Tire and Natural rubber Industry - FPTS

88

Tire and Natural rubber Industry “… The low cost of Radial tire manufacturing, being attributed the dramatic reduction in Rubber prices, enables domestic enterprises to foster sustainable development, thereby helping to put Vietnam tire brands on the world map…” Luan Ngo Kinh Senior Analyst E: [email protected] P: (08) - 6290 8686 - Ext: 7595 Oct 2014 POTENTIAL GROWTH IN TIMES OF HARDSHIP

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Tire and Natural rubber Industry - FPTS

Tire and Natural

rubber Industry

“… The low cost of Radial tire manufacturing, being attributed the dramatic reduction in Rubber prices, enables domestic enterprises to foster sustainable

development, thereby helping to put Vietnam tire brands on the world map…”

Luan Ngo Kinh

Senior Analyst

P: (08) - 6290 8686 - Ext: 7595

Oct 2014

POTENTIAL GROWTH IN

TIMES OF HARDSHIP

Tires and Natural Rubber

CONTENT

A. NATURAL RUBBER AND TIRES 4

I. Overview of the Natural Rubber 4

1. The Global Rubber Value chain 7

2. Vietnam’s Natural Rubber Industry 9

3. Value chain of Natural rubber industry of Vietnam 12

4. The position of Vietnam Natural rubber industry 14

5. The difference among Vietnam and the 3 neighboring countries Thailand,

Malaysia and Indonesia 15

6. Exporting – Importing of natural rubber of Vietnam 18

7. Analysis of the 5-Forces model of Vietnam Natural Rubber Industry 21

8. Policies related to Natural Rubber 22

9. Natural rubber industry outlook (NR) 23

II. Tire Industry 24

1. Overview of global tire industry 24

2. The Tire industry in Vietnam 28

3. Tire industry value chain in Vietnam 34

4. Era of Radial tire 37

5. SWOT Analysis of Tire industry in Vietnam 39

6. Policies related to tire industry 41

7. Tire industry outlook 42

B. UPDATED TIRE & RUBBER COMPANIES 43

I. Overview of listed companies in the industry 43

II. Opposite Business Performance between Natural rubber and Tire 48

III. Financial Analysis 52

C. INVESTMENT RECOMMENDATION 57

D. APPENDIX 64

NA

TU

RA

L R

UB

BE

R

TIR

ES

E

NT

ER

PR

ISE

S

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 1

SUMMARY The world’s natural rubber industry

In the period of 2003-2013, the global production and consumption reach the CAGR of 4.2% and 3.7%, respectively.

The rubber plantation and the tapping production are largely located in Asia (93%) By the end of 2013, 88.85% of natural rubber’s global production is attributable to 6 countries including:

Thailand (34.41%); Indonesia (25.6%); Vietnam (7.89%); China (7.11%); India (6.99%) and Malaysia (6.85%).

About 68.7% of total NR demand of the world is consumed by China (36.65%), India (8.46%), US (8.06%), Japan (6.23%), Indonesia (4.72%) and Thailand (4.59%)

The supply surplus is expected to continue until the end of 2016. It shows that the motivation for price increase is quite low. Hardly any factor can apparently promote price increase in the years to come.

Vietnam’s natural rubber industry

Rubber planting area in 2013 was 955,700 ha (+4.1% yoy), production volume was 949,100 tons (an +8.2% yoy).

In the ten-year phase of 2003-2013, CAGR of rubber area was 8.0%/year with exploitation volume reaching 10.1%/year.

Vietnam ranks the fifth in the world in terms of rubber area and the third in term of production volume of natural rubber. In 2013, Vietnam surpassed its competitor – India, becoming one of the leading countries in exploiting capacity – 1.74 tons/ha.

56% of rubber area is in the Southeast of Vietnam.

Up to 2013, rubber area of Vietnam in Laos and Cambodia were 28,000 ha and 89,000 ha, respectively. Especially, HAGL possessed an area of 36,130 ha in the 2 countries above, and Gemadept JSC was planting 29,500 ha of rubber trees in Cambodia.

Domestic consumption of rubber is only 15-16% of the total supply.

There still remains a vast distinction in operation between Vietnam and neighbouring countries like Thailand, Malaysia, and Indonesia.

In the first 6 months of 2014, export volume decreased by 8.7% and export value reduced by more than 32% yoy.

In the first 6 months of 2014, Vietnam imported about 44,557 tons natural rubber with value of 82.9 mil USD, a decrease of 12.1% in quantity and 35.4% in value yoy.

Prospects of domestic natural rubber are not proved very bright considering the excess supply situation will continue at a high level and will not stop until 2016.

The world’s tire industry

The world’s tire industry is categorized into 2 segments: OEM (25-27%) and Replacement tires (73-75%).

70% of global market share is dominated by the top 5 countries such as Japan (23.9%), France (14.2%), the USA (13.1%), China (13.5%).

In terms of auto tire production: 60-61% of global products belongs to the Asia.

Regarding consumption: Consumption of the Asia, Europe and North America in combination is 86% of global consumption.

Currently, Radial tires are dominating the world’s consuming market.

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 2

Vietnam’s Tire industry

There are about 830 enterprises operating in the tire industry in Vietnam.

Tires for bicycles in Vietnam are close to saturation while tires for motorbikes can satisfy only 80% of

the demand. As for automobile tires, 80-90% of the volume is for export.

61% of the truck tire market share in the country is traced back from the 5 enterprises as follows:

Bridgestone (importation), Michelin (exportation), Da Nang rubber (DRC), Casumina (CSM) and

Yokohama (manufacturing and importing).

Speaking of tire market share in the country: Casumina makes up for 33% followed by DRC (25%),

SRC (10%) and others (31%).

For Radial tires, 90% of the market share is dominated by FDI corporations and imported tires.

According to the statistics of the first 6 months of 2014, export value achieved USD 217 mil, an increase

of 12.9% yoy. Import value of tires of Vietnam was 140.57 mil USD, decreasing by 16% yoy.

The year of 2014 has witnessed the initial penetration of Radial tires of DRC and CSM. In the phase of

2015-2016, it is predicted that sales will grow and market share of both DRC and CSM for this segment

will increase accordingly.

Recommendation

Phuoc Hoa Rubber JSC. (PHR – HOSE) NEUTRAL, TARGET PRICE: 30,300 VND/share (+4.5%. Revenue in 2014 is expected to reduce by 16-20% yoy. EAT is estimated to be around 221-245 bn VND, 8-17% lower than 2014 plan – a decrease of 49-54% yoy. With the above estimation, EPS 2014 will be 2,154-2,388 VND/share. Accordingly, PHR is trading with PE forward of 11x, which is relatively higher than the average. The

target price measured by FCFF is 30,300 VND/share. (More details)

Dong Phu Rubber JSC. (DPR – HOSE) NEUTRAL, TARGET PRICE: 35,400 VND/share (-16%) Revenue in 2014 is expected to be around VND 925-940 bn, achieving 92% of the plan for the whole

year.

EBT of the whole year is about VND 211-221 bn, achieving 85-89% of the 2014 plan, a decrease of

46% yoy.

With this estimation, EPS 2014 will achieve 4,565 – 4,723 VND/share. Short-term target price is 35,400

VND/share, 16% lower than the market price. Currently DPR price can range from 40,000 – 50,000

VND/share thanks to the purchase of 2,000,000 shares. We, thus, recommend a NEUTRAL for this

stock. (More details)

Tay Ninh Rubber JSC. (TRC – HOSE) NEUTRAL, TARGET PRICE: 33,200 VND/share (+3.8%) Revenue yield from rubber business will be about 532 bn VND making a total revenue of the year of 573 bn VND, achieving 80% of the plan. EBT is estimated to be around VND 168 bn, exceeding 23% of the plan and decreasing by 37% yoy. Accordingly, EPS achieves 4,740 VND/share. In terms of PE, target price of TRC is 33,200 VND, equivalent to PE of 7.0x. (More details)

Hoa Binh Rubber JSC. (HRC – HOSE) SELL With more than 50% of aged rubber trees, low productivity and ineffective business activity, the future does not look very positive. Revenue of the year is VND 230.7 bn, achieving 88% of the plan. EAT this year will be about VND 53.7

bn, achieving 77% of the plan – a decrease of 17% yoy.

EPS 2014 will achieve 3,110 VND/share. At the current price of 39,000 VND/share (dated Sep 30,

2014), HRC is trading at PE forward of 12.5x, which is relatively higher than the average of 7.0x. We

recommend SELLING this stock. (More details)

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 3

Thong Nhat Rubber JSC. (TNC – HOSE) SELL Business activities involve a number of unstable business fields, let alone small-scale plantation, low

productivity and inefficient business performance.

TNC is not as highly recognized as other listed corporations.

EPS 2014 is expected to be 694 VND/share. The company is now trading at PE forward of 17x, which

is relatively higher than the average of 7x. We recommend SELLING this stock. (More details)

Da Nang Rubber (DRC – HOSE) – HOLD, target price at the middle of 2015 is 60,300 VND/share (- 4,3%) The sale volume of both Bias tires and Radial tires increases quickly. The EAT is VND 369 – 383 bn,

declining by 2% yoy because the company recognizes the depreciation and interest expenses of Radial

factory.

It is very potential for the high growth of Radial tires in near future.

The estimated EPS of 2014 is about 4,450 – 4,615 VND/share. The target price of this year is 54,000

VND/share and 60,300 VND/share by the mid-2015. (More details)

Casumina (CSM–HOSE) – HOLD, the 12-month target price is 48,200 – 51,500 VND/share (increase from 3.4% to 10%). We forecast that the selling volume will highly rise, however, the profit will decrease because the

depreciation and interest expenses of Radial factory will be recognized next year.

The company will have an infrequent contribution from real estate in both 2014 and 2015.

It is very potential for the high growth of Radial tires in near future.

EPS of 2014 will be 4,820 VND/share (excluding the real estate transfer) and is 5,150 VND/share

(including the real estate transfer). (More details)

Sao Vang Rubber (SRC – HOSE) ADD, the year-end target price is 30,600 VND/share (+9%) We expect that the business result will be more positive than that of last year thanks to high growth

of demand of the market in general and SRC in particular on tires.

The selling quantity achieved the high growth in the first eight months of this year. Bicycle tires rose by

10%; motorcycle tires increased by 40%.

We forecast that the revenue of 2014 will reach VND 959 bn, PBT is VND 95.3 bn, increasing by 10%

yoy. Consequently, the EPS of 2014 will be 4,081 VND/share. The target price of this year is 30,600

VND/share. (More details)

Abbreviation

ANRPC : Association of Natural Rubber Producing Countries

IRSG : International Rubber Study Group

VRA : Vietnam Rubber Association

VRG : Vietnam Rubber Group

AFET : Agricultural Futures Exchange of Thailand

LMC : LMC Automotive

ASP : Average Selling Price

NR : Natural Rubber

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 4

A. Natural Rubber and Tire

I. Overview of the Natural Rubber

The world natural rubber’s production and consumption are 12.04 and 11.32 million ton respectively in 2013, increasing by 2.67% and 3.73%, respectively compared to that of 2012.

