Bills of Exchange LEARNING OBJECTIVES

66

CHAPTER 6 Bills of Exchange LEARNING OBJECTIVES After studying this chapter, you will be able to: ● state the meaning of bill of exchange and promissory note; ● describe features of bill of exchange and promissory note; ● identify the parties to a bill of exchange and a promissory note; ● distinguish between a bill of exchange and a promissory note; ● explain the meaning of different terms involved in the bill transaction, i.e. term of bill and days of grace, date of maturity, bill after date, negotiation, endorsement, discounting of bill, dishonour and noting of bill, insolvency of acceptor, retirement and renewal of a bill; and ● record accounting transactions of bills of exchange.

Transcript of Bills of Exchange LEARNING OBJECTIVES

180 ACCOUNTANCY

CHAPTER 6

Bills of Exchange

LEARNING OBJECTIVES

After studying this chapter, you will be able to:

● state the meaning of bill of exchange and promissory note;

● describe features of bill of exchange and promissory note;

● identify the parties to a bill of exchange and a promissorynote;

● distinguish between a bill of exchange and a promissorynote;

● explain the meaning of different terms involved in thebill transaction, i.e. term of bill and days of grace, date ofmaturity, bill after date, negotiation, endorsement,discounting of bill, dishonour and noting of bill, insolvencyof acceptor, retirement and renewal of a bill; and

● record accounting transactions of bills of exchange.

181BILLS OF EXCHANGE

Goods can be sold or bought for cashor on credit. When goods are sold orbought for cash, payment is received/made immediately .On the other handwhen goods are sold/bought on creditthen payment is deferred to a futuredate. In such a situation, instrumentsof credit are used through which thebuyer assures the seller that thepayment shall be made according tothe agreed conditions as stated in theinstrument of credit. The instrumentsof credit in India have been in use sincetime immemorial and are popularlyknown as Hundies .The hundies arewritten in Indian languages. Now-a-days these instruments of credit arecalled as bills of exchange orpromissory notes. The most importantpoint about these instruments is thatthey contain an unconditional orderto pay a certain amount on an agreeddate in case of bills of exchange andan unconditional promise to pay acertain sum of money on a certain datein case of promissory notes. Theseinstruments in India are governed bythe Indian Negotiable Instruments Act1881.

6.1 Meaning of Bills of Exchange

According to the Negotiable Instru-ments Act 1881, a bill of exchange isdefined as an instrument in writingcontaining an unconditional order,signed by the maker, directing acertain person to pay a certain sum ofmoney only to, or to the order of acertain person or to the bearer of theinstrument. The following features ofa bill of exchange emerge out on the

basis of this definition.

● A bill of exchange must be inwriting and not oral.

● It is an order to make payment.● The order to make payment is

unconditional.● The maker of the bill of

exchange must sign it.● The payment to be made must

be certain.● The date on which payment is

made must also be certain.● The bill of exchange must be

payable to a certain person.● The amount mentioned in the

bill of exchange is payable eitheron demand or on the expiry of afixed period of time.

● It must be stamped as per therequirement of law.

According to the Negotiable Instru-ments Act, a bill of exchange isgenerally drawn by the creditor on hisdebtor. It has to be accepted by thedebtor or someone else on his behalf.It is called a draft before its acceptance.Therefore, one of the underlyingfeatures of a bill of exchange is that ithas to be accepted either by the personupon whom it is drawn or by someoneelse on his/her behalf. For example,Amit sold goods to Rohit on credit forRs.10,000 for three months. If agreedso, Amit can draw a bill of exchangeupon Rohit for Rs. 10,000 payable afterthree months. Before it is accepted byRohit it will be called a draft. It willbecome a bill of exchange only whenRohit writes the word “accepted” on itand puts his signature to commu-nicate the acceptance.

182 ACCOUNTANCY

6.1.1 Parties to a Bill ofExchange

There are three parties to a bill ofexchange:

● Drawer is the maker of the billof exchange. A seller/creditorwho is entitled to receive moneyfrom the debtor can draw a billof exchange upon the buyer/debtor. The drawer after writingthe bill of exchange has to signit as maker of the bill.

● Drawee is the person uponwhom the bill of exchange isdrawn. Drawee is purchaser ofthe goods upon whom the billof exchange is drawn. The daweehas to write the word “accepted”if he accepts to make thepayment given in the bill on thedue date and has to put hissignatures on it. After thedrawee of a bill has signed hisassent on the face of the bill, heis called the acceptor and thisprocess is called acceptance. Abill of exchange becomes a legaldocument after acceptance andbinds the drawee to honour thebill on the due date. Acceptancehowever may be general orqualified. The general accep-tance requires signatures of theacceptor only without statingany conditions, thereto. However,mention of a bank or a specifiedplace of payment or partpayment thereof, makes theacceptance qualified.A qualified acceptance varies theexpress terms of the bill as

originally drawn and thereby thedrawer can refuse to considerthe bill as accepted. Sometimesthe bill of exchange may beaccepted by another person onbehalf of the drawee. Forexample a bill of exchangedrawn by Ram upon Shyam maybe accepted by Ghanshyam.

● Payee is the person to whom thepayment is made. The drawer ofthe bill himself will be the payeeif he keeps the bill with him tillthe date of its payment. Thepayee may change in thefollowing situations.

● In case the drawer has got thebill discounted, the person whohas discounted the bill willbecome the payee;

● In case the bill is transferred infavour of a creditor of the drawerthen the creditor will become thepayee.

Normally, the drawer and the payeeis the same person. Similarly, thedrawee and the acceptor is normallythe same person.

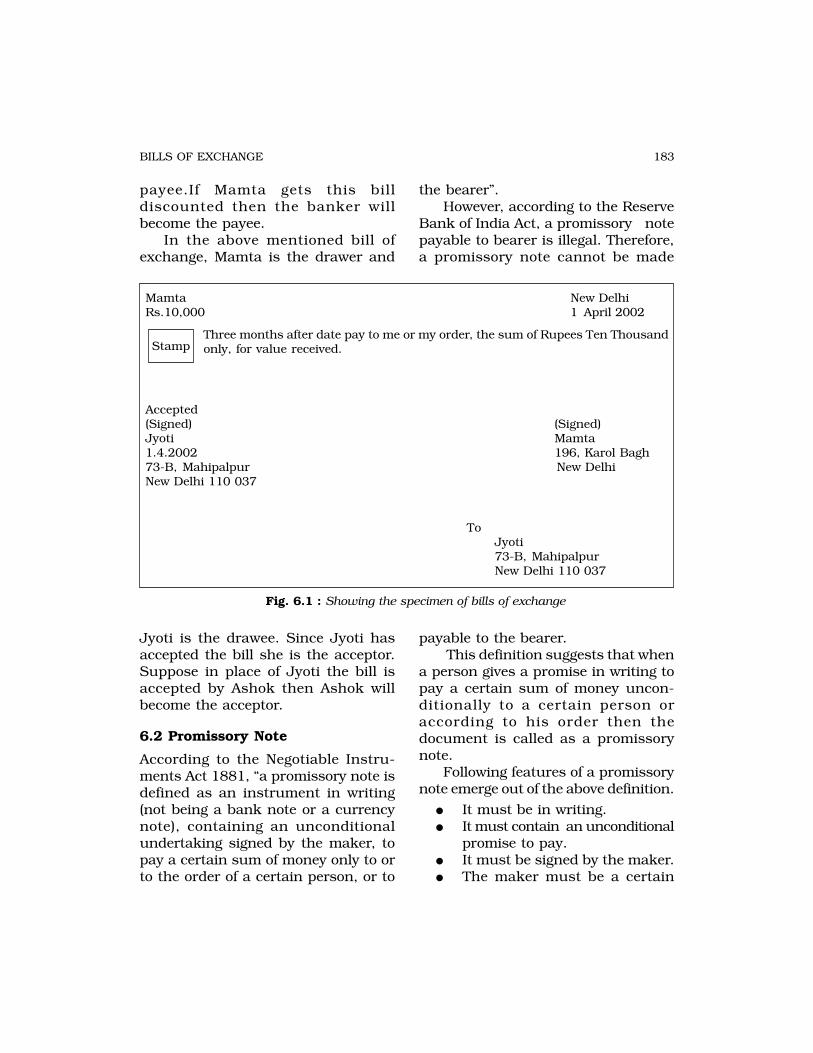

For example, Mamta sold goodsworth Rs.10, 000 to Jyoti and drewa bill of exchange upon her for thesame amount payable after threemonths. Here Mamta is the drawerof the bill and Jyoti is the drawee. Ifthe bill is retained by Mamta forthree months and the amount ofRs.10,000 is received by her on thedue date than Mamta will be thepayee.

If Mamta gives away this bill to hercreditor, Ruchi then Ruchi will be the

183BILLS OF EXCHANGE

payee.If Mamta gets this billdiscounted then the banker willbecome the payee.

In the above mentioned bill ofexchange, Mamta is the drawer and

Mamta New DelhiRs.10,000 1 April 2002

Three months after date pay to me or my order, the sum of Rupees Ten Thousandonly, for value received.

Accepted(Signed) (Signed)Jyoti Mamta1.4.2002 196, Karol Bagh73-B, Mahipalpur New DelhiNew Delhi 110 037

ToJyoti73-B, MahipalpurNew Delhi 110 037

Fig. 6.1 : Showing the specimen of bills of exchange

the bearer”.However, according to the Reserve

Bank of India Act, a promissory notepayable to bearer is illegal. Therefore,a promissory note cannot be made

Stamp

Jyoti is the drawee. Since Jyoti hasaccepted the bill she is the acceptor.Suppose in place of Jyoti the bill isaccepted by Ashok then Ashok willbecome the acceptor.

6.2 Promissory Note

According to the Negotiable Instru-ments Act 1881, “a promissory note isdefined as an instrument in writing(not being a bank note or a currencynote), containing an unconditionalundertaking signed by the maker, topay a certain sum of money only to orto the order of a certain person, or to

payable to the bearer. This definition suggests that when

a person gives a promise in writing topay a certain sum of money uncon-ditionally to a certain person oraccording to his order then thedocument is called as a promissorynote.

Following features of a promissorynote emerge out of the above definition.

● It must be in writing.● It must contain an unconditional

promise to pay.● It must be signed by the maker.● The maker must be a certain

184 ACCOUNTANCY

person.● The person to whom payment is

to be made must also be certain.● The sum payable must also be

certain.

● It should be properly stamped.

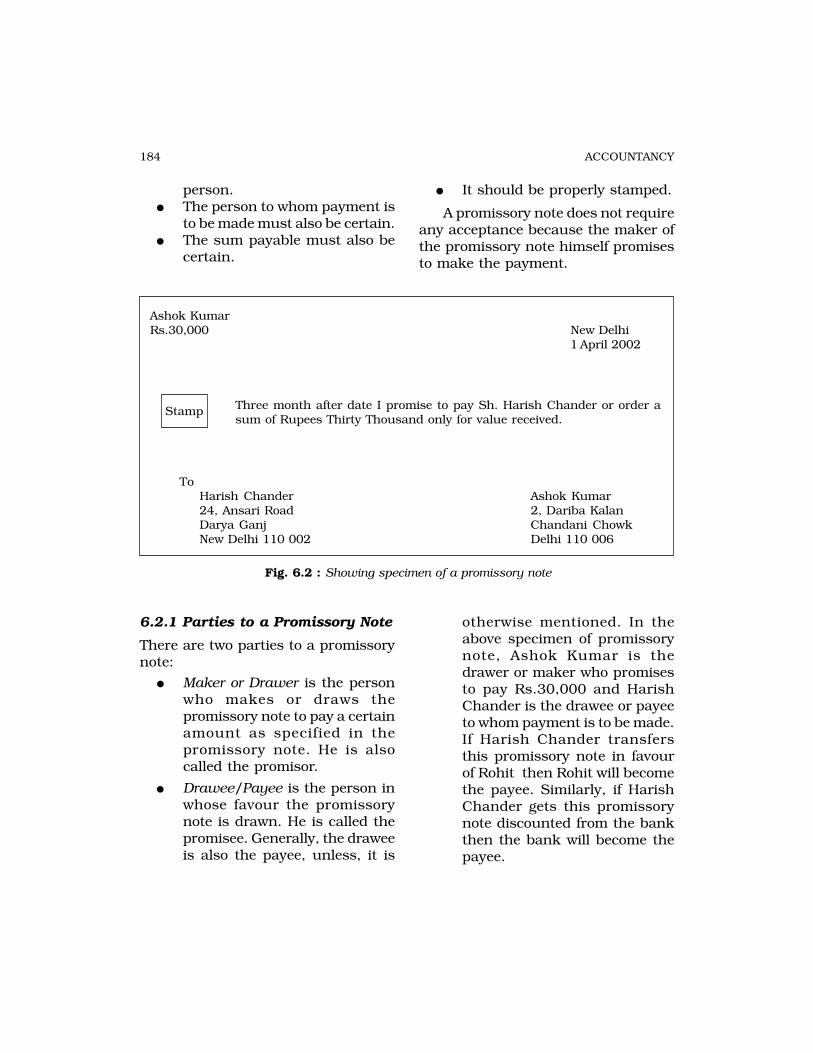

A promissory note does not requireany acceptance because the maker ofthe promissory note himself promisesto make the payment.

Ashok Kumar Rs.30,000 New Delhi

1 April 2002

Three month after date I promise to pay Sh. Harish Chander or order asum of Rupees Thirty Thousand only for value received.

ToHarish Chander Ashok Kumar24, Ansari Road 2, Dariba KalanDarya Ganj Chandani ChowkNew Delhi 110 002 Delhi 110 006

Fig. 6.2 : Showing specimen of a promissory note

Stamp

6.2.1 Parties to a Promissory Note

There are two parties to a promissorynote:

● Maker or Drawer is the personwho makes or draws thepromissory note to pay a certainamount as specified in thepromissory note. He is alsocalled the promisor.

● Drawee/Payee is the person inwhose favour the promissorynote is drawn. He is called thepromisee. Generally, the draweeis also the payee, unless, it is

otherwise mentioned. In theabove specimen of promissorynote, Ashok Kumar is thedrawer or maker who promisesto pay Rs.30,000 and HarishChander is the drawee or payeeto whom payment is to be made.If Harish Chander transfersthis promissory note in favourof Rohit then Rohit will becomethe payee. Similarly, if HarishChander gets this promissorynote discounted from the bankthen the bank will become thepayee.

185BILLS OF EXCHANGE

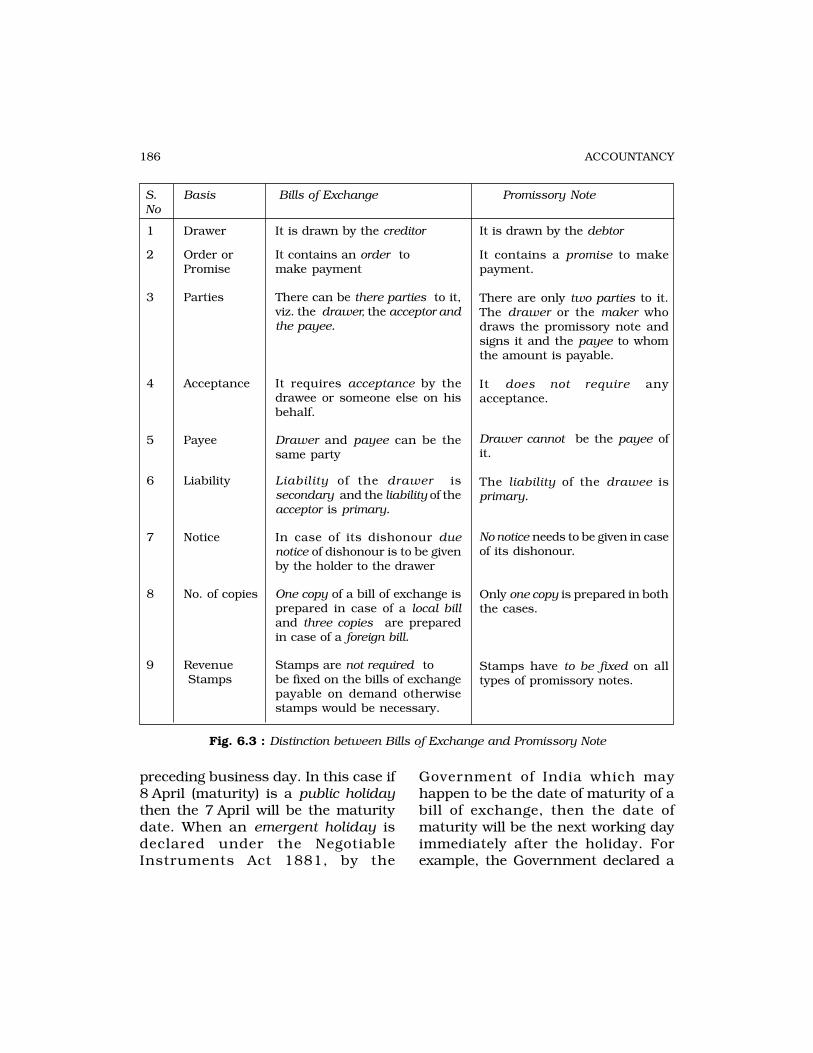

6.3 Distinction between a Bill ofExchange and a PromissoryNote

Both a bill of exchange and apromissory note are instruments ofcredit and are similar in many ways.However, there are certain basicdifferences between the two (fig. 6.3).

6.4 Advantages

The bills of exchange as instrumentsof credit are used frequently inbusiness because of the followingadvantages.

● Frame for Relationship: A bill ofexchange represents a device,which provides a framework forenabling the credit transactionbetween the seller /creditor andbuyer/debtor on an agreedbasis.

● Certainty of Terms and Conditions:The creditor knows the timewhen he would receive themoney so also debtor is fullyaware of the date by which hehas to pay the money. This isdue to the fact that terms andconditions of the relationshipbetween debtor and creditorsuch as amount required to bepaid; date of payment; interestto be paid, if any; place ofpayment are clearly mentionedin the bill of exchange.

● Convenient Mode of Credit: A billof exchange enables the buyerto buy the goods on credit andpay after the period of credit.However, the seller of goods evenafter extension of credit can get

payment immediately either bydiscounting the bill with thebank or by endorsing it in favourof a third party.

● Conclusive Proof: The bill ofexchange is a legal evidence ofa credit transaction implyingthereby that during the courseof trade buyer has obtainedcredit from the seller of thegoods, therefore, he is liable topay to the seller. In the event ofrefusal of making the payment,the law requires the creditor toobtain a certificate from theNotary to make it a conclusiveevidence of the happening.

● Easy Transferability: A debt canbe settled by transferring a billof exchange through endor-sement and delivery.

6.5 Maturity

When a bill of exchange or a promi-ssory note is not payable on demand,the payment is deferred to the date ofmaturity of the instrument. It is thedate on which the instrument becomesdue for payment. In arriving at thematurity date three days, known asdays of grace, must be added to thedate on which the instrument ispayable. Thus, if a bill dated March 5is payable 30 days after date it fallsdue on April 7, i.e. 33 days after March5. However, if it were payable onemonth after date, the due date wouldbe April 8, i.e. one month and 3 daysafter March 5. But where the date ofmaturity is a public holiday, theinstrument will become due on the

186 ACCOUNTANCY

S. Basis Bills of Exchange Promissory NoteNo

1 Drawer It is drawn by the creditor

2 Order or It contains an order toPromise make payment

3 Parties There can be there parties to it,viz. the drawer, the acceptor andthe payee.

4 Acceptance It requires acceptance by thedrawee or someone else on hisbehalf.

5 Payee Drawer and payee can be thesame party

6 Liability Liability of the drawer issecondary and the liability of theacceptor is primary.

7 Notice In case of its dishonour duenotice of dishonour is to be givenby the holder to the drawer

8 No. of copies One copy of a bill of exchange isprepared in case of a local billand three copies are preparedin case of a foreign bill.

