Third Capital Market Development Program (Second Tranche)

27

Progress Report on Tranche Release Project Number: 45253–002 Loan Number: 3318/3319 January 2020 Bangladesh: Third Capital Market Development Program (Second Tranche) Distribution of this document is restricted until it has been approved by the Board of Directors. Following such approval, ADB will disclose the document to the public in accordance with ADB’s Access to Information Policy.

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Third Capital Market Development Program (Second Tranche)

Progress Report on Tranche Release

Project Number: 45253–002 Loan Number: 3318/3319 January 2020

Bangladesh: Third Capital Market Development Program (Second Tranche) Distribution of this document is restricted until it has been approved by the Board of Directors. Following such approval, ADB will disclose the document to the public in accordance with ADB’s Access to Information Policy.

CURRENCY EQUIVALENTS (as of 06 January 2020)

Currency unit – taka (Tk) Tk1.00 = $0.01179 $1.00 = Tk84.780

ABBREVIATIONS

ADB – Asian Development Bank BSEC – Bangladesh Securities and Exchange Commission CCP – central counterparty CDMC – Cash and Debt Management Committee CMDP – Capital Market Development Program CMT – Capital Market Tribunal CSE – Chittagong Stock Exchange DSE – Dhaka Stock Exchange FRC – Financial Reporting Council FRTB – floating rate treasury bond GDP – gross domestic product IAD – Internal Audit Department ICT – information and communication technology IDRA – Insurance Development and Regulatory Authority IPO – initial public offering NSC – national saving certificate TA – technical assistance

NOTE

(i) The fiscal year (FY) of the Government of Bangladesh and its agencies ends on 30 June. “FY” before a calendar year denotes the year in which the fiscal year ends, e.g., FY2019 ended on 30 June 2019.

(ii) In this report, “$” refers to United States dollars.

Vice-President Shixin Chen, Operations 1 Director General Hun Kim, South Asia Department (SARD) Director Takeo Konishi, Public Management, Financial Sector and Trade

Division, SARD Team leader Takuya Hoshino, Financial Sector Specialist, SARD

Team members Monica Mei Carino-Young, Project Analyst, SARD M. M. Zimran Khan, Associate Project Analyst, SARD

Jackie Moreno, Senior Project Assistant, SARD Douglas Perkins, Principal Counsel, Office of the General Counsel Dongdong Zhang, Principal Financial Sector Specialist, SARD

In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area

CONTENTS

Page

I. INTRODUCTION ............................................................................................................ 1

II. RECENT MACROECONOMIC AND POLITICAL DEVELOPMENTS.............................. 2

III. STATUS OF PROGRAM IMPLEMENTATION ................................................................ 3

A. Summary of Compliance Status .......................................................................... 3

B. Program Implementation ..................................................................................... 3

C. Review of the Associated Technical Assistance .................................................10

IV. CONCLUSION ..............................................................................................................10

V. THE PRESIDENT’S RECOMMENDATION ...................................................................12

APPENDIXES

1. Country Economic Indicators 13

2. Status of Second Tranche Policy Actions 14

3. Summary of Progress Under Design and Monitoring Framework 18

4. Bangladesh Capital Market Performance 22

I. INTRODUCTION 1. On 20 November 2015, the Asian Development Bank (ADB) approved a program loan to Bangladesh totaling $250 million equivalent for the Third Capital Market Development Program (CMDP3). CMDP3 comprises (i) a program loan to support vital capital market reforms and (ii) an associated technical assistance (TA) grant of $700,000 to assist the implementation of key reform actions under the program.1 2. Capital markets are important for financial intermediation and resource mobilization, specifically for raising long-term financing and risk capital for infrastructure and entrepreneurial activities. Well-functioning capital markets can reduce the private sector’s dependency on bank financing. Bangladesh’s capital market needs to be larger, deeper, and more dynamic to encourage enough private sector investment to spur economic growth and enable the country to achieve middle-income status. The Government of Bangladesh has shown strong ownership of reforms that enable capital market development.2 Its Vision 2021 calls for capital markets to be further liberalized, reformed, and deepened to raise capital to support industry growth.3 ADB has been supporting this government-owned reform agenda through the Second Capital Market Development Program (CMDP2) and the follow-on CMDP3 since 2012. 3. CMDP2 was introduced after the turbulence in the stock market in December 2010 to regain market confidence and pull the capital market back onto a sustainable development path. The program first brought in market stabilization measures such as (i) regulations on margin lending and the equity exposure of banks; and (ii) stronger oversight by Bangladesh Bank (the banking regulator) and the Bangladesh Securities and Exchange Commission (BSEC, the securities regulator) as well as policy coordination between the two entities. Second, CMDP2 laid the foundation for sustainable market development by tackling structural deficiencies in a comprehensive and sequential manner. This resulted in a long-term national capital market master plan, with strong ownership of the government. 4 In addition, critical legislations and amendments to tax codes strengthened the policy framework for (i) new financial instruments, (ii) better corporate governance, (iii) reliable financial reporting and auditing, and (iv) stronger operational and financial efficiency of BSEC. The demutualization of the Dhaka and Chittagong stock exchanges, undertaken through a special act with time-bound action plans, aligned the broader incentives of capital market development with those of brokers and dealers. Parliament passed the Financial Reporting Act (FRA) on 6 September 2015 to set up an independent regulatory agency, the Financial Reporting Council (FRC), improve the quality of financial reporting, and upgrade accounting and auditing standards. The reform under the FRA was expected to promote more informed investment decisions based on reliable financial reports. 4. CMDP3 was introduced in 2015 to broaden and deepen the reform outreach and overcome the remaining constraints to sustainable market development. In fact, the government,

1 ADB. 2015. Report and Recommendation of the President to the Board of Directors: Proposed Loan to the People’s Republic of Bangladesh for the Third Capital Market Development Program. Manila.

2 ADB’s first program for capital market development in Bangladesh was approved in 1997 to restore investor confidence, which was significantly damaged when the Bangladesh stock market crashed in 1996 because of excessive speculation. The program’s key achievements were: (i) strengthened market regulation and supervision, such as by strengthening regulatory authority of the Bangladesh Securities Exchange Commission; (ii) developed capital market infrastructure, including strengthened governance framework for market intermediaries, and (iii) modernized capital market support facilities, including establishment of automated depository and trading systems.

3 Government of Bangladesh, Planning Commission. 2012. Perspective Plan of Bangladesh 2010–2021. Dhaka. 4 Bangladesh Securities and Exchange Commission. 2012. Bangladesh Capital Market Development Master Plan

2012–2022. Dhaka.

2

in its 7th Five Year Plan, called for more measures to further improve the overall capital market performance with a strong emphasis on reducing malpractices and governance deficits.5 In line with the five-year plan, the government and ADB agreed to build on the stabilization measures introduced by CMDP2 and to support the timely implementation of the capital market development master plan. In particular, CMDP3 was to focus on the actual implementation of regulatory and institutional reforms mandated by the legislations introduced under CMDP2, such as demutualizing the two stock exchanges, establishing the FRC, strengthening the human resource capacity of BSEC, and operationalizing the Capital Market Tribunal (CMT). CMDP3 was considered critical in maintaining the reform momentum by continuing to take various actions and successfully delivering outputs with strong engagement by the different stakeholders. 5. The reforms under CMDP3 were implemented from January 2015 to November 2019. CMDP3 comprises an $80 million first tranche against 8 policy actions and a $170 million second tranche against 18 policy actions. The policy actions supported four program outputs: (i) strengthened market stability, (ii) enhanced market facilitation, (iii) enhanced supply measures, and (iv) enhanced demand measures. The first tranche was released upon loan effectiveness on 11 December 2015. While the release of the second and final tranche was originally expected 18 months after the first tranche (i.e., in June 2017), the program was extended to March 2020 to achieve a satisfactory fulfillment of the corresponding tranche release conditions. 6. This report focuses on the progress achieved under the second tranche.

II. RECENT MACROECONOMIC AND POLITICAL DEVELOPMENTS 7. Bangladesh has experienced strong economic growth since 2015 (Appendix 1). Its average annual real gross domestic product (GDP) growth rate was 7.2% during FY2015–FY2018, and accelerated to 7.9% in FY2018, driven by higher private sector consumption, private sector investment, and exports. Continued political stability, improved power supply, and higher growth in private sector credit facilitated the fastest economic expansion in Bangladesh since 1974. 8. The election in December 2018 was won by the ruling party, giving the government an extended period of continuity to pursue selected policy reforms while continuing to implement policies from its Vision 2021 and 7th Five Year Plan. 9. Monetary policy has been supportive of continued economic growth. Broad money grew at an average 12.2% during FY2015–FY2018. Inflation was contained broadly within the central bank’s target range at an annual average of 5.8%. Average tax revenue stood at 8.7% of GDP, and public investment was at 7.2% of GDP (6.8% in FY2015, 8.0% in FY2018), both below the government’s targets.6 The fiscal deficit stayed within a 5% band as underperformance in project implementation on the expenditure side balanced out underperformance in tax collection on the revenue side. 10. Private sector investment increased in line with GDP growth during FY2015–FY2018. As a result, the share of private investment to GDP remained consistent at about 23% (22.1% in FY2015, 23.3% in FY2018). Private sector credit grew at an annual average of 15.7% during the period. Despite this strong economic growth, the country’s banking industry continuously

5 Government of Bangladesh, Planning Commission. 2015. The 7th Five Year Plan, FY2016–FY2020: Accelerating Growth, Empowering Citizens. Dhaka.

6 In FY2018, the total tax revenue was originally budgeted at 13.0% of GDP, but it was actually at 9.6%. The total expenditure was originally budgeted at 18.0% of GDP, but it was actually at 14.3% (Source: Ministry of Finance).

3

underperformed—with a high gross nonperforming loan ratio of about 10% (9.7% in FY2015, 10.3% in FY2018).7 The high level of stressed assets is going to limit the banks’ ability to provide new lending to the private sector.

11. Maintaining robust economic performance will require an increase in productive investments by the private sector, supported by a strong financial market, including banking and capital markets.

III. STATUS OF PROGRAM IMPLEMENTATION

A. Summary of Compliance Status 12. The government has remained strongly committed to the program’s policy reforms. All but one of the 18 second-tranche policy actions were fully complied with (Appendix 2). The one policy action not complied with became irrelevant because of a change in market factors that occurred after the ADB Board approval of the program (para. 33). ADB closely monitored the program implementation through 13 loan review missions during 2015–2019. The compliance of the 8 first-tranche policy actions has been maintained. It found no issues regarding compliance with the loan covenants.8 13. The government conducted periodic monitoring and oversight in accordance with the loan covenants. However, the program implementation was delayed by more than 2 years for the following reasons:

(i) Inadequate staffing of BSEC and the insurance regulator, Insurance Development and Regulatory Authority (IDRA), stalled formulation of new regulations.

