Secured Transactions Law Reform, Priorities and the Nature ...

Upload

khangminh22Category

view

4download

0

WHEN "EQUALITY" IS NOT "EQUITY":

A COMPARATIVE LEGAL AND ECONOMIC PERSPECTIVE FOR

JUDICIAL REVIEW OF THE STATUS OF SECURED CREDITORS INPHILIPPINE CORPORATE REHABILITATION PROCEEDINGS

Diane A. Desierto"

Rehabilitation contemplates a continuance of corporate life andactivities in an effort to restore and reinstate the corporation to its formerposition of successful operation and solveny. When a distressed company isplaced under rehabilitation, the appointment of a management committeefollows to avoid collusion between the previous management and creditors itmight favor, to the prejudice of the other creditors. All assets of a corporationunder rehabilitation receivershp are held in trust for the equal benefit of allcreditors to preclude one from obtaining an advantage or preference overanother by the expedieny of attachment, execution or otherwise. As betweenthe creditors, the key phrase is equality in equity. Once the corporationthreatened by bankrupty is taken over by a receiver, all the creditors ought tostand on equal footing. Not any one of them should be paid ahead of theothers. This is precise4 the reason for suspending all pending claims againstthe corporation under receivershjo.

- Ruby Industrial Corporation et al. v. Court of AppealsG.R. Nos. 124185-87, 20 January 1998

Supreme Court Second Division

Sec.5. Rehabilitation Plan. - The rehabilitation plan shallinclude xxx xxx xxx (b) the terms and conditions of such rehabilitation,which shall include the manner of its implementation, giving due regardto the interests of secured creditors; xxx

- Interim Rules of Procedure on Corporate Rehabilitation(A.M. No. 00-8-10-SC)

Law Reform Specialist, Institute of International Legal Studies (ILLS), University of the PhilippinesLaw Center; Professorial Lecturer in Legal History and Agency & Partnership Law, University of thePhilippines College of Law; Professorial Lecturer in Public International Law and Administrative Law,Lyceum of the Philippines College of Law; B.S. Economics, summa cum kwde, School of Economics, Universityof the Philippines; LL.B., eum laude, College of Law, University of the Philippines.

CORE Metadata, citation and similar papers at core.ac.uk

Provided by ScholarSpace at University of Hawai'i at Manoa

STATUS OF SECURED CREDITORS

INTRODUCTION

Since the Supreme Court's promulgation of the Interim Rules ofProcedure on Corporate Rehabilitation in 2000 ("Interim Rules"), unsecuredcreditors have latched on to the oft-cited Ruby Industrial dictum' to assert a status ofequality with secured creditors with respect to rehabilitation plan payments. Thisraises several threshold questions. Does giving "due regard" (as mandated in RuleIV, Section 5(b) of the Interim Rules) to the interests of secured creditorscontemplate a prohibition against the use or distribution of the propertyconstituting the security under the terms of a court-approved rehabilitation plan? Ifthe use or distribution of the property constituting the security is permitted, couldsecured creditors be "adequately protected", as contemplated in the Interim Rules,against the erosion of their security interests? If so, what modes of judicial actionare permissible to abate or mitigate such erosion?

The extreme interpretation of the Ruby Industrial dictum can lead tounsecured creditors claiming that "all assets" of the corporation under rehabilitationform part of the entire corpus of assets from which rehabilitation plan payments aremade. All of these assets are purportedly "held in trust for the equal benefit of allcreditors to preclude one from obtaining an advantage or preference over anotherby the expediency of attachment, execution or otherwise". Relying on the RubyIndustrial dictum's claim of "equality is equity", unsecured creditors therefore insiston their "equal" status with secured creditors for any payments to be made undercourt-approved rehabilitation plans. Whether payments are to be sourced fromproperties comprising security or other assets of the corporation, unsecuredcreditors maintain that all such properties (secured or unsecured) form part of the"distributable assets" of a corporation in a rehabilitation proceeding.

The result of this "extreme" interpretation of perceived "equality" underthe Ruby Industrial dictum is that secured creditors can end up losing theproperty/ies subject of their security to the distribution scheme approved under therehabilitation plan. Unsecured creditors can end up recovering their claims evenfrom the disposition of (or income from) secured assets - a pool of corporate assetsunsecured creditors would ordinarily not have had access to without corporaterehabilitation proceedings. In the meantime, due to the Stay Order 2 in force duringrehabilitation, secured creditors will be unable to foreclose over their security. Thenet effect of the "extreme" interpretation of the Ruby Industrial dictum is that

O Other recent citations of the Ru/ lndustrial dictum include: Metropolitan Bank & TrustCompany v. ASB Holdings Inc. ct al., G.R. No. 166197, February 27, 2007; New Frontier SugarCorporation v. Regional Trial Court, Branch 39, Iloilo City, et al., G.R. No. 165001, January 31,2007; Spouses Sobrejuanite v. ASB DevelopmentT Corporation, G.R. No. 165675, September 30,2005.

" "ee Rule IV, SLction 6 of the Interim Rules.

20071

PHILIPPINE LAWJOURNAL

unsecured creditors could also profit from a distribution or payment schemeinvolving secured assets, reinforced by the suspension of enforcement of securedcreditors' foreclosure rights. At its worst, the "extreme" interpretation of "equality"the Ruby Industrial dictum could be basis for rehabilitation courts to approverehabilitation plans that dispose of secured assets (without correspondingreplacement) and transmit the proceeds of disposition to all creditors, secured orunsecured. Since courts are authorized under the Interim Rules to a "cramdown"of the rehabilitation plan even over the objections of creditors, 3 there is noguarantee that secured creditors' security interests could be preserved duringrehabilitation. By the time rehabilitation has terminated, there could be no property(if any) over which secured creditors could exercise their foreclosure right.

Secured creditors can expectedly object to the decimation of their securityunder a court-approved payments distribution to all creditors (secured orunsecured) in the rehabilitation plan. Arguing from the standpoint of both policyand law, secured creditors foreseeably can insist on the protection of their securityinterests even during corporate rehabilitation.4 Otherwise, the perceiveddestruction of security interests in corporate rehabilitation proceedings willultimately incentivize secured creditors to immediately initiate insolvencyproceedings against the subject corporation, in order to enable secured creditors tomaximize recovery on their loans to the corporation and the security intended toguarantee such loans.

Clearly, the interpretation and application of the Ruby Industrial dictum is apivotal case for judicial balancing of interests,5 and an opportunity for courts toreview the relative status of secured and unsecured creditors in corporaterehabilitations under the Interim Rules. Part I of this paper examines thejurisprudential antecedents of the Ruby Industrial dictum in relation to the content

Interim Rules, Rule IV, Section 23.4 See Villanueva, Cesar L. Judtcal Aivim in Commerdal Laws, at p. 8 found at:

http://www.deanclv.net/newsdata/13/oboect/iudicial activism.doc (last visited 5 January 2008):

"Perhaps the more controversial areas of the Interim Rules are those that haveconstitutional repercussion, thus:

(a) Lumping together both secured and unsecured creditors and makingtheir vote to the adoption of the rehabilitation plan a condition precedent; and

(b) Non-protection of the property value of secured creditors under therehabilitation plan with the cramdown power of the Regional Trial Courts

xxx xxx xxxAs the argument goes, secured creditors have property rights under their existing

security arrangements with the debtor that cannot be put asunder without their consentor unless in exchange for valuable consideration that preserves at least the value of theirproperty rights."

See Kahn, Peter L. The Poktics of Unregulation: Pubic Choice and the Limits of Government, 75

CORNELL L. REv. 280 (anuary 1990).

[VOL 82

STATUS OF SECURED CREDITO)RS

and purpose of the "due regard" provision of the Interim Rules (and comparableprovisions in the former SEC Interim Rules on Corporate Recovery). In Part II,the scope of the "due regard" provision is also explored from comparativeinternational best practices on corporate rehabilitations and/or reorganizations todetermine the relative status of secured and unsecured creditors in these types ofproceedings. As will be later shown, there appears to be a heavy legalpreponderance in favor of maintaining and preserving security interests toaccomplish the objects and purposes of corporate rehabilitations. Bothinternational practice and Philippine jurisprudence affirm that security interestsshould not be destroyed in corporate rehabilitation.

