The World Bank FOR OFFICIAL USE ONLY - Afghanistan ...

112

Document of The World Bank FOR OFFICIAL USE ONLY PROJECT PAPER ON A PROPOSED ARTF GRANT IN THE AMOUNT OF US$ 73 MILLION TO THE ISLAMIC REPUBLIC OF AFGHANISTAN FOR A SECOND PUBLIC FINANCIAL MANAGEMENT REFORM PROJECT (PFMR II) May 25, 2011 This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of The World Bank FOR OFFICIAL USE ONLY - Afghanistan ...

Document ofThe World Bank

FOR OFFICIAL USE ONLY

PROJECT PAPER

ON A

PROPOSED ARTF GRANT

IN THE AMOUNT OF US$ 73 MILLION

TO THE

ISLAMIC REPUBLIC OF AFGHANISTAN

FOR A

SECOND PUBLIC FINANCIAL MANAGEMENT REFORM PROJECT (PFMR II)

May 25, 2011

This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

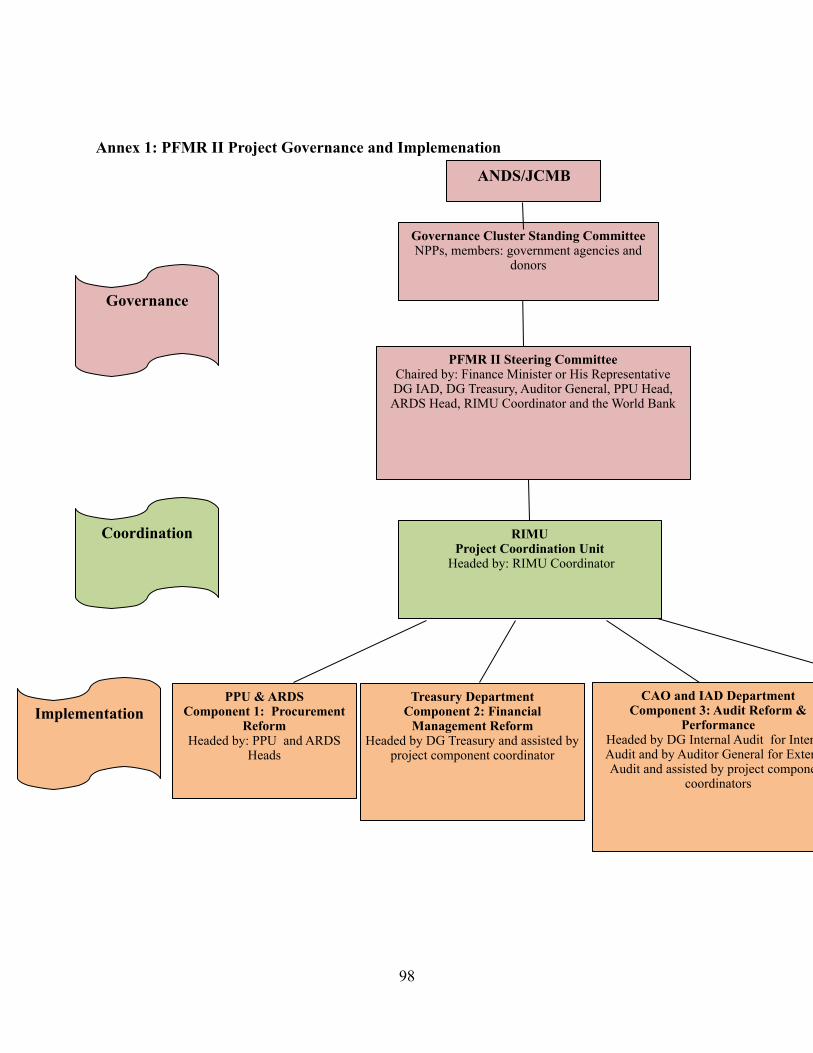

CURRENCY EQUIVALENTS(Exchange Rate Effective XXX, 2011)

Currency Unit= Afghani (AFN)AFN XX= US$1

FISCAL YEARMarch 21 – March 20

ABBREVIATIONS AND ACRONYMS

ACCA

ACSIADBAFMIS

ANDS

Association of Certified Chartered Accountants Afghanistan Civil Service InstituteAsian Development BankAfghanistan Financial Management Information SystemAfghanistan National Development Strategy

APAPARDS

Afghanistan Parliament Assistance ProgramAfghanistan Reconstruction and Development Services

ARTF Afghanistan Reconstruction Trust FundATPCAS

Audit Training ProgramCountry Assistance Strategy

CATCIPS

CMUDADAB

Certified Accounting TechnicianChartered Institute of Procurement and SupplyContract Management UnitDesignated AccountDa Afghanistan Bank

DFIDDPG

Department for International DevelopmentDevelopment Policy Grant

EA Environmental AssessmentFM Financial ManagementFMCGDP

Financial Management ConsultantGross Domestic Product

GOA Government of Afghanistan HRHRCDP

HRMD

IADIARCSC

Human ResourcesHuman Resource Capacity DevelopmentProgramHuman Resource Management DepartmentInternal Audit DepartmentIndependent Afghanistan Reform andCivil Service Commission

IDA International Development Association of the WBG

IFACIMF

International Federation of AccountantsInternational Monetary Fund

IPSAS

IT

International Public Sector AccountingStandardsInformation Technology

ISN Interim Strategy NoteLANM&E

Local Area NetworkMonitoring and Evaluation

MAIL Ministry of Agriculture Irrigation and Livestock

MCMEW

Management CommitteeMinistry of Energy and Water

MIS Management Information SystemMOFMOE

Ministry of Finance Ministry of Economy

MRRD Ministry of Rural Rehabilitation and Development

NSCO&M

National Steering CommitteeOperation and Maintenance

ORAFPACB

Operational Risk Assessment FrameworkPublic Admin Capacity Building Project

PCBOPCUPDOs

Procurement Capacity Building OfficerProject Coordiation UnitProject Development Objectives

PEFA

PFCPFMPFMRPFMRII

Public Expenditure and Financial Accountability Procurement Facilitation ConsultantPublic Financial ManagementPublic Financial Management Reform ProjectSecond Public Financial Management Reform Project

PPU Public Procurement UnitPSC Project Steering CommitteeRIMUROSC

Reform Implementation and Management UnitReport on Observation of Standards and Codes

SBDSSDUSPCSIGAR

Standard Bidding DocumentsSpecial Disbursements UnitSpecial Procurement UnitSpecial Inspector General Afghanistan Reconstruction

TA Technical AssistanceTOR Terms of ReferenceUSAID

VPP

United States Agency for International DevlopmentVerified Payroll Program

WBG World Bank Group

Vice President: Isabel M. GuerreroCountry Director: Nicholas J. Krafft

Sector Manager: Jennifer K. ThomsonTask Team Leader: Paul Sisk

AFGHANISTANSecond Public Financial Management Reform Project

CONTENTSPage

..................................................................................................................................Introduction 4

Emergency Challenge: Country Context, Government’s PFM Performance & Road Map and ....................................................................................................Rationale for Proposed Project 5

...................................................................................................................................The Project 8

..................................................................................................Appraisal of Project Activities 10

..................................................................Implementation Arrangements and Financing Plan 13

.................................................................................................Risks and Mitigating Measures 18

...........................................................Annex 1: Detailed Description of Project Components 20

.........................................................................Annex 2: Results Framework and Monitoring 36

.......................................................................Annex 3: Summary of Estimated Project Costs 37

................................................................................Project Cost Summary - Component wise 37

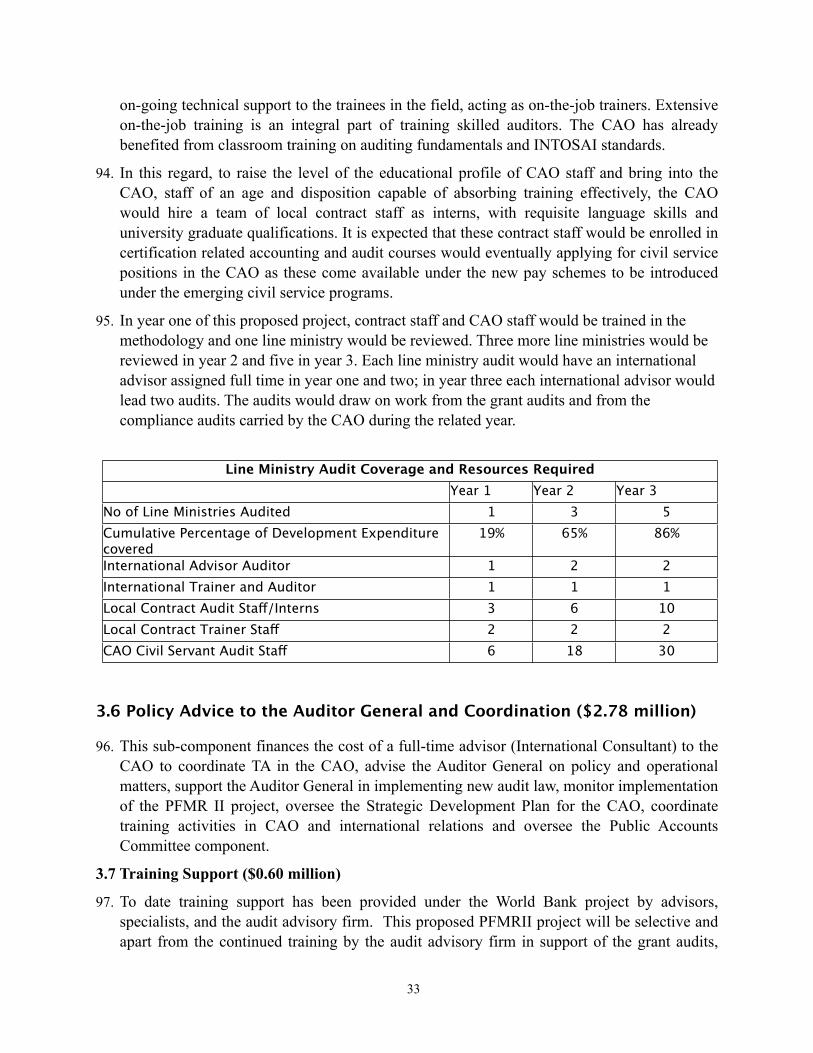

.....................................Annex 5: Financial Management and Disbursement Arrangements 53

.......................................................................................Annex 6: Procurement Arrangements 64

......................................................Annex 7: Implementation and Monitoring Arrangements 94

........................................................................Annex 8: Governance and Accountability Plan 99

.............................................Annex 9: Project Preparation and Appraisal Team Members 105

....................................................................................Annex 12: Documents in Project Files 107

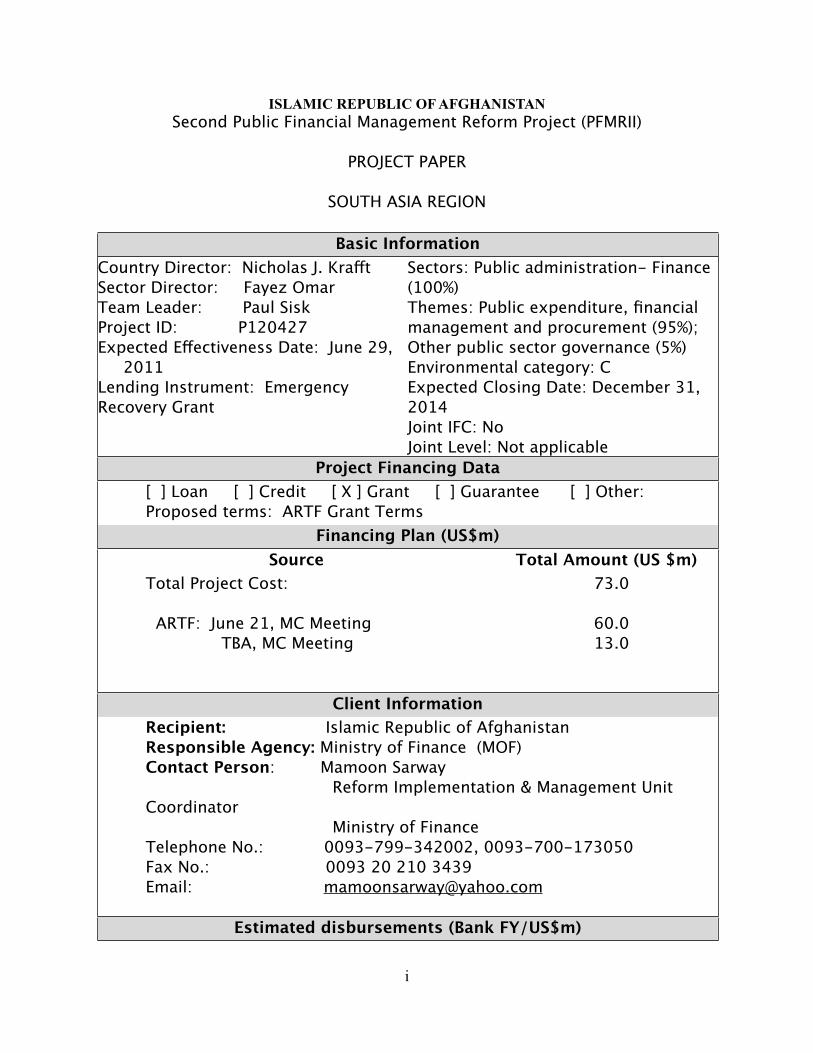

ISLAMIC REPUBLIC OF AFGHANISTANSecond Public Financial Management Reform Project (PFMRII)

PROJECT PAPER

SOUTH ASIA REGION

Basic InformationBasic InformationBasic InformationBasic InformationBasic InformationBasic InformationBasic InformationBasic InformationBasic InformationBasic InformationCountry Director: Nicholas J. KrafftSector Director: Fayez OmarTeam Leader: Paul Sisk Project ID: P120427Expected Effectiveness Date: June 29,