In the period of 2003-2013, the production achieves the CAGR of 3.7% higher than that of consumption of 3.4%.

The supply surplus of the world rose continuously from 2011 to 2013 by 243 thousand

tons, 524 thousand tons and 640 thousand tons, respectively.

The rubber plantation and the tapping production are the most densely in Asia (93%),

followed by Africa (4-5%) and Latin America (2-3%).

Asia is the largest consumer of natural rubber accounting for about 72% of total

demand, followed by Europe (12%); North of America (10%); 6% of others.

Supply – Demand of Global Natural Rubber

Source: IRSG and ANRPC

Source: IRSG

(600)

(400)

(200)

-

200

400

600

800

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Production

Consumption

Supply Surplus

93.4%

4.3% 2.5%

Asia

Africa

Latin America 72%

12%

10%

5%

1%

Asia

Europe

North of America

Latin America

Africa

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 5

By the end of 2013, 88.85% of total natural rubber’s production of the world comes from

6 countries including: Thailand (34.41%); Indonesia (25.6%); Vietnam (7.89%); China

(7.11%); India (6.99%) and Malaysia (6.85%). Last year, Vietnam surpassed Malaysia

and India to make it to the top 3 of the largest rubber producers of the world.

By the end of 2013, Indonesia owned the largest rubber plantation of the world

accounting for 3.49 million tons with Thailand ranking the second (3.43) and China;

Malaysia holding the third and the fourth place (1.16 and 1.06 respectively). The fifth

and sixth position belong to Vietnam and India (955,700 ha and 776,000 ha

respectively).

About 68.7% of total NR demand of the world consumed by China (36.65%), India

(8.46%), US (8.06%), Japan (6.23%), Indonesia (4.72%) and Thailand (4.59%). In

particularly, China occupied about 32% of total NR consumption and 25% of total NR

export value of the world for the last 5-year.

Approximately 87-94% of total NR export volume of the world belongs to Thailand (3.66

million tons), Indonesia (2.72 million tons), Malaysia (1.38 million tons) and Vietnam

(1.07 million tons).

Top 4 of Natural rubber exporters in 2013

Source: The Rubber Economist

Source: ANRPC

Natural rubber production’s structure

by country in 2013

Natural rubber consumption’s

structure by country in 2013

Country 1,000 Ton % Proportion

Thailand 4,141 34.4

Indonesia 3,081 25.6

Vietnam 950 7.89

China 856 7.11

India 842 6.99

Malaysia 825 6.85

Cote d'Ivoire 275 2.29

Brazil 173 1.44

Myanmar 147 1.22

Sri Lanka 131 1.08

Philippines 111 0.92

Others 26- 4.20

Country 1,000 Ton % Proportion

China 4,150.0 36.65

India 958.2 8.46

USA 913.0 8.06

Japan 705.4 6.23

Indonesia 534.0 4.72

Thailand 520.0 4.59

Malaysia 434.1 3.83

Korea 396.0 3.50

Brazil 395.3 3.49

Germany 249.5 2.20

Vietnam 154.0 1.36

Others 1,718.5 16.91

Country 1,000 ton % Proportion

Thailand 3,664 40.5%

Indonesia 2,719 30.1%

Malaysia 1,380 15.3%

Vietnam 1,076 11.9%

Others 201 2.2%

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 6

Natural Rubber price volatility based on the economic events of 2008-2014

Based on the structure of global NR consumption and production as described above and the events that happened in the past, we could see that the NR price is always influenced by economic and social events, disasters, etc. in developed countries which has a great effect on the demand and supply of NR from countries like US, Japan, China, Thailand, Malaysia, etc.

Natural Rubber price forecast

According to the data of The Rubber Economist and IRSG, it shows that the supply surplus will continue until the end of 2016. Massive influx of countries joining rubber plantation in the period 2007-2009 (the positive price uptrend period) results in the current oversupply. The supply will increase quickly from 2013 to 2016 when all rubber in the period of 2007-2009 is tapped. From 2013-2016, the production is estimated to grow 2% per year lower than the 3% of consumption. It would narrow the gap between supply and demand for the next 3 years. However, it shows that the motivation for price increase is quite low. Hardly can any factor apparently promote price increase in the years to come.

Source: The Rubber Economist Report

Supply-Demand of Global Natural Rubber of 2012-2016

0

1000

2000

3000

4000

5000

6000

7000T

1

T3

T5

T7

T9

T1

1

T1

T3

T5

T7

T9

T1

1

T1

T3

T5

T7

T9

T1

1

T1

T3

T5

T7

T9

T1

1

T1

T3

T5

T7

T9

T1

1

T1

T3

T5

T7

T9

T1

1

T1

T3

T5

T7

2008 2009 2010 2011 2012 2013 2014

Thailand Malaysia Vietnam

Source: VRG, AFET, Malaysia Rubber

Natural Rubber price’s performance in the period of 2008 - 2014

Global financial

crisis

Flood in Thailand Tsunami in Japan

Debt crisis in Europe

QE in US, Japan,

China The highest rubber inventory in China

Crisis in China US reduced QE

Thailand, Malaysia, Indonesia together reduce supply volume for supporting the natural rubber price

-

100

200

300

400

500

600

700

10,000

10,500

11,000

11,500

12,000

12,500

13,000

2012 2013 2014 2015 2016

Production Consumption Supply Surplus

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 7

1. The Global Rubber Value chain

a.1 Materials: This is the most critical part of the value chain with capital and land

investment being demanded on a long-term basis. This, accordingly, builds a

major barrier for any would-be entrepreneurs in this industry. Natural rubber trees

grow well primarily in tropical regions that feature the 4 factors as follows:

temperature of higher than 260C, an annual 1,800 mm of rain, humidity range of

well above 80%, 1-metre soil layer and elevation of lower than 300m. Business

efficiency is subject to the tapping productivity. At the present, 88.85% of the

world’s total natural rubber production comes from the 6 countries namely:

Thailand, Indonesia, Vietnam, China, India and Malaysia. These countries also

have the dominant acreage constituting 80-90% of the total globe’s land area.

a.2 Purchasing: This involves the transporting natural rubber from the plantations to

processing factories with profit margin being quite modest. Natural rubber are also

known to be a popular commodity frequently traded at world-renowned

commodities exchanges such as Tocom, Sicom, AFET, Malaysia, to name just a

few. Therefore, purchases will be made via these commodities exchanges with

intermediate traders taking part in or otherwise paid for by processing factories in

those countries. In addition, the Government of such countries will make purchase

of natural rubber and keep it in reserve as following their national policy to

stabilize prices.

Large holder (State-owned

corporation,

Government)

)

International

merchant Technical

rubber (block,

sheet)

Latex

processing

(liquid)

Processing Manufacturers Materials

Imported rubber

Smallholder (Private

companies,

households)

Purchasing

Collectors

Processing

companies

State-owned

corporation,

Government

Others

International

producers

Domestic

merchant

Domestic

producers

Synthetic rubber (Raw Oil)

Synthetic

rubber

(Butadiene,

Styrene,...)

Retails/Distribution

Distributors/St

ores

Retails chain

Import –

Export

companies

Industrial

manufacturers

Consumer petrochemical

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 8

a.3 Processing: after being tapped, latex will be sent to processing factories to

manufacture mid-stream products available for related industries in the value

chain. Profit margin yielded from this stage secures a significant proportion of 21-

40% with the percentage varying depending on rubber’s seasonal prices.

However, experience shows that large-scale businesses are often owners of a

chain of materials and processing. Such profit margin is higher than that earned

from each segment of the chain separately. Typical products are latex concentrate

(for manufacture of pillows, mattress, and medical gloves); block rubber (for

manufacture of tires, conveyor belts, etc.)

a.4 Industrial manufacture: the added value is greater than that of the processing

segment. Processed rubber is used in this segment to produce consumer

products like: tires, gloves, mattress, condoms, conveyor belts, seat belts, shoes

and sporting equipment. This segment features some giant corporations namely

Michelin (France), Bridgestone (Japan), Top Gloves (Malaysia), Kossan

(Malaysia), Durex (USA), Trojan (USA), Bata Shoes (Thailand, Aquatex (USA),

etc.

Currently, tire industry is proved to be the largest consumption of natural rubber,

accounting for 65% of global consumption. Molding products and mattresses

occupy 17% and 11% respectively. With tire production playing the dominant role

in consumption of natural rubber, this industry is given top priority in this report.

Besides natural rubber, synthetic rubber is also known to be well consumed

worldwide (14.8 million tons) with consumption sometimes exceeding that of

natural rubber (11.1 million tons). As for synthetic rubber, the disparity in supply

and demand within the past 5 years has been so modest that it has managed to

sustain the supply and demand balance. Synthetic rubber is generated by

refineries and used together with natural rubber to manufacture tires and other

products.

Global natural rubber consumption’s

structure by product

Source: VRA

Global consumption Structure Global production Structure

Source: ANRPC, The Rubber Economist

36.7

8.5

8.1 6.2

4.7

4.6

31.3

China

India

US

Japan

Indonesia

Thailand

Others

34.4

25.6

7.9

7.1

7.0

6.9

11.2 Thailand

Indonesia

Vietnam

China

India

Malaysia

Others

65%

17%

11%5%

1% 1%

Tires

Molding products

Foam, Pillow, Packaging

Rubber tubes & Conveyor Belt

Shoes

Others

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 9

a.5 Retailing: Finished products will be distributed to consumers or other

manufacturing factories as their input materials to make conveyor belts, curoa

bando or assembling automobiles.

As depicted above, the segments can be divided into 2 main groups with the Upstream group including materials and processing and the Downstream group involving manufacturing and consuming. Evidently, the Upstream group proves to earn more added value than the Downstream group.

2. Vietnam’s Natural Rubber Industry

Total rubber area reached 955,700 ha at the end of 2013, increasing by 4.1% yoy

(equivalent to 37,800 ha). The tapping area occupied 57% of total rubber area

equivalent to 545,600 ha. In the last 10 years, the CAGR of Vietnam’s rubber area

achieves 8.0% per year higher than the 7.4% of tapping area.

Besides, there is the new rubber area planted in Cambodia (89,000 ha) and Laos (28,000 ha) of Vietnam Rubber Group (VRG). In particular, Hoang Anh Gia Lai Corporation (HAG) planted by around 36,130 ha in these countries and about 29,500 ha rubber is underway in Gemadept Co. (GMD) in Cambodia. Moreover, there are a lot of unofficial statistic rubber areas planted by many other Vietnam’s companies across of Cambodia and Laos.

