The Statement of Cash Flows Chapter 14 Learning Objectives

34

8/28/2019 1 Chapter 14 The Statement of Cash Flows Chapter 14 Learning Objectives 1. Identify the purposes of the statement of cash flows and distinguish among operating, investing, and financing cash flows 2. Prepare the statement of cash flows by the indirect method 14-2 © 2018 Pearson Education, Inc. 1 2

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of The Statement of Cash Flows Chapter 14 Learning Objectives

8/28/2019

1

Chapter 14The Statement of Cash Flows

Chapter 14 Learning Objectives

1. Identify the purposes of the statement of cash flows and distinguish among operating, investing, and financing cash flows

2. Prepare the statement of cash flows by the indirect method

14-2© 2018 Pearson Education, Inc.

1

2

8/28/2019

2

Chapter 14 Learning Objectives

3. Use free cash flow to evaluate business performance

4. Prepare the statement of cash flows by the direct method (Appendix 14A)

5. Prepare the statement of cash flows by the indirect method using a spreadsheet (Appendix 14B)

14-3© 2018 Pearson Education, Inc.

Learning Objective 1

Identify the purposes of the statement of cash flows and distinguish among operating, investing, and financing cash flows

14-4© 2018 Pearson Education, Inc.

3

4

8/28/2019

3

WHAT IS THE STATEMENT OF CASH FLOWS?

• The statement of cash flows reports on a business’s cash receipts and cash payments for a specific period.

• This statement does the following:– Reports on the cash flows of a business– Reports why cash increased or decreased

during the period– Covers a span of time and is dated the same

as the income statement

14-5© 2018 Pearson Education, Inc.

Purpose of the Statement of Cash Flows

• The statement of cash flows explains why net income as reported on the income statement does not equal the change in the cash balance.

• The statement of cash flows helps:– Predict future cash flows– Evaluate management – Predict ability to pay debts and dividends

14-6© 2018 Pearson Education, Inc.

5

6

8/28/2019

4

Classification of Cash Flows

• There are three basic types of cash flows, and the statement of cash flows has a section for each: – Operating activities– Investing activities– Financing activities

14-7© 2018 Pearson Education, Inc.

Operating Activities

• Operating activities is the first section on the statement of cash flows.

• This section reports on activities that create revenue or expense in the entity’s business.

• This is often the most important category.

14-8© 2018 Pearson Education, Inc.

7

8

8/28/2019

5

Investing Activities

• Investing activities is the second category listed on the statement of cash flows.

• This section reports cash receipts and cash payments that increase or decrease long-term assets.

• It includes the cash inflow from selling and the cash outflow from purchasing long-term assets.

14-9© 2018 Pearson Education, Inc.

Financing Activities

• Financing activities is the last category listed on the statement of cash flows.

• Financing activities include cash inflows and outflows involved in long-term liabilities and equity.

• Financing activities include issuing stock, paying dividends, and buying and selling treasury stock.

14-10© 2018 Pearson Education, Inc.

9

10

8/28/2019

6

Classification of Cash Flows

14-11© 2018 Pearson Education, Inc.

Non-cash Investing and Financing Activities

• Companies make investments that do not require cash.

• Such transactions are called non-cash investing and financing activities.

• These activities appear as a separate schedule at the bottom of the statement of cash flows or in the notes to the financial statements.

14-12© 2018 Pearson Education, Inc.

11

12

8/28/2019

7

14-13© 2018 Pearson Education, Inc.

Non-cash Investing

and Financing Activities

Two Formats for Operating Activities

Indirect method

Starts with accrual income and adjusts to

net cash

Uses account relationships to determine changes in

cash

Direct method

Restates the income in

terms of cash

Shows actual cash receipts and cash payments

14-14© 2018 Pearson Education, Inc.

13

14

8/28/2019

8

Learning Objective 2

Prepare the statement of cash flows by the indirect method

14-15© 2018 Pearson Education, Inc.

HOW IS THE STATEMENT OF CASH FLOWS PREPARED USING

THE INDIRECT METHOD?

Items needed:– Income statement for the current year– Balance sheet from current year– Balance sheet from prior year– Additional information based on review of

transactions

14-16© 2018 Pearson Education, Inc.

15

16

8/28/2019

9

HOW IS THE STATEMENT OF CASH FLOWS PREPARED USING

THE INDIRECT METHOD?

14-17© 2018 Pearson Education, Inc.

Prepare in five steps:1. Complete the cash flows from operating

activities.2. Complete the cash flows from investing

activities section.3. Complete the cash flows from financing

activities section. 4. Compute the change in cash. 5. Prepare a schedule for non-cash activities.