2011Lending Instrument: Emergency Recovery Grant

Country Director: Nicholas J. KrafftSector Director: Fayez OmarTeam Leader: Paul Sisk Project ID: P120427Expected Effectiveness Date: June 29,

2011Lending Instrument: Emergency Recovery Grant

Country Director: Nicholas J. KrafftSector Director: Fayez OmarTeam Leader: Paul Sisk Project ID: P120427Expected Effectiveness Date: June 29,

2011Lending Instrument: Emergency Recovery Grant

Sectors: Public administration- Finance (100%)Themes: Public expenditure, financial management and procurement (95%); Other public sector governance (5%)Environmental category: CExpected Closing Date: December 31, 2014Joint IFC: NoJoint Level: Not applicable

Sectors: Public administration- Finance (100%)Themes: Public expenditure, financial management and procurement (95%); Other public sector governance (5%)Environmental category: CExpected Closing Date: December 31, 2014Joint IFC: NoJoint Level: Not applicable

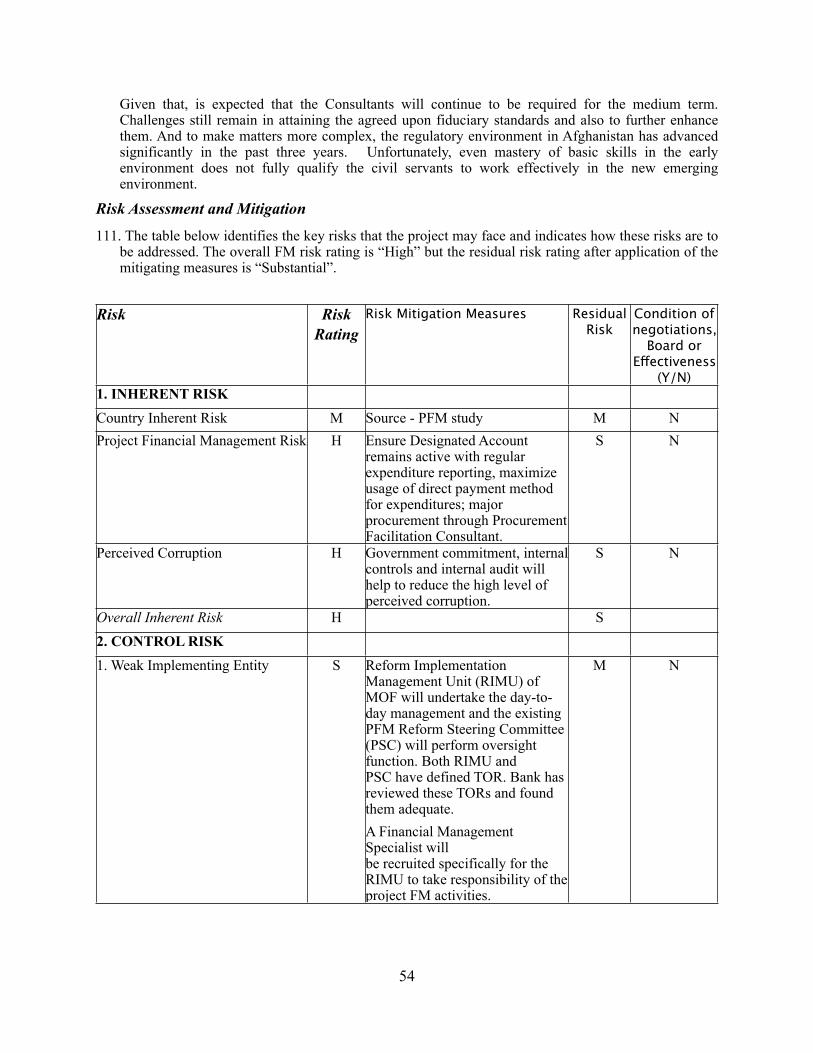

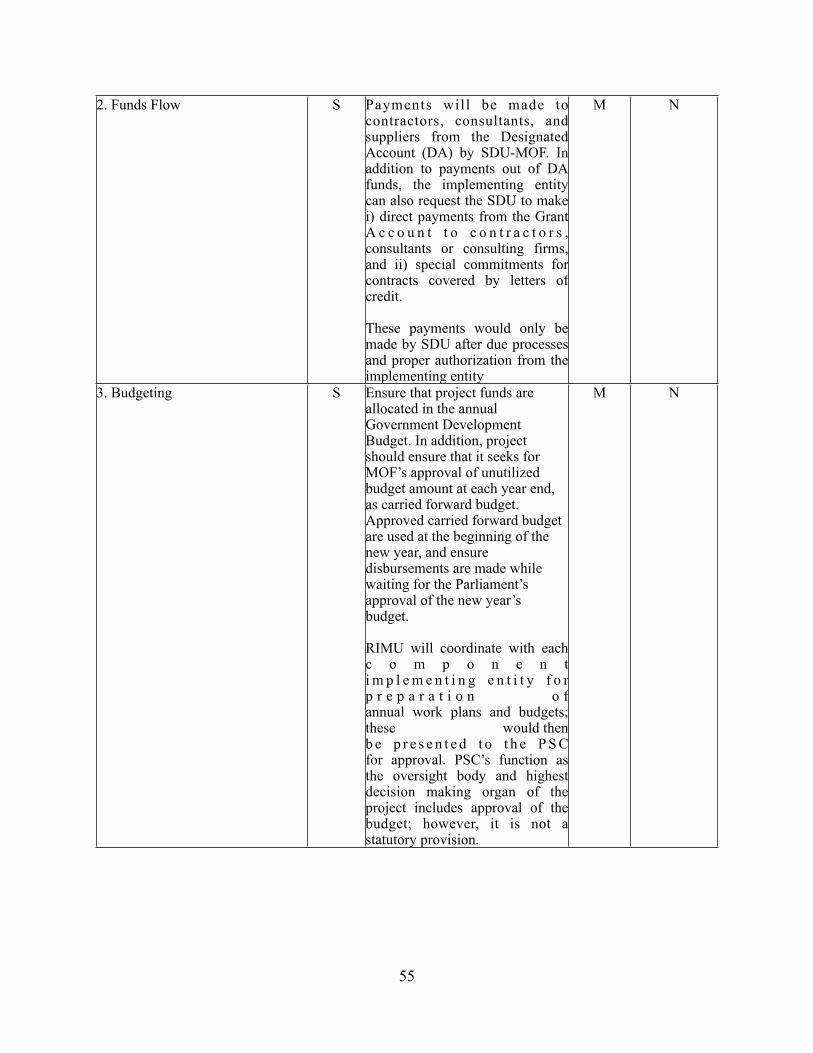

Sectors: Public administration- Finance (100%)Themes: Public expenditure, financial management and procurement (95%); Other public sector governance (5%)Environmental category: CExpected Closing Date: December 31, 2014Joint IFC: NoJoint Level: Not applicable

Sectors: Public administration- Finance (100%)Themes: Public expenditure, financial management and procurement (95%); Other public sector governance (5%)Environmental category: CExpected Closing Date: December 31, 2014Joint IFC: NoJoint Level: Not applicable

Sectors: Public administration- Finance (100%)Themes: Public expenditure, financial management and procurement (95%); Other public sector governance (5%)Environmental category: CExpected Closing Date: December 31, 2014Joint IFC: NoJoint Level: Not applicable

Sectors: Public administration- Finance (100%)Themes: Public expenditure, financial management and procurement (95%); Other public sector governance (5%)Environmental category: CExpected Closing Date: December 31, 2014Joint IFC: NoJoint Level: Not applicable

Sectors: Public administration- Finance (100%)Themes: Public expenditure, financial management and procurement (95%); Other public sector governance (5%)Environmental category: CExpected Closing Date: December 31, 2014Joint IFC: NoJoint Level: Not applicable

Project Financing DataProject Financing DataProject Financing DataProject Financing DataProject Financing DataProject Financing DataProject Financing DataProject Financing DataProject Financing DataProject Financing Data[ ] Loan [ ] Credit [ X ] Grant [ ] Guarantee [ ] Other:[ ] Loan [ ] Credit [ X ] Grant [ ] Guarantee [ ] Other:[ ] Loan [ ] Credit [ X ] Grant [ ] Guarantee [ ] Other:[ ] Loan [ ] Credit [ X ] Grant [ ] Guarantee [ ] Other:[ ] Loan [ ] Credit [ X ] Grant [ ] Guarantee [ ] Other:[ ] Loan [ ] Credit [ X ] Grant [ ] Guarantee [ ] Other:[ ] Loan [ ] Credit [ X ] Grant [ ] Guarantee [ ] Other:[ ] Loan [ ] Credit [ X ] Grant [ ] Guarantee [ ] Other:[ ] Loan [ ] Credit [ X ] Grant [ ] Guarantee [ ] Other:[ ] Loan [ ] Credit [ X ] Grant [ ] Guarantee [ ] Other:Proposed terms: ARTF Grant TermsProposed terms: ARTF Grant TermsProposed terms: ARTF Grant TermsProposed terms: ARTF Grant TermsProposed terms: ARTF Grant TermsProposed terms: ARTF Grant TermsProposed terms: ARTF Grant TermsProposed terms: ARTF Grant TermsProposed terms: ARTF Grant TermsProposed terms: ARTF Grant Terms

Financing Plan (US$m)Financing Plan (US$m)Financing Plan (US$m)Financing Plan (US$m)Financing Plan (US$m)Financing Plan (US$m)Financing Plan (US$m)Financing Plan (US$m)Financing Plan (US$m)Financing Plan (US$m)SourceSourceSourceSourceSource Total Amount (US $m)Total Amount (US $m)Total Amount (US $m)Total Amount (US $m)Total Amount (US $m)

Total Project Cost:

ARTF: June 21, MC Meeting TBA, MC Meeting

Total Project Cost:

ARTF: June 21, MC Meeting TBA, MC Meeting

Total Project Cost:

ARTF: June 21, MC Meeting TBA, MC Meeting

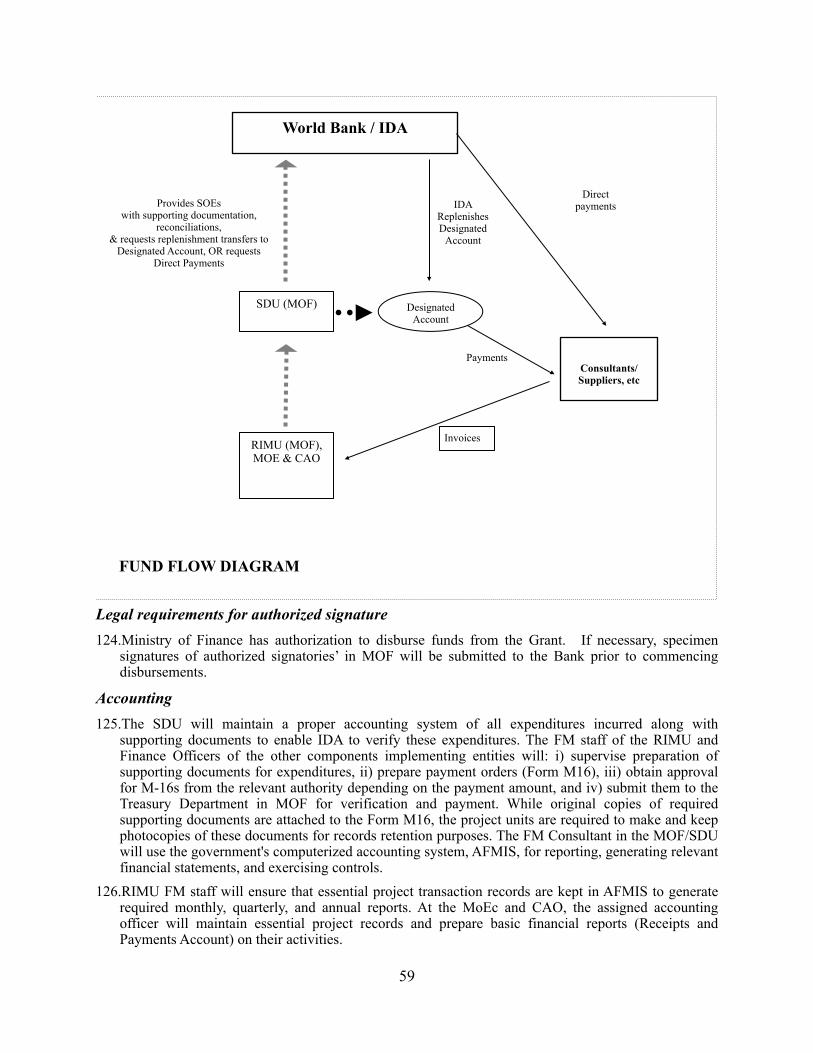

Total Project Cost:

ARTF: June 21, MC Meeting TBA, MC Meeting

Total Project Cost:

ARTF: June 21, MC Meeting TBA, MC Meeting

73.0

60.0 13.0

73.0

60.0 13.0

73.0

60.0 13.0

73.0

60.0 13.0

73.0

60.0 13.0

Client InformationClient InformationClient InformationClient InformationClient InformationClient InformationClient InformationClient InformationClient InformationClient InformationRecipient: Islamic Republic of AfghanistanResponsible Agency: Ministry of Finance (MOF)Contact Person: Mamoon Sarway Reform Implementation & Management Unit Coordinator Ministry of FinanceTelephone No.: 0093-799-342002, 0093-700-173050Fax No.: 0093 20 210 3439Email: [email protected]

Recipient: Islamic Republic of AfghanistanResponsible Agency: Ministry of Finance (MOF)Contact Person: Mamoon Sarway Reform Implementation & Management Unit Coordinator Ministry of FinanceTelephone No.: 0093-799-342002, 0093-700-173050Fax No.: 0093 20 210 3439Email: [email protected]

