natural and social phenomena exhibit power law

on the length and width of the “tail” of such distributions.20 A

deeper base of knowledge in this area could move us from thinking

overly simply about concentration thresholds, to a more nuanced

and multidimensional understanding of how different sizes of

firms influence different kinds of innovation and competition.

Relatedly, it would be useful for us to have a richer

understanding of how different levels of organizational slack

influence the amount and types of innovation produced in

different kinds of industries. In industries with greater risk or

longer payoff horizons for innovation, for instance, we may need

mechanisms that ensure firms have more organizational slack.

B. Hatch Waxman and automatic substitution laws

In 1984, the United States passed The Drug Price Competition

and Patent Term Restoration Act (known as the Hatch-Waxman Act)

in hopes of increasing competition by generic drugs. Under the

Act, generic drugs can avoid the regular clinical testing process

distributions. For example, the number of cities tends to vary as a power of the size of the city, creating a distribution that has a peak at a relatively small size but has a long right tail because there are some cities that are very large.

20 RL Axtell. Zipf distribution of U.S. firm sizes. 293 SCIENCE (5536):1818 (2001); X Gabaix, YM Ioannides, Chapter 53 The evolution of city size distributions. 4 HANDBOOK OF REGIONAL AND URBAN ECONOMICS, 2341 (2004).

– their manufacturers need only submit an Abbreviated New Drug

Application (ANDA) to prove the product is “bioequivalent” to the

original branded drug. A drug is considered to be bioequivalent

if its bioavailability is between 80% to 120% of the original

drug. Manufacturers can only apply for an ANDA and enter the

market after the original branded drug’s patent has expired. Once

generic substitutes are available for a branded drug, automatic

substitution laws in most states either permit (or even require)

pharmacists to automatically substitute a generic for a patient’s

branded drug prescription. At this point there is little left for

the branded drug maker to do but to abandon the drug – money

spent on promoting the drug will be wasted as the drug will be

swapped out for that of another manufacturer at point of sale.

Though patent protection in the drug industry is considered

relatively strong (compared to, for example, electronics where it

is easier to “invent around” a patent),21 it can still be

difficult for pharmaceutical firms to appropriate the returns to

21 R Levin, A Klevorick, R Nelson, & S Winter, Appropriating the Returns from Industrial Research and Development, 3 BROOKINGS PAPERS ON ECONOMIC ACTIVITY, MICROECONOMICS 783 (1987).

their drug development investments. First, because patents are

applied for before the drug enters the clinical testing process,

by the time a drug reaches the market, its patent protection is

surprisingly brief. In the US, new drugs are commonly awarded a

patent of roughly twenty years, but approximately half of those

years will be spent in pre-clinical testing and clinical trials.

The firm can apply for up to five years extension of its patent

to make up for some of that time spent in the approval process,

but the average drug ends up with only seven to twelve years to

recoup its development expense under patent protection before

generics enter the market and drive the price of the drug down by

as much as 80%. Because generics spend significantly less on

development and testing, and also choose to spend little on

marketing (because they only enter markets where physicians and

caregivers have already been educated about the value of an

existing drug), they have an enormous cost advantage over the

branded pharmaceutical manufacturer who developed the drug.

It is also important to note that many drugs face

competition from substitute treatments even before their patents

expire, because other branded pharmaceutical companies may offer

treatments that address the same problem via different compounds,

route of administration (e.g., dissolvable tablets, liquid oral

suspension, extended release capsules), or with other

pharmokinetic or pharmacodynamic properties. For example, in the

cholesterol medication market, Pfizer’s Lipitor, AstraZeneca’s

Crestor, Merck’s Zocor and Vytorin all competed against each

other as patented products. Pfizer’s Lipitor (atorvastatin) had

an early mover advantage that by 2003 had made it the best-

selling pharmaceutical of all time. However, other statins

quickly and successfully entered the market and took share away

from Lipitor by offering functional alternatives and enhancements

to the product long before its patent had expired.

As a consequence of the extremely challenging nature of drug

development, competition among branded pharmaceutical companies,

and competition with generic pharmaceutical companies, the

industry has relatively slim returns given its level of risk. In

2013, for example, the median return on assets (ROA) in the U.S.

pharmaceutical industry was 2.04%. The top branded pharmaceutical

firms earned returns that averaged between 7% and 11% over the

last five years. Those are not exceptional returns; in every year

but one their returns were exceeded by the Standard & Poor’s 500

index, which averaged nearly 18% over the same five years (see

Figure 4).