In 2013, total of rubber production of Vietnam is 949,100 tons, increasing by 8.2% yoy.

Last year, the Vietnam’s rubber yield reached the highest rate for the past 10 years of 1.74 tons/ha marking the 5 successive years having the yield above 1.7 tons/ha. Therefore, Vietnam officially surpassed India to make it to the top 3 of highest yield on the world.

Source: ANRPC, FPTS

Rubber plantation and Tapping Area Tapping volume and Tapping yield

483 522

556

631 678

749

834

911 956

334 356 373 399 422 439 472

506 546

-

200

400

600

800

1,000

1,200

2005 2006 2007 2008 2009 2010 2011 2012 2013

Total Plantation Tapping Area

29

1

31

3

29

8

36

4

41

9

48

2

55

5

60

2

66

0

72

4

75

2

81

2

86

4

95

0

1,25

1,30

1,23

1,36 1,39 1,44

1,56 1,61

1,65

1,72

1,71

1,72 1,71

1,74

-

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

-

100

200

300

400

500

600

700

800

900

1,000

2000 2002 2004 2006 2008 2010 2012

Tapping Volume Yield

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 10

Natural Rubber plantation in Vietnam

South East area is considered as the largest rubber

region of Vietnam, occupying 56% of total rubber area

in Vietnam. It is followed by Highland, Central Coast

and the North.

Binh Phuoc and Binh Duong provinces have the

highest rubber yield in Vietnam. Binh Phuoc province

occupies about 22% of total nationwide rubber area

and nearly 36% of total rubber plantation of the South

East area.

Binh Duong province holds 18%, Tay Ninh province

takes up 10%, followed by Gia Lai and Dong Nai with

the rate of 11% and 6%, respectively. The highest

yield belongs to Binh Phuoc, Tay Ninh and Binh

Duong which reaches the average of 2 tons/ha higher

than the nationwide average yield of 1.74 tons/ha.

At the end of 2013, total rubber area of Vietnam

planted in Laos and Cambodia is 28,000 ha and

89,000 ha, respectively. In Laos, total rubber area

of Vietnam is located in the South region adjacent

to Quang Nam province, KonTum city, Hue city,

etc. Vietnamese enterprises and VRG in

particularly make an effort to plant rubber to reach

the area of 30,000 ha as permitted by Laos’s

Government before. In Cambodia, we plan to finish

planting a total of 100,000 ha in 2014.

Structure of Natural rubber plantation

Source: VRA, FPTS

Currently, HAGL is the private enterprise of Vietnam has the

largest rubber plantation in Laos and Cambodia with total area

of 36,130 ha located in Attepeu, Sekong and Ratanakiri

province.

(More details)

8.000 ha

5.000 ha

36.000 ha

25.300 ha

8.000 ha

7.600 ha

19.000 ha

38.400 ha

South East 535,514 ha 1.86 ton/ha

Central 140,775 ha 1.28 ton/ha

Highland 258,396 ha 1.56 ton/ha

North 25,102 ha

Kampongthom

SiemRiep

Ratanakiri

Kratie

Savanakhet

Sekong

Champasak

Attapeu

56%27%

15%3%

South East Highland Central Coast North

-

0.50

1.00

1.50

2.00

2.50

BinhPhuoc

Tay Ninh BinhDuong

DongNai

Gia Lai Daklak Averageof

Vietnam

Tapping yield by provinces in Vietnam

Source: VRA

Rubber area of VRG’s members and Hoang Anh Gia Lai Group

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 11

317 364

422

490 522

560 604

612

667

714

796

-

100

200

300

400

500

600

700

800

900

1,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Supply Demand Supply Surplus

Production and consumption of Natural rubber in Vietnam

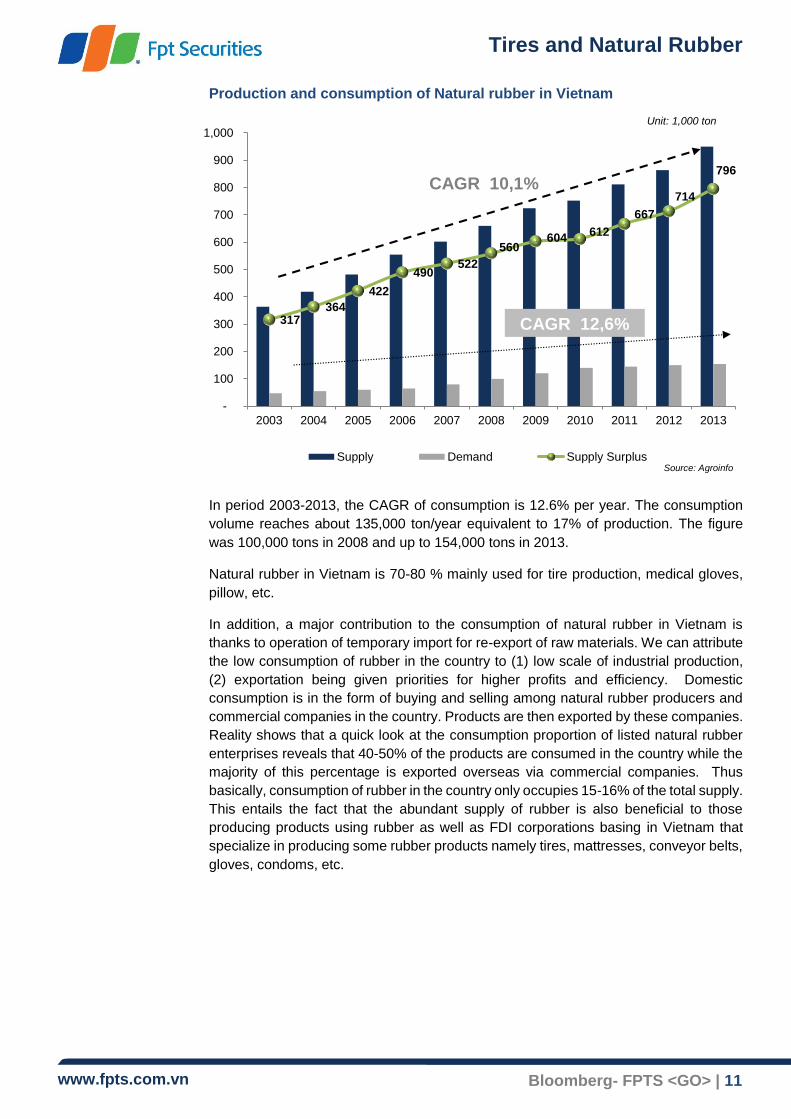

In period 2003-2013, the CAGR of consumption is 12.6% per year. The consumption

volume reaches about 135,000 ton/year equivalent to 17% of production. The figure

was 100,000 tons in 2008 and up to 154,000 tons in 2013.

Natural rubber in Vietnam is 70-80 % mainly used for tire production, medical gloves,

pillow, etc.

In addition, a major contribution to the consumption of natural rubber in Vietnam is

thanks to operation of temporary import for re-export of raw materials. We can attribute

the low consumption of rubber in the country to (1) low scale of industrial production,

(2) exportation being given priorities for higher profits and efficiency. Domestic

consumption is in the form of buying and selling among natural rubber producers and

commercial companies in the country. Products are then exported by these companies.

Reality shows that a quick look at the consumption proportion of listed natural rubber

enterprises reveals that 40-50% of the products are consumed in the country while the

majority of this percentage is exported overseas via commercial companies. Thus

basically, consumption of rubber in the country only occupies 15-16% of the total supply.

This entails the fact that the abundant supply of rubber is also beneficial to those

producing products using rubber as well as FDI corporations basing in Vietnam that

specialize in producing some rubber products namely tires, mattresses, conveyor belts,

gloves, condoms, etc.

CAGR 10,1%

CAGR 12,6%

Source: Agroinfo

Unit: 1,000 ton

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 12

3. Value chain of Natural rubber industry of Vietnam

Materials and processing (Upstream) (Click here for more further details)

High profit margin: Dong Nai Rubber Corporation (26.8%), PHR (31%), DPR (41%), TRC (36%), Kuala Lumpur Kepong (20.6%); HwaFong Thai Rubber (24.5%).

Materials and processing: Natural rubber industry of Vietnam as well as the global is categorized into 2 groups namely Upstream and Downstream with the former including planting, exploiting and processing companies and the latter involving companies with industrial products such as tires and tube, gloves, mattresses, conveyor belts, etc. The downstream group, as comparable to the world’s, yields a greater number of products with higher added value than that of the upstream group. Reality shows that in Vietnam, large holder farmers and smallholder farmers takes up the share of rubber planting area of 53% and 47% respectively. On an annual basis, large corporations have to purchase rubber from these farmers for (1) the sufficiency of input rubber for processing and (2) the economic support for the local farmers as a policy implemented by the Province and the Government.

Nguồn: FPTS tổng hợp

Source: FPTS collected

Industrial products:

Chemical products:

Condom

Gloves

Others Consumer product: Balloon, Foam, Pillow, Toys, Shoes, ball, etc.

Rubber plantation

Distribution:

Direct export

Traders

Manufacturers

Others

SVR

Latex

Automobile

kits

Rubber band Rubber belt Curoa bando

Typical companies: Vu Minh, Vuong Hung, Giai Phong, Ruthimex

Tires

Tires for bicycle, motorcycle, truck, agriculture vehicle,OTR,etc.

Typical companies: DRC, CSM, SRC

Construction

materials

Rubber floor

Glue, rubber tubes, etc.

Typical companies: Giai Phong, Rubber No.75, Rubtechco

Conveyor belt

Rubber cover of Wire Conveyor belt, etc.

Typical companies:

BenThanh rubber,

Rubber No.75,etc.

Others

Rubber shoes Sport tools Others Typical companies: Doc Lap Co., GeruSport, Dong Luc Co., Ruthimex, etc.

Smallholder (individual-owned plantation, small private companies). Large holder (VRG, Joint stock Co.: Dau Tieng, Dong Nai, Hoang Anh Gia Lai Group, Phuoc Hoa, Dong Phu, Tay Ninh,etc.)

Materials Processing Industrial

Manufacture

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 13

Large corporations in this upstream group are Dong Nai Rubber Corporation, Dau Tieng Rubber Co. Ltd., Phu Rieng Co. Ltd. and the 5 listed rubber companies namely PHR, DPR, TRC, HRC, TNC, etc. Besides, HAGL Corporation (HAG) also makes an investment of around 44,500 ha across the 3 countries of Vietnam – Laos – Cambodia. It is also known to have the largest privately owned rubber area in Vietnam up to now.