9 Revenue Stamps are not required to Stamps be fixed on the bills of exchange

payable on demand otherwisestamps would be necessary.

It is drawn by the debtor

It contains a promise to makepayment.

There are only two parties to it.The drawer or the maker whodraws the promissory note andsigns it and the payee to whomthe amount is payable.

It does not require anyacceptance.

Drawer cannot be the payee ofit.

The liability of the drawee isprimary.

No notice needs to be given in caseof its dishonour.

Only one copy is prepared in boththe cases.

Stamps have to be fixed on alltypes of promissory notes.

Fig. 6.3 : Distinction between Bills of Exchange and Promissory Note

preceding business day. In this case if8 April (maturity) is a public holidaythen the 7 April will be the maturitydate. When an emergent holiday isdeclared under the NegotiableInstruments Act 1881, by the

Government of India which mayhappen to be the date of maturity of abill of exchange, then the date ofmaturity will be the next working dayimmediately after the holiday. Forexample, the Government declared a

187BILLS OF EXCHANGE

holiday on April 5, which happened tobe the day on which a bill of exchangedrawn by X upon Y for Rs.20,000became due for payment. Since 5 Aprilhas been declared a holiday under theNegotiable Instruments Act, therefore,April 6 will be the date of maturity forthis bill.

6.6 Negotiability

Negotiability means that the holder ofthe instrument can transfer the title.Bills of exchange and promissory notesare negotiable instruments within themeaning of Section 13 of NegotiableInstruments Act 1881, however in caseof promissory note the negotiation isrestricted, but it does not render it tothe status of not-negotiable instru-ment. This implies that a bill ofexchange can be transferred bynegotiation but a promissory notecannot be. However, this is subject tothe condition that the holder acquiresthem–

● without notice of defect in thetitle of the transferor, i.e. in goodfaith,

● for a consideration, and● before maturity.

If these conditions are met, it doesnot matter if the title of the transferorwas defective. Thus, if Rakesh steals abill of exchange and transfers it toRajesh who is not aware of Rakesh’smode of acquiring the bill and he takesit over for value and before the date ofits maturity, Rajesh will be entitled toget payment on the bill of exchange.However, if the words ‘or order’ areomitted from the bill, it cannot be

negotiated and becomes payable to theperson named therein and to himalone. Bills of exchange and promi-ssory notes can be passed on from oneperson to another by endorsement anddelivery. If a bill of exchange or apromissory note is dishonoured, thatis if payment is not made on the duedate by the drawee, the amount ofbill can be claimed from any of theprevious endorsers.

6.7 Endorsement of Bill

Any holder may transfer a bill unlessits transfer is restricted, i.e. the bill hasbeen negotiated containing wordsprohibiting its transfer.

The bill can be initially endorsedby the drawer by putting his signaturesat the back of the bill along with thename of the party to whom it isbeing transferred. The act of signingand transferring the bill is called‘endorsement’.

6.7.1 Effects of Endorsement

● Once an endorsement has beenmade, the person endorsing thebill is called an ‘endorser’. Theperson to whom the bill isendorsed is known as an‘endrosee’ and the bill is said tohave been ‘endorsed’.

● After a bill has been endorsedand delivered to a third person(endorsee), it would becomepayable to him instead oforiginal holder (endorsee). Theendorsee may again endorse itin favour of a fourth person(unless endorsement is restricted)

188 ACCOUNTANCY

and this may continue to anyextent till the date of maturity.

● An unrestricted endorsementprovides a mechanism forsettling the business payments.

6.7.2 Types of Endorsement

A bill may be endorsed in any one ofthe following ways:

● Blank Endorsement : It requiressignatures to be put by thetransferor, as follows:

Signed“Raja Ram”

This makes the bill transferable bymere delivery.

● Special Endorsement: Specialendorsement necessitates wri-ting the name of the party inwhose favour the property rightsof the bill are endorsed underthe signature of the endorser. Suppose Vishal & Co wantsto endorse a bill in favour ofArun & Co., it will be shown atthe back of the bill as follows.

“Pay Arun & Co. or order” Vishal & Co.

Official Signatory or Stamp

● Restricted Endorsement: This isan endorsement in favour of adefinite person, and to himalone. This restricts furtherendorsement of the bill. This isexpressed as follows:

“Pay Rakesh only”SignedAjay

● Endorsement Sans Recourse(i.e. Without recourse): Theendorsement of the bill in thismanner enables the endorser torelieve himself from the liabilityto all subsequent endorseesindicated by the word “SansRecourse” added to the signa-tures. This is generally made bypersons who acts in a repre-sentative capacity as agents andnot as principal. The endorse-ment is done in the following way;

“Pay Varun or order”SignedAnkit

Sans Recource

● Facultative Endorsement: Thisis the endorsement by whichthe endorser waives some of therights to which he is entitled.The right which is given up isclearly stated as a part of theendorsement itself. The endorse-ment is effected in the followingmanner:

“Pay Aleem or orderNotice of dishonour waived”

SignedRaja Ram

The implication of this is that thenotice of dishonour need not be givenby the endorsee before demanding thepayment from the endorser.

6.8 Accounting Treatment

For the person who draws the bill ofexchange and gets it back, after its due

189BILLS OF EXCHANGE

acceptance, it becomes a billreceivable. For the person who acceptsit, the same becomes bills payable.In case of a promissory note for themaker it is a bills payable and for theperson in whose favour the promissorynote is drawn it is a note receivable.Bills/Notes receivables are assets andBills/Notes payables are liabilities.

Bills and Notes are usedinterchangeably.

6.8.1 Books of ReceiverA bill receivable can be treated in thefollowing four ways by its receiver.

● He can retain it till the date ofmaturity, and(i) get it collected on date of

maturity directly, or(ii) get it collected through the

banker.● He can get the bill discounted

from the bank.● He can endorse the bill in favour

of his Creditor.● He can pledge the bill receivable

as a security for obtaining cashcredit and overeraft facilities.

The accounting treatment in thebooks of receiver under all the fouralternatives is given below under theassumption that the bill is dulyhonoured on maturity by the acceptor.

1. (a) When the bill of exchange isretained by the receiver withhim till the date of its maturity,the following journal entriesare passed.

On receiving the billBills Receivables A/c Dr.

Debtors. A/c

On maturity of the bill

Cash/Bank A/c Dr. Bills Receivable A/c

(b) When the bill of exchange isretained by the receiver with himand sent to bank for collection afew days before maturity.

For sending the bill for collection

Bills sent for collection A/c Dr. Bills Receivable A/c

(c) On receiving the advice from thebank that the bill has beencollectedBank A/c Dr. Bills sent for collection A/c

1. When the receiver gets the billdiscounted from the bank.

On receiving the bill

Bills Receivable A/c Dr.Debtors. A/c

On discounting the billBank A/c Dr.Discount A/c Dr.

Bills Receivable A/cOn maturity

No Entry

Since the bill becomes the property ofthe bank, therefore, the bank willcollect the amount of the bill from theacceptor and no journal entry will bepassed in the books of the receiver.

2. When the bill is endorsed by thereceiver in favour of his Creditor–

On receiving the bill

Bills Receivable A/c Dr. Debtor’s A/c

On endorsing the bill

Creditor A/c Dr. Bills Receivable A/c

On maturityNo Entry

190 ACCOUNTANCY

Since the bill has been transferred infavour of the creditor, therefore thecreditor becomes its owner and willreceive the payment on maturity.Hence, no entry will be passed in thebooks of the receiver.

3. For pledging the bills receivables asa security for obtaining cash creditand overdraft facilities:

Pledging of the bill is a legal-cum-financial arrangement with thebank, whereby the bank authorizesthe customer to make withdrawalsup to a specific amount. This factis noted as a marking on theaccount of the customer in thebank’s ledger and no journal entryis required until the customeractually withdraws the money.However, such a pledged bill isalways collected through the bankonly because bank has the firstright to claim the amount of thebill. The journal entries to bepassed for this are as follows:

On Pledging the billNo Entry

On Maturity

(i) Bills sent for collection A/c Dr. Bills Receivable A/c

(ii) Bank A/c Dr. Bills sent for collection A/c

6.9 Books of Acceptor/Promissor

The following journal entries arepassed in the books of the acceptorunder all the four circumstancesdiscussed above.

On accepting the billCreditor’s A/c Dr. Bills payable A/c

On maturity of the billBills payable A/c Dr. Bank A/c

The journal entries in the books ofthe drawer and the acceptor under allthe four cases have been given in theform of a table for better understanding.

1. When the drawer retains the bill with him till the date of its maturity and gets thesame collected directly.

Transaction Books of Books ofCreditor/Drawer Debtor/Acceptor

Sale/Purchase of Debtor’s A/c Dr. Purchase A/c Dr.goods Sales A/c Creditor’s A/c

Receiving/Accepting Bills Receivable A/c Dr. Creditor’s A/c Dr.the bill Debtor’s A/c Bills Payable A/c

Collection of the bill Cash/Bank A/c Dr. Bills Payable A/c Dr. Bills Receivable A/c Dr. Cash/Bank A/c

191BILLS OF EXCHANGE

2. When the bill is retained by the drawer with him and sent to bank for collection afew days before maturity.

Transaction Books of Books ofCreditor/Drawer Debtor/Acceptor

Sale/Purchase of Debtor’s A/c Dr. Purchase A/c Dr.goods Sales A/c Creditor’s A/c

Receiving/Accepting Bills Receivable A/c Dr. Creditor’s A/c Dr.the bill Debtor’s A/c Bills Payable A/c

Sending the bill Bills sent for collection A/c No Entryfor collection Bill Receivable A/c Dr.

On Receiving the Bank A/c Dr. Bills Payable A/c Dr.bank advice that the Bill sent for collection A/c Bank A/cbill has been collected

3. When the drawer gets the bill discounted from the bank.

Transaction Books of Books ofCreditor/Drawer Debtor/Acceptor

Sale/Purchase of Debtor’s A/c Dr. Purchase A/c Dr.goods Sales A/c Creditor’s A/c

Receiving/Accepting Bills Receivable A/c Dr. Creditor’s A/c Dr.the bill Debtor’s A/c Bills Payable A/c

Discounting the bill Bank A/c Dr.Discount A/c Dr. No Entry Bill Receivable A/c

On maturity of the No Entry Bills Payable A/c Dr.bill Bank A/c

4. When the bill is endorsed by the drawer in favour of his creditor.

Transaction Books of Books ofCreditor/Drawer Debtor/Acceptor

Sale/Purchase of Debtor’s A/c Dr. Purchase A/c Dr.goods Sales A/c Creditor’s A/c

Receiving/Accepting Bills Receivable A/c Dr. Creditor’s A/c Dr.the bill Debtor’s A/c Bills Payable A/c

Endorsing the bill Creditor’s A/c Dr. No Entry Bill Receivable A/c

On maturity of the No Entry Bills Payable A/c Dr.bill Bank A/c

192 ACCOUNTANCY

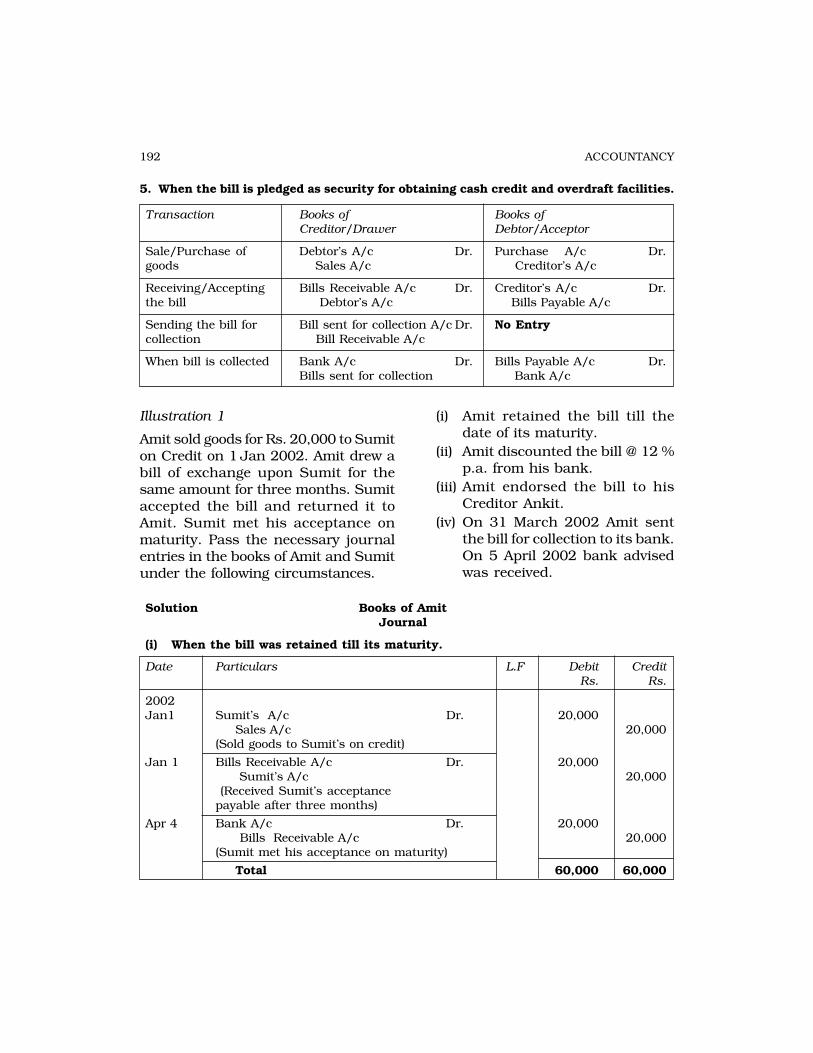

5. When the bill is pledged as security for obtaining cash credit and overdraft facilities.

Transaction Books of Books ofCreditor/Drawer Debtor/Acceptor

Sale/Purchase of Debtor’s A/c Dr. Purchase A/c Dr.goods Sales A/c Creditor’s A/c

Receiving/Accepting Bills Receivable A/c Dr. Creditor’s A/c Dr.the bill Debtor’s A/c Bills Payable A/c

Sending the bill for Bill sent for collection A/c Dr. No Entrycollection Bill Receivable A/c

When bill is collected Bank A/c Dr. Bills Payable A/c Dr.Bills sent for collection Bank A/c

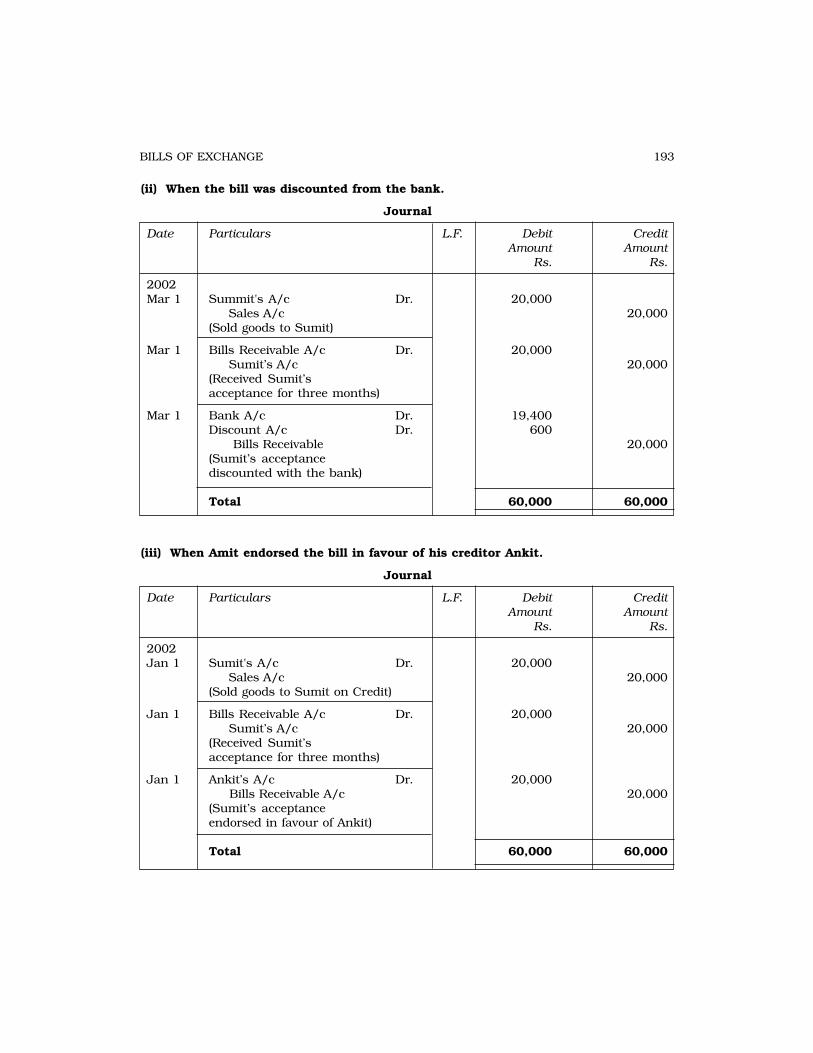

Illustration 1

Amit sold goods for Rs. 20,000 to Sumiton Credit on 1 Jan 2002. Amit drew abill of exchange upon Sumit for thesame amount for three months. Sumitaccepted the bill and returned it toAmit. Sumit met his acceptance onmaturity. Pass the necessary journalentries in the books of Amit and Sumitunder the following circumstances.

(i) Amit retained the bill till thedate of its maturity.

(ii) Amit discounted the bill @ 12 %p.a. from his bank.

(iii) Amit endorsed the bill to hisCreditor Ankit.

(iv) On 31 March 2002 Amit sentthe bill for collection to its bank.On 5 April 2002 bank advisedwas received.

Solution Books of AmitJournal

(i) When the bill was retained till its maturity.

Date Particulars L.F Debit CreditRs. Rs.

2002Jan1 Sumit’s A/c Dr. 20,000

Sales A/c 20,000(Sold goods to Sumit’s on credit)

Jan 1 Bills Receivable A/c Dr. 20,000 Sumit’s A/c 20,000 (Received Sumit’s acceptancepayable after three months)

Apr 4 Bank A/c Dr. 20,000 Bills Receivable A/c 20,000(Sumit met his acceptance on maturity)

Total 60,000 60,000

193BILLS OF EXCHANGE

(ii) When the bill was discounted from the bank.

Journal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2002Mar 1 Summit's A/c Dr. 20,000

Sales A/c 20,000(Sold goods to Sumit)

Mar 1 Bills Receivable A/c Dr. 20,000 Sumit’s A/c 20,000(Received Sumit’sacceptance for three months)

Mar 1 Bank A/c Dr. 19,400Discount A/c Dr. 600 Bills Receivable 20,000(Sumit’s acceptancediscounted with the bank)

Total 60,000 60,000

(iii) When Amit endorsed the bill in favour of his creditor Ankit.