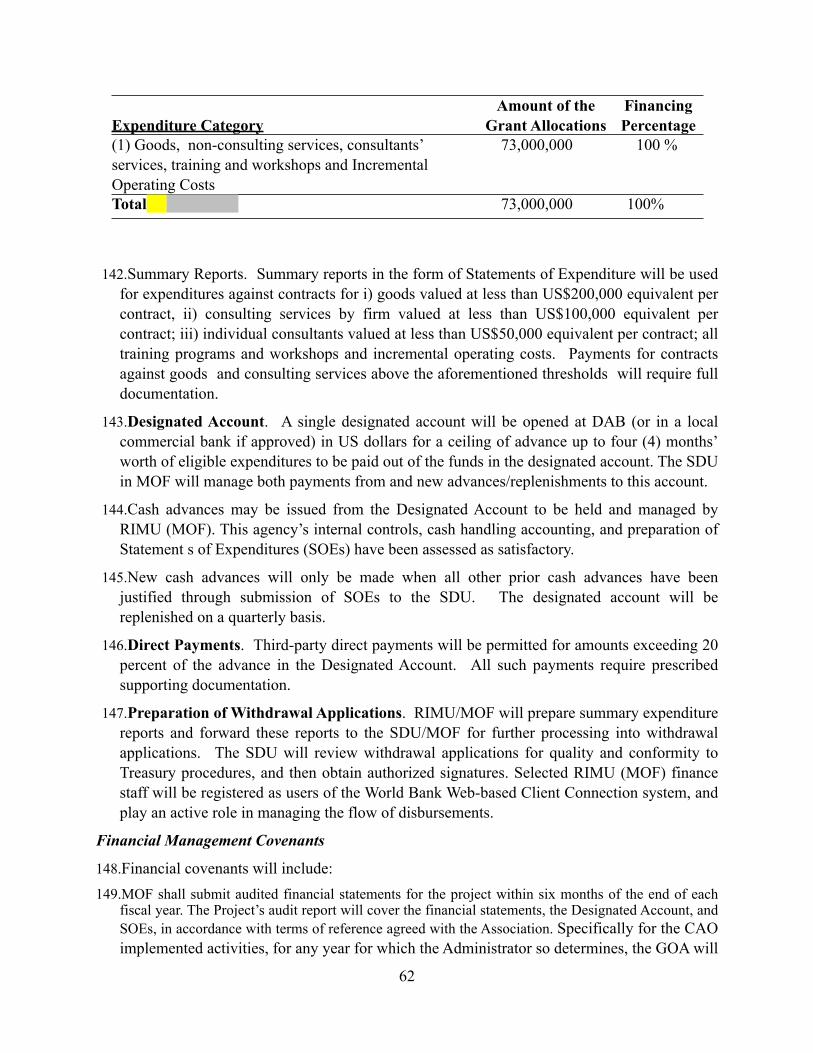

Recipient: Islamic Republic of AfghanistanResponsible Agency: Ministry of Finance (MOF)Contact Person: Mamoon Sarway Reform Implementation & Management Unit Coordinator Ministry of FinanceTelephone No.: 0093-799-342002, 0093-700-173050Fax No.: 0093 20 210 3439Email: [email protected]

Recipient: Islamic Republic of AfghanistanResponsible Agency: Ministry of Finance (MOF)Contact Person: Mamoon Sarway Reform Implementation & Management Unit Coordinator Ministry of FinanceTelephone No.: 0093-799-342002, 0093-700-173050Fax No.: 0093 20 210 3439Email: [email protected]

Recipient: Islamic Republic of AfghanistanResponsible Agency: Ministry of Finance (MOF)Contact Person: Mamoon Sarway Reform Implementation & Management Unit Coordinator Ministry of FinanceTelephone No.: 0093-799-342002, 0093-700-173050Fax No.: 0093 20 210 3439Email: [email protected]

Recipient: Islamic Republic of AfghanistanResponsible Agency: Ministry of Finance (MOF)Contact Person: Mamoon Sarway Reform Implementation & Management Unit Coordinator Ministry of FinanceTelephone No.: 0093-799-342002, 0093-700-173050Fax No.: 0093 20 210 3439Email: [email protected]

Recipient: Islamic Republic of AfghanistanResponsible Agency: Ministry of Finance (MOF)Contact Person: Mamoon Sarway Reform Implementation & Management Unit Coordinator Ministry of FinanceTelephone No.: 0093-799-342002, 0093-700-173050Fax No.: 0093 20 210 3439Email: [email protected]

Recipient: Islamic Republic of AfghanistanResponsible Agency: Ministry of Finance (MOF)Contact Person: Mamoon Sarway Reform Implementation & Management Unit Coordinator Ministry of FinanceTelephone No.: 0093-799-342002, 0093-700-173050Fax No.: 0093 20 210 3439Email: [email protected]

Recipient: Islamic Republic of AfghanistanResponsible Agency: Ministry of Finance (MOF)Contact Person: Mamoon Sarway Reform Implementation & Management Unit Coordinator Ministry of FinanceTelephone No.: 0093-799-342002, 0093-700-173050Fax No.: 0093 20 210 3439Email: [email protected]

Recipient: Islamic Republic of AfghanistanResponsible Agency: Ministry of Finance (MOF)Contact Person: Mamoon Sarway Reform Implementation & Management Unit Coordinator Ministry of FinanceTelephone No.: 0093-799-342002, 0093-700-173050Fax No.: 0093 20 210 3439Email: [email protected]

Estimated disbursements (Bank FY/US$m)Estimated disbursements (Bank FY/US$m)Estimated disbursements (Bank FY/US$m)Estimated disbursements (Bank FY/US$m)Estimated disbursements (Bank FY/US$m)Estimated disbursements (Bank FY/US$m)Estimated disbursements (Bank FY/US$m)Estimated disbursements (Bank FY/US$m)Estimated disbursements (Bank FY/US$m)Estimated disbursements (Bank FY/US$m)

i

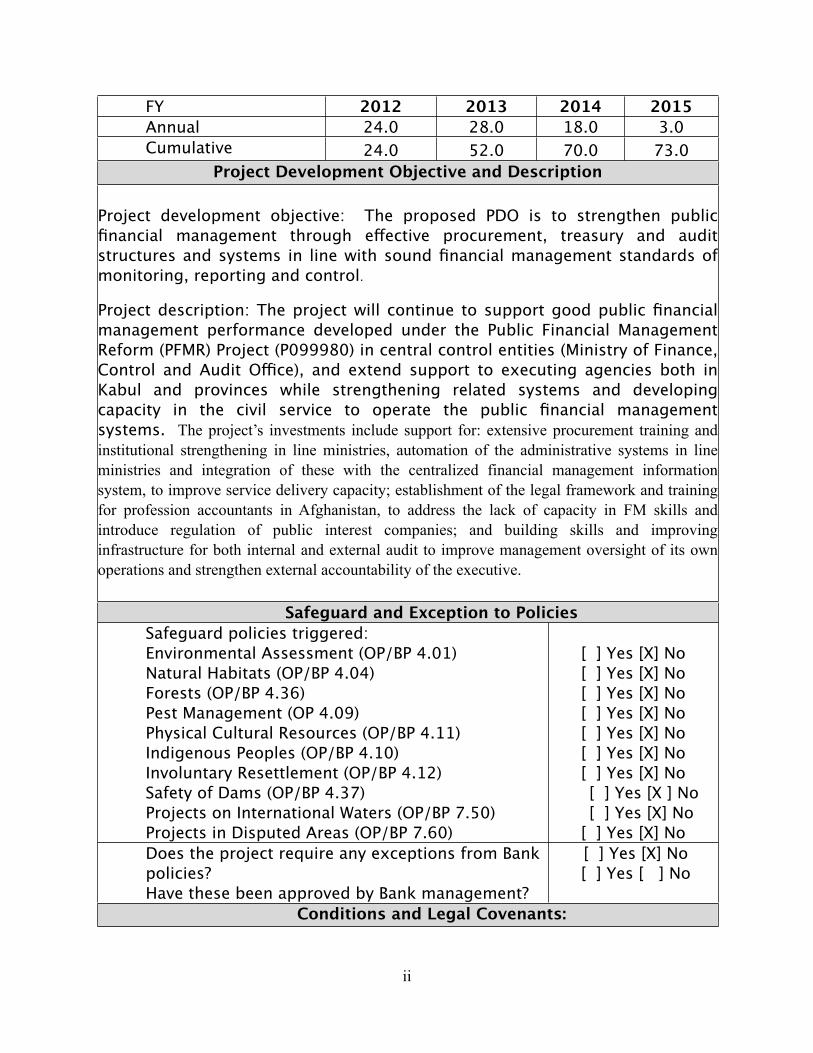

FYFY 20122012 20132013 201420142014 2015AnnualAnnual 24.024.0 28.028.0 18.018.018.0 3.0CumulativeCumulative 24.024.0 52.052.0 70.070.070.0 73.0

Project Development Objective and DescriptionProject Development Objective and DescriptionProject Development Objective and DescriptionProject Development Objective and DescriptionProject Development Objective and DescriptionProject Development Objective and DescriptionProject Development Objective and DescriptionProject Development Objective and DescriptionProject Development Objective and DescriptionProject Development Objective and Description

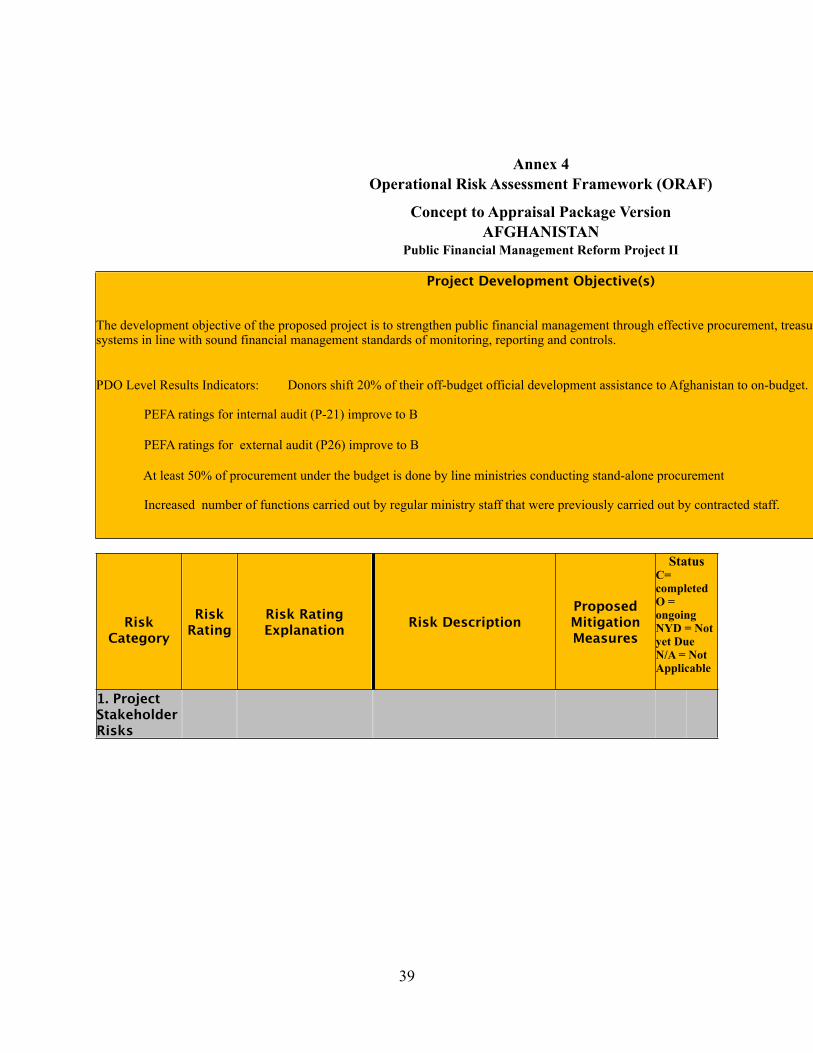

Project development objective: The proposed PDO is to strengthen public financial management through effective procurement, treasury and audit structures and systems in line with sound financial management standards of monitoring, reporting and control.

Project description: The project will continue to support good public financial management performance developed under the Public Financial Management Reform (PFMR) Project (P099980) in central control entities (Ministry of Finance, Control and Audit Office), and extend support to executing agencies both in Kabul and provinces while strengthening related systems and developing capacity in the civil service to operate the public financial management systems. The project’s investments include support for: extensive procurement training and institutional strengthening in line ministries, automation of the administrative systems in line ministries and integration of these with the centralized financial management information system, to improve service delivery capacity; establishment of the legal framework and training for profession accountants in Afghanistan, to address the lack of capacity in FM skills and introduce regulation of public interest companies; and building skills and improving infrastructure for both internal and external audit to improve management oversight of its own operations and strengthen external accountability of the executive.

Project development objective: The proposed PDO is to strengthen public financial management through effective procurement, treasury and audit structures and systems in line with sound financial management standards of monitoring, reporting and control.

Project description: The project will continue to support good public financial management performance developed under the Public Financial Management Reform (PFMR) Project (P099980) in central control entities (Ministry of Finance, Control and Audit Office), and extend support to executing agencies both in Kabul and provinces while strengthening related systems and developing capacity in the civil service to operate the public financial management systems. The project’s investments include support for: extensive procurement training and institutional strengthening in line ministries, automation of the administrative systems in line ministries and integration of these with the centralized financial management information system, to improve service delivery capacity; establishment of the legal framework and training for profession accountants in Afghanistan, to address the lack of capacity in FM skills and introduce regulation of public interest companies; and building skills and improving infrastructure for both internal and external audit to improve management oversight of its own operations and strengthen external accountability of the executive.

Project development objective: The proposed PDO is to strengthen public financial management through effective procurement, treasury and audit structures and systems in line with sound financial management standards of monitoring, reporting and control.

Project description: The project will continue to support good public financial management performance developed under the Public Financial Management Reform (PFMR) Project (P099980) in central control entities (Ministry of Finance, Control and Audit Office), and extend support to executing agencies both in Kabul and provinces while strengthening related systems and developing capacity in the civil service to operate the public financial management systems. The project’s investments include support for: extensive procurement training and institutional strengthening in line ministries, automation of the administrative systems in line ministries and integration of these with the centralized financial management information system, to improve service delivery capacity; establishment of the legal framework and training for profession accountants in Afghanistan, to address the lack of capacity in FM skills and introduce regulation of public interest companies; and building skills and improving infrastructure for both internal and external audit to improve management oversight of its own operations and strengthen external accountability of the executive.