(ii) Inadequate coordination between government agencies delayed the government’s approval of a new BSEC organogram and ADB’s attached TA in support of program implementation.

(iii) Resistance from vested interests meant that it took longer than anticipated to build consensus on asset investment rules for insurance companies and on risk-based capital rules for market intermediaries.

14. Despite these challenges, all but one of the second-tranche policy actions were duly implemented and the program’s objective was successfully achieved, as paras. 15–39 confirm. Appendix 3 also provides the progress of achieving results based on the program’s design and monitoring framework.

B. Program Implementation 15. The following is a summary of progress made under each tranche release action, classified according to the expected outputs and associated objectives.

1. Strengthened Market Stability 16. Building on the efforts made under CMDP2 (para. 3), CMDP3 aimed to further strengthen market stability by deepening BSEC’s regulatory capacity with more human resources, a new information and communication technology (ICT) system, and better internal governance;

7 The average gross nonperforming loan ratio of the state-owned commercial banks was 28.2% in FY2018; that of the

private commercial banks was 6.0% in FY2018 (Source: Bangladesh Bank). 8 No changes in policy actions occurred, and the safeguard classifications remained category C during the program

implementation.

4

introducing new regulations on public issuance and share acquisition; and setting up a clearing and settlement company to facilitate securities transactions. 17. Tranche 2, policy action 1: Government to approve BSEC’s revised organogram (complied with). On 16 October 2019, the government approved the creation of 180 new positions at BSEC, supplementary to the existing staff positions (about 100). The government also approved a new pay-scale structure, comparable to that of Bangladesh Bank, more closely in line with private sector compensation practices for recruiting better-qualified candidates. The additional BSEC staff and the new pay-scale structure had become legally possible when the revised Securities and Exchange Commission Act 1993 (clause 9) was introduced under CMDP2. However, the government’s approval was pending for several years. This policy action was intended to implement clause 9 so as to enhance BSEC’s regulatory and enforcement capacity and promote market stability. It was seen as being critical for market development in view of novel and more complex financial instruments such as sukuk (para. 29) and derivatives (para. 30). These recent market developments require BSEC to strengthen its ability to formulate better regulations and exercise more stringent supervision to ensure market confidence and promote market innovation. 18. Tranche 2, policy action 2: BSEC to operationalize the Office of Internal Control and Compliance (complied with). BSEC approved the establishment of the Internal Audit Department (IAD) on 24 August 2015. IAD is mandated to provide reasonable assurance on reliable information, policy and regulatory compliance, safeguarding of assets, functional efficiency, achievement of objectives, and integrity and ethical value by evaluating and improving the effectiveness of reputational risk management, and the internal control and governance processes of BSEC. The head of IAD reports directly to the Chairman, a board member. BSEC appointed an executive director as the head of IAD on 18 October 2015 and an assistant director on 9 May 2016. IAD will be expanded and fully functional as new staff is added under the new BSEC organogram (para. 17) to play a more significant role in ensuring internal governance as BSEC’s operations are scaled up. 19. Tranche 2, policy action 3: BSEC to amend Securities and Exchange Commission (Public Issue) Rules, 2006, including (i) IPO book-building procedures to make the price discovery method more effective and (ii) reduction of the IPO lock-in period from 3 years to 1 year for BSEC-licensed private equity investors (complied with). BSEC issued the Bangladesh Securities and Exchange Commission (Public Issue) Rules, 2006 on 28 December 2015. Before then, initial public offerings (IPOs) were carried out exclusively through the fixed price method, whereby an issuer offers its securities at par value. The book-building method allows an issuer to offer its securities at prices determined through auction by institutional investors. The book-building method is intended to make price discovery more effective and transparent to reflect market demand. During 2016–2019, 7 large-sized IPOs out of 30 IPOs overall were conducted through book-building, accounting for 66% of the total issuance amount.9 The new rules also allow a 1-year IPO lock-in period for qualified alternative investment funds, including venture capital funds or private equity funds.10 The shorter IPO lock-in period enables these strategic investors to exit earlier to realize capital gains, which is anticipated to spur venture capital and private equity fund activity and further develop an entrepreneurial finance ecosystem as a source of quality equity issuance.

9 The average value of an IPO through book-building was Tk1,762 million; for an IPO under the fixed-price method, it

was Tk280 million (Source: Bangladesh Securities Exchange Commission). 10 As a first-tranche policy action of CMDP3, the Bangladesh Securities and Exchange Commission (Alternative

Investment) Rules, 2015 created the new investor category of alternative investment funds.

5

20. Tranche 2, policy action 4: BSEC to (i) issue risk-based capital rules for intermediaries, and (ii) adopt and initiate the implementation of a capital restructuring plan for intermediaries (complied with). BSEC issued the Bangladesh Securities and Exchange Commission (Risk and Capital Adequacy) Rules, 2019 on 22 May 2019, which include risk-based capital rules for market intermediaries, such as brokers and dealers, and sets clear milestones and a timeline for rectification for undercapitalized intermediaries. BSEC was to activate enforcement actions for noncompliance in 2 years after the issuance of the rules. Enforcement actions may include obliging noncompliant entities to submit reconstruction plans, and potentially suspending the licenses for entities that continue to be noncompliant. The new rules and its stringent enforcement are intended to ensure that the market intermediaries hold enough capital in proportion to the level of risks that the entities are exposed to from different types of market activities. The enforcement of capital adequacy measures ensures the financial stability of the market intermediaries and limits the build-up of systemic risk.11 The market intermediaries are required to submit quarterly reports on their risk-based capital to BSEC, accounting for their exposure to credit, operational, and concentration risk as well as liquidity mismatches. The increase in BSEC’s staff and ICT capacity will help it in supervising the risk-based capital rules.12 21. Tranche 2, policy action 5: BSEC to issue merger and takeover rules (complied with). BSEC issued the Bangladesh Securities and Exchange Commission Rules, 2018 (as regards acquisition and ownership of a sufficient number of shares) on 3 June 2018. These are intended to streamline and clarify the procedures for (i) the acquisition of shares of 10% or more in a publicly listed company and (ii) bailout takeovers of financially distressed companies, which were previously governed by BSEC’s Substantial Acquisition and Takeover Rules (2002). The 2002 rule did not have clear provisions and placed buyers at risk of an invalid acquisition. The lower legal risk and simplified procedure under the new regulatory framework will foster a more active market for corporate control and make trade sales a more attractive exit option for potential investors. 22. Tranche 2, policy action 6: BSEC to initiate installation of its ICT system, which includes the following elements: (i) electronic reporting by listed companies and intermediaries; (ii) electronic internal communication system (filing, retrieval, and analysis of documents); and (iii) case-tracking system for investigations and enforcement cases (complied with). BSEC approved the procurement plan for the new ICT system with functional and technical specifications for a regulatory information system and enterprise resource planning package at the commission meeting on 29 May 2019. The attached TA supported drafting of the procurement plan and will further support BSEC in procuring and installing the new ICT system in 2020. BSEC’s operations are currently paper based, except for market surveillance. The new ICT system will strengthen the administrative capacity of BSEC with digital enterprise resource planning, while the regulatory information system will enable regulated entities to submit documents online, and ensure more efficient risk-based supervision on the part of BSEC. 23. Tranche 2, policy action 7: Finalize legal framework to grant license for establishing a clearing and settlement company by way of approval by BSEC or by submission of a draft bill to Parliament, as necessary (complied with). The policy action was intended to facilitate the establishment of a clearing and settlement company that would eventually function as the central counterparty (CCP) entity for settlement guarantees. The CCP will be a key market

11 Systemic risk is the risk of a cascading failure in the finance sector caused by links within the financial system,

resulting in a severe economic downturn or market crash. 12

With the introduction of more complex financial instruments, such as derivatives and short-selling, market intermediaries must maintain adequate capital to protect themselves from the volatility of the trading book, given that the trading book is influenced by market risk, e.g., equity, commodity, interest rate, and foreign exchange risk.

6

infrastructure to reduce the counterparty risk of individual transactions, especially derivatives transactions, provided it is well capitalized and has a better risk management system.13 BSEC issued the Bangladesh Securities and Exchange Commission (Clearing and Settlement) Regulations, 2017 on 13 June 2017. They defined the key concepts of CCP operations; set a formal registration process for a new clearing and settlement company; set key organizational parameters for the new company—capital structure, ownership composition, governance structure, and risk management structure—as necessary requirements for business registration, and to ensure its effective functioning as a CCP. The new company was set up on 14 January 2019 in accordance with the new regulations. The preparations for introducing the CCP function in 2020 are ongoing, such as specifications for the ICT system and the development of a risk management framework.

2. Market Facilitation 24. The program aimed to enhance market facilitation by expediting the adjudication of enforcement actions, upgrading the accounting and auditing standards, and pursuing the demutualization of the two stock exchanges. The legal frameworks were established under CMDP2 and were to be operationalized under CMDP3. 25. Tranche 2, policy action 8: Establish an independent Financial Reporting Council (FRC) with the purpose of initiating the adoption of international accounting and auditing standards for public interest entities (complied with). As per Subsection (1) of Article 3 of the Financial Reporting Act (FRA), 2015, the government established on 23 April 2016 an independent oversight authority, the Financial Reporting Council (FRC), to guide the introduction of international standards on financial reporting, accounting, and auditing for public interest entities and professional accountants, and to monitor their practices.14 The FRC was set up in compliance with the objectives, powers and functions, governance structure, and organizational structure set forth in the FRA. On financial reporting, the FRC conducts on-site and off-site inspections of public interest entities. On auditing and accounting practices, the FRC exercises its authority over professional accountants through two self-regulating organizations, the Institute of Chartered Accountants of Bangladesh and the Institute of Cost and Management Accountants of Bangladesh. The FRC is operational with a chairman, 4 executive directors, and 10 staff as of July 2019. Each executive director oversees a key functional area: (i) standard setting, (ii) financial report monitoring, (iii) audit practice review, and (iv) enforcement. The FRC is recruiting additional staff to fill in 250 positions under the existing FRC organogram. 26. Tranche 2, policy action 9: Transfer of capital market-related cases from the regular courts to the special tribunal for capital markets (complied with). To complement BSEC’s enforcement capacity, the Capital Markets Tribunal (CMT) was to expedite the adjudication of any enforcement actions that require highly technical expertise. The CMT was set up on 7 January 2014 as a policy action of CMDP2, and started operations on 21 June 2015 as a first-tranche release action of CMDP3. By 6 November 2016, all 17 special cases had been transferred from the regular courts to the CMT. By mid-2017, 25 cases had been referred to the CMT. The cases related to the two stock market turbulences of the late 1990s and early 2010s, had become entrenched in the regular court process, and needed to be resolved promptly. Even though the

13 The CCP concentrates the risk of settlement failures onto itself and isolates the effects of a failure of a market

participant through the process of novation, whereby the original contract between the buyer and seller is extinguished and replaced by two new contracts—one between the CCP and the buyer, the other between the CCP and the seller. Given the nature of risk retention, the CCP must be well capitalized and must have a sound risk management system to efficiently absorb the risk.