Journal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2002Jan 1 Sumit's A/c Dr. 20,000

Sales A/c 20,000(Sold goods to Sumit on Credit)

Jan 1 Bills Receivable A/c Dr. 20,000 Sumit’s A/c 20,000(Received Sumit’sacceptance for three months)

Jan 1 Ankit’s A/c Dr. 20,000 Bills Receivable A/c 20,000(Sumit’s acceptanceendorsed in favour of Ankit)

Total 60,000 60,000

194 ACCOUNTANCY

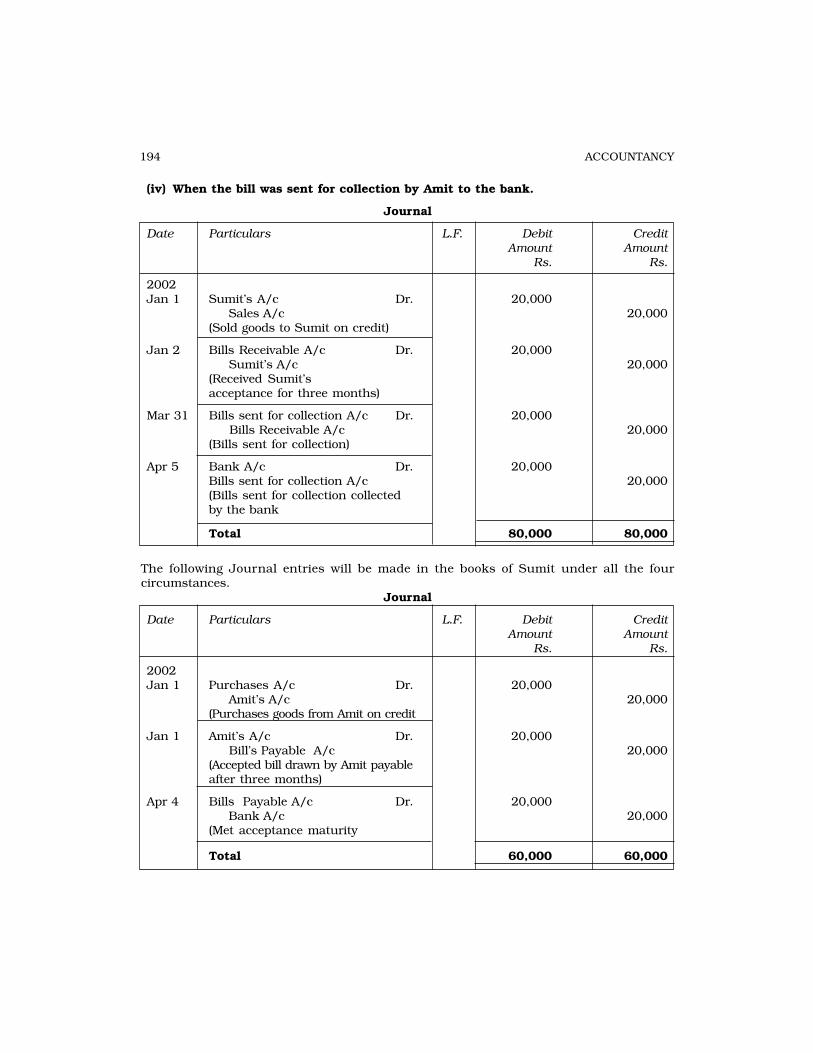

(iv) When the bill was sent for collection by Amit to the bank.

Journal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2002Jan 1 Sumit’s A/c Dr. 20,000

Sales A/c 20,000(Sold goods to Sumit on credit)

Jan 2 Bills Receivable A/c Dr. 20,000 Sumit’s A/c 20,000(Received Sumit’sacceptance for three months)

Mar 31 Bills sent for collection A/c Dr. 20,000 Bills Receivable A/c 20,000(Bills sent for collection)

Apr 5 Bank A/c Dr. 20,000Bills sent for collection A/c 20,000(Bills sent for collection collectedby the bank

Total 80,000 80,000

The following Journal entries will be made in the books of Sumit under all the fourcircumstances.

Journal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2002Jan 1 Purchases A/c Dr. 20,000

Amit’s A/c 20,000(Purchases goods from Amit on credit

Jan 1 Amit’s A/c Dr. 20,000 Bill’s Payable A/c 20,000(Accepted bill drawn by Amit payableafter three months)

Apr 4 Bills Payable A/c Dr. 20,000 Bank A/c 20,000(Met acceptance maturity

Total 60,000 60,000

195BILLS OF EXCHANGE

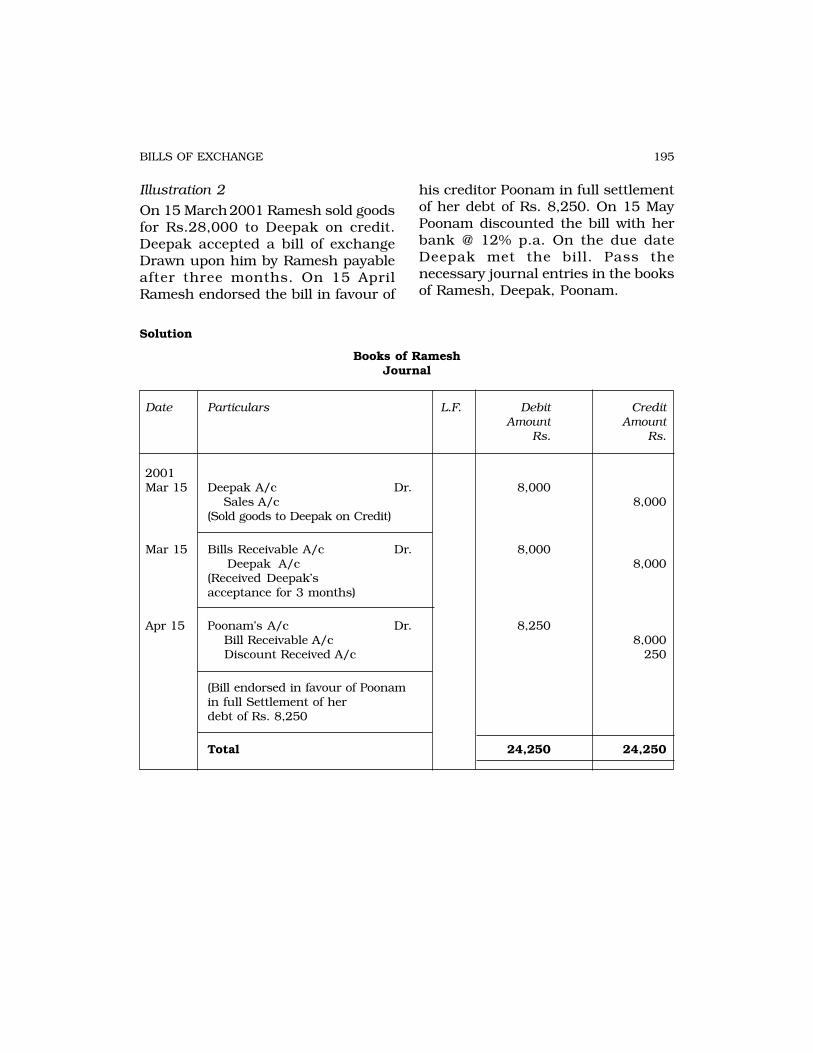

his creditor Poonam in full settlementof her debt of Rs. 8,250. On 15 MayPoonam discounted the bill with herbank @ 12% p.a. On the due dateDeepak met the bill. Pass thenecessary journal entries in the booksof Ramesh, Deepak, Poonam.

Illustration 2

On 15 March 2001 Ramesh sold goodsfor Rs.28,000 to Deepak on credit.Deepak accepted a bill of exchangeDrawn upon him by Ramesh payableafter three months. On 15 AprilRamesh endorsed the bill in favour of

Solution

Books of RameshJournal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2001Mar 15 Deepak A/c Dr. 8,000

Sales A/c 8,000(Sold goods to Deepak on Credit)

Mar 15 Bills Receivable A/c Dr. 8,000 Deepak A/c 8,000(Received Deepak’sacceptance for 3 months)

Apr 15 Poonam’s A/c Dr. 8,250 Bill Receivable A/c 8,000 Discount Received A/c 250

(Bill endorsed in favour of Poonamin full Settlement of herdebt of Rs. 8,250

Total 24,250 24,250

196 ACCOUNTANCY

Books of DeepakJournal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2001Mar 5 Purchase A/c Dr. 8,000

Ramesh A/c 8,000(Purchased goods on creditfrom Ramesh)

Mar 5 Ramesh’s A/c Dr. 8,000 Bills Payable A/c 8,000(Accepted Ramesh’s draftpayable after 3 months)

June 18 Bills Payable A/c Dr. 8,000 Bank A/c 8,000(Met the acceptance in favourof Ramesh on maturity)

Total 24,000 24,000

Books of PoonamJournal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2001May 15 Bills Receivable A/c Dr. 8,000

Discount Allowed A/c Dr. 250 (Ramesh’s A/c 8,250(Ramesh endrosed Deepak’sacceptance in our favour fordischarge has debt of Rs. 8,250in full settlement)

May 15 Bank A/c Dr. 7,920 Discount allowed A/c Dr. 80 Bills Receivable A/c 8,000

Total 16,250 16,250

197BILLS OF EXCHANGE

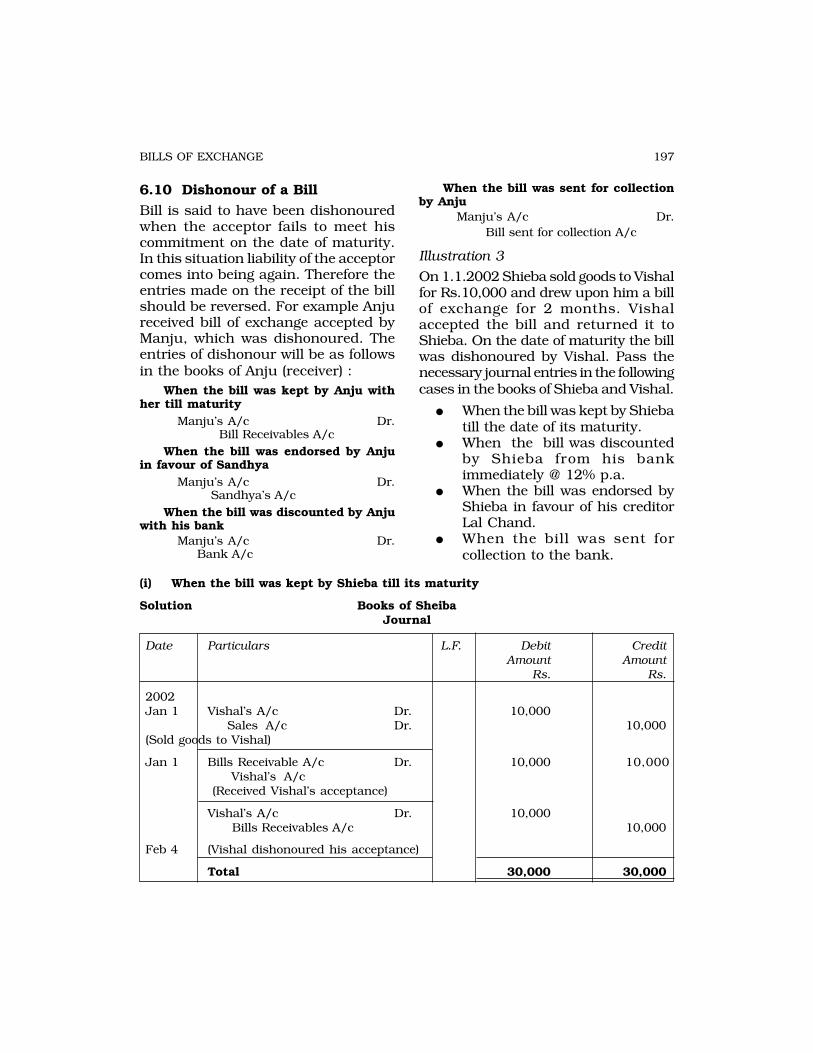

6.10 Dishonour of a BillBill is said to have been dishonouredwhen the acceptor fails to meet hiscommitment on the date of maturity.In this situation liability of the acceptorcomes into being again. Therefore theentries made on the receipt of the billshould be reversed. For example Anjureceived bill of exchange accepted byManju, which was dishonoured. Theentries of dishonour will be as followsin the books of Anju (receiver) :

When the bill was kept by Anju withher till maturity

Manju’s A/c Dr. Bill Receivables A/cWhen the bill was endorsed by Anju

in favour of SandhyaManju’s A/c Dr.

Sandhya’s A/cWhen the bill was discounted by Anju

with his bankManju’s A/c Dr. Bank A/c

When the bill was sent for collectionby Anju

Manju’s A/c Dr. Bill sent for collection A/c

Illustration 3

On 1.1.2002 Shieba sold goods to Vishalfor Rs.10,000 and drew upon him a billof exchange for 2 months. Vishalaccepted the bill and returned it toShieba. On the date of maturity the billwas dishonoured by Vishal. Pass thenecessary journal entries in the followingcases in the books of Shieba and Vishal.

● When the bill was kept by Shiebatill the date of its maturity.

● When the bill was discountedby Shieba from his bankimmediately @ 12% p.a.

● When the bill was endorsed byShieba in favour of his creditorLal Chand.

● When the bill was sent forcollection to the bank.

(i) When the bill was kept by Shieba till its maturity

Solution Books of SheibaJournal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2002Jan 1 Vishal’s A/c Dr. 10,000

Sales A/c Dr. 10,000(Sold goods to Vishal)

Jan 1 Bills Receivable A/c Dr. 10,000 10,000 Vishal’s A/c (Received Vishal’s acceptance)

Vishal’s A/c Dr. 10,000 Bills Receivables A/c 10,000

Feb 4 (Vishal dishonoured his acceptance)

Total 30,000 30,000

198 ACCOUNTANCY

(ii) When the bill was discounted by Shieba

Journal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2002Jan 1 Vishal’s A/c Dr. 10,000

Sales A/c Dr. 10,000(Sold goods to Vishal)

Jan 1 (Bills Receivable A/c) Dr. 10,000 Vishal’s A/c 10,000 (Received Vishal’s acceptance)

Jan 1 Bank A/c Dr. 9,800 Discount A/c Dr. 200Bills Receivable A/c 10,000(Vishal’s Bill discounted)

Mar 4 Vishal’s A/c Dr. 10,000 Bank A/c 10,000(Discounted bill dishonouredby Vishal)

Total 40,000 40,000

(iii) When the bill was endorsed by Shieba to Lal Chand

Journal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2002Jan 1 Vishal’s A/c Dr. 10,000

Sales A/c 10,000(Sold goods to Vishal)

Jan 1 Bills Receivable A/c Dr. 10,000 Vishal’s A/c 10,000(Receivable Vishal’s acceptance

Jan 1 Lal Chand’s A/c Dr. 10,000 Bills Receivable A/c 10,000(Vishal’s acceptance endorsed infavour of Lal Chand)

Mar 4 Vishal’s A/c Dr. 10,000 Lal Chand’s A/c 10,000(Endorsed bill dishonoured by Vishal)

Total 40,000 40,000

199BILLS OF EXCHANGE

The following entires will be passed in the books of Vishal in all the four cases

Books of Vishal Journal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2002Jan 1 Purchases A/c Dr. 10,000

Shieba’s A/c 10,000(Purchased goods from Shieba)

Jan 1 Shieba’s A/c Dr. 10,000 Bills Payable A/c 10,000(Accepted Shieba’s draft)

Mar 4 Bills Payable A/ Dr. 10,000 Shieba’s A/c 10,000(Acceptance in favour ofShieba dishonoured)

Total 30,000 30,000

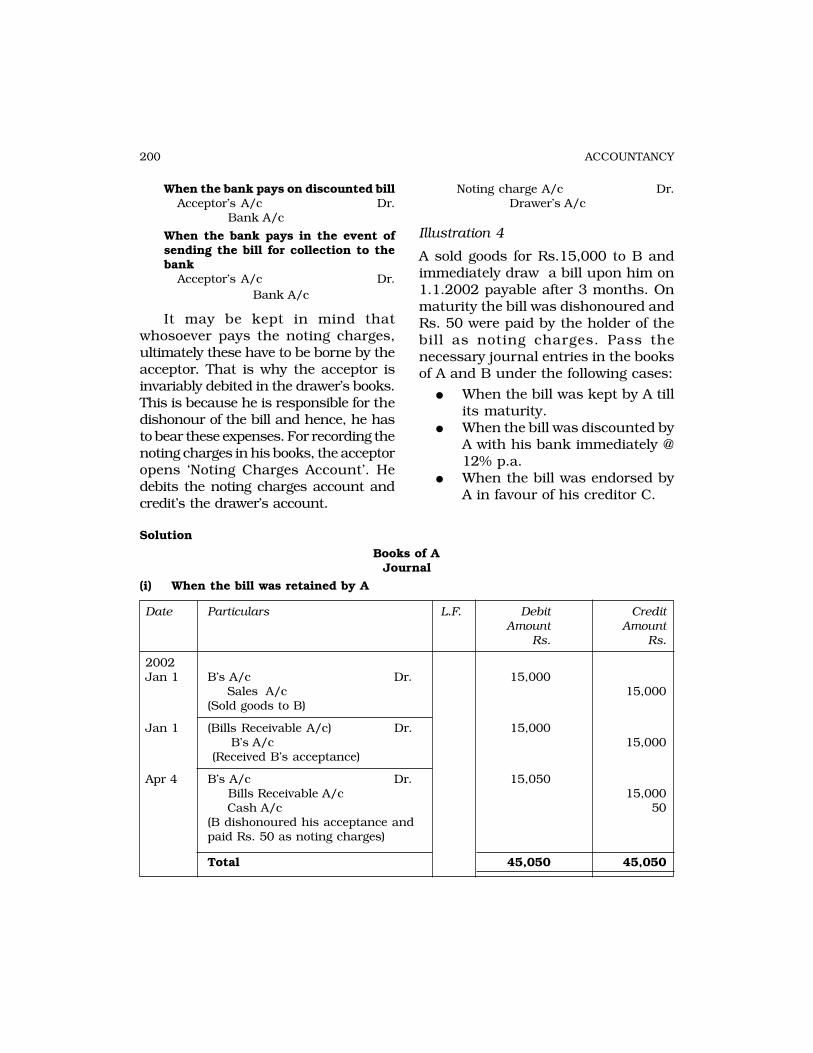

6.11 Noting Charges

A bill of exchange should be dulypresented for payment on the date ofits maturity. Acceptor is absolved ofhis liability if the bill is not dulypresented. Proper presentation of thebill means that it should be presentedon the date of maturity to theacceptor during business workinghours. To establish beyond doubtthat the bill was dishonoured, despiteits due presentation, it has gotpreferably to be “noted” by ‘NotaryPublic’. Therefore, ‘Noting’ authen-ticates the facts of dishonour. Forproviding this service, a fees ischarged which is called “NotingCharges”.

The following facts are generallynoted by the Notary:

● Date, fact and reasons ofdishonour,

● If the bill is not expresslydishonoured, the reasons whyhe treats it as dishonoured,and

● The amount of noting charges.

The entries for noting charges inthe drawers books will be as follows:

When Drawer himself paysAcceptor’s A/c Dr. Cash A/c

Where endorsee paysAcceptor’s A/c Dr. Endorsee A/c

200 ACCOUNTANCY

When the bank pays on discounted billAcceptor’s A/c Dr. Bank A/c

When the bank pays in the event ofsending the bill for collection to thebank

Acceptor’s A/c Dr. Bank A/c

It may be kept in mind thatwhosoever pays the noting charges,ultimately these have to be borne by theacceptor. That is why the acceptor isinvariably debited in the drawer’s books.This is because he is responsible for thedishonour of the bill and hence, he hasto bear these expenses. For recording thenoting charges in his books, the acceptoropens ‘Noting Charges Account’. Hedebits the noting charges account andcredit’s the drawer’s account.