14-18© Pearson Education, Inc.

HOW IS THE STATEMENT OF CASH FLOWS

PREPARED USING THE INDIRECT METHOD?

17

18

8/28/2019

10

14-19© 2018 Pearson Education, Inc.

HOW IS THE STATEMENT OF CASH FLOWS

PREPARED USING THE INDIRECT METHOD?

14-20© 2018 Pearson Education, Inc.

HOW IS THE STATEMENT OF CASH FLOWS

PREPARED USING THE INDIRECT METHOD?

19

20

8/28/2019

11

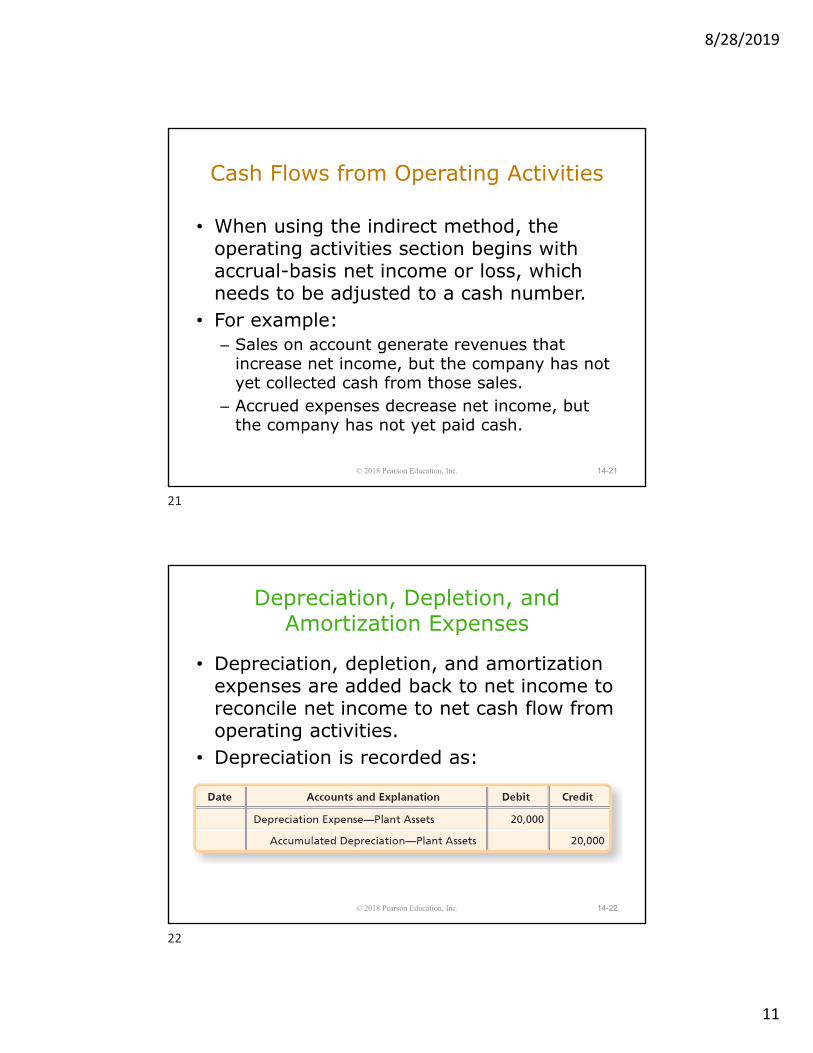

Cash Flows from Operating Activities

• When using the indirect method, the operating activities section begins with accrual-basis net income or loss, which needs to be adjusted to a cash number.

• For example:– Sales on account generate revenues that

increase net income, but the company has not yet collected cash from those sales.

– Accrued expenses decrease net income, but the company has not yet paid cash.

14-21© 2018 Pearson Education, Inc.

Depreciation, Depletion, and Amortization Expenses

• Depreciation, depletion, and amortization expenses are added back to net income to reconcile net income to net cash flow from operating activities.

• Depreciation is recorded as:

14-22© 2018 Pearson Education, Inc.

21

22

8/28/2019

12

Depreciation, Depletion, and Amortization Expenses

• Depreciation does not affect cash.• To go from net income to net cash flows, we

must remove depreciation by adding it back to net income.

14-23© 2018 Pearson Education, Inc.

Gains and Losses on the Disposal of Long-term Assets

Disposals from long-term assets create a gain or loss that must be removed from net income, which is in the operating activities section.

14-24© 2018 Pearson Education, Inc.

23

24

8/28/2019

13

Changes in Current Assets and Current Liabilities

Most current assets and current liabilities result from operating activities.

14-25© 2018 Pearson Education, Inc.