Project development objective: The proposed PDO is to strengthen public financial management through effective procurement, treasury and audit structures and systems in line with sound financial management standards of monitoring, reporting and control.

Project description: The project will continue to support good public financial management performance developed under the Public Financial Management Reform (PFMR) Project (P099980) in central control entities (Ministry of Finance, Control and Audit Office), and extend support to executing agencies both in Kabul and provinces while strengthening related systems and developing capacity in the civil service to operate the public financial management systems. The project’s investments include support for: extensive procurement training and institutional strengthening in line ministries, automation of the administrative systems in line ministries and integration of these with the centralized financial management information system, to improve service delivery capacity; establishment of the legal framework and training for profession accountants in Afghanistan, to address the lack of capacity in FM skills and introduce regulation of public interest companies; and building skills and improving infrastructure for both internal and external audit to improve management oversight of its own operations and strengthen external accountability of the executive.

Project development objective: The proposed PDO is to strengthen public financial management through effective procurement, treasury and audit structures and systems in line with sound financial management standards of monitoring, reporting and control.

Project description: The project will continue to support good public financial management performance developed under the Public Financial Management Reform (PFMR) Project (P099980) in central control entities (Ministry of Finance, Control and Audit Office), and extend support to executing agencies both in Kabul and provinces while strengthening related systems and developing capacity in the civil service to operate the public financial management systems. The project’s investments include support for: extensive procurement training and institutional strengthening in line ministries, automation of the administrative systems in line ministries and integration of these with the centralized financial management information system, to improve service delivery capacity; establishment of the legal framework and training for profession accountants in Afghanistan, to address the lack of capacity in FM skills and introduce regulation of public interest companies; and building skills and improving infrastructure for both internal and external audit to improve management oversight of its own operations and strengthen external accountability of the executive.

Project development objective: The proposed PDO is to strengthen public financial management through effective procurement, treasury and audit structures and systems in line with sound financial management standards of monitoring, reporting and control.

Project description: The project will continue to support good public financial management performance developed under the Public Financial Management Reform (PFMR) Project (P099980) in central control entities (Ministry of Finance, Control and Audit Office), and extend support to executing agencies both in Kabul and provinces while strengthening related systems and developing capacity in the civil service to operate the public financial management systems. The project’s investments include support for: extensive procurement training and institutional strengthening in line ministries, automation of the administrative systems in line ministries and integration of these with the centralized financial management information system, to improve service delivery capacity; establishment of the legal framework and training for profession accountants in Afghanistan, to address the lack of capacity in FM skills and introduce regulation of public interest companies; and building skills and improving infrastructure for both internal and external audit to improve management oversight of its own operations and strengthen external accountability of the executive.

Project development objective: The proposed PDO is to strengthen public financial management through effective procurement, treasury and audit structures and systems in line with sound financial management standards of monitoring, reporting and control.

Project description: The project will continue to support good public financial management performance developed under the Public Financial Management Reform (PFMR) Project (P099980) in central control entities (Ministry of Finance, Control and Audit Office), and extend support to executing agencies both in Kabul and provinces while strengthening related systems and developing capacity in the civil service to operate the public financial management systems. The project’s investments include support for: extensive procurement training and institutional strengthening in line ministries, automation of the administrative systems in line ministries and integration of these with the centralized financial management information system, to improve service delivery capacity; establishment of the legal framework and training for profession accountants in Afghanistan, to address the lack of capacity in FM skills and introduce regulation of public interest companies; and building skills and improving infrastructure for both internal and external audit to improve management oversight of its own operations and strengthen external accountability of the executive.

Project development objective: The proposed PDO is to strengthen public financial management through effective procurement, treasury and audit structures and systems in line with sound financial management standards of monitoring, reporting and control.

Project description: The project will continue to support good public financial management performance developed under the Public Financial Management Reform (PFMR) Project (P099980) in central control entities (Ministry of Finance, Control and Audit Office), and extend support to executing agencies both in Kabul and provinces while strengthening related systems and developing capacity in the civil service to operate the public financial management systems. The project’s investments include support for: extensive procurement training and institutional strengthening in line ministries, automation of the administrative systems in line ministries and integration of these with the centralized financial management information system, to improve service delivery capacity; establishment of the legal framework and training for profession accountants in Afghanistan, to address the lack of capacity in FM skills and introduce regulation of public interest companies; and building skills and improving infrastructure for both internal and external audit to improve management oversight of its own operations and strengthen external accountability of the executive.

Project development objective: The proposed PDO is to strengthen public financial management through effective procurement, treasury and audit structures and systems in line with sound financial management standards of monitoring, reporting and control.

Project description: The project will continue to support good public financial management performance developed under the Public Financial Management Reform (PFMR) Project (P099980) in central control entities (Ministry of Finance, Control and Audit Office), and extend support to executing agencies both in Kabul and provinces while strengthening related systems and developing capacity in the civil service to operate the public financial management systems. The project’s investments include support for: extensive procurement training and institutional strengthening in line ministries, automation of the administrative systems in line ministries and integration of these with the centralized financial management information system, to improve service delivery capacity; establishment of the legal framework and training for profession accountants in Afghanistan, to address the lack of capacity in FM skills and introduce regulation of public interest companies; and building skills and improving infrastructure for both internal and external audit to improve management oversight of its own operations and strengthen external accountability of the executive.

Project development objective: The proposed PDO is to strengthen public financial management through effective procurement, treasury and audit structures and systems in line with sound financial management standards of monitoring, reporting and control.

Project description: The project will continue to support good public financial management performance developed under the Public Financial Management Reform (PFMR) Project (P099980) in central control entities (Ministry of Finance, Control and Audit Office), and extend support to executing agencies both in Kabul and provinces while strengthening related systems and developing capacity in the civil service to operate the public financial management systems. The project’s investments include support for: extensive procurement training and institutional strengthening in line ministries, automation of the administrative systems in line ministries and integration of these with the centralized financial management information system, to improve service delivery capacity; establishment of the legal framework and training for profession accountants in Afghanistan, to address the lack of capacity in FM skills and introduce regulation of public interest companies; and building skills and improving infrastructure for both internal and external audit to improve management oversight of its own operations and strengthen external accountability of the executive.

Safeguard and Exception to PoliciesSafeguard and Exception to PoliciesSafeguard and Exception to PoliciesSafeguard and Exception to PoliciesSafeguard and Exception to PoliciesSafeguard and Exception to PoliciesSafeguard and Exception to PoliciesSafeguard and Exception to PoliciesSafeguard and Exception to PoliciesSafeguard and Exception to PoliciesSafeguard policies triggered:Environmental Assessment (OP/BP 4.01) Natural Habitats (OP/BP 4.04) Forests (OP/BP 4.36) Pest Management (OP 4.09) Physical Cultural Resources (OP/BP 4.11) Indigenous Peoples (OP/BP 4.10) Involuntary Resettlement (OP/BP 4.12)Safety of Dams (OP/BP 4.37)Projects on International Waters (OP/BP 7.50) Projects in Disputed Areas (OP/BP 7.60)

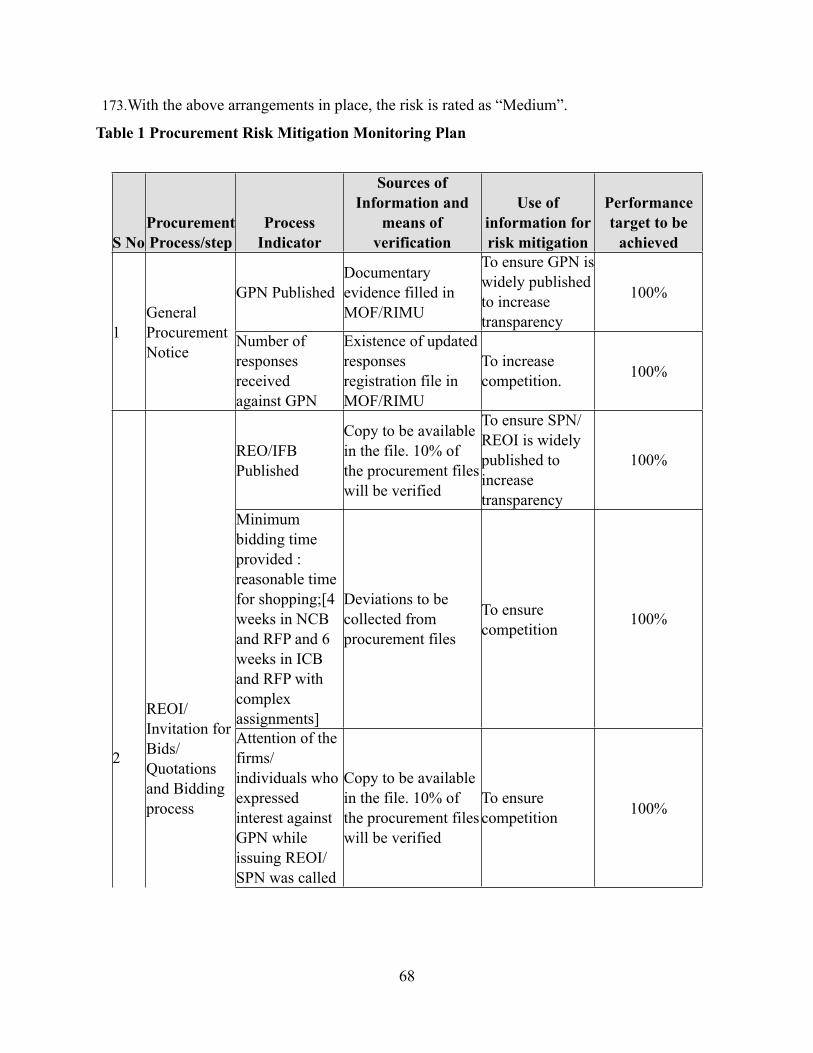

Safeguard policies triggered:Environmental Assessment (OP/BP 4.01) Natural Habitats (OP/BP 4.04) Forests (OP/BP 4.36) Pest Management (OP 4.09) Physical Cultural Resources (OP/BP 4.11) Indigenous Peoples (OP/BP 4.10) Involuntary Resettlement (OP/BP 4.12)Safety of Dams (OP/BP 4.37)Projects on International Waters (OP/BP 7.50) Projects in Disputed Areas (OP/BP 7.60)

Safeguard policies triggered:Environmental Assessment (OP/BP 4.01) Natural Habitats (OP/BP 4.04) Forests (OP/BP 4.36) Pest Management (OP 4.09) Physical Cultural Resources (OP/BP 4.11) Indigenous Peoples (OP/BP 4.10) Involuntary Resettlement (OP/BP 4.12)Safety of Dams (OP/BP 4.37)Projects on International Waters (OP/BP 7.50) Projects in Disputed Areas (OP/BP 7.60)

Safeguard policies triggered:Environmental Assessment (OP/BP 4.01) Natural Habitats (OP/BP 4.04) Forests (OP/BP 4.36) Pest Management (OP 4.09) Physical Cultural Resources (OP/BP 4.11) Indigenous Peoples (OP/BP 4.10) Involuntary Resettlement (OP/BP 4.12)Safety of Dams (OP/BP 4.37)Projects on International Waters (OP/BP 7.50) Projects in Disputed Areas (OP/BP 7.60)

Safeguard policies triggered:Environmental Assessment (OP/BP 4.01) Natural Habitats (OP/BP 4.04) Forests (OP/BP 4.36) Pest Management (OP 4.09) Physical Cultural Resources (OP/BP 4.11) Indigenous Peoples (OP/BP 4.10) Involuntary Resettlement (OP/BP 4.12)Safety of Dams (OP/BP 4.37)Projects on International Waters (OP/BP 7.50) Projects in Disputed Areas (OP/BP 7.60)

Safeguard policies triggered:Environmental Assessment (OP/BP 4.01) Natural Habitats (OP/BP 4.04) Forests (OP/BP 4.36) Pest Management (OP 4.09) Physical Cultural Resources (OP/BP 4.11) Indigenous Peoples (OP/BP 4.10) Involuntary Resettlement (OP/BP 4.12)Safety of Dams (OP/BP 4.37)Projects on International Waters (OP/BP 7.50) Projects in Disputed Areas (OP/BP 7.60)

Safeguard policies triggered:Environmental Assessment (OP/BP 4.01) Natural Habitats (OP/BP 4.04) Forests (OP/BP 4.36) Pest Management (OP 4.09) Physical Cultural Resources (OP/BP 4.11) Indigenous Peoples (OP/BP 4.10) Involuntary Resettlement (OP/BP 4.12)Safety of Dams (OP/BP 4.37)Projects on International Waters (OP/BP 7.50) Projects in Disputed Areas (OP/BP 7.60)

[ ] Yes [X] No[ ] Yes [X] No[ ] Yes [X] No[ ] Yes [X] No[ ] Yes [X] No[ ] Yes [X] No[ ] Yes [X] No

[ ] Yes [X ] No [ ] Yes [X] No

[ ] Yes [X] No

[ ] Yes [X] No[ ] Yes [X] No[ ] Yes [X] No[ ] Yes [X] No[ ] Yes [X] No[ ] Yes [X] No[ ] Yes [X] No

[ ] Yes [X ] No [ ] Yes [X] No

[ ] Yes [X] No

[ ] Yes [X] No[ ] Yes [X] No[ ] Yes [X] No[ ] Yes [X] No[ ] Yes [X] No[ ] Yes [X] No[ ] Yes [X] No

[ ] Yes [X ] No [ ] Yes [X] No

[ ] Yes [X] NoDoes the project require any exceptions from Bank policies?Have these been approved by Bank management?

Does the project require any exceptions from Bank policies?Have these been approved by Bank management?

Does the project require any exceptions from Bank policies?Have these been approved by Bank management?