Noting charge A/c Dr. Drawer’s A/c

Illustration 4

A sold goods for Rs.15,000 to B andimmediately draw a bill upon him on1.1.2002 payable after 3 months. Onmaturity the bill was dishonoured andRs. 50 were paid by the holder of thebill as noting charges. Pass thenecessary journal entries in the booksof A and B under the following cases:

● When the bill was kept by A tillits maturity.

● When the bill was discounted byA with his bank immediately @12% p.a.

● When the bill was endorsed byA in favour of his creditor C.

Solution

Books of AJournal

(i) When the bill was retained by A

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2002Jan 1 B’s A/c Dr. 15,000

Sales A/c 15,000(Sold goods to B)

Jan 1 (Bills Receivable A/c) Dr. 15,000 B’s A/c 15,000 (Received B’s acceptance)

Apr 4 B’s A/c Dr. 15,050 Bills Receivable A/c 15,000 Cash A/c 50(B dishonoured his acceptance andpaid Rs. 50 as noting charges)

Total 45,050 45,050

201BILLS OF EXCHANGE

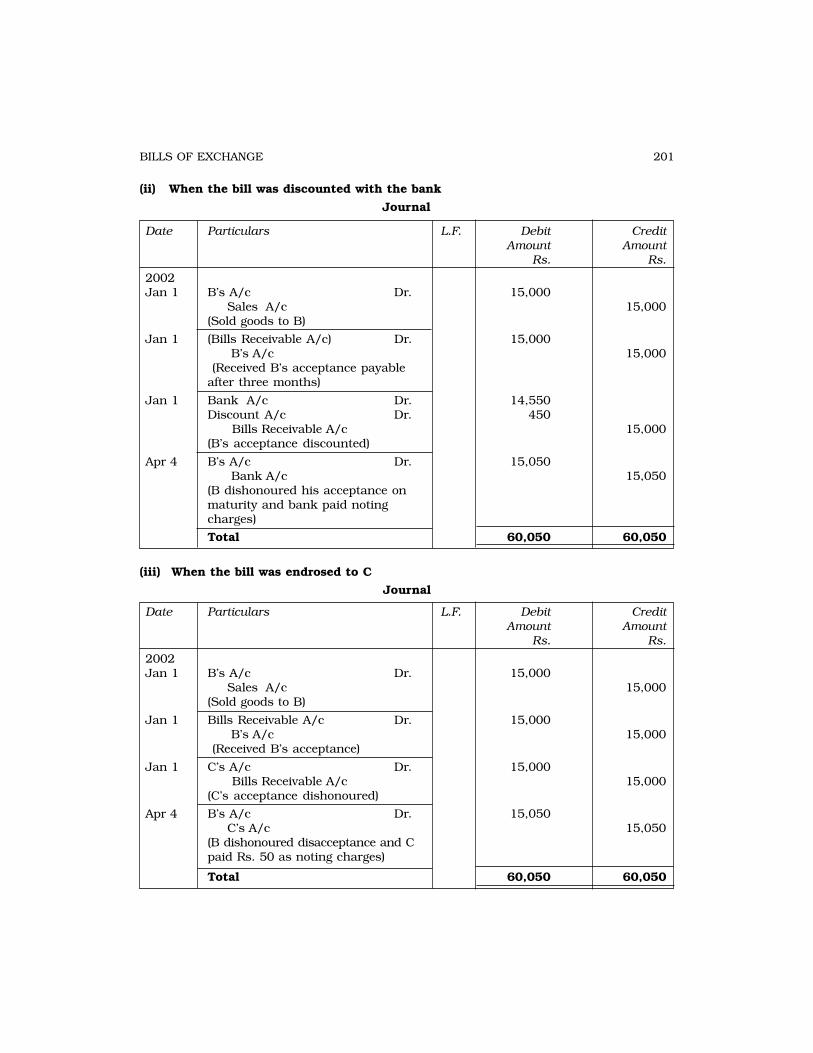

(ii) When the bill was discounted with the bank

Journal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2002Jan 1 B’s A/c Dr. 15,000

Sales A/c 15,000(Sold goods to B)

Jan 1 (Bills Receivable A/c) Dr. 15,000 B’s A/c 15,000 (Received B’s acceptance payableafter three months)

Jan 1 Bank A/c Dr. 14,550Discount A/c Dr. 450 Bills Receivable A/c 15,000(B’s acceptance discounted)

Apr 4 B’s A/c Dr. 15,050 Bank A/c 15,050(B dishonoured his acceptance onmaturity and bank paid notingcharges)

Total 60,050 60,050

(iii) When the bill was endrosed to C

Journal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2002Jan 1 B’s A/c Dr. 15,000

Sales A/c 15,000(Sold goods to B)

Jan 1 Bills Receivable A/c Dr. 15,000 B’s A/c 15,000 (Received B’s acceptance)

Jan 1 C’s A/c Dr. 15,000 Bills Receivable A/c 15,000(C’s acceptance dishonoured)

Apr 4 B’s A/c Dr. 15,050 C’s A/c 15,050(B dishonoured disacceptance and Cpaid Rs. 50 as noting charges)

Total 60,050 60,050

202 ACCOUNTANCY

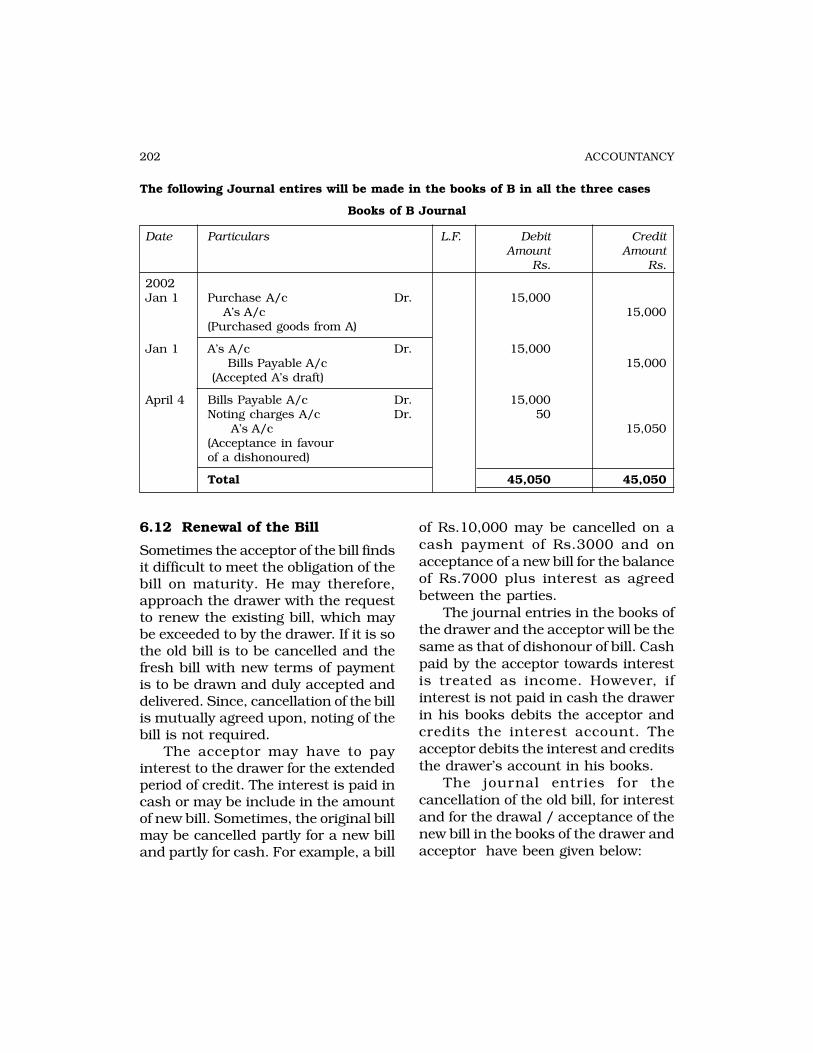

The following Journal entires will be made in the books of B in all the three cases

Books of B Journal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2002Jan 1 Purchase A/c Dr. 15,000

A’s A/c 15,000(Purchased goods from A)

Jan 1 A’s A/c Dr. 15,000 Bills Payable A/c 15,000 (Accepted A’s draft)

April 4 Bills Payable A/c Dr. 15,000Noting charges A/c Dr. 50 A’s A/c 15,050(Acceptance in favourof a dishonoured)

Total 45,050 45,050

6.12 Renewal of the Bill

Sometimes the acceptor of the bill findsit difficult to meet the obligation of thebill on maturity. He may therefore,approach the drawer with the requestto renew the existing bill, which maybe exceeded to by the drawer. If it is sothe old bill is to be cancelled and thefresh bill with new terms of paymentis to be drawn and duly accepted anddelivered. Since, cancellation of the billis mutually agreed upon, noting of thebill is not required.

The acceptor may have to payinterest to the drawer for the extendedperiod of credit. The interest is paid incash or may be include in the amountof new bill. Sometimes, the original billmay be cancelled partly for a new billand partly for cash. For example, a bill

of Rs.10,000 may be cancelled on acash payment of Rs.3000 and onacceptance of a new bill for the balanceof Rs.7000 plus interest as agreedbetween the parties.

The journal entries in the books ofthe drawer and the acceptor will be thesame as that of dishonour of bill. Cashpaid by the acceptor towards interestis treated as income. However, ifinterest is not paid in cash the drawerin his books debits the acceptor andcredits the interest account. Theacceptor debits the interest and creditsthe drawer’s account in his books.

The journal entries for thecancellation of the old bill, for interestand for the drawal / acceptance of thenew bill in the books of the drawer andacceptor have been given below:

203BILLS OF EXCHANGE

Transaction Books of Drawer Books of Acceptor

Cancellation Acceptor’s A/c Dr. Bills Payable A/c Dr.of old bill Bills Receivable A/c Drawer’s A/c

Interest Acceptor’s A/c Dr. Interest A/c Dr. Interest A/c Drawer’s A/c

New Bill Bill Receivable A/c Dr. Drawer’s A/c Dr. Acceptor’s A/c Bills Payable A/c

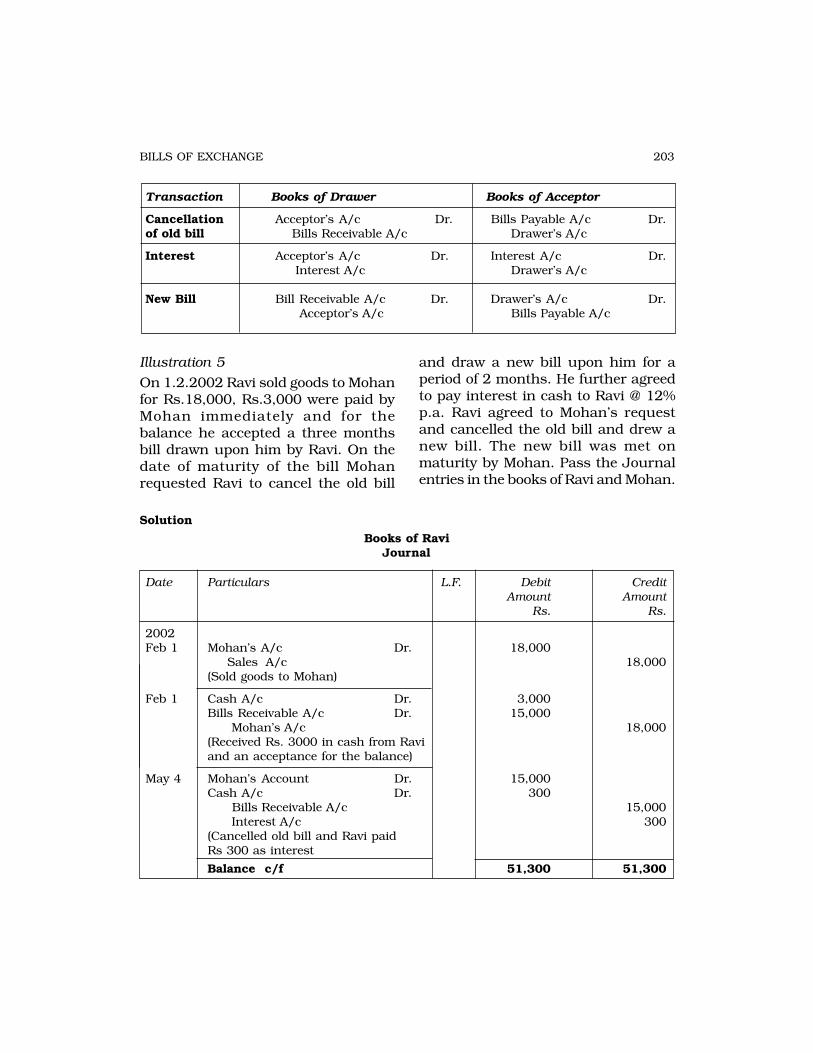

Illustration 5

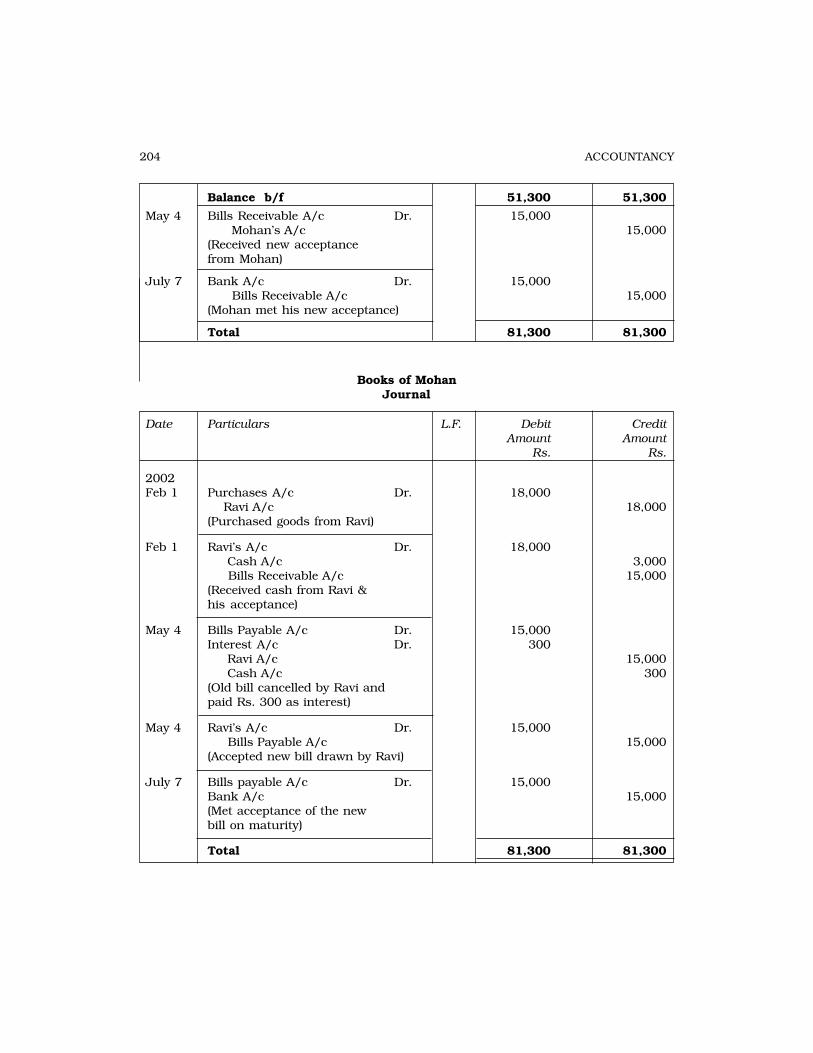

On 1.2.2002 Ravi sold goods to Mohanfor Rs.18,000, Rs.3,000 were paid byMohan immediately and for thebalance he accepted a three monthsbill drawn upon him by Ravi. On thedate of maturity of the bill Mohanrequested Ravi to cancel the old bill

and draw a new bill upon him for aperiod of 2 months. He further agreedto pay interest in cash to Ravi @ 12%p.a. Ravi agreed to Mohan’s requestand cancelled the old bill and drew anew bill. The new bill was met onmaturity by Mohan. Pass the Journalentries in the books of Ravi and Mohan.

Solution

Books of RaviJournal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2002Feb 1 Mohan’s A/c Dr. 18,000

Sales A/c 18,000(Sold goods to Mohan)

Feb 1 Cash A/c Dr. 3,000Bills Receivable A/c Dr. 15,000 Mohan’s A/c 18,000(Received Rs. 3000 in cash from Raviand an acceptance for the balance)

May 4 Mohan’s Account Dr. 15,000Cash A/c Dr. 300 Bills Receivable A/c 15,000 Interest A/c 300(Cancelled old bill and Ravi paidRs 300 as interest

Balance c/f 51,300 51,300

204 ACCOUNTANCY

Balance b/f 51,300 51,300

May 4 Bills Receivable A/c Dr. 15,000 Mohan’s A/c 15,000(Received new acceptancefrom Mohan)

July 7 Bank A/c Dr. 15,000 Bills Receivable A/c 15,000(Mohan met his new acceptance)

Total 81,300 81,300

Books of MohanJournal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2002Feb 1 Purchases A/c Dr. 18,000

Ravi A/c 18,000(Purchased goods from Ravi)

Feb 1 Ravi’s A/c Dr. 18,000 Cash A/c 3,000 Bills Receivable A/c 15,000(Received cash from Ravi &his acceptance)

May 4 Bills Payable A/c Dr. 15,000Interest A/c Dr. 300 Ravi A/c 15,000 Cash A/c 300(Old bill cancelled by Ravi andpaid Rs. 300 as interest)

May 4 Ravi’s A/c Dr. 15,000 Bills Payable A/c 15,000(Accepted new bill drawn by Ravi)

July 7 Bills payable A/c Dr. 15,000Bank A/c 15,000(Met acceptance of the newbill on maturity)

Total 81,300 81,300

205BILLS OF EXCHANGE

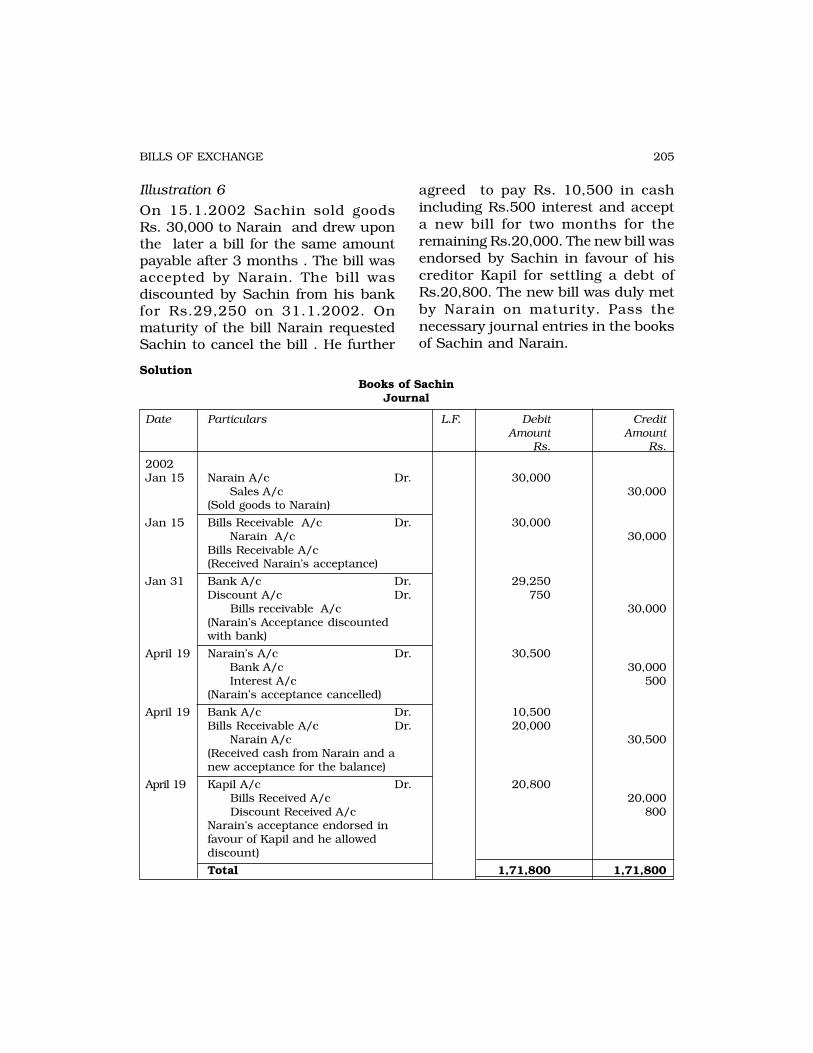

Illustration 6

On 15.1.2002 Sachin sold goodsRs. 30,000 to Narain and drew uponthe later a bill for the same amountpayable after 3 months . The bill wasaccepted by Narain. The bill wasdiscounted by Sachin from his bankfor Rs.29,250 on 31.1.2002. Onmaturity of the bill Narain requestedSachin to cancel the bill . He further

agreed to pay Rs. 10,500 in cashincluding Rs.500 interest and accepta new bill for two months for theremaining Rs.20,000. The new bill wasendorsed by Sachin in favour of hiscreditor Kapil for settling a debt ofRs.20,800. The new bill was duly metby Narain on maturity. Pass thenecessary journal entries in the booksof Sachin and Narain.