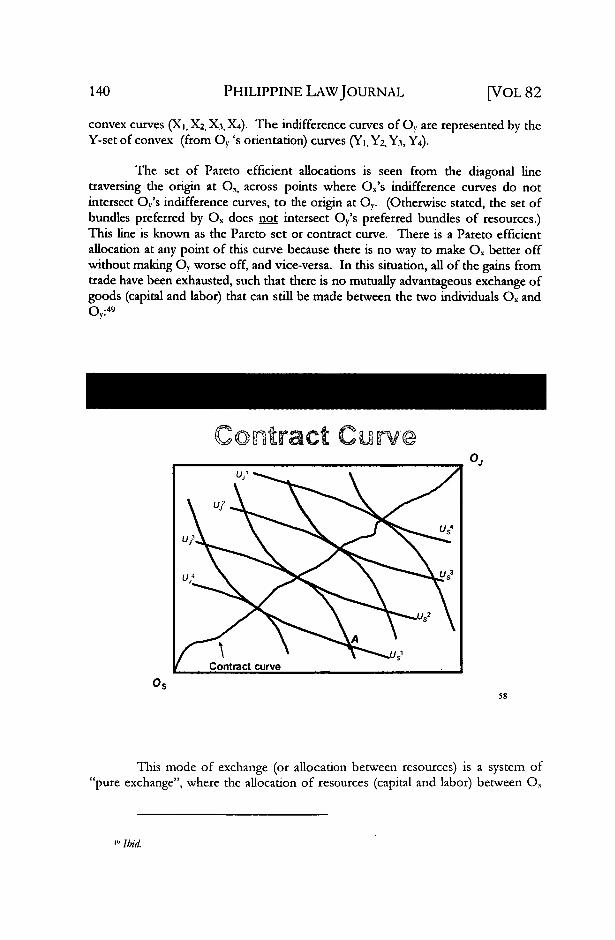

Part III of this paper then uses a basic efficiency allocation model forcourts to consider before approving rehabilitation plans that call for distribution ofproperties comprising security in order to pay off all of the corporation's creditors,secured or unsecured. The question of distribution is ultimately one of efficiency inthe allocation of corporate resources for creditor payments and corporate expenses- how best to derive the optimal distribution of corporate assets in payment tocreditors (secured or unsecured) that most feasibly ensures the corporation'srestoration to financial and operational viability. The Pareto efficient allocation forcourts to consider in the payment distribution under a rehabilitation plan is clearlythe allocation when "there is no way to make some individual better off withoutmaking someone else worse off".6

As will be subsequently shown, however, the Interim Rules (specifically the"due regard" and "adequate protection" clauses in Rule 4, Section 5(b) and Rule 4,Section 12 of the Interim Rules) create an in-built constraint that forces courts tochoose a Pareto-efficient allocation in the interior of the Pareto set or contractcurve, and not at the origin (where one set of creditors enjoys full recovery fromsecured assets to the complete exclusion of the other set of creditors). The courts,as the virtual "auctioneer" in the "exchange" between secured and unsecuredcreditors (best exemplified in the creditors' meetings with the rehabilitationreceiver), can set the "relative prices" for creditor recovery on their claims -through court approval of valuation of corporate assets, court approval of theestimated debt burden of the corporation under rehabilitation, and, among others,court-sanctioned 'transaction costs' that make it incrementally difficult for creditorsto recover the full amount of their claim from the corporation. While Paretoefficiency can theoretically contemplate a situation where one set of creditors(unsecured creditors) are able to recover the full amount of their claim from bothsecured and unsecured assets of the corporation while secured assets can beexhausted under the payment scheme in the rehabilitation plan, the Interim Rulesprevent this situation by prohibiting the destruction of security interests.

Thus, as will be seen from international best practices, Philippinejurisprudence, and economic efficiency analysis, rehabilitation courts cannot

SSee ',ARthN, I AIR. IN NiI I A)I,\'r MI(:I ()I( :)N(OMICS." (2-1 cd., 1990.). at 480.

2007]

PHILIPPINE LAWJOURNAL

interpret the Ruby Industrial dictum in a manner that permits the obliteration ordestruction of assets comprising the security, without requiring the corporationsubject of rehabilitation to replace such assets with others comparable in value. The"equality is equity" dictum in Ruby Industrial simply contemplates a stay in theenforcement of claims of all creditors, whether secured or unsecured. It cannotauthorize the distribution of secured assets to all creditors (secured or unsecured)without a corresponding and appropriate replacement of such assets. Rehabilitationdoes not intend the destruction of security interests.

I. RETRACING THE RUBYINDUSTRIAL DICTUM: FROMSEC CORPORATE RECOVERY RULES AND ALEMAR'S SIBAL & SONS,

TO THE INTERIM RULES AND NEW FRONTIER

Ruby Industrial Corp. et al v. Court of Appeal et aL, (hereafter, Ruby Industria)7

was decided by the Second Division of the Supreme Court two (2) years before itspromulgation of the Interim Rules of Procedure on Corporate Rehabilitations. Thecase originated from a Petition for Suspension of Payments filed by Ruby Industrialwith the Securities and Exchange Commission (SEC) in 1983. When the SECdeclared Ruby Industrial under suspension of payments, Ruby Industrial wasenjoined, pending hearing on the Petition, from disposing of its properties or frommaking payments outside of the necessary or legitimate expenses of its business.

After the SEC Hearing Panel approved the rehabilitation plan proposed byRuby Industrial's majority stockholders ("Benhar/Ruby plan"), the minoritystockholders appealed. The SEC en banc then issued a writ of preliminaryinjunction against the enforcement of the Benhar/Ruby plan. The Supreme Courtlater upheld the injunction.

Problems arose when it was discovered that Ruby Industrial had partlyimplemented the Benhar/Ruby plan before its approval by the SEC Hearing Panel.One of Ruby Industrial's secured creditors (Far East Bank & Trust Company, orFEBTC) had been paid off, and FEBTC had executed a deed of assignment infavor of the majority stockholder, Benhar. Despite the injunction, Benhar paid offRuby Industrial's other secured creditors who later assigned their credits to Benhar.Upon motion of Ruby Industrial's unsecured creditors, the SEC nullified the deedsof assignment to Benhar. The SEC's orders were affirmed by the Court of Appeals,and thereafter, the Supreme Court.

Ruby Industrial then submitted a revised rehabilitation plan to the SEC,which provided for reimbursement to Benhar for payments it had made to Ruby

G.R. Nos. 124185-87,January 20, 1998.

[VOL 82

STATUS OF SECURED CREDITORS

Industrial's secured creditors. Ruby Industrial's creditors objected, claiming that therevised plan would legitimize the entry of Benhar as the new (and biggest) creditorof Ruby, and the revised plan would put Ruby's assets beyond the reach ofunsecured creditors and the minority stockholders.

The SEC approved this revised plan. The Court of Appeals reversed,stating that the revised plan circumvented its earlier decision nullifying the deeds ofassignment executed by Ruby's secured creditors in favor of Benhar.

The Supreme Court affirmed the Court of Appeals' decision, anchoring itsreasoning on the final declaration of nullity of the deeds of assignment. Suchassignments being entirely void, Benhar could not derive rights as against RubyIndustrial as to entitle Benhar to payments as a 'creditor'. Otherwise stated, theCourt affirmed that Benhar could not assert any entitlement to repayment fromRuby Industrial for Benhar's void act of paying off Ruby's secured creditors whilean injunction against such dispositions was subsisting. The Court then admonished,in its now oft-cited dictum, that:

"Rehabilitation contemplates a continuance of corporate life andactivities in an effort to restore and reinstate the corporation to its formerposition of successful operation and solvency. (citing New York Title andMortgage Co., vs. Friedman, 276 N.Y.S. 72, 153, Misc. 697) When adistressed company is placed under rehabilitation, the appointment of amanagement committee follows to avoid collusion between the previousmanagement and creditors it might favor, to the prejudice of the othercreditors. All assets of a corporation under rehabilitation receivership areheld in trust for the equal benefit of all creditors to preclude one fromobtaining an advantage or preference over another by the expediency ofattachment, execution or otherwise. As between the creditors, the key phraseis equality in equity. Once the corporation threatened by bankruptcy is takenover by a receiver, all the creditors ought to stand on equal footing. Not anyone of them should be paid ahead of the others. This is precisely the reasonfor suspending all pending claims against the corporation under receivership.(citing Araneta vs. Court of Appeals, G.R. No. 95253, July 10, 1992, 211SCRA 390; Rizal Commercial Banking Corporation vs. IAC and BF Homes,Inc., G.R. No. 74851, September 14, 1992,213 SCRA 830)."

Thus, as clearly seen from Ruby Industrial, the Supreme Court simplyaffirmed.the prohibition against disposition of corporate assets in favor of one classof creditors (secured creditors) before approval of the rehabilitation plan. The RubyIndustrial dictum precisely affirms that what is suspended is the enforcement ofclaims against the corporation, and thus, "not any one of [the creditors] should bepaid ahead of the others". The Ruby Industrial dictum did not destroy the distinctionbetween the claims of secured creditors and unsecured creditors.