Does the project require any exceptions from Bank policies?Have these been approved by Bank management?

Does the project require any exceptions from Bank policies?Have these been approved by Bank management?

Does the project require any exceptions from Bank policies?Have these been approved by Bank management?

Does the project require any exceptions from Bank policies?Have these been approved by Bank management?

[ ] Yes [X] No [ ] Yes [ ] No [ ] Yes [X] No [ ] Yes [ ] No [ ] Yes [X] No [ ] Yes [ ] No

Conditions and Legal Covenants:Conditions and Legal Covenants:Conditions and Legal Covenants:Conditions and Legal Covenants:Conditions and Legal Covenants:Conditions and Legal Covenants:Conditions and Legal Covenants:Conditions and Legal Covenants:Conditions and Legal Covenants:Conditions and Legal Covenants:

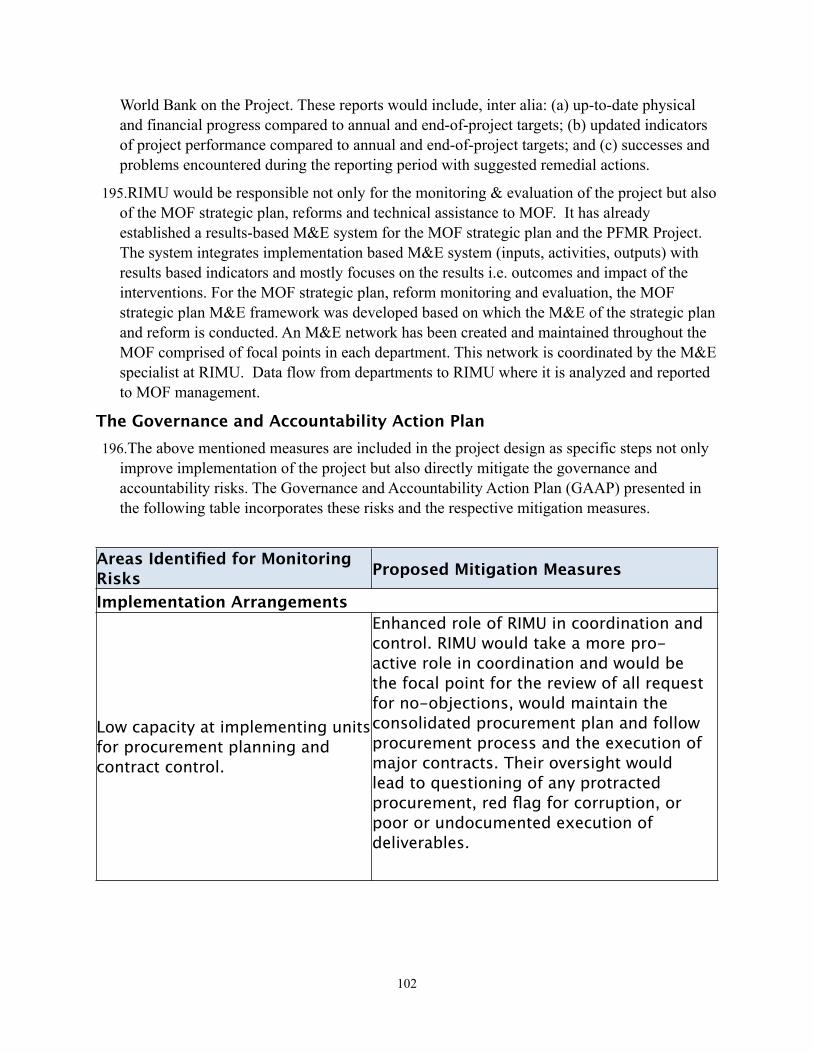

ii

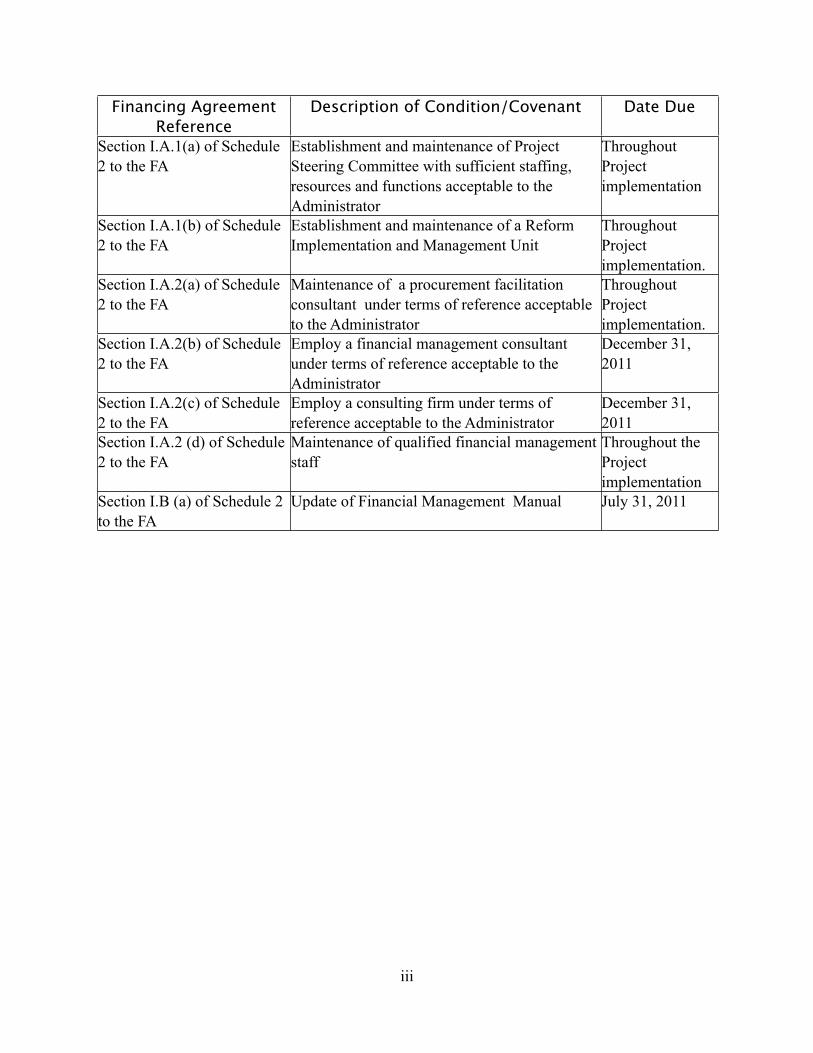

Financing Agreement Reference

Description of Condition/CovenantDescription of Condition/CovenantDescription of Condition/CovenantDescription of Condition/CovenantDescription of Condition/CovenantDescription of Condition/CovenantDescription of Condition/Covenant Date DueDate Due

Section I.A.1(a) of Schedule 2 to the FA

Establishment and maintenance of Project Steering Committee with sufficient staffing, resources and functions acceptable to the Administrator

Establishment and maintenance of Project Steering Committee with sufficient staffing, resources and functions acceptable to the Administrator

Establishment and maintenance of Project Steering Committee with sufficient staffing, resources and functions acceptable to the Administrator

Establishment and maintenance of Project Steering Committee with sufficient staffing, resources and functions acceptable to the Administrator

Establishment and maintenance of Project Steering Committee with sufficient staffing, resources and functions acceptable to the Administrator

Establishment and maintenance of Project Steering Committee with sufficient staffing, resources and functions acceptable to the Administrator

Establishment and maintenance of Project Steering Committee with sufficient staffing, resources and functions acceptable to the Administrator

Throughout Project implementation

Throughout Project implementation

Section I.A.1(b) of Schedule 2 to the FA

Establishment and maintenance of a Reform Implementation and Management UnitEstablishment and maintenance of a Reform Implementation and Management UnitEstablishment and maintenance of a Reform Implementation and Management UnitEstablishment and maintenance of a Reform Implementation and Management UnitEstablishment and maintenance of a Reform Implementation and Management UnitEstablishment and maintenance of a Reform Implementation and Management UnitEstablishment and maintenance of a Reform Implementation and Management Unit

Throughout Project implementation.

Throughout Project implementation.

Section I.A.2(a) of Schedule 2 to the FA

Maintenance of a procurement facilitation consultant under terms of reference acceptable to the Administrator

Maintenance of a procurement facilitation consultant under terms of reference acceptable to the Administrator

Maintenance of a procurement facilitation consultant under terms of reference acceptable to the Administrator

Maintenance of a procurement facilitation consultant under terms of reference acceptable to the Administrator

Maintenance of a procurement facilitation consultant under terms of reference acceptable to the Administrator

Maintenance of a procurement facilitation consultant under terms of reference acceptable to the Administrator

Maintenance of a procurement facilitation consultant under terms of reference acceptable to the Administrator

Throughout Project implementation.

Throughout Project implementation.

Section I.A.2(b) of Schedule 2 to the FA

Employ a financial management consultant under terms of reference acceptable to the Administrator

Employ a financial management consultant under terms of reference acceptable to the Administrator

Employ a financial management consultant under terms of reference acceptable to the Administrator

Employ a financial management consultant under terms of reference acceptable to the Administrator

Employ a financial management consultant under terms of reference acceptable to the Administrator

Employ a financial management consultant under terms of reference acceptable to the Administrator

Employ a financial management consultant under terms of reference acceptable to the Administrator

December 31, 2011December 31, 2011

Section I.A.2(c) of Schedule 2 to the FA

Employ a consulting firm under terms of reference acceptable to the AdministratorEmploy a consulting firm under terms of reference acceptable to the AdministratorEmploy a consulting firm under terms of reference acceptable to the AdministratorEmploy a consulting firm under terms of reference acceptable to the AdministratorEmploy a consulting firm under terms of reference acceptable to the AdministratorEmploy a consulting firm under terms of reference acceptable to the AdministratorEmploy a consulting firm under terms of reference acceptable to the Administrator

December 31, 2011December 31, 2011

Section I.A.2 (d) of Schedule 2 to the FA

Maintenance of qualified financial management staff Maintenance of qualified financial management staff Maintenance of qualified financial management staff Maintenance of qualified financial management staff Maintenance of qualified financial management staff Maintenance of qualified financial management staff Maintenance of qualified financial management staff

Throughout the Project implementation

Throughout the Project implementation

Section I.B (a) of Schedule 2 to the FA

Update of Financial Management Manual Update of Financial Management Manual Update of Financial Management Manual Update of Financial Management Manual Update of Financial Management Manual Update of Financial Management Manual Update of Financial Management Manual July 31, 2011July 31, 2011

iii

4

A. Introduction

1. This Project Paper seeks the approval of the Afghanistan Reconstruction Trust Fund (ARTF) Management Committee (MC) to provide a Grant in an amount of US$ 73.0 million to the Islamic Republic of Afghanistan for the proposed Second Public Financial Management Reform Project.

2. The proposed Project builds on the outcomes of a series of IDA operations and bilateral donor technical assistance projects that have been aimed at assisting the government of Afghanistan (GOA) to establish the legal framework for public financial management (PFM) and put in place the capacity at the central government level to operate the PFM systems and processes for budget planning, execution and monitoring. The Project’s development objective is to strengthen public financial management through effective procurement, treasury and audit structures and systems in line with sound financial management standards of monitoring, reporting and control.

3. As such, the proposed project responds to the desire of major donor agencies and GOA to channel more official development assistance through the budget, as donors transition out of direct implementation, by ensuring continued high level PFM performance through direct operational support in the form of expert advisors for the core public financial management systems - treasury and budget operations, public sector procurement and grant external audits. Now while, a sound basis has been established for PFM performance, progress has been slow in building civil servant capacity, automation of administrative processes, management oversight via internal audit and external accountability. To address these areas, the proposed project will build on the foundations in place by focusing on development of PFM systems development in line ministries and intensive training in procurement, financial management and audit across government. Similarly, support for the establishment of an accounting profession in Afghanistan and activities to create demand for public sector accountability are proposed. The operation will not address any reform in budget formulation, outside of integrating the budget system with AFMIS, in revenue, outside of the oversight through internal and external audit, or in the financial sector supervision, which is the mandate of the Central Bank.

4. The project would therefore extend technical assistance to (a) further build the capacity of central government (Ministry of Finance, Control and Audit Office) to ensure integrity, transparency and accountability of public expenditures, with particular focus on internal and external audit; and (b) develop the organizational infrastructure, systems, processes and staff capacity in the line ministries and the provincial offices of the Treasury for them to discharge their PFM functions and responsibilities with efficiency and accountability.

5. The Project’s key outcomes would be measured using the following indicators: (a) donors channel increased portion of development assistance to Afghanistan through the government

5

budget; (b) improved internal audit i.e. quality of standards applied, management responses and coverage; (c) improved external audit i.e. quality of standards applied, improved response and coverage; (d) at least 50% of procurement under the budget is done by line ministries without the support of ARDS; and (e) increased number of functions carried out by regular ministry staff that were previously carried out by contracted staff. The project is slated for ARTF in accordance with the financing strategy of the ARTF endorsed by the GOA and ARTF donors.

B.Emergency Challenge: Country Context, Government’s PFM Performance & Road Map and Rationale for Proposed Project

Country Context

6. After several decades of wars and civil strife, building an effective state - one that can provide security and services to the people - has been at the heart of the reconstruction effort in Afghanistan. The government has made remarkable progress in many areas such as primary education, basic health services, irrigation rehabilitation, and rural development. However, the country remains extremely fragile. Security remains a serious obstacle to the delivery of reconstruction assistance and implementation of reconstruction programs. Afghanistan’s poverty and social indicators remain among the lowest in the world. Government capacity is weak despite improvements and the pace of implementation of reconstruction programs has been short of popular expectations. Strengthening the country’s public financial management to accelate aid utilization, provide faster and better services to Afghan people, and ensure transparency and accountability of public expenditure is a top priority for the government in taking the reconstruction agenda forward.