Distributing and commercial trading (Midstream) (Click here for more further details)

This group is reported to yield a rather modest and unstable profit margin of 1-5% with

the majority of money procured from production.

There are 2 basic procedures with (1) rubber processing and exploiting companies (Dau Tieng, Dong Nai, PHR, DPR, TRC, HAGL, etc.) selling their product directly to domestic customers or overseas and (2) commercial companies specializing in purchasing processed rubber to export thus making profit from price errors as well as typical companies among the top 50 in the industry (Binh Phuoc General Import and Export JSC, Viet Phu Thinh, Trung Chinh, Hoa Sen Vang, etc. ) Due to their typical commercial trading, corporations of group (2), without their own rubber plantations, are facing the risk of a heavy dependence on the market. Profits by and large are not stable.

Industrial production (Downstream)

A good amount of gross profit.

Purchased natural rubber is the input of manufacturing industrial products. In Vietnam, its main purpose is for production of tires (60-70% or production) with the remaining share going to medical gloves, mattresses, conveyor belts, etc. There are 29 tire manufacturing companies, 15 glove manufacturing companies and 6 mattress manufacturing companies and other miscellaneous products such as shoe soles, rubber bands, sporting balls, etc… within the nation. In terms of proportion of natural rubber production as well as industrial production corporation, tire manufacturing takes up the largest share. We, therefore, carried out an in-depth analysis of the tire industry in this report.

Gross profit margin by sectors

Company Tires Conveyor Belt Gloves Rubber shoes Condom

Domestic DRC: 21%; CSM: 19%; SRC: 14% BRC:23% NA NA NA

Foreign Michelin: 30.5%

Bridgestone: 33.6%

Apollo: 21-25%

Doublecoin:14.3%

Chengshin:20%

Kenda: 20-28%

Titan International: 14.3%

Somi Conveyor: 29%

Nippon conveyor: 16.3%

Top Glove: 17.6%

Kossan: 27-33%

Hartalega: 34.45%

Supermax: 20-30%

BataShoe

Thailand: 35%

Durex: 35%

Karex: 20.6%

Source: Bloomberg

Source: Vietnam Rubber Business Directory

Number of rubber product manufacturers in Vietnam Domestic Typical companies:

1. Tires: DaNang Rubber JSC. (DRC), Casumina

(CSM), Sao Vang Rubber JSC. (SRC),etc.

2. Conveyor Belt: Ben Thanh Rubber JSC.(BRC),

Rubber 17/05 Co,etc.

3. Gloves: VRG Khai Hoan, Showa Glove (Japan),

Nam Cuong, Nam Long,netc.

4. Condom: Merufa, Laprodex,etc

5. Foam, piilow: KymDan, Dong Phu Rubber (DPR),

Van Thanh, Lien A, etc.

6. Sports: Geru Star Sport, Dong Luc,etc.

0

5

10

15

20

25

30

35

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 14

4. The position of Vietnam Natural rubber industry

In 2013, Vietnam was ranked the 5th all over the world with rubber planting area of

955,700 ha and surpassed Malaysia, India and China to take the third place in the world

in terms of rubber exploiting (949,100 tons). Exploiting productivity was 1.71 and 1.74

ton/ha in 2012 and 2013 respectively beating India to be among the top countries of

rubber exploiting worldwide.

Global natural rubber in 2013 was 11.5 mil tons with 88.85% acquired from the 6

following countries: Thailand (1.14 mil tons); Indonesia (3.08 mil tons), Vietnam (0.95

mil tons), China (0.86 mil tons), India (0.84 mil tons), Malaysia (0.83 mil tons). Vietnam,

together with the 3 neighboring countries Thailand, Indonesia, Malaysia is among the

top 4 leading exporter of natural rubber the world over with the total export volume being

85-93% of the global export volume (Thailand (3.66 mil tons), Indonesia (2.7 mil tons),

Malaysia (1.38 mil tons), Vietnam (1.07 mil tons). As for Vietnam, export volume

increases by 24.4% yoy. Favorable climate, soil and agricultural advantages as well as

seed researching projects also enable the 6 countries to secure the leading positions in

the world in terms of area, exploitation and export volume over the decade.

Top 6 countries of Natural rubber in the world in 2013

Top 5 of natural rubber producers in the world Top 5 of natural rubber exporters in the world

Source: ANRPC

Source: ANRPC

3.428 3.492

1.167

1.057 956

776

4.170

3.180

856 826 949

849

1,72

1,10 1,25

1,40

1,74

1,64

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Thailand Indonesia China Malaysia Vietnam India

To

n/h

a

Th

ou

san

d t

on

-h

a

Rubber area

Tapping Volume

Tapping Yield

36%

27%

7%

7%

8%

14%

Thailand

Indonesia

Malaysia

India

Vietnam

Others

41%

30%

15%

12%2%

Thailand

Indonesia

Malaysia

Vietnam

Others

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 15

5. The difference in the natural rubber operating process among Vietnam and

the 3 neighboring countries Thailand, Malaysia and Indonesia

Management

Currently, the rubber industry of Vietnam has yet to be under any direct management

of the State, which reflects the difference from other neighboring countries. Meanwhile,

the rubber industry of the 3 aforementioned countries is governed by the General

Department of Rubber or other institutes for this industry of its own. In Vietnam, it is

misunderstood that Vietnam rubber group (VRG) is the representative organization of

the State while in truth, VRG is only a state-owned corporation as well as a holder of

the majority of shares. VRG does not constitute a governmental management of the

domestic rubber industry. The natural rubber industry of Vietnam is in fact just under

the Ministry of Agriculture and only by the Department of Agricultural and Forestry

Products Processing has the natural rubber industry of Vietnam as well as other

produce been governed so far. Consequently, there exists no separate structural

governance of the industry itself which inevitably leads to the lack of harmony in

planning areas of rubber plantation nationwide as well as distributing and assessing

rubbery products within regions and overseas. (Click here for more details)

Quality

Smallholder farmers, known to constitute a hefty 47% of total rubber plantation

nationwide, fails to closely observe every regulation and standard of rubber processing

workflow and sustain the required quality. Reality shows that, privately-owned

organizations are prone to cut out the quality control stage to lower cost unless there is

a request of quality certificates from their foreign importers. Consequently, the inequality

of quality of domestic and exported rubbery products, to some extent, has destroyed

the reputation of Vietnam’s Rubber Industry, thus bringing down the price of exported

rubber which is usually lower than that of Thailand, Malaysia and Indonesia.

(Click here for more details)

Natural Rubber structure by owner of Top 4 countries

Source: FPTS’s data

0 0.2 0.4 0.6 0.8 1

Thailand

Indonesia

Malaysia

Vietnam

Largeholder (state-owned or private)

Smallholder

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 16

Unit: 1,000 ton

Flag Country Production Consumption Export Import

Thailand 4,170 519 3,664 0.9

Indonesia 3,180 603 2,719 26

Malaysia 826 456 1,380 955

Vietnam 950 155 1,076 280

India 849 953 26 292

China 856 4,150 15 3,701

Others 675 4,293 - -

Global 11,505 11,128 - -

Source: ANRPC

Exploiting productivity

One more favorable feature of the natural rubber industry of Vietnam than the other 3

countries is the fair balance in ownership between smallholder and large holder farmers

(47%-53%). The percentage of smallholder farmers is by contrast 85% and 90% for

Indonesia and Thailand, irrespectively. Vietnam is also ranked among the top 3 in the

world for the invention of new seeds of high quality every year.

What’s more, large rubber plantation of VRG corporation also fosters the pilot planting

of new seeds and popularizes it to smallholder farmers. This, if successful, can shorten

the usual time spent of new seed pilot planting and simultaneously enhance the

productivity over the country. Today, Vietnam is still among the group of countries with

the highest rubber’s exploiting productivity all over the globe (the average figure is

above 1.7 ton/ha for the past 3 years). (Click here for more details)

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 17

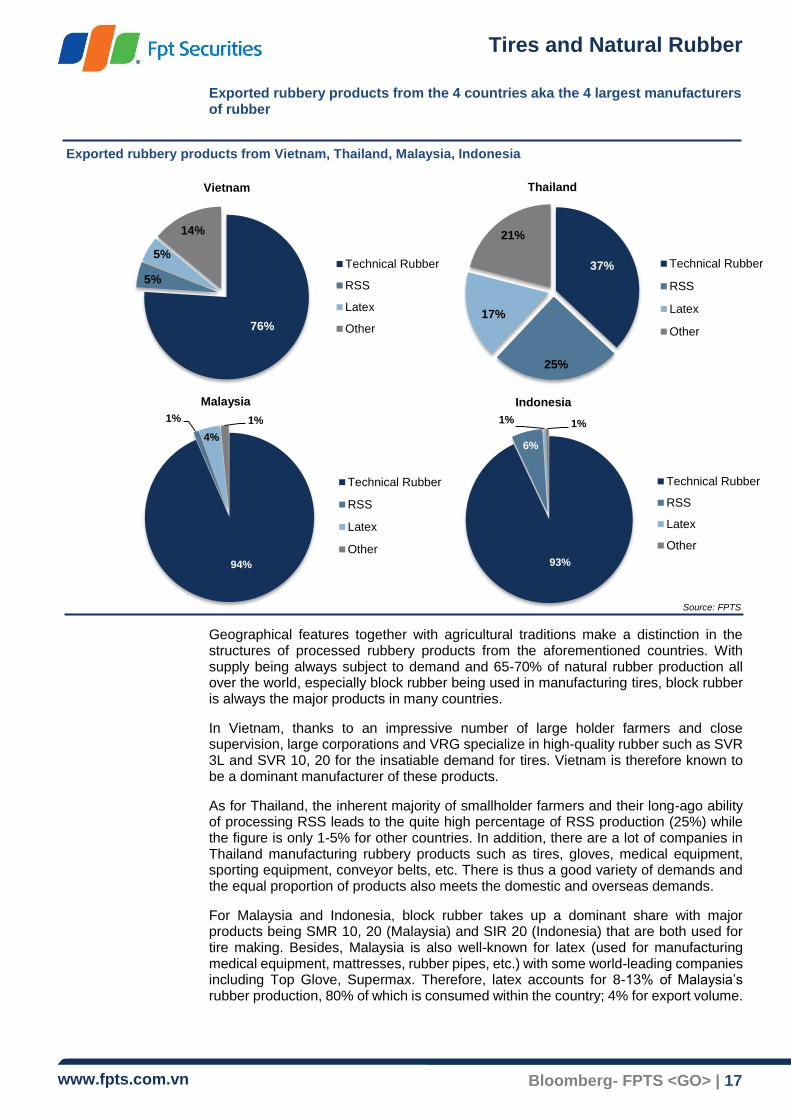

Exported rubbery products from the 4 countries aka the 4 largest manufacturers of rubber

Geographical features together with agricultural traditions make a distinction in the structures of processed rubbery products from the aforementioned countries. With supply being always subject to demand and 65-70% of natural rubber production all over the world, especially block rubber being used in manufacturing tires, block rubber is always the major products in many countries.