SolutionBooks of Sachin

Journal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2002Jan 15 Narain A/c Dr. 30,000

Sales A/c 30,000(Sold goods to Narain)

Jan 15 Bills Receivable A/c Dr. 30,000 Narain A/c 30,000Bills Receivable A/c(Received Narain’s acceptance)

Jan 31 Bank A/c Dr. 29,250Discount A/c Dr. 750 Bills receivable A/c 30,000(Narain’s Acceptance discountedwith bank)

April 19 Narain’s A/c Dr. 30,500 Bank A/c 30,000 Interest A/c 500(Narain’s acceptance cancelled)

April 19 Bank A/c Dr. 10,500Bills Receivable A/c Dr. 20,000 Narain A/c 30,500(Received cash from Narain and anew acceptance for the balance)

April 19 Kapil A/c Dr. 20,800 Bills Received A/c 20,000 Discount Received A/c 800Narain’s acceptance endorsed infavour of Kapil and he alloweddiscount)

Total 1,71,800 1,71,800

206 ACCOUNTANCY

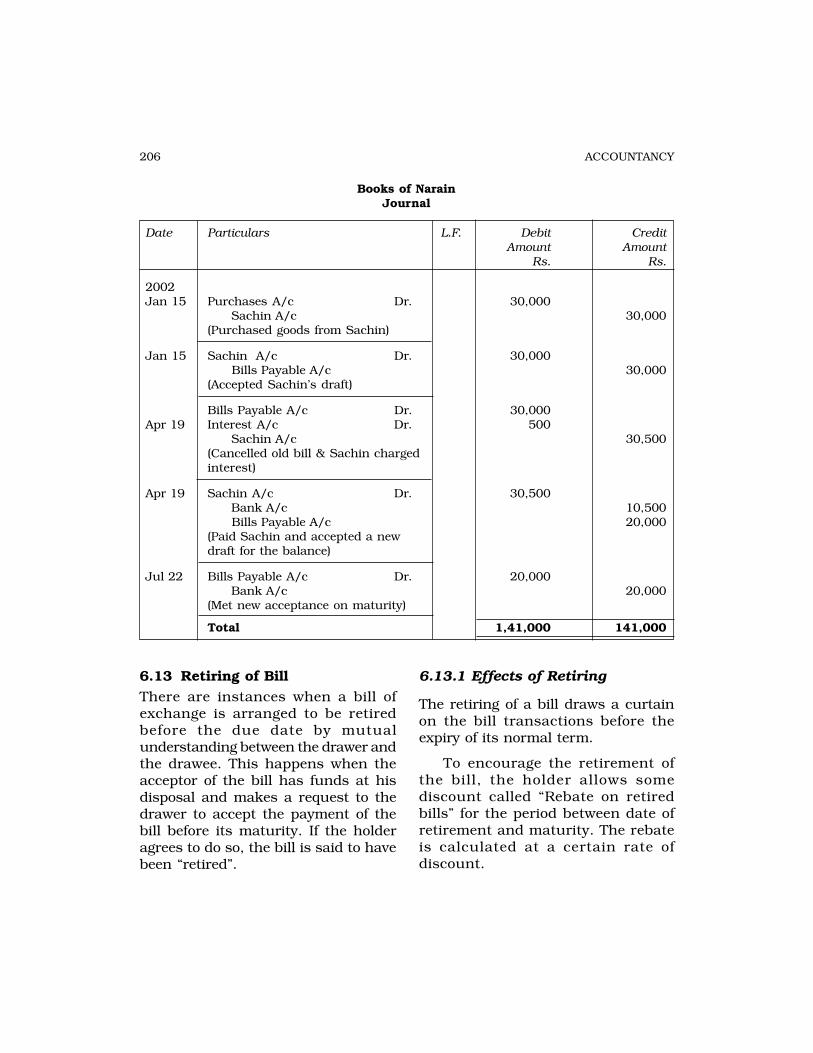

6.13 Retiring of BillThere are instances when a bill ofexchange is arranged to be retiredbefore the due date by mutualunderstanding between the drawer andthe drawee. This happens when theacceptor of the bill has funds at hisdisposal and makes a request to thedrawer to accept the payment of thebill before its maturity. If the holderagrees to do so, the bill is said to havebeen “retired”.

6.13.1 Effects of Retiring

The retiring of a bill draws a curtainon the bill transactions before theexpiry of its normal term.

To encourage the retirement ofthe bill, the holder allows somediscount called “Rebate on retiredbills” for the period between date ofretirement and maturity. The rebateis calculated at a certain rate ofdiscount.

Books of NarainJournal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2002Jan 15 Purchases A/c Dr. 30,000

Sachin A/c 30,000(Purchased goods from Sachin)

Jan 15 Sachin A/c Dr. 30,000 Bills Payable A/c 30,000(Accepted Sachin’s draft)

Bills Payable A/c Dr. 30,000Apr 19 Interest A/c Dr. 500

Sachin A/c 30,500(Cancelled old bill & Sachin chargedinterest)

Apr 19 Sachin A/c Dr. 30,500 Bank A/c 10,500 Bills Payable A/c 20,000(Paid Sachin and accepted a newdraft for the balance)

Jul 22 Bills Payable A/c Dr. 20,000 Bank A/c 20,000(Met new acceptance on maturity)

Total 1,41,000 141,000

207BILLS OF EXCHANGE

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2001Jan 1 B’s A/c Dr. 10,000

Sales A/c 10,000(Sold goods to B)

Jan 1 Bills Receivable A/c Dr. 10,000 B’s A/c 10,000(Received B’s acceptance for threemonths)

Mar 4 Cash A/c Dr. 9,950Rebate on bills A/c Dr. 50 Bills Receivable A/c 10,000(B tried his acceptance and rebateallowed to him)

Total 30,000 30,000

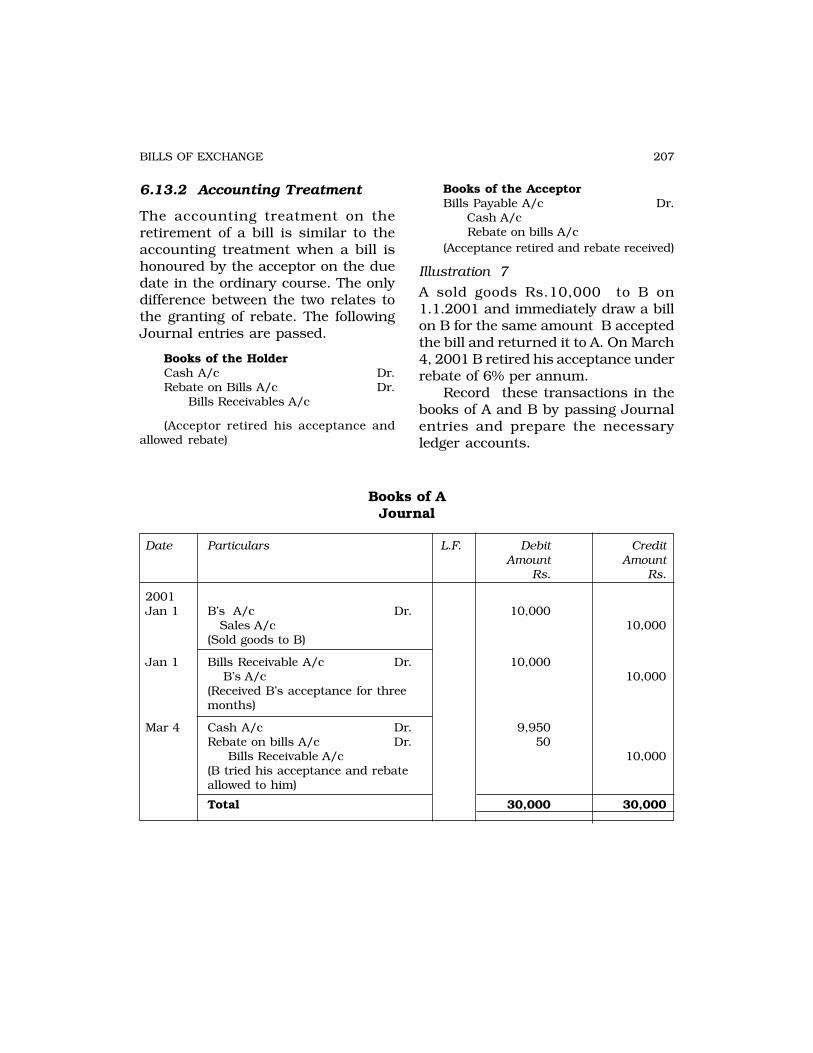

6.13.2 Accounting Treatment

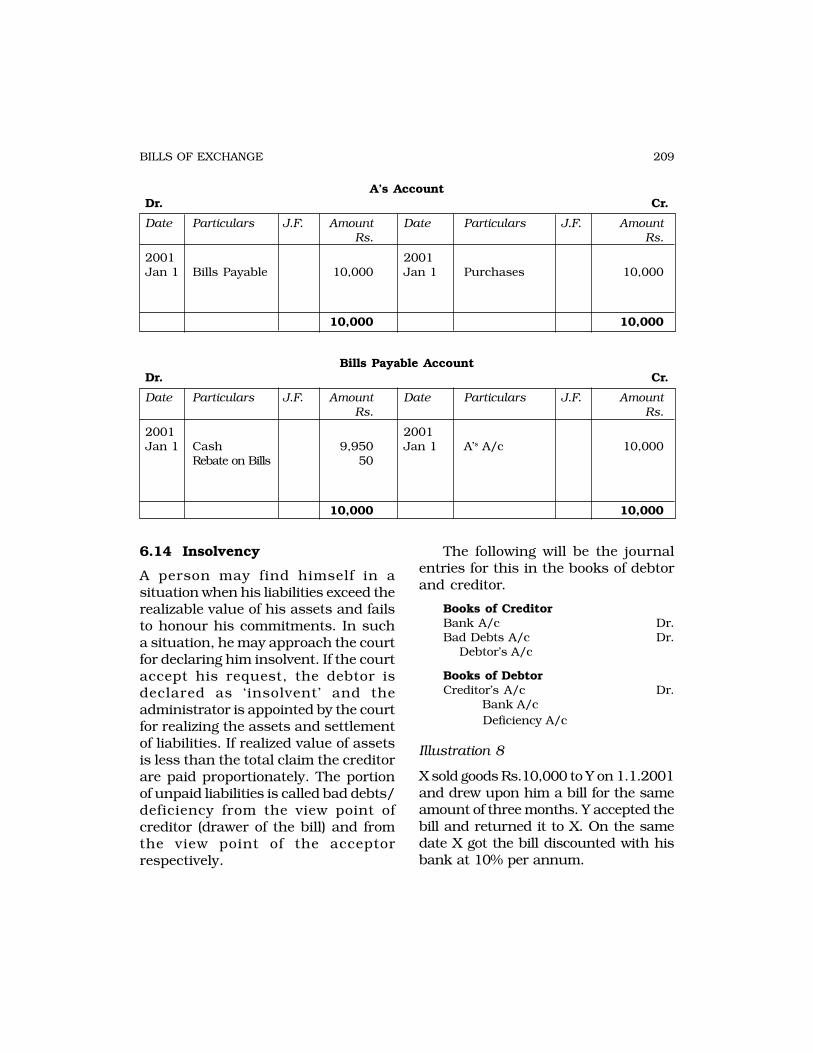

The accounting treatment on theretirement of a bill is similar to theaccounting treatment when a bill ishonoured by the acceptor on the duedate in the ordinary course. The onlydifference between the two relates tothe granting of rebate. The followingJournal entries are passed.

Books of the HolderCash A/c Dr.Rebate on Bills A/c Dr. Bills Receivables A/c

(Acceptor retired his acceptance andallowed rebate)

Books of the AcceptorBills Payable A/c Dr. Cash A/c Rebate on bills A/c(Acceptance retired and rebate received)

Illustration 7

A sold goods Rs.10,000 to B on1.1.2001 and immediately draw a billon B for the same amount B acceptedthe bill and returned it to A. On March4, 2001 B retired his acceptance underrebate of 6% per annum.

Record these transactions in thebooks of A and B by passing Journalentries and prepare the necessaryledger accounts.

Books of AJournal

208 ACCOUNTANCY

B’s Account

Dr. Cr.

Date Particulars J.F Amount Date Particulars J.F AmountRs. Rs.

2001 Sales 10,000 2001 Bills Receivable 10,000Jan 1 Jan1

10,000 10,000

Bill Receivable AccountDr. Cr.

Date Particulars J.F Amount Date Particulars J.F AmountRs. Rs.

2001 B’s A/c 10,000 2001 Cash 9,950Jan 1 Mar 4 Rebate on Bills 50

10,000 10,000

Books of BJournal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2001Jan 1 Purchases A/c Dr. 10,000

A’s A/c 10,000(Purchased goods from A)

Jan 1 A’s A/c Dr. 10,000 Bill’s Payable A/c 10,000(Accepted A’s draft payable afterthree months)

Mar 4 Bills Payable A/c Dr. 10,000 Cash A/c 9,950 Rebate on Bills A/c 50(Acceptance in favour of A retired andrebate received)

Total 30,000 30,000

209BILLS OF EXCHANGE

A’s AccountDr. Cr.

Date Particulars J.F. Amount Date Particulars J.F. AmountRs. Rs.

2001 2001Jan 1 Bills Payable 10,000 Jan 1 Purchases 10,000

10,000 10,000

6.14 Insolvency

A person may find himself in asituation when his liabilities exceed therealizable value of his assets and failsto honour his commitments. In sucha situation, he may approach the courtfor declaring him insolvent. If the courtaccept his request, the debtor isdeclared as ‘insolvent’ and theadministrator is appointed by the courtfor realizing the assets and settlementof liabilities. If realized value of assetsis less than the total claim the creditorare paid proportionately. The portionof unpaid liabilities is called bad debts/deficiency from the view point ofcreditor (drawer of the bill) and fromthe view point of the acceptorrespectively.

The following will be the journalentries for this in the books of debtorand creditor.

Books of CreditorBank A/c Dr.Bad Debts A/c Dr. Debtor’s A/c

Books of DebtorCreditor’s A/c Dr. Bank A/c Deficiency A/c

Illustration 8

X sold goods Rs.10,000 to Y on 1.1.2001and drew upon him a bill for the sameamount of three months. Y accepted thebill and returned it to X. On the samedate X got the bill discounted with hisbank at 10% per annum.

Bills Payable AccountDr. Cr.

Date Particulars J.F. Amount Date Particulars J.F. AmountRs. Rs.

2001 2001Jan 1 Cash 9,950 Jan 1 A’s A/c 10,000

Rebate on Bills 50

10,000 10,000

210 ACCOUNTANCY

The bill was dishonoured on thedue date and the bank paid Rs. 50 asnoting charges. X agreed to accept asum of Rs. 5,300 in cash from Y andagreed to draw two new bills on Y. onefor Rs. 3,000 for two months and theother for Rs. 2,000 for three monthsin full satisfaction of his claim.

Y accepted the bills and returnedterm to X.

X endorsed the first bill to Z andthe same was duly paid on maturity.

The second bill was dishonouredas Y became insolvent and a dividendof 25 paise in the rupees was receivedfrom his estate.

Pass necessary journal entries torecord these transactions in the booksof X and Y and prepare Y’s account inthe books of X and X’s account in thebooks of Y.

Books of XJournal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2001Jan 1 Y’s A/c Dr. 10,000

Sales A/c 10,000(Sold goods to Y)

Jan 1 Bills Receivable A/c Dr. 10,000 Y A/c 10,000(Received Y’s acceptance)

Jan 1 Cash A/c Dr. 9,750Discount A/c Dr. 250 Bills Receivable A/c 10,000Y’s acceptance discount with bank)

Jan 1 Y’s A/c Dr. 10,050 Bank A/c 10,050(Y dishonoured his acceptance onmaturity and back paid Rs. 50 asnoting charges

April 4 Cash A/c Dr. 5,300 Y’s A/c 5,300(Partial payment received from Y)

April 4 Y’s A/c Dr. 250Interest A/c 250(Interest for the entendedperiod debited to Y)

April 4 Bill Receivable A/c Dr. 5,000Y’s A/c 5,000(Received two acceptance from Y)

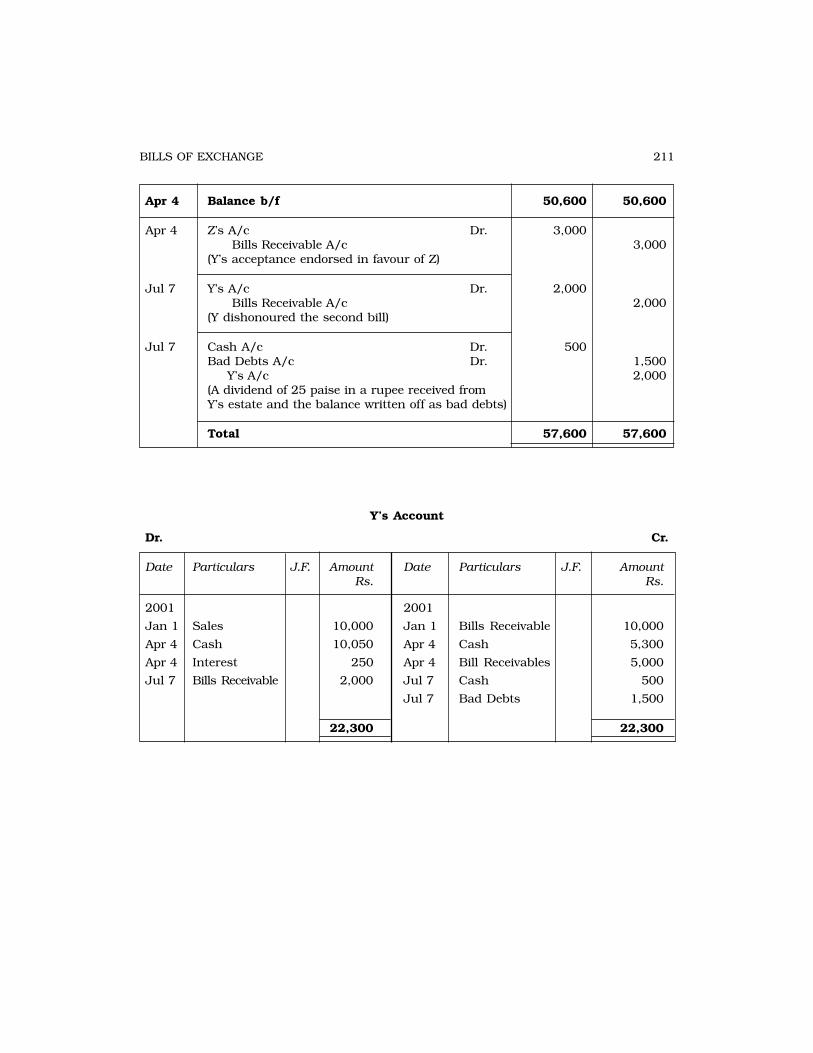

Balance c/f 50,600 50,600

211BILLS OF EXCHANGE

Apr 4 Balance b/f 50,600 50,600

Apr 4 Z’s A/c Dr. 3,000 Bills Receivable A/c 3,000(Y’s acceptance endorsed in favour of Z)

Jul 7 Y’s A/c Dr. 2,000 Bills Receivable A/c 2,000(Y dishonoured the second bill)

Jul 7 Cash A/c Dr. 500Bad Debts A/c Dr. 1,500 Y’s A/c 2,000(A dividend of 25 paise in a rupee received fromY’s estate and the balance written off as bad debts)

Total 57,600 57,600

Y’s Account

Dr. Cr.