Government’s PFM Performance

7. With assistance of IDA and other donors, the government has made significant progress over recent years in establishing a functioning public financial management (PFM) system under the direction of Ministry of Finance, which has been the single, most crucial enabling factor for the implementation of government budget. The legal framework underpinning PFM (Public Finance and Expenditure Management Law and Public Procurement Law) has been established. Through a series of IDA grant operations, specialized international firms have been engaged and have been providing direct operational support to the Treasury of Ministry of Finance, the Afghanistan Reconstruction and Development Services (ARDS) for public sector procurement management, and the Control and Audit office (CAO) for carrying out external audits for all IDA and ARTF funded operations in Afghanistan .

8. The government-wide PFM systems were assessed using the Public Expenditures and Financial Accountability (PEFA) Public Financial Management Performance Measurement Framework in 2005 and 2007. Afghanistan’s ratings against the PEFA indicators portray a public sector where public finances are, by and large, being used for their intended purposes as authorized by the budget; and the budget is processed with transparency and has contributed to aggregrate fiscal discipline. A comparison of Afghanistan’s 2008 results

6

indicates that it now ranks higher than middle income countries in several key areas of PFM. Moreover, the comparison between the first and second assessment shows significant improvements within Afghan PFM systems. Out of total 28 performance indicators, 17 indicators improved and four deteriorated, while seven remained unchanged.

9. The government–wide PFM systems have generated the following outcomes: (a) all transactions under the budget are now effected on-line in real time through the Afghanistan Financial Management Information System (AFMIS) with the corresponding benefits of automated controls; (b) since 2008, monthly financial statements covering central government have been published and operating units can produce on their from AFMIS at any time updated budget execution reports; (c) every year since 2006, the audited annual appropriation statements of the Government (Qatia) have been submitted to Parliament within six months of the end of the fiscal year in accordance with public financial management law; and (d) 450,000 government employees have been registered under the verified payroll program of whom 290,000 are receiving salary through direct transfer to their bank accounts. Treasury staffing has also improved since 2005 when only a few key civil service positions in the Treasury Department were filled and those few civil servants working in the department were incapable of carrying out the basic functional responsibilities of their roles. Currently, the majority of key civil service positions are filled and civil service personnel do most of the day-to-day work of the Treasury Department.

10. While the December 2007 PEFA-based PFM performance assessment reported significant positive developments in Afghanistan’s PFM systems since the 2005 assessment, it also highlighted a number of weaknesses which must be addressed. To improve Afghanistan’s PFM performance, actions in the following areas are critical:

i) PFM capacity outside the Ministry of Finance: Capacity development in line ministries, as executing agencies of expenditures, is critical. Compared with the progress in the Ministry of Finance, developments in most line ministries lag behind. Particularly, capacity building on public procurement should be accelerated so that line ministries can progressively take greater responsibility for procurement activities.

ii) Internal and external audit: Internal audit work in line ministries does not meet recognized professional standards. In addition to in-house training in the ministries, formal academic/professional training in auditing should be made available for staff in internal audit departments. Also, most internal audit manuals are very outdated and need to be revised based on modern internal audit practices that also take into account the current context in Afghanistan. Likewise, capacity for external audit needs to be further developed along with a revised legal foundation based on international standards. Acceleration of the accounting and auditing certification process for all professional staff should be pursued.

Government’s PFM Roadmap

7

11. In the wake of discussions between the GOA and the donor community on a planned transition for the GOA to take greater responsibility in managing the reconstruction agenda, the GOA prepared and shared with donors at the Kabul Donor Conference in June, 2010 a PFM Roadmap. The PFM Roadmap is guided by the vision that (i) policies that reflect the aspirations and needs of the Afghan People, drive the Government Budget; (ii) a Government Budget assigns responsibility for development outcomes; (iii) efficient public finance and equitable allocation of resources sustain economic development; and (iv) accountable civil servants and equitable delivery of services build citizens’s trust in Government. The Roadmap sets out reforms which seek to ensure efficient, transparent and accountable use of public resources, increase aid absorption capacity and secure on-budget donor aid, and improve development outcomes. The strategy encompasses all major functions of the Ministry of Finance (MOF), CAO and PFM across government. Alongside steps to further strengthen the legal framework and PFM infrastructure and capacity of MOF and CAO, the Roadmap outlines a decisive further step in delegating responsibilities for budget making, spending decisions, and procurement to line ministries and provinces under the supervision of the MOF, in order to reduce the daily management of line ministries’ financial operations by the MOF itself when operating conditions in terms of acceptable standards of transparency and accountability in line ministries so permit. Such delegation will help strengthen ownership and results focus in budget preparation and execution. It would provide more incentive for line ministries to plan for and achieve results than to “game” the budget and treasury operations systems. Line ministries would accept increased responsibilities for results and become increasingly transparent with improved reporting and auditing.

Rationale for Proposed Project

12. During the reconstruction period, there has been effective coordination of support for PFM among the key donors. IDA has been leading in providing technical assistance in treasury, procurement and audit, with support from USAID and US Treasury advisors. DFID, along with UNDP, has provided both operations support and capacity building to the Budget Department of MOF while DFID and USAID have supported the Revenue Department. The Asian Development Bank (ADB) has contributed to the reorganization and development of procedures in the provincial offices of the MOF which dovetails with the IDA support of the centralized operations in Treasury and the roll-out of the centralized systems to Mostoufiats Coordination is facilitated by agreement on the government’s PFM Roadmap and its implementation. Given that the technical assistance to be provided by the proposed project represents a natural continuation and deepening of reforms supported by prior and ongoing IDA grant operations, GOA and donors have requested that the project be financed by ARTF with IDA providing supervison and implementation support.

13. Building core PFM capacity in government has been one of the fundamental thrusts of the Bank’s interim support strategy for Afghanistan. The Bank has gained valuable insight on PFM issues in Afghanistan both through the IDA funded technical assistance projects and the extensive analytical work on PFM. Given its successful record of providing technical assistance on PFM, the Bank has gained the recognition and confidence of the Government

8

and donors and is uniquely positioned to assist the Government in implementing the PFM Roadmap.

C. The Project

Project Development Objectives

14. The Project’s development objective is to strengthen public financial management through effective procurement, treasury and audit structures and systems in line with sound financial management standards of monitoring, reporting and control.

Summary of Project Components

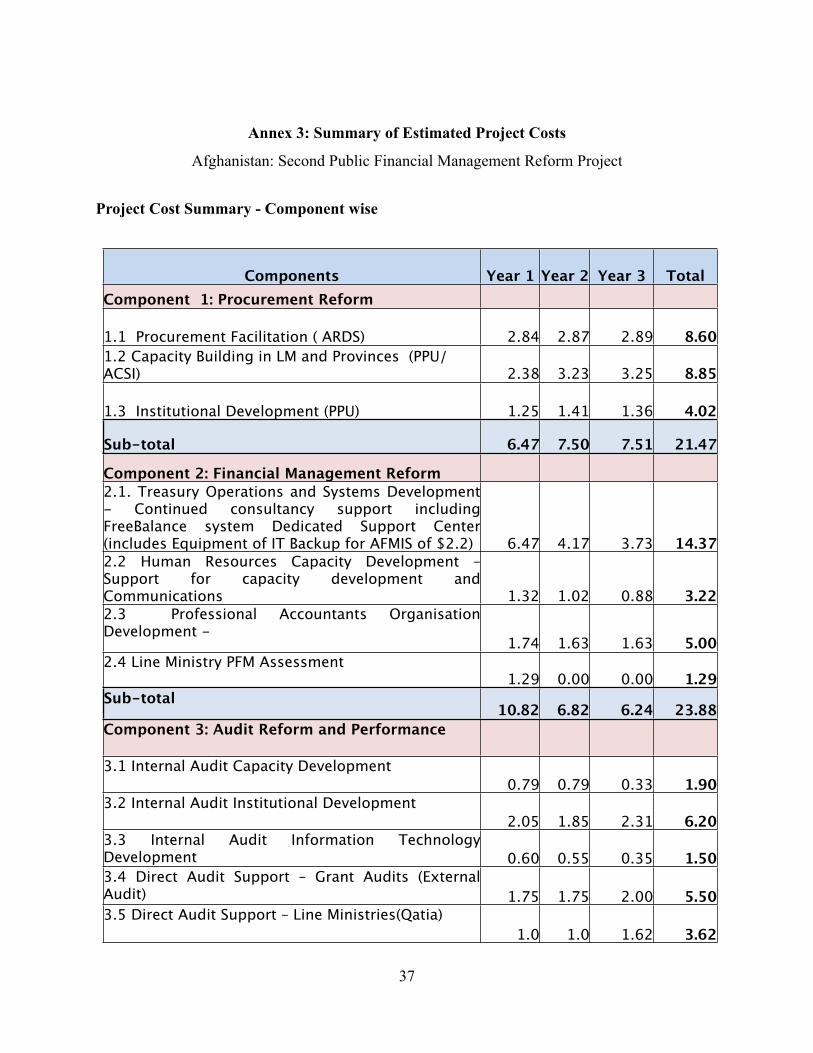

15. The project consists of the following four components.• Component 1: Procurement Reform (US$ 21.47 million): The component would provide

support to build procurement management capacity throughout government and institutional capacity in the public sector, and as far as practicable in the private sector, and to complete the legal and institutional framework for procurement. This improved in procurement knowledge, systems and institutions would contribute to better development budget execution. There are three sub-components:

Subcomponent 1.1 Procurement Facilitation: Provision of consultancy services of a Procurement Facilitation Consultant (PFC) to assist the ARDS in (i) processing civilian on-budget public procurement; (ii) completing regulatory and institutional frameworks for procurement; and (iii) capacity building through knowledge transfer to staff in line ministries.

Sub-component 1.2 Capacity Building in Line Ministries and Provinces comprising (i) support to the Public Procurement Unit (PPU) and the Afghanistan Civil Service Institutue (ACSI) to lead capacity building and institutional building activities; and (ii) the deployment of 3 groups of procurement specialists, under the PPU, to the line ministries a) to liase with central authorities on training and support the application of training in the day to day operations; b) to act as procurement controllers to contribute to the preparation of procurement plans, report on progress of the plans and coordinate input into the procurement MIS; and c) as procurement facilitators to assist on more complex procurement and accelerate budget execution.

Sub-component 1.3 Institutional Development: Support would be provided for completing the legal framework, preparing a compendium of all relevant legal documents and for operation of the Appeal & Review Committee and training on dispute resolution. Taking into account the lessons of the 7 ministries and 6 provinces already reorganized, the institutional development of the rest of the central and provincial budget units would be carried out. Support also would be provided for designing an effective and strategic communication and procurement disclosure policy to raise awareness, and to enhance and operate the procurement management information system (MIS). • Component 2: Financial Management Reform (US$ 23.88 million) The component aims

to support high level PFM performance and build staff and institutional PFM capacity

9

throughout government through support for training, systems development and process renewal. There are four sub-components:

Sub-component 2.1 Treasury Operations and Systems Development: Through the services of a Financial Management Consultant (FMC), direct operations support and systems development for treasury functions for more efficient delivery of treasury services and strengthened internal controls will be provided as well as counterpart training. This sub-component’s activities would also include the establishment of a disaster recovery plan and equipping an AFMIS IT back-up facility.

Sub-component 2.2 Human Resources Capacity Development: Support would be provided for developing job specific certifiable finance skills and general skills of treasury and finance staff of MOF and line ministries. A Treasury Communications Plan will be developed and implemented to support reforms.

Sub-component 2.3 Professional Accountants Organization Development: Support would be provided for establishing the legal framework and structures for development and regulation of an accounting and auditing profession and for the training of professional accountants in Afghanistan.

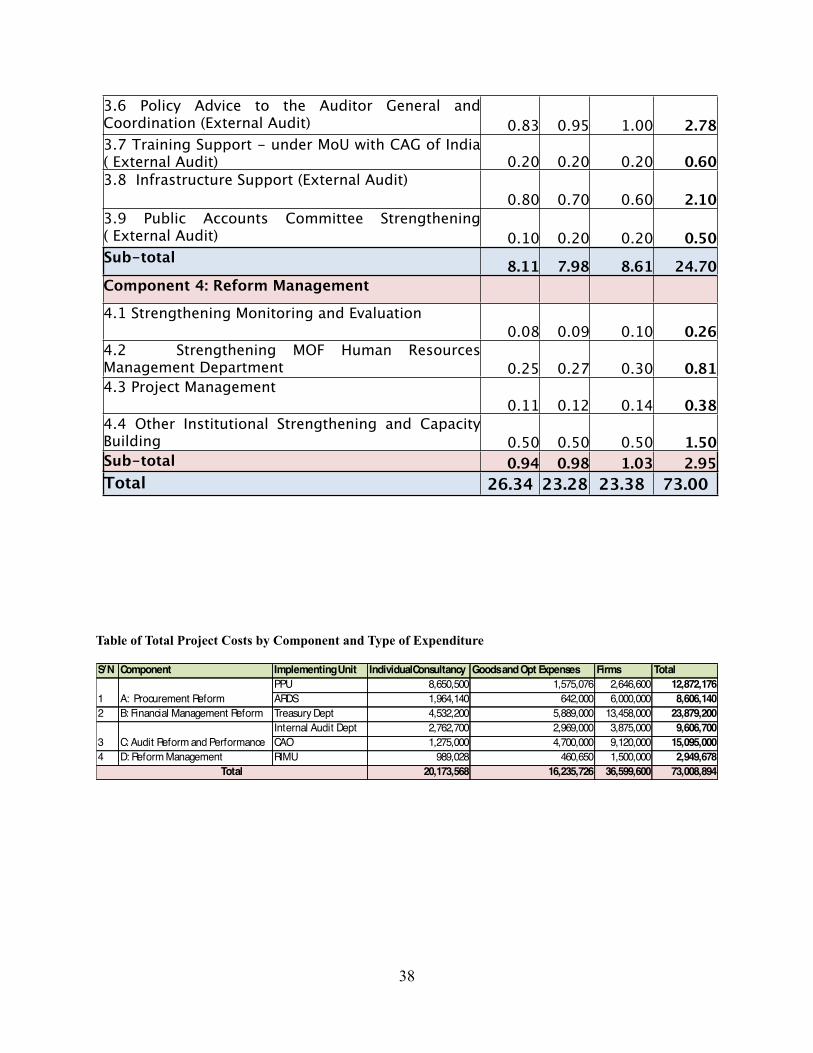

Sub-component 2.4 Line Ministry Public Financial Management Assessments: The project would finance a detailed review of internal control and public financial management performance of 7 line ministries; a first set of 7 line ministries is under review through the support of the PFMR project.• Component 3: Audit Reform and Performance (US $ 24.70 million) The component aims

to improve public sector governance through nine sub-components grouped under Internal Audit and External Audit.