14 Public interest entities include listed and unlisted companies, nongovernment organizations, financial institutions, and government agencies.

7

CMT was fully operational, it had to refer most of the transferred cases back to the regular court system because the defendants found ways to bring the cases outside the CMT jurisdiction. The government is now considering legislative amendments to expand the legal powers of the CMT, fill the loopholes, and ensure more proactive case resolutions, as originally envisioned. 27. Tranche 2, policy action 10: As part of the stock exchanges’ demutualization plan of action, BSEC to issue directives for the inclusion of strategic investors on Dhaka Stock Exchange (DSE) and Chittagong Stock Exchange (CSE) (complied with). Strategic investors in DSE and CSE would facilitate the development of technology infrastructure and promote market innovation. The Demutualization Act allowed the two exchanges to sell not more than 25% of the total shares to strategic investors. To expedite the process, BSEC issued directives to DSE and CSE on 9 December 2015, instructing them to sign a contract agreement with a strategic investor within 1 year. However, both CSE and DSE were deliberate in evaluating the proposals from potential strategic investors.15 On 4 September 2018, DSE transferred 25% of its ownership to a consortium of the Shenzhen and Shanghai stock exchanges after the contract agreement had been signed on 14 May 2018 upon BSEC’s approval.16 CSE continues to search for viable strategic investors with the right fit.

3. Supply Measures 28. While BSEC’s efforts to streamline issuance processes and expand the exit options for strategic investors (paras. 19 and 21) are intended to increase the supply of securities, the absence of alternative financial instruments limits the depth and breadth of Bangladesh’s capital market. The program aimed to introduce an enabling regulatory framework for new financial instruments suitable for different investor types having different risk–return profiles. 29. Tranche 2, policy action 11: BSEC to issue sukuk rules (complied with). To promote Islamic finance and increase the number of sukuk (Sharia-compliant bond) issuances, BSEC released the Bangladesh Securities and Exchange Commission (Investment Sukuk) Rules, 2019 on 22 May 2019. Based on the existing regulatory framework for public offerings and asset-backed securities developed under CMDP2, the new rules define special issuance procedures for securities to be certified as sukuk. 30. Tranche 2, policy action 12: BSEC to issue rules for derivatives (complied with). Derivatives are a well-recognized instrument to control the risk exposure of capital market participants by transferring specific types of risks to third parties in a cost-efficient manner. BSEC issued the Bangladesh Securities and Exchange Commission (Exchange Traded Derivatives) Rules, 2019 on 22 May 2019. The new regulations and the CCP (para. 23) are necessary market infrastructure components for the future introduction of derivative products.

4. Demand Measures 31. The program aimed to increase demand for capital market instruments by (i) developing liquid bond markets with a focus on government bonds; (ii) promoting a mutual fund industry by introducing exchange traded funds; and (iii) developing an insurance sector by strengthening IDRA and expediting the issuance of pending regulations, as required by the Insurance Act 2011.

15 In the case of DSE, its demutualization scheme set the following three areas for consideration in selecting strategic investors: (i) strategic fit in terms of industry experience, market experience, and credibility; (ii) financial consideration; and (iii) cultural compatibility.

16 The Consortium of Shenzhen Stock Exchange and Shanghai Stock Exchange is expected to advance long-term cooperation with DSE in the areas such as technology, market cultivation, and product development in an orderly manner (Source: Dhaka Stock Exchange Limited Press Release, 4 September 2018).

8

a. Developing Liquid Bond Markets

32. Tranche 2, policy action 13: Cash and Debt Management Committee (CDMC) to approve a manual for the introduction of floating rate notes (complied with); and Tranche 2, policy action 14: CDMC to approve guidelines on floating rate notes and Bangladesh Bank to issue floating rate notes in the government bond auction system on a pilot basis (complied with). Floating rate notes provide protection for investors against interest rate risk, and can capture new demand from government bond investors. To establish a reference rate for floating rate notes, Bangladesh Bank on 16 September 2015 began publishing the 91-day Bangladesh compounded rate (91-day BCR) on a daily basis as a first-tranche policy action of CMDP3. On 25 January 2018, CDMC approved Bangladesh Bank’s issuance of a floating rate treasury bond (FRTB) on a pilot basis.17 CDMC delegated the design of the FRTB issuance to its technical committee. The committee approved the manual for the auction of the FRTB, setting the procedures for auction, settlement, coupon payment, and redemption on maturity. On 10 May 2018, Bangladesh Bank published a notification to primary dealers that outlined the operational procedures for an FRTB issuance. The first FRTB was issued on 25 March 2019. Its tenor was 3 years and the maximum allocated amount was Tk5 billion ($59.07 million). The pilot FRTB issuance was reviewed and discussed at a consultative meeting (para. 34) between the government and primary dealers on 24 April 2019. 33. Tranche 2, policy action 15: CDMC/Bangladesh Bank to approve and introduce short-selling of primary dealer-owned government securities on a pilot basis (not complied with). As part of a strategy to develop a risk-free yield curve to serve as pricing benchmark for other fixed-income securities, including corporate bonds, the short-selling of government securities by primary dealers was originally planned to be introduced on a pilot basis to support primary dealers in market-making as a liquidity provider for the secondary government bond market. Short-selling would permit the investment positions of primary dealers to be hedged. However, during the program implementation, the supply of government bonds was not large enough for primary dealers to sell them to institutional investors in the secondary market. The majority of the government bonds were purchased by primary dealer banks to meet their statutory liquidity requirements and be held to maturity. The short supply of government bonds was caused partly by an increase in subscriptions to the national saving certificates (NSCs), which offered more attractive risk-free investment returns to individuals. 18 Given this unanticipated market development, the short-selling pilot was considered to be ineffective in creating liquidity in the secondary market. ADB alternatively proposed other measures to achieve the original objective of developing a risk-free yield curve; these are intended to enhance market readiness until the market conditions favor the introduction of short-selling in the future. 34. As a long-term solution, ADB proposed that the government rationalize NSC issuances, and as a short-term solution, the government, on ADB’s advice, successfully introduced two measures to upgrade the framework for government bond issuance. First, Bangladesh Bank and the Ministry of Finance started quarterly consultations with primary dealers to obtain market views on the government’s future debt management operations and to minimize market distortion. The first consultation was held on 27 December 2017. Second, CDMC on 25 January 2018 approved

17 CDMC is an interagency coordination committee chaired by the Finance Secretary with members from the Ministry

of Finance, Bangladesh Bank, and the National Board of Revenue, to oversee the government’s cash and debt management and coordinate fiscal policy decisions.

18 Net issuance of NSCs sharply increased by 32.6% in FY2017. NSCs provided about 5%–6% higher interest rates than 5-year government bonds. As of 30 June 2017, NSCs represented 54.4% of government domestic debt. In turn, government bonds accounted only for one-third of the NSCs issued in FY2017 (Source: Bangladesh Bank).

9

Bangladesh Bank’s buyback of already issued government bonds to facilitate consolidation, i.e., to reduce the number of bond series and create sufficient volume for each series to be actively traded as a standardized product.19 Furthermore, the government introduced a new operational framework for NSCs, including stringent enforcement of an upper limit for NSC holdings through a new ICT system for NSC transactions. The government plans to reduce NSC issuances and increase government bond issuances in FY2020.20 35. Moreover, to mainstream short-selling as typical market practice by securities dealers, BSEC on 22 May 2019 issued the Bangladesh Securities and Exchange Commission (Short-Sale) Rules, 2019 with ADB TA support. The new rules provide guidance to securities exchanges on their operational procedures for short-selling listed corporate and government securities, and lending and borrowing them. The rules will raise market awareness of the practice of short-selling and will be replicated for a new framework for future short-selling of government securities. Furthermore, short-selling and securities lending and borrowing require settlement through a CCP to minimize settlement failures (para. 23).

b. Promoting Mutual Funds 36. Tranche 2, policy action 16: BSEC to issue rules for the operation of exchange-traded funds (complied with). This policy action promotes a robust mutual fund industry by providing opportunities for passive investments by institutional and retail investors through exchange-traded funds. BSEC issued the Bangladesh Securities and Exchange Commission (Exchange Traded Funds) Rules, 2016 on 19 June 2016, to introduce an enabling regulatory framework for such funds. The newly introduced BSEC’s short-selling rules (para. 35) will support market makers provide vital liquidity and ensure efficient price discovery for exchange-traded funds through arbitrage.

c. Enhancing Institutional Investors’ Demand through Insurance Sector Development

37. The program aimed to boost the participation of insurance companies in the capital market by increasing the size of the insurance sector through stabilization measures, such as strengthening IDRA’s regulatory capacity and introducing regulatory measures as required by the Insurance Act, 2011. 38. Tranche 2, policy action 17: Government to approve the IDRA organogram (complied with). The government approved the creation of 155 new positions at IDRA on 30 June 2016 for 1 year until 31 May 2017, and then extended it for another 3 years to 31 May 2020. To ensure IDRA’s capacity enhancement with additional staff, the World Bank’s Insurance Sector Development Project will provide training to IDRA’s new staff and support the installation of IDRA’s new ICT system.21 39. Tranche 2, policy action 18: Issuance of the following rules or regulations: (i) paid-up capital and shareholdings of an insurance company; (ii) asset investment rules (including government securities, real estate, and equities) for life and non-life insurance

19 As of June 2017, 316 series of government bonds were outstanding, much more than the recommended number of

40–50 series. The number was reduced to 268 as of November 2019 (Source: Bangladesh Bank). 20 The total value of the primary issuance of treasury bills and treasury bonds in the period of January-November 2019

increased to Tk1,763 billion from Tk750 billion in the same period of 2018. The total value of the secondary trading of treasury bills and treasury bonds increased to Tk233 billion in the period of January-November 2019 from Tk110 billion in the same period of 2018 (Source: Bangladesh Bank).