In Vietnam, thanks to an impressive number of large holder farmers and close supervision, large corporations and VRG specialize in high-quality rubber such as SVR 3L and SVR 10, 20 for the insatiable demand for tires. Vietnam is therefore known to be a dominant manufacturer of these products.

As for Thailand, the inherent majority of smallholder farmers and their long-ago ability of processing RSS leads to the quite high percentage of RSS production (25%) while the figure is only 1-5% for other countries. In addition, there are a lot of companies in Thailand manufacturing rubbery products such as tires, gloves, medical equipment, sporting equipment, conveyor belts, etc. There is thus a good variety of demands and the equal proportion of products also meets the domestic and overseas demands.

For Malaysia and Indonesia, block rubber takes up a dominant share with major products being SMR 10, 20 (Malaysia) and SIR 20 (Indonesia) that are both used for tire making. Besides, Malaysia is also well-known for latex (used for manufacturing medical equipment, mattresses, rubber pipes, etc.) with some world-leading companies including Top Glove, Supermax. Therefore, latex accounts for 8-13% of Malaysia’s rubber production, 80% of which is consumed within the country; 4% for export volume.

Thái Lan

Indonesia

Malaysia Indonesia

Thailand Vietnam

Source: FPTS

Exported rubbery products from Vietnam, Thailand, Malaysia, Indonesia

76%

5%

5%

14%

Technical Rubber

RSS

Latex

Other

37%

25%

17%

21%

Technical Rubber

RSS

Latex

Other

93%

6%

1% 1%

Technical Rubber

RSS

Latex

Other

94%

1%

4%

1%

Technical Rubber

RSS

Latex

Other

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 18

6. Exporting – Importing of natural rubber of Vietnam

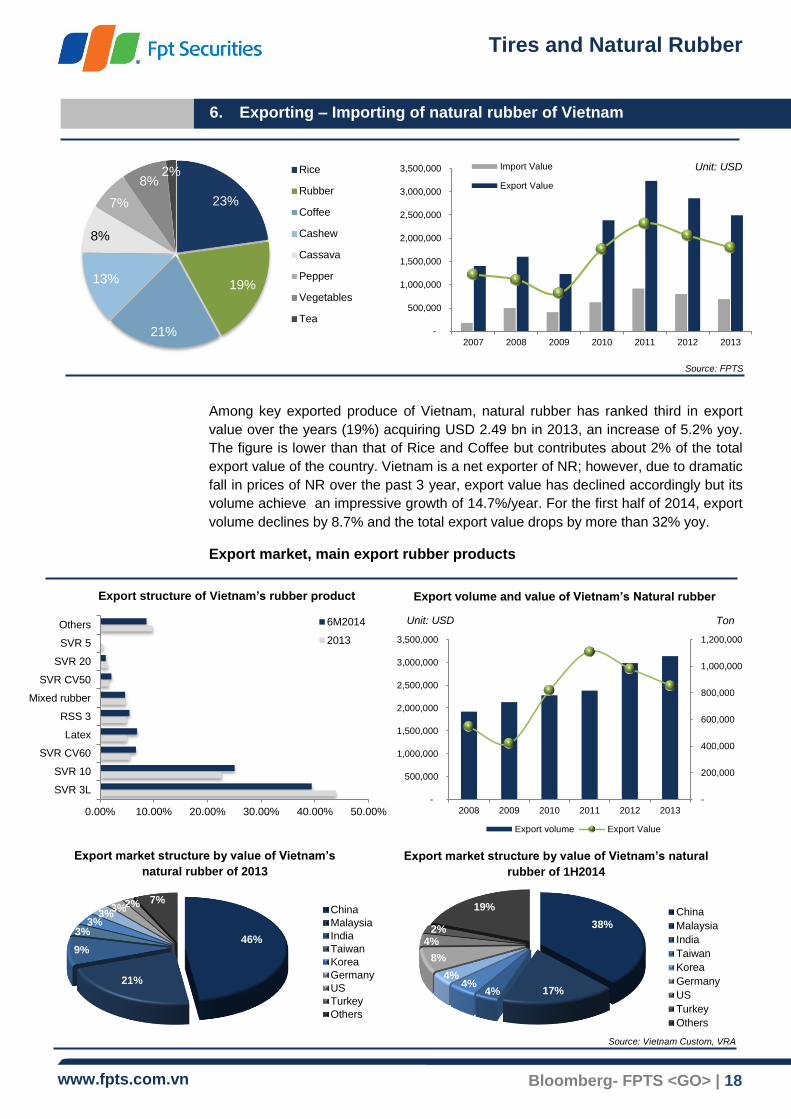

Among key exported produce of Vietnam, natural rubber has ranked third in export

value over the years (19%) acquiring USD 2.49 bn in 2013, an increase of 5.2% yoy.

The figure is lower than that of Rice and Coffee but contributes about 2% of the total

export value of the country. Vietnam is a net exporter of NR; however, due to dramatic

fall in prices of NR over the past 3 year, export value has declined accordingly but its

volume achieve an impressive growth of 14.7%/year. For the first half of 2014, export

volume declines by 8.7% and the total export value drops by more than 32% yoy.

Export market, main export rubber products

Unit: USD

Export structure of Vietnam’s rubber product Export volume and value of Vietnam’s Natural rubber

Export market structure by value of Vietnam’s

natural rubber of 2013

Export market structure by value of Vietnam’s natural

rubber of 1H2014

Source: Vietnam Custom, VRA

Source: FPTS

Ton Unit: USD

23%

19%

21%

13%

8%

7%

8%2% Rice

Rubber

Coffee

Cashew

Cassava

Pepper

Vegetables

Tea -

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

2007 2008 2009 2010 2011 2012 2013

Import Value

Export Value

0.00% 10.00% 20.00% 30.00% 40.00% 50.00%

SVR 3L

SVR 10

SVR CV60

Latex

RSS 3

Mixed rubber

SVR CV50

SVR 20

SVR 5

Others 6M2014

2013

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

2008 2009 2010 2011 2012 2013

Export volume Export Value

46%

21%

9%

3%3%

3%3%2% 7%

China

Malaysia

India

Taiwan

Korea

Germany

US

Turkey

Others

38%

17%4%4%

4%

8%

4%2%

19% China

Malaysia

India

Taiwan

Korea

Germany

US

Turkey

Others

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 19

In 2013, NR of Vietnam has been exported to more than 72 markets, 97,6% of which are major markets including the leading market in China (511,448 tons) accounting for 47.5% which is of the same volume in 2012 but a slight decrease compared to the 61% market share in 2011. Export value of NR in China also reduced from 59% in 2011 to 46% in 2013. Malaysia market ranks the second (acquiring 227,159 tons, a proportion of 21.1% higher than the figure of 19.6% in 2012) followed by India with a volume of 88,178 tons, attaining 8.2% compared to 7% in 2012. What caused the decrease of export market share to China is the restructuring and diversification of export markets of VRG for the sake of being less dependent upon the China market. This approach has enabled Vietnam NR industry to keep the output risk to a minimum and to encourage the flexibility needed in exporting practices and at the same time extending the customer base. Such was a great global demand for rubber that not resorting to a few particular markets will surely improve export volume and growth.

Export market of Natural rubber of 1H2014

Market 6M2014 % YoY

Volume (Ton)

%Proportion Value (1,000 USD)

Volume Value

China 138,542 39.7% 247,840 -23.6% -42.6%

Malaysia 64,624 18.5% 112,296 -13.4% -41.3%

India 24,998 7.2% 49,658 +23.9% -10.4%

Korea 14,921 4.3% 28,960 -0.4% -23.8%

US 12,987 3.7% 24,194 +19.1% -9.3%

Germany 11,618 3.3% 24,870 -12.3% -32.9%

Taiwan 10,935 3.1% 23,013 -18.4% -40.6%

Turkey 8,398 2.4% 16,154 +18.8% -9.4%

Others 61,584 17.8% 125,255 - -

Total 348,607 100% 652,241 -8.7% -32.2%

Adopting such an approach, VGR have experienced a dramatic change in export NR for the first 6 months of this year with export volume to China dropping by 23.6% and export value reducing by 42.6%. Export value to China now takes up a proportion of only 39.7% whereas the percentage substantially increases in some markets like India (by 23.9%), USA (19.1%), and Turkey (18.8%) yoy.

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 20

Vietnam’s import market of Natural rubber (NR) and its products

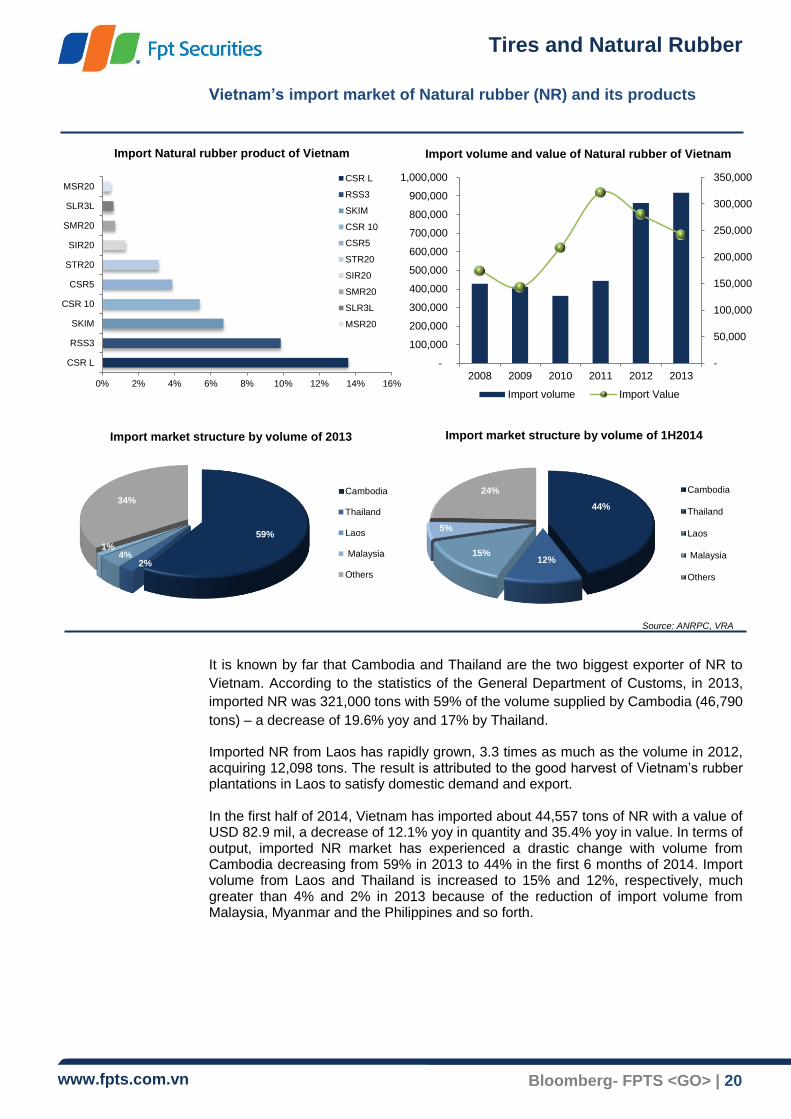

It is known by far that Cambodia and Thailand are the two biggest exporter of NR to

Vietnam. According to the statistics of the General Department of Customs, in 2013,

imported NR was 321,000 tons with 59% of the volume supplied by Cambodia (46,790

tons) – a decrease of 19.6% yoy and 17% by Thailand.