The prohibition against the mere enforcement of claims is further affirmedfrom the cases cited by the Supreme Court in the Ruby Industrial dictum:

2007]

PHILIPPINE LAWJOURNAL

1) Araneta v. Court of Appeals

Araneta involved a claim arising from Philfinance's sale of a security(promissory note) to the Aranetas. The security was under the custodianship ofPilipinas Bank. When the Aranetas sought to recover the security from PilipinasBank, the bank maintained that the security forms part of the assets of Philfinancewhich have been frozen by the SEC upon declaring Philfinance under suspensionof payments and receivership. In affirming the bank's refusal to turn over thesecurity to the Aranetas, the Supreme Court held that the declaration of suspensionof payments upon Philfnance was a 'supervening' event, and that the Aranetasshould properly file their claim under the SEC proceedings. The Supreme Courtnoted its decision in Alemar's Sibal & Sons Inc. v. Elbinias,9 to explain the rationalefor placing a corporation in a state of suspension of payments and receivership:

"It must be stressed that the SEC had earlier ordered thesuspension of all actions for claims against Alcmar's in order that all thcassets of said petitioner could be inventoried and kt intact for the purposeof ascertaining an equitable scheme of distribution among its creditors.

During rehabilitation receivership, the assets are held in trust for the equalbenefit of all creditors to preclude one from obtaining an advantage or preferenceover another by the expediency of an attachment, execution or otherwise. For whatwould prevent an alert creditor, upon learning of the receivership, from rushingposthaste to the courts to secure judgments for the satisfaction of its claims to theprejudice of the less alert creditors.

As between creditors, the key phrase is 'equality is equity (Central Bank vs.Morfe, 63 SCRA 114, citing Ramisch vs. Fulton, 41 Ohio App. 443, 180 N.E. 735).'When a corporation threatened by bankruptcy is taken over by a receiver, all thecreditors should stand on an equal footing. Not anyone of them should be givenay preference y payi one or some of them ahead of the others. This is preciselythe reason for the suspension of all pending claims against the corporation underreceivership. Instead of creditors vexing the courts with suits against the distressedfirm, they are directed to file their claims with the receiver who is a duly appointedofficer of the SEC."

As seen from the foregoing, what the Supreme Court simply intended instating that "all creditors should stand on equal footing" is the establishment of"equality" based on an across-the-board prohibition against any enforcement ofclaim by any creditor, secured or unsecured. Thus, this reasoning should infusejudicial appreciation of the Ruby Industrial dictum. The Ruby Industrial dictum shouldnot be read as having destroyed security interests in corporate rehabilitation, or

G.R. No. 95253,July 10, 1992.G.R. No. 75414,June 4, 1990. Imphasis and underscoring supplied.

[VOL 82

STATUS OF SECURED CREDITORS

vesting unsecured creditors-with the same corpus of rights over secured assets assecured creditors.

2) Rizal Commercial Banking Corporation (RCBC) v. IntermediateAppellate Court (IAC) et al."'

RCBC likewise affirms the same prohibition against enforcement of claimsby any creditor where a corporation is declared under suspension of payments. Inthis case, BF Homes filed a Petition for Rehabilitation and for Declaration andSuspension of Payments with the SEC. One of its creditors was RCBC. Before thepetition could be heard by the SEC, RCBC extrajudicially foreclosed on theproperties subject of BF Homes' real estate mortgage with RCBC. The propertieswere auctioned off at a public sale, on the sheriffs' claim that the SEC had not yetissued any injunction at the time of the sale. RCBC filed a petition for mandamusto compel the delivery of the Certificate of Sale of the auctioned properties. Thetrial court granted RCBC's petition. Thereafter, upon BF Homes' complaint withthe IAC for annulment of the trial court's judgment, the [AC set aside the writ ofmandamus issued and suspended issuance of new titles to RCBC pendingresolution of the rehabilitation petition with the SEC.

The Supreme Court denied RCBC's petition seeking annulment of the JACdecision. The Supreme Court affirmed the prohibition on the enforcement (orforeclosure) of the claim over the security pending rehabilitation:

"While it is recognized that RCBC is a preferred-creditor andlikewise the highest bidder at the auction sale, We have however stated thatwhenever a distressed corporation asks the SEC for rehabilitation andsuspension of payments, preferred creditors may no longer assert suchpreference, but as earlier stated, stand on equal footing with other creditors.Foreclosure shall be disallowed so as not o p orejudice 2hucreditors, orcause discrimination among them. If foreclosure is undertaken despite thefact that a petition for rehabilitation has been filed, the certificate of sale shallnot be delivered pendin rehabilitation. Likewise, if this has also been done,no transfer of title shall be effected also, within the period of rehabilitation.The rationale behind PD 902-A, as amended, is to effect a feasible and viablerehabilitation. This cannot be achieved if one creditor is preferred over theothers.

In this connection, the prohibition against foreclosure attaches assoon as a petition for rehabilitation is fied. Were it otherwise, what is toprevent the petitioner from delaying the creation of the ManagementCommittee and in the meantime dissipate all its assets. The sooner the SECtakes over and imposes a freeze on all the assets, the better for allconcerned.""

to G.R. No. 74851, September 14, 1992 (en banc).11 Emphasis and underscoring supplied.

20071

PHILIPPINE LAWJOURNAL

Clearly, the 'equality of footing' contemplated (between secured andunsecured creditors)dis hinged on the uniform prohibition against the enforcementof claims against the corporation pending rehabilitation. Read alongside itsjurisprudential antecedents in Alemar's Sibal & Sons Inc., Araneta, and RCBC, theRuby Industrial dictum should be understood simply as a prohibition against anycreditor's enforcement of a claim against the corporation pending rehabilitation(and approval of a rehabilitation plan). None of these cases collapsed thedistinction between secured creditors and unsecured creditors. The rights ofsecured creditors to foreclose over secured assets of the corporation (to theexclusion) of unsecured creditors), remain intact, but are simply rendered'unenforceable' during the pendency of corporate rehabilitation.

The foregoing interpretation is also consistent with the SEC Rules ofProcedure on Corporate Recovery ("SEC Corporate Recovery Rules"),12 whichantedated the Interim Rules. The SEC Corporate Recovery Rules werepromulgated "to carry out the objectives of Presidential Decree No. 902-Al3and toassist the parties in obtaining a just, expeditious, and inexpensive settlement ofcases". 14 Section 2-10 of the SEC Corporate Recovery Rules expressly classifiescreditors into secured and unsecured creditors.

Rule IV of the SEC Corporate Recovery Rules provides for the remedy ofrehabilitation. Rehabilitation can be initiated by the debtor corporation, its creditors,or stockholders, so long as it is -shown that the debtor corporation is "insolventbecause its assets are not sufficient to cover its liabilities, or [which is] technicallyinsolvent under Section 3-12 of these Rules, but which may still be rescued orrevived through the institution of some changes in its management, organization,policies, strategies, operations, or finances."' Is While the SEC Corporate RecoveryRules does not carry a similar "due regard" provision for secured creditors asindicated in the Interim Rules,' 6 the same SEC Corporate Recovery Rules recognize

12 SEC Rules of Procedure on Corporate Recovery, December 21, 1999.1- Presidential Decree No. 902-A ("REORGANIZATI()N OF THE SECURITIES AND

EXCHANGE COMMISSION WITH ADDITIONAL POWERS AND PLACING THE SAIDAGENCY UNDER THE ADMINISTRATIVE SUPERVISION OF THE OFFICE OF THPRESIDENT"), March 11, 1976, as amended.

"SEC Rules of Procedure on Corporate Recovery, Rule I, Section 1-2.'s Ibid, at Rule IV, Section 4-1.' See Interim Rules, Rule IV, Section 5(b) alongside Rule IV, Section 4-18 of the SEC Rules

of Procedure on Corporate Recovery:

Rule IV, Section 5 of the Interim Rules Rule IV, Section 4-18 of the SEC Rules ofof Procedure on Corporate Rehabilitation Procedure on Corporate Recovery

[VOL 82

STATUS OF SECURED CREDITORS

that a secured creditor is entitled to "adequate protection over property securing itsclaim."t

7

Section 5. Rehabilitation Plan. - Therehabilitation plan shall include: a) the desiredbusiness targets or goals and the duration andcoverage of the rehabilitation; b) the terms andconditions of such rehabilitation which shallinclude the manner of its implementation,giving due regard to the interests ofsecured creditors; (c) the material financial

commitments to support the rehabilitationplan; (d) the means for the execution of therehabilitation plan, which may includeconversion of the debts or any portion thereofto equity, restructuring of the debts, dadon enpago, or sale of assets or of the controllinginterest; (c) a liquidation analysis that estimatesthe proportion of the claims that the creditorsand shareholders would receive if the debtor'sproperties were liquidated; and (f) such otherrelevant information to enable a reasonableinvestor to make an informed decision on thefeasibility of the rehabilitation plan. (Emphasissupplied.)