Date Particulars J.F. Amount Date Particulars J.F. AmountRs. Rs.

2001 2001

Jan 1 Sales 10,000 Jan 1 Bills Receivable 10,000

Apr 4 Cash 10,050 Apr 4 Cash 5,300

Apr 4 Interest 250 Apr 4 Bill Receivables 5,000

Jul 7 Bills Receivable 2,000 Jul 7 Cash 500

Jul 7 Bad Debts 1,500

22,300 22,300

212 ACCOUNTANCY

Books of YJournal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2001 Purchases A/c Dr. 10,000Jan 1 X’s A/c 10,000

(Purchased goods from X)

Jan 1 X’s A/c Dr. 10,000 Bills Payable A/c 10,000 (Accepted X’s draft)

Apr 4 Bills Payable A/c Dr. 10,000Noting Charge A/c Dr. 50 X’s A/c 10,050 (Acceptance in favour of X dishonoured)

Apr 4 X’s A/c Dr. 5,300 Cash A/c 5,300 (Partial Payment made to X)

Apr 4 Interest A/c Dr. 250 X’s A/c 250 (Interested on extended Credit period allowed to X)

Apr 4 X’s A/c Dr. 5,000 Bills Payable A/c 5,000 (Accepted two drafts of X)

Jun 7 Bills Payable A/c Dr. 3,000 Cash A/c 3,000 (Met acceptance in favour of X on maturity)

Jul 7 Bills Payable A/c Dr. 2,000 X’s A/c 2,000 (Acceptance in favour of X dishonoured on becoming Insolvent)

Jul 7 X’s A/c Dr. 2,000 Cash A/c 500 Deficiency A/c 1,500(Dividend of 25 paise a rupee paid to X’saccount transferred to insolvent account)

Total 42,600 42,600

213BILLS OF EXCHANGE

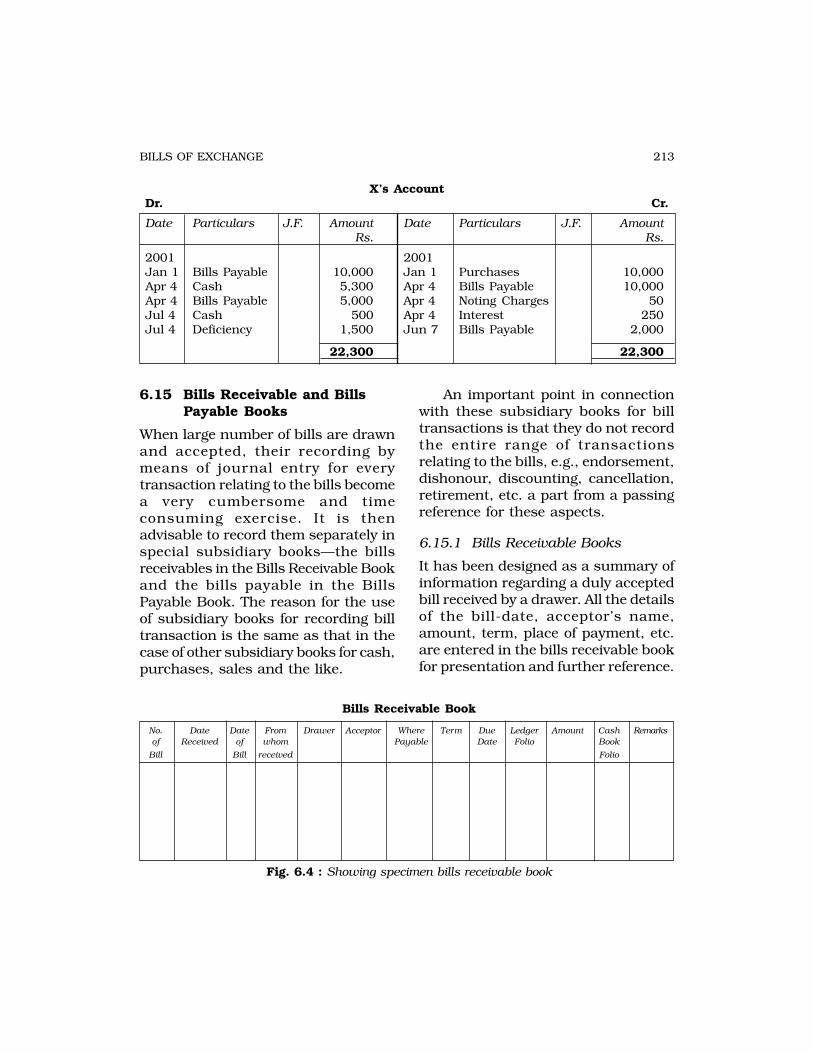

X’s AccountDr. Cr.

Date Particulars J.F. Amount Date Particulars J.F. AmountRs. Rs.

2001 2001Jan 1 Bills Payable 10,000 Jan 1 Purchases 10,000Apr 4 Cash 5,300 Apr 4 Bills Payable 10,000Apr 4 Bills Payable 5,000 Apr 4 Noting Charges 50Jul 4 Cash 500 Apr 4 Interest 250Jul 4 Deficiency 1,500 Jun 7 Bills Payable 2,000

22,300 22,300

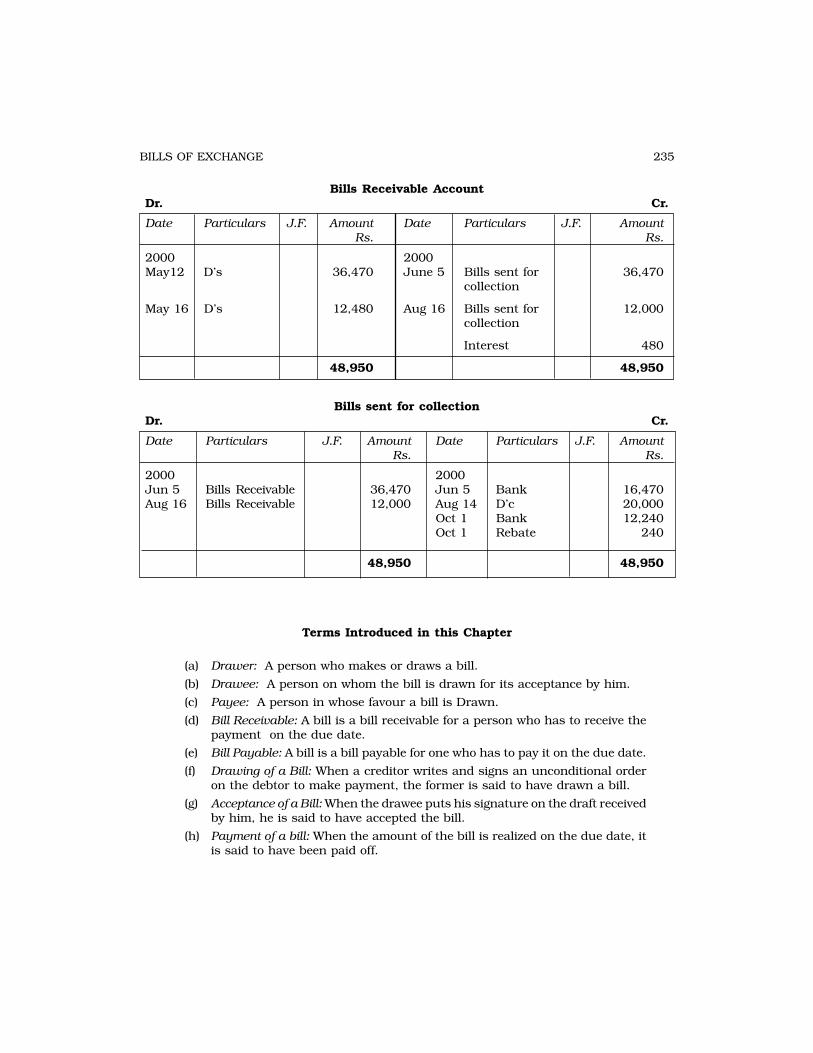

Bills Receivable Book

No. Date Date From Drawer Acceptor Where Term Due Ledger Amount Cash Remarksof Received of whom Payable Date Folio Book

Bill Bill received Folio

Fig. 6.4 : Showing specimen bills receivable book

6.15 Bills Receivable and BillsPayable Books

When large number of bills are drawnand accepted, their recording bymeans of journal entry for everytransaction relating to the bills becomea very cumbersome and timeconsuming exercise. It is thenadvisable to record them separately inspecial subsidiary books—the billsreceivables in the Bills Receivable Bookand the bills payable in the BillsPayable Book. The reason for the useof subsidiary books for recording billtransaction is the same as that in thecase of other subsidiary books for cash,purchases, sales and the like.

An important point in connectionwith these subsidiary books for billtransactions is that they do not recordthe entire range of transactionsrelating to the bills, e.g., endorsement,dishonour, discounting, cancellation,retirement, etc. a part from a passingreference for these aspects.

6.15.1 Bills Receivable Books

It has been designed as a summary ofinformation regarding a duly acceptedbill received by a drawer. All the detailsof the bill-date, acceptor’s name,amount, term, place of payment, etc.are entered in the bills receivable bookfor presentation and further reference.

214 ACCOUNTANCY

The proforma of a bills receivablebook is given on page 213.

The bills receivable book, like anyother subsidiary book, is totaledperiodically. This total is debited to the“Bills Receivable Account” where as theaccount of every individual debtor formwhom the bills received is credited inthe ledger. The bills receivable accountis the account of an asset and wouldalways have debit balance. Thisbalance on any date would representthe amount of bills receivableunmatured and on hand.

6.15.2 Bills Payable Book

It is maintained like a bills receivablebook. It is meant to record all thedetails, relating to the bills acceptedby a person or a party, which areretained for being use in the future, incase of need. The proforma of a billspayable book is given in (Figure 6.5).

The postings from this books areto the debit of the account of everycreditor to whom acceptance has beengiven and the periodical total of thebooks is credited to the ‘Bills PayableAccount’ in the ledger.

The Bills Payable Account,representing as it does the liability ofthe acceptor in respect of bills acceptedby him, always has a credit balance, ifany. The credit balance of this accounton any particular date must be thesame as the total amount worth of billspayable yet to be presented forpayment as ascertained from the billspayable book.

Illustration 9

Enter the following transactions in theBills Receivable and Bills Payablebooks maintained by a trader and postthem in the ledger as well:

2002Jan 7

Received from S. Mitra bill dulyaccepted for Rs. 1,325 dated January4, payable three months after date.

Jan 9

Accepted S.Warden’s draft for Rs. 970at two months.

Jan 13Pradhan drew on the trader at threemonths’ date and the same wasaccepted for Rs. 390.

Bills Payable Book

No. Date of To Drawer Payee Where Term Due Ledger Amount Date Cash Remarksof Bill whom Payable Date Folio Paid Book

Bill given Folio

Fig. 6.5 : Showing specimen bills payable

215BILLS OF EXCHANGE

Bills Receivable Book

No. Date Date of From Drawer Acceptor Where Term Due Ledger Amount Cash Re-of Received Bill whom payable Date Folio Rs Book marks

Bill received Folio

2002 2002 2002

1 Jan 7 Jan 4 S. Mitra Self S. Mitra Bombay 3 month Apr 17 1,325

2 Jan 15 Jan 14 R. Rakesh “” R. Rakesh Amritsar 1 month Feb 17 250

3 Jan 21 Jan 21 G. Ghosh “” G. Ghosh Calcutta 2 month Mar 24 310

4 Jan 22 Jan 17 D. Dhiman D. Dhiman A. Vakil Bombay 3 month Apr 20 200

5 Jan 23 Jan 23 D. Kanga Self K. Kanga Bangalore 1 month Feb 26 300

6 Jan 27 Jan 20 C. Shah M. Meyers P. Parson Madras 2 month Mar 23 350

Total : Rs. 2,735

Jan 14

Drew on R.Rakesh at one month for Rs.250 and he accepted the draft next day.

Jan 18

Gave acceptance at two months forRs. 420 to S.Parkar.

Jan 21

Received from G.Ghosh his acceptancefor Rs. 310 at two months.

Jan 22

Received from D. Dhiman, A. Vakil’sacceptance for Rs. 200 at three monthsfrom Jan 17.

Jan 23

K.Kanga accepted my draft at onemonth for Rs. 300.

Jan 27

Received from C.Shah bill for Rs. 350dated January 20, accepted by P.Parson and drawn by M. Meyers.,payable two months after date.

Jan 31

Gave acceptance for Rs. 215 at onemonth to A. Roberts.

Bills Payable Book

No. Date To whom Drawer Payee Where Term Due Ledger Amount Date Cash Remof of given Payable Date Folio Paid Book arks

Bill Bill Folio

2002 2002

1 Jan 9 S. Warden S. Warden – 2 month Mar 12 970

2 Jan 13 Pradhan Pradhan – 3 month Apr 16 390

3 Jan 18 S. Parkar S. Parkar – 2 month Mar 21 420

4 Jan 31 A. Roberts A. Roberts – 1 month Mar 3 215

Total : Rs. 1,995

216 ACCOUNTANCY

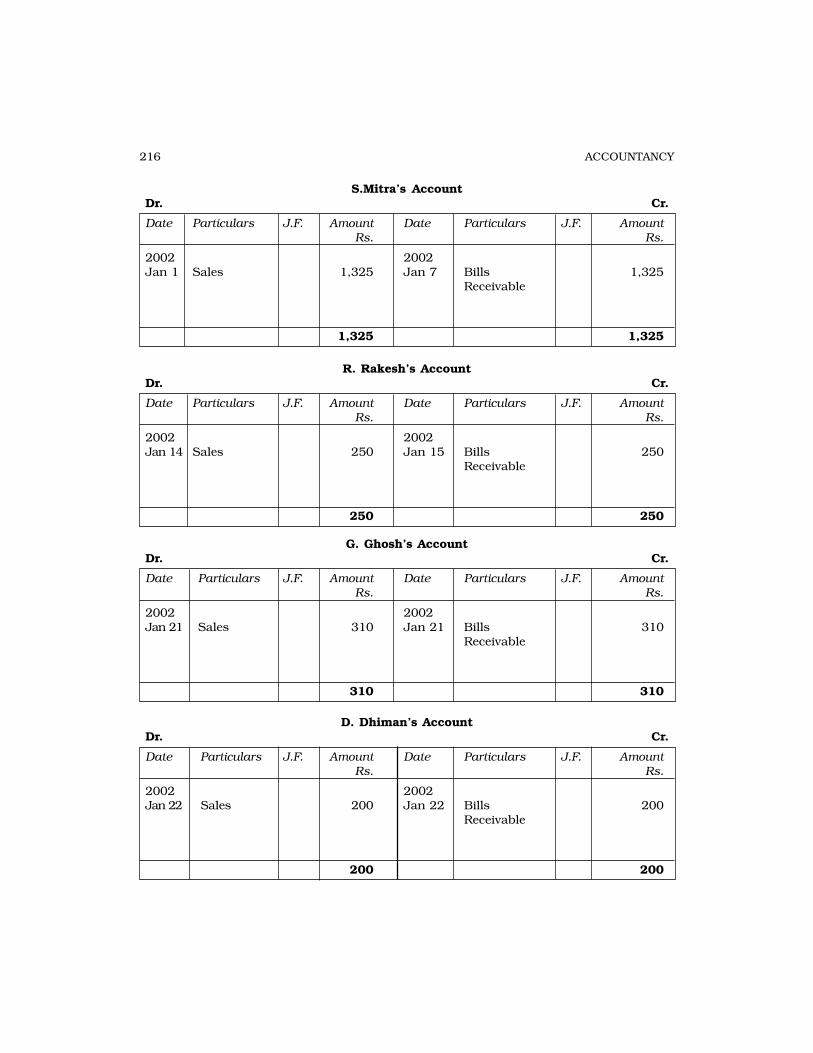

S.Mitra’s AccountDr. Cr.

Date Particulars J.F. Amount Date Particulars J.F. AmountRs. Rs.

2002 2002Jan 1 Sales 1,325 Jan 7 Bills 1,325

Receivable

1,325 1,325

R. Rakesh’s AccountDr. Cr.

Date Particulars J.F. Amount Date Particulars J.F. AmountRs. Rs.

2002 2002Jan 14 Sales 250 Jan 15 Bills 250

Receivable

250 250

G. Ghosh’s AccountDr. Cr.

Date Particulars J.F. Amount Date Particulars J.F. AmountRs. Rs.

2002 2002Jan 21 Sales 310 Jan 21 Bills 310

Receivable

310 310

D. Dhiman’s AccountDr. Cr.

Date Particulars J.F. Amount Date Particulars J.F. AmountRs. Rs.

2002 2002Jan 22 Sales 200 Jan 22 Bills 200

Receivable

200 200

217BILLS OF EXCHANGE

K. Kanga’s AccountDr. Cr.

Date Particulars J.F. Amount Date Particulars J.F. AmountRs. Rs.

2002 2002Jan 23 Sales 300 Jan 23 Bills 300

Receivable

300 300

C. Shah’s AccountDr. Cr.

Date Particulars J.F. Amount Date Particulars J.F. AmountRs. Rs.

2002 2002Jan 27 Sales 350 Jan 27 Bills 350

Receivable

350 350

Bill Receivables AccountDr. Cr.

Date Particulars J.F. Amount Date Particulars J.F. AmountRs. Rs.

2002 2002Jan 31 Sundries 2,735 Jan 31 Balance c/f 2,735

2,735 2,735

S. Warden’s AccountDr. Cr.

Date Particulars J.F. Amount Date Particulars J.F. AmountRs. Rs.

2002 2002Jan 9 Bill Payable 970 Jan 9 Purchases 970

970 970

218 ACCOUNTANCY

Pradhan’s AccountDr. Cr.