21 World Bank. Bangladesh Insurance Sector Development Project. 2017. Washington DC.

10

companies; (iii) life insurance policy and claim register; and (iv) life insurance policyholders’ security fund (complied with). This policy action aimed to increase insurance penetration by ensuring the stability of the insurance industry through regulatory reforms, as required by the new Insurance Act 2010 introduced under CMDP2. The growth of the industry will eventually increase the demand for capital market instruments. As per the requirements of the Insurance Act 2010, IDRA issued the (i) Paid-up Capital and Shareholding Rules 2016 on 19 September 2016; (ii) the Insurance (Asset investment of life insurers) Regulation, 2019 on 19 November 2019 and the Insurance (Asset investment and conversion of non-life insurer) Regulation, 2019 on 14 November 2019; (iii) Regulations for the Protection of the Insurers’ Register (Policy and Claims), 2017 on 26 November 2017; and (iv) Life Insurance Policy Owner Security Fund Regulations, 2016 on 21 November 2016. The paid-up capital rules and the asset investment rules are prudential measures for insurance companies to ensure financial stability and sustainability by requiring adequate capital and by limiting any excessive risk-taking in their investment decisions. The latter two regulations, (iii) and (iv), provide protection for policyholders and build the public’s trust in insurance services—one established a database that detects and prevents fraud; the other ensures claim payments to policyholders even if an insurance company becomes insolvent.

C. Review of the Associated Technical Assistance 40. The attached TA aimed to support the implementation of key reform actions under the program, such as the completion of four policy actions: (i) BSEC’s ICT procurement plan (para. 22), (ii) clearing and settlement company (para. 23), (iii) sukuk rule (para. 29), and (iv) derivatives rule (para. 30).22 41. ADB’s contribution of $700,000 was to be matched by government counterpart funds of $1.4 million, mainly for BSEC’s ICT procurement. The total TA amount of $2.1 million required the approval from the Planning Commission, which resulted in a significant delay. The government’s final approval of the TA did not materialize until 22 April 2018. BSEC decided to prepare its rules for a clearing and settlement company without TA support, but it requested to expand the TA scope to accommodate support for finalizing a draft of the risk-based capital rules for intermediaries (para. 20) and for drafting the rules on short-selling and securities lending and borrowing (para. 35). 42. Within about 1 year from the government approval, the TA had successfully supported BSEC in achieving the policy actions described in paras. 40 and 41, all of which required highly technical knowledge input. The TA is still ongoing until October 2020 to sustain the overall program outcome beyond the second-tranche policy action requirements. For example, the TA is supporting the procurement and installation of BSEC’s new ICT system.

IV. CONCLUSION 43. Compliance with second-tranche policy actions. Of the 18 second-tranche policy actions, 17 were fully complied with, while 1 was no longer relevant because of an unanticipated market development (para. 33). Despite various challenges (para. 13), the executing and implementing agencies remained committed to the completion of CMDP3 to develop Bangladesh’s capital market as a key driver of long-term economic growth.

22 Of the TA amount of $700,000, $300,000 was financed by the Republic of Korea e-Asia and Knowledge Partnership

Fund, and $400,000 from ADB’s Technical Assistance Special Fund (TASF-V).

11

44. Development results. The capital market was stable and grew steadily during the program period (Appendix 4). ADB’s long-term engagement through CMDP2 and CMDP3 fundamentally transformed the legal, regulatory, and institutional market frameworks in line with the government’s long-term capital market master plan. In particular, the two programs achieved:

(i) Stronger stability of the securities market. The successful implementation of a new supervisory framework for the securities market helped restore stability after the market turbulence in late 2010. Market governance will be further strengthened by (a) making the regulator, BSEC, more effective through the addition of 180 staff with technical capacity and an efficient new ICT system for risk-based supervision; (b) introducing risk-based capital rules for market intermediaries; and (c) operationalizing the FRC to boost confidence in financial reporting and auditing.

(ii) Enhanced stock market development. A demutualized DSE, with technological and knowledge transfer from its strategic investor, is expected to drive market development with new products and services, including derivatives and exchange-traded funds. The introduction of short-selling and securities lending and borrowing will enable market intermediaries to increase the liquidity of listed securities. The new rules for share acquisitions and for IPOs will expand the options for venture capital funds and provide growth-oriented enterprises with better access to capital market financing. A stronger entrepreneurial finance ecosystem will increase the pool of quality issuances in the long term.

(iii) Foundation for bond market development. The corporate bond market is still in its infancy because the government bond market is distorted by high interest-bearing NSCs and an ad hoc public debt management practice. As an interim solution until the government successfully rationalizes NSC issuance under the new operational framework (para. 34) and increases the supply of government bonds, the program created an enabling environment for the development of a risk-free yield curve by (a) consolidating multiple bond series through a buyback initiative, and (b) institutionalizing regular consultations between the government and primary dealers to facilitate informed government decisions on public debt management and avoid market distortion.

(iv) Insurance industry development. The legal, regulatory, and institutional frameworks for greater stability of the insurance industry were strengthened by approving the expanded IDRA organogram (para. 38) and issuing the rules and regulations required by the Insurance Act 2011 (para. 39).

45. ADB’s value addition. ADB supported the successful implementation of the government’s commitments to the program by (i) facilitating stakeholder coordination to overcome conflicts between the government and the private sector, and between different government ministries and agencies; and (ii) providing TA to strengthen the capacity of the government, give proper guidance on highly technical subjects, and ensure sustainability through regular policy dialogue based on international best practice. With regard to (i), CMDP3 assisted the government in resolving long-pending issues such as the new BSEC organogram (para. 17), risk-based capital rules for intermediaries (para. 20), and asset investment rules for insurance companies (para. 39). ADB also continuously communicated with the government on the importance of rationalizing NSCs, which is also in accordance with other development partners such as the International Monetary Fund, and ADB provided practical suggestions for achieving the expected outcome of developing a risk-free yield curve through alternative measures (para. 33). With regard to (ii), the attached TA supported the government in achieving highly technical policy actions (paras. 40–42). ADB’s core competence was leveraged for an in-depth diagnosis of market issues, especially in the government bond market, and for formulating alternative measures, to which the government fully committed (para. 33); and for the creation of a regional network of securities regulators through the promotion of regional cooperation across Asia and the Pacific, e.g., the

12

Asian Bond Market Initiative forum.23 Without ADB’s involvement, these reforms would not have happened given their complexity and the large requirement of resources and experts. 46. Moving forward. It is recommended that the government continue to solve pending items under the long-term capital market development master plan, with strong political will to sustain the reforms and avoid policy reversals. For the corporate securities market, governance should be stepped up under the strengthened regulatory and supervisory functions of BSEC and the FRC, and through stronger capacity and integrity of market players. Market development should be further promoted through fully demutualized stock exchanges and stronger policy formulation by BSEC. The jurisdiction of the CMT should be periodically updated to close loopholes. Market demand should be further increased through financial literacy training for retail investors and by expanding the institutional investor base, including insurance companies and pension funds. The supply should be encouraged through quality issuances by start-up companies, foreign investors, and possibly state-owned enterprises. To ensure bond market development, the government should further rationalize NSC issuance and consolidate the number of government bond series to create sufficient liquidity for each series. 47. Lessons. The program benefited from (i) the small number of implementing agencies, which made compliance monitoring more effective; (ii) the implementation of the long-term national capital market development master plan with strong government ownership; (iii) TA support for highly technical policy actions; and (iv) the enabling of tangible benefits for and visible impacts on the implementing agencies, such as the government’s approval of BSEC’s expanded organogram. The program implementation reconfirmed that a policy-based loan is the right modality to facilitate consensus-building among various stakeholders with conflicting interests, and to resolve long-standing issues within a fixed timeframe, e.g., new BSEC organogram, risk-based capital rules for market intermediaries, and asset investment rules for insurance companies. 48. The program implementation could have been expedited if all key authorities—e.g., the Planning Commission for the approval of the attached TA and the Ministry of Public Administration for the approval of the BSEC organogram—had been involved from the start. Monitoring and evaluation should be strengthened, with TA support, to periodically obtain views from private sector stakeholders on regulatory changes and market developments, which could inform midterm corrections in the approach to policy actions. Extensive monitoring from the field is critically important to ensuring timely access to regulatory information.

V. THE PRESIDENT’S RECOMMENDATION

49. In view of the significant progress made in the implementation of the overall program, as evidenced by full compliance with 17 of the 18 policy actions for the release of the second tranche, the President recommends that the Board approve

(i) the waiver of one tranche release policy action (policy action 15: Cash and Debt Management Committee and Bangladesh Bank to approve and introduce short-selling of primary dealer-owned government securities on a pilot basis); and

(ii) the release of the second tranche in the amount of $170,000,000 for the Third Capital Market Development Program in Bangladesh.24

23 During the program implementation, the program team obtained guidance from and collaborated with the Asian Bond

Market Initiative team. 24 Comprising $70 million from ordinary capital resources and $100 million from the concessional ordinary capital

resources lending (formerly Asian Development Fund).

Appendix 1 13

( ) = negative, FY = fiscal year, GDP = gross domestic product, Tk = taka. a Based on constant 2005/06 market prices. b Receipts (excluding grants) in comparison with GDP are 9.6% for 2015, 10.0% (2016), 10.2% (2017), 9.6% (2018),

and 12.5% (2019). c Fiscal deficits (excluding grants) in comparison with GDP are 3.9% for 2015, 3.8% (2016), 3.4% (2017), 4.7% (2018),

and 5.0% (2019). d The ratios of debt service to total foreign exchange earnings from exports of goods and nonfactor services, including

workers’ remittances, are 2.2% for 2015, 2.0% (2016), 2.2% (2017), 2.5% (2018), and 2.5% (2019). e Official estimates. Sources: Bangladesh Bureau of Statistics; Bangladesh Bank; Export Promotion Bureau; Ministry of Finance, and Asian Development Bank estimates.