Internal Audit: Through three sub-components, support would be given for institutional reforms in internal audit and capacity building to improve management oversight. Additionally, support is provided for the development of information systems and the purchase of and training in automated auditing tools.

External Audit: Through 6 sub-components support would be given for capacity building and for carrying out independent reviews of on-budget donor funded operations as well as of all operations under the budget of nine line ministries over the project period. Additionally, support would be provided for the Public Accounts Committee and the purchase of office and IT equipment for the new CAO offices.

• Component 4: Reform Management (US$ 2.95 million) The component aims to support improvement in monitoring and management of technical assistance and human resources in the MOF. Through 4 sub-components: 4.1 Strengthening Monitoring and Evaluation; 4.2 Strengthening MOF Human Resources Management Department; 4.3 Project Executive Management; and 4.4 Other Institutional Strengthening and Capacity Building, support would be provided for strengthening M&E, HR management development, and project management in MOF and for unforeseen needs for related technical assistance and analytical work.

10

Expected Outcomes

16. Key outcomes expected to be achieved through these activities include: (a) donors shift 20% of their off-budget official development assistance to Afghanistan to on-budget; (b) extension of internal audit coverage, done to professional standards, to 75% of the budget operations; (c) effecting external audit coverage of an acceptable standard to 75 % of the budget operations; (d) at least 50% of procurement under the budget is done by line ministries without the assistance of ARDS; and (e) increased numbers of regular ministry staff performing functions previously carried out by contracted staff.

D. Appraisal of Project Activities

Economic and Financial Analysis

17. Since the proposed operation is a technical assistance project, no economic analysis has been carried out. The project is expected to yield high benefits in that: (a) line ministries are able to execute budget and deliver services efficiently; (b) fast track capacity building of civil servants to operate the PFM systems contributes to sustainability of PFM; and (c) strengthened internal and external audit function and operation would contribute to good governance. Cumulatively, these benefits would lead to greater confidence on the part of the public, and donors, that Government is responsive to felt needs and that the apparatus of government is operating efficiently and transparently. It would then support the strategy of increasing the transfer of donor resources to the government system. As the project is focused on changing the institutional environment in a high risk country, establishing a trend is considered more important than reaching pre-determined targets.

Technical Aspects

18. Component 1: Procurement Reform. The component builds on the success of both centralized oversight of civilian procurement for the entire budget under the Afghanistan Reconstruction and Development Services (ARDS) and the development of the regulatory framework, institution and capacity building, started under the Public Administration Capacity Building Project (PACB) IDA-H1440 in 2005. ARDS oversight is key in supporting the aim to put more donor funds on-budget both for assurance of compliance and to achieve more development spending. The component’s approach to delivery of procurement training is considered best practice in Afghanistan as the training is delivered through the Afghanistan Civil Service Institute (ACSI), with the technical assistance and oversight of the Procurement Policy Unit of MOF, thereby strengthening the ACSI and building permanent training capacity. The component’s activities focus on support to line ministries for conducting procurement, reporting on compliance and applying knowledge from the classroom training. The training is critical to effect the restructuring of procurement units centrally and in provinces which will allow the delegation of procurement oversight as provided for in the law. Support to establish the long overdue appeal and review function will contribute to assurance on the fair application of the law. Development of a communication and disclosure

11

strategy also will contribute to awareness of the procurement reform agenda and the public’s interest in public procurement.

19. Component 2: Financial Management Reform. The Treasury Department’s performance in timeliness and reliability of reporting is already remarkable but as on-budget donors’ funds continue to surge, this good performance must continue. To support this good performance and to up-grade installations and underlying systems, an operations support consultant will be engaged to carry out the systems integration for putting in place administrative systems for service delivery units. Treasury’s performance and sustainable capacity will be strengthened with duty specific training while certification training in accounting will be offered to all financial management staff throughout Government. Support will be provided to begin establishing an administrative and legal framework for developing and regulating a sustainable accounting and auditing profession in Afghanistan to develop professionally recognized accountants and auditors which are needed in both the public and private sectors.

20. Component 3: Audit Reform and Performance. Improving management’s oversight by building internal audit is essential for sound PFM performance and governance. With the clarification of MOF’s mandate to conduct internal audit across government, MOF is poised to take this function to a new standard. Expectations for external audit are more modest; donor grant audits are already being conducted to a high standard but as funding grows the quality of audits of operations funded by all sources should be raised. Capacity will improve from both the training at and exposure to the supreme audit institution of India and the classroom training offered under the USAID technical assistance underway at the CAO.

21. Component 4: Reform Management. Monitoring and evaluation of progress under the project and reforms under the MOF rest on the work of the RIMU in MOF which is well equipped and poised to continue to effect this.

Institutional Aspects

22. While the project is operating in a weak capacity country environment, ownership and commitment by MOF for PFM reforms are strong. The implementation arrangements for the PACB and PFMR projects have worked well and these will be maintained for this proposed PFMRII Project. These arrangements include a project coordination unit (RIMU) in MOF assisted by a technical assistance team funded by the project, which will be responsible for overall project implementation, including back-up to the procurement and financial management units. Project implementation is supported by firms and local contract staff in all implementing units. The highly visible PFM reforms are closely monitored by the MOF through the ministry wide technical assistance monitoring process under RIMU and through the program monitoring progress under the National Priority Program for Finance and Economic Reform under the Deputy Minister for Policy. Donors groups, both under the government-wide mechanism and now under the ARTF donor groups, also monitor progress on government commitments on PFM.

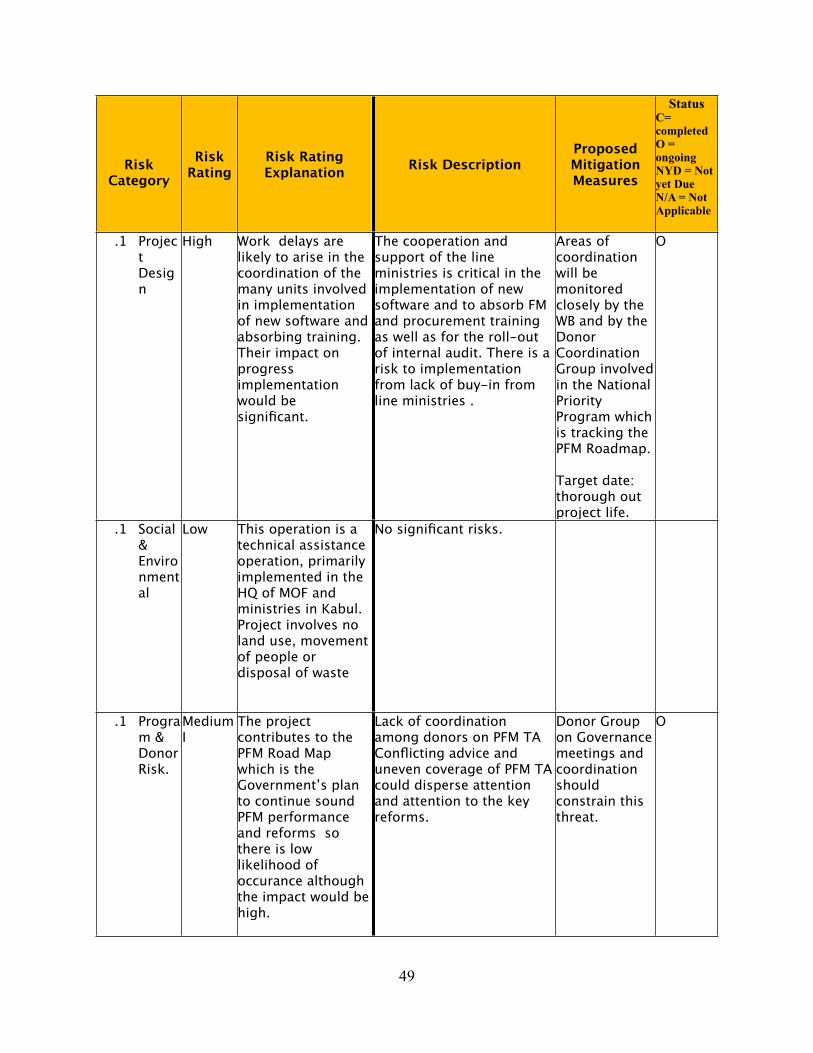

Lessons Learned and Reflected in Project Design

12

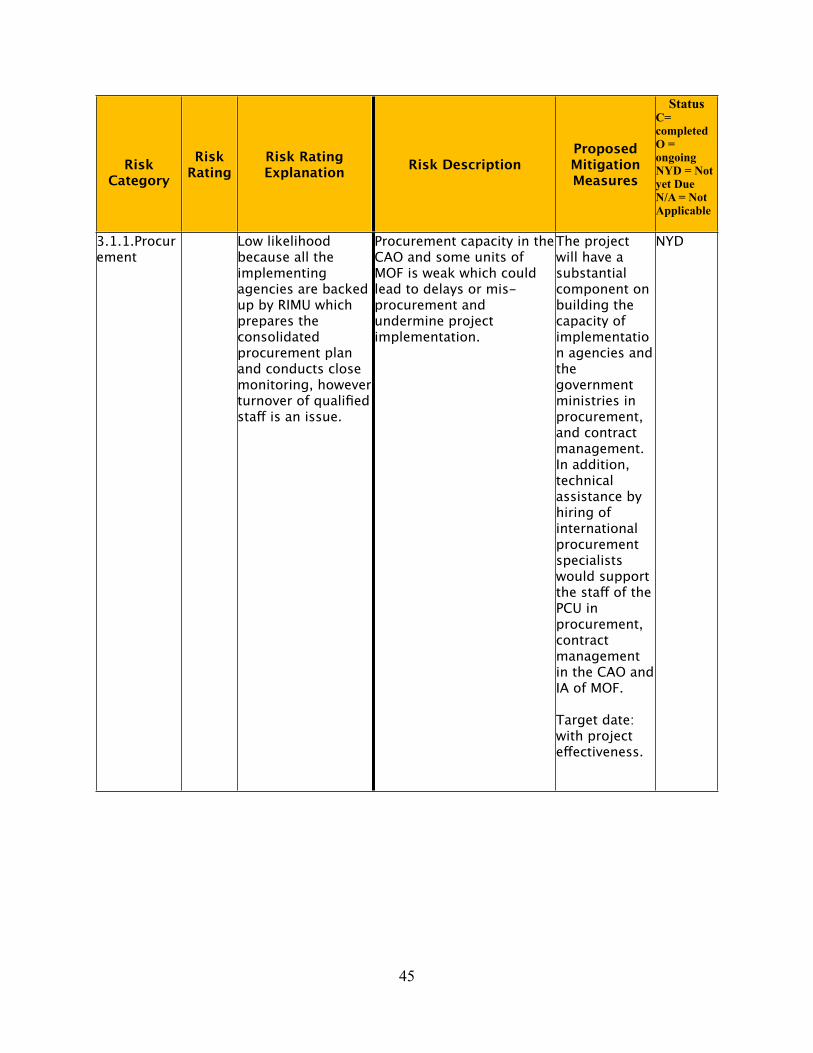

23. The Implementation Completion Report of the PACB Project highlighted a number of issues, which persist under the ongoing PFMR project that are addressed in the design of this proposed project. These issues also arise and were expanded on in the following analytical work by the Bank: World Bank and DFID, Afghanistan Public Expenditure Management Performance Assessment, June, 2008; World Bank and DFID, Public Expenditure Review 2010; World Bank, DFID and ADF, Vulnerability to Corruption Study, 2008.• Inadequate Human Resources, Capacity in PFM. Engaging international firms and local

consultants to perform basic PFM functions has been a default strategy. Sustainability and consolidation of achievements in PFM is challenged as trained local highly specialized advisors move from the ministries to work on projects outside the budget or in the private sector while civil servants cannot take over the related duties. Coordination with the proposed ARTF Capacity Building for Results Program project, which is under preparation, has led to the incorporation of a component for market related compensation for FM and procurement specialists. At the same time, intensive training of civil servants should provide an incentive and allow these civil servants to qualify for these salaries.

• Durability of PFM Reforms. The Government, while generally dedicated to making improvements, has taken unilateral action to reverse or restrain progress in the legal framework. Donor coordination around the ARTF Incentive Program and consultations on the PFM Roadmap have led to firm commitments to maintain and improve the legal framework.

• Limited Automation of PFM Processes. The current systems to support service delivery are largely manual, and lack some basic functions. The project supports the development of the related service delivery administrative processes.

• Corruption Risk. The country operating environment carries a high risk to perceived corruption. Further strengthening of procurement and audit including developing social accountability and support for the activities of the Public Accounts Committee should help address these issues

• Internal Audit. Management oversight is key to good governance. This oversight is constrained by the lack of an effectively operating internal audit function, except in the MOF. Building internal audit capacity in each line ministry cannot be done in the short term so implementing the approach provided in the Public Expenditure and Finance Law which entrusts MOF to establish internal audit throughout the government would be the most effective and expeditious route to establish the function across government, while at the same time supporting the development of internal audit in the line ministries, where feasible. This approach is supported by the proposed project.

• External Audit. The external accountability of the executive must be strengthened if confidence in its performance is to be built. Many achievements in PFM are discounted because there is little independent oversight or assurance that the reports and decisions of the executive deserve credibility, particularly given the perception of rising corruption. A

13

new legal framework, training for members of a public accounts committee and training and technical support to the CAO are needed and are included in the proposed project.