Section 4-18. Rehabilitation Plan. - Thepetitioner shall attach to the petition theproposed rehabilitation plan. If not soattached, the petitioner shall subniit it withinsuch time as the Commission may allowserving notice to each creditor of record thatthe Rehabilitation Plan has been filed with theCommission and that a copy thereof served on

the Interim Receiver is available forexamination and reproduction. TheRehabilitation Plan shall include (a) the desiredbusiness targets or goals and the duration andcoverage of the rehabilitation, (b) the termsand conditions of such rehabilitation whichshall include the manner of its implementation,(c) the material financial commitments tosupport the Rehabilitation Plan, (d) arepayment plan for all debts and liabilitiesincluding the source of repayment, (e) themeans for the execution of the RehabilitationPlan, which may include conversion of thedebts or any portion thereof to equity,restructuring of the debts, dadon enpago, or saleof the assets or of the controlling interest; and(0 such other relevant information to enable areasonable investor to make an informeddecision on the feasibility of the RehabilitationPlan.

'1 See Rule IV, Section 4-10 of the SEC Rules of Procedure on Corporate Recovery:

"Section 4-10. Refief from, moification or termination of Suspension Order.. - The Commissionmay, on motion or motu prop co, terminate, modify, or set conditions for the continuance of thesuspension order, or relieve a claim from the coverage thereof upon showing that (a) any of thcallegations in the petition, or any of the contents of any attachment, or the verification thereof hasceased to be true, (b) a creditor does not have adequate protection over property securingits claim, or (c) the debtor's secured obligation is more than the fair market value of the propertysubject of the stay and such property is not necessary for the rehabilitation of the debtor.

For purposes of this section, the creditor shall lack adequate protection if it can be shownthat:

a. the debtor is not honoring pre-existing agreement with the creditor to keep theproperty insured;

b. the debtor is failing to take commercially reasonable steps to maintain the property; or

2007]

" "1 € 14 ¢

124 PHILIPPINE LAWJOURNAL [VOL 82

Significantly, the SEC Corporate Recovery Rules (in conjunction withPresidential Decree No. 902-A) also appear to affirm the preservation of securityinterests during rehabilitation:

"May encumbered assets be disposed of?

In almost all rehabilitation proceedings, infusion of additionalcapital is an indispensable ingredient of the rehabilitation strategy. I Iowever,it is next to impossibility to find a bank willing to lend that additional capital.An investor may become interested but, as demonstrated in the case of PAL,that situation is rare.

Faced with the formidable predicament, the corporation may haveno choice but to dispose of some assets and use the proceeds to operate thebusiness. There will be no problem if the assets are unencumbered. Butcomplications will develop if they are. May the Commission allow thedisposition of encumbered assets?

I believe that the Commission has the authority to allow the liftingof the lien from an encumbered asset but only when a substitute security isgiven to the creditor. Rehabilitation, as a rule, merely postones the Liht ofthe creditors to fireclose on the security. I d= not work to remove thelien altocether. ''"

c. depreciation of the property is increasing to the extent that the creditor isundersecured.

Upon showing of a lack of adequate protection, the Commission shall order the debtor to (a)make arrangements to provide for the insurance or maintenance of the property, (b) to makepayments or otherwise provide an additional or replacement lien to the creditor to offset theextent that the depreciation of the property is increasing the extent that the creditor isundersecured. Provided, however, that the Commission may deny the creditor the remedies inthis paragraph if such remedies would prevent the continuation of the debtor as a going concernor otherwise prevent the approval and implementation of a Rehabilitation Plan."

18 " oncepcion, l)anilo I. Cotporate Rehabilitation: The Phiippine Experience, found at:http: / /web.worldbank.org/WBSI'F11 ,/IXTERNAL/TOPICS/LAtWANDIUSTICE/G ILD/ O..contentMDK:20154076-menuPK:146222-pagePK:64065425-1piPK:162156-theSitePK:215006.00.html. (last visited 15 January 2008) (Emphasis and underscoring supplied.).

See also Villanueva, Cesar I.. Revisiting the Phiippine 'Laws" on Corporate Rehabiltation,Professorial Chair Paper for the JUSTICE CARMEL() AlVENDIA ('HAIR INCOMMER(IAL L.AW for School Year 1998-1999:

"What may be clearly implied from the rulings of the Supreme Court is that the whole issueof "equality" among the creditors, both secured and unsecured, during the process ofrehabilitation, should pertain only to the non-availment of actions on claims against thepetitioning creditor during the period that rehabilitation is being pursued. But it cannot mean anactual treatment of the claims as "equal" to forgo the existence of contractual security rights infavor of secured creditors. A rehabilitation plan that "impairs" or destroys such security rightscannot be affirmed without the consent of the individual sccurLd creditors; otherwise it would bea constitutional violation of due process and non-impairment clause."

STATUS OF SECURED CREDITO)R.S

Likewise, the destruction of security interests (or any collapse in thedistinction between secured and unsecured creditors) does not appear to beconsistent with the express provisions of the Interim Rules, mandating thatrehabilitation plans must give 'due regard' to the interests of secured creditors, andproviding for adequate protection for secured creditors thus:

"Sec. 5. Rehabtilitation Plan. - The rehabilitation plan shall include:a) the desired business targets or goals and the duration and coverage of therehabilitation; b) the terms and conditions of such rehabilitation which shallinclude the manner of its implementation, giving due regard to the interestsof secured creditors; (c) the material financial commitments to support therehabilitation plan; (d) the means for the execution of the rehabilitation plan,which may include conversion of the debts or any portion thereof to equity,restructuring of the debts, dadon enpago, or sale of assets or of the controllinginterest; (e) a liquidation analysis that estimates the proportion of the claimsthat the creditors and shareholders would receive if the debtor's propertieswere liquidated; and (0 such other relevant information to enable. areasonable investor to make an informed decision on the feasibility of therehabilitation plan.

xxx xxx xxx

Sec.12. Re/ffrom, Modification, or Termination of Stay Order. - Thecourt may, on motion or motupropnio, terminate, modify, or set conditions forthe continuance of the stay order, or relieve a claim from the coveragethereof upon showing that: (a) any of the allegations in the petition, or anyof the contents of any attachment, or the verification thereof has ceased tobe true; (b) a creditor does not have adequate protection over propertysecuring its claim; or (c) the debtor's secured obligation is more than the fairmarket value of the property subject of the stay and such property is notnecessary fior the rehabilitation of the debtor.

Ior purposes of this section, the creditor shall lack adequateprotection if it can be shown that:

a. the debtor fails or refuses to honor a pre-existing agreement with thecreditor to keep the property insured;

b. the debtor fails or refuses to take commercially reasonable steps tomaintain the property; or

c. the property has depreciated to an extent that the creditor isundcrsccured.

Upon showing of a lack of adequate protection, the court shallorder the rehabilitation receiver to (a) make arrangements to provide for theinsurance or maintenance of the property, or (b) to make payments orotherwise provide additional or replacement security such that the obligationis fully secured. If such arrangements are not feasible, the court shall modify.

2007]

126 PHILIPPINE LAWJOURNAL [VOL 82

the stay order to allow the secured creditor lacking adequate protection toenforce its claim against the debtor; Provided, however, That the court may denythe creditor the remedies in this paragraph if such remedies would preventthe continuation of the debtor as a going concern or otherwise prevent theapproval and implementation of a rehabilitation plan."' 9

The Supreme Court has not had occasion yet to interpret the foregoing"due regard" and "adequate protection" clauses of the Interim Rules. The Court,however, has consistently upheld the preferred status of secured creditors overunsecured creditors in relation to properties subject of security, clarifying that whatis merely suspended during rehabilitation proceedings is the enforcement of theclaim over the property constituting the security. As the Court clarified inMetropolitan Bank & Trust Company v. ASB Holdings Inc. et al,21 mortgage liens areretained in corporate rehabilitations, and what is only suspended is the creditor'senforcement of such preference:

"We are not convinced that the approval of the Rehabilitation Planimpairs petitioner bank's lien over the mortgaged properties. Section 6(c) ofP.D. No. 902-A provides that 'upon appointment of a management committee,rehabiitation receiver, board or body, pursuant to this Decree, all actions for c/aims againstcorporations, partnerships or associations under management or receivership pending beforeany court, tribunal, board or body shall be suspended "

By that statutory provision, it is clear that the approval of theRehabilitation Plan and the appointment of a rehabilitation receiver merely suspendthe actions for claims against respondent corporations. Petitioner bank's preferredstatus over the unsecured creditors relative to the mortgage liens is retained, but theenforcement of such preference is suspended. The loan agreements between theparties have not been set aside and petitioner bank may still enforce its preferencewhen the assets of ASB Group of Companies will be liquidated. Considering thatthe provisions of the loan agreements are merely suspended, there is no impairmentof contracts, specifically its lien in the mortgaged properties.

As we stressed in RiZal Commercial Banking Corporation v. Intermediate AppellateCourt, such suspension "shall not prejudice or render ineffective the status of asecured creditor as compared to a totally unsecured creditor", for what P.D. No.902-A merely provides is that all actions for claims against the distressedcorporation, partnership or association shall be suspended. This arrangementprovided by law is intended to give the receiver a chance to rehabilitate thecorporation if there should still be a possibility for doing so, without beingunnecessarily disturbed by the creditors' actions against the distressed corporation.However, in the event that rehabilitation is no longer feasible and the claims againstthe distressed corporation would eventually have to be settled, the secured

19 Interim Rules, Rule IV, Sections 5 and 12. Emphasis supplied.

21 See Philippine Airlines Inc. et al. v. Zamora, G.R. No. 166996, February 6, 2007; Philippine

Airlines Inc. v. Philippine Airlines Employees Association, G.R. No. 142399,june 19, 2007.21 G.R. No. 166197, February 27, 2007.