---------------------------------Insert Figure 4 about here

-----------------------------------

As noted in the section on R&D portfolios, firms have to

balance their R&D investments across advanced R&D, breakthrough

projects, platform projects and derivative projects in a way that

balances their short-term cash flow needs and long-term strategic

momentum. Firms make long-term investments in breakthrough

innovation in order to avoid being technologically leapfrogged by

competitors who are also making investments in breakthrough

technology. This suggests that pharmaceutical firms invest in

developing fundamentally new drugs that offer major improvements

in functional performance in anticipation of, or response to,

competition from other branded pharmaceuticals who are making

similar investments. Generic drug manufacturers do not provide

this form of competition; they compete primarily on price. A

branded pharmaceutical’s best defense against price competition

from the generics is to find ways to extend their patent

protection for a given compound by developing improvements in the

product that are significant enough to meet the “useful, novel,

and non-obvious” requirement of the patent office. This is far

more easily accomplished with incremental improvements in things

like route of administration, extended release capabilities,

incorporation of additional features that address side effects

and similar derivative enhancements, than the development of a

fundamentally new compound that offers major improvements in

functional performance. This reveals that the balance between

generic and branded competition in the drug industry directly

influences the balance of incremental and breakthrough innovation

in the drug industry: greater competition from other branded

pharmaceuticals will tend to induce firms to invest in more

breakthrough innovation; greater competition from generic

pharmaceuticals will tend to induce firms to invest in more

incremental innovation.

Furthermore, generic competition can also induce a

deleterious gaming of the timing of innovation: A branded

pharmaceutical company that has discovered ways to make valuable

enhancements to its product that could justify a new patent is

incentivized to hold back those improvements until just before

patent expiration of the original product. By introducing its

enhancements just before patent expiry of its original product,

it maximizes the length of total patent protection from which the

product can benefit. Generic competition may thus not only induce

a focus on incremental innovation; it has the potential to cause

firms to delay the introduction of their innovations.

Competition between branded pharmaceutical competitors does

not induce such timing games. When competitors are competing

through the differential performance of patented products, there

is little to be gained, and much to be lost, in delaying entry.

First, in industries with strong patent protection, firms that

are innovating in similar technology domains must race to be

first to patent lest they be locked out by others who secure

patents that bar their entry.22 Second, firms that introduce a

superior product earlier capture revenues that they can reinvest

in innovation to get even further ahead of competitors.23 Such

reinvestment is one of the sources of increasing return to

adoption that can lead to long-lived market dominance.24 Third,

earlier entry can enable firms to capture advantages in brand

awareness and loyalty;25 this can be particularly valuable in the

pharmaceutical industry where physicians can be reluctant to

switch a patient’s medication once they have found a medication

that works well for them.

The preceding suggests that the combination of Hatch Waxman

and automatic substitution laws have the potential to shift the

balance of competition in the pharmaceutical industry in ways

that encourage incremental innovations that are timed to extend

patent protection, and to undermine incentives for platform and

22 W Mitchell, Whether and When? Probability of Incumbent’s Entry into Emerging Technical Subfields, 38 ADMINISTRATIVE SCI QUART. 208 (1989).

23 R. Makadok, Can First-Mover and Early-Mover Advantages Be Sustained in an Industry with Low Barriers to Entry/Imitation? 19 STRATEGIC MANAGEMENT J.683 (1998)

24 WB Arthur, Competing Technologies, Increasing Returns, and Lock-In by Historical Events, ECON J. March, 116 (1989).

25 M Lieberman & D Montgomery, First Mover Advantages: A Survey, 9 STRATEGIC MANAGEMENT J. 41 (1988).

breakthrough innovation. By doing so they could significantly

impair dynamic efficiency. A very large portion of the cost of

developing drugs in the Unites States is due to the clinical

testing process, and it thus makes sense to find ways to avoid

redundant testing of already proven drugs, as the Hatch Waxman

laws accomplish. The Hatch Waxman laws, however, result in

branded pharmaceutical companies being at a significant cost

disadvantage to generic manufacturers. Furthermore, automatic

substitution laws greatly amplify this disadvantage by a)

undermining the branded pharmaceutical company’s investment in

market education and brand reputation, and b) causing the loss of

market share to be sudden and extreme – a situation that is very

difficult for any company to manage. This suggests that we may

need to rethink how these laws are structured and employed.

Legislators and researchers should work together to revise the

laws so that they do not influence firms to focus too heavily on

incremental innovation, or to intentionally delay innovation.