• Accounting Profession. There is a very limited accounting and audit profession in Afghanistan due to an acute shortage of qualified professionals. There is no recognized body that represents or promotes the profession in Afghanistan, nor regulation of the profession. Accounting and auditing services are provided by expatriate accountants, but there is no oversight of these services. Auditors are not subject to civil liability under any legislation and there is no law that provides for auditors to obtain professional indemnity insurance. The only recognized accountancy training available is provided by the Afghan Chapter of the Association of Certified Chartered Accountants (ACCA). Due to the poor educational standards, Afghans students are opting to join the Certified Accounting Techncian (CAT) qualification of ACCA – a qualification that does not require a formal prior education history. This lack of accounting and auditing infrastructure and poor practice conditions undermine and perpetuate the limited pool of accounting and auditing skills for the public and private sectors and limit the oversight of public interest entities (many of which are public sector organizations). Support is included in the proposed project to develop the capacity of accounting and auditing in Afghanistan and establish a sustainable structure of effective regulation and oversight of the profession.

E. Implementation Arrangements and Financing Plan

24. As with the PACB and PFMR projects, the components would be implemented through four departments of the MOF, ARDS in the Ministry of Economy and the CAO. The Directors of the respective units would be responsible for implementation; each unit would have the support of the project implementation cells already staffed and operating under the PFMR project. The units would continue to support with transaction processing, contract control, and reporting. These cells have satisfactorily supported implementation in the past. The RIMU of the MOF would continue to coordinate and report on project activities. This RIMU has functioned with the authority of the Minister and has been supported by local advisors who demonstrated expertise in institutional development, change management and project implementation. The project would be implemented through an annual project work planning and budgeting process reflecting the input of the affected units and be subject to annual program reviews of achievements. Donor coordination would be part of the annual review and programming process. The detailed activity and procurement plans for the first year of the project are complete and were used as the basis for the budget submission for the coming fiscal year of the implementing units.

25. Project Reporting: Each implementing unit would report quarterly to RIMU on physical and financial progress. RIMU would maintain the overall project management information system and be responsible for collation of progress reports and reporting to the Project Steering Committee (PSC) and IDA. These reports would include, inter alia: (a) up-to-date physical and financial progress compared to annual and end-of-project targets; (b) updated indicators of project performance compared to annual and end-of-project targets; and (c)

14

successes and problems encountered during the reporting period with suggested remedial actions.

26. Project Coordination: The overall project coordination and oversight would rest with the PFMR Project Steering Committee (PSC), established in 2006 to provide cross-ministry oversight and guidance. The PSC was established to maintain focus on results, ensure good communications and provide a consolidated view of the reform under the project. It would be responsible to review progress and recommend any necessary changes to the reforms, component activities, implementation arrangements or performance measurements. The SC would be chaired by the Minister of Finance, or his delegate, and would receive secretariat support from RIMU. The Committee members comprise senior MOF departmental managers (Treasury, Budget, Internal Audit, Administration, and PPU), a representative of the Ministry of Economy (responsible for procurement operations support) and a representative of the CAO.

27. Project Monitoring and Evaluation: RIMU would be responsible for the monitoring & evaluation of the project as well as that of the MOF strategic plan, reforms and technical assistance (TA) to MOF. It has already established a results-based M&E system for the MOF strategic plan and the PFMR Project. The system integrates implementation based M&E system (inputs, activities, outputs) with results based indicators and mostly focuses on the results i.e. outcomes and impact of the interventions. The M&E specialists at RIMU would continue to conduct monitoring and evaluation of the MOF strategic plan, TA and the project with focus on institutionalization of the system and creating a permanent M&E Unit within the MOF. RIMU would report to MOF top management on strategic plan progress and to the PSC and Bank on the project progress.

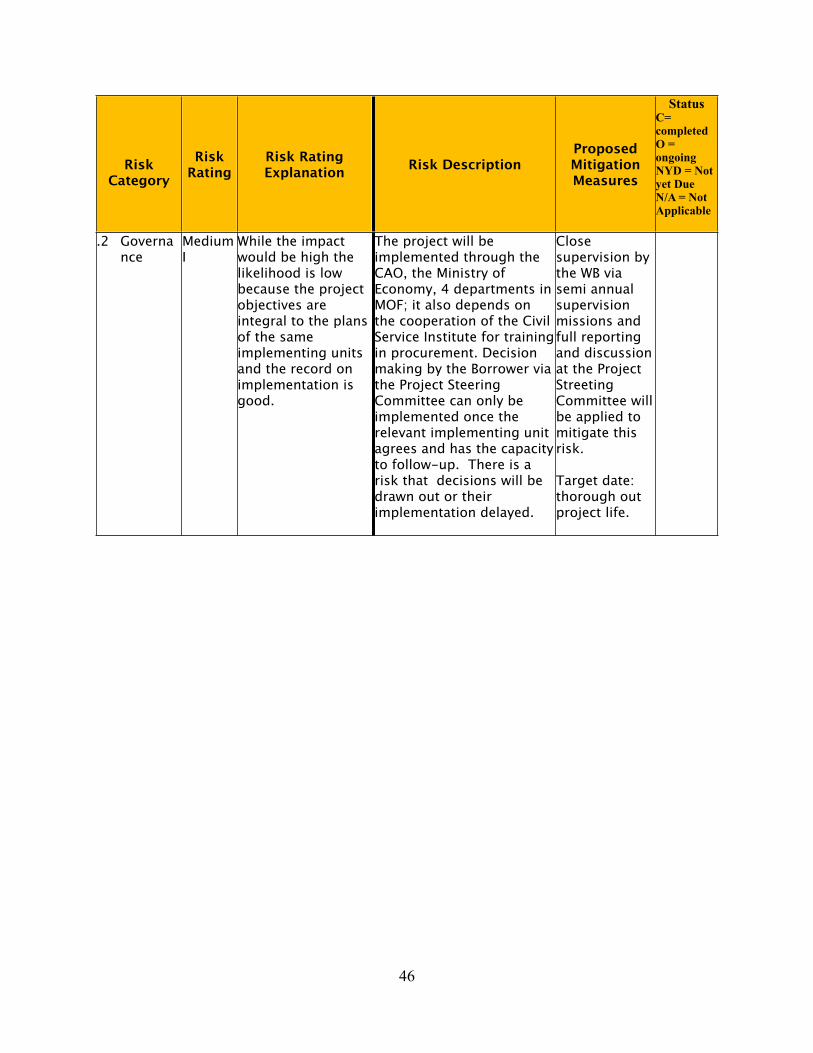

28. Governance and Accountability Action Plan. This proposed PFMR II Project would be implemented in a high risk environment. However, the very outputs of the project address relevant risks and include timely, reliable reporting on all operations under the budget, including all investment operations like the PFMR II Project, centralized oversight of all non-security procurement over a modest threshold and external audit done to a high standard of all IDA and ARTF investment operations. Similarly, the expansion of effective internal audit and capacity building of the CAO add depth to these arrangements. These measures contribute to good governance by improving both management oversight and improving transparency, while at the same time act to constrain corruption by reducing the opportunities for financial leakages and procurement corruption which are the two forms of corruption that most threaten donor funds directly1. Moreover, the Government of Afghanistan (GOA) is fully committed to the Project and further reforms which are also central to fiscal discipline and transparency and support channeling more development assistance through the budget.

29. Bank supervision is largely unencumbered since the project operations are concentrated in Kabul where supervision has not been affected by the security concerns, or in the provincial

1 The forms of corruption which drive the Transparency International perception index would include bribery, extortion, grand corruption and patronage which are not direct threats to donor funds on-budget and are not constrained by the PFM Framework.

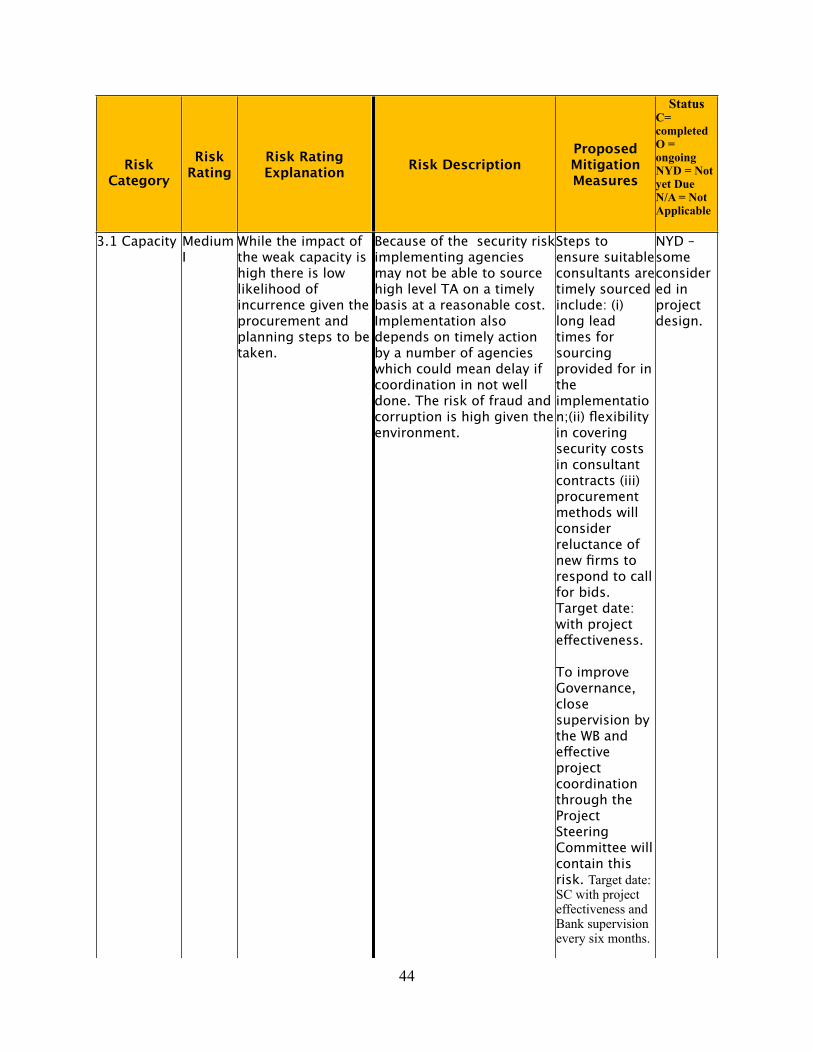

15

capitals where missions can be carried-out with due protection. Similarly, the nature of the project transactions, mostly involving consultant contracts, are subject to close supervision by the RIMU and the Bank. Nevertheless, to mitigate and guard against governance, corruption and fraud risks and improve transparency and accountability in implementation of this proposed PFMR II project, several measures have been incorporated in the implementation and monitoring arrangements. These measures are included in the Governance and Accountability Plan (GAAP) to identify and mitigate critical risks in achieving the development objectives. The GAAP measures include: (a) implementation arrangements for PFMRII Project that build upon the lessons learnt from PFMR project; (b) fiduciary processes including FM and Procurement which respond to the risk; and (c) enhanced monitoring and evaluation arrangements.

Project Costs and Financing Plan

30. The cost of this proposed project is estimated at US$ 73 million including physical and price contingencies. The project will be financed by an ARTF grant of US$ 73 million.

Financial Management, Disbursement and Audit Arrangements

31. At the project level, financial management will be coordinated by the RIMU of the MOF. The RIMU reports to the Minister of Finance and serves as the "secretariat" for the PFM Reform SC. The RIMU will recruit a Financial Management Specialist who will have responsibility for the financial management activities of the project including: preparing required monthly, quarterly and annual reports; coordinating with other component implementing entities to ensure that adequate financial management requirements are met; liaising with the Special Disbursements Unit (SDU) to ensure that the project’s Designated Account (DA) is replenished when due; and responding to project audits.

32. Quarterly unaudited Interim Financial Reports will be prepared by the RIMU accounting unit and submitted to the Bank within 45 days from the end of the quarter. Consolidated project reports will be prepared, reviewed, and approved by the MOF.

33. A DA will be opened at Da Afghanistan Bank (DAB, Central Bank) in the name of the project on terms and conditions satisfactory to IDA. The DA will be maintained by the MOF. Withdrawal applications for new advances and expenditure reports will be submitted monthly. Financial management arrangements for the project are set out in detail in Annex 5.

Fund Flows

34. Fund management for the Project will follow existing procedures. As with all public expenditure, all payments under the project will be routed through MOF. In keeping with current practices for other projects in Afghanistan, the DA will be operated by the SDU in the Treasury Department of MOF. Requests for payments from DA funds will be made to the SDU by the RIMU. In addition to payments from the DA funds, the RIMU can also request the SDU to make direct payments to consultants or consulting firms, and special commitments for contracts covered by letters of credit. Such requests will follow World

16

Bank’s procedures. All withdrawal applications to IDA, for advances, reimbursement, and direct payment applications, will be prepared and submitted by MOF.

Accounting and Reporting

35. The RIMU will ensure that project transaction records are reflected in the AFMIS to generate required monthly, quarterly and annual reports.

36. The FM Manual in place for the current PFMR project is to be updated/modified by the RIMU to reflect the arrangements for this proposed project, and is to be approved by the Bank. The FM Manual will outline guidelines for project activities including specific requirements for each component implementing entity and will include: i) roles and responsibilities for all FM staff, ii) documentation and approval procedures for payments, iii) project reporting requirements, and iv) quality assurance measures to help ensure that adequate internal controls and procedures are in place and are being followed.

37. The FM Manual also will establish project financial management in accordance with standard Afghan government policies and procedures including use of the Government Chart of Accounts to record project expenditures. The use of these procedures will enable adequate recording and reporting of project expenditures. Overall project accounts will be maintained centrally in SDU, which will be ultimately responsible for recording of all project expenditures and receipts in the Government’s accounting system. Reconciliation of project expenditure records with MOF records will be carried out monthly by the RIMU.