STATUS OF SECURED CREDITORS

creditors, like petitioner bank, shall enjoy preference over the unsecuredcreditors."22

Notably, the Supreme Court held in Metrobank that there was noimpairment of security interests under the approved rehabilitation plan, since thedacton en pago therein contemplates obtaining the consent of the secured creditors tothe disposition of the mortgaged properties. Since the dadon en pago transactionswould be based on "mutually agreed upon terms" between the debtor-corporationand secured creditors, the rehabilitation plan did not per se appear to indicateimpairment of the secured creditors' property and/or contractual rights. (Clearly,this was not even an instance involving a "cramdown" upon secured creditors of apayment distribution scheme calling for disposition of the corporation's mortgagedproperties.)

Finally, under the Interim Rules, the suspension of enforcement of creditorclaims comes into effect from the issuance of the Stay Order appointing arehabilitation receiver. As the Court explained in New Frontier Sugar Corporation v.Regional Trial Court of Iloilo City, Branch 39, et al,23 (a case whose original incidentswere already covered by the Interim Rules), the suspension of enforcement ofcreditor claims applies to both secured and unsecured creditors:

"Rehabilitation contemplates a continuance of corporate life andactivities in an effort to restore and reinstate the corporation to its formerposition of successful operation and solvency (citing Ruby Industrial Corporationv. CoArt of Appeal, 348 Phil. 480, 497 (1998). Presently, the applicable law onrehabilitation petitions filed by corporations, partnerships or associations,including rehabilitation cases transferred from the Securities and ExchangeCommission to the RTACs pursuant to Republic Act No. 8799 or theSecurities Regulation Code, is the Interim Rules of Procedure on CorporateRehabilitation (2000).

Under the Interim Rules, the RTC, within five (5) days from thefiling of the petition for rehabilitation and after finding that the petition issufficient in form and substance, shall issue a Stay Order appointing aRtehabilitation Receiver, suspending enforcement of all claims, prohibitingtransfers or encumbrances of the debtor's properties, prohibiting payment ofoutstanding liabilities, and prohibiting the withholding of supply of goodsand services from the debtor. Any transfer of property or any otherconveyance, sale, payment, or agreement made in violation of the Stay Orderor in violation of the Rules may be declared void by the court upon motionor motu proprio.

Further- the St Order is effective both aimns secured andunsecured creditors. This is in harony with the lrincilie of "equality is1gui& enunciated in Alemar's & alSons. Inc. v. Elbinias thus:

2Emphasis and italics in the original.2. G.R. No. 165001,January 31, 2007.

2007]

128 PHILIPPINE LAWJOURNAL [VOL 82

During rehabilitation receivership, the assets areheld in trust for the equal benefit of all creditors to precludeone from obtaining an advantage or preference over another bythe expediency of an attachment, execution or othenvise. Forwhat would prevent an alert creditor, upon learning of thereceivership, from rushing posthaste to the courts to securejudgments for the satisfaction of its claims to the prejudice ofthe less alert creditors.

As btween creditors, the key phrase is "equality iseluity." When a corporation threatened by bankruptcy is takenover by a receiver, all the creditors should stand on an equalfooting. Not anyone of them should be given any preference bypaying (me or soime of them ahead of the others. This isprecisely the reason for the suspension of all pending claimsagainst the corporation under receivership. Instead of creditorsvexing the courts with suits against the distregsed firm, they arcdirected to file their claims with the receiver who is a dulyappointed officer of the SEC. (Emphasis supplied)

Nevertheless, the suspension of the enforcement of all claimsagainst the corporation is subject to the rule that it shall commence onlyfrom the time the Rehabilitation Receiver is appointed. Thus, in RizalCommernial Bankin& Corporation v. Intermediate Appellate Court, the Court upheldthe right of RCBC to extrajudicially foreclose the mortgage on some of BFI tomes' properties, and reinstated the trial court's judgment ordering thesheriff to execute and deliver to RCBC the certificate of- auction saleinvolving the properties. The Court vacated its previous Decision renderedon September 14, 1992 in the same case, finding that RCBC can rightfullymove for the extrajudicial foreclosure of the mortgage since it was done onOctober 16, 1984, while the management committee was appointed only onMarch 18, 1985. The Court also took note of the SEC's denial of thepetitioner's cons6lidated motion to cite the sheriff and RCBC for contemptand to annul the auction proceedings and sale."

As seen from the foregoing recent clarification by the Supreme Court, itappears clear that the "equality is equity" dictum in Ruby Industrial (traceable toAkrar's Sibal & Sons) only refers to the stay order, or the suspension ofenforcement of claims against the corporation. It should not be construed ashaving destroyed the distinction between the rights of secured creditors vis-a-visunsecured creditors.

Thus, as seen from the jurisprudential antecedents of the Ruby Industrialdictum, the SEC Rules on Corporate Recovery, the express provisions of theInterim Rules, and recent jurisprudence, there is no basis for an "extreme"interpretation of the Ruby Industrial dictum by rehabilitation courts. The perceived"equality" of secured and unsecured creditors in rehabilitation proceedings stemsfrom the uniform suspension of enforcement of claims of all creditors. This"equality" does not extend to the use and disposition of secured assets (and withoutreplacement or comparable substitution of the assets) to pay off all creditors underthe rehabilitation plan, whether secured or unsecured. Security interests must stillbe respected and preserved during corporate rehabilitation.

STATUS OF SECURED CREDITORS

II. INTERNATIONAL BEST PRACTICES ON CORPORATEREHABILITATIONS/REORGANIZATIONS: RECONCILING THE 'PARI PASSU'

DOCTRINE WITH THE RUBY INDUSTRIAL DICTUM

The "extreme" interpretation of "equality" between creditors classes(secured and unsecured) in the Rub Industrial dictum has led to the argument thatsuch "equality" permits the distribution of all corporate assets (including securedassets) for indiscriminate payment to all creditors (secured or unsecured). It hasbeen argued that this "equality" is, in reality, consistent with the doctrine of paripassu treatment of creditors.

As internationally applied and understood in corporate restructuringproceedings, however, the pari passu doctrine contemplates equality only for classesof creditors that are similarly situated. The pari passu clause is a basic financialcovenant which, in modem cross-border credit instruments, typically states that theloan (to which the clause is attached) will rank equally in right of payment with allother similarly situated loans of the borrower: 24

"In a corporate context, this [paripassuJ clause is a statement thaton a forced insolvency, debts are, by law, paid ratably. It does not mean thatone debt cannot be paid before another in time.

In the state context, the meaning of the clause is uncertain becausethere is no hierarchy of payment which is legally enforced under abankruptcy regime. Probably the clause means that on a de facto inability topay external debt as it falls due, one creditor will not be preferred by virtue of.an allocation of international monetary assets achieved by a method goingbeyond contract; and (perhaps) that there will be no discrimination betweencreditors of the same class in the event of insolvency."2 5

Clearly, the paripassu clause does not mandate uniform payment treatmentfor what are obviously different creditor classes (secured and unsecured creditors).In devising a payment scheme during corporate restructuring, clear distinctionsmust be drawn between secured creditors and unsecured creditors, who not only

24 Buchheit, Lee C. and Jeremiah S. Pamn, The Pari Passu Clause in Sovereign Debt Instruments,found at http://wvw.law.gortdwn.edu/intemaional/documents/Pampdf (last visited on 31 March2005); See also WOOD, PHILIP R. LAW AND PRACTICE OF INTERNATIONAL FINANCE (1980), at Sec.6.3(2), pp. 155-156: "In the context of a corporate loan, the undertaking Eparipassu clause] is to beconstrued as a commitment or a warranty that on an insolvent liquidation or a forced distributionof assets unsecured creditors will be entitled to pro rata payment, and also that, on the occasionof judicial compromises or agreed debt settlements- the bondholders will not be discriminatedaginst." (Underscoring supplied.)

21 WOOD, PHILIP R., LAW AND PRACTICE OF INTERNATIQNAL FINANCE PROJECT FINANCE,SUBORDINATED DEBT & STATE LOANS (1995), at Sec. 16-12, p. 165. (Underscoring supplied.)