C. Collaborative relationships and merger analysis

In the preceding I argued that due to the high cost and risk

of some types of breakthrough innovation projects, they can

typically only be pursued by large firms. This points to an

important caveat, however: Through collaborative agreements

organizations can pool their resources and skills, and share the

risk of a project.26 By providing firms access to a wider range

of resources than they individually possess, technology

collaboration agreements enable firms to achieve much more than

they could achieve individually.27 Numerous large sample studies

have found that alliance relationships enhance the innovative

performance of firms.28 Even when controlling for changes in the

opportunity structure that might lead to alliances, it has been

26 R Gulati 1998 Alliances and networks. 19 STRATEGIC MANAGEMENT J. 293 (1998); WWPowell, D White, KW Koput & J Owen-Smith, Network Dynamics and Field Evolution: The Growth of Interorganizational Collaboration in the Life Sciences. AMER. J. SOCIOL. 110: 1132-1205(2005); FT Rothaermel, Incumbent’s advantage through exploiting complementary assets via interfirm cooperation. 22 STRATEGIC MANAGEMENT J. 687 (2001); MA Schilling & C Phelps, Interfirm Collaboration Networks: The Impact of Large-Scale Network Structure on Firm Innovation. 53 MANAGEMENT SCI. 1113 (2007).

27 KM Eisenhardt & CB Schoonhoven, Resource-based view of strategic alliance formation:Strategic and social effects in entrepreneurial firms. 7 ORGAN. SCI. 136 (1996); L Rosenkopf & P Almeida, Overcoming Local Search through Alliances and Mobility. 49 MANAGEMENT SCI. 751 (2003).

28 G Ahuja, Collaboration Networks, Structural Holes, and Innovation: A Longitudinal Study. 45 ADMIN. SCI. QUART. 425 (2000); DL Deeds, & CWL Hill, Strategic alliances and the rate of new product development: An empirical study of entrepreneurial firms. 11 J. BUS. VENTURING 41 (1996); DC Mowery, JE Oxley, & BS Silverman, Strategic alliances and interfirm knowledge transfer. 17 STRATEGIC MANAGEMENT J. 77 (1996).

shown that increases in alliances lead to a significant increase

in patents.29

Awareness of the opportunities for enhancing innovation

through collaboration agreements is what led to the passage of

the 1984 National Cooperative Research Act which relaxed

antitrust restrictions against cooperative R&D agreements between

otherwise competing firms.30 I do not know of any study that has

rigorously examined the influence of the NCRA on innovation

outcomes, but it is worth noting that the number of patent

applications filed with the US Patent and Trademark Office was

basically flat from 1963 to 1984, and then began to climb steeply

from 1984 onwards (see figure 5).

-----------------------------Insert Figure 5 about

here-----------------------------

Occasionally concerns are expressed that collaboration could

lead to a loss of requisite variety in innovation ideas –

seemingly superior ideas could diffuse so quickly and widely that

29 MA Schilling, Technology shocks, technological collaboration, and innovation outcomes. ORGANIZATION SCI (forthcoming).

30 DM Hart, 2001. Antitrust and technological innovation in the US: Ideas, institutions, decisions, and impacts, 1890-2000. 1286 RESEARCH POLICY 1 (2001).

they create technological monocultures that would extinguish

further innovation. Empirical evidence on industry-level and

global-level collaboration networks does not support this claim,

at least at the current time. Inter-firm collaboration networks

are typically sparse, resulting in loosely-coupled and/or

disconnected networks.31 Furthermore, collaboration between two

firms does not mean that both firms converge on a single solution

that dominates all of their other efforts. There is significant

variance in the degree to which firms are willing or able to

adopt the solutions used by other firms, and as discussed

previously many firms pursue a portfolio of technological paths

simultaneously.32 In terms March would have used, the world has

plenty of “slow learners,” that help to preserve requisite

variety. That said, this discussion suggests that it would be

worthwhile to monitor the collaboration structures of industries

to gain a better understanding of which structures have yielded

31 MA Schilling, Technology shocks, technological collaboration, and innovation outcomes. ORGANIZATION SCI (forthcoming).