Imported NR from Laos has rapidly grown, 3.3 times as much as the volume in 2012, acquiring 12,098 tons. The result is attributed to the good harvest of Vietnam’s rubber plantations in Laos to satisfy domestic demand and export. In the first half of 2014, Vietnam has imported about 44,557 tons of NR with a value of USD 82.9 mil, a decrease of 12.1% yoy in quantity and 35.4% yoy in value. In terms of output, imported NR market has experienced a drastic change with volume from Cambodia decreasing from 59% in 2013 to 44% in the first 6 months of 2014. Import volume from Laos and Thailand is increased to 15% and 12%, respectively, much greater than 4% and 2% in 2013 because of the reduction of import volume from Malaysia, Myanmar and the Philippines and so forth.

CSR L

RSS3

SKIM

CSR 10

CSR5

STR20

SIR20

SMR20

SLR3L

MSR20

0% 2% 4% 6% 8% 10% 12% 14% 16%

CSR L

RSS3

SKIM

CSR 10

CSR5

STR20

SIR20

SMR20

SLR3L

MSR20

Import Natural rubber product of Vietnam Import volume and value of Natural rubber of Vietnam

Import market structure by volume of 1H2014 Import market structure by volume of 2013

Source: ANRPC, VRA

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

2008 2009 2010 2011 2012 2013

Import volume Import Value

59%

2%4%

1%

34%Cambodia

Thailand

Laos

Malaysia

Others

44%

12%15%

5%

24% Cambodia

Thailand

Laos

Malaysia

Others

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 21

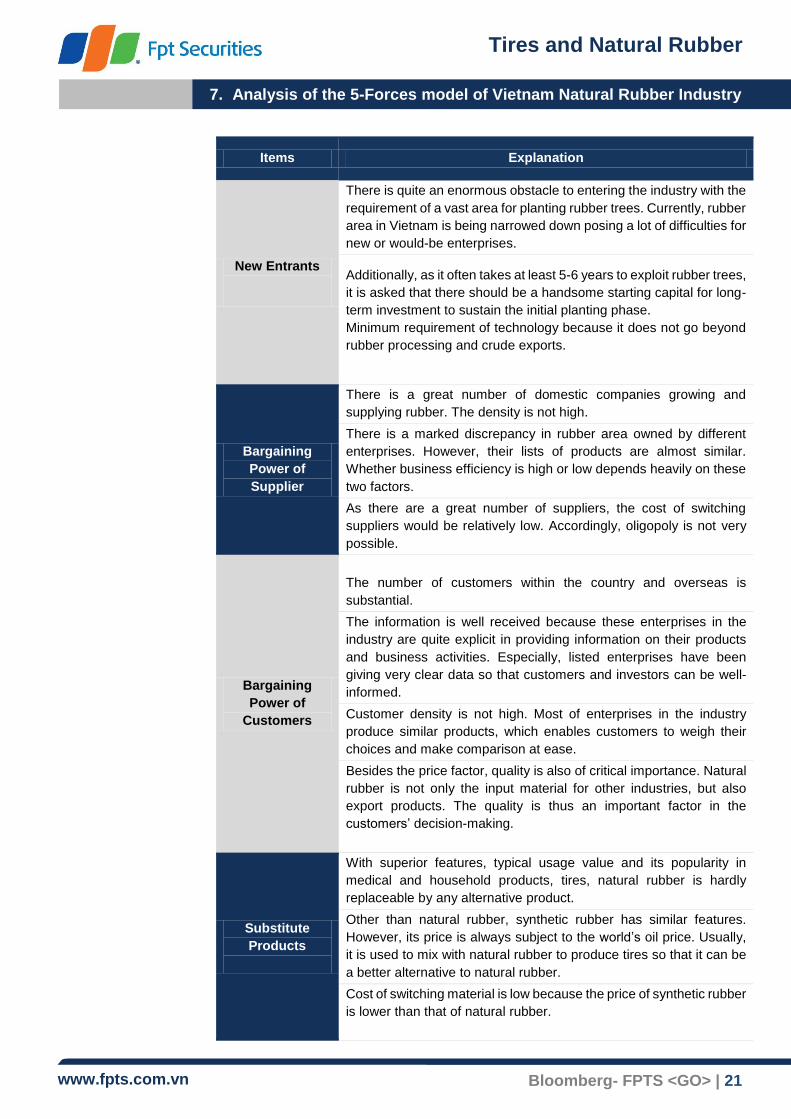

7. Analysis of the 5-Forces model of Vietnam Natural Rubber Industry

Items Explanation

New Entrants

There is quite an enormous obstacle to entering the industry with the

requirement of a vast area for planting rubber trees. Currently, rubber

area in Vietnam is being narrowed down posing a lot of difficulties for

new or would-be enterprises.

Additionally, as it often takes at least 5-6 years to exploit rubber trees,

it is asked that there should be a handsome starting capital for long-

term investment to sustain the initial planting phase.

Minimum requirement of technology because it does not go beyond

rubber processing and crude exports.

Bargaining

Power of

Supplier

There is a great number of domestic companies growing and

supplying rubber. The density is not high.

There is a marked discrepancy in rubber area owned by different

enterprises. However, their lists of products are almost similar.

Whether business efficiency is high or low depends heavily on these

two factors.

As there are a great number of suppliers, the cost of switching

suppliers would be relatively low. Accordingly, oligopoly is not very

possible.

Bargaining

Power of

Customers

The number of customers within the country and overseas is

substantial.

The information is well received because these enterprises in the

industry are quite explicit in providing information on their products

and business activities. Especially, listed enterprises have been

giving very clear data so that customers and investors can be well-

informed.

Customer density is not high. Most of enterprises in the industry

produce similar products, which enables customers to weigh their

choices and make comparison at ease.

Besides the price factor, quality is also of critical importance. Natural

rubber is not only the input material for other industries, but also

export products. The quality is thus an important factor in the

customers’ decision-making.

Substitute

Products

With superior features, typical usage value and its popularity in

medical and household products, tires, natural rubber is hardly

replaceable by any alternative product.

Other than natural rubber, synthetic rubber has similar features.

However, its price is always subject to the world’s oil price. Usually,

it is used to mix with natural rubber to produce tires so that it can be

a better alternative to natural rubber.

Cost of switching material is low because the price of synthetic rubber

is lower than that of natural rubber.

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 22

Intensity of

Rivalry

Added value of the industry is still low with most of it being yielded

from crude rubber export.

There is a minor difference in the products of various corporations in

the industry because the manufacturing process is similar so that it

is each company’s technology and experience that could make a

difference.

The selecting process is now going on mainly among smallholder

farmers. Because of large investment but low sales price, some

smallholder farmers have got rid of rubber trees to grow other

produce. However, this happens only in a small scale with little harm

to the industry.

Regulations on the floor price: the possibility of floor price imposition

is quite high and this depends on the decisions of VRG for the

purpose of maintaining a profitable margin and avoiding dumping

products among members in the industry. As for the price, most of

Vietnam’s rubber products are charged according to the world’s price

especially Malaysia, Thailand and Indonesia.

8. Policies related to Natural Rubber

Decision No. 1003 / QD-BNN-CB by the Ministry of Agriculture and Rural

Development Ministry of Finance decided to reduce export taxes for rubber products. Exemption from corporate income tax for individuals, households and rubber Establishment of rubber triangular area in Indochina

Decision 1003/QD-BNN-CB by the Ministry of Agriculture and Rural Development According to Decision 1003 / QD-BNN-CB by the Ministry of Agriculture and Rural

Development, signed on dated 13th May, 2014, government decided to raise added

values of agricultural, forestry and fisheries sector in processing and reduce post-

harvest losses. (More details)

Ministry of Finance decided to reduce export taxes for rubber products

The Ministry of Finance issued Circular No 111/2014 / TT-BTC in order to amend the

export tax rate for some rubber goods in group 40.01, 40.02, 40.05, stipulated in the

Export Tariff issued together with Circular No. 164/2013 / TT-BTC to 0 percent, and has

been applicable since 2nd, October 2014. (More details)

Exemption of personal income tax for rubber households and individuals

Deputy Minister of Finance, Mr. Tuan Hoang Anh Do has sent documents to Taxation

Department of the province or city, which is under Central Government to conduct about

income tax exemption for families and individuals, who plant rubber trees.

(More details)

Establishment of rubber triangular area in Indochina

To ensure sustainable development for the sector, Vietnam Rubber Group (VRG) has

been developed to promote cooperation of rubber plantation in Laos (30,000 hectares)

and Cambodia (100,000 hectares), in order to form triangular zones Indochinese with

development orientation becoming the world's largest rubber area. (More details)

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 23

9. Natural rubber industry outlook (NR)

Up to now, Natural Rubber Industry has observed a gradual decrease of rubber

price. From early this year, many supportive measures made from Thailand,

Malaysia and Indonesia such as export output cuts; limit of tapping volume in order

to reduce the supply volume. Vietnam reduce the export tax of rubber from 3% and

5% down to 0%; reschedule and restructure debt of NR export companies in trouble.

However, there is no prosperity of the rubber industry in nationwide and worldwide. At present, there is an inconsistency of the rubber master planning all over the world. So it is the reason for a strong oversupply of natural rubber from now to 2016.

In the period of 2007-2009, a lot of countries all over the world plant rubber because of very high rubber price. It makes the rubber plantation increase quickly. All of them are matured from now to 2016 and it will dramatically increase the supply. This is the main reason for price decline over the past 2 years and it puts the global rubber industry into trouble.