2007]

PHILIPPINE LAWJOURNAL

bear radically different legal rights and creditor status, but are also motivated bydisparate interests.26 As such, the pari pasmru clause is intended to address onlyborrower actions having the effect of changing the legal ranking of the debt orperhaps the earmarking of assets or revenue streams to benefit specific creditors.27

Notably, the 2004 United Nations Commission on International Trade Law(UNCITRAL) Legislative Guide on Insolvency Law (which includes the concept ofcorporate reorganization/restructuring/rehabilitation), defines the pari parsu clauseas "the principle according to which similarly situated creditors are treated andsatisfied proportionately to their claim out of the assets of the estate available fordistribution to creditors of their rank."

The importance of the distinction between the rights of secured andunsecured creditors has constitutional dimensions. As recently argued by scholarsand encapsulated in United States Supreme Court decisions, secured creditors havea property right in "hav[ing] the value of the collateral applied for payment of thesecured creditor's claim". 29 Where there is an impairment of this property right in acorporate reorganization plan that jeopardizes such property right (e.g. through a'most egregious' delay in the enforcement of a stay against a secured creditor duringcorporate reorganization, for example), it has been argued that there is a violationof the Takings Clause.3"

2 WOOD, PHILIP R., LAW AND PRACTICE OF INTERNATIONAL FINANCE: PRINCIPLES OF

INTERNATIONAL INSOLVENCY (1995 ed.), Secs. 1-15-1-44, pp. 10-26.27 Ibid., at p.5; See also distinctions betvieen-.lasses of creditors in corporate reorganizations

(or rehabilitations) in FLETCHER CYCLOPEDIA OF THE LAW OF PRIVATE CORPORATIONS (2000ed.), Volume 15A, Chapter 63, Sections 7634.27 to 7634.42. See also ScoTr, HAL S.,INTERNATIONAL FINANCE: TRANSACTIONS, POLICY ABD REGULATION (Foundation Press, 131h

ed., 2006), at pp. 840-843.Z" UNCITRAL Lqgislative Guide on Insolveng Law, p. 6. Found at:

http://www.iiiglobal.org/organizations/uncitral/UNCITRAL LeUislative Guide Insolvency La3 (last visited 15 January 2008)

29 Forrester, Julia Patterson. Bankrpt.yTakng.r, 51 FLA. L. REV. 851 (December 1999),at 877. This paper provides a comprehensive and updated refutation of the claim that security interestscould be completely invalidated in a bankruptcy or corporate reorganization setting, which claim wasdiscussed in the landmark article of Rogers, James Steven, The lmpairment of Securrd Crditorr' Rigbtr inReotgani,-ton: A Study of the Rekatotrhip Betaen the Fiftb Amendment and the Baxknepty Clau.r, 96 HARV. L REV.973, 973 (1983).

.1' Ibid, at 911:

"Current bankruptcy law for the most part protects property rights, including the rights ofsecured creditors. Secured creditors do experience delay in bankruptcy in their ability to realizeupon their security. However, only the most egregious case of delay could present asuccessful takings claim. Security interests are subject to avoidance in bankruptcy, but only inlimited circumstances that for various reasons do not present a takings problem.

Scholars have suggested that prospective legislation that invalidates security interests inbankruptcy would not create a takings problem. However, the constitutionality of this invalidationproposal is doubtful. All property owners would be affected by legislation that invalidated securityinterests in bankruptcy because they would not be able to create a security interest that could

[VOL 82

2007] STATUS OF SECURED CREDITORS

It should be noted further that international practices on corporaterehabilitations, restructuring, or reorganizations collectively affirm that thedistinction between creditor classes (secured and unsecured) must be preserved inany court-approved payment distribution scheme.31 In the United States, corporate

survive a bankruptcy filing. The right to convey a security interest may be a sufficientlyimportant strand in the bundle of property rights that its abrogation would constitute animpermissible taking. If, because of limitations on the availability of secured credit, theinvalidation proposal substantially interfered with the right of an owner to transfer land, it wouldmost certainly be an unconstitutional taking. In addition, the invalidation proposal may beunconstitutional from the point of view of the secured creditor. Because the proposalwould appropriate the secured creditor's property rights rather than regulate them, acourt could find the proposal unconstitutional without reaching the ad hoc test of PennCentral. Even if the ad hoc test is applicable, a court could find a taking. The extent of thesecured creditor's reasonable investment-backed expectations would be limited, but priornotice should not eliminate investment-backed expectations altogether where the securedcreditor is not taking the security interest in order to create a takings claim and has noability to avoid the possibility of loss. Furthermore, the economic impact of the proposalcould be substantial, and the character of the regulation, destruction of the secured creditor'sproperty rights, would be extraordinary. As a result, the constitutionality of the invalidationproposal is doubtful.

Although other proposals are not as onerous in affecting the property rights of ownersand 'secured parties, they do still raise substantial constitutional questions. The takings formula istoo fact dependent and takings law is still in too much of a muddle to make certain predictionsabout its application. Scholars making these proposals are ignoring significant and complextakings issues that may make their proposals unconstitutional. Since Professor Rogers' 1983article, courts and scholars have made assumptions about the bankruptcy takings problem, mostof which are based on his conclusions. However, their assumptions are not correct. The TakingsClause does limit the power of Congress to pass new bankruptcy legislation, even legislation thatis prospective. Security interests are interests in property, and new bankruptcy legislation cannotredefine the property interest of a secured creditor. Changes in the treatment of secured creditorsin bankruptcy do affect property owners as well as secured creditors, and their rights must beconsidered in assessing the constitutionality of new bankruptcy legislation, Finally, because thetakings formula, in the absence of a categorical taking, requires the application of a fact intensivead hoc test, the constitutionality of current limitations on the rights of secured creditors does notmean that different limitations would also pass constitutional muster. When the correctassumptions are made, the bankruptcy takings problem becomes much more complex and cannotbe dismissed with a short parag of current bankruptcy limitations on secured creditors. Thebankruptcy takings problem is still very much alive and must not be ignored." (Emphasissupplied.)

3, See Phelan, Robin F. and W. I verett. The Wretched Refuse -- Leading the Foreign Corporation toa Fresh Start in the United States, 59 CONSUMER FIN. L. Q. REP. 23 (Spring-Summer, 2005), at 36:

"The district court in Singer, discussed above, granted comity to the courts on the other sideof the Atlantic. Across the Pacific, the 1990s Asian financial crisis spurred interest in insolvencyand reorganization proceedings for Asian companies, and an increasing number of bankruptcyopinions here are recognizing foreign proceedings over there. For examle. Bankruptcy ludgaThomas E. Carlson recently recognized the Philippine rehabilitation law as worthy ofcomity. in an unpublished opinion ("In re Ancillary Petition regarding PhilippineAirlines Inc., a Philippine Corporation, No. 98-3-2705-TC (Bankr. N.D. Cal. 1998).Philippine Airlines Inc. (PALU, he national airline ofjth Republic of ths Philippines. filedA petition for suspension of payments and corporate rehabilitation with the Philippine

132 PHILIPPINE LAWJOURNAL [VOL 82

reorganizations expressly require a specification of creditor classes in theformulation of corporate reorganization plans:

"§7634.30 )esignation of classes of claims

A plan of reorganization is required to designate classes of claimsand classes of interests. A claim or interest rn l placed in a particula jaonlif it is substantially similar to the other claims rr interest, in the class.The plan may, however, designate a separate class of claims consisting ofevery unseccaed claim that is less than or reduced to an amount that thecourt approves as reasonable and necessary for administrative convenience.

Certain sorts of claims need not be designated, such asadministrative expenses, claims arising after the filing of an involuntarypetition and before the appointment of a trustee or the entry of an order forrelief, and certain claims for taxes and custom duties.

§ 7634.33 Designation of classes of interests

The reorganization plan must designate classes of interests.Although the term "interest" is not defined in the Bankruptcy Code, it isused to describe an ownership interest.

An interest may be placed in a particular class only if it issubstantially similar to the other interests in the class. ih plan must alsosp-ecify anyi classes o~f interest,,wic-a not impaired under the p-lan. and

ecifthe tatment of .n c off interests which impaired.

7634.36 Specification of claims or interests impaired

A reoranization must specify_ any class of claims or interestswhich is not impaired under the plan. and specify the treatment of any classof claims or interests which is impaired. The plan may impair or leaveunimpaired any class of claims, whether secured or unsecured, or any class ofinterests.

Securities and Exchange Commission (PSEC . Thereafter, the foreign representative of PAl,filed a section 304 petition in the Northern District of California, obtaining a preliminaryinjunction prohibiting actions against PAl, and its property in the United States. Objectingcreditors noted a 1981 presidential decree of President Marcos that transferred jurisdiction oversuspension-of-payments proceedings from the Philippine courts to the PSE'. According to theobjecting creditors, the suspensioo-of-payments proceeding was not subject to Philippineinsolvency law, and thus not worthy of comity under section 304.

The Philippines Airline court disagreed. noting imit 1hat Philippine insolveny lawprovides creditors procedures and protections similar to those found under the U.S.Bankruptcy Code, includig riori of claims, appellate review, a first meeting ofcreditors, an automatic sta. ygon gn plan confirmation. and recovery of preferences andfraudulent transfers. xxx" (mphasis and underscoring supplied.)