32 E Green, Parallel search as a competitive response: How technological positioning affects R&D strategy. ACADEMY OF MANAGEMENT PROCEEDINGS (2014), January; A Leiponen & CE Helfat, Innovation objectives, knowledge sources, and the benefits of breadth. 31 STRATEGIC MANAGEMENT J. 224 (2010); B Simonin, 1999. Ambiguity and the process of knowledge transferin strategic alliances. 20 STRATEGIC MANAGEMENT J. 595 (1999); G Szulanski, Exploring internal stickiness: Impediments to the transfer of best practice within the firm. 17 STRATEGIC MANAGEMENTJ. 27 (1996).

the most innovative advance, and identify opportunities to

improve collaborative structure through either greater

fragmentation or connectivity. There is an opportunity for

antitrust officials to play a more sophisticated role in

fostering industry innovation and growth through their influence

on license agreements, joint ventures, research consortia, and

standards coalitions.

The evidence on the relationship between mergers and

innovation is more equivocal. Many studies find mixed or negative

results for the influence of mergers on innovation. 33 This

should not be surprising – the potential benefits of a merger to

innovation (e.g., greater scale of R&D investment, knowledge

sharing, coordination between complementary technologies, etc.)

33 WS Comanor & FM Scherer, Mergers and innovation in the pharmaceutical industry. 32 J. HEALTH ECON. 106 (2013); C Ornaghi, Mergers and innovation in big pharma. 27 INTERNATIONAL J. INDUSTRIAL ORGANIZATION 70 (2009); M Cloodt, J Hagedoorn & H Van Kranenburg, Mergers and acquisitions: Their effect on the innovative performance of companies in high-tech industries. 35 RESEARCH POLICY 642 (2005); B Cassiman, MG Colombo, P Garrone & R. Veugelers. The impact of M&A on the R&D process, 34 RESEARCH POLICY 195 (2005); G Ahuja, & R Katila, Technological acquisitions and the innovation performance of acquiring firms: a longitudinal study, 22 STRATEGIC MANAGEMENT J. 197 (2001); MA Hitt, RE Hoskisson, RA Johnson & DD Moesel. The market for corporate control and firm innovation, 39 ACADEMY OF MANAGEMENT J. 1084 (1996); A Chakrabarti, J Hauschildt & C Sueverkruep, Does it pay to acquire technological firms?, 24 R&D MANAGEMENT 47 (1994); MA Hitt, RE Hoskisson, RD Ireland & JS Harrison, Effects of acquisitions on R&D inputs and outputs, 34 ACADEMY OF MANAGEMENT J. 693 (1991).

may be more than offset by the costs of mergers (e.g., cost and

difficulty of integration, loss of focus and flexibility,

significant managerial and employee churn due to elimination of

redundant roles, dilution of entrepreneurial incentives due to

greater firm size, etc.).

Furthermore, many of the innovation benefits that might be

sought through mergers can typically be obtained through

collaboration agreements that do not pose such high costs to the

firm nor impede long-term competition. Alliances have been

successful modes for innovation even when it requires the

exchange of highly sensitive and proprietary technology (see, for

example, the cooperative development of the B2 Stealth Bomber–

considered at the time to be “America’s biggest military secret

since the Atom Bomb”-- by Northrop, Boeing, Vaught, and General

Electric34), or when it requires the cooperation of firms that

compete vigorously head-to-head in their end markets (see, for

34 NS Argyres, The impact of information technology on coordination: Evidence from the B-2 “Stealth” Bomber. 10 ORGANIZATION SCIENCE, 162 (1999); B SCOTT, INSIDE THE STEALTH BOMBER: THE B-2 STORY (1991).

example, the development of the PowerPC by Apple, IBM, and

Motorola).

The preceding suggests that we do more to examine how firms

could be encouraged to use such temporary arrangements (while

retaining their incentives to compete individually) in lieu of

consolidation. Relatedly, it might also be useful to examine the

alliance databases (e.g., Thomson SDC Platinum, Recombinant

Capital, Bioscan, etc.) to create a framework of the kinds of

innovation projects that have been pursued through different

types of collaboration modes (e.g., R&D alliances, licensing,

outsourcing, joint ventures) to give antitrust enforcement

officials more evidence upon which to evaluate claims that a

merger is required to achieve a particular innovation outcome.

IV. CONCLUSION

There is growing consensus among those involved in antitrust

that we should be managing for dynamic efficiency: long-run

economic welfare requires striking an appropriate balance between

mechanisms that encourage short-run static efficiencies and the

long-term gains achievable through innovation. However, agreeing

on dynamic efficiency as an ideal does not necessarily lead to

consensus on how it should be achieved. Innovation is a

particularly complex and uncertain phenomenon. Innovation

projects are often long-term investments whose outcomes are

unknowable. New product development failure rates are extremely

high, yet even failed projects may give rise to important

knowledge or capabilities. Furthermore, innovation projects are

rarely one-shot investments whose costs and returns can be

assessed independently; rather innovation projects are more often

part of complex portfolios and lifecycles wherein some projects

lay groundwork for others, and each project has a different role

in a firm’s attempt to balance its long-term growth and short-

term cash flow needs.