COUNTRY ECONOMIC INDICATORS

Item

Fiscal Year

2015 2016 2017 2018 2019e

A. Income and Growth 1. GDP per capita ($, current) 1236.0 1385.0 1544.0 1675.0 1827.0 2. GDP growtha (%, in constant prices) 6.6 7.1 7.3 7.9 8.1 a. Agriculture 3.3 2.8 3.0 4.2 3.5 b. Industry 9.7 11.1 10.2 12.1 13.0 c. Services 5.8 6.3 6.7 6.4 6.5 B. Saving and Investment (current market prices, % of GDP) 1. Gross domestic investment 28.9 29.7 30.5 31.2 31.6 2. Gross domestic saving 22.2 25.0 25.3 22.8 23.9 C. Money and Inflation (annual % change) 1. Consumer price index (FY2006 base, average) 6.4 5.9 5.4 5.8 5.5 2. Total liquidity (M2) 12.4 16.4 10.9 9.2 9.9 D. Government Finance (% of GDP) 1. Revenue and grantsb 9.8 10.1 10.2 9.7 12.6 2. Expenditure and onlending 13.5 13.8 13.6 14.3 17.4 3. Overall fiscal deficitc (3.7) (3.7) (3.4) (4.6) (4.8) E. Balance of Payments 1. Merchandise trade balance (% of GDP) (3.6) (2.8) (3.8) (6.6) (5.1) 2. Current account balance (% of GDP) 1.8 1.9 (0.5) (3.5) (1.7) 3. Merchandise export ($ million) 30,697.0 33,441.0 34,019.0 36,285.0 39,945.0 Growth (annual % change) 3.1 8.9 1.7 6.7 10.1 4. Merchandise import ($ million) 37,662.0 39,901.0 43,491.0 54,463.0 55,439.0 Growth (annual % change) 3.0 5.9 9.0 25.2 1.8 F. External Payments Indicators 1. Gross official reserves (including gold,

$ million) 25,025.3 30,168.2 33,406.6

32,916.5

32,751.0 Weeks of current year’s imports of goods and

services 24.8 31.6 32.0

24.8

24.0 2. External debt service (% of exports of goods

and services)d 3.2 2.8 3.0

3.5

3.4 3. Total external debt (% of GDP) 12.2 11.9 11.4 12.2 12.3 G. Memorandum Items 1. GDP (current prices, Tk billion) 15,158.0 17,328.6 19,758.2 22,504.8 25,361.8 2. Exchange rate (Tk/$, average) 77.7 78.3 79.1 82.1 84.0 3. Midyear population (million) 157.9 159.9 161.8 163.7 165.6

14 Appendix 2

STATUS OF SECOND TRANCHE POLICY ACTIONS

Second-Tranche Policy Actions Compliance Status

A. Market Stability Objective: to promote more robust, resilient and stable capital markets

(1) Government to approve the revised BSEC organogram. (MOF-FID) Complied with. The government approved an additional 180 staff at BSEC,

with a new pay-scale structure comparable to that that of Bangladesh Bank, on

16 October 2019.

(2) BSEC to operationalize the Office of Internal Control and

Compliance. (BSEC)

Complied with. BSEC approved the establishment of IAD on 24 August 2015.

IAD is mandated to provide reasonable assurance on reliable information,

policy and regulatory compliance, safeguarding of assets, functional efficiency,

achievement of objectives, and integrity and ethical value by evaluating and

improving the effectiveness of reputational risk management, and internal

control and governance processes of BSEC. BSEC appointed an executive

director (as the head of IAD) on 18 October 2015 and an assistant director on

9 May 2016.

(3) BSEC to amend Securities and Exchange Commission (Public

Issue) Rules, 2006, including (i) IPO book-building procedures to

make the price discovery method more effective and (ii) reduction of

the IPO lock-in period from 3 years to 1 year for BSEC-licensed

private equity investors. (BSEC)

Complied with. BSEC issued the Bangladesh Securities and Exchange

Commission (Public Issue) Rules, 2006 on 28 December 2015, reintroducing

the IPO book-building procedures. Section 10-(5) of the new rules allows a 1-

year IPO lock-in period for alternative investment funds.

(4) BSEC to (i) issue risk-based capital rules for intermediaries, and (ii)

adopt and initiate implementation of capital restructuring plan for

intermediaries. (BSEC)

Complied with. BSEC issued risk-based capital rules for intermediaries on

22 May 2019, including clear milestones and a timeline for rectification for

undercapitalized intermediaries (Section 4).

(5) BSEC to issue merger and takeover rules. (BSEC) Complied with. BSEC issued the Bangladesh Securities and Exchange

Commission (gain, acquisition and ownership of a sufficient number of shares)

Rules, 2018 on 3 June 2018. These new rules streamline and clarify the

procedures for share acquisitions.

(6) BSEC to initiate installation of its ICT system, which includes the

following elements: (i) electronic reporting by listed companies and

intermediaries; (ii) electronic internal communication system (filing,

retrieval, and analysis of documents); and (iii) case-tracking system for

investigations and enforcement cases. (BSEC)

Complied with. BSEC approved a procurement plan for the new ICT system

with technical specifications for a regulatory information system and enterprise

resource package on 29 May 2019.

Appendix 2 15

Second-Tranche Policy Actions Compliance Status

(7) Finalize legal framework to grant license for establishing a clearing

and settlement company by way of approval by BSEC or by

submission of a draft bill to Parliament, as necessary. (MOF-FID and

BSEC)

Complied with. BSEC issued the Bangladesh Securities and Exchange

Commission (Clearing and Settlement) Regulations, 2017 on 13 June 2017.

These (i) define the key concepts of CCP operations; (ii) set a formal

registration process for a new CCP company; (iii) set key organizational

parameters for a CCP company—capital structure, ownership composition,

governance structure, and risk management structure—as necessary

requirements for business registration; and (iv) categorize different types of

participants.

B. Market Facilitation Objective: to support more effective and efficient mobilization and allocation of resources in the economy.

(8) Establish an independent financial reporting council with the

purpose of initiating the adoption of international accounting and

auditing standards for public interest entities. (MOF-FD)

Complied with. As per Subsection (1) of Article 3 of the Financial Reporting

Act, 2015, the government established the FRC as a statutory body on 23 April

2016. The FRC adheres to the objectives, powers and functions, governance

structure, and organizational structure set forth in the act. Currently, it is

operational with 4 board members and 10 staff as of July 2019.

(9) Transfer of capital market-related cases from the regular courts to

the special tribunal for capital markets. (BSEC)

Complied with. The CMT was established on 7 January 2014 as part of

CMDP2, and started its operation on 21 June 2015 as a T1 policy action of

CMDP3. As of 6 November 2016, all transferrable 17 cases were transferred

from the regular courts to the CMT.

(10) As part of the stock exchanges demutualization plan of action,

BSEC to issue directives for inclusion of strategic investors in DSE

and CSE. (BSEC)

Complied with. BSEC issued the two directives to the Dhaka and Chittagong

stock exchanges on 9 December 2015 to sign a contract agreement with the

strategic investor. After signing a contract agreement on 14 May 2018, DSE

transferred a 25% stake of its ownership to a consortium of the Shenzhen and

Shanghai stock exchanges on 4 September 2018.

C. Supply Measures Objective: to increase the supply of quality bonds and alternative financial instruments through the capital markets.

(11) BSEC to issue sukuk rules. (BSEC) Complied with. BSEC issued Bangladesh Securities and Exchange

Commission (Investment Sukuk) Rules, 2019 on 22 May 2019.

16 Appendix 2

Second-Tranche Policy Actions Compliance Status

(12) BSEC to issue rules for derivatives. (BSEC) Complied with. BSEC issued Bangladesh Securities and Exchange

Commission (Exchange Traded Derivatives) Rules, 2019 on 22 May 2019.

D. Demand Measures Objective: to support mobilization of capital market financing.

(13) CDMC to approve manual for introduction of floating rate notes.

(MOF-FD and BB)

Complied with. BB, on 16 September 2015, began publishing the 91-day BCR

on a daily basis as a T1 policy of CMDP3. CDMC approved BB’s issuance of an FRTB on a pilot basis on 25 January 2018. CDMC delegated the final

decision on the design of the FRTB issuance to its technical committee, the

CDMTC.

(14) CDMC to approve floating rate note guidelines and BB to issue

floating rate notes in the Government Bond Auction System on a pilot

basis. (MOF-FD and BB)

Complied with. After the approval by CDMTC, BB published on 10 May 2018

a notification to the primary dealers that described operational procedures for

FRTB issuance. The first FRTB was issued on 25 March 2019 (its tenor was

3 years and the maximum allocated amount was Tk5 billion).

(15) CDMC/BB to approve and introduce short-selling of primary

dealer-owned government securities on a pilot basis. (MOF-FD and

BB)

Not complied with. The supply of government securities was much smaller

than expected, which did not justify short-selling as an effective way for primary

dealers to create liquidity in the secondary market for developing a risk-free

yield curve.

To achieve the policy action’s objective nonetheless, the government

introduced two alternative measures to upgrade its debt operations. First, BB

and MOF-FD on 27 December 2017 started quarterly consultations with

primary dealers to obtain a market view on the government’s future debt

management operations. Second, CDMC on 25 January 2018 approved BB’s buyback of already issued government bonds to help reduce the number of

different bond series and create sufficient trading volume for each series. In

addition, BSEC on 22 May 2019 issued Bangladesh Securities and Exchange

Commission (Short-Sale) Rules, 2019 requiring DSE and CSE to issue their

own specific rules to regulate the short-selling of listed corporate and

government securities by market intermediaries. This will form the regulatory

foundation for the future introduction of short-selling of non-listed government

securities by primary dealers.

(16) BSEC to issue rules for operation of exchange traded funds.

(BSEC)

Complied with. BSEC issued the Bangladesh Securities and Exchange

Commission (Exchange Traded Funds) Rules, 2016 on 19 June 2016.