Evaluating Cash Flows from Operating Activities

The operating activities section starts with accrual net income, and then adjustments are made to reconcile net income to net cash.

14-26© 2018 Pearson Education, Inc.

25

26

8/28/2019

14

14-27© 2018 Pearson Education, Inc.

Evaluating Cash Flows from Operating Activities

Cash Flows from Investing Activities

• Investing activities affect long-term assets, such as: – Plant Assets – Investments– Notes Receivable

• It is helpful to evaluate the T-accounts for each long-term asset to determine if there was an acquisition or disposal.

14-28© 2018 Pearson Education, Inc.

27

28

8/28/2019

15

Cash Flows from Investing Activities

Let’s look at the Plant Assets and Accumulated Depreciation accounts for ShopMart.

14-29© 2018 Pearson Education, Inc.

Cash Flows from Investing Activities

14-30© 2018 Pearson Education, Inc.

Use the information available to determine the cash received from an asset disposal:

29

30

8/28/2019

16

Cash Flows from Investing Activities

14-31© 2018 Pearson Education, Inc.

Cash Flows from Financing Activities

• Financing activities affect the long-term liability and equity accounts:– Long-term Notes Payable– Bonds Payable– Common Stock– Retained Earnings

14-32© 2018 Pearson Education, Inc.

31

32

8/28/2019

17

Long-term Liabilities

The T-account for ShopMart’s Notes Payable is shown below.• Additional information:

– Received $90,000 cash from issuance of notes payable.

– Paid $10,000 cash to retire notes payable.

14-33© 2018 Pearson Education, Inc.

Long-term Liabilities

• A new issuance of notes payable is known to be a $90,000 cash receipt.

• In addition, ShopMart paid $10,000 cash to retire notes payable.

14-34© 2018 Pearson Education, Inc.

33

34

8/28/2019

18

Long-term Liabilities

The cash inflow and cash outflow associated with these notes payable are listed first in the cash flows from financing activities section.

14-35© 2018 Pearson Education, Inc.

Common Stock and Treasury Stock

• The amount of new issuances of stock is determined by analyzing the stock accounts and reviewing additional information:– Received $120,000 cash from issuing shares of

common stock.– Paid $20,000 cash for purchase of shares of

treasury stock.

14-36© 2018 Pearson Education, Inc.

35

36

8/28/2019

19

Common Stock and Treasury Stock

• The common stock account shows a new stock issuance of $120,000.

• Acquisition of treasury stock:

14-37© 2018 Pearson Education, Inc.

Common Stock and Treasury Stock

The $20,000 payment for treasury stock is shown as a cash outflow in the financing section of the statement of cash flows.

14-38© 2018 Pearson Education, Inc.

37

38

8/28/2019

20

Computing Dividend Payments

The amount of dividend payments can be computed by analyzing the Retained Earnings account. • ShopMart earned net income of $40,000

14-39© 2018 Pearson Education, Inc.

Computing Dividend Payments

Only cash dividends paid are reported on the statement of cash flows.

14-40© 2018 Pearson Education, Inc.

39

40

8/28/2019

21

Net Change in Cash and Cash Balances

14-41© 2018 Pearson Education, Inc.

Non-cash Investing and Financing Activities

• The last step is to prepare the non-cash investing and financing activities section.

• Let’s consider three non-cash transactions for The Outdoors, Inc.:1. Acquired $300,000 building by issuing

common stock.2. Acquired $70,000 land by issuing notes

payable. 3. Retired $100,000 notes payable by issuing

common stock.

14-42© 2018 Pearson Education, Inc.

41

42

8/28/2019

22

Non-cash Investing and Financing Activities

The Outdoors issues common stock of $300,000 to acquire a building. The journal entry to record the purchase would be as follows:

14-43© 2018 Pearson Education, Inc.

Non-cash Investing and Financing Activities

The second transaction listed indicates that The Outdoors acquired $70,000 of land by issuing a note. The journal entry to record the purchase would be as follows:

14-44© 2018 Pearson Education, Inc.

43

44

8/28/2019

23

Non-cash Investing and Financing Activities

The third transaction listed indicates that The Outdoors retired $100,000 of debt by issuing common stock. The journal entry to record the transaction would be as follows:

14-45© 2018 Pearson Education, Inc.

14-46© 2018 Pearson Education, Inc.

Non-cash Investing and Financing Activities

45

46

8/28/2019

24

Learning Objective 3

Use free cash flow to evaluate business performance

14-47© 2018 Pearson Education, Inc.

HOW DO WE USE FREE CASH FLOW TO EVALUATE BUSINESS PERFORMANCE?