Despite this high degree of uncertainty, we can use what we

know about the innovation process and innovation portfolios to

improve how we manage for dynamic efficiency. We know, for

example, that many of the innovation objectives that firms

purport to use mergers for can be achieved as well – if not

better – through collaboration agreements. Armed with this

knowledge we can develop better standards for merger analysis. We

also know that firms (and economies) benefit from having a

distribution of innovation types; any regulatory mechanism that

induces an undue amount of focus on a particular kind of

innovation will tend to undermine long-term technological

advance. Furthermore, we know that inadequate organizational

slack or weak appropriability mechanisms can undermine investment

in innovation – particularly in long-term or risky projects.

Fortunately, a considerable amount of research is being focused

on how intellectual property protection mechanisms influence

innovation around the world, and knowledge in this area is

accruing rapidly.

Table 1: Revenues, R&D Expenditures, and R&D Intensity for Select Industries and Firms, 2013(Data based on Publicly-Held North American Firms; Compustat)

Industry FirmsTotal R&D($millions)

TotalRevenues

($millions)

R&DIntensity

(R&D/Sales)

FirmsReporting

Nonzero R&DPharmaceuticals Mfr 486 110700 692424 0.160 459 (94%)Semiconductor Mfr 226 49045 434519 0.113 204 (90%)Communication Equip. Mfr 102 19990 182022 0.110 97 (95%)Computer SW 677 68863 808319 0.085 481 (71%)Medical Equipment Mfr 212 9283 120760 0.077 197 (93%)Scientific Instruments Mfr 101 9256 127689 0.072 94 (93%)Computer HW Mfr 92 33655 634943 0.053 88 (96%)Automotive Bodies & Parts Mfr 81 69901 1726074 0.040 65 (80%)Aircraft Bodies & PartsMfr 28 9368 278478 0.034 16 (57%)Food and Beverages Mfr 158 5591 946496 0.006 60 (38%)Apparel and Textiles Mfr 65 169 102729 0.002 14 (22%)Oil and Gas Exploration 389 475 438673 0.001 4 (1%)

Comparison of Individual FirmsMicrosoft 10411 77849 0.134Intuit 685 4171 0.164

Google 7952 59825 0.133

Toyota 8575 234327 0.037General Motors 7200 155427 0.046Volkswagen 14035 274454 0.051

Abbott Laboratories 1452 21848 0.066GlaxoSmithKline 6502 46434 0.140Mylan 526 6909 0.076Sangamo Biosciences 37 24 1.542

Figure 1: The Aggregate Project Planning Framework (or “R&D Map”), with Examples from Toyota’s Innovation Pipeline

Figure 2: The New Product Development Funnel in Pharmaceuticals

5,000 Compound

s

125 Leads

2-3 drugs tested

1 drug Rx

Discovery & Preclinical3-6 years

Clinical Trials6-7 years

Approval½-2 years

Table 3: Research Spending and New Drug Approvals35

CompanyNumber of drugsapproved

R&D Spending Per Drug($Mil)

Total R&D Spending 1997-2011 ($Mil)

AstraZeneca 5 11,790.93 58,955GlaxoSmithKline 10 8,170.81 81,708Sanofi 8 7,909.26 63,274Roche Holding 11 7,803.77 85,841Pfizer 14 7,727.03 108,178Johnson & Johnson 15 5,885.65 88,285Eli Lilly & Co 11 4,577.04 50,347Abbott Laboratories 8 4,496.21 35,970

Merck & Co Inc 16 4,209.99 67,360Bristol-Myers Squibb Co 11 4,152.26 45,675

Novartis 21 3,983.13 83,646Amgen Inc 9 3,692.14 33,229AVERAGE: 11.58 6,199.85 66,872.33

Sources: InnoThink Center For Research In Biomedical Innovation; Thomson Reuters Fundamentals via FactSet Research Systems

35 Herper, M. 2012. The truly staggering costs of inventing new drugs. Forbes, February 10th.

Figure 3: Return on Assets for Selected Pharma Firms and the S&P 500 Index, 2009-2013.

Figure 4: US Patent Applications, 1963-2013

1963

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

2011

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000