Appendix 2 17

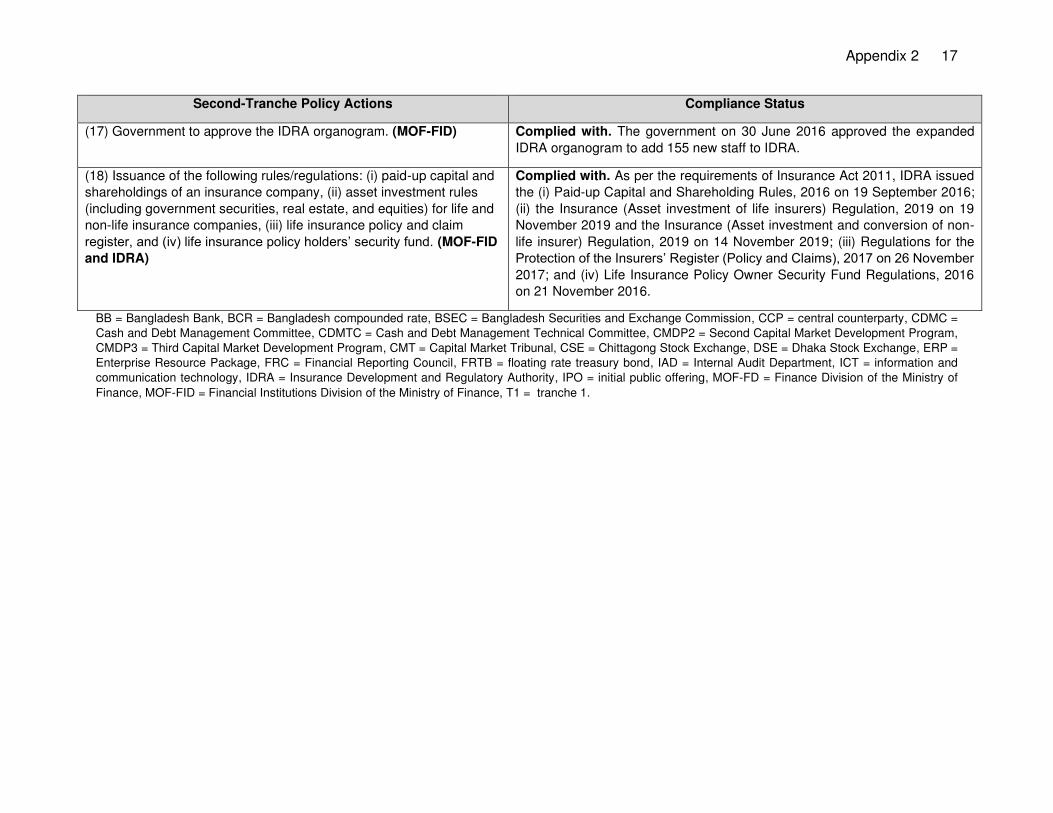

Second-Tranche Policy Actions Compliance Status

(17) Government to approve the IDRA organogram. (MOF-FID) Complied with. The government on 30 June 2016 approved the expanded

IDRA organogram to add 155 new staff to IDRA.

(18) Issuance of the following rules/regulations: (i) paid-up capital and

shareholdings of an insurance company, (ii) asset investment rules

(including government securities, real estate, and equities) for life and

non-life insurance companies, (iii) life insurance policy and claim

register, and (iv) life insurance policy holders’ security fund. (MOF-FID

and IDRA)

Complied with. As per the requirements of Insurance Act 2011, IDRA issued

the (i) Paid-up Capital and Shareholding Rules, 2016 on 19 September 2016;

(ii) the Insurance (Asset investment of life insurers) Regulation, 2019 on 19

November 2019 and the Insurance (Asset investment and conversion of non-

life insurer) Regulation, 2019 on 14 November 2019; (iii) Regulations for the

Protection of the Insurers’ Register (Policy and Claims), 2017 on 26 November 2017; and (iv) Life Insurance Policy Owner Security Fund Regulations, 2016

on 21 November 2016.

BB = Bangladesh Bank, BCR = Bangladesh compounded rate, BSEC = Bangladesh Securities and Exchange Commission, CCP = central counterparty, CDMC =

Cash and Debt Management Committee, CDMTC = Cash and Debt Management Technical Committee, CMDP2 = Second Capital Market Development Program,

CMDP3 = Third Capital Market Development Program, CMT = Capital Market Tribunal, CSE = Chittagong Stock Exchange, DSE = Dhaka Stock Exchange, ERP =

Enterprise Resource Package, FRC = Financial Reporting Council, FRTB = floating rate treasury bond, IAD = Internal Audit Department, ICT = information and

communication technology, IDRA = Insurance Development and Regulatory Authority, IPO = initial public offering, MOF-FD = Finance Division of the Ministry of

Finance, MOF-FID = Financial Institutions Division of the Ministry of Finance, T1 = tranche 1.

18 Appendix 3

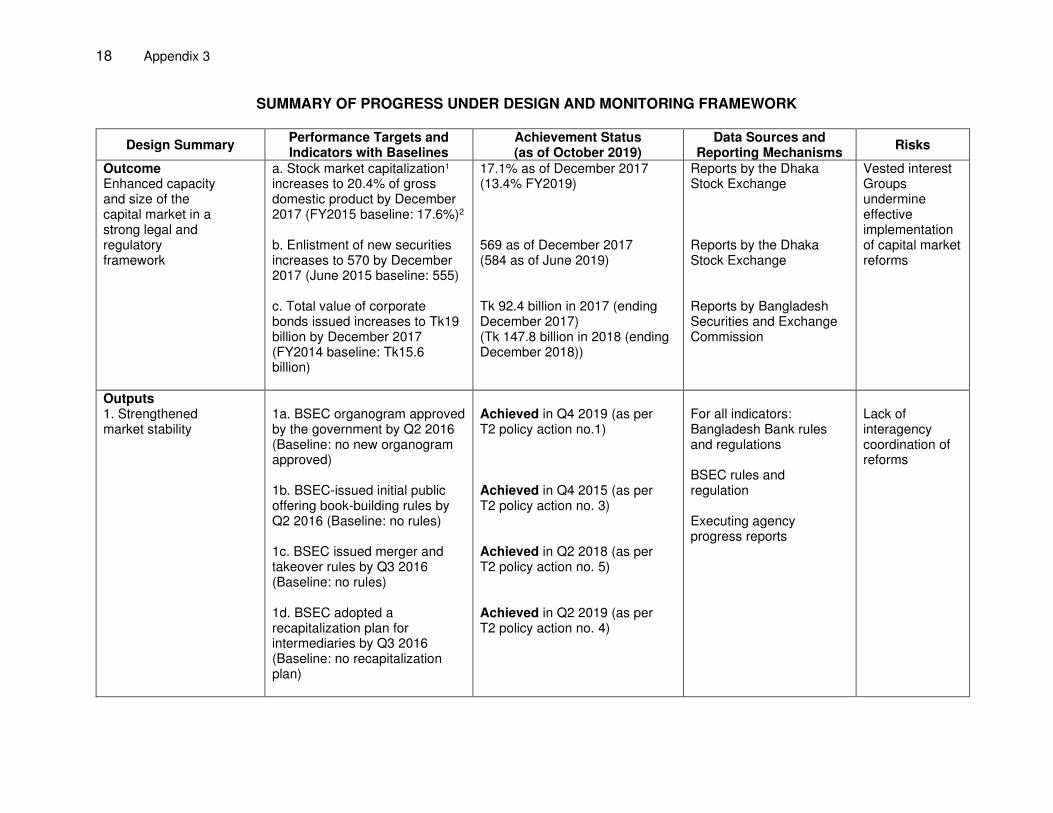

SUMMARY OF PROGRESS UNDER DESIGN AND MONITORING FRAMEWORK

Design Summary Performance Targets and Indicators with Baselines

Achievement Status (as of October 2019)

Data Sources and Reporting Mechanisms

Risks

Outcome Enhanced capacity and size of the capital market in a strong legal and regulatory framework

a. Stock market capitalization1 increases to 20.4% of gross domestic product by December 2017 (FY2015 baseline: 17.6%)2 b. Enlistment of new securities increases to 570 by December 2017 (June 2015 baseline: 555) c. Total value of corporate bonds issued increases to Tk19 billion by December 2017 (FY2014 baseline: Tk15.6 billion)

17.1% as of December 2017 (13.4% FY2019) 569 as of December 2017 (584 as of June 2019) Tk 92.4 billion in 2017 (ending December 2017) (Tk 147.8 billion in 2018 (ending December 2018))

Reports by the Dhaka Stock Exchange Reports by the Dhaka Stock Exchange Reports by Bangladesh Securities and Exchange Commission

Vested interest Groups undermine effective implementation of capital market reforms

Outputs 1. Strengthened market stability

1a. BSEC organogram approved by the government by Q2 2016 (Baseline: no new organogram approved) 1b. BSEC-issued initial public offering book-building rules by Q2 2016 (Baseline: no rules) 1c. BSEC issued merger and takeover rules by Q3 2016 (Baseline: no rules) 1d. BSEC adopted a recapitalization plan for intermediaries by Q3 2016 (Baseline: no recapitalization plan)

Achieved in Q4 2019 (as per T2 policy action no.1) Achieved in Q4 2015 (as per T2 policy action no. 3) Achieved in Q2 2018 (as per T2 policy action no. 5) Achieved in Q2 2019 (as per T2 policy action no. 4)

For all indicators: Bangladesh Bank rules and regulations BSEC rules and regulation Executing agency progress reports

Lack of interagency coordination of reforms

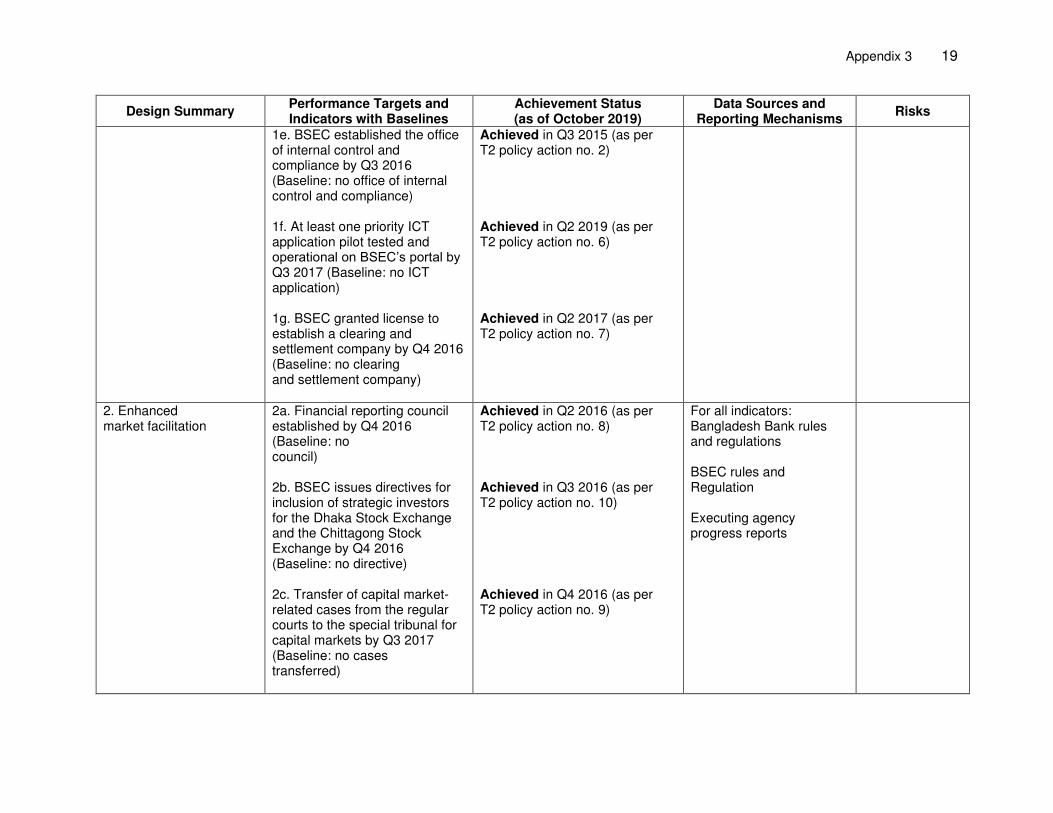

Appendix 3 19

Design Summary Performance Targets and Indicators with Baselines

Achievement Status (as of October 2019)