Global market

Under forecast of The Rubber Economist Ltd., the supply surplus will be 651,000 ton higher than the 640,000 tons of 2013 (+1,7%yoy) whereas forecast consumption volume increases about 2% yoy. It shows that the recovery for rubber price is unlikely to happen this year. In addition, the gap between supply and demand continues tobe high until 2016: 483,000 tons (2015) and 316,000 tons (2016).

Besides, according to the forecast of global HSBC, the demand of truck tires increases by 5.5% yoy (2014) and 5.7% (2015) higher than the rate 3.8% of PC and light truck tires (2014) and 4% (2015). This suggests that there is a recovery in demand for tires production. Nevertheless, the high supply surplus until 2016 will control the rising of rubber price. So it will be a slow recovery.

In addition, the global rubber storage reserves continue to increase. By the Rubber Economist Ltd., the reserve will reach 3.79 million tons at the end of 2014 and up to 4.33 million tons in 2015. The number of reserve month will rise from 2 months (2013) up to 4 months in 2016. We consider that the natural rubber industry continue to get into trouble for the next 2 years.

Domestic market

In our opinion, Vietnam is not out of difficult situation of the world. Because rubber is the commodity type so every country in the world will be affected similarly. Under the direction of the State and Vietnam Rubber Group (VRG), we have been diversifying the structure of export market to avoid depending on unique market like China before. It helps to reduce the risk for export activities of Vietnam rubber industry. Recently, VRG has been entering into a partnership with Japanese partners including: JTC Corporation and Shinichi Kato Officer to purchase natural rubber of Vietnam annually. Those partners are professional rubber trader for many famous Japan tire manufacturers such as: Bridgestone, Yokohama, etc. This is the positive factor to export natural rubber of Vietnam for the next years.

However, the efficiency is still the price of rubber. As discussed above, it completely depends on supply and demand of the world. We think that the rubber companies continue to face to the industrial difficulty for this year and 2015.

Domestic Consumption Forecast: We consider that the domestic demand of natural rubber will increase when VRG invest to expand the capacity of glove

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 24

factory of VRG Khai Hoan Company from 1.2 billion units/year to 3.2 billion units/year. In addition, two all-steel radial tire factories of DRC and CSM came into operation with the capacity of the 1st phase are 300,000 units/year and 350,000 units/year, respectively and up to 600,000 units/year and 1,000,000 units/year several next years. Moreover, in 2015, the factory of Kumho Tire (capacity of 3.15 million units/year up to 6.3 million unit/year) and the factory of Bridgestone (capacity of 24,700 – 49,000 units/day) will be in operation. The fact that the tires and gloves manufacture uses about 70-80% of total domestic consumption of NR shows that the aforementioned new factories will help to boost the local demand of NR in coming years. According to our estimation, total increased volume of NR will be around 433,000 tons. It helps Vietnam’s rubber companies increase the sale volume for domestic market and improve the added value for Vietnam rubber products. That the reason why we focus to analyze the tire segment which is one of the sectors of rubber industry’s value chain.

II. Tire Industry

1. Overview of global tire industry

The global tire industry is divided into 2 types of tires for Original Equipment Manufacturer (OEM – occupies 25-27%) and Replacement tires (around 73-75%).

The famous tire companies always research and develop new products with high technology, extreme quality and high profit margin such as semi-steel and all-steel radial tires for trucks, aircraft, luxury passenger car, etc. The small companies focus on niche market with lower profit margin such: motorcycle tires, bicycle tires, rubber’s spare parts, etc.

In tire industry, the product is divided into 3 types basing on quality and brand. Tier 1 is about famous brand, high-quality such as: Bridgestone, Michelin, Goodyear, Continental, Pirelli, etc. ; Tier 2 is middle-class brand such as: Kumho, Yokohama, Hankook, Apollo, etc. Tier 3 is acceptable products such as: Inoue, Chengshin, Double Coin, Kenda, etc.

Tires market share by country Tires market share by brand

Source: Tire Business, FPTS

23.9%

14.2%

13.5%13.1%

6.0%

5.8%

5.2%

4.5%3.6%

1.0% 9.2%Japan

France

China

US

Korea

Germany

India

Italy

Taiwan

Finland

Others

15.3%

14.2%

10.1%

5.8%4.1%4.1%

3.3%

3.0%

2.5%

2.4%2.2%

1.9%

1.5%

30%

Bridgestones

Michellin

GoodYear

Continental

Sumitomo

Pirelli

Hankook

Yokohama

Maxxis

HangZhou Zhongce

Cooper Tire

Kumho

Toyo

Others

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 25

The revenue of tier 1 group occupies 53% of global market share. Accordingly,

Bridgestone achieve the best seller for 5 consecutive years with the market share of

15%, followed by Michelin (14%) and Goodyear (10%), 60% of remains.

70% of market share is occupied by Japan (23.9%); France (14.2%); USA (13.1%);

China (13.5%).

Production and consumption

As categorized by regions: according to the statistics from LMC, China is now topping

the world in production of tires for passenger cars, light trucks and heavy trucks making

up for 27% of the total production of tires globally equal to 501 mil tires in 2013. The

USA and Japan are the second and the third largest producers with market share of

11% and 10% respectively. China also tops the list of countries with the highest

consumption of tires for heavy trucks with 34% equal to 51 mil tires in 2013, followed by

the USA (16%), Japan (5%), Germany (6%). The USA, on the other hand, dominates

the market of tires for passenger cars and light trucks with 22% equal to 316 mil tires in

2013, followed by China (14%) and Japan (8%).

Speaking of tire production, Asian countries supply up to 60-61% of the total volume

globally equal to 1.02 bn tires in 2013. The European countries, by comparison, only

account for 19%, equal to 317 bn tires, followed by North America, the USA and the

Africa with 11.5%, 6.5% and 1.5%, respectively.

Top 20 of tires manufacturers of the world (by sales)

Source: Tire Business, FPTS

Unit: million USD

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 26

As categorized by consumption volume: Consumption volume of Asia, Europe and

North America takes up a share of 86% of global consumption with Asia consuming

540 mil tires (36%), Europe using 383 mil tires (25%), North America consuming 192

mil tires (24%). The remainder of 14% is distributed to South America, Africa and the

Middle East.

As categorized by products: According to the statistics, the segment for passenger

cars, light trucks constitutes about 87-89% of global volume with the remaining 11-

13% is of tires for heavy trucks and buses.

Car tires production

Heavy truck proportion

Light truck and passenger car tires (< 9 seats)

Source: HSBC Global

Source: FPTS

60%25%

15%

Light Truck and Passenger Car (< 9 seats)

Heavy Truck and Passenger Car (> 9 seats)

Others

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 27

Based on the scale of global tire sales, tires for passenger cars (<=9 seats) and light

trucks takes the share of up to 60%, the remainder is divided into the group of heavy

trucks, buses and passenger cars (>9 seats) (25%) and that of specialty tires such as

agricultural tires, aircraft tires, solid tires (15%).

As categorized by purposes of usage: Replacement market achieves a dominant

proportion of 73-75% whereas OEM only occupies 25-27% of consumption products.

Supplies of tires for passenger cars (<=7 seats), light trucks have always exceeded

demands by 5% for the past 5 years. For tires for heavy trucks and buses, supplies are

outstripping demand by 17%.

As categorized by types – Bias vs Radial:

Radial tires are now dominating global demands being used by 92% of passenger cars

and light trucks; 53% of heavy trucks. Especially in North America, 96% of vehicles use

Radial tires, 72% in Africa and Middle East, and 79% in Europe. Particularly in Asia

Pacific including frontier and developing countries, the need for switching from Bias to

Radio tires is on the increase. The current proportion of them both is 52% (Radial) and

48% (Bias). In the near future, Radial tires are expected keep exceeding Bias tires and

Tires production and consumption for

light vehicle

Tires production and consumption for

heavy vehicle

Source:: LMC

Source: HSBC Global

23% 23%36%

24%14%

77% 77%64%

76%86%

0%

20%

40%

60%

80%

100%

120%

Europe North ofAmerica

Asean South ofAmerica

Africa

Replacement OEM

OEM27%

Replacement73%

-

200

400

600

800

1,000

1,200

1,400

1,600

2009 2010 2011 2012 2013

Production Consumption

-

20

40

60

80

100

120

140

160

180

200

2009 2010 2011 2012 2013

Production Consumption

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 28

maintain the stable growth corresponding with the economy well-being and the

infrastructure development in such countries.

2. The Tire industry in Vietnam

According to the statistics from Vietnam Rubber Association, our country has 830

entrepreneurs specializing in the tire industry including 30 tire-manufacturing

companies, 17 large-scale tire-manufacturing factories, 170 tire-trading companies, 170

exporters and 460 importers of all size. In 2013, there were 23.3 mil tires for bike, 30

mil tires for motorbikes and 6.3 mil tires for automobiles of all types manufactured.

Noticeably, there were well above 5.4 mil car tires exported from FDI companies like

Kumho, Chengshin, Kenda, Yokohama, etc.).

The domestic consumption of tires is now obviously heavy with 24 mil tires for bike, 37.5

mil for motorbikes and 5 mil for automobiles. Statistics show that there is a stable

balance between supply and demand with the market being saturated. Tires for

motorbike, on the other hand, are insufficient considering its capacity to satisfy only 80%

of the demand. With the segment of tires for motorbikes, domestic entrepreneurs are

only able to share the market of replacement tires rather than OEM which is almost

monopolized by FDI companies or imported brand-new motorbikes. As for automobile

tires, despite the massive domestic production volume, 80-90% of the products are for

exportation. Thus, the remaining production volume only satisfies 20-27% (radial) and

67% (Bias) of the domestic market. This suggests the unfulfilled potential of the

domestic tire market.

Additionally, as stated by many analysts, the rate of cars owned per 1,000 people in

Vietnam is still modest (17.8 cars/1,000 people) as compared to neighboring countries.

The rate is 77.7 in Thailand, 48.3 in Indonesia, 341 in Malaysia, 30 in the Philippines.

As said by AFTA convention, import tax rate for automobiles will plunge to 0% in 2018

onwards. With improved living standard and better transport infrastructure, more

Vietnamese consumers are believed to be more accessible to automobiles, thus

increasing the rate of owned automobiles. In the long run, it is firmly believed that there

is an ensured growth in replacement tires in supply for the increased number of cars

and current ones within the country.

Bias and Radial tires consumption structure by continents

Source: LMC

52%

96% 95%

65%

100%

80%72%

48%

4% 5%

35%20%

28%

0%

20%

40%

60%

80%

100%

120%

Asean Pacific North ofAmerica

South ofAmerica

Latin America West ofEurope

East ofEurope

Africa andCentral

Bias Radial

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 29

Domestic tire market share

In the domestic market, the 5 corporations namely Bridgestone (import), Michelin

(import), Danang rubber, Casumina, and Yokohama account for 61% of the market of

automobile tires. The remaining percentage is shared by other private domestic

entrepreneurs, FDI and other importers. Speaking of tires of all kinds consumed,

Casumina dominates the domestic market with 33% followed by DRC (25%), and SRC

(10%) and other companies (31%).