2007] STATUS OF SECURED CREDIT )RS 133

Fach claim or interest of a particular class must receive the sametreatment under the plan, unless the holder of a particular claim or interestaprces to a less favorable treatment. A plan may desi ,mate a separate class ofclaims consistinV only of unsecured claims less than a specified amount, orreduced to an amount which the court finds reasonable and necessary foradministrative convenience. Therefore. small and unsecured claims may beplaced in a separate class and need not be accorded the same treatment aslarge unsecured claims.

§ 7634.39 Priority claims

Claims for administrative expenses and claims arising during thegap period must be paid in full on the effective date of the plan, unless theholder of the claim agrees to a less favorable treatment. Tax claims may bepaid over a period of time, as may employee benefit claims, wage, salary andcommission claims, and claims for deposits on consumer purchases, underprescribed conditions.

It is fundamental that creditors take priority over stockholders.Even defrauded stockholders' claims are subordinate to the claims of generalunsecured creditors."

32

More importantly, international practice emphasizes that corporatereorganizations or rehabilitations should not cause 'excessive interference' with the

security as to altogether deprive the secured creditors of benefit from such

security:3 3

"If there is a stay on the enforcement of security, the main pointsto be considered are the period of the stay and whether the stay is limited toassets essential to the continuing business which are idiosyncratic (notsecurities, cash or ordinary commodities). The alleged object of the stay is tokeep the business together while the rehabilitation is allowed to work, e.g. bypreventing the mortgagee sale of the main factory, computer equipment, oran essential patent or unfinished inventory. But the effect f excessiveinterference in the u i ko the ce r f the benefit of thesecurty: the whole pupose of security is that it should be available on theinsolvency f the debtor ad t if the jurisdiction destroys the

s when it is most needed- the value and ufil of security tself isdemoted. Accordingly jurisdictions have to decide whether they desire theadvantages of security or whether they prefer the draconian rehabilitationprocedure, although middle courses are possible, e.g. a stay on enforcementfor a limited period.

The stay causes problems for perishable assets; volatile assets, suchas securities, commodities, and foreign currency deposits, especially margin

12 FLETCHER CYCLOPEDIA OF THE LAW OF PRIVATE CORPORATIONS, (1995 ed.) Vol. 15A, p.603, § 7634.30 to §7634.39. Emphasis and underscoring supplied.

33 See also Norton Jr., William L. f 110:9 Treatment of Holdes of Secured Claims, 5 NORTON

BANKR. L. & PRAc. 2d § 110:9 (October 2007).

134 PHILIPPINE LAWJOURNAL [VOL 82

collateral for market dealings; ships, aircraft and other assets which are inneed of special protection or which could attract an ."assets" bankruptcyjurisdiction just because they happen to be there or which can be spiritedaway to avoid a surprise attachment; liens covering small assets not essentialto the business; income-earning assets if the debtor can use the income, e.g.rent from land and equipment leases, dividends and interest on securities,recoveries on receivables, royalties and intellectual property rights (theincome may have been essential to service the creditors' interest); andpossessory pledges and liens since the security is lost if possession must besurrendered.

Other factors are: (1) a stay results in the erosion of security if itfalls in value or if interest continues to pile up - the period of the stay isgermane; (2) whether the debtor can use the secured assets for the purposeof the continuing business and the powers which the creditor has to preservethe asset; (3) whether the debtor can substitute alternative secured assets inorder to retain some essential asset; (4) whether a plan can bind dissentientsecured creditors to an extension of the maturity of the debt or a reduction inamounts or a change of currency; (5) whether the security is primed by thecosts of the administration (liabilities incurred in continuing the business,super-priority loans, employees, taxes) so that the creditor's security is erodedand its value highly unpredictable; (6) whether security expressed to coverafter-acquired property such as a floating charge over all present and futureassets or an aircraft mortgage over engines subsequently replaced can catchassets acquired by the debtor post-commencement; (7) the degree ofprotection given to secured creditors against unfair prejudice; (8) whethercash collateral can be taken away in the interests of financing the business;and (9) whether post-commencement interest continues to run and can beadded to the secured debt. A common problem is whether a creditor.whohas security over investments or receivables violates a stay if he receivespayment on the assets from the third party and applies it to the secured debt:this would be a violation of the US stay in BC 1978 s 362." .

14 Wo)I, PIIII.11 R., COMI'AI VEAII: I,AW OF SICURITY AND GUARANI'.1S(1995 ed.), Chapter

11 ("Security and Rehabilitation Proceedings"), at pp. 152-153; See Woo, PIIIlu' R., PRINCHI'LFSo1: INTEgRNATIONAI. INSOILVt:NC'Y (1995 ed.), at Chapter 11 ("Corporate RehabilitationProceedings: Ik'ngland, France, Japan, United States) p. 186-187:

"Grounds for petition and ease of entry

11-7 General The key issue here is the case of entry into the proceedings - case of entryprioritizes the formal proceedings over private work-outs. Factors are:

- whether the debtor must show actual insolvency or the likelihoodof insolvency, whether he is not required to prove insolvency at all, andwhether insolvency is a balance sheet test or a liquidity test or both. If theobjective of early rehabilitation is to be achieved before it is too late, thedebtor should not be required to show actual insolvency, but rather theprobability j f an impending insolvency:

2007] STATUS OF SECURED CREDITO)RS

Where there is an erosion of the security interest under thereorganization/rehabilitation plan, there must be 'adequate protection' given to theaffected (secured) creditor through corresponding liens or cash payments:

"11-12 Adequate protection Rather than allowing relief from thestay, the court may order the creditor to bc given adequate protection of itssecurity interest, e.g. additional licns or cash payments to match the fall invalue. The basic protection given to secured creditors is that thcy mustreceive indubitably adequate protection for their security.

The House Report indicated that the concept of adequateprotection is derived from the Fifth Amendment protection of propertyinterests and from a policy that secured creditors should not be deprived ofthe benefit of their bargain, so that if the secured creditor does not get theexact collateral (because, like a factory, it is needed for the debtor's business),he must get the equivalent in value. Case law shows that the creditor hasadequate protection if he is over-secured (to the extent of the cushion) or hasa recoverable guarantee from a third party, but not usually if the guarantee isunsecured. The US Supreme Court established in the Timbers case abovethat, if the creditor is undcr-secured, the creditor is entitled to cash payments(or the equivalent) if his collateral is decreasing in value, that he is notentitled to compensation for loss of the ability to reinvest proceeds from aforeclosure, and that the creditor should be granted relief from the stay if theproperty is not necessary for an effective reorganization which is feasible andin prospect."3

It is internationally recognized that judicial rehabilitations result in"increased complication, confrontation, delay and cost". The heavy involvement ofprofessionals - lawyers, accountants and consultants - and the "confrontations andlitigation caused by a rigid statutory framework, by the compulsory quelling ordivestment of creditor rights" makes formal proceedings in judicial rehabilitations

- whether the debtor must show that survival is feasible so as toavoid abuse of the process;

- whether entry is by court order or by unilateral initiation by thedebtor (Australia, but not Britain or the US). Judicial approval increases costbu controls abue and discourages an over-easy entQr with a view topronotin a work-out i.e. the proceeding is a a resort." (Underscoringsuplfied.)

. Ibid at pp. 156-157. Emphasis supplied. See Japanese practice in Tanaka, Wataru.Extinguishing Security Interests: Secured Claims in Japanese Business Reoganization Law and Some PoAhImplicationsfor U.S. Law, 22 EMORY BANKR. DEV. J. 427 .(Spring 2006), at 428-435. In Japan, adebtor can cancel security interests in any property necessary for continuation of its business bypaying the secured creditors the liquidation value of such property.

See aLro GROCI1AL, ALAN M. AND MEGAN K. MECHAK, PRACTICE MANUAL FOR TEMARYLAND LAWYER, 3rd ed. with 2006 Update, Volume 1, Chapter 4 ("Bankruptcy"), (2006ed.), at Part IV.G . (summary on Chapter 11 proceedings in the United States)."

PHILIPPINE LAWJOURNAL

costly for all stakeholders.3' These inherent costs only make it all the moreimperative that distinctions betveen secured and unsecured creditors should bebuilt into the court's approval of the rehabilitation or reorganization plan. To doothenvise would only invite further delay and cement opposition between creditorclasses - a situation prohibitive to the goal of expeditious, efficient, and non-adversarial rehabilitation envisioned in the Interim Rules.