Data Sources and Reporting Mechanisms

Risks

1e. BSEC established the office of internal control and compliance by Q3 2016 (Baseline: no office of internal control and compliance) 1f. At least one priority ICT application pilot tested and operational on BSEC’s portal by Q3 2017 (Baseline: no ICT application) 1g. BSEC granted license to establish a clearing and settlement company by Q4 2016 (Baseline: no clearing and settlement company)

Achieved in Q3 2015 (as per T2 policy action no. 2) Achieved in Q2 2019 (as per T2 policy action no. 6) Achieved in Q2 2017 (as per T2 policy action no. 7)

2. Enhanced market facilitation

2a. Financial reporting council established by Q4 2016 (Baseline: no council) 2b. BSEC issues directives for inclusion of strategic investors for the Dhaka Stock Exchange and the Chittagong Stock Exchange by Q4 2016 (Baseline: no directive) 2c. Transfer of capital market-related cases from the regular courts to the special tribunal for capital markets by Q3 2017 (Baseline: no cases transferred)

Achieved in Q2 2016 (as per T2 policy action no. 8) Achieved in Q3 2016 (as per T2 policy action no. 10) Achieved in Q4 2016 (as per T2 policy action no. 9)

For all indicators: Bangladesh Bank rules and regulations BSEC rules and Regulation Executing agency progress reports

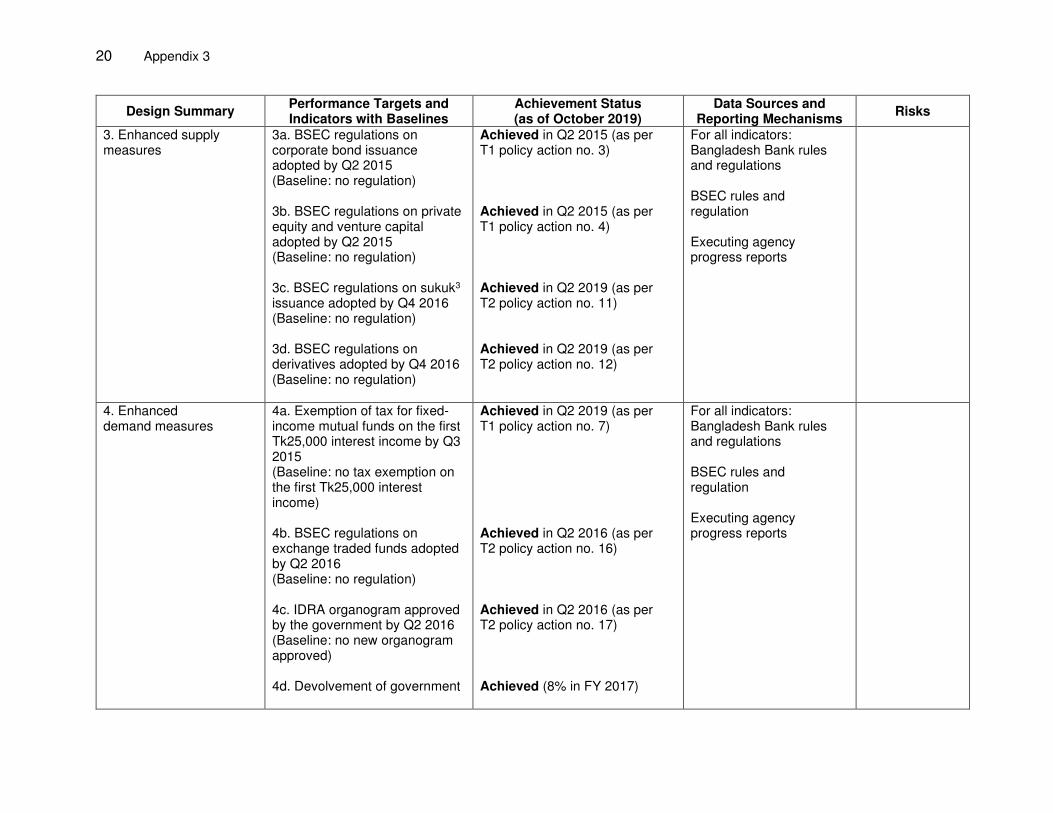

20 Appendix 3

Design Summary Performance Targets and Indicators with Baselines

Achievement Status (as of October 2019)

Data Sources and Reporting Mechanisms

Risks

3. Enhanced supply measures

3a. BSEC regulations on corporate bond issuance adopted by Q2 2015 (Baseline: no regulation) 3b. BSEC regulations on private equity and venture capital adopted by Q2 2015 (Baseline: no regulation) 3c. BSEC regulations on sukuk3 issuance adopted by Q4 2016 (Baseline: no regulation) 3d. BSEC regulations on derivatives adopted by Q4 2016 (Baseline: no regulation)

Achieved in Q2 2015 (as per T1 policy action no. 3) Achieved in Q2 2015 (as per T1 policy action no. 4) Achieved in Q2 2019 (as per T2 policy action no. 11) Achieved in Q2 2019 (as per T2 policy action no. 12)

For all indicators: Bangladesh Bank rules and regulations BSEC rules and regulation Executing agency progress reports

4. Enhanced demand measures

4a. Exemption of tax for fixed-income mutual funds on the first Tk25,000 interest income by Q3 2015 (Baseline: no tax exemption on the first Tk25,000 interest income) 4b. BSEC regulations on exchange traded funds adopted by Q2 2016 (Baseline: no regulation) 4c. IDRA organogram approved by the government by Q2 2016 (Baseline: no new organogram approved) 4d. Devolvement of government

Achieved in Q2 2019 (as per T1 policy action no. 7) Achieved in Q2 2016 (as per T2 policy action no. 16) Achieved in Q2 2016 (as per T2 policy action no. 17) Achieved (8% in FY 2017)

For all indicators: Bangladesh Bank rules and regulations BSEC rules and regulation Executing agency progress reports

Appendix 3 21

Design Summary Performance Targets and Indicators with Baselines

Achievement Status (as of October 2019)

Data Sources and Reporting Mechanisms

Risks

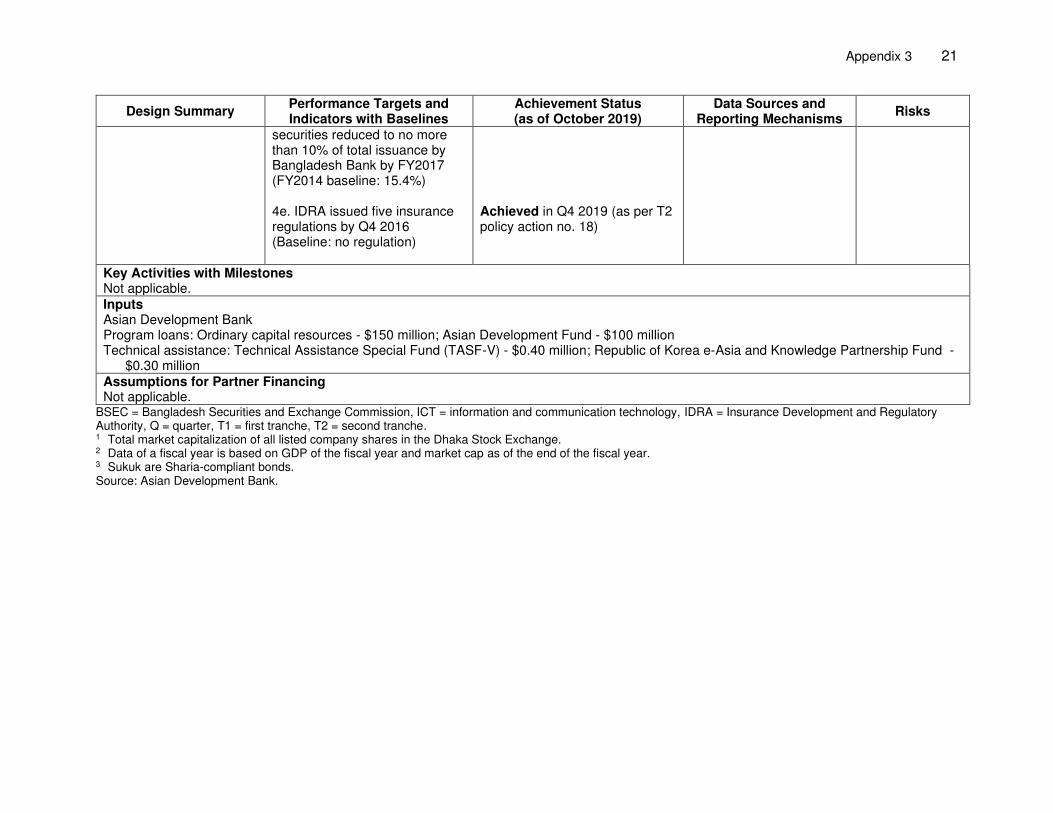

securities reduced to no more than 10% of total issuance by Bangladesh Bank by FY2017 (FY2014 baseline: 15.4%) 4e. IDRA issued five insurance regulations by Q4 2016 (Baseline: no regulation)

Achieved in Q4 2019 (as per T2 policy action no. 18)

Key Activities with Milestones Not applicable. Inputs Asian Development Bank Program loans: Ordinary capital resources - $150 million; Asian Development Fund - $100 million Technical assistance: Technical Assistance Special Fund (TASF-V) - $0.40 million; Republic of Korea e-Asia and Knowledge Partnership Fund -

$0.30 million Assumptions for Partner Financing Not applicable.