-10,000

-

10,000

20,000

30,000

40,000

50,000

60,000

-100 0 100 200 300 400

19%

15%

13%

8%6%

5%

5%

2%

3%

4%

20%

Bridgestone

Michelin

DRC

CSM

Yokohama

Maxxis

Double Coin

Chengshin

Kumho

SRC

Others

33%

25%

10%

32%CSM

DRC

SRC

Others

Vehicle consumption per 1,000 people Vehicle ownership per 1,000 people

Vehicle ownership per 1,000 people

and GDP per capita

Number of large-scale tire

factories in the world

Source: WorldBank, Asean Automobile Federation, FPTS

Source: Tyre Business, FPTS

Truck-tire market share in Domestic Tires market share in Domestic market

158

59

22 21 17 15 9 6 2

0

20

40

60

80

100

120

140

160

180

- 10 20 30 40

Thailand

Indonesia

Malaysia

Phillipines

India

Vietnam

Singapore

Car

Motorcycle

0 100 200 300 400

Thailand

Indonesia

Malaysia

Phillipines

India

Vietnam

Singapore

Car

Motorcycle

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 30

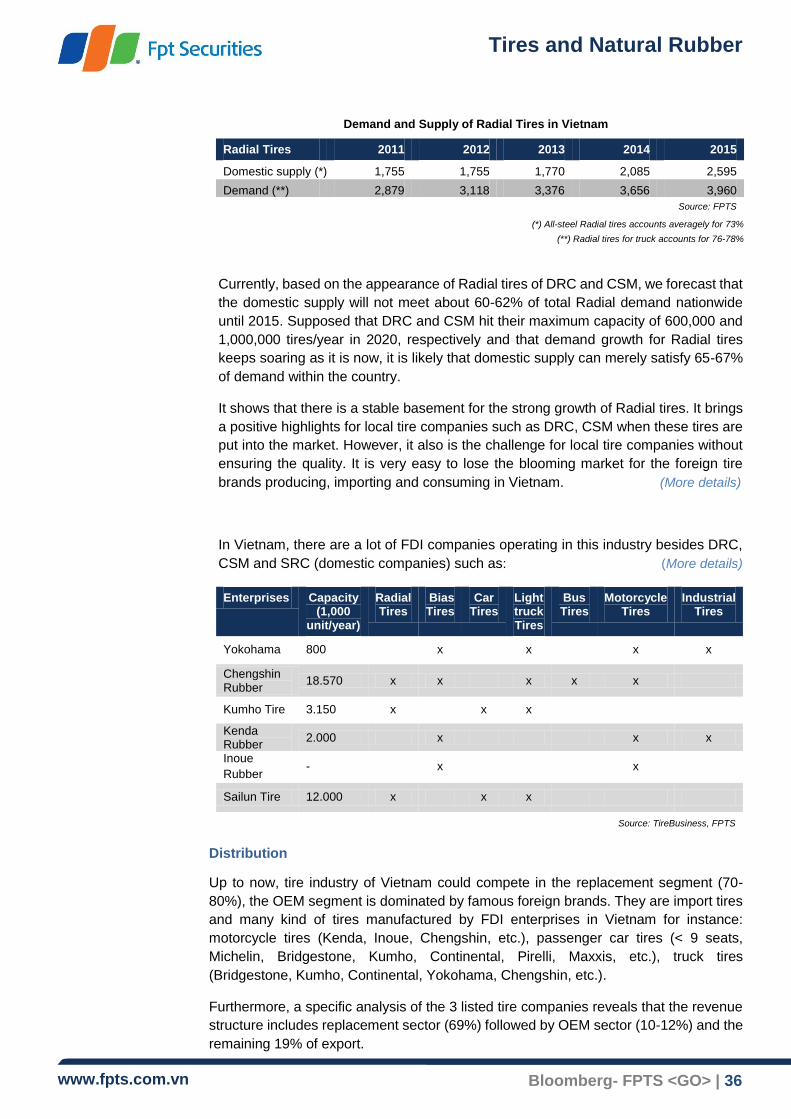

For Radial tires, FDI and importers claim to have 90% of market share. From 2014

onwards, all-steal Radial tires, however, are also manufactured by DRC and CSM with

their 2 factories with capacity of 600,000 tires/year and 1,000,000 tires/year,

respectively. At present, the two factories are having their phase 1 in progress which

expects to yield 300,000 tires/year and 350,000 tires/year. This segment is projected to

promise quite intense competition in the years to come.

Tire importation-exportation in Vietnam

In 2013, Vietnam’s tire export value is 363 mil USD, increasing by 8.1% yoy (335.7 mil

USD in 2012). For the past 3 years, export value has a CAGR of 8%/year. 2013 is the

fourth consecutive year when Vietnam has experienced exportation in surplus.

According to the statistics for the first 6 months of 2014, export value is 217 mil USD,

rising by 12.9% yoy. Net surplus in the first 6 months is 76.7 mil USD, 2.5 times as much

as the figure in the whole 2013 year. There is, thus, a tendency for exportation to

prosper this year.

Reality shows that the largest exporters of tires are still FDI corporations namely Kumho,

Chengshin, Chinh Tan, Kenda, Yokohama with 65% of export value. The three major

manufacturers of tires in Vietnam are DRC, CSM and SRC with 14% of export value.

As always, CSM is the largest exporter among the 3 listed corporations and ranks 67th

in revenue in the world scale according to 2013 statistics of Tire business.

Importation: For the past 3 years, export value has the CAGR of 18%. In the first 6 months of this year, tire export value of Vietnam is 140.57 mil USD, decreasing by 16% yoy.

Import – Export value of Tires in Vietnam

Source: VRA, Vietnam Custom, FPTS

309

336

363

217.25

239

327 332

140.57

0

10

20

30

40

50

60

70

80

90

0

50

100

150

200

250

300

350

400

2011 2012 2013 6M2014

Export Import Net Export

Tires and Natural Rubber

www.fpts.com.vn www.fpts.com.vn Bloomberg- FPTS <GO> | 31

Export market: in 2013, Vietnam’s rubbery products were exported to 115 countries.

The USA topped the export market with 62.5 mil USD (17.2%), followed by China with

39.2 mil USD (10.8%), Malaysia with 27.2 mil USD (7.5%), Japan with 19.6 mil USD

(5.4%), Arab with 17.1 mil USD (4.7%) and other 110 countries with 197 mil USD. These

percentage figures, however, went through some slight changes in the first 6 months

this year with Japan climbing to the highest of 11.2% (24.38 USD) and USA (10.4%)

and Malaysia (7.9%).

In terms of production volume, Brazil has the most imported capacity of 2.3 mil tires, most of which are tires for bikes and motorbikes with rather modest value.

Import market: In 2013, Vietnam imports a majority of tires from Thailand (43%), China

(12%), HongKong (12%), Indonesia (4%), and India (3%). Interestingly, the ranks of

these countries remained the same in the first 6 months this year with 40% of import

value equivalent to 78 mil USD from Thailand and 16% from China. Tires imported from

Thailand and China are mostly for automobiles with popular brands like Double Coin,

Transking, Chengshin (China-Taiwan) and Bridgestone, Michelin (Thailand). Besides,

the majority of tires for motorbike are also imported from Thailand with common brands

like Inoue, Vee Rubber, Deestone, etc. Products from Japan, also, are mostly tires for

trucks and passenger cars (<9 seats) with famous brands like Bridgestone, Yokohama,

etc. with import value of 13.7 mil USD, a 31% decrease yoy.

Tires export-market structure by value of

Vietnam in 2013

Source: VRA, Vietnam Custom, FPTS

Tires export - market structure by value of

Vietnam of 6M2014

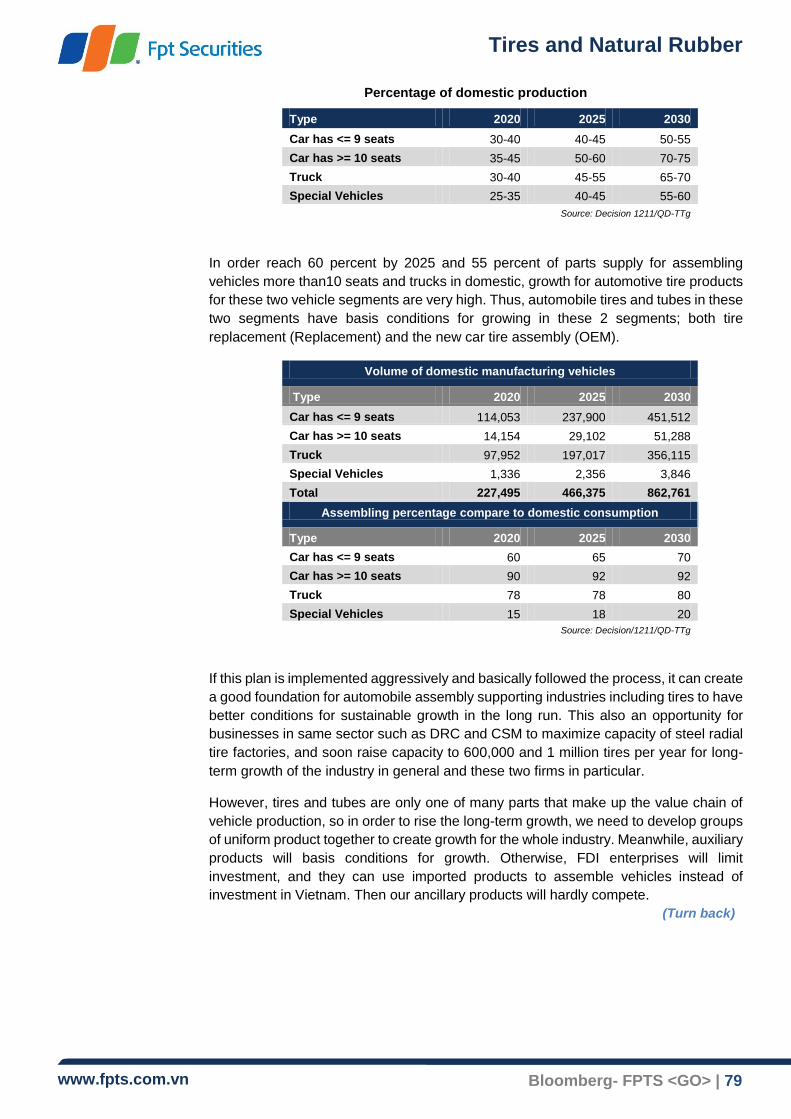

(*): excluding the data of China