Date Particulars J.F. Amount Date Particulars J.F. AmountRs. Rs.

2002 2002Jan 13 Bill Payable 390 Jan 13 Purchases 390

390 390

S. Parkar’s AccountDr. Cr.

Date Particulars J.F. Amount Date Particulars J.F. AmountRs. Rs.

2002 2002Jan18 Bill Payable 420 Jan 18 Purchases 420

420 420

A. Robert’s AccountDr. Cr.

Date Particulars J.F. Amount Date Particulars J.F. AmountRs. Rs.

2002 2002Jan31 Bill Payable 215 Jan 31 Purchases 215

Receivable

215 215

Bill Payables AccountDr. Cr.

Date Particulars J.F. Amount Date Particulars J.F. AmountRs. Rs.

2002 2002Jan 31 Balance c/f 1,995 Jan 31 Sundries 1,995

Receivable

1,995 1,995

Note : The drawings and acceptance of a bill always pre-supposes some background of sale or purchasetransaction. Therefore, in posting bill transactions from the two books to the accounts of deb-tors and creditors, it has been necessary sales and purchases have been effected.

219BILLS OF EXCHANGE

Illustration 10

On 1 Jan 2002 Vinay sold goods to Ravifor Rs. 8,000 and drew four bills ofexchange on him. The first forRs. 1,500 for one month the second forRs. 1,000 for two months. The third forRs. 2,000 for three months and thefourth for Rs. 3,500 for four months.Ravi accepted the bills and returned the

same to Vinay.The second bill wasdiscounted with the bank on 4 Jan at12% p.a and on the same day the thirdbill was endorsed to Ahmad. The firstbill was sent for collection on 30 Jan.On 4 Feb the bank informed that thebill had been collected. All the bills weremet by Ravi on maturity.Pass journalentries in the books of Vinay and Ravi.

Books of VinayJournal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2002 Ravi A/c Dr. 8,000Jan 1 Sale A/c 8,000

(Sold goods to Ravi on Credit)

Jan 1 Bill Receivable A/c Dr. 8,000 Ravi A/c 8,000(Four bills of Rs. 1,500, Rs. 1,000,Rs. 2,000 & Rs. 3,500 payable after onetwo, three, and four months respectivelyaccepted by Ravi)

Jan 4 Bank A/c Dr. 980Discount A/c Dr. 20 Bill Receivable A/c 1,000(Second bill discounted)

Jan 4 Ahmad A/c Dr. 2,000 Bills Receivable A/c 2,000(Third bill endorsed in favour of Ahmad)

Jan 30 Bills sent for collection A/c Dr. 1,500Bills Receivable A/c 1,500(First bill collected by Bank)

Feb 4 Bank A/c Dr. 1,500 Bills sent for collection A/c 1,500(First bill collected by Bank)

May 3 Bank A/c Dr. 3,500 Bills Receivable A/c 3,500(Fourth bill met by Ravi on marutity)

Total 25,500 25,500

220 ACCOUNTANCY

Books of VinayJournal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2002 Purchases A/c Dr. 8,000Jan 1 Vinay A/c 8,000

(Purchase goods on credit from Vinay)

Jan 1 Vinay’s A/c Dr. 8,000 Bills payable A/c 8,000(Accepted four bills drawn by Vinay)

Feb 3 Bill Payable A/c Dr. 1,500 Bank A/c 1,500(Met first acceptance in favour of Vinayon maturity)

Mar 3 Bill payable A/c Dr. 1,000 Bank A/c 1,000(Met 2nd acceptance in favour ofVinay on maturity

Apr 3 Bills payable A/c Dr. 2,000 Bank A/c 2,000(Met 3rd acceptance in favourof Vinay on maturity)

May 3 Bills Payable Dr. 3,500 Bank A/c 3,500(Met 4th bill in favour of Vinay onmaturity)

Total 24,000 24,000

Illustration 11

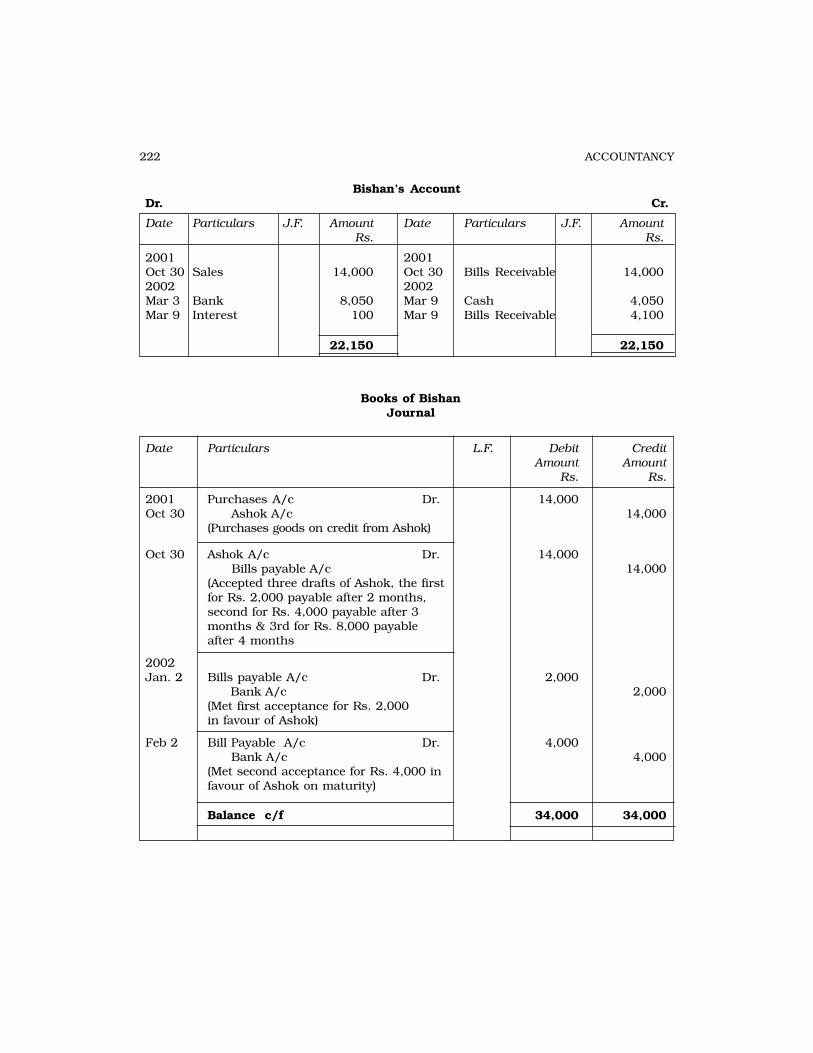

Ashok sold goods Rs. 14,000 toBishan on 30 October 2001 and drewthree bills for Rs.2,000, Rs.4,000 &Rs. 8,000 payable after two, three,and four months respectively. Thefirst bill was kept by Ashok with himtill maturity. He endorsed the secondbill in favour of his creditor Chetan.The third bill was discounted on 3December 2001 at 12% p.a. The firstand second bills were duly met onmaturity but the third bill was

dishonoured and the bank paid Rs.50as noting charges. On 8 March 2002Bishan paid Rs. 4,000 and notingcharges in cash and accepted a newbill at two months after date for thebalance plus interest Rs.100. Thenew bill was met on maturity byBishan.You are required to give thejournal entries in the books of bothAshok and Bishan and prepareBishan’s account in Ashok’s booksand Ashok’s account in Bishan’sbooks.

221BILLS OF EXCHANGE

Books of AshokJournal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2001 Bishan Dr. 14, 000Oct. 30 Sales A/c 14,000

(Sold goods to Bishan on Credit)

Oct. 30 Bills Receivable A/c Dr. 14,000 Bishan 14,000(Received three acceptances from Bishan.First for Rs. 2,000 payable after twomonths, second for 4,000 payable afterthree months and the third for Rs. 8,000payable after four months)

Oct. 30 Chetan A/c Dr. 4,000 Bills Receivable A/c 4,000(Endorsed second bill in favour ofcreditor Chetan)

Dec. 3 Bank A/c Dr. 7,760Discount A/c Dr. 240 Bills Receivable A/c 8,000(Third bill discounted at 12% p.a)

2002 Bank A/c Dr. 2,000Jan. 2 Bills Receivable A/c 2,000

(Bishan met his first acceptance on due date)

March 3 Bishan Dr. 8,050 Bank A/c 8,050(Bishan dishonoured his third acceptanceand bank paid Rs. 50 as noting charges

March 8 Cash A/c Dr. 4,050 Bishan 4,050(Cash Received from Bishan)

March 8 Bishan Dr. 100 Interest A/c 100(Interest charged from Bishan for theextended period

March 8 Bills Receivable A/c Dr. 4,100 Bishan 4,100(Received new acceptance from Bishanfor 2 months)

May Bank A/c Dr. 4,10012 Bills Receivable Account 4,100

(Bishan met his new acceptance on maturity)

Total 62,400 62,400

222 ACCOUNTANCY

Bishan’s AccountDr. Cr.

Date Particulars J.F. Amount Date Particulars J.F. AmountRs. Rs.

2001 2001Oct 30 Sales 14,000 Oct 30 Bills Receivable 14,0002002 2002Mar 3 Bank 8,050 Mar 9 Cash 4,050Mar 9 Interest 100 Mar 9 Bills Receivable 4,100

22,150 22,150

Books of BishanJournal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2001 Purchases A/c Dr. 14,000Oct 30 Ashok A/c 14,000

(Purchases goods on credit from Ashok)

Oct 30 Ashok A/c Dr. 14,000 Bills payable A/c 14,000(Accepted three drafts of Ashok, the firstfor Rs. 2,000 payable after 2 months,second for Rs. 4,000 payable after 3months & 3rd for Rs. 8,000 payableafter 4 months

2002Jan. 2 Bills payable A/c Dr. 2,000

Bank A/c 2,000(Met first acceptance for Rs. 2,000in favour of Ashok)

Feb 2 Bill Payable A/c Dr. 4,000 Bank A/c 4,000(Met second acceptance for Rs. 4,000 infavour of Ashok on maturity)

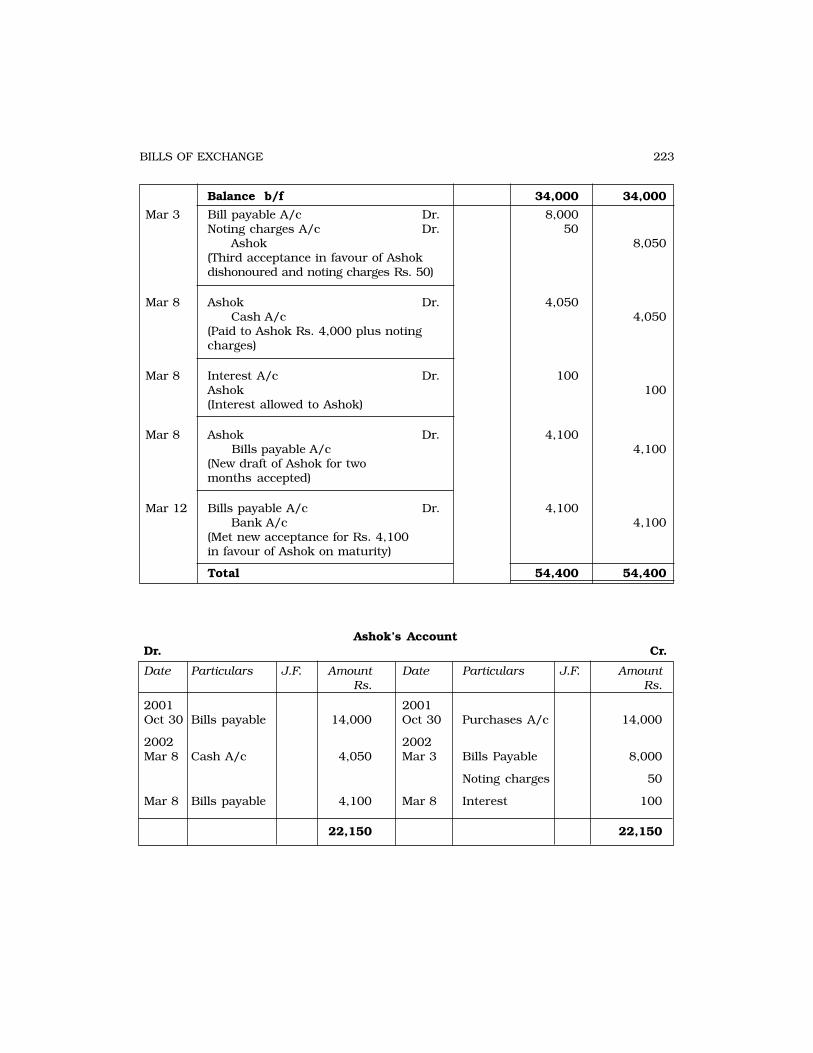

Balance c/f 34,000 34,000

223BILLS OF EXCHANGE

Balance b/f 34,000 34,000

Mar 3 Bill payable A/c Dr. 8,000Noting charges A/c Dr. 50 Ashok 8,050(Third acceptance in favour of Ashokdishonoured and noting charges Rs. 50)

Mar 8 Ashok Dr. 4,050 Cash A/c 4,050(Paid to Ashok Rs. 4,000 plus notingcharges)

Mar 8 Interest A/c Dr. 100Ashok 100(Interest allowed to Ashok)

Mar 8 Ashok Dr. 4,100 Bills payable A/c 4,100(New draft of Ashok for twomonths accepted)

Mar 12 Bills payable A/c Dr. 4,100 Bank A/c 4,100(Met new acceptance for Rs. 4,100in favour of Ashok on maturity)

Total 54,400 54,400

Ashok’s AccountDr. Cr.

Date Particulars J.F. Amount Date Particulars J.F. AmountRs. Rs.

2001 2001Oct 30 Bills payable 14,000 Oct 30 Purchases A/c 14,000

2002 2002Mar 8 Cash A/c 4,050 Mar 3 Bills Payable 8,000

Noting charges 50

Mar 8 Bills payable 4,100 Mar 8 Interest 100

22,150 22,150

224 ACCOUNTANCY

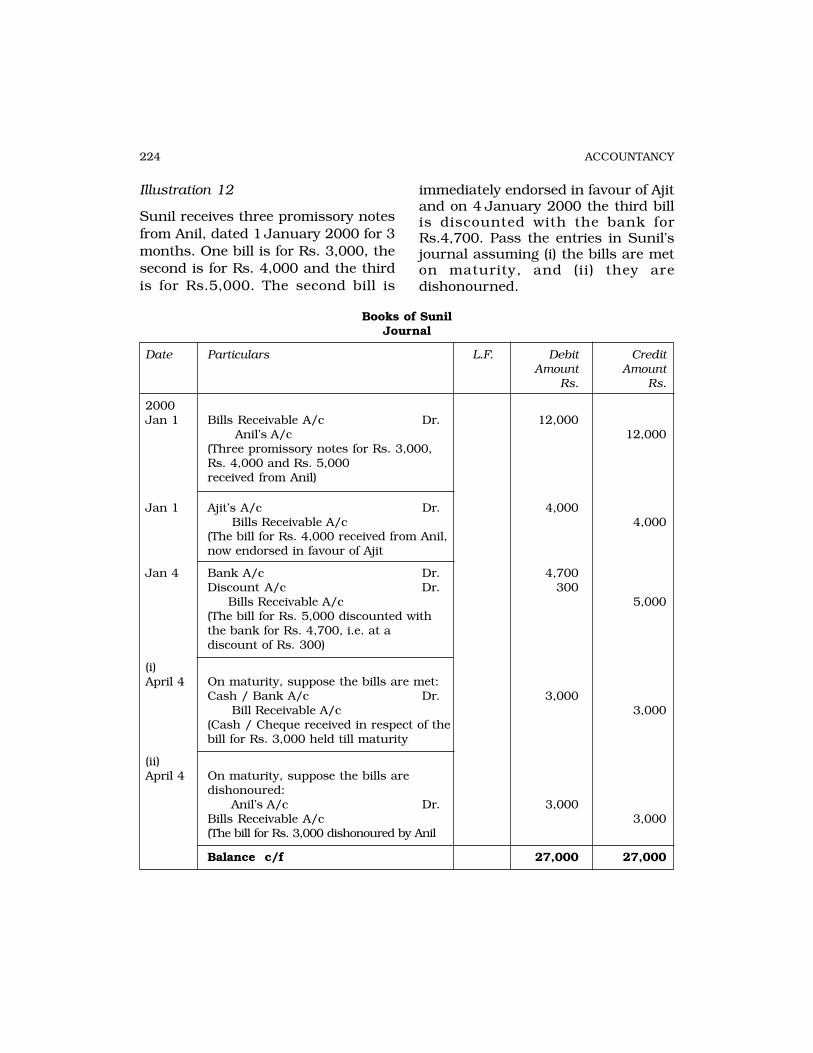

Illustration 12

Sunil receives three promissory notesfrom Anil, dated 1 January 2000 for 3months. One bill is for Rs. 3,000, thesecond is for Rs. 4,000 and the thirdis for Rs.5,000. The second bill is

immediately endorsed in favour of Ajitand on 4 January 2000 the third billis discounted with the bank forRs.4,700. Pass the entries in Sunil’sjournal assuming (i) the bills are meton maturity, and (ii) they aredishonourned.