BSEC = Bangladesh Securities and Exchange Commission, ICT = information and communication technology, IDRA = Insurance Development and Regulatory Authority, Q = quarter, T1 = first tranche, T2 = second tranche. 1 Total market capitalization of all listed company shares in the Dhaka Stock Exchange. 2 Data of a fiscal year is based on GDP of the fiscal year and market cap as of the end of the fiscal year. 3 Sukuk are Sharia-compliant bonds. Source: Asian Development Bank.

22 Appendix 4

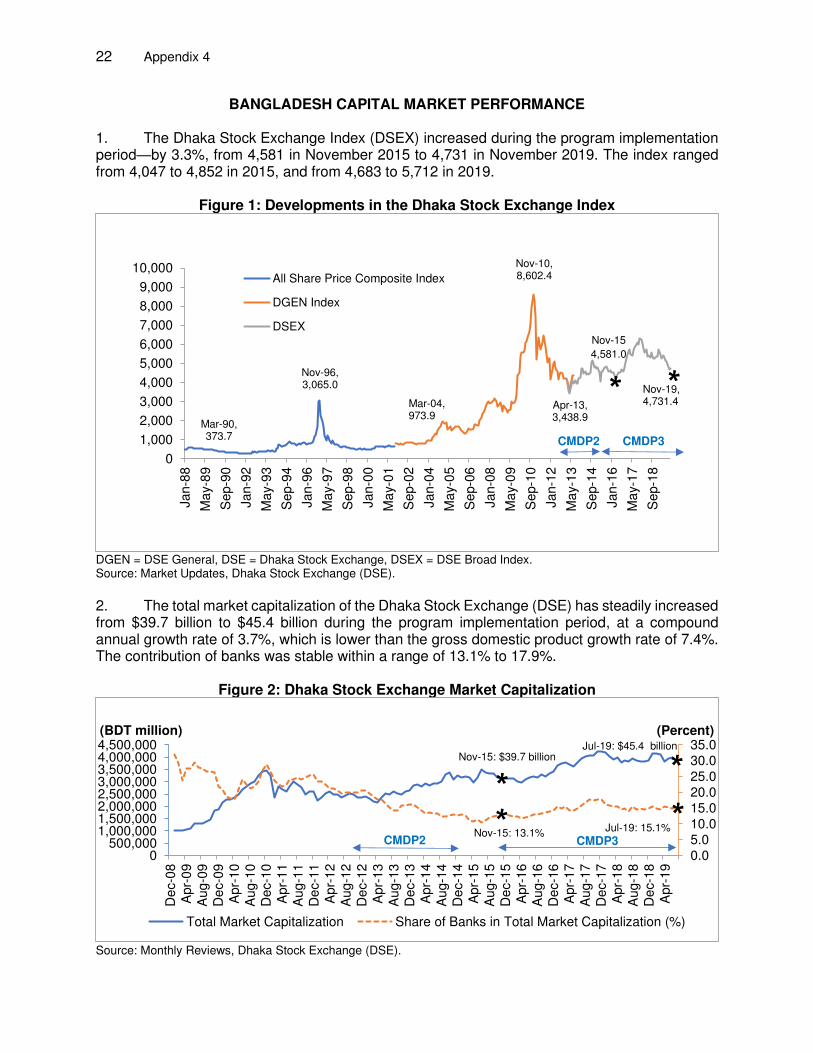

BANGLADESH CAPITAL MARKET PERFORMANCE

1. The Dhaka Stock Exchange Index (DSEX) increased during the program implementation period—by 3.3%, from 4,581 in November 2015 to 4,731 in November 2019. The index ranged from 4,047 to 4,852 in 2015, and from 4,683 to 5,712 in 2019.

Figure 1: Developments in the Dhaka Stock Exchange Index

DGEN = DSE General, DSE = Dhaka Stock Exchange, DSEX = DSE Broad Index. Source: Market Updates, Dhaka Stock Exchange (DSE).

2. The total market capitalization of the Dhaka Stock Exchange (DSE) has steadily increased from $39.7 billion to $45.4 billion during the program implementation period, at a compound annual growth rate of 3.7%, which is lower than the gross domestic product growth rate of 7.4%. The contribution of banks was stable within a range of 13.1% to 17.9%.

Figure 2: Dhaka Stock Exchange Market Capitalization

Source: Monthly Reviews, Dhaka Stock Exchange (DSE).

Mar-90, 373.7

Nov-96, 3,065.0

Apr-13, 3,438.9

Nov-10, 8,602.4

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Jan-8

8

Ma

y-8

9

Sep-9

0

Jan-9

2

Ma

y-9

3

Sep-9

4

Jan-9

6

Ma

y-9

7

Sep-9

8

Jan-0

0

Ma

y-0

1

Sep-0

2

Jan-0

4

Ma

y-0

5

Sep-0

6

Jan-0

8

Ma

y-0

9

Sep-1

0

Jan-1

2

Ma

y-1

3

Sep-1

4

Jan-1

6

Ma

y-1

7

Sep-1

8

All Share Price Composite Index

DGEN Index

DSEX

Nov-19, 4,731.4Mar-04,

973.9

Nov-15

4,581.0

0.05.010.015.020.025.030.035.0

0500,000

1,000,0001,500,0002,000,0002,500,0003,000,0003,500,0004,000,0004,500,000

De

c-0

8A

pr-

09

Aug-0

9D

ec-0

9A

pr-

10

Aug-1

0D

ec-

10

Apr-

11

Aug-1

1D

ec-1

1A

pr-

12

Aug-1

2D

ec-1

2A

pr-

13

Aug-1

3D

ec-

13

Apr-

14

Aug-1

4D

ec-1

4A

pr-

15

Aug-1

5D

ec-1

5A

pr-

16

Aug-1

6D

ec-1

6A

pr-

17

Aug-1

7D

ec-1

7A

pr-

18

Aug-1

8D

ec-1

8A

pr-

19

(Percent)(BDT million)

Total Market Capitalization Share of Banks in Total Market Capitalization (%)

CMDP2 CMDP3

CMDP2 CMDP3

Nov-15: $39.7 billion

Jul-19: $45.4 billion

Nov-15: 13.1% Jul-19: 15.1%

Appendix 4 23

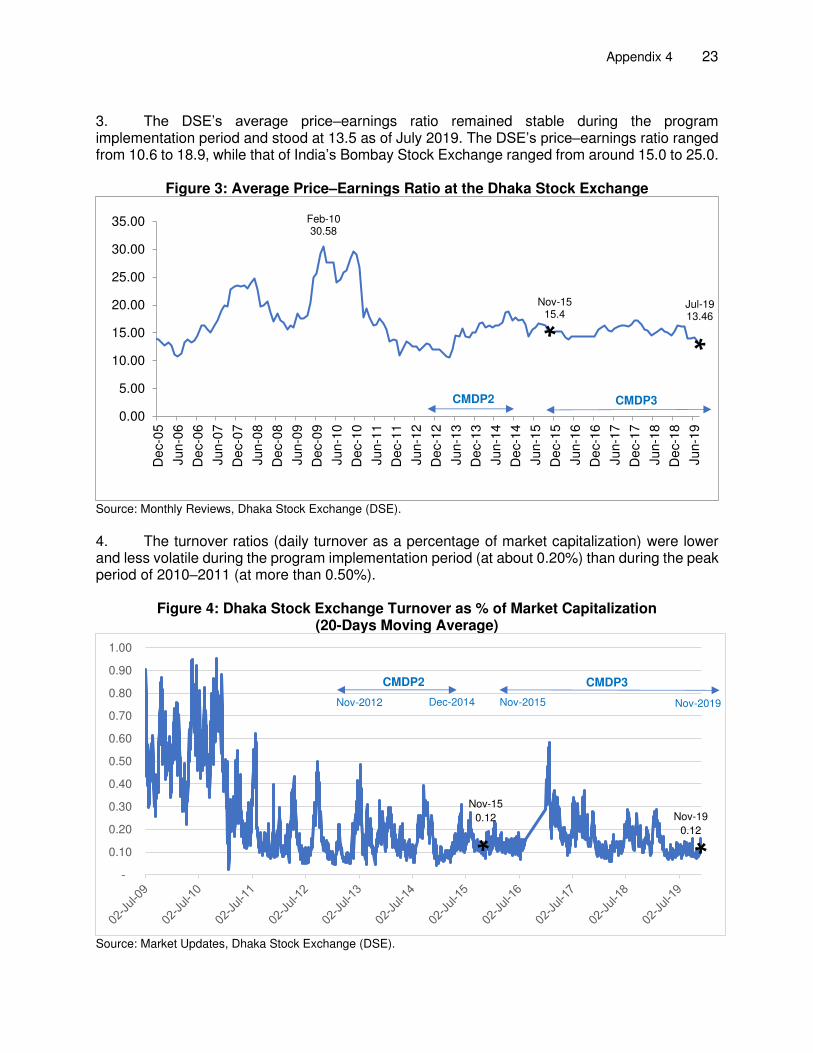

3. The DSE’s average price–earnings ratio remained stable during the program implementation period and stood at 13.5 as of July 2019. The DSE’s price–earnings ratio ranged from 10.6 to 18.9, while that of India’s Bombay Stock Exchange ranged from around 15.0 to 25.0.

Figure 3: Average Price–Earnings Ratio at the Dhaka Stock Exchange

Source: Monthly Reviews, Dhaka Stock Exchange (DSE).

4. The turnover ratios (daily turnover as a percentage of market capitalization) were lower and less volatile during the program implementation period (at about 0.20%) than during the peak period of 2010–2011 (at more than 0.50%).

Figure 4: Dhaka Stock Exchange Turnover as % of Market Capitalization (20-Days Moving Average)

Source: Market Updates, Dhaka Stock Exchange (DSE).

Feb-1030.58

Jul-1913.46

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

De

c-0

5

Jun-0

6

De

c-0

6

Jun-0

7

De

c-0

7

Jun-0

8

De

c-0

8

Jun-0

9

De

c-0

9

Jun-1

0

De

c-1

0

Jun-1

1

De

c-1

1

Jun-1

2

De

c-1

2

Jun-1

3

De

c-1

3

Jun-1

4

De

c-1

4

Jun-1

5

De

c-1

5

Jun-1

6

De

c-1

6

Jun-1

7

De

c-1

7

Jun-1

8

De

c-1

8

Jun-1

9

-

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

Nov-15

0.12 Nov-19

0.12

CMDP2 CMDP3

CMDP2 CMDP3

Dec-2014 Nov-2012 Nov-2019 Nov-2015

Nov-15 15.4

![[Second Edition,.]](https://static.fdokumen.com/doc/165x107/6322fad1887d24588e04752c/second-edition.jpg)