III. REHABILITATION COURTS AS 'AucTIONEERS' IN THE'CREDITOR' EXCHANGE OF DEMANDS:

HOW THE PARETO-EFFICIENT SET OF ALLOCATIONS OF CORPORATE ASSETSBETWEEN SECURED AND UNSECURED CREDITORS ARE CONSTRAINED BY

THE INTERIM RULES

Rehabilitation courts assume a more "interventionist" role in rehabilitationproceedings than in traditional civil or criminal litigation. In corporaterehabilitations, courts are mandated to approve rehabilitation plans that will mostfeasibly restore the corporation to financial viability. This task calls for a calibrationof competing interests in the mode and manner of distribution of corporate assets:1) the corporation's need for a sustainable supply of resources to support businessoperations, generate profits, and improve shareholder value; 2) secured creditors'demand for repayment of their loans, and in the interim (before full repayment), themaintenance or preservation of their security interests; and 3) unsecured creditors'demand for repayment of their loans. Clearly, thiis is not a pure system of "privatebargaining", which as envisioned under the Coase Theorem, should be the mostappropriate means of allocating resources when transactions costs are low.37

Instead, what transpires is a hybrid between private bargaining and public regulation(through the rehabilitation court's approval and implementation of therehabilitation plan and the Interim Rules).

Certainly bargaining does take place in corporate rehabilitation, perhapseven more so than most traditional litigation contexts. Under the Interim Rules, theRehabilitation Receiver may (and before submission of his evaluation of therehabilitation plan to the rehabilitation court) meet with the debtor, the creditors, orany interested party "to discuss the plan with a view to clarifying or resolving anymatter connected therewith". 38 Prior to the court's final approval of therehabilitation plan, revisions can be submitted by creditors, any interested party, as

u, See (illo \V' ( )l, PlII.IIp R. ]IRiN(CIPI.I~ ( )F I NI-I/NAII( )N A.I+ NS( mI.VI'NCYR IN (:1IP1I.1S ( )1I

INTI:IRNA'lI()N,\I. INS()I .VBNCY. (1995 ed.), at Chapter 11 ("Corporate RehabilitationProceedings: kngland, France,.lapan, United States"), pp. 302-303.

11 See (ooIt'lI. It. & TI IMAS L)I.I:N. ILA\' AND ]+CONNMICS (Pearson \ddison Wesley 2004.411, cd.), at p. 89.

18 Interim Rules, Rule IV, Section 21.

[VOL 82

STATUS OF SECURED CREDITORS

well as the debtor corporation. -9 Such "bargaining", therefore, occurs in a settinginstitutionally-mandated under the Interim Rules. (As discussed elsewhere by otherscholars, such institutionally-mandated bargaining under corporate reorganization isbased on the social desirability of coordinating debt collection activities, as well as acost-reduction motivation to mitigate or prevent creditor conflict.*)

The bargaining process entails the resolution of several issues of valuation(e.g. how much is the corporation's total debt burden; how much of the total debtburden is owed to each creditor class; how much is the corporation's total assets;and how much is the corporation's needed annual operational and capital expensesto reach the targeted level of financial solvency as would take the corporation out ofrehabilitation). Parties' options for restructuring corporate debt can range fromdebt cancellation or reduction, debt satisfaction (for less than the full amount, orwith "haircuts" borne by creditors), debt-for-debt exchanges, debt modification,debt-for-equity exchanges, or capital contribution of debt.41 Given limitedresources to service corporate debt, creditors can foreseeably bring their ownvaluations to the bargaining table, including the maximum portion of their creditthat they are willing to "retire" (or, as in some cases, convert to equity in thecorporation) for the sake of corporate rehabilitation. Following the RehabilitationReceiver's submission of his proposed rehabilitation plan and creditors' commentsand/or revisions to such plan, it is then the task of the rehabilitation court to

.1 bid at Rule IV, Section 22.4' Longhofer, Stanley D. and Stephen R. Peters, Protection for Whom? Creditor Confict and

Bankrupty, 6 AM. L. & ECON. REV. 249 (Fall 2004), at 273-274:

"xxx But, in the absence of an automatic stay on the unsecured creditor's debt-collection

efforts, it may be difficult after the fact to trace the line between the disposal of the assets servingas collateral and the payments made to the unsecured creditors. Thus, even collateralizedclaims depend on the basic elements of a bankruptcy system -- the automatic stay andpreference'provisions -- to ensure effective protection for the secured creditor.

There are private actions a secured creditor might take to protect its interests, even in the

absence of a bankruptcy system with these provisions. For example, it may impose restrictivecovenants on the firm's use of any assets serving as collateral, requiring prior approval before theymay be liquidated. Restrictions such as these, however, may prove more costly than they areworth. By limiting the firm's ability to misuse the assets, the creditor may also hamper the firm'sability to redirect these assets to their highest-valued use. In other words, the very restrictions thecreditor may require to protect its own interests may limit the firm's ability to maximize its profits.Furthermore, covenants restricting the use of collateralized assets must be monitored if they areto be effective in protecting the secured creditor's interests. Consequently, secured debt may beno more effective in reducing the costs of coordination than seniority and coordinationcovenants.

All of this suggests that, although collateral may effect coordination in some cases, it cannot

serve as a general replacement for a bankruptcy system that mandates creditor coordination.Thus, our primary conclusion is reconfirmed: A mandatory bankruptcy law that ensures allcreditors will coordinate their liquidation activities ex post improves social welfare better thanprivate contracting solutions." (Emphasis and underscoring supplied.)

41 Zarlenga, Lisa M. Restructuring Troubled Corporations, 789 PLI/Tax 769 (October-November

2007), at 780-786.

2007]

PHILIPPINE LAWJOURNAL

ascertain how to most efficiently allocate corporate resources (between debtservicing and financing corporate expenses) towards the goal of rehabilitation.

"Efficient" public regulation (through the rehabilitation court'senforcement of the Interim Rules) should therefore reduce the costs of enforcingand implementing the eventual "agreement" between creditors (spanning securedcreditors, unsecured creditors, and suppliers) and the debtor corporation under therehabilitation plan.42 As the "public regulator", courts conceivably appear as themost critical actors in the rehabilitation process. How rehabilitation courts willdecide on the sensitive issue of corporate asset/resource allocation between creditorclasses (and without sacrificing rehabilitation goals) is a veritable test case formodeling judicial methodology and reasoning.4

Intuitively, an "effective" corporate rehabilitation should be "capable ofswift implementation, as uncomplicated and inexpensive as possible, and flexible,providing alternative terms of dealing with the financial affairs of the company." 44

These intuitive generalities, however, are hardly informative for rehabilitation courtstasked to ascertain what "efficiency" is in the allocation of corporate resourcesduring rehabilitation. Does "efficiency" embrace the extreme interpretation of theRuby Industrial dictum, which is that secured and unsecured creditors are on "equalfooting" with respect to the pool of resources from which their debts will beserviced? Alternatively, does an "efficient" allocation mean that unsecuredcreditors can, along with secured creditors, be paid from the proceeds of sales ordispositions of secured assets, without the debtor corporation having to replacesuch properties comprising the security?

A. THE CONCEPT OF ECONOMIC EFFICIENCY

Answers to the foregoing questions depend on how rehabilitation courtsappreciate the concept of efficiency. Economic efficiency is described as "the bestuse of limited resources given people's tastes."'45 Intuitively, the optimal quantity ofany good, ceter paribus, is that "at which the value placed by society on the marginalunit equals its marginal social cost."'4f There is Pareto efficiency (also known as

42 See Ulen, Thomas S. Courts, Legislatures, and the General Theoy of Second Best in Law and

Economics, 73 0 II-KiNr. L. lRi:V. 189 (1998), at 198.11 1 or an interesting model proposing cognitive reflection as the schema for judicial decision-

making, see (uthrie, C. ct al. Blinking on the Bench: How Judges Decide Cases, 93 CORNELL L. RIV. I

(November 2007).44 Fisher, Richard. Rehabilitating Large and Complex Enterprises in Financial Dificulties,

DISCUSSION PAPI"-R BY Till: ClAilMAN OF PARINERS OF BLAKE DAWSONWA]L)RON, Sydney, Australia, 8 April 2004 fiund athtt2:// www.camc. ov.au/camac/camac.nsf/byl-eadfine/PDFSubmissions/Sfile/BDW.pdf (lastvisited 27 December 2007).

4, BARR, N i: R)IAS. 'I: I J,0N(MICkS OF TIE WEIFARI S'I'ATIE (Oxford University Press, 3rd

ed., 1998), at 70.4' Ibid,

[VOL 82

STATUS OF SECURED CREDITORS

Pareto optimality or allocative efficiency) when resources cannot be allocated ordistributed in any other way without making someone else worse off.47 In a marketof exchange, a "general equilibrium" exists when three (3) conditionssimultaneously hold: 1) productive efficieny (where maximum output is achieved froma given set of inputs); 2) efficiency in the product mix (the optimal combination of goodsthat should be produced given existing production technology and consumertastes); and 3) effciengy in consumption (consumers allocate their income in a way thatmaximizes their utility, given their incomes and the prices of goods).

Economic efficiency is best illustrated by the Edgeworth Box Diagram48 inmicroeconomics:

LEdgewcth Box iagramAt each efficient point, the RTS (of k for ) is equal in bothx and y production

Total Labor