• Investors want to know how much cash a company can “free up” for new opportunities.

• Free cash flow is the amount of cash available from operating activities after paying for planned investments in long-term assets and after paying dividends.

14-48© 2018 Pearson Education, Inc.

47

48

8/28/2019

25

• ShopMart expects net cash provided by operations of $200,000. It plans to spend $160,000 to modernize its retail facilities and pays $15,000 in cash dividends.

• ShopMart’s free cash flow is $25,000:($200,000 ‒ $160,000 ‒ $15,000)

14-49© 2018 Pearson Education, Inc.

HOW DO WE USE FREE CASH FLOW TO EVALUATE BUSINESS PERFORMANCE?

Learning Objective 4

Prepare the statement of cash flows by the direct method (Appendix 14A)

14-50© 2018 Pearson Education, Inc.

49

50

8/28/2019

26

HOW IS THE STATEMENT OF CASH FLOWS PREPARED USING THE DIRECT METHOD?

• The Financial Accounting Standards Board (FASB) prefers the direct method of reporting cash flows from operating activities.

• This method provides clearer information about the sources and uses of cash than the indirect method.

• Only the operating section differs between the two methods.

14-51© 2018 Pearson Education, Inc.

Cash Collections from Customers

Net Sales Revenue can be converted to cash receipts from customers as follows:

14-52© 2018 Pearson Education, Inc.

51

52

8/28/2019

27

Cash Collections from Customers

The cash ShopMart received from customers is the first item in the operating activities section of the direct-method statement of cash flows.

14-53© 2018 Pearson Education, Inc.

Cash Receipts of Interest Revenue

The income statement reports interest revenue of $12,000. Because there is no Interest Receivable account on the balance sheet, the interest revenue must have all been received in cash.

14-54© 2018 Pearson Education, Inc.

53

54

8/28/2019

28

Cash Receipts of Dividend Revenue

The income statement reports dividend revenue of $9,000. No Dividends Receivable indicates that all dividend revenue was received in cash.

14-55© 2018 Pearson Education, Inc.

Payments to Suppliers

• Payments to suppliers include all payments for the following:– Merchandise inventory– Operating expenses except employee

compensation, interest, and income taxes• Suppliers, also called vendors, are those entities

that provide the business with its merchandise inventory and essential services.

14-56© 2018 Pearson Education, Inc.

55

56

8/28/2019

29

Payments to Suppliers

Cash paid for inventory is calculated as follows:

14-57© 2018 Pearson Education, Inc.

Payments to Suppliers

Cash paid for operating expenses is calculated as follows:

14-58© 2018 Pearson Education, Inc.

57

58

8/28/2019

30

Payments to Suppliers

Total cash paid to suppliers = Cash paid for merchandise inventory + Cash paid for other operating expenses

14-59© 2018 Pearson Education, Inc.

Payments to Employees

This category includes payments for salaries, wages, and other forms of employee compensation.

14-60© 2018 Pearson Education, Inc.

59

60

8/28/2019

31

Payments for Interest Expense and Income Tax Expense

14-61© 2018 Pearson Education, Inc.

Non-cash Expenses and Gains or Losses on Disposal of

Long-term Assets

• Non-cash expenses and gains or losses on disposal of long-term assets are reported on the income statement but are not included in the operating activities when using the direct method.

• The Indirect Method adjusts Net Income for these items. The Direct Method does not start with Net Income, so we can skip over these items that are not cash transactions from operating activities.

14-62© 2018 Pearson Education, Inc.

61

62

8/28/2019

32

Net Cash Provided by Operating

Activities

To calculate net cash provided by operating activities using the direct method, we add all the cash receipts and cash payments described previously and find the difference.

14-63© 2018 Pearson Education, Inc.

Learning Objective 5

Prepare the statement of cash flows by the indirect method using a spreadsheet (Appendix 14B)

14-64© 2018 Pearson Education, Inc.

63

64

8/28/2019

33

HOW IS THE STATEMENT OF CASH FLOWS PREPARED USING THE INDIRECT METHOD

AND A SPREADSHEET?

• Most companies use a spreadsheet to prepare the statement of cash flows.

• This statement starts with the beginning balance sheet and concludes with the ending balance sheet.

• Columns labeled “Transaction Analysis” hold the data for the statement of cash flows.

14-65© 2018 Pearson Education, Inc.

14-66© 2018 Pearson Education, Inc.

HOW IS THE STATEMENT OF CASH FLOWS PREPARED USING THE INDIRECT METHOD

AND A SPREADSHEET?

65

66

8/28/2019

34

14-67© 2018 Pearson Education, Inc.

14-68© 2018 Pearson Education, Inc.

67

68