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2000Jan 1 Bills Receivable A/c Dr. 12,000

Anil’s A/c 12,000(Three promissory notes for Rs. 3,000,Rs. 4,000 and Rs. 5,000received from Anil)

Jan 1 Ajit’s A/c Dr. 4,000 Bills Receivable A/c 4,000(The bill for Rs. 4,000 received from Anil,now endorsed in favour of Ajit

Jan 4 Bank A/c Dr. 4,700Discount A/c Dr. 300 Bills Receivable A/c 5,000(The bill for Rs. 5,000 discounted withthe bank for Rs. 4,700, i.e. at adiscount of Rs. 300)

(i)April 4 On maturity, suppose the bills are met:

Cash / Bank A/c Dr. 3,000 Bill Receivable A/c 3,000(Cash / Cheque received in respect of thebill for Rs. 3,000 held till maturity

(ii)April 4 On maturity, suppose the bills are

dishonoured: Anil’s A/c Dr. 3,000Bills Receivable A/c 3,000(The bill for Rs. 3,000 dishonoured by Anil

Balance c/f 27,000 27,000

Books of SunilJournal

225BILLS OF EXCHANGE

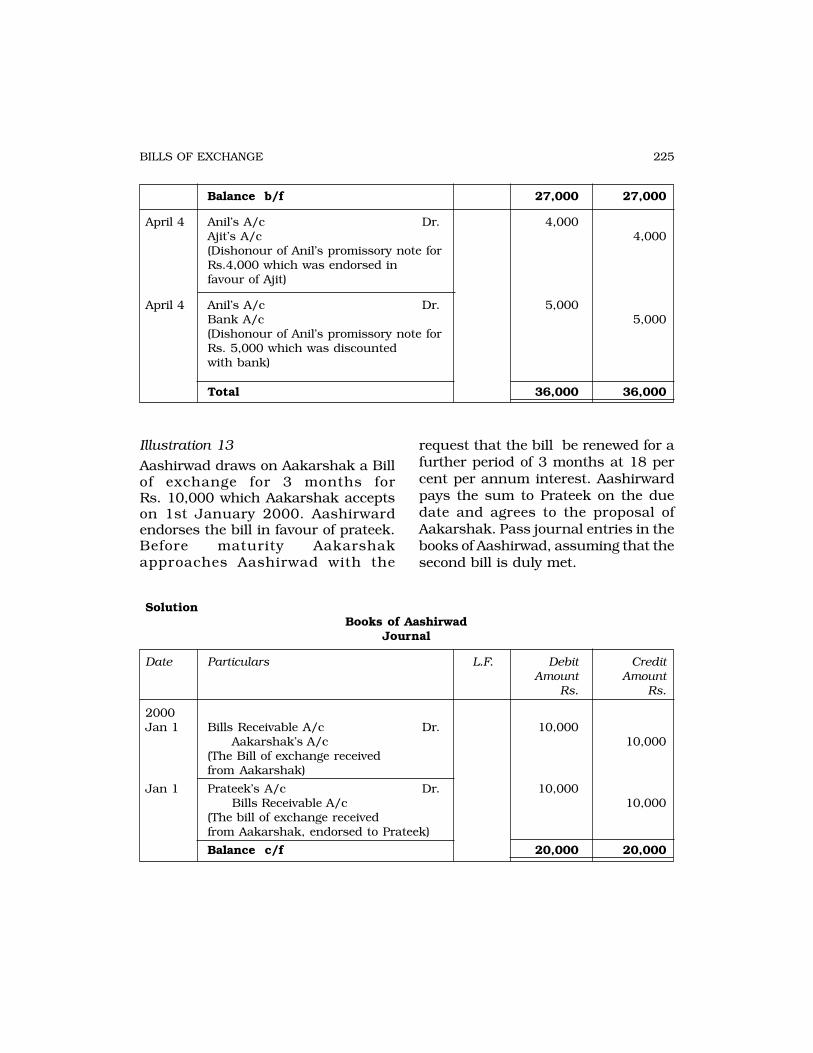

Balance b/f 27,000 27,000

April 4 Anil’s A/c Dr. 4,000Ajit’s A/c 4,000(Dishonour of Anil’s promissory note forRs.4,000 which was endorsed infavour of Ajit)

April 4 Anil’s A/c Dr. 5,000Bank A/c 5,000(Dishonour of Anil’s promissory note forRs. 5,000 which was discountedwith bank)

Total 36,000 36,000

SolutionBooks of Aashirwad

Journal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2000Jan 1 Bills Receivable A/c Dr. 10,000

Aakarshak’s A/c 10,000(The Bill of exchange receivedfrom Aakarshak)

Jan 1 Prateek’s A/c Dr. 10,000 Bills Receivable A/c 10,000(The bill of exchange receivedfrom Aakarshak, endorsed to Prateek)

Balance c/f 20,000 20,000

Illustration 13

Aashirwad draws on Aakarshak a Billof exchange for 3 months forRs. 10,000 which Aakarshak acceptson 1st January 2000. Aashirwardendorses the bill in favour of prateek.Before maturity Aakarshakapproaches Aashirwad with the

request that the bill be renewed for afurther period of 3 months at 18 percent per annum interest. Aashirwardpays the sum to Prateek on the duedate and agrees to the proposal ofAakarshak. Pass journal entries in thebooks of Aashirwad, assuming that thesecond bill is duly met.

226 ACCOUNTANCY

Balance b/f 20,000 20,000

Apr 4 Aakarshak’s A/c Dr. 10,000 Prateek’s A/c 10,000(Cancellation of the bill of exchangereceived from Aakarshak nowwith Prateek)

Apr 4 Prateek’s A/c Dr. 10,000 Bank A/c 10,000(Payment of the amount due to Prateek)

Apr 4 Aakarshak’s A/c Dr. 450 Interest A/c 450(Interest due from Aakarshak onRs. 10,000 for 3 months at 18% p.a.)

Apr 4 Bills Receivable A/c Dr. 10,450 Aakarshak’s A/c 10,450(The new bill recieved from Aakarshak forthe amount due for him.)

July 7 Bank A/c Dr. 10,450 Bills Receivable A/c 10,450(The amount received from Aakarshak inrespect of the renewed bill.)

Total 61,350 61,350

Illustration 14

Ankit owes Nikita a sum of Rs.6,000.On 1 April,2000 Ankit gives apromissory note for the amount for 3months to Nikita who gets itdiscounted with her bankers forRs.5,760. On the due date the bill isdishonoured, the bank paid Rs.15 asnoting charges. Ankit then pays

Rs.2,000 in cash and accepts a bill ofexchange drawn on him for thebalance together with Rs.100 asinterest. This bill of exchange is for 2months and on the due date the billis again dishonoured, Nikita paidRs.15 as noting charges. Draft thejournal entries to be passed inNikita’s books.

227BILLS OF EXCHANGE

SolutionBooks of Nikita

Journal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2000Apr Bills Receivable A/c Dr. 6,000

Ankit’s A/c 6,000(Ankit’s promissory note received insettlement of his account)

Apr 1 Bank A/c Dr. 5,760Discount A/c 240 Bills Receivable A/c 6,000(Ankit’s promissory note discountedfor Rs. 5,760)

July 4 Ankit A/c Dr. 6,015 Bank A/c 6,015(The promissory note dishonoured byAnkit the amount of the bill and thenoting charges recoverable from Ankitand payable to Bank)

Jul 4 Cash A/c Dr. 2,000 Ankit’s A/c 2,000(The amount received from Ankit)

Jul 4 Ankit’s A/c Dr. 100 Interest A/c 100(Interest due from Ankit for thesecond bill)

Jul 4 Bills Receivable A/c Dr. 4,115 Ankit’s A/c 4,115(Ankit’s acceptance for 2 months insettlement of amount due)

Sep 7 Ankit’s A/c Dr. 4,115 Bills Receivable A/c 4,115(The dishonour by Ankit of his acceptance)

Sep 7 Ankit’s A/c Dr. 15 Cash A/c 15(Payment of noting charges, recoverablefrom Ankit

Total 28,360 28,360

228 ACCOUNTANCY

Illustration 15

Mohit sends his promissory note for3 months to Rohit for Rs. 6,000 onMay 1, 2000. Rohit gets it discountedwith his bankers. at 18 per centperannum on 4 May. On the due date thebill is dishonoured, the bank payingRs.10 as noting charges. Rohit agreesto accept Rs. 2,170 in cash (Rs. 130for noting charges and interest) and

another promissory note for Rs.4,000at 2 months. On the due date, Mohitapproaches Rohit again and asks forrenewal of the bill for a further periodof 3 months. Rohit agrees to therequest, provided Mohit pays Rs.200as interest in cash. This last bill ispaid on maturity. Draft journalenteries in the books of Mohit andRohit.

SolutionBooks of Mohit

Journal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2000May 1 Rohit’s A/c Dr. 6,000

Bills Payable A/c 6,000(The amount of the promissory notesent to Rohit)

Aug 4 Bills payable A/c Dr. 6,000Noting Charges A/c Dr. 10 Rohit’s A/c 6,010(The dishonour of the promissory noteand Rs. 10 being payable as notingcharges to Rohit

Aug 4 Interest A/c Dr. 120 Rohit’s A/c 120(Interest due to Rohit for part renewalof the promissory note)

Aug 4 Rohit’s A/c Dr. 6,130 Bills Payable A/c 4,000 Cash A/c 2,130(Payment of Rs. 2,130 in cash and a newpromissory note For Rs. 4,000 sent toRohit to Settle his account)

Oct 7 Bills Payable A/c Dr. 4,000 Rohit’s A/c 4,000(Cancellation of the bill due today)

Balance c/f 22,260 22,260

229BILLS OF EXCHANGE

Balance b/f 22,260 22,260

Oct 7 Interest A/c Dr. 200 Rohit’s A/c 200(The amount due as interest to Rohiton the renewed bill)

Oct 7 Rohit’s A/c Dr. 4,200 Cash A/c 200 Bills Payable A/c 4,000(Payment to Rohit of Rs. 200 in cash andthe promissory note sent to him)

2001 Bills Payable A/c Dr. 4,000Jan 10 Cash A/c 4,000

(Payment made to meet the bill due this day)

Total 30,660 30,660

Books of RohitJournal

Dr. Cr.

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2000May 1 Bill Receivable A/c Dr. 6,000

Mohit’s A/c 6,000(Mohit’s promissory note receivedthis day)

May 4 Bank’s A/c Dr. 5,730Discount A/c Dr. 270 Bills Receivable A/c 6,000(The discounting of the promissory note byMohit at 18% on Rs. 6,000 for 3 months)

Aug 4 Mohit’s A/c Dr. 6,010 Bank A/c 6,010(The dishonour of the promissory noteby Mohit Rs. 10 being charged by bankfor noting charges)

Aug 4 Mohit’s A/c Dr. 120 Interest A/c 120(The amount agreed to be paid as interestby Mohit)

Balance c/f 18,130 18,130

230 ACCOUNTANCY

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

Balance b/f 18,130 18,130

Aug 4 Cash A/c Dr. 2,130Bill Receivable A/c Dr. 4,000 Mohit’s A/c 6,130(Cash and promissory note received fromMohit for the amount due from him)

Oct 7 Mohit’s A/c Dr. 4,000 Bills Receivable A/c 4,000Cancellation of Mohit’s promissory note

Oct 7 Mohit’s A/c Dr. 200 Interest A/c 200(The amout due from Mohit as interest)

Oct 7 Cash A/c Dr. 200Bills Receivable A/c Dr. 4,000 Mohit’s A/c 4,200(Cash and promissory note receivedfrom Mohit)

2001 Cash / Bank /A/c Dr. 4,000Jan 10 Bills Receivable A/c 4,000

(Mohit met his acceptance on maturity)

Total 36,660 36,660

Illustration 16

Journalize the following transactionsin the books of J. Jaggi:

(a) Our acceptance to M. Madan forRs. 3,000 retired before duedate, rebate allowed Rs.45.

(b) K. Kaku’s acceptance forRs.4,000 renewed for a furtherperiod of 3 months, interestcharged at 15 per cent.

(c) Our acceptance to P. Swamy forRs.8,000 renewed for 3 monthson the condition that Rs.2,000is paid in cash immediately andthe remaining balance to carry

out interest at 18 per cent.(d) D. Dutt’s promissory note for

Rs.7,000 which we had endorsedin favour of P. Mukerjeedishonoured. P. Mukerjee paidRs.10 as noting charges. We payP. Mukerjee by cheque and acceptfrom D. Dutt another bill for theamount due plus interest, Rs.315.

(e) Our promissory note in favourof A. Alam for Rs. 2,150 whichwe pay by cheque.

(f) Our promissory note forRs.5,000 in favour of Patelsettled by sending him Tanna’sacceptance for Rs.5,000

231BILLS OF EXCHANGE

SolutionBooks of J. Jaggi

Journal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

Bills Payable A/c Dr. 3,000 Bank A/c 2,955 Discount A/c 45(The amount paid and discount receivedon retirement of our acceptance beforedue date)

K. Kaku’s A/c Dr. 4,000 Bills receivable A/c 4,000(The Cancellation of K. Kaku’s acceptancein order to renew it)

K. Kaku’s A/c Dr. 150 Interest A/c 150(Interest due on renewal of bill for threemonths rate of interest being 15%)

Bills Receivable A/c Dr. 4,150 K. Kaku’s A/c 4,150(K. Kaku’s acceptance for the amount due)

Bills Payable A/c Dr. 8,000 P. Swamy’s A/c 8,000(Cancellation of our acceptance toP. Swamy prior renewal)

Interest A/c Dr. 270 P. Swamy A/c 270(Interest due to P. Swamy for hisreadiness to accept a new bill for theamount due which after paying Rs 2,000cash, will be Rs. 6,000)

P. Swamy’s A/c Dr 8,270 Cash 2,000 Bills Payable A/c 6,270(Settlement of P. Swamy’s account bypaying him cash Rs. 2,000 and thebalance by a bill of exchange)

Balance c/f 27,840 27,840

232 ACCOUNTANCY

Balance b/f 27,840 27,840

D. Dutt’s A/c Dr. 7,010 P. Mukerjee’s A/c 7,010(Dishonour of D. Dutt’s acceptance whichwas sent to P. Mukerjee who claimsanother Rs. 10 for noting charges)

P. Mukerjee’s A/c Dr. 7,010 Bank A/c 7,010(Amount paid to P. Mukerjee)

D. Dutt’s A/c Dr. 315Interest A/c 315

(Interest due from D. Dutt for renewalof his acceptance)

Bills Receivable A/c Dr. 7,325 D.Dutt’s A/c 7,325(Acceptance received from D. Dutt)

Bills Payable A/c Dr. 2,500 Noting Charge A/c Dr. 10 A. Alam A/c 2,510(A. Alam for dishonoured bill and notingcharges)

Bills Payable A/c Dr. 5,000 Bills Receivable A/c 5,000(Tanna’s acceptance of Rs. 5,000 sent toPatel settlement of own acceptance tohim for Rs. 5,000)

Total 59,520 59,520

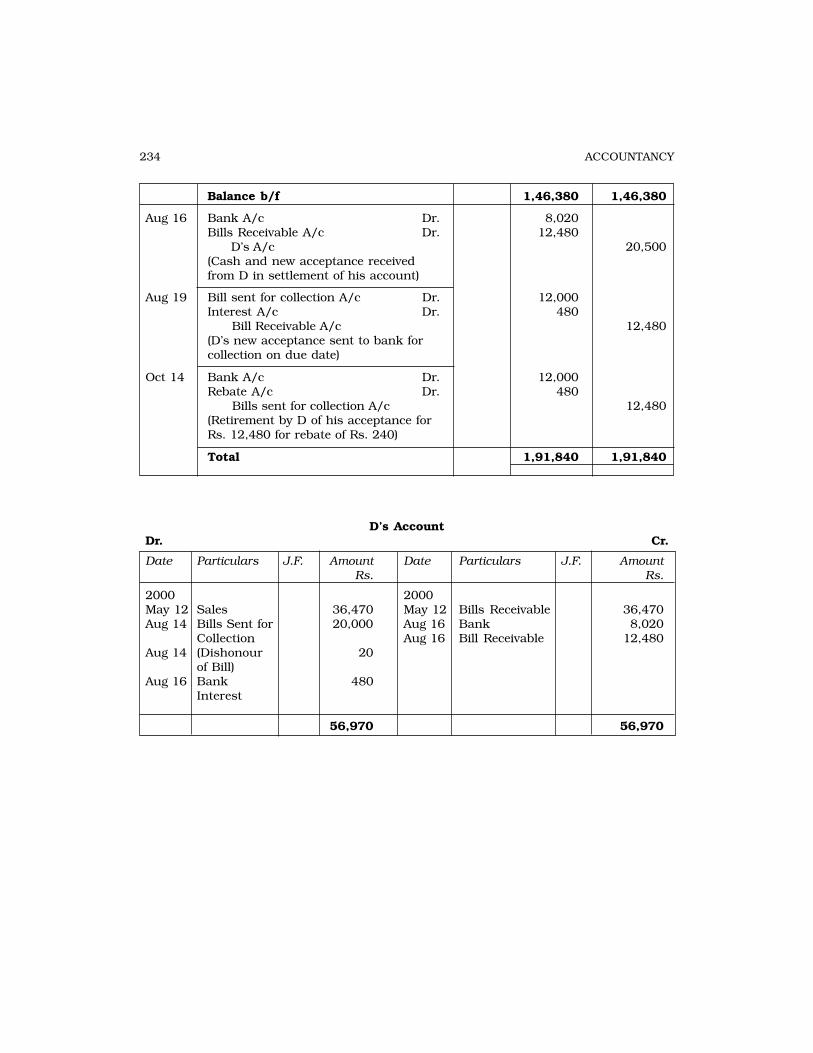

dates. The first bill was duly met. Butdue to some temporary financialdifficulties, C failed to honour hisacceptance for Rs.20,000 on the duedate and the bank had to pay Rs.20 asnoting charges. However, on 14 August2000 it was agreed between C and Dthat D would immediately pay Rs.8,020in cash and accept a new bill at three

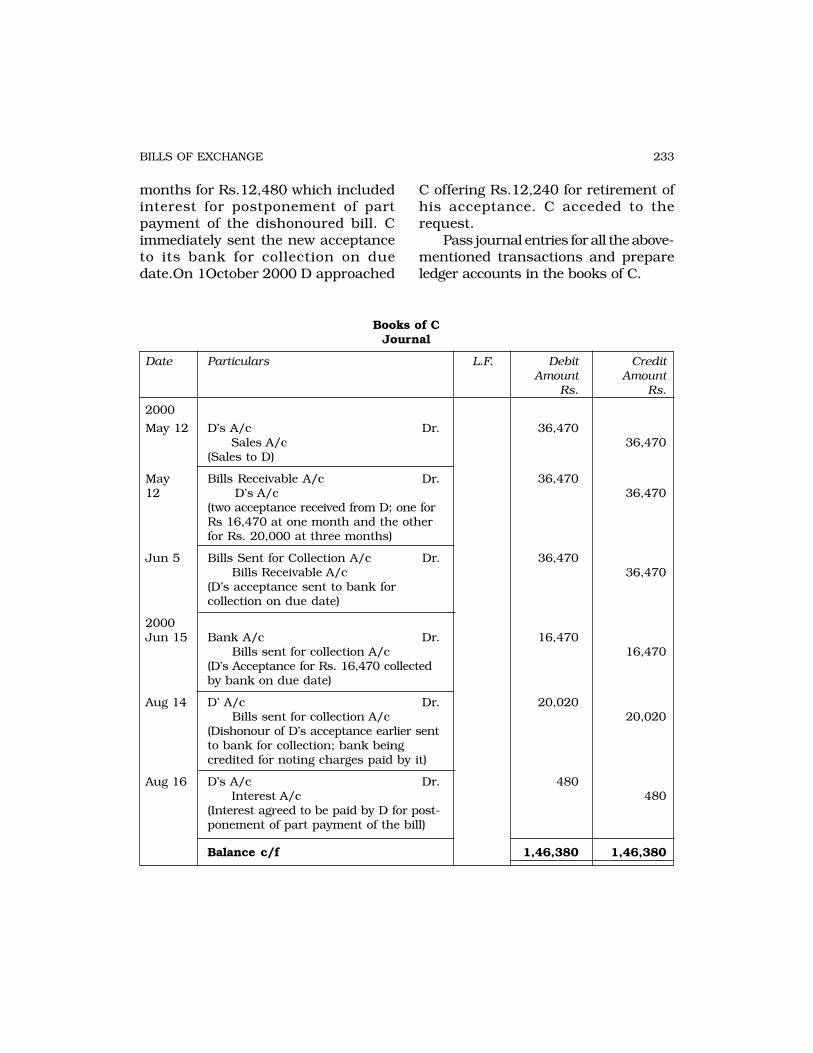

Illustration: 17

On 12 May 2000 C sold to D goods forRs. 36,470 and drew upon the lattertwo bills of exchange; One forRs.16,470 at one month and the otherfor Rs.20,000 at three months. Daccepted both the bills.

On 5 June 2000 C sent both thebills to his bank for collection on due

233BILLS OF EXCHANGE

months for Rs.12,480 which includedinterest for postponement of partpayment of the dishonoured bill. Cimmediately sent the new acceptanceto its bank for collection on duedate.On 1October 2000 D approached

C offering Rs.12,240 for retirement ofhis acceptance. C acceded to therequest.

Pass journal entries for all the above-mentioned transactions and prepareledger accounts in the books of C.

Books of CJournal

Date Particulars L.F. Debit CreditAmount Amount

Rs. Rs.

2000

May 12 D’s A/c Dr. 36,470 Sales A/c 36,470(Sales to D)

May Bills Receivable A/c Dr. 36,47012 D’s A/c 36,470